UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-03373 | |

SEGALL BRYANT & HAMILL TRUST

(Exact name of registrant as specified in charter)

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Maggie Bull, Secretary |

| Segall Bryant & Hamill Trust, 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (303) 623-2577 | |

| Date of fiscal year end: | December 31 | |

| | | |

| Date of reporting period: | December 31, 2022 | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| |

| |

| |

| |

| |

|

| |

| |

| Segall Bryant & Hamill Small Cap Value Fund |

| (Ticker Symbol: Retail - SBRVX; Institutional - SBHVX) |

| |

| Segall Bryant & Hamill Small Cap Growth Fund |

| (Ticker Symbol: Retail - WTSGX; Institutional - WISGX) |

| |

| Segall Bryant & Hamill Small Cap Core Fund |

| (Ticker Symbol: Retail - SBHCX; Institutional - SBASX) |

| |

| Segall Bryant & Hamill All Cap Fund |

| (Ticker Symbol: Retail - SBRAX; Institutional - SBHAX) |

| |

| Segall Bryant & Hamill Emerging Markets Fund |

| (Ticker Symbol: Retail - SBHEX; Institutional - SBEMX) |

| |

| Segall Bryant & Hamill International Small Cap Fund |

| (Ticker Symbol: Retail - SBHSX; Institutional - SBSIX) |

| |

| Segall Bryant & Hamill Fundamental International Small Cap Fund |

| (Ticker Symbol: Retail - WTIFX; Institutional - WIIFX) |

| |

| Segall Bryant & Hamill Global All Cap Fund |

| (Ticker Symbol: Retail - WTMVX; Institutional - WIMVX) |

| |

| Segall Bryant & Hamill Workplace Equality Fund |

| (Ticker Symbol: Retail - WEQRX; Institutional - WEQIX) |

| |

| Segall Bryant & Hamill Short Term Plus Fund |

| (Ticker Symbol: Retail - SBHPX; Institutional - SBAPX) |

| |

| Segall Bryant & Hamill Plus Bond Fund |

| (Ticker Symbol: Retail - WTIBX; Institutional - WIIBX) |

| |

| Segall Bryant & Hamill Quality High Yield Fund |

| (Ticker Symbol: Retail - WTLTX; Institutional - WILTX) |

| |

| Segall Bryant & Hamill Municipal Opportunities Fund |

| (Ticker Symbol: Retail - WTTAX; Institutional - WITAX) |

| |

| Segall Bryant & Hamill Colorado Tax Free Fund |

| (Ticker Symbol: Retail - WTCOX; Institutional - WICOX) |

| |

| |

| |

| SEGALL BRYANT & HAMILL |

| ANNUAL REPORT |

| DECEMBER 31, 2022 |

| SHAREHOLDER LETTER | 1 |

| FUND OVERVIEWS | |

| Segall Bryant & Hamill Small Cap Value Fund | 2 |

| Segall Bryant & Hamill Small Cap Growth Fund | 4 |

| Segall Bryant & Hamill Small Cap Core Fund | 6 |

| Segall Bryant & Hamill All Cap Fund | 8 |

| Segall Bryant & Hamill Emerging Markets Fund | 10 |

| Segall Bryant & Hamill International Small Cap Fund | 12 |

| Segall Bryant & Hamill Fundamental International Small Cap Fund | 14 |

| Segall Bryant & Hamill Global All Cap Fund | 16 |

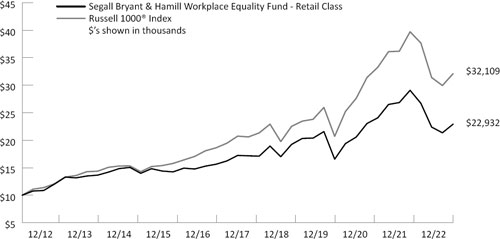

| Segall Bryant & Hamill Workplace Equality Fund | 18 |

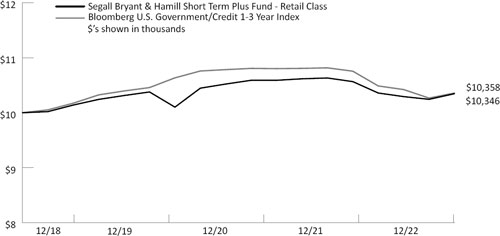

| Segall Bryant & Hamill Short Term Plus Fund | 20 |

| Segall Bryant & Hamill Plus Bond Fund | 22 |

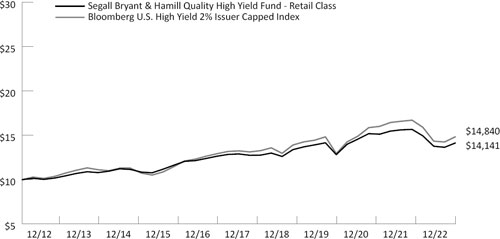

| Segall Bryant & Hamill Quality High Yield Fund | 24 |

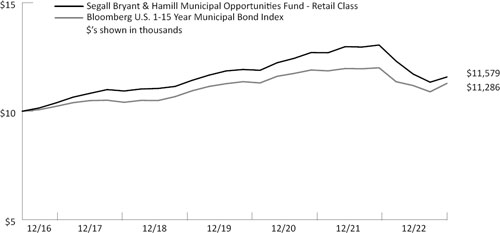

| Segall Bryant & Hamill Municipal Opportunities Fund | 26 |

| Segall Bryant & Hamill Colorado Tax Free Fund | 28 |

| FUND EXPENSES | 30 |

| IMPORTANT DISCLOSURES | 34 |

| TRUSTEES AND OFFICERS | 37 |

| FINANCIAL STATEMENTS | 40 |

| Statements of Investments | 40 |

| Statements of Assets and Liabilities | 89 |

| Statements of Operations | 93 |

| Statements of Changes in Net Assets | 97 |

| Financial Highlights | 102 |

| Notes to Financial Statements | 130 |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 147 |

| SHAREHOLDER TAX INFORMATION | 148 |

| OTHER IMPORTANT INFORMATION | 149 |

| Annual Report | December 31, 2022 | |  |

Intentionally Left Blank

| Segall Bryant & Hamill Funds | Shareholder Letter |

| | December 31, 2022 (Unaudited) |

Dear Fellow Shareholders:

What a difference a year makes. We entered 2022 coming off one of the most profitable two-year periods in the history of the U.S. financial markets. Shortly after the year began, the tides began to turn and by year end, the financial markets had posted steep losses, with many indices generating their worst performance since the financial crisis in 2008.

|  |

| | |

| Janice M. Teague | Carolyn B. Goldhaber |

| Chair | President |

The key underpinning of the economic environment of the last 12 years—the program of holding interest rates at or near zero percent—was ended by the Federal Reserve (Fed). The Fed felt compelled to end its program due to a rapid rise in inflation that most forecasters, including the Fed, thought would be “transitory.” That wasn’t the case. Various explanations—the COVID pandemic, supply chain shortages, changes in the labor force, and the war in Ukraine—were all offered as candidates for the source of the rapid rise in inflation. We believe that each of these were simply agents that accelerated or slowed the pace of inflation, thereby hastening or slowing the changes to be brought about in the economy. In our view, change will occur through a reduction of economic activity and prices of financial assets. While painful, such declines are needed before we can expect a new upswing in global economic growth that can then be reflected in the prices of financial assets.

