QuickLinks -- Click here to rapidly navigate through this documentExhibit 13

Financial Highlights

| |

| |

|

|---|

| | 2003

| | 2002

| | 2001

| | 2000*

| | 1999

|

|---|

| Operating Results (millions) | | | | | | | | | | | |

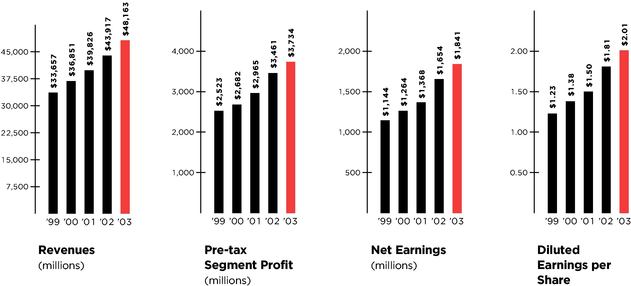

| Total revenues | | $ | 48,163 | | 43,917 | | 39,826 | | 36,851 | | 33,657 |

| Pre-tax segment profit | | $ | 3,734 | | 3,461 | | 2,965 | | 2,682 | | 2,523 |

| Net earnings | | $ | 1,841 | | 1,654 | | 1,368 | | 1,264 | | 1,144 |

| Per Common Share Data** | | | | | | | | | | | |

| Diluted earnings per share | | $ | 2.01 | | 1.81 | | 1.50 | | 1.38 | | 1.23 |

| Cash dividends declared | | $ | .270 | | .240 | | .225 | | .215 | | .200 |

| At Year-end (millions, except Number of stores) | | | | | | | | | | | |

| Common shares outstanding | | | 911.8 | | 909.8 | | 905.2 | | 897.8 | | 911.7 |

| Retail square feet | | | 188.6 | | 176.5 | | 161.6 | | 149.4 | | 139.4 |

| Number of stores | | | 1,553 | | 1,475 | | 1,381 | | 1,307 | | 1,243 |

- *

- Consisted of 53 weeks.

- **

- Earnings per share, dividends per share and common shares outstanding reflect our 2000 two-for-one common share split.

The Financial Highlights should be read in conjuction with the Notes to Consolidated Financial Statements throughout page 30-39.

| 01 Report to Shareholders | | 17 Financial Review |

| 04 Strategy Discussion | | 42 Shareholder Information |

MANAGEMENT'S DISCUSSION AND ANALYSIS

Analysis of Operations

Target Corporation operates large-format general merchandise stores in the United States, including discount stores, moderate-priced promotional stores and traditional department stores, and additionally operates a small, rapidly growing on-line business. We drive incremental merchandise sales and profitability through increases in our comparable-store sales and through contribution of new store growth at Target. Additionally, we benefit from our credit card operations which strategically support each of our retail segments. We focus on delighting our guests by offering both everyday essentials and fashionable, differentiated merchandise at exceptional prices. Our ability to deliver a shopping experience that is preferred by our guests is supported by our strong supply chain and technology network, a devotion to innovation which is ingrained in our organization and culture and our disciplined approach to managing our current business and investing in future growth. Though our industry is highly competitive and subject to macroeconomic conditions, we believe we are well-positioned to deliver continued profitable market share growth for many years to come.

On March 10, 2004, we began reviewing strategic alternatives for Mervyn's and Marshall Field's that include but are not limited to, the possible sale of one or both of these segments as ongoing businesses to existing retailers or other qualified buyers. The following Management's Discussion and Analysis, Consolidated Financial Statements, and Notes to Consolidated Financial Statements do not reflect any impact of any strategic alternatives as we are in the early stages of this review process.

Management's Discussion and Analysis is based on our Consolidated Financial Statements as shown on pages 26-29.

Revenues and Comparable-store Sales

Total revenues include retail sales and net credit card revenues. Net credit card revenues represent income derived from finance charges, late fees and other revenues from use of our Target Visa and proprietary credit cards. Comparable-store sales are sales from stores open longer than one year. Stores that were remodeled at their existing location and did not convert to a SuperTarget remain in the comparable-store sales calculation. Stores that have been converted to a SuperTarget or moved to a new location are included in the comparable-store sales calculation once they are open longer than one year.

In 2003, total revenues increased 9.7 percent and comparable-store sales increased 2.9 percent. Retail price deflation had a negative impact of approximately 3 percent on sales growth. At Target, which accounted for 86 percent of our total revenues, slightly more than half of our 12 percent increase in revenues was driven by new store expansion, while the rest of the increase resulted from a 4.4 percent increase in comparable-store sales and an increase in net credit card revenues. Mervyn's and Marshall Field's, which accounted for 7 percent and 5 percent of our total revenues, respectively, experienced a decline in revenues, primarily due to decreases in comparable-store sales.

In 2002, total revenues increased 10.3 percent and comparable-store sales increased 1.1 percent. Retail price deflation had a negative impact of approximately 3 percent on sales growth. At Target, which accounted for 84 percent of our total revenues, the increase was driven by new store expansion, an increase in net credit card revenues and a 2.2 percent increase in comparable-store sales. Mervyn's and Marshall Field's, which accounted for 9 percent and 6 percent of our total revenues, respectively, experienced a decline in revenues primarily due to decreases in comparable-store sales.

Revenues and Comparable-store Sales Growth

| | 2003

| | 2002

| | 2001

| |

|---|

| | Revenues

| | Comparable-

store

Sales

| | Revenues

| | Comparable-

store

Sales

| | Revenues

| | Comparable-

store

Sales

| |

|---|

| Target | | 12.0 | % | 4.4 | % | 13.3 | % | 2.2 | % | 13.1 | % | 4.1 | % |

| Mervyn's | | (6.9 | ) | (7.6 | ) | (5.2 | ) | (5.3 | ) | (1.7 | ) | (1.5 | ) |

| Marshall Field's | | (4.0 | ) | (2.6 | ) | (3.1 | ) | (3.7 | ) | (5.2 | ) | (5.7 | ) |

| | |

| |

| |

| |

| |

| |

| |

| Total | | 9.7 | % | 2.9 | % | 10.3 | % | 1.1 | % | 9.7 | % | 2.7 | % |

| | |

| |

| |

| |

| |

| |

| |

Revenues per Square Foot*

| | 2003

| | 2002

| | 2001

|

|---|

| Target | | $ | 282 | | $ | 278 | | $ | 274 |

| Mervyn's | | | 165 | | | 178 | | | 187 |

| Marshall Field's | | | 178 | | | 180 | | | 186 |

| | |

| |

| |

|

- *

- Thirteen-month average retail square feet.

In 2004, we expect revenues to increase due to new store growth and an increase in comparable-store sales and net credit card revenues.

Gross Margin Rate

Gross margin rate represents gross margin (sales less cost of sales) as a percent of sales. Cost of sales primarily includes purchases, markdowns and other costs associated with our merchandise. These costs are partially offset by various forms of consideration earned or received from our vendors, which we refer to as "vendor income."

17

In 2003, our consolidated gross margin rate increased 0.5 percent to a rate of 32.0 percent primarily due to the adoption of Emerging Issues Task Force (EITF) Issue No. 02-16 "Accounting by a Customer (Including a Reseller) for Certain Consideration Received from a Vendor." The adoption resulted in a reclassification of a portion of our vendor income from selling, general and administrative expenses to cost of sales and had a slight negative impact on net earnings as described in the Notes to Consolidated Financial Statements on page 30.

At Target, gross margin rate improved due to the vendor income reclassification. Mervyn's gross margin rate improvement was primarily a result of the vendor income reclassification and efforts to lower purchase costs through improved negotiating programs that resulted in markup improvement, partially offset by an increase in markdowns. Marshall Field's gross margin rate increased due to the vendor income reclassification and reductions in purchase costs which resulted in markup improvement. These improvements were partially offset by an increase in markdowns.

In 2002, our consolidated gross margin rate expanded by almost a full percentage point to a rate of 31.5 percent from 30.6 percent. The growth is attributable to rate expansion at Target and Mervyn's, primarily due to reductions in purchase costs and improvements in markup during the year. These increases were partially offset by additional markdowns at Mervyn's and Marshall Field's and the mix impact of growth at Target, our lowest gross margin rate division.

Consolidated gross margin rate in 2004 is expected to be approximately equal to 2003. Gross margin rate at Target is expected to remain essentially even with that of 2003. We expect modest gross margin rate expansion at both Mervyn's and Marshall Field's to be offset by the mix impact of faster growth at Target, our lowest gross margin rate division.

