UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-23700 |

| MassMutual AccessSM Pine Point Fund |

| (Exact name of registrant as specified in charter) |

| 1295 State Street, Springfield, MA | 01111 |

| (Address of principal executive offices) | (Zip code) |

| Karl Beinkampen | |

| 1295 State Street, Springfield, MA 01111 | |

| (Name and address of agent for service) | |

| Registrant's telephone number, including area code: | (413) 744-1000 |

| Date of fiscal year end: | 3/31/2022 | |

| Date of reporting period: | 3/31/2022 |

Item 1. Reports to Stockholders.

| (a) | The Report to Stockholders is attached herewith. |

Table of Contents | |

This material must be preceded or accompanied by a current prospectus (or summary prospectus, if available) for MassMutual AccessSM Pine Point Fund. Investors should consider the Fund’s investment objective, risks, and charges and expenses carefully before investing. This and other information about the investment company is available in the prospectus (or summary prospectus, if available). Read it carefully before investing.

[THIS PAGE INTENTIONALLY LEFT BLANK]

MassMutual AccessSM Pine Point Fund – President’s Letter to Shareholders (Unaudited) |

To Our Shareholders

Karl Beinkampen

President

March 31, 2022

I am pleased to present you with the first MassMutual AccessSM Pine Point Fund Annual Report.

The Fund’s investment objective is to generate long-term capital appreciation by investing in a broad cross section of private equity assets in order to seek, over time: long-term capital appreciation; regular, current income through quarterly distributions; a diversified portfolio of private equity assets; and an investment alternative for investors seeking to allocate a portion of their long-term portfolios primarily to middle and lower middle market buyout and growth equity assets through a single investment. Under normal market conditions, the Fund will invest primarily in and/or make capital commitments to private equity investments (“Private Equity Investments”), including primary and secondary investments in private equity funds (“Portfolio Funds”) and co-investments directly or indirectly in private portfolio companies (“Co-Investments”), investments intended to provide an investment return while offering better liquidity than private equity investments, and cash, cash equivalents, and other short-term investments. The Fund’s subadviser is Barings LLC (“Barings”), and the Fund’s sub-subadviser is Baring International Investment Limited (“BIIL”).

From inception on January 7, 2022 through March 31, 2022, the Fund’s shares returned 7.72%, outperforming the -5.90% return of the Russell 2000® Index* (the “benchmark”), which measures the performance of the small-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

A note to investors from Barings, the Fund’s subadviser:

As an inaugural management discussion and analysis for the MassMutual Access Pine Point Fund (the “Fund”), it is our pleasure as the Fund’s subadviser to provide a framework for the recently constructed portfolio as well as our expectations for the coming quarters. The private equity asset class, unlike public equity markets with daily pricing visibility, is, as the asset class suggests, made up of private companies with no readily tradable market. Investments are privately negotiated and subject to varying competitive conditions. Valuations are formally established on a quarterly basis, with intra-quarterly changes primarily reflecting cash movements and occasional material subsequent events, such as an announced sale; market dislocations, like a pandemic or military conflict; or material and measurable changes in the operations of the asset. Short-term value changes are typically nominal, with longer-term value creation strategies implemented and realized over time. The performance of each investment is driven by combinations of growth in revenue and earnings, deleveraging of the balance sheet, and prevailing market conditions. The weighting of each will vary based on the company, its sector, and the strategy deployed by the controlling equity participant.

The Fund’s investment mandate is to pursue a private equity strategy of investing through Co-Investments (minority equity stakes in companies), secondary vehicles (purchase of existing private equity fund assets), and primary funds (blind pool investment vehicles) in what we believe are attractive opportunities focused on small to medium-sized private companies in developed markets alongside of high-quality private equity sponsors. The portfolio, as of March 31, 2022, reflects that strategy.

* Indexes referenced, other than the MSCI Indexes, are unmanaged, do not incur fees, expenses, or taxes, and cannot be purchased directly for investment. The MSCI Indexes are unmanaged, do not incur fees or expenses, and cannot be purchased directly for investment.

(Continued)

1

MassMutual AccessSM Pine Point Fund – President’s Letter to Shareholders (Unaudited) (Continued) |

As of March 31, 2022, the Fund had over $105 million in investor capital and had committed $97.6 million across 18 investments alongside 16 discrete private equity sponsors, including, six Co-Investments, nine secondaries, and three primary funds. Secondaries have been a higher percentage of the portfolio mix (56% of total committed capital), as more private equity sponsors have used the secondary market to retain control of seasoned portfolio assets, offer existing investors liquidity, and raising additional capital for continued growth. The Fund has sought to benefit from this development by investing with strong sponsors in high-quality companies in which the sponsor has long-term familiarity. The Fund’s portfolio has a current weighting to lower- and middle-market companies (85% of total committed capital), North American geographic domiciles (87%), and buyout (100%) structures (control investments in established, cash flow-positive businesses where leverage may be used to support acquisition prices). The headline sector mix is skewed toward information technology (41% of total committed capital), but the underlying sub-sector, or second order segmentation is diversified across industries such as government services, health care compliance, consumer data management, payment systems, and financial services connectivity.

Performance for this newly constructed portfolio of assets is as we expected, with little change. The value creation strategies underwritten for each of the investments are in their early stages.

Looking forward, in a market of changing dynamics with increasing inflation, rising interest rates, labor shortages and supply chain disruptions, we believe the Fund’s portfolio is appropriately diversified and may be well positioned for continued growth, given its exposure to companies with leading competitive positions in strong end markets, high-margin, mission-critical products and services, and flexible capital structures with access to growth capital.

Over the remainder of the year, we believe the Fund has the potential for slow, but steady, value growth across the portfolio. The uncommitted investor capital will be targeted toward opportunities that we expect to be additive to the current portfolio mix and long-term performance, using a list of well-defined criteria to prioritize allocations.

Sincerely,

Karl Beinkampen

President

MassMutual Access Pine Point Fund

© 2022 Massachusetts Mutual Life Insurance Company (MassMutual®), Springfield, MA. All rights reserved. www.MassMutual.com Underwriter: MML Distributors, LLC. (MMLD) Member FINRA and SIPC (www.FINRA.org and www.SIPC.org), 1295 State Street, Springfield, MA 01111. MMLD is a wholly-owned subsidiary of MassMutual. Investment advisory services provided to the Fund by MML Investment Advisers, LLC (MML Advisers), a wholly-owned subsidiary of MassMutual.

The information provided is the opinion of MML Advisers as of 4/1/2022 and is subject to change without notice. It is not to be construed as tax, legal, or investment advice. Of course, past performance does not guarantee future results.

MM202305-301665

2

MassMutual AccessSM Pine Point Fund – Economic and Market Overview (Unaudited) |

March 31, 2022

Market Highlights

● | For the reporting period from January 7, 2022 (the inception date of the Fund) through March 31, 2022, U.S. stocks, as measured by the Russell 2000® Index, were down 5.90% in response to rising inflationary pressures, the Russian-Ukraine war, and the Federal Reserve Board (the “Fed”) taking the first steps in rolling back years of accommodative monetary policy. |

● | In the fourth quarter of 2021, expectations for strong economic and earnings growth in 2022, bolstered by the possibility of a $2 trillion economic stimulus and social spending plan, allowed investors to look past skyrocketing Omicron variant COVID-19 cases and heightened inflationary pressures. |

● | During the first quarter of 2022, investors in both stocks and bonds were challenged by the unexpected invasion of Ukraine by Russia, a stalled economic stimulus plan, and the Fed raising interest rates for the first time since 2018. |

● | Foreign stocks in both developed and emerging markets experienced losses in the reporting period, hindered by the unexpected economic impact of the Russian-Ukraine war and the strengthening of the U.S. dollar. |

● | U.S. bond investors experienced negative returns as the rollback of accommodative monetary policy drove yields higher and concerns over increased default risk due to the Russian-Ukraine war drove valuations lower. |

Market Commentary

For the reporting period from January 7, 2022 through March 31, 2022, global stock investors experienced negative returns. Despite the Russian-Ukraine war, U.S. stocks were only down slightly in the period, buoyed by rising expectations for strong economic growth, during a time when COVID-19 appeared to have peaked, and strong corporate earnings growth and balance sheets prevailed.

