First Quarter 2008

Earnings Conference Call

Exhibit 99.1

Proxy Statement Disclosure

On February 22, 2008, CSX Corporation ("CSX") filed with the SEC a revised preliminary proxy statement in connection

with its 2008 Annual Meeting. CSX plans to file with the SEC and furnish to its shareholders a definitive Proxy

Statement in connection with its 2008 Annual Meeting, and advises its security holders to read the definitive Proxy

Statement when it becomes available, because it will contain important information. Security holders may obtain a free

copy of the definitive Proxy Statement and other documents (when available) that CSX files with the SEC at the SEC’s

website at www.sec.gov. The definitive Proxy Statement and these other documents may also be obtained for free from

CSX by directing a request to CSX Corporation, Attn: Investor Relations, David Baggs, 500 Water Street C110,

Jacksonville, FL 32202.

CSX, its directors, director nominee and certain named executive officers and employees may be deemed to be

participants in the solicitation of CSX’s security holders in connection with its 2008 Annual Meeting. Security holders

may obtain information regarding the names, affiliations and interests of such individuals in CSX’s revised preliminary

proxy statement filed on February 22, 2008 with the SEC.

2

Executive Summary

Michael Ward

Chairman, President and

Chief Executive Officer

Forward-Looking Disclosure

This information and other statements by the company contain forward-looking statements within the meaning of the

Private Securities Litigation Reform Act with respect to, among other items: projections and estimates of earnings,

revenues, cost-savings, expenses, or other financial items; statements of management’s plans, strategies and

objectives for future operation, and management’s expectations as to future performance and operations and the time

by which objectives will be achieved; statements concerning proposed new products and services; and statements

regarding future economic, industry or market conditions or performance. Forward-looking statements are typically

identified by words or phrases such as “believe,” “expect,” “anticipate,” “project,” “estimate” and similar expressions.

Forward-looking statements speak only as of the date they are made, and the company undertakes no obligation to

update or revise any forward-looking statement. If the company does update any forward-looking statement, no

inference should be drawn that the company will make additional updates with respect to that statement or any other

forward-looking statements.

Forward-looking statements are subject to a number of risks and uncertainties, and actual performance or results could

differ materially from that anticipated by these forward-looking statements. Factors that may cause actual results to

differ materially from those contemplated by these forward-looking statements include, among others: (i) the company’s

success in implementing its financial and operational initiatives, (ii) changes in domestic or international economic or

business conditions, including those affecting the rail industry (such as the impact of industry competition, conditions,

performance and consolidation); (iii) legislative or regulatory changes; (iv) the inherent business risks associated with

safety and security; and (v) the outcome of claims and litigation involving or affecting the company.

Other important assumptions and factors that could cause actual results to differ materially from those in the forward-

looking statements are specified in the company’s SEC reports, accessible on the SEC’s website at www.sec.gov and

the company’s website at: http://investors.csx.com/

4

First quarter overview . . .

Delivered record Q1 revenues,

operating income and EPS

Raised safety and customer

service to record levels

Produced best-ever Q1

operating ratio of 77%

Increased dividend, buyback

and financial targets

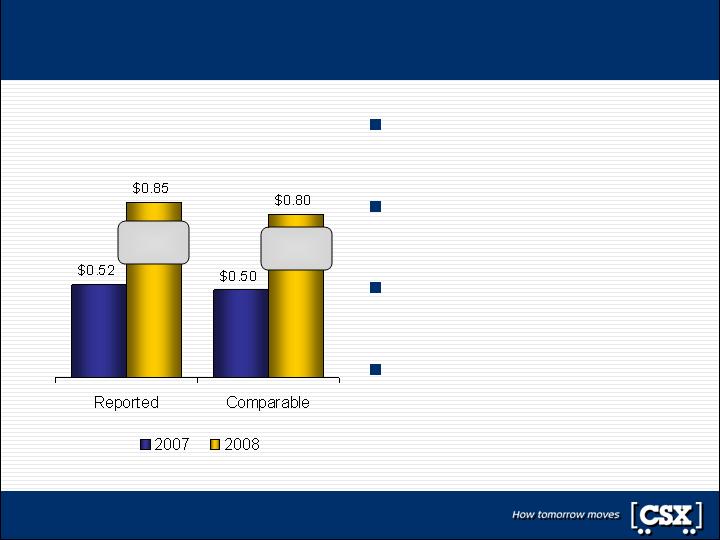

First Quarter

Earnings Per Share

60%

Increase

Note: Comparable results exclude gains from insurance recoveries and a non-cash equity earnings adjustment

