UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-02383

AB BOND FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: October 31, 2022

Date of reporting period: October 31, 2022

ITEM 1. REPORTS TO STOCKHOLDERS.

OCT 10.31.22

ANNUAL REPORT

AB ALL MARKET REAL RETURN PORTFOLIO

| Investment Products Offered | • Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed | |

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.abfunds.com or contact your AB representative. Please read the prospectus and/or summary prospectus carefully before investing.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Form N-PORT reports are available on the Commission’s website at www.sec.gov. AB publishes full portfolio holdings for the Fund monthly at www.abfunds.com.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

| FROM THE PRESIDENT |  |

Dear Shareholder,

We’re pleased to provide this report for the AB All Market Real Return Portfolio (the “Fund”). Please review the discussion of Fund performance, the market conditions during the reporting period and the Fund’s investment strategy.

At AB, we’re striving to help our clients achieve better outcomes by:

| + | Fostering diverse perspectives that give us a distinctive approach to navigating global capital markets |

| + | Applying differentiated investment insights through a connected global research network |

| + | Embracing innovation to design better ways to invest and leading-edge mutual-fund solutions |

Whether you’re an individual investor or a multibillion-dollar institution, we’re putting our knowledge and experience to work for you every day.

For more information about AB’s comprehensive range of products and shareholder resources, please log on to www.abfunds.com.

Thank you for your investment in AB mutual funds—and for placing your trust in our firm.

Sincerely,

Onur Erzan

President and Chief Executive Officer, AB Mutual Funds

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 1 | |

ANNUAL REPORT

December 6, 2022

This report provides management’s discussion of fund performance for the AB All Market Real Return Portfolio for the annual reporting period ended October 31, 2022.

The Fund’s investment objective is to maximize real return over inflation.

NAV RETURNS AS OF OCTOBER 31, 2022 (unaudited)

| 6 Months | 12 Months | |||||||

| AB ALL MARKET REAL RETURN PORTFOLIO | ||||||||

| Class 1 Shares1 | -10.95% | -6.85% | ||||||

| Class 2 Shares1 | -10.85% | -6.63% | ||||||

| Class A Shares | -11.00% | -7.01% | ||||||

| Class C Shares | -11.33% | -7.71% | ||||||

| Advisor Class Shares2 | -10.83% | -6.64% | ||||||

| Class R Shares2 | -11.15% | -7.32% | ||||||

| Class K Shares2 | -11.05% | -7.08% | ||||||

| Class I Shares2 | -10.86% | -6.75% | ||||||

| Class Z Shares2 | -10.85% | -6.64% | ||||||

| MSCI AC World Commodity Producers Index (net) | 0.72% | 16.97% | ||||||

| 1 | Class 1 shares are only available to Bernstein Global Wealth Management private client accounts. Class 2 shares are only available to the Adviser’s institutional clients or through other limited arrangements. |

| 2 | Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

INVESTMENT RESULTS

The table above shows the Fund’s performance compared to its benchmark, the Morgan Stanley Capital International All Country (“MSCI AC”) World Commodity Producers Index (net), for the six- and 12-month periods ended October 31, 2022.

All share classes of the Fund underperformed the benchmark for both periods, before sales charges. For the 12-month period, the strategic allocation detracted overall, relative to the benchmark, as real estate investment trusts (“REITs”), inflation-sensitive equities and commodity futures underperformed commodity producers. Security selection within commodity equities detracted, while selection within inflation-sensitive equities and REITs contributed. The Fund’s tactical underweight to REITs contributed, while tactical overweights to commodity futures detracted.

2 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

During the six-month period, the strategic allocation detracted overall, as REITs, inflation-sensitive equities and commodity futures all underperformed commodity producers. Security selection within commodity producers and inflation-sensitive equities contributed. The Fund’s modest overweights to commodity futures detracted, while tactical underweights to REITs and inflation-sensitive equities contributed.

The Fund utilized derivatives for hedging and investment purposes in the form of currency forwards and total return swaps, which added to absolute returns for both periods, while futures and inflation swaps added for the 12-month period and detracted for the six-month period; during the 12-month period, variance swaps added to returns.

MARKET REVIEW AND INVESTMENT STRATEGY

US, international and emerging-market stocks declined during the 12-month period ended October 31, 2022. Initially, positive earnings momentum overshadowed concerns surrounding coronavirus variants, supply chain disruptions and rising inflation. But the global economic outlook deteriorated as increasingly hawkish central banks elevated investor concern that rapidly rising borrowing costs would slow economic growth significantly and tip global economies into recession. The US Federal Reserve (the “Fed”) raised interest rates five times during the period, including three consecutive 0.75% increases, setting a course followed by other key central banks. Equity markets began to rise at the end of the period, after some central banks raised rates by less than expected and several Fed governors suggested the possibility of a shift toward a less reactive course in order to review the impact of higher rates over a longer time horizon. Against a backdrop of rising rates, growth stocks came under pressure throughout most of the period. Within large-cap markets, both growth and value stocks declined in absolute terms, but value stocks outperformed growth stocks significantly. Large-cap stocks outperformed small-cap stocks on a relative basis, but both declined in absolute terms.

Inflation assets were mixed over the six- and 12-month periods ended October 31, 2022. REITs fell meaningfully over both periods as the asset class faced headwinds from rising interest rates. Natural resource equities posted positive performance over the 12-month period and were close to neutral toward the end of the period. For both periods, natural resource equities outperformed broader equity markets. Elsewhere, commodities rose over the 12-month period but fell over the six-month period. While the ongoing conflict between Russia and Ukraine was initially supportive of higher prices (especially in oil, gas and agriculture), concerns regarding the impact of restrictive monetary policy on future economic growth weighed on sentiment toward the end of the period. Finally, inflation swaps were slightly negative over the trailing six-month period but remained positive over the 12-month period.

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 3 | |

The Fund’s Senior Investment Management Team continues to look for sources of value via asset allocation shifts, active security selection, risk overlay strategies and currency management. The Fund uses a blend of quantitative and fundamental research in order to determine overall portfolio risk, allocate risk across major real asset classes and identify idiosyncratic opportunities.

INVESTMENT POLICIES

The Fund seeks to maximize real return. Real return is the rate of return after adjusting for inflation. The Fund pursues an aggressive investment strategy involving a variety of asset classes. The Fund invests primarily in instruments that the Adviser expects to outperform broad equity indices during periods of rising inflation. Under normal circumstances, the Fund expects to invest its assets principally in the following instruments that, in the judgment of the Adviser, are affected directly or indirectly by the level and change in rate of inflation: inflation-indexed fixed-income securities, such as Treasury inflation-protected securities (“TIPS”) and similar bonds issued by governments outside of the United States; commodities; commodity-related equity securities; real estate equity securities; inflation-sensitive equity securities, which the Fund defines as equity securities of companies that the Adviser believes have the ability to pass along increasing costs to consumers and maintain or grow margins in rising inflation environments, including equity securities of utilities and infrastructure-related companies (“inflation-sensitive equities”); securities and derivatives linked to the price of other assets (such as commodities, stock indices and real estate); and currencies. The Fund expects its investments in fixed-income securities to have a broad range of maturities and quality levels.

The Fund seeks inflation protection from investments around the globe, both in developed- and emerging-market countries. In selecting securities for purchase and sale, the Adviser utilizes its qualitative and quantitative resources to determine overall inflation sensitivity, asset allocation and security selection. The Adviser assesses the securities’ risks and inflation sensitivity as well as the securities’ impact on the overall risks and inflation sensitivity of the Fund. When its analysis indicates that changes are necessary, the Adviser intends to implement them through a combination of changes to underlying positions and the use of inflation swaps and other types of derivatives, such as interest rate swaps.

The Fund anticipates that its targeted investment mix, other than its investments in inflation-indexed fixed-income securities, will focus on commodity-related equity securities, commodities and commodity

(continued on next page)

4 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

derivatives, real estate equity securities and inflation-sensitive equities to provide a balance between expected return and inflation protection. The Fund may vary its investment allocations among these asset classes, at times significantly. Its commodities investments will include significant exposure to energy commodities, but will also include agricultural products, and industrial and precious metals, such as gold. The Fund’s investments in real estate equity securities will include REITs and other real estate-related securities.

The Fund invests in both US and non-US dollar-denominated equity or fixed-income securities. The Fund may invest in currencies for hedging or investment purposes, both in the spot market and through long or short positions in currency-related derivatives. The Fund does not ordinarily expect to hedge its foreign currency exposure because it will be balanced by investments in US dollar-denominated securities, although it may hedge the exposure under certain circumstances.

The Fund may enter into derivatives, such as options, futures contracts, forwards, swaps or structured notes, to a significant extent, subject to the limits of applicable law. The Fund intends to use leverage for investment purposes through the use of cash made available by derivatives transactions to make other investments in accordance with its investment policies. In determining when and to what extent to employ leverage or enter into derivatives transactions, the Adviser considers factors such as the relative risks and returns expected of potential investments and the cost of such transactions. The Adviser considers the impact of derivatives in making its assessments of the Fund’s risks. The resulting exposures to markets, sectors, issuers or specific securities will be continuously monitored by the Adviser.

