UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-23715

OAKTREE DIVERSIFIED INCOME FUND INC.

(Exact name of registrant as specified in charter)

Brookfield Place

250 Vesey Street, 15th Floor

New York, New York 10281-1023

(Address of principal executive offices) (Zip code)

Brian F. Hurley, Esq.

Brookfield Public Securities Group LLC

Brookfield Place

225 Liberty Street, 35th Floor

New York, New York 10281

(Name and address of agent for service)

(855) 777-8001

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

Item 1. Reports to Stockholders.

(a)

2023

ANNUAL REPORT

DECEMBER 31, 2023

Oaktree Diversified Income Fund Inc.

* Please see inside front cover of the report for important information regarding delivery of shareholder reports.

IN PROFILE

Oaktree Fund Advisors, LLC (the "Adviser" or "Oaktree") is an investment adviser registered with the SEC and is also an affiliate and related adviser of Oaktree Capital Management, L.P., an investment adviser registered with the SEC. Oaktree serves as the investment adviser to the Fund. Oaktree was founded in April 1995 and is a leader among global investment managers specializing in alternative investments. Oaktree manages assets across a wide range of investment strategies within four asset classes: Credit, Private Equity, Real Assets, and Listed Equities. As of December 31, 2023, Oaktree had $189 billion in assets under management. Brookfield Public Securities Group LLC ("PSG") serves as the Administrator to the Fund. PSG is an indirect wholly-owned subsidiary of Brookfield Asset Management ULC with $900 billion of assets under management as of December 31, 2023, an unlimited liability company formed under the laws of British Columbia, Canada ("BAM ULC"). Brookfield Corporation, a publicly traded company (NYSE: BN; TSX: BN), holds a 75% interest in BAM ULC, while Brookfield Asset Management Ltd., a publicly traded company (NYSE: BAM; TSX: BAMA) ("Brookfield Asset Management"), holds a 25% interest in BAM ULC. In 2019, Brookfield acquired a majority interest in Oaktree.

Oaktree Diversified Income Fund Inc. (the "Fund") is managed by Oaktree Fund Advisors, LLC. The Fund uses its website as a channel of distribution of material company information. Financial and other material information regarding the Fund is routinely posted on and accessible at https://publicsecurities.brookfield.com/products/us-interval-funds/oaktree-diversified-income-fund?id=192692

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund's annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund's website (https://publicsecurities.brookfield.com/en), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker, investment adviser, bank or trust company) or, if you are a direct investor, by calling the Fund (toll-free) at 1-855-777-8001 or by sending an e-mail request to the Fund at publicsecurities.enquiries@brookfield.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you may call 1-855-777-8001 or send an email request to publicsecurities.enquiries@brookfield.com to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held within the fund complex if you invest directly with the Fund.

TABLE OF CONTENTS

Letter to Shareholders | 1 | ||||||

Management Discussion of Fund Performance | 3 | ||||||

| Portfolio Characteristics | 6 | ||||||

| Consolidated Schedule of Investments | 7 | ||||||

| Consolidated Statement of Assets and Liabilities | 42 | ||||||

| Consolidated Statement of Operations | 43 | ||||||

| Consolidated Statements of Changes in Net Assets | 44 | ||||||

| Consolidated Statement of Cash Flows | 45 | ||||||

| Consolidated Financial Highlights | 46 | ||||||

| Notes to Consolidated Financial Statements | 47 | ||||||

| Report of Independent Registered Public Accounting Firm | 61 | ||||||

| Tax Information | 62 | ||||||

| Information Concerning Directors and Officers | 63 | ||||||

| Dividend Reinvestment Plan | 66 | ||||||

| Joint Notice of Privacy Policy | 67 | ||||||

This report is for shareholder information. This is not a Prospectus intended for use in the purchase or sale of Fund shares.

NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED | |||||||||

[THIS PAGE IS INTENTIONALLY LEFT BLANK]

LETTER TO SHAREHOLDERS

Dear Shareholders,

We are pleased to provide the Annual Report for the Oaktree Diversified Income Fund (the "Fund") for the year ended December 31, 2023.

Personal Consumption Expenditure (PCE) inflation continued to ease in the latter half of the year, and the widely anticipated recession did not materialize. As a result, global equity and credit markets delivered strong returns, but with several ups and downs in what was a volatile and eventful year. Market participants grappled with fundamental data and its implications for interest rates across developed markets, especially in the U.S. where expectations for the future path of policy rates evolved drastically.

Looking back to the first half of the year, U.S. regional banking turmoil drove speculations about a potential pause in the Federal Reserve's hiking cycle. However, the central bank maintained its hawkish stance in the face of resilient economic data. Interest rates continued their climb in the second and third quarters, with the the 10-year U.S. Treasury yield peaking in October just under 5%. Meanwhile, the ECB also hiked its deposit rate to an all-time high of 4%. In the fourth quarter, we observed evidence of easing inflation, dovish rhetoric from the Fed, and a growing consensus among investors that the U.S. economy may avoid a recession. As a result, the yield on 10-year U.S. Treasurys fell 45 bps to end the year below 4% and 1-year inflation expectations fell to the Fed's target of 2.0%. Expectations of rate cuts in 2024 also increased — the Summary of Economic Projections from the December FOMC meeting suggested 75 bps of rate cuts in 2024, while futures markets priced in double that amount on September 30, 2023. Against this backdrop, global equities surged 4.9% in December. Fixed income markets also rallied in response to lower rates and tighter credit spreads: global investment grade and high yield bonds returned 3.7% and 3.5%, respectively, outperforming shorter-duration global senior loans, which gained 1.6% at year-end. Notably, this outperformance caused high yield bonds to outperform senior loans for the full year period, a reversal in trend from the first half of the year in which higher rates fueled the performance of floating-rate assets. Overall, it was a great period to be invested in credit, which delivered equity-like returns to investors, with less than commensurate risk.

The Fund's diversified asset mix of both public and private debt provided investors with a net return of 11.76% during the period. High income was generated from the portfolio's nearly 70% allocation to floating-rate debt given interest rates remain above the ten-year average. Collateralized loan obligations (CLOs) were standout performers, especially the BBB- and BB-rated tranches we emphasized. Other structured credit also performed well, including hospitality-related single asset single borrower (SASB) commercial mortgage-backed securities (CMBS). Senior loans and high yield bonds also contributed positively, earning an attractive coupon and benefitting from spread compression both in the U.S. and Europe. Falling rates late in the period were a tailwind for high yield bonds and other fixed rate assets in the portfolio. Steady private credit performance was attributed to strength in a variety of sectors, but consumer discretionary and information technology did particularly well. The portfolio's allocation to global convertibles also benefitted from strength in equity markets during the period, helped by exposures in the U.S., Europe, and Asia. Our emerging markets exposure was modestly negative in what was a volatile period, particularly for Chinese corporates.

Looking ahead to 2024, we remain optimistic about credit delivering equity-like returns. While the high yield market experienced a robust rally at the end of 2023, the asset class remains attractive due to several important factors: high expected return, quality, and convexity. The average yield-to-maturity in the asset class is near 8% — which is well above the ten-year average — and compelling compared to the roughly 5.0% offered in the investment grade bond market. Around half of the asset class is rated BB (the credit rating tier just below investment grade) and only 11% is rated CCC (the lowest tier), compared to 45% and 17%, respectively, a decade ago. This quality advantage partly reflects the increase in the average size of high yield bond issuers in the last decade. Additionally, leverage ratios in the asset class are fairly healthy compared to the pre-pandemic and long-term averages. U.S. high yield bonds also still trade at an average price of 92 cents on the dollar, and their average duration is 3.3 years, roughly half the average duration of investment grade bonds. Thus, high yield bonds should benefit meaningfully from the pull to par in the coming years as bonds mature. Additionally, all fixed rate assets, including high yield bonds, should be better positioned than they were in recent years now that the likelihood of near-term interest rate increases has fallen sharply.

2023 Annual Report

1

LETTER TO SHAREHOLDERS (continued)

We also expect opportunities to continue to emerge as a result of weakness in the banking system. In recent years, banks have had to contend with multiple challenges, including enormous sums of hung bridge debt, weak commercial real estate books, and uncertainty surrounding potential regulatory changes. Thus, banks have often reduced their lending activities, including in the areas they previously dominated. This has created the potential for alternative lenders to gain share in new markets that are uncorrelated or only modestly correlated with traditional corporate lending deals. We believe this should keep our pipeline of private credit opportunities strong. Overall, we believe the portfolio is well-positioned with a yield-to-worst over 11%, an average price in the mid-90s, and less than one year duration. We believe the Fund's emphasis on credit quality and its diversification may help mitigate risk, positioning it to seek long-term income and capital appreciation. We believe that a focus on potential downside risk is as important today as ever, and we are positioning the portfolio so that it will do well even if shocks develop. We believe this approach will prove especially beneficial in today's uncertain environment.

In addition to performance information and additional discussion of factors impacting the Fund, this report provides the Fund's audited financial statements and schedules of investments as of December 31, 2023.

We welcome your questions and comments and encourage you to contact our Investor Relations team at 1-855-777-8001 or visit us at https://publicsecurities.brookfield.com/en for more information.

Thank you for your support.

Sincerely,

|

| ||||||

Brian F. Hurley | David W. Levi, CFA | ||||||

President | Chief Executive Officer | ||||||

Oaktree Diversified Income Fund Inc. | Brookfield Public Securities Group LLC | ||||||

1 Yield reflects yield to worst. Yield to worst is a measure of the lowest possible yield that can be received on a bond that fully operates within the terms of its contract without defaulting.

These views represent the opinions of Oaktree Fund Advisors, LLC and are not intended to predict or depict the performance of any investment. These views are primarily as of the close of business on December 31, 2023, and subject to change based on subsequent developments.

Must be preceded or accompanied by a Prospectus.

Past performance is no guarantee of future results.

Investing involves risk. Principal loss is possible. Real assets includes real estate securities, infrastructure securities and natural resources securities. Property values may fall due to increasing vacancies or declining rents resulting from unanticipated economic, legal, cultural or technological developments. Infrastructure companies may be subject to a variety of factors that may adversely affect their business, including high interest costs, high leverage, regulation costs, economic slowdown, surplus capacity, increased competition, lack of fuel availability and energy conservation policies. Natural resources securities may be affected by numerous factors, including events occurring in nature, inflationary pressures and international politics.

