QuickLinks -- Click here to rapidly navigate through this documentExhibit 99.C.1

Hon Dr Michael Cullen

MINISTER OF FINANCE

DECEMBER ECONOMIC AND FISCAL UPDATE 2003

18 DECEMBER 2003

ISBN 0-478-18255-4

Contents

December Economic and Fiscal Update

| Statement of Responsibility | | |

Economic Outlook |

|

|

| |

Summary |

|

|

| |

Recent and Current Developments |

|

|

| |

Forecasts to June 2005 |

|

|

| |

2005/06 and the Medium Outlook |

|

|

Fiscal Outlook |

|

|

| |

Summary of the December Update |

|

|

| |

Comparison of OBERAC with Budget Update |

|

|

| |

Revenues and Expenses |

|

|

| |

Expenses |

|

|

| |

Risks to Forecasts |

|

|

Risks and Scenarios |

|

|

| |

Summary |

|

|

| |

Economic Risks |

|

|

| |

Economic Scenarios |

|

|

| |

Fiscal Scenarios |

|

|

| |

Fiscal Sensitivities |

|

|

Specific Fiscal Risks |

|

|

| |

Introduction |

|

|

| |

Specific fiscal risks |

|

|

| |

Contingent liabilities |

|

|

Generally Accepted Accounting Practice (GAAP) Series Tables |

|

|

| |

Statement of Accounting Policies and Forecast Assumptions |

|

|

| |

Reporting Entity as at 8 December 2003 |

|

|

| |

Forecast Statements |

|

|

| |

Notes to the Forecast Financial Statements |

|

|

Glossary of Terms |

|

|

Statement of Responsibility

On the basis of the economic and fiscal information available to it, the Treasury has used its best professional judgement in supplying the Minister of Finance with this Economic and Fiscal Update. The Update incorporates the fiscal and economic implications both of Government decisions and circumstances as at 8 December 2003 that were communicated to me, and of other economic and fiscal information available to the Treasury in accordance with the provisions of the Fiscal Responsibility Act 1994.

John Whitehead

Secretary to the Treasury

11 December 2003

This Economic and Fiscal Update has been prepared in accordance with the Fiscal Responsibility Act 1994. I accept overall responsibility for the integrity of the disclosures contained in this Update, and the consistency and completeness of the Update information in accordance with the requirements of the Fiscal Responsibility Act 1994.

To enable the Treasury to prepare this Update, I have ensured that the Secretary to the Treasury has been advised of all Government decisions and other circumstances as at 8 December 2003 of which I was aware and that had material economic or fiscal implications.

Hon Dr Michael Cullen

Minister of Finance

11 December 2003

1

Economic Outlook

Summary

- •

- The economy has grown strongly over the past two years. Annual growth was 4.0% in the year ended June. Employment growth has been strong, and the unemployment rate has fallen to 4.4%, which is lower than at any time since the late-1980s.

Figure 1.1—Real GDP growth

Sources: Statistics New Zealand, The Treasury

- •

- However, in the last year strong overall growth has come to be increasingly dominated by domestic demand.

- •

- The Iraq conflict, the SARS outbreak and drought have all been partly responsible for slower export growth, and also led to an overall "growth pause" over the June quarter.

- •

- But in general, strong domestic demand can be explained by strong employment and household wealth, and more immigration, while declining net export earnings can be explained by the increasing exchange rate.

- •

- Over the short term, GDP growth is expected to continue to be robust, owing to ongoing strong household and business spending. Housing investment growth will be particularly strong.

- •

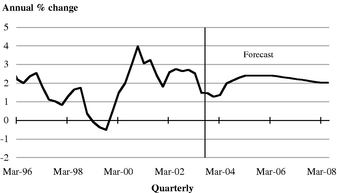

- The strong end to the year sees real GDP growth of 2.8% for the year to March 2004, compared with 2.2% forecast in the Budget Update.

- •

- As calendar 2004 progresses the pace of domestic demand growth is forecast to abate, with the housing investment cycle running its course and households easing back their other spending. Together with export growth remaining low quarterly GDP growth will slow. For the year ended March 2005, 2.8% growth is forecast, declining further to 2.5% by June.

- •

- From mid-2005, the rebound in global growth is forecast to provide a greater stimulus to exports, with the exchange rate acting as less of a drag given its assumed decline. Households are expected to continue to consolidate their financial position so that despite steady business investment and rising infrastructure investment, domestic demand will slow further, implying more balanced growth than has occurred over 2003. With import growth also slowing, GDP growth of around 3.4% is forecast for 2005/06 and 2006/07.

- •

- At the end of the forecast period, economic growth is expected to have been relatively robust for a decade. An economic growth cycle is forecast, with the period of slower growth in 2004/05 representing the trough, but the fluctuation is expected to be less than in past cycles.

- •

- Over most of the forecast period, annual CPI inflation is expected to fluctuate between 2.0% and 2.5%. Non-tradable inflation will persist for a time even after domestic demand growth

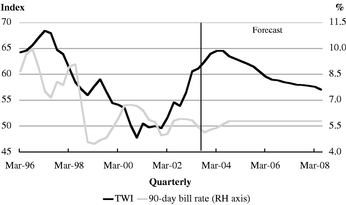

Figure 1.2—Monetary conditions

Sources: Reserve Bank of New Zealand, The Treasury

- •

- Monetary policy is assumed to lean against these inflation pressures. Modest increases in the Reserve Bank's Official Cash Rate (OCR) are expected to see 90-day bank bills at around 5.8% from the middle of 2004. This represents a modest interest rate cycle by historical standards.

- •

- The current account deficit is forecast to increase to 6% of GDP by early 2005, because of the strength of domestic demand and the high exchange rate, both of which will draw in imports. As growth becomes more balanced, however, the deficit will decrease to around 5% of GDP.

- •

- Overall, the view of the economy implied by this forecast is similar to that presented in the 2003 Budget Update. However, the level of nominal GDP is higher throughout the forecast period than forecast in the Budget Update, because of historical revisions and a higher starting level of labour market earnings. This implies higher tax revenue for the Government.

Table 1.1—Economic outlook: central forecast(1)

(Annual average % change, March years)

| | 2002

Actual

| | 2003

Actual

| | 2004

Forecast

| | 2005

Forecast

| | 2006

Forecast

| | 2007

Forecast

| | 2008

Forecast

|

|---|

| Private consumption | | 2.8 | | 3.8 | | 4.3 | | 3.1 | | 2.9 | | 2.9 | | 3.0 |

| Public consumption(2) | | 3.9 | | 5.0 | | 5.0 | | 3.5 | | 3.0 | | 4.5 | | 2.8 |

| Total Consumption | | 3.1 | | 4.1 | | 4.5 | | 3.2 | | 2.9 | | 3.3 | | 3.0 |

| | |

| |

| |

| |

| |

| |

| |

|

Residential investment |

|

3.3 |

|

23.3 |

|

20.3 |

|

5.2 |

|

- -7.9 |

|

- -1.6 |

|

0.9 |

| Market investment | | 5.4 | | 4.1 | | 9.1 | | 5.8 | | 5.7 | | 3.2 | | 4.1 |

| Non-market investment | | 3.7 | | 2.8 | | 5.1 | | 4.8 | | 9.7 | | 3.8 | | 2.8 |

| Total Investment | | 4.7 | | 8.6 | | 11.6 | | 5.6 | | 2.3 | | 2.1 | | 3.2 |

| | |

| |

| |

| |

| |

| |

| |

|

Stock change(3) |

|

0.3 |

|

- -0.4 |

|

0.0 |

|

0.1 |

|

0.2 |

|

- -0.2 |

|

- -0.1 |

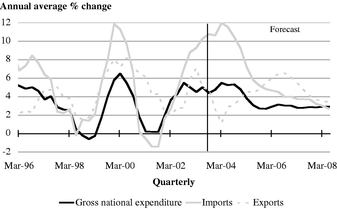

| Gross National Expenditure | | 3.7 | | 4.5 | | 5.4 | | 3.8 | | 2.9 | | 2.8 | | 2.9 |

| | |

| |

| |

| |

| |

| |

| |

|

Exports |

|

2.0 |

|

7.0 |

|

1.7 |

|

4.2 |

|

6.1 |

|

5.5 |

|

3.5 |

| Imports | | 2.4 | | 9.4 | | 11.9 | | 7.1 | | 4.7 | | 3.7 | | 3.0 |

| | |

| |

| |

| |

| |

| |

| |

|

| GDP (production measure) | | 3.4 | | 4.4 | | 2.8 | | 2.8 | | 3.4 | | 3.4 | | 3.0 |

| | |

| |

| |

| |

| |

| |

| |

|

| —annual % change | | 4.1 | | 4.0 | | 3.0 | | 2.3 | | 4.1 | | 3.0 | | 3.0 |

Nominal GDP (expenditure basis) |

|

7.9 |

|

4.0 |

|

4.7 |

|

5.6 |

|

5.3 |

|

5.2 |

|

5.1 |

| GDP deflator | | 3.7 | | -0.6 | | 2.3 | | 2.7 | | 1.9 | | 1.8 | | 2.0 |

Employment(4) |

|

2.5 |

|

2.6 |

|

3.0 |

|

1.4 |

|

0.9 |

|

1.4 |

|

1.4 |

| Unemployment(5) | | 5.2 | | 4.9 | | 4.4 | | 4.8 | | 4.9 | | 4.8 | | 4.8 |

Wages(6) |

|

3.5 |

|

2.9 |

|

3.7 |

|

4.2 |

|

3.9 |

|

3.6 |

|

3.6 |

| CPI inflation(7) | | 2.6 | | 2.5 | | 1.4 | | 2.4 | | 2.4 | | 2.2 | | 2.0 |

| Export prices(8) | | 3.1 | | -13.0 | | -9.8 | | -2.1 | | 3.4 | | 3.5 | | 1.2 |

| Import prices(8) | | -0.9 | | -7.2 | | -10.2 | | -2.2 | | 3.1 | | 3.2 | | 0.8 |