The most frequent question asked by our longtime clients and shareholders is how much longer we believe this transition will take. The only answer, of course, is we don’t know any more than anyone else. What we do know, however, is that our investment teams continue to apply our time-tested discipline of focusing on valuation, whether in our fundamental or our quantitative strategies, to seek mispriced opportunities. Importantly, our teams strive to include, as they always have, an estimate of downside risks in their assessments of the companies they consider, with the goal of protecting shareholder capital in down markets.

Lastly, the Board of Trustees would like to extend our sincere appreciation to Phil Hildebrandt who served as the President of the SBH Funds since May 1, 2018, and we wish him all the best in his retirement. We would also like to welcome Carolyn Goldhaber as the newly elected SBH Funds’ President. Since joining the adviser close to 10 years ago, Carolyn has served on its leadership committee and is currently the President of the firm.

Thank you for your continued investment in the SBH Funds.

The views of the authors and information discussed in the shareholder letter and manager commentaries are as of February 17, 2023, are subject to change, and may not reflect the writers’ current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation.

Neither Segall Bryant & Hamill, Segall Bryant & Hamill Funds, nor any Segall Bryant & Hamill Fund accept any liability for losses either direct or consequential caused by the use of this information. Diversification cannot guarantee gain or prevent losses.

| | |

| Annual Report | December 31, 2022 | | | 1 |

| Segall Bryant & Hamill Small Cap Value Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

Mark T. Dickherber, CFA, CPA Portfolio Manager

Shaun P. Nicholson Portfolio Manager

CFA is a trademark owned by CFA Institute.

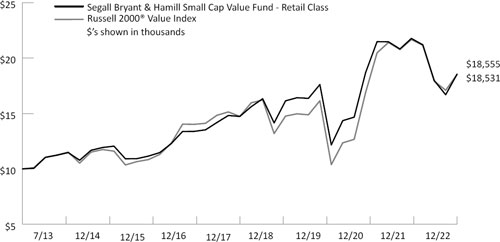

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of December each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class (SBRVX) | (14.76)% | 1.76% | 4.60% | — | 6.78% | 12/9/19 |

| Institutional Class (SBHVX) | (14.65)% | 1.87% | 4.73% | — | 6.93% | 7/31/13 |

| Russell 2000® Value Index | (14.48)% | 4.70% | 4.13% | — | 6.77% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Total - 1.04%

Institutional Class Annual Expense Ratio (per the current prospectus) – Total - 0.97%

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Industrials | 23.1% |

| | Financials | 13.7% |

| | Information Technology | 8.8% |

| | Health Care | 8.6% |

| | Materials | 8.3% |

| | Real Estate | 8.2% |

| | Consumer Discretionary | 6.9% |

| | Utilities | 6.3% |

| | Consumer Staples | 4.6% |

| | Energy | 3.8% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | | |

| | Equity Commonwealth | 4.5% |

| | Progress Software Corp. | 3.6% |

| | Regal Rexnord Corp. | 2.5% |

| | ICU Medical, Inc. | 2.5% |

| | Coty, Inc. | 2.5% |

| | Compass Minerals International, Inc. | 2.4% |

| | SPX Technologies, Inc. | 2.4% |

| | Belden, Inc. | 2.2% |

| | Orthofix Medical, Inc. | 2.1% |

| | SP Plus Corp. | 2.0% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

| | |

Performance data quoted represents past performance and does not guarantee future results. Performance information for the Retail Class shares prior to their inception is based on the performance of the Institutional Class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.14% and 0.99% to the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in larger-cap funds.

| | |

| 2 | | | www.sbhfunds.com |

| Segall Bryant & Hamill Small Cap Value Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For the year 2022, the Segall Bryant & Hamill Small Cap Value Fund returned -14.76% (Retail Class) compared to a return of -14.48% for its benchmark, the Russell 2000® Value Index.

While the easy monetary policy has abated with interest rates rising and, therefore, cost of capital higher, we believe the market has only reacted to the interest rates and not to the longer lagging effects on profit margins and funding requirements, and the impact on the economy. Throughout 2022, the market experienced significant volatility due to an array of events including an unexpected geopolitical event with the war in Ukraine, the Federal Reserve tightening cycle which began in March and continued throughout the year, and the resurgence of supply issues. There was a lot for investors to digest in a short time period and we believe 2023 will likely continue the cycle of volatility as interest rate hikes and a liquidity tightening cycle start to impact the economy more visibly. For us, investing with a Return on Invested Capital (ROIC) mindset remains at the center of our approach; investing the Fund’s capital with management teams that we believe can improve ROIC by becoming more efficient, divesting businesses not deemed core, and improving overall culture and governance matters at their respective companies.

Contributors to Return

Over the last twelve months, the three sectors in the Fund that contributed most to returns on a relative basis were Industrials, Real Estate, and Consumer Discretionary. Modine Manufacturing Co. (MOD), SPX Technologies, Inc. (SPXC), and Helmerich & Payne, Inc. (HP) generated the largest positive contribution to returns on an absolute basis. Modine, under a new CEO, has rapidly hired new talent in its management ranks as it works to execute upon an 80/20 simplification strategy. When this strategy is successfully adopted, we believe it may lead to less complexity, stronger customer relationships, and a greater focus on pricing and improvements. Although Modine is still early in this process, we have already started to see positive signs of its focus on profitability. SPX Technologies’ management has transformed its business by divesting non-core assets and redeploying those proceeds into niche, higher ROIC and higher margin businesses. In our view, the mix of the revenue is attractive with greater than 65% of the business driven by repair/replacement demand which has typically been stable in times of economic weakness. Helmerich & Payne has focused on optimizing its drilling fleet while also focusing capital allocation on debt reduction and shareholder returns. In our view, the team

at HP is focused on ROIC-additive investments and takes a long-term view when making capital decisions, which gives us optimism despite volatile energy markets making HP’s near-term returns less predictable.

Detractors from Return

The three sectors that detracted most over the last twelve months were Consumer Staples, Energy, and Materials. Hain Celestial Group, Inc. (HAIN), Glatfelter Corp. (GLT), and NCR Corp. (NCR) generated the weakest contributions to returns on an absolute basis. Hain suffered from rising energy prices in its U.K. market while also dealing with continued supply chain challenges. Though some of these headwinds are easing, the recovery could take longer than we originally expected. Glatfelter was also caught up in the energy crisis in Europe as it has significant operations in Germany which were impacted by rapidly rising energy prices. The integration of Glatfelter’s acquisition in 2021 has been a headwind to profitability. Glatfelter is now under a new CEO who is looking to quickly take out costs and raise prices to recapture profits lost due to inflation. NCR’s weakness stemmed from the company not being able to sell themselves to private equity as the debt markets were untenable to many. Management at NCR has decided to split the company into two separate businesses and remains open to being acquired if the opportunity arises.

