| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-228597-08 | ||

January 25, 2021

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,530,900,153

(Approximate Initial Mortgage Pool Balance)

$1,087,104,000

(Offered Certificates)

Benchmark 2021-B23 Mortgage Trust

As Issuing Entity

Citigroup Commercial Mortgage Securities Inc.

As Depositor

Commercial Mortgage Pass-Through Certificates, Series 2021-B23

Citi Real Estate Funding Inc.

JPMorgan Chase Bank, National Association

Goldman Sachs Mortgage Company

German American Capital Corporation

As Sponsors and Mortgage Loan Sellers

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Academy Securities, Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

| Citigroup | Goldman Sachs & Co. LLC | Deutsche Bank Securities | J.P. Morgan |

| Co-Lead Managers and Joint Bookrunners | |||

| Academy Securities | Drexel Hamilton |

| Co-Manager | Co-Manager |

| CERTIFICATE SUMMARY |

The securities offered by this structural and collateral term sheet (this “Term Sheet”) are described in greater detail in the preliminary prospectus, dated on or about January 25, 2021, included as part of our registration statement (SEC File No. 333-228597) (the “Preliminary Prospectus”). The Preliminary Prospectus contains material information that is not contained in this Term Sheet (including, without limitation, a summary of risks associated with an investment in the offered securities under the heading “Summary of Risk Factors” and a detailed discussion of such risks under the heading “Risk Factors”). The Preliminary Prospectus is available upon request from Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities, Inc. or Drexel Hamilton, LLC. This Term Sheet is subject to change.

For information regarding certain risks associated with an investment in this transaction, refer to “Summary of Risk Factors” and “Risk Factors” in the Preliminary Prospectus. Capitalized terms used but not otherwise defined in this Term Sheet have the respective meanings assigned to those terms in the Preliminary Prospectus.

The Securities May Not Be a Suitable Investment for You

The securities offered by this Term Sheet are not suitable investments for all investors. In particular, you should not purchase any class of securities unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with that class of securities. For those reasons and for the reasons set forth under the headings “Summary of Risk Factors” and “Risk Factors” in the Preliminary Prospectus, the yield to maturity of, the aggregate amount and timing of distributions on and the market value of the offered securities are subject to material variability from period to period and give rise to the potential for significant loss over the life of those securities. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered securities involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the securities. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered securities described in this Term Sheet.

The securities offered by these materials are being offered when, as and if issued. This Term Sheet is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this Term Sheet may not pertain to any securities that will actually be sold. The information contained in this Term Sheet may be based on assumptions regarding market conditions and other matters as reflected in this Term Sheet. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this Term Sheet should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this Term Sheet may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in this Term Sheet or derivatives thereof (including options). Information contained in this Term Sheet is current as of the date appearing on this Term Sheet only. Information in this Term Sheet regarding the securities and the mortgage loans backing any securities discussed in this Term Sheet supersedes all prior information regarding such securities and mortgage loans. None of Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Academy Securities, Inc. or Drexel Hamilton, LLC provides accounting, tax or legal advice.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

2

| CERTIFICATE SUMMARY |

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—General Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity and Other Aspects of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

3

| CERTIFICATE SUMMARY |

OFFERED CERTIFICATES

Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| Class A-1 | AAA(sf) / AAAsf / AAA(sf) | $21,244,000 | 30.000% | % | (6) | 2.33 | 3/21 – 4/25 |

| Class A-2 | AAA(sf) / AAAsf / AAA(sf) | $155,183,000 | 30.000% | % | (6) | 4.74 | 4/25 – 1/26 |

| Class A-4A1 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class A-5 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class A-AB | AAA(sf) / AAAsf / AAA(sf) | $19,922,000 | 30.000% | % | (6) | 7.10 | 1/26 – 3/30 |

| Class X-A | AAA(sf) / AAAsf / AAA(sf) | $1,181,663,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class A-S | AAA(sf) / AAAsf / AAA(sf) | $163,615,000 | 18.750% | % | (6) | 9.92 | 1/31 – 2/31 |

| Class B | AA-(sf) / AA-sf / NR | $59,992,000 | 14.625% | % | (6) | 9.99 | 2/31 – 2/31 |

| Class C | A-(sf) / A-sf / NR | $45,449,000 | 11.500% | % | (6) | 9.99 | 2/31 – 2/31 |

NON-OFFERED POOLED CERTIFICATES(10)

Non-Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| Class A-4A2 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class X-B | A-(sf) / A-sf / NR | $105,441,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-D | NR / BBB-sf / NR | $72,718,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-F | NR / BB-sf / NR | $32,723,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-G | NR / B-sf / NR | $14,543,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-H | NR / NR / NR | $47,267,145(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class D | NR / BBBsf / NR | $50,902,000 | 8.000% | % | (6) | 9.99 | 2/31 – 2/31 |

| Class E | NR / BBB-sf / NR | $21,816,000 | 6.500% | % | (6) | 9.99 | 2/31 – 2/31 |

| Class F | NR / BB-sf / NR | $32,723,000 | 4.250% | % | (6) | 9.99 | 2/31 – 2/31 |

| Class G | NR / B-sf / NR | $14,543,000 | 3.250% | % | (6) | 9.99 | 2/31 – 2/31 |

| Class H | NR / NR / NR | $47,267,145 | 0.000% | % | (6) | 9.99 | 2/31 – 2/31 |

| Class S(11) | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| Class R(11) | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

NON-OFFERED VERTICAL RISK RETENTION INTEREST(10)

Non-Offered Eligible Vertical Interest | Expected Ratings | Approximate Initial Combined VRR Interest Balance(2) | Approximate Initial Credit Support(3) | Initial Effective Interest Rate(4) | Effective Interest Rate Description | Expected | Expected Principal Window(5) |

| Combined VRR Interest(12) | NR / NR / NR | $76,545,008 | N/A(13) | % | (14) | 9.13 | 3/21 – 2/31 |

NON-OFFERED LOAN-SPECIFIC CERTIFICATES(10)(15)

Non-Offered Classes | Expected Ratings | Approximate Initial Certificate Balance(2) | Approximate Initial Credit Support(16) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| Class 360A | NR / NR / A(low)(sf) | $12,350,000 | 26.295% | % | (17) | 9.91 | 1/31 – 1/31 |

| Class 360B | NR / NR / BBB(low)(sf) | $16,387,000 | 15.496% | % | (17) | 9.91 | 1/31 – 1/31 |

| Class 360C | NR / NR / BB(low)(sf) | $16,388,000 | 4.696% | % | (17) | 9.91 | 1/31 – 1/31 |

| Class 360D | NR / NR / B(low)(sf) | $7,125,000 | 0.000% | % | (17) | 9.91 | 1/31 – 1/31 |

Non-Offered Vertical Risk Retention Interest | Expected Ratings | Approximate Initial Certificate Balance(2) | Approximate Initial Credit Support(16) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| 360RR Interest(18) | NR / NR / NR | $2,750,000 | N/A(19) | % | (20) | 9.91 | 1/31 – 1/31 |

(1) | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of S&P Global Ratings, a Standard & Poor’s Financial Services LLC business (“S&P”), Fitch Ratings, Inc. (“Fitch”) and DBRS, Inc. (“DBRS Morningstar”). Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. S&P, Fitch and DBRS Morningstar have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related rating agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the rating agencies on those websites. Credit ratings referenced throughout this Term Sheet are |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

4

| CERTIFICATE SUMMARY |

forward-looking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment.

