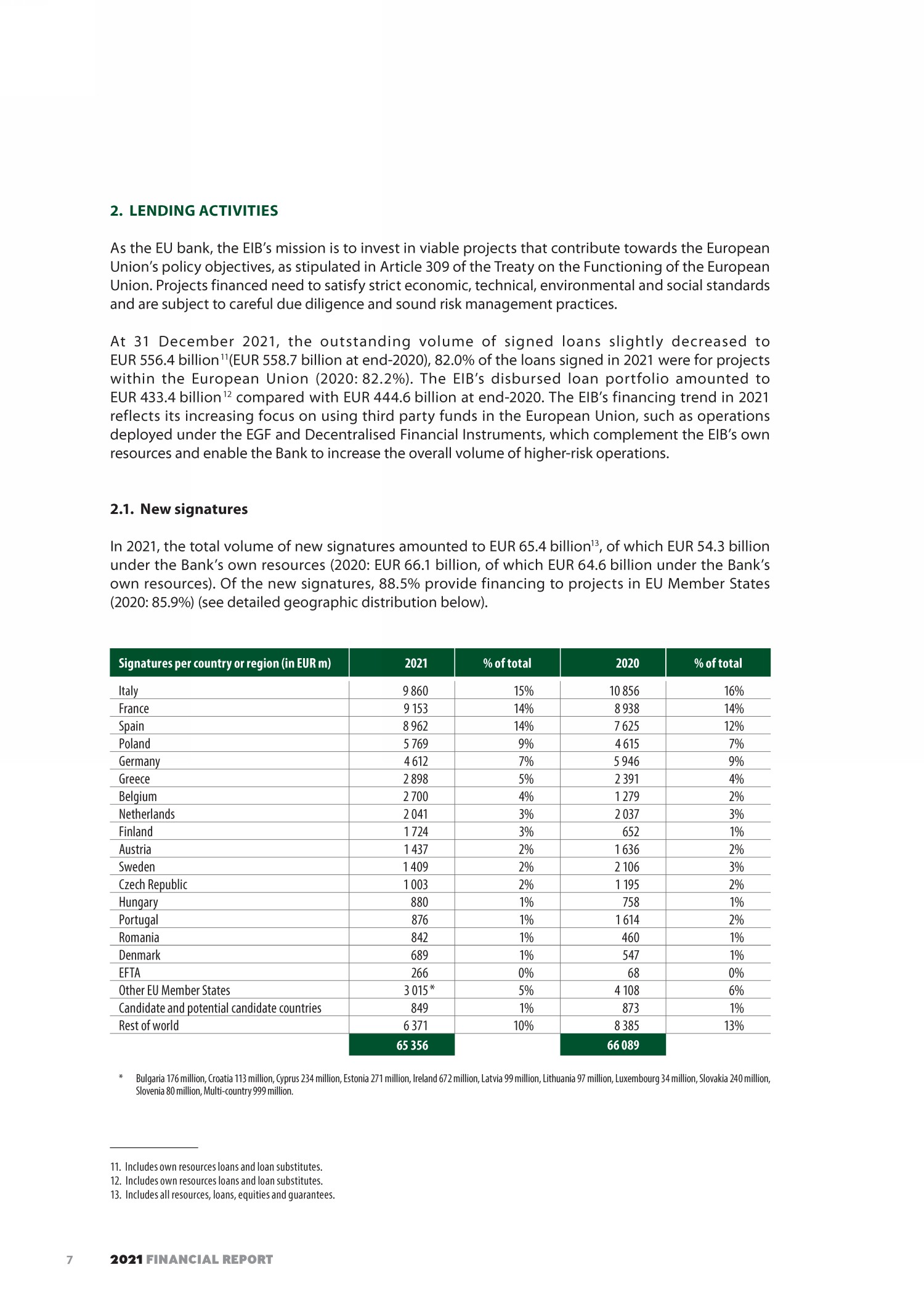

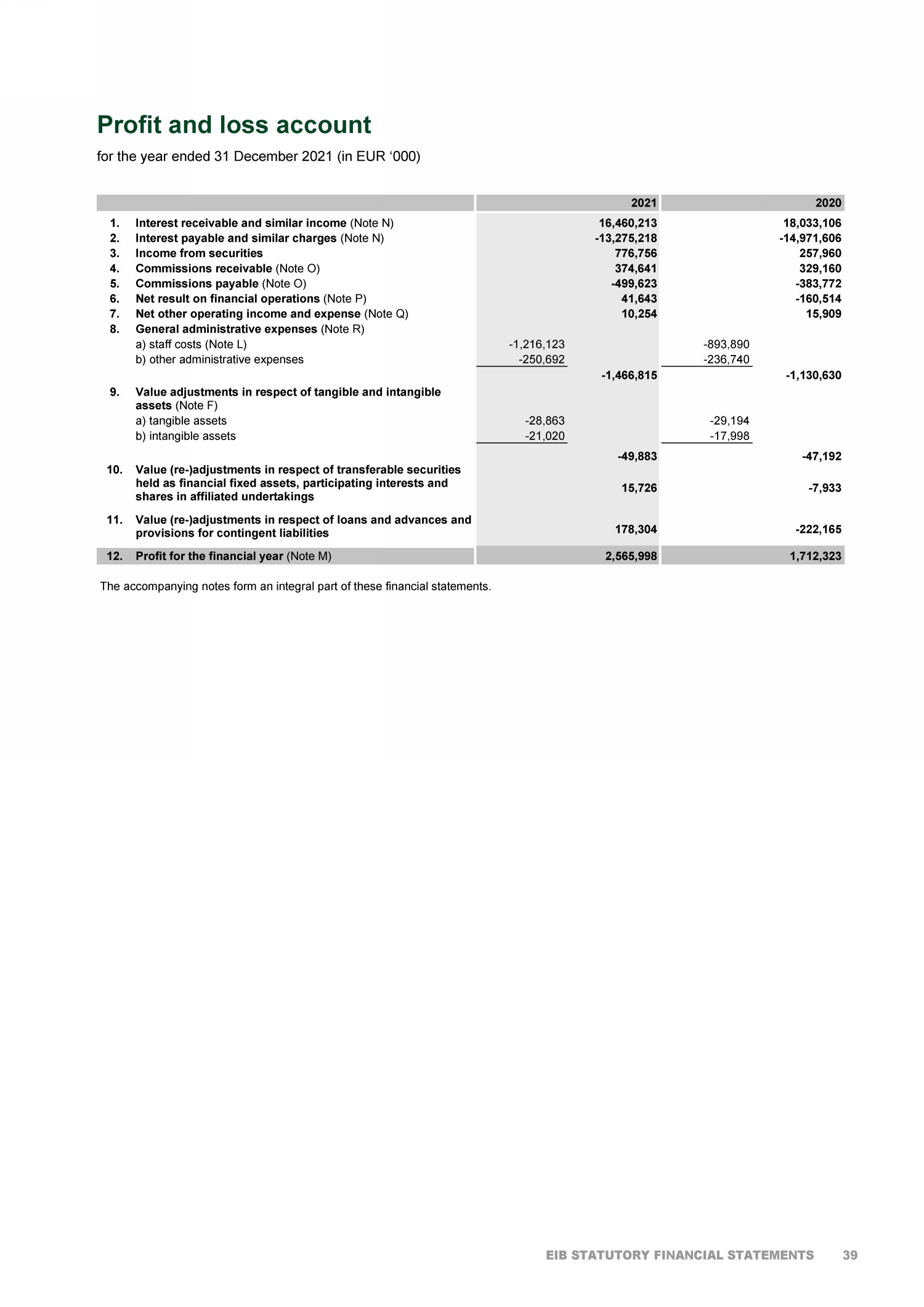

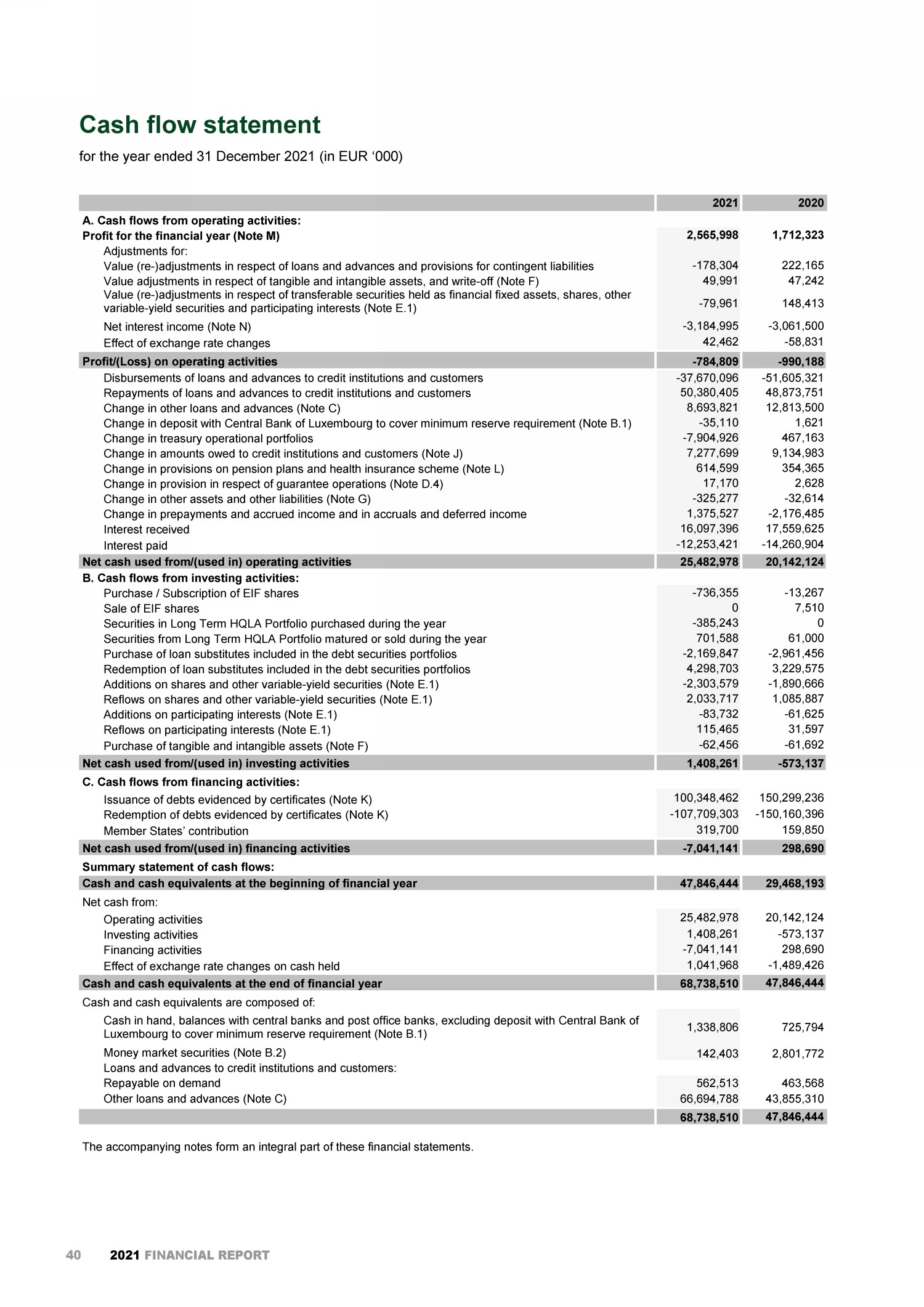

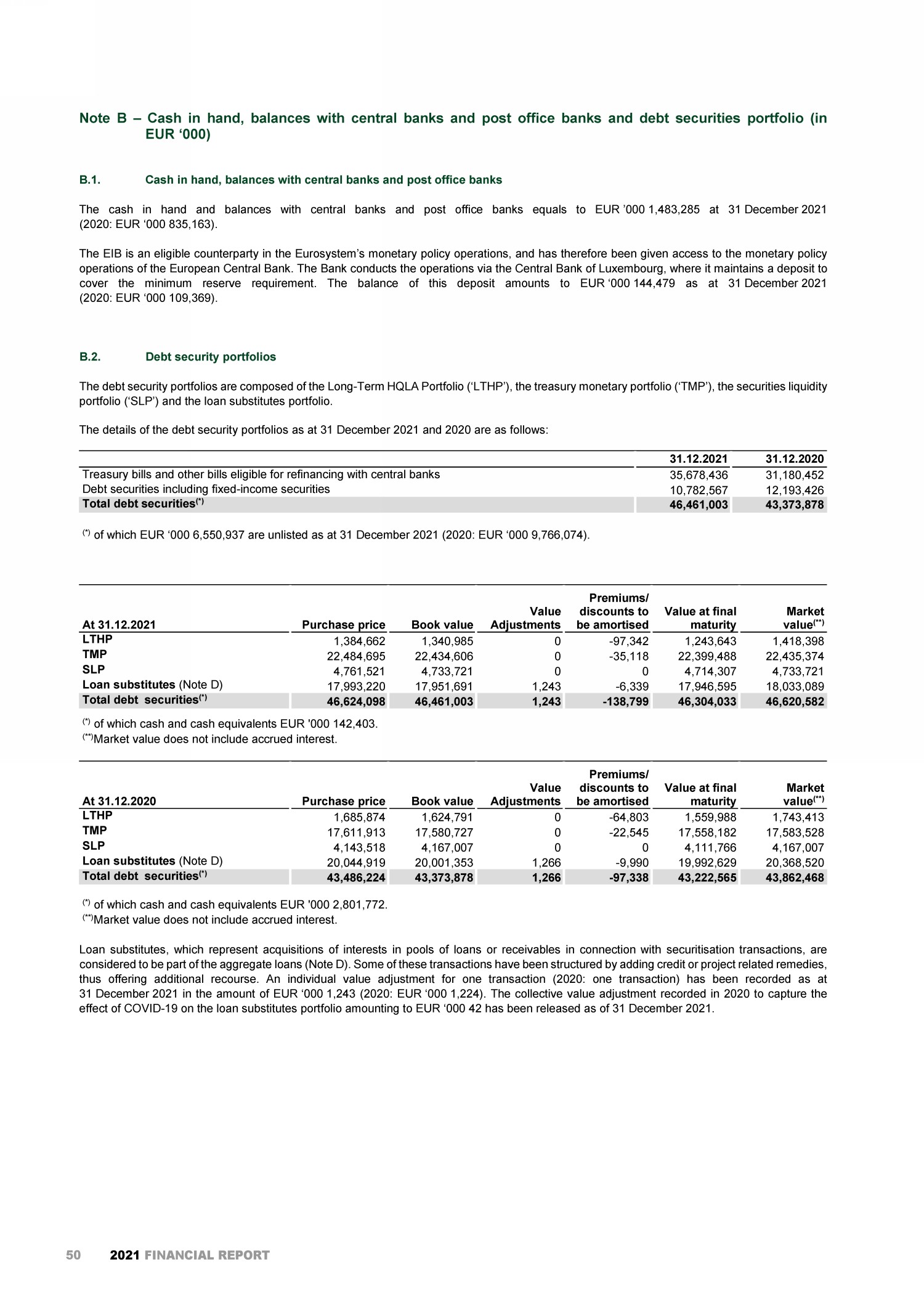

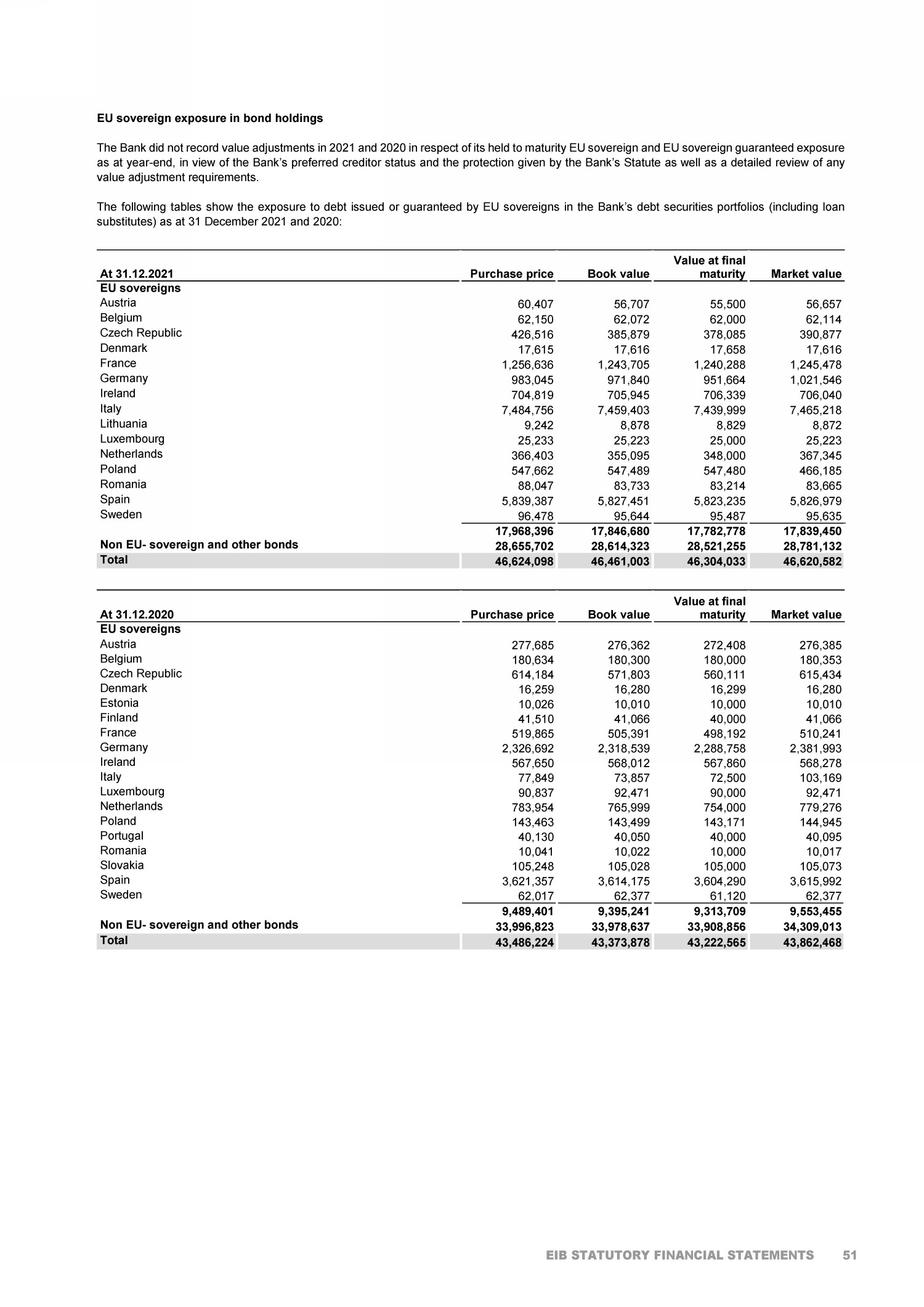

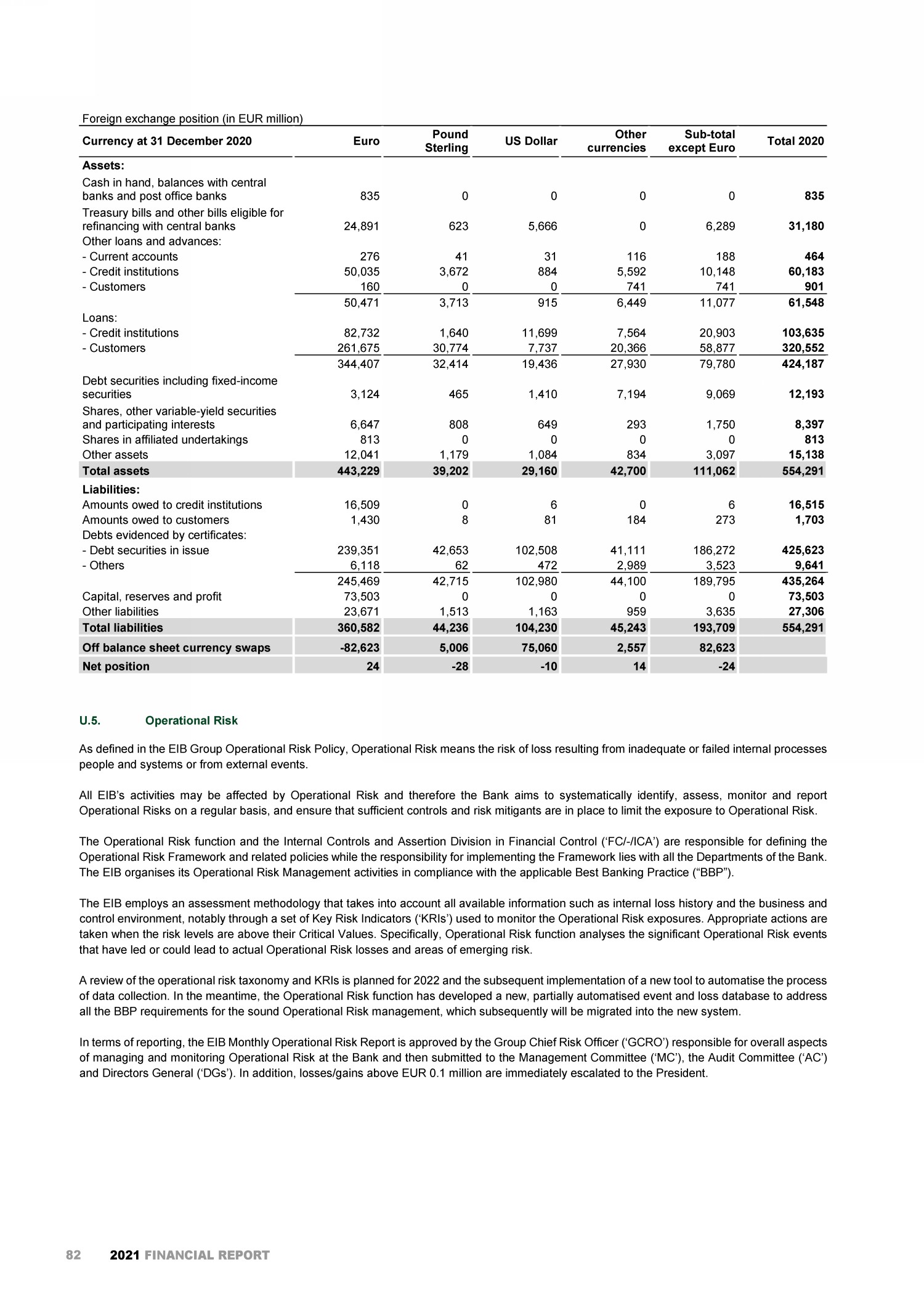

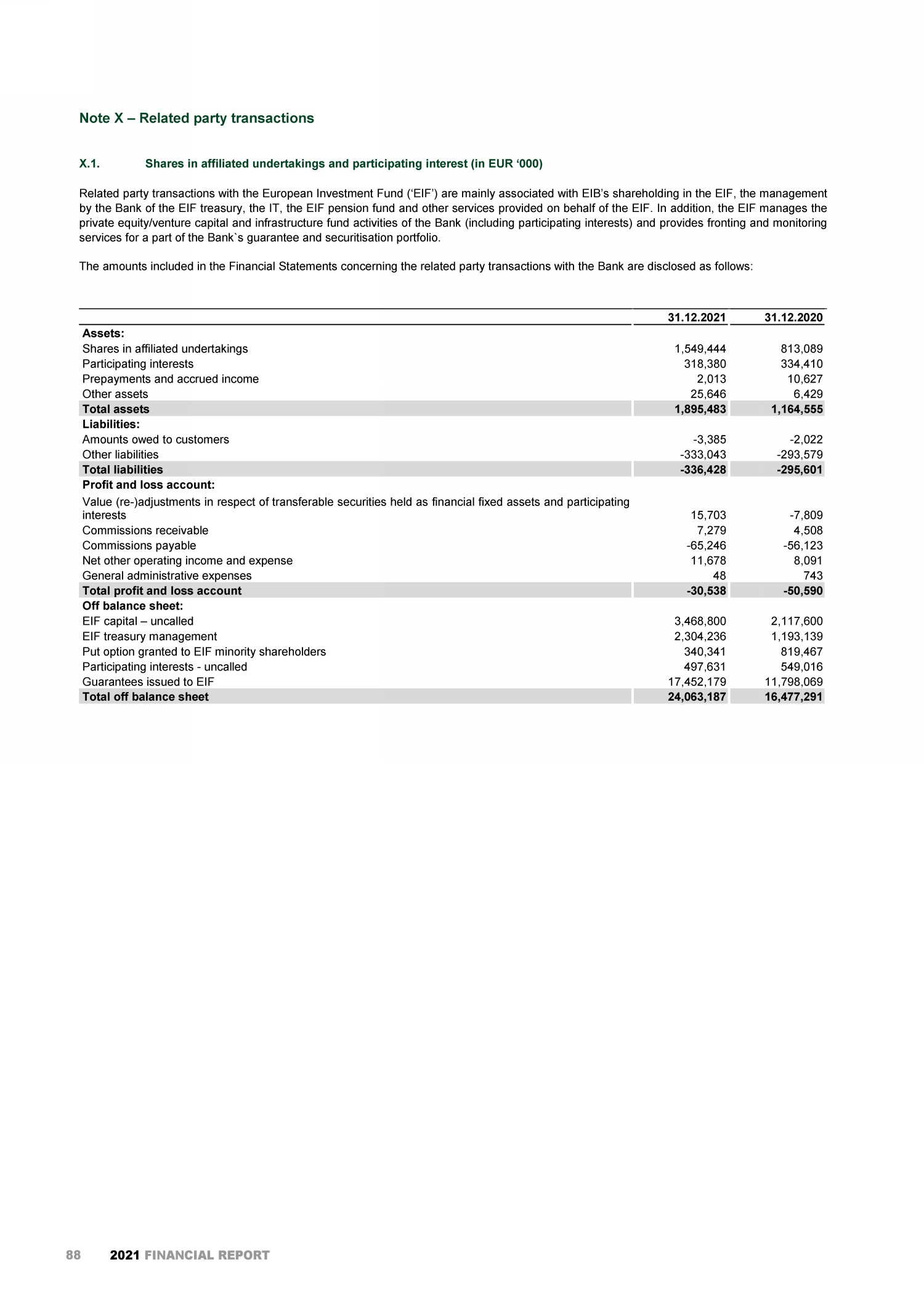

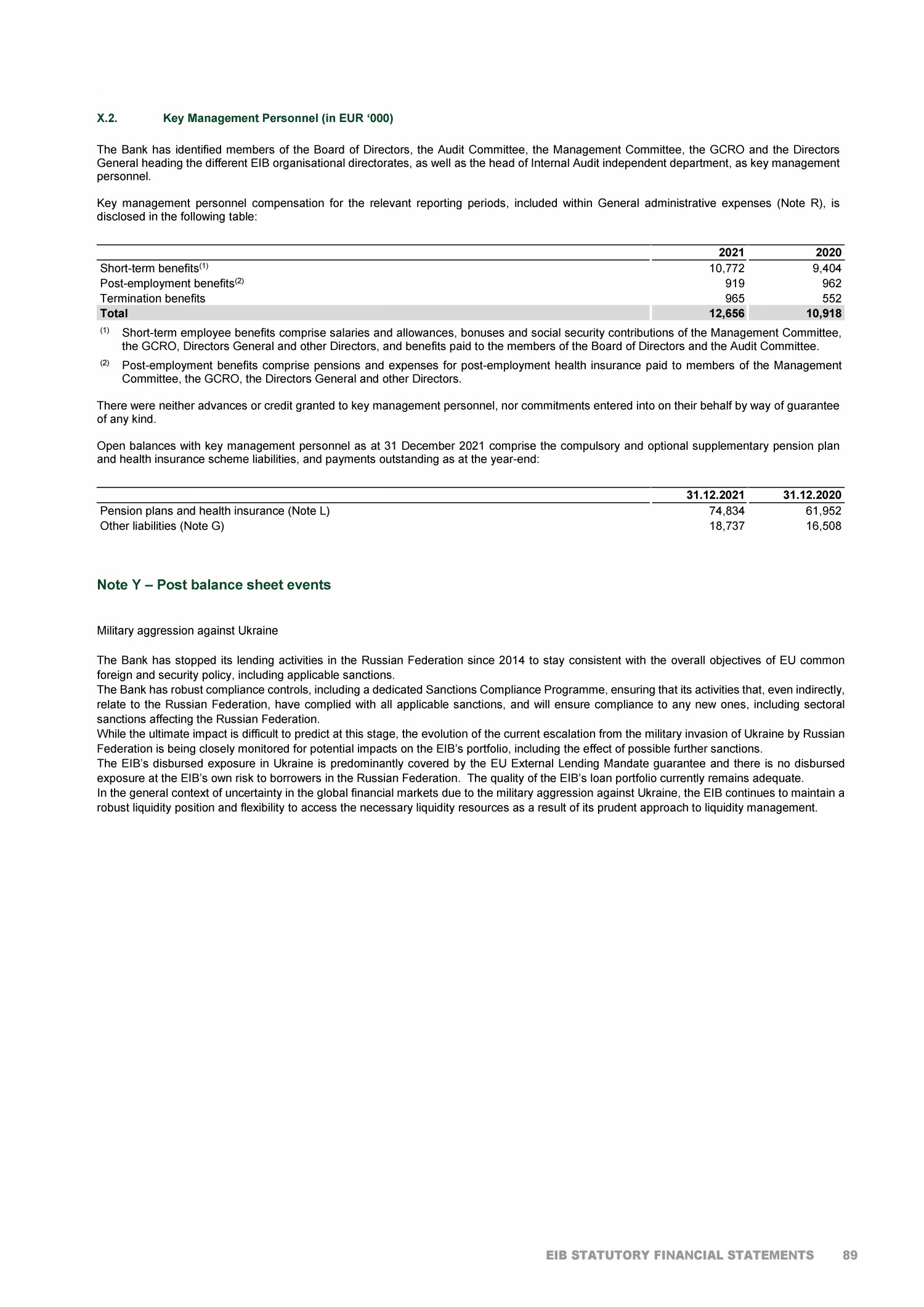

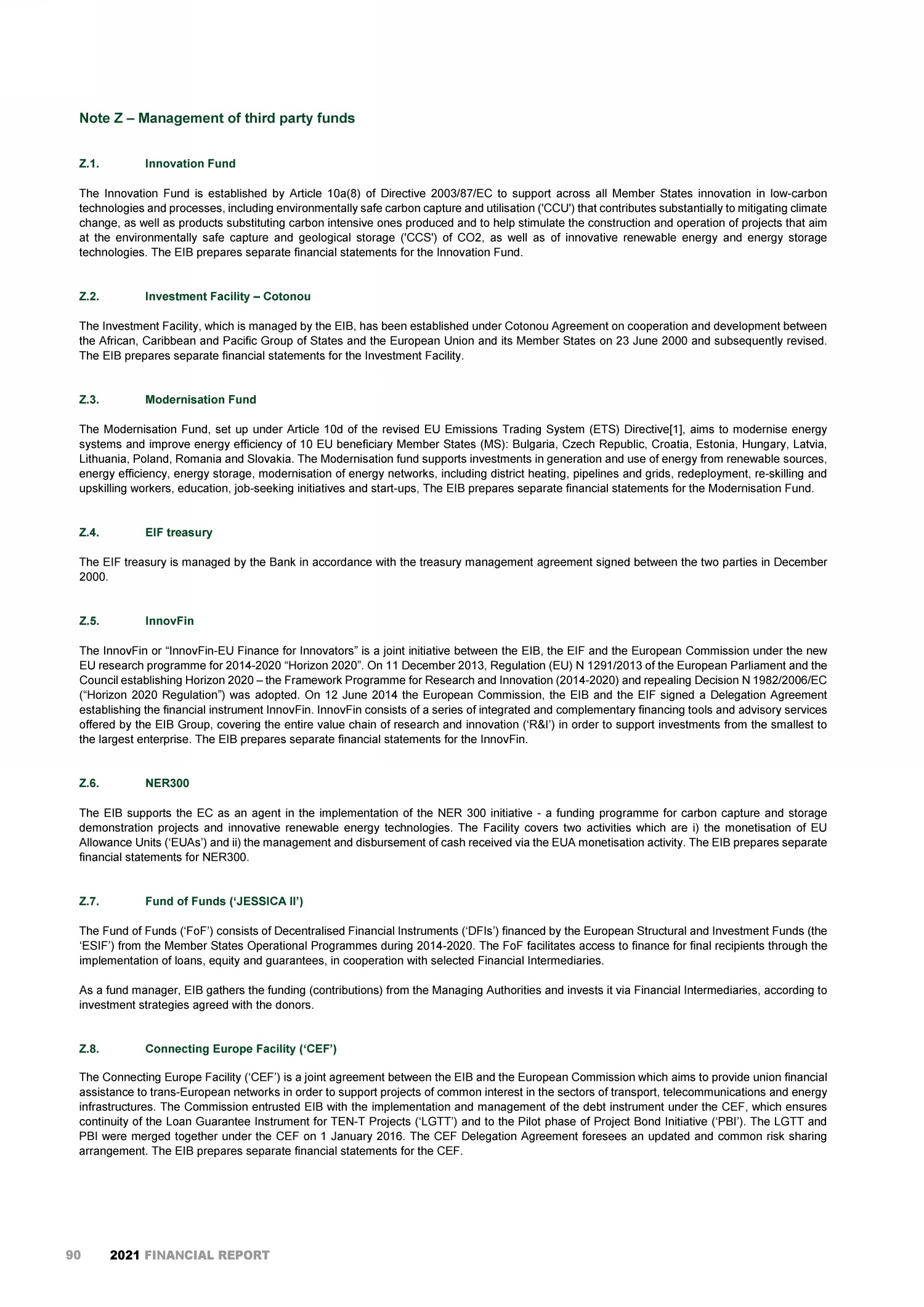

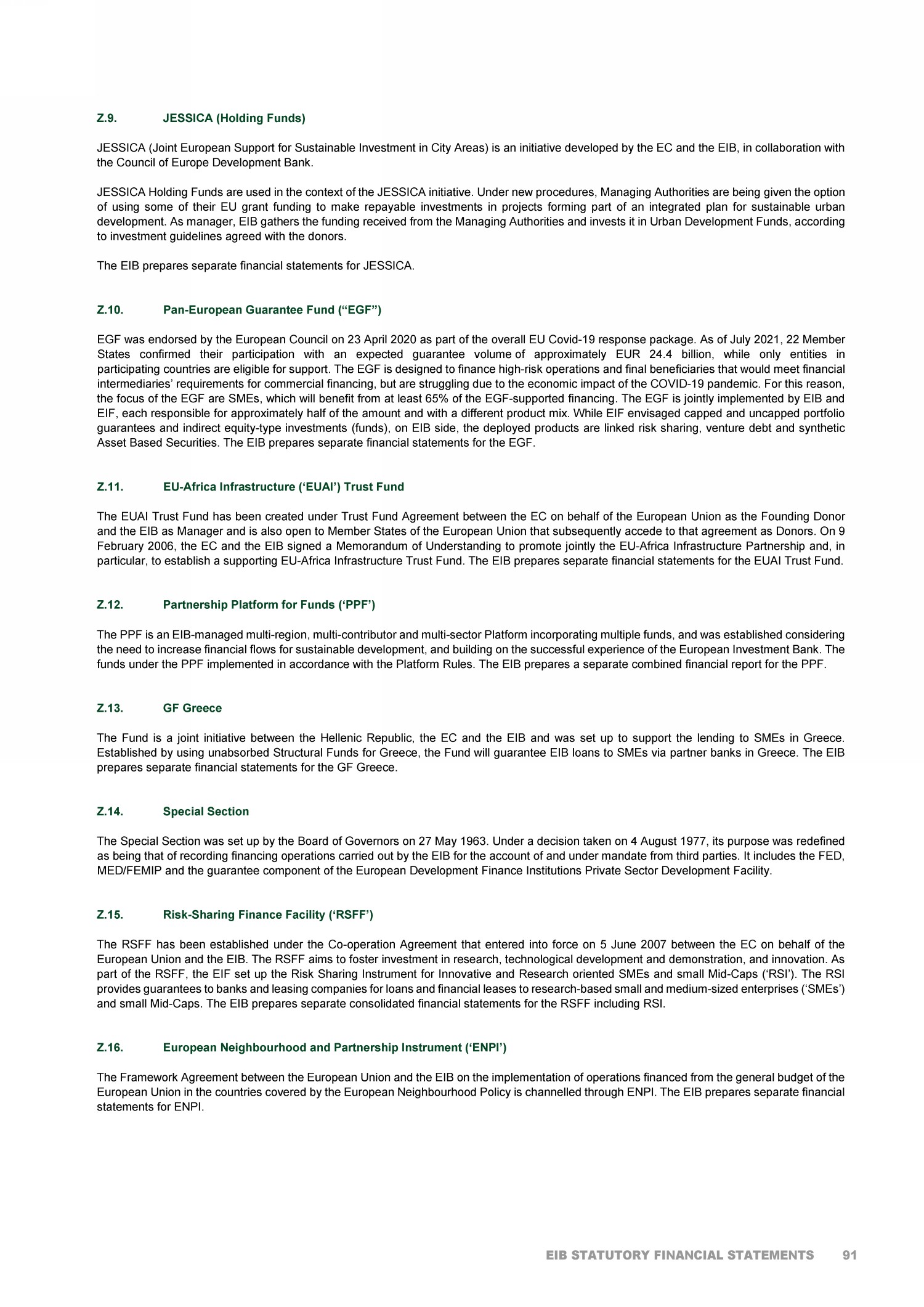

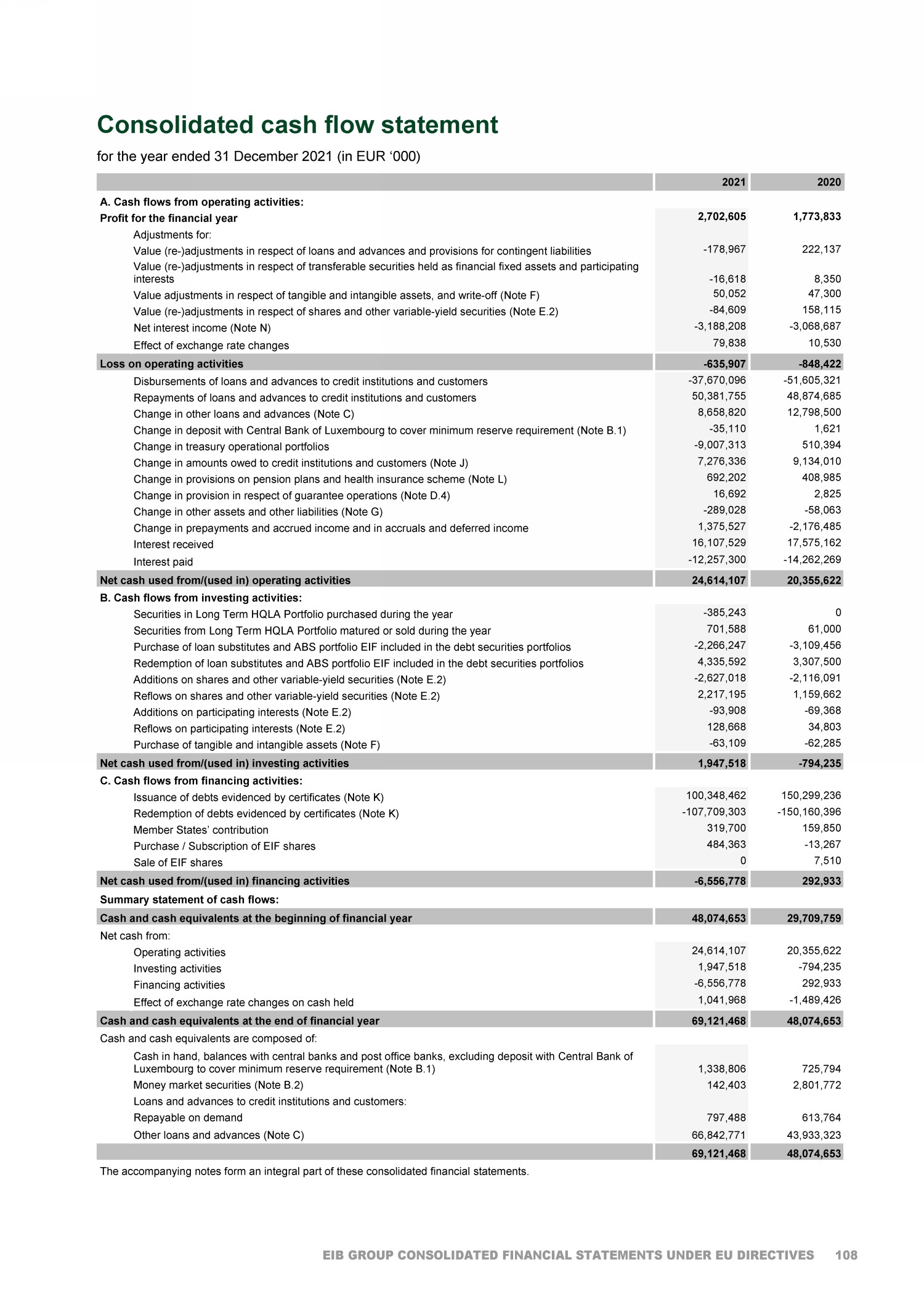

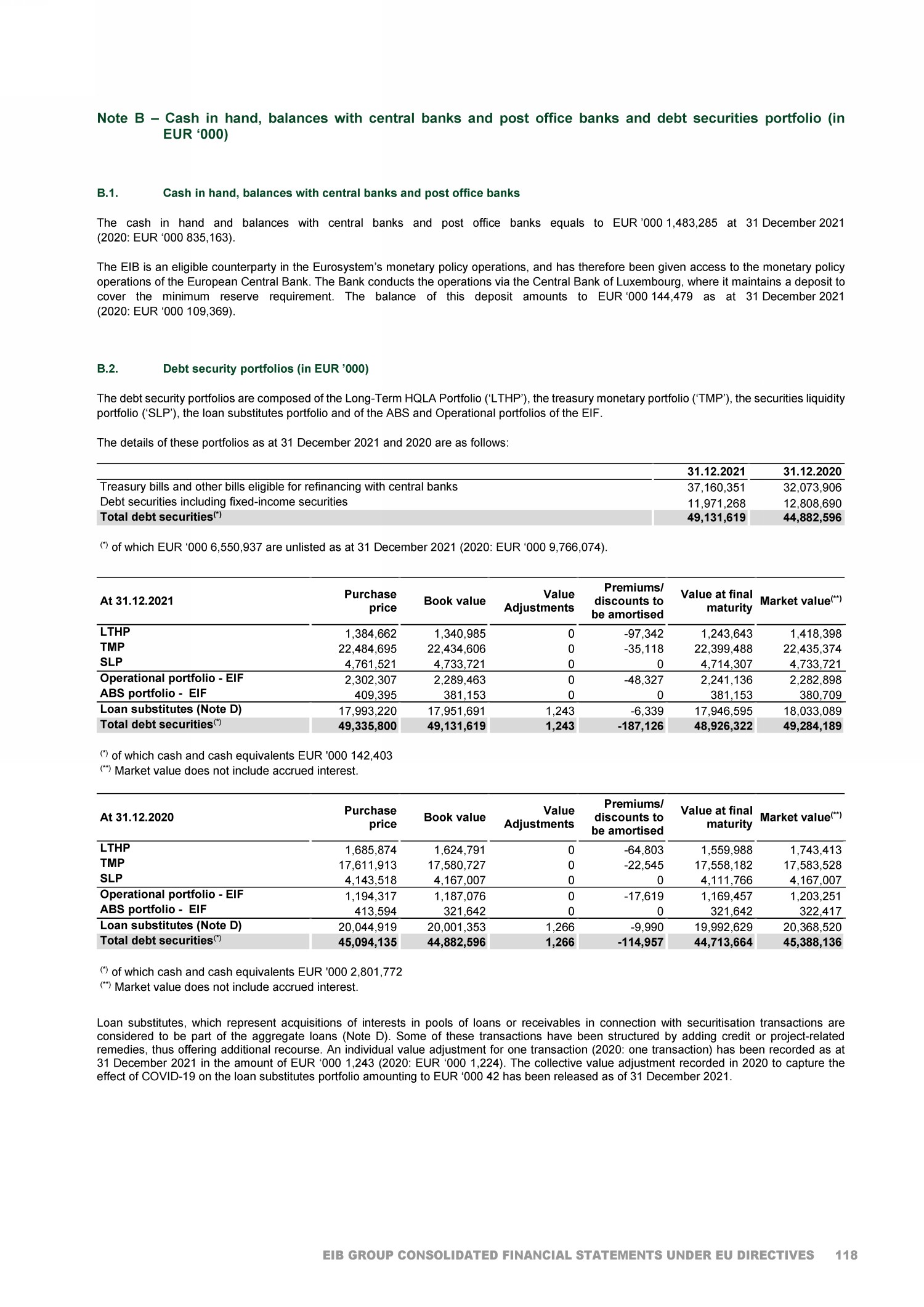

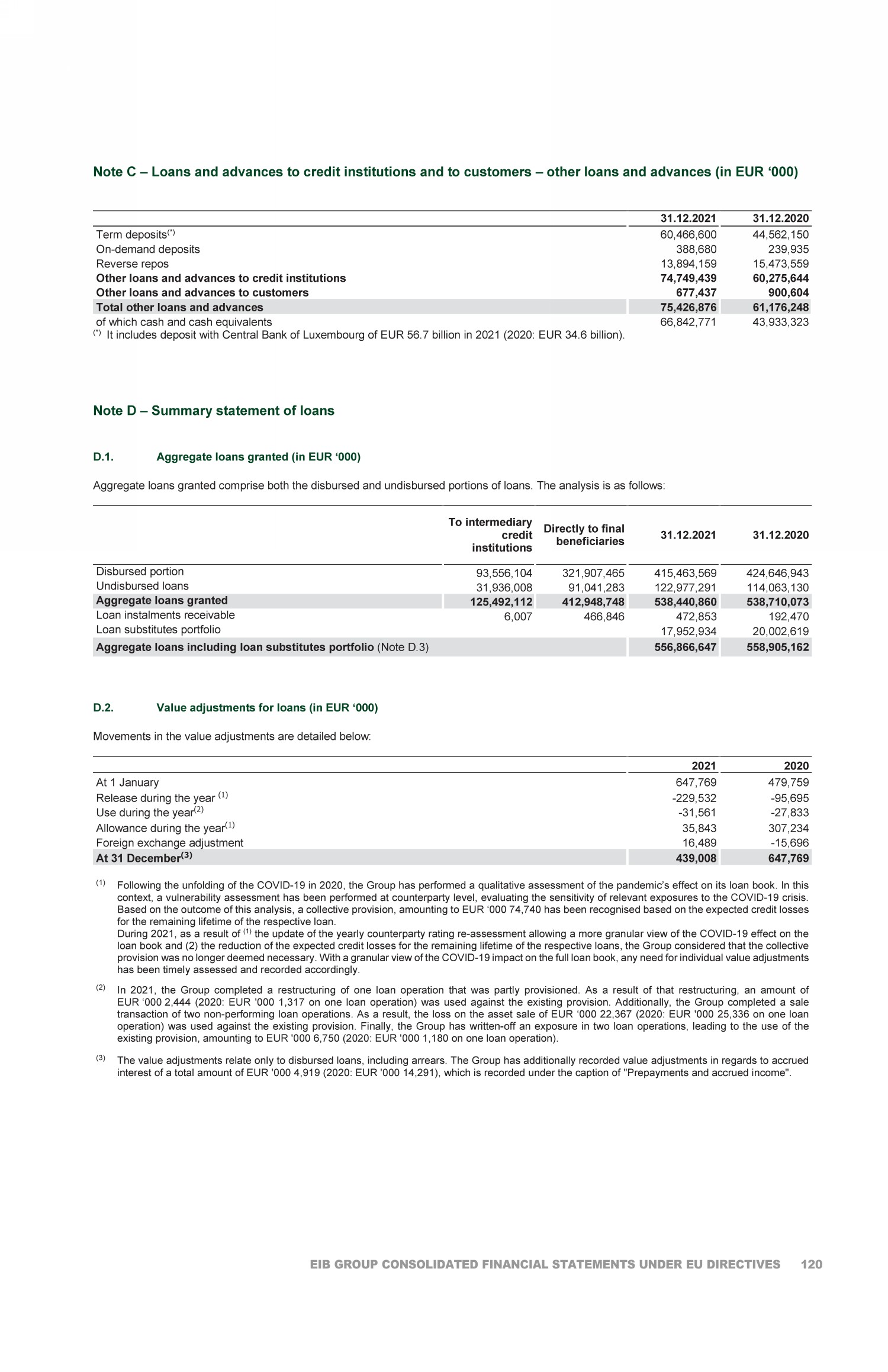

