© Fifth Third Bank | All Rights Reserved 4Q10 Earnings Conference Call January 19, 2011 Please refer to earnings release dated January 19, 2011 for further information. Exhibit 99.2 |

2 © Fifth Third Bank | All Rights Reserved Cautionary statement This report contains statements that we believe are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Rule 175 promulgated thereunder, and Section 21E of the Securities Exchange Act of 1934, as amended, and Rule 3b-6 promulgated thereunder. These statements relate to our financial condition, results of operations, plans, objectives, future performance or business. They usually can be identified by the use of forward-looking language such as “will likely result,” “may,” “are expected to,” “is anticipated,” “estimate,” “forecast,” “projected,” “intends to,” or may include other similar words or phrases such as “believes,” “plans,” “trend,” “objective,” “continue,” “remain,” or similar expressions, or future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” or similar verbs. You should not place undue reliance on these statements, as they are subject to risks and uncertainties, including but not limited to the risk factors set forth in our most recent Annual Report on Form 10-K. When considering these forward-looking statements, you should keep in mind these risks and uncertainties, as well as any cautionary statements we may make. Moreover, you should treat these statements as speaking only as of the date they are made and based only on information then actually known to us. There are a number of important factors that could cause future results to differ materially from historical performance and these forward- looking statements. Factors that might cause such a difference include, but are not limited to: (1) general economic conditions and weakening in the economy, specifically the real estate market, either nationally or in the states in which Fifth Third, one or more acquired entities and/or the combined company do business, are less favorable than expected; (2) deteriorating credit quality; (3) political developments, wars or other hostilities may disrupt or increase volatility in securities markets or other economic conditions; (4) changes in the interest rate environment reduce interest margins; (5) prepayment speeds, loan origination and sale volumes, charge-offs and loan loss provisions; (6) Fifth Third’s ability to maintain required capital levels and adequate sources of funding and liquidity; (7) maintaining capital requirements may limit Fifth Third’s operations and potential growth; (8) changes and trends in capital markets; (9) problems encountered by larger or similar financial institutions may adversely affect the banking industry and/or Fifth Third (10) competitive pressures among depository institutions increase significantly; (11) effects of critical accounting policies and judgments; (12) changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board (FASB) or other regulatory agencies; (13) legislative or regulatory changes or actions, or significant litigation, adversely affect Fifth Third, one or more acquired entities and/or the combined company or the businesses in which Fifth Third, one or more acquired entities and/or the combined company are engaged, including the recently enacted Dodd-Frank Wall Street Reform and Consumer Protection Act; (14) ability to maintain favorable ratings from rating agencies; (15) fluctuation of Fifth Third’s stock price; (16) ability to attract and retain key personnel; (17) ability to receive dividends from its subsidiaries; (18) potentially dilutive effect of future acquisitions on current shareholders’ ownership of Fifth Third; (19) effects of accounting or financial results of one or more acquired entities; (20) difficulties in separating Fifth Third Processing Solutions from Fifth Third; (21) loss of income from any sale or potential sale of businesses that could have an adverse effect on Fifth Third’s earnings and future growth;(22) ability to secure confidential information through the use of computer systems and telecommunications networks; and (23) the impact of reputational risk created by these developments on such matters as business generation and retention, funding and liquidity. You should refer to our periodic and current reports filed with the Securities and Exchange Commission, or “SEC,” for further information on other factors, which could cause actual results to be significantly different from those expressed or implied by these forward-looking statements. |

3 © Fifth Third Bank | All Rights Reserved 4Q10 in review Credit continuing to improve • Net charge-offs of $356 million (1.86 percent of loans and leases) vs. 3Q10 NCOs of $956 million (3Q10 included $510 million of losses on the sale or transfer of loans to held-for-sale and $446 million of losses on remaining loan portfolio) • Total NPAs of $2.5 billion including held-for-sale declined $313 million or 11 percent sequentially to lowest level since 2008 – Total delinquencies down 7% sequentially (lowest level since 1Q07) • Provision expense of $166 million • Loan loss allowance of 3.88%; coverage 138% of NPAs and 179% of NPLs Actions driving progress • Focusing on credit quality, portfolio management and loss mitigation strategies • Executing on customer satisfaction initiatives and improving customer loyalty • Enhancing breadth and profitability of offerings and relationships • Becoming an employer of choice in the industry by continuing to enhance employee engagement Continued strong operating results • Net income available to common shareholders of $270 million, $0.33 per diluted share • Period end loans and leases up $1.5 billion or 2% sequentially • Pre-provision net revenue (PPNR)* of $583 million reflecting solid net interest income, mortgage banking revenue, and corporate revenue results. • Return on average assets of 1.18%; return on average common equity of 10.4% • Strong capital ratios: Tier 1 common 7.50%, Tier 1 ratio 13.94%, Total capital ratio 18.14% • Extended $26 billion of new and renewed credit * Pre-provision net revenue: net interest income plus noninterest income minus noninterest expense |

4 © Fifth Third Bank | All Rights Reserved Financial summary • 4Q10 earnings $0.33 per diluted share, up 50% sequentially, demonstrating strong operating results and continued improvement in credit results • Return on average assets of 1.18% and return on average common equity of 10.4%. • Strong net interest income and net interest margin performance – Reflected ongoing CD repricing and deposit mix shift out of CDs, as well as higher average total loan balances and continued deposit pricing discipline, partially offset by effect of FTPS loan refinancing – Average core deposits up 6% year-over-year; up 2% sequentially, reflecting seasonally high DDA balances and includes decline in consumer CDs • 4Q10 NCO ratio of 1.86% reflecting continued improvement in the credit quality of loans as well as the benefit from 3Q10 credit actions Actual Seq. YOY ($ in millions) 4Q09 3Q10 4Q10 $ % $ % Average Balances Commercial loans $45,395 $43,861 $42,808 ($1,053) (2%) ($2,587) (6%) Consumer loans 32,206 32,756 33,428 671 2% 1,222 4% Total loans & leases (excl. held-for-sale) $77,601 $76,617 $76,236 ($381) 0% ($1,365) (2%) Core deposits $71,845 $75,202 $76,454 $1,252 2% $4,609 6% Income Statement Data Net interest income (taxable equivalent) $883 $916 $919 $3 0% $36 4% Provision for loan and lease losses 776 457 166 (290) (64%) (610) (79%) Noninterest income 651 827 656 (171) (21%) 4 1% Noninterest expense 967 979 987 8 1% 20 2% Net Income (loss) ($98) $238 $333 $95 40% $431 NM Diluted earnings after preferred dividends ($160) $175 $270 $95 54% $430 NM Pre-provision net revenue $562 $760 $583 ($177) (23%) $21 4% Earnings per share, basic ($0.20) $0.22 $0.34 $0.12 55% $0.54 NM Earnings per share, diluted ($0.20) $0.22 $0.33 $0.11 50% $0.53 NM Net interest margin 3.55% 3.70% 3.75% 5 bps 1% 20bps 6% Return on average assets (0.35%) 0.84% 1.18% 50bps 40% 153bps NM |

5 © Fifth Third Bank | All Rights Reserved Net interest income NII and NIM (FTE) • Sequential trends in net interest income and net interest margin (FTE) reflect CD repricing, deposit mix shift out of CDs, higher average total loan balances and continued deposit pricing discipline partially offset by effect of FTPS loan refinancing – NII up $3 million sequentially and up $36 million, or 4%, year-over-year – NIM up 5 bps sequentially and 20 bps year- over-year (bps) * Represents purchase accounting adjustments included in net interest income. Yields and rates ($mm) • Yield on interest-earning assets down 5 bps sequentially and down 9 bps year-over-year – Average loan and lease yield down 7 bps sequentially and up 1 bp versus prior year • Cost of interest-bearing liabilities down 9 bps sequentially and down 35 bps versus prior year |

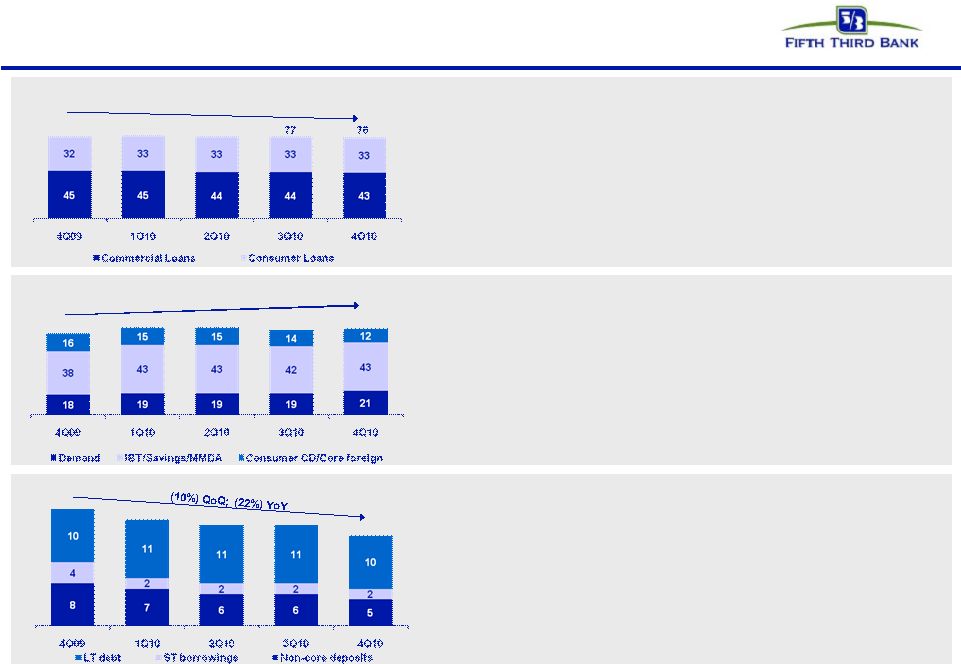

6 © Fifth Third Bank | All Rights Reserved Balance sheet • Extended $26 billion of new and renewed credit in 4Q10 • C&I loans flat sequentially and up 2% from the previous year • CRE loans down 8% sequentially and 18% from the previous year • Consumer loans up 2% sequentially and up 4% from the previous year • Warehoused residential mortgage loans held-for-sale were $2.3 billion at quarter end Flat QoQ; (2%) YoY +2% QoQ; +6% YoY • Core deposit to loan ratio of 100%, up from 93% in 4Q09 • DDAs up 9% sequentially and 16% year-over-year • Retail average transaction deposits up 4% sequentially and 14% from the previous year, driven by growth in demand deposit, savings, and interest checking account balances • Commercial average transaction deposits up 5% sequentially, driven by growth in demand deposit interest checking account balance – Excluding public funds balances, commercial average transaction deposits increased 6% sequentially and 33% over prior year Average loan growth ($B)^ Average core deposit growth ($B) 78 78 72 76 Average wholesale funding ($B) 20 22 • Reduced wholesale funding by $4.8 billion from the fourth quarter of 2009 – Non-core deposits down 20% sequentially and 41% from the previous year – Short term borrowings down 4% sequentially and 39% from the previous year – Long-term debt down 6% sequentially and 1% from the previous year ^ Excludes loans held-for-sale Note: Numbers may not sum due to rounding 77 77 19 19 75 76 17 |

7 © Fifth Third Bank | All Rights Reserved Noninterest income • Noninterest income of $656 million down $171 million, or 21%, from prior quarter; excluding 3Q10 BOLI settlement noninterest income decreased $19 million, or 3%, compared with 3Q10 noninterest income of $675 million driven by exceptionally strong third quarter mortgage results – Strong corporate banking revenue results; mortgage banking net revenue largely driven by originations of $7.4 billion • OREO write-downs, negative fair value adjustments, and gains/losses on loan sales recorded in other noninterest income continue to negatively impact noninterest income: Noninterest income Note: Numbers may not sum due to rounding Actual ($ in millions) 4Q09 3Q10 4Q10 Gain / (loss) on sale of loans 8 (1) 21 Commercial loans HFS FV adjustment (17) (9) (35) Gain / (loss) on sale of OREO properties (21) (29) (19) Mortgage repurchase costs (2) (2) (1) Total credit-related revenue ($42) ($34) Actual Seq. YOY 4Q09 3Q10 4Q10 $ % $ % ($ in millions) Service charges on deposits $159 $143 $140 ($3) (2%) ($19) (12%) Corporate banking revenue 89 86 103 17 20% 14 16% Mortgage banking revenue 132 232 149 (83) (36%) 17 13% Investment advisory services 86 90 93 3 3% 7 8% Card and processing revenue 76 77 81 4 5% 5 7% Other noninterest income 107 195 55 (140) (72%) (52) (49%) Securities gain (losses), net 2 4 21 17 NM 19 NM Securities gains, net - - - 14 14 14 non-qualifying hedges on MSRs NM NM Noninterest income $651 $827 $656 $ (171) (21%) $5 1% |

8 © Fifth Third Bank | All Rights Reserved Noninterest expense Noninterest expense • Noninterest expense of $987 million increased $8 million, or 1%, compared with 3Q10, driven by an increase in revenue-based incentives; 4Q10 included a $17 million charge related to termination of FHLB debt and 3Q10 included $25 million in legal expenses associated with the BOLI settlement – Year-over-year increase also impacted by growth in salaries, wages, and incentives due to higher levels of production and investment in sales force expansion • Credit related expenses declined but remain elevated: Note: Numbers may not sum due to rounding Actual Seq. YOY 4Q09 3Q10 4Q10 $ % $ % ($ in millions) Salaries, wages and incentives $331 $360 $385 $25 7% $54 16% Employee benefits 69 82 73 (9) (11%) 3 5% Net occupancy expense 75 72 76 4 5% 1 1% Technology and communications 47 48 52 4 8% 4 9% Equipment expense 31 30 32 2 5% 1 3% Card and processing expense 27 26 26 0 2% (1) (2%) Other noninterest expense 387 361 343 (19) (5%) (44) (11%) Noninterest expense $967 $979 $987 $8 1% $20 2% Actual ($ in millions) 4Q09 3Q10 4Q10 Mortgage repurchase expense $17 $45 $20 Provision for unfunded commitments 11 (23) (4) Derivative valuation adjustments (2) 8 (1) OREO expense 9 9 11 Other work-out related expenses 37 28 27 Total credit-related operating expenses $73 $67 $53 |