| (2) | Approximate, subject to a variance of plus or minus 5% and further subject to any additional variances described in the footnotes below. In addition, the notional amounts of the Class X-A, Class X-B, Class X-D, Class X-F, Class X-G and Class X-H certificates (collectively, the “Class X Certificates” or the “Pooled Class X Certificates”) may vary depending upon the final pricing of the classes of Pooled Principal Balance Certificates (as defined in footnote (13) below) whose certificate balances comprise such notional amounts, and, if as a result of such pricing (a) the pass-through rate of any class of Pooled Class X Certificates, as applicable, would be equal to zero at all times, such class of Pooled Class X Certificates will not be issued on the closing date of this securitization (the “Closing Date”) or (b) the pass-through rate of any class of Pooled Principal Balance Certificates whose certificate balance comprises such notional amount is at all times equal to the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time (the “WAC Rate”), the certificate balance of such class of Pooled Principal Balance Certificates may not be part of, and there would be a corresponding reduction in, such notional amount of the related class of Pooled Class X Certificates. |

| (3) | “Approximate Initial Credit Support” means, with respect to any class of Non-Vertically Retained Pooled Principal Balance Certificates (as defined in footnote (6) below), the quotient, expressed as a percentage, of (i) the aggregate of the initial certificate balances of all classes of Non-Vertically Retained Pooled Principal Balance Certificates, if any, junior to such class of Non-Vertically Retained Pooled Principal Balance Certificates, divided by (ii) the aggregate of the initial certificate balances of all classes of Non-Vertically Retained Pooled Principal Balance Certificates. The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-4A1, Class A-4A2, Class A-5 and Class A-AB certificates are represented in the aggregate. The approximate initial credit support percentages shown in the table above do not take into account the Combined VRR Interest (as defined in footnote (12) below). The approximate initial credit support percentage shown for each class of Non-Vertically Retained Pooled Principal Balance Certificates does not take into account the subordination provided by the trust subordinate companion loan (as defined in footnote (15) below), provided that payments on the trust subordinate companion loan are generally subordinate to payments on the related senior loan in the related Loan Combination as and to the extent provided in the related co-lender agreement. |

| (4) | Approximate per annum rate as of the Closing Date. |

| (5) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for any mortgage loan or the trust subordinate companion loan and based on the modeling assumptions described under “Yield, Prepayment and Maturity Considerations” in the Preliminary Prospectus. |

| (6) | For any distribution date, the pass-through rate for each class of the Class A-1, Class A-2, Class A-4A1, Class A-4A2, Class A-5, Class A-AB, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates (collectively, the “Non-Vertically Retained Pooled Principal Balance Certificates”, and collectively with the Pooled Class X Certificates and the Class S certificates, the “Non-Vertically Retained Pooled Certificates”, and the Non-Vertically Retained Pooled Certificates collectively with the Class VRR certificates, the “Pooled Certificates”) will generally be equal to one of (i) a fixed per annum rate, (ii) the WAC Rate, (iii) a rate equal to the lesser of a specified per annum rate and the WAC Rate, or (iv) the WAC Rate less a specified percentage, but no less than 0.000%. The trust subordinate companion loan will not be taken into account in determining pass-through rates on the Non-Vertically Retained Pooled Principal Balance Certificates. See “Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| (7) | The exact initial certificate balances of the Class A-4A1 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, weighted average lives and principal windows of the Class A-4A1, Class A-4A2 and Class A-5 certificates are expected to as set forth, or be within the applicable ranges reflected, in the following chart. The aggregate initial certificate balance of the Class A-4A1 and Class A-5 certificates is expected to be approximately $621,699,000, subject to a variance of plus or minus 5%. |

Class of Certificates | Initial Certificate Balance or Expected Range of Initial Certificate Balances | Expected Weighted Avg. Life or Expected Range of Weighted Avg. Lives (Yrs) | Expected Range of Principal Windows |

| Class A-4A1 | $60,000,000 – $200,000,000 | 9.39 – 9.57 | 3/30 – 12/30 / 3/30 – 1/31 |

| Class A-4A2 | $200,000,000 | 9.39 – 9.57 | 3/30 – 12/30 / 3/30 – 1/31 |

| Class A-5 | $561,699,000 – $421,699,000 | 9.91 | 12/30 – 1/31 / 1/31 – 1/31 |

| (8) | The Pooled Class X Certificates will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of Pooled Class X Certificates at the related pass-through rate based upon the related notional amount. The notional amount of each class of the Pooled Class X Certificates will be equal to the certificate balance or the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the Non-Vertically Retained Pooled Principal Balance Certificates identified in the same row as such class of Pooled Class X Certificates in the chart below (as to such class of Pooled Class X Certificates, the “Corresponding Principal Balance Certificates”): |

| Class of Pooled Class X Certificates | Class(es) of Corresponding Principal Balance Certificates |

| Class X-A | Class A-1, Class A-2, Class A-4A1, Class A-4A2, Class A-5, Class A-AB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D and Class E |

| Class X-F | Class F |

| Class X-G | Class G |

| Class X-H | Class H |

| (9) | The pass-through rate for each class of Pooled Class X Certificates will generally be a per annum rate equal to the excess, if any, of (i) the WAC Rate over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of Corresponding Principal Balance Certificates as in effect from time to time, as described in the Preliminary Prospectus. See “Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| (10) | The classes of certificates set forth below “Non-Offered Pooled Certificates”, “Non-Offered Vertical Risk Retention Interest” and “Non-Offered Loan-Specific Certificates” in the table are not offered by this Term Sheet. |

| (11) | Neither the Class S certificates nor the Class R certificates will have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date. A specified portion of the “excess interest” accruing after the related anticipated repayment date on any mortgage loan with an anticipated repayment date will, to the extent collected, be allocated to the Class S certificates as set forth in “Description of the Certificates—Distributions—Excess Interest” in the Preliminary Prospectus. The Class R certificates will represent the residual interests in each of five separate REMICs, as further described in the Preliminary Prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

5

| CERTIFICATE SUMMARY |

| (12) | In satisfaction of the risk retention obligations of Citi Real Estate Funding Inc. (“CREFI”) (as “retaining sponsor” for the securitization transaction constituted by the issuance of the Pooled Certificates and the Uncertificated VRR Interest), CREFI is expected to acquire (or cause one or more other retaining parties to acquire) from the depositor, on the Closing Date, portions of an “eligible vertical interest” in the form of a “single vertical security” with an initial principal balance of approximately $76,545,008 (the “Combined VRR Interest”), which is expected to represent at least 5% of the aggregate principal balance of all of the “ABS interests” (i.e. the sum of the aggregate initial certificate balance of all of the Pooled Certificates and the initial principal balance of the Uncertificated VRR Interest) issued by the issuing entity in connection with such securitization transaction on the Closing Date. The Combined VRR Interest will consist of the “Uncertificated VRR Interest” and the “Class VRR certificates” (each as defined under “Credit Risk Retention” in the Preliminary Prospectus). The Combined VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to such securitization transaction. “Retaining sponsor”, “eligible vertical interest”, “single vertical security” and “ABS interests” have the meanings given to such terms in Regulation RR. See “Credit Risk Retention” in the Preliminary Prospectus. The Combined VRR Interest is not offered hereby. |

| (13) | Although the approximate initial credit support percentages shown in the table above with respect to the Non-Vertically Retained Pooled Principal Balance Certificates do not take into account the Combined VRR Interest, losses incurred on the mortgage loans will be allocated between the Combined VRR Interest, on the one hand, and the Non-Vertically Retained Pooled Principal Balance Certificates, on the other hand, pro rata in accordance with the principal balance of the Combined VRR Interest (the “Combined VRR Interest Balance”) and the aggregate outstanding certificate balance of the Non-Vertically Retained Pooled Principal Balance Certificates, respectively. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. The Class VRR certificates and the Non-Vertically Retained Pooled Principal Balance Certificates are collectively referred to in this Term Sheet as the “Pooled Principal Balance Certificates”. |

| (14) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the Combined VRR Interest will be the WAC Rate. |

| (15) | The Class 360A, Class 360B, Class 360C and Class 360D certificates and the 360RR Interest are collectively referred to as the “Loan-Specific Certificates” or the “Loan-Specific Principal Balance Certificates” (and, collectively with the Pooled Principal Balance Certificates, constitute the “Principal Balance Certificates”). The Loan-Specific Certificates will only be entitled to receive distributions from, and will only incur losses with respect to, a junior promissory note secured by the 360 Spear mortgaged property (such junior promissory note, the “trust subordinate companion loan”). The trust subordinate companion loan will be included as an asset of the issuing entity but will not be part of the mortgage pool backing the Pooled Certificates. No class of Pooled Certificates will have any interest in the trust subordinate companion loan. See “Description of the Mortgage Pool—The Loan Combinations—The 360 Spear Pari Passu-AB Loan Combination”. |

| (16) | “Approximate Initial Credit Support” means, with respect to any class of Loan-Specific Certificates (other than the 360RR Interest), the quotient, expressed as a percentage, of (i) the aggregate of the initial certificate balances of all classes of Loan-Specific Certificates (other than the 360RR Interest), if any, that are junior to the subject class of Loan-Specific Certificates, divided by (ii) the sum of (A) the aggregate of the initial certificate balances of all classes of Loan-Specific Certificates (other than the 360RR Interest) and (B) 95% of the aggregate outstanding principal balance of the senior loans included in the 360 Spear loan combination. The approximate initial credit support percentages shown in the table above with respect to the Loan-Specific Certificates (other than the 360RR Interest) do not take into account the 360RR Interest. |

| (17) | The pass-through rates for the Loan-Specific Certificates (other than the 360RR Interest), in each case, will equal one of the following per annum rates: (i) a fixed rate, (ii) the net mortgage rate (adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) on the trust subordinate companion loan, (iii) the lesser of a specified rate and the net mortgage rate on the trust subordinate companion loan described in clause (ii), or (iv) the net mortgage rate on the trust subordinate companion loan described in clause (ii) less a specified rate. See “Description of the Certificates—Distributions—Pass-Through Rates”. |