Selling, General and Administrative Expense Rate

Our selling, general and administrative (SG&A) expense rate represents payroll, benefits, advertising, distribution, buying and occupancy, start-up and other expenses as a percentage of sales. SG&A expense excludes depreciation and amortization and expenses associated with our credit card operations, which are reflected separately in our Consolidated Results of Operations. In 2003, approximately $78 million of vendor income was recorded as an offset to SG&A expenses as it met the specific, incremental and identifiable criteria of EITF No. 02-16. Approximately $294 million and $272 million of vendor income was recorded as an offset to SG&A expenses in 2002 and 2001, respectively. This vendor income primarily represented advertising reimbursements.

In 2003, our SG&A expense rate increased to 22.9 percent compared to 22.0 percent in 2002. Over half of this increase is attributable to the reclassification of vendor income to cost of sales from SG&A expenses as described in the Notes to Consolidated Financial Statements on page 30. The remaining increase is principally due to a lack of sales leverage at both Mervyn's and Marshall Field's.

In 2002, our SG&A expense rate rose to 22.0 percent compared to 21.6 percent in 2001 because certain items such as medical expenses increased at a faster pace than sales. This effect was only partially offset by the mix impact of growth at Target, our lowest SG&A expense rate division.

In 2004, we expect our SG&A expense rate to increase slightly from 2003, reflecting our belief that a number of expenses will increase at a faster pace than sales. These include expenses related to our defined benefit plans, insurance and stock options, which we began expensing during 2003 under the prospective transition method in accordance with Statement of Financial Accounting Standards (SFAS) No. 148, "Accounting for Stock-Based Compensation—Transition and Disclosure." We expect the effect of these increased expenses to be partially offset by the mix impact of growth at Target, our lowest SG&A expense rate division.

Depreciation and Amortization

In 2003, depreciation and amortization increased 8.9 percent to $1,320 million compared to 2002. In 2002, depreciation and amortization increased 12.4 percent to $1,212 million compared to 2001. The increase in both years is primarily due to new store growth at Target.

Pre-tax Segment Profit

Pre-tax segment profit is our core measure of profitability for the three segments and is a required disclosure for segment reporting under accounting principles generally accepted in the United States (GAAP).

In 2003, pre-tax segment profit increased 7.9 percent to $3,734 million, compared with $3,461 million in 2002. The increase was driven by growth at Target, which produced 93 percent of consolidated pre-tax segment profit. Mervyn's and Marshall Field's experienced a decrease in pre-tax segment profit compared to 2002.

Pre-tax segment profit increased 16.7 percent in 2002 to $3,461 million, compared with $2,965 million in 2001. The increase was driven by growth at Target, which produced 89 percent of consolidated pre-tax segment profit. Marshall Field's pre-tax segment profit in 2002 was essentially equal to 2001, while Mervyn's experienced a decline in pre-tax segment profit in 2002 compared to 2001.

A reconciliation of pre-tax segment profit to pre-tax earnings follows. Our segment disclosures may not be consistent with disclosures of other companies in the same line of business.

18

Pre-tax Segment Profit and as a Percent of Revenues

| | Pre-tax Segment Profit

| | As a Percent of Revenues

| |

|---|

| | 2003

| | 2002

| | 2001

| | 2003

| | 2002

| | 2001

| |

|---|

| | (millions)

| |

|---|

| Target | | $ | 3,467 | | $ | 3,088 | | $ | 2,546 | | 8.4 | % | 8.4 | % | 7.8 | % |

| Mervyn's | | | 160 | | | 238 | | | 286 | | 4.5 | | 6.2 | | 7.1 | |

| Marshall Field's | | | 107 | | | 135 | | | 133 | | 4.1 | | 5.0 | | 4.8 | |

| | |

| |

| |

| |

| |

| |

| |

| Total pre-tax segment profit | | $ | 3,734 | | $ | 3,461 | | $ | 2,965 | | 7.9 | % | 8.0 | % | 7.5 | % |

| | |

| |

| |

| |

| |

| |

| |

| Securitization adjustments: | | | | | | | | | | | | | | | | |

| | Loss | | | — | | | — | | | (67 | ) | | | | | | |

| | Interest equivalent | | | — | | | — | | | (27 | ) | | | | | | |

| LIFO provision credit/(expense) | | | 27 | | | 12 | | | (8 | ) | | | | | | |

| Interest expense | | | (559 | ) | | (588 | ) | | (473 | ) | | | | | | |

| Other | | | (242 | ) | | (209 | ) | | (183 | ) | | | | | | |

| | |

| |

| |

| | | | | | | |

| Earnings before taxes | | $ | 2,960 | | $ | 2,676 | | $ | 2,207 | | | | | | | |

| | |

| |

| |

| | | | | | | |

In 2001, the $67 million pre-tax loss related to the required adoption of a new accounting standard applicable to securitized accounts receivable. The $27 million interest equivalent represented payments accrued to holders of sold securitized receivables prior to August 22, 2001 (discussed in detail in the Notes to Consolidated Financial Statements under Accounts Receivable and Receivable-backed Securities on page 31).

Interest Expense

In 2003, interest expense was $559 million, $29 million lower than in 2002. The decrease was due to a lower average portfolio interest rate and a smaller loss on debt called or repurchased, partially offset by higher average debt outstanding. The average portfolio interest rate in 2003 was 4.9 percent compared with 5.6 percent in 2002. The $297 million of debt called or repurchased during 2003 resulted in a loss of $15 million (approximately $.01 per share) and had an average interest rate of 7.8 percent and an average remaining life of 20 years.

In 2002, interest expense was $588 million, $88 million higher than the total of interest expense and interest equivalent in 2001. The increase was due to higher average debt outstanding and a greater loss on the early call or repurchase of debt, partially offset by a lower average portfolio interest rate. The average portfolio interest rate in 2002 was 5.6 percent compared with 6.4 percent in 2001. (For analytical purposes, the amounts that represented payments accrued to holders of sold securitized receivables prior to August 22, 2001 were considered interest equivalent as discussed in the Notes to Consolidated Financial Statements on page 31. After that date, such payments constituted interest expense.) In 2002 and 2001, we incurred losses of $34 million ($.02 per share) and $9 million (less than $.01 per share) from the early call or repurchase of $266 million and $144 million of debt, respectively. The debt called or repurchased had an average interest rate of 8.8 percent and 9.2 percent, respectively, and had an average remaining life of 19 years and 7 years, respectively.

We adopted SFAS No. 145, "Rescission of FASB Statements No. 4, 44 and 64, Amendment of FASB Statement No. 13 and Technical Corrections" in the first quarter of 2002. Under SFAS No. 145, gains and losses from the early extinguishment of debt are required to be included in interest expense and are not reflected as an extraordinary item. Prior year extraordinary items have been reclassified to reflect this change. The adoption of SFAS No. 145 had no impact on net earnings, cash flows or financial position. The requirements of SFAS No. 145 are discussed under New Accounting Pronouncements on page 25.

Excluding the effect of any early call or repurchase of debt, we expect interest expense in 2004 to remain essentially flat to 2003, as average debt outstanding and the average portfolio interest rate are not expected to change significantly.

Credit Card Operations

Through our proprietary store-brand credit card programs, some of which have been available for decades, and our Target Visa credit card that was introduced nationally in 2001, we offer credit to qualified guests in each of our business segments. Our credit card programs strategically support our core retail operations and are an integral component of each business segment. Our credit card products support earnings growth by driving sales at our stores and through improvements in our credit card financial performance.

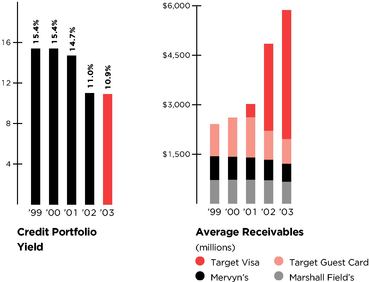

Our credit card revenues are primarily derived from finance charges, late fees and other revenues. Intracompany merchant fees are fees charged to our retail operations on a basis similar to fees charged by third-party credit card issuers. These fees are eliminated in consolidation. Third-party merchant fees are paid to us by merchants that have accepted the Target Visa credit card. In 2003, our credit card revenues increased to $1,479 million from $1,297 million, or 14 percent, due to continued growth in the Target Visa credit card portfolio. In 2002, our credit card revenues increased to $1,297 million from $899 million, or 44 percent, due primarily to additional revenues earned from the Target Visa credit card portfolio.

19

Credit card expenses include marketing and account service activities that support our credit card portfolio, as well as bad debt expense. In 2003, our credit card expense increased to $838 million from $765 million, or 9.6 percent, primarily due to growth in our bad debt expense commensurate with the growth in our accounts receivable. In 2002, our credit card expenses increased to $765 million from $454 million, or 69 percent, due to substantial growth in our accounts receivable resulting from the Target Visa portfolio.

In 2003, 2002 and 2001, allowance for doubtful accounts as a percent of year-end receivables was 6.8 percent, 6.7 percent and 6.4 percent, respectively. The increase in 2003 and 2002 was primarily due to higher accounts receivable balances and increases in the incidence and severity of personal bankruptcies, among other factors.