As a result, the broad market S&P 500® Index (the “S&P 500”) delivered a loss of 3.20% for the period. The technology-heavy NASDAQ Composite® Index also underperformed, losing 5.55% for the period. The more economically sensitive Dow Jones Industrial AverageSM was down 3.86%. During this period, small-cap stocks significantly underperformed their larger-cap peers, while value stocks significantly outperformed their growth counterparts.

The continued economic recovery, Fed interest rate hike in March, and the unexpected invasion of Ukraine by Russia affected sectors differently. The energy, materials, and utilities sectors fared the best during the period as investors expected these sectors to benefit the most from higher commodity prices. On the other hand, the communication services and information technology sectors lagged the other sectors, hurt by rising interest rates and rising inflationary pressures. West Texas Intermediate (WTI) crude oil prices ended the period at $100.28 per barrel, up 41% for the period.

Developed international stock markets, as measured by the MSCI EAFE® Index, trailed their domestic peers, falling 5.40% for the reporting period, negatively impacted by the Russian-Ukraine war and a stronger U.S. dollar. European stocks fared better than Japanese stocks, in part due to the Japanese economy’s great sensitivity to energy prices. Emerging-market stock markets, as measured by the MSCI Emerging Markets® Index, were also down, falling 5.84% for the period, with food and energy inflation affecting these countries to a greater degree.

The Fed has begun to unwind years of accommodative monetary policy now that the labor market has recovered and inflationary pressures are higher. The economic shock of the Russian-Ukraine war and the resulting rise in commodity prices may force the Fed to raise interest rates faster than planned which increases the risk of a policy mistake that leads to a recession. The proposed tax hike in the President’s budget proposal adds to the risk of a recession.

Investors entered the period in the midst of rising inflationary pressures and expectations that the Fed would start rolling back years of accommodative monetary policy. In this environment, bond yields rose, with the 10-year U.S. Treasury bond reaching 2.32% by the end of March 2022. Since rising yields drive bond prices down, the Bloomberg U.S. Aggregate Bond Index ended the period down 4.73%. Investment-grade bond prices fared even worse during the reporting period, as concerns of defaults increased, amplified by their generally longer maturities. The Bloomberg U.S. Corporate Bond Index, which tracks the

3

MassMutual AccessSM Pine Point Fund – Economic and Market Overview (Unaudited) (Continued) |

performance of investment-grade corporate bonds, ended the period down 6.18%. Below-investment-grade bonds, as represented by the Bloomberg U.S. Corporate High Yield Index, performed significantly better, ending the period down 4.15%, aided by generally shorter maturities and investors’ demand for bonds in the energy sector as the sharp rise in oil prices lessened the risk of default.

The same factors influencing the public markets slowed deal flow and transaction activity in the private markets in early 2022. Financing markets for leveraged transactions were down year over year, as spreads widened and activity slowed. Exits were constrained by volatility in the public markets and the Securities and Exchange Commission’s (“SEC”) increasing scrutiny on special purpose acquisition companies (SPACs). This activity level was consistent with that observed in the MassMutual Access Pine Point Fund. Health care and software remained among the more active sectors. Despite the slowdown in transaction activity, fundraising by private equity funds remained robust, with many funds returning to the market sooner than expected.

Review and maintain your strategy

MassMutual is committed to helping people secure their long-term future. While the return of volatility and the reality of market sell-offs can test an investor’s mettle, we’d like to remind you as an investor that it’s important to maintain perspective and have realistic expectations about the future performance of your investment accounts. As always, we recommend that you work with a personal financial professional, who can help you define an investment strategy that aligns with your comfort level with respect to market volatility, how you feel about investing, and your specific financial goals. Thank you for your confidence in MassMutual.

4

MassMutual AccessSM Pine Point Fund – Portfolio Manager Report (Unaudited) |

MassMutual AccessSM Pine Point Fund | |

United States | 87.6% |

Guernsey | 5.2% |

Luxembourg | 5.5% |

Total Investments | 98.3% |

MassMutual AccessSM Pine Point Fund | |

Secondary Fund | 44.2% |

Co-Investment | 19.1% |

Primary Fund | 10.2% |

Total Long-Term Investments | 73.5% |

Short-Term Investments and Other Assets and Liabilities | 26.5% |

Net Assets | 100.0% |

5

MassMutual AccessSM Pine Point Fund – Portfolio Manager Report (Unaudited) (Continued) |

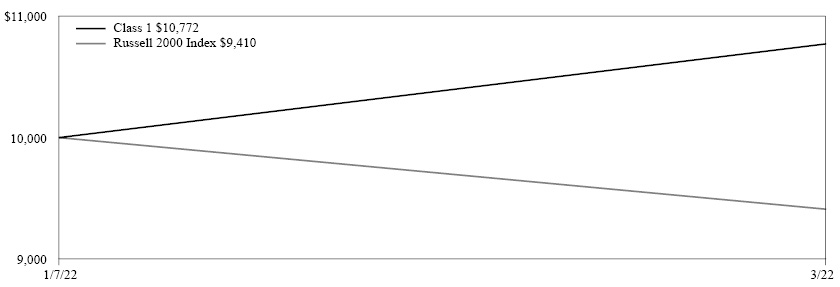

GROWTH OF $10,000 INVESTMENT SINCE INCEPTION - CLASS 1

The graph above illustrates a representative class of the Fund’s historical performance since the Fund’s inception in comparison to its benchmark index. The performance of other share classes will be greater than or less than the class depicted above.

Average Annual Total Returns (for the periods ended 03/31/2022) | |||||

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception |

Class 1 | 1/07/2022 | N/A | N/A | N/A | 7.72% |

Russell 2000 Index |

| -5.79% | 9.74% | 11.04% | -5.90% |

Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes only, and as such, the total return based on the unadjusted net asset value per share may differ from the total return reported in the financial highlights.

Performance data quoted represents past performance; past performance is not predictive of future results. The investment return and principal value of shares of the Fund will fluctuate with market conditions so that shares of the Fund, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-888-309-3539.

Investors should note that the Fund is a professionally managed closed-end fund, while the Russell 2000 Index is unmanaged, does not incur fees, expenses, or taxes, and cannot be purchased directly by investors. Investors should read the Fund’s prospectus with regard to the Fund’s investment objective, risks, and charges and expenses in conjunction with these financial statements. The performance tables and charts do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of the Fund shares.

6

MassMutual AccessSM Pine Point Fund – Consolidated Portfolio of Investments |

March 31, 2022 |

Name | Initial Acquisition | Geographic | Unfunded | Fair | ||||||||||||

Primary Fund Investments — 10.2%* | ||||||||||||||||

Bertram Growth Capital IV-A, LP(a) (c) | 1/07/2022 | North America | 2,626,346 | $ | 2,593,261 | |||||||||||

Gryphon Partners VI-A, LP (a) (c) | 1/07/2022 | North America | 4,033,110 | 3,466,890 | ||||||||||||

OceanSound Partners Fund, LP (a) (c) | 1/07/2022 | North America | 3,465,309 | 5,340,170 | ||||||||||||

Total (Cost $9,915,460) | $ | 11,400,321 | ||||||||||||||

Secondary Fund Investments — 44.2%* | ||||||||||||||||

AE Industrial Partners Extended Value Fund, LP (a) (b) (c) | 1/07/2022 | North America | 184,196 | $ | 1,531,027 | |||||||||||

BC Partners Galileo (1) LP (a) (b) (c) (d) | 1/07/2022 | Europe | — | 5,770,992 | ||||||||||||

FB HA Holdings LP (a) (b) (c) | 1/07/2022 | North America | — | 5,015,865 | ||||||||||||