The Fund may seek to gain exposure to physical commodities traded in the commodities markets through use of a variety of derivative instruments, including investments in commodity index-linked notes. The Adviser expects that the Fund will seek to gain exposure to commodities and commodity-related instruments and derivatives primarily through investments in AllianceBernstein Cayman Inflation Strategy, Ltd., a wholly owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). The Subsidiary is advised by the Adviser and has the same investment objective and substantially similar investment policies and restrictions as the Fund except that the Subsidiary, unlike the Fund, may invest, without limitation, in commodities and commodity-related instruments. The Fund is subject to the risks associated with the commodities, derivatives and other instruments in which the Subsidiary invests, to the extent of its investment in the Subsidiary. The Fund limits its investment in the

(continued on next page)

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 5 | |

Subsidiary to no more than 25% of its net assets. Investment in the Subsidiary is expected to provide the Fund with commodity exposure within the limitations of federal tax requirements that apply to the Fund.

The Fund is “non-diversified”, which means that it may concentrate its assets in a smaller number of issuers than a diversified fund.

6 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

DISCLOSURES AND RISKS

Benchmark Disclosure

The MSCI AC World Commodity Producers Index is unmanaged and does not reflect fees and expenses associated with the active management of a mutual fund portfolio. The MSCI AC World Commodity Producers Index is a free float-adjusted, market capitalization index designed to track the performance of global listed commodity producers, including emerging markets. Commodities sectors include: energy, grains, industrial metals, petroleum, precious metals and softs. MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI. Net returns include the reinvestment of dividends after deduction of non-US withholding tax. An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

Market Risk: The value of the Fund’s assets will fluctuate as the stock, commodity and bond markets fluctuate. The value of the Fund’s investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events, including public health crises (including the occurrence of a contagious disease or illness) and regional and global conflicts, that affect large portions of the market.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security and accrued interest. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

Interest-Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of existing investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest-rate risk is generally greater for fixed-income securities with longer maturities or durations. The Fund may be subject to greater risk of rising interest rates than would normally be the case due to the end of a recent period of historically low rates and the effect of potential government fiscal policy initiatives and resulting market reaction to those initiatives.

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 7 | |

DISCLOSURES AND RISKS (continued)

Commodity Risk: Investing in commodities and commodity-linked derivative instruments, either directly or through the Subsidiary, may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments.

Derivatives Risk: Derivatives may be difficult to price or unwind and leveraged so that small changes may produce disproportionate losses for the Fund. Derivatives, especially over-the-counter derivatives, are also subject to counterparty risk, which is the risk that the counterparty (the party on the other side of the transaction) on a derivative transaction will be unable or unwilling to honor its contractual obligations to the Fund.

Leverage Risk: To the extent the Fund uses leveraging techniques, its net asset value (“NAV”) may be more volatile because leverage tends to exaggerate the effect of changes in interest rates and any increase or decrease in the value of the Fund’s investments.

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Illiquid Investments Risk: Illiquid investments risk exists when certain investments are or become difficult to purchase or sell. Difficulty in selling such investments may result in sales at disadvantageous prices affecting the value of your investment in the Fund. Causes of illiquid investments risk may include low trading volumes and large positions. Foreign fixed-income securities may have more illiquid investments risk because secondary trading markets for these securities may be smaller and less well-developed and the securities may trade less frequently. Illiquid investments risk may be higher in a rising interest-rate environment, when the value and liquidity of fixed-income securities generally go down.

Foreign (Non-US) Risk: Investments in securities of non-US issuers may involve more risk than those of US issuers. These securities may fluctuate more widely in price and may be more difficult to trade due to adverse market, economic, political, regulatory or other factors.

Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments or reduce its returns.

8 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

DISCLOSURES AND RISKS (continued)

Subsidiary Risk: By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary’s investments. The derivatives and other investments held by the Subsidiary are generally similar to those that are permitted to be held by the Fund and are subject to the same risks that apply to similar investments if held directly by the Fund. The Subsidiary is not registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and, unless otherwise noted in the Fund’s prospectus, is not subject to all of the investor protections of the 1940 Act. However, the Fund wholly owns and controls the Subsidiary, and the Fund and the Subsidiary are managed by the Adviser, making it unlikely the Subsidiary will take actions contrary to the interests of the Fund or its shareholders.

Real Estate Risk: The Fund’s investments in real estate securities have many of the same risks as direct ownership of real estate, including the risk that the value of real estate could decline due to a variety of factors that affect the real estate market generally. Investments in REITs may have additional risks. REITs are dependent on the capability of their managers, may have limited diversification, and could be significantly affected by changes in taxes.

Non-Diversification Risk: The Fund may have more risk because it is “non-diversified”, meaning that it can invest more of its assets in a smaller number of issuers. Accordingly, changes in the value of a single security may have a more significant effect, either negative or positive, on the Fund’s NAV.

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the intended results. Some of these techniques may incorporate, or rely upon, quantitative models, but there is no guarantee that these models will generate accurate forecasts, reduce risk or otherwise perform as expected.

These risks are fully discussed in the Fund’s prospectus. As with all investments, you may lose money by investing in the Fund.

An Important Note About Historical Performance

The investment return and principal value of an investment in the Fund will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Performance shown in this report represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by visiting www.abfunds.com. For

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 9 | |

DISCLOSURES AND RISKS (continued)

Class 1 shares, go to www.bernstein.com and click on “Investments”, found in the footer, then “Mutual Fund Information—Mutual Fund Performance at a Glance.”

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.abfunds.com. For Class 1 shares, go to www.bernstein.com, click on “Investments”, found in the footer, then “Mutual Fund Information—Prospectuses, SAIs and Shareholder Reports.” Please read the prospectus and/or summary prospectus carefully before investing.

All fees and expenses related to the operation of the Fund have been deducted. NAV returns do not reflect sales charges; if sales charges were reflected, the Fund’s quoted performance would be lower. SEC returns reflect the applicable sales charges for each share class: a 4.25% maximum front-end sales charge for Class A shares and a 1% 1-year contingent deferred sales charge for Class C shares. Returns for the different share classes will vary due to different expenses associated with each class. Performance assumes reinvestment of distributions and does not account for taxes.

10 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

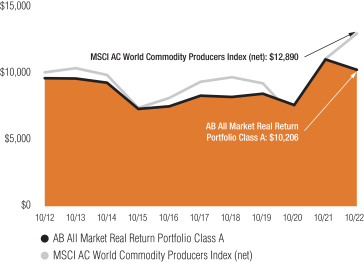

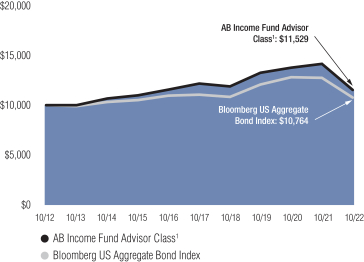

HISTORICAL PERFORMANCE

GROWTH OF A $10,000 INVESTMENT IN THE FUND (unaudited)

10/31/2012 TO 10/31/2022

This chart illustrates the total value of an assumed $10,000 investment in AB All Market Real Return Portfolio Class A shares (from 10/31/2012 to 10/31/2022) as compared to the performance of its benchmark. The chart reflects the deduction of the maximum 4.25% sales charge from the initial $10,000 investment in the Fund and assumes the reinvestment of dividends and capital gains distributions.

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 11 | |

HISTORICAL PERFORMANCE (continued)

AVERAGE ANNUAL RETURNS AS OF OCTOBER 31, 2022 (unaudited)

| NAV Returns | SEC Returns (reflects applicable sales charges) | |||||||

| CLASS 1 SHARES1 | ||||||||

| 1 Year | -6.85% | -6.85% | ||||||

| 5 Years | 4.54% | 4.54% | ||||||

| 10 Years | 0.80% | 0.80% | ||||||

| CLASS 2 SHARES1 | ||||||||

| 1 Year | -6.63% | -6.63% | ||||||

| 5 Years | 4.81% | 4.81% | ||||||

| 10 Years | 1.05% | 1.05% | ||||||

| CLASS A SHARES | ||||||||

| 1 Year | -7.01% | -10.96% | ||||||

| 5 Years | 4.34% | 3.43% | ||||||

| 10 Years | 0.64% | 0.20% | ||||||

| CLASS C SHARES | ||||||||

| 1 Year | -7.71% | -8.57% | ||||||

| 5 Years | 3.57% | 3.57% | ||||||

| 10 Years2 | -0.09% | -0.09% | ||||||

| ADVISOR CLASS SHARES3 | ||||||||

| 1 Year | -6.64% | -6.64% | ||||||

| 5 Years | 4.61% | 4.61% | ||||||

| 10 Years | 0.92% | 0.92% | ||||||

| CLASS R SHARES3 | ||||||||

| 1 Year | -7.32% | -7.32% | ||||||

| 5 Years | 4.04% | 4.04% | ||||||

| 10 Years | 0.39% | 0.39% | ||||||

| CLASS K SHARES3 | ||||||||

| 1 Year | -7.08% | -7.08% | ||||||

| 5 Years | 4.34% | 4.34% | ||||||

| 10 Years | 0.65% | 0.65% | ||||||

| CLASS I SHARES3 | ||||||||

| 1 Year | -6.75% | -6.75% | ||||||

| 5 Years | 4.78% | 4.78% | ||||||

| 10 Years | 1.03% | 1.03% | ||||||

| CLASS Z SHARES3 | ||||||||

| 1 Year | -6.64% | -6.64% | ||||||

| 5 Years | 4.81% | 4.81% | ||||||

| Since Inception4 | 1.57% | 1.57% | ||||||

(footnotes continued on next page)

