FRANKLIN CUSTODIAN FUNDS

| 1

Semiannual Report

Economic and Market Overview

The U.S. economy, as measured by gross domestic product growth, expanded during the six-month period ended March 31, 2012. The national unemployment rate for March 2012 stood at 8.2%, compared with 9.0% at the start of the period.1 Jobless claims touched a four-year low in February, and job creation was fairly robust. Consistent with employment trends, industrial production and manufacturing activity increased toward the end of the period. Automobile sales rose to their highest levels since February 2008, and consumer confidence climbed to pre-recession levels. Outside of the U.S., Greece secured bailout financing as bondholders agreed to concessions and the country enacted austerity measures. Although the long-term resolution of the European debt situation remained unclear, the European Central Bank’s plan to increase liquidity through loans was well received and seemed to improve investor sentiment.

At the end of the reporting period, however, challenges to the economy remained, including uncertainty surrounding deeply indebted European countries, soaring gas prices amid political turmoil in the Middle East, indications of reduced economic stimulus from the federal government, and continued malaise in the U.S. housing market. To help support mortgage market conditions, the Federal Reserve Board decided to reinvest principal received from certain debt securities into agency mortgage-backed securities. Additionally, federal lawmakers made efforts to strengthen the real estate market by removing some eligibility restrictions and charges associated with refinancing. Signs of China’s economic growth slowdown contributed to pessimism as, despite a higher overall level of U.S. exports, the U.S. trade deficit widened following decreases in exports to China and the eurozone.

For much of the period, investors sought the perceived safety of U.S. Treasuries. As U.S. economic data improved, however, investors shifted assets into equities, which drove bond prices lower and yields higher. The 10-year Treasury note yield rose from 1.92% on September 30, 2011, to 2.23% on March 31, 2012. U.S. stock markets soared amid the positive economic reports and reached multi-year highs in the first quarter of 2012. The Dow Jones Industrial Average

1. Source: Bureau of Labor Statistics.

Semiannual Report | 3

exceeded the 13,000 level for the first time since 2008, and the NASDAQ Composite Index hit an 11-year high. Sector leaders during the six-month period included financials, information technology and consumer discretionary. Conversely, utilities and telecommunication services lagged the broader market.

The foregoing information reflects our analysis and opinions as of March 31, 2012. The information is not a complete analysis of every aspect of any market, country, industry, security or fund. Statements of fact are from sources considered reliable.

4 | Semiannual Report

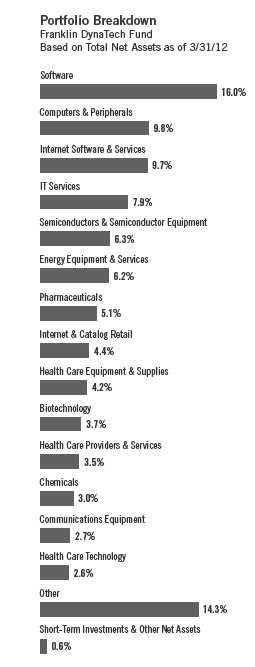

Franklin DynaTech Fund

Your Fund’s Goal and Main Investments: Franklin DynaTech Fund seeks capital

appreciation by investing substantially in equity securities of companies emphasizing scientific or

technological development or that are in fast-growing industries.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

We are pleased to bring you Franklin DynaTech Fund’s semiannual report for the period ended March 31, 2012.