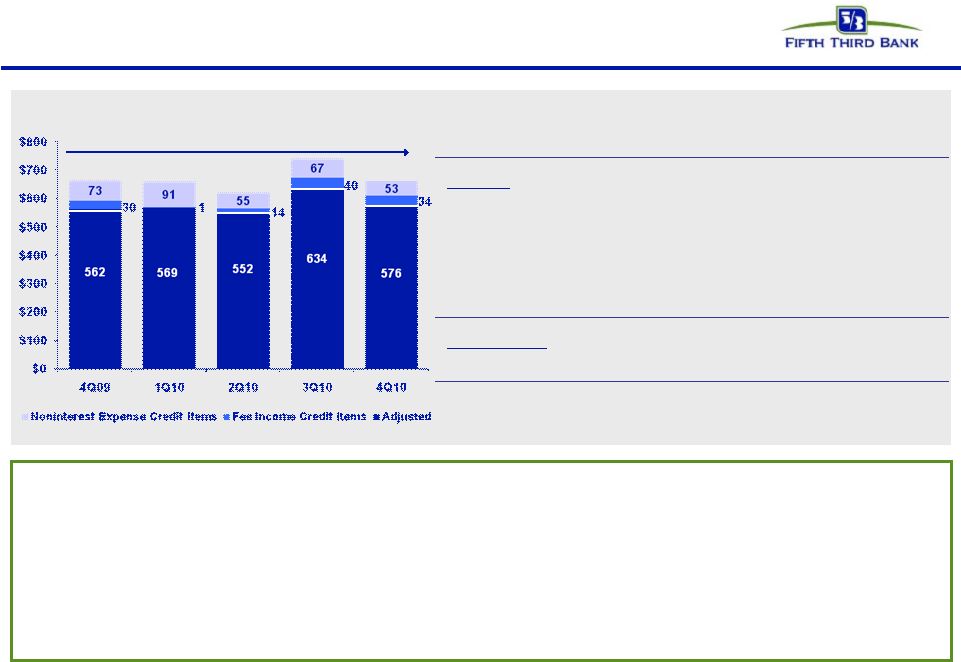

9 © Fifth Third Bank | All Rights Reserved Pre-tax pre-provision earnings Core PPNR trend Pre-provision net revenue (PPNR): net interest income plus noninterest income minus noninterest expense • Reported PPNR of $583 million down 23% from strong 3Q10 levels which included the BOLI litigation settlement and higher mortgage banking revenue, and up 4% over prior year reflecting solid net interest income and mortgage banking revenue results • Adjusted PPNR of $576 million, including adjustments totaling ($27) million, resulting in adjusted sequential decrease of 9% and year-over-year increase of 2% • Excluding the impact of credit-related adjustments ($87mm in 4Q10), PPNR down 11% versus 3Q10; stable versus 4Q09 Adjusted PPNR +2% Credit adjusted PPNR flat% Core PPNR reconciliation 4Q09 1Q10 2Q10 3Q10 4Q10 Reported PPNR $562 $568 $567 $760 $583 Adjustments: BOLI - - - (127) - Gain on sale of Visa shares - 9 - - - Divested merchant and EFT revenue (2) - - - - Securities gains/losses (2) (14) (8) (4) (21) Other litigation reserve expense 22 4 3 - - FTPS warrants + puts (20) 2 (10) 5 (3) Extinguishment of FHLB funding - - - - 17 Divested merchant and EFT expense (estimated) 2 - - - - Adjusted PPNR $562 $569 $552 $634 $576 Credit Related Items: OREO write-downs, FV adjs, & G/L on loan sales 31 1 15 42 34 Problem asset work-out expenses 73 91 55 67 53 Credit adjusted PPNR $666 $661 $622 $743 $663 |

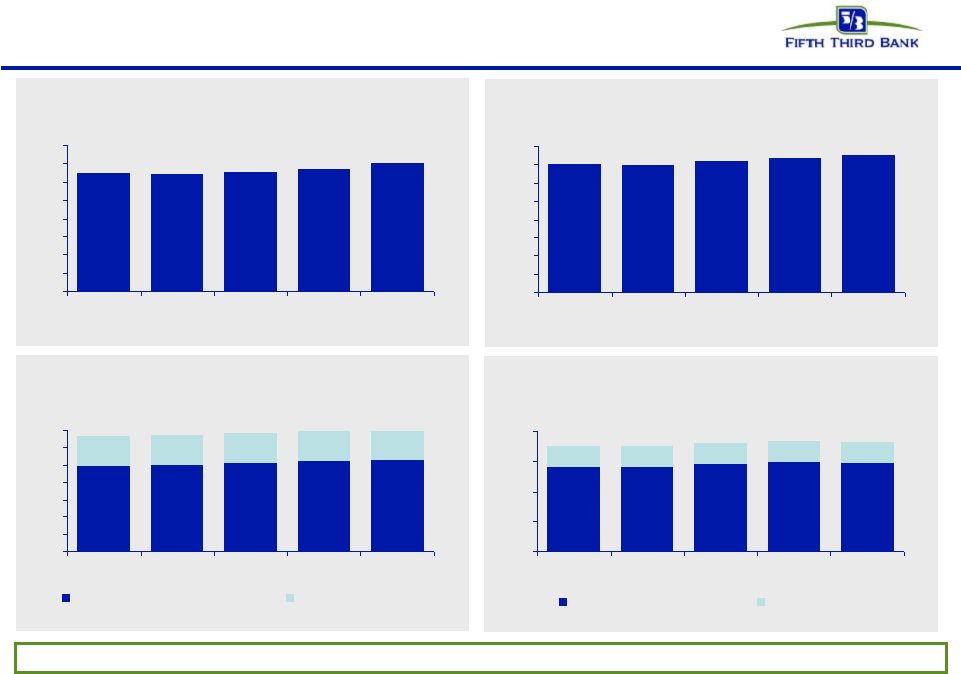

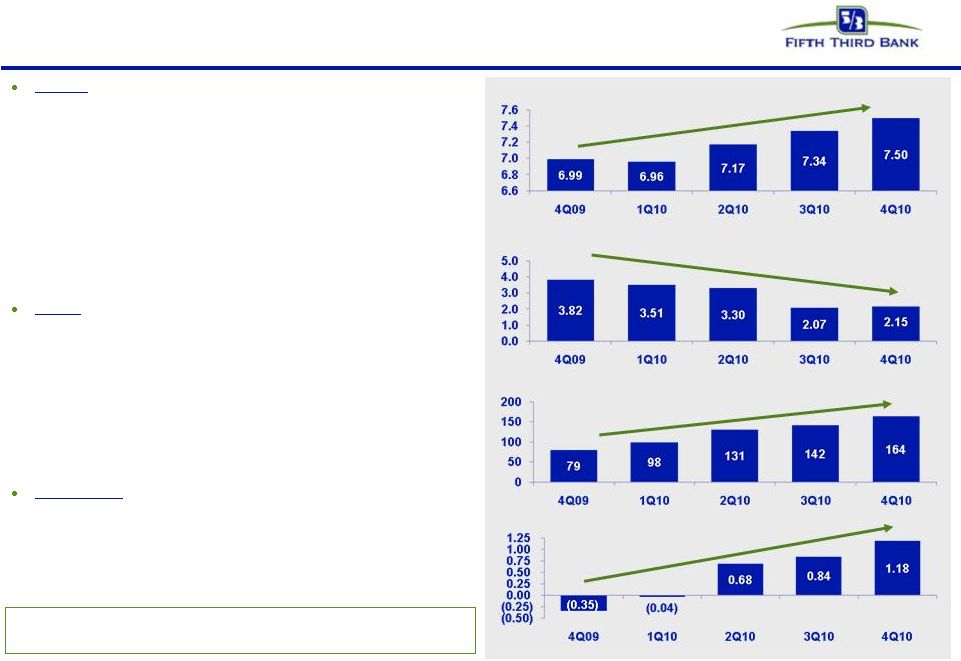

10 © Fifth Third Bank | All Rights Reserved Strong capital position ^ Tangible common equity ratio excludes unrealized securities gains/losses after-tax. Capital ratios remained strong during the quarter and increased from previous quarters 6.5% 6.4% 6.6% 6.7% 7.0% 0% 1% 2% 3% 4% 5% 6% 7% 8% 4Q09 1Q10 2Q10 3Q10 4Q10 Tangible common equity ratio^ 7.0% 7.0% 7.2% 7.3% 7.5% 0% 1% 2% 3% 4% 5% 6% 7% 8% 4Q09 1Q10 2Q10 3Q10 4Q10 Tier I common equity 9.9% 10.0% 10.3% 10.5% 10.5% 13.9% 13.3% 13.4% 13.7% 13.9% 0% 2% 4% 6% 8% 10% 12% 14% 4Q09 1Q10 2Q10 3Q10 4Q10 Tier 1 Capital Ratio ex-TARP Tier 1 Capital Ratio Tier I capital ratio 14.1% 14.1% 14.6% 14.9% 14.7% 18.3% 17.5% 17.5% 18.0% 18.1% 0% 5% 10% 15% 20% 4Q09 1Q10 2Q10 3Q10 4Q10 Total RBC ratio ex-TARP Total RBC ratio Total risk-based capital ratio |

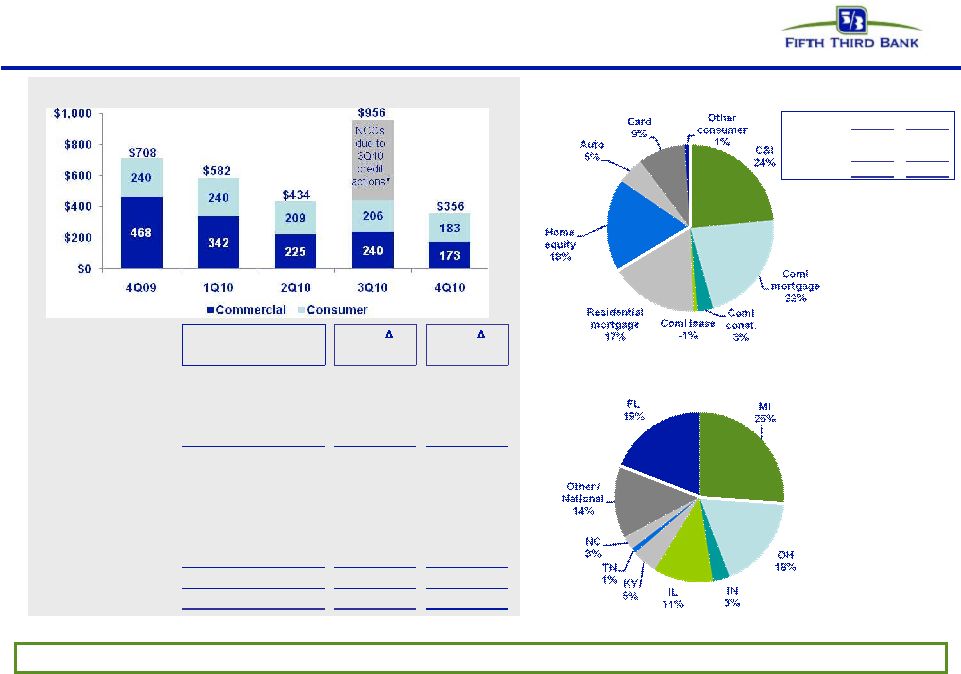

11 © Fifth Third Bank | All Rights Reserved Net charge-offs Net charge-offs by loan type Net charge-offs by geography Net charge-offs ($mm) $mm % Commercial $173 49% Consumer $183 51% Total $356 100% Actual Seq. YOY ($ in millions) 4Q09 3Q10 4Q10 $ % $ % C&I $183 $237 $85 ($152) (64%) ($98) (54%) Commercial mortgage 142 268 80 ($188) (70%) ($62) (44%) Commercial construction 135 121 11 ($110) (91%) ($124) (92%) Commercial lease 8 1 (3) ($4) (400%) ($11) (138%) Commercial $468 $627 $173 ($454) (72%) ($295) (63%) Residential mortgage loans 78 204 62 (142) (70%) (16) (21%) Home equity 82 66 65 (1) (2%) (17) (21%) Automobile 32 17 19 2 12% (13) (41%) Credit card 44 36 33 (3) (8%) (11) (25%) Other consumer 4 6 4 (2) (33%) 0 0% Consumer $240 $329 $183 ($146) (44%) ($57) (24%) Total net charge-offs $708 $956 $356 ($600) (63%) ($352) (50%) Charge-offs down due to improving credit trends and effect of 3Q10 credit actions* * See slide 36 for more information |