12 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

HISTORICAL PERFORMANCE (continued)

The Fund’s prospectus fee table shows the Fund’s total annual operating expense ratios as 1.13%, 0.87%, 1.18%, 1.93%, 0.92%, 1.60%, 1.31%, 0.88% and 0.88% for Class 1, Class 2, Class A, Class C, Advisor Class, Class R, Class K, Class I and Class Z shares, respectively, gross of any fee waivers or expense reimbursements. Contractual fee waivers and/or expense reimbursements limited the Fund’s total annual operating expense ratio (excluding extraordinary expenses, interest expense, and acquired fund fees and expenses other than the advisory fees of any AB mutual funds in which the Fund may invest) to 1.55% for Class R shares. These waivers/reimbursements may not be terminated before January 31, 2023, and may be extended by the Adviser for additional one-year terms. Absent reimbursements or waivers, performance would have been lower. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratios shown above may differ from the expense ratios in the Financial Highlights section since they are based on different time periods.

| 1 | Class 1 shares are only available to Bernstein Global Wealth Management private client accounts. Class 2 shares are only available to the Adviser’s institutional clients or through other limited arrangements. These share classes do not carry front-end sales charges; therefore, their respective NAV and SEC returns are the same. |

| 2 | Assumes conversion of Class C shares into Class A shares after eight years. |

| 3 | These share classes are offered at NAV to eligible investors and their SEC returns are the same as their NAV returns. Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

| 4 | Inception date: 1/31/2014. |

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 13 | |

HISTORICAL PERFORMANCE (continued)

SEC AVERAGE ANNUAL RETURNS

AS OF THE MOST RECENT CALENDAR QUARTER-END SEPTEMBER 30, 2022 (unaudited)

| SEC Returns (reflects applicable sales charges) | ||||

| CLASS 1 SHARES1 | ||||

| 1 Year | -7.41% | |||

| 5 Years | 3.73% | |||

| 10 Years | 0.19% | |||

| CLASS 2 SHARES1 | ||||

| 1 Year | -7.09% | |||

| 5 Years | 4.00% | |||

| 10 Years | 0.45% | |||

| CLASS A SHARES | ||||

| 1 Year | -11.40% | |||

| 5 Years | 2.66% | |||

| 10 Years | -0.39% | |||

| CLASS C SHARES | ||||

| 1 Year | -9.05% | |||

| 5 Years | 2.76% | |||

| 10 Years2 | -0.69% | |||

| ADVISOR CLASS SHARES3 | ||||

| 1 Year | -7.19% | |||

| 5 Years | 3.82% | |||

| 10 Years | 0.32% | |||

| CLASS R SHARES3 | ||||

| 1 Year | -7.85% | |||

| 5 Years | 3.25% | |||

| 10 Years | -0.20% | |||

| CLASS K SHARES3 | ||||

| 1 Year | -7.63% | |||

| 5 Years | 3.54% | |||

| 10 Years | 0.06% | |||

| CLASS I SHARES3 | ||||

| 1 Year | -7.22% | |||

| 5 Years | 3.98% | |||

| 10 Years | 0.43% | |||

| CLASS Z SHARES3 | ||||

| 1 Year | -7.21% | |||

| 5 Years | 3.98% | |||

| Since Inception4 | 0.99% | |||

(footnotes continued on next page)

14 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

HISTORICAL PERFORMANCE (continued)

| 1 | Class 1 shares are only available to Bernstein Global Wealth Management private client accounts. Class 2 shares are only available to the Adviser’s institutional clients or through other limited arrangements. These share classes do not carry front-end sales charges; therefore, their respective NAV and SEC returns are the same. |

| 2 | Assumes conversion of Class C shares into Class A shares after eight years. |

| 3 | Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

| 4 | Inception date: 1/31/2014. |

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 15 | |

EXPENSE EXAMPLE

(unaudited)

As a shareholder of a mutual fund, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

16 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

EXPENSE EXAMPLE (continued)

| Beginning Account Value May 1, 2022 | Ending Account Value October 31, 2022 | Expenses Paid During Period* | Annualized Expense Ratio* | Total Expenses Paid During Period+ | Total Annualized Expense Ratio+ | |||||||||||||||||||

| Class A | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 890.00 | $ | 5.67 | 1.19 | % | $ | 5.81 | 1.22 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,019.21 | $ | 6.06 | 1.19 | % | $ | 6.21 | 1.22 | % | ||||||||||||

| Class C | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 886.70 | $ | 9.37 | 1.97 | % | $ | 9.46 | 1.99 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,015.27 | $ | 10.01 | 1.97 | % | $ | 10.11 | 1.99 | % | ||||||||||||

| Advisor Class | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 891.70 | $ | 4.48 | 0.94 | % | $ | 4.58 | 0.96 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,020.47 | $ | 4.79 | 0.94 | % | $ | 4.89 | 0.96 | % | ||||||||||||

| Class R | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 888.50 | $ | 7.28 | 1.52 | % | $ | 7.33 | 1.54 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,017.49 | $ | 7.78 | 1.52 | % | $ | 7.83 | 1.54 | % | ||||||||||||

| Class K | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 889.50 | $ | 6.00 | 1.26 | % | $ | 6.14 | 1.29 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,018.85 | $ | 6.41 | 1.26 | % | $ | 6.56 | 1.29 | % | ||||||||||||

| Class I | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 891.40 | $ | 4.10 | 0.86 | % | $ | 4.20 | 0.88 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,020.87 | $ | 4.38 | 0.86 | % | $ | 4.48 | 0.88 | % | ||||||||||||

| Class 1 | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 890.50 | $ | 5.15 | 1.08 | % | $ | 5.29 | 1.11 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,019.76 | $ | 5.50 | 1.08 | % | $ | 5.65 | 1.11 | % | ||||||||||||

| Class 2 | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 891.50 | $ | 3.96 | 0.83 | % | $ | 4.05 | 0.85 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,021.02 | $ | 4.23 | 0.83 | % | $ | 4.33 | 0.85 | % | ||||||||||||

| Class Z | ||||||||||||||||||||||||

Actual | $ | 1,000 | $ | 891.50 | $ | 3.96 | 0.83 | % | $ | 4.05 | 0.85 | % | ||||||||||||

Hypothetical** | $ | 1,000 | $ | 1,021.02 | $ | 4.23 | 0.83 | % | $ | 4.33 | 0.85 | % | ||||||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| ** | Assumes 5% annual return before expenses. |

| + | In connection with the Fund’s investments in affiliated/unaffiliated underlying portfolios, the Fund incurs no direct expenses, but bears proportionate shares of the fees and expenses (i.e., operating, administrative and investment advisory fees) of the affiliated/unaffiliated underlying portfolios. The Adviser has contractually agreed to waive its fees from the Fund in an amount equal to the Fund’s pro rata share of certain acquired fund fees and expenses of the affiliated underlying portfolios. The Fund’s total expenses are equal to the classes’ annualized expense ratio plus the Fund’s pro rata share of the weighted average expense ratio of the affiliated/unaffiliated underlying portfolios in which it invests, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 17 | |

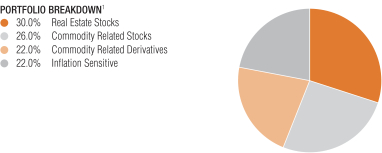

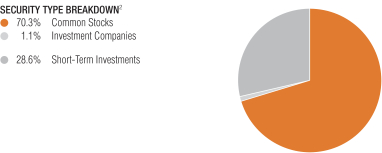

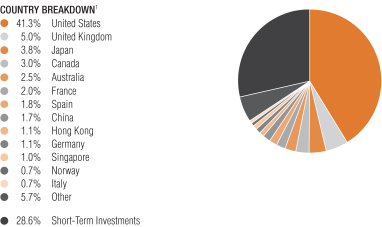

PORTFOLIO SUMMARY

October 31, 2022 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $1,029.7

| 1 | The portfolio breakdown is expressed as an approximate percentage of the Fund’s net assets inclusive of derivative exposure, based on the Adviser’s internal classification guidelines. |

| 2 | The Fund’s security type breakdown is expressed as a percentage of total investments (excluding security lending collateral) and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Consolidated Portfolio of Investments” section of the report for additional details). |

18 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

PORTFOLIO SUMMARY (continued)

October 31, 2022 (unaudited)

