UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-23758

Eagle Point Institutional Income Fund

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 202

Greenwich, CT 06830

(Address of principal executive offices) (Zip code)

Thomas P. Majewski

c/o Eagle Point Institutional Income Fund

600 Steamboat Road, Suite 202

Greenwich, CT 06830

(Name and address of agent for service)

Copies to

Thomas J. Friedmann

Philip Hinkle

Dechert LLP

One International Place, 40th Floor

100 Oliver Street

Boston, MA 02110

(617) 728-7120

Registrant’s telephone number, including area code: (203) 340-8500

Date of fiscal year end: December 31

Date of reporting period: June 30, 2024

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders

The Company’s Semiannual Report to stockholders for the six months ending June 30, 2024 is filed herewith.

Eagle Point Institutional Income Fund

Semiannual Report – June 30, 2024

Table of Contents

1

Letter to Shareholders and Management Discussion of Fund Performance

Dear Shareholders:

We are pleased to provide you with the enclosed report of Eagle Point Institutional Income Fund (“we,” “us,” “our” or the “Fund”) for the six months ended June 30, 2024.

The Fund is a closed-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”) and is advised by Eagle Point Credit Management LLC (the “Adviser”). The Fund is organized as a Delaware statutory trust and offers its shares of beneficial interest (“Shares”) to investors on a continuous basis at the Fund’s net asset value (“NAV”) per share plus any applicable sales load. The Fund’s primary investment objective is to generate high current income, with a secondary objective to generate capital appreciation. We seek to achieve these objectives by investing primarily in equity and junior debt tranches of collateralized loan obligations (“CLOs”). We may also invest in other securities or instruments that are related investments or that are consistent with our investment objectives.

The Adviser has significant expertise in CLO investing, including 62 years of combined CLO industry experience among the senior investment team, and over $10.0 billion of assets under management (including undrawn capital commitments)1 as of June 30, 2024. The Fund was formed in order to provide investors with access to institutional credit investment strategies in a continuously offered, SEC-registered and non-traded format.

In the first half of 2024, we:

| ■ | Exceeded $100 million of total assets, inclusive of available borrowings under a revolving credit facility. |

| ■ | Generated a net total return of 12.8% over the 12-month period ending June 30, 2024.2 |

| ■ | Paid consistent monthly distributions to shareholders totaling $0.483 per share during the first half of 2024, generating a 9.7% annualized distribution rate. This represents a 5.2% increase from the $0.459 per share distributed in the second half of 2023.3 |

| ■ | Opportunistically purchased CLO equity investments in the primary and secondary markets at a weighted average effective yield of 17.9%, and sustained a healthy weighted average remaining reinvestment period of the Fund’s CLO equity portfolio of 3.5 years as of June 30, 2024. |

Past performance is not indicative of, or a guarantee of, future performance.

Please see page 7 for endnotes.

2

| ■ | Increased the Fund’s NAV per share to $9.97 as of June 30, 2024, from $9.70 a year prior. |

The strong performance of our investment portfolio during the first half of 2024 enabled the Fund to distribute $3.1 million.3

We continue to prudently and actively manage the Fund’s investment portfolio while raising capital to take advantage of attractive investment opportunities. During the first half of 2024, we deployed $42.5 million into new CLO equity investments and loan accumulation facilities. We also sold three CLO debt investments and realized capital gains with a weighted average appreciation in price of 11.25%.

We believe our portfolio continues to have the potential for further meaningful upside. In our view, CLOs generally are not particularly sensitive to interest rate movements, as underlying broadly syndicated loans (“BSLs”), which generate the cash flows we receive as a CLO equity investor, and our financing from CLO debt are both principally floating rate.

The Fund’s investment portfolio as of June 30, 2024 consisted of 58 unique CLO investments. Importantly, nearly all of the Fund’s investments were also investments made by other institutional funds and accounts managed by the Adviser. To the extent that the Fund (along with other funds and accounts managed by the Adviser) owns a majority position in the equity tranche, our Adviser has the ability to exercise certain protective rights over the vehicle (such as the ability to call the CLO after the non-call period, to refinance/reprice certain CLO debt tranches after the non-call period and to influence potential amendments to the governing documents of the CLO) that may reduce our risk in these investments and/or enhance our economics.

For the first of half of 2024, the cash generation of the Fund’s CLO equity portfolio was steady and robust, with an annualized cash-on-cash return of 20.7%4 providing the Fund with valuable dry powder to deploy into new securities at attractive prices.

During the first half of 2024, the Fund raised $31.3 million through sales of shares and reinvestment of distributions. The Adviser intends to continue increasing the Fund’s equity by raising capital under the Fund’s continuous offering program.

On June 28, 2024, the Fund entered into an agreement that establishes a senior secured revolving credit facility, which provides $25 million of committed capital to the Fund. The Fund’s use of leverage through this credit facility is expected to be accretive to shareholders.

We also want to highlight the Fund’s distribution reinvestment plan for shareholders. This plan allows shareholders to have their distributions automatically reinvested into new shares at a 5% discount to NAV per share. We encourage all shareholders to carefully review the terms of the plan. See “Distribution Reinvestment Plan” in the enclosed report.

Past performance is not indicative of, or a guarantee of, future performance.

Please see page 7 for endnotes.

3

Market Overview5

Loan Market

For the first half of 2024, loan performance was stable. The Credit Suisse Leverage Loan Index6 (“CSLLI”), which is a broad index followed by many tracking the corporate loan market, generated a non-annualized total return of 4.44% in the first half of 2024. Interest rates remained elevated, helping to maintain the attractive current coupons on floating rate loans.

Average loan prices finished the first half of 2024 at 95.68, a modest increase from 95.32 at the beginning of the year.

Loan issuance totaled $289 billion for the first half of 2024, compared to $103 billion for the first half of 2023. Total institutional loans outstanding stood at $1.4 trillion as of June 30, 2024.

The trailing 12-month par-weighted default rate finished June at 0.92%, compared to 1.53% at the end of 2023, and remaining well below the long-term average of 2.65%.7 The Fund’s look through default exposure stood at 0.37% at the end of June.

While many CLO investors focus principally on default rates, we believe the market does not give enough consideration to loan repayment rates and the reinvestment period tenor within CLOs, which often allows CLOs to purchase loans at a discounted prices using par repayment proceeds. With over $44 billion of BSLs repaying at par in June, the 12-month trailing loan prepayment rate increased to 25.3% as of June 30, 2024.

Part of these repayments relate to refinancing of loans coming due. As of June 30, 2024, less than 3% of the loan market was set to mature prior to 2026 and the “maturity wall” continues to be pushed out; 2025 and 2026 maturities have each been reduced by over 50% since the beginning of the year. Only 2% of the loans in the portfolios of our underlying CLO equity positions mature prior to 2026.

CLO Market

The first half of 2024 saw CLO new issue at the fastest pace ever, with approximately $102 billion of volume. This is over 80% above new issue volume at the same time last year. Third party CLO equity investors (including us) have returned to the new issue market in 2024 as CLO AAAs have tightened. That tightening has also driven a large increase in CLO refinancing and reset activity to over $110 billion combined. We appear comfortably on pace to break the previous issuance records set in 2021.

Past performance is not indicative of, or a guarantee of, future performance.

Please see page 7 for endnotes.

4

In the first half of 2024, there were approximately $50 billion of CLO AAA paydowns, and we believe CLO AAA paydowns will continue. The brief bout of volatility in August has not materially affected the CLO market, so we expect tightening pressure on CLO AAA spreads to continue. We believe this trend will encourage more new issue, refinancing and reset activity.

As of June 30, 2024, CLO AAA discount margins, or DMs, averaged approximately 142 basis points over SOFR; this is 33 basis points tighter than the end of 2023.

The underlying fundamentals of CLO portfolios remain strong. The median market-wide CCC-rated loan exposure for U.S. CLOs was just 6.6%, with average OC cushions of 3.2% on June 30, 2024. For context, approximately 6.3% of U.S. CLOs recorded a breach of their overcollateralization test as of June 30, 2024. In other words, over 93% of U.S. CLOs continued to pay cash distributions to their CLO equity investors. All of our CLO equity positions with a payment date in July received a distribution

As we look into the second half of 2024, we expect continued tightening in CLO AAA spreads. This tightening trend, along with CLO equity investors directing liquidations of seasoned CLOs to capture higher loan prices, has led to AAA investors being redeemed out of paper despite the increased issuance activity. We believe many AAA investors will need to replenish their investment portfolios.

We remain excited about the investment opportunities within the CLO market – in particular, the equity portion of the capital structure.

