UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-2794

MFS SERIES TRUST III

(Exact name of registrant as specified in charter)

111 Huntington Avenue, Boston, Massachusetts 02199

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

111 Huntington Avenue

Boston, Massachusetts 02199

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: January 31

Date of reporting period: July 31, 2014

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

SEMIANNUAL REPORT

July 31, 2014

MFS® HIGH INCOME FUND

MFH-SEM

MFS® HIGH INCOME FUND

CONTENTS

The report is prepared for the general information of shareholders. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ NO BANK GUARANTEE

LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholders:

The U.S. economy has gathered momentum after a slow start to the year. Industrial output, consumer confidence and retail sales have all strengthened along with the labor market. However, the unemployment rate remains elevated and the housing

market has cooled off. With second-quarter economic growth rebounding strongly, economists have a favorable outlook for the rest of the year.

China’s economy has picked up again, and Japan is moving steadily towards Prime Minister Abe’s economic goals, including an inflation rate of 2% by next spring. The eurozone’s economy appears to have turned a corner, with renewed growth. However, historically high unemployment persists, deflation remains a risk and Russian sanctions could present a new obstacle to regional growth.

With corporate earnings surpassing expectations, the greatest concerns now are related to conflicts in the Middle East and Ukraine as well as growing speculation on when the U.S. Federal Reserve will begin increasing interest rates.

As always at MFS®, active risk management is integral to how we manage your investments. We use a collaborative process, sharing insights across asset classes, regions and economic sectors. Our global team of investment professionals uses a multidisciplined, long-term, diversified investment approach.

We understand that these are challenging economic times. We believe that we can serve you best by applying proven principles, such as asset allocation and diversification, over the long term. We are confident that this approach can serve you well as you work with your financial advisors to reach your goals in the years ahead.

Respectfully,

Robert J. Manning

Chairman and Chief Executive Officer

MFS Investment Management

September 15, 2014

The opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed.

1

PORTFOLIO COMPOSITION

Portfolio structure (i)

| | | | |

| Top five industries (i) | | | | |

| Energy-Independent | | | 8.8% | |

| Cable TV | | | 5.5% | |

| Midstream | | | 5.1% | |

| Medical & Health Technology & Services | | | 4.9% | |

| Metals & Mining | | | 4.8% | |

| | | | |

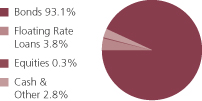

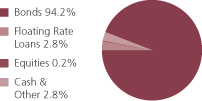

| Composition including fixed income credit quality (a)(i) | |

| BBB | | | 2.6% | |

| BB | | | 34.7% | |

| B | | | 46.9% | |

| CCC | | | 12.2% | |

| CC (o) | | | 0.0% | |

| C (o) | | | 0.0% | |

| D (o) | | | 0.0% | |

| Not Rated | | | 0.5% | |

| Non-Fixed Income | | | 0.3% | |

| Cash & Other | | | 2.8% | |

| |

| Portfolio facts (i) | | | | |

| Average Duration (d) | | | 4.5 | |

| Average Effective Maturity (m) | | | 7.0 yrs. | |

| (a) | For all securities other than those specifically described below, ratings are assigned to underlying securities utilizing ratings from Moody’s, Fitch, and Standard & Poor’s rating agencies and applying the following hierarchy: If all three agencies provide a rating, the middle rating (after dropping the highest and lowest ratings) is assigned; if two of the three agencies rate a security, the lower of the two is assigned. Ratings are shown in the S&P and Fitch scale (e.g., AAA). Securities rated BBB or higher are considered investment grade. All ratings are subject to change. Not Rated includes fixed income securities, including fixed income futures contracts, which have not been rated by any rating agency. Non-Fixed Income includes equity securities (including convertible bonds and equity derivatives) and commodities. The fund may not hold all of these instruments. The fund is not rated by these agencies. |

| (d) | Duration is a measure of how much a bond’s price is likely to fluctuate with general changes in interest rates, e.g., if rates rise 1.00%, a bond with a 5-year duration is likely to lose about 5.00% of its value due to the interest rate move. |

| (i) | For purposes of this presentation, the components include the value of securities, and reflect the impact of the equivalent exposure of derivative positions, if any. These amounts may be negative from time to time. Equivalent exposure is a calculated amount that translates the derivative position into a reasonable approximation of the amount of the underlying asset that the portfolio would have to hold at a given point in time to have the same price sensitivity that results from the portfolio’s ownership of the derivative contract. When dealing with derivatives, equivalent exposure is a more representative measure of the potential impact of a position on portfolio performance than value. The bond component will include any accrued interest amounts. |

2

Portfolio Composition – continued

| (m) | In determining an instrument’s effective maturity for purposes of calculating the fund’s dollar-weighted average effective maturity, MFS uses the instrument’s stated maturity or, if applicable, an earlier date on which MFS believes it is probable that a maturity-shortening device (such as a put, pre-refunding or prepayment) will cause the instrument to be repaid. Such an earlier date can be substantially shorter than the instrument’s stated maturity. |

Where the fund holds convertible bonds, these are treated as part of the equity portion of the portfolio.

Cash & Other can include cash, other assets less liabilities, offsets to derivative positions, and short-term securities.

Percentages are based on net assets as of 7/31/14.

The portfolio is actively managed and current holdings may be different.

3

EXPENSE TABLE

Fund expenses borne by the shareholders during the period, February 1, 2014 through July 31, 2014

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on certain purchase or redemption payments, and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period February 1, 2014 through July 31, 2014.

The expenses include the payment of a portion of the transfer-agent-related expenses of MFS funds that invest in the fund. For further information, please see the Notes to the Financial Statements.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

4

Expense Table – continued

| | | | | | | | | | | | | | | | | | |

Share

Class | | | | Annualized

Expense

Ratio | | | Beginning

Account Value

2/01/14 | | | Ending

Account Value

7/31/14 | | | Expenses

Paid During

Period (p)

2/01/14-7/31/14 | |

| A | | Actual | | | 0.91% | | | | $1,000.00 | | | | $1,028.77 | | | | $4.58 | |

| | Hypothetical (h) | | | 0.91% | | | | $1,000.00 | | | | $1,020.28 | | | | $4.56 | |

| B | | Actual | | | 1.66% | | | | $1,000.00 | | | | $1,024.96 | | | | $8.33 | |

| | Hypothetical (h) | | | 1.66% | | | | $1,000.00 | | | | $1,016.56 | | | | $8.30 | |

| C | | Actual | | | 1.66% | | | | $1,000.00 | | | | $1,024.96 | | | | $8.33 | |

| | Hypothetical (h) | | | 1.66% | | | | $1,000.00 | | | | $1,016.56 | | | | $8.30 | |

| I | | Actual | | | 0.66% | | | | $1,000.00 | | | | $1,030.07 | | | | $3.32 | |

| | Hypothetical (h) | | | 0.66% | | | | $1,000.00 | | | | $1,021.52 | | | | $3.31 | |

| R1 | | Actual | | | 1.66% | | | | $1,000.00 | | | | $1,024.93 | | | | $8.33 | |

| | Hypothetical (h) | | | 1.66% | | | | $1,000.00 | | | | $1,016.56 | | | | $8.30 | |

| R2 | | Actual | | | 1.16% | | | | $1,000.00 | | | | $1,027.51 | | | | $5.83 | |

| | Hypothetical (h) | | | 1.16% | | | | $1,000.00 | | | | $1,019.04 | | | | $5.81 | |

| R3 | | Actual | | | 0.91% | | | | $1,000.00 | | | | $1,025.93 | | | | $4.57 | |

| | Hypothetical (h) | | | 0.91% | | | | $1,000.00 | | | | $1,020.28 | | | | $4.56 | |

| R4 | | Actual | | | 0.66% | | | | $1,000.00 | | | | $1,030.07 | | | | $3.32 | |

| | Hypothetical (h) | | | 0.66% | | | | $1,000.00 | | | | $1,021.52 | | | | $3.31 | |

| R5 | | Actual | | | 0.59% | | | | $1,000.00 | | | | $1,027.59 | | | | $2.97 | |

| | Hypothetical (h) | | | 0.59% | | | | $1,000.00 | | | | $1,021.87 | | | | $2.96 | |

| 529A | | Actual | | | 0.95% | | | | $1,000.00 | | | | $1,025.78 | | | | $4.77 | |

| | Hypothetical (h) | | | 0.95% | | | | $1,000.00 | | | | $1,020.08 | | | | $4.76 | |

| 529B | | Actual | | | 1.71% | | | | $1,000.00 | | | | $1,021.85 | | | | $8.57 | |

| | Hypothetical (h) | | | 1.71% | | | | $1,000.00 | | | | $1,016.31 | | | | $8.55 | |

| 529C | | Actual | | | 1.71% | | | | $1,000.00 | | | | $1,024.70 | | | | $8.58 | |

| | Hypothetical (h) | | | 1.71% | | | | $1,000.00 | | | | $1,016.31 | | | | $8.55 | |

| (h) | 5% class return per year before expenses. |

| (p) | “Expenses Paid During Period” are equal to each class’s annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). Expenses paid do not include any applicable sales charges (loads). If these transaction costs had been included, your costs would have been higher. |

Notes to Expense Table

Each class with a Rule 12b-1 service fee is subject to a rebate of a portion of such fee. Such rebates are included in the expense ratios above. For Class A and Class 529A shares, this rebate reduced the expense ratios above by 0.01% and 0.02%, respectively. See Note 3 in the Notes to Financial Statements for additional information.

5

PORTFOLIO OF INVESTMENTS

7/31/14 (unaudited)

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| | | | | | | | |

| Bonds - 91.1% | | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Aerospace - 2.2% | | | | | | | | |

| Bombardier, Inc., 7.5%, 3/15/18 (n) | �� | $ | 3,280,000 | | | $ | 3,583,405 | |

| Bombardier, Inc., 7.75%, 3/15/20 (n) | | | 2,770,000 | | | | 2,991,600 | |

| Bombardier, Inc., 6.125%, 1/15/23 (n) | | | 5,020,000 | | | | 4,944,700 | |

| CPI International, Inc., 8.75%, 2/15/18 | | | 4,927,000 | | | | 5,148,715 | |

| Gencorp, Inc., 7.125%, 3/15/21 | | | 5,375,000 | | | | 5,817,363 | |

| Huntington Ingalls Industries, Inc., 7.125%, 3/15/21 | | | 6,395,000 | | | | 6,842,650 | |

| TransDigm, Inc., 6%, 7/15/22 (z) | | | 470,000 | | | | 472,350 | |

| TransDigm, Inc., 6.5%, 7/15/24 (z) | | | 1,975,000 | | | | 1,994,750 | |

| | | | | | | | |

| | | | $ | 31,795,533 | |

| Apparel Manufacturers - 0.4% | | | | | | | | |

| Hanesbrands, Inc., 6.375%, 12/15/20 | | $ | 2,990,000 | | | $ | 3,176,875 | |

| PVH Corp., 4.5%, 12/15/22 | | | 2,945,000 | | | | 2,849,288 | |

| | | | | | | | |

| | | | $ | 6,026,163 | |

| Asset-Backed & Securitized - 0.1% | | | | | | | | |

| Citigroup Commercial Mortgage Trust, FRN, 5.898%, 12/10/49 (d)(q) | | $ | 2,948,120 | | | $ | 405,661 | |

| CW Capital Cobalt Commercial Mortgage Trust, “E2”, CDO, 6%, 5/25/45 (a)(d)(p)(z) | | | 1,387,564 | | | | 192,996 | |

