| | | |

| | |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

|

| FORM N-CSR |

|

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

|

| Investment Company Act file number: (811-02675) | |

| |

| Exact name of registrant as specified in charter: | Putnam Tax Exempt Income Fund |

| |

| Address of principal executive offices: One Post Office Square, Boston, Massachusetts 02109 |

|

| Name and address of agent for service: | Beth S. Mazor, Vice President |

| | One Post Office Square |

| | Boston, Massachusetts 02109 |

| |

| Copy to: | | John W. Gerstmayr, Esq. |

| | Ropes & Gray LLP |

| | 800 Boylston Street |

| | Boston, Massachusetts 02199-3600 |

| |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| |

| Date of fiscal year end: September 30, 2011 | | |

| | |

| Date of reporting period: October 1, 2010 — March 31, 2011 |

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

Putnam

Tax Exempt

Income Fund

Semiannual report

3 | 31 | 11

| | |

| Message from the Trustees | 1 | |

| |

| About the fund | 2 | |

| |

| Performance snapshot | 4 | |

| |

| Interview with your fund’s portfolio manager | 5 | |

| |

| Your fund’s performance | 11 | |

| |

| Your fund’s expenses | 13 | |

| |

| Terms and definitions | 15 | |

| |

| Other information for shareholders | 16 | |

| |

| Financial statements | 17 | |

| |

Message from the Trustees

Dear Fellow Shareholder:

The U.S. economy and markets continue to improve, despite the many headwinds that they face. The stock market has shown resilience, recently hitting multiple-year highs. The number of U.S. companies paying dividends is significantly higher than a year ago, and corporate profits remain strong.

Even with this positive news, Putnam believes that volatility will continue to roil the markets in the months ahead. Federal budget issues, inflationary pressures, stubbornly high unemployment, and global developments from Japan to Libya have created a cloud of uncertainty. In addition, the U.S. fixed-income market faces the end of the Federal Reserve’s quantitative easing program and the prospects of a tighter monetary policy in the future. We believe, however, that Putnam’s active, research-intensive approach is well suited to uncovering opportunities in this environment.

In addition, Putnam would like to thank Richard B. Worley and Myra R. Drucker, who have retired from the Board of Trustees, for their many years of dedicated and thoughtful leadership.

Lastly, we would like to take this opportunity to welcome new shareholders to the fund and to thank all of our investors for your continued confidence in Putnam.

About the fund

Potential for income exempt from federal income tax

Municipal bonds finance important public projects, such as schools, roads, and hospitals, and they can help investors keep more of the income they receive from their investment. Putnam Tax Exempt Income Fund offers an additional advantage — the flexibility to invest in municipal bonds issued by any state in the country.

The income from a municipal bond is generally exempt from federal income tax. The bonds are backed by either the issuing city, town, or other government entity or by revenues collected from usage fees.

The fund’s portfolio managers can select bonds from a variety of state and local governments. Because a state’s fiscal health can affect the prices of its bonds, this flexibility is a distinct advantage. The fund also combines two types of bonds to increase income potential. In addition to investing in high-quality bonds, the managers allocate a smaller portion of the portfolio to lower-rated bonds, which may offer higher income in return for more risk.

The portfolio managers are backed by the resources of Putnam’s fixed-income organization, in which municipal bond analysts are grouped into sector teams and conduct ongoing, rigorous research. Once a bond has been purchased, the fund’s managers continue to monitor developments that affect the bond market, the sector, and the issuer of the bond.

The goal of this in-depth research and active management is to stay a step ahead of the industry and pinpoint opportunities for investors.

Consider these risks before investing: Capital gains, if any, are taxable for federal and, in most cases, state purposes. For some investors, investment income may be subject to the federal alternative minimum tax. Income from federally exempt funds may be subject to state and local taxes. Tax-free funds may not be suitable for IRAs and other non-taxable accounts. Funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses.

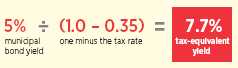

Understanding tax-equivalent yield

To understand the value of tax-free income, it is helpful to compare a municipal bond’s yield with the “tax-equivalent yield” — the before-tax yield that must be offered by a taxable bond in order to equal the municipal bond’s yield after taxes.

How to calculate tax-equivalent yield: The tax-equivalent yield equals the municipal bond’s yield divided by “one minus the tax rate.” For example, if a municipal bond’s yield is 5%, then its tax-equivalent yield is 7.7%, assuming the maximum 35% federal tax rate for 2011.

Results for investors subject to lower tax rates would not be as advantageous.

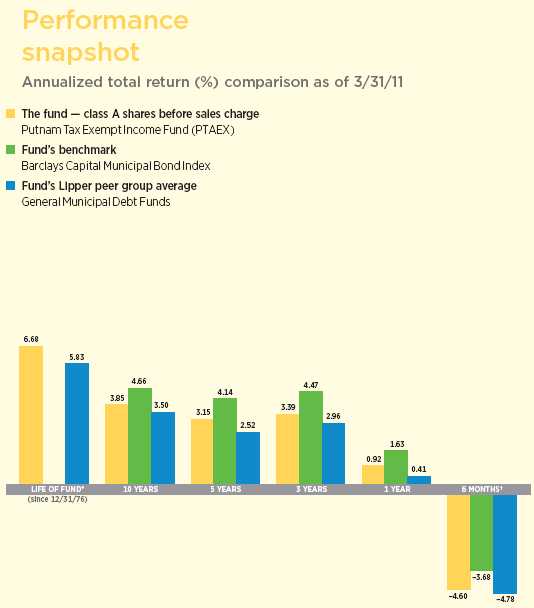

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 11–12 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

* The fund’s benchmark, the Barclays Capital Municipal Bond Index, was introduced on 12/31/79, which post-dates the inception of the fund’s class A shares.

† Returns for the six-month period are not annualized, but cumulative.

4

Interview with your fund’s portfolio manager

Thalia Meehan, CFA

The final months of 2010 were an unusually turbulent period for the bond markets. How did that volatility affect Putnam Tax Exempt Income Fund’s performance over the first half of its fiscal year?

It was a volatile period for the fixed-income markets, especially for municipal bonds. In early November, the Federal Reserve announced it would purchase $600 billion in Treasury bonds over the next several months in a second round of quantitative easing measures, designed in part to keep yields low and encourage investor risk-taking. Around this time, data also began to suggest that the U.S. economic recovery was gathering strength. Treasury market yields jumped higher, which in turn put pressure on interest rates in the municipal bond market.

In addition, the media’s coverage of state budget challenges took on a more dire tone during the final months of 2010, with predictions of widespread defaults becoming increasingly common. As a result, sentiment turned sharply negative, and investors pulled money out of municipal bond holdings at a rapid pace. In the first quarter of 2011, the municipal bond market was far more stable, but there is still a significant amount of investor uncertainty surrounding a number of issues — from interest rates to the potential for tax reform.

The past six months have been challenging, and while it is always difficult to report a loss, I am pleased to report that the fund has outperformed its Lipper peer group average over the 1-, 3-, 5-, and 10-year periods ended March 31, 2011.

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 3/31/11. See pages 4 and 11–12 for additional fund performance information. Index descriptions can be found on page 15.

5

What accounts for the difference between the fund’s performance and that of the benchmark?

The benchmark is constructed somewhat differently than the fund. As active managers, we look for what we believe are the most attractive areas of the market from a risk/return perspective. Throughout the past six months, we’ve held an overweight position in securities rated A and Baa, which have a somewhat higher perceived credit risk than AA-rated securities. For reference, AAA is the highest bond rating and indicates the lowest relative risk of default among rated securities. We believed that the A/Baa segment of the market generally was undervalued. When investors pulled money out of municipal bonds and municipal bond funds during the fourth quarter, the entire market declined, but since January, higher-rated bonds performed better than the lower-rated segments of the market. As a result, the benchmark index, which has a larger exposure to higher-rated securities, posted higher returns.

I should also point out that the benchmark is constructed so that the various maturity “buckets” — the short-, intermediate-, and long-term bonds tracked by the benchmark — all have a relatively equal contribution to the benchmark’s duration. Duration, as a reminder, measures a portfolio’s sensitivity to interest-rate changes. The fund, on the other hand, has a more limited exposure to shorter-term securities — specifically, those with maturities of less than five years. As a result, the fund’s slightly longer duration detracted from relative performance as interest rates rose during the period.

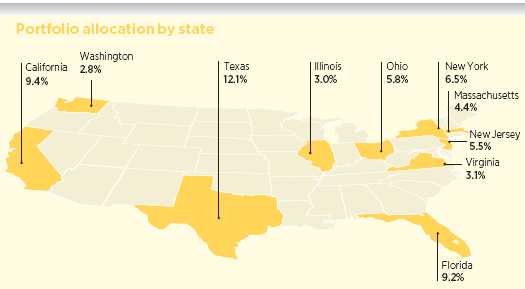

Top ten state allocations are shown as a percentage of the fund’s net assets as of 3/31/11. Investments in Puerto Rico represented 5.7% of net assets. Holdings will vary over time.

6

How has the increase in Treasury rates affected the municipal bond market?

By way of background, when interest rates increase, the prices of existing bonds generally decline as the fixed interest rates they offer become less attractive to investors. So when interest rates in the Treasury market change, the rest of the taxable fixed-income market generally moves with them.

Municipal bonds’ relation to Treasuries is a little more complex. Because municipal bonds offer tax-exempt income, their yields generally are lower than those of comparable Treasuries, whose interest is taxed as ordinary income. Over the long term, municipal bonds have offered yields between 85% and 100% of comparable Treasuries, broadly speaking. Since 2008, however, amid forced selling and some unusual supply/demand characteristics, pretax yields in the municipal market have often been at 100% or more of Treasuries.

That ratio continues to hover at or above the 100% threshold today for 30-year maturities. We believe that if interest rates continue to rise, municipal bonds won’t necessarily decline to the same degree as taxable bonds, given that high yield ratio.

