UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-03231

SEI Liquid Asset Trust

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

c/o CT Corporation

155 Federal St.

Boston, MA 02110

Registrant’s telephone number, including area code: 1-800-342-5734

Date of fiscal year end: June 30, 2016

Date of reporting period: June 30, 2016

| Item 1. | Reports to Stockholders. |

June 30, 2016

ANNUAL REPORT

SEI Liquid Asset Trust

➤ Prime Obligation Fund

| 1 | ||||

| 4 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 15 | ||||

| 16 | ||||

| 20 | ||||

Board of Trustees Considerations in Approving the Advisory Agreement | 21 | |||

| 24 | ||||

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarter of each fiscal year on Form N-Q within sixty days after the end of the period. The Trust’s Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

JUNE 30, 2016 (Unaudited)

To Our Shareholders:

The Fund’s fiscal year — July 1, 2015 through June 30, 2016 — was notable for several key themes: energy-sector volatility spread to other areas of the market amid continued oil-price weakness, followed by a partial recovery; major central-bank policies diverged, with the Federal Reserve (Fed) commencing rate increases while the European Central Bank (ECB), Bank of Japan (BOJ) and People’s Bank of China (PBOC) deepened their commitments to monetary accommodation; and, as a result of the diverging policies, major developed-market sovereign-bond yields continued to fall, with some edging into negative-rate territory. A vote (Brexit) by U.K. citizens in favor of leaving the European Union (EU) took place with roughly a week left in the reporting period, briefly upending global financial markets and presenting major questions about how the relationship will be dissolved.

Geopolitical events

Severe unrest continued in certain areas of the Middle East, driven by the sometimes-opposing and sometimes-overlapping interests of Islamic State, the Syrian regime, Syrian nationalists, Kurdish forces and the Iraqi military. Regional superpowers Iran, Saudi Arabia and Turkey also applied varying degrees of indirect influence. Broader involvement escalated, with Russia’s airpower commitment in early fall and a redoubled coalition of Western powers targeting Islamic State after a series of attacks by religious extremists across the globe. A U.S.-Russia-brokered ceasefire between the Syrian regime and nationalist rebels (excluding Islamic State and other terrorist groups) came into effect during late February, maintaining a questionable hold through the end of the reporting period. Iraqi forces, supported by U.S. air and ground resources, began to make notable progress in reversing Islamic State gains as the end of the reporting period approached; at the same time, incidences of terrorism appeared to increase in Africa, Asia, Europe, the Middle East and North America. While the conflict that originated in Syria and Iraq appears to have influenced destabilizing events elsewhere around the globe, and taken a terrible human toll, it has not had a significant impact on global markets or the economy at this point.

It will be interesting, however, to see the ultimate effects of the ensuing Syrian migrant crisis on the European Union (EU). Immigration served as one of the key points of contention leading up to Great Britain’s EU referendum, which resulted in a vote to leave the EU just before the end of the reporting period. U.K. Prime Minister David Cameron tendered his resignation as a result, and a litany of questions entered the public dialogue on topics ranging from when the government would commence the formal withdrawal process, to how negotiations would fare regarding trade agreements, and the likelihood that immigration goals espoused by the Leave campaign would come to pass.

Immigration-driven ballot-box uncertainty has also taken center stage in the U.S. presidential election, where the leading primary candidates of the two major political parties were essentially positioned to clinch their nominations at the end of the reporting period.

Despite the considerable aforementioned instability in the Middle East, the price of oil remained mostly insulated from regional developments. Oil-price weakness, which persisted for the first two-thirds of the reporting period, remained primarily attributable to oversupply: members of the Organization of Petroleum Exporting Countries failed to agree on production cuts; U.S. Congress approved the restoration of oil exports in mid-December; and Iran’s multilateral agreement on the scope of its nuclear program paved the way for its post-sanction return as a major low-cost oil supplier. The International Energy Agency, however, projected a return to supply-demand balance in 2017.

Energy-export-dependent Venezuela succumbed to the economically depressive effects of low oil prices during the fiscal year. Food shortages and a breakdown of the rule of law appeared to worsen as the reporting period concluded, despite a partial rebound in the price of oil. Brazil’s prospects also paled during the reporting period, as a corruption investigation centering on its lead state-run oil company enveloped a cross-section of political leaders — culminating in the impeachment of President Dilma Rousseff.

Economic performance

U.S. economic growth in the second quarter of 2015 bordered on impressive, due in large part to strong consumer activity. The pace of growth essentially halved during the third quarter amid slow sales and lackluster export activity. Fourth-quarter growth decelerated further, as industrial production and manufacturing came under pressure from the effects of U.S. dollar strength. Growth during the first quarter of 2016 slowed more still; although business activity improved toward the end of the quarter and early in the second quarter. Retail sales and consumer spending surged in April 2016, foreshadowing a potential rebound in second-quarter economic growth. At the end of the reporting

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 1 |

LETTER TO SHAREHOLDERS (Concluded)

JUNE 30, 2016 (Unaudited)

period, the Federal Reserve Bank of Atlanta projected second-quarter economic growth would roughly double the first quarter’s pace; while welcomed, it falls far short of the growth rate achieved during the second quarter of 2015. The labor market improved consistently for most of the fiscal year, with the unemployment rate declining from 5.3% in July 2015 to 4.9% in June 2016. Average hourly earnings and real personal incomes gained with relative steadiness, bouncing around a rough mean of about 0.2% per month over the reporting period. The Fed raised its target interest rate in mid-December for the first time since 2006, leaving behind a near-zero rate that had been in place since late 2008.

Market developments

Risk assets were treading water at the start of the fiscal year after spending June 2015 (immediately prior to the start of the reporting period) in a downtrend that originated with deep losses on China’s mainland stock exchanges. More severe declines in late summer, when China moderately devalued its currency, were followed by a partial recovery through October. As 2015 came to a close, the questionable health of U.S. energy companies (which was caused by a persistent, multi-year oil-price decline) raised concerns among high-yield bond investors.

The beginning of 2016 was marked by a global flight to quality, benefitting safe-haven assets at the expense of risk assets. A trend reversal took place in mid-February, with risk assets rallying into April, followed by mixed performance until late June. The price of oil, and commodities in general, also advanced sharply from mid-February into June. Brexit caused a major spike in global stock-market volatility, yields were driven downward to record levels on perceived safe-haven investments like developed-market government bonds, and the currencies at the center of the developments — sterling and the euro — weakened substantially relative to the U.S. dollar and Japanese yen. Most of the stock-market losses, however, were recovered within a week’s time as the reporting period drew to a close.

The U.S. dollar ended the fiscal year less than 1% higher against a trade-weighted basket of major currencies, having been as much as 6.5% higher in late January, and 2.5% lower in early May.

Global fixed income, as measured by the Barclays Global Aggregate Bond Index, advanced 8.87% in U.S. dollar terms during the fiscal year. Interest rates generally declined during the reporting period, as major central banks outside of the U.S. guided benchmark rates downward (into negative territory in some cases) and expanded their asset-purchase programs.

U.S. Treasuries generally performed well as the yield curve flattened (bond yields move inversely to prices) and rates fell across most maturities, with only the yields on treasuries with maturities shorter than two years increasing during the full reporting period.

U.S. investment-grade corporate debt performed well, and the high-yield market was modestly positive. The BofA Merrill Lynch US High Yield Constrained Index increased by 1.74% during the full fiscal year, although a sharp advance beginning in mid-February eliminated a double-digit decline by the end of the reporting period. Mortgage- and asset-backed securities also delivered positive returns during the reporting period.

Emerging-market debt delivered mixed gains. The J.P. Morgan GBI Emerging Markets Global Diversified Index, which tracks local-currency-denominated emerging-market bonds, increased by 2.24% in U.S. dollar terms during the reporting period, bolstered by an impressive late-period rally as U.S. dollar strength waned. The J.P. Morgan EMBI Global Diversified Index, which tracks emerging-market debt denominated in external currencies (such as the U.S. dollar), advanced by 9.79%.

