RiskMetrics Group Forum Presentation

Delivering Superior Value For All Shareholders

June 2008

Exhibit 99.1

CSX’s Board is

driving shareholder

value creation

CSX’s Board & Mgmt.

have transformed CSX

into an industry leader

CSX Board delivers results; TCI Group puts results at risk

TCI Group could

jeopardize CSX’s

momentum & success

CSX is on target

to become the best

railroad in N. America

Re-elect the CSX Board to ensure maximum shareholder value creation

TCI Group’s nominees bring a poor track record, limited

experience and no operating plan…

TCI Group’s proposals would put CSX’s future at risk

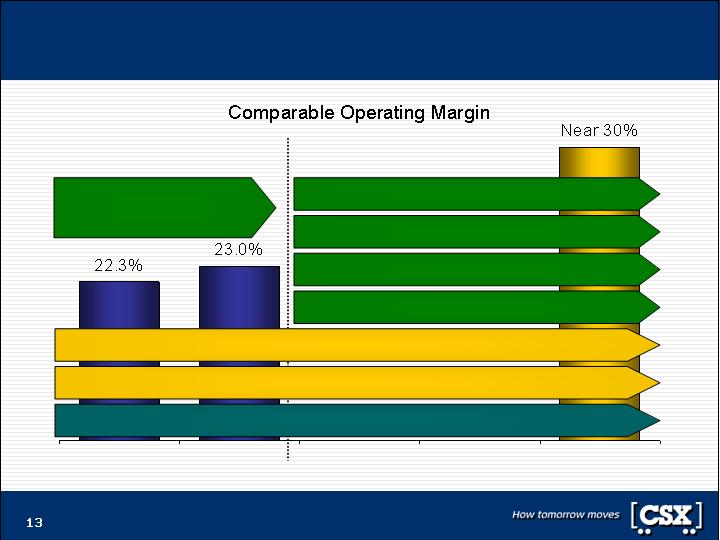

Long-term Board strategy targets industry-leading

operating margins

CSX has achieved unprecedented results with

industry-leading forward guidance

CSX Board and Management deliver superior

performance and leading governance

CSX’s Board and Management have

transformed CSX into an industry leader

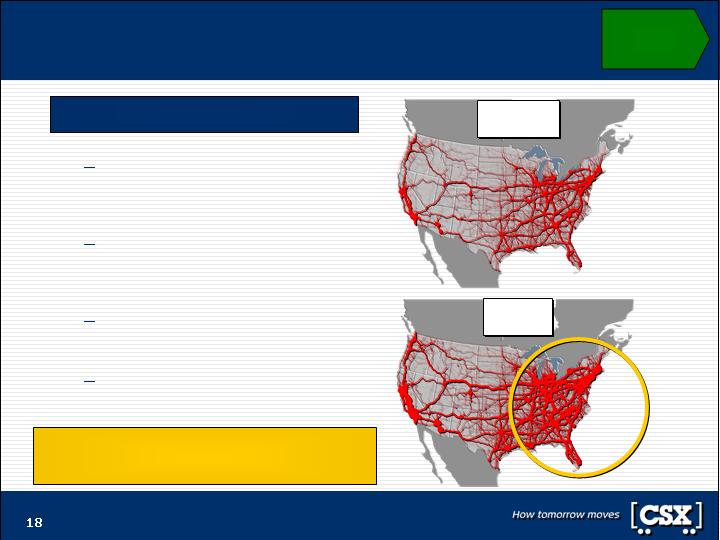

CSX provides a nation-critical service

CSX is an integral part of the

nation’s infrastructure

CSX operates approximately

21,000 route miles of track

Serves every major market in the

eastern U.S., with direct access to

all Atlantic and Gulf Coast ports

CSX is an economic driver

$10 billion of annual revenue

Over 35,000 employees

Ships life-essential goods and

serves national interest

2007 Population in Major Metropolitan Areas

GT 10 Million

5 – 10 Million

3 – 5 Million

1 – 2 Million

2 – 3 Million

New Orleans

Chicago

St Louis

Memphis

Source: Global Insight

Miami

New York

Jacksonville

Tampa

Orlando

Atlanta

Baltimore

Philadelphia

Washington

Boston

Note: Stock price performance as of May 30, 2008; adjusted for splits; Rail industry includes BNI, CNI, CP, NSC and UNP.

Outperformed all other Class I

rails over a one, two, three, four

and five year period

Outperformed 95% of the

S&P 500 since 2005

Operating margin tied for best

of U.S. railroads during

first quarter 2008

Industry-leading guidance and

aggressive capital structure

to maximize investment returns

CSX has delivered superior shareholder value

Total Shareholder Return

34%

221%

357%

4 Years

59%

245%

347%

5 Years

24%

123%

244%

3 Years

15%

50%

114%

2 Years

(7%)

19%

56%

1 Year

S&P

500

Rail

Industry

CSX

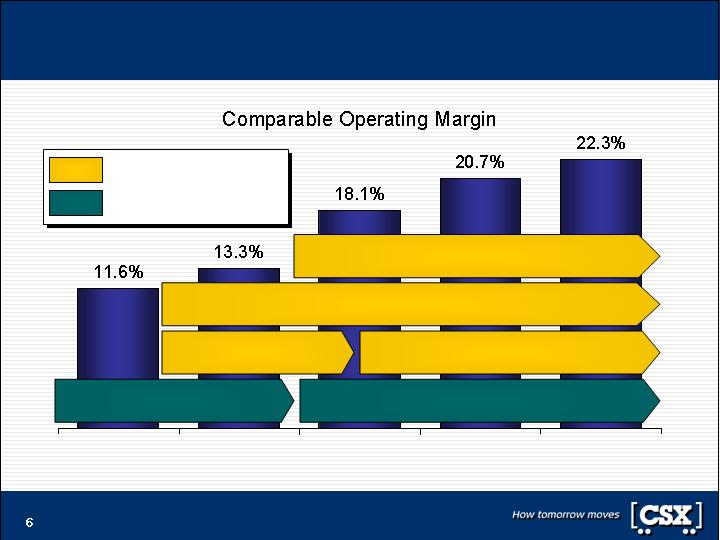

CSX has nearly doubled margins by building a

strong foundation and driving operational excellence

Assembling the Team &

Management Restructuring

“Safety First” Culture of Accountability

Pay for Performance

Note: See GAAP Reconciliation for details on Comparable Operating Margin.

