| | | FREE WRITING PROSPECTUS |

| | | FILED PURSUANT TO RULE 433 |

| | | REGISTRATION FILE NO.: 333-280224-05 |

| | | |

| Dated February 5, 2025 | BMO 2025-C11 |

| Structural and Collateral Term Sheet |

BMO 2025-C11 Mortgage Trust |

$906,918,176 (Approximate Mortgage Pool Balance) |

| |

$[] (Approximate Offered Certificates) |

| |

BMO Commercial Mortgage Securities LLC Depositor |

| |

Commercial Mortgage Pass-Through Certificates, Series 2025-C11 |

| |

| |

Bank of Montreal Societe Generale Financial Corporation Starwood Mortgage Capital LLC UBS AG German American Capital Corporation National Cooperative Bank, N.A. Citi Real Estate Funding Inc. Barclays Capital Real Estate Inc. LMF Commercial, LLC LoanCore Capital Markets LLC Goldman Sachs Mortgage Company Greystone Commercial Mortgage Capital LLC Natixis Real Estate Capital LLC Sponsors and Mortgage Loan Sellers |

BMO Capital

Markets | Deutsche

Bank

Securities | Citigroup | Barclays | Goldman

Sachs &

Co. LLC | UBS

Securities

LLC | Société

Générale |

| |

| Co-Lead Managers and Joint Bookrunners |

| | | | | |

| Academy Securities | Bancroft Capital, LLC | Drexel Hamilton | Mischler Financial | Natixis |

| Co-Managers |

| |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | | |

| Dated February 5, 2025 | BMO 2025-C11 |

This material is for your information, and none of BMO Capital Markets Corp., SG Americas Securities, LLC, Deutsche Bank Securities Inc., Citigroup Global Markets Inc., Barclays Capital Inc., Goldman Sachs & Co. LLC, UBS Securities LLC, Academy Securities, Inc., Bancroft Capital, LLC, Drexel Hamilton, LLC, Mischler Financial Group, Inc. and Natixis Securities Americas LLC (collectively, the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-280224) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or BMO Capital Markets Corp., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-888-200-0266. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2025-C11 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these Certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the Certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the Certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Europe p.l.c, and Bank of Montreal (China) Co. Ltd, the institutional broker dealer business of BMO Capital Markets Corp. (Member FINRA and SIPC) and the agency broker dealer business of Clearpool Execution Services, LLC (Member FINRA and SIPC) in the U.S., and the institutional broker dealer businesses of BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia, Bank of Montreal Europe p.l.c. (authorized and regulated by the Central Bank of Ireland) in Europe and BMO Capital Markets Limited (authorized and regulated by the Financial Conduct Authority) in the UK and Australia.

Securities and investment banking activities in the United States are performed by Deutsche Bank Securities Inc., a member of NYSE, FINRA and SIPC, and its broker-dealer affiliates. Lending and other commercial banking activities in the United States are performed by Deutsche Bank AG and its banking affiliates.

Société Générale is the marketing name for SG Americas Securities, LLC.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 2 | |

| Dated February 5, 2025 | BMO 2025-C11 |

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 3 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| Collateral Characteristics |

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate

Cut-off Date Balance | % of IPB | Roll-up Aggregate Cut-off Date Balance | Roll-up Aggregate % of Cut-off Date Balance |

| SGFC | 7 | 8 | $139,408,845 | 15.4% | $164,408,845 | 18.1% |

| BMO | 4 | 10 | $83,025,000 | 9.2% | $132,275,000 | 14.6% |

| SMC | 7 | 9 | $108,150,000 | 11.9% | $108,150,000 | 11.9% |

| UBS AG | 3 | 3 | $107,575,000 | 11.9% | $107,575,000 | 11.9% |

| GACC | 2 | 2 | $50,660,000 | 5.6% | $101,410,000 | 11.2% |

| NCB | 26 | 26 | $75,947,785 | 8.4% | $75,947,785 | 8.4% |

| CREFI | 2 | 2 | $61,000,000 | 6.7% | $61,000,000 | 6.7% |

| Barclays | 1 | 1 | $9,400,000 | 1.0% | $49,400,000 | 5.4% |

| LMF | 2 | 2 | $29,975,000 | 3.3% | $29,975,000 | 3.3% |

| LCM | 1 | 1 | $25,000,000 | 2.8% | $25,000,000 | 2.8% |

| GSMC | 1 | 1 | $19,956,546 | 2.2% | $19,956,546 | 2.2% |

| GCMC | 3 | 4 | $18,570,000 | 2.0% | $18,570,000 | 2.0% |

| Natixis | 1 | 1 | $13,250,000 | 1.5% | $13,250,000 | 1.5% |

| BMO, GACC | 2 | 2 | $100,000,000 | 11.0% | - | - |

| Barclays, SGFC | 1 | 1 | $65,000,000 | 7.2% | - | - |

| Total: | 63 | 73 | $906,918,176 | 100.0% | $906,918,176 | 100.0% |

| Loan Pool | |

| | Initial Pool Balance (“IPB”): | $906,918,176 |

| | Number of Mortgage Loans: | 63 |

| | Number of Mortgaged Properties: | 73 |

| | Average Cut-off Date Balance per Mortgage Loan: | $14,395,527 |

| | Weighted Average Current Mortgage Rate: | 6.73129% |

| | 10 Largest Mortgage Loans as % of IPB: | 50.8% |

| | Weighted Average Remaining Term to Maturity: | 119 months |

| | Weighted Average Seasoning: | 1 month |

| | | |

| Credit Statistics | |

| | Weighted Average UW NCF DSCR: | 2.10x |

| | Weighted Average UW NOI Debt Yield: | 15.8% |

| | Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”): | 54.9% |

| | Weighted Average Maturity Date/ARD LTV: | 52.6% |

| | | |

| Other Statistics | |

| | % of Mortgage Loans with Additional Debt: | 5.9% |

| | % of Mortgage Loans with Single Tenants(1): | 8.6% |

| | % of Mortgage Loans secured by Multiple Properties: | 12.0% |

| | |

| Amortization | |

| | Weighted Average Original Amortization Term: | 338 months |

| | Weighted Average Remaining Amortization Term: | 337 months |

| | % of Mortgage Loans with Interest-Only: | 65.1% |

| | % of Mortgage Loans with Amortizing Balloon: | 15.4% |

| | % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 11.2% |

| | % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon and Partial Interest-Only: | 6.5% |

| | % of Mortgage Loans with Fully Amortizing: | 1.8% |

| | | |

| Lockboxes | |

| | % of Mortgage Loans with Hard Lockboxes: | 48.6% |

| | % of Mortgage Loans with Springing Lockboxes: | 32.0% |

| | % of Mortgage Loans with Soft Lockbox: | 11.0% |

| | % of Mortgage Loans with No Lockbox: | 8.4% |

| | | |

| Reserves | |

| | % of Mortgage Loans Requiring Monthly Tax Reserves: | 69.9% |

| | % of Mortgage Loans Requiring Monthly Insurance Reserves: | 40.9% |

| | % of Mortgage Loans Requiring Monthly CapEx Reserves: | 59.8% |

| | % of Mortgage Loans Requiring Monthly TI/LC Reserves(2): | 39.2% |

(1) Excludes mortgage loans that are secured by multiple properties leased to separate single tenants.

(2) Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, industrial, mixed use, leased fee and multifamily (with commercial tenants) properties.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 4 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| Collateral Characteristics |

| Ten Largest Mortgage Loans |

| |

| No. | Loan Name | City, State | Mortgage Loan

Seller | No.

of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Units | Property Type | UW

NCF DSCR | UW NOI Debt Yield | Cut-off Date LTV | Maturity Date/ARD LTV |

| 1 | Shops at Mission Viejo | Mission Viejo, CA | Barclays, SGFC | 1 | $65,000,000 | 7.2% | 1,012,005 | Retail | 1.69x | 13.4% | 52.4% | 49.5% |

| 2 | UOVO QPN | Long Island City, NY | BMO, GACC | 1 | $65,000,000 | 7.2% | 281,494 | Self Storage | 1.47x | 9.7% | 60.9% | 60.9% |

| 3 | 340 Mt Kemble | Morris Township, NJ | SGFC | 1 | $59,000,000 | 6.5% | 413,261 | Office | 1.61x | 14.3% | 61.8% | 54.5% |

| 4 | Ali'i Place | Honolulu, HI | UBS AG | 1 | $46,575,000 | 5.1% | 337,370 | Office | 1.92x | 15.3% | 67.1% | 67.1% |

| 5 | 29-33 Ninth Avenue | New York, NY | UBS AG | 1 | $45,000,000 | 5.0% | 87,537 | Mixed Use | 1.30x | 9.0% | 58.4% | 58.4% |

| 6 | 360 Bowery | New York, NY | GACC | 1 | $40,000,000 | 4.4% | 8,707 | Other | 1.11x | 7.3% | 62.5% | 62.5% |

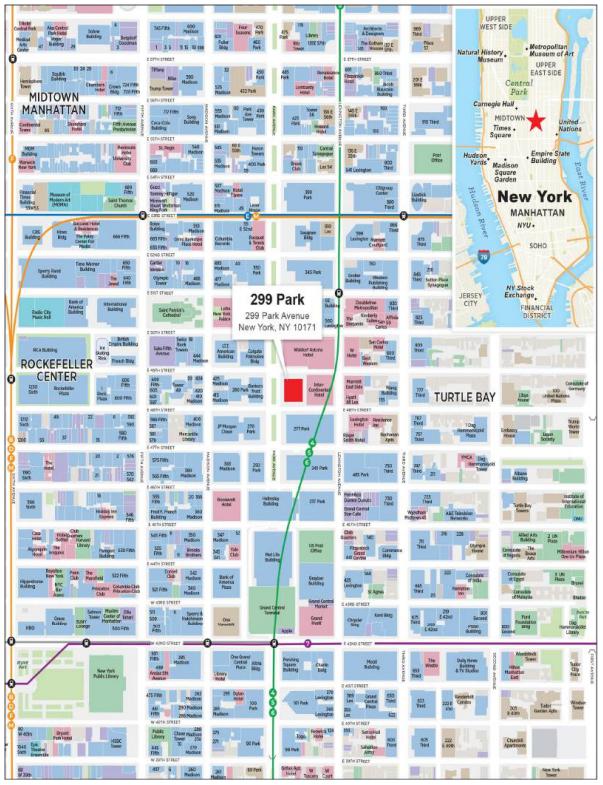

| 7 | 299 Park Avenue | New York, NY | CREFI | 1 | $36,000,000 | 4.0% | 1,176,837 | Office | 2.35x | 14.4% | 45.6% | 45.6% |