Current account balance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| —$ million | | -2,795 | | -5,035 | | -7,340 | | -8,488 | | -8,603 | | -8,660 | | -8,704 |

| —% of GDP | | -2.3 | | -3.9 | | -5.5 | | -6.0 | | -5.8 | | -5.5 | | -5.3 |

TWI(9) |

|

51.6 |

|

60.6 |

|

64.5 |

|

62.5 |

|

59.5 |

|

58.3 |

|

57.6 |

| 90-day bank bill rate(9) | | 5.0 | | 5.8 | | 5.4 | | 5.8 | | 5.8 | | 5.8 | | 5.8 |

| 10-year bond rate(9) | | 6.7 | | 6.0 | | 6.3 | | 6.4 | | 6.0 | | 6.0 | | 6.0 |

Sources: Statistics New Zealand, Reserve Bank of New Zealand, The Treasury

NOTES:

- (1)

- Forecasts finalised 21 November 2003. Text finalised 11 December 2003. Additional tables are available on the Internet at www.treasury.govt.nz/forecasts/defu/2003/.

- (2)

- The forecast profile for public consumption is influenced by government defence spending.

- (3)

- Contribution to GDP growth.

- (4)

- Household Labour Force Survey, full-time equivalent employment.

- (5)

- Household Labour Force Survey, percentage of the labour force, March quarter, seasonally adjusted.

- (6)

- Quarterly Employment Survey, average hourly ordinary time earnings.

- (7)

- Annual % change, March quarter

- (8)

- Overseas Trade Index basis, annual average percentage change, March quarter.

- (9)

- Average for the March quarter.

Assumptions Underlying the Central Forecast

Global economic activity—global economic growth, inflation and interest rate forecasts are assumed to conform to those presented in the November Asia Pacific Consensus Forecasts. Long-term forecasts (beyond 2004) are taken from the October Consensus Forecasts. For a more detailed discussion of the global outlook, see the 'Global economic growth' box on page 21.

Oil prices—oil prices are assumed to decline gradually over the short term, consistent with the price of oil futures at the time the forecasts were put together. Thereafter, oil prices are assumed to converge to a long-term average of around US$18.50 per barrel.

Net migration—the net number of migrants has started to decline from a peak early in 2003 and is assumed to continue declining to approximately 10,000 per year by 2005/06. This assumption is higher than the one used in the Budget Update.

Monetary conditions—from the middle of 2004, the exchange rate (TWI) is assumed to decline steadily to its estimated equilibrium of around 57. This is a technical assumption. The forecasts assume a neutral short-term interest rate of 5.8%.

Climate—agricultural growing conditions and the level of hydroelectricity storage lakes are assumed to be normal over the forecast period.

Recent and Current Developments

The economy as a whole has performed well over the past two years...

Annual real GDP growth was 4.0% in the year ended June 2003, following growth of 3.6% during the previous year. New Zealand's performance easily exceeded the OECD average over this period.

Nominal GDP growth is estimated to have been slightly slower at 3.8%. However, with Statistics New Zealand revising up official estimates of nominal GDP by approximately $1.5 billion dollars over two years, the level of nominal GDP is higher than the forecasts contained in the Budget Update. This helps explain the increase in tax revenue experienced over the past year.

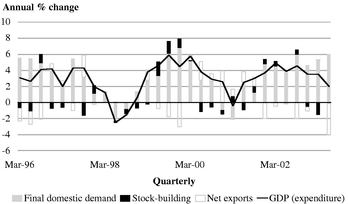

... but growth has become increasingly domestically based over the past year

Figure 1.3—Contributions to GDP growth

Sources: Statistics New Zealand, The Treasury

Digging more deeply into the GDP statistics, it is clear that some components of production, income and spending have grown faster than others.

Household and business spending has grown quickly...

Household spending grew rapidly over 2003/04, the result of more purchases of consumption items, but also vastly more investment in new housing. The value of houses constructed rose by almost 25% over the year ended June.

More jobs and steady wage increases have provided the foundation for household spending over this period. Employment growth has been healthy since the end of 2002, and became very rapid in mid-2003, driving the unemployment rate down to 4.4% by September. The unemployment rate has declined in spite of a growing number of people choosing to enter the labour force.

The strength of employment growth means that the level of employment at the beginning of the forecast period is considerably higher than expected in the Budget Update. Although the view of employment growth from this point on has not changed dramatically since the Budget, growth so far together with slightly faster wage growth is likely to translate into higher income tax receipts over the forecast period.

Greater household wealth has also provided a basis for more consumption and investment over the past year. The average price of houses, which are the most widely held of household assets, has gone up by 17%, not only encouraging more house building but also making householders more willing to purchase consumption items on credit.

Meanwhile, business investment has been given a boost by low prices for imported capital equipment. Computer prices, in particular, have fallen dramatically in real terms. Adding to the incentive to invest, capacity utilisation rates have been relatively high in recent quarters, particularly in the construction sector, implying a need for more investment. Overall utilisation peaked at a ten-year high of 91.4% in mid-2003. It has since declined slightly to 89.5% but remains above the average for the period since 1990 (88.9%).

As a consequence of more domestic spending, but also because of lower prices, demand for imports has been strong. The volume of imports rose 10.3% over the year ended June, although the value declined 0.3%.

Consumer price inflation ran at an annual rate of less than 1.5% over the middle of 2003. A rising exchange rate has caused import and export prices to decline, offsetting non-tradable inflation. The non-tradable inflation rate, which was 4.1% in September, has been driven up partly by housing and household operation costs.

... while export earnings growth has been slow

In contrast to domestic spending, export earnings have been declining. The volume of exports increased 5.0% over the year ended June 2003, but falling prices meant export receipts fell 5.9%.

Figure 1.4—Nominal export earnings

Sources: Statistics New Zealand, The Treasury

The important point here is that in contrast to household incomes and profits for most businesses, exporters' incomes have declined.

Falling New Zealand dollar prices have been widespread. The agricultural sector has been hit particularly hard over the last year, and farm incomes have declined from high levels in previous years.

Exporters of services, such as tourist operators and educational institutions, have been less affected by falling prices, but the quarterly volume of service exports was reduced over the period from March to June.

Unusual events explain some of the dichotomy between export earnings and domestic spending...

One of the reasons for the uneven growth of different parts of the economy is that a series of shocks that hit the economy over the first half of this year mostly affected exporters.

- •

- the US-Iraq conflict added to a climate of general geo-political uncertainty, caused oil prices to fluctuate and acted to delay global recovery

- •

- the outbreak of Severe Acute Respiratory Syndrome (SARS), principally in Asia, led to a marked fall in visitor arrivals

- •

- dry weather led to poor agricultural growing conditions, and reduced the level of hydroelectric storage lakes, causing some manufacturers to conserve energy by cutting back production.

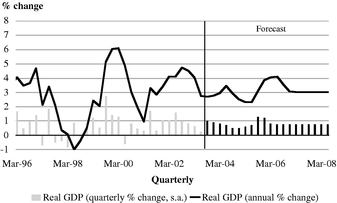

The quarterly GDP growth rate was reduced to 0.2% in June, following 0.6% in March. Quarterly export volumes fell by 3.1%, while domestic spending was largely unaffected.

These events were discussed in detail in the Budget Update, and their effects have been broadly as expected.

... but less fleeting influences have also been fundamental.

The shocks that hit the March and June quarters were temporary and, it appears, their effects were short-lived. But it is expected that the divide between domestic spending and net export growth will continue to widen for a time. This is because more fundamental forces have also been at work this year.

In the household sector, high levels of net migration have been increasing the demand for consumption goods and services in general, and housing in particular. The annual net number of migrants peaked at over 40,000 in the March quarter and has remained relatively high.

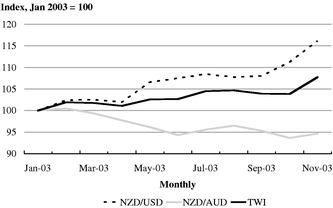

Figure 1.5—Exchange rates

Sources: Statistics of New Zealand, The Treasury

At the same time, a rising exchange rate has reduced the prices of both imports and exports. This has encouraged households and businesses to spend on imported goods, sometimes at the expense of domestic producers, and is also the main reason for lower incomes in the export sector.

Although export earnings have been significantly lower this year than in 2002, the effect of the exchange rate appreciation on overall GDP growth has been moderate so far, and the 4.0% growth rate over the year ended June is evidence of that. Partly, this is due to the fact that it can take a long time—one to two years is typical—for exchange rate developments to impact on export volumes and to flow through to the rest of the economy. This year's rise in the exchange rate is expected to have its greatest negative effect on economic activity from late-2004.