2003

2004

2005

2006

2007

Operational Excellence

Strong Foundation

Network Realignment and

Disciplined Investment in Core Assets

Process Excellence Teams and Value Pricing

One Plan Implementation

One Plan — Resource Alignment

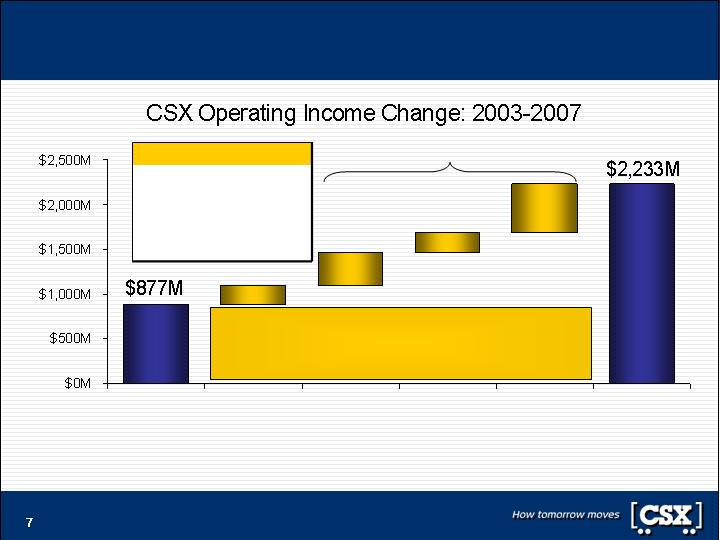

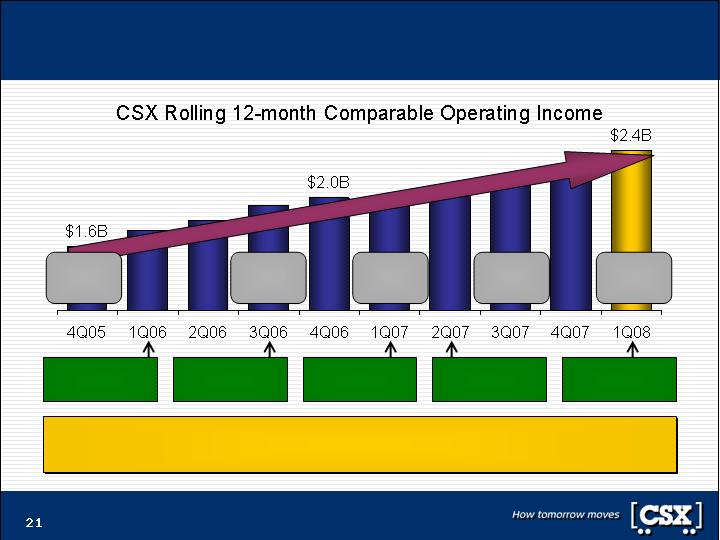

Operating income nearly tripled since 2003;

Management is driving price, volume and productivity gains

2003

Comparable

Operating

Income

2007

Comparable

Operating

Income

Net

Inflation

Real

Pricing

Volume

Productivity

28%

Real Pricing

16%

Volume

40%

16%

Net Inflation

Productivity

Sources of Income Growth

Sustained, industry leading price above inflation.

Volume is up 7% on RTM basis with favorable mix.

Productivity has exceeded $500M.

Note: Inflation assumed at 3.5% based on AAR’s ALL-LF index. Real pricing based on “same store sales” price

gains less inflation and net impact from fuel price. See GAAP Reconciliation for CSX data.

Management Action

CSX has delivered superior financial performance

39%

CAGR

8%

7

S&P 500

20%

6

NSC

22%

5

BNI

24%

4

CNI

32%

3

CP

34%

2

UNP

39%

1

CSX

2004-2007

CAGR

Rank/Company

Note: See GAAP Reconciliation for CSX data; peer comparisons based on First Call data.

CSX leads the industry across critical performance measures

NSC

CP

CP

NSC

CNI

NSC

CP

CNI

CNI

CP

CP

CNI

CNI

NSC

BNI

BNI

BNI

CP

BNI

UNP

NSC

CNI

UNP

BNI

UNP

BNI

UNP

UNP

CSX

UNP

CSX

CSX

CSX

CSX

NSC

CSX

Projected

Analyst EPS

Growth

through 2010

EPS

Growth

Margin

Expansion

Expense

Control

per RTM

Employee

Safety

Shareholder

Value

Creation

Worst

Best

Shareholder Value Creation based on Total Shareholder Return from Q1 2007 - Q1 2008. Safety based on 2007 FRA

Personal Injury statistics. Expense Control per Revenue Ton Mile, Margin Expansion and EPS Growth based on Q1 2007

vs. Q1 2008 results. CN and CP expenses have been adjusted for the impact from translation of U.S. dollar-denominated

expenses into Canadian dollars. Projected Analyst EPS Growth is 2007 through 2010 and is based on First Call data.