We expect our 2004 credit operations to grow at a more modest rate than the substantial growth we experienced in 2003 and 2002. Our pre-tax credit card contribution as a percent of total average receivables is expected to continue to be in the range of 10 to 11 percent in 2004.

Credit Card Contribution to Segment Profit

| | 2003

| | 2002

| | 2001

| |

|---|

| | (millions)

| |

|---|

| Revenues: | | | | | | | | | | |

| Finance charges, late fees and other revenues | | $ | 1,300 | | $ | 1,126 | | $ | 779 | |

| Merchant fees | | | | | | | | | | |

| | Intracompany | | | 97 | | | 102 | | | 102 | |

| | Third-party | | | 82 | | | 69 | | | 18 | |

| | |

| |

| |

| |

| | Total revenues | | | 1,479 | | | 1,297 | | | 899 | |

| | |

| |

| |

| |

| Expenses: | | | | | | | | | | |

| Bad debt provision | | | 532 | | | 460 | | | 230 | |

| Operations and marketing | | | 306 | | | 305 | | | 224 | |

| | |

| |

| |

| |

| | Total expenses | | | 838 | | | 765 | | | 454 | |

| | |

| |

| |

| |

| Pre-tax credit card contribution | | $ | 641 | | $ | 532 | | $ | 445 | |

| | |

| |

| |

| |

| As a percent of total average receivables | | | 10.9 | % | | 11.0 | % | | 14.7 | % |

| | |

| |

| |

| |

Receivables

| | 2003

| | 2002

| | 2001

| |

|---|

| | (millions)

| |

|---|

| Target | | | | | | | | | | |

| | Target Visa | | $ | 4,190 | | $ | 3,774 | | $ | 1,567 | |

| | Proprietary card | | | 783 | | | 827 | | | 1,063 | |

| Mervyn's proprietary card | | | 550 | | | 626 | | | 706 | |

| Marshall Field's proprietary card | | | 672 | | | 737 | | | 756 | |

| | |

| |

| |

| |

| Total year-end receivables | | $ | 6,195 | | $ | 5,964 | | $ | 4,092 | |

| | |

| |

| |

| |

| Past Due | | | | | | | | | | |

| Accounts with three or more payments past due as a percent of total year-end receivables: | | | | | | | | | | |

| Target Visa | | | 3.6 | % | | 3.1 | % | | 0.5 | % |

| Proprietary cards | | | 4.7 | % | | 5.1 | % | | 4.9 | % |

| | |

| |

| |

| |

| Total past due | | | 4.0 | % | | 3.8 | % | | 3.2 | % |

| | |

| |

| |

| |

Allowance for Doubtful Accounts

| | 2003

| | 2002

| | 2001

| |

|---|

| | (millions)

| |

|---|

| Allowance at beginning of year | | $ | 399 | | $ | 261 | | $ | 211 | |

| Bad debt provision | | | 532 | | | 460 | | | 230 | |

| Net write-offs | | | (512 | ) | | (322 | ) | | (180 | ) |

| | |

| |

| |

| |

| Allowance at end of year | | $ | 419 | | $ | 399 | | $ | 261 | |

| As a percent of year-end receivables | | | 6.8 | % | | 6.7 | % | | 6.4 | % |

| | |

| |

| |

| |

Other Credit Card Contribution Information*

| | 2003

| | 2002

| |

|---|

| | (millions)

| |

|---|

| Total Revenues | | | | | | | |

| | Target Visa | | $ | 857 | | $ | 626 | |

| | Proprietary cards | | $ | 622 | | $ | 671 | |

| | |

| |

| |

| Total revenues as a percent of average receivables: | | | | | | | |

| | Target Visa | | | 21.9 | % | | 23.8 | % |

| | Proprietary cards | | | 31.7 | % | | 30.4 | % |

| | |

| |

| |

| Net Write-offs | | | | | | | |

| | Target Visa | | $ | 359 | | $ | 151 | |

| | Proprietary cards | | $ | 153 | | $ | 171 | |

| | |

| |

| |

| Net write-offs as a percent of average receivables: | | | | | | | |

| | Target Visa | | | 9.2 | % | | 5.8 | % |

| | Proprietary cards | | | 7.8 | % | | 7.7 | % |

| | |

| |

| |

| Average Receivables | | | | | | | |

| | Target Visa | | $ | 3,907 | | $ | 2,635 | |

| | Proprietary cards | | | 1,960 | | | 2,206 | |

| | |

| |

| |

| Total average receivables | | $ | 5,867 | | $ | 4,841 | |

| | |

| |

| |

- *

- The Target Visa credit card does not reflect a full year of activity in 2001 and has been excluded due to lack of comparability.

Fourth Quarter Results

Due to the seasonal nature of our business, fourth quarter operating results typically represent a substantially larger share of total year revenues and earnings due to the inclusion of the holiday shopping season.

Fourth quarter 2003 net earnings were $832 million, compared with $688 million in 2002. Earnings per share were $.91 for the quarter, compared with $.75 in 2002. Total revenues increased 10.7 percent and 13-week comparable-store sales increased 4.9 percent. Our pre-tax segment profit increased 17.3 percent to $1,513 million, primarily driven by growth at Target.

20

Fourth Quarter Pre-tax Segment Profit and Percent Change from Prior Year

| | 2003

| | 2002

| | 2001

| |

|---|

| | (millions)

| |

|---|

| Target | | $ | 1,380 | | 18.5 | % | $ | 1,165 | | 8.0 | % | $ | 1,078 | | 20.9 | % |

| Mervyn's | | | 74 | | (0.3 | ) | | 75 | | (42.9 | ) | | 131 | | 20.8 | |

| Marshall Field's | | | 59 | | 15.6 | | | 51 | | (18.9 | ) | | 63 | | (20.2 | ) |

| | |

| |

| |

| |

| |

| |

| |

| Total | | $ | 1,513 | | 17.3 | % | $ | 1,291 | | 1.4 | % | $ | 1,272 | | 17.9 | % |

| | |

| |

| |

| |

| |

| |

| |

| LIFO provision | | | 27 | | | | | 12 | | | | | (8 | ) | | |

| Interest expense | | | (130 | ) | | | | (154 | ) | | | | (135 | ) | | |

| Other | | | (72 | ) | | | | (36 | ) | | | | (68 | ) | | |

| | |

| | | |

| | | |

| | | |

| Earnings before taxes | | $ | 1,338 | | | | $ | 1,113 | | | | $ | 1,061 | | | |

| | |

| | | |

| | | |

| | | |

Critical Accounting Estimates

Our analysis of operations and financial condition are based upon our consolidated financial statements, which have been prepared in accordance with GAAP. The preparation of these financial statements requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements, the reported amounts of revenues and expenses during the reporting period and the related disclosures of contingent assets and liabilities. In the Notes to Consolidated Financial Statements, we describe our significant accounting policies used in the preparation of the consolidated financial statements. We evaluate our estimates on an ongoing basis. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances. Actual results could differ from these estimates under different assumptions or conditions.

The following items in our consolidated financial statements require significant estimation or judgment:

Inventory and cost of sales We account for substantially all of our inventory and the related cost of sales under the retail inventory method using the LIFO basis. Under the retail inventory method, inventory is stated at cost, which is determined by applying a cost-to-retail ratio to each similar merchandise grouping's ending retail value. Since this inventory value is adjusted regularly to reflect market conditions, our inventory methodology reflects the lower of cost or market. We also reduce inventory for estimated losses related to shortage, based upon historical losses verified by prior physical inventory counts. Inventory also includes a LIFO provision that is calculated based on inventory levels, markup rates and internally generated retail price indices. Inventory is at risk of obsolescence if economic conditions change, such as shifting consumer demand, changing consumer credit markets, or increased competition, even though substantially all of our inventory sells in less than six months. Our vendor income and inventory are described in the Notes to Consolidated Financial Statements on pages 30 and 31, respectively.

Allowance for doubtful accounts When receivables are recorded, an allowance for doubtful accounts in an amount equal to anticipated future write-offs is recognized. The allowance includes provisions for uncollectible finance charges and other credit fees. We estimate future write-offs based on delinquencies, risk scores, aging trends, industry risk trends and our historical experience. The allowance for doubtful accounts was $419 million or 6.8 percent of year-end receivables at January 31, 2004, compared to $399 million or 6.7 percent of year-end receivables at February 1, 2003. Management believes that the allowance for doubtful accounts is adequate to cover anticipated losses in our credit card accounts receivable under current conditions; however, significant deterioration in any of the factors mentioned above or in general economic conditions could materially change these expectations. Our accounts receivable and related allowance are described in the Notes to Consolidated Financial Statements on page 31.

