UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-2794

MFS SERIES TRUST III

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: January 31

Date of reporting period: July 31, 2008

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

MFS® High Income Fund

Note to Shareholders: At the close of business on April 18, 2008, Class R shares and Class R2 shares converted into Class R3 shares.

Following this conversion, Class R3, Class R4, and Class R5 shares were renamed Class R2, Class R3, and Class R4 shares, respectively.

The report is prepared for the general information of shareholders. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ

NO BANK OR CREDIT UNION GUARANTEE Ÿ NOT A DEPOSIT Ÿ

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY OR

NCUA/NCUSIF

7/31/08

MFH-SEM

LETTER FROM THE CEO

Dear Shareholders:

Negative headlines tend to resonate during difficult markets, and we certainly have had more than our share of tough news recently. As a result consumer, and particularly investor, sentiment are at all-time lows. That said, I do think it is helpful to remember there are always silver linings in the storm clouds if you look hard enough.

Through all of the challenges we have faced, there are some positive underlying trends. In the United States, for example, institutional traders and credit market followers are just now showing increasing signs of confidence and are beginning to take on more risk. At the corporate level, earnings continue to be relatively strong as companies have reduced labor costs, controlled inventories, and relied less on debt to finance expansion. More broadly, low interest rates and strong demand for consumer goods and industrial equipment are good signs for the global economy.

While I do not mean to minimize the risks inherent in today’s markets, periods such as these allow the talented fund managers and research analysts we have at MFS® to test their convictions, reevaluate existing positions, and identify new investment ideas. Our investment process also includes a significant risk management component, with constant attention paid to monitoring market risk, so we can do our best to minimize any surprises to your portfolio.

For investors, this is a great time to check in with your advisor and make sure you have a sound investment plan in place — one that can keep your hard-earned money working over the long term through a strategy that involves asset allocation, diversification, and periodic portfolio rebalancing and reviews. A plan tailored to your distinct needs and goals continues to be the best approach to help you take advantage of the inevitable challenges — and opportunities — that present themselves over time.

Respectfully,

Robert J. Manning

Chief Executive Officer and Chief Investment Officer

MFS Investment Management®

September 15, 2008

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

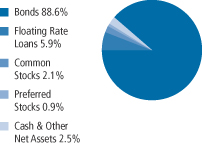

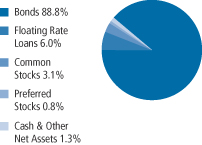

PORTFOLIO COMPOSITION

Portfolio structure (i)

| | |

| Top five industries (i) | | |

Medical & Health Technology

& Services | | 9.2% |

| Utilities - Electric Power | | 7.6% |

| Gaming & Lodging | | 7.5% |

| Broadcasting | | 6.7% |

| Energy - Independent | | 5.6% |

| | |

| Credit quality of bonds (r) | | |

| AAA | | 3.7% |

| AA | | 1.0% |

| A | | 1.5% |

| BBB | | 0.7% |

| BB | | 20.4% |

| B | | 50.7% |

| CCC | | 19.6% |

| D | | 0.1% |

| Not Rated | | 2.3% |

| |

| Portfolio facts | | |

| Average Duration (d)(i) | | 4.2 |

| Average Life (i)(m) | | 6.6 yrs. |

| Average Maturity (i)(m) | | 8.0 yrs. |

| Average Credit Quality of Rated Securities (long-term) (a) | | B+ |

| Average Credit Quality of Rated Securities (short-term) (a) | | A-1 |

| (a) | The average credit quality of rated securities is based upon a market weighted average of portfolio holdings that are rated by public rating agencies. |

| (d) | Duration is a measure of how much a bond’s price is likely to fluctuate with general changes in interest rates, e.g., if rates rise 1.00%, a bond with a 5-year duration is likely to lose about 5.00% of its value. |

| (i) | For purposes of this presentation, the bond component includes accrued interest amounts and may be positively or negatively impacted by the equivalent exposure from any derivative holdings, if applicable. |

| (m) | The average maturity shown is calculated using the final stated maturity on the portfolio’s holdings without taking into account any holdings which have been pre-refunded or pre-paid to an earlier date or which have a mandatory put date prior to the stated maturity. The average life shown takes into account these earlier dates. |

| (r) | Each security is assigned a rating from Moody’s Investors Service. If not rated by Moody’s, the rating will be that assigned by Standard & Poor’s. Likewise, if not assigned a rating by Standard & Poor’s, it will be based on the rating assigned by Fitch, Inc. For those portfolios that hold a security which is not rated by any of the three agencies, the security is considered Not Rated. Holdings in U.S. Treasuries and government agency mortgage-backed securities, if any, are included in the “AAA”-rating category. Percentages are based on the total market value of investments as of 7/31/08. |

Percentages are based on net assets as of 7/31/08, unless otherwise noted.

The portfolio is actively managed and current holdings may be different.

2

EXPENSE TABLE

Fund expenses borne by the shareholders during the period,

February 1, 2008 through July 31, 2008

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on certain purchase or redemption payments, and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period February 1, 2008 through July 31, 2008.

The actual expenses include the payment of a portion of the transfer-agent-related expenses of MFS funds that invest in the fund. For further information, please see the Notes to the Financial Statements.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

3

Expense Table – continued

| | | | | | | | | | |

Share

Class | | | | Annualized

Expense

Ratio | | Beginning

Account Value

2/01/08 | | Ending

Account Value

7/31/08 | | Expenses

Paid During

Period (p)

2/01/08-7/31/08 |

| A | | Actual | | 1.02% | | $1,000.00 | | $986.88 | | $5.04 |

| | Hypothetical (h) | | 1.02% | | $1,000.00 | | $1,019.79 | | $5.12 |

| B | | Actual | | 1.72% | | $1,000.00 | | $983.57 | | $8.48 |

| | Hypothetical (h) | | 1.72% | | $1,000.00 | | $1,016.31 | | $8.62 |

| C | | Actual | | 1.72% | | $1,000.00 | | $980.83 | | $8.47 |

| | Hypothetical (h) | | 1.72% | | $1,000.00 | | $1,016.31 | | $8.62 |

| I | | Actual | | 0.72% | | $1,000.00 | | $985.47 | | $3.55 |

| | Hypothetical (h) | | 0.72% | | $1,000.00 | | $1,021.28 | | $3.62 |

| R1 | | Actual | | 1.74% | | $1,000.00 | | $980.60 | | $8.57 |

| | Hypothetical (h) | | 1.74% | | $1,000.00 | | $1,016.21 | | $8.72 |

R2

(formerly R3) | | Actual | | 1.22% | | $1,000.00 | | $985.89 | | $6.02 |

| | Hypothetical (h) | | 1.22% | | $1,000.00 | | $1,018.80 | | $6.12 |

R3

(formerly R4) | | Actual | | 0.97% | | $1,000.00 | | $984.25 | | $4.79 |

| | Hypothetical (h) | | 0.97% | | $1,000.00 | | $1,020.04 | | $4.87 |

R4

(formerly R5) | | Actual | | 0.72% | | $1,000.00 | | $988.38 | | $3.56 |

| | Hypothetical (h) | | 0.72% | | $1,000.00 | | $1,021.28 | | $3.62 |

| 529A | | Actual | | 1.22% | | $1,000.00 | | $983.01 | | $6.02 |

| | Hypothetical (h) | | 1.22% | | $1,000.00 | | $1,018.80 | | $6.12 |

| 529B | | Actual | | 1.87% | | $1,000.00 | | $982.68 | | $9.22 |

| | Hypothetical (h) | | 1.87% | | $1,000.00 | | $1,015.56 | | $9.37 |

| 529C | | Actual | | 1.87% | | $1,000.00 | | $979.94 | | $9.21 |

| | Hypothetical (h) | | 1.87% | | $1,000.00 | | $1,015.56 | | $9.37 |

| (h) | 5% class return per year before expenses. |

| (p) | Expenses paid is equal to each class’ annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by the number of days in the year. Expenses paid do not include any applicable sales charges (loads). If these transaction costs had been included, your costs would have been higher. |

Expense Changes Impacting the Table

| | Effective March 1, 2008 the fund’s Class R1 retirement plan administration and services fee was terminated and the Class R1 distribution fee was increased (as described in Note 3 of the Notes to the Financial Statements). Had these fee changes been in effect throughout the entire six month period, the annualized expense ratio would have been 1.72%; the actual expenses paid during the period would have been approximately $8.47; and the hypothetical expenses paid during the period would have been approximately $8.62. |

| | Effective April 1, 2008 the fund’s Class 529A, Class 529B, and Class 529C shares program manager fee was reduced (as described in Note 3 of the Notes to Financial Statements). Had this fee change been in |

4

Expense Table – continued

| | effect throughout the entire six month period, the annualized expense ratio would have been 1.17%, 1.83%, and 1.82% for Class 529A, Class 529B, and Class 529C shares, respectively; the actual expenses paid during the period would have been approximately $5.77, $9.02, and $8.96 for Class 529A, Class 529B, and Class 529C shares, respectively; and the hypothetical expenses paid during the period would have been approximately $5.87, $9.17, and $9.12 for Class 529A, Class 529B, and Class 529C shares, respectively. |

5

PORTFOLIO OF INVESTMENTS

7/31/08 (unaudited)

