UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-2410 |

| |

| Dreyfus Liquid Assets, Inc. | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Michael A. Rosenberg, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 12/31 | |

Date of reporting period: | 12/31/2010 | |

| | | | | | | |

FORM N-CSR

Item 1. Reports to Stockholders.

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| | Contents |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Understanding Your Fund’s Expenses |

| 6 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 7 | Statement of Investments |

| 10 | Statement of Assets and Liabilities |

| 11 | Statement of Operations |

| 12 | Statement of Changes in Net Assets |

| 13 | Financial Highlights |

| 15 | Notes to Financial Statements |

| 23 | Report of Independent Registered Public Accounting Firm |

| 24 | Important Tax Information |

| 25 | Information About the Review and Approval of the Fund’s Management Agreement |

| 29 | Board Members Information |

| 31 | Officers of the Fund |

| | FOR MORE INFORMATION |

| | Back Cover |

Dreyfus

Liquid Assets, Inc.

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this semiannual report for Dreyfus Liquid Assets, Inc., covering the 12-month period from January 1, 2010, through December 31, 2010.

Although 2010 proved to be a volatile year for many longer-term assets, such as stocks and bonds, the reporting period ended with many asset categories producing respectable, positive returns. Investors’ early concerns regarding sovereign debt issues in Europe and stubbornly high unemployment in the United States later gave way to optimism that massive economic stimulus programs, robust growth in the world’s emerging markets, a strong holiday retail season and rising corporate earnings signaled better economic times ahead.

Although U.S. GDP growth was positive throughout the reporting period, the economic recovery has been milder than historical averages. Therefore, we are guardedly optimistic regarding the U.S. economy’s prospects in 2011, and many experts believe inflationary pressures and short-term interest rates should remain low over the near term, potentially preventing any significant rise in money market yields.What does this mean for your investment portfolio? We suggest talking to your financial advisor, who can help you review your allocations and your current liquid asset needs, and identify potential opportunities suitable for your individual needs and risk tolerance in today’s market environment.

For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

January 18, 2011

2

DISCUSSION OF FUND PERFORMANCE

For the period of January 1, 2010, through December 31, 2010, as provided by Patricia A. Larkin, Senior Portfolio Manager

Fund and Market Performance Overview

For the 12-month period ended December 31, 2010, Dreyfus Liquid Assets’ Class 1 shares produced a yield of 0.00%, and its Class 2 shares produced a yield of 0.16%. Taking into account the effects of compounding, the fund’s Class 1 and Class 2 shares provided effective yields of 0.00% and 0.16%, respectively, for the same period.1,2

Money market yields remained near historical lows throughout 2010 as the Federal Reserve Board (the “Fed”) left its target for short-term interest rates unchanged in a generally sluggish economic environment.

The Fund’s Investment Approach

The fund seeks as high a level of current income as is consistent with the preservation of capital.To pursue this goal, the fund invests in a diversified portfolio of high-quality, short-term debt securities, including securities issued or guaranteed by the U.S. government or its agencies or instrumentalities, certificates of deposit, time deposits, bankers’ acceptances, and other short-term securities issued by U.S. banks and foreign branches of U.S. banks, repurchase agreements, including tri-party repurchase agreements, asset-backed securities, commercial paper and other short-term corporate obligations of U.S. issuers.

Normally, the fund invests at least 25% of its net assets in bank obligations.

Recovery Strengthened but Fed Remained on Hold

The year 2010 began in the midst of an economic recovery fueled, in part, by an overnight federal funds rate that has remained unchanged since December 2008 in a range between 0.00% and 0.25%.While the economy expanded in the first quarter of 2010 at a relatively mild 3.7% annualized rate, it was encouraging news nonetheless for investors eager to see an end to recession. In fact, job creation began to improve during the first quarter after many months of losses.

DISCUSSION OF FUND PERFORMANCE (continued)

Investors were further cheered in May, when 431,000 additional new jobs were created, although many were temporary government workers hired for the 2010 Census. However, the economic outlook soon took a turn for the worse when a resurgent sovereign debt crisis in Europe rattled investors. U.S. industrial production moderated in June, and private-sector job growth proved more anemic than many analysts expected. U.S. GDP declined to an annualized 1.7% rate during the second quarter.

Yet, in July, the manufacturing and service sectors of the U.S. economy continued to expand. Still, total nonfarm payroll employment fell by 131,000 jobs in July, reflecting the end of temporary census hiring. Sales of new homes fell to a 47-year low in August, while purchases of existing homes plummeted to a 15-year low.The unemployment rate rose to 9.6%, as only 67,000 jobs were created in the private sector during August. Economic data released in September appeared to confirm that the economic recovery, while intact, remained tenuous as employment and housing data showed few signs of improvement. U.S. GDP grew at a 2.6% annualized rate in the third quarter of 2010.

In response to the sluggish rebound, the Fed indicated in September that it would embark on a second round of quantitative easing of monetary policy by purchasing $600 million of U.S.Treasury securities.This move was designed to fight deflationary forces and encourage lending by injecting more cash into the financial system. Indeed, October brought better economic news. The private sector added 159,000 jobs, with much of the gain coming from the services sector. However, issues regarding the banking industry’s foreclosure process further clouded an already murky outlook for home values.

Economic data remained encouraging in November, except for one critical measure: the economy created only 93,000 jobs during the month. Yet, the manufacturing and service sectors continued to improve, and even the housing market posted better sales data.

December continued to show signs of improvement, including better data from the labor market as new unemployment claims moderated and the unemployment rate eased to 9.4%. The manufacturing sector

4

expanded for the 17th consecutive month, and the holiday season proved to be a relatively healthy one for retailers, bolstering the services sector.

Quality and Liquidity Are Paramount

The low federal funds rate kept money market yields near zero percent, and with narrow yield differences along the market’s maturity spectrum, it continued to make little sense to incur the additional credit and interest-rate risks that longer-dated instruments typically entail.Therefore, we maintained the fund’s weighted average maturity in a range that was roughly in line with industry averages. As always, we focused exclusively on money market instruments meeting our stringent credit-quality criteria.

The economic recovery appears to be gathering momentum, and we are hopeful that money market yields will respond to a more constructive market environment in 2011. In the meantime, as we have for some time, we intend to maintain the fund’s focus on credit quality and liquidity.

