| | | FREE WRITING PROSPECTUS |

| | | FILED PURSUANT TO RULE 433 |

| | | REGISTRATION FILE NO.: 333-255934-09 |

| | | |

| Dated November 20, 2023 | BMO 2023-C7 |

| Structural and Collateral Term Sheet |

BMO 2023-C7 Mortgage Trust |

$739,304,766 (Approximate Mortgage Pool Balance) |

| |

$[ ] (Approximate Offered Certificates) |

| |

BMO Commercial Mortgage Securities LLC Depositor |

COMMERCIAL MORTGAGE PASS-THROUGH CERTIFICATES, SERIES 2023-C7 |

Bank of Montreal Citi Real Estate Funding Inc. UBS AG Starwood Mortgage Capital LLC RRECM Capital II, LLC (formerly known as Sabal Capital II, LLC) Greystone Commercial Mortgage Capital LLC KeyBank National Association Sponsors and Mortgage Loan Sellers |

| BMO Capital Markets | KeyBanc Capital Markets | UBS Securities LLC | Citigroup |

| Co-Lead Managers and Joint Bookrunners |

Academy Securities

Co-Manager | Bancroft Capital, LLC

Co-Manager | Drexel Hamilton

Co-Manager |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| |

| Dated November 20, 2023 | BMO 2023-C7 |

This material is for your information, and none of BMO Capital Markets Corp., Citigroup Global Markets Inc., KeyBanc Capital Markets Inc., UBS Securities LLC, Academy Securities, Inc., Bancroft Capital, LLC and Drexel Hamilton, LLC (collectively, the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-255934) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or BMO Capital Markets Corp., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-866-864-7760. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2023-C7 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these Certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the Certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the Certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Europe p.l.c, and Bank of Montreal (China) Co. Ltd, the institutional broker dealer business of BMO Capital Markets Corp. (Member FINRA and SIPC) and the agency broker dealer business of Clearpool Execution Services, LLC (Member FINRA and SIPC) in the U.S., and the institutional broker dealer businesses of BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia, Bank of Montreal Europe p.l.c. (authorized and regulated by the Central Bank of Ireland) in Europe and BMO Capital Markets Limited (authorized and regulated by the Financial Conduct Authority) in the UK and Australia.

| Dated November 20, 2023 | BMO 2023-C7 |

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 3 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| Collateral Characteristics |

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate

Cut-off Date Balance | |

| BMO | 8 | 27 | $240,850,000 | 32.6% |

| CREFI | 6 | 9 | $183,166,296 | 24.8% |

| UBS AG | 4 | 7 | $89,908,333 | 12.2% |

| SMC | 4 | 4 | $74,100,000 | 10.0% |

| Regions | 6 | 6 | $72,581,000 | 9.8% |

| GCMC | 3 | 3 | $42,699,137 | 5.8% |

| KeyBank | 1 | 29 | $36,000,000 | 4.9% |

| Total: | 32 | 85 | $739,304,766 | 100.0% |

| Loan Pool | |

| | Initial Pool Balance (“IPB”): | $739,304,766 |

| | Number of Mortgage Loans: | 32 |

| | Number of Mortgaged Properties: | 85 |

| | Average Cut-off Date Balance per Mortgage Loan: | $23,103,274 |

| | Weighted Average Current Mortgage Rate: | 7.20127% |

| | 10 Largest Mortgage Loans as % of IPB: | 53.9% |

| | Weighted Average Remaining Term to Maturity: | 108 months |

| | Weighted Average Seasoning: | 2 months |

| | | |

| Credit Statistics | |

| | Weighted Average UW NCF DSCR: | 1.69x |

| | Weighted Average UW NOI Debt Yield(1): | 13.2% |

| | Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”): | 53.4% |

| | Weighted Average Maturity Date/ARD LTV: | 52.1% |

| | | |

| Other Statistics | |

| | % of Mortgage Loans with Additional Debt: | 9.0% |

| | % of Mortgage Loans with Single Tenants(2): | 16.7% |

| | % of Mortgage Loans secured by Multiple Properties: | 34.8% |

| | |

| Amortization | |

| | Weighted Average Original Amortization Term: | 360 months |

| | Weighted Average Remaining Amortization Term: | 360 months |

| | % of Mortgage Loans with Interest-Only: | 77.1% |

| | % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 18.4% |

| | % of Mortgage Loans with Amortizing Balloon: | 4.6% |

| | | |

| Lockboxes | |

| | % of Mortgage Loans with Hard Lockboxes: | 67.7% |

| | % of Mortgage Loans with Springing Lockboxes: | 21.4% |

| | % of Mortgage Loans with Soft Lockboxes: | 10.8% |

| | | |

| Reserves | |

| | % of Mortgage Loans Requiring Monthly Tax Reserves: | 58.2% |

| | % of Mortgage Loans Requiring Monthly Insurance Reserves: | 45.3% |

| | % of Mortgage Loans Requiring Monthly CapEx Reserves: | 49.3% |

| | % of Mortgage Loans Requiring Monthly TI/LC Reserves(3): | 37.1% |

| (1) | In the case of Loan No. 7, the UW NOI Debt Yield (11.6%) is based on Cut-off Date Principal Balance after netting out a $4,200,000 holdback reserve. The UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve is 10.2%. |

| (2) | Excludes mortgage loans that are secured by multiple properties with multiple tenants. |

| (3) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, industrial, retail, data center and mixed use properties. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 4 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| Collateral Characteristics |

| Ten Largest Mortgage Loans |

| No. | Loan Name | City, State | Mortgage Loan Seller | No.

of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms / Units | Property Type | UW

NCF DSCR | UW NOI Debt Yield(1) | Cut-off Date LTV | Maturity Date/ARD LTV |

| 1 | Woodfield Mall | Schaumburg, IL | BMO | 1 | $68,000,000 | 9.2% | 1,064,590 | Retail | 2.02x | 14.4% | 42.4% | 42.4% |

| 2 | Arundel Mills and Marketplace | Hanover, MD | CREFI | 1 | $60,000,000 | 8.1% | 1,938,983 | Retail | 1.98x | 16.1% | 41.4% | 41.4% |

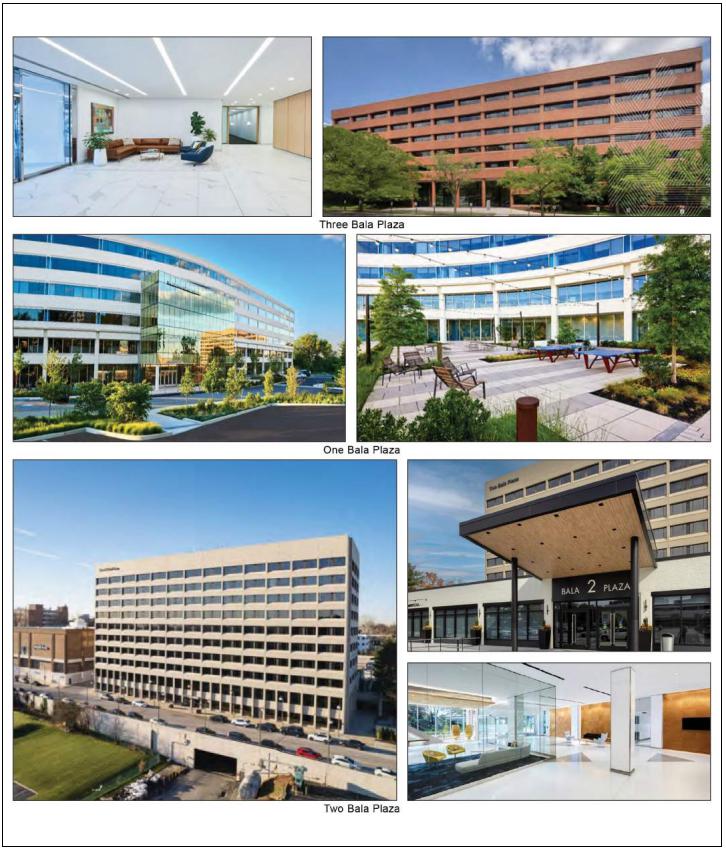

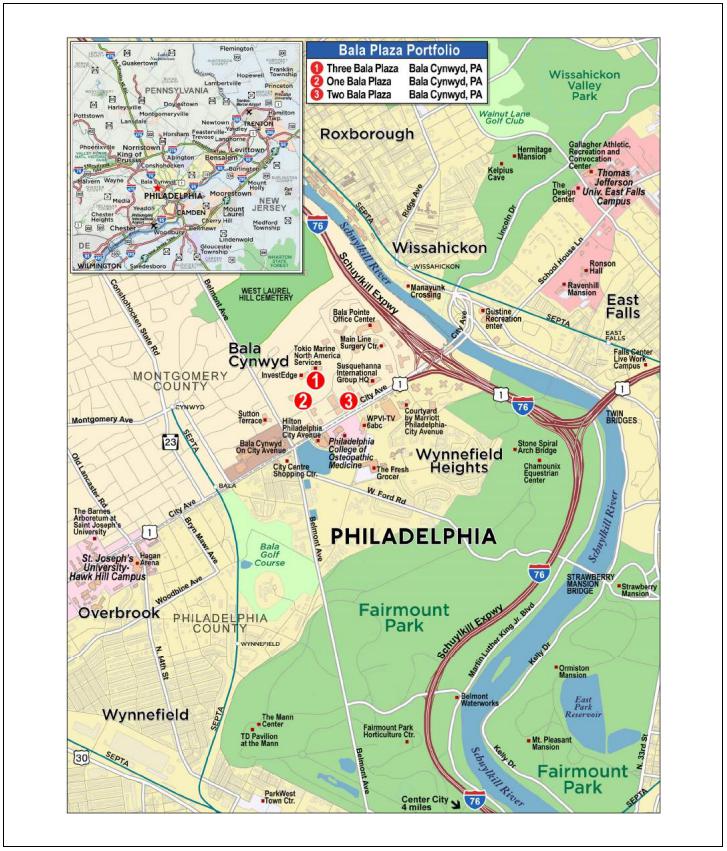

| 3 | Bala Plaza Portfolio | Bala Cynwyd, PA | CREFI | 3 | $40,000,000 | 5.4% | 1,136,771 | Various | 1.68x | 16.2% | 47.4% | 47.4% |