Icon Partners V, LP (a) (b) (c) | 1/07/2022 | North America | 2,592,593 | 7,406,150 | ||||||||||||

JFL-NG Continuation Fund, LP (a) (b) (c) | 1/07/2022 | North America | 2,163,177 | 11,296,540 | ||||||||||||

Montagu + SCSp (a) (b) (c) (e) | 1/07/2022 | Europe | 1,954,215 | 6,128,790 | ||||||||||||

NSH Verisma Holdco, LP (a) (b) (c) | 1/07/2022 | North America | 1,453,497 | 4,527,136 | ||||||||||||

Stork SPV, LP (a) (b) (c) | 1/07/2022 | North America | 2,025,277 | 3,214,385 | ||||||||||||

TSCP CV I, LP (a) (b) (c) | 1/07/2022 | North America | 918,568 | 4,412,482 | ||||||||||||

Total (Cost $42,683,304) | $ | 49,303,367 | ||||||||||||||

Co-Investments — 19.1%* | ||||||||||||||||

BSP-TS, LP (a) (b) (c) | 1/07/2022 | North America | — | $ | 4,987,655 | |||||||||||

EPP Holdings LLC (a) (b) (c) (f) | 1/07/2022 | North America | 1,196,000 | 1,404,000 | ||||||||||||

Gallant Screening Acquisition, LLC (a) (b) (c) | 1/07/2022 | North America | — | 4,996,926 | ||||||||||||

GoCanvas TopCo, LLC (a) (b) (c) | 1/07/2022 | North America | — | 1,718,735 | ||||||||||||

Home Services Aggregator LP (a) (b) (c) | 1/07/2022 | North America | 1,050,000 | 4,560,000 | ||||||||||||

OceanSound Partners Co-Invest II, LP (a) (b) (c) | 1/07/2022 | North America | — | 3,589,091 | ||||||||||||

Total (Cost $20,843,847) | $ | 21,256,407 | ||||||||||||||

The accompanying notes are an integral part of the consolidated financial statements.

7

MassMutual AccessSM Pine Point Fund – Consolidated Portfolio of Investments (Continued) |

Principal | Fair | |||||||

SHORT-TERM INVESTMENTS — 24.8%* | ||||||||

| ||||||||

Commercial Paper — 24.8%* | ||||||||

Agilent Technologies | ||||||||

0.700% 4/05/22 (g) | $ | 1,500,000 | $ | 1,499,889 | ||||

Amcor Flexibles North America | ||||||||

1.030% 4/11/22 (g) | 1,200,000 | 1,199,765 | ||||||

Bell Canada | ||||||||

0.964% 4/29/22 (g) | 1,500,000 | 1,499,369 | ||||||

Canadian Pacific | ||||||||

0.761% 4/12/22 (g) | 1,500,000 | 1,499,675 | ||||||

Enbridge (US), Inc. | ||||||||

1.116% 4/27/22 | 1,500,000 | 1,498,833 | ||||||

Enterprise Prods Operation LLC | ||||||||

0.730% 4/05/22 (g) | 1,500,000 | 1,499,884 | ||||||

Eversource Energy | ||||||||

0.964% 5/05/22 (g) | 1,500,000 | 1,499,173 | ||||||

Fidelity National Information Services | ||||||||

0.791% 4/12/22 (g) | 1,000,000 | 999,787 | ||||||

Fiserv, Inc. | ||||||||

0.710% 4/13/22 (g) | 1,500,000 | 1,499,632 | ||||||

Fortive Corporation | ||||||||

0.913% 4/20/22 (g) | 1,500,000 | 1,499,350 | ||||||

HP, Inc. | ||||||||

1.228% 4/25/22 (g) | 1,500,000 | 1,499,125 | ||||||

Ingredion, Inc. | ||||||||

0.811% 4/13/22 (g) | 500,000 | 499,881 | ||||||

0.933% 4/08/22 (g) | 1,000,000 | 999,876 | ||||||

Intercontinental Exchange, Inc. | ||||||||

1.015% 4/29/22 (g) | 1,500,000 | 1,498,735 | ||||||

Mohawk Industries, Inc. | ||||||||

0.812% 4/06/22 (g) | 1,000,000 | 999,906 | ||||||

OGE Energy Corp. | ||||||||

1.014% 4/04/22 (g) | 1,000,000 | 999,939 | ||||||

Spire, Inc. | ||||||||

0.913% 4/19/22 (g) | 1,000,000 | 999,597 | ||||||

Tampa Electric Co. | ||||||||

0.964% 4/08/22 (g) | 1,000,000 | 999,931 | ||||||

1.127% 4/28/22 (g) | 500,000 | 499,849 | ||||||

VF Corp. | ||||||||

0.710% 4/19/22 (g) | 1,500,000 | 1,499,644 | ||||||

Westrock Co. | ||||||||

0.913% 4/28/22 (g) | 1,500,000 | 1,498,950 | ||||||

XCEL Energy, Inc. | ||||||||

0.862% 4/12/22 (g) | 1,500,000 | 1,499,674 | ||||||

TOTAL SHORT-TERM INVESTMENTS (Cost $27,688,275) | $ | 27,690,464 | ||||||

TOTAL INVESTMENTS — 98.3% (Cost $101,130,886) | $ | 109,650,559 | ||||||

Other Assets/(Liabilities) — 1.7% | 1,845,309 | |||||||

NET ASSETS — 100.0% | $ | 111,495,868 | ||||||

Notes to Portfolio of Investments

* | Percentages are stated as a percent of net assets. |

(a) | Restricted security. |

(b) | Non-income producing security. |

(c) | Fair value estimated by management using significant unobservable inputs. |

(d) | Foreign security denominated in Eurodollars. Total commitment and remaining commitment are €4,200,000 and €0, respectively. Amounts converted to U.S. dollar. |

(e) | Foreign security denominated in Eurodollars. Total commitment and remaining commitment are €6,190,795 and €1,631,270, respectively. Amounts converted to U.S. dollar. |

(f) | Held in MassMutual Private Equity Funds Subsidiary LLC. (See Note 1 in the “Notes to Consolidated Financial Statements” section for more information on this entity). |

(g) | Security is exempt from registration under Regulation S or Rule 144A of the Securities Act of 1933. These securities are considered restricted and may be resold in transactions exempt from registration. At March 31, 2022, the aggregate market value of these securities amounted to $26,191,631 or 23.49% of net assets. |

(h) | See Note 1 in the “Notes to Consolidated Financial Statements”. |

The accompanying notes are an integral part of the consolidated financial statements.

8

MassMutual AccessSM Pine Point Fund – Consolidated Financial Statements |

Consolidated Statement of Assets and Liabilities |

Assets: | ||||

Investments, at value (Note 2) (a) | $ | 81,960,095 | ||

Short-term investments, at value (Note 2) (b) | 27,690,464 | |||

Total investments | 109,650,559 | |||

Cash | 2,286,751 | |||

Receivables from: | ||||

Investment adviser (Note 3) | 66,726 | |||

Other receivables | 45,487 | |||

Total assets | 112,049,523 | |||

Liabilities: | ||||

Payables for: | ||||

Affiliates (Note 3): | ||||

Administration fees | 23,014 | |||

Investment advisory fees | 273,445 | |||

Accrued expense and other liabilities | 257,196 | |||

Total liabilities | 553,655 | |||

Net assets | $ | 111,495,868 | ||

Net assets consist of: | ||||

Paid-in capital | $ | 103,407,582 | ||

Accumulated Gain (Loss) | 8,088,286 | |||

Net assets | $ | 111,495,868 |

(a) | Cost of investments: | $ | 73,442,611 | ||

(b) | Cost of short-term investments: | $ | 27,688,275 |

The accompanying notes are an integral part of the consolidated financial statements.