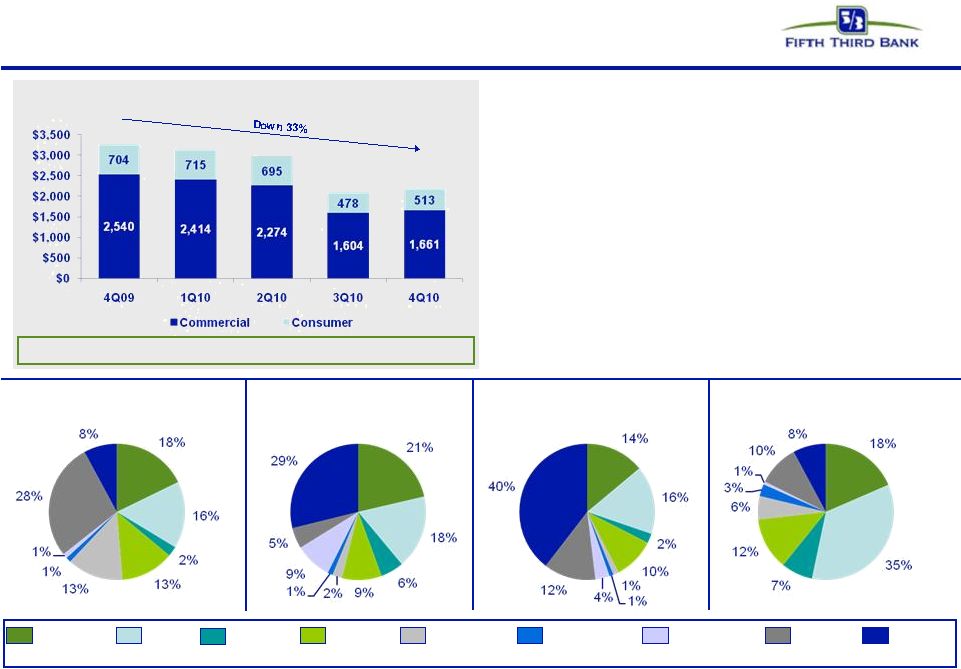

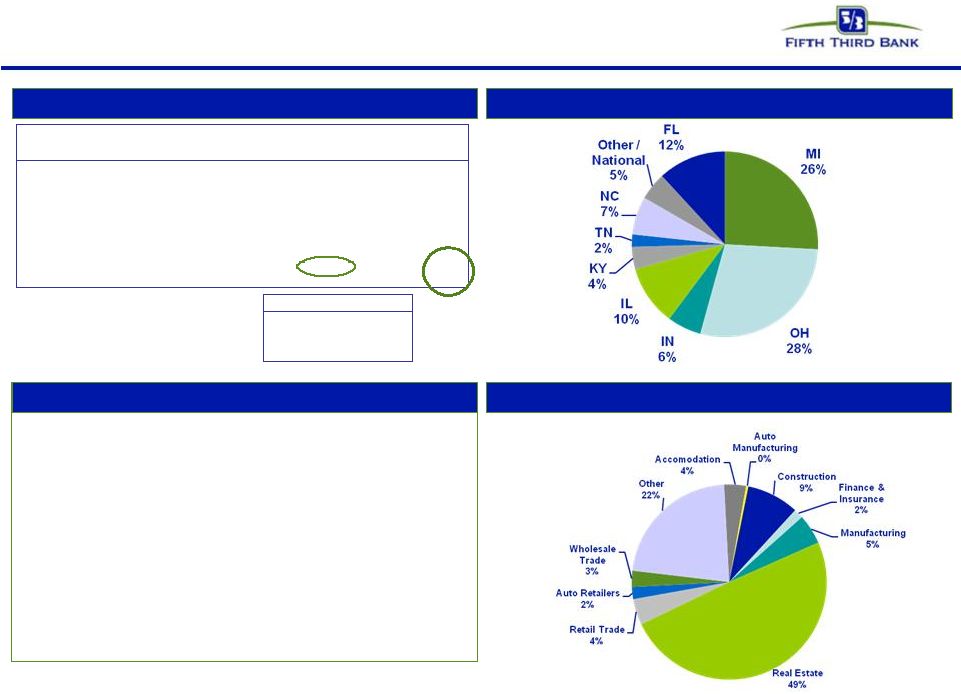

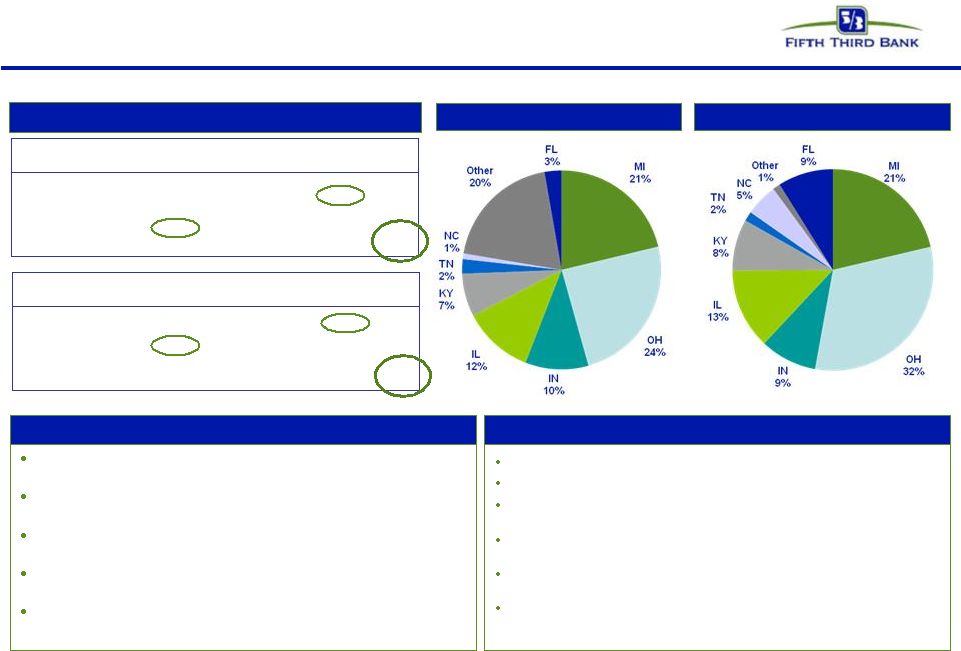

12 © Fifth Third Bank | All Rights Reserved Nonperforming assets • NPAs of $2.17B excluding held-for-sale • Commercial NPAs of $1.66B, down 35% from the previous year – Homebuilder/developer NPAs of $259mm; represent 16% of total NPAs • Consumer NPAs of $513mm, down 27% from the previous year • NPAs in held-for-sale of $294mm • Decline in 3Q10 largely driven by credit actions* C&I / Lease $723mm, 33% CRE $938mm, 43% Residential $440mm, 20% Other Consumer $73mm, 3% ILLINOIS INDIANA FLORIDA TENNESSEE KENTUCKY OHIO MICHIGAN NORTH CAROLINA OTHER / NATIONAL NPAs exclude loans held-for-sale. * See slide 36 for more information Nonperforming assets ($mm) $3,244 $3,129 Nonperforming assets continue to improve $2,969 $2,082 $2,174 |

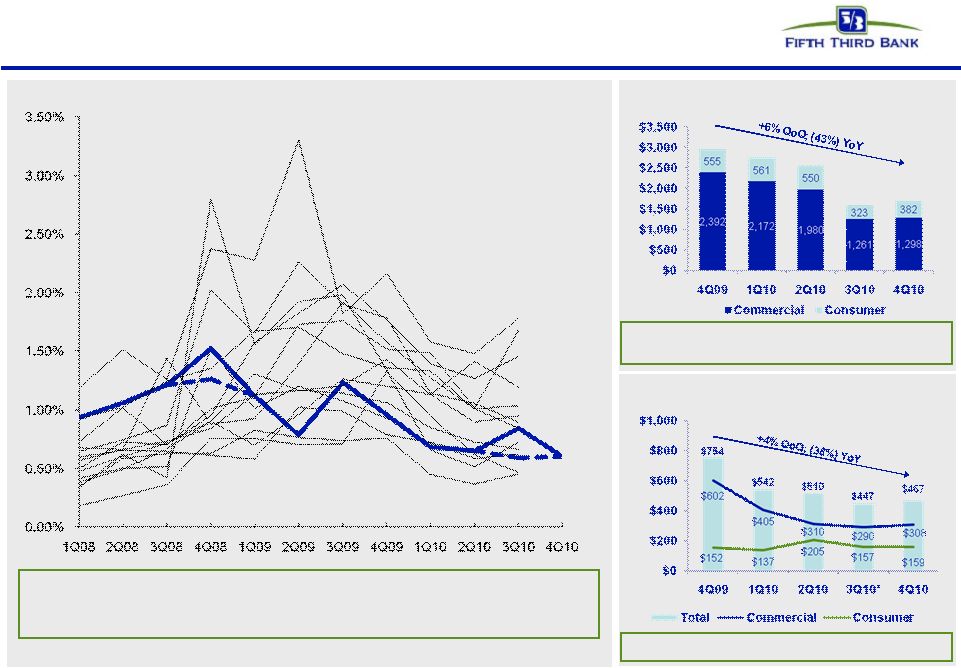

13 © Fifth Third Bank | All Rights Reserved NPL Rollforward Significant improvement in NPL inflows over past two years NPL HFI Rollforward Commercial 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 Beginning NPL Amount 1,406 1,937 2,110 2,430 2,392 2,172 1,980 1,261 New nonaccrual loans 799 544 832 602 405 310 290 308 Paydowns, payoffs, sales and net other activity (157) (190) (246) (332) (425) (401) (631) (169) Charge-offs (111) (181) (266) (308) (200) (100) (379) (103) Ending Commercial NPL 1,937 2,110 2,430 2,392 2,172 1,980 1,261 1,298 Consumer 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 Beginning NPL Amount 457 459 477 517 555 561 550 323 New nonaccrual loans 157 125 160 152 137 205 157 159 Net other activity (155) (107) (120) (114) (131) (216) (384) (100) Ending Consumer NPL 459 477 517 555 561 550 323 382 Total NPL 2,396 2,587 2,947 2,947 2,733 2,530 1,584 1,680 Total new nonaccrual loans - HFI 956 669 992 754 542 515 447 467 |

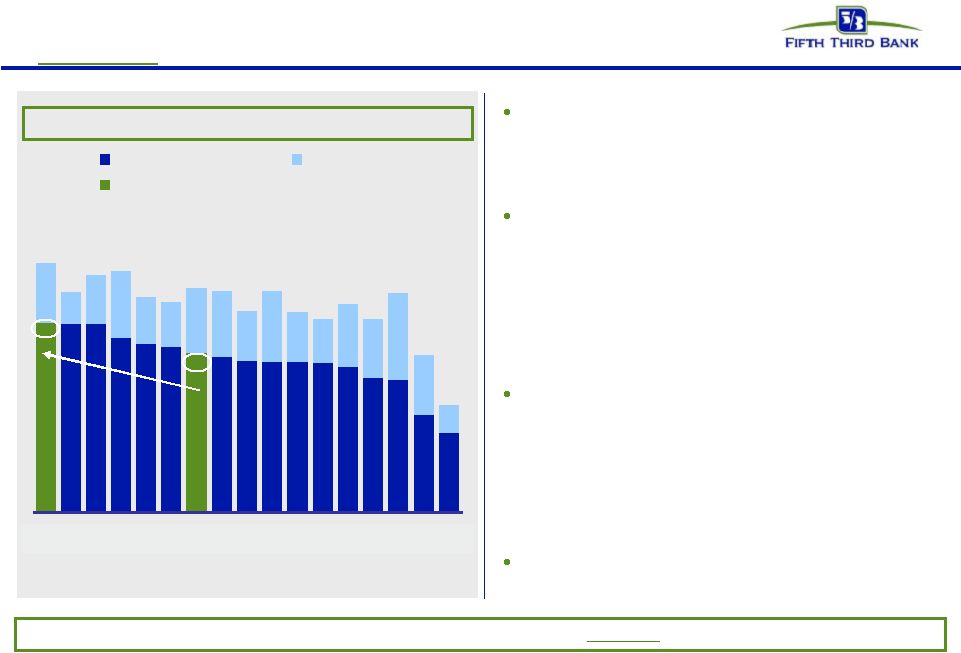

14 © Fifth Third Bank | All Rights Reserved Non-performing loans Non-performing loans ($mm) $2.9B $2.7B Non-performing loans improving with lower severity mix; benefit of sales/transfers $2.5B Fifth Third’s non-performing loan inflows (relative to loans) were higher than peers throughout 2008. More recently, FITB inflows have been proportionally lower than peers FITB NPL inflows (relative to loans) vs. peers FITB Source: SNL Financial and company filings. Peers include: BAC, BBT, C, CMA, HBAN, JPM, KEY, MI, MTB, PNC, RF, STI, USB, and WFC New HFI non-performing loan flows ($mm) NPL inflows have declined significantly $1.6B * 3Q10 inflows into NPLs HFS were $217mm, reflecting performing loans moved to held-for-sale in 3Q10 that were deemed impaired as a result of the decision to sell these loans FITB ex-HFS $1.7B |

15 © Fifth Third Bank | All Rights Reserved Troubled debt restructurings (TDR) overview Successive improvement in vintage performance during 2008 and 2009, even as volume of modification increased Fifth Third’s mortgage portfolio TDRs have redefaulted at a lower rate than other bank held portfolio modifications — Fifth Third’s TDRs less likely to redefault than modifications on GSE mortgages Of $1.8B in consumer TDRs, $1.6B were on accrual status and $206M were nonaccruals — $1.1 billion of TDRs are current and have been on the books 6 or more months; within that, nearly $800 million of TDRs are current and have been on the books for more than a year As current TDRs season, their default propensity declines significantly — We see much lower defaults on current loans after a vintage approaches 12 months since modification TDR performance has improved in newer vintages Outperforming redefault benchmarks Source: Fifth Third and OCC/OTS data through 3Q10 Mortgage TDR 60+ redefault trend by vintage 1Q08 $55 2Q08 $114 3Q08 $112 4Q08 $128 1Q09 $189 2Q09 $219 Months since modification Mortgage TDR 60+ redefault rate: Fifth Third comparison (January 1, 2008 through September 2010) Fannie Mae Industry portfolio loans Fifth Third Volume by vintage ($mm) Freddie Mac 3Q09 $269 Current consumer TDRs (%) 4Q09 $137 $1.1 billion 2008 2009 1Q10 $131 2Q10 $105 |