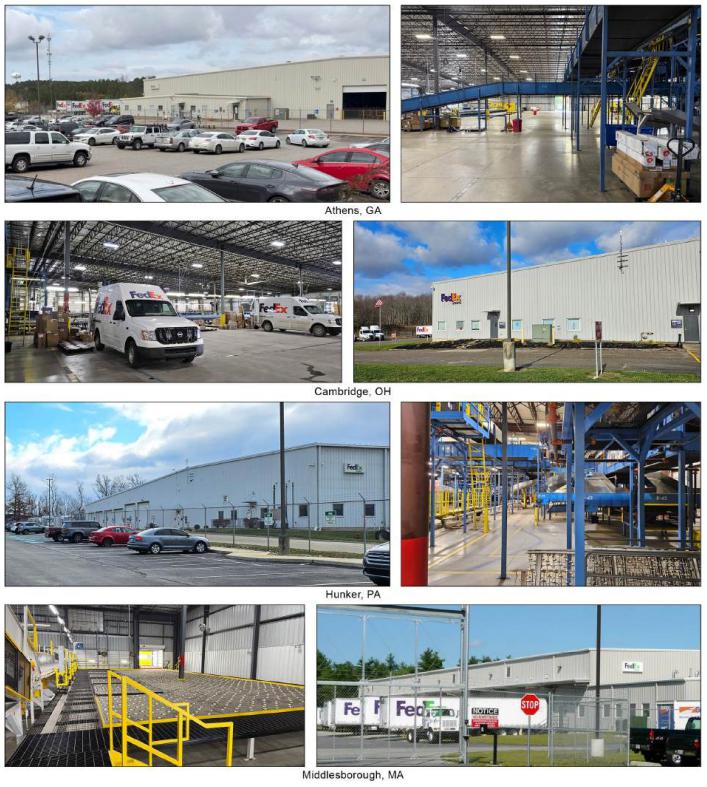

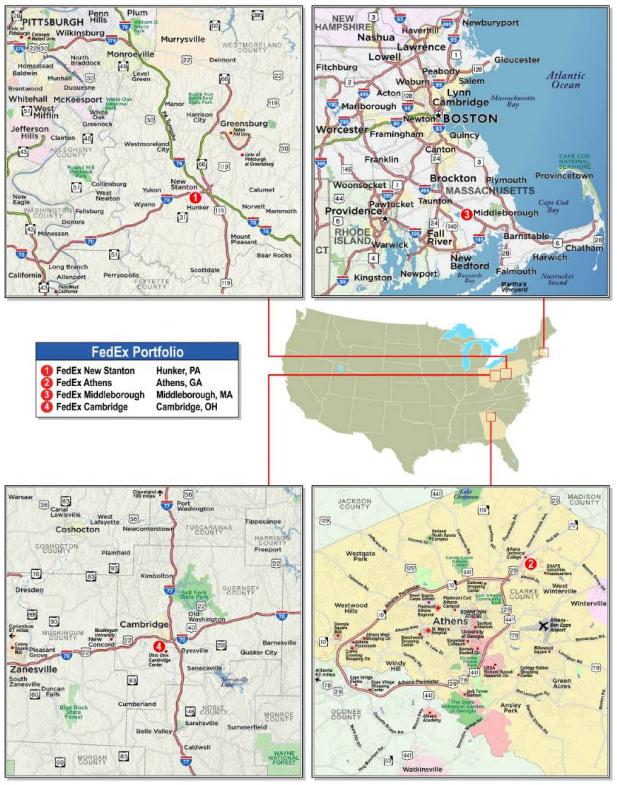

| 8 | FedEx Portfolio | Various, Various | BMO | 4 | $36,000,000 | 4.0% | 438,592 | Industrial | 1.51x | 10.9% | 69.8% | 69.8% |

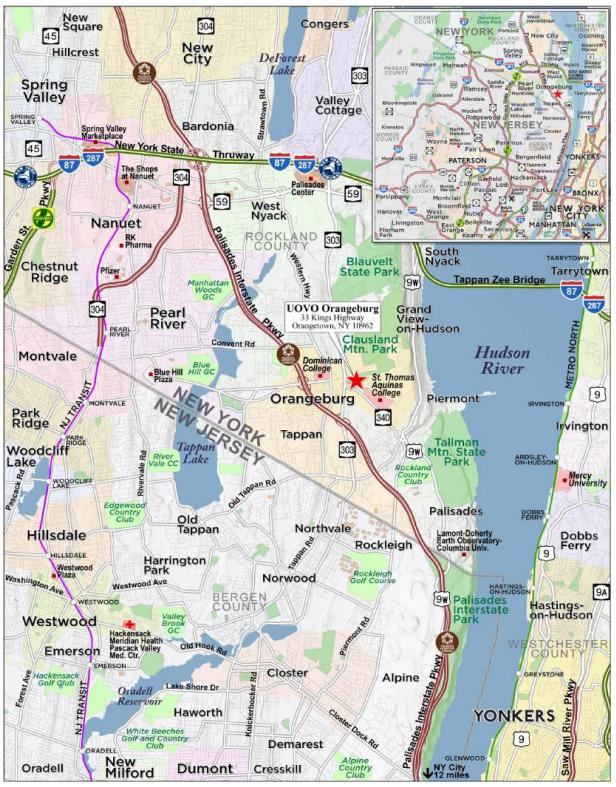

| 9 | UOVO Orangeburg | Orangetown, NY | BMO, GACC | 1 | $35,000,000 | 3.9% | 102,446 | Self Storage | 1.67x | 11.0% | 59.5% | 59.5% |

| 10 | 2481 Crotona Avenue | Bronx, NY | SMC | 1 | $33,250,000 | 3.7% | 90 | Multifamily | 1.25x | 9.7% | 59.3% | 54.2% |

| | | | | | | | | | | | | |

| | Top 3 Total/Weighted Average | | 3 | $189,000,000 | 20.8% | | | 1.59x | 12.4% | 58.3% | 55.0% |

| | Top 5 Total/Weighted Average | | 5 | $280,575,000 | 30.9% | | | 1.60x | 12.3% | 59.7% | 57.5% |

| | Top 10 Total/Weighted Average | | 13 | $460,825,000 | 50.8% | | | 1.59x | 11.7% | 59.6% | 57.9% |

| | Non-Top 10 Total/Weighted Average | | 60 | $446,093,176 | 49.2% | | | 2.63x | 20.1% | 50.1% | 47.1% |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 5 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| Collateral Characteristics |

| Pari Passu Companion Loan Summary |

| |

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Companion Loan(s) Original Balance |

| 1 | Shops at Mission Viejo | Barclays, SGFC | $65,000,000 | $115,000,000 | BBCMS 2025-C32 | Midland | Argentic | BBCMS 2025-C32

Future Securitization(s) | $90,000,000

$25,000,000 |

| 2 | UOVO QPN | BMO, GACC | $65,000,000 | $78,000,000 | WFCM 2025-C64 | Wells Fargo | Rialto | WFCM 2025-C64

Future Securitization(s) | $45,000,000

$33,000,000 |

| 3 | 340 Mt Kemble | SGFC | $59,000,000 | $13,950,000 | BMO 2025-C11 | Midland | KeyBank | Future Securitization(s) | $13,950,000 |

| 5 | 29-33 Ninth Avenue | UBS AG | $45,000,000 | $90,000,000 | BMO 2025-C11(1) | Midland(1) | KeyBank(1) | Future Securitization(s) | $90,000,000 |

| 7 | 299 Park Avenue | CREFI | $36,000,000 | $464,000,000 | NY 2025-299P | Wells Fargo | KeyBank | NY 2025-299P

