Table of Contents

Exhibit (99)(b)

QUARTERLY EARNINGS REPORT

APRIL 16, 2007

TABLEOF CONTENTS

| 1 | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 6 | ||

| 7 | ||

| 8 | ||

| 9 | ||

| 10 | ||

| 11 | ||

| 12 | ||

| 13-14 | ||

| 15 | ||

Note: World Savings Monthly Financial Highlights are located on Pages 27-28 of the Appendix | ||

| 16-41 | ||

Explanation of Our Use and Reconciliation of Certain Non-GAAP Financial Measures | 42-46 | |

| 47 | ||

| 48 |

READERSAREENCOURAGEDTOREFERTO WACHOVIA’SRESULTSFORTHEYEARENDED DECEMBER 31, 2006,PRESENTEDINACCORDANCEWITH U.S.GENERALLYACCEPTEDACCOUNTINGPRINCIPLES (“GAAP”),WHICHMAYBEFOUNDIN WACHOVIA’S 2006 ANNUAL REPORTON FORM 10-K.

ALLNARRATIVECOMPARISONSAREWITH FOURTH QUARTER 2006UNLESSOTHERWISENOTED.

THEINFORMATIONCONTAINEDHEREININCLUDESCERTAINNON-GAAPFINANCIALMEASURES. PLEASEREFERTOPAGES 42-46FORANIMPORTANTEXPLANATIONOFOURUSEOFNON-GAAPMEASURESANDRECONCILIATIONOFTHOSENON-GAAPMEASURESTO GAAP.

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

EXPLANATIONOF “COMBINED” RESULTS

CERTAINTABLESANDNARRATIVECOMPARISONSINTHIS QUARTERLY EARNINGS REPORTINCLUDEREFERENCESTO “COMBINED”RESULTSFORFIRSTQUARTER 2006ANDEARLIERPERIODS. “COMBINED”RESULTSFORTHEFIRSTQUARTEROF 2006ANDPRIORQUARTERSREPRESENT WACHOVIA’SACTUALRESULTSPLUSTHEACTUALRESULTSOF GOLDEN WEST. “COMBINED”RESULTSINCLUDEPURCHASEACCOUNTINGANDOTHERCLOSINGADJUSTMENTS (PAA)ASOFTHEACTUALCLOSINGDATEOF OCTOBER 1, 2006; “COMBINED”RESULTSFORPRIORPERIODSINCLUDEAMORTIZATION/ACCRETIONBASEDONPRELIMINARYFAIRVALUEPURCHASEACCOUNTINGADJUSTMENTSFORSECURITIES,LOANS,PREMISESANDEQUIPMENT,DEPOSITS,LONG-TERMDEBTANDDEPOSITBASEINTANGIBLE (DBI). INADDITION, “COMBINED”RESULTSALSOINCLUDEA “FUNDINGCOST”WHICHREPRESENTSINTERESTEXPENSECALCULATEDATARATEOF 5.35%ONTHECASHPORTIONOFTHEPURCHASEPRICEANDMERGER-RELATEDANDRESTRUCTURINGEXPENSES. READERSSHOULDNOTETHATSUCHPURCHASEACCOUNTINGADJUSTMENTSANDFUNDINGCOSTSMAYHAVEBEENDIFFERENTIFTHEMERGERHADBEENCOMPLETEDINPRIORPERIODS,ALTHOUGHFORPURPOSESOFPRESENTINGTHE “COMBINED”RESULTSWEHAVEASSUMEDTHEYWERENOTDIFFERENT.

THE “COMBINED”RESULTSAREFORILLUSTRATIVEPURPOSESONLYANDTHEPRESENTATIONOFRESULTSONTHIS “COMBINED”BASISISNOTAPRESENTATIONTHATCONFORMSWITHGENERALLYACCEPTEDACCOUNTINGPRINCIPLES. READERSAREENCOURAGEDTOREFERTO WACHOVIA’SRESULTSPRESENTEDINACCORDANCEWITHGENERALLYACCEPTEDACCOUNTINGPRINCIPLES,WHICHMAYBEFOUNDINEXHIBIT (99)(C) TO WACHOVIA’SCURRENTREPORTONFORM 8-K,FILEDON APRIL 16, 2007. ALLNARRATIVECOMPARISONSARETOWACHOVIA-ONLYRESULTSFORPRIORPERIODSUNLESSOTHERWISENOTED. SEEALSO “SUPPLEMENTAL ILLUSTRATIVE COMBINED INFORMATION”ONPAGE 48FORAFURTHERDISCUSSIONREGARDINGTHE “COMBINED”PRESENTATION.

IN 4Q06,ASARESULTOFPERFORMINGOUR STAFF ACCOUNTING BULLETIN NO. 108,CONSIDERINGTHE EFFECTSOF PRIOR YEAR MISSTATEMENTSWHENQUANTIFYING MISSTATEMENTSIN CURRENT YEAR FINANCIAL STATEMENTS, (SAB 108)REVIEW,WEELECTEDTORECORDCERTAINIMMATERIAL,PRIORYEARADJUSTMENTSWHICHAREUNRELATEDTO SAB 108ANDWHICHAREFURTHERDISCUSSEDANDOUTLINEDONPAGE 18. THESEADJUSTMENTSAREREFERREDTOAS “4Q06ADJUSTMENTS”ANDINSOMEINSTANCES,OURREPORTEDRESULTSAREDISCUSSEDEXCLUDINGTHEEFFECTOFTHESE 4Q06ADJUSTMENTSTOILLUSTRATETHEEFFECTSONCOREOPERATINGTRENDSWITHOUTSUCHADJUSTMENTS.

ALLNARRATIVECOMPARISONSOF “COMBINED”RESULTSPERTAINTO 1Q07 REPORTEDRESULTSVERSUS 1Q06 “COMBINED”RESULTSUNLESSOTHERWISENOTED. INADDITION, “COMBINED”RESULTSDONOTREFLECTTHEACQUISITIONOF WESTCORPAND WFS FINANCIAL INCCOMPLETEDON MARCH 1, 2006,FORPERIODSPRIORTOTHEACQUISITIONDATE.

FOREASEOFUSE,COMMENTSPERTAININGTO AS REPORTEDOR ACTUALRESULTSAREPRESENTEDINBOLDTYPE.

“COMBINED” SUMMARY

1Q06: | REPORTEDRESULTSPLUS GOLDEN WEST’SRESULTSPLUSTHREEMONTHSOF PAAAND DBIACCRETION/AMORTIZATIONANDFUNDINGCOSTS. |

Page-1

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

First Quarter 2007 Financial Highlights

| • | Earnings of $2.3 billion flat with 4Q06 and up 33% from 1Q06; EPS of $1.20 flat, and up 10% from 1Q06 |

| — | Excluding net merger-related and restructuring expenses, EPS of $1.20 down 1% from 4Q06 which included $0.02 gain from sale of corporate and institutional trust businesses; up 7% from 1Q06 |

| • | Segment results compared to 4Q06 reflect strength in Capital Management; weaker results in General Bank and Wealth Management, largely reflecting seasonality and environmental headwinds; and lower results in Corporate & Investment Bank from strong 4Q06 levels |

| — | Environmental factors largely mask underlying sales momentum and disciplined execution |

| Segment Earnings | ||||||

| vs. 4Q06 | vs. 1Q06 | |||||

General Bank | -8 | % | +41 | % | ||

Wealth Management | -11 | % | +14 | % | ||

Corporate & Investment Bank | -26 | % | -23 | % | ||

Capital Management | +19 | % | +42 | % | ||

1Q07 vs. Adjusted Reported 4Q06

The following chart adjusts 4Q06 Reported results to illustrate operating trends without the impact of 4Q06 Adjustments; additional detail is included on pages 7, 8 and 18.

(In millions) | A Reported 1Q07 | B Reported 4Q06 | C 4Q06 Adjustments | B+C Adjusted Reported 4Q06 | 1Q07 vs Adj 4Q06 | ||||||||

Net interest income(Tax-equivalent) | $ | 4,497 | 4,612 | (24 | ) | 4,588 | (2 | )% | |||||

Fee and other income | 3,741 | 3,980 | (115 | ) | 3,865 | (3 | ) | ||||||

Total revenue(Tax-equivalent) | 8,238 | 8,592 | (139 | ) | 8,453 | (3 | ) | ||||||

Provision for credit losses | 177 | 206 | — | 206 | (14 | ) | |||||||

Total noninterest expense | 4,588 | 4,931 | (198 | ) | 4,733 | (3 | ) | ||||||

Minority interest in income of consolidated subsidiaries | 136 | 125 | — | 125 | 9 | ||||||||

Pre-tax income from continuing operations(Tax-equivalent) | 3,337 | 3,330 | 59 | 3,389 | (2 | ) | |||||||

Income taxes(Tax-equivalent) | 1,035 | 1,075 | 72 | 1,147 | (10 | ) | |||||||

Income from continuing operations | 2,302 | 2,255 | (13 | ) | 2,242 | 3 | |||||||

Discontinued operations, net of income taxes | — | 46 | — | 46 | — | ||||||||

Net income | $ | 2,302 | 2,301 | (13 | ) | 2,288 | 1 | % | |||||

| • | Revenues down 3% from strong Adjusted 4Q06 levels; up 3% from Combined 1Q06 |

| — | Net interest income down 2% and margin decreased 7 bps to 3.01% from Adjusted 4Q06 of 3.08% |

| • | Results largely reflect growth in lower spread loans and the securitization warehouse and improved retail deposit pricing, lower income from maturing off-balance sheet positions, declines in trading-related net interest income and the effect of FSP 13-2/FIN 48 adoption |

| — | Fee income down 3% from strong Adjusted 4Q06 levels largely due to declines in structured products and principal investing gains somewhat offset by improvement in trading |

| • | Other noninterest expense down $83 million, or 2% from Adjusted 4Q06; up 3% from Combined 1Q06 |

| — | Excluding $93 million of retirement-eligible employee stock compensation expense in 1Q07, noninterest expense down 4% from Adjusted 4Q06 driven largely by lower revenue-based incentives and sundry expense as well as expense discipline |

| • | Average loans up 1% and up 59% from 1Q06;up 9% from Combined 1Q06 |

| • | Average core deposits grew 2% and 27% from 1Q06;up 5% from Combined 1Q06 |

| — | Strong momentum in retail checking account strategies |

| • | Nonperforming assets of $1.8 billion or 40 bps of loans |

| • | Net charge-offs of $155 million or 15 bps of loans |

| — | Provision expense of $177 million largely reflects loan growth including $10 million relating to credit card |

| • | Effective tax rate of 30.99% reflects updated information on certain tax matters |

| • | Tangible equity of 4.7% and leverage ratio of 6.1%; repurchased 5 million shares during the quarter |

Page-2

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Earnings Reconciliation

| 2007 | 2006 | 1Q07 EPS | |||||||||||||||||||||||||||

First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | vs | vs | |||||||||||||||||||||||

