Table of Contents

As filed with the Securities and Exchange Commission on June 15, 2023

File No.

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

PURSUANT TO SECTION 12(b) OR 12(g)

OF THE SECURITIES EXCHANGE ACT OF 1934

Apollo Infrastructure Company LLC

(Exact name of registrant as specified in charter)

| Delaware | 92-3084689 | |

| (State or other jurisdiction of incorporation or registration) | (I.R.S. Employer Identification No.) | |

9 West 57th Street, 42nd Floor, New York, NY | 10019 | |

| (Address of principal executive offices) | (Zip Code) | |

(212) 515-3200

(Registrant’s telephone number, including area code)

with copies to:

Rajib Chanda Ryan Brizek James Hahn Simpson Thacher & Bartlett LLP 900 G Street, N.W. Washington, DC 20001 | Richard Fenyes Mark Brod Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, NY 10017 |

Securities to be registered pursuant to Section 12(b) of the Act:

None

Securities to be registered pursuant to Section 12(g) of the Act:

Interests in Apollo Infrastructure Company LLC—Series I

Interests in Apollo Infrastructure Company LLC—Series II

(Title of class)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Table of Contents

| Page | ||||||

| Explanatory Note | i | |||||

| Special Note Regarding Forward-Looking Statements | iv | |||||

| Item 1. | 1 | |||||

| Item 1A | 44 | |||||

| Item 2. | 133 | |||||

| Item 3. | 143 | |||||

| Item 4. | Security Ownership of Certain Beneficial Owners and Management | 144 | ||||

| Item 5. | 144 | |||||

| Item 6. | 146 | |||||

| Item 7. | Certain Relationships and Related Transactions, and Director Independence | 146 | ||||

| Item 8. | 150 | |||||

| Item 9. | Market Price of and Dividends on the Registrant’s Common Equity and Related Stockholder Matters | 150 | ||||

| Item 10. | 151 | |||||

| Item 11. | 151 | |||||

| Item 12. | 163 | |||||

| Item 13. | 164 | |||||

| Item 14. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 164 | ||||

| Item 15. | 164 | |||||

Table of Contents

Apollo Infrastructure Company LLC is filing this registration statement on Form 10 (the “Registration Statement”) with the Securities and Exchange Commission (the “SEC”) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), to provide current public information to the investment community in anticipation of being required to register under Section 12(g) of the Exchange Act in the future, to comply with applicable requirements thereunder.

In this Registration Statement, except where the context suggests otherwise:

| • | the terms “we,” “us,” “our,” the “Company” and “AIC” refer to Apollo Infrastructure Company LLC or, where applicable, the Series I Issuer and/or the Series II Issuer; |

| • | the term “Operating Manager” refers to Apollo Manager, LLC, a Delaware limited liability company, our manager; |

| • | the term “Apollo” refers collectively to Apollo Asset Management, Inc. and its subsidiaries; |

| • | the term “Apollo Clients” refers to the applicable fund, account, entity, vehicle, product and/or similar arrangement sponsored, managed or advised by Apollo; |

| • | the terms “Series I Issuer” and “Series I” refer to Apollo Infrastructure Company LLC—Series I, a registered series of the Company; |

| • | the terms “Series II Issuer” and “Series II” refer to Apollo Infrastructure Company LLC—Series II, a registered series of the Company; |

| • | the term “Series” refers collectively to Series I Issuer and Series II Issuer; |

| • | each of the terms “S Shares,” “I Shares,” “F-S Shares,” “F-I Shares,” “A-I Shares,” “A-II Shares,” “E Shares” and “V Shares,” unless otherwise indicated, refers collectively to the applicable type of Shares of both Series I Issuer and Series II Issuer. Each type of Shares described herein represents the applicable type of limited liability company interest in each of Series I Issuer and Series II Issuer. The same type of each Series will have the same terms with respect to each Series unless otherwise indicated; |

| • | the term “Series I Shareholders” refers to holders of our Series I Shares (as defined below). There are six types of shares available to Shareholders through Series I: S Shares, I Shares, F-S Shares, F-I Shares, A-I Shares and A-II Shares (collectively, the “Series I Investor Shares”); |

| • | the term “Series II Shareholders” refers to holders of our Series II Shares (as defined below). There are six types of shares available to Shareholders through Series II: S Shares, I Shares, F-S Shares, F-I Shares, A-I Shares and A-II Shares (collectively, the “Series II Investor Shares” and, together with the Series I Investor Shares, the “Investor Shares”); |

| • | E Shares and V Shares of Series I (collectively, “Series I Apollo Shares” and together with the Series I Investor Shares, the “Series I Shares”) will be held only by Apollo, certain of its affiliates and, in the case of the E Shares, also by our and our affiliates’ employees (if any), officers and directors; neither E Shares or V Shares are being offered to other investors; |

| • | E Shares and V Shares of Series II (collectively, “Series II Apollo Shares” and together with the Series II Investor Shares, the “Series II Shares”) will be held only by Apollo, certain of its affiliates and, in the case of the E Shares, also by our and our affiliates’ employees (if any), officers and directors; neither E Shares or V Shares are being offered to other investors; |

| • | the term “Apollo Shares” refers collectively to Series I Apollo Shares and Series II Apollo Shares; |

| • | the term “Shareholders” refers, individually and collectively, to Series I Shareholders and/or Series II Shareholders, as the context requires; |

i

Table of Contents

| • | the term “Shares” refers, individually and collectively, to Series I Shares and/or Series II Shares, as the context requires; |

| • | the term “Infrastructure Assets” refers, individually and collectively, to the infrastructure businesses or other assets owned by the Company and its direct or indirect subsidiaries, including as the context requires, infrastructure businesses or other assets, holding companies, special purpose vehicles, equity acquisitions, corporate carve outs, any investments made by us in any other infrastructure-related entities or assets not controlled by the Company and any other entities through which infrastructure assets or businesses will be held; and |

| • | the term “Assets Under Management” refers to the assets of the funds, partnerships and accounts to which Apollo provides investment management, advisory or certain other investment related services, including, without limitation, capital that such funds, partnerships and accounts have the right to call from investors pursuant to capital commitments; Apollo’s Assets Under Management equals the sum of: (i) the net asset value plus used or available leverage and/or capital commitments, or gross assets plus capital commitments, of the yield and certain hybrid funds, partnerships and accounts for which Apollo provides investment management or advisory services, other than certain collateralized loan obligations, collateralized debt obligations and certain perpetual capital vehicles, which have a fee-generating basis other than the mark-to-market value of the underlying assets; for certain perpetual capital vehicles in yield, gross asset value plus available financing capacity; (ii) the fair value of the investments of the equity and certain hybrid funds, partnerships and accounts Apollo manages or advises plus the capital that such funds, partnerships and accounts are entitled to call from investors pursuant to capital commitments, plus portfolio level financings; (iii) the gross asset value associated with the reinsurance investments of the portfolio company assets Apollo manages or advises; and (iv) the fair value of any other assets that Apollo manages or advises for the funds, partnerships and accounts to which Apollo provides investment management, advisory or certain other investment-related services, plus unused credit facilities, including capital commitments to such funds, partnerships and accounts for investments that may require pre-qualification or other conditions before investment plus any other capital commitments to such funds, partnerships and accounts available for investment that are not otherwise included in the clauses above. Apollo’s Assets Under Management measure includes assets under management for which it charges either nominal or zero fees. Apollo’s Assets Under Management measure also includes assets for which Apollo does not have investment discretion, including certain assets for which Apollo earns only investment-related service fees, rather than management or advisory fees. Apollo’s definition of Assets Under Management is not based on any definition of assets under management contained in its governing documents or in any management agreements of the funds Apollo manages. Apollo considers multiple factors for determining what should be included in its definition of Assets Under Management. Such factors include but are not limited to (1) its ability to influence the investment decisions for existing and available assets; (2) its ability to generate income from the underlying assets in the funds it manages; and (3) the assets under management measures that Apollo uses internally or believe are used by other investment managers. Given the differences in the investment strategies and structures among other alternative investment managers, Apollo’s calculation of Assets Under Management may differ from the calculations employed by other investment managers and, as a result, this measure may not be directly comparable to similar measures presented by other investment managers. Apollo’s calculation also differs from the manner in which its affiliates registered with the SEC report “Regulatory Assets Under Management” on Form ADV and Form PF in various ways. Apollo uses “Assets Under Management” as a performance measurement of its investment activities, as well as to monitor fund size in relation to professional resource and infrastructure needs. |

