UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: (811- 02742 )

Exact name of registrant as specified in charter: Putnam Equity Income Fund

Address of principal executive offices: One Post Office Square, Boston, Massachusetts 02109

| Name and address of agent for service: | Beth S. Mazor, Vice President |

| One Post Office Square | |

| Boston, Massachusetts 02109 | |

| Copy to: | John W. Gerstmayr, Esq. |

| Ropes & Gray LLP | |

| One International Place | |

| Boston, Massachusetts 02110 | |

Registrant’s telephone number, including area code: (617) 292-1000

Date of fiscal year end: November 30, 2006

Date of reporting period: December 1, 2005— May 31, 2006

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

What makes Putnam different?

In 1830, Massachusetts Supreme Judicial Court Justice Samuel Putnam established The Prudent Man Rule, a legal foundation for responsible money management.

THE PRUDENT MAN RULE

All that can be required of a trustee to invest is that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

A time-honored tradition in money management

Since 1937, our values have been rooted in a profound sense of responsibility for the money entrusted to us.

A prudent approach to investing

We use a research-driven team approach to seek consistent, dependable, superior investment results over time, although there is no guarantee a fund will meet its objectives.

Funds for every investment goal

We offer a broad range of mutual funds and other financial products so investors and their financial representatives can build diversified portfolios.

A commitment to doing what’s right for investors

We have below-average expenses and stringent investor protections, and provide a wealth of information about the Putnam funds.

Industry-leading service

We help investors, along with their financial representatives, make informed investment decisions with confidence.

| Putnam Equity Income Fund |

| 5| 31| 06 Semiannual Report |

| Message from the Trustees | 2 |

| About the fund | 4 |

| Report from the fund managers | 7 |

| Performance | 12 |

| Expenses | 15 |

| Portfolio turnover | 17 |

| Risk | 18 |

| Your fund’s management | 19 |

| Terms and definitions | 22 |

| Trustee approval of management contract | 24 |

| Other information for shareholders | 29 |

| Financial statements | 30 |

| Brokerage commissions | 50 |

| Cover photograph: © White-Packert Photography |

| Message from the Trustees |

Dear Fellow Shareholder

Investors continue to keep a close watch on the course of the economy. Globally, it appears that, assuming economic growth exceeds 4% in 2006, we will have seen the strongest economic performance over a four-year period in over thirty years. Corporate profits have boomed around the world, business capacity utilization rates have moved up, and unemployment rates have come down. Given such a sustained period of robust growth, it is not surprising that prices have begun to rise, inflation rates have crept up, and central banks in many countries, particularly the Federal Reserve (the Fed) in the United States, have pushed interest rates higher.

In recent weeks, investors have worried that these higher rates could threaten the fundamentals of the global economy, prompting a widespread sell-off. However, we believe that today’s higher interest rates, far from being a threat to global economic fundamentals, are in fact an integral part of them. Higher interest rates are bringing business borrowing costs closer to the rate of return available from investments. In our view, this should help provide the basis for a longer and more durable business expansion and a continued healthy investment environment.

You can be assured that the investment professionals managing your fund are closely monitoring the factors that influence the performance of the securities in which your fund invests. Moreover, Putnam Investments’ management team, under the leadership of Chief Executive Officer Ed Haldeman, continues to focus on investment performance and remains committed to putting the interests of shareholders first.

2

In the following pages, members of your fund’s management team discuss the fund’s performance and strategies for the fiscal period ended May 31, 2006, and provide their outlook for the months ahead. As always, we thank you for your support of the Putnam funds.

| Putnam Equity Income Fund: seeking to harness the power of dividends |

When a company is in a building phase, profits are generally reinvested in areas such as research or infrastructure. However, a large mature company that has progressed beyond the growth stage will often use a portion of its profits for dividends, paid directly to its shareholders. Putnam Equity Income Fund is composed primarily of stocks of midsize and large companies that pay dividends to their shareholders.

The issuance of dividends can be a positive indicator, often signaling that a company is profitable and has excess funds after its expenses are paid. It also represents management’s confi-dence in continued financial corporate health. Dividends can act as tangible evidence of a company’s ability and commitment to create shareholder value. In addition, dividends can also act as an incentive for investors to hold stock in a stable company that is not experiencing a great deal of growth.

Investors have historically turned to dividend-paying stocks for several reasons. They can offer a cash-in-hand return (versus future capital appreciation that may or may not occur), even in a bear market. They can also be reinvested, allowing an investor to take advantage of the power of compounding, which can serve as a valuable wealth-building benefit. And, should individual stocks decline in price, their dividend-paying counterparts can provide a cushion for portfolio returns, lessening the impact of other holdings’ losses. Dividend-paying stocks have traditionally played an important part in retirement planning by offering an income stream for investors on fixed incomes.

| Dividends can bolster price appreciation or help offset share price declines. |

By targeting undervalued stocks of dividend-paying companies, Putnam Equity Income Fund’s management team seeks to construct a portfolio of stocks whose issuing companies are undervalued and poised for positive change. The goal is to uncover stocks that will appreciate in value as the market recognizes their long-term worth. From the universe of U.S. mid- and large-capitalization value stocks, the team, together with Putnam’s equity analysts, seeks companies that are not only well established with solid fundamentals, but that continue to find ways to grow and remain profitable — and offer above-average dividends.

This fund may invest a portion of its assets in small and/or midsize companies. Such investments increase the risk of greater price fluctuations. Value investing seeks underpriced stocks, but there is no guarantee that a stock’s price will rise.

| In-depth analysis is key to successful stock selection. |

Drawing on the expertise of a dedicated team of stock analysts, the fund’s management team seeks attractive value stocks. Once a stock is selected for the portfolio, it is regularly assessed by members of the team to ensure that it continues to meet their criteria, including:

Valuation They carefully consider how each stock is valued, seeking stocks whose valuations are attractive relative to the company’s profit potential.

Change They focus on company fundamentals against the broader context of industry trends to identify whether individual companies possess a catalyst for positive change.

Quality They look for high-quality companies, seeking characteristics such as sound balance sheets, profitable business models, and competent management.

Putnam Equity Income Fund seeks to invest in undervalued stocks of mid-and large-cap companies that are poised to experience positive change that may improve financial performance. The fund targets stocks of mature companies that pay above-average dividend yields, and it may be appropriate for conservative investors who seek capital appreciation and current income.

| Highlights * For the six months ended May 31, 2006, Putnam Equity Income Fund’s class A shares returned 4.77% without sales charges. * Over the same period, the fund’s benchmark, the Russell 1000 Value Index, returned 6.53% . * The average return for the fund’s Lipper category, Equity Income Funds, was 5.24% . * Additional fund performance, comparative performance, and Lipper data can be found in the performance section beginning on page 12. |

Performance

Total return for class A shares for periods ended 5/31/06

Since the fund’s inception (6/15/77), average annual return is 10.91% at NAV and 10.70% at POP.

| Average annual return | Cumulative return | ||||

| NAV | POP | NAV | POP | ||

| 10 years | 9.30% | 8.71% | 143.23% | 130.55% | |

| 5 years | 5.51 | 4.38 | 30.77 | 23.91 | |

| 3 years | 12.77 | 10.76 | 43.41 | 35.87 | |

| 1 year | 10.60 | 4.78 | 10.60 | 4.78 | |

| 6 months | — | — | 4.77 | –0.75 | |

Data is historical. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Returns at NAV do not reflect a sales charge of 5.25% . For the most recent month-end performance, visit www.putnam.com. A short-term trading fee of up to 2% may apply.