63%

Increase

5

Operations Review

Tony Ingram

Executive Vice President

Chief Operating Officer

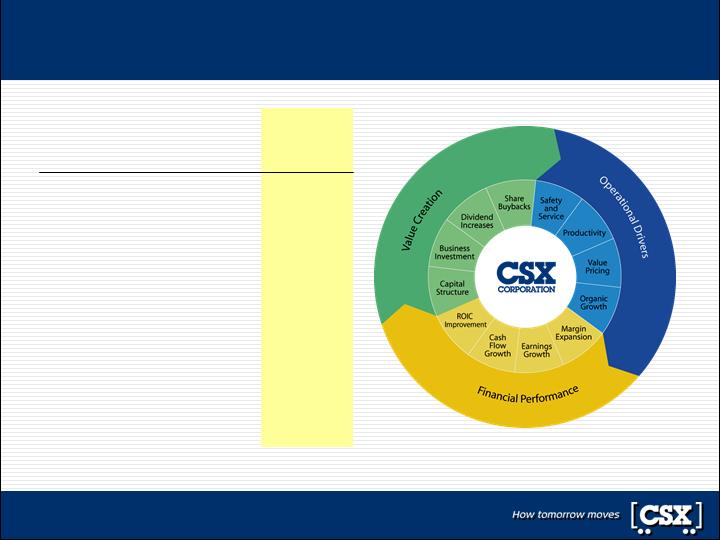

Leadership, discipline and execution

Safety performance improves

to record levels

Productivity helping drive the

operating ratio lower

Customer service improves

to record levels

Safety

Productivity

Service

Leadership

Discipline

Execution

Performance

Excellence

7

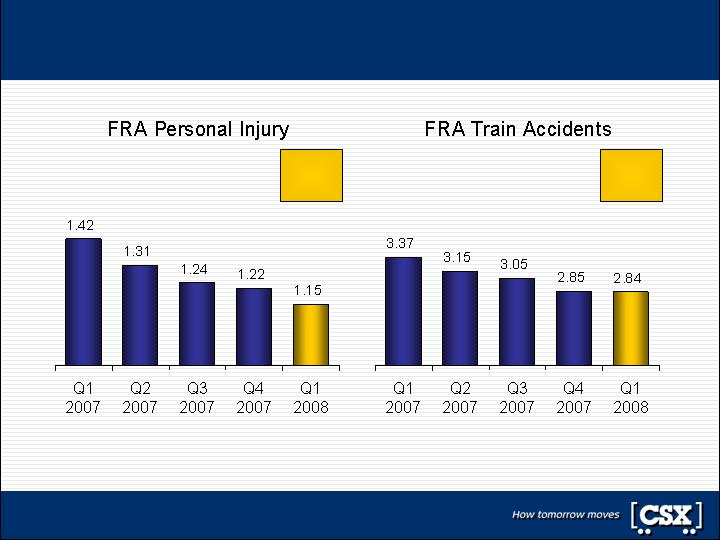

Helping lead one of the nation’s safest industries

Rolling 12-Month Averages

13 Week

Average

1.10

13 Week

Average

3.04

8

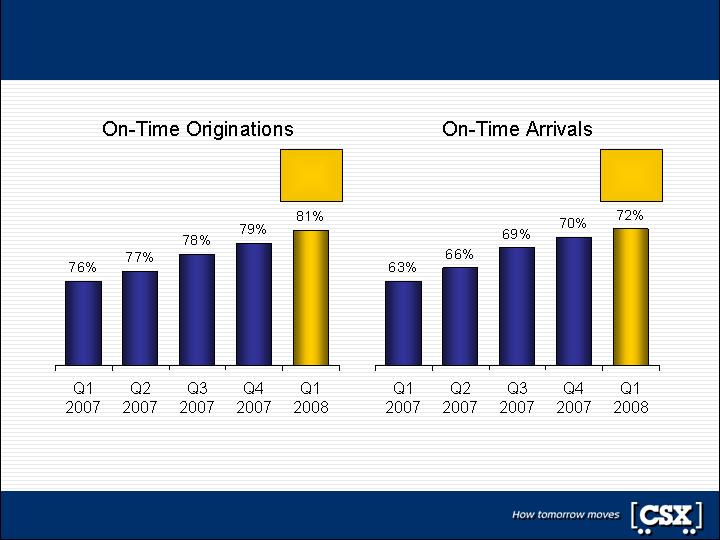

On-time performance at all-time highs

Rolling 12-Month Averages

13 Week

Average

79%

13 Week

Average

69%

9

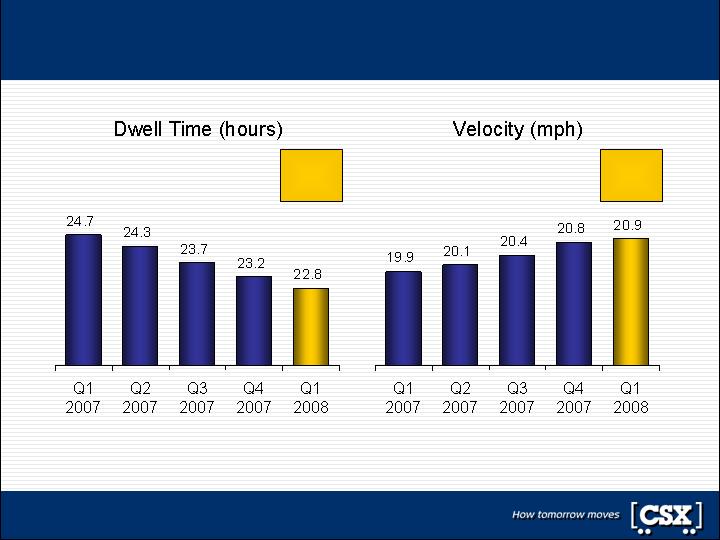

Network efficiency provides strong service product

Rolling 12-Month Averages

13 Week

Average

20.8 mph

13 Week

Average

22.7 hrs

10

Operations wrap-up . . .