Outlook and Positioning

We would describe 2022 as quietly chaotic with many unexpected macro circumstances. We believe that the market has only adjusted to some of the cost of capital increases. We also believe a recession is highly probable and 2023 will show us how the market will react to contracting profit margins, a factor which usually accompanies economic downturns. It is our view that the key to the market ending 2023 on a strong note will be increased liquidity. We believe there is currently more downside than upside risk in the market; however, 2023 should be full of opportunities to buy quality companies with strong management teams. We think companies with strong balance sheets and stable free cash flow will remain important. We have an ROIC philosophy and seek to find like-minded management teams focused on improving ROIC. We learned much in 2022, not simply about the market, but about resilience in the face of volatile times. This business is not for the faint of heart. Experience is the best teacher, and we believe we are stronger investors entering 2023.

Stock Performance (12/31/2021 to 12/31/2022)

| | Average | Contribution |

| 5 Highest | Weight | To Return |

| Modine Manufacturing Co. | 0.82 | 0.67 |

| SPX Technologies, Inc. | 2.38 | 0.57 |

| Helmerich & Payne, Inc. | 1.00 | 0.56 |

| Alamos Gold, Inc. | 0.75 | 0.42 |

| SP Plus Corp. | 1.73 | 0.38 |

| | Average | Contribution |

| 5 Lowest | Weight | To Return |

| Orthofix Medical, Inc. | 2.49 | -1.25 |

| FARO Technologies, Inc. | 1.32 | -1.25 |

| NCR Corp. | 2.44 | -1.37 |

| Glatfelter Corp. | 0.94 | -1.66 |

| Hain Celestial Group, Inc. | 2.81 | -2.68 |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Fund’s Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call (800) 392-2673.

Please see page 35 for a description of the methodology used to construct this table.

| | |

| Annual Report | December 31, 2022 | | | 3 |

| Segall Bryant & Hamill Small Cap Growth Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

Brian C. Fitzsimons, CFA Portfolio Manager

Mitch S. Begun, CFA Portfolio Manager

CFA is a trademark owned by CFA Institute.

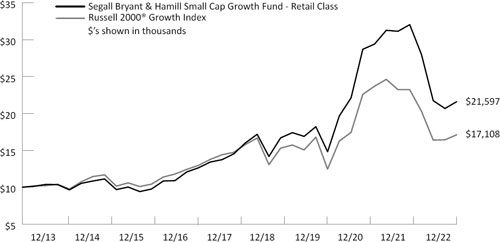

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class (WTSGX) | (32.59)% | 5.86% | 9.48% | — | 8.90% | 12/20/13 |

| Institutional Class (WISGX) | (32.48)% | 6.01% | 9.68% | — | 9.15% | 12/20/13 |

| Russell 2000® Growth Index | (26.36)% | 0.65% | 3.51% | — | 6.13% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Total: 1.03%

Institutional Class Annual Expense Ratio (per the current prospectus) — Total: 0.87%

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Information Technology | 24.9% |

| | Health Care | 23.3% |

| | Industrials | 18.5% |

| | Consumer Discretionary | 9.0% |

| | Financials | 7.6% |

| | Materials | 3.7% |

| | Real Estate | 3.1% |

| | Energy | 2.9% |

| | Consumer Staples | 1.7% |

| | Communication Services | 1.2% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | |

| | Tetra Tech, Inc. | 2.5% |

| | Novanta, Inc. | 2.2% |

| | Envestnet, Inc. | 2.2% |

| | MAXIMUS, Inc. | 2.2% |

| | Option Care Health, Inc. | 2.1% |

| | Ensign Group, Inc. (The) | 2.0% |

| | Endava PLC | 2.0% |

| | Workiva, Inc. | 2.0% |

| | Integra LifeSciences Holdings Corp. | 1.9% |

| | CONMED Corp. | 1.9% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

| | |

| | |

Performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.14% and 0.99% for the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in larger-cap funds.

| | |

| 4 | | | www.sbhfunds.com |

| Segall Bryant & Hamill Small Cap Growth Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For 2022, the Segall Bryant & Hamill Small Cap Growth Fund returned -32.59% (Retail Class) compared to the Fund’s benchmark, the Russell 2000® Growth Index’s -26.36% return. While nearly all asset classes struggled in 2022 due to rapidly rising interest rates and higher levels of inflation, growth stocks were particularly battered. The benchmark posted its worst year since the financial crisis of 2008. Additionally, for the second year in a row, growth stocks were trounced by their value counterparts, lagging the Russell 2000® Value Index by more than 11% in 2022 and 25% in 2021.

The mantra over the last decade has been growth at all costs, particularly in Silicon Valley, where technology investors were happily rewarded for higher growth that was based, in many cases, on only promises of future cash flows down the road. As interest rates have risen, the valuation of these types of growth companies has appropriately come under immense pressure. Meanwhile, investors have favored companies in cyclical sectors in this inflationary backdrop, particularly Energy, Industrials, and Materials. Historically, during economic slowdowns, these have been some of the hardest-hit sectors; however, the resilience in cash flows, especially relative to typical growth sectors, has been impressive. The Fund underperformed for the year largely due to its positioning in the aforementioned cyclical sectors.

Contributors to Return

Two sectors contributed positively to the Fund’s performance relative to its benchmark during the year, Real Estate and Information Technology. The three strongest performing stocks, which all rallied in the period, were biotechnology company Turning Point Therapeutics, Inc. (TPTX), enterprise planning software provider Anaplan, Inc. (PLAN), and provider of outsourced clinical development services Medpace Holdings, Inc. (MEDP). Turning Point Therapeutics was acquired by pharmaceutical company Bristol-Myers Squibb Co. (BMY) and Anaplan was bought by private equity firm Thoma Bravo. Despite fears around a slowing funding environment for early-stage biotechnology companies, Medpace continued to see strong demand for its services. The company expects growth to remain strong into 2023, fueled by its large and growing backlog of contracted business. Both Turning Point Therapeutics and Anaplan were sold in the period, while Medpace remained in the Fund at the end of 2022.

Detractors from Return

The three sectors that detracted most from the Fund’s performance relative to its benchmark in the period were Energy, Financials, and Industrials. The three weakest stocks, which all fell in the period, were pharmacy automation tools and services provider Omnicell, Inc. (OMCL), independent insurance agency Goosehead Insurance, Inc. (GSHD), and information technology services provider Endava PLC (DAVA). Omnicell reported an abrupt and unexpected slowdown in customer demand. The company’s customer base of large health systems is under considerable financial strain and is slowing implementation of Omnicell’s products and services. We sold the Fund’s position given the highly uncertain outlook over the next 12-18 months. Goosehead was weak as continued growth investments have created margin pressure. Additionally, investors have concerns that a slowdown in housing could reduce demand for new policies. Despite strong growth and profitability, Endava underperformed largely due to a compression in valuations for growth companies as interest rates have risen. We believe the long-term growth prospects for digital transformation services remain attractive.