TEN LARGEST HOLDINGS2

| Company | U.S. $ Value | Percent of Net Assets | ||||||

| Shell PLC | $ | 21,133,068 | 2.1 | % | ||||

| Prologis, Inc. | 17,578,351 | 1.7 | ||||||

| Exxon Mobil Corp. | 17,102,304 | 1.7 | ||||||

| Equinix, Inc. | 12,002,863 | 1.2 | ||||||

| ConocoPhillips | 10,971,847 | 1.1 | ||||||

| Public Storage | 10,804,080 | 1.0 | ||||||

| EOG Resources, Inc. | 9,458,788 | 0.9 | ||||||

| Mitsui Fudosan Co., Ltd. | 8,400,387 | 0.8 | ||||||

| TotalEnergies SE | 8,366,193 | 0.8 | ||||||

| Chevron Corp. | 7,614,624 | 0.7 | ||||||

| $ | 123,432,505 | 12.0 | % | |||||

| 1 | The Fund’s country breakdown is expressed as a percentage of total investments (excluding security lending collateral) and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). “Other” country weightings represent 0.6% or less in the following: Austria, Belgium, Brazil, Denmark, Finland, India, Ireland, Israel, Luxembourg, Mexico, Netherlands, New Zealand, Philippines, Russia, South Africa, South Korea, Sweden, Switzerland, Thailand, United Arab Emirates, United Republic of Tanzania and Zambia. |

| 2 | Long-term investments. |

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 19 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS

October 31, 2022

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

COMMON STOCKS – 67.8% |

| |||||||

Real Estate – 26.4% |

| |||||||

Diversified Real Estate Activities – 1.7% | ||||||||

Ayala Land, Inc. | 2,554,100 | $ | 1,133,482 | |||||

City Developments Ltd. | 295,500 | 1,593,221 | ||||||

Daito Trust Construction Co., Ltd. | 8,700 | 861,507 | ||||||

Mitsui Fudosan Co., Ltd. | 438,700 | 8,400,387 | ||||||

Nomura Real Estate Holdings, Inc. | 14,900 | 336,797 | ||||||

Sun Hung Kai Properties Ltd. | 435,000 | 4,674,648 | ||||||

Tokyu Fudosan Holdings Corp. | 233,300 | 1,183,665 | ||||||

|

| |||||||

| 18,183,707 | ||||||||

|

| |||||||

Diversified REITs – 1.6% |

| |||||||

Alexander & Baldwin, Inc. | 99,800 | 1,944,104 | ||||||

Armada Hoffler Properties, Inc. | 250,690 | 2,930,566 | ||||||

Charter Hall Long Wale REIT | 606,580 | 1,691,336 | ||||||

Essential Properties Realty Trust, Inc. | 153,440 | 3,302,029 | ||||||

Growthpoint Properties Ltd.(a) | 2,072,622 | 1,461,202 | ||||||

ICADE | 29,880 | 1,111,502 | ||||||

Merlin Properties Socimi SA | 278,910 | 2,364,201 | ||||||

United Urban Investment Corp. | 1,519 | 1,607,144 | ||||||

|

| |||||||

| 16,412,084 | ||||||||

|

| |||||||

Health Care REITs – 1.9% | ||||||||

Assura PLC | 2,490,200 | 1,595,505 | ||||||

Cofinimmo SA | 13,570 | 1,125,434 | ||||||

Medical Properties Trust, Inc. | 288,010 | 3,297,714 | ||||||

Ventas, Inc. | 145,390 | 5,689,111 | ||||||

Welltower, Inc. | 124,340 | 7,589,713 | ||||||

|

| |||||||

| 19,297,477 | ||||||||

|

| |||||||

Hotel & Resort REITs – 0.8% | ||||||||

Invincible Investment Corp. | 9,400 | 2,950,786 | ||||||

Park Hotels & Resorts, Inc. | 234,690 | 3,069,745 | ||||||

RLJ Lodging Trust | 159,880 | 1,945,740 | ||||||

|

| |||||||

| 7,966,271 | ||||||||

|

| |||||||

Industrial REITs – 4.3% | ||||||||

Americold Realty Trust, Inc. | 78,680 | 1,907,990 | ||||||

CapitaLand Ascendas REIT | 825,200 | 1,526,777 | ||||||

Centuria Industrial REIT | 913,830 | 1,775,892 | ||||||

Dream Industrial Real Estate Investment Trust | 303,414 | 2,438,715 | ||||||

GLP J-Reit(b) | 1,146 | 1,188,496 | ||||||

Industrial & Infrastructure Fund Investment Corp. | 1,115 | 1,177,597 | ||||||

Mapletree Logistics Trust(a) | 1,205,318 | 1,293,631 | ||||||

Mitsui Fudosan Logistics Park, Inc.(b) | 479 | 1,589,253 | ||||||

Plymouth Industrial REIT, Inc. | 70,946 | 1,308,244 | ||||||

Prologis, Inc. | 158,721 | 17,578,351 | ||||||

Rexford Industrial Realty, Inc. | 64,600 | 3,571,088 | ||||||

20 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Segro PLC | 575,272 | $ | 5,177,447 | |||||

STAG Industrial, Inc. | 122,160 | 3,859,035 | ||||||

|

| |||||||

| 44,392,516 | ||||||||

|

| |||||||

Office REITs – 1.2% | ||||||||

Alexandria Real Estate Equities, Inc. | 7,540 | 1,095,562 | ||||||

City Office REIT, Inc. | 231,540 | 2,458,955 | ||||||

Cousins Properties, Inc. | 121,065 | 2,876,504 | ||||||

Daiwa Office Investment Corp. | 602 | 2,844,007 | ||||||

Derwent London PLC | 66,190 | 1,638,156 | ||||||

Kenedix Office Investment Corp.(a) | 648 | 1,476,147 | ||||||

|

| |||||||

| 12,389,331 | ||||||||

|

| |||||||

Real Estate Development – 0.9% | ||||||||

China Overseas Land & Investment Ltd. | 743,500 | 1,420,768 | ||||||

China Resources Land Ltd. | 678,000 | 2,121,315 | ||||||

CK Asset Holdings Ltd. | 284,000 | 1,570,113 | ||||||

Emaar Properties PJSC | 686,820 | 1,133,771 | ||||||

Instone Real Estate Group SE(c) | 81,039 | 589,854 | ||||||

Megaworld Corp. | 17,716,000 | 639,126 | ||||||

Midea Real Estate Holding Ltd.(a)(c) | 2,151,600 | 1,503,466 | ||||||

|

| |||||||

| 8,978,413 | ||||||||

|

| |||||||

Real Estate Operating Companies – 1.6% | ||||||||

Azrieli Group Ltd. | 14,750 | 1,092,761 | ||||||

CA Immobilien Anlagen AG | 58,719 | 1,854,600 | ||||||

Central Pattana PCL | 411,500 | 743,316 | ||||||

CTP NV(c) | 96,979 | 1,005,870 | ||||||

Hongkong Land Holdings Ltd. | 441,000 | 1,697,799 | ||||||

Hulic Co., Ltd. | 146,600 | 1,064,953 | ||||||

Shurgard Self Storage SA | 27,430 | 1,194,328 | ||||||

TAG Immobilien AG | 117,450 | 735,566 | ||||||

Vonovia SE | 176,274 | 3,897,525 | ||||||

Wihlborgs Fastigheter AB | 489,360 | 3,205,908 | ||||||

|

| |||||||

| 16,492,626 | ||||||||

|

| |||||||

Real Estate Services – 0.1% | ||||||||

Unibail-Rodamco-Westfield(b) | 20,600 | 974,738 | ||||||

|

| |||||||

Residential REITs – 4.0% | ||||||||

American Homes 4 Rent – Class A | 141,480 | 4,518,871 | ||||||

Equity LifeStyle Properties, Inc. | 44,010 | 2,814,880 | ||||||

Equity Residential | 102,510 | 6,460,180 | ||||||

Essex Property Trust, Inc. | 22,830 | 5,073,739 | ||||||

Independence Realty Trust, Inc. | 240,000 | 4,022,400 | ||||||

Kenedix Residential Next Investment Corp. | 538 | 788,746 | ||||||

Killam Apartment Real Estate Investment Trust | 272,860 | 3,162,520 | ||||||

Minto Apartment Real Estate Investment Trust(c) | 150,500 | 1,472,577 | ||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 21 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Sun Communities, Inc. | 46,857 | $ | 6,318,666 | |||||

