UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3221

Fidelity Charles Street Trust

(Exact name of registrant as specified in charter)

82 Devonshire St., Boston, Massachusetts 02109

(Address of principal executive offices) (Zip code)

Eric D. Roiter, Secretary

82 Devonshire St.

Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-563-7000

Date of fiscal year end: | September 30 |

| |

Date of reporting period: | September 30, 2005 |

Item 1. Reports to Stockholders

| | Annual Report

September 30, 2005

|

| Contents | | | | | | |

| |

| Chairman’s Message | | A-4 | | Ned Johnson’s message to shareholders. |

| Performance | | A-5 | | How the fund has done over time. |

| Management’s Discussion | | A-6 | | The manager’s review of fund |

| | | | | | | performance, strategy and outlook. |

| Shareholder Expense | | A-7 | | An example of shareholder expenses. |

| Example | | | | | | |

| Investment Changes | | A-9 | | A summary of major shifts in the fund’s |

| | | | | | | investments over the past six months. |

| Investments | | A-10 | | A complete list of the fund’s investments |

| | | | | | | with their market values. |

| Financial Statements | | A-26 | | Statements of assets and liabilities, |

| | | | | | | operations, and changes in net assets, |

| | | | | | | as well as financial highlights. |

| Notes | | A-30 | | Notes to the financial statements. |

| Report of Independent | | A-38 | | |

| Registered Public | | | | | | |

| Accounting Firm | | | | | | |

| Trustees and Officers | | A-39 | | |

| Distributions | | A-51 | | |

| Board Approval of | | A-52 | | |

| Investment Advisory | | | | | | |

| Contracts and | | | | | | |

| Management Fees | | | | | | |

| Central Fund Investments | | A- | 61 | | | Complete list of investments for Fidelity’s |

| | | | | | | Fixed-Income Central Funds. |

To view a fund’s proxy voting guidelines and proxy voting record for the 12 month period

ended June 30, visit www.fidelity.com/proxyvotingresults or visit the Securities and Exchange

Commission’s (SEC) web site at www.sec.gov. You may also call 1-800-544-8544 to request a free

copy of the proxy voting guidelines.

Standard & Poor’s, S&P and S&P 500 are registered service marks of The McGraw Hill Companies, Inc.

and have been licensed for use by Fidelity Distributors Corporation.

Other third party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks

of FMR Corp. or an affiliated company.

|

Annual Report A-2

This report and the financial statements contained herein are submitted for the general information

of the shareholders of the fund. This report is not authorized for distribution to prospective investors

in the fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third

quarters of each fiscal year on Form N Q. Forms N Q are available on the SEC’s web site at

http://www.sec.gov. A fund’s Forms N Q may be reviewed and copied at the SEC’s Public Reference

Room in Washington, DC. Information regarding the operation of the SEC’s Public Reference

Room may be obtained by calling 1-800-SEC-0330. For a complete list of a fund’s portfolio

holdings, view the most recent quarterly holdings report, semiannual report, or annual report

on Fidelity’s web site at http://www.fidelity.com/holdings.

NOT FDIC INSURED · MAY LOSE VALUE · NO BANK GUARANTEE

Neither the fund nor Fidelity Distributors Corporation is a bank.

|

Chairman’s Message

(photograph of Edward C. Johnson 3d)

Dear Shareholder:

During the past year or so, much has been reported about the mutual fund industry, and much of it has been more critical than I believe is warranted. Allegations that some companies have been less than forthright with their shareholders have cast a shadow on the entire industry. I continue to find these reports disturbing, and assert that they do not create an ac curate picture of the industry overall. Therefore, I would like to remind every one where Fidelity stands on these issues. I will say two things specifically regarding allegations that some mutual fund compa nies were in violation of the Securities and Exchange Commission’s forward pricing rules or were involved in so called “market timing” activities.

First, Fidelity has no agreements that permit customers who buy fund shares after 4 p.m. to obtain the 4 p.m. price. This is not a new policy. This is not to say that some one could not deceive the company through fraudulent acts. However, we are extremely diligent in preventing fraud from occurring in this manner and in every other. But I underscore again that Fidelity has no so called “agreements” that sanction illegal practices.

Second, Fidelity continues to stand on record, as we have for years, in opposition to predatory short term trading that adversely affects shareholders in a mutual fund. Back in the 1980s, we initiated a fee which is returned to the fund and, therefore, to investors to discourage this activity. Further, we took the lead several years ago in developing a Fair Value Pricing Policy to prevent market timing on foreign securities in our funds. I am confident we will find other ways to make it more difficult for predatory traders to operate. However, this will only be achieved through close cooperation among regulators, legislators and the industry.

Yes, there have been unfortunate instances of unethical and illegal activity within the mutual fund industry from time to time. That is true of any industry. When this occurs, confessed or convicted offend ers should be dealt with appropriately. But we are still concerned about the risk of over regulation and the quick application of simplistic solutions to intricate problems. Every system can be improved, and we support and applaud well thought out improvements by regulators, legislators and industry representatives that achieve the common goal of building and protecting the value of investors’ holdings.

For nearly 60 years, Fidelity has worked very hard to improve its products and service to justify your trust. When our family founded this company in 1946, we had only a few hundred customers. Today, we serve more than 18 million customers in cluding individual investors and participants in retirement plans across America.

Let me close by saying that we do not take your trust in us for granted, and we real ize that we must always work to improve all aspects of our service to you. In turn, we urge you to continue your active participation with your financial matters, so that your interests can be well served.

Best regards,

/s/ Edward C. Johnson 3d

Edward C. Johnson 3d

Annual Report A-4

Performance: The Bottom Line

Average annual total return reflects the change in the value of an investment, assuming reinvestment of the fund’s dividend income and capital gains (the profits earned upon the sale of securities that have grown in value) and assuming a constant rate of perfor mance each year. The $10,000 table and the fund’s returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. During periods of reimbursement by Fidelity, a fund’s total return will be greater than it would be had the reimbursement not occurred. How a fund did yesterday is no guarantee of how it will do tomorrow.

| Average Annual Total Returns | | | | | | |

| Periods ended September 30, 2005 | | Past 1 | | Past 5 | | Past 10 |

| | | year | | years | | years |

| Fidelity® Asset ManagerSM | | 7.15% | | 1.27% | | 7.89% |

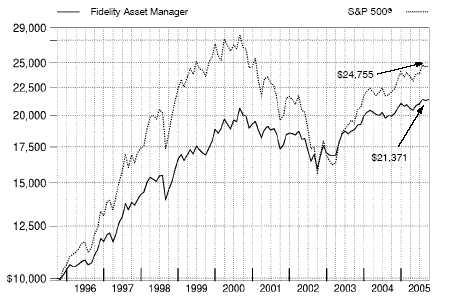

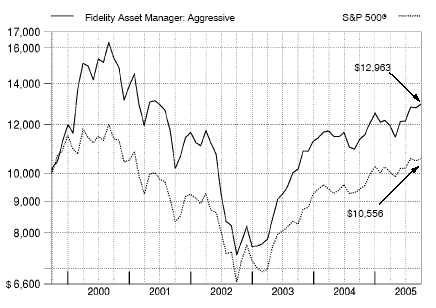

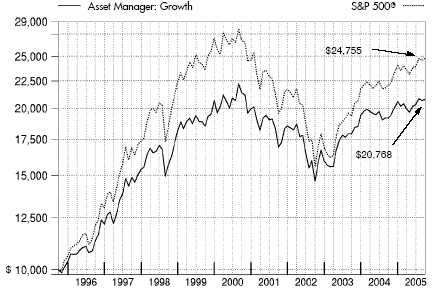

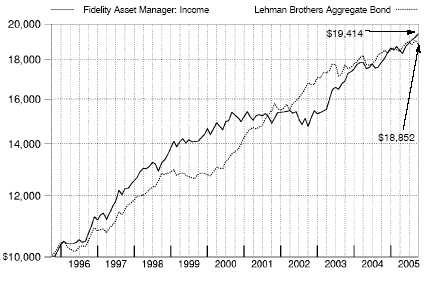

$10,000 Over 10 Years

Let’s say hypothetically that $10,000 was invested in Fidelityr Asset ManagerSM on September 30, 1995. The chart shows how the value of your investment would have changed, and also shows how the Standard & Poor’s 500SM Index performed over the same period.

A-5 Annual Report

A-5

Management’s Discussion of Fund Performance

Comments from Richard Habermann, Portfolio Manager of Fidelity® Asset ManagerSM

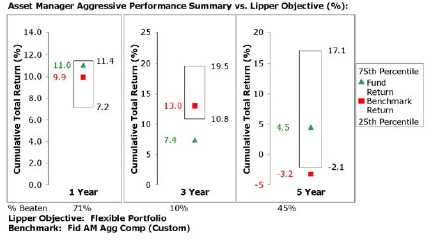

Stocks and bonds had positive returns for the 12 months ending September 30, 2005. Equities did significantly better, as the majority of bellwether stock market measures had gains in the low to mid teens, compared to low single digits for bonds. Energy and utilities were the top performing sectors and drove about a third of the stock market’s return on the strength of record high oil prices. It was a fairly conducive investment environment for equities, as continued strength in consumer spending and corporate profits led to steady economic growth. Against this backdrop, the Standard & Poor’s 500SM Index returned 12.25%, the NASDAQ Composite® Index rose 14.19% and the Dow Jones Industrial AverageSM gained 7.23% . In the bond market, a flattening yield curve surprised many. Despite eight interest rate hikes in the past year, longer term yields were relatively stable, resulting in a narrowing yield gap compared to rising short term rates. Overall, the Federal Reserve Board’s monetary policy and inflation concerns tempered debt returns, as shown by the modest 2.80% rise in the Lehman Brothersr Aggregate Bond Index.