(After-tax in millions, except per share data) | Amount | EPS | Amount | EPS | Amount | EPS | Amount | EPS | Amount | EPS | 4Q06 | 1Q06 | |||||||||||||||||

Net income (GAAP) | $ | 2,302 | 1.20 | 2,301 | 1.20 | 1,877 | 1.17 | 1,885 | 1.17 | 1,728 | 1.09 | — | % | 10 | |||||||||||||||

Net merger-related and restructuring expenses | 6 | — | 29 | 0.01 | 25 | 0.02 | 15 | 0.01 | 46 | 0.03 | (100 | ) | (100 | ) | |||||||||||||||

Earnings excluding merger-related and restructuring expenses | 2,308 | 1.20 | 2,330 | 1.21 | 1,902 | 1.19 | 1,900 | 1.18 | 1,774 | 1.12 | (1 | ) | 7 | ||||||||||||||||

Discontinued operations, net of income taxes | — | — | (46 | ) | (0.02 | ) | �� | — | — | — | — | — | — | — | |||||||||||||||

Earnings excluding merger-related and restructuring expenses, and discontinued operations | 2,308 | 1.20 | 2,284 | 1.19 | 1,902 | 1.19 | 1,900 | 1.18 | 1,774 | 1.12 | 1 | 7 | |||||||||||||||||

Deposit base and other intangible amortization | 76 | 0.04 | 90 | 0.05 | 59 | 0.04 | 64 | 0.04 | 59 | 0.04 | (20 | ) | — | ||||||||||||||||

Earnings excluding merger-related and restructuring expenses, other intangible amortization and discontinued operations | $ | 2,384 | 1.24 | 2,374 | 1.24 | 1,961 | 1.23 | 1,964 | 1.22 | 1,833 | 1.16 | — | % | 7 | |||||||||||||||

KEY POINTS

| • | Expect remaining 2007 intangible amortization of $0.09 per share: 2Q07 $0.03; 3Q07 $0.03; 4Q07 $0.03, based on 1Q07 average diluted shares outstanding of 1,925 million |

Page-3

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Earnings Summary

| 2007 | 2006 | 1Q07 vs 4Q06 | 1Q07 vs 1Q06 | Combined | |||||||||||||||||||||

(In millions, except per share data) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | 1Q06 | 1Q07 vs 1Q06 | ||||||||||||||||||

Net interest income(Tax-equivalent) | $ | 4,497 | 4,612 | 3,578 | 3,675 | 3,539 | (2 | )% | 27 | $ | 4,441 | 1 | % | ||||||||||||

Fee and other income | 3,741 | 3,980 | 3,465 | 3,583 | 3,517 | (6 | ) | 6 | 3,545 | 6 | |||||||||||||||

Total revenue(Tax-equivalent) | 8,238 | 8,592 | 7,043 | 7,258 | 7,056 | (4 | ) | 17 | 7,986 | 3 | |||||||||||||||

Provision for credit losses | 177 | 206 | 108 | 59 | 61 | (14 | ) | 190 | 65 | 172 | |||||||||||||||

Other noninterest expense | 4,460 | 4,741 | 3,915 | 4,139 | 4,079 | (6 | ) | 9 | 4,350 | 3 | |||||||||||||||

Merger-related and restructuring expenses | 10 | 49 | 38 | 24 | 68 | (80 | ) | (85 | ) | 68 | (85 | ) | |||||||||||||

Other intangible amortization | 118 | 141 | 92 | 98 | 92 | (16 | ) | 28 | 131 | (10 | ) | ||||||||||||||

Total noninterest expense | 4,588 | 4,931 | 4,045 | 4,261 | 4,239 | (7 | ) | 8 | 4,549 | 1 | |||||||||||||||

Minority interest in income of consolidated subsidiaries | 136 | 125 | 104 | 90 | 95 | 9 | 43 | 95 | 43 | ||||||||||||||||

Income from continuing operations before income taxes(Tax-equivalent) | 3,337 | 3,330 | 2,786 | 2,848 | 2,661 | — | 25 | 3,277 | 2 | ||||||||||||||||

Income taxes(Tax-equivalent) | 1,035 | 1,075 | 909 | 963 | 933 | (4 | ) | 11 | 1,175 | (12 | ) | ||||||||||||||

Income from continuing operations | 2,302 | 2,255 | 1,877 | 1,885 | 1,728 | 2 | 33 | 2,102 | 10 | ||||||||||||||||

Discontinued operations, net of income taxes | — | 46 | — | — | — | — | — | — | — | ||||||||||||||||

Net income | $ | 2,302 | 2,301 | 1,877 | 1,885 | 1,728 | — | % | 33 | $ | 2,102 | 10 | % | ||||||||||||

Diluted earnings per common share from continuing operations | $ | 1.20 | 1.18 | 1.17 | 1.17 | 1.09 | 2 | % | 10 | ||||||||||||||||

Diluted earnings per common share based on net income | $ | 1.20 | 1.20 | 1.17 | 1.17 | 1.09 | — | 10 | |||||||||||||||||

Dividend payout ratio on common shares | 46.67 | % | 46.67 | 47.86 | 43.59 | 46.79 | — | — | |||||||||||||||||

Return on average common stockholders’ equity | 13.47 | 13.09 | 14.85 | 15.41 | 14.62 | — | — | ||||||||||||||||||

Return on average assets | 1.34 | 1.31 | 1.34 | 1.39 | 1.34 | — | — | ||||||||||||||||||

Overhead efficiency ratio(Tax-equivalent) | 55.70 | % | 57.38 | 57.44 | 58.71 | 60.07 | — | — | 56.96 | % | — | ||||||||||||||

Operating leverage(Tax-equivalent) | $ | (13 | ) | 665 | 1 | 180 | 436 | — | % | — | |||||||||||||||

KEY POINTS

| • | Net interest income decreased 2% as benefits from loan and securitization warehouse growth and improved retail deposit pricing were more than offset by lower income from maturing off-balance sheet positions, 4Q06 Adjustments and trading-related net interest income, as well as the effect of FSP 13-2/FIN 48 adoption |

| — | The positive effect of retail deposit pricing strategies was somewhat negatively impacted by the effect of seasonally lower corporate deposit balances and continued migration to off-balance sheet alternatives |

| — | Net interest income up 1% from Combined 1Q06 reflecting growth in earning assets, including Westcorp, largely offset by a shift in deposit mix to lower spread categories and the impact of the interest rate environment |

(See Appendix, pages 19-23 for further detail)

Page-4

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Performance Highlights

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||

(Dollars in millions, except per share data) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||

Earnings excluding merger-related and restructuring expenses, and discontinued operations (a)(b) | ||||||||||||||||||

Net income | $ | 2,308 | 2,284 | 1,902 | 1,900 | 1,774 | 1 | % | 30 | |||||||||

Return on average assets | 1.35 | % | 1.30 | 1.36 | 1.40 | 1.38 | — | — | ||||||||||

Return on average common stockholders’ equity | 13.50 | 12.98 | 15.02 | 15.52 | 15.01 | — | — | |||||||||||

Overhead efficiency ratio(Tax-equivalent) | 55.57 | 56.81 | 56.90 | 58.39 | 59.10 | — | — | |||||||||||

Overhead efficiency ratio excluding brokerage(Tax-equivalent) | 52.37 | % | 53.55 | 53.29 | 54.85 | 55.20 | — | — | ||||||||||

Operating leverage(Tax-equivalent) | $ | (51 | ) | 675 | 16 | 135 | 446 | — | % | — | ||||||||

Earnings excluding merger-related and restructuring expenses, other intangible amortization and discontinued operations (a)(b) | ||||||||||||||||||

Net income | $ | 2,384 | 2,374 | 1,961 | 1,964 | 1,833 | — | % | 30 | |||||||||

Dividend payout ratio on common shares | 45.16 | % | 45.16 | 45.53 | 41.80 | 43.97 | — | — | ||||||||||

Return on average tangible assets | 1.48 | 1.43 | 1.47 | 1.52 | 1.49 | — | — | |||||||||||

Return on average tangible common stockholders’ equity | 33.27 | 31.58 | 30.79 | 32.63 | 30.64 | — | — | |||||||||||

Overhead efficiency ratio(Tax-equivalent) | 54.15 | 55.17 | 55.60 | 57.03 | 57.81 | — | — | |||||||||||

Overhead efficiency ratio excluding brokerage(Tax-equivalent) | 50.65 | % | 51.61 | 51.73 | 53.21 | 53.63 | — | — | ||||||||||

Operating leverage(Tax-equivalent) | $ | (75 | ) | 725 | 8 | 142 | 444 | — | % | — | ||||||||

Other financial data | ||||||||||||||||||

Net interest margin | 3.01 | % | 3.09 | 3.03 | 3.18 | 3.21 | — | — | ||||||||||

Fee and other income as % of total revenue | 45.41 | 46.32 | 49.20 | 49.37 | 49.84 | — | — | |||||||||||

Effective tax rate (c) | 30.22 | 31.74 | 31.71 | 33.05 | 33.84 | — | — | |||||||||||

Effective tax rate(Tax-equivalent) (c) (d) | 30.99 | % | 32.46 | 32.61 | 33.84 | 35.06 | — | — | ||||||||||

Asset quality | ||||||||||||||||||

Allowance for loan losses as % of loans, net | 0.80 | % | 0.80 | 1.03 | 1.07 | 1.08 | — | — | ||||||||||

Allowance for loan losses as % of nonperforming assets | 194 | 246 | 396 | 421 | 389 | — | — | |||||||||||

Allowance for credit losses as % of loans, net | 0.84 | 0.84 | 1.09 | 1.13 | 1.14 | — | — | |||||||||||

Net charge-offs as % of average loans, net | 0.15 | 0.14 | 0.16 | 0.08 | 0.09 | — | — | |||||||||||

Nonperforming assets as % of loans, net, foreclosed properties and loans held for sale | 0.40 | % | 0.32 | 0.26 | 0.25 | 0.28 | — | — | ||||||||||

Capital adequacy | ||||||||||||||||||

Tier 1 capital ratio (e) | 7.4 | % | 7.4 | 7.7 | 7.8 | 7.9 | — | — | ||||||||||

Tangible capital ratio(including FAS 115/133/158) | 4.4 | 4.5 | 4.9 | 4.5 | 4.8 | — | — | |||||||||||

Tangible capital ratio(excluding FAS 115/133/158) | 4.7 | 4.8 | 5.1 | 5.0 | 5.1 | — | — | |||||||||||

Leverage ratio (e) | 6.1 | % | 6.0 | 6.6 | 6.6 | 6.9 | — | — | ||||||||||

Other | ||||||||||||||||||

Average diluted common shares(In millions) | 1,925 | 1,922 | 1,600 | 1,613 | 1,586 | — | % | 21 | ||||||||||