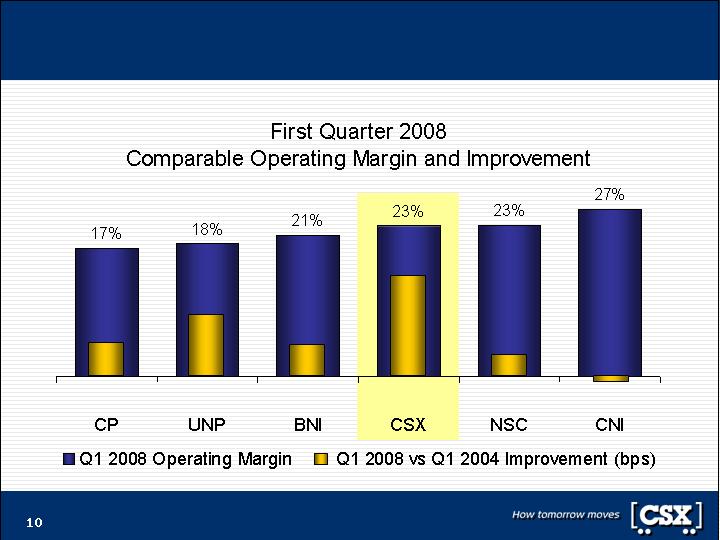

First quarter results confirm industry-leading momentum

420

760

410

1,240

270

(30)

Note: See GAAP Reconciliation for CSX data; peer comparisons based on First Call data.

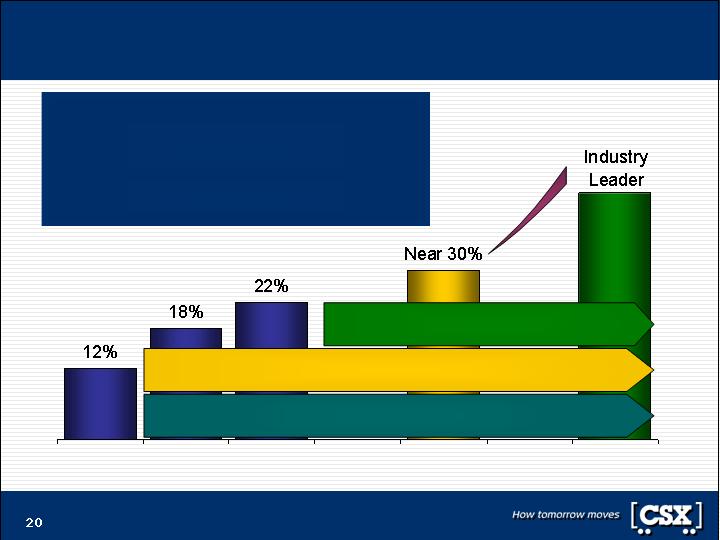

CSX is on target to become the best railroad

in North America

How Tomorrow Moves…

Exceed $1B

in 2010

Free Cash Flow

Before Dividends

Near 30%

By 2010

Operating Margin

18%–21%

CAGR

Earnings Per Share

13%–15%

CAGR

Operating Income

2008–2010

Targets

Note: Compound annual growth rates are off comparable 2007 results; EPS targets are stated before share buybacks.

Guidance is based on:

$400M+ of Productivity through 2010

6+% Pricing guidance in 2008

CSX creates value for

shareholders through

balanced capital deployment

Strategic volume growth in key markets

Strategic initiatives to drive record margins

Strong Foundation: “Safety First,” Accountability, Pay for Performance

Note: See GAAP Reconciliation for details. 2010 target based on low-70’s CSX Operating Ratio guidance.

2007

1Q 2008

2008

2009

2010

Total Service Integration

Operational Excellence: Process Excellence & Value Pricing

Operational Excellence: One Plan, Resource Alignment, Core Asset Investment

CSX leveraging a foundation

of excellence to achieve

targeted 30% margins

Capture strategic growth

Technology – Building the railroad of the future

Proven leaders to meet future business goals

CSX to deliver $400M+ of productivity through 2010

Implementing on-board fuel saving systems

Effective deployment of fuel-efficient processes

Fuel Efficiency

Utilization gains through reduced dwell

Improved reclaim and settlement reduces cost

Car Fleet Utilization

Utilization gains with advanced planning tools,

distributed power and Total Service Integration

Driving maintenance efficiency and reliability

Locomotive Fleet

Management

Technology drives terminal and customer efficiency

Driving infrastructure maintenance productivity with

process and technology

Labor Productivity

Continuous focus on plan design efficiency

TSI building reliable and productive service products

Network Efficiency/

Total Service Integration

Strategies for achieving targets

Key focus area

Disciplined process excellence teams have continuously delivered on

clear productivity targets and have a pipeline of specific initiatives

Operational

Excellence

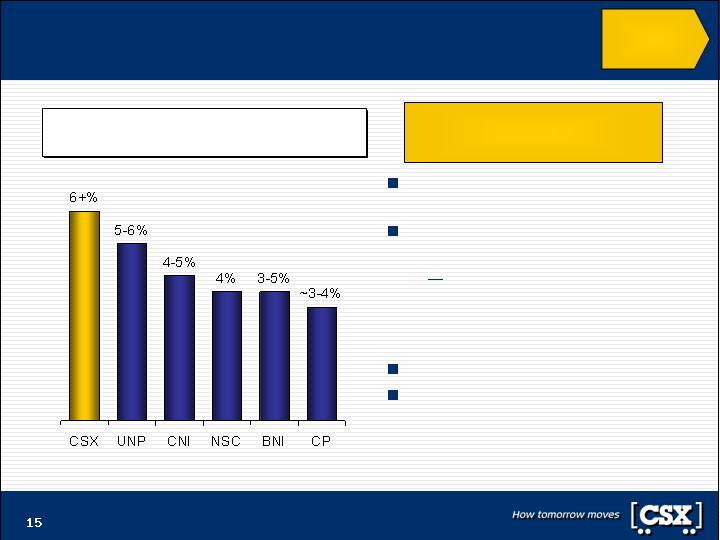

CSX to continue delivering strong price gains

Increasingly reliable service

product drives value

External factors continue to

favor rail

Globalization, shifting

supply chains, higher

trucking costs, increasing

commodity prices

Test price ceilings

Internal targets and rewards are

based on bottom-line impact

CSX has the highest price guidance

in the rail industry for 2008

Drivers of continued

strong pricing

Note: Peer railroad price guidance given by rail executives on analyst calls.

