UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

o Registration statement pursuant to Section 12(b) or 12(g) of the Securities Exchange Act of 1934

or

x Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2006

or

o Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

or

o Shell company report pursuant to section 13 or 15(d) of the securities Exchange Act of 1934

Date of event requiring this shell company report

For the transition period from to

Commission file number: 1-8382

AKTIEBOLAGET SVENSK EXPORTKREDIT

(Exact name of Registrant as Specified in Its Charter)

(SWEDISH EXPORT CREDIT CORPORATION)

(Translation of Registrant’s Name into English)

Kingdom of Sweden

(Jurisdiction of incorporation or organization)

Västra Trädgårdsgatan 11 B, Stockholm, Sweden

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

5.721% Redeemable Notes due 2020

(Title of Class)

Securities registered or to be registered pursuant to Section 12 (g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Medium-Term Notes Series D

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Class A shares | | 640,000 |

Class B shares | | 350,000 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

x Yes oNo

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

o Yes xNo

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o Non-accelerated filer x

Indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 o Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o Yes xNo

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

o Yes oNo

In this Report, unless otherwise specified, all amounts are expressed in Swedish kronor (“Skr”). See Item 3, “Key Information”, for a description of historical exchange rates and other matters relating to the Swedish kronor. On March 30, 2007, the exchange rate for into Swedish kronor per U.S. dollars based on the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York was Skr X.XXX per U.S. dollar. No representation is made that Swedish kronor amounts have been, could have been or could be converted into U.S. dollars at that rate.

INTRODUCTORY NOTES

In this Report, unless otherwise indicated, all descriptions and financial information relate to Aktiebolaget Svensk Exportkredit (Swedish Export Credit Corporation) (“SEK” or the “Company”) as a whole, and include both “SEK exclusive of the S-system” and the “State Support System” (the “S-system”), each of which is described in detail herein. In certain instances, information relating to the S-system on a stand-alone basis is provided separately.

SEK is a “public company” according to the Swedish Companies Act. A Swedish company, even if its shares are not listed on an exchange and are not publicly traded, may choose to declare itself a “public company”. Only public debt companies are allowed to raise funds from the public through the issuance of debt instruments. In certain cases, a public company is required to add the denotation “publ” to its name.

FORWARD-LOOKING STATEMENTS

This Report contains forward-looking statements. In addition, the Company may make forward-looking statements in its periodic reports to the U.S. Securities and Exchange Commission (the “SEC”) on Form 6-K, in its annual and interim reports, offering circulars and prospectuses, press releases and other written information. The Board of Directors, officers and employees may also make oral forward-looking statements to third parties, including financial analysts. Forward-looking statements are statements that are not historical facts. Examples of forward-looking statements include:

· financial projections and estimates and their underlying assumptions;

· statements regarding plans, objectives and expectations relating to future operations and services;

· statements regarding the impact of regulatory initiatives on the Company’s operations;

· statements regarding general industry and macroeconomic growth rates and the Company’s performance relative to them; and

· statements regarding future performance.

Forward-looking statements generally are identified by the words “expect”, “anticipate”, “believe”, “intend”, “estimate”, “should”, and similar expressions.

Forward-looking statements are based on current plans, estimates and projections, and therefore you should not place too much reliance on them. Forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update any forward-looking statement in light of new information or future events, although the Company intends to continue to meet its ongoing disclosure obligations under the U.S. securities laws (such as the obligations to file annual reports on Form 20-F and reports on Form 6-K) and under other applicable laws. Forward-looking statements involve inherent risks and uncertainties, most of which are difficult to predict and generally beyond the Company’s control. You are cautioned that a number of important factors could cause actual results or outcomes to differ materially from those expressed in, or implied by, the forward-looking statements. These factors include, among others, the following:

· changes in general economic business conditions, especially in Sweden;

· changes and volatility in currency exchange and interest rates;

· dislocations in one or more segments of the financial markets; and

· changes in government policy and regulations and in political and social conditions.

ii

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not required as this 20-F is filed as an Annual Report.

Item 2. Offer Statistics and Expected Timetable

Not required as this 20-F is filed as an Annual Report.

1

Item 3. �� Key Information

a. General

The following selected financial data at and for the years ended December 31, 2006, 2005, 2004, 2003 and 2002 have been derived from SEK’s consolidated financial statements prepared in accordance with generally accepted accounting principles in Sweden (Swedish GAAP). SEK prepares its accounts in accordance with Swedish GAAP, which differs in significant respects from generally accepted accounting principles in the United States (U.S. GAAP). Information relating to the nature and effect of such differences is presented in Note 37 to the Consolidated Financial Statements.

The economic purpose of holding a derivative is consistently reflected in the accounting treatment under Swedish GAAP, both when applying deferral hedge accounting and when carried at fair value. Therefore, there is under Swedish GAAP no measurement or recognition inconsistency (sometimes referred to as an accounting mismatch or mixed measurement attributes) that would otherwise arise from measuring assets, liabilities or derivatives or recognizing the gains and losses on them on different bases.

Based on its experience and knowledge of the functioning of SEK’s economic hedging, management believes Swedish GAAP better reflects the effects of the economic hedge relationships on net income and shareholders’ funds. That is the case, for example, regarding the Skr 647.8 million positive adjustment in 2006, reflected in Note 37 to the Consolidated Financial Statements as a reconciling adjustment, to U.S. GAAP to shareholders’ funds as of year-end. It only applies because SEK did not qualify for hedge accounting under U.S. GAAP from January 1, 2001, until June 30, 2002. This amount is correctly presented based on the rules of SFAS 133, Accounting for Derivatives Instruments and Hedging Activities, but would not in management’s opinion have appeared under Swedish GAAP.

There are further significant differences between SEK’s net profit and shareholders’ funds calculated under Swedish GAAP as compared to these items calculated under U.S. GAAP. These differences arise primarily from the requirements of U.S. GAAP that (1) changes in the fair value of derivatives that are not part of a qualifying fair value hedge relationship are required to be recognized currently in the income statement while the contract which the derivative is economically hedging is carried at amortized cost and (2) changes in currency exchange rates affecting the fair value of foreign-currency instruments in the available-for-sale portfolio that are not eligible for hedge accounting are reported only as increases or decreases in shareholders’ funds, while the largely offsetting changes in the Swedish kronor position of the related funding must be recognized currently in the income statement.

The following information should be read in conjunction with the more detailed discussion contained in Item 5 “Operating and Financial Review and Prospects”.

Selected Financial Data

| | Year Ended December 31, | |

| | | | | | | | | | | |

(In Skr million, unless otherwise stated) | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

INCOME STATEMENT DATA | | | | | | | | | | | |

| | | | | | | | | | | |

Net interest revenues/(expenses): | | | | | | | | | | | |

SEK excluding the S-system | | 797.8 | | 759.1 | | 801.7 | | 757.5 | | 798.2 | |

S-system(A) | | (13.8 | ) | 48.9 | | 33.9 | | (67.5 | ) | (193.9 | ) |

| | | | | | | | | | | |

Operating profit | | 543.2 | | 498.1 | | 611.8 | | 595.3 | | 664.4 | |

| | | | | | | | | | | |

Net profit (Swedish GAAP) | | 385.6 | | 346.9 | | 439.6 | | 427.5 | | 479.7 | |

| | | | | | | | | | | |

After-tax return on equity (%) | | 10.5 | % | 10.6 | % | 14.9 | % | 13.6 | % | 14.0 | % |

Earnings per share (Swedish GAAP) (Skr) | | 389 | | 350 | | 444 | | 432 | | 485 | |

Dividend per share (Skr) (C) | | — | | — | | — | | 1,252 | | 364 | |

| | | | | | | | | | | |

Net profit (loss) (U.S. GAAP) (D) (E) | | 2,146.2 | | (1,537.9 | ) | 1,076.7 | | 643.2 | | 2,613.4 | |

Comprehensive income (U.S. GAAP) (G) | | 719.3 | | 283.9 | | 336.5 | | 70.9 | | 429.5 | |