The Fed’s policy of keeping short-term interest rates near zero continued to depress money market fund yields during the period. In December 2015, the Fed raised the target Fed funds rate for the first time in nine years to a range of 0.25%-0.50% and, as a result, Treasury rates moved higher on the front end of the curve. In subsequent meetings, the Fed has left rates unchanged, pointing to concerns about the state of the global economy.

In addition, the finalization of the Securities and Exchange Commission’s money market rule reform in July 2014 is expected to have significant impacts on the scope of money market fund management and operations. Shares of institutional prime funds will be required to adopt a floating net asset value (NAV), replacing the traditional stable one dollar per share price. Retail prime funds and government funds are exempt from the floating NAV requirement. In addition, prime funds (both institutional and retail) will be required to impose liquidity fees and redemption gates

| 2 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

under certain circumstances, while government funds will be able to elect to opt out of those gates and fees. The deadline for these funds to comply with the new rules is October 2016. SEI has designed a plan to restructure our existing money market fund offerings and made the decision to liquidate the SLAT Prime Obligation fund on July 22, 2016.

A combination of subdued inflation and dollar strength began to ease in the latter part of the reporting period, reducing headwinds to the performance of inflation-sensitive assets such as Treasury inflation-protected securities and commodities. The latter declined by 15% over the Fund’s fiscal year, according to the TR/CC CRB Commodities Total Return Index, but dropped by almost 32% as recently as mid-February before staging a steep partial recovery.

Our view

The U.S. has remained resilient despite numerous shocks over the past seven years, and we expect this resilience will once again be on display following the U.K. vote. May’s employment figure was the weakest since 2010, but other labor-market data are not quite as downbeat. Job openings remain in a solid uptrend, rising well beyond the previous cycle’s peak in mid-2007. The first hints of wage pressure have appeared, with a moderate acceleration in wages and total labor compensation apparent on a year-over-year basis. As corporate margins get squeezed by the pick-up in labor costs, the pressure to raise prices will likely intensify.

This puts the Fed in something of a quandary, since the Brexit shock has seemingly upended any possibility of a near-term rise in the funds rate. Market-implied expectations for the next policy-rate move have been pushed out to late 2017; in fact, futures traders have priced in the mild possibility of a rate cut in the near term. Yet, we admit to a growing uneasiness that the central bank may be a falling behind the inflation curve.

We understand that the still-soggy global economy and the shock delivered by the U.K. vote argue for a very cautious process of interest-rate normalization. But if the upward trend in labor costs is sustained, a more aggressive response by the U.S. central bank eventually will be justified.

On behalf of SEI Investments, I want to thank you for your continued confidence. We are working every day to maintain that confidence, and we look forward to serving your investment needs in the future.

Sincerely,

William T. Lawrence, CFA

Managing Director, Portfolio Management Team

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 3 |

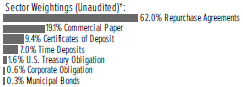

SCHEDULE OF INVESTMENTS

June 30, 2016

Prime Obligation Fund

| ||||||

†Percentages are based on total investments. | ||||||

| Description |

Face Amount |

Value | ||||||

COMMERCIAL PAPER (A)(B) — 18.3% |

| |||||||

ASB Finance | ||||||||

0.807%, 07/14/2016 (D) | $ | 3,076 | $ | 3,076 | ||||

Chevron | ||||||||

0.586%, 07/07/2016 | 8,000 | 7,999 | ||||||

0.511%, 07/11/2016 | 20,000 | 19,997 | ||||||

0.521%, 07/13/2016 | 10,000 | 9,999 | ||||||

DNB Bank | ||||||||

0.692%, 07/15/2016 | 17,000 | 16,995 | ||||||

Fairway Finance | ||||||||

0.652%, 07/05/2016 | 8,010 | 8,009 | ||||||

JP Morgan Securities | ||||||||

0.682%, 07/01/2016 | 604 | 604 | ||||||

0.672%, 07/08/2016 | 2,000 | 2,000 | ||||||

0.854%, 07/21/2016 | 3,926 | 3,924 | ||||||

Liberty Street Funding | ||||||||

0.591%, 07/13/2016 | 6,389 | 6,388 | ||||||

MetLife Short Term Funding | ||||||||

0.581%, 07/01/2016 | 11,000 | 11,000 | ||||||

0.611%, 07/05/2016 | 1,619 | 1,619 | ||||||

0.581%, 07/08/2016 | 15,000 | 14,998 | ||||||

0.581%, 07/11/2016 | 15,000 | 14,998 | ||||||

National Australia Funding Delaware |

| |||||||

0.652%, 07/01/2016 | 5,000 | 5,000 | ||||||

Nordea Bank | ||||||||

0.646%, 07/11/2016 | 7,000 | 6,999 | ||||||

0.652%, 07/20/2016 | 10,175 | 10,171 | ||||||

Old Line Funding | ||||||||

0.652%, 07/05/2016 | 8,016 | 8,016 | ||||||

0.732%, 07/19/2016 | 4,342 | 4,340 | ||||||

Sumitomo Mitsui Banking | ||||||||

0.350%, 07/05/2016 | 20,000 | 19,999 | ||||||

Sumitomo Mitsui Trust Bank Limited |

| |||||||

0.485%, 07/05/2016 | 20,000 | 19,999 | ||||||

Thunder Bay Funding | ||||||||

0.687%, 07/08/2016 | 9,359 | 9,358 | ||||||

Total Capital Canada | ||||||||

0.611%, 07/05/2016 | 17,000 | 16,999 | ||||||

Toyota Motor Credit | ||||||||

0.632%, 07/01/2016 | 14,000 | 14,000 | ||||||

| Description |

Face Amount |

Value | ||||||

COMMERCIAL PAPER (A)(B) (continued) |

| |||||||

0.632%, 07/15/2016 | $ | 8,000 | $ | 7,998 | ||||

|

| |||||||

Total Commercial Paper |

| 244,485 | ||||||

|

| |||||||

CERTIFICATES OF DEPOSIT — 9.0% |

| |||||||

ASB Finance | ||||||||

0.797%, 07/11/2016 (D) | 2,491 | 2,491 | ||||||

Bank of Nova Scotia | ||||||||

0.798%, 07/21/2016 (D) | 10,000 | 10,000 | ||||||

Bank of Tokyo-Mitsubishi UFJ NY |

| |||||||

0.620%, 07/01/2016 | 24,700 | 24,700 | ||||||

Canadian Imperial Bank of Commerce |

| |||||||

0.690%, 07/08/2016 | 10,000 | 10,000 | ||||||

Sumitomo Mitsui Trust Bank Limited |

| |||||||

0.700%, 07/21/2016 | 11,581 | 11,581 | ||||||

Svenska Handelsbanken | ||||||||

0.545%, 07/06/2016 | 11,000 | 11,000 | ||||||

0.655%, 07/07/2016 | 15,000 | 15,000 | ||||||

0.655%, 07/14/2016 | 12,000 | 12,000 | ||||||

0.805%, 07/15/2016 | 6,000 | 6,000 | ||||||

Toronto-Dominion Bank | ||||||||

0.792%, 07/15/2016 (D) | 5,750 | 5,750 | ||||||

Wells Fargo Bank | ||||||||

0.813%, 07/06/2016 (D) | 2,000 | 2,000 | ||||||

0.797%, 07/14/2016 (D) | 5,000 | 5,000 | ||||||

Westpac Banking | ||||||||

0.617%, 07/01/2016 (D) | 5,000 | 5,000 | ||||||

|

| |||||||

Total Certificates of Deposit |

| 120,522 | ||||||

|

| |||||||

TIME DEPOSITS — 6.7% |

| |||||||

National Australia Funding Delaware |

| |||||||

0.300%, 07/01/2016 | 20,500 | 20,500 | ||||||

Skandinaviska Enskilda Banken |

| |||||||

0.290%, 07/01/2016 | 29,500 | 29,500 | ||||||

Swedbank | ||||||||

0.300%, 07/01/2016 | 40,000 | 40,000 | ||||||

|

| |||||||

Total Time Deposits |

| 90,000 | ||||||

|

| |||||||

| 4 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

| Description |

Face Amount |

Value | ||||||

U.S. TREASURY OBLIGATION — 1.5% |

| |||||||

United States Treasury Bill | ||||||||

0.100%, 07/14/2016 (C)