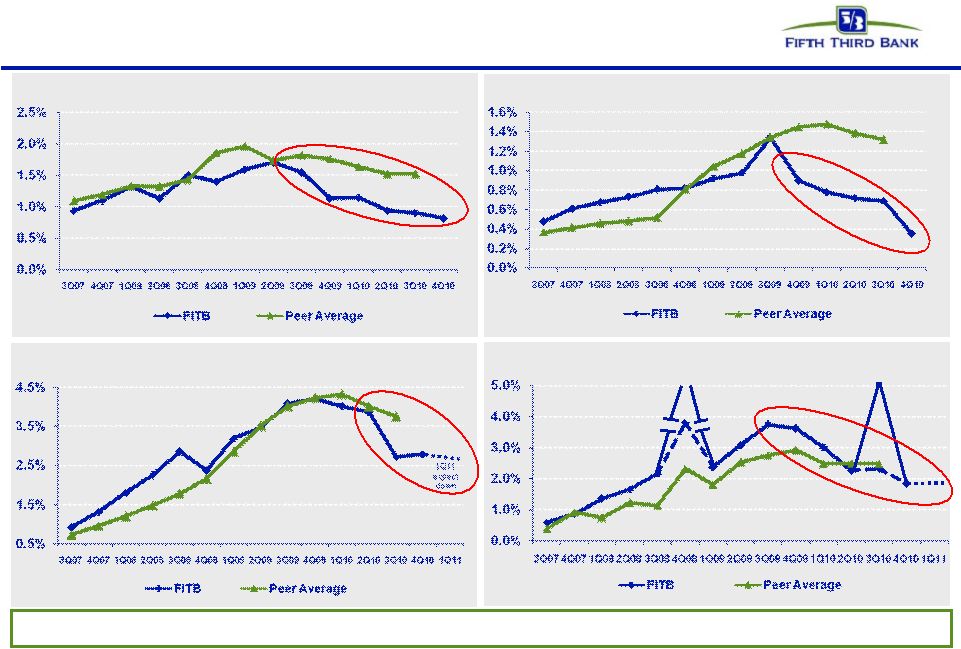

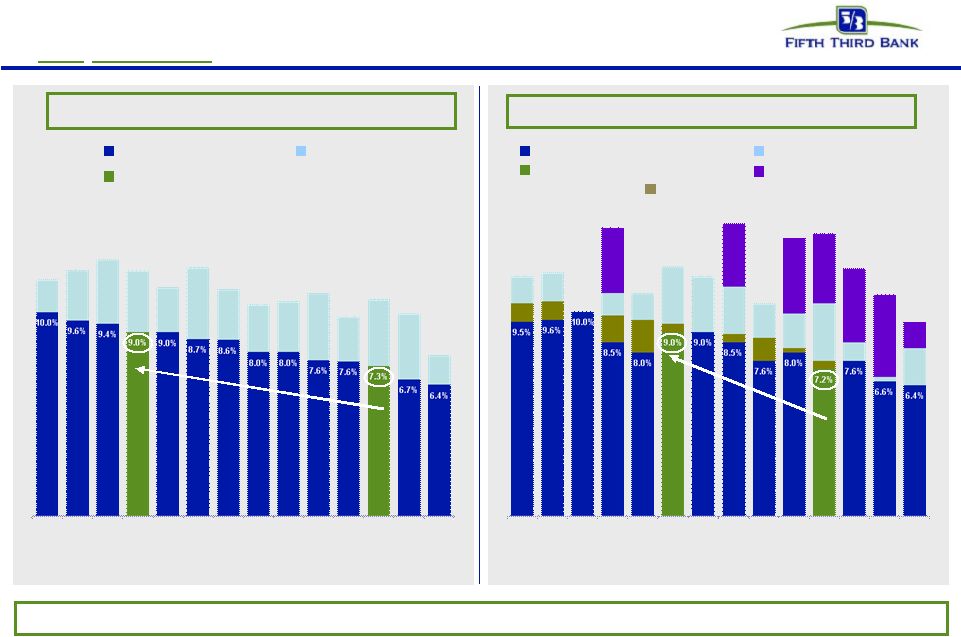

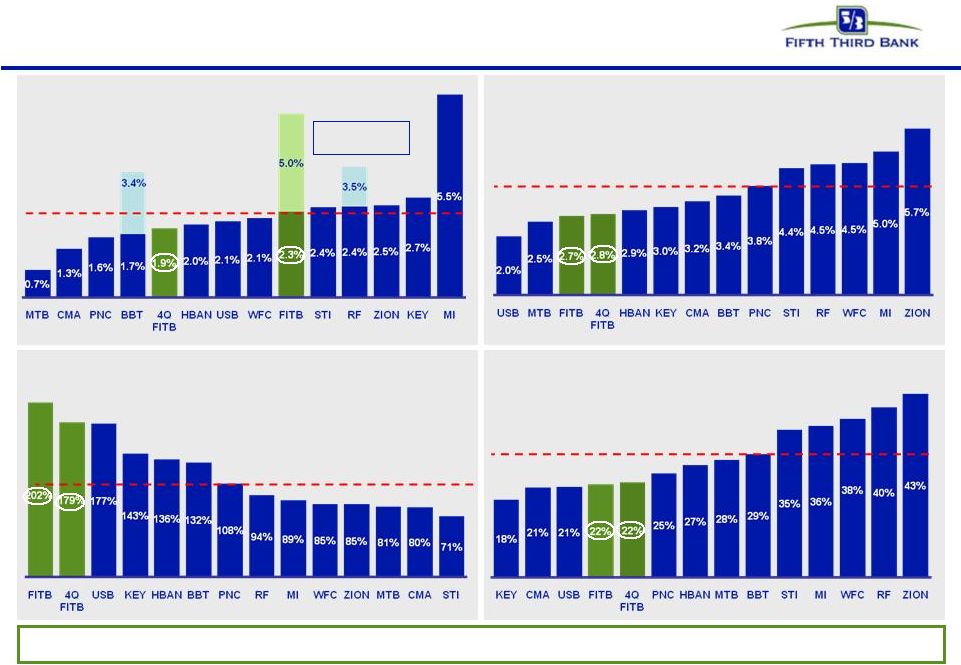

16 © Fifth Third Bank | All Rights Reserved Strong relative credit trends FITB credit metrics are now generally better than peers NPA ratio vs. peers Net charge-off ratio vs. peers Loans 90+ days delinquent % vs. peers Loans 30-89 days delinquent % vs. peers (7.5%)* (HFS transfer) 3.8% Before credit actions 5.0% 1Q11 expect stable 2.3%* Before credit actions Source: SNL Financial and company filings. NPA and NCO ratios exclude loans held-for-sale and covered assets for peers where appropriate. * 4Q08 NCOs included $800mm in NCOs related to commercial loans moved to held-for-sale; 3Q10 NCOs included $510mm in NCOs related to loans sold or moved to held-for-sale |

17 © Fifth Third Bank | All Rights Reserved Strong reserve position 4Q10 coverage ratios strong relative to peers (3Q10) $708 $582 $434 $956 $356 $68 $8 ($109) ($499) ($190) 4.88% 4.91% 4.85% 3.88% 4.20% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 4Q09 1Q10 2Q10 3Q10 4Q10 ($600) ($400) ($200) $0 $200 $400 $600 $800 $1,000 $1,200 Net Charge-offs Additional Provision Reserves Industry leading reserve levels 89% 138% Reserves / NPAs 107% 179% Reserves / NPLs 179% Fifth Third (4Q10) Peer Average (3Q10) Source: SNL and company reports. NPAs/NPLs exclude held-for-sale portion for all banks as well as covered assets for BBT, USB, and ZION. |

18 © Fifth Third Bank | All Rights Reserved $4.1B Realized credit losses have been significantly below SCAP submissions; expect further improvement Actual $2.6B Actual $2.7B $2.8B 2009 SCAP scenarios vs. current loss expectations under internally-specified scenarios Internal Base Case Updated internal stress analysis vs. SCAP scenarios Fifth Third’s realized credit losses were significantly below its SCAP submitted baseline and more adverse scenarios – In SCAP submissions, we incorporated significant conservatism, given then prevailing negative economic and industry trends and extreme uncertainty in potential loss outcomes – Economic and credit market conditions have been much better than expected in Spring 2009 2010 charge-offs of $2.3bn (included $510mm on sale / transfer of $900mm of NPLs in 3Q10) – 16% lower than baseline submission, 53% below adverse scenario under SCAP 2011 charge-offs expected lower than 2010 – Reflects aggressive actions to address / dispose of problem credits – 3Q10 dispositions alone expected to reduce 2011 charge-offs by ~$300mm³ Base Red SCAP line represents more adverse scenario as adjusted by supervisors for additional assumed two-year losses. Supervisory estimates of total two-year losses under more adverse scenario were not allocated by period. Estimate allocates total two-year supervisory losses using the allocation under Fifth Third’s submission. Moody’s Economy.com scenarios; macroeconomic scenarios and estimates as of November 2010 (probabilities assigned by Moody’s). It is not known what, if any, losses taken in 2010 due to 3Q10 credit actions would have been taken in 2011 through “normal” charge-off recognition processes 1 2 3 |

19 © Fifth Third Bank | All Rights Reserved Well-positioned for the future • Holding company cash currently sufficient for more than two years of obligations; no holding company or Bank debt maturities until 2013 • Bank level capital ratios significantly above most peers • After TARP repayment, Fifth Third will have completely exited all crisis-era government support programs – Fifth Third is one of the few large banks that have no TLGP-guaranteed debt Superior capital and liquidity position • $1.2bn problem assets addressed through loan sales and transfer to HFS in 3Q10 • NCOs below 2%; 213% reserves / annualized NCOs • Substantial reduction in exposure to CRE since 1Q09; relatively low CRE exposure versus peers Proactive approach to risk management • Traditional commercial banking franchise built on customer-oriented localized operating model • Strong market share in key markets with focus on further improving density • Fee income ~40% of total revenues Diversified traditional banking platform • PPNR has remained strong throughout the credit cycle • PPNR substantially exceeds annual net charge-offs (164% PPNR / NCOs in 4Q10) • 1.18% ROAA in 4Q10 Strong industry leader in earnings power |

20 © Fifth Third Bank | All Rights Reserved Appendix 1 – Capital plan |

21 © Fifth Third Bank | All Rights Reserved Overview and rationale Following extensive dialogue with our regulators, the company believes that now is the appropriate time to redeem TARP ($3.408bn), given its strong foundation for future growth: — $1.7bn common equity issuance — Planned senior debt issuance — Internally available funds (expected to be the predominant source of additional liquidity necessary for TARP redemption) After TARP repayment, intend to negotiate for with Treasury repurchase of warrants; if mutually agreeable value not reached, will evaluate participation in auction — Incorporated into capital plans (but not pro formas) Strong capital levels provide strategic flexibility and capital deployment optionality (9.0% pro forma Tier 1 common) Pro forma capital structure provides additional flexibility in capital deployment |

22 © Fifth Third Bank | All Rights Reserved Pro forma capital ratios Refer to Regulation G Non-GAAP Reconciliation in appendix Note: Pro forma capital ratios net of write-off of discount accretion on TARP preferred stock of $164mm and underwriting fees of approximately $51mm. ¹ Pro forma ratios include $1,700mm common equity issuance ² Pro forma ratios also assume repurchase of the Bancorp’s Fixed Rate Cumulative Perpetual Preferred Stock, Series F, issued under TARP CPP subject to U.S. Treasury approval. 3 Also includes proposed phase-out of trust preferred securities under Dodd-Frank Act and Basel III 4 Peers include BBT, CMA, HBAN, KEY, RF, MI, MTB, PNC, STI, USB, WFC, ZION Post-offering capital position creates foundation for future growth TCE / TA (incl. unrealized gains) Tier 1 common Tier 1 capital Total capital 7.1% 7.3% 13.9% 18.3% 7.3% 7.5% 13.9% 18.1% 4Q10 4Q10 $1.7bn offering pro forma 3Q10 Consolidated Bank Tier 1 common Tier 1 capital 14.5% 13.2% 14.5% 13.2% 8.8% 9.1% 15.6% 19.8% 13.2% 13.2% 7.1% 8.3% 11.7% 15.2% 3Q10 Peer Median 4 10.1% 10.1% TCE / TA (excl. unrealized gains) 6.7% 7.0% 8.6% 7.1% including phase-out of TRUPS 11.1% 11.2% 12.8% 8.9% Tier 1 leverage 12.5% 12.8% 14.3% 9.4% 4Q10 TARP redemption pro forma 8.7% 9.0% 12.2% 16.4% 13.2% 13.2% 8.4% 9.4% 11.2% 2 1 3 |

23 © Fifth Third Bank | All Rights Reserved Pro forma capital position vs. peers (not adjusted for Basel III) Fifth Third’s capital position will be well in excess of any established standards and most peers Red: repaid TARP Tier 1 common (peers) Tier 1 common (FITB) Reserves (Tier 1 common + reserves) RWA Red: repaid TARP Tier 1 capital ex-TPS & TARP (peers) Tier 1 capital ex-TPS & TARP (FITB) Tier 1 capital ratio Trust preferred TARP CPP Preferred equity 11.6% 12.0% 12.5% 12.0% 12.2% 11.1% 11.2% 10.5% 10.9% 9.8% 10.6% 9.9% 7.9% 10.3% CMA PNC PF PF BBT ZION KEY STI WFC RF USB FITB MI MTB HBAN¹ FITB² 10.5% 11.9% 14.0% 10.8% 9.7% 12.2% 10.9% 9.6% 11.7% 8.9% 11.2% 14.3% 13.6% 11.7% 13.9% 12.1% 10.8% 9.5% 10.3% 9.9% 10.4% 8.5% 6.8% 8.2% 8.6% 8.2% 10.4% 7.6% PF PNC CMA ZION WFC PF BBT KEY USB STI FITB RF MI MTB HBAN¹ FITB² Ranked in order of Tier 1 capital from instruments not being phased out 9.4% Source: SNL Financial and company filings (financial data as of 3Q10). Common equity ratios for non-TARP repayers exclude discount accretion from attribution of TARP value (included in “TARP CPP” at top of bars). 1 Consolidated capital ratios pro forma adjusted for common equity and subordinated debt issuance. HBAN reported 3Q10 Tier 1 common ratio of 7.4% and Tier 1 capital ratio of 12.8% 2 Pro forma for TARP redemption and issuance of $1.7bn of common equity net of associated items. FITB reported 4Q10 Tier 1 common ratio of 7.5% and Tier 1 capital ratio of 13.9%. Refer to Regulation G Non-GAAP Reconciliation in appendix. |

24 © Fifth Third Bank | All Rights Reserved Pro forma capital position including TARP repayment (adjusted for Basel III*) Source: SNL Financial, company filings, and third-party estimates. Financial data as of 3Q10, not adjusted for potential mitigation efforts. Note: Four large peers include estimated Basel III RWA impact based on BIS proposals * Estimates based on current Basel III rules released by the Basel Committee ¹ Pro forma for TARP redemption, issuance of $1.7bn of common equity, net of associated items, and phase-out of trust-preferred securities. Reported 4Q10 Tier 1 common ratio of 7.5%. Tier 1 common ratio (+ reserves / RWA) Adjusted for Basel III, Fifth Third’s pro forma capital position would be strongest among peers in level and quality Reserves Tier 1 common (peers) Tier 1 common (FITB) 12.3% Note: Peers not in order of prior slide; estimated Unlike other SCAP commercial banks, Fifth Third does not expect adverse effect to common capital ratios from Basel III — Improvement of relative capital position Potentially net positive impact on regulatory capital — Limited deductions for mortgage servicing rights and deferred tax assets — Potentially positive impact from the absence of an adjustment for unrealized gains and losses Do not expect significant risk weighted assets impact — Low level of financial counterparty interconnectedness — Daily Value-at-Risk less than $500 thousand — Fifth Third is not a Basel II bank 9.7% Tier 1 capital ratio on fully phased-in basis* — Top of peer group under Basel III 11.1% PF Bank Bank Bank Bank Bank FITB Bank Bank Bank Bank Bank Bank Bank Bank Bank Bank FITB¹ 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 9.3% 7.8% |

25 © Fifth Third Bank | All Rights Reserved Capital management philosophy • Return excess capital to shareholders after assessment of other capital deployment alternatives and maintenance of buffers over targeted and required capital levels • Evaluate any share repurchases in context of stock price level • Not expected in near term Share repurchases* • Prudently expand franchise or increase density in core markets via disciplined acquisition evaluation • Attain top 3 market position in 65% of markets or more Strategic opportunities* • Strong levels of profitability would support significantly higher dividend than current dividend • Subject to consideration and approval of plans submitted under CCPR** Return to more normal dividend policy* • Support growth of core banking franchise • Improving loan demand in recovering economy Organic growth opportunities * Subject to Board of Directors and regulatory approval ** Comprehensive Capital Plan Review by Federal Reserve Internal Tier 1 common equity target of 8% range |

26 © Fifth Third Bank | All Rights Reserved Potential effects of capital plan and TARP repayment on income statement and earnings per share Fifth Third has not provided earnings or earnings per share guidance The comments below relate to the expected effects of our capital plan on our earnings and earnings per share. — Write-off of discount accretion and avoidance of accretion of discount: when we recorded the TARP preferred in our books, we were required to allocate the $3.408 billion to the value of the preferred stock and to the associated warrants. The amortized value of the discount assigned to the preferred stock was $153 million as of 12/31/10. This will be written-off at the time of TARP redemption through an increase in “preferred dividends” and reduce income available to common shareholders by the amount of the write-off. We will avoid future accretion of discount ($11 million in 4Q10) — TARP preferred dividend: The TARP preferred dividend is 5% of $3.408 billion ($170.4 million a year or $42.6 million a quarter). It represents approximately $0.20 per common share on an annual basis and approximately $0.05 per common share on a quarterly basis. Net income available to common shareholders will begin to benefit from the elimination of this dividend at the time of TARP repayment. — Net interest income would be modestly reduced by the net effect of our capital plan and TARP repayment. This would be driven by the following factors: – Our announced common stock offering will be “free funds” from a net interest income perspective. However, TARP preferred stock is also free funds from a net interest income perspective. – We intend to fund the remainder of TARP repayment primarily from available funds but also with a planned debt offering. The cost of replacing available funds with other sources of similar funding is currently very low in this interest rate environment. The effect of the planned debt offering is yet to be determined and will depend on the size of that offering, its cost, and the time of that offering and any associated hedges. — Earnings per share*: Will be affected by the above effects on any period, and the effect of the addition of the shares expected to be issued in our announced common stock offering. Our average fully diluted share count for fourth quarter 2010 was approximately 836 million (actual shares were approximately 796 million). Using our closing share price on January 18, 2011 of $14.86, the contemplated $1.7 billion offering would involve the issuance of approximately 114 million shares. Thus, our announced offering would increase our average fully diluted share count on an annualized basis by the shares issued, and increase the number of fully diluted shares by approximately 12 percent (number of actual shares by approximately 12.5 percent). * Excludes effect of any over-allotment option and associated equity forward agreement |

27 © Fifth Third Bank | All Rights Reserved Appendix 2 – Other information Note that data does not include any pro forma impact of the proposed offering and TARP repayment unless indicated otherwise. |

