UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

| |

| (Mark One) | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 2014 |

| OR |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from to |

Commission File Number 1-8641

COEUR MINING, INC.

(Exact name of registrant as specified in its charter)

|

| |

| Delaware | 82-0109423 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

104 S. Michigan Ave. Suite 900 Chicago, IL (Address of principal executive offices) | 60603 (Zip Code) |

Registrant’s telephone number, including area code: (312) 489-5800

Securities Registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | New York Stock Exchange |

| Warrants Exercisable for Common Stock (expiring April 16, 2017) | | New York Stock Exchange/Toronto Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | |

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

$945,619,031

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

As of February 19, 2015, 103,342,296 shares of Common Stock, par value $0.01 per share

DOCUMENTS INCORPORATED BY REFERENCE

Certain information called for by Part III of the Form 10-K is incorporated by reference from the registrant’s definitive proxy statement for the 2015 Annual Meeting of Stockholders which will be filed pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this report.

COEUR MINING, INC.

FORM 10-K

INDEX

|

| | |

| PART I |

| | |

| | |

| | |

| | |

| | |

| | |

| PART II |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART III |

| | |

| | |

| | |

| | |

| | |

| PART IV |

| | |

| |

PART I

INTRODUCTION

Coeur Mining, Inc. (“Coeur”,“the Company”, or "we") is a large silver producer with significant gold production and mines located in the United States, Mexico, and Bolivia; a silver streaming interest in Australia; and exploration projects in Mexico and Argentina. The Company operates the Palmarejo mine, San Bartolomé mine, Kensington mine, and Rochester mine and also owns Coeur Capital, which is primarily comprised of the Endeavor silver stream, other precious metal royalties, and strategic investments. The Company’s principal sources of revenue are its operating mines and the Endeavor silver stream.

Coeur was incorporated as an Idaho corporation in 1928 under the name Coeur d'Alene Mines Corporation. On May 16, 2013, Coeur changed its state of incorporation from the State of Idaho to the State of Delaware and changed its name to Coeur Mining, Inc.

OVERVIEW OF MINING PROPERTIES AND INTERESTS

The Company’s operating properties and interests are described below:

| |

| • | Coeur owns 100% of Coeur Mexicana S.A. de C.V. ("Coeur Mexicana"), which has operated the underground and surface Palmarejo silver and gold complex in Mexico since 2009. Palmarejo produced 6.6 million ounces of silver and 86,673 ounces of gold in 2014. The Company controls a large land position around its existing operations. In 2009, Coeur Mexicana entered into a gold production royalty with Franco-Nevada Corporation covering 50% of the Palmarejo life of mine gold production. In 2014, Coeur Mexicana terminated the gold production royalty effective upon completion of the minimum ounce delivery requirement and subsequently entered into a gold stream agreement with a subsidiary of Franco-Nevada Corporation. In December 2014, the Company announced the acquisition of Paramount Gold and Silver Corp. ("Paramount"), which owns the San Miguel project that is adjacent to Coeur's Palmarejo mine. The transaction is expected to close in the second quarter of 2015. |

| |

| • | Coeur owns 100% of Coeur Rochester, Inc. ("Coeur Rochester"), which has operated the Rochester mine, a silver and gold surface mining operation located in northwestern Nevada, since 1986. Rochester produced 4.2 million ounces of silver and 44,888 ounces of gold in 2014. Coeur Rochester is obligated to pay a 3.4% net smelter returns ("NSR") royalty on up to 39.4 million silver equivalent ounces produced and sold from a portion of the Rochester mine effective in 2014. |

| |

| • | Coeur owns 100% of Empresa Minera Manquiri S.A. ("Manquiri"), a Bolivian company that controls the mining rights for the San Bartolomé mine, which is a surface silver mine in Bolivia where Coeur commenced commercial production in 2008. San Bartolomé produced 5.9 million ounces of silver in 2014. |

| |

| • | Coeur owns 100% of Coeur Alaska, Inc. ("Coeur Alaska"), which owns the Kensington mine, an underground gold mine located north of Juneau, Alaska. The Kensington mine began commercial production in 2010. Kensington produced 117,823 ounces of gold in 2014. |

| |

| • | Coeur owns 100% of Coeur Capital, Inc. (“Coeur Capital”), which holds the Company's streaming and royalty interests, along with its portfolio of strategic equity investments. The Endeavor silver stream, acquired in 2005 for $44.0 million, consists of all silver production and reserves (up to 20.0 million payable ounces) at the Endeavor mine in New South Wales, Australia, which is owned and operated by Cobar Operations Pty. Limited, a wholly-owned subsidiary of CBH Resources Ltd. (“CBH”). The Endeavor mine is an underground zinc, lead and silver mine, which has been in production since 1983. Endeavor produced 0.6 million ounces of silver in 2014. At December 31, 2014, the Company has received a total of 5.4 million ounces under the streaming agreement. |

Coeur Capital also holds a tiered royalty on McEwen Mining Inc.’s El Gallo/Magistral mine in Mexico, currently paying a 3.5% NSR royalty, a 1.5% NSR royalty on Dynasty Metals & Mining, Inc.’s Zaruma mine in Ecuador, a 2.0% NSR royalty on Mandalay Resources Corp.’s Cerro Bayo mine in Chile, and other non-producing royalties.

| |

| • | Another Coeur subsidiary owns an 80% interest in a 2.5% royalty on Newmont Mining Corporation's Correnso mine in New Zealand. |

| |

| • | Coeur owns 100% of the La Preciosa silver-gold exploration project in Durango state, Mexico. In 2014, the Company announced results of a feasibility study for the project and has deferred construction activities based on its disciplined capital deployment philosophy and commitment to retaining a flexible, liquid balance sheet. |

| |

| • | Coeur owns 100% of the Joaquin silver and gold exploration project located in the Santa Cruz province of southern Argentina. The Company commenced exploration of this large property located north of the Company's Martha silver mine in 2007 and has since defined silver and gold mineralization in two deposits. |

| |

| • | In January 2015, the Company announced the acquisition of the Wharf gold mine located near Lead, South Dakota. The transaction is expected to close in the first quarter of 2015. |

| |

| • | Coeur owns 100% of Coeur Argentina S.R.L., which operated the Martha mine located in Argentina through 2012. |

The Company also has interests in exploration stage properties located in the United States, Chile, Argentina, Bolivia, and Mexico with no mineable ore reserves.

SILVER AND GOLD PRICES

The Company’s operating results are substantially dependent upon the market prices of silver and gold, which can fluctuate widely. The volatility of such prices is illustrated by the following table, which sets forth the high and low prices of silver (fixing price as reported by the London Bullion Market Association) and gold (PM fixing price as reported by London Gold Market Fixing Limited) per ounce during the periods indicated:

|

| | | | | | | | | | | |

| | Year Ended December 31, |

| | 2014 | | 2013 | | 2012 |

| | High | | Low | | High | | Low | | High | | Low |

| Silver | $22.05 | | $15.28 | | $32.23 | | $18.61 | | $37.23 | | $26.67 |

| Gold | $1,385 | | $1,142 | | $1,694 | | $1,192 | | $1,792 | | $1,540 |

MARKETING

All of the Company's mining operations produce silver and gold in doré form except the Kensington mine which produces a gold concentrate. The Endeavor mine, in which Coeur Capital holds a silver stream, produces lead and zinc concentrates with a high silver content, from which the Company recovers its payable silver ounces. The Company refines its precious metals doré and concentrates using a geographically diverse group of third party refiners and smelters in the United States, Switzerland, China, and Japan.

