UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03231

SEI Liquid Asset Trust

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

c/o CT Corporation

155 Federal St.

Boston, MA 02110

Registrant’s telephone number, including area code: 1-800-342-5734

Date of fiscal year end: June 30, 2015

Date of reporting period: June 30, 2015

| Item 1. | Reports to Stockholders. |

June 30, 2015

ANNUAL REPORT

SEI Liquid Asset Trust

➤ Prime Obligation Fund

| 1 | ||||

| 4 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 16 | ||||

| 17 | ||||

| 20 | ||||

Board of Trustees Considerations in Approving the Advisory and Sub-Advisory Agreements | 21 | |||

| 24 | ||||

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“Commission”) for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Trust’s Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

SEI LIQUID ASSET TRUST — JUNE 30, 2015 (Unaudited)

At the beginning of the Fund’s fiscal year — which ran from July 1, 2014 through June 30, 2015 — SEI’s view was that global economic recovery was a work in progress. We anticipated continued strength in equity markets and their outperformance over bonds. We also expected a cautious approach by the U.S. Federal Open Market Committee in raising interest rates. While the market had its ups, downs and inbetweens during the fiscal year, our view was largely accurate.

In the first half of 2014, there was an easing of the geopolitical standoff between Russia, Ukraine and Europe; and certain high-risk areas of the market (such as high-yield and emerging-market debt and equities) continued the recoveries they had begun in late 2013 and early 2014. By the end of the second quarter of 2014, U.S. economic growth was recovering from its surprisingly weak start, and key measures of volatility and investor risk aversion was reaching extreme lows by the end of June 2014.

These dynamics changed considerably in mid-2014 due to shocks in commodities and currency markets as well as divergent central bank policies. These developments fostered rising uncertainty and volatility, as well as divergent behavior within and across asset classes. Despite the intrigue, most fixed-income and equity asset classes in the U.S. produced positive returns for the one-year period ending June 30, 2015. Results were more of a mixed bag in other asset classes and outside the U.S., as a significantly stronger dollar weighed on commodity and international-asset returns.

Geopolitical events

In contrast to the Fund’s previous fiscal year, the conflict between Russia and Ukraine (and, by extension, between Russia and western powers such as Europe and the U.S.) simmered but did not boil over. There was continued (and in some cases intensifying) strife in several Middle Eastern and African nations, including Syria, Iraq, Libya and Nigeria. However, disruptions within the latter three countries, which are net oil producers, were not sufficient to stop the price of crude oil from falling sharply during the period. In fact, some of the most interesting geopolitical wrangling occurred within the oil markets. Faced with a dramatic increase in North American oil production in recent years, the Organization of Petroleum Exporting Countries (OPEC) decided to maintain, rather than cut, existing production targets, despite “an extremely well-supplied market.”3 This decision reflected an intense battle for market share that began during 2014 between Saudi Arabia, the oil market’s key producer, and North America, where significant investments have been made in unconventional (but costlier) forms of oil-and-gas production. Although not necessarily related, the Obama administration invested a great deal of diplomatic time and effort during the year in reaching a deal with Iran — which happens to be Saudi Arabia’s key rival in the region — in an attempt to check its nuclear ambitions while easing the west’s economic sanctions. Although Iran has vast amounts of oil reserves, most energy analysts do not believe the agreement will have an immediate impact on either the country’s oil production or the global price of oil. Still, Saudi Arabia has been willing to allow the price of oil to fall in order to recover market share, even running down its foreign-currency reserves and increasing its borrowing to cover government expenditures. We believe these oil-market dynamics could continue to have diverse and meaningful impacts on the world’s economies and financial markets.

Economic performance

In the U.S., recovery from a first-quarter contraction began in the second quarter of 2014. Growth slowed a bit in the fourth quarter before contracting once again in the first quarter of 2015. This year’s first-quarter disappointment was driven by extreme winter weather in certain parts of the U.S., as well as sluggish demand from abroad. The latter factor was made worse by a stronger dollar (which makes imports from the U.S. more expensive to foreign buyers) and increasingly contentious labor negotiations in several west-coast ports that, at times, prevented the smooth flow of goods into and out of the country. While overall U.S. growth was not terribly impressive for the full period, it remained positive and, encouragingly, the labor market continued to strengthen. Initial claims for unemployment benefits maintained their sharp, downward trajectory from the highs of 2009, and the U.S. unemployment rate fell from 6.3% at the end of May 2014 to 5.3% at the end of June 2015, according to the Bureau of Labor Statistics. The proportion of working-age individuals participating in the labor force, which declined sharply

| 3 | “OPEC 166th Meeting concludes,” Organization of the Petroleum Exporting Countries, November 27, 2014, <http://www.opec.org/opec_web/en/press_room/2938.htm>. |

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 1 |

from 2008 to 2013, continued to show signs of stabilizing. Employee compensation also exhibited steady growth, although the pace remained below its long-term average. While the U.S. economy appears to have rebounded in the second quarter of 2015, there have nonetheless been additional signs of sluggishness. For example, after a solid run during the first half of the Fund’s fiscal year, industrial production, capacity utilization and consumer-sentiment measures have been trending down since the start of 2015. Lower oil prices, historically a boon for U.S. consumers, have had a more mixed impact this time around. As global oil prices fell, many higher-cost North American producers began to struggle, as did states and regions where heavy energy investments were made in recent years. Still, the overall story during the reporting period was one of slow but continued growth. As a result, the Fed ended its asset-purchase programs (also known as quantitative easing) in 2014, which caused some volatility in fixed-income markets during the period. Most market observers still expect the Fed to begin hiking interest rates sometime in late 2015, which should be positive for short-term fixed-income investors. However, these recent signs of economic sluggishness have pushed the expected start date of Federal Reserve (Fed) interest rate hikes further into the future.

Market developments

In U.S. fixed-income markets, inflation-protected securities lagged as inflation expectations fell in the face of lower commodity prices, a stronger dollar and sluggish growth. The U.S. Treasury yield curve flattened; shorter-term rates rose on expectations of a Fed rate hike in the near future, while longer-term rates fell on disappointing economic results, falling inflation expectations and bouts of risk aversion. Long rates reversed course in a choppy fashion from February 2015 but still ended the period slightly lower. This meant positive returns in longer-dated Treasurys, as Treasury bond yields and prices move inversely. Interest rate volatility was notably higher once the Fed ended its quantitative-easing efforts.

Most non-Treasury sectors performed well. Non-agency mortgage-backed securities (MBS), commercial MBS (CMBS) and asset-backed securities (ABS) outperformed comparably dated Treasurys. Non-agency MBS outperformance was driven by the ongoing U.S. housing recovery, limited supply and attractive risk-adjusted returns. CMBS outperformance, driven by ongoing improvement in commercial real estate fundamentals, was reflected in tightening yield spreads over Treasurys. (Spread is the additional yield offered by a security over a benchmark security, such as a Treasury, of similar maturity; when the spread narrows, it indicates that the higher-risk security has outperformed, and when it widens, it implies that the benchmark or risk-free security has outperformed.) Within ABS, securitized credit card and automobile loans were outperformers.

Investment-grade and high-yield corporate debt underperformed Treasurys, as spreads widened in both sectors. The struggles of the energy sector (especially issues related to oil, gas and coal production) played a significant role in the underperformance. Industrial issues also performed poorly overall. Within investment-grade, financials outperformed (especially banks, where bondholders have benefited from stricter capital regulations and sturdier balance sheets). Healthcare was also positive, thanks to solid corporate fundamentals and strong merger-and-acquisition (M&A) activity. Within high yield, collateralized loan obligations outperformed, primarily due to a supply-and-demand imbalance, as strong investor demand was met by sluggish loan production. Taxable municipal debt also performed well compared to corporates.

The Fed’s policy of keeping short-term interest rates near zero continued to depress money market fund yields during the period. In addition, the finalization of the Securities and Exchange Commission’s money market rule reform in July 2014 is expected to have significant impacts on the scope of money market fund management and operations. Shares of institutional prime funds will be required to adopt a floating net asset value (NAV), replacing the traditional stable one dollar per share price. Retail prime funds and government funds are exempt from the floating NAV requirement. In addition, prime funds (both institutional and retail) will be required to impose liquidity fees and redemption gates under certain circumstances, while government funds will be able to elect to opt out of those gates and fees. Funds have until October 2016 to come into compliance with the new rules, and SEI is designing a plan to restructure our existing money market fund offerings.

