| | |

United States Securities and Exchange Commission Washington, DC 20549 | | Form 10-K |

| ( X ) | | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the Fiscal Year Ended December 31, 2008 |

or

| ( ) | | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the Transition Period from to |

Commission file number 001-05519

| | |

| CDI Corp. | | (Exact name of Registrant as specified in its charter) |

| | |

Pennsylvania (State of incorporation) 1717 Arch Street, 35th Floor, Philadelphia, PA 19103-2768 (Address of principal executive offices) 23-2394430 (I.R.S. Employer Identification Number) (215) 569-2200 (Registrant’s telephone number, including area code) | | Securities registered pursuant to Section 12(b) of the Act: Common stock, $.10 par value (Title of each class) New York Stock Exchange (Name of exchange on which registered) |

Indicate by a check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES[ ] NO [ X ]

Indicate by a check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES[ ] NO [ X ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [ X ] NO[ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | |

| Large accelerated filer [ ] | | Accelerated filer [ X ] |

| Non-accelerated filer [ ] | | Smaller reporting company [ ] |

| (Do not check if a smaller reporting company) | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) YES [ ] NO [ X ]

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on June 30, 2008, the last business day of the registrant’s most recently completed second fiscal quarter, as reported on the New York Stock Exchange, was $353,186,878:

The number of shares outstanding of each of the registrant’s classes of common stock as of February 27, 2009 was as follows:

| | |

Common stock, $.10 par value Class B common stock, $.10 par value | | 18,906,576 Shares None |

Documents Incorporated By Reference

Portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission in connection with the registrant’s 2009 annual meeting of shareholders are incorporated by reference into Part III of this report on Form 10-K.

Part I

Caution Concerning Forward-Looking Statements

This report (including Management’s Discussion and Analysis of Financial Condition and Results of Operations) contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements that address expectations or projections about the future, including statements about the Company’s strategies for growth and future financial results (such as revenues, pre-tax profit and tax rates), are forward-looking statements. Some of the forward-looking statements can be identified by words like “anticipates,” “believes,” “expects,” “may,” “will,” “could,” “should”, intends,” “plans,” “estimates,” and similar expressions. These statements are not guarantees of future performance and involve a number of risks, uncertainties and assumptions that are difficult to predict. Because these forward-looking statements are based on estimates and assumptions that are subject to significant business, economic and competitive uncertainties, many of which are beyond the Company’s control or are subject to change, actual outcomes and results may differ materially from what is expressed or forecasted in these forward-looking statements. Important factors that could cause actual results to differ materially from the forward-looking statements include, but are not limited to: continued deterioration in general economic conditions and levels of capital spending by customers in the industries that the Company serves; further weakness in the financial and capital markets which may result in the postponement or cancellation of the CDI’s customers’ capital projects or the inability of CDI’s customers to pay the Company’s fees; competitive market pressures; the Company’s ability to maintain and grow its revenue base; the availability and cost of qualified labor; adverse consequences arising out of the U.K. Office of Fair Trading investigation; the Company’s level of success in attracting, training and retaining qualified management personnel and other staff employees; changes in customers’ attitudes towards outsourcing; credit risks associated with the Company’s customers; changes in tax laws and other government regulations; the possibility of incurring liability for the Company’s activities, including the activities of the Company’s temporary employees; the Company’s performance on customer contracts; and government policies or judicial decisions adverse to the Company’s businesses. More detailed information about some of these risks and uncertainties may be found in the Company’s filings with the SEC, particularly in the “Risk Factors” section in Part I, Item 1A. of this Annual Report on Form 10-K. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company assumes no obligation to update such statements, whether as a result of new information, future events or otherwise, except as required by law.

Unless the context otherwise requires, all references herein to “CDI,” the “Registrant,” the “Company,” “we,” “us,” or “our” are to CDI Corp. and its consolidated subsidiaries.

General

CDI Corp. (the “Company” or “CDI”) (NYSE:CDI) was incorporated in Pennsylvania on July 30, 1985. It is the successor registrant to CDI Corporation, which was incorporated in Pennsylvania on September 16, 1950. The Company, which provides engineering and information technology outsourcing solutions and professional staffing, derives the majority of its revenues by providing services to Fortune 1000 companies and equivalent non-US-based companies, primarily in the US, UK, Canada, Mexico and Australia. Its services can be described in the following broad categories:

| | Ÿ | | Project outsourcing services - Project outsourcing services include engineering and information technology projects, usually performed at a CDI facility, which provide a deliverable work product or service to the customer. |

| | | In the CDI Engineering Solutions segment, these outsourcing projects can range in duration from several months to multiple years and generally include analysis of a customer’s engineering needs and development of solutions in one or more areas of a facility’s design and start-up supply chain. This supply chain includes such functions as feasibility studies, program and projectmanagement, technology and process design, front end engineering design, detailed design, construction management, equipment procurement and facility start-up services. Additional services can include life cycle plant maintenance. |

| | | In the CDI Information Technology Solutions segment, outsourcing projects can range from several months to multiple years and include problem analysis and execution of business application services, testing and quality assurance, program management and process outsourcing. |

| | | The CDI AndersElite and Management Recruiters International segments do not provide project outsourcing services. |

| | Ÿ | | Staffing services - Staffing services include assigning the Company’s skilled engineering, information technology, project management, architecture, construction and other professionals to work at a customer’s location under the supervision of customer personnel on a contractual basis for assignments that could range from several months to over one year. The Company also provides managed staffing services where the Company assumes overall management of a customer’s contract staffing functions. All of the Company’s four business segments provide customers with staffing services. |

2

| | Ÿ | | Professional services - Professional services include search, recruitment and permanent placement of technical, professional and managerial personnel; sales of new franchises; and services provided to franchisees to help them generate permanent placements. All of the Company’s four business segments provide customers with professional services. |

Reporting Segments

Through December 31, 2006, the Company operated through four reporting segments: Business Solutions (“BS”), CDI AndersElite (“Anders”), Todays Staffing (“Todays”), and Management Recruiters International (“MRI”). As of January 1, 2007, the Company began separately reporting CDI Engineering Solutions (“ES”) and CDI Information Technology Solutions (“ITS”), which together previously comprised the BS segment. This change reflected the Company’s new operating structure and was intended to provide investors with additional information on the Company’s engineering versus its information technology revenue and operating profit. Please see Note 21—Reporting Segments, in the notes to the consolidated financial statements, for further information about reporting segments.

As discussed in Note 9—Discontinued Operations, in the notes to the consolidated financial statements, the Company sold its Todays business segment in the third quarter of 2007. This was a significant step in the Company’s efforts over the past few years to refocus CDI’s business on engineering and IT project outsourcing and professional staffing services. Since September 30, 2007, the Company has four reporting segments: ES, MRI, Anders and ITS.

CDI Engineering Solutions (“ES”)

ES is a full service engineering, procurement, construction management, technical outsourcing and technical staffing firm providing project outsourcing, staffing and professional services through a global network of offices and alliance partners. In most engineering project engagements, the Company seeks to utilize technical resources at the most cost-effective CDI offices or alliance facilities. Work is generally performed at CDI engineering centers in the US and Canada, as well as at an alliance facility in Mexico. Approximately 22% of ES’s total revenue was generated outside the US in 2008.