The Company's doré is refined into gold and silver bullion according to benchmark standards set by the London Bullion Market Association, which regulates the acceptable requirements for bullion traded in the London precious metals markets. The Company then sells its silver and gold bullion to multi-national banks, bullion trading houses, and refiners across the globe. The Company has seven trading counterparties and the sales of metals to these companies amounted to approximately 63%, 72%, and 91% of total metal sales for the years ended December 31, 2014, 2013, and 2012, respectively. Generally, the loss of a single bullion trading counterparty would not adversely affect the Company due to the liquidity of the markets and the availability of alternative trading counterparties.

The Company's concentrates are sold to smelters under purchase and sale agreements, and the smelters pay the Company for the gold or silver recovered from the concentrates. The Company currently has seven trading counterparties for its concentrates, and the sales to these companies amounted to approximately 37%, 28%, and 9% of total metal sales for the years ended December 31, 2014, 2013, and 2012, respectively. While the loss of any one smelter may have a material adverse effect if alternate smelters are not available, the Company believes that there is sufficient global capacity available to address the loss of a smelter.

HEDGING ACTIVITIES

The Company’s strategy is to provide stockholders with exposure to silver and gold prices by selling silver and gold production at market prices. The Company has entered into derivative contracts to protect the selling price for certain anticipated silver and gold production and to manage risks associated with foreign currencies. For additional information see "Item 7A. Quantitative and Qualitative Disclosures About Market Risk" and Note 11 -- Derivative Financial Instruments in the notes to the consolidated financial statements.

GOVERNMENT REGULATION

General

The Company’s activities are subject to extensive federal, state and local laws governing the protection of the environment, prospecting, development, production, taxes, labor standards, occupational health, mine safety, toxic substances and other matters. The costs associated with compliance with such regulatory requirements are substantial and possible future legislation and regulations could cause additional expense, capital expenditures, restrictions and delays in the development and continued operation of the Company’s properties, the extent of which cannot be predicted. In the context of environmental permitting, including the approval of reclamation plans, the Company must comply with known standards and regulations which may entail significant costs and delays. Although the Company has been recognized for its commitment to environmental responsibility and believes it is in substantial compliance with applicable laws and regulations, amendments to current laws and regulations, more stringent

application or interpretation of these laws and regulations through judicial review or administrative action or the adoption of new laws could have a material adverse effect upon the Company and its results of operations.

Estimated future reclamation costs are based primarily on legal and regulatory requirements. At December 31, 2014, $67.2 million was accrued for reclamation costs relating to currently developed and producing properties. The Company is also involved in several matters concerning environmental obligations associated with former mining activities. Based upon the Company’s best estimate of its liabilities for these items, $3.6 million was accrued at December 31, 2014. These amounts are included in reclamation and mine closure liabilities on the consolidated balance sheet.

Federal Environmental Laws

Certain mining wastes from extraction and beneficiation of ores would be considered hazardous waste under the Resource Conservation and Recovery Act (“RCRA”) and state law equivalents, but are currently exempt from the extensive set of Environmental Protection Agency (“EPA”) regulations governing hazardous waste. If the Company’s mine wastes were treated as hazardous waste under RCRA or such wastes resulted in operations being designated as “Superfund” sites under the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) or state law equivalents for cleanup, material expenditures could be required for the construction of additional waste disposal facilities, for other remediation expenditures, or for natural resource damages. Under CERCLA, any present or past owners or operators of a Superfund site generally may be held liable and may be forced to undertake remedial cleanup action or to pay for the government’s cleanup efforts. Such owners or operators may also be liable to governmental entities for the cost of damages to natural resources, which may be substantial. Additional regulations or requirements may also be imposed upon the Company’s operations and tailings and waste disposal areas in Alaska and Nevada under the Clean Water Act (“CWA”) and state law equivalents. Air emissions are subject to the Clean Air Act and its state equivalents as well. The Company has reviewed and considered current federal legislation relating to climate change and does not believe it to have a material effect on its operations. Future changes in federal or state laws or regulations could have a material adverse effect upon the Company and its results of operations.

Proposed Mining Legislation

A portion of the Company’s U.S. mining properties are on unpatented mining claims on federal lands. Legislation has been introduced regularly in the U.S. Congress over the last decade to change the Mining Law of 1872 as amended (the "Mining Law"), under which the Company holds these unpatented mining claims. It is possible that the Mining Law may be amended or replaced by less favorable legislation in the future. Previously proposed legislation contained a production royalty obligation, new environmental standards and conditions, additional reclamation requirements and extensive new procedural steps which would likely result in delays in permitting. The ultimate content of future proposed legislation, if enacted, is uncertain. If a royalty on unpatented mining claims were imposed, the profitability of the Company’s U.S. operations could be materially adversely affected. In addition, the U.S. Forest Service and the U.S. Bureau of Land Management ("BLM") have considered revising regulations governing operations under the Mining Law on federal lands they administer, which, if implemented, may result in additional procedures and environmental conditions and standards on those lands. The majority of the Company’s operations are either outside of the United States or on private patented lands and would be unaffected by potential legislation.

Any such reform of the Mining Law or BLM and U.S. Forest Service regulations thereunder could increase the costs of mining activities on unpatented mining claims, or could materially impair the ability of the Company to develop or continue operations which derive ore from federal lands, and as a result could have an adverse effect on the Company and its results of operations. Until such time, if any, as new reform legislation or regulations are enacted, the ultimate effects and costs of compliance on the Company cannot be estimated.

Foreign Government Regulations

Bolivia, where the San Bartolomé mine is located, and Mexico, where the Palmarejo mine and the La Preciosa exploration project are located, have both adopted laws and guidelines for environmental permitting that are similar to those in effect in the United States and other South American countries. The permitting process requires a thorough study to determine the baseline condition of the mining site and surrounding area, an environmental impact analysis, and proposed mitigation measures to minimize and offset the environmental impact of mining operations. The Company has received all permits required to operate the San Bartolomé and Palmarejo mines, and has received all permits necessary for its exploration activities at the La Preciosa exploration project.

The mining properties of the Company that are located in Argentina are subject to various government laws and regulations pertaining to the protection of the air, surface and ground water, and the environment in general, as well as the health of the work force, labor standards and the socio-economic impacts of mining facilities upon the communities. The Company believes it is in substantial compliance with all applicable laws and regulations to which it is subject in Argentina.

The Company does not directly hold any interest in mining properties in Australia. However, the Company owns a silver stream on CBH's Endeavor mine. CBH is responsible for the mining operation and compliance with laws and regulations, and the Company is not responsible for compliance. The Company is, however, at risk for any production stoppages resulting from non-compliance. CBH’s mining property is subject to a range of laws and regulations pertaining to the protection of the air, surface water, ground water, noise, site rehabilitation and the environment in general, as well as the occupational health and safety of the work force, labor standards and the socio-economic impacts of mining facilities among local communities. In addition, the various federal and state native title laws and regulations recognize and protect the rights and interests in Australia of Aboriginal and Torres Strait Islander people in land and waters and may restrict mining and exploration activity and/or result in additional costs. CBH is required to deal with a number of governmental departments in connection with the development and exploitation of its mining property. The Company is not aware of any substantial non-compliance with applicable laws and regulations to which CBH is subject in Australia.