Future Securitization(s) | $435,000,000

$29,000,000 |

| 17 | Outlet Shoppes of the Bluegrass | GSMC | $19,956,546 | $45,900,055 | WFCM 2025-C64 | Wells Fargo | Rialto | WFCM 2025-C64 | $46,000,000 |

| 23 | Twin Cities Premium Outlets | Natixis | $13,250,000 | $81,750,000 | BBCMS 2024-C30 | Midland | Rialto | BBCMS 2024-C30 WFCM 2025-C64 | $61,750,000 $20,000,000 |

| (1) | In the case of Loan No. 5, until the securitization of the related controlling pari passu companion loan, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement for the BMO 2025-C11 securitization transaction by the parties thereto. Upon the securitization of the related controlling pari-passu companion loan, servicing of the related whole loan will shift to the servicers under the servicing agreement with respect to such future securitization transaction, which servicing agreement will become the Controlling Pooling/Trust & Servicing Agreement. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 6 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| Collateral Characteristics |

| Mortgaged Properties by Type |

| | | | | | Weighted Average |

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW

NCF DSCR | UW

NOI DY | Cut-off Date LTV | Maturity Date/ARD LTV |

| Multifamily | Garden | 12 | $107,678,845 | 11.9% | 1.30x | 10.4% | 59.4% | 55.6% |

| | Cooperative | 26 | 75,947,785 | 8.4 | 7.79x | 58.3% | 12.9% | 11.6% |

| | Mid Rise | 2 | 39,700,000 | 4.4 | 1.43x | 9.7% | 65.5% | 65.5% |

| | High Rise | 1 | 33,250,000 | 3.7 | 1.25x | 9.7% | 59.3% | 54.2% |

| | Townhomes | 1 | 3,750,000 | 0.4 | 1.20x | 10.1% | 62.2% | 59.1% |

| | Subtotal: | 42 | $260,326,630 | 28.7% | 3.21x | 24.2% | 46.8% | 44.1% |

| Office | CBD | 2 | $82,575,000 | 9.1% | 2.11x | 14.9% | 57.7% | 57.7% |

| | Suburban | 1 | 59,000,000 | 6.5 | 1.61x | 14.3% | 61.8% | 54.5% |

| | Urban | 1 | 10,000,000 | 1.1 | 1.78x | 12.6% | 47.4% | 47.4% |

| | Subtotal: | 4 | $151,575,000 | 16.7% | 1.89x | 14.5% | 58.6% | 55.8% |

| Retail | Super Regional Mall | 1 | $65,000,000 | 7.2% | 1.69x | 13.4% | 52.4% | 49.5% |

| | Anchored | 3 | 48,535,000 | 5.4 | 1.43x | 10.8% | 62.4% | 62.4% |

| | Outlet Center | 2 | 33,206,546 | 3.7 | 1.84x | 14.2% | 55.1% | 50.3% |

| | Subtotal: | 6 | $146,741,546 | 16.2% | 1.64x | 12.7% | 56.3% | 54.0% |

| Self Storage | Self Storage | 3 | $105,100,000 | 11.6% | 1.61x | 10.6% | 59.1% | 59.1% |

| Industrial | Warehouse/Distribution | 6 | $48,700,000 | 5.4% | 1.51x | 11.1% | 67.1% | 67.1% |

| | Distribution/Manufacturing | 4 | 28,925,000 | 3.2 | 1.91x | 12.9% | 61.5% | 61.5% |

| | Subtotal: | 10 | $77,625,000 | 8.6% | 1.66x | 11.8% | 65.0% | 65.0% |

| Mixed Use | Retail | 1 | $45,000,000 | 5.0% | 1.30x | 9.0% | 58.4% | 58.4% |

| | Retail/Office | 1 | 22,250,000 | 2.5 | 1.42x | 10.2% | 60.0% | 60.0% |

| | Multifamily/Retail | 1 | 6,000,000 | 0.7 | 1.28x | 10.6% | 66.7% | 58.6% |

| | Subtotal: | 3 | $73,250,000 | 8.1% | 1.33x | 9.5% | 59.6% | 58.9% |

| Hospitality | Full Service | 2 | $41,000,000 | 4.5% | 2.06x | 20.4% | 42.7% | 28.0% |

| Other | Leased Fee | 1 | $40,000,000 | 4.4% | 1.11x | 7.3% | 62.5% | 62.5% |

| Manufactured Housing | RV Park | 1 | $6,027,000 | 0.7% | 1.73x | 12.5% | 53.8% | 53.8% |

| | Manufactured Housing/RV Park | 1 | 5,273,000 | 0.6 | 1.73x | 12.5% | 53.8% | 53.8% |

| | Subtotal: | 2 | $11,300,000 | 1.2% | 1.73x | 12.5% | 53.8% | 53.8% |

| Total / Weighted Average: | 73 | $906,918,176 | 100.0% | 2.10x | 15.8% | 54.9% | 52.6% |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 7 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

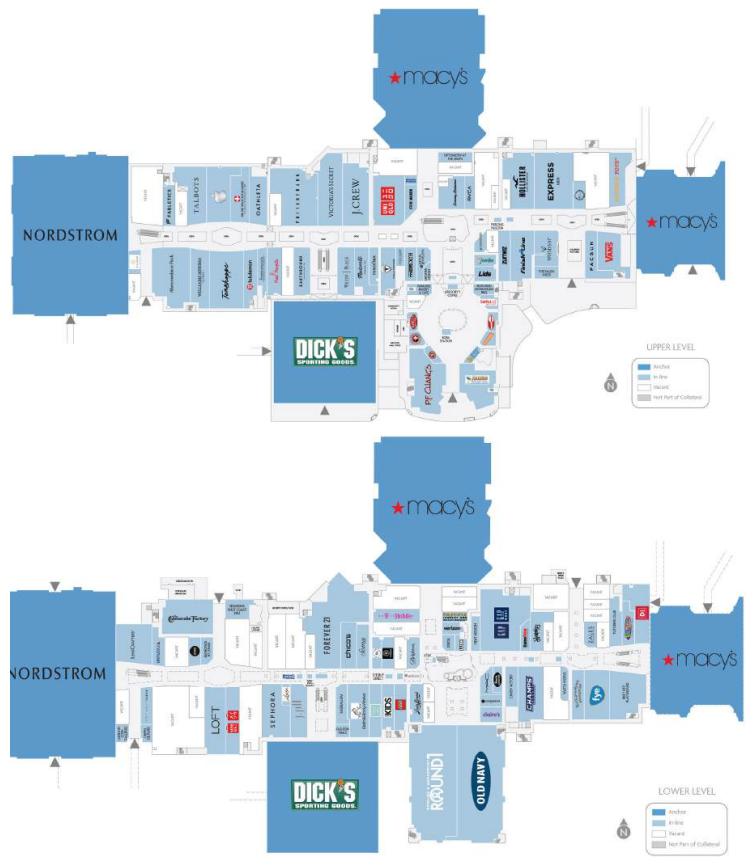

| No. 1 – Shops at Mission Viejo |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 8 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 9 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 10 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Seller: | Barclays, SGFC | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $65,000,000 | | Title: | Fee |

| Cut-off Date Principal Balance(1): | $65,000,000 | | Property Type – Subtype: | Retail – Super Regional Mall |

| % of IPB: | 7.2% | | Net Rentable Area (SF)(3): | 1,012,005 |

| Loan Purpose: | Refinance | | Location: | Mission Viejo, CA |

| Borrower: | Shops at Mission Viejo, LLC | | Year Built / Renovated: | 1979 / 2000, 2021 |

| Borrower Sponsors: | Simon Property Group, L.P. and Institutional Mall Investors LLC | | Occupancy: | 89.8% |

| Interest Rate: | 6.72500% | | Occupancy Date: | 10/23/2024 |

| Note Date: | 12/4/2024 | | 4th Most Recent NOI (As of): | $25,868,237 (12/31/2021) |

| Maturity Date: | 1/1/2035 | | 3rd Most Recent NOI (As of): | $24,750,051 (12/31/2022) |

| Interest-only Period: | 60 months | | 2nd Most Recent NOI (As of)(4): | $25,221,490 (12/31/2023) |

| Original Term: | 120 months | | Most Recent NOI (As of)(4): | $24,142,803 (TTM 9/30/2024) |

| Original Amortization Term: | 360 months | | UW Economic Occupancy: | 85.7% |

| Amortization Type: | Interest Only, Amortizing Balloon | | UW Revenues: | $32,946,299 |

| Call Protection: | L(25),D(88),O(7) | | UW Expenses: | $8,771,579 |

| Lockbox / Cash Management: | Hard / Springing | | UW NOI: | $24,174,721 |

| Additional Debt(1): | Yes | | UW NCF: | $23,570,815 |

| Additional Debt Balance(1): | $115,000,000 | | Appraised Value / Per SF: | $343,600,000 / $340 |

| Additional Debt Type(1): | Pari Passu | | Appraisal Date: | 10/30/2024 |

| | | | | |

| Escrows and Reserves(2) | | Financial Information(1) |

| | Initial | Monthly | Initial Cap | | Cut-off Date Loan / SF: | $178 |

| Taxes: | $0 | Springing | N/A | | Maturity Date Loan / SF: | $168 |

| Insurance: | $0 | Springing | N/A | | Cut-off Date LTV: | 52.4% |

| Replacement Reserves: | $0 | Springing | N/A | | Maturity Date LTV: | 49.5% |

| TI/LC Reserve: | $0 | Springing | N/A | | UW NCF DSCR: | 1.69x |

| Gap Rent Reserve: | $429,705 | $0 | N/A | | UW NOI Debt Yield: | 13.4% |

| Outstanding TI/LC: | $1,981,224 | $0 | N/A | | | |

| Major Tenant Reserve: | $0 | Springing | N/A | | | |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | | Uses | Proceeds | % of Total |

| Whole Loan(1) | $180,000,000 | 62.8 | % | | Loan Payoff | $282,626,868 | 98.5 | % |

| Borrower Sponsor Equity | 106,843,216 | 37.2 | | | Upfront Reserves | 2,410,929 | 0.8 | |

| | | | | Closing Costs | 1,805,418 | 0.6 | |

| Total Sources | $286,843,216 | 100.0 | % | | Total Uses | $286,843,216 | 100.0 | % |

| (1) | The Shops at Mission Viejo Mortgage Loan (as defined below) is part of a whole loan evidenced by 10 pari passu promissory notes with an aggregate outstanding principal balance as of the Cut-off Date of $180.0 million (the “Shops at Mission Viejo Whole Loan”). The Financial Information in the chart above reflects the Shops at Mission Viejo Whole Loan. |

| (2) | For a full description of Escrows and Reserves, please refer to “Escrows and Reserves” below. |

| (3) | The Shops at Mission Viejo Property (as defined below) is part of a larger retail development consisting of a total of 1,236,320 square feet (“SF”). Macy’s operates 193,500 SF at the Shops at Mission Viejo Property through a ground lease and has another suite consisting of 224,315 SF that is not part of the collateral. |

| (4) | The decrease from 2nd Most Recent NOI to Most Recent NOI is primarily driven by occupancy (including temporary tenants) decreasing from 98.8% as of the end of 2023 to 96.3% as of October 23, 2024. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 11 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

