Lind Capital Partners Municipal Credit Income Fund

Filed: 10 Apr 23, 2:12pm

united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-23711

Lind Capital Partners Municipal Credit Income Fund

(Exact name of registrant as specified in charter)

500 Davis Center Suite 1004 Evanston, IL 60201

(Address of principal executive offices) (Zip code)

Karen Jacoppo-Wood, Ultimus Fund Solutions, LLC.

225 Pictoria Drive Suite 450, Cincinnati, OH 45246

(Name and address of agent for service)

Registrant's telephone number, including area code: 513-577-1693

Date of fiscal year end: 1/31

Date of reporting period: 1/31/23

Item 1. Reports to Stockholders.

|

| LIND CAPITAL PARTNERS MUNICIPAL CREDIT INCOME FUND |

| (Symbol:LCPMX) |

| Annual Report |

| January 31, 2023 |

| 1-833-615-3031 |

| www.LCPMX.com |

| Distributed by Ultimus Fund Distributors, LLC |

| Member FINRA |

Letter from the President

Dear Shareholder,

It has been an eventful and interesting year for Lind Capital Partners. Following the successful conversion of the Backcountry Investment Partnership LPs into the Lind Capital Partners Municipal Credit Income Fund (“LCPMX”) interval fund, in which existing LP investors provided the seed capital for the fund, the municipal bond market endured one of the most difficult market environments in recent memory. While not immune to negative performance experienced across almost all asset classes during 2022, our credit and portfolio management team worked diligently to navigate a very challenging environment.

We believe the Fund is well positioned to take advantage of the new market environment that can be broadly characterized with significantly higher rates and diminished liquidity. In December, LCPMX became available to advisors through the Fidelity FundsNetwork, and it recently became available on the Schwab Mutual Fund Marketplace. The availability of the Fund for advisors on both platforms provides the roadmap for growth of the Fund, which benefits all investors. Our team looks forward to the investment opportunities this new market environment will bring in the coming year. As always, we thank our investors for their continued confidence in Lind Capital Partners and we will work diligently to maintain that trust. On the subsequent pages, we detail specific fund performance and market factors affecting that performance.

Sincerely,

J. Robert Lind Jr.

President

1

Portfolio Management Discussion & Analysis (Unaudited)

The 12-month period ending January 31, 2023, presented one of the most challenging environments for municipal market participants since the Great Financial Crisis of 2008. Volatility rattled the financial markets throughout 2022, with nearly all asset classes (aside from cash and commodities) posting negative returns. Investors struggled to discern the path of the U.S. economy, as the country continued to emerge from the severe disruption caused by the COVID-19 pandemic but faced historically high inflation, increased fears of recession, and heightened geopolitical tension. Persistently high inflation caused the Federal Reserve to embark on an aggressive monetary tightening policy. The target Federal Funds rate began the year at 0.25% and ended January 2023 at 4.50%. The 425 basis point increase within a 12-month period was much steeper than many market participants predicted heading into 2022. This resulted in the 10-year U.S. Treasury yield increasing from 1.81% on February 1, 2022, to 3.53% on January 31, 2023. The broad municipal market largely followed suit, with the 10-year AAA municipal yield increasing from 1.56% to 2.22% during the same period. Investor concerns regarding the path of interest rates drove relentless outflows from municipal bond mutual funds and ETFs. During calendar year 2022, investors withdrew over $121 billion. Only a handful of weeks throughout the year experienced net positive inflows. As the page turned to 2023, municipal investors have shown a glimmer of confidence, returning $2.3 billion in inflows to mutual funds and ETFs during January. However, it is yet to be determined if this confidence has true conviction or if volatility in the coming 12 months will continue to make investors uneasy.

The direction of the high yield municipal market has largely mimicked the broader municipal market. Investors withdrew over $19 billion from high yield mutual funds and ETFs during the calendar year 2022 but returned over $1.7 billion in January 2023. For the 12-months ending January 31, 2023, the Bloomberg High Yield Municipal Bond Index (the “Index”) returned (6.63%). Despite unrelenting selling pressure from outflows for most of the period, the high yield market caught a bit of reprieve during the last few months, which included a monthly return of +4.44% in January 2023. The recent support level found in the market has largely been driven by decreased primary market supply, as overall higher cost of capital has kept many potential borrowers on the sidelines and the traditional “January Effect” with seasonally high coupon and principal reinvestment. We view the sell-off in the high yield market as largely driven by technical market factors, rather than a reflection of deteriorating credit. In fact, we believe fundamental credit is broadly stronger than it has been since the onset of the COVID-19 pandemic. This market dynamic, increasing yields and improving credit, has resulted in what we believe to be many “undervalued” credits within the high yield municipal market.

2

Portfolio Management Discussion & Analysis (continued)(Unaudited)

For the 12-months ending January 31, 2023, the Fund outperformed the Index, with a total return of (6.27%) versus (6.63%) for the Index. Outperformance was largely driven by the following contributors:

| ● | Individual credit selection outperformance. |

| ● | The Fund’s strategy to intentionally underweight “bellwether” credits such as Puerto Rico and Tobacco Securitization bonds. |

| ● | Outperformance in the Higher Education sector. |

| ● | Favorable credit outcomes with several holdings being advanced refunded. The Fund was able to sell these positions at a significant premium and redeploy the proceeds into an advantageous rising-rate environment, increasing portfolio yield. |

| ● | Stable performance in Utilities sector, particularly rural fiber internet networks. |

For the 12-months ending January 31, 2023, detractors to the Fund’s performance included:

| ● | Broad municipal market sell-off. |

| ● | The Fund’s overweight to senior living sectors. |

| ● | Low coupon and longer duration credits underperformed. |

| ● | Select credits underperformed. However, we hold a favorable view on the long-term recovery value of these positions. |

Effects of derivatives and leverage on Fund performance:

| ● | None. The Fund intentionally does not utilize derivatives or leverage. |

Throughout the 12-month period, there was no material change to the Fund’s investment strategy or sector allocations. Our exhaustive credit research approach continually identifies developing credit risks, which have resulted in more nuanced sub-sector allocation shifts. For example, challenges within the labor market, particularly nursing labor, have caused expense pressure in healthcare related industries. As such, we have gradually shifted senior living exposure to borrowers who focus more heavily on independent living services versus skilled nursing and higher levels of care. In addition, we have been particularly cognizant of risks associated with new construction projects, such as cost overruns, supply chain disruptions, delays, and labor shortages. These nuanced allocation shifts allow us to proactively manage credit risk exposure within the portfolio.

3

Portfolio Management Discussion & Analysis (continued)(Unaudited)

A staple of the Fund’s strategy, which is enabled by the Fund’s interval fund structure, is to capitalize on periods of retail outflows and market dislocation for the benefit of long-term investors. The past 12 months presented an extremely attractive period to deploy long-term capital and we found ample opportunity to purchase quality, undervalued credits within our target sectors. Through the entire period, the weighted-average yield-to-worst on portfolio purchases was 5.70%. However, the opportunities grew even more attractive as time went on, with weighted-average yield-to-worst on purchases over the last 6 months of 7.11%.

As the Fund reaches its one-year anniversary, we are confident in the portfolio as currently constructed and are excited about the opportunity ahead. We expect the favorable market conditions discussed to persist into 2023, which should contribute to the growth of the Fund. To further aid in the growth of the Fund, we are pleased to announce that the Fund is now available to RIAs utilizing both the Fidelity and Schwab custodial platforms, giving advisors seamless access to the strategy.

Consider the investment objectives, risks, and charges and expenses of the fund carefully before investing. The prospectus contains this and other information about the fund and may be obtained by calling 888-615-3031. The prospectus should be read carefully before investing. The fund is distributed by Ultimus Fund Distributors, LLC. Lind Capital Partners and Ultimus Fund Distributors, LLC are not affiliated.