Maintenance of Claims

United States

At mining properties in the United States, including the Rochester and Kensington mines, operations are conducted upon both patented and unpatented mining claims. Pursuant to applicable federal law it is necessary to pay to the Secretary of the Interior, on or before August 31 of each year, a claim maintenance fee of $140 per claim. This claim maintenance fee is in lieu of the assessment work requirement contained in applicable mining laws. In addition, Nevada holders of unpatented mining claims are required to pay the county recorder of the county in which the claim is situated an annual fee of $8.50 per claim. For unpatented claims in Alaska, the Company is required to pay a variable, annual rental fee based on the age of the claim and must perform annual labor or make an annual payment in lieu of annual labor. No maintenance fees are payable for federal patented claims. Patented claims are similar to land held by an owner who is entitled to the entire interest in the property with unconditional power of disposition and are subject to local ad valorem property taxes.

Mexico

In order to carry out mining activities in Mexico, the Company is required to obtain a mining concession from the General Bureau of Mining, which belongs to the Ministry of Economy of the Federal Government, or be assigned previously granted concession rights, and both must be recorded with the Public Registry of Mining. In addition, mining works may have to be authorized by other authorities when performed in certain areas, including ejidos (communal owners of land recognized by the federal laws in Mexico), villages, dams, channels, general communications ways, submarine shelves of islands, islets and reefs, marine beds and subsoil and federal maritime-terrestrial zones. Reports have to be filed with the General Bureau of Mining in May of each year, evidencing previous calendar year mining investment and works. Annual reports, detailing production results, must be submitted by January 30 for each concession bearing production and all concessions over six years of age. Bi-annual mining duties are payable in January and July of each year and, beginning in 2014, holders of mining concessions must pay annually and no later than the last business day of March a special mining fee based on 7.5% of the income before interest and certain other permitted deductions derived from the transfer or sale of minerals, plus 0.5% of gross revenues from sales of gold, silver and platinum. Failure to pay any of these duties and submit the required reports could lead to cancellation of the concessions. Upon expiration or cancellation of the concession, certain obligations remain, such as filing technical reports and ground support.

Bolivia

The Bolivian state owns the resources at San Bartolomé. The Bolivian state-owned mining organization, Corporación Minera de Bolivia (“COMIBOL”), is the underlying manager of all of the mining rights relating to the San Bartolomé mine. Bolivia’s ownership derives from the Supreme Decree 3196 issued in October 1952, when the government nationalized most of the mines in Potosí. COMIBOL has leased the mining rights for the surface silver and tin bearing sediment to several Potosí cooperatives. The cooperatives have subleased their mining rights to Coeur’s subsidiary, Manquiri, through a series of “joint venture” contracts. In addition to those agreements with the cooperatives, Manquiri holds additional mining rights under lease agreements directly with COMIBOL. All of Manquiri’s mining and surface rights collectively constitute the San Bartolomé project. For additional information regarding the maintenance of its claims to the San Bartolomé mine, see "Item 2. Properties -- Silver and Gold Mining Properties, Bolivia-San Bartolomé."

Argentina

Minerals are owned by the provincial governments, which impose a maximum 3% mine-mouth royalty on mineral production. The first step in acquiring mining rights is filing an exploration permit ("Cateo"), which gives exclusive prospecting rights for the requested area for a period of time, generally up to three years. The maximum size of each Cateo is 10,000 hectares; a maximum of 20 Cateos, or 200,000 hectares, can be held by a single entity in any one province.

The holder of a Cateo has exclusive right to establish a discovery concession ("Manifestacion de Descubrimiento" or “MD”) on that Cateo, but MDs can also be set without a Cateo on any land not covered by another party's Cateo. MDs are filed

as either a vein or disseminated discovery. A square protection zone can be declared around the discovery of up to 840 hectares for a vein MD, or up to 7,000 hectares for a disseminated MD. The protection zone grants the discoverer exclusive rights for an indefinite period, during which the discoverer must provide an annual report presenting a program of exploration work and investments related to the protection zone. An MD can be upgraded to an exploitation concession ("Concesion de Explotacion or "Mina"), which gives the holder the right to begin commercial extraction of minerals.

Australia

At the Endeavor mining property in Australia operated by CBH, operations are conducted on designated mining leases issued by the relevant state government mining department. Mining leases are issued for a specific term and include a range of environmental and other conditions including the payment of production royalties, annual lease fees and the use of cash or a bank guarantee as security for reclamation liabilities. The amounts required to be paid to secure reclamation liabilities are determined on a case by case basis. In addition, according to public sources, CBH holds a range of exploration titles and permits, which are also issued by the respective state government mining departments for specified terms and require payment of annual fees and completion of designated expenditure programs to maintain title. In Australia, minerals in the ground are owned by the state until severed from the ground through mining operations.

EMPLOYEES

The number of full-time employees of the Company at December 31, 2014 was:

|

| | |

| U.S. Corporate and Other | 69 |

|

| Rochester Mine | 295 |

|

| Kensington Mine | 322 |

|

San Bartolomé Mine(1) | 361 |

|

| Palmarejo Mine | 821 |

|

| Total | 1,868 |

|

| |

| (1) | The Company maintains a labor agreement in South America with Sindicato de Trabajadorés Mineras de la Empresa Manquiri S.A. at the San Bartolomé mine in Bolivia. The San Bartolomé mine labor agreement is in effect for 2015. At December 31, 2014, approximately 12% of the Company’s global labor force was covered by collective bargaining agreements. |

BUSINESS STRATEGY AND COMPETITIVE STRENGTHS

Management believes the following strengths provide the Company with significant competitive advantages:

Strong track record of developing and operating mines

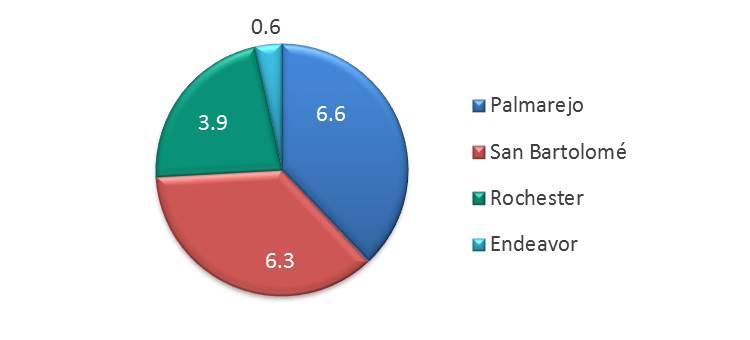

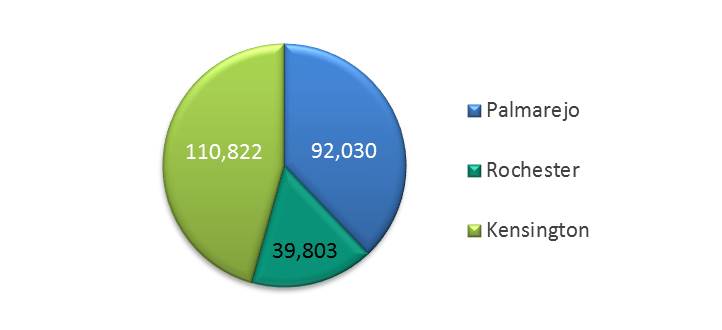

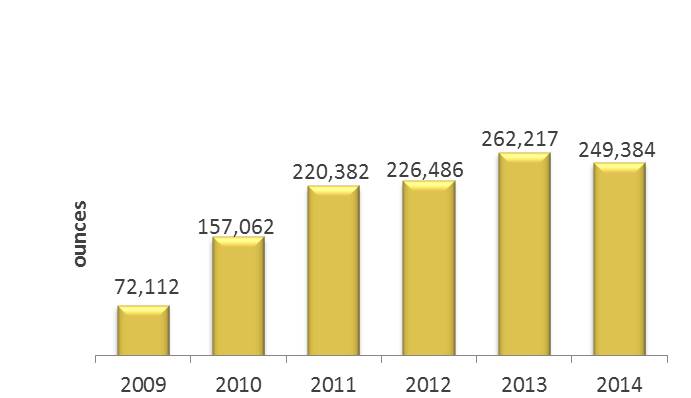

The Company has successfully acquired, developed, and operated a portfolio of operating mines since its founding in 1928. In 2014, it produced 17.2 million ounces of silver and 249,384 ounces of gold at costs applicable to sales of $14.71 per silver equivalent ounce at its primary silver mines and $951 per ounce of gold at its Kensington mine.