Credit qualities are shown as a percentage of net assets as of 3/31/11. A bond rated Baa or higher (MIG3/VMIG3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s or, if unrated by S&P, by Fitch, and then included in the closest equivalent Moody’s rating. Ratings will vary over time. Credit qualities are included for portfolio securities and are not included for derivative instruments and cash. The fund itself has not been rated by an independent rating agency.

7

What effect has recent legislation — both enacted and proposed — had on the tax-exempt bond market?

It has been a very busy period from a policy perspective. First, at the end of 2010, the popular Build America Bonds — or “BABs” — program expired. The program was authorized by the 2009 stimulus bill to allow states and municipalities to issue bonds in the taxable market by offering an accompanying subsidy payment to the municipal issuer from the federal government. All 50 states issued BABs during the life of the program, and, despite some speculation that the program might be extended, it was allowed to expire on December 31, 2010.

The expiration of the BABs program caused a significant spike in supply at the end of 2010. To lock in the federal subsidy BABs offered, many states pushed up new issuance into the fourth quarter of 2010 — issuance that was originally slated for 2011. Because excess supply can lead to lower prices when demand fails to keep pace, some investors worried that the expiration of BABs would translate into significantly higher tax-free issuance in 2011, undermining price stability. We believed the first few months of 2011 would bring lighter issuance, and, in fact, issuance year to date has been even lower than expected, which has helped price stability recently.

Speculation about changes to tax policy also has affected the market. Given the ongoing struggle to reduce the federal deficit, a number of proposals are now on the table. Simplification of the tax code is one possibility, with changes to a number of the existing marginal rates. In a market dominated by individual investors, the relative attractiveness of municipal bonds is driven

This chart shows how the fund’s top weightings have changed over the past six months. Weightings are shown as a percentage of net assets. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities and the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings will vary over time.

8

in large part by income tax rates, and any changes to those rates could affect investors’ decisions as they reexamine their portfolios.

Investors also should be aware that there are a number of proposals under consideration in Washington, D.C. that could affect the way that municipal bonds are issued in the future. For example, one proposal suggests replacing traditional tax-exempt bonds with tax credit bonds. It is very important to note that no current proposal would affect the tax-exempt nature of currently outstanding bonds, which is to say they would be grandfathered. It is difficult to say how these proposals will fare as part of the overall attempts to reduce the federal deficit, but the debate could add to investor uncertainty.

How did you position the portfolio during the past six months?

Adhering to a strategy we have held for some time, we continued to position the portfolio to benefit from improving fundamentals in the municipal bond market. As I mentioned earlier, we believed essential service revenue bonds remained attractive, and we held an overweight position in A- and Baa-rated securities relative to the fund’s benchmark. Over the period, this detracted from returns relative to the benchmark, as lower-rated securities lagged the overall market’s returns. Within our credit positioning strategy, the fund’s overweight exposure to California state general obligation bonds helped relative returns. Our holdings in Puerto Rico bonds produced more mixed results. Puerto Rico securities tend to be highly liquid, heavily traded positions in the municipal bond market, and the territory’s bonds generally lagged the market over the past six months.

We continued to limit the fund’s exposure to local general obligation bonds, or “G.O.s,” which are securities issued at the city or county level that are not tied to any particular revenue stream. We believe that as the federal government looks to reduce transfer payments to the states and as states, in turn, seek to close their deficits by reducing spending, these types of bonds are at risk for downgrades or other headline-driven price volatility. Unlike state general obligation bonds, local G.O.s rely more on property tax revenue rather than income or sales taxes. With real estate prices still under pressure in many markets, property taxes have been slower to recover than other tax sources. For those reasons, limiting our exposure in this area of the market generally has been beneficial.

We have also been maintaining a modestly larger cash position than is usual. We believe that given the heightened uncertainty in the market and the potential for ongoing volatility, adopting a slightly more defensive stance is prudent. This positioning also gives us greater flexibility to purchase attractive bonds without necessarily having to sell an existing position to raise cash.

What is your outlook for the municipal bond market?

We believe that while the financial challenges faced by many states remain significant, the likelihood of a default at the state level is quite remote. Generally, debt service is one of the top priorities of payment for a state. For example, debt service payments in California are second only to education. Debt service for states is also normally a small part of the budget. While some states will continue to wrestle with large pension deficits, we believe that the fiscal condition of most state governments gradually will continue to improve along with the broader U.S. economy.

Still, various factors will continue to affect the municipal bond market’s supply-and-demand balance. Although we expect overall supply to contract in 2011 compared with last year — and although it has been lighter than expected year to date — the market is

9

anticipating an uptick in new issuance, which could put pressure on yield levels.

Moreover, there is increased uncertainty surrounding the future of tax rates. Although the Bush-era tax rates were extended in December 2010 for another two years, legislators are now discussing a tax code overhaul, and it’s unclear what future rates will be, particularly for top income earners. In addition to the uncertainty at the federal level, state budget shortfalls and pension liabilities could increase pressure to raise state income taxes. Additionally, government policymakers are showing increased interest in states’ financial conditions, which could spur more media attention and add volatility to the municipal bond market.

All in all, we anticipate that price volatility in the municipal bond market could continue over the short term, but for investors with longer time horizons, we remain confident that our actively managed approach remains a prudent way to generate attractive total returns in the tax-free bond market.

Thank you, Thalia, for bringing us up to date.

The views expressed in this report are exclusively those of Putnam Management. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Thalia Meehan is Team Leader of Tax Exempt Fixed Income at Putnam. She holds a B.A. from Williams College. A CFA charterholder, Thalia joined Putnam in 1989 and has been in the investment industry since 1983.

In addition to Thalia, your fund is managed by Paul Drury and Susan McCormack.

IN THE NEWS

Municipal bonds’ tax-exempt income status is under fire by Washington lawmakers. A recently proposed bill would change the tax treatment of municipal bonds’ distributions, taxing all interest payments but also offering a tax credit for 25% of the interest income earned. The bill would likely make municipal bonds a less attractive option for individual investors, particularly those in the top three income tax brackets. But it could encourage institutional and foreign buyers to re-enter the municipal market. Both had been a significant source of demand for bonds issued under the now-expired Build America Bonds program. This is not the first time lawmakers have considered revoking the tax exemption for municipal bonds in order to generate more revenue, but each time the effort has failed.

10

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended March 31, 2011, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 3/31/11

| | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

| (inception dates) | (12/31/76) | (1/4/93) | (7/26/99) | (2/16/95) | (1/2/08) |

|

| | NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV |

|

| Annual average | | | | | | | | | |

| (life of fund) | 6.68% | 6.56% | 5.89% | 5.89% | 5.82% | 5.82% | 6.27% | 6.16% | 6.71% |

|

| 10 years | 45.89 | 39.91 | 37.09 | 37.09 | 34.74 | 34.74 | 41.64 | 37.02 | 47.11 |

| Annual average | 3.85 | 3.42 | 3.20 | 3.20 | 3.03 | 3.03 | 3.54 | 3.20 | 3.94 |

|

| 5 years | 16.78 | 12.18 | 13.30 | 11.43 | 12.16 | 12.16 | 14.99 | 11.26 | 17.76 |

| Annual average | 3.15 | 2.33 | 2.53 | 2.19 | 2.32 | 2.32 | 2.83 | 2.16 | 3.32 |

|

| 3 years | 10.52 | 6.15 | 8.55 | 5.67 | 7.89 | 7.89 | 9.48 | 6.03 | 11.28 |

| Annual average | 3.39 | 2.01 | 2.77 | 1.86 | 2.56 | 2.56 | 3.07 | 1.97 | 3.63 |

|

| 1 year | 0.92 | –3.11 | 0.30 | –4.53 | 0.13 | –0.84 | 0.64 | –2.59 | 1.16 |

|

| 6 months | –4.60 | –8.37 | –4.90 | –9.56 | –4.95 | –5.88 | –4.72 | –7.77 | –4.48 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns (public offering price, or POP) for class A and M shares reflect a maximum 4.00% and 3.25% load, respectively. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C shares reflect a 1% CDSC for the first year that is eliminated thereafter. Class Y shares have no initial sales charge or CDSC. Performance for class B, C, M, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance does not reflect conversion to class A shares.

11

Comparative index returns For periods ended 3/31/11

| | |

| | Barclays Capital Municipal | Lipper General Municipal Debt Funds |

| | Bond Index | category average* |

|

| Annual average (life of fund) | — † | 5.83% |

|

| 10 years | 57.65% | 41.46 |

| Annual average | 4.66 | 3.50 |

|

| 5 years | 22.49 | 13.47 |

| Annual average | 4.14 | 2.52 |

|

| 3 years | 14.01 | 9.22 |

| Annual average | 4.47 | 2.96 |

|

| 1 year | 1.63 | 0.41 |

|

| 6 months | –3.68 | –4.78 |

|

Index and Lipper results should be compared to fund performance at net asset value.

* Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 3/31/11, there were 264, 259, 229, 201, 169, and 9 funds, respectively, in this Lipper category.

† The fund’s benchmark, the Barclays Capital Municipal Bond Index, was introduced on 12/31/79, which post-dates the inception of the fund’s class A shares.

Fund price and distribution information For the six-month period ended 3/31/11

| | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class Y |

|

| Number | 6 | 6 | 6 | 6 | 6 |

|

| Income 1 | $0.191090 | $0.164772 | $0.158893 | $0.179830 | $0.200314 |

|

| Capital gains 2 | — | — | — | — | — |

|

| Total | $0.191090 | $0.164772 | $0.158893 | $0.179830 | $0.200314 |

|

| Share value | NAV | POP | NAV | NAV | NAV | POP | NAV |

|

| 9/30/10 | $8.71 | $9.07 | $8.71 | $8.72 | $8.73 | $9.02 | $8.72 |

|

| 3/31/11 | 8.12 | 8.46 | 8.12 | 8.13 | 8.14 | 8.41 | 8.13 |

|

| Current yield (end of period) | NAV | POP | NAV | NAV | NAV | POP | NAV |

|

| Current dividend rate 3 | 4.78% | 4.58% | 4.14% | 3.99% | 4.49% | 4.35% | 4.99% |

|

| Taxable equivalent 4 | 7.35 | 7.05 | 6.37 | 6.14 | 6.91 | 6.69 | 7.68 |

|

| Current 30-day SEC yield 5 | N/A | 4.14 | 3.68 | 3.53 | N/A | 3.90 | 4.59 |

|

| Taxable equivalent 4 | N/A | 6.37 | 5.66 | 5.43 | N/A | 6.00 | 7.06 |

|

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

1 For some investors, investment income may be subject to the federal alternative minimum tax.

2 Capital gains, if any, are taxable for federal and, in most cases, state purposes.

3 Most recent distribution, excluding capital gains, annualized and divided by NAV or POP at end of period.

4 Assumes maximum 35.00% federal tax rate for 2011. Results for investors subject to lower tax rates would not be as advantageous.

