Exhibit 99.3

Roadmap to Front-end Peer Group Profitability

28 April 2008

© 2008 ASM

Proprietary Information

Safe Harbour Statements

All matters discussed in this document, except for any historical data, are forward-looking statements. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements. These include, but are not limited to, economic conditions and trends in the semiconductor industry generally and the timing of the industry cycles specifically, currency fluctuations, the timing of significant orders, market acceptance of new products, competitive factors, litigation involving intellectual property, shareholder and other issues, commercial and economic disruption due to natural disasters, terrorist activity, armed conflict or political instability, epidemics and other risks indicated in the Company’s filings from time to time with the U.S. Securities and Exchange Commission. All statements are made as of the date provided and we assume no obligation nor intend to update or revise any forward-looking statements to reflect future developments or circumstances.

© 2008 ASM

Proprietary Information

April 2008

2 |

|

Agenda

Introduction

Current situation FE

Roadmap to peer profitability FE in 2009

Concluding remarks

Appendix

FE and BE convergence

Peer selection criteria

© 2008 ASM

Proprietary Information

April 2008

3 |

|

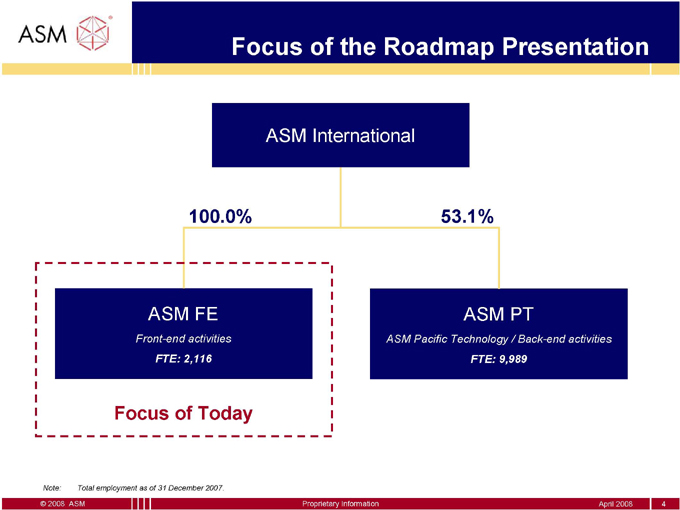

Focus of the Roadmap Presentation

ASM International

100.0%

53.1%

ASM FE ASM PT

Front-end activities ASM Pacific Technology / Back-end activities

FTE: 2,116 FTE: 9,989

Focus of Today

Note: Total employment as of 31 December 2007.

© 2008 ASM Proprietary Information April 2008 4

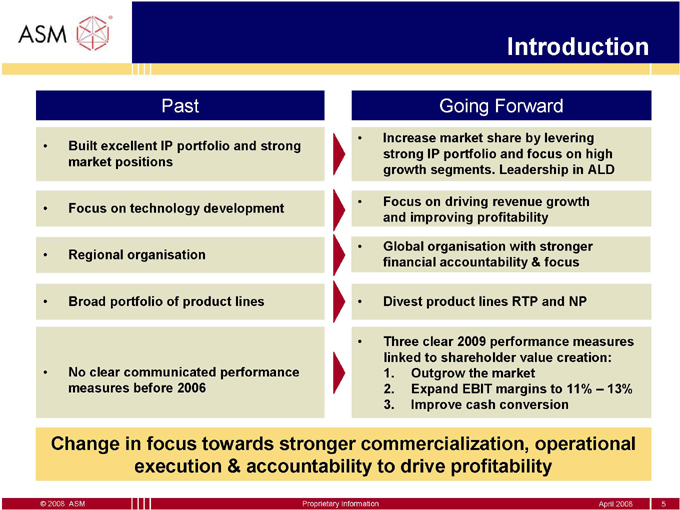

Past

Built excellent IP portfolio and strong market positions

Focus on technology development

Regional organisation

Broad portfolio of product lines

No clear communicated performance measures before 2006

Introduction

Going Forward

Increase market share by levering strong IP portfolio and focus on high growth segments. Leadership in ALD

Focus on driving revenue growth and improving profitability

Global organisation with stronger financial accountability & focus

Divest product lines RTP and NP

Three clear 2009 performance measures linked to shareholder value creation:

1. Outgrow the market

2. Expand EBIT margins to 11% – 13%

3. Improve cash conversion

Change in focus towards stronger commercialization, operational execution & accountability to drive profitability

© 2008 ASM

Proprietary Information

April 2008

5 |

|

Agenda

Introduction

Current situation FE

Roadmap to peer profitability FE in 2009

Concluding remarks

Appendix

FE and BE convergence

Peer selection criteria

© 2008 ASM

Proprietary Information

April 2008

6 |

|

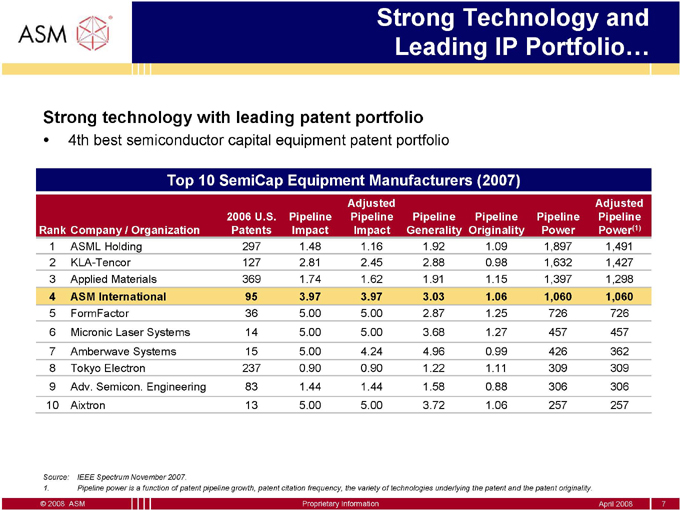

Strong Technology and

Leading IP Portfolio…

Strong technology with leading patent portfolio

• 4th best semiconductor capital equipment patent portfolio

Top 10 SemiCap Equipment Manufacturers (2007)

Adjusted Adjusted 2006 U.S. Pipeline Pipeline Pipeline Pipeline Pipeline Pipeline Rank Company / Organization Patents Impact Impact Generality Originality Power Power(1)

1 |

| ASML Holding 297 1.48 1.16 1.92 1.09 1,897 1,491 |

2 |

| KLA-Tencor 127 2.81 2.45 2.88 0.98 1,632 1,427 |

3 |

| Applied Materials 369 1.74 1.62 1.91 1.15 1,397 1,298 |

4 |

| ASM International 95 3.97 3.97 3.03 1.06 1,060 1,060 |

5 |

| FormFactor 36 5.00 5.00 2.87 1.25 726 726 |

6 |

| Micronic Laser Systems 14 5.00 5.00 3.68 1.27 457 457 |

7 |

| Amberwave Systems 15 5.00 4.24 4.96 0.99 426 362 |

8 |

| Tokyo Electron 237 0.90 0.90 1.22 1.11 309 309 |

9 Adv. Semicon. Engineering 83 1.44 1.44 1.58 0.88 306 306

10 Aixtron 13 5.00 5.00 3.72 1.06 257 257

Source: IEEE Spectrum November 2007.

1. Pipeline power is a function of patent pipeline growth, patent citation frequency, the variety of technologies underlying the patent and the patent originality.