6

Report from the fund managers

The period in review

Domestic stock market gains during the first half of your fund’s 2006 fiscal year were somewhat modest, possibly reflecting the dampening effects of rising interest rates and inflationary pressures. Your fund posted what we consider a respectable return, yet lagged its benchmark. The fund’s focus on stocks with above-average dividend yields did not help during the period because stocks with low or no yields continued to outperform. The fund also lagged the average for its peer group, Lipper Equity Income Funds. We believe this may be due to a combination of factors, including the fund’s greater exposure to larger-cap stocks within its investment universe, as well as weaker-than-expected results from certain portfolio holdings during the period. Based on our fundamental and quantitative analysis, we believe these holdings are poised to offer attractive returns over the longer term.

Market overview

Productivity growth in the United States was slowed by the steady braking effect of the Fed’s numerous interest-rate increases. As of its meeting on May 10, 2006, the Fed had raised the federal funds rate 16 times since it began to tighten the money supply in June 2004. As of the end of the fund’s fiscal period, the federal funds rate stood at 5%, and Fed Chairman Ben Bernanke has signaled that further hikes could be necessary to sustain economic growth while staving off inflation.

Despite Fed action, rising energy and materials costs caused an uptick in general inflation as businesses began to pass higher costs on to consumers, who consequently reined in their spending on discretionary items. Consumer confi-dence began to wane. Businesses, on the other hand, increased their capital spending, which was made possible by continued strong profit growth. In the financial markets, gains were not as robust as they had been in the prior six months. Major market indexes posted single-digit returns, with the exception of international stocks, which continued to outperform with strong gains. Stocks outpaced bonds. Large-cap stocks moved

7

ahead for a few brief periods, but small caps dominated overall. Investors continued to prefer value stocks, despite broad speculation that growth stocks would begin to outperform. The market seemed indifferent to stocks offering dividends. The best-performing sectors during the period were transportation, capital goods, basic materials, and energy. The worst-performing sectors were conglomerates, utilities, technology, and consumer cyclicals.

Strategy overview

Your fund invests in a well-diversified portfolio of undervalued large-cap stocks that we believe offer both attractive dividend income and the potential for long-term capital appreciation. During the period, we made slight adjustments to various sector weightings in an effort to enhance absolute and relative returns. Within transportation, the best-performing sector, we favored railroad stocks, which offered more attractive dividend yields than those of airlines. Railroad stocks performed well, but we were slightly underweighted versus the benchmark, which dampened relative performance. However, relative to the benchmark, the fund had nearly twice the allocation to capital goods, the second-strongest sector for the period, a weighting that contributed positively to performance. Within the basic materials sector, we favored large-cap chemical companies because of their attractive dividend yields. During this time period,

Market sector performance

These indexes provide an overview of performance in different market sectors for the six months ended 5/31/06.

| Equities | |

| Russell 1000 Value Index (large-company value stocks) | 6.53% |

| S&P 500 Index (broad stock market) | 2.60% |

| MSCI EAFE Index (international stocks) | 15.30% |

| Russell Midcap Growth Index (midsize-company growth stocks) | 4.11% |

| Bonds | |

| Lehman Government Bond Index (U.S. Treasury and agency securities) | –0.25% |

| JP Morgan Global High Yield Index (global high-yield corporate bonds) | 4.56% |

| Lehman Credit Index (corporate bonds) | –0.74% |

8

however, lower-yielding mid-cap metals and mining companies delivered stronger results.

The portfolio was slightly underweighted in the energy sector, which continued to outperform but did so by a much smaller margin than it had last year. Nevertheless, our stock selection within this sector contributed favorably to returns. Our emphasis on conglomerates detracted from performance, as the sector faltered. Likewise, our overweight exposure to the technology and consumer cyclical sectors had a negative effect on returns. The portfolio had an underweight exposure to utilities, consumer staples, and financials.

In general, we lessened exposure to large-cap stocks somewhat and lowered the fund’s average market capitalization, as we sought and discovered value opportunities in the smaller-cap range of the fund’s investment universe.

Your fund’s holdings

Lockheed Martin was among the portfolio’s top performers for the period. This aerospace and defense contractor, whose largest customer is the U.S. government, benefited from robust defense procurement spending and aerospace spending over the past several years. We believed the stock was intrinsically cheap. We trimmed the position by a small amount during the period to lock in some profits.

Consistently high energy prices and strong demand made Amerada Hess

Comparison of top industry weightings

This chart shows how the fund’s top weightings have changed over the last six months.

Weightings are shown as a percentage of net assets. Holdings will vary over time.

9

and Marathon Oil two of the fund’s best-performing positions over the period. These diversified energy companies extract, refine, transport, and market petroleum products and are also involved in exploration for new sources of supply. Both significantly increased their revenues and earnings during the period. In addition, we believe both companies have demonstrated fundamental improvements in production growth, and their management teams are focused on providing shareholders with higher returns. We sold shares of Amerada Hess throughout the period to lock in strong gains. We added to the fund’s position in Marathon Oil. We expect the company will enhance its rate of production in coming years.

Intel was among the stocks that detracted from returns. This large semiconductor company is best known for its Pentium processors. However, it lost market share to Advanced Micro Devices. Swings in market share are not unusual in the technology sector, and they generally result in innovative new products being brought to market. Intel has plans and a strategy that we believe will improve its market share over the next several months. We had been building the position on weakness, and we anticipated that the share price could drop further. We continue to use this opportunity to build the fund’s position.

Top holdings

This table shows the fund’s top holdings, and the percentage of the fund’s net assets that each comprised, as of 5/31/06. The fund’s holdings will change over time.

| Holding (percent of fund's net assets) | Industry |

| Bank of America Corp. (5.6%) | Banking |

| Citigroup, Inc. (4.9%) | Financial |

| Exxon Mobil Corp. (4.5%) | Oil and gas |

| Chevron Corp. (4.3%) | Oil and gas |

| U.S. Bancorp (4.1%) | Banking |

| Tyco International, Ltd. (2.4%) | Conglomerates |

| Marathon Oil Corp. (2.4%) | Oil and gas |

| Freddie Mac (2.4%) | Financial |

| Masco Corp. (2.3%) | Building materials |

| Lockheed Martin Corp. (2.2%) | Aerospace and defense |

10

Property and casualty insurer ACE Limited also detracted from results, but we think its longer-term outlook is favorable. The company’s management team successfully reined in expenses and was able to raise prices following the brutal hurricane season of 2005. Also, we believe the company will be able to increase its share of the property and casualty market in 2006.

Tyco International also disappointed during the period. Although the market did not react significantly to Tyco’s decision to split the conglomerate into three distinct units, Tyco’s electronics division, which is a supplier to the auto industry, suffered when that industry fell on hard times. In our view, Tyco’s varied divisions are well managed and attractively valued. Tyco repurchased approximately $1 billion in shares in the first quarter of 2006, and further repurchases are anticipated. The dividend yield is over 1%, and we believe the company’s long-term prospects remain very favorable. We continue to hold a fairly large position.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future.

| The outlook for your fund |

The following commentary reflects anticipated developments that could affect your fund over the next six months, as well as your management team’s plans for responding to them.

Our near-term outlook is reasonably optimistic. We foresee economic expansion continuing through 2006. We believe the economy is going through a fairly normal cycle, with a bit of infla-tion. The Fed will need to raise short-term interest rates enough to contain inflation and, in our view, this objective may be accomplished relatively soon. It is conceivable that we could see a rate cut by the end of the fund’s fiscal year, in November. If that were the case, we would expect the yield curve, a graphical depiction of bond yields over various maturities, to steepen.

