Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Information Required in Proxy Statement

Schedule 14A Information

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☒ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to §240.14a-12 |

RMG Acquisition Corp. III

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a6(i)(l) and 0-11. |

Table of Contents

RMG ACQUISITION CORP. III

57 Ocean, Suite 403

5775 Collins Avenue

Miami Beach, Florida 33140

PROXY STATEMENT FOR EXTRAORDINARY GENERAL MEETING

OF

RMG ACQUISITION CORP. III

Dear Shareholders of RMG Acquisition Corp. III:

You are cordially invited to attend the Extraordinary General Meeting (the “Extraordinary General Meeting”) of RMG Acquisition Corp. III, a Cayman Islands exempted company (the “Company,” “RMG III,” “we,” “us” or “our”), to be held on January 10, 2023, at 9:00 AM, Central Time, at the offices of Latham & Watkins LLP, located at 811 Main St., Suite 3700, Houston, Texas 77002, or at such other time, on such other date and at such other place to which the meeting may be postponed or adjourned, or to attend virtually via the Internet. You will be able to attend the Extraordinary General Meeting online, vote, and submit your questions during the Extraordinary General Meeting by visiting https://www.cstproxy.com/rmgiii/2023. While shareholders are encouraged to attend the meeting virtually, you will be permitted to attend the Extraordinary General Meeting in person at the offices of Latham & Watkins LLP. The accompanying proxy statement is dated December 1, 2022, and is first being mailed to shareholders of the Company on or about December 2, 2022.

Even if you are planning on attending the Extraordinary General Meeting online, please promptly submit your proxy vote by completing, dating, signing and returning the enclosed proxy, so that your shares will be represented at the Extraordinary General Meeting. It is strongly recommended that you complete and return your proxy card before the Extraordinary General Meeting date to ensure that your shares will be represented at the Extraordinary General Meeting. Instructions on how to vote your shares are on the proxy materials you received for the Extraordinary General Meeting.

The Extraordinary General Meeting is being held to consider and vote upon the following proposals:

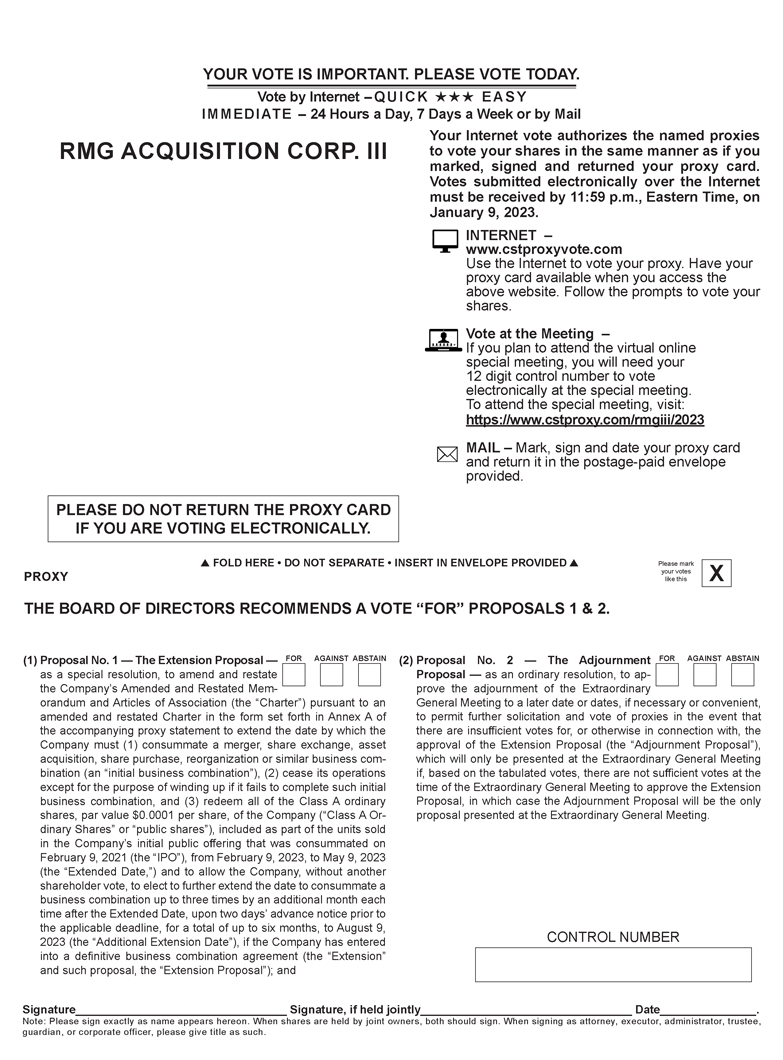

(a) Proposal No. 1 – The Extension Proposal – a proposal, by special resolution, to amend and restate the Company’s Amended and Restated Memorandum and Articles of Association (the “Charter”) pursuant to an amended and restated Charter in the form set forth in Annex A of the accompanying proxy statement to extend the date by which the Company must (1) consummate a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination (an “initial business combination”), (2) cease its operations except for the purpose of winding up if it fails to complete such initial business combination, and (3) redeem all of the Class A ordinary shares, par value $0.0001 per share, of the Company (“Class A Ordinary Shares” or “public shares”), included as part of the units sold in the Company’s initial public offering that was consummated on February 9, 2021 (the “IPO”), from February 9, 2023 to May 9, 2023 (the “Extended Date,”) and to allow the Company, without another shareholder vote, to elect to further extend the date to consummate a business combination up to three times by an additional month each time after the Extended Date, upon two days’ advance notice prior to the applicable deadline, for a total of up to six months, to August 9, 2023 (the “Additional Extension Date”), if the Company has entered into a definitive business combination agreement (the “Extension” and such proposal, the “Extension Proposal”); and

(b) Proposal No. 2 – The Adjournment Proposal – a proposal, by ordinary resolution, to approve the adjournment of the Extraordinary General Meeting to a later date or dates, if necessary or convenient, to permit further solicitation and vote of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Extension Proposal (the “Adjournment Proposal”), which will only be presented at the Extraordinary General Meeting if, based on the tabulated votes, there are not sufficient votes at the time of the Extraordinary General Meeting to approve the Extension Proposal, in which case the Adjournment Proposal will be the only proposal presented at the Extraordinary General Meeting.

Each of the Extension Proposal and the Adjournment Proposal is more fully described in the accompanying proxy statement, which you are encouraged to read carefully.

Table of Contents

THE BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS A VOTE “FOR” THE EXTENSION PROPOSAL AND, IF PRESENTED, THE ADJOURNMENT PROPOSAL.

The sole purpose of the Extension Proposal is to provide the Company with sufficient time to complete an initial business combination.

The Charter provides that the Company has 24 months from the consummation of the IPO (such date being February 9, 2023) within which to complete an initial business combination. While the Company is currently in discussions regarding various business combination opportunities, the Company’s board of directors (the “Board”) has determined that there may not be sufficient time before February 9, 2023 to complete an initial business combination. Therefore, the Board has determined that it is in the best interests of the Company to extend the date by which the Company has to complete an initial business combination.