Silver Production Gold Production

Operating and commodity diversity

The Company's silver and gold production comes from five operating mines located in four countries. The Company operates the Palmarejo silver and gold mine in Mexico, the San Bartolomé silver mine in Bolivia, the Kensington gold mine in Alaska, and the Rochester silver and gold mine in Nevada. In addition, the Company owns a silver stream on the Endeavor mine in Australia. The Company also owns the La Preciosa and Joaquin silver and gold exploration projects in Mexico and Argentina, respectively. In December 2014, the Company announced the acquisition of Paramount, which owns the San Miguel project that is adjacent to Coeur's Palmarejo mine. The transaction is expected to close in the second quarter of 2015. In January 2015, the

Company announced the acquisition of the Wharf gold mine located near Lead, South Dakota. The transaction is expected to close in the first quarter of 2015. The Company's metal sales breakdown by operating mine and metal is set out below:

2014 Silver Sales by Mine (millions of ounces) 2014 Gold Sales by Mine (ounces)

Experienced management team

The Company has built a high-caliber management team of devoted professionals with extensive mining industry expertise. President and Chief Executive Officer, Mitchell Krebs, Senior Vice President and Chief Financial Officer, Peter Mitchell, and Senior Vice President and Chief Operating Officer, Frank Hanagarne, each has significant experience in the mining industry. The board of directors also brings diverse industry backgrounds and a depth of professional experience to the Company.

Capitalizing on prior development program

The Company has spent significant capital in commissioning or expanding its four operating mines. The following table provides the percentage contribution to the Company’s total revenues by mine during the past five years, excluding discontinued operations:

|

| | | | | | | | | | | | | | | | | |

| | | Coeur Percentage Ownership at December 31, | | Percentage of Total Revenues For The Year Ended December 31, |

| Mine/Location | | 2014 | | 2014 | | 2013 | | 2012 | | 2011 | | 2010 |

| Palmarejo Mine, Mexico | | 100% | | 38 | % | | 43 | % | | 49 | % | | 50 | % | | 45 | % |

| San Bartolomé Mine, Bolivia | | 100% | | 19 |

| | 19 |

| | 20 |

| | 26 |

| | 28 |

|

| Kensington Mine, United States | | 100% | | 22 |

| | 20 |

| | 12 |

| | 15 |

| | 4 |

|

| Rochester Mine, United States | | 100% | | 20 |

| | 16 |

| | 15 |

| | 6 |

| | 11 |

|

| Martha Mine, Argentina | | 100% | | — |

| | — |

| | 2 |

| | 1 |

| | 10 |

|

Coeur Capital(1) | | 100% | | 1 |

| | 2 |

| | 2 |

| | 2 |

| | 2 |

|

| | | | | 100 | % | | 100 | % | | 100 | % | | 100 | % | | 100 | % |

| |

| (1) | Primarily revenue from the Endeavor silver stream (Australia). |

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This report contains numerous forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) relating to the Company’s gold and silver mining business, including statements regarding potential acquisitions, mineral reserve and mineralized material estimates, exploration and development efforts, estimated production, costs, capital expenditures, expenses, metals prices, sufficiency of assets, ability to discharge liabilities, and initiatives to maximize net cash flow, enhance revenues, reduce operating and non-operating costs, future economic benefits generated by assets relative to current valuations (see p. 37 impairment discussion), manage working capital efficiently, liquidity management, financing needs, and environmental compliance expenditures. Such forward-looking statements are identified by the use of words such as “believes,” “intends,” “expects,” “hopes,” “may,” “should,” “plan,” “projected,” “contemplates,” “anticipates” or similar words. Actual results could differ materially from those projected in the forward-looking statements. The factors that could cause actual results to differ materially from those projected in the forward-looking statements include (i) the risk factors set forth below under Item 1A and in Management’s Discussion and Analysis of Financial Condition and Results of Operations under Item 7, (ii) the risk that regulatory and other approvals for pending acquisition transactions are not obtained on the proposed terms and on schedule and the risk that pending acquisition transactions will not be consummated, (iii) the risks and hazards inherent in the mining business (including risks inherent in developing large-scale mining projects, environmental hazards, industrial accidents, weather or geologically related conditions), (iv) changes in the market prices of gold and silver and a sustained lower price environment, (v) the uncertainties inherent in the Company’s production, exploratory and developmental activities, including risks relating to permitting and regulatory delays, ground conditions and grade variability, (vi) any future labor disputes or work stoppages (involving the Company and its subsidiaries or third parties), (vii) the uncertainties inherent in the estimation of gold and silver

reserves and mineralized material, (viii) changes that could result from the Company’s future acquisition of new mining properties or businesses, (ix) reliance on third parties to operate certain mines where the Company owns silver production and reserves, (x) the absence of control over mining operations in which the Company or any of its subsidiaries holds royalty or streaming interests and risks related to these mining operations (including results of mining and exploration activities, environmental, economic and political risks, and changes in mine plans and project parameters); (xi) the loss of access to any third-party smelter to which the Company markets silver and gold, (xii) the effects of environmental and other governmental regulations, (xiii) the risks inherent in the ownership or operation of or investment in mining properties or businesses in foreign countries, and (xiv) the Company’s ability to raise additional financing necessary to conduct its business, make payments or refinance its debt. Readers are cautioned not to put undue reliance on forward-looking statements. The Company disclaims any intent or obligation to update publicly these forward-looking statements, whether as a result of new information, future events or otherwise.

CAUTIONARY NOTE REGARDING DISCLOSURE OF MINERAL PROPERTIES

Reserves, Resources and Mineralized Material

Coeur Mining, Inc. is subject to the reporting requirements of the Exchange Act and applicable Canadian securities laws, and as a result we report our mineral reserves according to two different standards. Canadian reporting requirements for disclosure of mineral properties are governed by National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”). The definitions of NI 43-101 are adopted from those given by the Canadian Institute of Mining, Metallurgy and Petroleum. U.S. reporting requirements, however, are governed by Securities and Exchange Commission ("SEC") Industry Guide 7 (“Guide 7”). Both sets of reporting standards have similar goals in terms of conveying an appropriate level of confidence in the disclosures being reported, but embody different approaches and definitions. Under Guide 7, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made.