28 © Fifth Third Bank | All Rights Reserved Balance Sheet: Average loans & leases (incl. HFS) Average core deposits Income Statement: Net interest income* Net interest margin* Noninterest income Noninterest expense Pre-provision net revenue Asset Quality: Net charge-offs Loan loss allowance Nonperforming assets^ Returns: ROA ROACE Capital Ratios: Tier I common equity Tier I leverage Tier I capital Total risk-based capital Category Fifth Third: First quarter 2011 outlook 1Q11 Outlook $79.1 billion $76.4 billion Down $5-10mm Up 5-10bps $600mm +/- ~$950mm range ~$550-560mm range Please see cautionary statement for risk factors related to forward-looking statements. * Presented on a fully-taxable equivalent basis. ^ Ratios as a percent of loans excluding held-for-sale; allowance expectation assumes current expectation for credit and economic trends and is subject to review at quarter-end. Does not incorporate effects of proposed offering 4Q10 Actual Results Outlook as of January 19, 2011 Continued growth Modest decline Stable Lower Lower Building $919 million 3.75% $656 million $987 million $583 million 7.5% 12.8% 13.9% 18.1% $356 million $3.0 billion (3.88%) $2.2 billion (2.79%) 1.18% 10.3% 1%+ (normalized 1.3%-1.5%) 10% vicinity Includes 1Q seasonality |

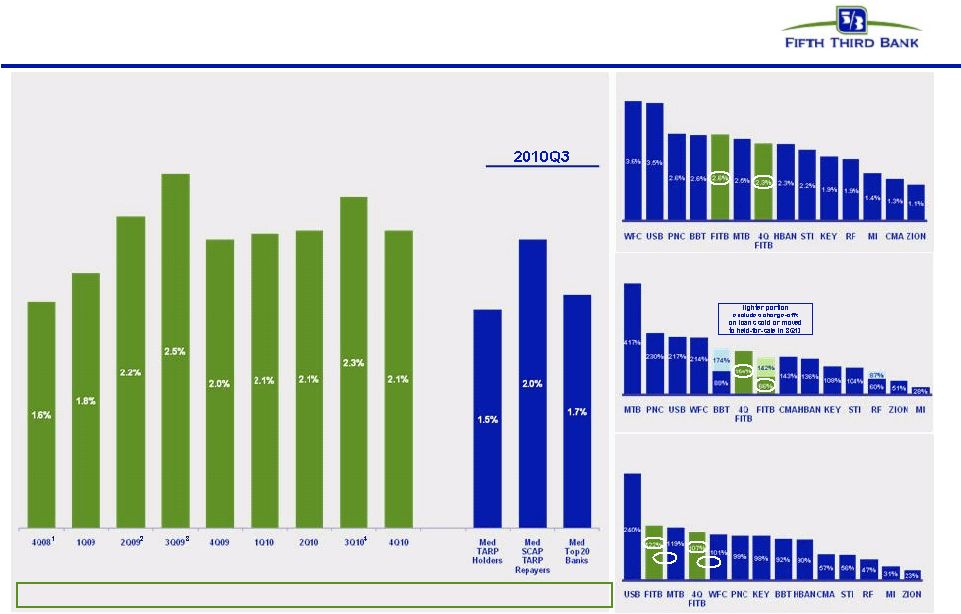

A foundation of continued growth Capital – foundation for continued growth — Tier 1 common capital has increased 313bps or $2.6bn 1 — Capital base transformed through series of capital actions – 9.4% pro forma Tier 1 ratio excluding trust preferred securities to be phased-out beginning 2013 2 — Capital levels supplemented by strong reserve levels – Loan loss reserves 3.88% of loans and 179% of NPLs — 9.0% pro forma Tier 1 common ratio 2 is $1.0bn in excess of internal 8.0% target Credit – ongoing discipline driving steady improvement — Broad-based improvements in problem loans – 72% reduction in 90+ day delinquent loans since 3Q09 – NCO ratio of 1.86%, first time below 2.0% since 2Q08 – 164% PPNR 3 / NCOs in 4Q10 — Balance sheet risk lowered through asset sales, resolutions – $1.3bn (43%) decline in NPLs since 4Q09 Profitability – recent results support positive momentum — PPNR remained stable throughout cycle — 5 consecutive quarters of increasing earnings with 3 consecutive profitable quarters — Return on assets 1.18%; Return on average common equity 10.4% in 4Q10 Tier 1 common ratio (%) NPL / Loans 4 (%) PPNR / Net charge-offs (%) Return on assets (%) 5 Well positioned due to combination of strong PPNR trends, robust reserves and strong Tier 1 common capital 29 © Fifth Third Bank | All Rights Reserved 1 Since December 31, 2008 2 See page 22 3 Pre-provision net revenue (PPNR): net interest income plus noninterest income minus noninterest expense; refer to Regulation G Non-GAAP Reconciliation in appendix 4 Nonperforming loans and leases as a percent of portfolio loans, leases and other assets, including other real estate owned (excludes nonaccrual loans held-for-sale) 5 Excluding $510mm net charge-offs attributable to credit actions and $127mm in net BOLI settlement gains |

Pre-provision net revenue: Strong in crisis and growing since Source: SNL Financial. Peers include – Med TARP Holders: BOK, FHN, HBAN, KEY, MI, MTB, RF, SNV, STI, ZION; Med SCAP TARP Repayers: BAC, BBT, C, CMA, COF, JPM, PNC, USB, WFC; Med Top 20 Banks by Total Assets as of 3Q10 Pre-provision net revenue (PPNR): net interest income plus noninterest income minus noninterest expense; refer to Regulation G Non-GAAP Reconciliation in appendix ¹ Excluding $965mm goodwill impairment 2 Excluding $1.8bn FTPS gain 3 Excluding $187mm Visa gain 4 3Q10 PPNR Excluding $127mm in net BOLI settlement gains 5 Includes and excludes net charge-offs related to loans sold or moved to held-for-sale during 3Q10 for FITB ($510mm), RF ($233mm), and BBT ($432mm) 30 © Fifth Third Bank | All Rights Reserved PPNR / Tangible assets Robust profitability provides first line of defense against credit losses PPNR 4 / Risk-weighted assets 4 PPNR 4 / Net charge-offs 5 PPNR 4 / HFI Nonperforming assets |

31 © Fifth Third Bank | All Rights Reserved Well-positioned for changed financial landscape Fifth Third’s business model is driven by traditional banking activities — Largest bank headquartered within Fifth Third’s core Midwest footprint — Focused on expansion and development of businesses where regional leadership matters — Capital investments, management talent, and added focus on businesses where (1) regional leadership creates an advantage (i.e., retail, small business, and mid- market commercial), and (2) select national lines where the bank has a distinctive element (i.e., Fifth Third Processing Solutions, Indirect Auto, Healthcare) No significant business at Fifth Third impaired during crisis; core business activities not generally limited by financial reform — Didn’t / don’t originate / sell CDOs or securitize loans on behalf of others; no mortgage securitizations outstanding (except <$150mm HELOC from 2003) — Didn’t / don’t originate / sell subprime mortgages or Option ARMs — Low level of financial system “interconnectedness” (e.g., Fifth Third loss in Lehman bankruptcy should be less than $2mm) — Little to no impact from Volcker rule (de minimis market maker in derivatives, proprietary trading); daily VaR less than $500 thousand – Small private equity portfolio ~$100mm (holding company subsidiary) Fifth Third’s businesses have performed well through the crisis, and we expect reintermediation and the landscape to evolve further toward our traditional strengths |

32 © Fifth Third Bank | All Rights Reserved Potential impact of key elements of Dodd-Frank Act and other recent financial legislation* Scope of activity Potential impact** Volcker Rule / Derivatives • Vast majority of derivatives activities are exempted (FITB generally not a market maker) • Any proprietary trading de minimis • “P/E” fund investments ~$100mm (<1% of Tier 1 capital) • Expect minimal financial impact from loss of existing revenue • Potentially higher compliance costs despite small levels of non-exempt activities Debit Interchange (Durbin Amendment) • 2010 debit interchange revenue of $204mm • 2010 debit interchange $ volume: $15.7B – Signature $12.2B, PIN $3.5B • 2010 debit interchange transaction volume: 433mm – Signature 347mm, PIN 86mm • Fed has proposed limits on debt interchange; proposal currently out for comment • Proposals would apply caps of $0.12 or $0.07 per transaction (e.g., on volume which in 2010 was 433 million transactions) • If proposal implemented as written, we would expect substantial mitigation of any reduction in revenue through actions by FITB and competitors to recapture costs of providing this service to customers and merchants Deposit Insurance • Current assessed base (Deposits): ~$78B • Proposed assessed base (Assets-TE): ~$97B • FITB rate under new industry assessment, based upon large bank scorecard, less than rate under old assessment • Lower due to reduced share of assessed base Reg. E • Requires customers to “opt-in” to allow non-recurring electronic overdrafts (e.g. debit, ATM) from accounts • Estimated quarterly impact of $17mm ($68mm annualized) to deposit service charges, before effect of mitigation; in full run-rate for 4Q10 Potential impact of these and other elements of financial regulatory reform, such as CFPA activities and many other aspects, are unknown at this time TRUPs exclusion (Collins Amendment) • ~280 bps of non-common Tier 1 capital in capital structure • >300 bps of non-common Tier 1 currently – Expected to be more than needed post-Basel III • 3-year transition period begins 2013 • Will manage capital structure to desired composition * Based on current understanding of legislation. ** Potential impact, as noted above, is not intended to be inclusive of all potential impacts that may result from implementation of legislation and does not include benefit of mitigation activities. Please refer also to cautionary statement. |

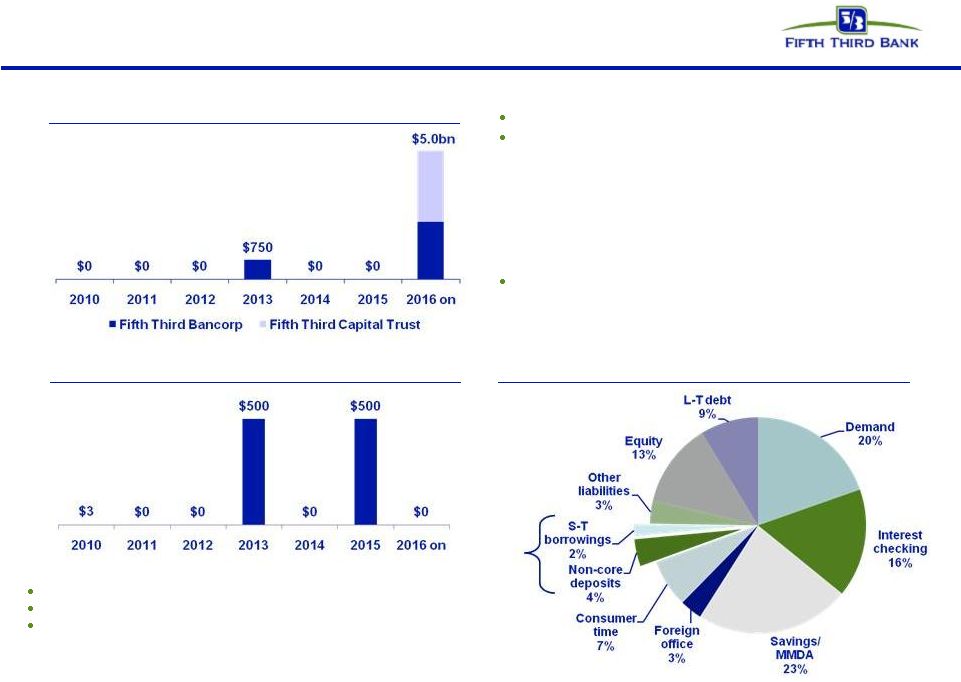

33 © Fifth Third Bank | All Rights Reserved Strong liquidity profile Retail Brokered CD maturities: $17.6mm in 2011 FHLB borrowings $1.5bn 12/31 unused avail. capacity $25.3bn ($19.5bn in Fed and $5.8bn in FHLB) Holding Company cash at 12/31/10: $2.3bn* Expected cash obligations over the next 12 months (assuming no TARP repayment)* — $0 debt maturities — ~$32mm common dividends — ~$205mm annual preferred dividends (~$35mm Series G, ~$170mm TARP prior to repayment) — ~$376mm interest and other expenses Cash currently sufficient to satisfy all fixed obligations** for more than two years without accessing capital markets/subsidiary dividends/asset sales Bank unsecured debt maturities ($mm – excl. Brokered CDs) Heavily core funded Holding company unsecured debt maturities ($mm) * Does not incorporate effects of proposed offering ** Debt maturities, common and preferred dividends, interest and other expenses S-T wholesale 6% |

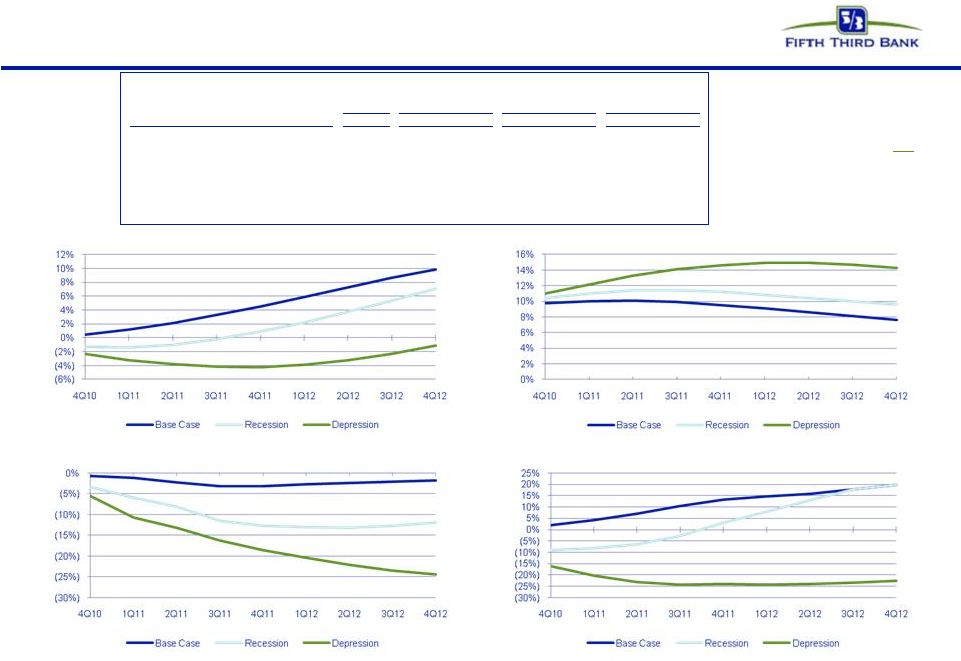

FITB’s internal macroeconomic assumptions Source: Moody's Economy.com *3Q10 Data Unemployment Cumulative HPI Growth Cumulative GDP Growth Cumulative Equity Price Index Growth OFHEO Index OFHEO Index OFHEO Index S&P 500 S&P 500 S&P 500 Current Base Case Moody's 25% probability Recession Moody's 4% probability Depression Economic Assumptions 4Q10 2011 2012 2011 2012 2011 2012 Average Unemployment 9.6% 9.9% 8.3% 11.3% 10.2% 13.5% 14.7% YoY GDP Growth 3.1%* 4.1% 5.1% 2.2% 6.1% (2.0%) 3.3% YoY Change in Housing Prices (1.6%)* (2.4%) 1.4% (9.6%) 0.9% (13.9%) (7.2%) Avg Effective Fed Funds 0.2% 0.2% 1.4% 0.2% 0.9% 0.1% 0.3% Avg Capacity Utilization 75.5% 74.8% 78.1% 72.0% 76.4% 67.2% 68.9% Avg Consumer Confidence 52.2 62.9 83.4 68.2 72.2 51.6 44.9 Avg YoY Equity Price Index Growth 12.8% 11.2% 5.8% 13.5% 16.1% (9.5%) 1.9% Note: These internally-specified scenarios are from Moody’s Economy.com and do not reflect the supervisory- specified stress scenarios provided to 19 U.S. banks in November 34 © Fifth Third Bank | All Rights Reserved |

