UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 26, 2015

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to ________.

Commission File Number 0-2585

The Dixie Group, Inc.

(Exact name of registrant as specified in its charter)

| Tennessee | 62-0183370 | |

| (State or other jurisdiction of incorporation of organization) | (I.R.S. Employer Identification No.) | |

| 475 Reed Road, Dalton, GA 30720 | (706) 876-5800 | |

| (Address of principal executive offices and zip code) | (Registrant's telephone number, including area code) | |

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Title of Class | Name of each exchange on which registered | |

| Common Stock, $3.00 par value | NASDAQ Stock Market, LLC | |

| Securities registered pursuant to Section 12(g) of the Act: | ||

| Title of class | ||

| None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes þ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. ¨ Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). þ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer þ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes þ No

The aggregate market value of the Common Stock held by non-affiliates of the registrant on June 26, 2015 (the last business day of the registrant's most recently completed fiscal second quarter) was $155,424,559. The aggregate market value was computed by reference to the closing price of the Common Stock on such date. In making this calculation, the registrant has assumed, without admitting for any purpose, that all executive officers, directors, and holders of more than 10% of a class of outstanding Common Stock, and no other persons, are affiliates. No market exists for the shares of Class B Common Stock, which is neither registered under Section 12 of the Act nor subject to Section 15(d) of the Act.

Indicate the number of shares outstanding of each of the registrant's classes of Common Stock as of the latest practicable date.

| Class | Outstanding as of February 26, 2016 | ||||

| Common Stock, $3.00 Par Value | 15,155,273 | shares | |||

| Class B Common Stock, $3.00 Par Value | 851,693 | shares | |||

| Class C Common Stock, $3.00 Par Value | 0 | shares | |||

DOCUMENTS INCORPORATED BY REFERENCE

Specified portions of the following document are incorporated by reference:

Proxy Statement of the registrant for annual meeting of shareholders to be held May 3, 2016 (Part III).

THE DIXIE GROUP, INC.

Index to Annual Report

on Form 10-K for

Year Ended December 26, 2015

| PART I | Page | |

| Item 1. | ||

| Item 1A. | ||

| Item 1B. | ||

| Item 2. | ||

| Item 3. | ||

| Item 4. | ||

| PART II | ||

| Item 5. | ||

| Item 6. | ||

| Item 7. | ||

| Item 7A. | ||

| Item 8. | ||

| Item 9. | ||

| Item 9A. | ||

| Item 9B. | ||

| PART III | ||

| Item 10. | ||

| Item 11. | ||

| Item 12. | ||

| Item 13. | ||

| Item 14. | ||

| PART IV | ||

| Item 15. | ||

FORWARD-LOOKING INFORMATION

This Report contains statements that may be considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements include the use of terms or phrases such as "expects," "estimates," "projects," "believes," "anticipates," "intends," and similar terms and phrases. Such forward-looking statements relate to, among other matters, our future financial performance, business prospects, growth strategies or liquidity. The following important factors may affect our future results and could cause those results to differ materially from our historical results; these factors include, in addition to those "Risk Factors" detailed in Item 1A of this report, and described elsewhere in this document, the cost and availability of capital, raw material and transportation costs related to petroleum price levels, the cost and availability of energy supplies, the loss of a significant customer or group of customers, materially adverse changes in economic conditions generally in carpet, rug and floorcovering markets we serve and other risks detailed from time to time in our filings with the Securities and Exchange Commission.

PART I.

| Item 1. | BUSINESS |

General

Our business consists principally of marketing, manufacturing and selling carpet and rugs to high-end residential and commercial customers through our various sales forces and brands. A small portion of our manufacturing capacity is used to provide carpet and yarn related services to other manufacturers.

From 1920 until 1993 we were exclusively in the textile business. We sold our textile assets and began acquiring floorcovering businesses in 1993. We focus exclusively on the upper-end of the soft floorcovering market where we believe we have strong brands and competitive advantages with our style and design capabilities and customer relationships.

Our business is concentrated in areas of the soft floorcovering markets where innovative styling, design, color, quality and service, as well as limited distribution, are welcomed and rewarded. Our Fabrica, Masland, and Dixie Home brands have a significant presence in the high-end residential soft floorcovering markets. Our Atlas Carpet Mills, Masland Contract and Masland Hospitality brands, participate in the upper end specified commercial marketplace. Dixie International sells all of our brands outside of the North American market. Our brands are well known, highly regarded and complementary; by being differentiated, we offer meaningful alternatives to the discriminating customer.

We have one line of business, carpet and rug manufacturing.

Our Brands

Fabrica markets and manufactures luxurious residential carpet and custom rugs, at selling prices that we believe are approximately five times the average for the residential soft floorcovering industry. Its primary customers are interior decorators and designers, selected retailers and furniture stores, luxury home builders and manufacturers of luxury motor coaches and yachts. Fabrica is among the leading premium brands in the domestic marketplace and is known for styling innovation and unique colors and patterns. Fabrica consists of made-to-order, hand-crafted, extremely high quality carpets and area rugs in both nylon and wool, with a wide variety of patterns and textures. Fabrica is viewed by the trade as the premier quality brand for very high-end carpet and enjoys an established reputation as a styling trendsetter and a market leader in providing both custom and designer products to the very high-end residential sector.

Masland Residential, founded in 1866, markets and manufactures design-driven specialty carpets and rugs for the high-end residential marketplace. Its residential and commercial broadloom carpet products are marketed at selling prices that we believe are over three times the average for the residential soft floorcovering industry. Its products are marketed through the interior design community, as well as to consumers through specialty floorcovering retailers. Masland Residential has strong brand recognition within the upper-end residential market. Masland Residential competes through innovative styling, color, product design, quality and service with products made of both wool and nylon.

Dixie Home provides stylishly designed, differentiated products that offer affordable fashion to residential consumers. Dixie Home markets an array of tufted broadloom residential and commercial carpet to selected retailers and home centers under the Dixie Home and private label brands. Its objective is to make the Dixie Home brand the choice for styling, service and quality in the more moderately priced sector of the high-end broadloom residential carpet market. Its products are marketed at selling prices which we believe average two times the soft floorcovering industry's average selling price.

Atlas Carpet Mills, acquired in 2014, is our premium commercial brand. Atlas has long been known for superior style and design. Atlas’ focus is the specified design community including architects and designers who serve the upper end commercial marketplace. The Atlas brand has unique styling, as evident in both its broadloom and modular carpet tile product offerings. Atlas’ high quality offerings are manufactured utilizing just in time manufacturing techniques in our California operations.

Masland Contract markets and manufactures broadloom and modular carpet tile for the specified commercial marketplace. Its commercial products are marketed to the architectural and specified design community and directly to commercial end users, as well as to consumers through specialty floorcovering retailers. Masland Contract has strong brand recognition within the upper-end contract market, and competes through innovative styling, color, patterns, quality and service.

Masland Hospitality, a new commercial business launched in 2014, is designed to focus on the hospitality market with both custom designed and running line products. Utilizing the computerized yarn placement technology we acquired with our Burtco acquisition in 2014, as well as offerings utilizing our state of the art Infinity tufting technology, this brand provides excellent service and design flexibility to the hospitality market serving upper-end hotels, conference centers and senior living markets. Its broadloom and rug product offerings are designed for the interior designer in the upper-end of the hospitality market who appreciates sophisticated texture, color and patterns with excellent service.

Industry

The carpet and rug industry has two primary markets, residential and commercial, with the residential market making up the largest portion of the industry's sales. A substantial portion of industry shipments is made in response to replacement demand. Residential products consist of broadloom carpets and rugs in a broad range of styles, colors and textures. Commercial products consist primarily of broadloom carpet and modular carpet tile for a variety of institutional applications such as office buildings, restaurant chains, schools and other commercial establishments. The carpet industry also manufactures carpet for the automotive, recreational vehicle, small boat and other industries.

The Carpet and Rug Institute (the "CRI") is the national trade association representing carpet and rug manufacturers. Information compiled by the CRI suggests that the domestic carpet and rug industry is comprised of fewer than 100 manufacturers, with a significant majority of the industry's production concentrated in a limited number of manufacturers focused on the lower end of the price curve. We believe that this industry focus provides us with opportunities to capitalize on our competitive strengths in selected markets where innovative styling, design, product differentiation, focused service and limited distribution add value.

Competition

The floorcovering industry is highly competitive. We compete with other carpet and rug manufacturers and other types of floorcoverings. In addition, the industry provides multiple floorcovering surfaces such as wood, luxury vinyl tile and laminate. Though soft floorcovering is still the dominant floorcovering surface, it has gradually lost market share to hard floorcovering surfaces over the last 25 years. We believe our products are among the leaders in styling and design in the high-end residential and high-end commercial carpet markets. However, a number of manufacturers produce competitive products and some of these manufacturers have greater financial resources than we do.