Pension and postretirement health care accounting We fund and maintain three qualified defined benefit pension plans and maintain certain related non-qualified plans as well. Our pension costs are determined based on actuarial calculations using key assumptions including our expected long-term rate of return on qualified plan assets, discount rate and our estimate of future compensation increases. We also maintain a postretirement health care plan for certain retired employees. Postretirement health care costs are calculated based on actuarial calculations using key assumptions including a discount rate and health care cost trend rates. Our pension and postretirement health care benefits are further described in the Notes to Consolidated Financial Statements on pages 36-37.

Insurance/self-insurance We retain a portion of the risk related to certain general liability, workers' compensation, property loss and employee medical and dental claims. Liabilities associated with these losses are calculated for claims filed, and claims incurred but not yet reported, at our estimate of their ultimate cost, based upon analysis of historical data and actuarial estimates. General liability and workers' compensation liabilities are recorded at our estimate of their net present value; other liabilities are not discounted. Our expected loss accruals are based on estimates, and while we believe the amounts accrued are adequate, the ultimate loss may differ from the amounts provided. We maintain stop-loss coverage to limit the exposure related to certain risks.

Income taxes We pay income taxes based on the tax statutes, regulations and case law of the various jurisdictions in which we operate. Our effective income tax rate was 37.8 percent, 38.2 percent and 38.0 percent in 2003, 2002 and 2001, respectively. The income tax provision includes estimates for certain unresolved matters in dispute with state and federal tax authorities. Management believes the resolution of such disputes will not have a material impact on our financial statements. Our effective income tax rate in 2004 is expected to be approximately 37.8 percent. Our income taxes are further described in the Notes to Consolidated Financial Statements on page 34.

21

Analysis of Financial Condition

Liquidity and Capital Resources

Our financial condition remains strong. In assessing our financial condition, management considers factors such as cash flows provided by operations, capital expenditures and debt service obligations. Cash flow provided by operations increased to $3.2 billion in 2003 from $1.6 billion in 2002, primarily due to a smaller increase in our gross accounts receivable balance and a higher net income.

During 2003, our total gross year-end receivables increased 3.9 percent, or $231 million, to $6,195 million. The growth in year-end receivables was driven by modest growth in issuance and usage of the Target Visa credit card during 2003. Average total receivables in 2003 increased 21 percent reflecting the substantial growth of the Target Visa credit card portfolio throughout 2002.

During 2003, inventory levels increased $583 million, or 12.2 percent. This growth was more than fully funded by the $764 million increase in accounts payable over the same period. The increase in inventory was primarily a result of our store square footage growth.

In January 1999 and March 2000, our Board of Directors authorized the aggregate repurchase of $2 billion of our common stock. Since that time, we have repurchased a total of 42 million shares of our common stock at a total cost of $1,247 million ($29.39 per share), net of the premium from exercised and expired put options. In 2001, common stock repurchases were essentially suspended. Consequently, common stock repurchases did not have a material impact on our 2003 or 2002 net earnings and financial position.

Our financing strategy is to ensure liquidity and access to capital markets, to manage the amount of floating-rate debt and to maintain a balanced spectrum of debt maturities. Within these parameters, we seek to minimize our cost of borrowing.

A key to our access to liquidity and capital markets is maintaining strong investment-grade debt ratings.

Credit Ratings

| | Moody's

| | Standard and Poor's

| | Fitch

|

|---|

| Long-term debt | | A2 | | A+ | | A |

| Commercial paper | | P-1 | | A-1 | | F1 |

| Securitized receivables | | Aaa | | AAA | | n/a |

Interest Coverage Ratio

We view interest coverage as an important indicator of our creditworthiness.

Interest coverage ratio represents the ratio of pre-tax earnings before fixed charges to fixed charges (interest expense and the interest portion of rent expense). Our interest coverage ratio was 5.5x, 4.9x and 4.7x in 2003, 2002 and 2001, respectively.

Further liquidity is provided by $1.6 billion of committed lines of credit obtained through a group of 26 banks. Of these credit lines, an $800 million credit facility expires in June 2004 but includes a one-year term-out option to June 2005. The remaining $800 million credit facility expires in June 2008. There were no balances outstanding at any time during 2003 or 2002 under these agreements. These committed credit lines as well as most of our long-term debt obligations contain certain financial covenants. We are, and expect to remain, well within the compliance requirements of these covenants. No material debt instrument contains provisions requiring acceleration of payment upon a debt rating downgrade.

Management believes that cash flows from operations, proceeds from long-term financing activities and issuance of short-term debt will be sufficient to fund any seasonal buildup in inventories and meet other cash requirements, including the refinancing of existing long-term debt, growth in receivables and projected capital expenditures.

Capital Expenditures

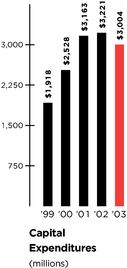

Capital expenditures were $3,004 million in 2003, compared with $3,221 million in 2002 and $3,163 million in 2001. Our modestly lower spending level in 2003 is due to a larger mix of leased stores and our ability to accomplish our expansion plans with less capital. Investment in Target accounted for 90 percent of capital expenditures in 2003 and 92 percent of capital expenditures in both 2002 and 2001. Net property and equipment increased $1,662 million in 2003, compared with an increase of $1,774 million in 2002. Over the past five years, Target's net retail square footage has grown at a compound annual rate of 10 percent, at the higher end of our objective of 8 to 10 percent in new net growth annually.

Approximately 74 percent and 66 percent of total capital expenditures in 2003 and 2002, respectively, were for new stores, expansions and remodels. Other capital investments were for information system hardware and software, distribution capacity and other infrastructure to support store growth, primarily at Target.

22

Number of Stores

| | February 1,

2003

| | Opened

| | Closed

| | January 31,

2004

|

|---|

| Target* | | 1,147 | | 101 | | 23 | | 1,225 |

| Mervyn's | | 264 | | 3 | | 1 | | 266 |

| Marshall Field's | | 64 | | — | | 2 | | 62 |

| | |

| |

| |

| |

|

| Total | | 1,475 | | 104 | | 26 | | 1,553 |

| | |

| |

| |

| |

|

- *

- Target includes 118 and 94 SuperTargets at January 31, 2004 and February 1, 2003, respectively.

In 2004, we expect to invest $3.2 billion to $3.4 billion, mostly in new square footage for Target stores and the distribution infrastructure and systems to support this growth. Our estimated 2004 store opening program at Target reflects net square footage growth of approximately 8 to 9 percent, or 95 to 100 total new stores partially offset by closings and relocations. In addition, we expect to remodel approximately 70 stores in 2004.

Owned and Leased Store Locations

At year-end 2003, owned, leased and "combined" (generally an owned building on leased land) store locations by operating segment were as follows:

| | Owned

| | Leased

| | Combined

| | Total

|

|---|

| Target | | 987 | | 87 | | 151 | | 1,225 |

| Mervyn's | | 155 | | 62 | | 49 | | 266 |

| Marshall Field's | | 49 | | 11 | | 2 | | 62 |

| | |

| |

| |

| |

|

| Total | | 1,191 | | 160 | | 202 | | 1,553 |

| | |

| |

| |

| |

|

Commitments and Contingencies

At January 31, 2004, our debt, lease and royalty contractual obligations were as follows:

Payments Due by Period

Contractual Obligations

| | Total

| | Less than

1 Year

| | 1-3

Years

| | 3-5

Years

| | After 5

Years

|

|---|

| | (millions)

|

|---|

| Long-term debt* | | $ | 10,828 | | $ | 857 | | $ | 1,254 | | $ | 2,774 | | $ | 5,943 |

| Interest payments** | | | 6,062 | | | 587 | | | 1,103 | | | 912 | | | 3,460 |

| Capital lease obligations*** | | | 264 | | | 21 | | | 39 | | | 38 | | | 166 |

| Operating leases*** | | | 1,778 | | | 163 | | | 286 | | | 236 | | | 1,093 |

| Royalties | | | 80 | | | 42 | | | 38 | | | — | | | — |

| | |

| |

| |

| |

| |

|

| Contractual cash obligations | | $ | 19,012 | | $ | 1,670 | | $ | 2,720 | | $ | 3,960 | | $ | 10,662 |

| | |

| |

| |

| |

| |

|

- *

- Required principal payments only. Excludes SFAS No. 133, "Accounting for Derivative Instruments and Hedging Activities," fair market value adjustments recorded in long-term debt.

- **

- Includes payments on $1.5 billion of floating rate long-term debt secured by credit card receivables, of which $750 million matures in July 2004 and $750 million matures in 2007. These payments are calculated assuming rates of 1.25%, 2.25%, 3.25% and 4.25% for 2004, 2005, 2006 and 2007, respectively. Excludes payments received or made relating to interest rate swaps discussed on pages 33-34.

- ***

- Total contractual lease payments.