Operational

Excellence

TSI takes service execution to the next level

Total Service Integration

initiative aims to achieve:

Longer trains

Faster loading/unloading

More unit trains

Fewer handlings

As a result, customers will

experience:

Increased reliability

Superior service

Quicker turn times

Total Service Integration aligns

customer needs with operational capabilities

Execution of Total Service

Integration will deliver:

1)

Increased capacity to serve

more customers

2)

Ability to capture volume

growth through superior

service and flexibility

3)

Sustained pricing gains and

improved return on capital

Total Service

Integration

“Smart” Cars

Safety & Asset Utilization

Electronically Controlled Pneumatic (ECP)

Brakes Safety & Fuel Efficiency

Technology drives productivity, reliability, safety

Positive Train Control and

Locomotive Optimization

Ensures optimum safety and plan

compliance

Proactively adjusts speed to optimize

fuel economy

Drives increased velocity and asset

reliability

Yard Automation

Proactive labor and material planning

Robotics perform routine maintenance

Benefits include labor and asset

productivity, as well as improved

service reliability

Asset Tracking

Enhanced fuel efficiency, labor

productivity and safety through

precise tracking of assets and people

Technologies in the pipeline will

also drive benefits:

Wayside Detection Technologies

Safety & Reliability

Optical Joint Bar Detection

Technologies Safety & Reliability

Vehicle Mounted Track Inspection

Devices Safety & Asset Utilization

Advanced

Technology

Emerging Advanced Technologies

Today

CSX

Territory

2020

Macro trends create an opportunity for CSX

1)

Trucking industry is challenged

Highway congestion is bad and getting

worse; higher fuel costs and

environmental advantage favor rail

2)

Global consumption is rising

Population growth and globalization drive

rising demand for energy, food and other

commodities

3)

East Coast ports are growing

Panama Canal expansion & West Coast

port congestion create an opportunity

4)

Rail is valued by the public

Increase in public funding facilitates

development of expanded, improved

service products

Key trends favor CSX

Source: USDOT FHWA Freight Analysis Framework

CSX’s ability to capitalize on key macro

trends depends on appropriate investment

Capture

Strategic

Growth

Investments and alliances target long-term growth

CSX launched the National Gateway

Initiative to connect ports, gateways and

markets through a world-class

double-stack network

Provides meaningful connections and

enables expedited traffic flows across

the CSX network

CSX is building long-term network

solutions with trucking companies

Partnerships are cost-efficient for mid-

and long-haul moves

Addresses truck driver shortage

To fund growth, CSX is also exploring:

Public Partnerships and Grants

Asset-based business alliances

to enable growth

New York

Wilmington

Key CSX Port

Jacksonville

Savannah

Charleston

Virginia

Ports

Baltimore

New Orleans

Expansion

Clearances

New Construction

Capture

Strategic

Growth

CSX is capitalizing on real opportunities while the

TCI Group wants to freeze strategic capital spending

Continued focus on excellence is expected to achieve

industry-leading operating margins

2003

2005

2007

2010

Target

CSX

Vision

Strong Foundation: Remains the same—safety leadership

and a culture that empowers leaders to perform

New Initiatives: Drive sustained strategic

long-term volume growth across markets

Operational Excellence: Discipline and excellence drive

continued long-term productivity and inflation-plus pricing

1)

Strong Foundation remains in place

2)

Operational Excellence delivers results

3)

New Initiatives take CSX to the next level

CSX can achieve industry-leading margins

through consistent, continuous improvement.

Note: See GAAP Reconciliation for CSX historical data.

Industry-leading operational performance drives ability to

deliver significant value to shareholders

$3B addl. share

buyback by 2010

Raised to $3B

buyback by 2008

$2B share

buyback by 2008

Between 2007 and 2010, CSX plans to return at least $6.5B of value

to shareholders through dividends and share repurchases

Note: See GAAP Reconciliation for Comparable Operating Income.

54%

dividend

increase

20%

dividend

increase

25%

dividend

increase

20% 2Q08

dividend

increase

30%

dividend

increase

$500M share

buyback

$150M share

buyback

CSX has an aggressive approach to leverage and

return of capital

CSX has the most aggressive capital structure of any major

Class I railroad

Only BBB- rated railroad

CSX has a history of returning significant capital to shareholders

Repurchased nearly $3 billion of stock since 2006; targeting

another $3 billion by 2009

Nearly tripled quarterly dividends since 2005

CSX balance sheet policy is efficient and prudent

Lowest long-term cost of capital

Provides financial flexibility and continued access to

capital markets

CSX’s capital structure achieves

lowest cost of capital and supports business strategy

CSX’s balanced approach is well known and well executed

Capital

Investment

Investing $5B through

2010 to support

long-term growth

Share

Buybacks

Repurchased nearly

$3B since 2006

Targeting another $3B

by year-end 2009

Dividends

Nearly tripled the

quarterly dividend

since 2005

. . . While maintaining an investment grade profile

Growing Free Cash Flow and

Improving Return on Invested Capital . . .