January 18, 2011

| |

| | An investment in the fund is not insured or guaranteed by the FDIC or any other government |

| | agency.Although the fund seeks to preserve the value of your investment at $1.00 per share, it is |

| | possible to lose money by investing in the fund. |

| | Short-term corporate and asset-backed securities holdings while rated in the highest rating category |

| | by one or more NRSRO (or unrated, if deemed of comparable quality by Dreyfus), involve credit |

| | and liquidity risks and risk of principal loss. |

| 1 | Effective yield is based upon dividends declared daily and reinvested monthly. Past performance is |

| | no guarantee of future results. Yields fluctuate. Yields provided for the fund’s Class 1 shares reflect |

| | the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an agreement in |

| | effect through May 1, 2011, at which time it may be extended, terminated or modified without |

| | notice. Had these expenses not been absorbed, fund yields would have been lower, and |

| | in some cases, 7-day yields during the reporting period would have been negative absent the |

| | expense absorption. |

| 2 | Effective yield is based upon dividends declared daily and reinvested monthly. Past performance is |

| | no guarantee of future results.Yields fluctuate.Yields provided for the fund’s Class 2 shares reflect |

| | the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an agreement in |

| | which shareholders will be given at least 90 days’ notice prior to the time such absorption may be |

| | terminated. Class 2 shares of the fund are available only to certain eligible financial institutions. |

| | Had these expenses not been absorbed, fund yields would have been lower, and in some cases, |

| | 7-day yields during the reporting period would have been negative absent the expense absorption. |

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Liquid Assets, Inc. from July 1, 2010 to December 31, 2010. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | |

| Expenses and Value of a $1,000 Investment | |

| assuming actual returns for the six months ended December 31, 2010 | |

| | Class 1 Shares | Class 2 Shares |

| Expenses paid per $1,000† | $ 1.81 | $ .81 |

| Ending value (after expenses) | $1,000.00 | $1,001.00 |

|

| COMPARING YOUR FUND’S EXPENSES |

| WITH THOSE OF OTHER FUNDS (Unaudited) |

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | |

| Expenses and Value of a $1,000 Investment | |

| assuming a hypothetical 5% annualized return for the six months ended December 31, 2010 |

| | Class 1 Shares | Class 2 Shares |

| Expenses paid per $1,000† | $ 1.84 | $ .82 |

| Ending value (after expenses) | $1,023.39 | $1,024.40 |

† Expenses are equal to the fund’s annualized expense ratio of .36% for Class 1, and .16% for Class 2, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

6

|

| STATEMENT OF INVESTMENTS |

| December 31, 2010 |

| | |

| | Principal | |

| Negotiable Bank Certificates of Deposit—1.1% | Amount ($) | Value ($) |

| Citibank N.A. | | |

| 0.36%, 2/24/11 | | |

| (cost $50,000,000) | 50,000,000 | 50,000,000 |

| | | |

| Commercial Paper—38.5% | | | |

| Credit Agricole NA | | | |

| 0.30%, 1/28/11 | 200,000,000 | | 199,955,000 |

| Deutsche Bank Financial LLC | | | |

| 0.40%, 2/14/11 | 200,000,000 | | 199,902,222 |

| Fortis Funding LLC | | | |

| 0.47%, 6/7/11 | 200,000,000 | a | 199,590,056 |

| General Electric Capital Services Inc. | | | |

| 0.25%, 3/16/11 | 200,000,000 | | 199,897,222 |

| ING (US) Funding LLC | | | |

| 0.22%, 1/6/11 | 200,000,000 | | 199,993,889 |

| JPMorgan Chase & Co. | | | |

| 0.35%, 2/1/11 | 70,000,000 | a | 69,978,903 |

| Nordea North America Inc. | | | |

| 0.18%, 1/5/11 | 200,000,000 | | 199,996,000 |

| Societe Generale N.A. Inc. | | | |

| 0.41%, 4/8/11 | 100,000,000 | | 99,889,528 |

| Toronto-Dominion Holdings USA Inc. | | | |

| 0.25%, 3/30/11 | 125,000,000 | a | 124,923,611 |

| UBS Finance Delaware Inc. | | | |

| 0.22%, 1/6/11 | 200,000,000 | | 199,993,889 |

| Total Commercial Paper | | | |

| (cost $1,694,120,320) | | | 1,694,120,320 |

| |

| Asset-Backed Commercial Paper—38.8% | | | |

| Amsterdam Funding Corp. | | | |

| 0.27%—0.40%, 1/7/11—3/8/11 | 77,475,000 | a | 77,454,305 |

| Atlantis One Funding Corp. | | | |

| 0.35%—0.51%, 1/20/11—3/8/11 | 225,000,000 | a | 224,864,938 |

| CAFCO | | | |

| 0.41%, 2/22/11 | 100,000,000 | a | 99,940,778 |

| Cancara Asset Securitization | | | |

| 0.29%—0.30%, 1/18/11—3/8/11 | 200,000,000 | a | 199,951,958 |

| CHARTA | | | |

| 0.38%, 4/4/11 | 50,000,000 | a | 49,950,917 |

| CIESCO LLC | | | |

| 0.40%, 3/4/11—3/21/11 | 100,000,000 | a | 99,921,667 |

STATEMENT OF INVESTMENTS (continued)

| | |

| | Principal | |

| Asset-Backed Commercial Paper (continued) | Amount ($) | Value ($) |

| | | |

| Clipper Receivables Co., LLC | | | |

| 0.30%, 1/25/11 | 200,000,000 | a | 199,960,000 |

| CRC Funding | | | |

| 0.30%, 1/21/11 | 100,000,000 | a | 99,983,333 |

| Falcon Asset Securitization Corp. | | | |

| 0.25%—0.48%, 1/18/11—1/28/11 | 135,000,000 | a | 134,972,812 |

| FCAR Owner Trust, Ser. I | | | |

| 0.30%—0.35%, 1/5/11—2/1/11 | 136,000,000 | | 135,963,300 |

| Govco | | | |

| 0.25%, 1/3/11 | 100,000,000 | a | 99,998,611 |

| Grampian Funding LLC | | | |

| 0.32%—0.37%, 1/24/11—3/4/11 | 200,000,000 | a | 199,915,833 |

| Victory Receivables Corp. | | | |

| 0.29%, 1/14/11 | 85,000,000 | a | 84,991,099 |

| Total Asset-Backed Commercial Paper | | | |

| (cost $1,707,869,551) | | | 1,707,869,551 |

| |

| |

| Time Deposit—1.4% | | | |

| Wells Fargo Bank, NA (Grand Cayman) | | | |

| 0.03%, 1/3/11 | | | |

| (cost $60,000,000) | 60,000,000 | | 60,000,000 |

| |

| |

| U.S. Government Agencies—5.4% | | | |

| Federal Home Loan Bank | | | |

| 0.001%-0.09%, 1/3/11-1/19/11 | 220,000,000 | | 219,990,999 |

| Straight-A Funding LLC | | | |

| 0.25%, 3/7/11 | 20,000,000 | a | 19,990,972 |

| Total U.S. Government Agencies | | | |

| (cost $239,981,971) | | | 239,981,971 |

| |

| |

| Repurchase Agreements—14.8% | | | |

| Barclays Capital, Inc. | | | |

| 0.25%, dated 12/31/10, due 1/3/11 in the amount of | | | |

| $7,000,146 (fully collateralized by $21,507,320 | | | |

| U.S. Treasury Strips, due 5/15/34, value $7,140,000) | 7,000,000 | | 7,000,000 |