| (18) | German American Capital Corporation (“GACC”) is the only sponsor (and will act as “retaining sponsor” (as such term is defined in Regulation RR)) with respect to the securitization transaction constituted by the issuance of the Loan-Specific Certificates. In connection therewith, GACC is expected to acquire from the depositor on the closing date an “eligible vertical interest” (as such term is defined in Regulation RR) in the form of a single vertical security with an initial certificate balance of approximately $2,750,000 (the “360RR Interest”), which is expected to represent 5.0% of the aggregate initial certificate balance of all Loan-Specific Certificates. The 360RR Interest is expected to be retained by GACC or its “majority-owned affiliate” (as such term is defined in Regulation RR) in accordance with the credit risk retention rules applicable to such securitization transaction. The 360RR Interest is a class of certificates, but is not offered hereby. |

| (19) | Although the approximate initial credit support percentages shown in the table with respect to the Loan-Specific Certificates (other than the 360RR Interest) do not take into account the 360RR Interest, losses incurred on the trust subordinate companion loan will be allocated between the 360RR Interest, on the one hand, and the other classes of Loan-Specific Certificates, on the other hand, pro rata in accordance with their respective outstanding certificate balances. |

| (20) | Except for tax reporting purposes, the 360RR Interest does not have a specified pass-through rate; however, the effective interest rate on the 360RR Interest will be a per annum rate equal to the net mortgage rate (adjusted, if necessary, to accrue interest on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time on the trust subordinate companion loan. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

6

| MORTGAGE POOL CHARACTERISTICS |

| Mortgage Pool Characteristics(1) | ||

| Initial Pool Balance(2) | $1,530,900,153 | |

| Number of Mortgage Loans | 53 | |

| Number of Mortgaged Properties | 65 | |

| Average Cut-off Date Balance | $28,884,909 | |

| Weighted Average Mortgage Rate | 3.21322% | |

| Weighted Average Remaining Term to Maturity/ARD (months)(3) | 112 | |

| Weighted Average Remaining Amortization Term (months)(4) | 360 | |

| Weighted Average Cut-off Date LTV Ratio(5) | 53.5% | |

| Weighted Average Maturity Date/ARD LTV Ratio(3)(5) | 51.6% | |

| Weighted Average UW NCF DSCR(6)(7) | 3.14x | |

| Weighted Average Debt Yield on Underwritten NOI(7)(8) | 11.6% | |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon | 3.8% | |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only then Amortizing Balloon | 12.0% | |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon then Interest Only | 6.8% | |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only | 69.7% | |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only – ARD | 7.6% | |

| % of Initial Pool Balance of Mortgaged Properties with Single Tenants | 16.9% | |

| % of Initial Pool Balance of Mortgage Loans with Mezzanine Debt | 14.5% | |

| % of Initial Pool Balance of Mortgage Loans with Subordinate Debt | 21.9% | |

| (1) | The Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Unit / Room information for each mortgage loan is presented in this Term Sheet (i) if such mortgage loan is part of a loan combination (as defined under “Collateral Overview—Loan Combination Summary” below), based on both that mortgage loan and any related pari passu companion loan(s) but, unless otherwise specifically indicated, without regard to any related subordinate companion loan(s), and (ii) unless otherwise specifically indicated, without regard to any other indebtedness (whether or not secured by the related mortgaged property, ownership interests in the related borrower or otherwise) that currently exists or that may be incurred by the related borrower or its owners in the future. The mortgage pool does not include, and the terms “mortgage loan” and “mortgage loans” (as used in this Term Sheet) are not intended to refer to the trust subordinate companion loan. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | Unless otherwise indicated, mortgage loans with anticipated repayment dates are presented as if they were to mature on the anticipated repayment date. |

| (4) | Excludes mortgage loans that are interest-only for the entire term. |

| (5) | The Cut-off Date LTV Ratios and Maturity Date/ARD LTV Ratios presented in this Term Sheet are generally based on the “as-is” appraised values of the related mortgaged properties (as set forth on Annex A to the Preliminary Prospectus), provided that such LTV ratios may be calculated based on (i) “as-stabilized” or similar values in certain cases where the completion of certain hypothetical conditions or other events at the property are assumed and/or where reserves have been established at origination to satisfy the applicable condition or event that is expected to occur, or (ii) the Cut-off Date Balance or Balloon Balance, as applicable, net of a related earnout or holdback reserve, or (iii) the “as-is” appraised value for a portfolio of mortgaged properties that includes a premium relating to the valuation of the portfolio of mortgaged properties as a whole rather than as the sum of individually valued mortgaged properties, in each case as further described in the definitions of “Appraised Value”, “Cut-off Date LTV Ratio” and “Maturity Date/ARD LTV Ratio” under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (6) | The UW NCF DSCR for each mortgage loan is generally calculated by dividing the UW NCF for the related mortgaged property or mortgaged properties by the annual debt service for such mortgage loan, as adjusted in the case of mortgage loans with a partial interest only period by using the first 12 amortizing payments due instead of the actual interest only payment due. |

| (7) | The UW NCF DSCR, Debt Yield on Underwritten NOI and Debt Yield on Underwritten NCF on the MGM Grand & Mandalay Bay mortgage loan are each calculated based on the master lease annual rent of $292,000,000. |

| (8) | The Debt Yield on Underwritten NOI for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NOI divided by the Cut-off Date Balance of such mortgage loan, and the Debt Yield on Underwritten NCF for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NCF divided by the Cut-off Date Balance of such mortgage loan. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

7

| MORTGAGE POOL CHARACTERISTICS |

| COVID-19 Update | ||||||||||||||

| Loan Number | Property Name | Mortgage Loan Seller | Property Type | Information as of Date | First Payment Date | December Debt Service Payment Received (Y/N) | January Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested (Y/N) | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Occupied SF or Unit Count Making Full November Rent Payment (%) | UW November Base Rent Paid (%) | Occupied SF or Unit Count Making Full December Rent Payment (%) | UW December Base Rent Paid (%) |

| 1 | 860 Washington(1) | JPMCB, GACC | Mixed Use | 1/1/2021 | 2/6/2021 | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 2 | Millennium Corporate Park | GSMC | Office | 1/14/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 3 | 360 Spear(2) | GACC | Office | 1/15/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

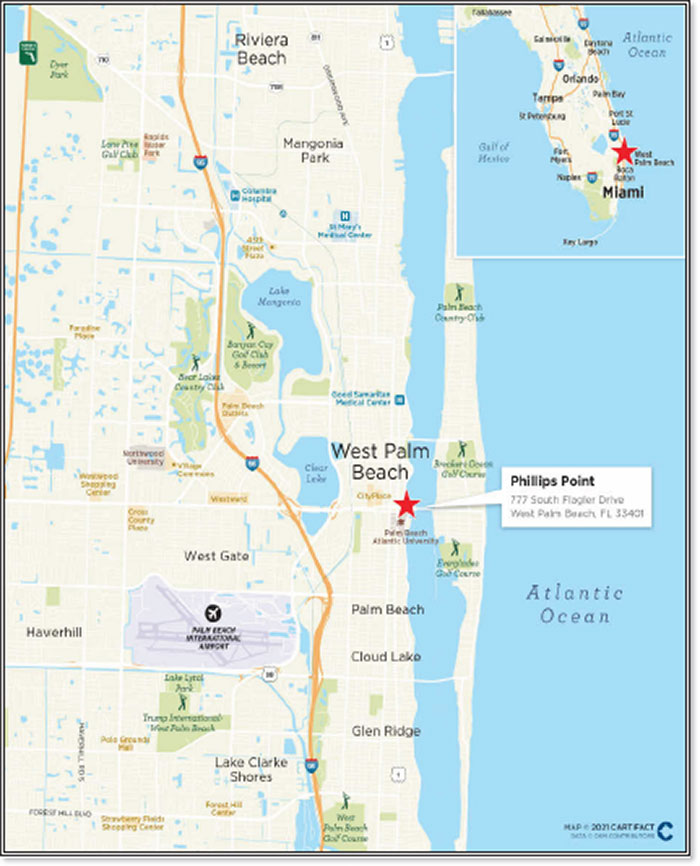

| 4 | Phillips Point | GSMC | Office | 1/20/2021 | 3/6/2021 | NAP | NAP | No | No | No | 99.0% | 99.0% | 100.0% | 100.0% |