5 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

12

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Total annual operating expenses for the fiscal year | | | | | |

| ended 9/30/10* | 0.75% | 1.38% | 1.53% | 1.03% | 0.53% |

|

| Annualized expense ratio for the six-month period | | | | | |

| ended 3/31/11 | 0.75% | 1.38% | 1.53% | 1.03% | 0.53% |

|

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

* Restated to reflect projected expenses under a new management contract effective 1/1/10.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from October 1, 2010, to March 31, 2011. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000*† | $3.65 | $6.71 | $7.44 | $5.01 | $2.58 |

|

| Ending value (after expenses) | $954.00 | $951.00 | $950.50 | $952.80 | $955.20 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/11. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

13

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended March 31, 2011, use the following calculation method. To find the value of your investment on October 1, 2010, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000*† | $3.78 | $6.94 | $7.70 | $5.19 | $2.67 |

|

| Ending value (after expenses) | $1,021.19 | $1,018.05 | $1,017.30 | $1,019.80 | $1,022.29 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/11. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

14

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. NAVs fluctuate with market conditions. NAV is calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Public offering price (POP) is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. POP performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Current yield is the annual rate of return earned from dividends or interest of an investment. Current yield is expressed as a percentage of the price of a security, fund share, or principal investment.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Barclays Capital U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

Barclays Capital Municipal Bond Index is an unmanaged index of long-term fixed-rate investment-grade tax-exempt bonds.

BofA (Bank of America) Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

15

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with SEC regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2010, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of March 31, 2011, Putnam employees had approximately $376,000,000 and the Trustees had approximately $69,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

16

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

17

| |

| The fund’s portfolio 3/31/11 (Unaudited) | |

| | |

| Key to holding’s abbreviations | |

| AGM Assured Guaranty Municipal Corporation | FRB Floating Rate Bonds |

| AGO Assured Guaranty, Ltd. | G.O. Bonds General Obligation Bonds |

| AMBAC AMBAC Indemnity Corporation | GNMA Coll. Government National Mortgage |

| Cmnwlth. of PR Gtd. Commonwealth of | Association Collateralized |

| Puerto Rico Guaranteed | NATL National Public Finance Guarantee Corp. |

| COP Certificates of Participation | PSFG Permanent School Fund Guaranteed |

| FGIC Financial Guaranty Insurance Company | Radian Insd. Radian Group Insured |

| FHA Insd. Federal Housing Administration Insured | SGI Syncora Guarantee, Inc. |

| FHLMC Coll. Federal Home Loan Mortgage | U.S. Govt. Coll. U.S. Government Collateralized |

| Corporation Collateralized | VRDN Variable Rate Demand Notes |

| FNMA Coll. Federal National Mortgage | |

| Association Collateralized | |

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* | Rating** | Principal amount | Value |

|

| Alabama (1.0%) | | | |

| AL Hsg. Fin. Auth. Rev. Bonds (Single Fam. Mtge.), | | | |

| Ser. G, GNMA Coll., FNMA Coll., FHLMC Coll., | | | |

| 5 1/2s, 10/1/37 | Aaa | $1,600,000 | $1,651,600 |

|

| Courtland, Indl. Dev. Board Env. Impt. Rev. Bonds | | | |

| (Intl. Paper Co.), Ser. A, 5s, 11/1/13 | BBB | 1,500,000 | 1,581,705 |

|

| Cullman Cnty., Hlth. Care Auth. Rev. Bonds | | | |

| (Cullman Regl. Med. Ctr.), Ser. A, 7s, 2/1/36 | Ba1 | 5,000,000 | 4,588,650 |

|

| Selma, Indl. Dev. Board Rev. Bonds (Gulf Opportunity | | | |

| Zone Intl. Paper Co.), Ser. A, 6 1/4s, 11/1/33 | BBB | 3,500,000 | 3,536,750 |

|

| | | | 11,358,705 |

| Arizona (2.0%) | | | |

| Casa Grande, Indl. Dev. Auth. Rev. Bonds (Casa | | | |

| Grande Regl. Med. Ctr.), Ser. A, 7 5/8s, 12/1/29 | BB–/P | 3,850,000 | 3,594,591 |

|

| Cochise Cnty., Indl. Dev. Auth. Rev. Bonds (Sierra | | | |

| Vista Regl. Hlth. Ctr.), Ser. A, 6.2s, 12/1/21 | BBB+/P | 5,255,000 | 5,332,196 |

|

| Coconino Cnty., Poll. Control Rev. Bonds (Tucson | | | |

| Elec. Pwr. Co. — Navajo), Ser. A, 5 1/8s, 10/1/32 | Baa3 | 2,000,000 | 1,723,220 |

|

| Glendale, Indl. Dev. Auth. Rev. Bonds (Midwestern U.), | | | |

| 5 1/8s, 5/15/40 | A– | 3,500,000 | 3,084,270 |

|

| Maricopa Cnty., Poll. Control Rev. Bonds (El Paso | | | |

| Elec. Co.), Ser. A, 7 1/4s, 2/1/40 | Baa2 | 3,300,000 | 3,560,535 |

|

| Mesa, Util. Syst. Rev. Bonds, FGIC, NATL, | | | |

| 7 1/4s, 7/1/12 | AA– | 3,635,000 | 3,915,368 |

|

| Yavapai Cnty., Indl. Dev. Auth. Hosp. Fac. Rev. Bonds | | | |

| (Yavapai Regl. Med. Ctr.), Ser. A, 6s, 8/1/33 | Baa2 | 500,000 | 488,535 |

|

| | | | 21,698,715 |

| California (9.3%) | | | |

| Bay Area Toll Auth. of CA Rev. Bonds (San Francisco | | | |

| Bay Area), Ser. F-1, 5s, 4/1/39 | AA | 5,000,000 | 4,624,850 |

|

| CA Edl. Fac. Auth. Rev. Bonds | | | |

| (Scripps College), 5s, 8/1/31 | A1 | 500,000 | 469,015 |

| (Lutheran U.), Ser. C, 5s, 10/1/24 | Baa1 | 1,215,000 | 1,140,047 |

|

18

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| CA Hsg. Fin. Agcy. Rev. Bonds (Home Mtge.), | | | |

| Ser. K, 4 3/4s, 8/1/36 | A | $5,750,000 | $4,531,690 |

|

| CA Infrastructure & Econ. Dev. Bank Rev. Bonds | | | |

| (Science Ctr. Phase II), Ser. B, FGIC, NATL, | | | |

| 5s, 5/1/23 | BBB | 640,000 | 599,283 |

|

| CA Muni. Fin. Auth. COP (Cmnty. Hosp. Central CA), | | | |

| 5 1/4s, 2/1/37 | Baa2 | 4,100,000 | 3,239,861 |

|

| CA State G.O. Bonds | | | |

| 6 1/2s, 4/1/33 | A1 | 10,000,000 | 10,807,100 |

| 5 3/4s, 4/1/31 | A1 | 15,000,000 | 15,376,050 |

| 5 1/2s, 3/1/40 | A1 | 10,300,000 | 9,924,462 |

| 5s, 11/1/30 | A1 | 5,000 | 4,807 |

| FGIC, NATL, 5s, 6/1/26 | A1 | 5,000,000 | 5,018,050 |

|

| CA State Dept. of Wtr. Resources Rev. Bonds | | | |

| (Central Valley), Ser. AE, 5s, 12/1/29 | AAA | 5,000,000 | 5,114,350 |

|

| CA State Pub. Wks. Board Rev. Bonds | | | |

| Ser. I-1, 6 5/8s, 11/1/34 | A2 | 10,000,000 | 10,440,700 |

| Ser. I-1, 6 1/8s, 11/1/29 | A2 | 2,000,000 | 2,073,360 |

| Ser. A-1, 6s, 3/1/35 | A2 | 3,100,000 | 3,104,030 |

|

| Chula Vista, Indl. Dev. Rev. Bonds (San Diego Gas), | | | |

| Ser. B, 5s, 12/1/27 | Aa3 | 200,000 | 192,332 |

|

| Golden State Tobacco Securitization Corp. Rev. | | | |

| Bonds (Tobacco Settlement), Ser. B, AMBAC, FHLMC | | | |

| Coll., 5s, 6/1/38 (Prerefunded 6/1/13) | Aaa | 530,000 | 575,326 |

|

| Los Angeles, Unified School Dist. G.O. Bonds, Ser. I, | | | |

| 5s, 7/1/26 | Aa2 | 5,000,000 | 4,999,600 |

|

| M-S-R Energy Auth. Rev. Bonds, Ser. A, | | | |

| 6 1/2s, 11/1/39 | A | 2,250,000 | 2,285,145 |

|

| Port Oakland, Rev. Bonds, Ser. L, FGIC, NATL | | | |

| 5 3/8s, 11/1/27 | A2 | 7,930,000 | 7,264,594 |

| 5 3/8s, 11/1/27 (Prerefunded 11/1/12) | A2 | 990,000 | 1,060,943 |

|

| Riverside Cnty., Asset Leasing Corp. Leasehold Rev. | | | |

| Bonds (Riverside Cnty. Hosp.), NATL, zero %, 6/1/25 | A2 | 4,000,000 | 1,418,360 |