© 2008 ASM Proprietary Information April 2008 7

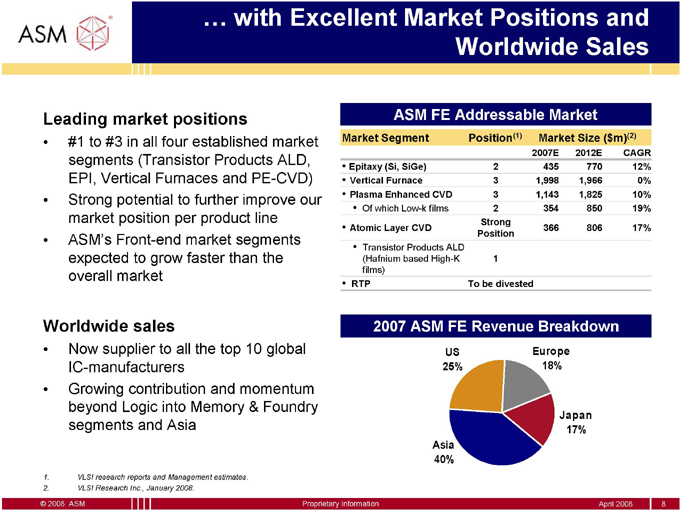

… with Excellent Market Positions and

Worldwide Sales

Leading market positions

#1 to #3 in all four established market segments (Transistor Products ALD, EPI, Vertical Furnaces and PE-CVD)

Strong potential to further improve our market position per product line

ASM’s Front-end market segments expected to grow faster than the overall market

Worldwide sales

• Now supplier to all the top 10 global IC-manufacturers

• Growing contribution and momentum beyond Logic into Memory & Foundry segments and Asia

1. VLSI research reports and Management estimates.

2. VLSI Research Inc., January 2008.

ASM FE Addressable Market

Market Segment Position(1) Market Size ($m)(2)

2007E 2012E CAGR

• Epitaxy (Si, SiGe) 2 435 770 12%

• Vertical Furnace 3 1,998 1,966 0%

• Plasma Enhanced CVD 3 1,143 1,825 10%

• Of which Low-k films 2 354 850 19% Strong

• Atomic Layer CVD 366 806 17% Position

• Transistor Products ALD

(Hafnium based High-K 1 films)

• RTP To be divested

2007 ASM FE Revenue Breakdown

US Europe 25% 18%

Japan

17%

Asia

40%

© 2008 ASM

Proprietary Information April 2008

8 |

|

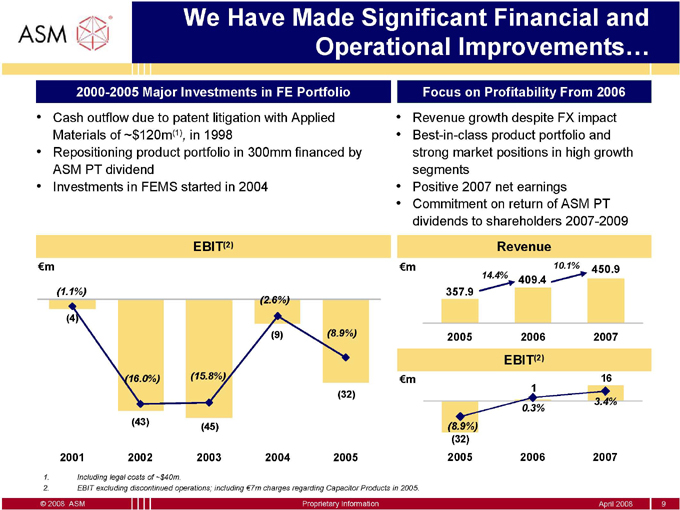

We Have Made Significant Financial and

Operational Improvements…

2000-2005 Major Investments in FE Portfolio

Focus on Profitability From 2006

Cash outflow due to patent litigation with Applied Materials of ~$120m(1), in 1998

Repositioning product portfolio in 300mm financed by ASM PT dividend

Investments in FEMS started in 2004

Revenue growth despite FX impact

Best-in-class product portfolio and strong market positions in high growth segments

Positive 2007 net earnings

Commitment on return of ASM PT dividends to shareholders 2007-2009

EBIT(2) Revenue

€m €m 10.1% 450.9

14.4%

409.4

(1.1%) 357.9

(2.6%)

(4) |

|

(9) |

| (8.9%) 2005 2006 2007 |

EBIT(2)

(16.0%) (15.8%) €m 16 1 (32) 3.4%

0.3%

(43) |

|

(45) |

| (8.9%) |

(32) |

|

2001 2002 2003 2004 2005 2005 2006 2007

Including legal costs of ~$40m.

EBIT excluding discontinued operations; including €7m charges regarding Capacitor Products in 2005.

© 2008 ASM

Proprietary Information

April 2008

9

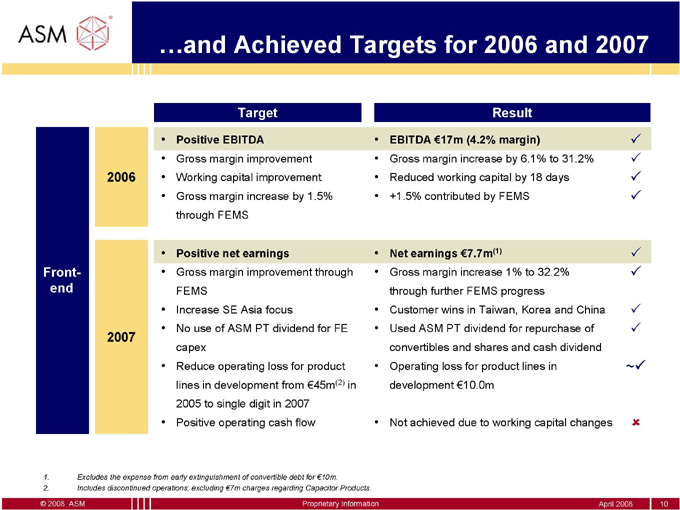

…and Achieved Targets for 2006 and 2007

Target

• Positive EBITDA

• Gross margin improvement 2006 • Working capital improvement

• Gross margin increase by 1.5% through FEMS

• Positive net earnings

Front- • Gross margin improvement through end FEMS

• Increase SE Asia focus

2007 • No use of ASM PT dividend for FE capex

• Reduce operating loss for product lines in development from €45m(2) in 2005 to single digit in 2007

• Positive operating cash flow

Excludes the expense from early extinguishment of convertible debt for €10m.

Includes discontinued operations; excluding €7m charges regarding Capacitor Products.