Driving safety momentum to record levels

Rightsizing resources to current business levels

On-track with Total Service Integration roll-out

Taking service and productivity to the next level

11

Sales and Marketing Review

Clarence Gooden

Executive Vice President

Sales and Marketing

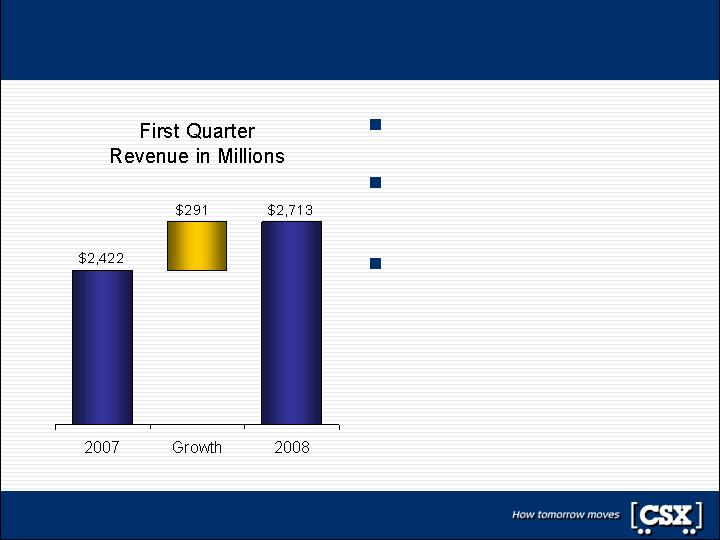

Revenues increased 12% to over $2.7 billion

Record first quarter revenues

Strong service continues to

drive revenue growth

Yield management and fuel

recovery offset softer volume

13

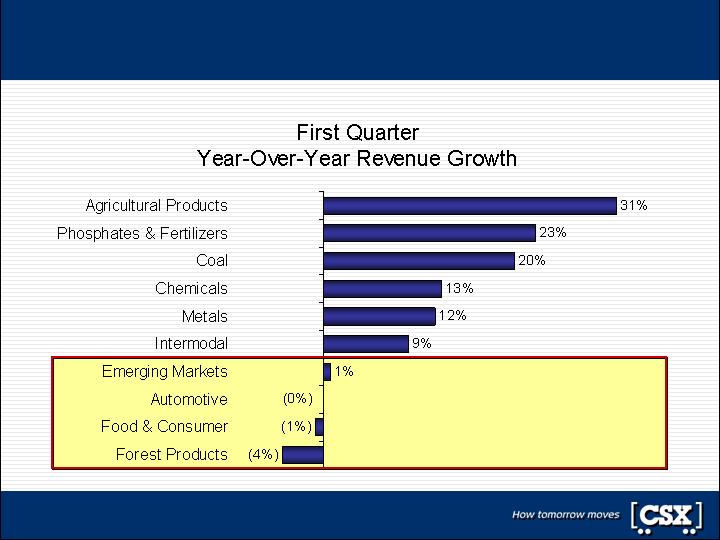

Revenue growth is strong across most markets

Revenues impacted by

the continued softness in

the housing and automotive

sectors of the economy

14

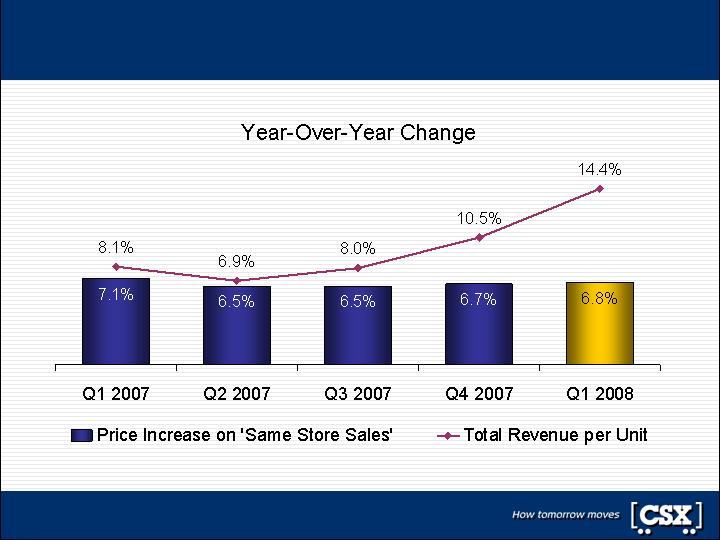

Price continues to drive RPU growth

Note: ‘Same Store Sales’ price increases exclude impacts from fuel and mix

15

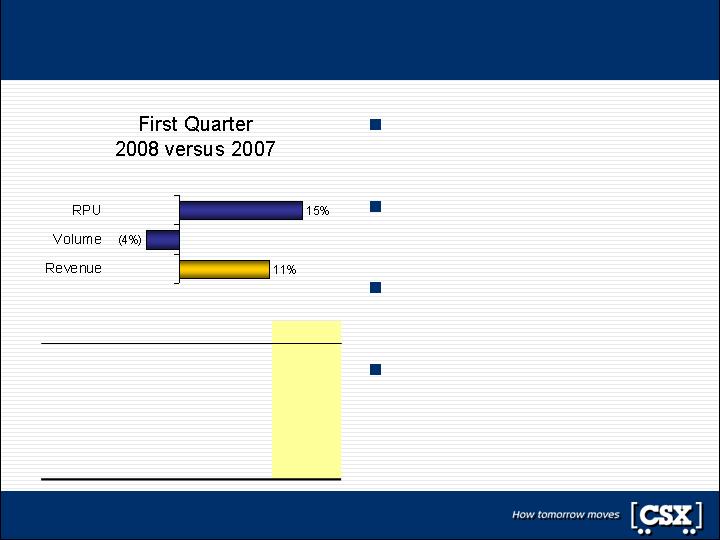

Merchandise revenue increases 11%

Yield management continues

to offset softer volumes

Continued softness in