Additional Information

In addition to the Fund’s regulatory requirement to file certain quarterly and annual portfolio information as described further in the enclosed report, the Fund makes certain additional financial information available to investors via our website (www.EPIIF.com).

About Our Adviser

Eagle Point Credit Management LLC is a specialist asset manager focused on investing in CLO securities and other income-oriented credit investments. As of June 30, 2024, our Adviser and its affiliates have over $10 billion of assets under management (inclusive of undrawn capital commitments).1

Subsequent Developments

Pursuant to the Fund’s continuous offering, during the period from July 1, 2024 through July 31, 2024, the Fund issued shares for total net proceeds to the Fund of $5.9 million.

Past performance is not indicative of, or a guarantee of, future performance.

Please see page 7 for endnotes.

5

For the month of July 2024, the Fund declared and paid a distribution in the amount of $0.083 per share, representing a 10% annualized distribution rate3 based on the Fund’s NAV per share of $9.97 as of June 30, 2024.

* * * *

Management remains keenly focused on continuing to create value for our shareholders. We appreciate the trust and confidence our shareholders have placed in the Fund.

Thomas Majewski

Chairman and Chief Executive Officer

This letter is intended to assist shareholders in understanding the Fund’s performance during the six months ended June 30, 2024. The views and opinions in this letter were current as of July 31, 2024. Statements other than those of historical facts included herein may constitute forward-looking statements and are not guarantees of future performance or results and involve a number of risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result of a number of factors. The Fund undertakes no duty to update any forward-looking statement made herein. Information contained on our website is not incorporated by reference into this shareholder letter and you should not consider information contained on our website to be part of this shareholder letter or any other report we file with the Securities and Exchange Commission.

Past performance is not indicative of, or a guarantee of, future performance.

Please see page 7 for endnotes.

6

Notes

| 1 | Assets under management is as of June 30, 2024. Calculated in the aggregate with certain affiliated advisers. |

| 2 | Past performance is not indicative of, or a guarantee of, future performance. Total return reflects the percent change in NAV per share from the beginning of the period, plus the amount of any distribution per share paid in the period. Return calculation assumes reinvestment of distributions pursuant to the Fund’s distribution reinvestment plan and is net of all Fund expenses, including general and administrative expenses, transaction related expenses, amortization of offering costs, management and incentive fees, and expense limitation being in effect during the performance periods (if any). The Fund charges a maximum upfront sales load of 6.75%. Total return does not reflect the Fund’s upfront sales load. If reflected, the Fund’s total return would have been lower. Return information is not a measure used under GAAP. Valuations based upon unaudited reports may not correspond to realized value and may not accurately reflect the price at which assets could be liquidated. Performance reflects certain expense limitation arrangements in effect during the periods shown. Absent these arrangements, the Fund’s performance would have been lower. Certain expenses paid by Eagle Point Credit Management or its affiliates on the Fund’s behalf are subject to reimbursement by the Fund for up to three years (which reimbursement would have the effect of reducing the Fund’s performance). Performance does not reflect the impact of federal, state or local taxation to which an investor may be subject. |

| 3 | Annualized distribution rate reflects distributions paid during the period, annualized, and divided by the period end NAV. The annualized distribution rate is not a guarantee of future returns and future performance may vary. The timing and frequency of distribution payments is not guaranteed. Such variance may be material and adverse, including the potential for full loss of principal and no distributions. In considering returns, investors should bear in mind that historical performance is not a guarantee, projection or prediction and is not indicative of future results. Actual net returns in any given year may be lower than the historical returns. Investment return and principal value of any investment will fluctuate and may be worth more or less than the amount initially invested. Distribution payments are not guaranteed. Distributions may be comprised of any combination of 1) net investment income and/or 2) net capital gain, and, if the Fund distributes an amount in excess of net investment income and net capital gains, a portion of such distribution will constitute a return of capital. A distribution comprised in whole or in part by a return of capital does not necessarily reflect the Fund’s investment performance and should not be confused with “yield” or “income.” A return of capital distribution may reduce the amount of investable funds. The actual components of the Fund’s distributions for U.S. tax reporting purposes can only be finally determined as of the end of each fiscal year of the Fund and are thereafter reported to shareholders on Form 1099-DIV. |

| 4 | Cash-on-cash return represents the total amount of recurring distributions received from investments for the period over the Fund’s average beginning NAV for the period, annualized. |

| 5 | Market data and statistics summarized herein are sourced from JPMorgan Chase & Co., S&P Capital IQ, S&P LCD, and Credit Suisse. |

| 6 | The CSLLI tracks the investable universe of the US dollar-denominated leveraged loan market. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index. |

| 7 | “Par-weighted default rate” represents the rate of obligors who fail to remain current on their loans based on the par amount. |

7

Page Intentionally Left Blank

Important Information about this Report and Eagle Point Institutional Income Fund

This report is transmitted to the shareholders of Eagle Point Institutional Income Fund (“we”, “us”, “our” or the “Fund”) and is furnished pursuant to certain regulatory requirements. This report and the information and views herein do not constitute investment advice, or a recommendation or an offer to enter into any transaction with the Fund or any of its affiliates. This report is provided for informational purposes only, does not constitute an offer to sell securities of the Fund and is not a prospectus. From time to time, the Fund may have a registration statement relating to one or more of its securities on file with the US Securities and Exchange Commission (“SEC”). Any registration statement that has not yet been declared effective by the SEC, and any prospectus relating thereto, is not complete and may be changed. Any securities that are the subject of such a registration statement may not be sold until the registration statement filed with the SEC is effective.

The information and its contents are the property of Eagle Point Credit Management LLC (the “Adviser”) and/or the Fund. Any unauthorized dissemination, copying or use of this presentation is strictly prohibited and may be in violation of law. This presentation is being provided for informational purposes only.

Investors should read the Fund’s prospectus and SEC filings (which are publicly available on the EDGAR Database on the SEC website at www.sec.gov) carefully and consider their investment goals, time horizons and risk tolerance before investing in the Fund. Investors should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing in securities of the Fund. There is no guarantee that any of the goals, targets or objectives described in this report will be achieved.

An investment in the Fund is not appropriate for all investors. The investment program of the Fund is speculative, entails substantial risk and includes investment techniques not employed by traditional mutual funds. An investment in the Fund is not intended to be a complete investment program. Past performance is not indicative of, or a guarantee of, future performance. The performance and certain other portfolio information quoted herein represents information as of June 30, 2024. Nothing herein should be relied upon as a representation as to the future performance or portfolio holdings of the Fund. Investment return and principal value of an investment will fluctuate, and shares, when sold, may be worth more or less than their original cost. The Fund’s performance is subject to change since the end of the period noted in this report and may be lower or higher than the performance data shown herein.

Liquidity will be provided by the Fund only through limited repurchase offers described below (if at all). An investment in the Fund is suitable only for investors who can bear the risks associated with the limited liquidity of the Shares and should be viewed as a long-term investment. The Fund’s shares will not be publicly traded and an investor should not expect to be able to sell shares regardless of how the Fund performs.

Neither the Adviser nor the Fund provide legal, accounting or tax advice. Any statement regarding such matters is explanatory and may not be relied upon as definitive advice. Investors should consult with their legal, accounting and tax advisors regarding any potential investment. The information presented herein is as of the dates noted herein and is derived from financial and other information of the Fund, and, in certain cases, from third party sources and reports (including reports of third party custodians, CLO managers and trustees) that have not been independently verified by the Fund. As noted herein, certain of this information is estimated and unaudited, and therefore subject to change. We do not represent that such information is accurate or complete, and it should not be relied upon as such.

Forward-Looking Statements

This report may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Statements other than statements of historical facts included in this report may constitute forward-looking statements and are not guarantees of future performance or results and involve a number of risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result of a number of factors, including those described in the Fund’s filings with the SEC. The Fund undertakes no duty to update any forward-looking statement made herein. All forward-looking statements speak only as of the date of this report.

9

Summary of Certain Unaudited Portfolio Characteristics

The summary of portfolio characteristics reflected below is as of June 30, 2024. The information presented below is on a look–through basis to the collateralized loan obligation, or “CLO”, equity held by the Fund as of June 30, 2024 (except as otherwise noted) and reflects the aggregate underlying exposure of the Fund based on the portfolios of those investments. The data is estimated and unaudited and is derived from CLO trustee reports received by the Fund relating to June 2024 and from custody statements and/or other information received from CLO collateral managers, or other third party sources.