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| | | | | | |

| Bonds - 86.4% | | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Aerospace - 1.2% | | | | | | |

| Hawker Beechcraft Acquisition Co. LLC, 9.75%, 2017 | | $ | 4,800,000 | | $ | 4,740,000 |

| Vought Aircraft Industries, Inc., 8%, 2011 | | | 6,690,000 | | | 6,171,523 |

| | | | | | |

| | | | | | $ | 10,911,523 |

| Airlines - 0.7% | | | | | | |

| Continental Airlines, Inc., 7.339%, 2014 | | $ | 5,719,000 | | $ | 4,289,250 |

| Continental Airlines, Inc., 6.9%, 2017 | | | 991,856 | | | 803,403 |

| Continental Airlines, Inc., 6.748%, 2017 | | | 1,595,724 | | | 1,244,665 |

| | | | | | |

| | | | | | $ | 6,337,318 |

| Asset Backed & Securitized - 5.4% | | | | | | |

| Airlie LCDO Ltd., CDO, FRN, 4.701%, 2011 (z) | | $ | 2,326,000 | | $ | 1,505,387 |

| Anthracite Ltd., CDO, 6%, 2037 (z) | | | 5,148,000 | | | 2,574,000 |

| Babson Ltd., CLO, “D”, FRN, 4.291%, 2018 (n) | | | 2,385,000 | | | 1,469,160 |

| Banc of America Commercial Mortgage, Inc., 5.39%, 2045 | | | 1,550,377 | | | 1,370,462 |

| Banc of America Commercial Mortgage, Inc., FRN, 5.772%, 2051 | | | 6,400,848 | | | 5,614,014 |

| Banc of America Commercial Mortgage, Inc., FRN, 5.812%, 2051 | | | 1,514,262 | | | 1,343,796 |

| Citigroup Commercial Mortgage Trust, FRN, 5.7%, 2049 | | | 2,948,120 | | | 1,820,596 |

| Credit Suisse Mortgage Capital Certificate, 5.343%, 2039 | | | 1,467,534 | | | 1,285,808 |

| CWCapital Cobalt Ltd., CDO, “E2”, 6%, 2045 (z) | | | 1,000,000 | | | 400,000 |

| CWCapital Cobalt Ltd., CDO, “F”, FRN, 4.095%, 2050 (z) | | | 610,000 | | | 158,758 |

| CWCapital Cobalt Ltd., CDO, “G”, FRN, 4.295%, 2050 (z) | | | 1,890,000 | | | 431,940 |

| Falcon Franchise Loan LLC, FRN, 3.421%, 2025 (i)(z) | | | 13,457,716 | | | 1,400,289 |

| First Union National Bank Commercial Mortgage Trust, 6.75%, 2032 | | | 2,000,000 | | | 1,659,214 |

| JPMorgan Chase Commercial Mortgage Securities Corp., 5.44%, 2045 | | | 4,479,655 | | | 3,967,955 |

| JPMorgan Chase Commercial Mortgage Securities Corp., 5.372%, 2047 | | | 2,288,482 | | | 2,012,801 |

JPMorgan Chase Commercial Mortgage Securities Corp., FRN,

5.466%, 2047 | | | 3,063,359 | | | 2,657,939 |

JPMorgan Chase Commercial Mortgage Securities Corp., FRN,

6.062%, 2051 | | | 2,285,000 | | | 1,630,799 |

Lehman Brothers Commercial Conduit Mortgage Trust, FRN,

0.811%, 2030 (i) | | | 12,965,339 | | | 442,118 |

| Merrill Lynch Mortgage Trust, FRN, 5.829%, 2050 | | | 2,285,000 | | | 1,610,466 |

Merrill Lynch/Countrywide Commercial Mortgage Trust, FRN,

5.204%, 2049 | | | 4,845,929 | | | 4,220,529 |

Merrill Lynch/Countrywide Commercial Mortgage Trust, FRN,

5.749%, 2050 | | | 1,241,000 | | | 1,098,113 |

| Morgan Stanley Capital I, Inc., 1.444%, 2039 (i)(n) | | | 23,489,233 | | | 614,243 |

6

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Asset Backed & Securitized - continued | | | | | | |

| TIERS Beach Street Synthetic, CLO, FRN, 6.788%, 2011 (z) | | $ | 2,750,000 | | $ | 2,092,750 |

| Wachovia Bank Commercial Mortgage Trust, FRN, 5.752%, 2047 | | | 1,738,692 | | | 1,182,516 |

| Wachovia Bank Commercial Mortgage Trust, FRN, 5.903%, 2051 | | | 4,834,564 | | | 4,311,834 |

| Wachovia Credit, CDO, FRN, 4.154%, 2026 (z) | | | 1,320,000 | | | 462,000 |

| | | | | | |

| | | | | | $ | 47,337,487 |

| Automotive - 3.0% | | | | | | |

| Allison Transmission, Inc., 11%, 2015 (n) | | $ | 7,145,000 | | $ | 6,466,225 |

| Fce Bank PLC, 7.125%, 2012 | | EUR | 4,950,000 | | | 6,406,179 |

| Ford Motor Credit Co. LLC, 12%, 2015 | | $ | 5,568,000 | | | 4,692,566 |

| Ford Motor Credit Co. LLC, 8%, 2016 | | | 5,045,000 | | | 3,565,407 |

| Ford Motor Credit Co. LLC, FRN, 4.361%, 2010 | | | 3,005,000 | | | 2,568,866 |

| General Motors Corp., 8.375%, 2033 | | | 5,225,000 | | | 2,573,313 |

| | | | | | |

| | | | | | $ | 26,272,556 |

| Broadcasting - 5.9% | | | | | | |

| Allbritton Communications Co., 7.75%, 2012 | | $ | 6,515,000 | | $ | 5,993,800 |

| Bonten Media Acquisition Co., 9%, 2015 (n)(p) | | | 4,420,000 | | | 3,359,200 |

| CanWest MediaWorks LP, 9.25%, 2015 (n) | | | 2,890,000 | | | 2,239,750 |

| DIRECTV Holdings LLC, 7.625%, 2016 (n) | | | 4,895,000 | | | 4,858,287 |

| Lamar Media Corp., 6.625%, 2015 | | | 4,660,000 | | | 4,194,000 |

| Lamar Media Corp., “C”, 6.625%, 2015 | | | 2,950,000 | | | 2,655,000 |

| LBI Media, Inc., 8.5%, 2017 (n) | | | 3,205,000 | | | 2,455,831 |

| LIN TV Corp., 6.5%, 2013 | | | 6,610,000 | | | 5,750,700 |

| Local TV Finance LLC, 9.25%, 2015 (n)(p) | | | 4,820,000 | | | 3,663,200 |

| Newport Television LLC, 13%, 2017 (n)(p) | | | 5,600,000 | | | 4,788,000 |

| Nexstar Broadcasting Group, Inc., 7%, 2014 | | | 5,375,000 | | | 4,420,938 |

| Univision Communications, Inc., 9.75%, 2015 (n)(p) | | | 9,000,000 | | | 6,862,500 |

| Young Broadcasting, Inc., 8.75%, 2014 | | | 1,640,000 | | | 701,100 |

| | | | | | |

| | | | | | $ | 51,942,306 |

| Brokerage & Asset Managers - 0.5% | | | | | | |

| Nuveen Investments, Inc., 10.5%, 2015 (n) | | $ | 5,265,000 | | $ | 4,738,500 |

| | |

| Building - 1.5% | | | | | | |

| Associated Materials, Inc., 9.75%, 2012 | | $ | 1,460,000 | | $ | 1,438,100 |

| Associated Materials, Inc., 0% to 2009, 11.25% to 2014 | | | 2,360,000 | | | 1,445,500 |

| Building Materials Corp. of America, 7.75%, 2014 | | | 3,270,000 | | | 2,550,600 |

| Nortek Holdings, Inc., 10%, 2013 (n) | | | 2,270,000 | | | 2,031,650 |

| Nortek Holdings, Inc., 8.5%, 2014 | | | 3,865,000 | | | 2,188,556 |

| Ply Gem Industries, Inc., 9%, 2012 | | | 4,640,000 | | | 2,412,800 |

| Ply Gem Industries, Inc., 11.75%, 2013 (n) | | | 1,660,000 | | | 1,485,700 |

| | | | | | |

| | | | | | $ | 13,552,906 |

7

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Business Services - 0.7% | | | | | | |

| SunGard Data Systems, Inc., 10.25%, 2015 | | $ | 6,493,000 | | $ | 6,590,395 |

| | |

| Cable TV - 3.8% | | | | | | |

| CCH I Holdings LLC, 11%, 2015 | | $ | 2,030,000 | | $ | 1,537,725 |

| CCH II Holdings LLC, 10.25%, 2010 | | | 7,675,000 | | | 7,310,437 |

| CCO Holdings LLC, 8.75%, 2013 | | | 14,135,000 | | | 13,074,875 |

| CSC Holdings, Inc., 6.75%, 2012 | | | 3,550,000 | | | 3,381,375 |

| CSC Holdings, Inc., 8.5%, 2015 (n) | | | 1,370,000 | | | 1,349,450 |

| Mediacom LLC, 9.5%, 2013 | | | 1,890,000 | | | 1,786,050 |

| NTL Cable PLC, 9.125%, 2016 | | | 5,428,000 | | | 5,020,900 |

| | | | | | |

| | | | | | $ | 33,460,812 |

| Chemicals - 3.5% | | | | | | |

| Innophos, Inc., 8.875%, 2014 | | $ | 5,530,000 | | $ | 5,530,000 |

| KI Holdings, Inc., 0% to 2009, 9.875% to 2014 | | | 7,030,000 | | | 6,327,000 |

| Koppers Holdings, Inc., 9.875%, 2013 | | | 4,665,000 | | | 4,892,419 |

| Momentive Performance Materials, Inc., 9.75%, 2014 | | | 1,460,000 | | | 1,292,100 |

| Momentive Performance Materials, Inc., 11.5%, 2016 | | | 5,901,000 | | | 4,543,770 |

| Nalco Co., 7.75%, 2011 | | | 1,485,000 | | | 1,499,850 |

| Nalco Co., 8.875%, 2013 | | | 6,215,000 | | | 6,416,988 |

| | | | | | |

| | | | | | $ | 30,502,127 |

| Computer Software - 0.6% | | | | | | |

| First Data Corp., 9.875%, 2015 (n) | | $ | 5,850,000 | | $ | 5,177,250 |

| | |

| Consumer Goods & Services - 2.6% | | | | | | |

| Corrections Corp. of America, 6.25%, 2013 | | $ | 2,330,000 | | $ | 2,277,575 |