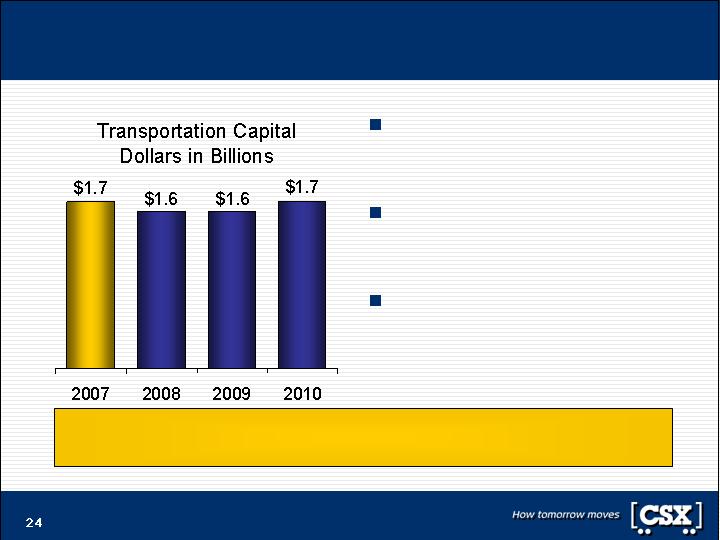

Key investments will support long-term growth

Note: Excludes Katrina-related capital. 2007 includes $200M of locomotive refinancing.

CSX’s disciplined capital

spending is consistent with

strategic objectives

Economics, scientific

modeling and safety

drive investment

Level of capital investment is

in line with industry peers

Disciplined capital analysis aims to

maximize investment returns on replacement cost basis

CSX’s Board is driving shareholder

value creation

More than 100 years of Board experience in rail, financial, energy and

industrial companies

CSX, Honeywell, Altria, Hartford, Dominion Resources,

Southern Company, Ashland, PNC, Bank of New York Mellon,

SunTrust, Smithfield, Constellation, Exelon and HCA

Need for diverse experience reflects regulated history and attributes

of railroads

Seven current and former CEOs, including Michael Ward

CEO and COO experience spans rail, financial and industrial

companies

CSX, Illinois Central, Florida East Coast, Southern Company,

Haskell, PHH, Citi Alternative Investments, Mercantile

Bankshares, AEGON, Cendant

Michael Ward and nominee John McPherson each have at least 30

years of railroad experience

Elizabeth Bailey was a key leader in airline deregulation and is

nationally recognized as a transportation and economics policy expert

John Breaux is a transportation policy expert with strong U.S. Senate

experience

CSX Board expert, diverse and performance driven

Compelling

Transportation

Experience

Blue Chip

Business

Experience

Governance and

Policy Expertise

CSX has an exceptional governance foundation

No poison pill

Opted out of anti-takeover statutes

Annual election of entire board by majority vote

No supermajority vote requirements

Presiding independent director with delineated duties

Board comprised entirely of outside directors other than CEO

CSX is a leader in Corporate Governance

Board and management driving proactive changes

Most aggressive capital

structure among its peers

Repurchased nearly $3

billion of stock since 2006

Targeting further $3 billion

buyback through 2009

Nearly tripled quarterly

dividend since 2005

ONE Plan implemented

during 2004

Rebuilt safety and

service culture

Now rank among industry

leaders in safety and

customer service

Initiating Total Service

Integration (TSI) to take

operations to next level

Michael Ward elected

Chairman & CEO in 2003

New executive team put in

place during 2003-2004

Reduced management

positions nearly 20%

Restructured incentive

pay plans to be 100%

performance-earned

Hired new talent to

diversify workforce

Acquired New York

Central assets of Conrail

Divested American

Commercial Lines

Sold Sea-Land

International assets

Sold CTI Logistics

Divested Horizon Lines

Sold CSX World Terminals

Corporate

Restructuring

New

Management

Operational

Improvement

Balance Sheet

Optimization

Over last three years, delivered 244% shareholder return, more than

doubled operating income, and nearly tripled earnings per share

Note: Stock price performance as of May 30, 2008 and adjusted for splits; operating income and EPS data is 2004 – 2007

TCI Group could jeopardize CSX’s

momentum and success

TCI Group’s demands would impair value

Investing for long-term

growth and value

creation

Freeze

expansion

capital spending

Managing regulatory

concerns; pricing to the

market reflecting value of

service

Increase

customer prices

7% annually

Repurchased nearly $3B

since 2006; further $3B

targeted by year-end

2009

Annual stock

buyback of 20%

for five years

CSX stock price has

significantly exceeded

proposed LBO price

Leveraged

Buyout

CSX Status

Negative

Credit

Impacts

Ignores

Risk Impacts

Flawed

Assumptions

Sacrifices

LT Potential

Proposal

Statements made by Chris Hohn and TCI have fueled support in

Congress for re-regulation, which would destroy shareholder value

CSX is investing for future strategic growth; TCI Group

prefers to freeze all investments & take CSX debt to junk

Invested in Southeast

Expressway to support capacity

expansion in key growth markets

Developed a clear strategy to

leverage growing Eastern ports

Unveiled National Gateway

initiative to connect ports with

key population centers and

Western gateways

Targeted investments in

advanced technology to drive

productivity, reliability and safety

TCI Group has advocated that “it

is prudent to freeze expansion

capex.”

TCI Founding Partner

Snehal Amin, 3/5/08

TCI Group has “no detailed

operating plan” and no capital

investment strategy for CSX

TCI Group would take CSX to

junk status, which would inhibit

investment to spur future growth

CSX

TCI Group

TCI Group’s $2.2B “productivity” claim for CSX is flawed

Flawed analysis; relies on theoretical volume growth.

$2,220M

Total TCI Group Value

CSX targets $400M+ productivity in 3 years; lower TCI Group

target is over 5-10 years and is based on flawed assumptions.

$380M

Productivity Value

Analysis flawed; CSX more productive per RTM than NS.

$150M

Labor Productivity

CSX is most fuel efficient RR when adjusted for length of haul.

$130M

Fuel Efficiency

Accurate analysis shows $35M gap to NS; initiatives in place.

$100M

Locomotive

Maintenance

$1.8B refers not to productivity, but entirely to volume growth.