Result

EBITDA €17m (4.2% margin) 333

Gross margin increase by 6.1% to 31.2% 333

Reduced working capital by 18 days 333

+1.5% contributed by FEMS 333

• Net earnings €7.7m(1) 33 3

• Gross margin increase 1% to 32.2% 33 3 through further FEMS progress

• Customer wins in Taiwan, Korea and China 33 3

• Used ASM PT dividend for repurchase of 33 3 convertibles and shares and cash dividend

• Operating loss for product lines in ~33 3 development €10.0m

• Not achieved due to working capital changes 33 3

© 2008 ASM

Proprietary Information

April 2008

10

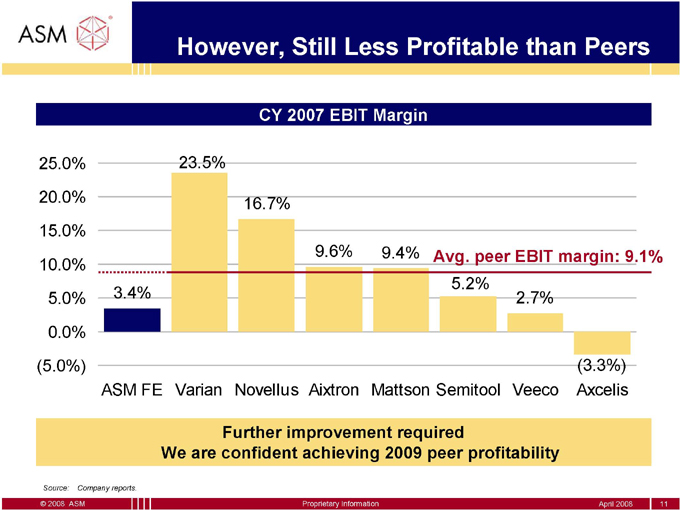

However, Still Less Profitable than Peers

CY 2007 EBIT Margin

25.0% 23.5%

20.0%

16.7%

15.0%

9.6% 9.4% Avg. peer EBIT margin: 9.1%

10.0%

5.2%

5.0% 3.4% 2.7%

0.0%

(5.0%) (3.3%) ASM FE Varian Novellus Aixtron Mattson Semitool Veeco Axcelis

Further improvement required

We are confident achieving 2009 peer profitability

Source: Company reports.

© 2008 ASM Proprietary Information April 2008 11

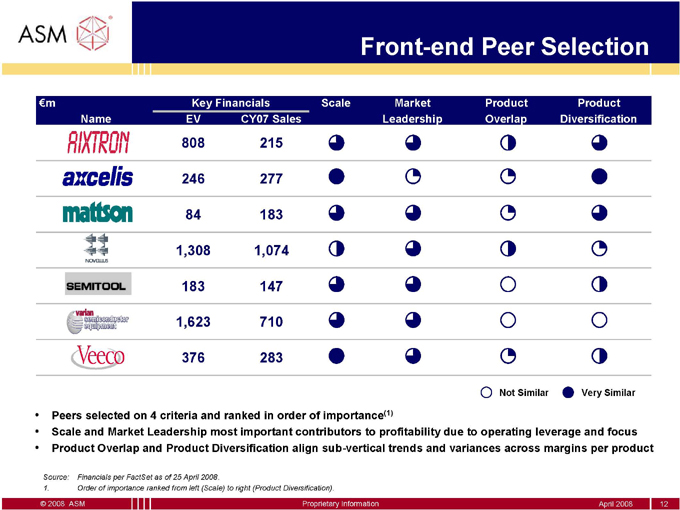

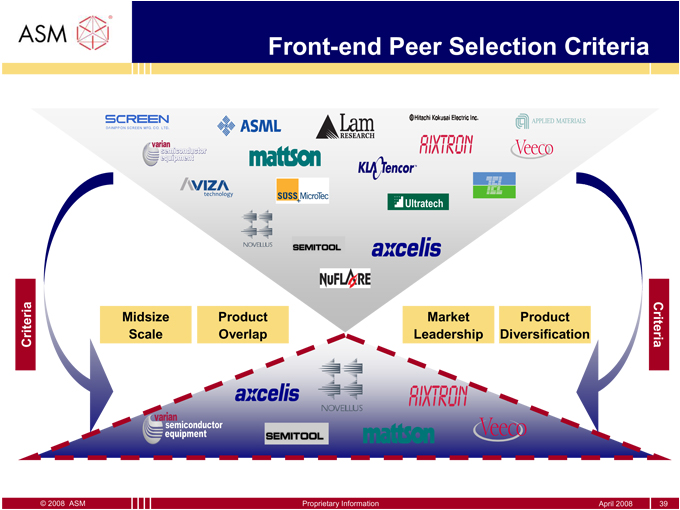

Front-end Peer Selection

€m Key Financials Scale Market Product Product Name EV CY07 Sales Leadership Overlap Diversification

808 215

246 277

84 183 1,308 1,074 183 147 1,623 710 376 283

Not Similar Very Similar

Peers selected on 4 criteria and ranked in order of importance(1)

Scale and Market Leadership most important contributors to profitability due to operating leverage and focus

Product Overlap and Product Diversification align sub-vertical trends and variances across margins per product

Source: Financials per FactSet as of 25 April 2008.

1. Order of importance ranked from left (Scale) to right (Product Diversification).

© 2008 ASM Proprietary Information April 2008 12

Agenda

Introduction

Current situation FE

Roadmap to peer profitability FE in 2009

Concluding remarks

Appendix

FE and BE convergence

Peer selection criteria

© 2008 ASM

Proprietary Information

April 2008

13

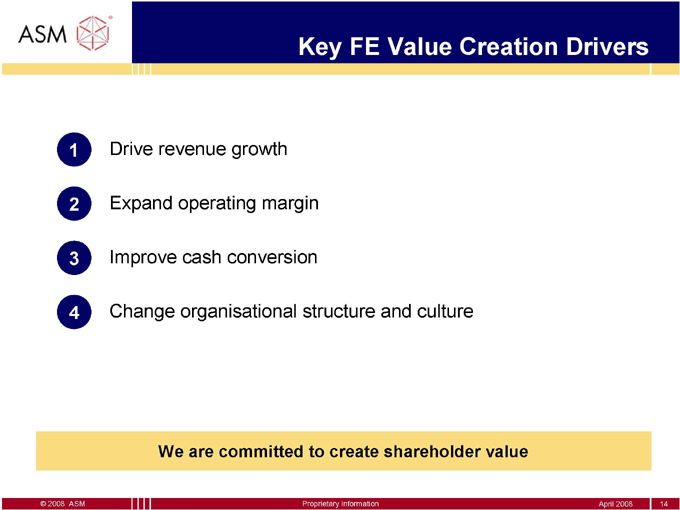

Key FE Value Creation Drivers

1. Drive revenue growth

2. Expand operating margin

3. Improve cash conversion

4. Change organisational structure and culture

We are committed to create shareholder value

© 2008 ASM

Proprietary Information

April 2008

14

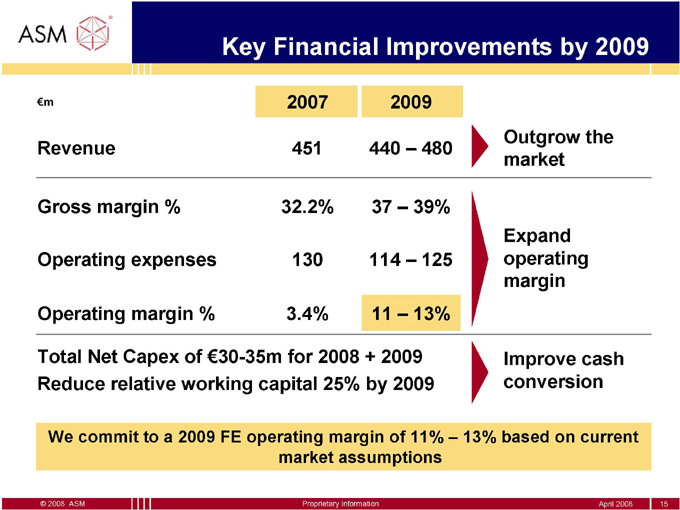

Key Financial Improvements by 2009

€m 2007 2009

Outgrow the Revenue 451 440 – 480 market

Gross margin % 32.2% 37 – 39%

Expand Operating expenses 130 114 – 125 operating margin

Operating margin % 3.4% 11 – 13%

Total Net Capex of €30-35m for 2008 + 2009 Improve cash Reduce relative working capital 25% by 2009 conversion