Another reason why the effect of the rising exchange rate on total GDP might not so far have been as large as expected is that components of the Trade Weighted Index (TWI) have been moving in opposite directions. On one hand, compared with most major currencies, the US dollar has been losing value, and the New Zealand dollar has consequently been gaining value. On the other hand, since the beginning of 2003, the New Zealand dollar has lost ground to the Australian dollar. Exporters of primary commodities will generally be worse off because of the weakening US dollar, since their exports are priced in that currency. But some manufacturing exporters, particularly those which buy raw materials in US dollars and sell finished products in Australian dollars, could be better off.

Growth appears to have been strong over the second half of 2003

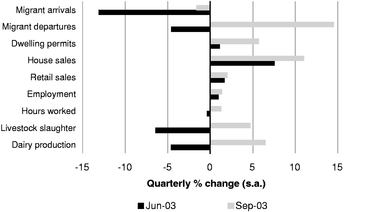

Turning to the very recent past, most indicators of economic activity are indicating a rebound in GDP growth over the September quarter.

Figure 1.6—Selected real activity indicators

Sources: Statistics New Zealand, Real Estate Institute of New Zealand, Fonterra, The Treasury

Retail trade turnover and the number of building permits granted for new houses both rose significantly, suggesting that household spending continued to grow rapidly, supported by increased job security and further house price rises.

Agricultural production also appears to have increased, and tourist numbers have rebounded, following sharp declines over the June quarter. Export prices are still subdued, but it seems that exporters did increase their real output over the quarter.

Global economic growth also accelerated over the September quarter, following concerns that the recovery of several of New Zealand's trading partners' economies would stall as a result of geo-political uncertainty and disease. The 2.0% rate of quarterly expansion in the US was the fastest in a decade. See box, "Global economic growth" on page 21, for a summary of international growth developments and forecasts.

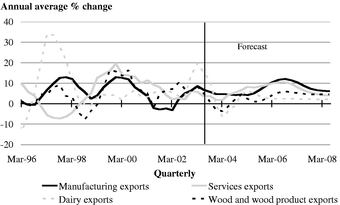

Export Performance

The performance of the export sector is an important component of the economic outlook. Exports fell sharply in the June quarter of 2003. This in part reflected the effect of dry climatic conditions over the beginning of 2003, which saw dairy production fall and a surge in meat slaughtering in the March quarter, followed by a slump in June. The outbreak of SARS had a negative impact on the exports of some foods, particularly seafood, while visitor arrivals fell sharply.

The unwinding of these negative factors is expected to see a lift in export volumes in the September quarter, with services exports in particular bouncing back.

Export volume growth is forecast to be subdued over the final quarter of 2003 and over much of 2004, as this year's exchange rate appreciation impacts on exporters' competitiveness, despite stronger global growth. The greatest impact of the appreciation of the exchange rate is likely to be on non-commodity exports, particularly manufactured goods, forestry and services. Analysis suggests that there is a lag of around 11/2 years between a rise in the currency and any impact on export volumes.

A further complication is that it is the bilateral exchange rate between New Zealand and trading partners that is important when considering competitiveness. With Australia accounting for around 50% of New Zealand's manufactured goods exports, and an important source of visitor arrivals, the smaller appreciation in the New Zealand/Australian exchange rate compared to the New Zealand/United States rate will mitigate some of the impact of the appreciation of the TWI. The central forecast sees annual average manufactures export growth slow to 4.6% and 4.2% in the March 2004 and 2005 years, down from 8.5% in the year to March 2003, and substantially weaker than expected at the time of the Budget Update. It will also be lower than the average since 1990 of about 8%. Forestry export volumes are forecast to fall 3.8% in the year to March 2004, with growth recovering to just 2.3% in the year to March 2005.

A return to normal growing conditions in the agricultural sector is expected to boost primary exports and help offset some of the weakness described above.

Figure 1.7—Export volume growth

Sources: Statistics NZ, The Treasury

The level of the TWI means that New Zealand dollar prices and exporter receipts will be weak for a while yet, although an improved outlook for the world prices of many of New Zealand's exports will provide some offset.

As the rebound in global growth becomes embedded and the exchange rate becomes less of a drag, export volume and receipts growth are forecast to lift, with manufacturing, forestry and services exports all contributing to a solid 6.1% rise in export volumes in the March 2006 year.

Global Economic Growth

Consensus Forecasts based forecasts of trading partner growth point to growth returning to a little above its long-term average in 2004, and then to around its average, following three years of being below-par. The expected rebound in 2004 is pretty much across the board with better growth in the US, Australia and non-Japan Asia, offsetting only modest growth in Japan and Europe. These are consistent with other views the Treasury monitors.

Calendar years

| | 2002(a)

| | 2003(e)

| | 2004(f)

| | 2005(f)

| | 2006(f)

| | 2007(f)

| | 2008(f)

|

|---|

| Australia | | 3.6 | | 2.5 | | 3.8 | | 3.7 | | 3.5 | | 3.4 | | 3.6 |

| Japan | | 0.2 | | 2.4 | | 1.3 | | 0.9 | | 1.9 | | 1.8 | | 1.9 |

| US | | 2.4 | | 2.7 | | 4.0 | | 3.5 | | 3.3 | | 3.3 | | 3.2 |

| Europe* | | 1.1 | | 1.0 | | 2.0 | | 2.1 | | 2.1 | | 2.0 | | 2.0 |

| Non-Japan Asia** | | 5.3 | | 4.3 | | 5.7 | | 5.7 | | 5.6 | | 5.4 | | 5.2 |

Trading partner growth |

|

2.8 |

|

2.7 |

|

3.6 |

|

3.5 |

|

3.5 |

|

3.4 |

|

3.4 |

- *

- UK, Germany, Italy, France (weighted by export share).

- **

- Korea, Taiwan, China, Malaysia, Hong Kong, Singapore (weighted by export share).

- (a)

- Actual.

- (e)

- Estimate.

- (f)

- Forecast.

However, other scenarios are also plausible. In the short term, for example, there is a risk that Consensus Forecasts are underestimating the momentum that major economies—and particularly the US—are building up. If this were the case, trading partner growth could be materially higher than that underpinning the central forecast over the next year or so.

Figure 1.8—Quarterly GDP growth

Sources: Datastream, The Treasury

Alternatively, the rebound in growth currently underway could give way to weaker growth, either because of unforeseen shocks or because of structural imbalances present in some countries acting as a constraint to ongoing growth.

For instance, the US has large government budget and current account deficits. These look to be a factor behind the current depreciation in the US dollar. Thus far the decline has been orderly and a necessary part of unwinding these imbalances, but if sentiment around lending to American consumers and businesses were to change significantly for the worse a less benign adjustment path is possible. This could make exporters in other countries uncompetitive (especially if the exchange rate adjustment is pushed onto a small group of countries) and lead to sharply reduced export earnings and in those

countries where economic recoveries are fragile (like Europe and Japan), spark a relapse into slow growth or recession. Moreover, some of these countries also face their own structural challenges with regard to increasing trend growth above the 2% level that many see currently (see table above).

A retreat from open markets would also lead in the same direction, hurting future productivity and growth prospects in developed countries as well harming global development objectives.

Forecasts to June 2005

The pace and composition of GDP growth are expected to change gradually over the next two years

Through to mid-2004 the economy is forecast to record robust, though moderating growth. From mid-2004, a period of slower growth is forecast, and the gap between household and business spending growth and export earnings growth is expected to begin to close. The amplitude of the economic cycle will seem quite small by historical standards, but this will conceal larger—partly offsetting—movements of the components of GDP.

Figure 1.9—Forecasts of GDP components

Sources: Statistics New Zealand, The Treasury

The exact timing and depth of the growth slowdown are sources of uncertainty in this forecast. An alternative scenario, incorporating a more substantial slowing of growth, is examined in Chapter 3.

Business and household spending will continue to provide the short-term impetus...

Household spending and business investment will continue to increase rapidly.

Steady employment growth is expected to continue, keeping the unemployment rate at current levels, which are the lowest in over a decade. And because employees will be harder to find, annual wage inflation is forecast to pick up too.

The residential construction boom is projected to persist. House prices are likely to continue to head upward at a fast rate, partly owing to the momentum they have built up already, and this is predicted to contribute directly to greater household wealth.

Business investment is forecast to benefit from a relatively low cost of capital, but also the commencement of investment projects which were delayed during the period of slower growth—and increased economic uncertainty—in the first half of 2003. Relatively high rates of capacity utilisation and healthy corporate balance sheets are also reasons for more business investment.

The healthy state of domestic demand, combined with low import prices, will push import volumes steadily upward.

Meanwhile, export volumes will begin to grow again following the contraction during the June quarter. But the recovery will not be underpinned by rising earnings, because prices will still be weak.

Global economic growth is expected to be more firmly established by this time, and this should boost demand for New Zealand's exports, but the high and rising exchange rate will undermine New-Zealand-dollar returns.

As a consequence of the continuing uneven performance of the economy, with domestic demand pulling in imports and export growth still not convincing, the annual current account deficit is expected to exceed 5.5% of GDP by the middle of 2004, with the quarterly deficit at 6.0% of GDP.

The CPI annual inflation rate is expected to rise over the next nine months too, from the current rate of 1.5% to about 2.0%, despite only modest quarterly increases in December and March, and even though import and export prices will be falling. Prices for housing and household operation will be rising particularly rapidly because of the residential property boom.