Performance Overview

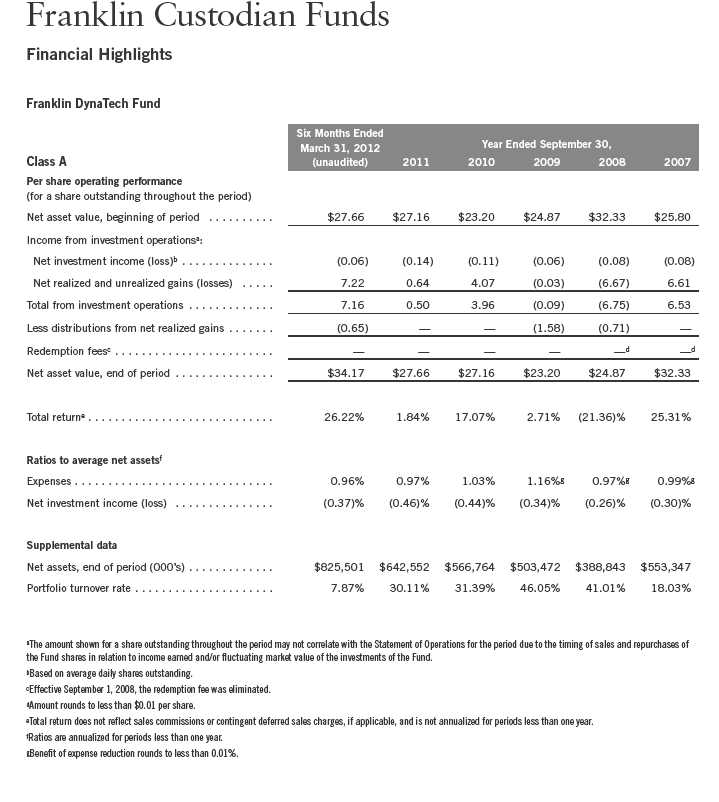

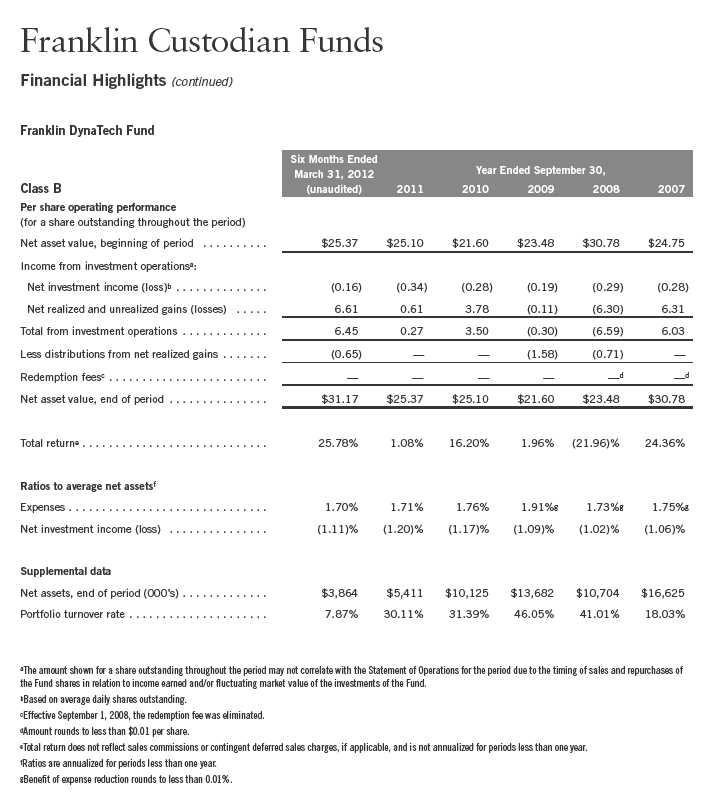

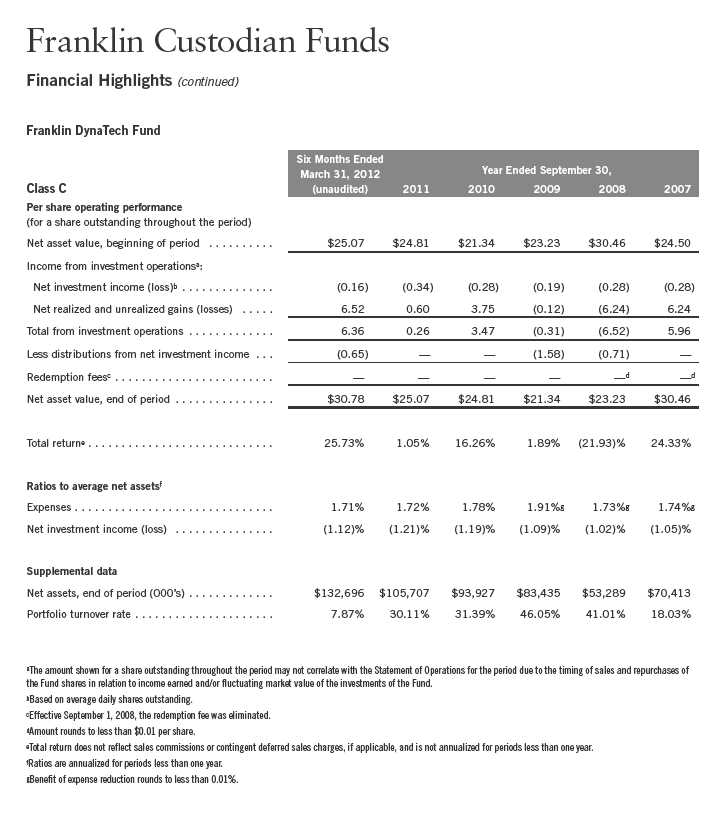

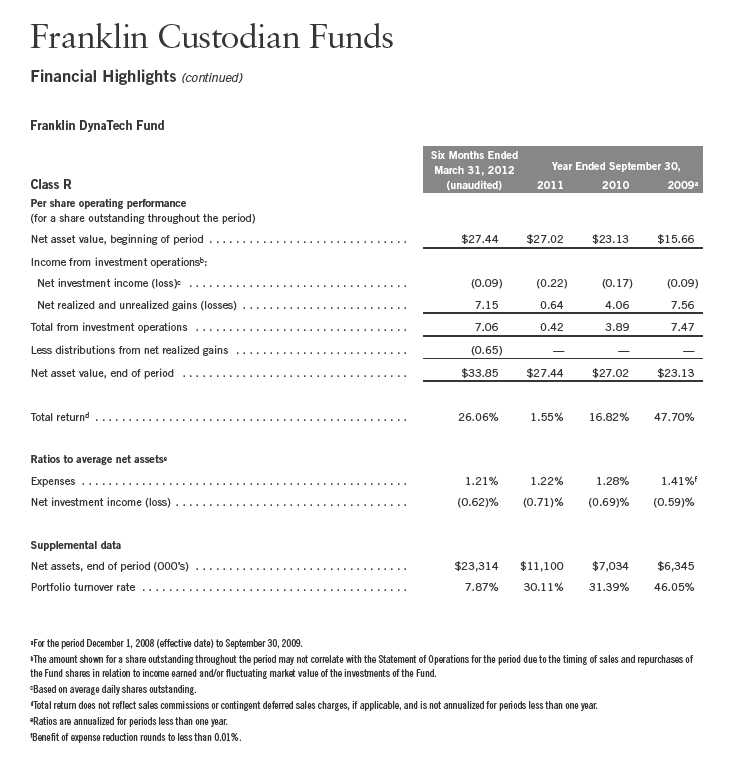

Franklin DynaTech Fund – Class A delivered a +26.22% cumulative total return for the six months under review. For the same period, the Fund performed comparably to the +26.85% total return of the Russell 1000® Growth Index, which measures performance of the largest companies in the Russell 3000® Index with higher price-to-book ratios and higher forecasted growth values.1 Also for comparison, the Fund performed comparably to the broad U.S. stock market as measured by the +25.89% total return of the Standard & Poor’s 500® Index (S&P 500®), but underperformed domestic and international-based stocks as measured by the NASDAQ Composite Index’s +28.70% total return.1 You can find the Fund’s long-term performance data in the Performance Summary beginning on page 8.

