| | | FREE WRITING PROSPECTUS |

| | | FILED PURSUANT TO RULE 433 |

| | | REGISTRATION FILE NO.: 333-280224-03 |

| | | |

| Dated November 25, 2024 | BMO 2024-5C8 |

| Structural and Collateral Term Sheet |

BMO 2024-5C8 Mortgage Trust |

$991,839,388 (Approximate Mortgage Pool Balance) |

| |

$[] (Approximate Offered Certificates) |

| |

BMO Commercial Mortgage Securities LLC Depositor |

| |

Commercial Mortgage Pass-Through Certificates, Series 2024-5C8 |

| |

| |

Bank of Montreal Goldman Sachs Mortgage Company German American Capital Corporation Starwood Mortgage Capital LLC Citi Real Estate Funding Inc. UBS AG Societe Generale Financial Corporation Greystone Commercial Mortgage Capital LLC Barclays Capital Real Estate Inc. Natixis Real Estate Capital LLC Sponsors and Mortgage Loan Sellers |

BMO Capital

Markets | Deutsche Bank

Securities | Citigroup | Société

Générale | Barclays | UBS

Securities LLC | Goldman Sachs

& Co. LLC |

| Co-Lead Managers and Joint Bookrunners |

| Academy Securities | Bancroft Capital, LLC | | Drexel Hamilton | Natixis |

Co-Managers |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | | |

| Dated November 25, 2024 | BMO 2024-5C8 |

This material is for your information, and none of BMO Capital Markets Corp., Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., Citigroup Global Markets Inc., SG Americas Securities, LLC, Barclays Capital Inc., UBS Securities LLC, Academy Securities, Inc., Bancroft Capital, LLC, Drexel Hamilton, LLC and Natixis Securities Americas LLC (collectively, the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-280224) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or BMO Capital Markets Corp., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-888-200-0266. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2024-5C8 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these Certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the Certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the Certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Europe p.l.c, and Bank of Montreal (China) Co. Ltd, the institutional broker dealer business of BMO Capital Markets Corp. (Member FINRA and SIPC) and the agency broker dealer business of Clearpool Execution Services, LLC (Member FINRA and SIPC) in the U.S., and the institutional broker dealer businesses of BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia, Bank of Montreal Europe p.l.c. (authorized and regulated by the Central Bank of Ireland) in Europe and BMO Capital Markets Limited (authorized and regulated by the Financial Conduct Authority) in the UK and Australia.

Securities and investment banking activities in the United States are performed by Deutsche Bank Securities Inc., a member of NYSE, FINRA and SIPC, and its broker-dealer affiliates. Lending and other commercial banking activities in the United States are performed by Deutsche Bank AG and its banking affiliates.

Société Générale is the marketing name for SG Americas Securities, LLC.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 2 | |

| Dated November 25, 2024 | BMO 2024-5C8 |

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 3 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| Collateral Characteristics |

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate

Cut-off Date Balance | % of IPB | Roll-up Aggregate Cut-off Date Balance | Roll-up Aggregate % of Cut-off Date Balance |

| BMO | 6 | 8 | $128,200,000 | 12.9% | $250,749,780 | 25.3% |

| GSMC | 3 | 27 | $136,300,000 | 13.7% | $195,260,651 | 19.7% |

| GACC | 4 | 4 | $70,500,000 | 7.1% | $172,846,957 | 17.4% |

| SMC | 5 | 6 | $74,400,000 | 7.5% | $118,150,000 | 11.9% |

| CREFI | 5 | 7 | $95,490,000 | 9.6% | $95,490,000 | 9.6% |

| UBS AG | 5 | 5 | $54,200,000 | 5.5% | $54,200,000 | 5.5% |

| SGFC | 3 | 3 | $49,200,000 | 5.0% | $49,200,000 | 5.0% |

| GCMC | - | - | - | - | $23,584,000 | 2.4% |

| Barclays | - | - | - | - | $23,583,000 | 2.4% |

| Natixis | 1 | 2 | $8,775,000 | 0.9% | $8,775,000 | 0.9% |

| BMO, GACC, GSMC | 2 | 2 | $131,000,000 | 13.2% | - | - |

| BMO, GCMC, Barclays | 1 | 1 | $70,750,000 | 7.1% | - | - |

| SMC, BMO | 2 | 3 | $70,000,000 | 7.1% | - | - |

| GACC, GSMC | 1 | 6 | $64,000,000 | 6.5% | - | - |

| GSMC, BMO | 1 | 23 | $26,389,388 | 2.7% | - | - |

| GACC, BMO | 1 | 1 | $12,635,000 | 1.3% | - | - |

| Total: | 40 | 98 | $991,839,388 | 100.0% | $991,839,388 | 100.0% |

| Loan Pool | |

| | Initial Pool Balance (“IPB”): | $991,839,388 |

| | Number of Mortgage Loans: | 40 |

| | Number of Mortgaged Properties: | 98 |

| | Average Cut-off Date Balance per Mortgage Loan: | $24,795,985 |

| | Weighted Average Current Mortgage Rate: | 6.58110% |

| | 10 Largest Mortgage Loans as % of IPB: | 54.6% |

| | Weighted Average Remaining Term to Maturity: | 59 months |

| | Weighted Average Seasoning: | 1 month |

| | | |

| Credit Statistics | |

| | Weighted Average UW NCF DSCR: | 1.68x |

| | Weighted Average UW NOI Debt Yield: | 11.6% |

| | Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”): | 58.1% |

| | Weighted Average Maturity Date/ARD LTV: | 58.1% |

| | | |

| Other Statistics | |

| | % of Mortgage Loans with Additional Debt: | 8.0% |

| | % of Mortgage Loans with Single Tenants(1): | 15.6% |

| | % of Mortgage Loans secured by Multiple Properties: | 25.5% |

| | |

| Amortization | |

| | Weighted Average Original Amortization Term: | 360 months |

| | Weighted Average Remaining Amortization Term: | 360 months |

| | % of Mortgage Loans with Interest-Only: | 97.0% |

| | % of Mortgage Loans with Amortizing Balloon: | 3.0% |

| | | |

| Lockboxes | |

| | % of Mortgage Loans with Hard Lockboxes: | 52.5% |

| | % of Mortgage Loans with Springing Lockboxes: | 25.4% |

| | % of Mortgage Loans with Soft Lockboxes: | 18.2% |

| | % of Mortgage Loans with Soft (Residential); Hard (Commercial) Lockboxes: | 3.8% |

| | | |

| Reserves | |

| | % of Mortgage Loans Requiring Monthly Tax Reserves: | 70.9% |

| | % of Mortgage Loans Requiring Monthly Insurance Reserves: | 36.9% |

| | % of Mortgage Loans Requiring Monthly CapEx Reserves: | 82.9% |

| | % of Mortgage Loans Requiring Monthly TI/LC Reserves(2): | 57.3% |

| (1) | Excludes mortgage loans that are secured by multiple properties leased to separate single tenants. |

| (2) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, industrial, mixed use and multifamily (with commercial tenants) properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 4 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| Collateral Characteristics |

| Ten Largest Mortgage Loans |

| |

| No. | Loan Name | City, State | Mortgage Loan Seller | No.

of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Units | Property Type | UW

NCF DSCR | UW NOI Debt Yield | Cut-off Date LTV | Maturity Date/ARD LTV |

| 1 | Queens Center | Elmhurst, NY | BMO, GACC, GSMC | 1 | $71,000,000 | 7.2% | 412,033 | Retail | 1.84x | 10.2% | 49.5% | 49.5% |

| 2 | 310 Grand Concourse | Bronx, NY | BMO, GCMC, Barclays | 1 | $70,750,000 | 7.1% | 150 | Multifamily | 1.26x | 8.0% | 69.4% | 69.4% |

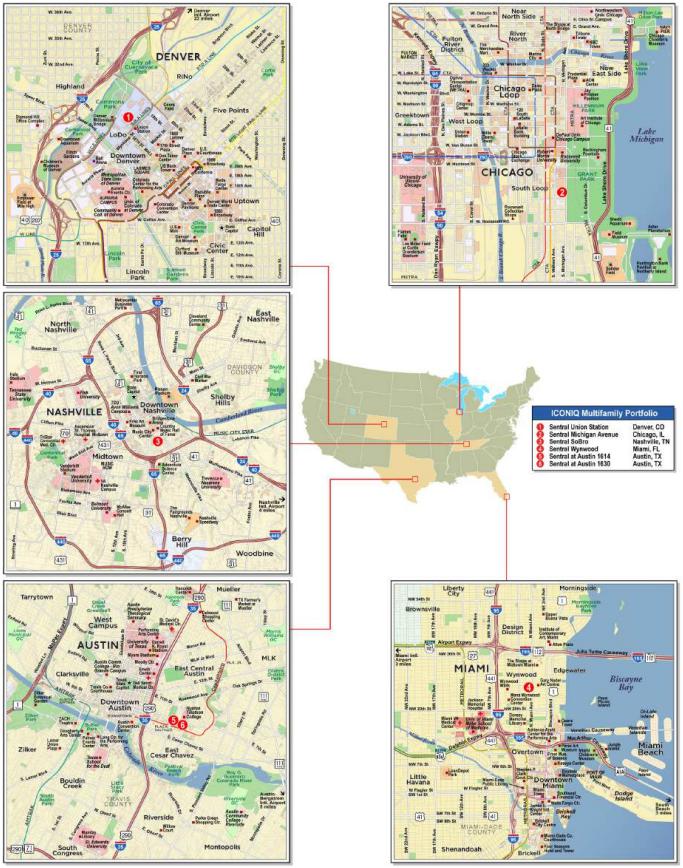

| 3 | ICONIQ Multifamily Portfolio | Various, Various | GACC, GSMC | 6 | $64,000,000 | 6.5% | 1,790 | Multifamily | 2.43x | 14.6% | 36.1% | 36.1% |

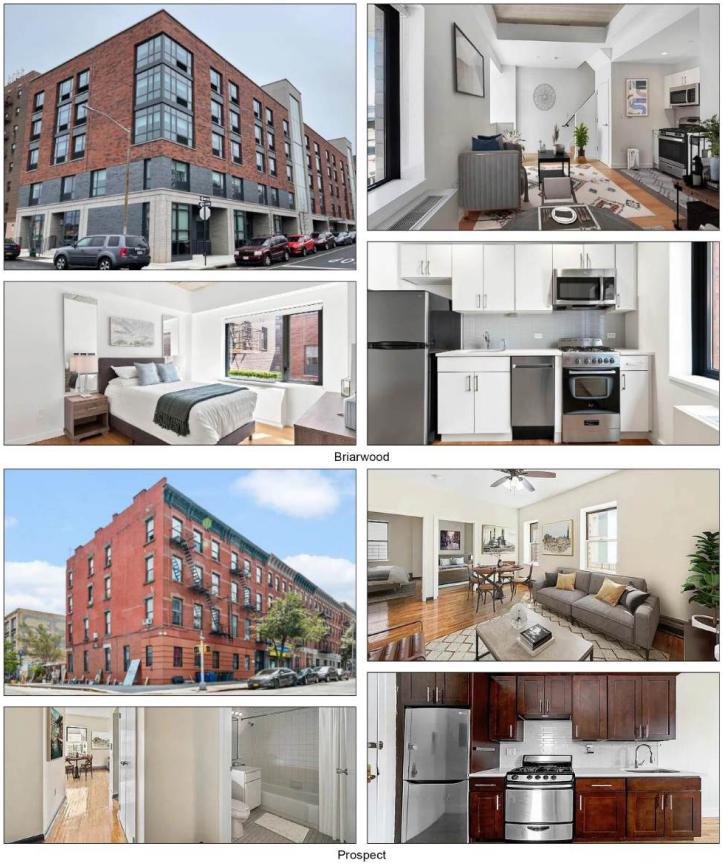

| 4 | Black Spruce - Briarwood and Prospect | Various, NY | GSMC | 2 | $64,000,000 | 6.5% | 488 | Multifamily | 1.20x | 8.1% | 70.0% | 70.0% |