| $

| 20,000

|

| $

| 19,999

|

| ||

|

| |||||||

Total U.S. Treasury Obligation |

| 19,999 | ||||||

|

| |||||||

CORPORATE OBLIGATION — 0.7% |

| |||||||

Canadian Imperial Bank of Commerce |

| |||||||

1.350%, 07/18/2016 | 9,000 | 9,003 | ||||||

|

| |||||||

Total Corporate Obligation | 9,003 | |||||||

|

| |||||||

MUNICIPAL BONDS (D) — 0.3% |

| |||||||

Massachusetts — 0.1% |

| |||||||

Simmons College, RB | ||||||||

0.440%, 07/07/2016 (B) | 480 | 480 | ||||||

|

| |||||||

Minnesota — 0.1% |

| |||||||

Minnesota Office of Higher Education, Ser A, RB | ||||||||

0.430%, 07/07/2016 (B) | 1,780 | 1,780 | ||||||

|

| |||||||

New Jersey — 0.1% |

| |||||||

North Hudson Sewerage Authority, RB Callable 07/05/2016 @ 100 | ||||||||

0.450%, 07/07/2016 (B) | 665 | 665 | ||||||

|

| |||||||

New York — 0.0% |

| |||||||

New York State Housing Finance Agency, Various Housing Project, RB Callable 07/04/2016 @ 100 | ||||||||

0.420%, 07/06/2016 (B) | 440 | 440 | ||||||

|

| |||||||

Wisconsin — 0.0% |

| |||||||

Wisconsin Housing & Economic Development | ||||||||

0.570%, 07/06/2016 | 125 | 125 | ||||||

Wisconsin Housing & | ||||||||

0.500%, 07/07/2016 | 260 | 260 | ||||||

|

| |||||||

|

385 |

| ||||||

|

| |||||||

| Description |

Face Amount |

Value | ||||||

MUNICIPAL BONDS (continued) |

| |||||||

Total Municipal Bonds |

| $ | 3,750 | |||||

|

| |||||||

REPURCHASE AGREEMENTS (E) — 59.3% |

| |||||||

Bank of Montreal | $ | 159,000 | 159,000 | |||||

Goldman Sachs | 50,000 | 50,000 | ||||||

Mitsubishi | 280,000 | 280,000 | ||||||

TD Bank | 145,000 | 145,000 | ||||||

TD Securities | 160,000 | 160,000 | ||||||

|

| |||||||

Total Repurchase Agreements |

| 794,000 | ||||||

|

| |||||||

Total Investments — 95.8% |

| $ | 1,281,759 | |||||

|

| |||||||

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 5 |

SCHEDULE OF INVESTMENTS

June 30, 2016

Prime Obligation Fund (Concluded)

| Percentages are based on a Net Assets of $1,338,007 ($ Thousands). |

| (A) | The rate reported is the effective yield at time of purchase. |

| (B) | Securities are held in connection with a letter of credit issued by a major bank. |

| (C) | Zero coupon security. The rate shown on the schedule of investments represents the security’s effective yield at the time of purchase. |

| (D) | Floating Rate Instrument. The rate reflected on the Schedule of Investments is the rate in effect as of June 30, 2016. The demand and interest rate reset feature gives this security a shorter effective maturity date. |

| (E) | Tri-Party Repurchase Agreement. |

FMAC — Financial Management Advisory Committee

FNMA — Federal National Mortgage Association

GNMA — Government National Mortgage Association

RB — Revenue Bond

Ser — Series

The accompanying notes are an integral part of the financial statements.

| 6 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

STATEMENT OF ASSETS AND LIABILITIES ($ Thousands)

As of June 30, 2016

| Prime Obligation Fund | ||||

ASSETS: | ||||

Investments, at value (Cost $487,759) | $ | 487,759 | ||

Repurchase agreements, at value (Cost $794,000) | 794,000 | |||

Cash | 56,509 | |||

Accrued income | 260 | |||

Prepaid expenses | 1 | |||

Total Assets | 1,338,529 | |||

LIABILITIES: | ||||

Payable due to administrator | 328 | |||

Payable due to investment adviser | 47 | |||

Trustees’ fees payable | 7 | |||

Chief Compliance Officer fees payable | 2 | |||

Accrued expenses | 138 | |||

Total Liabilities | 522 | |||

Net Assets | $ | 1,338,007 | ||

NET ASSETS CONSIST OF: | ||||

Paid-in Capital | $ | 1,338,006 | ||

Distributions in excess of net investment income | (5 | ) | ||

Accumulated net realized gain on investments | 6 | |||

Net Assets | $ | 1,338,007 | ||

Net Asset Value, Offering and Redemption Price Per Share — Class A ($1,338,007,392 ÷ 1,338,006,616 shares) | | $1.00 | | |

The accompanying notes are an integral part of the financial statements.

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 7 |

STATEMENT OF OPERATIONS ($ Thousands)

For the year ended June 30, 2016

| Prime Obligation Fund | ||||

Investment Income: | ||||

Interest Income | $ | 5,356 | ||

Expenses: | ||||

Administration Fees | 4,106 | |||

Shareholder Servicing Fees — Class A | 3,416 | |||

Investment Advisory Fees | 589 | |||

Trustees’ Fees | 24 | |||

Chief Compliance Officer Fees | 7 | |||

Printing Fees | 355 | |||

Professional Fees | 79 | |||

Custodian/Wire Agent Fees | 65 | |||

Registration Fees | 52 | |||

Other Expenses | 39 | |||

Total Expenses | 8,732 | |||

Less, Waiver of: | ||||

Administration Fees | (449 | ) | ||

Shareholder Servicing Fees — Class A | (3,416 | ) | ||

Net Expenses | 4,867 | |||

Net Investment Income | 489 | |||

Net Realized Gain on Investments | 4 | |||

Net Increase in Net Assets Resulting from Operations | $ | 493 | ||

The accompanying notes are an integral part of the financial statements.

| 8 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

STATEMENTS OF CHANGES IN NET ASSETS ($ Thousands)

For the years ended June 30,

Prime Obligation Fund | ||||||||

| 2016 | 2015 | |||||||

Operations: | ||||||||

Net Investment Income | $ | 489 | $ | 113 | ||||

Net Realized Gain on Investments | 4 | — | ||||||

Net Increase in Net Assets Resulting from Operations | 493 | 113 | ||||||

Dividends From: | ||||||||

Net Investment Income: | ||||||||

Class A | (489 | ) | (113 | ) | ||||

Total Dividends | (489 | ) | (113 | ) | ||||

Capital Share Transactions (all at $ 1.00 per share) | ||||||||

Class A: | ||||||||

Proceeds from Shares Issued | 10,449,545 | 8,010,610 | ||||||

Reinvestment of Dividends | 486 | 111 | ||||||

Cost of Shares Redeemed | (10,254,477 | ) | (7,964,288 | ) | ||||

Net Increase in Net Assets Derived from Capital Shares Transactions | 195,554 | 46,433 | ||||||

Net Increase in Net Assets | 195,558 | 46,433 | ||||||

Net Assets: | ||||||||

Beginning of Year | 1,142,449 | 1,096,016 | ||||||

End of Year | $ | 1,338,007 | $ | 1,142,449 | ||||

Distributions in Excess of Net Investment Income | $ | (5 | ) | $ | (5 | ) | ||

The accompanying notes are an integral part of the financial statements.