We have long anticipated a decline in consumer spending, and recent data indicates that it has, in fact, slowed. With its emphasis on capital goods, the portfolio is positioned to benefit from corporate capital spending, and we have seen solid evidence that this trend has begun to gain some traction, except within the technology sector. We continue to see greater value in larger-cap stocks, many of which offer attractive dividend yields. As always, we target stocks of well-managed companies offering higher-than-average equity income because we believe they offer strong potential for attractive returns over time.

The views expressed in this report are exclusively those of Putnam Management. They are not meant as investment advice.

The fund may invest a portion of its assets in small and/or midsize companies. Such investments increase the risk of fluctuations in the value of your investment. Value investing seeks underpriced stocks, but there is no guarantee that a stock’s price will rise.

11

| Your fund’s performance |

This section shows your fund’s performance for periods ended May 31, 2006, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance as of the most recent calendar quarter-end. Performance should always be considered in light of a fund’s investment strategy. Data represents past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. For the most recent month-end performance, please visit www.putnam.com or call Putnam at 1-800-225-1581. Class Y shares are generally only available to corporate and institutional clients. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

| Fund performance | ||||||||||

| Total return for periods ended 5/31/06 | ||||||||||

| Class A | Class B | Class C | Class M | Class R | Class Y | |||||

| (inception dates) | (6/15/77) | (9/13/93) | (2/1/99) | (12/2/94) | (1/21/03) | (10/1/98) | ||||

| NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV | |

| Annual average | ||||||||||

| (life of fund) | 10.91% | 10.70% | 9.95% | 9.95% | 10.07% | 10.07% | 10.22% | 10.10% | 10.63% | 10.98% |

| 10 years | 143.23 | 130.55 | 125.59 | 125.59 | 125.67 | 125.67 | 131.27 | 123.79 | 137.27 | 147.79 |

| Annual average | 9.30 | 8.71 | 8.48 | 8.48 | 8.48 | 8.48 | 8.75 | 8.39 | 9.02 | 9.50 |

| 5 years | 30.77 | 23.91 | 25.96 | 23.96 | 25.96 | 25.96 | 27.53 | 23.41 | 29.22 | 32.41 |

| Annual average | 5.51 | 4.38 | 4.72 | 4.39 | 4.72 | 4.72 | 4.98 | 4.30 | 5.26 | 5.78 |

| 3 years | 43.41 | 35.87 | 40.24 | 37.24 | 40.17 | 40.17 | 41.29 | 36.66 | 42.31 | 44.47 |

| Annual average | 12.77 | 10.76 | 11.93 | 11.13 | 11.91 | 11.91 | 12.21 | 10.97 | 12.48 | 13.05 |

| 1 year | 10.60 | 4.78 | 9.78 | 4.78 | 9.78 | 8.78 | 10.03 | 6.42 | 10.32 | 10.87 |

| 6 months | 4.77 | –0.75 | 4.36 | –0.64 | 4.36 | 3.36 | 4.48 | 1.07 | 4.61 | 4.84 |

Performance assumes reinvestment of distributions and does not account for taxes. Returns at public offering price (POP) for class A and M shares reflect a sales charge of 5.25% and 3.25%, respectively. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining to 1% in the sixth year, and is eliminated thereafter. Class C shares reflect a 1% CDSC the first year that is eliminated thereafter. Class R and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and, except for class Y shares, the higher operating expenses for such shares.

A 2% short-term trading fee may be applied to shares exchanged or sold within 5 days of purchase.

12

Comparative index returns

For periods ended 5/31/06

| Lipper Equity | ||

| Russell 1000 | Income Funds | |

| Value Index | category average* | |

| Annual average | ||

| (life of fund) | —† | 11.92% |

| 10 years | 178.52% | 129.74 |

| Annual average | 10.79 | 8.54 |

| 5 years | 35.61 | 24.68 |

| Annual average | 6.28 | 4.34 |

| 3 years | 55.82 | 44.98 |

| Annual average | 15.93 | 13.09 |

| 1 year | 12.61 | 10.81 |

| 6 months | 6.53 | 5.24 |

| Index and Lipper results should be compared to fund performance at net asset value. * Over the 6-month and 1-, 3-, 5-, and 10-year periods ended 5/31/06, there were 239, 223, 156, 121, and 73 funds, respectively, in this Lipper category. † The inception date of the Russell 1000 Value Index was 12/31/78. |

13

Fund price and distribution information

For the six-month period ended 5/31/06

| Distributions* | Class A | Class B | Class C | Class M | Class R | Class Y | ||

| Number | 2 | 2 | 2 | 2 | 2 | 2 | ||

| Income | $0.126 | $0.061 | $0.063 | $0.083 | $0.107 | $0.147 | ||

| Capital gains | — | — | — | — | — | — | ||

| Total | $0.126 | $0.061 | $0.063 | $0.083 | $0.107 | $0.147 | ||

| Share value: | NAV | POP | NAV | NAV | NAV | POP | NAV | NAV |

| 11/30/05 | $16.71 | $17.64 | $16.56 | $16.61 | $16.59 | $17.15 | $16.67 | $16.72 |

| 5/31/06 | 17.38 | 18.34 | 17.22 | 17.27 | 17.25 | 17.83 | 17.33 | 17.38 |

| Current yield | ||||||||

| (end of period) | ||||||||

| Current | ||||||||

| dividend rate1 | 1.45% | 1.37% | 0.67% | 0.69% | 0.95% | 0.92% | 1.22% | 1.70% |

| Current 30-day | ||||||||

| SEC yield2 | 1.71 | 1.62 | 0.95 | 0.96 | 1.21 | 1.17 | 1.46 | 1.96 |

| * Dividend sources are estimated and may vary based on final tax calculations after the fund’s fiscal year-end. 1 Most recent distribution, excluding capital gains, annualized and divided by NAV or POP at end of period. 2 Based only on investment income, calculated using SEC guidelines. |

Fund performance for most recent calendar quarter

Total return for periods ended 6/30/06

| Class A | Class B | Class C | Class M | Class R | Class Y | |||||

| (inception dates) | (6/15/77) | (9/13/93) | (2/1/99) | (12/2/94) | (1/21/03) | (10/1/98) | ||||

| NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV | |

| Annual average | ||||||||||

| (life of fund) | 10.88% | 10.68% | 9.93% | 9.93% | 10.05% | 10.05% | 10.20% | 10.08% | 10.61% | 10.96% |

| 10 years | 142.76 | 130.08 | 125.29 | 125.29 | 125.36 | 125.36 | 131.03 | 123.53 | 136.98 | 147.47 |

| Annual average | 9.27 | 8.69 | 8.46 | 8.46 | 8.46 | 8.46 | 8.73 | 8.38 | 9.01 | 9.48 |

| 5 years | 32.57 | 25.58 | 27.72 | 25.72 | 27.71 | 27.71 | 29.34 | 25.10 | 30.99 | 34.31 |

| Annual average | 5.80 | 4.66 | 5.02 | 4.68 | 5.01 | 5.01 | 5.28 | 4.58 | 5.55 | 6.08 |

| 3 years | 42.27 | 34.83 | 39.2 | 36.2 | 39.13 | 39.13 | 40.18 | 35.62 | 41.22 | 43.44 |

| Annual average | 12.47 | 10.47 | 11.66 | 10.85 | 11.64 | 11.64 | 11.92 | 10.69 | 12.19 | 12.78 |

| 1 year | 9.38 | 3.62 | 8.61 | 3.64 | 8.56 | 7.56 | 8.83 | 5.31 | 9.09 | 9.66 |

| 6 months | 4.24 | -1.23 | 3.92 | -1.08 | 3.87 | 2.87 | 4.01 | 0.63 | 4.13 | 4.38 |

14

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund limited these expenses; had it not done so, expenses would have been higher. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial advisor.