In connection with the Extension, public shareholders may elect to redeem their shares for a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account established in connection with the IPO (the “Trust Account”), including interest earned on the funds held in the Trust Account and not previously released to the Company, divided by the number of then-issued and outstanding Class A Ordinary Shares, regardless of how such public shareholders vote on the Extension Proposal or if they vote at all. If the Extension is approved by the requisite vote of shareholders, the remaining public shareholders will retain their right to redeem their Class A Ordinary Shares upon consummation of our initial business combination when it is submitted to a vote of the shareholders, subject to any limitations set forth in the Charter, as amended. In addition, public shareholders will be entitled to have their shares redeemed for cash if the Company has not completed an initial business combination by the Extended Date or the Additional Extension Date, as applicable.

Based upon the amount held in the Trust Account as of September 30, 2022, which was $485,865,952, and estimated interest income and taxes post-September 30, 2022, the Company estimates that the per-share price at which public shares may be redeemed from cash held in the Trust Account will be approximately $10.08 at the time of the Extraordinary General Meeting. The closing price of a Class A Ordinary Share on November 30, 2022, was $10.02. The Company cannot assure shareholders that they will be able to sell their Class A Ordinary Shares in the open market, even if the market price per share is higher than the redemption price stated above, as there may not be sufficient liquidity in its securities when such shareholders wish to sell their shares.

Pursuant to the Charter, a public shareholder may request that the Company redeem all or a portion of such public shareholder’s public shares for cash if the Extension Proposal is approved. You will be entitled to receive cash for any public shares to be redeemed only if you:

(1) (a) hold public shares or (b) hold public shares as part of units and elect to separate such units into the underlying public shares and public warrants prior to exercising your redemption rights with respect to the public shares; and

(2) prior to 5:00 p.m., Central Time, on January 6, 2023 (two business days prior to the vote at the Extraordinary General Meeting), (a) submit a written request to Continental Stock Transfer & Trust Company, the Company’s transfer agent, that the Company redeem your public shares for cash and (b) deliver your public shares to the transfer agent, physically or electronically through The Depository Trust Company.

Holders of units of the Company must elect to separate the underlying public shares and public warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate the units into the underlying public shares and public warrants, or if a holder holds units registered in its, his or her own name, the holder must contact the transfer agent directly and instruct it to do so. Public shareholders may elect to redeem all or a portion of their public shares even if they vote for the Extension Proposal.

Table of Contents

If the Extension is not approved and we do not consummate an initial business combination by February 9, 2023, we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible but not more than ten business days thereafter subject to lawfully available funds therefor, redeem 100% of the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company (less taxes payable, expenses relating to the administration of the trust account, amounts withdrawn to fund the Company’s working capital requirements and up to $100,000 of interest to pay dissolution expenses), divided by the total number of then-issued and outstanding public shares, which redemption will completely extinguish public shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), and (iii) as promptly as reasonably possible following such redemption, subject to the approval of the remaining public shareholders and the Board, liquidate and dissolve, subject in each case to the Company’s obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law. There will be no redemption rights or liquidating distributions with respect to our warrants, which will expire worthless if we fail to complete our initial business combination by February 9, 2023, or by the applicable deadline as may be extended.

Approval of the Extension Proposal requires a special resolution under Cayman Islands law, being the affirmative vote of the holders of at least two-thirds of the Class A Ordinary Shares and Class B ordinary shares, par value $0.0001 per share, of the Company (“Class B Ordinary Shares” and, together with the Class A Ordinary Shares, the “Ordinary Shares”) who, being present in person (including virtually) or represented by proxy and entitled to vote thereon and who do so in person or by proxy at the Extraordinary General Meeting. Ordinary Shares that are present virtually during the Extraordinary General Meeting constitute Ordinary Shares represented “in person.”

The Adjournment Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of a majority of the Ordinary Shares who, being present in person (including virtually) or represented by proxy and entitled to vote thereon and who do so in person or by proxy at the Extraordinary General Meeting.

The Board has fixed the close of business on November 22, 2022, as the record date for the Extraordinary General Meeting. Only shareholders of record on November 22, 2022, are entitled to notice of and to vote at the Extraordinary General Meeting or any postponement or adjournment thereof. Further information regarding voting rights and the matters to be voted upon is presented in the accompanying proxy statement.

You are not being asked to vote on an initial business combination at this time. If the Extension is implemented and you do not elect to redeem your public shares in connection with the Extension, you will retain the right to vote on an initial business combination if and when such transaction is submitted to shareholders and the right to redeem your public shares for cash from the Trust Account in the event a proposed initial business combination is approved and completed or the Company has not consummated an initial business combination by the Extended Date or the Additional Extension Date, as applicable. If an initial business combination is not consummated by the Extended Date or the Additional Extension Date, as applicable, assuming the Extension is implemented, and the Company does not obtain an additional extension, the Company will redeem its public shares.

All RMG III shareholders are cordially invited to attend the Extraordinary General Meeting via the Internet at https://www.cstproxy.com/rmgiii/2023. To ensure your representation at the Extraordinary General Meeting, however, you are urged to complete, sign, date and return your proxy card as soon as possible. If your shares are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares. You may revoke your proxy card at any time prior to the Extraordinary General Meeting.

A shareholder’s failure to vote in person or by proxy will not be counted towards the number of Ordinary Shares required to validly establish a quorum. Abstentions and broker non-votes will be counted in connection with the determination of whether a valid quorum is established but will have no effect on the outcome of any of the Proposals.

YOUR VOTE IS IMPORTANT. Please sign, date and return your proxy card as soon as possible. You are requested to carefully read the proxy statement and accompanying Notice of Extraordinary General Meeting for a more complete statement of matters to be considered at the Extraordinary General Meeting.

Table of Contents

If you have any questions or need assistance voting your ordinary shares, please contact Morrow Sodali LLC, our proxy solicitor, by calling (800) 662-5200, or banks and brokers can call collect at (203) 658-9400, or by emailing RMGC.info@investor.morrowsodali.com.

On behalf of our board of directors, we would like to thank you for your support of RMG Acquisition Corp. III.

December 1, 2022

By Order of the Board,

/s/ D. James Carpenter

D. James Carpenter

Chairman

If you return your proxy card signed and without an indication of how you wish to vote, your shares will be voted “FOR” each of the proposals.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST (1) IF YOU HOLD CLASS A ORDINARY SHARES AS PART OF UNITS, ELECT TO SEPARATE YOUR UNITS INTO THE UNDERLYING PUBLIC SHARES AND PUBLIC WARRANTS PRIOR TO EXERCISING YOUR REDEMPTION RIGHTS WITH RESPECT TO THE PUBLIC SHARES, (2) SUBMIT A WRITTEN REQUEST TO THE TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE EXTRAORDINARY GENERAL MEETING THAT YOUR PUBLIC SHARES BE REDEEMED FOR CASH AND (3) DELIVER YOUR CLASS A ORDINARY SHARES TO THE TRANSFER AGENT, PHYSICALLY OR ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM, IN EACH CASE IN ACCORDANCE WITH THE PROCEDURES AND DEADLINES DESCRIBED IN THE ACCOMPANYING PROXY STATEMENT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

This proxy statement is dated December 1, 2022 and is first being mailed to our shareholders with the form of proxy on or about December 2, 2022.

Table of Contents

IMPORTANT

Whether or not you expect to attend the Extraordinary General Meeting, you are respectfully requested by the Company’s board of directors (the “Board”) to sign, date and return the enclosed proxy promptly, or follow the instructions contained in the proxy card or voting instructions provided by your broker. If you grant a proxy, you may revoke it at any time prior to the Extraordinary General Meeting.