| GEO Group, Inc., 8.25%, 2013 | | | 4,290,000 | | | 4,354,350 |

| Jarden Corp., 7.5%, 2017 | | | 2,325,000 | | | 2,022,750 |

| KAR Holdings, Inc., 10%, 2015 | | | 3,440,000 | | | 2,855,200 |

| Service Corp. International, 7.375%, 2014 | | | 2,220,000 | | | 2,147,850 |

| Service Corp. International, 7%, 2017 | | | 7,550,000 | | | 7,002,625 |

| Ticketmaster, 10.75%, 2016 (z) | | | 1,975,000 | | | 2,044,125 |

| | | | | | |

| | | | | | $ | 22,704,475 |

| Containers - 1.5% | | | | | | |

| Crown Americas LLC, 7.625%, 2013 | | $ | 3,075,000 | | $ | 3,121,125 |

| Graham Packaging Co. LP, 9.875%, 2014 | | | 3,335,000 | | | 2,851,425 |

| Greif, Inc., 6.75%, 2017 | | | 3,415,000 | | | 3,244,250 |

| Owens-Brockway Glass Container, Inc., 8.25%, 2013 | | | 3,985,000 | | | 4,084,625 |

| | | | | | |

| | | | | | $ | 13,301,425 |

8

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Defense Electronics - 1.0% | | | | | | |

| L-3 Communications Corp., 6.125%, 2014 | | $ | 4,685,000 | | $ | 4,427,325 |

| L-3 Communications Corp., 5.875%, 2015 | | | 4,475,000 | | | 4,150,563 |

| | | | | | |

| | | | | | $ | 8,577,888 |

| Electronics - 0.8% | | | | | | |

| Avago Technologies Finance, 11.875%, 2015 | | $ | 2,340,000 | | $ | 2,492,100 |

| Flextronics International Ltd., 6.25%, 2014 | | | 2,430,000 | | | 2,247,750 |

| Spansion LLC, 11.25%, 2016 (n) | | | 3,575,000 | | | 2,216,500 |

| | | | | | |

| | | | | | $ | 6,956,350 |

| Emerging Market Sovereign - 0.5% | | | | | | |

| Republic of Argentina, FRN, 3.092%, 2012 | | $ | 4,942,500 | | $ | 4,003,005 |

| | |

| Energy - Independent - 5.5% | | | | | | |

| Chaparral Energy, Inc., 8.875%, 2017 | | $ | 3,225,000 | | $ | 2,781,562 |

| Chesapeake Energy Corp., 7%, 2014 | | | 2,147,000 | | | 2,114,795 |

| Chesapeake Energy Corp., 6.375%, 2015 | | | 5,625,000 | | | 5,315,625 |

| Forest Oil Corp., 7.25%, 2019 | | | 2,760,000 | | | 2,594,400 |

| Forest Oil Corp., 7.25%, 2019 (n) | | | 780,000 | | | 733,200 |

| Hilcorp Energy I LP, 7.75%, 2015 (n) | | | 450,000 | | | 412,875 |

| Hilcorp Energy I LP, 9%, 2016 (n) | | | 2,215,000 | | | 2,170,700 |

| Mariner Energy, Inc., 8%, 2017 | | | 2,775,000 | | | 2,615,438 |

| Newfield Exploration Co., 6.625%, 2014 | | | 3,715,000 | | | 3,510,675 |

| OPTI Canada, Inc., 8.25%, 2014 | | | 6,360,000 | | | 6,407,700 |

| Plains Exploration & Production Co., 7%, 2017 | | | 6,490,000 | | | 6,068,150 |

| Quicksilver Resources, Inc., 7.125%, 2016 | | | 7,100,000 | | | 6,123,750 |

| SandRidge Energy, Inc., 8.625%, 2015 (n)(p) | | | 1,840,000 | | | 1,856,100 |

| SandRidge Energy, Inc., 8%, 2018 (n) | | | 2,630,000 | | | 2,603,700 |

| Southwestern Energy Co., 7.5%, 2018 (n) | | | 2,855,000 | | | 2,926,375 |

| | | | | | |

| | | | | | $ | 48,235,045 |

| Entertainment - 0.5% | | | | | | |

| AMC Entertainment, Inc., 11%, 2016 | | $ | 2,935,000 | | $ | 2,971,688 |

| Marquee Holdings, Inc., 12%, 2014 | | | 2,295,000 | | | 1,818,788 |

| | | | | | |

| | | | | | $ | 4,790,476 |

| Financial Institutions - 0.6% | | | | | | |

| General Motors Acceptance Corp., 6.875%, 2011 | | $ | 4,897,000 | | $ | 3,233,499 |

| General Motors Acceptance Corp., 8%, 2031 | | | 4,380,000 | | | 2,454,298 |

| | | | | | |

| | | | | | $ | 5,687,797 |

| Food & Beverages - 1.9% | | | | | | |

| ARAMARK Corp., 8.5%, 2015 | | $ | 2,046,000 | | $ | 2,038,327 |

| B&G Foods, Inc., 8%, 2011 | | | 3,570,000 | | | 3,498,600 |

9

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Food & Beverages - continued | | | | | | |

| Dean Foods Co., 7%, 2016 | | $ | 4,625,000 | | $ | 4,185,625 |

| Del Monte Corp., 6.75%, 2015 | | | 3,920,000 | | | 3,665,200 |

| Michael Foods, Inc., 8%, 2013 | | | 3,105,000 | | | 3,066,188 |

| | | | | | |

| | | | | | $ | 16,453,940 |

| Forest & Paper Products - 2.5% | | | | | | |

| Buckeye Technologies, Inc., 8%, 2010 | | $ | 993,000 | | $ | 995,482 |

| Buckeye Technologies, Inc., 8.5%, 2013 | | | 7,725,000 | | | 7,705,687 |

| Georgia-Pacific Corp., 7.125%, 2017 (n) | | | 2,605,000 | | | 2,403,113 |

| Georgia-Pacific Corp., 8%, 2024 | | | 1,490,000 | | | 1,370,800 |

| Graphic Packaging International Corp., 9.5%, 2013 | | | 2,340,000 | | | 2,176,200 |

| JSG Funding PLC, 7.75%, 2015 | | | 525,000 | | | 472,500 |

| Millar Western Forest Products Ltd., 7.75%, 2013 | | | 4,885,000 | | | 2,857,725 |

| NewPage Holding Corp., 10%, 2012 | | | 125,000 | | | 119,688 |

| Smurfit-Stone Container Corp., 8%, 2017 | | | 4,285,000 | | | 3,502,987 |

| | | | | | |

| | | | | | $ | 21,604,182 |

| Gaming & Lodging - 6.3% | | | | | | |

| Firekeepers Development Authority, 13.875%, 2015 (z) | | $ | 2,950,000 | | $ | 2,714,000 |

| Fontainebleau Las Vegas Holdings LLC, 10.25%, 2015 (n) | | | 6,865,000 | | | 3,638,450 |

| Harrah’s Operating Co., Inc., 5.5%, 2010 | | | 2,795,000 | | | 2,431,650 |

| Harrah’s Operating Co., Inc., 5.375%, 2013 | | | 660,000 | | | 353,100 |

| Harrah’s Operating Co., Inc., 10.75%, 2016 (n) | | | 8,245,000 | | | 6,224,975 |

| Harrah’s Operating Co., Inc., 10.75%, 2018 (n)(p) | | | 3,865,000 | | | 2,589,550 |

| Host Marriott LP, 7.125%, 2013 | | | 2,770,000 | | | 2,548,400 |

| Host Marriott LP, 6.75%, 2016 | | | 1,380,000 | | | 1,179,900 |

| Mandalay Resort Group, 9.375%, 2010 | | | 3,525,000 | | | 3,436,875 |

| MGM Mirage, 8.5%, 2010 | | | 3,075,000 | | | 2,959,688 |

| MGM Mirage, 8.375%, 2011 | | | 4,045,000 | | | 3,650,613 |

| MGM Mirage, 6.75%, 2013 | | | 4,020,000 | | | 3,356,700 |

| MGM Mirage, 5.875%, 2014 | | | 3,010,000 | | | 2,377,900 |

| Pinnacle Entertainment, Inc., 7.5%, 2015 | | | 6,360,000 | | | 4,738,200 |

| Station Casinos, Inc., 6%, 2012 | | | 1,395,000 | | | 934,650 |

| Station Casinos, Inc., 6.5%, 2014 | | | 8,305,000 | | | 4,007,162 |

| Station Casinos, Inc., 6.875%, 2016 | | | 7,690,000 | | | 3,498,950 |

| Trump Entertainment Resorts Holdings, Inc., 8.5%, 2015 | | | 9,875,000 | | | 4,863,437 |

| | | | | | |

| | | | | | $ | 55,504,200 |

| Industrial - 1.4% | | | | | | |

| Blount, Inc., 8.875%, 2012 | | $ | 3,955,000 | | $ | 4,004,437 |

| JohnsonDiversey, Inc., 9.625%, 2012 | | EUR | 1,405,000 | | | 2,103,116 |

| JohnsonDiversey, Inc., “B”, 9.625%, 2012 | | $ | 5,965,000 | | | 6,069,388 |

| | | | | | |

| | | | | | $ | 12,176,941 |

10

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Insurance - Property & Casualty - 0.3% | | | | | | |

| USI Holdings Corp., 9.75%, 2015 (n) | | $ | 3,165,000 | | $ | 2,555,738 |

| | |

| Machinery & Tools - 0.6% | | | | | | |

| Case New Holland, Inc., 7.125%, 2014 | | $ | 5,565,000 | | $ | 5,384,137 |

| | |

| Major Banks - 1.2% | | | | | | |

| Bank of America Corp., 8% to 2018, FRN to 2059 | | $ | 4,515,000 | | $ | 4,165,088 |

| JPMorgan Chase & Co., 7.9% to 2018, FRN to 2049 | | | 6,505,000 | | | 6,017,255 |

| | | | | | |

| | | | | | $ | 10,182,343 |

| Medical & Health Technology & Services - 8.4% | | | | | | |

| Biomet, Inc., 10%, 2017 | | $ | 3,195,000 | | $ | 3,434,625 |

| Biomet, Inc., 11.625%, 2017 | | | 6,305,000 | | | 6,659,655 |

| Community Health Systems, Inc., 8.875%, 2015 | | | 10,360,000 | | | 10,437,700 |

| Cooper Cos., Inc., 7.125%, 2015 | | | 4,305,000 | | | 4,132,800 |

| DaVita, Inc., 7.25%, 2015 | | | 7,980,000 | | | 7,850,325 |

| HCA, Inc., 6.375%, 2015 | | | 8,905,000 | | | 7,302,100 |

| HCA, Inc., 9.25%, 2016 | | | 16,355,000 | | | 16,845,650 |

| Psychiatric Solutions, Inc., 7.75%, 2015 | | | 3,970,000 | | | 3,880,675 |

| U.S. Oncology, Inc., 10.75%, 2014 | | | 6,330,000 | | | 6,219,225 |

| Universal Hospital Services, Inc., 8.5%, 2015 (p) | | | 3,330,000 | | | 3,330,000 |