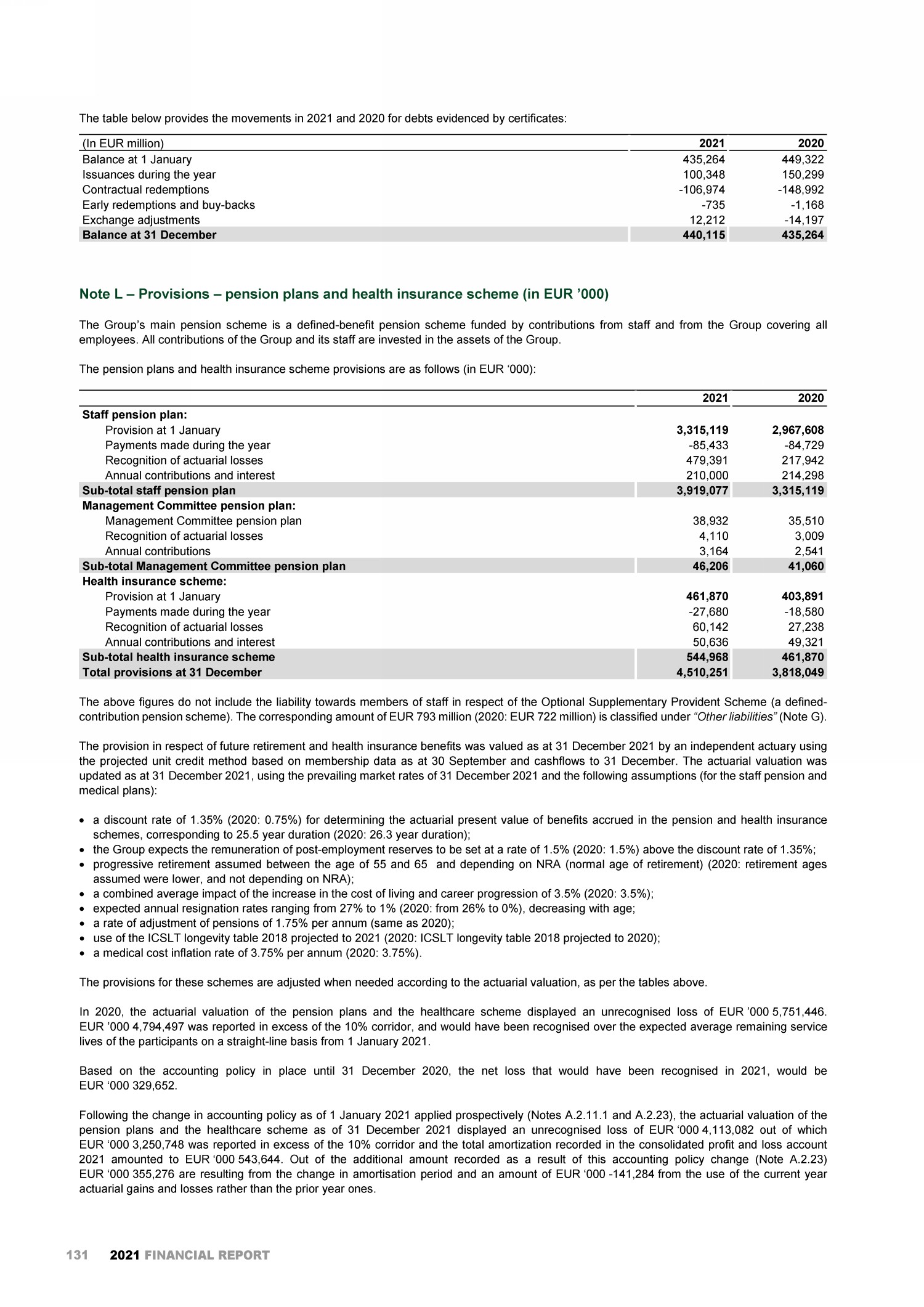

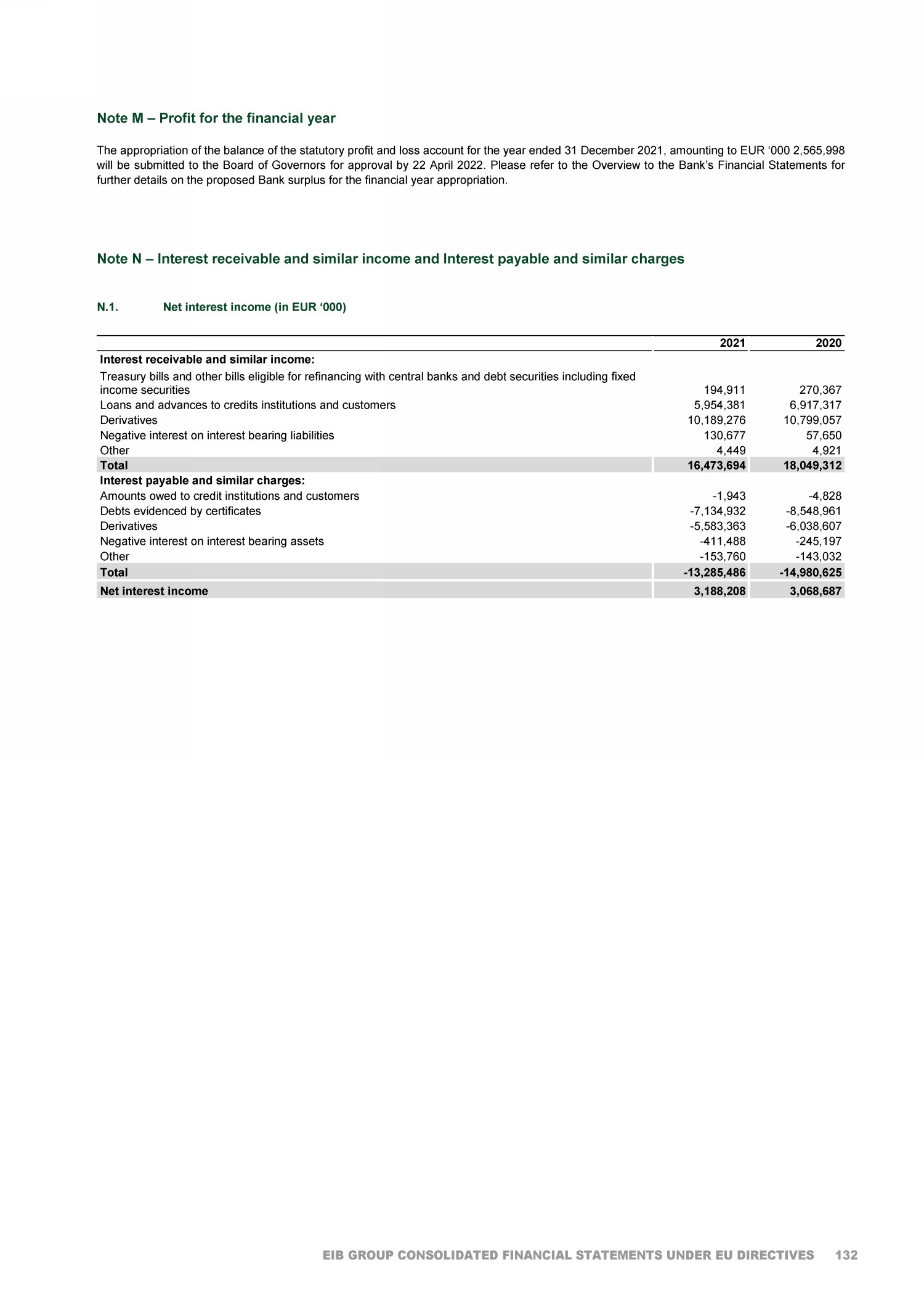

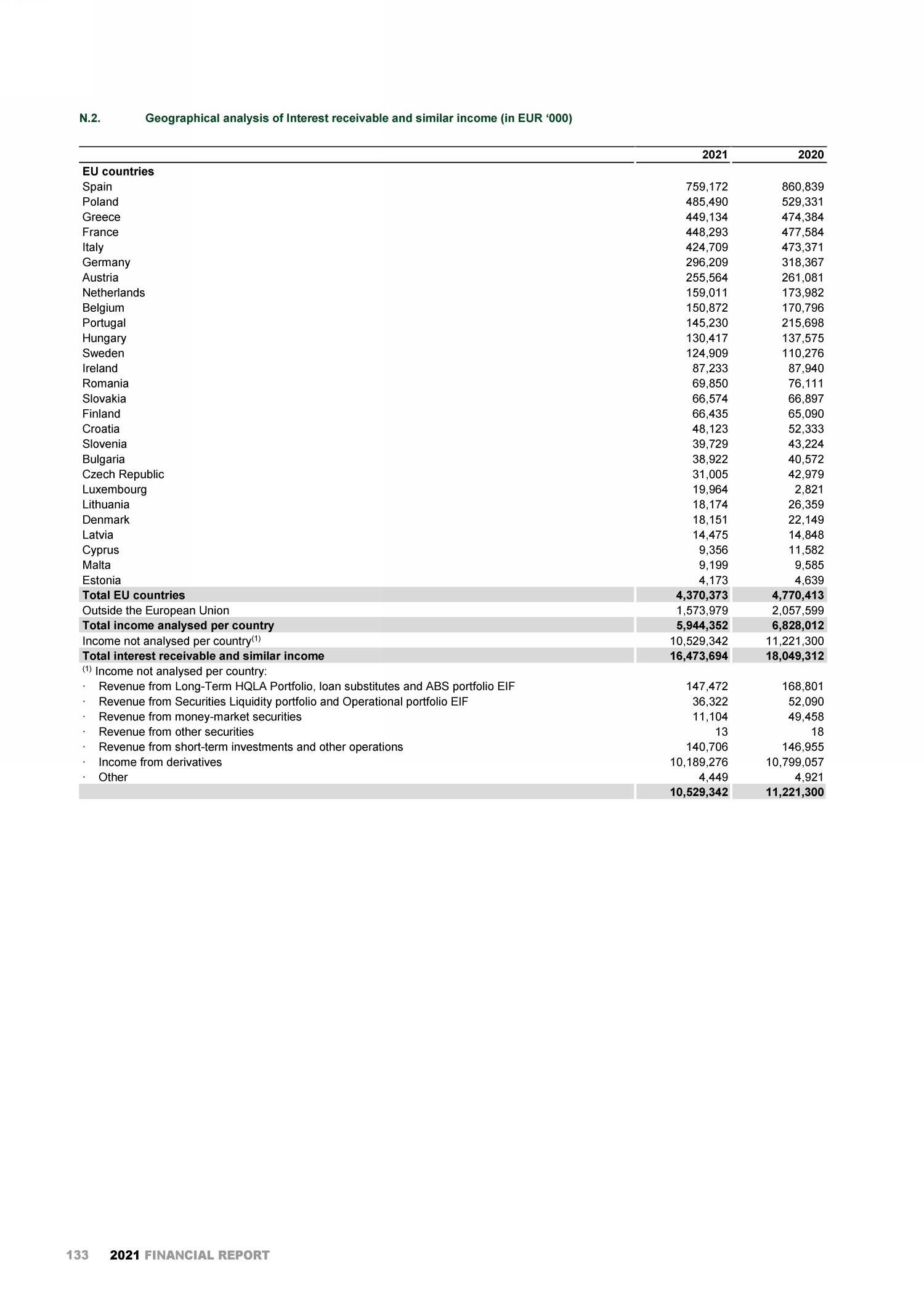

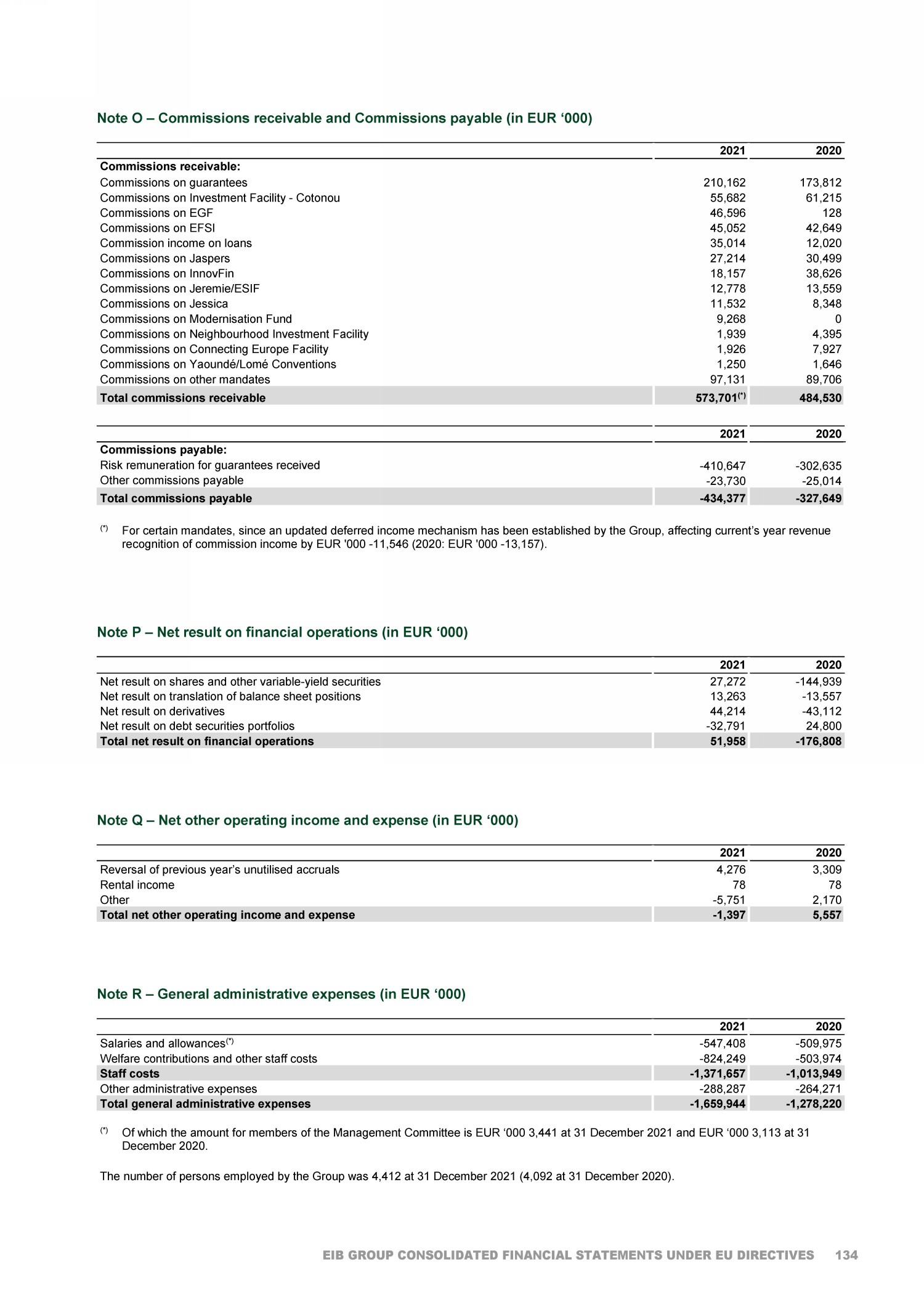

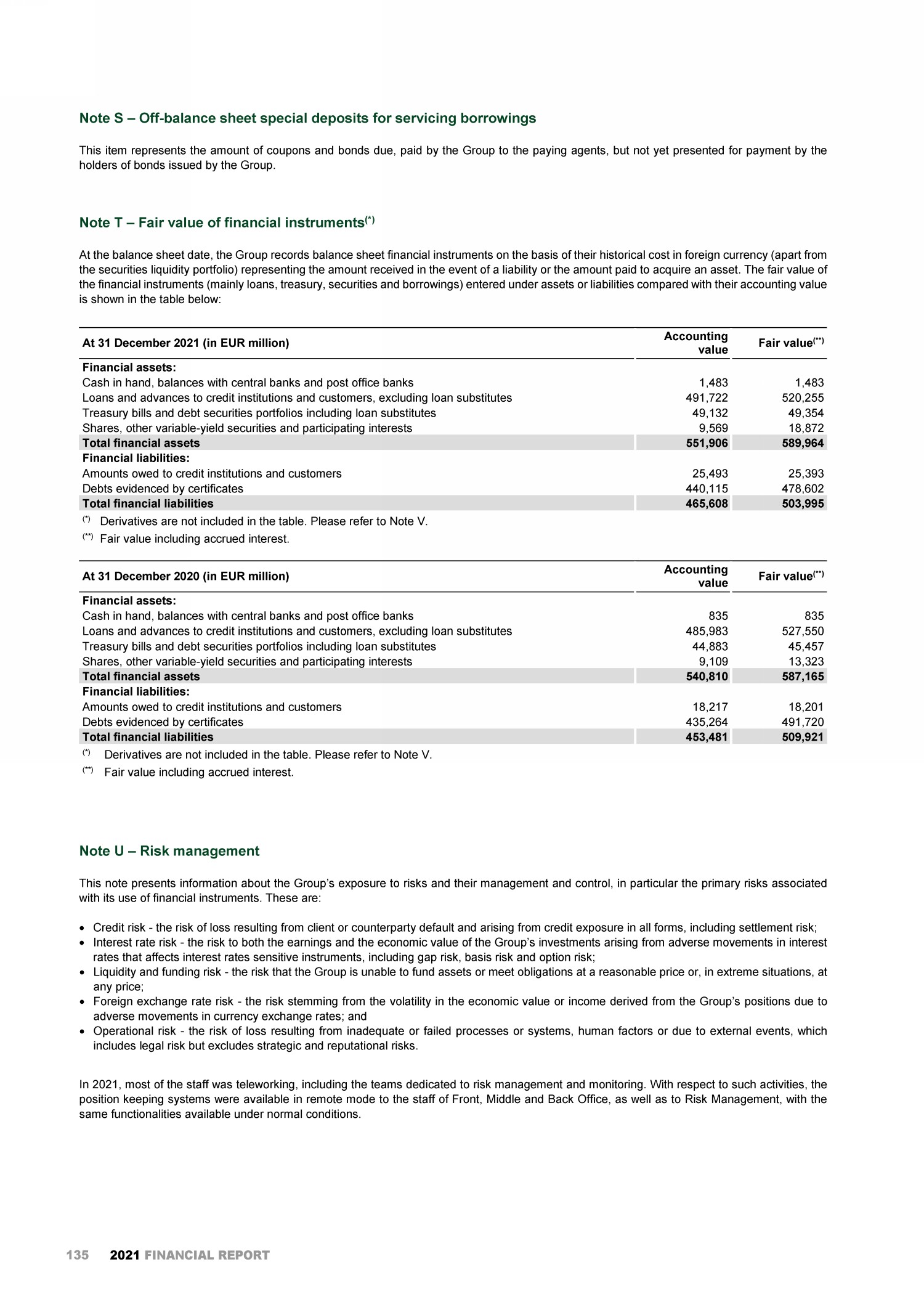

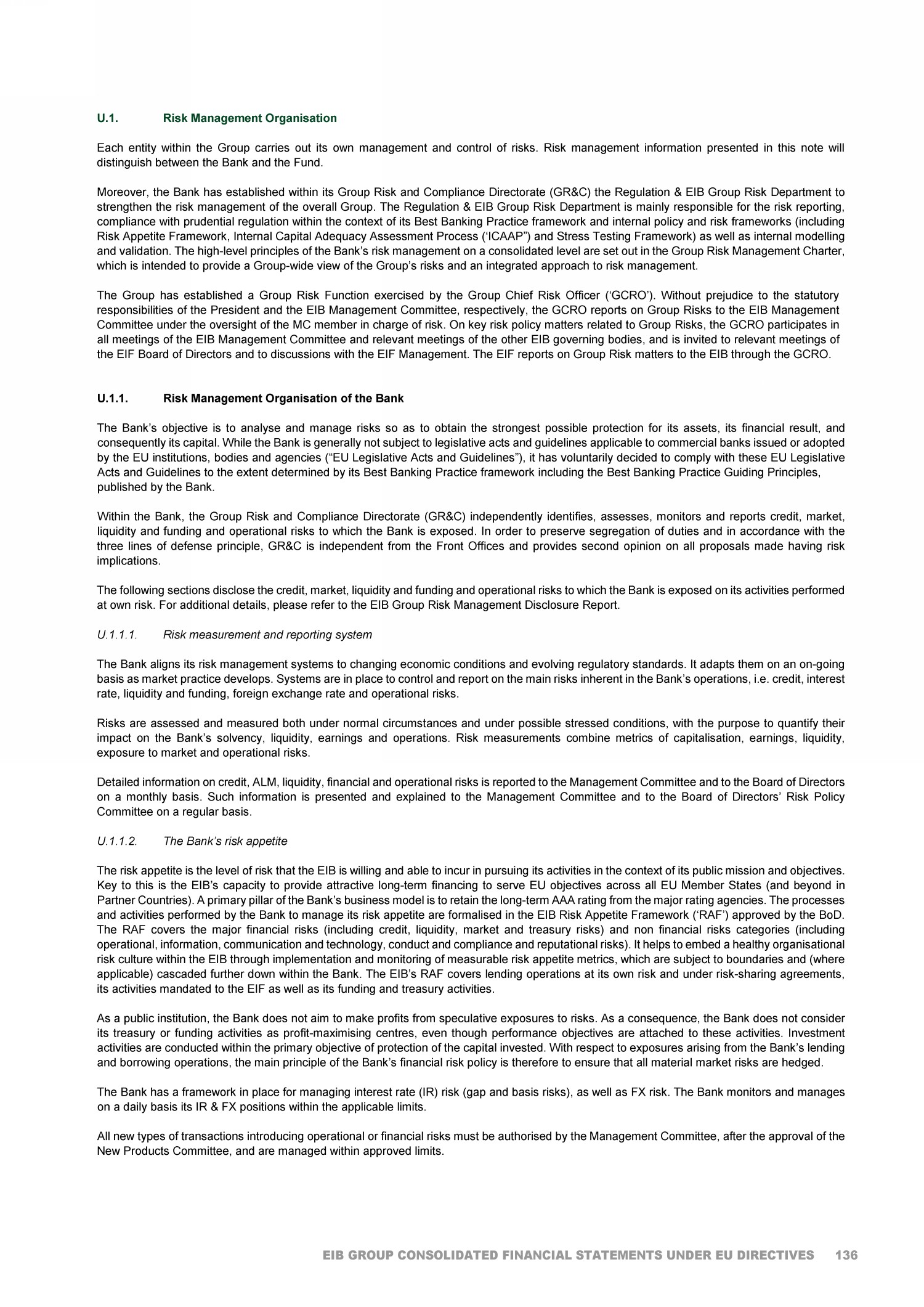

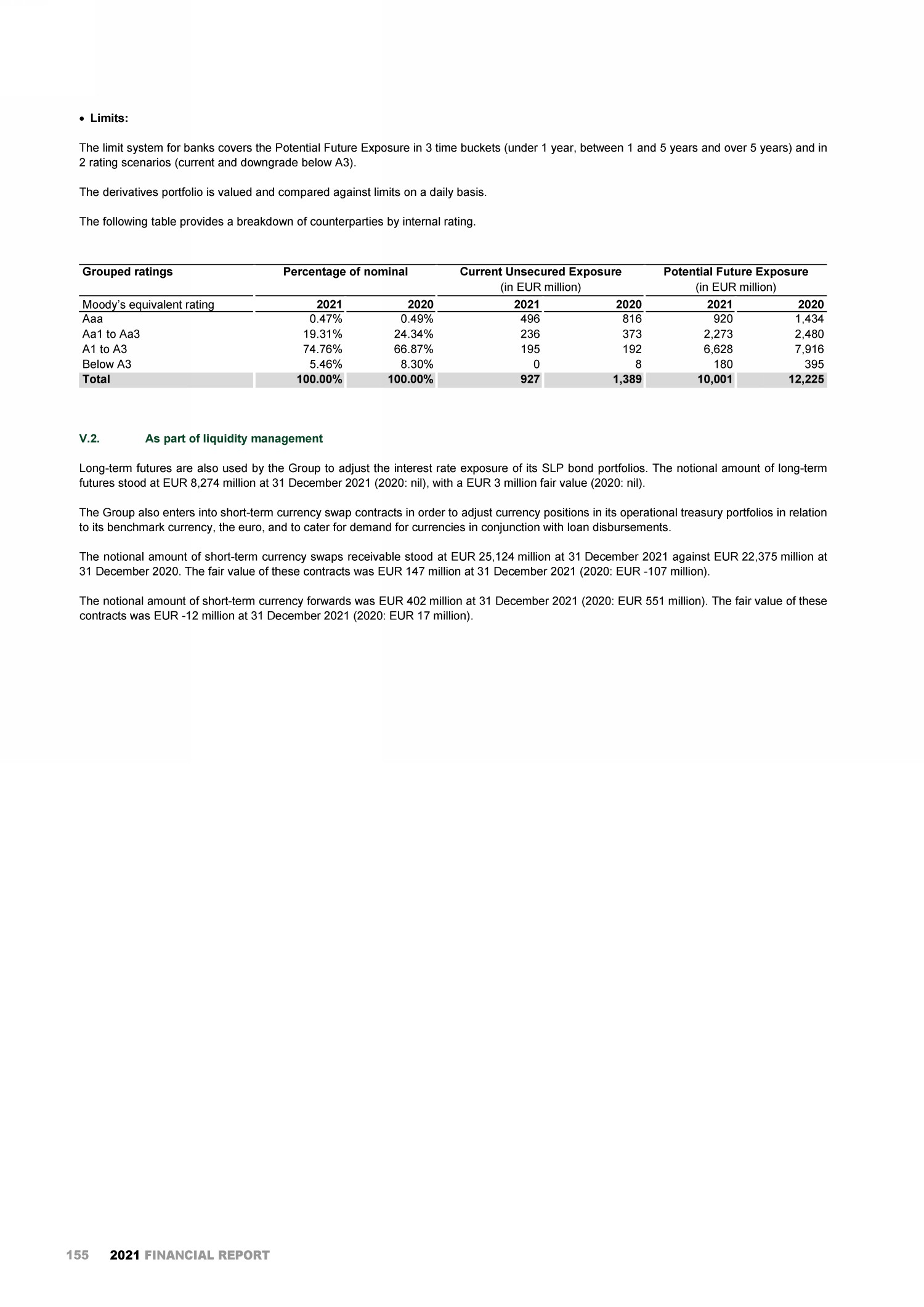

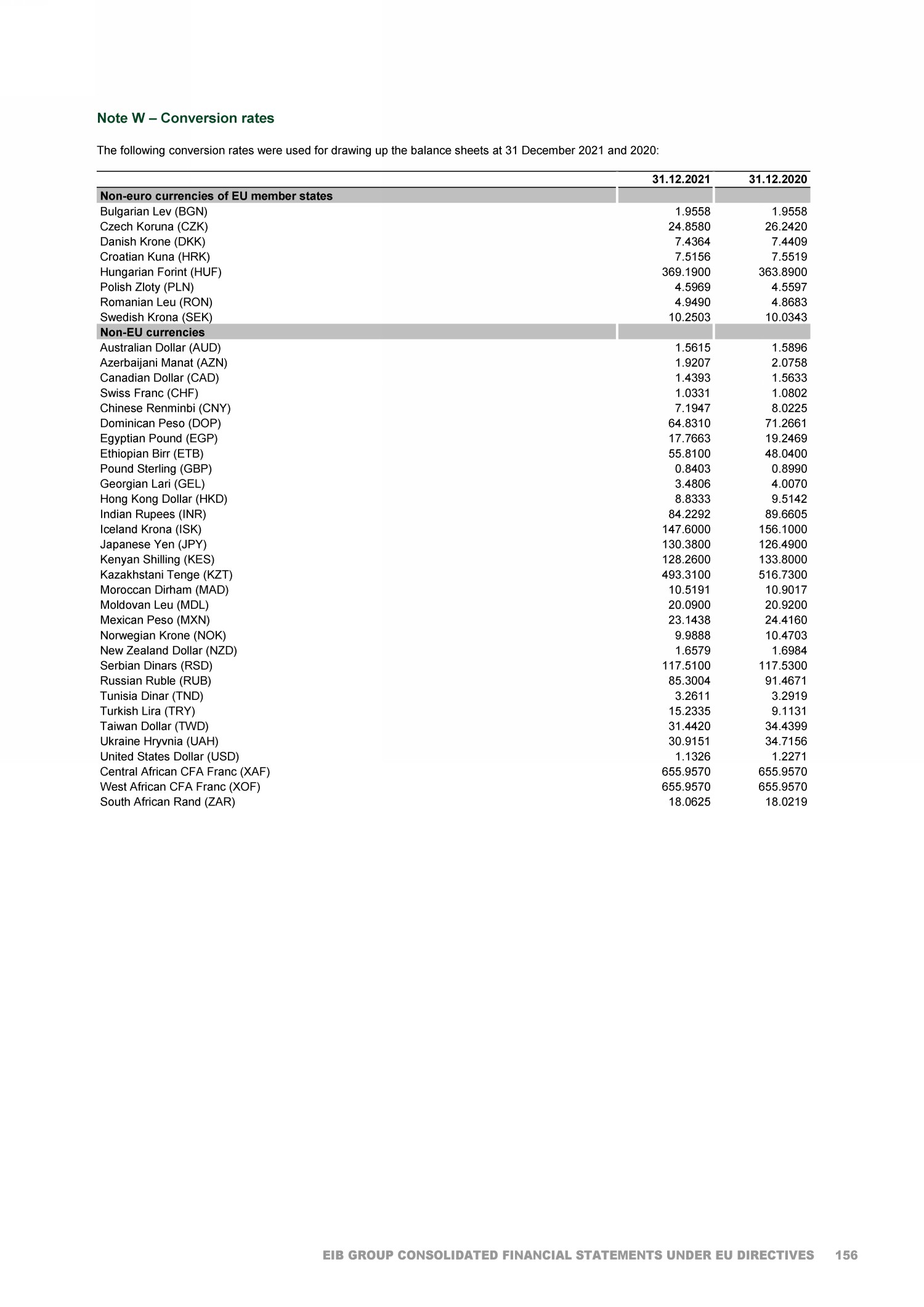

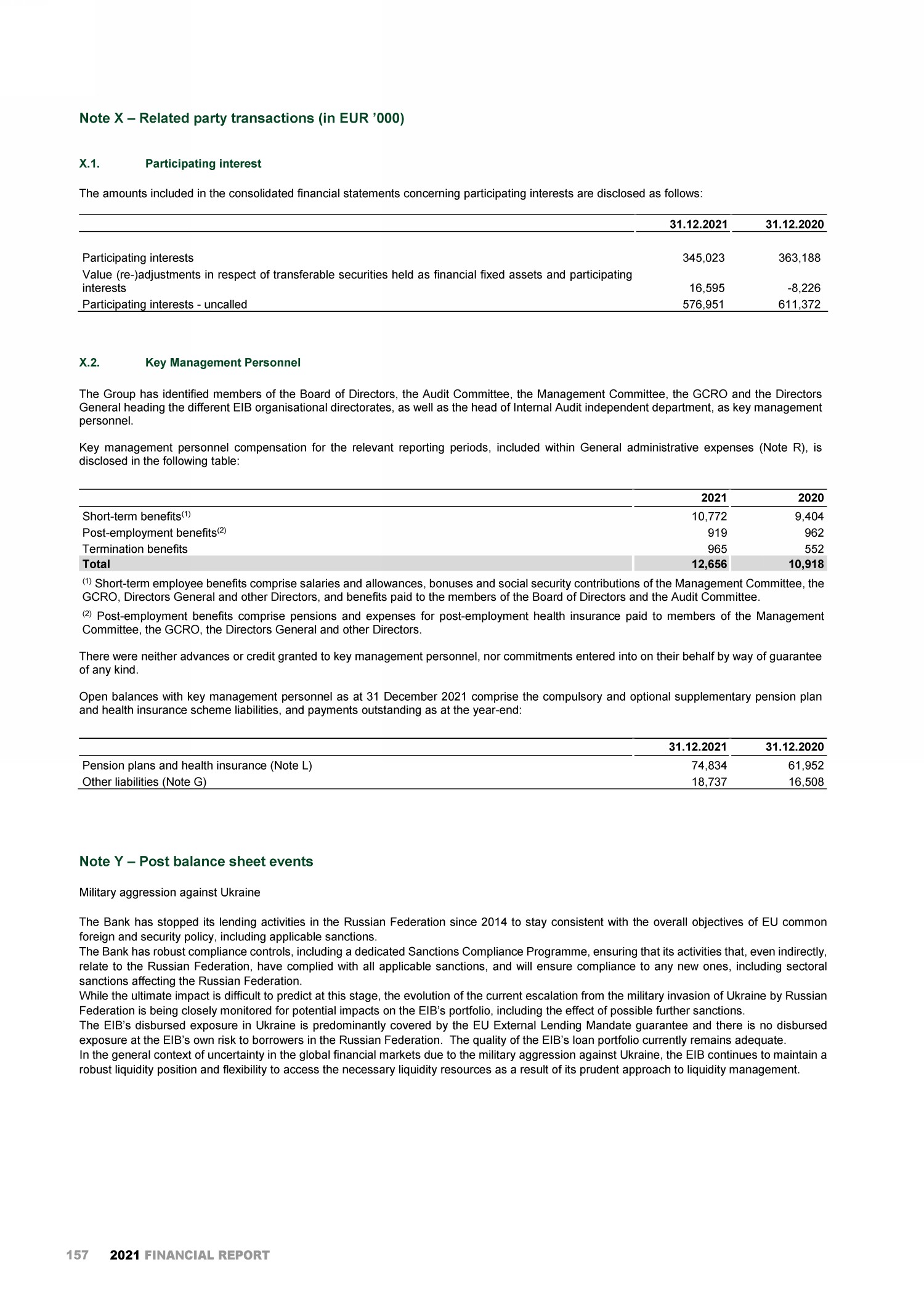

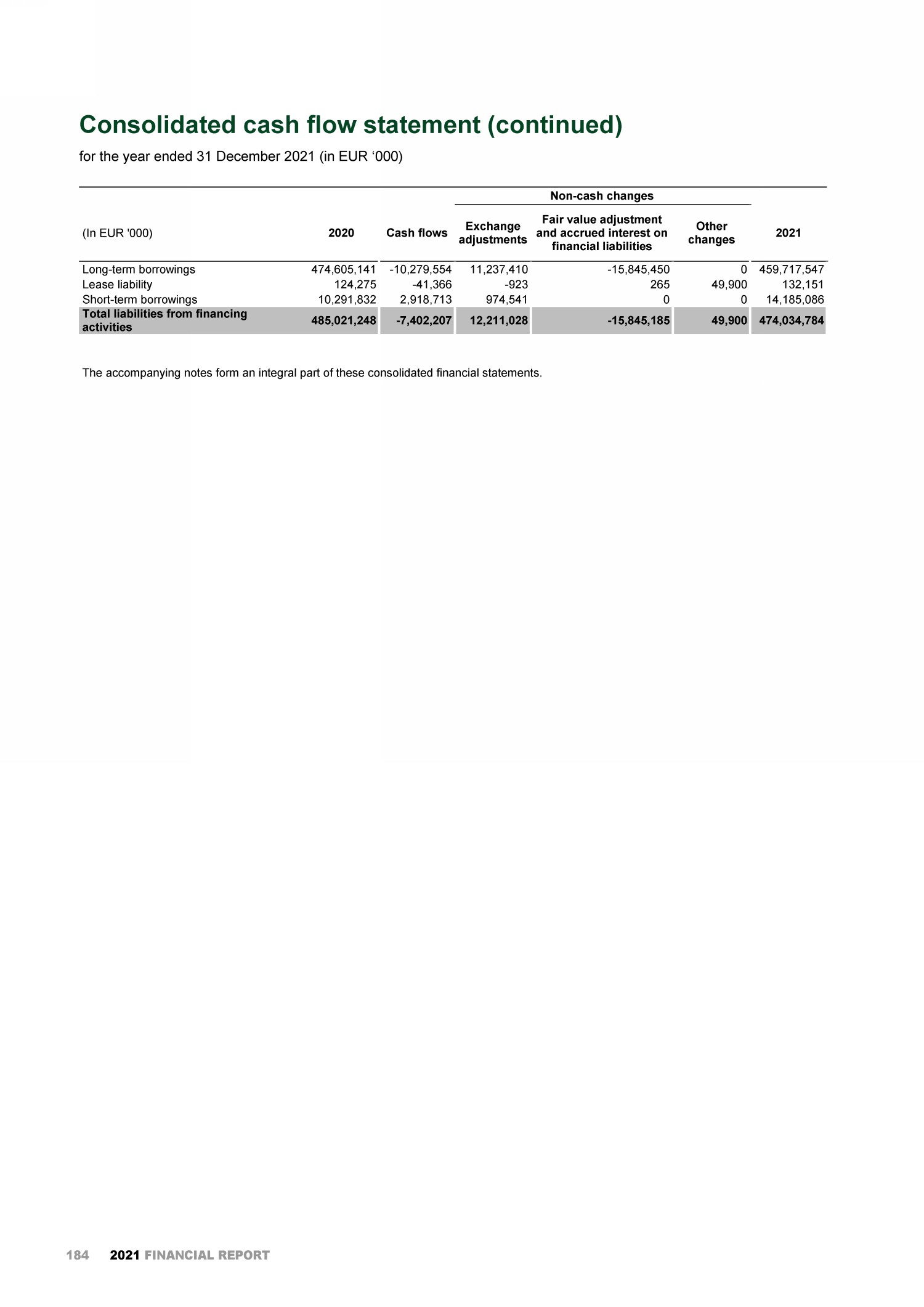

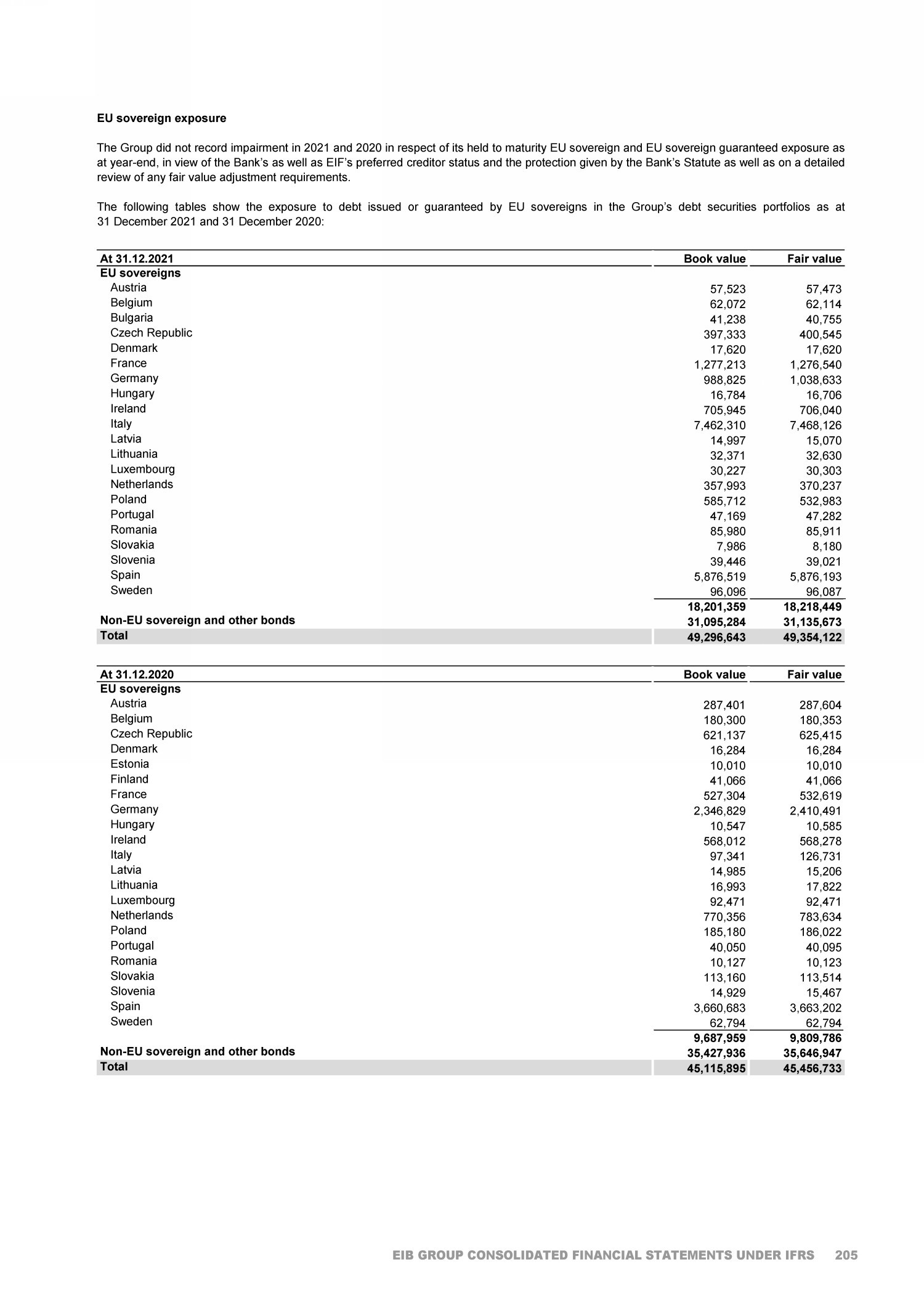

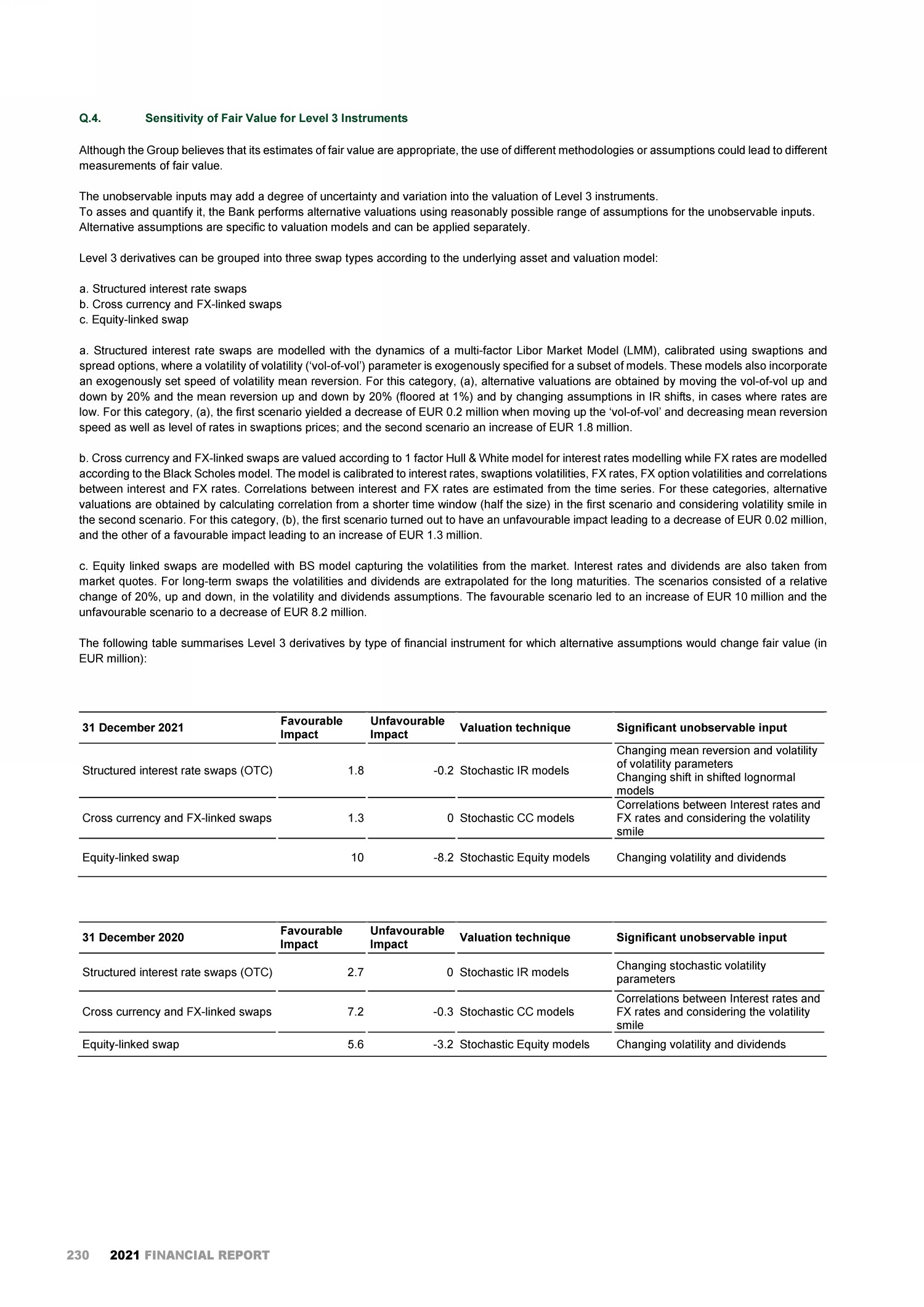

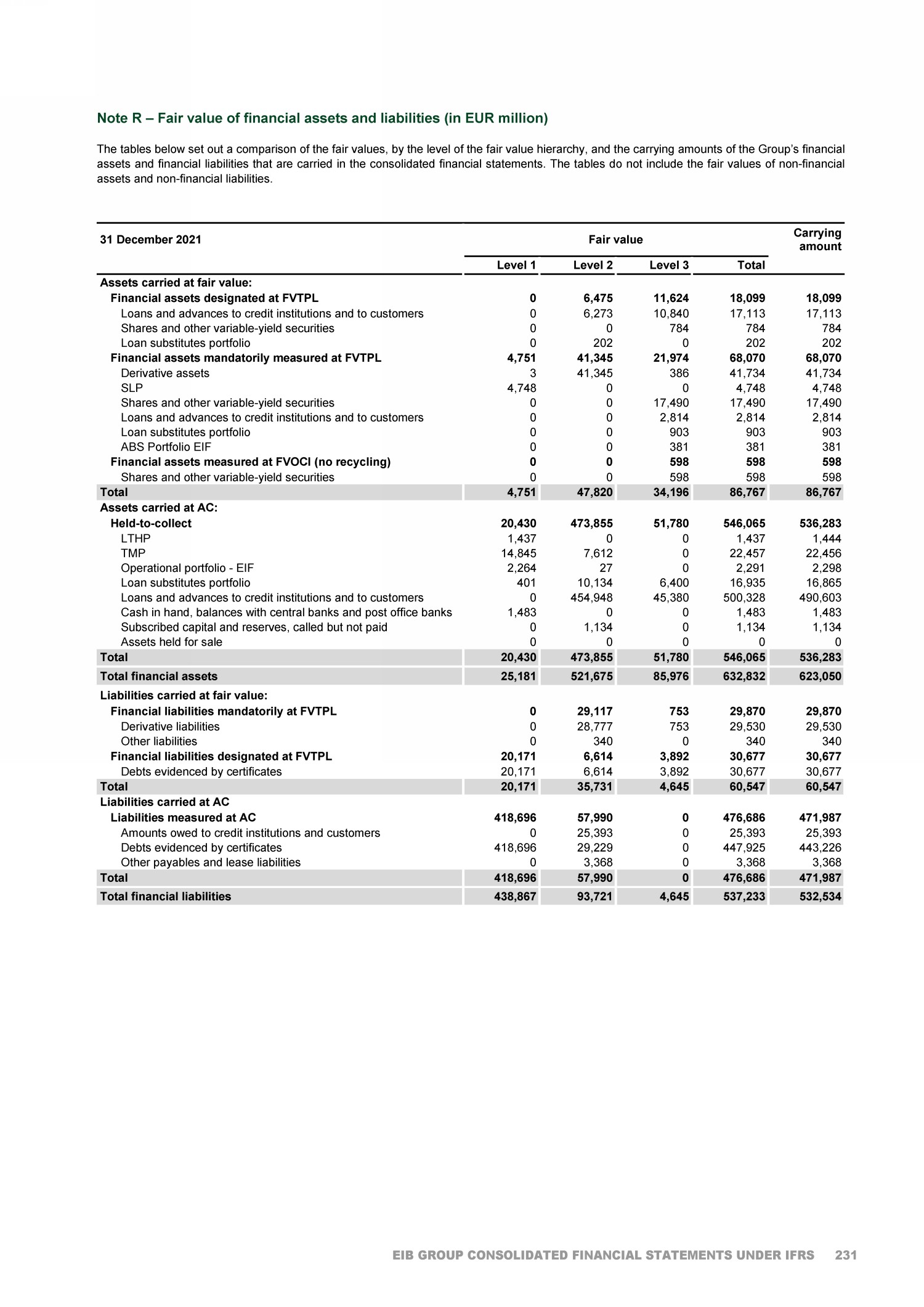