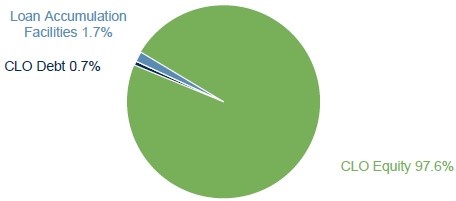

| Summary of Portfolio Investments1 |

| Number of CLO Securities | 58 |

| Number of Collateral Managers | 23 |

| Fair Value of CLO Equity Securities | $77,148,769 |

| Fair Value of Loan Accumulation Facility Securities | $1,367,944 |

| Fair Value of CLO Debt Securities | $546,095 |

| Summary of Underlying Portfolio Characteristics2 | |

| Number of Unique Underlying Loan Obligors | 1,293 |

| Largest Exposure to an Individual Obligor | 0.63% |

| Average Individual Loan Obligor Exposure | 0.08% |

| Top 10 Loan Obligors Exposure | 5.07% |

| Aggregate Indirect Exposure to Senior Secured Loans3 | 97.32% |

| Weighted Average Market Value of Loan Collateral | 97.51% |

| Weighted Average Stated Loan Spread | 3.63% |

| Weighted Average Loan Maturity | 4.7 years |

| Weighted Average Remaining CLO Reinvestment Period | 3.5 years |

Please see footnote disclosure on Page 11.

10

Notes

| 1 | The summary of portfolio investments shown is based on the estimated fair value of the underlying positions as of June 30, 2024. |

| 2 | The information presented herein is on a look-through basis to the collateralized loan obligation, or “CLO”, equity held by the Fund as of June 30, 2024 (except as otherwise noted) and reflects the aggregate underlying exposure of the Fund based on the portfolios of those investments. The data is estimated and unaudited and is derived from CLO trustee reports received by the Fund relating to June 2024 and from custody statements and/or other information received from CLO collateral managers and other third party sources. Information relating to the market price of underlying collateral is as of month end; however, with respect to other information shown, depending on when such information was received, the data may reflect a lag in the information reported. As such, while this information was obtained from third party data sources, June 2023 trustee reports and similar reports, other than market price, it does not reflect actual underlying portfolio characteristics as of June 30, 2024 and this data may not be representative of current or future holdings. The weighted average remaining reinvestment period information is based on the fair value of CLO equity investments held by the Fund as of June 30, 2024. |

| 3 | We obtain exposure in underlying senior secured loans indirectly through CLOs and related investments. |

11

Consolidated Financial Statements for the Six Months Ended

June 30, 2024 (Unaudited)

12

Eagle Point Institutional Income Fund & Subsidiaries

Consolidated Statement of Assets and Liabilities

As of June 30, 2024

(expressed in U.S. dollars)

(Unaudited)

| ASSETS | ||||

| Investments, at fair value (cost $81,299,030) | $ | 79,062,808 | ||

| Cash and cash equivalents | 2,878,804 | |||

| Interest receivable | 2,605,007 | |||

| Due from Adviser (Note 4) | 1,665,553 | |||

| Deferred offering costs (Note 4) | 572,453 | |||

| Other assets | 53,721 | |||

| Prepaid expenses | 47,847 | |||

| Total Assets | 86,886,193 | |||

| LIABILITIES | ||||

| Payable for securities purchased | 6,014,679 | |||

| Incentive fee payable (Note 4) | 1,548,578 | |||

| Management fee payable (Note 4) | 918,402 | |||

| Professional fees payable | 267,144 | |||

| Administration fees payable | 124,767 | |||

| Trustees’ fees payable | 53,153 | |||

| Transfer agent fees payable | 42,961 | |||

| Other expenses payable | 56,939 | |||

| Total Liabilities | 9,026,623 | |||

| COMMITMENTS AND CONTINGENCIES (Note 7) | ||||

| NET ASSETS applicable to common stock, 94,000,000 shares authorized, 7,813,240 shares issued and outstanding | $ | 77,859,570 | ||

| NET ASSETS consist of: | ||||

| Paid-in capital (Note 5) | $ | 78,185,698 | ||

| Aggregate distributable earnings (losses) | (326,128 | ) | ||

| Total Net Assets | $ | 77,859,570 | ||

| Shares issued and outstanding | 7,813,240 | |||

| Net asset value per share | $ | 9.97 | ||

See accompanying notes to the consolidated financial statements

13

Eagle Point Institutional Income Fund & Subsidiaries

Consolidated Schedule of Investments

As of June 30, 2024

(expressed in U.S. dollars)

(Unaudited)

| Issuer (1) | Investment (2) | Acquisition Date (3) | Principal Amount | Cost | Fair Value (4) | % of Net Assets | ||||||||||||||

| Investments at Fair Value (5) | ||||||||||||||||||||

| CLO Debt (6) | ||||||||||||||||||||

| Structured Finance | ||||||||||||||||||||

| United States | ||||||||||||||||||||

| Tralee CLO VII, Ltd. | Secured Note - Class E, 12.98% (3M SOFR + 7.65%, due 04/25/2034) | 06/02/22 | $ | 550,000 | $ | 492,852 | $ | 546,095 | 0.70 | % | ||||||||||

| Total CLO Debt | 492,852 | 546,095 | 0.70 | % | ||||||||||||||||

| CLO Equity (7) | ||||||||||||||||||||

| Structured Finance | ||||||||||||||||||||

| United States | ||||||||||||||||||||

| Ares LXII CLO Ltd. | Subordinated Note (effective yield 19.28%, maturity 01/25/2034) ⁽⁸⁾ | 01/18/24 | 4,750,000 | 3,223,390 | 3,124,277 | 4.01 | % | |||||||||||||

| Ares LXIV CLO Ltd. | Subordinated Note (effective yield 20.16%, maturity 04/15/2035) ⁽⁸⁾ | 01/26/23 | 600,000 | 447,428 | 462,375 | 0.59 | % | |||||||||||||

| Ares LXV CLO Ltd. | Subordinated Note (effective yield 20.67%, maturity 07/25/2034) ⁽⁸⁾ | 04/16/24 | 675,000 | 461,256 | 488,396 | 0.63 | % | |||||||||||||

| Ares LXIX CLO Ltd. | Income Note (effective yield 23.20%, maturity 04/15/2037) ⁽⁸⁾ ⁽⁹⁾ | 01/31/24 | 4,850,000 | 3,495,686 | 4,276,684 | 5.49 | % | |||||||||||||

| Ares LXXII CLO Ltd. | Income Note (effective yield 19.10%, maturity 07/15/2036) ⁽⁸⁾ ⁽⁹⁾ | 06/21/24 | 4,050,000 | 2,982,779 | 2,982,779 | 3.83 | % | |||||||||||||

| Ares Loan Funding IV, Ltd. | Subordinated Note (effective yield 17.24%, maturity 10/15/2036) ⁽⁸⁾ | 04/23/24 | 4,925,000 | 3,656,813 | 3,537,431 | 4.54 | % | |||||||||||||

| Bain Capital Credit CLO 2021-2, Limited | Subordinated Note (effective yield 22.17%, maturity 07/16/2034) ⁽⁸⁾ | 08/09/23 | 2,750,000 | 1,447,232 | 1,286,063 | 1.65 | % | |||||||||||||

| Bain Capital Credit CLO 2021-7, Limited | Subordinated Note (effective yield 20.12%, maturity 01/22/2035) ⁽⁸⁾ | 09/05/23 | 3,450,000 | 2,027,731 | 1,687,150 | 2.17 | % | |||||||||||||

| Bardot CLO, Ltd. | Subordinated Note (effective yield 34.85%, maturity 10/22/2032) ⁽⁸⁾ ⁽⁹⁾ | 11/22/22 | 275,000 | 156,751 | 124,095 | 0.16 | % | |||||||||||||

| Barings CLO Ltd. 2021-II | Subordinated Note (effective yield 18.15%, maturity 07/15/2034) ⁽⁸⁾ | 09/07/22 | 600,000 | 416,559 | 357,128 | 0.46 | % | |||||||||||||

| Barings CLO Ltd. 2022-II | Income Note (effective yield 32.08%, maturity 07/15/2072) ⁽⁸⁾ ⁽⁹⁾ | 06/21/22 | 1,000,000 | 366,930 | 522,485 | 0.67 | % | |||||||||||||

| Barings CLO Ltd. 2024-II | Income Note (effective yield 18.30%, maturity 07/15/2039) ⁽⁸⁾ ⁽⁹⁾ | 05/31/24 | 4,300,000 | 2,971,900 | 2,971,899 | 3.82 | % | |||||||||||||