2

Ratios of earnings to fixed charges (Swedish GAAP) (H) | | 1.09 | | 1.10 | | 1.14 | | 1.16 | | 1.16 | |

| | | | | | | | | | | |

Ratios of earnings to fixed charges (U.S. GAAP) (H) | | 1.48 | | 0.59 | | 1.34 | | 1.22 | | 1.96 | |

| | | | | | | | | | | |

Earnings (loss) per share (U.S. GAAP) (Skr) | | 2,168 | | (1,553 | ) | 1,088 | | 650 | | 2,640 | |

| | At December 31, | |

(Skr million) | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

BALANCE SHEET DATA | | | | | | | | | | | |

Total Credits Outstanding (I) | | 91,148.5 | | 78,147.4 | | 57,931.9 | | 60,870.5 | | 65,470.1 | |

| | | | | | | | | | | |

of which SEK excluding the S-system (I) | | 82,023.6 | | 67,808.1 | | 51,191.6 | | 53,140.5 | | 53,988.9 | |

| | | | | | | | | | | |

of which S-system (I) | | 9,124.9 | | 10,339.3 | | 6,740.3 | | 7,730.0 | | 11,481.2 | |

| | | | | | | | | | | |

Total assets | | 229,200.9 | | 207,493.2 | | 162,066.2 | | 151,800.5 | | 132,538.5 | |

| | | | | | | | | | | |

Total debt | | 209,535.1 | | 191,713.5 | | 143,895.3 | | 135,565.9 | | 114,838.2 | |

| | | | | | | | | | | |

of which subordinated debt | | 2,857.9 | | 3,254.9 | | 2,764.7 | | 3,001.0 | | 2,224.6 | |

| | | | | | | | | | | |

Deferred taxes related to untaxed reserves (B) | | 357.0 | | 370.7 | | 373.8 | | 376.5 | | 380.8 | |

| | | | | | | | | | | |

Shareholders’ funds (Swedish GAAP) (C) | | 4,124.3 | | 3,738.7 | | 3,391.8 | | 2,952.2 | | 3,764.7 | |

| | | | | | | | | | | |

Total liabilities and shareholders’ funds | | 229,200.9 | | 207,493.2 | | 162,066.2 | | 151,800.5 | | 132,538.5 | |

| | | | | | | | | | | |

Shareholders’ funds (U.S. GAAP) (D) (E) (F) | | 5,219.3 | | 4,500.0 | | 4,216.1 | | 3,879.6 | | 5,048.7 | |

(A) The difference between interest revenues, net commission revenues and any net foreign exchange gains related to lending and liquid assets under the S-system, on the one hand, and interest expenses related to borrowing, all financing costs and any net foreign exchange losses incurred by SEK under the S-system, on the other hand, is reimbursed by or, as applicable, paid to the Swedish State and, therefore, has no impact on operating profit or net profit.

(B) In accordance with Swedish GAAP, no untaxed reserves are reported in separate line items in the Consolidated Balance Sheet nor are changes in untaxed reserves reported in the Consolidated Income Statement. Instead, in the Consolidated Balance Sheet, the untaxed reserves are presented as (i) an after-tax portion, included in non-distributable capital, and (ii) a portion representing deferred taxes, reported as one component of allocations. (See Notes 25 and 27 to the Consolidated Financial Statements.)

(C) In connection with the sale of the Class B shares to the Swedish State on June 30, 2003, SEK paid a total dividend in 2003 of Skr 1,240 million solely to ABB Structured Finance Investment AB, the former holder of the Class B shares that represented approximately 35.5% of the Company’s share capital. There was no dividend paid in 2006, 2005 or 2004 to the Swedish State, which now owns all of the shares of SEK.

(D) The effect of SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities, and SFAS No. 138, Accounting for Certain Derivative Instruments and Certain Hedging Activities results in significant adjustments in computing net profit and shareholders’ funds according to U.S. GAAP. This is a result of having to mark at fair value in the balance sheet certain derivatives which do not qualify for hedge accounting. However, the variability in net income related to the instruments that qualify for hedge accounting is to some extent reduced because the Company is able to apply hedge accounting to certain assets and liabilities. (See Note 37 to the Consolidated Financial Statements.)

(E) SEK holds securities in a number of different currencies which are classified as available for sale for U.S. GAAP purposes. No net foreign exchange exposures arise from these holdings because, although the value of the assets in Swedish kronor terms changes according to the relevant exchange rates, there is an largely offsetting change in the Swedish kronor value of the related funding. Under Swedish GAAP both the assets and the liabilities are translated at closing exchange rates and the differences between historical book value and current value are reflected in foreign exchange effects in earnings, where they offset each other. This reflects the economic substance of

3

holding assets in a certain currency, financed by liabilities in that currency. However, under U.S. GAAP, the valuation effects of changes in currency exchange rates on the value of the investments classified as available for sale and not otherwise hedged by a derivative in a fair value hedging relationship are taken directly to equity whereas the offsetting changes in Swedish kronor terms of the borrowing are reflected in earnings. This leads to an accounting result which in management’s view does not reflect either the underlying risk position or the economics of the transactions. The result of the foregoing is that for the year 2006 SEK’s U.S. GAAP net profit reflects the addition, before tax effects, of Skr 2,302.9 million of foreign exchange difference on available-for-sale securities, which amount is not reflected in Swedish GAAP net profit (2005: deduction of Skr 2,617.9 million, 2004: addition of Skr 1,000.0 million). There is no difference in total shareholders’ funds between Swedish GAAP and U.S. GAAP as a result of this treatment (although there are differences in individual components of shareholders’ funds). (See Note 37 to the Consolidated Financial Statements.)

(F) At January 1, 2001, the carrying value of certain assets and liabilities that qualified for hedge accounting under previous U.S. GAAP standards was adjusted by Skr 1.6 billion with an offsetting recognition of the fair value of derivative instruments formerly designated in fair value type hedge relationships. Changes in the fair value of the previously designated derivatives are being recognized in income while the adjustment to the carrying value of the assets and liabilities is being accreted to income. The result of the foregoing is that for the year 2006 SEK’s U.S. GAAP shareholders’ funds reflects the addition of Skr 647.8 million before tax effects (2005: addition of Skr 819.7 million; 2004 addition of Skr 991.6 million). (See Note 37 to the Consolidated Financial Statements.)

(G) Comprehensive income (loss) (U.S. GAAP) comprises net profit (loss) (U.S. GAAP) and other comprehensive income (U.S. GAAP). (See Note 37 to the Consolidated Financial Statements.)

(H) For the purpose of calculating ratios of earnings to fixed charges, earnings consist of net profit for the year, plus taxes and fixed charges. Fixed charges consist of interest expenses, including borrowing costs, in SEK exclusive of the S-system.

(I) Amounts of credits as reported under the “old format”. The old format includes all credits — i.e., credits documented as interest-bearing securities (which are not included in the amounts reported as credits under the “new format”), as well as credits granted against traditional documentation. The amounts reported under the old format, in SEK’s opinion, reflect the real credit/lending volumes of SEK. The comments regarding lending volumes included in this report therefore refer to amounts based on the old format unless otherwise stated. (See Item 5c Operating and Financial Review and Prospects — Assets and Business Volume and Note 17 to the Consolidated Financial Statements.)

4

Foreign Exchange Rates

The Company publishes its financial statements in Swedish kronor (“Skr”). The following table sets forth for the years indicated certain information concerning the exchange rate for Swedish kronor as against the U.S. dollar (“USD”) based on the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York.

Calendar Year | | High | | Low | | Average(A) | | Period End | |

2007 | | 7.1060 | | 6.7818 | | 6.9823 | | 6.9837 | |

2006 | | 7.9656 | | 6.7674 | | 7.3098 | | 6.8342 | |

2005 | | 8.2434 | | 6.6855 | | 7.5170 | | 7.9370 | |

2004 | | 7.7725 | | 6.5939 | | 7.3480 | | 6.6687 | |

2003 | | 8.7920 | | 7.1950 | | 8.0351 | | 7.1950 | |

2002 | | 10.7290 | | 8.6950 | | 9.6571 | | 8.6950 | |

(A) The average of the exchange rates on the last day of each month during the period.

The following table sets forth for the months indicated certain information concerning the exchange rate for Swedish kronor as against the U.S. dollar based on the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York.