Actual common shares(In millions) | 1,913 | 1,904 | 1,581 | 1,589 | 1,608 | — | 19 | |||||||||||

Dividends paid per common share | $ | 0.56 | 0.56 | 0.56 | 0.51 | 0.51 | — | 10 | ||||||||||

Book value per common share | 36.47 | 36.61 | 32.37 | 30.75 | 30.95 | — | 18 | |||||||||||

Common stock price | 55.05 | 56.95 | 55.80 | 54.08 | 56.05 | (3 | ) | (2 | ) | |||||||||

Market capitalization | $ | 105,330 | 108,443 | 88,231 | 85,960 | 90,156 | (3 | ) | 17 | |||||||||

Common stock price to book value | 151 | % | 156 | 172 | 176 | 181 | (3 | ) | (17 | ) | ||||||||

FTE employees (f) | 110,369 | 109,460 | 97,060 | 97,316 | 97,134 | 1 | 14 | |||||||||||

Total financial centers/brokerage offices | 4,167 | 4,126 | 3,870 | 3,847 | 3,889 | 1 | 7 | |||||||||||

ATMs | 5,146 | 5,212 | 5,163 | 5,134 | 5,179 | (1 | )% | (1 | ) | |||||||||

| (a) | See tables on page 3, and on pages 42 through 46 for reconciliation to earnings prepared in accordance with GAAP. |

| (b) | See page 3 for the most directly comparable GAAP financial measure and pages 42 through 46 for reconciliation to earnings prepared in accordance with GAAP. |

| (c) | 4Q06 includes taxes on discontinued operations. |

| (d) | The tax-equivalent tax rate applies to fully tax-equivalized revenues. |

| (e) | The first quarter of 2007 is based on estimates. |

| (f) | Amount presented in the fourth quarter of 2006 has been restated to conform with the presentation in 2007. |

KEY POINTS

| • | Cash overhead efficiency ratio declined 102 bps to 54.15% reflecting expense discipline |

| • | Net interest margin declined to 3.01% as benefits of the improved retail deposit pricing were more than offset by growth in lower-spread assets, lower contributions from maturing off-balance sheet positions, lower trading-related net interest income and the continued effect of the yield curve |

| • | Effective tax rate of 30.99% reflects updated information on certain tax matters |

| • | Tangible capital ratio of 4.7% largely reflects the adoption of FSP 13-2/FIN 48 |

| • | Average diluted shares up 3 million reflecting the net effect of employee stock option and restricted share activity somewhat offset by the repurchase of 5 million shares during the quarter at an average cost of $56.72 per share and the ongoing effect of 4Q06 repurchases |

(See Appendix, pages 16-23 for further detail)

Page-5

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Average Balance Sheet Data

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | Combined | |||||||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | 1Q06 | 1Q07 vs 1Q06 | ||||||||||||||||

Assets | |||||||||||||||||||||||

Trading assets | $ | 29,681 | 31,069 | 31,160 | 29,252 | 27,240 | (4 | )% | 9 | $ | 27,240 | 9 | % | ||||||||||

Securities | 108,071 | 108,543 | 122,152 | 124,102 | 117,944 | — | (8 | ) | 119,421 | (10 | ) | ||||||||||||

Commercial loans, net | |||||||||||||||||||||||

General Bank | 95,653 | 92,990 | 90,837 | 88,729 | 85,614 | 3 | 12 | 85,746 | 12 | ||||||||||||||

Corporate and Investment Bank | 40,938 | 41,064 | 39,797 | 37,730 | 36,867 | — | 11 | 36,867 | 11 | ||||||||||||||

Other | 20,697 | 20,252 | 19,932 | 19,882 | 19,988 | 2 | 4 | 20,182 | 3 | ||||||||||||||

Total commercial loans, net | 157,288 | 154,306 | 150,566 | 146,341 | 142,469 | 2 | 10 | 142,795 | 10 | ||||||||||||||

Consumer loans, net | 257,973 | 258,255 | 130,544 | 128,924 | 118,105 | — | 118 | 236,856 | 9 | ||||||||||||||

Total loans, net | 415,261 | 412,561 | 281,110 | 275,265 | 260,574 | 1 | 59 | 379,651 | 9 | ||||||||||||||

Loans held for sale | 16,748 | 11,928 | 12,130 | 9,320 | 8,274 | 40 | 102 | 8,378 | 100 | ||||||||||||||

Other earning assets (a) | 24,552 | 32,792 | 25,587 | 25,293 | 28,495 | (25 | ) | (14 | ) | 32,090 | (23 | ) | |||||||||||

Total earning assets | 594,313 | 596,893 | 472,139 | 463,232 | 442,527 | — | 34 | 566,780 | 5 | ||||||||||||||

Cash | 12,260 | 12,418 | 11,973 | 12,055 | 12,762 | (1 | ) | (4 | ) | 13,217 | (7 | ) | |||||||||||

Other assets | 88,875 | 89,376 | 71,052 | 68,325 | 66,920 | (1 | ) | 33 | 82,850 | 7 | |||||||||||||

Total assets | $ | 695,448 | 698,687 | 555,164 | 543,612 | 522,209 | — | % | 33 | $ | 662,847 | 5 | % | ||||||||||

Liabilities and Stockholders’ Equity | |||||||||||||||||||||||

Core interest-bearing deposits | $ | 308,294 | 299,402 | 227,674 | 226,140 | 225,724 | 3 | % | 37 | $ | 286,746 | 8 | % | ||||||||||

Foreign and other time deposits | 33,605 | 32,953 | 35,133 | 36,300 | 32,616 | 2 | 3 | 32,634 | 3 | ||||||||||||||

Total interest-bearing deposits | 341,899 | 332,355 | 262,807 | 262,440 | 258,340 | 3 | 32 | 319,380 | 7 | ||||||||||||||

Short-term borrowings | 55,669 | 65,239 | 71,030 | 69,069 | 70,014 | (15 | ) | (20 | ) | 76,296 | (27 | ) | |||||||||||

Long-term debt | 141,979 | 139,364 | 80,726 | 71,725 | 56,052 | 2 | 153 | 111,114 | 28 | ||||||||||||||

Total interest-bearing liabilities | 539,547 | 536,958 | 414,563 | 403,234 | 384,406 | — | 40 | 506,790 | 6 | ||||||||||||||

Noninterest-bearing deposits | 60,976 | 63,025 | 63,553 | 65,498 | 64,490 | (3 | ) | (5 | ) | 64,636 | (6 | ) | |||||||||||

Other liabilities | 25,605 | 28,979 | 26,905 | 25,817 | 25,387 | (12 | ) | 1 | 25,861 | (1 | ) | ||||||||||||

Total liabilities | 626,128 | 628,962 | 505,021 | 494,549 | 474,283 | — | 32 | 597,287 | 5 | ||||||||||||||

Stockholders’ equity | 69,320 | 69,725 | 50,143 | 49,063 | 47,926 | (1 | ) | 45 | 65,560 | 6 | |||||||||||||

Total liabilities and stockholders’ equity | $ | 695,448 | 698,687 | 555,164 | 543,612 | 522,209 | — | % | 33 | $ | 662,847 | 5 | % | ||||||||||

(a) Includes interest-bearing bank balances, federal funds sold and securities purchased under resale agreements. |

| ||||||||||||||||||||||

Memoranda | |||||||||||||||||||||||

Low-cost core deposits | $ | 253,008 | 250,569 | 238,875 | 243,249 | 243,905 | 1 | % | 4 | $ | 259,175 | (2 | )% | ||||||||||

Other core deposits | 116,262 | 111,858 | 52,352 | 48,389 | 46,309 | 4 | 151 | 92,207 | 26 | ||||||||||||||

Total core deposits | $ | 369,270 | 362,427 | 291,227 | 291,638 | 290,214 | 2 | % | 27 | $ | 351,382 | 5 | % | ||||||||||

KEY POINTS

| • | Securities relatively stable, down 10% from Combined 1Q06 largely reflecting $13.2 billion of sales relating to the Golden West merger |

| • | Commercial loans increased $3.0 billion, or 2%, as strength in middle-market and business banking, commercial real estate portfolios and foreign loans was somewhat offset by a $1.9 billion decline in leasing including $1.4 billion relating to the adoption of FSP 13-2/FIN 48; up 10% from 1Q06 |

| • | Consumer loans remained relatively stable as growth in real estate-secured and auto was more than offset by the $1.4 billion average effect of securitization and sales; increased $139.9 billion from 1Q06 driven by the addition of Golden West;Consumer loans up 9% from Combined 1Q06 largely reflecting growth in real estate-secured and auto, including the impact of Westcorp, and strength in credit card |

| • | Loans held for sale increased $4.8 billion largely reflecting growth in the commercial mortgage securitization warehouse |

| • | Other earning assets down $8.2 billion driven by lower fed funds sold and repos reflecting temporary excess 4Q06 liquidity related to balance sheet repositioning, including deleveraging, in connection with the Golden West merger |

| • | Long-term debt (original maturity > 12 months) increased $2.6 billion driven by the effect of 1Q07 issuances of $12.4 billion and the continuing effect of 4Q06 issuances of $10.4 billion |

| • | Core deposits increased $6.8 billion, or 2%, reflecting strength in retail CDs, interest-bearing and foreign; up 27% from 1Q06 driven by merger activity |

| — | Up $17.9 billion, or 5%, from Combined 1Q06 driven by strength in retail CDs, NOW and foreign |

(See Appendix, pages 19 - 21 for further detail)

Page-6

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Fee and Other Income

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | Combined | |||||||||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | 1Q06 | 1Q07 vs 1Q06 | ||||||||||||||||||

Service charges | $ | 614 | 646 | 638 | 622 | 574 | (5 | )% | 7 | $ | 576 | 7 | % | ||||||||||||

Other banking fees | 416 | 452 | 427 | 449 | 428 | (8 | ) | (3 | ) | 443 | (6 | ) | |||||||||||||

Commissions | 659 | 633 | 562 | 588 | 623 | 4 | 6 | 630 | 5 | ||||||||||||||||

Fiduciary and asset management fees | 920 | 856 | 823 | 808 | 761 | 7 | 21 | 761 | 21 | ||||||||||||||||

Advisory, underwriting and other investment banking fees | 407 | 433 | 292 | 318 | 302 | (6 | ) | 35 | 302 | 35 | |||||||||||||||

Trading account profits | 168 | 29 | 123 | 164 | 219 | — | (23 | ) | 219 | (23 | ) | ||||||||||||||

Principal investing | 48 | 142 | 91 | 189 | 103 | (66 | ) | (53 | ) | 103 | (53 | ) | |||||||||||||

Securities gains (losses) | 53 | 47 | 94 | 25 | (48 | ) | 13 | — | (48 | ) | — | ||||||||||||||

Other income | 456 | 742 | 415 | 420 | 555 | (39 | ) | (18 | ) | 559 | (18 | ) | |||||||||||||