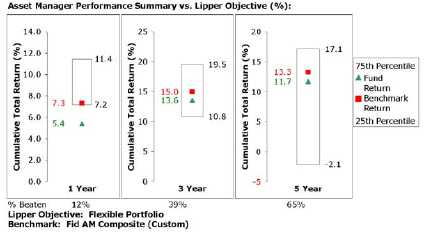

The fund was up 7.15% during the past year, versus 7.52% for the Fidelity Asset Manager Composite Index and 11.66% for the LipperSM Flexible Portfolio Funds Average. Relative to the index, weak results from our domestic equity holdings more than offset favorable asset allocation overall and solid outperformance in the fixed income subportfolio. In an environ ment that favored riskier assets, it paid to overweight stocks and high yield securities relative to investment grade debt. Within the equity allocation, modest exposure to foreign stocks was helpful, as overseas markets easily beat their U.S. counterparts. Overweighting cash detracted slightly relative to the index, but the fund enjoyed signifi cantly higher yields than in recent periods. Our U.S. equities trailed the S&P 500® by nearly three percentage points, largely due to underweightings in the energy and utilities sectors. Stock selection in financials also hurt, as two major positions mortgage finance giant Fannie Mae and insurer American International Group wilted amid regulatory issues. Conversely, some good picks in consumer staples and health care provided most of the upside, led by pharmacy chain CVS and medical supplier Cardinal Health, respectively. In fixed income, we benefited mainly from good sector selection, and our high yield and investment grade holdings through the use of central investment portfolios comfortably outpaced the Lehman Brothers index. The strategic cash portion of the fund topped its benchmark as well.

The views expressed in this statement reflect those of the portfolio manager only through the end of the period of the report as stated on the cover and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (April 1, 2005 to September 30, 2005).

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, the fund, as a share holder in underlying affiliated central funds, will indirectly bear its pro rata share of the fees and expenses incurred by the underlying affiliated central funds. These fees and expenses are not included in the fund’s annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the share holder reports of the other funds. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, the fund as a shareholder in underlying affiliated central funds, will indirectly bear its pro rata share of the fees and expenses incurred by the underlying affiliated central funds. These fees and expenses are not included in the fund’s annualized expense ratio used to calculate the expense estimate in the table below.

Shareholder Expense Example continued

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| | | | | | | | | | | Expenses Paid |

| | | | | | | | | | | During Period* |

| | | | | Beginning | | | | Ending | | April 1, 2005 |

| | | | | Account Value | | | | Account Value | | to September 30, |

| | | | | April 1, 2005 | | | | September 30, 2005 | | 2005 |

| Actual | | | | $ 1,000.00 | | | | $ 1,038.20 | | $ 3.73 |

| Hypothetical (5% return per year | | | | | | | | | | |

| before expenses) | | | | $ 1,000.00 | | | | $1,021.41 | | $ 3.70 |

* Expenses are equal to the Fund’s annualized expense ratio of .73%; multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one half year period). The fees and expenses of the underlying affiliated central funds in which the fund invests are not included in the fund’s annualized expense ratio.

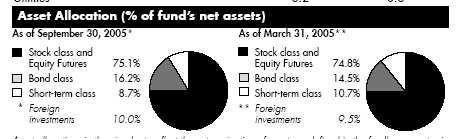

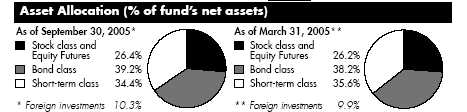

Investment Changes

| Top Five Stocks as of September 30, 2005 | | |

| | | % of fund’s | | % of fund’s net assets |

| | | net assets | | 6 months ago |

| Cardinal Health, Inc. | | 3.1 | | 2.6 |

| American International Group, Inc. | | 2.7 | | 2.2 |

| Home Depot, Inc. | | 2.5 | | 2.4 |

| Microsoft Corp. | | 2.5 | | 2.2 |

| Wyeth | | 2.1 | | 1.8 |

| | | 12.9 | | |

| Top Five Bond Issuers as of September 30, 2005 | | |

| (with maturities greater than one year) | | % of fund’s | | % of fund’s net assets |

| | | net assets | | 6 months ago |

| Fannie Mae | | 6.9 | | 7.7 |

| U.S. Treasury Obligations | | 2.3 | | 2.4 |

| Freddie Mac | | 2.0 | | 2.4 |

| Government National Mortgage Association | | 0.3 | | 0.8 |

| United Mexican States | | 0.3 | | 0.4 |

| | | 11.8 | | |

| Top Five Market Sectors as of September 30, 2005 | | |

| | | % of fund’s | | % of fund’s net assets |

| | | net assets | | 6 months ago |

| Financials | | 14.3 | | 14.8 |

| Information Technology | | 9.2 | | 8.6 |

| Consumer Discretionary | | 8.8 | | 8.0 |

| Health Care | | 8.8 | | 8.7 |

| Industrials | | 5.8 | | 5.2 |

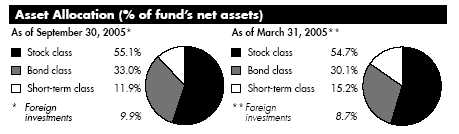

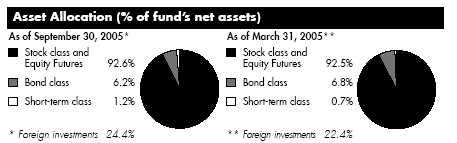

Asset allocations in the pie charts reflect the categorization of assets as defined in the fund’s prospectus in effect as of the time periods indicated above. Financial Statement categorizations conform to accounting standards and will differ from the pie chart. Percentages are adjusted for the effect of futures contracts and swap contracts, if applicable.

The information in the above tables is based on the combined investments of the fund and its pro rata share of the investments of Fidelity’s fixed income central funds.

A-9 Annual Report

| Investments September 30, 2005 | | |

| Showing Percentage of Net Assets | | | | | | |

| |

| Common Stocks 49.3% | | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| CONSUMER DISCRETIONARY – 6.4% | | | | | | |

| Auto Components 0.0% | | | | | | |

| Aisin Seiki Co. Ltd. | | 37,600 | | | | $ 1,074 |

| Cheng Shin Rubber Industry Co. Ltd. | | 437,000 | | | | 356 |

| NOK Corp. | | 32,400 | | | | 972 |

| Stanley Electric Co. Ltd. | | 122,100 | | | | 1,862 |

| Sumitomo Rubber Industries Ltd. | | 78,000 | | | | 934 |

| Tong Yang Industry Co. Ltd. | | 595,000 | | | | 714 |

| | | | | | | 5,912 |

| Automobiles – 0.2% | | | | | | |

| Honda Motor Co. Ltd. | | 13,800 | | | | 784 |

| Hyundai Motor Co. | | 44,730 | | | | 3,494 |

| Kia Motors Corp. | | 84,880 | | | | 1,586 |

| Renault SA | | 40,700 | | | | 3,856 |

| Toyota Motor Corp. | | 149,900 | | | | 6,923 |

| | | | | | | 16,643 |

| Distributors – 0.0% | | | | | | |

| Doshisha Co. Ltd. | | 27,600 | | | | 566 |

| Diversified Consumer Services – 0.0% | | | | | | |

| ABC Learning Centres Ltd. | | 200,260 | | | | 956 |

| Raffles Education Corp. Ltd. | | 1,483,000 | | | | 754 |

| YBM Sisa.com, Inc. | | 18,565 | | | | 311 |

| | | | | | | 2,021 |

| Hotels, Restaurants & Leisure 0.5% | | | | | | |

| Carnival Corp. unit | | 118,900 | | | | 5,943 |

| Hilton Group PLC | | 894,600 | | | | 4,965 |

| McDonald’s Corp. | | 833,200 | | | | 27,904 |

| Royal Caribbean Cruises Ltd. | | 105,900 | | | | 4,575 |

| St. Marc Co. Ltd. | | 2,500 | | | | 120 |

| William Hill PLC | | 451,100 | | | | 4,641 |

| | | | | | | 48,148 |

| Household Durables – 0.2% | | | | | | |

| Barratt Developments PLC | | 109,700 | | | | 1,462 |

| Casio Computer Co. Ltd. | | 66,000 | | | | 966 |

| Chitaly Holdings Ltd. | | 1,114,000 | | | | 632 |

| George Wimpey PLC | | 438,700 | | | | 3,313 |

| HTL International Holdings Ltd. | | 1,371,000 | | | | 1,045 |

| Koninklijke Philips Electronics NV (NY Shares) | | 171,500 | | | | 4,576 |

| LG Electronics, Inc. | | 13,220 | | | | 886 |

| Matsushita Electric Industrial Co. Ltd. | | 109,000 | | | | 1,865 |

See accompanying notes which are an integral part of the financial statements.