One-Month Period Ended | | High | | Low | |

March 31, 2007 | | 7.1060 | | 6.9622 | |

February 28, 2007 | | 7.0823 | | 6.9436 | |

January 31, 2007 | | 7.0829 | | 6.7818 | |

December 31, 2006 | | 6.9204 | | 6.7674 | |

November 30, 2006 | | 7.2096 | | 6.8331 | |

October 31, 2006 | | 7.4200 | | 7.2111 | |

September 30, 2006 | | 7.3450 | | 7.2410 | |

The noon buying rate on March 30, 2007 was USD 1 = Skr 6.9837

No representation is made that Swedish kronor amounts have been, could have been or could be converted into U.S. dollars at the foregoing rates on any of the dates indicated.

5

d. Risk factors

SEK’s financial performance is affected by borrower and counterparty credit quality and general economic conditions.

Risks arising from the credit quality of borrowers and counterparties and the recoverability of loans and amounts due from counterparties in derivative transactions are inherent in SEK’s businesses. Adverse changes in the credit quality of SEK’s borrowers and counterparties or a general deterioration in the economic conditions, or arising from systemic risks in the financial systems could affect the recoverability and value of its assets and require an increase in SEK’s provision for bad and doubtful debts and other provisions. SEK has developed guidelines to mitigate and manage these risks, which mainly entail the strict selection of borrowers and counterparties and the use of guarantees and credit derivatives. Over-the-counter derivative transactions under ISDA Master Agreements are only entered into with the provision of collateral or mark-to-market agreements.

A credit-rating downgrade may substantially reduce SEK’s earnings.

The Company is dependent on access to the international capital markets to fund its capital requirements. The cost and availability of financing is generally dependent on SEK’s credit rating. The Company currently has favorable credit ratings from various credit rating agencies. The Company’s credit rating depends on many factors, some of which are outside of its control. Factors that are significant in determining SEK’s credit ratings or that otherwise could affect its ability to raise financing include ownership structure, asset quality, liquidity profile, capital ratios, prudent banking, government support and public policy role. A deterioration in any of these factors or combination of these factors may lead rating agencies to downgrade SEK’s credit rating. If the Company was to receive a downgrade in its credit rating, it would likely become necessary to offer increased interest rates in the capital markets in order to obtain financing, which would likely substantially lower the Company’s profit margins and earnings and negatively affect the Company’s business.

Reduced accessibility to the international capital markets at a desired interest rate could lower SEK’s profit margins.

Any situation that impairs the Company’s access to the capital markets or increases the cost of financing could have a negative effect on its profit margin. For instance, the Company must compete with domestic and foreign financial institutions in the capital markets for financing. This competition could raise the cost of financing to the Company by forcing it to offer higher interest rates in order to attract investors.

Changes in interest rates may reduce SEK’s earnings.

Increases in interest rates may force the Company to respond by offering higher interest rates to investors when seeking financing in the capital markets. Furthermore, market conditions may result in lower interest rates on loans extended by the Company and on its investments. Any decrease in the average interest income on SEK’s assets relative to the average interest expense on its liabilities will reduce the Company’s net income. In recent years there has been a decline in the Company’s average margin on debt-financed assets as well as in the earnings on the investment of its equity capital.

SEK’s hedging strategies may not prevent losses.

SEK is constantly attempting to manage interest rate, currency, credit and other market-related risks, as well as refinancing risks. If any of the variety of instruments and strategies the Company uses to hedge its exposure to these various types of risk is not effective, the Company may incur losses. The Company may not be able to obtain economically efficient hedging opportunities that will enable it to carry on its present policies with respect to new assets and liabilities.

Fluctuations in foreign currency exchange rates could harm SEK’s profit margins.

As an international lending institution, the Company is subject to currency risk. The Company’s earnings may fluctuate due to currency translations, and changes in currency exchange rates adverse to the Company could cause a reduction in profits.

Additionally, as the Company’s financial statements are reported in Swedish kronor, a majority of the items presented in the balance sheet are subject to fluctuations as a result of changes in the U.S. dollar/Swedish kronor and the euro/Swedish kronor exchange rate. Even though the Company is carefully

6

monitoring and hedging its foreign currency exposures changes in currency exchange rates adverse to the Company could cause a reduction in profits. Also, a strengthening of the kronor against other currencies may reduce demand for the products of SEK’s customers and thus reduce demand for its loans.

Increasing competition may adversely affect SEK’s income and business.

Competition in the Company’s business is based on service, product innovation, product features, price, commission structure, financial strength and name recognition. The Company competes with a large number of other credit institutions, including domestic and foreign banks. Some of these institutions offer a broader array of products, have more competitive pricing and may have greater financial resources with which to compete. Increasing competition may have significant negative effects on the Company’s results if the Company is unable to match the products and services of its competitors.

Operational risks are inherent in SEK’s businesses.

SEK’s businesses are dependent on the ability to process complex transactions efficiently and accurately. Operational risk and losses can result from fraud, errors by employees, failure to document transactions properly or to obtain proper internal authorization, equipment failures, natural disasters or the failure of external systems, for example, those of SEK’s suppliers or counterparties. The extensive risk management conducted by SEK is often complicated and therefore leads to additional operational risk that is minimized in a corresponding manner. There is also a risk that SEK’s reputation will be damaged if SEK fails to comply with current legislation and best practice or in another manner fails to meet its commitments, even those that are not explicit. Although such risks are reduced through active efforts relating to risk culture, compliance with regulations and corporate governance, it is only possible to be reasonably, but not absolutely, certain that such procedures will be effective in controlling each of the operational risks.

SEK’s business is subject to regulation and regulatory oversight. Any significant regulatory developments could have an effect on how SEK conducts its business and on SEK’s results of operations.

SEK is subject to financial services laws, regulations, administrative actions and policies in each location in which SEK operates. This supervision and regulation, in particular in Sweden, if changed could materially affect SEK’s business, the products and services it offers or the value of its assets.

Item 4. Information on the Company

a. General

SEK is a public stock corporation organized under the Swedish Companies Act. It is wholly-owned by the Swedish State through the Ministry of Foreign Affairs (“Sweden” or the “State”).

SEK was founded in 1962 in order to strengthen the competitiveness of the Swedish export industry by meeting the need for long-term credits. SEK’s objective is to engage in financing activities in accordance with the Swedish Banking and Financing Business Act and in connection therewith primarily to promote the development of Swedish commerce and industry as well as otherwise engage in Swedish and international financing activities on commercial grounds.

SEK provides long-term sustainable financial solutions for the private and public sectors with the aim of promoting the development and international competitiveness of Swedish industry and trade. SEK’s mission is to secure access to financial solutions for export and infrastructure. Business activities include export credits, lending, structured financing, project financing, leasing, capital market products and financial advisory services. SEK offers its solutions to corporations and financial institutions as well as domestic and international investors. SEK extends credits, or loans, on commercial terms at prevailing fixed or floating market rates of interest in “SEK exclusive of the S-system”, and credits on State-supported terms at fixed rates of interest that may be lower than prevailing fixed market rates in the “State Support System” (the “S-system”). The S-system is administered on behalf of the State by SEK against compensation.

From its roots and base in export credits, SEK’s product range has expanded to promote the development of Swedish commerce and industry and the Swedish export industry. Over the years, SEK has

7

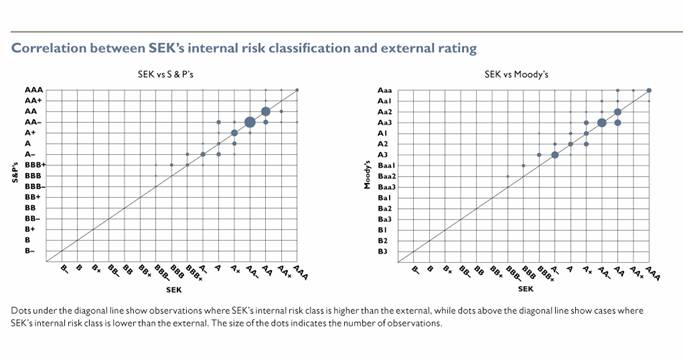

been active in the creation of new financial solutions. SEK’s clear niche specialization in long-term financial products, combined with its financial capacity and flexible organization, are key factors in the management of its operations. SEK’s borrowing activities in the international capital markets have given SEK expertise in financial instruments, an expertise that has earned international awards from financial publications on several occasions. This experience, together with maintaining credit quality and credit ratings (as of March 2007: AA+ from Standard & Poors and Aa1 from Moody’s Investors Service), has allowed SEK to offer its customers tailored products and what SEK believes are highly competitive terms.

