Exhibit 99.1

|

Board of Directors

500 Water Street, C160

Jacksonville, Florida 32202

November 16, 2007

Chris Hohn, Managing Partner

Snehal Amin, Partner

The Children’s Investment Master Fund

7 Clifford Street

London, England

Dear Mr. Hohn and Mr. Amin:

We are pleased to provide the response of the CSX Corporation Board of Directors to the correspondence from The Children’s Investment Master Fund dated October 16 and October 22, 2007.

Board Engagement: As background, this Board is very familiar with TCI’s views of the U.S. rail industry and of CSX. CSX and its representatives have been in regular communication with TCI throughout this year, and TCI’s proposals have been shared with, and thoroughly analyzed by the Board.

Throughout the year, CSX and its representatives have repeatedly made TCI aware that the Board has spent a great deal of time considering its views. In fact, those views have been considered during more than a dozen full Board and committee meetings to date in 2007. In July, the CSX Board formally invited TCI to submit its proposals for consideration and analysis.

Furthermore, there have also been dozens of telephone calls, e-mail exchanges and face-to-face meetings between CSX, and its advisors, and TCI since late 2006, and Mr. Amin had a private meeting with two members of the company’s senior management team in March.

CSX Quality: In any event, TCI’s recent letters and public statements express the view that there is a fundamental lack of quality in CSX’s business results, management and Board. The Board respectfully disagrees.

The measures of quality for a public company are well understood. For an operating company such as CSX, those measures generally are shareholder return, financial performance, balance sheet, safety, customer service and governance. By any of those measures, the Board believes that CSX is an excellent company, and the Board unanimously supports the company’s strategy and management.

Since the current management team undertook major restructuring initiatives in 2004, CSX shares have significantly outperformed all major North American railroads and the broader market. That performance reflects the improvement CSX has achieved over that period in every relevant area. Simply put, the Board believes this performance record demonstrates unequivocally that CSX is a well run company with continuously improving results.

-1-

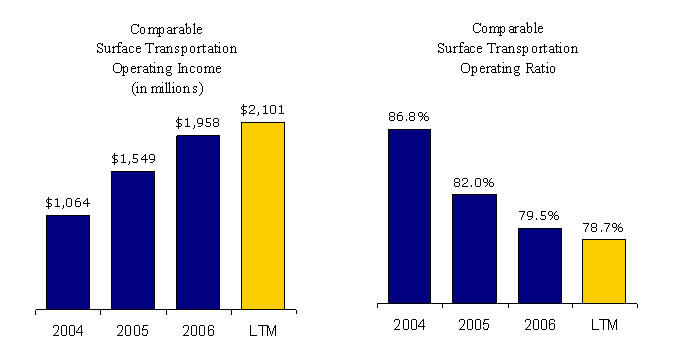

Exceptional Earnings and Shareholder Value Creation: Since 2004, CSX operating income has risen steadily as the management team implemented key restructuring initiatives. From 2004 through today, CSX operating income nearly doubled. At the same time, productivity and revenue improvement initiatives have lowered the CSX operating ratio to its best level in a decade.

Excludes provision for management restructuring and insurance recoveries

LTM – last twelve months through September 2007

As reflected in the company’s projections for EPS, operating income, operating ratio, and cash flow, which is among the most extensive guidance in the industry, CSX expects these positive trends to continue as it executes on its proven operating plan. Supporting these targets are plans for continued pricing above inflation, volume growth and productivity gains.

Furthermore, the Board is confident that CSX shareholders appreciate the value that CSX has created on the strength of its steadily increasing earnings. The value of CSX stock has increased nearly 150 percent in the past three years, providing shareholders with a return better than the rest of the North American rail industry and 89 percent of all S&P 500 companies.

-2-

Stock performance through Oct. 31, 2007

Class I Rails includes BNI, CNI, CP, NSC and UNP

CSX also continues to generate value for shareholders through a $3 billion share repurchase program. The program was announced early this year and is already more than halfway complete. Additionally, the quarterly dividend has tripled over the past two years. It is curious that TCI would reduce these important components of CSX shareholder value creation to a footnote in its letter, when the share buyback program is consistent with a position that TCI previously advanced.

In light of recent developments in the credit markets, the Board understands TCI’s apparent abandonment of its suggestion that CSX take on extraordinary debt to repurchase more shares and reduce the CSX credit rating to “junk” – a suggestion the Board prudently rejected at the time it was made.