Annual Report A-10

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| CONSUMER DISCRETIONARY – continued | | | | | | |

| Household Durables – continued | | | | | | |

| Sony Corp. | | 33,400 | | | | $ 1,109 |

| Sumitomo Forestry Co. Ltd. | | 140,000 | | | | 1,430 |

| Techtronic Industries Co. Ltd. | | 782,000 | | | | 2,001 |

| Tsann Kuen Enterprise Co. Ltd. | | 237,880 | | | | 381 |

| Wilson Bowden PLC | | 77,000 | | | | 1,584 |

| | | | | | | 21,250 |

| Leisure Equipment & Products – 0.0% | | | | | | |

| Aruze Corp. | | 30,000 | | | | 488 |

| Asia Optical Co., Inc. | | 100,076 | | | | 639 |

| Li Ning Co. Ltd. | | 1,296,000 | | | | 773 |

| Mars Engineering Corp. | | 24,500 | | | | 756 |

| Sankyo Co. Ltd. (Gunma) | | 13,600 | | | | 722 |

| Sega Sammy Holdings, Inc. | | 28,000 | | | | 1,113 |

| Sega Sammy Holdings, Inc. New | | 28,000 | | | | 1,093 |

| | | | | | | 5,584 |

| Media – 2.6% | | | | | | |

| Bandai Visual Co. Ltd. | | 190 | | | | 649 |

| Beijing Media Corp. Ltd. (H Shares) | | 126,000 | | | | 211 |

| Clear Channel Communications, Inc. | | 5,653,191 | | | | 185,933 |

| Cyber Agent Ltd. | | 238 | | | | 437 |

| Cyber Agent Ltd. New (a) | | 238 | | | | 424 |

| E.W. Scripps Co. Class A | | 124,731 | | | | 6,233 |

| ITV PLC | | 2,471,958 | | | | 4,929 |

| Lagardere S.C.A. (Reg.) | | 76,900 | | | | 5,459 |

| livedoor MARKETING Co. Ltd. (a) | | 6,264 | | | | 264 |

| Macquarie Communications Infrastructure Group unit | | 231,300 | | | | 1,046 |

| Modern Times Group AB (MTG) (B Shares) (a) | | 40,650 | | | | 1,532 |

| News Corp.: | | | | | | |

| Class A | | 1,942,100 | | | | 30,277 |

| Class B unit | | 219 | | | | 4 |

| Omnicom Group, Inc. | | 292,000 | | | | 24,420 |

| Oricon, Inc. | | 205 | | | | 262 |

| Seek Ltd. | | 450,800 | | | | 1,014 |

| Television Broadcasts Ltd. | | 170,000 | | | | 1,040 |

| Yedang Entertainment Co. Ltd. (a) | | 47,742 | | | | 686 |

| | | | | | | 264,820 |

| Multiline Retail – 0.0% | | | | | | |

| Don Quijote Co. Ltd. | | 4,500 | | | | 291 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | |

| |

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| CONSUMER DISCRETIONARY – continued | | | | | | |

| Specialty Retail – 2.8% | | | | | | |

| Esprit Holdings Ltd. | | 477,000 | | | | $ 3,566 |

| Hikari Tsushin, Inc. | | 16,200 | | | | 1,035 |

| Home Depot, Inc. | | 6,782,700 | | | | 258,692 |

| Pertama Holdings Ltd. | | 2,253,000 | | | | 473 |

| TJX Companies, Inc. | | 916,400 | | | | 18,768 |

| Tsutsumi Jewelry Co. Ltd. | | 20,700 | | | | 641 |

| USS Co. Ltd. | | 14,220 | | | | 1,017 |

| | | | | | | 284,192 |

| Textiles, Apparel & Luxury Goods – 0.1% | | | | | | |

| Adidas Salomon AG | | 11,800 | | | | 2,051 |

| Asics Corp. | | 71,000 | | | | 603 |

| Billabong International Ltd. | | 117,000 | | | | 1,165 |

| Ted Baker PLC | | 267,600 | | | | 2,276 |

| | | | | | | 6,095 |

| |

| TOTAL CONSUMER DISCRETIONARY | | | | | | 655,522 |

| |

| CONSUMER STAPLES 3.7% | | | | | | |

| Beverages – 0.3% | | | | | | |

| Asahi Breweries Ltd. | | 76,800 | | | | 979 |

| C&C Group PLC | | 423,000 | | | | 2,533 |

| PepsiCo, Inc. | | 350,570 | | | | 19,881 |

| Pernod-Ricard | | 47,000 | | | | 8,301 |

| Takara Holdings, Inc. | | 134,000 | | | | 850 |

| Yantai Changyu Pioneer Wine Co. (B Shares) | | 423,500 | | | | 751 |

| | | | | | | 33,295 |

| Food & Staples Retailing – 2.2% | | | | | | |

| Aeon Co. Ltd. | | 30,000 | | | | 607 |

| CVS Corp. | | 3,504,700 | | | | 101,671 |

| Safeway, Inc. | | 1,216,000 | | | | 31,130 |

| Wal-Mart Stores, Inc. | | 1,963,300 | | | | 86,032 |

| Wumart Stores, Inc. (H Shares) | | 102,000 | | | | 220 |

| | | | | | | 219,660 |

| Food Products 0.0% | | | | | | |

| Binggrea Co. Ltd. | | 16,400 | | | | 657 |

| China Mengniu Dairy Co. Ltd. | | 520,000 | | | | 429 |

| Global Bio-Chem Technology Group Co. Ltd. | | 1,892,000 | | | | 866 |

| Global Bio-Chem Technology Group Co. Ltd. warrants | | | | | | |

| 5/31/07 (a) | | 85,000 | | | | 1 |

See accompanying notes which are an integral part of the financial statements.

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| CONSUMER STAPLES – continued | | | | | | |

| Food Products – continued | | | | | | |

| Hokuto Corp. | | 16,600 | | | | $ 291 |

| Orion Corp. | | 9,400 | | | | 1,667 |

| People’s Food Holdings Ltd. | | 772,000 | | | | 502 |

| | | | | | | 4,413 |

| Household Products – 0.1% | | | | | | |

| Colgate-Palmolive Co. | | 228,300 | | | | 12,052 |

| LG Household & Health Care Ltd. | | 18,450 | | | | 1,059 |

| Uni-Charm Corp. | | 10,600 | | | | 461 |

| | | | | | | 13,572 |

| Personal Products 0.3% | | | | | | |

| Alberto-Culver Co. | | 617,600 | | | | 27,638 |

| Hengan International Group Co. Ltd. | | 162,000 | | | | 155 |

| | | | | | | 27,793 |

| Tobacco 0.8% | | | | | | |

| Altria Group, Inc. | | 1,043,100 | | | | 76,887 |

| |

| TOTAL CONSUMER STAPLES | | | | | | 375,620 |

| |

| ENERGY 2.7% | | | | | | |

| Energy Equipment & Services – 1.4% | | | | | | |

| Diamond Offshore Drilling, Inc. | | 591,800 | | | | 36,248 |

| ENSCO International, Inc. | | 544,300 | | | | 25,359 |

| Expro International Group PLC | | 129,500 | | | | 1,250 |

| GlobalSantaFe Corp. | | 910,901 | | | | 41,555 |

| Ocean RIG ASA (a) | | 404,500 | | | | 4,646 |

| Petroleum Geo-Services ASA (a) | | 161,600 | | | | 5,143 |

| Transocean, Inc. (a) | | 563,100 | | | | 34,524 |

| WorleyParsons Ltd. | | 59,600 | | | | 465 |

| | | | | | | 149,190 |

| Oil, Gas & Consumable Fuels – 1.3% | | | | | | |

| BG Group PLC | | 785,600 | | | | 7,458 |

| BowLeven PLC | | 104,600 | | | | 1,347 |

| CNOOC Ltd. | | 2,239,000 | | | | 1,616 |

| ConocoPhillips | | 416,500 | | | | 29,118 |

| Cosmo Oil Co. Ltd. | | 169,000 | | | | 922 |

| ENI Spa | | 537,100 | | | | 15,909 |

| ENI Spa sponsored ADR | | 32,500 | | | | 4,813 |

| Exxon Mobil Corp. | | 560,500 | | | | 35,614 |

| Formosa Petrochemical Corp. | | 234,286 | | | | 450 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | |

| |

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| ENERGY – continued | | | | | | |

| Oil, Gas & Consumable Fuels – continued | | | | | | |

| GS Holdings Corp. | | 17,684 | | | | $ 451 |

| Nippon Mining Holdings, Inc. | | 203,500 | | | | 1,625 |

| PetroChina Co. Ltd. (H Shares) | | 1,544,000 | | | | 1,287 |

| Statoil ASA | | 355,200 | | | | 8,811 |

| Total SA sponsored ADR | | 159,300 | | | | 21,636 |

| | | | | | | 131,057 |

| |

| TOTAL ENERGY | | | | | | 280,247 |

| |

| FINANCIALS – 10.7% | | | | | | |

| Capital Markets 1.7% | | | | | | |

| Credit Suisse Group (Reg.) | | 99,284 | | | | 4,416 |

| DAB Bank AG | | 196,700 | | | | 1,577 |

| E*Trade Securities Co. Ltd. (d) | | 180 | | | | 797 |

| Goldman Sachs Group, Inc. | | 351,500 | | | | 42,735 |

| JAFCO Co. Ltd. | | 15,700 | | | | 1,035 |

| kiwoom.com Securities Co. Ltd. | | 28,332 | | | | 502 |

| Korea Investment Holdings Co. Ltd. | | 24,650 | | | | 720 |

| Macquarie Bank Ltd. | | 45,000 | | | | 2,586 |

| Merrill Lynch & Co., Inc. | | 867,500 | | | | 53,221 |

| Monex Beans Holdings, Inc. (d) | | 737 | | | | 876 |

| Morgan Stanley | | 950,600 | | | | 51,275 |

| Nikko Cordial Corp. | | 86,500 | | | | 1,008 |

| Nuveen Investments, Inc. Class A | | 270,600 | | | | 10,659 |

| | | | | | | 171,407 |

| Commercial Banks – 1.9% | | | | | | |

| Banca Intesa Spa | | 736,188 | | | | 3,431 |

| Banco Bilbao Vizcaya Argentaria SA | | 131,600 | | | | 2,308 |

| Bank of America Corp. | | 2,880,920 | | | | 121,287 |

| Hokuhoku Financial Group, Inc. | | 292,000 | | | | 1,109 |

| Kookmin Bank | | 24,810 | | | | 1,462 |

| Mitsui Trust Holdings, Inc. | | 190,000 | | | | 2,650 |

| Mizuho Financial Group, Inc. | | 464 | | | | 2,972 |

| Nishi-Nippon City Bank Ltd. (a) | | 114,000 | | | | 569 |

| Shinhan Financial Group Co. Ltd. | | 41,320 | | | | 1,437 |

| Standard Chartered PLC (United Kingdom) | | 338,300 | | | | 7,301 |

| Sumitomo Mitsui Financial Group, Inc. | | 534 | | | | 5,069 |

| Synovus Financial Corp. | | 262,100 | | | | 7,265 |

| Tokyo Tomin Bank Ltd. | | 24,800 | | | | 814 |

| Wachovia Corp. | | 615,435 | | | | 29,289 |

See accompanying notes which are an integral part of the financial statements.