We commit to a 2009 FE operating margin of 11% – 13% based on current market assumptions

© 2008 ASM

Proprietary Information

April 2008

15

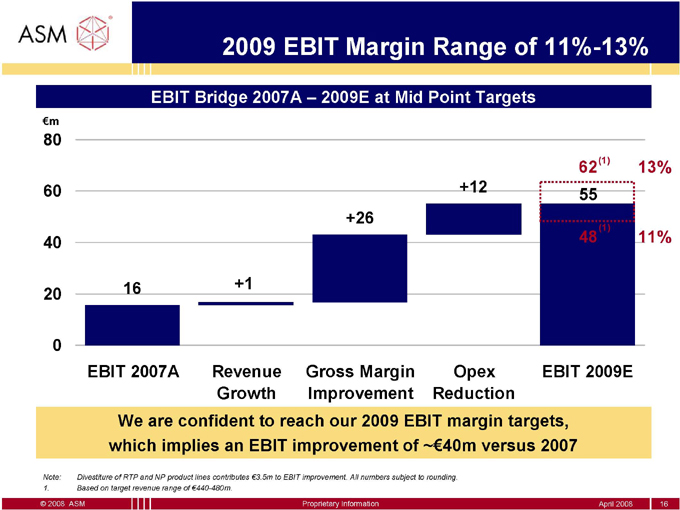

2009 EBIT Margin Range of 11%-13%

EBIT Bridge 2007A – 2009E at Mid Point Targets

€m

80

(1) |

|

62 13%

60 +12

55 +26 (1)

40 48 11%

16 +1 20

0

EBIT 2007A Revenue Gross Margin Opex EBIT 2009E Growth Improvement Reduction

We are confident to reach our 2009 EBIT margin targets, which implies an EBIT improvement of ~€40m versus 2007

Note: Divestiture of RTP and NP product lines contributes €3.5m to EBIT improvement. All numbers subject to rounding.

1. Based on target revenue range of €440-480m.

© 2008 ASM Proprietary Information April 2008 16

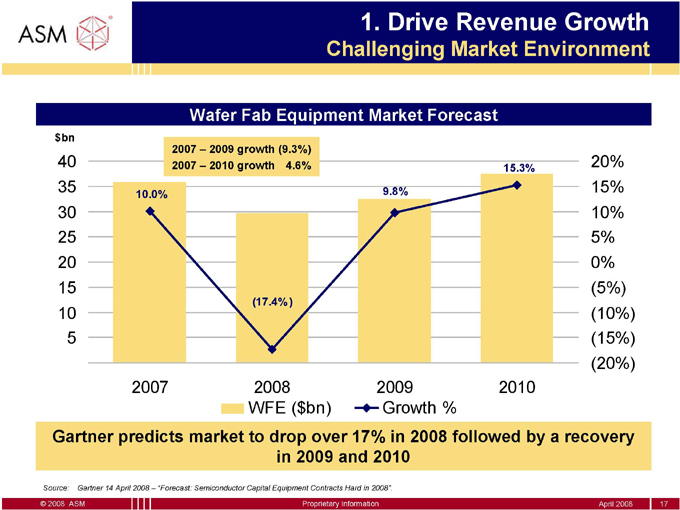

1. Drive Revenue Growth

Challenging Market Environment

Wafer Fab Equipment Market Forecast

$bn

2007 – 2009 growth (9.3%)

40 2007 – 2010 growth 4.6% 15.3% 20%

35 9.8% 15%

10.0%

30 10%

25 5%

20 0%

15 (5%)

(17.4% )

10 (10%)

5 |

| (15%) |

(20%)

2007 2008 2009 2010

WFE ($bn) Growth %

Gartner predicts market to drop over 17% in 2008 followed by a recovery in 2009 and 2010

Source: Gartner 14 April 2008 – “Forecast: Semiconductor Capital Equipment Contracts Hard in 2008”.

© 2008 ASM Proprietary Information April 2008 17

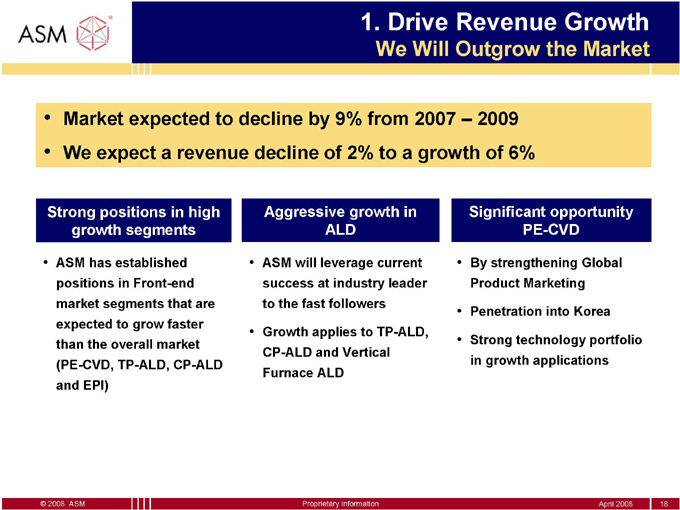

1. Drive Revenue Growth

We Will Outgrow the Market

Market expected to decline by 9% from 2007 – 2009

We expect a revenue decline of 2% to a growth of 6%

Strong positions in high growth segments

ASM has established positions in Front-end market segments that are expected to grow faster than the overall market (PE-CVD, TP-ALD, CP-ALD and EPI)

Aggressive growth in ALD

ASM will leverage current success at industry leader to the fast followers

Growth applies to TP-ALD, CP-ALD and Vertical Furnace ALD

Significant opportunity PE-CVD

By strengthening Global Product Marketing

Penetration into Korea

Strong technology portfolio in growth applications

© 2008 ASM

Proprietary Information

April 2008

18

1. Change of

Sales Organization

2. Appointment

VP Global Sales & Service

3 |

| Focus and Penetration |

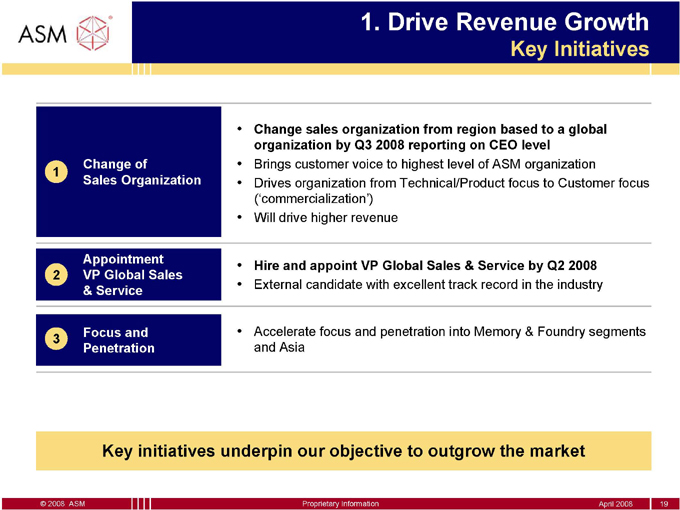

1. Drive Revenue Growth

Key Initiatives

Change sales organization from region based to a global organization by Q3 2008 reporting on CEO level