Quasar Distributors, LLC is the distributor of Oaktree Diversified Income Fund Inc.

2

OAKTREE DIVERSIFIED INCOME FUND INC.

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

The Oaktree Diversified Income Fund (the "Fund") Class D shares returned 11.76% for the year ended December 31, 2023 (net of fees). The Fund generated high income from its nearly 70% allocation to floating-rate debt given higher interest rates. Collateralized loan obligations (CLOs) were standout performers, especially the BBB- and BB-rated tranches we emphasized. Other structured credit also performed well, including hospitality-related single asset single borrower (SASB) commercial mortgage-backed securities (CMBS). Senior loans and high yield bonds also contributed positively, earning an attractive coupon and benefitting from spread compression both in the U.S. and Europe. Falling rates late in the year were also a tailwind for high yield bonds and other fixed-rate assets in the portfolio. Steady private credit performance was attributed to strength in a variety of sectors, but consumer discretionary and information technology did particularly well. The portfolio's allocation to global convertibles also benefitted from strength in equity markets during the period, helped by exposures in the U.S., Europe, and Asia. Our emerging markets exposure was modestly negative in what was a volatile period, particularly for Chinese corporates.

The Fund's largest sector allocations at the end of 2023 were software (8.5%), hotels, restaurants & leisure (5.9%), commercial services & supplies (5.4%), and healthcare providers and services (4.4%). At the end of 2023, the Fund's investments had an average yield of 11.15%1 an average price in the mid-90s, and an effective duration of less than one year. We believe this profile reflects significant upside potential for both yield and return, balanced against the risk that interest rates could continue rising.

GLOBAL CREDIT MARKET OVERVIEW

Inflationary pressures eased in 2023, and the widely anticipated recession did not materialize. As a result, global equity and credit markets delivered strong returns, but with several ups and downs in what was a volatile and eventful year. Market participants grappled with fundamental data and its implications for interest rates across developed markets, driving volatility in bond markets as expectations on the future path of policy rates continued to evolve throughout the year. A strong rally in risk assets at the start of the year stumbled in February and March as i) evidence of persistent inflation-biased rates higher and ii) the highly publicized collapse of Silicon Valley Bank and takeover of Credit Suisse led to fears of contagion across the financial system. The regional banking turmoil also drove speculations about a potential pause in the central banks' hiking cycle, which were soon disappointed by their continued hawkish stance amid resilient economic data. Interest rates continued to climb in the second and third quarters, with the ECB hiking its deposit rate to an all-time high of 4% and the 10-year U.S. Treasury yield peaking in October just under 5%. However, evidence of decelerating inflation led the Fed to turn more dovish at the December FOMC meeting, prompting a material rally in interest rates and risk assets through the end of the year amid growing optimism among investors that a soft landing can be achieved. In all, credit markets performed well despite interest rate volatility: Global senior loans and high yield bonds gained 13.5% and 13.0%, respectively, outperforming global investment grade bonds, which returned 9.0%.

OUTLOOK

Looking ahead to 2024, we remain optimistic about credit delivering equity-like returns. We continue to look for opportunities to balance a high current income with the potential for price appreciation across credit asset classes. As we assess relative value opportunities within our core strategies, we are currently favoring high yield bonds relative to senior loans for incremental deployment. Within our alpha strategies, CLOs and private credit continue to offer some of the most attractive risk-adjusted return potential in the portfolio over the next 12 months. Overall, we believe that the Fund is well-positioned heading into the new year and that its focus on credit quality and diversification may help mitigate risk, positioning it to seek long-term income and capital appreciation. We believe that a focus on potential downside risk is as important today as ever, and we are positioning the portfolio so that it will do well even if shocks develop. We believe this approach will prove especially beneficial in today's uncertain environment.

1 Source: Oaktree. Yield reflects yield to worst. Yield to worst is a measure of the lowest possible yield that can be received on a bond that fully operates within the terms of its contract without defaulting.

Past performance is no guarantee of future results.

2023 Annual Report

3

OAKTREE DIVERSIFIED INCOME FUND INC.

AVERAGE ANNUAL TOTAL RETURNS

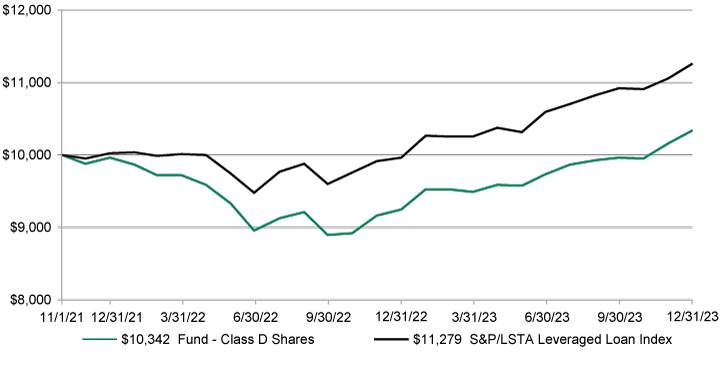

As of December 31, 2023 | 1 Year | Since Inception* | |||||||||

Class D Shares | 11.76 | % | 1.56 | % | |||||||

S&P/LSTA Leveraged Loan Index | 13.11 | % | 5.72 | % | |||||||

* Class D Shares commenced operations on November 1, 2021.

The graph below illustrates a hypothetical investment of $10,000 in the Fund from the commencement of investment operations on November 1, 2021 to December 31, 2023 compared to the S&P/LSTA Leverage Loan Index.

The table and graphs do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Disclosure

All returns shown in USD.

S&P/LSTA (Loans Syndications and Trading Association) Leveraged Loan Index tracks the largest leveraged-loan-to-market facilities, considering market weightings, spreads and interest payments.

An index does not reflect any fees, expenses or sales charges. It is not possible to invest directly in an index. Index performance is shown for illustrative purposes only and does not predict or depict the performance of the Fund.

The Fund's portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance includes the reinvestment of income, dividends and capital gain distributions. To obtain performance

4

OAKTREE DIVERSIFIED INCOME FUND INC.

information current to the most recent month-end, please call 1-855-862-5873. Performance reflects management fees and other fund expenses.

An investor should consider the Fund's investment objectives, risks, charges and expenses carefully before investing.

The Fund is subject to investment risks, including the possible loss of principal invested. Investing involves risk, and principal loss is possible. The Adviser employs an active approach to allocation across multiple credit sectors, but there is no guarantee that such allocation techniques will produce the desired results. General interest rate fluctuations may have a substantial negative impact on the Fund's investments and investment opportunities, and, accordingly, may have a material adverse effect on the Fund's rate of return. The Fund may invest in foreign securities, including, but not limited to, risk related to exchange rate changes, political and economic upheaval, and relatively low market liquidity, all of which are magnified in emerging markets. The Fund intends to invest in illiquid investments which can face significant difficulties and delays associated with such transactions, and the Fund may be unable to sell other illiquid investments when it desires to do so, resulting in the Fund obtaining a lower price or being required to retain the investment. Investments in derivatives involve special risks including correlation, counterparty, liquidity, operational, accounting and tax risks. These risks, in certain cases, may be greater than the risks presented by more traditional investments.

High-yield debt securities rated below investment grade are commonly referred to as "junk bonds" and are considered speculative. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. Bank loans (including senior loans) are usually rated below investment grade, and the market for bank loans may be subject to irregular trading activity, wide bid/ask spreads, restrictions on resale, and extended trade settlement periods. The Fund's investments in senior loans may be subject to greater levels of credit risk, call risk, settlement risk and liquidity risk than funds that do not invest in such securities. The Fund may invest in distressed securities of corporate issuers that are the subject of bankruptcy proceedings or otherwise in default as to the repayment of principal and/or interest or in significant risk of being in such default which is speculative and involves significant risk. Distressed Securities frequently do not produce income while they are outstanding and may require the Fund to bear certain extraordinary expenses in order to protect and recover its investment. The Fund may invest in loans that may be "covenant-lite," generally loans that do not have financial maintenance covenants, which can cause the Fund to have fewer rights against a borrower and may have a greater risk of loss on such investments.

The Fund may invest in a variety of mortgage related and other asset-backed securities, which are subject to greater price volatility in relation to interest rate movements. Residential mortgage backed securities (RMBS) may be subject to prepayment risk, meaning that securities may be paid off more quickly than originally anticipated and the Fund will have to invest the proceeds in securities with lower yields. Commercial mortgage backed securities (CMBS) may be subject to extension risk, meaning that the value of CMBS may be adversely affected in rising interest rate environments when payments on underlying mortgages do not occur as anticipated, resulting in the extension of the security's effective maturity and the related increase in interest rate sensitivity of a longer-term instrument. Investments in collateralized loan obligations (CLOs) carry additional risks including, but not limited to: 1) the possibility that distributions from collateral securities will not be adequate to make interest or other payments; 2) the quality of the collateral may decline in value or default; 3) the possibility that the Fund may invest in CLOs that are subordinate to other classes; and 4) the complex structure of the security may produce disputes with the issuer or unexpected investment results.

Short term performance in particular is not a good indication of the Fund's future performance and an investment should not be made based solely on returns.

These views represent the opinions of Oaktree Fund Advisors, LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2023 and subject to change based on subsequent developments.

2023 Annual Report

5

OAKTREE DIVERSIFIED INCOME FUND INC.