Commitments for the purchase, construction, lease or remodeling of real estate, facilities and equipment were approximately $545 million at year-end 2003.

Throughout the year, we enter into various commitments to purchase inventory. In addition to the accounts payable reflected in our Statements of Financial Position on page 27, we had commitments with various vendors for the purchase of inventory as of January 31, 2004. The previous table excludes these commitments because these purchase commitments are cancelable by their terms.

Legal Proceedings

We are exposed to claims and litigation arising out of the ordinary course of business and use various methods to resolve those matters in a manner that serves the best interest of our shareholders and other constituents. The dispute resolution methods that we use include vigorous litigation, when necessary, and alternatives such as settlement discussions, where appropriate, to reduce the costs of litigation. Our policy is to fully disclose pending lawsuits and other known claims that we expect may have a material impact on our results of operations or financial condition. After consulting with legal counsel, management does not believe that any currently identified claims or litigation meet this criterion.

Market Risk

Our exposure to market risk results primarily from fluctuations in interest rates on our debt obligations and from the effect of equity market returns on our non-qualified defined contribution plans. We hold derivative instruments primarily to manage our exposure to these risks and all derivative instruments are matched against specific debt obligations or other liabilities. There have been no material changes in the primary risk exposures or management of the risks since the prior year. Our debt and interest rate swap instruments outstanding at January 31, 2004, including applicable interest rates, are discussed in the Notes to Consolidated Financial Statements on pages 33-34.

The annualized effect of a one percentage point change in floating interest rates on our interest rate swap agreements and other floating rate debt obligations at January 31, 2004, would be to change interest expense by approximately $36 million. The annualized effect of a one percentage point change in equity market returns on our non-qualified defined contribution plans (inclusive of the effect of derivative instruments used to hedge or manage these exposures) would not be significant.

23

Performance Objectives

Shareholder Return

Our primary objective is to maximize shareholder value over time through a combination of share price appreciation and dividend income while maintaining a prudent and flexible capital structure. Our total annualized return to shareholders (including reinvested dividends) over the last five years averaged 4.2 percent, returning about $123 for each $100 invested in our stock at the beginning of this period. The peer group we refer to in the adjacent graph represents those companies included in the S&P 500 Retailing and S&P 500 Food and Drug Retailing Indices, and is the group we refer to in our proxy statement.

Measuring Value Creation

We measure value creation internally using a form of Economic Value Added (EVA), which we define as after-tax segment profit less a capital charge for all investment employed. The capital charge is an estimate of our after-tax cost of capital adjusted for the age of our stores, recognizing that mature stores inherently have higher returns than newly opened stores. We use a benchmark of 9 percent for the estimated after-tax cost of capital invested in our retail operations and a benchmark of 5 percent for capital invested in our credit card operations, as a result of its ability to support higher debt levels. We expect to continue to generate returns in excess of these benchmarks, thereby producing EVA.

EVA is used to evaluate our performance and to guide capital investment decisions. A significant portion of executive incentive compensation is tied to the achievement of targeted levels of annual EVA generation. We believe that managing our business with a focus on EVA helps achieve our objective of average annual earnings per share growth of 15 percent or more over time. Earnings per share has grown at a compound annual rate of 15 percent over the last five years.

New Accounting Pronouncements

2004 Adoptions

In January 2003, the Financial Accounting Standards Board issued Interpretation No. 46, "Consolidation of Variable Interest Entities, an interpretation of Accounting Research Bulletin No. 51" (FIN No. 46). FIN No. 46 will be effective no later than the end of the first reporting period that ends after March 15, 2004. FIN No. 46 requires the consolidation of entities in which an enterprise absorbs a majority of the entity's expected losses, receives a majority of the entity's expected residual returns, or both, as a result of ownership, contractual or other financial interest in the entity. Currently, entities are generally consolidated by an enterprise when it has a controlling financial interest through ownership of a majority voting interest in the entity. We do not expect the adoption of FIN No. 46 to have a material impact on our net earnings, cash flows or financial position.

2003 Adoptions

In the first quarter of 2003, we adopted EITF No. 02-16, "Accounting by a Customer (Including a Reseller) for Certain Consideration Received from a Vendor." Under the new guidance, cash consideration received from a vendor is presumed to be a reduction of the prices of the vendor's products or services and should be classified as a reduction in cost of sales. If the cash consideration is for assets or services delivered to the vendor, it should be characterized as revenue. If the cash consideration is a reimbursement of costs incurred to sell the vendor's products, it should be characterized as a reduction of that cost. This guidance had no material impact on sales, cash flows or financial position for any period, and had a slight negative impact on net earnings. Our accounting policy regarding vendor income is discussed in the Notes to Consolidated Financial Statements on page 30.

In the first quarter of 2003, we adopted SFAS No. 123, "Accounting for Stock-Based Compensation," in accordance with the prospective transition method prescribed in SFAS No. 148, "Accounting for Stock-Based Compensation—Transition and Disclosure." The fair value based method has been applied prospectively to awards granted subsequent to February 1, 2003 (the last day of our 2002 fiscal year). The adoption of this method increased compensation expense by less than $.01 per share in 2003. Our accounting policy regarding stock-based compensation is discussed in the Notes to Consolidated Financial Statements on page 30.

In the first quarter of 2003, we adopted SFAS No. 143, "Accounting for Asset Retirement Obligations." The adoption did not have an impact on current year or previously reported net earnings, cash flows or financial position.

In the first quarter of 2003, we adopted SFAS No. 146, "Accounting for Costs Associated with Exit or Disposal Activities." SFAS No. 146 requires that a liability for a cost associated with an exit or disposal activity be recognized when the liability is incurred

24

instead of recognizing the liability at the date of commitment to an exit plan as was previously allowed. The adoption of SFAS No. 146 did not have a material impact on current year or previously reported net earnings, cash flows or financial position.

In the second quarter of 2003, we adopted SFAS No. 149, "Amendment of Statement 133 on Derivative Instruments and Hedging Activities." SFAS No. 149 amends and clarifies accounting for derivative instruments, and is effective for contracts entered into or modified after June 30, 2003. The adoption of SFAS No. 149 had no material impact on current year or previously reported net earnings, cash flows or financial position.

In the third quarter of 2003, we adopted SFAS No. 150, "Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity." SFAS No. 150 clarifies the classification and measurement of certain financial instruments with characteristics of both liabilities and equity, and is effective for financial instruments entered into or modified after May 31, 2003, or otherwise for the first interim period beginning after June 15, 2003. The adoption of SFAS No. 150 had no material impact on current year or previously reported net earnings, cash flows or financial position.

In the fourth quarter of 2003, we adopted EITF's Issue No. 03-10 "Application of Issue 02-16 by Resellers to Sales Incentives Offered to Consumers by Manufacturers" (EITF No. 03-10) which amends EITF No. 02-16. According to the amended guidance, if certain criteria are met, consideration received by a reseller in the form of reimbursement from a vendor for honoring the vendor's sales incentives offered directly to consumers (i.e. manufacturer's coupons) should not be recorded as a reduction of the cost of the reseller's purchases from the vendor. The adoption of EITF No. 03-10 did not have a material impact on current year or previously reported net earnings, cash flows or financial position. Our accounting policy regarding vendor income is discussed in the Notes to Consolidated Financial Statements on page 30.

In the fourth quarter of 2003, we adopted SFAS No. 132(R), "Employers' Disclosures about Pensions and Other Postretirement Benefits—an amendment of FASB Statements No. 87, 88 and 106," which revises the annual and interim disclosure requirements about pension and other postretirement benefits.

2002 Adoptions

In the first quarter of 2002, we adopted SFAS No. 142, "Goodwill and Other Intangible Assets," which superseded Accounting Principles Board (APB) Opinion No. 17, "Intangible Assets." Under the new statement, goodwill and intangible assets that have indefinite useful lives are no longer amortized but rather reviewed at least annually for impairment, or more frequently if impairment indicators arise. In both 2003 and 2002, the adoption of this statement reduced annual amortization expense by approximately $10 million (less than $.01 per share). Our accounting policy regarding intangible assets is discussed in the Notes to Consolidated Financial Statements on page 32.

In the first quarter of 2002, we adopted SFAS No. 144, "Accounting for the Impairment or Disposal of Long-Lived Assets." The guidance requires companies to review long-lived assets when events or changes in circumstances indicate that the carrying value of the asset may not be recoverable. In both 2003 and 2002, impairment losses resulted in a financial statement impact of less than $.01 per share. Our accounting policy regarding impairment of long-lived assets is discussed in the Notes to Consolidated Financial Statements on page 32.