UDR, Inc. | 119,730 | 4,760,465 | ||||||

UNITE Group PLC (The) | 156,180 | 1,595,371 | ||||||

|

| |||||||

| 40,988,415 | ||||||||

|

| |||||||

Retail REITs – 3.7% | ||||||||

AEON REIT Investment Corp. | 1,654 | 1,780,738 | ||||||

Brixmor Property Group, Inc. | 172,880 | 3,684,073 | ||||||

CapitaLand Integrated Commercial Trust | 3,103,460 | 4,118,769 | ||||||

Frasers Centrepoint Trust | 513,100 | 754,054 | ||||||

Kite Realty Group Trust | 168,660 | 3,312,482 | ||||||

Link REIT | 511,301 | 3,022,102 | ||||||

Mercialys SA | 122,148 | 1,057,716 | ||||||

NETSTREIT Corp. | 144,266 | 2,715,086 | ||||||

Phillips Edison & Co., Inc. | 103,350 | 3,114,969 | ||||||

Realty Income Corp. | 14,250 | 887,348 | ||||||

Shopping Centres Australasia Property Group | 772,030 | 1,344,657 | ||||||

Simon Property Group, Inc. | 34,378 | 3,746,514 | ||||||

SITE Centers Corp. | 314,880 | 3,898,215 | ||||||

Spirit Realty Capital, Inc. | 91,430 | 3,550,227 | ||||||

Waypoint REIT Ltd. | 467,450 | 816,164 | ||||||

|

| |||||||

| 37,803,114 | ||||||||

|

| |||||||

Specialized REITs – 4.6% | ||||||||

American Tower Corp. | 13,394 | 2,775,103 | ||||||

Crown Castle, Inc. | 12,458 | 1,660,153 | ||||||

CubeSmart | 115,710 | 4,844,778 | ||||||

Digital Realty Trust, Inc. | 9,160 | 918,290 | ||||||

Equinix, Inc. | 21,190 | 12,002,863 | ||||||

Iron Mountain, Inc. | 25,600 | 1,281,792 | ||||||

National Storage Affiliates Trust | 45,180 | 1,927,379 | ||||||

Public Storage | 34,880 | 10,804,080 | ||||||

Safestore Holdings PLC | 224,530 | 2,326,216 | ||||||

SBA Communications Corp. | 3,104 | 837,770 | ||||||

VICI Properties, Inc. | 220,100 | 7,047,602 | ||||||

Weyerhaeuser Co. | 45,585 | 1,409,944 | ||||||

|

| |||||||

| 47,835,970 | ||||||||

|

| |||||||

| 271,714,662 | ||||||||

|

| |||||||

Energy – 11.2% |

| |||||||

Coal & Consumable Fuels – 0.1% | ||||||||

Cameco Corp. | 26,821 | 636,194 | ||||||

|

| |||||||

Integrated Oil & Gas – 6.5% | ||||||||

Cenovus Energy, Inc.(a) | 17,389 | 351,520 | ||||||

Chevron Corp. | 42,093 | 7,614,624 | ||||||

Equinor ASA | 142,609 | 5,195,776 | ||||||

Exxon Mobil Corp. | 154,339 | 17,102,304 | ||||||

Gazprom PJSC(d) | 818,956 | – 0 | – | |||||

LUKOIL PJSC(d) | 20,541 | – 0 | – | |||||

22 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Repsol SA(b) | 532,416 | $ | 7,243,235 | |||||

Shell PLC | 762,883 | 21,133,068 | ||||||

Suncor Energy, Inc. | 6,237 | 214,530 | ||||||

TotalEnergies SE | 153,358 | 8,366,193 | ||||||

|

| |||||||

| 67,221,250 | ||||||||

|

| |||||||

Oil & Gas Drilling – 0.2% | ||||||||

China Oilfield Services Ltd. – Class H | 1,648,000 | 1,855,185 | ||||||

|

| |||||||

Oil & Gas Equipment & Services – 0.1% | ||||||||

Halliburton Co. | 26,015 | 947,466 | ||||||

|

| |||||||

Oil & Gas Exploration & Production – 3.1% | ||||||||

ConocoPhillips | 87,016 | 10,971,847 | ||||||

Coterra Energy, Inc. | 48,350 | 1,505,136 | ||||||

EOG Resources, Inc. | 69,285 | 9,458,788 | ||||||

Hess Corp. | 31,848 | 4,493,116 | ||||||

Texas Pacific Land Corp. | 620 | 1,428,399 | ||||||

Tourmaline Oil Corp.(a) | 13,858 | 780,813 | ||||||

Williams Cos., Inc. (The) | 35,053 | 1,147,285 | ||||||

Woodside Energy Group Ltd. | 91,483 | 2,114,945 | ||||||

|

| |||||||

| 31,900,329 | ||||||||

|

| |||||||

Oil & Gas Refining & Marketing – 0.3% |

| |||||||

Marathon Petroleum Corp. | 13,509 | 1,534,893 | ||||||

Neste Oyj | 11,223 | 491,887 | ||||||

Valero Energy Corp. | 11,950 | 1,500,322 | ||||||

|

| |||||||

| 3,527,102 | ||||||||

|

| |||||||

Oil & Gas Storage & Transportation – 0.9% | ||||||||

Antero Midstream Corp. | 9,634 | 102,602 | ||||||

Cheniere Energy, Inc. | 7,186 | 1,267,682 | ||||||

Enbridge, Inc.(a) | 71,454 | 2,783,997 | ||||||

EnLink Midstream LLC(b) | 7,164 | 85,108 | ||||||

Gibson Energy, Inc. | 5,174 | 88,300 | ||||||

Keyera Corp.(a) | 7,799 | 167,160 | ||||||

Kinder Morgan, Inc. | 57,035 | 1,033,474 | ||||||

Koninklijke Vopak NV | 2,307 | 47,137 | ||||||

New Fortress Energy, Inc. | 1,373 | 75,611 | ||||||

ONEOK, Inc. | 12,855 | 762,559 | ||||||

Pembina Pipeline Corp.(a) | 19,593 | 646,892 | ||||||

Targa Resources Corp. | 6,517 | 445,567 | ||||||

TC Energy Corp. | 35,711 | 1,568,574 | ||||||

|

| |||||||

| 9,074,663 | ||||||||

|

| |||||||

| 115,162,189 | ||||||||

|

| |||||||

Materials – 6.0% |

| |||||||

Aluminum – 0.1% |

| |||||||

Alcoa Corp. | 20,672 | 806,828 | ||||||

|

| |||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 23 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Commodity Chemicals – 0.5% | ||||||||

Beijing Haixin Energy Technology Co., Ltd. – Class A | 1,735,085 | $ | 952,315 | |||||

Corteva, Inc. | 41,683 | 2,723,567 | ||||||

Ecopro Co., Ltd. | 8,277 | 821,674 | ||||||

LG Chem Ltd. | 1,416 | 621,395 | ||||||

W-Scope Corp.(a)(b) | 19,600 | 253,243 | ||||||

|

| |||||||

| 5,372,194 | ||||||||

|

| |||||||

Construction Materials – 0.2% |

| |||||||

GCC SAB de CV | 258,717 | 1,614,092 | ||||||

|

| |||||||

Copper – 0.2% |

| |||||||

First Quantum Minerals Ltd. | 85,965 | 1,516,306 | ||||||

OZ Minerals Ltd.(a) | 37,029 | 573,358 | ||||||

|

| |||||||

| 2,089,664 | ||||||||

|

| |||||||

Diversified Chemicals – 0.1% |

| |||||||

Sumitomo Chemical Co., Ltd. | 316,200 | 1,064,727 | ||||||

|

| |||||||

Diversified Metals & Mining – 1.6% |

| |||||||

Allkem Ltd.(b) | 74,824 | 691,348 | ||||||

Anglo American PLC | 132,981 | 3,983,339 | ||||||

BHP Group Ltd. | 43,087 | 1,034,958 | ||||||

CMOC Group Ltd. – Class H(a) | 1,368,000 | 440,430 | ||||||

Ganfeng Lithium Group Co., Ltd – Class A | 50,480 | 546,534 | ||||||

Glencore PLC | 726,435 | 4,164,702 | ||||||

MMC Norilsk Nickel PJSC (ADR)(d)(e) | 66,074 | – 0 | – | |||||

Rio Tinto PLC | 72,754 | 3,802,242 | ||||||

Teck Resources Ltd. – Class B | 55,531 | 1,690,364 | ||||||

Zhejiang Huayou Cobalt Co., Ltd. – Class A | 53,270 | 398,377 | ||||||

|

| |||||||

| 16,752,294 | ||||||||

|

| |||||||

Fertilizers & Agricultural Chemicals – 0.5% | ||||||||

CF Industries Holdings, Inc. | 38,154 | 4,054,244 | ||||||

OCI NV | 35,167 | 1,345,063 | ||||||

|

| |||||||

| 5,399,307 | ||||||||

|

| |||||||

Forest Products – 0.0% |

| |||||||

Interfor Corp.(b) | 28,218 | 501,248 | ||||||

|

| |||||||

Gold – 0.8% |

| |||||||

Agnico Eagle Mines Ltd. | 61,135 | 2,689,339 | ||||||

Barrick Gold Corp. | 143,570 | 2,157,857 | ||||||

Endeavour Mining PLC | 122,275 | 2,126,768 | ||||||

Northern Star Resources Ltd. | 71,866 | 401,091 | ||||||

Regis Resources Ltd. | 301,971 | 294,427 | ||||||

St. Barbara Ltd.(b) | 412,784 | 134,387 | ||||||

|

| |||||||

| 7,803,869 | ||||||||

|

| |||||||

24 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Industrial Gases – 0.2% |

| |||||||

Air Liquide SA | 4,613 | $ | 603,443 | |||||

Air Products and Chemicals, Inc. | 2,547 | 637,769 | ||||||

Linde PLC | 2,065 | 614,028 | ||||||

|

| |||||||

| 1,855,240 | ||||||||

|

| |||||||

Paper Packaging – 0.1% |

| |||||||

Sealed Air Corp. | 26,931 | 1,282,454 | ||||||

|

| |||||||

Paper Products – 0.2% |

| |||||||

Stora Enso Oyj – Class R | 94,140 | 1,227,473 | ||||||

Suzano SA | 105,200 | 1,083,466 | ||||||

|

| |||||||

| 2,310,939 | ||||||||

|

| |||||||

Specialty Chemicals – 0.7% |

| |||||||

Albemarle Corp. | 2,888 | 808,265 | ||||||

Danimer Scientific, Inc.(a)(b) | 167,875 | 439,833 | ||||||

Ecolab, Inc. | 3,149 | 494,613 | ||||||

Evonik Industries AG | 49,372 | 909,517 | ||||||

IMCD NV | 4,070 | 527,856 | ||||||

Johnson Matthey PLC | 31,809 | 706,083 | ||||||

Livent Corp.(a)(b) | 26,870 | 848,286 | ||||||

Shanghai Putailai New Energy Technology Co., Ltd. – Class A | 60,520 | 414,260 | ||||||