In addition to this strong financial performance, safety and service levels at CSX are consistently improving. In 2004 CSX began implementing significant operational changes and publicly stated that the company would focus on improving two things: safety and on-time train originations. The record demonstrates that CSX has achieved precisely what it set out to do three years ago – dramatically improve both the safety of the railroad and the on-time performance for its customers.

Committed to Improving Safety: Although TCI did not discuss CSX safety advances in its letter, safety is and will continue to be a core value of the company, and CSX will continue to make the important investments in the network to support and maintain safety improvements.

-3-

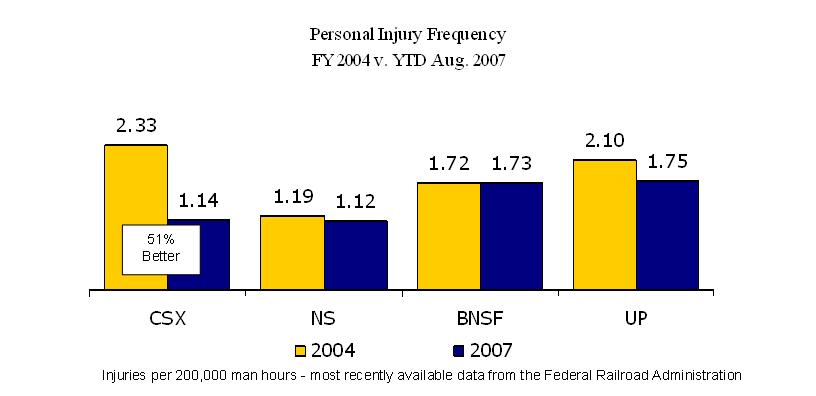

Since 2004, CSX has achieved a decrease in personal injuries of more than 50 percent, an industry leading improvement.

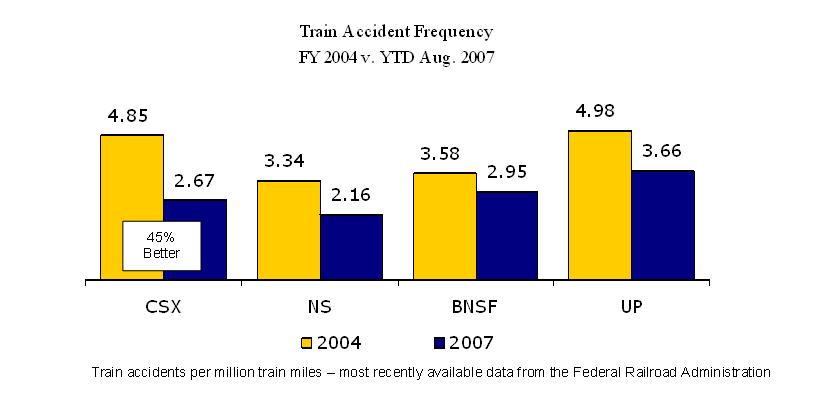

CSX has also reduced train accidents by 45 percent over the past three years and by 23 percent year-to-date, both industry leading improvements.

The safety of CSX employees, customers and communities is a top priority of the Board, and the company’s actions will continue to demonstrate the strength of that commitment.

-4-

Disciplined Operational and Customer Service Improvements: The Board believes that CSX operational and service performance has been outstanding under Michael Ward and the senior management team. In the past three years CSX has achieved substantial improvements in important operating metrics and is committed to making its operations even better.1

In addition to achieving industry-leading safety improvements, the company has improved its rate of both on-time originations and arrivals by nearly 30 percent since 2004. From the third quarter of 2004 through the third quarter of 2007, CSX improved its velocity more than any other U.S. railroad.

Data from the Association of American Railroads

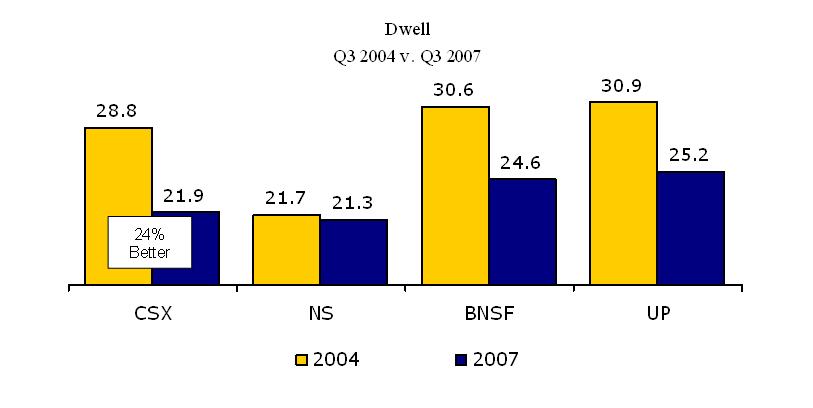

Similarly, CSX has shortened dwell time, another key operating metric, by 24 percent over the same period.