Portfolio Characteristics (Unaudited)

December 31, 2023

ASSETS BY SECTOR1 | |||||||

Corporate Credit | |||||||

| — Senior Loans (Syndicated) | 29.7 | % | |||||

| — High Yield | 19.0 | % | |||||

| — Emerging Markets | 2.4 | % | |||||

| — Convertible Bonds | 0.6 | % | |||||

| — Investment Grade | 0.0 | % | |||||

Total Corporate Credit | 51.7 | % | |||||

Structured Credit | |||||||

| — Collateralized Loan Obligations | 15.9 | % | |||||

| — Commercial Mortgage-Backed Securities | 3.9 | % | |||||

| — Residential Mortgage-Backed Securities | 2.4 | % | |||||

| — Asset-Backed Securities | 4.0 | % | |||||

Total Structured Credit | 26.2 | % | |||||

Private Credit | |||||||

| — Senior Loans | 18.2 | % | |||||

| — Preferred Stock | 0.8 | % | |||||

| — Common Stock | 0.1 | % | |||||

| — Warrants | 0.0 | % | |||||

Total Private Credit | 19.1 | % | |||||

Money Market Fund | 3.0 | % | |||||

Total | 100.0 | % | |||||

ASSETS BY GEOGRAPHY1 | |||||||

North America | 82.9 | % | |||||

Europe Ex UK | 8.3 | % | |||||

UK | 4.7 | % | |||||

Asia Ex Japan | 2.2 | % | |||||

South America | 1.6 | % | |||||

Africa | 0.3 | % | |||||

Total | 100.0 | % | |||||

1 Percentages are based on total market value of investments.

6

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT – 59.6% | |||||||||||||||

Senior Loans (Syndicated) – 34.1% | |||||||||||||||

Aerospace & Defense – 1.2% | |||||||||||||||

| AI Convoy Luxembourg Sarl, First Lien Tranche B Term Loan 7.08% (3 Month EURIBOR + 3.75%), 01/18/27 (b) | Luxembourg | € | 240,000 | $ | 259,511 | ||||||||||

| Cobham Ultra US Company Borrower LLC, First Lien Tranche B Term Loan 9.36% (6 Month SOFR + 3.50%), 11/16/28 (b) | Luxembourg | $ | 738,811 | 729,944 | |||||||||||

| Dynasty Acquisition Company, Inc., First Lien Tranche B2 Term Loan 9.35% (1 Month SOFR + 4.00%), 08/31/28 (b) | United States | 193,022 | 193,763 | ||||||||||||

| Dynasty Acquisition Company, Inc., First Lien Tranche B1 Term Loan 9.35% (1 Month SOFR + 4.00%), 08/31/38 (b) | United States | 450,385 | 452,113 | ||||||||||||

| Peraton Corp, First Lien Tranche B Term Loan 9.20% (1 Month SOFR + 3.75%), 02/01/28 (b) | United States | 562,928 | 565,039 | ||||||||||||

| TransDigm, First Lien Tranche I Term Loan 8.64% (3 Month SOFR + 3.25%), 08/15/28 (b) | United States | 621,867 | 625,477 | ||||||||||||

Total Aerospace & Defense | 2,825,847 | ||||||||||||||

Automobile Components – 0.2% | |||||||||||||||

| First Brands Group LLC, First Lien Tranche B Term Loan 10.88% (6 Month SOFR + 5.00%), 03/24/27 (b) | United States | 494,911 | 491,817 | ||||||||||||

Automobiles – 0.2% | |||||||||||||||

| MajorDrive Holdings IV LLC, First Lien Tranche B Term Loan 9.65% (3 Month SOFR + 4.00%), 06/01/28 (b) | United States | 497,449 | 496,828 | ||||||||||||

Beverages – 0.7% | |||||||||||||||

| Pegasus Bidco BV, First Lien Tranche B Term Loan 8.03% (3 Month EURIBOR + 4.25%), 07/12/29 (b) | Netherlands | € | 250,000 | 277,337 | |||||||||||

9.63% (3 Month SOFR + 4.25%), 04/20/29 (b) | Netherlands | $ | 495,000 | 496,005 | |||||||||||

| Triton Water Holdings, Inc., First Lien Tranche B Term Loan 8.90% (3 Month SOFR + 3.25%), 03/31/28 (b) | United States | 733,085 | 727,586 | ||||||||||||

Total Beverages | 1,500,928 | ||||||||||||||

Building Products – 0.1% | |||||||||||||||

| Aquiles Spain Bidco SA, First Lien Tranche B Term Loan 8.14% (6 Month EURIBOR + 4.85%), 02/19/29 (b) | Spain | € | 300,000 | 314,556 | |||||||||||

Chemicals – 1.0% | |||||||||||||||

| Ineos Enterprises Holdings II Ltd., First Lien Tranche B Term Loan 7.96% (3 Month EURIBOR + 4.00%), 06/23/30 (b) | United States | 250,000 | 275,771 | ||||||||||||

| INEOS Finance PLC, First Lien Tranche B Term Loan 7.85% (1 Month EURIBOR + 4.00%), 11/03/27 (b) | Luxembourg | 247,403 | 273,365 | ||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

7

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| Ineos Quattro Holdings UK Ltd., First Lien Tranche B Term Loan 8.35% (1 Month EURIBOR + 4.50%), 04/03/29 (b) | United States | € | 250,000 | $ | 271,847 | ||||||||||

| SCIH Salt Holdings, Inc., First Lien Tranche B Term Loan 9.44% (1 Month SOFR + 4.00%), 03/16/27 (b) | United States | $ | 904,007 | 906,620 | |||||||||||

| Windsor Holdings III LLC, First Lien Tranche B Term Loan 8.38% (1 Month EURIBOR + 4.50%), 08/01/30 (b) | United States | € | 160,000 | 178,011 | |||||||||||

9.82% (1 Month SOFR + 4.50%), 08/01/30 (b) | United States | $ | 299,250 | 301,868 | |||||||||||

Total Chemicals | 2,207,482 | ||||||||||||||

Commercial Services & Supplies – 2.7% | |||||||||||||||

| Access CIG LLC, First Lien Term Loan 10.39% (3 Month SOFR + 5.00%), 08/15/28 (b) | United States | 947,625 | 950,392 | ||||||||||||

| Allied Universal Holdco LLC, First Lien Tranche B Term Loan 9.20% (1 Month SOFR + 3.75%), 05/12/28 (b) | United States | 822,799 | 820,668 | ||||||||||||

| American Auto Auction Group LLC, Second Lien Term Loan 14.14% (3 Month SOFR + 8.75%), 12/30/28 (b) | United States | 483,000 | 451,605 | ||||||||||||

| Apleona Holding GmbH, First Lien Tranche B Term Loan 8.65% (3 Month EURIBOR + 4.70%), 04/28/28 (b) | Germany | € | 145,000 | 160,823 | |||||||||||

| Atlas Luxco 4 SARL, First Lien Tranche B Term Loan 7.62% (1 Month EURIBOR + 3.75%), 05/12/28 (b) | Luxembourg | 246,843 | 265,315 | ||||||||||||

| Freshworld Holding III GMBH, First Lien Tranche B Term Loan 7.49% (3 Month EURIBOR + 3.75%), 10/02/26 (b) | Germany | 250,000 | 273,211 | ||||||||||||

| Garda World Security Corp., First Lien Tranche B Term Loan 9.75% (3 Month SOFR + 4.25%), 10/30/26 (b) | Canada | $ | 1,000,000 | 1,003,049 | |||||||||||

| Restaurant Technologies, Inc., First Lien Tranche B Term Loan 9.64% (3 Month SOFR + 4.25%), 03/17/29 (b) | United States | 875,282 | 869,155 | ||||||||||||

| TMS International Corp., First Lien Tranche B Term Loan 10.11% (1 Month SOFR + 4.75%), 03/07/30 (b) | United States | 496,250 | 499,972 | ||||||||||||

| Trugreen LP, First Lien Tranche B Term Loan 9.45% (1 Month SOFR + 4.00%), 10/29/27 (b) | United States | 610,575 | 590,884 | ||||||||||||

| USIC Holdings Inc., First Lien Tranche B Term Loan 8.94% (3 Month SOFR + 3.50%), 05/31/28 (b) | United States | 322,351 | 320,417 | ||||||||||||

Total Commercial Services & Supplies | 6,205,491 | ||||||||||||||

Communications Equipment – 0.6% | |||||||||||||||

| Genesys Cloud Services Holdings II LLC, First Lien Tranche B Term Loan 9.46% (1 Month SOFR + 4.00%), 12/01/27 (b) | United States | 745,532 | 749,323 | ||||||||||||

| Sorenson Communications LLC, First Lien Tranche B Term Loan 10.96% (1 Month SOFR + 5.50%), 03/17/26 (b) | United States | 619,399 | 618,111 | ||||||||||||

Total Communications Equipment | 1,367,434 | ||||||||||||||

See Notes to Consolidated Financial Statements.

8

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Construction & Engineering – 1.1% | |||||||||||||||

| ADB Companies LLC, First Lien Term Loan 12.00% (3 Month SOFR + 6.50%), 12/18/25 (b) (c) | United States | $ | 1,199,966 | $ | 1,172,487 | ||||||||||

| Artera Services LLC, First Lien Term Loan 8.99% (3 Month SOFR + 3.50%), 03/06/25 (b) | United States | 585,461 | 552,804 | ||||||||||||

| Tiger Acquisition LLC, First Lien Tranche B Term Loan 8.70% (1 Month SOFR + 3.25%), 06/01/28 (b) | United States | 736,809 | 734,584 | ||||||||||||

Total Construction & Engineering | 2,459,875 | ||||||||||||||

Consumer Staples Distribution & Retail – 0.1% | |||||||||||||||

| Bellis Acquisition Company PLC, First Lien Tranche B Term Loan 6.06% (6 Month EURIBOR + 2.75%), 02/16/26 (b) | United Kingdom | € | 250,000 | 274,855 | |||||||||||

Containers & Packaging – 1.1% | |||||||||||||||

| Charter Next Generation, Inc., First Lien Tranche B Term Loan 9.21% (1 Month SOFR + 3.75%), 12/01/27 (b) | United States | $ | 994,891 | 1,000,647 | |||||||||||

| Clydesdale Acquisition Holdings, Inc., First Lien Tranche B Term Loan 9.62% (1 Month SOFR + 4.18%), 06/30/29 (b) | United States | 474,037 | 476,703 | ||||||||||||

| Kouti BV, First Lien Tranche B Term Loan 8.53% (3 Month EURIBOR + 4.75%), 08/31/28 (b) | Netherlands | € | 200,000 | 221,963 | |||||||||||

| ProAmpac LLC, First Lien Tranche B Term Loan 9.87% (3 Month SOFR + 4.50%), 09/15/28 (b) | United States | $ | 913,644 | 916,499 | |||||||||||