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| FINANCIALS – continued | | | | | | |

| Commercial Banks – continued | | | | | | |

| Wells Fargo & Co. | | 24,700 | | | | $ 1,447 |

| Woori Finance Holdings Co. Ltd. | | 57,010 | | | | 825 |

| | | | | | | 189,235 |

| Consumer Finance – 0.2% | | | | | | |

| Capital One Financial Corp. | | 79,400 | | | | 6,314 |

| Credit Saison Co. Ltd. | | 27,100 | | | | 1,197 |

| MBNA Corp. | | 271,600 | | | | 6,692 |

| Nissin Co. Ltd. | | 592,300 | | | | 793 |

| Nissin Co. Ltd. New (a) | | 592,300 | | | | 778 |

| ORIX Corp. | | 14,600 | | | | 2,655 |

| SFCG Co. Ltd. | | 6,740 | | | | 1,752 |

| UCS Co. Ltd. | | 10,000 | | | | 360 |

| | | | | | | 20,541 |

| Diversified Financial Services – 0.9% | | | | | | |

| Banca Italease Spa | | 287,100 | | | | 6,902 |

| Citigroup, Inc. | | 1,630,366 | | | | 74,214 |

| Deutsche Boerse AG | | 25,546 | | | | 2,442 |

| Gemina Spa (a) | | 791,400 | | | | 1,983 |

| ING Groep NV (Certificaten Van Aandelen) | | 135,100 | | | | 4,025 |

| OMX AB (a)(d) | | 153,600 | | | | 1,898 |

| | | | | | | 91,464 |

| Insurance – 5.1% | | | | | | |

| ACE Ltd. | | 623,200 | | | | 29,334 |

| AFLAC, Inc. | | 114,000 | | | | 5,164 |

| Allianz AG (Reg.) | | 63,200 | | | | 8,538 |

| AMBAC Financial Group, Inc. | | 385,300 | | | | 27,765 |

| American International Group, Inc. | | 4,509,769 | | | | 279,425 |

| Amlin PLC | | 857,100 | | | | 3,150 |

| AMP Ltd. | | 139,800 | | | | 793 |

| AXA SA | | 122,100 | | | | 3,361 |

| Baloise Holdings AG (Reg.) | | 31,017 | | | | 1,558 |

| Chaucer Holdings PLC | | 2,793,400 | | | | 2,649 |

| Hartford Financial Services Group, Inc. | | 1,067,680 | | | | 82,393 |

| MBIA, Inc. | | 406,900 | | | | 24,666 |

| MetLife, Inc. | | 712,300 | | | | 35,494 |

| Ping An Insurance (Group) Co. of China, Ltd. (H Shares) | | 489,500 | | | | 855 |

| Prudential PLC | | 460,600 | | | | 4,182 |

| QBE Insurance Group Ltd. | | 117,685 | | | | 1,677 |

| Skandia Foersaekrings AB | | 660,100 | | | | 3,441 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | |

| |

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| FINANCIALS – continued | | | | | | |

| Insurance – continued | | | | | | |

| Sompo Japan Insurance, Inc | | 181,000 | | | | $ 2,414 |

| T&D Holdings, Inc. | | 30,500 | | | | 1,829 |

| | | | | | | 518,688 |

| Real Estate 0.1% | | | | | | |

| Ascendas Real Estate Investment Trust (A REIT) | | 529,200 | | | | 685 |

| British Land Co. PLC | | 249,400 | | | | 4,139 |

| CapitaLand Ltd. | | 549,000 | | | | 1,019 |

| China Overseas Land & Investment Ltd. | | 2,878,000 | | | | 863 |

| Japan Logistics Fund, Inc | | 121 | | | | 816 |

| KK daVinci Advisors (a) | | 145 | | | | 556 |

| Shun Tak Holdings Ltd. | | 1,374,000 | | | | 1,142 |

| Sumitomo Realty & Development Co. Ltd. | | 69,000 | | | | 1,030 |

| Wharf Holdings Ltd. | | 253,000 | | | | 987 |

| | | | | | | 11,237 |

| Thrifts & Mortgage Finance – 0.8% | | | | | | |

| Fannie Mae | | 1,316,100 | | | | 58,988 |

| MGIC Investment Corp. | | 397,400 | | | | 25,513 |

| Washington Mutual, Inc. | | 12,700 | | | | 498 |

| | | | | | | 84,999 |

| |

| TOTAL FINANCIALS | | | | | | 1,087,571 |

| |

| HEALTH CARE – 8.4% | | | | | | |

| Biotechnology – 0.0% | | | | | | |

| Actelion Ltd. (Reg.) (a) | | 17,309 | | | | 1,866 |

| Health Care Equipment & Supplies – 0.1% | | | | | | |

| Axis Shield PLC (a) | | 311,700 | | | | 1,799 |

| Cochlear Ltd. | | 13,800 | | | | 413 |

| Miraca Holdings, Inc. | | 48,500 | | | | 1,123 |

| Phonak Holding AG | | 92,775 | | | | 3,975 |

| Pihsiang Machinery Manufacturing Co. | | 183,820 | | | | 297 |

| ResMed, Inc. CHESS Depositary Interests (a) | | 180,600 | | | | 716 |

| Sysmex Corp. | | 9,200 | | | | 321 |

| Sysmex Corp. New (a) | | 9,200 | | | | 319 |

| Terumo Corp. | | 31,000 | | | | 1,004 |

| | | | | | | 9,967 |

| Health Care Providers & Services – 3.4% | | | | | | |

| Cardinal Health, Inc. | | 4,970,480 | | | | 315,320 |

See accompanying notes which are an integral part of the financial statements.

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| HEALTH CARE – continued | | | | | | |

| Health Care Providers & Services – continued | | | | | | |

| Sonic Healthcare Ltd. | | 94,800 | | | | $ 1,121 |

| UnitedHealth Group, Inc. | | 567,000 | | | | 31,865 |

| | | | | | | 348,306 |

| Pharmaceuticals – 4.9% | | | | | | |

| Astellas Pharma, Inc. | | 52,900 | | | | 2,004 |

| AstraZeneca PLC sponsored ADR | | 136,300 | | | | 6,420 |

| Chugai Pharmaceutical Co. Ltd. | | 53,900 | | | | 1,035 |

| Eisai Co. Ltd. | | 26,200 | | | | 1,127 |

| GlaxoSmithKline PLC | | 277,500 | | | | 7,115 |

| GlaxoSmithKline PLC sponsored ADR | | 70,500 | | | | 3,615 |

| Johnson & Johnson | | 1,610,900 | | | | 101,938 |

| Novartis AG: | | | | | | |

| (Reg.) | | 199,589 | | | | 10,179 |

| sponsored ADR | | 34,800 | | | | 1,775 |

| Pfizer, Inc. | | 5,399,100 | | | | 134,816 |

| Sanofi-Aventis sponsored ADR | | 63,100 | | | | 2,622 |

| Takeda Pharamaceutical Co. Ltd. | | 30,100 | | | | 1,805 |

| Tong Ren Tang Technologies Co. Ltd. (H Shares) | | 218,000 | | | | 415 |

| Wyeth | | 4,720,900 | | | | 218,436 |

| | | | | | | 493,302 |

| |

| TOTAL HEALTH CARE | | | | | | 853,441 |

| |

| INDUSTRIALS – 4.8% | | | | | | |

| Aerospace & Defense – 0.6% | | �� | | | | |

| BAE Systems PLC | | 665,200 | | | | 4,032 |

| Honeywell International, Inc. | | 645,970 | | | | 24,224 |

| Lockheed Martin Corp. | | 287,700 | | | | 17,561 |

| United Technologies Corp. | | 366,200 | | | | 18,984 |

| | | | | | | 64,801 |

| Building Products 0.0% | | | | | | |

| Daikin Industries Ltd. | | 31,700 | | | | 855 |

| Commercial Services & Supplies – 0.2% | | | | | | |

| ChoicePoint, Inc. (a) | | 276,856 | | | | 11,952 |

| Citiraya Industries Ltd. (a) | | 716,000 | | | | 0 |

| Downer EDI Ltd. | | 345,361 | | | | 1,591 |

| INSUN ENT Co. Ltd. | | 22,600 | | | | 301 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | |

| |

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| INDUSTRIALS – continued | | | | | | |