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and we will take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”).

ii

Table of Contents

This Registration Statement does not constitute an offer of securities of Apollo Infrastructure Company LLC, any of its Series or any other entity. Once this Registration Statement has been deemed effective, we will be subject to the requirements of Section 13(a) of the Exchange Act, including the rules and regulations promulgated thereunder, which will require us, among other things, to file annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and we will be required to comply with all other obligations of the Exchange Act applicable to issuers filing registration statements pursuant to Section 12(g) of the Exchange Act.

iii

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements in this Registration Statement constitute forward-looking statements because they relate to future events or our future performance or financial condition. The forward-looking statements contained in this Registration Statement may include statements as to:

| • | our future operating results; |

| • | our business prospects and the prospects of the Infrastructure Assets we acquire, control and manage; |

| • | our ability to raise sufficient capital to execute our acquisition and lending strategies; |

| • | the ability of the Operating Manager to source adequate acquisition and lending opportunities to efficiently deploy capital; |

| • | the ability of our Infrastructure Assets to achieve their objectives; |

| • | our current and expected financing arrangements; |

| • | changes in the general interest rate environment; |

| • | the adequacy of our cash resources, financing sources and working capital; |

| • | the timing and amount of cash flows, distributions and dividends, if any, from our Infrastructure Assets; |

| • | our contractual arrangements and relationships with third parties; |

| • | actual and potential conflicts of interest with the Operating Manager or any of its affiliates; |

| • | the dependence of our future success on the general economy and its effect on the industries in which we acquire, control and manage Infrastructure Assets; |

| • | our use of financial leverage; |

| • | the ability of the Operating Manager to identify, acquire and manage our Infrastructure Assets; |

| • | the ability of the Operating Manager or its affiliates to attract and retain highly talented professionals; |

| • | our ability to structure acquisitions in a tax-efficient manner and the effect of changes to tax legislation and our tax position; and |

| • | the tax status of the enterprises through which we acquire, control and manage Infrastructure Assets. |

In addition, words such as “anticipate,” “believe,” “expect” and “intend” indicate a forward-looking statement, although not all forward-looking statements include these words. The forward-looking statements contained in this Registration Statement involve risks and uncertainties. Our actual results could differ materially from those implied or expressed in the forward-looking statements for any reason, including the factors set forth in “Item 1A. Risk Factors” and elsewhere in this Registration Statement. Other factors that could cause actual results to differ materially include:

| • | changes in the economy; |

| • | risks associated with possible disruption in our operations or the economy generally due to terrorism, natural disasters, epidemics or other events having a broad impact on the economy; and |

| • | future changes in laws or regulations and conditions in our operating areas. |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this Registration Statement should not be regarded as a representation by us that our plans and objectives will be achieved. These forward-looking statements apply only as of the date of this Registration Statement. Moreover, we assume no duty and do not undertake to update the forward-looking statements.

iv

Table of Contents

The following is only a summary of the principal risks that may materially adversely affect our business, financial condition, results of operations and cash flows. The following should be read in conjunction with the complete discussion of risk factors we face, which are set forth in “Item 1A. Risk Factors.”

Risks Related to our Company and an Investment in our Shares

| • | We face heightened risks because we are a newly formed entity with no history or record. |

| • | Our Infrastructure Assets may not achieve our business objectives or generate returns for Shareholders. |

| • | Many services related to acquiring, owning and operating our Infrastructure Assets, including conducting due diligence before an acquisition, rely on third parties which creates risks, including a lack of control of the process and a lack of alignment with our goals. Additionally, if the Operating Manager is unable to timely engage third-party providers or if a transaction must, for commercial or other reasons, be conducted on an expedited basis, its ability to evaluate and acquire more complex targets could be adversely affected. |

| • | Our ability to achieve our business objectives depends on the Operating Manager because the Operating Manager has significant discretion as to the implementation of the Company’s objectives and policies. |

| • | We face heightened risk from working with Affiliated Service Providers since key personnel will not devote their full time or attention to the Company and could leave the Affiliated Service Provider at any time. |

Risks Related to the Company’s Infrastructure Assets and Owning and Managing Infrastructure Assets Generally

| • | We face heightened risks relating to owning and managing Infrastructure Assets. |

| • | Our acquisitions and assets are affected by the general economy and recent events, including market volatility, inflation and public health crises such as COVID-19. |

| • | Financial instruments which the Company will acquire may be impacted by the high volatility of the market which may be beyond the control of the Company and could adversely impact the Company’s ability to generate attractive returns. |

| • | Our Infrastructure Assets may also be impacted by interest rate fluctuations which may be beyond the control of the Company. |

| • | The success of the Company depends on our ability to navigate the acquisitions and competition of the market. It is possible that competition for appropriate acquisition opportunities may increase, thus reducing the number of opportunities available to the Company and adversely affecting the terms, including pricing, upon which Infrastructure Assets can be acquired. |

Risks Related to our Primary Operating Strategies

Risks Related to Acquiring Long-Term Control-Oriented Infrastructure Assets

| • | Government contracts can be uncertain. For example, the U.S. government can, in some circumstances, unilaterally suspend its contractors from receiving new contracts in the event of certain violations of law or regulation. |

| • | The Company faces the risk of eminent domain and governmental takings. |

| • | Infrastructure Assets we purchase may face issues relating to labor relations, which could result in those Infrastructure Assets being subjected to labor disputes, difficulties relating to the negotiation of collective bargaining agreements and complex laws and regulations. |

| • | Our business may be adversely affected by commodity price risk and energy industry market dislocation. |

| • | Compliance with environmental laws and regulations may result in substantial costs to the Company. |

Risks Related to Infrastructure Asset Financings

| • | There is no restriction on credit quality for Company acquisitions of debt instruments and the amount and timing of payments with respect to loans are not guaranteed, which may cause losses. |

| • | Loans we acquire may not receive an investment-grade rating, or may be unrated, which can result in additional risk that can adversely affect our returns. |

v

Table of Contents

| • | Acquiring subordinated loans or securities can be associated with the increased risks of unrated or below investment-grade assets including an increased risk of default during periods of economic downturn, the possibility that the obligor may not be able to meet its debt payments and limited secondary market support, among other risks. |

| • | The Company faces risks by originating loans if then unable to sell, assign or close transactions for that loan. |

| • | Our business may be affected by prepayment risk. The frequency at which prepayments (including voluntary prepayments by obligors and accelerations due to defaults) occur on bonds and loans will be affected by a variety of factors, including the prevailing level of interest rates and spreads, as well as economic, demographic, tax, social, legal and other factors. |