housing and auto sectors

All-time record revenue in

agriculture products

Further strength in fertilizer,

chemicals and metals

2007

Change

2008

RPU

$ 1,791

$ 274

$ 2,065

Volume

(thousands)

675

(25)

650

Revenue

(millions)

$ 1,209

$ 133

$ 1,342

16

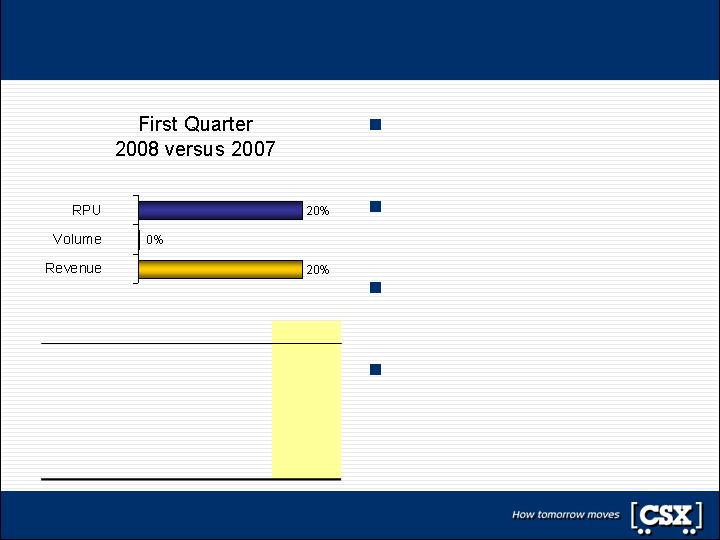

Coal revenue increases 20%

Strength in exports offset

decline in utility market

Tons shipped increase 1% on

flat carload volume

Price, fuel recovery and mix

drove strong revenue growth

Overall pricing environment

remains favorable

2007

Change

2008

RPU

$ 1,370

$ 276

$ 1,646

Volume

(thousands)

462

1

463

Revenue

(millions)

$ 633

$ 129

$ 762

17

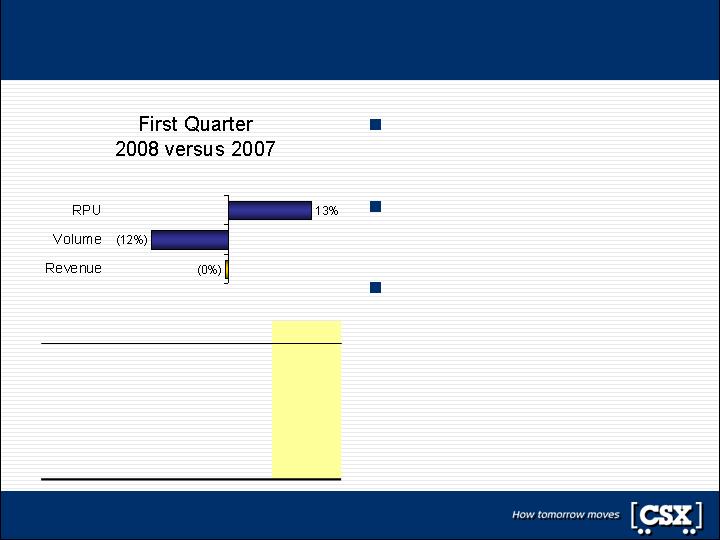

Automotive revenue flat

Softer demand and tight

credit impacting auto sales

Lower production at CSX

plants impacted volumes

Revenues flat on higher

prices and fuel recovery

2007

Change

2008

RPU

$ 1,862

$ 242

$ 2,104

Volume

(thousands)

109

(13)

96

Revenue

(millions)

$ 203

($ 1)