| Universal Hospital Services, Inc., FRN, 6.303%, 2015 | | | 1,015,000 | | | 943,950 |

| VWR Funding, Inc., 10.25%, 2015 (p) | | | 2,835,000 | | | 2,601,113 |

| | | | | | |

| | | | | | $ | 73,637,818 |

| Metals & Mining - 4.7% | | | | | | |

| Arch Western Finance LLC, 6.75%, 2013 | | $ | 3,570,000 | | $ | 3,561,075 |

| FMG Finance Ltd., 10.625%, 2016 (n) | | | 7,395,000 | | | 8,578,200 |

| Freeport-McMoRan Copper & Gold, Inc., 8.375%, 2017 | | | 12,055,000 | | | 12,627,612 |

| Freeport-McMoRan Copper & Gold, Inc., FRN, 5.883%, 2015 | | | 4,988,000 | | | 5,012,042 |

| Peabody Energy Corp., 5.875%, 2016 | | | 4,440,000 | | | 4,229,100 |

| Peabody Energy Corp., 7.375%, 2016 | | | 3,600,000 | | | 3,672,000 |

| PNA Group, Inc., 10.75%, 2016 | | | 2,950,000 | | | 3,503,125 |

| | | | | | |

| | | | | | $ | 41,183,154 |

| Municipals - 0.5% | | | | | | |

| Regional Transportation Authority, IL, “A”, MBIA, 4.5%, 2035 | | $ | 4,335,000 | | $ | 4,010,092 |

| | |

| Natural Gas - Distribution - 0.8% | | | | | | |

| AmeriGas Partners LP, 7.125%, 2016 | | $ | 4,575,000 | | $ | 4,151,812 |

| Inergy LP, 6.875%, 2014 | | | 3,625,000 | | | 3,262,500 |

| | | | | | |

| | | | | | $ | 7,414,312 |

11

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Natural Gas - Pipeline - 2.1% | | | | | | |

| Atlas Pipeline Partners LP, 8.125%, 2015 | | $ | 2,865,000 | | $ | 2,800,537 |

| Atlas Pipeline Partners LP, 8.75%, 2018 (n) | | | 2,775,000 | | | 2,726,437 |

Deutsche Bank (El Paso Performance-Linked Trust, CLN),

7.75%, 2011 (n) | | | 4,380,000 | | | 4,432,236 |

| El Paso Corp., 7.25%, 2018 | | | 2,840,000 | | | 2,811,600 |

| Transcontinental Gas Pipe Line Corp., 7%, 2011 | | | 1,094,000 | | | 1,137,760 |

| Williams Partners LP, 7.25%, 2017 | | | 4,285,000 | | | 4,274,288 |

| | | | | | |

| | | | | | $ | 18,182,858 |

| Network & Telecom - 3.5% | | | | | | |

| Cincinnati Bell, Inc., 8.375%, 2014 | | $ | 6,315,000 | | $ | 6,015,037 |

| Citizens Communications Co., 9.25%, 2011 | | | 4,461,000 | | | 4,639,440 |

| Nordic Telephone Co. Holdings, 8.875%, 2016 (n) | | | 3,965,000 | | | 3,826,225 |

| Qwest Capital Funding, Inc., 7.25%, 2011 | | | 5,935,000 | | | 5,653,088 |

| Qwest Corp., 7.875%, 2011 | | | 715,000 | | | 704,275 |

| Qwest Corp., 8.875%, 2012 | | | 5,210,000 | | | 5,196,975 |

| Windstream Corp., 8.625%, 2016 | | | 4,395,000 | | | 4,449,938 |

| | | | | | |

| | | | | | $ | 30,484,978 |

| Oil Services - 0.8% | | | | | | |

| Basic Energy Services, Inc., 7.125%, 2016 | | $ | 5,755,000 | | $ | 5,380,925 |

| GulfMark Offshore, Inc., 7.75%, 2014 | | | 1,340,000 | | | 1,319,900 |

| | | | | | |

| | | | | | $ | 6,700,825 |

| Printing & Publishing - 2.8% | | | | | | |

| American Media Operations, Inc., 10.25%, 2009 (z) | | $ | 167,910 | | $ | 131,809 |

| American Media Operations, Inc., “B”, 10.25%, 2009 | | | 4,618,000 | | | 3,625,130 |

| Dex Media West LLC, 9.875%, 2013 | | | 1,025,000 | | | 804,625 |

| Dex Media, Inc., 0% to 2008, 9% to 2013 | | | 9,895,000 | | | 5,937,000 |

| Dex Media, Inc., 0% to 2008, 9% to 2013 | | | 6,115,000 | | | 3,669,000 |

| Idearc, Inc., 8%, 2016 | | | 7,309,000 | | | 3,325,595 |

| Nielsen Finance LLC, 10%, 2014 | | | 4,545,000 | | | 4,579,088 |

| Nielsen Finance LLC, 0% to 2011, 12.5% to 2016 | | | 615,000 | | | 419,738 |

| Quebecor World, Inc., 6.125%, 2013 (d) | | | 2,190,000 | | | 766,500 |

| R.H. Donnelley Corp., 8.875%, 2016 | | | 2,670,000 | | | 1,288,275 |

| | | | | | |

| | | | | | $ | 24,546,760 |

| Retailers - 0.2% | | | | | | |

| Couche-Tard, Inc., 7.5%, 2013 | | $ | 705,000 | | $ | 657,412 |

| Sally Holdings LLC, 10.5%, 2016 | | | 930,000 | | | 895,125 |

| | | | | | |

| | | | | | $ | 1,552,537 |

12

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Bonds - continued | | | | | | |

| Specialty Stores - 0.3% | | | | | | |

| Payless ShoeSource, Inc., 8.25%, 2013 | | $ | 3,290,000 | | $ | 2,961,000 |

| | |

| Supermarkets - 0.1% | | | | | | |

| Stater Brothers Holdings, Inc., 7.75%, 2015 | | $ | 664,000 | | $ | 634,120 |

| | |

| Telecommunications - Wireless - 1.7% | | | | | | |

| Alltel Corp., 7%, 2012 | | $ | 4,894,000 | | $ | 5,016,350 |

| MetroPCS Wireless, Inc., 9.25%, 2014 | | | 5,430,000 | | | 5,267,100 |

| Wind Acquisition Finance S.A., 10.75%, 2015 (n) | | | 4,720,000 | | | 4,885,200 |

| | | | | | |

| | | | | | $ | 15,168,650 |

| Transportation - Services - 0.3% | | | | | | |

| Hertz Corp., 8.875%, 2014 | | $ | 3,020,000 | | $ | 2,770,850 |

| | |

| Utilities - Electric Power - 6.2% | | | | | | |

| Dynegy Holdings, Inc., 7.5%, 2015 | | $ | 2,135,000 | | $ | 2,022,912 |

| Edison Mission Energy, 7%, 2017 | | | 6,865,000 | | | 6,487,425 |

| Mirant Americas Generation LLC, 8.3%, 2011 | | | 2,900,000 | | | 2,958,000 |

| Mirant North America LLC, 7.375%, 2013 | | | 4,870,000 | | | 4,870,000 |

| NRG Energy, Inc., 7.375%, 2016 | | | 19,260,000 | | | 18,682,200 |

| Reliant Energy, Inc., 6.75%, 2014 | | | 1,555,000 | | | 1,586,100 |

| Reliant Energy, Inc., 7.875%, 2017 | | | 6,675,000 | | | 6,441,375 |

| Sierra Pacific Resources, 8.625%, 2014 | | | 536,000 | | | 561,461 |

| Texas Competitive Electric Holdings LLC, 10.25%, 2015 (n) | | | 11,095,000 | | | 11,095,000 |

| | | | | | |

| | | | | | $ | 54,704,473 |

| Total Bonds (Identified Cost, $830,809,023) | | | | | $ | 758,893,549 |

| | |

| Floating Rate Loans - 5.9% (g)(r) | | | | | | |

| Aerospace - 0.6% | | | | | | |

| Hawker Beechcraft Acquisition Co., Letter of Credit, 4.8%, 2014 | | $ | 203,875 | | $ | 189,540 |

| Hawker Beechcraft Acquisition Co., Term Loan B, 4.8%, 2014 | | | 5,076,310 | | | 4,719,385 |

| | | | | | |

| | | | | | $ | 4,908,925 |

| Automotive - 1.2% | | | | | | |

| Federal Mogul Corp., Term Loan B, 4.4%, 2014 | | $ | 3,751,524 | | $ | 2,926,189 |

| Ford Motor Co., Term Loan B, 5.46%, 2013 | | | 7,730,635 | | | 6,063,717 |

| Mark IV Industries, Inc., Second Lien Term Loan, 11.39%, 2011 | | | 3,476,611 | | | 1,408,027 |

| | | | | | |

| | | | | | $ | 10,397,933 |

| Broadcasting - 0.5% | | | | | | |

| Young Broadcasting, Inc., Term Loan, 5.31%, 2012 | | $ | 3,642,319 | | $ | 3,132,395 |

| Young Broadcasting, Inc., Term Loan B-1, 5.31%, 2012 | | | 1,356,995 | | | 1,167,016 |

| | | | | | |

| | | | | | $ | 4,299,411 |

13

Portfolio of Investments (unaudited) – continued

| | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | | |

| Floating Rate Loans (g)(r) - continued | | | | | | |

| Computer Software - 0.5% | | | | | | |

| First Data Corp., Term Loan B-1, 5.24%, 2014 | | $ | 4,936,458 | | $ | 4,537,429 |

| | |

| Forest & Paper Products - 0.1% | | | | | | |

| Abitibi-Consolidated, Inc., Term Loan, 11.5%, 2009 | | $ | 1,265,104 | | $ | 1,258,778 |