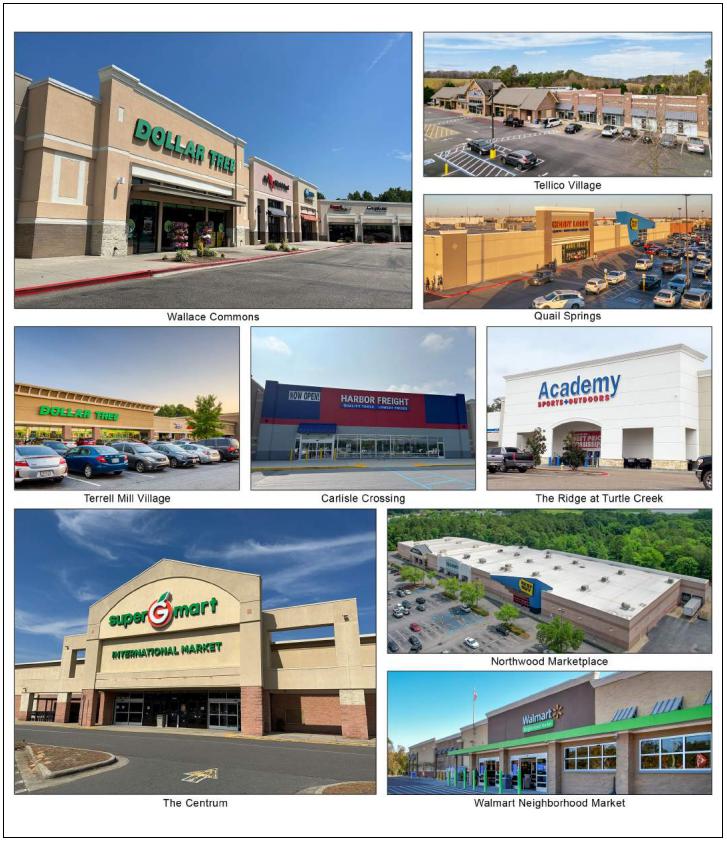

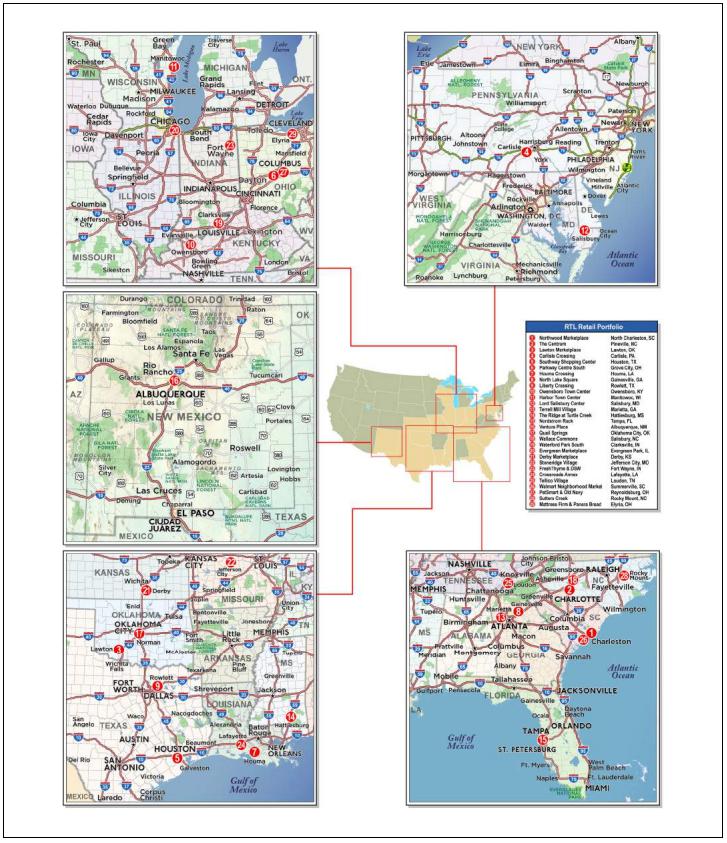

| 4 | RTL Retail Portfolio | Various, Various | KeyBank | 29 | $36,000,000 | 4.9% | 3,117,102 | Retail | 1.97x | 13.8% | 51.2% | 51.2% |

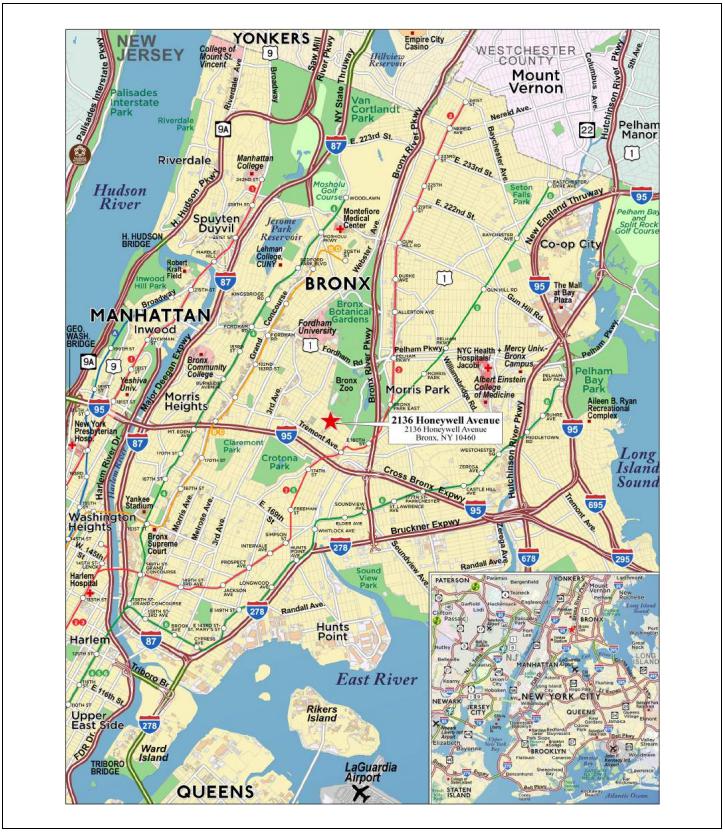

| 5 | 2136 Honeywell Avenue | Bronx, NY | SMC | 1 | $36,000,000 | 4.9% | 101 | Multifamily | 1.20x | 9.9% | 59.1% | 54.6% |

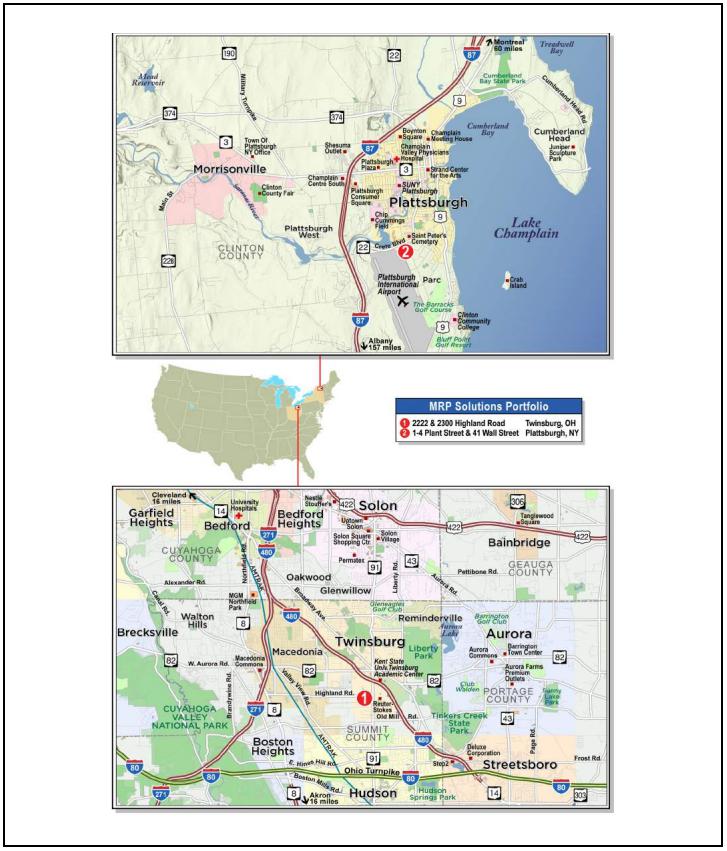

| 6 | MRP Solutions Portfolio | Various, Various | BMO | 2 | $34,000,000 | 4.6% | 560,141 | Industrial | 1.78x | 11.0% | 59.4% | 59.4% |

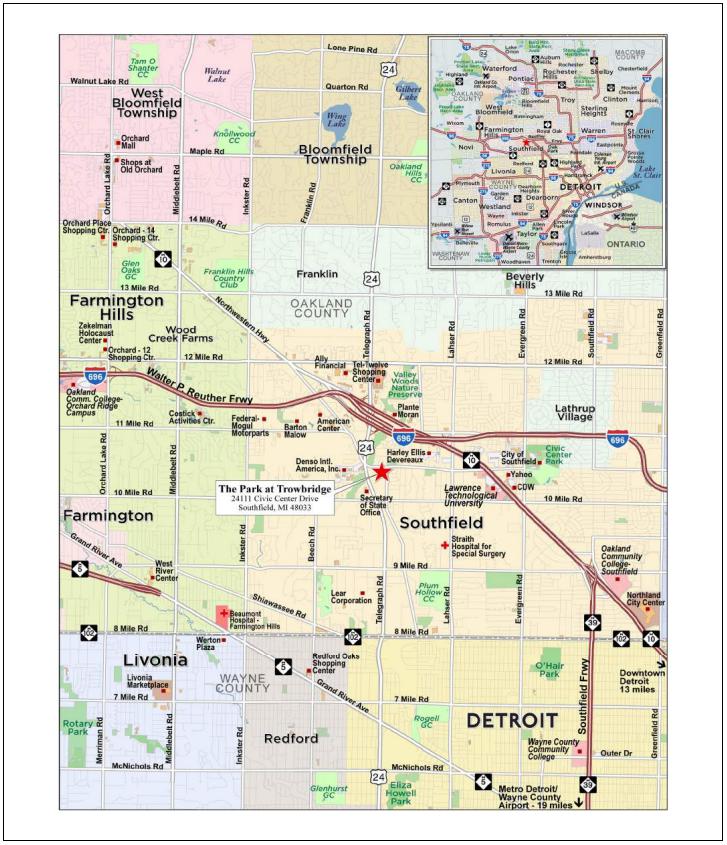

| 7 | The Park at Trowbridge | Southfield, MI | BMO | 1 | $33,000,000 | 4.5% | 320 | Multifamily | 1.34x | 11.6% | 45.2% | 45.2% |

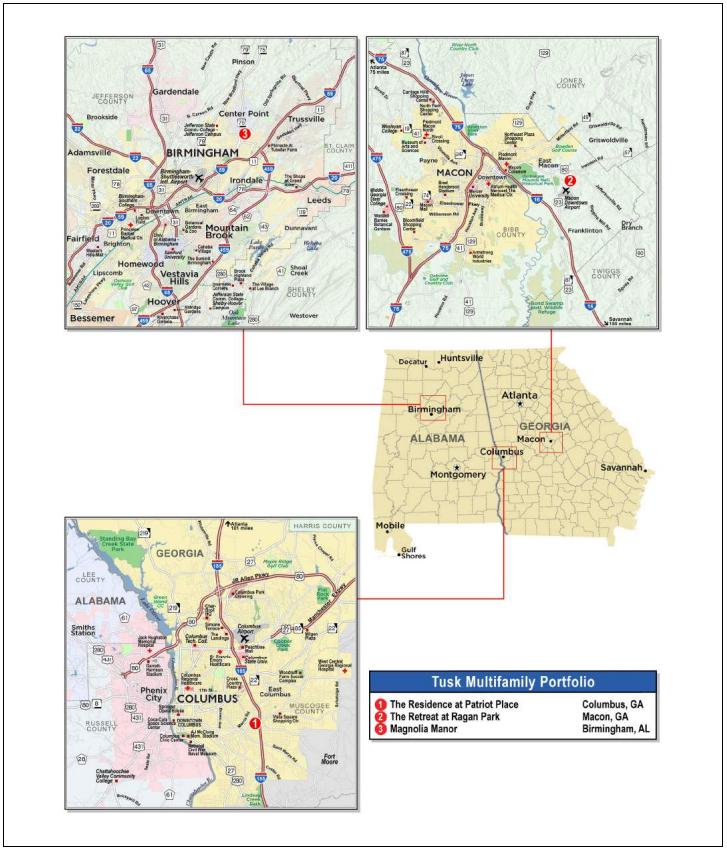

| 8 | Tusk Multifamily Portfolio | Various, Various | UBS AG | 3 | $33,000,000 | 4.5% | 523 | Multifamily | 1.25x | 8.9% | 63.5% | 63.5% |