| HSBC USA Inc. | | | |

| 0.27%, dated 12/31/10, due 1/3/11 in the amount of | | | |

| $100,002,250 (fully collateralized by $98,545,000 | | | |

| Corporate Bonds, 0%-1.75%, due 7/17/14-10/6/15, value | | | |

| $102,166,031 and $835,000 Inter-American Development | | | |

| Bank, 1.52%, due 3/16/11, value $835,969) | 100,000,000 | | 100,000,000 |

8

| | |

| | Principal | |

| Repurchase Agreements (continued) | Amount ($) | Value ($) |

| RBC Capital Markets | | |

| 0.275%, dated 12/31/10, due 1/3/11 in the amount of | | |

| $100,002,292 (fully collateralized by $149,318,523 | | |

| Corporate Bonds, 0%-12.75%, due 3/15/11-7/1/47, | | |

| value $103,500,001) | 100,000,000 | 100,000,000 |

| RBS Securities, Inc. | | |

| 0.18%-0.275%, dated 12/31/10, due 1/3/11 in the | | |

| amount of $246,005,273 (fully collateralized by | | |

| $148,844,240 Corporate Bonds, 0%-5.05%, due | | |

| 11/12/13-6/25/47, value $67,460,715, $235,644,634 | | |

| Federal Home Loan Mortgage Corp., 5%-6.50%, due | | |

| 4/1/24-1/1/41, value $137,589,128 and $47,280,000 | | |

| U.S. Treasury Notes, 2.75%, due 2/15/19, | | |

| value $46,921,734) | 246,000,000 | 246,000,000 |

| TD Securities (USA) LLC | | |

| 0.22%, dated 12/31/10, due 1/3/11 in the amount of | | |

| $200,003,667 (fully collateralized by $162,622,200 | | |

| U.S. Treasury Inflation Protected Securities, 1.88%, | | |

| due 7/15/13-7/15/15, value $204,000,072) | 200,000,000 | 200,000,000 |

| Total Repurchase Agreements | | |

| (cost $653,000,000) | | 653,000,000 |

| |

| Total Investments (cost $4,404,971,842) | 100.0% | 4,404,971,842 |

| |

| Cash and Receivables (Net) | .0% | 886,108 |

| |

| Net Assets | 100.0% | 4,405,857,950 |

|

| a Securities exempt from registration under Rule 144A of the Securities Act of 1933.These securities may be resold in |

| transactions exempt from registration, normally to qualified institutional buyers.At December 31, 2010, these |