Commodity markets were routed badly during the Fund’s fiscal year. As already noted, the oil market was hit especially hard due to substantial increases in global supply, driven by a massive expansion of North American production and OPEC’s refusal to cut output. Oil prices fell by more than half from mid-2014 through the start of 2015 and ended the period more than 40% lower. Most other commodities were also hit hard, as they: fell in sympathy with oil; reacted to concerns about slowing growth in China and other large emerging markets; and responded to a sharply stronger U.S. dollar. (Most commodity trading takes place in U.S. dollars; thus, as the dollar’s value increases, the prices of most commodities tend to fall.) The Bloomberg Commodity Index fell by roughly 25% over the Fund’s fiscal year. Although lower oil prices may be supportive of economic activity in the longer term, these developments have had negative short-term impacts on the dollar value of global trade and economic activity in certain energy-producing regions of North America. They have also helped keep a lid on inflation pressures. As a result, short-term interest rates have remained near zero for longer than many market participants expected.

| 2 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

Our View

Toward the end of the Fund’s fiscal year, there were indications that the U.S. economy had returned to growth, but the immediate rebound was not as strong as the one seen in the second quarter of 2014. Whether its momentum improves remains to be seen, and the outcome could influence the Fed’s policy decisions later in 2015. In fixed-income markets, low-risk and risk-free sovereign-government debt still looks expensive to us, but credit markets should continue to offer relative-value opportunities.

On behalf of SEI Investments, I want to thank you for the confidence you have in the SEI Liquid Asset Trust. We are working every day to maintain that confidence, and we look forward to serving your investment needs in the future.