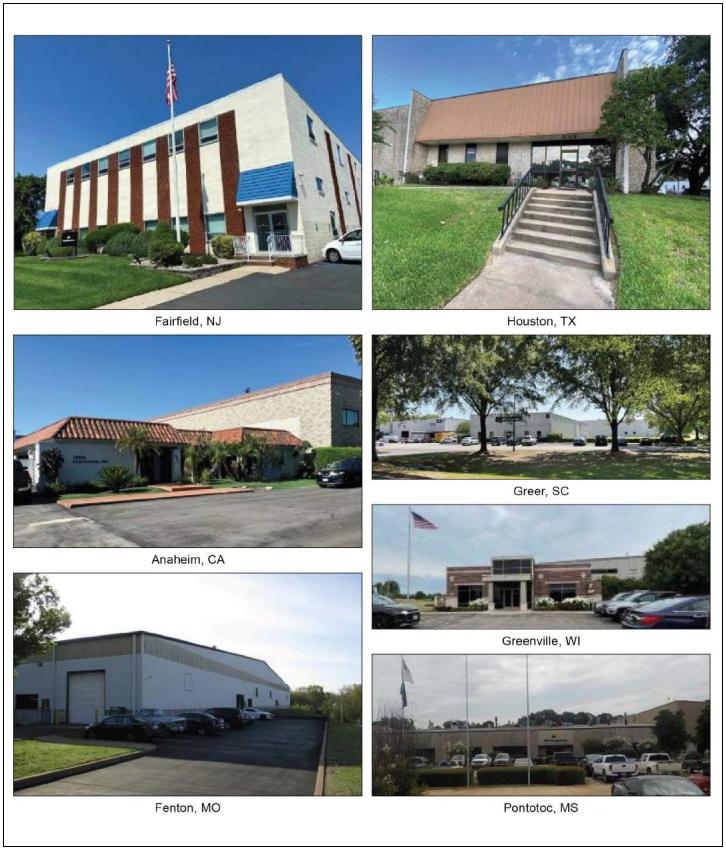

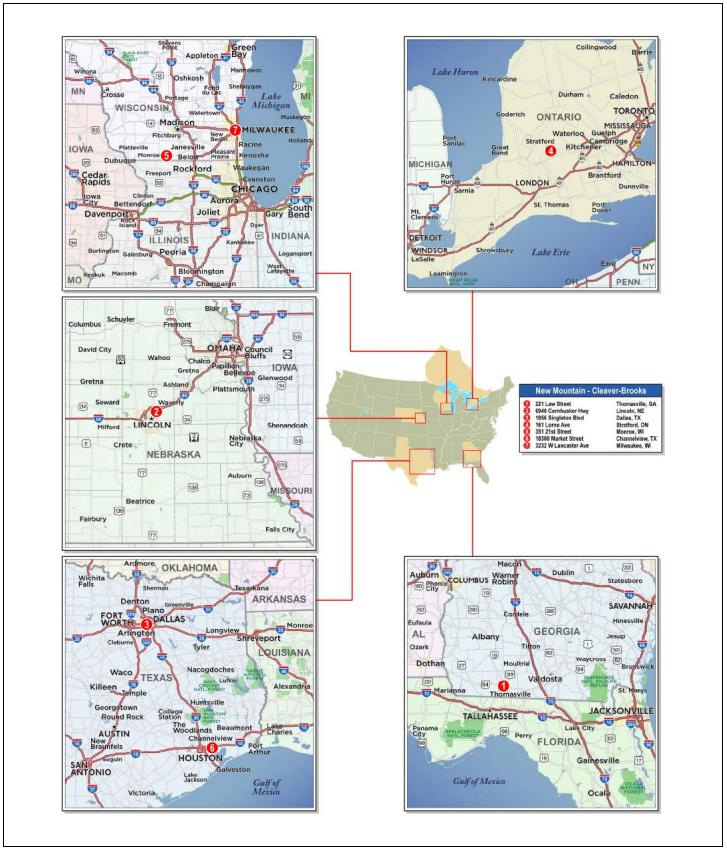

| 9 | New Mountain - Cleaver Brooks | Various, Various | BMO | 7 | $31,350,000 | 4.2% | 799,679 | Industrial | 1.95x | 13.6% | 53.8% | 53.8% |

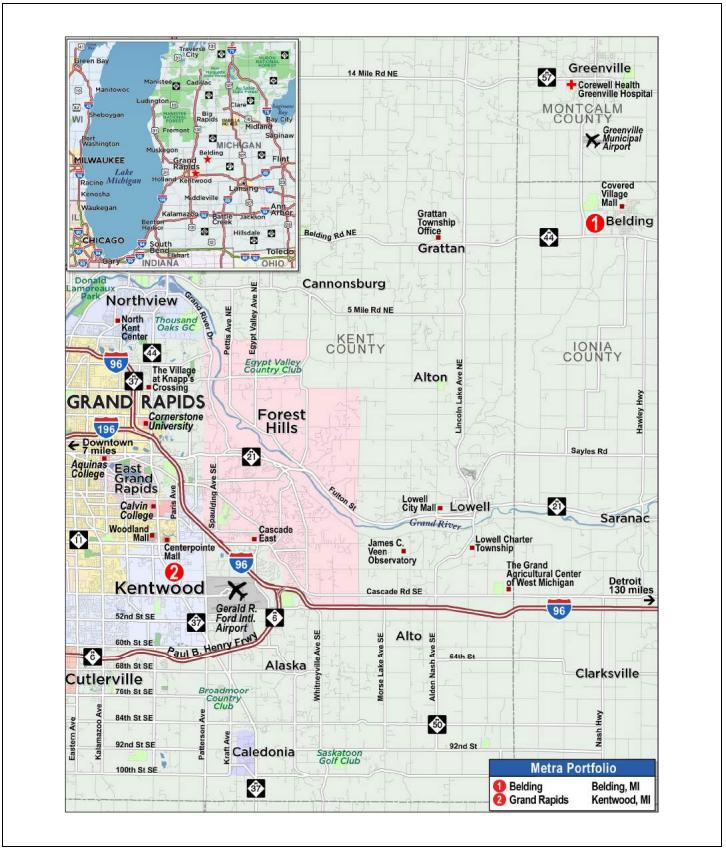

| 10 | Metra Portfolio | Various, MI | CREFI | 2 | $27,216,296 | 3.7% | 450,104 | Industrial | 1.30x | 11.6% | 59.4% | 55.1% |

| | | | | | | | | | | | | |

| | Top 3 Total/Weighted Average | 5 | $168,000,000 | 22.7% | | | 1.92x | 15.4% | 43.2% | 43.2% |

| | Top 5 Total/Weighted Average | 35 | $240,000,000 | 32.5% | | | 1.82x | 14.4% | 46.8% | 46.1% |

| | Top 10 Total/Weighted Average | 50 | $398,566,296 | 53.9% | | | 1.71x | 13.1% | 50.5% | 49.8% |

| | Non-Top 10 Total/Weighted Average | 35 | $340,738,470 | 46.1% | | | 1.66x | 13.3% | 56.7% | 54.8% |

| (1) | In the case of Loan No. 7, the UW NOI Debt Yield (11.6%) is based on Cut-off Date Principal Balance after netting out a $4,200,000 holdback reserve. The UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve is 10.2%. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 5 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| Collateral Characteristics |

| Pari Passu Companion Loan Summary |

No. | Loan Name | | Trust Cut-off Date Balance | Aggregate Pari Passu Loan Cut-off Date Balance | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Loan(s) Original Balance |

| 1 | Woodfield Mall | BMO | $68,000,000 | $226,000,000 | BMO 2023-C7(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $226,000,000 |

| 2 | Arundel Mills and Marketplace | CREFI | $60,000,000 | $300,000,000 | BMO 2023-C7(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $300,000,000 |

| 3 | Bala Plaza Portfolio | CREFI | $40,000,000 | $59,500,000 | BMO 2023-C7(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $59,500,000 |

| 4 | RTL Retail Portfolio | KeyBank | $36,000,000 | $224,000,000 | BBCMS 2023-C22 | Midland | Rialto | BBCMS 2023-C21

BBCMS 2023-C22

Future Securitization(s) | $62,500,000

$68,833,334

$92,666,666 |

| 12 | 11 West 42nd Street | UBS AG | $26,333,333 | $247,666,667 | BANK5 2023-5YR3 | Wells Fargo | Greystone | BMO 2023-5C1

BMO 2023-C6

BMO 2023-5C2

BANK5 2023-5YR3

BBCMS 2023-C21

BBCMS 2023-5C23(2)

Future Securitization(s) | $62,500,000

$25,000,000

$18,833,333

$75,000,000

$15,000,000

$20,000,000

$31,333,334 |

| 13 | OPI Portfolio | UBS AG | $25,000,000 | $29,300,000 | BMO 2023-C7(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $29,300,000 |

| 14 | Creekside Town Center | BMO | $24,000,000 | $47,525,000 | BMO 2023-C7(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $47,525,000 |

| 18 | 60 Hudson | BMO | $20,000,000 | $260,000,000 | BBCMS 2023-C22(3) | Midland(3) | Rialto(3) | BBCMS 2023-C22

Future Securitization(s) | $40,000,000

$220,000,000 |

| 19 | Knoll Ridge Apartments | BMO | $17,500,000 | $25,000,000 | BBCMS 2023-C22 | Midland | Rialto | BBCMS 2023-C22 | $25,000,000 |

| 20 | 645 North Michigan Avenue | CREFI | $17,000,000 | $38,000,000 | BMO 2023-C7(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $38,000,000 |

| 25 | Regency Retail Portfolio | BMO | $13,000,000 | $40,000,000 | BBCMS 2023-C22 | Midland | Rialto | BBCMS 2023-C22 | $40,000,000 |

| (1) | In the case of Loan Nos. 1, 2, 3, 13, 14 and 20, until the securitization of the related controlling pari passu companion loan, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement for the BMO 2023-C7 securitization transaction by the parties thereto. Upon the securitization of the related controlling pari-passu companion loan, servicing of the related whole loan will shift to the servicers under the servicing agreement with respect to such future securitization transaction, which servicing agreement will become the Controlling Pooling/Trust & Servicing Agreement. |

| (2) | Based on a publicly available prospectus. The BBCMS 2023-5C23 transaction is expected to close prior to the closing of this securitization transaction. |

| (3) | In the case of Loan No. 18, until the securitization of the related controlling pari passu companion loan, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement for the BBCMS 2023-C22 securitization transaction by the parties thereto. Upon the securitization of the related controlling pari-passu companion loan, servicing of the related whole loan will shift to the servicers under the servicing agreement with respect to such future securitization transaction, which servicing agreement will become the Controlling Pooling/Trust & Servicing Agreement. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 6 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| Collateral Characteristics |

| Mortgaged Properties by Type |

| | | | | | Weighted Average |

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW

NCF DSCR | UW

NOI DY(1) | Cut-off Date LTV | Maturity Date/ARD LTV |

| Retail | Anchored | 41 | $149,904,467 | 20.3% | 1.62x | 12.4% | 59.9% | 57.6% |

| | Super Regional Mall | 2 | 128,000,000 | 17.3 | 2.00x | 15.2% | 41.9% | 41.9% |

| | Unanchored | 3 | 13,765,000 | 1.9 | 2.12x | 16.0% | 49.8% | 47.8% |

| | Shadow Anchored | 3 | 2,511,533 | 0.3 | 1.80x | 12.7% | 58.3% | 58.3% |

| | Subtotal: | 49 | $294,181,000 | 39.8% | 1.81x | 13.8% | 51.6% | 50.3% |

| Multifamily | Garden | 7 | $73,500,000 | 9.9% | 1.29x | 9.5% | 64.6% | 64.6% |

| | Mid Rise | 2 | 69,000,000 | 9.3 | 1.27x | 10.7% | 52.5% | 50.1% |

| | Subtotal: | 9 | $142,500,000 | 19.3% | 1.28x | 10.1% | 58.7% | 57.6% |

| Industrial | Warehouse/Manufacturing | 9 | $65,350,000 | 8.8% | 1.86x | 12.2% | 56.7% | 56.7% |

| | Manufacturing | 3 | 32,791,296 | 4.4 | 1.40x | 11.7% | 59.2% | 55.7% |

| | Subtotal: | 12 | $98,141,296 | 13.3% | 1.71x | 12.1% | 57.6% | 56.4% |

| Office | Suburban | 4 | $56,530,111 | 7.6% | 1.69x | 14.8% | 48.7% | 48.7% |

| | CBD | 2 | 33,477,900 | 4.5 | 1.47x | 12.1% | 49.2% | 49.2% |

| | Subtotal: | 6 | $90,008,011 | 12.2% | 1.60x | 13.8% | 48.9% | 48.9% |

| Hospitality | Full Service | 2 | $33,500,000 | 4.5% | 1.50x | 15.6% | 56.9% | 55.1% |

| | Limited Service | 2 | 20,550,000 | 2.8 | 1.47x | 14.9% | 65.0% | 60.6% |

| | Subtotal: | 4 | $54,050,000 | 7.3% | 1.49x | 15.4% | 60.0% | 57.2% |

| Mixed Use | Medical Office/Retail | 1 | $17,000,000 | 2.3% | 1.57x | 14.2% | 57.9% | 51.3% |

| | Office/Retail | 2 | 9,424,459 | 1.3 | 1.60x | 15.7% | 49.8% | 49.0% |

| | Subtotal: | 3 | $26,424,459 | 3.6% | 1.58x | 14.7% | 55.0% | 50.5% |

| Other | Data Center | 1 | $20,000,000 | 2.7% | 3.92x | 24.2% | 17.5% | 17.5% |

| Self Storage | Self Storage | 1 | $14,000,000 | 1.9% | 1.33x | 10.3% | 59.6% | 59.6% |

| Total / Weighted Average: | 85 | $739,304,766 | 100.0% | 1.69x | 13.2% | 53.4% | 52.1% |