9

MassMutual AccessSM Pine Point Fund – Consolidated Financial Statements (Continued) |

Consolidated Statement of Assets and Liabilities |

Class 1 shares: | ||||

Net assets | $ | 111,495,868 | ||

Shares outstanding (a) | 10,350,808 | |||

Net asset value, and redemption price per share | $ | 10.77 |

(a) | Authorized unlimited number of shares with no par value. |

The accompanying notes are an integral part of the consolidated financial statements.

10

Investment income (Note 2): | ||||

Dividends | $ | 3,498 | ||

Interest | 106,993 | |||

Total investment income | 110,491 | |||

Expenses (Note 3): | ||||

Investment advisory fees | 273,445 | |||

Custody fees | 622 | |||

Audit fees | 85,241 | |||

Legal fees | 55,815 | |||

Proxy fees | 484 | |||

Other fees | 23,014 | |||

Shareholder reporting fees | 6,904 | |||

Trustees’ fees | 80,230 | |||

Registration and filing fees | 25,315 | |||

Transfer agent fees | 57,534 | |||

Total expenses | 608,604 | |||

Expenses waived (Note 3): | ||||

Fees reimbursed by adviser | (66,726 | ) | ||

Net expenses: | 541,878 | |||

Net investment income (loss) | (431,387 | ) | ||

Realized and unrealized gain (loss): | ||||

Net change in unrealized appreciation (depreciation) on: | ||||

Investment transactions | 8,519,673 | |||

Net change in unrealized appreciation (depreciation) | 8,519,673 | |||

Net realized gain (loss) and change in unrealized appreciation (depreciation) | 8,519,673 | |||

Net increase (decrease) in net assets resulting from operations | $ | 8,088,286 |

The accompanying notes are an integral part of the consolidated financial statements.

11

Increase (Decrease) in Net Assets: | ||||

Operations: | ||||

Net investment income (loss) | $ | (431,387 | ) | |

Net realized gain (loss) | — | |||

Net change in unrealized appreciation (depreciation) | 8,519,673 | |||

Net increase (decrease) in net assets resulting from operations | 8,088,286 | |||

Net fund share transactions (Note 5): | ||||

Class 1 | 103,307,582 | |||

Increase (decrease) in net assets from fund share transactions | 103,307,582 | |||

Total increase (decrease) in net assets | 111,395,868 | |||

Net assets | ||||

Beginning of period | 100,000 | |||

End of year | $ | 111,495,868 |

The accompanying notes are an integral part of the consolidated financial statements.

12

Cash flows from operating activities: | ||||

Net increase (decrease) in net assets resulting from operations | $ | 8,088,286 | ||

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by (used in) operating activities: | ||||

Investments purchased | (1,302,808 | ) | ||

Net proceeds from investments | 2,149,673 | |||

(Purchase) Sale of short-term investments, net | (27,688,275 | ) | ||

Increase (Decrease) in payable for administration fees | 23,014 | |||

Increase (Decrease) in other receivables | (45,487 | ) | ||

Increase (Decrease) in receivable for investment adviser | (66,726 | ) | ||

Increase (Decrease) in payable for investment advisory fees | 273,445 | |||

Increase (Decrease) in payable for accrued expenses and other liabilities | 257,196 | |||

Net change in unrealized (appreciation) depreciation on investments | (8,519,673 | ) | ||

Net cash used in operating activities | (26,831,355 | ) | ||

Cash flows from (used in) financing activities: | ||||

Proceeds from shares sold | 29,018,106 | |||

Net cash from (used in) financing activities | 29,018,106 | |||

Net increase (decrease) in cash | 2,186,751 | |||

Cash at beginning of period | 100,000 | |||

Cash at end of period | $ | 2,286,751 | ||

Supplemental Disclosure of Cash Flow Information | ||||

Non-Cash Transactions: | ||||

In-Kind Transfer of Investments | $ | 74,289,476 |

The accompanying notes are an integral part of the consolidated financial statements.

13

MassMutual AccessSM Pine Point Fund – Consolidated Financial Statements (Continued) |

Consolidated Financial Highlights (For a share outstanding throughout the period) |

Income (loss) from investment | Ratios / Supplemental Data | |||||||||||||||||||||||||||||||||||||||

Net | Net | Net | Total | Net | Total | Net | Ratio of | Ratio of | Net | |||||||||||||||||||||||||||||||

Class 1 | ||||||||||||||||||||||||||||||||||||||||

3/31/22i | $ | 10.00 | $ | (0.05 | ) | $ | 0.82 | $ | 0.77 | $ | 10.77 | 7.72 | %b | $ | 111,496 | 2.86 | %a | 2.54 | %a | (2.02 | %)a | |||||||||||||||||||

Period ended | |

Portfolio turnover rate | 0% |

a | Annualized. |

b | Percentage represents the results for the period and is not annualized. |

c | Per share amount calculated on the average shares method. |

i | Fund commenced operations on January 7, 2022. |

The accompanying notes are an integral part of the consolidated financial statements.

14

MassMutual AccessSM Pine Point Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified, closed-end management investment company. The Fund is organized under the laws of the State of Delaware as a Delaware statutory trust pursuant to a Certificate of Trust dated May 24, 2021, as amended and restated on December 13, 2021, as it may be further amended from time to time. The Fund intends to qualify as a regulated investment company (a “RIC”). The Fund had no operations prior to January 7, 2022 other than when Massachusetts Mutual Life Insurance Company (“MassMutual”) made a seed investment of $100,000 and received 10,000 common shares.

The Fund currently offers Class 1 shares on a continuous basis at the net asset value (“NAV”) per share. The minimum investment is $1,000,000 and there is no sales charge associated with the share class. MassMutual owns 100% of the outstanding Class 1 shares.

The Fund’s investment objective is to generate long-term capital appreciation. In pursuing its investment objective, the Fund intends to invest primarily and/or make capital commitments in private equity investments (“Private Equity Investments”), including primary and secondary private equity funds (“Portfolio Funds”) and co-investments, directly or indirectly in private portfolio companies (“Co-Investments”); investments intended to provide an investment return while offering better liquidity than private equity investments; and cash, cash equivalents and other short-term investments. Capital not invested in private equity may be invested in short-term debt securities, public equities or money market funds pending investment pursuant to the Fund’s investment objective and strategies. In addition, subject to applicable law, the Fund may maintain a portion of its assets in cash or short-term debt securities or money market funds to meet operational and liquidity needs or for temporary defensive purposes.

Basis of Consolidation – On January 7, 2022, MassMutual performed an in-kind purchase transaction whereby it contributed the assets and liabilities of MassMutual Private Equity Funds LLC (“MMPEF”) and its subsidiary, MassMutual Private Equity Funds Subsidiary LLC (“MMPEF Subsidiary”) to the Fund in exchange for shares of the Fund. The consolidated financial statements of the Fund include MMPEF and MMPEF Subsidiary in which the Fund invests and the results of which are reported on a consolidated basis with the Fund. Both MMPEF and MMPEF Subsidiary are wholly owned subsidiaries of the Fund; therefore, all intercompany accounts and transactions have been eliminated. MMPEF and MMPEF Subsidiary will hold all of the Fund’s Private Equity Investments and Co-Investments, while short-term investments are held directly by the Fund. As of March 31, 2022, MMPEF and MMPEF Subsidiary hold investments in the amount of $80,556,095 and $1,404,000, respectively.

2. Significant Accounting Policies:

The following is a summary of significant accounting policies followed consistently by the Fund in the preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America (“generally accepted accounting principles”). The preparation of the financial statements in accordance with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board Accounting Standards Codification Topic 946, Financial Services – Investment Companies.

Investment Valuation Policies:

The NAV of the Fund’s shares is determined as of the close of business on the last business day of each month, as of the date of any distribution, and at such other times as the Fund’s Board of Trustees shall determine fair value securities in accordance with procedures approved annually by the Board of Trustees (“Trustees”), and under the general oversight of the Trustees.