Total fee and other income | $ | 3,741 | 3,980 | 3,465 | 3,583 | 3,517 | (6 | )% | 6 | $ | 3,545 | 6 | % | ||||||||||||

KEY POINTS

| • | Fee and other income decreased 6%; grew 6% vs. 1Q06 which included $133 million relating to MBNA fee and Archipelago/NYSE gain |

| — | Fee income up 11% from 1Q06 exclusive of the above mentioned one-time fee and gain |

Fee and Other Income

(In millions) | A Reported 1Q07 | B Reported 4Q06 | C 4Q06 | B+C Adjusted Reported 4Q06 | 1Q07 vs Adj 4Q06 | ||||||||

Service charges | $ | 614 | 646 | (22 | ) | 624 | (2 | )% | |||||

Securities gains | 53 | 47 | — | 47 | 13 | ||||||||

Other income | 3,074 | 3,287 | (93 | ) | 3,194 | (4 | ) | ||||||

Total fee and other income | $ | 3,741 | 3,980 | (115 | ) | 3,865 | (3 | )% | |||||

| — | Down 3% vs. strong Adjusted 4Q06 levels which included robust commercial mortgage securitization income and principal investing gains, as well as fiduciary and asset management fees and record advisory and underwriting fees |

| • | Service charges down 5%; rose 7% from 1Q06 |

| — | Service charges decreased 2% vs. Adjusted 4Q06 as strength in commercial was more than offset by seasonally lower consumer volumes |

| • | Other banking fees declined 8% driven by the effect of the HomEq divestiture and declines in consumer and commercial mortgage banking fees as well as seasonally lower interchange fees; down 3% from 1Q06 as strength in interchange was more than offset by lower mortgage banking fees |

| • | Commissions increased 4% and 6% from 1Q06 on strength in retail brokerage transaction activity driven by higher equity syndicate volumes |

| • | Fiduciary and asset management fees grew 7% driven by the addition of European Credit Management (“ECM”) and continued growth in retail brokerage managed account fees; up 21% from 1Q06 |

| — | Results vs. 1Q06 largely reflect strength in retail brokerage managed account fees and the effect of acquisitions |

| • | Advisory, underwriting and other investment banking fees decreased $26 million, or 6%, from robust 4Q06 levels; up 35% from 1Q06 on strength in equities reflecting enhanced CIB/CMG partnership, and growth in high yield and loan syndications |

| • | Trading account profits increased $139 million driven by strength in global rate and credit products |

| • | Principal investing net gains of $48 million decreased $94 million from strong 4Q06 levels |

| • | Other income decreased $286 million driven by $133 million decline in commercial mortgage securitization activity, $93 million relating to 4Q06 Adjustments and $49 million decrease in consumer loan securitization activity |

(See Appendix, pages 22-23 for further detail)

Page-7

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Noninterest Expense

Noninterest Expense

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | Combined | |||||||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | 1Q06 | 1Q07 vs 1Q06 | ||||||||||||||||

Salaries and employee benefits | $ | 2,972 | 3,023 | 2,531 | 2,652 | 2,697 | (2 | )% | 10 | $ | 2,889 | 3 | % | ||||||||||

Occupancy | 312 | 323 | 284 | 291 | 275 | (3 | ) | 13 | 294 | 6 | |||||||||||||

Equipment | 307 | 314 | 291 | 299 | 280 | (2 | ) | 10 | 300 | 2 | |||||||||||||

Advertising | 61 | 47 | 54 | 56 | 47 | 30 | 30 | 52 | 17 | ||||||||||||||

Communications and supplies | 173 | 166 | 158 | 162 | 167 | 4 | 4 | 180 | (4 | ) | |||||||||||||

Professional and consulting fees | 177 | 239 | 200 | 184 | 167 | (26 | ) | 6 | 174 | 2 | |||||||||||||

Sundry expense | 458 | 629 | 397 | 495 | 446 | (27 | ) | 3 | 461 | (1 | ) | ||||||||||||

Other noninterest expense | 4,460 | 4,741 | 3,915 | 4,139 | 4,079 | (6 | ) | 9 | 4,350 | 3 | |||||||||||||

Merger-related and restructuring expenses | 10 | 49 | 38 | 24 | 68 | (80 | ) | (85 | ) | 68 | (85 | ) | |||||||||||

Other intangible amortization | 118 | 141 | 92 | 98 | 92 | (16 | ) | 28 | 131 | (10 | ) | ||||||||||||

Total noninterest expense | $ | 4,588 | 4,931 | 4,045 | 4,261 | 4,239 | (7 | )% | 8 | $ | 4,549 | 1 | % | ||||||||||

KEY POINTS

| • | Other noninterest expense decreased 6%; rose 9% vs. 1Q06 driven by merger activity |

| — | Other noninterest expense down $83 million, or 2%, from Adjusted 4Q06 reflecting expense discipline despite $93 million higher employee stock compensation expense |

Noninterest Expense

(In millions) | A Reported 1Q07 | B Reported 4Q06 | C 4Q06 | B+C Adjusted Reported 4Q06 | 1Q07 vs Adj 4Q06 | ||||||||

Salaries and employee benefits | $ | 2,972 | 3,023 | (99 | ) | 2,924 | 2 | % | |||||

Sundry expense | 458 | 629 | (99 | ) | 530 | (14 | ) | ||||||

Other expense | 1,030 | 1,089 | — | 1,089 | (5 | ) | |||||||

Other noninterest expense | $ | 4,460 | 4,741 | (198 | ) | 4,543 | (2 | )% | |||||

| — | 1Q07 results include $16 million relating to efficiency initiative spending, $31 million associated with de novo expansion and branch consolidations and $26 million relating to credit card |

| • | Salaries and employee benefits decreased 2% and up 10% from 1Q06;up $48 million from Adjusted 4Q06 as $93 million increase in employee stock compensation expense more than offset lower revenue-based incentives |

| • | Professional and consulting fees decreased 26% reflecting discipline and reductions from seasonally high 4Q06 levels |

| • | Sundry expense decreased 27%, down 14% from Adjusted 4Q06 |

| — | 1Q07 sundry expense reflects lower legal costs and expense discipline in travel and entertainment expense and other areas |

(See Appendix, page 23 for further detail)

Page-8

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

This segment includes Retail and Small Business, and Commercial.

General Bank

Performance Summary

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | Combined | |||||||||||||||||||||

(Dollars in millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | 1Q06 | 1Q07 vs 1Q06 | ||||||||||||||||||

Income statement data | |||||||||||||||||||||||||

Net interest income(Tax-equivalent) | $ | 3,705 | 3,764 | 2,819 | 2,779 | 2,531 | (2 | )% | 46 | $ | 3,483 | 6 | % | ||||||||||||

Fee and other income | 862 | 946 | 891 | 847 | 868 | (9 | ) | (1 | ) | 884 | (2 | ) | |||||||||||||

Intersegment revenue | 48 | 58 | 48 | 48 | 43 | (17 | ) | 12 | 43 | 12 | |||||||||||||||

Total revenue(Tax-equivalent) | 4,615 | 4,768 | 3,758 | 3,674 | 3,442 | (3 | ) | 34 | 4,410 | 5 | |||||||||||||||

Provision for credit losses | 162 | 147 | 122 | 95 | 62 | 10 | — | 62 | 161 | ||||||||||||||||

Noninterest expense | 2,030 | 1,996 | 1,676 | 1,737 | 1,656 | 2 | 23 | 1,901 | 7 | ||||||||||||||||

Income taxes(Tax-equivalent) | 884 | 958 | 715 | 673 | 629 | (8 | ) | 41 | 894 | (1 | ) | ||||||||||||||

Segment earnings | $ | 1,539 | 1,667 | 1,245 | 1,169 | 1,095 | (8 | )% | 41 | $ | 1,553 | (1 | )% | ||||||||||||

Performance and other data | |||||||||||||||||||||||||

Economic profit | $ | 1,159 | 1,283 | 982 | 896 | 854 | (10 | )% | 36 | ||||||||||||||||

Risk adjusted return on capital (RAROC) | 48.22 | % | 51.94 | 57.44 | 54.76 | 58.38 | — | — | |||||||||||||||||

Economic capital, average | $ | 12,622 | 12,439 | 8,384 | 8,218 | 7,308 | 1 | 73 | |||||||||||||||||

Cash overhead efficiency ratio(Tax-equivalent) | 43.98 | % | 41.86 | 44.59 | 47.29 | 48.10 | — | — | 43.13 | % | — | % | |||||||||||||

Lending commitments | $ | 145,326 | 139,940 | 128,380 | 121,181 | 115,788 | 4 | 26 | |||||||||||||||||

Average loans, net | 326,808 | 324,168 | 196,396 | 191,769 | 177,458 | 1 | 84 | $ | 297,145 | 10 | % | ||||||||||||||

Average core deposits | $ | 292,389 | 288,578 | 216,591 | 214,666 | 211,169 | 1 | 38 | $ | 272,263 | 7 | % | |||||||||||||

FTE employees | 57,224 | 56,556 | 45,250 | 44,973 | 44,927 | 1 | % | 27 | |||||||||||||||||

General Bank Key Metrics

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||

| First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | ||||||||||||

Customer overall satisfaction score (a) | 6.63 | 6.64 | 6.62 | 6.61 | 6.62 | — | % | — | ||||||||

New/Lost ratio | 1.26 | 1.29 | 1.30 | 1.31 | 1.27 | (2 | ) | (1 | ) | |||||||

Online active customers(In thousands)(b) | 4,103 | 3,997 | 3,833 | 3,634 | 3,421 | 3 | 20 | |||||||||

Financial centers | 3,399 | 3,375 | 3,133 | 3,109 | 3,159 | 1 | % | 8 | ||||||||

| (a) | Gallup survey measured on a 1-7 scale; 6.4 = “best in class”. |

| (b) | Retail and small business. |

SEGMENTEARNINGSOF $1.5BILLIONDOWN 8%ANDUP 41%FROM 1Q06

| • | Revenue of $4.6 billion down 3%, and up 34% from 1Q06 driven by acquisitions and strong loan and deposit growth |

| — | Net interest income down $59 million, or 2%, largely reflecting $15 million relating to day count, $15 million relating to lower mortgage loans and $29 million due to narrowing spreads on loans and deposits; up 6% from Combined 1Q06 |

| — | Fees down $84 million as lower branch and loan sale gains, seasonally lower consumer service charges and interchange fees more than offset improvement in commercial service charges |

| • | Excluding the 1Q06 $100 million MBNA fee, fees up $94 million, or 12%, driven by strength in consumer and commercial service charges and interchange fees |

| • | Expenses up $34 million, or 2%, as benefits of strong expense control were more than offset by $46 million of higher employee stock compensation expense; up 23% from 1Q06 driven largely by merger activity |

| — | Reflects $31 million due to de novo expansion and branch consolidation costs and $26 million relating to credit card |

| • | Average loans up 1% and up 84% from 1Q06 reflecting merger activity; loans up 10% from Combined 1Q06 |

| — | Commercial loans up 3% on growth in business banking, middle-market and commercial real estate |

| — | Consumer loans flat as strength in credit card and auto offset by decreases in real estate-secured |

| • | Average core deposits up 1% and up 38% from 1Q06 reflecting merger activity |

| — | Core deposits up 7% from Combined 1Q06 driven by growth in retail CDs and commercial deposits |

| — | Retail net new checking account sales up 44% to 270,000 including 38,000 in World Savings network |

| • | Opened 29 de novo branches during the quarter; 21 California branches now branded Wachovia |