Sincerely,

William Lawrence

Managing Director, Portfolio Management Group

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 3 |

Prime Obligation Fund

June 30, 2015

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

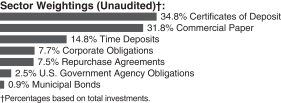

CERTIFICATES OF DEPOSIT (A) — 34.8% |

| |||||||

ANZ New Zealand International (B) (D) | ||||||||

0.263%, 07/05/15 | $ | 10,484 | $ | 10,484 | ||||

Bank of Montreal IL | ||||||||

0.275%, 07/04/15 (D) | 10,000 | 10,000 | ||||||

0.250%, 09/16/15 | 4,750 | 4,750 | ||||||

Bank of Nova Scotia (D) | ||||||||

0.270%, 07/01/15 | 12,000 | 12,000 | ||||||

0.260%, 07/01/15 | 10,000 | 10,000 | ||||||

Bank of Tokyo-Mitsubishi UFJ NY | ||||||||

0.324%, 07/01/15 (D) | 4,000 | 4,000 | ||||||

0.314%, 07/01/15 (D) | 750 | 750 | ||||||

0.336%, 07/29/15 (D) | 9,900 | 9,900 | ||||||

0.310%, 07/29/15 | 2,000 | 2,000 | ||||||

0.464%, 09/04/15 (D) | 7,000 | 7,003 | ||||||

BNZ International Funding (B) (D) | ||||||||

0.010%, 07/02/15 | 4,794 | 4,794 | ||||||

Canadian Imperial Bank Commerce | ||||||||

0.100%, 07/01/15 | 36,742 | 36,742 | ||||||

0.377%, 08/13/15 (D) | 326 | 326 | ||||||

DNB Bank (D) (B) | ||||||||

0.286%, 07/14/15 | 10,000 | 10,000 | ||||||

Fairway Finance (D) (B) | ||||||||

0.267%, 07/20/15 | 1,500 | 1,500 | ||||||

0.258%, 07/24/15 | 13,500 | 13,500 | ||||||

General Electric Capital (D) | ||||||||

0.280%, 07/01/15 | 4,750 | 4,750 | ||||||

0.260%, 07/24/15 | 5,000 | 5,000 | ||||||

HSBC Bank | ||||||||

0.200%, 08/10/15 | 11,000 | 11,000 | ||||||

0.230%, 09/01/15 | 5,500 | 5,500 | ||||||

JPMorgan Securities (D) | ||||||||

0.305%, 07/04/15 | 11,250 | 11,250 | ||||||

0.327%, 07/31/15 | 5,850 | 5,850 | ||||||

Mizuho Bank | ||||||||

0.250%, 07/01/15 | 5,672 | 5,672 | ||||||

0.260%, 07/13/15 | 4,000 | 4,000 | ||||||

0.260%, 08/07/15 | 10,000 | 10,000 | ||||||

0.270%, 08/11/15 | 5,374 | 5,374 | ||||||

0.270%, 09/10/15 | 8,000 | 8,000 | ||||||

National Australia Bank (B) (D) | ||||||||

0.264%, 07/07/15 | 9,854 | 9,854 | ||||||

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

National Bank of Canada (D) | ||||||||

0.416%, 09/11/15 | $ | 455 | $ | 455 | ||||

Nordea Bank | ||||||||

0.245%, 09/17/15 | 1,058 | 1,058 | ||||||

Old Line Funding (D) | ||||||||

0.275%, 07/20/15 | 2,000 | 2,000 | ||||||

0.275%, 07/20/15 | 2,000 | 2,000 | ||||||

0.267%, 07/26/15 | 7,000 | 7,000 | ||||||

Skandinaviska Enskilda Banken NY | ||||||||

0.250%, 07/02/15 | 941 | 941 | ||||||

0.240%, 07/06/15 | 10,000 | 10,000 | ||||||

0.240%, 09/10/15 | 2,028 | 2,028 | ||||||

Sumitomo Mitsui Banking | ||||||||

0.250%, 07/01/15 | 4,000 | 4,000 | ||||||

0.314%, 07/02/15 (D) | 9,000 | 9,000 | ||||||

0.335%, 07/14/15 (D) | 4,000 | 4,000 | ||||||

0.336%, 07/15/15 (D) | 4,000 | 4,000 | ||||||

0.337%, 07/23/15 (D) | 3,125 | 3,125 | ||||||

0.327%, 07/23/15 (D) | 7,500 | 7,500 | ||||||

Svenska Handelsbanken | ||||||||

0.205%, 07/15/15 | 10,000 | 10,000 | ||||||

0.225%, 08/28/15 | 8,000 | 8,000 | ||||||

0.205%, 09/01/15 | 22,000 | 22,000 | ||||||

Toronto-Dominion Bank | ||||||||

0.235%, 07/06/15 | 3,027 | 3,027 | ||||||

0.220%, 09/17/15 | 11,500 | 11,500 | ||||||

0.280%, 09/18/15 | 5,000 | 5,000 | ||||||

Toyota Motor Credit (D) | ||||||||

0.268%, 07/19/15 | 4,437 | 4,437 | ||||||

0.266%, 07/27/15 | 7,190 | 7,190 | ||||||

Wells Fargo Bank (D) | ||||||||

0.270%, 07/01/15 | 5,000 | 5,000 | ||||||

0.250%, 07/01/15 | 5,700 | 5,700 | ||||||

0.555%, 07/02/15 | 3,200 | 3,201 | ||||||

0.264%, 07/07/15 | 6,000 | 6,000 | ||||||

0.264%, 07/08/15 | 8,500 | 8,500 | ||||||

0.296%, 07/11/15 | 263 | 263 | ||||||

0.265%, 07/17/15 | 7,810 | 7,810 | ||||||

0.312%, 09/03/15 | 1,029 | 1,029 | ||||||

Westpac Securities NZ (B) (D) | ||||||||

0.276%, 07/15/15 | 5,210 | 5,210 | ||||||

0.187%, 07/21/15 | 6,235 | 6,235 | ||||||

|

| |||||||

Total Certificates of Deposit | 401,208 | |||||||

|

| |||||||

COMMERCIAL PAPER (A) (C) — 31.8% |

| |||||||

Albion Capital (B) | ||||||||

0.150%, 07/02/15 | 5,000 | 5,000 | ||||||

0.220%, 07/27/15 | 412 | 412 | ||||||

0.240%, 08/17/15 | 2,000 | 1,999 | ||||||

0.240%, 08/21/15 | 9,750 | 9,747 | ||||||

0.240%, 08/26/15 | 1,793 | 1,792 | ||||||

| 4 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

ANZ New Zealand International (B) | ||||||||

0.264%, 07/02/15 (D) | $ | 2,000 | $ | 2,000 | ||||

0.346%, 12/29/15 | 11,225 | 11,225 | ||||||

Bank of Nova Scotia (B) | ||||||||

0.285%, 08/10/15 | 2,962 | 2,961 | ||||||

Bank of Tokyo-Mitsubishi UFJ NY | ||||||||

0.310%, 07/01/15 | 1,300 | 1,300 | ||||||

BNZ International Funding (B) | ||||||||

0.270%, 07/15/15 | 6,262 | 6,261 | ||||||

0.230%, 09/14/15 | 17,000 | 16,992 | ||||||

CAFCO (B) | ||||||||

0.210%, 09/08/15 | 5,000 | 4,998 | ||||||

Caisse Centrale Desjardins (B) | ||||||||

0.128%, 07/02/15 | 29,000 | 29,000 | ||||||

Chariot Funding (B) | ||||||||

0.270%, 07/15/15 | 1,058 | 1,058 | ||||||

0.250%, 09/10/15 | 775 | 775 | ||||||

0.401%, 12/16/15 | 7,000 | 6,987 | ||||||

Charta (B) | ||||||||

0.250%, 08/28/15 | 1,360 | 1,359 | ||||||

0.270%, 09/01/15 | 800 | 800 | ||||||

Ciesco (B) | ||||||||

0.250%, 09/01/15 | 1,761 | 1,760 | ||||||

Coca-Cola (B) | ||||||||

0.220%, 07/27/15 | 4,750 | 4,749 | ||||||

0.300%, 09/09/15 | 5,000 | 4,997 | ||||||

CRC Funding (B) | ||||||||

0.200%, 09/14/15 | 2,955 | 2,954 | ||||||

Fairway Finance (B) | ||||||||

0.230%, 07/02/15 | 4,114 | 4,114 | ||||||

0.230%, 07/06/15 | 3,989 | 3,989 | ||||||

0.260%, 07/16/15 | 7,620 | 7,619 | ||||||

0.266%, 07/29/15 (D) | 7,290 | 7,290 | ||||||

0.205%, 08/05/15 | 10,000 | 9,998 | ||||||

0.250%, 09/14/15 | 2,136 | 2,135 | ||||||

HSBC Bank (B) (D) | ||||||||

0.264%, 07/08/15 | 11,000 | 11,000 | ||||||

JPMorgan Securities (B) | ||||||||

0.300%, 07/24/15 | 2,000 | 2,000 | ||||||

0.300%, 08/04/15 | 361 | 361 | ||||||

0.270%, 09/08/15 | 7,750 | 7,746 | ||||||

0.376%, 09/19/15 (D) | 9,130 | 9,132 | ||||||

0.341%, 11/17/15 | 10,000 | 9,987 | ||||||

Jupiter Securitization (B) | ||||||||

0.330%, 12/01/15 | 7,753 | 7,742 | ||||||

0.371%, 12/08/15 | 10,000 | 9,984 | ||||||

Liberty Street Funding (B) | ||||||||

0.300%, 10/26/15 | 2,268 | 2,266 | ||||||

0.341%, 11/12/15 | 966 | 965 | ||||||

Manhattan Asset Funding (B) | ||||||||

0.200%, 07/06/15 | 5,000 | 5,000 | ||||||

0.190%, 07/16/15 | 1,829 | 1,829 | ||||||

0.240%, 07/27/15 | 2,700 | 2,699 | ||||||

0.280%, 07/31/15 | 1,000 | 1,000 | ||||||

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

0.280%, 08/05/15 | $ | 3,189 | $ | 3,188 | ||||

0.250%, 09/18/15 | 7,000 | 6,996 | ||||||

National Bank of Canada (B) | ||||||||

0.280%, 09/17/15 | 14,000 | 13,991 | ||||||

Nestle Capital (B) | ||||||||

0.225%, 07/14/15 | 3,000 | 3,000 | ||||||

Old Line Funding (B) | ||||||||

0.240%, 09/01/15 | 4,627 | 4,625 | ||||||

0.240%, 09/04/15 | 4,590 | 4,588 | ||||||

0.230%, 09/09/15 | 1,675 | 1,674 | ||||||

0.401%, 12/16/15 | 12,000 | 11,978 | ||||||

Prudential Funding | ||||||||

0.070%, 07/01/15 | 3,102 | 3,102 | ||||||

Regency Markets No. 1 (B) | ||||||||

0.120%, 07/02/15 | 4,077 | 4,077 | ||||||

0.170%, 07/24/15 | 23,225 | 23,222 | ||||||

Thunder Bay Funding (B) | ||||||||

0.230%, 09/09/15 | 5,148 | 5,146 | ||||||

0.280%, 09/21/15 | 3,058 | 3,056 | ||||||

Toyota Motor Credit | ||||||||

0.270%, 07/30/15 | 10,000 | 9,998 | ||||||

0.270%, 07/31/15 | 5,675 | 5,674 | ||||||

Victory Receivables (B) | ||||||||

0.200%, 07/23/15 | 3,260 | 3,260 | ||||||

Westpac Securities NZ (B) | ||||||||

0.280%, 07/07/15 | 10,000 | 9,999 | ||||||

0.275%, 07/10/15 (D) | 880 | 880 | ||||||

0.275%, 07/15/15 | 5,000 | 4,999 | ||||||

Working Capital Management (B) | ||||||||

0.130%, 07/01/15 | 3,066 | 3,066 | ||||||

0.130%, 07/02/15 | 3,266 | 3,266 | ||||||

0.153%, 07/06/15 | 6,664 | 6,664 | ||||||

0.130, 07/07/15 | 2,596 | 2,596 | ||||||

0.200%, 07/10/15 | 1,390 | 1,390 | ||||||

|

| |||||||

Total Commercial Paper | 366,417 | |||||||

|

| |||||||

TIME DEPOSITS — 14.8% |

| |||||||

Bank of Montreal IL (D) | ||||||||

0.275%, 07/04/15 | 6,381 | 6,381 | ||||||

Citibank | ||||||||

0.090%, 07/01/15 | 35,642 | 35,642 | ||||||

Lloyds Bank PLC | ||||||||

0.060%, 07/01/15 | 56,000 | 56,000 | ||||||

Svenska Handelsbanken | ||||||||

0.040%, 07/01/15 | 16,000 | 16,000 | ||||||

Swedbank | ||||||||

0.060%, 07/01/15 | 56,500 | 56,500 | ||||||

|

| |||||||

Total Time Deposits | 170,523 | |||||||

|

| |||||||

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 5 |

SCHEDULE OF INVESTMENTS

Prime Obligation Fund (Continued)

