Relentless Pursuit of Excellence

May 2008

Exhibit 99.1

Proxy Statement Disclosure

Important Information

In connection with the 2008 annual meeting of shareholders, CSX Corporation ("CSX") has filed with the SEC and is

mailing to shareholders a definitive Proxy Statement dated April 25, 2008. Security holders are strongly advised to read

the definitive Proxy Statement because it contains important information. Security holders may obtain a free copy of the

definitive Proxy Statement and any other documents filed by CSX with the SEC at the SEC’s website at www.sec.gov.

The definitive Proxy Statement and these other documents may also be obtained for free from CSX by directing a

request to CSX Corporation, Attn: Investor Relations, David Baggs, 500 Water Street C110, Jacksonville, FL 32202.

Certain Information Concerning Participants

CSX, its directors, director nominee and certain named executive officers and employees may be deemed to be

participants in the solicitation of CSX’s security holders in connection with its 2008 Annual Meeting. Security holders

may obtain information regarding the names, affiliations and interests of such individuals in CSX’s definitive Proxy

Statement.

2

Forward-Looking Disclosure

This presentation and other statements by the company contain forward-looking statements within the meaning of the

Private Securities Litigation Reform Act with respect to, among other items: projections and estimates of earnings,

revenues, cost-savings, expenses, or other financial items; statements of management’s plans, strategies and

objectives for future operation, and management’s expectations as to future performance and operations and the time

by which objectives will be achieved; statements concerning proposed new products and services; and statements

regarding future economic, industry or market conditions or performance. Forward-looking statements are typically

identified by words or phrases such as “believe,” “expect,” “anticipate,” “project,” “estimate,” and similar expressions.

Forward-looking statements speak only as of the date they are made, and the company undertakes no obligation to

update or revise any forward-looking statement. If the company does update any forward-looking statement, no

inference should be drawn that the company will make additional updates with respect to that statement or any other

forward-looking statements.

Forward-looking statements are subject to a number of risks and uncertainties, and actual performance or results could

differ materially from that anticipated by these forward-looking statements. Factors that may cause actual results to

differ materially from those contemplated by these forward-looking statements include, among others: (i) the company’s

success in implementing its financial and operational initiatives; (ii) changes in domestic or international economic or

business conditions, including those affecting the rail industry (such as the impact of industry competition, conditions,

performance and consolidation); (iii) legislative or regulatory changes; (iv) the inherent business risks associated with

safety and security; and (v) the outcome of claims and litigation involving or affecting the company. Other important

assumptions and factors that could cause actual results to differ materially from those in the forward-looking statements

are specified in the company’s SEC reports, accessible on the SEC’s website at www.sec.gov and the company’s

website at www.csx.com.