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 9 |

FINANCIAL HIGHLIGHTS

For the years ended June 30,

For a share outstanding throughout each year

| Net Asset Value, Beginning of Year | Net Investment | Net (Losses) on Securities | Total from | Dividends Investment | Distributions From Net Realized Gains | Net Asset Value, End of Year | Total Return† | Net Assets ($ Thousands) | Ratio of Expenses to Average Net Assets | Ratio of Expenses to Average Net Assets (Excluding Waivers) | Ratio of Net to Average | |||||||||||||||||||||||||||||||

Prime Obligation Fund | ||||||||||||||||||||||||||||||||||||||||||

Class A: | ||||||||||||||||||||||||||||||||||||||||||

2016 | $1.00 | $—(2) | $— | $—(2) | $—(2) | $— | $1.00 | 0.03 | % | $1,338,007 | 0.36%* | 0.64% | 0.04% | |||||||||||||||||||||||||||||

2015 | 1.00 | —(2) | —(2) | —(2) | — | — | 1.00 | 0.01 | 1,142,449 | 0.18* | 0.67 | 0.01 | ||||||||||||||||||||||||||||||

2014 | 1.00 | —(2) | —(2) | —(2) | — | — | 1.00 | 0.01 | 1,096,016 | 0.17* | 0.75 | 0.01 | ||||||||||||||||||||||||||||||

2013 | 1.00 | —(2) | —(2) | —(2) | —(2) | —(2) | 1.00 | 0.01 | 1,034,769 | 0.24* | 0.76 | 0.01 | ||||||||||||||||||||||||||||||

2012 | 1.00 | —(2) | —(2) | —(2) | —(2) | — | 1.00 | 0.01 | 886,342 | 0.25* | 0.77 | 0.01 | ||||||||||||||||||||||||||||||

| † | Returns are for the period indicated and have not been annualized. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (1) | Per share calculations were performed using average shares. |

| (2) | Amount represents less than $0.01 per share. |

| * | The Administrator has voluntarily agreed to waive and reduce their fee and/or reimburse certain expenses of the Fund in order to limit the one-day net income yield of the Fund to not less than 0.01% of the Fund’s average net assets. Had these waivers been excluded, the ratio would have been at the expense ratio cap figure of 0.44%. See Note 3 of the Notes to Financial Statements. |

Amounts designated as “—” are zero or have been rounded to zero.

The accompanying notes are an integral part of the financial statements.

| 10 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

NOTES TO FINANCIAL STATEMENTS

June 30, 2016

1. ORGANIZATION

SEI Liquid Asset Trust (the “Trust”) was organized as a Massachusetts business trust under a Declaration of Trust dated July 20, 1981.

The Trust is registered under the Investment Company Act of 1940, as amended, as a diversified, open-end management investment company with one fund: the Prime Obligation Fund (the “Fund”). The Trust is registered to offer Class A shares of the Fund. A description of the Fund’s investment objectives, policies, and strategies are provided in the prospectus.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Trust.

Use of Estimates—The preparation of financial statements, in conformity with U.S. generally accepted accounting principles, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Security Valuation — Investment securities are stated at amortized cost which approximates market value. Under this valuation method, purchase discounts and premiums are accreted and amortized to maturity and are included in interest income. The Fund’s use of amortized cost is subject to its compliance with certain conditions as specified by Rule 2a-7 of the 1940 Act.

In accordance with U.S. generally accepted accounting principles, fair value is defined as the price that the Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. A three-tier hierarchy has been established to maximize the use of the observable market data and minimize the use of unobservable inputs and to establish classification of the fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including such a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s

own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

Level 1 — quoted prices in active markets for identical investments

Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risks, etc.)

Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The valuation techniques used by the Fund to measure fair value during the year ended June 30, 2016 maximized the use of observable inputs and minimized the use of unobservable inputs.

As of June 30, 2016, all of the Fund’s investments are Level 2. During the year ended June 30, 2016, there were no transfers between levels.

For the year ended June 30, 2016, there have been no significant changes to the fair valuation methodologies.

Illiquid Securities — To the extent consistent with its investment objective and strategies, the Fund may invest in illiquid securities. A security is considered illiquid if it cannot be sold or disposed of in the ordinary course of business within seven days or less for its approximate carrying value on the books of the Fund. Valuations of illiquid securities may differ significantly from the values that would have been used had an active market value for these securities existed. At June 30, 2016, the Fund did not own any illiquid securities.

Restricted Securities — To the extent consistent with its investment objective and strategies, the Fund may own private placement investments purchased through private offerings or acquired through initial public offerings that could not be sold without prior registration under the Securities Act of 1933 or pursuant to an exemption there from. In addition, the Fund may generally agree to further restrictions on the disposition of certain holdings as set forth in various agreements entered into in connection with the purchase of those investments. These investments generally would be valued at amortized cost as determined in accordance with the procedures approved by the Board of Trustees (the “Board”). At June 30, 2016, the Fund did not own any restricted securities.

Repurchase Agreements — To the extent consistent with its investment objective and strategies, the Fund

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 11 |

NOTES TO FINANCIAL STATEMENTS (Continued)

June 30, 2016

may invest in tri-party repurchase agreements. Securities held as collateral for tri-party repurchase agreements are maintained in a segregated account by the broker’s custodian bank. Provisions of the agreements and the Trust’s policies ensure that the market value of the collateral, including accrued interest thereon, is sufficient to cover interest and principal in the event of default by the counterparty. If the counterparty defaults and the value of the collateral declines or if the counterparty enters an insolvency proceeding, realization of the collateral by the Fund may be delayed or limited. At June 30, 2016, the Fund held Repurchase Agreements in the amount of $794,000 ($ Thousands). Please refer to the Schedule of Investments for more information.

Expenses — Expenses that are directly related to the Fund are charged directly to the Fund.

Security Transactions and Investment Income — Security transactions are accounted for on the trade date. Costs used in determining realized gains and losses on the sale of investment securities are on the basis of specific identification. Interest income is recognized using the accrual basis of accounting.

All amortization and accretion is calculated using the straight line method over the holding period of the security. Amortization of premiums and accretion of discounts are included in interest income.

Dividends and Distributions to Shareholders — Dividends from net investment income are declared on a daily basis and are payable on the first business day of the following month. Any net realized capital gains of the Fund are distributed to the shareholders of the Fund annually.

3. INVESTMENT ADVISORY, ADMINISTRATION AND DISTRIBUTION AGREEMENTS AND OTHER TRANSACTIONS WITH AFFILIATES

Investment Advisory, Administration and Distribution Agreements — SEI Investments Management Corporation (“SIMC”) serves as the Fund’s investment adviser (the “Adviser”) and “manager of managers” under an investment advisory agreement.

BlackRock Advisors, LLC (“BAL”), serves as sub-adviser to the Fund under an investment sub-advisory agreement with SIMC. SIMC compensates BAL out of the fee it receives from the Fund.

SEI Investments Global Funds Services (the “Administrator”) provides administrative and transfer agency services for an annual fee, which is calculated daily and paid monthly, of 0.30% of the average daily net assets of the Fund.

SEI Investments Distribution Co. (the “Distributor”), a wholly owned subsidiary of SEI Investments Company

(“SEI”) and a registered broker-dealer, acts as the Distributor of the shares of the Trust under a Distribution Agreement. The Trust has adopted a shareholder servicing plan for its Class A shares (the “Class A Plan”) pursuant to which a shareholder servicing fee of up to 0.25% of the average daily net assets attributable to Class A shares will be paid to the Distributor. Under the Class A Plan, the Distributor may perform, or may compensate other service providers for performing, certain shareholder and administrative services.

The Distributor may retain as a profit any difference between the fee it receives and the amount it pays to third parties.

The Administrator has contractually agreed to waive its administration fees and/or to reimburse expenses of the Fund as necessary to keep total operating expenses (excluding interest, taxes and certain non-routine expenses, and net of SIMC and (the Distributor’s) fee) of the Fund from exceeding an annual rate of 0.44%.

The Adviser and/or Distributor have voluntarily agreed to waive a portion of their fees in order to keep total direct operating expenses (exclusive of interest from borrowings, brokerage commissions, taxes, Trustee fees, prime broker fees, interest and dividend expenses related to short sales and extraordinary expenses not incurred in the ordinary course of the Fund’s business) at a specified level.

The waivers by the Adviser, Administrator and/or Distributor are limited to the Fund’s direct operating expenses and, therefore, do not apply to indirect expenses incurred by the Fund, such as acquired fund fees and expenses. The waivers are voluntary with the exception of the Administrator contractual waiver mentioned above and the Adviser, Administrator and/ or Distributor may discontinue all or part of any of these waivers at any time.