June 30, 2015

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

CORPORATE OBLIGATIONS — 7.7% |

| |||||||

American Honda Finance (B) | ||||||||

1.000%, 08/11/15 | $ | 1,516 | $ | 1,517 | ||||

ANZ New Zealand International (B) | ||||||||

3.125%, 08/10/15 | 301 | 302 | ||||||

1.850%, 10/15/15 | 3,521 | 3,536 | ||||||

Bank of Montreal IL | ||||||||

0.265%, 07/18/15 (D) | 3,500 | 3,500 | ||||||

0.755%, 09/11/15 (D) | 2,197 | 2,199 | ||||||

0.532%, 09/24/15 (D) | 2,613 | 2,614 | ||||||

0.800%, 11/06/15 | 102 | 102 | ||||||

Bank of Nova Scotia | ||||||||

0.260%, 07/02/15 (D) | 4,900 | 4,900 | ||||||

0.254%, 07/02/15 (D) | 1,068 | 1,068 | ||||||

0.255%, 07/10/15 (D) | 323 | 323 | ||||||

0.254%, 07/15/15 (D) | 269 | 269 | ||||||

0.726%, 09/11/15 (D) | 315 | 315 | ||||||

0.340%, 09/25/15 (D) | 8,000 | 8,000 | ||||||

2.050%, 10/07/15 | 326 | 328 | ||||||

0.750%, 10/09/15 | 1,261 | 1,263 | ||||||

Bank of Tokyo-Mitsubishi UFJ NY (B) | ||||||||

2.450%, 09/11/15 | 576 | 578 | ||||||

Caisse Centrale Desjardins (B) | ||||||||

2.650%, 09/16/15 | 1,376 | 1,383 | ||||||

Canadian Imperial Bank of Commerce | ||||||||

0.900%, 10/01/15 | 2,595 | 2,598 | ||||||

2.350%, 12/11/15 | 3,325 | 3,353 | ||||||

DNB Bank (D) | ||||||||

0.277%, 07/15/15 | 5,000 | 5,000 | ||||||

General Electric Capital | ||||||||

1.625%, 07/02/15 | 8,802 | 8,802 | ||||||

1.301%, 07/02/15 (D) | 2,400 | 2,400 | ||||||

0.651%, 07/10/15 (D) | 249 | 249 | ||||||

4.375%, 09/21/15 | 374 | 377 | ||||||

International Business Machines (D) | ||||||||

0.309%, 07/02/15 | 827 | 827 | ||||||

Metropolitan Life Global Funding (B) | ||||||||

2.500%, 09/29/15 | 4,829 | 4,854 | ||||||

National Australia Bank (B) | ||||||||

1.600%, 08/07/15 | 2,034 | 2,037 | ||||||

1.406%, 08/07/15 (D) | 5,203 | 5,209 | ||||||

2.750%, 09/28/15 | 2,326 | 2,340 | ||||||

Royal Bank of Canada | ||||||||

0.800%, 10/30/15 | 740 | 741 | ||||||

Sumitomo Mitsui Banking (B) | ||||||||

3.150%, 07/22/15 | 916 | 917 | ||||||

Toyota Motor Credit | ||||||||

0.875%, 07/17/15 | 338 | 338 | ||||||

0.436%, 09/18/15 (D) | 235 | 235 | ||||||

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

US Bancorp | ||||||||

2.450%, 07/27/15 | $ | 1,102 | $ | 1,104 | ||||

Wal-Mart Stores | ||||||||

4.500%, 07/01/15 | 2,745 | 2,745 | ||||||

2.250%, 07/08/15 | 335 | 335 | ||||||

Wells Fargo Bank (D) | ||||||||

0.265%, 07/04/15 | 980 | 980 | ||||||

Westpac Banking | ||||||||

1.041%, 07/10/15 (D) | 826 | 828 | ||||||

3.000%, 08/04/15 | 4,603 | 4,614 | ||||||

1.125%, 09/25/15 | 1,981 | 1,985 | ||||||

3.000%, 12/09/15 | 3,005 | 3,038 | ||||||

|

| |||||||

Total Corporate Obligations |

| 88,103 | ||||||

|

| |||||||

U.S. GOVERNMENT AGENCY OBLIGATIONS — 2.5% |

| |||||||

FFCB (D) | ||||||||

0.208%, 07/11/15 | 7,810 | 7,811 | ||||||

0.180%, 07/16/15 | 10,000 | 10,000 | ||||||

0.197%, 07/23/15 | 9,000 | 9,000 | ||||||

0.237%, 07/24/15 | 2,250 | 2,251 | ||||||

|

| |||||||

Total U.S. Government Agency Obligations |

| 29,062 | ||||||

|

| |||||||

MUNICIPAL BONDS (D) — 0.9% |

| |||||||

Arizona — 0.1% | ||||||||

Pima County, Industrial Development Authority, RB | ||||||||

0.090%, 07/01/15 | 1,200 | 1,200 | ||||||

|

| |||||||

Colorado — 0.1% |

| |||||||

Colorado State, Housing & Finance Authority, Multi-Family Housing Program, Ser A-1, RB | ||||||||

0.120%, 07/01/15 | 710 | 710 | ||||||

|

| |||||||

Illinois — 0.0% | ||||||||

University of Illinois, Ser S, RB | ||||||||

0.150%, 07/02/15 | 330 | 330 | ||||||

|

| |||||||

Iowa — 0.2% | ||||||||

Iowa State, Finance Authority, Ser C, RB | ||||||||

0.160%, 07/02/15 | 1,320 | 1,320 | ||||||

Iowa State, Finance Authority, Ser G, RB | ||||||||

0.160%, 07/02/15 | 15 | 15 | ||||||

Iowa State, Finance Authority, Ser M, RB | ||||||||

0.140%, 07/02/15 | 450 | 450 | ||||||

|

| |||||||

| 1,785 | ||||||||

|

| |||||||

| 6 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

Massachusetts — 0.0% | ||||||||

Simmons College, Higher Education Authority, RB | ||||||||

0.140%, 07/02/15 | $ | 530 | $ | 530 | ||||

|

| |||||||

Michigan — 0.3% | ||||||||

Kent, Hospital Finance Authority, Ser C, RB | ||||||||

0.070%, 07/01/15 | 2,875 | 2,875 | ||||||

|

| |||||||

Minnesota — 0.2% | ||||||||

Minnesota State, Office of Higher Education, Ser A, RB | ||||||||

0.120%, 07/02/15 | 1,780 | 1,780 | ||||||

|

| |||||||

New Hampshire — 0.0% | ||||||||

New Hampshire State, Health & Educational Facilities Authority, Dartmouth College Project, Ser C, RB | ||||||||

0.160%, 07/01/15 | 390 | 390 | ||||||

|

| |||||||

New York — 0.0% | ||||||||

New York State, Housing Finance Agency, RB | ||||||||

0.220%, 07/07/15 | 440 | 440 | ||||||

|

| |||||||

Wisconsin — 0.0% | ||||||||

Wisconsin Housing & Economic Development Authority, Ser B, RB | ||||||||

0.170%, 07/04/15 | 155 | 155 | ||||||

Wisconsin State, Housing & Economic Development Authority, Wheaton Franciscan System Project, Ser B, RB | ||||||||

0.140%, 07/02/15 | 285 | 285 | ||||||

|

| |||||||

| 440 | ||||||||

|

| |||||||

Total Municipal Bonds |

| 10,480 | ||||||

|

| |||||||

REPURCHASE AGREEMENTS (E) — 7.5% |

| |||||||

Goldman Sachs | 23,000 | 23,000 | ||||||

| Description | Face Amount ($ Thousands) | Value ($ Thousands) | ||||||

RBC Capital | $ | 8,399 |

| $ | 8,399 |

| ||

RBC Capital | 6,363 | 6,363 | ||||||

TD Securities | 17,000 | 17,000 | ||||||

Wells Fargo | 23,000 | 23,000 | ||||||

Wells Fargo | 1,622 | 1,622 | ||||||

Wells Fargo | 6,489 | 6,489 | ||||||

|

| |||||||

Total Repurchase Agreements | 85,873 | |||||||

|

| |||||||

Total Investments — 100.8% | $ | 1,151,666 | ||||||

|

| |||||||

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 7 |

SCHEDULE OF INVESTMENTS

Prime Obligation Fund (Concluded)

June 30, 2015

| * | A list of the corporate obligations used to collateralize repurchase agreements entered into by the Fund at June 30, 2015, is as follows: |

| Counterparty | Corporate Obligation | Rate | Maturity Date | Par Amount ($ Thousands) | ||||||||||

| RBC | BNP Paribas | 2.450 | % | 03/17/19 | $ | — | ||||||||

| Cantor Fitzgerald | 7.875 | 02/26/16 | 15 | |||||||||||

| Caterpillar Financial | 0.522 | 02/26/16 | 293 | |||||||||||

| CBRE Services | 5.000 | 03/15/23 | 46 | |||||||||||

| Credit Agricole | 4.375 | 03/17/25 | 9 | |||||||||||

| Credit Suisse | 0.969 | 01/29/18 | 1,490 | |||||||||||

| Credit Suisse | 3.750 | 03/26/25 | 1,316 | |||||||||||

| Daimler Finance | 0.632 | 03/10/17 | — | |||||||||||

| Deutsche Bank | 0.886 | 02/13/17 | 27 | |||||||||||

| General Electric | 3.450 | 05/15/24 | 226 | |||||||||||

| HSBC | 3.500 | 06/23/24 | 305 | |||||||||||

| JPMorgan | 3.200 | 01/25/23 | 291 | |||||||||||

| KKR Group | 6.375 | 09/29/20 | 19 | |||||||||||

| Lam Reserarch | 2.750 | 03/15/20 | 144 | |||||||||||

| LyondellBasell | 5.750 | 04/15/24 | 13 | |||||||||||

| Mckesson | 3.796 | 03/15/24 | 3 | |||||||||||

| Morgan Stanley | 2.800 | 06/16/20 | 997 | |||||||||||

| National Rural Utility | 0.582 | 11/23/16 | 839 | |||||||||||

| Paccar Financial | 1.100 | 06/06/17 | 65 | |||||||||||

| Puttable Floating Option | 6.500 | 05/15/21 | 630 | |||||||||||

| Synchrony | 3.750 | 08/15/21 | — | |||||||||||

| SYSCO | 2.600 | 06/12/22 | 3 | |||||||||||

| Union Pacific | 2.750 | 04/15/23 | 1,908 | |||||||||||

| Verizon Communications | 1.053 | 06/17/19 | — | |||||||||||

| XL Capital | 5.750 | 10/01/21 | 177 | |||||||||||

| Wells Partnership II | 5.875 | 04/01/18 | — | |||||||||||

Percentages are based on Net Assets of $1,142,449 ($ Thousands).

| (A) | Securities are held in connection with a letter of credit issued by a major bank. |

| (B) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” These securities have been determined to be liquid under guidelines established by the Board of Trustees. |

| (C) | The rate reported is the effective yield at time of purchase. |

| (D) | Floating Rate Instrument. The rate reflected on the Schedule of Investments is the rate in effect on June 30, 2015. The demand and interest rate reset features give this security a shorter effective maturity date. |

| (E) | Tri-Party Repurchase Agreement. |

FFCB — Federal Farm Credit Bank

FMAC — Financial Management Advisory Committee

FNMA — Federal National Mortgage Association

RB — Revenue Bond

Ser — Series

The accompanying notes are an integral part of the financial statements.

| 8 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

Statement of Assets and Liabilities ($ Thousands)

As of June 30, 2015

| Prime Obligation Fund | ||||

ASSETS: | ||||

Investments, at value (Cost $1,065,793) | $ | 1,065,793 | ||

Repurchase agreements, at value (Cost $85,873) | 85,873 | |||

Accrued income | 476 | |||

Receivable for investment securities sold | 20 | |||

Prepaid expenses | 23 | |||

Total Assets | 1,152,185 | |||

LIABILITIES: | ||||

Payable for investment securities purchased | 9,504 | |||

Payable due to administrator | 89 | |||

Payable due to investment adviser | 40 | |||

Trustees’ fees payable | 3 | |||

Chief Compliance Officer fees payable | 1 | |||

Accrued expenses | 99 | |||

Total Liabilities | 9,736 | |||

Net Assets | $ | 1,142,449 | ||

NET ASSETS CONSIST OF: | ||||

Paid-in Capital | $ | 1,142,452 | ||

Distributions in excess of net investment income | (5 | ) | ||

Accumulated net realized gain on investments | 2 | |||

Net Assets | $ | 1,142,449 | ||

Net Asset Value, Offering and Redemption Price Per Share — Class A | $ | 1.00 | ||

( $1,142,443,624 ÷ 1,142,452,703 shares) | ||||

The accompanying notes are an integral part of the financial statements.