| CW Capital Cobalt Commercial Mortgage Trust, “F”, CDO, FRN, 1.535%, 4/26/50 (a)(d)(p)(z) | | | 659,687 | | | | 7 | |

| CW Capital Cobalt Commercial Mortgage Trust, “G”, CDO, FRN, 1.735%, 4/26/50 (a)(d)(p)(z) | | | 2,063,671 | | | | 21 | |

| Falcon Franchise Loan LLC, FRN, 16.08%, 1/05/25 (i)(z) | | | 743,158 | | | | 245,242 | |

| First Union National Bank Commercial Mortgage Trust, 6.75%, 10/15/32 (d)(q) | | | 1,447,046 | | | | 724,572 | |

| G-Force LLC, CDO, “A2”, 4.83%, 8/22/36 (z) | | | 1,891 | | | | 1,936 | |

| LB Commercial Conduit Mortgage Trust, FRN, 1.248%, 2/18/30 (i) | | | 1,964,768 | | | | 46,946 | |

| Morgan Stanley Capital I, Inc., FRN, 1.414%, 4/28/39 (i)(z) | | | 5,276,328 | | | | 34,903 | |

| | | | | | | | |

| | | | $ | 1,652,284 | |

| Automotive - 2.9% | | | | | | | | |

| Accuride Corp., 9.5%, 8/01/18 | | $ | 6,635,000 | | | $ | 6,966,750 | |

| Allison Transmission, Inc., 7.125%, 5/15/19 (n) | | | 6,660,000 | | | | 7,059,600 | |

| Goodyear Tire & Rubber Co., 6.5%, 3/01/21 | | | 6,650,000 | | | | 7,032,375 | |

| Goodyear Tire & Rubber Co., 7%, 5/15/22 | | | 1,340,000 | | | | 1,453,900 | |

| Jaguar Land Rover PLC, 8.125%, 5/15/21 (n) | | | 7,060,000 | | | | 7,818,950 | |

| Jaguar Land Rover PLC, 5.625%, 2/01/23 (n) | | | 1,055,000 | | | | 1,102,475 | |

6

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Automotive - continued | | | | | | | | |

| Lear Corp., 8.125%, 3/15/20 | | $ | 1,350,000 | | | $ | 1,444,500 | |

| Lear Corp., 4.75%, 1/15/23 | | | 3,035,000 | | | | 2,987,578 | |

| Schaeffler Finance B.V., 6.875%, 8/15/18 (n)(p) | | | 3,050,000 | | | | 3,202,500 | |

| Schaeffler Finance B.V., 4.75%, 5/15/21 (z) | | | 2,795,000 | | | | 2,836,925 | |

| | | | | | | | |

| | | | $ | 41,905,553 | |

| Broadcasting - 2.3% | | | | | | | | |

| AMC Networks, Inc., 7.75%, 7/15/21 | | $ | 3,641,000 | | | $ | 3,986,895 | |

| Clear Channel Communications, Inc., 9%, 3/01/21 | | | 3,262,000 | | | | 3,372,093 | |

| Clear Channel Worldwide Holdings, Inc., “A”, 6.5%, 11/15/22 | | | 830,000 | | | | 867,350 | |

| Clear Channel Worldwide Holdings, Inc., “B”, 6.5%, 11/15/22 | | | 3,080,000 | | | | 3,234,000 | |

| Liberty Media Corp., 8.5%, 7/15/29 | | | 4,285,000 | | | | 4,756,350 | |

| Liberty Media Corp., 8.25%, 2/01/30 | | | 40,000 | | | | 44,200 | |

| Netflix, Inc., 5.375%, 2/01/21 | | | 3,625,000 | | | | 3,742,813 | |

| Nexstar Broadcasting, Inc., 6.875%, 11/15/20 | | | 3,920,000 | | | | 4,155,200 | |

| Univision Communications, Inc., 6.875%, 5/15/19 (n) | | | 3,455,000 | | | | 3,627,750 | |

| Univision Communications, Inc., 7.875%, 11/01/20 (n) | | | 3,145,000 | | | | 3,380,875 | |

| Univision Communications, Inc., 8.5%, 5/15/21 (n) | | | 870,000 | | | | 939,600 | |

| | | | | | | | |

| | | | $ | 32,107,126 | |

| Brokerage & Asset Managers - 0.6% | | | | | | | | |

| E*TRADE Financial Corp., 6.375%, 11/15/19 | | $ | 7,590,000 | | | $ | 8,064,375 | |

|

| Building - 3.4% | |

| Allegion U.S. Holding Co., Inc., 5.75%, 10/01/21 | | $ | 5,631,000 | | | $ | 5,912,550 | |

| Building Materials Holding Corp., 6.875%, 8/15/18 (n) | | | 950,000 | | | | 983,250 | |

| Building Materials Holding Corp., 7%, 2/15/20 (n) | | | 1,150,000 | | | | 1,206,063 | |

| Building Materials Holding Corp., 6.75%, 5/01/21 (n) | | | 4,385,000 | | | | 4,675,506 | |

| CEMEX Espana S.A., 9.25%, 5/12/20 | | | 3,215,000 | | | | 3,480,238 | |

| CEMEX Espana S.A., 9.25%, 5/12/20 (n) | | | 1,180,000 | | | | 1,277,350 | |

| CEMEX S.A.B. de C.V., 5.875%, 3/25/19 (n) | | | 669,000 | | | | 680,708 | |

| CEMEX S.A.B. de C.V., 6.5%, 12/10/19 (n) | | | 546,000 | | | | 569,888 | |

| CEMEX S.A.B. de C.V., 7.25%, 1/15/21 (n) | | | 910,000 | | | | 964,600 | |

| Gibraltar Industries, Inc., 6.25%, 2/01/21 | | | 2,755,000 | | | | 2,816,988 | |

| HD Supply, Inc., 8.125%, 4/15/19 | | | 2,470,000 | | | | 2,667,600 | |

| HD Supply, Inc., 7.5%, 7/15/20 | | | 6,440,000 | | | | 6,874,700 | |

| Headwaters, Inc., 7.25%, 1/15/19 | | | 2,210,000 | | | | 2,309,450 | |

| Headwaters, Inc., 7.625%, 4/01/19 | | | 1,455,000 | | | | 1,527,750 | |

| Nortek, Inc., 8.5%, 4/15/21 | | | 4,750,000 | | | | 5,153,750 | |

| Roofing Supply Group LLC/Roofing Supply Finance, Inc., 10%, 6/01/20 (n) | | | 3,690,000 | | | | 3,929,850 | |

| USG Corp., 7.875%, 3/30/20 (n) | | | 1,570,000 | | | | 1,705,413 | |

| USG Corp., 5.875%, 11/01/21 (n) | | | 910,000 | | | | 937,300 | |

| | | | | | | | |

| | | | $ | 47,672,954 | |

7

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Business Services - 1.4% | | | | | | | | |

| Equinix, Inc., 4.875%, 4/01/20 | | $ | 3,670,000 | | | $ | 3,697,525 | |

| Equinix, Inc., 5.375%, 4/01/23 | | | 1,955,000 | | | | 1,964,775 | |

| Fidelity National Information Services, Inc., 5%, 3/15/22 | | | 3,080,000 | | | | 3,261,674 | |

| Iron Mountain, Inc., 8.375%, 8/15/21 | | | 1,729,000 | | | | 1,793,838 | |

| Iron Mountain, Inc., 6%, 8/15/23 | | | 3,350,000 | | | | 3,492,375 | |

| Lender Processing Services, Inc., 5.75%, 4/15/23 | | | 1,415,000 | | | | 1,515,465 | |

| NeuStar, Inc., 4.5%, 1/15/23 | | | 4,795,000 | | | | 4,075,750 | |

| | | | | | | | |

| | | | $ | 19,801,402 | |

| Cable TV - 5.2% | | | | | | | | |

| CCO Holdings LLC/CCO Holdings Capital Corp., 8.125%, 4/30/20 | | $ | 6,590,000 | | | $ | 7,026,588 | |

| CCO Holdings LLC/CCO Holdings Capital Corp., 7.375%, 6/01/20 | | | 1,305,000 | | | | 1,393,088 | |

| CCO Holdings LLC/CCO Holdings Capital Corp., 6.5%, 4/30/21 | | | 5,360,000 | | | | 5,574,400 | |

| CCO Holdings LLC/CCO Holdings Capital Corp., 5.75%, 1/15/24 | | | 4,205,000 | | | | 4,183,975 | |

| Cequel Communications Holdings, 6.375%, 9/15/20 (n) | | | 5,065,000 | | | | 5,216,950 | |

| DISH DBS Corp., 6.75%, 6/01/21 | | | 3,410,000 | | | | 3,751,000 | |

| DISH DBS Corp., 5%, 3/15/23 | | | 2,975,000 | | | | 2,915,500 | |

| Intelsat Jackson Holdings S.A., 6.625%, 12/15/22 | | | 3,660,000 | | | | 3,696,600 | |

| Intelsat Jackson Holdings S.A., 5.5%, 8/01/23 | | | 6,225,000 | | | | 5,976,000 | |

| Intelsat Luxembourg S.A., 8.125%, 6/01/23 | | | 4,615,000 | | | | 4,799,600 | |

| Lynx I Corp., 5.375%, 4/15/21 (n) | | | 1,575,000 | | | | 1,590,750 | |

| Lynx II Corp., 6.375%, 4/15/23 (n) | | | 2,635,000 | | | | 2,766,750 | |

| Numericable Group S.A., 6%, 5/15/22 (n) | | | 5,325,000 | | | | 5,351,625 | |

| SIRIUS XM Radio, Inc., 4.25%, 5/15/20 (n) | | | 1,020,000 | | | | 981,750 | |

| SIRIUS XM Radio, Inc., 5.875%, 10/01/20 (n) | | | 460,000 | | | | 470,350 | |

| SIRIUS XM Radio, Inc., 4.625%, 5/15/23 (n) | | | 2,535,000 | | | | 2,357,550 | |

| SIRIUS XM Radio, Inc., 6%, 7/15/24 (z) | | | 2,340,000 | | | | 2,351,700 | |

| Telenet Finance Luxembourg, 6.375%, 11/15/20 (n) | | EUR | 1,875,000 | | | | 2,668,291 | |

| Unitymedia Hessen, 5.5%, 1/15/23 (n) | | $ | 4,235,000 | | | | 4,256,175 | |

| UPCB Finance III Ltd., 6.625%, 7/01/20 (n) | | | 3,833,000 | | | | 4,043,815 | |

| Ziggo Bond Co. B.V., 8%, 5/15/18 (n) | | EUR | 2,225,000 | | | | 3,262,130 | |

| | | | | | | | |

| | | | $ | 74,634,587 | |

| Chemicals - 3.0% | | | | | | | | |

| Celanese U.S. Holdings LLC, 5.875%, 6/15/21 | | $ | 4,178,000 | | | $ | 4,522,685 | |

| Celanese U.S. Holdings LLC, 4.625%, 11/15/22 | | | 1,760,000 | | | | 1,751,200 | |

| Flash Dutch 2 B.V./U.S. Coatings Acquisition, 7.375%, 5/01/21 (n) | | | 3,365,000 | | | | 3,575,313 | |

| Hexion U.S. Finance Corp., 6.625%, 4/15/20 | | | 2,190,000 | | | | 2,277,600 | |

| Hexion U.S. Finance Corp./Hexion Nova Scotia Finance, 8.875%, 2/01/18 | | | 4,005,000 | | | | 4,133,160 | |

| Huntsman International LLC, 8.625%, 3/15/21 | | | 4,280,000 | | | | 4,654,500 | |

| INEOS Finance PLC, 8.375%, 2/15/19 (n) | | | 4,145,000 | | | | 4,476,600 | |

| INEOS Group Holdings S.A., 6.125%, 8/15/18 (n) | | | 3,665,000 | | | | 3,701,650 | |

