Exhibit 99.2

Item 1

The Children’s Investment (TCI) Fund CSX The Children’s Investment (TCI) Fund Management (UK) LLP January 22, 2007 Prepared for Nelson Walsh This presentation is private and confidential

TCI Fund Management (UK) LLP, 7 Clifford Street, London, WIS 2WE, UK Tel: +44 20 7440 2330 Plaintiff’s Exhibit 37 TCI0153568 ATTORNEYS’ EYES ONLY

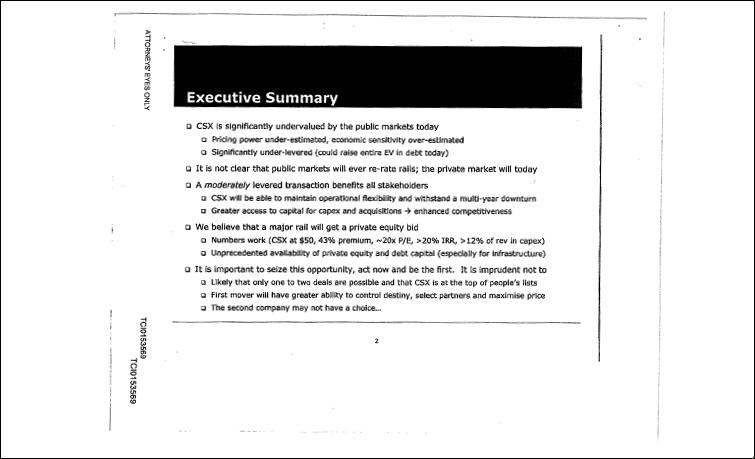

Executive Summary CSX is significantly undervalued by the public markets today Pricing power under-estimated,-economic sensitivity over-estimated Significantly under-levered (could raise entire EV in debt today) It is not clear that public markets will ever re-rate rails; the private market will today A moderately levered transaction benefits all stakeholders CSX will be able to maintain operational flexibility and withstand a multi-year downturn Greater access to capital for capex and acquisitions → enhanced competitiveness We believe that a major rail will get a private equity bid Numbers work (CSX at $50, 43% premium, ~20x P/E, >20% IRR, >12% of rev in capex) Unprecedented availability of private equity and debt capital (especially for infrastructure) It is important to seize this opportunity, act now and be the first. it is imprudent not to Likely that only one to two deals are possible and that CSX is at the top of people’s lists First mover will have greater ability to control destiny, select partners and maximise price The second company may not have a choice... TCI0153569 ATTORNEYS EYES ONLY

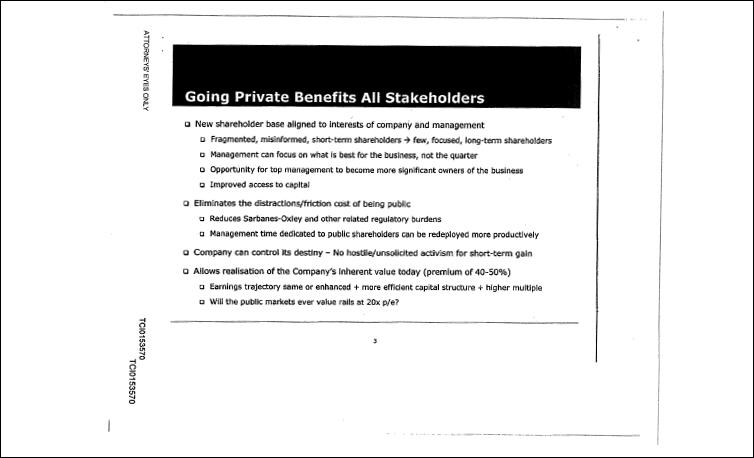

Going Private Benefits All Stakeholders New shareholder base aligned to interests of company and management Fragmented, misinformed, short-term shareholders → few, focused, long-term shareholders

Management can focus on what is best for the business, not the quarter Opportunity for top management to become more significant owners of the business Improved access to capital

Eliminates the distractions/friction cost of being public Reduces Sarbanes-Oxley and other related regulatory burdens Management time dedicated to public shareholders can be redeployed more productively

Company can control its destiny - No hostile/unsolicited activism for short-term gain Allows realisation of the Company’s inherent value today (premium of 40-50%) Earnings trajectory same or enhanced + more efficient capital structure + higher multiple Will the public markets ever value rails at 20x p/e? TCI0153570 ATTORNEYS’ EYES ONLY

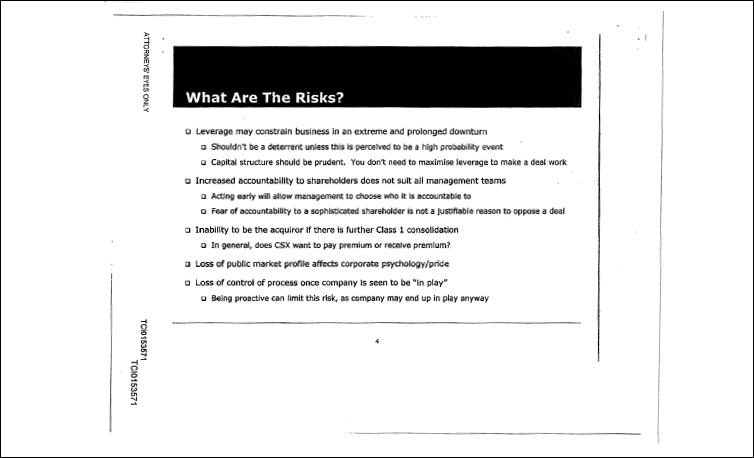

What Are The Risks? Leverage may constrain business in an extreme and prolonged downturn Shouldn’t be a deterrent unless this is perceived to be a high probability event Capital structure should be prudent. You don’t need to maximise leverage to make a deal work Increased accountability to shareholders does not suit all management teams Acting early will, allow management to choose who it is accountable to Fear of accountability to a sophisticated shareholder is not a justifiable reason to oppose a deal Inability to be the acquiror if there is further Class 1 consolidation In general, does CSX want to pay premium or receive premium? Loss of public market profile affects corporate psychology/pride Loss of control of process once company is seen to be “in play” Being proactive can limit this risk, as company may end up in play anyway TCI0153571 ATTORNEYS’ EYES ONLY

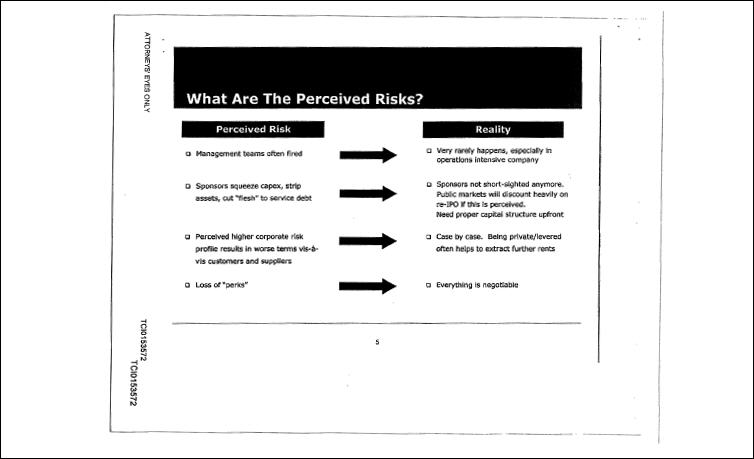

What Are The Perceived Risks? Perceived Risk Management teams often fired Sponsors squeeze capex, strip assets, cut “flesh” to service debt Perceived higher corporate risk profile results in worse terms vis-á- vis customers and suppliers Loss of “perks” Reality Very rarely happens, especially in operations intensive company Sponsors not short-sighted anymore. Public markets will discount heavily on re-IPO if this is perceived. Need proper capital structure upfront Case by case. Being private/levered often helps to extract further rents Everything is negotiable TCI0153572 ATTORNEYS’ EYES ONLY

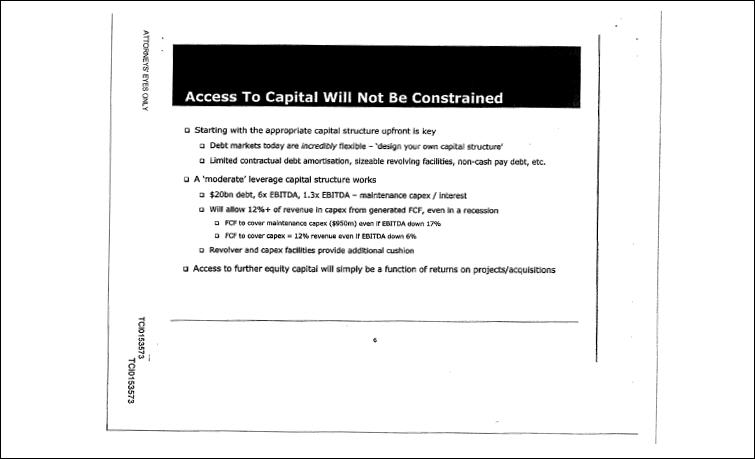

Access To Capital Will Not Be Constrained Starting with the appropriate capital structure upfront is key Debt markets today are incredibly flexible - ‘design your own capital structure’Limited contractual debt amortisation, sizeable revolving facilities, non-cash pay debt, etc. A ‘moderate’ leverage capital structure works $20bn debt, 6x EBITDA, 1.3x EBITDA - maintenance capex / interest Will allow 12%+ of revenue in capex from generated FCF, even in a recession FCF to cover maintenance capex ($950m) even if EBITDA down 17% FCF to cover capex = 12% revenue even If EBITDA down 6% Revolver and capex facilities provide additional cushion Access to further equity capital will simply be a function of returns on projects/acquisitions TCI0153573 ATTORNEYS’ EYES ONLY

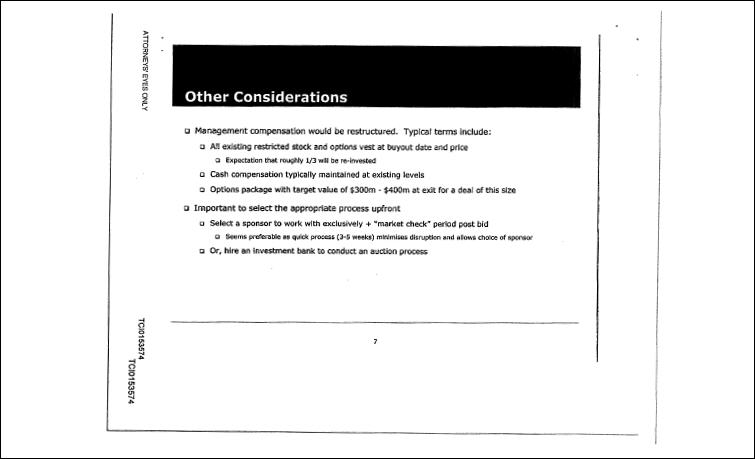

Other Considerations Management compensation would be restructured. Typical terms include: All existing restricted stock and options vest at buyout date and price Expectation that roughly 1/3 will be re-invested Cash compensation typically maintained at existing levels Options package with target value of $300m - $400m at exit for a deal of this size Important to select the appropriate process upfront Select a sponsor to work with exclusively + “market check” period post bid Seems preferable as quick process (3-5 weeks) minimises disruption and allows choice of sponsor Or, hire an investment bank to conduct an auction process TCI0153574 ATTORNEYS’ EYES ONLY