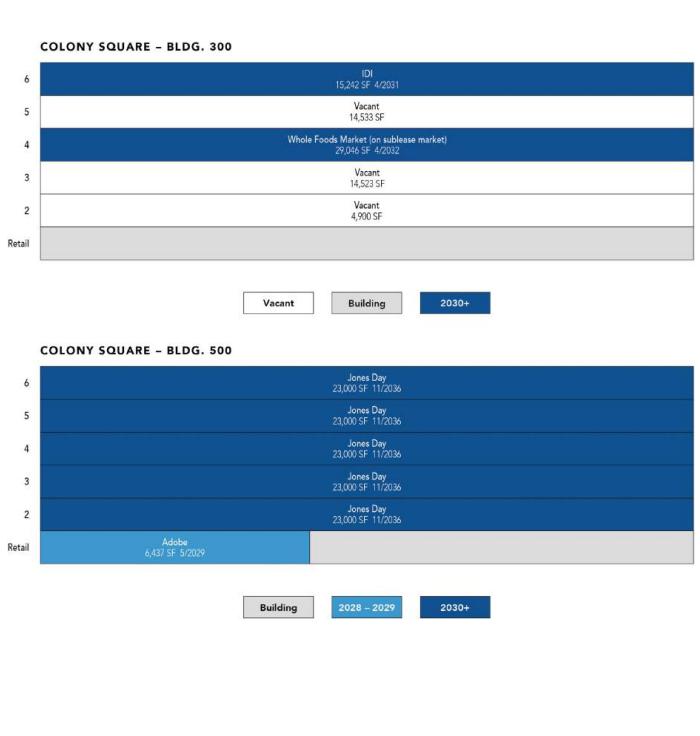

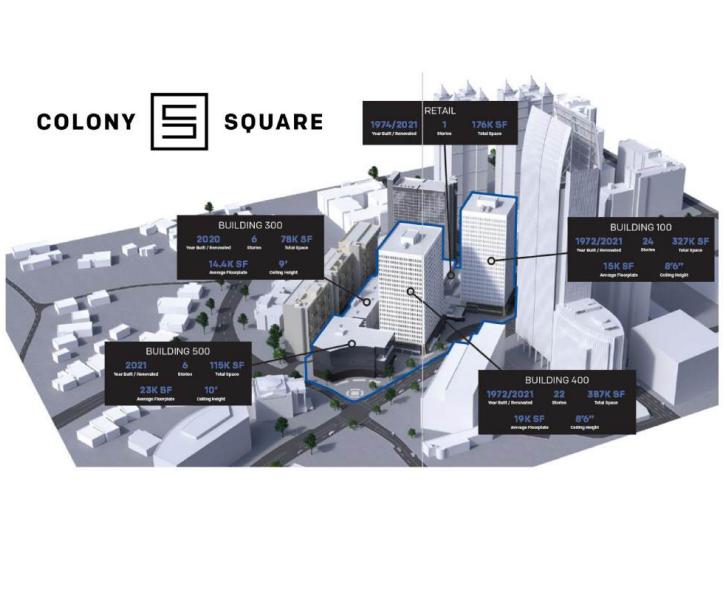

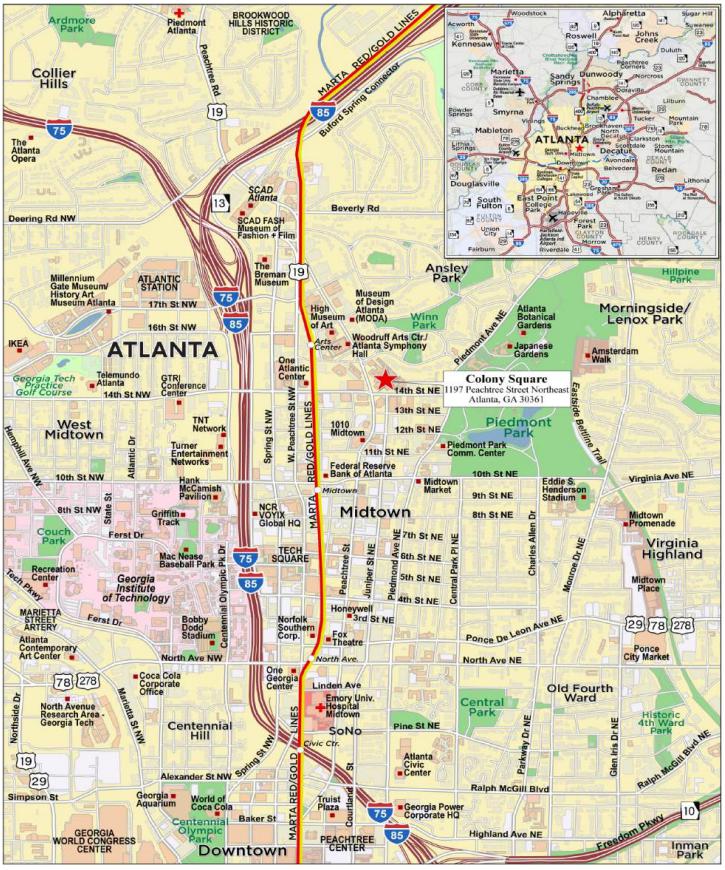

| 5 | Colony Square | Atlanta, GA | BMO, GACC, GSMC | 1 | $60,000,000 | 6.0% | 1,085,612 | Mixed Use | 1.51x | 11.8% | 50.4% | 50.4% |

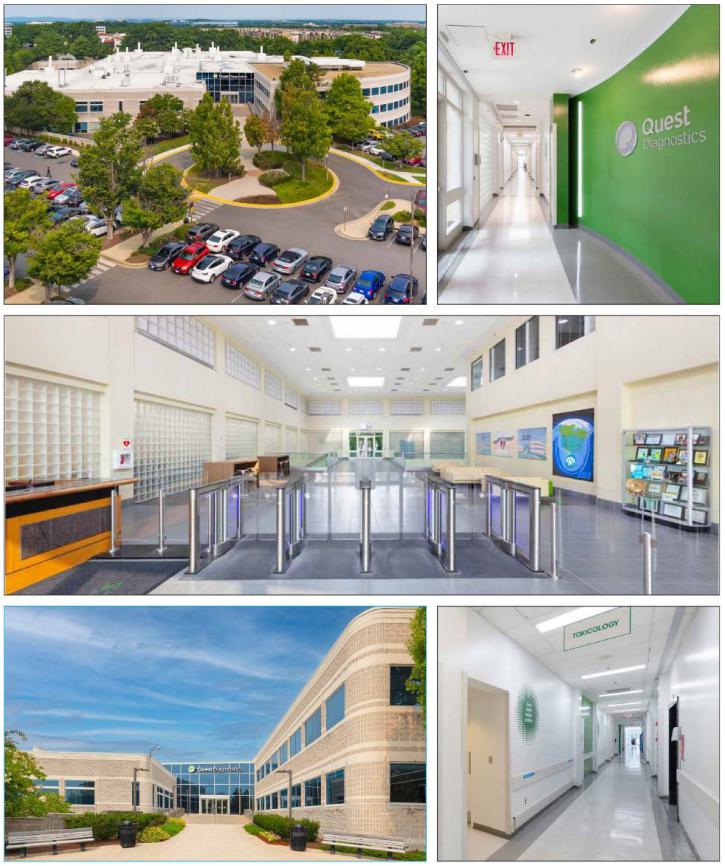

| 6 | Quest Diagnostics - Chantilly | Chantilly, VA | GSMC | 1 | $57,300,000 | 5.8% | 248,186 | Mixed Use | 1.77x | 10.2% | 70.7% | 70.7% |

| 7 | Woodland Mall | Kentwood, MI | SMC, BMO | 1 | $50,000,000 | 5.0% | 563,041 | Retail | 1.93x | 15.0% | 53.0% | 53.0% |

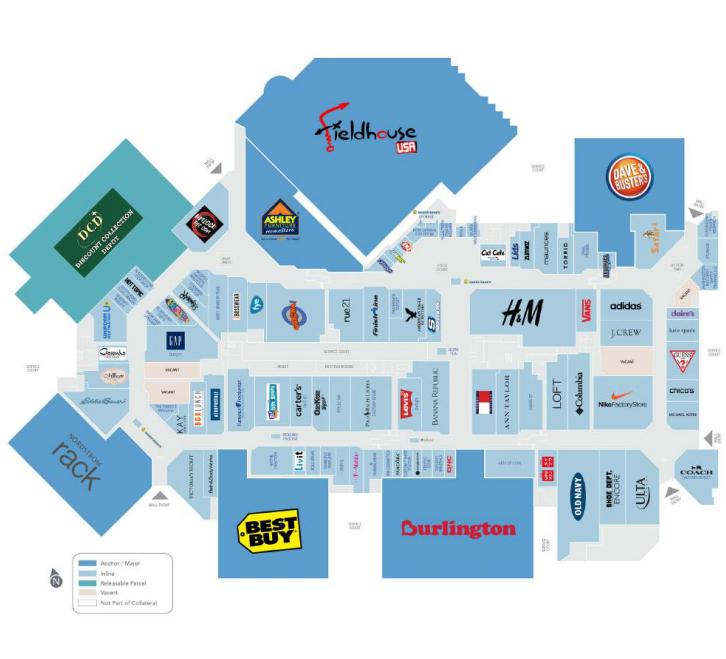

| 8 | The Outlet Collection Seattle | Auburn, WA | CREFI | 1 | $35,970,000 | 3.6% | 913,033 | Retail | 2.40x | 19.5% | 50.3% | 50.3% |

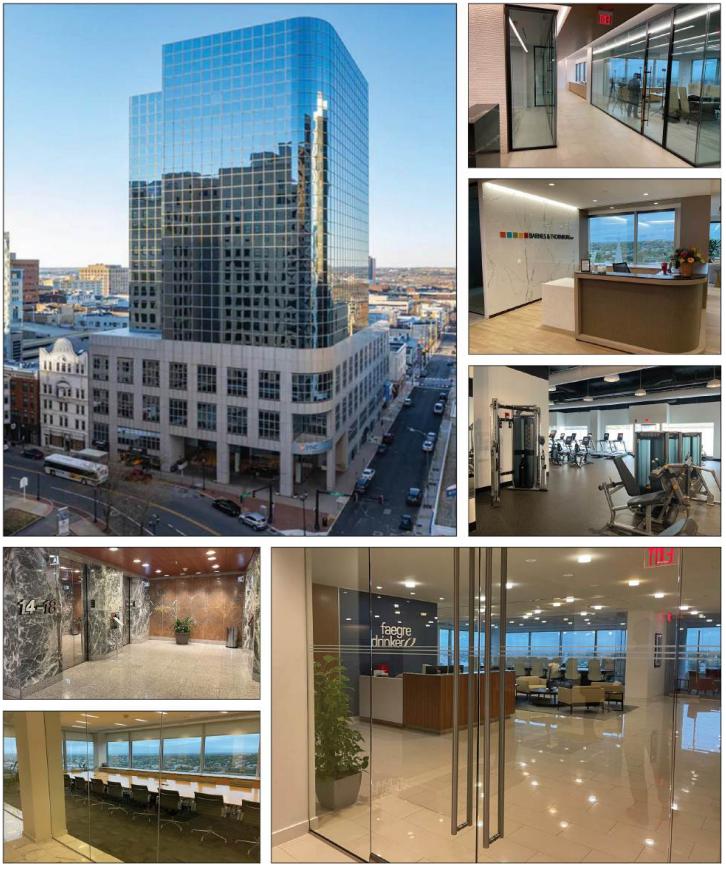

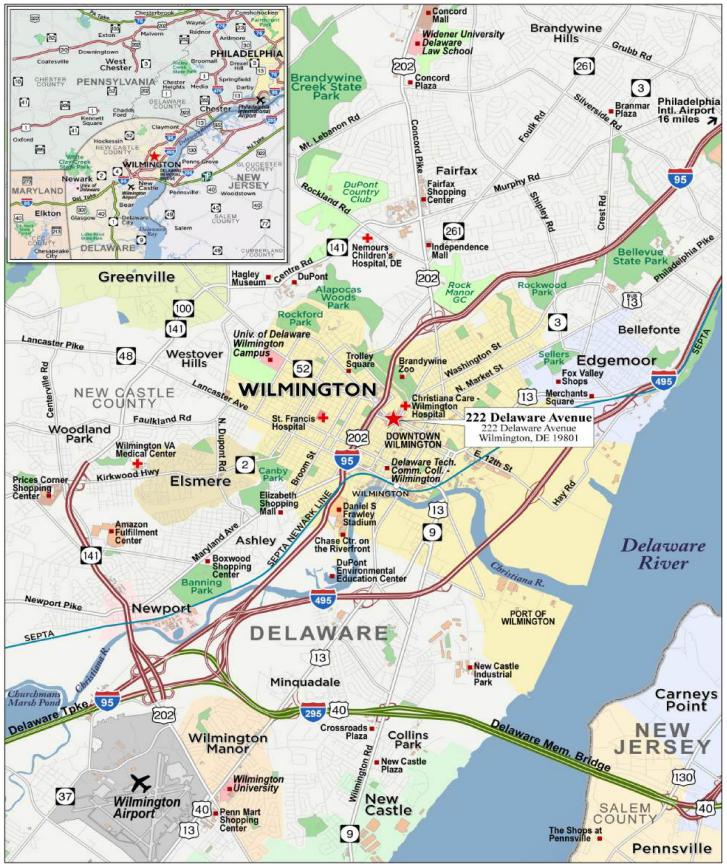

| 9 | 222 Delaware Avenue | Wilmington, DE | BMO | 1 | $35,500,000 | 3.6% | 294,417 | Office | 1.75x | 14.2% | 64.8% | 64.8% |