Risks Related to Opportunistic Investments in Infrastructure Assets

| • | We may acquire structured products where the performance of such assets is uncertain because they are subject to greater volatility than acquiring an asset or other security directly from the underlying market. |

| • | For a portion of our assets, we are at risk of having a limited ability to control an asset when we hold a non-controlling interest in that asset. |

| • | We may participate in proposed transactions where the value of securities can decline if the transaction is not consummated. |

| • | If an Infrastructure Asset is involved in a bankruptcy proceeding, the Company could be adversely affected. |

| • | We may acquire or invest in Infrastructure Assets in distressed securities or entities that are in or may become bankrupt, which typically involves elevated risk. For example, such securities are typically subject to adverse changes in general economic conditions, changes in the financial condition of their issuers and price fluctuation in response to changes in interest rates. |

Risks Related to Regulatory Matters

| • | We would not be able to operate our business according to our business plans if we are required to register as an investment company under the Investment Company Act. |

| • | Legal, regulatory and tax changes associated with alternative investment structures could cause adverse impacts to the Company. |

| • | We will have certain reporting obligations not applicable to private companies. We will need to make significant capital expenditures to be in compliance with certain regulations not applicable to private companies. Failure to comply with such regulations may have an adverse effect on our business. |

| • | We face the risk that the Operating Manager or any affiliated entities may experience a compliance failure, which would adversely affect us. |

| • | We face the risk that the legal and regulatory fields will change in a manner which adversely affects the Company. |

Tax Risks Related to the Company, the Shares and the Company’s Investments

| • | Our acquisition decisions will be based on economic considerations which could result in adverse tax consequences. |

| • | Series II Shareholders may be subject to taxes on phantom income relating to certain investments where taxable income allocated to a Shareholder may exceed cash distributions. |

| • | We face the risk of owning SPVs in a manner that is not fully tax efficient because certain jurisdictional rules or other factors may limit our ability to do so. |

| • | If the Series II Issuer were to be treated as a corporation for U.S. federal income tax purposes, the value of our Series II Issuer Shares might be adversely affected. |

| • | The Series II Issuer and its corporate subsidiaries face the risk of a tax audit which may have adverse consequences for the Series II Issuer and/or the Series II Shareholders. |

| • | The Series I Issuer faces the risk of a tax audit which may have adverse consequences for the Series I Issuer and/or the Series I Shareholders. |

vi

Table of Contents

| ITEM 1. | BUSINESS |

Business Overview

We are a holding company whose mission is to be a leading owner, operator and capital provider to Infrastructure Assets across global private markets. In doing so, our objective is to generate excess returns per unit of risk for our Shareholders consisting of both current income and long-term capital appreciation. We plan to establish operations and provide capital across power and renewables, transportation, communications, and social infrastructure sectors (collectively, the “Target Sectors”). We intend to have a global footprint, focusing primarily on opportunities in North America, countries in Western Europe and member states of the Organization for Economic Co-operation and Development (“OECD”).

We formed separate Series pursuant to the Delaware Limited Liability Company Act (as amended from time to time, the “LLC Act”), each of which is intended to be treated as a separate entity, and have a different tax classification, for U.S. federal income tax purposes. Under Delaware law, to the extent the records maintained for a Series account for the assets associated with such Series separately from the other assets of the Company or any other Series, the debts, liabilities, obligations and expenses incurred, contracted for or otherwise existing with respect to such Series are segregated and enforceable only against the assets of such Series and not against the assets of the Company generally or any other Series. The Series I Issuer has elected to be treated as a corporation for U.S. federal income tax purposes and the Series II Issuer is intended to be treated as a partnership for U.S. federal income tax purposes. We intend to conduct our operations so that we are not required to register as an investment company under the U.S. Investment Company Act of 1940, as amended (the “Investment Company Act”). See “Item 1A. Risk Factors—Risks Related to Regulatory Matters—We would not be able to operate our business according to our business plans if we are required to register as an investment company under the Investment Company Act.”

We are sponsored by Apollo and expect to benefit from its asset sourcing, operations, and portfolio management capabilities pursuant to an operating agreement with the Operating Manager (the “Operating Agreement”). Prior to accepting any subscriptions for Shares from unaffiliated investors of the Company, we will appoint the Operating Manager to manage the Company on a day-to-day basis, together with our executive officers, and provide certain management, administrative and advisory services related to identifying, acquiring, owning, controlling and providing capital to Infrastructure Assets and to a lesser extent the other investments described below.

Business Strategies

We plan to build and manage a portfolio of Infrastructure Assets using three key strategies.

| (1) | Long-Term Control-Oriented Infrastructure Assets. We plan to acquire, own, control and operate Infrastructure Assets across our Target Sectors. We will rely on Apollo’s Infrastructure Platform (defined below) to source and manage these Infrastructure Assets. Our executive officers, with the assistance of our Operating Manager, will actively oversee operations through board seats and shareholder governance across our control-oriented Infrastructure Assets with a focus on driving operational improvement, capital structure enhancements and long-term value creation. Over time, we may expand our operations through additional mergers and acquisitions. We plan to own these assets primarily through controlled operating company subsidiaries. |

| (2) | Infrastructure Asset Financings. We will pursue Infrastructure Asset financing opportunities across project finance, corporate debt and green loans. In addition to Apollo’s Infrastructure Team (defined below), we will leverage Apollo Credit (as defined below) and Apterra, Apollo’s infrastructure debt origination platform, to participate in private direct origination opportunities. We plan to hold these debt assets primarily through controlled lending company subsidiaries. |

| (3) | Opportunistic Investments in Infrastructure Assets. To a lesser extent, we also plan to participate in other opportunistic investments originated by Apollo’s Infrastructure Team. These investments will |

1

Table of Contents

| include allocations to equity buyouts and corporate carve outs originated by the Apollo Infrastructure Team. We expect these assets to carry a higher risk-return profile than the Infrastructure Assets that we will seek to own and control long-term. Our participation structure in these investments will depend on the facts and circumstances of each opportunity. |

Across our Infrastructure Assets, we will seek to emphasize downside protection by targeting contracted or partially contracted Infrastructure Assets and businesses that are operationally mature, provide essential services, typically operate in regulated environments and benefit from dominant and defensive market positions. These assets and businesses are generally characterized by stable and predictable cash flows that are often inflation-linked. We may also participate in Infrastructure Asset financings or opportunistic investments in Infrastructure Assets that demonstrate a significant potential growth profile due to factors such as project development, construction and business expansion, while seeking to mitigate downside risk, often by investing in securities that are senior to common equity in the capital structure.

We expect that over the long-term, Infrastructure Assets will make up a substantial portion of our assets. Additionally, we expect that the remainder of our assets will consist of cash and cash equivalents, U.S. Treasury securities, U.S. government agency securities, municipal securities, other sovereign debt, investment grade credit, and other investments including high yield credit, asset backed securities, mortgage backed securities, collateralized loan obligations, leveraged loans and/or debt of companies or assets (collectively, the “Liquidity Portfolio”) in each case to facilitate capital deployment and provide a potential source of liquidity. These types of liquid assets may exceed AIC’s target investment allocations, if any, at any given time due to distributions from, or dispositions of, Infrastructure Assets or for other reasons as our Operating Manager determines.