Data from the Association of American Railroads

The company’s operational improvement over the past three years shows that the existing operating plan is effective and will continue to advance the interests of CSX shareholders. The Board expects that the operating performance of CSX will continue to improve with the benefit of ongoing investments in capacity and productivity initiatives, and, in the Board’s view, it would be imprudent and counterproductive to reduce planned capital investment at this time.

Strong Corporate Governance: TCI’s statements that CSX does not practice good corporate governance are simply incorrect. CSX has an ISS ranking in the top 3 percent of transportation companies. This high governance ranking reflects the quality of corporate governance practices currently in place at CSX. These include, but are not limited to:

· Election of the entire board annually;

· Majority vote election of the board in uncontested elections;

· Majority vote (rather than supermajority as allowed by Virginia law) on major events impacting the shareholders such as charter amendments and mergers;

· No poison pill; and

· Cap for senior executive severance payments.

Highly Experienced, Engaged and Independent Board: TCI stated in its letter to CSX that “over half of the independent directors have been on the Board for over a decade.” In fact, as the most recent CSX proxy statement clearly shows, the majority of independent directors have been on the Board for less than six years. Moreover, the eleven independent directors of CSX have considerable public company experience and a wide range of views and backgrounds, encompassing, among other fields, the financial sector, railroad customers, insurance, manufacturing, government, transportation regulation, higher education and health care.

TCI also calls for CSX to split the roles of Chairperson of the Board and CEO. That proposition was put to a vote of CSX shareholders at the 2006 annual meeting, where it was rejected by a margin of roughly 109 million votes (nearly 5 votes against for every 1 vote in favor). Almost two-thirds of companies in the S&P 500 combine the two positions. CSX believes that an independent board and a presiding independent director, the prevailing practice in the United States, provides more meaningful oversight of management when combined with the strong counterbalancing governance structures in place at CSX. These governance structures include: established governance guidelines, independent presiding director with delineated duties, 11 out of 12 directors independent, and key Board committees comprised solely of independent directors.

Executive Compensation Directly Linked to Performance: At CSX, like every major American railroad, the independent members of the Board annually determine the compensation of management based on the recommendation of the Compensation Committee. The Board relies on advice from an independent consultant who reports directly to the fully-independent Compensation Committee. Contrary to TCI’s suggestion, 100 percent of CSX’s short and long term incentive compensation for CSX executives is tied to company performance that drives shareholder value. We believe CSX is in a minority of companies that can make that statement.

-6-

The Compensation Committee and the Board selected operating ratio as the performance metric for the current long-term incentive compensation program based on an analysis of nearly 15 years of CSX stock performance. The analysis showed that operating ratio had a strong correlation to creation of shareholder value. Also, the Board believes that operating ratio provides a readily identifiable and understandable goal to focus performance for the company’s management employees with diverse responsibilities.

Focused and Strategic Capital Investment: Two important points must be made to correct TCI’s characterizations of CSX’s capital spending plan. First, the industry typically measures capital expenditures as a percentage of revenue, and CSX’s current capital expenditures are equivalent to those of other Class I railroads, which over the past five years have averaged from 15 to 17 percent of revenue. Second, CSX has consistently stated that important strategic decisions about investing in the rail network are dependent on the ability of railroads to earn adequate returns on investment. As Michael Ward stated in a hearing before the Surface Transportation Board (STB) in April of this year,

| It’s not a coincidence that our company’s record-setting infrastructure investments in 2006 and 2007 come at a time when we’re just beginning to approach revenue adequacy…That investment of course requires strong earnings, earnings that must remain strong both to make the necessary money and to justify reinvestment in the railroad business…Ill-considered calls to re-regulate the rail industry by whatever name are the greatest threat to the railroad industry’s ability to reach sustained revenue adequacy and to continue to reinvest into the future. |

CSX makes decisions about capital spending today that will have profound implications for the company and the nation’s critical transportation infrastructure for decades to come. In doing so, CSX carefully evaluates the return on investment that can be achieved from capital spending and the necessity of replacing long-lived railroad assets. Like the rest of the industry, the company’s investments in new equipment and technology to improve asset utilization, train handling and fuel efficiency are critical to providing sustainable profits and enhanced customer service.