The Loan. The largest mortgage loan (the “Shops at Mission Viejo Mortgage Loan”) is part of a fixed rate whole loan secured by the borrower’s fee interest in a super-regional mall located in Mission Viejo, California (the “Shops at Mission Viejo Property”). The Shops at Mission Viejo Whole Loan consists of 10 pari passu promissory notes and accrues interest at a rate of 6.72500% per annum on an Actual/360 basis. The Shops at Mission Viejo Whole Loan has a 10-year term and is interest only for the first 60 months followed by amortization based on a 30 year schedule for the remaining term. The Shops at Mission Viejo Whole Loan was co-originated on December 4,2024 by Barclays, SGFC and Citi Real Estate Funding Inc. The Shops at Mission Viejo Mortgage Loan is evidenced by non-controlling Notes A-1-2 and A-1-3, contributed by Barclays, and non-controlling Notes A-3-2 and A-3-3, contributed by SGFC, with an aggregate original principal balance of $65,000,000. The Shops at Mission Viejo Whole Loan is expected to be serviced pursuant to the pooling and servicing agreement for the BBCMS 2025-C32 trust. See “Description of the Mortgage Pool—The Whole Loans—The Outside Serviced Pari Passu Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus.

| Whole Loan Summary |

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1-1 | $35,000,000 | $35,000,000 | BBCMS 2025-C32 | Yes |

| A-1-2 | $25,000,000 | $25,000,000 | BMO 2025-C11 | No |

| A-1-3 | $15,000,000 | $15,000,000 | BMO 2025-C11 | No |

| A-1-4 | $10,000,000 | $10,000,000 | BBCMS 2025-C32 | No |

| A-1-5 | $5,000,000 | $5,000,000 | BBCMS 2025-C32 | No |

| A-2-1 | $25,000,000 | $25,000,000 | WFCM 2025-C64 | No |

| A-2-2 | $20,000,000 | $20,000,000 | BBCMS 2025-C32 | No |

| A-3-1 | $20,000,000 | $20,000,000 | BBCMS 2025-C32 | No |

| A-3-2 | $15,000,000 | $15,000,000 | BMO 2025-C11 | No |

| A-3-3 | $10,000,000 | $10,000,000 | BMO 2025-C11 | No |

| Whole Loan | $180,000,000 | $180,000,000 | | |

The Property. The Shops at Mission Viejo Property is a Class A, two-story, enclosed super-regional mall on a 66.70-acre site in Mission Viejo in Orange County, California. The Shops at Mission Viejo Property consists of a 1,012,005 square foot portion of a larger retail development consisting of 1,236,320 total SF. The Shops at Mission Viejo Property benefits from three anchor tenants: two Macy’s units (one of which is collateral), Dick’s Sporting Goods (“Dick’s”) and Nordstrom. Notable inline tenants include, among others, Apple, Tesla, Sephora, Lululemon, Steve Madden, Pandora and J. Crew. Food and beverage offerings at the food court include SmashBurger, Chipotle Mexican Grill and Cheesecake Factory. One Macy‘s unit representing 224,315 SF is not part of the collateral. The Shops at Mission Viejo Property was constructed in 1979 and was most recently renovated in 2021 that involved a $17.6 million interior and exterior redevelopment of the Dick’s space to allow for Dick’s to take occupancy on a build-to-suit basis.

As of October 23, 2024, the Shops at Mission Viejo Property was 89.8% leased to 116 unique tenants (excluding temporary tenants), including one medical office tenant (1.0% of underwritten base rent). Other than the three retail anchor tenants and one medical office tenant, no other tenant accounts for greater than 2.1% of net rentable area and 3.9% of underwritten base rent. In the trailing-12 month period ending September 30, 2024, the tenants at the Shops at Mission Viejo Property generated approximately $245.0 million in total sales (excluding Tesla, whose sales have been excluded from all sales data due to historical reporting variances in methodology), with comparable inline sales of $566 per square foot (less than 10,000 SF excluding Apple and Tesla) and $665 per square foot (less than 10,000 SF).

The Shops at Mission Viejo Property has benefitted from positive leasing momentum with 11 unique tenants totaling 43,868 SF (4.3% of collateral SF) and approximately $1.8 million of underwritten rent (9.2% of total underwritten rent) of recently executed leases since the beginning of 2024. Such new leasing includes two major tenants, Round 1 Bowling and Amusement and Uniqlo, collectively representing 32,196 SF.

Major Retail Tenants.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 12 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

Macy’s (193,500 SF; 19.1% of NRA; 0.0% of underwritten base rent): Founded in 1858 and headquartered in New York, New York, Macy’s (Fitch/Moody’s/S&P: BBB-/Ba2/BB+) is a department store chain that operates approximately 735 stores in the United States as well as Guam and Puerto Rico. Macy’s has three banners that include Macy’s, bluemercury and Bloomingdale’s (and accompanying e-commerce sites), which sell men's, women's and children's apparel and accessories, cosmetics and home furnishings, among other merchandise. Macy’s, as ground lessee, occupies the Shops at Mission Viejo Property pursuant to a ground lease from the borrower, as ground lessor, with an expiration date of February 2030 and has five, 10-year renewal options remaining with no termination options. Ground rent will remain $10 during any renewal periods. Simon Property Group, L.P. (“Simon”) estimated Macy’s sales to be $11,100,000, or $57 per square foot, for the 193,500 SF of collateral space and $20,100,000, or $90 per square foot, for the 224,315 SF of non-collateral space from the trailing-12 month period through September 2024. The 224,315 SF non-collateral space is occupied by Macy’s pursuant to a ground lease through 2069. Macy’s has been in occupancy of such space since the Shops at Mission Viejo Property opened in 1977.

Nordstrom (165,000 SF; 16.3% of NRA; 0.0% of underwritten base rent): Nordstrom (Fitch/Moody’s/S&P: BB+/Ba2/BB) was founded in 1901 as a retail shoe business in Seattle, Washington. Nordstrom is a leading fashion designer offering clothing, shoes and accessories for men, women and kids. Nordstrom has more than 350 Nordstrom, Nordstrom Local and Nordstrom Rack locations. Nordstrom was added to the Shops at Mission Viejo Property upon executing a ground lease in January 1999 that was part of a significant renovation and expansion with an original cost of $20 million. The ground lease has an initial expiration date on February 2030. Nordstrom has seven, 10-year extension options remaining. Ground rent will remain $1 during any renewal periods. For the trailing-12 month period through September 2024, Nordstrom reported sales of approximately $49.4 million, which equates to approximately $299 per square foot.

Dick's (80,000 SF; 7.9% of NRA; 7.9% of underwritten base rent): Dick’s (Fitch/Moody's/S&P: NR/Baa2/BBB) was founded in 1948 as a bait-and-tackle shop in Binghamton, New York, and has since grown to become an omnichannel sporting goods retailer, with a primary focus on sports equipment, apparel, footwear and accessories. Headquartered in Coraopolis, Pennsylvania, Dick’s offers a wide range of products through its main and specialty concept stores, including Dick’s Sporting Goods, Public Lands, Moosejaw and Going Going Gone!. Dick’s has been in occupancy at the Shops at Mission Viejo Property since May 2020 and has a lease expiration date of January 2032. Dick’s has three, five-year extension options remaining. For the trailing-12 month period through September 2024, Dick’s reported sales of approximately $19.1 million, which equates to approximately $239 per square foot.

Major Medical Office Tenant.

Welltower Mission Viejo Medical (104,500 SF; 10.3% of NRA; 1.0% of underwritten base rent): Welltower Mission Viejo Medical (“Welltower”) is an outparcel medical office that is being operated as an outpatient center with a focus on cancer care. The medical office also includes an array of health and medical services in partnership with Providence Mission Viejo Hospital that is located adjacent to Welltower. Providence Mission Viejo Hospital is the largest employer in the city of Mission Viejo and is currently undergoing a $712 million expansion. Welltower is a real estate investment trust and S&P 500 company headquartered in Toledo, Ohio. Welltower invests with senior housing operators, post-acute providers and health systems to fund the real estate infrastructure needed for health care operations. Founded in 1970, Welltower currently has a portfolio of over 430 medical properties totaling approximately 26 million square feet with locations across all 50 states. Welltower, as ground lessee, occupies the Shops at Mission Viejo Property pursuant to a ground lease from the borrower, as ground lessor, with an expiration date of January 2074 with two, 10-year renewal options remaining.

| Historical and Current Occupancy(1) |

| | 2019 | 2020 | 2021 | 2022 | 2023 | Current(2) |

| Inc. Temp Tenants | 88.7% | 96.6% | 95.3% | 98.5% | 98.8% | 96.3% |

| Excl. Temp Tenants | 85.2% | 90.6% | 88.4% | 88.2% | 90.8% | 89.8% |

| (1) | Based on December 31 of each respective year. |

| (2) | Based on the underwritten rent roll as of October 23, 2024. Temporary tenants are underwritten as vacant, however, income from such tenants is included in underwritten income. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 13 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

| Top Tenant Summary(1) |

| Tenant | Ratings

(Fitch/Moody’s/S&P)(2) | Net Rentable Area (SF) | % of

Total NRA | UW Base Rent PSF(1) | UW Base Rent(1) | % of Total

UW Base Rent(1) | Lease

Expiration Date |

| Anchor Tenants | | | | | | | |

| Macy’s(3) | NR/Ba2/BB+ | 193,500 | 19.1% | $0.00 | $10 | 0.0% | 2/2/2030 |

| Nordstrom(3) | BB+/Ba2/BB | 165,000 | 16.3% | $0.00 | $0 | 0.0% | 2/28/2030 |

| Dick’s | NR/Baa2/BBB | 80,000 | 7.9% | $19.50 | $1,560,000 | 7.9% | 1/31/2032 |

| Anchor Tenants Subtotal / Wtd. Avg. | | 438,500 | 43.3% | $3.56 | $1,560,010 | 7.9% | |

