UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM N-CSR

Investment Company Act file number: 811-02671

DWS Municipal Trust

(Exact Name of Registrant as Specified in Charter)

345 Park Avenue

New York, NY 10154-0004

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (212) 250-3220

Paul Schubert

60 Wall Street

New York, NY 10005

(Name and Address of Agent for Service)

| Date of fiscal year end: | 5/31 |

| Date of reporting period: | 5/31/2013 |

| ITEM 1. | REPORT TO STOCKHOLDERS |

MAY 31, 2013 Annual Report to Shareholders |

| DWS Managed Municipal Bond Fund |

|

Contents

4 Letter to Shareholders 5 Portfolio Management Review 12 Performance Summary 15 Investment Portfolio 47 Statement of Assets and Liabilities 49 Statement of Operations 50 Statement of Cash Flows 51 Statement of Changes in Net Assets 52 Financial Highlights 57 Notes to Financial Statements 68 Report of Independent Registered Public Accounting Firm 69 Information About Your Fund's Expenses 70 Tax Information 71 Summary of Management Fee Evaluation by Independent Fee Consultant 75 Board Members and Officers 80 Account Management Resources |

This report must be preceded or accompanied by a prospectus. To obtain a summary prospectus, if available, or prospectus for any of our funds, refer to the Account Management Resources information provided in the back of this booklet. We advise you to consider the fund's objectives, risks, charges and expenses carefully before investing. The summary prospectus and prospectus contain this and other important information about the fund. Please read the prospectus carefully before you invest.

Bond investments are subject to interest-rate and credit risks. When interest rates rise, bond prices generally fall. Credit risk refers to the ability of an issuer to make timely payments of principal and interest. Investments in lower-quality ("junk bonds") and non-rated securities present greater risk of loss than investments in higher-quality securities. The fund invests in inverse floaters, which are derivatives that involve leverage and could magnify the fund's gains or losses. Although the fund seeks income that is exempt from federal income taxes, a portion of the fund's distributions may be subject to federal, state and local taxes, including the alternative minimum tax. See the prospectus for details.

DWS Investments is part of the Deutsche Asset & Wealth Management division of Deutsche Bank AG.

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

Dear Investor:

The first half of 2013 brought welcome evidence that the U.S. economic recovery is gaining traction. Consumer confidence reached its highest level since 2007, U.S. stock market indexes marked a series of record highs and the housing market continues its recovery.

According to Asoka Wohrmann, co-chief investment officer for Deutsche Asset & Wealth Management, "The revival of the employment market, good asset performance with rising home and share prices, and an expansive monetary policy gives further growth momentum to the real economy. Accordingly, U.S. economic growth could accelerate in the coming months."

Nevertheless, concerns about the European and emerging-market economies persist. Closer to home, the outlook remains guarded when it comes to the eventual end of government intervention in the bond market and the full effects of reduced government spending on employment.

Where does this leave you? That depends on a variety of factors, including your overall portfolio allocation. Given the uncertainties in today's bond and stock markets, it may be time for a thoughtful evaluation of your strategy.

Talk with a trusted advisor to determine whether any adjustments may be in order, given your specific objectives and risk tolerance. We believe even the most sophisticated investor can benefit from the assistance of a trusted, objective financial professional.

Remember that Deutsche Asset & Wealth Management gives you access to Deutsche Bank's global network of economists, analysts and investment professionals. Insights are always at your fingertips at dws-investments.com.

Best regards,

Douglas Beck, CFA President, DWS Funds |

Overview of Market and Fund Performance

All performance information below is historical and does not guarantee future results. Returns shown are for Class A shares, unadjusted for sales charges. Investment return and principal fluctuate, so your shares may be worth more or less when redeemed. Current performance may differ from performance data shown. Please visit www.dws-investments.com for the most recent month-end performance of all share classes. Fund performance includes reinvestment of all distributions. Unadjusted returns do not reflect sales charges and would have been lower if they had. Please refer to pages 12 through 14 for more complete performance information.

DWS Managed Municipal Bond Fund posted a return of 4.01% over the 12 months ended May 31, 2013, while the overall municipal bond market, as measured by the unmanaged Barclays Municipal Bond Index, delivered a total return of 3.05% for the same period. The average fund in the Morningstar Muni National Long category returned 3.80% for the 12 months.

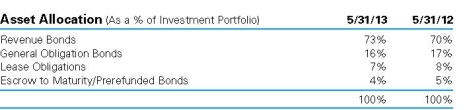

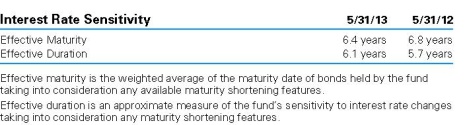

Investment Strategy The fund invests in a wide variety of municipal bonds. These include general obligation bonds, for which payments of principal and interest are secured by the full faith and credit of the issuer and usually supported by the issuer's taxing power. In addition, securities held may include revenue bonds, for which principal and interest are secured by revenues from tolls, rents or other fees gained from the facility that was built with the bond issue proceeds. The fund's management team seeks to hold municipal bonds that appear to offer the best opportunity to meet the fund's objective of earning tax-exempt income. A number of factors influence the performance of municipal bonds. These include supply and demand, the direction of overall interest rates, and the perceived credit risk associated with an individual municipal issuer. In selecting securities, the managers weigh the impact of the economic outlook and potential interest rate movements on municipal bonds as well as characteristics specific to securities such as coupons, maturity dates and call dates, and supply and demand of the municipal market. Finally, the managers may seek to take advantage if they believe the municipal yield curve presents an opportunity to gain incremental income with limited additional interest rate risk. Although portfolio management may adjust the fund's duration (a measure of sensitivity to interest rates) over a wider range, they generally intend to keep it similar to that of the Barclays Municipal Bond Index, generally between five and nine years. |

As the period began, with the U.S. Federal Reserve Board (the Fed) maintaining short-term rates anchored near zero, fixed-income markets were closely following developments in the European debt crisis as well as the stream of U.S. economic data. Europe would soon become less of a fulcrum for market sentiment as the European Central Bank (ECB) implemented strong measures to support refinancing by troubled governments. As the period progressed, U.S. housing data seemed to confirm that prices had finally reached a bottom and were beginning to strengthen. In addition, with employment data continuing to disappoint, there was speculation that the Fed would announce further bond purchases under quantitative easing. This speculation was borne out at the Fed's mid-September meeting. The net result was an increased willingness on the part of investors to assume credit risk in exchange for yields higher than the extraordinarily low rates offered from U.S. Treasuries.

As November 2012 approached, U.S. fixed-income markets were focused primarily on the presidential election, against a backdrop of wrangling over solutions to the country's fiscal dilemma. The strong demand municipals experienced over the prior several months continued as investors sought tax-exempt income that was attractive relative to taxable U.S. Treasury yields. However, December 2012 saw a retreat in municipal demand levels as institutional investors engaged in selling to lock in gains before year-end and amid some concern over proposals to limit the tax exemption on municipals as part of any budget deal.

As 2013 unfolded, the interest rate environment became less favorable for bond prices overall. Investors shrugged off the lack of meaningful progress in the budget standoff, and U.S. Treasury rates began to trend somewhat higher on optimism over prospects for the economy. Municipals experienced their greatest yield increases and price weakness in the last weeks of the fiscal period. Economic data continued to strengthen and there was mounting speculation that the Fed would begin to scale back its bond purchases that had helped keep longer-term rates in check. In addition, a rising stock market attracted strong investor interest, perhaps drawing flows that may have otherwise gone towards fixed-income securities. Municipal bond funds experienced large outflows as investors found the historically low yields on offer unappealing and sought to minimize exposure to rising interest rates.

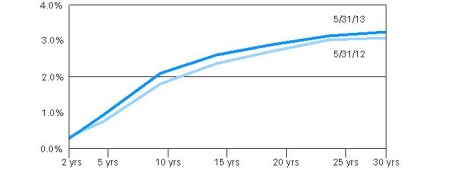

Municipal Bond Yield Curve (as of 5/31/13 and 5/31/12) |

|

This chart is for illustrative purposes only and is not intended to represent the yield of any DWS fund. Performance is historical and does not guarantee future results.

Throughout the period ended May 31, 2013, the Fed kept short-term rates anchored near zero. Along the municipal yield curve, the two-year bond yield decreased 4 basis points over the full 12 months, from 0.33% to 0.29%, while the 30-year yield rose 16 basis points, from 3.08% to 3.24%, resulting in a total steepening of 20 basis points. However, the middle of the yield curve experienced the brunt of the impact of curve steepening, with increases of 30 and 24 basis points for the 10-year and 15-year bond, respectively. (See the graph above for municipal bond yield changes from the beginning to the end of the period.) Credit spreads — the yield differential provided by lower-quality issues vs. AAA-rated issues — generally narrowed for the 12 months as investors sought incremental yield.

| "As economic data continued to strengthen in 2013, there was increasing speculation that the U.S. Federal Reserve Board (the Fed) would begin to scale back its bond purchases." |

Positive and Negative Contributors to Fund Performance

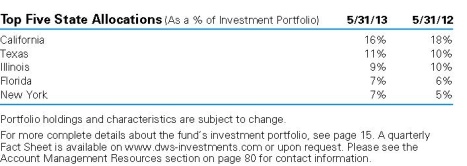

With a relatively steep yield curve as the period began, we had a tilt in the portfolio towards longer-term issues in the 20-to-30-year maturity range. This exposure added to relative performance as longer-term issues provided incremental income. In addition, with credit spreads at attractive levels, we maintained significant exposure to lower-quality issues in the BBB or A range. This helped performance relative to the benchmark as credit spreads narrowed and prices rose for many of these issues. In particular, exposure to airport revenue bonds and healthcare-related issues added to performance. In addition, the fund had a significant position in California state general obligation bonds, which outperformed as California succeeded in addressing its budgetary imbalance by raising revenue, leading to a ratings upgrade.

Performance relative to the benchmark was constrained to a degree by some of our long-standing, higher-coupon holdings as they rolled down into the 10-to-15-year area of the yield curve, which was most impacted by interest rate increases.

For some of the period, we hedged a portion of the fund's assets against interest rate changes using LIBOR (London Interbank Offered Rate, a benchmark for taxable interest rates) swaps. With a LIBOR swap, we in effect take a short position against the taxable market in order to manage the fund's overall duration and interest rate sensitivity. This helped the fund's return as municipal rates decreased and LIBOR rates increased during the period the hedge was on.

Outlook and Positioning

Municipal yields, while reasonably attractive relative to U.S. Treasuries, remain at very low levels by historical standards despite the recent uptick in rates. At the end of May 2013, the 10-year municipal bond yield of 2.09% was 98% of the comparable-maturity U.S. Treasury bond yield before taking into account the tax advantage of municipals. The 30-year municipal yield of 3.24% was 99% of the comparable U.S. Treasury yield. Longer-term issues continue to carry a substantial yield advantage and we are continuing to focus purchases on bonds with maturities in the 20-to-30-year range, while seeking exposure to premium coupon issues that can provide a degree of protection against rising interest rates. While credit spreads have narrowed over the last several quarters, we continue to see opportunities, mostly among issues in the A-quality range.

The national economic backdrop continues to show gradual improvement, and many state and local governments have continued to show progress in stabilizing their finances. Nonetheless, there remain troubled pockets, and there are also significant uncertainties with respect to the ongoing U.S. budget negotiations as well as Europe's sovereign debt crisis. As a result we believe the expertise we bring to researching municipal sectors and individual issues continues to be of critical importance. For new purchases, we are taking a very cautious approach with respect to general obligation bonds issued by localities, given uncertain levels of state support going forward.

Portfolio Management Team

Philip G. Condon, Managing Director

Co-Lead Portfolio Manager of the fund. Joined the fund in 1990.