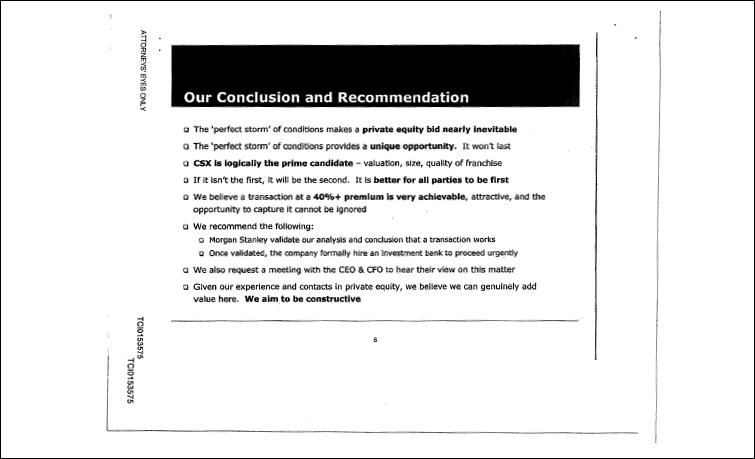

Our Conclusion and Recommendation The ‘perfect storm’ of conditions makes a private equity bid nearly inevitable The perfect storm’ of conditions provides a unique opportunity. It won’t last CSX is logically the prime candidate - valuation, size, quality of franchise If it isn’t the first, it will be the second. it is better for all parties to be first We believe a transaction at a 40%+ premium is very achievable, attractive, and the opportunity to capture it cannot be ignored We recommend the following: Morgan Stanley validate our analysis and conclusion that a transaction works Once validated, the company formally hire an investment bank to proceed urgently We also request a meeting with the CEO & CFO to hear their view on this matter Given our experience and contacts in private equity, we believe we can genuinely add value here. We aim to be constructive TCI0153575 ATTORNEYS’ EYES ONLY

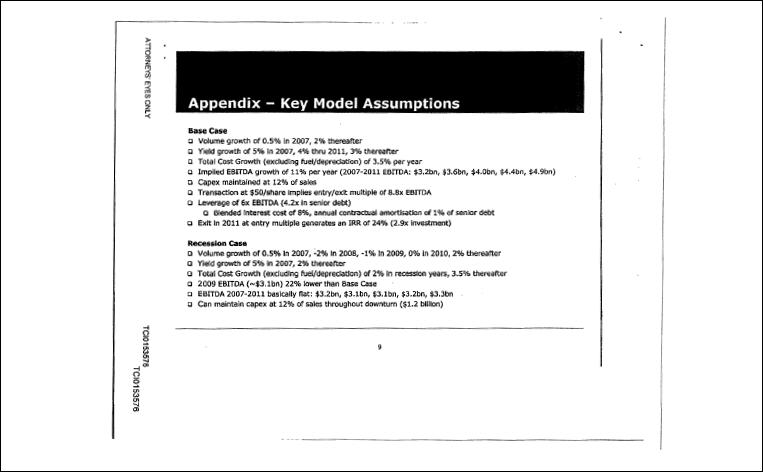

Appendix - - Key Model Assumptions Base Case Volume growth of 0.5% in 2007, 2% thereafter Yield growth of 5% in 2007, 4% thru 2011, 3% thereafter Total Cost Growth (excluding fuel/depreciation) of 3.5% per year Implied EBITDA growth of 11% per year (2007-2011 EBITDA: $3.2bn, $3.6bn, $4.0bn, $4.4bn, $4.9bn) Capex maintained at 12% of sales Transaction at $50/share implies entry/exit multiple of 8.8x EBITDA Leverage of 6x EBITDA (4.2x in senior debt) Blended Interest cost of 8%, annual contractual amortisation of 1% of senior debt Exit in 2011 at entry multiple generates an IRR of 24% (2.9x investment) Recession Case Volume growth of 0.5% in 2007, -2% in 2008, -1% in 2009, 0% in 2010, 2% thereafter Yield growth of 5% in 2007, 2% thereafter Total Cost Growth (excluding fuel/depreciation) of 2% in recession years, 3.5% thereafter 2009 EBITDA (~$3.1bn) 22% lower than Base Case EBITDA 2007-2011 basically flat: $3.2bn, $3.1bn, $3.1bn, $3.2bn, $3.3bn Can maintain capex at 12% of sales throughout downturn ($1.2 billion) TCI0153576 ATTORNEYS’ EYES ONLY

Disclaimer This document is being issued by The Children’s Investment Fund Management (UK) LLP and is for private circulation only. The Information contained in this document is strictly confidential and is only for the use of the company, firm or individual to whom it is sent and whose name appears on the face of this document. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of The Children’s Investment Fund Management (UK) LLP. The Children’s Investment Fund Management (UK) LLP is Authorised and Regulated by the Financial Services Authority to carry on regulated activities in the UK. The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore. No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of The Children’s Investment Fund Management (UK) LLP, its partners or employees and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. This document is being communicated by The Children’s Investment Fund Management (UK) LLP only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. The summary description of The Children’s Investment Fund Management (UK) LLP included herein and other materials provided to you are intended only for discussion purposes. This information is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. You should consult your tax, legal, accounting or other advisors about the issues discussed herein. A potential investor expressing an interest to invest in the transaction will be provided with an offering memorandum and subscription agreement (together, the “Fund Documents”) for the investment and an opportunity to review the documentation relating to the investment. Prospective investors must review the Fund Documents, including the risk factors, before making a decision to invest and should rely only on the information contained in the Fund Documents in making their investment decision. Investing in financial markets and securities involves risk. There can be no assurance that the investment objectives described herein will be achieved. Past performance is not a guarantee of future results. Investment losses may occur from time to time and investors could lose some or all of their investment. Distribution of this information to any person other than the person to whom this information was originally delivered and to such person’s advisors is unauthorised and any reproduction of these materials, in whole or in part, or the divulgence of any of their contents, without the prior consent of The Children’s Investment Fund Management (UK) LLP. In each such instance is prohibited. Notwithstanding anything to the contrary herein, each shareholder (and each employee, representative, or other agent of such shareholder) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of (i) The Children’s Investment Fund Management (UK) LLP and (ii) any of its transactions, and all materials of any kind (including opinions or other tax analyses) that are provided to the shareholder relating to such tax treatment and tax structure. These materials are accurate as of this date, and no representation or warranty is made as to its continued accuracy after such date. TCI0153577 ATTORNEYS’ EYES ONLY

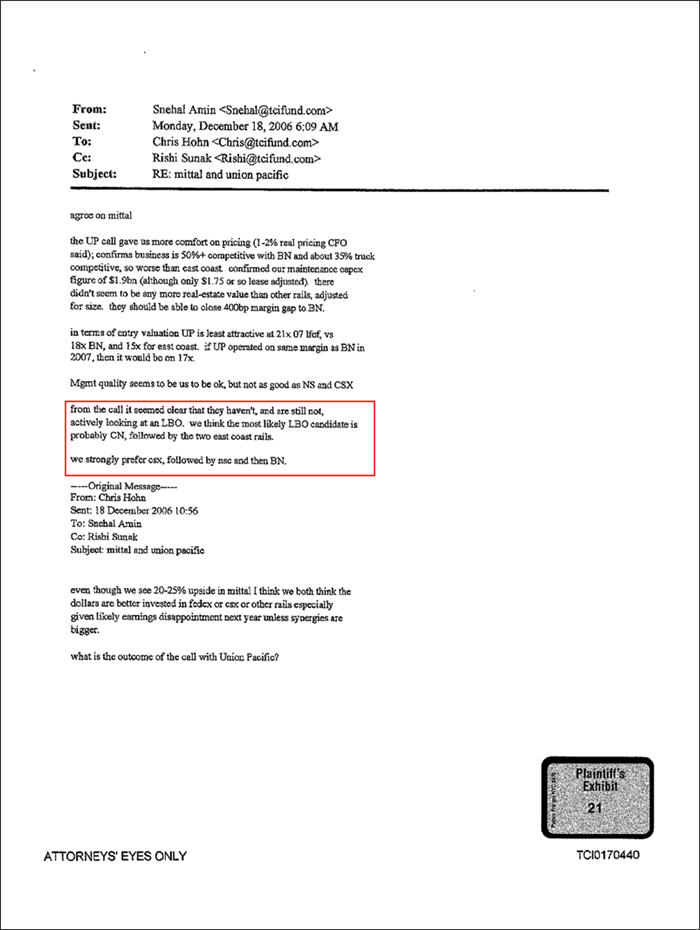

From: Snehal Amin <Snehal@tcifund.com> Sent: Monday, December 18, 2006 6:09 AM To: Chris Hohn <Chris@tcifund.com> Cc: Rishi Sunak <Rishi@tcifund.com> Subject: RE: mittal and union pacific agree on mittal The UP call gave us more comfort on pricing (1-2% real pricing CFO said); confirms business is 50%+ competitive with BN and about 35% truck competitive, so worse than east coast confirmed our maintenance capex figure of $1.9bn (although only $1.75 or so lease adjusted). There didn’t seem to be any more real-estate value than other rails, adjusted for size. They should be able to close 400bp margin gap to BN. in terms of entry valuation UP is least attractive at 21x 07 lfcf, vs 18x BN, and 15x for east coast. if UP operated on same margin as BN in 2007, then it would be on 17x. Mgmt quality seems to be us to be ok, but not as good as NS and CSX from the call it seemed clear that they haven’t, and are still not, actively looking at an LBO. we think the most likely LBO candidate is probably CN, followed by the two east coast rails. we strongly prefer CSX, followed by NSC and then BN. ----Original Message---- From: Chris Hohn Sent: 18 December 2006 10:56 To: Snehal Amin Cc: Rishi Sunak Subject: mittal and union pacific even though we see 20-25% upside in mittal I think we both think the dollars are better invested in FEDEX or CSX or other rails especially given likely earnings disappointment next year unless synergies are bigger. what is the outcome of the call with Union Pacific? Plaintiff’s Exhibit 21 TCI0170440 ATTORNEYS’ EYES ONLY