8

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Chemicals - continued | | | | | | | | |

| INEOS Group Holdings S.A., 5.875%, 2/15/19 (n) | | $ | 2,745,000 | | | $ | 2,772,450 | |

| Taminco Global Chemical Corp., 9.75%, 3/31/20 (n) | | | 3,745,000 | | | | 4,110,138 | |

| Tronox Finance LLC, 6.375%, 8/15/20 | | | 7,175,000 | | | | 7,246,750 | |

| | | | | | | | |

| | | | $ | 43,222,046 | |

| Computer Software - 0.4% | | | | | | | | |

| Syniverse Holdings, Inc., 9.125%, 1/15/19 | | $ | 1,453,000 | | | $ | 1,525,650 | |

| VeriSign, Inc., 4.625%, 5/01/23 | | | 4,260,000 | | | | 4,153,500 | |

| | | | | | | | |

| | | | $ | 5,679,150 | |

| Computer Software - Systems - 0.7% | | | | | | | | |

| Audatex North America, Inc., 6%, 6/15/21 (n) | | $ | 3,560,000 | | | $ | 3,729,100 | |

| Audatex North America, Inc., 6.125%, 11/01/23 (n) | | | 835,000 | | | | 872,575 | |

| CDW LLC/CDW Finance Corp., 8.5%, 4/01/19 | | | 3,795,000 | | | | 4,032,188 | |

| CDW LLC/CDW Finance Corp., 6%, 8/15/22 | | | 1,915,000 | | | | 1,915,000 | |

| | | | | | | | |

| | | | $ | 10,548,863 | |

| Conglomerates - 2.0% | | | | | | | | |

| Amsted Industries Co., 5%, 3/15/22 (n) | | $ | 5,085,000 | | | $ | 5,046,863 | |

| BC Mountain LLC, 7%, 2/01/21 (n) | | | 3,290,000 | | | | 3,158,400 | |

| Dynacast International LLC, 9.25%, 7/15/19 | | | 2,295,000 | | | | 2,513,025 | |

| Entegris, Inc., 6%, 4/01/22 (n) | | | 5,505,000 | | | | 5,683,913 | |

| Renaissance Acquisition, 6.875%, 8/15/21 (n) | | | 5,585,000 | | | | 5,626,888 | |

| Rexel S.A., 6.125%, 12/15/19 (n) | | | 3,200,000 | | | | 3,312,000 | |

| Silver II Borrower, 7.75%, 12/15/20 (n) | | | 3,195,000 | | | | 3,346,763 | |

| | | | | | | | |

| | | | $ | 28,687,852 | |

| Construction - 0.3% | | | | | | | | |

| Empresas ICA S.A.B. de C.V., 8.875%, 5/29/24 (n) | | $ | 1,546,000 | | | $ | 1,580,785 | |

| Empresas ICA Sociedad Controladora S.A. de C.V., 8.9%, 2/04/21 | | | 2,555,000 | | | | 2,682,750 | |

| | | | | | | | |

| | | | $ | 4,263,535 | |

| Consumer Products - 0.9% | | | | | | | | |

| Elizabeth Arden, Inc., 7.375%, 3/15/21 | | $ | 4,411,000 | | | $ | 4,554,358 | |

| Prestige Brands, Inc., 8.125%, 2/01/20 | | | 1,531,000 | | | | 1,676,445 | |

| Prestige Brands, Inc., 5.375%, 12/15/21 (n) | | | 3,135,000 | | | | 3,135,000 | |

| Spectrum Brands, Inc., 6.375%, 11/15/20 | | | 3,270,000 | | | | 3,441,675 | |

| | | | | | | | |

| | | | $ | 12,807,478 | |

| Consumer Services - 1.6% | | | | | | | | |

| ADT Corp., 6.25%, 10/15/21 | | $ | 4,995,000 | | | $ | 5,169,825 | |

| ADT Corp., 4.125%, 6/15/23 | | | 1,585,000 | | | | 1,434,425 | |

| Garda World Security Corp., 7.25%, 11/15/21 (z) | | | 2,905,000 | | | | 2,955,838 | |

9

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Consumer Services - continued | | | | | | | | |

| Garda World Security Corp., 7.25%, 11/15/21 (z) | | $ | 1,200,000 | | | $ | 1,221,000 | |

| Grupo Posadas S.A.B. de C.V., 7.875%, 11/30/17 | | | 2,125,000 | | | | 2,156,875 | |

| Monitronics International, Inc., 9.125%, 4/01/20 | | | 3,885,000 | | | | 4,079,250 | |

| Service Corp. International, 7%, 6/15/17 | | | 2,630,000 | | | | 2,912,725 | |

| Service Corp. International, 5.375%, 5/15/24 (n) | | | 2,120,000 | | | | 2,167,700 | |

| | | | | | | | |

| | | | $ | 22,097,638 | |

| Containers - 3.0% | | | | | | | | |

| Ardagh Packaging Finance PLC, 7%, 11/15/20 (n) | | $ | 748,235 | | | $ | 737,012 | |

| Ardagh Packaging Finance PLC, 9.125%, 10/15/20 (n) | | | 4,110,000 | | | | 4,418,250 | |

| Ardagh Packaging Finance PLC, 9.125%, 10/15/20 (n) | | | 400,000 | | | | 432,000 | |

| Ardagh Packaging Finance PLC, 6%, 6/30/21 (z) | | | 2,845,000 | | | | 2,716,975 | |

| Ball Corp., 5%, 3/15/22 | | | 1,624,000 | | | | 1,619,940 | |

| Ball Corp., 4%, 11/15/23 | | | 2,735,000 | | | | 2,523,038 | |

| Berry Plastics Group, Inc., 5.5%, 5/15/22 | | | 5,470,000 | | | | 5,333,250 | |

| Crown American LLC, 4.5%, 1/15/23 | | | 7,310,000 | | | | 6,907,950 | |

| Greif, Inc., 6.75%, 2/01/17 | | | 1,410,000 | | | | 1,533,375 | |

| Greif, Inc., 7.75%, 8/01/19 | | | 795,000 | | | | 898,350 | |

| Reynolds Group, 7.125%, 4/15/19 | | | 2,925,000 | | | | 3,034,688 | |

| Reynolds Group, 9.875%, 8/15/19 | | | 1,030,000 | | | | 1,109,825 | |

| Reynolds Group, 5.75%, 10/15/20 | | | 2,760,000 | | | | 2,815,200 | |

| Reynolds Group, 8.25%, 2/15/21 | | | 5,025,000 | | | | 5,326,500 | |

| Signode Industrial Group, 6.375%, 5/01/22 (z) | | | 3,440,000 | | | | 3,388,400 | |

| | | | | | | | |

| | | | $ | 42,794,753 | |

| Defense Electronics - 0.4% | | | | | | | | |

| Ducommun, Inc., 9.75%, 7/15/18 | | $ | 5,106,000 | | | $ | 5,629,365 | |

|

| Electronics - 1.7% | |

| Advanced Micro Devices, Inc., 6.75%, 3/01/19 (n) | | $ | 4,010,000 | | | $ | 4,110,250 | |

| Advanced Micro Devices, Inc., 7.5%, 8/15/22 | | | 1,500,000 | | | | 1,552,500 | |

| Advanced Micro Devices, Inc., 7%, 7/01/24 (z) | | | 1,165,000 | | | | 1,135,875 | |

| Micron Technology, Inc., 5.875%, 2/15/22 (n) | | | 3,305,000 | | | | 3,470,250 | |

| Micron Technology, Inc., 5.5%, 2/01/25 (z) | | | 2,290,000 | | | | 2,278,550 | |

| Nokia Corp., 5.375%, 5/15/19 | | | 1,075,000 | | | | 1,139,500 | |

| Nokia Corp., 6.625%, 5/15/39 | | | 1,345,000 | | | | 1,435,788 | |

| NXP B.V., 5.75%, 2/15/21 (n) | | | 1,770,000 | | | | 1,840,800 | |

| NXP B.V., 5.75%, 3/15/23 (n) | | | 3,430,000 | | | | 3,541,475 | |

| Sensata Technologies B.V., 6.5%, 5/15/19 (n) | | | 3,770,000 | | | | 3,939,650 | |

| | | | | | | | |

| | | | $ | 24,444,638 | |

| Energy - Independent - 8.5% | | | | | | | | |

| American Energy-Permian Basin LLC, 7.125%, 11/01/20 (z) | | $ | 1,790,000 | | | $ | 1,727,350 | |

| American Energy-Permian Basin LLC, 7.375%, 11/01/21 (z) | | | 1,495,000 | | | | 1,442,675 | |

10

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Energy - Independent - continued | | | | | | | | |

| Antero Resources Finance Corp., 6%, 12/01/20 | | $ | 3,740,000 | | | $ | 3,898,950 | |

| Antero Resources Finance Corp., 5.375%, 11/01/21 | | | 2,650,000 | | | | 2,683,125 | |

| Athlon Holdings LP/Athlon Finance Corp., 6%, 5/01/22 (z) | | | 4,080,000 | | | | 4,090,200 | |

| Baytex Energy Corp., 5.125%, 6/01/21 (z) | | | 585,000 | | | | 580,613 | |

| Baytex Energy Corp., 5.625%, 6/01/24 (z) | | | 2,985,000 | | | | 2,940,225 | |

| Bill Barrett Corp., 7%, 10/15/22 | | | 3,950,000 | | | | 4,048,750 | |

| BreitBurn Energy Partners LP, 8.625%, 10/15/20 | | | 1,395,000 | | | | 1,499,625 | |

| BreitBurn Energy Partners LP, 7.875%, 4/15/22 | | | 6,375,000 | | | | 6,661,875 | |

| Chaparral Energy, Inc., 7.625%, 11/15/22 | | | 3,770,000 | | | | 3,949,075 | |

| Chesapeake Energy Corp., 5.75%, 3/15/23 | | | 1,345,000 | | | | 1,435,788 | |

| Concho Resources, Inc., 6.5%, 1/15/22 | | | 4,690,000 | | | | 4,994,850 | |

| Concho Resources, Inc., 5.5%, 4/01/23 | | | 4,295,000 | | | | 4,445,325 | |

| Denbury Resources, Inc., 4.625%, 7/15/23 | | | 3,755,000 | | | | 3,510,925 | |

| EP Energy LLC, 6.875%, 5/01/19 | | | 1,435,000 | | | | 1,503,163 | |

| EP Energy LLC, 9.375%, 5/01/20 | | | 5,265,000 | | | | 5,830,988 | |

| EP Energy LLC, 7.75%, 9/01/22 | | | 6,260,000 | | | | 6,823,400 | |

| EPL Oil & Gas, Inc., 8.25%, 2/15/18 | | | 4,555,000 | | | | 4,759,975 | |

| Halcon Resources Corp., 8.875%, 5/15/21 | | | 5,825,000 | | | | 6,043,438 | |

| Harvest Operations Corp., 6.875%, 10/01/17 | | | 3,985,000 | | | | 4,293,838 | |

| Hilcorp Energy I/Hilcorp Finance Co., 8%, 2/15/20 (n) | | | 1,870,000 | | | | 1,991,550 | |