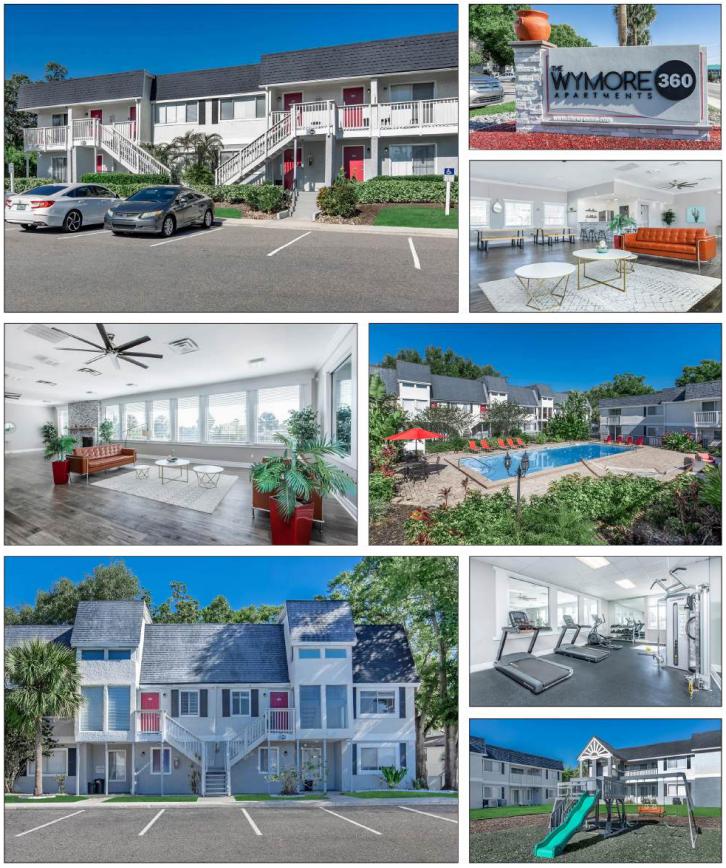

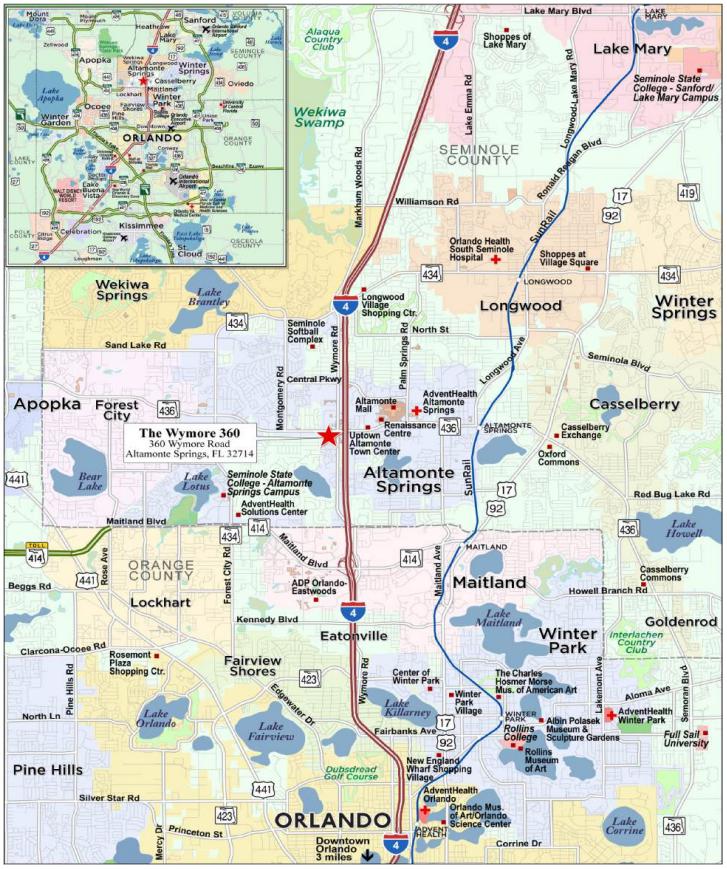

| 10 | The Wymore 360 | Altamonte Springs, FL | GACC | 1 | $33,000,000 | 3.3% | 200 | Multifamily | 1.36x | 9.6% | 71.0% | 71.0% |

| | | | | | | | | | | | | |

| | Top 3 Total/Weighted Average | | 8 | $205,750,000 | 20.7% | | | 1.82x | 10.8% | 52.2% | 52.2% |

| | Top 5 Total/Weighted Average | | 11 | $329,750,000 | 33.2% | | | 1.65x | 10.5% | 55.3% | 55.3% |

| | Top 10 Total/Weighted Average | | 16 | $541,520,000 | 54.6% | | | 1.72x | 11.6% | 58.0% | 58.0% |

| | Non-Top 10 Total/Weighted Average | | 82 | $450,319,388 | 45.4% | | | 1.62x | 11.6% | 58.3% | 58.2% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 5 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| Collateral Characteristics |

| Pari Passu Companion Loan Summary |

| |

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Controlling Pooling/Trust & Servicing Agreement | Master

Servicer | Special

Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Companion Loan(s) Original Balance |

| 1 | Queens Center | BMO, GACC, GSMC | $71,000,000 | $454,000,000 | Future Securitization(1) | Midland(1) | LNR(1) | WFCM 2024-5C2 BANK5 2024-5YR11 BANK5 2024-5YR12 Future Securitization(s) | $30,000,000 $75,000,000 $85,000,000 $264,000,000 |

| 3 | ICONIQ Multifamily Portfolio | GACC, GSMC | $64,000,000 | $236,000,000 | ICNQ 2024-MF | Wells Fargo | KeyBank | ICNQ 2024-MF WCFM 2024-5C2 Future Securitization(s) | $170,000,000 $26,000,000 $40,000,000 |

| 4 | Black Spruce - Briarwood and

Prospect | GSMC | $64,000,000 | $27,230,000 | BMO 2024-5C8 | Wells Fargo | Greystone | Future Securitization(s) | $27,230,000 |

| 5 | Colony Square | BMO, GACC,

GSMC | $60,000,000 | $200,000,000 | BMO 2024-5C8 | Wells Fargo | Greystone | BMO 2024-5C7 Benchmark 2024-V11 Future Securitization(s) | $60,000,000 $70,000,000 $70,000,000 |

| 7 | Woodland Mall | SMC, BMO | $50,000,000 | $30,000,000 | BMO 2024-5C8 | Wells Fargo | Greystone | Future Securitization(s) | $30,000,000 |

| 8 | The Outlet Collection Seattle | CREFI | $35,970,000 | $17,297,500 | BMO 2024-5C8 | Wells Fargo | Greystone | Future Securitization(s) | $17,297,500 |

| 11 | Newport on the Levee | BMO | $30,000,000 | $12,000,000 | BMO 2024-5C8 | Wells Fargo | Greystone | Future Securitization(s) | $12,000,000 |

| 14 | Tank Holding Portfolio | GSMC, BMO | $26,389,388 | $60,000,000 | BMO 2024-5C7 | Midland | Greystone | BMO 2024-5C7 | $60,000,000 |

| 16 | Signum at 375 Dean | BMO | $24,000,000 | $60,000,000 | BMO 2024-5C7 | Midland | Greystone | BMO 2024-5C7 | $60,000,000 |

| 18 | Riverwalk West | SMC, BMO | $20,000,000 | $60,000,000 | Future Securitization(2) | Midland(2) | LNR(2) | Future Securitization(s) | $60,000,000 |

| 23 | Atrium Hotel Portfolio 24 Pack | GSMC | $15,000,000 | $449,800,000 | AHPT 2024-ATRM | Wells Fargo | CWC Capital

Asset

Management

LLC | AHPT 2024-ATRM Benchmark 2024-V11 WFCM 2024-5C2 BANK5 2024-5YR11 | $835,000,000 $50,000,000 $35,000,000 $50,000,000 |

| 28 | 125 Summer | GACC, BMO | $12,635,000 | $90,000,000 | BMO 2024-5C7 | Midland | Greystone | BMO 2024-5C7 Future Securitization(s) | $60,000,000 $30,000,000 |

| 30 | GRM South Brunswick | SMC | $12,000,000 | $60,000,000 | BMO 2024-5C7 | Midland | Greystone | BMO 2024-5C7 | $60,000,000 |

| 33 | Linx | SGFC | $10,000,000 | $84,000,000 | BMO 2024-5C6 | Midland | LNR | BMO 2024-5C6 BMO 2024-5C7 Future Securitization(s) | $53,000,000 $6,000,000 $25,000,000 |

| 36 | Northbridge Centre | BMO | $5,000,000 | $91,000,000 | BMO 2024-5C6 | Midland | LNR | BMO 2024-5C6 BMO 2024-5C7 BBCMS 2024-5C29 | $53,000,000 $8,000,000 $30,000,000 |

| (1) | In the case of Loan No. 1, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement of the securitization of the related controlling pari-passu companion loan, which securitization transaction is expected to close on or prior to the closing date for this securitization transaction, at which time the related servicing agreement will be the Controlling Pooling/Trust & Servicing Agreement. |

| (2) | In the case of Loan No. 18, until the securitization of the related controlling pari passu companion loan, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement for a securitization transaction expected to close on or prior to the closing date for this securitization transaction, at which time the related servicing agreement will be the Controlling Pooling/Trust & Servicing Agreement. Upon the securitization of the related controlling pari-passu companion loan, servicing of the related whole loan will shift to the servicers under the servicing agreement with respect to such future securitization transaction, which servicing agreement will become the Controlling Pooling/Trust & Servicing Agreement. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 6 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| Collateral Characteristics |

| Mortgaged Properties by Type |

| | | | | | Weighted Average |

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW

NCF DSCR | UW

NOI DY | Cut-off Date LTV | Maturity Date/ARD LTV |

| Multifamily | High Rise | 6 | $172,096,667 | 17.4% | 1.63x | 10.1% | 55.2% | 55.2% |

| | Mid Rise | 14 | 137,408,333 | 13.9 | 1.37x | 9.2% | 65.0% | 65.0% |

| | Garden | 7 | 100,636,379 | 10.1 | 1.36x | 9.7% | 66.8% | 66.8% |

| | Townhome | 1 | 10,063,621 | 1.0 | 1.41x | 10.5% | 60.5% | 60.5% |

| | Low Rise | 1 | 2,570,000 | 0.3 | 1.36x | 10.2% | 64.0% | 64.0% |

| | Subtotal / Weighted Average: | 29 | $422,775,000 | 42.6% | 1.48x | 9.7% | 61.3% | 61.3% |