In the first quarter of 2002, we adopted SFAS No. 145, "Rescission of FASB Statements No. 4, 44 and 64, Amendment of FASB Statement No. 13, and Technical Corrections." Previously, all gains and losses from the early extinguishment of debt were required to be aggregated and classified as an extraordinary item in the Consolidated Results of Operations, net of the related tax effect. Under SFAS No. 145, gains and losses from the early extinguishment of debt are included in interest expense. Prior year extraordinary items have been reclassified to reflect this change. The adoption of SFAS No. 145 had no impact on net earnings, cash flows or financial position.

Forward-looking Statements

This Annual Report, including the preceding Management's Discussion and Analysis, contains forward-looking statements regarding our performance, liquidity and the adequacy of our capital resources. Those statements are based on our current assumptions and expectations and are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected. We caution that the forward-looking statements are qualified by the risks and challenges posed by increased competition (including the effects of competitor liquidation activities), shifting consumer demand, changing consumer credit markets, changing health care costs, changing capital markets and general economic conditions, hiring and retaining effective team members, sourcing merchandise from domestic and international vendors, investing in new business strategies, achieving our growth objectives, the review of strategic alternatives, the outbreak of war and other significant national and international events, and other risks and uncertainties. As a result, while we believe that there is a reasonable basis for the forward-looking statements, you should not place undue reliance on those statements. You are encouraged to review Exhibit (99)C attached to our Form 10-K Report for the year-ended January 31, 2004, which contains additional important factors that may cause actual results to differ materially from those projected in the forward-looking statements.

25

CONSOLIDATED RESULTS OF OPERATIONS

| | 2003

| | 2002

| | 2001

|

|---|

| | (millions, except per share data)

|

|---|

| Sales | | $ | 46,781 | | $ | 42,722 | | $ | 39,114 |

| Net credit card revenues | | | 1,382 | | | 1,195 | | | 712 |

| | |

| |

| |

|

| | Total revenues | | | 48,163 | | | 43,917 | | | 39,826 |

| | |

| |

| |

|

| Cost of sales | | | 31,790 | | | 29,260 | | | 27,143 |

| Selling, general and administrative expense | | | 10,696 | | | 9,416 | | | 8,461 |

| Credit card expense | | | 838 | | | 765 | | | 463 |

| Depreciation and amortization | | | 1,320 | | | 1,212 | | | 1,079 |

| Interest expense | | | 559 | | | 588 | | | 473 |

| | |

| |

| |

|

| Earnings before income taxes | | | 2,960 | | | 2,676 | | | 2,207 |

| Provision for income taxes | | | 1,119 | | | 1,022 | | | 839 |

| | |

| |

| |

|

| Net earnings | | $ | 1,841 | | $ | 1,654 | | $ | 1,368 |

| | |

| |

| |

|

| Basic earnings per share | | $ | 2.02 | | $ | 1.82 | | $ | 1.52 |

| | |

| |

| |

|

| Diluted earnings per share | | $ | 2.01 | | $ | 1.81 | | $ | 1.50 |

| | |

| |

| |

|

| Weighted average common shares outstanding: | | | | | | | | | |

| | Basic | | | 911.0 | | | 908.0 | | | 901.5 |

| | Diluted | | | 917.1 | | | 914.0 | | | 909.8 |

| | |

| |

| |

|

See Notes to Consolidated Financial Statements throughout pages 30-39.

26

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

| | January 31,

2004

| | February 1,

2003

| |

|---|

| | (millions)

| |

|---|

| Assets | | | | | | | |

| Cash and cash equivalents | | $ | 716 | | $ | 758 | |

| Accounts receivable, net | | | 5,776 | | | 5,565 | |

| Inventory | | | 5,343 | | | 4,760 | |

| Other | | | 1,093 | | | 852 | |

| | |

| |

| |

| | Total current assets | | | 12,928 | | | 11,935 | |

| Property and equipment | | | | | | | |

| | Land | | | 3,629 | | | 3,236 | |

| | Buildings and improvements | | | 13,091 | | | 11,527 | |

| | Fixtures and equipment | | | 5,432 | | | 4,983 | |

| | Construction-in-progress | | | 995 | | | 1,190 | |

| | Accumulated depreciation | | | (6,178 | ) | | (5,629 | ) |

| | |

| |

| |

| | Property and equipment, net | | | 16,969 | | | 15,307 | |

| Other | | | 1,495 | | | 1,361 | |

| | |

| |

| |

| Total assets | | $ | 31,392 | | $ | 28,603 | |

| | |

| |

| |

| Liabilities and shareholders' investment | | | | | | | |

| Accounts payable | | $ | 5,448 | | $ | 4,684 | |

| Accrued liabilities | | | 1,618 | | | 1,545 | |

| Income taxes payable | | | 382 | | | 319 | |

| Current portion of long-term debt and notes payable | | | 866 | | | 975 | |

| | |

| |

| |

| | Total current liabilities | | | 8,314 | | | 7,523 | |

| Long-term debt | | | 10,217 | | | 10,186 | |

| Deferred income taxes and other | | | 1,796 | | | 1,451 | |

| Shareholders' investment | | | | | | | |

| | Common stock* | | | 76 | | | 76 | |

| | Additional paid-in-capital | | | 1,341 | | | 1,256 | |

| | Retained earnings | | | 9,645 | | | 8,107 | |

| | Accumulated other comprehensive income | | | 3 | | | 4 | |

| | |

| |

| |

| | Total shareholders' investment | | | 11,065 | | | 9,443 | |

| | |

| |

| |

| Total liabilities and shareholders' investment | | $ | 31,392 | | $ | 28,603 | |

| | |

| |

| |

*Common Stock Authorized 6,000,000,000 shares, $.0833 par value; 911,808,051 shares issued and outstanding at January 31, 2004; 909,801,560 shares issued and outstanding at February 1, 2003.

Preferred Stock Authorized 5,000,000 shares, $.01 par value; no shares were issued or outstanding at January 31, 2004 or February 1, 2003.

See Notes to Consolidated Financial Statements throughout pages 30-39.

27

CONSOLIDATED STATEMENTS OF CASH FLOWS

| | 2003

| | 2002

| | 2001

| |

|---|

| | (millions)

| |

|---|

| Operating activities | | | | | | | | | | |

| Net earnings | | $ | 1,841 | | $ | 1,654 | | $ | 1,368 | |

| Reconciliation to cash flow: | | | | | | | | | | |

| | Depreciation and amortization | | | 1,320 | | | 1,212 | | | 1,079 | |

| | Bad debt provision | | | 532 | | | 460 | | | 230 | |

| | Deferred tax provision | | | 249 | | | 248 | | | 49 | |

| | Loss on disposal of fixed assets, net | | | 54 | | | 67 | | | 52 | |

| | Other non-cash items affecting earnings | | | 11 | | | 159 | | | 160 | |

| | Changes in operating accounts providing/(requiring) cash: | | | | | | | | | | |

| | | Accounts receivable | | | (744 | ) | | (2,194 | ) | | (1,193 | ) |

| | | Inventory | | | (583 | ) | | (311 | ) | | (201 | ) |

| | | Other current assets | | | (255 | ) | | 15 | | | (91 | ) |

| | | Other assets | | | (196 | ) | | (174 | ) | | (178 | ) |

| | | Accounts payable | | | 764 | | | 524 | | | 584 | |

| | | Accrued liabilities | | | 57 | | | (21 | ) | | 29 | |

| | | Income taxes payable | | | 91 | | | (79 | ) | | 124 | |

| | Other | | | 19 | | | 30 | | | — | |

| | |

| |

| |

| |

| | Cash flow provided by operations | | | 3,160 | | | 1,590 | | | 2,012 | |

| | |

| |

| |

| |

| Investing activities | | | | | | | | | | |

| | Expenditures for property and equipment | | | (3,004 | ) | | (3,221 | ) | | (3,163 | ) |

| | Increase in receivable-backed securities | | | — | | | — | | | (174 | ) |

| | Proceeds from disposals of property and equipment | | | 85 | | | 32 | | | 32 | |

| | Other | | | — | | | — | | | (5 | ) |

| | |

| |

| |

| |

| | Cash flow required for investing activities | | | (2,919 | ) | | (3,189 | ) | | (3,310 | ) |

| | |

| |

| |

| |

| Financing activities | | | | | | | | | | |

| | Decrease in notes payable, net | | | (100 | ) | | — | | | (808 | ) |

| | Additions to long-term debt | | | 1,200 | | | 3,153 | | | 3,250 | |

| | Reductions of long-term debt | | | (1,172 | ) | | (1,071 | ) | | (793 | ) |

| | Dividends paid | | | (237 | ) | | (218 | ) | | (203 | ) |

| | Repurchase of stock | | | — | | | (14 | ) | | (20 | ) |

| | Other | | | 26 | | | 8 | | | 15 | |

| | |

| |

| |

| |

| | Cash flow (required for)/provided by financing activities | | | (283 | ) | | 1,858 | | | 1,441 | |

| | |

| |

| |

| |

| Net (decrease)/increase in cash and cash equivalents | | | (42 | ) | | 259 | | | 143 | |

| Cash and cash equivalents at beginning of year | | | 758 | | | 499 | | | 356 | |

| | |

| |

| |

| |

| Cash and cash equivalents at end of year | | $ | 716 | | $ | 758 | | $ | 499 | |

| | |

| |

| |

| |

Amounts presented herein are on a cash basis and therefore may differ from those shown in other sections of this Annual Report. Cash paid for income taxes was $781 million, $853 million and $666 million during 2003, 2002 and 2001, respectively. Cash paid for interest (including interest capitalized) was $550 million, $526 million and $477 million during 2003, 2002 and 2001, respectively.