• Head of US Retail Fixed Income.

• Joined Deutsche Asset & Wealth Management in 1983.

• BA and MBA, University of Massachusetts at Amherst.

Ashton P. Goodfield, CFA, Managing Director

Co-Lead Portfolio Manager of the fund. Joined the fund in 1998.

• Joined Deutsche Asset & Wealth Management in 1986.

• BA, Duke University.

Matthew J. Caggiano, CFA, Managing Director

Portfolio Manager of the fund. Joined the fund in 1999.

• Joined Deutsche Asset & Wealth Management in 1989.

• BS, Pennsylvania State University; MS, Boston College.

Michael J. Generazo, Director

Portfolio Manager of the fund. Joined the fund in 2010.

• Joined Deutsche Asset & Wealth Management in 1999.

• BS, Bryant College; MBA, Suffolk University.

The views expressed reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The management team's views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Past performance is no guarantee of future results. Current and future portfolio holdings are subject to risk.

Terms to Know

The Barclays Municipal Bond Index is an unmanaged, market-value-weighted measure of municipal bonds issued across the United States. Index issues have a credit rating of at least Baa and a maturity of at least two years.

Index returns do not reflect fees or expenses and it is not possible to invest directly into an index.

The Morningstar Muni National Long category consists of funds that invest in municipal bonds issued by various state and local governments to fund public projects and are free from federal taxes. These funds spread their assets across many states and sectors and focus on bond durations of seven years or more.

Quantitative easing is a government monetary policy often used when interest rates are at or near zero. With this policy government or other securities are purchased from the market, causing the price of the securities purchased to rise and the yield or interest rates on the securities purchased to fall. For the companies whose bonds the central banks are willing to purchase, it means having to pay lower interest rates on new bonds issued to replace existing bonds that have matured. With lower borrowing costs, the central banks hope that consumers will be encouraged to spend more, thus helping the overall economy, and improving the balance sheets for the companies providing the goods and services on which consumers are spending their money.

The yield curve is a graph with a left-to-right line that shows how high or low yields are, from the shortest to the longest maturities. Typically (and when the yield curve is characterized as "steep," this is especially true), the line rises from left to right as investors who are willing to tie up their money for a longer period are rewarded with higher yields.

One basis point equals 1/100 of a percentage point.

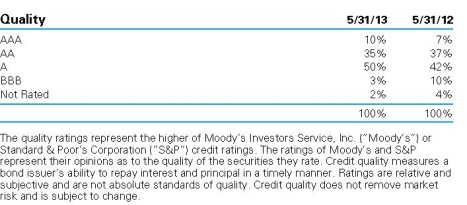

Credit quality measures a bond issuer's ability to repay interest and principal in a timely manner. Rating agencies assign letter designations, such as AAA, AA and so forth. The lower the rating the higher the probability of default. Credit quality does not remove market risk and is subject to change.

Credit spread is the additional yield provided by municipal bonds rated AA and below vs. municipals rated AAA with comparable effective maturity.

Duration, which is expressed in years, measures the sensitivity of the price of a bond or bond fund to a change in interest rates.

Sovereign debt is debt that is issued by a national government.

| Class A | 1-Year | 5-Year | 10-Year | |||||||||

Average Annual Total Returns as of 5/31/13 | ||||||||||||

| Unadjusted for Sales Charge | 4.01 | % | 6.04 | % | 4.63 | % | ||||||

| Adjusted for the Maximum Sales Charge (max 2.75% load) | 1.15 | % | 5.45 | % | 4.34 | % | ||||||

Barclays Municipal Bond Index† | 3.05 | % | 5.70 | % | 4.68 | % | ||||||

| Class B | 1-Year | 5-Year | 10-Year | |||||||||

Average Annual Total Returns as of 5/31/13 | ||||||||||||

| Unadjusted for Sales Charge | 3.14 | % | 5.15 | % | 3.81 | % | ||||||

| Adjusted for the Maximum Sales Charge (max 4.00% CDSC) | 0.14 | % | 4.99 | % | 3.81 | % | ||||||

Barclays Municipal Bond Index† | 3.05 | % | 5.70 | % | 4.68 | % | ||||||

| Class C | 1-Year | 5-Year | 10-Year | |||||||||

Average Annual Total Returns as of 5/31/13 | ||||||||||||

| Unadjusted for Sales Charge | 3.21 | % | 5.24 | % | 3.84 | % | ||||||

| Adjusted for the Maximum Sales Charge (max 1.00% CDSC) | 3.21 | % | 5.24 | % | 3.84 | % | ||||||

Barclays Municipal Bond Index† | 3.05 | % | 5.70 | % | 4.68 | % | ||||||

| Class S | 1-Year | 5-Year | 10-Year | |||||||||

Average Annual Total Returns as of 5/31/13 | ||||||||||||

| No Sales Charges | 4.19 | % | 6.21 | % | 4.86 | % | ||||||

Barclays Municipal Bond Index† | 3.05 | % | 5.70 | % | 4.68 | % | ||||||

| Institutional Class | 1-Year | 5-Year | 10-Year | |||||||||

Average Annual Total Returns as of 5/31/13 | ||||||||||||

| No Sales Charges | 4.25 | % | 6.30 | % | 4.89 | % | ||||||

Barclays Municipal Bond Index† | 3.05 | % | 5.70 | % | 4.68 | % | ||||||

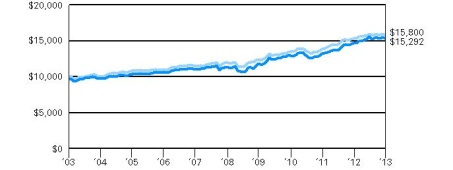

Performance in the Average Annual Total Returns table(s) above and the Growth of an Assumed $10,000 Investment line graph that follows is historical and does not guarantee future results. Investment return and principal fluctuate, so your shares may be worth more or less when redeemed. Current performance may differ from performance data shown. Please visit www.dws-investments.com for the Fund's most recent month-end performance. Fund performance includes reinvestment of all distributions. Unadjusted returns do not reflect sales charges and would have been lower if they had.

The gross expense ratios of the Fund, as stated in the fee table of the prospectus dated October 1, 2012 are 0.82%, 1.63%, 1.59%, 0.64% and 0.56% for Class A, Class B, Class C, Class S and Institutional Class shares, respectively, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report.

Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index.

Performance figures do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

A portion of the Fund's distributions may be subject to federal, state and local taxes and the alternative minimum tax.

Growth of an Assumed $10,000 Investment (Adjusted for Maximum Sales Charge) |

|

|

| Yearly periods ended May 31 |

The Fund's growth of an assumed $10,000 investment is adjusted for the maximum sales charge of 2.75%. This results in a net initial investment of $9,725.

The growth of $10,000 is cumulative.

Performance of other share classes will vary based on the sales charges and the fee structure of those classes.

† The Barclays Municipal Bond Index covers the U.S.-dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds.

| Class A | Class B | Class C | Class S | Institutional Class | ||||||||||||||||

| Net Asset Value | ||||||||||||||||||||

| 5/31/13 | $ | 9.40 | $ | 9.40 | $ | 9.40 | $ | 9.41 | $ | 9.40 | ||||||||||

| 5/31/12 | $ | 9.40 | $ | 9.40 | $ | 9.40 | $ | 9.41 | $ | 9.40 | ||||||||||

Distribution Information as of 5/31/13 | ||||||||||||||||||||

| Income Dividends, Twelve Months | $ | .37 | $ | .29 | $ | .30 | $ | .39 | $ | .39 | ||||||||||

| May Income Dividend | $ | .0289 | $ | .0235 | $ | .0226 | $ | .0303 | $ | .0311 | ||||||||||

| Capital Gain Distributions, Twelve Months | $ | .004 | $ | .004 | $ | .004 | $ | .004 | $ | .004 | ||||||||||

SEC 30-day Yield‡‡ | 1.88 | % | 1.12 | % | 1.14 | % | 2.10 | % | 2.20 | % | ||||||||||

Tax Equivalent Yield‡‡ | 2.89 | % | 1.72 | % | 1.75 | % | 3.23 | % | 3.38 | % | ||||||||||

Current Annualized Distribution Rate‡‡ | 3.69 | % | 3.00 | % | 2.89 | % | 3.86 | % | 3.97 | % | ||||||||||

‡‡ The SEC yield is net investment income per share earned over the month ended May 31, 2013, shown as an annualized percentage of the maximum offering price per share on the last day of the period. The SEC yield is computed in accordance with a standardized method prescribed by the Securities and Exchange Commission. Tax equivalent yield is based on the Fund's yield and a marginal federal income tax rate of 35%. Current annualized distribution rate is the latest monthly dividend shown as a percentage of net asset value on May 31, 2013. Distribution rate simply measures the level of dividends and is not a complete measure of performance. Yields and distribution rates are historical, not guaranteed and will fluctuate.

| Principal Amount ($) | Value ($) | |||||||

| Municipal Bonds and Notes 94.9% | ||||||||

| Alabama 0.9% | ||||||||

| Alabama, State Public School & College Authority, Capital Improvement, 5.0%, 12/1/2023 | 35,000,000 | 40,784,100 | ||||||

| Tuscaloosa County, AL, Industrial Development Authority, Gulf Opportunity Zone, Hunt Refining Project, Series C, 0.15%**, 12/1/2027, LOC: Bank of Nova Scotia | 10,000,000 | 10,000,000 | ||||||

| 50,784,100 | ||||||||

| Alaska 0.2% | ||||||||

| Alaska, State Industrial Development & Export Authority Revenue, Providence Health Services, Series A, 5.5%, 10/1/2041 | 11,000,000 | 12,582,020 | ||||||

| Arizona 1.5% | ||||||||

| Arizona, Salt Verde Financial Corp., Gas Revenue: | ||||||||

| 5.0%, 12/1/2032 | 1,600,000 | 1,783,008 | ||||||

| 5.0%, 12/1/2037 | 8,405,000 | 9,303,411 | ||||||

| Arizona, State Health Facilities Authority Revenue, Banner Health System: | ||||||||

| Series A, 5.0%, 1/1/2043 | 7,000,000 | 7,650,300 | ||||||

| Series D, 5.375%, 1/1/2032 | 12,000,000 | 13,225,200 | ||||||

| Arizona, Water Infrastructure Finance Authority Revenue, Water Quality, Series A, 5.0%, 10/1/2030 | 6,250,000 | 7,346,625 | ||||||

| Phoenix, AZ, Civic Improvement Corp., Airport Revenue: | ||||||||

| Series A, 5.0%, 7/1/2040 | 22,775,000 | 24,420,949 | ||||||

| Series A, 5.25%, 7/1/2033 | 20,885,000 | 23,111,550 | ||||||

| 86,841,043 | ||||||||

| Arkansas 0.1% | ||||||||

| North Little Rock, AR, Electric Revenue, Series A, ETM, 6.5%, 7/1/2015, INS: NATL | 8,335,000 | 8,847,519 | ||||||

| California 14.5% | ||||||||

| Banning, CA, Water & Sewer Revenue, 1989 Water System Improvement Project, ETM, 8.0%, 1/1/2019, INS: AMBAC | 520,000 | 605,654 | ||||||

| Banning, CA, Water & Sewer Revenue, Water System Reference & Improvement Project, ETM, 8.0%, 1/1/2019, INS: AMBAC | 285,000 | 346,021 | ||||||

| California, Bay Area Toll Authority, Toll Bridge Revenue, San Francisco Bay Area: | ||||||||

| Series F-1, 5.5%, 4/1/2043 | 13,000,000 | 14,798,160 | ||||||

| Series F-1, 5.625%, 4/1/2044 | 11,500,000 | 13,008,685 | ||||||

| California, Educational Facilities Authority Revenue, University of Southern California, Series A, 5.0%, 10/1/2038 | 6,925,000 | 7,839,654 | ||||||