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 9 |

Statement of Operations ($ Thousands)

For the year ended June 30, 2015

| Prime Obligation Fund | ||||

Investment Income: | ||||

Interest Income | $ | 2,122 | ||

Expenses: | ||||

Administration Fees | 3,719 | |||

Shareholder Servicing Fees — Class A | 2,818 | |||

Investment Advisory Fees | 492 | |||

Trustees’ Fees | 17 | |||

Chief Compliance Officer Fees | 5 | |||

Printing Fees | 259 | |||

Professional Fees | 61 | |||

Custodian/Wire Agent Fees | 59 | |||

Registration Fees | 46 | |||

Other Expenses | 33 | |||

Total Expenses | 7,509 | |||

Less, Waiver of: | ||||

Administration Fees | (2,682 | ) | ||

Shareholder Servicing Fees — Class A | (2,818 | ) | ||

Net Expenses | 2,009 | |||

Net Investment Income | 113 | |||

Net Increase in Net Assets Resulting from Operations | $ | 113 | ||

The accompanying notes are an integral part of the financial statements.

| 10 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

Statements of Changes in Net Assets ($ Thousands)

For the years ended June 30,

| Prime Obligation Fund | ||||||||

| 2015 | 2014 | |||||||

Operations: | ||||||||

Net Investment Income | $ | 113 | $ | 108 | ||||

Net Increase in Net Assets Resulting from Operations | 113 | 108 | ||||||

Dividends From: | ||||||||

Net Investment Income: | ||||||||

Class A | (113 | ) | (108 | ) | ||||

Total Dividends | (113 | ) | (108 | ) | ||||

Capital Share Transactions (all at $1.00 per share): | ||||||||

Class A: | ||||||||

Proceeds from Shares Issued | 8,010,610 | 7,723,124 | ||||||

Reinvestment of Dividends | 111 | 105 | ||||||

Cost of Shares Redeemed | (7,964,288 | ) | (7,661,982 | ) | ||||

Net Increase in Net Assets Derived from Capital Shares Transactions | 46,433 | 61,247 | ||||||

Net Increase in Net Assets | 46,433 | 61,247 | ||||||

Net Assets: | ||||||||

Beginning of Year | 1,096,016 | 1,034,769 | ||||||

End of Year | $ | 1,142,449 | $ | 1,096,016 | ||||

Distributions in Excess of Net Investment Income | $ | (5 | ) | $ | (5 | ) | ||

The accompanying notes are an integral part of the financial statements.

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 11 |

For the years ended June 30,

For a Share Outstanding Throughout Each Year

| Net Asset Value, Beginning of Year | Net Investment Income(1) | Net Realized and Unrealized Gains (Losses) On Securities | Total from Investment Operations | Dividends from Net Investment Income | Distributions From Net Realized Gains | Net Asset Value, End of Period | Total Return† | Net Assets End of Year ($ Thousands) | Ratio of Expenses to Average Net Assets | Ratio of Expenses to Average Net Assets (Excluding Waivers) | Ratio of Net Investment Income to Average Net Assets | |||||||||||||||||||||||||||||||||||||

Prime Obligation Fund |

| |||||||||||||||||||||||||||||||||||||||||||||||

Class A: |

| |||||||||||||||||||||||||||||||||||||||||||||||

2015 | $ | 1.00 | $ | — | (2) | $ | — | (2) | $ | — | (2) | $ | — | $ | — | $ | 1.00 | 0.01 | % | $ | 1,142,449 | 0.18 | %* | 0.67 | % | 0.01 | % | |||||||||||||||||||||

2014 | 1.00 | — | (2) | — | (2) | — | (2) | — | — | 1.00 | 0.01 | 1,096,016 | 0.17 | * | 0.75 | 0.01 | ||||||||||||||||||||||||||||||||

2013 | 1.00 | — | (2) | — | (2) | — | (2) | — | (2) | — | (2) | 1.00 | 0.01 | 1,034,769 | 0.24 | * | 0.76 | 0.01 | ||||||||||||||||||||||||||||||

2012 | 1.00 | — | (2) | — | (2) | — | (2) | — | (2) | — | 1.00 | 0.01 | 886,342 | 0.25 | * | 0.77 | 0.01 | |||||||||||||||||||||||||||||||

2011 | 1.00 | — | (2) | — | (2) | — | (2) | — | (2) | — | 1.00 | 0.01 | �� | 904,457 | 0.31 | * | 0.77 | 0.01 | ||||||||||||||||||||||||||||||

| * | The Administrator has voluntarily agreed to waive and reduce their fee and/or reimburse certain expenses of the Fund in order to limit the one-day net income yield of the Fund to not less than 0.01% of the Fund’s daily average net assets. Had these waivers been excluded, the ratio would have been at the expense cap figure of 0.44%. See Note 3 of the Notes to Financial Statements. |

| (1) | Per share calculations were performed using average shares. |

| (2) | Amount represents less than $0.01 per share. |

| † | Returns are for the period indicated and have not been annualized. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

Amounts designated as “—” are zero or have been rounded to zero.

The accompanying notes are an integral part of the financial statements.

| 12 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

June 30, 2015

1. ORGANIZATION

SEI Liquid Asset Trust (the “Trust”) was organized as a Massachusetts business trust under a Declaration of Trust dated July 20, 1981.

The Trust is registered under the Investment Company Act of 1940, as amended, as a diversified, open-end management investment company with one fund: the Prime Obligation Fund (the “Fund”). The Trust is registered to offer Class A shares of the Fund. A description of the Fund’s investment objectives, policies, and strategies are provided in the prospectus.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Trust.

Use of Estimates — The preparation of financial statements, in conformity with U.S. generally accepted accounting principles, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Security Valuation — Investment securities are stated at amortized cost which approximates market value. Under this valuation method, purchase discounts and premiums are accreted and amortized to maturity and are included in interest income. The Fund’s use of amortized cost is subject to its compliance with certain conditions as specified by Rule 2a-7 of the 1940 Act.

In accordance with U.S. generally accepted accounting principles, fair value is defined as the price that the Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. A three-tier hierarchy has been established to maximize the use of the observable market data and minimize the use of unobservable inputs and to establish classification of the fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including such a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

Level 1 — quoted prices in active markets for identical investments

Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risks, etc.)

Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The valuation techniques used by the Fund to measure fair value during the year ended June 30, 2015 maximized the use of observable inputs and minimized the use of unobservable inputs.

As of June 30, 2015, all of the Fund’s investments are Level 2. During the year ended June 30, 2015, there were no transfers between Level 1 and Level 2.

For the year ended June 30, 2015, there have been no significant changes to the fair valuation methodologies.

Illiquid Securities — To the extent consistent with its investment objective and strategies, the Fund may invest in illiquid securities. A security is considered illiquid if it cannot be sold or disposed of in the ordinary course of business within seven days or less for its approximate carrying value on the books of the Fund. Valuations of illiquid securities may differ significantly from the values that would have been used had an active market value for these securities existed. At June 30, 2015, the Fund did not own any illiquid securities.

Restricted Securities — To the extent consistent with its investment objective and strategies, the Fund may own private placement investments purchased through private offerings or acquired through initial public offerings that could not be sold without prior registration under the Securities Act of 1933 or pursuant to an exemption there from. In addition, the Fund may generally agree to further restrictions on the disposition of certain holdings as set forth in various agreements entered into in connection with the purchase of those investments. These investments would be valued at amortized cost as determined in accordance with the procedures approved by the Board of Trustees. At June 30, 2015, the Fund did not own any restricted securities.

Repurchase Agreements — To the extent consistent with its investment objective and strategies, the Fund may invest in tri-party repurchase agreements. Securities held as collateral for tri-party repurchase agreements are maintained in a segregated account by the broker’s custodian bank. Provisions of the agreements and the Trust’s policies ensure that the market value of the collateral, including accrued interest thereon, is sufficient to cover interest and principal in the event of default by the counterparty. If the counterparty defaults and the value of the collateral declines or if the counterparty enters an insolvency proceeding, realization of the collateral by the Fund may be delayed or limited. At June 30, 2015, the Fund held Repurchase Agreements in the amount of $85,873 ($ Thousands). Please refer to the Schedule of Investments for more information.