| Commercial Services & Supplies – continued | | | | | | |

| S1 Corp. | | 12,770 | | | | $ 616 |

| Taiwan Secom Co. | | 312,120 | | | | 445 |

| | | | | | | 14,905 |

| Construction & Engineering – 0.1% | | | | | | |

| Bilfinger & Berger Bau AG | | 42,700 | | | | 2,290 |

| Chiyoda Corp. | | 76,000 | | | | 1,409 |

| Commuture Corp. | | 89,000 | | | | 786 |

| Doosan Heavy Industries & Construction Co. Ltd. | | 54,260 | | | | 1,024 |

| Hyundai Engineering & Construction Co. Ltd. (a) | | 23,870 | | | | 755 |

| Keangnam Enterprises (a) | | 33,600 | | | | 308 |

| Paul Y ITC Construction Holdings Ltd. | | 6,594,000 | | | | 1,267 |

| United Group Ltd. | | 163,060 | | | | 1,317 |

| | | | | | | 9,156 |

| Electrical Equipment – 0.0% | | | | | | |

| Dongfang Electrical Machinery Co. Ltd. (H Shares) | | 110,000 | | | | 121 |

| Kumho Electric Co. Ltd. | | 18,017 | | | | 1,162 |

| Kumho Electric Co. Ltd. rights 11/3/05 (a) | | 1,481 | | | | 33 |

| Shanghai Electric (Group) Corp. (H Shares) | | 1,914,000 | | | | 648 |

| Sumitomo Electric Industries Ltd. | | 98,400 | | | | 1,336 |

| | | | | | | 3,300 |

| Industrial Conglomerates – 3.2% | | | | | | |

| 3M Co. | | 873,200 | | | | 64,058 |

| General Electric Co. | | 5,409,660 | | | | 182,143 |

| Hutchison Whampoa Ltd. | | 159,000 | | | | 1,645 |

| Keppel Corp. Ltd. | | 203,000 | | | | 1,524 |

| Shanghai Industrial Holdings Ltd. Class H | | 251,000 | | | | 508 |

| Tyco International Ltd. | | 2,729,400 | | | | 76,014 |

| | | | | | | 325,892 |

| Machinery – 0.5% | | | | | | |

| Bradken Ltd. | | 456,996 | | | | 1,223 |

| Hyundai Mipo Dockyard Co. Ltd. | | 9,400 | | | | 676 |

| Ingersoll-Rand Co. Ltd. Class A | | 908,200 | | | | 34,720 |

| Kinik Co. | | 17,250 | | | | 37 |

| Koyo Seiko Co. Ltd. | | 65,000 | | | | 987 |

| Lung Kee (Bermuda) Holdings | | 164,000 | | | | 125 |

| MAN AG | | 78,800 | | | | 4,043 |

| Metso Corp. | | 171,200 | | | | 4,345 |

| Nittoku Engineering Co. Ltd. | | 54,000 | | | | 447 |

| Taewoong Co. Ltd. | | 39,300 | | | | 544 |

See accompanying notes which are an integral part of the financial statements.

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| INDUSTRIALS – continued | | | | | | |

| Machinery – continued | | | | | | |

| TSM Tech Co. Ltd. | | 70,400 | | | | $ 874 |

| Weichai Power Co. Ltd. (H Shares) | | 271,000 | | | | 603 |

| | | | | | | 48,624 |

| Marine – 0.0% | | | | | | |

| Alexander & Baldwin, Inc. | | 74,700 | | | | 3,977 |

| Road & Rail 0.0% | | | | | | |

| East Japan Railway Co | | 298 | | | | 1,713 |

| Hamakyorex Co. Ltd. | | 53,500 | | | | 1,732 |

| | | | | | | 3,445 |

| Trading Companies & Distributors – 0.1% | | | | | | |

| Mitsubishi Corp. | | 129,500 | | | | 2,574 |

| Mitsui & Co. Ltd. | | 197,000 | | | | 2,484 |

| | | | | | | 5,058 |

| Transportation Infrastructure 0.1% | | | | | | |

| ConnectEast Group unit | | 1,794,807 | | | | 1,109 |

| Kamigumi Co. Ltd. | | 87,000 | | | | 699 |

| Macquarie Airports unit | | 272,935 | | | | 683 |

| Macquarie Infrastructure Group unit | | 819,620 | | | | 2,507 |

| | | | | | | 4,998 |

| |

| TOTAL INDUSTRIALS | | | | | | 485,011 |

| |

| INFORMATION TECHNOLOGY – 8.6% | | | | | | |

| Communications Equipment – 1.7% | | | | | | |

| Cisco Systems, Inc. (a) | | 5,679,914 | | | | 101,841 |

| Comverse Technology, Inc. (a) | | 315,700 | | | | 8,293 |

| Lightron Fiber-Optic Devices, Inc. | | 46,100 | | | | 294 |

| Motorola, Inc. | | 126,400 | | | | 2,792 |

| Nokia Corp. sponsored ADR | | 2,113,700 | | | | 35,743 |

| QUALCOMM, Inc. | | 292,200 | | | | 13,076 |

| TANDBERG ASA | | 144,400 | | | | 1,929 |

| TANDBERG Television ASA (a) | | 631,400 | | | | 8,216 |

| | | | | | | 172,184 |

| Computers & Peripherals – 1.4% | | | | | | |

| Acer, Inc. | | 465,340 | | | | 925 |

| Dell, Inc. (a) | | 1,632,900 | | | | 55,845 |

| EMC Corp. (a) | | 559,000 | | | | 7,233 |

| Fujitsu Ltd. | | 252,000 | | | | 1,672 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | |

| |

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| INFORMATION TECHNOLOGY – continued | | | | | | |

| Computers & Peripherals – continued | | | | | | |

| GES International Ltd. | | 927,000 | | $ | | 501 |

| Hanny Holdings Ltd. | | 970,000 | | | | 500 |

| Hewlett-Packard Co. | | 302,100 | | | | 8,821 |

| International Business Machines Corp. | | 806,800 | | | | 64,721 |

| | | | | | | 140,218 |

| Electronic Equipment & Instruments – 0.3% | | | | | | |

| Flextronics International Ltd. (a) | | 654,400 | | | | 8,409 |

| Hon Hai Precision Industry Co. Ltd. (Foxconn) | | 126,511 | | | | 589 |

| Hoya Corp. | | 12,400 | | | | 415 |

| Hoya Corp. New | | 37,200 | | | | 1,274 |

| Jabil Circuit, Inc. (a) | | 92,400 | | | | 2,857 |

| KH Vatec Co. Ltd. | | 27,065 | | | | 668 |

| Kingboard Chemical Holdings Ltd. | | 458,000 | | | | 1,142 |

| Nidec Corp. | | 8,100 | | | | 485 |

| Nidec Corp. New | | 6,900 | | | | 408 |

| Nippon Chemi-con Corp. | | 190,000 | | | | 1,087 |

| Nippon Electric Glass Co. Ltd. | | 223,000 | | | | 4,046 |

| Optimax Technology Corp. | | 250,910 | | | | 408 |

| Phoenix Precision Technology Corp. | | 572,000 | | | | 696 |

| SFA Engineering Corp. | | 70,700 | | | | 1,755 |

| Yageo Corp. (a) | | 1,903,000 | | | | 645 |

| Yaskawa Electric Corp. (a) | | 108,000 | | | | 833 |

| | | | | | | 25,717 |

| Internet Software & Services – 0.1% | | | | | | |

| Dip Corp. (a) | | 204 | | | | 326 |

| Easynet Group PLC (a) | | 1,797,900 | | | | 3,061 |

| livedoor Co. Ltd. (a) | | 289,061 | | | | 1,146 |

| NHN Corp. (a) | | 18,492 | | | | 3,145 |

| Softbank Corp. | | 61,500 | | | | 3,437 |

| Telewave, Inc. | | 135 | | | | 739 |

| Yahoo! Japan Corp | | 249 | | | | 294 |

| Yahoo! Japan Corp. New | | 249 | | | | 298 |

| | | | | | | 12,446 |

| IT Services – 0.0% | | | | | | |

| Computershare Ltd. | | 389,900 | | | | 1,963 |

| Office Electronics – 0.0% | | | | | | |

| Konica Minolta Holdings, Inc. | | 98,000 | | | | 897 |

| Semiconductors & Semiconductor Equipment – 1.7% | | | | | | |

| Advanced Semiconductor Engineering, Inc. | | 877,000 | | | | 592 |

See accompanying notes which are an integral part of the financial statements.

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| INFORMATION TECHNOLOGY – continued | | | | | | |

| Semiconductors & Semiconductor Equipment – continued | | | | | | |

| Analog Devices, Inc. | | 85,000 | | | | $ 3,157 |

| Applied Materials, Inc. | | 1,784,300 | | | | 30,262 |

| ASM Pacific Technology Ltd. | | 117,000 | | | | 569 |

| Chipbond Technology Corp. | | 615,040 | | | | 778 |

| Core Logic, Inc. | | 23,094 | | | | 863 |

| Holtek Semiconductor, Inc. | | 436,784 | | | | 505 |

| Intel Corp. | | 3,418,300 | | | | 84,261 |

| KLA Tencor Corp. | | 207,800 | | | | 10,132 |

| Lam Research Corp. (a) | | 302,400 | | | | 9,214 |

| Linear Technology Corp. | | 77,050 | | | | 2,896 |

| MediaTek, Inc. | | 69,300 | | | | 654 |

| Novellus Systems, Inc. (a) | | 191,300 | | | | 4,798 |

| Phoenix PDE Co. Ltd. | | 158,600 | | | | 830 |

| Samsung Electronics Co. Ltd. | | 5,570 | | | | 3,139 |

| Sanken Electric Co. Ltd. | | 45,000 | | | | 520 |

| Solomon Systech Ltd. | | 2,968,000 | | | | 1,071 |

| Taiwan Semiconductor Manufacturing Co. Ltd. sponsored ADR | | 637,318 | | | | 5,239 |

| United Microelectronics Corp. | | 1,857,327 | | | | 1,192 |

| United Microelectronics Corp. sponsored ADR | | 1,862,500 | | | | 6,705 |

| Xilinx, Inc. | | 52,800 | | | | 1,470 |

| | | | | | | 168,847 |

| Software 3.4% | | | | | | |

| BEA Systems, Inc. (a) | | 1,490,652 | | | | 13,386 |

| Intelligent Wave, Inc. | | 538 | | | | 1,537 |

| KOEI Co. Ltd. | | 8,400 | | | | 208 |

| Microsoft Corp. | | 9,722,015 | | | | 250,147 |

| NCsoft Corp. (a) | | 8,880 | | | | 731 |

| SAP AG | | 20,700 | | | | 3,588 |

| Springsoft, Inc. | | 450,149 | | | | 757 |

| Symantec Corp. (a) | | 3,454,272 | | | | 78,274 |

| Trend Micro, Inc. | | 21,000 | | | | 669 |

| | | | | | | 349,297 |

| |

| TOTAL INFORMATION TECHNOLOGY | | | | | | 871,569 |

| |

| MATERIALS 0.5% | | | | | | |

| Chemicals – 0.4% | | | | | | |

| BASF AG | | 185,600 | | | | 13,994 |

| Bayer AG | | 199,000 | | | | 7,323 |

| Ise Chemical Corp. | | 107,000 | | | | 597 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | |

| |

Common Stocks continued

| | | | | | |

| | | Shares | | Value (Note 1) |

| | | | | (000s) |

| |

| MATERIALS – continued | | | | | | |

| Chemicals – continued | | | | | | |

| JSR Corp. | | 44,400 | | | | $ 930 |

| Kaneka Corp. | | 21,000 | | | | 276 |

| Nitto Denko Corp. | | 34,500 | | | | 1,956 |

| Praxair, Inc. | | 278,900 | | | | 13,368 |

| Syngenta AG (Switzerland) | | 53,851 | | | | 5,639 |

| Teijin Ltd | | 235,000 | | | | 1,380 |

| | | | | | | 45,463 |

| Containers & Packaging – 0.0% | | | | | | |

| Vision Grande Group Holdings Ltd. | | 738,000 | | | | 469 |

| Metals & Mining – 0.1% | | | | | | |

| BHP Billiton Ltd. | | 325,200 | | | | 5,558 |

| Newcrest Mining Ltd. | | 103,500 | | | | 1,656 |

| | | | | | | 7,214 |

| |

| TOTAL MATERIALS | | | | | | 53,146 |

| |

| TELECOMMUNICATION SERVICES – 3.4% | | | | | | |

| Diversified Telecommunication Services – 3.1% | | | | | | |

| BellSouth Corp. | | 1,561,700 | | | | 41,073 |

| BT Group PLC | | 987,500 | | | | 3,914 |

| Completel Europe NV (a) | | 73,475 | | | | 3,626 |

| FASTWEB Spa (a) | | 101,500 | | | | 4,547 |

| Qwest Communications International, Inc. (a) | | 7,043,600 | | | | 28,879 |

| SBC Communications, Inc. | | 8,645,600 | | | | 207,235 |

| Telefonica SA sponsored ADR | | 50,232 | | | | 2,477 |

| Verizon Communications, Inc. | | 858,000 | | | | 28,048 |

| | | | | | | 319,799 |

| Wireless Telecommunication Services – 0.3% | | | | | | |

| Far EasTone Telecommunications Co. Ltd. | | 587,150 | | | | 665 |

| Millicom International Cellular SA unit (a) | | 209,000 | | | | 3,857 |

| Sprint Nextel Corp. | | 631,566 | | | | 15,019 |

| Vodafone Group PLC | | 2,542,200 | | | | 6,602 |

| Vodafone Group PLC sponsored ADR | | 196,200 | | | | 5,095 |

| | | | | | | 31,238 |

| |

| TOTAL TELECOMMUNICATION SERVICES | | | | | | 351,037 |

See accompanying notes which are an integral part of the financial statements.

Common Stocks continued

| | | | | | | | | | |

| | | | | | | Shares | | Value (Note 1) |

| | | | | | | | | (000s) |

| |

| UTILITIES – 0.1% | | | | | | | | | | |

| Electric Utilities – 0.1% | | | | | | | | | | |

| E.ON AG | | | | | | 80,400 | | | | $ 7,417 |

| Gas Utilities 0.0% | | | | | | | | | | |

| Hong Kong & China Gas Co. Ltd. | | | | | | 426,000 | | | | 879 |

| Xinao Gas Holdings Ltd. | | | | | | 722,000 | | | | 568 |

| | | | | | | | | | | 1,447 |

| |

| TOTAL UTILITIES | | | | | | | | | | 8,864 |

| |

| TOTAL COMMON STOCKS | | | | | | | | | | |

| (Cost $4,550,391) | | | | | | | | | | 5,022,028 |

| |

| Nonconvertible Preferred Stocks 0.1% | | | | | | | | |

| |

| CONSUMER DISCRETIONARY – 0.1% | | | | | | | | | | |

| Automobiles – 0.1% | | | | | | | | | | |

| Porsche AG (non-vtg.) | | | | | | 7,130 | | | | 5,484 |

| TOTAL NONCONVERTIBLE PREFERRED STOCKS | | | | | | | | |

| (Cost $4,680) | | | | | | | | | | 5,484 |

| |

| Convertible Bonds 0.0% | | | | | | | | | | |

| | | | | | | Principal | | | | |

| | | | | | | Amount (000s) | | | | |

| |

| INFORMATION TECHNOLOGY – 0.0% | | | | | | | | | | |

| Communications Equipment – 0.0% | | | | | | | | | | |

| CIENA Corp. 3.75% 2/1/08 | | | | | | $ 2,490 | | | | 2,275 |

| TOTAL CONVERTIBLE BONDS | | | | | | | | | | |

| (Cost $2,115) | | | | | | | | | | 2,275 |

| |

| U.S. Treasury Obligations 0.3% | | | | | | | | | | |

| |

| U.S. Treasury Bills, yield at date of purchase 3.17% to | | | | | | | | |

| 3.47% 10/13/05 to 12/22/05 (e) | | | | | | | | | | |

| (Cost $31,446) | | | | | | 31,600 | | | | 31,461 |

See accompanying notes which are an integral part of the financial statements.

| Investments continued | | | | | | | | |

| |

Fixed Income Funds 31.7%

| | | | | | | | |

| | | | | Shares | | Value (Note 1) |

| | | | | | | (000s) |

| Fidelity Floating Rate Central Investment Portfolio (b) | | 1,816,765 | | | | $ 182,785 |

| Fidelity High Income Central Investment Portfolio 1 (b) | | 5,570,762 | | | | 542,035 |

| Fidelity Tactical Income Central Investment Portfolio (b) | | 25,355,003 | | | | 2,504,314 |

| TOTAL FIXED INCOME FUNDS | | | | | | | | |

| (Cost $3,190,654) | | | | | | | | 3,229,134 |

| Money Market Funds 18.5% | | | | | | |

| Fidelity Cash Central Fund, 3.82% (b) | | | | 1,461,708,632 | | | | 1,461,709 |

| Fidelity Money Market Central Fund, 3.82% (b) | | 425,013,442 | | | | 425,013 |

| Fidelity Securities Lending Cash Central Fund, | | | | | | |

| 3.84% (b)(c) | | | | 190,575 | | | | 191 |

| TOTAL MONEY MARKET FUNDS | | | | | | | | |

| (Cost $1,886,913) | | | | | | | | 1,886,913 |

| TOTAL INVESTMENT PORTFOLIO 99.9% | | | | | | |

| (Cost $9,666,199) | | | | | | 10,177,295 |

| |

| NET OTHER ASSETS – 0.1% | | | | | | | | 12,652 |

| NET ASSETS 100% | | | | | | $ 10,189,947 |

| |

| Futures Contracts | | | | | | | | |

| | | Expiration | | Underlying | | Unrealized |

| | | Date | | Face Amount | | Appreciation/ |

| | | | | at Value (000s) | | (Depreciation) |

| | | | | | | (000s) |

| Purchased | | | | | | | | |

| Equity Index Contracts | | | | | | | | |

| 1,902 S&P 500 Index Contracts | | Dec. 2005 | | $ 586,910 | | | | $ (3,608) |

| |

| The face value of futures purchased as a percentage of net assets – 5.8% | | | | |

See accompanying notes which are an integral part of the financial statements.

Legend

(a) Non-income producing

(b) Affiliated fund that is available only to

investment companies and other

accounts managed by Fidelity

Investments. The rate quoted is the

annualized seven-day yield of the fund

at period end. A complete unaudited

listing of the money market fund’s

holdings as of its most recent quarter

end is available upon request. A

complete unaudited listing of the

fixed-income central fund’s holdings is

provided at the end of this report.

(c) Investment made with cash collateral

received from securities on loan.

(d) Security or a portion of the security is on

loan at period end.

(e) Security or a portion of the security was

pledged to cover margin requirements

for futures contracts. At the period end,

the value of securities pledged

amounted to $31,461,000.

|

Other Information

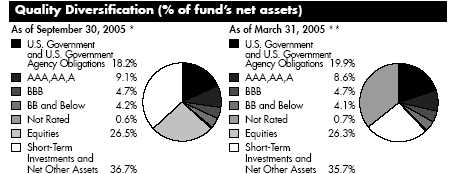

The composition of credit quality ratings as a percentage of net assets is as follows (ratings are unaudited):

| U.S.Government and | | |

| U.S.Government Agency | | |

| Obligations | | 11.8% |

| AAA, AA, A | | 7.5% |

| BBB | | 4.0% |

| BB | | 3.4% |

| B | | 3.2% |

| CCC, CC, C | | 0.6% |

| Not Rated | | 0.6% |

| Equities | | 55.1% |

| Short Term Investments and Net | | |

| Other Assets | | 13.8% |

| | | 100.0% |

We have used ratings from Moody’s® Investors Services, Inc. Where Moody’s ratings are not available, we have used S&P® ratings. Percentages are adjusted for the effect of futures contracts, if applicable.

The information in the above table is based on the combined investments of the fund and its pro-rata share of the investments of Fidelity’s fixed-income Central Funds.

See accompanying notes which are an integral part of the financial statements.