RMG Acquisition Corp. III

57 Ocean, Suite 403

5775 Collins Avenue

Miami Beach, Florida 33140

NOTICE OF THE EXTRAORDINARY GENERAL MEETING

TO BE HELD ON JANUARY 10, 2023

Dear Shareholders of RMG Acquisition Corp. III:

NOTICE IS HEREBY GIVEN that an Extraordinary General Meeting (the “Extraordinary General Meeting”) of shareholders of RMG Acquisition Corp. III, a Cayman Islands exempted company (the “Company”), will be held on January 10, 2023, at 9:00 AM Central Time, at the offices of Latham & Watkins LLP, located at 811 Main St., Suite 3700, Houston, Texas 77002, or at such other time, on such other date and at such other place to which the meeting may be postponed or adjourned, and will be available to attend virtually via the Internet. You will be able to attend the Extraordinary General Meeting online, vote and submit your questions during the Extraordinary General Meeting by visiting. While shareholders are encouraged to attend the meeting virtually, you will be permitted to attend the Extraordinary General Meeting in person at the offices of Latham & Watkins LLP. The Extraordinary General Meeting will be held to consider and vote upon the following proposals:

(1) Proposal No. 1—The Extension Proposal—a proposal, by special resolution, to amend and restate the Company’s Amended and Restated Memorandum and Articles of Association (the “Charter”) pursuant to an amended and restated Charter in the form set forth in Annex A of the accompanying proxy statement to extend the date by which the Company must (1) consummate a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination (an “initial business combination”), (2) cease its operations except for the purpose of winding up if it fails to complete such initial business combination, and (3) redeem all of the Class A ordinary shares, par value $0.0001 per share, of the Company (“Class A Ordinary Shares” or “public shares”), included as part of the units sold in the Company’s initial public offering that was consummated on February 9, 2021 (the “IPO”), from February 9, 2023 to May 9, 2023 (such date the “Extended Date”) and to allow the Company, without another shareholder vote, to elect to further extend the date to consummate a business combination up to three times by an additional month each time after the Extended Date, upon two days’ advance notice prior to the applicable deadline, for a total of up to six months, to August 9, 2023 (the “Additional Extension Date”), if the Company has entered into a definitive business combination agreement (the “Extension” and such proposal, the “Extension Proposal”); and

(2) Proposal No. 2—The Adjournment Proposal—a proposal, by ordinary resolution, to approve the adjournment of the Extraordinary General Meeting to a later date or dates, if necessary or convenient, to permit further solicitation and vote of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Extension Proposal (the “Adjournment Proposal”), which will only be presented at the Extraordinary General Meeting if, based on the tabulated votes, there are not sufficient votes at the time of the Extraordinary General Meeting to approve the Extension Proposal, in which case the Adjournment Proposal will be the only proposal presented at the Extraordinary General Meeting.

The above matters are more fully described in the accompanying proxy statement. We urge you to read carefully the accompanying proxy statement in its entirety.

The sole purpose of the Extension Proposal is to provide the Company with sufficient time to complete an initial business combination.

Approval of the Extension Proposal is a condition to the implementation of the Extension. In addition, we will not proceed with the Extension if the number of redemptions of our public shares causes us to have less than $5,000,001 of net tangible assets following approval of the Extension.

Table of Contents

Approval of the Extension Proposal requires a special resolution under Cayman Islands law, being the affirmative vote of the holders of a majority of at least two-thirds of the Class A Ordinary Shares and Class B ordinary shares, par value $0.0001 per share, of the Company (“Class B Ordinary Shares” and together with the Class A Ordinary Shares, the “Ordinary Shares”) who, being present in person (including virtually) or by proxy and entitled to vote thereon and who do so in person or by proxy at the Extraordinary General Meeting. Ordinary Shares that are present virtually during the Extraordinary General Meeting constitute Ordinary Shares represented “in person.”

Approval of the Adjournment Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of a majority of the Ordinary Shares who, being present in person (including virtually) or represented by proxy and entitled to vote thereon and who vote at the Extraordinary General Meeting.

In connection with the Extension, public shareholders may elect to redeem their shares for a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account established in connection with the IPO (the “Trust Account”), including interest earned on the funds held in the Trust Account and not previously released to the Company to pay its taxes or fund the Company’s for working capital requirements, divided by the number of then-issued and outstanding Class A Ordinary Shares, regardless of how such public shareholders vote on the Extension Proposal, or if they vote at all. If the Extension is approved by the requisite vote of shareholders, the remaining public shareholders will retain their right to redeem their Class A Ordinary Shares upon consummation of our initial business combination when it is submitted to a vote of the shareholders, subject to any limitations set forth in the Charter. In addition, public shareholders will be entitled to have their shares redeemed for cash if the Company has not completed an initial business combination by the Extended Date or the Additional Extension Date, as applicable.

Pursuant to the Charter, a public shareholder may request that the Company redeem all or a portion of such public shareholder’s public shares for cash if the Extension is approved. You will be entitled to receive cash for any public shares to be redeemed only if you:

(1) (a) hold public shares or (b) hold public shares as part of units and elect to separate such units into the underlying public shares and public warrants prior to exercising your redemption rights with respect to the public shares; and

(2) prior to 5:00 p.m., Central Time, on January 6, 2023 (two business days prior to the vote at the Extraordinary General Meeting), (a) submit a written request to Continental Stock Transfer & Trust Company, the Company’s transfer agent, that the Company redeem your public shares for cash and (b) deliver your public shares to the transfer agent, physically or electronically through The Depository Trust Company.

Holders of units must elect to separate the underlying public shares and public warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate the units into the underlying public shares and public warrants, or if a holder holds units registered in its, his or her own name, the holder must contact the transfer agent directly and instruct it to do so. Public shareholders may elect to redeem all or a portion of their public shares even if they vote for the Extension Proposal.

If the Extension is not approved and we do not consummate an initial business combination by February 9, 2023, we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible but not more than ten business days thereafter subject to lawfully available funds therefor, redeem 100% of the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company (less taxes payable, expenses relating to the administration of the trust account, amounts withdrawn to fund the Company’s working capital requirements and up to $100,000 of interest to pay dissolution expenses), divided by the total number of then-issued and outstanding public shares, which redemption will completely extinguish public shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), and (iii) as promptly as reasonably possible following such redemption, subject to the approval of the remaining shareholders and the Board, liquidate and dissolve, subject in each case to the Company’s obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law.

Table of Contents

The Company’s sponsor is RMG Sponsor III, LLC, a Delaware limited liability company (the “Sponsor”). The Sponsor and the Company’s directors and officers have agreed to waive their respective rights to liquidating distributions from the Trust Account in respect of any Class B Ordinary Shares held by it or them, as applicable, if the Company fails to complete an initial business combination by February 9, 2023, or by the applicable deadline as may be extended, although they will be entitled to liquidating distributions from the Trust Account with respect to any Class A Ordinary Shares they hold if the Company fails to complete its initial business combination by such date. There will be no redemption rights or liquidating distributions with respect to our warrants, which will expire worthless if we fail to complete our initial business combination by February 9, 2023 or by the applicable deadline as may be extended.