SEK has intensified the broadening of both its range of services and customer base in recent years in response to changes in demand and the opportunities created by the development of new forms of cooperation and financial instruments. Among other things SEK has increased its financing of infrastructure projects with Swedish regional and local authorities, with the aim of supporting the development and competitiveness of Swedish commerce and industry. SEK also intermediates capital market products to third party investors, and has also to a greater extent become involved as a financial advisor for international projects. The expansion of SEK’s services and customer base reflects SEK’s efforts to become a broader-range finance house with specialists in certain areas, while continuing to emphasize its traditional role as a long-term lender.

The increasing integration of business in the Nordic countries is consistent with SEK’s goal of having a position in the Nordic countries within its niche: long-term financial solutions. SEK has a representative office in Helsinki, which, with its focus on major Finnish companies and local authorities, furthers this development. The operations in Helsinki are important for strengthening SEK’s position in the Nordic market.

Since the early 1990s, SEK has been involved in Sweden’s fast-growing trade with the countries in the Baltic region. The overall goal is to contribute to a continued positive economic development in the region, while strengthening the presence of Swedish and other Nordic business. Within the framework of these activities there are also increased business opportunities that have been created by the enlargement in 2004 of the European Union to include new members from the Baltic region and Eastern Europe.

SEK’s relationship with domestic, Nordic and other international investors and partners strengthen its ability to develop financial solutions which meet its customers’ requirements. This network enables SEK to participate in co-financing arrangements and advisory assignments, as well as in benchmarking and cooperation in areas such as risk management and business systems.

The address of the Company’s principal executive office is AB Svensk Exportkredit (Swedish Export Credit Corporation), Västra Trädgårdsgatan 11B, Stockholm, Sweden, and the Company’s telephone number is 011-46-8-613-8300. The Company’s authorized representative in the United States is the Consulate General of Sweden, One Dag Hammarskjöld Plaza, 885 Second Avenue, New York, NY 10017, and the telephone number is (212) 583-2550.

The following table summarizes SEK’s credits outstanding and debt outstanding at December 31, 2006, 2005 and 2004:

| | At December 31, | |

(Skr million) | | 2006 | | 2005 | | 2004 | |

| | | | | | | |

Total credits outstanding (old format)(A) | | 91,148 | | 78,147 | | 57,932 | |

Of which S-system | | 9,125 | | 10,339 | | 6,740 | |

| | | | | | | |

Total debt outstanding | | 209,535 | | 191,714 | | 143,895 | |

Of which S-system | | 6 | | 278 | | 526 | |

(A) Amounts of credits as reported under the “old format”. The old format includes all credits — i.e., credits documented as interest-bearing securities (which are not included in the amounts reported as credits under the “new format”), as well as credits granted against traditional credit agreement documentation. These amounts, in SEK’s opinion, reflect the real credit/lending volumes of SEK. The comments regarding lending volumes included in this report therefore refer to amounts based on the old format unless otherwise stated. (See also Note 17 to the Consolidated Financial Statements.)

8

b. Lending Operations — General

The following table sets forth certain data regarding the Company’s lending operations during the five-year period ended December 31, 2006:

| | Year ending December 31, | |

(Skr million) | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | | | | | | | | | |

Offers of long-term credits accepted (A) | | 56,923 | | 37,525 | | 22,748 | | 18,960 | | 13,365 | |

of which S-system (B) | | 8,537 | | 3,195 | | 2,619 | | 1,939 | | 172 | |

Total credit disbursements | | 24,022 | | 20,981 | | 11,459 | | 9,954 | | 7,896 | |

of which S-system | | 2,037 | | 4,493 | | 1,732 | | 1,032 | | 1,377 | |

Total credit repayments, including effects of currency translations | | 12,970 | | 6,878 | | 14,396 | | 17,334 | | 14,599 | |

of which S-system | | 3,306 | | 894 | | 2,721 | | 4,784 | | 5,357 | |

Total net increase / (decrease) in credits outstanding | | 12,741 | | 10,671 | | (8,050 | ) | 1,739 | | (6,478 | ) |

of which S-system | | (1,219 | ) | 3,603 | | (1,516 | ) | (3,238 | ) | (3,981 | ) |

| | | | | | | | | | | |

Credits outstanding at December 31: | | | | | | | | | | | |

Credits outstanding (old format)(A) | | 91,148 | | 78,147 | | 57,932 | | 60,870 | | 65,470 | |

of which S-system | | 9,125 | | 10,339 | | 6,740 | | 7,730 | | 11,481 | |

Credits outstanding (new format)(A) | | 56,134 | | 43,393 | | 32,722 | | 40,772 | | 39,033 | |

of which S-system | | 9,132 | | 10,351 | | 6,748 | | 8,264 | | 11,502 | |

Total credit commitments outstanding at December 31 | | 21,889 | | 15,114 | | 16,353 | | 14,358 | | 11,849 | |

of which S-system | | 14,163 | | 9,067 | | 10,226 | | 10,025 | | 10,124 | |

(A) Amounts of credits reported under the “old format” include all credits — i.e., credits granted against documentation in the form of interest-bearing securities (which are not included in the credits reported as credits under the “new format”), as well as credits granted against traditional credit agreement documentation. Amounts of credits under new format includes credits granted against traditional credit agreement documentation, deposits with banks and states, repurchase agreements, and cash on demand. Credits under new format is a presentation in accordance with Swedish GAAP, while credits under old format is a non-GAAP presentation. Amounts reported under the old format, in SEK’s opinion, reflect the real credit/lending volumes of SEK. SEK views credits granted against documentation in the form of interest-bearing securities as real credit volumes, while deposits with banks and states, repurchase agreements, and cash on demand in SEK’s opinion is a part of liquidity volumes. The comments regarding lending volumes included in this report, therefore, refer to amounts based on the old format unless otherwise stated. (See also Item 5. c. “Operating and Financial Review and Prospects — Assets and Business Volume” and Note 17 to the Consolidated Financial Statements.)

(B) SEK offers S-system financing at CIRR (Commercial Interest Reference Rate) rates. The CIRR-rates for new credits are subject to periodic review and adjustment by the OECD. As described below under “—S-system”, the OECD Consensus stipulates that credit offers will be valid for acceptance during a period of not more than four months. Thereafter the CIRR rate can be locked in for a maximum period of six months in order for the credit agreement to be finalized. The attractiveness of an S-system credit offer is, therefore, dependent on the general movement of interest rates during the relevant four month period which is, in turn, a significant factor contributing to the year-to-year differences in offers of long-term credits accepted in the S-system.

Most of the credits granted by SEK are related to Swedish exports. Measured by revenues, the largest markets for the export of goods from Sweden are Western Europe and North America. However, exports to other, including less developed, markets are also important. Accordingly, the need for export financing may be related to transactions involving buyers in many different countries, with varying levels of creditworthiness. Pursuant to its counterparty risk exposure policy, SEK is selective in accepting any type of risk exposure. This policy seeks to ensure that SEK is neither dependent on the creditworthiness of individual buyers of Swedish goods and services, nor on the countries in which they are domiciled, but on the creditworthiness of individual counterparties to whom SEK accepts counterparty risk exposure.