In our public filings in Canada and in certain other announcements not filed with the SEC, we disclose measured, indicated and inferred resources, each as defined in NI 43-101, in addition to our mineral reserves. U.S. investors are cautioned that, while the terms “measured mineral resources,” “indicated mineral resources” and “inferred mineral resources” are recognized and required by Canadian securities laws, Guide 7 does not recognize them. The estimation of measured resources and indicated resources involve greater uncertainty as to their existence and economic feasibility than the estimation of proven and probable reserves, and therefore U.S. investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into Guide 7 compliant reserves. The estimation of inferred resources involves far greater uncertainty as to their existence and economic viability than the estimation of other categories of resources, and therefore it cannot be assumed that all or any part of inferred resources will ever be upgraded to a higher category. Therefore, investors are cautioned not to assume that all or any part of inferred resources exist, or that they can be mined legally or economically.

In this Annual Report on Form 10-K and in our other filings with the SEC, we modify our estimates made in compliance with NI 43-101 to conform to Guide 7 for reporting in the United States. In this Form 10-K, we use the term “mineralized material” to describe mineralization in mineral deposits that do not constitute “reserves” under U.S. standards. “Mineralized material” is substantially equivalent to measured and indicated mineral resources (exclusive of reserves) as disclosed for reporting purposes in Canada, except that the SEC only permits issuers to report "mineralized material" in tonnage and average grade without reference to contained ounces. We provide disclosure of mineralized material to allow a means of comparing our projects to those of other companies in the mining industry, many of which are Canadian and report pursuant to NI 43-101, and to comply with applicable disclosure requirements. We caution you not to assume that all or any part of mineralized material will ever be converted into Guide 7 compliant reserves.

Technical Reports and Qualified Persons

As required by Canadian securities laws, we hereby notify Canadian investors that the scientific and technical information concerning our mineral projects in this Form 10-K have been reviewed and approved by a “qualified person” under NI 43-101, namely our Vice President, Technical Services, W. David Tyler. For a description of the key assumptions, parameters and methods used to estimate mineral reserves included in this Form 10-K, as well as data verification procedures and a general discussion of the extent to which the estimates may be affected by any known environmental, permitting, legal, title, taxation, socio-political, marketing or other relevant factors, Canadian investors may view technical reports prepared for each of our properties as filed on SEDAR at http://www.sedar.com. Neither the technical reports nor the statements of any qualified person filed with the Canadian securities regulatory authorities are included in, or incorporated by reference in, this Form 10-K. Because the definitions and standards of NI 43-101 differ from those of Guide 7, investors are cautioned that information contained in reports prepared pursuant to NI 43-101, like the technical reports, may not be comparable to similar information that we can disclose in this Form 10-K or the other reports we file with the SEC.

AVAILABLE INFORMATION

Coeur makes available, free of charge, on its website (http://www.coeur.com), its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and Proxy Statements, as well as Forms 3, 4 and 5 with respect to its common stock, as soon as reasonably practicable after such reports are electronically filed with the SEC. Copies of Coeur’s Corporate Governance Guidelines, charters of the key committees of the Board of Directors (Audit, Compensation, Nominating and Corporate Governance, and Environmental, Health, Safety, and Social Responsibility Committees) and its Code of Business Conduct and Ethics, applicable to the Chief Executive Officer, Chief Financial Officer and Chief Accounting Officer, among others, are available at the Company’s website. Information contained on the Company’s website is not a part of this report.

The Company's results of operations, cash flows and operating costs are highly dependent upon the market prices of silver and gold and other commodities, which are volatile and beyond the Company's control. The Company's use of derivative contracts to protect against such volatility exposes us to risk of opportunity loss, mark-to-market accounting adjustments and exposure to counterparty credit risk.

Silver and gold are exchange-traded commodities, and their prices are volatile. During the twelve months ended December 31, 2014, the price of silver ranged from a low of $15.28 per ounce to a high of $22.05 per ounce, and the price of gold ranged from a low of $1,142 per ounce to a high of $1,385 per ounce. The closing market prices of silver and gold on February 19, 2015 were $16.73 per ounce and $1,208 per ounce, respectively.

Silver and gold prices are affected by many factors beyond the Company’s control, including U.S. dollar strength or weakness, prevailing interest rates and returns on other asset classes, expectations regarding inflation, speculation, global currency values, governmental decisions regarding the disposal of precious metals stockpiles, global and regional demand and production, political and economic conditions and other factors. In addition, Exchange Traded Funds (“ETFs”), which have substantially facilitated the ability of large and small investors to buy and sell precious metals, have become significant holders of gold and silver. Factors that are generally understood to contribute to a decline in the prices of silver and gold include a strengthening of the U.S. dollar, net outflows from gold and silver ETFs, bullion sales by private and government holders and global economic conditions and/or fiscal policies that negatively impact large consumer markets.

Because the Company derives all of its revenues from sales of silver and gold, its results of operations and cash flows will fluctuate as the prices of these metals increase or decrease. A period of significant and sustained lower gold and silver prices would materially and adversely affect the results of operations and cash flows. Additionally, if market prices for silver and gold decline or remain at relatively low levels for a sustained period of time, the Company may have to revise its operating plans, including reducing operating costs and capital expenditures, terminating or suspending mining operations at one or more of its properties and discontinuing certain exploration and development plans. The Company may be unable to decrease its costs in an amount sufficient to offset reductions in revenues, and may incur losses.

Operating costs at the Company’s mines are also affected by the price of input commodities, such as fuel, electricity, labor, chemical reagents, explosives, steel and concrete. Prices for these input commodities are volatile and can fluctuate due to conditions that are difficult to predict, including global competition for resources, currency fluctuations, consumer or industrial demand and other factors. Continued volatility in the prices of commodities and other supplies the Company purchases could lead to higher costs, which would adversely affect results of operations and cash flows.

The significant and sustained decline in gold and silver prices during 2013 and 2014 caused the Company to write down certain of its long-lived assets and, in the future, such declines could cause one or more of the Company’s mining properties to become less profitable, which could require the Company to record additional write-downs of long-lived assets. Such write-downs may adversely affect the Company’s results of operations and financial condition.

The Company reviews its long-lived assets for recoverability pursuant to the Financial Accounting Standard Board’s Accounting Standards Codification Section 360 (“ASC 360”). Under that standard, the Company reviews the recoverability of its long-lived assets, such as its mining properties, upon a triggering event. Such review involves the Company estimating the future undiscounted cash flows expected to result from the use and eventual disposition of the asset. Impairment, measured by comparing an asset’s carrying value to its fair value, must be recognized when the carrying value of the asset exceeds these cash flows. The Company conducts a review of the financial performance of its mines in connection with the preparation of its financial statements for each reported period and determines whether any triggering events are indicated.

The Company’s assessment of the recoverability of its long-lived assets at December 31, 2014 and 2013 under ASC 360 indicated that write-downs of its long-lived assets of $1,472.7 million and $773.0 million, respectively, were required. These non-cash impairment charges resulted in write-downs in the Company's Statement of Comprehensive Income (Loss) and reduced the carrying value of Mining properties and Property, plant, and equipment on the Company’s balance sheet at December 31, 2014 and 2013. See Note 4 -- Write-Downs in the notes to the Consolidated Financial Statements for further detail.

If there are further significant and sustained declines in silver and gold prices or if the currently low silver or gold prices remain at such prices, or if the Company fails to control production and operating costs or realize the mineable ore reserves at its mining properties, the Company may terminate or suspend mining operations at one or more of its properties. These events could require a further write-down of the carrying value of the Company’s assets. Any such actions would adversely affect the Company’s results of operations and financial condition.