Total Containers & Packaging | 2,615,812 | ||||||||||||||

Distributors – 0.5% | |||||||||||||||

| American Tire Distributors, Inc., First Lien Tranche B Term Loan 11.91% (3 Month SOFR + 6.25%), 10/08/28 (b) | United States | 434,222 | 365,506 | ||||||||||||

| Dealer Tire Financial LLC, First Lien Tranche B2 Term Loan 9.85% (1 Month SOFR + 4.50%), 12/14/27 (b) | United States | 654,600 | 657,670 | ||||||||||||

Total Distributors | 1,023,176 | ||||||||||||||

Diversified Consumer Services – 2.6% | |||||||||||||||

| AI Aqua Merger Sub, Inc., First Lien Tranche B Term Loan 9.07% (1 Month SOFR + 3.75%), 07/31/28 (b) | United States | 495,082 | 496,078 | ||||||||||||

9.58% (CME Term SOFR 1 Month + 4.25%), 07/31/28 (b) | United States | 400,000 | 402,500 | ||||||||||||

| Houghton Mifflin Harcourt Co., First Lien Tranche B Term Loan 10.70% (1 Month SOFR + 5.25%), 04/04/29 (b) | United States | 344,265 | 338,548 | ||||||||||||

| KUEHG Corp., First Lien Term Loan 10.39% (3 Month SOFR + 5.00%), 05/31/30 (b) | United States | 652,365 | 656,035 | ||||||||||||

| Lakeshore Learning, First Lien Tranche B Term Loan 8.96% (1 Month SOFR + 3.50%), 09/29/28 (b) | United States | 497,462 | 497,619 | ||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

9

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| Renaissance Holdings Corp., First Lien Term Loan 10.10% (1 Month SOFR + 4.75%), 06/02/25 (b) | United States | $ | 498,750 | $ | 501,174 | ||||||||||

| University Support Services LLC, First Lien Tranche B Term Loan 8.70% (1 Month SOFR + 3.25%), 09/30/28 (b) | Canada | 2,725,888 | 2,729,636 | ||||||||||||

| Verisure Holding AB, First Lien Tranche B Term Loan 6.97% (3 Month EURIBOR + 3.00%), 03/27/28 (b) | Sweden | € | 250,000 | 274,608 | |||||||||||

Total Diversified Consumer Services | 5,896,198 | ||||||||||||||

Diversified Telecommunication Services – 0.7% | |||||||||||||||

| Altice France SA, First Lien Tranche B Term Loan 8.66% (3 Month EURIBOR + 5.00%), 10/28/27 (b) | Luxembourg | 228,275 | 245,893 | ||||||||||||

| CCI Buyer, Inc., First Lien Tranche B Term Loan 9.39% (3 Month SOFR + 4.00%), 12/31/27 (b) | United States | $ | 742,366 | 741,305 | |||||||||||

| Cincinnati Bell, Inc., First Lien Tranche B2 Term Loan 8.70% (CME Term SOFR 1 Month + 3.25%), 12/29/28 (b) | United States | 525,000 | 521,252 | ||||||||||||

| Numericable U.S. LLC, First Lien Tranche B14-EXT Term Loan 9.46% (3 Month EURIBOR + 5.50%), 08/17/28 (b) | France | € | 199,000 | 197,899 | |||||||||||

Total Diversified Telecommunication Services | 1,706,349 | ||||||||||||||

Electric Utilities – 0.2% | |||||||||||||||

| Lackawanna Energy Center LLC, First Lien Tranche B2 Term Loan 10.32% (1 Month SOFR + 5.00%), 07/20/29 (b) | United States | $ | 409,199 | 405,449 | |||||||||||

Electronic Equipment Instruments & Components – 0.6% | |||||||||||||||

| LTI Holdings, Inc., First Lien Tranche B Term Loan 8.94% (1 Month SOFR + 3.50%), 09/06/25 (b) | United States | 976,804 | 945,263 | ||||||||||||

| Sonicwall US Holdings Inc, First Lien Term Loan 10.40% (CME Term SOFR 1 Month + 5.00%), 05/31/28 (b) | United States | 500,000 | 496,250 | ||||||||||||

Total Electronic Equipment Instruments & Components | 1,441,513 | ||||||||||||||

Entertainment – 0.4% | |||||||||||||||

| City Football Group Ltd., First Lien Tranche B Term Loan 8.46% (1 Month SOFR + 3.00%), 07/21/28 (b) | United Kingdom | 893,680 | 891,075 | ||||||||||||

Financial Services – 0.3% | |||||||||||||||

| Boost Newco Borrower LLC, First Lien Tranche B Term Loan 3.75% (CME Term SOFR 1 Month + 3.00%), 09/21/30 (b) | United States | 575,000 | 578,235 | ||||||||||||

Food Products – 0.4% | |||||||||||||||

| Froneri International Ltd., First Lien Tranche B Term Loan 7.70% (1 Month SOFR + 2.25%), 01/29/27 (b) | United States | 429,773 | 430,762 | ||||||||||||

See Notes to Consolidated Financial Statements.

10

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| Upfield USA Corp., First Lien Tranche B7 Term Loan 9.93% (CME Term SOFR 1 Month + 4.75%), 01/03/28 (b) | Netherlands | $ | 500,000 | $ | 492,375 | ||||||||||

Total Food Products | 923,137 | ||||||||||||||

Health Care Equipment & Supplies – 0.5% | |||||||||||||||

| Bausch + Lomb Corp., First Lien Tranche B Term Loan 8.76% (1 Month SOFR + 3.25%), 05/05/27 (b) | United States | 895,081 | 887,812 | ||||||||||||

| Medline Borrower LP, First Lien Tranche B Term Loan 8.46% (1 Month SOFR + 3.00%), 09/29/28 (b) | United States | 240,552 | 242,036 | ||||||||||||

Total Health Care Equipment & Supplies | 1,129,848 | ||||||||||||||

Health Care Providers & Services – 2.4% | |||||||||||||||

| Baart Programs, Inc., Second Lien Tranche DD Delay Draw Term Loan 14.15% (3 Month SOFR + 8.50%), 06/11/28 (b) (c) | United States | 584,156 | 514,641 | ||||||||||||

| Baart Programs, Inc., First Lien Tranche DD Delay Draw Term Loan 10.65% (3 Month SOFR + 5.00%), 06/11/27 (b) (c) | United States | 418,690 | 403,198 | ||||||||||||

| CHG Healthcare Services, Inc., First Lien Term Loan 8.71% (1 Month SOFR + 3.25%), 10/31/28 (b) | United States | 497,455 | 498,811 | ||||||||||||

9.06% (3 Month SOFR + 3.75%), 09/29/28 (b) | United States | 500,000 | 501,615 | ||||||||||||

| Covetrus, Inc., First Lien Term Loan 10.39% (3 Month SOFR + 5.00%), 09/20/29 (b) | United States | 908,032 | 908,746 | ||||||||||||

| Electron Bidco, Inc., First Lien Term Loan 8.46% (1 Month SOFR + 3.00%), 10/31/28 (b) | United States | 497,468 | 499,334 | ||||||||||||

| HomeVi SASU, First Lien Tranche B Term Loan 7.71% (3 Month EURIBOR + 4.00%), 10/31/26 (b) | France | € | 250,000 | 256,706 | |||||||||||

| IVC Acquisition Ltd., First Lien Tranche B Term Loan 8.98% (3 Month EURIBOR + 5.00%), 11/17/28 (b) | United Kingdom | 250,000 | 276,246 | ||||||||||||

| Nidda Healthcare Holding GmbH, First Lien Tranche F Term Loan 7.31% (3 Month EURIBOR + 3.50%), 08/21/26 (b) | Germany | 250,000 | 274,846 | ||||||||||||

| Schon Klinik SE, Tranche B Term Loan 4.50%, 11/27/30 | Germany | 115,000 | 126,954 | ||||||||||||

| Southern Veterinary Partners LLC, First Lien Term Loan 9.46% (1 Month SOFR + 4.00%), 10/01/27 (b) | United States | $ | 846,408 | 844,821 | |||||||||||

| Surgery Center Holdings, Term Loan 8.86%, 12/05/30 | United States | 100,000 | 100,532 | ||||||||||||

| Vetstrategy Canada Holdings Inc, Tranche B Term Loan 10.87%, 11/16/28 | United States | 400,000 | 402,165 | ||||||||||||

Total Health Care Providers & Services | 5,608,615 | ||||||||||||||

Health Care Technology – 1.2% | |||||||||||||||

| athenaHealth Group, Inc., First Lien Tranche B Term Loan 8.60% (1 Month SOFR + 3.25%), 02/15/29 (b) | United States | 680,562 | 678,521 | ||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

11

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| FinThrive Software Intermediate Holdings, Inc., Second Lien Term Loan 12.21% (1 Month SOFR + 6.75%), 12/17/29 (b) | United States | $ | 2,082,000 | $ | 1,255,966 | ||||||||||

| Polaris Newco LLC, First Lien Tranche B Term Loan 7.87% (1 Month EURIBOR + 4.00%), 06/02/28 (b) | United States | € | 244,375 | 263,427 | |||||||||||

9.46% (1 Month SOFR + 4.00%), 06/02/28 (b) | United States | $ | 550,025 | 543,355 | |||||||||||

Total Health Care Technology | 2,741,269 | ||||||||||||||

Hotels Restaurants & Leisure – 2.1% | |||||||||||||||

| Alterra Mountain Co., First Lien Tranche B Term Loan 8.96% (1 Month SOFR + 3.50%), 08/17/28 (b) | United States | 920,663 | 923,158 | ||||||||||||

| Carnival Corp., First Lien Tranche B Term Loan 8.32% (1 Month SOFR + 3.00%), 08/02/27 (b) | United States | 746,250 | 749,048 | ||||||||||||

| Entain Holdings Gibraltar Ltd., First Lien Tranche B2 Term Loan 8.99% (3 Month SOFR + 3.50%), 10/18/29 (b) | United Kingdom | 263,341 | 264,164 | ||||||||||||

| Flutter Financing BV, First Lien Tranche B Term Loan 8.90% (3 Month SOFR + 3.25%), 07/04/28 (b) | Ireland | 106,557 | 107,060 | ||||||||||||

| Flynn Restaurant Group LP, First Lien Tranche B Term Loan 9.71% (1 Month SOFR + 4.25%), 11/22/28 (b) | United States | 980,000 | 986,125 | ||||||||||||

| Inspire Brands, First Lien Tranche B Term Loan 8.45% (1 Month SOFR + 3.00%), 12/15/27 (b) | United States | 497,468 | 498,888 | ||||||||||||

| Kingpin Intermediate Holdings LLC, First Lien Tranche B Term Loan 8.85% (1 Month SOFR + 3.50%), 02/08/28 (b) | United States | 223,875 | 224,155 | ||||||||||||

| Ontario Gaming GTA LP, First Lien Tranche B Term Loan 9.64% (3 Month SOFR + 4.25%), 07/20/30 (b) | Canada | 375,000 | 377,076 | ||||||||||||

| Whatabrands LLC, First Lien Tranche B Term Loan 8.46% (1 Month SOFR + 3.00%), 08/03/28 (b) | United States | 782,351 | 784,659 | ||||||||||||