| Laredo Petroleum, Inc., 5.625%, 1/15/22 | | | 1,440,000 | | | | 1,465,200 | |

| Laredo Petroleum, Inc., 7.375%, 5/01/22 | | | 1,155,000 | | | | 1,258,950 | |

| LINN Energy LLC, 8.625%, 4/15/20 | | | 2,050,000 | | | | 2,165,313 | |

| LINN Energy LLC, 7.75%, 2/01/21 | | | 3,166,000 | | | | 3,316,385 | |

| MEG Energy Corp., 6.5%, 3/15/21 (n) | | | 2,285,000 | | | | 2,347,838 | |

| MEG Energy Corp., 7%, 3/31/24 (n) | | | 3,245,000 | | | | 3,431,588 | |

| Northern Blizzard Resources, Inc., 7.25%, 2/01/22 (n) | | | 4,205,000 | | | | 4,425,763 | |

| Oasis Petroleum, Inc., 6.875%, 3/15/22 (n) | | | 5,605,000 | | | | 6,067,413 | |

| Range Resources Corp., 5%, 8/15/22 | | | 5,535,000 | | | | 5,673,375 | |

| Sanchez Energy Corp., 6.125%, 1/15/23 (z) | | | 2,985,000 | | | | 2,977,538 | |

| SandRidge Energy, Inc., 8.125%, 10/15/22 | | | 4,415,000 | | | | 4,701,975 | |

| SM Energy Co., 6.5%, 11/15/21 | | | 4,230,000 | | | | 4,536,675 | |

| | | | | | | | |

| | | | $ | 121,523,716 | |

| Entertainment - 1.7% | | | | | | | | |

| Activision Blizzard, Inc., 6.125%, 9/15/23 (n) | | $ | 2,970,000 | | | $ | 3,200,175 | |

| Cedar Fair LP, 5.25%, 3/15/21 | | | 4,270,000 | | | | 4,312,700 | |

| Cedar Fair LP, 5.375%, 6/01/24 (n) | | | 1,790,000 | | | | 1,790,000 | |

| Cinemark USA, Inc., 5.125%, 12/15/22 | | | 2,805,000 | | | | 2,826,038 | |

| Cinemark USA, Inc., 4.875%, 6/01/23 | | | 2,495,000 | | | | 2,438,863 | |

| Seven Seas Cruises S. DE R.L., 9.125%, 5/15/19 | | | 4,755,000 | | | | 5,135,400 | |

| Six Flags Entertainment Corp., 5.25%, 1/15/21 (n) | | | 4,115,000 | | | | 4,094,425 | |

| | | | | | | | |

| | | | $ | 23,797,601 | |

11

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Financial Institutions - 4.8% | | | | | | | | |

| Aircastle Ltd., 4.625%, 12/15/18 | | $ | 3,385,000 | | | $ | 3,444,238 | |

| Aircastle Ltd., 5.125%, 3/15/21 | | | 1,815,000 | | | | 1,819,538 | |

| Aviation Capital Group, 4.625%, 1/31/18 (n) | | | 2,300,000 | | | | 2,433,959 | |

| Aviation Capital Group, 6.75%, 4/06/21 (n) | | | 3,515,000 | | | | 3,958,442 | |

| CIT Group, Inc., 5.25%, 3/15/18 | | | 3,330,000 | | | | 3,513,150 | |

| CIT Group, Inc., 6.625%, 4/01/18 (n) | | | 5,369,000 | | | | 5,919,323 | |

| CIT Group, Inc., 5.5%, 2/15/19 (n) | | | 5,562,000 | | | | 5,937,435 | |

| CIT Group, Inc., 5%, 8/15/22 | | | 4,690,000 | | | | 4,842,425 | |

| Icahn Enterprises LP, 6%, 8/01/20 | | | 3,730,000 | | | | 3,888,525 | |

| Icahn Enterprises LP, 5.875%, 2/01/22 | | | 5,785,000 | | | | 5,897,084 | |

| International Lease Finance Corp., 7.125%, 9/01/18 (n) | | | 2,634,000 | | | | 3,015,930 | |

| Nationstar Mortgage LLC/Capital Corp., 6.5%, 8/01/18 | | | 2,615,000 | | | | 2,588,850 | |

| Nationstar Mortgage LLC/Capital Corp., 7.875%, 10/01/20 | | | 5,115,000 | | | | 5,217,300 | |

| SLM Corp., 4.875%, 6/17/19 | | | 930,000 | | | | 936,975 | |

| SLM Corp., 8%, 3/25/20 | | | 6,735,000 | | | | 7,610,550 | |

| SLM Corp., 7.25%, 1/25/22 | | | 4,225,000 | | | | 4,626,375 | |

| SLM Corp., 6.125%, 3/25/24 | | | 2,140,000 | | | | 2,086,500 | |

| | | | | | | | |

| | | | $ | 67,736,599 | |

| Food & Beverages - 1.4% | | | | | | | | |

| B&G Foods, Inc., 4.625%, 6/01/21 | | $ | 2,800,000 | | | $ | 2,730,000 | |

| Constellation Brands, Inc., 3.75%, 5/01/21 | | | 525,000 | | | | 511,875 | |

| Constellation Brands, Inc., 4.25%, 5/01/23 | | | 3,885,000 | | | | 3,836,438 | |

| Darling Ingrediants, Inc., 5.375%, 1/15/22 (n) | | | 4,595,000 | | | | 4,721,363 | |

| H.J. Heinz Co., 4.25%, 10/15/20 | | | 2,610,000 | | | | 2,593,688 | |

| Sun Merger Sub, Inc., 5.875%, 8/01/21 (n) | | | 4,560,000 | | | | 4,788,000 | |

| | | | | | | | |

| | | | $ | 19,181,364 | |

| Forest & Paper Products - 0.4% | | | | | | | | |

| Appvion, Inc., 9%, 6/01/20 (n) | | $ | 3,130,000 | | | $ | 2,989,150 | |

| Tembec Industries, Inc., 11.25%, 12/15/18 | | | 2,880,000 | | | | 3,088,800 | |

| | | | | | | | |

| | | | $ | 6,077,950 | |

| Gaming & Lodging - 2.3% | | | | | | | | |

| CCM Merger, Inc., 9.125%, 5/01/19 (n) | | $ | 3,945,000 | | | $ | 4,161,975 | |

| Chester Downs & Marina LLC, 9.25%, 2/01/20 (n) | | | 1,750,000 | | | | 1,662,500 | |

| Greektown Holdings LLC, 8.875%, 3/15/19 (n) | | | 3,515,000 | | | | 3,497,425 | |

| Hilton Worldwide Finance Co., 5.625%, 10/15/21 (n) | | | 4,025,000 | | | | 4,216,188 | |

| Isle of Capri Casinos, Inc., 8.875%, 6/15/20 | | | 1,965,000 | | | | 2,082,900 | |

| Isle of Capri Casinos, Inc., 5.875%, 3/15/21 | | | 715,000 | | | | 732,875 | |

| MGM Resorts International, 6.625%, 12/15/21 | | | 3,540,000 | | | | 3,827,625 | |

| Pinnacle Entertainment, Inc., 8.75%, 5/15/20 | | | 2,545,000 | | | | 2,716,788 | |

| Pinnacle Entertainment, Inc., 6.375%, 8/01/21 | | | 2,185,000 | | | | 2,250,550 | |

| Ryman Hospitality Properties, Inc., REIT, 5%, 4/15/21 | | | 3,870,000 | | | | 3,840,975 | |

12

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Gaming & Lodging - continued | | | | | | | | |

| Wynn Las Vegas LLC, 7.75%, 8/15/20 | | $ | 3,830,000 | | | $ | 4,126,825 | |

| | | | | | | | |

| | | | $ | 33,116,626 | |

| Health Maintenance Organizations - 0.0% | | | | | | | | |

| Wellcare Health Plans, Inc., 5.75%, 11/15/20 | | $ | 244,000 | | | $ | 248,880 | |

| | |

| Industrial - 1.3% | | | | | | | | |

| Dematic S.A., 7.75%, 12/15/20 (n) | | $ | 5,925,000 | | | $ | 6,339,750 | |

| Howard Hughes Corp., 6.875%, 10/01/21 (n) | | | 5,615,000 | | | | 5,909,788 | |

| Hyva Global B.V., 8.625%, 3/24/16 (n) | | | 2,489,000 | | | | 2,576,115 | |

| SPL Logistics Escrow LLC, 8.875%, 8/01/20 (n) | | | 3,320,000 | | | | 3,676,900 | |

| | | | | | | | |

| | | | $ | 18,502,553 | |

| International Market Quasi-Sovereign - 0.3% | | | | | | | | |

| Eksportfinans A.S.A., 5.5%, 5/25/16 | | $ | 1,090,000 | | | $ | 1,153,765 | |

| Eksportfinans A.S.A., 5.5%, 6/26/17 | | | 2,745,000 | | | | 2,946,291 | |

| | | | | | | | |

| | | | $ | 4,100,056 | |

| Machinery & Tools - 1.3% | | | | | | | | |

| H&E Equipment Services Co., 7%, 9/01/22 | | $ | 4,955,000 | | | $ | 5,363,788 | |

| Jurassic Holdings III, Inc., 6.875%, 2/15/21 (n) | | | 4,025,000 | | | | 4,004,875 | |

| Light Tower Rentals, Inc., 8.125%, 8/01/19 (z) | | | 1,785,000 | | | | 1,816,238 | |

| RSC Equipment Rental, Inc., 8.25%, 2/01/21 | | | 2,910,000 | | | | 3,175,538 | |

| United Rentals North America, Inc., 7.625%, 4/15/22 | | | 3,667,000 | | | | 4,042,868 | |

| | | | | | | | |

| | | | $ | 18,403,307 | |

| Major Banks - 1.1% | | | | | | | | |

| Bank of America Corp., FRN, 5.2%, 12/31/49 | | $ | 5,305,000 | | | $ | 4,973,438 | |

| JPMorgan Chase & Co., 6% to 8/01/23, FRN to 12/31/49 | | | 4,920,000 | | | | 4,993,800 | |

| Royal Bank of Scotland Group PLC, 6.99% to 10/04/17, FRN to 12/31/49 (n) | | | 1,370,000 | | | | 1,572,075 | |

| Royal Bank of Scotland Group PLC, 7.648% to 9/30/31, FRN to 12/31/49 | | | 3,320,000 | | | | 3,951,464 | |

| | | | | | | | |

| | | | $ | 15,490,777 | |

| Medical & Health Technology & Services - 4.7% | | | | | | | | |

| CHS/Community Health Systems, Inc., 5.125%, 8/01/21 (z) | | $ | 840,000 | | | $ | 846,300 | |

| CHS/Community Health Systems, Inc., 6.875%, 2/01/22 (z) | | | 6,985,000 | | | | 7,142,163 | |

| Davita, Inc., 6.625%, 11/01/20 | | | 5,625,000 | | | | 5,906,250 | |

| Davita, Inc., 5.125%, 7/15/24 | | | 2,205,000 | | | | 2,171,925 | |

| Fresenius Medical Care Capital Trust III, 5.625%, 7/31/19 (n) | | | 2,410,000 | | | | 2,566,650 | |

| Fresenius Medical Care Capital Trust III, 5.875%, 1/31/22 (n) | | | 1,710,000 | | | | 1,868,175 | |