$ 202

18

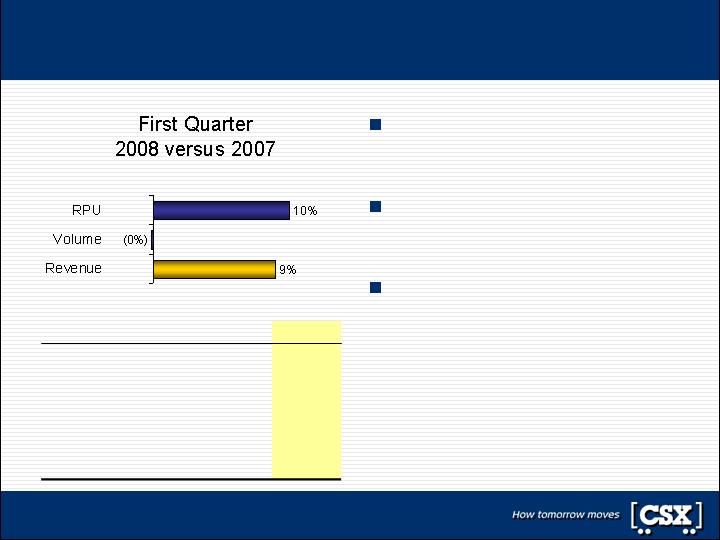

Intermodal revenue increases 9%

RPU increase driven by fuel

recovery and mix

Domestic traffic gains offset

International weakness

Domestic revenue increased

on Transcontinental growth

2007

Change

2008

RPU

$ 625

$ 60

$ 685

Volume

(thousands)

509

(1)

508

Revenue

(millions)

$ 318

$ 30

$ 348

19

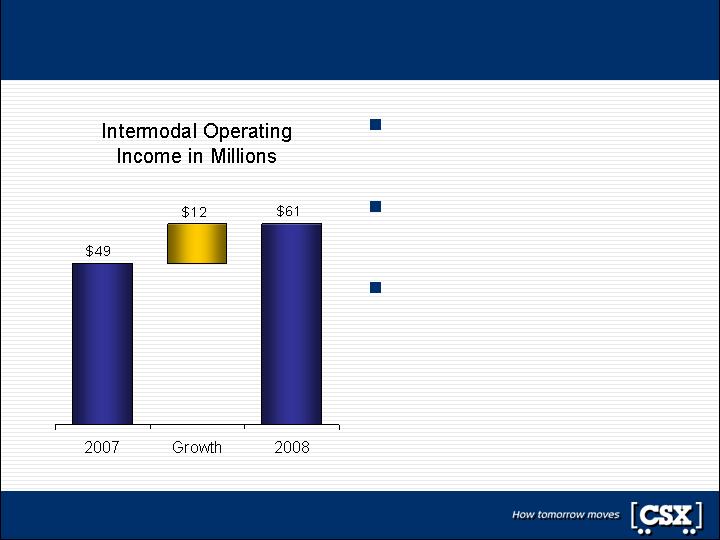

Intermodal reports strong first quarter profit

Bottom-line focus increases

operating income nearly 25%

Operating initiatives continue

to offset rising fuel costs

Operating ratio improves

210 bps to 82.5%

20

Second quarter revenue outlook is positive

Favorable

Neutral

Unfavorable

Agricultural Products

Chemicals

Coal, Coke & Iron Ore

Metals

Phosphate & Fertilizer

Emerging Markets

Food & Consumer

Intermodal

Automotive

Forest Products

21

Financial Results

Oscar Munoz

Executive Vice President

Chief Financial Officer

Double-digit growth in operating income and EPS

Variance

2007

2008

Dollars in millions, except EPS

$ 141

$ 485

$ 626

Operating Income

48.0

$ 0.33

463.2

$ 0.52

415.2

$ 0.85

Fully Diluted Shares in Millions

Earnings Per Share

$ 111

$ 240

$ 351

Net Income

)

)

63

(20

(73

)

)

)

(8

(99

(138

)

)

55

(119

(211

Other Income (net)

Interest Expense

Income Taxes

)

$ 291

(150

$ 2,422

1,937

$ 2,713

2,087

Revenue

Expense

First Quarter Results

23

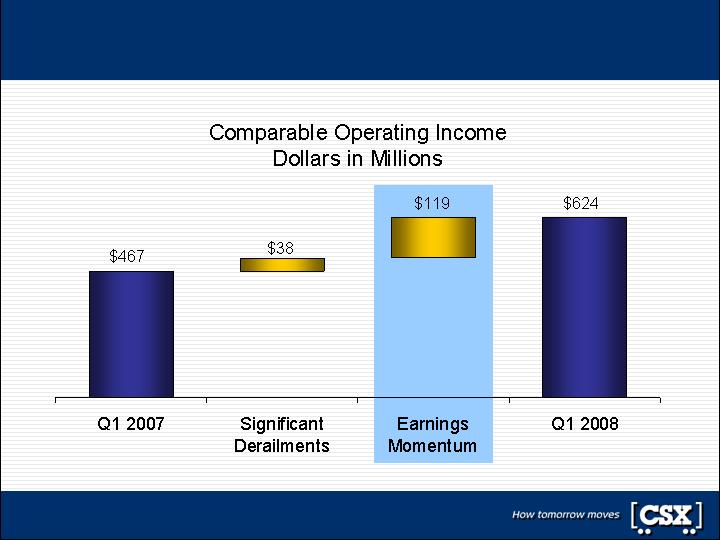

Comparable earnings per share increase 60%

Variance

2007

2008

Dollars in millions, except EPS

$ 0.30

$ 0.50

$ 0.80

Comparable Earnings Per Share

$ 157

$ 467

$ 624

Comparable Operating Income

$ 141

16

)