If the Company liquidates, the Sponsor has agreed that it will be liable to us if and to the extent any claims by a third party (other than our independent auditors) for services rendered or products sold to us, or a prospective target business with which we have discussed entering into a transaction agreement, reduce the amount of funds in the trust account to below (1) $10.00 per public share or (2) such lesser amount per public share held in the trust account as of the date of the liquidation of the trust account due to reductions in the value of the trust assets, in each case net of the interest which may be withdrawn to pay taxes, expenses relating to the administration of the trust account and limited withdrawals for working capital, except as to any claims by a third party who executed a waiver of any and all rights to seek access to the trust account and except as to any claims under our indemnity of the underwriters of the IPO against certain liabilities, including liabilities under the Securities Act of 1933, as amended. The per-share liquidation price for the public shares is anticipated to be approximately $10.05 (based on the amount held in the Trust Account as of September 30, 2022 and estimated interest income and taxes post-September 30, 2022). Nevertheless, the Company cannot assure you that the per share distribution from the Trust Account, if the Company liquidates, will not be less than $10.05 due to unforeseen claims of potential creditors.

If the Extension Proposal is approved, such approval will constitute consent for the Company to (i) remove from the Trust Account an amount (the “Withdrawal Amount”) equal to the number of public shares properly redeemed multiplied by the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company, divided by the number of then outstanding public shares and (ii) deliver to the holders of such redeemed public shares their portion of the Withdrawal Amount. The funds remaining in the Trust Account after the removal of such Withdrawal Amount shall be available for use by the Company to complete an initial business combination on or before the Extended Date or the Additional Extension Date, as applicable. Holders of public shares who do not redeem their public shares now will retain their redemption rights and their ability to vote on an initial business combination through the Extended Date or the Additional Extension Date, if applicable, if the Extension Proposal is approved.

The withdrawal of the Withdrawal Amount will reduce the amount held in the Trust Account, and the amount remaining in the Trust Account may be significantly less than the $485,865,952 that was in the Trust Account as of September 30, 2022. In such an event, the Company may need to obtain additional funds to complete its initial business combination, and there can be no assurance that such funds will be available on terms acceptable to the parties or at all.

Only shareholders of record of the Company as of the close of business on November 22, 2022, are entitled to notice of, and to vote at, the Extraordinary General Meeting or any adjournment or postponement thereof. Each Ordinary Share entitles the holder thereof to one vote. On the record date, there were 60,375,000 Ordinary Shares issued and outstanding, including 48,300,000 Class A Ordinary Shares and 12,075,000 Class B Ordinary Shares. The Company’s warrants do not have voting rights in connection with the proposals.

Your vote is important. Proxy voting permits shareholders unable to attend the Extraordinary General Meeting in person to vote their shares through a proxy. By appointing a proxy, your shares will be represented and voted in accordance with your instructions. You can vote your shares by completing and returning your proxy card or by completing the voting instruction form provided to you by your broker. Proxy cards that are signed and returned but do not include voting instructions will be voted by the proxy as recommended by the Board. You can change your voting instructions or revoke your proxy at any time prior to the Extraordinary General Meeting by following the instructions included in this proxy statement and on the proxy card.

Table of Contents

It is strongly recommended that you complete and return your proxy card before the Extraordinary General Meeting date to ensure that your shares will be represented at the Extraordinary General Meeting. You are urged to review carefully the information contained in the enclosed proxy statement prior to deciding how to vote your shares. If you have any questions or need assistance voting your Ordinary Shares, please contact Morrow Sodali LLC, our proxy solicitor, by calling (800) 662-5200, or banks and brokers can call collect at (203) 658-9400, or by emailing RMGC.info@investor.morrowsodali.com.

By Order of the Board,

/s/ D. James Carpenter |

| D. James Carpenter |

| Chairman |

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE EXTRAORDINARY GENERAL MEETING TO BE HELD ON JANUARY 10, 2023

This Notice of Extraordinary General Meeting and Proxy Statement are available at https://www.cstproxy.com/rmgiii/2023.

Table of Contents

| 1 | ||||

QUESTIONS AND ANSWERS ABOUT THE EXTRAORDINARY GENERAL MEETING | 2 | |||

| 12 | ||||

| 16 | ||||

| 27 | ||||

| 28 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| A-1 |

Table of Contents

RMG Acquisition Corp. III

PROXY STATEMENT

FOR THE EXTRAORDINARY GENERAL MEETING

To Be Held at 9:00 AM, Central Time, on January 10, 2023

This proxy statement and the enclosed form of proxy are furnished in connection with the solicitation of proxies by the board of directors (the “Board”) for use at the extraordinary general meeting of RMG Acquisition Corp. III, a Cayman Islands exempted company (the “Company,” “RMG III,” “we,” “us” or “our”), and any postponements, adjournments or continuations thereof (the “Extraordinary General Meeting”). The Extraordinary General Meeting will be held on January 10, 2023, at 9:00 AM, Central Time, at the offices of Latham & Watkins LLP, located at 811 Main St., Suite 3700, Houston, Texas 77002, and will be available to attend virtually via the Internet. You will be able to attend the Extraordinary General Meeting online, vote and submit your questions during the Extraordinary General Meeting by visiting https://www.cstproxy.com/rmgiii/2023. While shareholders are encouraged to attend the meeting virtually, you will be permitted to attend the Extraordinary General Meeting in person at the offices of Latham & Watkins LLP.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This proxy statement contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) that are not historical facts, and involve risks and uncertainties that could cause actual results to differ materially from those expected and projected. All statements, other than statements of historical fact included in this proxy statement including, without limitation, regarding the Company’s financial position, business strategy and the plans and objectives of management for future operations, are forward-looking statements. Words such as “expect,” “believe,” “anticipate,” “intend,” “estimate,” “seek” and variations and similar words and expressions are intended to identify such forward-looking statements. Such forward-looking statements relate to future events or future performance, but reflect management’s current beliefs, based on information currently available. A number of factors could cause actual events, performance or results to differ materially from the events, performance and results discussed in the forward-looking statements. For information identifying important factors that could cause actual results to differ materially from those anticipated in the forward-looking statements, please refer to the Risk Factors section of our Annual Report on Form 10-K for the year ended December 31, 2021 filed with the U.S. Securities and Exchange Commission (the “SEC”) on March 31, 2022, the Company’s subsequent Quarterly Reports on Form 10-Q and elsewhere in our filings with the SEC. The Company’s securities filings can be accessed on the EDGAR section of the SEC’s website at www.sec.gov. Except as expressly required by applicable securities law, the Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

1

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE EXTRAORDINARY GENERAL MEETING

These Questions and Answers are only summaries of the matters they discuss. They do not contain all of the information that may be important to you. You should read carefully the entire document, including any annexes to this proxy statement.

Why am I receiving this proxy statement?

This proxy statement and the enclosed proxy card are being sent to you in connection with the solicitation of proxies by our Board for use at the Extraordinary General Meeting to be held in person or virtually on January 10, 2023, or at any adjournments or postponement thereof. This proxy statement summarizes the information that you need to make an informed decision on the proposals to be considered at the Extraordinary General Meeting.

RMG III is a blank check company incorporated on December 23, 2020 as a Cayman Islands exempted company for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses (an “initial business combination”).

In December 2020, the Sponsor paid an aggregate of $25,000 to cover for certain expenses on behalf of the Company in exchange for issuance of 10,062,500 Class B ordinary shares, par value $0.0001 per share, of the Company (the “Class B Ordinary Shares”). On January 30, 2021, the Company effectuated a 5-for-6 share split of the Class B Ordinary Shares, resulting in an aggregate outstanding amount of 12,075,000 Class B Ordinary Shares.