$1,840M

Capacity/Volume Value

Flawed analysis based on anecdotal benchmarks.

$300M

Reduce load/unload time

TCI Group overstates the number of handlings at CSX by 50%.

$400M

Reduce handlings

CSX and CN dwell already identical when correctly adjusted.

$200M

Reduce dwell

Impact overstated. Velocity exceeds NS in nearly all markets.

$40M

Increase velocity

Benefits solely derived from volume growth.

$900M

Increase cars per train

Flaw to TCI Group Analysis

Est.

Value

TCI Group

“Opportunity” Source

TCI Group brings poor track record, minimal

experience

CSX targeted directors have nearly twice

the rail board experience as TCI Group nominees

Gilbert Lamphere

Chaired a publicly traded company sold through a distressed sale, and has a career characterized by

buyouts and leverage.

Gary Wilson

Led Northwest Airlines into bankruptcy and sold more than 75% of his shares in the months immediately

leading up to the bankruptcy filing. Yahoo! board member.

Timothy O’Toole

No U.S. public board experience. Transitional CEO as Conrail was converted to a switching operator. As

Managing Director of London Underground, performance is down sharply and need for government

funding is up 600%.

Alexandre Behring

No U.S. public board experience. Led Brazilian railroad a fraction of CSX’s size with an abysmal safety

record. Has said the TCI Group has “no detailed operating plan for CSX.”

Christopher Hohn

Demands for CSX, if implemented, could have impaired shareholder value. Made statements raising

significant regulatory concerns in Washington. No U.S. public board experience. Resigned from a UK board

amid allegations of conflict of interest.

Others don’t think TCI Group’s slate is world-class

On Christopher Hohn : “The interlude with Hohn was nerve-wracking, especially

because he would say one thing one day and another the next…His demands

changed quicker than the time of day.���

Former Deutsche Börse CEO Werner Seifert, writing in “Invasion der Heuschrecken” (or

“Invasion of the Locusts”), translated from the original German edition

On Gary Wilson: “Until now I naively believed that self-destructive doomsday

machines were fictional devices found only in James Bond movies. I never believed

that anyone would actually create and activate one in real life. I guess I never knew

about Yang and the Yahoo! Board.”

Carl Icahn, activist investor, writing on the value-destructive actions of Wilson and the

Yahoo! Board

On Timothy O’Toole : “It is widely known that Tim O’Toole’s abrasive manner

played a significant role in the breakdown of relationships between the Treasury

and Transport for London.”

UK Treasury Department Official, speaking of O’Toole’s relationships with other

government officials

Dissidents have a mixed record and fractured relationships

CSX believes dissidents would not add value to the Board

TCI Group nominees fail to represent the best interests of all shareholders

TCI Group’s desire to leverage CSX’s balance sheet to create a fast exit opportunity is

not in the best interest of the company or its shareholders

Credit default swaps would financially benefit TCI Group at the expense of

CSX shareholders

TCI Group has misrepresented its nominees

TCI Group nominees represent a track record of abysmal safety, bankruptcy and poor

operational performance; three nominees have no U.S. Board experience

TCI Group has overstated its nominees’ rail operating experience

TCI Group’s slate has provided no business plan or strategic insights

Proposals to date have been constantly changing, reflecting a lack of consistent vision

Proposals to date do not reflect significant understanding of U.S. railroad industry, its

regulatory environment or CSX’s business

Election of TCI Group slate will interrupt the value creation from CSX’s

strategic plan

It became apparent through negotiations that the TCI Group’s interests were not aligned

with value creation for all shareholders

The TCI Group could disrupt CSX’s momentum and success

Closing Remarks

CSX’s Board is

driving shareholder

value creation

CSX’s Board & Mgmt.

have transformed CSX

into an industry leader

CSX Board delivers results; TCI Group puts results at risk

TCI Group could

jeopardize CSX’s

momentum & success

CSX is on target

to become the best

railroad in N. America

Re-elect the CSX Board to ensure maximum shareholder value creation

TCI Group’s nominees bring a poor track record, limited

experience and no operating plan…

TCI Group’s proposals would put CSX’s future at risk

Long-term Board strategy targets industry-leading

operating margins

CSX has achieved unprecedented results with

industry-leading forward guidance

CSX Board and Management deliver superior

performance and leading governance

Based on all criteria, the CSX Board should be re-elected

Strong governance standards

Engaged board with diverse skill sets

Aggressive capital structure

Concrete plan for future performance enhancement

Superior performance relative to competitors

Significant return of capital to shareholders

Superior stock price performance

Vote the White Proxy Card

Appendix and GAAP Reconciliation

Recognized leader in transportation policy in the US

Served as a commissioner of the Civil Aeronautics Board, where she oversaw the deregulation of the

airline industry

During her tenure with Altria oversaw many consolidating acquisitions as well as the shareholder

value creating spin-offs of Kraft Foods ($49 billion) and Philip Morris International ($107 billion)

During her almost 20 year tenure on the Altria board, the company has generated annualized returns

of over 19% for shareholders

Altria: Director

Brookings Institution: Trustee

National Bureau of Economic Research: Board of Trustees

Teachers Insurance and Annuity Association: Director

Elizabeth E. Bailey

Founder and president of Aguila International, a business-consulting firm specializing in human

resources and leadership development

Appointed by President Reagan to serve as chief national spokesperson and administrator for federal

volunteerism programs during the second Reagan administration

During her tenure at CCA, Forbes named it the “Best Managed Company” in Business Services and

Supplies

During her almost 5 year tenure as a director of CCA, the company has generated annualized returns

of over 25%

Aguila International: President

Quest International: President & CEO

Park National Bank: Director (Chair, Audit Committee)