9

The following table shows the geographic distribution of SEK’s credits outstanding and committed (old format) by domicile of borrower at December 31, 2006. The table further shows, by domicile and category, the related risk counterparties to whom SEK’s counterparty risk exposures are allocated when taking into account prevailing guarantees and collateral. The table at December 31, 2006 includes both credits outstanding and credits committed while the tables at December 31, 2005 and 2004 only include credits outstanding. The addition in 2006 of credits committed in the table is made to better reflect the geographical distribution of all credit related amounts, both outstanding and those that may in the near future be disbursed.

| | | | Domicile and category of the related counterparties, to whom SEK is risk exposed | |

| | | | Sweden | | Other Nordic Area | | Other Western Europe & U.S. | | Asia & Latin America (A) | |

at December 31, 2006 | | | | | | Govern- | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

(Skr billion) | | | | | | ment & | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Total | | | | Munici- | | | | Corpo- | | | | Govern- | | | | Corpo- | | | | Govern- | | | | Corpo- | | | | Govern- | | | | Corpo- | |

Domicile of SEK´s borrowers | | amount | | Sum | | palities | | Bank | | ration | | Sum | | ment | | Bank | | ration | | Sum | | ment | | Bank | | ration | | Sum | | ment | | Bank | | ration | |

Africa | | 1.5 | | 1.4 | | 1.4 | | | | | | | | | | | | | | 0.1 | | | | 0.1 | | | | | | | | | | | |

Asia | | 21.5 | | 12.9 | | 12.8 | | | | 0.1 | | 0.1 | | 0.1 | | | | | | 8.5 | | 7.9 | | 0.6 | | | | | | | | | | | |

Latin America | | 6.9 | | 3.4 | | 3.2 | | 0.2 | | | | | | | | | | | | 3.3 | | 2.5 | | 0.8 | | | | 0.2 | | | | | | 0.2 | |

North America | | 0.6 | | 0.2 | | 0.2 | | | | | | | | | | | | | | 0.4 | | | | | | 0.4 | | | | | | | | | |

Sweden | | 44.7 | | 41.7 | | 18.5 | | 15.9 | | 7.3 | | 0.4 | | 0.4 | | | | | | 2.3 | | 0.4 | | 1.7 | | 0.2 | | 0.3 | | | | | | 0.3 | |

Other Nordic Area | | 21.0 | | 0.7 | | | | 0.7 | | | | 18.7 | | 8.1 | | 5.3 | | 5.3 | | 1.6 | | | | 1.6 | | | | | | | | | | | |

Other Western Europe | | 13.8 | | 1.8 | | 1.8 | | | | | | | | | | | | | | 12.0 | | 7.4 | | 3.1 | | 1.5 | | | | | | | | | |

Baltic Area | | 0.7 | | | | | | | | | | | | | | | | | | 0.7 | | | | 0.7 | | | | | | | | | | | |

Other Eastern Europe | | 2.9 | | 1.3 | | 1.3 | | | | | | 0.3 | | 0.3 | | | | | | 1.1 | | 0.8 | | 0.3 | | | | 0.2 | | 0.2 | | | | | |

Total | | 113.6 | | 63.4 | | 39.2 | | 16.8 | | 7.4 | | 19.5 | | 8.9 | | 5.3 | | 5.3 | | 30.0 | | 19.0 | | 8.9 | | 2.1 | | 0.7 | | 0.2 | | 0.0 | | 0.5 | |

(A) SEK had insignificant credits outstanding in Asia & Latin America prior to 2006.

The following tables show the geographic distribution of SEK’s credits outstanding (old format) by domicile of borrower at December 31, 2005, and 2004. The tables further show, by domicile and category, the related risk counterparties to whom SEK’s counterparty risk exposures are allocated when taking into account prevailing guarantees and collateral.

| | | | Domicile and category of the related counterparties, to whom SEK is risk exposed | |

| | | | Sweden | | Other Nordic Area | | Other Western Europe & U.S. | |

at December 31, 2005 | | | | | | Govern- | | | | | | | | | | | | | | | | | | | | | |

Skr billion) | | | | | | ment & | | | | | | | | | | | | | | | | | | | | | |

Domicile of SEK´s

borrowers | | Total

amount | | Sum | | Muni-

cipalities | | Bank | | Corpo-

ration | | Sum | | Govern-

ment | | Bank | | Corpo-

ration | | Sum | | Govern-

ment | | Bank | | Corpo-

ration | |

Africa | | 1.5 | | 1.4 | | 1.4 | | | | | | | | | | | | | | 0.1 | | | | 0.1 | | | |

Asia | | 9.5 | | 5.2 | | 5.0 | | 0.1 | | 0.1 | | 0.3 | | 0.3 | | | | | | 4.0 | | 3.4 | | 0.6 | | | |

Latin America | | 5.9 | | 4.3 | | 4.0 | | 0.3 | | | | | | | | | | | | 1.6 | | 1.0 | | 0.4 | | 0.2 | |

North America | | 0.8 | | 0.2 | | 0.2 | | | | | | | | | | | | | | 0.6 | | | | 0.3 | | 0.3 | |

Sweden | | 36.8 | | 32.9 | | 12.0 | | 15.1 | | 5.8 | | 0.4 | | | | 0.4 | | | | 3.5 | | | | 3.2 | | 0.3 | |

Other Nordic Area | | 14.9 | | 0.1 | | 0.1 | | | | | | 12.6 | | 5.4 | | 4.5 | | 2.7 | | 2.2 | | | | 2.2 | | | |

Other Western Europe | | 6.9 | | 1.9 | | 1.9 | | | | | | | | | | | | | | 5.0 | | 1.1 | | 3.2 | | 0.7 | |

Baltic Area | | 0.4 | | | | | | | | | | | | | | | | | | 0.4 | | 0.3 | | 0.1 | | | |

Other Eastern Europe | | 1.4 | | 0.5 | | 0.5 | | | | | | 0.4 | | 0.4 | | | | | | 0.5 | | 0.4 | | 0.1 | | | |

Total | | 78.1 | | 46.5 | | 25.1 | | 15.5 | | 5.9 | | 13.7 | | 6.1 | | 4.9 | | 2.7 | | 17.9 | | 6.2 | | 10.2 | | 1.5 | |

10

| | | | Domicile and category of the related counterparties, towhom SEK is risk exposed | |

| | | | Sweden | | Other Nordic Area | | Other Western Europe & U.S. | |

at December 31, 2004 | | | | | | Govern- | | | | | | | | | | | | | | | | | | | | | |

Skr billion) | | | | | | ment & | | | | | | | | | | | | | | | | | | | | | |

Domicile of borrowers | | Total

amount | | Sum | | Muni-

cipalities | | Bank | | Corpo-

ration | | Sum | | Govern-

ment | | Bank | | Corpo-

ration | | Sum | | Govern-

ment | | Bank | | Corpo-

ration | |

Africa | | 1.5 | | 1.4 | | 1.4 | | | | | | | | | | | | | | 0.1 | | | | 0.1 | | | |

Asia | | 6.0 | | 4.7 | | 4.5 | | 0.1 | | 0.1 | | 0.5 | | 0.5 | | | | | | 0.8 | | 0.2 | | 0.6 | | | |

Latin America | | 3.0 | | 2.4 | | 2.2 | | 0.2 | | | | | | | | | | | | 0.6 | | 0.2 | | 0.4 | | | |

North America | | 0.8 | | 0.3 | | 0.3 | | | | | | | | | | | | | | 0.5 | | | | 0.1 | | 0.4 | |

Sweden | | 31.4 | | 27.0 | | 10.5 | | 10.3 | | 6.2 | | 0.1 | | | | 0.1 | | | | 4.3 | | | | 4.3 | | | |

Other Nordic Area | | 10.2 | | | | | | | | | | 8.1 | | 1.9 | | 3.1 | | 3.1 | | 21 | | | | 2.1 | | | |

Other Western Europe | | 4.1 | | | | | | | | | | | | | | | | | | 4.1 | | 0.7 | | 2.2 | | 1.2 | |

Baltic Area | | 0.0 | | | | | | | | | | | | | | | | | | 0.0 | | | | 0.0 | | | |

Other Eastern Europe | | 0.9 | | 0.5 | | 0.5 | | | | | | | | | | | | | | 0.4 | | 0.2 | | 0.2 | | | |

Total | | 57.9 | | 36.3 | | 19.4 | | 10.6 | | 6.3 | | 8.7 | | 2.4 | | 3.2 | | 3.1 | | 12.9 | | 1.3 | | 10.0 | | 1.6 | |

As most credits are supported by elements from more than one category, resulting in more than one party being responsible for the same payments to SEK, the above tables reflect the counterparty (either borrower or guarantor) that SEK believes to be the stronger credit.

SEK exclusive of the S-system

SEK exclusive of the S-system reports credits in the following categories:

1. Medium and long-term export financing of durable goods and services.

2. Lines of credit for the refinancing of finance companies’, banks’ and exporting companies’ portfolios of revolving export receivables. Refinancing of export leasing agreements and short-term export finance. Credits for direct market investments abroad that will promote exports of Swedish goods and services. Credits for research and development, to promote Swedish industry and commerce.

3. Credits for investments in infrastructure to promote Swedish industry and commerce.

SEK’s lending also includes financing in cooperation with intergovernmental organizations and foreign export credit agencies. (These credits are included under the relevant underlying type of credit).

The Company also extends export financing by establishing credit lines or protocols, principally with countries in Eastern Europe and Asia. (These credits are included under the relevant underlying type of credit).