On February 9, 2021, the Company consummated its initial public offering (“IPO”) of 48,300,000 units at $10.00 per unit. Each unit consists of one Class A ordinary share, par value $0.0001 per share, of the Company (“Class A Ordinary Shares” or “public shares”) and one-fifth of one redeemable warrant to purchase one Class A Ordinary Share. Simultaneously with the consummation of the IPO, RMG III completed the private placement of 8,216,330 private placement warrants (the “Private Placement” and collectively the “Private Placement Warrants”) at a purchase price of $1.50 per Private Placement Warrant to the Sponsor, generating gross proceeds to us of approximately $12.3 million. Following the closing of the IPO and the Private Placement, a total of $483.0 million ($10.00 per unit) of the net proceeds from its IPO and the Private Placement were placed in a trust account at Citibank N.A. (the “Trust Account”) with Continental Stock Transfer & Trust Company (“Continental”) acting as trustee. Our charter provides for the return of the IPO proceeds held in the Trust Account to the holders of public shares if we do not complete our initial business combination by February 9, 2023.

While the Company is currently in discussions regarding various business combination opportunities, the Board has determined that there may not be sufficient time before February 9, 2023 to complete an initial business combination. Therefore, the Board has determined that it is in the best interests of the Company’s shareholders to extend the date by which the Company has to complete an initial business combination to the Extended Date or up to the Additional Extension Date, if the Company has entered into a definitive business combination agreement, in order that the Company’s shareholders are given the chance to participate in an investment opportunity.

What is being voted on?

You are being asked to vote on the following proposals:

(1) A proposal, by special resolution, to amend and restate the Company’s Amended and Restated Memorandum and Articles of Association (the “Charter”) pursuant to an amended and restated Charter in the form set forth in Annex A of the accompanying proxy statement to extend the date by which the Company must (a) consummate an initial business combination, (b) cease its operations except for the purpose of winding up if it fails to complete such initial business combination, and (c) redeem all of the Class A Ordinary Shares included as part of the units sold in the IPO, from February 9, 2023 to May 9, 2023 (the “Extended Date”), with optional additional extensions of up to three (3) times by an additional month each time (the “Additional Extension Date”), if the Company has entered into a definitive business combination agreement (the “Extension,” and such proposal, the “Extension Proposal”); and

(2) A proposal, by ordinary resolution, to approve the adjournment of the Extraordinary General Meeting to a later date or dates, if necessary or convenient, to permit further solicitation and vote of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Extension Proposal (the “Adjournment Proposal”), which will only be presented at the Extraordinary General Meeting if, based on the tabulated votes, there are not sufficient votes at the time of the Extraordinary General Meeting to approve the Extension Proposal, in which case the Adjournment Proposal will be the only proposal presented at the Extraordinary General Meeting.

2

Table of Contents

You are not being asked to vote on an initial business combination at this time. If the Extension is implemented and you do not elect to redeem your public shares, you will retain the right to vote on our initial business combination if and when it is submitted to shareholders and the right to redeem your public shares for cash in the event an initial business combination is approved and completed or the Company has not consummated an initial business combination by the Extended Date or the Additional Extension Date, as applicable.

What is the effect of giving a proxy?

Proxies are solicited by and on behalf of our Board. Robert S. Mancini and Wesley Sima have been designated as proxies by our Board. When proxies are properly dated, executed and returned, the shares represented by such proxies will be voted at the Extraordinary General Meeting in accordance with the instructions of the shareholder. If no specific instructions are given, however, the shares will be voted in accordance with the recommendations of our Board as described below. If any matters not described in this proxy statement are properly presented at the Extraordinary General Meeting, the proxy holders will use their own judgment to determine how to vote the shares. If the Extraordinary General Meeting is adjourned, the proxy holders can vote the shares on the new Extraordinary General Meeting date as well, unless you have properly revoked your proxy instructions, as described elsewhere herein.

Can I attend the Extraordinary General Meeting?

The Extraordinary General Meeting will be held at 9:00 AM, Central Time, on January 10, 2023, at the offices of Latham & Watkins LLP, located at 811 Main St., Suite 3700, Houston, Texas 77002, or virtually via live webcast. You will be able to attend the Extraordinary General Meeting online, vote and submit your questions during the Extraordinary General Meeting by visiting https://www.cstproxy.com/rmgiii/2023. The Extraordinary General Meeting will comply with the meeting rules of conduct. The rules of conduct will be posted on the virtual meeting web portal. We encourage you to access the Extraordinary General Meeting webcast prior to the start time. Online check-in will begin fifteen minutes prior to the start time of the Extraordinary General Meeting, and you should allow ample time for the check-in procedures. While shareholders are encouraged to attend the meeting virtually, you will be permitted to attend the Extraordinary General Meeting in person at the offices of Latham & Watkins LLP. You may submit your proxy by completing, signing, dating and returning the enclosed proxy card in the accompanying pre-addressed postage-paid envelope. If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or nominee, you should contact your broker, bank or nominee to ensure that votes related to the shares you beneficially own are properly counted. In this regard, you must provide the broker, bank or nominee with instructions on how to vote your shares.

Why should I vote to approve the Extension?

Our Board believes shareholders will benefit from the Company consummating an initial business combination and is proposing the Extension to extend the date by which the Company has to complete an initial business combination until the Extended Date, and up until the Additional Extension Date if applicable. The Extension would give the Company the opportunity to complete its initial business combination.

The Charter currently provides that if the Company does not complete an initial business combination by February 9, 2023, we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible but not more than ten business days thereafter subject to lawfully available funds therefor, redeem 100% of the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company (less taxes payable, expenses relating to the administration of the trust account, amounts withdrawn to fund the Company’s working capital requirements and up to $100,000 of interest to pay dissolutions expenses) divided by the total number of then-issued and outstanding public shares, which redemption will completely extinguish public shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), and (iii) as promptly as reasonably possible following such redemption, subject to the approval of the remaining public shareholders and the Board, liquidate and dissolve, subject in each case to the Company’s obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law.

3

Table of Contents

We believe that the provisions of the Charter described in the preceding paragraph were included to protect the Company’s shareholders from having to sustain their investments for an unreasonably long period if the Company failed to find a suitable initial business combination in the timeframe contemplated by the Charter. We also believe, however, that given the Company’s expenditure of time, effort and money on pursuing an initial business combination and our belief that an initial business combination offers an attractive investment for our shareholders, the Extension is warranted.

In connection with the Extension, public shareholders may elect to redeem their shares for a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company to pay its taxes or to fund the Company’s working capital requirements, divided by the number of then-issued and outstanding Class A Ordinary Shares, regardless of how such public shareholders vote on the Extension Proposal, or if they vote at all. We will not proceed with the Extension if redemptions of public shares cause us to have less than $5,000,001 of net tangible assets following approval of the Extension Proposal.

Liquidation of the Trust Account is a fundamental obligation of the Company to the public shareholders and the Company is not proposing and will not propose to change that obligation to the public shareholders. If holders of public shares do not elect to redeem their public shares, such holders shall retain redemption rights in connection with an initial business combination. Assuming the Extension is approved, the Company will have until the Extended Date or the Additional Extension Date, as applicable, to complete an initial business combination, unless the Company obtains any additional extension.

Our Board recommends that you vote in favor of the Extension Proposal, but expresses no opinion as to whether you should redeem your public shares.