| Retail | Super Regional Mall | 2 | $121,000,000 | 12.2% | 1.88x | 12.2% | 50.9% | 50.9% |

| | Anchored | 3 | 44,000,000 | 4.4 | 1.59x | 12.4% | 56.1% | 56.1% |

| | Outlet Center | 1 | 35,970,000 | 3.6 | 2.40x | 19.5% | 50.3% | 50.3% |

| | Single Tenant | 1 | 3,750,000 | 0.4 | 1.34x | 9.6% | 60.2% | 60.2% |

| | Subtotal / Weighted Average: | 7 | $204,720,000 | 20.6% | 1.90x | 13.5% | 52.1% | 52.1% |

| Mixed Use | Office/Retail | 2 | $73,550,000 | 7.4% | 1.51x | 11.7% | 52.5% | 52.5% |

| | Lab/Office | 2 | 67,300,000 | 6.8 | 1.86x | 10.8% | 65.9% | 65.9% |

| | Retail/Office | 1 | 30,000,000 | 3.0 | 1.68x | 16.6% | 39.9% | 38.3% |

| | Multifamily/Retail | 1 | 11,320,000 | 1.1 | 1.73x | 12.1% | 65.1% | 65.1% |

| | Subtotal / Weighted Average: | 6 | $182,170,000 | 18.4% | 1.68x | 12.2% | 56.1% | 55.9% |

| Office | CBD | 4 | $82,135,000 | 8.3% | 1.75x | 13.1% | 63.6% | 63.6% |

| | Suburban/R&D | 1 | 6,450,000 | 0.7 | 1.50x | 11.1% | 61.6% | 61.6% |

| | Subtotal / Weighted Average: | 5 | $88,585,000 | 8.9% | 1.73x | 13.0% | 63.4% | 63.4% |

| Industrial | Warehouse Distribution/Light Manufacturing | 23 | $26,389,388 | 2.7% | 2.25x | 11.8% | 65.0% | 65.0% |

| | Flex/R&D | 1 | 26,000,000 | 2.6 | 1.27x | 10.5% | 56.8% | 56.8% |

| | Warehouse | 1 | 12,000,000 | 1.2 | 1.37x | 10.0% | 57.1% | 57.1% |

| | Subtotal / Weighted Average: | 25 | $64,389,388 | 6.5% | 1.69x | 10.9% | 60.2% | 60.2% |

| Hospitality | Full Service | 18 | $13,337,315 | 1.3% | 4.17x | 26.7% | 32.1% | 32.1% |

| | Extended Stay | 1 | 10,500,000 | 1.1 | 1.60x | 14.7% | 55.6% | 55.6% |

| | Limited Service/Extended Stay | 3 | 865,477 | 0.1 | 4.17x | 26.7% | 32.1% | 32.1% |

| | Select Service | 3 | 797,208 | 0.1 | 4.17x | 26.7% | 32.1% | 32.1% |

| | Subtotal / Weighted Average: | 25 | $25,500,000 | 2.6% | 3.11x | 21.8% | 41.8% | 41.8% |

| Self Storage | Self Storage | 1 | $3,700,000 | 0.4% | 1.30x | 9.2% | 68.1% | 68.1% |

| Total / Weighted Average: | 98 | $991,839,388 | 100.0% | 1.68x | 11.6% | 58.1% | 58.1% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 7 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

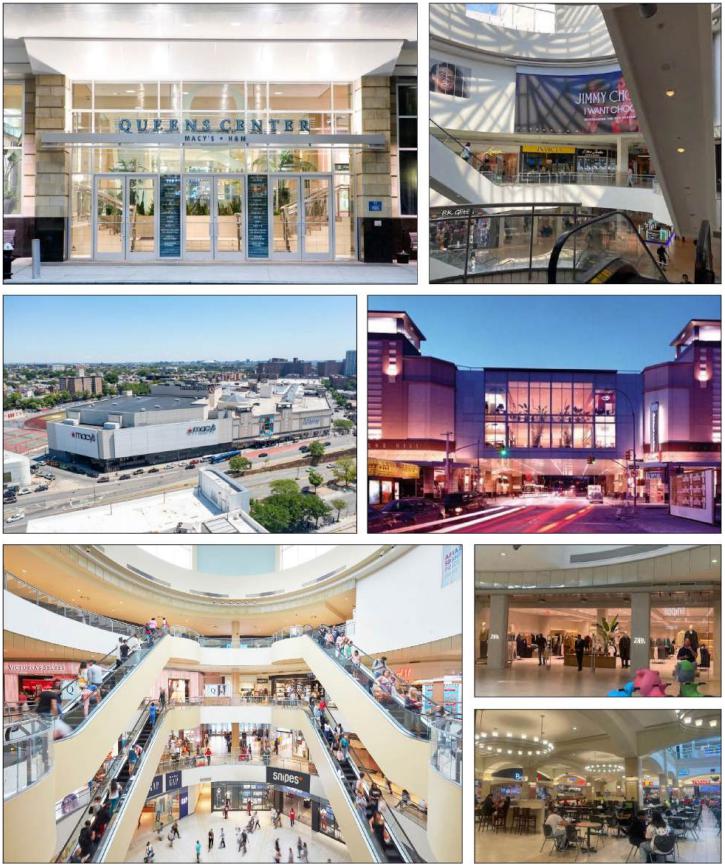

| No. 1 – Queens Center |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 8 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 9 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 10 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 11 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 12 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

| Mortgage Loan Information | | Property Information |

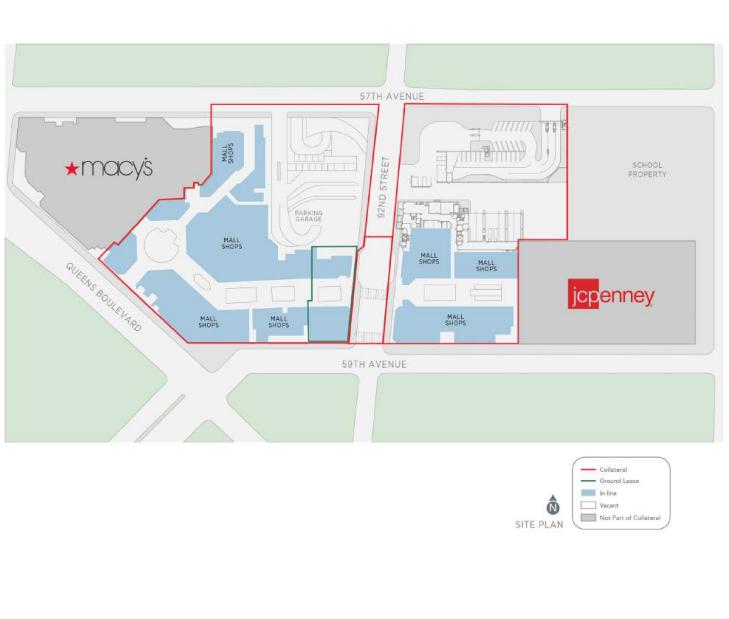

| Mortgage Loan Sellers: | GACC, BMO, GSMC | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $71,000,000 | | Title(5): | Fee/Leasehold |

| Cut-off Date Principal Balance(1): | $71,000,000 | | Property Type – Subtype: | Retail – Super Regional Mall |

| % of IPB: | 7.2% | | Net Rentable Area (SF)(6): | 412,033 |

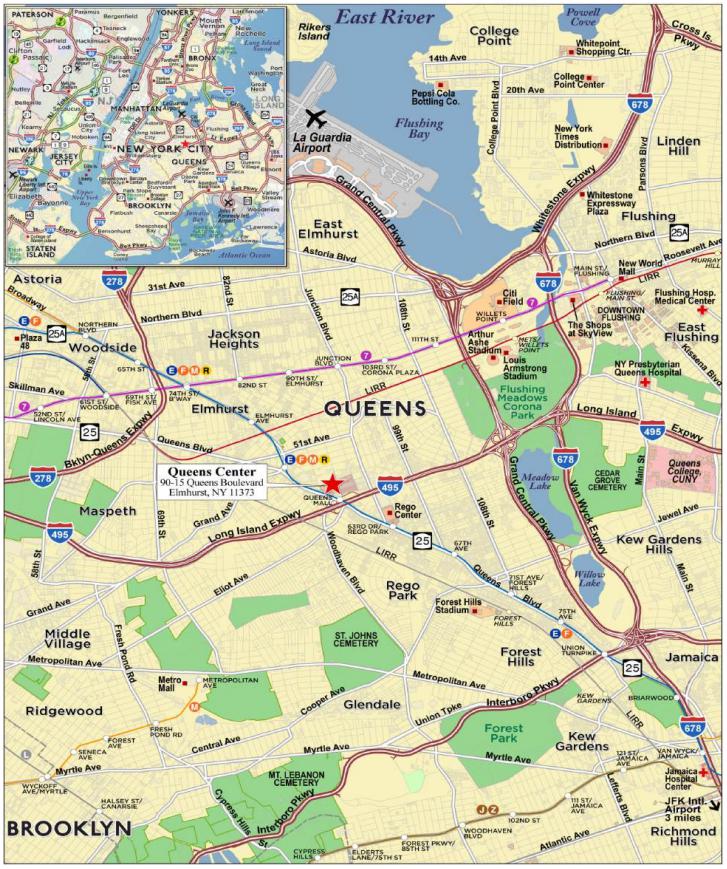

| Loan Purpose: | Refinance | | Location: | Elmhurst, NY |

| Borrower: | Queens Center SPE LLC and Queens Center Pledgor LLC | | Year Built / Renovated: | 1973 / 2004 |

| Borrower Sponsor: | The Macerich Partnership, L.P. | | Occupancy: | 95.4% |

| Interest Rate(2): | 5.37000% | | Occupancy Date: | 10/7/2024 |

| Note Date: | 10/28/2024 | | 4th Most Recent NOI (As of): | $51,866,594 (12/31/2021) |

| Maturity Date: | 11/6/2029 | | 3rd Most Recent NOI (As of): | $55,476,544 (12/31/2022) |

| Interest-only Period: | 60 months | | 2nd Most Recent NOI (As of): | $52,482,275 (12/31/2023) |

| Original Term: | 60 months | | Most Recent NOI (As of): | $49,730,304 (9/30/2024 TTM) |

| Original Amortization Term: | None | | UW Economic Occupancy: | 95.8% |

| Amortization Type: | Interest Only | | UW Revenues: | $100,774,128 |

| Call Protection(2): | L(25),DorYM1(28),O(7) | | UW Expenses: | $47,153,562 |

| Lockbox / Cash Management: | Hard / Springing | | UW NOI: | $53,620,566 |

| Additional Debt(1): | Yes | | UW NCF: | $52,532,319 |

| Additional Debt Balance(1): | $454,000,000 | | Appraised Value / Per SF(1): | $1,060,000,000 / $2,573 |

| Additional Debt Type(1)(3): | Pari Passu | | Appraisal Date: | 9/19/2024 |

| | | | | |

| Escrows and Reserves(4) | | Financial Information(1) |

| | Initial | Monthly | Cap | | Cut-off Date Loan / SF: | $1,274 |

| Taxes: | $0 | Springing | N/A | | Maturity Date Loan / SF: | $1.274 |

| Insurance: | $0 | Springing | N/A | | Cut-off Date LTV: | 49.5% |

| Replacement Reserves: | $0 | Springing | $206,017 | | Maturity Date LTV: | 49.5% |

| TI / LC Reserve: | $0 | Springing | $641,476 | | UW NCF DSCR: | 1.84x |

| Other Reserve(7): | $12,211,534 | N/A | N/A | | UW NOI Debt Yield: | 10.2% |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | Uses | Proceeds | % of Total |

| Whole Loan Amount(1): | $525,000,000 | 85.2 | % | | Loan Payoff: | $601,802,949 | 97.7 | % |

| Sponsor Equity: | 91,238,851 | 14.8 | | | Reserves | 12,211,534 | 2.0 | |

| | | | | Closing Costs: | 2,224,368 | 0.4 | |

| Total Sources: | $616,238,851 | 100.0 | % | | Total Uses: | $616,238,851 | 100.0 | % |

| (1) | The Queens Center Mortgage Loan (as defined below) is part of a whole loan evidenced by 30 pari passu promissory notes with an aggregate original principal balance of $525,000,000. The financial information presented in the chart above is based on the Queens Center Whole Loan (as defined below). |

| (2) | The lockout period will be at least 25 payment dates beginning with and including the first payment date on December 6, 2024. Defeasance of the Queens Center Whole Loan in full is permitted at any time after the earlier to occur of (i) November 6, 2027 and (ii) the date that is two years from the closing date of the securitization that includes the last pari passu note to be securitized (the ”Lockout Release Date”). In addition, on any business day from and after the Lockout Release Date, voluntary prepayment of the Queens Center Whole Loan is permitted in whole (but not in part), together with, if such voluntary prepayment occurs prior to the monthly payment date that occurs prior to May 6, 2029, a prepayment fee equal to the greater of (x) 1.00% of the principal amount of the Queens Center Whole Loan being prepaid and (y) a yield maintenance premium. The assumed lockout period of 25 payments is based on the anticipated closing date of the BMO 2024-5C8 securitization closing date in December 2024. The actual lockout period may be longer. |

| (3) | See "The Loan" below for further discussion of additional mortgage debt. |

| (4) | Please see “Escrows and Reserves” below for further discussion of reserve information. |

| (5) | See “Ground Lease” below for further discussion of reserve requirements. |

| (6) | Net Rentable Area (SF) is exclusive of 556,724 square feet associated with Macy’s and JCPenney, both of which are non-collateral anchor tenants. |

| (7) | Other Reserve is comprised of $11,562,092 for outstanding tenant improvements and leasing commissions and $649,442 for gap rent. |