A-25 Annual Report

| Financial Statements | | | | | | | | |

| |

| |

| Statement of Assets and Liabilities | | | | | | | | |

| Amounts in thousands (except per share amount) | | | | | | September 30, 2005 |

| |

| Assets | | | | | | | | |

| Investment in securities, at value (including securities | | | | | | | | |

| loaned of $182) (cost $9,666,199) See | | | | | | | | |

| accompanying schedule | | | | | | $ | | 10,177,295 |

| Receivable for investments sold | | | | | | | | 27,071 |

| Receivable for fund shares sold | | | | | | | | 5,639 |

| Dividends receivable | | | | | | | | 5,711 |

| Interest receivable | | | | | | | | 20,501 |

| Receivable for daily variation on futures contracts | | | | | | | | 1,189 |

| Prepaid expenses | | | | | | | | 6 |

| Other affiliated receivables | | | | | | | | 121 |

| Other receivables | | | | | | | | 264 |

| Total assets | | | | | | | | 10,237,797 |

| |

| Liabilities | | | | | | | | |

| Payable for investments purchased | | $ | | 14,589 | | | | |

| Payable for fund shares redeemed | | | | 26,471 | | | | |

| Accrued management fee | | | | 4,450 | | | | |

| Other affiliated payables | | | | 2,010 | | | | |

| Other payables and accrued expenses | | | | 139 | | | | |

| Collateral on securities loaned, at value | | | | 191 | | | | |

| Total liabilities | | | | | | | | 47,850 |

| |

| Net Assets | | | | | | $ | | 10,189,947 |

| Net Assets consist of: | | | | | | | | |

| Paid in capital | | | | | | $ | | 9,418,618 |

| Undistributed net investment income | | | | | | | | 70,280 |

| Accumulated undistributed net realized gain (loss) on | | | | | | | | |

| investments and foreign currency transactions | | | | | | | | 193,574 |

| Net unrealized appreciation (depreciation) on | | | | | | | | |

| investments and assets and liabilities in foreign | | | | | | | | |

| currencies | | | | | | | | 507,475 |

| Net Assets, for 625,943 shares outstanding | | | | | | $ | | 10,189,947 |

| Net Asset Value, offering price and redemption price per | | | | | | |

| share ($10,189,947 ÷ 625,943 shares) | | | | | | $ | | 16.28 |

See accompanying notes which are an integral part of the financial statements.

| Statement of Operations | | | | | | |

| Amounts in thousands | | | | Year ended September 30, 2005 |

| |

| Investment Income | | | | | | |

| Dividends | | | | $ | | 94,688 |

| Special Dividends | | | | | | 28,846 |

| Interest | | | | | | 222,176 |

| Security lending | | | | | | 306 |

| Total income | | | | | | 346,016 |

| |

| Expenses | | | | | | |

| Management fee | | $ | | 55,269 | | |

| Transfer agent fees | | | | 19,969 | | |

| Accounting and security lending fees | | | | 1,337 | | |

| Independent trustees’ compensation | | | | 53 | | |

| Appreciation in deferred trustee compensation account | | | | 7 | | |

| Custodian fees and expenses | | | | 352 | | |

| Registration fees | | | | 53 | | |

| Audit | | | | 215 | | |

| Legal | | | | 37 | | |

| Miscellaneous | | | | 138 | | |

| Total expenses before reductions | | | | 77,430 | | |

| Expense reductions | | | | (1,250) | | 76,180 |

| |

| Net investment income (loss) | | | | | | 269,836 |

| Realized and Unrealized Gain (Loss) | | | | | | |

| Net realized gain (loss) on: | | | | | | |

| Investment securities | | | | 205,425 | | |

| Foreign currency transactions | | | | 99 | | |

| Futures contracts | | | | 42,752 | | |

| Swap agreements | | | | 372 | | |

| Total net realized gain (loss) | | | | | | 248,648 |

| Change in net unrealized appreciation (depreciation) on: | | | | |

| Investment securities | | | | 214,359 | | |

| Assets and liabilities in foreign currencies | | | | (106) | | |

| Futures contracts | | | | 1,260 | | |

| Swap agreements | | | | (542) | | |

| Total change in net unrealized appreciation | | | | | | |

| (depreciation) | | | | | | 214,971 |

| Net gain (loss) | | | | | | 463,619 |

| Net increase (decrease) in net assets resulting from | | | | | | |

| operations | | | | $ | | 733,455 |

See accompanying notes which are an integral part of the financial statements.

| Financial Statements continued | | | | | | | | |

| |

| |

| Statement of Changes in Net Assets | | | | | | | | |

| | | | | Year ended | | | | Year ended |

| | | | | September 30, | | | | September 30, |

| Amounts in thousands | | | | 2005 | | | | 2004 |

| Increase (Decrease) in Net Assets | | | | | | | | |

| Operations | | | | | | | | |

| Net investment income (loss) | | | | $ 269,836 | | | | $ 237,534 |

| Net realized gain (loss) | | | | 248,648 | | | | 133,333 |

| Change in net unrealized appreciation (depreciation) . | | | | 214,971 | | | | 279,447 |

| Net increase (decrease) in net assets resulting | | | | | | | | |

| from operations | | | | 733,455 | | | | 650,314 |

| Distributions to shareholders from net investment income . | | | | (267,576) | | | | (193,241) |

| Share transactions | | | | | | | | |

| Proceeds from sales of shares | | | | 912,849 | | | | 1,305,615 |

| Reinvestment of distributions | | | | 260,003 | | | | 187,749 |

| Cost of shares redeemed | | | | (2,352,097) | | | | (1,859,651) |

| Net increase (decrease) in net assets resulting from | | | | | | | | |

| share transactions | | | | (1,179,245) | | | | (366,287) |

| Total increase (decrease) in net assets | | | | (713,366) | | | | 90,786 |

| |

| Net Assets | | | | | | | | |

| Beginning of period | | | | 10,903,313 | | | | 10,812,527 |

| End of period (including undistributed net investment | | | | | | | | |

| income of $70,280 and undistributed net investment | | | | | | | | |

| income of $69,579, respectively) | | | | $ 10,189,947 | | | | $ 10,903,313 |

| |

| Other Information | | | | | | | | |

| Shares | | | | | | | | |

| Sold | | | | 56,990 | | | | 83,085 |

| Issued in reinvestment of distributions | | | | 16,382 | | | | 11,877 |

| Redeemed | | | | (147,136) | | | | (118,489) |

| Net increase (decrease) | | | | (73,764) | | | | (23,527) |

See accompanying notes which are an integral part of the financial statements.

| Financial Highlights | | | | | | | | | | |

| |

| Years ended September 30, | | 2005 | | 2004 | | 2003 | | 2002 | | 2001 |

| Selected Per Share Data | | | | | | | | | | |

| Net asset value, beginning of | | | | | | | | | | |

| period | | $ 15.58 | | $ 14.95 | | $ 13.01 | | $ 14.72 | | $ 19.11 |

| Income from Investment | | | | | | | | | | |

| Operations | | | | | | | | | | |

| Net investment income (loss)B | | 41D | | .33 | | .40 | | .49F | | .59 |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) | | 69 | | .57 | | 1.95 | | (1.62)F | | (3.03) |

| Total from investment operations | | 1.10 | | .90 | | 2.35 | | (1.13) | | (2.44) |

| Distributions from net investment | | | | | | | | | | |

| income | | (.40) | | (.27) | | (.41) | | (.58) | | (.61) |

| Distributions from net realized | | | | | | | | | | |

| gain | | — | | — | | — | | | | (1.34) |

| Total distributions | | (.40) | | (.27) | | (.41) | | (.58) | | (1.95) |

| Net asset value, end of period | | $ 16.28 | | $ 15.58 | | $ 14.95 | | $ 13.01 | | $ 14.72 |

| Total ReturnA | | 7.15% | | 6.00% | | 18.26% | | (8.17)% | | (13.63)% |

| Ratios to Average Net AssetsC,E | | | | | | | | | | |

| Expenses before expense | | | | | | | | | | |

| reductions | | 73% | | .74% | | .75% | | .75% | | .73% |

| Expenses net of voluntary | | | | | | | | | | |

| waivers, if any | | 73% | | .74% | | .75% | | .75% | | .73% |

| Expenses net of all reductions | | 72% | | .73% | | .74% | | .73% | | .71% |

| Net investment income (loss) | | 2.55%D | | 2.12% | | 2.82% | | 3.31%F | | 3.51% |

| Supplemental Data | | | | | | | | | | |

| Net assets, end of period (in | | | | | | | | | | |

| millions) | | $10,190 | | $10,903 | | $10,813 | | $ 9,594 | | $11,177 |

| Portfolio turnover rate | | 32% | | 78% | | 120% | | 129% | | 133% |

A Total returns would have been lower had certain expenses not been reduced during the periods shown.

B Calculated based on average shares outstanding during the period.

C Amounts do not include the activity of the underlying funds.

D Investment income per share reflects a special dividend which amounted to $.04 per share. Excluding the special dividend, the ratio of net

investment income to average net assets would have been 2.28% .

E Expense ratios reflect operating expenses of the fund. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or

reductions from brokerage service arrangements or other expense offset arrangements and do not represent the amount paid by the fund during

periods when reimbursements or reductions occur. Expenses net of any voluntary waivers reflect expenses after reimbursement by the investment

adviser but prior to reductions from brokerage service arrangements or other expense offset arrangements. Expenses net of all reductions repre

sent the net expenses paid by the fund.

F Effective October 1, 2001, the fund adopted the provisions of the AICPA Audit and Accounting Guide for Investment Companies and began

amortizing premium and discount on all debt securities. Per share data and ratios for periods prior to adoption have not been restated to reflect

this change.

|

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements

| | For the period ended September 30, 2005

(Amounts in thousands except ratios)

|

1. Significant Accounting Policies.

Fidelity Asset Manager (the fund) is a fund of Fidelity Charles Street Trust (the trust) and is authorized to issue an unlimited number of shares. The trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open end management investment company organized as a Massachusetts business trust. The fund may invest in affiliated money market central funds (Money Market Central Funds) and fixed income Central Investment Portfolios (CIPs), collectively referred to as Central Funds, which are open end investment companies available to investment companies and other accounts managed by Fidelity Management & Research Company (FMR) and its affiliates. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which require manage ment to make certain estimates and assumptions at the date of the financial statements. The following summarizes the significant accounting policies of the fund, which are also consistently followed by the Central Funds:

Security Valuation. Net asset value per share (NAV calculation) is calculated as of the close of business of the New York Stock Exchange, normally 4:00 p.m. Eastern time. Equity securities, including restricted securities, for which market quotations are available are valued at the last sale price or official closing price (closing bid price or last evaluated quote if no sale has occurred) on the primary market or exchange on which they trade. Debt securities, including restricted securities, for which quotations are readily available are valued at their most recent bid prices (sales prices if the principal market is an exchange) in the principal market in which such securities are normally traded, as determined by recognized dealers in such securities, or securities are valued on the basis of information provided by a pricing service. Pricing services use valuation matrices that incorporate both dealer supplied valuations and valuation models. If prices are not readily available or do not accurately reflect fair value for a security, or if a security’s value has been materially affected by events occurring after the close of the exchange or market on which the security is principally traded, that security may be valued by another method that the Board of Trustees believes accurately reflects fair value. A security’s valuation may differ depending on the method used for determining value. Price movements in futures contracts and ADRs, market and trading trends, the bid/ask quotes of brokers and off exchange institutional trading may be reviewed in the course of making a good faith determination of a security’s fair value. Short term securi ties with remaining maturities of sixty days or less for which quotations are not readily available are valued on the basis of amortized cost. Investments in open end investment companies, including Central Funds, are valued at their net asset value each business day.