Important Risk Information

Investment involves risk, including loss of principal. There is no guarantee that the fund will achieve its investment objectives.

An investment in the fund is appropriate for investors who can bear the risks associated with the limited liquidity of the fund’s shares and should be viewed as a long-term investment. Investors will not be able to redeem shares daily because the fund is a closed-end fund operating as an interval fund. The fund’s shares are not traded on an active market and there is currently no secondary market for the shares, nor does the fund expect a secondary market in the shares to develop.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income prices will fall. Credit risk is the risk that issuers and counter parties will not make payments on securities and other investments held by the fund, resulting in losses to the fund. Generally, the longer the maturity and the lower the credit quality of a security, the more sensitive it is to credit risk. The fund invests in high yield securities, also known as “high yield” or “junk bonds.” High yield securities provide greater income and opportunity for gain but entail greater risk of loss of principal.

The fund is subject to municipal bond risk, which is the risk that the fund may be affected significantly by the economic, regulatory or political developments affecting the ability of obligors of municipal bonds to pay interest or repay principal. While the fund intends to invest in municipal bond free from federal income tax, income from municipal bonds held by the fund could be declared taxable because of, among other things, unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer or other obligated party. Investments in taxable municipal bonds and certain derivatives utilized by the fund may cause the fund to have taxable investment income.

There is a risk that a particular investment may be difficult to purchase or sell and that the fund may be unable to sell illiquid investments at an advantageous time or price or achieve its desired level of exposure to a certain sector. Illiquid securities may trade at a discount from comparable, more liquid investments. The fund is non-diversified, which means it may be invested in a limited number of issuers and susceptible to any economic, political and regulatory events than a more diversified fund. The fund is newly organized and has no operating or trading history.

Glossary of Terms:

Yield to Worst: A measure of the lowest possible yield that can be received on a bond without defaulting, taking into consideration contractual call provisions.

16504819-UFD-03012023

4

Lind Capital Partners Municipal Credit Income Fund

PORTFOLIO REVIEW (Unaudited)

January 31, 2023

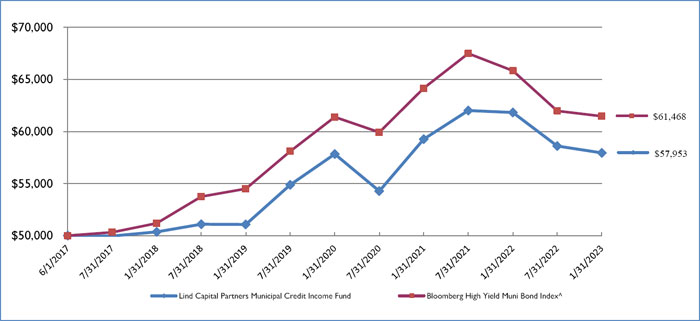

The Fund’s performance figures(*) for the period ended January 31, 2023, compared to its benchmark:

| Annualized | |||

| 1 Year** | 5 Year** | Since Inception** | |

| Lind Capital Partners Municipal Credit Income Fund | (6.27)% | 2.85% | 2.68% |

| Bloomberg High Yield Muni Bond Index^ | (6.63)% | 3.73% | 3.76% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Per the fee table in the prospectus dated February 2, 2022 the Fund’s total annual operating expenses are 1.39%. For performance information current to the most recent month-end, please call toll-free 1-833-615-3031 or visit www.LCPMX.com. |

| ** | The Fund acquired all of the assets and liabilities of Backcountry Investment Partners 3 LP (the “Predecessor Fund”) in a tax free reorganization on February 2, 2022. In connection with this acquisition, shares of the Predecessor Fund were exchanged for shares of the Fund. The Fund’s investment objective, policies and guidelines are in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies and guidelines. The Predecessor Fund commenced operations on June 1, 2017. Updated performance information will be available at no cost by calling 1-833-615-3031 or visiting the Fund’s website at www.LCPMX.com. |

| ^ | Bloomberg High Yield Muni Bond Index covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. You cannot invest directly in an index and unmanaged index returns do not reflect any fees, expenses or sales charges. |

Comparison of the Change in Value of a $50,000 Investment

| Portfolio Composition+ as of January 31, 2023: | ||||

| Municipal Bonds | ||||

| Wisconsin | 13.4 | % | ||

| New Jersey | 12.6 | % | ||

| Indiana | 8.9 | % | ||

| Texas | 8.4 | % | ||

| Pennsylvania | 7.9 | % | ||

| Colorado | 5.7 | % | ||

| Michigan | 5.5 | % | ||

| Vermont | 5.2 | % | ||

| Kentucky | 5.1 | % | ||

| Other Assets in Excess of Liabilities | 27.3 | % | ||

| 100.0 | % | |||

| + | Based on Total Net Assets as of January 31, 2023 |

Please refer to the Schedule of Investments in this report for a detailed listing of the Fund’s holdings.

5

| LIND CAPITAL PARTNERS MUNICIPAL CREDIT INCOME FUND |

| SCHEDULE OF INVESTMENTS |

| January 31, 2023 |

| Principal | Coupon Rate | |||||||||||

| Amount ($) | (%) | Maturity | Fair Value | |||||||||

| MUNICIPAL BONDS — 95.8% | ||||||||||||

| ARIZONA — 3.3% | ||||||||||||

| 100,000 | Arizona Industrial Development Authority | 4.5000 | 07/15/29 | $ | 98,078 | |||||||

| 200,000 | Arizona Industrial Development Authority | 5.6250 | 10/01/49 | 194,733 | ||||||||

| 150,000 | Industrial Development Authority of the County of Pima | 5.7500 | 05/01/50 | 144,982 | ||||||||

| 100,000 | Industrial Development Authority of the County of Pima | 6.8750 | 11/15/52 | 104,066 | ||||||||

| 541,859 | ||||||||||||

| COLORADO — 5.7% | ||||||||||||

| 750,000 | Colorado Health Facilities Authority | 8.0000 | 08/01/43 | 760,909 | ||||||||

| 165,000 | Fiddlers Business Improvement District | 5.5500 | 12/01/47 | 168,095 | ||||||||

| 929,004 | ||||||||||||

| FLORIDA — 3.1% | ||||||||||||

| 340,000 | Capital Trust Agency, Inc. | 6.0000 | 07/01/42 | 287,339 | ||||||||

| 125,000 | Collier County Industrial Development Authority | 8.2500 | 05/15/49 | 72,500 | ||||||||

| 405,000 | Highlands County Health Facilities Authority | 6.0000 | 04/01/38 | 141,750 | ||||||||

| 501,589 | ||||||||||||

| GEORGIA — 3.0% | ||||||||||||

| 450,000 | Fulton County Residential Care Facilities for the Elderly Authority | 4.0000 | 04/01/56 | 303,013 | ||||||||

| 175,000 | Macon-Bibb County Urban Development Authority | 5.8750 | 06/15/47 | 177,437 | ||||||||

| 480,450 | ||||||||||||

| INDIANA — 8.9% | ||||||||||||

| 1,530,000 | City of Anderson IN | 6.0000 | 10/01/42 | 1,443,983 | ||||||||

| IOWA — 1.7% | ||||||||||||

| 290,000 | Iowa Higher Education Loan Authority | 5.5000 | 11/01/51 | 273,242 | ||||||||

| KENTUCKY — 5.1% | ||||||||||||

| 465,000 | Kentucky Economic Development Finance Authority | 5.5000 | 11/15/27 | 436,092 | ||||||||

| 335,000 | Kentucky Economic Development Finance Authority | 6.0000 | 11/15/36 | 292,235 | ||||||||

| 115,000 | Kentucky Economic Development Finance Authority | 6.2500 | 11/15/46 | 94,032 | ||||||||

| 822,359 | ||||||||||||

| LOUISIANA — 0.5% | ||||||||||||

| 100,000 | Louisiana Public Facilities Authority | 5.2500 | 06/01/51 | 87,385 | ||||||||

| MICHIGAN — 5.5% | ||||||||||||

| 725,000 | Grand Rapids Economic Development Corporation | 5.5000 | 04/01/39 | 569,839 | ||||||||

| 435,000 | Grand Rapids Economic Development Corporation | 5.7500 | 04/01/49 | 323,803 | ||||||||

| 893,642 | ||||||||||||

See accompanying notes to financial statements.