The Loan. The largest mortgage loan (the “Queens Center Mortgage Loan”) is part of a whole loan evidenced by 30 pari passu promissory notes with an aggregate outstanding principal balance as of the Cut-off Date of $525,000,000 (the “Queens Center Whole Loan”). The Queens Center Whole Loan is secured by the borrowers’ non-overlapping fee and leasehold interests in a 412,033 SF retail property located in Elmhurst, New York (the “Queens Center Property”) as well as the Pledgor Borrower’s (as defined below) membership interest in the Property Borrower (as defined below). The Queens Center Mortgage Loan is evidenced by the non-controlling notes A-1-4-1, A-1-5, A-2-2-2, A-2-3, A-4-1-2 and A-4-2 with an

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 13 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

outstanding principal balance as of the Cut-off Date of $71,000,000. The Queens Center Whole Loan was originated by German American Capital Corporation (“GACC”), Goldman Sachs Bank USA (“GS”), JPMorgan Chase Bank, National Association (“JPMCB”), Bank of Montreal (“BMO”) and Morgan Stanley Bank, N.A. (“MSBNA”) on October 28, 2024. GACC is selling Notes A-1-4-1 and A-1-5 with an outstanding principal balance as of the Cut-off Date of $31,000,000. BMO is selling Notes A-4-1-2 and A-4-2 with an outstanding principal balance as of the Cut-off Date of $20,000,000. GS is selling Notes A-2-2-2 and A-2-3 with an outstanding principal balance as of the Cut-off Date of $20,000,000. The Queens Center Whole Loan will be serviced pursuant to the pooling and servicing agreement for a future securitization trust. See “Description of the Mortgage Pool—The Serviced Pari Passu Whole Loans” and “The Pooling and Servicing Agreement” in the Preliminary Prospectus.

The table below identifies the promissory notes that comprise the Queens Center Whole Loan:

| Whole Loan Summary |

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1-1 | $50,000,000 | $50,000,000 | Future Securitization(1) | Yes |

| A-1-2(1) | $25,000,000 | $25,000,000 | DBRI | No |

| A-1-3(1) | $25,000,000 | $25,000,000 | DBRI | No |

| A-1-4-1 | $16,000,000 | $16,000,000 | BMO 2024-5C8 | No |

| A-1-4-2 | $4,000,000 | $4,000,000 | DBRI | No |

| A-1-5 | $15,000,000 | $15,000,000 | BMO 2024-5C8 | No |

| A-1-6(1) | $15,000,000 | $15,000,000 | DBRI | No |

| A-2-1 | $15,000,000 | $15,000,000 | WFCM 2024-5C2 | No |

| A-2-2-1(1) | $10,000,000 | $10,000,000 | GS | No |

| A-2-2-2 | $5,000,000 | $5,000,000 | BMO 2024-5C8 | No |

| A-2-3 | $15,000,000 | $15,000,000 | BMO 2024-5C8 | No |

| A-2-4(1) | $15,000,000 | $15,000,000 | GS | No |

| A-2-5(1) | $15,000,000 | $15,000,000 | GS | No |

| A-2-6(1) | $25,000,000 | $25,000,000 | GS | No |

| A-3-1 | $43,000,000 | $43,000,000 | BANK5 2024-5YR11 | No |

| A-3-2(1) | $20,000,000 | $20,000,000 | JPMCB | No |

| A-3-3 | $15,000,000 | $15,000,000 | WFCM 2024-5C2 | No |

| A-3-4(1) | $15,000,000 | $15,000,000 | JPMCB | No |

| A-3-5(1) | $7,000,000 | $7,000,000 | JPMCB | No |

| A-4-1-1 | $10,000,000 | $10,000,000 | Future Securitization(1) | No |

| A-4-1-2 | $5,000,000 | $5,000,000 | BMO 2024-5C8 | No |

| A-4-2 | $15,000,000 | $15,000,000 | BMO 2024-5C8 | No |

| A-4-3(1) | $15,000,000 | $15,000,000 | BMO | No |

| A-4-4(1) | $15,000,000 | $15,000,000 | BMO | No |

| A-4-5(1) | $15,000,000 | $15,000,000 | BMO | No |

| A-4-6 | $25,000,000 | $25,000,000 | Future Securitization(1) | No |

| A-5-1 | $32,000,000 | $32,000,000 | BANK5 2024-5YR11 | No |

| A-5-2(1) | $20,000,000 | $20,000,000 | MSBNA | No |

| A-5-3(1) | $15,000,000 | $15,000,000 | MSBNA | No |

| A-5-4(1) | $8,000,000 | $8,000,000 | MSBNA | No |

| Total | $525,000,000 | $525,000,000 | | |

| (1) | Expected to be contributed to one or more future securitization transactions. In the case of the notes where the holder is indicated as “Future Securitization”, the related note(s) are expected to be included in a securitization transaction that has not been announced but is expected to close on or prior to the closing date for this securitization transaction. |

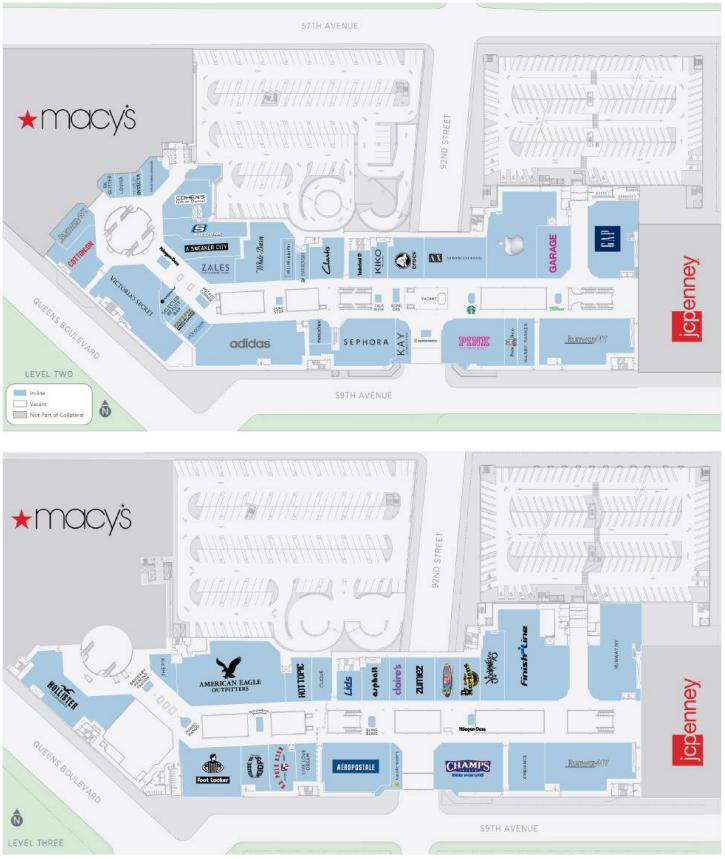

The Property. Built in 1973 and renovated in 2004, Queens Center (the “Queens Center Mall”) is a 968,757 square foot (412,033 collateral square feet) super regional mall located in Elmhurst, New York situated on an 11.21-acre parcel with 8.41 acres of owned acreage and 1,903 parking spaces or 4.6 parking spaces per 1,000 square feet. Of the 968,757 total SF, 412,033 SF constitutes the collateral for the Queens Center Whole Loan, with the remaining non-collateral areas of the Queens Center Mall occupied by Macy’s and JCPenney and owned by third parties.

Representing the sole enclosed super-regional shopping center in Queens, the Queens Center Mall attracts 9.4 million visitors annually and has a trade area of 2.4 million people as of 2022. The Queens Center Mall has historically benefited from high tenant demand with occupancy averaging nearly 99% over the last 10 years. Further, the Queens Center Property is currently 95.4% leased and features a mix of 120 national and regional tenants. Since 2022, the borrower sponsor has

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 14 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

been able to re-tenant or renew over 60% of the collateral SF. Recently, the borrower sponsor has leased to several new high-performing tenants including Primark (54,832 square feet), ZARA (36,463 square feet) and H&M (19,694 square feet).

The Queens Center Mall was originally acquired by the borrower sponsor in 1995. In 2004, the borrower sponsor invested $275.0 million to fully redevelop and expand the Queens Center Property. The expansion featured the addition of 250,000 in-line square feet and JCPenney’s development of an approximately 204,000 square foot box, which JCPenney subsequently sold to Ashkenazy Acquisition Corporation in January 2022. Since 2019, the Borrowers have invested $65.2 million in leasing capital, common area renovations, and operational upgrades with plans to invest an additional $13.0 million by the end of 2024 (such additional investment is not required or reserved for under the Queens Center Whole Loan documents). Of the $78.2 million spent or budgeted from 2019 through year end 2024, $15.2 million has been allocated toward buildout of ZARA’s new 36,463 square foot store, which combined 10 in-line units across two floors. Furthermore, the borrower sponsor has invested $19.7 million and $6.3 million in tenant allowances and buildout costs for Primark (54,832 SF) and H&M (19,694 SF), respectively.

According to the appraisal, the Queens Center Mall is a top-producing center in New York City, attracting significant foot traffic and generating over $500 million in annual sales. The Queens Center Mall’s sales PSF are significantly higher than the national average, with comparable mall shop sales reported at $1,731 PSF ($1,165 PSF excluding Apple). According to the borrower sponsor, as of TTM July 2024 the non-collateral Macy’s and JCPenney reported annual sales of $132,000,000 and $26,000,000, respectively.

Major Tenants. The four largest tenants by underwritten base rent at Queens Center Property are Primark, American Eagle Outfitters, ZARA and H&M.

Primark (54,832 square feet; 13.3% of NRA; 5.6% of underwritten base rent): Founded in 1969, Primark is an international fashion retailer that offers affordable fashion, home goods and accessories. Primark operates over 450 stores across 17 countries across Europe and the United States. The Queens Center Property hosts Primark’s newest location in the Tri-State area. Primark is not yet in occupancy and is expected to take possession of its space in December 2024. Primark’s lease expires in January 2035, has two, five-year extension options remaining and contains a termination option in the event that gross sales between December 2027 and November 2028 do not exceed $23,000,000, provided it gives notice within 90 days following November 30, 2028.