$ 485

(18

)

$ 626

(2

Operating Income

Less Gain on Insurance Recoveries

)

$ 0.33

0.02

(0.05

)

$ 0.52

(0.02

-

)

$ 0.85

-

(0.05

Earnings Per Share

Less Gain on Insurance Recoveries

Less Equity Earnings Adjustment

First Quarter Results

24

Core earning power increases 25%

Note: Comparable operating income excludes gains from insurance recoveries

25

Operating ratio improves 370 basis points

Margin expansion driven by:

Yield management

Operating efficiencies

Diversity of portfolio helps

overcome softer economy

370 bps

Improvement

Note: Comparable operating ratio excludes gains from insurance recoveries

26

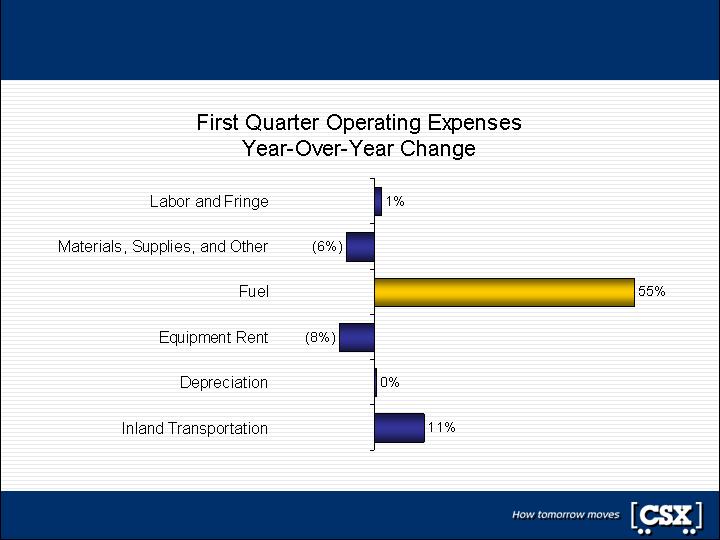

Expenses up 7% overall; down 1% excluding fuel

Note: Results exclude gains from insurance recoveries

27

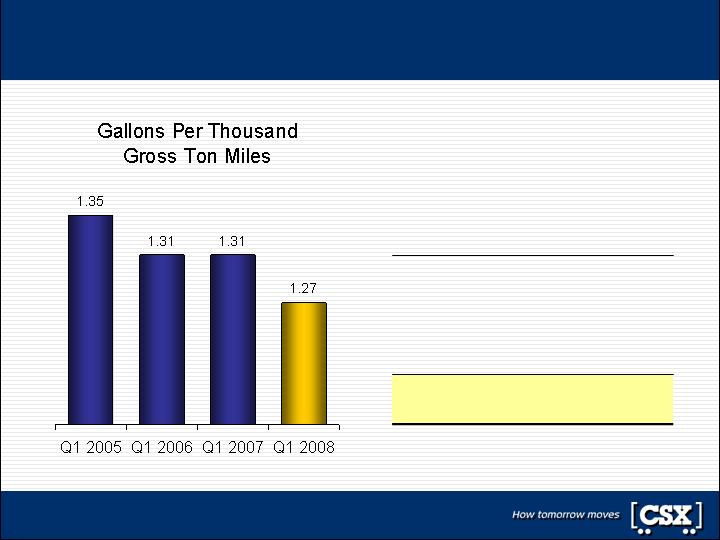

Fuel price more than offsets efficiency and volume

$ 441

2008 Fuel Expense

)

)