Significantly improved credit metrics Reserves / NPLs Source: SNL Financial and company reports. Data as of 3Q10. NPLs and NPAs exclude loans held-for-sale. * Includes and excludes net charge-offs related to loans sold or moved to held-for-sale during 3Q10 for FITB ($510mm), RF ($233mm), and BBT ($432mm) Texas Ratio (HFI NPAs + Over 90s) / (Reserves + TCE) Well positioned from credit and coverage standpoint Net charge-off ratio* (Annualized) HFI NPA ratio Peer average: 3.8% Peer average: 107% Peer average: 30% Peer average: 2.3% Lighter portion includes charge-offs on loans sold or moved to held- for-sale in 3Q10 35 © Fifth Third Bank | All Rights Reserved |

36 © Fifth Third Bank | All Rights Reserved Aggressive portfolio actions in 3Q10 Furthered problem asset resolution and reduced future losses • Residential mortgage loan sale – $228 million of balances sold – $205 million of balances were nonaccrual – $123 million of NCOs realized • Commercial HFS transfer – $961 million of balances transferred – $694 million of balances were nonaccrual – $387 million of NCOs realized – $267 million of performing loans ($217 million of NPLs transferred into held-for-sale) • Reserve reduction – Approximately $337 million related to sale or transfer of loans to held-for- sale Residential mortgages sold Balances NCO Florida $141 $72 Ohio 25 15 Illinois 15 9 Michigan 15 8 Indiana 10 6 Other 23 13 Total $228 $123 Commercial HFS transfers - O/S Florida Michigan Other Total Commercial mortgage $174 $45 $267 $486 Commercial construction 32 12 123 167 C&I 51 38 219 308 Total $257 $95 $609 $961 Commercial HFS transfers - nonaccruals Florida Michigan Other Total Commercial mortgage $106 $38 $183 $327 Commercial construction 32 11 86 129 C&I 49 35 154 238 Total $187 $84 $423 $694 Commercial HFS transfers - NCO (marks) Florida Michigan Other Total Commercial mortgage $75 $20 $107 $202 Commercial construction 20 6 51 77 C&I 26 10 72 108 Total $121 $36 $230 $387 Net charge-off composition Credit Actions Remaining Portfolio Total Consumer $123 $206 $329 Commercial 387 240 627 Total $510 $446 $956 Fifth Third’s past portfolio management activity has accelerated loss recognition and reduced potential future losses |

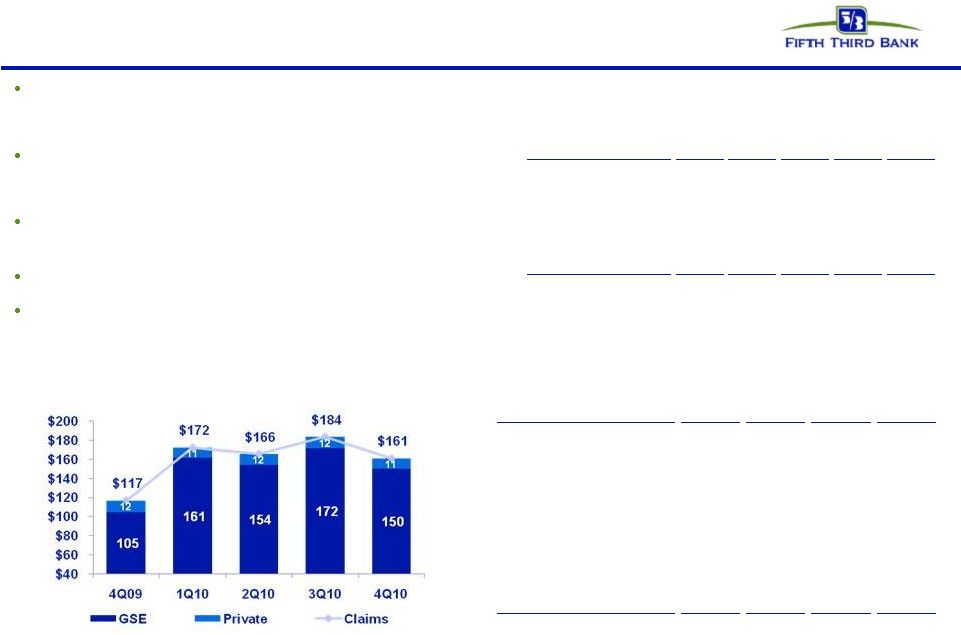

37 © Fifth Third Bank | All Rights Reserved Mortgage repurchase overview Demand requests and repurchase losses remain volatile and near-term repurchase losses are expected to remain elevated — Number of outstanding demand requests (units) down 9% from Q3 2010, outstanding demand requests ($) down13% Virtually all sold loans and new claims relate to GSEs or GNMA — 98% of outstanding balance of loans sold — 92% of outstanding claims Majority of new claims and repurchase losses relate to 2006 through 2008 vintages — 75% of new claims for 2010 YTD Majority of outstanding balances of the serviced for others portfolio relates to origination activity in 2009 and later Claims and exposure related to whole loan sales (no outstanding first mortgage securitizations) Repurchase Reserves* ($ in millions) Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Beginning balance $48 $58 $84 $85 $103 Net reserve additions 25 39 19 47 21 Repurchase losses (15) (13) (18) (29) (23) Ending balance $58 $84 $85 $103 $101 Outstanding Counterparty Claims ($ in millions) Outstanding Balance of Sold Loans ($ in millions) GSE GNMA Private Total 2005 and prior $8,497 $333 $705 $9,535 2006 2,194 71 333 2,598 2007 3,591 105 285 3,981 2008 3,746 847 - 4,593 2009 and later 25,355 7,173 - 32,527 Total $43,382 $8,529 $1,323 $53,234 * Includes reps and warranty reserve ($85mm) and reserve for loans sold with recourse ($16mm). |

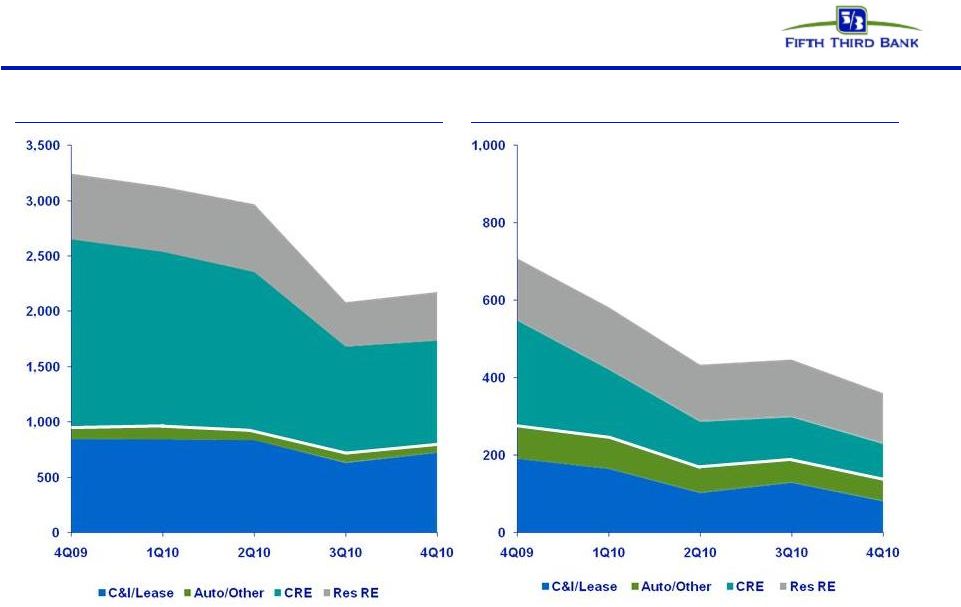

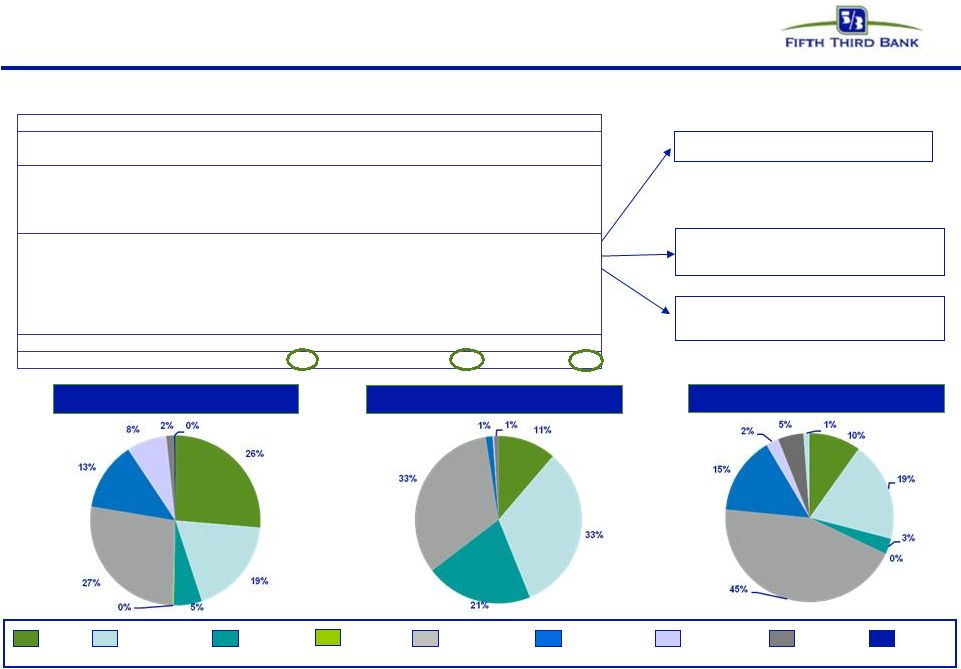

38 © Fifth Third Bank | All Rights Reserved Non-performing assets and net charge-offs: Product view* Total NPAs Total NCOs *NPAs exclude loans held-for-sale. 3Q10 NCOs exclude $510mm loans sold of moved to held-for-sale in 3Q10 |

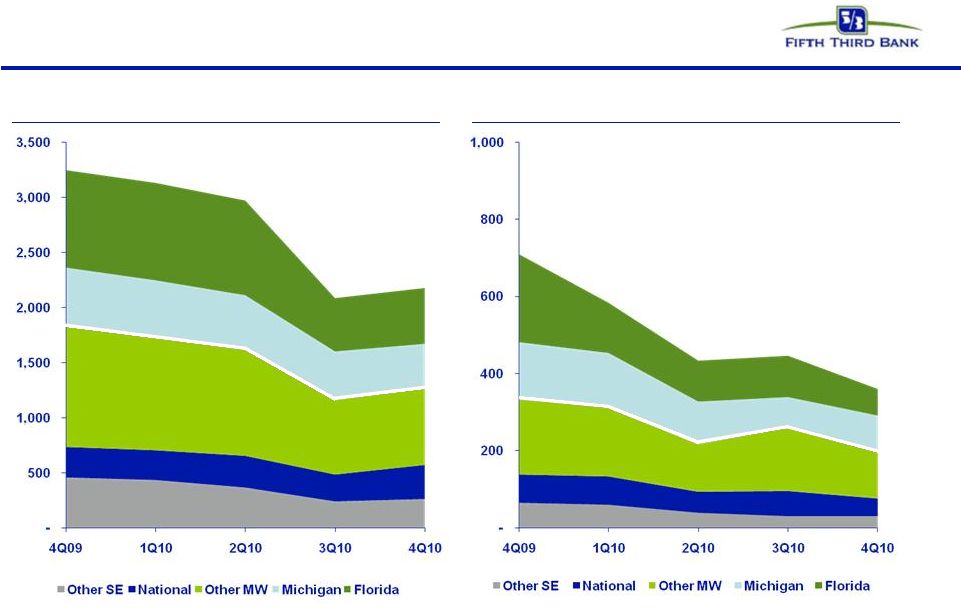

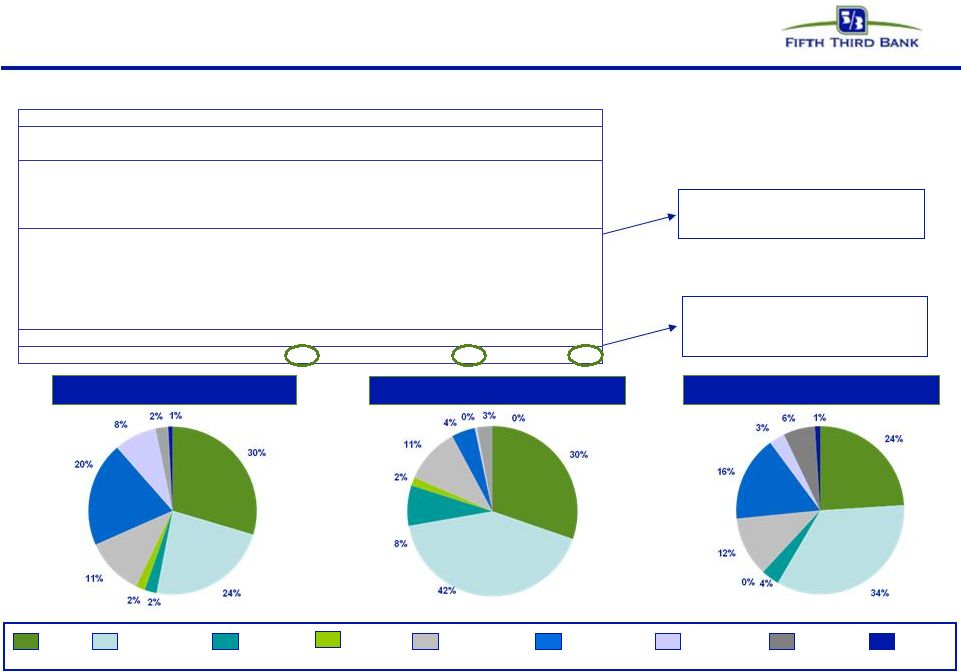

39 © Fifth Third Bank | All Rights Reserved Total NPAs Total NCOs Non-performing assets and net charge-offs: Geographic view* *NPAs exclude loans held-for-sale. 3Q10 NCOs exclude $510mm loans sold of moved to held-for-sale in 3Q10 39 |