American Eagle Outfitters (10,268 square feet; 2.5% of NRA; 3.4% of underwritten base rent): Founded in 1977, American Eagle Outfitters is a global specialty retailer that offers various types of apparel, intimates, activewear, accessories, and personal care products. With over 1,000 stores worldwide, American Eagle Outfitters focuses on providing a unique shopping experience for the 15 to 25 year-old consumer demographic. American Eagle Outfitters reported annual sales for the TTM July 2024 period of $10,541,311 ($1,027 PSF). American Eagle Outfitters’ lease at the Queens Center Property expires in September 2032 and has no extension or termination options.

ZARA (36,463 square feet; 8.8% of NRA; 3.2% of underwritten base rent): Founded in 1974, ZARA is an international fashion retailer and part of the Inditex Group. ZARA operates approximately 3,000 stores in 96 countries, offering a wide range of fashion-forward apparel. ZARA’s forecasted reported annual sales for the TTM July 2024 period are $23,559,201 ($646 PSF). ZARA’s lease expires in November 2033, with one, five-year extension option remaining and contains a termination option in the event that ZARA gives notice 270 days prior to either (i) December 31, 2028 or (ii) May 31, 2031 with the payment of a termination fee in an amount equal to the unamortized portion, as of the end of 2028 the fifth lease year or the last day of the 90th full calendar month, of the sum of certain allowance for construction work amortized on a straight-line basis over the period from the rent commencement date through the effective date of termination.

H&M (19,694 SF; 4.8% of NRA; 2.8% of underwritten base rent): Founded in 1947, H&M, part of the H&M Group, is a global fashion retailer offering a broad range of clothing and accessories for men, women, and children. H&M has over 3,800 stores across 77 markets worldwide, H&M is known for its commitment to affordable fashion. H&M’s lease expires in January 2035, has two, 4-year extension options remaining and contains options to terminate its lease if its gross sales (i) between January 2028 and December 2028 do not exceed $16,000,000 or (ii) between January 2031 and December 2031 do not exceed $18,000,000, in each case, provided that it gives notice within 120 days following such period.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 15 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

The following information presents certain information relating to the historical and current occupancy of the Queens Center Property:

| Historical and Current Occupancy(1) |

| 2021 | 2022 | 2023 | Current(2) |

| 97.6% | 98.7% | 98.9% | 95.4% |

| (1) | Historical occupancies are as of December 31 of each respective year. |

| (2) | Current occupancy is based on the underwritten rent roll as of October 7, 2024. |

The following table presents certain information relating to the sales history for the Queens Center Property:

| Comparable Sales History(1) |

| | 2019 | 2021 | 2022 | 2023 | TTM July 2024 |

| Comparable Inline (<10,000 SF) Sales PSF | $1,581 | $1,615 | $1,717 | $1,751 | $1,731 |

| Comparable Inline (<10,000 SF excluding Apple) Sales PSF | $1,145 | $1,122 | $1,189 | $1,147 | $1,165 |

| Comparable Inline (<10,000 SF excluding Apple) Occupancy Cost(2) | 22.5% | 21.7% | 21.1% | 22.8% | 22.1% |

| Non-collateral Anchor Sales(3) | $173,300,000 | $159,700,000 | $164,000,000 | $164,000,000 | $158,000,000 |

| Comparable Total Queens Center Mall Sales | $616,120,375 | $536,343,372 | $561,506,309 | $562,896,033 | $533,839,416 |

| (1) | All sales information presented above is based upon information provided by the borrower sponsor. In certain instances, sales figures represent estimates because the tenants are not required to report, or otherwise may not have reported sales information on a timely basis. Further, because sales are self-reported, such information is not independently verified by the borrower sponsor. 2020 numbers are excluded due to the COVID-19 pandemic. |

| (2) | Occupancy Cost is calculated based on gross sales divided by the sum of (i) contractual rent and (ii) reimbursements, each based on the underwritten rent roll dated October 7, 2024. |

| (3) | Includes sales of Macy’s and JCPenney, both of which are non-collateral anchors, as provided by the borrower sponsor. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 16 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

The following table presents certain information relating to the major tenants at the Queens Center Property:

| Top Tenant Summary(1) |

| Tenant | Ratings

Moody’s/S&P/Fitch(2) | Net Rentable Area (SF) | % of

Total NRA | UW Base Rent PSF | UW Base Rent | % of Total

UW Base Rent | Lease

Exp. Date |

| Major Tenants | | | | | | | |

| Primark(3) | NR/NR/NR | 54,832 | 13.3 | % | $54.12 | $2,967,306 | 5.6 | % | 1/31/2035 |

| American Eagle Outfitters | NR/NR/NR | 10,268 | 2.5 | | $172.69 | 1,773,181 | 3.4 | | 9/30/2032 |

| ZARA(4) | NR/NR/NR | 36,463 | 8.8 | | $46.62 | 1,700,000 | 3.2 | | 11/30/2033 |

| H&M(5) | NR/NR/NR | 19,694 | 4.8 | | $75.00 | 1,477,050 | 2.8 | | 1/31/2035 |

| Subtotal/Wtd. Avg. | | 121,257 | 29.4 | % | $65.30 | $7,917,537 | 15.0 | % | |

| Select In-Line < 10,000 SF | | | | | | | |

| Finish Line | NR/NR/NR | 8,625 | 2.1 | | $193.61 | $1,669,923 | 3.2 | | 8/31/2025 |

| Apple Store | Aaa/AA+/NR | 8,706 | 2.1 | % | $178.96 | 1,558,044 | 3.0 | % | 7/31/2025 |

| Victoria’s Secret | NR/NR/NR | 7,767 | 1.9 | % | $165.55 | 1,285,796 | 2.4 | % | 1/31/2033 |

| Adidas(6) | NR/NR/NR | 8,183 | 2.0 | | $135.00 | 1,104,705(7) | 2.1 | | 1/31/2029 |

| Hollister Co. | NR/NR/NR | 8,028 | 1.9 | | $109.50 | 879,028 | 1.7 | | 1/31/2027 |

| The Cheesecake Factory | NR/NR/NR | 8,077 | 2.0 | | $105.00 | 848,085 | 1.6 | | 1/31/2037 |

| Subtotal/Wtd. Average | 49,386 | 12.0 | % | 148.74 | $7,345,580 | 13.9 | % | |

| Other Tenants | | 222,284 | 53.9 | | $168.84 | 37,530,596 | 71.1 | | |

| Occupied Collateral Total | | 392,927 | 95.4 | % | $134.36 | $52,793,713 | 100.0 | % | |

| Vacant Space(8) | | 19,106 | 4.6 | % | | | | |

| Collateral Total | | 412,033 | 100.0 | % | | | | |

| | | | | | | | |

| (1) | Based on the underwritten rent roll dated as of October 7, 2024 and exclusive of 556,724 square feet associated with Macy’s and JCPenney, both of which are non-collateral anchors. |

| (2) | Certain ratings are those of the parent company whether or not the parent guarantees the lease. |

| (3) | Primark has the right to terminate its lease if its gross sales between December 2027 and November 2028 do not exceed $23,000,000, provided it gives notice within 90 days following November 30, 2028, with the payment of a termination fee in an amount equal to the unamortized portion, as of the end of the fifth lease year, of the sum of certain allowances for construction and other interior work amortized on a straight-line basis over the period from the rent commencement date through the effective date of termination. |

| (4) | ZARA has the right to terminate its lease, provided it gives notice 270 days prior to either (i) December 31, 2028 or (ii) May 31, 2031, with the payment of a termination fee in an amount equal to the unamortized portion, as of the end of the fifth lease year, of the sum of certain allowance for construction work amortized on a straight-line basis over the period from the rent commencement date through the effective date of termination. |

| (5) | H&M has the right to terminate its lease if its gross sales (i) between January 2028 and December 2028 do not exceed $16,000,000 or (ii) between January 2031 and December 2031 do not exceed $18,000,000, in each case, provided that it gives notice within 120 days following such period, with the payment of a termination fee in an amount equal to 50% (if terminated based on sales in 2028) or 25% (if terminated based on sales in 2031) of the unamortized portion of the sum of certain allowance for construction and other interior work amortized on a straight-line basis over the period from the rent commencement date through the effective date of termination. |

| (6) | If Adidas' gross sales for calendar year 2024 (the "Test Period") do not exceed $7,000,000, any time during the 60-day period immediately following the Test Period, Adidas will have the one-time right to terminate its lease upon 90 days' prior written notice and the payment of termination fee in an amount equal to five times the monthly fixed minimum rent and monthly amount of the tenant's share of variable costs as set forth in the lease and in effect on the date of tenant's notice to terminate its lease. Adidas' sales for the TTM July 2024 period were $5,438,309. |

| (7) | During the period commencing January 2024 and continuing through December 2024 (“Rent Reduction Period”), in lieu of fixed minimum rent and percentage rent set forth in the lease, Adidas benefits from reduced monthly rent in the amount of (a) $92,058.75 plus (b) the product obtained by multiplying 6% by annual gross sales in excess of $14,452,452.47. |

| (8) | Vacant Space includes 8,351 square feet currently occupied by tenants known to be vacacting that is underwritten as vacant. The Queens Center Property was 97.4% physically occupied inclusive of such tenants as of October 7, 2024. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 17 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

The following table presents certain information relating to the lease rollover schedule at the Queens Center Property:

| Lease Rollover Schedule(1)(2) |

| Year | Number of Leases Expiring | Net Rentable Area Expiring(3) | % of NRA Expiring(3) | UW Base

Rent

Expiring | % of UW Base Rent Expiring | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring(3) | Cumulative UW Base Rent Expiring | Cumulative % of UW Base Rent Expiring |

| Vacant | NAP | 19,106 | 4.6 | % | NAP | NAP | | 19,106 | 4.6% | NAP | NA | P |

| 2024 & MTM | 10 | 21,754 | 5.3 | | $4,334,114 | 8.2 | % | 40,860 | 9.9% | $4,334,114 | 8.2% | |

| 2025 | 28 | 77,642 | 18.8 | | 9,690,548 | 18.4 | | 118,502 | 28.8% | $14,024,662 | 26.6% | |

| 2026 | 17 | 37,142 | 9.0 | | 7,896,124 | 15.0 | | 155,644 | 37.8% | $21,920,786 | 41.5% | |

| 2027 | 13 | 25,249 | 6.1 | | 3,456,921 | 6.5 | | 180,893 | 43.9% | $25,377,707 | 48.1% | |

| 2028 | 11 | 19,816 | 4.8 | | 3,090,862 | 5.9 | | 200,709 | 48.7% | $28,468,570 | 53.9% | |

| 2029 | 16 | 32,294 | 7.8 | | 6,424,947 | 12.2 | | 233,003 | 56.5% | $34,893,516 | 66.1% | |

| 2030 | 5 | 8,572 | 2.1 | | 1,167,451 | 2.2 | | 241,575 | 58.6% | $36,060,968 | 68.3% | |

| 2031 | 1 | 389 | 0.1 | | 175,873 | 0.3 | | 241,964 | 58.7% | $36,236,841 | 68.6% | |

| 2032 | 2 | 11,788 | 2.9 | | 1,966,221 | 3.7 | | 253,752 | 61.6% | $38,203,062 | 72.4% | |

| 2033 | 8 | 52,114 | 12.6 | | 3,599,219 | 6.8 | | 305,866 | 74.2% | $41,802,281 | 79.2% | |

| 2034 | 10 | 12,981 | 3.2 | | 3,290,888 | 6.2 | | 318,847 | 77.4% | $45,093,170 | 85.4% | |

| 2035 & Beyond | 8 | 93,186 | 22.6 | | 7,700,543 | 14.6 | | 412,033 | 100.0% | $52,793,713 | 100.0% | |

| Total | 129 | 412,033 | 100.0 | % | $52,793,713 | 100.0 | % | | | | |

| (1) | Based on the underwritten rent roll as of October 7, 2024. |

| (2) | Certain tenants may have lease termination options that were not taken into account in the Lease Rollover Schedule. |

| (3) | Net Rentable Area Expiring, % of NRA Expiring and Cumulative % of NRA Expiring are exclusive of 556,724 square feet associated with Macy’s and JCPenney, both of which are non-collateral anchor tenants. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 18 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