Services

Through December 31, 2007, the ES segment operated through four verticals: CDI-Process and Industrial, CDI-Life Sciences, CDI-Government Services and CDI-Aerospace. In the second quarter of 2008, management decided to re-align the management and operations of the CDI-Life Sciences vertical into the CDI-Process and Industrial vertical. As a result, ES now offers its services through the following three key verticals:

| | Ÿ | | CDI-Process and Industrial (“P&I”) - Provides a full range of engineering, design, project management, professional staffing and outsourcing solutions to firms in oil, gas, refining, alternative energy, power generation and energy transmission, nuclear, chemicals and heavy manufacturing industries. In addition, P&I offers facility design, project management, engineering, professional staffing and facility start-up services to customers in the pharmaceutical, bio-pharmaceutical and regulated medical services industries. |

| | Ÿ | | CDI-Government Services (“Government Services”) - Provides engineering, design and logistics services to the defense industry, particularly in marine design, systems development and military aviation support. |

| | Ÿ | | CDI-Aerospace (“Aerospace”) - Provides a full range of engineering, design, project management, professional staffing and outsourcing solutions to both the commercial and military aerospace markets. |

ES’s project outsourcing services are high value-added engineering services that typically involve managing a discrete portion or portions of a customer’s capital project, including, but not limited to, feasibility studies, basic engineering or detailed plant design and construction management, validation and commissioning of a facility and life cycle support. To the extent such activities entail design and planning work, they are typically performed at CDI’s offices. However, construction management, commissioning and life cycle support activities are generally performed on-site at customers’ facilities. ES performs these engagements under contracts that are generally more than a year in duration.

ES’s staffing service is tailored to the needs of the customer. The most basic service provides skilled professionals to work at a single customer location on a temporary basis. In providing these services, the segment recruits and hires employees and provides personnel to customers for assignments that, on average, last close to one year. ES personnel perform the vast majority of these services at the customers’ facilities. Customers use ES’s employees to provide additional capabilities in times of expansion and change and to work on projects requiring specialized skills. At the end of the project, ES assigns the employees to another project for the customer, assigns the employees to perform services for another customer or terminates the employment of the employees.

This segment’s highest-value staffing service is customized managed staffing solutions, under which ES oversees the customer’s entire contract staffing needs as well as certain human resource functions required to manage the customer’s contract workforce. In these instances, ES frequently establishes on-site offices at one or more of the customer’s facilities, provides staffing and links that office into the segment’s business systems. If desired by the customer, managed staffing services utilize web-based technology to help accelerate and streamline the procurement, management and supervision of contract

3

employees. ES is responsible for administrative matters, benefits and employment taxes for these temporary employees.

ES also provides permanent placement services to meet the needs of its customers. Customers provide a position specification to ES, and candidates are identified through traditional advertising, the Company’s website, networking, public job boards or targeted recruiting. ES has developed professional recruitment outsourcing (“PRO”) services to manage a customer’s entire permanent recruitment process. PRO services provide domestic and multi-national customers with a single source of professional and technical permanent placements across an entire organization. ES also offers assessment services to study a customer’s permanent placement hiring processes and provides recommendations to improve critical hiring metrics. Those metrics include time to hire, cost to hire and quality of hired candidates.

Pricing

ES generally prices its project outsourcing services using either a mark-up or a multiplier of its employees’ hourly rates of pay or bill rates. Contracts generally do not obligate the customer to pay for any fixed number of hours. To a lesser extent, ES prices these services on a fixed-price basis. For the majority of its temporary and managed staffing contracts, ES determines the pricing based on either mark-ups of its employees’ hourly rates of pay or bill rates. Contracts generally do not obligate the customer to pay for any fixed number of hours. Generally, the customer has the right to terminate the project outsourcing or staffing contract on short notice. ES maintains the right to terminate its employees at will.

Permanent placement revenues are contingent upon filling an assigned position. If the customer hires the candidate, ES receives a fee based upon an agreed-upon rate, which generally amounts to a percentage of the candidate’s first-year compensation.

Customers typically invite several companies to bid for contracts, which the Company believes are awarded primarily on the basis of prior performance, reputation, value-added services, technological capability and price. Customers frequently grant multi-vendor contracts.

All pricing is subject to negotiation and agreement with the customer.

Customers / Markets

ES’s customers are primarily large, multinational corporations, spanning several industries. P&I customers are in the oil, gas, refining, alternative energy, power generation and energy transmission, nuclear, chemicals, heavy manufacturing, pharmaceutical, bio-pharmaceutical and regulated medical service industries. Government Services customers are in the defense industry. Aerospace customers are in the commercial and military aviation industries. Business under government contracts, which may be terminated by the government forconvenience at any time, represented approximately 18% of ES’s total segment revenues in 2008, mostly in the Government Services vertical.

ES’s management conducts business development activities to identify opportunities in specific vertical markets and geographical areas. Business development professionals identify the potential markets for services and develop these markets through personal contact with existing and prospective customers, as well as other business and trade contacts. The segment’s operating management seeks to stay abreast of emerging demand for services and expands or redirects their efforts to take advantage of potential business in either established or new marketing areas.

Management Recruiters International (“MRI”)

MRI is a global franchisor that does business as MRINetwork® and provides the use of its trademarks, business systems and training and support services to its franchisees to enable them to engage in the search and recruitment of managerial, professional, executive, administrative and technical personnel for employment by their customers. MRI brand names include Management Recruiters®, Sales Consultants®, CompuSearch® and OfficeMates 5®. MRI’s trademarks provide value by distinguishing its services from those of its competitors, being connected to its successful service offering and providing MRI with the legal ability to prevent unauthorized use of its brands. The trademarks have indefinite lives. MRI also provides training and back-office services to enable franchisees to provide temporary contract staffing services to their customers.

As of December 31, 2008, MRI had approximately 790 franchised offices in the US and two master franchises, one covering the Japanese market and one covering the rest of the international markets. In April 2006, MRI sold an international master franchise to MRI Worldwide Network, Limited (“Worldwide”), whereby MRI assigned the rights to all of its existing international franchise agreements as well as the right to enter into any new franchise agreements outside the US, with the exception of existing or future franchises in Japan. The Company entered into a master franchise agreement for the Japanese market in 2004. On January 22, 2009, the Company terminated its master franchise agreement with MRI Worldwide Network, Limited and had assigned to it the benefit of the franchise agreements of MRI Worldwide Network, Limited’s sub-franchisees. Subsequently, the Company has been operating the business. MRI believes that the international marketplace provides opportunity for franchise expansion and the potential for franchise sales and royalty revenue flows. There are approximately 150 franchised offices in 39 countries throughout the world. MRI reported less than 1% of its total revenue from sources outside the US in 2008.

4

Services

MRI provides training and administrative support primarily from offices in Philadelphia, Pennsylvania and Cleveland, Ohio for domestic franchise operations and in the UK and Japan for the international franchise operations. The broad geographic scope of operations and underlying support and related systems enables franchisees to provide their customers with global permanent placement services through a worldwide inter-office referral network.