1. Significant Accounting Policies continued

Foreign Currency. The fund uses foreign currency contracts to facilitate transactions in foreign denominated securities. Losses from these transactions may arise from changes in the value of the foreign currency or if the counterparties do not perform under the contracts’ terms.

Foreign denominated assets, including investment securities, and liabilities are trans lated into U.S. dollars at the exchange rate at period end. Purchases and sales of invest ment securities, income and dividends received and expenses denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transac tion date.

The effects of exchange rate fluctuations on investments are included with the net realized and unrealized gain (loss) on investment securities. Other foreign currency transactions resulting in realized and unrealized gain (loss) are disclosed separately.

Investment Transactions and Income. Security transactions, including the fund’s investment activity in the Central Funds, are accounted for as of trade date. Gains and losses on securities sold are determined on the basis of identified cost and may include proceeds received from litigation. Dividend income is recorded on the ex dividend date, except for certain dividends from foreign securities where the ex dividend date may have passed, which are recorded as soon as the fund is informed of the ex dividend date. Non cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Distributions received on securities that represent a return of capital or capital gain are recorded as a reduction of cost of investments and/or as a realized gain. The fund estimates the components of distributions received that may be considered return of capital distributions or capital gain distributions. Large, non recurring dividends recognized by the fund are presented separately on the Statement of Operations as “Special Dividends” and the impact of these dividends is presented in the Financial Highlights. Interest income, including distributions from the Central Funds, is accrued as earned. Interest income includes coupon interest and amortization of pre mium and accretion of discount on debt securities. Investment income is recorded net of foreign taxes withheld where recovery of such taxes is uncertain.

Expenses. Most expenses of the trust can be directly attributed to a fund. Expenses which cannot be directly attributed are apportioned among each fund in the trust.

Deferred Trustee Compensation. Under a Deferred Compensation Plan (the Plan), independent Trustees must defer receipt of a portion of, and may elect to defer receipt of an additional portion of, their annual compensation. Deferred amounts are treated as though equivalent dollar amounts had been invested in shares of the fund or are invested in a cross section of other Fidelity funds, and are marked to market. Deferred amounts remain in the fund until distributed in accordance with the Plan.

Notes to Financial Statements continued

(Amounts in thousands except ratios)

|

1. Significant Accounting Policies continued

Income Tax Information and Distributions to Shareholders. Each year, the fund intends to qualify as a regulated investment company by distributing all of its taxable income and realized gains under Subchapter M of the Internal Revenue Code. As a result, no provision for income taxes is required in the accompanying financial statements. Foreign taxes are provided for based on the fund’s understanding of the tax rules and rates that exist in the foreign markets in which it invests.

Distributions are recorded on the ex dividend date. Income and capital gain distribu tions are determined in accordance with income tax regulations, which may differ from generally accepted accounting principles. In addition, the fund will claim a portion of the payment made to redeeming shareholders as a distribution for income tax purposes.

Capital accounts within the financial statements are adjusted for permanent book tax differences. These adjustments have no impact on net assets or the results of operations. Temporary book tax differences will reverse in a subsequent period.

Book tax differences are primarily due to futures transactions, swap agreements, foreign currency transactions, passive foreign investment companies (PFIC), prior period premium and discount on debt securities, market discount, partnerships (including allocations from the CIPs), non taxable dividends, deferred trustees compensation and losses deferred due to wash sales.

The tax basis components of distributable earnings and the federal tax cost as of period end were as follows:

| Unrealized appreciation | | $ | | 750,857 |

| Unrealized depreciation | | | | (304,745) |

| Net unrealized appreciation (depreciation) | | | | 446,112 |

| Undistributed ordinary income | | | | 116,850 |

| Undistributed long term capital gain | | | | 190,583 |

| |

| Cost for federal income tax purposes | | $ | | 9,731,183 |

The tax character of distributions paid was as follows:

| | | | | September 30, | | | | September 30, |

| | | | | 2005 | | | | 2004 |

| Ordinary Income | | | | $ 267,576 | | | | $ 193,241 |

Annual Report A-32

Repurchase Agreements. FMR has received an Exemptive Order from the Securities and Exchange Commission (the SEC) which permits the fund and other affiliated entities of FMR to transfer uninvested cash balances into joint trading accounts which are then invested in repurchase agreements. The fund may also invest directly with institutions in repurchase agreements. Repurchase agreements are collateralized by government or non government securities. Collateral is held in segregated accounts with custodian banks and may be obtained in the event of a default of the counterparty. The fund monitors, on a daily basis, the value of the collateral to ensure it is at least equal to the principal amount of the repurchase agreement (including accrued interest). In the event of a default by the counterparty, realization of the collateral proceeds could be delayed, during which time the value of the collateral may decline.

Futures Contracts. The fund may use futures contracts to manage its exposure to the stock market. Buying futures tends to increase a fund’s exposure to the underlying instrument, while selling futures tends to decrease a fund’s exposure to the underlying instrument or hedge other fund investments. Futures contracts involve, to varying degrees, risk of loss in excess of any futures variation margin reflected in the Statement of Assets and Liabilities. The underlying face amount at value of any open futures contracts at period end is shown in the Schedule of Investments under the caption “Futures Contracts.” This amount reflects each contract’s exposure to the underlying instrument at period end. Losses may arise from changes in the value of the underlying instruments or if the counterparties do not perform under the contracts’ terms. Gains (losses) are realized upon the expiration or closing of the futures contracts. Futures contracts are valued at the settlement price established each day by the board of trade or exchange on which they are traded.

Swap Agreements. The fund may invest in swaps for the purpose of managing its exposure to credit or market risk.

Total return swaps are agreements to exchange the return generated by one instrument or index for the return generated by another instrument, for example, the agreement to pay interest in exchange for a market linked return based on a notional amount. To the extent the total return of the index exceeds the offsetting interest obligation, a fund will receive a payment from the counterparty. To the extent it is less, a fund will make a payment to the counterparty. Periodic payments received or made by the fund are recorded in the accompanying Statement of Operations as realized gains or losses, respectively.

Notes to Financial Statements continued

(Amounts in thousands except ratios)

2. Operating Policies continued

Swap Agreements - continued

|

Credit default swaps involve the exchange of a fixed rate premium for protection against the loss in value of an underlying debt instrument in the event of a defined credit event (such as payment default or bankruptcy). Under the terms of the swap, one party acts as a “guarantor” receiving a periodic payment that is a fixed percentage applied to a no tional principal amount. In return the party agrees to purchase the notional amount of the underlying instrument, at par, if a credit event occurs during the term of the swap. The fund may enter into credit default swaps in which either it or its counterparty act as guarantors. By acting as the guarantor of a swap, a fund assumes the market and credit risk of the underlying instrument including liquidity and loss of value.

Swaps are marked to market daily based on dealer supplied valuations and changes in value are recorded as unrealized appreciation (depreciation). Gains or losses are realized upon early termination of the swap agreement. Collateral, in the form of cash or securities, may be required to be held in segregated accounts with a fund’s custodian in compliance with swap contracts.

3. Purchases and Sales of Investments.

Purchases and sales of securities, other than short term securities and U.S. government securities and in kind transactions, aggregated $2,260,711 and $3,267,716, respectively.

4. Fees and Other Transactions with Affiliates.

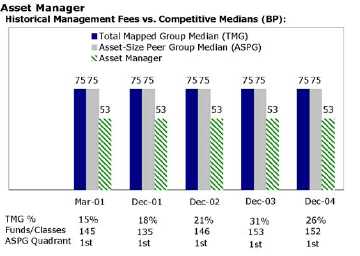

Management Fee. FMR and its affiliates provide the fund with investment manage ment related services for which the fund pays a monthly management fee. The manage ment fee is the sum of an individual fund fee rate that is based on an annual rate of .25% of the fund’s average net assets and a group fee rate that averaged .27% during the period. The group fee rate is based upon the average net assets of all the mutual funds advised by FMR. The group fee rate decreases as assets under management increase and increases as assets under management decrease. For the period, the total annual man agement fee rate was .52% of the fund’s average net assets.

Transfer Agent Fees. Fidelity Service Company, Inc. (FSC), an affiliate of FMR, is the fund’s transfer, dividend disbursing and shareholder servicing agent. FSC receives account fees and asset based fees that vary according to account size and type of ac count. FSC pays for typesetting, printing and mailing of shareholder reports, except proxy statements. For the period, the transfer agent fees were equivalent to an annual rate of .19% of average net assets.

4. Fees and Other Transactions with Affiliates continued

Accounting and Security Lending Fees. FSC maintains the fund’s accounting rec ords. The accounting fee is based on the level of average net assets for the month. Under a separate contract, FSC administers the security lending program. The security lending fee is based on the number and duration of lending transactions.

Affiliated Central Funds. The fund may invest in Money Market Central Funds which seek preservation of capital and current income and are managed by Fidelity Invest ments Money Management, Inc. (FIMM), an affiliate of FMR.