Outlook and Positioning

Valuation compression in less profitable, higher growth companies is just one consequence of the current backdrop. More importantly, we have seen a sharp fundamental deterioration in many profitable bellwether companies (particularly in the Technology sector) as years of aggressive hiring have now created margin headwinds as growth rapidly slows. As it turns out, companies fueled by near-zero interest rates with little consequence for a focus on returns on invested capital are now pivoting. The ramifications, we believe, will be long-lasting and affect all sectors of the economy. We are focused, as always, on building a portfolio of companies that can demonstrate fundamentally stable growth and cash flow characteristics over the long term.

As of the end of 2022, the Fund was overweight primarily in the Information Technology and Financials sectors and underweight primarily in the Energy and Consumer Staples sectors.

Thank you for your continued interest and support.

Stock Performance (12/31/2021 to 12/31/2022)

| | Average | Contribution |

| 5 Highest | Weight | To Return |

| Turning Point Therapeutics, Inc. | 0.40 | 0.67 |

| Anaplan, Inc. | 0.63 | 0.52 |

| Medpace Holdings, Inc. | 1.29 | 0.50 |

| Silk Road Medical, Inc. | 1.25 | 0.42 |

| Inspire Medical Systems, Inc. | 1.81 | 0.29 |

| | Average | Contribution |

| 5 Lowest | Weight | To Return |

| AZEK Co., Inc. | 1.61 | -1.23 |

| Rapid7 Inc. | 0.79 | -1.32 |

| Endava PLC | 2.14 | -1.42 |

| Goosehead Insurance, Inc. | 1.29 | -1.52 |

| Omnicell, Inc. | 1.62 | -1.86 |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Fund’s Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call (800) 392-2673.

Please see page 35 for a description of the methodology used to construct this table.

| | |

| Annual Report | December 31, 2022 | | | 5 |

| Segall Bryant & Hamill Small Cap Core Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

Jeffrey C. Paulis, CFA, Portfolio Manager

Mark T. Dickherber, CFA, CPA Portfolio Manager

CFA is a trademark owned by CFA Institute.

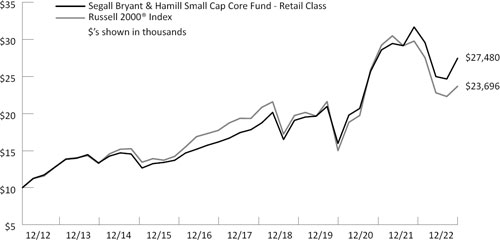

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns*

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class (SBHCX) | (13.26)% | 9.44% | 9.53% | 10.64% | 8.77% | 12/31/19 |

| Institutional Class (SBASX) | (13.12)% | 9.62% | 9.71% | 10.81% | 8.94% | 12/15/03 |

| Russell 2000® Index | (20.44)% | 3.10% | 4.13% | 9.01% | 7.66% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.35%, Net: 1.14%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.10%, Net: 0.99%

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Industrials | 23.2% |

| | Information Technology | 16.8% |

| | Consumer Discretionary | 12.4% |

| | Health Care | 11.2% |

| | Materials | 8.7% |

| | Financials | 8.2% |

| | Consumer Staples | 5.7% |

| | Energy | 3.7% |

| | Real Estate | 1.7% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | |

| | KBR, Inc. | 2.3% |

| | Graphic Packaging Holding Co. | 2.1% |

| | EnPro Industries, Inc. | 2.0% |

| | Carlisle Cos., Inc. | 2.0% |

| | WNS Holdings, Ltd. | 1.9% |

| | Pure Storage, Inc. | 1.8% |

| | EMCOR Group, Inc. | 1.7% |

| | Insulet Corp. | 1.7% |

| | Agilysys, Inc. | 1.7% |

| | Casella Water Systems, Inc. | 1.7% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| * | The quoted performance of the Fund reflects the past performance of Lower Wacker Small Cap Investment Fund, LLC (the “Partnership”), an unregistered limited partnership managed by the portfolio managers of the Fund. The Partnership was organized into the Institutional Class shares on December 31, 2019, the date the Fund commenced operations. The Fund has been managed in the same style since the Partnership’s inception on December 15, 2003. The Fund’s annual returns and long-term performance reflect the actual fees and expenses that were charged when the Fund was a limited partnership. From its inception on December 15, 2003 through December 31, 2019, the Partnership was not subject to certain investment restrictions, diversification requirements and other restrictions of the Investment Company Act of 1940, as amended or Subchapter M of the Internal Revenue Code of 1986, as amended, which, if they had been applicable, might have adversely affected the Fund’s performance. |

Performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.14% and 0.99% to the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in larger-cap funds.

| | |

| 6 | | | www.sbhfunds.com |

| Segall Bryant & Hamill Small Cap Core Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For 2022, the Segall Bryant & Hamill Small Cap Core Fund returned -13.26% (Retail Class) compared to the Fund’s benchmark, the Russell 2000® Index’s -20.44% return. The market pulled back in 2022 as higher inflation led to a rise in interest rates while the outbreak of the Russia/Ukraine war increased uncertainty. As interest rates rose, market multiples contracted, particularly in longer duration assets, as alternative investment options to equities resurfaced. Further, as the cost of capital increased and uncertainty related to the war and global economies grew, higher Return on Invested Capital (ROIC) companies outperformed.

Contributors to Return

On a sector level, Health Care, Information Technology, and Industrials were the largest contributors to the Fund’s performance relative to the benchmark. Agilysys, Inc. (AGYS), a software solutions provider to the hospitality industry, was the largest individual contributor to the Fund’s return. A complete refresh of Agilysys’s software positioned the company to benefit as consumers returned to travel with the COVID-19 pandemic waning. Agilysys’s improved competitive position was punctuated towards the end of 2022 when Marriott chose its software for a multi-year rollout, potentially its largest win ever. Model N, Inc. (MODN), a software provider to Health Care and IT companies, was another large contributor. The transition of Model N’s customers to the cloud reached an inflection point driving organic growth acceleration which, combined with less macroeconomic sensitivity, resulted in multiple expansion.

Detractors From Return

On a sector level, Energy and Utilities were the largest relative detractors from the Fund’s performance. Hain Celestial Group, Inc. (HAIN), a manufacturer of organic and natural food products, was the largest detractor. Hain incurred multiple headwinds through the year including slowing demand in Europe, supply chain issues, and higher input costs which pressured growth and margins. Endava PLC (DAVA), a digital technology outsourcer, was another detractor. Endava’s share price suffered as growing macroeconomic concern and layoffs at its customers created uncertainty about the sustainability of its revenue growth rate.

Outlook and Positioning

We enter 2023 with a sense of caution. While corporate earnings held up reasonably well through 2022, buoyed by excess consumer savings and solid backlogs, there are increasing signs of slowing in economic indicators and corporate commentary. We expect inflation to continue to soften in 2023 which, combined with softer economic conditions as the year progresses, should allow the U.S. Federal Reserve to stop raising interest rates. As inflation likely cools through 2023, however, earnings expectations are likely to continue to fall as the lagged effect of the interest rate increases materializes.