| | | | | | | | |

| Medical Office Tenant | | | | | | | |

| Welltower(3) | NR/Baa1/BBB+ | 104,500 | 10.3% | $1.89 | $198,000 | 1.0% | 1/31/2074 |

| | | | | | | | |

| Major Tenants | | | | | | | |

| Old Navy | NR/NR/NR | 21,196 | 2.1% | $22.64 | $479,945 | 2.4% | 1/31/2026 |

| Round 1 Bowling and Amusement | NR/NR/NR | 20,465 | 2.0% | $37.63 | $770,000 | 3.9% | 1/31/2035 |

| Forever 21 | NR/NR/NR | 13,141 | 1.3% | $11.78 | $154,757 | 0.8% | 1/31/2027 |

| Uniqlo(4) | NR/NR/NR | 11,731 | 1.2% | $37.30 | $437,566 | 2.2% | 8/31/2035 |

| The Gap/Gap Body | NR/B1/BB | 10,617 | 1.0% | $59.94 | $636,422 | 3.2% | 1/31/2027 |

| Pottery Barn | NR/NR/NR | 10,048 | 1.0% | $35.64 | $358,138 | 1.8% | 1/31/2025 |

| Express Men | NR/NR/NR | 9,748 | 1.0% | $14.53 | $141,638 | 0.7% | 1/31/2029 |

| Abercrombie & Fitch | NR/NR/BB | 9,350 | 0.9% | $40.88 | $382,222 | 1.9% | 1/31/2026 |

| Tenshoppe | NR/NR/NR | 8,681 | 0.9% | $25.43 | $220,758 | 1.1% | 11/30/2025 |

| Victoria's Secret | NR/B1/BB- | 7,709 | 0.8% | $41.23 | $317,842 | 1.6% | 1/31/2033 |

| Major Tenants Subtotal / Wtd. Avg. | | 122,686 | 12.1% | $31.78 | $3,899,289 | 19.6% | |

| Remaining Occupied | | 243,443 | 24.1% | $58.31 | $14,194,421 | 71.5% | |

| Occupied Collateral Total / Wtd. Avg. | | 909,129 | 89.8% | $21.84 | $19,851,720 | 100.0% | |

| | | | | | | | |

| Vacant Space | | 102,876 | 10.2% | | | | |

| | | | | | | | |

| Collateral Total | | 1,012,005 | 100.0% | | | | |

| | | | | | | | |

| (1) | Based on the underwritten rent roll dated October 23, 2024, inclusive of rent steps through December 2025. |

| (2) | In certain instances, ratings provided are those of the parent company of the entity shown, whether or not the parent company guarantees the lease. |

| (3) | Nordstrom, Macy’s and Welltower are subject to ground leases. |

| (4) | In the event that Uniqlo does not achieve sales of at least $4,271,726 during the 12 month period from September 1, 2027 through August 31, 2028 (the “Sales Measuring Period”), Uniqlo has the right to terminate its lease by providing notice within 90 days of the end of the Sales Measuring Period and the lease termination would be effective one year after providing such notice. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 14 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

| Tenant Sales(1)(2) |

| | 2019 | 2021 | 2022 | 2023 | TTM(3) |

| Gross Mall Sales | $293,240,349 | $211,527,376 | $241,604,693 | $252,622,256 | $244,989,630 |

| Sales PSF (Inline < 10,000 SF) | $715 | $569 | $653 | $684 | $665 |

| Sales PSF (Inline < 10,000 SF, Ex-Apple / Tesla) | $553 | $501 | $565 | $580 | $566 |

| Occupancy Cost (Inline < 10,000 SF) | 13.5% | 16.4% | 13.8% | 13.4% | 12.8% |

| Occupancy Cost (Inline < 10,000 SF, Ex-Apple / Tesla) | 17.2% | 18.4% | 15.8% | 15.7% | 14.9% |

| (1) | Includes the borrower sponsor’s provided estimates for non-reporting anchor tenants and/or non-collateral tenants. Macy’s does not report sales for its collateral and non-collateral spaces. |

| (2) | 2020 sales are excluded due to the adverse impact of the COVID-19 pandemic. Tesla sales are excluded from all sales data due to historical reporting variances. |

| (3) | Based on the trailing-12 month period as of September 30, 2024. |

| Major Tenant Sales(1)(2) |

| Tenant Name | SF | 2019 | 2021 | 2022 | 2023 | 9/30/2024 TTM | Occupancy Cost | 9/30/2024 TTM

Sales PSF |

| Anchor Tenants | | | | | | | | |

| Macy’s(3) | 193,500 | $13,100,000 | $11,800,000 | $11,700,000 | $11,100,000 | $11,100,000 | 0.6% | $57 |

| Nordstrom | 165,000 | $55,450,000 | $45,699,000 | $62,174,000 | $54,767,955 | $49,364,357 | 0.3% | $299 |

| Dick’s | 80,000 | NAV | NAV | $17,566,000 | $17,398,683 | $19,100,000 | 9.9% | $239 |

| Major Tenants | | | | | | | | |

| Old Navy | 21,196 | $3,813,000 | $3,041,000 | $2,809,000 | $2,855,915 | $2,925,013 | 20.2% | $138 |

| Forever 21 | 13,141 | NAV | $506,000 | $1,651,000 | $1,406,717 | $1,282,319 | 14.0% | $98 |

| The Gap/Gap Body | 10,617 | $2,601,000 | $1,960,000 | $2,010,000 | $2,163,548 | $2,542,138 | 45.0% | $239 |

| Pottery Barn | 10,048 | $6,880,000 | $7,500,000 | $8,801,000 | $7,556,008 | $7,153,671 | 10.2% | $712 |

| Signature Tenants | | | | | | | | |

| Abercrombie & Fitch | 9,350 | $1,731,000 | $1,954,000 | $2,071,000 | $2,557,750 | $3,036,791 | 14.7% | $325 |

| Victoria's Secret | 7,709 | $4,824,000 | $3,789,000 | $3,878,000 | $3,480,655 | $4,553,559 | 12.9% | $591 |

| J. Crew | 7,100 | $1,791,000 | $1,903,000 | $2,144,000 | $2,588,908 | $2,817,790 | 11.1% | $397 |

| Cheesecake Factory | 6,927 | $9,980,000 | $10,015,000 | $10,861,000 | $10,730,469 | $10,516,158 | 6.4% | $1,518 |

| Apple | 6,195 | $50,363,000 | $19,693,000 | $24,418,000 | $28,302,090 | $26,569,865 | 2.4% | $4,289 |

| Sephora | 5,338 | $7,128,000 | $4,576,000 | $6,627,000 | $8,894,692 | $9,298,805 | 7.7% | $1,742 |

| Williams-Sonoma | 4,718 | $2,485,000 | $3,080,000 | $3,168,000 | $3,260,723 | $3,434,306 | 10.9% | $728 |

| Tommy Bahama | 3,387 | $2,395,000 | $2,479,000 | $2,827,000 | $2,533,608 | $2,402,062 | 19.6% | $709 |

| Lululemon | 3,099 | $6,836,000 | $5,010,000 | $6,194,000 | $6,685,376 | $6,742,842 | 5.7% | $2,176 |

| Lego | 2,321 | $1,665,000 | $2,985,000 | $3,319,000 | $3,052,182 | $2,965,632 | 10.3% | $1,278 |

| (1) | All sales information presented herein with respect to the Shops at Mission Viejo Property is based upon information provided by the borrower sponsor. In certain instances, sales figures represent estimates because the tenants are not required to report, or otherwise may not have reported sales information on a timely basis. Further, because sales are self-reported, such information is not independently verified by the borrower sponsor. |

| (2) | 2020 excluded due to the adverse impact of the COVID-19 pandemic on the Shops at Mission Viejo Property. |

| (3) | Based on estimates provided by the borrower sponsor as Macy’s does not report sales. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 15 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

| Lease Rollover Schedule(1)(2) |

| Year | Number of Leases Expiring | Net Rentable Area Expiring | % of NRA Expiring | UW Base Rent Expiring | % of UW Base Rent Expiring | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring | Cumulative UW Base Rent Expiring | Cumulative % of UW Base Rent Expiring |

| Vacant | NAP | 102,876 | 10.2% | NAP | NAP | 102,876 | 10.2% | NAP | NAP |

| 2025 & MTM | 27 | 75,833 | 7.5% | $2,824,046 | 14.2% | 178,709 | 17.7% | $2,824,046 | 14.2% |

| 2026 | 25 | 94,348 | 9.3% | $4,893,766 | 24.7% | 273,057 | 27.0% | $7,717,812 | 38.9% |

| 2027 | 18 | 51,790 | 5.1% | $2,746,512 | 13.8% | 324,847 | 32.1% | $10,464,324 | 52.7% |

| 2028 | 8 | 12,949 | 1.3% | $1,037,348 | 5.2% | 337,796 | 33.4% | $11,501,673 | 57.9% |

| 2029 | 12 | 30,543 | 3.0% | $1,168,107 | 5.9% | 368,339 | 36.4% | $12,669,780 | 63.8% |

| 2030 | 12 | 387,629 | 38.3% | $2,119,516 | 10.7% | 755,968 | 74.7% | $14,789,296 | 74.5% |

| 2031 | 4 | 8,022 | 0.8% | $540,251 | 2.7% | 763,990 | 75.5% | $15,329,547 | 77.2% |

| 2032 | 4 | 89,093 | 8.8% | $2,100,725 | 10.6% | 853,083 | 84.3% | $17,430,273 | 87.8% |

| 2033 | 3 | 14,333 | 1.4% | $463,498 | 2.3% | 867,416 | 85.7% | $17,893,771 | 90.1% |

| 2034 | 3 | 4,808 | 0.5% | $416,273 | 2.1% | 872,224 | 86.2% | $18,310,044 | 92.2% |

| 2035 | 2 | 32,196 | 3.2% | $1,207,566 | 6.1% | 904,420 | 89.4% | $19,517,610 | 98.3% |

| 2036 & Thereafter | 2 | 107,585 | 10.6% | $334,110 | 1.7% | 1,012,005 | 100.0% | $19,851,720 | 100.0% |

| Total | 120 | 1,012,005 | 100.0% | $19,851,720 | 100.0% | | | | |

| (1) | Based on the underwritten rent roll dated October 23, 2024 inclusive of rent steps through December 2025. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the Lease Rollover Schedule. |