(See Appendix, pages 25 - 29 for further discussion of business unit results

Page-9

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Wealth Management

Performance Summary

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||

(Dollars in millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||

Income statement data | ||||||||||||||||||

Net interest income(Tax-equivalent) | $ | 146 | 149 | 148 | 149 | 150 | (2 | )% | (3 | ) | ||||||||

Fee and other income | 195 | 200 | 197 | 194 | 188 | (3 | ) | 4 | ||||||||||

Intersegment revenue | 1 | 3 | 1 | 1 | 1 | (67 | ) | — | ||||||||||

Total revenue(Tax-equivalent) | 342 | 352 | 346 | 344 | 339 | (3 | ) | 1 | ||||||||||

Provision for credit losses | — | — | — | 2 | — | — | — | |||||||||||

Noninterest expense | 241 | 236 | 235 | 249 | 248 | 2 | (3 | ) | ||||||||||

Income taxes(Tax-equivalent) | 36 | 43 | 41 | 33 | 34 | (16 | ) | 6 | ||||||||||

Segment earnings | $ | 65 | 73 | 70 | 60 | 57 | (11 | )% | 14 | |||||||||

Performance and other data | ||||||||||||||||||

Economic profit | $ | 46 | 53 | 52 | 41 | 39 | (13 | )% | 18 | |||||||||

Risk adjusted return on capital (RAROC) | 43.63 | % | 47.58 | 46.77 | 40.61 | 39.34 | — | — | ||||||||||

Economic capital, average | $ | 566 | 574 | 568 | 563 | 556 | (1 | ) | 2 | |||||||||

Cash overhead efficiency ratio(Tax-equivalent) | 70.22 | % | 67.38 | 67.85 | 72.30 | 73.25 | — | — | ||||||||||

Lending commitments | $ | 6,686 | 6,504 | 6,481 | 6,285 | 6,229 | 3 | 7 | ||||||||||

Average loans, net | 17,180 | 16,794 | 16,469 | 16,016 | 15,603 | 2 | 10 | |||||||||||

Average core deposits | $ | 14,037 | 14,208 | 13,775 | 14,265 | 14,609 | (1 | ) | (4 | ) | ||||||||

FTE employees | 4,393 | 4,474 | 4,530 | 4,727 | 4,758 | (2 | )% | (8 | ) | |||||||||

| Wealth Management Key Metrics | ||||||||||||||||||

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||

(Dollars in millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||

Investment assets under administration | $ | 135,562 | 143,879 | 138,915 | 135,817 | 134,293 | (6 | )% | 1 | |||||||||

Assets under management (a) | $ | 76,214 | 75,297 | 72,397 | 71,184 | 71,120 | 1 | 7 | ||||||||||

Wealth Management advisors | 940 | 951 | 970 | 996 | 973 | (1 | )% | (3 | ) | |||||||||

| (a) | These assets are managed by and reported in Capital Management. |

SEGMENTEARNINGSOF $65MILLION,DOWN 11%ANDUP 14%FROM 1Q06

| • | Revenue of $342 million decreased 3%; up 1% from 1Q06 |

| — | Net interest income was down 2% reflecting lower core deposits and narrowing spreads which offset loan growth |

| — | Fee and other income decreased 3% from strong 4Q06 levels driven by lower insurance commissions, which more than offset growth in fiduciary and asset management fees |

| • | Expenses up 2% as lower salaries and benefits were more than offset by $8 million in higher employee stock compensation expense; down 3% from 1Q06 driven by lower salaries, benefits and incentives |

| • | Assets under management increased 1%, and 7% from 1Q06, on market gains |

| — | 78% acceptance rate on introduction of new investment platform |

(See Appendix, page 30 for further discussion of business unit results)

Page-10

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

This segment includes Corporate Lending, Investment Banking, and Treasury and International Trade Finance.

Corporate and Investment Bank

Performance Summary

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||||||

(Dollars in millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||||||

Income statement data | ||||||||||||||||||||||

Net interest income(Tax-equivalent) | $ | 453 | 512 | 450 | 468 | 463 | (12 | )% | (2 | ) | ||||||||||||

Fee and other income | 1,088 | 1,355 | 992 | 1,217 | 1,242 | (20 | ) | (12 | ) | |||||||||||||

Intersegment revenue | (42 | ) | (56 | ) | (43 | ) | (42 | ) | (37 | ) | (25 | ) | 14 | |||||||||

Total revenue(Tax-equivalent) | 1,499 | 1,811 | 1,399 | 1,643 | 1,668 | (17 | ) | (10 | ) | |||||||||||||

Provision for credit losses | — | 5 | (5 | ) | (33 | ) | 1 | — | — | |||||||||||||

Noninterest expense | 903 | 999 | 797 | 886 | 893 | (10 | ) | 1 | ||||||||||||||

Income taxes(Tax-equivalent) | 217 | 294 | 222 | 288 | 283 | (26 | ) | (23 | ) | |||||||||||||

Segment earnings | $ | 379 | 513 | 385 | 502 | 491 | (26 | )% | (23 | ) | ||||||||||||

Performance and other data | ||||||||||||||||||||||

Economic profit | $ | 159 | 290 | 167 | 275 | 301 | (45 | )% | (47 | ) | ||||||||||||

Risk adjusted return on capital (RAROC) | 20.10 | % | 27.14 | 20.88 | 27.98 | 31.15 | — | — | ||||||||||||||

Economic capital, average | $ | 7,088 | 7,117 | 6,707 | 6,499 | 6,066 | — | 17 | ||||||||||||||

Cash overhead efficiency ratio(Tax-equivalent) | 60.20 | % | 55.16 | 57.02 | 53.90 | 53.55 | — | — | ||||||||||||||

Lending commitments | $ | 106,578 | 107,155 | 102,698 | 106,105 | 103,812 | (1 | ) | 3 | |||||||||||||

Average loans, net | 40,946 | 41,069 | 39,801 | 37,733 | 36,871 | — | 11 | |||||||||||||||

Average core deposits | $ | 28,948 | 26,993 | 26,223 | 26,346 | 25,568 | 7 | 13 | ||||||||||||||

FTE employees | 5,959 | 6,040 | 6,049 | 6,227 | 5,994 | (1 | )% | (1 | ) | |||||||||||||

Corporate and Investment Bank

Sub-segment Revenue | ||||||||||||||||||||||

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||||||

Investment Banking | $ | 968 | 1,269 | 868 | 1,093 | 1,102 | (24 | )% | (12 | ) | ||||||||||||

Corporate Lending | 282 | 281 | 269 | 285 | 315 | — | (10 | ) | ||||||||||||||

Treasury and International Trade Finance | 249 | 261 | 262 | 265 | 251 | (5 | ) | (1 | ) | |||||||||||||

Total revenue(Tax-equivalent) | $ | 1,499 | 1,811 | 1,399 | 1,643 | 1,668 | (17 | )% | (10 | ) | ||||||||||||

Memoranda | ||||||||||||||||||||||

Total net trading revenue(Tax-equivalent) | $ | 218 | 182 | 225 | 281 | 361 | 20 | % | (40 | ) | ||||||||||||

SEGMENTEARNINGSOF $379MILLION,DOWN 26%AND 23%FROM 1Q06

| • | Revenue of $1.5 billion decreased 17% and 10% from 1Q06 |

| — | Net interest income down 12% driven by lower trading-related net interest income and narrowing spreads |

| — | Fee and other income declined 20% from strong 4Q06 driven by lower results in structured products and M&A from record levels as well as lower principal investing results, somewhat offset by improvement in trading results |

| • | Strong origination revenues and underlying momentum in commercial mortgage securititization activity muted by the effect of higher 4Q06 asymmetrical hedge gains on the warehouse |

| • | Expenses decreased 10% driven by lower revenue-based incentives and professional and consulting fees; up 1% from 1Q06 |

| — | 1Q07 results include $20 million higher employee stock compensation expense |

| • | Average loans were relatively stable; up 11% from 1Q06 |

| • | Average core deposits grew 7% on an increase in lower-spread money market deposits; up 13% from 1Q06 |

| • | Origination pipelines showed continued strong improvement during the quarter |

(See Appendix, pages 31-34 for further discussion of business unit results)

Page-11

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

This segment includes Asset Management and Retail Brokerage Services.

Capital Management

Performance Summary

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||||||

(Dollars in millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||||||

Income statement data | ||||||||||||||||||||||

Net interest income(Tax-equivalent) | $ | 265 | 259 | 247 | 260 | 250 | 2 | % | 6 | |||||||||||||

Fee and other income | 1,458 | 1,353 | 1,231 | 1,225 | 1,230 | 8 | 19 | |||||||||||||||

Intersegment revenue | (8 | ) | (8 | ) | (8 | ) | (9 | ) | (8 | ) | — | — | ||||||||||

Total revenue(Tax-equivalent) | 1,715 | 1,604 | 1,470 | 1,476 | 1,472 | 7 | 17 | |||||||||||||||

Provision for credit losses | — | — | — | — | — | — | — | |||||||||||||||

Noninterest expense | 1,236 | 1,200 | 1,097 | 1,118 | 1,135 | 3 | 9 | |||||||||||||||

Income taxes(Tax-equivalent) | 175 | 148 | 136 | 131 | 123 | 18 | 42 | |||||||||||||||

Segment earnings | $ | 304 | 256 | 237 | 227 | 214 | 19 | % | 42 | |||||||||||||

Performance and other data | ||||||||||||||||||||||

Economic profit | $ | 261 | 215 | 198 | 187 | 175 | 21 | % | 49 | |||||||||||||

Risk adjusted return on capital (RAROC) | 77.48 | % | 67.52 | 66.78 | 63.64 | 59.88 | — | — | ||||||||||||||

Economic capital, average | $ | 1,592 | 1,504 | 1,410 | 1,428 | 1,450 | 6 | 10 | ||||||||||||||

Cash overhead efficiency ratio(Tax-equivalent) | 72.07 | % | 74.86 | 74.58 | 75.80 | 77.08 | — | — | ||||||||||||||