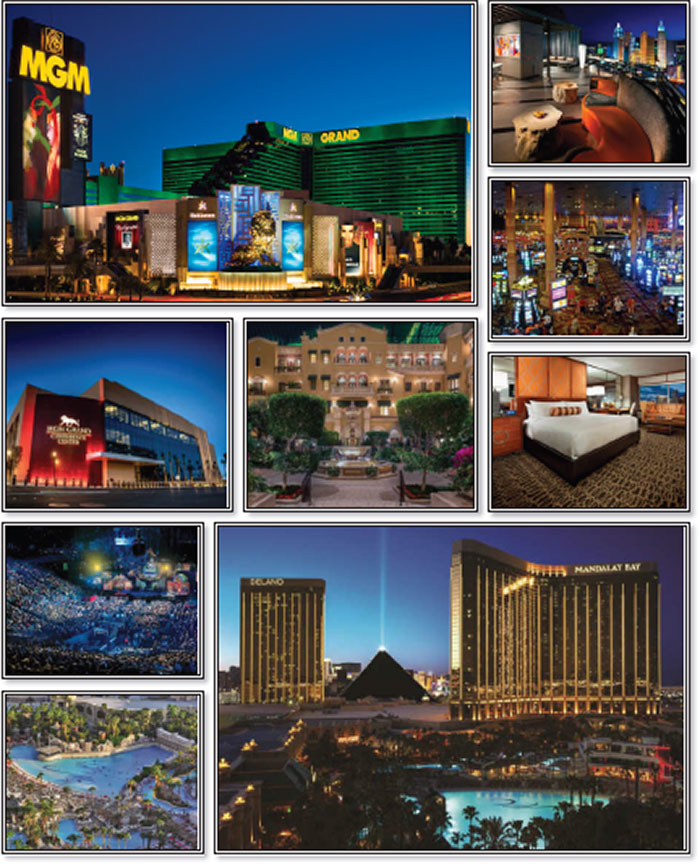

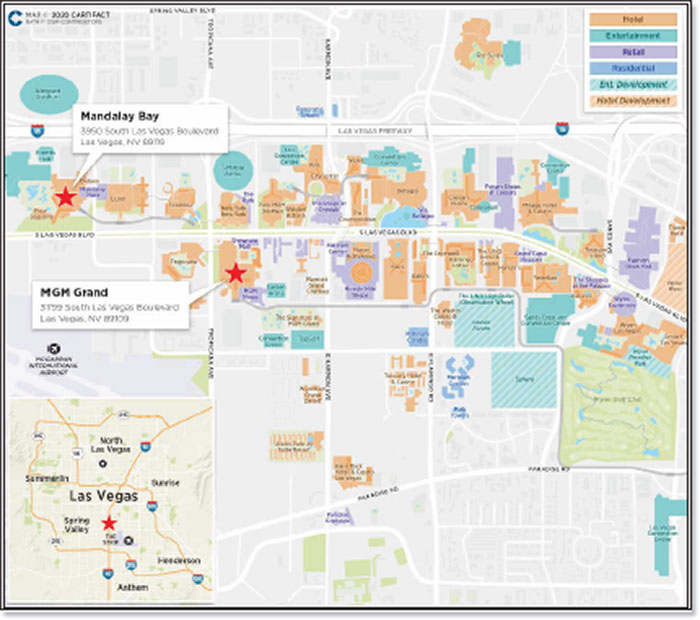

| 5 | MGM Grand & Mandalay Bay(3) | CREFI, GACC | Hospitality | 1/15/2021 | 4/5/2020 | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

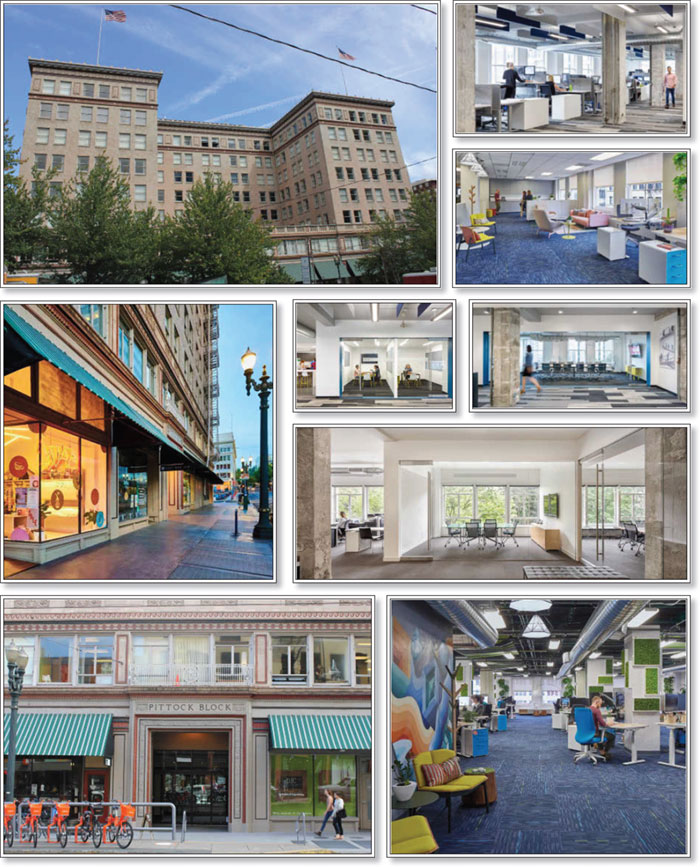

| 6 | Pittock Block(4) | JPMCB | Mixed Use | 1/18/2021 | 2/1/2021 | NAP | NAP | No | No | Yes | 67.0% | 74.0% | 68.2% | 82.0% |

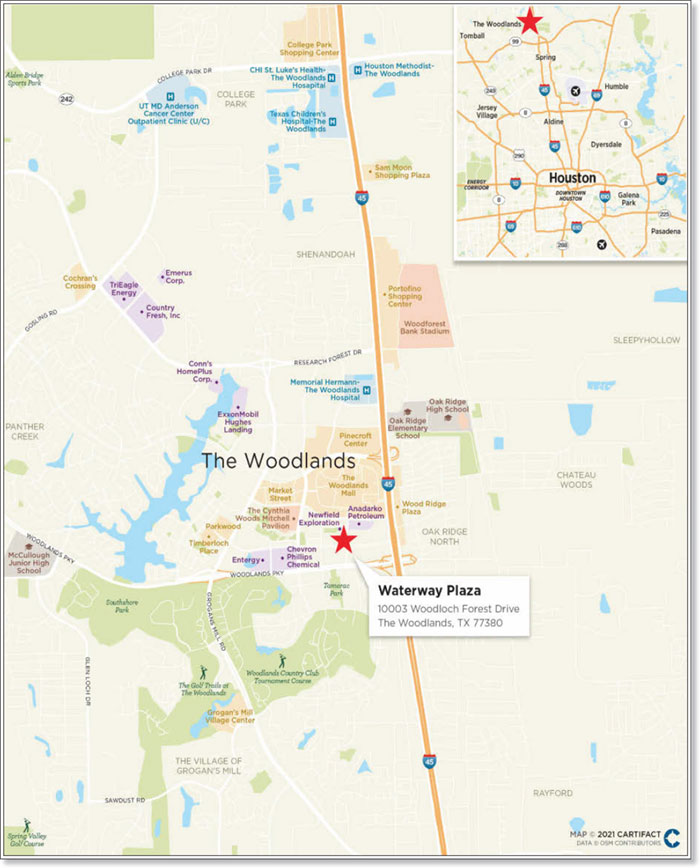

| 7 | Waterway Plaza | GSMC | Office | 1/14/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 8 | Leonardo DRS Industrial | CREFI | Industrial | 2/6/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