How do the Company insiders intend to vote their shares?

The Sponsor, the Company’s directors, officers and initial shareholders and their permitted transferees (collectively, the “Initial Shareholders”) are expected to vote any Class A Ordinary Shares and Class B Ordinary Shares (together, the “Ordinary Shares”) over which they have voting control in favor of the Extension Proposal and, if presented, the Adjournment Proposal.

The Initial Shareholders are not entitled to redeem any Ordinary Shares held by them. On the record date, the Initial Shareholders beneficially owned and were entitled to vote 12,075,000 Ordinary Shares, which represents 20% of the Company’s issued and outstanding Ordinary Shares.

Subject to applicable securities laws (including with respect to material nonpublic information), the Sponsor, the Company’s directors, officers, advisors or any of their respective affiliates may (i) purchase public shares from institutional and other investors (including those who vote, or indicate an intention to vote, against any of the proposals presented at the Extraordinary General Meeting, or elect to redeem, or indicate an intention to redeem, public shares), (ii) enter into transactions with such investors and others to provide them with incentives to not redeem their public shares, or (iii) execute agreements to purchase such public shares from such investors or enter into non-redemption agreements in the future. In the event that the Sponsor, the Company’s directors, officers, advisors or any of their respective affiliates purchase public shares in situations in which the tender offer rules restrictions on purchases would apply, they (a) would purchase the public shares at a price no higher than the price offered through the Company’s redemption process (i.e., approximately $10.05 per share, based on the amounts held in the Trust Account as of September 30, 2022); (b) would represent in writing that such public shares will not be voted in favor of approving the Extension; and (c) would waive in writing any redemption rights with respect to the public shares so purchased.

4

Table of Contents

To the extent any such purchases by the Sponsor, the Company’s directors, officers, advisors or any of their respective affiliates are made in situations in which the tender offer rules restrictions on purchases apply, the Company will disclose in a Current Report on Form 8-K prior to the Extraordinary General Meeting the following: (i) the number of public shares purchased outside of the redemption offer, along with the purchase price(s) for such public shares; (ii) the purpose of any such purchases; (iii) the impact, if any, of the purchases on the likelihood that the Extension will be approved; (iv) the identities of the securityholders who sold to the Sponsor, the Company’s directors, officers, advisors or any of their respective affiliates (if not purchased on the open market) or the nature of the securityholders (e.g., 5% security holders) who sold such public shares; and (v) the number of Ordinary Shares for which the Company has received redemption requests pursuant to its redemption offer.

The purpose of such share purchases and other transactions would be to increase the likelihood of (i) otherwise limiting the number of public shares electing to redeem and (ii) the Company’s net tangible assets (as determined in accordance with Rule 3a51(g)(l) of the Exchange Act) being at least $5,000,001.

If such transactions are effected, the consequence could be to cause the Extension to be effectuated in circumstances where such effectuation could not otherwise occur. Consistent with SEC guidance, purchases of shares by the persons described above would not be permitted to be voted for the Extension at the Extraordinary General Meeting and could decrease the chances that the Extension would be approved. In addition, if such purchases are made, the public “float” of our securities and the number of beneficial holders of our securities may be reduced, possibly making it difficult to maintain or obtain the quotation, listing or trading of our securities on a national securities exchange.

The Company hereby represents that any Company securities purchased by the Sponsor, the Company’s directors, officers, advisors or any of their respective affiliates in situations in which the tender offer rules restrictions on purchases would apply would not be voted in favor of approving the Extension Proposal.

Who is the Company’s Sponsor?

The Company’s sponsor is RMG Sponsor III, LLC, a Delaware limited liability company. The Sponsor currently owns an aggregate of 12,075,000 Ordinary Shares, all of which are Class B Ordinary Shares. The Sponsor is controlled by its manager, MKC Investments LLC (the “Manager”). Robert S. Mancini, the Company’s Chief Executive Officer and a Member of the Board, D. James Carpenter, the Chairman of the Board, and Philip Kassin, the Company’s President, Chief Operating Officer, and a member of the Board, are the managing members of the Manager. Each of the Company’s directors and officers, and each of the managing members of the Manager, is a U.S. citizen. The Sponsor is not controlled by and does not have substantial ties with a non-US person.

The Company’s ability to complete an initial business combination with a U.S. target company may be impacted if such initial business combination is subject to U.S. foreign investment regulations and review by a U.S. government entity, such as the Committee on Foreign Investment in the United States (“CFIUS”), and ultimately prohibited.

The Sponsor, RMG Sponsor III, LLC, is a Delaware limited liability company. The Company does not believe the Sponsor would be considered a foreign person because it is organized in a U.S. jurisdiction, is controlled and majority-owned by U.S. nationals and does not have substantial ties with a non-U.S. person.

In the event the Sponsor is considered a foreign person, however, the Company could also be considered a foreign person and would continue to be considered as such in the future for so long as the Sponsor has the ability to exercise control over the Company for purposes of CFIUS’s regulations. The Company could likewise be considered a foreign person if a foreign investor acquires a significant interest in the Company and is viewed as having the ability to exercise control over the Company. As such, an initial business combination with a U.S. business may be subject to CFIUS review, the scope of which includes controlling investments as well as certain non-passive, non-controlling investments in sensitive U.S. businesses and certain acquisitions of real estate even with no underlying U.S. business. If the Company’s potential initial business combination with a U.S. business falls within CFIUS’s jurisdiction, the Company may determine that it is required to make a mandatory filing or that it will submit a voluntary filing to CFIUS, or to proceed with the initial business combination without notifying CFIUS and risk CFIUS intervention, before or after closing the initial business combination. CFIUS may decide to delay the initial business combination, impose conditions to mitigate national security concerns with respect to such initial business combination or recommend that the U.S. president block the initial business combination or order the Company to divest all or a portion of a U.S. business of the combined company, which may limit the attractiveness of or prevent the Company from pursuing certain initial business combination opportunities that it believes would otherwise be beneficial to the Company and its shareholders. As a result, the pool of potential targets with which the Company could complete an initial business combination may be impacted, and it may be adversely affected in terms of competing with other special purpose acquisition companies which do not have similar foreign ownership issues.

Moreover, the process of government review, whether by the CFIUS or otherwise, could be lengthy and the Company has limited time to complete its initial business combination. If the Company cannot complete its initial business combination by February 9, 2023 or by the Extended Date or the Additional Extension Date, as applicable, if the Extension is approved, or such later date that may be approved by the Company’s shareholders, because the review process extends beyond such timeframe or because the initial business combination is ultimately prohibited by CFIUS or another U.S. government entity, the Company may be required to liquidate. If the Company liquidates, its public shareholders may only receive approximately $10.05 per share (based on the amount held in the Trust Account as of September 30, 2022 and estimated interest income and taxes post-September 30, 2022, and assuming the Extension is not approved), and the Company’s warrants will expire worthless. This will also cause you to lose the investment opportunity in a target company and the chance of realizing future gains on your investment through any price appreciation in the combined company.

What vote is required to approve the Extension Proposal?

Approval of the Extension Proposal requires a special resolution under Cayman Islands law, being the affirmative vote of the holders of a majority of at least two-thirds of the Ordinary Shares who, being present in person (including virtually) or represented by proxy and entitled to vote thereon and who do so in person or by proxy at the Extraordinary General Meeting. Ordinary Shares that are present virtually during the Extraordinary General Meeting constitute Ordinary Shares represented “in person.”