Figure 1.10—Consumer price inflation forecasts

Sources: Statistics New Zealand, The Treasury

Because prices in some areas will have been rising rapidly for a prolonged period, there is a risk that inflation expectations will begin to be raised. Once changed, expectations can resist moving again. Consistent with the inflation outlook, the Reserve Bank is expected to increase its Official Cash Rate slightly over this period. Even so, the rate of inflation for non-tradable goods and services is expected to remain quite high for a prolonged period.

... but the economy will lose some momentum from the September quarter of 2004

By mid-2004, the rate of economic growth is expected to slow. Over the year ended June 2005, GDP growth of 2.5% is forecast, below the average of recent years although not especially low for the trough of an economic cycle.

A period of less house building and buying will be influential...

Growth in house prices and new house construction is forecast to run its course over 2004 and some modest falls in activity are expected in 2005. The housing cycle will be the second greatest negative influence on GDP growth over the year to June 2005, behind the rising volume of imports.

As house prices stop rising, further household wealth growth will be constrained. And to the extent that households were counting on further capital gains, spending plans are likely to be cut back.

Employment growth is also forecast to be relatively slow from mid-2004, as businesses look to maintain profitability in the face of slower overall economic growth and higher wages.

Businesses are likely to cut back on investment as well as employment, although investment will still grow faster than GDP. The price of imported capital equipment will still be low, particularly relative to labour costs, and firms will be making an effort to increase labour productivity by building up the capital stock.

... and the improvement in exporters' prospects will be gradual at this stage

Exporters will begin to see an improvement in their incomes over 2004/05, as export prices (in New Zealand dollars) rise. Export volumes will also grow steadily, but still not as fast as import volumes until the following year. Recovering exports of dairy products and services (tourism) will provide a solid base for growth.

Reasons for slower growth will include fewer immigrants and more debt

The net number of migrants is assumed to decline from about 40,000 per year now to 15,000 by June 2005 and 10,000 at the beginning of 2006. This will translate directly into slower population growth, with a consequent effect on the demand for housing, as well as for other goods and services. This is likely to be a key influence on house construction and prices over the period of slower GDP growth.

Figure 1.11—Net immigration

Sources: Statistics New Zealand, The Treasury

Other housing-related variables are also relevant, however. Interest rates will be marginally higher, and households in aggregate have built up significant debt to finance investment in housing and consumption over recent years. In an environment in which house prices are no longer increasing, and slower population growth is increasing the chance of rental housing lying empty, higher debt servicing costs are likely to mean households will cut back on discretionary spending.

But government spending will provide some support...

Government consumption and investment are expected to increase steadily through the whole forecast. Non-market investment is likely to be boosted by infrastructure investment, including spending on roads, although the precise timing and magnitude are uncertain.

... and the seeds of an export recovery will have been sown

The exchange rate is assumed to decline from about June 2004. The exchange rate path used in the forecasts is purely technical, but a decline at some stage over the forecast period would be consistent with a growing balance of payments deficit, a smaller gap between New Zealand's GDP growth and that of New Zealand's trading partners, and reduced interest rate differentials.

The lower exchange rate will eventually lead to a gradual reduction of the real net export deficit, as export and import prices increase. This is unlikely to happen before the end of 2005, but there will be some signs of improved export earnings and volumes before that.

Export volumes will not respond faster because many exporters have exchange rate hedges in place, and because it takes time to increase productive capacity, particularly in the agricultural and silvicultural industries.

Similarly, import volumes will continue to increase steadily over much of 2005, because it will take time for households and businesses to find domestic sources of production for some goods and services previously imported. In some cases, those sources of production will not exist and will need to be established.

Higher export and import prices will contribute to steady CPI inflation over 2005, in spite of lower housing costs.

Quarterly GDP growth is not expected to slow dramatically

Through the entire period of slower economic growth—from mid-2004 to mid-2005—it is important to note that the quarterly GDP growth rate is not expected to be slower than 0.5%. This is only slightly below the long-term average of about 0.8%.

The growth recession is therefore mild.

Figure 1.12—GDP growth

Sources: Statistics NZ, The Treasury

But as noted earlier, this does conceal some larger cyclical movements of the different components of GDP. The annual Gross National Expenditure growth rate is expected to slow from more than 5% in mid-2004 to about 3% by mid-2005. And the contribution of net exports to total GDP will move from a strongly negative one to one that is almost neutral.

Over the year to June 2005, nominal GDP growth will be 5.0%. Slower real economic growth will be partly offset by higher inflation, as import and export prices rise.

Recent Labour Market Developments

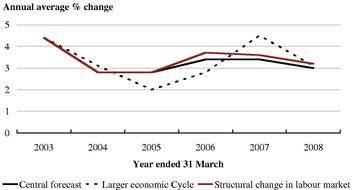

Statistics New Zealand and business survey data through 2003 has shown a labour market characterised by strong employment growth, high participation rates, and very low unemployment, combined with moderate wage pressure.

Together the latest Quarterly Employment Survey and Household Labour Force Survey results show a labour market continuing to operate with little slack. Fulltime equivalent employment grew 2.5% in the year to September, with an increase of 1.4% in the September quarter. The big sectoral employment gains have tended to come from the non-tradable sector, which is consistent with the sources of GDP growth. To date, however, wage inflation has risen only slightly. A further mild increase is forecast (to over 4% from the current 3.1% pace), but wage outturns appear well anchored.

The impact of fast employment growth on overall labour market conditions has been somewhat eased by high participation rates, currently at 66.6%. The ongoing strength of the labour market has pulled additional people into the labour force, particularly women.

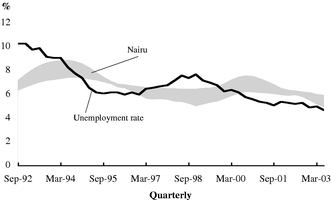

With strong increases in employment, the seasonally adjusted unemployment rate fell to 4.4% in the September quarter. The unemployment rate is at its lowest level since December 1987 when it was 4.2% and is the 5th lowest rate in the OECD. The extent to which these low levels of unemployment flow through to wages represents a key area of uncertainty in these forecasts.

The rate of unemployment that the economy can sustain without a marked increase in wage or price pressure is commonly referred as the NAIRU—or non-accelerating inflation rate of unemployment. In other words, at what level of unemployment will wage or price inflation begin to rise? If the NAIRU falls over time then medium term trend growth will rise as the workforce can increase (and vice versa) without generating extra inflation.

New Zealand's current low unemployment rate combined with wage and price developments raises the question about whether it has fallen below its NAIRU. While estimation of the NAIRU is imprecise as it cannot be directly observed, it appears to have changed over time. Work by the OECD published in 2000 suggested that New Zealand's NAIRU may have fallen by around 1/2% per annum over the last decade.

Figure 1.13—A range of NAIRU estimates using the Kalman filter

Sources: Statistics New Zealand, The Treasury

More recent work by the Treasury backs this up and is suggestive of structural unemployment continuing to fall over recent years. The analysis used a number of models of the NAIRU with different model specifications and various measures of inflation. The filtering process uses the rule that stable inflation implies an unemployment rate that is at the NAIRU but rising (falling) inflation is suggestive of an unemployment rate that is below (above) the NAIRU. Figure 1.13 indicates the range estimates generated using Kalman Filter specifications (note that these estimates also have large standard error bands around them).

The results indicate that: the concept of the NAIRU appears to be valid to the extent that estimates indicate that the rate of unemployment does have some impact on inflation; the spread of results indicates that estimates of the NAIRU are imprecise; and the NAIRU appears to have fallen over the estimation period.

While the modelling process does not examine the reasons for a falling NAIRU, there are a number of plausible factors that may have contributed, including strong growth, population demographics, labour market reforms, improved information technology and matching services from Work and Income New Zealand reducing frictional unemployment, and more appropriate skills.

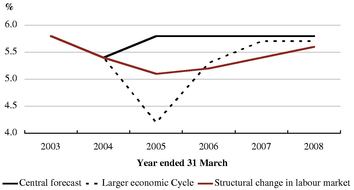

A falling structural unemployment rate is included as one of the scenarios in the Risks and Scenarios chapter.

2005/06 and the Medium-term Outlook

From mid-2005, economic conditions and growth are expected to become more balanced

Economic growth is forecast to rebound to around 31/2% over 2005/06 and 2006/07, with the negative contribution net exports made from 2001/02 to 2004/05 disappearing, and domestic demand growth stabilising.

Over 2005 and 2006, export earnings will accelerate

From about the end of 2005, export earnings and the volume of exports are expected to begin to increase rapidly. Nominal growth of 9.2% over the year to March 2006 and real growth of 6.1% will be higher than the averages (5.7% and 4.9% respectively) for the period since 1990.

Exporters will have had time to increase production to take advantage of the higher prices which will have been prevailing for several quarters by this time.

Domestic spending will also increase steadily, although not as fast as export earnings

Consumer and business spending will also grow faster over the end of 2005 and in 2006, following the period of sluggishness in the previous year. But rather than returning to the rapid rates of 2003/04, consumption and investment growth is likely to return only to the long term average.

Employment growth will remain gradual rather than impressive over this period, partly because annual wage inflation is forecast to persist at 31/2% or so, encouraging businesses to keep improving labour productivity. But the unemployment rate will start to edge down from 5.0%, which it reached during the period of slower growth in 2004/05.