Under a typical MRI franchise agreement, the franchisee is entitled to the use of MRI’s intellectual property, such as trademarks and trade names, as well as ongoing field service and public relations support, training and vendor purchasing programs. Franchisees also have access to MRI’s extensive performance development curriculum, which is designed specifically for the recruitment industry, and an inter-office referral network that provides franchisees with a searchable database of assignments and candidates to facilitate office cooperation in search and recruiting activities. MRI does not control the business operations of its franchisees.

In conjunction with MRI, franchisees can also offer professional and administrative temporary staffing services to their customers. Franchisees are responsible for selling these services to their customers and for recruiting the temporary personnel. MRI performs payroll services, billing and collection functions for the franchisees. The franchisee receives a portion of the gross profit generated from the temporary staffing service accounts.

Pricing

Ongoing royalties and initial franchise fees are key components of MRI’s revenues. MRI receives ongoing royalty fees based on a contractual percentage of the franchisee’s permanent placement service fees and any other revenue collected. New franchise agreements generally have a term of 10 years. Individual franchises and international master franchises may be acquired by qualified candidates both in the US and internationally. In 2008, new franchisees located in the US paid an initial fee of approximately $100,000 and MRI was entitled to receive a portion of the initial fee paid by new subfranchisees located outside the US. Beginning in 2009, MRI implemented a new pricing structure with an initial fee of approximately $40,000, a total service fee, payable monthly for the first twelve months of operation, totaling $24,000 and a revised royalty rate schedule.

For the majority of its professional and administrative temporary staffing services, pricing is based on mark-ups of the hourly rates payable to the temporary personnel. Arrangements generally do not obligate the customer to pay for any fixed number of hours. Generally, the customer has the right to terminate the arrangement on short notice.

Customers / Markets

MRI’s primary objective is to provide valuable trademarks and business systems, as well as superior service, training, supportand ancillary services to its franchisees, to enable them to be successful in their businesses. Its secondary objective is to sell new franchises and renew existing franchises. New franchisees have been brought into the MRI network primarily on a referral basis. The ability of MRI’s franchisees to compete successfully with other contingent recruitment firms is important to this segment’s changes in revenue. MRI’s business is not dependent on any single franchisee.

CDI AndersElite (“Anders”)

Anders provides contract and permanent placement candidates to customers in the infrastructure environment seeking staff in building, construction and related professional services through a network of Company offices. The Company maintains offices in the UK and Australia, and many candidates that Anders places in the UK are recruited from Australia and New Zealand. Customer disciplines include architecture, building services, rail, commercial and industrial construction, consulting engineering, facilities management, interior design, surveying and town planning projects in both private and government-funded capital infrastructure investments. In 2008, Anders generated approximately 3% of its total revenue from its Australian operations.

Services

Anders provides temporary workers at customer jobsites to work on projects. Anders contracts for the temporary workers’ services either with the individual workers directly or with a limited company that employs the worker. In the case of individual workers, Anders is responsible for related tax deductions and national insurance contributions, whereas in the case of limited company workers, the limited company employer is responsible for such deductions and contributions. The customer has supervisory control and responsibility for the performance of the temporary workers. The period of assignment depends on the customer’s need for the individual worker’s skills and can range up to many months. The average duration ranges from 12 to 14 weeks. At the end of the project, Anders seeks to find the workers new assignments, or terminates the relationship with the workers.

Additionally, Anders recruits candidates to meet the permanent placement requirements of its customers. Typically customers provide a candidate specification to Anders and Anders in turn recruits the candidate, primarily through the Company’s website, external candidate databases or referrals.

Pricing

Anders determines its pricing for the supply of temporary workers based on mark-ups of the hourly rates payable to the temporary workers. Pricing is subject to negotiation and agreement with the customer. Arrangements with the customer generally do not obligate the customer to pay for any fixed number of hours. Permanent placement revenues are con-

5

tingent upon filling an assigned position. If the customer hires the candidate, Anders receives a fee equal to a percentage of the candidate’s first-year compensation.

Customers / Markets

Anders provides services to national and regional UK-based customers that operate within the public and private sectors. These customers span the industrial, commercial, government and defense, housing and rail industries. The service industries in which Anders competes are highly competitive and are subject to strong pricing pressures from customers and competition.

The segment’s operating results are affected by the seasonality of its customers’ businesses. This seasonality is due to weather and daylight limitations, as well as governmental budget constraints. Demand for Anders’ staffing services is generally lower in the first and fourth quarters of the calendar year and increases during the second and third quarters. Anders provides services to the government sector. Business under government contracts, which may be terminated by the government for convenience at any time, represented approximately 23% of Anders total segment revenues in 2008.

CDI Information Technology Solutions (“ITS”)

ITS provides a variety of information technology (“IT”) related services to its customers, which are primarily Fortune 1000 customers with high volume information technology requirements and/or the need to augment their own staff on a flexible basis. Services include staffing augmentation, permanent placement, outsourcing (both on-site and off-site) and consulting.

Services

ITS provides three types of services to key functions.

| | Ÿ | | IT staffing - To provide IT specialists to assist in the completion of special projects or to address peak seasonal, project or business cycle demands through the addition of contract IT professionals or through a managed staffing solution. |

| | Ÿ | | IT outsourcing - To improve process management of complex or labor-intensive IT functions such as testing and quality assurance, Help Desk operations and other business application services. |

| | Ÿ | | IT consulting - To provide subject matter expertise in selected IT domains, improve IT process efficiency, reduce implementation time and obtain knowledgeable assessments from the Company’s subject matter experts. |

IT outsourcing and IT consulting provide quality assurance management and testing, application development and maintenance, program, portfolio and project management services, service desk application and infrastructure support, IT riskmanagement services and IT security services. In providing IT outsourcing services, this segment usually provides its own employees to the customer’s technical department and manages and monitors the results of the department. In most instances, the managed department is located on-site at the customer’s premises, but in some cases the customer may prefer an off-site location. In this case, the segment may maintain a stand-alone operation. ITS performs these engagements under contracts that span from several months to more than a year in duration.

IT staffing provides skilled professionals to work on a temporary basis on customer projects at their facilities. The customer’s need for the individual employee’s skills dictates the period of assignment. The average duration of an assignment is approximately six to nine months. At the end of the assignment, ITS assigns the employees to perform services for another customer or terminates the employment of the employees.

Additionally, IT permanent placement recruits candidates to meet the permanent placement requirements of its customers. Typically customers provide a candidate specification to ITS. The candidate is then found primarily through the Company’s website, a candidate database or a referral program.

Pricing

For the majority of its IT staffing augmentation contracts, ITS determines the pricing based on bill rates or mark-ups of its employees’ hourly rates of pay. Contracts generally do not obligate the customer to pay for any fixed number of hours. Generally, the customer has the right to terminate the contract on short notice. ITS maintains the right to terminate its employees at will.

Permanent placement revenues are contingent upon filling an assigned position. If the customer hires the candidate, ITS receives a fee based upon an agreed-upon rate, which generally amounts to a percentage of the candidate’s first-year compensation.

ITS generally prices its project outsourcing services using a mark-up or a multiplier of its employees’ hourly rates of pay or bill rates. Contracts generally do not obligate the customer to pay for any fixed number of hours. ITS also prices these services, to a lesser extent, on a fixed-price basis.