What vote is required to approve the Adjournment Proposal?

Approval of the Adjournment Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of a majority of the Ordinary Shares who, being present in person (including virtually) or represented or by proxy and entitled to vote thereon and who do so in person or by proxy at the Extraordinary General Meeting.

What if I want to vote against or don’t want to vote for any of the proposals?

If you do not want any of the proposals to be approved, you must abstain, not vote or vote against such proposal. A shareholder’s failure to vote by proxy or to vote in person at the Extraordinary General Meeting will not be counted towards the number of Ordinary Shares required to validly establish a quorum. Abstentions will be counted in connection with the determination of whether a valid quorum is established.

5

Table of Contents

What happens if the Extension Proposal is not approved?

If the Extension Proposal is not approved and we do not consummate an initial business combination by February 9, 2023, we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible but not more than ten business days thereafter subject to lawfully available funds therefor, redeem 100% of the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company (less amounts withdrawn to fund the Company’s taxes payable, expenses relating to the administration of the trust account and limited withdrawals for working capital requirements and up to $100,000 of interest to pay dissolution expenses), divided by the total number of then-issued and outstanding public shares, which redemption will completely extinguish public shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), and (iii) as promptly as reasonably possible following such redemption, subject to the approval of the remaining public shareholders and the Board, liquidate and dissolve, subject in each case to the Company’s obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law.

The Initial Shareholders have agreed to waive their respective rights to liquidating distributions from the Trust Account in respect of any Class B Ordinary Shares held by it or them, as applicable, if the Company fails to complete an initial business combination by February 9, 2023, or by the applicable deadline as may be extended, although they will be entitled to liquidating distributions from the Trust Account with respect to any Class A Ordinary Shares they hold if the Company fails to complete its initial business combination by such date. There will be no redemption rights or liquidating distributions with respect to our warrants, which will expire worthless if we fail to complete our initial business combination by February 9, 2023 or by the applicable deadline as may be extended. The Company will pay the costs of liquidation from its remaining assets outside of the Trust Account.

If the Extension is approved, what happens next?

The Company is continuing its efforts to complete its initial business combination. The Company is seeking approval of the Extension because the Company may not be able to complete an initial business combination prior to February 9, 2023. If the Extension is approved, the Company expects to continue evaluating business combination opportunities in pursuit of entering into a business combination agreement and seeking shareholder approval of an initial business combination. If shareholders approve an initial business combination, the Company expects to consummate such initial business combination as soon as possible following shareholder approval and satisfaction of the other conditions to the consummation of such initial business combination.

Upon approval of the Extension Proposal by a special resolution under Cayman Islands law, being the affirmative vote of the holders of a majority of at least two-thirds of the Ordinary Shares present in person (including virtually) or represented by proxy and entitled to vote thereon and who do so at the Extraordinary General Meeting, the Company will file an amended and restated Charter with the Cayman Islands Registrar of Companies (the “Cayman Registrar”) in the form attached as Annex A hereto. The Company will remain a reporting company under the Exchange Act, and its units, Class A Ordinary Shares and public warrants will remain publicly traded.

If the Extension is approved, any removal of any Withdrawal Amount (defined as an amount equal to the number of public shares properly redeemed multiplied by the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company to pay its taxes or fund the Company’s working capital requirements, from the Trust Account will reduce the amount remaining in the Trust Account and increase the percentage interest of Ordinary Shares held by the Sponsor through the Class B Ordinary Shares. We will not proceed with the Extension if redemptions of public shares cause us to have less than $5,000,001 of net tangible assets following approval of the Extension.

If the Extension is approved, an affiliate of our Sponsor will continue to have the right to receive payments from the Company of $20,000 per month for office space, administrative and support services until the earlier of the Company’s consummation of an initial business combination or the Company’s liquidation pursuant to the Administrative Services Agreement, dated as of February 4, 2021, by and between the Company and the Sponsor (the “Administrative Services Agreement”).

Where will I be able to find the voting results of the Extraordinary General Meeting?

We will announce preliminary voting results at the Extraordinary General Meeting. We will also disclose voting results on a Current Report on Form 8-K that we will file with the SEC within four business days after the Extraordinary General Meeting. If final voting results are not available to us in time to file a Current Report on Form 8-K within four business days after the Extraordinary General Meeting, we will file a Current Report on Form 8-K to publish preliminary results and will provide the final results in an amendment to such Current Report on Form 8-K as soon as they become available.

6

Table of Contents

Would I still be able to exercise my redemption rights in connection with a vote to approve a proposed initial business combination?

Yes. Assuming you are a shareholder as of the record date for voting on a proposed initial business combination, you will be able to vote on a proposed initial business combination if and when it is submitted to shareholders. If you disagree with an initial business combination, you will retain your right to redeem your public shares upon consummation of such initial business combination, subject to any limitations set forth in our Charter.

How do I change my vote?

Shareholders may send a later-dated, signed proxy card to the Company at 57 Ocean, Suite 403, 5775 Collins Ave., Miami Beach, Florida 33140, attn.: Chief Operating Officer, so that it is received prior to the vote at the Extraordinary General Meeting (which is scheduled to take place on January 10, 2023). Shareholders also may revoke their proxy by sending a notice of revocation to the Company’s Chief Operating Officer, which must be received prior to the vote at the Extraordinary General Meeting, or by attending the Extraordinary General meeting, revoking their proxy and voting in person. However, if your shares are held in “street name” by your broker, bank or another nominee, you must contact your broker, bank or other nominee to change your vote.

How are votes counted?

Votes will be counted by the inspector of election appointed for the meeting, who will separately count “FOR” and “AGAINST” votes, for each of the proposals. A shareholder’s failure to vote by proxy or to vote in person at the meeting will not be counted towards the number of Ordinary Shares required to validly establish a quorum. Abstentions and broker non-votes will be counted in connection with the determination of whether a valid quorum is established but will have no effect on the outcome on any of the Proposals.

If my shares are held in “street name,” will my broker automatically vote them for me?

If you do not give instructions to your broker, your broker can vote your shares with respect to “discretionary” items, but not with respect to “non-discretionary” items. We believe that each of the proposals are “non-discretionary” items.

Your broker can vote your shares with respect to “non-discretionary” items only if you provide instructions on how to vote. You should instruct your broker to vote your shares. Your broker can tell you how to provide these instructions. If you do not give your broker instructions, your shares will be treated as broker non-votes with respect to all proposals. Abstentions and broker non-votes, while considered present for the purposes of establishing a quorum, will not count as votes cast at the Extraordinary General Meeting and will have no outcome on any of the Proposals.

What is a quorum?

A quorum is the minimum number of shares required to be present at the Extraordinary General Meeting for the Extraordinary General Meeting to be properly held under our Charter and the Companies Act (As Revised) of the Cayman Islands (the “Companies Act”). The presence, in person, by proxy, or if a corporation or other non-natural person, by its duly authorized representative or proxy, of the holders of a majority of the issued and outstanding Ordinary Shares entitled to vote at the Extraordinary General Meeting constitutes a quorum. Proxies that are marked “abstain” and proxies relating to “street name” shares that are returned to us but marked by brokers as “not voted” (so-called “broker non-votes”) will be treated as shares present for purposes of determining the presence of a quorum on all matters but will have no effect on the outcome of the Proposals. If a shareholder does not give the broker voting instructions, under applicable self-regulatory organization rules, its broker may not vote its shares on “non-discretionary” matters. We believe that each of the proposals is a “nondiscretionary” matter.