From: John Ho <john.ho@tcifund.com> Sent: Thursday, February 1, 2007 4:33 AM To: Snehal Amin <Snehal@tcifund.com> Subject: RE: Today’s Trading I know exactly what you mean by Chris getting on 1 call and got scared because management was bearish!!!!!!! We own this utility called Chubu Electric in Japan and he also had 1 call with management after we studied stock for 6 months and he wanted to sell the entire position after that call. Luckily we didn’t because stock went up 30% since then....... I suspect this would happen to NSC. We really stuck our neck out in Chubu (and he also said we had enough Jap utility exposure due to J-power) and we kept hammering away and we got him to talk with a JAPANESE analyst who he likes telling him mgt was just very conservative and that this analyst also called the company and got this confirmed. So I know exactly what you mean. From: Snehal Amin Sent: Thursday, February 01, 2007 5:18 PM To: John Ho Subject: RE: Today’s Trading we had a call with the NSC CFO who was bearish and scared the crap out of Chris (and they missed q4 consensus and market hammered stock, which didn’t help, but of course means now is also the wrong time to sell). this CFO is notoriously conservative, but because that was the only call Chris was on it tainted his picture of NSC and he didn’t want to keep adding rail exposure. CSX is much better we all agree (20%+ more fundamental upside, better chance of being taken out) so we are now swapping into it. NSC still has 40% absolute upside - ----Original Message From: John Ho Sent: 01 February 2007 00:52 To: Snehal Amin Plaintiff’s Exhibit 40 TCI0024086 CONFIDENTIAL

Sieger, Christopher From: Ha, Gil Sent: Thursday, April 05, 2007 11:36 AM To: Bryson, Nancy; Saglio, Jesse Cc: Mestre, Eduardo G. Subject: FW: CSX Attachments: CSX.xls; Bain conclusions.ppt CSX.xls (394 KB) Bain Conclusions.ppt (2 MB) Let’s sit down this afternoon and chat. I will propose a call tomorrow morning our time for them to walk us through their materials. ----Original Message--- From: Snehal Amin [mailto:Snehal@tcifund.com] Sent Thursday, April 05, 2007 8:47 AM To: Ha, Gil Cc: Chris Hohn; Rishi Sunak Subject CSX Gil I work with Chris at TCI. Please find attached our analysis- on CSX (operating model, LBO model, recap/buyback model) as well as the conclusions from the Bain study. We kindly ask that you not forward the attached to anyone until we have discussed disclosure with our lawyer; we don’t anticipate any issues; but we would like to check with him first and we trust that you will keep this confidential until then (hopefully later today). We wanted to get it out to you asap though so we could start discussing and moving forward. I think the best way to explain the models and how they work is over the phone. When would you be available for a call, ideally together with Chris and myself? If you let us know what times work for you we will accommodate as best we can. We are anxious-to discuss this with you asap. Here are the key things to know about the model: 1. ‘CSX Model’ is our base operating model. This assumes status quo capital structure. They key assumptions are 4-5% pricing growth per year (3% inflation + 1% real pricing + 1% ‘reversionary pricing’ from legacy contracts for each of the next 5 years), 1.5% volume growth, and non-fuel cost growth of 3% (labor + materials mostly) excluding volume. The output of this is circa 6% revenue growth and 15% EBIT growth over the next 5 years. The main difference versus management’s announced LT guidance looks to be 1% more price per year, which translates to 4-5% more EBIT growth. We have high conviction in higher pricing based on the level of captivity of the customer base (65% as per our work, per management and also per Bain), pricing now relative to the value of what is being shipped, and pricing rate relative to what the rails used to charge 20 years ago; in fact if anything we believe there is more pricing than what we assume. I was just in Washington DC yesterday and even the shippers lobbyists believe 5-6% annual pricing is likely going forward, and if the shippers are saying that then it must be conservative! We assume capex of 12% of sales to accommodate the 1.5% volume growth (management says 12-13%. of sales accumulates 2-3% volume). We assume maintenance capex of $1bn (slightly higher than management) Plaintiff’s Exhibit 71 EVR 00277

2. ‘Scenario Analysis’ is our recap/buyback analysis. You can change either the operating assumption or the recap assumption in cells O31 and O37. (Please note that when running the TCI operating case here the numbers will not be exactly in line with CSX Model sheet as we needed to accommodate being able to change the operating assumptions here without to much complexity, but they are close enough to make the point). The buyback/recap cases are: (1) TCI Base which is a 20% buyback per year, (2)Management Base which is the announced $2bn buyback over 2 years, (3)Initial Recap to 5x EBITDA with proceeds used to buyback stock immediately and delivering from there, (4) initial recap to 5x EBITDA and maintaining that leverage. We believe 5x EBITDA is the appropriate leverage for CSX as a public company as it allows EBITDA to fall roughly 30% (as seen in line 23) while still meeting interest and mairat caper requirements, and we feel 30% is very ample headroom given the stability of the business and pricing power; it also is comfortable on other leverage/coverage measures. The net result of this analysis is the share price trajectory in line 55, also graphed in upper right hand cornet of sheet. We assume the shares always trade at 15x forward P/E. What you can see is if the company just does what it says the stock should trade to roughly $65 by y/e 2010, while if it does what we think it can in pricing and maintains 5x EBITDA leverage the stock should trade above $120. That is a difference of nearly $55, 20% of which comes from our better pricing and 80% of which comes from leverage. $55 of upside is a lot when the stock is trading at $40, which is why we are so keen to engage management in a dialogue on leverage. 3. ‘CSX LBO’ is a simple LBO analysis. It will run off of whichever operating model you choose in ‘Scenario Analysis’. They key assumptions here are leverage (we have high conviction that banks will underwrite 7x EBITDA leverage in an LBO today) and exit valuation (we assume circa 15x earnings again). The result is a 20% IRR over 5 years if taken out at $55 per share on the TCI operating case; we think sponsors will view pricing similarly, but likely have more cost efficiencies than we model so their returns will in fact look higher. Based in discussions we have had, we believe LBO sponsors would accept high teens returns and infrastructure funds low teens returns for a business like CSX and to invest capital in this size. This gives us conviction that in a competitive process, CSX could sell for $55-60 per share. I hope this is a helpful start, and we look forward to speaking with you as soon as you are available. Kind regards Snehal Snehal K. Amin Partner The Children’s Investment Fund 7 Clifford Street, London W1S 2WE, UK +44 207 440 2330 (general) +44 207 440 2346 (direct) +44 207 440 2333 (fax) +44 774E 112 344 (mobile) snehal@tcifund.com The Children’s Investment Fund Management (UK) LLP (“TCI”) is authorised and regulated by the Financial Services Authority and is registered with the US Securities and Exchange Commission. The sender of this email is EVR 00278

Snehal Amin at Bear Stearns, May 8, 2007 Global Transportation Conference It has generated the net returns to its investors of over 300%. It’s also donated hundreds of millions of dollars to its foundation, which funds children’s causes in the developing world. TCI’s success is, in no small part, to key activist roles it has taken around the world with companies such as Deutsche Borse, ABM Amro in Europe, Arcelor Brasil in Brazil and J-Power in Japan. Recently, TCI has announced its investment in U.S. railroads, including a recent Hart-Scott-Rodino filing as an activist investor with a larger than $500 million investment in CSX. Mr. Amin oversees the investment strategies for the Americas, which includes both the U.S. and Latin America. And prior to his involvement with TCI, Mr. Amin was Vice President of the Merchant Banking Division of Goldman Sachs. Like I said, I’ve been looking forward to this presentation and I thank Snehal for agreeing to share his thoughts here with us at the Bear Stearns Global Transportation Conference. (inaudible) [Next speaker] Just for that kind intro we promise not to call publicly for the break up or sale of Bear Stearns. (laughter) At least not this week. [inaudible] In all seriousness, TCI was found not to be an activist fund. It was founded to be a fundamental investor to invest as owners of businesses and not stocks. On that basis, we’ve invested over a billion dollars in the U.S. rails. It’s unfortunate that this strategy sometimes results in public collisions with managements and boards. When that happens, when the boards and managements forget the most basic tenet of corporate governance and that’s managements are operators, boards are trustees and the shareholders are the owners. We’ve learned the hard way that when this relationship

breaks down, boards lose accountability, managements can get lazy and businesses underperform their potential. We fear that this is the state of the U.S. railroads and we can’t accept this and neither should anyone in this room. One could argue that these rail managements have done a good job. Pricing is strong, but that was inherited. Operational metrics are improving, but offer very low base. Stocks have done well, but they still trade at half of what they’re worth. We believe in judging growth potential and not the past. So we say to the management teams that it’s time to stop looking in the rear-view mirror. If you don’t understand the potential of your business, if you don’t have conviction in it, or you don’t have the talent to realize it, you should question, as we will, whether you’re the right people to run it. We believe that, relative to potential, these rails are failing and it’s costing all of us. It’s costing labor because the trains aren’t as safe as they should be. It’s costing shippers because the trains aren’t as reliable as they should be. It’s costing shareholders because the trains aren’t as profitable as they should be. U.S. companies usually set the benchmark globally and it’s time for that to start happening for the rails. So, here’s our vision. We firmly believe, that in five years, the U.S. rails can be safer, more reliable and less capacity-constrained than they are today, and, in the process, can earn four times as much, four times as much per share as they do today. Getting there is not about reading, it’s not about cutting cutbacks or laying off employees. It’s not about liquidating lines. It’s about three very fundamental things. First, it’s ending the 25-year subsidy that we have provided the shippers. Over the past 25 years, the value of the goods the shippers are shipping has doubled, truck rates have doubled and yet rail rates have gone down. Rails provide an absolutely essential

service to the shippers. The next best alternative truck charges five times as much and our networks are vastly constrained. All this, and yet the rails are in an appalling 2% under replacement value of their business, lower, I suspect, than any other customers. So raising rates isn’t wrong, it’s fair. I see no good reason why the 6 to 7% peer price increases that rails are achieving today isn’t sustainable for at least the next 10 years. Second, it’s being relentless on the cost and operations. I’ve heard all the arguments as far as U.S. rails aren’t CN but when CN went public in 1996, people thought CN wasn’t a U.S. rail. Here’s a quote from back then: “CN. It’s going to be very difficult for them to compete. Look at them. Miles and miles of inefficient track, operating ratio of 85. I’m sure they’re in the high 90’s three years ago. But the leader is south of the border at 78 and it’s proven. They’re a railroad. How can they catch up? They can’t.” Those “leaders” south of the border are still at operating ratios in the 70’s while CN’s gone from 85 to 60. Literally from worst to first. CN has the lowest accident rate, lowest dwell time, highest velocity and highest labor productivity of any of the big five rails. And the worst part about it is the gap between them and U.S. rails isn’t narrowing, it’s widening. I think the biggest difference between CN and U.S. rails isn’t the simplicity of CN’s network or nationalized healthcare in Canada. It’s CN’s management. They’re visionary, they’re relentless and they’re not victims of group think. If you don’t want to take my word for it, you can take Hunter Harrison’s. He says on why the U.S. rails don’t perform like CN, “…perhaps the most ingrained barrier is human nature, the tendency to stick with the familiar and the comfortable, is the key to doing things the way that we’ve always done them.”