See Notes to Consolidated Financial Statements throughout pages 30-39.

28

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' INVESTMENT

| | Common

Stock

Shares

| | Common

Stock

| | Additional

Paid-in

Capital

| | Retained

Earnings

| | Accumulated

Other

Comprehensive

Income

| | Total

| |

|---|

| | (millions, except footnotes)

| |

|---|

| February 3, 2001 | | 897.8 | | $ | 75 | | $ | 902 | | $ | 5,542 | | $ | — | | $ | 6,519 | |

| Consolidated net earnings | | — | | | — | | | — | | | 1,368 | | | — | | | 1,368 | |

| Dividends declared | | — | | | — | | | — | | | (203 | ) | | — | | | (203 | ) |

| Repurchase of stock | | (.5 | ) | | — | | | — | | | (20 | ) | | — | | | (20 | ) |

| Issuance of stock for ESOP | | 2.6 | | | — | | | 89 | | | — | | | — | | | 89 | |

| Stock options and awards: | | | | | | | | | | | | | | | | | | |

| | Tax benefit | | — | | | — | | | 63 | | | — | | | — | | | 63 | |

| | Proceeds received, net | | 5.3 | | | — | | | 44 | | | — | | | — | | | 44 | |

| | |

| |

| |

| |

| |

| |

| |

| February 2, 2002 | | 905.2 | | | 75 | | | 1,098 | | | 6,687 | | | — | | | 7,860 | |

| Consolidated net earnings | | — | | | — | | | — | | | 1,654 | | | — | | | 1,654 | |

| Other comprehensive income | | — | | | — | | | — | | | — | | | 4 | | | 4 | |

| | | | | | | | | | | | | | | | |

| |

| Total comprehensive income | | | | | | | | | | | | | | | | | 1,658 | |

| Dividends declared | | — | | | — | | | — | | | (218 | ) | | — | | | (218 | ) |

| Repurchase of stock | | (.5 | ) | | — | | | — | | | (16 | ) | | — | | | (16 | ) |

| Issuance of stock for ESOP | | 3.0 | | | 1 | | | 105 | | | — | | | — | | | 106 | |

| Stock options and awards: | | | | | | | | | | | | | | | | | | |

| | Tax benefit | | — | | | — | | | 26 | | | — | | | — | | | 26 | |

| | Proceeds received, net | | 2.1 | | | — | | | 27 | | | — | | | — | | | 27 | |

| | |

| |

| |

| |

| |

| |

| |

| February 1, 2003 | | 909.8 | | | 76 | | | 1,256 | | | 8,107 | | | 4 | | | 9,443 | |

| Consolidated net earnings | | — | | | — | | | — | | | 1,841 | | | — | | | 1,841 | |

| Other comprehensive income | | — | | | — | | | — | | | — | | | (1 | ) | | (1 | ) |

| | | | | | | | | | | | | | | | |

| |

| Total comprehensive income | | | | | | | | | | | | | | | | | 1,840 | |

| Dividends declared | | — | | | — | | | — | | | (246 | ) | | — | | | (246 | ) |

| Repurchase of stock | | (1.5 | ) | | — | | | — | | | (57 | ) | | — | | | (57 | ) |

| Issuance of stock for ESOP | | 0.6 | | | — | | | 17 | | | — | | | — | | | 17 | |

| Stock options and awards: | | | | | | | | | | | | | | | | | | |

| | Tax benefit | | — | | | — | | | 28 | | | — | | | — | | | 28 | |

| | Proceeds received, net | | 2.9 | | | — | | | 40 | | | — | | | — | | | 40 | |

| | |

| |

| |

| |

| |

| |

| |

| January 31, 2004 | | 911.8 | | $ | 76 | | $ | 1,341 | | $ | 9,645 | | $ | 3 | | $ | 11,065 | |

| | |

| |

| |

| |

| |

| |

| |

Common Stock Authorized 6,000,000,000 shares, $.0833 par value; 911,808,051 shares issued and outstanding at January 31, 2004; 909,801,560 shares issued and outstanding at February 1, 2003; 905,164,702 shares issued and outstanding at February 2, 2002.

In January 1999 and March 2000, our Board of Directors authorized the aggregate repurchase of $2 billion of our common stock. In 2001, common stock repurchases under our program were essentially suspended. Our common stock repurchases are recorded net of the premium received from put options. Repurchases are made primarily in open market transactions, subject to market conditions.

Our common stock repurchase program has included the sale of put options that entitle the holder to sell shares of our common stock to us, at a specified price, if the holder exercises the option. No put options were sold during or were outstanding at the end of 2003, 2002 or 2001.

Preferred Stock Authorized 5,000,000 shares, $.01 par value; no shares were issued or outstanding at January 31, 2004, February 1, 2003 or February 2, 2002.

Junior Preferred Stock Rights In 2001, we declared a distribution of preferred share purchase rights. Terms of the plan provide for a distribution of one preferred share purchase right for each outstanding share of our common stock. Each right will entitle shareholders to buy one twelve-hundredth of a share of a new series of junior participating preferred stock at an exercise price of $125.00, subject to adjustment. The rights will be exercisable only if a person or group acquires ownership of 20 percent or more of our common stock or announces a tender offer to acquire 30 percent or more of our common stock.

Dividends Dividends declared per share were $0.27, $0.24 and $0.225 in 2003, 2002 and 2001, respectively.

See Notes to Consolidated Financial Statements throughout pages 30-39.

29

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Summary of Accounting Policies

Organization Target Corporation (the Corporation) is a general merchandise retailer, comprised of three operating segments: Target, Mervyn's and Marshall Field's. Our segments are primarily determined by the nature of the products and services offered to our guests. Target, an upscale discount chain located in 47 states, contributed 86 percent of our 2003 total revenues. Mervyn's, a middle-market promotional department store located in 14 states in the West, South and Midwest, contributed 7 percent of total revenues. Marshall Field's (including stores formerly named Dayton's and Hudson's), a traditional department store located in 8 states in the upper Midwest, contributed 5 percent of total revenues. Management measures segment performance based on pre-tax segment profit, which includes credit card operations. Credit card operations drive revenue growth at each segment and are considered an integral component of our retail operations. Business segment comparisons are presented on page 38.

Consolidation The financial statements include the balances of the Corporation and its subsidiaries after elimination of material intercompany balances and transactions. All material subsidiaries are wholly owned.

Use of Estimates The preparation of our financial statements, in conformity with accounting principles generally accepted in the United States (GAAP), requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. Actual results may differ from those estimates.

Fiscal Year Our fiscal year ends on the Saturday nearest January 31. Unless otherwise stated, references to years in this report relate to fiscal years rather than to calendar years. Fiscal years 2003, 2002 and 2001 each consisted of 52 weeks.

Reclassifications Certain prior year amounts have been reclassified to conform to the current year presentation.

Stock-based Compensation In 2003, we adopted Statement of Financial Accounting Standards (SFAS) No. 123, "Accounting for Stock-Based Compensation," in accordance with the prospective transition method prescribed in SFAS No. 148, "Accounting for Stock-Based Compensation—Transition and Disclosure" and began recognizing compensation expense for stock options granted during the year. Compensation expense is reflected in selling, general and administrative expenses. Prior to 2003, we accounted for stock option awards under the intrinsic value method prescribed in Accounting Principles Board (APB) No. 25, "Accounting for Stock Issued to Employees" which resulted in no compensation expense because the exercise price of the stock options was equal to the fair market value of the underlying stock on the grant date. The pro forma impact of accounting for those awards at fair value is disclosed on page 35.

Revenues

Revenue from retail sales is recognized at the time of sale. Commissions earned on sales generated by leased departments are included within sales and were $38 million in 2003, $33 million in 2002 and $37 million in 2001. Net credit card revenues are comprised of finance charges and late fees from credit card holders, as well as third-party merchant fees earned from the use of our Target Visa credit card. Net credit card revenues are recognized according to the contractual provisions of each applicable credit card agreement. If an account is written-off, any uncollected finance charges or late fees are recorded as a reduction of credit card revenue. The amount of our retail sales charged to our credit cards was $5.3 billion, $5.4 billion and $5.6 billion in 2003, 2002 and 2001, respectively. Prior to August 22, 2001, net credit card revenues are net of the payments made to holders of publicly held receivable-backed securities.