15

Notes to Consolidated Financial Statements (Continued) |

The fair value of Private Equity Investments held by the Fund is generally based on the NAV of that investment reported by its investment manager on a quarterly basis. Adjustments are made to reported NAV for contributions by the Fund to a private equity investment and distributions to the Fund from a private equity investment after the reported valuation date. In the case of new investments where a NAV has not yet been received, the fair value is typically held at cost of the investment.

The Private Equity Investments are not subject to the public company disclosure, timing, and reporting standards as other investments held by the Fund. Typically, the most recently available information for a Private Equity Investments is as of a date that is earlier than the date the Fund is calculating its net asset value. This factor may result in a difference between the value of the investment and the price the Fund could receive upon the sale of the investment.

For direct investments in equity issued by privately held companies and any other investments fair valued using significant unobservable inputs, as described below, the fair valuation approaches used by the Fund utilizes one or a combination of, but not limited to, the following approaches:

● | (i) Recent market transactions, including subsequent rounds of financing, in the underlying investment or comparable issuers; (ii) recapitalizations and other transactions across the capital structure; and (iii) market multiples of comparable issuers, adjusted for illiquidity and other factors such as minority ownership. |

● | Future cash flows discounted to present value and adjusted as appropriate for liquidity, credit, and/or market risks. |

● | Cost of the investment when that is determined to be a fair approximate value of the investment. |

Equity securities that are actively traded on a national securities exchange are valued on the basis of information furnished by a pricing service, which provides the last reported sale price, or the official closing price on the NASDAQ National Market System (“NASDAQ System”), or in the case of over-the-counter (“OTC”) securities for which an official closing price is unavailable or not reported on the NASDAQ System, the last reported bid price. Portfolio securities traded on more than one national securities exchange are valued at the last price at the close of the exchange representing the principal market for such securities. Debt securities are valued on the basis of valuations furnished by a pricing service, which generally determines valuations taking into account factors such as institutional-size trading in similar securities, yield, quality, coupon rate, maturity, type of issue, trading characteristics, and other market data. Shares of open-end mutual funds are valued at their closing net asset values as reported on each business day.

Investments for which market quotations are readily available are marked to market based on those quotations. Market quotations may be provided by third-party vendors or market makers, and may be determined on the basis of a variety of factors, such as broker quotations, financial modeling, and other market data, such as market indexes and yield curves, counterparty information, and foreign exchange rates. U.S. Government and agency securities may be valued on the basis of market quotations or using a model that may incorporate market observable data such as reported sales of similar securities, broker quotes, yields, bids, offers, quoted market prices, and reference data. The fair values of OTC derivative contracts, including forward, swap, and option contracts related to interest rates, foreign currencies, credit standing of reference entities, equity prices, or commodity prices, may be based on market quotations or may be modeled using a series of techniques, including simulation models, depending on the contract and the terms of the transaction. The fair values of asset-backed securities and mortgage-backed securities are estimated based on models that consider the estimated cash flows of each debt tranche of the issuer, established benchmark yield, and estimated tranche-specific spread to the benchmark yield based on the unique attributes of the tranche, including, but not limited to, prepayment speed assumptions and attributes of the collateral.

Investments for which a pricing service or other approved source either does not supply a quotation, price, or market based valuation, or supplies a quotation, price, or market based valuation that is believed by the primary pricing service or MML Advisers to be unreliable, will be valued according to fair value of those investments determined in good faith by the Fund’s Trustees. The Fund has adopted valuation policies that relate to the fair valuation of the Fund’s securities. The valuation policies are based on the fair value policies of Barings, the Fund’s subadviser. In general, fair value represents a good faith approximation of the current value of an asset and will be used when there is no public market or possibly no market at all for the asset. The fair values of one or more assets may not be the prices at which those assets are ultimately sold and the differences may be significant.

16

Notes to Consolidated Financial Statements (Continued) |

The Fund may invest in securities that are traded principally in foreign markets and that trade on weekends and other days when the Fund does not price their shares. As a result, the values of the Fund’s portfolio securities may change on days when the prices of the Fund’s shares are not calculated. The prices of the Fund’s shares will reflect any such changes when the prices of the Fund’s shares are next calculated. The Fund may use fair value pricing more frequently for securities primarily traded in foreign markets because, among other things, most foreign markets close well before the Fund values its securities. The earlier close of these foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim. The Fund’s investments may be priced based on fair values provided by a third-party vendor, based on certain factors and methodologies applied by such vendor, in the event that there is movement in the U.S. market, between the close of the foreign market and the time the Fund calculates its net asset values. All assets and liabilities expressed in foreign currencies are converted into U.S. dollars at the mean between the buying and selling rates of such currencies against the U.S. dollar at the end of each business day.

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. A three-tier hierarchy is utilized to maximize the use of observable market data inputs and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value (such as a pricing model) and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability and are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability and are developed based on the best information available in the circumstances. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below. The inputs or methodology used for valuing investments are not necessarily an indication of the risk associated with investing in those investments and the determination of the significance of a particular input to the fair value measurement in its entirety requires judgment and consideration of factors specific to each security.

Level 1 – quoted prices (unadjusted) in active markets for identical investments that the Fund can access at the measurement date

Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

Level 3 – significant unobservable inputs, to the extent observable inputs are not available (including the Fund’s own assumptions in determining the fair value of investments)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

Changes in valuation techniques may result in transfers in or out of an investment’s assigned Level within the hierarchy. In addition, in periods of market dislocation, the observability of prices and inputs may be reduced for many instruments. This condition, as well as changes related to liquidity of investments, could cause a security to be reclassified between Levels.

In certain cases, the inputs used to measure fair value may fall into different Levels of the fair value hierarchy. In such cases, for disclosure purposes, the Level in the fair value hierarchy within which the fair value measurement falls is determined based on the lowest Level input that is significant to the overall fair value measurement.

17

Notes to Consolidated Financial Statements (Continued) |

The following is the aggregate value by input level, as of March 31, 2022 for the Fund’s investments:

Level 1 | Level 2 | Level 3 | Investments | Total | ||||||||||||||||

Private Equity Investments | $ | — | $ | — | $ | — | $ | 81,960,095 | $ | 81,960,095 | ||||||||||

Short-Term Investments | — | 27,690,464 | — | — | 27,690,464 | |||||||||||||||

Total Investments | $ | — | $ | 27,690,464 | $ | — | $ | 81,960,095 | $ | 109,650,559 | ||||||||||

The Fund does not have the right to redeem private equity investments and therefore, they are considered illiquid.

Unfunded Commitments:

As of March 31, 2022, the Fund had total unfunded commitments of $23,662,288 which consist of $10,124,765 for primary private equity funds, $11,291,523 for secondary private equity funds and $2,246,000 for co-investments.

Accounting for Investment Transactions:

Investment transactions are accounted for on the trade date. Realized gains and losses on sales of investments and unrealized appreciation and depreciation of investments are computed by the specific identification cost method. Proceeds received from litigation, if any, are included in realized gains on investment transactions for any investments that are no longer held in the portfolio and as a reduction in cost for investments that continue to be held in the portfolio. Interest income, adjusted for amortization of discounts and premiums on debt securities, is earned from the settlement date and is recorded on the accrual basis. Dividend income and realized capital gain distributions are recorded on the ex-dividend date. Non-cash dividends received in the form of stock are recorded as dividend income at market value. Withholding taxes on foreign interest, dividends, and capital gains have been provided for in accordance with the applicable country’s tax rules and rates. Foreign dividend income is recorded on the ex-dividend date or as soon as practicable after the Fund determines the existence of a dividend declaration after exercising reasonable due diligence. Distributions received on securities that represent a return of capital or capital gains are recorded as a reduction of cost of investments and/or as a realized gain.

Dividends and Distributions to Shareholders:

Dividends from net investment income and distributions of any net realized capital gains of the Fund are declared and paid annually and at other times as may be required to satisfy tax or regulatory requirements. Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from generally accepted accounting principles. As a result, net investment income and net realized capital gains on investment transactions for a reporting period may differ significantly from distributions during such period.