| Battalion CLO XXIII Ltd. | Income Note (effective yield 18.81%, maturity 07/15/2036) ⁽⁸⁾ ⁽⁹⁾ | 05/19/22 | 600,000 | 414,662 | 293,557 | 0.38 | % | |||||||||||||

| Bear Mountain Park CLO, Ltd. | Income Note (effective yield 18.03%, maturity 07/15/2035) ⁽⁸⁾ ⁽⁹⁾ | 07/13/22 | 550,000 | 447,622 | 553,365 | 0.71 | % | |||||||||||||

| Belmont Park CLO, Ltd. | Income Note (effective yield 17.46%, maturity 04/15/2037) ⁽⁸⁾ ⁽⁹⁾ | 02/21/24 | 3,450,000 | 2,499,629 | 2,590,606 | 3.33 | % | |||||||||||||

| BlueMountain CLO XXIV Ltd. | Subordinated Note (effective yield 18.68%, maturity 04/20/2034) ⁽⁸⁾ | 05/31/22 | 750,000 | 455,429 | 336,896 | 0.43 | % | |||||||||||||

| Carlyle US CLO 2021-10, Ltd. | Subordinated Note (effective yield 17.59%, maturity 10/20/2034) ⁽⁸⁾ | 08/16/23 | 1,400,000 | 889,290 | 769,201 | 0.99 | % | |||||||||||||

| Carlyle US CLO 2022-2, Ltd. | Subordinated Note (effective yield 18.95%, maturity 04/20/2035) ⁽⁸⁾ | 08/15/23 | 2,775,000 | 1,959,326 | 1,846,739 | 2.37 | % | |||||||||||||

| Carlyle US CLO 2023-3, Ltd. | Income Note (effective yield 13.46%, maturity 10/15/2036) ⁽⁸⁾ ⁽⁹⁾ | 07/06/23 | 1,000,000 | 731,548 | 643,924 | 0.83 | % | |||||||||||||

| CIFC Funding 2019-V, Ltd. | Subordinated Note (effective yield 19.56%, maturity 01/15/2035) ⁽⁸⁾ | 02/07/23 | 650,000 | 462,515 | 450,292 | 0.58 | % | |||||||||||||

| CIFC Funding 2020-II, Ltd. | Subordinated Note (effective yield 21.68%, maturity 10/20/2034) ⁽⁸⁾ | 12/14/22 | 650,000 | 451,924 | 450,220 | 0.58 | % | |||||||||||||

| CIFC Funding 2022-IV, Ltd. | Subordinated Note (effective yield 18.59%, maturity 07/16/2035) ⁽⁸⁾ | 10/23/23 | 2,400,000 | 1,926,842 | 1,850,564 | 2.38 | % | |||||||||||||

| CIFC Funding 2022-VI, Ltd. | Income Note (effective yield 13.71%, maturity 07/16/2035) ⁽⁸⁾ ⁽⁹⁾ | 08/01/22 | 600,000 | 478,191 | 518,746 | 0.67 | % | |||||||||||||

| CIFC Funding 2023-I, Ltd. | Income Note (effective yield 19.75%, maturity 10/15/2037) ⁽⁸⁾ ⁽⁹⁾ | 09/14/23 | 4,350,000 | 3,388,293 | 3,692,650 | 4.74 | % | |||||||||||||

| Clover CLO 2019-1 Ltd. | Subordinated Note (effective yield 17.73%, maturity 04/18/2035) ⁽⁸⁾ | 02/15/24 | 1,831,800 | 1,299,567 | 1,293,618 | 1.66 | % | |||||||||||||

| Clover CLO 2021-2, Ltd. | Subordinated Note (effective yield 20.55%, maturity 07/20/2034) ⁽⁸⁾ | 08/09/23 | 2,150,000 | 1,423,512 | 1,494,691 | 1.92 | % | |||||||||||||

| Dryden 94 CLO, Ltd. | Income Note (effective yield 16.98%, maturity 07/15/2037) ⁽⁸⁾ ⁽⁹⁾ | 04/28/22 | 3,000,000 | 2,105,711 | 1,565,164 | 2.01 | % | |||||||||||||

| Dryden 109 CLO, Ltd. | Subordinated Note (effective yield 15.68%, maturity 04/20/2035) ⁽⁸⁾ | 02/15/23 | 775,000 | 582,713 | 440,317 | 0.57 | % | |||||||||||||

| Eaton Vance CLO 2020-1, Ltd. | Subordinated Note (effective yield 17.59%, maturity 10/15/2034) ⁽⁸⁾ | 08/08/23 | 1,985,000 | 1,403,385 | 1,281,295 | 1.65 | % | |||||||||||||

| Eaton Vance CLO 2020-2, Ltd. | Subordinated Note (effective yield 19.73%, maturity 01/15/2035) ⁽⁸⁾ | 09/16/22 | 650,000 | 436,683 | 412,144 | 0.53 | % | |||||||||||||

| Elmwood CLO 14 Ltd. | Subordinated Note (effective yield 19.11%, maturity 04/20/2035) ⁽⁸⁾ | 06/06/23 | 1,000,000 | 701,553 | 755,447 | 0.97 | % | |||||||||||||

| Elmwood CLO 17 Ltd. | Subordinated Note (effective yield 18.64%, maturity 07/17/2035) ⁽⁸⁾ | 04/25/23 | 650,000 | 468,164 | 516,316 | 0.66 | % | |||||||||||||

| Elmwood CLO 21 Ltd. | Subordinated Note (effective yield 14.33%, maturity 10/20/2036) ⁽⁸⁾ | 10/26/23 | 2,900,000 | 1,867,874 | 1,777,150 | 2.28 | % | |||||||||||||

| Generate CLO 3 Ltd. | Subordinated Note (effective yield 16.18%, maturity 10/20/2036) ⁽⁸⁾ | 04/23/24 | 5,874,000 | 3,377,550 | 3,254,164 | 4.18 | % | |||||||||||||

| Generate CLO 9 Ltd. | Subordinated Note (effective yield 24.06%, maturity 10/20/2034) ⁽⁸⁾ | 05/31/22 | 600,000 | 436,918 | 467,076 | 0.60 | % | |||||||||||||

| Kings Park CLO, Ltd. | Subordinated Note (effective yield 26.10%, maturity 01/21/2035) ⁽⁸⁾ | 04/27/23 | 925,000 | 543,489 | 594,780 | 0.76 | % | |||||||||||||

| Madison Park Funding XXXIV, Ltd. | Subordinated Note (effective yield 21.85%, maturity 04/25/2048) ⁽⁸⁾ | 09/27/22 | 750,000 | 436,739 | 433,915 | 0.56 | % | |||||||||||||

| Madison Park Funding LII, Ltd. | Subordinated Note (effective yield 16.51%, maturity 01/22/2035) ⁽⁸⁾ | 03/13/24 | 4,200,000 | 2,868,799 | 2,644,912 | 3.40 | % | |||||||||||||

| Madison Park Funding LXII, Ltd. | Subordinated Note (effective yield 13.53%, maturity 07/17/2036) ⁽⁸⁾ | 07/27/23 | 1,300,000 | 974,625 | 858,328 | 1.10 | % | |||||||||||||

| Morgan Stanley Eaton Vance CLO 2023-20, Ltd. | Subordinated Note (effective yield 15.33%, maturity 01/20/2037) ⁽⁸⁾ | 05/08/24 | 3,780,000 | 3,175,200 | 2,996,832 | 3.85 | % | |||||||||||||

| OCP CLO 2020-20, Ltd. | Subordinated Note (effective yield 18.09%, maturity 04/18/2037) ⁽⁸⁾ | 04/25/24 | 2,000,000 | 1,528,700 | 1,455,615 | 1.87 | % | |||||||||||||

| OCP CLO 2021-22, Ltd. | Preferred Share (effective yield 13.78%, maturity 12/02/2034) ⁽⁸⁾ | 05/08/24 | 1,650,000 | 1,256,063 | 1,131,149 | 1.45 | % | |||||||||||||

| OCP CLO 2021-22, Ltd. | Subordinated Note (effective yield 13.78%, maturity 12/02/2034) ⁽⁸⁾ | 05/08/24 | 1,500,000 | 1,141,875 | 1,028,317 | 1.32 | % | |||||||||||||

| OCP CLO 2023-30, Ltd. | Subordinated Note (effective yield 13.18%, maturity 01/24/2037) ⁽⁸⁾ | 05/10/24 | 3,600,000 | 2,992,500 | 2,690,117 | 3.46 | % | |||||||||||||