Brings customer voice to highest level of ASM organization

Drives organization from Technical/Product focus to Customer focus (‘commercialization’)

Will drive higher revenue

Hire and appoint VP Global Sales & Service by Q2 2008

External candidate with excellent track record in the industry

Accelerate focus and penetration into Memory & Foundry segments and Asia

Key initiatives underpin our objective to outgrow the market

© 2008 ASM

Proprietary Information

April 2008

19

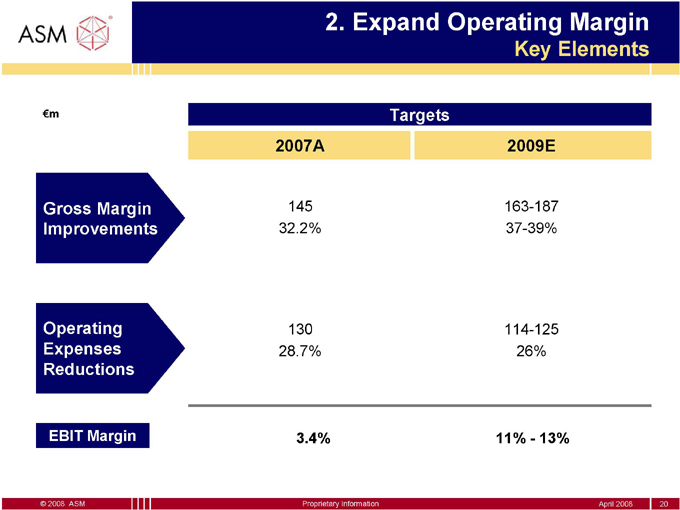

2. Expand Operating Margin

Key Elements

€m Targets

2007A 2009E

Gross Margin 145 163-187 Improvements 32.2% 37-39%

Operating 130 114-125 Expenses 28.7% 26% Reductions

EBIT Margin

3.4%

11%—13%

© 2008 ASM

Proprietary Information

April 2008

20

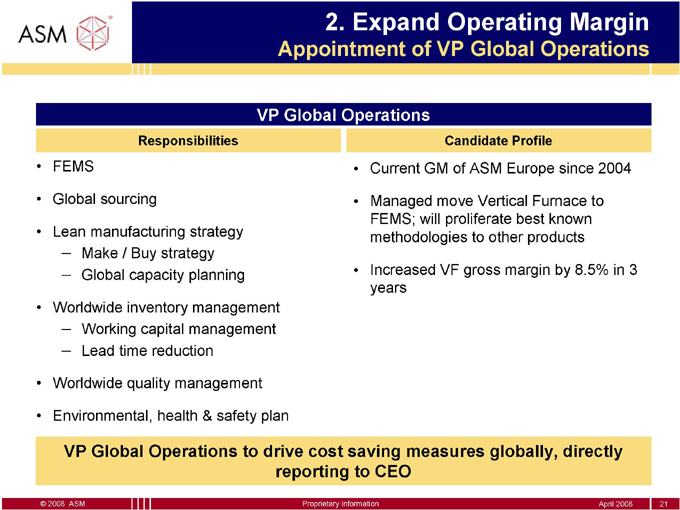

2. Expand Operating Margin

Appointment of VP Global Operations

VP Global Operations

Responsibilities

FEMS

Global sourcing

Lean manufacturing strategy

Make / Buy strategy

Global capacity planning

Worldwide inventory management

Working capital management

Lead time reduction

Worldwide quality management

Environmental, health & safety plan

•

•

•

Candidate Profile

Current GM of ASM Europe since 2004

Managed move Vertical Furnace to FEMS; will proliferate best known methodologies to other products

Increased VF gross margin by 8.5% in 3 years

VP Global Operations to drive cost saving measures globally, directly reporting to CEO

© 2008 ASM

Proprietary Information

April 2008

21

2. Expand Operating Margin

Gross Margin – FEMS

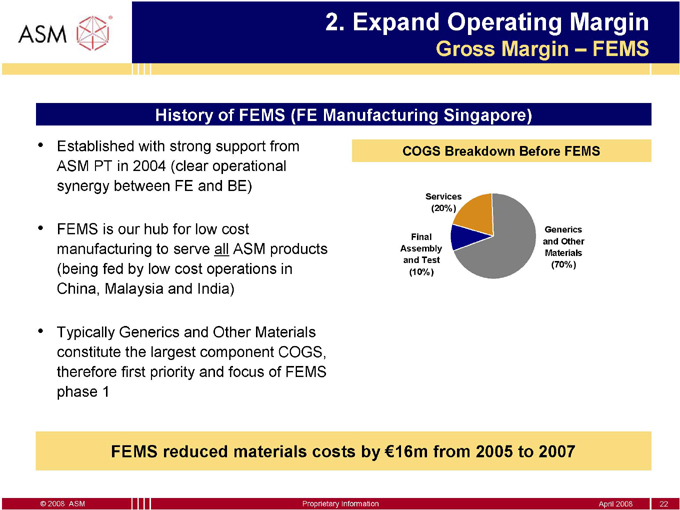

History of FEMS (FE Manufacturing Singapore)

Established with strong support from ASM PT in 2004 (clear operational synergy between FE and BE)

FEMS is our hub for low cost manufacturing to serve all ASM products (being fed by low cost operations in China, Malaysia and India)

Typically Generics and Other Materials constitute the largest component COGS, therefore first priority and focus of FEMS phase 1

COGS Breakdown Before FEMS

Services (20% )

Generics Final and Other Assembly Materials and Test (70% ) (10% )

FEMS reduced materials costs by €16m from 2005 to 2007

© 2008 ASM

Proprietary Information

April 2008

22

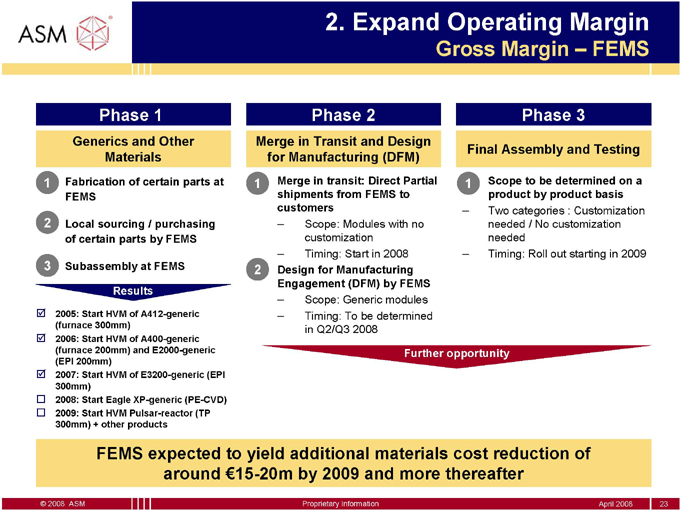

Phase 1

Generics and Other Materials

• Fabrication of certain parts at FEMS

• Local sourcing / purchasing of certain parts by FEMS

• Subassembly at FEMS

Results

2005: Start HVM of A412-generic (furnace 300mm)

2006: Start HVM of A400-generic (furnace 200mm) and E2000-generic (EPI 200mm)

2007: Start HVM of E3200-generic (EPI 300mm)

2008: Start Eagle XP-generic (PE-CVD)