|

| Sacramento, City Fin. Auth. Tax Alloc. Bonds, | | | |

| Ser. A, FGIC, NATL, zero %, 12/1/22 | A | 7,500,000 | 3,451,800 |

|

| Solano, Cmnty. College Dist. G.O. Bonds (Election | | | |

| of 2002), Ser. B, FGIC, NATL, zero %, 8/1/26 | Aa3 | 9,560,000 | 3,722,090 |

|

| | | | 101,437,845 |

| Colorado (1.9%) | | | |

| CO Edl. & Cultural Fac. Auth. VRDN (National | | | |

| Jewish Federation Bond), Ser. A1, 0.23s, 9/1/33 | VMIG1 | 7,245,000 | 7,245,000 |

|

| CO Hlth. Fac. Auth. Rev. Bonds | | | |

| (Valley View Assn.), 5 1/4s, 5/15/42 | BBB | 1,500,000 | 1,225,350 |

| (Evangelical Lutheran), 5 1/4s, 6/1/22 | A3 | 1,000,000 | 987,480 |

| (Evangelical Lutheran), 5s, 6/1/16 | A3 | 1,000,000 | 1,043,750 |

|

| CO Pub. Hwy. Auth. Rev. Bonds (E-470 Pub. Hwy.), | | | |

| Ser. C1, NATL, 5 1/2s, 9/1/24 | Baa1 | 1,750,000 | 1,651,615 |

|

| CO Springs, Hosp. Rev. Bonds | | | |

| 6 3/8s, 12/15/30 | A3 | 2,520,000 | 2,482,225 |

| 6 1/4s, 12/15/33 | A3 | 3,000,000 | 3,027,660 |

|

19

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Colorado cont. | | | |

| E-470 Pub. Hwy. Auth. Rev. Bonds, Ser. A, NATL, | | | |

| zero %, 9/1/34 | A | $13,000,000 | $1,964,040 |

|

| Regl. Trans. Dist. Rev. Bonds (Denver Trans. Partners), | | | |

| 6s, 1/15/41 | Baa3 | 750,000 | 675,473 |

|

| | | | 20,302,593 |

| Connecticut (0.4%) | | | |

| CT State Dev. Auth. 1st. Mtg. Gross Rev. Hlth. Care | | | |

| Rev. Bonds (Elim Street Park Baptist, Inc.), | | | |

| 5.85s, 12/1/33 | BBB+ | 650,000 | 590,207 |

|

| CT State Dev. Auth. Poll. Control Rev. Bonds | | | |

| (Western MA Electric Co.), Ser. A, 5.85s, 9/1/28 | Baa2 | 3,000,000 | 2,986,860 |

|

| Hamden, Fac. Rev. Bonds (Whitney Ctr.), Ser. B, | | | |

| 6 1/8s, 1/1/14 | BB/P | 1,000,000 | 999,510 |

|

| | | | 4,576,577 |

| Delaware (0.5%) | | | |

| DE St. Econ. Dev. Auth. Rev. Bonds | | | |

| (Delmarva Pwr.), 5.4s, 2/1/31 | BBB+ | 1,700,000 | 1,651,533 |

| (Indian River Pwr.), 5 3/8s, 10/1/45 | Baa3 | 4,200,000 | 3,563,154 |

|

| | | | 5,214,687 |

| District of Columbia (0.7%) | | | |

| DC G.O. Bonds, Ser. A, AGM, 5s, 6/1/26 | AA+ | 5,005,000 | 5,138,684 |

|

| DC Ballpark Rev. Bonds, Ser. B-1, FGIC, NATL, | | | |

| 5s, 2/1/25 | A3 | 1,035,000 | 1,014,693 |

|

| Metro. Washington, Arpt. Auth. Dulles Toll Rd. | | | |

| Rev. Bonds (Metrorail), Ser. A, zero %, 10/1/37 | Baa1 | 11,000,000 | 1,706,540 |

|

| | | | 7,859,917 |

| Florida (9.0%) | | | |

| Brevard Cnty., Hlth. Care Fac. Auth. Rev. Bonds | | | |

| (Health First, Inc.), 7s, 4/1/39 | A3 | 4,000,000 | 4,240,480 |

|

| Cape Coral, Wtr.& Swr. Rev. Bonds, AMBAC, | | | |

| 5s, 10/1/26 | A1 | 2,500,000 | 2,513,075 |

|

| Escambia Cnty., Hlth. Fac. Auth. Rev. Bonds | | | |

| (Baptist Hosp., Inc.), Ser. A, 5 3/4s, 8/15/29 | Baa1 | 2,500,000 | 2,315,575 |

|

| FL Hsg. Fin. Corp. Rev. Bonds | | | |

| Ser. G, GNMA Coll., FNMA Coll., FHLMC Coll., | | | |

| 5 3/4s, 1/1/37 | Aa1 | 1,040,000 | 1,086,426 |

| (Noah’s Landing Apts.), Ser. H-1, AGM, 5 3/8s, | | | |

| 12/1/41 | AA+ | 1,710,000 | 1,601,637 |

| (Homeowner Mtge.), Ser. 2, GNMA Coll, FNMA Coll, | | | |

| FHLMC Coll., 4.95s, 7/1/37 | Aa1 | 1,240,000 | 1,178,769 |

|

| FL State Muni. Pwr. Agcy. Rev. Bonds, Ser. A, | | | |

| 5s, 10/1/31 | A1 | 3,300,000 | 3,181,134 |

|

| Hernando Cnty., Rev. Bonds (Criminal Justice | | | |

| Complex Fin.), FGIC, NATL, 7.65s, 7/1/16 | BBB | 18,500,000 | 21,509,580 |

|

| Highlands Cnty., Hlth. Fac. Auth. Rev. Bonds | | | |

| (Adventist Sunbelt), Ser. A, 6s, 11/15/31 | | | |

| (Prerefunded 11/15/11) | AAA/P | 1,000,000 | 1,043,670 |

|

| Hillsborough Cnty., Cmnty. Investment Tax Rev. | | | |

| Bonds, AMBAC, 5s, 5/1/24 | AA+ | 1,250,000 | 1,307,775 |

|

| Hillsborough Cnty., Indl. Dev. Auth. Poll. | | | |

| Control Mandatory Put Bonds | | | |

| (9/1/13) (Tampa Elec. Co.), Ser. B, 5.15s, 9/1/25 | Baa1 | 1,125,000 | 1,194,154 |

| (3/15/12) AMBAC, 5s, 12/1/34 | Baa1 | 1,350,000 | 1,386,410 |

|

20

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Florida cont. | | | |

| Kissimmee, Util. Auth. Rev. Bonds, AGM, 5 1/4s, | | | |

| 10/1/18 | Aa3 | $2,270,000 | $2,391,036 |

|

| Lee Cnty., Rev. Bonds, SGI, 5s, 10/1/25 | Aa2 | 5,500,000 | 5,589,595 |

|

| Lee Cnty., Indl. Dev. Auth. Hlth. Care Fac. Rev. Bonds | | | |

| (Cypress Cove Hlth. Pk.), Ser. A, 6 3/8s, 10/1/25 | BB–/P | 2,500,000 | 1,927,625 |

|

| Leesburg, Cap. Impt. Rev. Bonds, FGIC, NATL, | | | |

| 5 1/4s, 10/1/27 | A1 | 1,600,000 | 1,615,712 |

|

| Miami Beach, Hlth. Fac. Auth. Hosp. Rev. Bonds | | | |

| (Mount Sinai Med. Ctr.), Ser. A | | | |

| 6.8s, 11/15/31 | Ba1 | 1,000,000 | 957,370 |

| 6.7s, 11/15/19 | Ba1 | 3,700,000 | 3,728,194 |

|

| Miami-Dade Cnty., G.O. Bonds (Parks Program), | | | |

| NATL, 5s, 11/1/25 | Aa2 | 5,000,000 | 5,065,000 |

|

| Miami-Dade Cnty., Aviation Rev. Bonds, Ser. B, | | | |

| 5s, 10/1/41 | A2 | 5,000,000 | 4,302,900 |

|

| Miami-Dade Cnty., Expressway Auth. Toll Syst. | | | |

| Rev. Bonds, Ser. B, FGIC, NATL, 5 1/4s, 7/1/26 | A | 3,000,000 | 3,040,710 |

|

| Orange Cnty., Hlth. Fac. Auth. Rev. Bonds | | | |

| (Orlando Regl. Hlth. Care), Ser. A, NATL, | | | |

| 6 1/4s, 10/1/18 | A2 | 3,000,000 | 3,336,690 |

|

| Palm Beach Cnty., Hlth. Fac. Auth. Rev. Bonds | | | |

| (Acts Retirement-Life Cmnty.), 5 1/2s, 11/15/33 | BBB+ | 5,000,000 | 4,454,800 |