Governance and Management

The Company’s board of directors’ (the “Board”) corporate governance responsibilities will be based on our third amended and restated limited liability company agreement (the “LLC Agreement”). The Board will oversee the management of the Company and the performance of the Operating Manager. See “Item 5. Directors and Executive Officers.” Actual or potential conflicts of interest will arise from time to time between the Company, Apollo and other Apollo Clients. See “Item 7. Certain Relationships and Related Transactions, and Director Independence—Potential Conflicts of Interest” and “Item 11. Description of Registrant’s Securities to be Registered—Summary of the LLC Agreement.” The Company will have protocols for handling actual and potential conflicts of interest and our independent directors may be called upon from time to time to approve specific conflicts as members of the Company’s audit committee (the “Audit Committee”) or the conflict may be otherwise addressed in accordance with our LLC Agreement.

AIC will be led by its Chief Executive Officer (“CEO”) Dylan Foo who has over 20 years of experience investing in the infrastructure space globally.

AIC, through its relationship with the Operating Manager, will be supported by the Apollo Infrastructure Platform, which includes an infrastructure investment team and asset management professionals (the “Apollo Infrastructure Team”) as well as a broader suite of professionals who will support asset origination, active asset and operations management and value creation.

The Apollo Infrastructure Team has proven experience (i) underwriting, acquiring, and managing Infrastructure Assets on a long-term basis, (ii) sourcing and structuring Infrastructure Asset financings and (iii) opportunistically investing in Infrastructure Assets across equity, structured equity and other parts of the capital structure. AIC will benefit from the Apollo Infrastructure Team’s relationship-based asset sourcing for AIC. Importantly, the Apollo Infrastructure Team adopts a “full lifecycle” approach to asset management seeking to build strong relationships, accountability and alignment from the onset of gaining control over Infrastructure Assets, which Apollo believes promotes continuity and consistency of results.

2

Table of Contents

AIC, through its relationship with the Operating Manager, will also have access to the broader Apollo platform’s proprietary deal flow, direct debt origination, capital structure expertise and asset management capabilities. Apollo’s credit platform (“Apollo Credit”), Apterra, Apollo’s infrastructure debt origination platform, and Apollo Capital Solutions (“ACS”) will provide AIC access to proprietary loan origination, transaction structuring and warehousing and syndication services. Furthermore, AIC will leverage Apollo Portfolio Performance Solutions (“APPS”), Apollo’s in-house team dedicated to engaging with and driving impact at portfolio companies through operational improvements and transformational initiatives based on Apollo’s institutionalized best practices. APPS provides access to Apollo’s network of senior advisors, with capabilities across policy, macroeconomics, value creation and ESG (as defined below), and broader industry relationships to support operations management and value creation.

The Operating Manager

Pursuant to the terms of the Operating Agreement, the Operating Manager, a subsidiary of Apollo, which is expected to be an investment adviser registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940, as amended, will manage the Company on a day-to-day basis and provide certain management, administrative and advisory services to the Company related to identifying, acquiring, owning, controlling and providing capital to Infrastructure Assets.

Founded in 1990, Apollo is a high-growth, global alternative asset manager with $597.7 billion of Assets Under Management as of March 31, 2023. As of March 31, 2023, Apollo’s asset management business had over 2,500 employees with offices throughout the world. Apollo seeks to provide its clients excess return at every point along the risk-reward spectrum from investment grade debt to private equity. Apollo Global Management, Inc. is led by its Chief Executive Officer, Marc Rowan, and its asset management business is led by Apollo’s Co-Presidents, Scott Kleinman and James Zelter.

Apollo maintains an integrated approach to investing, which it believes distinguishes Apollo from other similarly situated alternative asset managers. Apollo places particular emphasis on value across its investing business, which adheres closely to the principles of “buying complexity and selling simplicity” and “purchase price matters.” By collaborating across disciplines, with each business unit contributing to, and drawing from, its shared knowledge and experience, Apollo believes it is well-suited to serve the financial return objectives of its clients and offer innovative capital solutions to businesses. Furthermore, Apollo believes that its capabilities in tackling complexity, creative deal structuring and rigorous underwriting standards are key differentiators and competitive advantages in the alternative asset industry. We believe that the Operating Manager’s integrated approach and platform-wide capabilities will enable AIC to access a specialized set of skills, sourcing networks and structuring know-how to enable AIC to execute its strategy.

The Apollo Infrastructure Team sits within Apollo’s Sustainability and Infrastructure Group, which is co-led by Dylan Foo and Olivia Wassenaar, Apollo’s Head of Natural Resources and Sustainable Investing. The combined group brings together Apollo’s expertise across infrastructure, sustainability and impact strategies. We expect many of our Infrastructure Assets to support the energy transition and plan to embed sustainability and ESG considerations into our asset management approach. As such, we believe access to Apollo’s broader Sustainability and Infrastructure Group will provide AIC with opportunities for attractive capital deployment and continued value creation.

Market Opportunity

We believe that the infrastructure market represents a large, sustainable and compelling opportunity. Within the infrastructure market, we have identified four Target Sectors for AIC, although we may evaluate other opportunities we consider to be infrastructure outside of these sectors:

| • | Power and Renewables. AIC will target opportunities within power and renewables across all aspects of the value chain including: generation, transmission/distribution and storage of electricity. We |

3

Table of Contents

believe there are many attractive opportunities for both regulated and unregulated projects. We believe regulated projects are characterized by higher barriers to entry and more predictable profit margins. We believe regulated projects will enable the Company to deploy significant capital at a regulated rate of return. For unregulated projects, we believe demand is quickly growing from commercial and industrial (“C&I”) offtakers where suppliers require private investment for their power needs (under long-term contracts). Notably, we expect opportunities to develop from highly scalable “platform” companies underpinned by contracts with C&I customers, whether for power generation, energy efficiency or other infrastructure-related services. Generally, investments in these assets benefit from long-term contracts (power purchase agreements, hedges, capacity or services contracts), which generally provide for stable, predictable cash flows. |

For energy transition investment, we believe private capital will continue to play an integral role in achieving decarbonization targets, not only in electricity generation, but in the build-out of related infrastructure like electric vehicle charging networks, as well as industrial decarbonization and carbon mitigation strategies. Aside from private capital investment, energy transition will also be largely influenced by policy measures and timing pressure to achieve net zero carbon emissions targets by 2050. The current inflationary and rising rate environment, geopolitical instability, supply chain issues and more make it apparent to us that there is an urgent need to invest in energy transition, which we believe can drive outsized returns.

| • | Transportation. The transportation sector continues to expand as the world’s economies grow, together with increasing globalization and efficiency in modes of moving goods and people across the world. Historically, countries have largely funded surface transportation (i.e., rails, motorways) development with public finance, though the deterioration and poor maintenance of existing infrastructure has forced transportation authorities to open the doors to privatization. Additionally, airports and aviation have been under-allocated in terms of government investment due to shortfalls in federal and local grants or aid programs. We believe there are several compelling opportunities for value creation in niche subsectors of transportation. For example, there are opportunities to enable the electrification of transportation through highly scalable platforms, such as partnerships with municipalities to replace high-pollutant, diesel-fueled, public buses with electric ones (and to provide the necessary charging infrastructure). Existing port infrastructure is already over-utilized and will require massive investment for expansion or improvement through capital expenditures. With respect to these niche opportunity sets, we believe there is a high potential for investments in North America, countries in Western Europe and members of the OECD. |