The third facet of our vision is buy-backs. We firmly believe that the rails should buy back 20% of their stock a year until they reach five times EBITDA. Why raise debt to buy back stock? Because borrowing at 4% to buy something that returns over 20%. That’s seems to us like a blindingly obvious decision. And I acknowledge that CSX this morning increased its buy-back program and I think that’s a good first step and I guess if I do four speeches a year, we’ll probably get what we want. But it’s not enough. It’s not enough. So what is the appropriate level of leverage? We say it’s five times and how do we get there? Because leverage should be a function of the strength and the predictability of businesses. It shouldn’t be determined by credit analysts. It shouldn’t be aimed to minimize the cost of debt and it shouldn’t be judged by antiquated measures like debt to cap. The key question when determining leverage is how much can EBITDA fall before you have a problem and what’s the likelihood of that event. At five-times leverage, EBITDA can fall for CSX 30%, 3-0, and you still cover up all of your expenses and maintenance CAP EX. So we challenge any of you in this room to construct a scenario where EBITDA realistically falls at 30%. To put a 30% fall EBITDA into context even in the midst of the physical Conrail integration, and during years when the rails didn’t have the strong pricing that we do today, CSX’s EBITDA over a three-year period, from peak to trough, didn’t fall 30%. One other thing to note about that period is when CSX and Norfolk bought Conrail, they levered the four-times and six-times EBITDA respectively. Now there are two-times in a much better rail environment. It’s curious how the debt capacity seems to come and go so opportunistically. If CSX, for example, were to accomplish these three things, which are, increase its prices 7% a year, improving the operating ratio by 1% a

Item 3

There’s no clear hero or villain in this stock battle TRAINS Don Phillips June 2008 The Children’s Investment Fund has been painted as the grinch who is trying to steal railroading. Most of you probably believe that this multi-billion dollar British hedge fund wants CSX to borrow lots of money, cut back on needed infrastructure improvements, and jack up the value of the railroad to its shareholders. You may also believe that the idea would then be for the Children’s Fund to cash out quickly at a big profit, leaving CSX in worse shape than before. I subscribed to some of those suspicions myself, and I’m still not sure that some of the Children’s Fund’s ideas would be good for CSX. However, after sitting through a congressional hearing on March 5 and spending several private sessions with Children’s Fund partner Snehal Amin, I see that the plan is more complicated and less threatening than it has been painted. On June 25 in New Orleans, the CSX annual shareholder’s meeting will take place, and we will know whether the Children’s Fund slate of board members was elected. In the meantime, I want to try my best to put the CSX-Children’s Fund battle into perspective. First, let’s get a couple of facts straight: Despite what you may have heard, the Children’s Fund is not trying to “take over” CSX. Basically, the group wants one of its own as a member of the board, and wants several other prominent railroad people elected to the board. While those railroad experts have been suggested by the Children’s Fund, they would receive no compensation from the Children’s Fund. Even if the entire Children’s Fund slate is elected, they would be a board minority. Current CSX management would continue to run CSX. However, CSX managers would be facing several new board members who arrive with suspicions about CSX’s plans. What’s more, CSX would be forced to release to its board — and, therefore, to the Children’s Fund — a lot of inside information that it is keeping secret. Second, although it is not well known, the Children’s Fund has had extensive conferences with top management at Norfolk Southern, Union Pacific, and BNSF Railway. The two Western roads gave the fund extensive financial and

operations information that persuaded the fund that their extensive level of capital spending is proper. Norfolk Southern, like CSX, would not open its books to the fund, but the fund’s managers came away from a meeting with NS persuaded that it should trust NS management. For reasons that are not fully clear to me, CSX management has refused to talk to the fund’s management. The only time that Amin and CSX Chairman Michael Ward have sat at the same table was at the congressional hearing. That hearing, frankly, was sad. With the exception of one member, Rep. James Oberstar, D.- Minn., the subcommittee hearing consisted of one dumb and uninformed question after another. All of those questions were hostile to the fund, and a great number made little sense. But Amin handled himself well. He never became frustrated or upset by the parade of nasty questions, and in fact, did quite a good job fielding the questions. Every answer made sense, and every answer popped out of his head with no prompting from aides and almost no reference to any paperwork. Oberstar’s statement was masterful. The man knows his railroading, even when one disagrees with his conclusions. Oberstar clearly had spent extensive time talking with Amin, and understood Amin’s positions. Nonetheless, Oberstar said he could not support the fund because he had seen too many instances in which such assurances later disappeared. In other words, he understood the subject matter, he understood what Amin was saying, and he understood the stakes for the industry. He simply had a different opinion from Amin. What do I think after listening extensively to both sides? My basic conclusion is that there’s no clear right or wrong in this one. No one is the hero and no one is the villain. However, I did draw two fairly firm conclusions about the Children’s Fund. First, and perhaps most important, is that this British-based fund is terribly naïve about American politics. Amin and his people stuck their heads into a political buzzsaw when they called for substantial freight rate increases, a position guaranteed to make enemies, which it did. Second, the fund called for a slowdown in spending on CSX infrastructure until there was more clarity about what Congress would do to reregulate railroads. For CSX, which underspent terribly on infrastructure in the 1980s and 1990s, that could be a disaster, although Amin made it clear he was talking about future projects and not ongoing projects. But what blew me away was that the Children’s Fund had a clear argument that it was not out to make a quick hit, take the money, and run. These sometimes-

naїve Brits didn’t know what a powerful argument they had that they were investing for the long run. Almost as an aside, Amin called for spending money to re-equip the entire U.S. freight fleet with electric brakes. He estimated that would increase rail capacity 20 percent even if no money were spent on new infrastructure. But implementing electronically controlled pneumatic brakes nationwide is an expensive proposition that would take more than five years to complete; and until it’s done, a lot of money would be spent with little return. That’s hardly a formula for jacking up stock prices and getting out fast. DON PHILLIPS, a newspaper reporter for more than four decades, writes the exclusive monthly column for Trains.

Item 4

FINAL TRANSCRIPT Thomson StreetEvents CSX - Q4 2007 CSX Corporation Earnings Conference Call Event Date/Time: Jan. 22. 2008 / 8:30 AM ET THOMSON www.streetevents.com Contact Us © 2008 Thomson Financial. Republished with permission. No part of this publication may be reproduced or transmitted in any form or by any means without the prior written consent of Thomson Financial.

FINAL TRANSCRIPT Jan. 22. 2008 / 8:30 AM. CSX - Q4 2007 CSX Corporation Earnings Conference Call Michael Ward - CSX Corporation - Chairman, President, CEO Well thank you, Oscar. Those of you that have been with us for the last three years have seen your share value rise by 120%. That’s better than any of our appears and better than 90% of the S&P 500. We’re creating that value by leveraging the resiliency of our industry and combining that the with even stronger operations. This team has reduced the Company’s operating ratio by nearly 900 basis points over the past three years to its best level in a decade. This success is due to the top line growth and aggressive process improvements which have produced more than $400 million of savings over the last three years. Over the next three years, we will drive even greater efficiency as we target a mid to low 70’s operating ratio by 2010. At the same time, we must and will make strategic targeted investments to capitalize on the growth potential of our industry. Long term, that potential is driven by growing and shifting populations, increasing global trade, and traffic congestion on the highways. Near term, we will build on our momentum to again deliver record results for 2008. For this team, it’s not enough to just participate in the rail renaissance. We want to lead it, by creating a 21st century freight transportation network that is best-in-class. As I’ve said before, you cannot and should not underestimate the importance of this critical service we provide to the country. This means that we have to be responsive to the safety, security, and economic needs of the nation. That takes investment, discipline, and dedicated employees. We have all three. By just about every measure of safety, service, and financial performance, your Company, CSX, is the fastest improving Company in an extremely attractive industry. Today, in fact, we rank among the industries best in safety and service and have created more shareholder value than any other railroad over the past three years. We’re going to continue on that path. And along the way we will become the best Company in more and more categories while remaining relentless in our pursuit of excellence across-the-board. With that we’ll take your questions and ask that you please identify yourself and your affiliation for the benefit of all the participants on the call. Operator, we’re ready to take calls at this point. QUESTIONS AND ANSWERS Operator Thank you. The first question comes from Tom Wadewitz with JPMorgan. Your line is open. Tom Wadewitz - JPMorgan - Analyst Yes, good morning. Definitely impressive results this morning, so congratulations on that. Michael Ward - CSX Corporation - Chairman, President, CEO Thank you, Tom. Tom Wadewitz - JPMorgan - Analyst I wanted to understand a little bit in terms of your conviction and visibility on the pricing outlook for 2008, if you could just give a sense of how much of that is already locked in or carryover from 2007 and how much is still you need to go out and fight for and get put into contracts? THOMSON www.streetevents.com Contact Us © 2008 Thomson Financial. Republished with permission. No part of this publication may be reproduced or transmitted in any form or by any means without the prior written consent of Thomson Financial.