| | |

| Gaming & Lodging - 0.3% | | | | | | |

Green Valley Ranch Gaming LLC, Second Lien Term Loan,

5.89%, 2014 (o) | | $ | 4,910,923 | | $ | 2,848,335 |

| | |

| Medical & Health Technology & Services - 0.6% | | | | | | |

Community Health Systems, Inc., Delayed Draw Term Loan B,

2014 (q) | | $ | 88,142 | | $ | 83,392 |

| Community Health Systems, Inc., Term Loan, 4.85%, 2014 | | | 1,723,423 | | | 1,630,549 |

| HCA, Inc., Term Loan B, 5.05%, 2013 | | | 4,015,350 | | | 3,772,755 |

| | | | | | |

| | | | | | $ | 5,486,696 |

| Printing & Publishing - 0.5% | | | | | | |

| Idearc, Inc., Term Loan B, 4.79%, 2014 | | $ | 461,220 | | $ | 341,687 |

| Tribune Co., Term Loan B, 2014 (o) | | | 5,724,803 | | | 3,889,317 |

| | | | | | |

| | | | | | $ | 4,231,004 |

| Retailers - 0.1% | | | | | | |

| Burlington Coat Factory, Term Loan B, 2013 (o) | | $ | 1,578,668 | | $ | 1,253,726 |

| | |

| Specialty Stores - 0.2% | | | | | | |

| Michaels Stores, Inc., Term Loan B, 4.75%, 2013 | | $ | 1,767,551 | | $ | 1,419,197 |

| | |

| Telecommunications - Wireless - 0.3% | | | | | | |

| Alltel Corp., Term Loan B-2, 2015 (o) | | $ | 2,530,406 | | $ | 2,498,303 |

| | |

| Utilities - Electric Power - 1.0% | | | | | | |

| Calpine Corp., Term Loan, 5.69%, 2014 | | $ | 4,046,172 | | $ | 3,795,455 |

| TXU Corp. Term Loan B-3, 6.26%, 2014 | | | 5,227,099 | | | 4,893,056 |

| | | | | | |

| | | | | | $ | 8,688,511 |

| Total Floating Rate Loans (Identified Cost, $57,268,278) | | | | | $ | 51,828,248 |

| | |

| Common Stocks - 2.1% | | | | | | |

| Automotive - 0.0% | | | | | | |

| Oxford Automotive, Inc. (a) | | | 1,087 | | $ | 0 |

14

Portfolio of Investments (unaudited) – continued

| | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | |

| Common Stocks - continued | | | | | |

| Cable TV - 0.8% | | | | | |

| Cablevision Systems Corp., “A” (a) | | 41,600 | | $ | 1,010,048 |

| Comcast Corp., “A” | | 228,100 | | | 4,703,422 |

| Time Warner Cable, Inc. (a) | | 59,500 | | | 1,691,585 |

| | | | | |

| | | | | $ | 7,405,055 |

| Consumer Goods & Services - 0.0% | | | | | |

| Central Garden & Pet Co. (a) | | 47,600 | | $ | 219,912 |

| | |

| Electronics - 0.1% | | | | | |

| Intel Corp. | | 20,700 | | $ | 459,333 |

| | |

| Energy - Integrated - 0.1% | | | | | |

| Chevron Corp. | | 9,500 | | $ | 803,320 |

| | |

| Forest & Paper Products - 0.1% | | | | | |

| Louisiana-Pacific Corp. | | 52,900 | | $ | 447,534 |

| | |

| Gaming & Lodging - 0.3% | | | | | |

| MGM Mirage (a) | | 25,700 | | $ | 745,814 |

| Pinnacle Entertainment, Inc. (a) | | 131,800 | | | 1,489,340 |

| | | | | |

| | | | | $ | 2,235,154 |

| Major Banks - 0.1% | | | | | |

| Bank of America Corp. | | 24,700 | | $ | 812,630 |

| JPMorgan Chase & Co. | | 12,000 | | | 487,560 |

| | | | | |

| | | | | $ | 1,300,190 |

| Printing & Publishing - 0.0% | | | | | |

| Golden Books Family Entertainment, Inc. (a) | | 206,408 | | $ | 0 |

| | |

| Real Estate - 0.1% | | | | | |

| Host Hotels & Resorts, Inc., REIT | | 102,500 | | $ | 1,343,775 |

| | |

| Telephone Services - 0.2% | | | | | |

| Windstream Corp. | | 151,600 | | $ | 1,807,072 |

| | |

| Utilities - Electric Power - 0.3% | | | | | |

| Reliant Energy, Inc. (a) | | 123,500 | | $ | 2,236,585 |

| Total Common Stocks (Identified Cost, $24,175,932) | | | | $ | 18,257,930 |

15

Portfolio of Investments (unaudited) – continued

| | | | | |

| Preferred Stocks - 0.9% | | | | | |

| Issuer | | Shares/Par | | Value ($) |

| | | | | |

| Broadcasting - 0.2% | | | | | |

| Spanish Broadcasting Systems, Inc., “B”, 10.75% (p) | | 2,034 | | $ | 1,281,420 |

| | |

| Brokerage & Asset Managers - 0.7% | | | | | |

| Merrill Lynch Co., Inc., 8.625% (a) | | 304,150 | | $ | 6,250,283 |

| Total Preferred Stocks (Identified Cost, $9,604,506) | | | | $ | 7,531,703 |

| | |

| Money Market Funds (v) - 3.8% | | | | | |

MFS Institutional Money Market Portfolio, 2.57%,

at Cost and Net Asset Value | | 33,545,765 | | $ | 33,545,765 |

| Total Investments (Identified Cost, $955,403,504) | | | | $ | 870,057,195 |

| | |

| Other Assets, Less Liabilities - 0.9% | | | | | 7,729,474 |

| Net Assets - 100.0% | | | | $ | 877,786,669 |

| (a) | Non-income producing security. |

| (d) | Non-income producing security – in default. |

| (g) | The rate shown represents a weighted average coupon rate on settled positions at period end, unless otherwise indicated. |

| (i) | Interest only security for which the fund receives interest on notional principal (Par amount). Par amount shown is the notional principal and does not reflect the cost of the security. |

| (n) | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in the ordinary course of business in transactions exempt from registration, normally to qualified institutional buyers. At period end, the aggregate value of these securities was $117,433,520, representing 13.4% of net assets. |

| (o) | All or a portion of this position has not settled. Upon settlement date, interest rates will be determined. |

| (p) | Payment-in-kind security. |

| (q) | All or a portion of this position represents an unfunded loan commitment. The rate shown represents a weighted average coupon rate on the full position, including the unfunded loan commitment which has no current coupon rate. |

| (r) | Remaining maturities of floating rate loans may be less than stated maturities shown as a result of contractual or optional prepayments by the borrower. Such prepayments cannot be predicted with certainty. These loans may be subject to restrictions on resale. Floating rate loans generally have rates of interest which are determined periodically by reference to a base lending rate plus a premium. |

| (v) | Underlying fund that is available only to investment companies managed by MFS. The rate quoted is the annualized seven-day yield of the fund at period end. |

16

Portfolio of Investments (unaudited) – continued

| (z) | Restricted securities are not registered under the Securities Act of 1933 and are subject to legal restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are subsequently registered. Disposal of these securities may involve time-consuming negotiations and prompt sale at an acceptable price may be difficult. The fund holds the following restricted securities: |

| | | | | | |

| Restricted Securities | | Acquisition

Date | | Cost | | Current

Market

Value |

| Airlie LCDO Ltd., CDO, FRN, 4.701%, 2011 | | 10/13/06 | | $2,326,000 | | $1,505,387 |

American Media Operations, Inc.,

10.25%, 2009 | | 1/18/08 | | 161,775 | | 131,809 |

| Anthracite Ltd., CDO, 6%, 2037 | | 5/14/02 | | 4,237,977 | | 2,574,000 |

| CWCapital Cobalt Ltd., CDO, “E2”, 6%, 2045 | | 3/20/06 | | 958,428 | | 400,000 |

| CWCapital Cobalt Ltd., CDO, “F”, FRN, 4.095%, 2050 | | 4/12/06 | | 610,000 | | 158,758 |

| CWCapital Cobalt Ltd., CDO, “G”, FRN, 4.295%, 2050 | | 4/12/06 | | 1,890,000 | | 431,940 |

Falcon Franchise Loan LLC, FRN,

3.421%, 2025 | | 1/29/03 | | 1,681,031 | | 1,400,289 |

| Firekeepers Development Authority, 13.875%, 2015 | | 4/22/08 | | 2,866,296 | | 2,714,000 |

| TIERS Beach Street Synthetic, CLO, FRN, 6.788%, 2011 | | 5/17/06 | | 2,750,000 | | 2,092,750 |

| Ticketmaster, 10.75%, 2016 | | 7/16/08-7/17/08 | | 1,995,881 | | 2,044,125 |

| Wachovia Credit, CDO, FRN, 4.154%, 2026 | | 6/08/06 | | 1,320,000 | | 462,000 |

| Total Restricted Securities | | | | | | $13,915,058 |

| % of Net Assets | | | | | | 1.6% |

Derivative Contracts at 7/31/08

Forward Foreign Currency Exchange Contracts at 7/31/08

| | | | | | | | | | | | | |

| Type | | Currency | | Contracts to

Deliver/Receive | | Settlement

Date Range | | In Exchange

For | | Contracts

at Value | | Net

Unrealized

Appreciation

(Depreciation) | |

| Appreciation | | | | | | | | | | | | | |

BUY | | EUR | | 1,555,723 | | 8/25/08 | | $2,416,410 | | $2,423,038 | | $6,628 | |

SELL | | EUR | | 4,302,212 | | 8/25/08 | | 6,773,550 | | 6,700,695 | | 72,855 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | $79,483 | |

| | | | | | | | | | | | | |

| | | | | | |

| Depreciation | | | | | | | | | | | | | |

SELL | | EUR | | 2,701,892 | | 8/25/08 | | $4,195,185 | | $4,208,196 | | $(13,011 | ) |

| | | | | | | | | | | | | |

17

Portfolio of Investments (unaudited) – continued

Swap Agreements at 7/31/08

| | | | | | | | | | | | | | | |

| Expiration | | Notional

Amount | | | Counterparty | | Cash Flows

to Receive | | | Cash Flows to

Pay | | Value | |

| Credit Default Swaps | | | | | | | | | | | |

| 6/20/09 | | USD | | 4,200,000 | | | JPMorgan Chase Bank | | 4.10% (fixed rate | ) | | (1) | | $(740,737 | ) |