| (1) | In the case of Loan No. 7, the UW NOI Debt Yield (11.6%) is based on Cut-off Date Principal Balance after netting out a $4,200,000 holdback reserve. The UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve is 10.2%. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 7 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 8 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 9 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 10 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 11 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 12 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Seller: | BMO | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $68,000,000 | | Title: | Fee Simple / Leased Fee |

| Cut-off Date Principal Balance(1): | $68,000,000 | | Property Type – Subtype: | Retail – Super-Regional Mall |

| % of IPB: | 9.2% | | Net Rentable Area (SF): | 1,064,590 |

| Loan Purpose: | Refinance | | Location: | Schaumburg, Illinois |

| Borrower: | Woodfield Mall LLC | | Year Built / Renovated: | 1971, 1995 / 2015, 2016, 2018 |

| Borrower Sponsors: | International Mall Investors LLC and Simon Property Group, L.P. | | Occupancy(4): | 96.1% |

| Interest Rate: | 6.85000% | | Occupancy Date: | 11/14/2023 |

| Note Date: | 11/21/2023 | | 4th Most Recent NOI (As of): | $27,546,528 (12/31/2020) |

| Maturity Date: | 12/1/2033 | | 3rd Most Recent NOI (As of): | $37,229,630 (12/31/2021) |

| Interest-only Period: | 120 months | | 2nd Most Recent NOI (As of): | $36,506,153 (12/31/2022) |

| Original Term: | 120 months | | Most Recent NOI (As of): | $36,477,631 (TTM 10/31/2023) |

| Original Amortization Term: | None | | UW Economic Occupancy: | 95.5% |

| Amortization Type: | Interest Only | | UW Revenues: | $75,029,161 |

| Call Protection: | L(24),DorYM1(89),O(7) | | UW Expenses: | $32,816,238 |

| Lockbox / Cash Management(2): | Hard / Springing | | UW NOI: | $42,212,924 |

| Additional Debt(1): | Yes | | UW NCF: | $41,153,257 |

| Additional Debt Balance(1): | $226,000,000 | | Appraised Value / Per SF: | $694,000,000 / $652 |

| Additional Debt Type(1): | Pari Passu | | Appraisal Date: | 10/27/2023 |

| | | | | |

| Escrows and Reserves(3) | | Financial Information(1) |

| | Initial | Monthly | Initial Cap | | Cut-off Date Loan / SF: | $272.16 |

| Taxes: | $0 | Springing | NAP | | Maturity Date Loan / SF: | $272.16 |

| Insurance: | $0 | Springing | NAP | | Cut-off Date LTV(5): | 42.4% |

| Replacement Reserves: | $0 | Springing | NAP | | Maturity Date LTV(5): | 42.4% |

| Deferred Maintenance: | $0 | NAP | NAP | | UW NCF DSCR: | 2.02x |

| TI/LC: | $5,445,975 | Springing | NAP | | UW NOI Debt Yield: | 14.4% |

| Other(4): | $1,603,122 | NAP | NAP | | | |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | | Uses | Proceeds | % of Tot | al |

| Whole Loan | $294,000,000 | 77.1 | % | | Loan Payoff | $372,898,903 | 97.7 | % |

| Sponsor Equity | 87,509,237 | 22.9 | | | Upfront Reserves | 7,049,097 | 1.9 | |

| | | | | Closing Costs | 1,561,237 | 0.4 | |

| Total Sources | $381,509,237 | 100.0 | % | | Total Uses | $381,509,237 | 100.0 | % |

| (1) | The Woodfield Mall Mortgage Loan (as defined below) is part of a whole loan evidenced by 16 pari passu notes with an aggregate original principal balance of $294,000,000. Financial Information in the chart above reflects the Woodfield Mall Whole Loan (as defined below). For additional information, see “The Loan” below. |

| (2) | The borrower is required to cause rents to be deposited into a lockbox account established at origination under the Woodfield Mall Whole Loan documents, and the borrower will have access to the funds in the lockbox account and use the lockbox account as an operating account so long as no Lockbox Event (as defined below) continues. During the continuance of a Lockbox Event, the borrower will not have any further access to the funds in the lockbox account except as otherwise expressly provided in the Woodfield Mall Whole Loan documents. |

| (3) | For a full description of Escrows and Reserves, please refer to “Escrows and Reserves” below. |

| (4) | Other Initial Escrows and Reserves consist of (i) $638,391 for a gap rent reserve and (ii) $964,731 for an upfront free rent reserve. |

| (5) | Occupancy for the Woodfield Mall Property (as defined below) includes temporary tenants. As of November 14, 2023, the Woodfield Mall Property was 87.5% occupied excluding temporary tenants. As of November 14, 2023, occupancy for the Woodfield Mall (as defined below) including temporary tenants was 98.1% and excluding temporary tenants was 98.0%. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 13 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

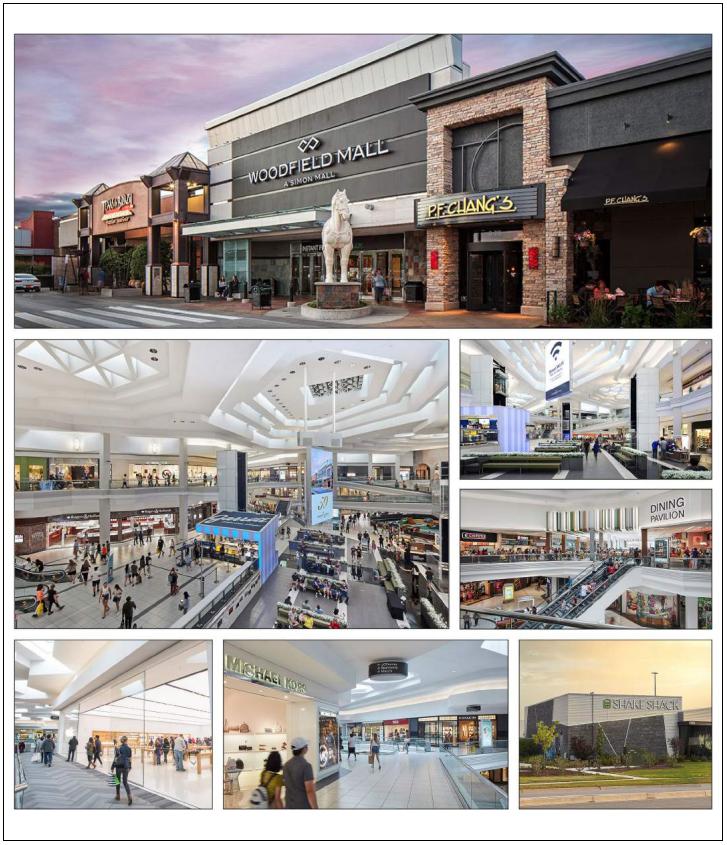

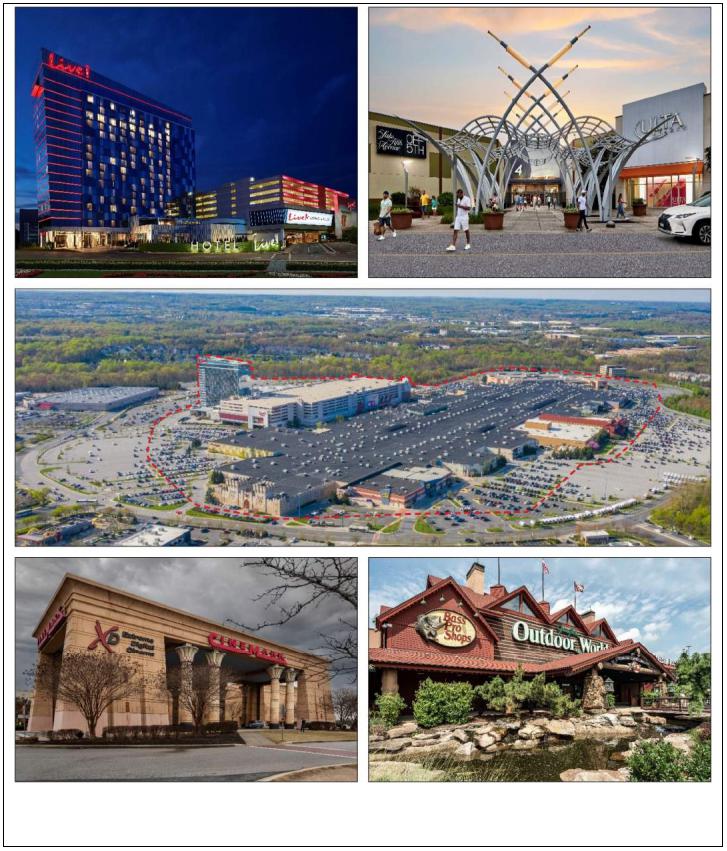

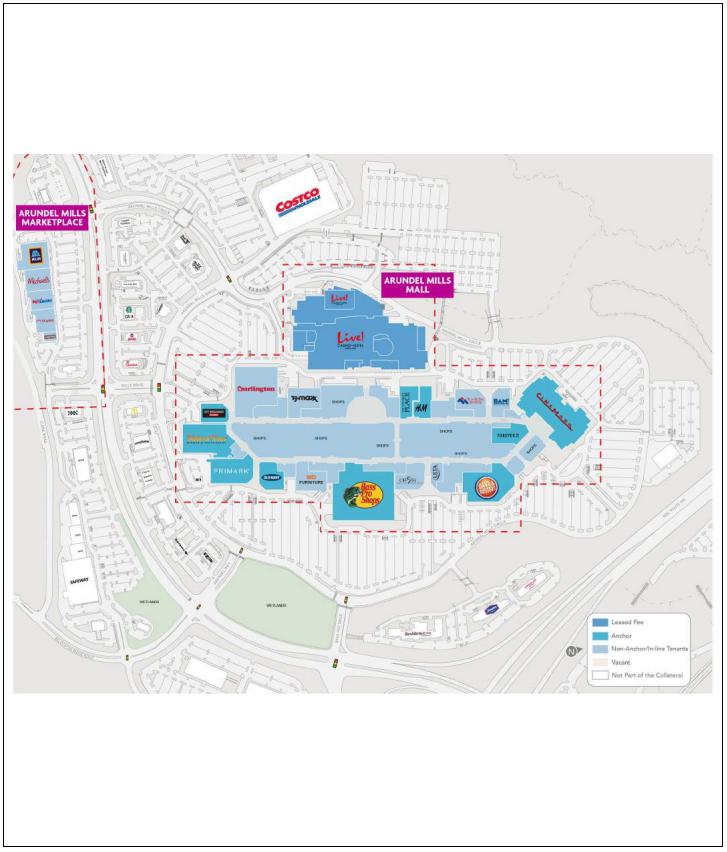

The Loan. The largest mortgage loan (the “Woodfield Mall Mortgage Loan”) is part of a whole loan (the “Woodfield Mall Whole Loan”) evidenced by 16 pari passu promissory notes in the aggregate original principal amount of $294,000,000. The Woodfield Mall Mortgage Loan is evidenced by two non-controlling notes which have an aggregate outstanding principal balance as of the Cut-off Date of $68,000,000. The Woodfield Mall Mortgage Loan will be included in the BMO 2023-C7 securitization trust and represent approximately 9.2% of the Initial Pool Balance. The Woodfield Mall Whole Loan was co-originated on November 21, 2023 by Bank of Montreal (“BMO”), Barclays Capital Real Estate Inc. (“Barclays”) and Bank of America, N.A. (“BANA”). The Woodfield Mall Whole Loan is secured by the borrower’s fee interest and leased fee interest in a portion of the super-regional mall (the “Woodfield Mall”) located in Schaumburg, Illinois (such portion of the mall securing the Woodfield Mall Whole Loan, the “Woodfield Mall Property”). The borrower owns the fee interest in the Woodfield Mall Property. The borrower ground leased a portion of the Woodfield Mall (the “Nordstrom Parcel”) to Nordstrom pursuant to the ground lease (the “Nordstrom Ground Lease”) between Nordstrom as ground lessor and the borrower as ground lessee. The Woodfield Mall Property collectively represents approximately 49.5% of the total 2,152,069 square feet of net rentable area at the Woodfield Mall (the “Total Mall NRA”).