11

Credits outstanding (exclusive of those under the S-System) at December 31, 2006, 2005 and 2004 were distributed among SEK’s various categories of credits as follows:

Credits outstanding, type of credits | | 2006 | | 2005 | | 2004 | |

(Skr million) | | | | | | | |

| | | | | | | |

Financing of capital goods exports | | 22,383 | | 14,082 | | 9,149 | |

Other export related credits | | 40,482 | | 37,880 | | 29,260 | |

Infrastructure | | 19,158 | | 15,846 | | 12,783 | |

Total | | 82,023 | | 67,808 | | 51,192 | |

Offers granted by the Company for credits that borrowers accepted (exclusive of those under the S-System) during the years ended December 31, 2006, 2005 and 2004 were distributed among SEK’s various categories of credits as follows:

Offers accepted, type of credit | | 2006 | | 2005 | | 2004 | |

(Skr million) | | | | | | | |

| | | | | | | |

Financing of capital goods exports | | 16,136 | | 7,767 | | 4,171 | |

Other export related credits | | 16,499 | | 15,858 | | 10,178 | |

Infrastructure | | 15,751 | | 10,705 | | 5,781 | |

Total | | 48,386 | | 34,330 | | 20,130 | |

A long-term trend has been the reduction in importance of the traditional financing of durable goods in Sweden’s export industry. SEK’s services have therefore changed over time to meet customers’ needs. This means that a credit granted could be either in the form of capital goods export financing or another category of export related credits such as direct lending to export companies through acquisitions of securities issued under the companies’ capital markets programs. As SEK is a relatively small player in the market, the changes in volumes from year to year are more the effect of specific business opportunities than the effect of fluctuation in the overall volume of the markets for export credits.

The volume of infrastructure credits reflects the decision of the shareholders, including the Swedish Government, in 1996 to broaden SEK’s mandate to include infrastructure financing that directly or indirectly enhances the Swedish export industry. In that connection municipalities and other public authorities in Sweden and elsewhere in the Nordic region have become an increasingly important sector of business that SEK targets.

Export financing is extended at prevailing market rates of interest. The Company normally makes credit offers at a quoted interest rate that is subject to change prior to acceptance of the credit offer (an “indicative credit offer”). However, credit offers can also be made at a binding interest rate (a “firm credit offer”), but such credit offers have until now rarely been made and are then only valid for short periods. When a borrower accepts an indicative credit offer, the interest rate is set and a binding credit commitment by the Company arises.

Before the Company makes any credit commitment, it ensures that the currency in which the credit is to be funded is expected to be available for the entire credit period at an interest rate (taking into account the costs of currency swaps) that, as of the day the commitment is made, results in a margin that the Company deems sufficient. Except for the portion of the Company’s credits in Swedish kronor that are financed by the Company’s shareholders’ funds and untaxed reserves, the Company borrows, on an aggregate basis, at maturities corresponding to or exceeding those of prospective credits. The Company may accordingly decide not to hedge for movements in interest rate risk particular credit commitments until some time after they are made. Interest rate risks associated with such uncovered commitments are monitored closely and may not exceed interest rate risk limits established by the Board of Directors. The Company’s policies with regard to counterparty exposures are described in Item 11.b “Quantitative and Qualitative Disclosures about Market Risk — Risk Management”.

12

The Company’s initial credit offer and subsequent credit commitment set forth the maximum principal amount of the credit, the currency in which the credit will be denominated, the repayment schedule and the disbursement schedule.

The following table shows the currency breakdown of credit offers accepted for credits with maturities exceeding one year for each year in the three-year period ended December 31, 2006.

| | Percentage of credit offers accepted | |

Currency in which credit is denominated | | 2006 | | 2005 | | 2004 | |

Swedish kronor | | 40 | % | 49 | % | 43 | % |

Euro | | 41 | % | 41 | % | 36 | % |

U.S. dollars | | 18 | % | 7 | % | 20 | % |

Other | | 1 | % | 3 | % | 1 | % |

Total | | 100 | % | 100 | % | 100 | % |

The decrease in the Swedish kronor component of new credit offers accepted in 2006 reflects a slowdown in new infrastructure lending by SEK. The increase in the U.S. dollar component of new credit offers accepted in 2006 reflects a trend toward increased demand for traditional export credits from Swedish companies which is often denominated in U.S. dollar and increased volumes of new credits to Finnish companies and municipalities. The increase in the Swedish kronor component of new credit offers accepted in 2005 reflected increased infrastructure lending by SEK that year. The decline in the U.S. dollar component of new credit offers accepted in 2005 reflects a trend toward increased demand for euro-denominated credits from Swedish companies, and increased volumes of new credits to Finnish companies and municipalities.

S-system

The S-system was established by the State on July 1, 1978, as a State-sponsored export financing program designed to maintain the competitive position of Swedish exporters of capital goods and services in world markets. After a trial period, in April 1984 the Swedish Parliament extended the S-system indefinitely. The S-system today comprises the normal export financing program at CIRR (Commercial Interest Reference Rate) rates and a tied aid credit program. Pursuant to arrangements established in 1978 and amended from time to time thereafter, the Company administers the S-system on behalf of the State against compensation based mainly on outstanding credit volumes.

Pursuant to agreements between SEK and the State, as long as any credits or borrowings remain outstanding under the S-system, the difference between interest revenues and net commission revenues related to lending and liquid assets under the S-system, on the one hand, and interest expenses related to borrowing, all other financing costs and any net foreign exchange losses incurred by SEK under the S-system, on the other hand, are reimbursed by (or paid to) the State. SEK treats the S-system as a separate operation for accounting purposes, with its own income statement. Although the deficits (surpluses) of programs under the S-system are reimbursed by (or paid to) the State, any credit losses that may be incurred under such programs are not reimbursed by the State. Accordingly, SEK has to obtain appropriate credit support for these credits as well, all of which are reported on SEK’s balance sheet.

The S-system is designed to comply with the Arrangement on Guidelines for Officially Supported Export Credits of the Organization for Economic Cooperation and Development (the “OECD Consensus”), of which Sweden is a member. The OECD Consensus establishes minimum interest rates, required down payments and maximum credit periods for government-supported export credit programs. Terms vary according to the per capita income of the importing country.

SEK offers S-system financing at CIRR rates. The CIRR-rates for new credits are subject to periodic review and adjustment by the OECD. The OECD Consensus stipulates that credit offers can be valid for a period of not more than four months, during which period the commercial contract shall be signed. Thereafter the CIRR rate can be locked in for a maximum period of six months in order for the credit agreement to be finalized. No commitment fee is charged for Swedish CIRR credits. The arranging bank receives compensation of 0.25 percent per annum, based on the outstanding credit amount, to cover its costs for arranging and managing the credit.

13

The OECD Consensus also provides eligibility standards for tied or partially tied concessionary credits. In principle, such credits are not permitted to be extended to countries whose per capita GNP for at least two consecutive years have exceeded the World Bank threshold for 17-year loans. Tied or partially tied concessionary credits to other countries are not permitted to be extended to finance public or private projects that normally would be commercially viable if financed on market or OECD Consensus terms.

SEK participates with government agencies in a State-sponsored export financing program (the “Concessionary Credit Program”) for exports to certain developing countries, presently incorporating a foreign aid element of at least 35 percent. The foreign aid element is granted in the form of lower rates of interest and/or deferred repayment schedules, and the State reimburses SEK in the S-system for the costs incurred as a result of SEK’s participation in such program. In general, credits under the program are made with State guarantees administered by the Exportkreditnämnden (EKN) (Sweden’s Export Credits Guarantee Board). All such credits granted by SEK must also undergo SEK’s customary approval process.