| securities amounted to $1,986,389,793 or 45.1% of net assets. |

| | | |

| Portfolio Summary (Unaudited)† | | |

| |

| | Value (%) | | Value (%) |

| Banking | 36.4 | U.S. Government Agencies | 5.4 |

| Asset-Backed/Banking | 18.4 | Finance | 4.6 |

| Asset-Backed/Multi-Seller Programs | 17.3 | Asset-Backed/Single Seller | 3.1 |

| Repurchase Agreements | 14.8 | | 100.0 |

| |

| † Based on net assets. | | | |

| See notes to financial statements. | | | |

|

| STATEMENT OF ASSETS AND LIABILITIES |

| December 31, 2010 |

| | |

| | Cost | Value |

| Assets ($): | | |

| Investments in securities—See Statement of Investments | | |

| (including repurchase agreements of | | |

| $653,000,000)—Note 1(b) | 4,404,971,842 | 4,404,971,842 |

| Cash | | 4,105,096 |

| Interest receivable | | 69,092 |

| Prepaid expenses | | 607,272 |

| | | 4,409,753,302 |

| Liabilities ($): | | |

| Due to The Dreyfus Corporation and affiliates—Note 2(b) | | 663,510 |

| Payable for shares of Common Stock redeemed | | 2,984,033 |

| Accrued expenses | | 247,809 |

| | | 3,895,352 |

| Net Assets ($) | | 4,405,857,950 |

| Composition of Net Assets ($): | | |

| Paid-in capital | | 4,405,857,950 |

| Net Assets ($) | | 4,405,857,950 |

| |

| |

| Net Asset Value Per Share | | |

| | Class 1 Shares | Class 2 Shares |

| Net Assets ($) | 1,066,646,838 | 3,339,211,112 |

| Shares Outstanding | 1,066,704,599 | 3,339,573,396 |

| Net Asset Value Per Share ($) | 1.00 | 1.00 |

| |

| See notes to financial statements. | | |

10

|

| STATEMENT OF OPERATIONS |

| Year Ended December 31, 2010 |

| |

| Investment Income ($): | |

| Interest Income | 14,576,154 |

| Expenses: | |

| Management fee—Note 2(a) | 21,671,729 |

| Shareholder servicing costs—Note 2(b) | 4,561,212 |

| Prospectus and shareholders’ reports | 1,090,174 |

| Custodian fees—Note 2(b) | 237,398 |

| Registration fees | 205,723 |

| Professional fees | 108,600 |

| Directors’ fees and expenses—Note 2(c) | 75,401 |

| Miscellaneous | 78,704 |

| Total Expenses | 28,028,941 |

| Less—reduction in management fee due to undertaking—Note 2(a) | (16,528,661) |

| Less—reduction in expenses due to undertaking—Note 2 (a) | (2,331,154) |

| Less—reduction in fees due to earnings credits—Note 2(b) | (9,171) |

| Net Expenses | 9,159,955 |

| Investment Income—Net | 5,416,199 |

| Net Realized Gain (Loss) on Investments—Note 1(b) ($) | 10,798 |

| Net Increase in Net Assets Resulting from Operations | 5,426,997 |

| See notes to financial statements. | |

STATEMENT OF CHANGES IN NET ASSETS

| | |

| | Year Ended December 31, |

| | 2010 | 2009 |

| Operations ($): | | |

| Investment income—net | 5,416,199 | 11,237,290 |

| Net realized gain (loss) on investments | 10,798 | (84,659,583) |

| Net unrealized appreciation | | |

| (depreciation) on investments | — | 25,385,182 |

| Net increase from payment by affiliate—Note 1(e) | — | 72,979,914 |

| Net Increase (Decrease) in Net Assets | | |

| Resulting from Operations | 5,426,997 | 24,942,803 |

| Dividends to Shareholders from ($): | | |

| Investment income—net: | | |

| Class 1 Shares | (447) | (2,280,997) |

| Class 2 Shares | (5,415,752) | (8,974,897) |

| Total Dividends | (5,416,199) | (11,255,894) |

| Capital Stock Transactions ($1.00 per share): | | |

| Net proceeds from shares sold: | | |

| Class 1 Shares | 444,381,456 | 545,593,194 |

| Class 2 Shares | 2,999,504,649 | 2,707,444,657 |

| Capital contribution from affiliate:† | | |

| Class 1 Shares | 3,397,294 | — |

| Class 2 Shares | 8,704,766 | — |

| Dividends reinvested: | | |

| Class 1 Shares | 33 | 2,172,803 |

| Class 2 Shares | 24,488 | 246,974 |

| Cost of shares redeemed: | | |

| Class 1 Shares | (704,399,006) | (845,484,534) |

| Class 2 Shares | (2,929,450,952) | (3,450,884,475) |

| Increase (Decrease) in Net Assets | | |

| from Capital Stock Transactions | (177,837,272) | (1,040,911,381) |

| Total Increase (Decrease) in Net Assets | (177,826,474) | (1,027,224,472) |

| Net Assets ($): | | |

| Beginning of Period | 4,583,684,424 | 5,610,908,896 |

| End of Period | 4,405,857,950 | 4,583,684,424 |

| |

| † See note 2(d). | | |

| See notes to financial statements. | | |

12

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated. All information reflects financial results for a single fund share. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | |

| | | Year Ended December 31, | |

| Class 1 Shares | 2010 | 2009 | 2008 | 2007 | 2006 |

| Per Share Data ($): | | | | | |

| Net asset value, | | | | | |

| beginning of period | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Investment Operations: | | | | | |

| Investment income—net | .000a | .001 | .026 | .047 | .044 |

| Distributions: | | | | | |

| Dividends from | | | | | |

| investment income—net | (.000)a | (.001) | (.026) | (.047) | (.044) |

| Net asset value, end of period | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Total Return (%) | .00b | .14c | 2.58 | 4.76 | 4.45 |

| Ratios/Supplemental Data (%): | | | | | |

| Ratio of total expenses | | | | | |

| to average net assets | .87 | .77 | .68 | .67 | .69 |

| Ratio of net expenses | | | | | |

| to average net assets | .31 | .52 | .67 | .67 | .69 |

| Ratio of net investment income | | | | | |

| to average net assets | .00b | .15 | 2.59 | 4.66 | 4.37 |

| Net Assets, end of period | | | | | |

| ($ x 1,000) | 1,066,647 | 1,323,118 | 1,617,316 | 1,798,630 | 1,816,411 |

| |

| a | Amount represents less than $.001 per share. |

| b | Amount represents less than .01%. |

| c | If payment pursuant to the Capital Support Agreement was not made, total return would have been (1.86%). |

| See notes to financial statements. |

FINANCIAL HIGHLIGHTS (continued)

| | | | | |

| | | Year Ended December 31, | |

| Class 2 Shares | 2010 | 2009 | 2008 | 2007 | 2006 |

| Per Share Data ($): | | | | | |

| Net asset value, | | | | | |

| beginning of period | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Investment Operations: | | | | | |

| Investment income—net | .002 | .002 | .027 | .048 | .045 |

| Distributions: | | | | | |

| Dividends from | | | | | |

| investment income—net | (.002) | (.002) | (.027) | (.048) | (.045) |

| Net asset value, end of period | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Total Return (%) | .16 | .23a | 2.72 | 4.87 | 4.61 |

| Ratios/Supplemental Data (%): | | | | | |

| Ratio of total expenses | | | | | |

| to average net assets | .52 | .58 | .55 | .56 | .55 |

| Ratio of net expenses | | | | | |

| to average net assets | .16 | .42 | .54 | .55 | .55 |

| Ratio of net investment income | | | | | |

| to average net assets | .16 | .25 | 2.69 | 4.77 | 4.54 |

| Net Assets, end of period | | | | | |

| ($ x 1,000) | 3,339,211 | 3,260,567 | 3,993,593 | 4,030,504 | 3,478,902 |

|

| a If payment pursuant to the Capital Support Agreement was not made, total return would have been (1.78%). |

| See notes to financial statements. |

14

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Liquid Assets, Inc. (the “fund”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as a diversified open-end management investment company. The fund’s investment objective is to seek as high a level of current income as is consistent with the preservation of capital.The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares. The fund is authorized to issue 30 billion shares of $.001 par value Common Stock.The fund currently offers two classes of shares: Class 1 (23.5 billion shares authorized) and Class 2 (6.5 billion shares authorized). Class 1 and Class 2 shares are identical except for the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs and certain voting rights. Class 2 shares are offered only to certain eligible financial institutions. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

It is the fund’s policy to maintain a continuous net asset value per share of $1.00; the fund has adopted certain investment, portfolio valuation and dividend and distribution policies to enable it to do so.There is no assurance, however, that the fund will be able to maintain a stable net asset value per share of $1.00.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accor-

NOTES TO FINANCIAL STATEMENTS (continued)

dance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: Investments in securities are valued at amortized cost in accordance with Rule 2a-7 of the Act, which has been determined by the fund’s Board of Directors to represent the fair value of the fund’s investments.

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e. the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

16

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, money market securities are valued using amortized cost, in accordance with rules under the Act. Generally, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected as Level 2.

The following is a summary of the inputs used as of December 31, 2010 in valuing the fund’s investments:

| |

| | Short-Term |

| Valuation Inputs | Investments ($)† |

| Level 1—Unadjusted Quoted Prices | — |

| Level 2—Other Significant Observable Inputs | 4,404,971,842 |

| Level 3—Significant Unobservable Inputs | — |

| Total | 4,404,971,842 |

| † See Statement of Investments for additional detailed categorizations. | |

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Interest income, adjusted for accretion of discount and amortization of premium on investments, is earned from settlement date and is recognized on the accrual basis. Cost of investments represents amortized cost.