Customers typically invite several companies to bid for contracts, which the Company believes are awarded primarily on the basis of prior performance, value-added services, technological capability and price. Many times customers grant multi-vendor contracts.

Customers / Markets

ITS customers are primarily Fortune 1000 companies. Major customers are predominantly in the technology, auto and financial services industries. ITS also has smaller projects with customers in a variety of other industries.

6

ITS seeks to provide incremental services to existing customers. ITS also grows its business in its major markets by developing business and trade contacts with prospective customers. The market demand for ITS’s services is heavily dependent upon the pace of technology change and the changes in business requirements and practices of its customers. The IT services industry is highly competitive and is subject to strong pricing pressures from customers and competition.

The segment’s operating results are affected by the seasonality of its customers’ businesses. This seasonality is due to customers’ vacation and holiday schedules. Demand for ITS’s staffing and project outsourcing services is typically subject to seasonal slowdown at the end of the fourth quarter and beginning of the first quarter of each year, as well as a modest downturn during heavy vacation periods in the third quarter of each year. Revenue from one customer, International Business Machines Corporation, accounted for 48% of total segment revenue in 2008.

Other Information

Competition

The Company competes in global, national, regional and local markets with numerous engineering and information technology outsourcing companies and with temporary staffing and permanent placement firms. All segments of the Company’s operations face competition in attracting both customers and high-quality specialized employment candidates. The temporary and permanent placement businesses are very competitive and highly fragmented, with limited barriers to entry into the market. In many areas, the local companies are the strongest competitors. Price competition among companies in CDI’s staffing services industry and pricing pressures from customers are significant. The trend of customers who consolidate their purchases of engineering and IT outsourcing and staffing services with a single provider or with a small number of providers continues. This trend to consolidate purchases may make it more difficult for the Company to obtain or retain customers. The Company believes it derives a competitive advantage from its lengthy experience with and long-standing commitment to the industries it serves, long-term relationships with its customers, technical capabilities, national presence, and various marketing activities.

In 2008, CDI’s largest competitors by segment included:

| | Ÿ | | ES - Aerotek, Inc., Belcan Corporation, Day & Zimmerman, Inc., Gibbs and Cox, Inc., Jacobs Engineering Group Inc. and The Shaw Group Inc. |

| | Ÿ | | MRI - Heidrick & Struggles International, Inc., Korn/Ferry International, Robert Half International Inc., and SRA International, Inc. |

| | Ÿ | | ITS - Aerotek, Inc., CIBER, Inc., Computer Task Group, Inc., MPS Group, Inc. and Volt Information Sciences, Inc. |

Financial Information about Segments

Please see Note 21—Reporting Segments, in the notes to the consolidated financial statements, for further information about reporting segments.

Safeguards—Business, Disaster and Contingency Planning

CDI has a number of safeguards to protect the Company from various system-related risks. Given the significant amount of data generated in the Company’s key processes, including customer related projects, recruiting, payroll, and customer invoicing, CDI has implemented fault tolerant processing capability within the Company’s primary data center. This mitigates the risks related to hardware failure. Additionally, CDI has contracted with a third-party provider to restore its primary data center operations in the event of a disruption. Finally, the Company maintains site disaster plans for a majority of its operating offices as well as maintaining data back-up requirements throughout the Company.

Employees

As of December 31, 2008, CDI had approximately 1,200 staff employees. In addition, CDI had approximately 9,200 employees and workers engaged as billable personnel. The number of billable employees and workers varies in relation to the number of projects and assignments in progress at any particular time.

Access to Company Information

CDI makes available, free of charge, through its website or by responding to requests addressed to the Company’s Vice President of Corporate Communications, its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports filed by the Company with the Securities and Exchange Commission (“SEC”) pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended. These reports are available as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. CDI’s website address ishttp://www.cdicorp.com. CDI posts its Audit Committee, Compensation Committee, Finance Committee, Executive Committee and Governance and Nominating Committee charters, Corporate Governance Principles and Code of Conduct on the Company’s website. The information contained on the Company’s website, or on other websites linked to the Company’s website, is not part of this document. The public may also read and copy any materials the Company has filed with the SEC at the SEC’s Public Reference Room located at 100 F Street N.E., Washington, D.C., 20549. In order to obtain information about the operation of the Public Reference Room, a person may call the SEC at 1-800-732-0330. The SEC also maintains a website on the Internet that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The SEC’s website is http://www.sec.gov.

7

CDI’s business involves a number of risks, many of which are beyond its control. The risks and uncertainties described below could individually or collectively have a material adverse effect on the Company’s business, assets, profitability or prospects. While these are not the only risks and uncertainties the Company faces, management believes that the more significant risks and uncertainties are as follows:

CDI’s business is heavily dependent on capital spending by customers in the industries it serves, and cuts in capital spending and economic downturns may result in the loss of revenues and profitability.

The demand for the Company’s services is highly dependent upon the level of capital spending by the Company’s customers, especially in the ES segment. The pace of customer capital spending programs, new product launches and similar activities have a direct impact on the need for project outsourcing and both temporary and permanent employees. There have been and may continue to be delays and cancellations of projects due to potential credit constraints and weak economic conditions experienced by CDI’s customers, which has and could continue to adversely affect the Company’s revenue stream. Further weakening of the economic condition of the US or any of the foreign countries in which the Company does business, or in any specific industry served, could have a further negative effect on the Company’s business, financial condition, cash flows or results of operations.

Unfavorable economic conditions could negatively affect CDI’s business.

As widely reported, financial markets in the US, Europe and Asia have been experiencing extreme disruption in recent months, including severely tightened credit availability, increases in unemployment and general declines in the US economy and economies around the world. Given the current economic conditions, many companies may choose to decrease their spending on staffing, both permanent and temporary, which in turn could have a material and adverse effect on the Company’s financial and operating performance.

The Anders and MRI segments earn revenue when qualified candidates accept open positions held by potential employers, generally corporate entities. These corporate entities may cut back on hiring in efforts to cut costs. In addition, as a result of the economic downturn, candidates may be less likely to take the risk of seeking new employment, creating a lack of qualified candidates. Both of these could have a material and adverse effect on the Company’s financial and operating performance.

In addition, the MRI segment derives royalty revenue from franchisees. If persons hoping to start MRI franchises are unable to obtain credit, they could be prevented from doing so, whichcould impede CDI’s growth in that sector. If current franchisees are unable to obtain credit, it could cause downsizing in their organizations, in turn negatively affecting the Company’s royalty revenue, potentially having a material and adverse effect on the Company’s financial and operating performance.

The Company’s continued success is dependent on its ability to hire and retain qualified employees, both management and billable personnel. The loss of key personnel could have a material adverse effect on the Company’s business.

CDI depends upon its ability to attract qualified personnel who possess the skills and experience required by its customers and to successfully bid for new customer projects. CDI must continually evaluate its base of available qualified personnel to keep pace with changing customer needs and emerging technologies. Competition for individuals with proven professional or technical skills always exists, and the demand for such individuals (particularly in certain engineering disciplines and geographic areas) is expected to remain strong in the foreseeable future. There is always uncertainty as to whether qualified personnel will continue to be available to CDI in sufficient numbers and on terms of employment acceptable to CDI.