Item 5

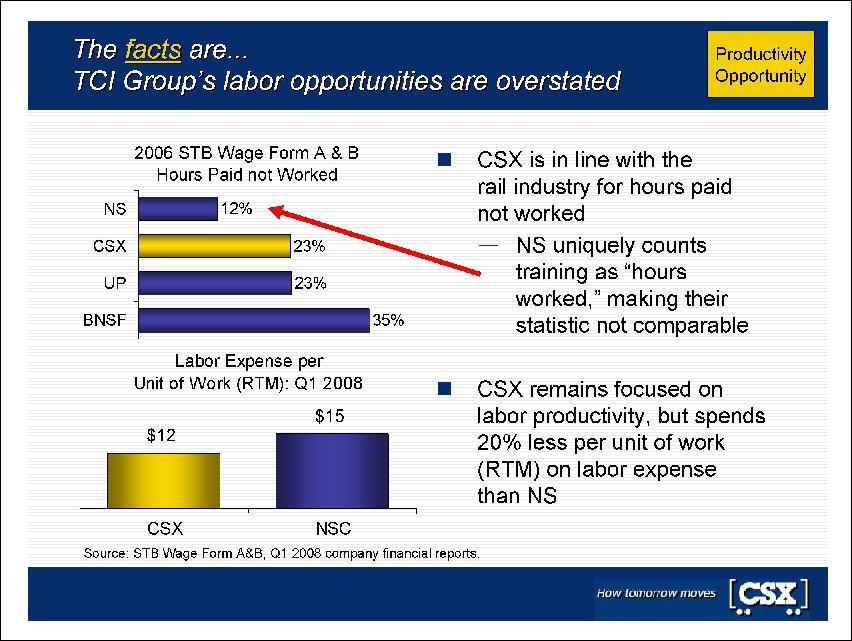

The facts are… TCI Group’s labor opportunities are overstated Productivity Opportunity 2006 STB Wage Form A & B Hours Paid not Worked NS 12% CSX 23% UP 23% BNSF 35% Labor Expense per Unit of Work (RTM): Q1 2008 $12 CSX $15 NSC Source: STB Wage Form A&B, Q1 2008 company financial reports. CSX is in line with the rail industry for hours paid not worked NS uniquely counts training as “hours worked,” making their statistic not comparable CSX remains focused on labor productivity, but spends 20% less per unit of work (RTM) on labor expense than NS How tomorrow moves [CSX]

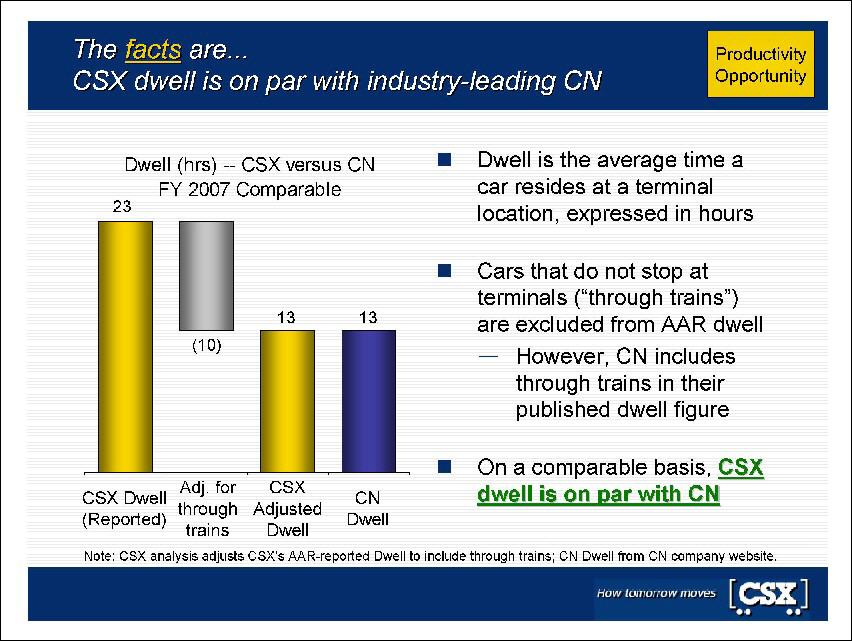

The facts are… CSX dwell is on par with industry-leading CN Productivity Opportunity Dwell (hrs) -- CSX versus CN FY 2007 Comparable 23 CSX Dwell (Reported) (10) Adj. for through trains 13 CSX Adjusted Dwell 13 CN Dwell Dwell is the average time a car resides at a terminal location, expressed in hours Cars that do not stop at terminals (“through trains”) are excluded from AAR dwell However, CN includes through trains in their published dwell figure On a comparable basis, CSX dwell is on par with CN Note: CSX analysis adjusts CSX’s AAR-reported Dwell to include through trains; CN Dwell from CN company website. How tomorrow moves [CSX]

Item 6

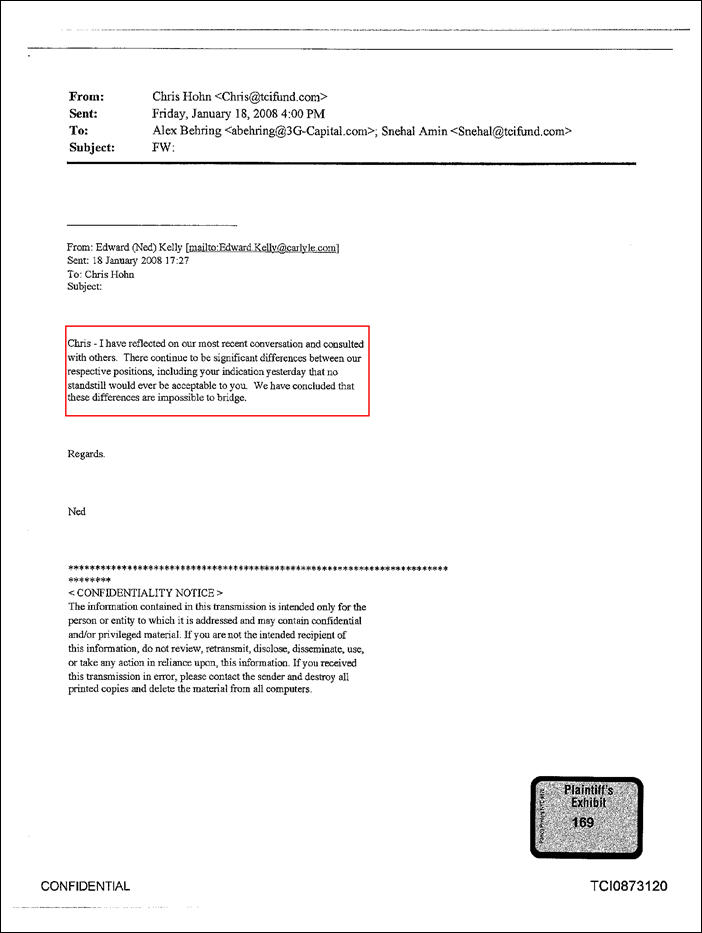

From: Chris Hohn Chris@tcifund.com Sent: Friday, January 18, 2008 4:00 PM To: Alex Behring<abehring@3G-Capital.com>, Snehal AminSnelhal@tcifund.com Subject: FW: From: Edward (Ned) Kelly [mailto: Edward.Kelly@carlyle.com] Sent: 18 January 2008 17:27 To: Chris Hohn Subject: Chris - I have reflected on our most recent conversation and consulted with others. There continue to be significant differences between our respective positions, including your indication yesterday that no standstill would ever be acceptable to you. We have concluded that these differences are impossible to bridge. Regards. Ned <CONFIDENTIALITY NOTICES> The information contained in this transmission is intended only for the person or entity to which it is addressed and may contain confidential and/or privileged material. If you are not the intended recipient of this information, do not review, retransmit, disclose, disseminate, use, or take any action in reliance upon, this information. If you received this transmission in error, please contact the sender and destroy all printed copies and delete the material from all computers. Plaintiff’s Exhibit 169 Confidential TCI0873120

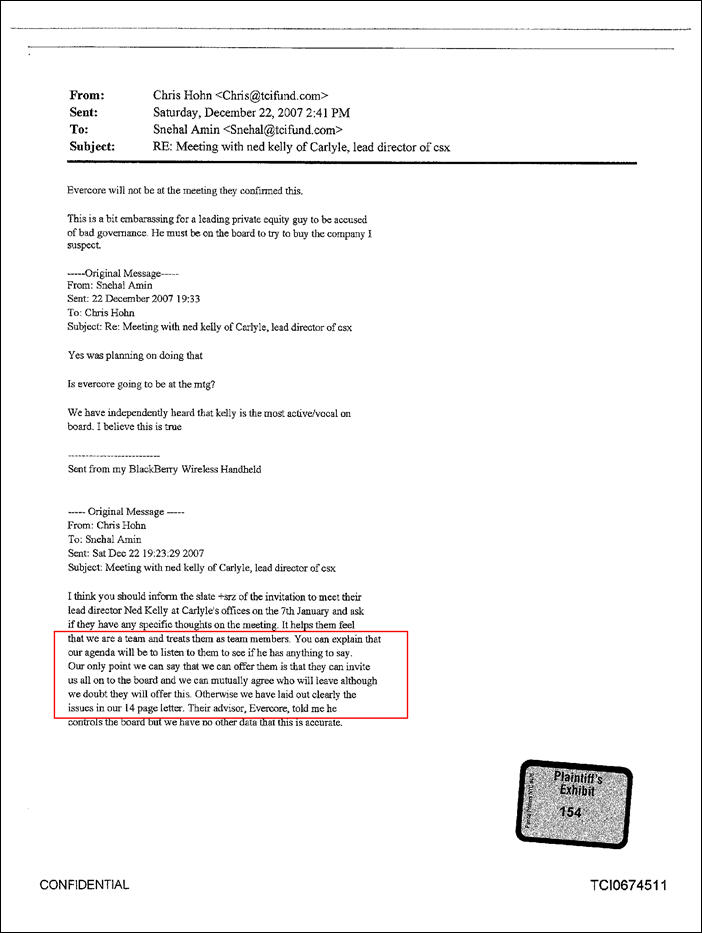

From: Chris Hohn Chris@tcifund.com Sent: Saturday, December 22, 2007 2:41 PM To: Snehal Amin Snehal<@tcifund.com> Subject: RE: Meeting with ned Kelly of Carlyle, lead director of csx Evercore will not be at the meeting they confirmed this. This is a bit embarrassing for a leading private equity guy to be accused of bad governance. He must be on the board to try to buy the company I suspect. Original Message From: Snehal Amin Sent: 22 December 2007 19:33 To: Chris Hohn Subject Re: Meeting with ned Kelly of Carlyle, lead director of csx Yes was planning on doing that Is evercore going to be at the mtg? We have independently heard that Kelly is the most active/vocal on board. I believe this is true Sent from my BlackBerry Wireless Handheld Original Message From: Chris Hohn To: Snehal Amin Sent: Sat Dec 22 19:23:29 2007 Subject: Meeting with ned Kelly of Carlyle, lead director of csx I think you should inform the slate +srz of the invitation to meet their lead director Ned Kelly at Carlyle’s offices on the 7th January and ask if they have any specific thoughts on the meeting. It helps them feel that we are a team and treats them as team members. You can explain that our agenda will be to listen to them to see if he has anything to say. Our only point we can say that we can offer them is that they can invite us all on to the board and we can mutually agree who will leave although we doubt they will offer this. Otherwise we have laid out clearly the issues in our 14 page letter. Their advisor, Evercore, told me he controls the board but we have no other data that this is accurate. Plaintiff’s Exhibit 154 Confidential TCI0674511