Decarbonization, urbanization, supply chain security and technological advances are also driving substantial need for investment in transportation infrastructure that supports the global movement of both goods and people. Furthermore, the deterioration and poor maintenance of existing transportation infrastructure that has historically been funded by public finance provides an opportunity for private capital to bridge the funding gap in an efficient manner. While some progress has begun in the road segment through investment in electric vehicles and related charging infrastructure, we believe the investment opportunity exists across all modes of transportation. These clean energy transportation alternatives will require significant private sector investment to facilitate mass adoption.

| • | Communications. Communications infrastructure provides the mission-critical backbone for global communications between countries, public and private enterprises and individual consumers. The proliferation of wireless devices and mobile data usage, together with the advancement/complexity of data applications and the “internet of things,” have highlighted the need for continuous investment in high-quality communications and digital infrastructure. The basic infrastructure assets—data centers, fiber, wireless towers, small cells, and distributed antenna systems—all serve to store or transmit data across networks. Despite the evolution of cloud technology, every single bit of data produced and consumed in the world needs to travel across physical infrastructure in order to be sent by or retrieved from any device. |

4

Table of Contents

The COVID-19 pandemic helped to shed light on the weaknesses and vulnerabilities of our existing digital infrastructure. As a result of these dynamics, investment in digital infrastructure is that much more important for private capital allocators. Building out and upgrading legacy fiber networks, data centers and macro cell towers represents a significant opportunity to deploy capital to enable digital connectivity. The opportunity set is especially evident in underserved or rural areas, where the need for investment is more critical. Furthermore, in areas where providers operate an extensive legacy network, the cost of upgrading the existing infrastructure will be high.

| • | Social Infrastructure. The water, waste and social infrastructure subsectors are similar to transportation in that they historically represent projects that have been largely funded with public finance due to the essential functions they serve for municipalities. Given the difference in prevalence of public-private partnerships (“PPPs”) between the United States and other countries, we expect the Operating Manager to review mainly private opportunities in the United States, with a heavier mix of PPPs and private opportunities abroad. The Operating Manager will consider opportunities across the water value chain, such as wastewater collection, storage, transportation, filtration, de-salination, treatment and recycling. Furthermore, social infrastructure is a relatively new subsector in the United States, but we believe there is significant unaddressed need due to the degraded state of schools, hospitals, stadiums and other municipal buildings across the country. |

We believe the size and growth trajectory of AIC’s Target Sectors will be primarily driven by secular trends such as the steady growth in population and improvements in living standards, as well as the aging of existing infrastructure, prompting governments across developed economies to prioritize their maintenance and support via private sector investment to fill the large financing gap. Furthermore, environmental and social priorities are accelerating the replacement and innovation of certain infrastructure as economies around the world transition from fossil fuel-based energy to renewable and clean energy. In the communications sector, a similar megatrend is occurring around digital adoption rates and data usage, driving significant acquisitions of infrastructure to support the buildout of networks, data centers, fiber, towers and similar assets. We expect that the significant infrastructure financing gap will continue to present further opportunities for private capital.

We have identified four key themes that we believe will generate a meaningful number of attractive acquisition opportunities for AIC:

| • | Supporting the accelerated global energy transition. In the face of a continually growing body of evidence about the effects of carbon-emitting energy sources on our climate, we believe there is an imminent and urgent need to finance the transition from carbon-emitting energy sources to clean energy sources, with up to $150 trillion of investment required over the next three decades. New renewable energy assets will replace older, inefficient, carbon-emitting assets and also serve new electric demand from economic expansion and the transition to electric vehicles. Importantly, it is increasingly evident that private capital will play an integral role in achieving ambitious—but necessary—decarbonization targets. Potential areas of opportunity for AIC within this theme include: traditional clean energy generation (e.g., wind, water and solar), grid stability (energy storage), transmission assets, microgrid or “energy-as-a-service” assets and renewable royalties. |

| • | Enhancing connectivity through digital infrastructure. There exists a growing “digital divide” between urbanized parts of North America and Europe and more rural areas that are lagging in terms of access to modern information and communications technology. For example, it is estimated that the most densely populated parts of the United States enjoy average broadband speeds of two to three times the speeds of rural and very rural areas, which contributes hundreds of productivity hours lost per person annually. The stark contrast between demographics with stronger internet connectivity and those without was particularly apparent during the “stay at home” periods of the COVID-19 pandemic in 2020, and in the years that have followed, the importance of adequate access to the internet has never been more well-understood. Correcting this inequality in the near-to-medium term through |

5

Table of Contents

investment in communications and digital infrastructure aims to make larger portions of populations more integrated via the internet, allowing for a more rapid development of digital skills and literacy society-wide. These factors, combined with an estimated 50% increase in demand for data centers over the next five years, make acquisition of digital infrastructure that much more important for private capital allocators. Apollo has been active in investing in communications and digital infrastructure assets in cell towers, enterprise fiber and communications infrastructure and fiber. Potential areas of opportunity for AIC within this theme include: macro cell towers, fiber, data centers, managed wi-fi, spectrum and fixed wireless. |

| • | Connecting economies through the global supply chain and sustainable mobility. Beyond the need to upgrade and repair aging infrastructure, increasing global trade and efficiency in modes of moving goods and people across the world has long been driving the need for transportation infrastructure acquisition. Moreover, shocks to the global supply chain and mobility caused by the COVID-19 pandemic showed that there is substantial room for improvement among alternatives to traditional methods of transportation. Incremental supply routes must be created, requiring significant investment in air, shipping and rail lines as well as newly constructed logistics centers and hubs to accommodate new trade flows. We anticipate the competing forces of globalization and deglobalization to create both risks and opportunities in our target market. We believe private infrastructure investors will be well-positioned to help build and finance the next wave of transportation infrastructure to keep the global economy on track. Potential areas of opportunity for AIC within this theme include: cold-chain logistics, e-commerce infrastructure and port, aviation and rail development in support of changing trade patterns. |

| • | The future of sustainable living. Consumer products and services are increasingly focused on sustainable means of care, production, reduction and reuse. The goal of sustainable living is to simultaneously encourage and enhance the health of a growing, more demanding population, while also improving environmental health in various forms. Achieving this goal will require further investments in the circular economy, which aims to reduce the production of new inputs by “closing the loop” on material production, supply and consumption—in essence, reducing or eliminating waste and pollution by maximizing the amounts of materials recovered, reused and recycled at all stages. In addition to reducing the impact from new production, further investment is required to support the sustainable delivery of critical services to a growing population. Globally, aging populations are requiring increasingly complex care, while educational needs are accelerating and evolving to teach children the skills required to thrive in our changing world. Significant acquisitions are also needed to improve the environmental footprint of agriculture and food production. To feed the growing global population and ensure food security, food production needs to increase in scale and productivity while also reducing negative environmental impacts. While an emerging area of focus within infrastructure, potential areas of opportunity for AIC within this theme include: waste recovery and recycling services and facilities, water and wastewater treatment, aged care and healthcare infrastructure, educational development and essential investment in the sustainable food and agriculture value chain. |

Our Approach to Building a Portfolio of Infrastructure Assets

Apollo has a long history of evaluating and providing capital to infrastructure and infrastructure-related assets in its equity, yield and hybrid strategies. Apollo believes its flexible and value-oriented approach, with a willingness to embrace complexity and a focus on downside protection, has enabled it to successfully deploy capital across various asset classes and market environments. AIC, through its relationship with the Operating Manager, will have access to the expertise, sourcing networks and structuring capabilities of Apollo’s broader resources, and the Operating Manager will apply Apollo’s approach to sourcing and evaluating opportunities for AIC’s strategy.