Foreign Currency Translation:

The books and records of the Fund are maintained in U.S. dollars. The market values of foreign currencies, foreign securities, and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars at the mean of the buying and selling rates of such currencies against the U.S. dollar at the end of each business day. Purchases and sales of foreign securities and income and expense items are translated at the rates of exchange prevailing on the respective dates of such transactions. The Fund does not isolate that portion of the results of operations arising from changes in the exchange rates from that portion arising from changes in the market prices of securities. Net realized foreign currency gains and losses resulting from changes in exchange rates include foreign currency gains and losses between trade date and settlement date on investment securities transactions, foreign currency transactions, and the difference between the amounts of dividends or interest recorded on the books of the Fund and the amount actually received.

18

Notes to Consolidated Financial Statements (Continued) |

Indemnifications:

Under the Fund’s organizational documents, current and former Trustees and Officers are provided with specified rights to indemnification against liabilities arising in connection with the performance of their duties to the Fund, and shareholders shall not be subject to any personal liability for obligations of the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

3. General Risks

General Risks. An investment in the Fund involves a considerable amount of risk. An investor may lose money. Before making an investment decision, a prospective shareholder should (i) consider the suitability of this investment with respect to the shareholder’s investment objectives and personal situation and (ii) consider factors such as the investor’s personal net worth, income, age, risk tolerance and liquidity needs. The Fund is an illiquid investment. Shareholders have no right to require the Fund to redeem their shares of the Fund.

Unlisted Closed-End Structure; Liquidity Limited to Repurchases of Shares. The Fund has been organized as a non-diversified, closed-end management investment company and designed primarily for long-term investors. An investor should not invest in the Fund if the investor needs a liquid investment. Closed-end funds differ from open-end management investment companies (commonly known as mutual funds) in that investors in a closed-end fund do not have the right to redeem their shares on a daily basis. Unlike most closed-end funds, which typically list their shares on a securities exchange, the Fund does not intend to list the shares for trading on any securities exchange, and the Fund does not expect any secondary market to develop for the shares. Although the Fund intends to offer a limited degree of liquidity by conducting quarterly repurchase offers, a shareholder may not be able to tender its shares in the Fund promptly after it has made a decision to do so. There is no assurance that you will be able to tender your shares when or in the amount that you desire or that the Fund will repurchase shares quarterly. In addition, with very limited exceptions, shares are not transferable, and liquidity will be provided only through quarterly repurchase offers made by the Fund. The Fund expects any quarterly repurchase offer to apply to no more than 5% of the net assets of the Fund. Shares are considerably less liquid than shares of funds that trade on a stock exchange or shares of open-end registered investment companies, and are therefore suitable only for investors who can bear the risks associated with the limited liquidity of shares, and should be viewed as a long-term investment.

There will be a substantial period of time between the date as of which shareholders must submit a request to have their shares repurchased and the date they can expect to receive payment for their shares from the Fund. The Fund currently intends, under normal market conditions, to provide payment with respect to 95% of the tender offer proceeds within 65 days of the expiration of the tender offer, and may hold back 5% of the tender offer proceeds until after the Fund’s year-end audit. Shareholders whose shares are accepted for repurchase bear the risk that the Fund’s NAV may fluctuate significantly between the time that they submit their repurchase requests and the date as of which such Shares are valued for purposes of such repurchase. Shareholders will have to decide whether to request that the Fund repurchase their shares without the benefit of having current information regarding the value of shares on a date proximate to the date on which shares are valued by the Fund for purposes of effecting such repurchases.

Repurchases of shares, if any, may be suspended, postponed or terminated by the Board under certain circumstances. An investment in the Fund is suitable only for investors who can bear the risks associated with the limited liquidity of shares and the underlying investments of the Fund. Also, because shares are not listed on any securities exchange, the Fund is not required, and does not intend, to hold annual meetings of its shareholders unless required under the provisions of the 1940 Act.

Dependence on MML Advisers. MML Advisers contracts with Barings to help manage the Fund. Subject to the oversight of the Board, MML Advisers has the ultimate responsibility to oversee any subadviser of the Fund and to recommend the hiring, termination, and replacement of any subadviser of the Fund. This responsibility includes, but is not limited to, analysis and review of subadviser performance, as well as assistance in the identification and vetting of new or replacement subadvisers. In addition, MML Advisers maintains responsibility for a number of other important obligations, including, among other things, board reporting, assistance in the annual advisory contract renewal process, and, in general, the performance of all obligations

19

Notes to Consolidated Financial Statements (Continued) |

not delegated to a subadviser. MML Advisers also provides advice and recommendations to the Board, and performs such review and oversight functions as the Board may reasonably request, as to the continuing appropriateness of the investment objective, strategies, and policies of the Fund, valuations of portfolio securities, and other matters relating generally to the investment program of the Fund.

Dependence on Barings. Barings is responsible for selecting Fund investments as opportunities arise. The Fund and, accordingly, shareholders, must rely upon the ability of Barings to identify and implement Fund investments consistent with the Fund’s investment objective. Shareholders will not receive or otherwise be privy to due diligence or risk information prepared by or for Barings in respect of Fund investments and Co-Investments. Barings has the authority and responsibility for asset allocation, the selection of Fund investments and all other investment decisions for the Fund. The success of the Fund depends upon the ability of Barings to develop and implement investment strategies that achieve the investment objective of the Fund. Shareholders will have no right or power to participate in the management or control of the Fund or Fund investments, or the terms of any such investments. There can be no assurance that Barings will be able to select or implement successful strategies or achieve the Fund’s investment objectives. No person should invest in the Fund unless such person is willing to entrust all aspects of the investment decisions of the Fund to Barings.

Liquidity and Valuation Risk. Liquidity risk is the risk that securities may be difficult or impossible to sell at the time the Fund would like or at the price it believes the security is currently worth. Liquidity risk may be increased for certain Fund investments, including those investments in funds with gating provisions or other limitations on investor withdrawals and restricted or illiquid securities. The Fund’s current Private Equity Investments do not have provisions which permit the Fund to redeem its investment. To the extent that the Fund seeks to reduce or sell out of its investment at a time or in an amount that is prohibited, the Fund may not have the liquidity necessary to participate in other investment opportunities or may need to sell other investments that it may not have otherwise sold.

The Fund may also invest in securities that, at the time of investment, are illiquid, as determined by using the SEC’s standard applicable to registered investment companies (i.e., securities that cannot be disposed of by the Fund within seven calendar days in the ordinary course of business at approximately the amount at which the Fund has valued the securities). Illiquid and restricted securities may be difficult to dispose of at a fair price at the times when the Fund believes it is desirable to do so. The market price of illiquid and restricted securities generally is more volatile than that of more liquid securities, which may adversely affect the price that the Fund pays for or recovers upon the sale of such securities. Investment of the Fund’s assets in illiquid and restricted securities may also restrict the Fund’s ability to take advantage of market opportunities.

Valuation risk is the risk that one or more of the securities in which the Fund invests are priced differently than the value realized upon such security’s sale. In times of market instability, valuation may be more difficult, in which case the Funds’ judgment may play a greater role in the valuation process.

Concentration of Investments. Except to the extent required by applicable law and the Fund’s fundamental policies, there are no limitations imposed on Barings as to the amount of Fund assets that may be invested in (i) any one geography, (ii) any one Fund Investment, (iii) in a Private Equity Investment managed by a particular general partner or its affiliates, (iv) indirectly in any single industry or (v) in any issuer. In addition, a Portfolio Fund’s investment portfolio may consist of a limited number of companies and may be concentrated in a particular industry area or group, and Co-Investments are typically single company positions. Accordingly, the Fund’s investment portfolio may at times be significantly concentrated, both as to managers, geographies, industries and individual companies. Such concentration could offer a greater potential for capital appreciation as well as increased risk of loss. Such concentration may also be expected to increase the volatility of the Fund’s investment portfolio. The Fund’s investment portfolio is, however, subject to the asset diversification requirements applicable to RICs, and may thus be limited by the Fund’s intention to qualify and be eligible to be treated as such. The Fund will consider the then-existing concentration of Portfolio Funds, to the extent they are known to the Fund, when making additional investments.