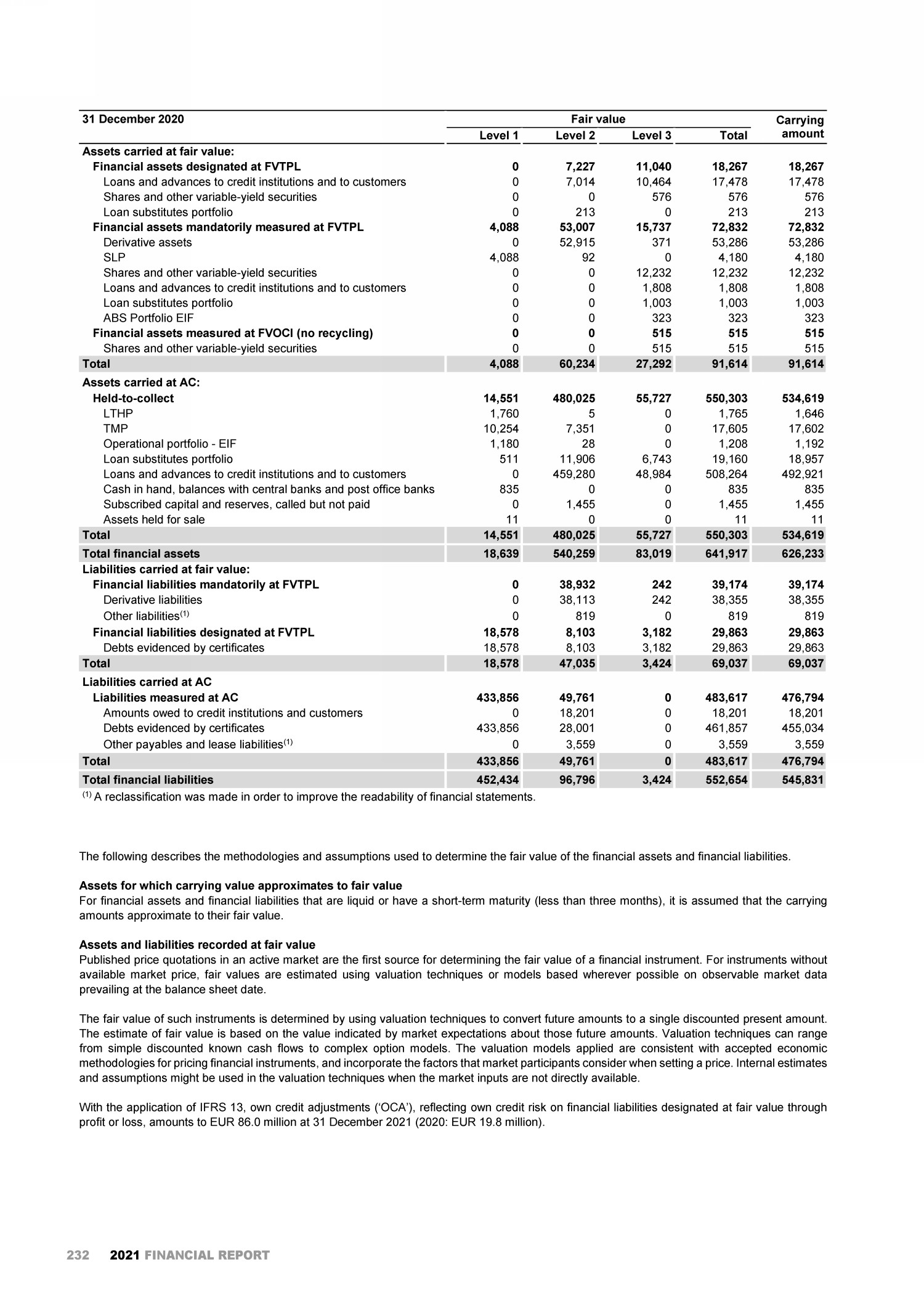

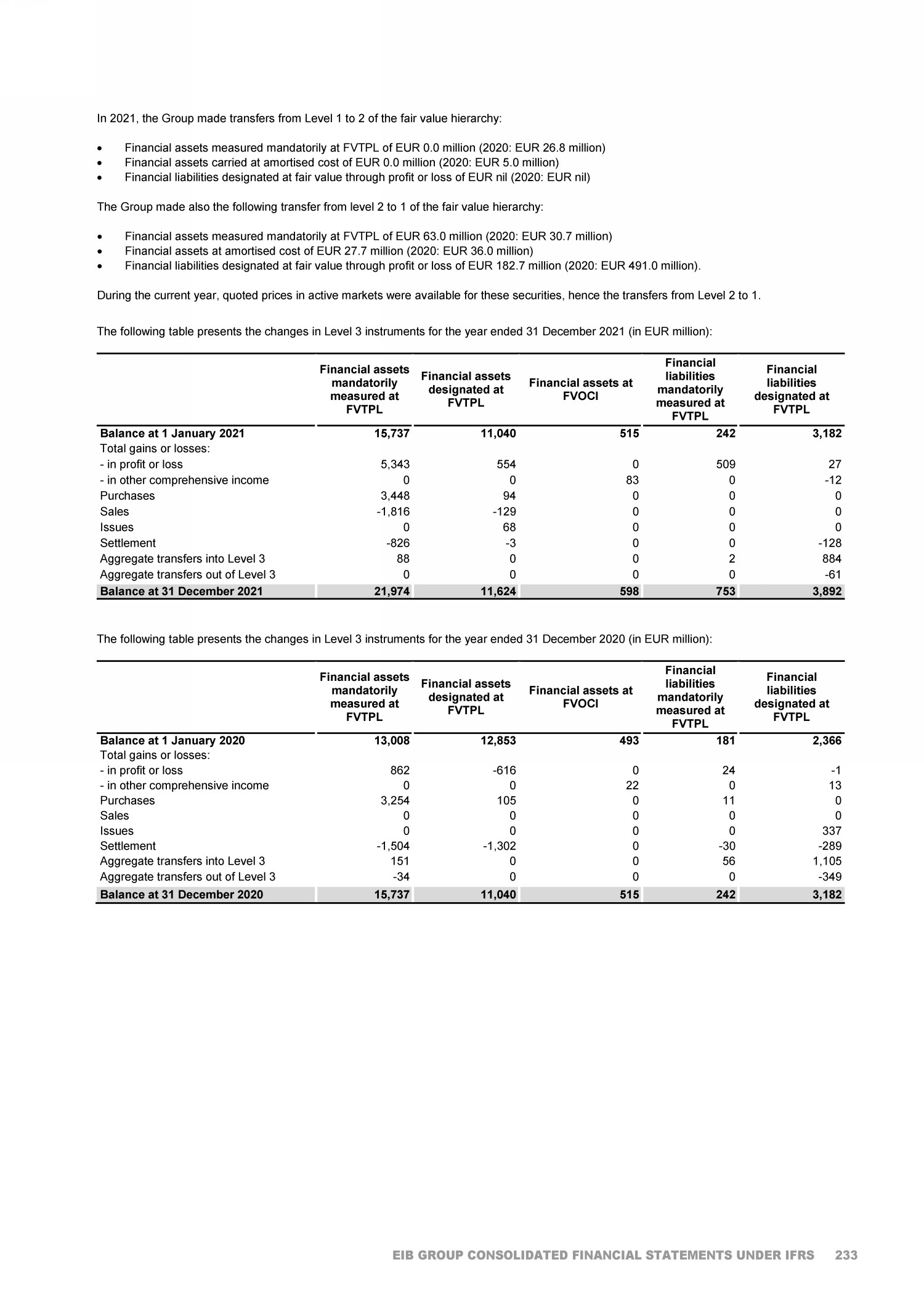

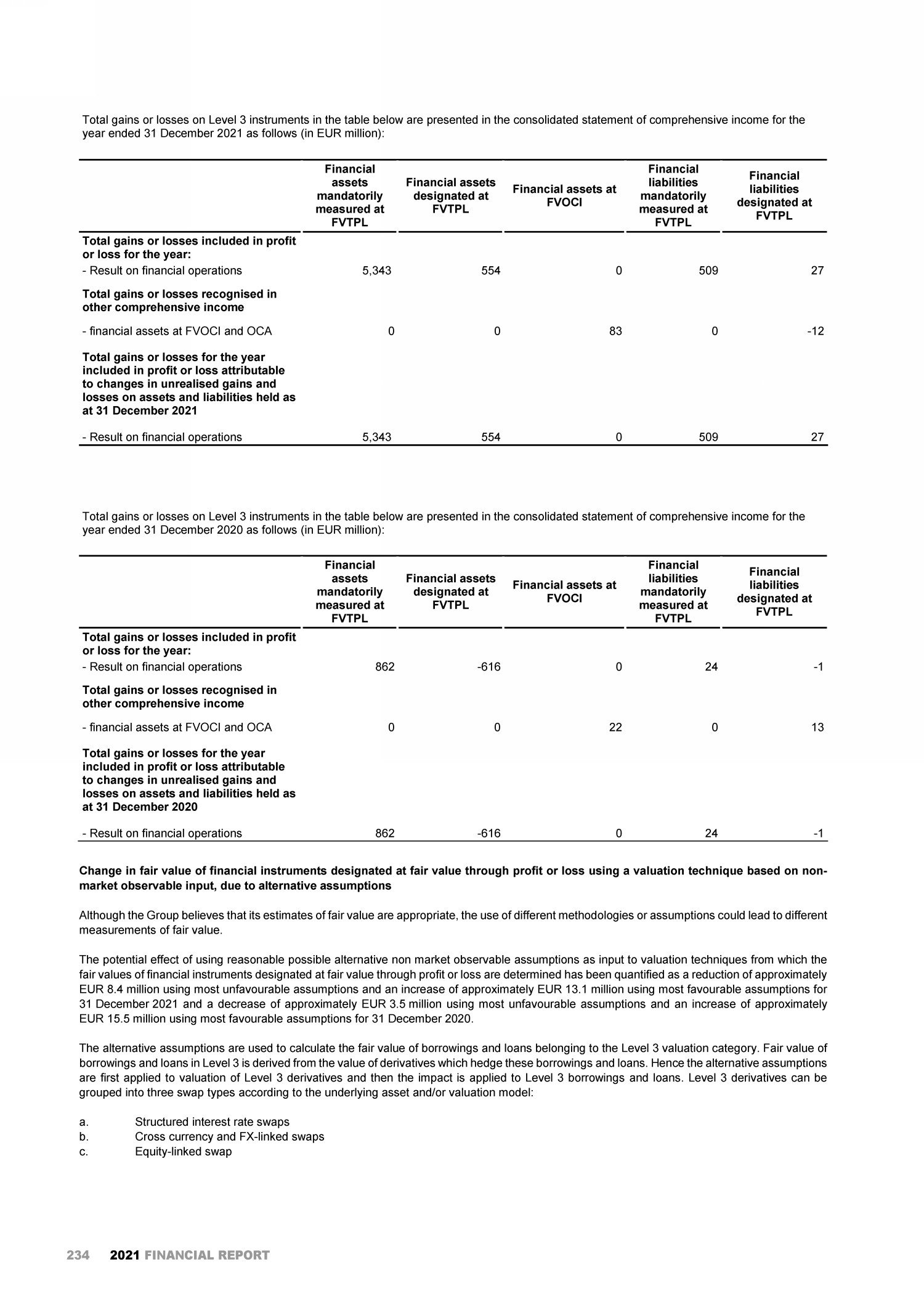

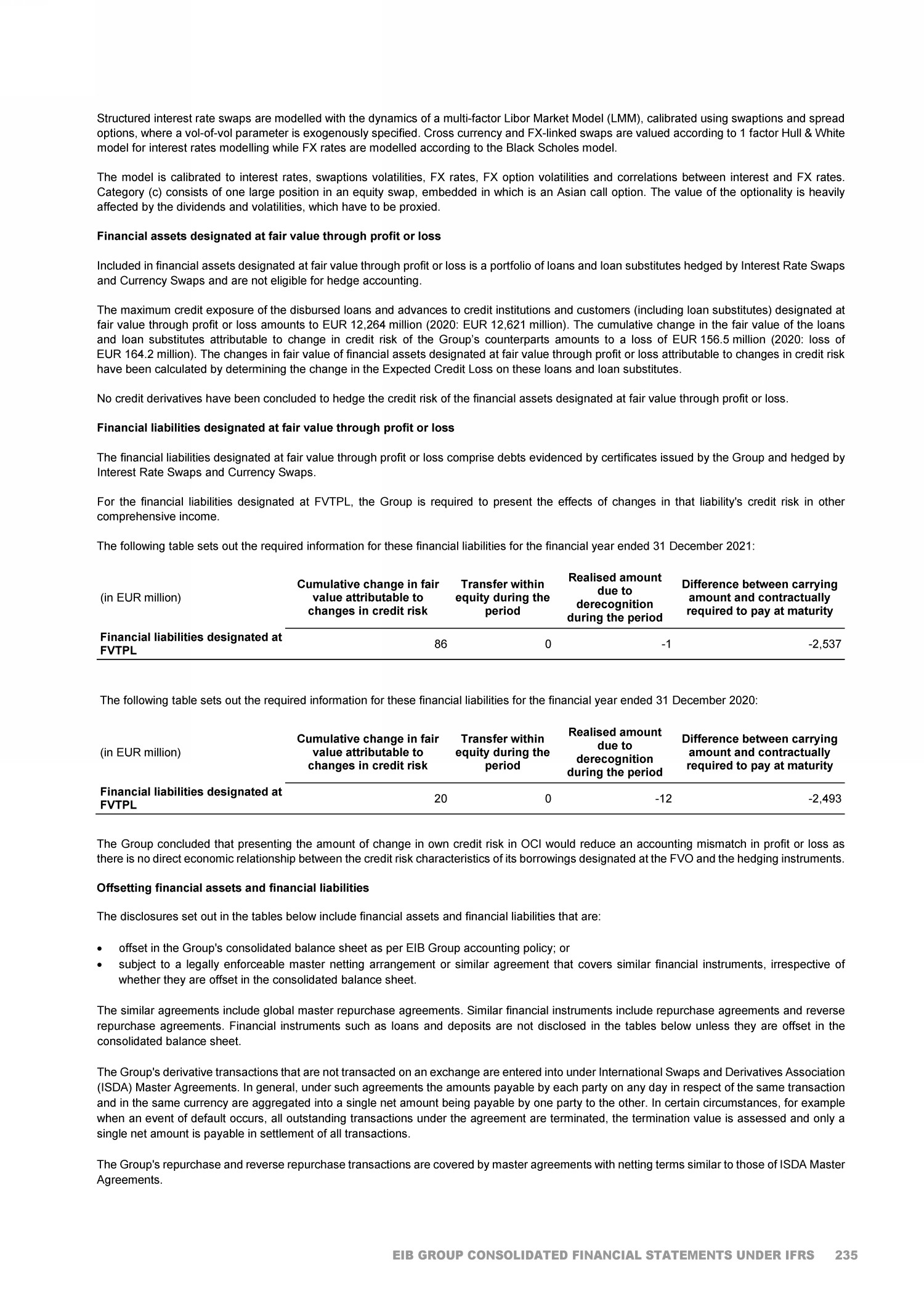

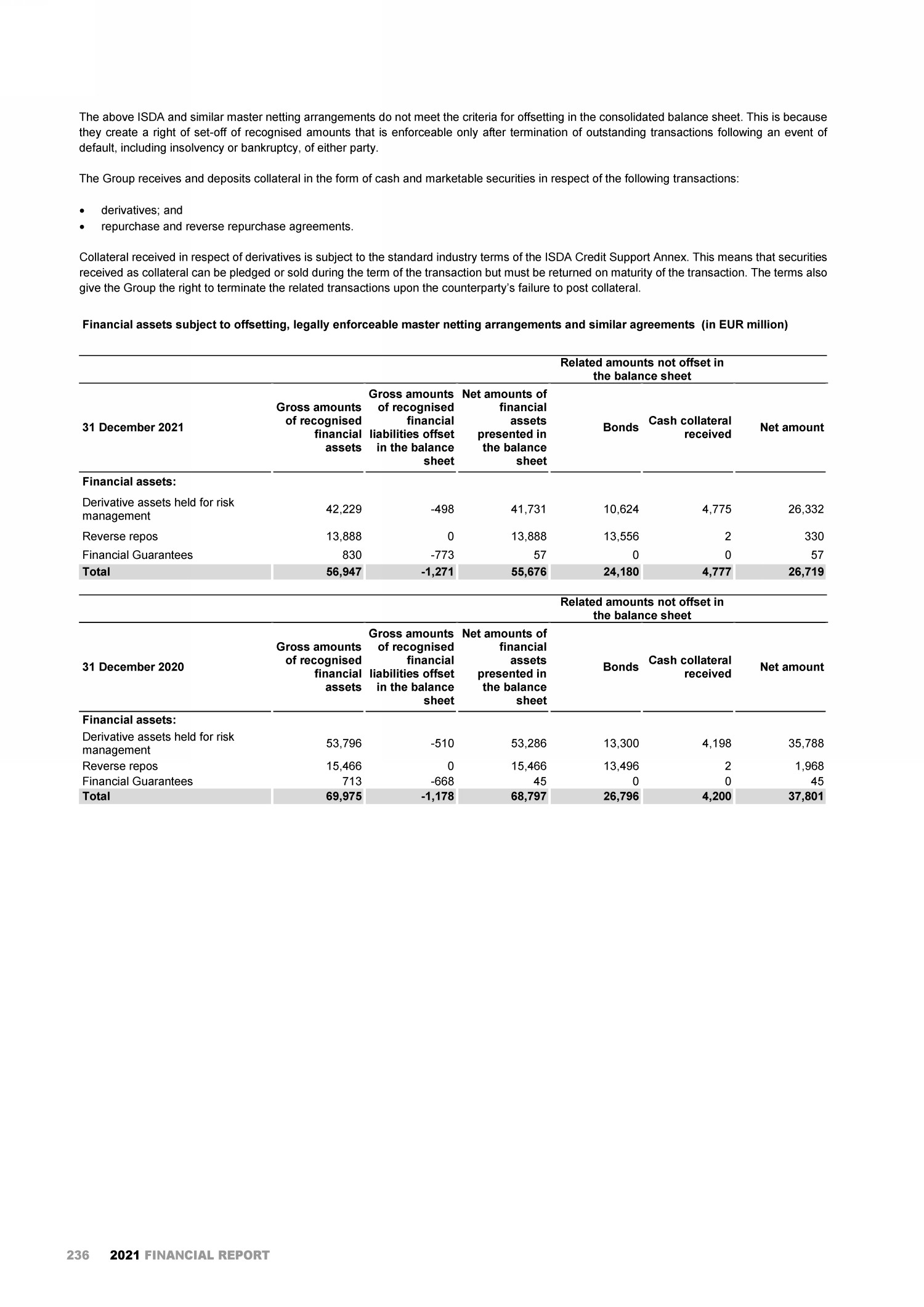

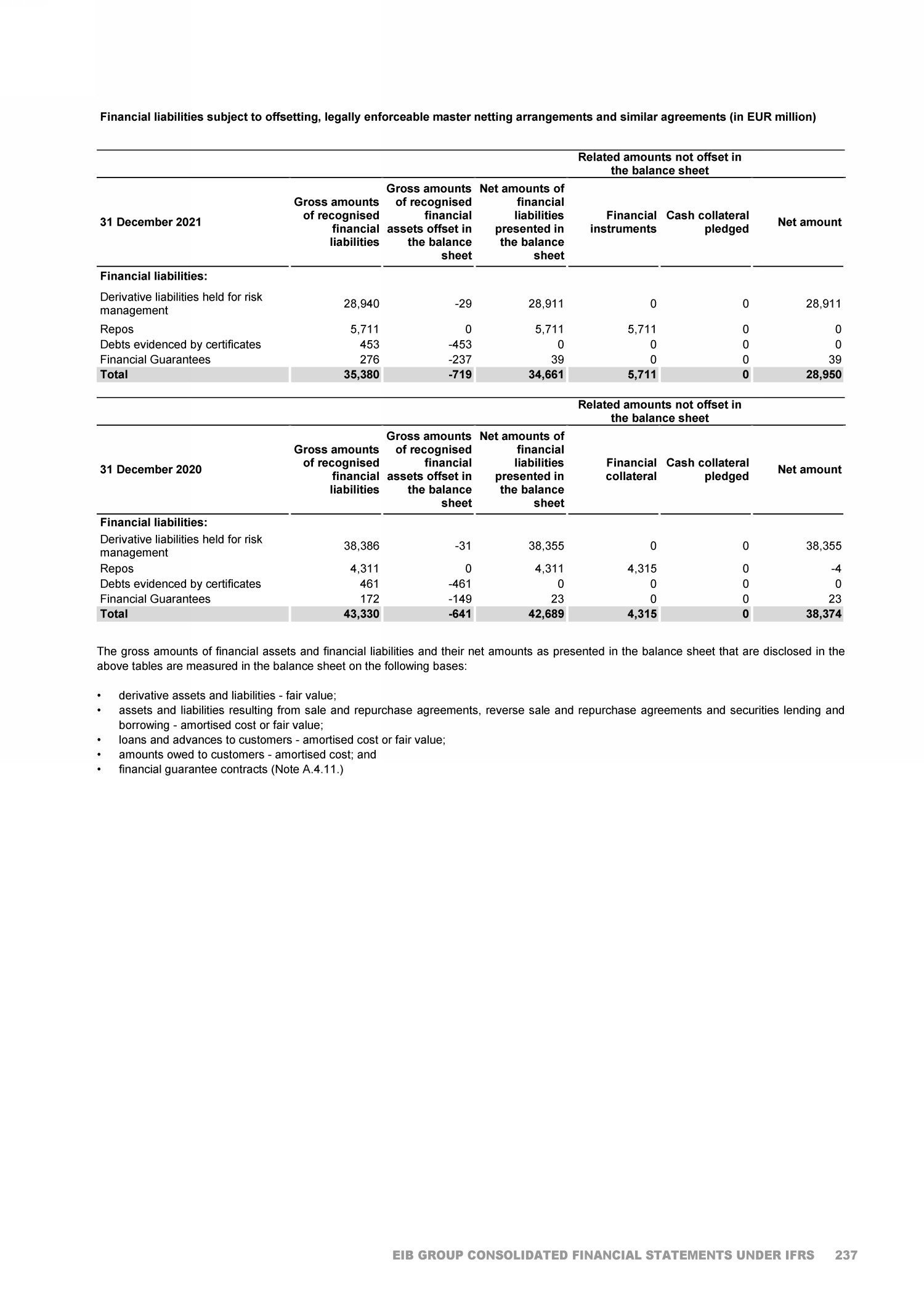

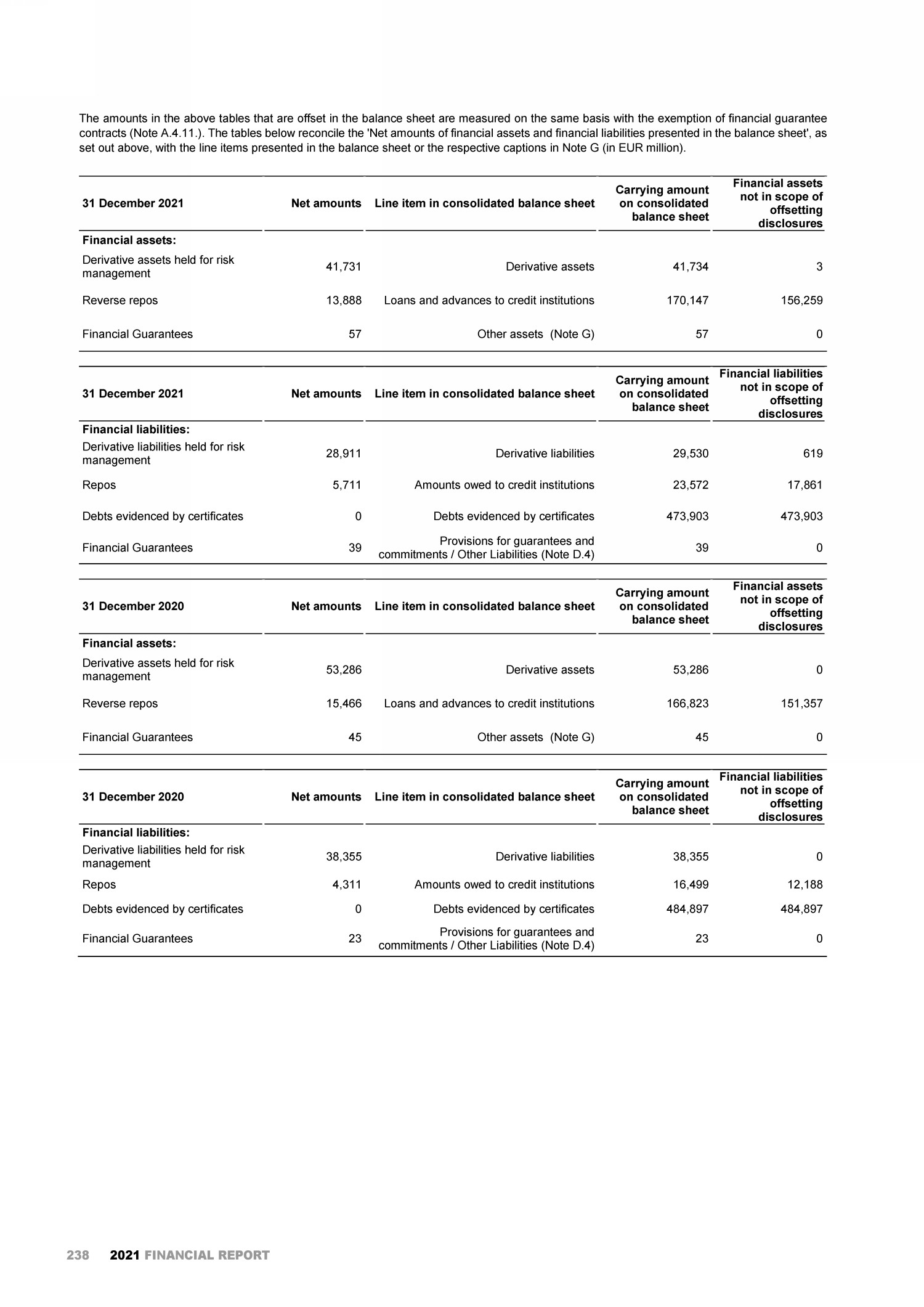

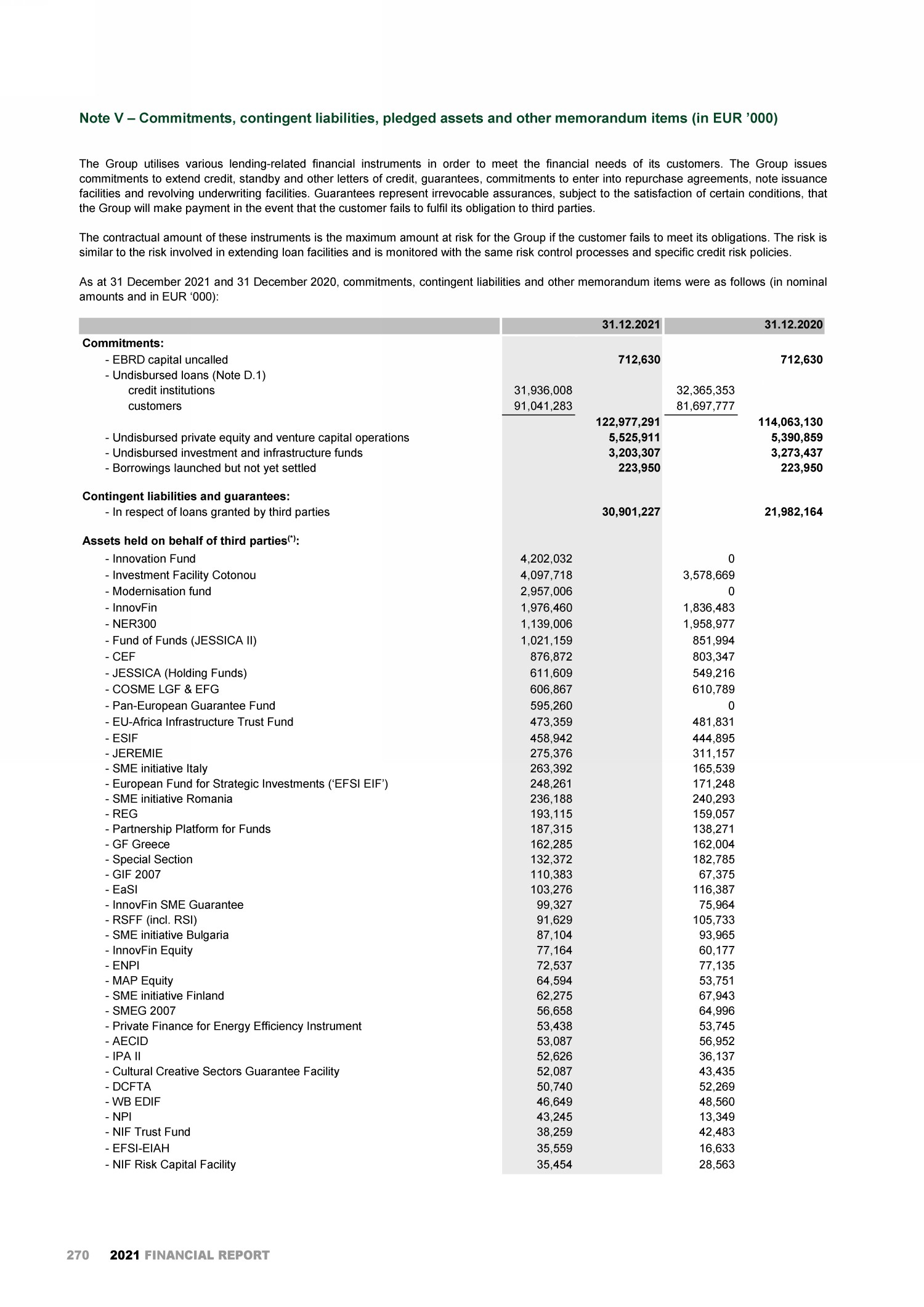

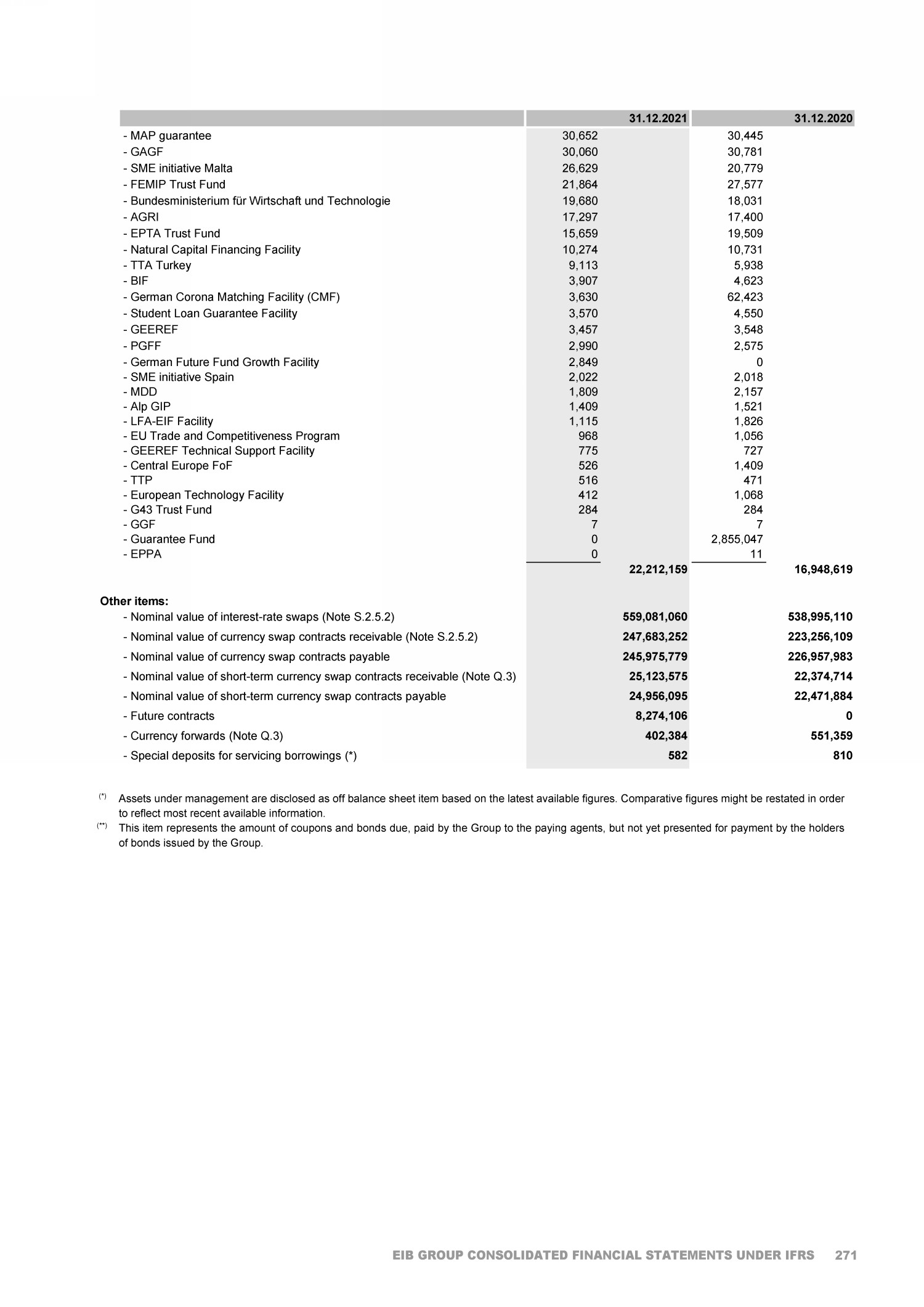

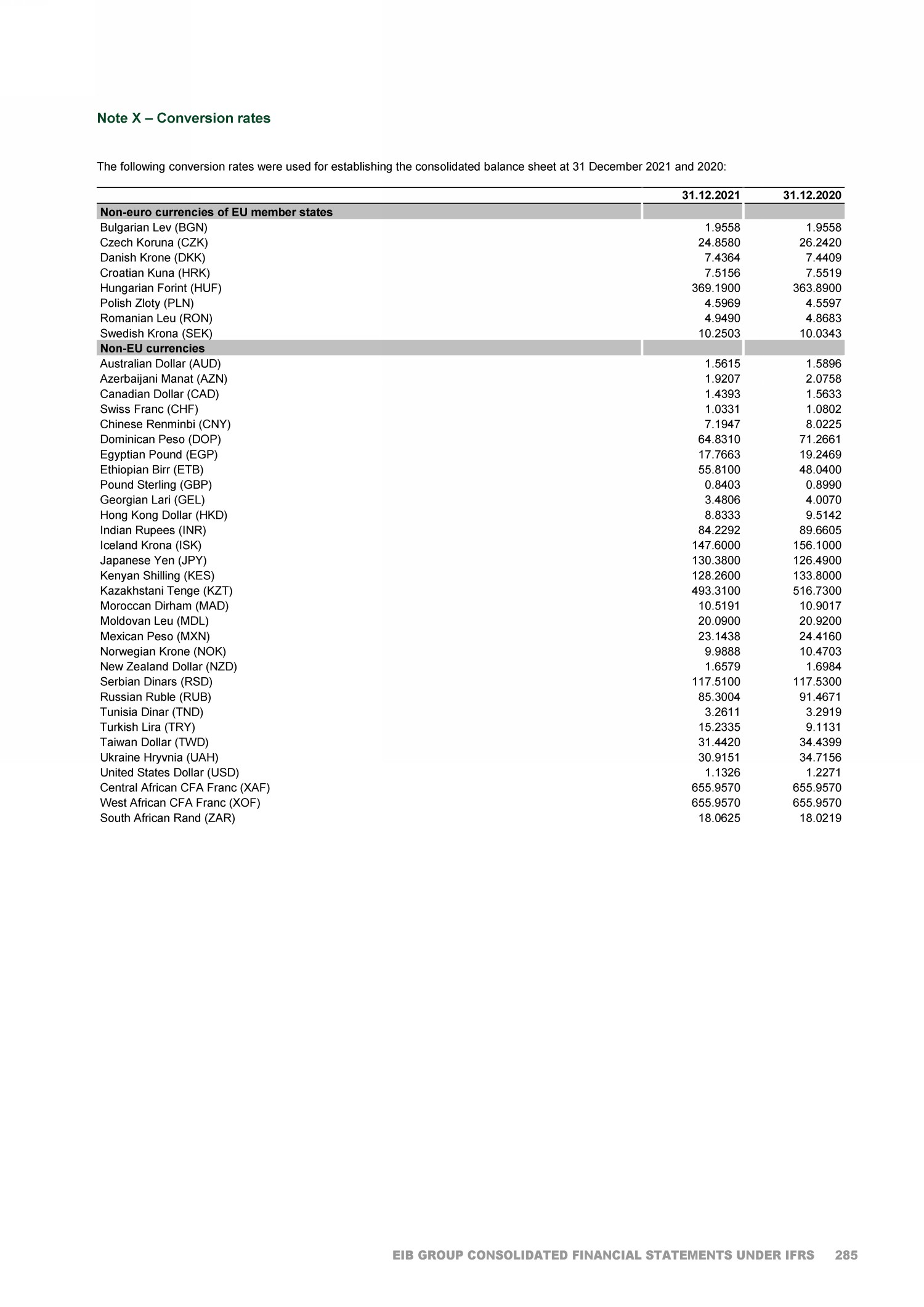

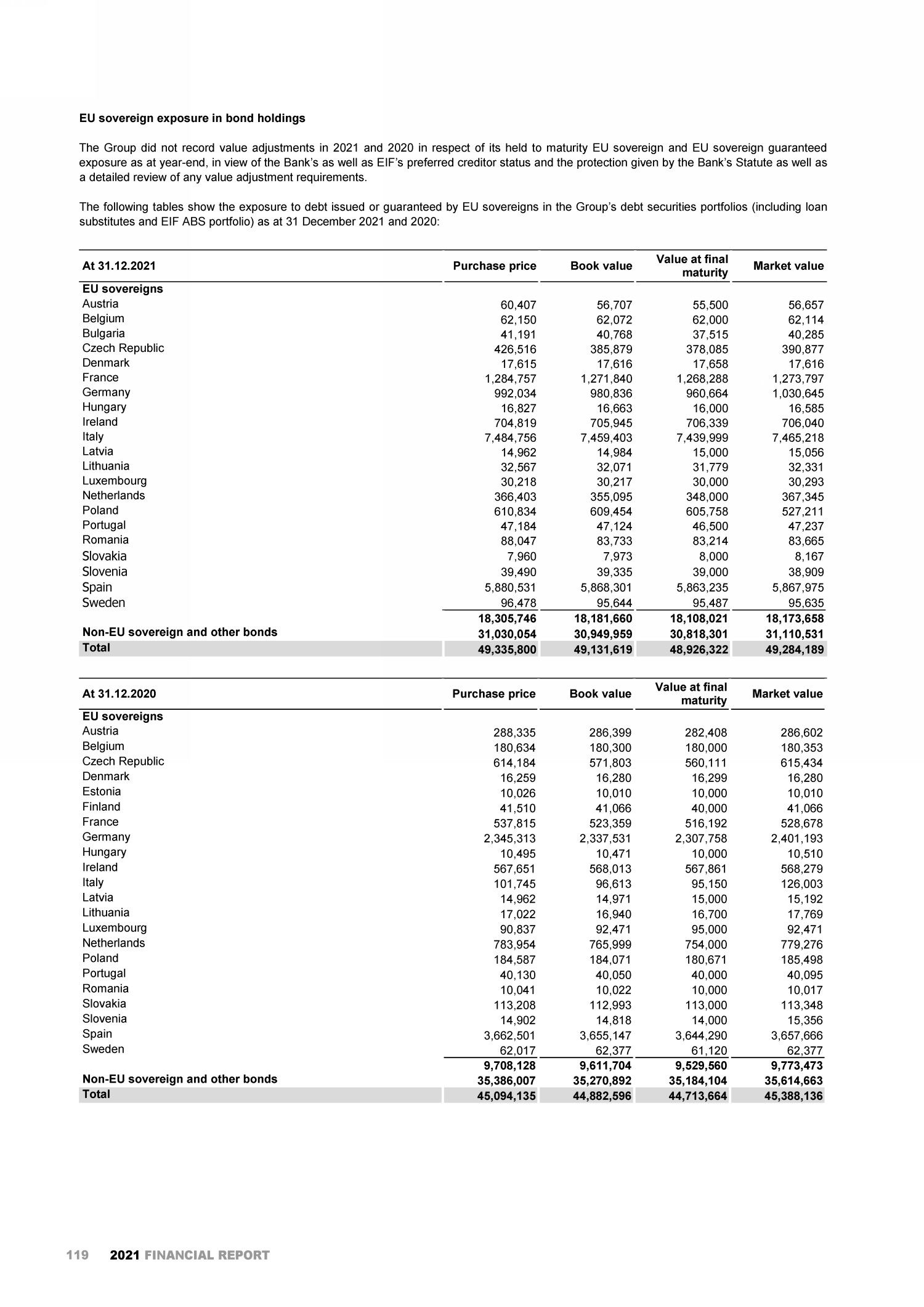

| 2021 FINANCIAL REPORT EU sovereign exposure in bond holdings The Group did not record