The Company may record other types of additional mining property charges in the future if it sells a property for a price less than its carrying value or has to increase reclamation liabilities in connection with the closure and reclamation of a property. Any additional write-downs of mining properties could adversely affect the Company’s results of operations and financial condition.

The Company’s future growth will depend upon its ability to develop new mines, either through exploration at existing properties or by acquisition from other mining companies.

Because mines have limited lives based on proven and probable ore reserves, an important element of the Company’s business strategy is the opportunistic acquisition of silver and gold mines, properties and businesses or interests therein. The Company’s ability to achieve significant additional growth in revenues and cash flows will depend upon success in further developing existing properties and developing or acquiring new mining properties. During 2011, the Company successfully constructed a new leach pad at the Company’s Rochester mine. Development of other major mining properties at Palmarejo, San Bartolomé and Kensington has been substantially completed. Since December 2012, the Company has owned 100% of the Joaquin silver-gold exploration project located in the Santa Cruz province of southern Argentina. As a result of its acquisition of Orko (now Coeur La Preciosa Silver Corp.) in April 2013, the Company also holds the La Preciosa silver-gold exploration project in the state of Durango, Mexico. In addition, the Company announced in December 2014 the acquisition of Paramount and in January 2015 the acquisition of the Wharf gold mine, both of which are expected to close in the first half of 2015. These strategies are inherently risky, and the Company cannot assure that it will be able to successfully develop existing or new mining properties or acquire additional mining properties on favorable economic terms or at all.

The Company may be unable to complete and successfully integrate an announced acquisition, including the recently announced Paramount and Wharf gold mine acquisitions.

The Company expects to continue to evaluate acquisition opportunities and pursue those opportunities it believes are in the Company’s long-term best interests. There can be no assurance that the anticipated benefits of any such acquisition will be realized. The success of any acquisition will depend upon the Company’s ability to effectively manage the integration and operations of entities or properties it acquires and to realize other anticipated benefits. The process of managing acquired businesses may involve unforeseen difficulties and may require a disproportionate amount of management resources, which may divert management’s focus and resources from other strategic opportunities and from operational matters during this process.

Any acquisition would be accompanied by risks, including:

| |

| • | a significant change in commodity prices after the Company has committed to complete the transaction and established the purchase price or exchange ratio; |

| |

| • | a material orebody may prove to be below expectations; |

| |

| • | difficulties integrating and assimilating the operations and personnel of any acquired companies, realizing anticipated synergies and maximizing the financial and strategic position of the combined enterprise, and maintaining uniform standards, policies and controls across the organization; and |

| |

| • | the acquired business or assets may have unknown liabilities which may be significant. |

In addition, in connection with an acquisition, the Company may incur indebtedness or issue equity securities or securities convertible into equity securities, resulting in increased interest expense, or dilution of the percentage ownership of existing stockholders. The Company cannot predict the impact of future acquisitions on the price of its common stock, or assure that it would be able to obtain any necessary financing on acceptable terms. Unprofitable acquisitions, or additional indebtedness or issuances of securities in connection with such acquisitions, may negatively affect results of operations.

The completion of the previously announced Paramount and Wharf gold mine acquisitions are subject to us obtaining all required third party regulatory and governmental approvals and the satisfaction or waiver of all other conditions to completion of the acquisitions, and, in the case of the Paramount acquisition, obtaining approval of the Company’s stockholders. There can be no assurance that the Company or the acquisition counterparty will be able to satisfy these conditions on a timely basis or at all. In addition, the Company’s systems, procedures and controls may be inadequate to support the expansion of our operations resulting from these acquisitions. The Company’s future operating results could be affected by the ability of its officers and key employees to manage the changing business conditions and to integrate the Paramount assets and the Wharf gold mine operation into Coeur. There may also be liabilities, such as environmental liabilities, or significant capital expenditures that the Company failed to discover or have underestimated in connection with these announced acquisitions. Any such liabilities or capital expenditure requirements could have a material adverse effect on the Company’s business, financial condition or future prospects.

The Company’s use of derivative contracts to protect against market price volatility exposes it to risk of opportunity loss, mark-to-market fair value adjustments and exposure to counterparty credit risk.

From time to time, the Company may enter into price risk management contracts to protect against fluctuations in the price of gold and silver and changes in the prices of fuel and other input costs. These contracts could include forward sales or purchase contracts, futures contracts, purchased or sold put and call options and other derivative instruments.

Any use of forward or futures contracts can expose the Company to risk of an opportunity loss. The use of derivative contracts may also result in significant mark-to-market fair value adjustments, which may have a material adverse impact on reported financial results. The Company is exposed to credit risk with contract counterparties, including, but not limited to, sales contracts and derivative contracts. In the event of nonperformance in connection with a contract, the Company could be exposed to a loss of value for that contract.

The Company is an international company and is exposed to political and social risks in the countries in which it has significant operations or interests.

A majority of the Company’s revenues are generated by operations outside the United States, and it is subject to significant risks inherent in mineral extraction by foreign companies and contracts with government owned entities. Exploration, development, production and closure activities in many countries are potentially subject to heightened political and social risks that are beyond the Company’s control. These risks include the possible unilateral cancellation or forced renegotiation of contracts, unfavorable changes in foreign laws and regulations, royalty and tax increases, claims by governmental entities or indigenous communities, expropriation or nationalization of property and other risks arising out of foreign sovereignty over areas in which operations are conducted. The right to export silver and gold may depend on obtaining certain licenses and quotas, which could be delayed or denied at the discretion of the relevant regulatory authorities. In addition, the Company’s rights under local law may be less secure in countries where judicial systems are susceptible to manipulation and intimidation by government agencies, non-governmental organizations or civic groups.

Any of these developments could require the Company to curtail or terminate operations at its mines, incur significant costs to meet newly-imposed environmental or other standards, pay greater royalties or higher prices for labor or services and recognize higher taxes, which could materially and adversely affect financial condition, results of operations and cash flows.

These risks may be higher in developing countries in which the Company may expand its exploration for and development of mineral deposits. Potential operations in these areas increase the Company’s exposure to risks of war, local economic conditions, political disruption, civil disturbance and governmental policies that may disrupt its operations.

The Company’s ongoing and future success depends on developing and maintaining productive relationships with the communities, including indigenous peoples, and other stakeholders in its operating locations. The Company believes its operations can provide valuable benefits to surrounding communities, in terms of direct employment, training and skills development and other benefits associated with ongoing payment of taxes. In addition, the Company seeks to maintain its partnerships and relationships with local communities and stakeholders in a variety of ways, including in-kind contributions, volunteer time, sponsorships and donations. Notwithstanding the Company’s ongoing efforts, local communities and stakeholders can become dissatisfied with its activities, which may result in civil unrest, protests, direct action or campaigns against it. Any such occurrences could materially and adversely affect the Company’s financial condition, results of operations and cash flows.

The Company’s operations outside the United States also expose it to economic and operational risks.

The Company’s operations outside the United States also expose it to economic and operational risks. Local economic conditions can cause shortages of skilled workers and supplies, increase costs and adversely affect the security of operations. In addition, higher incidences of criminal activity and violence in the area of some of the Company’s foreign operations, including drug-cartel related violence in Mexico, could adversely affect the Company’s ability to operate in an optimal fashion and may impose greater risks of theft and greater risks as to personnel and property security. These conditions could lead to lower productivity and higher costs, which would adversely affect results of operations and cash flows. The Company sells gold and silver doré in U.S. dollars, but it conducts operations outside the United States in local currency. Currency exchange movements could also adversely affect results of operations.