| 6/20/09 | | USD | | 2,100,000 | | | JPMorgan Chase Bank | | 4.80% (fixed rate | ) | | (1) | | (357,227 | ) |

| 6/20/12 | | USD | | 4,200,000 | | | Morgan Stanley Capital Services, Inc. | | 3.76% (fixed rate | ) | | (2) | | (1,213,743 | ) |

| 6/20/12 | | USD | | 2,100,000 | | | Morgan Stanley Capital Services, Inc. | | 4.15% (fixed rate | ) | | (2) | | (587,174 | ) |

| 6/20/13 | | USD | | 4,045,000 | (a) | | Goldman Sachs International | | 5.00% (fixed rate | ) | | (3) | | (1,439,657 | ) |

| 6/20/13 | | USD | | 16,000,000 | (b) | | Morgan Stanley Capital Services, Inc. | | (4)

|

| | 5.00% (fixed rate) | | 900,888 | |

| 9/20/13 | | USD | | 3,400,000 | | | JPMorgan Chase Bank | | 5.30% (fixed rate | ) | | (5) | | 73,070 | |

| | | | | | | | | | | | | | $(3,364,580 | ) |

| | | | | | | | | | | | | | | |

| (1) | Fund to pay notional amount upon a defined credit event by Abitibi-Consolidated, Inc., 8.375%, 4/01/15. |

| (2) | Fund to pay notional amount upon a defined credit event by Bowater, Inc. 6.5%, 6/15/13. |

| (3) | Fund to pay notional amount upon a defined credit event by Station Casino’s, Inc., 6%, 4/01/12. |

| (4) | Fund to receive notional amount upon a defined credit event by a reference obligation specified in the CDX High Yield Index. |

| (5) | Fund to pay notional amount upon a defined credit event by Aramark Services, 8.5%, 2/01/15. |

| (a) | Net unamortized premiums received by the fund amounted to $702,819. |

| (b) | Net unamortized premiums paid by the fund amounted to $1,070,000. |

At July 31, 2008, the fund had sufficient cash and/or other liquid securities to cover any commitments under these derivative contracts.

The following abbreviations are used in this report and are defined:

| CDO | | Collateralized Debt Obligation |

| CLO | | Collateralized Loan Obligation |

| FRN | | Floating Rate Note. Interest rate resets periodically and may not be the rate reported at period end. |

| REIT | | Real Estate Investment Trust |

Insurers

| MBIA | | MBIA Insurance Corp. |

Abbreviations indicate amounts shown in currencies other than the U.S. dollar. All amounts are stated in U.S. dollars unless otherwise indicated. A list of abbreviations is shown below:

See Notes to Financial Statements

18

Financial Statements

STATEMENT OF ASSETS AND LIABILITIES

At 7/31/08 (unaudited)

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| | | | | |

Assets | | | | | |

Investments - | | | | | |

Non-affiliated issuers, at value

(identified cost, $921,857,739) | | $836,511,430 | | | |

Underlying funds, at cost and value | | 33,545,765 | | | |

Total investments, at value (identified cost, $955,403,504) | | | | | $870,057,195 |

Cash | | $10,966 | | | |

Restricted cash | | 1,875,580 | | | |

Receivable for forward foreign currency exchange contracts | | 79,483 | | | |

Receivable for investments sold | | 5,893,556 | | | |

Receivable for fund shares sold | | 234,469 | | | |

Interest and dividends receivable | | 18,601,390 | | | |

Swaps, at value (net unamortized premiums paid, $1,070,000) | | 973,958 | | | |

Other assets | | 4,560 | | | |

Total assets | | | | | $897,731,157 |

Liabilities | | | | | |

Distributions payable | | $1,236,017 | | | |

Payable for forward foreign currency exchange contracts | | 13,011 | | | |

Payable for investments purchased | | 12,302,984 | | | |

Payable for fund shares reacquired | | 1,567,570 | | | |

Swaps, at value (net unamortized premiums received, $702,819) | | 4,338,538 | | | |

Payable to affiliates | | | | | |

Management fee | | 22,056 | | | |

Shareholder servicing costs | | 276,427 | | | |

Distribution and service fees | | 16,106 | | | |

Administrative services fee | | 688 | | | |

Program manager fees | | 8 | | | |

Payable for independent trustees’ compensation | | 119,675 | | | |

Accrued expenses and other liabilities | | 51,408 | | | |

Total liabilities | | | | | $19,944,488 |

Net assets | | | | | $877,786,669 |

Net assets consist of | | | | | |

Paid-in capital | | $1,408,439,184 | | | |

Unrealized appreciation (depreciation) on investments and

translation of assets and liabilities in foreign currencies | | (89,015,079 | ) | | |

Accumulated net realized gain (loss) on investments and foreign currency transactions | | (436,978,274 | ) | | |

Accumulated distributions in excess of net investment income | | (4,659,162 | ) | | |

Net assets | | | | | $877,786,669 |

Shares of beneficial interest outstanding | | | | | 258,392,312 |

19

Statement of Assets and Liabilities (unaudited) – continued

| | | | |

Class A shares | | | | |

Net assets | | $461,740,008 | | |

Shares outstanding | | 135,988,076 | | |

Net asset value per share | | | | $3.40 |

Offering price per share (100/95.25 × net asset value per share) | | | | $3.57 |

Class B shares | | | | |

Net assets | | $88,907,240 | | |

Shares outstanding | | 26,105,835 | | |

Net asset value and offering price per share | | | | $3.41 |

Class C shares | | | | |

Net assets | | $60,182,219 | | |

Shares outstanding | | 17,638,293 | | |

Net asset value and offering price per share | | | | $3.41 |

Class I shares | | | | |

Net assets | | $250,196,227 | | |

Shares outstanding | | 73,726,316 | | |

Net asset value, offering price, and redemption price per share | | | | $3.39 |

Class R1 shares | | | | |

Net assets | | $1,157,629 | | |

Shares outstanding | | 340,287 | | |

Net asset value, offering price, and redemption price per share | | | | $3.40 |

Class R2 shares (formerly Class R3 shares) | | | | |

Net assets | | $5,938,578 | | |

Shares outstanding | | 1,746,585 | | |

Net asset value, offering price, and redemption price per share | | | | $3.40 |

Class R3 shares (formerly Class R4 shares) | | | | |

Net assets | | $8,221,736 | | |

Shares outstanding | | 2,422,103 | | |

Net asset value, offering price, and redemption price per share | | | | $3.39 |

Class R4 shares (formerly Class R5 shares) | | | | |

Net assets | | $56,808 | | |

Shares outstanding | | 16,731 | | |

Net asset value, offering price, and redemption price per share | | | | $3.40 |

20

Statement of Assets and Liabilities (unaudited) – continued

| | | | |

Class 529A shares | | | | |

Net assets | | $788,987 | | |

Shares outstanding | | 232,442 | | |

Net asset value and redemption price per share | | | | $3.39 |

Offering price per share (100/95.25 × net asset value per share) | | | | $3.56 |

Class 529B shares | | | | |

Net assets | | $258,546 | | |

Shares outstanding | | 76,149 | | |

Net asset value and offering price per share | | | | $3.40 |

Class 529C shares | | | | |

Net assets | | $338,691 | | |

Shares outstanding | | 99,495 | | |

Net asset value and offering price per share | | | | $3.40 |

On sales of $50,000 or more, the offering prices of Class A and Class 529A shares are reduced. A contingent deferred sales charge may be imposed on redemptions of Class A, Class B, Class C, Class 529B, and Class 529C shares.

See Notes to Financial Statements

21

Financial Statements

STATEMENT OF OPERATIONS

Six months ended 7/31/08 (unaudited)