Environmental. According to the Phase I environmental site assessment dated November 5, 2024, there was no evidence of any recognized environmental conditions at the Shops at Mission Viejo Property.

| Operating History and Underwritten Net Cash Flow(1) | |

| | 2021) | 2022 | 2023(2) | TTM 9/30/2024(2) | Underwritten | Per SF | %(3) |

| Base Rent | $20,285,085 | $19,884,382 | $19,881,736 | $19,292,499 | $19,487,194 | $19.26 | 52.8% |

| Contractual Rent Steps(4) | 0 | 0 | 0 | 0 | 364,526 | $0.36 | 1.0 |

| Credit Tenant Rent Steps | 0 | 0 | 0 | 0 | 121,892 | $0.12 | 0.3 |

| Temporary Tenant Rent | 1,568,156 | 2,041,575 | 2,193,164 | 2,015,799 | 2,101,000 | $2.08 | 5.7 |

| Percentage in Lieu Rent | 344,873 | 110,773 | 299,278 | 281,009 | 248,573 | $0.25 | 0.7 |

| Overage Rent | 926,893 | 1,599,365 | 1,334,111 | 1,266,529 | 862,043 | $0.85 | 2.3 |

| Other Rental Income | 205,717 | 205,944 | 189,833 | 196,947 | 202,000 | $0.20 | 0.5 |

| Gross-Up Vacant Rent | 0 | 0 | 0 | 0 | 4,465,543 | $4.41 | 12.1 |

| Net Rental Income | $23,330,724 | $23,842,039 | $23,898,122 | $23,052,783 | $27,852,771 | $27.52 | 75.5% |

| Total Recoveries | 8,741,330 | 7,737,820 | 8,631,027 | 8,571,797 | 9,056,105 | $8.95 | 24.5 |

| Gross Potential Income | $32,072,054 | $31,579,859 | $32,529,149 | $31,624,580 | $36,908,876 | $36.47 | 100.0% |

| Vacancy & Bad Debt | 0 | 0 | 0 | 0 | (5,283,576) | (5.22) | (14.3) |

| Miscellaneous Income | 1,028,204 | 1,018,361 | 1,213,703 | 1,146,579 | 1,321,000 | $1.31 | 3.6 |

| Effective Gross Income | $33,100,258 | $32,598,220 | $33,742,852 | $32,771,159 | $32,946,299 | $32.56 | 89.3% |

| Taxes | 1,501,687 | 1,719,161 | 1,748,385 | 1,757,126 | 1,780,005 | $1.76 | 5.4 |

| Insurance | 966,390 | 1,058,211 | 1,195,409 | 1,318,030 | 1,363,648 | $1.35 | 4.1 |

| Management Fee | 993,121 | 1,007,385 | 1,002,899 | 983,193 | 988,329 | $0.98 | 3.0 |

| Other Expenses | 3,770,823 | 4,063,412 | 4,574,669 | 4,570,007 | 4,639,596 | $4.58 | 14.1 |

| Total Expenses | 7,232,021 | 7,848,169 | 8,521,362 | 8,628,356 | 8,771,579 | $8.67 | 26.6% |

| Net Operating Income | $25,868,237 | $24,750,051 | $25,221,490 | $24,142,803 | $24,174,721 | $23.89 | 73.4% |

| Capital Expenditures | 0 | 0 | 0 | 0 | 54,901 | $0.05 | 0.2 |

| TI/LC | 0 | 0 | 0 | 0 | 549,005 | $0.54 | 1.7 |

| Net Cash Flow | $25,868,237 | $24,750,051 | $25,221,490 | $24,142,803 | $23,570,815 | $23.29 | 71.5% |

| (1) | Based on the underwritten rent roll dated October 23, 2024. |

| (2) | The decrease from 2023 NOI to TTM 9/30/2024 NOI is primarily driven by occupancy (including temporary tenants) decreasing from 98.8% as of the end of 2023 to 96.3% as of October 23, 2024. |

| (3) | % column represents percentage of Gross Potential Income for all revenue lines and represents percentage of Effective Gross Income for the remaining fields. |

| (4) | Contractual Rent Steps were taken through December 2025. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 16 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

The Market. The Shops at Mission Viejo Property is located in the South submarket of the broader Orange County retail market. The Shops at Mission Viejo Property benefits from its accessible location as it is adjacent to Interstate 5, which is a main thoroughfare throughout Orange County and allows for direct access to Los Angeles. Residential development dominates the area surrounding the Shops at Mission Viejo Property. Additionally, the Shops at Mission Viejo Property is the southernmost mall in the competitive set as identified in the appraisal. Providence Mission Hospital and Saddleback College, the two largest employers in Mission Viejo, are both located across the street from the Shops at Mission Viejo Property. Providence Mission Hospital is in the midst of a $712 million expansion and Saddleback College, which consists of approximately 26,000 students, recently completed an expansion project in March of 2024 that added a $60 million facility dedicated to student services.

The South retail submarket consists of approximately 9.7 million SF and is the second largest of the five submarkets within the approximately 41.6 million SF Orange County market. As of the second quarter of 2024, the 6.5% vacancy rate in the submarket is lower than the 6.7% vacancy rate for the Orange County retail market. Additionally, the South submarket asking rent of $39.34 per square foot is greater than the Orange County market asking rent of $34.68 per square foot. Asking rent in the submarket and market have grown each year since 2021.

According to the appraisal, the estimated 2023 population within a five-, seven- and 10-mile radius was 293,855, 469,899 and 651,466, respectively. Additionally, for the same period, the average household income within the same radii was $164,778, $166,335 and $167,972, respectively.

The following table presents certain information relating to the appraiser’s market rent conclusions for the Shops at Mission Viejo– Property:

| Market Rent Summary(1) |

| | Market Rent (PSF) | Lease Term (Yrs.) | Rent Increase Projections | New Tenant Improvements |

| 0 – 1,200 SF | $80.00 | 8 | 3.0% | $40.00 |

| 1,201 – 2,000 SF | $60.00 | 8 | 3.0% | $40.00 |

| 2,001 – 3,500 SF | $45.00 | 8 | 3.0% | $40.00 |

| 3,501 – 5,000 SF | $35.00 | 8 | 3.0% | $40.00 |

| 5,001 – 10,000 SF | $27.00 | 8 | 3.0% | $40.00 |

| 10,000 SF + | $30.00 | 8 | 3.0% | $40.00 |

| Restaurants | $45.00 | 10 | 3.0% | $75.00 |

| Jewelers | $80.00 | 8 | 3.0% | $40.00 |

| Food Court | $100.00 | 8 | 3.0% | $40.00 |

| Kiosk | $400.00 | 5 | 3.0% | $40.00 |

| ATM | $600.00 | 5 | 3.0% | $40.00 |

| (1) | Based on the appraisal. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 17 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

The following table presents certain information relating to comparable retail centers for the Shops at Mission Viejo Property:

| Competitive Retail Center Summary(1) |

| Property / Location | Year Built / Renovated or Expanded | Total NRA (SF) | Occupancy | Distance to Subject | Sales PSF | Anchor Tenants |

Shops at Mission Viejo Mission Viejo, CA | 1979 / 2000, 2021 | 1,012,005(2)(3) | 89.8%(2)(3) | NAP | $665(4) | Macy’s, Nordstrom, Dick’s |

Irvine Spectrum Center Irvine, CA | 1995 / 2016 | 1,388,737 | 95% | 11 miles | $1,100 - $1,200(5) | Nordstrom, Target, Regal Cinemas, Dave & Busters, Newfound Market |

Fashion Island Newport Beach, CA | 1967 / 2003, 2017 | 1,573,000 | 96% | 15 miles | $1,400 - $1,600(5) | Nordstrom, Macy’s, Bloomingdale’s, Neiman Marcus, Whole Foods, Cinema |

South Coast Plaza Costa Mesa, CA | 1967 / 1999 | 2,740,000 | 95% | 18 miles | $1,300 - $1,500(5) | Bloomingdale’s, Macy’s, Saks Fifth Avenue, Nordstrom |

Marketplace at Laguna Niguel and Plaza De La Paz Laguna Niguel, CA | 1990 & 1994 / 1994 | 811,000 | 94% | 4 miles | NAV | Kohl’s, Costco, The Home Depot, Hobby Lobby, Walmart, Marshall’s, Old Navy |

Outlets at San Clemente San Clemente, CA | 2015 / NAP | 369,500 | 85% | 11 miles | $500 - $550 | Metropolitan Theatres, Nike, H&M |

| (1) | Based on the appraisal. |

| (2) | Based on the underwritten rent roll as of October 23, 2024. |

| (3) | Total NRA (SF) and Occupancy exclude the non-collateral Macy’s space. |

| (4) | Represents sales per square foot as of September 30, 2024 for in-line tenants. All sales information presented herein with respect to the Shops at Mission Viejo Property is based upon information provided by the borrower sponsor. |

| (5) | Includes sales attributed to Apple. |

The Borrower. The borrower for the Shops at Mission Viejo Whole Loan is Shops at Mission Viejo, LLC, a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the Shops at Mission Viejo Whole Loan.