6

Table of Contents

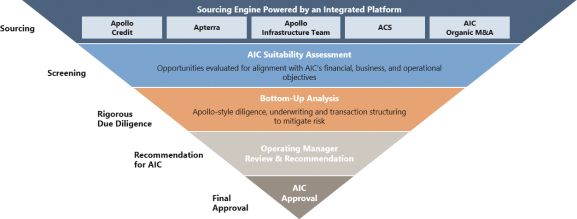

AIC’s Rigorous Acquisition Process

Please refer to the following graphic for an illustration of our rigorous acquisition process for Infrastructure Assets. All three of our capital deployment strategies, (i) control-oriented Infrastructure Asset acquisitions, (ii) Infrastructure Asset financings, and (iii) opportunistic investments in Infrastructure Assets, will follow the acquisition process described below.

| • | Sourcing. Given the integrated nature of Apollo, we believe AIC will benefit from the significant origination and sourcing capabilities of Apollo’s entire platform. Unlike most peers, Apollo generally operates without information barriers across its asset management business units, which Apollo believes helps to generate differentiated acquisition ideas across the capital structure. Apollo believes the collaboration across equity, yield and hybrid strategies enables the Apollo Infrastructure Team to more successfully source and diligence opportunities. As a result of its scale, Apollo sees an active channel of infrastructure opportunities across both debt and equity. |

The Apollo Infrastructure Team utilizes its deep networks across the infrastructure landscape to consistently source high-quality, relationship-driven opportunities. In addition to sourcing driven exclusively by the Apollo Infrastructure Team and its relationships, we believe AIC will benefit from cooperation with Apollo’s broader platform, including Apterra, Apollo Credit and ACS, to identify opportunities that fit AIC’s mandate. As AIC grows, we expect attractive organic merger and acquisition opportunities to develop which will flow through the same process used to screen Infrastructure Asset opportunities sourced by other parts of Apollo’s platform.

| • | Screening. AIC’s target asset portfolio, operational footprint, capital availability and cost of capital, along with other financial, business and operational factors, will be considered when determining whether an acquisition opportunity is suitable for AIC. The Operating Manager will actively monitor these considerations and adjust our screening process where necessary based on macro and micro factors. Ultimately, our goal is to ensure AIC is building a portfolio that is well diversified, inflation protected and expected to generate low volatility and stable cash flows for our Shareholders. |

| • | Rigorous Due Diligence. We believe the Operating Manager’s approach to due diligence of acquisition opportunities is distinguished by Apollo’s consensus-driven philosophy whereby the collective knowledge of the professionals is maximized and a variety of perspectives are considered as an acquisition opportunity proceeds through the various stages of approval. In addition, consistent with Apollo’s conservative approach and overall objective of achieving attractive risk-adjusted returns, AIC will place a significant amount of emphasis on mitigating downside risks and the preservation of capital. |

| • | Operating Manager Recommendation and AIC Approval. The Operating Manager will consider the input from other Apollo professionals, operating executives and/or various other industry experts as |

7

Table of Contents

part of its decision-making process. Throughout the rigorous and iterative acquisition process, objections and concerns are typically raised early, such that any acquisition that would reach the final approval stage is expected to already have the support of the broader team. If, following the screening and diligence processes, an opportunity is deemed appropriate, the Operating Manager will recommend the acquisition to us. |

| • | Final Approval. One or more officers or directors of AIC will approve all acquisition opportunities for AIC. |

Operations Management and Value Creation

Apollo Infrastructure Platform’s Asset Management Capabilities

Our Operating Manager has an extensive network of resources that will support the Apollo Infrastructure Team in driving value creation across our Infrastructure Assets, (collectively, the “Infrastructure Platform”). Apollo will seek to add value to the Infrastructure Assets by focusing on enhancements to the assets’ operations through working closely with such network of resources outlined below. Apollo also relies on its deep credit orientation and seeks to optimize the capital structure of the Infrastructure Assets.

| • | Apollo Portfolio Performance Solutions (“APPS”): The Apollo Infrastructure Team works closely with portfolio company management teams, as well as APPS, and other key strategic partners to build better, more sustainable and streamlined businesses. APPS is Apollo’s in-house team dedicated to engaging with and driving impact at portfolio companies through operational improvements and transformational initiatives, works alongside investment teams and portfolio companies to, among other things, transform portfolio company operational and functional capabilities throughout all stages of the investment lifecycle. These functional priorities include operational excellence, commercial excellence, talent management and organizational effectiveness, digital and data analytics, innovation, technology transformation, finance and portfolio analytics and environmental, social and governance impact. By seeking to institutionalize best practices across APPS’s functional areas of focus, Apollo believes it can achieve more rapid execution, more consistent underwriting and quicker identification and realization of value-add opportunities. |

| • | Apollo Capital Solutions (“ACS”): Apollo’s capital solutions business, which it refers to as ACS, operates through Apollo’s affiliated broker-dealer, Apollo Global Securities, LLC (“AGS”), and other affiliated entities to provide (at additional expense) underwriting, structuring, arrangement and placement of debt and equity securities, syndication, advisory, sourcing and origination services to Apollo Clients and their portfolio companies, as well as third parties. The Apollo Infrastructure Team works closely with ACS. Apollo believes its ability to structure and directly place financings remains critical to both the sourcing process as well as value creation post-acquisition. Through ACS, Apollo looks to optimize the capital structures of its clients’ portfolio companies through creative financing solutions, which provide greater flexibility to invest for growth and enhanced capital preservation during periods of economic volatility. In tougher market environments, ACS seeks to leverage its deep credit experience and relationships to provide successful deal execution when traditional financing sources are unavailable. |

| • | Apollo Credit: The Apollo Infrastructure Team also collaborates with Apollo Credit, which helps companies access flexible, low-cost capital solutions to fund their growth and achieve their corporate objectives. Apollo Credit has expertise across corporate fixed income, direct lending, structured credit and commercial real estate debt and has two key asset class segments: (i) corporate credit where the platform identifies opportunities within the public and private corporate lending areas and (ii) asset-backed finance where the platform funds, finances and structures asset-backed originations and structured solutions, including for infrastructure assets. Apollo believes its proprietary platforms and |

8

Table of Contents

corporate solutions capabilities enable it to originate high-quality and safe-yielding assets for its investors. Most of the Apollo Credit services are also provided by ACS, which structures, originates and distributes those opportunities. |

| • | Apterra: AIC will also benefit from access to debt originated by Apterra. “Apterra” is Apollo’s infrastructure debt origination platform launched earlier this year that will seek to create proprietary infrastructure debt opportunities for the Company. Apterra is led by a team of professionals with extensive experience in origination and syndication. Apterra primarily will seek to originate first lien senior secured loans across project finance, corporate infrastructure and energy transition loans. The Apterra team, which has extensive experience across all power, midstream and infrastructure industry sub-sectors, plans to initially focus on energy-transition-related sectors, including renewables and liquefied natural gas. |

| • | Apollo ESG: Apollo views sustainable investment to be the strategy and practice of incorporating environmental, social and governance (“ESG”) factors and sustainability outcomes into its investment decisions, practices and ownership, to the extent they are deemed to be material to financial performance and consistent with fiduciary obligations. Apollo believes that managing relevant ESG risks and realizing ESG opportunities can make it a better investor and better steward of its investors’ money by positioning portfolio companies and other investments of Apollo-managed products for sustainable financial success. Apollo believes that sustainability can be a core function for building better businesses and help it deliver superior risk-adjusted returns to investors, and that companies that proactively manage ESG risks and seize ESG opportunities can be more sustainable and better positioned for the long-term. Accordingly, Apollo aims to integrate ESG into investment decision-making and monitoring processes, as necessary and appropriate, and consistent with fiduciary obligations. |

| • | Apollo Infrastructure Operating Advisors and Access to Apollo Industry and Sector Expertise: Since its inception, Apollo has developed significant expertise investing in AIC’s Target Sectors. In the process of screening, executing and monitoring investments in the Target Sectors, Apollo has developed valuable relationships with infrastructure operating advisors, leading management teams, consultants, senior advisors and other intermediaries who may or may not be exclusive to Apollo and are not employees of Apollo. Apollo’s relationships with infrastructure operating advisors are crucial across all aspects of the investment process, from sourcing and due diligence to value creation within owned and controlled operations. We believe the active participation of these advisory relationships within AIC’s Target Sectors will allow the Company to benefit from high-quality, proprietary deal flow and access to extensive executive-level contacts with sector expertise. Apollo believes that its industry specialization provides Apollo with advantages in sourcing and evaluating new opportunities and adding value to its clients’ assets post-acquisition. |