The following table presents certain information relating to the historical operating results and underwritten cash flows of the Queens Center Property:

| Operating History and Underwritten Net Cash Flow |

| | 2019 | 2020 | 2021 | 2022 | 2023 | TTM(1) | Underwritten | Per Square Foot | %(2)

|

Rents in Place(3) | $67,057,833 | $59,301,650 | $52,916,768 | $51,918,944 | $52,818,458 | $51,520,695 | $52,793,713 | $128.13 | 50.2 | % |

| Rent Steps | 0 | 0 | 0 | 0 | 0 | 0 | 1,247,807 | 3.03 | 1.2 | |

| Vacant Income | 0 | 0 | 0 | 0 | 0 | 0 | 4,370,011 | 10.61 | 4.2 | |

| Gross Potential Income | $67,057,833 | $59,301,650 | $52,916,768 | $51,918,944 | $52,818,458 | $51,520,695 | $58,411,531 | $141.76 | 55.6 | % |

| Reimbursements | 30,790,847 | 29,765,742 | 27,453,264 | 29,305,910 | 29,580,066 | 30,900,451 | 31,470,373 | 76.38 | 29.9 | |

| Percentage Rent | 87,927 | 284,409 | 1,504,768 | 1,176,649 | 211,061 | 4,663 | 0 | 0.00 | 0.0 | |

| Other Income(4) | 18,077,641 | 9,515,462 | 14,790,599 | 20,746,611 | 16,405,772 | 15,580,030 | 15,262,235 | 37.04 | 14.5 | |

| Net Rental Income | $116,014,248 | $98,867,263 | $96,665,399 | $103,148,114 | $99,015,357 | $98,005,839 | $105,144,139 | $255.18 | 100.0 | % |

| (Vacancy/Bad Debt)(5) | (482,316) | (7,429,704) | 3,086,693 | (396,362) | 285,757 | (1,035,603) | (4,370,011) | (10.61) | (4.2 | ) |

| Effective Gross Income | $115,531,932 | $91,437,559 | $99,752,092 | $102,751,752 | $99,301,114 | $96,970,236 | $100,774,128 | $244.58 | 95.8 | % |

| Real Estate Taxes | 28,285,488 | 29,999,255 | 29,577,588 | 27,309,540 | 26,831,221 | 26,587,630 | 26,925,545 | 65.35 | 26.7 | |

| Insurance | 254,934 | 356,236 | 424,981 | 453,227 | 419,257 | 486,435 | 531,957 | 1.29 | 0.5 | |

| Management Fee | 1,106,734 | 952,496 | 923,502 | 1,003,129 | 876,335 | 860,247 | 1,000,000 | 2.43 | 1.0 | |

| Ground Rent Expense | 441,719 | 441,719 | 461,478 | 471,358 | 471,358 | 502,544 | 608,041 | 1.48 | 0.6 | |

| Other Operating Expenses | 17,087,387 | 11,923,051 | 16,497,949 | 18,037,954 | 18,220,668 | 18,803,076 | 18,088,019 | 43.90 | 17.9 | |

| Total Expenses | $47,176,262 | $43,672,757 | $47,885,498 | $47,275,208 | $46,818,839 | $47,239,932 | $47,153,562 | $114.44 | 46.8 | % |

| Net Operating Income | $68,355,670 | $47,764,802 | $51,866,594 | $55,476,544 | $52,482,275 | $49,730,304 | $53,620,566 | $130.14 | 53.2 | % |

| Capital Expenditures | 0 | 0 | 0 | 0 | 0 | 0 | 119,490 | 0.29 | 0.1 | |

| TI/LC | 0 | 0 | 0 | 0 | 0 | 0 | 968,757 | 2.35 | 1.0 | |

| Net Cash Flow(6) | $68,355,670 | $47,764,802 | $51,866,594 | $55,476,544 | $52,482,275 | $49,730,304 | $52,532,319 | $127.50 | 52.1 | % |

| (1) | TTM represents the trailing 12-month period ending September 30, 2024. |

| (2) | % column represents percent of Net Rental Income for all revenue lines and represents percent of Effective Gross Income for the remainder of fields. |

| (3) | Based on the underwritten rent roll as of October 7, 2024. |

| (4) | Other Income is based on the borrower sponsor’s budget and includes income from parking, business development/advertising, specialty leasing, overage rent and other miscellaneous income. |

| (5) | Vacancy/Bad Debt reflects bad debt for historical periods and vacancy for Underwritten. Positive periods reflect recovery of bad debt. |

| (6) | The decrease in Net Cash Flow from 2019 to 2020 and subsequent increase from 2020 to 2021 is primarily attributable to impacts from the COVID-19 pandemic. |

Appraisal. According to the appraisal, the Queens Center Property had an “as-is” appraised value of $1,060,000,000 as of September 19, 2024. The table below shows the appraisal’s “as-is” conclusions:

| Appraisal Valuation Summary(1) |

| Appraisal Approach | Appraised Value | Capitalization Rate(2) |

| Direct Capitalization Approach | $1,060,000,000 | 5.25% |

| (2) | The appraisal used a discounted cash flow approach to arrive at the appraised value. The capitalization rate shown above represents the overall capitalization rate. |

Environmental. According to the Phase I environmental site assessment dated October 18, 2024, there was no evidence of any recognized environmental conditions at the Queens Center Property.

The Market. The Queens Center Property is located in the Elmhurst neighborhood of Queens, New York. Elmhurst is a densely populated area with a mix of residential and commercial developments. The neighborhood is well-connected via public transportation, including the Long Island Rail Road and New York City subway system, providing access to Manhattan and other parts of the city. The area is characterized by a diverse population and a variety of housing types, including multi-tenant rentals and cooperative apartments. In 2023, the average household income in a one-, three- and five-mile radius was $86,791, $92,204 and $98,765, respectively. In 2023, the population within the same radii was 191,469, 907,210, and 2,357,847, respectively.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 19 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

The Queens Center Mall benefits from its location and strong tenant mix, making it a key retail center in the region. Notably, Apple is a significant draw, with TTM July 2024 sales of approximately $130 million. According to the appraisal, the Queens retail market, as of the second quarter of 2024, had a total inventory is approximately 5.7 million square feet with an 11.3% vacancy rate.

As the only enclosed super regional shopping center in Queens County, the Queens Center Property serves a trade area of 2.4 million people and approximately 861,000 households. Queens County spans 108.1 square miles and is home to 2.4 million residents, making Queens the 4th densest county in the United States. The Queens Center Mall’s trade area is characterized by a dynamic and culturally rich population with an average household income approximately of $104,000. The Queens Center Mall has four power centers and four super-regional retail centers in its market; however, the Queens Center Mall offers superior access via car, bus, subway or foot, as it is located adjacent to a highly trafficked subway station and the intersection of Queens Boulevard, Woodhaven Boulevard, and the Long Island Expressway.

The following table presents certain information relating to the appraisal’s market rent conclusions for the Queens Center Property:

| Market Rent Summary(1) |

| | Market Rent (PSF) | Lease Term (Yrs.) | Rent Increase Projections | New Tenant Improvements PSF | Renewal Tenant Improvements PSF |

| 0 – 1,000 SF | $225.00 | 5 | 3% per annum | $100.00 | $25.00 |

| 1,001 – 2,000 SF | $200.00 | 5 | 3% per annum | $100.00 | $25.00 |

| 2,001 – 3,000 SF | $200.00 | 5 | 3% per annum | $100.00 | $25.00 |

| 3,001 – 5,000 SF | $175.00 | 5 | 3% per annum | $100.00 | $25.00 |

| 5,001 – 7,500 SF | $150.00 | 10 | 3% per annum | $100.00 | $25.00 |

| 7,501+ SF | $150.00 | 10 | 3% per annum | $100.00 | $25.00 |

| Jewelry | $400.00 | 10 | 3% per annum | $100.00 | $25.00 |

| Food Court | $410.00 | 10 | 3% per annum | $250.00 | $75.00 |

| Kiosk 0-100 SF | $2,000.00 | 5 | 3% per annum | $0.00 | $0.00 |

| Kiosk 100+ SF | $650.00 | 5 | 3% per annum | $0.00 | $0.00 |

| Major | $75.00 | 10 | 10% in Year 6 | $100.00 | $25.00 |

| Junior Anchor | $50.00 | 10 | 10% in Year 6 | $100.00 | $25.00 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 20 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

The table below presents certain information relating to retail centers comparable to the Queens Center Property identified by the appraisal:

| Competitive Set(1) |

| Property Name | Year Built/Renovated | Total NRA | Total Occupancy | Anchor / Major Tenants | Distance to Queens Center Property |

| Queens Center | 1973 / 2004 | 412,033(2) | 95.4%(2) | Primark, ZARA(2) | NAP |

| Queens Place Retail Center | 1965 / 1999, 2001 | 445,953 | 96.0% | Target, Macy’s Furniture Store, DSW Shoes, Best Buy, Lidl | One Block North |

| Rego Park Center I | 1996 / 2005 | 342,869 | 75.0% | Burlington, Marshalls | Two Blocks South |

| Rego Park Center II | 2010 / NAP | 616,820 | 100.0% | Costco, At Home, Aldi, Petco, TJ Maxx | Two Blocks South |

| The Shops at Atlas Park | 2006 / NAP | 372,000 | 95.0% | Ashley Furniture, Forever 21, HomeGoods, NYSC, Regal Cinemas, Ulta, TJ Maxx | 1.8 Miles South |

| Kings Plaza(3) | 1969 / 2018 | 1,146,035 | 88.0% | Burlington, Lowe’s, Macy’s, Target, Primark | 10.0 Miles South |

| Green Acres Mall(3) | 1956 / 2016 | 2,075,000 | 93.0% | Macy’s, Kohl’s, Primark | 11.0 Miles Southeast |

| Staten Island Mall(3) | 1972 / 2018 | 1,700,000 | 94.0% | Primark, JC Penney, Macy’s, Lidl, AMC Theatres | 22.0 Miles Southwest |

| Roosevelt Field | 1956 / 2014 | 2,330,000 | 98.0% | Bloomingdale’s, JC Penney, Primark, Macy’s, Nordstrom, Dick’s Sporting Goods, Neiman Marcus | 15.0 Miles East |

| Weighted Average | | | 93.9%(4) | | |

| (1) | Source: Appraisal, unless otherwise specified. |

| (2) | Based on the underwritten rent roll dated as of October 7, 2024 and does not include 556,724 SF of space associated with Macy’s and JCPenney which are non-collateral anchor tenants. |

| (3) | Owned by the borrower sponsor. |

| (4) | Weighted Average excludes the Queens Center Property. |

The Borrowers. The borrowers are Queens Center SPE LLC (the “Property Borrower”) and Queens Center Pledgor LLC (the “Pledgor Borrower”; together with the Property Borrower, the “Borrowers”), each a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the Borrowers delivered a non-consolidation opinion in connection with the origination of the Queens Center Whole Loan.

The Borrower Sponsor. The borrower sponsor and non-recourse carveout guarantor is The Macerich Partnership, L.P., which is a subsidiary of The Macerich Company (“Macerich”). Macerich is a fully integrated, self-managed and self-administered real estate investment trust. Developing and managing properties that serve as community cornerstones, Macerich currently owns 44 million square feet of real estate consisting primarily of interests in 41 retail centers.

Property Management. The Queens Center Property is currently managed by Macerich Property Management Company, LLC an affiliate of the Borrowers.

Escrows and Reserves. On the loan origination date, the Borrowers were required to make an upfront deposit of $11,562,092 into a reserve for outstanding tenant improvements and leasing commissions and $649,442 for gap rent.

Real Estate Taxes – During the continuance of an Trigger Period (as defined below), the Borrowers are required to deposit into a real estate tax reserve, on a monthly basis, an amount equal to 1/12th of the real estate taxes that the lender estimates will be payable during the next ensuing 12 months (initially estimated to be approximately $2,243,795 monthly).

Insurance – During the continuance of a Trigger Period, unless the Queens Center Property is insured under an acceptable blanket policy and no event of default for which the lender has commenced an enforcement action is continuing, the Borrowers are required to escrow 1/12th of the annual estimated insurance payments on a monthly basis. A blanket insurance policy was in place at closing.