40 © Fifth Third Bank | All Rights Reserved Source: SNL Financial and company filings Note: Ratios exclude outstanding TARP CRE / Total RBC Reduced exposure to high-risk loan categories C&D Loans / Total RBC Non-owner Occupied CRE / Total RBC 3Q10 PNC 18.0% Wells Fargo 21.9% KeyCorp 23.4% SunTrust 32.4% Fifth Third 34.3% U.S. Bancorp 34.5% Huntington 35.5% Comerica 38.4% Regions 49.1% M&T 56.1% BB&T 67.1% Zions 82.2% M&I 91.3% Peer median 36.9% Peer average 45.8% 3Q10 Wells Fargo 64.4% Fifth Third 71.4% PNC 74.9% SunTrust 77.2% Comerica 87.4% KeyCorp 93.6% U.S. Bancorp 109.2% BB&T 131.7% Huntington 138.8% Regions 162.1% M&T 219.8% Zions 224.2% M&I 271.7% Peer median 120.4% Peer average 137.9% 3Q10 SunTrust 27.3% Fifth Third 28.4% Wells Fargo 29.9% Comerica 31.3% PNC 38.6% KeyCorp 40.3% U.S. Bancorp 51.2% BB&T 51.4% Regions 67.9% Huntington 78.4% M&T 115.8% Zions 118.8% M&I 119.0% Peer median 51.3% Peer average 64.1% Fifth Third has relatively low CRE exposure that has been significantly reduced over past 3+ years FITB Peer median 3Q10 ratios; all ratios exclude TARP capital for all BHCs |

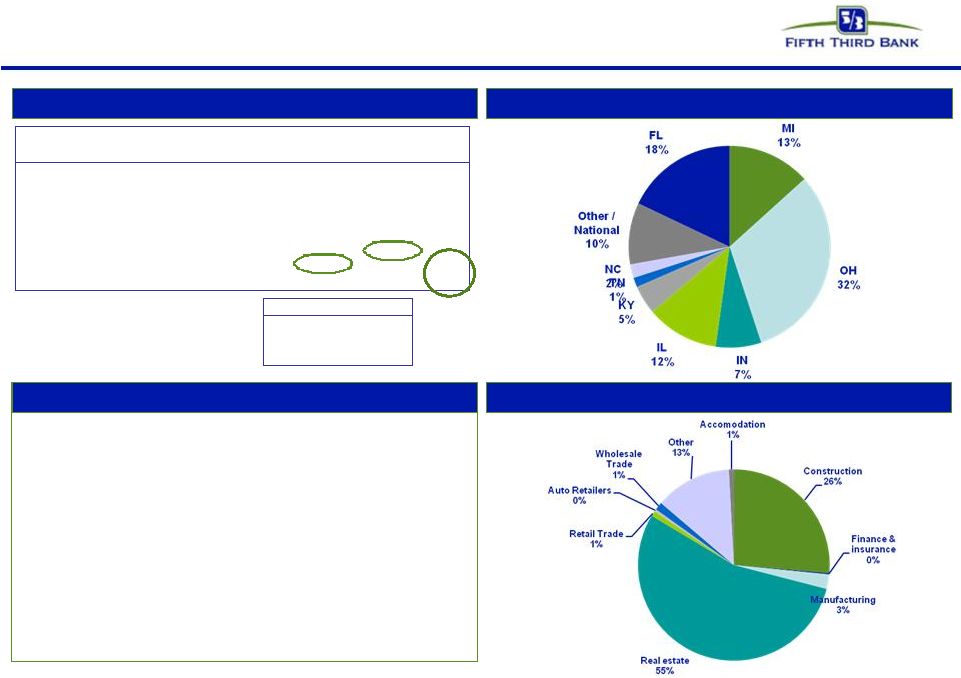

Commercial & industrial* Loans by geography Credit trends Loans by industry Comments • Commercial & industrial loans represented 35% of total loans and 24% of net charge-offs • 24% of 4Q10 losses on loans to companies in real estate related industries – Loans to real estate related industries of $2.9B (10%); 3Q10 NCO ratio of 2.8% • FL represented 8% of 4Q10 losses, 6% of loans; MI represented 27% of losses, 13% of loans * NPAs exclude loans held-for-sale. 3Q10 includes losses on loans transferred to held-for-sale ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $25,683 $26,131 $26,008 $26,302 $27,191 90+ days delinquent $118 $63 $49 $28 $16 as % of loans 0.46% 0.24% 0.19% 0.11% 0.06% NPAs $781 $788 $792 $594 $696 as % of loans 3.04% 3.02% 3.05% 2.26% 2.56% Net charge-offs $183 $161 $104 $237 $85 as % of loans 2.81% 2.49% 1.58% 3.57% 1.27% C&I Non-core: $108 Core: $129 Core NCO Rate: 1.94% 3Q10 NCO Breakout 41 © Fifth Third Bank | All Rights Reserved |

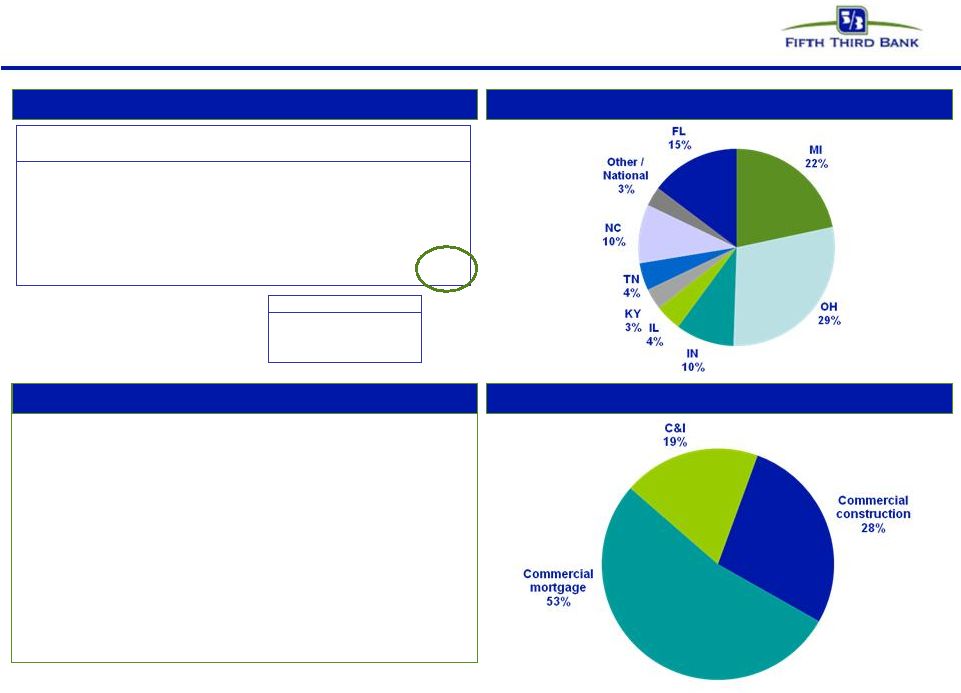

Commercial mortgage* Loans by geography Credit trends Loans by industry Comments * NPAs exclude loans held-for-sale. 3Q10 includes losses on loans transferred to held-for-sale • Commercial mortgage loans represented 14% of total loans and 22% of net charge-offs • Owner occupied 4Q10 NCO ratio of 1.3%, other non-owner occupied 4Q10 NCO ratio of 4.3% • Loans from FL/MI represented 38% of portfolio loans, 58% of portfolio losses in 4Q10 ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $11,803 $11,744 $11,481 $10,985 $10,845 90+ days delinquent $59 $44 $53 $29 $11 as % of loans 0.50% 0.38% 0.46% 0.26% 0.10% NPAs $985 $1,002 $956 $679 $679 as % of loans 8.34% 8.53% 8.33% 6.19% 6.26% Net charge-offs $142 $99 $78 $268 $79 as % of loans 4.69% 3.42% 2.68% 9.34% 2.86% Commercial mortgage Non-core: $202 Core: $66 Core NCO Rate: 2.30% 3Q10 NCO Breakout 42 © Fifth Third Bank | All Rights Reserved |

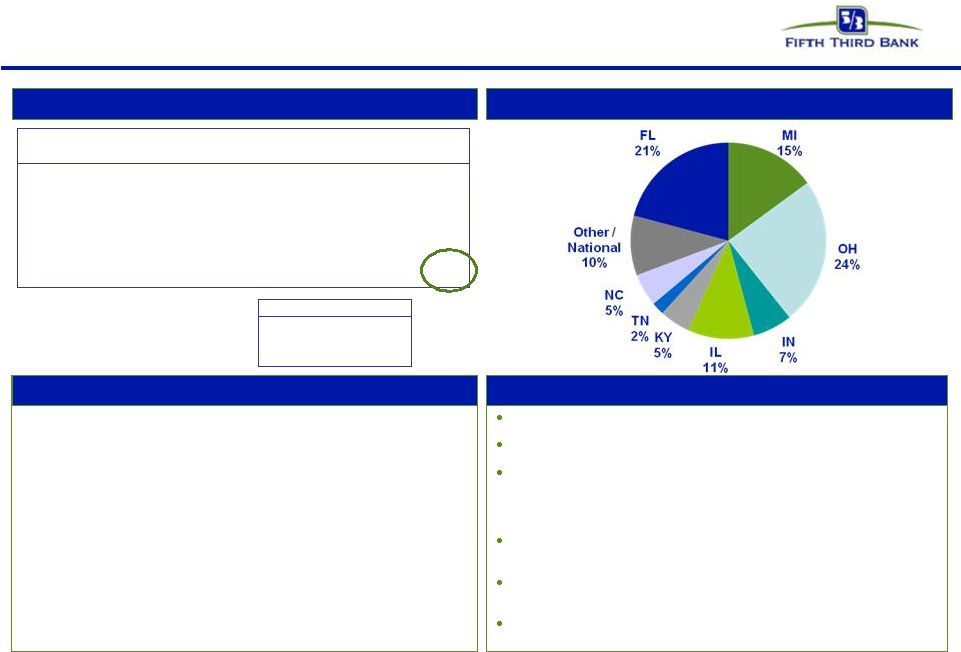

Commercial construction* Loans by geography Credit trends Loans by industry Comments * NPAs exclude loans held-for-sale. 3Q10 includes losses on loans transferred to held-for-sale • Commercial construction loans represented 3% of total loans and 3% of net charge-offs • Loans from FL/MI represented 31% of portfolio loans, 52% of portfolio losses in 4Q10 ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $3,784 $3,277 $2,965 $2,349 $2,048 90+ days delinquent $16 $9 $37 $5 $3 as % of loans 0.44% 0.28% 1.24% 0.21% 0.13% NPAs $707 $569 $482 $291 $259 as % of loans 18.68% 17.36% 16.26% 12.40% 12.65% Net charge-offs $135 $78 $43 $121 $10 as % of loans 13.28% 8.57% 5.46% 16.58% 1.88% Commercial construction Non-core: $77 Core: $44 Core NCO Rate: 5.99% 3Q10 NCO Breakout 43 © Fifth Third Bank | All Rights Reserved |

Homebuilders/developers* Loans by geography Credit trends Loans by industry Comments • Originations of builder/developer loans suspended in 2007 • Remaining portfolio balance of $699mm, down 79% from peak of $3.3B in 2Q08; represents approximately 1% of total loans and 2% of commercial loans • $19mm of NCOs (53% commercial mortgage, 36% commercial construction, 11% C&I) • $259mm of NPAs (62% commercial mortgage, 33% commercial construction, 4% C&I), down $20mm sequentially * NPAs exclude loans held-for-sale. 3Q10 includes losses on loans transferred to held-for-sale Non-core: $95 Core: $32 Core NCO Rate: 12.25% 3Q10 NCO Breakout ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $1,563 $1,324 $1,207 $824 $699 90+ days delinquent $19 $6 $12 $3 $1 as % of loans 1.19% 0.43% 1.03% 0.37% 0.12% NPAs $548 $520 $431 $280 $259 as % of loans 35.09% 39.28% 35.68% 33.97% 37.12% Net charge-offs $110 $81 $48 $127 $19 as % of loans 26.25% 22.89% 15.01% 48.74% 10.08% Homebuilders/developers 44 © Fifth Third Bank | All Rights Reserved |

45 © Fifth Third Bank | All Rights Reserved Residential mortgage 1 liens: 100%; weighted average LTV: 76% Weighted average origination FICO: 739 Origination FICO distribution: <660 9%; 660-689 7%; 690-719 11%; 720-749 14%; 750+ 42%; Other ^ 17% (note: loans <660 includes CRA loans and FHA/VA loans) Origination LTV distribution: <=70 32%; 70.1-80 40%; 80.1-90 9%; 90.1-95 5%; >95 14% Vintage distribution: 2010 28%; 2009 6%; 2008 9%; 2007 11%; 2006 11%; 2005 17%; 2004 and prior 18% % through broker: 14%; performance similar to direct Loans by geography Credit trends Portfolio details Comments ^ Includes acquired loans where FICO at origination is not available 3Q10 includes losses on loans sold During 1Q09 the Bancorp modified its nonaccrual policy to exclude TDR loans less than 90 days past due because they were performing in accordance with restructured terms. For comparability purposes, prior periods were adjusted to reflect this reclassification. • Residential mortgage loans represented 12% of total loans and 18% of net charge-offs • FL portfolio 21% of residential mortgage loans driving 49% of portfolio losses • FL lots ($196mm) running at 27% annualized loss rate (YTD) Non-core: $123 Core: $81 Core NCO Rate: 4.10% 3Q10 NCO Breakout ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $8,035 $7,918 $7,707 $7,975 $8,956 90+ days delinquent $189 $157 $107 $111 $100 as % of loans 2.35% 1.98% 1.38% 1.39% 1.12% NPAs $523 $521 $549 $328 $368 as % of loans 6.51% 6.57% 7.12% 4.11% 4.11% Net charge-offs $78 $88 $85 $204 $62 as % of loans 3.82% 4.46% 4.35% 10.37% 2.93% Residential mortgage st |

46 © Fifth Third Bank | All Rights Reserved Home equity 1st liens: 30%; 2 liens: 70% Weighted average origination FICO: 749 Origination FICO distribution^: <660 4%; 660-689 7%; 690-719 13%; 720-749 17%; 750+ 50%; Other 9% Average CLTV: 75% Origination CLTV distribution: <=70 38%; 70.1-80 22%; 80.1-90 18%; 90.1-95 7%; >95 14% Vintage distribution: 2010 4%; 2009 5%; 2008 11%; 2007 12%; 2006 15%; 2005 14%; 2004 and prior 40% % through broker channels: 15% WA FICO: 734 brokered, 751 direct; WA CLTV: 88% brokered; 72% direct Portfolio details Comments Brokered loans by geography Direct loans by geography Credit trends Home equity loans represented 15% of total loans and 18% of net charge-offs Approximately 15% of portfolio in broker product driving 38% total loss Approximately one third of Fifth Third 2 liens are behind Fifth Third 1 liens 2005/2006 vintages represent approximately 30% of portfolio; account for 52% of losses Aggressive home equity line management strategies in place Note: Brokered and direct home equity net charge-off ratios are calculated based on end of period loan balances ^ Includes acquired loans where FICO at origination is not available ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $1,948 $1,906 $1,838 $1,770 $1,698 90+ days delinquent $33 $29 $29 $26 $25 as % of loans 1.72% 1.53% 1.57% 1.46% 1.46% Net charge-offs $34 $30 $24 $26 $25 as % of loans 7.02% 6.45% 5.29% 5.87% 5.74% Home equity - brokered ($ in millions) 4Q09 1Q10 2Q10 3Q10 4Q10 Balance $10,226 $10,280 $10,149 $10,004 $9,815 90+ days delinquent $65 $60 $61 $61 $59 as % of loans 0.64% 0.58% 0.60% 0.61% 0.60% Net charge-offs $48 $43 $37 $40 $40 as % of loans 1.85% 1.68% 1.45% 1.57% 1.61% Home equity - direct nd nd st |