Investment Strategy

We use fundamental, bottom-up research to seek companies meeting our criteria of growth potential, quality and valuation. In seeking sustainable growth characteristics, we look for companies we believe can produce sustainable earnings and cash flow growth, evaluating the long-term market opportunity and competitive structure of an industry to target leaders and emerging leaders. We define quality companies as those with strong and improving competitive positions in attractive markets. We also believe important attributes of quality are experienced and talented management teams as well as financial strength reflected in the capital structure, gross and operating margins, free cash flow generation

1. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. RUSSELL® is a trademark of the Frank Russell Company. STANDARD & POOR’S®, S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC. The indexes are unmanaged and include reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

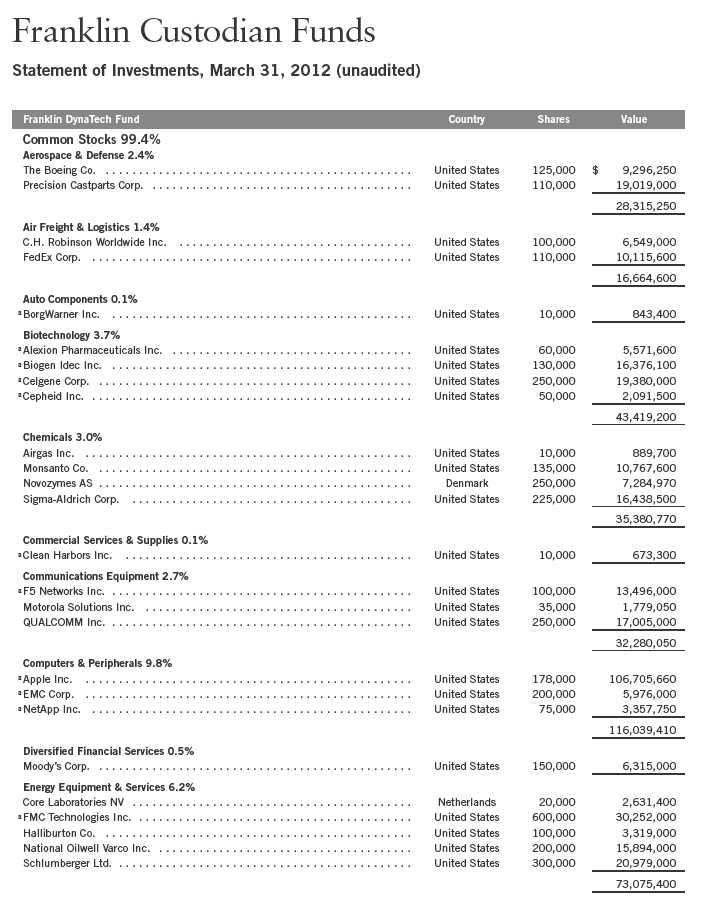

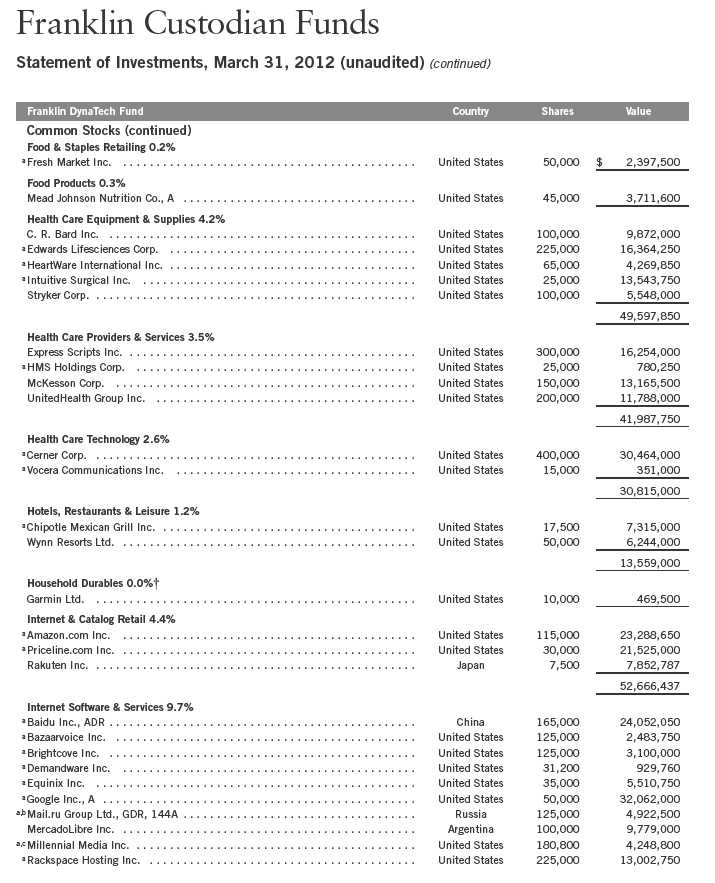

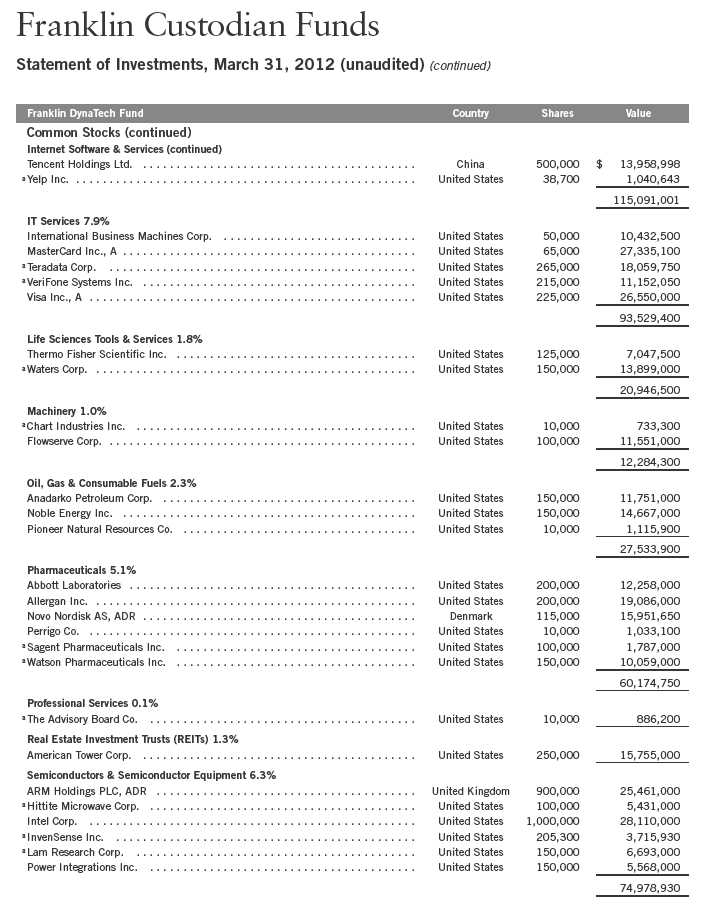

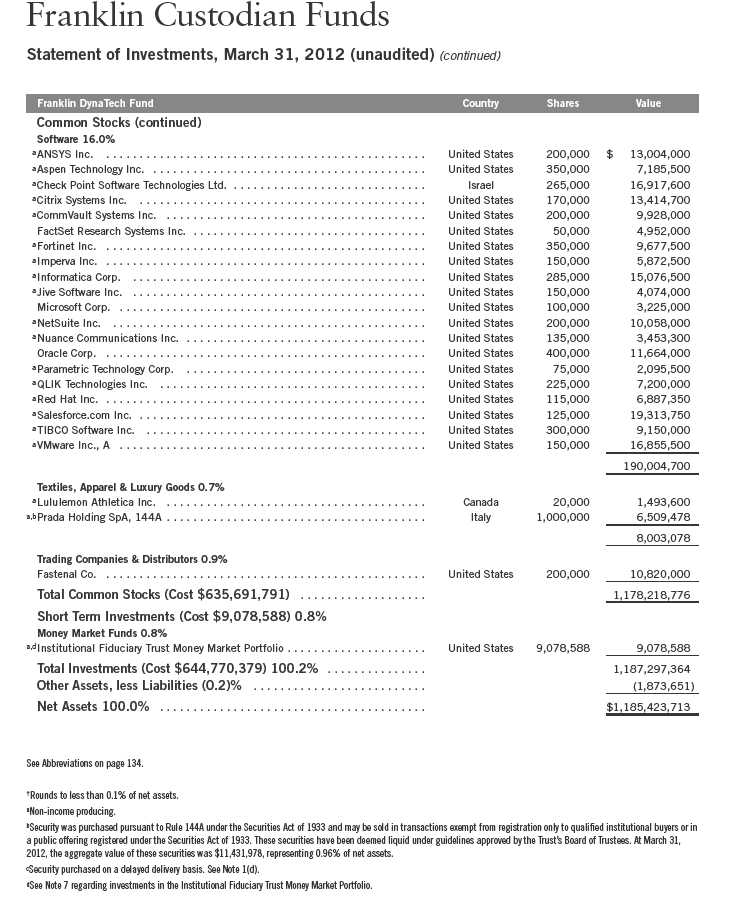

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 52.

Semiannual Report | 5

and returns on capital employed. Our valuation analysis includes a range of potential outcomes based on an assessment of multiple scenarios. In assessing value, we consider whether security prices fully reflect the balance of the sustainable growth opportunities relative to business and financial risks.

Manager’s Discussion