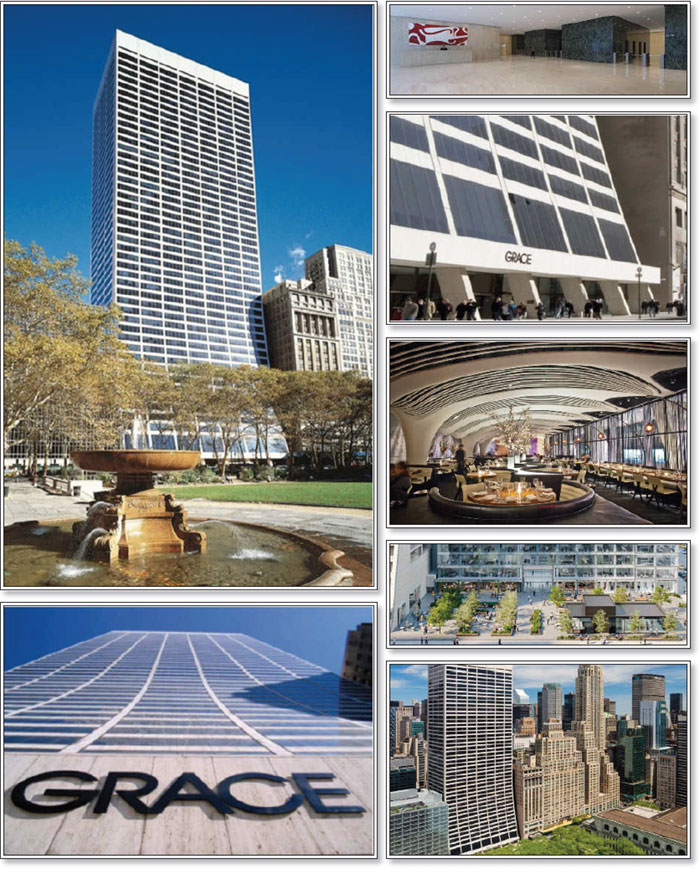

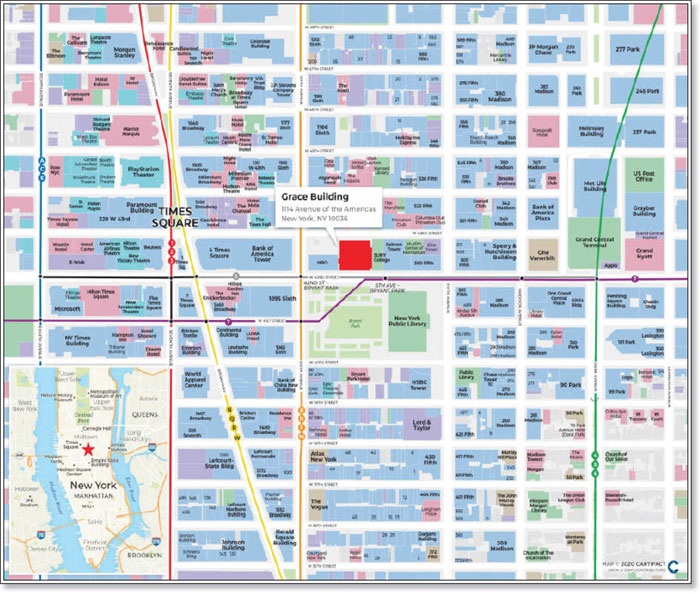

| 9 | The Grace Building(5) | JPMCB, GACC | Office | 1/19/2021 | 1/6/2021 | NAP | Yes | No | No | Yes | 98.0% | 97.1% | 95.0% | 89.7% |

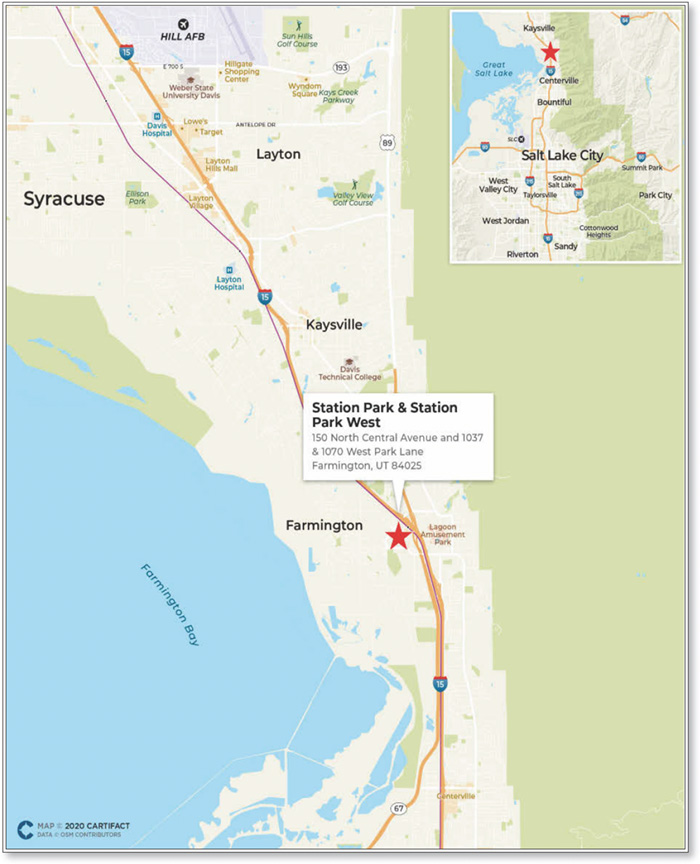

| 10 | Station Park & Station Park West(5) | JPMCB | Mixed Use | 1/1/2021 | 1/5/2021 | NAP | Yes | No | No | Yes | 85.7% | 85.7% | 84.7% | 84.7% |

| 11 | First Central Tower | CREFI | Office | 1/15/2021 | 3/6/2021 | NAP | NAP | No | No | Yes | 95.3% | 95.3% | 95.0% | 95.0% |

| 12 | Knitting Mills | CREFI | Office | 1/6/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 13 | First Republic Center(7) | GACC | Mixed Use | 12/30/2020 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 14 | Rugby Pittsburgh Portfolio | JPMCB | Office | 1/1/2021 | 2/1/2021 | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 15 | Amazon Chicago-Pullman | JPMCB | Industrial | 1/1/2021 | 2/1/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 16 | JW Marriott Nashville(8) | GSMC | Hospitality | 1/14/2021 | 4/6/2020 | Yes | Yes | Yes | Yes | Yes | NAP | NAP | NAP | NAP |

| 17 | The Village at Meridian(9) | JPMCB | Retail | 1/1/2021 | 3/5/2021 | NAP | NAP | No | No | Yes | 80.2% | 80.2% | 79.2% | 79.2% |

| 18 | Selig Office Portfolio(10) | GSMC | Office | 12/29/2020 | 5/6/2015 | NAP | Yes | No | No | Yes | 96.4% | 99.5% | 96.4% | 99.5% |

| 19 | The Trails at Silverdale(11) | JPMCB | Retail | 1/1/2021 | 2/5/2021 | NAP | NAP | No | No | Yes | 99.9% | 99.9% | 96.1% | 96.1% |

| 20 | 711 Fifth Avenue(12) | GSMC | Mixed Use | 1/1/2021 | 4/6/2020 | Yes | Yes | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 21 | Hotel ZaZa Houston Museum District(13) | CREFI | Hospitality | 1/6/2021 | 4/6/2020 | Yes | Yes | No | Yes | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 22 | 360 Neptune Avenue | CREFI | Mixed Use | 1/15/2021 | 3/6/2021 | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 23 | Central Missouri Distribution Center | CREFI | Industrial | 1/11/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 24 | Treasure Valley Marketplace(14) | JPMCB | Retail | 1/1/2021 | 2/5/2021 | NAP | NAP | No | No | Yes | 98.0% | 98.0% | 99.0% | 99.0% |

| 25 | 2601 Wilshire | GACC | Office | 1/19/2020 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 26 | Brookfield Place Richmond | CREFI | Office | 1/15/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 27 | 104 Delancey Street | CREFI | Office | 1/15/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 28 | 880 Butler Drive | GSMC | Industrial | 12/31/2020 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 29 | 1400 North 25th Avenue | CREFI | Industrial | 1/10/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 30 | Luna Apartments | CREFI | Multifamily | 1/12/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 31 | 63 West 104th Street | CREFI | Multifamily | 1/15/2021 | 2/6/2021 | NAP | NAP | No | No | No | 88.9% | 88.9% | 88.4% | 88.4% |

| 32 | 2300 Route 33 | JPMCB | Office | 1/1/2021 | 2/1/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 33 | Backlot Apartments(15) | GACC | Multifamily | 1/24/2021 | 3/6/2021 | NAP | NAP | No | No | No | 90.2% | 92.2% | 87.1% | 90.4% |

| 34 | 1623 Flatbush | CREFI | Mixed Use | 1/13/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 35 | Trepte Industrial Park | GSMC | Industrial | 12/31/2020 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 36 | 206-20 Linden Boulevard | CREFI | Office | 1/13/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 37 | Rent A Space Portfolio | CREFI | Self Storage | 1/13/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 38 | The Centre at Stirling & Palm | CREFI | Office | 1/18/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 99.2% |

| 39 | Baxter International Production Center | GSMC | Industrial | 12/21/2020 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