Portfolio Funds Not Registered. The Fund is registered as an investment company under the 1940 Act. The 1940 Act is designed to afford various protections to investors in pooled investment vehicles. However, the Portfolio Funds in which the Fund is expected to invest are not subject to the provisions of the 1940 Act. Some Portfolio Fund managers may not be registered as

20

Notes to Consolidated Financial Statements (Continued) |

investment advisers under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). As an indirect investor in the Portfolio Funds managed by managers that are not registered as investment advisers, the Fund will not have the benefit of certain of the protections of the Advisers Act.

In addition, many Portfolio Funds do not maintain their securities and other assets in the custody of a bank or a member of a securities exchange, as generally required of RICs, in accordance with certain SEC rules. The Portfolio Funds in which the Fund will invest may maintain custody of their assets with brokerage firms which do not separately segregate such customer assets as would be required in the case of RICs, or may not use a custodian to hold their assets. Under the provisions of the Securities Investor Protection Act of 1970, as amended, the bankruptcy of any brokerage firm used to hold Portfolio Fund assets could have a greater adverse effect on the Fund than would be the case if custody of assets were maintained in accordance with the requirements applicable to RICs. There is also a risk that a Portfolio Fund manager could convert assets committed to it by the Fund to its own use or that a custodian could convert assets committed to it by a Portfolio Fund manager to its own use. There can be no assurance that the Portfolio Fund managers or the entities they manage will comply with all applicable laws and that assets entrusted to the Portfolio Fund managers will be protected.

Valuations of Private Equity Investments; Valuations Subject to Adjustment. A large percentage of the securities in which the Fund invests will not have a readily determinable market price and will be fair valued.

In addition, a large percentage of the securities in which the Portfolio Funds invest and the Co-Investments will not have a readily determinable market price and will be valued periodically by the Portfolio Fund managers or the Co-Investment or Co-Investment sponsor. In this regard, a Portfolio Fund manager or a Co-Investment sponsor may face a conflict of interest in valuing the securities, as their value may affect the Portfolio Fund manager’s or the Co-Investment sponsor’s compensation or the manager’s or sponsor’s ability to raise additional funds in the future.

Prior to investing in any Private Equity Investment, Barings will generally conduct a due diligence review of the valuation methodology used by the Portfolio Fund manager. No assurances can be given regarding the valuation methodology or the sufficiency of systems utilized by any Portfolio Fund manager or Co-Investment or Co-Investment sponsor, the accuracy of the valuations provided by the Portfolio Fund managers, the Co-Investment or the Co-Investment sponsor, that the Portfolio Fund managers, Co-Investments or Co-Investment sponsors will comply with their own internal policies or procedures for keeping records or making valuations, or that the Portfolio Fund managers’, the Co-Investments or the Co-Investment sponsors’ policies and procedures and systems will not change without notice to the Fund. As a result, valuations of the securities may be subjective and could subsequently prove to have been inaccurate, potentially by significant amounts.

Under the 1940 Act, the Board is responsible for determining the fair valuation of any investments directly held by the Fund for which market quotations are not readily available or reliable; to the extent permitted under applicable rules and guidance, the Board may assign the determination to a “valuation designee,” subject to certain conditions and oversight requirements.

The valuation methodology set forth in the Fund Valuation Procedures incorporates general private equity pricing principles. Based on the methodology, Barings may recommend that the Board adjust a Portfolio Fund manager’s periodic valuation of a Portfolio Fund, or a Co-Investment’s valuation, as appropriate. The Fund runs the risk that its valuation techniques will fail to produce the desired results. Any imperfections, errors, or limitations in any methodology that is used could affect the ability of the Fund to accurately value Portfolio Fund or Co-Investment assets. While any methodology that may be used would be designed to assist in confirming or adjusting valuation recommendations, the Fund generally will not have sufficient information in order to be able to confirm with certainty the accuracy of valuations provided by a Portfolio Fund manager, a Co-Investment or a Co-Investment sponsor until the Fund receives the Portfolio Funds’ or the Co-Investment’s audited annual financial statements. Moreover, Portfolio Fund managers, Co-Investments and Co-Investment sponsors typically provide estimated valuations on a quarterly basis whereas Barings will consider valuations on an ongoing basis and will recommend valuations on a monthly basis. In addition, MML Advisers, Barings, and BIIL (collectively, “Advisers”) face conflicts of interest in assisting with the valuation of the Fund’s investments, as the value of the Fund’s investments will affect the Advisers’ compensation. The Fund Valuation Procedures are designed to help eliminate or at least minimize the risk of such a conflicts of interest.

21

Notes to Consolidated Financial Statements (Continued) |

A Portfolio Fund’s or a Co-Investment’s information could be inaccurate due to fraudulent activity, misevaluation, or inadvertent error. In any case, the Fund may not uncover errors for a significant period of time, if ever. Even if Barings elects to cause the Fund to sell its interests in such a Portfolio Fund or Co- Investment, the Fund may be unable to sell such interests quickly, if at all, and could therefore be obligated to continue to hold such interests for an extended period of time. In such a case, the Portfolio Fund’s valuations of such interests or the Co-Investment’s valuation could remain subject to such fraud or error, and the Board may, in its sole discretion, determine to discount the value of the interests or value them at zero.

Investors should be aware that situations involving uncertainties as to the valuations by Portfolio Funds or Co-Investments could have a material adverse effect on the Fund if judgments regarding valuations should prove incorrect. Persons who are unwilling to assume such risks should not make an investment in the Fund.

The valuations reported by the Portfolio Funds and Co-Investments based upon which the Fund determines its month-end NAV may be subject to later adjustment or revision. For example, NAV calculations may be revised as a result of fiscal year-end audits. Other adjustments may occur from time to time. Because such adjustments or revisions, whether increasing or decreasing the NAV of the Fund, at the time they occur, relate to information available only at the time of the adjustment or revision, the adjustment or revision may not affect the amount of the repurchase proceeds of the Fund received by investors who had their shares repurchased prior to such adjustments and received their repurchase proceeds, subject to the ability of the Fund to adjust or recoup the repurchase proceeds received by shareholders under certain circumstances. As a result, to the extent that such subsequently adjusted valuations from the Portfolio Funds, Co-Investments, direct private equity investments or the Fund adversely affect the Fund’s NAV, the outstanding shares may be adversely affected by prior repurchases to the benefit of shareholders who had their shares repurchased at a NAV higher than the adjusted amount. Conversely, any increases in the NAV resulting from such subsequently adjusted valuations may be entirely for the benefit of the outstanding shares and to the detriment of shareholders who previously had their shares repurchased at a NAV lower than the adjusted amount. The same principles apply to the purchase of shares. New shareholders may be affected in a similar way.

Repurchase Offers Risk. To provide liquidity to shareholders, the Fund may, from time to time, offer to repurchase Shares pursuant to written tenders by shareholders. Repurchases will be made at such times, in such amounts and on such terms as may be determined by the Board, in its sole discretion. With respect to any future repurchase offer, Shareholders tendering Shares for repurchase must do so by a date specified in the notice describing the terms of the repurchase offer, which will generally be approximately 75 days prior to the date that the Shares to be repurchased are valued by the Fund (the “Valuation Date”). Shareholders that elect to tender any shares for repurchase will not know the price at which such shares will be repurchased until the Fund’s NAV as of the Valuation Date is able to be determined.

A 2.00% early repurchase fee will be charged by the Fund with respect to any repurchase of shares from a shareholder at any time prior to the day immediately preceding the one-year anniversary of the shareholder’s purchase of shares. Such repurchase fee will be retained by the Fund and will benefit the Fund’s remaining shareholders. Shares tendered for repurchase will be treated as having been repurchased on a “first in-first out” basis. An early repurchase fee payable by a shareholder may be waived by the Fund in circumstances where the Board determines that doing so is in the best interests of the Fund. For example, an Early Repurchase Fee may not be charged where shares are tendered for repurchase due to shareholder death or disability.