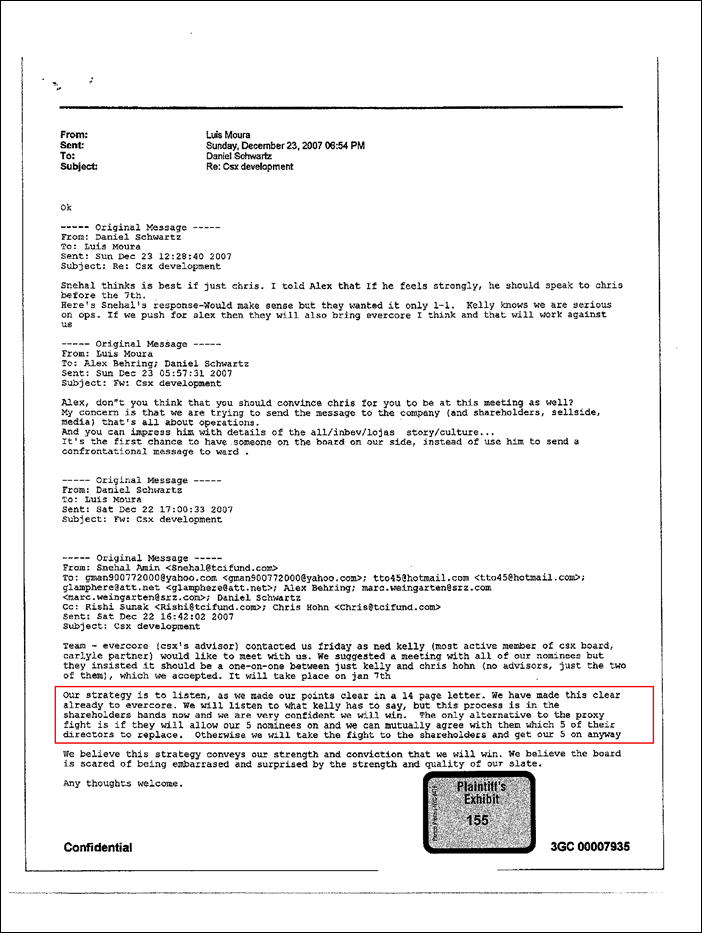

From: Luis Moura Sent: Sunday, December 23, 2007 06:54 PM To: Daniel Schwartz Subject: Re: Csx development Ok Original Message From: Daniel Schwartz To: Luis Moura Sent: Sun Dec 23 12:28:40 2007 Subject: Re: Csx development Snehal thinks is best if just chris. I told Alex that If he feels strongly, he should speak to chris before the 7th. Here’s Snehal’s response-Would make sense but they wanted it only 1-1. Kelly knows we are serious on ops. If we push for alex then they will also bring evercore I think and that will work against us Original Message From: Luis Moura To: Alex Behring; Daniel Schwartz Sent: Sun Dec 23 05:57:31 2007 Subject: Fw: Csx development Alex, don’t you think that you should convince chris for you to be at this meeting as well? My concern is that we are trying to send the message to the company (and shareholders, sellside, media) that’s all about operations. And you can impress him with details of the all/inbev/lojas story/culture... It’s the first chance to have someone on the board on our side, instead of use him to send a confrontational message to ward .. Original Message From: Daniel Schwartz To: Luis Moura Sent: Sat Dec 22 17:00:33 2007 Subject: Fw: Csx development Original Message From: Snehal Amin Snehal@tcifund.com To: gman900772000@yahoo.com; <gman900772000@yahoo.com>; tto45@hotmail.com <tto45@hotmail.com>; glamphere@att.net <glamphere@att.net>; Alex Behring; marc.weingarten@srz.com <marc.weingarten@srz.com>; Daniel Schwartz Cc: Rishi Sunak <Rishi@tcifund.com›; Chris Hohn <chris@tcifund.com> Sent: Sat Dec 22 16:42:02 2007 Subject: Csx development Team - evercore (csx’s advisor) contacted us friday as ned kelly (most active member of csx board, carlyle partner) would like to meet with us. We suggested a meeting with all of our nominees but they insisted it should be a one-on-one between just kelly and chris hohn (no advisors, just the two of them), which we accepted. It will take place on jan 7th Our strategy is to listen, as we made our points clear in a 14 page letter. We have made this clear already to evercore. We will listen to what kelly has to say, but this process is in the shareholders hands now and we are very confident we will win. The only alternative to the proxy fight is if they will allow our 5 nominees on and we can mutually agree with them which 5 of their directors to replace. Otherwise we will take the fight to the shareholders and get our 5 on anyway We believe this strategy conveys our strength and conviction that we will win. We believe the board is scared of being embarrased and surprised by the strength and quality of our slate. Any thoughts welcome. Plaintiff’s Exhibit 155 Confidential 3GC 00007935

Item 7

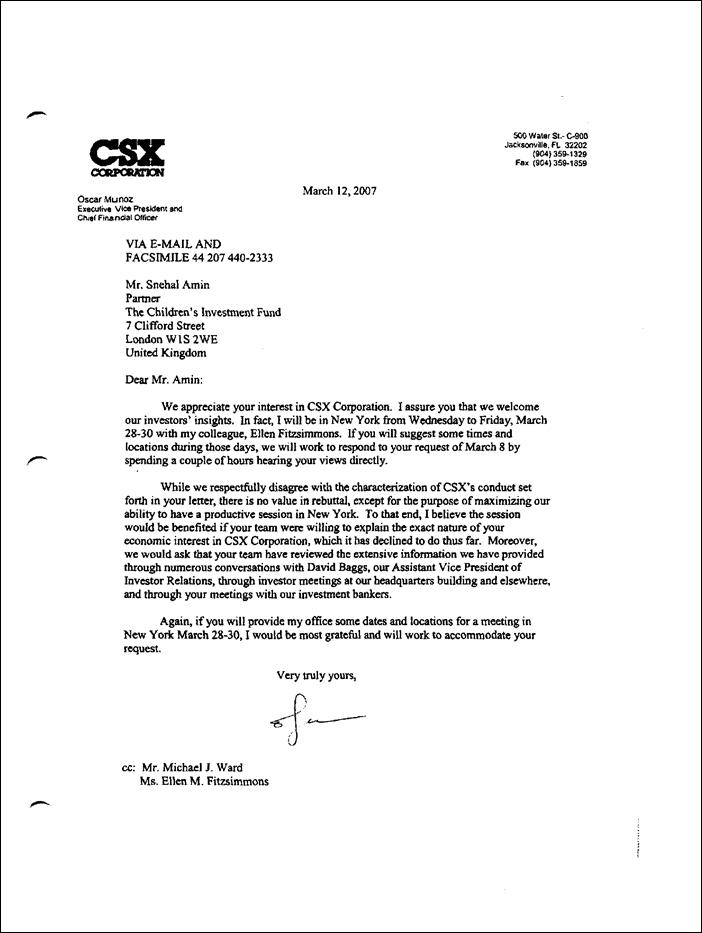

CSX Corporation 500 Water St. - C-900, Jacksonville, FL 32202 (904) 359-1329 Fax (904) 359-1859 March 12, 2007 Oscar Munoz Executive Vice President and Chief Financial Officer VIA E-MAIL AND FACSIMILE 44 207 440-2333 Mr. Snehal Amin Partner The children’s Investment Fund 7 Clifford Street London W1S 2WE United Kingdom Dear Mr. Amin: We appreciate your interest in CSX Corporation. I assure you that we welcome our investors’ insights. In fact, I will be in New York from Wednesday to Friday, March 28-30 with my colleague, Ellen Fitzsimmons. If you will suggest some times and locations during those days, we will work to respond to your request of March 8 by spending a couple of hours hearing your views directly. While we respectfully disagree with the characterization of CSX’s conduct set forth in your letter, there is no value in rebuttal, except for the purpose of maximizing our ability to have a productive session in New York. To that end, I believe the session would be benefited if your team were willing to explain the exact nature of your economic interest in CSX Corporation, which it has declined to do thus far. Moreover, we would ask that your team have reviewed the extensive information we have provided through numerous conversations with David Baggs, our Assistant Vice President of Investor Relations, through investor meetings at our headquarters building and elsewhere, and through your meetings with our investment bankers. Again, if you will provide my office some dates and locations for a meeting in New York March 28-30, I would be most grateful and will work to accommodate your request. Very truly yours, cc: Mr. Michael J. Ward Ms. Ellen M. Fitzsimmons

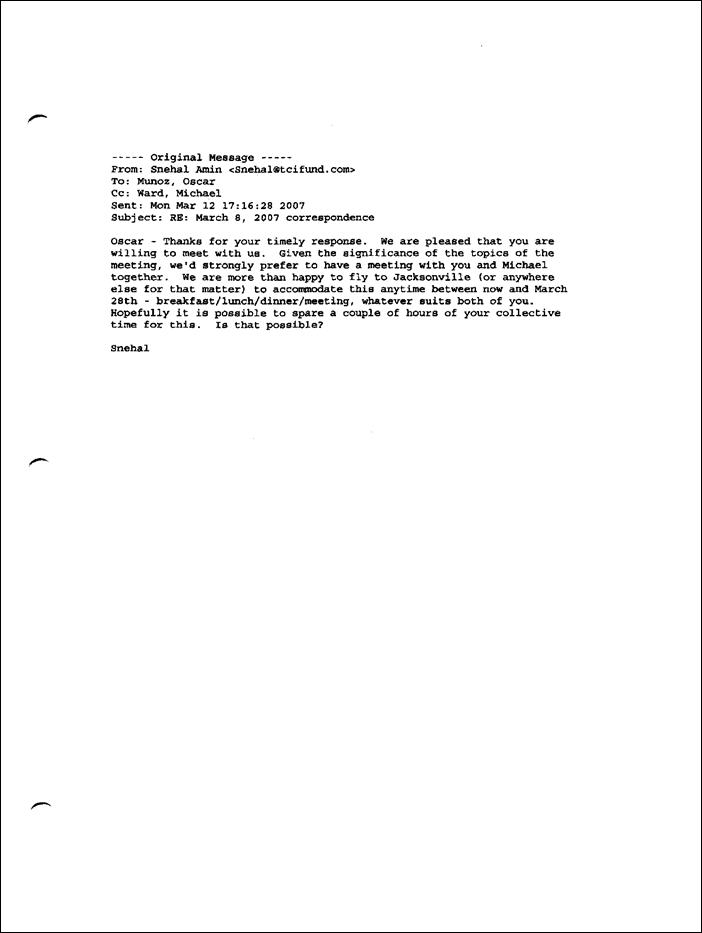

Original Message From: Snehal Amin Snehal@tcifund.com To: Munoz, Oscar Cc: Ward, Michael Sent: Mon Mar 12 17:16:28 2007 Subject: RE: March 8, 2007 correspondence Oscar - Thanks for your timely response. We are pleased that you are willing to meet with us. Given the significance of the topics of the meeting, we’d strongly prefer to have a meeting with you and Michael together. We are more than happy to fly to Jacksonville (or anywhere else for that matter) to accommodate this anytime between now and March 28th - breakfast/lunch/dinner/meeting, whatever suits both of you. Hopefully it is possible to spare a couple of hours of your collective time for this. Is that possible? Snehal