The following table sets forth the volumes of offers accepted, undisbursed credits at year end, new credits disbursed and credits outstanding at year end under the various programs in the S-system for each year in the three-year period ended December 31, 2006. The increase in volumes of offers accepted and undisbursed credits at year end under the CIRR-credits program was related to an increased demand of traditional export credits with terms that are eligible in the CIRR-system. The increase in volumes of offers accepted and undisbursed credits at year-end under the concessionary credit program in 2005 was primarily related to a single transaction.

| | Concessionary

Credit Program | | CIRR-credits | | Total | |

(Skr million) | | 2006 | | 2005 | | 2004 | | 2006 | | 2005 | | 2004 | | 2006 | | 2005 | | 2004 | |

| | | | | | | | | | | | | | | | | | | |

Offers accepted | | 38 | | 126 | | 17 | | 8,499 | | 3,069 | | 2,602 | | 8,537 | | 3,195 | | 2,619 | |

Undisbursed credits at year-end | | 16 | | 107 | | 43 | | 14,147 | | 8,960 | | 10,183 | | 14,163 | | 9,067 | | 10,226 | |

New credits disbursed | | 102 | | 59 | | 34 | | 1,935 | | 4,435 | | 1 698 | | 2,037 | | 4,494 | | 1,732 | |

Credits outstanding at year-end | | 858 | | 1,265 | | 1,410 | | 8,267 | | 9,074 | | 5,330 | | 9,125 | | 10,339 | | 6,740 | |

Credit Support for Outstanding Credits

The Company’s policies with regard to counterparty exposures are described in Item 11.b “Quantitative and Qualitative Disclosures about Market Risk — Risk Management”.

14

The following table shows the credit support by category for the Company’s outstanding credits for the five-year period ended December 31, 2006. As most credits are supported by elements from more than one category, resulting in more than one party being responsible for the same payments to SEK, this table reflects the counterparty (either borrower or guarantor) that SEK believes to be the stronger credit.

| | Percentage of Total Credits | |

| | Outstanding at December 31, | |

Consolidated Group | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Credits with Swedish State guarantees via EKN (A) | | 14 | % | 17 | % | 16 | % | 20 | % | 26 | % |

Credits with Swedish State guarantees via National Debt Office (B) | | 1 | % | 1 | % | 2 | % | 3 | % | 3 | % |

Credits with Swedish State guarantees (total) | | 15 | % | 18 | % | 18 | % | 23 | % | 29 | % |

Credits to or guaranteed by Swedish credit institutions (C) | | 17 | % | 19 | % | 17 | % | 15 | % | 15 | % |

Credits to or guaranteed by foreign bank groups or governments (D) | | 35 | % | 33 | % | 28 | % | 28 | % | 25 | % |

Credits to or guaranteed by other Swedish counterparties, primarily corporations (E) | | 7 | % | 8 | % | 10 | % | 10 | % | 14 | % |

Credits to or guaranteed by Municipalities | | 17 | % | 17 | % | 18 | % | 14 | % | 7 | % |

Credits to or guaranteed by other foreign counterparties, primarily corporations | | 9 | % | 5 | % | 9 | % | 10 | % | 10 | % |

Total | | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % |

See “Lending Operations — General” for information on the geographical distribution of borrowers.

(A) EKN guarantees are in substance credit insurance against losses caused by the default of a foreign borrower or buyer in meeting its contractual obligations in connection with the purchase of Swedish goods or services. In the case of a foreign private borrower or buyer, coverage is for “commercial” and, in most cases, “political” risks. Coverage for “commercial” risk refers to losses caused by events such as the borrower’s or buyer’s insolvency or failure to make required payments within a certain time period (usually six months). Coverage for “political” risk refers to losses caused by events such as a moratorium, revolution or war in the importing country or the imposition of import or currency control measures in such country.

Generally, an EKN guarantee covers 85-90 percent of losses incurred due to covered risks. Disputed claims must be resolved by a court judgment or arbitral award, unless otherwise agreed by EKN. In the table above, only the percentages guaranteed have been included.

EKN is a State agency whose obligations are backed by the full faith and credit of Sweden.

(B) State guarantees issued by the National Debt Office are unconditional obligations backed by the full faith and credit of Sweden.

(C) At December 31, 2006, credits in this category amounting to approximately 6 % (2005: 8, 2004: 10) of total credits were obligations of the four largest commercial bank groups in Sweden including credit guarantees in the form of bank guarantees or credit derivatives.

(D) Principally obligations of other Nordic, Western European or North American bank groups, together with obligations of Western European governments including credit guarantees in the form of bank guarantees or credit derivatives.

(E) At December 31, 2006, approximately 66% (2005: 79, 2004: 71) of credits in this category represented credits to or guarantees issued by ten large Swedish corporations.

15

See also Item 11. b) “Quantitative and Qualitative Disclosures about Market Risk — Risk Management” for a discussion of how bank guarantees and credit derivatives are used to mitigate credit exposures.

The decline in credits guaranteed by the Swedish Government is a result of SEK’s diversification strategy. Under this strategy, SEK’s intention is to reduce the relative proportion of its risk exposure towards Swedish counterparties, although the reduction in Swedish Government exposure has been largely offset by the increase in exposure to Swedish municipalities.

c. Organization

SEK organizes its activities into three main business areas: Corporate & Structured Finance, Capital Markets and SEK Securities.

Corporate & Structured Finance. The Corporate & Structured Finance group is responsible for all activities in general lending, export credits, project finance, leasing and other structured finance projects, as well as origination and advisory services. The business area Corporate has overall responsibility for SEK’s relationships with its customers. The business area Structured Finance is responsible for structured finance solutions, project financing and leasing products. As a complement to SEK’s lending activity, the business area Financial Advisors offers independent consulting services to both the private and public sectors based on SEK’s experience in various areas, especially export credits and project finance, risk management and capital markets.

Capital Markets. The Capital Markets group comprises four sub-functions: Funding, Liquidity Management, Syndication and Credit Investments. Funding is responsible for managing SEK’s borrowing program and Liquidity Management is responsible for the investment of SEK’s liquidity portfolio. See also Item 5, “Operating and Financial Review and Prospects — Liquidity, Capital Resources and Funding — Liquidity”. Syndication handles risk syndication and risk cover solutions. Credit Investments handles corporate bond investment and trading.

SEK Securities. AB SEK Securities is a wholly-owned subsidiary with a license from the Swedish Financial Supervisory Authority to conduct a securities business. AB SEK Securities intermediates capital markets products to third party investors principally in the primary market via private placements.

In addition, SEK maintains a risk control unit that operates independently of the business areas. See Item 11b, “Quantitative and Qualitative Disclosures About Market Risk—Risk Management”.

d. Swedish Government Supervision

The Company operates as a credit market institution within the meaning of the Swedish Banking and Financing Business Act (the “Act”). As such, it is subject to supervision and regulation by the Swedish Financial Supervisory Authority (the “Supervisory Authority”), which licenses and monitors the activities of credit market companies to ensure their compliance with the Act and regulations thereunder and their corporate charters.

Among other things, the Supervisory Authority requires SEK to submit reports on a three-month, six-month and twelve-month basis and may conduct periodic inspections. The Supervisory Authority also may (and currently does) appoint an external auditor to participate with SEK’s independent auditors in examining the Company’s financial statements and the management of the Company.

As a credit market institution, SEK is also subject to regulation of its capital adequacy and limits on credit to a single customer pursuant to the Capital Adequacy and Large Exposures (Credit Institutions and Securities Companies) Act, as amended.

The capital adequacy requirements under Swedish law comply with international guidelines, including the recommendations issued by the Basel Committee on Banking Regulation and Supervisory Practices at the Bank for International Settlements (the “Basel Committee”). The principal measure of capital adequacy is a capital to risk asset ratio, which compares the capital base to the total of assets and off-balance sheet items. The capital base is divided into two components, one of them being “core” or “Tier

16

1” capital, which includes equity capital and, with certain limitations, non-cumulative preferred shares and similar instruments. Non-cumulative preferred shares and similar instruments may not be included in Tier 1 capital to the extent they exceed 15% of the Tier 1 capital other than non-cumulative preferred shares and similar instruments. The other component in the capital base is “supplementary” or “Tier 2” capital, which includes non-cumulative preferred shares and similar instruments not included in core capital, plus subordinated obligations with an original term of at least five years (with a deduction of 20% for each of the last five years prior to maturity). Until December 31, 2006 assets were assigned a weighting based on relative credit risk (0%, 10%, 20%, 50% or 100%) depending on the debtor or the type of collateral, if any, securing the assets. The minimum capital ratio requirement was 8%, and not more than 50% of an institution’s regulatory capital may comprise supplementary capital. SEK’s policy is to maintain a strong capital base, well in excess of the regulatory minimum. At December 31, 2006, SEK’s total regulatory capital ratio was 13.8% and its Tier 1 ratio was 9.4%. See also Item 5, “Operating and Financial Review and Prospects — Liquidity, Capital Resources and Funding — Capital Adequacy.”