The fund may enter into repurchase agreements with financial institutions, deemed to be creditworthy by the Manager, subject to the seller’s agreement to repurchase and the fund’s agreement to resell such securities at a mutually agreed upon price. Securities purchased subject to repurchase agreements are deposited with the fund’s custodian and, pursuant to the terms of the repurchase agreement, must have an aggregate market value greater than or equal to the repurchase price plus accrued interest at all times. If the value of the underlying securities falls below the value of the repurchase price plus accrued interest, the fund will require the seller to deposit additional collateral by the next business day. If the request for additional collateral is not

NOTES TO FINANCIAL STATEMENTS (continued)

met, or the seller defaults on its repurchase obligation, the fund maintains the right to sell the underlying securities at market value and may claim any resulting loss against the seller.

(c) Dividends to shareholders: It is the policy of the fund to declare dividends daily from investment income-net. Such dividends are paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains.

(d) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended December 31, 2010, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the four-year period ended December 31, 2010 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At December 31, 2010, the components of accumulated earnings on a tax basis were substantially the same as for financial reporting purposes.

The tax character of distributions paid to shareholders during the fiscal periods ended December 31, 2010 and December 31, 2009 were all ordinary income.

During the period ended December 31, 2010, as a result of permanent book to tax differences, primarily due to capital contributions by an affiliate, the fund increased accumulated net realized gain (loss) on investments by $11,668,871 and decreased paid-in capital by the

18

same amount. Net assets and net asset value per share were not affected by this reclassification.

At December 31, 2010, the cost of investment for federal income tax purposes was substantially the same as the cost for financial reporting purposes (see the Statement of Investments).

(e) Capital Support Agreement: The fund held notes (the “Notes”) issued by Lehman Brothers Holdings, Inc. (“Lehman”). In order to mitigate the negative impact of holding these securities in light of the bankruptcy of Lehman, on September 16, 2008, the fund entered into a Capital Support Agreement (the “Agreement”) with BNY Mellon, the parent company of the fund’s adviser. Pursuant to the Agreement, BNY Mellon had agreed to provide capital support to the fund, subject to a maximum amount of $100 million (the “Maximum Capital Support Payment”), if any of the following events resulted in the fund’s net asset value falling below $0.9950:

| (i) | Any final sale or other final liquidation of the Notes by the fund for cash in an amount, after deduction of costs, which is less than the amortized cost value of the Notes as of the date such sale or liquidation is consummated; |

| (ii) | Receipt by the fund of final payment on the Notes in cash in an amount less than the amortized cost value of the Notes less costs in respect thereof, as of the date such final payment is received; and |

| (iii) | The date upon which a court of competent jurisdiction over the matter discharges Lehman from liability in respect of the Notes, and such discharge results in the receipt of aggregate pay- ments on the Notes in an amount less than the amortized cost value of the Notes, less costs in respect thereof, as of the date such final payment is received. |

On September 9, 2009, the fund sold the Notes it held in Lehman which obligated BNY Mellon to make payments to the fund pursuant to the terms of the Agreement.The fund received payments amounting to $72,979,914 and the Agreement was terminated.

NOTES TO FINANCIAL STATEMENTS (continued)

NOTE 2—Management Fee and Other Transactions With Affiliates:

(a) Pursuant to a management agreement with the Manager, the management fee is based on the value of the fund’s average daily net assets and is computed at the following annual rates: .50% of the first $1.5 billion; .48% of the next $500 million; .47% of the next $500 million; and .45% over $2.5 billion.The fee is payable monthly.The agreement provides that if in any full fiscal year the aggregate expenses (exclusive of taxes, brokerage fees, interest on borrowings and extraordinary expenses) exceed 1% of the value of the fund’s average daily net assets, the Manager will refund to the fund, or bear, the excess over 1%. The Manager has undertaken, from January 1, 2010 until May 1, 2011, to waive receipt of its fees and/or assume the expenses of the fund’s Class 1 shares, so that direct annual fund operating expenses (excluding taxes, interest, brokerage commissions, commitment fees and extraordinary expenses) do not exceed .69% of the value of Class 1’s average daily net assets.The Manager has also undertaken to waive receipt of its fees and/or assume the expenses of the fund’s Class 2 shares, so that direct annual fund operating expenses (excluding taxes, interest, brokerage commissions, commitment fees and extraordinary expenses) do not exceed .55% of the value of Class 2’s average daily net assets.The Manager may terminate this undertaking upon at least 90 days prior notice to investors.

The Manager currently is limiting Class 1’s direct expense limit to .70% of the value of Class 1’s average daily net assets, in addition limiting the management fee to .16% of the value of Class 1’s average daily net assets and waiving non-class specific expenses.The Manager also is limiting Class 2’s current direct expense limit to .16% of the value of Class 2’s average daily net assets.These expense limitations and waivers are voluntary, not contractual, and may be terminated at any time.The waiver of fees, pursuant to these undertakings, amounted to $4,210,017 for Class 1 shares and $12,318,644 for Class 2 shares during the period ended December 31, 2010.

20

The Manager has undertaken to reimburse expenses in the event that current yields drop below a certain level. Such expense limitations may fluctuate daily, are voluntary and not contractual and may be terminated at any time.The expense reimbursement, pursuant to this undertaking amounted to $2,331,154 for Class 1 shares during the period ended December 31, 2010.

(b) Under the Shareholder Services Plan, Class 1 shares pay the Distributor at an annual rate of .25% of the value of Class 1’s average daily net assets for certain allocated expenses of providing personal services and/or maintaining shareholder accounts.The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. During the period ended December 31, 2010, Class 1 shares were charged $2,984,330 pursuant to the Shareholder Services Plan.

The fund compensates DreyfusTransfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing personnel and facilities to perform transfer agency services for the fund. During the period ended December 31, 2010, the fund was charged $1,137,852 pursuant to the transfer agency agreement, which is included in Shareholder servicing costs in the Statement of Operations.

The fund has arrangements with the custodian and cash management bank whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset custody and cash management fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates The Bank of NewYork Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, under a cash management agreement for performing cash management services related to fund subscriptions and redemptions. During the period ended December 31, 2010, the fund was charged $118,513 pursuant to the cash man-

NOTES TO FINANCIAL STATEMENTS (continued)

agement agreement, which is included in Shareholder servicing costs in the Statement of Operations. These fees were partially offset by earnings credits of $7,190.

The fund also compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. During the period ended December 31, 2010, the fund was charged $237,398 pursuant to the custody agreement.These fees were partially offset by earnings credits of $1,981.

During the period ended December 31, 2010, the fund was charged $6,243 for services performed by the Chief Compliance Officer.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $1,757,840, shareholder services fees $228,730, custodian fees $79,913, chief compliance officer fees $1,728 and transfer agency per account fees $188,268, which are offset against an expense reimbursement currently in effect in the amount of $1,592,969.