| Octagon Investment Partners 45, Ltd. | Subordinated Note (effective yield 21.03%, maturity 04/15/2035) ⁽⁸⁾ | 07/27/23 | 1,600,000 | 928,680 | 809,961 | 1.04 | % | |||||||||||||

| Octagon 58, Ltd. | Income Note (effective yield 19.81%, maturity 07/15/2037) ⁽⁸⁾ ⁽⁹⁾ | 04/21/22 | 3,000,000 | 2,032,076 | 1,855,332 | 2.38 | % | |||||||||||||

| Point Au Roche Park CLO, Ltd. | Subordinated Note (effective yield 23.15%, maturity 07/20/2034) ⁽⁸⁾ | 08/07/23 | 2,275,000 | 1,417,561 | 1,442,249 | 1.85 | % | |||||||||||||

| Regatta XXI Funding Ltd. | Subordinated Note (effective yield 16.29%, maturity 10/20/2034) ⁽⁸⁾ | 06/10/22 | 650,000 | 450,001 | 434,942 | 0.56 | % | |||||||||||||

| Regatta XXII Funding Ltd. | Subordinated Note (effective yield 22.44%, maturity 07/20/2035) ⁽⁸⁾ | 06/20/23 | 1,000,000 | 693,474 | 811,827 | 1.04 | % | |||||||||||||

| Regatta XXIV Funding Ltd. | Subordinated Note (effective yield 18.74%, maturity 01/20/2035) ⁽⁸⁾ | 02/14/23 | 700,000 | 435,223 | 447,042 | 0.57 | % | |||||||||||||

| Rockford Tower CLO 2022-3, Ltd. | Subordinated Note (effective yield 19.41%, maturity 01/20/2035) ⁽⁸⁾ | 07/27/23 | 1,400,000 | 995,750 | 1,276,784 | 1.64 | % | |||||||||||||

| RR 23 Ltd. | Subordinated Note (effective yield 17.11%, maturity 10/15/2035) ⁽⁸⁾ | 10/12/23 | 3,250,000 | 1,913,767 | 1,982,864 | 2.55 | % | |||||||||||||

| Shackleton 2019-XIV CLO, Ltd. | Subordinated Note (effective yield 21.54%, maturity 07/20/2034) ⁽⁸⁾ | 01/24/24 | 3,800,000 | 2,873,911 | 2,851,598 | 3.66 | % | |||||||||||||

| Venture 45 CLO, Ltd. | Subordinated Note (effective yield 14.39%, maturity 07/20/2035) ⁽⁸⁾ | 09/19/22 | 700,000 | 507,583 | 301,398 | 0.39 | % | |||||||||||||

| Wind River 2022-1 CLO Ltd. | Subordinated Note (effective yield 21.49%, maturity 07/20/2035) ⁽⁸⁾ | 08/15/23 | 3,118,610 | 2,005,980 | 1,699,357 | 2.18 | % | |||||||||||||

| Wind River 2022-2 CLO Ltd. | Income Note (effective yield 17.95%, maturity 07/20/2035) ⁽⁸⁾ ⁽⁹⁾ | 06/03/22 | 600,000 | 408,576 | 326,546 | 0.42 | % | |||||||||||||

| Total CLO Equity | 79,443,928 | 77,148,769 | 99.09 | % | ||||||||||||||||

| Loan Accumulation Facilities (10) | ||||||||||||||||||||

| Structured Finance | ||||||||||||||||||||

| United States | ||||||||||||||||||||

| Steamboat XLVIII Ltd. | Loan Accumulation Facility ⁽⁸⁾ | 04/08/24 | 887,250 | 887,250 | 892,754 | 1.15 | % | |||||||||||||

| Steamboat XLIX Ltd. | Loan Accumulation Facility ⁽⁸⁾ | 06/03/24 | 475,000 | 475,000 | 475,190 | 0.61 | % | |||||||||||||

| Total Loan Accumulation Facilities | 1,362,250 | 1,367,944 | 1.76 | % | ||||||||||||||||

| Total investments at fair value as of June 30, 2024 | $ | 81,299,030 | $ | 79,062,808 | 101.55 | % | ||||||||||||||

| Net assets above (below) fair value of investments | (1,203,238 | ) | ||||||||||||||||||

| Net Assets as of June 30, 2024 | $ | 77,859,570 | ||||||||||||||||||

(1) The Fund is not affiliated with, nor does it “control” (as such term is defined in the Investment Fund Act of 1940 (the “1940 Act”)), any of the issuers listed. In general, under the 1940 Act, the Fund would be presumed to “control” an issuer if it owned 25% or more of its voting securities.

(2) All securities exempt from registration under the Securities Act of 1933, and are deemed to be “restricted securities”.

(3) Acquisition date represents the initial purchase date of investment.

(4) Fair value is determined by the Adviser in accordance with written valuation policies and procedures, subject to oversight by the Fund’s Board of Trustees, in accordance with Rule 2a-5 under the 1940 Act.

(5) Country represents the principal country of risk where the investment has exposure.

(6) Variable rate investment. Interest rate shown reflects the rate in effect at the reporting date. Investment description includes the reference rate and spread.

(7) CLO subordinated notes and income notes are considered CLO equity positions. CLO equity positions are entitled to recurring distributions which are generally equal to the remaining cash flow of payments made by underlying assets less contractual payments to debt holders and fund expenses. The effective yield is estimated based upon the current projection of the amount and timing of these recurring distributions in addition to the estimated amount of terminal principal payment. It is the Fund's policy to update the effective yield for each CLO equity position held within the Fund’s portfolio at the initiation of each investment and each subsequent quarter thereafter. The effective yield and investment cost may ultimately not be realized. As of June 30, 2024, the Fund's weighted average effective yield on its aggregate CLO equity positions, based on current amortized cost, was 18.45%.

(8) Classified as Level III investments. See Note 3 “Investments” for further discussion.

(9) Fair value includes the Fund's interest in fee rebates on CLO subordinated and income notes.

(10) Loan accumulation facilities are financing structures intended to aggregate loans that may be used to form the basis of a CLO vehicle.

| Reference Key: | |

| SOFR | Secured Overnight Financing Rate |

See accompanying notes to the consolidated financial statements

14

Eagle Point Institutional Income Fund & Subsidiaries

Consolidated Statement of Operations

For the six months ended June 30, 2024

(expressed in U.S. dollars)

(Unaudited)

| INVESTMENT INCOME | ||||

| Interest income | $ | 5,451,787 | ||

| Other income | 109,029 | |||

| Total Investment Income | 5,560,816 | |||

| EXPENSES | ||||

| Incentive fee (Note 4) | 842,532 | |||

| Management fee (Note 4) | 572,822 | |||

| Amortization of offering costs (Note 4) | 427,162 | |||

| Administration fees (Note 4) | 227,084 | |||

| Professional fees | 226,392 | |||

| Transfer agent fees | 114,509 | |||

| Trustees’ fees | 53,153 | |||

| Tax Expense | 50,000 | |||

| Other expenses | 104,198 | |||

| Total Expenses | 2,617,852 | |||

| NET INVESTMENT INCOME | 2,942,964 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | ||||

| Net realized gain (loss) on investments | 97,688 | |||

| Net change in unrealized appreciation (depreciation) on investments | (2,093,049 | ) | ||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | (1,995,361 | ) | ||

| NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | $ | 947,603 | ||

See accompanying notes to the consolidated financial statements

15

Eagle Point Institutional Income Fund & Subsidiaries

Consolidated Statements of Changes in Net Assets

(expressed in U.S. dollars, except share amounts)

(Unaudited)

| For the | For the | |||||||

| six months ended | year ended | |||||||

| June 30, 2024 | December 31, 2023 | |||||||

| Net Increase (decrease) in net assets resulting from operations: | ||||||||

| Net investment income | $ | 2,942,964 | $ | 3,691,383 | ||||

| Net realized gain (loss) on investments | 97,688 | 130,199 | ||||||

| Net change in unrealized appreciation (depreciation) on investments | (2,093,049 | ) | (91,023 | ) | ||||

| Total net increase (decrease) in net assets resulting from operations | 947,603 | 3,730,559 | ||||||

| Distributions to shareholders: | ||||||||

| Total earnings distributed | (3,097,749 | ) | (2,401,908 | ) | ||||

| Distributions from tax return of capital | — | — | ||||||

| Total distributions to shareholders | (3,097,749 | ) | (2,401,908 | ) | ||||

| Capital share transactions: | ||||||||

| Proceeds from shares sold | 30,147,643 | 32,544,606 | ||||||

| Reinvestment of distributions resulting in the issuance of shares | 1,123,295 | 1,360,921 | ||||||

| Repurchase of shares proceeds | (408,432 | ) | (60,866 | ) | ||||

| Total capital share transactions: | 30,862,506 | 33,844,661 | ||||||

| Total increase (decrease) in net assets | 28,712,360 | 35,173,312 | ||||||

| Net assets at beginning of period | 49,147,210 | 13,973,898 | ||||||

| Net assets at end of period | $ | 77,859,570 | $ | 49,147,210 | ||||

| Capital share activity: | ||||||||

| Shares sold | 2,937,114 | 3,271,466 | ||||||

| Shares sold pursuant to the Fund’s distribution reinvestment plan | 112,529 | 136,251 | ||||||

| Repurchase of shares | (39,771 | ) | (5,961 | ) | ||||

| Total increase (decrease) in capital share activity | 3,009,872 | 3,401,756 | ||||||