The Fund’s information technology sector drove performance during the reporting period, a combination of our holdings’ robust performance and the Fund’s sizable sector allocation.2 As in the previous reporting period, computer manufacturer Apple was a stalwart performer and led contributors. During the six-month period, the company announced it was initiating a regular dividend on its common stock, and sales of iPhones and iPads more than doubled year-over-year for the quarter ended December 31, 2011. Semiconductor manufacturer Intel also benefited Fund performance, as did payment technology firm Visa. Positions in the health care and energy sectors also generated solid returns, led by pharmaceutical claims processor Express Scripts and FMC Technologies, a technology products and services firm serving the oil and gas industry.3 In the consumer discretionary sector, travel discounter Priceline.com posted impressive results and boosted performance.4

While healthy gains for most equities characterized the six-month period, certain Fund holdings declined in value. Online retailer Amazon.com, risk management provider RPX5 and oil services diagnostic services firm CARBO Ceramics5 were among the positions weighing on performance.

As managers of Franklin DynaTech Fund, at period-end we were encouraged by the relative abundance of leading science and technology companies that we believe have strong long-term growth prospects trading at what we perceive to be attractive valuations. We believe it is these innovative, thought-leading companies that may promote economic advancement over the longer term.

2. The information technology sector comprises communications equipment, computers and peripherals, Internet software and services, IT services, semiconductors and semiconductor equipment, and software in the SOI.

3. The health care sector comprises biotechnology, health care equipment and supplies, health care providers and services, health care technology, life sciences tools and services, and pharmaceuticals in the SOI. The energy sector comprises energy equipment and services; and oil, gas and consumable fuels in the SOI.

4. The consumer discretionary sector comprises auto components; hotels, restaurants and leisure; household durables; Internet and catalog retail; specialty retail; and textiles, apparel and luxury goods in the SOI.

5. Sold by period-end.

Thank you for your continued participation in Franklin DynaTech Fund.

We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of March 31, 2012, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Performance Summary as of 3/31/12

Franklin DynaTech Fund

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

8 | Semiannual Report

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Average annual total return and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class B: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only; Class R/Advisor Class: no sales charges.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Semiannual Report | 9

Performance Summary (continued)

Endnotes

All investments involve risks, including possible loss of principal. The Fund’s investments in fast-growing industries, including the technology and telecommunications sectors (which have historically been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement. The Fund may also invest in small- and mid-capitalization companies, which can be particularly sensitive to changing economic conditions, and their prospects for growth are less certain than those of larger, more established companies. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class B: Class C: | These shares have higher annual fees and expenses than Class A shares. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Class R: | Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not been annualized.