| HCA, Inc., 7.25%, 9/15/20 | | | 1,010,000 | | | | 1,068,075 | |

| HCA, Inc., 7.5%, 2/15/22 | | | 5,995,000 | | | | 6,789,338 | |

| HCA, Inc., 5.875%, 3/15/22 | | | 6,325,000 | | | | 6,736,125 | |

13

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Medical & Health Technology & Services - continued | |

| HCA, Inc., 5%, 3/15/24 | | $ | 2,930,000 | | | $ | 2,908,025 | |

| HealthSouth Corp., 8.125%, 2/15/20 | | | 5,915,000 | | | | 6,240,325 | |

| Lifepoint Hospitals, Inc., 5.5%, 12/01/21 (n) | | | 6,310,000 | | | | 6,451,975 | |

| Tenet Healthcare Corp., 8%, 8/01/20 | | | 6,500,000 | | | | 6,938,750 | |

| Tenet Healthcare Corp., 4.5%, 4/01/21 | | | 5,265,000 | | | | 5,120,213 | |

| Universal Health Services, Inc., 7.625%, 8/15/20 | | | 3,560,000 | | | | 3,631,200 | |

| | | | | | | | |

| | | | $ | 66,385,489 | |

| Medical Equipment - 0.7% | | | | | | | | |

| Biomet, Inc., 6.5%, 8/01/20 | | $ | 2,248,000 | | | $ | 2,424,805 | |

| Physio-Control International, Inc., 9.875%, 1/15/19 (n) | | | 1,767,000 | | | | 1,939,283 | |

| Teleflex, Inc., 6.875%, 6/01/19 | | | 2,975,000 | | | | 3,146,063 | |

| Teleflex, Inc., 5.25%, 6/15/24 (n) | | | 2,700,000 | | | | 2,740,500 | |

| | | | | | | | |

| | | | $ | 10,250,651 | |

| Metals & Mining - 4.6% | | | | | | | | |

| ArcelorMittal S.A., 6.75%, 2/25/22 | | $ | 1,130,000 | | | $ | 1,223,225 | |

| ArcelorMittal S.A., 7.25%, 3/01/41 | | | 2,945,000 | | | | 3,003,900 | |

| Arch Coal, Inc., 8%, 1/15/19 (n) | | | 2,045,000 | | | | 1,973,425 | |

| Arch Coal, Inc., 7.25%, 10/01/20 | | | 2,560,000 | | | | 1,702,400 | |

| Century Aluminum Co., 7.5%, 6/01/21 (n) | | | 4,715,000 | | | | 4,997,900 | |

| Commercial Metals Co., 4.875%, 5/15/23 | | | 3,048,000 | | | | 2,933,700 | |

| Consol Energy, Inc., 8.25%, 4/01/20 | | | 3,985,000 | | | | 4,244,025 | |

| Consol Energy, Inc., 6.375%, 3/01/21 | | | 1,545,000 | | | | 1,622,250 | |

| Consol Energy, Inc., 5.875%, 4/15/22 (n) | | | 3,910,000 | | | | 3,953,988 | |

| First Quantum Minerals Ltd., 7.25%, 10/15/19 (n) | | | 7,343,000 | | | | 7,636,720 | |

| First Quantum Minerals Ltd., 7.25%, 5/15/22 (n) | | | 2,698,000 | | | | 2,775,568 | |

| FMG Resources, 6.875%, 4/01/22 (n) | | | 1,070,000 | | | | 1,138,213 | |

| Fortescue Metals Group Ltd., 8.25%, 11/01/19 (n) | | | 5,220,000 | | | | 5,598,450 | |

| GrafTech International Co., 6.375%, 11/15/20 | | | 4,385,000 | | | | 4,483,663 | |

| Molycorp, Inc., 10%, 6/01/20 | | | 1,205,000 | | | | 1,072,450 | |

| Peabody Energy Corp., 6%, 11/15/18 | | | 2,295,000 | | | | 2,289,263 | |

| Steel Dynamics, Inc., 5.25%, 4/15/23 | | | 2,850,000 | | | | 2,871,375 | |

| Suncoke Energy Partners LP/Suncoke Energy Partners Finance Corp., 7.375%, 2/01/20 (z) | | | 1,440,000 | | | | 1,519,200 | |

| Suncoke Energy, Inc., 7.625%, 8/01/19 | | | 3,270,000 | | | | 3,466,200 | |

| TMS International Corp., 7.625%, 10/15/21 (n) | | | 2,855,000 | | | | 3,026,300 | |

| Walter Energy, Inc., 9.5%, 10/15/19 (n) | | | 1,960,000 | | | | 1,950,200 | |

| Walter Energy, Inc., 8.5%, 4/15/21 | | | 3,680,000 | | | | 1,766,400 | |

| | | | | | | | |

| | | | $ | 65,248,815 | |

| Midstream - 5.1% | | | | | | | | |

| Access Midstream Partners Co., 5.875%, 4/15/21 | | $ | 1,180,000 | | | $ | 1,241,950 | |

| Access Midstream Partners Co., 4.875%, 5/15/23 | | | 5,245,000 | | | | 5,402,350 | |

14

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Midstream - continued | | | | | | | | |

| AmeriGas Finance LLC, 6.75%, 5/20/20 | | $ | 6,375,000 | | | $ | 6,709,688 | |

| Atlas Pipeline Partners LP/Atlas Pipeline, 4.75%, 11/15/21 | | | 1,050,000 | | | | 992,250 | |

| Atlas Pipeline Partners LP/Atlas Pipeline, 5.875%, 8/01/23 | | | 4,155,000 | | | | 4,082,288 | |

| Crestwood Midstream Partners LP, 6%, 12/15/20 | | | 3,815,000 | | | | 3,929,450 | |

| Crestwood Midstream Partners LP, 6.125%, 3/01/22 (n) | | | 2,420,000 | | | | 2,498,650 | |

| El Paso Corp., 7.75%, 1/15/32 | | | 8,280,000 | | | | 9,149,360 | |

| Energy Transfer Equity LP, 7.5%, 10/15/20 | | | 4,955,000 | | | | 5,537,213 | |

| Ferrellgas LP/Ferrellgas Finance Corp., 6.5%, 5/01/21 | | | 1,735,000 | | | | 1,791,388 | |

| Ferrellgas LP/Ferrellgas Finance Corp., 6.75%, 1/15/22 (n) | | | 5,720,000 | | | | 5,963,100 | |

| MarkWest Energy Partners LP, 5.5%, 2/15/23 | | | 3,325,000 | | | | 3,449,688 | |

| MarkWest Energy Partners LP, 4.5%, 7/15/23 | | | 3,644,000 | | | | 3,589,340 | |

| Sabine Pass Liquefaction LLC, 5.625%, 2/01/21 | | | 3,800,000 | | | | 3,933,000 | |

| Sabine Pass Liquefaction LLC, 5.625%, 4/15/23 | | | 6,670,000 | | | | 6,770,050 | |

| Sabine Pass Liquefaction LLC, 5.75%, 5/15/24 (z) | | | 2,130,000 | | | | 2,161,950 | |

| Summit Midstream Holdings LLC/Summit Midstream Finance Corp., 7.5%, 7/01/21 | | | 2,490,000 | | | | 2,707,875 | |

| Summit Midstream Holdings LLC/Summit Midstream Finance Corp., 5.5%, 8/15/22 | | | 2,260,000 | | | | 2,260,000 | |

| | | | | | | | |

| | | | $ | 72,169,590 | |

| Municipals - 0.2% | | | | | | | | |

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., “A-1”, 4.5%, 6/01/27 | | $ | 1,545,000 | | | $ | 1,370,091 | |

| New Jersey Tobacco Settlement Financing Corp., “1-A”, 4.5%, 6/01/23 | | | 1,635,000 | | | | 1,598,801 | |

| | | | | | | | |

| | | | | | | $ | 2,968,892 | |

| Network & Telecom - 1.9% | | | | | | | | |

| Centurylink, Inc., 6.45%, 6/15/21 | | $ | 4,205,000 | | | $ | 4,520,375 | |

| Centurylink, Inc., 6.75%, 12/01/23 | | | 1,205,000 | | | | 1,307,425 | |

| Centurylink, Inc., 7.65%, 3/15/42 | | | 3,030,000 | | | | 3,030,000 | |

| Citizens Communications Co., 9%, 8/15/31 | | | 4,755,000 | | | | 5,064,075 | |

| Frontier Communications Corp., 8.125%, 10/01/18 | | | 1,030,000 | | | | 1,179,350 | |

| Telecom Italia Capital, 6%, 9/30/34 | | | 1,515,000 | | | | 1,484,700 | |

| Telecom Italia S.p.A., 5.303%, 5/30/24 (n) | | | 3,990,000 | | | | 3,870,300 | |

| TW Telecom Holdings, Inc., 5.375%, 10/01/22 | | | 2,580,000 | | | | 2,792,850 | |

| TW Telecom Holdings, Inc., 5.375%, 10/01/22 | | | 1,100,000 | | | | 1,190,750 | |

| Windstream Corp., 7.75%, 10/15/20 | | | 2,615,000 | | | | 2,798,050 | |

| | | | | | | | |

| | | | $ | 27,237,875 | |

| Oil Services - 1.3% | | | | | | | | |

| Bristow Group, Inc., 6.25%, 10/15/22 | | $ | 5,435,000 | | | $ | 5,733,925 | |

| Pacific Drilling S.A., 5.375%, 6/01/20 (n) | | | 4,675,000 | | | | 4,452,938 | |

| Shale-Inland Holdings LLC/Finance Co., 8.75%, 11/15/19 (n) | | | 3,290,000 | | | | 3,409,263 | |

15

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Oil Services - continued | | | | | | | | |

| Unit Corp., 6.625%, 5/15/21 | | $ | 4,525,000 | | | $ | 4,751,250 | |

| | | | | | | | |

| | | | $ | 18,347,376 | |

| Oils - 0.1% | | | | | | | | |

| CITGO Petroleum Corp., 6.25%, 8/15/22 (z) | | $ | 1,475,000 | | | $ | 1,519,250 | |

| | |

| Other Banks & Diversified Financials - 0.4% | | | | | | | | |

| Groupe BPCE S.A., 12.5% to 8/6/19, FRN to 12/31/49 (n) | | $ | 3,791,000 | | | $ | 5,203,148 | |

| | |

| Pharmaceuticals - 1.7% | | | | | | | | |

| Endo Finance LLC/Endo Finco, Inc., 7.25%, 1/15/22 (z) | | $ | 5,255,000 | | | $ | 5,557,163 | |

| Mallinckrodt International Finance S.A., 5.75%, 8/01/22 (n) | | | 3,170,000 | | | | 3,185,850 | |

| Salix Pharmaceuticals Ltd., 6%, 1/15/21 (n) | | | 1,995,000 | | | | 2,084,775 | |

| Valeant Pharmaceuticals International, Inc., 7%, 10/01/20 (n) | | | 6,495,000 | | | | 6,787,275 | |

| Valeant Pharmaceuticals International, Inc., 7.25%, 7/15/22 (n) | | | 3,850,000 | | | | 4,081,000 | |

| Vantage Point Imaging, 7.5%, 7/15/21 (n) | | | 2,850,000 | | | | 3,078,000 | |

| | | | | | | | |

| | | | $ | 24,774,063 | |

| Precious Metals & Minerals - 0.6% | | | | | | | | |

| Aurico Gold, Inc., 7.75%, 4/01/20 (z) | | $ | 2,550,000 | | | $ | 2,581,875 | |