Sika AG (REG) | 2,054 | 463,127 | ||||||

Umicore SA | 18,303 | 603,375 | ||||||

Wacker Chemie AG | 5,147 | 599,241 | ||||||

|

| |||||||

| 6,814,456 | ||||||||

|

| |||||||

Steel – 0.8% |

| |||||||

ArcelorMittal SA | 174,554 | 3,901,919 | ||||||

Commercial Metals Co. | 20,956 | 953,498 | ||||||

Steel Dynamics, Inc. | 15,744 | 1,480,723 | ||||||

Vale SA (Sponsored ADR) | 138,199 | 1,788,295 | ||||||

|

| |||||||

| 8,124,435 | ||||||||

|

| |||||||

| 61,791,747 | ||||||||

|

| |||||||

Capital Goods – 4.5% |

| |||||||

Aerospace & Defense – 0.3% |

| |||||||

BAE Systems PLC | 108,753 | 1,017,228 | ||||||

Hexcel Corp. | 13,775 | 767,268 | ||||||

Huntington Ingalls Industries, Inc. | 5,361 | 1,378,152 | ||||||

|

| |||||||

| 3,162,648 | ||||||||

|

| |||||||

Agricultural & Farm Machinery – 0.3% |

| |||||||

Deere & Co. | 2,279 | 902,074 | ||||||

Lindsay Corp. | 4,466 | 756,094 | ||||||

Toro Co. (The) | 8,093 | 853,245 | ||||||

|

| |||||||

| 2,511,413 | ||||||||

|

| |||||||

Building Products – 0.6% |

| |||||||

A O Smith Corp. | 12,800 | 701,184 | ||||||

Carrier Global Corp. | 18,733 | 744,824 | ||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 25 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Cie de Saint-Gobain | 26,986 | $ | 1,103,213 | |||||

Kingspan Group PLC | 11,474 | 578,481 | ||||||

Lennox International, Inc. | 2,335 | 545,386 | ||||||

Nibe Industrier AB – Class B | 59,623 | 475,599 | ||||||

Owens Corning | 14,873 | 1,273,277 | ||||||

Zurn Elkay Water Solutions Corp. | 18,797 | 441,542 | ||||||

|

| |||||||

| 5,863,506 | ||||||||

|

| |||||||

Construction & Engineering – 0.2% |

| |||||||

Ferrovial SA | 17,604 | 430,213 | ||||||

MDU Resources Group, Inc. | 5,849 | 166,580 | ||||||

Vinci SA | 18,979 | 1,746,769 | ||||||

|

| |||||||

| 2,343,562 | ||||||||

|

| |||||||

Construction & Farm Machinery & Heavy Trucks – 0.1% | ||||||||

Cummins, Inc. | 4,099 | 1,002,246 | ||||||

|

| |||||||

Electrical Components & Equipment – 1.3% | ||||||||

Acuity Brands, Inc. | 7,334 | 1,346,302 | ||||||

Advent Technologies Holdings, Inc.(a)(b) | 278,432 | 629,256 | ||||||

Ballard Power Systems, Inc.(a)(b) | 80,904 | 458,457 | ||||||

Beijing Easpring Material Technology Co., Ltd. – Class A | 53,500 | 434,679 | ||||||

Blink Charging Co.(a)(b) | 19,644 | 290,731 | ||||||

Camel Group Co., Ltd. – Class A | 546,200 | 639,253 | ||||||

Contemporary Amperex Technology Co., Ltd. – Class A | 8,900 | 456,745 | ||||||

EnerSys | 16,176 | 1,072,307 | ||||||

First Solar, Inc.(b) | 7,443 | 1,083,478 | ||||||

FuelCell Energy, Inc.(a)(b) | 146,061 | 455,710 | ||||||

Gotion High-tech Co., Ltd. – Class A | 121,200 | 501,112 | ||||||

Hubbell, Inc. | 3,554 | 844,004 | ||||||

Legrand SA | 10,424 | 794,357 | ||||||

nVent Electric PLC | 30,848 | 1,125,952 | ||||||

Plug Power, Inc.(a)(b) | 23,424 | 374,316 | ||||||

Prysmian SpA | 23,685 | 770,902 | ||||||

Signify NV(c) | 39,231 | 1,086,901 | ||||||

SunPower Corp.(a)(b) | 22,852 | 422,534 | ||||||

Sunrun, Inc.(b) | 28,997 | 652,722 | ||||||

|

| |||||||

| 13,439,718 | ||||||||

|

| |||||||

Heavy Electrical Equipment – 0.5% |

| |||||||

Bloom Energy Corp. – Class A(b) | 19,157 | 358,428 | ||||||

CS Wind Corp. | 14,045 | 578,576 | ||||||

ITM Power PLC(a)(b) | 213,956 | 202,118 | ||||||

Ming Yang Smart Energy Group Ltd. – Class A | 188,696 | 645,860 | ||||||

NARI Technology Co., Ltd. – Class A | 168,609 | 566,285 | ||||||

NEL ASA(b) | 333,613 | 407,785 | ||||||

26 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Nordex SE(b) | 52,303 | $ | 487,577 | |||||

Siemens Energy AG(b) | 75,800 | 883,647 | ||||||

TPI Composites, Inc.(b) | 31,683 | 315,563 | ||||||

Vestas Wind Systems A/S | 24,079 | 474,685 | ||||||

|

| |||||||

| 4,920,524 | ||||||||

|

| |||||||

Industrial Conglomerates – 0.1% |

| |||||||

General Electric Co. | 13,929 | 1,083,815 | ||||||

|

| |||||||

Industrial Machinery – 1.0% |

| |||||||

Chart Industries, Inc.(b) | 3,225 | 718,788 | ||||||

Energy Recovery, Inc.(b) | 25,889 | 666,124 | ||||||

Evoqua Water Technologies Corp.(b) | 14,600 | 572,028 | ||||||

Illinois Tool Works, Inc. | 7,222 | 1,542,114 | ||||||

John Bean Technologies Corp. | 6,165 | 562,248 | ||||||

McPhy Energy SA(b) | 32,420 | 367,775 | ||||||

Mueller Industries, Inc. | 11,185 | 700,628 | ||||||

NGK Insulators Ltd. | 66,500 | 775,793 | ||||||

Pentair PLC | 17,361 | 745,655 | ||||||

Snap-on, Inc. | 6,315 | 1,402,246 | ||||||

SPX Technologies, Inc.(b) | 15,185 | 999,781 | ||||||

Watts Water Technologies, Inc. – Class A | 5,198 | 760,779 | ||||||

Xylem, Inc./NY | 7,142 | 731,555 | ||||||

|

| |||||||

| 10,545,514 | ||||||||

|

| |||||||

Trading Companies & Distributors – 0.1% | ||||||||

WW Grainger, Inc. | 2,433 | 1,421,724 | ||||||

|

| |||||||

| 46,294,670 | ||||||||

|

| |||||||

Utilities – 4.4% |

| |||||||

Electric Utilities – 1.1% |

| |||||||

Avangrid, Inc.(a) | 22,721 | 924,290 | ||||||

Constellation Energy Corp. | 1 | 95 | ||||||

Edison International | 10,973 | 658,819 | ||||||

Elia Group SA/NV | 1,271 | 160,695 | ||||||

Enel SpA | 505,112 | 2,256,511 | ||||||

Eversource Energy | 9,966 | 760,206 | ||||||

Exelon Corp. | 14,729 | 568,392 | ||||||

Fortis, Inc./Canada | 16,892 | 659,016 | ||||||

Hydro One Ltd.(c) | 11,198 | 280,782 | ||||||

Iberdrola SA | 82,974 | 843,785 | ||||||

NextEra Energy, Inc. | 4,547 | 352,393 | ||||||

NRG Energy, Inc. | 31,429 | 1,395,448 | ||||||

Orsted AS(c) | 5,787 | 477,461 | ||||||

PG&E Corp.(b) | 46,315 | 691,483 | ||||||

Red Electrica Corp. SA | 15,275 | 247,084 | ||||||

SSE PLC | 34,755 | 621,102 | ||||||

Terna – Rete Elettrica Nazionale | 49,652 | 329,275 | ||||||

|

| |||||||

| 11,226,837 | ||||||||

|

| |||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 27 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Gas Utilities – 0.8% |