We believe the principal competitive factors in our primary soft floorcovering markets are styling, color, product design, quality and service. In the high-end residential and high-end commercial markets, carpet competes with various other types of floorcoverings. Nevertheless, we believe we have competitive advantages in several areas. We have an attractive portfolio of brands that we believe are well known, highly regarded by customers and complementary; by being differentiated, we offer meaningful alternatives to the discriminating customer. We believe our investment in new yarns, such as Stainmaster's® TruSoft™ and PetProtect™, and innovative tufting and dyeing technologies, strengthens our ability to offer product differentiation to our customers. In addition, we have established longstanding relationships with key suppliers in our industry and customers in most of our markets. Finally, our reputation for innovative design excellence and our experienced management team enhance our competitive position. See "Risk Factors" in Item 1A of this report.

Backlog

Sales order backlog is not material to understanding our business, due to relatively short lead times for order fulfillment in the markets for the vast majority of our products.

Trademarks

Our floorcovering businesses own a variety of trademarks under which our products are marketed. Among such trademarks, the names "Fabrica", "Masland", "Dixie Home", “Atlas Carpet Mills”, “Masland Contract” and "Masland Hospitality" are of greatest importance to our business. We believe that we have taken adequate steps to protect our interest in all significant trademarks.

Customer and Product Concentration

As a percentage of our net sales, one customer, Lowe's, a mass merchant, accounted for approximately 9% in 2015, 9% in 2014 and 13% in 2013. No other customer was more than 10 percent of our sales during the periods presented. During 2015, sales to our top ten customers accounted for 15% percent of our sales and our top 20 customers accounted for 18% percent of our sales. We do not make a material amount of sales in foreign countries.

We do not have any single class of products that accounts for more than 10 percent of our sales. However, sales of our floorcovering products may be classified by significant end-user markets into which we sell, and such information for the past three years is summarized as follows:

| 2015 | 2014 | 2013 | ||||||

| Residential floorcovering products | 64 | % | 67 | % | 73 | % | ||

| Commercial floorcovering products | 36 | % | 33 | % | 27 | % | ||

Seasonality

Our sales historically have normally reached their lowest level in the first quarter (approximately 23% of our annual sales), with the remaining sales being distributed relatively equally among the second, third and fourth quarters. Working capital requirements have normally reached their highest levels in the third and fourth quarters of the year.

Environmental

Our operations are subject to federal, state and local laws and regulations relating to the generation, storage, handling, emission, transportation and discharge of materials into the environment. The costs of complying with environmental protection laws and regulations have not had a material adverse impact on our financial condition or results of operations in the past and are not expected to have a material adverse impact in the future. See "Risk Factors” in Item 1A of this report.

Raw Materials

Our primary raw material is yarn. Nylon is the primary yarn we utilize and, to a lesser extent, wool and polyester yarn is used. Additionally, we utilize polypropylene carpet backing, latex, dyes and chemicals, and man-made topical applications in the construction of our products. Our synthetic yarns are purchased primarily from domestic fiber suppliers and wool is purchased from a number of domestic and international sources. Our other raw materials are purchased primarily from domestic suppliers. Where possible, we pass raw material price increases through to our customers; however, there can be no assurance that price increases can be passed through to customers and that increases in raw material prices will not have an adverse effect on our profitability. See "Risk Factors” in Item 1A of this report. We purchase a significant portion of our primary raw material (nylon yarn) from one supplier. We believe there are other sources of nylon yarn; however, an unanticipated termination or interruption of our supply arrangements could adversely affect our supplies of raw materials and could have a material effect on our operations. See "Risk Factors” in Item 1A of this report.

Utilities

We use electricity as our principal energy source, with oil or natural gas used in some facilities for dyeing and finishing operations as well as heating. We have not experienced any material problem in obtaining adequate supplies of electricity, natural gas or oil. Energy shortages of extended duration could have an adverse effect on our operations, and price volatility could negatively impact future earnings. See "Risk Factors” in Item 1A of this report.

Working Capital

We are required to maintain significant levels of inventory in order to provide the enhanced service levels demanded by the nature of our business and our customers, and to ensure timely delivery of our products. Consistent and dependable sources of liquidity are required to maintain such inventory levels. Failure to maintain appropriate levels of inventory could materially adversely affect our relationships with our customers and adversely affect our business. See "Risk Factors” in Item 1A of this report.

Employment Level

At December 26, 2015, we employed 1,822 associates in our operations.

Available Information

Our internet address is www.thedixiegroup.com. We make the following reports filed by us with the Securities and Exchange Commission available, free of charge, on our website under the heading "Investor Relations":

| 1. | annual reports on Form 10-K; |

| 2. | quarterly reports on Form 10-Q; |

| 3. | current reports on Form 8-K; and |

| 4. | amendments to the foregoing reports. |

The contents of our website are not a part of this report.

Item 1A. RISK FACTORS

In addition to the other information provided in this Report, the following risk factors should be considered when evaluating the results of our operations, future prospects and an investment in shares of our Common Stock. Any of these factors could cause our actual financial results to differ materially from our historical results, and could give rise to events that might have a material adverse effect on our business, financial condition and results of operations.

The floorcovering industry is sensitive to changes in general economic conditions and a decline in residential or commercial construction activity or corporate remodeling and refurbishment could have a material adverse effect on our business.

The floorcovering industry, in which the Company participates, is highly dependent on general economic conditions, such as consumer confidence and income, corporate and government spending, interest rate levels, availability of credit and demand for housing. The Company derives a majority of its sales from the replacement segment of the market. Therefore, economic changes that result in a significant or prolonged decline in spending for remodeling and replacement activities could have a material adverse effect on the Company’s business and results of operations.

The floorcovering industry is highly dependent on construction activity, including new construction, which is cyclical in nature, and experienced a downturn in 2008. The 2008 downturn in the U.S. and global economies, along with the residential and commercial markets in such economies, negatively impacted the floorcovering industry and the Company’s business. Although the impact of a decline in new construction activity is typically accompanied by an increase in remodeling and replacement activity, these activities lagged during the downturn. Although the difficult economic conditions have improved, there may be additional downturns that could cause the industry to deteriorate in the foreseeable future. A significant or prolonged decline in residential or commercial construction activity could have a material adverse effect on the Company’s business and results of operations.

We have significant levels of sales in certain channels of distribution and reduction in sales through these channels could adversely affect our business.

A significant amount of our sales are generated through certain retail and mass merchant channels of distribution. A significant reduction of sales through such channels could adversely affect our business.

We have significant levels of indebtedness that could result in negative consequences to us.

We have a significant amount of indebtedness relative to our equity. Insufficient cash flow, profitability or the value of our assets securing our loans could materially adversely affect our ability to generate sufficient funds to satisfy the terms of our senior loan agreements and other debt obligations. Additionally, the inability to access debt or equity markets at competitive rates in sufficient amounts to satisfy our obligations could adversely impact our business.

Uncertainty in the credit market or downturns in the economy and our business could affect our overall availability and cost of credit.

Uncertainty in the credit markets could affect the availability and cost of credit. Despite recent improvement in overall economic conditions, market conditions could impact our ability to obtain financing in the future, including any financing necessary to refinance existing indebtedness. The cost and terms of such financing is uncertain. These and other economic factors could have a material adverse effect on demand for our products and on its financial condition and operating results.

We face intense competition in our industry, which could decrease demand for our products and could have a material adverse effect on our profitability.

The floorcovering industry is highly competitive. We face competition from a number of domestic manufacturers and independent distributors of floorcovering products and, in certain product areas, foreign manufacturers. Significant consolidation within the floorcovering industry has caused a number of our existing and potential competitors to grow significantly larger and have greater access to resources and capital than we do. Maintaining our competitive position may require us to make substantial additional investments in our product development efforts, manufacturing facilities, distribution network and sales and marketing activities. These additional investments may be limited by our access to capital, as well as restrictions set forth in our credit facilities. Competitive pressures, both from other providers of soft surfaces and the growth of hard surface alternatives, may also result in decreased demand for our products and in the loss of market share. In addition, we face, and will continue to face, competitive pressures on our sales price and cost of our products. As a result of any of these factors, there could be a material adverse effect on our sales and profitability.

If we are unable to anticipate consumer preferences and successfully develop and introduce new, innovative and updated products, we may not be able to maintain or increase our net revenues and profitability.