As of January 1, 2007, the revised capital adequacy rules of the Basel Committee, referred to as Basel II, became applicable to credit institutions in Sweden and the EU, including SEK. In July 2005, SEK submitted an application to the Supervisory Authority related to the use of the Internal Ratings Based Approach when calculating risk-weighted claims under Basel II. The application was approved subject to legislation being fully implemented in Sweden. In March 2007, the Supervisory Authority finally determined that SEK can use an Internal Rating Based Approach when calculating risk-weighted claims under Basel II based on legislation adopted in Sweden in the beginning of 2007. The quantitative analysis regarding Pillar I (methods for calculating minimum capital requirements for certain risks) was implemented in 2005. During 2006 the required capital base, depending on the Company’s risk profile with regard to all relevant risks, was established (Pillar II). Reporting under the new rules will be made for the first time as of March 31, 2007. See also item 11. “Quantitative and Qualitative Disclosures About Market Risks” for a discussion regarding Basel II and its effects.

Under the regulatory rules for large exposures, a “large exposure” is defined as a (risk-weighted) exposure to a single counterparty (or counterparty group) that exceeds 10% of the institution’s regulatory total capital base. These rules state that no individual large exposure may exceed 25% of the regulatory total capital base of the institution, and that the aggregate amount of large exposures may not exceed 800% of the institution’s regulatory total capital base. The aggregate amount of SEK’s large exposures on December 31, 2006, was 148% of SEK’s regulatory total capital base, and consisted of risk-weighted exposures to eleven different counterparties (or counterparty groups). These counterparties (or counterparty groups) were all rated by at least one of the major rating agencies, Moody’s and Standard & Poor’s, with ratings of not lower than investment grade.

The Company’s subsidiary, AB SEK Securities, is licensed to conduct a securities business and as such is regulated by the Swedish Financial Supervisory Authority under the Securities Operations Act.

e. Competition

SEK is the only institution authorized by the State to make export financing credits under the S-system. In that connection, and with support from the Swedish State, SEK helps Swedish export companies compete with other export companies within OECD member countries which have similar support from their respective domestic export credit agencies, who also provide government-supported export credits. Lending from SEK exclusive of the S-system, including infrastructure credits mainly to municipalities, faces competition from other Swedish and foreign financial institutions, as well as from direct or indirect financing programs of exporters themselves. Deregulation and globalization of the world’s financial markets have resulted in an increasingly competitive environment for financial institutions, including SEK, for both lending opportunities and funding sources.

f. Property, Plants and Equipment

The Company owns, through its wholly-owned subsidiary AB SEKTIONEN, an office building in the City of Stockholm. The major part of the building is used by the Company as its headquarters.

Item 4A. Unresolved Staff Comments

None.

17

Item 5. Operating and Financial Review and Prospects

a. Overview

Substantially all of SEK’s revenues and net income derive from the net interest revenues earned on its credits and interest-bearing securities. Funding for these assets comes from shareholders’ funds and debt securities issued in the international capital markets. Accordingly, key elements in SEK’s profits from year to year are the spread, or difference, between the rate of interest earned on its debt-financed assets and the cost of that debt, the rate of interest earned on the investment of its shareholders’ funds and the outstanding volumes of credits and interest-bearing securities in the balance sheet, as well as the relative proportions of its assets funded by debt and shareholders’ funds.

In recent years SEK’s profit under Swedish GAAP has mainly been declining, however, with a break in the trend in 2006, which showed higher operating and net profits than the year before. The decline reflects several factors, including (1) reduction in shareholders’ funds in 2003 in connection with changes in SEK’s ownership, resulting in a higher portion of SEK’s assets being funded through debt financing, and (2) the lower interest rate environment in recent years that has resulted in maturing investments of the Company’s shareholders funds being reinvested at lower rates. However, both of these factors impact on operating profit has diminished during 2005 and 2006. One of the additional factors affecting net profit has been higher volumes of debt-financed interest-bearing assets in the balance sheet, however at lower margins. The margin on new business improved somewhat during 2006 but that has not yet provided any significant effect on net profit. Furthermore, increased costs related to new and pending regulations, particularly Basel II and IFRS, have affected net profit negatively in recent years, especially during 2005 and 2006.

The Company has continued to rebuild shareholder’s funds through retained earnings and a restrictive dividend policy. In recent years SEK has also expanded into business areas that may produce non-interest revenue, although commission income has not thus far made a material contribution to SEK’s revenues and profits.

b. Critical Accounting Policies and Estimates

Critical Accounting Policies and Estimates under Swedish GAAP

The Company has identified the followings critical accounting policies according to Swedish GAAP:

· Deferral hedge accounting

· Valuation principles when securities and derivatives are carried at fair value

· Foreign currency exchange revaluation

· Provisions for probable credit losses

The economic purpose of holding a derivative is consistently reflected in the accounting treatment under Swedish GAAP, both when applying deferral hedge accounting and when carried at fair value. Therefore, there is under Swedish GAAP no measurement or recognition inconsistency (sometimes referred to as an accounting mismatch or mixed measurement attributes) that would otherwise arise from measuring assets, liabilities or derivatives or recognizing the gains and losses on them on different bases.

Deferral hedge accounting

The Company has identified as critical accounting policies those accounting policies regarding the application of deferral hedge accounting according to Swedish GAAP. For accounting policies regarding deferral hedge accounting according to Swedish GAAP see the discussion below and Notes 1(j) and 1(q) to the Consolidated Financial Statements.

Certain of the Company’s lending and investing transactions are hedged on-balance sheet or off-balance sheet by transactions with matching principal or notional amounts, interest rates, currencies and other relevant factors, such that the Company’s exposure to changes in net fair values of such transactions due to

18

movements in interest and/or exchange rates is hedged. Under Swedish GAAP, SEK applies deferral hedge accounting for all transactions that are economically hedged. Economic hedging is done primarily on a contract-by-contract basis but in some cases on a portfolio basis.

For transactions without matched and offsetting balance sheet positions, SEK enters into derivative transactions, in order to achieve an effective economic hedge. These instruments include interest-rate basis related, currency related and other agreements that SEK uses for the purpose of hedging or eliminating mainly interest rate and currency exchange rate exposures as well as exposures related to embedded derivatives.

SEK accounts for derivatives in accordance with deferral hedge accounting rules under Swedish GAAP. If deferral hedge accounting is applicable, the change in the amortized cost of the derivative is recorded in earnings, which corresponds to a similar but opposite change in the amortized cost of the underlying assets or liabilities, also recorded in earnings. For the major part of transactions on or off balance sheet, both derivatives and underlying instruments are recorded at amortized cost.

Where the securities are carried at amortized cost, changes in their estimated fair values, arising from changes in management’s assessment of the underlying assumptions, may result in the recording of a permanent diminution in their value. In such case, it would also be necessary for SEK’s management to exercise judgment as to whether or not changes in the underlying valuation assumptions are only temporary. SEK monitors on an ongoing basis the validity of such assumptions.

Valuation principles when securities and derivatives are carried at fair value

For financial instruments classified as held-for-trading both derivatives and underlying instruments are marked-to-market. In reporting the amounts of its assets and derivatives, and its revenues and expenses, the Company must make assumptions and estimates in assessing the fair value of certain assets and derivatives, especially where unquoted or illiquid securities or other debt instruments are involved. If the conditions underlying these assumptions and estimates were to change, the amounts reported could be different.

When the securities are carried at fair value, fair value is calculated with the use of market quotations, pricing models and discounted cash flows. Certain of the Company’s securities are not publicly traded, and quoted market prices are not readily available. However, different pricing models or assumptions or changes in relevant current information could produce different valuation results. Furthermore, the estimated fair value of a security may, under certain market conditions, differ significantly from the amount that could be realized if the security were sold immediately.

When the derivative instruments are carried at fair value, fair value is calculated based upon internally established valuations that are consistent with external valuation models, quotations furnished by dealers in such instruments or market quotations. However, different pricing models or assumptions or changes in relevant current information could produce different valuation results.

Although variability is inherent in these estimates, when carrying instruments at fair value for securities and derivatives, management believes the amounts presented in the financial statements under Swedish GAAP will be appropriate based upon the facts available.

Foreign currency exchange revaluation