Given the headwinds seen in the data and emerging in corporate earnings results, as we enter 2023, we have weighted the Fund more towards companies that we believe have higher ROIC businesses and solid balance sheets, and that we assess have the ability to generate free cash flow. Lower ROIC companies have been underperforming as interest rates have risen and the outlook has become more uncertain. We would expect lower ROIC companies to continue to underperform should the economy worsen from here. Should fundamental weakness begin to accelerate and translate into a further market sell-off over the next quarter or two, we may begin to rotate out of higher ROIC companies and into smaller market cap, improving/lower ROIC companies that would disproportionately benefit from an economic recovery. Of course, these improving ROIC companies would be augmented with additional key attributes within our philosophical approach such as niche market positioning with defendable competitive advantages and strong management teams. Combined, we believe these attributes have the potential to produce powerful results over market cycles but also allow the Fund to be prepared for risks and surprises – of which we are sure 2023 could be full!

Stock Performance (12/31/2021 to 12/31/2022)

| | Average | Contribution |

| 5 Highest | Weight | To Return |

| Agilysys, Inc. | 1.00 | 0.88 |

| Devon Energy Corp. | 2.41 | 0.68 |

| Model N, Inc. | 1.01 | 0.52 |

| Badger Meter, Inc. | 0.66 | 0.44 |

| EMCOR Group, Inc. | 0.61 | 0.39 |

| Average | Contribution |

| 5 Lowest | Weight | To Return |

| Heska Corp. | 0.62 | -0.77 |

| Pegasystems, Inc. | 0.46 | -0.83 |

| Allegiant Travel Co. | 0.84 | -0.91 |

| Endava PLC | 1.60 | -1.07 |

| Hain Celestial Group, Inc. | 1.41 | -1.35 |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Fund’s Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call (800) 392-2673.

Please see page 35 for a description of the methodology used to construct this table.

| | |

| Annual Report | December 31, 2022 | | | 7 |

| Segall Bryant & Hamill All Cap Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

Ralph M. Segall, CFA, CIC Portfolio Manager

Suresh Rajagopal, CFA Portfolio Manager

CFA is a trademark owned by CFA Institute.

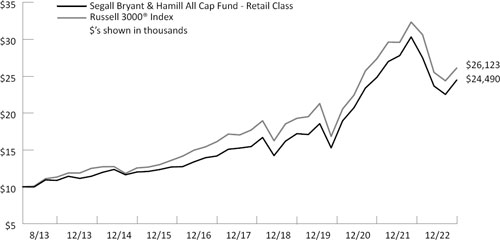

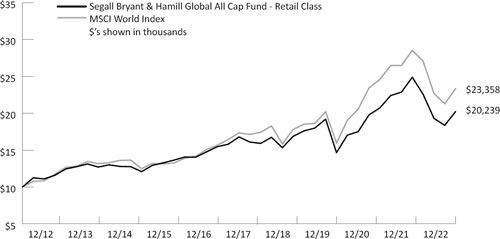

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class (SBRAX) | (19.23)% | 9.68% | 10.17% | — | 9.98% | 12/9/19 |

| Institutional Class (SBHAX) | (19.21)% | 9.71% | 10.25% | — | 10.10% | 7/31/13 |

| Russell 3000® Index | (19.21)% | 7.07% | 8.79% | — | 10.73% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Total: 0.83%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 0.87%, Net: 0.84%

| | |

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Information Technology | 16.4% |

| | Financials | 15.9% |

| | Health Care | 15.7% |

| | Consumer Discretionary | 14.0% |

| | Industrials | 12.6% |

| | Consumer Staples | 7.7% |

| | Energy | 6.3% |

| | Materials | 4.4% |

| | Communication Services | 3.1% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | | |

| | Microsoft Corp. | 4.1% |

| | Quanta Services, Inc. | 3.6% |

| | Alphabet, Inc. | 3.2% |

| | Reinsurance Group of America, Inc. | 3.0% |

| | UnitedHealth Group, Inc. | 2.8% |

| | Raytheon Technologies Corp. | 2.8% |

| | Chevron Corp. | 2.8% |

| | Visa, Inc. | 2.6% |

| | Globe Life, Inc. | 2.5% |

| | Novo Nordisk | 2.3% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

Performance data quoted represents past performance and does not guarantee future results. Performance information for the Retail Class shares prior to their inception is based on the performance of the Institutional Class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 0.99% and 0.84% to the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

| | |

| 8 | | | www.sbhfunds.com |

| Segall Bryant & Hamill All Cap Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For 2022, the Segall Bryant & Hamill All Cap Fund returned -19.23% (Retail Class) compared to the Fund’s benchmark, the Russell 3000® Index’s -19.21% return. Security selection detracted from relative performance while sector allocation contributed, as did the Fund’s allocation to cash. As a reminder, a key element of the Fund’s strategy is to participate in all markets by investing in companies that we believe possess strong management teams, can generate High Return on Invested Capital (ROIC), and produce quality financial metrics (e.g., free cash flow growth, consistent earnings growth, and margin expansion).

Contributors to Return

At the sector level, the strategy’s best performing areas relative to the benchmark during the year were Consumer Discretionary, Financials, and Communication Services. Outperformance in the Consumer Discretionary sector was driven by favorable stock selection as the Fund held outperforming retail positions while also avoiding the negative performance of Tesla, Inc. (TSLA). Outperformance in Financials reflected an improvement in COVID-related mortality trends within life insurers Globe Life (GL) and Reinsurance Group of America, Inc. (RGA). Communication Services performance was aided by avoiding ownership in many sector names that underperformed during the year. These included Meta Platforms Inc. (META) and many other media companies tied to digital advertising that declined significantly during the year due to a weakening economy. At the individual stock level, Quanta Services, Inc. (PWR) outperformed as power grid and renewables spending continues to propel earnings growth and positive sentiment in shares. In addition, Chevron Corp. (CVX) saw outperformance as supportive commodity prices and disciplined spending drove strong cash returns at major energy companies during the year.

Detractors from Returns

Health Care, Information Technology, and Consumer Staples were the largest relative detractors on a sector level for the year. Health Care underperformance was linked to unfavorable stock selection as the Fund had positions that delivered weaker-than-anticipated earnings updates. Information Technology underperformance was tied to many of the Fund’s technology holdings underperforming throughout the year after significant outperformance during 2021. Specifically, rising rates had an outsized negative impact on many of

the Fund’s software holdings and increasing concerns related to an inventory correction in semiconductor holdings weighed on results. Consumer Staples underperformance was due to unfavorable stock selection as the Fund held names that experienced a margin squeeze from a challenging cost environment and adverse operating conditions in China due to COVID. At the individual stock level, underperformance was driven by Alphabet, Inc. (GOOG) as difficult comparisons relative to 2021 and a pullback by advertisers in many categories significantly reduced growth. In addition, profitability was impacted more than expected due to continued headcount growth and investments in the cloud. Underperformance by Marvell Technology, Inc. (MRVL) was tied to concerns related to a semiconductor inventory correction and a slowdown in data center capex spending.