3

Presentation Outline

Executive Summary

Safety and Service Performance

Financial Performance

Corporate Governance

GAAP Reconciliation Disclosure

Appendix

4

Executive Summary

CSX Corporation is a high-performance company

Delivering superior value for all shareholders

Leads industry and S&P 500 over one, three and five years

Fastest growing company in an attractive industry

An industry leader in safety, service and financial performance

Driving exceptional long-term financial performance

Most extensive and aggressive guidance in the industry

CSX’s strong Board and governance is the

foundation of the company’s superior performance

6

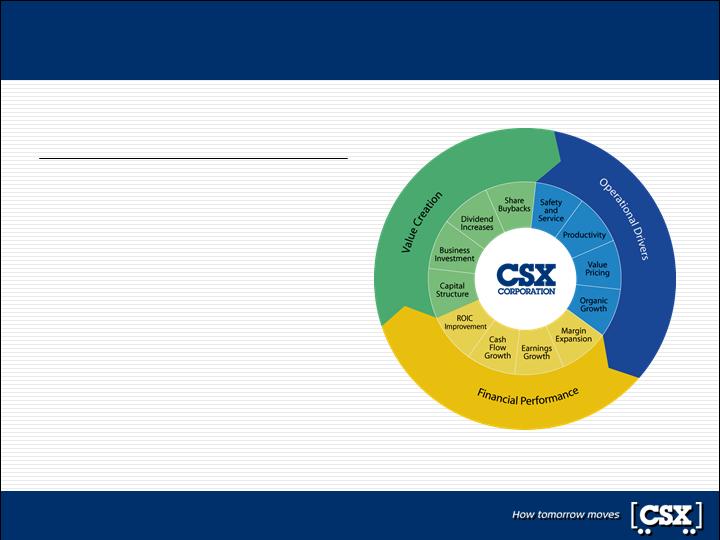

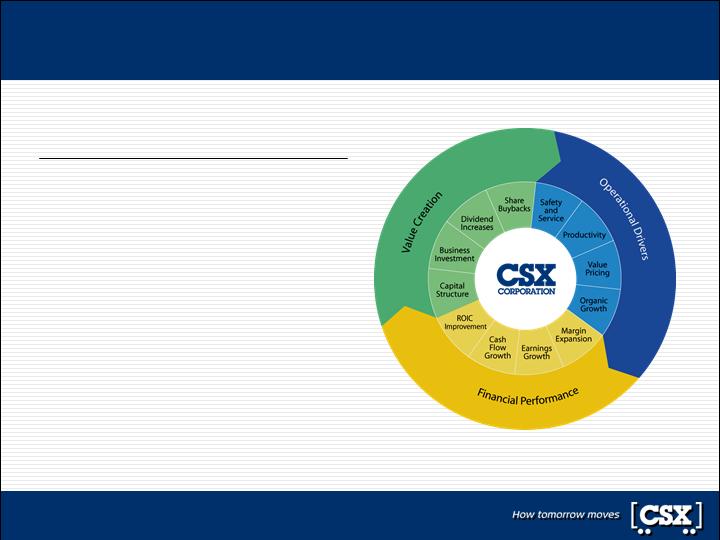

CSX leads in value creation

Our record speaks for itself

Delivering strong operating and financial performance

Driving fastest rate of growth in an attractive industry

Returning capital to shareholders at most aggressive rate among our peers

Proof is in shareholder returns – stock appreciation and dividend growth

We are committed to maximizing shareholder

returns and remain fully accountable to all shareholders

7

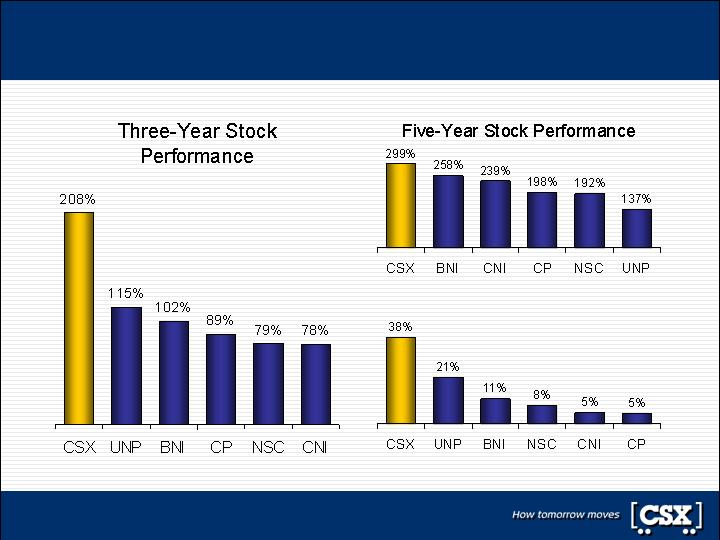

CSX delivering industry-leading shareholder value

Note: Stock price performance as of April 25, 2008; adjusted for splits

One-Year Stock Performance

8

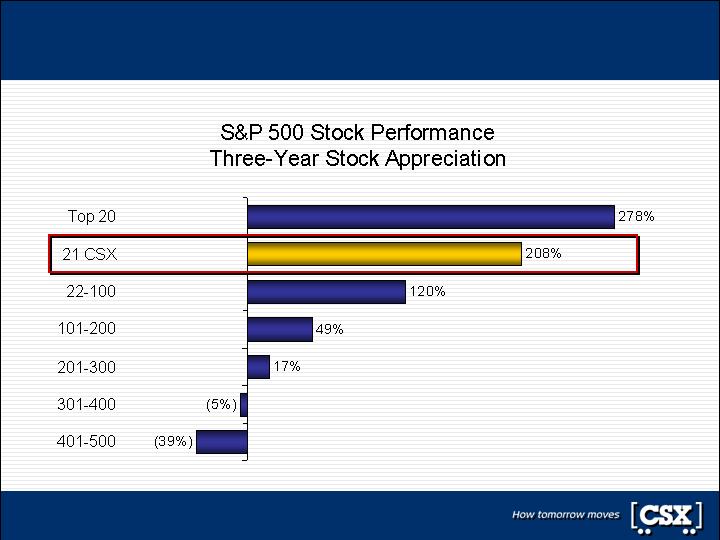

CSX ranks in top 4% of S&P 500 over three years

Note: Stock price performance as of April 25, 2008; adjusted for splits

9

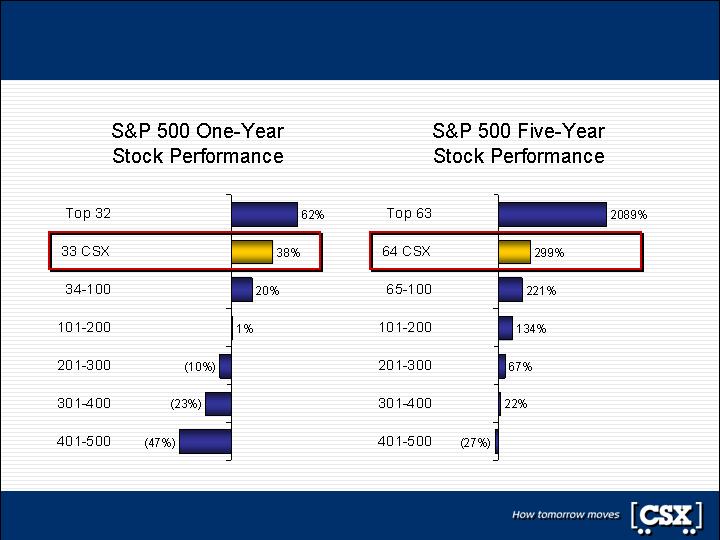

CSX is also market leader over one and five years

Note: Stock price performance as of April 25, 2008; adjusted for splits

10

Industry-leading improvements drive performance

3

4

2

5

6

1

Earnings Per Share

3

5

2

6

4

1

Operating Margin

3

5

1

4

6

2

Operating Income

1

4

3

5

6

2

Terminal Dwell

6

4

3

2

5

1

Network Velocity

5

6

3

4

2

1

Train Accidents

4

2

3

6

5

1

Personal Injuries

CP

CNI

UNP

BNI

NSC

CSX

Key Measures

2004 – 2007 Growth/Improvement Rankings

11

First quarter confirms industry-leading momentum

420

760

410

1,240

270

(30)

12

Controlling costs through productivity

1Q04–1Q08 CAGR

4.6%

1.4%

2.5%

2.2%

0.2%

0.0%

Excluding

Fuel

8.7%

6

NSC

6.8%

5

BNI

6.6%

4

UNP

5.8%

3

CNI

3.9%

2

CSX

3.6%

1

CP

Expense

per RTM

Rank/Company

Note: See GAAP reconciliation for CSX data; peer comparisons based on First Call data