value adjustments in 2021 and 2020 in respect of its held to maturity EU sovereign and EU sovereign guaranteed exposure as at year-end, in view of the Bank’s as well as EIF’s preferred creditor status and the protection given by the Bank’s Statute as well as a detailed review of any value adjustment requirements. The following tables show the exposure to debt issued or guaranteed by EU sovereigns in the Group’s debt securities portfolios (including loan substitutes and EIF ABS portfolio) as at 31 December 2021 and 2020: At 31.12.2021 Purchase price Book value Value at final maturity Market value EU sovereigns Austria 60,407 56,707 55,500 56,657 Belgium 62,150 62,072 62,000 62,114 Bulgaria 41,191 40,768 37,515 40,285 Czech Republic 426,516 385,879 378,085 390,877 Denmark 17,615 17,616 17,658 17,616 France 1,284,757 1,271,840 1,268,288 1,273,797 Germany 992,034 980,836 960,664 1,030,645 Hungary 16,827 16,663 16,000 16,585 Ireland 704,819 705,945 706,339 706,040 Italy 7,484,756 7,459,403 7,439,999 7,465,218 Latvia 14,962 14,984 15,000 15,056 Lithuania 32,567 32,071 31,779 32,331 Luxembourg 30,218 30,217 30,000 30,293 Netherlands 366,403 355,095 348,000 367,345 Poland 610,834 609,454 605,758 527,211 Portugal 47,184 47,124 46,500 47,237 Romania 88,047 83,733 83,214 83,665 Slovakia 7,960 7,973 8,000 8,167 Slovenia 39,490 39,335 39,000 38,909 Spain 5,880,531 5,868,301 5,863,235 5,867,975 Sweden 96,478 95,644 95,487 95,635 18,305,746 18,181,660 18,108,021 18,173,658 Non-EU sovereign and other bonds 31,030,054 30,949,959 30,818,301 31,110,531 Total 49,335,800 49,131,619 48,926,322 49,284,189 At 31.12.2020 Purchase price