The Woodfield Mall Whole Loan proceeds were used to refinance the existing debt on the Woodfield Mall Property, fund upfront reserves and pay origination costs. The Woodfield Mall Whole Loan accrues interest at a fixed rate of 6.85000% per annum. The table below summarizes the promissory notes that comprise the Woodfield Mall Whole Loan. The relationship between the holders of the Woodfield Mall Whole Loan is governed by a co-lender agreement as described under “Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans” and “Description of the Mortgage Pool —The Whole Loans—The Outside Serviced Pari Passu Whole Loans” in the Preliminary Prospectus. The Woodfield Mall Whole Loan will be serviced pursuant to the pooling and servicing agreement for the BMO 2023-C7 trust.

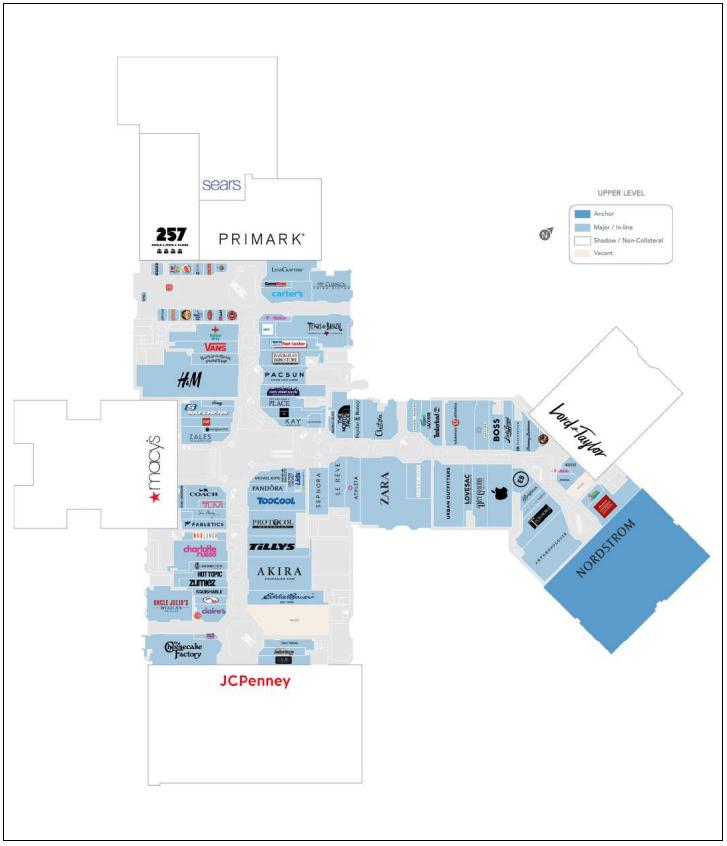

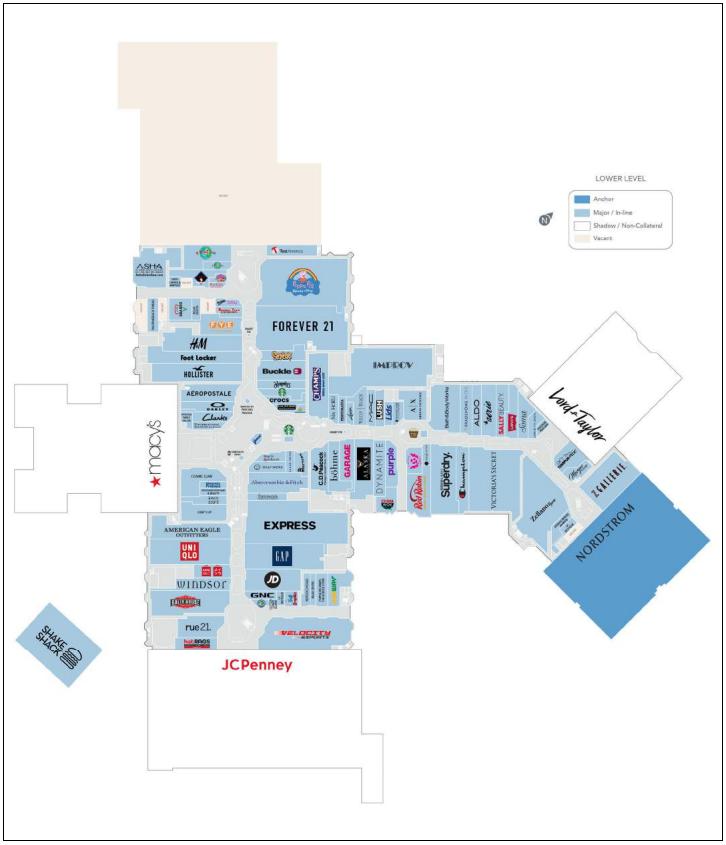

The Property. The Woodfield Mall is a two- and three-story partially enclosed Class “A” super-regional mall, totaling 2,152,069 square feet on an approximately 133.05-acre site in Schaumburg, Illinois. Woodfield Mall was built in 1971 by Taubman Centers and expanded in 1995, and with renovations occurring in 2015, 2016 and 2018. The Woodfield Mall provides parking via 8,949 surface parking and parking garage spaces, resulting in a parking ratio of approximately 4.2 spaces per 1,000 square feet of Total Mall NRA. The Woodfield Mall Property consists of 1,064,590 square feet of net rentable area (approximately 49.5% of the Total Mall NRA).

As of November 14, 2023, the Woodfield Mall Property was 96.1% occupied by over 200 tenants (including temporary tenants, which occupy approximately 8.6% of the Woodfield Mall Property (the “Total Collateral NRA”)). No underwritten base rent is attributable to such temporary tenants. Approximately 47.8% of the Total Collateral NRA is occupied by 20 major tenants (each of which occupies 10,000 or more square feet of net rentable area) and one collateral anchor tenant (Nordstrom).

The portion of the Woodfield Mall occupied by six anchor tenants, namely Macy’s, J.C. Penney, Sears, Primark, Level 257 and Lord & Taylor (the “Non-Collateral Anchors”), representing approximately 50.5% of the Total Mall NRA, and is not part of the collateral securing the Woodfield Mall Mortgage Loan. As used in this term sheet, the term “Woodfield Mall Property” collectively refers to the portion of the mall securing the Woodfield Mall Whole Loan and does not include any portion of the mall owned and occupied by the Non-Collateral Anchors, and the term “Woodfield Mall” collectively refers to the entire mall including the portion of the mall occupied by the Non-Collateral Anchors that is not part of the collateral securing the Woodfield Mall Whole Loan. The information relating to the Woodfield Mall Property in this term sheet does not include any space occupied by the Non-Collateral Anchors, unless otherwise expressly stated herein.

The most recent expansion of the Woodfield Mall Property occurred in 1995, and such expansion included Nordstrom and the mall shops leading to Nordstrom. Renovations of the Woodfield Mall Property occurred in 2015, 2016 and 2018, with the most recent renovation involving a food court.

Major Tenants. The three largest tenants at the Woodfield Mall Property based on underwritten base rent are H&M, Zara and Victoria’s Secret/Pink.

H&M (27,320 square feet; 2.6% NRA; 6.1% of underwritten base rent): H&M Hennes & Mauritz (“H&M”) is a global retailer offering affordable apparel for men, women, and children. H&M was incorporated in 1947 and remains under the control of the family of founder Erling Persson. H&M group’s brands are H&M, H&M Home, COS, Weekday, Monki, & Other Stories, ARKET, Afound and Singular Society. As of 2022, H&M operated over 4,000 stores across 79 markets with approximately

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 14 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

150,000 employees. H&M has been a tenant at the Woodfield Mall Property since 2014 under a lease with an expiration date of January 31, 2029 and no renewal or termination options.

Victoria’s Secret/Pink (18,269 SF, 1.7% of NRA, 3.7% of underwritten base rent). Victoria’s Secret & Co. (“Victoria’s Secret/Pink”) is a Fortune 500 specialty retailer of modern, fashion-inspired collections including signature bras, panties, lingerie, casual sleepwear, athleisure and swim, as well as award-winning prestige fragrances and body care. Victoria’s Secret comprises two brands, Victoria’s Secret and PINK, founded in 1977 by Roy and Gaye Raymond. Victoria’s Secret employs over 30,000 associates across approximately 1,360 retail stores in approximately 70 countries. Victoria’s Secret has been a tenant at the Woodfield Mall Property since 2013 under a lease with an expiration date of January 31, 2028 and no renewal or termination options.

Zara (21,759 square feet; 2.0% NRA; 3.6% of underwritten base rent): Zara is a global clothing retailer having approximately 3,000 stores across 96 countries. Zara is the flagship brand of the Inditex Group. Inditex Group has a variety of brands including Zara, Pull&Bear, Massimo Dutti, Bershka, Stradivarius and Oysho Y Zara, located across 213 markets worldwide. The United States has 98 Inditex Group stores as of January 2019. Zara has been a tenant at the Woodfield Mall Property since 2015 under a lease with an expiration date of October 31, 2028 and no renewal or termination options.

The two largest tenants at the Woodfield Mall based on net rentable area are Macy’s (a Non-Collateral Anchor Tenant) and J.C. Penney (a Non-Collateral Anchor Tenant), and the largest tenant at the Woodfield Mall Property based on net rentable area is Nordstrom.

Nordstrom (200,000 square feet, 18.8% of Total Collateral NRA, 0.0% of underwritten base rent): Nordstrom (Moody’s/S&P/Fitch: Ba1/BB+/BBB-) was founded in 1901 as a retail shoe business in Seattle, Washington. Nordstrom offers an extensive selection of brand-name and private label merchandise for women, men, young adults and children focused on apparel, shoes, beauty, accessories and home goods. The Nordstrom Ground Lease at the Woodfield Mall Property has an original commencement date of March 3, 1995 and expiration date of March 2, 2025. The Nordstrom Ground Lease has seven, 10-year renewal options remaining. Nordstrom does not pay base rent.

Macy’s (Non-Collateral Anchor, 315,498 square feet, 0.0% of Total Collateral NRA, 0.0% of underwritten base rent): Founded in 1858 and headquartered in New York, New York, Macy’s (Moody’s/S&P/Fitch: Ba2/BB+/BBB-) is a department store chain that operates approximately 725 stores in the United States and Washington, D.C., as well as Guam and Puerto Rico. Macy’s has three banners that include Macy’s, bluemercury, and Bloomingdale’s (and accompanying e-commerce sites), that sell men's, women's, and children's apparel and accessories, cosmetics, and home furnishings, among other merchandise. Macy’s has a lease expiration date of December 31, 2050.

J.C. Penney (Non-Collateral Anchor, 288,550 square feet, 0.0% of Total Collateral NRA, 0.0% of underwritten base rent): Founded in 1902 and headquartered in Plano, Texas, J.C. Penney (Moody’s/S&P/Fitch: NR/NR/NR) is a department store chain with approximately 10,000 employees. J.C. Penney sells products including family apparel, footwear, accessories, fine and fashion jewelry, home furnishings, and beauty products through Sephora. J.C. Penney is an original tenant at the Woodfield Mall Property having been a tenant since October 10, 1971. J.C. Penney has a lease expiration date of December 31, 2050.