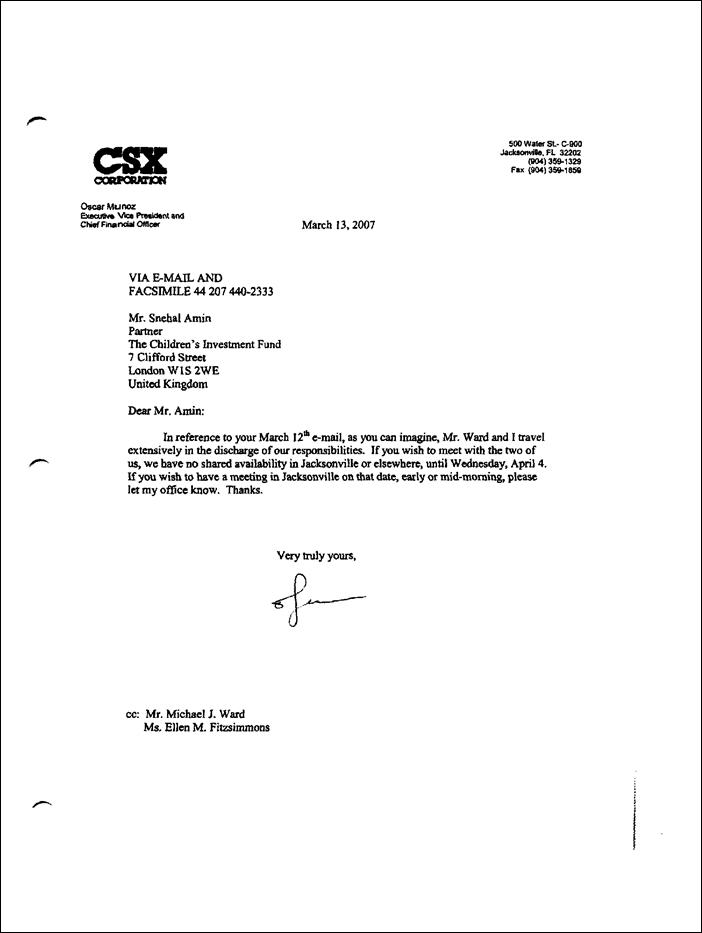

CSX Corporation 500 Water St. - C-900, Jacksonville, FL 32202 (904) 359-1329 Fax (904) 359-1859 March 13, 2007 Oscar Munoz Executive Vice President and Chief Financial Officer VIA E-MAIL AND FACSIMILE 44 207 440-2333 Mr. Snehal Amin Partner The children’s Investment Fund 7 Clifford Street London W1S 2WE United Kingdom Dear Mr. Amin: In reference to your March 12th e-mail, as you can imagine, Mr. Ward and I travel extensively in the discharge of our responsibilities. If you wish to meet with the two of us, we have no shared availability in Jacksonville or elsewhere, until Wednesday, April 4. If you wish to have a meeting in Jacksonville on that date, early or mid-morning, please let my office know. Thanks. Very truly yours, cc: Mr. Michael J. Ward Ms. Ellen M. Fitzsimmons

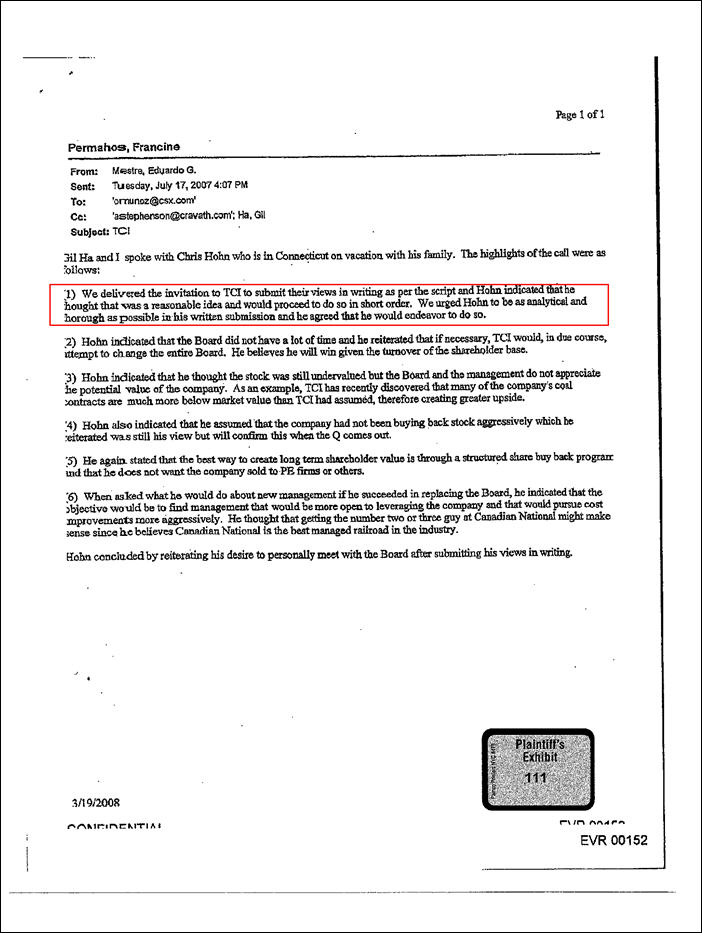

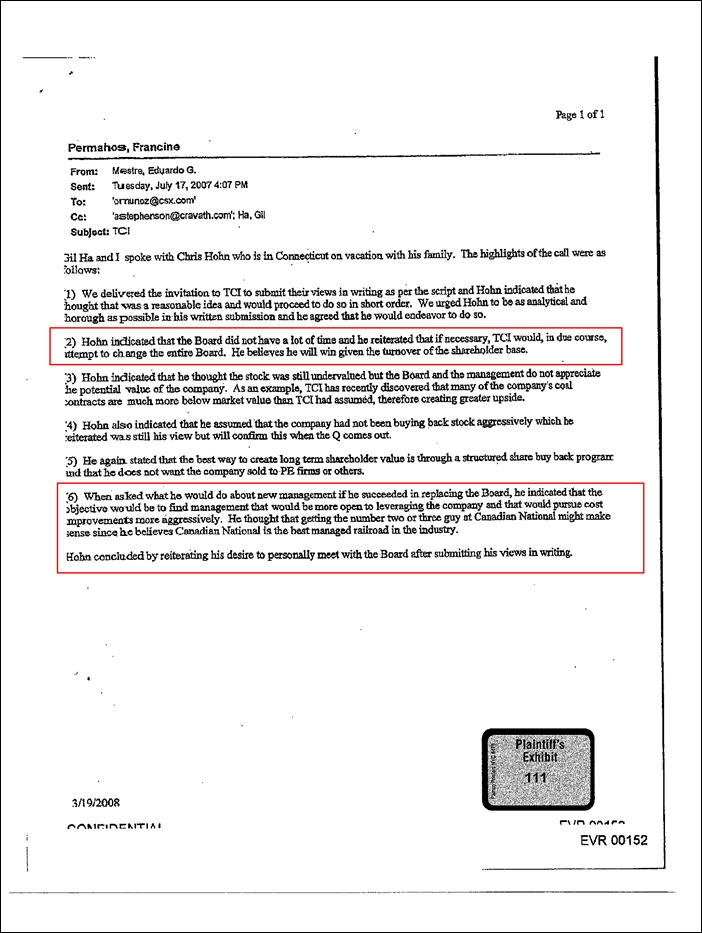

Page 1 of 1 Permahos, Francine From: Mestre, Eduardo G. Sent: Tuesday, July 17, 2007 4:07 PM To: ‘ornunoz@csx.com’ Cc: ‘astephenson@cravath.com’; Ha, Gil Subject: TCI Gil Ha and I spoke with Chris Hohn who is in Connecticut on vacation with his family. The highlights of the call were as follows: 1) We delivered the invitation to TCI to submit their views in writing as per the script and Hohn indicated that he thought that was a reasonable idea and would proceed to do so in short order. We urged Hohn to be as analytical and thorough as possible in his written submission and he agreed that he would endeavor to do so. 2) Hohn indicated that the Board did not have a lot of time and he reiterated that if necessary, TCI would, in due course, attempt to change the entire Board. He believes he will win given the turnover of the shareholder base. 3) Hohn indicated that he thought the stock was still undervalued but the Board and the management do not appreciate the potential value of the company. As an example, TCI has recently discovered that many of the company’s coal contracts are much more below market value than TCI had assumed, therefore creating greater upside. 4) Hohn also indicated that he assumed that the company had not been buying back stock aggressively which he reiterated was still his view but will confirm this when this Q comes out. 5) He again stated that the best way to create long term shareholder value is through a structured share buy back program and that he does not want the company sold to PE firms or others. 6) When asked what he would do about new management if he succeeded in replacing the Board, he indicated that the objective would be to find management that would be more open to leveraging the company and that would pursue cost improvements more aggressively. He thought that getting the number two or three guy at Canadian National might make sense since he believes Canadian National is the best managed railroad in the industry. Hohn concluded by reiterating his desire to personally meet with the Board after submitting his views in writing. 3/19/2008 Plaintiff’s Exhibit 111 Confidential EVR 00152