The Borrower Sponsor. The borrower sponsors are Simon (51% interest) and Institutional Mall Investors LLC (“IMI”) (49% interest). Simon is the non-recourse carveout guarantor. So long as the non-recourse carveout guarantor is either Simon, Simon Property Group, Inc., a Delaware corporation, or an IMI Key Principal (as defined below), the liability under the guaranty is limited to 20% ($36,000,000) of the original principal amount of the Shops at Mission Viejo Whole Loan, plus all reasonable out-of-pocket costs and expenses incurred in the enforcement of the guaranty or preservation of the lenders’ rights under the guaranty. There is no separate environmental indemnity for the Shops at Mission Viejo Whole Loan; however, the non-recourse carveout guaranty provides loss recourse for breaches of representations, warranties and indemnification provisions in the Shops at Mission Viejo Whole Loan agreement concerning environmental laws and hazardous materials (subject to the aforementioned 20% cap).

Simon is the operating partnership of Simon Property Group Inc. (NYSE: SPG / S&P: A-), an S&P 100 company and owner of shopping, dining, entertainment and mixed-use destinations. As of March 31, 2024, Simon owned or held an interest in 195 income-producing properties in the United States, including 93 malls, 69 premium outlets, 14 Mills-branded shopping centers, six lifestyle centers and 13 other retail properties. Simon also owns an 84% non-controlling interest in The Taubman Realty Group, LLC, or TRG, which has an interest in 23 regional, super-regional and outlet malls in the United States and Asia. Additionally, Simon has a 22.4% ownership interest in Klépierre SA, a publicly traded, Paris-based real estate company, which owns shopping centers in 14 European countries. As of December 12, 2024, Simon had an equity market capitalization of approximately $57.8 billion.

IMI is a co-investment venture owned by an affiliate of Miller Capital Advisory and California Public Employees’ Retirement System (“CalPERS”), the nation’s largest public pension fund. IMI focuses on high-quality, fashion-oriented retail properties throughout the United States. As of September 2024, IMI’s portfolio included approximately 20.6 million SF of retail space and over approximately 1.2 million SF of prime office space.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 18 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

“IMI Key Principal” means one or more of IMI, CalPERS or any person of which CalPERS owns, directly or indirectly, at least 50% of the capital and profits.

Property Management. The Shops at Mission Viejo Property is managed by Simon Management Associates, LLC, an affiliate of the borrower sponsor.

Escrows and Reserves. At origination, the borrower was required to deposit into escrow (i) $1,981,224 for outstanding tenant improvement allowances and leasing commissions and (ii) $429,705 for outstanding gap rent.

Tax Escrows – On a monthly basis, during the continuance of a Reserve Trigger Period (as defined below) or at any time taxes are not paid by the borrower prior to the assessment of any penalty, the borrower is required to escrow 1/12th of the annual estimated tax payments payable during the next ensuing 12 months.

Insurance Escrows – During the continuance of a Reserve Trigger Period, except if the Shops at Mission Viejo Property is insured under an acceptable blanket policy, the borrower is required to escrow 1/12th of the annual estimated insurance payments on a monthly basis.

Replacement Reserves – During the continuance of a Reserve Trigger Period, the borrower is required to escrow approximately $12,000 on a monthly basis for replacements and repairs to be made at the Shops at Mission Viejo Property.

TI/LC Reserves – During the continuance of a Reserve Trigger Period, the borrower is required to escrow approximately $79,000 on a monthly basis for ongoing leasing reserves.

Major Tenant Reserve – During the continuance of a Major Tenant Trigger Event (as defined below), the borrower is required to escrow an amount equal to 1/12th of the applicable Major Tenant Threshold Amount (as defined below) on a monthly basis until such Major Tenant Threshold Amount is reached.

A “Reserve Trigger Period” commences upon the net operating income debt yield (the “NOI Debt Yield”) falling below 10.50% for two consecutive calendar quarters, and cures upon the NOI Debt Yield reaching 10.50% for two consecutive calendar quarters.

A “Major Tenant Trigger Event” commences upon the earlier to occur of (i) a Major Tenant (as defined below) bankruptcy event, (ii) a Major Tenant vacates its space or goes dark for a period of at least 90 days or (iii) a Major Tenant Renewal Event (as defined below).

Such Major Tenant Trigger Event will be cured with respect to (a) clause (i) above, upon the resolution of the bankruptcy event, the Major Tenant Threshold Amount has been deposited into the Major Tenant reserve account or a permitted guarantor has delivered to the lenders a Major Tenant guaranty with liability limited to the applicable Major Tenant Threshold Amount, (b) clause (ii) above, the Major Tenant reopens for 30 consecutive days or, if applicable, the Major Tenant Threshold Amount has been deposited into the Major Tenant reserve account or (c) clause (iii) above, a Major Tenant Renewal Event Cure (as defined below).

A “Major Tenant” means Macy’s (193,500 SF of collateral space), Nordstrom, Dick’s or any replacement tenant occupying at least 50% of the space occupied by one or more of the foregoing.

A “Major Tenant Renewal Event” means, unless such Major Tenant lease has been renewed or extended, the earlier of (x) the date on which such Major Tenant gives notice that it will not be renewing its lease and (y) the date that is six months prior to the date of such Major Tenant’s lease expiration.

A Major Tenant Renewal event will be cured upon (a) such Major Tenant renews and/or extends the Major Tenant lease, (b) not less than 50% of the space demised by the Major Tenant lease has been leased to one or more new tenants, (c) the applicable notice of intent not to renew has been rescinded, (d) the applicable Major Tenant Threshold Amount has been deposited into the Major Tenant Reserve Account or (e) at the borrower’s election, a permitted guarantor has delivered to the lenders a Major Tenant guaranty with liability limited to the applicable Major Tenant Threshold Amount (collectively, a “Major Tenant Renewal Event Cure”).

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 19 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 1 – Shops at Mission Viejo |

“Major Tenant Threshold Amount” means the amount, with respect to (i) the Macy’s collateral space, of $9,675,000, (ii) the space occupied by Nordstrom, of $8,250,000 and (iii) the space occupied by Dick’s, of $4,000,000.

Lockbox / Cash Management. The Shops at Mission Viejo Whole Loan is structured with a hard lockbox and springing cash management. The borrower and property manager are required to direct the tenants to pay rent directly into the lockbox account, and to deposit any rents otherwise received into such account within two business days after receipt. During the continuance of a Lockbox Event Period (as defined below), all funds in the lockbox account are required to be swept on a weekly basis to a lender-controlled cash management account. Funds in the cash management account are required to be applied to debt service and the reserves and escrows described above, with any excess funds (i) to be deposited into an excess cash flow reserve account held by the lenders as cash collateral for the Shops at Mission Viejo Whole Loan or (ii) if no Lockbox Event Period is continuing, disbursed to the borrower.

A “Lockbox Event Period” means the period commencing upon the occurrence of (i) an event of default, (ii) a bankruptcy action of the borrower or property manager (if the property manager is an affiliate of the borrower) and the property manager is not replaced within 60 days with a qualified manager or (iii) the NOI Debt Yield being less than 10.50% for two consecutive calendar quarters. A Lockbox Event Period will end with respect to (a) clause (i) above, if the cure of the event of default has been accepted by the lenders, (b) clause (ii) above, if the property manager is replaced within 60 days or the bankruptcy action with respect to the property manager is dismissed within 90 days without adverse consequences to the Shops at Mission Viejo Property or (c) clause (iii) above, if (A) the NOI Debt Yield is greater than or equal to 10.50% for two consecutive calendar quarters, (B) the borrower prepays a portion of the Shops at Mission Viejo Whole Loan in accordance with the Shops at Mission Viejo Whole Loan documents in an amount sufficient such that the debt yield is no less than 10.50%, together with, if prior to the open period, the yield maintenance premium or (C) the borrower delivers to the lenders (1) cash, (2) U.S. obligations, (3) other securities having a rating reasonably acceptable to the lenders and for which a rating agency confirmation has been received or (4) a letter of credit, in each case, in an amount which, if applied to the repayment of the Shops at Mission Viejo Whole Loan would result in a debt yield equal to 10.50%.

Subordinate and Mezzanine Debt. None.

Permitted Future Subordinate or Mezzanine Debt. Not permitted. However, the Shops at Mission Viejo Whole Loan documents permit the borrower to enter into a Property Assessed Clean Energy loan for an amount not to exceed $5,000,000, subject to the consent of the lenders and delivery of a rating agency confirmation.

Partial Release. The Shops at Mission Viejo Whole Loan documents permit the borrower to obtain the release of non-income producing portions of the Shops at Mission Viejo Property in connection with a transfer to third parties or affiliates of the borrower without the payment of a release price provided that, among other conditions, the borrower satisfies customary REMIC requirements.

Additionally, the borrower is permitted to release the proposed space for a planned 50,000 square foot lifestyle development that is expected to break ground in the near future without the payment of a release price provided that, among other conditions, the borrower satisfies the REMIC requirements. The proposed expansion space is expected to be located between Dick’s and Macy’s.