| California, Golden State Tobacco Securitization Corp., Tobacco Settlement Revenue, Series A, 5.0%, 6/1/2045, INS: AGC | 10,275,000 | 10,688,261 | ||||||

| California, Health Facilities Financing Authority Revenue, Adventist Health System, Series A, 5.75%, 9/1/2039 | 5,000,000 | 5,745,800 | ||||||

| California, Health Facilities Financing Authority Revenue, Catholic Healthcare West: | ||||||||

| Series A, 6.0%, 7/1/2034 | 10,000,000 | 11,892,100 | ||||||

| Series A, 6.0%, 7/1/2039 | 7,500,000 | 8,919,075 | ||||||

| California, Infrastructure & Economic Development Bank Revenue, California Independent Systems Operator Corp., Series A, 6.25%, 2/1/2039 | 7,800,000 | 8,380,242 | ||||||

| California, M-S-R Energy Authority, Series B, 7.0%, 11/1/2034 | 15,315,000 | 21,251,094 | ||||||

| California, Port of Oakland, Series P, AMT, 5.0%, 5/1/2033 | 7,590,000 | 8,294,200 | ||||||

| California, State General Obligation: | ||||||||

| Series B, 144A, 0.11%**, 5/1/2040, LOC: JPMorgan Chase Bank NA | 1,000,000 | 1,000,000 | ||||||

| 5.0%, 2/1/2032 | 35,000,000 | 39,102,000 | ||||||

| 5.0%, 9/1/2032 | 10,000,000 | 10,876,500 | ||||||

| 5.0%, 2/1/2033 | 8,000,000 | 8,905,840 | ||||||

| 5.25%, 4/1/2035 | 15,340,000 | 17,382,674 | ||||||

| 6.0%, 4/1/2038 | 22,915,000 | 27,153,588 | ||||||

| 6.25%, 11/1/2034 | 20,655,000 | 25,336,869 | ||||||

| California, State General Obligation, Various Purposes: | ||||||||

| 5.0%, 6/1/2023, INS: AGMC | 25,000,000 | 28,579,500 | ||||||

| 5.0%, 12/1/2031, INS: NATL | 1,045,000 | 1,083,038 | ||||||

| Prerefunded, 5.125%, 11/1/2024 | 5,000,000 | 5,102,400 | ||||||

| 5.25%, 9/1/2026 | 18,765,000 | 22,086,968 | ||||||

| 5.25%, 9/1/2030 | 5,000,000 | 5,767,200 | ||||||

| 5.25%, 10/1/2032 | 25,000,000 | 28,672,500 | ||||||

| 6.0%, 11/1/2039 | 50,000,000 | 60,068,000 | ||||||

| 6.5%, 4/1/2033 | 58,440,000 | 72,034,313 | ||||||

| California, State Housing Finance Agency, Multi-Family Housing Revenue: | ||||||||

| Series C, AMT, 0.11%**, 8/1/2040, LOC: Fannie Mae, Freddie Mac | 4,625,000 | 4,625,000 | ||||||

| Series C, AMT, 0.14%**, 2/1/2037, LOC: Fannie Mae, Freddie Mac | 2,200,000 | 2,200,000 | ||||||

| California, State Kindergarten, Series B4, 0.1%**, 5/1/2034, LOC: Citibank NA | 6,130,000 | 6,130,000 | ||||||

| California, State Public Works Board, Lease Revenue, Capital Projects, Series I-1, 6.375%, 11/1/2034 | 10,000,000 | 12,286,100 | ||||||

| California, State Public Works Board, Lease Revenue, Department of Corrections, Series C, Prerefunded, 5.5%, 6/1/2021 | 2,500,000 | 2,566,125 | ||||||

| California, State Public Works Board, Lease Revenue, Department of General Services, Buildings 8 & 9, Series A, 6.125%, 4/1/2029 | 2,000,000 | 2,406,220 | ||||||

| California, State Public Works Board, Lease Revenue, Department of Mental Health: | ||||||||

| Series A, Prerefunded, 5.5%, 6/1/2021 | 5,275,000 | 5,552,043 | ||||||

| Series A, Prerefunded, 5.5%, 6/1/2022 | 1,400,000 | 1,473,528 | ||||||

| California, State Revenue Lease, Public Works Board, Department of Corrections: | ||||||||

| Series C, 5.0%, 6/1/2025 | 2,500,000 | 2,546,025 | ||||||

| Series C, Prerefunded, 5.5%, 6/1/2020 | 5,000,000 | 5,132,250 | ||||||

| California, State University Revenue, Series A, 5.25%, 11/1/2038 | 10,000,000 | 11,224,500 | ||||||

| California, Statewide Communities Development Authority Revenue, Kaiser Permanente, Kaiser Foundation, Series A, 5.0%, 4/1/2042 | 5,295,000 | 5,753,229 | ||||||

| East Bay, CA, Municipal Utility District, Wastewater Systems Revenue, Series A, 5.0%, 6/1/2037, INS: AMBAC | 13,085,000 | 14,703,091 | ||||||

| Foothill, CA, Eastern Corridor Agency, Toll Road Revenue: | ||||||||

| Series A, ETM, Zero Coupon, 1/1/2015 | 10,000,000 | 9,925,200 | ||||||

| Series A, ETM, Zero Coupon, 1/1/2017 | 5,000,000 | 4,859,850 | ||||||

| Series A, ETM, Zero Coupon, 1/1/2018 | 21,890,000 | 20,868,831 | ||||||

| Irvine, CA, Unified School District Special Tax, Community Facilities District, Series 1-B, 0.13%**, 9/1/2051, LOC: Bank of America NA | 12,570,000 | 12,570,000 | ||||||

| Los Angeles, CA, Community College District, Election of 2008, Series C, 5.25%, 8/1/2039 | 12,000,000 | 14,115,480 | ||||||

| Los Angeles, CA, Department of Airports Revenue, Series A, 5.25%, 5/15/2039 | 5,000,000 | 5,703,250 | ||||||

| Los Angeles, CA, Department of Airports Revenue, Los Angeles International Airport, Series A, 5.0%, 5/15/2040 | 25,000,000 | 27,744,750 | ||||||

| Murrieta Valley, CA, School District General Obligation, Unified School District, Series A, Zero Coupon, 9/1/2014, INS: FGIC, NATL | 4,235,000 | 4,190,914 | ||||||

| Oakland, CA, Special Assessment Revenue, Oakland Convention Centers, 5.5%, 10/1/2014, INS: AMBAC | 2,000,000 | 2,100,680 | ||||||

| Orange County, CA, Airport Revenue: | ||||||||

| Series A, 5.25%, 7/1/2039 | 16,000,000 | 17,683,200 | ||||||

| Series B, 5.25%, 7/1/2039 | 12,000,000 | 13,262,400 | ||||||

| Roseville, CA, School District General Obligation, Junior High, Series B, Zero Coupon, 8/1/2015, INS: FGIC, NATL | 1,000,000 | 983,240 | ||||||

| Sacramento, CA, Municipal Utility District, Electric Revenue: | ||||||||

| Series U, 5.0%, 8/15/2026, INS: AGMC | 10,455,000 | 11,712,109 | ||||||

| Series U, 5.0%, 8/15/2028, INS: AGMC | 8,175,000 | 9,060,271 | ||||||

| San Diego County, CA, Regional Airport Authority Revenue, Series A, 5.0%, 7/1/2034 | 7,000,000 | 7,582,680 | ||||||

| San Diego, CA, Community College District General Obligation, Election of 2002, 5.25%, 8/1/2033 | 5,000,000 | 5,933,400 | ||||||

| San Diego, CA, Community College District, Election of 2006, 5.0%, 8/1/2036 | 6,100,000 | 6,871,711 | ||||||

| San Diego, CA, School District General Obligation, Series A, Zero Coupon, 7/1/2014, INS: FGIC, NATL | 1,000,000 | 994,870 | ||||||

| San Francisco, CA, City & County Airports Commission, International Airport Revenue: | ||||||||

| Series 32-G, 5.0%, 5/1/2026, INS: FGIC, NATL | 8,565,000 | 9,416,961 | ||||||

| Series F, 5.0%, 5/1/2035 | 27,500,000 | 30,022,575 | ||||||

| Series E, 6.0%, 5/1/2039 | 35,000,000 | 42,372,400 | ||||||

| San Francisco, CA, City & County Certificates of Participation, Multiple Capital Improvement Projects, Series A, 5.25%, 4/1/2031 | 7,860,000 | 8,846,666 | ||||||

| San Joaquin County, CA, County General Obligation Lease, Facilities Project, 5.5%, 11/15/2013, INS: NATL | 1,390,000 | 1,416,549 | ||||||

| San Joaquin Hills, CA, Transportation/Tolls Revenue, Transportation Corridor Agency, Toll Road Revenue, Series A, Zero Coupon, 1/15/2014, INS: NATL | 14,905,000 | 14,667,265 | ||||||

| Walnut, CA, Energy Center Authority Revenue, Series A, 5.0%, 1/1/2040 | 10,000,000 | 10,641,900 | ||||||

| 835,065,599 | ||||||||

| Colorado 4.0% | ||||||||

| Colorado, E-470 Public Highway Authority Revenue: | ||||||||

| Series B, Zero Coupon, 9/1/2016, INS: NATL | 5,000,000 | 4,624,200 | ||||||

| Series A-1, 5.5%, 9/1/2024, INS: NATL | 4,000,000 | 4,319,400 | ||||||

| Colorado, Health Facilities Authority Revenue, Covenant Retirement Communities, Inc., 5.0%, 12/1/2035 | 15,000,000 | 15,312,300 | ||||||

| Colorado, Public Energy Authority, Natural Gas Purchase Revenue, 6.5%, 11/15/2038, GTY: Merrill Lynch & Co., Inc. | 30,000,000 | 40,362,600 | ||||||

| Colorado, State Building Excellent Schools Today, Certificates of Participation, Series G, 5.0%, 3/15/2032 | 8,630,000 | 9,583,097 | ||||||

| Colorado, Transportation/Tolls Revenue: | ||||||||

| Series B, Zero Coupon, 9/1/2014, INS: NATL | 6,380,000 | 6,217,438 | ||||||

| Series B, Zero Coupon, 9/1/2015, INS: NATL | 17,120,000 | 16,293,275 | ||||||

| Series B, Zero Coupon, 9/1/2017, INS: NATL | 8,000,000 | 7,157,680 | ||||||

| Series B, Zero Coupon, 9/1/2018, INS: NATL | 20,560,000 | 17,707,711 | ||||||

| Series B, Zero Coupon, 9/1/2019, INS: NATL | 36,500,000 | 29,970,880 | ||||||

| Series B, Zero Coupon, 9/1/2020, INS: NATL | 7,000,000 | 5,481,350 | ||||||

| Series A, 5.75%, 9/1/2014, INS: NATL | 14,700,000 | 15,444,702 | ||||||

| Colorado Springs, CO, Utilities Revenue, System Improvement, Series A, 0.12%**, 11/1/2038, SPA: Bank of America NA | 3,700,000 | 3,700,000 | ||||||

| Douglas County, CO, School District General Obligation, 7.0%, 12/15/2013, INS: NATL | 2,500,000 | 2,590,750 | ||||||

| University of Colorado, Enterprise Revenue, 5.25%, 6/1/2036 | 11,500,000 | 13,235,580 | ||||||

| University of Colorado, Hospital Authority Revenue, Series A, 5.0%, 11/15/2042 | 36,010,000 | 39,191,124 | ||||||