Our success depends on our ability to identify and originate product trends as well as to anticipate and react to changing consumer demands in a timely manner. All of our products are subject to changing consumer preferences that cannot be predicted with certainty. In addition, long lead times for certain of our products may make it hard for us to quickly respond to changes in consumer demands. Our new products may not receive consumer acceptance as consumer preferences could shift rapidly to different types of flooring products or away from these types of products altogether, and our future success depends in part on our ability to anticipate and respond to these changes. Failure to anticipate and respond in a timely manner to changing consumer preferences could lead to, among other things, lower sales and excess inventory levels, which could have a material adverse effect on our financial condition.

Raw material prices may vary and the inability to either offset or pass on such cost increases or avoid passing on decreases larger than the cost decrease to our customers could materially adversely affect our business, results of operations and financial condition.

We require substantial amounts of raw materials to produce our products, including nylon and polyester yarn, as well as wool yarns, synthetic backing, latex, and dyes. Substantially all of the raw materials we require are purchased from outside sources. The prices of raw materials and fuel-related costs vary significantly with market conditions. The fact that we source a significant amount of raw materials means that several months of raw materials and work in process are moving through our supply chain at any point in time. We are not able to predict whether commodity costs will significantly increase or decrease in the future. If commodity costs increase in the future and we are not able to reduce or eliminate the effect of the cost increases by reducing production costs or implementing price increases, our profit margins could decrease. If commodity costs decline, we may experience pressures from customers to reduce our selling prices. The timing of any price reductions and decreases in commodity costs may not align. As a result, our margins could be affected.

Unanticipated termination or interruption of our arrangements with third-party suppliers of nylon yarn could have a material adverse effect on us.

Nylon yarn is the principal raw material used in our floorcovering products. A significant portion of such yarn is purchased from one supplier. Our yarn supplier is one of the leading fiber suppliers within the industry and is the exclusive supplier of certain innovative branded fiber technology upon which we rely. We believe our offerings of this innovative fiber technology contribute materially to the competitiveness of our products. While we believe there are other sources of nylon yarns, an unanticipated termination or interruption of our current supply of nylon yarn could have a material adverse effect on our ability to supply our product to our customers and have a material adverse impact on our competitiveness if we are unable to replace our nylon supplier with another supplier that can offer similar innovative fiber products. An interruption in the supply of these or other raw materials or sourced products used in the Company’s business or in the supply of suitable substitute materials or products would disrupt the Company’s operations, which could have a material adverse effect on the Company’s business.

We may experience certain risks associated with internal expansion, acquisitions, joint ventures and strategic investments.

We have recently embarked on several strategic and tactical initiatives, including aggressive internal expansion, acquisitions and investment in new products, to strengthen our future and to enable us to return to sustained growth and profitability. Growth through expansion and acquisition involves risks, many of which may continue to affect us after the acquisition or expansion. An acquired company, operation or internal expansion may not achieve the levels of revenue, profitability and production that we expect. The combination of an acquired company’s business with ours involves risks. Further, internally generated growth that involves expansion involves risks as well. Such risks include the integration of computer systems, alignment of human resource policies and the retention of valued talent. Reported earnings may not meet expectations because of goodwill and intangible asset impairment, other asset impairments, increased interest costs and issuance of additional securities or debt as a result of these acquisitions. We may also face challenges in consolidating functions and integrating our organizations, procedures, operations and product lines in a timely and efficient manner.

The diversion of management attention and any difficulties encountered in the transition and integration process could have a material adverse effect on our revenues, level of expenses and operating results. Failure to successfully manage and integrate an acquisition with our existing operations or expansion of our existing operations could lead to the potential loss of customers of the acquired or existing business, the potential loss of employees who may be vital to the new or existing operations, the potential loss of business opportunities or other adverse consequences that could have a material adverse effect on our business, financial condition and results of operations. Even if integration occurs successfully, failure of the expansion or acquisition to achieve levels of anticipated sales growth, profitability or productivity, or otherwise perform as expected, may have a material adverse effect on our business, financial condition and results of operations.

We are subject to various environmental, safety and health regulations that may subject us to costs, liabilities and other obligations, which could have a material adverse effect on our business, results of operations and financial condition.

We are subject to various environmental, safety and health and other regulations that may subject us to costs, liabilities and other obligations which could have a material adverse effect on our business. The applicable requirements under these laws are subject to amendment, to the imposition of new or additional requirements and to changing interpretations of agencies or courts. We could incur material expenditures to comply with new or existing regulations, including fines and penalties and increased costs of its operations. Additionally, future laws, ordinances or regulations could give rise to additional compliance or remediation costs that

could have a material adverse effect on our business, results of operations and financial condition. For example, producer responsibility regulations regarding end-of-life disposal could impose additional cost and complexity to our business.

Various federal, state and local environmental laws govern the use of our current and former facilities. These laws govern such matters as:

| • | Discharge to air and water; |

| • | Handling and disposal of solid and hazardous substances and waste, and |

| • | Remediation of contamination from releases of hazardous substances in our facilities and off-site disposal locations. |

Our operations also are governed by laws relating to workplace safety and worker health, which, among other things, establish noise standards and regulate the use of hazardous materials and chemicals in the workplace. We have taken, and will continue to take, steps to comply with these laws. If we fail to comply with present or future environmental or safety regulations, we could be subject to future liabilities. However, we cannot ensure that complying with these environmental or health and safety laws and requirements will not adversely affect our business, results of operations and financial condition.

We may be exposed to litigation, claims and other legal proceedings in the ordinary course of business relating to our products or business, which could have a material adverse effect on our business, results of operations and financial condition.

In the ordinary course of business, we are subject to a variety of work-related and product-related claims, lawsuits and legal proceedings, including those relating to product liability, product warranty, product recall, personal injury, and other matters that are inherently subject to many uncertainties regarding the possibility of a loss to our business. Such matters could have a material adverse effect on our business, results of operations and financial condition if we are unable to successfully defend against or resolve these matters or if our insurance coverage is insufficient to satisfy any judgments against us or settlements relating to these matters. Although we have product liability insurance, the policies may not provide coverage for certain claims against us or may not be sufficient to cover all possible liabilities. Further, we may not be able to maintain insurance at commercially acceptable premium levels. Additionally, adverse publicity arising from claims made against us, even if the claims are not successful, could adversely affect our reputation or the reputation and sales of our products.

Our business operations could suffer significant losses from natural disasters, catastrophes, fire or other unexpected events.

Many of our business activities involve substantial investments in manufacturing facilities and many products are produced at a limited number of locations. These facilities could be materially damaged by natural disasters, such as floods, tornadoes, hurricanes and earthquakes, or by fire or other unexpected events such as adverse weather conditions or other disruptions to our facilities, supply chain or our customer's facilities. We could incur uninsured losses and liabilities arising from such events, including damage to our reputation, and/or suffer material losses in operational capacity, which could have a material adverse impact on our business, financial condition and results of operations.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

| Item 2. | PROPERTIES |

The following table lists our facilities according to location, type of operation and approximate total floor space as of February 26, 2016:

| Location | Type of Operation | Approximate Square Feet | |||

| Administrative: | |||||

| Saraland, AL | Administrative | 29,000 | |||

| Commerce, CA* | Administrative | 21,800 | |||

| Santa Ana, CA | Administrative | 4,000 | |||

| Calhoun, GA | Administrative | 10,600 | |||

| Dalton, GA* | Administrative | 47,900 | |||

| Chattanooga, TN* | Administrative | 3,500 | |||

| Total Administrative | 116,800 | ||||

| Manufacturing and Distribution: | |||||

| Atmore, AL | Carpet Manufacturing, Distribution | 610,000 | |||

| Roanoke, AL | Carpet Yarn Processing | 204,000 | |||

| Saraland, AL | Carpet Tile Manufacturing, Distribution | 384,000 | |||

| Saraland, AL* | Samples and Rug Manufacturing, Distribution | 132,000 | |||

| Commerce, CA* | Carpet Manufacturing, Distribution | 51,700 | |||

| Commerce, CA* | Carpet Manufacturing | 250,000 | |||

| Santa Ana, CA | Carpet and Rug Manufacturing, Distribution | 200,000 | |||

| Adairsville, GA | Samples and Rug Manufacturing, Distribution | 292,000 | |||

| Calhoun, GA * | Carpet Wool Manufacturing | 99,000 | |||

| Calhoun, GA | Carpet Dyeing & Processing | 193,300 | |||

| Chickamauga, GA* | Carpet Manufacturing | 107,000 | |||

| Eton, GA | Carpet Manufacturing, Distribution | 408,000 | |||

| Total Manufacturing and Distribution | 2,931,000 | ||||

| * Leased properties | TOTAL | 3,047,800 | |||

In addition to the facilities listed above, we lease a small amount of office space in various locations.