Expenses — Expenses that are directly related to the Fund are charged directly to the Fund.

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 13 |

Notes to Financial Statements (Continued)

June 30, 2015

Security Transactions and Investment Income — Security transactions are accounted for on the trade date. Costs used in determining realized gains and losses on the sale of investment securities are on the basis of specific identification. Interest income is recognized using the accrual basis of accounting.

All amortization is calculated using the straight line method over the holding period of the security. Amortization of premiums and accretion of discounts are included in interest income.

Dividends and Distributions to Shareholders — Dividends from net investment income are declared on a daily basis and are payable on the first business day of the following month. Any net realized capital gains of the Fund are distributed to the shareholders of the Fund annually.

3. INVESTMENT ADVISORY, ADMINISTRATION AND DISTRIBUTION AGREEMENTS AND OTHER TRANSACTIONS WITH AFFILIATES

Investment Advisory, Administration and Distribution Agreements — SEI Investments Management Corporation (“SIMC”) serves as the Fund’s investment adviser (the “Adviser”) and “manager of managers” under an investment advisory agreement.

BofA Advisors, LLC (“BofA”), serves as sub-adviser to the Fund under an investment sub-advisory agreement with SIMC. SIMC compensates BofA out of the fee it receives from the Fund.

SEI Investments Global Funds Services (the “Administrator”) provides administrative and transfer agency services for an annual fee, which is calculated daily and paid monthly, of 0.30% of the average daily net assets of the Fund.

SEI Investments Distribution Co. (the “Distributor”), a wholly owned subsidiary of SEI Investments Company (“SEI”) and a registered broker-dealer, acts as the Distributor of the shares of the Trust under a Distribution Agreement. The Trust has adopted a shareholder servicing plan for its Class A shares (the “Class A Plan”) pursuant to which a shareholder servicing fee of up to 0.25% of the average daily net assets attributable to Class A shares will be paid to the Distributor. Under the Class A Plan, the Distributor may perform, or may compensate other service providers for performing, certain shareholder and administrative services.

The Distributor may retain as a profit any difference between the fee it receives and the amount it pays to third parties.

The Administrator has contractually agreed to waive its administration fees and/or to reimburse expenses of the Fund as necessary to keep total operating expenses (excluding interest, taxes and certain non-routine expenses, and net of SIMC and (the Distributor’s) fee) of the Fund from exceeding an annual rate of 0.44%.

The Adviser and/or Distributor have voluntarily agreed to waive a portion of their fees in order to keep total direct operating expenses

(exclusive of interest from borrowings, brokerage commissions, taxes, Trustee fees, prime broker fees, interest and dividend expenses related to short sales and extraordinary expenses not incurred in the ordinary course of the Fund’s business) at a specified level.

The waivers by the Adviser, Administrator and/or Distributor are limited to the Fund’s direct operating expenses and, therefore, do not apply to indirect expenses incurred by the Fund, such as acquired fund fees and expenses. The waivers are voluntary with the exception of the Administrator contractual waiver mentioned above and the Adviser, Administrator and/or Distributor may discontinue all or part of any of these waivers at any time.

In addition, the Administrator has voluntarily agreed to waive and reduce their fee and/or reimburse certain expenses of the Fund in order to limit the one-day net income yield of the Fund to not less than 0.01% of the Fund’s average daily net assets. For the year ended June 30, 2015, the amount of this waiver totaled $2,682 ($ Thousands).

The following is a summary of annual fees payable to the Adviser, Administrator and Distributor and the voluntary expense limitations for the Fund:

| Advisory Fees | Administration Fees | Shareholder Servicing Fees | Expense Limitations | |||||||||||||

Class A | 0.075 | %(1) | 0.30 | %(2) | 0.25 | % | 0.44 | % | ||||||||

| (1) | The Adviser receives an annual fee equal to 0.075% of the Trust’s average daily net assets up to $500 million and 0.02% of such net assets in excess of $500 million |

| (2) | Prior to October 1, 2014 the administration fees were 0.42%. |

Other — Certain officers and/or trustees of the Trust are also officers and/or directors of the Administrator, the Distributor or SIMC. Compensation of officers and affiliated trustees of the Trust is paid by the Administrator and/or the Distributor.

The services provided by the Chief Compliance Officer (“CCO”) and his staff, whom are employees of the Administrator, are paid for by the Trust as incurred. The services include regulatory oversight of the Trust’s adviser, sub-advisors and service providers as required by Securities Exchange Commission (“SEC”) regulations. The CCO’s services have been approved by and are reviewed annually by the Board.

Interfund Lending — The SEC has granted an exemption that permits the Trust to participate in an interfund lending program (the “Program”) with existing or future open ended investment companies registered under the 1940 Act that are advised by SIMC (the “SEI Funds”). The Program allows the SEI Funds to lend money to and borrow money from each other for temporary or emergency purposes. Participation in the Program is voluntary for both borrowing and lending funds. Interfund loans may be made only when the rate of interest to be charged is more favorable to the lending fund than an investment in overnight repurchase agreements (“Repo Rate”), and more favorable to the borrowing fund than the rate of interest that would be charged by a bank for short-term borrowings (“Bank Loan Rate”). The Bank Loan Rate will be determined

| 14 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

using a formula reviewed annually by the SEI Funds’ Board of Trustees. The interest rate imposed on interfund loans is the average of the Repo Rate and the Bank Loan Rate.

During the year ended June 30, 2015, the Trust loaned funds from the Fund to the SEI Funds. The amount of lending was $705,968 ($ Thousands) and the interest received on the lending and the corresponding interest rate were $8 ($ Thousands) and 0.22%-0.32%, respectively. The average amount of lending during the year ended June 30, 2015 was $24,344 ($ Thousands). The Trust had no outstanding loans under the interfund lending agreement at June 30, 2015.

4. FEDERAL INCOME TAXES

It is the Fund’s intention to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income. Accordingly, no provision for Federal income taxes is required. The timing and characterization of certain income and capital gains distributions are determined annually in accordance with Federal tax regulations which may differ from U.S. generally accepted accounting principles. As a result, net investment income (loss) and net realized gain (loss) on investment transactions for the reporting period may differ from distributions during such period. These book/tax differences may be temporary or permanent in nature. To the extent these differences are permanent, they are charged or credited to paid-in capital, undistributed net investment income or accumulated net realized gain, as appropriate, in the period that the differences arise.

Accordingly, no permanent differences have been reclassified during the year ended June 30, 2015, (as there were none).

The tax character of dividends paid to Class A shareholders during the years ended June 30, 2015 and June 30, 2014 were as follows ($ Thousands):

| Ordinary Income | ||||

2015 | $ | 113 | ||

2014 | $ | 108 | ||

As of June 30, 2015, the components of distributable earnings (accumulated losses) on a tax basis were as follows ($ Thousands):

| Undistributed Ordinary Income | $ | 6 | ||

| Other Temporary Differences | (9 | ) | ||

|

| |||

| Total Accumulated Losses | $ | (3 | ) | |

|

|

For Federal income tax purposes, capital loss carryforwards represent realized losses of the Fund that may be carried forward for a maximum period of eight years and applied against future capital gains.

Under the Regulated Investment Company Modernization Act of 2010, the Fund is permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period. However, any losses incurred during those future taxable years

are required to be utilized prior to the losses incurred in pre-enactment taxable years. As a result of this ordering rule, pre-enactment capital loss carryforwards may be more likely to expire unused. Additionally, post-enactment capital losses that are carried forward will retain their character as either short-term or long-term capital losses rather than being considered all short-term as under previous law.

The cost basis of securities for Federal income tax purposes is equal to the cost basis used for financial reporting purposes.

Management has analyzed the Fund’s tax positions taken on the federal tax returns for all open tax years and has concluded that as of June 30, 2015, no provision for income tax is required in the Fund’s financial statements.

5. NEW ACCOUNTING PRONOUNCEMENT

In May 2015, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2015-07 regarding “Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share”. The amendments in this update are effective for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. ASU No. 2015-07 will eliminate the requirement to categorize investments in the fair value hierarchy if their fair value is measured at net asset value (NAV) per share (or its equivalent) using the practical expedient in the FASB’s fair value measurement guidance. At this time, management is evaluating the implications of ASU No. 2015-07 and its impact on the financial statement disclosures has not yet been determined.

6. REGULATORY MATTERS

On July 23, 2014, the SEC adopted amendments to the rules that govern money market mutual funds. In part, the amendments will require structural changes to most types of money market funds to one extent or another; however, the SEC provided for an extended 2-year transition period to comply with such structural requirements. At this time, management is evaluating the reforms adopted and the manner for implementing these reforms over time and its impact on the financial statements.