|

| Palm Coast Pk. Cmnty. Dev. Dist. Special Assmt. | | | |

| Bonds, 5.7s, 5/1/37 | B+/P | 280,000 | 162,756 |

|

| South Broward, Hosp. Dist. Rev. Bonds, NATL, | | | |

| 4 3/4s, 5/1/28 | Aa3 | 2,000,000 | 1,864,220 |

|

| South Village, Cmnty. Dev. Dist. Rev. Bonds, Ser. A, | | | |

| 5.7s, 5/1/35 | B/P | 455,000 | 314,542 |

|

| St. Lucie Cnty., School Board COP, Ser. A, AGM, | | | |

| 5s, 7/1/23 | AA+ | 4,300,000 | 4,325,198 |

|

| Sumter Cnty., School Dist. Rev. Bonds | | | |

| (Multi-Dist. Loan Program), AGM, 7.15s, 11/1/15 | | | |

| (Escrowed to maturity) | AA+ | 4,800,000 | 5,830,368 |

|

| Sunrise, Util. Syst. Rev. Bonds, AMBAC | | | |

| 5.2s, 10/1/22 | AA– | 3,405,000 | 3,687,785 |

| 5.2s, 10/1/22 (Prerefunded 10/1/18) | AA– | 2,590,000 | 2,907,456 |

|

| Tolomato, Cmnty. Dev. Dist. Special Assmt. Bonds, | | | |

| 5.4s, 5/1/37 | BB–/P | 100,000 | 73,322 |

|

| Verandah, West Cmnty. Dev. Dist. Rev. Bonds | | | |

| (Cap. Impt.), Ser. A, 6 5/8s, 5/1/33 | BB/P | 870,000 | 789,281 |

|

| | | | 98,923,245 |

| Georgia (1.4%) | | | |

| Atlanta, Arpt. Rev. Bonds (Hartsfield-Jackson | | | |

| Intl. Arpt.), Ser. A, 5s, 1/1/35 | A1 | 2,000,000 | 1,859,580 |

|

| Atlanta, Wtr. & Waste Wtr. Rev. Bonds, Ser. A, | | | |

| 6 1/4s, 11/1/39 | A1 | 4,500,000 | 4,662,675 |

|

| Forsyth Cnty., Hosp. Auth. Rev. Bonds (Baptist | | | |

| Hlth. Care Syst.), U.S. Govt. Coll., 6 1/4s, | | | |

| 10/1/18 (Escrowed to maturity) | AAA | 845,000 | 985,278 |

|

| GA State Private College & U. Auth. Rev. Bonds | | | |

| (Emory U.), Ser. B, 5s, 9/1/29 | Aa2 | 2,250,000 | 2,321,550 |

|

21

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Georgia cont. | | | |

| Main St. Natural Gas, Inc. Rev. Bonds (GA Gas), | | | |

| Ser. A, 5 1/2s, 9/15/21 | A+ | $370,000 | $370,570 |

|

| Marietta, Dev. Auth. Rev. Bonds (U. Fac. — | | | |

| Life U., Inc.), 7s, 6/15/39 | Ba3 | 3,450,000 | 3,136,533 |

|

| Richmond Cnty., Dev. Auth. Rev. Bonds (Amt.-Intl. | | | |

| Paper Co.), Ser. A, 6 1/4s, 2/1/25 | BBB | 1,950,000 | 1,953,101 |

|

| | | | 15,289,287 |

| Illinois (3.0%) | | | |

| Chicago, O’Hare Intl. Arpt. Rev. Bonds, Ser. F, | | | |

| 5s, 1/1/40 | A1 | 3,700,000 | 3,169,827 |

|

| Chicago, Waste Wtr. Transmission VRDN, Ser. C-2, | | | |

| 0.22s, 1/1/39 | VMIG1 | 1,210,000 | 1,210,000 |

|

| Chicago, Wtr. Rev. Bonds, AGM, 5s, 11/1/25 | AA+ | 4,750,000 | 4,797,548 |

|

| Cook Cnty., G.O. Bonds, Ser. B, NATL, 5s, 11/15/29 | Aa2 | 1,250,000 | 1,218,888 |

|

| IL Edl. Fac. Auth. Rev. Bonds (Northwestern U.), | | | |

| 5s, 12/1/33 | Aaa | 2,250,000 | 2,269,328 |

|

| IL Fin. Auth. Rev. Bonds | | | |

| (Rush U. Med. Ctr.), Ser. A, 7 1/4s, 11/1/38 | A2 | 350,000 | 370,188 |

| (Rush U. Med. Ctr.), Ser. B, 7 1/4s, 11/1/38 | A2 | 2,520,000 | 2,665,354 |

| (Silver Cross Hosp. & Med. Ctr.), 7s, 8/15/44 | BBB | 5,500,000 | 5,457,210 |

| (IL Rush U. Med Ctr.), Ser. C, 6 5/8s, 11/1/39 | A2 | 1,075,000 | 1,100,187 |

| (Roosevelt U.), 6 1/2s, 4/1/39 | Baa2 | 4,000,000 | 3,884,680 |

| (Elmhurst Memorial), Ser. A, 5 5/8s, 1/1/37 | Baa1 | 1,000,000 | 853,710 |

| (Newman Foundation), Radian Insd., 5s, 2/1/32 | BBB/P | 3,000,000 | 2,380,380 |

|

| IL State Toll Hwy. Auth. Rev. Bonds, Ser. A-1, | | | |

| AGM, 5s, 1/1/22 | AA+ | 1,000,000 | 1,016,500 |

|

| Railsplitter, Tobacco Settlement Auth. Rev. | | | |

| Bonds, 6s, 6/1/28 | A– | 2,150,000 | 2,093,713 |

|

| | | | 32,487,513 |

| Indiana (2.0%) | | | |

| IN Bk. Special Program Gas Rev. Bonds, Ser. A, | | | |

| 5 1/4s, 10/15/21 | Aa3 | 6,150,000 | 6,239,360 |

|

| IN Hlth. Fac. Fin. Auth. VRDN (Fayette Memorial | | | |

| Hosp. Assn.), Ser. A, 0.23s, 10/1/32 | A–1+ | 1,775,000 | 1,775,000 |

|

| IN State Fin. Auth. Edl. Fac. Rev. Bonds | | | |

| (Valparaiso U.), 5s, 10/1/27 | A2 | 1,405,000 | 1,425,190 |

|

| IN State Fin. Auth. Edl. Fac. VRDN | | | |

| (Depauw U.), Ser. A, 0 1/4s, 7/1/36 | VMIG1 | 500,000 | 500,000 |

| Ser. A-1, 0.21s, 2/1/37 | VMIG1 | 1,100,000 | 1,100,000 |

|

| Indianapolis, Arpt. Auth. Rev. Bonds (Federal | | | |

| Express Corp.), 5.1s, 1/15/17 | Baa2 | 4,500,000 | 4,815,090 |

|

| Jasper Cnty., Indl. Poll. Control Rev. Bonds | | | |

| AMBAC, 5.7s, 7/1/17 | Baa2 | 2,500,000 | 2,696,650 |

| NATL, 5.6s, 11/1/16 | Baa1 | 2,750,000 | 2,967,745 |

|

| Jasper Hosp. Auth. Rev. Bonds (Memorial Hosp.), | | | |

| Radian Insd., 5 1/2s, 11/1/32 | A– | 500,000 | 443,460 |

|

| | | | 21,962,495 |

| Iowa (1.0%) | | | |

| IA Fin. Auth. Rev. Bonds (Single Fam. Mtge.), Ser. D, | | | |

| GNMA Coll., FNMA Coll., 5s, 1/1/36 | Aaa | 200,000 | 204,496 |

|

| IA Fin. Auth. Hlth. Care Fac. Rev. Bonds (Care | | | |

| Initiatives), 9 1/4s, 7/1/25 (Prerefunded 7/1/11) | AAA | 7,095,000 | 7,449,750 |

|

22

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Iowa cont. | | | |

| IA Fin. Auth. Hlth. Fac. Rev. Bonds (Care Initiatives), | | | |

| Ser. A, 5 1/2s, 7/1/21 | BB+ | $2,500,000 | $2,195,525 |

|

| Tobacco Settlement Auth. of IA Rev. Bonds, | | | |

| Ser. C, 5 3/8s, 6/1/38 | BBB | 750,000 | 539,438 |

|

| | | | 10,389,209 |

| Kansas (0.8%) | | | |

| KS State Dev. Fin. Auth. Rev. Bonds | | | |

| Ser. K, NATL, 5 1/4s, 11/1/26 | Aa2 | 1,355,000 | 1,446,354 |

| Ser. K, NATL, 5 1/4s, 11/1/25 | Aa2 | 1,620,000 | 1,735,004 |

| (Lifespace Cmnty’s. Inc.), Ser. S, 5s, 5/15/30 | A/F | 2,900,000 | 2,572,648 |

|

| KS State Dev. Fin. Auth. Hlth. Fac. Rev. Bonds | | | |

| (Stormont-Vail Hlthcare, Inc.), Ser. L, NATL, | | | |

| 5 1/8s, 11/15/32 | A2 | 1,260,000 | 1,184,942 |

|

| Lenexa, Hlth. Care Rev. Bonds (LakeView Village), | | | |

| Ser. C, 6 7/8s, 5/15/32 (Prerefunded 5/15/12) | AAA | 500,000 | 541,185 |

|

| Lenexa, Hlth. Care Fac. Rev. Bonds, 5 1/2s, 5/15/39 | BB/P | 1,500,000 | 1,039,230 |

|

| | | | 8,519,363 |

| Kentucky (0.9%) | | | |

| Breckinridge Cnty., Lease Program VRDN, Ser. A, | | | |

| 0.22s, 2/1/32 | VMIG1 | 675,000 | 675,000 |

|

| Christian Cnty., Assn. of Cnty. Leasing Trust | | | |

| VRDN, Ser. B, 0.22s, 8/1/37 | VMIG1 | 770,000 | 770,000 |

|

| KY Econ. Dev. Fin. Auth. Rev. Bonds | | | |

| (Louisville Arena), Ser. A-1, AGO, 6s, 12/1/42 | AA+ | 3,500,000 | 3,511,760 |

|

| Louisville & Jefferson Cnty., Metro. Govt. Hlth. Syst. | | | |

| Rev. Bonds (Norton Hlth. Care, Inc.), 5s, 10/1/30 | A– | 4,000,000 | 3,519,680 |