A lower exchange rate and a sustained global recovery will help achieve this balance

More balanced growth—with net exports making a slightly positive contribution to overall GDP growth—will be largely the result of global economic growth and the exchange rate acting as less of a drag on growth.

By 2006, the TWI is assumed to have fallen to less than 60.0, and will be steadily declining.

Meanwhile, household and business spending will be rising slightly faster.

By 2007/08, both the rate and composition of growth are assumed to be back to "normal"...

Because it is not possible to predict unexpected shocks, and because the effects of past shocks will have mostly worked their way through the economy, forecasts for the latter year or so of the forecast period flow from assumptions made about the long-term determinants of economic growth.

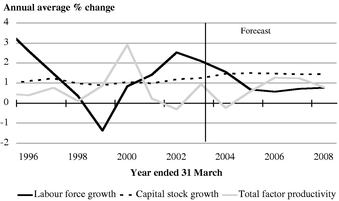

By 2007/08, domestic demand is forecast to be growing at approximately the same rate as total GDP, and the real value of net exports is predicted to be close to zero. Real GDP growth of 3.0% is forecast, and nominal GDP growth will be rising at a rate of approximately 5% per annum.

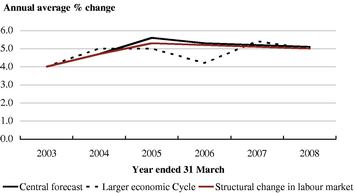

Real GDP growth will come from approximately equal parts labour force growth, capital stock growth, and multi-factor productivity. This is in line with the contributions observed over the last decade.

Figure 1.14—Contributions to annual average GDP growth

Sources: Statistics New Zealand, The Treasury

Employment and labour force growth are assumed to have stabilised, with the unemployment rate settling at just under 5%, around the level at which wage inflation is expected to be relatively stable. However, it is acknowledged that wage pressures could be either stronger than forecast, or weaker. The effects of an ongoing fall in the rate of unemployment the economy can sustain without generating increased inflation are considered in Chapter 3. Also see the box, "Recent labour market developments and implications" on page 26.

The balance of payments deficit will be about 5% of GDP, which is expected to be sustainable over the long run without increasing the nation's debt-to-GDP ratio.

CPI inflation is forecast to gradually decline to about 2% per year, the mid-point of the Reserve Bank's 1-3% target.

... because many of the determinants of growth will be "at trend"

The contribution of net migration to population is assumed to have stabilised at around 10,000 people per year.

Interest rates are expected to be at "neutral" levels of around 53/4% for short-term rates and 6% for long-term rates. The exchange rate (TWI) is also expected to have moved down to its assumed equilibrium of around 57.

Figure 1.15—Investment to GDP ratio (excluding housing investment)

Sources: Statistics New Zealand, The Treasury

The rate of global economic growth will be approximately the same as the historical average. Furthermore, it will have been there for some years.

The capital-to-labour ratio is expected to rise over the whole forecast period. With real wage inflation running at around 1.5% per year over much of the forecast, and the price of imported capital equipment rising by considerably less, there is expected to be an incentive to increase investment.

The other ratio which is expected to still be changing at the end of the forecast period is the household debt-servicing ratio. Household spending is forecast to outpace disposable income growth consistently. At some point the gap between the two may prompt households to cut back their spending significantly.

Fiscal Impulse and Structural Fiscal Balances

The government's spending actions show up in the economic forecasts discussed in this Chapter in a number of ways. Public consumption incorporates government spending on employees and purchases of other goods and services, including military equipment. Non-market investment includes new physical investment undertaken by the government in areas like education, health and on roads. Other government spending such as transfers (e.g., New Zealand Superannuation and unemployment benefits) flows through the household sector and into private consumption. In addition, the government withdraws money from the economy through income tax, corporate tax and GST.

Fiscal impulse is a measure of whether changes in fiscal policy are adding to, or subtracting from, aggregate demand pressures in the economy. In Figure 1.16, a positive fiscal impulse represents a tightening of policy relative to the previous year. The fiscal impulse indicator presented here removes estimated cyclical influences and net interest payments to provide a measure of "discretionary" fiscal policy changes. Fiscal impulse is calculated as the change in the estimated structural primary cash balance. (The concept of a structural fiscal balance is discussed below.) The fiscal impulse indicator treats selected capital items as components of expenditure and is derived from (Core Crown) cash flow information.

Figure 1.16—Estimates of fiscal impulse

Sources: Statistics New Zealand, The Treasury

Indicators based on fiscal aggregates have limitations. At best they can only provide an indication of the first round impact of changes in fiscal policy. They focus only on the net impact of tax and spending decisions and so do not take into account the composition of changes in fiscal policy. Aggregate indicators do not allow for any supply side effects of the fiscal policy change (which may be relevant for the assessment of inflationary impacts).

Ex post estimates of fiscal impulse may differ from the ex ante (or "real time") view because of revisions to the evolution of the structural component of the fiscal balance and changes in the implementation of spending plans. For example, the Budget Update estimate of fiscal impulse for the year ended June 2003 was neutral. Subsequent information suggests the outturn provided a small contractionary impulse. Forecast impulses across the years 2005 to 2008 are on average expansionary, at around a third of a percent of GDP. Fiscal impulses are sensitive to the cyclical adjustment and the

removal of net interest payments. For example, removing the forecast cycle and net interest impact for the year ended June 2006 reduces the impulse by just under 1/2 percent of GDP.

The fiscal forecasts in the next Chapter focus on aggregates such as the OBERAC. The structural (or cyclically-adjusted) fiscal balance adjusts the actual fiscal balance for fluctuations of output around trend output. This provides a picture of the underlying fiscal position—that is, what the fiscal balance would be if the economy was operating at trend.(1)

- (1)

- Treasury's approach to estimating structural fiscal balances and fiscal impulses is set out in Treasury Working Papers 01/10 and 02/30. The 2002 December Update discussed some of the alternative techniques used to estimate trend output.

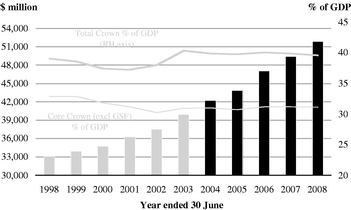

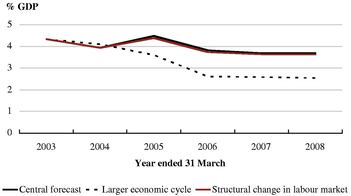

The forecast fiscal surplus (not shown) is close to the forecast structural surplus because forecast deviations from trend output are relatively small. The increase in the structural fiscal surplus relative to the Budget Update reflects the view that the increase in tax revenues seen over the past few years is likely to be more structural than previously thought. Figure 1.17 also indicates that changes to fiscal plans in the latter years of the forecast period result in a change in the trajectory of the structural balance (see the 2004 Budget Policy Statement).

Figure 1.17—Estimates of the structural fiscal balance, OBERAC basis (ex net NZS Fund returns)

Sources: Statistics New Zealand, The Treasury

Fiscal Forecasts—Finalisation Dates and Key Assumptions

Finalisation Dates

| Economic outlook (refer Chapter 1) | | 21 November |

| Tax revenue forecasts | | 27 November |

| Fiscal forecasts | | 8 December |

| Government decisions and circumstances | | 8 December |

| Actual asset revaluations | | 31 October |

| Foreign exchange rates | | 31 October |

| Specific fiscal risks (refer Chapter 4) | | 8 December |

| Contingent liabilities and commitments (refer Chapter 4) | | 31 October |

Key assumptions

The fiscal forecasts have been prepared in accordance with the Fiscal Responsibility Act 1994. They are based on the Crown's accounting policies and assumptions (refer page 88 of the GAAP tables). As with all assumptions, there is a degree of uncertainty surrounding them. This uncertainty increases as the forecast horizon extends. A summary of the key economic assumptions that are

particularly relevant to the fiscal forecasts is provided below (on a June-year-end basis to align with the Crown's balance date of 30 June):

| | 2003/04

| | 2004/05

| | 2005/06

| | 2006/07

| | 2007/08

|

|---|

June Years

|

|---|

| | BEFU

| | DEFU

| | DEFU

| | DEFU

| | DEFU

| | DEFU

|

|---|

| Real GDP (P) (ann avg % chg) | | 2.1 | | 3.0 | | 2.5 | | 3.8 | | 3.2 | | 3.0 |

| Nominal GDP (E) ($m) | | 134,034 | | 136,112 | | 142,932 | | 150,944 | | 158,512 | | 166,744 |

| CPI (ann avg %) | | 1.7 | | 1.5 | | 2.3 | | 2.4 | | 2.2 | | 2.1 |

| Govt 10-year bonds (qty avg %) | | 6.2 | | 6.4 | | 6.3 | | 6.0 | | 6.0 | | 6.0 |

| 90-day bill rate (qty avg %) | | 5.3 | | 5.6 | | 5.8 | | 5.8 | | 5.8 | | 5.8 |

Unemployment rate (HLFS) basis

(ann avg %) | | 5.5 | | 4.4 | | 4.7 | | 4.9 | | 4.8 | | 4.8 |

Full-time equivalent employment

(ann avg %) | | 1.0 | | 3.2 | | 0.9 | | 1.1 | | 1.4 | | 1.4 |

| Current account (% of GDP) | | -5.1 | | -5.7 | | -6.1 | | -5.6 | | -5.7 | | -5.2 |

Source: The Treasury

New Zealand Superannuation (NZS) Fund

The estimated annual contribution to the NZS Fund for the year ending 30 June 2005 is $1.979 billion. The contribution to the NZS Fund is calculated over a 40-year rolling horizon to ensure superannuation entitlements over the next 40 years could be met if the contribution rate were to be held constant at that level for 40 years.