The Fund may be limited in its ability to liquidate its holdings in portfolio funds to meet repurchase requests. Repurchase offers principally will be funded by cash and cash equivalents, as well as by the sale of certain liquid securities. Accordingly, the Fund may tender fewer shares than shareholders may wish to sell, resulting in the proration of shareholder repurchases, or the Fund may need to suspend or postpone repurchase offers if it is required to dispose of interests in portfolio funds and is not able to do so in a timely manner.

Substantial requests for the Fund to repurchase shares could require the Fund to liquidate certain of its investments more rapidly than otherwise desirable for the purpose of raising cash to fund the repurchases and could cause Barings to sell investments at different times than similar investments are sold by other investment vehicles advised by Barings. This could have a material adverse effect on the value of the shares and the performance of the Fund. In addition, substantial repurchases of shares may decrease the Fund’s total assets and accordingly may increase its expenses as a percentage of average net assets. If a repurchase offer is oversubscribed by shareholders who tender shares, the Fund may extend the repurchase offer, repurchase a pro rata

22

Notes to Consolidated Financial Statements (Continued) |

portion of the shares tendered, or take any other action permitted by applicable law. If a repurchase offer is oversubscribed, or if the Fund does not conduct a repurchase offer in any particular quarter, investors will have to wait until the next repurchase offer to make another repurchase request. As a result, investors may be unable to liquidate all or a given percentage of their investment in the Fund during a particular quarter.

Currency Risk. Although the Fund intends to invest significantly in the United States, the Fund’s portfolio is anticipated to include investments in a select number of different currencies. Any returns on, and the value of such investments may, therefore, be materially affected by exchange rate fluctuations, local exchange control, limited liquidity of the relevant foreign exchange markets, the convertibility of the currencies in question and/or other factors. A decline in the value of the currencies in which Fund Investments are denominated against the U.S. Dollar may result in a decrease the Fund’s NAV. Barings generally does not expect to hedge the value of investments made by the Fund against currency fluctuations, and even if Barings deems hedging appropriate, it may not be possible or practicable to hedge currency risk exposure. Accordingly, the performance of the Fund could be adversely affected by such currency fluctuations.

Market Disruption and Geopolitical Risk. The Fund is subject to the risk that geopolitical events will disrupt securities markets and adversely affect global economies and markets. War, terrorism, and related geopolitical events (and their aftermath) have led, and in the future may lead, to increased short-term market volatility and may have adverse long-term effects on U.S. and world economies and markets generally. Likewise, natural and environmental disasters, such as, for example, earthquakes, fires, floods, hurricanes, tsunamis and weather-related phenomena generally, as well as the spread of infectious illness or other public health issues, including widespread epidemics or pandemics such as the COVID-19 outbreak, and systemic market dislocations can be highly disruptive to economies and markets. Those events as well as other changes in non-U.S. and domestic economic and political conditions also could adversely affect individual issuers or related groups of issuers, securities markets, interest rates, credit ratings, inflation, investor sentiment, and other factors affecting the value of Fund investments.

The COVID-19 outbreak has resulted in travel restrictions and disruptions, closed borders, enhanced health screenings at ports of entry and elsewhere, disruption of and delays in healthcare service preparation and delivery, quarantines, event cancellations and restrictions, service cancellations or reductions, disruptions to business operations, supply chains and customer activity, lower consumer demand for goods and services, as well as general concern and uncertainty that has negatively affected the economic environment. The impact of this outbreak and any other epidemic or pandemic that may arise in the future could adversely affect the economies of many nations or the entire global economy, the financial performance of individual issuers, borrowers and sectors and the health of capital markets and other markets generally in potentially significant and unforeseen ways. This crisis or other public health crises may also exacerbate other pre-existing political, social and economic risks in certain countries or globally. The duration of the COVID-19 outbreak and its effects cannot be determined with certainty. The foregoing could lead to a significant economic downturn or recession, increased market volatility, a greater number of market closures, higher default rates and adverse effects on the values and liquidity of securities or other assets. Such impacts, which may vary across asset classes, may adversely affect the performance of the private equity investments, the Fund and a shareholder’s investment in the Fund.

Eurozone Risk. The Fund may invest directly or indirectly from time to time in European companies and assets and companies and assets that may be affected by the Eurozone economy. Ongoing concerns regarding the sovereign debt of various Eurozone countries, including the potential for investors to incur substantial write-downs, reductions in the face value of sovereign debt and/or sovereign defaults, as well as the possibility that one or more countries might leave the European Union (“EU”) or the Eurozone create risks that could materially and adversely affect the Fund Investments. Sovereign debt defaults and EU and/or Eurozone exits could have material adverse effects on the Fund’s investments in European companies and assets, including, but not limited to, the availability of credit to support such companies’ financing needs, uncertainty and disruption in relation to financing, increased currency risk in relation to contracts denominated in Euros and wider economic disruption in markets served by those companies, while austerity and/or other measures introduced to limit or contain these issues may themselves lead to economic contraction and resulting adverse effects for the Fund. Legal uncertainty about the funding of Euro-denominated obligations following any breakup or exits from the Eurozone, particularly in the case of investments in companies and assets in affected countries, could also have material adverse effects on the Fund.

23

Notes to Consolidated Financial Statements (Continued) |

Nature of Portfolio Companies. The private equity investments will include direct and indirect investments in portfolio companies. This may include portfolio companies in the early phases of development, which can be highly risky due to the lack of a significant operating history. The private equity investments may also include portfolio companies that are in a state of distress or which have a poor record, and which are undergoing restructuring or changes in management, and there can be no assurances that such restructuring or changes will be successful. The management of such portfolio companies may depend on one or two key individuals, and the loss of the services of any of such individuals may adversely affect the performance of such portfolio companies.

4. Advisory Fee and Other Transactions:

Investment Advisory and Investment Subadviser:

MML Investment Advisers, LLC (“MML Advisers”), a wholly-owned subsidiary of Massachusetts Mutual Life Insurance Company (“MassMutual”), serves as investment adviser to the Fund. Under an investment advisory agreement between MML Advisers and the Fund, MML Advisers is responsible for providing investment management services for the Fund. In return for these services, MML Advisers receives an advisory fee at an annual rate of 1.30% of the net assets of the Fund as of the end of each month.

MML Advisers has entered into an investment subadvisory agreement with Barings LLC (“Barings”), an indirect wholly-owned subsidiary of MassMutual, on behalf of the Fund. This agreement provides that Barings manage the investment and reinvestment of assets of the Fund. Barings receives a subadvisory fee from MML Advisers, based upon the Fund’s average monthly net assets, at an annual rate of 0.55% on the first $500 million of net assets, 0.45% on the next $500 million of net assets and 0.40% on net assets over $1 billion. Barings has agreed to pay Barings International Investment Limited, under a sub-subadvisory agreement, a fee in an amount equal to 10% of the subadvisory fee received by Barings.

MML Advisers has also entered into an administrative and shareholding services agreement to provides the Fund certain administration, accounting, and compliance services. The Fund does not incur charges associated with these services

Expense Caps and Waivers:

MML Advisers has agreed to cap the fees and expenses of the Fund (including organizational and offering expenses, but excluding extraordinary legal and other expenses, Acquired Fund Fees and Expenses, interest expense, expenses related to borrowings, securities lending, leverage, taxes, and brokerage, short sale dividend and loan expense, or other non-recurring or unusual expenses such as shareholder meeting expenses, as applicable) through January 7, 2023, to the extent that Total Annual Fund Operating Expenses after Expense Reimbursement would otherwise exceed the applicable class of shares of the Fund, as follows:

Class 1 | |||||

| 2.55% | |||||

Expense caps and waiver amounts are reflected as a reduction of expenses on the Consolidated Statement of Operations.