|

| Louisville/Jefferson Cnty., Metro. Govt. College | | | |

| Rev. Bonds (Bellarmine U.), Ser. A, 6s, 5/1/38 | Baa3 | 855,000 | 822,903 |

|

| Owen Cnty., Wtr. Wks. Syst. Rev. Bonds (American | | | |

| Wtr. Co.), Ser. A, 6 1/4s, 6/1/39 | BBB+ | 1,000,000 | 1,026,210 |

|

| | | | 10,325,553 |

| Louisiana (0.6%) | | | |

| LA Pub. Fac. Auth. Rev. Bonds (Entergy LA LLC), | | | |

| 5s, 6/1/30 | A3 | 5,000,000 | 4,926,950 |

|

| Tobacco Settlement Fin. Corp. Rev. Bonds, | | | |

| Ser. 01-B, 5 1/2s, 5/15/30 | A | 2,275,000 | 2,161,387 |

|

| | | | 7,088,337 |

| Maine (—%) | | | |

| ME Hlth. & Higher Edl. Fac. Auth. Rev. Bonds, | | | |

| Ser. C, AGM, 5 3/4s, 7/1/30 | AA+ | 50,000 | 50,549 |

|

| | | | 50,549 |

| Maryland (0.3%) | | | |

| MD Econ. Dev. Corp. Poll. Control Rev. Bonds | | | |

| (Potomac Electric Power Co.), 6.2s, 9/1/22 | A | 1,100,000 | 1,237,984 |

|

| MD State Hlth. & Higher Edl. Fac. Auth. Rev. | | | |

| Bonds (Washington Cnty. Hosp.) | | | |

| 6s, 1/1/43 | BBB– | 1,590,000 | 1,461,703 |

| 5 3/4s, 1/1/38 | BBB– | 1,000,000 | 900,700 |

|

| | | | 3,600,387 |

23

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Massachusetts (4.3%) | | | |

| MA Edl. Fin. Auth. Rev. Bonds, Ser. B, 5.7s, 1/1/31 | AA | $5,195,000 | $4,986,577 |

|

| MA State Dept. Trans. Rev. Bonds (Metro Hwy. Syst.), | | | |

| Ser. B, 5s, 1/1/37 | A | 6,750,000 | 6,168,623 |

|

| MA State Dev. Fin. Agcy. Rev. Bonds | | | |

| (Sabis Intl.), Ser. A, 8s, 4/15/39 | BBB | 920,000 | 983,784 |

| (Wheelock College), Ser. C, 5 1/4s, 10/1/29 | BBB | 3,300,000 | 3,060,486 |

| (Suffolk U.), 5 1/8s, 7/1/40 | Baa2 | 2,000,000 | 1,676,000 |

|

| MA State Hlth. & Edl. Fac. Auth. Rev. Bonds | | | |

| (Civic Investments/HPHC), Ser. A, 9s, 12/15/15 | | | |

| (Prerefunded 12/15/12) | AAA/P | 525,000 | 588,940 |

| (Jordan Hosp.), Ser. E, 6 3/4s, 10/1/33 | BB– | 2,950,000 | 2,726,272 |

| (UMass Memorial), Ser. C, 6 5/8s, 7/1/32 | Baa1 | 4,750,000 | 4,751,378 |

| (UMass Memorial), Ser. C, 6 1/2s, 7/1/21 | Baa1 | 900,000 | 902,466 |

| (Berkshire Hlth. Syst.), Ser. E, 6 1/4s, 10/1/31 | BBB+ | 1,000,000 | 980,760 |

| (Hlth. Care Syst.-Covenant Hlth.), 6s, 7/1/31 | A/F | 1,065,000 | 1,067,545 |

| (Suffolk U.), Ser. A, 5 3/4s, 7/1/39 | Baa2 | 4,000,000 | 3,827,680 |

| (Baystate Med. Ctr.), Ser. I, 5 3/4s, 7/1/36 | A+ | 2,000,000 | 1,910,220 |

| (Springfield College), 5 5/8s, 10/15/40 | Baa1 | 1,000,000 | 918,740 |

| (Springfield College), 5 1/2s, 10/15/31 | Baa1 | 600,000 | 567,546 |

| (Milton Hosp.), Ser. D, 5 3/8s, 7/1/35 | BB– | 450,000 | 333,873 |

| (Care Group), Ser. B-2, NATL, 5 3/8s, 2/1/26 | A3 | 1,050,000 | 1,009,974 |

| (Sterling & Francine Clark), Ser. A, 5s, 7/1/36 | Aa2 | 3,305,000 | 3,258,102 |

| (Northeastern U.), Ser. A, 5s, 10/1/35 | A2 | 4,100,000 | 3,820,790 |

|

| MA State Hlth. & Edl. Fac. Auth. VRDN | | | |

| (Museum of Fine Arts), Ser. A2, 0.23s, 12/1/37 | VMIG1 | 550,000 | 550,000 |

|

| MA State Port Auth. Rev. Bonds, 13s, 7/1/13 | AA–/P | 2,800,000 | 3,236,800 |

|

| | | | 47,326,556 |

| Michigan (2.4%) | | | |

| Detroit, G.O. Bonds | | | |

| Ser. A-1, AMBAC, 5 1/4s, 4/1/24 | BB | 500,000 | 396,345 |

| (Cap. Impt.), Ser. A-1, 5s, 4/1/15 | BB | 3,120,000 | 2,841,290 |

|

| Detroit, Wtr. Supply Syst. Rev. Bonds, Ser. B, | | | |

| AGM, 6 1/4s, 7/1/36 | AA+ | 4,040,000 | 4,254,564 |

|

| Flint, Hosp. Bldg. Auth. Rev. Bonds (Hurley Med. Ctr.), | | | |

| 7 3/8s, 7/1/35 | Ba1 | 2,500,000 | 2,405,650 |

|

| Garden City, Hosp. Fin. Auth. Rev. Bonds (Garden | | | |

| City Hosp.), Ser. A, 5 3/4s, 9/1/17 | Ba3 | 535,000 | 514,210 |

|

| MI Higher Ed. Fac. Auth. VRDN (U. of Detroit), | | | |

| 0.23s, 11/1/36 | VMIG1 | 675,000 | 675,000 |

|

| MI State Hosp. Fin. Auth. Rev. Bonds | | | |

| Ser. A, 6 1/8s, 6/1/39 | A1 | 2,500,000 | 2,503,725 |

| (Henry Ford Hlth. Syst.), Ser. A, 5 1/4s, 11/15/46 | A1 | 8,160,000 | 6,828,533 |

| (Chelsea Cmnty. Hosp. Oblig.), 5s, 5/15/25 | | | |

| (Prerefunded 5/15/15) | AAA | 915,000 | 1,036,338 |

|

| MI State Strategic Fund Mandatory Put Bonds | | | |

| (6/2/14) (Dow Chemical), Ser. A-1, 6 3/4s, | | | |

| 12/1/28 | BBB– | 700,000 | 753,949 |

|

| MI State Strategic Fund, Ltd. Mandatory Put Bonds | | | |

| (6/1/13) (Dow Chemical), 5 1/2s, 12/1/28 | Baa3 | 3,500,000 | 3,654,315 |

|

| U. of MI VRDN (Hosp.), Ser. A, 0.22s, 12/1/37 | VMIG1 | 700,000 | 700,000 |

|

| | | | 26,563,919 |

24

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Minnesota (0.9%) | | | |

| Douglas Cnty., Gross Hlth. Care Fac. Rev. Bonds | | | |

| (Douglas Cnty. Hosp.), Ser. A, 6 1/4s, 7/1/38 | BBB– | $1,600,000 | $1,608,768 |

|

| Minneapolis, Rev. Bonds (National Marrow Donor | | | |

| Program), 4 7/8s, 8/1/25 | BBB | 2,000,000 | 1,882,740 |

|

| MN Agricultural & Econ. Dev. Board Rev. Bonds | | | |

| (Evangelical Lutheran), 6s, 2/1/27 | A3 | 1,625,000 | 1,639,495 |

|

| MN State Higher Ed. Fac. Auth. VRDN (St. Olaf | | | |

| College), Ser. 5-M2, 0.23s, 10/1/20 | VMIG1 | 805,000 | 805,000 |

|

| MN State Hsg. Fin. Agcy. Rev. Bonds (Res. Hsg.), | | | |

| Ser. H, 4.3s, 1/1/13 | Aa1 | 565,000 | 577,622 |

|

| St. Paul, Hsg. & Redev. Auth. Hlth. Care Fac. | | | |

| Rev. Bonds (HealthPartners Oblig. Group), | | | |

| 5 1/4s, 5/15/36 | A3 | 2,155,000 | 1,910,903 |

|

| St. Paul, Hsg. & Redev. Auth. Hosp. Rev. Bonds | | | |

| (Healtheast), 6s, 11/15/35 | Ba1 | 1,250,000 | 1,076,813 |

|

| St. Paul, Port Auth. VRDN (MN Pub. Radio), | | | |

| Ser. 7, 0.24s, 5/1/25 | VMIG1 | 250,000 | 250,000 |

|

| Winona, Hlth. Care Fac. Rev. Bonds (Winona Hlth. | | | |

| Oblig. Group), Ser. A, 6s, 7/1/34 | BBB– | 500,000 | 467,345 |

|

| | | | 10,218,686 |

| Mississippi (0.4%) | | | |

| MS Bus. Fin. Corp. Poll. Control Rev. Bonds | | | |

| (Syst. Energy Resources, Inc.), 5 7/8s, 4/1/22 | BBB | 3,000,000 | 2,927,760 |

|

| MS Home Corp. Rev. Bonds (Single Fam. Mtge.), | | | |

| Ser. B-2, GNMA Coll., FNMA Coll., 6.45s, 12/1/33 | Aaa | 1,285,000 | 1,344,701 |

|

| | | | 4,272,461 |

| Missouri (0.4%) | | | |

| MO State Hlth. & Edl. Fac. Auth. Rev. Bonds | | | |

| (Washington U. (The)), Ser. A, 5 3/8s, 3/15/39 | Aaa | 2,250,000 | 2,330,955 |

|

| MO State Hlth. & Edl. Fac. Auth. VRDN | | | |

| (Washington U. (The)), Ser. A, 0 1/4s, 9/1/30 | VMIG1 | 1,500,000 | 1,500,000 |