| 231,192,087 | ||||||||

| Connecticut 1.0% | ||||||||

| Connecticut, Harbor Point Infrastructure Improvement District, Special Obligation Revenue, Harbor Point Project, Series A, 7.875%, 4/1/2039 | 13,000,000 | 14,721,720 | ||||||

| Connecticut, State Health & Educational Facilities Authority Revenue, Hartford Healthcare, Series A, 5.0%, 7/1/2041 | 20,000,000 | 21,333,600 | ||||||

| Connecticut, State Health & Educational Facilities Authority Revenue, Stamford Hospital, Series J, 5.125%, 7/1/2035 | 18,000,000 | 19,636,380 | ||||||

| 55,691,700 | ||||||||

| Delaware 0.1% | ||||||||

| Delaware, State Economic Development Authority Revenue, YMCA Delaware Project, 0.12%**, 5/1/2036, LOC: PNC Bank NA | 4,785,000 | 4,785,000 | ||||||

| District of Columbia 0.7% | ||||||||

| District of Columbia, Income Tax Secured Revenue, Series G, 5.0%, 12/1/2036 | 27,475,000 | 30,901,682 | ||||||

| District of Columbia, National Public Radio Revenue, Series A, 5.0%, 4/1/2035 | 5,000,000 | 5,428,350 | ||||||

| District of Columbia, Water & Sewer Revenue, Public Utility Revenue, 5.5%, 10/1/2023, INS: AGMC | 5,000,000 | 6,333,850 | ||||||

| 42,663,882 | ||||||||

| Florida 6.2% | ||||||||

| Broward County, FL, Airport Systems Revenue, Series Q-1, 5.0%, 10/1/2037 | 39,000,000 | 42,694,860 | ||||||

| Clearwater, FL, Water & Sewer Revenue, Series A, 5.25%, 12/1/2039 | 2,000,000 | 2,225,860 | ||||||

| Florida, Capital Trust Agency Housing Revenue, Atlantic Housing Foundation, Series A, 0.15%**, 7/15/2024, LIQ: Fannie Mae | 19,000,000 | 19,000,000 | ||||||

| Florida, Jacksonville Electric Authority, Water & Sewer Revenue, Series A, 5.0%, 10/1/2032 | 5,000,000 | 5,606,150 | ||||||

| Florida, Village Center Community Development District, Utility Revenue, ETM, 6.0%, 11/1/2018, INS: FGIC | 1,250,000 | 1,473,162 | ||||||

| Fort Pierce, FL, Utilities Authority Revenue, Series B, Zero Coupon, 10/1/2018, INS: AMBAC | 2,000,000 | 1,769,880 | ||||||

| Hillsborough County, FL, Industrial Development Authority Revenue, University Community Hospital, ETM, 6.5%, 8/15/2019, INS: NATL | 1,000,000 | 1,221,290 | ||||||

| Lee County, FL, Airport Revenue, Series A, AMT, 5.375%, 10/1/2032 | 1,750,000 | 1,907,850 | ||||||

| Marco Island, FL, Utility Systems Revenue: | ||||||||

| Series A, 5.0%, 10/1/2034 | 1,000,000 | 1,093,860 | ||||||

| Series A, 5.0%, 10/1/2040 | 1,000,000 | 1,085,120 | ||||||

| Melbourne, FL, Water & Sewer Revenue, ETM, Zero Coupon, 10/1/2016, INS: FGIC | 1,350,000 | 1,316,075 | ||||||

| Miami-Dade County, FL, Aviation Revenue: | ||||||||

| Series A, AMT, 5.0%, 10/1/2030 | 7,355,000 | 8,039,677 | ||||||

| Series A, AMT, 5.0%, 10/1/2031 | 3,495,000 | 3,800,288 | ||||||

| Series A, AMT, 5.0%, 10/1/2032 | 9,050,000 | 9,781,602 | ||||||

| Series B, 5.0%, 10/1/2035, INS: AGMC | 15,000,000 | 16,756,950 | ||||||

| Series A, 5.5%, 10/1/2041 | 30,000,000 | 33,825,000 | ||||||

| Miami-Dade County, FL, Aviation Revenue, Miami International Airport: | ||||||||

| Series C, AMT, 5.25%, 10/1/2022, INS: AGMC | 20,000,000 | 22,988,400 | ||||||

| Series A-1, 5.375%, 10/1/2035 | 1,000,000 | 1,117,560 | ||||||

| Series A-1, 5.375%, 10/1/2041 | 19,290,000 | 21,465,526 | ||||||

| Miami-Dade County, FL, Double Barreled Aviation, 5.0%, 7/1/2041 | 6,700,000 | 7,283,838 | ||||||

| Miami-Dade County, FL, Transit Sales Surtax Revenue, 5.0%, 7/1/2037 | 16,500,000 | 18,201,810 | ||||||

| Miami-Dade County, FL, Water & Sewer Systems Revenue, 5.0%, 10/1/2034 | 17,800,000 | 19,676,654 | ||||||

| North Brevard County, FL, Hospital District Revenue, Parrish Medical Center Project, 5.75%, 10/1/2043 | 10,000,000 | 10,950,500 | ||||||

| Orange County, FL, Health Facilities Authority Revenue: | ||||||||

| Series 2006-A, 6.25%, 10/1/2016, INS: NATL | 1,100,000 | 1,199,726 | ||||||

| Series 2006-A, ETM, 6.25%, 10/1/2016, INS: NATL | 70,000 | 79,402 | ||||||

| Orange County, FL, Health Facilities Authority Revenue, Orlando Regional Healthcare System: | ||||||||

| Series B, 5.25%, 12/1/2029, INS: AGMC | 6,500,000 | 7,232,940 | ||||||

| Series A, 6.25%, 10/1/2018, INS: NATL | 500,000 | 611,940 | ||||||

| Series C, 6.25%, 10/1/2021, INS: NATL | 6,000,000 | 7,300,560 | ||||||

| Orange County, FL, Health Facilities Authority, Orlando Regional Facilities, Series A, ETM, 6.25%, 10/1/2016, INS: NATL | 2,830,000 | 3,210,097 | ||||||

| Orlando & Orange County, FL, Expressway Authority Revenue: | ||||||||

| Series C, 5.0%, 7/1/2035 | 16,215,000 | 17,627,975 | ||||||

| Series A, 5.0%, 7/1/2040 | 11,895,000 | 12,846,600 | ||||||

| Palm Beach County, FL, Airport Systems Revenue: | ||||||||

| 5.75%, 10/1/2013, INS: NATL | 3,770,000 | 3,837,332 | ||||||

| 5.75%, 10/1/2014, INS: NATL | 755,000 | 805,842 | ||||||

| Palm Beach County, FL, Criminal Justice Facilities Revenue, 7.2%, 6/1/2015, INS: FGIC, NATL | 110,000 | 123,345 | ||||||

| Port St. Lucie, FL, Utility System Revenue: | ||||||||

| 5.0%, 9/1/2035, INS: AGC | 2,600,000 | 2,878,018 | ||||||

| 5.25%, 9/1/2035, INS: AGC | 3,000,000 | 3,425,880 | ||||||

| Sunrise, FL, Water & Sewer Revenue, Utility Systems, ETM, 5.5%, 10/1/2018, INS: AMBAC | 12,500,000 | 14,649,875 | ||||||

| Tallahassee, FL, Energy System Revenue, 5.5%, 10/1/2016, INS: AMBAC | 1,005,000 | 1,155,830 | ||||||

| Tampa, FL, Sports Authority Revenue, Sales Tax-Tampa Bay Arena Project, 5.75%, 10/1/2020, INS: NATL | 2,075,000 | 2,281,276 | ||||||

| Tampa, FL, Utility Tax Revenue: | ||||||||

| Zero Coupon, 10/1/2014, INS: AMBAC | 375,000 | 371,250 | ||||||

| ETM, Zero Coupon, 10/1/2014, INS: AMBAC | 2,790,000 | 2,778,115 | ||||||

| Tampa-Hillsborough County, FL, Expressway Authority, Series A, 5.0%, 7/1/2037 | 18,430,000 | 20,137,171 | ||||||

| 355,835,086 | ||||||||

| Georgia 4.8% | ||||||||

| Atlanta, GA, Airport Revenue: | ||||||||

| Series A, 5.0%, 1/1/2035 | 2,470,000 | 2,688,373 | ||||||

| Series B, 5.0%, 1/1/2037 | 720,000 | 798,610 | ||||||

| Atlanta, GA, Metropolitan Rapid Transit Authority, Sales Tax Revenue, 5.0%, 7/1/2039 | 5,000,000 | 5,594,900 | ||||||

| Atlanta, GA, Water & Sewer Revenue, Series A, 5.5%, 11/1/2019, INS: FGIC, NATL | 13,000,000 | 15,955,160 | ||||||

| Atlanta, GA, Water & Wastewater Revenue, Series B, 5.375%, 11/1/2039, INS: AGMC | 40,000,000 | 44,579,600 | ||||||

| Burke County, GA, Development Authority Pollution Control Revenue, Oglethorpe Power Corp. Vogtle Project: | ||||||||

| Series A, 5.3%, 1/1/2033, INS: AGMC | 10,000,000 | 11,258,300 | ||||||

| Series B, 5.5%, 1/1/2033 | 4,000,000 | 4,375,800 | ||||||

| Burke County, GA, Development Authority, Georgia Power Co., Plant Vogtle Project, AMT, 0.1%**, 11/1/2052 | 11,000,000 | 11,000,000 | ||||||

| De Kalb County, GA, Water & Sewer Revenue: | ||||||||

| Series A, 5.25%, 10/1/2032 | 2,180,000 | 2,507,109 | ||||||

| Series A, 5.25%, 10/1/2033 | 3,635,000 | 4,168,981 | ||||||

| Series A, 5.25%, 10/1/2036 | 11,115,000 | 12,651,982 | ||||||

| Series A, 5.25%, 10/1/2041 | 13,000,000 | 14,676,610 | ||||||

| Gainesville & Hall County, GA, Hospital Authority Revenue, Anticipation Certificates, Northeast Georgia Healthcare: | ||||||||

| Series A, 5.375%, 2/15/2040 | 8,225,000 | 8,941,891 | ||||||

| Series A, 5.5%, 2/15/2045 | 20,000,000 | 21,951,400 | ||||||

| Georgia, Main Street Natural Gas, Inc., Gas Project Revenue: | ||||||||

| Series A, 5.0%, 3/15/2019 | 17,440,000 | 20,126,806 | ||||||

| Series B, 5.0%, 3/15/2019 | 5,000,000 | 5,673,000 | ||||||

| Series A, 5.0%, 3/15/2020 | 2,700,000 | 3,114,450 | ||||||

| Series B, 5.0%, 3/15/2020 | 5,000,000 | 5,694,950 | ||||||

| Series A, 5.0%, 3/15/2022 | 17,340,000 | 19,930,249 | ||||||

| Series A, 5.5%, 9/15/2023 | 5,000,000 | 5,979,550 | ||||||

| Series A, 5.5%, 9/15/2024 | 4,635,000 | 5,578,686 | ||||||

| Series A, 5.5%, 9/15/2027 | 5,000,000 | 6,113,650 | ||||||

| Series A, 5.5%, 9/15/2028 | 5,000,000 | 6,072,150 | ||||||

| Georgia, Medical Center Hospital Authority Revenue, Anticipation Certificates, Columbus Regional Healthcare Systems, 6.5%, 8/1/2038, INS: AGC | 18,700,000 | 21,098,462 | ||||||

| Georgia, Municipal Electric Authority Power Revenue, Series W, 6.6%, 1/1/2018, INS: NATL | 8,575,000 | 9,483,264 | ||||||

| Georgia, State Municipal Electric Authority, Series GG, 5.0%, 1/1/2039 | 5,695,000 | 6,285,173 | ||||||