Lending commitments | $ | 303 | 219 | 263 | 250 | 237 | 38 | 28 | ||||||||||||||

Average loans, net | 1,554 | 1,419 | 1,235 | 1,039 | 856 | 10 | 82 | |||||||||||||||

Average core deposits | $ | 31,683 | 30,100 | 30,114 | 31,827 | 33,583 | 5 | (6 | ) | |||||||||||||

FTE employees | 17,704 | 17,515 | 17,289 | 17,242 | 17,147 | 1 | % | 3 | ||||||||||||||

| Capital Management Key Metrics | ||||||||||||||||||||||

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||||||

(Dollars in billions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||||||

Equity assets | $ | 106.3 | 103.6 | 96.4 | 93.5 | 90.1 | 3 | % | 18 | |||||||||||||

Fixed income assets | 144.0 | 114.0 | 106.7 | 101.4 | 106.0 | 26 | 36 | |||||||||||||||

Money market assets | 64.3 | 61.2 | 49.7 | 45.2 | 45.0 | 5 | 43 | |||||||||||||||

Total assets under management (a) | 314.6 | 278.8 | 252.8 | 240.1 | 241.1 | 13 | 30 | |||||||||||||||

Gross fluctuating mutual fund sales | $ | 3.7 | 3.0 | 2.0 | 2.9 | 3.7 | 23 | — | ||||||||||||||

Full-service financial advisors series 7 | 8,166 | 8,091 | 7,972 | 7,973 | 7,926 | 1 | 3 | |||||||||||||||

Financial center advisors series 6 | 2,521 | 2,497 | 2,477 | 2,541 | 2,454 | 1 | 3 | |||||||||||||||

Broker client assets (b) | $ | 773.0 | 760.0 | 729.9 | 704.3 | 689.1 | 2 | 12 | ||||||||||||||

Customer receivables including margin loans | $ | 4.7 | 4.8 | 4.9 | 5.3 | 5.6 | (2 | ) | (16 | ) | ||||||||||||

Traditional brokerage offices | 768 | 751 | 737 | 738 | 730 | 2 | 5 | |||||||||||||||

Banking centers with brokerage services (c) | 1,850 | 1,824 | 1,825 | 1,867 | 1,883 | 1 | % | (2 | ) | |||||||||||||

| (a) | Includes $76 billion in assets managed for Wealth Management, which are also reported in that segment. Beginning in 4Q06, assets under management include assets retained from the divested Corporate and Institutional Trust business, which were reported in the Parent in previous quarters. |

| (b) | Beginning in 2Q06, certain mutual funds assets were added to the overall client asset total. Prior periods have not been restated. |

| (c) | Amounts presented in 2006 have been restated to conform to the presentation in 2007. |

RECORDSEGMENTEARNINGSOF $304MILLION,UP 19%AND 42%FROM 1Q06

| • | Revenue of $1.7 billion grew 7%; up 17% from 1Q06 |

| — | Net interest income increased 2% driven by strong core deposit growth |

| — | Fee and other income rose 8% primarily driven by higher retail brokerage transaction activity and equity syndicate distribution fees, the addition of ECM, and managed account fees |

| • | Results include successful launch of new investment products reflecting strong partnership with Corporate and Investment Bank |

| • | Expenses increased 3% driven by higher commissions, $17 million higher employee stock compensation expense, the addition of ECM, and increased fund distribution costs partially offset by decreases in sundry and equipment expense |

| — | Retail brokerage pre-tax profit margin of 29% |

| • | Assets under management increased 13% driven by the addition of $26.2 billion from ECM and net asset inflows |

| • | Series 7 advisors of 8,166 reflects strong recruiting and retention efforts; net new hires of 75 during the quarter |

(See Appendix, pages 35-36 for further discussion of business unit results)

Page-12

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Asset Quality

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | |||||||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||||||||

Nonperforming assets | ||||||||||||||||||||||

Nonaccrual loans | $ | 1,584 | 1,234 | 578 | 619 | 672 | 28 | % | — | |||||||||||||

Foreclosed properties | 155 | 132 | 181 | 99 | 108 | 17 | 44 | |||||||||||||||

Total nonperforming assets | $ | 1,739 | 1,366 | 759 | 718 | 780 | 27 | % | — | |||||||||||||

as % of loans, net and foreclosed properties | 0.41 | % | 0.32 | 0.26 | 0.25 | 0.28 | 27 | 48 | ||||||||||||||

Nonperforming assets in loans held for sale | $ | 26 | 16 | 23 | 23 | 24 | 63 | % | 8 | |||||||||||||

Total nonperforming assets in loans and in loans held for sale | $ | 1,765 | 1,382 | 782 | 741 | 804 | 28 | % | — | |||||||||||||

as % of loans, net, foreclosed properties and loans held for sale | 0.40 | % | 0.32 | 0.26 | 0.25 | 0.28 | — | — | ||||||||||||||

Allowance for credit losses (a) | ||||||||||||||||||||||

Allowance for loan losses, beginning of period | $ | 3,360 | 3,004 | 3,021 | 3,036 | 2,724 | 12 | % | 23 | |||||||||||||

Balance of acquired entities at purchase date | — | 303 | — | — | 300 | — | — | |||||||||||||||

Net charge-offs | (155 | ) | (140 | ) | (116 | ) | (51 | ) | (59 | ) | 11 | — | ||||||||||

Allowance relating to loans acquired, transferred to loans held for sale or sold | (3 | ) | (18 | ) | (15 | ) | (18 | ) | 12 | (83 | ) | — | ||||||||||

Provision for credit losses related to loans transferred to loans held for sale or sold (b) | 1 | 7 | (4 | ) | 5 | — | (86 | ) | — | |||||||||||||

Provision for credit losses | 175 | 204 | 118 | 49 | 59 | (14 | ) | 197 | ||||||||||||||

Allowance for loan losses, end of period | 3,378 | 3,360 | 3,004 | 3,021 | 3,036 | 1 | 11 | |||||||||||||||

Reserve for unfunded lending commitments, beginning of period | 154 | 159 | 165 | 160 | 158 | (3 | ) | (3 | ) | |||||||||||||

Provision for credit losses | 1 | (5 | ) | (6 | ) | 5 | 2 | — | (50 | ) | ||||||||||||

Reserve for unfunded lending commitments, end of period | 155 | 154 | 159 | 165 | 160 | 1 | (3 | ) | ||||||||||||||

Allowance for credit losses | $ | 3,533 | 3,514 | 3,163 | 3,186 | 3,196 | 1 | % | 11 | |||||||||||||

Allowance for loan losses | ||||||||||||||||||||||

as % of loans, net | 0.80 | % | 0.80 | 1.03 | 1.07 | 1.08 | — | — | ||||||||||||||

as % of nonaccrual and restructured loans (c) | 213 | 272 | 520 | 488 | 452 | — | — | |||||||||||||||

as % of nonperforming assets (c) | 194 | 246 | 396 | 421 | 389 | — | — | |||||||||||||||

Allowance for credit losses | ||||||||||||||||||||||

as % of loans, net | 0.84 | % | 0.84 | 1.09 | 1.13 | 1.14 | — | — | ||||||||||||||

Net charge-offs | $ | 155 | 140 | 116 | 51 | 59 | 11 | % | — | |||||||||||||

Commercial, as % of average commercial loans | 0.07 | % | 0.04 | 0.03 | (0.06 | ) | 0.05 | — | — | |||||||||||||

Consumer, as % of average consumer loans | 0.20 | 0.19 | 0.32 | 0.23 | 0.14 | — | — | |||||||||||||||

Total, as % of average loans, net | 0.15 | % | 0.14 | 0.16 | 0.08 | 0.09 | — | — | ||||||||||||||

Past due loans, 90 days and over, and nonaccrual loans (c) | ||||||||||||||||||||||

Commercial, as a % of loans, net | 0.28 | % | 0.23 | 0.28 | 0.28 | 0.32 | — | — | ||||||||||||||

Consumer, as a % of loans, net | 0.66 | % | 0.59 | 0.61 | 0.64 | 0.62 | — | — | ||||||||||||||

| (a) | The allowance for credit losses is the sum of the allowance for loan losses and the reserve for unfunded lending commitments. |

| (b) | The provision related to loans transferred or sold includes recovery of lower of cost or market losses. |

| (c) | These ratios do not include nonperforming assets included in loans held for sale. |

| • | Total NPAs of $1.8 billion rose $383 million driven by growth in consumer real estate secured and commercial loans; up 8 bps to 40 bps of loans |

| — | World Savings well-collateralized real estate secured portfolio contributed $194 million to nonaccrual loan increase; World Savings foreclosed properties up only $4 million |

| • | Provision expense of $177 million, largely reflecting loan growth and includes $10 million relating to credit card |

| — | Net charge-offs of $155 million, or 15 bps of average loans, increased $15 million driven by growth in commercial reflecting lower recoveries |

| • | Allowance for credit losses of $3.5 billion, or 0.84% of net loans, increased $19 million |

| — | Allowance for commercial credit losses to loans down 3 bps to 1.22% of loans; allowance for consumer credit losses up 1 bp to 0.53% of loans |

| — | Allowance as a percentage of nonaccruals and restructured loans declined to 213% from 272% largely reflecting the historically low loss content of World Savings well-collateralized real estate secured portfolio |

| • | Average LTV of consumer real estate secured nonperforming loans (assets) of 76% |

(See Appendix, pages 38-39 for further detail)

Page-13

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

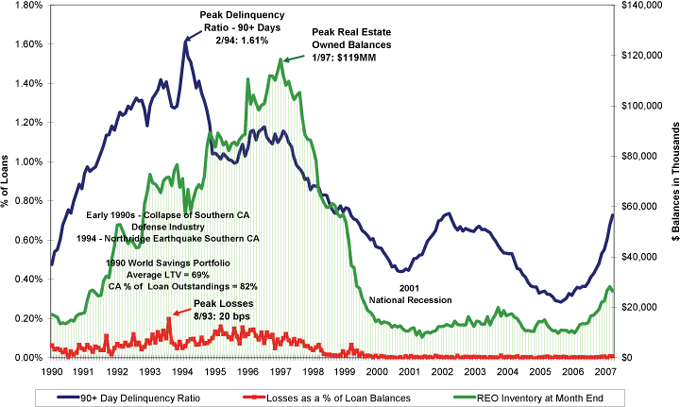

World Savings Historical Credit Trends

HISTORICALLY, SPIKESIN WORLD SAVINGS NPAS HAVE NOT MANIFESTED AS SIGNIFICANTLY HIGHER LOSSES

PERIOD-END 1Q07

| • | World Savings NPAs of $899 million or 74 bps of total loans |

| — | 74% average LTV on NPAs vs. 71% for the total portfolio |

| • | World Savings foreclosed properties totaled $23 million |

| — | 141 properties |

| — | 77% average LTV |

Page-14

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Wachovia 2007 Full-Year Outlook