2009: Start HVM Pulsar-reactor (TP 300mm) + other products

2. Expand Operating Margin

Gross Margin – FEMS

•2 |

| Design for Manufacturing |

Engagement (DFM) by FEMS

– Scope: Generic modules

– Timing: To be determined

in Q2/Q3 2008

Further opportunity

FEMS expected to yield additional materials cost reduction of around €15-20m by 2009 and more thereafter

© 2008 ASM

Proprietary Information

April 2008

23

Phase 2

Merge in Transit and Design for Manufacturing (DFM)

•1 |

| Merge in transit: Direct Partial shipments from FEMS to customers |

– Scope: Modules with no customization

– Timing: Start in 2008

Phase 3

Final Assembly and Testing

•1 |

| Scope to be determined on a product by product basis |

– Two categories : Customization needed / No customization needed

– Timing: Roll out starting in 2009

2. Expand Operating Margin

Gross Margin – Global Sourcing

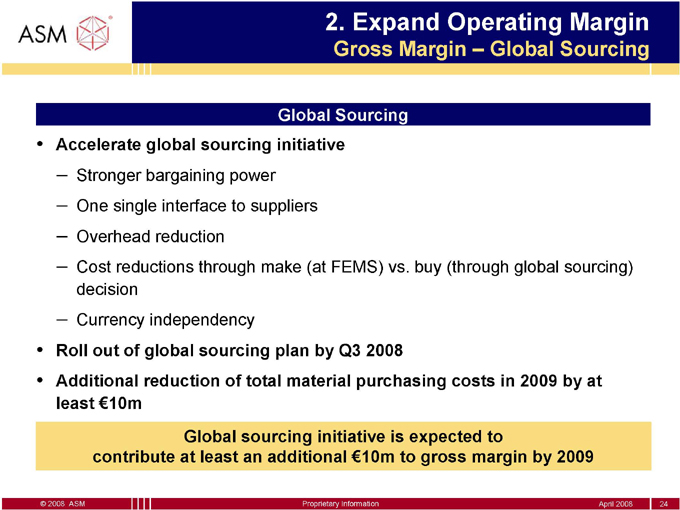

Global Sourcing

Accelerate global sourcing initiative

Stronger bargaining power

One single interface to suppliers

Overhead reduction

Cost reductions through make (at FEMS) vs. buy (through global sourcing) decision

Currency independency

Roll out of global sourcing plan by Q3 2008

Additional reduction of total material purchasing costs in 2009 by at least €10m

Global sourcing initiative is expected to contribute at least an additional €10m to gross margin by 2009

© 2008 ASM

Proprietary Information

April 2008

24

2. Expand Operating Margin

Gross Margin – Platform Consolidation

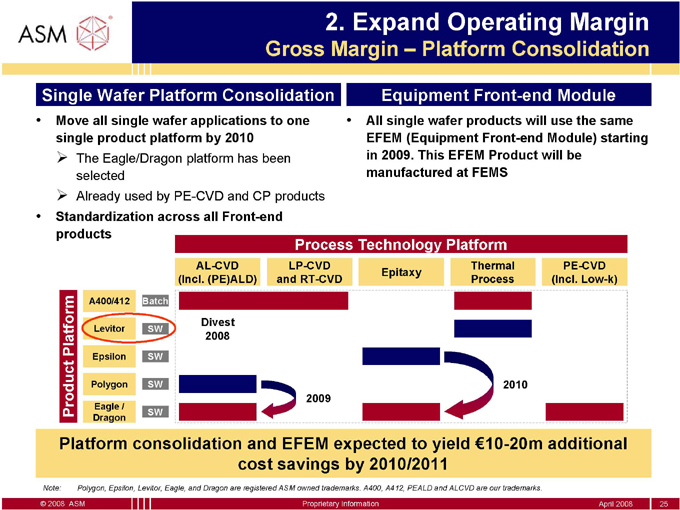

Single Wafer Platform Consolidation Equipment Front-end Module

• Move all single wafer applications to one • All single wafer products will use the same single product platform by 2010 EFEM (Equipment Front-end Module) starting

3 |

| The Eagle/Dragon platform has been in 2009. This EFEM Product will be selected manufactured at FEMS |

3 |

| Already used by PE-CVD and CP products |

• Standardization across all Front-end products

Process Technology Platform

AL-CVD LP-CVD Thermal PE-CVD Epitaxy (Incl. (PE)ALD) and RT-CVD Process (Incl. Low-k)

A400/412 Batch

Divest

Platform Levitor SW 2008 Epsilon SW

Polygon SW 2010

2009

Eagle /

Product SW

Dragon

Platform consolidation and EFEM expected to yield €10-20m additional cost savings by 2010/2011

Note: Polygon, Epsilon, Levitor, Eagle, and Dragon are registered ASM owned trademarks. A400, A412, PEALD and ALCVD are our trademarks.

© 2008 ASM Proprietary Information April 2008 25

2. Expand Operating Margin

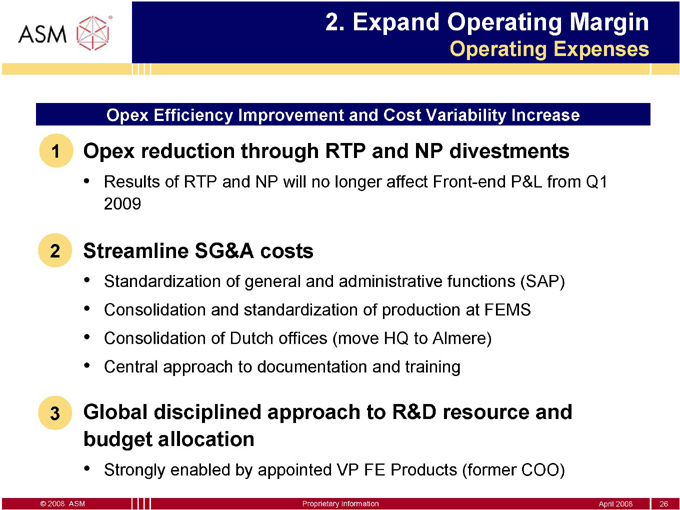

Operating Expenses

Opex Efficiency Improvement and Cost Variability Increase

1 |

| Opex reduction through RTP and NP divestments |

Results of RTP and NP will no longer affect Front-end P&L from Q1 2009

2 |

| Streamline SG&A costs |

Standardization of general and administrative functions (SAP)

Consolidation and standardization of production at FEMS

Consolidation of Dutch offices (move HQ to Almere)

Central approach to documentation and training

3 |

| Global disciplined approach to R&D resource and |

budget allocation

• Strongly enabled by appointed VP FE Products (former COO)