| (Sisters of Mercy Hlth.), Ser. B, 0.22s, 6/1/16 | VMIG1 | 660,000 | 660,000 |

|

| MO State Hsg. Dev. Comm. Mtge. Rev. Bonds | | | |

| (Single Fam. Homeowner Loan), Ser. B-1, GNMA | | | |

| Coll., FNMA Coll., 7.45s, 9/1/31 | AAA | 150,000 | 154,458 |

| (Single Fam. Home Ownership Loan), Ser. A-1, | | | |

| GNMA Coll., FNMA Coll., 6 3/4s, 3/1/34 | AAA | 160,000 | 168,480 |

|

| | | | 4,813,893 |

| Montana (0.2%) | | | |

| MT Fac. Fin. Auth. VRDN (Sisters of Charity), | | | |

| Ser. A, 0.23s, 12/1/25 | VMIG1 | 1,750,000 | 1,750,000 |

|

| | | | 1,750,000 |

| Nebraska (—%) | | | |

| Central Plains, Energy Rev. Bonds (NE Gas No. 1), | | | |

| Ser. A, 5 1/4s, 12/1/18 | Ba3 | 370,000 | 363,803 |

|

| | | | 363,803 |

| Nevada (0.8%) | | | |

| Clark Cnty., Indl. Dev. Rev. Bonds (Southwest | | | |

| Gas Corp.), Ser. A, AMBAC, 5 1/4s, 7/1/34 | Baa2 | 7,570,000 | 6,681,509 |

|

| Clark Cnty., Local Impt. Dist. Special Assmt. | | | |

| Bonds (No. 142), 6.1s, 8/1/18 | BB+/P | 1,635,000 | 1,638,499 |

|

| | | | 8,320,008 |

25

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| New Hampshire (0.6%) | | | |

| NH Higher Edl. & Hlth. Fac. Auth. Rev. Bonds | | | |

| (Rivermead at Peterborough), 5 3/4s, 7/1/28 | BB+/P | $1,000,000 | $844,040 |

|

| NH Hlth. & Ed. Fac. Auth. Rev. Bonds (Hlth. Care | | | |

| Syst.-Covenant Hlth.), 6 1/8s, 7/1/31 | | | |

| (Prerefunded 1/1/12) | A | 4,000,000 | 4,196,600 |

|

| NH State Bus. Fin. Auth. Rev. Bonds (Elliot Hosp. | | | |

| Oblig. Group), Ser. A, 6 1/8s, 10/1/39 | Baa1 | 2,000,000 | 1,910,720 |

|

| | | | 6,951,360 |

| New Jersey (5.4%) | | | |

| Middlesex Cnty., Impt. Auth. Lease Rev. Bonds (Perth | | | |

| Amboy Muni. Complex), FGIC, NATL, 5s, 3/15/31 | BBB–/P | 3,500,000 | 2,991,240 |

|

| NJ Econ. Dev. Auth. Rev. Bonds | | | |

| (Cedar Crest Village, Inc.), Ser. A, U.S. Govt. | | | |

| Coll., 7 1/4s, 11/15/31 (Prerefunded 11/15/11) | AAA/F | 3,150,000 | 3,314,588 |

| (MSU Student Hsg.), 5 7/8s, 6/1/42 | Baa3 | 3,840,000 | 3,436,570 |

| (Cigarette Tax), 5 1/2s, 6/15/24 | BBB | 9,750,000 | 9,035,715 |

| (School Fac. Construction), Ser. AA, 5 1/4s, | | | |

| 12/15/33 | Aa3 | 5,500,000 | 5,399,405 |

| (Motor Vehicle), Ser. A, NATL, 5s, 7/1/27 | A | 7,000,000 | 6,984,040 |

|

| NJ Econ. Dev. Auth. Wtr. Fac. Rev. Bonds | | | |

| (NJ American Wtr.), Ser. B, 5.6s, 11/1/34 | A2 | 2,000,000 | 1,906,920 |

| (American Wtr. Co.), Ser. D, 4 7/8s, 11/1/29 | A2 | 1,100,000 | 1,019,381 |

|

| NJ Hlth. Care Fac. Fin. Auth. Rev. Bonds | | | |

| (St. Joseph Hlth. Care Syst.), 6 5/8s, 7/1/38 | BBB– | 6,250,000 | 6,024,438 |

| (St. Peter’s U. Hosp.), 5 3/4s, 7/1/37 | Baa3 | 2,000,000 | 1,686,660 |

| (Holy Name Hosp.), 5s, 7/1/36 | Baa2 | 3,000,000 | 2,370,570 |

|

| NJ State Rev. Bonds (Trans. Syst.), Ser. C, | | | |

| AMBAC, zero %, 12/15/24 | AA– | 8,760,000 | 3,801,227 |

|

| NJ State Higher Ed. Assistance Auth. Rev. Bonds | | | |

| (Student Loan), Ser. A, 5 5/8s, 6/1/30 | AA | 2,250,000 | 2,252,880 |

|

| NJ State Tpk. Auth. Rev. Bonds, Ser. E, | | | |

| 5 1/4s, 1/1/40 | A+ | 3,000,000 | 2,904,660 |

|

| Tobacco Settlement Fin. Corp. Rev. Bonds | | | |

| 6 3/4s, 6/1/39 (Prerefunded 6/1/13) | Aaa | 2,000,000 | 2,257,000 |

| 6 3/8s, 6/1/32 (Prerefunded 6/1/13) | Aaa | 1,775,000 | 1,947,654 |

| 6 1/8s, 6/1/42 (Prerefunded 6/1/12) | Aaa | 1,600,000 | 1,704,912 |

|

| | | | 59,037,860 |

| New Mexico (0.7%) | | | |

| Farmington, Poll. Control Rev. Bonds | | | |

| (San Juan), Ser. B, 4 7/8s, 4/1/33 | Baa3 | 2,110,000 | 1,767,948 |

| (AZ Pub. Svc. Co.), Ser. B, 4.7s, 9/1/24 | Baa2 | 4,500,000 | 4,247,145 |

|

| U. of NM Rev. Bonds (Hosp. Mtg.), AGM, FHA Insd., | | | |

| 5s, 1/1/24 | AA+ | 2,000,000 | 2,021,280 |

|

| | | | 8,036,373 |

| New York (6.4%) | | | |

| Metro. Trans. Auth. Dedicated Tax Rev. Bonds, | | | |

| Ser. A, 5 1/2s, 11/15/39 | AA | 2,000,000 | 2,027,160 |

|

| NY City, Indl. Dev. Agcy. Rev. Bonds (Queens | | | |

| Baseball Stadium — Pilot), AMBAC, 5s, 1/1/23 | Ba1 | 300,000 | 281,688 |

|

| NY City, Indl. Dev. Agcy. Special Arpt. Fac. Rev. | | | |

| Bonds (Airis JFK I LLC), Ser. A, 6s, 7/1/27 | BBB– | 10,510,000 | 9,423,371 |

|

26

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| New York cont. | | | |

| NY City, Indl. Dev. Agcy. Special Fac. Rev. Bonds | | | |

| (British Airways PLC), 5 1/4s, 12/1/32 | BB– | $200,000 | $157,338 |

|

| NY State Dorm. Auth. Rev. Bonds | | | |

| (Construction City U. Syst.), Ser. A, 6s, 7/1/20 | Aa3 | 10,900,000 | 12,400,494 |

| (City U.), Ser. A, 5 3/4s, 7/1/18 | Aa3 | 12,485,000 | 14,275,099 |

| (Winthrop-U. Hosp. Assn.), Ser. A, 5 1/2s, 7/1/32 | Baa1 | 600,000 | 578,124 |

| (Winthrop Nassau U.), 5 1/2s, 7/1/23 | Baa1 | 750,000 | 751,028 |

| (State U. Edl. Fac.), Ser. A, 5 1/2s, 5/15/19 | Aa3 | 23,100,000 | 26,201,406 |

| (Brooklyn Law School), Ser. B, SGI, 5 3/8s, 7/1/22 | Baa1 | 1,000,000 | 1,010,300 |

|

| NY State Dorm. Auth. Personal Income Tax Rev. | | | |

| Bonds (Ed.), Ser. B, 5 3/4s, 3/15/36 | AAA | 500,000 | 536,515 |

|

| Orange Cnty., Indl. Dev. Agcy. Rev. Bonds (Arden | | | |

| Hill Care Ctr. Newburgh), Ser. C, 7s, 8/1/31 | B/P | 750,000 | 602,820 |

|

| Port Auth. NY & NJ Special Oblig. Rev. Bonds | | | |

| (Kennedy Intl. Arpt. — 5th Installment), 6 3/4s, | | | |

| 10/1/19 | BB+/P | 2,200,000 | 2,074,072 |

| (Kennedy Intl. Arpt. — 4th Installment), 6 3/4s, | | | |

| 10/1/11 | BB+/P | 75,000 | 75,239 |

|

| | | | 70,394,654 |

| North Carolina (1.5%) | | | |

| NC Eastern Muni. Pwr. Agcy. Syst. Rev. Bonds | | | |

| Ser. C, 6 3/4s, 1/1/24 | A– | 1,250,000 | 1,405,900 |

| AMBAC, 6s, 1/1/18 | Baa1 | 7,000,000 | 7,974,470 |

|

| NC Hsg. Fin. Agcy. FRB (Homeownership), Ser. 26, | | | |

| Class A, 5 1/2s, 1/1/38 | Aa2 | 605,000 | 620,912 |

|

| NC Med. Care Cmnty. Hlth. Care Fac. Rev. Bonds | | | |

| (Deerfield), Ser. A, 6s, 11/1/33 | BBB+/F | 2,345,000 | 2,170,579 |

|

| NC Med. Care Comm. Retirement Fac. Rev. Bonds | | | |

| (First Mtge.-Forest at Duke), 6 3/8s, 9/1/32 | | | |

| (Prerefunded 9/1/12) | AAA/P | 3,000,000 | 3,229,740 |

|

| NC State Muni. Pwr. Agcy. Rev. Bonds (No. 1, | | | |

| Catawba Elec.), Ser. A, 5s, 1/1/30 | A2 | 1,200,000 | 1,189,824 |

|

| | | | 16,591,425 |

| Ohio (5.7%) | | | |

| Allen Cnty., Hosp. Fac. VRDN (Catholic Hlth. Care), | | | |

| Ser. B, 0.22s, 10/1/31 | VMIG1 | 1,600,000 | 1,600,000 |

|

| American Muni. Pwr. — Ohio, Inc. Rev. Bonds | | | |

| (Prairie State Energy Campus), Ser. A, 5s, 2/15/38 | A1 | 5,000,000 | 4,677,550 |