Total Hotels Restaurants & Leisure | 4,914,333 | ||||||||||||||

Household Durables – 0.1% | |||||||||||||||

| Hunter Douglas, Inc., First Lien Tranche B Term Loan 8.89% (3 Month SOFR + 3.50%), 02/09/29 (b) | Netherlands | 301,030 | 300,428 | ||||||||||||

Independent Power and Renewable Electricity Producers – 1.4% | |||||||||||||||

| Eastern Power LLC, First Lien Tranche B Term Loan 9.21% (1 Month SOFR + 3.75%), 10/02/25 (b) | United States | 500,000 | 492,850 | ||||||||||||

| Generation Bridge Northeast LLC, First Lien Tranche B Term Loan 9.60% (1 Month SOFR + 4.25%), 08/31/29 (b) | United States | 489,509 | 492,060 | ||||||||||||

| Granite Generation LLC, First Lien Tranche B Term Loan 9.21% (CME Term SOFR 1 Month + 3.75%), 11/09/26 (b) | United States | 750,000 | 749,476 | ||||||||||||

See Notes to Consolidated Financial Statements.

12

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| Helix Gen Funding LLC, First Lien Tranche B Term Loan 10.10% (3 Month SOFR + 4.75%), 12/31/27 (b) | United States | $ | 233,149 | $ | 234,141 | ||||||||||

| Lackawanna Energy Center LLC, First Lien Tranche C Term Loan 10.32% (1 Month SOFR + 5.00%), 07/20/29 (b) | United States | 88,745 | 87,931 | ||||||||||||

| Parkway Generation LLC, First Lien Tranche B Term Loan 10.18% (3 Month SOFR + 4.75%), 11/06/28 (b) | United States | 678,277 | 653,930 | ||||||||||||

| Parkway Generation LLC, First Lien Tranche C Term Loan 10.18% (3 Month SOFR + 4.75%), 11/06/28 (b) | United States | 89,876 | 86,650 | ||||||||||||

| Talen Energy Supply LLC, First Lien Tranche TLC-EXIT Term Loan 9.88% (3 Month SOFR + 4.50%), 04/20/30 (b) | United States | 123,095 | 123,967 | ||||||||||||

| Talen Energy Supply LLC, First Lien Tranche TLB-EXIT Term Loan 9.88% (3 Month SOFR + 4.50%), 04/20/30 (b) | United States | 350,145 | 352,626 | ||||||||||||

Total Independent Power and Renewable Electricity Producers | 3,273,631 | ||||||||||||||

Insurance – 0.4% | |||||||||||||||

| Asurion LLC, First Lien Tranche B10 Term Loan 9.45% (1 Month SOFR + 4.00%), 08/31/28 (b) | United States | 241,389 | 240,709 | ||||||||||||

| Asurion LLC, Second Lien Tranche B3 Term Loan 10.71% (1 Month SOFR + 5.25%), 01/31/28 (b) | United States | 350,000 | 334,541 | ||||||||||||

| HUB International Ltd., First Lien Tranche B Term Loan 9.66% (3 Month SOFR + 4.25%), 06/08/30 (b) | United States | 374,063 | 376,141 | ||||||||||||

Total Insurance | 951,391 | ||||||||||||||

Interactive Media & Services – 0.7% | |||||||||||||||

| Ancestry.com, Inc., First Lien Term Loan 9.36% (1 Month SOFR + 5.50%), 12/12/33 (b) | United States | 1,637,000 | 1,612,445 | ||||||||||||

Leisure Products – 0.4% | |||||||||||||||

| Gibson Brands, Inc., First Lien Tranche B Term Loan 10.66% (3 Month SOFR + 5.00%), 08/11/28 (b) | United States | 392,000 | 351,493 | ||||||||||||

| Peloton Interactive, First Lien Term Loan 12.48% (6 Month SOFR + 7.00%), 05/17/27 (b) | United States | 641,740 | 646,392 | ||||||||||||

Total Leisure Products | 997,885 | ||||||||||||||

Life Sciences Tools & Services – 0.4% | |||||||||||||||

| Catalent Pharma Solutions, First Lien Tranche B4 Term Loan 8.36% (1 Month SOFR + 3.00%), 02/22/28 (b) | United States | 300,000 | 300,750 | ||||||||||||

| Sotera Health Holdings LLC, First Lien Tranche B Term Loan 9.09% (1 Month SOFR + 3.75%), 12/11/26 (b) | United States | 497,500 | 498,435 | ||||||||||||

Total Life Sciences Tools & Services | 799,185 | ||||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

13

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Machinery – 0.4% | |||||||||||||||

| Delachaux Group SA, First Lien Tranche B Term Loan 8.15% (3 Month EURIBOR + 4.25%), 04/16/29 (b) | United States | € | 239,144 | $ | 264,388 | ||||||||||

| Emerald Debt Merger Sub LLC, First Lien Tranche B Term Loan 8.35% (1 Month SOFR + 3.00%), 04/17/30 (b) | United States | $ | 250,373 | 251,547 | |||||||||||

| SPX FLOW, Inc., First Lien Tranche B Term Loan 9.95% (1 Month SOFR + 4.50%), 04/05/29 (b) | United States | 500,000 | 502,292 | ||||||||||||

Total Machinery | 1,018,227 | ||||||||||||||

Media – 1.9% | |||||||||||||||

| Aragorn Parent Corp., First Lien Tranche B Term Loan 9.57% (CME Term SOFR 1 Month + 4.25%), 12/14/28 (b) | United States | 650,111 | 650,316 | ||||||||||||

| Century DE Buyer LLC, First Lien Term Loan 9.58% (CME Term SOFR 1 Month + 4.00%), 09/19/30 (b) | United States | 350,000 | 351,531 | ||||||||||||

| Directv Financing LLC, First Lien Term Loan 10.65% (3 Month SOFR + 5.00%), 08/02/27 (b) | United States | 797,500 | 798,948 | ||||||||||||

| Gray Television, Inc., First Lien Tranche D Term Loan 8.46% (1 Month SOFR + 3.00%), 11/30/28 (b) | United States | 497,462 | 494,781 | ||||||||||||

| McGraw-Hill Education, Inc., First Lien Tranche B Term Loan 10.21% (1 Month SOFR + 4.75%), 07/28/28 (b) | United States | 473,096 | 473,245 | ||||||||||||

| Univision Communications, Inc., First Lien Tranche B Term Loan 9.59% (3 Month SOFR + 4.25%), 06/24/29 (b) | United States | 494,975 | 496,955 | ||||||||||||

| Virgin Media SFA Finance Ltd., First Lien Tranche L Term Loan 8.47% (Daily SONIA + 3.25%), 01/15/27 (b) | United Kingdom | £ | 135,000 | 170,981 | |||||||||||

| Virgin Media, Inc., Term Loan 7.33%, 10/15/31 | United Kingdom | € | 115,000 | 127,166 | |||||||||||

| WideOpenWest Finance, First Lien Tranche B Term Loan 8.39% (3 Month SOFR + 3.00%), 12/31/28 (b) | United States | $ | 746,826 | 694,029 | |||||||||||

Total Media | 4,257,952 | ||||||||||||||

Metals & Mining – 0.5% | |||||||||||||||

| American Rock Salt Company LLC, First Lien Tranche B Term Loan 9.46% (1 Month SOFR + 4.00%), 06/05/28 (b) | United States | 493,671 | 468,062 | ||||||||||||

| Arsenal AIC Parent, First Lien Tranche B Term Loan 9.85% (1 Month SOFR + 4.50%), 08/18/30 (b) | United States | 299,250 | 300,933 | ||||||||||||

| Vibrantz Technologies, Inc., First Lien Tranche B Term Loan 9.81% (3 Month SOFR + 4.25%), 03/30/29 (b) | United States | 470,050 | 451,591 | ||||||||||||

Total Metals & Mining | 1,220,586 | ||||||||||||||

See Notes to Consolidated Financial Statements.