Corrections Corporation of America: Director

Donna M. Alvarado

Sold Mercantile Bankshares to PNC Financial Services for $5.9 billion after successfully

reorganizing the firm and growing the company from $11 billion in assets in 2002 to $18 billion in

assets in 2006

Director at Hartford Financial Services during decisions to repurchase $1.8 billion in stock

Citi Alternative Investments: President & CEO

The Carlyle Group: Managing Director

PNC Financial Services Group: Vice Chairman

Mercantile Bankshares: Chairman, CEO & President

Edward J. Kelly, III

Presiding Director

Drove superior stock performance, nearly tripled dividends, targeting nearly $6 billion of buybacks

between 2006 and 2009

Presiding over fastest growing company in an attractive industry

CSX: Chairman, President & CEO

Association of American Railroads: Director

Center for Energy and Economic Development: Director

Ashland, Inc.: Director

Michael J. Ward

Chairman

Until retiring from public service in 2005, Senator Breaux represented Louisiana in Congress for three

consecutive terms, beginning in 1987. Prior to his tenure as Senator, he served in the U.S. House of

Representatives from 1972 to 1987

Recognized as a non-partisan consensus builder while serving as a member of the Senate

committees on Finance and Commerce

U.S. Senate: Member

U.S. House of Representatives: Member

President’s Advisory Panel on Federal Tax Reform: Co-Chair

John B. Breaux

Director

Company / Position Experience

Key Accomplishments

Highly experienced, qualified and independent CSX Board

Assisted in the sale of Cendant’s vehicle leasing and fleet management unit to Avis Rent A

Car. Process included returning significant capital to shareholders through a "Dutch Auction“

self-tender offer to repurchase up to 50 million shares of Cendant stock

After leaving the Board of Cendant, Mr. Kunisch continued as a senior advisor to the Cendant

management team through July 2006 when Cendant refocused its portfolio by spinning off

Wyndham Worldwide ($7 billion) and Realogy Corporation ($7 billion) and selling Travelport to

Blackstone ($4 billion)

ABS Capital Partners: Special Partner & Senior Advisor

Cendant Corporation: Vice Chairman & Director

PHH Corporation: Chairman & CEO

Johns Hopkins Medical: Trustee

Robert D. Kunisch

Focused on five principles at FEC: customer service, managing expenses carefully, investing

capital wisely, utilizing assets productively, and safety

Increased customer satisfaction ratings, revenue per employee, intermodal volume, net

income, and earned Gold Harriman Awards for safety

Florida East Coast Railway: President & COO

Illinois Central Railroad: President & COO

Santa Fe Railroad: Regional VP & Assistant VP for Safety

John D. McPherson

Grew Southern Company’s reputation for excellent customer service, high reliability, and retail

electric prices significantly below the national average; Listed the top ranking U.S. electric

service provider in customer satisfaction for eight consecutive years

Maintained seven straight years of common stock dividend increases

Successfully sold non-core natural gas business in 2005 to focus on core business lines

Southern Company: Chairman, President, CEO

Georgia Power: President & CEO

Federal Reserve Bank of Atlanta: Chairman

David M. Ratcliffe

Member of Board integration committee overseeing Bank of New York’s acquisition of Mellon

Financial Corporation ($17 Billion)

Director at Exelon during decisions to repurchase $1.75 billion in stock

President of Johns Hopkins University before leading Kellogg Foundation, one of the world’s

largest philanthropic foundations ($7 billion endowment and nearly $300 million in annual

grants)

Kellogg Company: Director

Bank of New York Mellon: Director

Exelon Corporation: Director

William C. Richardson

Nearly doubled revenues since becoming CEO of the design-build company, positioning the

award-winning firm not only as an infrastructure leader in the Southeast U.S. but also an

emerging leader in North America

The Haskell Company: President & CEO

Construction Industry Roundtable: Director

National Center for Construction Education and

Research: Chairman

Steven T. Halverson

Director

Company / Position Experience

Key Accomplishments

Highly experienced, qualified and independent CSX Board

Led AEGON to a nearly 39% increase in net income and 10% increase in revenue in 2003, his first

full year as chairman

Oversaw AEGON’s acquisition of Transamerica Corporation ($21 billion) in 1999 as well as the

recent sale of Getronics ($1.8 billion on 10/12/07), the acquisition of Merrill Lynch Insurance ($1.3

billion on 12/31/07) and a share buyback ($1.5 billion on 11/19/07)

AEGON: Chairman & CEO

PNC Financial Services Group: Director

U.S. Chamber of Commerce: Vice-Chairman

Donald J. Shepard

As an active member of the compensation committees of corporate boards, has been a major

advocate of tying management pay to operating improvements and aligning management with long-

term shareholder interests

Oversaw SunTrust’s acquisition of National Commerce Financial ($7 billion) and Crestar Financial

($9 billion)

Oversaw over $13 billion in asset divestitures at Dominion Resources over the course of 2007 and

a subsequent $5.3 billion Dutch Auction share repurchase in August 2007 as well as a $4 billion

share buyback in 2005

SunTrust Bank: Director

Dominion Resources: Director

Smithfield Foods: Director

Hospital Corporation of America: Director

Chesapeake Corp: Director

Frank S. Royal

Director

Company / Position Experience

Key Accomplishments

Highly experienced, qualified and independent CSX Board

Proxy Statement Disclosure

Important Information

In connection with the 2008 annual meeting of shareholders, CSX Corporation ("CSX") has filed with the SEC and mailed to shareholders a definitive Proxy Statement dated April 25, 2008. Security holders are strongly advised to read the definitive Proxy Statement because it contains important information. Security holders may obtain a free copy of the definitive Proxy Statement and any other documents filed by CSX with the SEC at the SEC’s website at www.sec.gov. The definitive Proxy Statement and these other documents may also be obtained for free from CSX by directing a request to CSX Corporation, Attn: Investor Relations, David Baggs, 500 Water Street C110, Jacksonville, FL 32202. CSX, its directors, director nominee and certain named executive officers and employees may be deemed to be participants in the solicitation of CSX’s security holders in connection with its 2008 Annual Meeting. Security holders may obtain information regarding the names, affiliations and interests of such individuals in CSX’s definitive Proxy Statement and its May 15, 2008 letter to shareholders filed with the SEC as definitive additional soliciting materials.