157

(1

(10

11

Increase in Price

Change in Volume/Mix

Fuel Efficiency

Net Non-locomotive Fuel

$ 284

2007 Fuel Expense

First Quarter

Fuel Analysis in Millions

28

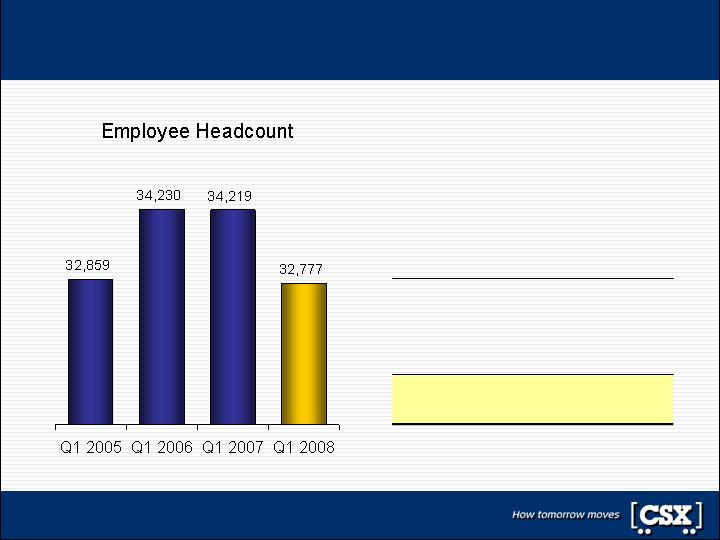

Labor and Fringe held to 1% increase

Note: Headcount reflects the company’s transportation businesses only

$ 745

2008 Labor Expense

)

22

12

(23

Wage & Benefit Inflation

Incentive Compensation

Labor Productivity, Other

$ 734

2007 Labor Expense

First Quarter

Labor Analysis in Millions

29

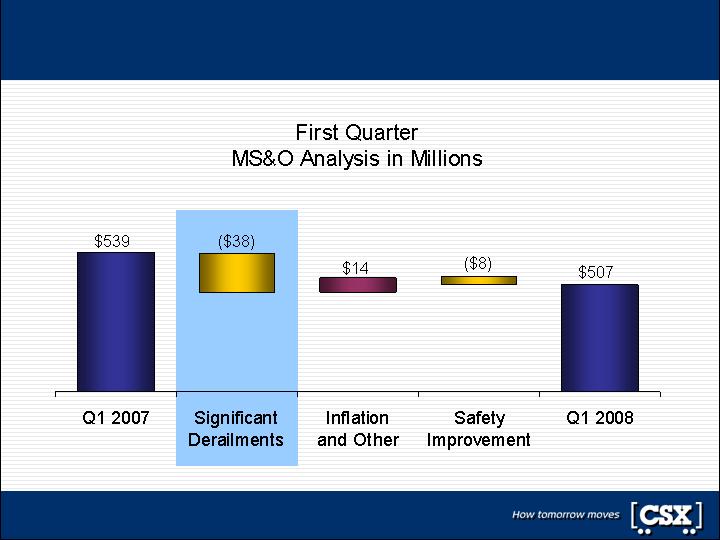

MS&O declines 6% on lower derailment costs

30

Rent expenses decline 8%

Note: Reflects equipment utilization in the carload network on freight cars where CSX incurs rent

$ 111

2008 Rent Expense

)

1

(12

2

Inflation

Volume/Other

Equipment Utilization

$ 120

2007 Rent Expense

First Quarter

Rents Analysis in Millions

31

Other expenses increase 3%

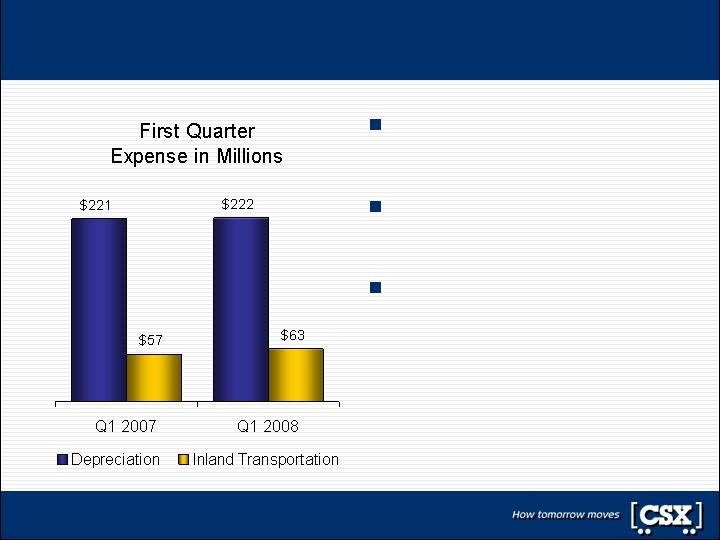

Higher capital base increased

depreciation expense

Mostly offset by lower rates

from asset life studies

Inland Transportation driven

by transcontinental volumes

32

Nearly $3 billion of stock repurchased since 2006

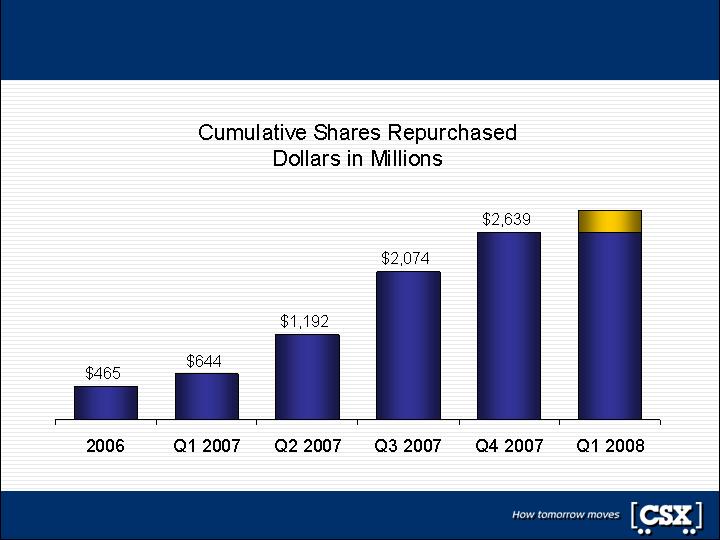

$2,939

Note: Includes $2.4B purchased under the $3.0 billion program authorized in 2007 and $0.5B under prior programs