| |||||||

AltaGas Ltd. | 17,530 | $ | 316,154 | |||||

APA Group | 323,138 | 2,175,490 | ||||||

Atmos Energy Corp. | 4,024 | 428,757 | ||||||

Beijing Enterprises Holdings Ltd. | 16,913 | 42,907 | ||||||

Chesapeake Utilities Corp. | 510 | 63,434 | ||||||

China Gas Holdings Ltd. | 105,593 | 93,712 | ||||||

China Resources Gas Group Ltd. | 31,847 | 81,566 | ||||||

Enagas SA | 8,783 | 142,582 | ||||||

ENN Energy Holdings Ltd. | 26,732 | 265,771 | ||||||

Hong Kong & China Gas Co., Ltd. | 381,933 | 294,382 | ||||||

Italgas SpA | 17,156 | 88,392 | ||||||

Kunlun Energy Co., Ltd. | 140,561 | 84,009 | ||||||

Naturgy Energy Group SA(a) | 40,971 | 1,051,419 | ||||||

New Jersey Resources Corp. | 2,768 | 123,564 | ||||||

Northwest Natural Holding Co. | 1,001 | 48,138 | ||||||

ONE Gas, Inc. | 1,557 | 120,636 | ||||||

Snam SpA | 72,348 | 321,696 | ||||||

Southwest Gas Holdings, Inc. | 1,773 | 129,553 | ||||||

Spire, Inc. | 1,510 | 105,413 | ||||||

Toho Gas Co., Ltd. | 3,491 | 65,044 | ||||||

Tokyo Gas Co., Ltd. | 14,473 | 258,654 | ||||||

Towngas Smart Energy Co., Ltd. | 39,098 | 13,694 | ||||||

UGI Corp. | 38,767 | 1,369,638 | ||||||

|

| |||||||

| 7,684,605 | ||||||||

|

| |||||||

Independent Power and Renewable Electricity Producers – 0.7% | ||||||||

Atlantica Sustainable Infrastructure PLC | 22,761 | 630,707 | ||||||

Azure Power Global Ltd.(a)(b) | 58,369 | 337,956 | ||||||

Boralex, Inc. – Class A | 17,325 | 491,258 | ||||||

Brookfield Renewable Corp. – Class A | 15,520 | 482,227 | ||||||

China Longyuan Power Group Corp. Ltd. – Class H | 436,000 | 498,204 | ||||||

EDP Renovaveis SA | 81,512 | 1,715,215 | ||||||

Innergex Renewable Energy, Inc. | 52,473 | 577,748 | ||||||

NextEra Energy Partners LP(a) | 9,801 | 725,960 | ||||||

Ormat Technologies, Inc.(a) | 7,255 | 656,215 | ||||||

Solaria Energia y Medio Ambiente SA(b) | 30,463 | 481,806 | ||||||

TransAlta Renewables, Inc.(a) | 61,898 | 664,710 | ||||||

Xinyi Energy Holdings Ltd.(a) | 1,580,000 | 402,437 | ||||||

|

| |||||||

| 7,664,443 | ||||||||

|

| |||||||

Independent Power Producers & Energy Traders – 0.5% | ||||||||

AES Corp. (The) | 28,600 | 748,176 | ||||||

Clearway Energy, Inc. – Class A | 18,541 | 599,431 | ||||||

Drax Group PLC | 104,811 | 625,891 | ||||||

ERG SpA | 24,584 | 771,122 | ||||||

28 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Guangxi Guiguan Electric Power Co., Ltd. – Class A | 778,700 | $ | 668,481 | |||||

Northland Power, Inc. | 21,941 | 638,412 | ||||||

RWE AG | 22,706 | 874,070 | ||||||

|

| |||||||

| 4,925,583 | ||||||||

|

| |||||||

Multi-Utilities – 0.7% |

| |||||||

ACEA SpA | 1,503 | 18,939 | ||||||

Algonquin Power & Utilities Corp. | 56,518 | 625,604 | ||||||

CenterPoint Energy, Inc. | 18,109 | 518,099 | ||||||

Consolidated Edison, Inc. | 10,200 | 897,192 | ||||||

DTE Energy Co. | 6,684 | 749,343 | ||||||

E.ON SE | 67,344 | 563,938 | ||||||

National Grid PLC | 136,793 | 1,490,376 | ||||||

NiSource, Inc. | 11,678 | 300,008 | ||||||

NorthWestern Corp. | 1,615 | 85,320 | ||||||

Sempra Energy | 12,677 | 1,913,466 | ||||||

United Utilities Group PLC | 24,063 | 259,307 | ||||||

Unitil Corp. | 461 | 24,299 | ||||||

|

| |||||||

| 7,445,891 | ||||||||

|

| |||||||

Water Utilities – 0.6% |

| |||||||

American States Water Co. | 7,480 | 676,641 | ||||||

American Water Works Co., Inc. | 9,061 | 1,316,925 | ||||||

Beijing Enterprises Water Group Ltd. | 3,070,538 | 645,114 | ||||||

California Water Service Group | 14,893 | 924,260 | ||||||

China Water Affairs Group Ltd. | 30,530 | 21,623 | ||||||

Cia de Saneamento Basico do Estado de Sao Paulo (ADR) | 12,060 | 139,414 | ||||||

Essential Utilities, Inc. | 6,860 | 303,349 | ||||||

Middlesex Water Co. | 3,851 | 344,549 | ||||||

Pennon Group PLC | 9,208 | 88,486 | ||||||

Severn Trent PLC | 8,939 | 256,547 | ||||||

SJW Group | 16,297 | 1,151,872 | ||||||

|

| |||||||

| 5,868,780 | ||||||||

|

| |||||||

| 44,816,139 | ||||||||

|

| |||||||

Pharmaceuticals & Biotechnology – 1.9% | ||||||||

Biotechnology – 0.3% |

| |||||||

AbbVie, Inc. | 6,902 | 1,010,453 | ||||||

Amgen, Inc. | 1,716 | 463,921 | ||||||

Moderna, Inc.(b) | 4,536 | 681,897 | ||||||

Neurocrine Biosciences, Inc.(b) | 5,444 | 626,713 | ||||||

Regeneron Pharmaceuticals, Inc.(b) | 1,116 | 835,605 | ||||||

|

| |||||||

| 3,618,589 | ||||||||

|

| |||||||

Life Sciences Tools & Services – 0.5% | ||||||||

Danaher Corp. | 3,046 | 766,587 | ||||||

Eurofins Scientific SE | 12,537 | 802,553 | ||||||

Mettler-Toledo International, Inc.(b) | 1,117 | 1,412,927 | ||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 29 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Sartorius Stedim Biotech | 489 | $ | 155,179 | |||||

Waters Corp.(b) | 5,979 | 1,788,737 | ||||||

|

| |||||||

| 4,925,983 | ||||||||

|

| |||||||

Pharmaceuticals – 1.1% |

| |||||||

Bayer AG (REG) | 22,622 | 1,189,488 | ||||||

Elanco Animal Health, Inc.(b) | 62,566 | 825,245 | ||||||

Eli Lilly & Co. | 6,176 | 2,236,268 | ||||||

Johnson & Johnson | 300 | 52,191 | ||||||

Novo Nordisk A/S – Class B | 17,095 | 1,858,761 | ||||||

Pfizer, Inc. | 40,807 | 1,899,566 | ||||||

Roche Holding AG (Roche) | 1,269 | 515,074 | ||||||

Roche Holding AG (Genusschein) | 4,707 | 1,561,774 | ||||||

Takeda Pharmaceutical Co., Ltd. | 16,700 | 441,030 | ||||||

Zoetis, Inc. | 3,810 | 574,472 | ||||||

|

| |||||||

| 11,153,869 | ||||||||

|

| |||||||

| 19,698,441 | ||||||||

|

| |||||||

Software & Services – 1.9% |

| |||||||

Application Software – 0.5% |

| |||||||

Autodesk, Inc.(b) | 3,735 | 800,411 | ||||||

Cadence Design Systems, Inc.(b) | 9,649 | 1,460,762 | ||||||

Dropbox, Inc. – Class A(b) | 63,208 | 1,374,774 | ||||||

Fair Isaac Corp.(b) | 1,541 | 737,892 | ||||||

Roper Technologies, Inc. | 2,559 | 1,060,808 | ||||||

|

| |||||||

| 5,434,647 | ||||||||

|

| |||||||

Data Processing & Outsourced Services – 0.4% | ||||||||

Mastercard, Inc. – Class A | 6,728 | 2,207,995 | ||||||

Visa, Inc. – Class A | 6,229 | 1,290,400 | ||||||

|

| |||||||

| 3,498,395 | ||||||||

|

| |||||||

Internet Services & Infrastructure – 0.1% | ||||||||

VeriSign, Inc.(b) | 6,730 | 1,349,096 | ||||||

|

| |||||||

IT Consulting & Other Services – 0.1% | ||||||||

Gartner, Inc.(b) | 4,620 | 1,394,870 | ||||||

Kyndryl Holdings, Inc.(b) | 606 | 5,860 | ||||||

|

| |||||||

| 1,400,730 | ||||||||

|

| |||||||

Systems Software – 0.8% | ||||||||

Fortinet, Inc.(b) | 22,356 | 1,277,869 | ||||||

Microsoft Corp. | 21,408 | 4,969,439 | ||||||

Palo Alto Networks, Inc.(b) | 3,978 | 682,585 | ||||||

ServiceNow, Inc.(b) | 2,069 | 870,511 | ||||||

|

| |||||||

| 7,800,404 | ||||||||

|

| |||||||

| 19,483,272 | ||||||||

|

| |||||||

30 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Food Beverage & Tobacco – 1.6% | ||||||||