(c) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

(d) During the period ended December 31, 2010, BNY Mellon made voluntary capital contributions of $12,102,060 to the fund.These contributions were made to reimburse the fund for previous realized losses experienced by the fund.

22

|

| REPORT OF INDEPENDENT REGISTERED |

| PUBLIC ACCOUNTING FIRM |

Shareholders and Board of Directors

Dreyfus Liquid Assets, Inc.

We have audited the accompanying statement of assets and liabilities of Dreyfus Liquid Assets, Inc., including the statement of investments, as of December 31, 2010, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and financial highlights for each of the years indicated therein. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2010 by correspondence with the custodian and others. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Liquid Assets, Inc. at December 31, 2010, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the indicated years, in conformity with U.S. generally accepted accounting principles.

|

| New York, New York |

| February 28, 2011 |

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes the fund hereby designates 99.20% of ordinary income dividends paid during the fiscal year ended December 31, 2010 as qualifying “interest related dividends”.

24

|

| INFORMATION ABOUT THE REVIEW AND APPROVAL |

| OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited) |

At a meeting of the fund’s Board of Directors held on July 14 and 15, 2010, the Board considered the re-approval for an annual period (through August 31, 2011) of the fund’s Management Agreement with Dreyfus, pursuant to which Dreyfus provides the fund with investment advisory and administrative services. The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from representatives of Dreyfus.

Analysis of Nature, Extent and Quality of Services Provided to the Fund.The Board members received a presentation from representatives of Dreyfus regarding services provided to the fund and other funds in the Dreyfus fund complex, and discussed the nature, extent and quality of the services provided to the fund by Dreyfus pursuant to the Management Agreement. Dreyfus’ representatives reviewed the fund’s distribution of accounts and the relationships Dreyfus has with various intermediaries and the different needs of each. Dreyfus’ representatives noted the distribution channels for the fund as well as the diversity of distribution among the funds in the Dreyfus fund complex, and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each distribu tion channel, including those of the fund. Dreyfus also provided the number of shareholder accounts in the fund, as well as the fund’s asset size.

The Board members also considered Dreyfus’ research and portfolio management capabilities and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements. The Board members also considered Dreyfus’ extensive administrative, accounting and compliance infrastructure.

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio.The Board members reviewed the fund’s performance and comparisons to a group of retail no-load money market funds (the “Performance Group”) and to a larger universe of funds, consisting of all retail money market funds (the “Performance

|

| INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE |

| FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued) |

Universe”), selected and provided by Lipper, Inc., an independent provider of investment company data.The Board was provided with a description of the methodology Lipper used to select the Performance Group and Performance Universe, as well as the Expense Group and Expense Universe (discussed below). The Board members discussed the results of the comparisons for various periods ended May 31, 2010. The Board members noted that, while the fund’s total return performance was below the Performance Group medians for all periods, the fund’s performance generally was in close proximity to the Performance Group medians, and that the fund’s total return performance was above the Performance Universe medians for all periods except the one-year period ended May 31, 2010, when it was below the Performance Universe median.

The Board members also discussed the fund’s management fee and expense ratio and reviewed the range of management fees and expense ratios as compared to a comparable group of funds (the “Expense Group”) and a broader group of funds (the “Expense Universe”), each selected and provided by Lipper. The Board members noted that the fund’s contractual management fee was higher than the Expense Group median, the fund’s actual management fee was lower than the Expense Group and Expense Universe medians and the fund’s total expense ratio was at the Expense Group median and lower than the Expense Universe median. The Board considered the current fee waiver and expense reimbursement arrangement undertaken by Dreyfus.

Representatives of Dreyfus reviewed with the Board members the advisory fees paid by mutual funds managed by Dreyfus or its affiliates with similar investment objectives, policies and strategies, and included within the fund’s Lipper category (the “Similar Funds”). Representatives of Dreyfus also noted that there were no other accounts managed by Dreyfus or its affiliates with similar investment objectives, policies and strategies as the fund.The Board members considered the relevance of the fee information provided for the Similar Funds to evaluate the appropriateness and reasonableness of the fund’s management fee.

26

Analysis of Profitability and Economies of Scale. Dreyfus’ representatives reviewed the dollar amount of expenses allocated and profit received by Dreyfus and the method used to determine such expenses and profit. The Board previously had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus mutual fund complex.The Board members also had been informed that the methodology had been reviewed by an independent registered public accounting firm which, like the consultant, found the methodology to be reasonable. The consulting firm also analyzed where any economies of scale might emerge in connection with the management of the fund.The Board members evaluated the profitability an alysis in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows and whether fee levels reflect these economies of scale for the benefit of fund investors. The Board members also considered potential benefits to Dreyfus from acting as investment adviser and noted that there were no soft dollar arrangements with respect to trading the fund’s investments.

It was noted that the Board members should consider Dreyfus’ profitability with respect to the fund as part of their evaluation of whether the fee under the Management Agreement bears a reasonable relationship to the mix of services provided by Dreyfus, including the nature, extent and quality of such services and that a discussion of economies of scale is predicated on increasing assets and that, if a fund’s assets had been decreasing, the possibility that Dreyfus may have realized any economies of scale would be less. It also was noted that the profitability percentage for managing the fund was within the range determined by appropriate court cases to be reasonable given the services rendered.The Board also noted the Capital Support Agreement payment made during the prior 12-month period and its effect on Dreyfus’ profitability.

|

| INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE |

| FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued) |

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to continuation of the Management Agreement. Based on the discussions and considerations as described above, the Board made the following conclusions and determinations.

The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

The Board generally was satisfied with the fund’s overall relative performance.

The Board concluded that the fee paid by the fund to Dreyfus was reasonable in light of the services provided, comparative performance, expense and management fee information (including fee waiver and expense reimbursement arrangements), costs of the services provided and profits to be realized and benefits derived or to be derived by Dreyfus from its relationship with the fund.

The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the manage- ment of the fund had been adequately considered by Dreyfus in connection with the management fee rate charged to the fund and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

The Board members considered these conclusions and determinations, along with information received on a routine and regular basis throughout the year, and, without any one factor being dispositive, the Board determined that re-approval of the Management Agreement was in the best interests of the fund and its shareholders.