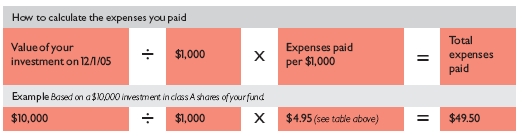

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Putnam Equity Income Fund from December 1, 2005, to May 31, 2006. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| Class A | Class B | Class C | Class M | Class R | Class Y | |

| Expenses paid per $1,000* | $ 4.95 | $ 8.76 | $ 8.76 | $ 7.49 | $ 6.22 | $ 3.68 |

| Ending value (after expenses) | $1,047.70 | $1,043.60 | $1,043.60 | $1,044.80 | $1,046.10 | $1,048.40 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of net assets for the six months ended 5/31/06. The expense ratio may differ for each share class (see the table at the bottom of the next page). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year. Does not reflect the effect of a non-recurring reimbursement by Putnam. If this amount had been reflected in the table above, expenses for each share class would have been lower.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended May 31, 2006, use the calculation method below. To find the value of your investment on December 1, 2005, go to www.putnam.com and log on to your account. Click on the “Transaction History” tab in your Daily Statement and enter 12/01/2005 in both the “from” and “to” fields. Alternatively, call Putnam at 1-800-225-1581.

15

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| Class A | Class B | Class C | Class M | Class R | Class Y | |

| Expenses paid per $1,000* | $ 4.89 | $ 8.65 | $ 8.65 | $ 7.39 | $ 6.14 | $ 3.63 |

| Ending value (after expenses) | $1,020.09 | $1,016.36 | $1,016.36 | $1,017.60 | $1,018.85 | $1,021.34 |

| * Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of net assets for the six months ended 5/31/06. The expense ratio may differ for each share class (see the table at the bottom of this page). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year. Does not reflect the effect of a non-recurring reimbursement by Putnam. If this amount had been reflected in the table above, expenses for each share class would have been lower. |

Compare expenses using industry averages

You can also compare your fund’s expenses with the average of its peer group, as defined by Lipper, an independent fund-rating agency that ranks funds relative to others that Lipper considers to have similar investment styles or objectives. The expense ratio for each share class shown below indicates how much of your fund’s net assets have been used to pay ongoing expenses during the period.

| Class A | Class B | Class C | Class M | Class R | Class Y | |

| Your fund's annualized | ||||||

| expense ratio* | 0.97% | 1.72% | 1.72% | 1.47% | 1.22% | 0.72% |

| Average annualized expense | ||||||

| ratio for Lipper peer group† | 1.23% | 1.98% | 1.98% | 1.73% | 1.48% | 0.98% |

| * Does not reflect the effect of a non-recurring reimbursement by Putnam. If this amount had been reflected in the table above, the expense ratio for each share class would have been lower. † Simple average of the expenses of all front-end load funds in the fund’s Lipper peer group, calculated in accordance with Lipper’s standard method for comparing fund expenses (excluding 12b-1 fees and without giving effect to any expense offset and brokerage service arrangements that may reduce fund expenses). This average reflects each fund’s expenses for its most recent fiscal year available to Lipper as of 3/31/06. To facilitate comparison, Putnam has adjusted this average to reflect the 12b-1 fees carried by each class of shares other than class Y shares, which do not incur 12b-1 fees. The peer group may include funds that are significantly smaller or larger than the fund, which may limit the comparability of the fund’s expenses to the simple average, which typically is higher than the asset-weighted average. |

16

| Your fund’s portfolio turnover |

Putnam funds are actively managed by teams of experts who buy and sell securities based on intensive analysis of companies, industries, economies, and markets. Portfolio turnover is a measure of how often a fund’s managers buy and sell securities for your fund. A portfolio turnover of 100%, for example, means that the managers sold and replaced securities valued at 100% of a fund’s assets within a one-year period. Funds with high turnover may be more likely to generate capital gains and dividends that must be distributed to shareholders as taxable income. High turnover may also cause a fund to pay more brokerage commissions and other transaction costs, which may detract from performance.

| Turnover comparisons | |||||

| Percentage of holdings that change every year | |||||

| 2005 | 2004 | 2003 | 2002* | 2001* | |

| Putnam Equity Income Fund | 52% | 46% | 65% | 59% | 70% |

| Lipper Equity Income Funds | |||||

| category average | 45% | 46% | 51% | 53% | 56% |

Turnover data for the fund is calculated based on the fund’s fiscal-year period, which ends on November 30. Turnover data for the fund’s Lipper category is calculated based on the average of the turnover of each fund in the category for its fiscal year ended during the indicated year. Fiscal years vary across funds in the Lipper category, which may limit the comparability of the fund’s portfolio turnover rate to the Lipper average. Comparative data for 2005 is based on information available as of 12/31/05.

* Portfolio turnover excludes certain Treasury note transactions executed in connection with a short-term trading strategy.

17

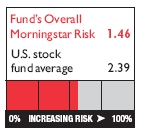

Your fund’s risk

This risk comparison is designed to help you understand how your fund compares with other funds. The comparison utilizes a risk measure developed by Morningstar, an independent fund-rating agency. This risk measure is referred to as the fund’s Overall Morningstar Risk.

Your fund’s Overall Morningstar® Risk

Your fund’s Overall Morningstar Risk is shown alongside that of the average fund in its broad asset class, as determined by Morningstar. The risk bar broadens the comparison by translating the fund’s Overall Morningstar Risk into a percentile, which is based on the fund’s ranking among all funds rated by Morningstar as of June 30, 2006. A higher Overall Morningstar Risk generally indicates that a fund’s monthly returns have varied more widely.

Morningstar determines a fund’s Overall Morningstar Risk by assessing variations in the fund’s monthly returns — with an emphasis on downside variations — over 3-, 5-, and 10-year periods, if available. Those measures are weighted and averaged to produce the fund’s Overall Morningstar Risk. The information shown is provided for the fund’s class A shares only; information for other classes may vary. Overall Morningstar Risk is based on historical data and does not indicate future results. Morningstar does not purport to measure the risk associated with a current investment in a fund, either on an absolute basis or on a relative basis. Low Overall Morningstar Risk does not mean that you cannot lose money on an investment in a fund. Copyright 2006 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

18

Your fund’s management

Your fund is managed by the members of the Putnam Large-Cap Value and Core Fixed-Income teams. Bartlett Geer is the Portfolio Leader and Kevin Cronin and Austin Kairnes are Portfolio Members of your fund. The Portfolio Leader and Portfolio Members coordinate the teams’ management of the fund.

For a complete listing of the members of the Putnam Large-Cap Value and Core Fixed-Income teams, including those who are not Portfolio Leaders or Portfolio Members of your fund, visit Putnam’s Individual Investor Web site at www.putnam.com.

Fund ownership by the Portfolio Leader and Portfolio Members

The table below shows how much the fund’s current Portfolio Leader and Portfolio Members have invested in the fund (in dollar ranges). Information shown is as of May 31, 2006, and May 31, 2005.

| $1 – | $10,001 – | $50,001 – | $100,001 – | $500,001 – | $1,000,001 | |||

| Year | $0 | $10,000 | $50,000 | $100,000 | $500,000 | $1,000,000 | and over | |

| Bartlett Geer | 2006 | * | ||||||

| Portfolio Leader | 2005 | * | ||||||

| Kevin Cronin | 2006 | * | ||||||

| Portfolio Member | 2005 | * | ||||||

| Austin Kairnes | 2006 | * | ||||||

| Portfolio Member | N/A | |||||||

N/A indicates the individual was not a Portfolio Leader or Portfolio Member as of 5/31/05.