In our opinion, our manufacturing facilities are well maintained and our machinery is efficient and competitive. Operations of our facilities generally vary between 120 and 168 hours per week. Substantially all of our owned properties are subject to mortgages, which secure the outstanding borrowings under our senior credit facilities.

| Item 3. | LEGAL PROCEEDINGS |

The Company is one of multiple parties to two lawsuits, both filed in Madison County Illinois, styled Sandra D. Watts, Individually and as Special Administrator of the Estate of Dianne Averett, Deceased vs. 4520 Corp., Inc. f/k/a Benjamin F. Shaw Company, et al No. 12-L-2032 and styled Brenda Bridgeman, Individually and as Special Administrator of the Estate of Robert Bridgeman, Deceased, vs. American Honda Motor Co., Inc., f/k/a Metropolitan Life Insurance Co., et al No. 15-L-374. Each lawsuit has a claim for damages to be determined in excess of $50,000 filed on behalf of the estate of an individual which alleges that the deceased contracted mesothelioma as a result of exposure to asbestos while employed by the Company. Discovery in both matters is ongoing, and tentative trial dates of February 2017 and January 2018 have been set. The Company has denied liability, is defending the matters vigorously and is unable to estimate its potential exposure to loss, if any, at this time.

| Item 4. | MINE SAFETY DISCLOSURES |

Not applicable

Pursuant to instruction G of Form 10-K the following is included as an unnumbered item to PART I.

EXECUTIVE OFFICERS OF THE REGISTRANT

The names, ages, positions and offices held by the executive officers of the registrant as of February 26, 2016, are listed below along with their business experience during the past five years.

| Name, Age and Position | Business Experience During Past Five Years | |

Daniel K. Frierson, 74 Chairman of the Board, and Chief Executive Officer, Director | Director since 1973, Chairman of the Board since 1987 and Chief Executive Officer since 1980. He is the Chairman of the Company's Executive Committee. He is currently Chairman of The Carpet and Rug Institute. He serves as Director of Astec Industries, Inc. headquartered in Chattanooga, Tennessee; and Louisiana-Pacific Corporation headquartered in Nashville, Tennessee. | |

D. Kennedy Frierson, Jr., 49 Vice President and Chief Operating Officer | Director since 2012 and Vice President and Chief Operating Officer since August 2009. Vice President and President Masland Residential from February 2006 to July 2009. President Masland Residential from December 2005 to January 2006. Executive Vice President and General Manager, Dixie Home, 2003 to 2005. Business Unit Manager, Bretlin, 2002 to 2003. | |

Jon A. Faulkner, 55 Vice President and Chief Financial Officer | Vice President and Chief Financial Officer since October 2009. Vice President of Planning and Development from February 2002 to September 2009. Executive Vice President of Sales and Marketing for Steward, Inc. from 1997 to 2002. | |

Paul B. Comiskey, 65 Vice President and President, Dixie Residential | Vice President and President of Dixie Residential since August 2009. Vice President and President, Dixie Home from February 2007 to July 2009. President, Dixie Home from December 2006 to January 2007.Senior Vice President of Residential Sales, Mohawk Industries, Inc. from 1998 to 2006. Executive Vice President of Sales and Marketing for World Carpets from 1996 to 1998. | |

V. Lee Martin, 64 Vice President and President, Masland Contract | President, Masland Contract since August 2012 and Vice President since February 2013. President, Step 2 Surfaces, LLC from 2011 to August 2012. Corporate Vice President, Sales and Marketing, for J & J Industries from 1994 to 2011. | |

W. Derek Davis, 65 Vice President, Human Resources and Corporate Secretary | Vice President of Human Resources since January 1991 and Corporate Secretary since January 2016. Corporate Employee Relations Director, 1988 to 1991. | |

The executive officers of the registrant are generally elected annually by the Board of Directors at its first meeting held after each annual meeting of our shareholders.

PART II.

| Item 5. | MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our Common Stock trades on the NASDAQ Global Market under the symbol DXYN. No market exists for our Class B Common Stock.

As of February 26, 2016, the total number of holders of our Common Stock was approximately 3,000 including an estimated 2,550 shareholders who hold our Common Stock in nominee names. The total number of holders of our Class B Common Stock was 11.

Recent Sales of Unregistered Securities

None.

Issuer Purchases of Equity Securities

On August 8, 2007, we announced an authorization to repurchase up to $10 million of our Common Stock. There were no repurchases of shares of our Common Stock during the three months ended December 26, 2015. Approximately $2.5 million remains for purchasing pursuant to the authorization.

Quarterly Financial Data, Dividends and Price Range of Common Stock

Following are quarterly financial data, dividends and price range of Common Stock for the four quarterly periods in the years ended December 26, 2015 and December 27, 2014. Due to rounding, the totals of the quarterly information for each of the years reflected below may not necessarily equal the annual totals. The discussion of restrictions on payment of dividends is included in Note 10 to the Consolidated Financial Statements included herein.

| THE DIXIE GROUP, INC. | ||||||||||||||||

| QUARTERLY FINANCIAL DATA, DIVIDENDS AND PRICE RANGE OF COMMON STOCK | ||||||||||||||||

| (unaudited) (dollars in thousands, except per share data) | ||||||||||||||||

| 2015 | 1ST | 2ND | 3RD | 4TH | ||||||||||||

| Net sales | $ | 95,855 | $ | 109,957 | $ | 108,908 | $ | 107,763 | ||||||||

| Gross profit | 23,339 | 29,306 | 27,265 | 26,320 | ||||||||||||

| Operating income (loss) | (2,683 | ) | 2,177 | 1,253 | 1,243 | |||||||||||

| Income (loss) from continuing operations | (2,380 | ) | 516 | 84 | (498 | ) | ||||||||||

| Loss from discontinued operations | (88 | ) | (12 | ) | (18 | ) | (30 | ) | ||||||||

| Net income (loss) | $ | (2,468 | ) | $ | 504 | $ | 66 | $ | (528 | ) | ||||||

| Basic earnings (loss) per share: | ||||||||||||||||

| Continuing operations | $ | (0.15 | ) | $ | 0.03 | $ | 0.01 | $ | (0.03 | ) | ||||||

| Discontinued operations | (0.01 | ) | — | — | — | |||||||||||

| Net income (loss) | $ | (0.16 | ) | $ | 0.03 | $ | 0.01 | $ | (0.03 | ) | ||||||

| Diluted earnings (loss) per share: | ||||||||||||||||

| Continuing operations | $ | (0.15 | ) | $ | 0.03 | $ | 0.01 | $ | (0.03 | ) | ||||||

| Discontinued operations | (0.01 | ) | — | — | — | |||||||||||

| Net income (loss) | $ | (0.16 | ) | $ | 0.03 | $ | 0.01 | $ | (0.03 | ) | ||||||

| Common Stock Prices: | ||||||||||||||||

| High | $ | 9.60 | $ | 11.40 | $ | 11.50 | $ | 9.89 | ||||||||

| Low | 7.77 | 8.76 | 8.81 | 4.75 | ||||||||||||

| 2014 | 1ST (1) | 2ND | 3RD | 4TH (2) | ||||||||||||

| Net sales | $ | 85,082 | $ | 107,926 | $ | 109,006 | $ | 104,574 | ||||||||

| Gross profit | 18,101 | 26,671 | 26,599 | 24,126 | ||||||||||||

| Operating income (loss) | (2,241 | ) | 588 | 832 | (4,415 | ) | ||||||||||

| Income (loss) from continuing operations | 4,821 | (510 | ) | (8 | ) | (3,630 | ) | |||||||||

| Loss from discontinued operations | (193 | ) | (135 | ) | (177 | ) | (103 | ) | ||||||||

| Loss on disposal of discontinued operations | $ | — | $ | — | $ | — | $ | (1,467 | ) | |||||||

| Net income (loss) | $ | 4,628 | $ | (645 | ) | $ | (185 | ) | $ | (5,200 | ) | |||||

| Basic earnings per share: | ||||||||||||||||

| Continuing operations | $ | 0.36 | $ | (0.04 | ) | $ | — | $ | (0.24 | ) | ||||||

| Discontinued operations | (0.02 | ) | (0.01 | ) | (0.01 | ) | (0.01 | ) | ||||||||

| Disposal of discontinued operations | $ | — | $ | — | $ | — | $ | (0.10 | ) | |||||||

| Net income (loss) | $ | 0.34 | $ | (0.05 | ) | $ | (0.01 | ) | $ | (0.35 | ) | |||||

| Diluted earnings (loss) per share: | ||||||||||||||||

| Continuing operations | $ | 0.36 | $ | (0.04 | ) | $ | — | $ | (0.24 | ) | ||||||

| Discontinued operations | (0.02 | ) | (0.01 | ) | (0.01 | ) | (0.01 | ) | ||||||||

| Disposal of discontinued operations | $ | — | $ | — | $ | — | $ | (0.10 | ) | |||||||

| Net income (loss) | $ | 0.34 | $ | (0.05 | ) | $ | (0.01 | ) | $ | (0.35 | ) | |||||

| Common Stock Prices: | ||||||||||||||||

| High | $ | 16.80 | $ | 18.41 | $ | 10.78 | $ | 9.44 | ||||||||

| Low | 12.10 | 9.77 | 7.42 | 6.00 | ||||||||||||

| (1) | The first quarter of 2014 included a pre-tax bargain purchase of $10,937 related to the acquisition of Atlas Carpet Mills, Inc. |

| (2) | The fourth quarter of 2014 included a loss of $1,467, net of tax, on the disposal of the Carousel specialty tufting and weaving operation that was part of the 2013 Robertex, Inc. acquisition. |