8

| MORTGAGE POOL CHARACTERISTICS |

| COVID-19 Update | ||||||||||||||

| Loan Number | Property Name | Mortgage Loan Seller | Property Type | Information as of Date | First Payment Date | December Debt Service Payment Received (Y/N) | January Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested (Y/N) | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Occupied SF or Unit Count Making Full November Rent Payment (%) | UW November Base Rent Paid (%) | Occupied SF or Unit Count Making Full December Rent Payment (%) | UW December Base Rent Paid (%) |

| 40 | Holiday Inn & Suites Memphis/Germantown(16) | JPMCB | Hospitality | 1/1/2021 | 2/1/2021 | NAP | NAP | No | No | No | NAP | NAP | NAP | NAP |

| 41 | Spring Glen Apartments | GACC | Multifamily | 1/15/2021 | 2/6/2021 | NAP | NAP | No | No | No | 91.4% | 90.8% | 89.4% | 88.8% |

| 42 | Fountainbleau Self Storage | CREFI | Self Storage | 1/12/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 43 | Tesla Schaumberg | GACC | Retail | 1/19/2020 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 44 | 211 Saw Mill | GACC | Industrial | 1/20/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 45 | E&B Brewery Lofts | CREFI | Mixed Use | 1/15/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 46 | 4 Storage - Bristol | CREFI | Self Storage | 1/13/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 47 | Excess Self Storage | GACC | Self Storage | 1/19/2021 | 2/6/2021 | NAP | NAP | No | No | No | 76.7% | 100.0% | 79.5% | 100.0% |

| 48 | Mechanicsburg Self Storage | CREFI | Self Storage | 1/13/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 49 | VanWest Storage Portfolio | CREFI | Self Storage | 1/13/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 50 | Walgreens Bradenton | CREFI | Retail | 1/12/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 51 | Woodbridge Group HQ | CREFI | Industrial | 1/13/2021 | 3/6/2021 | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 52 | Secure Store Self Storage | CREFI | Self Storage | 1/13/2021 | 2/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 53 | 30222 Esperanza | CREFI | Industrial | 1/19/2021 | 3/6/2021 | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| (1) | 860 Washington – As of January 18, 2021, the 860 Washington Property is open and operational; however, the majority of the building’s tenants are working remotely. As of November 2020, the 860 Washington Property was 96.6% leased. Since March 2020, tenants at the 860 Washington Property have paid 100.0% of contractual rent. Reportedly, [Tesla asked for rent deferrals across many of its showrooms including the 860 Washington Property, but that request was denied by the borrower sponsor. No other tenant has requested rent relief.] |

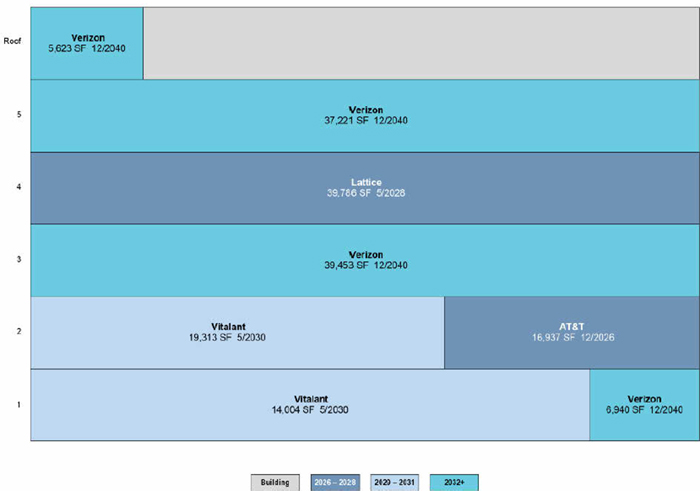

| (2) | 360 Spear – Verizon (in its existing space) and AT&T were the only tenants required to pay rent during the months of November and December. The remaining tenants were either in a free rent period or did not yet have executed leases in place. |

| (3) | MGM Grand & Mandalay Bay – Based on the adjusted September 2020 TTM EBITDAR of approximately $222.0 million and the initial master lease rent of $292.0 million, the MGM Grand & Mandalay Bay Whole Loan results in a September 2020 TTM EBITDAR to rent coverage ratio of 0.76x. |

| (4) | Pittock Block – As of January 18, 2021 the Pittock Block Property is open for business; however, a majority of the tenants are working remotely. 11 tenants, representing approximately 26.625 SF (8.9% NRA) have requested rent relief. |

| (5) | The Grace Building – As a result of the COVID-19 pandemic, four retail tenants (2.0% of NRA and 2.9% of U/W Base Rent) have not made rent payments for the past several months. The borrower sponsor is in the process of negotiating rent deferrals with full rental payments anticipated to commence in late 2021 or early 2022. The parking tenant has not paid the required monthly rental payments since March and an event of default is continuing under the lease. The borrower sponsor is in the process of replacing the current operator and plans to employ a new operator under a management agreement. The borrower deposited $1,608,940 with the lender at origination for anticipated parking rent shortfalls. See The Grace Building “COVID-19 Update” herein for additional information. |

| (6) | Station Park & Station Park West – As a result of COVID-19, the borrower sponsor negotiated rent deferrals on a tenant-by-tenant basis and ultimately provided between two to three months of deferred rent spanning April 2020 to December 2020 to 31 tenants totaling 293,362 sq. ft. and amounting to $909,200 of rent deferment. Leases for these tenants were amended such that the deferred rent will be recouped by the borrower sponsor via 12 equal installments in 2021. In addition, as a result of COVID-19, the borrower sponsor provided partial rent abatements to three tenants spanning April 2020 to June 2020. At origination, a $3,958,133 gap rent reserve was established, representing the aggregate amount of base rent for the succeeding 12-months for tenants who have not paid in-full base rent due pursuant to each such tenant’s underlying lease as of the origination date. Such amounts will not be released to the borrower until, among other conditions, (i) collections exceed 95% of the full rent payable from all tenants in place as of the origination date for a period of 12 consecutive months and (ii) the Station Park & Station Park West property is at least 80% occupied based on total square footage, provided no event of default or cash sweep event then exists. See the Station Park & Station Park West “COVID-19 Update” herein for additional information. |

| (7) | First Republic Center – Two tenants at the First Republic Center mortgaged property had abated rent in the months of November and December. One tenant (3.3% of NRA and 2.4% of U/W Base Rent) made a rent relief request to the prior owner of the First Republic Center mortgaged property, which was not granted. The same tenant has not made all CAM reimbursements required pursuant to the terms of its lease. One tenant (5.1% of NRA and 5.1% of U/W Base Rent) made a rent relief request to the prior owner of the First Republic Center mortgaged property, which was granted and reflected in its lease. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

9

| MORTGAGE POOL CHARACTERISTICS |

| (8) | JW Marriott Nashville – In April 2020, the mortgage loan was modified to permit the use of FF&E reserve funds to pay debt service, and the borrower sponsor provided a 6-month guaranty for debt service, taxes and insurance payments that expired in October 2020. In October 2020, the mortgage loan was further modified to waive the requirement to fund the FF&E reserve until April 2021, waive the cash management debt yield trigger through the second quarter of 2022, and otherwise permanently decrease the debt yield trigger level from 10% to 7.5%, in exchange for the borrower funding an 18-monthdebt service reserve to be applied to monthly payments from October 2020 through March 2022. |

| (9) | The Village at Meridian – As a result of COVID-19, the borrower sponsor negotiated rent deferrals on a tenant-by-tenant basis and ultimately provided between one to five months of deferred rent spanning April 2020 to December 2020 to 30 tenants totaling 186,026 sq. ft., amounting to $909,200 of rent deferment. Leases for these tenants were amended such that the deferred rent will be recouped by the borrower sponsor via 12 equal installments in 2021. In addition, as a result of COVID-19, the borrower sponsor provided partial or full rent abatements to eight tenants spanning May 2020 to December 2020. At origination, a $3,742,823 gap rent reserve was established, representing the aggregate amount of base rent for the succeeding 12-months for tenants who have not paid in-full base rent due pursuant to each such tenant’s underlying lease as of the origination date. Such amounts will not be released to the borrower until, among other conditions, (i) collections exceed 95% of the full rent payable from all tenants in place as of the origination date for a period of 12 consecutive months and (ii) The Village at Meridian property is at least 80% occupied based on total square footage, provided no event of default or cash sweep event then exists. |

| (10) | Selig Office Portfolio - Seven tenants, representing 3.2% of the SF have requested rent relief. |

| (11) | The Trails at Silverdale – As a result of COVID-19, the borrower sponsor offered most of their non-essential tenants a two-month rent deferral for either the months of April, May or June such that the deferred rent will be recouped by the borrower sponsor via 12 equal installments in 2021. The landlord negotiated on a tenant-by-tenant basis provided two months of deferred rent in spanning April 2020 to June 2020 to 11 tenants totaling 88,234 sq. ft. and amounting to approximately $290,000 of rent deferment. Leases for these tenants were amended such that the deferred rent will be recouped by the borrower sponsor via 12 equal installments in 2021. At origination, a $225,000 gap rent reserve was established, representing the aggregate amount of base rent for the succeeding 12-months for tenants who have not paid in-full base rent due pursuant to each such tenant’s underlying lease as of the origination date. Such amounts will not be released to the borrower until, among other conditions, (i) collections exceed 95% of the full rent payable from all tenants in place as of the origination date for a period of 12 consecutive months and (ii) The Trails at Silverdale property is at least 80% occupied based on total square footage, provided no event of default or cash sweep event then exists. |