| Georgia, Water & Sewer Revenue, Municipal Electric Authority Power Revenue, Series W, ETM, 6.6%, 1/1/2018, INS: NATL | 100,000 | 116,620 | ||||||

| 276,415,726 | ||||||||

| Hawaii 0.6% | ||||||||

| Hawaii, State Airports Systems Revenue, Series A, 5.0%, 7/1/2039 | 16,800,000 | 18,165,840 | ||||||

| Hawaii, State Department of Budget & Finance, Special Purpose Revenue, Hawaiian Electric Co., Inc., 6.5%, 7/1/2039, GTY: Hawaiian Electric Co., Inc. | 6,000,000 | 7,035,780 | ||||||

| Honolulu City & County, HI, Wastewater Systems Revenue, Series A, 5.25%, 7/1/2036 | 10,285,000 | 11,803,580 | ||||||

| 37,005,200 | ||||||||

| Idaho 0.2% | ||||||||

| Idaho, Health Facilities Authority Revenue, St. Luke's Regional Medical Center, 6.75%, 11/1/2037 | 10,060,000 | 11,695,152 | ||||||

| Illinois 9.6% | ||||||||

| Channahon, IL, Morris Hospital Revenue, Series A, 0.13%**, 12/1/2034, LOC: U.S. Bank NA | 6,780,000 | 6,780,000 | ||||||

| Chicago, IL, Core City General Obligation, Zero Coupon, 1/1/2017, INS: FGIC, NATL | 20,000,000 | 18,833,000 | ||||||

| Chicago, IL, General Obligation: | ||||||||

| Series B, 5.125%, 1/1/2015, INS: AMBAC | 1,470,000 | 1,538,605 | ||||||

| Series B, Prerefunded, 5.125%, 1/1/2015, INS: AMBAC | 490,000 | 503,931 | ||||||

| Series A, 5.25%, 1/1/2035 | 10,125,000 | 10,990,283 | ||||||

| Chicago, IL, O'Hare International Airport Revenue: | ||||||||

| Series A-2, AMT, 5.75%, 1/1/2019, INS: AGMC | 12,975,000 | 13,369,310 | ||||||

| Series C, 6.5%, 1/1/2041 | 26,700,000 | 33,982,425 | ||||||

| Chicago, IL, O'Hare International Airport Revenue, Third Lien: | ||||||||

| Series A, 5.75%, 1/1/2039 | 13,650,000 | 15,684,533 | ||||||

| Series B, 6.0%, 1/1/2041 | 25,000,000 | 29,563,250 | ||||||

| Chicago, IL, Sales & Special Tax Revenue, 5.375%, 1/1/2014, INS: AMBAC | 1,105,000 | 1,136,636 | ||||||

| Chicago, IL, School District General Obligation Lease, Board of Education: | ||||||||

| Series A, 6.0%, 1/1/2016, INS: NATL | 11,025,000 | 12,452,958 | ||||||

| Series A, 6.0%, 1/1/2020, INS: NATL | 46,340,000 | 53,774,326 | ||||||

| Series A, 6.25%, 1/1/2015, INS: NATL | 15,225,000 | 15,948,188 | ||||||

| Chicago, IL, Water & Sewer Revenue, Zero Coupon, 11/1/2018, INS: AMBAC | 5,165,000 | 4,656,248 | ||||||

| Chicago, IL, Water Revenue, 5.0%, 11/1/2023, INS: AGMC | 10,000,000 | 11,710,100 | ||||||

| Cook County, IL, County General Obligation, 6.5%, 11/15/2014, INS: FGIC, NATL | 18,560,000 | 20,191,424 | �� | |||||

| Cook County, IL, Forest Preservation District, Series C, 5.0%, 12/15/2037 | 3,155,000 | 3,515,080 | ||||||

| Illinois, Finance Authority Revenue, Advocate Health Care Network: | ||||||||

| Series B, 5.375%, 4/1/2044 | 5,500,000 | 6,089,435 | ||||||

| Series A, 5.5%, 4/1/2044 | 5,500,000 | 6,200,755 | ||||||

| Series D, 6.5%, 11/1/2038 | 4,085,000 | 4,892,564 | ||||||

| Illinois, Finance Authority Revenue, Elmhurst Memorial Healthcare, Series A, 5.625%, 1/1/2037 | 8,000,000 | 8,836,880 | ||||||

| Illinois, Finance Authority Revenue, Memorial Health Systems: | ||||||||

| 5.5%, 4/1/2034 | 12,100,000 | 13,295,964 | ||||||

| 5.5%, 4/1/2039 | 4,800,000 | 5,232,240 | ||||||

| Illinois, Finance Authority Revenue, Northwest Community Hospital, Series A, 5.5%, 7/1/2038 | 22,990,000 | 24,763,908 | ||||||

| Illinois, Higher Education Revenue, Zero Coupon, 4/1/2015, INS: NATL | 3,300,000 | 3,243,900 | ||||||

| Illinois, Hospital & Healthcare Revenue, Health Facilities Authority: | ||||||||

| 6.25%, 8/15/2013, INS: NATL | 655,000 | 662,336 | ||||||

| Series A, 6.25%, 1/1/2015, INS: AMBAC | 5,050,000 | 5,289,875 | ||||||

| Illinois, Metropolitan Pier & Exposition Authority, Dedicated State Tax Revenue, McCormick Capital Appreciation: | ||||||||

| Zero Coupon, 6/15/2013, INS: NATL | 4,045,000 | 4,044,555 | ||||||

| ETM, Zero Coupon, 6/15/2013, INS: NATL | 3,520,000 | 3,519,718 | ||||||

| Illinois, Metropolitan Pier & Exposition Authority, Dedicated State Tax Revenue, McCormick Place Expansion: | ||||||||

| Series A, Zero Coupon, 6/15/2016, INS: FGIC, NATL | 7,035,000 | 6,779,418 | ||||||

| Series A, ETM, Zero Coupon, 6/15/2016, INS: FGIC, NATL | 2,965,000 | 2,901,608 | ||||||

| Illinois, Municipal Electric Agency Power Supply: | ||||||||

| Series A, 5.25%, 2/1/2023, INS: FGIC, NATL | 3,500,000 | 3,980,305 | ||||||

| Series A, 5.25%, 2/1/2024, INS: FGIC, NATL | 2,500,000 | 2,843,075 | ||||||

| Illinois, Pollution Control Revenue, Development Finance Authority, 5.85%, 1/15/2014, INS: AMBAC | 5,000,000 | 5,150,250 | ||||||

| Illinois, Project Revenue, Zero Coupon, 1/1/2014, INS: AGMC | 17,975,000 | 17,897,168 | ||||||

| Illinois, Railsplitter Tobacco Settlement Authority, 6.0%, 6/1/2028 | 17,315,000 | 20,679,304 | ||||||

| Illinois, Regional Transportation Authority: | ||||||||

| Series B, 5.75%, 6/1/2033, INS: NATL | 7,000,000 | 8,815,030 | ||||||

| Series A, 6.7%, 11/1/2021, INS: FGIC, NATL | 23,910,000 | 28,348,652 | ||||||

| Illinois, Sales & Special Tax Revenue: | ||||||||

| 6.25%, 12/15/2020, INS: AMBAC | 6,380,000 | 7,232,559 | ||||||

| Series P, 6.5%, 6/15/2013 | 405,000 | 405,996 | ||||||

| Illinois, Special Assessment Revenue, Metropolitan Pier and Exposition Authority, Series A, Zero Coupon, 12/15/2018, INS: NATL | 6,660,000 | 6,007,653 | ||||||

| Illinois, State Finance Authority Revenue, Ascension Health Credit Group: | ||||||||

| Series A, 5.0%, 11/15/2032 | 2,435,000 | 2,737,257 | ||||||

| Series A, 5.0%, 11/15/2037 | 3,440,000 | 3,800,237 | ||||||

| Illinois, State Finance Authority Revenue, OSF Healthcare Systems, Series A, 5.0%, 5/15/2041 | 13,155,000 | 14,111,237 | ||||||

| Illinois, State Finance Authority Revenue, Resurrection Health, Series C, 0.13%**, 5/15/2035, LOC: Barclays Bank PLC | 5,000,000 | 5,000,000 | ||||||

| Illinois, State Toll Highway Authority, Series A, 5.0%, 1/1/2038 | 14,695,000 | 16,180,518 | ||||||

| Lake Cook Kane & McHenry Counties, IL, School District General Obligation, 6.3%, 12/1/2017, INS: AGMC | 1,885,000 | 2,324,639 | ||||||

| Lake County, IL, Higher Education Revenue, District No. 117: | ||||||||

| Series B, Zero Coupon, 12/1/2013, INS: FGIC, NATL | 5,880,000 | 5,861,831 | ||||||

| Series B, Zero Coupon, 12/1/2014, INS: FGIC, NATL | 5,985,000 | 5,888,582 | ||||||

| Springfield, IL, Water Revenue, 5.0%, 3/1/2037 | 3,640,000 | 4,073,014 | ||||||

| University of Illinois, Health Services Facilities Systems, Series B, 0.13%**, 10/1/2026, LOC: JPMorgan Chase Bank NA | 10,600,000 | 10,600,000 | ||||||

| Will County, IL, County General Obligation: | ||||||||

| Series B, Zero Coupon, 12/1/2013, INS: FGIC, NATL | 12,030,000 | 12,013,038 | ||||||

| Series B, Zero Coupon, 12/1/2014, INS: FGIC, NATL | 10,255,000 | 10,188,855 | ||||||

| Will County, IL, School District General Obligation, Community Unit School District No. 365-U, Series B, ETM, Zero Coupon, 11/1/2015, INS: AGMC | 8,000,000 | 7,888,160 | ||||||

| 552,410,813 | ||||||||

| Indiana 1.3% | ||||||||

| Indiana, Electric Revenue, Municipal Power Agency, Series B, 5.5%, 1/1/2016, INS: NATL | 10,160,000 | 10,743,184 | ||||||

| Indiana, Finance Authority Hospital Revenue, Deaconess Hospital Obligation, Series A, 6.75%, 3/1/2039 | 5,230,000 | 6,121,349 | ||||||

| Indiana, Hospital & Healthcare Revenue, Health Facilities Financing Authority: | ||||||||

| ETM, 6.0%, 7/1/2013, INS: NATL | 1,230,000 | 1,235,916 | ||||||

| ETM, 6.0%, 7/1/2013, INS: NATL | 390,000 | 391,541 | ||||||

| ETM, 6.0%, 7/1/2014, INS: NATL | 410,000 | 428,364 | ||||||

| ETM, 6.0%, 7/1/2014, INS: NATL | 1,310,000 | 1,390,775 | ||||||

| ETM, 6.0%, 7/1/2015, INS: NATL | 440,000 | 478,130 | ||||||

| ETM, 6.0%, 7/1/2015, INS: NATL | 1,385,000 | 1,544,663 | ||||||

| 6.0%, 7/1/2016, INS: NATL | 465,000 | 520,860 | ||||||

| ETM, 6.0%, 7/1/2016, INS: NATL | 1,470,000 | 1,710,904 | ||||||

| 6.0%, 7/1/2017, INS: NATL | 490,000 | 559,242 | ||||||

| ETM, 6.0%, 7/1/2017, INS: NATL | 1,560,000 | 1,888,052 | ||||||

| 6.0%, 7/1/2018, INS: NATL | 520,000 | 605,155 | ||||||

| ETM, 6.0%, 7/1/2018, INS: NATL | 1,655,000 | 2,059,499 | ||||||

| Indiana, State Finance Authority Revenue, Community Foundation of Northwest Indiana, 5.0%, 3/1/2041 | 17,395,000 | 18,358,509 | ||||||