6

| LIND CAPITAL PARTNERS MUNICIPAL CREDIT INCOME FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| January 31, 2023 |

| Principal | Coupon Rate | |||||||||||

| Amount ($) | (%) | Maturity | Fair Value | |||||||||

| MUNICIPAL BONDS — 95.8% (Continued) | ||||||||||||

| MINNESOTA — 1.8% | ||||||||||||

| 330,000 | City of Blaine MN | 6.1250 | 07/01/45 | $ | 214,500 | |||||||

| 125,000 | City of Blaine MN | 6.1250 | 07/01/50 | 81,250 | ||||||||

| 295,750 | ||||||||||||

| NEW HAMPSHIRE — 0.8% | ||||||||||||

| 50,000 | New Hampshire Business Finance Authority | 5.6250 | 07/01/46 | 47,715 | ||||||||

| 85,000 | New Hampshire Business Finance Authority | 5.7500 | 07/01/54 | 81,084 | ||||||||

| 128,799 | ||||||||||||

| NEW JERSEY — 12.6% | ||||||||||||

| 2,715,000 | Middlesex County Improvement Authority | 5.0000 | 01/01/32 | 1,820,636 | ||||||||

| 275,000 | New Jersey Economic Development Authority | 5.7500 | 07/01/47 | 223,801 | ||||||||

| 2,044,437 | ||||||||||||

| NEW YORK — 1.0% | ||||||||||||

| 200,000 | Ulster County Capital Resource Corporation | 5.2500 | 09/15/42 | 162,947 | ||||||||

| OHIO — 2.8% | ||||||||||||

| 450,000 | Columbus-Franklin County Finance Authority | 6.5000 | 03/01/48 | 368,286 | ||||||||

| 225,000 | County of Montgomery OH | 6.2500 | 04/01/49 | 78,750 | ||||||||

| 447,036 | ||||||||||||

| OKLAHOMA — 1.9% | ||||||||||||

| 315,000 | Oklahoma County Finance Authority | 6.1250 | 07/01/48 | 310,871 | ||||||||

| PENNSYLVANIA — 7.9% | ||||||||||||

| 75,000 | Philadelphia Authority for Industrial Development | 5.6250 | 08/01/36 | 77,751 | ||||||||

| 250,000 | Philadelphia Authority for Industrial Development | 6.3750 | 06/01/40 | 249,582 | ||||||||

| 950,000 | Philadelphia Authority for Industrial Development | 6.5000 | 06/01/45 | 951,106 | ||||||||

| 1,278,439 | ||||||||||||

| PUERTO RICO — 0.0%(a) | ||||||||||||

| 6,000 | Puerto Rico Sales Tax Financing Corp Sales Tax | 4.5360 | 07/01/53 | 5,523 | ||||||||

| SOUTH CAROLINA — 0.3% | ||||||||||||

| 50,000 | South Carolina Jobs-Economic Development Authority | 5.0000 | 11/01/42 | 47,854 | ||||||||

| TENNESSEE — 1.5% | ||||||||||||

| 230,000 | Shelby County Health Educational & Housing | 5.7500 | 10/01/49 | 169,898 | ||||||||

| 100,000 | Shelby County Health Educational & Housing | 5.7500 | 10/01/54 | 71,604 | ||||||||

| 241,502 | ||||||||||||

| �� | ||||||||||||

See accompanying notes to financial statements.

7

| LIND CAPITAL PARTNERS MUNICIPAL CREDIT INCOME FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| January 31, 2023 |

| Principal | Coupon Rate | |||||||||||

| Amount ($) | (%) | Maturity | Fair Value | |||||||||

| MUNICIPAL BONDS — 95.8% (Continued) | ||||||||||||

| TEXAS — 8.4% | ||||||||||||

| 325,000 | Clifton Higher Education Finance Corporation | 6.1250 | 08/15/48 | $ | 332,901 | |||||||

| 35,000 | New Hope Cultural Education Facilities Finance | 5.7500 | 07/15/52 | 33,749 | ||||||||

| 250,000 | New Hope Cultural Education Facilities Finance | 5.5000 | 01/01/57 | 186,883 | ||||||||

| 170,000 | Newark Higher Education Finance Corporation | 5.7500 | 08/15/45 | 175,865 | ||||||||

| 375,000 | Port Beaumont Navigation District | 8.0000 | 02/01/39 | 366,428 | ||||||||

| 325,000 | San Antonio Education Facilities Corporation | 5.0000 | 10/01/51 | 273,760 | ||||||||

| 1,369,586 | ||||||||||||

| UTAH — 1.4% | ||||||||||||

| 235,000 | Utah Infrastructure Agency | 5.0000 | 10/15/46 | 229,298 | ||||||||

| VERMONT — 5.2% | ||||||||||||

| 650,000 | East Central Vermont Telecommunications District | 6.1250 | 12/01/40 | 666,624 | ||||||||

| 175,000 | East Central Vermont Telecommunications District | 5.6000 | 12/01/43 | 175,910 | ||||||||

| 842,534 | ||||||||||||

| WISCONSIN — 13.4% | ||||||||||||

| 100,000 | Public Finance Authority | 4.6500 | 12/01/35 | 86,493 | ||||||||

| 325,000 | Public Finance Authority | 5.0000 | 04/01/47 | 291,407 | ||||||||

| 515,254 | Public Finance Authority | 5.7500 | 12/01/48 | 468,398 | ||||||||

| 1,522 | Public Finance Authority | 5.5000 | 12/01/48 | 472 | ||||||||

| 425,000 | Public Finance Authority | 5.7500 | 05/01/54 | 365,020 | ||||||||

| 470,000 | Public Finance Authority | 5.0000 | 01/01/57 | 417,637 | ||||||||

| 175,000 | Public Finance Authority | 5.0000 | 02/01/62 | 168,070 | ||||||||

| 250,000 | Wisconsin Health & Educational Facilities | 5.0000 | 08/01/37 | 216,401 | ||||||||

| 225,000 | Wisconsin Health & Educational Facilities | 7.0000 | 07/01/43 | 155,464 | ||||||||

| 2,169,362 | ||||||||||||

| TOTAL MUNICIPAL BONDS (Cost $16,794,971) | 15,547,451 | |||||||||||

| Shares | ||||||||

| SHORT-TERM INVESTMENTS — 2.2% | ||||||||

| MONEY MARKET FUNDS - 2.2% | ||||||||

| 356,443 | Federated Institutional Tax-Free Cash Trust, 1.42% (Cost $356,443)(b) | 356,443 | ||||||

| TOTAL INVESTMENTS – 98.0% (Cost $17,151,414) | $ | 15,903,894 | ||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES - 2.0% | 323,092 | |||||||

| NET ASSETS - 100.0% | $ | 16,226,986 | ||||||

| (a) | Percentage rounds to less than 0.1%. |

| (b) | Rate disclosed is the seven day effective yield as of January 31, 2023. |

See accompanying notes to financial statements.