Western

Rails

Eastern

Rails

Canadian

Rails

13

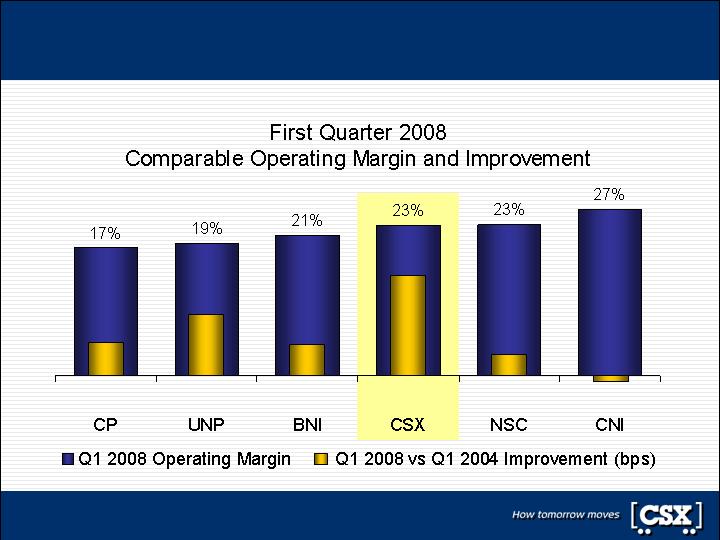

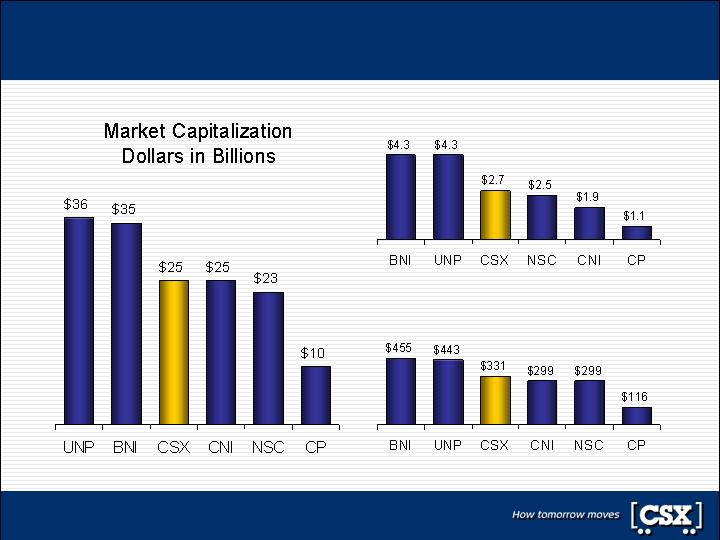

CSX now third most valuable and profitable railroad

Note: Market capitalization as of April 25, 2008; comparable earnings based on GAAP reconciliation and First Call data

Comparable Q1 2008 Net Earnings

Dollars in Millions

Q1 2008 Revenues in Billions

14

Superior financial performance to continue

Exceed $1B

in 2010

Free Cash Flow

Before Dividends

Near 30%

By 2010

Operating Margin

18%–21%

CAGR

Earnings Per Share

13%–15%

CAGR

Operating Income

2008–2010

Targets

Note: CAGR’s are off comparable 2007 results; EPS targets are stated before the impact of share buybacks

15

Driving value through strategic capital deployment

Capital

Investment

Investing $5B through

2010 to support

long-term growth

Share

Buybacks

Repurchased nearly

$3B since 2006

Targeting another $3B

by year-end 2009

Dividends

Nearly tripled the

quarterly dividend

since 2005

. . . While maintaining an investment grade profile

Growing Free Cash Flow and

Improving Return on Invested Capital . . .

16

TCI Group’s baseless attacks ignore reality

Under this management team, CSX’s earnings and margins have

been the fastest growing in an attractive industry

Stock performance over the last one, three and five years is

industry leading and top-tier across the broader S&P 500

CSX is recognized by RiskMetrics and others as a leader in

corporate governance

CSX is recognized as an industry leader in safety, customer

service and financial performance

Given the CSX Board and management track record, support of

TCI Group’s dissident slate could harm the value of your investment

17

TCI Group’s demands would impair value

Investing for long-term growth

and value creation

Freeze expansion

capital spending

Current Board has presided

over industry-leading

performance

Replace current

Board of Directors

Managing regulatory concerns;

pricing to the market reflecting

value of service

Increase customer

prices 7% annually

Repurchased nearly $3B since

2006; further $3B targeted by

year-end 2009

Annual stock

buyback of 20%

for five years

CSX stock price has significantly

exceeded proposed LBO price

Leveraged Buyout

CSX Status

Negative

Credit Impacts

Ignores

Risk Impacts

Flawed

Assumptions

Sacrifices

LT Potential

Proposal

Statements made by Chris Hohn and TCI have fueled support in

Congress for re-regulation, which would destroy shareholder value

18

Red flags surround TCI Group’s candidates

Chris Hohn

As evidenced by the wide ranging demands of CSX, he has a “special interest” agenda. We note that he resigned

from a U.K. board in the face of allegations of conflict of interest last year

Alex Behring

Only relevant experience comes from Brazilian railroad that is both a fraction of the size of CSX and has a safety

record that is abysmal compared to all U.S. railroads

Tim O’Toole

During the period that he has led the London Underground subway system, its service performance has declined

sharply and government funding required for operations has increased over 600%

Gary Wilson

Led Northwest Airlines into bankruptcy and sold more than 75% of his shares in the months immediately leading

up to the bankruptcy filing

Gil Lamphere

Chaired a publicly traded company sold through a distressed sale, and has a career characterized by buyouts

The choice between director slates is clear

19

Red flags surround TCI’s governance approach

Chris Hohn alleges TCI is only seeking a “shareholder voice”

Yet, Hohn and TCI representatives have provided insight into how

the group would use the Board voting block it is seeking

TCI has said it will “go to war” and that there are “no limits” to what they will

do if CSX does not comply with their demands

TCI has said it would ultimately undertake to change out the entire CSX

Board if necessary to achieve its undisclosed agenda

The choice between director slates is clear

20

CSX Board expert, diverse and performance driven

Compelling

Transportation

Experience

Blue Chip

Business

Experience

Governance and

Policy Expertise

Over 100 years of Board experience in rail, financial and industrial companies

CSX, Honeywell, Altria, Hartford, Dominion Resources, Southern Company,

Ashland, PNC, Bank of New York, SunTrust, Smithfield, Constellation

Need for diverse experience reflects regulated history and attributes of railroads

Seven current and former CEO’s; including Michael Ward

CEO and COO experience spans rail, financial and industrial companies

CSX, Illinois Central, Florida East Coast, Southern Company, Haskell, PHH

Citi Alternative Investments, Mercantile Bankshares, AEGON, Cendant

Michael Ward and John McPherson each have 30 years of railroad experience

Elizabeth Bailey was a key leader in airline deregulation and is nationally

recognized as a transportation and economics policy expert

John Breaux is a transportation policy expert with strong U.S. Senate experience

The choice between director slates is clear

21

Incumbents targeted by TCI provide strong expertise

Elizabeth Bailey

Key role in the deregulation of the airline industry as Vice Chairman of the Civil Aeronautics Board. She is a

nationally recognized transportation and economics policy expert, and her Board experience includes