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| | | | | | |

Net investment income | | | | | | |

Income | | | | | | |

Interest | | $37,488,652 | | | | |

Dividends from underlying funds | | 485,718 | | | | |

Dividends | | 341,977 | | | | |

Foreign taxes withheld | | (4,829 | ) | | | |

Total investment income | | | | | $38,311,518 | |

Expenses | | | | | | |

Management fee | | $2,141,190 | | | | |

Distribution and service fees | | 1,606,092 | | | | |

Program manager fees | | 1,020 | | | | |

Shareholder servicing costs | | 874,818 | | | | |

Administrative services fee | | 62,727 | | | | |

Retirement plan administration and services fees | | 338 | | | | |

Independent trustees’ compensation | | 14,363 | | | | |

Custodian fee | | 80,800 | | | | |

Shareholder communications | | 61,277 | | | | |

Auditing fees | | 31,075 | | | | |

Legal fees | | 8,661 | | | | |

Miscellaneous | | 83,591 | | | | |

Total expenses | | | | | $4,965,952 | |

Reduction of expenses by investment adviser | | (2,740 | ) | | | |

Net expenses | | | | | $4,963,212 | |

Net investment income | | | | | $33,348,306 | |

Realized and unrealized gain (loss) on investments

and foreign currency transactions | | | | | | |

Realized gain (loss) (identified cost basis) | | | | | | |

Investment transactions: | | | | | | |

Non-affiliated issuers | | $(17,704,643 | ) | | | |

Futures contracts | | 203,269 | | | | |

Swap transactions | | 1,005,931 | | | | |

Foreign currency transactions | | (309,262 | ) | | | |

Net realized gain (loss) on investments

and foreign currency transactions | | | | | $(16,804,705 | ) |

Change in unrealized appreciation (depreciation) | | | | | | |

Investments | | $(27,073,364 | ) | | | |

Futures contracts | | (270,563 | ) | | | |

Swap transactions | | (2,103,094 | ) | | | |

Translation of assets and liabilities in foreign currencies | | 80,448 | | | | |

Net unrealized gain (loss) on investments

and foreign currency translation | | | | | $(29,366,573 | ) |

Net realized and unrealized gain (loss) on investments

and foreign currency | | | | | $(46,171,278 | ) |

Change in net assets from operations | | | | | $(12,822,972 | ) |

See Notes to Financial Statements

22

Financial Statements

STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| | | | | | |

| | | Six months ended

7/31/08 | | | Year ended

1/31/08 | |

| Change in net assets | | (unaudited) | | | | |

From operations | | | | | | |

Net investment income | | $33,348,306 | | | $79,939,917 | |

Net realized gain (loss) on investments and foreign

currency transactions | | (16,804,705 | ) | | (1,809,178 | ) |

Net unrealized gain (loss) on investments and foreign

currency translation | | (29,366,573 | ) | | (90,378,874 | ) |

Change in net assets from operations | | $(12,822,972 | ) | | $(12,248,135 | ) |

Distributions declared to shareholders | | | | | | |

From net investment income | | | | | | |

Class A | | $(18,942,894 | ) | | $(48,029,574 | ) |

Class B | | (3,567,935 | ) | | (11,005,810 | ) |

Class C | | (2,286,751 | ) | | (5,876,268 | ) |

Class I | | (10,271,804 | ) | | (21,291,854 | ) |

Class R (b) | | (12,425 | ) | | (243,806 | ) |

Class R1 | | (41,937 | ) | | (56,111 | ) |

Former Class R2 (b) | | (11,420 | ) | | (38,427 | ) |

Class R2 (formerly Class R3) | | (216,905 | ) | | (261,511 | ) |

Class R3 (formerly Class R4) | | (315,672 | ) | | (587,093 | ) |

Class R4 (formerly Class R5) | | (2,294 | ) | | (4,732 | ) |

Class 529A | | (30,555 | ) | | (66,936 | ) |

Class 529B | | (7,994 | ) | | (15,465 | ) |

Class 529C | | (11,441 | ) | | (28,036 | ) |

Total distributions declared to shareholders | | $(35,720,027 | ) | | $(87,505,623 | ) |

Change in net assets from fund share transactions | | $(35,942,342 | ) | | $(157,432,891 | ) |

Total change in net assets | | $(84,485,341 | ) | | $(257,186,649 | ) |

Net assets | | | | | | |

At beginning of period | | 962,272,010 | | | 1,219,458,659 | |

At end of period (including accumulated distributions in excess of net investment income of $4,659,162 and $2,287,441, respectively) | | $877,786,669 | | | $962,272,010 | |

| (b) | At the close of business on April 18, 2008, Class R and Class R2 shares converted into Class R3 shares. Following the conversion, Class R3 shares were renamed Class R2 shares. |

See Notes to Financial Statements

23

Financial Statements

FINANCIAL HIGHLIGHTS

The financial highlights table is intended to help you understand the fund’s financial performance for the semiannual period and the past 5 fiscal years (or life of a particular share class, if shorter). Certain information reflects financial results for a single fund share. The total returns in the table represent the rate by which an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class A | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.58 | | | $3.92 | | | $3.82 | | | $3.98 | | | $3.98 | | | $3.52 | |

Income (loss) from

investment operations | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | $0.13 | | | $0.27 | | | $0.27 | | | $0.27 | | | $0.29 | | | $0.30 | |

Net realized and

unrealized gain (loss)

on investments and

foreign currency | | (0.18 | ) | | (0.31 | ) | | 0.11 | | | (0.13 | ) | | 0.01 | (g) | | 0.46 | |

Total from investment

operations | | $(0.05 | ) | | $(0.04 | ) | | $0.38 | | | $0.14 | | | $0.30 | | | $0.76 | |

Less distributions declared

to shareholders | | | | | | | | | | | | | | | | | | |

From net investment

income | | $(0.13 | ) | | $(0.30 | ) | | $(0.28 | ) | | $(0.30 | ) | | $(0.30 | ) | | $(0.30 | ) |

Redemption fees added to

paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) | | $0.00 | (w) | | $— | |

Net asset value, end of

period | | $3.40 | | | $3.58 | | | $3.92 | | | $3.82 | | | $3.98 | | | $3.98 | |

Total return (%) (r)(s)(t) | | (1.31 | )(n) | | (1.20 | ) | | 10.30 | | | 3.61 | | | 7.74 | | | 22.83 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | |

Expenses before expense

reductions (f) | | 1.02 | (a) | | 0.97 | | | 1.00 | | | 1.00 | | | 0.99 | | | 0.99 | |

Expenses after expense

reductions (f) | | 1.02 | (a) | | 0.97 | | | 1.00 | | | 1.00 | | | 0.99 | | | N/A | |

Net investment income | | 7.18 | (a) | | 7.17 | | | 7.09 | | | 6.85 | | | 7.31 | | | 7.87 | |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | | | 68 | | | 81 | |

Net assets at end of period

(000 Omitted) | | $461,740 | | | $504,159 | | | $671,019 | | | $703,305 | | | $799,651 | | | $934,958 | |

See Notes to Financial Statements

24

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class B | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.59 | | | $3.93 | | | $3.83 | | | $3.99 | | | $3.99 | | | $3.53 | |

Income (loss) from

investment operations | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | $0.11 | | | $0.25 | | | $0.25 | | | $0.24 | | | $0.26 | | | $0.27 | |

Net realized and

unrealized gain (loss)

on investments and

foreign currency | | (0.17 | ) | | (0.32 | ) | | 0.10 | | | (0.13 | ) | | 0.01 | (g) | | 0.47 | |

Total from investment

operations | | $(0.06 | ) | | $(0.07 | ) | | $0.35 | | | $0.11 | | | $0.27 | | | $0.74 | |

Less distributions declared

to shareholders | | | | | | | | | | | | | | | | | | |

From net investment

income | | $(0.12 | ) | | $(0.27 | ) | | $(0.25 | ) | | $(0.27 | ) | | $(0.27 | ) | | $(0.28 | ) |

Redemption fees added to

paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) | | $0.00 | (w) | | $— | |

Net asset value, end of

period | | $3.41 | | | $3.59 | | | $3.93 | | | $3.83 | | | $3.99 | | | $3.99 | |

Total return (%) (r)(s)(t) | | (1.64 | )(n) | | (1.87 | ) | | 9.53 | | | 2.90 | | | 7.10 | | | 21.65 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | |

Expenses before expense

reductions (f) | | 1.72 | (a) | | 1.67 | | | 1.71 | | | 1.72 | | | 1.69 | | | 1.69 | |

Expenses after expense

reductions (f) | | 1.72 | (a) | | 1.67 | | | 1.71 | | | 1.72 | | | 1.69 | | | N/A | |

Net investment income | | 6.47 | (a) | | 6.47 | | | 6.40 | | | 6.26 | | | 6.63 | | | 7.18 | |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | | | 68 | | | 81 | |

Net assets at end of period

(000 Omitted) | | $88,907 | | | $113,331 | | | $195,028 | | | $275,363 | | | $379,253 | | | $471,520 | |

See Notes to Financial Statements

25

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class C | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.60 | | | $3.94 | | | $3.84 | | | $4.00 | | | $4.00 | | | $3.54 | |

Income (loss) from

investment operations | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | $0.11 | | | $0.25 | | | $0.24 | | | $0.24 | | | $0.26 | | | $0.27 | |

Net realized and

unrealized gain (loss)

on investments and

foreign currency | | (0.18 | ) | | (0.32 | ) | | 0.11 | | | (0.13 | ) | | 0.01 | (g) | | 0.47 | |

Total from investment

operations | | $(0.07 | ) | | $(0.07 | ) | | $0.35 | | | $0.11 | | | $0.27 | | | $0.74 | |

Less distributions declared

to shareholders | | | | | | | | | | | | | | | | | | |

From net investment

income | | $(0.12 | ) | | $(0.27 | ) | | $(0.25 | ) | | $(0.27 | ) | | $(0.27 | ) | | $(0.28 | ) |

Redemption fees added to

paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) | | $0.00 | (w) | | $— | |

Net asset value, end of

period | | $3.41 | | | $3.60 | | | $3.94 | | | $3.84 | | | $4.00 | | | $4.00 | |

Total return (%) (r)(s)(t) | | (1.92 | )(n) | | (1.84 | ) | | 9.52 | | | 2.91 | | | 7.10 | | | 21.61 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | |

Expenses before expense

reductions (f) | | 1.72 | (a) | | 1.67 | | | 1.70 | | | 1.72 | | | 1.69 | | | 1.69 | |

Expenses after expense

reductions (f) | | 1.72 | (a) | | 1.67 | | | 1.70 | | | 1.72 | | | 1.69 | | | N/A | |

Net investment income | | 6.45 | (a) | | 6.46 | | | 6.39 | | | 6.26 | | | 6.63 | | | 7.18 | |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | | | 68 | | | 81 | |

Net assets at end of period

(000 Omitted) | | $60,182 | | | $69,505 | | | $92,050 | | | $108,181 | | | $148,073 | | | $214,915 | |

See Notes to Financial Statements

26

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class I | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.58 | | | $3.92 | | | $3.82 | | | $3.98 | | | $3.98 | | | $3.52 | |

Income (loss) from

investment operations | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | $0.13 | | | $0.29 | | | $0.28 | | | $0.28 | | | $0.29 | | | $0.30 | |

Net realized and

unrealized gain (loss)

on investments and

foreign currency | | (0.18 | ) | | (0.32 | ) | | 0.11 | | | (0.13 | ) | | 0.02 | (g) | | 0.47 | |

Total from investment

operations | | $(0.05 | ) | | $(0.03 | ) | | $0.39 | | | $0.15 | | | $0.31 | | | $0.77 | |

Less distributions declared

to shareholders | | | | | | | | | | | | | | | | | | |

From net investment

income | | $(0.14 | ) | | $(0.31 | ) | | $(0.29 | ) | | $(0.31 | ) | | $(0.31 | ) | | $(0.31 | ) |

Redemption fees added to

paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) | | $0.00 | (w) | | $— | |

Net asset value, end of

period | | $3.39 | | | $3.58 | | | $3.92 | | | $3.82 | | | $3.98 | | | $3.98 | |

Total return (%) (r)(s) | | (1.45 | )(n) | | (0.90 | ) | | 10.62 | | | 3.92 | | | 8.17 | | | 22.88 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | |

Expenses before expense

reductions (f) | | 0.72 | (a) | | 0.67 | | | 0.70 | | | 0.71 | | | 0.68 | | | 0.69 | |