19

| Fund manager compensation |

The total 2005 fund manager compensation that is attributable to your fund is approximately $2,500,000. This amount includes a portion of 2005 compensation paid by Putnam Management to the fund managers listed in this section for their portfolio management responsibilities, calculated based on the fund assets they manage taken as a percentage of the total assets they manage. The compensation amount also includes a portion of the 2005 compensation paid to the Chief Investment Officer of the team and the Group Chief Investment Officers of the fund’s broader investment categories for their oversight responsibilities, calculated based on the fund assets they oversee taken as a percentage of the total assets they oversee. This amount does not include compensation of other personnel involved in research, trading, administration, systems, compliance, or fund operations; nor does it include non-compensation costs. These percentages are determined as of the fund’s fiscal period-end. For personnel who joined Putnam Management during or after 2005, the calculation reflects annualized 2005 compensation or an estimate of 2006 compensation, as applicable.

Other Putnam funds managed by the Portfolio Leader and Portfolio Members

Kevin Cronin is also a Portfolio Leader of Putnam American Government Income Fund, Putnam Global Income Trust, Putnam Income Fund, Putnam Limited Duration Government Income Fund, and Putnam U.S. Government Income Trust.

Bartlett Geer, Kevin Cronin, and Austin Kairnes may also manage other accounts and variable trust funds advised by Putnam Management or an affiliate.

Changes in your fund’s Portfolio Leader and Portfolio Members

During the year ended May 31, 2006, Austin Kairnes became a Portfolio Member of your fund. Coincident with this appointment, Portfolio Member Jeanne Mockard left the management team, though she continues in her other fund management roles at Putnam.

20

Fund ownership by Putnam’s Executive Board

The table below shows how much the members of Putnam’s Executive Board have invested in the fund (in dollar ranges). Information shown is as of May 31, 2006, and May 31, 2005.

| $1 – | $10,001 – | $50,001– | $100,001 | ||||

| Year | $0 | $10,000 | $50,000 | $100,000 | and over | ||

| Philippe Bibi | 2006 | * | |||||

| Chief Technology Officer | 2005 | * | |||||

| Joshua Brooks | 2006 | * | |||||

| Deputy Head of Investments | 2005 | * | |||||

| William Connolly | 2006 | * | |||||

| Head of Retail Management | N/A | ||||||

| Kevin Cronin | 2006 | * | |||||

| Head of Investments | 2005 | * | |||||

| Charles Haldeman, Jr. | 2006 | * | |||||

| President and CEO | 2005 | * | |||||

| Amrit Kanwal | 2006 | * | |||||

| Chief Financial Officer | 2005 | * | |||||

| Steven Krichmar | 2006 | * | |||||

| Chief of Operations | 2005 | * | |||||

| Francis McNamara, III | 2006 | * | |||||

| General Counsel | 2005 | * | |||||

| Richard Robie, III | 2006 | * | |||||

| Chief Administrative Officer | 2005 | * | |||||

| Edward Shadek | 2006 | * | |||||

| Deputy Head of Investments | 2005 | * | |||||

| Sandra Whiston | 2006 | * | |||||

| Head of Institutional Management | N/A | ||||||

N/A indicates the individual was not a member of Putnam’s Executive Board as of 5/31/05.

21

| Terms and definitions |

| Important terms |

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. NAVs fluctuate with market conditions. NAV is calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Public offering price (POP) is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. POP performance figures shown here assume the 5.25% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

| Share classes |

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain defined contribution plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are only available to eligible purchasers, including eligible defined contribution plans or corporate IRAs.

22

| Comparative indexes |

JP Morgan Global High Yield Index is an unmanaged index of global high-yield fixed-income securities.

Lehman Credit Index is an unmanaged index of investment-grade corporate bonds.

Lehman Government Bond Index is an unmanaged index of U.S. Treasury and agency securities.

Morgan Stanley Capital International (MSCI) EAFE Index is an unmanaged index of equity securities from developed countries in Western Europe, the Far East, and Australasia.

Russell 1000 Value Index is an unmanaged index of those companies in the large-cap Russell 1000 Index chosen for their value orientation.

Russell Midcap Growth Index is an unmanaged index of those companies in the Russell Midcap Index chosen for their growth orientation.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

23

| Trustee approval of management contract |

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Management. In this regard, the Board of Trustees, with the assistance of its Contract Committee consisting solely of Trustees who are not “interested persons” (as such term is defined in the Investment Company Act of 1940, as amended) of the Putnam funds (the “Independent Trustees”), requests and evaluates all information it deems reasonably necessary under the circumstances. Over the course of several months beginning in March and ending in June 2005, the Contract Committee met five times to consider the information provided by Putnam Management and other information developed with the assistance of the Board’s independent counsel and independent staff. The Contract Committee reviewed and discussed key aspects of this information with all of the Independent Trustees. Upon completion of this review, the Contract Committee recommended and the Independent Trustees approved the continuance of your fund’s management contract, effective July 1, 2005.

This approval was based on the following conclusions:

| * That the fee schedule currently in effect for your fund represents reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds and the costs incurred by Putnam Management in providing such services, and * That such fee schedule represents an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels. |

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the fee arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that certain aspects of such arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements in prior years.

24

Model fee schedules and categories; total expenses

The Trustees’ review of the management fees and total expenses of the Putnam funds focused on three major themes:

| * Consistency. The Trustees, working in cooperation with Putnam Management, have devel- oped and implemented a series of model fee schedules for the Putnam funds designed to ensure that each fund’s management fee is consistent with the fees for similar funds in the Putnam family of funds and compares favorably with fees paid by competitive funds spon- sored by other investment advisors. Under this approach, each Putnam fund is assigned to one of several fee categories based on a combination of factors, including competitive fees and perceived difficulty of management, and a common fee schedule is implemented for all funds in a given fee category. The Trustees reviewed the model fee schedule then in effect for your fund, including fee levels and breakpoints, and the assignment of the fund to a particular fee category under this structure. (“Breakpoints” refer to reductions in fee rates that apply to additional assets once specified asset levels are reached.) The Trustees concluded that no changes should be made in the fund’s current fee schedule at this time. |

| * Competitiveness. The Trustees also reviewed comparative fee and expense information for competitive funds, which indicated that, in a custom peer group of competitive funds selected by Lipper Inc., your fund ranked in the 10th percentile in management fees and in the 14th percentile in total expenses (less any applicable 12b-1 fees) as of December 31, 2004 (the first percentile being the least expensive funds and the 100th percentile being the most expensive funds). (Because the fund’s custom peer group is smaller than the fund’s broad Lipper Inc. peer group, this expense comparison may differ from the Lipper peer expense information found elsewhere in this report.) The Trustees noted that expense ratios for a number of Putnam funds, which show the percentage of fund assets used to pay for manage- ment and administrative services, distribution (12b-1) fees and other expenses, had been increasing recently as a result of declining net assets and the natural operation of fee break- points. They noted that such expense ratio increases were currently being controlled by expense limitations implemented in January 2004 and which Putnam Management, in consul- tation with the Contract Committee, had committed to maintain at least through 2006. The Trustees expressed their intention to monitor this information closely to ensure that fees and expenses of the Putnam funds continue to meet evolving competitive standards. |

| * Economies of scale. The Trustees concluded that the fee schedule currently in effect for your fund represents an appropriate sharing of economies of scale at current asset levels. Your fund currently has the benefit of breakpoints in its management fee that provide shareholders with significant economies of scale, which means that the effective management fee rate of a fund (as a percentage of fund assets) declines as a fund grows in size and crosses specified asset thresholds. The Trustees examined the existing breakpoint structure of the Putnam |