Fortune-500 companies in the transportation, banking, technology, agricultural and food products industries

Steven Halverson

Chief Executive Officer of a major commercial development firm, with substantial infrastructure expertise in the

eastern U.S. He presides over a company that is involved in a diverse array of industries, including ethanol,

real estate development, and building products, which are critical to CSX’s business strategies

Robert Kunisch

Career spans private equity and CEO of a major business services provider. His Board experience includes

Fortune-500 companies in the transportation, aerospace, financial services and banking industries

William Richardson

As an economics policy expert, he is the former president of Johns Hopkins University and former Chairman

and President of the W.K. Kellogg Foundation. His Board experience includes Fortune-500 companies in the

transportation, energy and banking industries

Frank Royal

As a medical and healthcare expert, he has served as Chairman of the National Medical Association. His

diverse Board experience includes Fortune-500 companies in the transportation, energy, banking, healthcare,

and food products industries

The choice between director slates is clear

22

CSX’s governance ranks among best-in-class

No poison pill

Board is elected annually; majority vote

in uncontested elections

Special shareholder meetings can be

called by investors holding 15% of

outstanding common shares

No supermajority vote required

Strong independent board (11 of 12

members are outside directors)

Presiding independent director with

delineated responsibilities

Executive severance payments limited

to 2.99 annual compensation

“Holy Trinity” of

Takeover Defenses

Does Not Apply at CSX

Other Provisions

Are Key to a Strong

Governance Foundation

RiskMetrics

Corporate Governance Quotient

Transportation Industry 99.0%

S&P 500 93.2%

23

CSX is building lasting shareholder value

CSX is driving superior performance for all shareholders

Safety, service, financial and value creation

Significant momentum is expected to continue

Striving for industry leadership across full spectrum

This Board of Directors and management team have