Outlook and Positioning

As we enter 2023, the focus of many investors is on assessing the durability of inflationary pressures and the intentions of the Federal Reserve with respect to interest rates. Determining the timing at the macro level and whether the U.S. enters a recession is nearly an impossible task. Fortunately for us, macro concerns are not a principal part of the selection process in our approach. A key aspect of our approach is to assess company-specific business models against the impact of a new regime of deglobalization, which we expect will reduce ROIC and free cash flow as the global economy is going to labor under building new supply chains and transitioning away from fossil fuels. Both are costly and inflationary and, as a result, company profits are likely to be hit much harder than consensus expectations. For example, we believe the reshoring of semiconductor supply chains should increase chip prices significantly due to rising inventory levels and diversifying suppliers. In addition, sluggish growth—or even a marked decline in inflation—could create negative operating leverage and result in lower margins. All that said, this will not stop us from buying stocks as they move into an attractive valuation range. It always has been, and will always remain, a market of stocks rather than a stock market. In our view, there will always be investments to make in companies with the right set of investment characteristics, priced at valuations that present an attractive opportunity to reach our long-term investment goals.

Thank you for your consideration and continued support.

Stock Performance (12/31/2021 to 12/31/2022)

| | Average | Contribution |

| 5 Highest | Weight | To Return |

| Quanta Services, Inc. | 3.37 | 0.80 |

| Chevron Corp. | 2.36 | 0.79 |

| McKesson Corp. | 1.63 | 0.76 |

| Reinsurance Group of America, Inc. | 2.51 | 0.69 |

| Novo Nordisk | 0.57 | 0.57 |

| | Average | Contribution |

| 5 Lowest | Weight | To Return |

| Catalent, Inc. | 1.53 | -1.33 |

| Zebra Technologies Corp. | 1.67 | -1.49 |

| Amazon.com, Inc. | 2.53 | -1.62 |

| Marvell Technology, Inc. | 2.13 | -1.77 |

| Alphabet, Inc. | 3.96 | -1.80 |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Fund’s Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call (800) 392-2673.

Please see page 35 for a description of the methodology used to construct this table.

| | |

| Annual Report | December 31, 2022 | | | 9 |

| Segall Bryant & Hamill Emerging Markets Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

Scott E. Decatur, Ph.D. Portfolio Manager

Nicholas C. Fedako, CFA Portfolio Manager

CFA is a trademark owned by CFA Institute.

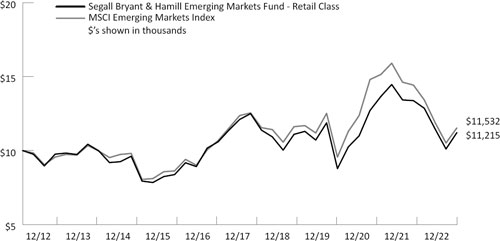

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class* (SBHEX) | (16.17)% | (1.89)% | (1.52)% | 1.15% | 0.77% | 6/30/14 |

| Institutional Class** (SBEMX) | (16.08)% | (1.73)% | (1.33)% | 1.34% | 0.97% | 6/30/11 |

| MSCI Emerging Markets Index | (20.10)% | (2.69)% | (1.40)% | 1.44% | 0.85% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.86%, Net: 1.38%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.69%, Net: 1.23%

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Financials | 22.6% |

| | Information Technology | 18.9% |

| | Consumer Discretionary | 14.1% |

| | Communication Services | 9.8% |

| | Materials | 8.7% |

| | Consumer Staples | 6.2% |

| | Industrials | 6.0% |

| | Energy | 5.2% |

| | Health Care | 3.9% |

| | Utilities | 3.0% |

| | Real Estate | 1.9% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | |

| | Taiwan Semiconductor Manufacturing Co., Ltd. | 4.8% |

| | Tencent Holdings, Ltd. | 3.2% |

| | Samsung Electronics Co., Ltd. | 2.4% |

| | Alibaba Group Holding, Ltd. | 1.6% |

| | Bank of China, Ltd. | 1.4% |

| | Fubon Finacial Holdings Co., Ltd. | 1.3% |

| | Vipshop Holdings, Ltd. | 1.2% |

| | China Construction Bank Corp. | 1.2% |

| | Vale S.A. | 1.2% |

| | China Tower Corp., Ltd. | 1.1% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

Performance data quoted represents past performance and does not guarantee future results. Performance information for the Retail Class shares prior to their inception is based on the performance of the Institutional Class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.38% and 1.23% to the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

Investing in foreign companies are subject to special risks, including currency fluctuations, social, economic, and political uncertainties, which could increase volatility.

| | |

| 10 | | | www.sbhfunds.com |

| Segall Bryant & Hamill Emerging Markets Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For 2022, the Segall Bryant & Hamill Emerging Markets Fund returned -16.17% (Retail Class) compared to the Fund’s benchmark, the MSCI Emerging Markets Index’s -20.09% return. The benchmark’s annual return was its worst since the 2008 financial crisis as concerns about higher inflation, supply chain disruptions, rising interest rates, and slowing global growth following the pandemic were exacerbated by Russia’s invasion of Ukraine in March. Regional performance within the benchmark was mixed as Latin America finished in positive territory while Europe, the Middle East, and Africa (EMEA) and Asia ended the year lower. Within Latin America, commodity exporting nations including Chile and Brazil benefited from sanctions imposed on Russia. Asia finished lower as China’s COVID restrictions, housing market troubles, and tensions with the U.S. increased uncertainty regarding global economic activity. China ended the year down and dragged on other Asian nations including Taiwan and Korea. EMEA was the worst-performing region as the trading of Russian securities was suspended and removed from the benchmark at no value, negatively impacting the benchmark’s return. Hungary and Poland were also a drag for the region over concerns about the war’s effect on Ukraine’s neighbors. Turkey notably ended the year as the best performing country in the benchmark as Turkish investors bought domestic stocks to hedge against the country’s high inflation. All 11 sectors in the benchmark ended the year lower. Information Technology was the worst performer as semiconductor stocks struggled due to weaker PC and smartphone demand. Utilities, a more defensive sector, and Financials, where earnings could benefit from higher interest rates, were the most resilient.

The Fund outperformed its benchmark for the second year in a row with positive security selection in Asia, EMEA, and Latin America. Within Asia, China and India were the top performers while Taiwan was modestly lower. Security selection in Saudi Arabia was the primary driver of positive returns in EMEA and South Africa also contributed. In Latin America, positive stock selection in Mexico and Brazil more than offset negative selection in Peru, Colombia, and Chile. At the sector level, stock selection in Financials, Communication Services, and Health Care added the most to relative returns. Consumer Discretionary and Industrials were the largest detractors.

Outlook and Positioning

Exiting the fiscal year, we are optimistic about the Fund’s performance potential as we look forward given the substantial discounts on certain key valuation measures. The Fund’s holdings at year end have an average price-to-earnings (P/E) ratio of 5.34x, a price-to-book (P/B) ratio of 0.86x, with a dividend yield (DY) of 5.93%. This compares favorably to the MSCI Emerging Markets Index, which at year end had a P/E of 10.93x, P/B of 1.57x and a DY of 3.33%. The strategy is even more attractively valued when viewed in contrast to what is currently observed in domestic U.S. markets, represented by the S&P 500® Index, which trades at 18.17x P/E, 3.84x P/B, and a DY of 1.73%.