| (12) | 711 Fifth Avenue - Includes one tenant, representing 4.2% of the SF and 37.3% of UW Base Rent of the 711 Fifth Avenue property who paid their rent in accordance with an agreement to pay 50% abated rent for the months of April, May and June. The abated rent will be paid back 50% by the end of 2020 and the remainder by the end of Q1 2021. |

| (13) | Hotel ZaZa Houston Museum District – The Hotel ZaZa Houston Museum District loan was recently modified to create a $2,311,667 debt service reserve by converting approximately $945,384 in existing FF&E reserves as well as a $1,248,110 new cash contribution by the sponsor, and an additional deposit to be received from the borrower on the monthly payment date occurring in January 2021 of $118,173. The debt service reserve will only be released upon the Hotel ZaZa Houston Museum District property achieving a 9.5% net cash flow debt yield on a trailing 12 month basis for two consecutive quarters, with approximately $1.16 million being allocated back to FF&E reserve and approximately $1.16 million being remitted back to the borrower. The FF&E reserve monthly deposits will be waived for the 2021 calendar year, after which the FF&E reserve will follow the step-up structure of 2.50% in 2022, 3.25% in 2023, and 4.00% in 2024 and thereafter. Lastly, the debt yield cash management trigger will be temporarily waived until January 2023, however, cash management will still be enforced if an event of default occurs. |

| (14) | Treasure Valley Marketplace – As a result of COVID-19, the borrower sponsor offered most of their non-essential tenants a two-month rent deferral for either the months of April, May or June such that the deferred rent will be recouped by the borrower sponsor via 12 equal installments in 2021. The landlord negotiated on a tenant-by-tenant basis and ultimately provided two months of deferred rent in April and May to nine tenants totaling approximately 49,000 sq. ft. and amounting to approximately $1.0 million of rent deferment. Leases for these tenants were amended such that the deferred rent will be recouped by the borrower sponsor via 12 equal installments in 2021. In addition, as a result of COVID-19, the borrower sponsor provided partial or full rent abatements to three tenants spanning April 2020 to July 2020. At origination, a $330,566 gap rent reserve was established, representing the aggregate amount of base rent for the succeeding 12-months for tenants who have not paid in-full base rent due pursuant to each such tenant’s underlying lease as of the origination date. Such amounts will not be released to the borrower until, among other conditions, (i) collections exceed 95% of the full rent payable from all tenants in place as of the origination date for a period of 12 consecutive months and (ii) Treasure Valley Market Place property is at least 80% occupied based on total square footage, provided no event of default or cash sweep event then exists. |

| (15) | Backlot Apartments - According to the borrower, in November and December, the borrower allowed certain of such tenants to apply their security deposits to monthly rent, which is not included in the calculations. |

| (16) | Holiday Inn & Suites Memphis/Germantown – As of January 12, 2021 the Holiday Inn & Suites Memphis/Germantown loan is not subject to any forbearance or debt service relief requests. At origination the loan was structured with an 18-month debt service reserve fund in the amount of approximately $742,933. The debt service reserve will be released upon the following conditions (i) if the sponsor has not drawn upon the debt service reserve for a period of 12 months, six months of the debt service reserve can be released upon the property achieving a DSCR of 1.30x on a trailing three month basis and (ii) if the sponsor has not drawn upon the debt service reserve for a period of 15 months, nine months of the debt service reserve can be released upon the property achieving a DSCR of 1.85x on a trailing 12 month basis. At loan maturity three months of the debt service will be remaining. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

10

| KEY FEATURES OF THE CERTIFICATES |

| Co-Lead Managers and Joint Bookrunners: | Citigroup Global Markets Inc. J.P. Morgan Securities LLC Goldman Sachs & Co. LLC Deutsche Bank Securities Inc.

|

| Co-Managers: | Academy Securities, Inc. Drexel Hamilton, LLC

|

| Depositor: | Citigroup Commercial Mortgage Securities Inc.

|

| Initial Pool Balance: | $1,530,900,153 |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association

|

| Special Servicers: | CWCapital Asset Management, LLC (with respect to all serviced loans (other than the Pittock Block loan combination)) and Situs Holdings, LLC (with respect to the Pittock Block loan combination) |

| Certificate Administrator: | Citibank, N.A. |

| Trustee: | Wilmington Trust, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Risk Retention Consultation Parties: | Citi Real Estate Funding Inc., Goldman Sachs Mortgage Company and JPMorgan Chase Bank, National Association |

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by Citi Real Estate Funding Inc., as retaining sponsor for the securitization transaction constituted by the issuance of the Pooled Certificates and the Uncertificated VRR Interest, see “Credit Risk Retention” in the Preliminary Prospectus. Note that the securitization transaction constituted by the issuance of the Pooled Certificates and the Uncertificated VRR Interest is not structured to satisfy European or United Kingdom risk retention and due diligence requirements. |

| Closing Date: | On or about February 18, 2021 |

| Cut-off Date: | With respect to each mortgage loan, the due date in February 2021 for that mortgage loan (or, in the case of any mortgage loan or trust subordinate companion loan that has its first due date subsequent to February 2021, the date that would have been its due date in February 2021 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) |

| Determination Date: | The 11th day of each month or next business day, commencing in March 2021 |

| Distribution Date: | The 4th business day after the Determination Date, commencing in March 2021 |

| Interest Accrual: | Preceding calendar month |

| ERISA Eligible: | The offered certificates are expected to be ERISA eligible, subject to the exemption conditions described in the Preliminary Prospectus |

| SMMEA Eligible: | No |

| Payment Structure: | Sequential Pay |

| Day Count: | 30/360 |

| Tax Structure: | REMIC |

| Rated Final Distribution Date: | February 2054 |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

11

| KEY FEATURES OF THE CERTIFICATES |

| Cleanup Call: | 1.0% |

| Minimum Denominations: | $10,000 minimum for the offered certificates (other than the Class X-A certificates); $1,000,000 minimum for the Class X-A certificates; and integral multiples of $1 thereafter for all the offered certificates |

| Delivery: | Book-entry through DTC |

| Bond Information: | Cash flows are expected to be modeled by TREPP, INTEX, BLOOMBERG and Moody’s Analytics |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

12

| TRANSACTION HIGHLIGHTS |

| ■ | $1,087,104,000 (Approximate) New-Issue Multi-Borrower CMBS: |

| — | Overview: The mortgage pool consists of 53 fixed-rate commercial mortgage loans that have an aggregate Cut-off Date Balance of $1,530,900,153 (the “Initial Pool Balance”), have an average mortgage loan Cut-off Date Balance of $28,884,909 and are secured by 65 mortgaged properties located throughout 23 states. |

| — | LTV: 53.5% weighted average Cut-off Date LTV Ratio |

| — | DSCR: 3.14x weighted average Underwritten NCF Debt Service Coverage Ratio |

| — | Debt Yield: 11.6% weighted average Debt Yield on Underwritten NOI |

| — | Credit Support: 30.000% credit support to Class A-1 / A-2 / A-4A1/ A-4A2 / A-5 / A-AB |

| ■ | Loan Structural Features: |

| — | Amortization: 22.7% of the mortgage loans by Initial Pool Balance have scheduled amortization: |

| – | 3.8% of the mortgage loans by Initial Pool Balance have amortization for the entire term with a balloon payment due at maturity |

| – | 12.0% of the mortgage loans by Initial Pool Balance have scheduled amortization following a partial interest only period with a balloon payment due at maturity |

| – | 6.8% of the mortgage loans by Initial Pool Balance have scheduled amortization followed by a partial interest only period with a balloon payment due at maturity |

| — | Hard Lockboxes: 82.9% of the mortgage loans by Initial Pool Balance have a Hard Lockbox in place |

| — | Cash Traps: 93.2% of the mortgage loans by Initial Pool Balance have cash traps triggered by certain declines in cash flow, all at levels equal to or greater than (i) a 1.10x coverage or (ii) a 5.75% debt yield, that fund an excess cash flow reserve |

| — | Reserves: The mortgage loans require amounts to be escrowed for reserves as follows: |

| – | Real Estate Taxes: 36 mortgage loans representing 51.4% of the Initial Pool Balance |

| – | Insurance: 22 mortgage loans representing 26.7% of the Initial Pool Balance |

| – | Replacement Reserves (Including FF&E Reserves): 32 mortgage loans representing 39.2% of the Initial Pool Balance |

| – | Tenant Improvements / Leasing Commissions: 15 mortgage loans representing 36.4% of the portion of the Initial Pool Balance that is secured by office, retail, industrial and mixed use properties and two self storage properties with commercial tenants. |

| — | Predominantly Defeasance Mortgage Loans: 84.4% of the mortgage loans by Initial Pool Balance permit defeasance only after an initial lockout period |