The Company’s operations also depend on the continued efforts of its executives and senior management. The loss of key members of CDI’s management team may cause a significant disruption to the Company’s business. CDI also depends on the performance and productivity of its local managers and sales and recruiting personnel. The Company’s ability to attract and retain new business is significantly affected by local relationships and the quality of service rendered. The loss of key managers and field personnel may also jeopardize existing customer relationships, which could cause revenues to decline.

The Company may experience adverse consequences arising out of an ongoing investigation by the UK Office of Fair Trading.

In June 2006, the United Kingdom’s Office of Fair Trading (“OFT”) opened an investigation into alleged anti-competitive behavior by Anders and a number of its competitors in the UK construction recruitment industry. The allegations being investigated include, among others, the competitors agreeing to minimum fees in their contracts with UK intermediary recruitment companies and declining to work with one particular UK intermediary recruitment company. The Company has fully cooperated with the OFT in the investigation under the OFT’s corporate leniency program. On October 21, 2008, the OFT issued a Statement of Objections in which the OFT proposes to make a finding that Anders violated the UK Competition Act of 1998. In response to the Statement of Objections, on January 16, 2009 the Company submitted written representations to the OFT and on February 18, 2009 the Company made an oral presentation to the OFT. Although the Statement of Objections does not propose a specific fine, based on the contents of the Statement of Objections, the Company continues to believe that a fine will be imposed and that the amount of such

8

fine could be material. The Company believes it is reasonably possible that the OFT will levy a fine in the near term. The Company does not believe the Statement of Objections provides sufficient new information for the Company to determine, with any reliability, the amount of the fine or an estimated range of the fine, nor does the document make it clear when the Company might be able to reach a reliable estimate. However, a significant fine could have a material adverse effect on the Company’s financial position and results of operations. The Company has not made any provision for any fine or other liabilities relating to this matter in the Company’s consolidated financial statements as of December 31, 2008.

It is also possible that third-party civil lawsuits may be filed against Anders in connection with this matter. Anders has incurred legal fees and could incur significant incremental legal fees in connection with the OFT investigation and in defending any third-party lawsuits. Furthermore, this matter and the related publicity could materially and adversely affect the reputation of Anders and the Company. Senior management at Anders and the Company has devoted and will likely need to continue to devote a significant amount of time with regard to this matter, which could distract them from day-to-day business operations.

CDI is engaged in highly competitive businesses. Pricing pressures and increasing consolidation of purchasing by its customers could reduce the Company’s market share and profits.

The engineering, IT and professional staffing businesses are highly competitive and fragmented, with limited barriers to entry for staffing services. CDI competes in global, national, regional and local markets with numerous engineering and IT outsourcing companies and with temporary staffing and permanent placement firms. Price competition among companies in CDI’s industry and pricing pressures from customers are significant. The number of customers which consolidate their purchases of engineering and IT outsourcing and staffing services with a single provider or with a small number of providers has continued to rise. This trend to consolidate purchases may make it more difficult for the Company to obtain or retain customers in the future. The Company could also face the risk that certain customers may decide to provide similar services internally. Additionally, pricing pressures have intensified as customers have continued to competitively bid new contracts and seek price reductions on existing contracts. This trend is expected to continue for the foreseeable future, which could limit CDI’s ability to maintain or increase its market share or profitability.

The Company’s revenues are subject to uncertainties. CDI’s results of operations depend on, among other factors, new contract awards, and the selection process and timing for performing these contracts are subject to contingencies beyond the Company’s control. In addition, the Company’s customer contracts and arrangements may be adjusted, cancelled or suspended by its customers, in some cases on short notice.

A significant portion of revenues is directly or indirectly derived from awards of long-term contracts. It is difficult to predict whether and when the Company will receive such awards due to the lengthy and complex bidding and selection process, which is affected by a number of factors, such as market conditions, financing arrangements and governmental approvals. Because a meaningful portion of revenues is generated from these contracts, the Company’s results of operations and cash flows can fluctuate from quarter to quarter depending on the timing of contract awards.

Furthermore, substantially all of the Company’s contracts are subject to cancellation or termination at the discretion of the customer. In addition, project contracts are generally subject to changes in the scope of services to be provided. CDI, particularly in the Government Services vertical of its ES segment, is a party to prime contracts and subcontracts involving the federal government. Contracts with the US and other governments and their respective agencies are subject to particular uncertainties, restrictions and regulations. The US Government is under no obligation to maintain funding at any specific level, and funds for a program can be eliminated. Accordingly, the Company does not have a guaranteed backlog of business.

The failure of customers to pay amounts owed to CDI could cause the Company to experience significant losses.

Accounts receivable represent the largest asset on CDI’s balance sheet. While the Company takes steps to evaluate and manage the credit risks relating to its customers, economic downturns or events like those that are currently being experienced, could affect particular customers’ or industries’ ability to pay, which could reduce CDI’s ability to collect all amounts due from customers. In particular, the chemical and auto industries have been severely impacted by the global economic downturn in 2008 and the Company’s December 31, 2008 accounts receivable balance related to customers in these industries totaled approximately $13 million. If conditions continue to decline in these two industries, customers may have difficulty in paying their balances. In addition, in the staffing business, there are sometimes intermediaries between CDI and the customer, and therefore financial problems involving the intermediary company could pose credit risks to CDI.

CDI faces competition from global outsourcing companies, which may result in a loss of market share and reduced profitability.

There is increasing pressure from customers on their suppliers to outsource certain areas of their businesses to low-cost offshore

9

locations. Many engineering and IT outsourcing and staffing companies already have or are seeking an offshore solution to support their technology and business process functions, and as a result, a significant amount of domestic technology and engineering project work may utilize offshore capabilities as alternatives to domestic resources. CDI has established lower cost outsourcing centers and has partnered with offshore companies to provide additional lower cost options to its customers. Conducting business through offshore arrangements entails additional compliance and regulatory issues and may result in additional costs. CDI’s partnering arrangements are subject to the Company’s ability to maintain good working relationships with its foreign partners and on its partners’ ability to fulfill their obligations under CDI’s agreements with them. Changes in the supply and demand for offshore personnel with the training to perform the IT and engineering services sought by CDI’s customers, as well as other factors affecting offshore labor costs, could raise CDI’s costs which would put pressure on its margins. Also, other offshore solution providers could develop direct relationships with CDI’s customers resulting in a significant loss of the Company’s market share and revenue.

Foreign currency fluctuations, weak foreign economies and unfavorable political developments in connection with CDI’s international operations could seriously harm its financial condition.

CDI’s international operations are important to its business and the Company expects that it will continue to account for an increasing portion of its total revenues. At a minimum, its reported financial condition and results of operations are exposed to the effects (both positive and negative) that fluctuating exchange rates have on the process of translating the financial statements of international operations, which are denominated in currencies other than the US dollar, into the US dollar. CDI’s exposure to foreign currency fluctuations relates primarily to operations denominated in British pounds sterling, Canadian dollars and Australian dollars. Exchange rate fluctuations impact the US dollar value of reported earnings derived from these foreign operations as well as the Company’s investment in the net assets related to these operations. The Company has and may continue to engage in hedging activities with respect to certain of its foreign operations.