|

| Buckeye, Tobacco Settlement Fin. Auth. Rev. Bonds, | | | |

| Ser. A-2 | | | |

| 5 3/4s, 6/1/34 | Baa3 | 27,100,000 | 18,682,740 |

| 5 1/8s, 6/1/24 | Baa3 | 4,905,000 | 3,740,063 |

|

| Hamilton Cnty., Swr. Syst. Rev. Rev. Bonds | | | |

| (Metro. Swr. Dist.), Ser. A, NATL, 5s, 12/1/28 | AA+ | 6,130,000 | 6,296,613 |

|

| Lorain Cnty., Hosp. Rev. Bonds (Catholic), | | | |

| Ser. C-2, AGM, 5s, 4/1/24 | AA+ | 5,000,000 | 5,032,400 |

|

| Midview, Local School Dist. COP (Elementary | | | |

| School Bldg. Fac.), 5 1/4s, 11/1/30 | A1 | 3,500,000 | 3,527,020 |

|

| OH Hsg. Fin. Agcy. Rev. Bonds (Single Fam. | | | |

| Mtge.), Ser. 1, 5s, 11/1/28 | Aaa | 2,000,000 | 2,140,320 |

|

27

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Ohio cont. | | | |

| OH State Higher Edl. Fac. Mandatory Put Bonds | | | |

| (7/1/15) (Kenyon College), 4.95s, 7/1/37 | A1 | $5,300,000 | $5,695,168 |

|

| OH State Higher Edl. Fac. Rev. Bonds (Case Western | | | |

| Reserve U.), 5 1/2s, 10/1/22 (Prerefunded 10/1/12) | AA– | 1,000,000 | 1,075,160 |

|

| OH State Higher Edl. Fac. Commn. Rev. Bonds | | | |

| (U. Hosp. Hlth. Syst.), Ser. 09-A, 6 3/4s, 1/15/39 | A2 | 5,000,000 | 5,153,400 |

|

| Scioto Cnty., Hosp. Rev. Bonds (Southern Med. Ctr.), | | | |

| 5 1/2s, 2/15/28 | A2 | 5,000,000 | 4,834,400 |

|

| | | | 62,454,834 |

| Oklahoma (0.9%) | | | |

| OK Hsg. Fin. Agcy. Single Fam. Rev. Bonds | | | |

| (Homeownership Loan), Ser. B, 4.2s, 9/1/25 | Aaa | 475,000 | 463,904 |

|

| OK State Tpk. Auth. VRDN | | | |

| Ser. E, 0.22s, 1/1/28 | VMIG1 | 5,600,000 | 5,600,000 |

| Ser. F, 0.22s, 1/1/28 | VMIG1 | 2,000,000 | 2,000,000 |

|

| Tulsa, Arpt. Impt. Trust Rev. Bonds, Ser. A, | | | |

| 5 3/8s, 6/1/24 | A3 | 2,200,000 | 2,218,964 |

|

| | | | 10,282,868 |

| Oregon (0.2%) | | | |

| OR Hlth. Sciences U. Rev. Bonds, Ser. A, | | | |

| 5 3/4s, 7/1/39 | A1 | 2,000,000 | 2,012,840 |

|

| OR State Hsg. & Cmnty. Svcs. Dept. Rev. Bonds | | | |

| (Single Fam. Mtge.), Ser. J, 4.7s, 7/1/30 | Aa2 | 60,000 | 60,390 |

|

| | | | 2,073,230 |

| Pennsylvania (2.6%) | | | |

| Allegheny Cnty., Hosp. Dev. Auth. Rev. Bonds | | | |

| (UPMC Hlth.), Ser. B, NATL, 6s, 7/1/24 | Aa3 | 2,210,000 | 2,404,016 |

| (Hlth. Syst.-West PA), Ser. A, 5 3/8s, 11/15/40 | BB– | 2,650,000 | 1,810,136 |

|

| Chester Cnty., Hlth. & Ed. Fac. Auth. Rev. Bonds | | | |

| (Jenners Pond, Inc.), 7 1/4s, 7/1/24 | | | |

| (Prerefunded 7/1/12) | AAA/P | 500,000 | 551,030 |

|

| Cumberland Cnty., Muni. Auth. Rev. Bonds | | | |

| (Presbyterian Homes Oblig.), Ser. A | | | |

| 5 1/4s, 1/1/19 | BBB+ | 1,465,000 | 1,455,683 |

| 5.15s, 1/1/18 | BBB+ | 665,000 | 663,078 |

|

| East Stroudsburg, Area School Dist. G.O. Bonds, | | | |

| AGM, 5s, 9/1/27 | Aa3 | 5,500,000 | 5,599,330 |

|

| Erie, Higher Ed. Bldg. Auth. Rev. Bonds | | | |

| (Mercyhurst College), 5 1/2s, 3/15/38 | BBB | 1,275,000 | 1,152,626 |

|

| Franklin Cnty., Indl. Dev. Auth. Rev. Bonds | | | |

| (Chambersburg Hosp.), 5 3/8s, 7/1/42 | A2 | 1,000,000 | 913,480 |

|

| Montgomery Cnty., Indl. Dev. Auth. Wtr. Fac. Rev. | | | |

| Bonds (Aqua PA, Inc.), Ser. A, 5 1/4s, 7/1/42 | AA– | 3,250,000 | 2,954,315 |

|

| PA Rev. Bonds (Philadelphia Biosolids Fac.), | | | |

| 6 1/4s, 1/1/32 | BBB+/F | 500,000 | 510,735 |

|

| PA Econ. Dev. Fin. Auth. Rev. Bonds (Amtrak), | | | |

| Ser. A , 6 1/4s, 11/1/31 | A1 | 1,000,000 | 1,004,040 |

|

| PA Hsg. Fin. Agcy. Rev. Bonds (Single Fam. Mtge.), | | | |

| Ser. 110B, 4 3/4s, 10/1/39 | AA+ | 2,400,000 | 2,235,360 |

|

| PA State Higher Edl. Fac. Auth. Rev. Bonds | | | |

| (Edinboro U. Foundation), 6s, 7/1/43 | Baa3 | 1,000,000 | 953,420 |

|

28

| | | |

| MUNICIPAL BONDS AND NOTES (97.8%)* cont. | Rating** | Principal amount | Value |

|

| Pennsylvania cont. | | | |

| Philadelphia, Arpt. Rev. Bonds, Ser. D, 5 1/4s, | | | |

| 6/15/25 | A+ | $2,750,000 | $2,687,933 |

|

| Philadelphia, Hosp. & Higher Ed. Fac. Auth. Rev. | | | |

| Bonds (Graduate Hlth. Syst.), 7 1/4s, 7/1/11 | | | |

| (In default) † | D/P | 5,415,577 | 542 |

|

| Pittsburgh & Allegheny Cnty., Passports & Exhib. | | | |

| Auth. Hotel Rev. Bonds, AGM, 5s, 2/1/35 | AA+ | 3,000,000 | 2,793,270 |

|

| West Shore, Area Hosp. Auth. Rev. Bonds | | | |

| (Holy Spirit Hosp.), 6 1/4s, 1/1/32 | BBB+ | 500,000 | 476,525 |

|

| | | | 28,165,519 |

| Puerto Rico (5.6%) | | | |

| Cmnwlth. of PR, G.O. Bonds | | | |

| Ser. B, 6s, 7/1/39 | A3 | 7,000,000 | 6,697,040 |

| Ser. A, 5 1/4s, 7/1/22 | A3 | 850,000 | 830,195 |

|

| Cmnwlth. of PR, Aqueduct & Swr. Auth. Rev. Bonds, | | | |

| Ser. A, 6s, 7/1/44 | Baa1 | 3,400,000 | 3,147,618 |

|

| Cmnwlth. of PR, Elec. Pwr. Auth. Rev. Bonds | | | |

| Ser. XX, 5 1/4s, 7/1/40 | A3 | 3,000,000 | 2,586,000 |

| Ser. TT, 5s, 7/1/37 | A3 | 5,000,000 | 4,192,800 |

| Ser. RR, FGIC, NATL, 5s, 7/1/23 | A3 | 4,395,000 | 4,292,465 |

|

| Cmnwlth. of PR, Govt. Dev. Bank Rev. Bonds, | | | |

| Ser. B, 5s, 12/1/13 | A3 | 250,000 | 264,235 |

|

| Cmnwlth. of PR, Hwy. & Trans. Auth. Rev. Bonds, | | | |

| Ser. K, 5s, 7/1/17 | A3 | 2,900,000 | 2,950,721 |

|

| Cmnwlth. of PR, Indl. Tourist Edl. Med. & Env. | | | |

| Control Facs. Rev. Bonds | | | |

| (Cogen. Fac.-AES), 6 5/8s, 6/1/26 | Baa3 | 250,000 | 250,458 |

| (Auxilio Mutuo Oblig. Group), Ser. A, NATL, | | | |

| 6 1/4s, 7/1/16 | A– | 3,015,000 | 3,025,040 |

|

| Cmnwlth. of PR, Muni. Fin. Agcy. G.O. Bonds, | | | |

| Ser. A, 5 1/4s, 8/1/24 | A3 | 750,000 | 723,053 |

|

| Cmnwlth. of PR, Pub. Bldg. Auth. Rev. Bonds | | | |

| (Govt. Fac.) | | | |

| Ser. M, Cmnwlth. of PR Gtd., 6 1/4s, 7/1/31 | A3 | 1,895,000 | 1,918,744 |

| Ser. P, Cmnwlth. of PR Gtd., 6 1/8s, 7/1/23 | A3 | 8,000,000 | 8,418,880 |

| Ser. I, Cmnwlth. of PR Gtd., 5s, 7/1/36 | A3 | 2,220,000 | 1,859,872 |

|