Appraisal. According to the appraisal, Woodfield Mall Property had an “as-is” appraised value of $694,000,000 as of October 27, 2023. The table below shows the appraiser’s “as-is” conclusions.

| Appraisal Valuation Summary(1) |

| Appraisal Approach | Appraised Value | Capitalization Rate(2) |

| Income Capitalization Approach | $694,000,000 | 6.00% |

| (2) | The appraiser used a discounted cash flow approach to arrive at the appraised value. The capitalization rates shown above represent the overall capitalization rate. |

Environmental. According to the Phase I environmental assessment dated November 7, 2023, there was no evidence of any recognized environmental conditions at the Woodfield Mall Property.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 15 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

The following table presents certain information relating to the historical occupancy of the Woodfield Mall Property:

| Historical and Current Occupancy |

| 2020(1) | 2021(1) | 2022(1) | Current(2) |

| 91.0% | 93.0% | 95.0% | 96.1% |

| (1) | Historical Occupancies are as of December 31 of each respective year and include temporary tenants. Occupancy does not include net rentable area for Non-Collateral Anchor Tenants. |

| (2) | Based on the underwritten rent roll dated November 14, 2023. Current occupancy of the in-line tenants less than 10,000 square feet is 95.2% |

The following table presents certain information relating to the major tenants based on the net rentable area of the Woodfield Mall:

| Top Tenant Summary(1) |

| Tenant | Ratings

Moody’s/S&P/Fitch(2) | Total Mall NRA (SF) | % of

Total Collateral NRA(3) | UW Base Rent PSF(1) | UW Base Rent(1) | % of Total

UW Base Rent(1) | TTM September 2023 Sales $(4) | Sales PSF(4) | Occ Cost | Lease

Expiration Date |

| Non-Collateral Anchor Tenants | | | | | | | | | | |

| Macy's | Ba2/BB+/BBB- | 315,498 | NAP | | $0.00 | $0 | 0.0 | % | $45,400,000 | $144 | NAV | 12/31/2050 |

| J.C. Penney(5) | NR/NR/NR | 288,550 | NAP | | $0.00 | 0 | 0.0 | | $16,500,000 | $57 | 3.6% | 12/31/2050 |

| Sears(6) | NR/NR/NR | 272,678 | NAP | | $0.00 | 0 | 0.0 | | NAV | NAV | NAV | 12/31/2050 |

| Primark(6) | NR/NR/NR | 50,000 | NAP | | $0.00 | 0 | 0.0 | | NAV | NAV | NAV | NAV |

| Level 257(6) | NR/NR/NR | 42,094 | NAP | | $0.00 | 0 | 0.0 | | NAV | NAV | NAV | NAV |

| Lord & Taylor(5) | NR/NR/NR | 118,659 | NAP | | $0.00 | 0 | 0.0 | | NAV | NAV | NAV | 12/31/2050 |

| Non-Collateral Anchor Tenants Subtotal / Wtd. Avg. | | 1,087,479 | NAP | | $0.00 | $0 | 0.0 | % | | | | |

| Collateral Anchor Tenant | | | | | | | | | | |

| Nordstrom | Ba1/BB+/BBB- | 200,000 | 18.8 | % | $0.00 | $0 | 0.0 | % | $17,037,470 | $85 | NAV | 03/02/2025 |

| Major Tenants | | | | | | | | | | |

| H&M | NR/NR/NR | 27,320 | 2.6 | % | $82.62 | 2,257,171 | 6.1 | $10,374,930 | $379.76 | 21.9% | 01/31/2029 |

| Victoria's Secret/Pink | NR/NR/NR | 18,269 | 1.7 | | $75.00 | 1,370,175 | 3.7 | $11,569,094 | $633.26 | 20.9% | 01/31/2028 |

| Zara | NR/NR/NR | 21,759 | 2.0 | | $61.59 | 1,340,243 | 3.6 | $16,127,709 | $741.20 | 9.3% | 10/31/2028 |

| Express/Express Men | NR/NR/NR | 20,176 | 1.9 | | $57.84 | 1,166,913 | 3.2 | $5,307,887 | $263.08 | 24.1% | 04/30/2029 |

| Cheesecake Factory | NR/NR/NR | 11,879 | 1.1 | | $67.80 | 805,432 | 2.2 | $13,685,994 | $1,152.12 | 7.8% | 01/31/2026 |

| Urban Outfitters | NR/NR/NR | 10,775 | 1.0 | | $66.63 | 717,884 | 1.9 | NAV | NAV | NAV | 08/31/2033 |

| The Gap/Gap Kids | NR/NR/NR | 11,202 | 1.1 | | $57.43 | 643,379 | 1.7 | $2,409,049 | $215.06 | 29.1% | 01/31/2027 |

| Hollister Co. | NR/NR/NR | 9,210 | 0.9 | | $65.83 | 606,304 | 1.6 | $6,343,726 | $688.79 | 20.0% | 01/31/2024 |

| Velocity Esports | NR/NR/NR | 15,360 | 1.4 | | $35.81 | 550,000 | 1.5 | NAV | NAV | NAV | 05/31/2036 |

| Uniqlo | NR/NR/NR | 11,384 | 1.1 | | $47.54 | 541,216 | 1.5 | $9,919,451 | $871.35 | 8.5% | 01/31/2029 |

| Major Tenants Subtotal / Wtd. Avg. | | 157,334 | 14.8 | % | $63.55 | $9,998,717 | 27.1 | % | | | | |

| Remaining Occupied | | 665,850 | 62.5 | % | $40.33 | $26,855,145 | 72.9 | % | | | | |

| Occupied Collateral Total | | 1,023,184 | 96.1 | % | $36.02 | $36,853,862 | 100.0 | % | | | | |

| Vacant | | 41,406 | 3.9 | | | | | | | | |

| Collateral Total / Wtd. Avg. | | 1,064,590 | 100.0 | % | | $36,853,862 | 100.0 | % | | | | |

| | | | | | | | | | | |

| Collateral + Non Collateral Total | | 2,152,069 | 100.0 | % | | | | | | | |

| | | | | | | | | | | |

| (1) | Based on the underwritten rent roll dated November 14, 2023 inclusive of rent steps through November 30, 2024. |

| (2) | In certain instances, ratings provided are those of the parent company of the entity shown, whether or not the parent company guarantees the lease. |

| (3) | % of Total Collateral NRA refers only to the Woodfield Mall Property and does not include the portion of the Woodfield Mall occupied by the Non-Collateral Anchors. |

| (4) | All information regarding sales and occupancy costs presented in this termsheet with respect to the Woodfield Mall is based upon information provided by the borrower sponsor. In certain instances, sales figures represent estimates because the tenants are not required to report, or otherwise may not have reported, sales information on a timely basis. Further, because sales are self-reported, such information is not independently verified by the borrower sponsor. Sales are as of the 12 months ended September 2023. |

| (5) | J.C. Penney and Lord & Taylor do not pay rent but pay certain reimbursements. |

| (6) | Sears has subleased 50,000 square feet to Primark, and 42,094 square feet to Level 257. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 16 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

The following table presents certain information relating to the tenant sales of the Woodfield Mall Property:

| Comparable In-line Sales(1) |

| Tenants < 10,000 SF | 2019 | 2020(2) | 2021 | 2022 | TTM September 2023 |

| Gross Mall Sales | $274,505,000 | NAP | $269,467,000 | $269,130,000 | $294,883,000 |

| Gross Mall Sales (Ex-Apple) | $220,566,000 | NAP | $240,722,000 | $233,070,000 | $256,280,000 |

| Sales PSF (Inline < 10,000 SF) | $726 | NAP | $755 | $807 | $820 |

| Sales PSF (Inline < 10,000 SF, Ex-Apple) | $597 | NAP | $691 | $717 | $730 |

| Occupancy Cost (Inline < 10,000 SF)(3) | 17.4% | NAP | 16.6% | 15.4% | 14.7% |

| Occupancy Cost (Inline < 10,000 SF, Ex-Apple)(3) | 21.2% | NAP | 18.2% | 17.3% | 16.5% |

| (1) | All information regarding sales and occupancy costs presented herein with respect to the Woodfield Mall Property is based upon information provided by the borrower sponsor. In certain instances, sales figures represent estimates because the tenants are not required to report, or otherwise may not have reported sales information on a timely basis. Further, because sales are self-reported, such information is not independently verified by the borrower sponsor. |

| (2) | The Woodfield Mall Property was closed due to the COVID-19 pandemic through a portion of 2022. |

| (3) | Occupancy Cost is calculated by the sum of base rents, percentage rents and all expense recoveries divided by annual sales. |

The following table presents certain information relating to the major tenant sales of the Woodfield Mall:

| Major Tenant Sales by Type(1) |

| Tenant Name | 2019 | 2020(2) | 2021 | 2022 | TTM September 2023 |

| Macy's(3) | $51,000,000 | $28,100,000 | $45,900,000 | $45,400,000 | $45,400,000 |

| Nordstrom | $53,600,000 | $37,500,000 | $40,100,000 | $42,000,000 | $42,000,000 |

| J.C. Penney(3) | $21,900,000 | $13,700,000 | $15,100,000 | $16,500,000 | $16,500,000 |

| Department Stores | $126,500,000 | $79,300,000 | $101,100,000 | $103,900,000 | $103,900,000 |

In-Line Tenants | $337,753,000 | $210,500,000 | $353,998,000 | $362,968,000 | $380,594,000 |

| Apple | $53,939,000 | $21,311,000 | $28,745,000 | $36,060,000 | $38,603,000 |

| Total Woodfield Mall | $518,192,000 | $311,111,000 | $483,843,000 | $502,928,000 | $523,097,000 |

| (1) | All sales information presented herein with respect to the Woodfield Mall Property is based upon information provided by the borrower sponsor. In certain instances, sales figures represent estimates because the tenants are not required to report, or otherwise may not have reported sales information on a timely basis. Further, because sales are self-reported, such information is not independently verified by the borrower sponsor. |

| (2) | The Woodfield Mall Property was closed due to the COVID-19 pandemic through a portion of 2022. |

| (3) | Macy’s and J.C. Penney are Non-Collateral Anchors. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 17 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

The following table presents certain information relating to the tenant lease expirations at the Woodfield Mall Property:

| Lease Rollover Schedule(1)(2) |

| Year | Number of Leases Expiring | Net Rentable Area Expiring | % of NRA Expiring | UW Base Rent Expiring(3) | % of UW Base Rent Expiring(3) | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring | Cumulative UW Base Rent Expiring(3) | Cumulative % of UW Base Rent Expiring(3) |

| Vacant | NAP | 41,406 | 3.9 | % | NAP | NA | P | 41,406 | | 3.9% | NAP | NA | P |

| 2023 & MTM | 7 | 21,886 | 2.1 | | $1,181,355 | 3.2 | % | 63,292 | | 6.0% | $1,181,355 | 3.2% | |

| 2024 | 25 | 78,764 | 7.4 | | 4,516,592 | 12.3 | | 142,056 | | 13.3% | $5,697,946 | 15.5% | |

| 2025 | 23 | 265,320 | 24.9 | | 3,242,897 | 8.8 | | 407,376 | | 38.3% | $8,940,844 | 24.3% | |

| 2026 | 38 | 144,818 | 13.6 | | 6,168,658 | 16.7 | | 552,194 | | 51.9% | $15,109,502 | 41.0% | |

| 2027 | 18 | 57,775 | 5.4 | | 3,089,980 | 8.4 | | 609,969 | | 57.3% | $18,199,482 | 49.4% | |

| 2028 | 18 | 80,709 | 7.6 | | 5,357,144 | 14.5 | | 690,678 | | 64.9% | $23,556,626 | 63.9% | |

| 2029 | 20 | 105,967 | 10.0 | | 6,255,091 | 17.0 | | 796,645 | | 74.8% | $29,811,716 | 80.9% | |

| 2030 | 7 | 28,745 | 2.7 | | 1,479,397 | 4.0 | | 825,390 | | 77.5% | $31,291,113 | 84.9% | |

| 2031 | 4 | 7,102 | 0.7 | | 395,209 | 1.1 | | 832,492 | | 78.2% | $31,686,322 | 86.0% | |

| 2032 | 5 | 18,655 | 1.8 | | 614,059 | 1.7 | | 851,147 | | 80.0% | $32,300,381 | 87.6% | |

| 2033 | 14 | 43,869 | 4.1 | | 2,661,904 | 7.2 | | 895,016 | | 84.1% | $34,962,285 | 94.9% | |

| 2034 | 7 | 39,914 | 3.7 | | 1,041,577 | 2.8 | | 934,930 | | 87.8% | $36,003,862 | 97.7% | |

| 2035 & Beyond | 2 | 38,323 | 3.6 | | 850,000 | 2.3 | | 973,253 | | 91.4% | $36,853,862 | 100.0% | |

| Temporary Tenants | 24 | 91,337 | 8.6 | | 0 | 0.0 | | 1,064,590 | | 100.0% | $36,853,862 | 100.0% | |

| Total Collateral | 212 | 1,064,590 | 100.0 | % | $36,853,862 | 100.0 | % | | | | |

| (1) | Based on the underwritten rent roll dated November 14, 2023. |

| (2) | Certain leases may have termination options that are exercisable prior to the originally stated expiration date of the lease and that are not considered in this Lease Rollover Schedule. |

| (3) | UW Base Rent Expiring, % of UW Base Rent Expiring and Cumulative UW Base Rent Expiring and Cumulative % of UW Base Rent Expiring include contractual rent steps through November 2024. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 18 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