3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

5. Effective 5/15/08, the Fund began offering Advisor Class shares, which do not have sales charges or a Rule 12b-1 plan. Performance quotations for this class reflect the following methods of calculation: (a) For periods prior to 5/15/08, a restated figure is used based upon the Fund’s Class A performance, excluding the effect of Class A’s maximum initial sales charge, but reflecting the effect of the Class A Rule 12b-1 fees; and (b) for periods after 5/15/08, actual Advisor Class performance is used reflecting all charges and fees applicable to that class. Since 5/15/08 (commencement of sales), the cumulative and average annual total returns of Advisor Class shares were +23.59% and +5.62%.

10 | Semiannual Report

Your Fund’s Expenses

Franklin DynaTech Fund

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

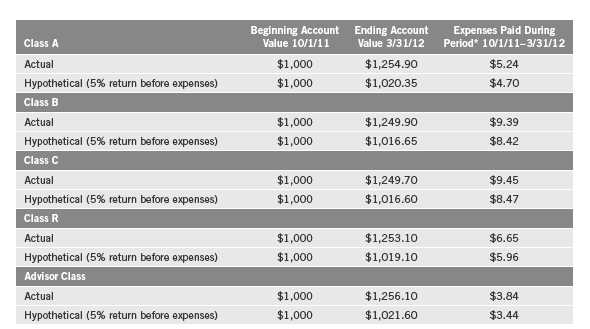

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. | |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 11

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 0.96%; B: 1.70%; C: 1.71%; R: 1.21%; and Advisor: 0.71%), multiplied by the average account value over the period, multiplied by 183/366 to reflect the one-half year period.