8

| Lind Capital Partners Municipal Credit Income Fund |

| STATEMENT OF ASSETS AND LIABILITIES |

| January 31, 2023 |

| ASSETS | ||||

| Investment securities: | ||||

| At cost | $ | 17,151,414 | ||

| At fair value | $ | 15,903,894 | ||

| Interest receivable | 373,952 | |||

| Due from Adviser | 16,021 | |||

| Prepaid expenses | 3,657 | |||

| TOTAL ASSETS | 16,297,524 | |||

| LIABILITIES | ||||

| Distribution payable | 9,471 | |||

| Payable to related parties | 31,104 | |||

| Other Accrued expenses | 29,963 | |||

| TOTAL LIABILITIES | 70,538 | |||

| NET ASSETS | $ | 16,226,986 | ||

| Net Assets Consist Of: | ||||

| Paid in capital | $ | 18,236,812 | ||

| Accumulated deficit | (2,009,826 | ) | ||

| NET ASSETS | $ | 16,226,986 | ||

| Net Asset Value Per Share: | ||||

| Shares: | ||||

| Net Assets | $ | 16,226,986 | ||

| Shares of beneficial interest outstanding ($0 par value. unlimited shares authorized) | 1,811,164 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | $ | 8.96 | ||

See accompanying notes to financial statements.

9

| Lind Capital Partners Municipal Credit Income Fund |

| STATEMENT OF OPERATIONS |

| For the Period Ended January 31, 2023 (a) |

| INVESTMENT INCOME | ||||

| Interest | $ | 978,412 | ||

| TOTAL INVESTMENT INCOME | 978,412 | |||

| EXPENSES | ||||

| Investment advisory fees | 168,976 | |||

| Administrative services fees | 105,376 | |||

| Transfer agent fees | 59,769 | |||

| Professional fees | 41,386 | |||

| Trustees fees and expenses | 31,479 | |||

| Legal fees | 31,460 | |||

| Offering costs | 20,571 | |||

| Audit fees | 20,039 | |||

| Printing | 12,949 | |||

| Custodian fees | 6,833 | |||

| Registration fees | 1,063 | |||

| Other expenses | 7,280 | |||

| TOTAL EXPENSES | 507,181 | |||

| Less: Fees waived/reimbursed by the Adviser | (296,039 | ) | ||

| NET EXPENSES | 211,142 | |||

| NET INVESTMENT INCOME | 767,270 | |||

| REALIZED AND UNREALIZED GAIN (LOSS) FROM INVESTMENTS | ||||

| Net realized (loss) from investments | (154,839 | ) | ||

| Net change in unrealized depreciation on investments | (1,903,409 | ) | ||

| NET REALIZED AND UNREALIZED (LOSS) FROM INVESTMENTS | (2,058,248 | ) | ||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (1,290,978 | ) | |

| (a) | Commencement of operations was February 2, 2022 |

See accompanying notes to financial statements.

10

| Lind Capital Partners Municipal Credit Income Fund |

| STATEMENT OF CHANGES IN NET ASSETS |

| Period Ended | ||||

| January 31, 2023 (a) | ||||

| FROM OPERATIONS | ||||

| Net investment income | $ | 767,270 | ||

| Net realized loss from investments | (154,839 | ) | ||

| Net change in unrealized depreciation on investments | (1,903,409 | ) | ||

| Net decrease in net assets resulting from operations | (1,290,978 | ) | ||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||

| Total distribution paid: | (718,848 | ) | ||

| Decrease in net assets from distributions to shareholders | (718,848 | ) | ||

| FROM SHARES OF BENEFICIAL INTEREST | ||||

| Proceeds from shares sold | 20,040,709 | |||

| Reinvestment of distributions to shareholders | 590,072 | |||

| Payments for shares redeemed | (2,493,969 | ) | ||

| Net increase in net assets from shares of beneficial interest | 18,136,812 | |||

| TOTAL INCREASE IN NET ASSETS | 16,126,986 | |||

| NET ASSETS | ||||

| Beginning of Period | 100,000 | |||

| End of Period | $ | 16,226,986 | ||

| SHARE ACTIVITY | ||||

| Shares Sold | 2,009,080 | |||

| Shares Reinvested | 65,281 | |||

| Shares Redeemed | (273,197 | ) | ||

| Net increase from share activity | 1,801,164 | |||

| (a) | Commencement of operations was February 2, 2022 |

See accompanying notes to financial statements.

11

| Lind Capital Partners Municipal Credit Income Fund |

| FINANCIAL HIGHLIGHTS |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout the Period Presented |

| Period Ended | ||||

| January 31, | ||||

| 2023(a) | ||||

| Net asset value, beginning of period | $ | 10.00 | ||

| Activity from investment operations: | ||||

| Net investment income (b) | 0.41 | |||

| Net realized and unrealized gain (loss) on investments | (1.06 | ) | ||

| Total from investment operations | (0.65 | ) | ||

| Less distributions from: | ||||

| Net investment income | (0.38 | ) | ||

| Net realized gains | (0.01 | ) | ||

| Total distributions | (0.39 | ) | ||

| Net asset value, end of period | $ | 8.96 | ||

| Total return (c) | (6.51 | )% (d) | ||

| Net assets, end of period (000s) | $ | 16,227 | ||

| Ratio of gross expenses to average net assets | 3.00 | % (e) | ||

| Ratio of net expenses to average net assets | 1.25 | % (e) | ||

| Ratio of net investment income to average net assets | 4.54 | % (e) | ||

| Portfolio Turnover Rate | 30 | % (d) | ||

| (a) | Lind Capital Partners Municipal Credit Income Fund Commencement of operations was February 2, 2022. |

| (b) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (c) | Total return is calculated assuming a purchase of shares at net asset value on the first day and a sale at net asset value on the last day of the period. Distributions are assumed, for the purpose of this calculation, to be reinvested at the ex-dividend date net asset value per share on their respective payment dates. |

| (d) | Not annualized. |

| (e) | Annualized. |

See accompanying notes to financial statements.

12

Lind Capital Partners Municipal Credit Income Fund

NOTES TO FINANCIAL STATEMENTS

January 31, 2023

| 1. | ORGANIZATION |

Lind Capital Partners Municipal Credit Income Fund (the “Fund”) was organized as a Delaware statutory trust on May 13, 2021 and is registered under the Investment Company Act of 1940, as amended, (the “1940 Act”), as a non-diversified, closed-end management investment company that operates as an interval fund with a continuous offering of Fund shares. The investment objective of the Fund is to generate high current income from investments in municipal securities exempt from federal income tax and capital preservation. Additional return via capital appreciation is a secondary investment objective of the Fund.

On February 2, 2023, Backcountry Investment Partnership, LP (the “Predecessor 1 Fund”) and Backcountry Investment Partnership 3, LP (the “Predecessor 3 Fund” collectively the “Predecessor Funds”) each reorganized and transferred substantially all its assets into the Fund. The Predecessor Funds maintained an investment objective, strategies, policies, guidelines, and restrictions that are, in all material respects, equivalent to those of the Fund. The Fund and the Predecessor Funds share the same investment manager and portfolio managers. The conversion was accomplished through a tax-free exchange of 1,908,348 shares of the Fund, for the value of $19,083,476. The investment portfolio of Predecessor 1 Fund with a fair value of $9,999,543, identified cost of $9,569,397 and unrealized appreciation of $430,146 and the Predecessor 3 Fund with a fair value of $7,533,904, identified cost of $7,308,354 and unrealized appreciation of $225,550 at February 2, 2023, was the principal asset acquired by the Fund. For financial reporting purposes, assets received and shares issued by the Fund were recorded at fair value. However, the cost basis of the investments received from the Predecessor Funds was carried forward to align ongoing reporting of Funds realized and unrealized gains and losses with amounts distributable to shareholders for tax purposes.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies”.