Forward-Looking Disclosure

This presentation and other statements by the company contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act with respect to, among other items: projections and estimates of earnings, revenues, cost-savings, expenses, or other financial items; statements of management’s plans, strategies and objectives for future operation, and management’s expectations as to future performance and operations and the time by which objectives will be achieved; statements concerning proposed new products and services; and statements regarding future economic, industry or market conditions or performance. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,” “project,” “estimate,” and similar expressions. Forward-looking statements speak only as of the date they are made, and the company undertakes no obligation to update or revise any forward-looking statement. If the company does update any forward-looking statement, no inference should be drawn that the company will make additional updates with respect to that statement or any other forward-looking statements.

Forward-looking statements are subject to a number of risks and uncertainties, and actual performance or results could differ materially from that anticipated by these forward-looking statements. Factors that may cause actual results to differ materially from those contemplated by these forward-looking statements include, among others: (i) the company’s success in implementing its financial and operational initiatives; (ii) changes in domestic or international economic or business conditions, including those affecting the rail industry (such as the impact of industry competition, conditions, performance and consolidation); (iii) legislative or regulatory changes; (iv) the inherent business risks associated with safety and security; and (v) the outcome of claims and litigation involving or affecting the company. Other important assumptions and factors that could cause actual results to differ materially from those in the forward-looking statements are specified in the company’s SEC reports, accessible on the SEC’s website at www.sec.gov and the company’s website at www.csx.com.

GAAP Reconciliation Disclosure

CSX reports its financial results in accordance with generally accepted accounting principles (“GAAP”). However, management believes that certain non-GAAP financial measures used to manage the company’s business that fall within the meaning of Regulation G (Disclosure of Non-GAAP Financial Measures) by the SEC may provide users of the financial information with additional meaningful comparisons to prior reported results.

CSX has provided operating income, margin and earnings per share adjusted for certain items, which are non-GAAP financial measures. The company’s management evaluates its business and makes certain operating decisions (e.g., budgeting, forecasting, employee compensation, asset management and resource allocation) using these adjusted numbers

Likewise, this information facilitates comparisons to financial results that are directly associated with ongoing business operations as well as provides comparable historical information. Lastly, earnings forecasts prepared by stock analysts and other third parties generally exclude the effects of items that are difficult to predict or measure in advance and are not directly related to CSX’s ongoing operations. A reconciliation between GAAP and the non-GAAP measure is provided. These non-GAAP measures should not be considered a substitute for GAAP measures.

GAAP Reconciliation to comparable results

23.0%

$ 624

-

-

-

(2)

2,087

$ 2,713

Q108

23.2%

22.3%

20.7%

18.1%

13.3%

11.6%

Comparable Operating Margin

$ 2,390

$ 2,233

$ 1,981

$ 1,556

$ 1,068

$ 877

Comparable Operating Income

-

-

-

-

-

108

Plus Additional Loss on Sale

-

-

-

-

-

232

Plus Provision for Casualty

Claims

-

-

-

-

71

22

Plus Restructuring Charge

(11)

(27)

(168)

-

-

-

Less Pretax Gain on

Insurance Recoveries

7,920

7,770

7,417

7,062

7,043

7,058

Operating Expense

$ 10,321

$ 10,030

$ 9,566

$ 8,618

$ 8,040

$ 7,573

Operating Revenue

Q108

LTM*

2007

2006

2005

2004

2003

Dollars in millions

* LTM is last twelve months (Q2 07 – Q1 08)

GAAP Reconciliation to comparable results

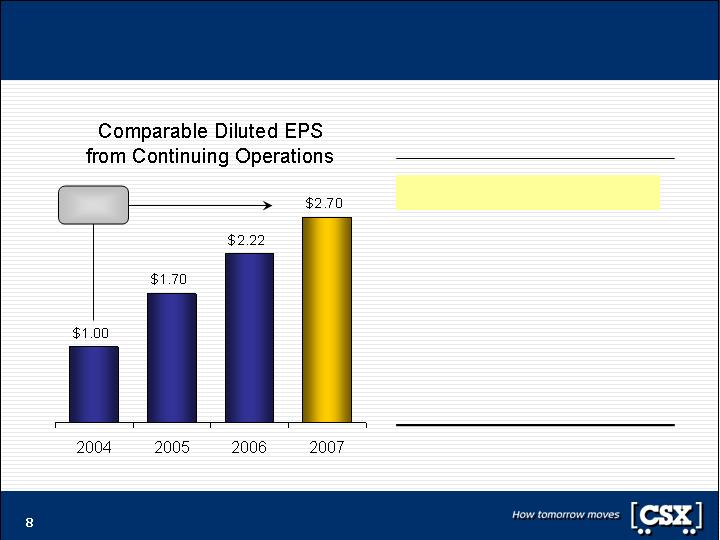

$ 2.70

$ 2.22

$ 1.70

$ 1.00

Comparable Diluted EPS From

Continuing Operations

)

$ 2.74

(0.04

-

-

-

-

)

)

)

$ 2.82

(0.22

(0.06

(0.32

-

-

)

$ 1.59

-

-

(0.16

0.27

-

)

$ 0.94

-

(0.04

-

-

0.10

Diluted EPS From Continuing Operations

Less Gain on Insurance Recoveries

Less Gain on Conrail Property

Less Income Tax Benefits

Plus Debt Repurchase Expense

Plus Restructuring Charge

2007

2006

2005

2004