presided over this substantial performance

CSX’s Board of Directors’ transportation and governance

experience is world-class

Board oversight and management team execution

are delivering superior performance for shareholders

24

Safety and Service Performance

Recognized industry leader in safety and service

Safety performance has improved significantly

CSX ranks among leaders in one of nation’s safest industries

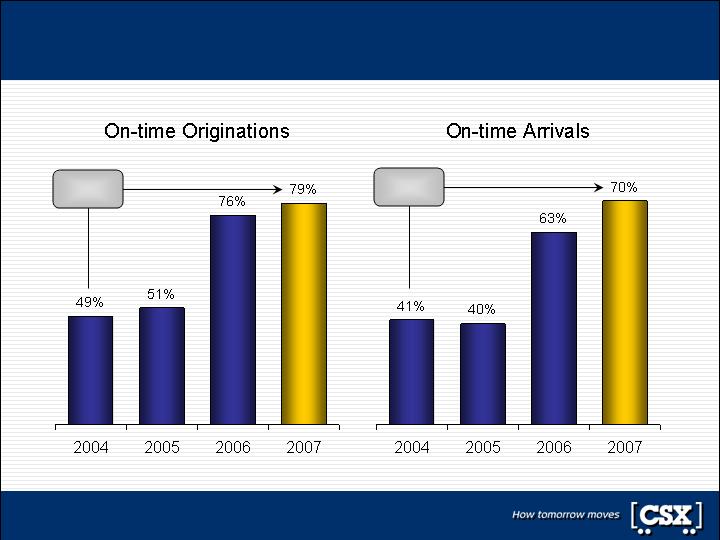

On-time performance at all-time highs

On-time originations up 61% and arrivals up 71%

Network reliability driving greater efficiency

Shipments are moving more quickly across the network

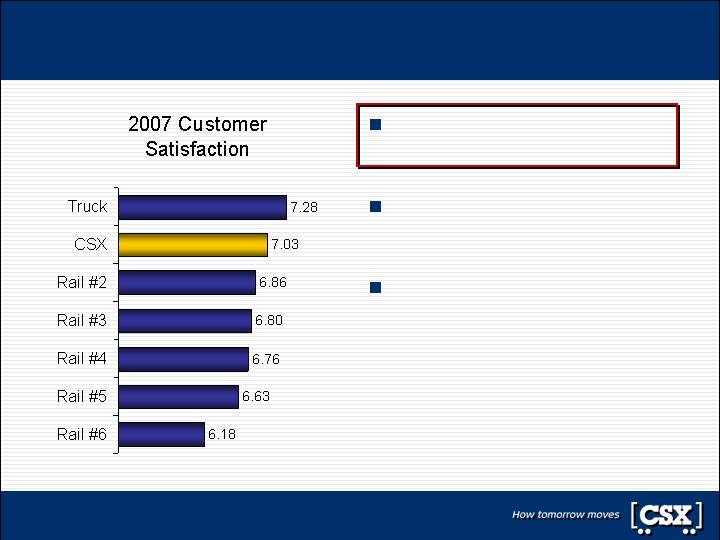

Overall customer satisfaction at all-time highs

CSX ranks among industry leaders in overall service quality

26

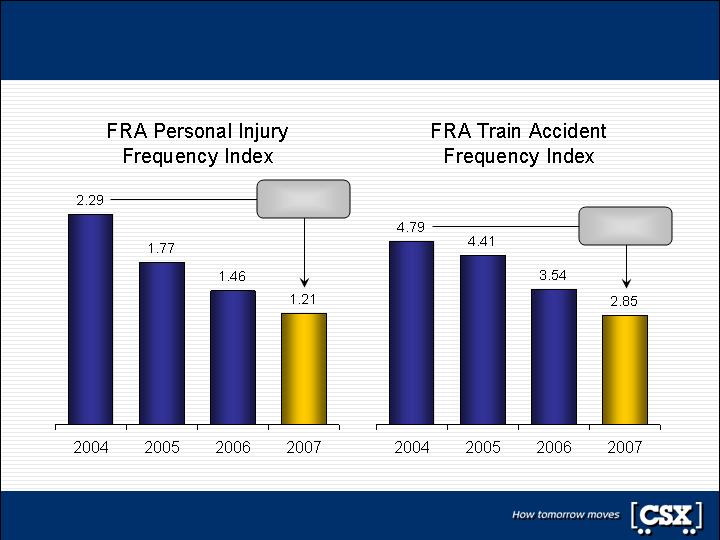

Safety measures improved significantly since 2004

41%

Improvement

47%

Improvement

Source: Federal Railroad Administration Data

27

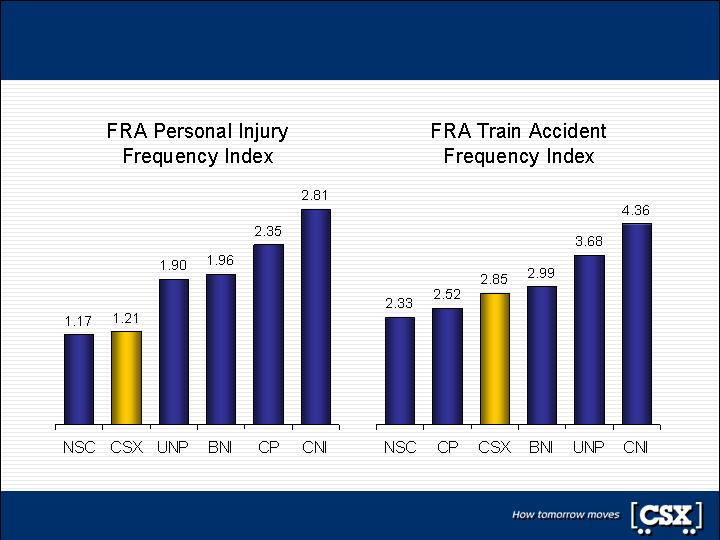

Improvements position CSX as an industry leader . . .

Source: 2007 Federal Railroad Administration Data

28

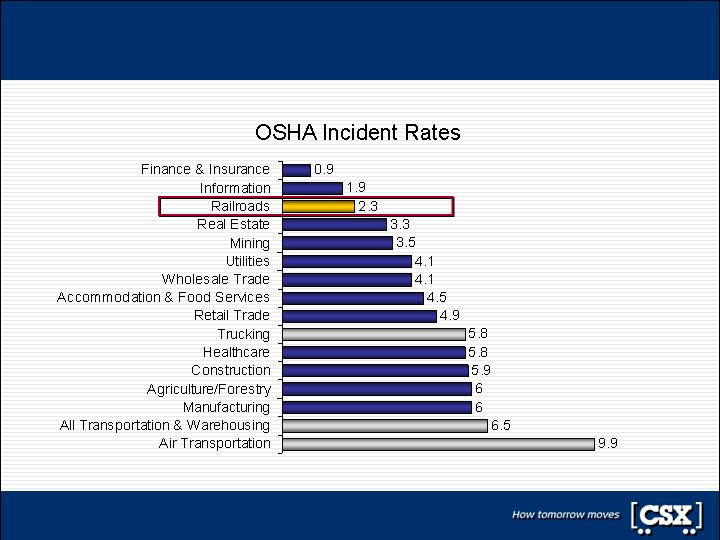

. . . in one of the nation’s safest industries

Note: Incidence rates of total recordable cases of nonfatal occupational injuries and illnesses are per 100 full-time workers

29

On-time performance at all-time highs

61%

Increase

71%

Increase

30

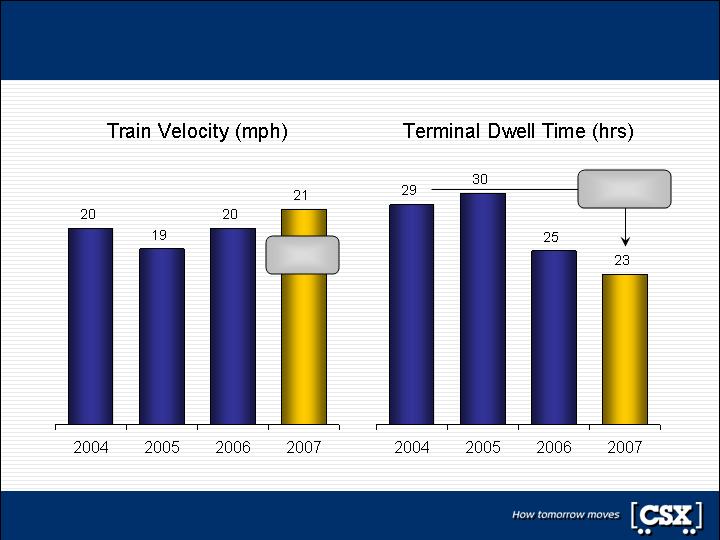

Network efficiency approaching all-time best levels

21%

Improvement

5%

Increase

31

Customers recognize CSX’s excellent performance

CSX ranks among industry

leaders in overall satisfaction

Correlates to internal

operating measure gains

Strong service supports

pricing initiatives

Source: Survey of CSX customers by a leading independent third-party surveyor

32

Customer awards are numerous and diverse

Schneider National names CSX carrier of the year (2007)

Ford names CSX carrier of the year (2007)

Landstar Global Logistics names CSX carrier of the year (2006)

C.H. Robinson names CSX carrier of the year (2007)

Hyundai recognizes CSX with Club Elite award for superior

service (2006-2007)