Optimizing Value at Exit within Opportunistic Investments

Through its integrated platform, Apollo believes it has access to in-depth expertise and insight into broader infrastructure market dynamics, which benefit Apollo’s investment professionals as they assess the potential timing and method of exit. For AIC’s opportunistic investment portfolio, the Operating Manager will seek to identify potential exit opportunities prior to consummating an acquisition, analyzing the benefits of various exit options. Apollo is an experienced seller and possesses longstanding relationships with potential buyers of infrastructure assets and businesses more broadly, including both strategic acquirers and financial sponsors. Particularly in relation to infrastructure and infrastructure-related assets, we believe Apollo has a demonstrated ability to monetize value and exit assets through different pathways, including through trade sales, refinancings, dividends and sales to sponsors.

9

Table of Contents

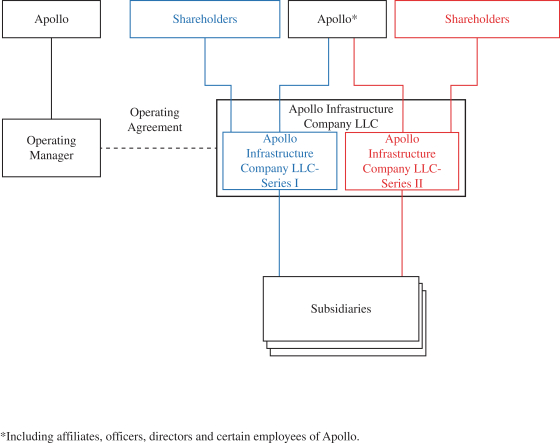

Our Structure

The following is a summary chart of our corporate structure.

The Board of Directors and Executive Officers

Overall responsibility for the Company’s and each Series’ oversight rests with the Board. To the extent permitted by applicable law, the Board may delegate any of its rights, powers and authority to, among others, any committee of the Board, the officers of the Company or the Operating Manager. The Board will consist of four members, two of whom are expected to be independent directors, as such term is defined in Section 303A.02 of the New York Stock Exchange Listed Company Manual. See “Item 5. Directors and Executive Officers.”

Our executive officers include our Chief Executive Officer. The executive officers (pursuant to a delegation of authority from the Board), and in certain instances the Board or a committee of the Board, are responsible for making capital allocation and acquisition decisions proposed by the Operating Manager. Together with the Board, our executive officers oversee the management and control of the Company’s Infrastructure Assets. Our Chief Executive Officer is Dylan Foo.

Operating Agreement

The description below of the Operating Agreement is only a summary and is not necessarily complete. The description set forth below is qualified in its entirety by reference to the Operating Agreement which has been filed as an exhibit to this Registration Statement.

10

Table of Contents

We will enter into the Operating Agreement pursuant to which the Operating Manager will manage the Company on a day-to-day basis. Under the terms of the Operating Agreement, the Operating Manager is responsible for, among others, the following:

| • | originating and recommending opportunities to acquire Infrastructure Assets and to finance Infrastructure Assets, consistent with the business objectives and strategy of the Company; |

| • | monitoring and evaluating our Infrastructure Assets; |

| • | analyzing and investigating potential dispositions of Infrastructure Assets, including identification of potential acquirers and evaluations of offers made by such potential acquirers; |

| • | structuring of acquisitions and financings of Infrastructure Assets; |

| • | identifying bank and institutional sources of financing for each Series and its Infrastructure Assets, arrangement of appropriate introductions and marketing of financial proposals; |

| • | supervising the preparation and review of all documents required in connection with the acquisition, disposition or financing of each Infrastructure Asset; |

| • | administering the day-to-day operations and performing and supervising the performance of such other administrative functions necessary to the management of the Company and its affiliates as may be agreed upon by the Operating Manager and the Board, including, without limitation, the collection of revenues and the payment of the debts and obligations of the Company and our subsidiaries and maintenance of appropriate computer services to perform such administrative functions, in each case, for which the Company will reimburse the Operating Manager; |

| • | monitoring the performance of Infrastructure Assets and, where appropriate, providing advice regarding the management of Infrastructure Assets; |

| • | arranging and coordinating the services of other professionals and consultants, including Apollo personnel; |

| • | making recommendations to the Company with respect to the Company’s repurchase offers; |

| • | originating, recommending opportunities to form, acquiring, structuring, coordinating and assisting with managing operations of any joint venture or Infrastructure Assets held by the Company and conducting all matters with the joint venture partners consistent with the business objectives and strategies of the Company (including, for the avoidance of doubt, the power to structure joint ventures that provide that any controlling interest of the Company shall be forfeited upon termination of the Operating Agreement); |

| • | advising the Company on, preparing, negotiating and entering into, on behalf of the Company, applications and agreements relating to programs established by the U.S. government; |

| • | arranging marketing materials, advertising, industry group activities (such as conference participations and industry organization memberships) and other promotional efforts designed to promote the Company’s business; |

| • | communicating on behalf of the Company and our subsidiaries with the holders of any of their equity or debt securities as required to satisfy the reporting and other requirements of any governmental bodies or agencies or trading markets and to maintain effective relations with such holders; |

| • | counseling the Company in connection with policy decisions to be made by the Board; |

| • | evaluating and recommending to the Board hedging strategies and engaging in hedging activities on behalf of the Company and our subsidiaries, consistent with such strategies as so modified from time to time; |

| • | counseling the Company and our subsidiaries regarding the maintenance of their exclusion from the definition of an investment company under the Investment Company Act, monitoring compliance with |