25

funds’ management fees in light of competitive industry practices. The Trustees considered various possible modifications to the Putnam funds’ current breakpoint structure, but ultimately concluded that the current breakpoint structure continues to serve the interests of fund shareholders. Accordingly, the Trustees continue to believe that the fee schedules currently in effect for the funds represent an appropriate sharing of economies of scale at current asset levels. The Trustees noted that significant redemptions in many Putnam funds, together with significant changes in the cost structure of Putnam Management, have altered the economics of Putnam Management’s business in significant ways. In view of these changes, the Trustees intend to consider whether a greater sharing of the economies of scale by fund shareholders would be appropriate if and when aggregate assets in the Putnam funds begin to experience meaningful growth.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services to be provided and profits to be realized by Putnam Management and its affiliates from the relationship with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability with respect to the funds’ management contracts, allocated on a fund-by-fund basis.

| Investment performance |

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the funds’ investment process and performance by the work of the Investment Oversight Committees of the Trustees, which meet on a regular monthly basis with the funds’ portfolio teams throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — as measured by the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to such personnel, and in general the ability of Putnam Management to attract and retain high-quality personnel — but also recognize that this does not guarantee favorable investment results for every fund in every time period. The Trustees considered the investment performance of each fund over multiple time periods and considered information comparing the fund’s performance with various benchmarks and with the performance of competitive funds. The Trustees noted the satisfactory investment performance of many Putnam funds. They also noted the disappointing investment performance of certain funds in recent years and continued to discuss with senior management of Putnam Management the factors contributing to such underperformance and actions being taken to improve performance. The Trustees recognized that, in recent years, Putnam Management has made significant changes in its investment personnel and processes and in the fund product line

26

to address areas of underperformance. The Trustees indicated their intention to continue to monitor performance trends to assess the effectiveness of these changes and to evaluate whether additional remedial changes are warranted.

In the case of your fund, the Trustees considered that your fund’s class A share cumulative total return performance at net asset value was in the following percentiles of its Lipper Inc. peer group (Lipper Equity Income Funds) for the one-, three-, and five-year periods ended December 31, 2004 (the first percentile being the best-performing funds and the 100th percentile being the worst-performing funds):

| One-year period | Three-year period | Five-year period |

| 56th | 32nd | 24th |

(Because of the passage of time, these performance results may differ from the performance results for more recent periods shown elsewhere in this report. Over the one-, three-, and five-year periods ended December 31, 2004, there were 237,164, and 134 funds, respectively, in your fund’s Lipper peer group.* Past performance is no guarantee of future performance.)

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance problems. The Trustees believe that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. Based on the responsiveness of Putnam Management in the recent past to Trustee concerns about investment performance, the Trustees believe that it is preferable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of terminating a management contract and engaging a new investment advisor for an underperforming fund would entail significant disruptions and would not provide any greater assurance of improved investment performance.

Brokerage and soft-dollar allocations; other benefits

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include principally benefits related to brokerage and soft-dollar allocations, whereby a portion of the commissions paid by a fund for brokerage is earmarked to pay for research services that may be utilized by a fund’s investment advisor, subject to the obligation to seek best execution. The Trustees believe that soft-dollar credits and other potential benefits associated with the allocation of fund brokerage, which pertains mainly to funds investing in equity securities,

| * The percentile rankings for your fund’s class A share annualized total return performance in the Lipper Equity Income Funds category for the one-, five-, and ten-year periods ended June 30, 2006, were 54%, 32%, and 37%, respectively. Over the one-, five-, and ten-year periods ended June 30, 2006, the fund ranked 120th out of 225, 40th out of 124, and 28th out of 76 funds, respectively. Note that this more recent information was not available when the Trustees approved the continuance of your fund’s management contract. |

27

represent assets of the funds that should be used for the benefit of fund shareholders. This area has been marked by significant change in recent years. In July 2003, acting upon the Contract Committee’s recommendation, the Trustees directed that allocations of brokerage to reward firms that sell fund shares be discontinued no later than December 31, 2003. In addition, commencing in 2004, the allocation of brokerage commissions by Putnam Management to acquire research services from third-party service providers has been significantly reduced, and continues at a modest level only to acquire research that is customarily not available for cash. The Trustees will continue to monitor the allocation of the funds’ brokerage to ensure that the principle of “best price and execution” remains paramount in the portfolio trading process.

The Trustees’ annual review of your fund’s management contract also included the review of its distributor’s contract and distribution plan with Putnam Retail Management Limited Partnership and the custodian agreement and investor servicing agreement with Putnam Fiduciary Trust Company, all of which provide benefits to affiliates of Putnam Management.

Comparison of retail and institutional fee schedules

The information examined by the Trustees as part of their annual contract review has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, etc. This information included comparison of such fees with fees charged to the funds, as well as a detailed assessment of the differences in the services provided to these two types of clients. The Trustees observed, in this regard, that the differences in fee rates between institutional clients and the mutual funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients reflect to a substantial degree historical competitive forces operating in separate market places. The Trustees considered the fact that fee rates across all asset sectors are higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to institutional clients of the firm, but have not relied on such comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

28

| Other information for shareholders |

Important notice regarding delivery of shareholder documents

In accordance with SEC regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

| Proxy voting |

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2005, are available on the Putnam Individual Investor Web site, www.putnam.com/individual, and on the SEC’s Web site, www.sec.gov. If you have questions about finding forms on the SEC’s Web site, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

| Fund portfolio holdings |

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s Web site at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s Web site or the operation of the Public Reference Room.

29

| Financial statements |

| A guide to financial statements |

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and noninvestment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlight table also includes the current reporting period.