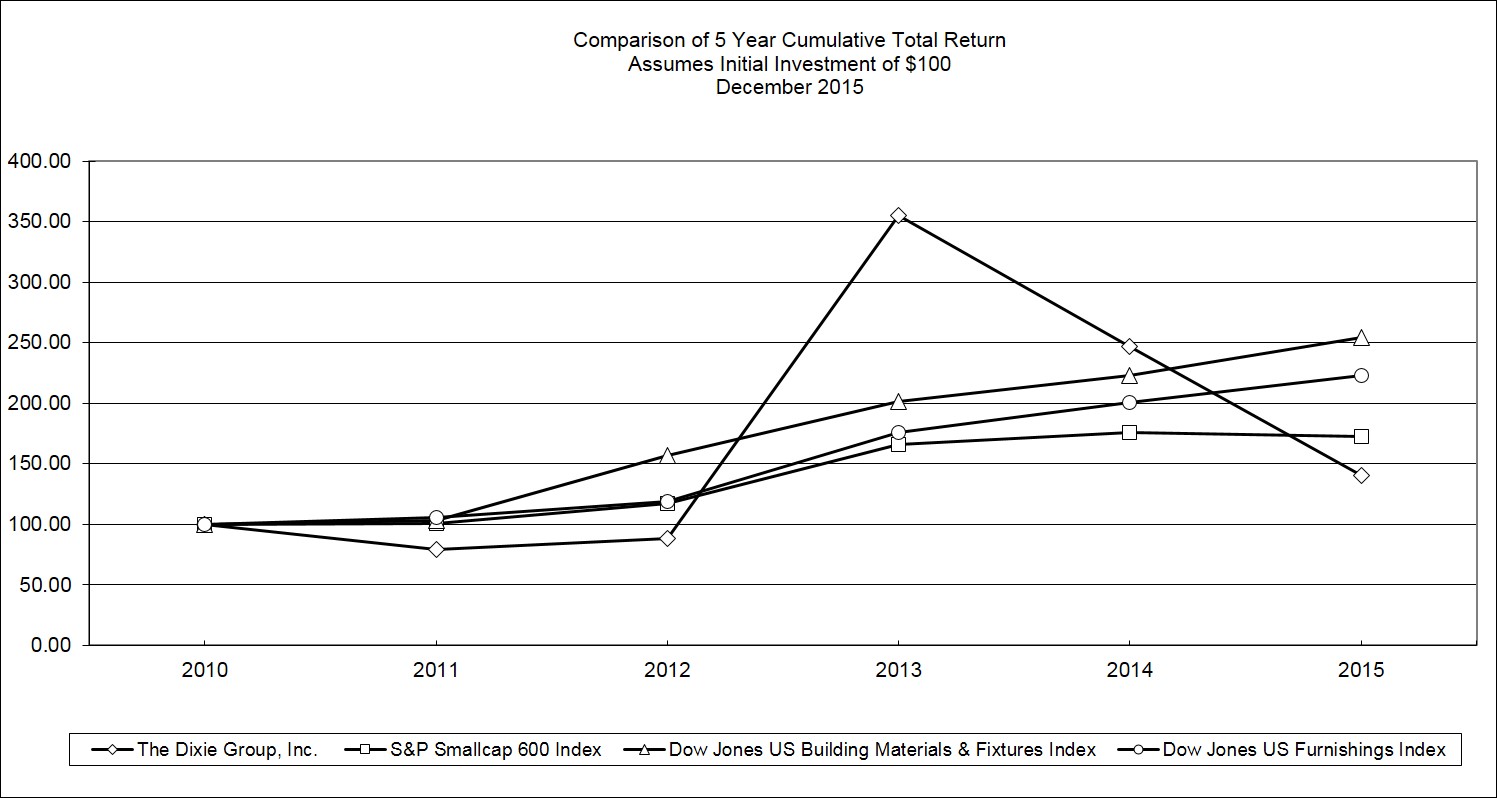

Shareholder Return Performance Presentation

We compare our performance to two different industry indexes published by Dow Jones, Inc. The first of these is the Dow Jones Furnishings Index, which is composed of publicly traded companies classified by Dow Jones in the furnishings industry. The second is the Dow Jones Building Materials & Fixtures Index, which is composed of publicly traded companies classified by Dow Jones in the building materials and fixtures industry.

In accordance with SEC rules, set forth below is a line graph comparing the yearly change in the cumulative total shareholder return on our Common Stock against the total return of the Standard & Poor's 600 Stock Index, plus both the Dow Jones Furnishings Index and the Dow Jones Building Materials & Fixtures Index, in each case for the five year period ended December 26, 2015. The comparison assumes that $100.00 was invested on December 25, 2010, in our Common Stock, the S&P 600 Index, and each of the two Peer Groups, and assumes the reinvestment of dividends.

The foregoing shareholder performance presentation shall not be deemed "soliciting material" or to be "filed" with the Commission subject to Regulation 14A, or subject to the liabilities of Section 18 of the Exchange Act.

| Item 6. | SELECTED FINANCIAL DATA |

Selected financial data for the periods presented have been restated to classify the results of Carousel operations discontinued in December 2014 as discontinued operations.

| The Dixie Group, Inc. | ||||||||||||||||||||

| Historical Summary | ||||||||||||||||||||

| (dollars in thousands, except share and per share data) | ||||||||||||||||||||

| FISCAL YEARS | 2015 (1) | 2014 (2)(3) | 2013 (4) | 2012 | 2011 (5) | |||||||||||||||

| OPERATIONS | ||||||||||||||||||||

| Net sales | $ | 422,483 | $ | 406,588 | $ | 344,374 | $ | 266,372 | $ | 270,110 | ||||||||||

| Gross profit | 106,230 | 95,497 | 85,570 | 65,372 | 65,506 | |||||||||||||||

| Operating income (loss) | 1,990 | (5,236 | ) | 8,855 | 1,815 | 5,668 | ||||||||||||||

| Income (loss) from continuing operations before taxes | (2,992 | ) | 1,726 | 4,979 | (1,054 | ) | 1,956 | |||||||||||||

| Income tax provision (benefit) | (714 | ) | 1,053 | (577 | ) | (401 | ) | 684 | ||||||||||||

| Income (loss) from continuing operations | (2,278 | ) | 673 | 5,556 | (653 | ) | 1,272 | |||||||||||||

| Depreciation and amortization | 14,119 | 12,850 | 10,230 | 9,396 | 9,649 | |||||||||||||||

| Dividends | — | — | — | — | — | |||||||||||||||

| Capital expenditures | 6,826 | 9,492 | 11,438 | 3,386 | 6,740 | |||||||||||||||

| Assets purchased under capital leases & notes, including deposits utilized and accrued purchases | 5,403 | 23,333 | 1,865 | 666 | 14 | |||||||||||||||

| FINANCIAL POSITION | ||||||||||||||||||||

| Total assets (6) | $ | 298,218 | $ | 290,447 | $ | 243,557 | $ | 196,820 | $ | 176,779 | ||||||||||

| Working capital (6) | 98,632 | 100,602 | 89,057 | 71,343 | 60,557 | |||||||||||||||

| Long-term debt (6) | 115,907 | 117,153 | 100,521 | 79,040 | 63,998 | |||||||||||||||

| Stockholders' equity | 90,804 | 92,977 | 70,771 | 64,046 | 64,385 | |||||||||||||||