The Government is making the required annual contribution for 2003/04 as calculated by the formula set out in the NZS Fund Act.

$ billion (June year end)

| | 2002

| | 2003

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

|

|---|

| Required contribution | | N/A | | N/A | | 1.879 | | 1.979 | | 2.156 | | 2.265 | | 2.410 |

| Intended contribution | | 600 | | 1.200 | | 1.879 | | 1.979 | | 2.156 | | 2.265 | | 2.410 |

The underlying assumptions in calculating the contribution are the nominal GDP series to 2048, the New Zealand Superannuation (NZS) expense series to 2048, and the expected long run net after-tax annual return of the NZS Fund (6.8%) (7.0% Budget Update). The forecast rate-of-return is based on the forecasts of the Guardians of NZS. The GDP and NZS expense series were projected using the assumptions stated on page 29 of the 2003 FSR.

The Treasury website contains further information on the NZS Fund, as well as a copy of the NZS Fund model.

2

Fiscal Outlook

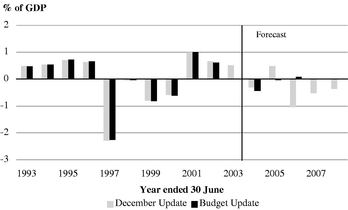

Summary of the December Update

The forecast fiscal outlook is stronger in the earlier forecast years than that contained in the Budget Update. Key influences on the operating balance/OBERAC and debt tracks include:

- •

- a stronger starting position due to higher-than-forecast OBERAC and cash flows in 2002/03

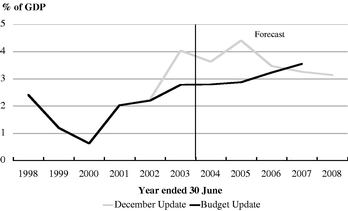

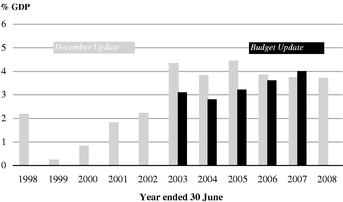

Figure 2.1—OBERAC comparison

Source: The Treasury

- •

- a slightly stronger actual and forecast economic position, resulting in lower benefit expenses and stronger tax revenues; tax revenues are also forecast to be higher based on recent outturns indicating a stronger corporate tax base

- •

- the Government's decision to increase spending consistent with the proposals in the 2003 FSR, produces a relatively flat OBERAC trend from 2005/06 onwards, compared to a rising profile in the Budget Update. The extent of the change is outlined in the 2004 BPS and on page 43.

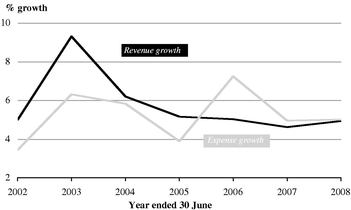

Figure 2.2—Core Crown revenue growth and expense growth (excluding Government Superannuation Fund (GSF) valuation)

Source: The Treasury

These influences translate into:

- •

- an OBERAC forecast at $5.2 billion (3.8% of GDP) in 2003/04; lower than last year largely due to Crown entity surpluses (excluding valuations) expected to be lower in 2003/04

- •

- an OBERAC that rises in 2004/05 to 4.4% of GDP ($6.3 billion) due to revenue growth outpacing expense growth, before decreasing to 3.8% of GDP in 2005/06 as the trend reverses

Figure 2.3—Debt comparison

Source: The Treasury

- •

- an improved net cash position from 2002/03 and 2003/04 reduces debt during 2003/04 compared with the Budget Update

- •

- in nominal terms, debt is forecast to decrease from $36 billion towards $33 billion by 2005/06 (due to the improved cash position from last year and the current year). Over the remaining forecast horizon debt remains stable between $33 billion and $34 billion

- •

- gross sovereign-issued debt is forecast to fall from 28% of GDP in 2002/03 to 20.4% of GDP by 2007/08

- •

- as a result of the improved overall cash position through last year and the current year, the Government's domestic bond programme has been lowered for 2003/04 to $2.2 billion (from $3.2 billion). In addition, the forecast bond programme for 2004/05 has also been lowered to $2.3 billion (from $3.5 billion)

- •

- Tables of the key indicators are located on pages 44 and 45.

Key Trends

OBERAC rises before flattening towards the end of the forecast horizon ...

The OBERAC is forecast at $5.2 billion (3.8% of GDP) in the current year, rising to $6.3 billion (4.4% of GDP) in 2004/05 before reducing to between $5.8 billion and $6.2 billion (3.7% of GDP) by 2007/08. The OBERAC, as a percentage of GDP, falls from 2004/05 due to the inclusion in the forecasts of additional new spending (previously signalled in the 2003 FSR).

The amount of additional spending included in the fiscal forecasts is more than signalled in the 2003 FSR, however the tax forecasts are also higher and so the OBERAC remains above 3% of GDP.

... enabling the Government to apply operating cash flows to its investment programme ...

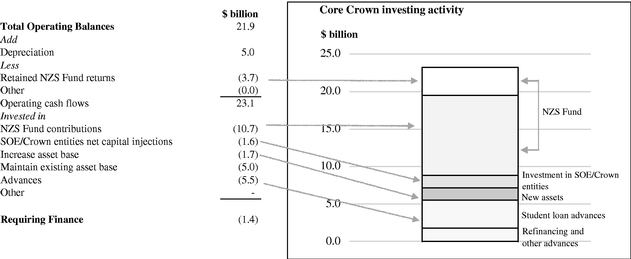

The core Crown operating balance sums to around $21.9 billion over the 2003/04 to 2007/08 period, which generates cash for the core Crown of around $23.1 billion over the same period.

As outlined in Table 2.1, this cash is invested primarily in NZS Fund contributions of $10.7 billion, advances of $5.5 billion (mainly student loans and refinancing existing private sector debt of the health and housing sectors) and purchases of physical assets of $6.7 billion (schools, hospitals, defence equipment, for example). There is a residual financing requirement of around $1.4 billion, which is primarily met by reducing the holdings of marketable securities and deposits which have accumulated from 2002/03. To see the year-on-year capital programme relative to the annual OBERAC and operating cash flows, refer to figure 1 in the BPS.

Table 2.1—Impact of core Crown operating surpluses on the balance sheet from 2003/04 to 2007/08

Source: The Treasury

... while gross debt as a percentage of GDP continues to fall

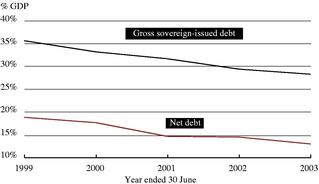

Gross sovereign-issued debt falls in nominal terms until 2004/05, and then remains relatively stable between $33 billion and $34 billion. As a percentage of GDP, debt falls from 28% in 2002/03 to 20.4% by 2007/08.

Figure 2.4—Gross sovereign-issued debt (% of GDP and $ million)

Source: The Treasury

The initial decrease in debt reflects surplus cash from the strong OBERAC results in 2002/03 and the expected result in 2003/04, and then remains flat as the cash flows from the OBERAC and surplus financial assets are broadly sufficient to fund all capital spending.

Net Crown debt reduces over the forecast horizon from around 13% of GDP in 2002/03 towards 8% of GDP by 2007/08.

The improved cash position for 2002/03 and 2003/04 has resulted in a decrease to the Government's 2003/04 and forecast 2004/05 bond programmes. The improved cash position (reflected in holdings of financial assets) has effectively been spread over the two programmes. The 2003/04 bond programme has been reduced to $2.2 billion, compared with $3.2 billion at the Budget Update. The forecast 2004/05 programme has been reduced to $2.3 billion from the $3.5 billion previously forecast.

Comparison of OBERAC with Budget Update

Compared with the Budget Update the OBERAC was stronger in 2002/03 than forecast and is expected to be stronger in 2003/04 and 2004/05, largely reflecting improvements to tax revenue.

From 2005/06, the OBERAC/operating balance is broadly similar in nominal terms to the Budget Update forecasts, reflecting improved tax revenues and SOEs'/Crown entities' surpluses, offset by increases to forecast new spending. However, the OBERAC is flatter as a percentage of GDP, whereas the Budget Update forecasts had a rising profile.