See accompanying notes to the consolidated financial statements

16

Eagle Point Institutional Income Fund & Subsidiaries

Consolidated Statement of Cash Flows

For the six months ended June 30, 2024

(expressed in U.S. dollars)

(Unaudited)

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||

| Net increase (decrease) in net assets from operations | $ | 947,603 | ||

| Adjustments to reconcile net increase (decrease) in net assets from operations to net cash provided by (used in) operating activities: | ||||

| Purchase of investments | (36,493,164 | ) | ||

| Proceeds from sales of investments and repayments of principal (1) | 2,834,314 | |||

| Net realized (gain) loss on investments | (97,688 | ) | ||

| Net change in unrealized (appreciation) depreciation on investments | 2,093,049 | |||

| Amortization (accretion) of premiums or discounts on CLO debt securities | (4,572 | ) | ||

| Change in assets and liabilities: | ||||

| Interest receivable | (857,022 | ) | ||

| Other assets | (53,721 | ) | ||

| Prepaid expenses | 25,049 | |||

| Incentive fee payable | 327,770 | |||

| Management fee payable | 473,657 | |||

| Professional fees payable | 99,827 | |||

| Administration fees payable | 65,828 | |||

| Trustees' fees payable | (97 | ) | ||

| Transfer agent fees payable | 31,024 | |||

| Other expenses payable | 43,977 | |||

| Net cash provided by (used in) operating activities | (30,564,166 | ) | ||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||

| Distributions to shareholders | (3,097,749 | ) | ||

| Proceeds from shares sold | 30,147,643 | |||

| Reinvestment of distributions resulting in the issuance of shares | 1,123,295 | |||

| Repurchase of shares | (408,432 | ) | ||

| Offering costs paid and deferred | (263,854 | ) | ||

| Net cash provided by (used in) financing activities | 27,500,903 | |||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | (3,063,263 | ) | ||

| CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | 5,942,067 | |||

| CASH AND CASH EQUIVALENTS, END OF PERIOD | $ | 2,878,804 | ||

(1) Proceeds from sales or maturity of investments includes $1,708,408 of return of capital on CLO equity investments from recurring cash flows.

See accompanying notes to the consolidated financial statements

17

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

| 1. | ORGANIZATION |

Eagle Point Institutional Income Fund (the “Fund”) was formed as a Delaware statutory trust on October 22, 2021, and is an externally managed, non-diversified closed-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund’s primary investment objective is to generate high current income, with a secondary objective to generate capital appreciation. The Fund seeks to achieve its investment objectives by investing primarily in equity and junior debt tranches of collateralized loan obligations (“CLOs”) that are collateralized by a portfolio consisting primarily of below investment grade U.S. senior secured loans with a large number of distinct underlying borrowers across various industry sectors. The Fund may also invest in other related securities and instruments or other securities and instruments that Eagle Point Credit Management LLC (the “Adviser”) believes are consistent with the Fund’s investment objectives, including senior debt tranches of CLOs, loan accumulation facilities (“LAFs”) and securities and instruments of corporate issuers. From time to time, in connection with the acquisition of CLO equity, the Fund may receive fee rebates from the CLO issuer. The CLO securities in which the Fund primarily seeks to invest are unrated or rated below investment grade and are considered speculative with respect to timely payment of interest and repayment of principal.

The Fund commenced operations on June 1, 2022 and is offering its shares of beneficial interest (“Shares”) on a continuous basis at the applicable period end net asset value (“NAV”) per share plus any applicable sales loads.

The Fund intends to operate so as to qualify to be taxed as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”), for federal income tax purposes.

The Adviser is the investment adviser of the Fund and manages the investments of the Fund subject to the supervision of the Fund’s Board of Trustees (the “Board”). The Adviser is registered as an investment adviser with the U.S. Securities and Exchange Commission (the “SEC”) under the Investment Advisers Act of 1940, as amended. Eagle Point Administration LLC, an affiliate of the Adviser, is the administrator of the Fund (the “Administrator”).

The consolidated financial statements include the accounts of the Fund and its wholly-owned subsidiaries: EPIIF Sub (Cayman) Ltd. (“Sub I”), a Cayman Islands exempted company, and EPIIF Sub II (Cayman) Ltd. (“Sub II”), a Cayman Islands exempted company. All intercompany accounts and transactions have been eliminated upon consolidation. As of June 30, 2024, Sub I and Sub II represented 0.59% and 1.60% of the Fund’s net assets, respectively.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

Basis of Accounting

The consolidated financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”). The Fund is an investment company and follows the accounting and reporting guidance applicable to investment companies in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946 Financial Services – Investment Companies. Items included in the consolidated financial statements are measured and presented in United States dollars.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions which affect the reported amounts included in the consolidated financial statements and accompanying notes as of the reporting date. Actual results may differ from those estimates.

Valuation of Investments

The most significant estimate inherent in the preparation of the consolidated financial statements is the valuation of investments.

18

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

The Fund accounts for its investments in accordance with U.S. GAAP, and fair values its investment portfolio in accordance with the provisions of the FASB ASC Topic 820, Fair Value Measurements and Disclosures, which defines fair value, establishes a framework for measuring fair value and requires enhanced disclosures about fair value measurements. Investments are reflected in the consolidated financial statements at fair value. Fair value is the estimated amount that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date (i.e., the exit price).

Pursuant to Rule 2a-5 under the 1940 Act adopted by the SEC in December 2020 (“Rule 2a-5”), the Board has elected to designate the Adviser as “valuation designee” to perform fair value determinations, subject to Board oversight and certain other conditions. In the absence of readily available market quotations, as defined by Rule 2a-5, the Adviser determines the fair value of the Fund’s investments in accordance with its written valuation policy approved by the Board. There is no single method for determining fair value in good faith. As a result, determining fair value requires judgment be applied to the specific facts and circumstances of each portfolio investment while employing a consistently applied valuation process for the types of investments held by the Fund. Due to the uncertainty of valuation, this estimate may differ significantly from the value that would have been used had a ready market for the investments existed, and the differences could be material.

The Fund determines fair value based on assumptions that market participants would use in pricing an asset or liability in an orderly transaction at the measurement date. When considering market participant assumptions in fair value measurements, the following fair value hierarchy prioritizes and ranks the level of market price observability used in measuring investments:

Level I – Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund is able to access as of the reporting date.

Level II – Inputs, other than quoted prices included in Level I, that are observable either directly or indirectly as of the reporting date. These inputs may include (a) quoted prices for similar assets in active markets, (b) quoted prices for identical or similar assets in markets that are not active, (c) inputs other than quoted prices that are observable for the asset, or (d) inputs derived principally from or corroborated by observable market data by correlation or other means.

Level III – Pricing inputs are unobservable for the investment and little, if any, active market exists as of the reporting date. Fair value inputs require significant judgment or estimation from the Adviser.

In certain cases, inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the determination of which category within the fair value hierarchy is appropriate for any given investment is based on the lowest level of input significant to that fair value measurement. The assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and consideration of factors specific to the investment.

Market price observability is impacted by a number of factors, including the type of investment, the characteristics specific to the investment and the state of the marketplace (including the existence and transparency of transactions between market participants). Investments with readily available actively quoted prices, or for which fair value can be measured from actively quoted prices in an orderly market, will generally have a higher degree of market price observability and a lesser degree of judgment used in measuring fair value.

Investments for which observable, quoted prices in active markets do not exist are reported at fair value based on Level III inputs. The amount determined to be fair value may incorporate the Adviser’s own assumptions (including assumptions the Adviser believes market participants would use in valuing investments and assumptions relating to appropriate risk adjustments for nonperformance and lack of marketability), as provided for in the Adviser’s valuation policy.