OVERALL VIEWOF FULL YEAR 2007 EARNINGS REMAINS RELATIVELY UNCHANGED FROM LAST UPDATE

FOR REFERENCE PURPOSES ONLY

ECONOMIC ASSUMPTIONSFOR FULL-YEAR 2007

| ESTIMATE | |||

REAL GDP GROWTH | 2.30 | % | |

FED FUNDS (AT DEC 2007) | 5.00 | % | |

10 YEAR TREASURY BOND (AT DEC 2007) | 4.75 | % |

Denotes update |

(VERSUS FULL-YEAR ADJUSTED COMBINED 2006 UNLESS OTHERWISE NOTED)

ADJUSTED COMBINED 2006# | 2007 OUTLOOK | |||||

NET INTEREST INCOME (TE) | $ 18.1 BILLION | RELATIVELYFLATTO 2%GROWTH | ||||

FEE INCOME | $ 14.5 BILLION | EXPECTLOW-DOUBLE-DIGIT %GROWTH | ||||

NONINTEREST EXPENSE* | $ 18.1BILLION | EXPECTMID-SINGLE-DIGIT %GROWTH;MARGINALLYLOWERTHANREVENUE | ||||

– TARGETINGYEAR-END 2007OVERHEADEFFICIENCYRATIOOF 51.5% – 53.5%** | ||||||

MINORITY INTEREST EXPENSE* | $ 414 MILLION | EXPECTHIGH-SINGLE-DIGIT %GROWTH | ||||

LOANS | $ 398.4 BILLION | EXPECTHIGH-SINGLE-DIGIT %GROWTH | ||||

CONSUMER | $ 249.6 BILLION | MID-SINGLE-DIGIT %GROWTH | ||||

COMMERCIAL | $ 148.8 BILLION | LOW-DOUBLE-DIGIT %GROWTH | ||||

NET CHARGE-OFFS | 8BPS | EXPECTMID-TEENSBPSRANGEOFAVERAGENETLOANS | ||||

PROVISIONMAYBEMODESTLYHIGHER | ||||||

EFFECTIVE TAX RATE (TE) | APPROXIMATELY 33% | |||||

LEVERAGE RATIO | TARGET > 6.0% | |||||

TANGIBLE CAPITAL RATIO (EXCLUDES FAS 115/133ANDPENSION) | TARGET > 4.7% | |||||

DIVIDEND PAYOUT RATIO | 40%–50%OFEARNINGS** | |||||

EXCESS CAPITAL | OPPORTUNISTICALLYREPURCHASESHARES;AUTHORIZATIONFOR 36.5MILLIONSHARESREMAINING | |||||

FINANCIALLYATTRACTIVE,SHAREHOLDERFRIENDLYACQUISITIONS | ||||||

| # | WACHOVIA’S 2006 REPORTED RESULTS AS FOOTNOTED BELOW PLUS GOLDEN WEST’S 3Q06 YTD RESULTS PLUS THE EFFECT OF PURCHASE ACCOUNTING AND INTANGIBLE ACCRETION/AMORTIZATION AND EXCLUDING 4Q06 ADJUSTMENTS AND GOLDEN WEST’S 3Q06 CHARITABLE CONTRIBUTION. |

| * | BEFORE NET MERGER-RELATED AND RESTRUCTURING EXPENSES. |

| ** | BEFORE NET MERGER-RELATED AND RESTRUCTURING EXPENSES, AND OTHER INTANGIBLE AMORTIZATION. |

Page-15

Table of Contents

TABLEOF CONTENTS

| 16 | ||

| 19 | ||

| 22 | ||

| 23 | ||

| 24 | ||

| 25 | ||

| 30 | ||

| 31 | ||

| 35 | ||

| 37 | ||

| 38 | ||

| 40 | ||

Explanation of Our Use of Certain Non-GAAP Financial Measures | 42 | |

| 43 | ||

| 47 | ||

| 48 |

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Business segment results are presented excluding (i) merger-related and restructuring expenses, (ii) deposit base intangible and other intangible amortization expense, (iii) amounts presented as discontinued operations, and (iv) the cumulative effect of a change in accounting principle. This is the basis on which we manage and allocate capital to our business segments. We continuously assess assumptions, methodologies and reporting classifications to better reflect the true economics of our business segments.

We continuously update segment information for changes that occur in the management of our businesses. In 1Q07, we moved our cross-border leveraged leases, consisting of our portfolios of Lease-In, Lease-Out and Sale-In, Lease-Out transactions, from the Corporate and Investment Bank to the Parent to reflect the way in which these portfolios are now managed. We have updated information for 2006 to reflect this change. The impact to segment earnings for full year 2006 as a result of this and other changes was a $3 million decrease in the General Bank, a $3 million increase in Capital Management, a $7 million decrease in Wealth Management, a $91 million decrease in the Corporate and Investment Bank and a $98 million increase in the Parent.

In a rising rate environment, Wachovia benefits from a widening spread between deposit costs and wholesale funding costs. However, our funds transfer pricing (“FTP”) system, described below, credits this benefit to deposit-providing business units on a lagged basis. The effect of the FTP system results in rising charges to business units for funding to support predominantly floating-rate assets. This benefit of higher rates earned on floating-rate assets and lagging rates on longer duration deposits is captured in the central money book in the Parent segment.

In order to remove interest rate risk from each core business segment, the management reporting model employs an FTP system. The FTP system matches the duration of the funding used by each segment to the duration of the assets and liabilities contained in each segment. Matching the duration, or the effective term until an instrument can be repriced, allocates interest income and/or interest expense to each segment so its resulting net interest income is insulated from interest rate risk.

On January 1, 2007, we adopted FASB Staff Position FAS 13-2, “Accounting for a Change or Projected Change in the Timing of Cash Flows Relating to Income Taxes Generated by a Leveraged Lease Transaction” (FSP 13-2), FASB Interpretation (FIN) No. 48, “Accounting for Uncertainty in Income Taxes—an amendment of FAS Statement No 109,” SFAS No. 155, “Accounting for Certain Hybrid Financial Instruments—an amendment of FASB Statements No. 133 and 140,” and Emerging Issues Task Force (EITF) Issue No, 06-5, “Accounting for Purchases of Life Insurance—Determining the Amount That Could Be Realized in Accordance with FASB Technical Bulletin No. 85-4, ‘Accounting for Purchases of Life Insurance’”. For all of these new standards, the cumulative effect of adoption is recorded as an adjustment, net of applicable taxes, to beginning retained earnings.

FSP 13-2 amends SFAS 13, “Accounting for Leases,” such that changes that affect the timing of cash flows but not the total net income under a leveraged lease will trigger a recalculation of the lease. FIN 48 clarifies the criteria for recognition of income tax benefits in accordance with SFAS No. 109.

We have two primary classes of leveraged lease transactions that are affected by FSP 13-2: Lease-In, Lease-Out transactions (LILOs) and a second group of transactions that are broadly referred to as Sale-In, Lease-Out transactions (SILOs). SILOs principally include service contract and qualified technological equipment leases. We settled with the IRS in June 2004 on all matters relating to our portfolio of LILOs. On SILOs, we have concluded that it is possible that, upon ultimate resolution of a potential dispute with the IRS, we may not realize all of the income tax benefits originally recorded. On January 1, 2007, we recorded a $1.4 billion after-tax charge to beginning retained earnings entirely related to our portfolio of LILOs and SILOs. The amount of this reduction to beginning retained earnings will be recognized in earnings over the remaining terms of the affected leases, generally 35 years to 40 years. The impact on 2007 results of this charge is a reduction to net income of $98 million after-tax. We remain well capitalized for regulatory capital purposes following the reduction to retained earnings relating to the affected leases. The impact of the adoption of FIN 48 for other matters amounted to a $4 million reduction in beginning retained earnings.

SFAS 155 permits companies to record certain hybrid financial instruments at fair value with corresponding changes in fair value recorded in the results of operations. Hybrid financial instruments are those containing an embedded derivative. SFAS 155 also provides a one-time opportunity to elect to record certain hybrid financial instruments existing on January 1, 2007, at fair value. We did not elect to carry any such financial instruments at fair value, and accordingly, had no cumulative effect adjustment from the adoption.

Page-16

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

EITF Issue No. 06-5 addresses the accounting for certain corporate and bank-owned life insurance policies. The impact of adoption of this standard amounted to a $4 million reduction in beginning retained earnings.

Please see pages 40-41 of Exhibit (13) to Wachovia’s Annual Report on Form 10-K for a more detailed discussion of these matters.

In September 2006, the FASB issued SFAS 157, “Fair Value Measurement,” (SFAS 157), which establishes a framework for measuring fair value under U.S. GAAP, expands disclosures about fair value measurement and provides new income recognition criteria for certain derivative contracts. SFAS 157 does not establish any new fair value measurements itself, but applies under other accounting standards that require the use of fair value for recognition or disclosure. In February 2007, the FASB issued SFAS 159, “The Fair Value Option for Financial Assets and Financial Liabilities.” SFAS 159 permits companies to elect to carry certain financial instruments at fair value with corresponding changes in fair value recorded in the results of operations. Both SFAS 157 and SFAS 159 are effective January 1, 2008, with early adoption permitted on January 1, 2007. We will adopt these standards on January 1, 2008, and are currently assessing the impact of adoption on our consolidated financial position and results of operations. The effect of adopting SFAS 157 will be recorded either directly to results of operations or as a cumulative effect of a change in accounting principle through an adjustment to beginning retained earnings on January 1, 2008, depending on the nature of the financial instrument to which fair value is being applied. The transition adjustment for SFAS 159 will be recorded as a cumulative effect of a change in accounting principle through an adjustment to beginning retained earnings.

SFAS No. 123R, “Share-Based Payments,” which we adopted on January 1, 2006, requires that compensation costs relating to share-based payment transactions be recognized in income, as has been our accounting policy since January 1, 2002. SFAS 123R, however, also requires a different treatment of awards to retirement-eligible employees in situations where the award automatically vests upon retirement, which is the case for substantially all of our awards. Beginning in 2006, these awards to retirement-eligible employees must be expensed in full at the date of grant, or from the date of grant to the date that an employee will be retirement-eligible, if that is before the end of the stated vesting period. In 1Q07 and in 1Q06 (2Q06 for Capital Management), we made our annual stock grants. Total stock compensation expense was $212 million and $194 million in 1Q07 and 1Q06, respectively, and $101 million in 4Q06. Of these amounts, $93 million in 1Q07 and $98 million in 1Q06 related to awards to retirement-eligible employees. The majority of the linked quarter variance in stock compensation expense in the business units is attributable to the incremental expense for retirement-eligible employees. Note: Unless otherwise noted, references in this document to employee stock compensation expense refer only to the retirement-eligible portion of overall employee stock compensation expense.