Table 2.2—Operating balance reconciliation (explains changes to the operating balance since the Budget Update)

($ million)

| | 2002/03

Actual

| | 2003/04

Forecast

| | 2004/05

Forecast

| | 2005/06

Forecast

| | 2006/07

Forecast

| |

|---|

| Operating balance 2003 Budget Update | | 1,361 | | 3,761 | | 4,474 | | 4,929 | | 6,181 | |

| Changes (core Crown revenues and net SOEs/CEs) | | | | | | | | | | | |

| Tax revenue forecasting changes | | 395 | | 1,600 | | 1,741 | | 1,730 | | 1,727 | |

| Other sovereign revenue | | (13 | ) | 70 | | 123 | | 113 | | 99 | |

| Investment income | | 420 | | 154 | | 274 | | 332 | | 302 | |

| Other revenue | | 135 | | 41 | | 86 | | 80 | | 90 | |

| Other change to SOEs and Crown entities (excluding ACC valuation change) | | 637 | | 179 | | 225 | | 634 | | 310 | |

| Valuation changes (GSF and ACC liability movements) | | (889 | ) | 694 | | — | | — | | — | |

Changes (core Crown expenses excl GSF 2003/04) |

|

|

|

|

|

|

|

|

|

|

|

| Change to future operating spending | | — | | — | | (383 | ) | (1,572 | ) | (2,367 | ) |

| Welfare benefits | | 47 | | 233 | | 401 | | 270 | | 237 | |

| Education | | 136 | | 37 | | (28 | ) | (112 | ) | (143 | ) |

| Health | | 85 | | (69 | ) | (22 | ) | (21 | ) | 76 | |

| Transport | | (4 | ) | (119 | ) | (67 | ) | (82 | ) | (150 | ) |

| Other core Crown functional expenses | | (36 | ) | (288 | ) | (467 | ) | (490 | ) | (433 | ) |

| Finance costs | | (308 | ) | (201 | ) | (19 | ) | (16 | ) | (11 | ) |

| | |

| |

| |

| |

| |

| |

| Total core Crown expense change | | (80 | ) | (407 | ) | (585 | ) | (2,023 | ) | (2,791 | ) |

| | |

| |

| |

| |

| |

| |

| Total Changes | | 605 | | 2,331 | | 1,864 | | 866 | | (263 | ) |

| | |

| |

| |

| |

| |

| |

| Operating balance 2003 December Update | | 1,966 | | 6,092 | | 6,338 | | 5,795 | | 5,918 | |

Source: The Treasury

Major changes to the components within the operating balance forecasts include:

- •

- tax revenue is higher over the forecast horizon. The following section contains an outline of the reasons for the improved tax forecasts

- •

- the SOE and Crown entity surpluses were higher in 2002/03, reflecting strength in SOEs and surpluses in the transport sector (as more was spent on capital rather than operating activity for example). From 2003/04 forward, the improvement against Budget Update is more muted, largely reflecting a mix of higher SOE forecasts and the transport sector forecasting to spend more of its revenue on capital expenditure rather than operating (which is debt neutral)

- •

- the valuation of the GSF and ACC unfunded liabilities are lower in 2003/04 compared with the Budget Update, primarily due to the increase in discount rates since the time of the Budget valuations, partially offset by updated scheme data for the GSF liability calculation

- •

- future new operating spending has been increased from previous forecasts from 2004/05 onwards, reflecting the Government moving on its previously signalled intentions to increase spending should economic and fiscal conditions continue as previously forecast (some of which has already been allocated to baselines). Refer page 43 for further details

- •

- welfare benefit costs are lower over the forecast period primarily through lower unemployment benefits reflecting lower unemployment levels than forecast in the Budget Update

- •

- transport expenses have increased reflecting forecast changes, though these are somewhat offset by additional revenues

- •

- net finance costs (investment income less finance costs) are effectively lower across the forecast horizon, reflecting a lower net debt position. While this appears to be reflected in higher investment income rather than lower finance costs, the movements since the Budget Update also reflect a gross up to both investment income and finance costs (reflecting a change in disclosure)

- •

- the change in other functional expenses (education, health and other core Crown functional expense in Table 2.2) represent forecast changes largely driven by demographics (impacting on GSF expenses and education expenses) and the specific allocation of new policy spending since the Budget Update (refer Table 2.3).

Table 2.3—Specific decisions for new policy since the 2003 Budget Update

($ million)

| | 2003/04

| | 2004/05

| | 2005/06

| | 2006/07

|

|---|

| Review of Child Youth and Family Services | | 29 | | 61 | | 66 | | 66 |

| Large budget film subsidies | | 40 | | 40 | | 40 | | 40 |

| State sector employment based superannuation | | 1 | | 19 | | 33 | | 33 |

| NZDF contribution to operation enduring freedom | | 28 | | 5 | | — | | — |

| Solomon Islands deployment | | 22 | | 5 | | — | | — |

| Painted Apple Moth | | 24 | | — | | — | | — |

| Other decisions | | 199 | | 177 | | 162 | | 118 |

| | |

| |

| |

| |

|

| Total decisions since the 2003 Budget Update (GST inclusive) | | 342 | | 307 | | 301 | | 257 |

Source: The Treasury

Revenue and Expenses

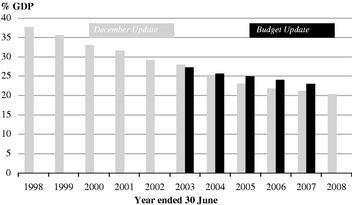

Table 2.4—Revenue and expenses comparison with Budget Update

Revenue and Expenses

(% of GDP)

| | 2003

Actual

| | 2004

Forecast

| | 2005

Forecast

| | 2006

Forecast

| | 2007

Forecast

| | 2008

Forecast

|

|---|

| Core Crown Revenue | | | | | | | | | | | | |

| December Update | | 33.9 | | 34.0 | | 34.1 | | 33.9 | | 33.8 | | 33.7 |

| Budget Update | | | | 33.2 | | 32.9 | | 33.0 | | 33.1 | | |

Total Tax Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

| December Update | | 30.9 | | 31.0 | | 30.9 | | 30.5 | | 30.2 | | 30.1 |

| Budget Update | | | | 30.3 | | 30.0 | | 30.0 | | 29.8 | | |

Total Crown Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

| December Update | | 44.3 | | 43.7 | | 44.2 | | 43.9 | | 43.6 | | 43.3 |

| Budget Update | | | | 42.7 | | 42.6 | | 42.6 | | 42.5 | | |

Core Crown Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

| December Update | | 32.4 | | 30.8 | | 30.7 | | 31.2 | | 31.2 | | 31.1 |

| Budget Update | | | | 31.1 | | 30.7 | | 30.4 | | 30.1 | | |

Total Crown Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

| December Update | | 42.9 | | 39.3 | | 39.8 | | 40.1 | | 39.9 | | 39.6 |

| Budget Update | | | | 40.0 | | 39.5 | | 39.1 | | 38.5 | | |

Source: The Treasury

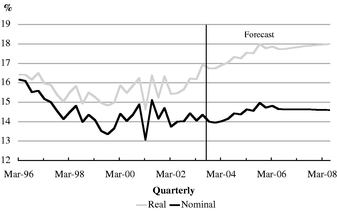

Over the forecast period, the total Crown revenue-to-GDP and expenses-to-GDP ratios are reasonably stable, though tend to drift down slowly.

The revenue-to-GDP trend of the total Crown is driven mainly from the trend in "core Crown" revenue forecasts, which are discussed in more detail under tax revenue.

The core Crown expenses-to-GDP ratio rises marginally in 2005/06 reflecting the impact of the increased budget package (refer following expense section) and then levels out at around 31.2% of GDP.

Tax Revenue

Table 2.5—Tax revenue indicators

Tax Revenue

| | 2003

Actual

| | 2004

Forecast

| | 2005

Forecast

| | 2006

Forecast

| | 2007

Forecast

| | 2008

Forecast

|

|---|

| ($ million) | | | | | | | | | | | | |

| Total Crown | | 39,785 | | 42,251 | | 44,114 | | 46,043 | | 47,944 | | 50,140 |

(% GDP) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Crown | | 30.9 | | 31.0 | | 30.9 | | 30.5 | | 30.2 | | 30.1 |

Source: The Treasury

The tax revenue forecasts have been increased substantially in every year of the forecast period.

Table 2.6—Change in tax revenue forecasts since Budget Update

($ million)

| | 2002/03

Actual

| | 2003/04

Forecast

| | 2004/05

Forecast

| | 2005/06

Forecast

| | 2006/07

Forecast

| |

|---|

| Tax revenue 2003 Budget Update Changes | | 39,390 | | 40,651 | | 42,373 | | 44,313 | �� | 46,217 | |

| Corporate taxes | | 234 | | 897 | | 694 | | 756 | | 778 | |

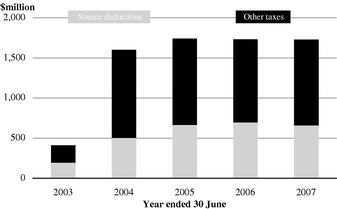

| Source deductions | | 194 | | 501 | | 662 | | 694 | | 658 | |

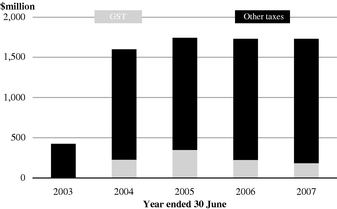

| Goods and services tax | | (28 | ) | 224 | | 347 | | 219 | | 183 | |

| Resident withholding tax | | 38 | | 89 | | 90 | | 77 | | 77 | |

| Other persons tax | | (63 | ) | (166 | ) | (138 | ) | (127 | ) | (91 | ) |

| Other | | 20 | | 55 | | 86 | | 111 | | 122 | |

| Total Changes | | 395 | | 1,600 | | 1,741 | | 1,730 | | 1,727 | |

| | |

| |

| |

| |

| |

| |

| Tax Revenue 2003 December Update | | 39,785 | | 42,251 | | 44,114 | | 46,043 | | 47,944 | |

Source: The Treasury

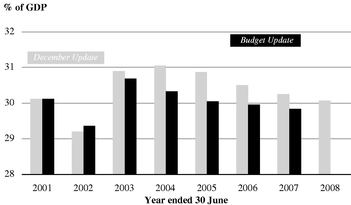

Tax-to-GDP higher than Budget Update

In the Budget Update forecasts, the ratio of tax to GDP was expected to peak at 30.7% in 2002/03. At the time, we believed that the sudden, sharp rise in the tax-to-GDP ratio was something of an anomaly and that the spike would eventually be smoothed out by a combination of revisions to GDP and a moderation in future tax revenue growth.