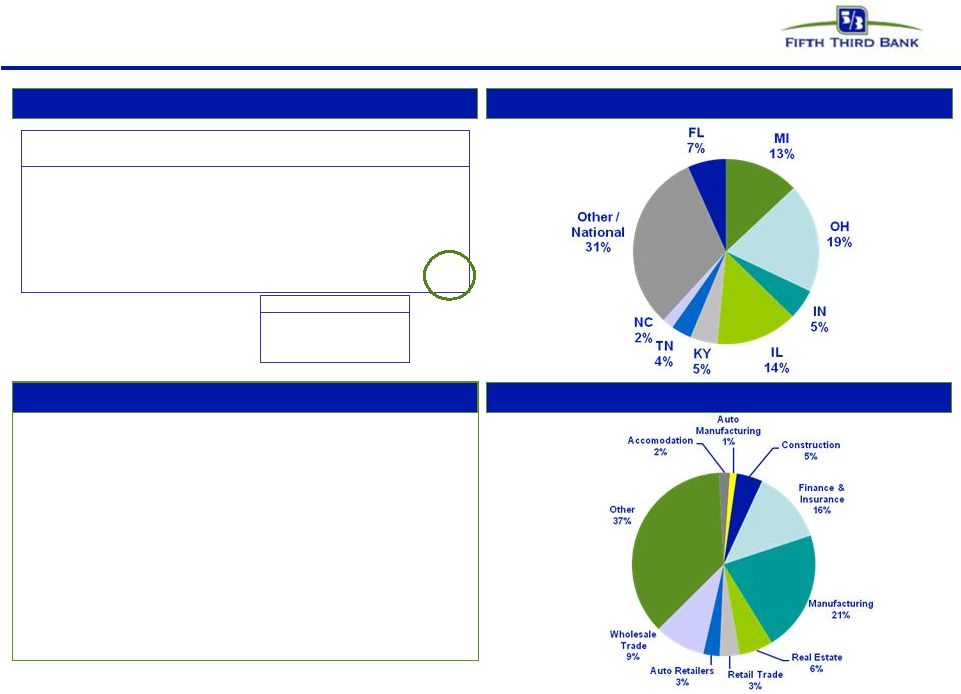

47 © Fifth Third Bank | All Rights Reserved Florida market* Deterioration in real estate values having effect on credit trends as evidenced by increased NPA/NCOs in real estate related products COML MORTGAGE C&I RESI MORTGAGE OTHER CONS COML CONST COML LEASE HOME EQUITY AUTO CREDIT CARD Total Loans NPAs NCOs *NPAs exclude loans held-for-sale. Loans ($B) % of FITB NPAs ($M) % of FITB NCOs ($M) % of FITB Commercial loans 1.8 7% 57 8% 7 8% Commercial mortgage 1.3 12% 166 24% 13 17% Commercial construction 0.4 18% 105 40% 2 20% Commercial lease 0.0 1% 0 0% 0 0% Commercial 3.5 8% 328 20% 22 13% Mortgage 1.9 21% 167 45% 31 49% Home equity 0.9 8% 7 9% 10 16% Auto 0.5 5% 1 8% 2 9% Credit card 0.1 5% 4 8% 3 10% Other consumer 0.0 2% 0 37% 1 11% Consumer 3.4 10% 180 35% 47 25% Total 6.9 9% 507 23% 69 19% Florida Weak commercial real estate market Losses due to significant declines in valuations Valuations; relatively small home equity portfolio |

48 © Fifth Third Bank | All Rights Reserved Michigan market* Deterioration in home price values coupled with weak economy impacting credit trends due to frequency of defaults and severity COML MORTGAGE C&I RESI MORTGAGE OTHER CONS COML CONST COML LEASE HOME EQUITY AUTO CREDIT CARD Total Loans NPAs NCOs *NPAs exclude loans held-for-sale. Loans ($B) % of FITB NPAs ($M) % of FITB NCOs ($M) % of FITB Commercial loans 3.5 13% 122 18% 23 27% Commercial mortgage 2.8 26% 169 25% 33 41% Commercial construction 0.3 13% 31 12% 3 32% Commercial lease 0.2 6% 6 23% 0 0% Commercial 6.8 16% 329 20% 59 34% Mortgage 1.3 15% 43 12% 11 18% Home equity 2.4 21% 18 25% 16 24% Auto 1.0 9% 2 11% 3 15% Credit card 0.3 15% 12 21% 6 17% Other consumer 0.1 14% 0 0% 1 13% Consumer 5.1 15% 75 15% 36 19% Total 11.9 15% 404 19% 95 27% Michigan Negative impact from housing valuations, economy, unemployment Economic weakness impacts commercial real estate market |

49 © Fifth Third Bank | All Rights Reserved Regulation G Non-GAAP reconciliation Fifth Third believes that pre-tax pre-provision earnings is useful as a tool to help evaluate availability to provide for credit costs through operations. Fifth Third believes that information adjusted for the impact of certain items may be useful due to the extent to which the items are not indicative of our ongoing operations. Fifth Third Bancorp and Subsidiaries Regulation G Non-GAAP Reconciliation $ in millions (unaudited) December September June March December September June March December 2010 2010 2010 2010 2009 2009 2009 2009 2008 Net interest income 914 912 882 897 878 869 831 776 892 Noninterest income 656 827 620 627 651 851 2,583 697 642 Noninterest expense 987 979 935 956 967 876 1,021 962 2,022 Pre-tax, pre-provision net revenue 583 760 567 568 562 844 2,393 511 (488) Goodwill impairment charge (965) Gain on sale of processing stake (6) 1,764 Gain on sale of Visa class B shares 187 Gain on BOLI settlement 127 Adjusted PPNR 583 633 567 568 562 663 629 511 477 Annualized Adjusted PPNR (a) 2,332 2,532 2,268 2,272 2,248 2,652 2,516 2,044 1,908 Tangible Assets (b) 108,528 109,833 109,525 110,140 110,857 108,204 113,434 116,536 116,972 Risk Weighted Assets (c) 100,204 98,904 Net charge-offs 356 956 434 582 708 756 626 521 1,652 Portfolio action net charge-offs - 510 - - - - - - 800 Adjust net charge-offs 356 446 434 582 708 756 626 521 852 Annualized net charge-offs (d) 1,424 3,824 1,736 2,328 2,832 3,024 2,504 2,084 6,608 Annualized adjusted NCO (e) 1,424 1,784 1,736 2,328 2,832 3,024 2,504 2,084 3,408 HFI Nonperforming Asssets (f) 2,174 2,082 Ratios: PPNR / Tangible Assets (a) / (b) 2.1% 2.3% 2.1% 2.1% 2.0% 2.5% 2.2% 1.8% 1.6% PPNR / RWA (a) / (c) 2.3% 2.6% PPNR / NCO (a) / (d) 164% 66% 131% 98% 79% PPNR / Adjusted NCO (a) / (e) 164% 142% 131% 98% 79% PPNR / HFI NPA (a) / (f) 107% 122% For the Three Months Ended |

50 © Fifth Third Bank | All Rights Reserved Regulation G Non-GAAP reconciliation Fifth Third Bancorp and Subsidiaries Regulation G Non-GAAP Reconcilation $ and shares in millions Pro forma Pro forma (unaudited) Common Share Issuance, TARP Common Share Issuance December December December September June March December 2010 2010 2010 2010 2010 2010 2009 Total Bancorp shareholders' equity (U.S. GAAP) 12,292 15,700 14,051 13,884 13,701 13,408 13,497 Less: Preferred stock (398) (3,654) (3,654) (3,642) (3,631) (3,620) (3,609) Goodwill (2,417) (2,417) (2,417) (2,417) (2,417) (2,417) (2,417) Intangible assets (62) (62) (62) (72) (83) (94) (106) Tangible common equity, including unrealized gains / losses (a) 9,415 9,567 7,918 7,753 7,570 7,277 7,365 Less: Accumulated other comprehensive income / loss (314) (314) (314) (432) (440) (288) (241) Tangible common equity, excluding unrealized gains / losses (b) 9,101 9,253 7,604 7,321 7,130 6,989 7,124 Add back: Preferred stock 398 3,654 3,654 3,642 3,631 3,620 3,609 Tangible equity (c) 9,499 12,907 11,258 10,963 10,761 10,609 10,733 Total assets (U.S. GAAP) 111,007 111,007 111,007 112,322 112,025 112,651 113,380 Less: Goodwill (2,417) (2,417) (2,417) (2,417) (2,417) (2,417) (2,417) Intangible assets (62) (62) (62) (72) (83) (94) (106) Tangible assets, including unrealized gains / losses (d) 108,528 108,528 108,528 109,833 109,525 110,140 110,857 Less: Accumulated other comprehensive income / loss, before tax (483) (483) (483) (665) (677) (443) (370) Tangible assets, excluding unrealized gains / losses (e) 108,045 108,045 108,045 109,168 108,848 109,697 110,487 Total Bancorp shareholders' equity (U.S. GAAP) 12,292 15,700 14,051 13,884 13,701 13,408 13,497 Goodwill and certain other intangibles (2,546) (2,546) (2,546) (2,525) (2,537) (2,556) (2,565) Unrealized gains (314) (314) (314) (432) (440) (288) (241) Qualifying trust preferred securities 2,763 2,763 2,763 2,763 2,763 2,763 2,763 Other 11 11 11 8 (25) (30) (26) Tier I capital 12,206 15,614 13,965 13,698 13,462 13,297 13,428 Less: Preferred stock (398) (3,654) (3,654) (3,642) (3,631) (3,620) (3,609) Qualifying trust preferred securities (2,763) (2,763) (2,763) (2,763) (2,763) (2,763) (2,763) Qualifying noncontrolling interest in consolidated subsidiaries (30) (30) (30) (30) - - - Tier I common equity (f) 9,015 9,167 7,518 7,263 7,068 6,914 7,056 Common shares outstanding (g) 796 796 796 796 796 795 795 Risk-weighted assets, determined in accordance with prescribed regulatory requirements (h) 100,193 100,193 100,193 98,904 98,604 99,281 100,933 Ratios: Tangible equity (c) / (e) 8.79% 11.95% 10.42% 10.04% 9.89% 9.67% 9.71% Tangible common equity (excluding unrealized gains/losses) (b) / (e) 8.42% 8.56% 7.04% 6.70% 6.55% 6.37% 6.45% Tangible common equity (including unrealized gains/losses) (a) / (d) 8.68% 8.82% 7.30% 7.06% 6.91% 6.61% 6.64% Tangible common equity as a percent of risk-weighted assets (excluding unrealized gains/losses) (b) / (h) 9.08% 9.24% 7.59% 7.40% 7.23% 7.04% 7.06% Tangible book value per share (a) / (g) 11.83 12.02 9.94 9.74 9.51 9.16 9.26 Tier I common equity (f) / (h) 9.00% 9.14% 7.50% 7.34% 7.17% 6.96% 6.99% For the Three Months Ended |

51 © Fifth Third Bank | All Rights Reserved Regulation G Non-GAAP reconciliation Common offering and TARP repay 4Q10 Common share offering only 4Q10 Tier 1 Capital ratio Tier 1 Capital ratio Tier 1 capital 13,964,857 $ Tier 1 capital 13,964,857 $ TARP repay (3,408,000) $ Equity raise 1,648,830 $ Equity raise 1,648,830 $ 12,205,687 $ 15,613,687 $ RWA 100,193,435 $ RWA 100,193,435 $ Asset increase - $ Asset increase - $ 100,193,435 $ 100,193,435 $ Tier 1 13.9% Tier 1 13.9% Tier 1 pro forma 12.2% Tier 1 pro forma 15.6% Total RBC ratio Total RBC ratio Total RBC 18,173,452 $ Total rbc 18,173,452 $ TARP repay (3,408,000) $ Equity raise 1,648,830 $ Equity raise 1,648,830 $ 16,414,282 $ 19,822,282 $ RWA 100,193,435 $ RWA 100,193,435 $ Asset increase - $ Asset increase - $ 100,193,435 $ 100,193,435 $ Total RBC 18.1% Total RBC 18.1% Total RBC pro forma 16.4% Total RBC 19.8% pro forma Tier 1 leverage Tier 1 leverage Tier 1 capital 13,964,857 $ Tier 1 capital 13,964,857 $ TARP repay (3,408,000) $ Equity raise 1,648,830 $ Equity raise 1,648,830 $ 12,205,687 $ 15,613,687 $ Quarterly Avg Assets 109,207,711 $ Quarterly Avg Assets 109,207,711 $ Asset increase - $ Asset increase - $ 109,207,711 $ 109,207,711 $ Tier 1 lev 12.8% Tier 1 lev 12.8% Tier 1 lev pro forma 11.2% Tier 1 lev pro forma 14.3% |

52 © Fifth Third Bank | All Rights Reserved Regulation G Non-GAAP reconciliation The Bancorp considers various measures when evaluating capital utilization and adequacy, including the tangible equity ratio, tangible common equity ratio and tier I common equity ratio, in addition to capital ratios defined by banking regulators. These calculations are intended to complement the capital ratios defined by banking regulators for both absolute and comparative purposes. Because U.S. GAAP does not include capital ratio measures, the Bancorp believes there are no comparable U.S. GAAP financial measures to these ratios. Tier I common equity is not formally defined by U.S. GAAP or codified in the federal banking regulations and, therefore, is considered to be a non-GAAP financial measure. Since analysts and banking regulators may assess the Bancorp’s capital adequacy using these ratios, the Bancorp believes they are useful to provide investors the ability to assess its capital adequacy on this same basis. The Bancorp believes these non-GAAP measures are important because they reflect the level of capital available to withstand unexpected market conditions. Additionally, presentation of these measures allows readers to compare certain aspects of the Bancorp’s capitalization to other organizations. However, because there are no standardized definitions for these ratios, the Bancorp’s calculations may not be comparable with other organizations, and the usefulness of these measures to investors may be limited. As a result, the Bancorp encourages readers to consider its Condensed Consolidated Financial Statements in their entirety and not to rely on any single financial measure. Phase out of TRUPs (Equity raise) 4Q10 Tier 1 Capital ratio Tier 1 capital 13,964,857 $ TARP repay TRUPs (2,762,782) Equity raise 1,648,830 $ 12,850,905 $ RWA 100,193,435 $ Asset increase - $ 100,193,435 $ Tier 1 13.9% Tier 1 pro forma 12.8% Phase out of TRUPs (TARP, Equity raise) 4Q10 Tier 1 Capital ratio Tier 1 capital 13,964,857 $ TARP repay (3,408,000) $ TRUPs (2,762,782) Equity raise 1,648,830 $ 9,442,905 $ RWA 100,193,435 $ Asset increase - $ 100,193,435 $ Tier 1 13.9% Tier 1 pro forma 9.4% Common share offering only 4Q10 Tangible Common Equity ratio Tangible CE 7,603,486 $ Equity raise 1,648,830 $ 9,252,316 $ Tangible Assets 108,044,298 $ Asset increase - $ 108,044,298 $ TCE 7.0% TCE pro forma 8.6% Tier 1 Common Tier 1 common 7,518,667 $ Equity raise 1,648,830 $ 9,167,497 $ RWA 100,193,435 $ Asset increase - $ 100,193,435 $ Tier 1 common 7.5% Tier 1 common 9.1% pro forma |