7

Table of Contents

Who can vote at the Extraordinary General Meeting?

Holders of our Ordinary Shares as of the close of business on November 22, 2022, the record date, are entitled to vote at the Extraordinary General Meeting. As of the record date, there were 60,375,000 Ordinary Shares issued and outstanding, consisting of 48,300,000 Class A Ordinary Shares and 12,075,000 Class B Ordinary Shares. In deciding all matters at the Extraordinary General Meeting, each shareholder will be entitled to one vote for each share held by them on the record date. Holders of Class A Ordinary Shares and holders of Class B Ordinary Shares will vote together as a single class on all matters submitted to a vote of our shareholders except as required by law. The Initial Shareholders own all of our issued and outstanding Class B Ordinary Shares, constituting approximately 20% of our issued and outstanding Ordinary Shares.

Registered Shareholders. If our shares are registered directly in your name with our transfer agent, Continental, you are considered the shareholder of record with respect to those shares. As the shareholder of record, you have the right to grant your voting proxy directly to the individuals listed on the proxy card or to vote in person at the Extraordinary General Meeting.

Street Name Shareholders. If our shares are held on your behalf in a brokerage account or by a bank or other nominee, you are considered the beneficial owner of those shares held in “street name,” and your broker or nominee is considered the shareholder of record with respect to those shares. As the beneficial owner, you have the right to direct your broker or nominee as to how to vote your shares. However, since a beneficial owner is not the shareholder of record, you may not vote your Ordinary Shares at the Extraordinary General Meeting unless you follow your broker’s procedures for obtaining a legal proxy. Throughout this proxy, we refer to shareholders who hold their shares through a broker, bank or other nominee as “street name shareholders.”

Does the Board recommend voting for the approval of the proposals?

Yes. After careful consideration of the terms and conditions of these proposals, the Board has determined that each of the proposals are in the best interests of the Company and its shareholders. The Board recommends that the Company’s shareholders vote “FOR” each of the proposals.

What interests do the Sponsor and the Company’s directors and officers have in the approval of the proposals?

The Sponsor and the Company’s directors and officers have interests in the proposals that may be different from, or in addition to, your interests as a shareholder. These interests include ownership of Class B Ordinary Shares and Private Placement Warrants that may become exercisable in the future and the possibility of future compensatory arrangements. See the section entitled “Proposal No. 1 — The Extension Proposal—Interests of the Sponsor and the Company’s Directors and Officers.”

Are there any dissenter’s or appraisal or similar rights for dissenting shareholders?

Neither the Companies Act nor our Charter provide for appraisal or other similar rights for dissenting shareholders in connection with any of the proposals to be voted upon at the Extraordinary General Meeting. Accordingly, our shareholders will have no right to dissent and obtain payment for their shares.

What happens to the Company’s warrants if the Extension is not approved?

If the Extension is not approved and we do not consummate an initial business combination by February 9, 2023, we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible but not more than ten business days thereafter subject to lawfully available funds therefor, redeem 100% of the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company (less taxes payable, expenses relating to the administration of the trust account, amounts withdrawn to fund the Company’s working capital requirements and up to $100,000 of interest to pay dissolution expenses) divided by the total number of then-issued and outstanding public shares, which redemption will completely extinguish public shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), subject to applicable law, and (iii) as promptly as reasonably possible following such redemption, subject to the approval of the remaining public shareholders and the Board, liquidate and dissolve, subject in each case to the Company’s obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law. There will be no redemption rights or liquidating distributions with respect to our warrants, which will expire worthless if we fail to complete our initial business combination by February 9, 2023 or by the applicable deadline as may be extended.

8

Table of Contents

What happens to the Company’s warrants if the Extension is approved?

If the Extension is approved, the Company will continue to attempt to consummate an initial business combination until the Extended Date and up to the Additional Extension Date, as applicable, and will retain the blank check company restrictions previously applicable to it. The warrants will remain outstanding in accordance with their terms.

How are the funds in the Trust Account currently being held?

With respect to the regulation of special purpose acquisition companies like the Company (“SPACs”), on March 30, 2022, the SEC issued proposed rules (the “SPAC Rule Proposals”) relating to, among other items, disclosures in business combination transactions involving SPACs and private operating companies; the condensed financial statement requirements applicable to transactions involving shell companies; the use of projections by SPACs in SEC filings in connection with proposed business combination transactions; the potential liability of certain participants in proposed business combination transactions; and the extent to which SPACs could become subject to regulation under the Investment Company Act of 1940, as amended (the “Investment Company Act”), including a proposed rule that would provide SPACs a safe harbor from treatment as an investment company if they satisfy certain conditions that limit a SPAC’s duration, asset composition, business purpose and activities.

Following the IPO, the funds in the Trust Account were held in U.S. government treasury obligations with a maturity of 185 days or less or in money market funds investing solely in U.S. government treasury obligations and meeting certain conditions under Rule 2a-7 under the Investment Company Act. In the fourth quarter of 2022, to mitigate the risk of us being deemed to have been operating as an unregistered investment company (including under the subjective test of Section 3(a)(1)(A) of the Investment Company Act), we instructed Continental, the trustee with respect to the Trust Account, to liquidate the U.S. government treasury obligations or money market funds held in the Trust Account and thereafter to hold all funds in the Trust Account in cash until the earlier of consummation of our initial business combination or liquidation. As a result, following such liquidation, we expect to receive minimal interest, if any, on the funds held in the Trust Account, which would reduce the dollar amount our public shareholders would receive upon any redemption or liquidation of the Company.

How do I vote?

If you are a holder of record of Ordinary Shares on November 22, 2022, the record date for the Extraordinary General Meeting, you may vote in person or by virtual attendance at the Extraordinary General Meeting or by submitting a proxy for the Extraordinary General Meeting. You may submit your proxy by completing, signing, dating and returning the enclosed proxy card in the accompanying pre-addressed postage-paid envelope. If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or nominee, you should contact your broker, bank or nominee to ensure that votes related to the shares you beneficially own are properly counted. In this regard, you must provide the broker, bank or nominee with instructions on how to vote your shares or, if you wish to attend the Extraordinary General Meeting and vote in person, obtain a valid proxy from your broker, bank or nominee.

How do I redeem my Ordinary Shares?

Pursuant to the Charter, a public shareholder may request that the Company redeem all or a portion of such public shareholder’s public shares for cash if the Extension Proposal is approved. You will be entitled to receive cash for any public shares to be redeemed only if you:

(1) (a) hold public shares or (b) hold public shares as part of units and elect to separate such units into the underlying public shares and public warrants prior to exercising your redemption rights with respect to the public shares; and

(2) prior to 5:00 p.m., Central Time, on January 6, 2023 (two business days prior to the vote at the Extraordinary General Meeting), (a) submit a written request to Continental, the Company’s transfer agent, that the Company redeem your public shares for cash and (b) deliver your public shares to the transfer agent, physically or electronically through The Depository Trust Company.

9

Table of Contents

Holders of units must elect to separate the underlying public shares and public warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate the units into the underlying public shares and public warrants, or if a holder holds units registered in its own name, the holder must contact the transfer agent directly and instruct it to do so. Public shareholders may elect to redeem all or a portion of their public shares even if they vote for the Extension Proposal.