33

Recent actions reflect long-term confidence

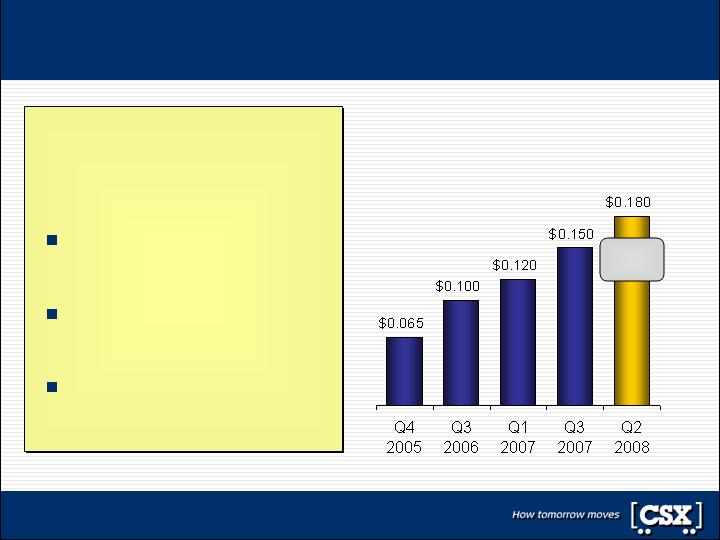

$3.0 Billion

Share Buyback Program

Targeting completion by

fiscal year-end 2009

Builds on nearly $3 billion

repurchased since 2006

Consistent with BBB-/Baa3

capital structure objectives

20%

Increase

Quarterly Dividend

Nearly Tripled Since 2005

34

Full-year earnings per share guidance driven by:

Same store sales price growth of 6%+

Continued productivity gains

Diverse portfolio of business

Targeting high-end of $3.40 – $3.60 EPS range

on a comparable basis

Update on full-year 2008 earnings guidance . . .

35

Long-term financial targets through 2010 . . .

Exceed $1B

in 2010

$800M– $1B

in 2010

Free Cash Flow

Before Dividends

Low 70’s

By 2010

Mid-Low

70’s by 2010

Operating Ratio

18%–21%

CAGR

15%–17%

CAGR

Earnings Per Share

13%–15%

CAGR

10%–12%

CAGR

Operating Income

Current

2008–2010

Targets

Previous

2008–2010

Targets

Note: Compound annual growth rates are off comparable 2007 results; EPS targets are stated before share buybacks

36

Concluding Remarks

Michael Ward

Chairman, President and

Chief Executive Officer

Relentless pursuit of excellence . . .

38

Appendix

GAAP Reconciliation Disclosure

CSX reports its financial results in accordance with generally accepted accounting principles (“GAAP”). However,

management believes that certain non-GAAP financial measures used to manage the company’s business that fall

within the meaning of Regulation G (Disclosure of Non-GAAP Financial Measures) by the SEC may provide users of

the financial information with additional meaningful comparisons to prior reported results.

In press releases and presentation slides for stock analysts, CSX has provided operating income, operating ratio and

earnings per share adjusted for certain items, which are non-GAAP financial measures. The company’s management

evaluates its business and makes certain operating decisions (e.g. budgeting, forecasting, employee compensation,

asset management, and resource allocation) using these adjusted numbers.

Likewise, this information facilitates comparisons to financial results that are directly associated with ongoing

business operations as well as provides comparable historical information. Lastly, earnings forecasts prepared by

stock analysts and other third parties generally exclude the effects of items that are difficult to predict or measure in

advance and are not directly related to CSX’s ongoing operations. A reconciliation between GAAP and non-GAAP

measures is provided on the following slide. These non-GAAP measures should not be considered a substitute for

the company’s GAAP measures.

40

GAAP reconciliation to comparable results

)

$ 291

(150

$ 2,422

1,937

$ 2,713

2,087

Revenue

Expense

$ 0.30

$ 0.50

$ 0.80

Comparable Earnings Per Share

)

$ 0.33

0.02

(0.05

)

$ 0.52

(0.02

-

)

$ 0.85

-

(0.05

Earnings Per Share

Less Gain on Insurance Recoveries

Less Equity Earnings Adjustment

$ 157

3.7%

$ 467

80.7%

$ 624

77.0%

Comparable Operating Income

Comparable Operating Ratio

$ 141

16

)

$ 485

(18

)

$ 626

(2

Operating Income

Less Gain on Insurance Recoveries

Variance

2007

2008

41

First Quarter 2008

Earnings Conference Call