| PER SHARE | ||||||||||||||||||||

| Income (loss) from continuing operations: | ||||||||||||||||||||

| Basic | $ | (0.15 | ) | $ | 0.03 | $ | 0.42 | $ | (0.05 | ) | $ | 0.10 | ||||||||

| Diluted | (0.15 | ) | 0.03 | 0.42 | (0.05 | ) | 0.10 | |||||||||||||

| Dividends: | ||||||||||||||||||||

| Common Stock | — | — | — | — | — | |||||||||||||||

| Class B Common Stock | — | — | — | — | — | |||||||||||||||

| Book value | 5.67 | 5.90 | 5.32 | 4.88 | 4.99 | |||||||||||||||

| GENERAL | ||||||||||||||||||||

| Weighted-average common shares outstanding: | ||||||||||||||||||||

| Basic | 15,535,980 | 14,381,601 | 12,736,835 | 12,637,657 | 12,585,396 | |||||||||||||||

| Diluted | 15,535,980 | 14,544,073 | 12,851,917 | 12,637,657 | 12,623,054 | |||||||||||||||

| Number of shareholders (7) | 3,000 | 3,000 | 2,350 | 1,800 | 1,750 | |||||||||||||||

| Number of associates | 1,822 | 1,740 | 1,423 | 1,200 | 1,171 | |||||||||||||||

| (1) | Includes expenses of $2,946, or $2,243 net of tax, for facility consolidation expenses in 2015. |

| (2) | Includes the results of operations of Atlas Carpet Mills, Inc. and Burtco Enterprises, Inc. subsequent to their acquisitions on March 19, 2014 and September 22, 2014, respectively. |

| (3) | Includes expenses of $5,514, or $3,364 net of tax, for facility consolidation expenses, $1,133, or $691 net of tax, for impairment of assets and income of $11,110, or $6,777 net of tax, for bargain purchases on the acquisitions of Atlas Carpet Mills and Burtco Enterprises. |

| (4) | Includes the results of operations of Robertex, Inc subsequent to its acquisition on June 30, 2013. |

| (5) | Includes income of $563, or $356 net of tax, for facility consolidation expenses in 2011. |

| (6) | Amounts have been retrospectively adjusted for the adoption of Accounting Standards Update No. 2015-03 for debt issuance costs and Accounting Standards Update No. 2015-17 for deferred taxes. (See Note 2 in the Consolidated Financial Statements) |

| (7) | The approximate number of record holders of our Common Stock for 2011 through 2015 includes Management's estimate of shareholders who held our Common Stock in nominee names as follows: 2011 - 1,250 shareholders; 2012 - 1,255 shareholders; 2013 - 1,900 shareholders; 2014 - 2,550 shareholders; 2015 - 2,550 shareholders. |

Item 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read in conjunction with our consolidated financial statements and related notes appearing elsewhere in this report.

OVERVIEW

Our business consists principally of marketing, manufacturing and selling carpet and rugs to high-end residential and commercial customers through our various sales forces and brands. We focus exclusively on the upper-end of the soft floorcovering market where we believe we have strong brands and competitive advantages with our style and design capabilities and customer relationships. Our Fabrica, Masland, and Dixie Home brands have a significant presence in the high-end residential soft floorcovering markets. Our Atlas Carpet Mills, Masland Contract and Masland Hospitality brands, participate in the upper end specified commercial marketplace. Dixie International sells all of our brands outside of the North American market.

During 2015, our net sales increased 3.9% compared with 2014. Sales of residential products decreased 0.4% in 2015 versus 2014, while, we estimate, the industry was down slightly. We anticipate the residential remodeling market to have marginal growth for next year. Commercial product sales increased 14.4% during 2015, while, we believe, the industry reflected an increase in the low single digits. We anticipate the commercial market to have moderate growth for next year.

We have completed the bulk of our capacity expansion and consolidation initiatives. However, during these endeavors, we experienced high training, quality and waste costs. We experienced a dramatically changed labor market in 2014 and 2015 as we no longer could easily recruit individuals with previous industry experience; therefore, our new hires required extensive training. In addition, we had significantly higher labor turnover than we had experienced in the period immediately prior to our expansion. We believe we have significantly improved our quality throughout 2015 as our new associates became trained in their new roles; however, we are still experiencing higher waste and claims cost from inventory produced during this period of consolidation. The status of our restructuring and facilities consolidation plans are discussed below.

Our Warehousing, Distribution & Manufacturing Consolidation Plan was developed to align our warehousing, distribution and manufacturing with our growth and manufacturing strategy. The plan was designed to create a better cost structure as well as improve distribution capabilities and customer service. In June of 2014, the Board of Directors approved a modification of this plan to include the elimination of both carpet dyeing and yarn dyeing in our Atmore, Alabama facility. Elimination of dyeing at this facility was designed to more fully accommodate our distribution and manufacturing realignment. Accordingly, the dyeing operations in Atmore were moved to our Colormaster continuous dyeing facility, our Calhoun Wool skein dyeing operation and other outside dyeing processors.

Total expenses of the Warehousing, Distribution & Manufacturing Consolidation Plan are anticipated to be approximately $6.5 million. Expenses incurred in 2015 were $2.0 million and $6.1 million since initiation of the plan in 2014. We estimate additional spending primarily related to the movement of our Saraland, Alabama rug operation moving from a rented facility into a company-owned facility of approximately $406 thousand under this plan through early 2016. These expenses of the plan primarily consist of moving and relocating inventory and equipment, facility restoration, information technology expenses and expenses relating to conversion and realignment of equipment. We also incurred non-cash asset impairment charges of $1.1 million subsequent to the first quarter of 2014 related to manufacturing changes and equipment taken out of service in our facilities.

On March 19, 2014, we acquired Atlas Carpet Mills. As a part of the Atlas acquisition, we discontinued operations at the Atlas dyeing facility in Los Angeles and moved the carpet dyeing of their products to our Susan Street dyeing operation located in Santa Ana, California. We initiated an Atlas Integration Plan to accommodate the dyeing move and address the modification of computer systems. The costs of these initiatives were $1.7 million. This plan was completed in the second quarter of 2015.

In April 2015, the Company's Board of Directors approved the Corporate Office Consolidation Plan, to cover the costs of consolidating three of the Company's existing leased divisional and corporate offices to a single leased facility located in Dalton, Georgia. The Company paid a fee to terminate one of the leases, did not renew a second facility and vacated the third facility. Related to the vacated facility, the Company recorded the estimated costs related to the fulfillment of its contractual lease obligation and on-going facilities maintenance, net of an estimate of sub-lease expectations. Costs related to the consolidation include the lease termination fee, contractual lease obligations and moving costs. Expenses of this plan were $728 thousand in 2015 with estimated remaining costs to be approximately $60 thousand.

RESULTS OF OPERATIONS

Fiscal Year Ended December 26, 2015 Compared with Fiscal Year Ended December 27, 2014

| Fiscal Year Ended | ||||||||||||||

| December 26, 2015 | % of Net Sales | December 27, 2014 | % of Net Sales | Increase (Decrease) | % Change | |||||||||

| Net sales | 422,483 | 100.0 | % | 406,588 | 100.0 | % | 15,895 | 3.9 | % | |||||

| Cost of sales | 316,253 | 74.9 | % | 311,091 | 76.5 | % | 5,162 | 1.7 | % | |||||

| Gross profit | 106,230 | 25.1 | % | 95,497 | 23.5 | % | 10,733 | 11.2 | % | |||||

| Selling and administrative expenses | 100,422 | 23.8 | % | 93,182 | 22.9 | % | 7,240 | 7.8 | % | |||||

| Other operating expense, net | 872 | 0.2 | % | 904 | 0.2 | % | (32 | ) | (3.5 | )% | ||||

| Facility consolidation expenses | 2,946 | 0.7 | % | 5,514 | 1.4 | % | (2,568 | ) | (46.6 | )% | ||||

| Impairment of assets | — | — | % | 1,133 | 0.3 | % | (1,133 | ) | (100.0 | )% | ||||

| Operating income (loss) | 1,990 | 0.4 | % | (5,236 | ) | (1.3 | )% | 7,226 | (138.0 | )% | ||||

| Interest expense | 4,935 | 1.2 | % | 4,302 | 1.1 | % | 633 | 14.7 | % | |||||

| Other (income) expense, net | 47 | — | % | (154 | ) | — | % | 201 | (130.5 | )% | ||||

| Gain on purchase of businesses | — | — | % | (11,110 | ) | (2.7 | )% | 11,110 | (100.0 | )% | ||||

| Income (loss) before taxes | (2,992 | ) | (0.8 | )% | 1,726 | 0.3 | % | (4,718 | ) | (273.3 | )% | |||

| Income tax provision (benefit) | (714 | ) | (0.2 | )% | 1,053 | 0.3 | % | (1,767 | ) | (167.8 | )% | |||

| Income (loss) from continuing operations | (2,278 | ) | (0.6 | )% | 673 | — | % | (2,951 | ) | (438.5 | )% | |||

| Loss from discontinued operations | (148 | ) | — | % | (608 | ) | (0.1 | )% | 460 | (75.7 | )% | |||

| Loss on disposal of discontinued operations | — | — | % | (1,467 | ) | (0.4 | )% | 1,467 | (100.0 | )% | ||||

| Net income (loss) | (2,426 | ) | (0.6 | )% | (1,402 | ) | (0.5 | )% | (1,024 | ) | 73.0 | % | ||