| Eldorado Gold Corp., 6.125%, 12/15/20 (n) | | | 4,155,000 | | | | 4,248,488 | |

| IAMGOLD Corp., 6.75%, 10/01/20 (n) | | | 1,627,000 | | | | 1,496,840 | |

| | | | | | | | |

| | | | $ | 8,327,203 | |

| Printing & Publishing - 0.8% | | | | | | | | |

| American Media, Inc., 13.5%, 6/15/18 (z) | | $ | 297,449 | | | $ | 312,321 | |

| Gannett Co., Inc., 6.375%, 10/15/23 (n) | | | 3,430,000 | | | | 3,618,650 | |

| Gannett Co., Inc., 5.125%, 7/15/20 | | | 1,645,000 | | | | 1,661,450 | |

| Lamar Media Corp., 5%, 5/01/23 | | | 3,160,000 | | | | 3,132,350 | |

| Nielsen Finance LLC, 5%, 4/15/22 (n) | | | 2,765,000 | | | | 2,723,525 | |

| | | | | | | | |

| | | | $ | 11,448,296 | |

| Railroad & Shipping - 0.2% | | | | | | | | |

| Watco Cos. LLC, 6.375%, 4/01/23 (n) | | $ | 2,710,000 | | | $ | 2,750,650 | |

|

| Real Estate - Healthcare - 0.9% | |

| Aviv Healthcare Properties LP/Aviv Healthcare, 6%, 10/15/21 | | $ | 4,880,000 | | | $ | 5,124,000 | |

| MPT Operating Partnership LP, REIT, 6.875%, 5/01/21 | | | 3,435,000 | | | | 3,692,625 | |

| MPT Operating Partnership LP, REIT, 6.375%, 2/15/22 | | | 3,810,000 | | | | 4,057,650 | |

| | | | | | | | |

| | | | $ | 12,874,275 | |

| Real Estate - Other - 1.3% | | | | | | | | |

| CNL Lifestyle Properties, Inc., REIT, 7.25%, 4/15/19 | | $ | 3,105,000 | | | $ | 3,167,100 | |

| DuPont Fabros Technology LP, REIT, 5.875%, 9/15/21 | | | 6,085,000 | | | | 6,206,700 | |

16

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Real Estate - Other - continued | | | | | | | | |

| ERP Properties, REIT, 7.75%, 7/15/20 | | $ | 3,050,000 | | | $ | 3,698,833 | |

| ERP Properties, REIT, 5.75%, 8/15/22 | | | 815,000 | | | | 884,828 | |

| Felcor Lodging LP, REIT, 5.625%, 3/01/23 | | | 4,255,000 | | | | 4,255,000 | |

| | | | | | | | |

| | | | $ | 18,212,461 | |

| Retailers - 1.8% | | | | | | | | |

| Best Buy Co., Inc., 5.5%, 3/15/21 | | $ | 5,555,000 | | | $ | 5,707,763 | |

| Bon Ton Stores, Inc., 8%, 6/15/21 | | | 2,990,000 | | | | 2,720,900 | |

| Burlington Coat Factory Warehouse Corp., 10%, 2/15/19 | | | 3,540,000 | | | | 3,887,380 | |

| Jo-Ann Stores Holdings, Inc., 9.75%, 10/15/19 (n)(p) | | | 3,060,000 | | | | 3,090,600 | |

| Limited Brands, Inc., 7%, 5/01/20 | | | 1,520,000 | | | | 1,717,600 | |

| Limited Brands, Inc., 6.95%, 3/01/33 | | | 1,080,000 | | | | 1,123,200 | |

| Rite Aid Corp., 9.25%, 3/15/20 | | | 4,640,000 | | | | 5,196,800 | |

| Sally Beauty Holdings, Inc., 6.875%, 11/15/19 | | | 1,755,000 | | | | 1,869,075 | |

| | | | | | | | |

| | | | $ | 25,313,318 | |

| Specialty Chemicals - 0.3% | | | | | | | | |

| Chemtura Corp., 5.75%, 7/15/21 | | $ | 4,245,000 | | | $ | 4,329,900 | |

| | |

| Specialty Stores - 0.5% | | | | | | | | |

| Group 1 Automotive, Inc., 5%, 6/01/22 (n) | | $ | 3,340,000 | | | $ | 3,289,900 | |

| Men’s Wearhouse, Inc., 7%, 7/01/22 (z) | | | 1,510,000 | | | | 1,570,400 | |

| Michaels Stores, Inc., 5.875%, 12/15/20 (n) | | | 2,905,000 | | | | 2,861,425 | |

| | | | | | | | |

| | | | $ | 7,721,725 | |

| Telecommunications - Wireless - 4.2% | | | | | | | | |

| Crown Castle International Corp., 4.875%, 4/15/22 | | $ | 1,445,000 | | | $ | 1,430,550 | |

| Crown Castle International Corp., 5.25%, 1/15/23 | | | 3,860,000 | | | | 3,898,600 | |

| Digicel Group Ltd., 8.25%, 9/01/17 (n) | | | 3,050,000 | | | | 3,118,625 | |

| Digicel Group Ltd., 8.25%, 9/30/20 (n) | | | 1,430,000 | | | | 1,540,825 | |

| Digicel Group Ltd., 6%, 4/15/21 (n) | | | 1,535,000 | | | | 1,561,863 | |

| Digicel Group Ltd., 7.125%, 4/01/22 (n) | | | 2,189,000 | | | | 2,221,835 | |

| Eileme 2 AB, 11.625%, 1/31/20 (n) | | | 2,149,000 | | | | 2,522,389 | |

| Sprint Capital Corp., 6.875%, 11/15/28 | | | 4,745,000 | | | | 4,626,375 | |

| Sprint Corp., 7.875%, 9/15/23 (n) | | | 4,665,000 | | | | 4,991,550 | |

| Sprint Corp., 7.125%, 6/15/24 (n) | | | 5,175,000 | | | | 5,278,500 | |

| Sprint Nextel Corp., 9%, 11/15/18 (n) | | | 2,120,000 | | | | 2,485,700 | |

| Sprint Nextel Corp., 6%, 11/15/22 | | | 3,600,000 | | | | 3,546,000 | |

| T-Mobile USA, Inc., 6.125%, 1/15/22 | | | 565,000 | | | | 581,244 | |

| T-Mobile USA, Inc., 6.5%, 1/15/24 | | | 1,715,000 | | | | 1,787,888 | |

| T-Mobile USA, Inc., 6.464%, 4/28/19 | | | 1,760,000 | | | | 1,834,800 | |

| T-Mobile USA, Inc., 6.25%, 4/01/21 | | | 6,685,000 | | | | 6,985,825 | |

| T-Mobile USA, Inc., 6.633%, 4/28/21 | | | 3,350,000 | | | | 3,517,500 | |

| Wind Acquisition Finance S.A., 4.75%, 7/15/20 (n) | | | 3,950,000 | | | | 3,861,125 | |

17

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Telecommunications - Wireless - continued | | | | | | | | |

| Wind Acquisition Finance S.A., 7.375%, 4/23/21 (z) | | $ | 4,430,000 | | | $ | 4,618,275 | |

| | | | | | | | |

| | | | $ | 60,409,469 | |

| Telephone Services - 0.2% | | | | | | | | |

| Cogent Communications Group, Inc., 8.375%, 2/15/18 (n) | | $ | 1,240,000 | | | $ | 1,314,400 | |

| Level 3 Financing, Inc., 8.625%, 7/15/20 | | | 1,315,000 | | | | 1,430,063 | |

| | | | | | | | |

| | | | $ | 2,744,463 | |

| Transportation - Services - 2.2% | | | | | | | | |

| Aguila American Resources Ltd., 7.875%, 1/31/18 (n) | | $ | 4,795,000 | | | $ | 5,016,769 | |

| Jack Cooper Holdings Corp., 9.25%, 6/01/20 (n) | | | 5,805,000 | | | | 6,356,475 | |

| Navios Logistics Finance (U.S.), Inc., 7.25%, 5/01/22 (n) | | | 677,000 | | | | 690,540 | |

| Navios Maritime Acquisition Corp., 8.125%, 11/15/21 (n) | | | 3,914,000 | | | | 3,962,925 | |

| Navios Maritime Holding, Inc., 7.375%, 1/15/22 (n) | | | 4,270,000 | | | | 4,344,725 | |

| Stena AB, 7%, 2/01/24 (n) | | | 6,510,000 | | | | 6,868,050 | |

| Syncreon Group BV/Syncre, 8.625%, 11/01/21 (n) | | | 2,545,000 | | | | 2,554,544 | |

| Ultrapetrol (Bahamas) Ltd., 8.875%, 6/15/21 | | | 953,000 | | | | 1,022,093 | |

| | | | | | | | |

| | | | $ | 30,816,121 | |

| Utilities - Electric Power - 1.8% | | | | | | | | |

| AES Corp., 7.375%, 7/01/21 | | $ | 2,560,000 | | | $ | 2,918,400 | |

| Calpine Corp., 5.375%, 1/15/23 | | | 2,225,000 | | | | 2,180,500 | |

| Covanta Holding Corp., 7.25%, 12/01/20 | | | 4,425,000 | | | | 4,734,750 | |

| Covanta Holding Corp., 6.375%, 10/01/22 | | | 1,520,000 | | | | 1,615,000 | |

| InterGen N.V., 7%, 6/30/23 (n) | | | 2,775,000 | | | | 2,761,125 | |

| NRG Energy, Inc., 8.25%, 9/01/20 | | | 4,950,000 | | | | 5,321,250 | |

| NRG Energy, Inc., 6.25%, 7/15/22 (n) | | | 1,740,000 | | | | 1,792,200 | |

| NRG Energy, Inc., 6.625%, 3/15/23 | | | 4,080,000 | | | | 4,202,400 | |

| | | | | | | | |

| | | | $ | 25,525,625 | |

| Total Bonds (Identified Cost, $1,284,177,471) | | | $ | 1,296,593,379 | |

| | |

| Floating Rate Loans (g)(r) - 3.7% | | | | | | | | |

| Aerospace - 0.2% | | | | | | | | |

| TransDigm, Inc., Term Loan C, 3.75%, 2/28/20 | | $ | 2,864,098 | | | $ | 2,843,640 | |

| | |

| Building - 0.4% | | | | | | | | |

| ABC Supply Co., Inc., Term Loan B, 3.5%, 4/16/20 | | $ | 4,227,594 | | | $ | 4,197,870 | |

| HD Supply, Term Loan B, 6/28/18 (o) | | | 2,319,361 | | | | 2,316,462 | |

| | | | | | | | |

| | | | $ | 6,514,332 | |

| Cable TV - 0.2% | | | | | | | | |

| Cequel Communications LLC, Term Loan, 2/14/19 (o) | | $ | 2,325,940 | | | $ | 2,310,433 | |