Item 8

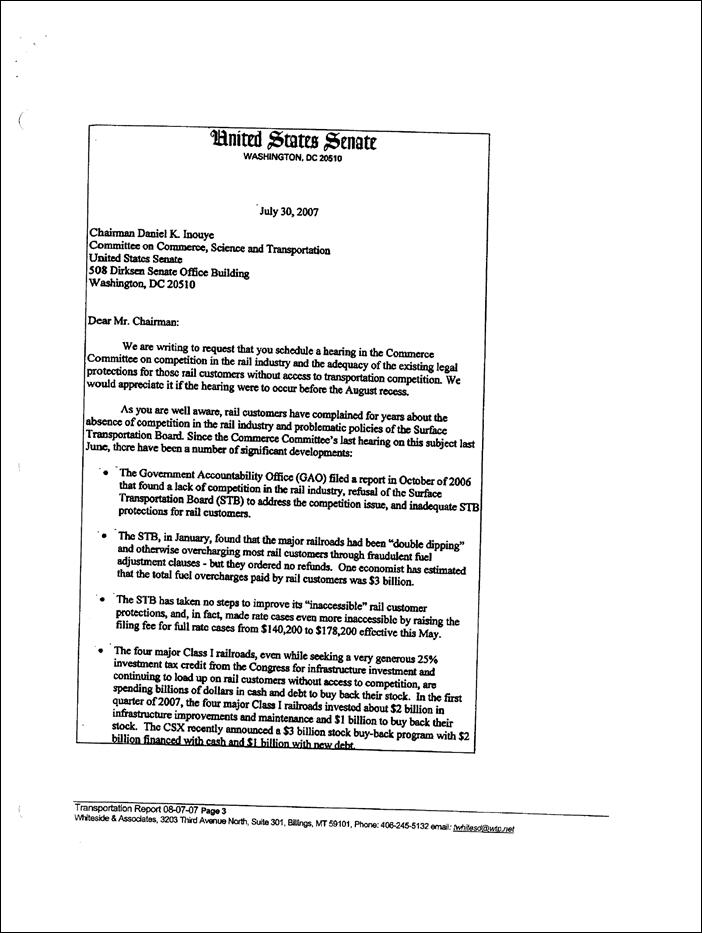

United States Senate Washington, DC 20510 July 30, 2007 Chairman Daniel K. Inouye Committee on Commerce, Science and Transportation United States Senate 508 Dirksen Senate Office Building Washington, DC 20510 Dear Mr. Chairman: We are writing to request that you schedule a hearing in the Commerce Committee on competition in the rail industry and the adequacy of the existing legal protections for those rail customers without access to transportation competition. We would appreciate if the hearing were to occur before the August recess. As you are well aware, rail customers have complained for years about the absence of competition in the rail industry and problematic policies of the Surface Transportation Board. Since the Commerce Committee’s last hearing on this subject last June, there have been a number of significant developments: · The Government Accountability Office (GAO) filed a report in October of 2006 that found a lack of competition in the rail industry, refusal of the Surface Transportation Board (STB) to address to competition issue, and inadequate STB protections for rail customers. · The STB, in January, found that the major railroads had been “double dipping” and otherwise overcharging most rail customers through fraudulent fuel adjustment clauses - but they ordered no refunds. One economist has estimated that the total fuel overcharges paid by rail customers was $3 billion. · The STB has taken no steps to improve its “inaccessible” rail customer protections, and, in fact, made rate cases even more inaccessible by raising the filing fee for full rate cases from $140,200 to $178,200 effective this May. · The four major Class I railroads, even while seeking a very generous 25% investment tax credit from the Congress for infrastructure investment and continuing to load up on rail customers without access to competition, are spending billions of dollars in cash and debt to buy back their stock. In the first quarter of 2007, the four major Class I railroads invested about $2 billion in infrastructure improvements and maintenance and $1 billion to buy back their stock. The CSX recently announced a $3 billion stock buy-back progress with $2 billion financed with cash and $1 billion with new debt.

· Finally, this year, hedge funds and other aggressive investors have discovered the stock of the major railroads. These investors have bought major quantities of stock in each of the large Class I railroads. At a recent gathering of railroad investors hosted by Bear Stearns on Wall Street, a London-based hedge fund investor, who was the keynote speaker, called for the railroads to double their rates over the next decade, continue to cut their costs and spend their cash buying back their stock. This investor made clear that he and other hedge fund investors are going to hold railroad management accountable if these goals are not achieved. All of these developments, Mr. Chairman, suggest that the Committee needs to consider whether the national rail system is developing as it should and whether current law is working as intended by Congress. Thank you for your attention to this matter that is of such fundamental interest to our constituents and to the future of our nation. Sincerely, John D. Rockefeller IV United States Senator Byron L. Dorgan United States Senator

Item 9

From: Chris Hohn Chris@tcifund.com Sent: Monday, April 9, 2007 1:39 PM To: john@mccallmacbain.com Subject: Hunter Harrison John I am interested to approach this legendary rail roader to see if he would be interested in coming in as CEO of CSX if he is not too old. Does your pension fund contact know him well enough to introduce us? Warren Buffett just filed in 3 of the 4 US rail roads. We have 22pc of our fund in them now. I will respond in the next day or two on Hal’s email Chris Sent from my BlackBerry Wireless Handheld Plaintiff’s Exhibit 36 Confidential TCI0397175

Permahos, Francine From: Mestre, Eduardo G. Sent: Tuesday, July 17, 2007 4:07 PM To: ‘ornunoz@csx.com’ Cc: ‘astephenson@cravath.com’; Ha, Gil Subject: TCI Gil Ha and I spoke with Chris Hohn who is in Connecticut on vacation with his family. The highlights of the call were as follows: 1) We delivered the invitation to TCI to submit their views in writing as per the script and Hohn indicated that he thought that was a reasonable idea and would proceed to do so in short order. We urged Hohn to be as analytical and thorough as possible in his written submission and he agreed that he would endeavor to do so. 2) Hohn indicated that the Board did not have a lot of time and he reiterated that if necessary, TCI would, in due course, attempt to change the entire Board. He believes he will win given the turnover of the shareholder base. 3) Hohn indicated that he thought the stock was still undervalued but the Board and the management do not appreciate the potential value of the company. As an example, TCI has recently discovered that many of the company’s coal contracts are much more below market value than TCI had assumed, therefore creating greater upside. 4) Hohn also indicated that he assumed that the company had not been buying back stock aggressively which he reiterated was still his view but will confirm this when this Q comes out. 5) He again stated that the best way to create long term shareholder value is through a structured share buy back program and that he does not want the company sold to PE firms or others. 6) When asked what he would do about new management if he succeeded in replacing the Board, he indicated that the objective would be to find management that would be more open to leveraging the company and that would pursue cost improvements more aggressively. He thought that getting the number two or three guy at Canadian National might make sense since he believes Canadian National is the best managed railroad in the industry. Hohn concluded by reiterating his desire to personally meet with the Board after submitting his views in writing. 3/19/2008 Plaintiff’s Exhibit 111 Confidential EVR 00152

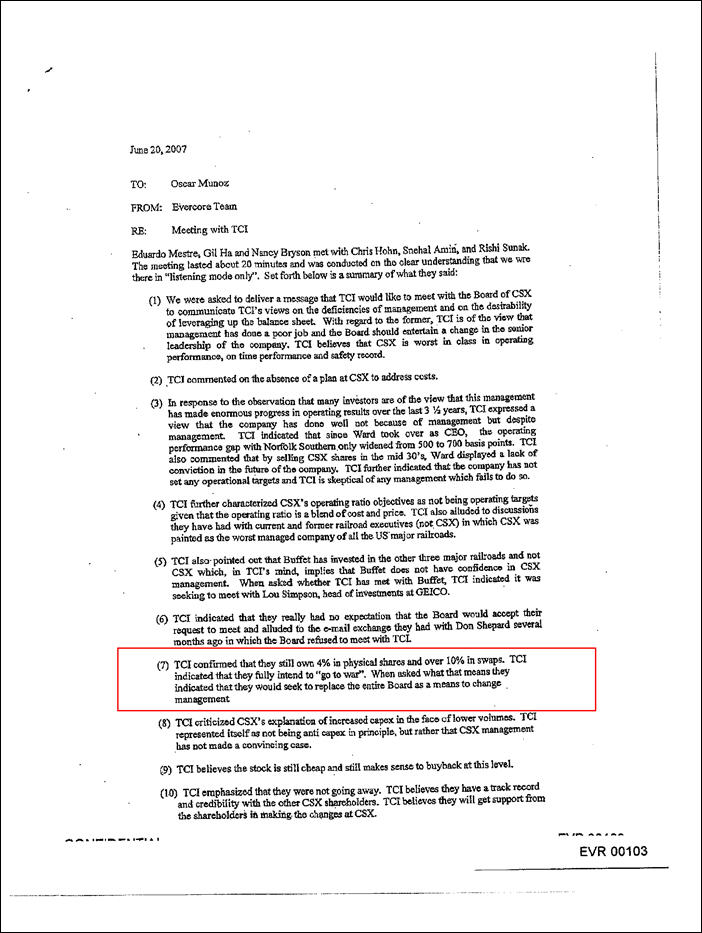

June 20, 2007 To: Oscar Munoz From: Evercore Team Re: Meeting with TCI Eduardo Mestre, Gil Ha and Nancy Bryson met with Chris Hohn, Snehal Amin, and Rishi Sunak. The meeting lasted about 20 minutes and was conducted on the clear understanding that we were there in “listening mode only”. Set forth below is a summary of what they said: (1) We were asked to deliver a message that TCI would like to meet with the Board of CSX to communicate TCI’s views on the deficiencies of management and on the desirability of leveraging up the balance sheet. With regard to the former, TCI is of the view that management has done a poor job and the Board should entertain a change in the senior leadership of the company. TCI believes that CSX is worst in class in operating performance, on time performance and safety record. (2) TCI commented on the absence of a plan at CSX to address costs. (3) In response to the observation that many investors are of the view that this management has made enormous progress in operating results over the last 3 1/2 years, TCI expressed a view that the company has done well not because of management but despite management. TCI indicated that since Ward took over as CEO, the operating performance gap with Norfolk Southern only widened from 500 to 700 basis points. TCI also commented that by selling CSX shares in the mid 30’s, Ward displayed a lack of conviction in the future of the company. TCI further indicated that the company has not set any operational targets and TCI is skeptical of any management which fails to do so. (4) TCI further characterized CSX’s operating ratio objectives as not being operating targets given that the operating ratio is a blend of cost and price. TCI also alluded to discussions they have had with current and former railroad executives (not CSX) in which CSX was painted as the worst managed company of all the US major railroads. (5) TCI also pointed out that Buffet has invested in the other three major railroads and not CSX which, in TCI’s mind, implies that Buffet does not have confidence in CSX management. When asked whether TCI has met with Buffet, TCI indicated it was seeking to meet with Lou Simpson, head of investments at GEICO. (6) TCI indicated that they really had no expectation that the Board would accept their request to meet and alluded to the e-mail exchange they had with Don Shepard several months ago in which the Board refused to meet with TCL. (7) TCI confirmed that they still own 4% in physical shares and over 10% in swaps. TCI indicated that they fully intend to “go to war”. When asked what that means they indicated that they would seek to replace the entire Board as a means to change management. (8) TCI criticized CSX’s explanation of increased capex in the face of lower volumes. TCI represented itself as not being anti capex in principle, but rather that CSX management has not made a convincing case. (9) TCI believes the stock is still cheap and still makes sense to buyback at this level. (10) TCI emphasized that they were not going away. TCI believes they have a track record and credibility with the other CSX shareholders. TC believes they will get support from the shareholders in making the changes at CSX.