Security Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the primary exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price. In the absence of a sale such securities shall be valued at the mean between the current bid and ask prices on the day of valuation. Debt securities not traded on an exchange may be valued at prices supplied by a pricing agent(s) based on broker or dealer supplied valuations or matrix pricing, a method of valuing securities by reference to the value of other securities with similar characteristics, such as rating, interest rate and maturity. Short-term debt obligations having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost.

When the Fund uses fair valuation to determine the value of a portfolio security or other asset for purposes of calculating its net asset value (“NAV”), such investments will not be priced on the basis of quotes from the primary market in which they are traded, but rather may be priced by the valuation designee. Fair valuation may require subjective determinations about the value of a security. Although the Fund’s policy is intended to result in a calculation of the Fund’s NAV that fairly reflects security values as of the time of pricing, the Fund cannot ensure that fair values determined by the Board of Trustees (the “Board”) or persons acting at its direction will accurately reflect the price that the Fund could obtain for a security if it were to dispose of that security as of the time of pricing (for instance, in a forced or distressed sale). The prices used by the Fund may differ from the value that would be realized if the securities were sold.

There is no single standard for determining fair value of a security. Rather, the valuation designee’s fair value calculations will involve significant professional judgment in the application of both observable and unobservable attributes, and as a result, the fair value determined for a security may differ from its actual realizable value or future fair value. As part of its due diligence, the Valuation Designee will attempt to obtain current information on an ongoing basis from market sources or issuers to value all fair valued securities.

13

Lind Capital Partners Municipal Credit Income Fund

NOTES TO FINANCIAL STATEMENTS (Continued)

January 31, 2023

The Fund utilizes various methods to measure the fair value of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of January 31, 2023 for the Fund’s assets measured at fair value:

| Assets* | Level I | Level 2 | Level 3 | Total | ||||||||||||

| Municipal Bonds | $ | — | $ | 15,547,451 | $ | — | $ | 15,547,451 | ||||||||

| Short-Term Investment | 356,443 | — | — | 356,443 | ||||||||||||

| Total | $ | 356,443 | $ | 15,547,451 | $ | — | $ | 15,903,894 | ||||||||

| * | Refer to the Schedule of Investments for industry classifications. |

The Fund did not hold any level 3 securities.

Security Transactions and Investment Income – Investment security transactions are accounted for on a trade date basis. Cost is determined and gains and losses are based upon the specific identification method for both financial statement and federal income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on the accrual basis. Purchase discounts and premiums on securities are accreted and amortized over the life of the respective securities using the effective interest method.

Federal Income Taxes – The Fund intends to comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and will distribute all of its taxable income, if any, to shareholders. Accordingly, no provision for Federal income taxes is required in the financial statements.

The Fund recognizes the tax benefits of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken or expected to be taken in the Fund’s January 31, 2023 tax return. The Fund identifies its major tax jurisdiction as U.S. Federal. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the period ended January 31, 2023, the Fund did not incur any interest or penalties. Generally, tax authorities can examine tax returns filed for the last three years.

14

| Lind Capital Partners Municipal Credit Income Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| January 31, 2023 |

Distributions to Shareholders – Distributions from investment income are declared and recorded on a daily basis and paid monthly. Distributions from net realized capital gains, if any, are declared and paid annually and are recorded on the ex- dividend date. The character of income and gains to be distributed is determined in accordance with income tax regulations, which may differ from GAAP. These “book/tax” differences are considered either temporary (e.g., deferred losses) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require reclassification.

All or a portion of a distribution may consist of return of capital, shareholders should not assume that the source of a distribution is net income.

Indemnification – The Fund indemnifies its officers and Trustees for certain liabilities that may arise from the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be remote.

Organizational and Offering Costs - Organizational costs are charged to expense as incurred. Offering costs incurred by the Fund are treated as deferred charges until operations commence and thereafter will be amortized into expense over 12 months using the straight-line method.

| 3. | PRINCIPAL INVESTMENT RISKS |

Credit Risk – the risk that the Fund could lose money if the issuer, guarantor, or insurers of a fixed-income security, or the counterparty to a derivative considered primarily speculative regarding the issuer’s continuing ability to make principal and interest payments and may be more volatile than higher-rated securities of similar maturity. Changes in the actual or perceived creditworthiness of an issuer, or a downgrade or default affecting any of the Fund’s securities could affect the Fund’s performance. Generally, the longer the maturity and the lower the credit quality of a security, the more sensitive it is to credit risk.

Municipal Bond Risk – the risk that a Fund may be affected significantly by the economic, regulatory, or political developments affecting the ability of obligors of Municipal Bonds to pay interest or repay principal. The values of Municipal Bonds held by the Fund may be adversely affected by local political and economic conditions and developments. The Fund may make significant investments in a particular segment of the municipal bond market or in the debt of issuers located in the same state or territory. Adverse conditions in such industry or location could have a correspondingly adverse effect on the financial condition of issuers. These conditions may cause the value of the Fund’s shares to fluctuate more than the values of shares of funds that invest in a greater variety of investments. The amount of public information available about municipal bonds is generally less than for certain corporate equities or bonds, meaning that the investment performance of the Fund may be more dependent on the analytical abilities of the Fund’s Adviser than funds that invest in stock or other corporate investments.

Interest Rate Risk – the risk that fixed-income securities will decline in value because of an increase in interest rates. The values of debt instruments, including Municipal Bonds, usually rise and fall in response to changes in interest rates. Declining interest rates generally increase the value of existing debt instruments, and rising interest rates generally decrease the value of existing debt instruments. Securities with floating interest rates generally are less sensitive to interest rate changes but may decline in value if their interest rates do not rise as much, or as quickly, as interest rates in general. Conversely, floating rate instruments will not generally increase in value if interest rates decline. Changes in interest rates will also affect the amount of interest income the fund earns on its floating rate investments.

High Yield Risk – Lower-quality bonds, known as “high yield” or “junk” bonds, present greater risk than bonds of higher quality, including an increased risk of default. Such bonds are considered predominantly speculative and may be questionable as to principal and interest payments. An economic downturn or period of rising interest rates could adversely affect the market for these bonds and reduce the Fund’s ability to sell its bonds. The lack of a liquid market for these bonds could decrease the Fund’s share price. Unrated municipal bonds determined by the Fund’s Adviser to be of comparable quality to rated municipal bonds which the Fund may purchase may pay a higher interest rate than such rated municipal bonds and be subject to a greater

15

| Lind Capital Partners Municipal Credit Income Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| January 31, 2023 |

risk of illiquidity or price changes. Less public information is typically available about unrated municipal bonds or issuers than rated bonds or issuers.

Liquidity Risk – the risk that a particular investment may be difficult to purchase or sell and that the Fund may be unable to sell illiquid investments at an advantageous time or price or achieve its desired level of exposure to a certain sector. Liquidity risk may result from the lack of an active market, reduced number and capacity of traditional market participants to make a market in fixed income securities. Inventories of municipal bonds held by brokers and dealers have decreased in recent years, lessening their ability to make a market in these securities. This reduction in market making capacity has the potential to decrease the Fund’s ability to buy or sell bonds, and increase bond price volatility and trading costs, particularly during periods of economic or market stress. In addition, recent federal banking regulations may cause certain dealers to reduce their inventories of municipal bonds, which may further decrease the Fund’s ability to buy or sell bonds. As a result, the Fund may be forced to accept a lower price to sell a security, to sell other securities to raise cash, or to give up an investment opportunity, any of which could have a negative effect on performance. If the Fund needed to sell large blocks of bonds to raise cash (such as to meet heavy shareholder redemptions), those sales could further reduce the bonds’ prices and hurt performance. The Fund may invest in securities which are, or which become, illiquid. Illiquid securities may trade at a discount from comparable, more liquid investments, and may be subject to wide fluctuations in market value. Also, the Fund may not be able to dispose readily of illiquid securities when that would be beneficial at a favorable time or price or at prices approximating those at which the Fund currently values them. Further, the lack of an established secondary market for illiquid securities may make it more difficult to value such securities, which may negatively affect the price the Fund would receive upon disposition of such securities.

| 4. | INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES |

Advisory Fees – Lind Capital Partners, LLC (“Lind”) serves as the Fund’s investment adviser (the “Adviser”). Pursuant to an investment advisory agreement with the Trust, on behalf of the Fund, the Adviser, under the oversight of the Board, directs the daily operations of the Fund and supervises the performance of administrative and professional services provided by others. As compensation for these services and the related expenses borne by the Adviser, the Fund has agreed to pay the Adviser as compensation under the Investment Management Agreement (the “Management Fee”). The management fee is calculated and payable monthly in arrears at the annual rate of 1.00% of the Fund’s average daily net assets.