18

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Floating Rate Loans (g)(r) - continued | | | | | | | | |

| Conglomerates - 0.5% | | | | | | | | |

| Entegris, Inc., Term Loan B, 3.5%, 2/04/21 | | $ | 3,809,837 | | | $ | 3,771,739 | |

| Silver II U.S. Holdings LLC, Term Loan B, 4%, 12/13/19 | | | 2,804,308 | | | | 2,791,602 | |

| | | | | | | | |

| | | | $ | 6,563,341 | |

| Consumer Services - 0.2% | | | | | | | | |

| Realogy Corp., Term Loan B, 3.75%, 3/05/20 | | $ | 2,775,739 | | | $ | 2,774,873 | |

| | |

| Containers - 0.1% | | | | | | | | |

| Berry Plastics, Term Loan E, 1/06/21 (o) | | $ | 2,164,128 | | | $ | 2,143,164 | |

| | |

| Electronics - 0.3% | | | | | | | | |

| Avago Technologies Ltd., Term Loan B, 3.75%, 5/06/21 | | $ | 3,808,811 | | | $ | 3,799,860 | |

| | |

| Energy - Independent - 0.1% | | | | | | | | |

| MEG Energy Corp., Term Loan B, 3.75%, 3/31/20 | | $ | 1,612,289 | | | $ | 1,611,425 | |

| | |

| Entertainment - 0.1% | | | | | | | | |

| Cedar Fair LP, Term Loan B, 3.25%, 3/06/20 | | $ | 1,503,073 | | | $ | 1,507,567 | |

| | |

| Food & Beverages - 0.1% | | | | | | | | |

| H.J. Heinz Co., Term Loan B2, 3.5%, 6/07/20 | | $ | 1,027,119 | | | $ | 1,026,569 | |

| | |

| Gaming & Lodging - 0.3% | | | | | | | | |

| Hilton Worldwide, Term Loan B, 3.5%, 10/25/20 | | $ | 3,834,534 | | | $ | 3,814,564 | |

| | |

| Medical & Health Technology & Services - 0.1% | | | | | | | | |

| Community Health Systems, Inc., Term Loan, 4.25%, 1/16/21 | | $ | 653,155 | | | $ | 654,425 | |

| Davita Healthcare, Term Loan B, 3.5%, 5/29/21 | | | 1,481,536 | | | | 1,478,097 | |

| | | | | | | | |

| | | | $ | 2,132,522 | |

| Metals & Mining - 0.1% | | | | | | | | |

| Fortescue Metals Group Ltd., Term Loan B, 4.25%, 6/30/19 | | $ | 2,018,849 | | | $ | 2,011,279 | |

| | |

| Printing & Publishing - 0.2% | | | | | | | | |

| CBS Outdoor, Term Loan B, 3%, 1/31/21 | | $ | 2,698,235 | | | $ | 2,681,371 | |

| | |

| Retailers - 0.1% | | | | | | | | |

| Rite Aid Corp., Term Loan, 4.87%, 6/21/21 | | $ | 1,149,016 | | | $ | 1,159,070 | |

| | |

| Specialty Stores - 0.2% | | | | | | | | |

| Mens Wearhouse, Inc., Term Loan B, 4.5%, 4/16/21 | | $ | 3,076,336 | | | $ | 3,099,408 | |

| | |

| Transportation - Services - 0.3% | | | | | | | | |

| American Commercial Lines, Inc., Term Loan, 7.5%, 9/15/19 | | $ | 4,104,700 | | | $ | 4,120,093 | |

19

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Floating Rate Loans (g)(r) - continued | | | | | | | | |

| Utilities - Electric Power - 0.2% | |

| Calpine Construction Finance Co., Term Loan B, 3%, 5/03/20 | | $ | 3,595,367 | | | $ | 3,520,652 | |

| Total Floating Rate Loans (Identified Cost, $53,811,689) | | | $ | 53,634,163 | |

| | |

| Common Stocks - 0.0% | | | | | | | | |

| Automotive - 0.0% | | | | | | | | |

| Accuride Corp. (a) | | | 65,068 | | | $ | 325,340 | |

| | |

| Printing & Publishing - 0.0% | | | | | | | | |

| American Media Operations, Inc. (a) | | | 76,223 | | | $ | 13,682 | |

| Total Common Stocks (Identified Cost, $2,168,949) | | | $ | 339,022 | |

| | |

| Convertible Bonds - 0.1% | | | | | | | | |

| Network & Telecom - 0.1% | | | | | | | | |

Nortel Networks Corp., 2.125%, 4/15/15

(Identified Cost, $821,790) (a)(d) | | $ | 828,000 | | | $ | 840,420 | |

| | |

| Preferred Stocks - 0.2% | | | | | | | | |

| Other Banks & Diversified Financials - 0.2% | | | | | | | | |

| Ally Financial, Inc., 7% (Identified Cost, $2,370,188) (z) | | | 2,489 | | | $ | 2,476,555 | |

| | |

| Money Market Funds - 3.6% | | | | | | | | |

MFS Institutional Money Market Portfolio, 0.09%,

at Cost and Net Asset Value (v) | | | 50,845,650 | | | $ | 50,845,650 | |

| Total Investments (Identified Cost, $1,394,195,737) | | | $ | 1,404,729,189 | |

| |

| Other Assets, Less Liabilities - 1.3% | | | | 18,768,800 | |

| Net Assets - 100.0% | | | $ | 1,423,497,989 | |

| (a) | Non-income producing security. |

| (d) | In default. Interest and/or scheduled principal payment(s) have been missed. |

| (g) | The rate shown represents a weighted average coupon rate on settled positions at period end, unless otherwise indicated. |

| (i) | Interest only security for which the fund receives interest on notional principal (Par amount). Par amount shown is the notional principal and does not reflect the cost of the security. |

| (n) | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in the ordinary course of business in transactions exempt from registration, normally to qualified institutional buyers. At period end, the aggregate value of these securities was $446,619,178 representing 31.4% of net assets. |

| (o) | All or a portion of this position has not settled. Upon settlement date, interest rates for unsettled amounts will be determined. The rate shown, if any, represents the weighted average coupon rate for settled amounts. |

20

Portfolio of Investments (unaudited) – continued

| (p) | Payment-in-kind security for which interest income may be received in additional securities and/or cash. During the period, the following amount of interest income was received in additional securities and/or cash: |

| | | | | | |

| Payment-in-kind Securities | | Cash | | Additional

Securities | |

| Jo-Ann Stores Holdings, Inc., 9.75%, 10/15/19 | | $149,175 | | | $— | |

| Schaeffler Finance B.V., 6.875%, 8/15/18 | | — | | | — | |

| Total | | $149,175 | | | $— | |

| (q) | Interest received was less than stated coupon rate. |

| (r) | Remaining maturities of floating rate loans may be less than stated maturities shown as a result of contractual or optional prepayments by the borrower. Such prepayments cannot be predicted with certainty. These loans may be subject to restrictions on resale. Floating rate loans generally have rates of interest which are determined periodically by reference to a base lending rate plus a premium. |

| (v) | Underlying affiliated fund that is available only to investment companies managed by MFS. The rate quoted for the MFS Institutional Money Market Portfolio is the annualized seven-day yield of the fund at period end. |

| (z) | Restricted securities are not registered under the Securities Act of 1933 and are subject to legal restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are subsequently registered. Disposal of these securities may involve time-consuming negotiations and prompt sale at an acceptable price may be difficult. The fund holds the following restricted securities: |

| | | | | | | | | | |

| Restricted Securities | | Acquisition

Date | |

Cost | | | Value | |

| Advanced Micro Devices, Inc., 7%, 7/01/24 | | 6/02/14 | | | $1,165,000 | | | | $1,135,875 | |

| Ally Financial, Inc., 7% (Preferred Stock) | | 4/13/11-11/27/12 | | | 2,370,188 | | | | 2,476,555 | |

| American Energy-Permian Basin LLC, 7.125%, 11/01/20 | | 7/16/14 | | | 1,790,000 | | | | 1,727,350 | |

| American Energy-Permian Basin LLC, 7.375%, 11/01/21 | | 7/16/14 | | | 1,495,000 | | | | 1,442,675 | |

| American Media, Inc., 13.5%, 6/15/18 | | 12/28/10 | | | 300,469 | | | | 312,321 | |

| Ardagh Packaging Finance PLC, 6%, 6/30/21 | | 6/20/14-6/24/14 | | | 2,865,552 | | | | 2,716,975 | |

| Athlon Holdings LP/Athlon Finance Corp., 6%, 5/01/22 | | 4/16/14-5/13/14 | | | 4,136,651 | | | | 4,090,200 | |

| Aurico Gold, Inc., 7.75%, 4/01/20 | | 6/27/14-7/15/14 | | | 2,568,331 | | | | 2,581,875 | |

| Baytex Energy Corp., 5.125%, 6/01/21 | | 5/29/14 | | | 585,000 | | | | 580,613 | |

| Baytex Energy Corp., 5.625%, 6/01/24 | | 5/29/14-6/05/14 | | | 3,002,843 | | | | 2,940,225 | |

| CHS/Community Health Systems, Inc., 5.125%, 8/01/21 | | 1/15/14 | | | 840,000 | | | | 846,300 | |

| CHS/Community Health Systems, Inc., 6.875%, 2/01/22 | | 1/15/14-4/24/14 | | | 7,191,954 | | | | 7,142,163 | |

| CITGO Petroleum Corp., 6.25%, 8/15/22 | | 7/23/14 | | | 1,475,000 | | | | 1,519,250 | |

| CW Capital Cobalt Commercial Mortgage Trust, “E2”, CDO, 6%, 5/25/45 | | 3/20/06-5/25/14 | | | 1,348,101 | | | | 192,996 | |

| CW Capital Cobalt Commercial Mortgage Trust, “F”, CDO, FRN, 1.535%, 4/26/50 | | 4/12/06-4/26/14 | | | 657,150 | | | | 7 | |

21

Portfolio of Investments (unaudited) – continued

| | | | | | | | | | |

| Restricted Securities – continued | | Acquisition

Date | |

Cost | | | Value | |

| CW Capital Cobalt Commercial Mortgage Trust, “G”, CDO, FRN, 1.735%, 4/26/50 | | 4/12/06-4/26/14 | | | $2,054,697 | | | | $21 | |

| Endo Finance LLC/Endo Finco, Inc., 7.25%, 1/15/22 | | 9/24/13-6/02/14 | | | 5,601,681 | | | | 5,557,163 | |

| Falcon Franchise Loan LLC, FRN, 16.08%, 1/05/25 | | 1/29/03 | | | 54,276 | | | | 245,242 | |

| G-Force LLC, CDO, “A2”, 4.83%, 8/22/36 | | 2/14/11 | | | 1,843 | | | | 1,936 | |

| Garda World Security Corp., 7.25%, 11/15/21 | | 5/21/14-5/22/14 | | | 1,270,645 | | | | 1,221,000 | |

| Garda World Security Corp., 7.25%, 11/15/21 | | 4/24/14 | | | 3,053,429 | | | | 2,955,838 | |

| Light Tower Rentals, Inc., 8.125%, 8/01/19 | | 7/16/14 | | | 1,785,000 | | | | 1,816,238 | |

| Men’s Wearhouse, Inc., 7%, 7/01/22 | | 6/11/14-6/20/14 | | | 1,560,915 | | | | 1,570,400 | |

| Micron Technology, Inc., 5.5%, 2/01/25 | | 7/23/14 | | | 2,290,000 | | | | 2,278,550 | |

| Morgan Stanley Capital I, Inc., FRN, 1.414%, 4/28/39 | | 7/20/04 | | | 285,614 | | | | 34,903 | |

| SIRIUS XM Radio, Inc., 6%, 7/15/24 | | 5/01/14-5/13/14 | | | 2,372,484 | | | | 2,351,700 | |

| Sabine Pass Liquefaction LLC, 5.75%, 5/15/24 | | 12/12/13-5/13/14 | | | 2,130,000 | | | | 2,161,950 | |

| Sanchez Energy Corp., 6.125%, 1/15/23 | | 6/13/14-6/30/14 | | | 3,039,927 | | | | 2,977,538 | |

| Schaeffler Finance B.V., 4.75%, 5/15/21 | | 7/10/14-7/11/14 | | | 2,878,375 | | | | 2,836,925 | |

| Signode Industrial Group, 6.375%, 5/01/22 | | 4/07/14-4/25/14 | | | 3,469,111 | | | | 3,388,400 | |

| Suncoke Energy Partners LP/Suncoke Energy Partners Finance Corp., 7.375%, 2/01/20 | | 4/29/14 | | | 1,513,031 | | | | 1,519,200 | |

| TransDigm, Inc., 6%, 7/15/22 | | 5/20/14 | | | 470,000 | | | | 472,350 | |

| TransDigm, Inc., 6.5%, 7/15/24 | | 5/20/14-5/21/14 | | | 1,984,800 | | | | 1,994,750 | |

| Wind Acquisition Finance S.A., 7.375%, 4/23/21 | | 4/08/14 | | | 4,430,000 | | | | 4,618,275 | |

| Total Restricted Securities | | | | | | | | | $67,707,759 | |

| % of Net assets | | | | | | | | | 4.8% | |

The following abbreviations are used in this report and are defined:

| CDO | | Collateralized Debt Obligation |

| FRN | | Floating Rate Note. Interest rate resets periodically and may not be the rate reported at period end. |

| PLC | | Public Limited Company |

| REIT | | Real Estate Investment Trust |

Abbreviations indicate amounts shown in currencies other than the U.S. dollar. All amounts are stated in U.S. dollars unless otherwise indicated. A list of abbreviations is shown below:

Derivative Contracts at 7/31/14

Forward Foreign Currency Exchange Contracts at 7/31/14

| | | | | | | | | | | | | | | | | | | | | | | | |

| Type | | Currency | | Counter-

party | | Contracts

to

Deliver/

Receive | | | Settlement

Date Range | | | In

Exchange

for | | | Contracts

at Value | | | Net

Unrealized

Appreciation

(Depreciation) | |

| Asset Derivatives | | | | | | | | | | | | | | | |

| SELL | | EUR | | Credit Suisse Group | | | 8,111,201 | | | | 10/10/14 | | | | $11,044,617 | | | | $10,863,796 | | | | $180,821 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

22

Portfolio of Investments (unaudited) – continued

Forward Foreign Currency Exchange Contracts at 7/31/14 - continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| Type | | Currency | | Counter-

party | | Contracts

to

Deliver/

Receive | | | Settlement

Date Range | | | In

Exchange

for | | | Contracts

at Value | | | Net

Unrealized

Appreciation

(Depreciation) | |

| Liability Derivatives | | | | | | | | | | | | | | | |

| BUY | | EUR | | Deutsche Bank AG | | | 2,067,000 | | | | 10/10/14 | | | | $2,820,883 | | | | $2,768,452 | | | | $(52,431 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Futures Contracts Outstanding at 7/31/14

| | | | | | | | | | | | | | | | | | |

| Description | | Currency | | | Contracts | | | Value | | Expiration

Date | | | Unrealized

Appreciation

(Depreciation) | |

| Asset Derivatives | | | | | | | | | | | |

| Interest Rate Futures | | | | | | | | | | | |

| U.S. Treasury Note 10 yr (Short) | | | USD | | | | 110 | | | $13,707,031 | | | September - 2014 | | | | $119,870 | |

| | | | | | | | | | | | | | | | | | |

Swap Agreements at 7/31/14

| | | | | | | | | | | | | | | | | | |

| Expiration | | | | | Notional

Amount | | | Counterparty | | Cash Flows

to Receive | | Cash Flows

to Pay | | Fair

Value | |

| Asset Derivatives | | | | | | | | | | | |

| Credit Default Swap Agreements | | | | | | | | |

| 12/20/17 | | | USD | | | | 12,761,100 | | | Goldman Sachs International (a) | | 5.0% (fixed rate) | | (1) | | | $1,088,369 | |

| 12/20/17 | | | USD | | | | 4,950,000 | | | JPMorgan Chase Bank, N.A. (b) | | 5.0% (fixed rate) | | (1) | | | 422,175 | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | $1,510,544 | |

| | | | | | | | | | | | | | | | | | |

| (1) | Fund, as protection seller, to pay notional amount upon a defined credit event by a reference obligation specified in the Markit CDX North America Investment Grade Index, a B rated credit default index. The fund entered into the contract to manage market/sector exposure. |

| (a) | Net unamortized premiums paid by the fund amounted to $443,448. |

| (b) | Net unamortized premiums paid by the fund amounted to $175,779. |

The credit ratings presented here are an indicator of the current payment/performance risk of the related swap agreement, the reference obligation for which may be either a single security or, in the case of a credit default index, a basket of securities issued by corporate or sovereign issuers. Ratings are assigned to each reference security, including each individual security within a reference basket of securities, utilizing ratings from Moody’s, Fitch, and Standard & Poor’s rating agencies and applying the following hierarchy: If all three agencies provide a rating, the middle rating (after dropping the highest and lowest ratings) is assigned; if two of the three agencies rate a security, the lower of the two is assigned. Ratings are shown in the S&P and Fitch scale (e.g., AAA). The ratings for a credit default index are calculated by MFS as a weighted average of the external credit ratings of the individual securities that compose the index’s reference basket of securities.

At July 31, 2014, the fund had cash collateral of $521,947 to cover any commitments for certain derivative contracts. Cash collateral is comprised of “Restricted cash” in the Statement of Assets and Liabilities.

See Notes to Financial Statements

23

Financial Statements

STATEMENT OF ASSETS AND LIABILITIES

At 7/31/14 (unaudited)

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| | | | |

| Assets | | | | |

Investments- | | | | |

Non-affiliated issuers, at value (identified cost, $1,343,350,087) | | | $1,353,883,539 | |

Underlying affiliated funds, at cost and value | | | 50,845,650 | |

Total investments, at value (identified cost, $1,394,195,737) | | | $1,404,729,189 | |

Cash | | | 1,882,648 | |

Restricted cash | | | 521,947 | |

Receivables for | | | | |

Forward foreign currency exchange contracts | | | 180,821 | |

Daily variation margin on open futures contracts | | | 148,155 | |

Investments sold | | | 12,604,894 | |

Fund shares sold | | | 1,304,583 | |

Interest | | | 24,122,908 | |

Swaps, at value (net unamortized premiums paid, $619,227) | | | 1,510,544 | |

Other assets | | | 2,723 | |

Total assets | | | $1,447,008,412 | |

| Liabilities | | | | |

Payables for | | | | |

Distributions | | | $351,145 | |

Forward foreign currency exchange contracts | | | 52,431 | |

Investments purchased | | | 15,332,841 | |

Fund shares reacquired | | | 6,818,123 | |

Payable to affiliates | | | | |

Investment adviser | | | 30,648 | |

Shareholder servicing costs | | | 754,433 | |

Distribution and service fees | | | 12,505 | |

Program manager fees | | | 15 | |

Payable for independent Trustees’ compensation | | | 55,375 | |

Accrued expenses and other liabilities | | | 102,907 | |

Total liabilities | | | $23,510,423 | |

Net assets | | | $1,423,497,989 | |

| Net assets consist of | | | | |

Paid-in capital | | | $1,587,065,499 | |

Unrealized appreciation (depreciation) on investments and translation of assets and liabilities in foreign currencies | | | 11,669,714 | |

Accumulated net realized gain (loss) on investments and foreign currency | | | (172,342,624 | ) |

Accumulated distributions in excess of net investment income | | | (2,894,600 | ) |

Net assets | | | $1,423,497,989 | |

Shares of beneficial interest outstanding | | | 395,890,290 | |

24

Statement of Assets and Liabilities (unaudited) – continued

| | | | | | | | | | | | |

| | | Net assets | | | Shares

outstanding | | | Net asset value per share (a) | |

Class A | | | $464,065,263 | | | | 129,052,328 | | | | $3.60 | |

Class B | | | 30,268,529 | | | | 8,404,012 | | | | 3.60 | |

Class C | | | 73,819,576 | | | | 20,460,542 | | | | 3.61 | |

Class I | | | 73,230,825 | | | | 20,402,992 | | | | 3.59 | |

Class R1 | | | 1,369,966 | | | | 380,468 | | | | 3.60 | |

Class R2 | | | 3,212,450 | | | | 892,932 | | | | 3.60 | |

Class R3 | | | 7,025,519 | | | | 1,954,635 | | | | 3.59 | |

Class R4 | | | 565,606 | | | | 157,250 | | | | 3.60 | |

Class R5 | | | 764,386,951 | | | | 212,641,085 | | | | 3.59 | |

Class 529A | | | 3,413,181 | | | | 949,678 | | | | 3.59 | |

Class 529B | | | 346,532 | | | | 96,390 | | | | 3.60 | |

Class 529C | | | 1,793,591 | | | | 497,978 | | | | 3.60 | |

| (a) | Maximum offering price per share was equal to the net asset value per share for all share classes, except for Classes A and 529A, for which the maximum offering prices per share were $3.78 [100 / 95.25 x $3.60] and $3.77 [100 / 95.25 x $3.59], respectively. On sales of $50,000 or more, the maximum offering prices of Class A and Class 529A shares are reduced. A contingent deferred sales charge may be imposed on redemptions of Class A, Class B, Class C, Class 529B, and Class 529C shares. Redemption price per share was equal to the net asset value per share for Classes I, R1, R2, R3, R4, R5, and 529A. |

See Notes to Financial Statements

25

Financial Statements

STATEMENT OF OPERATIONS

Six months ended 7/31/14 (unaudited)

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| | | | |

| Net investment income | |

Income | | | | |

Interest | | | $43,856,802 | |

Dividends | | | 133,622 | |

Dividends from underlying affiliated funds | | | 21,701 | |

Total investment income | | | $44,012,125 | |

Expenses | | | | |

Management fee | | | $3,201,787 | |

Distribution and service fees | | | 1,155,376 | |

Program manager fees | | | 2,725 | |

Shareholder servicing costs | | | 822,313 | |

Administrative services fee | | | 85,359 | |

Independent Trustees’ compensation | | | 18,314 | |

Custodian fee | | | 95,925 | |

Shareholder communications | | | 31,986 | |

Audit and tax fees | | | 38,114 | |

Legal fees | | | 7,115 | |

Miscellaneous | | | 96,751 | |

Total expenses | | | $5,555,765 | |

Fees paid indirectly | | | (435 | ) |

Reduction of expenses by investment adviser and distributor | | | (50,702 | ) |

Net expenses | | | $5,504,628 | |

Net investment income | | | $38,507,497 | |

Realized and unrealized gain (loss) on investments and

foreign currency | | | | |

Realized gain (loss) (identified cost basis) | | | | |

Investments | | | $15,428,663 | |

Futures contracts | | | (225,317 | ) |

Swap agreements | | | 189,481 | |

Foreign currency | | | 20,169 | |

Net realized gain (loss) on investments and foreign currency | | | $15,412,996 | |

Change in unrealized appreciation (depreciation) | | | | |

Investments | | | $(14,867,843 | ) |

Futures contracts | | | 119,870 | |

Swap agreements | | | 64,390 | |

Translation of assets and liabilities in foreign currencies | | | (8,735 | ) |

Net unrealized gain (loss) on investments and foreign currency translation | | | $(14,692,318 | ) |

Net realized and unrealized gain (loss) on investments and foreign currency | | | $720,678 | |

Change in net assets from operations | | | $39,228,175 | |

See Notes to Financial Statements

26

Financial Statements