The Company’s international operations are subject to a variety of other risks, including, but not limited to, the following:

| | Ÿ | | Recessions in foreign economies and the impact on costs of doing business in those countries; |

| | Ÿ | | Difficulties in staffing and managing foreign operations; |

| | Ÿ | | Changes in regulatory requirements; |

| | Ÿ | | The adoption of new, and the expansion of existing, trade restrictions and the failure to comply with US export control laws; |

| | Ÿ | | The lack of well-developed legal systems and less established or traditional business practices in some countries, which could make it difficult for CDI to enforce its contractual rights; |

| | Ÿ | | Exposure to liability under the Foreign Corrupt Practices Act; |

| | Ÿ | | Social, political and economic instability, including risks of loss due to civil strife, acts of war, insurrection and terrorism; |

| | Ÿ | | Limitations on the movement of cash and the ability to repatriate foreign earnings; and |

| | Ÿ | | Logistical and communications challenges. |

CDI’s projects may encounter difficulties that result in additional costs, reductions in revenues, claims, disputes and the payment of damages.

CDI’s projects often involve complex design and engineering, significant procurement of equipment and supplies and broad construction management. The Company may encounter difficulties in the design or engineering, equipment and supply delivery, schedule changes and other factors, some of which are beyond its control, that impact its ability to complete the project in accordance with the original delivery schedule. In addition, the Company often relies on third-party equipment manufacturers as well as other third-party subcontractors to assist with the completion of its contracts. Any delay by these equipment manufacturers or subcontractors to complete their respective portions of a project, or any failure by subcontractors to satisfactorily complete their respective portions of a project, as well as other factors beyond the Company’s control, may result in delays in the overall progress of such project, cause CDI to incur additional costs or both. These delays and additional costs may be substantial, and the Company may be required to compensate the customer for these delays. While CDI may recover these additional costs from the responsible vendor, subcontractor or other third-party, the Company may not be able to recover all of these costs in all circumstances.

In addition, some contracts may require CDI’s customers to provide it with design or engineering information or with equipment or materials to be used on the project. In some cases, the customer may provide CDI with deficient design or engineering information or equipment or may provide the information or equipment to it later than required by the project schedule. The customer may also determine, after commencement of the project, to change various elements of the project. CDI is subject to the risk that it might be unable to obtain, through negotiation, arbitration, litigation or otherwise, adequate amounts to compensate it for the additional work or expenses incurred due to customer requested change orders or failure by the customer to timely provide required items. A failure to obtain adequate compensation for these matters could require CDI to record an adjustment to amounts of revenues

10

and gross profit that were recognized in prior periods. Any such adjustments could have a material adverse effect on the Company’s results of operations and financial condition.

The Company bears the risk of cost overruns in fixed-price contracts.

CDI sometimes enters into fixed-price contracts with customers, primarily for engineering project services. Revenue recognized under fixed-price contracts accounts for less than 5% of consolidated revenue in each of the past three years. Under these fixed-price contracts, prices are established based on cost and scheduling estimates, which in turn are based in part on assumptions about the prices and availability of skilled personnel, equipment, and materials. If the Company’s price estimates for a particular project prove to be inaccurate, then cost overruns may occur, and CDI could experience reduced profits or a loss for that project and the Company’s reputation could be harmed. Cost overruns may also be caused by changes in the scope of the project after the contract has been entered into or by a failure of the parties to adequately define and agree upon the entire scope of the project at inception. In those cases, there may be disputes between the parties over who should pay for the cost overruns. The Company will attempt to negotiate change orders to recover the additional costs, but there can be no assurance that the Company will be successful in its negotiations with its customers. In general, fixed-price contracts can offer greater profit potential but also entail more inherent risk—both in terms of possible financial losses and the potential for significant disputes with customers—than contracts containing pricing on a time-and-materials basis.

The Company’s project outsourcing services expose it to potential professional liability, product liability, warranty and other claims.

In connection with certain of its project outsourcing services, the Company engineers and performs services in various types of facilities, including major industrial facilities, where accidents or system failures can be disastrous. Any catastrophic occurrences in excess of insurance limits relating to locations or products which are engineered by the Company or locations where its services are performed could result in significant professional liability, product liability, warranty and other claims against the Company.

Furthermore, the project outsourcing services CDI provides expose it to additional risks including equipment failures, personal injuries, property damage and unforeseen engineering, architectural and environmental problems, each of which could significantly impact the Company’s performance and materially impact its financial statements.

Changes in government regulations could result in loss of business and/or increased costs.

CDI’s business is subject to regulation or licensing in many states and in certain foreign countries. There can be no assurance the Company will be able to continue to obtain all necessary licenses or approvals or that the cost of compliance will not prove to be material in the future. Any inability to comply with government regulation or licensing requirements, or increase in the cost of compliance, could materially and adversely impact the Company. New government regulations could disrupt or reduce existing business done by the Company, though it can also provide new business opportunities. Changes in government regulations could result in the imposition of new or additional benefits, licensing or tax requirements, thereby increasing CDI’s costs of doing business. There can be no assurance that CDI would be able to increase the fees charged to its customers in a timely manner or in a sufficient amount to cover increased costs as a result of any of the foregoing. Staffing services entail employing individuals on a temporary basis and placing such individuals in customers’ workplaces. Therefore, increased government regulation of the workplace or of the employer-employee relationship could materially and adversely impact the Company.

The outcome of pending and future claims and litigation could have a material adverse effect on the Company’s business.

From time to time, various types of legal claims arise in connection with the ordinary course of CDI’s business. Employees of the Company may make a variety of claims including workplace injury claims and employment-related claims such as discrimination, harassment, and wage and hour claims. Since the Company’s staffing business involves employing individuals on a temporary basis and placing them in customer workplaces where CDI has limited ability to control the workplace environment, these types of claims may arise more frequently in those business operations. The Company’s customers may make claims based on the Company’s alleged failure to perform in accordance with contract requirements. Since the Company’s project business often involves responsibility to produce specified deliverables, these types of claims may arise more frequently in those business operations. Customers in the staffing business may allege claims based on the conduct of staffing employees assigned to the customer’s worksite. Customers and subcontractors may make claims alleging the Company’s failure to abide by certain contract provisions. In addition, the Company is subject to possible government claims or fines for violations of various laws. See Note 15—Legal Proceedings and Claims, in the notes to the consolidated financial statements, for more information.

CDI has significant payroll-related costs, such as workers’ compensation, unemployment taxes and health benefits, which are subject to increases caused by government regulation and other factors, and such increases could reduce its profits.

In conducting its business, CDI pays a number of payroll and related costs and expenses, including unemployment taxes, workers’ compensation and medical insurance for its personnel. Unemployment insurance premiums paid by employers typically

11

increase during periods of increased levels of unemployment. Workers’ compensation costs may increase in the future if states raise benefit levels and liberalize allowable claims. The Company self-insures a portion of the exposure for losses related to workers’ compensation. The Company has established reserves for workers’ compensation claims based on historical loss statistics and periodic independent actuarial valuations. While management believes that its assumptions and estimates are appropriate, significant differences in actual experience or significant changes in assumptions may materially and adversely affect the Company’s future financial results. CDI’s future earnings could also be materially and adversely affected if it is not able to increase the fees charged to customers to absorb the increased costs related to unemployment insurance, workers’ compensation and medical benefits. In addition, its future earnings could also be materially and adversely affected by future cost increases.