14

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Oil Gas & Consumable Fuels – 0.4% | |||||||||||||||

| AL NGPL Holdings LLC, First Lien Tranche B Term Loan 8.85% (CME Term SOFR 1 Month + 3.75%), 04/14/28 (b) | United States | $ | 297,406 | $ | 297,965 | ||||||||||

| Freeport LNG Investments LLP, First Lien Tranche B Term Loan 9.09% (3 Month SOFR + 3.50%), 11/17/28 (b) | United States | 674,305 | 674,969 | ||||||||||||

Total Oil Gas & Consumable Fuels | 972,934 | ||||||||||||||

Passenger Airlines – 0.7% | |||||||||||||||

| AAdvantage Loyalty IP Ltd., First Lien Term Loan 10.43% (CME Term SOFR 3 Month + 4.75%), 04/20/28 (b) | United States | 500,000 | 514,415 | ||||||||||||

| Air Canada, First Lien Tranche B Term Loan 9.13% (3 Month SOFR + 3.50%), 08/11/28 (b) | Canada | 541,253 | 543,577 | ||||||||||||

| Mileage Plus Holdings LLC, First Lien Tranche B Term Loan 10.80% (3 Month SOFR + 5.25%), 07/30/27 (b) | United States | 141,400 | 146,450 | ||||||||||||

| United Airlines, Inc., First Lien Tranche B Term Loan 9.21% (1 Month SOFR + 3.75%), 04/21/28 (b) | United States | 389,940 | 391,890 | ||||||||||||

Total Passenger Airlines | 1,596,332 | ||||||||||||||

Pharmaceuticals – 0.4% | |||||||||||||||

| AI Sirona Luxembourg Acquisition Sarl, First Lien Tranche B Term Loan 8.85% (3 Month EURIBOR + 5.00%), 09/29/28 (b) | Czech Republic | € | 250,000 | 276,958 | |||||||||||

| Curium Bidco Sarl, First Lien Tranche B Term Loan 9.89% (3 Month SOFR + 4.50%), 07/31/29 (b) | Luxembourg | $ | 323,375 | 323,579 | |||||||||||

| Pharmanovia Bidco Ltd., First Lien Tranche B Term Loan 7.78% (3 Month EURIBOR + 4.00%), 08/07/26 (b) | United Kingdom | € | 250,000 | 276,462 | |||||||||||

Total Pharmaceuticals | 876,999 | ||||||||||||||

Professional Services – 0.7% | |||||||||||||||

| DTI Holdco, Inc., First Lien Tranche B Term Loan 9.80% (3 Month SOFR + 4.75%), 04/23/29 (b) | United States | $ | 142,639 | 141,340 | |||||||||||

| Element Materials Technology Group US Holdings, Inc., First Lien Tranche DD Delay Draw Term Loan 9.74% (3 Month SOFR + 4.25%), 09/28/29 (b) | United States | 88,191 | 87,640 | ||||||||||||

| Element Materials Technology Group US Holdings, Inc., First Lien Tranche B Term Loan 9.74% (3 Month SOFR + 4.25%), 04/12/29 (b) | United States | 191,081 | 189,887 | ||||||||||||

| Project Alpha Intermediate Holding, Inc., First Lien Tranche B Term Loan 10.09% (1 Month SOFR + 4.75%), 10/18/30 (b) | United States | 350,000 | 352,588 | ||||||||||||

| Skopima Consilio Parent LLC, First Lien Tranche B Term Loan 9.46% (1 Month SOFR + 4.00%), 05/31/28 (b) | United States | 917,573 | 915,852 | ||||||||||||

Total Professional Services | 1,687,307 | ||||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

15

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Software – 3.4% | |||||||||||||||

| Capstone Borrower, Inc., First Lien Tranche B Term Loan 9.08% (3 Month SOFR + 3.75%), 06/17/30 (b) | United States | $ | 431,787 | $ | 432,867 | ||||||||||

| Castle US Holding Corp., First Lien Tranche B Term Loan 7.17% (3 Month EURIBOR + 3.75%), 01/29/27 (b) | United States | € | 244,289 | 191,812 | |||||||||||

9.36% (3 Month SOFR + 4.00%), 01/29/27 (b) | United States | $ | 983,228 | 687,276 | |||||||||||

| Claudius Finance Sarl, First Lien Tranche B Incremental Term Loan 3.75% (3 Month EURIBOR + 3.75%), 07/10/28 (b) | Luxembourg | € | 190,000 | 208,988 | |||||||||||

| Epicor Software Corp., First Lien Tranche D Incremental Term Loan 9.10% (1 Month SOFR + 3.75%), 07/30/27 (b) | United States | $ | 500,000 | 505,000 | |||||||||||

| eResearchTechnology, Inc., First Lien Tranche B Term Loan 9.96% (1 Month SOFR + 4.50%), 02/04/27 (b) | United States | 893,838 | 894,047 | ||||||||||||

| I-Logic Technologies Bidco Ltd., First Lien Tranche B Term Loan 7.96% (3 Month EURIBOR + 4.00%), 02/16/28 (b) | United Kingdom | € | 194,501 | 212,196 | |||||||||||

| Instructure Holdings, Inc., First Lien Tranche B Term Loan 8.68% (CME Term SOFR 1 Month + 2.75%), 10/30/28 (b) | United States | $ | 285,000 | 286,781 | |||||||||||

| ION Corporate Solutions Finance Sarl, First Lien Tranche B Term Loan 7.72% (3 Month EURIBOR + 3.75%), 03/13/28 (b) | Luxembourg | € | 250,000 | 274,723 | |||||||||||

| ION Trading Technologies Sarl, First Lien Tranche B Term Loan 8.22% (3 Month EURIBOR + 4.25%), 03/31/28 (b) | Ireland | 250,000 | 267,017 | ||||||||||||

| McAfee Corp., First Lien Tranche B Term Loan 7.85% (3 Month EURIBOR + 3.75%), 02/02/29 (b) | United States | 246,875 | 269,282 | ||||||||||||

9.19% (CME Term SOFR 1 Month + 3.75%), 03/01/29 (b) | United States | $ | 498,734 | 498,009 | |||||||||||

| Mitchell International, Inc., First Lien Tranche B Term Loan 9.40% (3 Month SOFR + 3.75%), 10/02/28 (b) | United States | 558,847 | 559,411 | ||||||||||||

| Planview Parent, Inc., First Lien Term Loan 9.65% (3 Month SOFR + 4.00%), 12/17/27 (b) | United States | 318,968 | 316,954 | ||||||||||||

| Proofpoint, First Lien Tranche B Term Loan 8.71% (1 Month SOFR + 3.25%), 06/09/28 (b) | United States | 497,462 | 498,308 | ||||||||||||

| Quartz Acquireco LLC, First Lien Tranche B Term Loan 8.85% (1 Month SOFR + 3.50%), 06/28/30 (b) | United States | 299,250 | 300,559 | ||||||||||||

| Seine Finance SARL, Tranche B Term Loan 8.50%, 11/15/30 | France | € | 135,000 | 149,732 | |||||||||||

| TIBCO Software, Inc., First Lien Tranche A Term Loan 9.99% (3 Month SOFR + 4.50%), 09/29/28 (b) | United States | $ | 191,376 | 187,115 | |||||||||||

| TIBCO Software, Inc., First Lien Tranche B Term Loan 9.99% (3 Month SOFR + 4.50%), 03/19/29 (b) | United States | 466,286 | 456,641 | ||||||||||||

See Notes to Consolidated Financial Statements.

16

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| UKG, Inc., Second Lien Term Loan 10.76% (3 Month SOFR + 5.25%), 05/03/27 (b) | United States | $ | 500,000 | $ | 501,920 | ||||||||||

Total Software | 7,698,638 | ||||||||||||||

Specialty Retail – 0.6% | |||||||||||||||

| Global Blue Acquisition BV, First Lien Term Loan 8.96% (3 Month EURIBOR + 5.00%), 12/05/30 (b) | United States | € | 160,000 | 176,632 | |||||||||||

| Great Outdoors Group LLC, First Lien Tranche B2 Term Loan 9.40% (1 Month SOFR + 3.75%), 03/31/28 (b) | United States | $ | 493,687 | 494,303 | |||||||||||

| Harbor Freight Tools USA, Inc., First Lien Tranche B Term Loan 8.21% (1 Month SOFR + 2.75%), 10/19/27 (b) | United States | 487,610 | 487,698 | ||||||||||||

| Motor Fuel Group, First Lien Tranche B5 Term Loan 11.29% (Daily SONIA + 6.00%), 06/21/28 (b) | United States | £ | 250,000 | 313,235 | |||||||||||

Total Specialty Retail | 1,471,868 | ||||||||||||||

Textiles Apparel & Luxury Goods – 0.1% | |||||||||||||||

| Amer Sports Holding Oy, First Lien Tranche B Term Loan 7.65% (3 Month EURIBOR + 4.00%), 03/30/26 (b) | Finland | € | 250,000 | 277,060 | |||||||||||

Transportation Infrastructure – 0.7% | |||||||||||||||

| Apple Bidco LLC, First Lien Tranche B Term Loan 8.85% (CME Term SOFR 1 Month + 4.00%), 09/22/28 (b) | United States | $ | 997,500 | 1,002,178 | |||||||||||

| Brown Group Holding LLC, First Lien Tranche B2 Term Loan 9.13% (3 Month SOFR + 3.75%), 06/30/29 (b) | United States | 497,481 | 499,486 | ||||||||||||

Total Transportation Infrastructure | 1,501,664 | ||||||||||||||

Total Senior Loans (Syndicated) | 78,534,654 | ||||||||||||||

High Yield – 22.0% | |||||||||||||||

Aerospace & Defense – 0.4% | |||||||||||||||

| Bombardier, Inc. 6.00%, 02/15/28 (d) | Canada | 313,000 | 305,325 | ||||||||||||

7.13%, 06/15/26 (d) | Canada | 187,000 | 186,297 | ||||||||||||

8.75%, 11/15/30 (d) | Canada | 155,000 | 165,223 | ||||||||||||

| Spirit AeroSystems, Inc. 9.38%, 11/30/29 (d) | United States | 135,000 | 147,896 | ||||||||||||

9.75%, 11/15/30 (d) | United States | 160,000 | 172,196 | ||||||||||||

Total Aerospace & Defense | 976,937 | ||||||||||||||

Automobile Components – 0.3% | |||||||||||||||

| Dana Financing Luxembourg Sarl 3.00%, 07/15/29 | United States | € | 200,000 | 195,668 | |||||||||||

| IHO Verwaltungs GmbH 8.75%, 05/15/28 (e) (f) (g) | Germany | 200,000 | 241,067 | ||||||||||||

| Renk AG 5.75%, 07/15/25 | Germany | 200,000 | 220,069 | ||||||||||||

Total Automobile Components | 656,804 | ||||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

17

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Automobiles – 0.3% | |||||||||||||||

| Ford Motor Company 3.25%, 02/12/32 | United States | $ | 340,000 | $ | 282,921 | ||||||||||

6.10%, 08/19/32 | United States | 305,000 | 307,601 | ||||||||||||

Total Automobiles | 590,522 | ||||||||||||||

Beverages – 0.1% | |||||||||||||||

| Primo Water Holdings, Inc. 3.88%, 10/31/28 | Canada | € | 200,000 | 213,637 | |||||||||||

Chemicals – 0.8% | |||||||||||||||

| INEOS Finance PLC 6.63%, 05/15/28 (e) (g) | Luxembourg | 175,000 | 198,735 | ||||||||||||

| Nufarm Australia Ltd. 5.00%, 01/27/30 (d) | Australia | $ | 445,000 | 413,227 | |||||||||||

| Olympus Water US Holding Corp. 4.25%, 10/01/28 (d) | United States | 280,000 | 252,269 | ||||||||||||