19

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

An estimate of fair value is made for each investment at least monthly taking into account information available as of the reporting date.

See Note 3 “Investments” for further discussion relating to the Fund’s investments.

Investment Income Recognition

Interest income from investments in CLO debt is recorded using the accrual basis of accounting to the extent such amounts are expected to be collected. Interest income on investments in CLO debt is generally expected to be received in cash. The Fund applies the provisions of Accounting Standards Update No. 2017-08 Premium Amortization on Purchased Callable Debt Securities (“ASU 2017-08”) in calculating amortization of premium for purchased CLO debt securities. Amortization of premium or accretion of discount is recognized using the effective interest method.

In certain circumstances, interest income may be paid in the form of additional investment principal, often referred to as payment-in-kind (“PIK”) interest. PIK interest is included in interest income and interest receivable through the payment date. The PIK interest rate for CLO debt securities represents the coupon rate at payment date when PIK interest is received. On the payment date, interest receivable is capitalized as additional investment principal in the CLO debt security. To the extent the Fund does not believe it will ultimately be able to collect PIK interest, the CLO debt security will be placed on non-accrual status, and previously recorded PIK interest income will be reversed. The Fund had no investments with PIK interest as of June 30, 2024.

CLO equity investments and fee rebates recognize investment income for U.S. GAAP purposes on the accrual basis utilizing an effective interest methodology based upon an effective yield to maturity utilizing projected cash flows. ASC Topic 325-40, Beneficial Interests in Securitized Financial Assets, requires investment income from CLO equity investments and fee rebates to be recognized under the effective interest method, with any difference between cash distributed and the amount calculated pursuant to the effective interest method being recorded as an adjustment to the cost basis of the investment. It is the Fund’s policy to update the effective yield for each CLO equity position held within the Fund’s portfolio at the initiation of each investment and each subsequent quarter thereafter.

LAFs recognize interest income according to the guidance noted in ASC Topic 325-40-35-1, Beneficial Interest in Securitized Financial Assets, which states that the holder of a beneficial interest in securitized financial assets shall determine interest income over the life of the beneficial interest in accordance with the effective yield method, provided such amounts are expected to be collected. FASB ASC 325-40-20 further defines “beneficial interests,” among other things, as “rights to receive all or portions of specified cash inflows received by a trust or other entity.” FASB ASC 325-40-15-7 also states that for income recognition purposes, beneficial interests in securitized financial assets (such as those in LAFs) are within the scope of ASC 325-40 because it is customary for certain industries, such as investment companies, to report interest income as a separate item in their income statements even though the investments are accounted for at fair value. The amount of interest income from LAFs recorded for the six months ended June 30, 2024 was $16,353.

Other Income

Other income includes the Fund’s share of income under the terms of fee rebate agreements.

Securities Transactions

The Fund records the purchase and sale of securities on trade date. Realized gains and losses on investments sold are recorded on the basis of the specific identification method.

Cash and Cash Equivalents

The Fund has defined cash and cash equivalents as cash and short-term, highly liquid investments with original maturities of three months or less from the date of purchase. The Fund maintains its cash in bank accounts, which, at times, may exceed federal insured limits. The Adviser monitors the performance of the financial institution where the accounts are held in order to manage any risk associated with such accounts.

20

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

Expense Recognition

Expenses are recorded on the accrual basis of accounting.

Prepaid Expenses

Prepaid expenses consist primarily of insurance premiums and state registration fees. Insurance premiums are amortized over the term of the current policy. State registration fees are amortized over twelve months from the time of payment.

Offering Costs

Offering costs of the Fund are capitalized and amortized to expense over the twelve month period following such capitalization on a straight line basis. Since inception of the Fund, a portion of the offering costs incurred by the Fund have been paid for by the Adviser, for which the Adviser has not yet sought reimbursement. See Note 4 “Related Party Transactions” for further discussion of the Fund’s offering costs.

Organization Costs

Organizational costs of the Fund are expensed as incurred. Since inception, organizational costs incurred by the Fund have been paid for the by the Adviser, for which it has not yet sought reimbursement. See Note 4 “Related Party Transactions” for further discussion of the Fund’s organizational costs.

Federal and Other Taxes

The Fund intends to operate so as to qualify to be taxed as a RIC under subchapter M of the Code and, as such, to not be subject to federal income tax on the portion of its taxable income and gains distributed to shareholders. To qualify for RIC tax treatment, among other requirements, the Fund is required to distribute at least 90% of its investment company taxable income, as defined by the Code.

Because U.S. federal income tax regulations differ from U.S. GAAP, distributions in accordance with tax regulations may differ from net investment income and realized capital gains recognized for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the consolidated financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain or loss are recognized at some time in the future. Differences in classification may also result from the treatment of short-term capital gains as ordinary income for federal income tax purposes. The tax basis components of distributable earnings differ from the amounts reflected in the Consolidated Statement of Assets and Liabilities due to temporary book/tax differences arising primarily from partnerships and passive foreign investment company investments.

As of June 30, 2024, the federal income tax cost and net unrealized depreciation on securities were as follows:

| Cost for federal income tax purposes | $ | 76,633,494 | ||

| Gross unrealized appreciation | $ | 4,758,659 | ||

| Gross unrealized depreciation | (2,329,345 | ) | ||

| Net unrealized appreciation | $ | 2,429,314 |

Distributions

The composition of distributions paid to shareholders from net investment income and capital gains are determined in accordance with U.S. federal income tax regulations, which differ from U.S. GAAP. Distributions to shareholders can be comprised of net investment income, net realized capital gains and return of capital for U.S. federal income tax purposes and are intended to be paid monthly. Distributions payable to shareholders are recorded as a liability on ex-dividend date. If a shareholder opts-in to the Fund’s distribution reinvestment plan (the “DRIP”), distributions are automatically reinvested in full shares of the Fund as of the payment date, pursuant to the DRIP. The Fund’s shareholders who choose not to participate in the DRIP generally will receive all distributions in cash.

21

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

In addition to the regular monthly distributions, and subject to available taxable earnings of the Fund, the Fund may make periodic special distributions representing the excess of the Fund’s net taxable income over the Fund’s aggregate monthly distributions paid during the year (or for other purposes).

The characterization of distributions paid to shareholders, as set forth in the Consolidated Financial Highlights, reflect estimates made by the Fund for federal income tax purposes. Such estimates are subject to change once the final determination of the source of all distributions has been made by the Fund.

For the six months ended June 30, 2024, the Fund declared distributions to shareholders of $3,097,749 or $0.483 per share.

| 3. | INVESTMENTS |

Fair Value Measurement

The following tables summarize the valuation of the Fund’s investments measured and reported at fair value under the fair value hierarchy levels described in Note 2 “Summary of Significant Accounting Policies” as of June 30, 2024:

| Investments at Fair Value | Level I | Level II | Level III | Total | ||||||||||||

| CLO Debt | $ | — | $ | 546,095 | $ | — | $ | 546,095 | ||||||||

| CLO Equity | — | — | 77,148,769 | 77,148,769 | ||||||||||||

| Loan Accumulation Facilities | — | — | 1,367,944 | 1,367,944 | ||||||||||||

| Total Investments at Fair Value | $ | — | $ | 546,095 | $ | 78,516,713 | $ | 79,062,808 | ||||||||

Significant Unobservable Inputs

The following table summarizes the quantitative inputs and assumptions used for investments categorized within Level III of the fair value hierarchy as of June 30, 2024:

| Quantitative Information about Level III Fair Value Measurements | ||||||||||||

| Assets | Fair Value | Valuation Techniques/Methodologies | Unobservable Inputs | Range / Weighted Average (1) | ||||||||

| CLO Equity | $ | 71,194,091 | Discounted Cash Flows | Annual Default Rate (2) | 0.00% - 4.56% | |||||||

| Annual Prepayment Rate (3) | 25.00% | |||||||||||

| Reinvestment Spread | 3.38% - 3.96% / 3.57% | |||||||||||

| Reinvestment Price | 99.50% | |||||||||||

| Recovery Rate | 68.89% - 70.00% / 69.70% | |||||||||||

| Expected Yield (4) | 9.53% - 55.71% / 18.50% | |||||||||||

(1) Weighted average calculations are based on the fair value of investments.

(2) A weighted average is not presented as the input in the discounted cash flow model varies over the life of an investment.

(3) 0% is assumed for defaulted and non-performing assets.

(4) Represents yield based on fair value and projected future cash flow.