Estimates of the Company’s income tax liabilities are subject to various uncertainties and actual results could vary significantly from these estimates.

When financial statements are prepared, CDI estimates its income tax liabilities with respect to the various jurisdictions in which the Company does business. Significant judgment is required in determining the provision for income tax liabilities in the financial statements and in forecasting CDI’s effective income tax rate in a given period. The provision for income taxes and tax liability in the future could be materially and adversely affected by numerous factors, including changes in tax laws, regulations or accounting principles, changes in the valuation of deferred tax assets and liabilities and audits by taxing authorities.

Future acquisitions may not be successful.

The Company may selectively pursue acquisitions as an element of its growth strategy, but it can not provide assurances that it will be able to locate suitable acquisitions or that it will be able to consummate any such transactions on terms and conditions acceptable to the Company, or that such transactions will be successful. Acquisitions involve a number of risks, including the diversion of management’s attention from its existing operations, the failure to retain key personnel or customers of an acquired business, the failure to realize anticipated benefits, such as cost savings and revenue enhancements, the potentially substantial transaction costs associated with acquisitions, the assumption of unknown liabilities of the acquired business, and the inability to successfully integrate the business. There can be no assurance that any future acquired businesses will generate anticipated revenues or earnings.

Disasters could interfere with CDI’s ability to operate its business. Certain of the Company’s customers operate in areas that may be impacted by severe weather conditions.

Various types of natural or man-made disasters could interfere with the Company’s continued ability to operate its businessnormally. For example, the Company’s ability to protect its data centers and information systems against damage from fire, power loss, telecommunications failure and other disasters is critical. In order to provide many of its services, CDI must be able to store, retrieve, process and manage large databases and periodically expand and upgrade its capabilities. Any damage to the Company’s data centers or any failure of the Company’s telecommunication links that interrupts its operations or results in an inadvertent loss of data could adversely affect CDI’s ability to meet its customers’ needs and their confidence in utilizing CDI for future services. While the Company has developed various backup plans and disaster recovery plans, there can be no assurance that the Company would be able to continue to operate its business smoothly in the face of certain natural or man-made disasters. Such business interruptions could materially and adversely affect CDI’s financial results and future prospects.

The Company services the oil, gas and chemical industries, each of which has a significant concentration of activities in the Gulf Coast of the US. This area has been impacted by several hurricanes in the past, and could be further impacted by severe weather in the future, negatively impacting CDI’s customers and its ability to serve them.

The Company relies on information systems in its operations. Failure to protect these systems against security breaches could materially and adversely affect CDI’s business and results of operations. Additionally, if these systems fail or become unavailable for any significant period of time, the Company’s business could be harmed.

The efficient operation of CDI’s business is dependent on computer hardware and software systems. Information systems are vulnerable to security breaches by computer hackers and cyber terrorists. The Company relies on industry accepted security measures and technology to securely maintain confidential and proprietary information maintained on its information systems. However, these measures and technology may not always be adequate to properly prevent security breaches. In addition, the unavailability of the information systems or the failure of these systems to perform as anticipated for any reason could disrupt CDI’s business and could result in decreased performance and increased overhead costs, causing the Company’s business and results of operations to suffer. Any significant interruption or failure of CDI’s information systems or any significant breach of security could adversely affect its business and results of operations.

CDI relies on outside suppliers to perform certain administrative services.

CDI outsources certain data processing, payroll and other administrative functions to companies that specialize in performing those services. The failure of such outside service providers to adequately perform such services could have a material adverse effect on CDI’s business and operations.

12

If CDI fails to maintain an effective system of internal controls over financial reporting, it may not be able to accurately report its financial results or prevent fraud. As a result, investors could lose confidence in the Company’s financial reporting, which would harm its business and the trading price of its stock.

Effective internal controls are necessary for CDI to provide reliable financial reports and prevent fraud. If the Company cannot provide reliable financial reports or prevent fraud, its operating results could be harmed. CDI devotes significant attention to establishing and maintaining effective internal controls. Any failure to implement required new or improved controls or difficulties encountered in their implementation could affect CDI’s operating results or cause it to fail to meet reporting obligations in future periods. Ineffective internal controls could also cause investors to lose confidence in the Company’s reported financial information, which could have a negative effect on the market price of CDI stock.

The Company may not be able to obtain the insurance coverages necessary to manage its risks.

The Company relies on insurance to help manage its risks and to limit the Company’s exposure to significant claims. The future availability and cost of such insurance is subject to market forces and CDI’s claims experience. There can be no assurance that the Company can always obtain and maintain appropriate insurance coverage, including errors and omissions insurance, in order to effectively manage the risks of its business.

A significant portion of the Company’s common stock is owned by related parties, and they could vote their shares in a way that is adverse to the interests of other shareholders.

Certain of CDI’s directors and trusts, for which some of the Company’s directors serve as trustee, own a substantial portion of the Company’s outstanding common stock. By virtue of this stock ownership, such shareholders have the power to significantly influence CDI’s affairs and are able to influence the outcome of matters required to be submitted to shareholders for approval, including the election of directors and the amendment of the Company’s Articles of Incorporation or Bylaws. Such shareholders could exercise influence over the Company in a manner adverse to the interests of CDI’s other shareholders.

The Company performs certain projects through joint ventures. Participation in joint ventures exposes the Company to additional risks and uncertainties.

As is common in the industry, CDI executes certain projects jointly with other contractors through joint ventures. These arrangements expose the Company to a number of risks, including the risk that CDI’s partners may not be able to fulfill their performance obligations under the joint venture agreements and related customer contracts. There is also a risk that CDI’s partners may be incapable of providing the required financialsupport to the partnerships. Disputes can arise not only between the Company and its joint venture partners, but also between the joint ventures and the customers.

Improper disclosure of employee and customer data could result in liabilities and harm the Company’s reputation.

The Company’s business involves the use, storage and transmission of information about its billable employees, permanent placement candidates and its customers. The Company has established policies and procedures to help protect the security and privacy of this information. The Company also, from time to time, exports sensitive customer data and technical information to recipients outside the US. The Company has a policy in place that requires an analysis prior to the export of any products, software, data, technology or other information from the Company’s systems to determine if any restrictions apply to the export.

It is possible that the Company’s security controls over personal and customer data and other practices that the Company follows may not prevent the improper access to or disclosure of personally identifiable and customer information. Such disclosure could harm the Company’s reputation and subject the Company to liability under its contracts and laws that protect personal and customer data, resulting in increased costs or loss of revenue.

The inability to meet the restrictive covenants included in the Company’s credit facility agreement could cause the Company to be unable to access facility funds, or default on the facility.

The Company has a credit facility, which requires that the Company comply with specified covenants, including certain minimum and maximum ratios that must be met or not be surpassed as well as a minimum level of shareholder’s equity. If the Company were to fail to meet any of these covenants, it would be unable to borrow under the credit facility. Failure to meet these covenants could also cause harm to the Company’s reputation and stock price.

| | |

| Item 1B. | | Unresolved Staff Comments |

Not applicable.