The Adviser and the Fund have entered into an expense limitation and reimbursement agreement (the “Expense Limitation Agreement”) under which the Adviser has agreed contractually to waive its fees and to pay or absorb the ordinary operating expenses of the Fund (excluding brokerage costs, taxes, interest, borrowing costs such as interest and dividend expenses on securities sold short, Acquired Fund fees and expenses, extraordinary expenses such as litigation and merger or reorganization costs, and other expenses not incurred in the ordinary course of such Fund’s business), to the extent that they exceed 1.25% per annum of the Fund’s average daily net assets of the Fund (the “Expense Limitation”). In consideration of the Adviser’s agreement to limit the Fund’s expenses, the Fund has agreed to repay the Adviser in the amount of any fees waived and Fund expenses paid or absorbed, subject to the limitations that: (1) the reimbursement for fees and expenses will be made only if payable not more than three years from when they were incurred; and (2) the reimbursement may not be made if it would cause the Expense Limitation (at the time of waiver/reimbursement or recapture) to be exceeded. The expense limitation will be in effect through April 30, 2025. During the period ended January 31, 2023, the Advisor waived $296,039 pursuant to the Expense Limitation Agreement and repayment of these waivers will expire January 31, 2026. The Fund had organizational costs of $47,500 which are recoupable until September 30, 2024.

Ultimus Fund Distributors, LLC (the “Distributor”) acts as the Fund’s distributor and principal underwriter in a continuous public offering of the Fund shares. During the year ended January 31, 2023, the Distributor received $0 in underwriting commissions.

In addition, certain affiliates of the Distributor provide services to the Fund as follows:

Ultimus Fund Solutions, LLC (“UFS”), an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to an administrative servicing agreement with UFS, the Fund pays UFS customary fees based on aggregate net assets of the Fund as described in the servicing agreement for providing administration, fund accounting, and

16

| Lind Capital Partners Municipal Credit Income Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| January 31, 2023 |

transfer agency services to the Fund. Certain officers of the Trust are also officers of UFS and are not paid any fees directly by the Fund for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”) - NLCS, an affiliate of UFS, provides a Chief Compliance Officer to the Fund, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Fund. Under the terms of such agreement, NLCS receives customary fees from the Fund.

Blu Giant, LLC (“Blu Giant”) – Blu Giant, an affiliate of UFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Fund on an ad-hoc basis. For the provision of these services, Blu Giant receives customary fees from the Fund.

| 5. | INVESTMENT TRANSACTIONS |

The cost of purchases and proceeds from the sale of securities, other than short-term securities, for the period ended January 31, 2023, amounted to $4,545,835 and $4,493,305 respectively.

| 6. | AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION – TAX BASIS |

The identified cost of investments in securities owned by the Fund for federal income tax purposes and its respective gross unrealized appreciation and depreciation at January 31, 2023, was as follows:

| Total Unrealized | ||||||||||||||

| Unrealized | Unrealized | Appreciation/ | ||||||||||||

| Cost | Appreciation | Depreciation | Depreciation | |||||||||||

| $ | 17,767,173 | $ | 223,276 | $ | (2,086,556 | ) | $ | (1,863,280 | ) | |||||

| 7. | DISTRIBUTIONS TO SHAREHOLDERS AND TAX COMPONENTS OF CAPITAL |

The tax character of fund distributions paid for the period ended January 31, 2023, was as follows:

| Fiscal Period Ended | ||||

| January 31, 2023 | ||||

| Ordinary Income | $ | — | ||

| Tax-exempt Income | 706,063 | |||

| Long-Term Capital Gain | 12,785 | |||

| Return of Capital | — | |||

| $ | 718,848 | |||

As of January 31, 2023, the components of accumulated earnings/ (deficit) on a tax basis were as follows:

| Tax-exempt | Undistributed | Undistributed | Post October | Capital Loss | Other | Unrealized | Total | |||||||||||||||||||||||

| Ordinary | Ordinary | Long-Term | Loss and | Carry | Book/Tax | Appreciation/ | Distributable Earnings/ | |||||||||||||||||||||||

| Income | Income | Gains | Late Year Loss | Forwards | Differences | (Depreciation) | (Accumulated Deficit) | |||||||||||||||||||||||

| $ | 9,471 | $ | — | $ | 21,063 | $ | (167,610 | ) | $ | — | $ | (9,471 | ) | $ | (1,863,279 | ) | $ | (2,009,826 | ) | |||||||||||

The difference between book basis and tax basis undistributed net investment income, accumulated net realized losses and unrealized depreciation is due to book/tax differences in the treatment of bond amortization. The difference between book basis and tax basis undistributed net investment income/(loss) and other book/tax adjustments is primarily attributable to the adjustments for accrued dividends payable.

Capital losses incurred after October 31 within the fiscal year are deemed to arise on the first business day of the following fiscal year for tax purposes. The Fund incurred and elected to defer such capital losses of $167,610.

17

Lind Capital Partners Municipal Credit Income Fund

NOTES TO FINANCIAL STATEMENTS (Continued)

January 31, 2023

| 8. | BENEFICIAL OWNERSHIP |

The beneficial ownership, either directly or indirectly, of 25% or more of the outstanding shares of a fund creates a presumption of control of the fund under Section 2(a)(9) of the 1940 Act. As of January 31, 2023, David M. Murdoch Trust was the record owner of 25.52% of the Fund’s outstanding shares. David M. Murdoch Trust may be the beneficial owner of some or all the shares or may hold the shares for the benefit of others. As a result, David M. Murdoch Trust may be deemed to control the Fund.

| 9. | REPURCHASE OFFERS |

The Fund is an “interval fund” and, in order to provide liquidity to shareholders, it intends to conduct quarterly repurchase offers of the outstanding shares at NAV, subject to approval of the Board. In each quarter, such repurchase offers will be at least 5% of its outstanding shares at NAV, pursuant to Rule 23c-3 under the 1940 Act. The Fund currently expects to conduct quarterly repurchase offers for 5% of its outstanding shares under ordinary circumstances. If shareholders tender for repurchase more than 5% of the outstanding Shares (the “Repurchase Offer Amount”), the Fund may, but is not required to, repurchase an additional amount of Shares not to exceed 2% of the outstanding Shares on the Repurchase Request Deadline. If the Fund determines not to repurchase more than the Repurchase Offer Amount, or if shareholders tender Shares in an amount exceeding the Repurchase Offer Amount plus 2% of the outstanding Shares on the Repurchase Request Deadline, the Fund will repurchase Shares pro rata based upon the number of Shares tendered by each shareholder. Repurchase offers and the need to fund repurchase obligations may affect the Fund’s ability to be fully invested or force the Fund to maintain a higher percentage of its assets in liquid investments, which may harm the Fund’s investment performance. Moreover, diminution in the size of the Fund through repurchases may result in untimely sales of portfolio securities (with associated imputed transaction costs, which may be significant), and may limit the ability of the Fund to participate in new investment opportunities or to achieve its investment objectives. The Fund may accumulate cash by holding back (i.e., not reinvesting) payments received in connection with the Fund’s investments.