Silver and gold mining involves significant production and operational risks.

Silver and gold mining involves significant production and operational risks, including those related to uncertain mineral exploration success, unexpected geological or mining conditions, the difficulty of development of new deposits, unfavorable climate conditions, equipment or service failures, current unavailability of or delays in installing and commissioning plants and equipment, import or customs delays and other general operating risks.

Commencement of mining can reveal mineralization or geologic formations, including higher than expected content of other minerals that can be difficult to separate from silver, which can result in unexpectedly low recovery rates. Problems also may arise due to the quality or failure of locally obtained equipment or interruptions to services (such as power, water, fuel or transport or processing capacity) or technical support, which could result in the failure to achieve expected target dates for exploration, or could cause production activities to require greater capital expenditure to achieve expected recoveries. Many of these production and operational risks are beyond the Company’s control. Delays in commencing successful mining activities at new or expanded mines, disruptions in production and low recovery rates could have adverse effects on the Company’s financial condition, results of operations and cash flows.

The estimation of ore reserves is imprecise and depends upon subjective factors. Estimated ore reserves may not be realized in actual production. The Company’s results of operations and financial position may be adversely affected by inaccurate estimates.

The ore reserve figures presented in the Company’s public filings are estimates made by the Company’s technical personnel and independent mining consultants with whom the Company contracts. Reserve estimates are a function of geological and engineering analyses that require the Company to make assumptions about production costs, recoveries and silver and gold market prices. Reserve estimation is an imprecise and subjective process. The accuracy of such estimates is a function of the quality of available data and of engineering and geological interpretation, judgment and experience. Assumptions about silver and gold market prices are subject to great uncertainty as those prices have fluctuated widely in the past. Declines in the market prices of silver or gold may render reserves containing relatively lower grades of ore uneconomic to exploit, and the Company may be required to reduce reserve estimates, discontinue development or mining at one or more of its properties or write down assets as impaired. Should the Company encounter mineralization or geologic formations at any of its mines or projects different from those predicted, it may adjust its reserve estimates and alter its mining plans. Either of these alternatives may adversely affect actual production and financial condition, results of operations and cash flows.

The Company’s estimates of future production, costs, and financial results are imprecise, depend upon subjective factors and may not be realized in actual production and such estimates speak only as of their respective dates.

The Company has in the past, and may in the future, provide estimates and projections of its future production, costs and financial results. Any such information is forward-looking. Such estimates are made by the Company’s management and technical personnel and depend on numerous assumptions, including assumptions about the availability, accessibility, sufficiency and quality of ore, the Company’s costs of production, the market prices of silver and gold, the Company’s ability to sustain and increase production levels, the sufficiency of its infrastructure, the performance of its personnel and equipment, its ability to maintain and obtain mining interests and permits and its compliance with existing and future laws and regulations. Actual results and experience may differ materially from these assumptions. Any such production, cost, or financial results estimates speak only as of the date on which they are made, and the Company disclaims any intent or obligation to update such estimates, whether as a result of new information, future events or otherwise.

Forward sales and royalty arrangements can result in limiting the Company’s ability to take advantage of increased metal prices while increasing its exposure to lower metal prices.

The Company has in the past entered into, and may in the future enter into, arrangements under which it has agreed to make royalty or similar payments to lenders or other third parties in amounts that are based on expected production and price levels for gold or silver. The Company enters into such arrangements when it concludes that they provide it with necessary capital to develop a specific mining property on favorable terms or to achieve other business objectives. Royalty or similar payment obligations, however, can limit the Company’s ability to realize the full effects of rising gold or silver prices and require the Company to make potentially significant cash payments if the mine fails to achieve specified minimum production levels.

The Company’s future operating performance may not generate cash flows sufficient to meet debt payment obligations.

As of December 31, 2014, the Company had approximately $478.4 million of outstanding indebtedness. In addition, the Company's total debt excludes $34.0 million for future minimum estimated gold production royalty payments due from Coeur Mexicana to Franco-Nevada. The liabilities associated with these gold production royalty payments increase as the price of gold increases. The Company’s ability to make scheduled debt payments on outstanding indebtedness will depend on future results of operations and cash flows. The Company’s results of operations and cash flows, in part, are subject to economic factors beyond its control, including the market prices of silver and gold. The Company may not be able to generate enough cash flow to meet obligations and commitments. If the Company cannot generate sufficient cash flow from operations to service debt, it may need to further refinance debt, dispose of assets or issue equity to obtain the necessary funds.

The Company cannot predict whether it would be able to refinance debt, issue equity or dispose of assets to raise funds on a timely basis or on satisfactory terms.

The Company might be unable to raise additional financing necessary to meet capital needs, conduct business, make payments when due or refinance debt.

The Company might need to raise additional funds in order to meet capital needs, implement its business plan, refinance debt or acquire complementary assets. Any required additional financing might not be available on commercially reasonable terms, or at all. If the Company raises additional funds by issuing equity securities or securities convertible into equity securities, holders of its common stock could experience significant dilution of their ownership interest, and these securities could have rights senior to those of the holders of common stock.

Any downgrade in the credit ratings assigned to the Company’s debt securities could increase future borrowing costs and adversely affect the availability of new financing.

There can be no assurance that any rating currently assigned by Standard & Poor’s Rating Services or Moody’s Investors Service to the Company will remain unchanged for any given period of time or that a rating will not be lowered if, in that rating agency’s judgment, future circumstances relating to the basis of the rating so warrant. If the Company is unable to maintain its outstanding debt and financial ratios at levels acceptable to the credit rating agencies, or should the Company’s business prospects or financial results deteriorate, our ratings could be downgraded by the rating agencies. A downgrade by the rating agencies could adversely affect the value of the Company’s outstanding debt securities, its existing debt and its ability to obtain new financing on favorable terms, if at all, and increase borrowing costs, which in turn could impair the Company’s results of operations and financial position.

The Company’s ability to recognize the benefits of deferred tax assets is dependent on future taxable income.

The Company recognizes the expected future tax benefit from deferred tax assets when the tax benefit is considered to be more likely than not of being realized, otherwise, a valuation allowance is applied against deferred tax assets. Assessing the recoverability of deferred tax assets requires management to make significant estimates related to expectations of future taxable income and the application of existing tax laws in each jurisdiction. To the extent that taxable income differs significantly from estimates, the Company’s ability to realize the deferred tax assets could be impacted. Additionally, future changes in tax laws could limit the Company’s ability to obtain the future tax benefits represented by our deferred tax assets. At December 31, 2014, the Company’s current and long-term deferred tax assets were $7.4 million and $60.2 million, respectively.

The Company’s business is subject to U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery laws, a breach or violation of which could lead to civil and criminal fines and penalties, loss of licenses or permits and reputational harm.

The Company operates in certain jurisdictions that have experienced governmental and private sector corruption to some degree. For example, the U.S. Foreign Corrupt Practices Act and anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments for the purpose of obtaining or retaining business or other commercial advantage. The Company’s Code of Business Ethics and Conduct and other corporate policies mandate compliance with these anti-bribery laws, which often carry substantial penalties. There can be no assurance that the Company’s internal control policies and procedures always will protect it from recklessness, fraudulent behavior, dishonesty or other inappropriate acts committed by the Company’s affiliates, employees or agents. As such, the Company’s corporate policies and processes may not prevent all potential breaches of law or other governance practices. Violations of these laws, or allegations of such violations, could lead to civil and criminal fines and penalties, litigation, and loss of operating licenses or permits, and may damage the Company’s reputation, which could have a material adverse effect on the Company’s business, financial position and results of operations.