Book value Value at final maturity Market value EU sovereigns Austria 288,335 286,399 282,408 286,602 Belgium 180,634 180,300 180,000 180,353 Czech Republic 614,184 571,803 560,111 615,434 Denmark 16,259 16,280 16,299 16,280 Estonia 10,026 10,010 10,000 10,010 Finland 41,510 41,066 40,000 41,066 France 537,815 523,359 516,192 528,678 Germany 2,345,313 2,337,531 2,307,758 2,401,193 Hungary 10,495 10,471 10,000 10,510 Ireland 567,651 568,013 567,861 568,279 Italy 101,745 96,613 95,150 126,003 Latvia 14,962 14,971 15,000 15,192 Lithuania 17,022 16,940 16,700 17,769 Luxembourg 90,837 92,471 95,000 92,471 Netherlands 783,954 765,999 754,000 779,276 Poland 184,587 184,071 180,671 185,498 Portugal 40,130 40,050 40,000 40,095 Romania 10,041 10,022 10,000 10,017 Slovakia 113,208 112,993 113,000 113,348 Slovenia 14,902 14,818 14,000 15,356 Spain 3,662,501 3,655,147 3,644,290 3,657,666 Sweden 62,017 62,377 61,120 62,377 9,708,128 9,611,704 9,529,560 9,773,473 Non-EU sovereign and other bonds 35,386,007 35,270,892 35,184,104 35,614,663 Total 45,094,135 44,882,596 44,713,664 45,388,136 119 |