Stock Performance (12/31/2021 to 12/31/2022)

| | Average | Contribution |

| 5 Highest | Weight | To Return |

| Vipshop Holdings Ltd. | 0.29 | 0.64 |

| Bank of Baroda | 0.45 | 0.36 |

| Grupo Comercial Chedraui S.A. de C.V. | 0.38 | 0.34 |

| Alinma Bank | 0.15 | 0.28 |

| Shandong Xinhua Pharmaceutical Co. Ltd. | 0.18 | 0.26 |

| | Average | Contribution |

| 5 Lowest | Weight | To Return |

| Brilliance China Automotive Holdings Ltd. | 0.72 | -0.60 |

| Gazprom PJSC | 0.13 | -0.67 |

| Samsung Electronics Co., Ltd. | 2.70 | -0.92 |

| Tencent Holdings Ltd. | 2.97 | -0.94 |

| Taiwan Semiconductor Manufacturing Co., Ltd. | 5.29 | -2.29 |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Fund’s Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call (800) 392-2673.

Please see page 35 for a description of the methodology used to construct this table.

| | |

| Annual Report | December 31, 2022 | | | 11 |

| Segall Bryant & Hamill International Small Cap Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

Scott E. Decatur, Ph.D. Portfolio Manager

Nicholas C. Fedako, CFA Portfolio Manager

CFA is a trademark owned by CFA Institute.

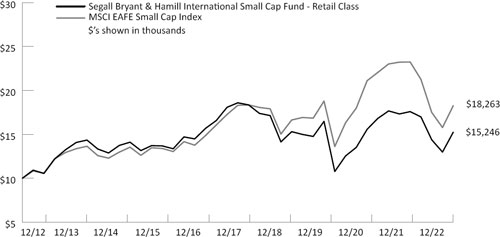

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class* (SBHSX) | (13.31)% | (2.55)% | (3.89)% | 4.31% | 3.57% | 6/30/14 |

| Institutional Class** (SBSIX) | (13.19)% | (2.39)% | (3.70)% | 4.52% | 3.79% | 5/31/11 |

| MSCI EAFE Small Cap Index | (21.39)% | (0.93)% | (0.05)% | 6.21% | 4.92% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.36%, Net: 1.18%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.13%, Net: 1.03%

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Industrials | 22.7% |

| | Consumer Discretionary | 12.2% |

| | Financials | 11.8% |

| | Real Estate | 10.4% |

| | Materials | 9.6% |

| | Information Technology | 9.3% |

| | Health Care | 6.8% |

| | Consumer Staples | 6.3% |

| | Communication Services | 3.5% |

| | Energy | 3.1% |

| | Utilities | 3.0% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | |

| | Incitec Pivot, Ltd. | 1.2% |

| | Galenica A.G. | 1.2% |

| | NRW Holdings, Ltd. | 1.0% |

| | D/S Norden A/S | 1.0% |

| | Bank of Georgia Group PLC | 1.0% |

| | Sojitz Corp. | 1.0% |

| | Helia Group, Ltd. | 1.0% |

| | TBC Bank Group PLC | 0.9% |

| | Betsson A.B. | 0.9% |

| | SANKYO Co., Ltd. | 0.9% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

Performance data quoted represents past performance and does not guarantee future results. Performance information for the Retail Class shares prior to their inception is based on the performance of the Institutional Class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.18% and 1.03% to the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in large-cap funds.

Investing in foreign companies are subject to special risks, including currency fluctuations, social, economic, and political uncertainties, which could increase volatility.

| | |

| 12 | | | www.sbhfunds.com |

| Segall Bryant & Hamill International Small Cap Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For 2022, the Segall Bryant & Hamill International Small Cap Fund returned -13.31% (Retail Class) compared to the Fund’s benchmark, the MSCI EAFE Small Cap Index, which returned -21.39%. The benchmark’s return was its worst annual return since the 2008 financial crisis as higher inflation driven by pandemic-related distortions and Russia’s invasion of Ukraine led to tighter monetary policies and increased recession fears from a slowdown in economic activity. After falling for the first three quarters of the year, stocks pared losses in the fourth quarter on optimism that inflation had peaked. During the year, the U.S. dollar strengthened versus the euro, pound, and yen as risk-off sentiment sent investors to the perceived safety of dollar assets. All four major benchmark regions ended lower led by the United Kingdom after newly elected prime minister Liz Truss announced a series of unfunded tax cuts that sent stocks and the pound tumbling. The chaos caused Truss to resign after six weeks and the reversal of many of her policies helped U.K. assets to stabilize. Europe also underperformed the broader market, led on the downside by Sweden and Germany, as investors worried that a gas and oil shortage would spark a major energy crisis. These concerns partially abated as the year ended due to warmer weather in the region. In the Far East, the region’s largest constituent, Australia, was the worst performer due in part to metal and mining companies falling on concerns of a global growth slowdown. Japan was the top performing region and ended the year 0.77% higher in local currency terms as the weaker yen benefited exporters. Ten of

11 sectors ended the year lower with the exception being Energy where coal companies gained from buyers seeking substitutes for Russian oil and gas.

The Fund outperformed its benchmark for the second year in a row with strong security selection in Europe, the Far East, the United Kingdom, and Japan. The Fund’s best relative performance within Europe came from Sweden, Norway, and Denmark, while in the Far East, Australia was the primary driver of positive returns. Stock selection was additive in nine of 11 sectors as Industrials, Financials, and Information Technology were the Fund’s top performers. Selection was modestly lower in Consumer Staples and Utilities.

Outlook and Positioning

Exiting the fiscal year, we are optimistic about the Fund’s performance potential as we look forward given the substantial discounts on certain key valuation measures. The Fund’s holdings at year end have an average price-to-earnings (P/E) ratio of 5.56x, a price-to-book (P/B) ratio of 0.85x, with a dividend yield (DY) of 5.63%. This compares favorably to the MSCI EAFE Small Cap Index which at year end had a P/E of 11.28x, P/B of 1.21x and a DY of 3.10%. The strategy is even more attractively valued when viewed in contrast to what is currently observed in domestic U.S. markets, represented by the Russell 2000® Index, which trades at 10.73x P/E, 1.94x P/B, and a DY of 1.49%.

Stock Performance (12/31/2021 to 12/31/2022)

| | Average | Contribution |

| 5 Highest | Weight | To Return |

| D/S Norden A/S | 0.67 | 0.79 |

| New Hope Corp. Ltd. | 0.61 | 0.78 |

| Bank of Georgia Group PLC | 0.78 | 0.60 |

| Whitehaven Coal Ltd. | 0.47 | 0.56 |

| Coronado Global Resources Inc. | 0.83 | 0.52 |

| | Average | Contribution |

| 5 Lowest | Weight | To Return |

| Marks and Spencer Group PLC | 0.45 | -0.49 |

| Computacenter PLC | 0.98 | -0.49 |

| Getinge AB | 0.48 | -0.51 |

| International Distributions Services PLC | 0.39 | -0.57 |

| Vistry Group PLC | 0.91 | -0.63 |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Fund’s Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call (800) 392-2673.