The Company presently maintains its principal executive offices at 1717 Arch Street, Philadelphia, Pennsylvania, in approximately 29,000 square feet of leased office space under leases expiring in 2012 and 2013. The Company also maintains offices at 1801 Market Street, Philadelphia, Pennsylvania, in approximately 50,000 square feet of leased office space under a lease expiring in 2016.

13

The Company maintains significant engineering centers in Houston, Texas (9800 Centre Parkway and 9555 W. Sam Houston Parkway) in approximately 100,000 square feet of leased space under various leases expiring through 2015, and in Baton Rouge, Louisiana at 4041 Essen Lane in approximately 49,000 square feet of leased space under a lease expiring in 2012. In addition, the Company operates a shared service center and engineering center at 3200 Kanawha Turnpike, South Charleston, West Virginia in approximately 54,000 square feet of leased space under a lease expiring in 2011. The Company also maintains additional offices at 200 Public Square, Cleveland, Ohio in approximately 52,000 square feet of leased office space under a lease expiring in 2011 and at 55 Merchant Square in Cincinnati, Ohio in approximately 53,000 square feet of leased office space under a lease expiring in 2011.

Additionally each reporting segment also has numerous other active facilities and locations under operating lease agreements. Most of the leased space is devoted to sales, marketing, engineering design, and administrative and back-office functions. These facilities are leased for terms ranging from five to ten years. The Company believes that its facilities are adequate to meet its current and near term needs.

A few of the Company’s offices accommodate more than one operating segment. In such cases, square-foot usage is allocated among the segments primarily based on utilization.

| | |

| Item 3. | | Legal Proceedings |

The Company has litigation and other claims pending which have arisen in the ordinary course of business.

In June 2006, the United Kingdom’s Office of Fair Trading (“OFT”) opened an investigation into alleged anti-competitive behavior by CDI AndersElite (“Anders”) and a number of its competitors in the UK construction recruitment industry. The Company has fully cooperated with the OFT in the investigation under the OFT’s corporate leniency program. On October 21, 2008, the OFT issued a Statement of Objections in which the OFT proposes to make a finding that Anders violated the UK Competition Act of 1998. In response to the Statement of Objections, on January 16, 2009 the Company submitted written representations to the OFT and on February 18, 2009 the Company made an oral presentation to the OFT. Although the Statement of Objections does not propose a specific fine, based on the contents of the Statement of Objections, the Company continues to believe that a fine will be imposed and that the amount of such fine could be material. The Company believes it is reasonably possible that the OFT will levy a fine in the near term. The Company does not believe the Statement of Objections provides sufficient new information for the Company to determine, with any reliability, the amount of the fine or an estimated range of the fine, nor does the document make it clear when the Company might be able to reach a reliable estimate. The Company has not made any provisions for any fine or other liabilities relating to this matter in its consolidated financial statements as of December 31, 2008.

| | |

| Item 4. | | Submission of Matters to a Vote of Security Holders |

There were no matters submitted to a vote of security holders during the fourth quarter of the year covered by this report.

14

Part II

| | |

| Item 5. | | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Shares of CDI’s common stock are traded on the New York Stock Exchange under the trading symbol “CDI”. The high and low sales price per share of the Company’s common stock for each quarter during the last two years are shown in the table below (all as reported by the Wall Street Journal), together with dividend information for each period.

| | | | | | | | | |

| | | High | | Low | | Dividends |

2008 | | | | | | | | | |

First quarter | | $ | 26.56 | | $ | 18.78 | | $ | 0.13 |

Second quarter | | | 28.96 | | | 24.60 | | | 0.13 |

Third quarter | | | 28.53 | | | 15.11 | | | 0.13 |

Fourth quarter | | | 22.51 | | | 7.88 | | | 0.13 |

| | | |

2007 | | | | | | | | | |

First quarter | | $ | 30.98 | | $ | 23.80 | | $ | 0.11 |

Second quarter | | | 33.87 | | | 28.35 | | | 0.11 |

Third quarter | | | 33.37 | | | 23.34 | | | 0.11 |

Fourth quarter | | | 30.09 | | | 23.53 | | | 0.13 |

Dividends

The declaration and payment of future dividends will be at the discretion of the Company’s Board of Directors and will depend upon many factors, including the Company’s earnings, financial condition and capital requirements.

Shareholders

As of February 27, 2009, there were 434 shareholders of record of the Company’s common stock. A single record shareholder account may however represent multiple beneficial owners, including holders of shares in street name accounts. Including those multiple beneficial owners, the total number of shareholders of the Company’s common stock on February 27, 2009 was approximately 5,000. See Note 10 – Stock-Based Compensation in the notes to the consolidated financial statements, for information relating to securities authorized for issuance under the Company’s equity compensation plans.

15

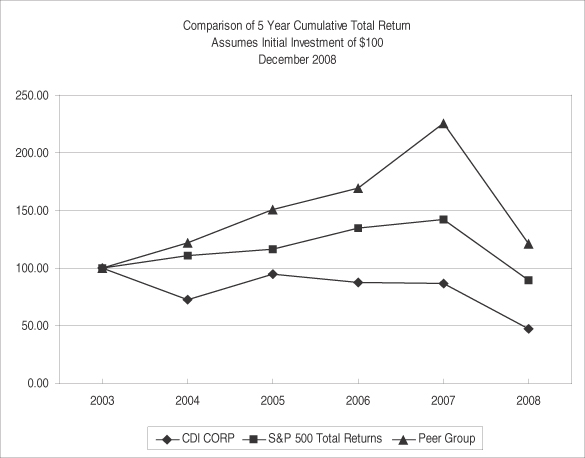

Comparative Stock Performance

The following graph sets forth the cumulative total shareholder return (assuming an investment of $100 on December 31, 2003 and the reinvestment of any dividends) for the last five fiscal years on (a) CDI stock, (b) the Standard & Poor’s (S&P) 500 Index and (c) CDI’s peer group index.

CDI’s peer group consists of the following nine companies: CIBER, Inc., Computer Task Group Inc., Heidrick & Struggles International Inc., Jacobs Engineering Group, Inc., Korn/Ferry International, MPS Group Inc., Robert Half International Inc., The Shaw Group Inc. and Volt Information Sciences Inc.

| | | | | | | | | | | | | | | | | | |

| | | Years ended December 31, |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 |

CDI Corp. | | $ | 100.00 | | $ | 72.65 | | $ | 94.81 | | $ | 87.63 | | $ | 86.73 | | $ | 47.55 |

S&P 500 Index—Total Return | | | 100.00 | | | 110.87 | | | 116.30 | | | 134.66 | | | 142.07 | | | 89.51 |

Peer Group | | | 100.00 | | | 121.92 | | | 150.62 | | | 169.11 | | | 225.27 | | | 121.10 |

16

Issuer Purchases of Equity Securities

A total of 1,489,469 shares of CDI Corp. common stock were repurchased by the Company at an average price of $20.13 during the year ended December 31, 2008. As of December 31, 2008, there remained an outstanding authorization to repurchase approximately $20.0 million of outstanding stock as represented in the table below:

| | | | | | | | | | |