11

Table of Contents

the requirements for maintaining such exclusion and using commercially reasonable efforts to cause them to maintain such exclusion from such status; |

| • | furnishing reports and statistical and economic research to the Company and our subsidiaries regarding their activities and services performed for the Company and our subsidiaries by the Operating Manager; |

| • | monitoring the operating performance of the Infrastructure Assets and providing periodic reports with respect thereto to the Board, including comparative information with respect to such operating performance and budgeted or projected operating results; |

| • | investing and reinvesting any moneys and securities of the Company and our subsidiaries (including investing in short-term Infrastructure Assets pending the acquisition of other Infrastructure Assets, payment of fees, costs and expenses, or payments of dividends or distributions to Shareholders of the Company and our subsidiaries) and advising the Company and our subsidiaries as to their capital structure and capital raising; |

| • | assisting the Company and our subsidiaries in retaining qualified accountants and legal counsel, as applicable, to assist in developing appropriate accounting systems and procedures, internal controls and other compliance procedures and testing systems with respect to financial reporting obligations and to conduct quarterly compliance reviews with respect thereto; |

| • | assisting the Company and our subsidiaries to qualify to do business in all applicable jurisdictions and to obtain and maintain all appropriate licenses; |

| • | assisting the Company and our subsidiaries in complying with all regulatory requirements applicable to them in respect of their business activities, including preparing or causing to be prepared all financial statements required under applicable regulations and contractual undertakings and all reports and documents, if any, required under the Exchange Act and the Securities Act; |

| • | assisting the Company and our subsidiaries in taking all necessary action to enable them to make required tax filings and reports; |

| • | placing, or facilitating the placement of, all orders pursuant to the Operating Manager’s acquisition determinations for the Company and our subsidiaries either directly with the issuer or with a broker or dealer (including any affiliated broker or dealer); |

| • | handling and resolving all claims, disputes or controversies (including all litigation, arbitration, settlement or other proceedings or negotiations) on the Company’s and/or the Subsidiaries’ behalf in which the Company and/or the Subsidiaries or their respective Infrastructure Assets, may be involved or to which they may be subject arising out of their day-to-day operations (other than with the Operating Manager or its affiliates), subject to such limitations or parameters as may be imposed from time to time by the Board; |

| • | using commercially reasonable efforts to cause expenses incurred by the Company and our subsidiaries or on their behalf to be commercially reasonable or commercially customary and within any budgeted parameters or expense guidelines set by the Board from time to time; |

| • | advising the Company and our subsidiaries with respect to and structuring long-term financing vehicles for the Infrastructure Assets, and offering and selling securities publicly or privately in connection with any such structured financing; |

| • | serving as the Company’s and the Subsidiaries’ consultant with respect to decisions regarding any of their financings, hedging activities or borrowings undertaken by the Company and our subsidiaries including (1) assisting the Company and our subsidiaries in developing criteria for debt and equity financing that are specifically tailored to their objectives, and (2) advising the Company and our subsidiaries with respect to obtaining appropriate financing for their acquisitions; |

12

Table of Contents

| • | providing the Company with such other services as the Board may, from time to time, appoint the Operating Manager to be responsible for and perform, consistent with the terms of the Operating Agreement; and |

| • | using commercially reasonable efforts to cause the Company and our subsidiaries to comply with all applicable laws. |

The Operating Manager’s services under the Operating Agreement will not be exclusive, and the Operating Manager will be free to furnish similar services to other entities, and it intends to do so, so long as its services to us are not impaired. For the avoidance of doubt, the oversight of management, policies and operations of the Company shall be the ultimate responsibility of the Board acting pursuant to and in accordance with the LLC Agreement.

The term of the Operating Agreement will continue indefinitely unless terminated as described below. The Operating Agreement may be terminated upon the affirmative vote of all of our independent directors, based upon unsatisfactory performance by the Operating Manager that is materially detrimental to us and our subsidiaries, taken as a whole. We will need to provide the Operating Manager 180 days’ written notice of any termination. We may also terminate the Operating Agreement “for cause,” as described in the Operating Agreement, subject to the terms thereof.

The Operating Manager may terminate the Operating Agreement if we become required to register as an investment company under the Investment Company Act, with such termination deemed to occur immediately prior to such event. The Operating Manager may also terminate the Operating Agreement by providing us with 180 days’ written notice. In addition, if we default in the performance or observance of any material term, condition or covenant contained in the Operating Agreement and the default continues for a period of 30 days after written notice to us requesting that the default be remedied within that period, the Operating Manager may terminate the Operating Agreement upon 60 days’ written notice.

In addition, if our Operating Agreement is terminated, the Operating Agreement will obligate us to forfeit our voting securities or other controlling interest in any Infrastructure Asset, which would likely require us to register as an investment company under the Investment Company Act and adversely affect an investment in our Shares. The Operating Agreement will require us to redeem any Apollo Shares if the Operating Agreement is terminated, which could require us to liquidate Infrastructure Assets at unfavorable times or prices, which may adversely affect an investment in our Shares.

We anticipate that the Operating Agreement will not be able to be terminated for any other reason, including if the Operating Manager or Apollo experience a change of control or due solely to the poor performance or under-performance of the Company’s operations or Infrastructure Assets, and the Operating Agreement continues in perpetuity, until terminated in accordance with its terms. Because the Operating Manager is an affiliate of Apollo and Apollo has a significant influence on the affairs of the Company, the Company may be unwilling to terminate the Operating Agreement, even in the case of a default. If the Operating Manager’s performance does not meet the expectations of Shareholders, and the Company is unable or unwilling to terminate the Operating Agreement, the Company is not entitled to terminate the agreement and the Company’s NAV per Share could decline.

Compensation of the Operating Manager

The compensation of the Operating Manager described below will apply with respect to each Series and will be the same for each Series unless otherwise indicated.

Management Fee

We will pay the Operating Manager a management fee (the “Management Fee”). The Management Fee is payable monthly in arrears in an amount equal to (i) 1.25% per annum of the month-end net asset value (“NAV”)

13

Table of Contents

attributable to S Shares and I Shares, (ii) 1.00% per annum of the month-end NAV attributable to the Founder Shares (iii) 0.75% per annum of the month-end NAV attributable to the A-I Shares until December 31, 2026 and 1.00% per annum of the month-end NAV attributable to the A-I Shares thereafter and (iv) 0.50% per annum of the month-end NAV attributable to the A-II Shares; provided, that this Management Fee will be reduced by any applicable Special Fees; provided, however, that this Management Fee will not be reduced for any Other Fees. In calculating the Management Fee, we will use our NAV before giving effect to accruals for the Management Fee, Performance Fee (as defined below), combined annual distribution fee and shareholder servicing fee or distributions payable on our Shares. We will not pay the Operating Manager a Management Fee on the Series I Apollo Shares and Series II Apollo Shares (each as defined below, collectively, the “Apollo Shares”), and as a result, it is an expense specific only to Investor Shares at the rates specified herein, which will result in the dilution of Investor Shares in proportion to the fees charged to different types of Investor Shares.

100% of any net consulting (including management consulting) or monitoring fees (including any early termination fee or acceleration of any such management consulting fee on a one-time basis that is approved by the Board), break-up fees (including, if applicable, the portion thereof described above in “Item 1A. Risk Factors—Risks Related to our Company and an Investment in our Shares—Our business may be affected by offering Co-Investments or opportunities to provide debt financing to any person”), directors’ fees, closing fees and merger and acquisition transaction advisory services fees related to the negotiation of the acquisition of an Infrastructure Asset (other than debt investments or investments with respect to which Apollo does not exercise direct control with respect to the decision to engage the services giving rise to the relevant fees, costs and expenses) and similar fees (including Bridge Financing fees), whether in cash or in kind, including options, warrants and other non-cash consideration paid to the Operating Manager or any of its affiliates or any employees of the foregoing in connection with actual or contemplated acquisitions or investments (and allocable to the Company) (collectively, “Special Fees”) that are allocable to those Shareholders who bear Management Fees, will be applied to reduce the Management Fees paid by such Management Fee-bearing Shareholders. As such, the portion of such Special Fees attributable to Apollo’s investment or to the investments of Shareholders that do not pay Management Fees will be retained by Apollo. In practice, the only fees that are generally expected to be paid and treated as Special Fees are mergers and acquisition transaction fees payable in connection with an acquisition and management consulting fees payable thereafter.

Performance Fee