9.75%, 11/15/28 (d) | United States | 380,000 | 403,805 | ||||||||||||

| SK Invictus Intermediate II Sarl 5.00%, 10/30/29 (d) | United States | 225,000 | 195,435 | ||||||||||||

| Windsor Holdings III LLC 8.50%, 06/15/30 (d) | United States | 285,000 | 298,189 | ||||||||||||

Total Chemicals | 1,761,660 | ||||||||||||||

Commercial Services & Supplies – 1.4% | |||||||||||||||

| Allied Universal Holdco LLC 3.63%, 06/01/28 | United States | € | 205,000 | 199,364 | |||||||||||

4.63%, 06/01/28 (d) | United States | $ | 690,000 | 628,063 | |||||||||||

| Aramark International Finance Sarl 3.13%, 04/01/25 | United States | € | 100,000 | 110,150 | |||||||||||

| Iron Mountain, Inc. 5.00%, 07/15/28 (d) | United States | $ | 435,000 | 418,342 | |||||||||||

| LABL, Inc. 5.88%, 11/01/28, (Acquired 11/1/2021 – 11/30/2021, cost $445,921) (d) (l) | United States | 445,000 | 404,016 | ||||||||||||

| Prime Security Services Borrower LLC 6.25%, 01/15/28 (d) | United States | 901,000 | 896,449 | ||||||||||||

| TMS International Corp. 6.25%, 04/15/29 (d) | United States | 330,000 | 272,697 | ||||||||||||

| WASH Multifamily Acquisition, Inc. 5.75%, 04/15/26 (d) | United States | 430,000 | 414,265 | ||||||||||||

Total Commercial Services & Supplies | 3,343,346 | ||||||||||||||

Communications Equipment – 0.1% | |||||||||||||||

| CommScope Technologies LLC 6.00%, 06/15/25 (d) | United States | 260,000 | 212,144 | ||||||||||||

| CommScope, Inc. 4.75%, 09/01/29 (d) | United States | 75,000 | 50,426 | ||||||||||||

6.00%, 03/01/26 (d) | United States | 95,000 | 84,759 | ||||||||||||

Total Communications Equipment | 347,329 | ||||||||||||||

Construction & Engineering – 0.3% | |||||||||||||||

| Great Lakes Dredge & Dock Corp. 5.25%, 06/01/29 (d) | United States | 340,000 | 289,422 | ||||||||||||

| Pike Corp. 5.50%, 09/01/28 (d) | United States | 440,000 | 419,720 | ||||||||||||

Total Construction & Engineering | 709,142 | ||||||||||||||

See Notes to Consolidated Financial Statements.

18

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Consumer Finance – 0.5% | |||||||||||||||

| FirstCash, Inc. 5.63%, 01/01/30 (d) | United States | $ | 702,000 | $ | 673,235 | ||||||||||

| Ford Motor Credit Company LLC 4.00%, 11/13/30 | United States | 445,000 | 399,623 | ||||||||||||

Total Consumer Finance | 1,072,858 | ||||||||||||||

Containers & Packaging – 0.9% | |||||||||||||||

| Ardagh Packaging Finance PLC 2.13%, 08/15/26 | United States | € | 180,000 | 177,718 | |||||||||||

4.13%, 08/15/26 (d) | United States | $ | 335,000 | 305,971 | |||||||||||

5.25%, 08/15/27 (d) | United States | 260,000 | 202,290 | ||||||||||||

| Fiber Bidco SpA 9.96% (3 Month EURIBOR + 6.00%), 10/25/27 (b) (d) | Italy | € | 100,000 | 112,491 | |||||||||||

| Graham Packaging Company, Inc. 7.13%, 08/15/28 (d) | United States | $ | 285,000 | 256,843 | |||||||||||

| Guala Closures SpA 7.93% (3 Month EURIBOR + 4.00%), 06/29/29 (b) (d) | Italy | € | 250,000 | 280,432 | |||||||||||

| Intelligent Packaging Limited Finco, Inc. 6.00%, 09/15/28 (d) | Canada | $ | 435,000 | 406,320 | |||||||||||

| Silgan Holdings, Inc. 2.25%, 06/01/28 | United States | € | 200,000 | 203,829 | |||||||||||

| Trivium Packaging Finance BV 3.75%, 08/15/26 | Netherlands | 100,000 | 107,254 | ||||||||||||

Total Containers & Packaging | 2,053,148 | ||||||||||||||

Diversified Consumer Services – 0.1% | |||||||||||||||

| Verisure Holding AB 3.88%, 07/15/26 | Sweden | 100,000 | 108,662 | ||||||||||||

| Verisure Midholding AB 5.25%, 02/15/29 | Sweden | 100,000 | 105,704 | ||||||||||||

Total Diversified Consumer Services | 214,366 | ||||||||||||||

Diversified Telecommunication Services – 1.3% | |||||||||||||||

| Altice Financing SA 3.00%, 01/15/28 | Luxembourg | 200,000 | 197,827 | ||||||||||||

| Altice France SA 3.38%, 01/15/28 | France | 100,000 | 87,916 | ||||||||||||

4.13%, 01/15/29 | France | 100,000 | 88,561 | ||||||||||||

| Cogent Communications Group, Inc. 7.00%, 06/15/27 (d) | United States | $ | 340,000 | 342,018 | |||||||||||

| Consolidated Communications, Inc. 6.50%, 10/01/28 (d) | United States | 380,000 | 329,650 | ||||||||||||

| Frontier Communications Holdings LLC 5.00%, 05/01/28 (d) | United States | 290,000 | 268,278 | ||||||||||||

6.75%, 05/01/29 (d) | United States | 155,000 | 138,763 | ||||||||||||

| Iliad Holding SASU 5.63%, 10/15/28 | France | € | 200,000 | 222,267 | |||||||||||

| Iliad SA 5.38%, 02/15/29 (e) (g) | France | 100,000 | 113,541 | ||||||||||||

| Level 3 Financing, Inc. 4.25%, 07/01/28 (d) | United States | $ | 330,000 | 163,683 | |||||||||||

| Lorca Telecom Bondco SA 4.00%, 09/18/27 | Spain | € | 200,000 | 216,097 | |||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

19

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| Telecom Italia SpA 6.88%, 02/15/28 (e) (g) | Italy | € | 100,000 | $ | 117,851 | ||||||||||

| Telefonica Europe BV 4.38% (5 Year Swap Rate EUR + 4.11%), Perpetual (b) | Spain | 200,000 | 219,588 | ||||||||||||

| TMNL Holding BV 3.75%, 01/15/29 | Netherlands | 195,000 | 204,931 | ||||||||||||

| Ziggo Bond Company BV 3.38%, 02/28/30 | Netherlands | 200,000 | 187,153 | ||||||||||||

Total Diversified Telecommunication Services | 2,898,124 | ||||||||||||||

Electrical Equipment – 0.1% | |||||||||||||||

| APX Group, Inc. 6.75%, 02/15/27 (d) | United States | $ | 290,000 | 289,684 | |||||||||||

Energy Equipment & Services – 0.2% | |||||||||||||||

| Howard Midstream Energy Partners LLC 8.88%, 07/15/28 (d) | United States | 180,000 | 189,117 | ||||||||||||

| Precision Drilling Corp. 7.13%, 01/15/26 (d) | Canada | 223,000 | 223,022 | ||||||||||||

Total Energy Equipment & Services | 412,139 | ||||||||||||||

Entertainment – 0.1% | |||||||||||||||

| Banijay (LOV Banijay SASU) 7.00%, 05/01/29 (e) (g) | France | € | 170,000 | 198,470 | |||||||||||

| Pinewood Finance Company Ltd. 3.25%, 09/30/25 | United Kingdom | £ | 100,000 | 124,243 | |||||||||||

Total Entertainment | 322,713 | ||||||||||||||

Financial Services – 0.9% | |||||||||||||||

| GTCR LLC 8.50%, 01/15/31 | Netherlands | 150,000 | 207,306 | ||||||||||||

| Nationstar Mortgage Holdings, Inc. 5.75%, 11/15/31 (d) | United States | $ | 700,000 | 653,683 | |||||||||||

6.00%, 01/15/27 (d) | United States | 140,000 | 139,094 | ||||||||||||

| NCR Atleos Escrow Corp. 9.50%, 04/01/29 (d) | United States | 415,000 | 441,299 | ||||||||||||

| Worldpay 7.50%, 01/15/31 (d) | United States | 530,000 | 560,407 | ||||||||||||

Total Financial Services | 2,001,789 | ||||||||||||||

Food Products – 0.4% | |||||||||||||||

| B&G Foods, Inc. 8.00%, 09/15/28 (d) | United States | 430,000 | 452,056 | ||||||||||||

| Post Holdings, Inc. 5.63%, 01/15/28 (d) | United States | 430,000 | 426,419 | ||||||||||||

Total Food Products | 878,475 | ||||||||||||||

Gas Utilities – 0.4% | |||||||||||||||

| CQP Holdco LP 5.50%, 06/15/31 (d) | United States | 165,000 | 156,587 | ||||||||||||

7.50%, 12/15/33 (d) | United States | 515,000 | 534,332 | ||||||||||||

| Suburban Propane Partners LP 5.00%, 06/01/31 (d) | United States | 220,000 | 199,777 | ||||||||||||

Total Gas Utilities | 890,696 | ||||||||||||||

See Notes to Consolidated Financial Statements.