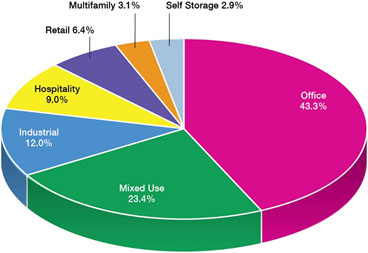

| ■ | Multiple-Asset Types > 5.0% of the Initial Pool Balance: |

| — | Office: 43.3% of the mortgaged properties by allocated Initial Pool Balance are office properties |

| — | Mixed Use: 23.4% of the mortgaged properties by allocated Initial Pool Balance are mixed use properties |

| — | Industrial: 12.0% of the mortgaged properties by allocated Initial Pool Balance are industrial properties |

| — | Hospitality: 9.0% of the mortgaged properties by allocated Initial Pool Balance are hospitality properties |

| — | Retail: 6.4% of the mortgaged properties by allocated Initial Pool Balance are retail properties (5.6% are anchored retail properties) |

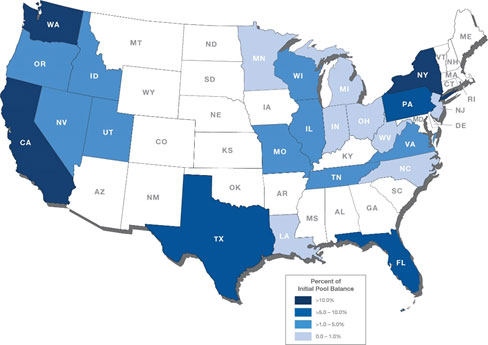

| ■ | Geographic Diversity: The 65 mortgaged properties are located throughout 23 states, with only three states having greater than 10.0% of the allocated Initial Pool Balance: New York (18.5%), California (12.3%) and Washington (11.2%) |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

13

| COLLATERAL OVERVIEW |

Mortgage Loans by Loan Seller

Mortgage Loan Seller | Mortgage Loans | Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance |

| Citi Real Estate Funding Inc. | 24 | 26 | $380,377,674 | 24.8% |

| Goldman Sachs Mortgage Company | 9 | 17 | 378,805,015 | 24.7 |

| JPMorgan Chase Bank, National Association | 9 | 10 | 316,395,105 | 20.7 |

| German American Capital Corporation | 8 | 8 | 204,322,359 | 13.3 |

| JPMorgan Chase Bank, National Association, German American Capital Corporation(1)(2) | 2 | 2 | 176,000,000 | 11.5 |

| Citi Real Estate Funding Inc., German American Capital Corporation(3) | 1 | 2 | 75,000,000 | 4.9 |

| Total | 53 | 65 | $1,530,900,153 | 100.0% |

| (1) | JPMorgan Chase Bank, National Association and German American Capital Corporation and are co-sponsors with respect to the 860 Washington mortgage loan (7.6%), which mortgage loan is evidenced by three (3) promissory notes: (i) notes A-1, A-2 and A-3, with an outstanding principal balance of $81,200,000 as of the cut-off date, as to which JPMorgan Chase Bank, National Association is acting as mortgage loan seller; and (ii) notes A-4 and A-5, with an outstanding principal balance of $34,800,000 as of the cut-off date, as to which German American Capital Corporation is acting as mortgage loan seller. |

| (2) | JPMorgan Chase Bank, National Association and German American Capital Corporation and are co-sponsors with respect to The Grace Building mortgage loan (3.9%), which mortgage loan is evidenced by two (2) promissory notes: (i) note A-2-4, with an outstanding principal balance of $30,000,000 as of the cut-off date, as to which JPMorgan Chase Bank, National Association is acting as mortgage loan seller; and (ii) note A-4-3, with an outstanding principal balance of $30,000,000 as of the cut-off date, as to which German American Capital Corporation is acting as mortgage loan seller. |

| (3) | Citi Real Estate Funding Inc. and German American Capital Corporation are co-sponsors with respect to the MGM Grand & Mandalay Bay mortgage loan (4.9%), which mortgage loan is evidenced by two (2) promissory notes: (i) note A-13-8 with an outstanding principal balance of $59,375,000 as of the cut-off date, as to which Citi Real Estate Funding Inc. is acting as mortgage loan seller; and (ii) note A-15-8, with an outstanding principal balance of $15,625,000 as of the cut-off date, as to which German American Capital Corporation is acting as mortgage loan seller. |

Ten Largest Mortgage Loans(1)(2)

# | Mortgage Loan Name | Cut-off Date Balance | % of Initial Pool Balance | Property Type | Property Size | Cut-off Date Balance Per SF/Unit/Room | UW NCF | UW | Cut-off Date LTV Ratio(3) |

| 1 | 860 Washington | $116,000,000 | 7.6% | Mixed Use | 117,230 | $990 | 4.58x | 12.0% | 48.3% |

| 2 | Millennium Corporate Park | 105,000,000 | 6.9 | Office | 537,046 | $246 | 3.13x | 10.0% | 60.9% |

| 3 | 360 Spear | 104,726,660 | 6.8 | Office | 179,277 | $584 | 2.13x | 13.1% | 40.3% |

| 4 | Phillips Point | 75,000,000 | 4.9 | Office | 448,885 | $442 | 2.78x | 9.7% | 68.7% |

| 5 | MGM Grand & Mandalay Bay(4) | 75,000,000 | 4.9 | Hospitality | 9,748 | $167,645 | 4.95x | 17.9% | 35.5% |

| 6 | Pittock Block | 75,000,000 | 4.9 | Mixed Use | 297,698 | $474 | 2.38x | 8.5% | 42.9% |

| 7 | Waterway Plaza | 66,000,000 | 4.3 | Office | 223,516 | $295 | 3.72x | 12.8% | 60.0% |

| 8 | Leonardo DRS Industrial | 63,700,000 | 4.2 | Industrial | 491,476 | $130 | 2.63x | 8.9% | 64.1% |

| 9 | The Grace Building | 60,000,000 | 3.9 | Office | 1,556,972 | $567 | 4.25x | 11.8% | 41.1% |

| 10 | Station Park & Station Park West | 58,700,000 | 3.8 | Mixed Use | 995,303 | $119 | 3.92x | 14.0% | 50.0% |

| Top 10 Total / Wtd. Avg. | $799,126,660 | 52.2% | 3.43x | 11.8% | 50.9% | ||||

| Remaining Total / Wtd. Avg. | 731,773,493 | 47.8 | 2.82x | 11.3% | 56.2% | ||||

| Total / Wtd. Avg. | $1,530,900,153 | 100.0% | 3.14x | 11.6% | 53.5% |

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | With respect to each mortgage loan that is part of a loan combination (as identified under “Collateral Overview—Loan Combination Summary” below), the Cut-off Date Balance Per SF/Unit/Room, UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s) or other indebtedness. |

| (3) | With respect to certain of the mortgage loans identified above, the Cut-off Date LTV Ratios have been calculated using “as-stabilized”, “portfolio premium” or similar hypothetical values. Such mortgage loans are identified under the definition of “Appraised Value” set forth under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (4) | The UW NCF DSCR and UW NOI Debt Yield on the MGM Grand & Mandalay Bay mortgage loan are each calculated based on the master lease annual rent of $292,000,000. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Academy Securities Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

14

| COLLATERAL OVERVIEW (continued) |

Loan Combination Summary

Mortgage Loan Name(1) | Mortgage Loan Cut-off Date Balance | Mortgage Loan as Approx. % of Initial Pool Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Loan Combination Cut-off Date Balance | Controlling Pooling/Trust and Servicing Agreement (“Controlling PSA”)(2) | Master Servicer / Outside Servicer | Special Servicer / Outside Special Servicer |

| Millennium Corporate Park | $105,000,000 | 6.9% | $27,000,000 | - | $132,000,000 | Benchmark 2021-B23 | Midland | CWCapital |

| 360 Spear | $104,726,660 | 6.8% | - | $55,000,000 | $159,726,660 | Benchmark 2021-B23 | Midland | CWCapital |

| Phillips Point | $75,000,000 | 4.9% | $123,520,000 | - | $198,520,000 | Benchmark 2021-B23 | Midland | CWCapital |