In September 2006, the SEC issued Staff Accounting Bulletin No. 108, “Considering the Effects of Prior Year Misstatements when Quantifying Misstatements in Current Year Financial Statements” (SAB 108). SAB 108 requires that both an income statement approach and a balance sheet approach be used when evaluating whether an error is material to an entity’s financial statements, based on all relevant quantitative and qualitative factors. The SEC staff issued SAB 108 to address what they identified as diversity in practice whereby entities were using either an income statement approach or a balance sheet approach, but not both. We have consistently used the income statement approach in prior periods. SAB 108 became effective December 31, 2006, and any material adjustments arising from the adoption of SAB 108 were recorded as a cumulative effect adjustment to beginning retained earnings.

Page-17

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

In 4Q06, we completed our analysis under SAB 108 using both the income statement and balance sheet approaches, and concluded that we have no prior year misstatements that were material to our financial statements. However, in the process of performing the above review, we elected to record certain prior year adjustments to a number of income statement line items that were not significant on an individual or aggregate basis. We recorded adjustments in 4Q06 to correct these items, which are shown in the table below and are referred to as “4Q06 Adjustments” in these materials.

4Q06 Adjustments

(In millions) | 4Q06 Impact | |||

Interest and fees on loans | $ | 56 | ||

Interest on deposits | (32 | ) | ||

Net interest income | 24 | |||

Service charges | 22 | |||

Other income | 93 | |||

Total fee and other income | 115 | |||

Salaries and employee benefits | (99 | ) | ||

Sundry expense | (99 | ) | ||

Total noninterest expense | (198 | ) | ||

Income before income taxes | (59 | ) | ||

Income taxes on above items | (23 | ) | ||

Income taxes | (49 | ) | ||

Total income taxes | (72 | ) | ||

Net income | $ | 13 | ||

We recorded adjustments to net interest income and service charges to reflect certain items that in the past had been recorded either when billed to the customer or on a lagged basis, but going forward will be recorded as earned. We recorded additional salaries and employee benefits expense to reflect the carryover of prior years’ unused paid time off and additional sundry expense relating to the prior year’s invoices received and processed after year-end, but for which the services had been rendered prior to year-end. We also recorded additional other noninterest income for amounts recorded in other comprehensive income relating to a hedging relationship that had been discontinued in a prior year. In the tax provision, we recorded the tax effect of the above-referenced items and certain other adjustments to current taxes payable. The net after-tax impact of all of these adjustments was a $13 million increase to net income.

On October 1, 2006, we completed the acquisition of Golden West Financial Corporation, a California-based financial services company. Under the purchase accounting method, Golden West is not included in our financial results prior to 4Q06.

In 4Q05, we completed the sale of most of our Corporate and Institutional Trust (CIT) businesses and recognized a pre-tax gain of $447 million ($214 million after-tax). In 4Q06, we recognized an additional pre-tax gain of $76 million ($46 million after-tax) based on the level of business retained in the 12-month period following the completion of the transaction. The gain on sale was presented, net of applicable taxes, as discontinued operations in the consolidated statement of income.

On March 1, 2006, we completed the acquisition of Westcorp and WFS Financial Inc, a California-based auto loan originator business and commercial bank. Financial results for 1Q06 include one month’s results of the acquired Westcorp entities under the purchase accounting method. The ongoing auto loan origination business activity is included in the Commercial sub-segment of the General Bank and the commercial banking business is included in the Retail and Small Business sub-segment of the General Bank.

We entered the credit card market as a direct issuer beginning in January 2006. This coincided with Wachovia terminating our existing joint marketing agreement with MBNA Corporation as a result of the Bank of America/MBNA merger, which closed on January 1, 2006. Upon consummation of that merger, MBNA paid us a $100 million termination fee, which was recorded in other income in 1Q06.

Page-18

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

(See Table on Page 6)

Net Interest Income Summary

| 2007 | 2006 | 1Q07 vs | 1Q07 vs | Combined | ||||||||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | 1Q06 | 1Q07 vs 1Q06 | |||||||||||||||||

Average earning assets | $ | 594,313 | 596,893 | 472,139 | 463,232 | 442,527 | — | % | 34 | $ | 566,780 | 5 | % | |||||||||||

Average interest-bearing liabilities | 539,547 | 536,958 | 414,563 | 403,234 | 384,406 | — | 40 | 506,790 | 6 | |||||||||||||||

Interest income(Tax-equivalent) | 10,185 | 10,405 | 7,821 | 7,438 | 6,756 | (2 | ) | 51 | 8,853 | 15 | ||||||||||||||

Interest expense | 5,688 | 5,793 | 4,243 | 3,763 | 3,217 | (2 | ) | 77 | 4,412 | 29 | ||||||||||||||

Net interest income(Tax-equivalent) | $ | 4,497 | 4,612 | 3,578 | 3,675 | 3,539 | (2 | )% | 27 | $ | 4,441 | 1 | % | |||||||||||

Average rate earned | 6.89 | % | 6.95 | 6.60 | 6.43 | 6.15 | — | — | ||||||||||||||||

Equivalent rate paid | 3.88 | 3.86 | 3.57 | 3.25 | 2.94 | — | — | |||||||||||||||||

Net interest margin | 3.01 | % | 3.09 | 3.03 | 3.18 | 3.21 | — | — | 3.14 | % | — | % | ||||||||||||

Net interest income of $4.5 billion decreased 2%, or $115 million, as the benefit of loan and securitization warehouse growth and improved retail deposit pricing were more than offset by lower income relating to 4Q06 Adjustments, the effect of FSP 13-2/FIN 48 adoption, and maturing off-balance sheet positions, as well as lower trading-related net interest income, and the shift in deposits to lower-spread categories. Net interest income grew 27% from 1Q06 driven by the addition of Golden West and Westcorp. Net interest income rose 1% from Combined 1Q06 as growth in earning assets including Westcorp was largely offset by the shift in deposit mix toward lower spread categories and the effect of the inverted yield curve.

Net interest margin of 3.01% decreased 8 bps as the benefit from retail deposit strategies and a reduction in lower-spread short-term investments was more than offset by lower income from maturing off-balance sheet positions, the effect of 4Q06 Adjustments, lower trading-related net interest income, the effect of FSP 13-2/FIN 48 adoption, growth in lower-spread commercial and consumer loans and securitization warehouses, and a continued shift in deposits toward lower-spread categories. The margin decreased 20 bps from 1Q06 on growth in lower-spread consumer and commercial loans and securities, a shift in deposits toward lower-spread categories, and the impact of acquisitions.Net interest margin decreased 13 bps from Combined 1Q06.

Average trading assets decreased $1.4 billion, or 4%. Average VAR increased to $23 million from $19 million in 4Q06.Average securities were down $472 million and decreased $9.9 billion, or 8%, from 1Q06 driven by the sale of $13.2 billion of securities relating to the Golden West merger. The average duration of the securities portfolio remained stable at 3.4 years in 1Q07. Average securities declined $11.4 billion from Combined 1Q06 driven by the above factors.

Average loans rose 1% and 59% from 1Q06 driven by merger activity.Average loans rose 9% from Combined 1Q06 driven by growth in commercial and consumer.Average commercial loans grew $3.0 billion, or 2%, on strength in middle-market and business banking, commercial real estate portfolios and foreign. This growth was somewhat offset by the $1.9 billion decrease in leases reflecting the $1.4 billion average effect of FSP 13-2/FIN 48 adoption and expected paydowns as well as the $400 million average effect of 4Q06 and 1Q07 loan sales. Commercial loans grew 10% from 1Q06.Average consumer loans remained relatively stable, down $282 million as growth in real estate secured and auto was more than offset by the $1.4 billion average effect of 4Q06 and 1Q07 loan sale and securitization activity. In 4Q06 we sold $1.7 billion of student loans and in late 1Q07 we sold or securitized a net $4.3 billion of consumer loans. Consumer loans grew $139.9 billion from 1Q06 largely driven by merger activity as well as growth in real estate secured, auto, student loans and credit card.Average consumer loans grew $21 billion, or 9%, from Combined 1Q06 driven by growth in auto, including the effect of Westcorp, as well as student loans and credit card.Net sale and securitization activity reduced average consumer loans by $8.2 billion from Combined 1Q06 levels.

Page-19

Table of Contents

Wachovia 1Q07 Quarterly Earnings Report

Loans Held for Sale

| 2007 | 2006 | |||||||||||||||

(In millions) | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | |||||||||||

Core business activity, beginning of period | $ | 12,566 | 9,030 | 7,740 | 7,846 | 6,388 | ||||||||||

Balance of acquired entities at purchase date | — | 193 | — | — | — | |||||||||||

Originations/purchases | 17,873 | 18,436 | 16,803 | 13,778 | 13,068 | |||||||||||

Transfers to (from) loans held for sale, net | (180 | ) | 127 | (154 | ) | (238 | ) | (70 | ) | |||||||

Lower of cost or market value adjustments | (3 | ) | — | — | — | — | ||||||||||

Performing loans sold or securitized | (14,745 | ) | (14,936 | ) | (15,137 | ) | (13,357 | ) | (11,397 | ) | ||||||

Other, principally payments | (481 | ) | (284 | ) | (222 | ) | (289 | ) | (143 | ) | ||||||

Core business activity, end of period | 15,030 | 12,566 | 9,030 | 7,740 | 7,846 | |||||||||||

Portfolio management activity, end of period | 2 | 2 | 9 | 10 | 13 | |||||||||||

Total loans held for sale (a) | $ | 15,032 | 12,568 | 9,039 | 7,750 | 7,859 | ||||||||||

| (a) | Nonperforming assets included in loans held for sale at March 31, 2007 and at December 31, September 30, June 30, and March 31, 2006, were $26 million, $16 million, $23 million, $23 million and $24 million, respectively. |

Average loans held for sale increased $4.8 billion driven by growth in the commercial mortgage securitization warehouse. In 1Q07 we sold/securitized $9.5 billion of commercial and $5.2 billion of consumer mortgages out of held for sale. In 1Q07 we originated $18.3 billion of consumer mortgages and delivered $5.2 billion to agencies/privates.

Average other earning assets decreased 25% driven by lower fed funds sold and repos, and were down 14% from 1Q06 reflecting temporary excess 4Q06 liquidity related to balance sheet repositioning, including deleveraging, in connection with the Golden West merger.Average other earning assets decreased $7.5 billion from Combined 1Q06.Total average earning assets were stable and rose 34% from 1Q06 driven by merger activity.Average earning assets increased 5% from Combined 1Q06.

Average core depositsincreased 2% on strength in CDs, interest-bearing checking and foreign deposits somewhat offset by decreases in DDA. Average core deposits grew 27% from 1Q06 driven by merger activity. Average core deposits increased 5% from Combined 1Q06 as growth in retail CDs, NOW, foreign and the effect of Westcorp more than offset declines in savings, DDA and interest checking.

Average short-term borrowings decreased 15% and 20% from 1Q06.

Average long-term debtincreased $2.6 billion and $85.9 billion from 1Q06 driven by merger activity.