In addition to the techniques and inputs noted in the above table, the Adviser may use other valuation techniques and methodologies when determining the fair value measurements of the Fund’s investments, as provided for in the Adviser’s valuation policy approved by the Board. Please refer to Note 2 “Valuation of Investments”. The table is not intended to be all-inclusive, but rather provides information on the significant Level III inputs as they

22

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

relate to the Fund’s fair value measurements as of June 30, 2024. Unobservable inputs and assumptions are reviewed at each measurement date and updated as necessary to reflect current market conditions.

Increases (decreases) in the annual default rate, reinvestment price and expected yield in isolation would result in a lower (higher) fair value measurement. Increases (decreases) in the reinvestment spread and recovery rate in isolation would result in a higher (lower) fair value measurement. Changes in the annual prepayment rate may result in a higher (lower) fair value, depending on the circumstances. Generally, a change in the assumption used for the annual default rate may be accompanied by a directionally opposite change in the assumption used for the annual prepayment rate and recovery rate.

Certain of the Fund’s Level III investments have been valued using unadjusted inputs that have not been internally developed by the Adviser, including third-party transactions, recent transactions and data reported by trustees. As a result, investments with a fair value of $7,322,622 have been excluded from the preceding table.

Change in Investments Classified as Level III

The changes in investments classified as Level III are as follows for the year ended June 30, 2024:

| CLO Equity | Loan Accumulation Facilities | |||||||

| Balance as of January 1, 2024 | $ | 39,773,103 | $ | — | ||||

| Purchases of investments | 41,145,593 | 1,362,250 | ||||||

| Proceeds from sales, maturity of investments or return of capital | (1,708,408 | )(1) | — | |||||

| Net realized gains (losses) and net change in unrealized appreciation (depreciation) | (2,061,519 | ) | 5,694 | |||||

| Balance as of June 30, 2024(2) | $ | 77,148,769 | $ | 1,367,944 | ||||

| Change in unrealized appreciation (depreciation) on investments still held as of June 30, 2024 | $ | (2,061,522 | ) | $ | 5,694 | |||

(1) Includes $1,708,408 of return of capital on CLO equity investments from recurring cash flows and distributions from called deals.

(2) There were no transfers into or out of level III investments during the period.

The net realized gains (losses) recorded for Level III investments are reported in the net realized gain (loss) on investments account in the Consolidated Statement of Operations, if applicable. Net changes in unrealized appreciation (depreciation) are reported in the net change in unrealized appreciation (depreciation) on investments account in the Consolidated Statement of Operations.

Fair Value – Valuation Techniques and Inputs

The Adviser establishes valuation processes and procedures to ensure the valuation techniques are fair and consistent, and valuation inputs are supportable. The Adviser has a Valuation Committee comprised of various senior personnel of the Adviser, the majority of which are not members of the Fund’s portfolio management function. The Valuation Committee is responsible for overseeing the valuation process, evaluating the overall fairness and consistent application of the Adviser’s written valuation policies approved by the Board. The Valuation Committee reviews and approves the valuation on a monthly basis.

Valuation of CLO Equity

The Adviser utilizes the output of a financial model to estimate the fair value of CLO equity investments. The model contains detailed information on the characteristics of each CLO, including recent information about assets and liabilities from data sources such as trustee reports, and is used to project future cash flows to the CLO note tranches, as well as management fees. Key inputs to the model, including, but not limited to assumptions for

23

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

future loan default rates, recovery rates, prepayment rates, reinvestment rates and discount rates are determined by considering both observable and third-party market data and prevailing general market assumptions and conventions as well as those of the Adviser. Additionally, a third-party independent valuation firm is used as an input by the Adviser to determine the fair value of the Fund’s investments in CLO equity. The valuation firm’s advice is only one factor considered in the valuation of such investments, and the Adviser does not solely rely on such advice in determining the fair value of the Fund’s investments in accordance with the 1940 Act.

The Adviser categorizes CLO equity as Level III investments. Certain pricing inputs may be unobservable. An active market may exist, but not necessarily for CLO equity investments that the Fund holds as of the reporting date.

Valuation of CLO Debt

The Fund’s investments in CLO debt have been valued using an independent pricing service. The valuation methodology of the independent pricing service includes incorporating data comprised of observable market transactions, executable bids, broker quotes from dealers with two sided markets, as well as transaction activity from comparable securities to those being valued. As the independent pricing service contemplates real time market data and no unobservable inputs or significant judgment has been used by the Adviser in the valuation of the Fund’s investment in CLO debt, such positions are considered Level II assets.

Valuation of Loan Accumulation Facilities

The Adviser determines the fair value of LAFs in accordance with FASB ASC Topic 820, Fair Value Measurements and Disclosures, utilizing the income approach as noted in ASC 820-10-55-3F (the “Income Approach”), in which fair value measurement reflects current market expectations about the receipt of future amounts (i.e., exit price). LAFs are typically short- to medium-term in nature and formed to acquire loans on an interim basis that are expected to form part of a specific CLO transaction. Pursuant to LAF governing documents, loans acquired by the LAF are typically required to be transferred to the contemplated CLO transaction at original cost plus accrued interest. In such situations, because the LAF will receive its full cost basis in the underlying loan assets and the accrued interest thereon upon the consummation of the CLO transaction, the Adviser determines the fair value of the LAF as follows: (A) the cost of the Fund’s investment (i.e., the principal amount invested), and (B) to the extent the LAF has realized gains (losses) on its underlying loan assets which are reported by the Trustee during the applicable reporting period, its attributable portion of such realized gains (losses).

In certain circumstances, the LAF documents can contemplate transferring the underlying loans at a price other than original cost plus accrued interest or the Adviser may determine that, despite the initial expectation that a CLO transaction would result from a LAF, such a transaction is in fact unlikely to occur and, accordingly, it is unlikely the loans held by the LAF will be transferred at cost. Rather, the loans held by the LAF will most likely be sold at market value. In such situations, the Adviser will continue to fair value the LAF consistent with the Income Approach, but modify the fair value measurement to reflect the change in exit strategy of the LAF to incorporate market expectations of the receipt of future amounts (i.e., exit price). As such, the fair value of the LAF is most appropriately determined by reference to the market value of the LAF’s underlying loans, which is reflective of the price at which the LAF could sell its loan assets in an orderly transaction between market participants. As such, in these situations, the Adviser will continue utilizing the Income Approach and determine the fair value of the LAF as follows: (A) the cost of the Fund’s investment (i.e., the principal amount invested), (B) the Fund’s attributable portion of the unrealized gain (loss) on the LAF’s underlying loan assets, and (C) to the extent the LAF has realized gains (losses) on its underlying loan assets which are reported by the Trustee during the applicable reporting period, its attributable portion of such realized gains (losses). The Adviser’s measure of the Fund’s attributable portion of the unrealized gain (loss) on the LAF’s underlying loan assets takes into account the Adviser’s current market expectations of the receipt of future amounts on such assets, which may be impacted by various factors including any applicable change in market conditions or new information.

The Adviser categorizes LAFs as Level III investments. There is no active market and prices are unobservable.

24

Eagle Point Institutional Income Fund & Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2024

(Unaudited)

Investment Risk Factors and Concentration of Investments

The following list is not intended to be a comprehensive list of all of the potential risks associated with the Fund. The Fund’s prospectus provides a detailed discussion of the Fund’s risks and considerations. The risks described in the prospectus are not the only risks the Fund faces. Additional risks and uncertainties not currently known to the Fund or that are currently deemed to be immaterial also may materially and adversely affect its business, financial condition and/or operating results.

Risks of Investing in CLOs and Other Structured Debt Securities

CLOs and other structured finance securities are generally backed by a pool of credit-related assets that serve as collateral. Accordingly, CLO and structured finance securities present risks similar to those of other types of credit investments, including default (credit), interest rate and prepayment risks. In addition, CLOs and other structured finance securities are often governed by a complex series of legal documents and contracts, which increases the risk of dispute over the interpretation and enforceability of such documents relative to other types of investments. There is also a risk that the trustee of a CLO does not properly carry out its duties to the CLO, potentially resulting in loss to the CLO. CLOs are also inherently leveraged vehicles and are subject to leverage risk.

Subordinated Securities Risk

CLO equity and junior debt securities that the Fund may acquire are subordinated to more senior tranches of CLO debt. CLO equity and junior debt securities are subject to increased risks of default relative to the holders of superior priority interests in the same CLO. In addition, at the time of issuance, CLO equity securities are under-collateralized in that the face amount of the CLO debt and CLO equity of a CLO at inception exceed its total assets. The Fund will typically be in a subordinated or first loss position with respect to realized losses on the underlying assets held by the CLOs in which the Fund is invested.

High Yield Investment Risk