The following table presents certain information relating to the operating history and underwritten cash flows of the Woodfield Mall Property:

| Operating History and Underwritten Net Cash Flow |

| | 2019 | 2020 | 2021 | 2022 | 10/31/2023 TTM(1) | Underwritten | Per Square Foot(2) | %(3) |

| Rents in Place | $41,174,170 | $37,184,667 | $34,297,836 | $31,325,141 | $31,995,485 | $36,145,721 | $33.95 | | 46.2 | % |

| Rent Steps | 0 | 0 | 0 | 0 | 0 | 708,141 | 0.67 | | 0.9 | |

| Percent in Lieu | 445,565 | 1,229,560 | 2,406,499 | 2,469,287 | 2,347,073 | 1,409,551 | 1.32 | | 1.8 | |

| Percent Rent | 811,987 | 341,531 | 3,278,507 | 4,355,569 | 4,441,146 | 4,032,529 | 3.79 | | 5.2 | |

| Vacant Income(4) | 0 | 0 | 0 | 0 | 0 | 3,244,349 | 3.05 | | 4.1 | |

| Gross Potential Rent | $42,431,722 | $38,755,758 | $39,982,842 | $38,149,997 | $38,783,704 | $45,540,290 | $42.78 | | 58.2 | % |

| Total Reimbursements | 35,104,199 | 23,802,491 | 25,870,805 | 28,065,713 | 26,816,583 | 26,220,282 | 24.63 | | 33.5 | |

| Temporary Tenants | 4,396,324 | 2,837,003 | 4,433,113 | 4,598,726 | 4,329,039 | 4,329,039 | 4.07 | | 5.5 | |

| Other Rents | 236,767 | 176,161 | 230,481 | 219,885 | 275,155 | 275,155 | 0.26 | | 0.4 | |

| Media Income | 1,309,770 | 709,843 | 1,251,746 | 1,471,910 | 1,480,496 | 1,480,496 | 1.39 | | 1.9 | |

| Lease Settlement Income | 472,562 | 909,740 | 1,585,822 | 1,797,721 | 304,962 | 0 | 0.00 | | 0.0 | |

| Deferred Rent | 485,119 | 12,837 | 0 | 170,470 | 0 | 0 | 0.00 | | 0.0 | |

| Other Income | 617,296 | 533,957 | 348,322 | 391,178 | 428,248 | 428,248 | 0.40 | | 0.5 | |

| Net Rental Income | $85,053,759 | $67,737,790 | $73,703,131 | $74,865,600 | $72,418,187 | $78,273,510 | $73.52 | | 100.0 | % |

| (Vacancy/Credit Loss)(5) | 0 | 0 | 0 | 0 | 0 | (3,244,349) | (3.05) | | (4.1 | ) |

| Effective Gross Income | $85,053,759 | $67,737,790 | $73,703,131 | $74,865,600 | $72,418,187 | $75,029,161 | $70.48 | | 95.9 | % |

| Total Expenses(6) | 34,048,763 | 40,191,262 | 36,473,501 | 38,359,447 | 35,940,556 | 32,816,238 | 30.83 | | 43.7 | |

| Net Operating Income | $51,004,996 | $27,546,528 | $37,229,630 | $36,506,153 | $36,477,631 | $42,212,924 | $39.65 | | 56.3 | % |

| Capital Expenditures | 0 | 0 | 0 | 0 | 0 | 195,077 | 0.18 | | 0.3 | |

| TI/LC | 0 | 0 | 0 | 0 | 0 | 864,590 | 0.81 | | 1.2 | |

| Net Cash Flow | $51,004,996 | $27,546,528 | $37,229,630 | $36,506,153 | $36,477,631 | $41,153,257 | $38.66 | | 54.8 | % |

| (1) | 10/31/2023 TTM reflects the trailing 12-month period ending October 31, 2023. Contractual rent steps are through November 2024. |

| (2) | Per Square Foot is calculated using the Total Collateral NRA. |

| (3) | % column represents percent of Net Rental Income for all revenue lines and represents percent of Effective Gross Income for the remainder of fields. |

| (4) | Vacant Income reflects the gross up of vacancy at average in-place rents. |

| (5) | The underwritten economic occupancy is 95.5%. The Woodfield Mall Property was 96.1% leased based on the November 14, 2023 underwritten rent roll, including leases executed by the origination date. |

| (6) | The management fee is underwritten to reflect 4.00% of below market rate, temporary and overage rents, capped at $1,000,000. Real estate taxes were underwritten based on the actual tax bills for all of the property tax parcels at the Woodfield Mall Property (including the Nordstrom Parcel), inclusive of any tax reimbursements. |

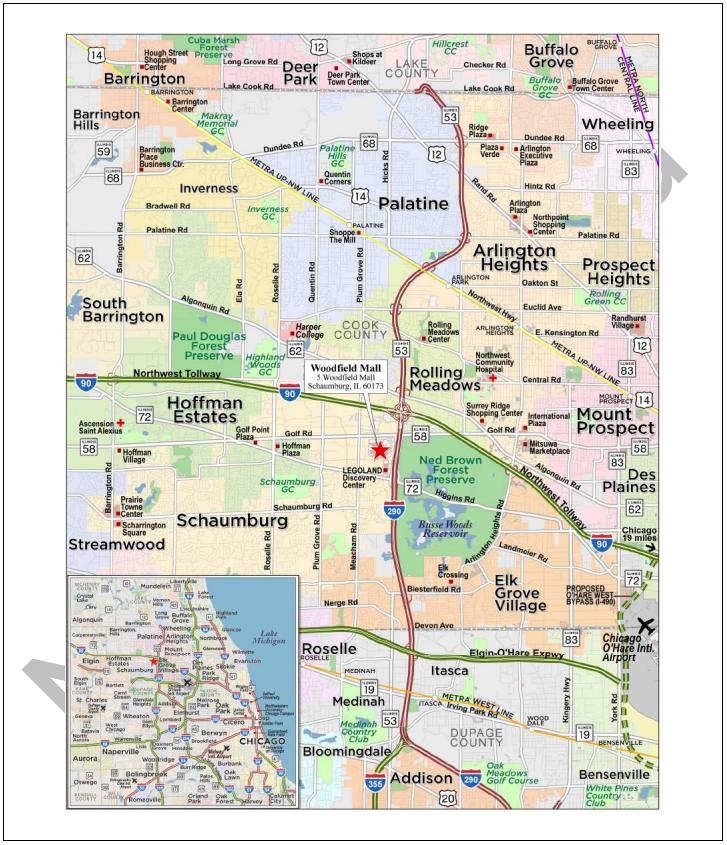

The Market. The Woodfield Mall Property is located in Schaumburg, Illinois, within the Chicago-Naperville-Elgin, IL-IN-WI core-based statistical area (the “Chicago CBSA”). Chicago is a major Great Lakes port and is considered the commercial, financial, industrial, and cultural center of the midwestern United States. The region surrounding Chicago is a major warehouse and distribution hub, supported by its comprehensive network of highway, water, rail, and air routes. The trade, transportation and utilities sector dominates Chicago CBSA as the largest employment sector with roughly 20.5% of the regional workforce.

The Woodfield Mall Property is located in Schaumburg, Illinois and is easily accessible from both Chicago and its surrounding suburbs. The Woodfield Mall Property is situated in the northwest Chicago suburb and is considered a desirable position within the Chicago MSA due to its proximity to the densely populated residential areas that surround the area and its easy access to both I-90 and I-290. Uses in the immediate area generally include a mixture of commercial, residential, hotel, and office. The Woodfield Mall Property is located approximately 27 miles from the central business district of Chicago. The O'Hare International Airport is located approximately 13 miles away from the Woodfield Mall Property. Public transit options are also readily available, with the Schaumburg Metra station providing a convenient train connection to Chicago. Additionally, Pace buses service the area, ensuring accessibility for those without personal vehicles.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 19 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

Schaumburg is home to 10 industrial parks, including 13.2 million square feet of space in over 400 facilities, 67 shopping centers totaling more than 9.5 million square feet of space, and 12.1 million square feet of office space spread throughout more than 90 buildings. Additional economic activity is generated by the Renaissance Schaumburg Hotel & Convention Center, with an additional 25 hotels supporting the community. The area is also home to numerous office complexes, including Two Century Centre, an office complex north of the Woodfield Mall Property, past Golf Road (Illinois Route 58), and east of N. Roosevelt Boulevard. In addition, the neighborhood is scattered with car dealerships, fast food chains, and gas stations.

According to the appraisal, the 2022 population within a 5-, 10- and 15-mile radius of the Woodfield Mall Property was 270,430, 949,592 and 2,109,255, respectively. Additionally, for the same time period, the average household income within the same radii was $119,090, $119,024 and $124,631, respectively.

According to the appraisal, the Woodfield Mall Property is located within the Chicago retail market and the Far Northwest retail submarket. As of the second quarter of 2023, the Chicago retail market contains 106,053,000 square feet of space and the overall vacancy rate was 12.7%, which is a decrease from 12.8% in 2018. As of the second quarter of 2023, the Far Northwest retail submarket contained approximately 6.9 million square feet of retail space inventory with a vacancy rate of 11.5% and an average asking rental rate of $18.20 per square foot.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 20 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

The following table presents certain information relating to comparable retail centers for the Woodfield Mall Property:

| Competitive Retail Center Summary(1) |

| Property Name/Location | Year Built / Renovated or Expanded | Total NRA (SF) | Total Occupancy | Distance to Subject | Sales PSF | Major Tenants |

Woodfield Mall 5 Woodfield Mall Schaumburg, IL | 1971, 1995 / 2015, 2016, 2018 | 1,064,590(2)(3) | 96.1% | NAP | $730(2) | Macy’s J.C. Penney Nordstrom Sears Lord & Taylor Primark Level 257 |

Streets of Woodfield 601 N Martingale Road Schaumburg, IL | 1991, 1993, 1997, 2009 / 2000 | 692,549 | 96.0% | 0.6 miles | NAV | Dick’s Sporting Goods RH Outlet AMC Loews (20 Screens) Whole Foods Crate & Barrel |

The Arboretum of South Barrington 100 W Higgins Road South Barrington, IL | 2007-2008, 2016, 2018, 2019, 2022 / NAP | 484,409 | 83.0% | 8.1 miles | NAV | L.L. Bean Star Cinema Grill Pinstripes DSW Arhaus |

Fashion Outlets of Chicago 5220 Fashion Outlets Way Rosemont, IL | 2013 / NAP | 538,735 | 99.0% | 12.9 miles | $1,036 | Forever 21 Nike Nordstrom rack Polo Ralph Lauren Bloomingdale’s Outlet Saks Fifth Avenue Off 5th |

Oakbrook Center 100 Oakbrook Center Oak Brook, IL | 1962, 2016, 2017, 2021 / 2014 | 1,886,885 | 92.0% | 15.3 miles | $1,326; $1,129 (Ex-Apple) | Macy’s Nordstrom Neiman Marcus AMC Theater (12 Screens) Crate & Barrel |

Westfield Old Orchard 4905 Old Orchard Center Skokie, IL | 1956 / 2022-2023 | 1,508,431 | 91.0% | 15.5 miles | $902; $830 (Ex-Apple) | Macy’s Nordstrom Bloomie’s Cinemex Crate & Barrel |

Northbrook Court 1515 Lake Cook Road Northbrook, IL | 1976 / 1996 | 1,014,506 | 92.0% | 19.2 miles | $833; $705 (Ex-Apple) | Neiman Marcus AMC (14 Screens) Crate & Barrel Forever 21 Gap |

Chicago Ridge Mall 444 Ridgeland Avenue Chicago Ridge, IL | 1981 / 2004 | 832,350 | 73.0% | 30.3 miles | $629 | Kohl’s Dick’s Sporting Goods AMC Theater (6 Screens) Michaels ALDI Old Navy Forever 21 |

| (1) | Source: Appraisal, unless stated otherwise. |

| (2) | Represents sales per square foot as of the 12 months ended September 2023 for in-line tenants (excluding Apple). |

| (3) | Total NRA (SF) includes only the Total Collateral NRA. |

The Borrower. The borrower for the Woodfield Mall Whole Loan is Woodfield Mall LLC, a single purpose entity with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the Woodfield Mall Whole Loan.

The Borrower Sponsors. The borrower sponsors and non-recourse carveout guarantors of the Woodfield Mall Whole Loan are International Mall Investors LLC (“IMI”) and Simon Property Group, L.P. (“Simon”). The Woodfield Mall Property ownership is a joint venture between IMI and Simon, with each owning 50%.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 21 | |

Not Funded

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 1 – Woodfield Mall |

Property Management. The Woodfield Mall Property is managed by Simon Management Associates, LLC, an affiliate of the borrower sponsor.