Please see page 35 for a description of the methodology used to construct this table.

| | |

| Annual Report | December 31, 2022 | | | 13 |

Segall Bryant & Hamill

Fundamental International Small Cap Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Investment Objective

The Fund seeks to achieve long-term capital appreciation.

Fund Management

John C. Fenley, CFA Portfolio Manager

CFA is a trademark owned by CFA Institute.

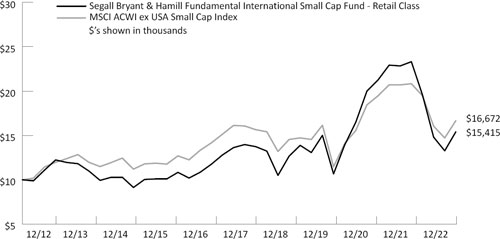

Cumulative Returns

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see index definitions beginning on page 34.

Average Annual Total Returns

| | | | | | Since | Inception |

| | 1 Year | 3 Years | 5 Years | 10 Years | Inception | Date |

| Retail Class (WTIFX) | (33.89)% | 0.89% | 2.50% | 4.42% | 5.17% | 12/15/99 |

| Institutional Class (WIIFX) | (33.74)% | 1.05% | 2.66% | 4.54% | 5.22% | 4/29/16 |

| MSCI ACWI ex USA Small Cap Index | (19.97)% | 1.07% | 0.67% | 5.24% | 6.10% | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.51%, Net: 1.25%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.36%, Net: 1.10%

| | Sector Allocation (as of 12/31/2022) |

| | |

| | Industrials | 33.4% |

| | Information Technology | 28.9% |

| | Consumer Discretionary | 19.6% |

| | Financials | 10.2% |

| | Health Care | 2.2% |

| | Communication Services | 1.9% |

| | Consumer Staples | 1.4% |

| | |

| | Sector classifications presented are based on the Global Industry Classification Standard (GICS) methodology. |

| | |

| | Percentages are based on Total Net Assets. |

| | |

| | The sector allocation table above does not include any cash or cash equivalents. |

| | |

| | Top Ten Holdings (as of 12/31/2022) |

| | | |

| | Brodrene A. & O. Johansen A/S | 5.5% |

| | Constellation Software, Inc. | 5.3% |

| | Epsilon Net S.A. | 5.0% |

| | GFL Environmental, Inc. | 4.8% |

| | PAX Global Technology, Ltd. | 4.6% |

| | Azimut Holdings S.p.A. | 4.6% |

| | Fluidra S.A. | 4.4% |

| | Evolution A.B. | 4.1% |

| | Topicus.com, Inc. | 3.9% |

| | Instalco A.B. | 3.6% |

| | |

| | Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments. Holdings are subject to change and may not reflect the current or future position of the Fund. |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

Performance data quoted represents past performance and does not guarantee future results. Performance information for the Institutional Class shares prior to their inception is based on the performance of the Retail Class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, visit www.sbhfunds.com. Average annual total returns reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements, if any. Without the fee waivers and expense reimbursements, total return figures would have been lower. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Segall Bryant & Hamill fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Until at least April 30, 2023, Segall Bryant & Hamill, LLC (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse other expenses, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.25% and 1.10% for the Fund’s Retail Class and Institutional Class, respectively, for such period. This agreement may not be terminated or modified by the Adviser prior to the termination date without the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in larger-cap funds.

Investing in foreign securities entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

| | |

| 14 | | | www.sbhfunds.com |

Segall Bryant & Hamill

Fundamental International Small Cap Fund | Fund Overview |

| | December 31, 2022 (Unaudited) |

Manager Commentary

Market Overview and Fund Performance

For 2022, the Segall Bryant & Hamill Fundamental International Small Cap Fund returned -33.89% (Retail Class) compared to the Fund’s benchmark, the MSCI ACWI ex USA Small-Cap Index’s -19.97% return. Faced with an abundance of global macroeconomic risks and concerns, including high inflation, rapidly rising interest rates, the war in Ukraine, and the COVID lockdowns in China, to name but a few, global equity markets struggled throughout the year.

Equity valuation levels, especially for companies with high growth rates compressed under the surging U.S. dollar, which explained most of the Fund’s negative performance. In our view, there was a difference between the stock price performance of these companies and their operating performance, which continued to be strong. We attribute this to our strict adherence to identify fundamentally strong companies.

Contributors to Return

The Fund’s relative outperformance and underweighting in Communication Services and its lack of exposure to Real Estate contributed to annual performance relative to the benchmark. From a holdings level, U.K.-based Clipper Logistics PLC (CLG.LN) was a contributor to performance. As one of the U.K.’s leading retail logistics companies, Clipper transformed its business model to accommodate the fast-changing demands of ecommerce retailers. The acceleration of ecommerce transactions due to COVID continued to propel Clipper’s earnings which garnered the attention of potential suitors. During the year, GXO Logistics (GXO) agreed to acquire Clipper at a 32% premium to Clipper’s three-month weighted-average share price.

Hong Kong-listed PAX Global Technology, Ltd. (PAX) contributed to performance as well. PAX is one of the world’s largest electronic-funds-transfer at point-of-sale (EFT-POS) terminal providers with a focus on emerging markets like Brazil. In 2021, speculation arose that PAX terminals may have been used in cyberattacks. Shares had been under pressure despite a lack of evidence of such claims. Our independent research supported maintaining the Fund’s position in PAX shares and we saw the benefits of our patience throughout 2022.

Detractors from Return

The Fund’s relative underperformance and overweighting in Industrials and Consumer Discretionary detracted from the Fund’s performance relative to the benchmark. From a holdings level, U.K.-based Victoria PLC (VCP) was a detractor to performance. Victoria manufactures and distributes primarily carpet, underlay, and tiles mostly for the European residential market. This market is highly fragmented, and Victoria has been a leading consolidator. We believe that the shares have been overlooked given that it operates in a cyclical and capital-intensive industry. We also believe the potential for continued value creative acquisitions is largely misunderstood and should provide opportunity for growth despite the negative sentiment in the industry stemming from inflationary pressures and supply chain issues.

Global pet nutrition company, Swedencare A.B. (publ), also negatively affected the Fund’s performance. The company’s two main product families, ProDen PlaqueOff and NutriScience, are sold in over 50 countries. We believe Swedencare has a significant opportunity to continue increasing penetration of its products in current markets and to launch new and existing products into fast-growing markets such as China. During the year, Swedencare reported strong top-line results but disappointed investors with below-guidance organic growth. Management cited tough comparables and large clients reducing inventory levels. While consumer sentiment remains challenged, exiting the fiscal year, we believe in maintaining the Fund’s position in Swedencare.

Outlook and Positioning