In addition, the Administrator has voluntarily agreed to waive and reduce their fee and/or reimburse certain expenses of the Fund in order to limit the one-day net income yield of the Fund to not less than 0.01% of the Fund’s average daily net assets. For the year ended June 30, 2016, the amount of this waiver totaled $449 ($ Thousands).

| 12 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

The following is a summary of annual fees payable to the Adviser, Administrator and Distributor and the voluntary expense limitations for the Fund:

| Advisory Fees* | Administration Fees | Shareholder Servicing Fees | Expense Limitations | |||||||||||||

Class A | 0.075% | 0.30% | 0.25% | 0.44% | ||||||||||||

| * | The Adviser receives an annual fee equal to 0.075% of the Trust’s average daily net assets up to $500 million and 0.02% of such net assets in excess of $500 million. |

Other — Certain officers and/or trustees of the Trust are also officers and/or directors of the Administrator, the Distributor or SIMC. Compensation of officers and affiliated trustees of the Trust is paid by the Administrator and/or the Distributor.

The services provided by the Chief Compliance Officer (“CCO”) and his staff, whom are employees of the Administrator, are paid for by the Trust as incurred. The services include regulatory oversight of the Trust’s adviser, sub-advisors and service providers as required by Securities Exchange Commission (“SEC”) regulations. The CCO’s services have been approved by and are reviewed annually by the Board.

Interfund Lending—The SEC has granted an exemption that permits the Trust to participate in an interfund lending program (the “Program”) with existing or future open ended investment companies registered under the 1940 Act that are advised by SIMC (the “SEI Funds”). The Program allows the SEI Funds to lend money to and borrow money from each other for temporary or emergency purposes. Participation in the Program is voluntary for both borrowing and lending funds. Interfund loans may be made only when the rate of interest to be charged is more favorable to the lending fund than an investment in overnight repurchase agreements (“Repo Rate”), and more favorable to the borrowing fund than the rate of interest that would be charged by a bank for short-term borrowings (“Bank Loan Rate”). The Bank Loan Rate will be determined using a formula reviewed annually by the SEI Funds’ Board of Trustees. The interest rate imposed on interfund loans is the average of the Repo Rate and the Bank Loan Rate.

During the year ended June 30, 2016, the Trust loaned funds from the Fund to the SEI Funds. The amount of lending was $85,709 ($ Thousands) and the interest received on the lending and the corresponding interest rate were $1 ($ Thousands) and 0.22%-0.49%, respectively. The average amount of lending during the year ended June 30, 2016 was $14,284 ($ Thousands). The Trust had no outstanding loans under the interfund lending agreement at June 30, 2016.

4. FEDERAL INCOME TAXES

It is the Fund’s intention to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income. Accordingly, no provision for Federal income taxes is required. The timing and characterization of certain income and capital gains distributions are determined annually in accordance with Federal tax regulations which may differ from U.S. generally accepted accounting principles. As a result, net investment income (loss) and net realized gain (loss) on investment transactions for the reporting period may differ from distributions during such period. These book/tax differences may be temporary or permanent in nature. To the extent these differences are permanent, they are charged or credited to paid-in capital, undistributed net investment income or accumulated net realized gain, as appropriate, in the period that the differences arise.

Accordingly, no permanent differences have been reclassified during the year ended June 30, 2016, (as there were none).

The tax character of dividends paid to Class A shareholders during the years ended June 30, 2015 and June 30, 2016 were as follows ($ Thousands):

| Ordinary Income | ||||

2016 | $489 | |||

2015 | $113 | |||

As of June 30, 2016, the components of distributable earnings (accumulated losses) on a tax basis were as follows ($ Thousands):

Undistributed Ordinary Income | $ | 20 | ||

Undistributed Long-Term Capital Gain | 4 | |||

Other Temporary Differences | (23 | ) | ||

|

| |||

Total Distributable Earnings | $ | 1 | ||

|

|

For Federal income tax purposes, capital loss carryforwards represent realized losses of the Fund that may be carried forward for a maximum period of eight years and applied against future capital gains.

Under the Regulated Investment Company Modernization Act of 2010, the Fund is permitted to

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 13 |

NOTES TO FINANCIAL STATEMENTS (Concluded)

June 30, 2016

carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period. However, any losses incurred during those future taxable years are required to be utilized prior to the losses incurred in preenactment taxable years. As a result of this ordering rule, preenactment capital loss carryforwards may be more likely to expire unused. Additionally, post-enactment capital losses that are carried forward will retain their character as either short-term or long-term capital losses rather than being considered all short-term as under previous law.

The cost basis of securities for Federal income tax purposes is equal to the cost basis used for financial reporting purposes.

Management has analyzed the Fund’s tax positions taken on the federal tax returns for all open tax years and has concluded that as of June 30, 2016, no provision for income tax is required in the Fund’s financial statements.

5. CONCENTRATION OF SHAREHOLDERS

SEI Private Trust Company (“SPTC”) and SIMC are subsidiaries of SEI Investments Company. As of June 30, 2016, SPTC held of record 99.50%.

SPTC is not a direct service provider to the Fund. However, SPTC performs a key role in the comprehensive investment solution that SEI provides to investors. SPTC holds the vast majority of shares in the Fund as custodian for shareholders that are clients of the advisors and financial planners. SPTC maintains accounts at SEI Institutional Transfer Agency (“SITA”), and operates in an omnibus fund account environment.

6. SUBSEQUENT EVENTS

The Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the financial statements were available to be issued.

On July 22, 2016, the Fund was liquidated and the proceeds of the Fund were distributed. At a meeting of the Board of the Trust held on August 11, 2016, the Board provided approval for the officers of the Trust to take such steps necessary and appropriate to affect the orderly dissolution/deregistration of the Trust with the Securities and Exchange Commission and the Commonwealth of Massachusetts.

| 14 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Trustees and Shareholders

SEI Liquid Asset Trust:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of SEI Liquid Asset Trust, comprised of the Prime Obligation Fund (the “Fund”), as of June 30, 2016, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of June 30, 2016, by correspondence with the custodian and brokers or other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Fund comprising SEI Liquid Asset Trust as of June 30, 2016, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

As discussed in Note 6, on July 22, 2016, the Fund was liquidated and the proceeds of the Fund were distributed.

| ||

| Philadelphia, Pennsylvania | ||

| August 26, 2016 | ||

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 15 |

TRUSTEES AND OFFICERS OF THE TRUST

The following chart lists Trustees and Officers as of June 30, 2016.

Set forth below are the names, addresses, ages, position with the Trust, Term of Office and Length of Time Served, the principal occupations for the last five years, number of portfolios in fund complex overseen by trustee, and other directorships outside the fund complex of each of the persons currently serving as Trustees and Officers of the Trust. The Trust’s Statement of Additional Information (“SAI”) includes additional information about the Trustees and Officers. The SAI may be obtained without charge by calling 1-800-342-5734.

| Name | Position(s) Held with Trusts | Term of Office and of Time Served 1 | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee 2 | Other Directorships Held by Trustee | |||||

| INTERESTED TRUSTEES | ||||||||||

| Robert A. Nesher One Freedom Valley Drive Oaks, PA 19456 68 yrs. old | Chairman of the Board of Trustees* | since 1995 | Currently performs various services on behalf of SEI for which Mr. Nesher is compensated. | 104 | Vice Chairman of The Advisors’ Inner Circle Fund III, O’Connor EQUUS, Winton Series Trust and Winton Diversified Opportunities Fund since 2014. Vice Chairman of Gallery Trust since 2015. President and Director of SEI Structured Credit Fund, LP. Director of SEI Global Master Fund plc, SEI Global Assets Fund plc, SEI Global Investments Fund plc, SEI Investments—Global Funds Services, Limited, SEI Investments Global, Limited, SEI Investments (Europe) Ltd., SEI Multi-Strategy Funds PLC, SEI Global Nominee Ltd and SEI Investments—Unit Trust Management (UK) Limited. Director and President of SEI Opportunity Fund, L.P. to 2010. Director of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Trustee of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, Bishop Street Funds and The KP Funds. | |||||

| William M. Doran One Freedom Valley Drive Oaks, PA 19456 74 yrs. old | Trustee* | since 1995 | Self-employed consultant since 2003. Partner, Morgan, Lewis & Bockius LLP (law firm) from 1976 to 2003, counsel to the Trust, SEI, SIMC, the Administrator and the Distributor. | 104 | Director of SEI since 1974;. Director of SEI Investments Distribution Co. since 2003.Director of SEI Investments— Global Funds Services, Limited, SEI Investments Global, Limited, SEI Investments (Europe), Limited, SEI Investments (Asia) Limited, SEI Global Nominee Ltd. and SEI Investments— Unit Trust Management (UK) Limited. Director of SEI Opportunity Fund, L.P. to 2010. Director of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Trustee/Director of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, The Advisors’ Inner Circle Fund III, O’Connor EQUUS, Winton Series Trust, Winton Diversified Opportunities Fund, Gallery Trust, Bishop Street Funds, and The KP Funds. | |||||

* Messrs. Nesher and Doran are Trustees who may be deemed as “interested” persons of the Trust as that term is defined in the 1940 Act by virtue of their affiliation with SIMC and the Trust’s Distributor.