7. SUBSEQUENT EVENTS

The Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the financial statements were available to be issued. This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments.

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 15 |

Report of Independent Registered Public Accounting Firm

The Board of Trustees and Shareholders

SEI Liquid Asset Trust:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of SEI Liquid Asset Trust, comprised of the Prime Obligation Fund (the “Fund”), as of June 30, 2015, and the related statements of operations for the year then ended, changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of June 30, 2015, by correspondence with the custodian and brokers or other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Fund comprising SEI Liquid Asset Trust as of June 30, 2015, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Philadelphia, Pennsylvania

August 28, 2015

| 16 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

TRUSTEES AND OFFICERS OF THE TRUST (Unaudited)

The following chart lists Trustees and Officers as of June 30, 2015.

Set forth below are the names, ages, addresses, position with the Fund, term of office and length of time served, the principal occupations for the last five years, number of portfolios in fund complex overseen by the directors, and other directorships outside the fund complex of each of the persons currently serving as Directors and Officers of the Fund. The Fund’s Statement of Additional Information (“SAI”) includes additional information about the Directors and Officers. The SAI may be obtained without charge by calling 1-800-342-5734.

Name Address, and Age | Position(s) Trusts | Term of Office and Length of Time Served1 | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee2 | Other Directorships Held by Trustee | |||||

| INTERESTED TRUSTEES | ||||||||||

Robert A. Nesher One Freedom Oaks, PA 19456 68 yrs. old | Chairman of the Board of Trustees* | since 1982 | Currently performs various services on behalf of SEI for which Mr. Nesher is compensated. | 101 | Trustee of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, Bishop Street Funds, Director of SEI Global Master Fund, plc, SEI Global Assets Fund, plc, SEI Global Investments Fund, plc, SEI Investments Global, Limited, SEI Investments — Global Fund Services, KP Funds, Limited, SEI Investments (Europe), Limited, SEI Global Nominee Ltd., SEI Structured Credit Fund, L.P. | |||||

William M. Doran One Freedom Valley Drive Oaks, PA 19456 74 yrs. old | Trustee* | since 1982 | Self-employed consultant since 2003. Partner, Morgan, Lewis & Bockius LLP (law firm) from 1976 to 2003, counsel to the Trust, SEI, SIMC, the Administrator and the Distributor. Secretary of SEI since 1978. | 101 | Trustee of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, The Advisors’ Inner Circle Fund III, Bishop Street Funds, The KP Funds, O’Connor EQUUS, Director of SEI since 1974. Director of the Distributor since 2003. Director of SEI Investments — Global Fund Services, Limited, SEI Investments Global, Limited, SEI Investments (Europe), Limited, SEI Investments (Asia), SEI Global Nominee Ltd., Limited and SEI Asset Korea Co., Ltd. | |||||

| TRUSTEES | ||||||||||

George J. Sullivan, Jr. One Freedom Valley Drive Oaks, PA 19456 72 yrs. old | Trustee | since 1996 | Retired since January 2012. Self-Employed Consultant, Newfound Consultants Inc. since April 1997-December 2011. | 101 | Trustee of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, Bishop Street Funds, State Street Navigator Securities Lending Trust, KP Funds and SEI Structured Credit Fund, L.P., member of the independent review committee for SEI’s Canadian-registered mutual funds. | |||||

| * | Messrs. Nesher and Doran are Trustees who may be deemed as “interested” persons of the Trust as that term is defined in the 1940 Act by virtue of their affiliation with SIMC and the Trust’s Distributor. |

| 1 | Each trustee shall hold office during the lifetime of this Trust until the election and qualification of his or her successor, or until he or she sooner dies, resigns or is removed in accordance with the Trust’s Declaration of Trust. |

| 2 | The Fund Complex includes the following Trusts: SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, Adviser Managed Trust, SEI Institutional International Trust, SEI Institutional Managed Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust , SEI Insurance Products Trust, New Covenant Funds and SEI Catholic Values Trust. |

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 17 |

TRUSTEES AND OFFICERS OF THE TRUST (Unaudited)

Name Address, and Age | Position(s) Trusts | Term of Office and Length of Time Served1 | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee2 | Other Directorships Held by Trustee | |||||

| TRUSTEES (continued) | ||||||||||

Nina Lesavoy One Freedom Valley Drive Oaks, PA 19456 57 yrs. old | Trustee | since 2003 | Founder and Managing Director, Avec Capital since 2008. Managing Director, Cue Capital from March 2002-March 2008. | 101 | Director of SEI Structured Credit Fund, L.P. | |||||

James M. Williams One Freedom Valley Drive Oaks, PA 19456 67 yrs. Old | Trustee | since 2004 | Vice President and Chief Investment Officer, J. Paul Getty Trust, Non-Profit Foundation for Visual Arts, since December 2002. | 101 | Trustee/Director of Ariel Mutual Funds, and SEI Structured Credit Fund, L.P. | |||||

Mitchell A. Johnson One Freedom Valley Drive Oaks, PA 19456 73 yrs. old | Trustee | since 2007 | Private Investor since 1994. | 101 | Trustee of the Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, and Bishop Street Funds and KP Funds | |||||

Hubert L. Harris, Jr. One Freedom Valley Drive Oaks, PA 19456 71 yrs. old | Trustee | since 2008 | Retired since December 2005. Chief Executive Officer and Chair of the Board of Directors, AMVESCAP Retirement, Inc., 1997-December 2005. Chief Executive Officer, INVESCO North America, September 2003-December 2005. | 101 | Director of Colonial BancGroup, Inc. and St. Joseph’s Translational Research Institute; Chair of the Board of Trustees, Georgia Tech Foundation, Inc. (nonprofit corporation); Board of Councilors of the Carter Center. | |||||

| OFFICERS | ||||||||||

Robert A. Nesher One Freedom Valley Drive Oaks, PA 19456 68 yrs. old | President and CEO | since 2005 | Currently performs various services on behalf of SEI for which Mr. Nesher is compensated. | N/A | N/A | |||||

Arthur Ramanjulu One Freedom Valley Drive Oaks, PA 19456 51 yrs. old | Controller and Chief Financial Officer | since 2015 | Director, Funds Accounting, SEI Investments Global Funds Services (March 2015); Senior Manager, Funds Accounting, SEI Global Funds Services (March 2007 to February 2015). | N/A | N/A | |||||

Russell Emery One Freedom Valley Drive Oaks, PA 19456 52 yrs. old | Chief Compliance Officer | since 2006 | Chief Compliance Officer of SEI Institutional Managed Trust, SEI Asset Allocation Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Institutional Investments Trust, The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, and Bishop Street Funds, since March 2006. Chief Compliance Officer of SEI Structured Credit Fund, LP and since June 2007. Chief Compliance Officer of Adviser Managed Trust since December 2010. Chief Compliance Officer of New Covenant Funds since February 2012. Chief Compliance Officer of SEI Insurance Products Trust and the KP Funds since 2013. Chief Compliance Officer of The Advisors’ Inner Circle Fund III, O’Connor EQUUS, Winton Series Trust and Winton Diversified Opportunities Fund since 2014. Chief Compliance Officer of SEI Catholic Values Trust since 2015. | N/A | N/A | |||||

| 18 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

Name Address, and Age | Position(s) Trusts | Term of Office and Length of Time Served1 | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee2 | Other Directorships Held by Trustee | |||||

| OFFICERS (continued) | ||||||||||

Timothy D. Barto One Freedom Valley Drive Oaks, PA 19456 47 yrs. old | Vice President and Secretary | since 2002 | General Counsel, Vice President and Secretary of SIMC and the Administrator since 2004. Vice President and Assistant Secretary of SEI since 2001. Vice President of SIMC and the Administrator since 1999. | N/A | N/A | |||||

Aaron Buser One Freedom Valley Drive Oaks, PA 19456 44 yrs. old | Vice President and Assistant Secretary | since 2008 | Vice President and Assistant Secretary of SIMC since 2007. Associate at Stark & Stark (2004-2007). | N/A | N/A | |||||

David F. McCann One Freedom Valley Drive Oaks, PA 19456 39 yrs. old | Vice President and Assistant Secretary | since 2009 | Vice President and Assistant Secretary of SIMC since 2008. Attorney, Drinker Biddle & Reath, LLP (law firm), May 2005-October 2008, Attorney, Pepper Hamilton, LLP (law firm), September 2001-May 2005. | N/A | N/A | |||||

Stephen G. MacRae One Freedom 47 yrs. old | Vice President | since 2012 | Director of Global Investment Product Management, January 2004 to present. | N/A | N/A | |||||

Bridget E. Sudall One Freedom Valley Drive Oaks, PA 19456 35 yrs. old | Anti-Money Laundering Compliance Officer and Privacy Officer | since 2015 | Anti-Money Laundering Compliance Officer and Privacy Officer since 2015. Senior Associate and AML Officer, Morgan Stanley Alternative Investment Partners, April 2011 to March 2015. Investor Services Team Lead, Morgan Stanley Alternative Investment Partners, July 2007 to April 2011. | N/A | N/A | |||||

| 1 | Each trustee shall hold office during the lifetime of this Trust until the election and qualification of his or her successor, or until he or she sooner dies, resigns or is removed in accordance with the Trust’s Declaration of Trust. |

| 2 | The Fund Complex includes the following Trusts: SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, Adviser Managed Trust, SEI Institutional International Trust, SEI Institutional Managed Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Insurance Products Trust, New Covenant Funds and SEI Catholic Values Trust. |

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 19 |

Disclosure of Fund Expenses (Unaudited)

All mutual funds have operating expenses. As a shareholder of a mutual fund, your investment is affected by these ongoing costs, which include (among others) costs for portfolio management, administrative services, and shareholder reports like this one. It is important for you to understand the impact of these costs on your investment returns.