© 2008 ASM

Proprietary Information

April 2008

26

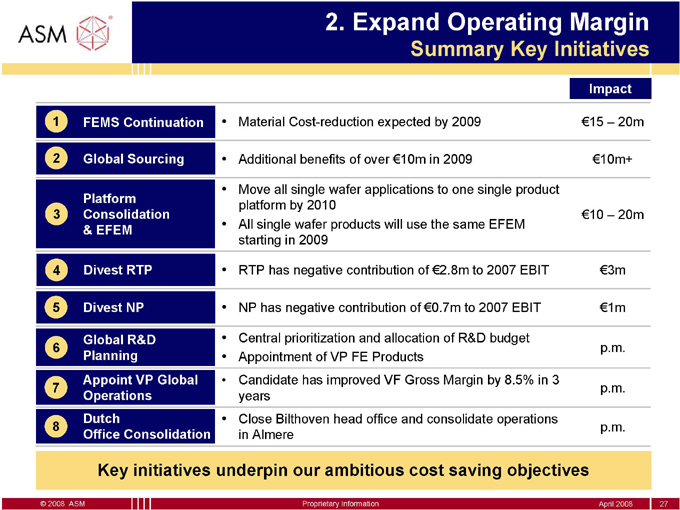

2. Expand Operating Margin

Summary Key Initiatives

Impact

1 |

| FEMS Continuation • Material Cost-reduction expected by 2009 €15 – 20m |

2 |

| Global Sourcing • Additional benefits of over €10m in 2009 €10m+ |

Platform • Move all single wafer applications to one single product

3 |

| Consolidation platform by 2010 €10 – 20m |

• All single wafer products will use the same EFEM

& EFEM starting in 2009

4 |

| Divest RTP • RTP has negative contribution of €2.8m to 2007 EBIT €3m |

5 |

| Divest NP • NP has negative contribution of €0.7m to 2007 EBIT €1m |

6 Global R&D • Central prioritization and allocation of R&D budget p.m. Planning • Appointment of VP FE Products Appoint VP Global • Candidate has improved VF Gross Margin by 8.5% in 3 7 p.m.

Operations years

Dutch • Close Bilthoven head office and consolidate operations

8 |

| p.m. |

Office Consolidation in Almere

Key initiatives underpin our ambitious cost saving objectives

© 2008 ASM

Proprietary Information

April 2008

27

2. Expand Operating Margin

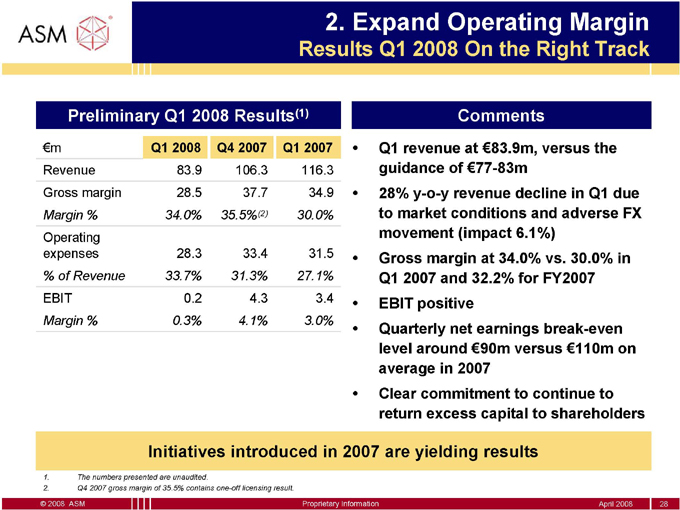

Results Q1 2008 On the Right Track

Preliminary Q1 2008 Results(1)

€m Q1 2008 Q4 2007 Q1 2007

Revenue 83.9 106.3 116.3

Gross margin 28.5 37.7 34.9

Margin % 34.0% 35.5%(2) 30.0%

Operating expenses 28.3 33.4 31.5

% of Revenue 33.7% 31.3% 27.1%

EBIT 0.2 4.3 3.4

Margin % 0.3% 4.1% 3.0%

Comments

Q1 revenue at €83.9m, versus the guidance of €77-83m

28% y-o-y revenue decline in Q1 due to market conditions and adverse FX movement (impact 6.1%)

Gross margin at 34.0% vs. 30.0% in Q1 2007 and 32.2% for FY2007

EBIT positive

Quarterly net earnings break-even level around €90m versus €110m on average in 2007

Clear commitment to continue to return excess capital to shareholders

Initiatives introduced in 2007 are yielding results

The numbers presented are unaudited.

Q4 2007 gross margin of 35.5% contains one-off licensing result.

© 2008 ASM

Proprietary Information

April 2008

28

3. Improve Cash Conversion

Focus on Working Capital and Capex

1 |

| Working capital reduction |

End of 2009 relative working capital will be at least 25% lower compared to the end of 2007 3 positive impact on cash level in excess of €30m

2 |

| Capital efficiency |

Net capex not to exceed depreciation in 2008 and 2009

Net capex not to exceed 4% of revenue in 2008 and 2009

Total net capex for 2008 + 2009 not to exceed €30m—€35m

© 2008 ASM

Proprietary Information

April 2008

29

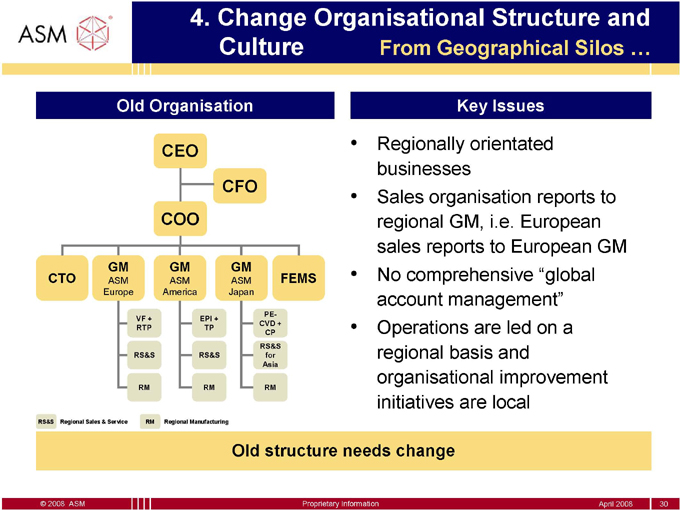

4. Change Organisational Structure and

Culture From Geographical Silos …

Old Organisation Key Issues

• Regionally orientated

CEO

businesses

CFO

• Sales organisation reports to COO regional GM, i.e. European sales reports to European GM

GM GM GM

CTO ASM ASM ASM FEMS • No comprehensive “global

Europe America Japan

account management”

PE-VF + EPI + CVD +

RTP TP • Operations are led on a

CP

RS&S

RS&S RS&S for regional basis and

Asia

organisational improvement

RM RM RM

initiatives are local

RS&S Regional Sales & Service RM Regional Manufacturing

Old structure needs change

© 2008 ASM

Proprietary Information

April 2008

30

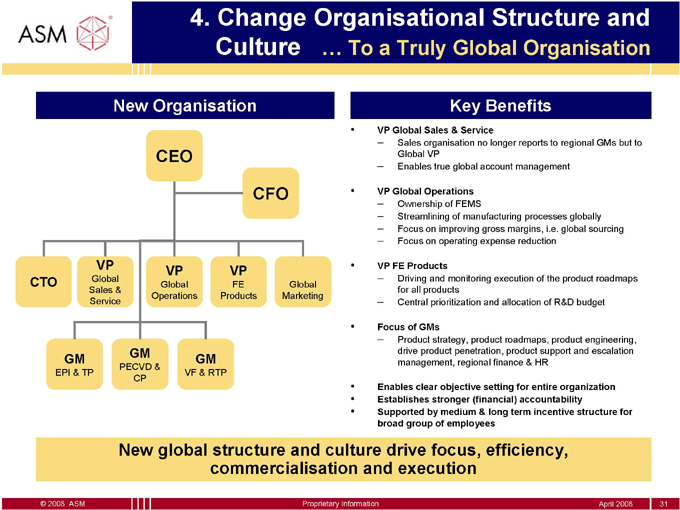

4. Change Organisational Structure and

Culture … To a Truly Global Organisation

New Organisation Key Benefits

• VP Global Sales & Service

??Sales organisation no longer reports to regional GMs but to CEO Global VP

??Enables true global account management

CFO • VP Global Operations

??Ownership of FEMS

??Streamlining of manufacturing processes globally

??Focus on improving gross margins, i.e. global sourcing

??Focus on operating expense reduction

VP • VP FE Products

Global VP VP ??Driving and monitoring execution of the product roadmaps CTO Global FE Global Sales & for all products Operations Products Marketing Service ??Central prioritization and allocation of R&D budget