Consideration Received from Vendors

We collect vendor income primarily as a result of our promotional, advertising and compliance programs. Promotional and advertising allowances are intended to offset our costs of promoting and selling the vendor's merchandise in our stores and are recognized when we incur the cost or complete the promotion. Under our compliance programs, vendors are charged for merchandise shipments that do not meet our requirements, such as late or incomplete shipments, and we record these allowances when the violation occurs. Vendor income either reduces our inventory costs or our operating expenses based on the requirements of Emerging Issues Task Force (EITF) Issue No. 02-16, "Accounting by a Customer (Including a Reseller) for Certain Consideration Received from a Vendor" as discussed below.

In the first quarter of 2003, we adopted EITF No. 02-16. In accordance with EITF No. 02-16, certain vendor income items have been reclassified from operating expenses to inventory purchases and recognized into income as the vendors' merchandise is sold. The guidance was applied on a prospective basis only as required by EITF No. 02-16. This reclassification had no material impact on sales, cash flows or financial position for any period, and had a slight negative impact on net earnings.

In the fourth quarter of 2003, we adopted EITF No. 03-10, "Application of Issue 02-16 by Resellers to Sales Incentives Offered to Consumers by Manufacturers," which amends EITF No. 02-16. The adoption of EITF No. 03-10 did not have a material impact on net earnings, cash flows or financial position. The requirements of EITF No. 02-16 and EITF No. 03-10 are discussed in Management's Discussion and Analysis on pages 24-25.

Buying and Occupancy Expenses

Buying expenses primarily consist of salaries and expenses incurred by the Corporation's merchandising operations, while our occupancy expenses primarily consist of rent, depreciation, property taxes and other operating costs of our retail and distribution facilities. Buying and occupancy expenses classified in selling, general and administrative expenses were $1.5 billion, $1.4 billion and $1.2 billion in 2003, 2002 and 2001, respectively. In addition, we recorded $1 billion, $934 million and $814 million of depreciation expense for our retail and distribution facilities in 2003, 2002 and 2001, respectively.

30

Advertising Costs

Advertising costs, included in selling, general and administrative expense, are expensed as incurred and were $1,249 million, $962 million and $924 million for 2003, 2002 and 2001, respectively. Advertising vendor income recorded within advertising expense was approximately $78 million, $251 million and $231 million for 2003, 2002 and 2001, respectively.

Earnings per Share

Basic earnings per share (EPS) is net earnings divided by the average number of common shares outstanding during the period. Diluted EPS includes the incremental shares that are assumed to be issued on the exercise of stock options. Shares issuable upon exercise of approximately 4.5 million options outstanding at January 31, 2004 were not included in the dilutive earnings per share calculation because the effect would have been antidilutive. At February 1, 2003, 13.2 million shares were excluded from the dilutive earnings per share calculation. No such shares were excluded from the dilutive earnings per share calculation at February 2, 2002.

| | Basic EPS

| | Diluted EPS

|

|---|

| | 2003

| | 2002

| | 2001

| | 2003

| | 2002

| | 2001

|

|---|

| | (millions, except per share data)

|

|---|

| Net earnings | | $ | 1,841 | | $ | 1,654 | | $ | 1,368 | | $ | 1,841 | | $ | 1,654 | | $ | 1,368 |

| Basic weighted average common shares outstanding | | | 911.0 | | | 908.0 | | | 901.5 | | | 911.0 | | | 908.0 | | | 901.5 |

| Stock options | | | — | | | — | | | — | | | 6.1 | | | 6.0 | | | 8.3 |

| | |

| |

| |

| |

| |

| |

|

| Weighted average common shares outstanding | | | 911.0 | | | 908.0 | | | 901.5 | | | 917.1 | | | 914.0 | | | 909.8 |

| | |

| |

| |

| |

| |

| |

|

| Earnings per share | | $ | 2.02 | | $ | 1.82 | | $ | 1.52 | | $ | 2.01 | | $ | 1.81 | | $ | 1.50 |

| | |

| |

| |

| |

| |

| |

|

Other Comprehensive Income

Other comprehensive income includes revenues, expenses, gains and losses that are excluded from net earnings under GAAP. In 2003 and 2002, it primarily included gains and losses on certain hedge transactions and the change in our minimum pension liability, net of related taxes.

Cash Equivalents

Cash equivalents represent short-term investments with a maturity of three months or less from the time of purchase and were $244 million, $357 million and $84 million in 2003, 2002 and 2001, respectively.

Accounts Receivable and Receivable-backed Securities

Accounts receivable is recorded net of an allowance for expected losses. The allowance, recognized in an amount equal to the anticipated future write-offs based on delinquencies, risk scores, aging trends, industry risk trends and our historical experience, was $419 million at January 31, 2004 and $399 million at February 1, 2003.

Through our special purpose subsidiary, Target Receivables Corporation (TRC), we transfer, on an ongoing basis, substantially all of our receivables to the Target Credit Card Master Trust (the Trust) in return for certificates representing undivided interests in the Trust's assets. TRC owns the undivided interest in the Trust's assets, other than the Trust's assets securing the financing transactions entered into by the Trust and the 2 percent of Trust assets held by Retailers National Bank (RNB). RNB is a wholly owned subsidiary of the Corporation that also services receivables. The Trust assets and the related income and expenses are reflected in each operating segment's assets and operating results based on the origin of the credit card giving rise to the receivable.

Concurrent with our August 22, 2001 issuance of receivable-backed securities from the Trust, SFAS No. 140 (which replaced SFAS No. 125, "Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities," in its entirety) became the accounting guidance applicable to such transactions. While this accounting requires secured financing treatment of the securities issued by the Trust on our consolidated financial statements, the assets within the Trust are still considered sold to our wholly owned, bankruptcy remote subsidiary, TRC, and are not available to general creditors of the Corporation.

Beginning on August 22, 2001, our consolidated financial statements reflected the obligation to holders of previously sold receivable-backed securities as debt of TRC and the receivables at fair value in place of the previously recorded retained interests related to the sold securities. This resulted in a pre-tax charge of $67 million ($.05 per share). On August 22, 2001, the Trust's entire portfolio of receivables was reflected on our consolidated financial statements at its fair value, which was based upon the expected performance of the underlying receivables portfolio. At that point in time, fair value was equivalent in amount to face value, net of an appropriate allowance.

Prior to August 22, 2001, income on the receivable-backed securities was accrued based on the effective interest rate applied to its cost basis, adjusted for accrued interest and principal paydowns. We monitored impairment of receivable-backed securities based on fair value. Permanent impairments were charged to earnings through credit expense in the period in which it was determined that the receivable-backed securities' carrying value was greater than their fair value. Permanent impairment charges on the receivables underlying the receivable-backed securities portfolio were $89 million in 2001. Permanent impairment charges in 2001 include only those losses prior to the consolidation of our special purpose entity on August 22, 2001.

Inventory

Substantially all of our inventory and the related cost of sales is accounted for under the retail inventory accounting method using the last-in, first-out (LIFO) basis. Inventory is stated at the lower of LIFO cost or market. The cumulative LIFO provision was $25 million and $52 million at year-end 2003 and 2002, respectively.

Inventory

| | January 31,

2004

| | February 1,

2003

|

|---|

| | (millions)

|

|---|

| Target | | $ | 4,282 | | $ | 3,748 |

| Mervyn's | | | 486 | | | 486 |

| Marshall Field's | | | 326 | | | 324 |

| Other | | | 249 | | | 202 |

| | |

| |

|

| Total inventory | | $ | 5,343 | | $ | 4,760 |

| | |

| |

|

31

Property and Equipment

Property and equipment are recorded at cost, less accumulated depreciation. Depreciation is computed using the straight-line method over estimated useful lives. Depreciation expense for the years 2003, 2002 and 2001 was $1,286 million, $1,183 million and $1,049 million, respectively. Accelerated depreciation methods are generally used for income tax purposes. Repair and maintenance costs were $453 million, $416 million and $386 million in 2003, 2002 and 2001, respectively.

Estimated useful lives by major asset category are as follows:

Asset

| | Life (in years)

|

|---|

| Buildings and improvements | | 8 - 39 |

| Fixtures and equipment | | 4 - 15 |

| Computer hardware and software | | 4 |

We adopted SFAS No. 144, "Accounting for the Impairment or Disposal of Long-Lived Assets" in the first quarter of 2002. In accordance with this guidance, all long-lived assets are reviewed when events or changes in circumstances indicate that the carrying value of the asset may not be recoverable. The requirements of SFAS No. 144 are discussed in Management's Discussion and Analysis on page 25.