28

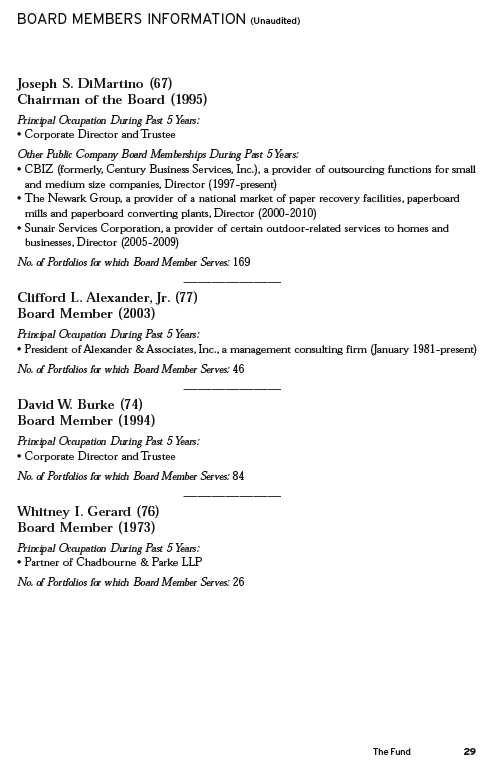

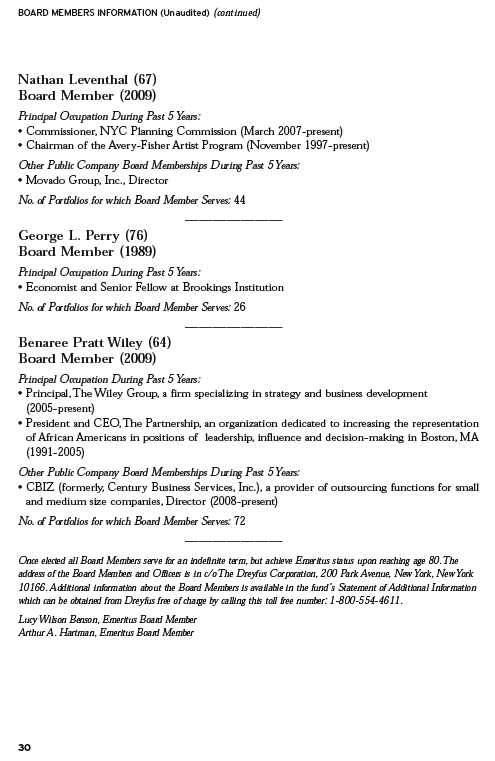

OFFICERS OF THE FUND (Unaudited)

BRADLEY J. SKAPYAK, President since January 2010.

Chief Operating Officer and a director of the Manager since June 2009. From April 2003 to June 2009, Mr. Skapyak was the head of the Investment Accounting and Support Department of the Manager. He is an officer of 76 investment companies (comprised of 169 portfolios) managed by the Manager. He is 52 years old and has been an employee of the Manager since February 1988.

PHILLIP N. MAISANO, Executive Vice President since July 2007.

Chief Investment Officer,Vice Chair and a director of the Manager, and an officer of 76 investment companies (comprised of 169 portfolios) managed by the Manager. Mr. Maisano also is an officer and/or Board member of certain other investment management subsidiaries of The Bank of New York Mellon Corporation, each of which is an affiliate of the Manager. He is 63 years old and has been an employee of the Manager since November 2006. Prior to joining the Manager, Mr. Maisano served as Chairman and Chief Executive Officer of EACM Advisors, an affiliate of the Manager, since August 2004.

MICHAEL A. ROSENBERG, Vice President and Secretary since August 2005.

Assistant General Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 50 years old and has been an employee of the Manager since October 1991.

KIESHA ASTWOOD, Vice President and Assistant Secretary since January 2010.

Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. She is 37 years old and has been an employee of the Manager since July 1995.

JAMES BITETTO, Vice President and Assistant Secretary since August 2005.

Senior Counsel of BNY Mellon and Secretary of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 44 years old and has been an employee of the Manager since December 1996.

JONI LACKS CHARATAN, Vice President and Assistant Secretary since August 2005.

Senior Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. She is 55 years old and has been an employee of the Manager since October 1988.

JOSEPH M. CHIOFFI, Vice President and Assistant Secretary since August 2005.

Senior Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 49 years old and has been an employee of the Manager since June 2000.

KATHLEEN DENICHOLAS, Vice President and Assistant Secretary since January 2010.

Senior Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. She is 36 years old and has been an employee of the Manager since February 2001.

JANETTE E. FARRAGHER, Vice President and Assistant Secretary since August 2005.

Assistant General Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. She is 48 years old and has been an employee of the Manager since February 1984.

OFFICERS OF THE FUND (Unaudited) (continued)

JOHN B. HAMMALIAN, Vice President and Assistant Secretary since August 2005.

Managing Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 47 years old and has been an employee of the Manager since February 1991.

M. CRISTINA MEISER, Vice President and Assistant Secretary since January 2010.

Senior Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. She is 40 years old and has been an employee of the Manager since August 2001.

ROBERT R. MULLERY, Vice President and Assistant Secretary since August 2005.

Managing Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 58 years old and has been an employee of the Manager since May 1986.

JEFF PRUSNOFSKY, Vice President and Assistant Secretary since August 2005.

Managing Counsel of BNY Mellon, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 45 years old and has been an employee of the Manager since October 1990.

JAMES WINDELS, Treasurer since November 2001.

Director – Mutual Fund Accounting of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 52 years old and has been an employee of the Manager since April 1985.

RICHARD CASSARO, Assistant Treasurer since January 2008.

Senior Accounting Manager – Money Market and Municipal Bond Funds of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 51 years old and has been an employee of the Manager since September 1982.

GAVIN C. REILLY, Assistant Treasurer since December 2005.

Tax Manager of the Investment Accounting and Support Department of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 42 years old and has been an employee of the Manager since April 1991.

ROBERT ROBOL, Assistant Treasurer since December 2002.

Senior Accounting Manager – Fixed Income Funds of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 46 years old and has been an employee of the Manager since October 1988.

ROBERT SALVIOLO, Assistant Treasurer since July 2007.

Senior Accounting Manager – Equity Funds of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 43 years old and has been an employee of the Manager since June 1989.

32

ROBERT SVAGNA, Assistant Treasurer since August 2005.

Senior Accounting Manager – Equity Funds of the Manager, and an officer of 77 investment companies (comprised of 194 portfolios) managed by the Manager. He is 43 years old and has been an employee of the Manager since November 1990.

JOSEPH W. CONNOLLY, Chief Compliance Officer since October 2004.

Chief Compliance Officer of the Manager and The Dreyfus Family of Funds (77 investment companies, comprised of 194 portfolios). From November 2001 through March 2004, Mr. Connolly was first Vice-President, Mutual Fund Servicing for Mellon Global Securities Services. In that capacity, Mr. Connolly was responsible for managing Mellon’s Custody, Fund Accounting and Fund Administration services to third-party mutual fund clients. He is 53 years old and has served in various capacities with the Manager since 1980, including manager of the firm’s Fund Accounting Department from 1997 through October 2001.