1 There is no stated term of office for the Trustees of the Trust. However, a Trustee must retire from the Board by the end of the calendar year in which the Trustee turns 75 provided that, although there shall be a presumption that each Trustee attaining such age shall retire, the Board may, if it deems doing so to be consistent with the best interest of the Trust, and with the consent of any Trustee that is eligible for retirement, by unanimous vote, extend the term of such Trustee for successive periods of one year.

2 The Fund Complex includes the following Trusts: SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, Adviser Managed Trust, SEI Institutional International Trust, SEI Institutional Managed Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Insurance Products Trust, New Covenant Funds and SEI Catholic Values Trust.

| 16 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

Name Address, and Age | Position(s) Held with Trusts | Term of Office Length of Time | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee 2 | Other Directorships Held by Trustee | |||||

TRUSTEES | ||||||||||

George J. Sullivan, Jr. One Freedom Valley Drive Oaks, PA 19456 72 yrs. old | Trustee | since 1996 | Retired since January 2012. Self-Employed Consultant, Newfound Consultants Inc. April 1997-December 2011. | 104 | Director of SEI Opportunity Fund, L.P. to 2010. Director of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Trustee/Director of State Street Navigator Securities Lending Trust, The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, Bishop Street Funds, and The KP Funds. | |||||

Nina Lesavoy One Freedom Valley Drive Oaks, PA 19456 57 yrs. old | Trustee | since 2003 | Founder and Managing Director, Avec Capital since 2008. Managing Director, Cue Capital from March 2002-March 2008. | 104 | Director of SEI Opportunity Fund, L.P. to 2010. Director of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Director of SEI Structured Credit Fund, L.P. | |||||

James M. Williams One Freedom Valley Drive Oaks, PA 19456 67 yrs. old | Trustee | since 2004 | Vice President and Chief Investment Officer, J. Paul Getty Trust, Non-Profit Foundation for Visual Arts, since December 2002. President, Harbor Capital Advisors and Harbor Mutual Funds, 2000-2002. Manager, Pension Asset Management, Ford Motor Company, 1997-1999. | 104 | Director of SEI Opportunity Fund, L.P. to 2010. Director of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Trustee/Director of Ariel Mutual Funds, and SEI Structured Credit Fund, L.P. | |||||

Mitchell A. Johnson One Freedom Valley Drive Oaks, PA 19456 73 yrs. old | Trustee | since 2007 | Retired Private Investor since 1994. | 104 | Director, Federal Agricultural Mortgage Corporation (Farmer Mac) since 1997. Director of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Trustee of the Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, and Bishop Street Funds and The KP Funds. | |||||

Hubert L. Harris, Jr. One Freedom Valley Drive Oaks, PA 19456 71 yrs. old | Trustee | since 2008 | Retired since December 2005. Owner of Harris Plantation, Inc. since 1995. Chief Executive Officer of Harris CAPM, a consulting asset and property management entity. Chief Executive Officer, INVESCO North America, August 2003-December 2005. Chief Executive Officer and Chair of the Board of Directors, AMVESCAP Retirement, Inc., January 1998- August 2003. | 104 | Director of AMVESCAP PLC from 1993-2004. Served as a director of a bank holding company, 2003-2009. Director, Aaron’s Inc., 2012-present. President and CEO, Oasis Ornamentals LLC, 2011-present. Serves as a member of the Board of Councilors of the Carter Center (nonprofit corporation) and served on the board of other non-profit organizations. Director of SEI Alpha Strategy Portfolios, LP from 2008 to 2013. | |||||

Susan C. Cote One Freedom Valley Drive Oaks, PA 19456 61 years old | Trustee | since 2015 | Retired since July 2015. Americas Director of Asset Management, Ernst & Young LLP from 2006-2013. Global Asset Management Assurance Leader, Ernst & Young LLP from 2006-2015. Partner, Ernst & Young LLP from 1997-2015. Prudential, 1983-1997. Member of Ernst & Young LLP Retirement Investment Committee. Treasurer and Chair of Finance, Investment and Audit Committee of the New York Women’s Foundation. Independent Consultant to SEI Liquid Asset Allocation Trust. | 104 | N/A | |||||

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 17 |

TRUSTEES AND OFFICERS OF THE TRUST (Concluded)

Name Address, and Age | Position(s) Held with Trusts | Term of Office and Length of Time | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee 2 | Other Directorships Held by Trustee | |||||

OFFICERS | ||||||||||

Robert A. Nesher One Freedom Valley Drive Oaks, PA 19456 68 yrs. old | President and CEO | since 2005 | Currently performs various services on behalf of SEI for which Mr. Nesher is compensated. | N/A | N/A | |||||

Arthur Ramanjulu One Freedom Valley Drive Oaks, PA 19456 51 yrs. old | Controller and Chief Financial Officer | since 2015 | Director, Funds Accounting, SEI Investments Global Funds Services (March 2015); Senior Manager, Funds Accounting, SEI Global Funds Services (March 2007 to February 2015). | N/A | N/A | |||||

Russell Emery One Freedom Valley Drive Oaks, PA 19456 52 yrs. old | Chief Compliance Officer | since 2006 | Chief Compliance Officer of SEI Institutional Investments Trust, SEI Asset Allocation Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Daily Income Trust, SEI Institutional Managed Trust, SEI Tax Exempt Trust, The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II and Bishop Street Funds since March 2006. Chief Compliance Officer of SEI Structured Credit Fund, LP since June 2007. Chief Compliance Officer of SEI Opportunity Fund, L.P. to 2010. Chief Compliance Officer of SEI Alpha Strategy Portfolios, LP from 2007 to 2013. Chief Compliance Officer of Adviser Managed Trust since December 2010. Chief Compliance Officer of New Covenant Funds since February 2012. Chief Compliance Officer of SEI Insurance Products Trust and The KP Funds since 2013. Chief Compliance Officer of The Advisors’ Inner Circle Fund III, O’Connor EQUUS, Winton Series Trust and Winton Diversified Opportunities Fund since 2014. Chief Compliance Officer of SEI Catholic Values Trust and Gallery Trust since 2015. | N/A | N/A | |||||

Timothy D. Barto One Freedom Valley Drive Oaks, PA 19456 47 yrs. old | Vice President and Secretary | since 2002 | Vice President and Secretary of SEI Institutional Transfer Agent, Inc. since 2009. General Counsel and Secretary of SIMC and the Administrator since 2004. Vice President of SIMC and the Administrator since 1999. Vice President and Assistant Secretary of SEI since 2001. | N/A | N/A | |||||

Aaron Buser One Freedom Valley Drive Oaks, PA 19456 44 yrs. old | Vice President and Assistant Secretary | since 2008 | Vice President and Assistant Secretary of SEI Institutional Transfer Agent, Inc. since 2009. Vice President and Assistant Secretary of SIMC since 2007. Attorney, Stark & Stark (law firm), March 2004-July 2007. | N/A | N/A | |||||

David F. McCann One Freedom Valley Drive Oaks, PA 19456 39 yrs. old | Vice President and Assistant Secretary | since 2009 | Vice President and Assistant Secretary of SEI Institutional Transfer Agent, Inc. since 2009. Vice President and Assistant Secretary of SIMC since 2008. Attorney, Drinker Biddle & Reath, LLP (law firm), May 2005-October 2008. | N/A | N/A | |||||

| 18 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

Name Address, and Age | Position(s) Held with Trusts | Term of Office and Length of Time | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee 2 | Other Directorships Held by Trustee | |||||

Stephen G. MacRae One Freedom Valley Drive Oaks, PA 19456 47 yrs. old | Vice President | since 2012 | Director of Global Investment Product Management, January 2004 to present. | N/A | N/A | |||||

Bridget E. Sudall One Freedom Valley Drive Oaks, PA 19456 35 yrs. old | Anti-Money Laundering Compliance Officer and Privacy Officer | since 2015 | Anti-Money Laundering Compliance Officer and Privacy Officer (since 2015), Senior Associate and AML Officer, Morgan Stanley Alternative Investment Partners, April 2011-March 2015, Investor Services Team Lead, Morgan Stanley Alternative Investment Partners, July 2007-April 2011. | N/A | N/A |

1 There is no stated term of office for the Trustees of the Trust. However, a Trustee must retire from the Board by the end of the calendar year in which the Trustee turns 75 provided that, although there shall be a presumption that each Trustee attaining such age shall retire, the Board may, if it deems doing so to be consistent with the best interest of the Trust, and with the consent of any Trustee that is eligible for retirement, by unanimous vote, extend the term of such Trustee for successive periods of one year.