During the year ended January 31, 2023, the Fund completed three quarterly repurchase offers. In those offers, the Fund offered to repurchase up to 5% of the number of its outstanding shares as of the Repurchase Pricing Dates. The Fund, under officer approval, increased the repurchase percentage above 5% on May 27, 2022 and August 26, 2022. The results of those repurchase offers were as follows:

| Repurchase Offer #1 | Repurchase Offer #2 | Repurchase Offer #3 | ||||||||||

| Commencement Date | May 2, 2022 | August 1, 2022 | October 31, 2022 | |||||||||

| Repurchase Request Deadline | May 27, 2022 | August 26, 2022 | November 28, 2022 | |||||||||

| Repurchase Pricing Date | May 27, 2022 | August 26, 2022 | November 28, 2022 | |||||||||

| Net Asset Value as of Repurchase Offer Date | $ | 9.25 | $ | 9.11 | $ | 8.78 | ||||||

| Amount Repurchased | $ | 1,006,228 | $ | 1,219,277 | $ | 268,465 | ||||||

| Percentage of Outstanding Shares Repurchased | 5.42 | % | 7.00 | % | 1.70 | % | ||||||

| 10. | SUBSEQUENT EVENTS |

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has determined that the below events or transactions occurred requiring adjustment or disclosure in the financial statements.

18

Lind Capital Partners Municipal Credit Income Fund

NOTES TO FINANCIAL STATEMENTS (Continued)

January 31, 2023

Subsequent to year end the Fund completed a quarterly repurchase offer. The results of this repurchase offer was as follows:

| Repurchase Offer | ||||

| Commencement Date | January 27, 2023 | |||

| Repurchase Request Deadline | February 24, 2023 | |||

| Repurchase Pricing Date | February 24, 2023 | |||

| Net Asset Value as of Repurchase Offer Date | $ | 8.76 | ||

| Amount Repurchased | $ | 172,419 | ||

| Percentage of Outstanding Shares Repurchased | 1.07 | % | ||

19

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Trustees of

Lind Capital Partners Municipal Credit Income Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Lind Capital Partners Municipal Credit Income Fund (the “Fund”) as of January 31, 2023, the related statements of operations and changes in net assets and the financial highlights for the period from February 2, 2022 (commencement of operations) through January 31, 2023, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of January 31, 2023, and the results of its operations, the changes in its net assets, and the financial highlights for the period indicated above, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of January 31, 2023, by correspondence with the custodian. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2023.

COHEN & COMPANY, LTD.

Philadelphia, Pennsylvania

March 31, 2023

COHEN & COMPANY, LTD.

800.229.1099 | 866.818.4538 fax | cohencpa.com

Registered with the Public Company Accounting Oversight Board

20

Lind Capital Partners Municipal Credit Income Fund

Change in Independent Registered Public Accounting Firm (unaudited)

January 31, 2023

On March 6, 2023, BBD LLP (“BBD”) ceased to serve as the independent registered public accounting firm of Lind Capital Partners Municipal Credit Income Fund (the “Fund”). The Audit Committee of the Board of Trustees approved the replacement of BBD as a result of Cohen & Company, Ltd.’s (“Cohen”) acquisition of BBD’s investment management group.

The report of BBD on the financial statements of the Fund as of and for the one day period ended September 21, 2021 did not contain an adverse opinion or a disclaimer of opinion, and were not qualified or modified as to uncertainties, audit scope or accounting principles. During the fiscal period ended January 31, 2023 and the interim period ended March 6, 2023: (i) there were no disagreements between the registrant and BBD on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of BBD, would have caused it to make reference to the subject matter of the disagreements in its report on the financial statements of the Fund/Funds for such years or interim period; and (ii) there were no “reportable events,” as defined in Item 304(a)(1)(v) of Regulation S-K under the Securities Exchange Act of 1934, as amended.

The registrant requested that BBD furnish it with a letter addressed to the U.S. Securities and Exchange Commission stating that it agrees with the above statements. A copy of such letter is filed as an exhibit hereto.

On February 24, 2023, the Audit Committee of the Board of Trustees also recommended and approved the appointment of Cohen as the Fund’s independent registered public accounting firm for the fiscal period ending January 31, 2023.

During the fiscal period January 31, 2023, and through the interim period March 6, 2023, neither the registrant, nor anyone acting on its behalf, consulted with Cohen on behalf of the Fund regarding the application of accounting principles to a specified transaction (either completed or proposed), the type of audit opinion that might be rendered on the Fund’s financial statements, or any matter that was either: (i) the subject of a “disagreement,” as defined in Item 304(a)(1)(iv) of Regulation S-K and the instructions thereto; or (ii) “reportable events,” as defined in Item 304(a)(1)(v) of Regulation S-K.

21

Lind Capital Partners Municipal Credit Income Fund

The tables below show, for each Trustee and executive officer of the Fund, his name, address, and age; the position held with the Fund; the length of time served as Trustee or officer of the Fund; the Trustee’s or officer’s principal occupations during the last five years; the number of portfolios in the Adviser’s fund complex overseen by the Trustee or for which a person served as an officer; and other directorships or trusteeships held by such Trustee. The address of each trustee and officer is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246.

| Name and Year of Birth | Position with the Fund | Term of Office and Length of Time Served | Principal Occupation(s) and Other Directorships/Trusteeships During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee |

| J. Robert Lind Year of Birth: 1961 | Interested Trustee and President | Since 2021 | Managing Director, Lind Capital Partners, LLC (2009 – Present). | 1 |

| Richard H. Adler Year of Birth: 1954 | Independent Trustee | Since 2021 | President/CEO, Red Arrow Capital, LLC (2014 – Present). | 1 |

| Thomas J. Schmidt Year of Birth: 1963 | Independent Trustee and Chairman | Since 2021 | Principal, Tom Schmidt & Associates Consulting, LLC (2015 – Present); Trustee, 360 Funds (2018 – Present) | 1 |

Information Regarding Officers

| Name and Year of Birth | Position with the Fund | Length of Time Served | Principal Occupation(s) During Past Five Years |

| Erik Naviloff Year of Birth: 1968 | Treasurer | Since 2021 | Vice President – Fund Administration, Ultimus Fund Solutions, LLC (2011 – Present). |

| William Kimme Year of Birth: 1962 | Chief Compliance Officer | Since 2021 | Senior Compliance Officer, Northern Lights Compliance Services, LLC (since 2011). |

| Khimmara Greer Year of Birth: 1983 | Secretary | Since 2021 | Vice President and Senior Legal Counsel of Ultimus Fund Solutions, LLC (2021 – Present); Vice President, Asset Servicing – Regulatory Administration of The Bank of New York Mellon (2019 – 2021); Vice President and Counsel of State Street Bank and Trust Company (2015 – 2019). |

| Deryk Jones Year of Birth: 1988 | Anti-Money Laundering Compliance Officer | Since 2021 | Compliance Analyst, Northern Lights Compliance Services, LLC (2018 – Present). |

The Funds’ SAI includes additional information about the Trustees and is available free of charge, upon request, by calling toll-free at 1-833-615-3031.