Agricultural Products – 0.3% | ||||||||

Archer-Daniels-Midland Co. | 11,204 | $ | 1,086,564 | |||||

Bunge Ltd. | 13,976 | 1,379,431 | ||||||

Darling Ingredients, Inc.(b) | 11,976 | 939,877 | ||||||

|

| |||||||

| 3,405,872 | ||||||||

|

| |||||||

Brewers – 0.1% | ||||||||

Carlsberg AS – Class B | 6,255 | 736,498 | ||||||

Kirin Holdings Co., Ltd. | 31,600 | 464,518 | ||||||

|

| |||||||

| 1,201,016 | ||||||||

|

| |||||||

Packaged Foods & Meats – 1.0% | ||||||||

Danone SA | 15,513 | 770,988 | ||||||

Hershey Co. (The) | 6,030 | 1,439,783 | ||||||

Hormel Foods Corp. | 15,728 | 730,566 | ||||||

JBS SA | 158,600 | 766,365 | ||||||

Maple Leaf Foods, Inc. | 49,198 | 729,113 | ||||||

Marfrig Global Foods SA | 389,700 | 807,238 | ||||||

Mowi ASA | 56,453 | 842,605 | ||||||

Nestle SA (REG) | 20,051 | 2,182,728 | ||||||

Pilgrim’s Pride Corp.(b) | 34,010 | 783,931 | ||||||

Sao Martinho SA | 118,800 | 620,276 | ||||||

Tyson Foods, Inc. – Class A | 11,981 | 818,901 | ||||||

|

| |||||||

| 10,492,494 | ||||||||

|

| |||||||

Tobacco – 0.2% |

| |||||||

Imperial Brands PLC | 64,211 | 1,564,120 | ||||||

|

| |||||||

| 16,663,502 | ||||||||

|

| |||||||

Technology Hardware & Equipment – 1.0% | ||||||||

Electronic Components – 0.1% | ||||||||

Samsung SDI Co., Ltd. | 1,355 | 699,065 | ||||||

TDK Corp. | 1,600 | 49,981 | ||||||

|

| |||||||

| 749,046 | ||||||||

|

| |||||||

Electronic Equipment & Instruments – 0.2% | ||||||||

Itron, Inc.(b) | 14,699 | 718,634 | ||||||

Landis+Gyr Group AG(b) | 14,851 | 855,818 | ||||||

|

| |||||||

| 1,574,452 | ||||||||

|

| |||||||

Technology Distributors – 0.0% | ||||||||

CDW Corp./DE | 2,581 | 446,023 | ||||||

|

| |||||||

Technology Hardware, Storage & Peripherals – 0.7% | ||||||||

Apple, Inc. | 49,183 | 7,541,721 | ||||||

|

| |||||||

| 10,311,242 | ||||||||

|

| |||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 31 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Commercial & Professional Services – 0.9% | ||||||||

Diversified Support Services – 0.2% | ||||||||

Brambles Ltd. | 112,577 | $ | 842,834 | |||||

Copart, Inc.(b) | 8,585 | 987,447 | ||||||

|

| |||||||

| 1,830,281 | ||||||||

|

| |||||||

Environmental & Facilities Services – 0.5% | ||||||||

Aker Carbon Capture ASA(b) | 209,829 | 236,125 | ||||||

Casella Waste Systems, Inc. – Class A(b) | 8,032 | 657,098 | ||||||

Clean Harbors, Inc.(b) | 9,646 | 1,181,249 | ||||||

Republic Services, Inc. | 6,397 | 848,370 | ||||||

Rollins, Inc. | 32,642 | 1,373,575 | ||||||

Tetra Tech, Inc. | 4,976 | 703,009 | ||||||

Waste Management, Inc. | 4,201 | 665,313 | ||||||

|

| |||||||

| 5,664,739 | ||||||||

|

| |||||||

Research & Consulting Services – 0.2% | ||||||||

Booz Allen Hamilton Holding Corp. | 12,001 | 1,306,309 | ||||||

Nihon M&A Center Holdings, Inc. | 28,200 | 318,203 | ||||||

Thomson Reuters Corp. | 4,286 | 455,829 | ||||||

|

| |||||||

| 2,080,341 | ||||||||

|

| |||||||

| 9,575,361 | ||||||||

|

| |||||||

Transportation – 0.9% | ||||||||

Air Freight & Logistics – 0.1% | ||||||||

CH Robinson Worldwide, Inc. | 3,539 | 345,831 | ||||||

Expeditors International of Washington, Inc. | 3,436 | 336,213 | ||||||

Kuehne & Nagel International AG (REG) | 1,634 | 347,823 | ||||||

|

| |||||||

| 1,029,867 | ||||||||

|

| |||||||

Airport Services – 0.2% | ||||||||

Aena SME SA(b)(c) | 2,594 | 304,876 | ||||||

Aeroports de Paris(b) | 978 | 132,256 | ||||||

Auckland International Airport Ltd.(b) | 42,616 | 190,511 | ||||||

Beijing Capital International Airport Co., Ltd. – Class H(b) | 59,027 | 31,965 | ||||||

Flughafen Zurich AG (REG)(b) | 672 | 104,251 | ||||||

Fraport AG Frankfurt Airport Services Worldwide(b) | 1,305 | 50,277 | ||||||

Grupo Aeroportuario del Centro Norte SAB de CV (ADR) | 1,201 | 76,588 | ||||||

Grupo Aeroportuario del Pacifico SAB de CV (ADR) | 1,281 | 198,632 | ||||||

Grupo Aeroportuario del Sureste SAB de CV (ADR) | 665 | 155,224 | ||||||

Japan Airport Terminal Co., Ltd.(a)(b) | 3,287 | 140,687 | ||||||

|

| |||||||

| 1,385,267 | ||||||||

|

| |||||||

32 | AB ALL MARKET REAL RETURN PORTFOLIO | abfunds.com | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Highways & Railtracks – 0.5% | ||||||||

Atlantia SpA | 17,776 | $ | 396,538 | |||||

Atlas Arteria Ltd. | 43,029 | 181,143 | ||||||

Getlink SE | 14,168 | 224,201 | ||||||

Jiangsu Expressway Co., Ltd. – Class H | 43,124 | 30,417 | ||||||

Shenzhen Expressway Corp. Ltd. – Class H | 21,630 | 15,528 | ||||||

Transurban Group(a) | 498,103 | 4,225,381 | ||||||

Yuexiu Transport Infrastructure Ltd. | 33,065 | 12,942 | ||||||

|

| |||||||

| 5,086,150 | ||||||||

|

| |||||||

Marine – 0.0% | ||||||||

SITC International Holdings Co., Ltd. | 101,000 | 165,418 | ||||||

|

| |||||||

Marine Ports & Services – 0.0% | ||||||||

China Merchants Port Holdings Co., Ltd. | 47,253 | 55,399 | ||||||

COSCO SHIPPING Ports Ltd. | 59,696 | 29,439 | ||||||

Hamburger Hafen und Logistik AG | 793 | 9,288 | ||||||

Hutchison Port Holdings Trust | 178,300 | 29,121 | ||||||

Westshore Terminals Investment Corp.(a) | 1,294 | 23,147 | ||||||

|

| |||||||

| 146,394 | ||||||||

|

| |||||||

Road & Rail – 0.1% | ||||||||

Aurizon Holdings Ltd. | 513,638 | 1,190,288 | ||||||

|

| |||||||

| 9,003,384 | ||||||||

|

| |||||||

Semiconductors & Semiconductor Equipment – 0.9% | ||||||||

Semiconductor Equipment – 0.5% | ||||||||

Applied Materials, Inc. | 11,454 | 1,011,274 | ||||||

ASML Holding NV | 3,124 | 1,465,427 | ||||||

Enphase Energy, Inc.(b) | 4,343 | 1,333,301 | ||||||

KLA Corp. | 1,092 | 345,563 | ||||||

SolarEdge Technologies, Inc.(b) | 1,804 | 414,974 | ||||||

Xinyi Solar Holdings Ltd. | 444,000 | 440,802 | ||||||

|

| |||||||

| 5,011,341 | ||||||||

|

| |||||||

Semiconductors – 0.4% | ||||||||

Canadian Solar, Inc.(b) | 19,902 | 674,678 | ||||||

LONGi Green Energy Technology Co., Ltd. – Class A(b) | 82,732 | 546,376 | ||||||

NVIDIA Corp. | 5,619 | 758,396 | ||||||

QUALCOMM, Inc. | 11,049 | 1,300,025 | ||||||

Wolfspeed, Inc.(a)(b) | 6,685 | 526,444 | ||||||

|

| |||||||

| 3,805,919 | ||||||||

|

| |||||||

| 8,817,260 | ||||||||

|

| |||||||

Health Care Equipment & Services – 0.9% | ||||||||

Health Care Distributors – 0.3% | ||||||||

AmerisourceBergen Corp. | 8,981 | 1,411,993 | ||||||

McKesson Corp. | 3,871 | 1,507,251 | ||||||

|

| |||||||

| 2,919,244 | ||||||||

|

| |||||||

| abfunds.com | AB ALL MARKET REAL RETURN PORTFOLIO | 33 | |

CONSOLIDATED PORTFOLIO OF INVESTMENTS (continued)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Health Care Equipment – 0.1% | ||||||||

ABIOMED, Inc.(b) | 1,321 | $ | 332,998 | |||||

Hologic, Inc.(b) | 5,168 | 350,390 | ||||||