Escrows and Reserves. At origination, the borrower was required to deposit into escrow (i) approximately $[5,449,975] for outstanding tenant improvement allowances and leasing commissions identified in a schedule to the related loan agreement, (ii) approximately $[638,391] for a gap rent reserve and (iii) approximately $[964,731] for a free rent reserve.

Tax Escrows – During the continuance of a Lockbox Event (as defined below), the borrower is required to escrow 1/12th of the annual estimated tax payments on a monthly basis.

Insurance Escrows – During the continuance of a Lockbox Event, the borrower is required to escrow 1/12th of the annual estimated insurance payments on a monthly basis, except if the Woodfield Mall Property is insured under a blanket policy meeting the requirements set forth in the related loan agreement (in which case, no insurance escrows will be required, notwithstanding the occurrence of a Lockbox Event).

Replacement Reserves – During the continuance of a Lockbox Event, the borrower is required to escrow approximately $[__].

Rollover Reserve – During the continuance of a Lockbox Event, the borrower is required to escrow an amount equal $[___] for lease rollover reserves.

Lockbox / Cash Management. The Woodfield Mall Whole Loan is structured with a hard lockbox and springing cash management. The borrower and property manager are required to direct the tenants to pay rent directly into the lockbox account, and to deposit any rents otherwise received in such account within two business days after receipt. So long as no Lockbox Event (as defined below) has occurred and is continuing, the borrower will have access to the funds in the lockbox account and may use the lockbox account as an operating account. During the continuance of a Lockbox Event, all funds in the lockbox account are required to be swept on a weekly basis to a lender-controlled cash management account. Funds in the cash management account are required to be applied to debt service and the reserves and escrows described above, with any excess funds (i) to be deposited into the TI/LC reserve, if the Lockbox Event is caused by a Tenant Trigger Event, or into an excess cash flow reserve account held by the lender as cash collateral for the Woodfield Mall Whole Loan, if the Lockbox Event is not solely caused by a Tenant Trigger Event, or if (ii) no Lockbox Event is continuing, disbursed to the borrower.

A “Lockbox Event” means the period commencing upon the occurrence of (i) an event of default, (ii) a bankruptcy action of the borrower or property manager, or (iii) a Debt Yield Trigger Event (as defined below). A Lockbox Event will end (a) with respect to the matters described in clause (i) above, if the event of default has been waived by the lender, (b) with respect to the matters described in clause (ii) above, if the applicable property manager is replaced within 60 days or the bankruptcy action is dismissed within 90 days without any adverse consequences to the Woodfield Mall Property, or (c) with respect to matters described in clause (iii) above, a cure of the Debt Yield Trigger Event occurs. A Lockbox Event may not be cured more than five times during the term of the Woodfield Mall Whole Loan

A “Debt Yield Trigger Event” will occur if as of any date of determination, the debt yield based on the trailing four calendar quarter period is less than 10.0% for two consecutive calendar quarters and will be cured upon the debt yield being greater than or equal to 10.0% for two consecutive calendar quarters.

Subordinate Debt. None. However, the borrower is permitted to obtain property assessed clean energy (PACE) or similar loans in an aggregate amount up to $5 million subject to lender’s approval.

Mezzanine Debt. None.

Partial Release. Not permitted.

Ground Lease. None.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 22 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 2 – Arundel Mills and Marketplace |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 23 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 2 – Arundel Mills and Marketplace |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 24 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 2 – Arundel Mills and Marketplace |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 25 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 2 – Arundel Mills and Marketplace |

| Loan Information | | Property Information |

| Loan Seller: | CREFI | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $60,000,000 | | Title: | Fee |

| Cut-off Date Principal Balance(1): | $60,000,000 | | Property Type – Subtype: | Retail – Super Regional Mall |

| % of IPB: | 8.1% | | Net Rentable Area (SF)(7): | 1,938,983 |

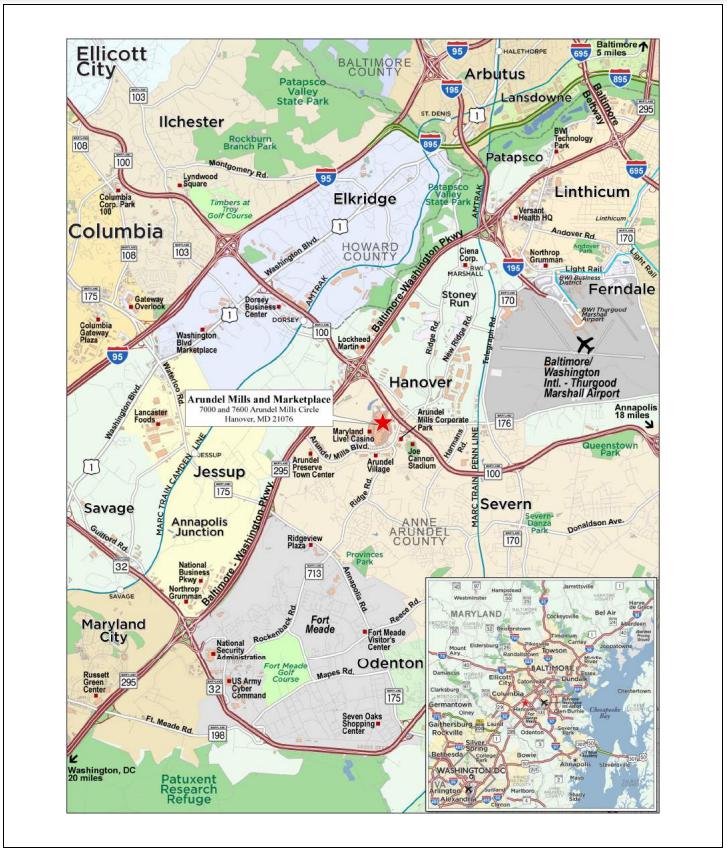

| Loan Purpose: | Refinance | | Location: | Hanover, MD |

| Borrowers: | Arundel Mills Limited Partnership and Arundel Mills Marketplace Limited Partnership | | Year Built / Renovated: | 2000, 2002, 2012 / NAP |

| Borrower Sponsor: | Simon Property Group, L.P. | | Occupancy(8): | 98.3% |

| Interest Rate: | 7.70100% | | Occupancy Date: | 6/15/2023 |

| Note Date: | 10/5/2023 | | 4th Most Recent NOI (As of)(9): | $42,286,167 (12/31/2020) |

| Maturity Date: | 11/1/2033 | | 3rd Most Recent NOI (As of)(9): | $52,018,087 (12/31/2021) |

| Interest-only Period: | 120 months | | 2nd Most Recent NOI (As of): | $52,750,256 (12/31/2022) |

| Original Term: | 120 months | | Most Recent NOI (As of)(10): | $51,525,734 (TTM 8/31/2023) |

| Original Amortization Term: | None | | UW Economic Occupancy: | 98.1% |

| Amortization Type: | Interest Only | | UW Revenues: | $74,354,670 |

| Call Protection(2): | L(25),D(89),O(6) | | UW Expenses: | $16,415,944 |

| Lockbox / Cash Management: | Hard / Springing | | UW NOI(10): | $57,938,726 |

| Additional Debt(1)(3)(4): | Yes | | UW NCF: | $55,557,554 |

| Additional Debt Balance(1)(3)(4): | $300,000,000 | | Appraised Value / Per SF(7): | $870,600,000 / $449 |

| Additional Debt Type(1)(3)(4): | Pari Passu | | Appraisal Date: | 9/1/2023 |

| | | | | |

| Escrows and Reserves(5) | | Financial Information(1) |

| | Initial | Monthly | Initial Cap | | | Whole Loan | |

| Taxes: | $0 | Springing | N/A | | Cut-off Date Loan / SF(7): | $186 | |

| Insurance: | $0 | Springing | N/A | | Maturity Date Loan / SF(7): | $186 | |

| Replacement Reserves: | $0 | Springing | N/A | | Cut-off Date LTV: | 41.4% | |

| TI/LC: | $0 | $231,942 | $5,566,608 | | Maturity Date LTV: | 41.4% | |

| Deferred Maintenance: | $0 | $0 | N/A | | UW NCF DSCR: | 1.98x | |

| Other(6): | $4,384,369 | $0 | N/A | | UW NOI Debt Yield: | 16.1% | |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | Uses | Proceeds | % of Total |

| Whole Loan(1) | $360,000,000 | 91.8 | % | | Loan Payoff | $384,870,923 | 98.1 | % |

| Sponsor Equity | 32,236,503 | 8.2 | | | Upfront Reserves | 4,384,369 | 1.1 | |

| | | | | Closing Costs | 2,981,210 | 0.8 | |

| Total Sources | $392,236,503 | 100.0 | % | | Total Uses | $392,236,503 | 100.0 | % |

| (1) | The Arundel Mills and Marketplace Mortgage Loan (as defined below) is part of the Arundel Mills and Marketplace Whole Loan (as defined below), which is comprised of 16 pari passu promissory notes with an aggregate original principal balance of $360,000,000. The financial information presented in the chart above shows the Cut-off Date Loan / SF, Maturity Date Loan / SF, Cut-off Date LTV, Maturity Date LTV, U/W NCF DSCR and U/W NOI Debt Yield based on the aggregate Cut-off Date principal balance of the Arundel Mills and Marketplace Whole Loan. |

| (2) | Defeasance of the Arundel Mills and Marketplace Whole Loan is permitted at any time after the earlier to occur of (a) the end of the two-year period commencing on the closing date of the securitization of the last promissory note representing a portion of the Arundel Mills and Marketplace Whole Loan to be securitized and (b) December 1, 2026. The assumed defeasance lockout period of 25 payments is based on the closing date of the BMO 2023-C7 transaction in December 2023. The actual defeasance lockout period may be longer. If any pari passu note has not been securitized for two years by December 1, 2026, the borrowers may prepay any note that has not been securitized for two years upon payment of a prepayment fee equal to the greater of (i) 1% of the prepaid amount or (ii) yield maintenance basis in conjunction with defeasance of any securitized pari passu note. In addition, the Arundel Mills and Marketplace Whole Loan may be prepaid in connection with a partial release, as described under “Partial Release” below. |

| (3) | See “The Loan” section below for further discussion of additional mortgage debt. |

| (4) | The Arundel Mills and Marketplace Property (as defined below) is subject to an existing property assessed clean energy loan in an original principal amount of $2,037,877.38 from Petros PACE Finance, LLC, a Texas limited liability company to the borrower. The PACE loan has a 16-year term with final payment occurring in November 2035. The annual debt service is $195,956.85 and the remaining balance, including all interest and administrative expenses, as of October 2023 was $1,633,579.73. Payments and any accrued interest are collected on the tax bill for the Arundel Mills and Marketplace Property and constitute a first lien on the Arundel Mills and Marketplace Property that has a priority over any mortgage loan. In addition, the Arundel Mills and Marketplace Whole Loan documents permit the borrowers to enter into an additional PACE loan for an amount not to exceed $5,000,000. |

| (5) | See “Escrows and Reserves” section below for further discussion of reserve requirements. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 26 | |

| Structural and Collateral Term Sheet | | BMO 2023-C7 |

| No. 2 – Arundel Mills and Marketplace |

| (6) | Other Initial Escrows and Reserves consist of (i) $3,796,478 for an outstanding tenant improvements and leasing commissions reserve, and (ii) $587,891 for an upfront gap rent reserve. |

| (7) | The Arundel Mills and Marketplace Property includes a larger mall and lifestyle center which consists of 1,391,652 square feet of owned improvements and 547,331 square feet of leased fee improvements. The Cut-off Date Loan / SF, Maturity Date Loan / SF, and Appraised Value / SF are based on the total square feet of 1,938,983. The Cut-off Date Loan / SF, Maturity Date Balance Loan / SF, and Appraised Value / Per SF based on the Owned SF (as defined below) of 1,391,652 is $258.69, $258.69, and $625.59, respectively. |

| (8) | Occupancy represents the occupancy excluding square footage from the leased fee tenant, Live Casino Hotel Maryland, and is based on the Owned SF totaling 1,391,652. Occupancy including Live Casino Hotel Maryland is 98.8%. |

| (9) | The increase from 4th Most Recent NOI to 3rd Most Recent NOI was primarily driven by an increase in bad debt/collection loss in 2020 due to the effect of the novel coronavirus pandemic. |

| (10) | The increase from the Most Recent NOI to UW NOI is driven by 18 new and renewal leases commencing in 2023 and 2024 totaling 113,039 square feet (5.8% of SF and 8.3% of underwritten rent) and rent steps of $604,665. |