The important investment decisions that CSX has made in the past several years have been integral to the safety and operational improvements that help drive shareholder returns. CSX will not compromise safety, service and efficiency by arbitrarily restricting investment as TCI suggests. The Board fully supports the disciplined infrastructure investment decisions that have allowed CSX to achieve the substantial safety, operational and financial advances of the past three years.

In addition to being a key measure of performance for CSX, return on invested capital is an important component of regulatory determinations by the STB. CSX fully appreciates the significance of pending proceedings before the STB on this subject. As CSX stated in its September submission to the STB,

| The [STB’s] proposal to change the regulatory cost of capital methodology without considering the true requirements that the rail industry is facing will lead to constrained capital spending at a time when the U.S. is facing a transportation capacity crisis. |

-7-

The fact is that replacement cost methodology should be considered in determining revenue adequacy for the purpose of railroad rate regulation, and, along with the entire railroad industry, CSX has repeatedly advanced that position. Having said that, CSX will not “threaten” to arbitrarily restrict capital spending on critical national infrastructure assets in a misguided and counterproductive effort to pressure legislative and regulatory authorities, as TCI has urged.

TCI’s Various Suggestions: As discussed earlier in this letter, CSX is committed to maintaining open communications with all of its shareholders. To that end, there have been dozens of exchanges between CSX and its advisors and TCI, starting in late 2006.

Each of TCI’s several different suggestions to CSX management has been conveyed to the Board and reviewed thoroughly and with the benefit of outside expert advice. For background, it is useful to walk through the major proposals that TCI has offered to CSX so far in 2007.

LBO Led by Current Management. Early this year, TCI suggested that CSX would make an attractive candidate for a leveraged buyout, and TCI urged the company to enter into discussions with private equity firms. Given that TCI’s proposal contemplated that the CEO and management team would continue to run the company following a leveraged buyout and, in fact, proffered substantial incentives to keep the management team in place, TCI’s suggestions were fairly viewed as a strong endorsement of the CSX management team. Nonetheless, the Board determined that the interests of CSX shareholders are best served by the company remaining publicly traded.

Junk Recapitalization. TCI next advocated that CSX dramatically increase leverage to fund additional share repurchases. Specifically, TCI suggested that the company repurchase 20 percent of outstanding shares each year until leverage reached five times EBITDA, more than doubling the company’s debt and reducing its credit rating to “junk” status. Although CSX has an aggressive share repurchase program in place, the company has repeatedly stressed the importance of maintaining an investment grade credit rating and the financial flexibility required for the capital intensive nature of the railroad business. The Board believes that developments in the credit markets since CSX rejected TCI’s “junk recapitalization” suggestion amply demonstrate that the company’s commitment to maintaining a strong balance sheet and an investment grade rating is the more prudent strategy for a company of this kind.

Rate Increases. TCI then publicly called for CSX, and the industry generally, to increase rates by 7 percent each year for the next 10 years. Putting aside the competitive dimensions of this announcement, the suggestion aroused the ire of customers and policymakers. In fact, customer advocates and members of the U.S. House of Representatives and the U.S. Senate pointed to TCI’s statements in calling for new regulation of the railroad industry.

Freezing Growth to Affect Legislation. In recent months, TCI has urged that CSX and the other railroads respond to re-regulation concerns in Washington by “freezing” expansion capital. Putting aside the competitive dimensions of such an announcement, the CSX Board believes that there are far more appropriate and effective ways to reach balanced legislative and regulatory solutions than abandoning core elements of long-term business strategy.

-8-

Now, in public letters, TCI criticizes corporate governance, operations and investment levels, notwithstanding CSX’s strong performance on the well understood measures of organizational quality. The Board believes that the suggestions outlined in these recent letters are not in the best interests of the company and its shareholders.

In conclusion, the Board is committed to acting in the best interest of all of the company’s shareholders. The Board supports the CEO and the management team in their effective efforts to deliver shareholder value, which also serves the company’s other shareholders.

Be assured that this Board constantly challenges the CSX management team to improve the company’s performance. As part of that process, the Board is always receptive to ideas from shareholders. The Board respects TCI’s right as a shareholder to express its opinions regarding CSX and will continue to keep an open mind. However, the Board believes that the approaches TCI has offered are not in the best interests of CSX shareholders and, in some cases, have damaged the industry.

Very truly yours,

The CSX Corporation Board of Directors

-9-