| Indiana, State Finance Authority, Hospital Revenue, Indiana University Health, Series D, 0.12%**, 3/1/2033, LOC: Northern Trust Co. | 6,115,000 | 6,115,000 | ||||||

| Indiana, State Finance Authority, Wastewater Utility Revenue, First Lien, Series A, 5.25%, 10/1/2038 | 8,000,000 | 9,081,360 | ||||||

| Indiana, Transportation/Tolls Revenue, Series A, 7.25%, 6/1/2015 | 1,350,000 | 1,429,582 | ||||||

| St. Joseph County, IN, Educational Facilities Revenue, Notre Dame du Lac Project, 5.0%, 3/1/2036 | 10,000,000 | 11,288,200 | ||||||

| 75,950,285 | ||||||||

| Iowa 0.0% | ||||||||

| Iowa, State Finance Authority, Single Family Revenue, Series C, AMT, 0.17%**, 1/1/2036, SPA: State Street Bank & Trust Co. | 1,700,000 | 1,700,000 | ||||||

| Kansas 0.7% | ||||||||

| Kansas, Pollution Control Revenue, Development Financing Authority, Series II, 5.5%, 11/1/2017 | 1,000,000 | 1,202,410 | ||||||

| Kansas, State Development Finance Authority Hospital Revenue, Adventist Health System: | ||||||||

| Series A, 5.0%, 11/15/2032 | 13,000,000 | 14,493,180 | ||||||

| Series A, 5.0%, 11/15/2034 | 8,465,000 | 9,382,352 | ||||||

| Olathe, KS, Health Facilities Revenue, Olathe Medical Center, Inc., 144A, 0.15%**, 9/1/2032, LOC: Bank of America NA | 12,655,000 | 12,655,000 | ||||||

| Wichita, KS, Hospital Revenue, Facilities Improvement, Series III-A, 5.0%, 11/15/2034 | 3,590,000 | 3,903,012 | ||||||

| 41,636,954 | ||||||||

| Kentucky 1.4% | ||||||||

| Kentucky, Economic Development Finance Authority, Health Systems Revenue, Norton Healthcare: | ||||||||

| Series C, 5.7%, 10/1/2013, INS: NATL | 5,495,000 | 5,591,602 | ||||||

| Series C, ETM, 5.7%, 10/1/2013, INS: NATL | 2,750,000 | 2,797,025 | ||||||

| Series C, 5.8%, 10/1/2014, INS: NATL | 3,420,000 | 3,510,733 | ||||||

| Series C, Prerefunded, 5.8%, 10/1/2014, INS: NATL | 1,710,000 | 1,758,718 | ||||||

| Series C, 5.85%, 10/1/2015, INS: NATL | 3,490,000 | 3,580,601 | ||||||

| Series C, Prerefunded, 5.85%, 10/1/2015, INS: NATL | 1,745,000 | 1,794,994 | ||||||

| Series C, 5.9%, 10/1/2016, INS: NATL | 4,330,000 | 4,440,155 | ||||||

| Series C, Prerefunded, 5.9%, 10/1/2016, INS: NATL | 2,170,000 | 2,232,539 | ||||||

| Kentucky, Economic Development Finance Authority, Hospital Facilities Revenue, Owensboro Medical Health Systems, Series A, 6.5%, 3/1/2045 | 11,000,000 | 12,858,340 | ||||||

| Kentucky, Economic Development Finance Authority, Louisville Arena Project Revenue, Series A-1, 6.0%, 12/1/2038, INS: AGC | 4,500,000 | 4,848,255 | ||||||

| Louisville & Jefferson County, KY, Metropolitan Government Health Systems Revenue, Norton Healthcare, Inc., 5.0%, 10/1/2030 | 15,000,000 | 15,684,600 | ||||||

| Louisville & Jefferson County, KY, Metropolitan Government Revenue, Catholic Health Initiatives, Series A, 5.0%, 12/1/2035 | 20,770,000 | 22,980,136 | ||||||

| 82,077,698 | ||||||||

| Louisiana 0.5% | ||||||||

| East Baton Rouge, LA, Sewer Commission Revenue, Series A, 5.25%, 2/1/2039 | 10,000,000 | 11,200,000 | ||||||

| Louisiana, Public Facilities Authority, Hospital Revenue, Lafayette General Medical Center, 5.5%, 11/1/2040 | 5,000,000 | 5,450,650 | ||||||

| Louisiana, St. John Baptist Parish Revenue, Marathon Oil Corp., Series A, 5.125%, 6/1/2037 | 12,000,000 | 12,666,960 | ||||||

| 29,317,610 | ||||||||

| Maine 0.2% | ||||||||

| Maine, Health & Higher Educational Facilities Authority Revenue, Series A, 5.0%, 7/1/2040 | 9,650,000 | 10,397,103 | ||||||

| Maryland 0.4% | ||||||||

| Maryland, State Economic Development Corp. Revenue, Senior Lien Project, Chesapeake Bay: | ||||||||

| Series A, 5.0%, 12/1/2016 | 860,000 | 748,200 | ||||||

| Series A, 5.0%, 12/1/2031 | 20,000,000 | 13,195,000 | ||||||

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Adventist Health Care, Series A, 0.13%**, 1/1/2035, LOC: Union Bank NA | 3,250,000 | 3,250,000 | ||||||

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Anne Arundel Health Systems, Series A, 6.75%, 7/1/2039 | 3,400,000 | 4,186,930 | ||||||

| 21,380,130 | ||||||||

| Massachusetts 3.7% | ||||||||

| Massachusetts, Bay Transportation Authority Revenue, Series B, 6.2%, 3/1/2016 | 7,065,000 | 7,599,750 | ||||||

| Massachusetts, Higher Education Revenue, College Building Authority Project, Series A, 7.5%, 5/1/2014 | 1,970,000 | 2,084,418 | ||||||

| Massachusetts, Industrial Development Revenue, Development Finance Agency, Series A, 7.1%, 7/1/2032 | 4,310,000 | 4,312,155 | ||||||

| Massachusetts, Port Authority Revenue, ETM, 13.0%, 7/1/2013 | 235,000 | 237,312 | ||||||

| Massachusetts, Sales & Special Tax Revenue, Federal Highway Grant, Series A, ETM, Zero Coupon, 12/15/2014 | 27,680,000 | 27,539,662 | ||||||

| Massachusetts, State College Building Authority Revenue: | ||||||||

| Series B, 5.0%, 5/1/2037 | 4,500,000 | 5,058,900 | ||||||

| Series B, 5.0%, 5/1/2043 | 4,125,000 | 4,600,324 | ||||||

| Massachusetts, State Department of Transportation, Metropolitan Highway Systems Revenue, Series B, 5.0%, 1/1/2032 | 28,800,000 | 31,791,744 | ||||||

| Massachusetts, State Development Finance Agency Revenue, Linden Ponds, Inc. Facility: | ||||||||

| Series A-2, 5.5%, 11/15/2046 | 63,235 | 50,699 | ||||||

| Series A-1, 6.25%, 11/15/2031 | 1,182,967 | 1,118,649 | ||||||

| Series B, 11/15/2056* | 314,524 | 2,214 | ||||||

| Massachusetts, State Development Finance Agency Revenue, Partners Healthcare System, Inc., Series L, 5.0%, 7/1/2036 | 13,680,000 | 15,240,888 | ||||||

| Massachusetts, State Health & Educational Facilities Authority Revenue, Hillcrest Extended Care Services, Inc., Series A, 0.17%**, 10/1/2026, LOC: Bank of America NA | 4,775,000 | 4,775,000 | ||||||

| Massachusetts, State Health & Educational Facilities Authority Revenue, Massachusetts Institute of Technology, Series K, 5.5%, 7/1/2022 | 9,000,000 | 11,678,400 | ||||||

| Massachusetts, State Health & Educational Facilities Authority Revenue, Suffolk University, Series A, 5.75%, 7/1/2039 | 14,285,000 | 15,837,922 | ||||||

| Massachusetts, State Port Authority Special Facilities Revenue, Delta Air Lines, Inc. Project: | ||||||||

| Series A, AMT, 5.5%, 1/1/2014, INS: AMBAC | 3,000,000 | 3,003,090 | ||||||

| Series A, AMT, 5.5%, 1/1/2015, INS: AMBAC | 3,000,000 | 3,002,970 | ||||||

| Series A, AMT, 5.5%, 1/1/2016, INS: AMBAC | 3,000,000 | 3,002,580 | ||||||

| Massachusetts, State School Building Authority, Sales Tax Revenue, Series B, 5.25%, 10/15/2035 | 12,000,000 | 13,922,760 | ||||||

| Massachusetts, State Water Resource Authority: | ||||||||

| Series B, 5.0%, 8/1/2041 | 5,500,000 | 6,149,715 | ||||||

| Series J, 5.5%, 8/1/2021, INS: AGMC | 5,685,000 | 7,193,572 | ||||||

| Massachusetts, Transportation/Tolls Revenue, Turnpike Authority, Series C, Zero Coupon, 1/1/2018, INS: NATL | 10,000,000 | 9,369,900 | ||||||

| Massachusetts, Water & Sewer Revenue, Water Authority, Series J, 5.5%, 8/1/2020, INS: AGMC | 14,315,000 | 17,939,272 | ||||||

| Massachusetts, Water & Sewer Revenue, Water Resource Authority, Series A, ETM, 6.5%, 7/15/2019 (a) | 13,710,000 | 16,027,401 | ||||||

| 211,539,297 | ||||||||

| Michigan 2.7% | ||||||||

| Detroit, MI, School District General Obligation, Series C, 5.25%, 5/1/2014, INS: FGIC | 1,000,000 | 1,042,240 | ||||||

| Detroit, MI, Sewer Disposal Revenue, Series B, 7.5%, 7/1/2033, INS: AGMC | 10,000,000 | 12,201,800 | ||||||

| Detroit, MI, Water & Sewer Revenue, Series A, Zero Coupon, 7/1/2015, INS: FGIC, NATL | 8,710,000 | 8,364,910 | ||||||

| Detroit, MI, Water Supply Systems Revenue, Series A, 5.75%, 7/1/2037 | 11,410,000 | 12,582,377 | ||||||

| Michigan, State Building Authority Revenue, Facilities Program: | ||||||||

| Series H, 5.125%, 10/15/2033 | 9,755,000 | 10,644,266 | ||||||

| Series I, 6.0%, 10/15/2038 | 9,000,000 | 10,716,390 | ||||||

| Michigan, State Grant Anticipation Bonds, 5.25%, 9/15/2023, INS: AGMC | 7,500,000 | 8,713,050 | ||||||

| Michigan, State Higher Education Facilities Authority, Limited Obligation, Hope College, Series B, 0.13%**, 4/1/2032, LOC: PNC Bank NA | 1,555,000 | 1,555,000 | ||||||

| Michigan, State Hospital Finance Authority Revenue, MidMichigan Health Obligation Group, Series A, 6.125%, 6/1/2039 | 4,000,000 | 4,585,960 | ||||||

| Michigan, State Hospital Finance Authority Revenue, Trinity Health, Series A, 6.5%, 12/1/2033 | 10,000,000 | 12,003,200 | ||||||

| Michigan, State Hospital Finance Authority, Trinity Health Credit Group, Series C, 5.0%, 12/1/2034 | 27,000,000 | 29,611,980 | ||||||

| Michigan, State Strategic Fund Ltd., Obligation Revenue, Consumers Energy Co., 0.13%**, 4/15/2018, LOC: JPMorgan Chase Bank NA | 17,000,000 | 17,000,000 | ||||||

| Royal Oak, MI, Hospital Finance Authority Revenue, William Beaumont Hospital, 8.25%, 9/1/2039 | 7,200,000 | 9,107,640 | ||||||

| Wayne County, MI, Airport Authority Revenue, Detroit Metropolitan Airport: | ||||||||