Expenses after expense

reductions (f) | | 0.72 | (a) | | 0.67 | | | 0.70 | | | 0.71 | | | 0.68 | | | N/A | |

Net investment income | | 7.50 | (a) | | 7.47 | | | 7.38 | | | 7.24 | | | 7.55 | | | 8.03 | |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | | | 68 | | | 81 | |

Net assets at end of period

(000 Omitted) | | $250,196 | | | $257,572 | | | $246,306 | | | $231,455 | | | $170,679 | | | $93,887 | |

See Notes to Financial Statements

27

Financial Highlights – continued

| | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class R1 | | | 2008 | | | 2007 | | | 2006 (i) | |

| | | (unaudited) | | | | | | | | | | |

Net asset value, beginning of period | | $3.59 | | | $3.93 | | | $3.83 | | | $3.89 | |

| Income (loss) from investment operations | | | | | | | | | | | | |

Net investment income (d) | | $0.11 | | | $0.24 | | | $0.24 | | | $0.19 | |

Net realized and unrealized gain (loss)

on investments and foreign currency | | (0.18 | ) | | (0.31 | ) | | 0.11 | | | (0.03 | )(g) |

Total from investment operations | | $(0.07 | ) | | $(0.07 | ) | | $0.35 | | | $0.16 | |

| Less distributions declared to shareholders | | | | | | | | | | | | |

From net investment income | | $(0.12 | ) | | $(0.27 | ) | | $(0.25 | ) | | $(0.22 | ) |

Redemption fees added to paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) |

Net asset value, end of period | | $3.40 | | | $3.59 | | | $3.93 | | | $3.83 | |

Total return (%) (r)(s) | | (1.94 | )(n) | | (1.96 | ) | | 9.41 | | | 4.28 | (n) |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | |

Expenses before expense reductions (f) | | 1.74 | (a) | | 1.77 | | | 1.89 | | | 1.91 | (a) |

Expenses after expense reductions (f) | | 1.74 | (a) | | 1.76 | | | 1.79 | | | 1.85 | (a) |

Net investment income | | 6.46 | (a) | | 6.35 | | | 6.27 | | | 6.08 | (a) |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | |

Net assets at end of period (000 Omitted) | | $1,158 | | | $1,273 | | | $361 | | | $231 | |

See Notes to Financial Statements

28

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class R2 (formerly Class R3) | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 (i) | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.58 | | | $3.93 | | | $3.83 | | | $3.98 | | | $3.98 | | | $3.85 | |

Income (loss) from

investment operations | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | $0.12 | | | $0.26 | | | $0.26 | | | $0.24 | | | $0.25 | | | $0.07 | |

Net realized and

unrealized gain (loss)

on investments and

foreign currency | | (0.17 | ) | | (0.32 | ) | | 0.10 | | | (0.11 | ) | | 0.03 | (g) | | 0.13 | (g) |

Total from investment

operations | | $(0.05 | ) | | $(0.06 | ) | | $0.36 | | | $0.13 | | | $0.28 | | | $0.20 | |

Less distributions declared

to shareholders | | | | | | | | | | | | | | | | | | |

From net investment

income | | $(0.13 | ) | | $(0.29 | ) | | $(0.26 | ) | | $(0.28 | ) | | $(0.28 | ) | | $(0.07 | ) |

Redemption fees added to

paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) | | $0.00 | (w) | | $— | |

Net asset value, end of

period | | $3.40 | | | $3.58 | | | $3.93 | | | $3.83 | | | $3.98 | | | $3.98 | |

Total return (%) (r)(s) | | (1.41 | )(n) | | (1.79 | ) | | 9.91 | | | 3.45 | | | 7.37 | | | 5.32 | (n) |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | |

Expenses before expense

reductions (f) | | 1.22 | (a) | | 1.30 | | | 1.44 | | | 1.46 | | | 1.49 | | | 1.43 | (a) |

Expenses after expense

reductions (f) | | 1.22 | (a) | | 1.29 | | | 1.34 | | | 1.42 | | | 1.49 | | | N/A | |

Net investment income | | 6.99 | (a) | | 6.83 | | | 6.71 | | | 6.61 | | | 6.58 | | | 7.07 | (a) |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | | | 68 | | | 81 | |

Net assets at end of period

(000 Omitted) | | $5,939 | | | $5,525 | | | $2,406 | | | $1,212 | | | $246 | | | $42 | |

See Notes to Financial Statements

29

Financial Highlights – continued

| | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class R3 (formerly Class R4) | | | 2008 | | | 2007 | | | 2006 (i) | |

| | | (unaudited) | | | | | | | | | | |

Net asset value, beginning of period | | $3.58 | | | $3.92 | | | $3.82 | | | $3.88 | |

| Income (loss) from investment operations | | | | | | | | | | | | |

Net investment income (d) | | $0.13 | | | $0.27 | | | $0.27 | | | $0.21 | |

Net realized and unrealized gain (loss)

on investments and foreign currency | | (0.18 | ) | | (0.31 | ) | | 0.10 | | | (0.02 | )(g) |

Total from investment operations | | $(0.05 | ) | | $(0.04 | ) | | $0.37 | | | $0.19 | |

| Less distributions declared to shareholders | | | | | | | | | | | | |

From net investment income | | $(0.14 | ) | | $(0.30 | ) | | $(0.27 | ) | | $(0.25 | ) |

Redemption fees added to paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) |

Net asset value, end of period | | $3.39 | | | $3.58 | | | $3.92 | | | $3.82 | |

Total return (%) (r)(s) | | (1.57 | )(n) | | (1.28 | ) | | 10.18 | | | 4.94 | (n) |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | |

Expenses before expense reductions (f) | | 0.97 | (a) | | 1.05 | | | 1.07 | | | 1.15 | (a) |

Expenses after expense reductions (f) | | 0.97 | (a) | | 1.05 | | | 1.07 | | | 1.15 | (a) |

Net investment income | | 7.24 | (a) | | 7.08 | | | 6.90 | | | 6.73 | (a) |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | |

Net assets at end of period (000 Omitted) | | $8,222 | | | $8,065 | | | $5,143 | | | $393 | |

See Notes to Financial Statements

30

Financial Highlights – continued

| | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class R4 (formerly Class R5) | | | 2008 | | | 2007 | | | 2006 (i) | |

| | | (unaudited) | | | | | | | | | | |

Net asset value, beginning of period | | $3.58 | | | $3.92 | | | $3.82 | | | $3.88 | |

| Income (loss) from investment operations | | | | | | | | | | |

Net investment income (d) | | $0.13 | | | $0.28 | | | $0.28 | | | $0.23 | |

Net realized and unrealized gain (loss)

on investments and foreign currency | | (0.17 | ) | | (0.31 | ) | | 0.11 | | | (0.03 | )(g) |

Total from investment operations | | $(0.04 | ) | | $(0.03 | ) | | $0.39 | | | $0.20 | |

| Less distributions declared to shareholders | | | | | | | | | | |

From net investment income | | $(0.14 | ) | | $(0.31 | ) | | $(0.29 | ) | | $(0.26 | ) |

Redemption fees added to paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) |

Net asset value, end of period | | $3.40 | | | $3.58 | | | $3.92 | | | $3.82 | |

Total return (%) (r)(s) | | (1.16 | )(n) | | (0.99 | ) | | 10.52 | | | 5.20 | (n) |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | |

Expenses before expense reductions (f) | | 0.72 | (a) | | 0.76 | | | 0.80 | | | 0.80 | (a) |

Expenses after expense reductions (f) | | 0.72 | (a) | | 0.76 | | | 0.80 | | | 0.80 | (a) |

Net investment income | | 7.49 | (a) | | 7.38 | | | 7.29 | | | 7.11 | (a) |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | |

Net assets at end of period (000 Omitted) | | $57 | | | $58 | | | $58 | | | $53 | |

See Notes to Financial Statements

31

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class 529A | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.58 | | | $3.92 | | | $3.82 | | | $3.98 | | | $3.98 | | | $3.52 | |

Income (loss) from

investment operations | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | $0.12 | | | $0.26 | | | $0.26 | | | $0.26 | | | $0.27 | | | $0.28 | |

Net realized and

unrealized gain (loss)

on investments and

foreign currency | | (0.18 | ) | | (0.31 | ) | | 0.11 | | | (0.14 | ) | | 0.02 | (g) | | 0.47 | |

Total from investment

operations | | $(0.06 | ) | | $(0.05 | ) | | $0.37 | | | $0.12 | | | $0.29 | | | $0.75 | |

Less distributions declared

to shareholders | | | | | | | | | | | | | | | | | | |

From net investment

income | | $(0.13 | ) | | $(0.29 | ) | | $(0.27 | ) | | $(0.28 | ) | | $(0.29 | ) | | $(0.29 | ) |

Redemption fees added to

paid-in capital (d) | | $— | | | $— | | | $0.00 | (w) | | $0.00 | (w) | | $0.00 | (w) | | $— | |

Net asset value, end of

period | | $3.39 | | | $3.58 | | | $3.92 | | | $3.82 | | | $3.98 | | | $3.98 | |

Total return (%) (r)(s)(t) | | (1.70 | )(n) | | (1.49 | ) | | 9.97 | | | 3.30 | | | 7.53 | | | 22.16 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | |

Expenses before expense

reductions (f) | | 1.22 | (a) | | 1.27 | | | 1.30 | | | 1.32 | | | 1.29 | | | 1.30 | |

Expenses after expense

reductions (f) | | 1.22 | (a) | | 1.27 | | | 1.30 | | | 1.32 | | | 1.29 | | | N/A | |

Net investment income | | 6.99 | (a) | | 6.87 | | | 6.78 | | | 6.65 | | | 6.97 | | | 7.42 | |

Portfolio turnover | | 39 | | | 66 | | | 89 | | | 51 | | | 68 | | | 81 | |

Net assets at end of period

(000 Omitted) | | $789 | | | $849 | | | $854 | | | $776 | | | $768 | | | $406 | |

See Notes to Financial Statements

32

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | |

| | | Six months

ended

7/31/08 | | | Years ended 1/31 | |

| Class 529B | | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning

of period | | $3.58 | | | $3.92 | | | $3.82 | | | $3.97 | | | $3.98 | | | $3.52 | |

Income (loss) from