30

| The fund’s portfolio 5/31/06 (Unaudited) | |||

| COMMON STOCKS (95.7%)* | |||

| Shares | Value | ||

| Aerospace and Defense (3.0%) | |||

| Boeing Co. (The) | 330,400 | $ | 27,505,800 |

| Lockheed Martin Corp. | 1,095,100 | 79,383,799 | |

| 106,889,599 | |||

| Banking (12.4%) | |||

| Bank of America Corp. | 4,140,900 | 200,419,560 | |

| U.S. Bancorp | 4,719,200 | 145,681,704 | |

| Wachovia Corp. | 1,293,200 | 69,186,200 | |

| Washington Mutual, Inc. | 580,300 | 26,641,573 | |

| 441,929,037 | |||

| Beverage (0.5%) | |||

| Coca-Cola Enterprises, Inc. | 887,400 | 17,446,284 | |

| Building Materials (3.7%) | |||

| Masco Corp. | 2,591,500 | 80,388,330 | |

| Sherwin-Williams Co. (The) | 1,094,000 | 52,916,780 | |

| 133,305,110 | |||

| Cable Television (0.9%) | |||

| Comcast Corp. Class A † (S) | 955,500 | 30,700,215 | |

| Chemicals (1.2%) | |||

| E.I. du Pont de Nemours & Co. | 162,800 | 6,923,884 | |

| Huntsman Corp. † | 406,800 | 7,627,500 | |

| PPG Industries, Inc. | 218,000 | 14,026,120 | |

| Rohm & Haas Co. (S) | 291,374 | 14,688,163 | |

| 43,265,667 | |||

| Commercial and Consumer Services (0.5%) | |||

| Cendant Corp. (S) | 1,186,600 | 19,187,322 | |

| Computers (3.3%) | |||

| Hewlett-Packard Co. | 2,258,400 | 73,126,992 | |

| IBM Corp. | 534,700 | 42,722,530 | |

| 115,849,522 | |||

| Conglomerates (5.2%) | |||

| General Electric Co. | 1,452,900 | 49,776,354 | |

| Honeywell International, Inc. | 1,012,600 | 41,698,868 | |

| Textron, Inc. (S) | 79,600 | 7,238,028 | |

| Tyco International, Ltd. (Bermuda) (S) | 3,212,038 | 87,078,350 | |

| 185,791,600 | |||

31

| COMMON STOCKS (95.7%)* continued | |||

| Shares | Value | ||

| Consumer Finance (2.4%) | |||

| Capital One Financial Corp. | 829,300 | $ | 68,641,161 |

| Countrywide Financial Corp. | 392,900 | 15,040,212 | |

| 83,681,373 | |||

| Consumer Goods (0.3%) | |||

| Procter & Gamble Co. (The) | 203,400 | 11,034,450 | |

| Electric Utilities (4.5%) | |||

| Dominion Resources, Inc. (S) | 210,000 | 15,241,800 | |

| Entergy Corp. | 450,100 | 31,556,511 | |

| Exelon Corp. | 623,900 | 35,318,979 | |

| PG&E Corp. (S) | 552,100 | 21,907,328 | |

| Public Service Enterprise Group, Inc. (S) | 621,100 | 39,582,703 | |

| Westar Energy, Inc. (S) | 348,300 | 7,422,273 | |

| Wisconsin Energy Corp. | 199,400 | 7,950,078 | |

| 158,979,672 | |||

| Electronics (1.5%) | |||

| Avnet, Inc. † | 422,900 | 9,337,632 | |

| Intel Corp. | 2,486,400 | 44,804,928 | |

| 54,142,560 | |||

| Financial (8.8%) | |||

| Allied Capital Corp. (S) | 668,000 | 20,093,440 | |

| Citigroup, Inc. | 3,543,100 | 174,674,830 | |

| Freddie Mac | 1,401,000 | 84,116,040 | |

| MGIC Investment Corp. (S) | 196,200 | 12,923,694 | |

| PMI Group, Inc. (The) | 481,900 | 21,926,450 | |

| 313,734,454 | |||

| Food (1.2%) | |||

| General Mills, Inc. | 807,300 | 41,890,797 | |

| Health Care Services (0.7%) | |||

| Cardinal Health, Inc. | 277,600 | 18,574,216 | |

| CIGNA Corp. | 50,500 | 4,683,370 | |

| 23,257,586 | |||

| Household Furniture and Appliances (1.0%) | |||

| Whirlpool Corp. (S) | 392,900 | 35,329,568 | |

| Insurance (7.3%) | |||

| ACE, Ltd. (Bermuda) | 1,493,600 | 77,323,672 | |

| AFLAC, Inc. | 161,000 | 7,534,800 | |

| Axis Capital Holdings, Ltd. (Bermuda) | 794,867 | 20,825,515 | |

| Berkshire Hathaway, Inc. Class B † | 2,660 | 8,163,540 | |

| Chubb Corp. (The) | 616,600 | 31,156,798 | |

| Endurance Specialty Holdings, Ltd. (Bermuda) | 238,400 | 7,283,120 | |

| Everest Re Group, Ltd. (Barbados) | 378,500 | 33,818,975 | |

| Fidelity National Title Group, Inc. Class A (S) | 354,300 | 7,737,912 | |

32

| COMMON STOCKS (95.7%)* continued | |||

| Shares | Value | ||

| Insurance continued | |||

| Genworth Financial, Inc. Class A | 313,720 | $ | 10,506,483 |

| PartnerRe, Ltd. (Bermuda) (S) | 439,199 | 26,975,603 | |

| Willis Group Holdings, Ltd. (United Kingdom) (S) | 793,500 | 27,574,125 | |

| 258,900,543 | |||

| Investment Banking/Brokerage (1.9%) | |||

| Morgan Stanley | 1,124,300 | 67,030,766 | |

| Machinery (1.0%) | |||

| Parker-Hannifin Corp. | 463,900 | 36,193,478 | |

| Manufacturing (0.9%) | |||

| Ingersoll-Rand Co., Ltd. Class A (Bermuda) (S) | 771,100 | 33,627,671 | |

| Media (1.1%) | |||

| Walt Disney Co. (The) (S) | 1,234,374 | 37,648,407 | |

| Medical Technology (1.6%) | |||

| Baxter International, Inc. | 293,200 | 11,053,640 | |

| Becton, Dickinson and Co. | 387,100 | 23,392,453 | |

| PerkinElmer, Inc. | 1,052,330 | 21,951,604 | |

| 56,397,697 | |||

| Metals (1.0%) | |||

| Alcoa, Inc. | 821,300 | 26,051,636 | |

| Freeport-McMoRan Copper & Gold, Inc. Class B (S) | 191,600 | 10,727,684 | |

| 36,779,320 | |||

| Oil & Gas (13.6%) | |||

| Chevron Corp. (S) | 2,562,400 | 153,205,896 | |

| Exxon Mobil Corp. | 2,622,300 | 159,724,293 | |

| Kerr-McGee Corp. (S) | 133,300 | 14,243,105 | |

| Marathon Oil Corp. | 1,156,600 | 86,802,830 | |

| Occidental Petroleum Corp. | 536,200 | 53,132,058 | |

| Valero Energy Corp. | 281,200 | 17,251,620 | |

| 484,359,802 | |||

| Pharmaceuticals (5.5%) | |||

| Johnson & Johnson | 1,189,500 | 71,631,690 | |

| Pfizer, Inc. (S) | 2,875,700 | 68,039,062 | |

| Wyeth | 1,258,500 | 57,563,790 | |

| 197,234,542 | |||

| Publishing (0.6%) | |||

| R. R. Donnelley & Sons Co. | 705,200 | 22,693,336 | |

| Railroads (0.9%) | |||

| Norfolk Southern Corp. | 640,400 | 33,787,504 | |

| Regional Bells (1.3%) | |||

| Verizon Communications, Inc. | 1,510,100 | 47,130,221 | |

33

| COMMON STOCKS (95.7%)* continued | |||

| Shares | Value | ||

| Restaurants (1.0%) | |||

| McDonald’s Corp. | 1,120,400 | $ | 37,163,668 |

| Retail (2.4%) | |||

| Foot Locker, Inc. | 704,500 | 17,027,765 | |

| OfficeMax, Inc. | 378,700 | 15,651,671 | |

| Supervalu, Inc. | 1,820,500 | 53,085,780 | |

| 85,765,216 | |||

| Software (1.2%) | |||

| Microsoft Corp. | 315,400 | 7,143,810 | |

| Oracle Corp. † | 2,185,600 | 31,079,232 | |

| Symantec Corp. † | 270,200 | 4,215,120 | |

| 42,438,162 | |||

| Telecommunications (1.6%) | |||

| Sprint Nextel Corp. | 2,527,318 | 53,604,415 | |

| Embarq Corp. † (S) | 126,365 | 5,265,630 | |

| 58,870,045 | |||

| Tobacco (1.5%) | |||

| Altria Group, Inc. | 755,900 | 54,689,365 | |

| Waste Management (0.2%) | |||

| Waste Management, Inc. (S) | 205,300 | 7,518,086 | |

| Total common stocks (cost $2,846,096,208) | $ | 3,414,642,645 | |

| CONVERTIBLE PREFERRED STOCKS (4.0%)* | |||

| Shares | Value | ||

| Amerada Hess Corp. $3.50 cv. pfd. | 95,474 | $ | 12,077,461 |

| Chubb Corp. (The) $1.75 cv. pfd. | 92,200 | 3,273,100 | |

| Citigroup Funding, Inc. Ser. GNW, 5.02% cv. pfd. | 276,133 | 8,714,757 | |

| Conseco, Inc. $1.38 cum. cv. pfd. | 220,122 | 6,300,992 | |

| General Motors Corp. Ser. A, $1.13 cv. pfd. (S) | 342,224 | 8,213,376 | |

| Hartford Financial Services Group, Inc. (The) $3.00 cv. pfd. | 140,403 | 10,898,783 | |