20

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Health Care Equipment & Supplies – 0.2% | |||||||||||||||

| Medline Borrower LP 5.25%, 10/01/29 (d) | United States | $ | 395,000 | $ | 372,847 | ||||||||||

Health Care Providers & Services – 0.4% | |||||||||||||||

| Avantor Funding, Inc. 3.88%, 07/15/28 | United States | € | 100,000 | 108,383 | |||||||||||

| Community Health Systems, Inc. 5.63%, 03/15/27 (d) | United States | $ | 205,000 | 190,741 | |||||||||||

10.88%, 01/15/32 (d) | United States | 260,000 | 272,059 | ||||||||||||

| Nidda Healthcare Holding GmbH 7.50%, 08/21/26 | Germany | € | 100,000 | 113,981 | |||||||||||

| Pediatrix Medical Group, Inc. 5.38%, 02/15/30 (d) | United States | $ | 295,000 | 263,093 | |||||||||||

Total Health Care Providers & Services | 948,257 | ||||||||||||||

Health Care Technology – 0.1% | |||||||||||||||

| MPH Acquisition Holdings LLC 5.50%, 09/01/28 (d) | United States | 160,000 | 143,449 | ||||||||||||

Hotels Restaurants & Leisure – 1.9% | |||||||||||||||

| Accor SA 7.25% (5 Year Swap Rate EUR + 4.11%), Perpetual (b) (e) (g) | France | € | 200,000 | 240,764 | |||||||||||

| Bloomin' Brands, Inc. 5.13%, 04/15/29 (d) | United States | $ | 665,000 | 614,093 | |||||||||||

| Brinker International, Inc. 8.25%, 07/15/30 (d) | United States | 392,000 | 410,451 | ||||||||||||

| Carnival Corp. 5.75%, 03/01/27 (d) | United States | 490,000 | 478,330 | ||||||||||||

10.50%, 06/01/30 (d) | United States | 80,000 | 87,562 | ||||||||||||

| Cirsa Finance International Sarl 7.88%, 07/31/28 (e) (g) | Spain | € | 160,000 | 184,837 | |||||||||||

8.45% (3 Month EURIBOR + 4.50%), 07/31/28 (b) (d) | Spain | 115,000 | 128,981 | ||||||||||||

| Everi Holdings, Inc. 5.00%, 07/15/29 (d) | United States | $ | 345,000 | 313,590 | |||||||||||

| Fertitta Entertainment LLC 6.75%, 01/15/30 (d) | United States | 160,000 | 140,664 | ||||||||||||

| Hilton Grand Vacations Borrower Escrow LLC 5.00%, 06/01/29 (d) | United States | 675,000 | 623,542 | ||||||||||||

| Legends Hospitality Holding Company LLC 5.00%, 02/01/26 (d) | United States | 440,000 | 439,616 | ||||||||||||

| Lottomatica S.P.A. 7.13%, 06/01/28 (e) (g) | Italy | € | 115,000 | 134,206 | |||||||||||

| Six Flags Entertainment Corp 7.25%, 05/15/31 (d) | United States | $ | 425,000 | 426,585 | |||||||||||

| TUI Cruises GmbH 6.50%, 05/15/26 | Germany | € | 200,000 | 218,585 | |||||||||||

Total Hotels Restaurants & Leisure | 4,441,806 | ||||||||||||||

Household Durables – 0.2% | |||||||||||||||

| Shea Homes LP 4.75%, 02/15/28 | United States | $ | 345,000 | 324,729 | |||||||||||

| Weekley Homes LLC 4.88%, 09/15/28 (d) | United States | 185,000 | 172,702 | ||||||||||||

Total Household Durables | 497,431 | ||||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

21

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

Independent Power and Renewable Electricity Producers – 0.4% | |||||||||||||||

| Calpine Corp. 5.13%, 03/15/28 (d) | United States | $ | 350,000 | $ | 335,791 | ||||||||||

| Talen Energy Supply LLC 8.63%, 06/01/30 (d) | United States | 250,000 | 265,819 | ||||||||||||

| Vistra Operations Company, LLC 7.75%, 10/15/31 (d) | United States | 315,000 | 327,392 | ||||||||||||

Total Independent Power and Renewable Electricity Producers | 929,002 | ||||||||||||||

Insurance – 0.2% | |||||||||||||||

| AssuredPartners, Inc. 5.63%, 01/15/29 (d) | United States | 250,000 | 233,664 | ||||||||||||

| HUB International Ltd. 5.63%, 12/01/29 (d) | United States | 120,000 | 114,628 | ||||||||||||

7.00%, 05/01/26 (d) | United States | 190,000 | 190,955 | ||||||||||||

Total Insurance | 539,247 | ||||||||||||||

Interactive Media & Services – 0.1% | |||||||||||||||

| QVC, Inc. 4.85%, 04/01/24 | United States | 310,000 | 307,137 | ||||||||||||

IT Services – 0.2% | |||||||||||||||

| Ahead DB Holdings LLC 6.63%, 05/01/28 (d) | United States | 340,000 | 296,567 | ||||||||||||

| Engineering – Ingegneria Informatica – SpA 5.88%, 09/30/26 | Italy | € | 200,000 | 216,946 | |||||||||||

Total IT Services | 513,513 | ||||||||||||||

Machinery – 0.8% | |||||||||||||||

| ProFrac Holdings II LLC 12.60% (CME Term SOFR 3 Month + 7.25%), 01/23/29 (b) (c) (d) | United States | $ | 1,316,000 | 1,302,840 | |||||||||||

| SPX FLOW, Inc. 8.75%, 04/01/30 (d) | United States | 453,000 | 453,521 | ||||||||||||

Total Machinery | 1,756,361 | ||||||||||||||

Media – 2.1% | |||||||||||||||

| AMC Networks, Inc. 4.25%, 02/15/29 | United States | 435,000 | 332,343 | ||||||||||||

| America Movil BV 0.00%, 03/02/24 | Mexico | € | 100,000 | 110,937 | |||||||||||

| Cablevision Lightpath LLC 5.63%, 09/15/28 (d) | United States | $ | 415,000 | 327,506 | |||||||||||

| CCO Holdings LLC 4.25%, 01/15/34 (d) | United States | 355,000 | 288,958 | ||||||||||||

4.50%, 06/01/33 (d) | United States | 494,000 | 418,634 | ||||||||||||

4.75%, 03/01/30 (d) | United States | 190,000 | 173,888 | ||||||||||||

6.38%, 09/01/29 (d) | United States | 140,000 | 138,249 | ||||||||||||

| CSC Holdings LLC 4.13%, 12/01/30 (d) | United States | 435,000 | 331,435 | ||||||||||||

| Directv Financing LLC 5.88%, 08/15/27 (d) | United States | 920,000 | 865,165 | ||||||||||||

| DISH DBS Corp. 5.25%, 12/01/26 (d) | United States | 195,000 | 167,432 | ||||||||||||

5.75%, 12/01/28 (d) | United States | 25,000 | 19,987 | ||||||||||||

See Notes to Consolidated Financial Statements.

22

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||

CORPORATE CREDIT (continued) | |||||||||||||||

| Gray Television, Inc. 4.75%, 10/15/30 (d) | United States | $ | 160,000 | $ | 120,626 | ||||||||||

| Scripps Escrow II, Inc. 5.38%, 01/15/31 (d) | United States | 130,000 | 95,557 | ||||||||||||

| Sirius XM Radio, Inc. 3.88%, 09/01/31 (d) | United States | 630,000 | 539,741 | ||||||||||||

5.50%, 07/01/29 (d) | United States | 214,000 | 207,134 | ||||||||||||

| Telenet Finance Luxembourg Notes Sarl 5.50%, 03/01/28 (d) | Belgium | 200,000 | 187,920 | ||||||||||||

| Virgin Media Secured Finance PLC 4.50%, 08/15/30 (d) | United Kingdom | 305,000 | 271,941 | ||||||||||||

5.25%, 05/15/29 | United Kingdom | £ | 100,000 | 118,935 | |||||||||||

| Virgin Media Vendor Financing Notes III DAC 4.88%, 07/15/28 | United Kingdom | 100,000 | 117,673 | ||||||||||||

Total Media | 4,834,061 | ||||||||||||||

Metals & Mining – 0.4% | |||||||||||||||

| Constellium SE 5.63%, 06/15/28 (d) | United States | $ | 260,000 | 254,043 | |||||||||||

| Mineral Resources Ltd. 8.50%, 05/01/30 (d) | Australia | 300,000 | 313,122 | ||||||||||||

9.25%, 10/01/28 (d) | Australia | 380,000 | 404,708 | ||||||||||||

Total Metals & Mining | 971,873 | ||||||||||||||

Mortgage Real Estate Investment Trusts – 0.3% | |||||||||||||||

| HAT Holdings I LLC 3.38%, 06/15/26 (d) | United States | 415,000 | 390,305 | ||||||||||||

3.75%, 09/15/30 (d) | United States | 150,000 | 126,524 | ||||||||||||

8.00%, 06/15/27 (d) | United States | 155,000 | 161,602 | ||||||||||||

Total Mortgage Real Estate Investment Trusts | 678,431 | ||||||||||||||

Oil Gas & Consumable Fuels – 0.8% | |||||||||||||||

| CITGO Petroleum Corp. 7.00%, 06/15/25 (d) | United States | 360,000 | 359,722 | ||||||||||||

| Civitas Resources, Inc. 8.63%, 11/01/30 (d) | United States | 200,000 | 212,313 | ||||||||||||

| CVR Energy, Inc. 5.25%, 02/15/25 (d) | United States | 305,000 | 304,706 | ||||||||||||

| Venture Global LNG, Inc. 8.13%, 06/01/28 (d) | United States | 255,000 | 257,756 | ||||||||||||

8.38%, 06/01/31 (d) | United States | 260,000 | 260,257 | ||||||||||||

9.50%, 02/01/29 (d) | United States | 335,000 | 354,695 | ||||||||||||

Total Oil Gas & Consumable Fuels | 1,749,449 | ||||||||||||||

Other – 1.0% | |||||||||||||||

| Nidda BondCo GmbH 7.25%, 09/30/25 | Germany | € | 71,616 | 79,063 | |||||||||||

| OWS Cre Funding I LLC 10.33% (1 Month LIBOR + 4.90%), 09/15/24 (b) (d) | United States | $ | 2,345,090 | 2,344,239 | |||||||||||

Total Other | 2,423,302 | ||||||||||||||

Paper & Forest Products – 0.2% | |||||||||||||||

| Mercer International, Inc. 5.50%, 01/15/26 | Germany | 385,000 | 368,973 | ||||||||||||

See Notes to Consolidated Financial Statements.

2023 Annual Report

23

OAKTREE DIVERSIFIED INCOME FUND INC.

Consolidated Schedule of Investments (continued)

December 31, 2023

Description | Country | Principal Amount | Value | ||||||||||||