Operating expenses such as these are deducted from the mutual fund‘s gross income and directly reduce its final investment return. These expenses are expressed as a percentage of the mutual fund’s average net assets; this percentage is known as the mutual fund’s expense ratio. The following examples use the expense ratio and are intended to help you understand the ongoing costs (in dollars) of investing in your Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The table below illustrates your Fund’s costs in two ways:

• Actual Fund Return. This section helps you to estimate the actual expenses after fee waivers that your Fund incurred over the period. The “Expenses Paid During Period” column shows the actual dollar expense cost incurred by a $1,000 investment in the Fund, and the “Ending Account Value” number is derived from deducting that expense cost from the Fund’s gross investment return.

You can use this information, together with the actual amount you invested in your Fund, to estimate the expenses you paid over that period. Simply divide your actual starting account value by $1,000 to arrive at a ratio (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply that ratio by the number shown for your Fund under “Expenses Paid During Period.”

• Hypothetical 5% Return. This section helps you compare your Fund’s costs with those of other mutual funds. It assumes that your Fund had an annual 5% return before expenses during the year, but that the expense ratio (Column 3) is unchanged. This example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to make this 5% calculation. You can assess your Fund’s comparative cost by comparing the hypothetical result for your Fund in the “Expenses Paid During Period” column with those that appear in the same charts in the shareholder reports for other mutual funds.

NOTE: Because the return is set at 5% for comparison purposes — NOT your Fund’s actual return — the account values shown do not apply to your specific investment.

| Beginning Account Value 1/1/15 | Ending Account Value 6/30/15 | Annualized Expense Ratios | Expenses Paid During Period* | |||||||||||||

Prime Obligation Fund |

| |||||||||||||||

Actual Fund Return |

| |||||||||||||||

Class A | $ | 1,000.00 | $ | 1,000.00 | 0.19 | % | $ | 0.94 | ||||||||

Hypothetical 5% Return |

| |||||||||||||||

Class A | $ | 1,000.00 | $ | 1,023.85 | 0.19 | % | $ | 0.95 | ||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period shown). |

| 20 | SEI Liquid Asset Trust / Annual Report / June 30, 2015 |

Board of Trustees Considerations in Approving the Advisory and Sub-Advisory Agreements (Unaudited)

SEI Liquid Asset Trust (the “Trust”) and SEI Investments Management Corporation (“SIMC”) have entered into an investment advisory agreement (the “Advisory Agreement”). Pursuant to the Advisory Agreement, SIMC is responsible for the investment advisory services provided to the sole series of the Trust (the “Fund”). Pursuant to a separate sub-advisory agreement with SIMC (the “Sub-Advisory Agreement” and, together with the Advisory Agreement, the “Investment Advisory Agreements”), and under the supervision of SIMC and the Trust’s Board of Trustees (the “Board”), the sub-adviser (the “Sub-Adviser”) provides security selection and certain other advisory services with respect to all or a discrete portion of the assets of the Fund. The Sub-Adviser is also responsible for managing its employees who provide services to the Fund. Sub-Advisers are selected based primarily upon the research and recommendations of SIMC, which evaluates quantitatively and qualitatively the Sub-Advisers’ skills and investment results in managing assets for specific asset classes, investment styles and strategies.

The Investment Company Act of 1940, as amended (the “1940 Act”) requires that the initial approval of, as well as the continuation of, the Fund’s Investment Advisory Agreements must be specifically approved: (i) by the vote of the Board or by a vote of the shareholders of the Fund; and (ii) by the vote of a majority of the Trustees who are not parties to the Investment Advisory Agreements or “interested persons” of any party (the “Independent Trustees”), cast in person at a meeting called for the purpose of voting on such approval(s). In connection with their consideration of such approval(s), the Fund’s Trustees must request and evaluate, and SIMC and the Sub-Adviser are required to furnish, such information as may be reasonably necessary to evaluate the terms of the Investment Advisory Agreements. In addition, the Securities and Exchange Commission takes the position that, as part of their fiduciary duties with respect to a mutual fund’s fees, mutual fund boards are required to evaluate the material factors applicable to a decision to approve an Investment Advisory Agreement.

Consistent with these responsibilities, the Board calls and holds meetings each year to consider whether to approve new and/or renew existing Investment Advisory Agreements between the Trust and SIMC and SIMC and the Sub-Adviser with respect to the Fund of the Trust. In preparation for these meetings, the Board requests and reviews a wide variety of materials provided by SIMC and the Sub-Adviser, including information about SIMC’s and the Sub-Adviser’s affiliates, personnel and operations and the services provided pursuant to the Investment Advisory Agreements. The Board also receives data from third parties. This information is provided in addition to the detailed information about the Fund that the Board reviews during the course of each year, including information that relates to Fund operations and Fund performance. The Trustees also receive a memorandum from counsel regarding the responsibilities of Trustees in connection with their consideration of whether to approve the Trust’s Investment Advisory Agreements. Finally, the Independent Trustees receive advice from independent counsel to the Independent Trustees, meet in executive sessions outside the presence of Fund management and participate in question and answer sessions with representatives of SIMC and the Sub-Adviser.

Specifically, during the course of the Trust’s fiscal year, the Board requested and received written materials from SIMC and the Sub-Adviser regarding: (i) the quality of SIMC’s and the Sub-Adviser’s investment management and other services; (ii) SIMC’s and the Sub-Adviser’s investment management personnel; (iii) SIMC’s and the Sub-Adviser’s operations and financial condition; (iv) SIMC’s and the Sub-Adviser’s brokerage practices (including any soft dollar arrangements) and investment strategies; (v) the level of the advisory fees that SIMC charges the Fund and the level of the sub-advisory fees that SIMC pays the Sub-Adviser, compared with fees each charge to comparable accounts; (vi) the advisory fees charged by SIMC and the Fund’s overall fees and operating expenses compared with peer groups of mutual funds prepared by Lipper, an independent provider of investment company data; (vii) the level of SIMC’s and the Sub-Adviser’s profitability from their Fund-related operations; (viii) SIMC’s and the Sub-Adviser’s compliance program, including a description of material compliance matters and material compliance violations; (ix) SIMC’s potential economies of scale; (x) SIMC’s and the Sub-Adviser’s policies on and compliance procedures for personal securities transactions; (xi) SIMC’s and the Sub-Adviser’s expertise and resources in domestic and/or international financial markets; and (xii) the Fund’s performance over various periods of time compared with peer groups of mutual funds prepared by Lipper and the Fund’s benchmark indices.

At the March 24-25, 2015 meeting of the Board of Trustees, the Trustees, including a majority of the Independent Trustees, approved the renewal of the Investment Advisory Agreements. In each case, the Board’s approvals were based on its

| SEI Liquid Asset Trust / Annual Report / June 30, 2015 | 21 |

Board of Trustees Considerations in Approving the Advisory and Sub-Advisory Agreements (Unaudited) (Continued)

consideration and evaluation of the factors described above, as discussed at the meeting and at prior meetings. The following

discusses some, but not all, of the factors that were considered by the Board in connection with its assessment of the Investment Advisory Agreements.

Nature, Extent and Quality of Services. The Board considered the nature, extent and quality of the services provided by SIMC and the Sub-Adviser to the Fund and the resources of SIMC and the Sub-Adviser and their affiliates dedicated to the Fund. In this regard, the Trustees evaluated, among other things, SIMC’s and the Sub-Adviser’s personnel, experience, track record and compliance program. Following evaluation, the Board concluded that, within the context of its full deliberations, the nature, extent and quality of services provided by SIMC and the Sub-Adviser to the Fund and the resources of SIMC and the Sub-Adviser and their affiliates dedicated to the Fund were sufficient to support renewal of the Investment Advisory Agreements. In addition to advisory services, the Board considered the nature and quality of certain administrative, transfer agency and other non-investment advisory services provided to the Fund by SIMC and/or its affiliates.