33

Financial Performance

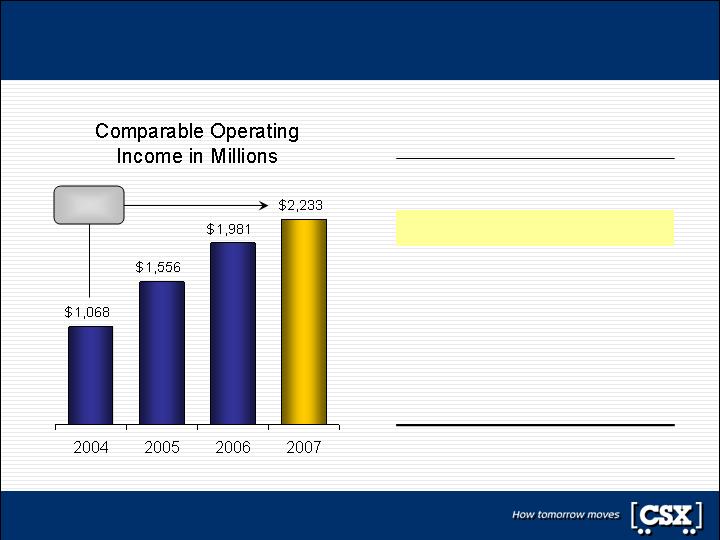

Producing superior financial performance

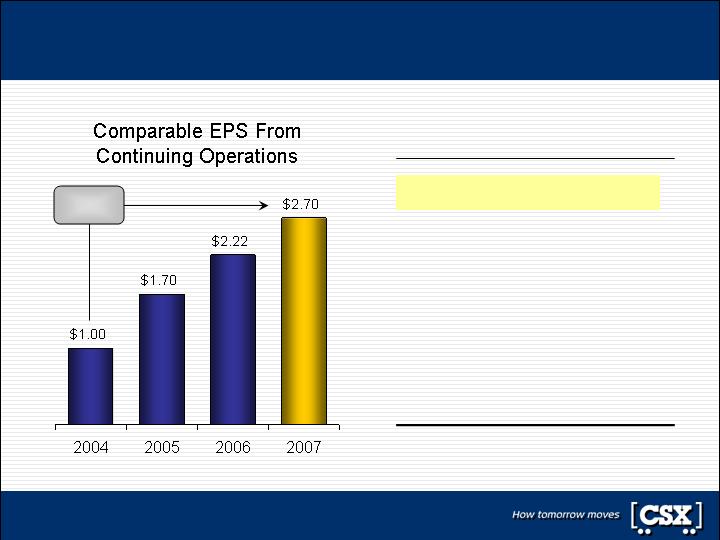

Significantly increasing core earning power

More than doubled operating income; nearly tripled earnings

per share from continuing operations since 2004

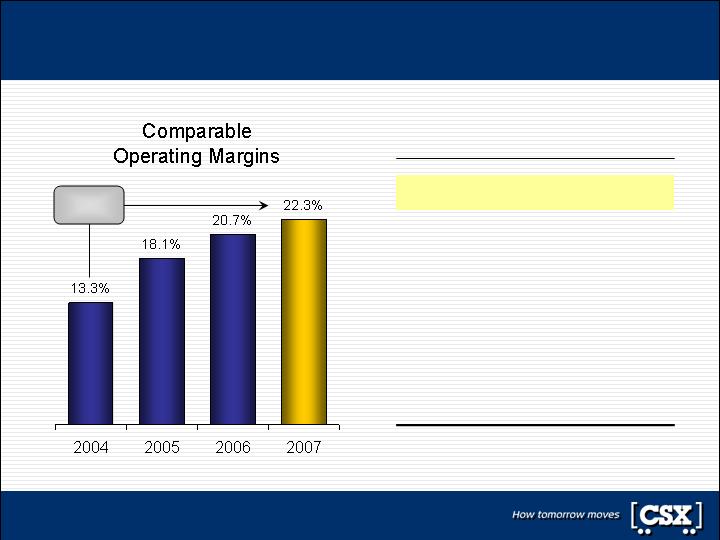

Driving margin expansion through price and productivity

Comparable operating margins nearly doubled since 2004

Targeting strong double-digit growth through 2010

Further margin expansion and Free Cash Flow generation

Note: See GAAP reconciliation for CSX data

35

Operating income more than doubled since 2004

28%

CAGR

11%

7

S&P 500

15%

6

NSC

17%

5

CNI

18%

4

BNI

22%

3

CP

28%

2

CSX

30%

1

UNP

2004-2007

CAGR

Rank/Company

Note: See GAAP reconciliation for CSX data; peer comparisons based on First Call data

36

Operating margins nearly doubled since 2004

900 bps

(90) bps

7

S&P 500

290 bps

6

BNI

330 bps

5

CNI

410 bps

4

NSC

450 bps

3

CP

810 bps

2

UNP

900 bps

1

CSX

2004-2007

Improvement

Rank/Company

Note: See GAAP reconciliation for CSX data; peer comparisons based on First Call data

37

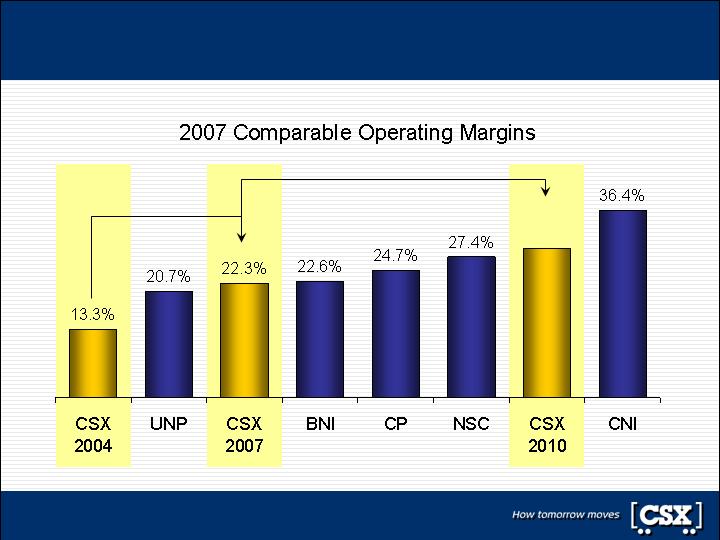

Targeting margins among industry leaders by 2010

Near

30%

900 bps

500 – 800 bps

Note: See GAAP reconciliation for CSX data; peer comparisons based on First Call data

38

Earnings per share nearly tripled since 2004

39%

CAGR

8%

7

S&P 500

20%

6

NSC

22%

5

BNI

24%

4

CNI

32%

3

CP

34%

2

UNP

39%

1

CSX

2004-2007

CAGR

Rank/Company

Note: See GAAP reconciliation for CSX data; peer comparisons based on First Call data

39

Continued strong financial performance expected

Exceed $1B

in 2010

Free Cash Flow

Before Dividends

Near 30%

By 2010

Operating Margin

18%–21%

CAGR

Earnings Per Share

13%–15%

CAGR

Operating Income

2008–2010

Targets

Note: CAGR’s are off comparable 2007 results; EPS targets are stated before the impact of share buybacks