• Focus of GMs

??Product strategy, product roadmaps, product engineering, GM GM GM drive product penetration, product support and escalation management, regional finance & HR

PECVD &

EPI & TP VF & RTP CP

• Enables clear objective setting for entire organization

• Establishes stronger (financial) accountability

• Supported by medium & long term incentive structure for broad group of employees

New global structure and culture drive focus, efficiency, commercialisation and execution

© 2008 ASM

Proprietary Information

April 2008

31

Agenda

Introduction

Current situation FE

Roadmap to peer profitability FE in 2009

Concluding remarks

Appendix

FE and BE convergence

Peer selection criteria

© 2008 ASM

Proprietary Information

April 2008

32

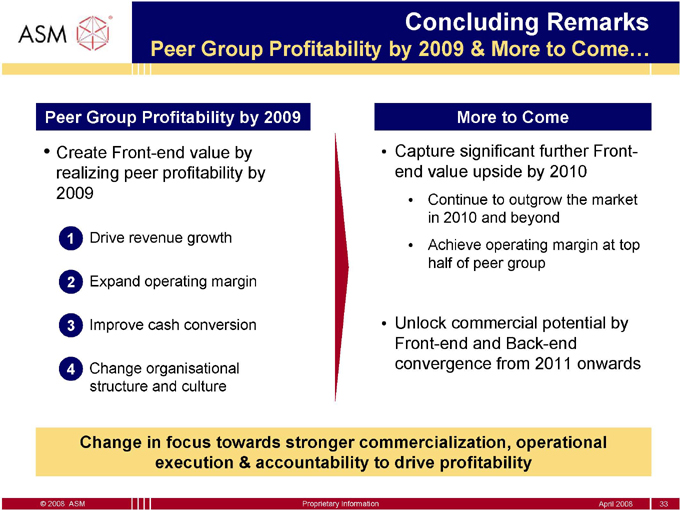

Concluding Remarks

Peer Group Profitability by 2009 & More to Come…

Peer Group Profitability by 2009 More to Come

• Create Front-end value by • Capture significant further Front-realizing peer profitability by end value upside by 2010 2009

• Continue to outgrow the market in 2010 and beyond 1 • Drive revenue growth

• Achieve operating margin at top half of peer group 2 • Expand operating margin

3 • Improve cash conversion • Unlock commercial potential by Front-end and Back-end 4 • Change organisational convergence from 2011 onwards

structure and culture

Change in focus towards stronger commercialization, operational execution & accountability to drive profitability

© 2008 ASM

Proprietary Information

April 2008

33

Agenda

Introduction

Current situation FE

Roadmap to peer profitability FE in 2009

Concluding remarks

Appendix

FE and BE convergence

Peer selection criteria

© 2008 ASM

Proprietary Information

April 2008

34

Convergence of FE and BE

Why 3D Integration?

Form Factor

Increases functionality per unit

Reduction of interconnect length improves device

Performance

speed and reduces power consumption

3D integration is less expensive than shrinking 2D Cost design rules, helped by the re-use of IP with improved modularity

3D technologies will enable performance, form factor and cost requirements to meet the demand of next generation devices

This requires integrated FE and BE process and manufacturing technologies

© 2008 ASM

Proprietary Information

April 2008

35

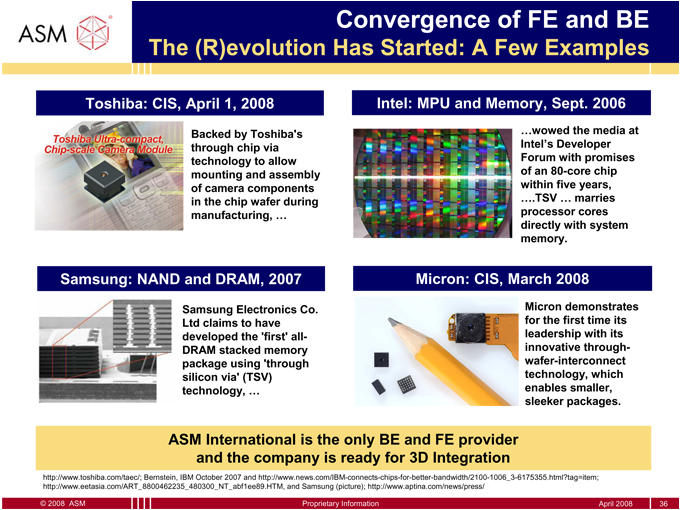

Convergence of FE and BE

The (R)evolution Has Started: A Few Examples

Toshiba: CIS, April 1, 2008 Intel: MPU and Memory, Sept. 2006

Backed by Toshiba’s …wowed the media at through chip via Intel’s Developer technology to allow Forum with promises mounting and assembly of an 80-core chip of camera components within five years, in the chip wafer during ….TSV … marries manufacturing, … processor cores directly with system memory.

Samsung: NAND and DRAM, 2007 Micron: CIS, March 2008

Samsung Electronics Co. Micron demonstrates Ltd claims to have for the first time its developed the ‘first’ all- leadership with its DRAM stacked memory innovative through-package using ‘through wafer-interconnect silicon via’ (TSV) technology, which technology, … enables smaller, sleeker packages.

ASM International is the only BE and FE provider and the company is ready for 3D Integration

http://www.toshiba.com/taec/; Bernstein, IBM October 2007 and http://www.news.com/IBM-connects-chips-for-better-bandwidth/2100-1006_3-6175355.html?tag=item; http://www.eetasia.com/ART_8800462235_480300_NT_abf1ee89.HTM, and Samsung (picture); http://www.aptina.com/news/press/

© 2008 ASM

Proprietary Information

April 2008

36

Convergence of FE and BE

ASM is Best Structured for 3D Integration

Building synergy and common vision is critical as this market is still emerging

ASM is the only company that has Front-end and Back-end products unified in a single company. Competitors are only able to provide one side of the solution.

ASM to focus on:

Front-end equipment with low Back-end cost

Back-end equipment with Front-end technology

Both groups have strengths to address and facilitate the 3D integration market

Front-end

Wafer level BEOL process and equipment technology

Interface chemistry

ALCVD and plasma processing knowledge

Fab equipment market knowledge

Back-end

Die level process

Wafer and die handling and alignment

Low cost manufacturing platforms and infrastructure

Packaging market knowledge

© 2008 ASM

Proprietary Information

April 2008

37

Agenda

Introduction

Current situation FE

Roadmap to peer profitability FE in 2009

Concluding remarks

Appendix

FE and BE convergence

Peer selection criteria

© 2008 ASM

Proprietary Information

April 2008

38

Front-end Peer Selection Criteria

Ultratech

Midsize Product Market Product

Criteria Scale Overlap Leadership Diversification Criteria

© 2008 ASM Proprietary Information April 2008 39