22

PRIVACY NOTICE

Lind Capital Partners

| FACTS | WHAT DOES LIND CAPITAL PARTNERS DO WITH YOUR PERSONAL INFORMATION? |

| Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some, but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. |

| What? | The types of personal information we collect and share depend on the product or service that you have with us. This information can include:

● Social Security number and wire transfer instructions

● account transactions and transaction history

● investment experience and purchase history

When you are no longer our customer, we continue to share your information as described in this notice. |

| How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons Lind Capital Parrtners chooses to share; and whether you can limit this sharing. |

| Reasons we can share your personal information: | Does Lind Capital Partners share information? | Can you limit this sharing? |

| For our everyday business purposes - such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus. | YES | NO |

| For our marketing purposes - to offer our products and services to you. | NO | We don’t share |

| For joint marketing with other financial companies. | NO | We don’t share |

| For our affiliates’ everyday business purposes -information about your transactions and records. | NO | We don’t share |

| For our affiliates’ everyday business purposes -information about your credit worthiness. | NO | We don’t share |

| For nonaffiliates to market to you | NO | We don’t share |

| QUESTIONS? | Call 1-312-361-3446 |

23

PRIVACY NOTICE

Lind Capital Partners

| What we do: | |

| How does Lind Capital Partners protect my personal information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings.

Our service providers are held accountable for adhering to strict policies and procedures to prevent any misuse of your nonpublic personal information. |

| How does Lind Capital Partners collect my personal information? | We collect your personal information, for example, when you

● open an account or deposit money

● direct us to buy securities or direct us to sell your securities

● seek advice about your investments

We also collect your personal information from others, such as credit bureaus, affiliates, or other companies. |

| Why can’t I limit all sharing? | Federal law gives you the right to limit only:

● sharing for affiliates’ everyday business purposes – information about your creditworthiness.

● affiliates from using your information to market to you.

● sharing for nonaffiliates to market to you.

State laws and individual companies may give you additional rights to limit sharing. |

| Definitions | |

| Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies.

● Lind Capital Partners does not share with our affiliates. |

| Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies.

● Lind Capital Partners does not share with nonaffiliates so they can market to you. |

| Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you.

● Lind Capital Partners isn’t joint market. |

24

How to Obtain Proxy Voting Information

Information regarding how the Fund votes proxies relating to portfolio securities during the most recent 12-month period ending June 30th as well as a description of the policies and procedures that the Fund used to determine how to vote proxies is available without charge, upon request, by calling 1-833-615-3031 or by referring to the Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov.

How to Obtain 1st and 3rd Fiscal Quarter Portfolio Holdings

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT, within sixty days after the end of the period. Form N-PORT reports are available on the SEC’s website at http://www.sec.gov. The information on Form N-PORT is available without charge, upon request, by calling 1-833-615-3031.

| Investment Adviser |

| Lind Capital Partners, LLC |

| 500 Davis Center, Suite 1004 |

| Evanston, Illinois 60201 |

| Administrator |

| Ultimus Fund Solutions, LLC |

| 225 Pictoria Drive, Suite 450 |

| Cincinnati, OH 45246 |

| Lind-AR23 |

Item 2. Code of Ethics.

(a) As of the end of the period covered by this report, the registrant has adopted a code of ethics that applies to the registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party.

(b) For purposes of this item, “code of ethics” means written standards that are reasonably designed to deter wrongdoing and to promote:

| (1) | Honest and ethical conduct, including the ethical handling of actual or apparent conflicts of interest between personal and professional relationships; |

| (2) | Full, fair, accurate, timely, and understandable disclosure in reports and documents that a registrant files with, or submits to, the Commission and in other public communications made by the registrant; |

(3) Compliance with applicable governmental laws, rules, and regulations;

| (4) | The prompt internal reporting of violations of the code to an appropriate person or persons identified in the code; and |

(5) Accountability for adherence to the code.

(c) Amendments: During the period covered by the report, there have not been any amendments to the provisions of the code of ethics.

(d) Waivers: During the period covered by the report, the registrant has not granted any express or implicit waivers from the provisions of the code of ethics.

(e) The Code of Ethics is not posted on Registrant’ website.

(f) A copy of the Code of Ethics is attached as an exhibit.

Item 3. Audit Committee Financial Expert.

(a) The Registrant’s board of trustees has determined that Richard H. Adler is an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr.Adler is independent for purposes of this Item.

Item 4. Principal Accountant Fees and Services.

| (a) | Audit Fees |

2023 - $17,000

| (b) | Audit-Related Fees |

2023- $0

| (c) | Tax Fees |

2023 - $3,000

Preparation of Federal & State income tax returns, assistance with calculation of required income, capital gain and excise distributions and preparation of Federal excise tax returns.

| (d) | All Other Fees |

2023 - $0

| (e) | (1) Audit Committee’s Pre-Approval Policies |

The registrant’s Audit Committee is required to pre-approve all audit services and, when appropriate, any non-audit services (including audit-related, tax and all other services) to the registrant. The registrant’s Audit Committee also is required to pre-approve, when appropriate, any non-audit services (including audit-related, tax and all other services) to its adviser, or any entity controlling, controlled by or under common control with the adviser that provides ongoing services to the registrant, to the extent that the services may be determined to have an impact on the operations or financial reporting of the registrant. Services are reviewed on an engagement by engagement basis by the Audit Committee.

| (2) | Percentages of Services Approved by the Audit Committee |

2023

Audit-Related Fees: 0.00%

Tax Fees: 0.00%

All Other Fees: 0.00%

| (f) | During the audit of registrant's financial statements for the most recent fiscal year, less than 50 percent of the hours expended on the principal accountant's engagement were attributed to work performed by persons other than the principal accountant's full-time, permanent employees. |

| (g) | The aggregate non-audit fees billed by the registrant's accountant for services rendered to the registrant, and rendered to the registrant's investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant: |

2023 - $3,000

(h) The registrant's audit committee has considered whether the provision of non-audit services to the registrant's investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant, that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X, is compatible with maintaining the principal accountant's independence.

Item 5. Audit Committee of Listed Companies. Not applicable

Item 6. Schedule of Investments. Schedule of investments in securities of unaffiliated issuers is included under Item 1.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Funds.

The Board has adopted Proxy Voting Policies and Procedures (“Policies”) on behalf of the Fund, which delegate the responsibility for voting proxies to the Adviser, subject to the Board’s continuing oversight. The Policies require that the Adviser elect to vote or not to vote proxies received in a manner consistent with the best interests of the Fund and shareholders. The Policies also require the Adviser to present to the Board, at least annually, the Adviser’s Proxy Policies and a record of each proxy voted or not voted by the Adviser on behalf of the Fund, including a report on the resolution of all proxies identified by the Adviser involving a conflict of interest.

Where a proxy proposal raises a material conflict between the interests of the Adviser, any affiliated person(s) of the Adviser, the Distributor or any affiliated person of the Distributor, or any affiliated person of the Fund and the Fund’s or its shareholder’s interests, the Adviser will resolve the conflict by voting in accordance with the policy guidelines or at the Fund’s directive using the recommendation of an independent third party. If the third party’s recommendations are not received in a timely fashion, the Adviser will abstain from voting.

Although it is uncommon given the fixed income nature of our investment strategy, Lind has the authority to vote proxies for the Fund. Proxies for high yield municipal bonds, often occur in restructures and workouts, if any. We vote the proxies in a way that we believe is consistent with our fiduciary duty to the Fund and that will cause the Fund’s securities to increase the most or decline the least in value. Lind does not have, per se, proxy vote guidelines as proxies for municipal securities are often unique and are not standardized. Consideration is provided to both long and short-term implications of the proposal to be voted upon when considering the vote that is in the best interest of the Fund.

Procedure

Lind goal is to act in the best interest of the Fund and its shareholders. Given the nature of the Fund’s investments, Lind does not have a formal proxy vote guideline or policy and procedure. We generally vote with management on standard matters (i.e., officers or directors, auditor, etc.). We separately evaluate other matters on a case-by-case basis. Lind Capital Partners will comply with the Fund’s policies and procedures related to the Fund’s Form N-PX filing requirements and maintains all records related to proxy ballots, including:

a. Date received.

b. Reconciliation to number of bonds in the Fund

c. Date voted and how we voted (typically, on line)