Replacement Reserve – During the continuance of a Trigger Period, the Borrowers are required to escrow approximately $8,584 on a monthly basis for replacement reserves, subject to a cap of $206,017.

TI/LC Reserve – During the continuance of a Trigger Period, the Borrowers are required to escrow approximately $26,728 on a monthly basis for ongoing rollover reserves, subject to a cap of $641,476.

Lockbox / Cash Management. The Queens Center Whole Loan is structured with a hard lockbox and springing cash management. The Borrowers and property manager, as applicable, are required to direct the tenants to pay rent directly

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 21 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

into the lockbox account, and to deposit any rents otherwise received in such account within three business days after receipt. So long as no Trigger Period is continuing, the Borrowers will have access to the funds deposited into the lockbox account, and may utilize the lockbox account as its operating account. During the continuance of a Trigger Period, the Borrowers will no longer have any further access to the funds in the lockbox account, and such funds in the lockbox account are required to be swept to a lender-controlled cash management account, and applied and disbursed in accordance with the Queens Center Whole Loan documents, with any excess funds (i) to be deposited into an excess cash flow reserve account held by the lender as cash collateral for the Queens Center Whole Loan during the continuance of such Trigger Period, or (ii) if no Trigger Period is continuing, disbursed to the Borrowers.

A “Trigger Period” means the period commencing upon the occurrence of (i) an event of default or (ii) the debt service coverage ratio is less than 1.40x for two consecutive calendar quarters. A Trigger Period will end (a) with respect to clause (i) above, if the cure of the event of default has been accepted by the lender or (b) with respect to clause (ii) above, (x) the debt service coverage ratio is greater than or equal to 1.40x for two consecutive calendar quarters, or (y) Borrowers will have (1) after the Lockout Release Date, prepaid the Queens Center Whole Loan in an amount that would result in a debt service coverage ratio of 1.40x in accordance with the Queens Center Whole Loan documents or (2) delivered to the lender cash or other securities acceptable to the lender in accordance with the Queens Center Whole Loan documents as additional collateral for the Queens Center Whole Loan in an amount that when added to underwritten net operating income would result in a debt service coverage ratio at least equal to 1.40x.

Subordinate and Mezzanine Debt. None.

Permitted Future Subordinate or Mezzanine Debt. Not permitted.

Partial Release. The Borrowers are permitted to obtain the free release (without prepayment or defeasance) of Out Parcels (as defined below) provided certain conditions are satisfied, including among others, (i) certification by the Borrowers that the release will not materially and adversely affect the use, operations, economic value of, or the revenue produced by (exclusive of the economic value or revenue lost attributable to the Out Parcel being released) the remaining improvements located on the Queens Center Property as a retail shopping center; (ii) the released Out Parcel constitutes a separate tax lot (or the owner of the released Out Parcel is contractually obligated to pay its share of taxes), (iii) compliance with all applicable laws, reciprocal easement and agreement and material leases, and (iv) compliance with REMIC related conditions.

“Out Parcels” means (A) certain real property that is as of the date of any potential release non-income producing and unimproved for tenant occupancy and the release of which does not have a material adverse effect on (i) the business, profits, operations or condition (financial) of the borrowers, (ii) the ability of the borrowers to repay the debt in accordance with the terms of the loan documents, or (iii) the ongoing operations of the remaining Queens Center Property; and (B) certain real property that is as of the date of any potential release non-income producing and improved by structures that (A) were vacant as of the origination date and (B) have been vacant and non-income producing continuously since the origination date and for at least three years prior to the date of any potential release.

Ground Lease. A 17,450 SF portion of the Queens Center Property located on the northeast corner of 92nd street and 59th Street (the “Ground Leased Parcel”) is subject to a ground lease (the “Ground Lease”) between Tiliakos Enterprises LLC, as the ground landlord (the “Ground Landlord”), and the Property Borrower, as the ground tenant (in such capacity, the “Ground Tenant”). The current annual base rent is $595,510, which is required to be adjusted every three years to the greater of (a) $325,000 (which was the initial annual base rent) or (b) the adjusted annual base rent based on the Consumer Price Index. The Ground Lease has a maturity date of May 31, 2048, with no renewal options, but with a purchase option for the Property Borrower, exercisable as follows: Between May 1, 2039 and April 30, 2046, the Ground Landlord must serve notice to the Ground Tenant for the Ground Tenant to purchase the ground-leased parcel (the “Put Right”), with the notice date being deemed to be March 2, 2046, if the Ground Landlord fails to provide such notice by April 30, 2046, and then the Ground Tenant will subsequently have three years to send notice of its acceptance of the Put Right beginning 60 days after Ground Landlord’s notice is sent (the “Call Right”). The Ground Landlord and the Ground Tenant are each required to appoint an appraiser, and to agree to a third, disinterested appraiser, to obtain a fair market value of the Ground Leased Parcel, and the average of the two closest valuations will be treated as the purchase price to be paid by the Ground Tenant for the Ground Leased Parcel.

Shared Tax Lot. A portion of the Queens Center Property to the west of 92nd Street and the Macy’s parcel together constitute a single tax lot (the “Shared Tax Lot”). The real estate taxes on the shared tax lot are allocated between Macy’s and the Property Borrower under a reciprocal easement agreement (the “REA”). Under the REA, Macy’s pays approximately

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 22 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 1 – Queens Center |

40% of the total property taxes assessed against the shared tax lot to the Property Borrower, who then makes the required tax payments. There are no other operating covenants in place governing the operation of the Shared Tax Lot.

In the event of default under the Queens Center Whole Loan documents, the lender has the right to require, among other related rights, the Borrowers to exercise the rights of the Property Borrower under the REA to pursue the creation of a separate tax lot for the portion of the Queens Center Property that is part of the Shared Tax Lot, such that no portion of the Queens Center Property shares a tax lot with any real property that is not subject to the lien of the Queens Center Whole Loan.

In September 2005, the City of New York advised that it would no longer accept deeds for recordation which affect only a portion of a tax lot, although the recordation of mortgages or instruments other than deeds is not affected by this advisement. The borrowers have provided a non-recourse carveout for any losses arising from the lender’s inability to foreclose on the portion of the Queens Center Property that is part of the Shared Tax Lot caused by (i) the City of New York’s refusal to accept for recordation a deed in foreclosure with respect to such portion of the Queens Center Property and (ii) the Borrowers’ failure to promptly pursue the creation of a separate tax lot for the portion of the Queens Center Property comprising the Shared Tax Lot.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 23 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

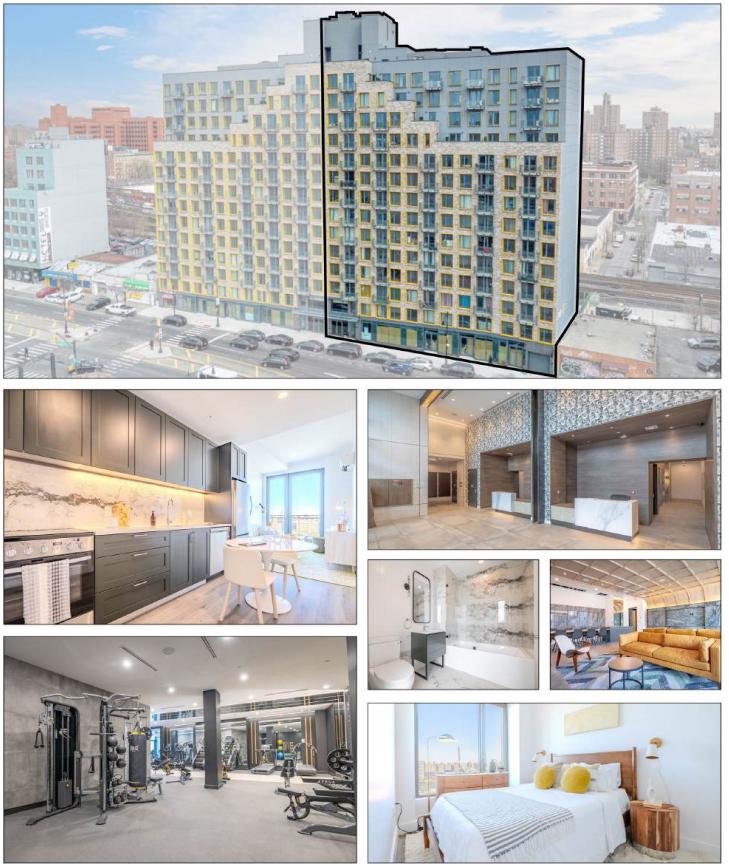

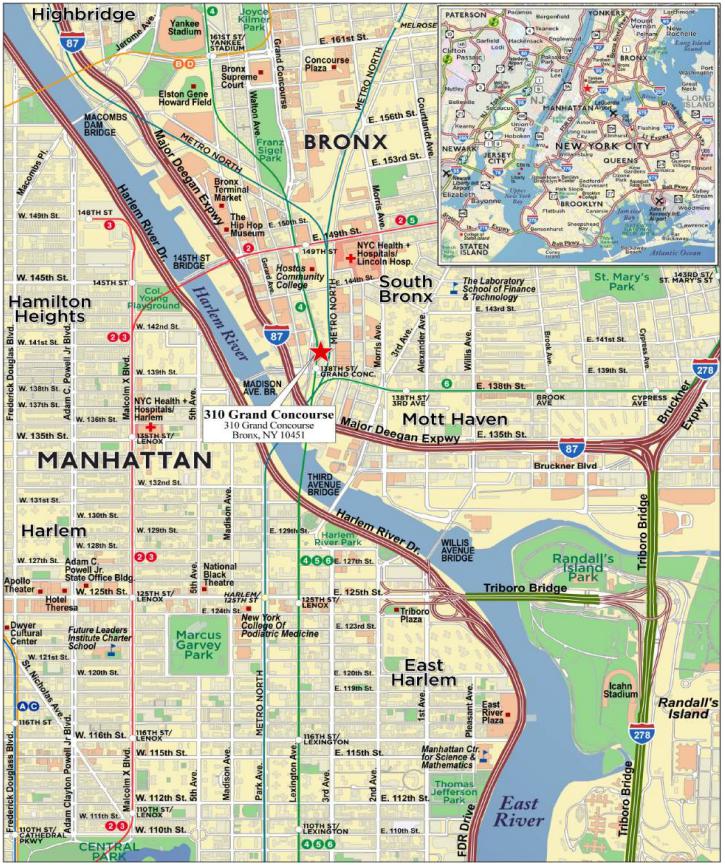

| No. 2 – 310 Grand Concourse |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 24 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 2 – 310 Grand Concourse |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 25 | |

| Structural and Collateral Term Sheet | | BMO 2024-5C8 |

| No. 2 – 310 Grand Concourse |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Seller: | BMO, GCMC, Barclays | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance: | $70,750,000 | | Title: | Fee |

| Cut-off Date Principal Balance: | $70,750,000 | | Property Type – Subtype: | Multifamily – High Rise |

| % of IPB: | 7.1% | | Net Rentable Area (Units)(1): | 150 |

| Loan Purpose: | Refinance | | Location: | Bronx, NY |

| Borrower: | 310 Grand Concourse LLC | | Year Built / Renovated: | 2023 / NAP |

| Borrower Sponsors: | Simon Kaufman and Yoel Kaufman | | Occupancy(2): | 96.7% |

| Interest Rate: | 6.21000% | | Occupancy Date: | 11/18/2024 |

| Note Date: | 11/20/2024 | | 4th Most Recent NOI (As of)(3): | NAP |

| Maturity Date: | 12/6/2029 | | 3rd Most Recent NOI (As of)(3): | NAP |

| Interest-only Period: | 60 months | | 2nd Most Recent NOI (As of)(3): | NAP |

| Original Term: | 60 months | | Most Recent NOI (As of): | $5,269,902 (T-3 10/31/2024 Ann.) |

| Original Amortization Term: | None | | UW Economic Occupancy(4): | 96.1% |

| Amortization Type: | Interest Only | | UW Revenues: | $6,294,352 |