Ground Lease. None.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 20 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

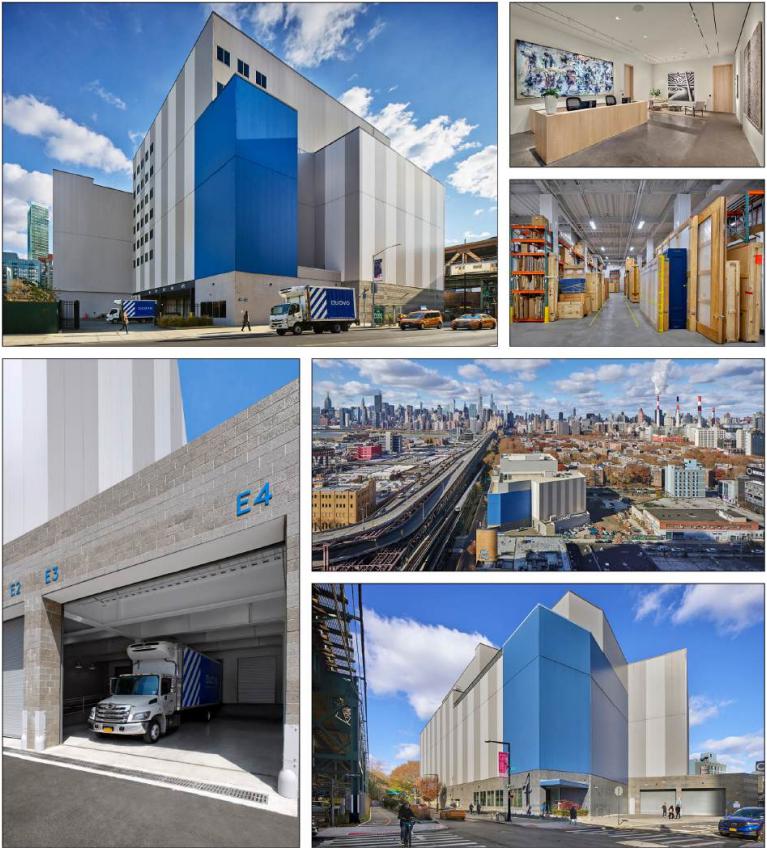

| No. 2 – UOVO QPN |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 21 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 2 – UOVO QPN |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 22 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 2 – UOVO QPN |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Sellers: | BMO, GACC | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $65,000,000 | | Title: | Fee |

| Cut-off Date Principal Balance(1): | $65,000,000 | | Property Type - Subtype: | Self-Storage – Self-Storage |

| % of IPB: | 7.2% | | Net Rentable Area (SF): | 281,494 |

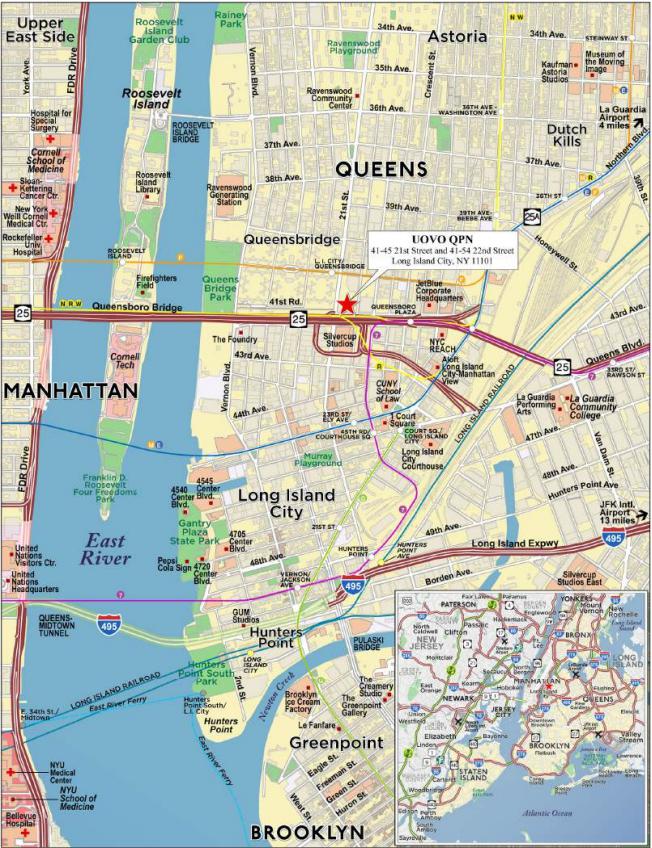

| Loan Purpose: | Refinance | | Location: | Long Island City, NY |

| Borrowers: | QPN 1 DE LLC and QPN 10 DE LLC | | Year Built / Renovated: | 2013 / NAP |

| Borrower Sponsor(2): | Steven J. Guttman | | Occupancy(5): | 87.3% |

| Interest Rate: | 6.48500% | | Occupancy Date: | 11/1/2024 |

| Note Date: | 1/22/2025 | | 4th Most Recent NOI (As of): | $11,871,108 (12/31/2021) |

| Maturity Date: | 2/6/2035 | | 3rd Most Recent NOI (As of): | $12,230,675 (12/31/2022) |

| Interest-only Period: | 120 months | | 2nd Most Recent NOI (As of): | $13,136,852 (12/31/2023) |

| Original Term: | 120 months | | Most Recent NOI (As of): | $12,841,638 (TTM 9/30/2024) |

| Original Amortization Term: | None | | UW Economic Occupancy: | 78.6% |

| Amortization Type: | Interest Only | | UW Revenues: | $17,547,845 |

| Call Protection(3): | L(24),DorYM1(89),O(7) | | UW Expenses: | $3,643,783 |

| Lockbox / Cash Management: | Soft / Springing | | UW NOI: | $13,904,062 |

| Additional Debt(1): | Yes | | UW NCF: | $13,861,838 |

| Additional Debt Balance(1): | $78,000,000 | | Appraised Value / Per SF: | $234,900,000 / $834 |

| Additional Debt Type(1): | Pari Passu | | Appraisal Date: | 12/16/2024 |

| | | | | |

| Escrows and Reserves(4) | | Financial Information(1) |

| | Initial | Monthly | Initial Cap | | Cut-off Date Loan / SF: | $508 | |

| Taxes: | $183,288 | $61,096 | N/A | | Maturity Date Loan / SF: | $508 | |

| Insurance: | $0 | Springing | N/A | | Cut-off Date LTV: | 60.9% | |

| Replacement Reserve: | $0 | Springing | N/A | | Maturity Date LTV: | 60.9% | |

| Immediate Repairs: | $14,300 | $0 | N/A | | UW NCF DSCR: | 1.47x | |

| | | | | | UW NOI Debt Yield: | 9.7% | |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | Uses | Proceeds | % of Total |

| Whole Loan | $143,000,000 | 100.0% | | Loan Payoff | $75,832,056 | 53.0 | % |

| | | | | Return of Equity | 63,964,738 | 44.7 | |

| | | | | Closing Costs | 3,005,619 | 2.1 | |

| | | | | Upfront Reserves | 197,588 | 0.1 | |

| Total Sources | $143,000,000 | 100.0% | | Total Uses | $143,000,000 | 100.0 | % |

| (1) | The UOVO QPN Mortgage Loan (as defined below) is part of the UOVO QPN Whole Loan (as defined below) which is comprised of six pari passu promissory notes with an aggregate original principal balance and Cut-off Date balance of $143,000,000. The UOVO QPN Whole Loan was originated by Bank of Montreal (“BMO”) on January 22, 2025. The financial information presented above is based on the UOVO QPN Whole Loan. |

| (2) | The borrower sponsor is also the borrower sponsor of the UOVO Orangeburg Mortgage Loan, which is also being contributed to the BMO 2025-C11 transaction. |

| (3) | The lockout period will be at least 24 payment dates beginning with and including the first payment date on March 6, 2025. Defeasance of the UOVO QPN Whole Loan is permitted after the date that is the earlier of (i) two years from the closing date of the securitization that includes the last note comprising a part of the UOVO QPN Whole Loan to be securitized and (ii) January 22, 2028. The assumed lockout period of 24 payments is based on the expected BMO 2025-C11 securitization closing date in February 2025. The actual lockout period may be longer. |

| (4) | See “Escrows and Reserves” below for further discussion of reserve information. |

| (5) | Occupancy represents the occupancy percentage for the private storage space (measured in square feet). The managed storage space is measured in cubic feet and is 55.4% leased as of November 1, 2024. See “The Property” below for further discussion of the property type. |

The Loan. The second largest mortgage loan (the “UOVO QPN Mortgage Loan”) is part of a whole loan (the “UOVO QPN Whole Loan”) secured by the borrowers’ fee interest in a 281,494 SF self-storage property located in Long Island City, New York (the “UOVO QPN Property”). The UOVO QPN Whole Loan is evidenced by six pari passu promissory notes with an aggregate outstanding principal balance as of the Cut-off Date of $143,000,000. The UOVO QPN Whole Loan was originated on January 22, 2025 by Bank of Montreal (“BMO”) and accrues interest at a fixed rate of 6.48500% per annum on an Actual/360 basis. On January 22, 2025, BMO transferred Notes A-4, A-5 and A-6, with an aggregate original principal

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 23 | |

| Structural and Collateral Term Sheet | | BMO 2025-C11 |

| No. 2 – UOVO QPN |

balance and Cut-off Date Balance of $50,050,000, to Deutsche Bank AG, New York Branch (“GACC”). The UOVO QPN Whole Loan has a 10-year term and is interest-only for the full term. The scheduled maturity date of the UOVO QPN Whole Loan is the payment date that occurs on February 6, 2035. The UOVO QPN Mortgage Loan is evidenced by the non-controlling Notes A-2 and A-4 with an aggregate outstanding principal balance as of the Cut-off Date of $65,000,000.

The relationship between the holders of the UOVO QPN Whole Loan is governed by a co-lender agreement as described under “Description of the Mortgage Pool— The Whole Loans—The Serviced Pari Passu Whole Loans” and “—The Outside Serviced Pari Passu Whole Loans” in the Preliminary Prospectus. The UOVO QPN Whole Loan will be serviced under the pooling and servicing agreement for the WFCM 2025-C64 securitization trust. See “The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans” in the Preliminary Prospectus.

The table below identifies the promissory notes that comprise the UOVO QPN Whole Loan:

| Whole Loan Summary |

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling

Piece |

| A-1 | $45,000,000 | $45,000,000 | WFCM 2025-C64 | Yes |

| A-2 | $26,500,000 | $26,500,000 | BMO 2025-C11 | No |

| A-3(1) | $21,450,000 | $21,450,000 | BMO | No |

| A-4 | $38,500,000 | $38,500,000 | BMO 2025-C11 | No |

| A-5(1) | $5,775,000 | $5,775,000 | GACC | No |

| A-6(1) | $5,775,000 | $5,775,000 | GACC | No |

| Whole Loan | $143,000,000 | $143,000,000 | | |

| (1) | Expected to be contributed to one or more future securitization transactions or may otherwise be transferred at any time. |