Net Sales. Net sales for the year ended December 26, 2015 were $422.5 million compared with $406.6 million in the year-earlier period, an increase of 3.9% for the year-over-year comparison. Sales for the carpet industry were down slightly for annual 2015 compared with the prior year. Our 2015 year-over-year carpet sales comparison reflected an increase of 4.5% in net sales. Sales of residential carpet were down 0.4% and sales of commercial carpet increased 14.4%. Revenue from carpet yarn processing and carpet dyeing and finishing services decreased 11.9% in 2015 compared with 2014. We believe our growth in both the residential and commercial sales were positively affected by the introduction of new and innovative product offerings.

Cost of Sales. Cost of sales, as a percentage of net sales, decreased 1.6 percentage points, as a percentage of net sales in 2015 compared with 2014. During the expansion and restructuring initiatives, we have experienced high training, quality and waste costs. These costs were offset by improvements in operating efficiencies and lower raw material costs.

Gross Profit. Gross profit, as a percentage of net sales, increased 1.6 percentage points in 2015 compared with 2014. The increase in gross profit as a percentage of net sales was attributable to the factors discussed above.

Selling and Administrative Expenses. Selling and administrative expenses were $100.4 million in 2015 compared with $93.2 million in 2014, or an increase of 0.9% as a percentage of sales. Our increase in selling and administrative expenses as a percentage of sales was primarily driven by the higher levels of investment in new products in our Residential and Commercial brands compared with the prior year.

Other Operating Expense, Net. Net other operating (income) expense was an expense of $872 thousand in 2015 compared with expense of $904 thousand in 2014.

Operating Income (Loss). Operations reflected operating income of $2.0 million in 2015 compared with an operating loss of $5.2 million in 2014. Facility consolidation expenses of $2.9 million and $5.5 million were included in the 2015 and 2014 results, respectively. In addition, related asset impairment expenses of $1.1 million were included in the 2014 operating results.

Interest Expense. Interest expense increased $633 thousand in 2015 principally due to higher interest rates associated with previously locked in future interest rate swaps from 2015 until 2021 to fix a portion of the Company's revolving credit facility.

Other (Income) Expense, Net. Other (income) expense, net was an expense of $47 thousand compared with income of $154 thousand in 2014. Earnings from equity investments of $209 thousand were included in 2014.

Gain on Purchase of Businesses. During 2014, we recognized gains of $11.1 million on business acquisitions. The acquisition of Atlas resulted in a gain of $10.9 million and the acquisition of Burtco resulted in a gain of $173 thousand.

Income Tax Provision (Benefit). Our effective income tax rate was a benefit of 23.9% in 2015. In 2015, we increased our valuation allowances by $977 thousand related to state income tax loss carryforwards and state income tax credit carryforwards. This was the result of a pretax loss in 2015 that put the Company in a three-year cumulative loss. Therefore, we cannot rely on future earnings to project the utilization of these carryforwards. Additionally, 2015 included approximately $441 thousand of federal tax credits. Our effective income tax rate was 61.0% in 2014 and included an increase of $569 thousand in increased valuation allowances related to state income tax carryforwards and state income tax credit carryforwards.

Loss from Discontinued Operations and Loss on Disposal of Discontinued Operations, net of tax. In the fourth quarter of 2014, we discontinued the Carousel specialty tufting and weaving operation that was part of the 2013 Robertex, Inc. acquisition. As a result, we recognized a loss on the disposal of the discontinued operation of $1.5 million, net of tax, which included the impairment of certain intangibles associated with Carousel and its related machinery and equipment. Additionally, 2014 included a loss from the discontinued Carousel operations of $598 thousand, net of tax.

Net Income (Loss). Continuing operations reflected a loss of $2.3 million, or $0.15 per diluted share in 2015, compared with income from continuing operations of $673 thousand, or $0.03 per diluted share in 2014. Our discontinued operations reflected a loss of $148 thousand, or $0.01 per diluted share in 2015 compared with a loss of $608 thousand, or $0.04 per diluted share, and a loss on disposal of discontinued operations of $1.5 million, or $0.10 per diluted share in 2014. Including discontinued operations, we had a net loss of $2.4 million, or $0.16 per diluted share, in 2015 compared with a net loss of $1.4 million, or $0.11 per diluted share, in 2014.

Fiscal Year Ended December 27, 2014 Compared with Fiscal Year Ended December 28, 2013

| Fiscal Year Ended | ||||||||||||||

| December 27, 2014 | % of Net Sales | December 28, 2013 | % of Net Sales | Increase (Decrease) | % Change | |||||||||

| Net sales | 406,588 | 100.0 | % | 344,374 | 100.0 | % | 62,214 | 18.1 | % | |||||

| Cost of sales | 311,091 | 76.5 | % | 258,804 | 75.2 | % | 52,287 | 20.2 | % | |||||

| Gross profit | 95,497 | 23.5 | % | 85,570 | 24.8 | % | 9,927 | 11.6 | % | |||||

| Selling and administrative expenses | 93,182 | 22.9 | % | 76,221 | 22.1 | % | 16,961 | 22.3 | % | |||||

| Other operating expense, net | 904 | 0.2 | % | 494 | 0.1 | % | 410 | 83.0 | % | |||||

| Facility consolidation expenses | 5,514 | 1.4 | % | — | — | % | 5,514 | 100.0 | % | |||||

| Impairment of assets | 1,133 | 0.3 | % | — | — | % | 1,133 | 100.0 | % | |||||

| Operating income (loss) | (5,236 | ) | (1.3 | )% | 8,855 | 2.6 | % | (14,091 | ) | (159.1 | )% | |||

| Interest expense | 4,302 | 1.1 | % | 3,756 | 1.1 | % | 546 | 14.5 | % | |||||

| Other (income) expense, net | (154 | ) | — | % | 26 | — | % | (180 | ) | (692.3 | )% | |||

| Gain on purchase of businesses | (11,110 | ) | (2.7 | )% | — | — | % | (11,110 | ) | 100.0 | % | |||

| Refinancing expenses | — | — | % | 94 | — | % | (94 | ) | (100.0 | )% | ||||

| Income (loss) before taxes | 1,726 | 0.3 | % | 4,979 | 1.5 | % | (3,253 | ) | (65.3 | )% | ||||

| Income tax provision (benefit) | 1,053 | 0.3 | % | (577 | ) | (0.2 | )% | 1,630 | (282.5 | )% | ||||

| Income (loss) from continuing operations | 673 | — | % | 5,556 | 1.7 | % | (4,883 | ) | (87.9 | )% | ||||

| Loss from discontinued operations | (608 | ) | (0.1 | )% | (266 | ) | (0.1 | )% | (342 | ) | 128.6 | % | ||

| Loss on disposal of discontinued operations | (1,467 | ) | (0.4 | )% | — | — | % | (1,467 | ) | 100.0 | % | |||

| Net income (loss) | (1,402 | ) | (0.5 | )% | 5,290 | 1.6 | % | (6,692 | ) | (126.5 | )% | |||

Net Sales. Net sales for the year ended December 27, 2014 were $406.6 million compared with $344.4 million in the year-earlier period, an increase of 18.1%, or 7.1% excluding Atlas, for the year-over-year comparison. Sales for the carpet industry were flat for annual 2014 compared with the prior year. Our 2014 year-over-year carpet sales comparison reflected an increase of 18.1% in net sales, or 7.5% excluding Atlas. Sales of residential carpet were up 8.2% and sales of commercial carpet increased 45.5%, or 5.5% excluding Atlas. Revenue from carpet yarn processing and carpet dyeing and finishing services increased $1.9 million in 2014 compared with 2013 primarily as a result of processing services performed by Atlas under an equity investment relationship. We

believe our growth in both the residential and commercial sales were positively affected by the introduction of new and innovative products and the expansion of our wool product offerings.