Significant investment risks and operational costs are associated with exploration, development and mining activities. These risks and costs may result in lower economic returns and may adversely affect the Company’s business.

The Company’s ability to sustain or increase its present production levels depends in part on successful exploration and development of new ore bodies and expansion of existing mining operations. Substantial expenditures are required to establish ore reserves, to extract metals from ores and, in the case of new properties, to construct mining and processing facilities.

Mineral exploration, particularly for silver and gold, involves many risks and is frequently unproductive. Even if mineral deposits are found, those deposits may be insufficient in quantity and quality to return a profit from production, or it may take a number of years until production is possible, during which time the economic viability of the project may change. Few properties that are explored are ultimately developed into producing mines. The commercial viability of a mineral deposit, once developed, depends on a number of factors, including: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; government regulations including taxes, royalties and land tenure; land use; importing and exporting of minerals; environmental protection; mineral prices; completion of favorable feasibility studies; issuance and maintenance of necessary permits; and receipt of adequate financing. Factors that affect adequacy of infrastructure include: reliability of roads, bridges, power sources and water supply; unusual or infrequent weather phenomena; sabotage; and government or other interference in the maintenance or provision of such infrastructure. All of these factors are highly cyclical. The exact effect of these factors cannot be accurately predicted, but the combination may result in not receiving an adequate return on invested capital.

In addition, exploration projects may have no operating history upon which to base estimates of future operating costs and capital requirements. Exploration project items such as estimates of reserves, metal recoveries and cash operating costs are to a large extent based upon the interpretation of geologic data, obtained from a limited number of drill holes and other sampling techniques, and feasibility studies. Estimates of cash operating costs are then derived based upon anticipated tonnage and grades of ore to be mined and processed, the configuration of the ore body, expected recovery rates of metals from the ore, comparable facility and equipment costs, anticipated climate conditions and other factors. As a result, actual operating costs and economic returns of any and all exploration projects may materially differ from the costs and returns estimated, and accordingly, the Company’s financial condition, results of operations and cash flows may be negatively affected.

A significant delay or disruption in sales of concentrates as a result of the unexpected discontinuation of purchases by smelter customers could have a material adverse effect on results of operations.

The Company currently markets gold concentrates to third-party smelters in China and Japan. The loss of any one smelter could have a material adverse effect on the Company if alternative smelters were unavailable. The Company cannot ensure that alternative smelters would be available if the need for them were to arise or that it would not experience delays or disruptions in sales that would materially and adversely affect results of operations.

There are significant hazards associated with mining activities, some of which may not be fully covered by insurance.

The mining business is subject to risks and hazards, including environmental hazards, industrial accidents, the encountering of unusual or unexpected geological formations, cave-ins, flooding, earthquakes and periodic interruptions due to inclement or hazardous weather conditions. These occurrences could result in damage to, or destruction of, mineral properties or production facilities, personal injury or death, environmental damage, reduced production and delays in mining, asset write-downs, monetary losses and possible legal liability.

Insurance fully covering many environmental risks, including potential liability for pollution or other hazards as a result of disposal of waste products occurring from exploration and production, is not generally available. Any liabilities that the Company incurs for these risks and hazards could be significant and could adversely affect results of operations, cash flows and financial condition.

The Company is subject to significant governmental regulations, including the Federal Mine Safety and Health Act, and related costs and delays may negatively affect its business.

Mining activities are subject to extensive federal, state, local and foreign laws and regulations governing environmental protection, natural resources, prospecting, development, production, post-closure reclamation, taxes, labor standards and occupational health and safety laws and regulations, including mine safety, toxic substances and other matters. The costs associated with compliance with such laws and regulations are substantial. Possible future laws and regulations, or more restrictive interpretations of current laws and regulations by governmental authorities, could cause additional expense, capital expenditures, restrictions on or suspensions of operations and delays in the development of new properties.

U.S. surface and underground mines like the Kensington and Rochester mines are continuously inspected by the U.S. Mine Safety and Health Administration (“MSHA”), which inspections often lead to notices of violation. Recently, the MSHA has been conducting more frequent and more comprehensive inspections of mining operations in general.

Failure to comply with applicable laws, regulations and permitting requirements may result in enforcement actions, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, which may require corrective measures including capital expenditures, installation of additional equipment or remedial actions. In addition, any of the Company’s U.S. mines could be subject to a temporary or extended shutdown as a result of a violation alleged by the MSHA. Parties engaged in mining operations or in the exploration or development of mineral properties may be required to compensate those suffering loss or damage by reason of the mining activities and may be subject to civil or criminal fines or penalties imposed for violations of applicable laws or regulations. Any such penalties, fines, sanctions or shutdowns could have a material adverse effect on the Company’s business and results of operations.

Compliance with environmental regulations and litigation based on environmental regulations could require significant expenditures.

Environmental regulations mandate, among other things, the maintenance of air and water quality standards and land reclamation, and set forth limitations on the generation, transportation, storage and disposal of solid and hazardous waste. Environmental legislation is evolving in a manner that may require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects, and a heightened degree of responsibility for mining companies and their officers, directors and employees. The Company may incur environmental costs that could have a material adverse effect on financial condition and results of operations. Any failure to remedy an environmental problem could require it to suspend operations or enter into interim compliance measures pending completion of the required remedy. The environmental standards that ultimately may be imposed at a mine site affect the cost of remediation and could exceed the financial accruals that the Company has made for such remediation. The potential exposure may be significant and could have a material adverse effect on the Company’s financial condition and results of operations.

Moreover, governmental authorities and private parties may bring lawsuits based upon damage to property and injury to persons resulting from the environmental, health and safety impacts of prior and current operations, including operations conducted by other mining companies many years ago at sites located on properties that the Company currently or formerly owned. These lawsuits could lead to the imposition of substantial fines, remediation costs, penalties and other civil and criminal sanctions. Substantial costs and liabilities, including for restoring the environment after the closure of mines, are inherent in the Company’s operations. The Company cannot assure that any such law, regulation, enforcement or private claim would not have a material adverse effect on its financial condition, results of operations or cash flows.

Some of the mining wastes from the Company’s U.S. mines currently are exempt to a limited extent from the extensive set of U.S. Environmental Protection Agency (the “USEPA”) regulations governing hazardous waste under the Resource Conservation and Recovery Act (“RCRA”). If the USEPA were to repeal this exemption, and designate these mining wastes as hazardous under RCRA, the Company would be required to expend additional amounts on the handling of such wastes and to make significant expenditures to construct hazardous waste storage or disposal facilities. In addition, if any of these wastes causes contamination in or damage to the environment at a U.S. mining facility, that facility could be designated as a “Superfund” site under the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”). Under CERCLA, any present owner or operator of a Superfund site or the owner or operator at the time of contamination may be held jointly and severally liable regardless of fault, and may be forced to undertake extensive remedial cleanup action or to pay for the cleanup efforts. The

owner or operator also may be liable to federal, state and tribal governmental entities for the cost of damages to natural resources, which could be substantial. Additional regulations or requirements also are imposed on the Company’s tailings and waste disposal areas in Alaska under the federal Clean Water Act (“CWA”) and in Nevada under the Nevada Water Pollution Control Law which implements the CWA.