40

Key investments will support long-term growth

Infrastructure 60%

Track

Structures

Equipment 20%

Locomotives

Freight cars

Strategic 20%

Technology

Network capacity

Terminal capacity

Note: Capital spending excludes capital related to Hurricane Katrina and The Greenbrier

41

Recent actions reflect strong confidence in CSX

$3.0 Billion

Share Buyback Program

Builds on nearly $3 billion

repurchased since 2006

Consistent with BBB-/Baa3

capital structure objectives

Targeting completion by

year-end 2009

20%

Increase

Quarterly Dividend

Nearly Tripled Since 2005

42

Corporate Governance

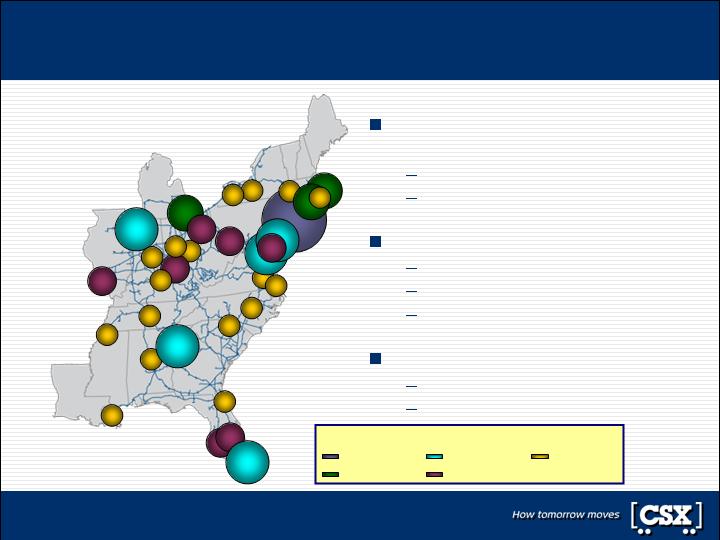

New Orleans

Chicago

St Louis

Memphis

Board presides over nation-critical business

Network serves all major

eastern U.S. markets

Two-thirds of U.S. population

Three-fourths of U.S. consumption

Ships life-essential goods that:

Build and power homes

Feed and clothe families

Support economic growth

Serves national interest

Carries most commuters/passengers

Largest shipper of U.S. military cargo

Source: Global Insight

2006 Population in Major Metropolitan Areas

GT 10 Million

5 – 10 Million

3 – 5 Million

1 – 2 Million

2 – 3 Million

Miami

New York

Jacksonville

Tampa

Orlando

Atlanta

Baltimore

Philadelphia

Washington

Boston

44

CSX Board expert, diverse and performance driven

Compelling

Transportation

Experience

Blue Chip

Business

Experience

Governance and

Policy Expertise

Mgmt Independence

And Performance

Driven

No social relationships exist between Board members and management

The Board has rigorous succession planning process

All executive incentive compensation programs are performance-based

Over 100 years of Board experience in rail, financial and industrial companies

CSX, Honeywell, Altria, Hartford, Dominion Resources, Southern Company,

Ashland, PNC, Bank of New York, SunTrust, Smithfield, Constellation

Need for diverse experience reflects regulated history and attributes of railroads

Seven current and former CEO’s; including Michael Ward

CEO and COO experience spans rail, financial and industrial companies

CSX, Illinois Central, Florida East Coast, Southern Company, Haskell, PHH

Citi Alternative Investments, Mercantile Bankshares, AEGON, Cendant

Michael Ward and John McPherson each have 30 years of railroad experience

Elizabeth Bailey was a key leader in airline deregulation and is nationally

recognized as a transportation and economics policy expert

John Breaux is a transportation policy expert with strong U.S. Senate experience

45

CSX’s Board is a leader in governance

CSX has presiding independent director with delineated duties

Consistent with prevailing practice in the United States

CSX has a strong independent board

CEO is the only management director, with eleven outside directors

Best practices already in place at CSX

Key Board committees are comprised solely of independent directors

Election of entire Board is conducted annually

Majority election of Board in uncontested elections is required

No supermajority vote required

Ability of 15% of shareholders to call a special meeting

Executive severance payments capped at 2.99 times annual compensation

No poison pill

46

Board and management driving proactive changes

Most aggressive capital

structure among its peers

Repurchased nearly $3

billion of stock since 2006

Targeting further $3 billion

buyback through 2009

Nearly tripled quarterly

dividend since 2005

ONE Plan implemented

during 2004

Rebuilt safety and

service culture

Now rank among industry

leaders in safety and

customer service

Initiating Total Service

Integration (TSI) to take

operations to next level

Michael Ward elected

Chairman & CEO in 2003

New executive team put in

place during 2003-2004

Management restructuring

completed in 2004

Reduced management

positions 25%

Hired new talent to

diversify workforce

Acquired New York

Central assets of Conrail

Divested American

Commercial Lines

Sold Sea-Land

International assets

Sold CTI Logistics

Divested Horizon Lines

Sold CSX World Terminals

Corporate

Restructuring

New

Management

Operational

Improvement

Balance Sheet

Optimization

Over last three years, increased stock price 208%, more than

doubled operating income, and nearly tripled earnings per share

Note: Stock price performance as of April 25, 2008 and adjusted for splits; operating income and EPS data is 2004 – 2007