| Huntsman Corp. $2.50 cv. pfd. | 695,140 | 28,935,203 | |

| Lehman Brothers Holdings, Inc. $1.563 cv. pfd. (S) | 300,600 | 8,078,625 | |

| MetLife, Inc. Ser. B, $1.594 cv. pfd. | 66,480 | 1,836,510 | |

| Platinum Underwriters Holdings, Ltd. Ser. A, | |||

| 6.00% cv. pfd. (Bermuda) | 337,776 | 9,246,618 | |

| Xerox Corp. $6.25 cv. pfd. | 299,570 | 34,038,641 | |

| XL Capital, Ltd. $1.75 cv. pfd. (Bermuda) | 398,150 | 9,706,897 | |

| Total convertible preferred stocks (cost $130,075,416) | $ | 141,320,963 | |

34

| UNITS (0.1%)* (cost $3,095,722) | |||||

| Units | Value | ||||

| Hercules, Inc. cv.sub.debs Ser. units, 6.50%, 2029 | 3,974,000 | $ | 3,218,940 | ||

| CORPORATE BONDS AND NOTES (—%)* (cost $8,604) | |||||

| Principal amount | Value | ||||

| York Power Funding 144A notes 12s, 2007 | |||||

| (Cayman Islands) (In default) (F) † | $8,032 | $ | 670 | ||

| SHORT-TERM INVESTMENTS (4.3%)* | |||||

| Principal amount/shares | Value | ||||

| Short-term investments held as collateral for loaned | |||||

| securities with yields ranging from 4.90% to 5.19% and | |||||

| due dates ranging from June 1, 2006 to June 29, 2006 (d) | $151,201,165 | $ | 150,971,932 | ||

| Putnam Prime Money Market Fund (e) | 2,851,514 | 2,851,514 | |||

| Total short-term investments (cost $153,823,446) | $ | 153,823,446 | |||

| TOTAL INVESTMENTS | |||||

| Total investments (cost $3,133,099,396) | $ | 3,713,006,664 | |||

| * Percentages indicated are based on net assets of $3,569,233,770. † Non-income-producing security. (S) Securities on loan, in part or in entirety, at May 31, 2006. (d) See Note 1 to the financial statements. (e) See Note 5 to the financial statements regarding investments in Putnam Prime Money Market Fund. (F) Security is valued at fair value following procedures approved by the Trustees. 144A after the name of an issuer represents securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. |

| The accompanying notes are an integral part of these financial statements. |

35

| Statement of assets and liabilities 5/31/06 (Unaudited) | |

| ASSETS | |

| Investments in securities, at value, including $146,779,817 of securities on loan (Note 1): | |

| Unaffiliated issuers (identified cost $3,130,247,882) | $3,710,155,150 |

| Affiliated issuers (identified cost $2,851,514) (Note 5) | 2,851,514 |

| Cash | 463 |

| Dividends, interest and other receivables | 10,550,192 |

| Receivable for shares of the fund sold | 2,514,369 |

| Receivable for securities sold | 54,159,830 |

| Total assets | 3,780,231,518 |

| LIABILITIES | |

| Payable for securities purchased | 42,451,953 |

| Payable for shares of the fund repurchased | 9,749,978 |

| Payable for compensation of Manager (Notes 2 and 5) | 4,577,738 |

| Payable for investor servicing and custodian fees (Note 2) | 961,085 |

| Payable for Trustee compensation and expenses (Note 2) | 209,821 |

| Payable for administrative services (Note 2) | 13,383 |

| Payable for distribution fees (Note 2) | 1,718,319 |

| Collateral on securities loaned, at value (Note 1) | 150,971,932 |

| Other accrued expenses | 343,539 |

| Total liabilities | 210,997,748 |

| Net assets | $3,569,233,770 |

| REPRESENTED BY | |

| Paid-in capital (Unlimited shares authorized) (Notes 1 and 4) | $2,832,243,195 |

| Undistributed net investment income (Note 1) | 28,054,427 |

| Accumulated net realized gain on investments (Note 1) | 129,028,880 |

| Net unrealized appreciation of investments | 579,907,268 |

| Total — Representing net assets applicable to capital shares outstanding | $3,569,233,770 |

| (Continued on next page) | |

36

| Statement of assets and liabilities (Continued) |

| COMPUTATION OF NET ASSET VALUE AND OFFERING PRICE | |

| Net asset value and redemption price per class A share | |

| ($2,473,843,180 divided by 142,347,372 shares) | $17.38 |

| Offering price per class A share | |

| (100/94.75 of $17.38)* | $18.34 |

| Net asset value and offering price per class B share | |

| ($630,773,289 divided by 36,634,729 shares)** | $17.22 |

| Net asset value and offering price per class C share | |

| ($89,276,264 divided by 5,168,709 shares)** | $17.27 |

| Net asset value and redemption price per class M share | |

| ($51,777,628 divided by 3,001,603 shares) | $17.25 |

| Offering price per class M share | |

| (100/96.75 of $17.25)* | $17.83 |

| Net asset value, offering price and redemption price per class R share | |

| ($3,003,533 divided by 173,343 shares) | $17.33 |

| Net asset value, offering price and redemption price per class Y share | |

| ($320,559,876 divided by 18,440,111 shares) | $17.38 |

| * On single retail sales of less than $50,000. On sales of $50,000 or more and on group sales, the offering price is reduced. ** Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

| The accompanying notes are an integral part of these financial statements. |

37

| Statement of operations Six months ended 5/31/06 (Unaudited) | |

| INVESTMENT INCOME | |

| Dividends | $ 44,693,426 |

| Interest (including interest income of $514,102 | |

| from investments in affiliated issuers) (Note 5) | 662,762 |

| Securities lending | 180,689 |

| Total investment income | 45,536,877 |

| EXPENSES | |

| Compensation of Manager (Note 2) | 9,041,605 |

| Investor servicing fees (Note 2) | 3,471,545 |

| Custodian fees (Note 2) | 114,371 |

| Trustee compensation and expenses (Note 2) | 77,575 |

| Administrative services (Note 2) | 44,666 |

| Distribution fees — Class A (Note 2) | 3,087,332 |

| Distribution fees — Class B (Note 2) | 3,471,082 |

| Distribution fees — Class C (Note 2) | 455,103 |

| Distribution fees — Class M (Note 2) | 199,465 |

| Distribution fees — Class R (Note 2) | 7,032 |

| Other | 364,314 |

| Non-recurring costs (Notes 2 and 6) | 33,293 |

| Costs assumed by Manager (Notes 2 and 6) | (33,293) |