Figure 2.5—Ratio of total tax revenue to nominal GDP

Source: The Treasury

Since the Budget Update, more data has come to hand that indicate the tax-to-GDP ratio may persist at its current level for some time yet.

There are two tax types that are mainly responsible for the recent rise in the tax-to-GDP ratio:

- •

- A recent run-down of corporate tax losses has contributed to rapid company tax revenue growth.

- •

- A rise in the average tax rate coupled with strong labour market growth has spurred growth in source deductions.

These are discussed in more detail in the relevant sections below.

The ratio of tax to GDP gradually subsides after 2004/05. This is because we have decided to exercise a little caution in the later years of the forecast period. For instance, it remains to be seen whether or not company tax loss utilisation will remain at relatively low levels. A sudden build-up of losses can have an adverse effect on the tax take, as explained in the section on corporate taxes below.

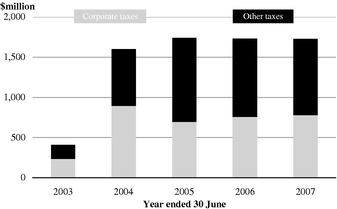

Corporate taxes contribute the largest portion of the increase to the forecast ...

Figure 2.6—Change in corporate tax forecasts since Budget Update

Source: The Treasury

As mentioned above, several new pieces of information have come to hand since the Budget Update forecasts were finalised:

- •

- Corporate tax outturns are running well ahead of forecast.

- •

- Provisional tax payments and assessments lodged for the 2004 tax year indicate that tax revenue for 2003/04 will be considerably higher than previously expected.

- •

- Annual tax returns lodged over the last six months or so indicate that the stock of tax losses available to be used to offset taxable income has dropped markedly over the last few years and is now much lower than previously thought.

Putting all of these factors together, the corporate tax forecast for 2003/04 is now about $900 million higher than at the Budget Update. With company profits forecast to continue to increase steadily each year, the relatively low level of loss utilisation is expected to persist, resulting in similar increases to the corporate tax forecast in the later years of the forecast period.

However, if the level of loss utilisation were to rise again, company tax could take a sharp fall, as happened in 1991, for instance, when losses built up in the early 1990s' recession contributed to a fall of nearly 30% in company tax. Since we are not certain of a continued low level of loss offset in the company tax base, we have taken a cautious approach to corporate tax growth further out. For this reason, forecast corporate tax growth is lower than forecast growth in corporate profits from 2005/06 onwards.

... and source deductions' forecasts are also much higher than Budget

Figure 2.7—Change in source deductions forecasts since Budget Update

Source: The Treasury

Source deductions' outturns to October are about $100 million above forecast. This follows on from 2002/03 when source deductions finished the year nearly $200 million above forecast.

There appears to be two factors causing this:

- •

- PAYE outturns indicate a notable rise in the average tax rate on employees' remuneration.

- •

- Growth in the labour market has been higher than forecast in the Budget Update.

The current variance from forecast is expected to continue to grow, reaching about $500 million by the end of 2003/04. This lift in the base flows through to the later forecast years, where source deductions' forecasts have been increased by between $650 million and $700 million each year.

With the labour market growing at a faster rate than total GDP over the past few years, employees' compensation now makes up a bigger part of total GDP than before. Since employees' compensation has a higher effective tax rate than most other tax bases, this will tend to drive up the overall tax-to-GDP ratio. Employees' compensation is forecast to remain at about 40% of GDP throughout the forecast period.

The GST forecasts are also up...

Figure 2.8—Change in GST forecasts since Budget Update

Source: The Treasury

Although nominal consumption is more or less in line with expectations, growth in residential investment has continued to outpace the Budget Update forecasts, providing an extra boost to the GST base in 2003/04. Our current view is that GST will finish the year around $220 million above the Budget Update forecast.

Rises in the forecast levels of domestic consumption and residential investment drive up the GST forecasts for 2004/05 and beyond by between $180 million and $350 million.

... but other persons tax forecasts have been lowered

At the time of the Budget Update, there was some uncertainty around the income levels of taxpayers in the other persons tax base. The tax outturns have subsequently come in below forecast, mainly as a result of farmers expecting their tax liability for the 2004 tax year to be somewhat lower than we had forecast. Thus the other persons tax forecast has been reduced by about $170 million for 2003/04.

With income levels in subsequent years now expected to be lower than forecast in the Budget Update, the other persons tax forecast has also been reduced slightly in later forecast years.

Effects on the tax forecasts of tax policy changes

One of the proposed changes to the Fiscal Responsibility Act (which is being merged with the Public Finance Act) will be the requirement for an annual statement on new government tax decisions that materially affect the tax revenue forecasts. Although disclosure of such information is not yet required, it has been included in the December Update.

The only new tax decision to materially affect the December Update forecasts was the decision to remove the freeze on tariff rates from 1 July 2006. This is expected to reduce customs duty by $20 million in 2006/07 and $50 million in 2007/08.

Inland Revenue's tax forecasts

In line with established practice, Inland Revenue has prepared an independent set of tax forecasts, based in the short term on more detailed analysis of taxpayer information, and in the longer term reflecting the same underlying macroeconomic trends that underpin the Treasury's tax forecasts.

Differing views on individuals' taxes are the major point of difference between the two sets of forecasts in 2003/04 and 2004/05. From 2005/06 onwards, the total Inland Revenue and Treasury tax forecasts are relatively close to each other (also refer www.treasury.govt.nz/forecasts/defu/2003/).

Table 2.7—Treasury and Inland Revenue tax revenue forecasts

($ million)

| | 2003/04

Forecast

| | 2004/05

Forecast

| | 2005/06

Forecast

| | 2006/07

Forecast

| | 2007/08

Forecast

| |

|---|

| Individuals' Taxes | | | | | | | | | | | |

| Treasury | | 21,791 | | 22,886 | | 24,060 | | 25,243 | | 26,518 | |

| Inland Revenue | | 21,580 | | 22,626 | | 23,863 | | 25,173 | | 26,514 | |

| | |

| |

| |

| |

| |

| |

| Difference | | 211 | | 260 | | 197 | | 70 | | 4 | |

Corporate Taxes |

|

|

|

|

|

|

|

|

|

|

|

| Treasury | | 6,832 | | 6,994 | | 7,268 | | 7,431 | | 7,747 | |

| Inland Revenue | | 6,876 | | 7,036 | | 7,331 | | 7,553 | | 7,862 | |

| | |

| |

| |

| |

| |

| |

| Difference | | (44 | ) | (42 | ) | (63 | ) | (122 | ) | (115 | ) |

Goods and services Tax |

|

|

|

|

|

|

|

|

|

|

|

| Treasury | | 9,338 | | 9,824 | | 10,179 | | 10,625 | | 11,145 | |

| Inland Revenue | | 9,304 | | 9,816 | | 10,206 | | 10,620 | | 11,068 | |

| | |

| |

| |

| |

| |

| |

| Difference | | 34 | | 8 | | (27 | ) | 5 | | 77 | |

Other Taxes |

|

|

|

|

|

|

|

|

|

|

|

| Treasury | | 4,290 | | 4,411 | | 4,536 | | 4,645 | | 4,730 | |

| Inland Revenue | | 4,296 | | 4,426 | | 4,546 | | 4,638 | | 4,713 | |

| | |

| |

| |

| |

| |

| |

| Difference | | (6 | ) | (15 | ) | (10 | ) | 7 | | 17 | |

Total Tax |

|

|

|

|

|

|

|

|

|

|

|

| Treasury | | 42,251 | | 44,115 | | 46,043 | | 47,944 | | 50,140 | |

| Inland Revenue | | 42,056 | | 43,904 | | 45,946 | | 47,984 | | 50,157 | |

| | |

| |

| |

| |

| |

| |

| Difference | | 195 | | 211 | | 97 | | (40 | ) | (17 | ) |

Source: The Treasury

Expenses

Table 2.8—Total expenses indicators

Expenses

| | 2003

Actual

| | 2004

Forecast

| | 2005

Forecast

| | 2006

Forecast

| | 2007

Forecast

| | 2008

Forecast

|

|---|

| ($ million) | | | | | | | | | | | | |

| Core Crown | | 41,749 | | 41,868 | | 43,877 | | 47,054 | | 49,385 | | 51,865 |

| Core Crown (excluding GSF valuation) | | 39,905 | | 42,232 | | 43,877 | | 47,054 | | 49,385 | | 51,865 |

| Total Crown | | 55,224 | | 53,508 | | 56,900 | | 60,508 | | 63,240 | | 66,022 |

(% of GDP) |

|

|

|

|

|

|

|

|

|

|

|

|

| Core Crown | | 32.4 | | 30.8 | | 30.7 | | 31.2 | | 31.2 | | 31.1 |