| Series A, 5.0%, 12/1/2037 | 9,255,000 | 10,091,282 | ||||||

| Series A, 5.0%, 12/1/2042 | 7,095,000 | 7,694,953 | ||||||

| 155,915,048 | ||||||||

| Minnesota 0.3% | ||||||||

| Minneapolis, MN, Health Care Systems Revenue, Fairview Health Services, Series A, 6.75%, 11/15/2032 | 6,440,000 | 7,773,402 | ||||||

| University of Minnesota, Higher Education Revenue: | ||||||||

| Series A, ETM, 5.75%, 7/1/2017 | 3,240,000 | 3,842,834 | ||||||

| Series A, ETM, 5.75%, 7/1/2018 (a) | 6,760,000 | 8,227,664 | ||||||

| 19,843,900 | ||||||||

| Mississippi 1.0% | ||||||||

| Mississippi, Development Bank Special Obligation, Department of Corrections, Series C, 5.25%, 8/1/2027 | 13,890,000 | 15,731,814 | ||||||

| Mississippi, State Business Finance Commission, Gulf Opportunity Zone, Chevron U.S.A., Inc. Project: | ||||||||

| Series B, 0.06%**, 12/1/2030, GTY: Chevron Corp. | 14,960,000 | 14,960,000 | ||||||

| Series B, 144A, 0.06%**, 11/1/2035, GTY: Chevron Corp. | 11,360,000 | 11,360,000 | ||||||

| Series K, 0.06%**, 11/1/2035, GTY: Chevron Corp. | 4,000,000 | 4,000,000 | ||||||

| Warren County, MS, Gulf Opportunity Zone, International Paper Co.: | ||||||||

| Series A, 5.5%, 9/1/2031 | 5,000,000 | 5,260,200 | ||||||

| Series A, 6.5%, 9/1/2032 | 7,420,000 | 8,457,613 | ||||||

| 59,769,627 | ||||||||

| Missouri 1.0% | ||||||||

| Cape Girardeau County, MO, Industrial Development Authority, Health Care Facilities Revenue, St. Francis Medical Center, Series A, 5.75%, 6/1/2039 | 2,150,000 | 2,384,608 | ||||||

| Cape Girardeau County, MO, Industrial Development Authority, St. Francis Medical Center, Series A, 5.0%, 6/1/2033 | 16,075,000 | 17,642,955 | ||||||

| Missouri, State Health & Educational Facilities Authority Revenue, Lutheran Senior Services, Series C, 5.0%, 2/1/2042 | 8,240,000 | 8,392,687 | ||||||

| Missouri, State Health & Educational Facilities Authority, Health Facilities Revenue, Lester E Cox Medical Centers, Series A, 5.0%, 11/15/2048 | 18,580,000 | 19,678,264 | ||||||

| St. Louis, MO, Industrial Development Authority Revenue, Convention Center Hotel, Zero Coupon, 7/15/2016, INS: AMBAC | 6,895,000 | 6,216,601 | ||||||

| St. Louis, MO, State General Obligation Lease, Industrial Development Authority, Convention Center Hotel, Zero Coupon, 7/15/2015, INS: AMBAC | 4,200,000 | 3,922,674 | ||||||

| 58,237,789 | ||||||||

| Montana 0.0% | ||||||||

| Forsyth, MT, Pollution Control Revenue, PacifiCorp Project, 0.09%**, 1/1/2018, LOC: JPMorgan Chase Bank NA | 2,200,000 | 2,200,000 | ||||||

| Nebraska 0.1% | ||||||||

| Omaha, NE, Public Power District Electric Revenue: | ||||||||

| Series A, 5.5%, 2/1/2033 | 1,000,000 | 1,139,880 | ||||||

| Series A, 5.5%, 2/1/2035 | 1,000,000 | 1,139,880 | ||||||

| Series A, 5.5%, 2/1/2039 | 1,000,000 | 1,139,880 | ||||||

| 3,419,640 | ||||||||

| Nevada 0.6% | ||||||||

| Clark County, NV, Airport Revenue: | ||||||||

| Series D-2B, 0.12%**, 7/1/2040, LOC: Royal Bank of Canada | 7,500,000 | 7,500,000 | ||||||

| Series B, 5.125%, 7/1/2036 | 5,000,000 | 5,460,100 | ||||||

| Las Vegas Monorail Co., Series A, 5.5%, 7/15/2019* (PIK) | 87,286 | 0 | ||||||

| Las Vegas Monorail Co., Series B, Step-up Coupon, 3.0% to 12/31/2015, 5.5% to 7/15/2055* (PIK) | 25,545 | 0 | ||||||

| Las Vegas Valley, NV, Water District, Series B, 5.0%, 6/1/2037 | 17,720,000 | 19,605,585 | ||||||

| 32,565,685 | ||||||||

| New Hampshire 0.2% | ||||||||

| New Hampshire, Health & Education Facilities Authority Revenue, Wentworth-Douglas Hospital, Series A, 6.5%, 1/1/2031 | 10,000,000 | 11,681,500 | ||||||

| New Jersey 3.7% | ||||||||

| New Jersey, Economic Development Authority Revenue, Cigarette Tax: | ||||||||

| Prerefunded, 5.5%, 6/15/2031 | 3,000,000 | 3,161,040 | ||||||

| Prerefunded, 5.75%, 6/15/2034 | 2,455,000 | 2,593,143 | ||||||

| New Jersey, Economic Development Authority Revenue, Motor Vehicle Surplus Revenue: | ||||||||

| Series A, 5.0%, 7/1/2022, INS: NATL | 7,140,000 | 7,460,015 | ||||||

| Series A, 5.0%, 7/1/2023, INS: NATL | 8,845,000 | 9,231,615 | ||||||

| New Jersey, Garden State Preservation Trust, Open Space & Farm Land, Series 2005-A, Prerefunded, 5.8%, 11/1/2023, INS: AGMC | 5,000,000 | 5,643,250 | ||||||

| New Jersey, Industrial Development Revenue, Economic Development Authority, Harrogate, Inc., Series A, 5.875%, 12/1/2026 | 1,000,000 | 1,000,660 | ||||||

| New Jersey, State Economic Development Authority Revenue, 5.0%, 6/15/2028 | 1,050,000 | 1,154,464 | ||||||

| New Jersey, State Economic Development Authority Revenue, School Facilities Construction: | ||||||||

| Series NN, 5.0%, 3/1/2030 | 27,000,000 | 30,236,760 | ||||||

| Series NN, 5.0%, 3/1/2031 | 14,775,000 | 16,455,952 | ||||||

| New Jersey, State Transportation Trust Fund Authority, Series A, 5.75%, 6/15/2020, INS: AMBAC | 11,000,000 | 13,612,720 | ||||||

| New Jersey, State Transportation Trust Fund Authority, Transportation Program, Series AA, 5.0%, 6/15/2038 | 12,565,000 | 13,694,091 | ||||||

| New Jersey, State Transportation Trust Fund Authority, Transportation Systems: | ||||||||

| Series B, 5.25%, 6/15/2036 | 15,940,000 | 17,790,953 | ||||||

| Series B, 5.5%, 6/15/2031 | 13,200,000 | 15,321,636 | ||||||

| Series A, 6.0%, 6/15/2035 | 6,000,000 | 7,156,620 | ||||||

| Series A, 6.0%, 12/15/2038 | 11,075,000 | 13,110,474 | ||||||

| Series A, Prerefunded, 6.0%, 12/15/2038 | 5,925,000 | 7,509,997 | ||||||

| New Jersey, State Turnpike Authority Revenue: | ||||||||

| Series A, 5.0%, 1/1/2035 | 6,025,000 | 6,575,504 | ||||||

| Series A, 5.0%, 1/1/2038 | 32,530,000 | 35,334,737 | ||||||

| Series E, 5.25%, 1/1/2040 | 5,250,000 | 5,760,982 | ||||||

| Series C, 6.5%, 1/1/2016, INS: AMBAC | 785,000 | 899,390 | ||||||

| Series C, ETM, 6.5%, 1/1/2016, INS: AMBAC | 425,000 | 490,429 | ||||||

| Series C-2005, ETM, 6.5%, 1/1/2016, INS: AMBAC | 425,000 | 490,429 | ||||||

| 214,684,861 | ||||||||

| New York 6.5% | ||||||||

| New York, Higher Education Revenue, Dormitory Authority, Series B, 5.25%, 5/15/2019, INS: FGIC | 6,000,000 | 6,732,900 | ||||||

| New York, Higher Education Revenue, Dormitory Authority, City University, Series B, 6.0%, 7/1/2014, INS: FGIC | 2,415,000 | 2,474,095 | ||||||

| New York, Metropolitan Transportation Authority Revenue: | ||||||||

| Series A, 5.0%, 11/15/2038 | 12,375,000 | 13,419,821 | ||||||

| Series E, 5.0%, 11/15/2042 | 10,140,000 | 10,968,945 | ||||||

| Series H, 5.0%, 11/15/2042 | 12,250,000 | 13,251,437 | ||||||

| New York, School District General Obligation, Dormitory Authority, City University, Series A, 5.5%, 5/15/2019 | 1,500,000 | 1,772,115 | ||||||

| New York, Senior Care Revenue, Dormitory Authority, City University, Series A, 5.25%, 5/15/2021 | 2,000,000 | 2,428,620 | ||||||

| New York, State Agency General Obligation Lease, Urban Development Corp., 5.7%, 4/1/2020 | 3,600,000 | 4,284,504 | ||||||

| New York, State Dormitory Authority, Personal Income Tax Revenue: | ||||||||

| Series F, 5.0%, 2/15/2035 | 5,000,000 | 5,642,950 | ||||||

| Series A, 5.0%, 3/15/2038 (a) | 8,750,000 | 9,804,550 | ||||||

| Series C, 5.0%, 3/15/2041 | 10,000,000 | 11,025,100 | ||||||

| New York, State General Obligation Lease, Urban Development Corp., State Facilities, 5.6%, 4/1/2015 | 3,185,000 | 3,376,419 | ||||||

| New York, State General Obligation, Tobacco Settlement Financing Corp., Series A-1, 5.25%, 6/1/2022, INS: AMBAC | 12,600,000 | 12,650,904 | ||||||

| New York, State Housing Finance Agency, 100 Maiden Lane Properties, Series A, 0.12%**, 5/15/2037, LIQ: Fannie Mae | 1,775,000 | 1,775,000 | ||||||

| New York, State Liberty Development Corp. Revenue, World Trade Center Port Authority Construction, 5.25%, 12/15/2043 | 40,000,000 | 44,986,400 | ||||||

| New York, State Thruway Authority Revenue, Series I, 5.0%, 1/1/2037 | 9,370,000 | 10,305,501 | ||||||

| New York, State Thruway Authority, Second Generation Highway & Bridge Trust Funding Authority: | ||||||||

| Series A, 5.0%, 4/1/2031 | 5,250,000 | 6,013,245 | ||||||

| Series A, 5.0%, 4/1/2032 | 4,000,000 | 4,561,600 | ||||||

| New York, Water & Sewer Revenue, Environmental Facilities Corp., State Water Pollution Control, Series E, 6.875%, 6/15/2014 | 1,260,000 | 1,266,968 | ||||||

| New York City, NY, Municipal Water Finance Authority, Water & Sewer Revenue: | ||||||||

| Series DD-1, 0.08%**, 6/15/2043, SPA: TD Bank NA | 5,325,000 | 5,325,000 | ||||||

| Series DD, 5.0%, 6/15/2035 | 32,000,000 | 36,308,800 | ||||||

| Series FF-2, 5.0%, 6/15/2040 | 2,270,000 | 2,483,607 | ||||||

| New York City, NY, Municipal Water Finance Authority, Water & Sewer Revenue, Second General Resolution: | ||||||||