2 The Fund Complex includes the following Trusts: SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, Adviser Managed Trust, SEI Institutional International Trust, SEI Institutional Managed Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Insurance Products Trust, New Covenant Funds and SEI Catholic Values Trust.

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 19 |

DISCLOSURE OF FUND EXPENSES

JUNE 30, 2016

All mutual funds have operating expenses. As a shareholder of a mutual fund, your investment is affected by these ongoing costs, which include (among others) costs for portfolio management, administrative services, and shareholder reports like this one. It is important for you to understand the impact of these costs on your investment returns.

Operating expenses such as these are deducted from the mutual fund‘s gross income and directly reduce its final investment return. These expenses are expressed as a percentage of the mutual fund’s average net assets; this percentage is known as the mutual fund’s expense ratio. The following examples use the expense ratio and are intended to help you understand the ongoing costs (in dollars) of investing in your Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The table below illustrates your Fund’s costs in two ways:

• Actual Fund Return. This section helps you to estimate the actual expenses after fee waivers that your Fund incurred over the period. The “Expenses Paid During Period” column shows the actual dollar expense cost incurred by a $1,000 investment in the Fund, and the “Ending Account Value” number is derived from deducting that expense cost from the Fund’s gross investment return.

You can use this information, together with the actual amount you invested in your Fund, to estimate the expenses you paid over that period. Simply divide your actual starting account value by $1,000 to arrive at a ratio (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply that ratio by the number shown for your Fund under “Expenses Paid During Period.”

• Hypothetical 5% Return. This section helps you compare your Fund’s costs with those of other mutual funds. It assumes that your Fund had an annual 5% return before expenses during the year, but that the expense ratio (Column 3) is unchanged. This example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to make this 5% calculation. You can assess your Fund’s comparative cost by comparing the hypothetical result for your Fund in the “Expenses Paid During Period” column with those that appear in the same charts in the shareholder reports for other mutual funds.

NOTE: Because the return is set at 5% for comparison purposes — NOT your Fund’s actual return — the account values shown do not apply to your specific investment.

| Beginning Account Value 1/1/16 | Ending Account Value 6/30/16 | Annualized Expense Ratios | Expenses Paid During Period * | |||||||||||||

Prime Obligation Fund | ||||||||||||||||

Actual Fund Return |

| |||||||||||||||

Class A Shares | $1,000.00 | $1,000.30 | 0.44 | % | $2.19 | |||||||||||

Hypothetical 5% Return |

| |||||||||||||||

Class A Shares | $1,000.00 | $1,022.68 | 0.44 | % | $2.21 | |||||||||||

* Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period,

multiplied by 182/366 (to reflect the one-half year period shown).

| 20 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

BOARD OF TRUSTEES’ CONSIDERATIONS IN APPROVING THE ADVISORY AGREEMENT

SEI Liquid Asset Trust (the “Trust”) and SEI Investments Management Corporation (“SIMC”) have entered into an investment advisory agreement (the “Advisory Agreement”). Pursuant to the Advisory Agreement, SIMC is responsible for the investment advisory services provided to the Prime Obligation Fund (the “Fund”), which was the sole series of the Trust until it commenced a liquidation of its portfolio and closed on July 22, 2016.

Pursuant to separate sub-advisory agreements with SIMC (each, a “Sub-Advisory Agreement” and, together with the Advisory Agreement, the “Investment Advisory Agreements”), and under the supervision of SIMC and the Trust’s Board of Trustees (the “Board”), two sub-advisers (each, a “Sub-Adviser”) at different points during the Trust’s fiscal year provided security selection and certain other advisory services with respect to all or a discrete portion of the assets of the Fund. Each Sub-Adviser is also responsible for managing its employees who provide services to the Fund. Sub-Advisers are selected based primarily upon the research and recommendations of SIMC, which evaluates quantitatively and qualitatively the Sub-Advisers’ skills and investment results in managing assets for specific asset classes, investment styles and strategies.

The Investment Company Act of 1940, as amended (the “1940 Act”), requires that the initial approval of, as well as the continuation of, the Fund’s Investment Advisory Agreements be specifically approved: (i) by the vote of the Board or by a vote of the shareholders of the Fund; and (ii) by the vote of a majority of the Trustees who are not parties to the Investment Advisory Agreements or “interested persons” of any party (the “Independent Trustees”), cast in person at a meeting called for the purpose of voting on such approval(s). In connection with their consideration of such approval(s), the Fund’s Trustees must request and evaluate, and SIMC and the Sub-Adviser are required to furnish, such information as may be reasonably necessary to evaluate the terms of the Investment Advisory Agreements. In addition, the Securities and Exchange Commission takes the position that, as part of their fiduciary duties with respect to a mutual fund’s fees, mutual fund boards are required to evaluate the material factors applicable to a decision to approve an Investment Advisory Agreement. An exemptive order obtained from the SEC permits SIMC, with the approval of the Board, to retain unaffiliated sub-advisers for the Fund without submitting the Sub-Advisory Agreements to a vote of the Fund’s shareholders.

Consistent with these responsibilities, the Board calls and holds meetings each year to consider whether to approve new and/or renew existing Investment Advisory Agreements between the Trust and SIMC and SIMC and the Sub-Adviser with respect to the Fund. In preparation for these meetings, the Board requests and reviews a wide variety of materials provided by SIMC and the Sub-Adviser, including information about SIMC’s and the Sub-Adviser’s affiliates, personnel and operations and the services provided pursuant to the Investment Advisory Agreements. The Board also receives data from third parties. This information is provided in addition to the detailed information about the Fund that the Board reviews during the course of each year, including information that relates to Fund operations and Fund performance. The Trustees also receive a memorandum from counsel regarding the responsibilities of Trustees in connection with their consideration of whether to approve the Trust’s Investment Advisory Agreements. Finally, the Independent Trustees receive advice from independent counsel to the Independent Trustees, meet in executive sessions outside the presence of Fund management and participate in question and answer sessions with representatives of SIMC and the Sub-Adviser(s).

Specifically, during the course of the Trust’s fiscal year, the Board requested and received written materials from SIMC and each Sub-Adviser regarding: (i) the quality of SIMC’s and the Sub-Adviser’s investment management and other services; (ii) SIMC’s and the Sub-Adviser’s investment management personnel; (iii) SIMC’s and the Sub-Adviser’s operations and financial condition; (iv) SIMC’s and the Sub-Adviser’s brokerage practices (including any soft dollar arrangements) and investment strategies; (v) the level of the advisory fees that SIMC charges the Fund and the level of the sub-advisory fees that SIMC pays the Sub-Adviser, compared with fees each charge to comparable accounts; (vi) the advisory fees charged by SIMC and the Fund’s overall fees and operating expenses compared with peer groups of mutual funds prepared by Broadridge, an independent provider of investment company data; (vii) the level of SIMC’s and the Sub-Adviser’s profitability from their Fund-related operations; (viii) SIMC’s and the Sub-Adviser’s compliance program, including a description of material compliance matters and material compliance violations; (ix) SIMC’s potential economies of scale; (x) SIMC’s and the Sub-Adviser’s policies on and compliance procedures for personal securities transactions; (xi) SIMC’s and the Sub-Adviser’s expertise and resources in domestic and/or international financial markets; and (xii) the Fund’s performance over various periods of time compared with peer groups of mutual funds prepared by Broadridge and the Fund’s benchmark indices.