Cost of Sales. Cost of sales, as a percentage of net sales, increased 1.3 percentage points, as a percentage of net sales in 2014 compared with 2013. The expansion and restructuring initiatives undertaken along with the expansion of our workforce negatively affected our operating results in the form of training costs, production inefficiencies, increased levels of waste and scrap and generally higher operating costs.

Gross Profit. Gross profit increased $9.9 million in 2014 compared with 2013. The increase in gross profit was primarily attributable to higher sales. However, the gross profit dollars in 2014 were negatively impacted by our actions taken to address our capacity constraints.

Selling and Administrative Expenses. Selling and administrative expenses were $93.2 million in 2014 compared with $76.2 million in 2013, or an increase of 0.7% as a percentage of sales. Our selling expense increase as a percentage of sales was primarily driven by the higher relative selling expense of Atlas and higher levels of investment in new products and marketing in our Masland Contract brand compared with the prior year.

Other Operating (Income) Expense, Net. Net other operating (income) expense was an expense of $904 thousand in 2014 compared with expense of $494 thousand in 2013. The change in 2014 was primarily a result of an increase in losses on currency valuations and the amortization of an intangible asset associated with the 2014 Atlas acquisition.

Operating Income (Loss). Operations reflected an operating loss of $5.2 million in 2014 compared with operating income of $8.9 million in 2013. Facility consolidation expenses of $5.5 million and related asset impairment expenses of $1.1 million were included in the 2014 operating results.

Interest Expense. Interest expense increased $546 thousand in 2014 principally due to higher levels of debt to support our growth and the acquisition of capital assets under various debt arrangements.

Other (Income) Expense, Net. Other (income) expense, net was income of $154 thousand in 2014 compared with expense of $26 thousand in 2013. $209 thousand of earnings from equity investments were included in 2014.

Gain on Purchase of Businesses. During 2014, we recognized gains of $11.1 million on business acquisitions. The acquisition of Atlas resulted in a gain of $10.9 million and the acquisition of Burtco resulted in a gain of $173 thousand.

Income Tax Provision (Benefit). Our effective income tax rate was 61.0% in 2014 and included an increase of $569 thousand in increased valuation allowances related to state income tax carryforwards and state income tax credit carryforwards. Our income tax provision was a benefit of $643 thousand in 2013 on positive earnings primarily as a result of the reversal of $1.2 million of previously established reserves for state income tax loss and tax credit carryforwards. The recognition or reversal of such reserves established by taxing jurisdiction is based on a number of factors including current and forecasted earnings. Additionally, 2013 included certain tax credits of approximately $520 thousand related to the years 2009 - 2011 determined to be available for utilization and $304 thousand of 2012 research and development tax credits that could not be recognized until the extension of the credit was approved by Congress in 2013.

Loss from Discontinued Operations and Loss on Disposal of Discontinued Operations, net of tax. In the fourth quarter of 2014, we discontinued the Carousel specialty tufting and weaving operation that was part of the 2013 Robertex, Inc. acquisition. As a result, we recognized a loss on the disposal of the discontinued operation of $1.5 million, net of tax, which included the impairment of certain intangibles associated with Carousel and its related machinery and equipment. Additionally, 2014 included a loss from the discontinued Carousel operations of $598 thousand, net of tax, compared with a loss of $198 thousand, net of tax in 2013.

Net Income (Loss). Continuing operations reflected income of $673 thousand, or $0.03 per diluted share in 2014, compared with income from continuing operations of $5.6 million, or $0.42 per diluted share in 2013. Our discontinued operations reflected a loss of $608 thousand, or $0.04 per diluted share, and a loss on disposal of discontinued operations of $1.5 million, or $0.10 per diluted share in 2014 compared with a loss from discontinued operations of $266 thousand, or $0.02 per diluted share in 2013. Including discontinued operations, we had a net loss of $1.4 million, or $0.11 per diluted share, in 2014 compared with net income of $5.3 million, or $0.40 per diluted share, in 2013.

LIQUIDITY AND CAPITAL RESOURCES

During the year ended December 26, 2015, cash provided by operations was $8.6 million. Inventories increased $10.9 million which was offset by an increase in accounts payable and accrued expenses of $7.6 million. Inventories were increased to improve service to our customers and to build inventories from a supplier that was going through a year-end software conversion.

Capital asset acquisitions for the year ended December 26, 2015 were $12.2 million; $6.8 million of cash used in investing activities, $3.3 million of equipment acquired under notes and capital leases, $1.9 million of previous deposits utilized for capital additions and $200 thousand for accrued purchases. Depreciation and amortization for the year ended December 26, 2015 were $14.1 million. We expect capital expenditures to be approximately $10.0 million in 2016 for capital expenditures while depreciation and amortization is expected to be approximately $13.5 million. Planned capital expenditures in 2016 are primarily for new equipment.

During the year ended December 26, 2015, cash used in financing activities was $2.0 million. In January 2015, we entered into a ten-year $6.3 million mortgage note payable to finance an owned facility in Saraland, Alabama. We had additional proceeds of $1.0 million from equipment notes payable. These proceeds are offset by payments on notes payable and lease obligations of $9.7 million.

We believe our operating cash flows, credit availability under our revolving credit facility and other sources of financing are adequate to finance our anticipated liquidity requirements. As of December 26, 2015, the unused borrowing availability under our revolving credit facility was $39.8 million. Our revolving credit facility requires us to maintain a fixed charge coverage ratio of 1.1 to 1.0 during any period that borrowing availability is less than $16.5 million. As of the date hereof, our fixed coverage ratio was less than 1.1 to 1.0, accordingly the unused availability accessible by us is the amount above $16.5 million. Significant additional cash expenditures above our normal liquidity requirements or significant deterioration in economic conditions could affect our business and require supplemental financing or other funding sources. There can be no assurance that such supplemental financing or other sources of funding can be obtained or will be obtained on terms favorable to us.

Debt Facilities

Revolving Credit Facility. The revolving credit facility provides for a maximum of $150.0 million of revolving credit, subject to borrowing base availability. The borrowing base is currently equal to specified percentages of the Company's eligible accounts receivable, inventories, fixed assets and real property less reserves established, from time to time, by the administrative agent under the facility. The revolving credit facility matures on March 14, 2019. The revolving credit facility is secured by a first priority lien on substantially all of our assets.

At our election, advances of the revolving credit facility bear interest at annual rates equal to either (a) LIBOR for 1, 2 or 3 month periods, as selected by us, plus an applicable margin of either 1.50%, 1.75% or 2.00%, or (b) the higher of the prime rate, the Federal Funds rate plus 0.5%, or a daily LIBOR rate plus 1.00%, plus an applicable margin of either 0.50%, 0.75% or 1.00%. The applicable margin is determined based on availability under our revolving credit facility with margins increasing as availability decreases. We pay an unused line fee on the average amount by which the aggregate commitments exceed utilization of the senior credit facility equal to 0.375% per annum. The weighted-average interest rate on borrowings outstanding under our revolving credit facility was 2.23% at December 26, 2015 and 2.29% at December 27, 2014.

The revolving credit facility includes certain affirmative and negative covenants that impose restrictions on our financial and business operations. The revolving credit facility requires us to maintain a fixed charge coverage ratio of 1.1 to 1.0 during any period that borrowing availability is less than $16.5 million. As of December 26, 2015, our unused borrowing availability under the revolving credit facility was $39.8 million. As of December 26, 2015, our fixed charge coverage ratio was less than 1.1 to 1.0, accordingly, the unused availability accessible by us is the amount above $16.5 million.

Notes Payable - Buildings. On November 7, 2014, we entered into a ten-year $8.3 million note payable to purchase a previously leased distribution center in Adairsville, Georgia. The note payable is scheduled to mature on November 7, 2024 and is secured by the distribution center. The note payable bears interest at a variable rate equal to one month LIBOR plus 2.0% and is payable in equal monthly installments of principal of $35 thousand, plus interest calculated on the declining balance of the note, with a final payment of $4.2 million due on maturity. In addition, we entered into an interest swap with an amortizing notional amount effective November 7, 2014 which effectively fixes the interest rate at 4.50%.

On January 23, 2015, we entered into a ten-year $6.3 million note payable to finance an owned facility in Saraland, Alabama. The note payable is scheduled to mature on January 7, 2025 and is secured by the facility. The note payable bears interest at a variable rate equal to one month LIBOR plus 2.0% and is payable in equal monthly installments of principal of $26 thousand, plus interest calculated on the declining balance of the note, with a final payment of $3.1 million due on maturity. In addition, we entered into a forward interest rate swap with an amortizing $5.7 million notional amount effective January 7, 2017 which effectively fixes the interest rate at 4.30%.