47

TCI does not meet business or shareholder needs

Advocated proposals that create an

“event” and sacrifice results

Certain proposals have drawn negative

rating agency and congressional reaction

Lacks understanding of CSX’s business

model and the rail industry in general

Has not brought forward any new ideas

that create sustainable shareholder value

Demands have changed dramatically and

cannot be reconciled with cogent strategy

TCI Group

CSX Corporation

Stock performance is industry leading and

top-tier across broader S&P 500

Credit profile optimized at BBB-/Baa3;

recognize all constituents vital to business

Industry-leading improvements in all

safety, service and financial measures

Strategies and plans are in place to drive

further industry-leading improvements

Business plans include aggressive return

of capital and best-in-class improvements

TCI Group nominees are not in the best interest of all shareholders

48

CSX Board and management delivering value

Proven record of delivering value to shareholders

Superior stock performance, investing for long-term growth, nearly tripled

dividends, targeting nearly $6 billion of buybacks between 2006 and 2009

Presiding over fastest growing company in an attractive industry

Leads industry in safety, service and financial improvement

Recognized among industry leaders in safety and service

Knowledge and expertise in place to continue strong improvement

Diverse background already in place for presiding over dynamic business

Corporate governance practices recognized among best-in-class

Constructive tension between Board and management in place to drive value

The CSX Board has a proven track record and is a market leader in

corporate governance. Support the CSX Board of Directors

49

GAAP Reconciliation Disclosure

GAAP Reconciliation Disclosure

CSX reports its financial results in accordance with generally accepted accounting principles (“GAAP”). However,

management believes that certain non-GAAP financial measures used to manage the company’s business that fall

within the meaning of Regulation G (Disclosure of Non-GAAP Financial Measures) by the SEC may provide users of

the financial information with additional meaningful comparisons to prior reported results.

CSX has provided operating income, operating margin and earnings per share adjusted for certain items, which are

non-GAAP financial measures. The company’s management evaluates its business and makes certain operating

decisions (e.g. budgeting, forecasting, employee compensation, asset management, and resource allocation) using

these adjusted numbers.

Likewise, this information facilitates comparisons to financial results that are directly associated with ongoing

business operations as well as provides comparable historical information. Lastly, earnings forecasts prepared by

stock analysts and other third parties generally exclude the effects of items that are difficult to predict or measure in

advance and are not directly related to CSX’s ongoing operations. A reconciliation between GAAP and non-GAAP

measures is provided on the following slide. These non-GAAP measures should not be considered a substitute for

the company’s GAAP measures.

51

GAAP reconciliation to comparable results

$ 2.70

$ 2.22

$ 1.70

$ 1.00

Comparable EPS From Continuing

Operations

)

$ 2.74

(0.04

-

-

-

-

)

)

)

$ 2.82

(0.22

(0.06

(0.32

-

-

)

$ 1.59

-

-

(0.16

0.27

-

)

$ 0.94

-

(0.04

-

-

0.10

EPS From Continuing Operations

Less Gain on Insurance Recoveries

Less Gain on Conrail Property

Less Income Tax Benefits

Plus Debt Repurchase Expense

Plus Restructuring Charge

$ 2,233

22.3%

$ 1,981

20.7%

$ 1,556

18.1%

$ 1,068

13.3%

Comparable Operating Income

Comparable Operating Margin

)

$ 2,260

(27

-

)

$ 2,149

(168

-

$ 1,556

-

-

$ 997

-

71

Operating Income

Less Pre-tax Gain on Insurance Recoveries

Plus Pre-tax Restructuring Charge

2007

2006

2005

2004

Dollars in millions, except earnings per share

52

Appendix

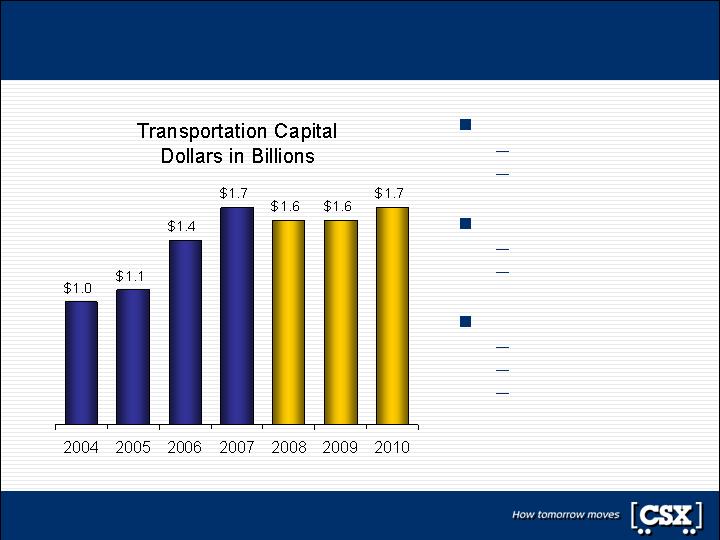

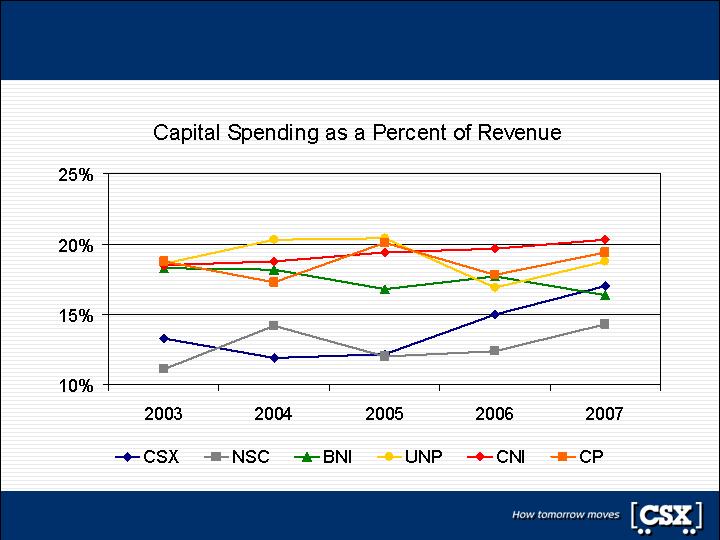

Comparison of capital spending relative to revenue

54

CSX demonstrates environmental leadership

First railroad to join EPA’s Climate Leaders program

Charter member of SmartWay Transport Partnership

EPA SmartWay Excellent Award winner in 2007

Association of American Railroads environmental leader

AAR Chafee Environmental Excellence Award for five of last eight years

AAR Professional Environmental Excellence Award in 2003, 2006 and 2007

55

CSX recognized as progressive employer

City Year National Sponsor – Supporting eight major cities

DiversityInc – Top 50 Company for Diversity

G.I. Jobs Magazine – Top 50 Company

Black MBA Magazine – Top Company for Black MBA’s to Work

CollegeGrad.com – Top 500 Entry Level Company

Hispanic Business Magazine – Top 60 Company

Wounded Warrior Project Sponsor – Warriors to Work Corporate Sponsor

56