NATALIA GRIBAS, Anti-Money Laundering Compliance Officer since July 2010.

Anti-Money Laundering Compliance Officer of the Distributor, and the Anti-Money Laundering Compliance Officer of 73 investment companies (comprised of 190 portfolios) managed by the Manager. She is 40 years old and has been an employee of the Distributor since September 2008.

Item 2. Code of Ethics.

The Registrant has adopted a code of ethics that applies to the Registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. There have been no amendments to, or waivers in connection with, the Code of Ethics during the period covered by this Report.

Item 3. Audit Committee Financial Expert.

The Registrant's Board has determined that Joseph S. DiMartino, a member of the Audit Committee of the Board, is an audit committee financial expert as defined by the Securities and Exchange Commission (the "SEC"). Joseph S. DiMartino is "independent" as defined by the SEC for purposes of audit committee financial expert determinations.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees. The aggregate fees billed for each of the last two fiscal years (the "Reporting Periods") for professional services rendered by the Registrant's principal accountant (the "Auditor") for the audit of the Registrant's annual financial statements or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $44,093 in 2009 and $45,293 in 2010.

(b) Audit-Related Fees. The aggregate fees billed in the Reporting Periods for assurance and related services by the Auditor that are reasonably related to the performance of the audit of the Registrant's financial statements and are not reported under paragraph (a) of this Item 4 were $5,276 in 2009 and $5,382 in 2010. These services consisted of one or more of the following: (i) agreed upon procedures related to compliance with Internal Revenue Code section 817(h), (ii) security counts required by Rule 17f-2 under the Investment Company Act of 1940, as amended, (iii) advisory services as to the accounting or disclosure treatment of Registrant transactions or events and (iv) advisory services to the accounting or disclosure treatment of the act ual or potential impact to the Registrant of final or proposed rules, standards or interpretations by the Securities and Exchange Commission, the Financial Accounting Standards Boards or other regulatory or standard-setting bodies.

The aggregate fees billed in the Reporting Periods for non-audit assurance and related services by the Auditor to the Registrant's investment adviser (not including any sub-investment adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the Registrant ("Service Affiliates"), that were reasonably related to the performance of the annual audit of the Service Affiliate, which required pre-approval by the Audit Committee were $0 in 2009 and $0 in 2010.

(c) Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by the Auditor for tax compliance, tax advice, and tax planning ("Tax Services") were $ 3,638 in 2009 and $3,181 in 2010. These services consisted of: (i) review or preparation of U.S. federal, state, local and excise tax returns; (ii) U.S. federal, state and local tax planning, advice and assistance regarding statutory, regulatory or administrative developments; (iii) tax advice regarding tax qualification matters and/or treatment of various financial instruments held or proposed to be acquired or held, and (iv) determination of Passive Foreign Investment Companies. The aggregate fees billed in the Reporting Periods for Tax Services by the Auditor to Service Affiliates, which required pre-approval by the Audit Committee were $0 in 2009 and $0 in 2010.

(d) All Other Fees. The aggregate fees billed in the Reporting Periods for products and services provided by the Auditor, other than the services reported in paragraphs (a) through (c) of this Item, were $1,686 in 2009 and $1,457 in 2010. [These services consisted of a review of the Registrant's anti-money laundering program].

The aggregate fees billed in the Reporting Periods for Non-Audit Services by the Auditor to Service Affiliates, other than the services reported in paragraphs (b) through (c) of this Item, which required pre-approval by the Audit Committee, were $0 in 2009 and $0 in 2010.

(e)(1) Audit Committee Pre-Approval Policies and Procedures. The Registrant's Audit Committee has established policies and procedures (the "Policy") for pre-approval (within specified fee limits) of the Auditor's engagements for non-audit services to the Registrant and Service Affiliates without specific case-by-case consideration. The pre-approved services in the Policy can include pre-approved audit services, pre-approved audit-related services, pre-approved tax services and pre-approved all other services. Pre-approval considerations include whether the proposed services are compatible with maintaining the Auditor's independence. Pre-approvals pursuant to the Policy are considered annually.

(e)(2) Note: None of the services described in paragraphs (b) through (d) of this Item 4 were approved by the Audit Committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) None of the hours expended on the principal accountant's engagement to audit the registrant's financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal account's full-time, permanent employees.

Non-Audit Fees. The aggregate non-audit fees billed by the Auditor for services rendered to the Registrant, and rendered to Service Affiliates, for the Reporting Periods were $24,975,296 in 2009 and $39,552,052 in 2010.

Auditor Independence. The Registrant's Audit Committee has considered whether the provision of non-audit services that were rendered to Service Affiliates, which were not pre-approved (not requiring pre-approval), is compatible with maintaining the Auditor's independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable. [CLOSED-END FUNDS ONLY]

Item 6. Investments.

(a) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable. [CLOSED-END FUNDS ONLY]

Item 9. Purchases of Equity Securities by Closed-End Management Investment Companies and Affiliated Purchasers.

Not applicable. [CLOSED-END FUNDS ONLY]

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no material changes to the procedures applicable to Item 10.

Item 11. Controls and Procedures.

(a) The Registrant's principal executive and principal financial officers have concluded, based on their evaluation of the Registrant's disclosure controls and procedures as of a date within 90 days of the filing date of this report, that the Registrant's disclosure controls and procedures are reasonably designed to ensure that information required to be disclosed by the Registrant on Form N-CSR is recorded, processed, summarized and reported within the required time periods and that information required to be disclosed by the Registrant in the reports that it files or submits on Form N-CSR is accumulated and communicated to the Registrant's management, including its principal executive and principal financial officers, as appropriate to allow timely decisions regarding required disclosure.

(b) There were no changes to the Registrant's internal control over financial reporting that occurred during the second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the Registrant's internal control over financial reporting.

Item 12. Exhibits.

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940.

(a)(3) Not applicable.

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this Report to be signed on its behalf by the undersigned, thereunto duly authorized.

Dreyfus Liquid Assets, Inc.

By: /s/ Bradley J. Skapyak |

Bradley J. Skapyak, President |

Date: | February 23, 2011 |

|

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this Report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated. |

|

By: /s/ Bradley J. Skapyak |

Bradley J. Skapyak, President |

Date: | February 23, 2011 |

|

By: /s/ James Windels |

James Windels, Treasurer |

Date: | February 23, 2011 |

|

EXHIBIT INDEX

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940. (EX-99.CERT)

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940. (EX-99.906CERT)