At the March 28-29, 2016 meeting of the Board, the Trustees, including a majority of the Independent Trustees, approved the renewal of the Advisory Agreement. Also at the March 28-29, 2016 meeting of the Board, the Board

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 21 |

BOARD OF TRUSTEES’ CONSIDERATIONS IN APPROVING THE ADVISORY AGREEMENT (Concluded)

terminated the Fund’s then-current Sub-Adviser and approved a Sub-Advisory Agreement with a new Sub-Adviser, to which the management of the Fund’s assets was subsequently transitioned. In each case, the Board’s approvals were based on its consideration and evaluation of the factors described above, as discussed at the meetings and at prior meetings. The following discusses some, but not all, of the factors that were considered by the Board in connection with its assessment of the Investment Advisory Agreements.

Nature, Extent and Quality of Services. The Board considered the nature, extent and quality of the services provided by SIMC and the Sub-Advisers to the Fund and the resources of SIMC and the Sub-Adviser and their affiliates dedicated to the Fund. In this regard, the Trustees evaluated, among other things, SIMC’s and the Sub-Adviser’s personnel, experience, track record and compliance program. In particular, the Board considered the fact that the investment management responsibilities of the Fund’s current Sub-Adviser were going to be transitioned to the Fund’s proposed replacement Sub-Adviser as part of a corporate acquisition. Following evaluation, the Board concluded that, within the context of its full deliberations, the nature, extent and quality of services provided by SIMC and the Sub-Adviser to the Fund and the resources of SIMC and the Sub-Adviser and their affiliates dedicated to the Fund were sufficient to support renewal of the Investment Advisory Agreements. In addition to advisory services, the Board considered the nature and quality of certain administrative, transfer agency and other non-investment advisory services provided to the Fund by SIMC and/or its affiliates.

Performance. In determining whether to renew SIMC’s Advisory Agreement, the Trustees considered the Fund’s performance relative to their peer groups and appropriate indices/benchmarks. The Trustees reviewed performance information for the Fund, noting that they receive performance reports that permit them to monitor the Fund’s performance at board meetings throughout the year. As part of this review, the Trustees considered the composition of each peer group and selection criteria. In assessing Fund performance, the Trustees considered a report compiled by Broadridge, an independent third-party, which was engaged to prepare an assessment of the Fund in connection with the renewal of the Advisory Agreement (the “Broadridge Report”). The Broadridge Report included metrics on risk analysis, volatility versus total return, net total return and performance consistency for the Fund and a universe of comparable funds. Based on the materials considered and discussed at the meetings, the Trustees found Fund performance satisfactory, or, where performance was materially below the benchmark and/or peer group, the Trustees were satisfied with the reasons provided to explain such performance. In connection with the approval of the Sub-Advisory Agreement, the Board considered the performance of the current Sub-Adviser relative to appropriate indices/benchmarks with the understanding that the proposed Sub-Adviser would be taking over the investment management responsibilities of the current Sub-Adviser. Following evaluation, the Board concluded that, within the context of its full deliberations, the performance of the Fund was sufficient to support renewal of SIMC’s Advisory Agreement, and the performance of the Sub-Adviser was sufficient to support approval of the Sub-Advisory Agreement.

Fees. With respect to the Fund’s expenses under the Investment Advisory Agreements, the Trustees considered the rate of compensation called for by the Investment Advisory Agreements and the Fund’s net operating expense ratio in comparison to those of the Fund’s respective peer groups. In assessing Fund expenses, the Trustees considered the information in the Broadridge Report, which included various metrics related to fund expenses, including, but not limited to, contractual management fees at various fee levels, actual management fees, and actual total expenses (including underlying fund expenses) for the Fund and a universe of comparable funds. Based on the materials considered and discussion at the meetings, the Trustees further determined that fees were either shown to be below the peer average in the comparative fee analysis, or that there was a reasonable basis for the fee level. The Trustees also considered the effects of SIMC’s waiver of management and other fees to prevent total Fund operating expenses from exceeding a specified cap and concluded that SIMC, through waivers, has maintained the Fund’s net operating expenses at competitive levels for their distribution channels. The Board also took into consideration compensation earned from the Fund by SIMC or its affiliates for non-advisory services, such as administration, transfer agency, shareholder services or brokerage, and considered whether SIMC and its affiliates may have realized other benefits from their relationship with the Fund, such as any research and brokerage services received under soft dollar arrangements. When considering fees to be paid to the proposed Sub-Adviser, the Board took into account the fact that the Sub-Adviser would be compensated by SIMC and not by the Fund directly, that such compensation with respect to any unaffiliated Sub-Adviser reflects an arms-length negotiation between the Sub-Adviser and SIMC, and the fees to be paid to the proposed Sub-Adviser compared to the fees paid to the current Sub-Adviser. Following evaluation, the Board concluded that, within the context of its full deliberations, the expenses of the Fund are reasonable and supported renewal of the Investment Advisory Agreements. The Board also considered whether the Sub-Adviser and its affiliates may have realized other benefits from their relationship with the Fund, such as any research and brokerage services received under soft dollar arrangements.

| 22 | SEI Liquid Asset Trust / Annual Report / June 30, 2016 |

Profitability. With regard to profitability, the Trustees considered compensation flowing to SIMC and the Sub-Adviser and their affiliates, directly or indirectly. The Trustees considered whether the levels of compensation and profitability were reasonable. As with the fee levels, when considering the profitability of the Sub-Adviser, the Board took into account the fact that compensation with respect to any unaffiliated Sub-Adviser reflects an arms-length negotiation between the Sub-Adviser and SIMC. In connection with the approval of the Sub-Advisory Agreement, the Board also took into consideration the impact that the fees paid to the Sub-Adviser have on SIMC’s advisory fee margin and profitability. Based on this evaluation, the Board concluded that, within the context of its full deliberations, the profitability of each of SIMC and the Sub-Adviser is reasonable and supported renewal of the Investment Advisory Agreements.

Economies of Scale. With respect to the Advisory Agreement, the Trustees considered whether any economies of scale were being realized by SIMC and its affiliates and, if so, whether the benefits of such economies of scale were passed along to the Fund’s shareholders through a graduated investment advisory fee schedule or other means, including any fee waivers by SIMC and its affiliates. The Trustees recognized that economies of scale are difficult to identify and quantify and are rarely identifiable on a fund-by-fund basis. Based on this evaluation, the Board determined that the fees were reasonable in light of the information that was provided by SIMC with respect to economies of scale.

Based on the Trustees’ deliberation and their evaluation of the information described above, the Board, including all of the Independent Trustees, with the assistance of Fund counsel and Independent Trustees’ counsel, unanimously approved the approval or renewal, as applicable, of the Investment Advisory Agreements and concluded that the compensation under the Investment Advisory Agreements is fair and reasonable in light of such services and expenses and such other matters as the Trustees considered to be relevant in the exercise of their reasonable judgment. In the course of its deliberations, the Board did not identify any particular factor (or conclusion with respect thereto) or single piece of information that was all-important, controlling or determinative of its decision, but considered all of the factors together, and each Trustee may have attributed different weights to the various factors (and conclusions with respect thereto) and information.

| SEI Liquid Asset Trust / Annual Report / June 30, 2016 | 23 |

NOTICE TO SHAREHOLDERS (Unaudited)

For shareholders that do not have a June 30, 2016 taxable year end, this notice is for informational purposes only. For shareholders with a June 30, 2016 taxable year end, please consult your tax adviser as to the pertinence of this notice.

For the fiscal year ended June 30, 2016, the Fund is making the following dividend designations with regard to distributions paid during the year as follows:

(A) Long Term Capital Gains Distributions (Tax Basis) | (B) Ordinary Income Distributions (Tax Basis) | Total Distributions (Tax Basis) | (C) Dividends Qualifying For Corporate Dividends Rec. Deduction (1) | |||