| Series B, 0.07%**, 6/15/2032, SPA: California State Teacher's Retirement System | 5,760,000 | 5,760,000 | ||||||

| Series EE, 5.375%, 6/15/2043 | 11,250,000 | 12,781,350 | ||||||

| New York City, NY, Transitional Finance Authority Revenue, Future Tax Secured: | ||||||||

| Series A-1, 144A, 0.11%**, 11/15/2028, SPA: TD Bank NA | 16,100,000 | 16,100,000 | ||||||

| Series D-1, 5.0%, 11/1/2038 | 10,000,000 | 11,150,700 | ||||||

| New York, NY, General Obligation: | ||||||||

| Series D-1, 5.0%, 10/1/2033 | 25,000,000 | 28,316,750 | ||||||

| Series D-1, 5.0%, 10/1/2034 | 5,000,000 | 5,645,750 | ||||||

| Series F-1, 5.0%, 3/1/2037 | 31,475,000 | 35,525,203 | ||||||

| Series I-1, 5.375%, 4/1/2036 | 7,000,000 | 8,250,130 | ||||||

| New York, NY, Triborough Bridge & Tunnel Authority Revenues, Series C, 5.0%, 11/15/2038 | 32,375,000 | 36,354,859 | ||||||

| Troy, NY, Capital Resource Corp. Revenue, Rensselaer Polytechnic Institute, Series A, 5.125%, 9/1/2040 | 2,000,000 | 2,168,420 | ||||||

| 372,911,643 | ||||||||

| North Carolina 1.7% | ||||||||

| Charlotte, NC, Airport Revenue, Series A, 5.5%, 7/1/2034 | 1,500,000 | 1,727,850 | ||||||

| Charlotte, NC, Core City General Obligation, 5.5%, 8/1/2018 | 4,165,000 | 4,242,677 | ||||||

| Charlotte-Mecklenberg, NC, Hospital Authority, Health Care System Revenue, Series A, 5.0%, 1/15/2039 | 28,015,000 | 30,832,469 | ||||||

| North Carolina, Electric Revenue, Eastern Municipal Power Agency: | ||||||||

| 6.0%, 1/1/2018, INS: AMBAC | 8,775,000 | 10,593,356 | ||||||

| Series B, 6.0%, 1/1/2022, INS: NATL | 18,775,000 | 23,714,890 | ||||||

| North Carolina, Lower Cape Fear Water & Sewer Authority, Special Facility Revenue, Bladen Bluffs Project, Recovery Zone Facility, 0.15%**, 12/1/2034, LOC: Rabobank International | 4,020,000 | 4,020,000 | ||||||

| North Carolina, Medical Care Commission, Health Care Facilities Revenue, University Health System, Series D, 6.25%, 12/1/2033 | 17,000,000 | 20,217,590 | ||||||

| North Carolina, Municipal Power Agency, No. 1 Catawba Electric Revenue, Series A, 5.0%, 1/1/2030 | 5,410,000 | 5,969,610 | ||||||

| 101,318,442 | ||||||||

| North Dakota 0.2% | ||||||||

| Fargo, ND, Sanford Health Systems Revenue, 6.25%, 11/1/2031 | 9,260,000 | 11,371,373 | ||||||

| Ohio 1.8% | ||||||||

| Avon, OH, School District General Obligation, 6.5%, 12/1/2015, INS: AMBAC | 940,000 | 1,026,179 | ||||||

| Beavercreek, OH, School District General Obligation, Local School District, 6.6%, 12/1/2015, INS: FGIC, NATL | 1,190,000 | 1,291,341 | ||||||

| Cleveland, OH, Airport Systems Revenue, Series A, 5.0%, 1/1/2030 | 1,000,000 | 1,099,840 | ||||||

| Cleveland, OH, Sales & Special Tax Revenue, Urban Renewal Tax Increment, Rock & Roll Hall of Fame and Museum Project, 6.75%, 3/15/2018 | 760,000 | 761,102 | ||||||

| Cuyahoga County, OH, County General Obligation, 5.65%, 5/15/2018 | 500,000 | 564,810 | ||||||

| Fayette County, OH, School District General Obligation, Rattlesnake Improvement Area Project, 5.9%, 12/1/2013 | 5,000 | 5,000 | ||||||

| Finneytown, OH, Other General Obligation, Local School District, 6.2%, 12/1/2017, INS: FGIC, NATL | 320,000 | 360,294 | ||||||

| Franklin County, OH, School District General Obligation, 6.5%, 12/1/2013 | 145,000 | 149,121 | ||||||

| Hancock County, OH, Hospital Revenue, Blanchard Valley Regional Health Center, 6.5%, 12/1/2030 | 14,425,000 | 17,260,522 | ||||||

| Kent, OH, State University Revenues, General Receipts, Series A, 5.0%, 5/1/2037 | 8,440,000 | 9,330,758 | ||||||

| Liberty Benton, OH, School District General Obligation, Zero Coupon, 12/1/2014, INS: AMBAC | 570,000 | 557,169 | ||||||

| Lucas County, OH, Hospital Revenue, Promedica Healthcare, Series A, 6.5%, 11/15/2037 | 6,000,000 | 7,404,000 | ||||||

| Ohio, Akron Bath Copley Joint Township Hospital District, Children's Hospital Medical Center of Akron, 5.0%, 11/15/2038 | 15,645,000 | 16,952,609 | ||||||

| Ohio, American Municipal Power, Inc. Revenue, Fremont Energy Center Project, Series B, 5.0%, 2/15/2037 | 13,090,000 | 14,259,461 | ||||||

| Ohio, Higher Education Revenue, Case Western Reserve University: | ||||||||

| 6.0%, 10/1/2014 | 1,000,000 | 1,072,010 | ||||||

| Series B, 6.5%, 10/1/2020 | 2,250,000 | 2,706,188 | ||||||

| Ohio, School District General Obligation, 6.0%, 12/1/2019, INS: AMBAC | 475,000 | 550,050 | ||||||

| Ohio, State Higher Educational Facility Commission Revenue, Summa Health Systems Project: | ||||||||

| Series 2010, 5.25%, 11/15/2035, INS: AGMC | 7,500,000 | 8,052,450 | ||||||

| Series 2010, 5.5%, 11/15/2030, INS: AGMC | 4,000,000 | 4,405,720 | ||||||

| Ohio, State Hospital Facility Revenue, Cleveland Clinic Health System, Series B, 5.5%, 1/1/2039 | 13,600,000 | 15,146,864 | ||||||

| Wayne, OH, School District General Obligation, 6.6%, 12/1/2016, INS: AMBAC | 175,000 | 194,983 | ||||||

| Wooster, OH, School District General Obligation, Zero Coupon, 12/1/2013, INS: AGMC | 930,000 | 928,084 | ||||||

| 104,078,555 | ||||||||

| Oklahoma 0.6% | ||||||||

| Oklahoma, State Municipal Power Authority, Supply System Revenue, Series A, 6.0%, 1/1/2038 | 8,625,000 | 9,962,824 | ||||||

| Oklahoma, Water & Sewer Revenue, McGee Creek Authority, 6.0%, 1/1/2023, INS: NATL | 23,125,000 | 26,527,843 | ||||||

| 36,490,667 | ||||||||

| Oregon 0.4% | ||||||||

| Port of Portland, OR, Special Obligation Revenue, Horizon Air Industries, Inc. Project, AMT, 0.11%**, 6/15/2027, LOC: Bank of America NA | 10,300,000 | 10,300,000 | ||||||

| Yamhill County, OR, Hospital Authority, Friendsview Manor, 0.13%**, 12/1/2034, LOC: U.S. Bank NA | 11,500,000 | 11,500,000 | ||||||

| 21,800,000 | ||||||||

| Pennsylvania 2.3% | ||||||||

| Allegheny County, PA, Airport Revenue, Pittsburgh International Airport, Series A-1, AMT, 5.75%, 1/1/2014, INS: NATL | 10,500,000 | 10,822,875 | ||||||

| Allegheny County, PA, Hospital Development Authority Revenue, University of Pittsburgh Medical, 5.625%, 8/15/2039 | 11,800,000 | 13,202,430 | ||||||

| Beaver County, PA, Industrial Development Authority, First Energy General Corp., Series C, AMT, 0.11%**, 6/1/2028, GTY: FirstEnergy Solutions, LOC: Bank of Nova Scotia | 5,000,000 | 5,000,000 | ||||||

| Berks County, PA, Hospital & Healthcare Revenue, Municipal Authority, Reading Hospital & Medical Center Project, 5.7%, 10/1/2014, INS: NATL | 370,000 | 380,756 | ||||||

| Delaware County, PA, Industrial Development Authority, Solid Waste System Revenue, Scott Paper Co., Series E, 0.13%**, 12/1/2018, GTY: Kimberly-Clark Corp. | 3,300,000 | 3,300,000 | ||||||

| Exeter Township, PA, School District General Obligation, Zero Coupon, 5/15/2017, INS: FGIC, NATL | 3,700,000 | 3,500,459 | ||||||

| Montgomery County, PA, Redevelopment Authority, Forge Gate Apartments Project, Series A, 0.15%**, 8/15/2031, LIQ: Fannie Mae | 1,510,000 | 1,510,000 | ||||||

| Pennsylvania, Central Bradford Progress Authority Revenue, Guthrie Healthcare System, 5.375%, 12/1/2041 | 12,550,000 | 13,950,329 | ||||||

| Pennsylvania, Commonwealth Financing Authority Revenue: | ||||||||

| Series B, 5.0%, 6/1/2036 | 5,475,000 | 5,987,131 | ||||||

| Series B, 5.0%, 6/1/2042 | 13,975,000 | 15,204,381 | ||||||

| Pennsylvania, Sales & Special Tax Revenue, Convention Center Authority, Series A, ETM, 6.0%, 9/1/2019, INS: FGIC | 2,200,000 | 2,749,868 | ||||||

| Pennsylvania, State Turnpike Commission Revenue, Series B, 5.75%, 6/1/2039 | 32,000,000 | 35,637,440 | ||||||

| Pennsylvania, State Turnpike Commission Revenue, Motor License Fund, Series A, 6.0%, 12/1/2036 | 3,000,000 | 3,572,700 | ||||||

| Pennsylvania, Water & Sewer Revenue, 5.25%, 11/1/2014, INS: NATL | 780,000 | 811,309 | ||||||

| Philadelphia, PA, Airport Revenue, Series A, 5.0%, 6/15/2035 | 7,080,000 | 7,548,484 | ||||||

| Philadelphia, PA, Water & Wastewater Revenue: | ||||||||

| Series A, 5.25%, 1/1/2032 | 3,000,000 | 3,295,200 | ||||||

| Series A, 5.25%, 1/1/2036 | 2,500,000 | 2,726,025 | ||||||

| Pittsburgh, PA, Core City General Obligation, Series A, 5.5%, 9/1/2014, INS: AMBAC | 555,000 | 568,764 | ||||||

| Pittsburgh, PA, Water & Sewer System, ETM, 7.25%, 9/1/2014, INS: FGIC | 40,000 | 41,908 | ||||||

| Westmoreland County, PA, Project Revenue, Zero Coupon, 8/15/2017, INS: NATL | 6,230,000 | 5,826,608 | ||||||

| 135,636,667 | ||||||||

| Puerto Rico 0.9% | ||||||||

| Puerto Rico, Sales Tax Financing Corp., Sales Tax Revenue: | ||||||||

| Series A, 5.375%, 8/1/2039 | 13,650,000 | 14,342,464 | ||||||

| Series A, 6.5%, 8/1/2044 | 35,000,000 | 39,788,700 | ||||||

| 54,131,164 | ||||||||

| Rhode Island 0.8% | ||||||||