12 | Semiannual Report

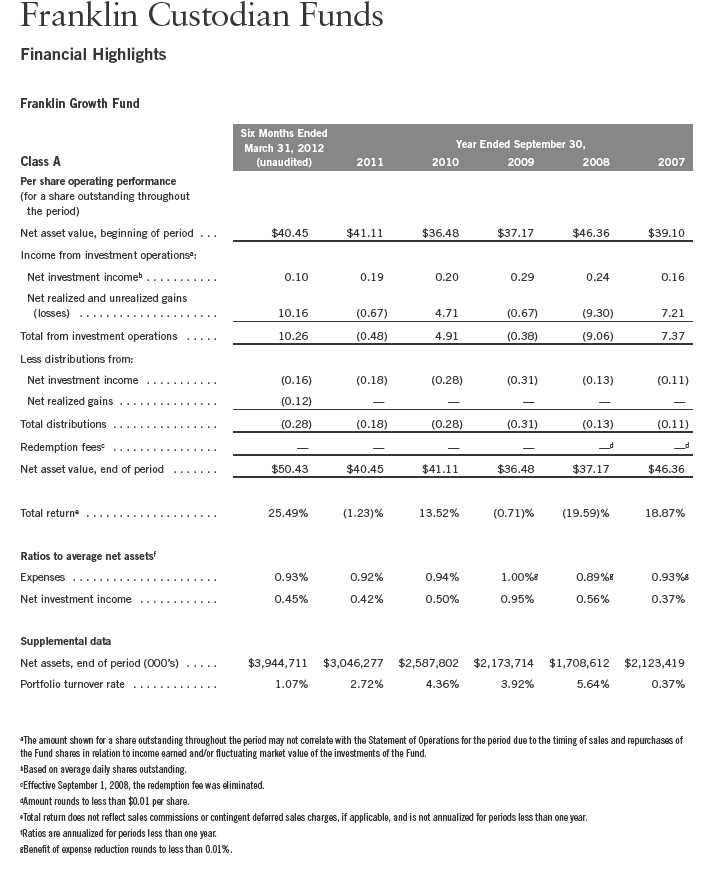

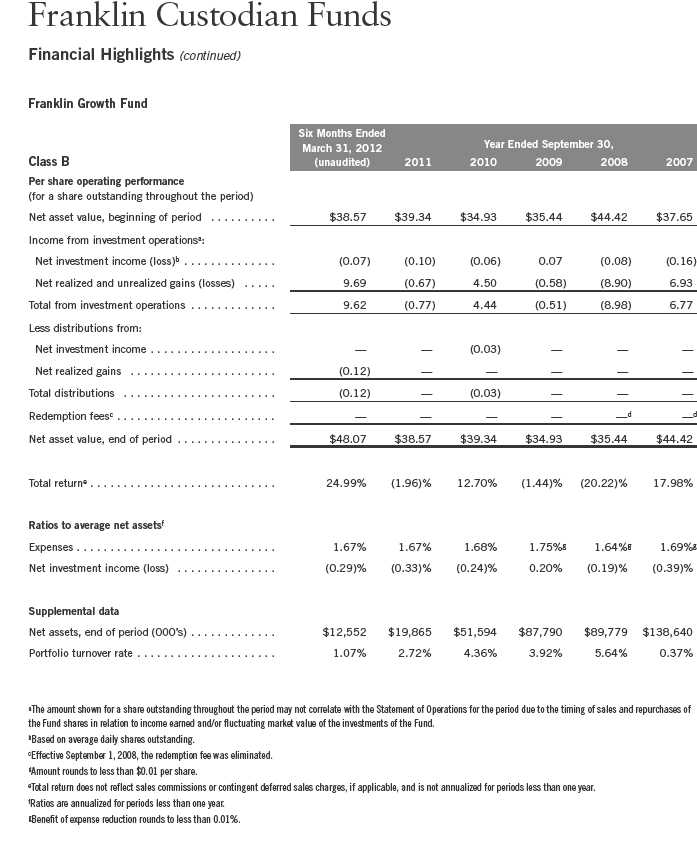

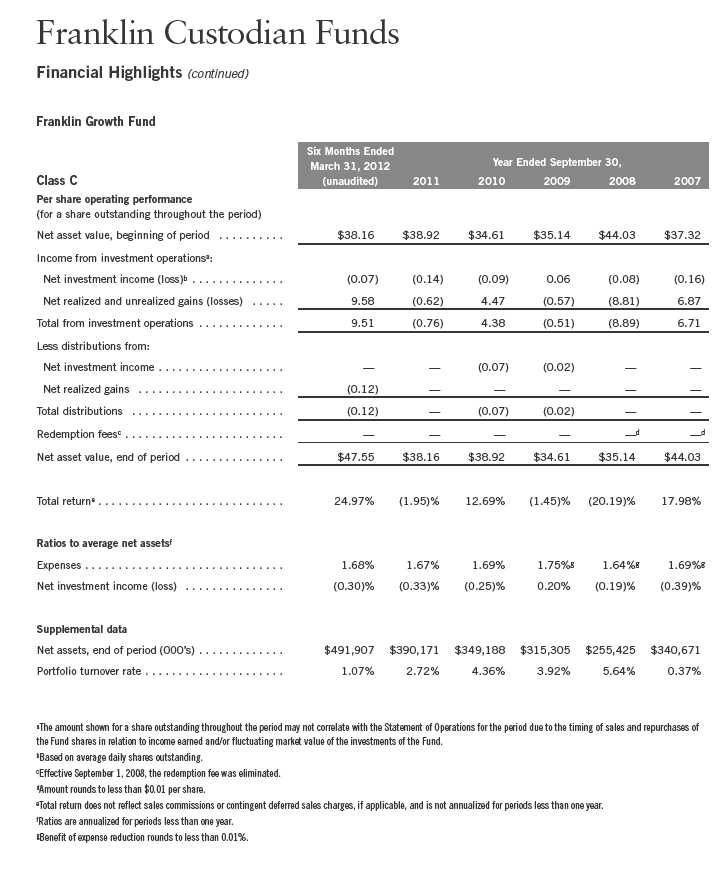

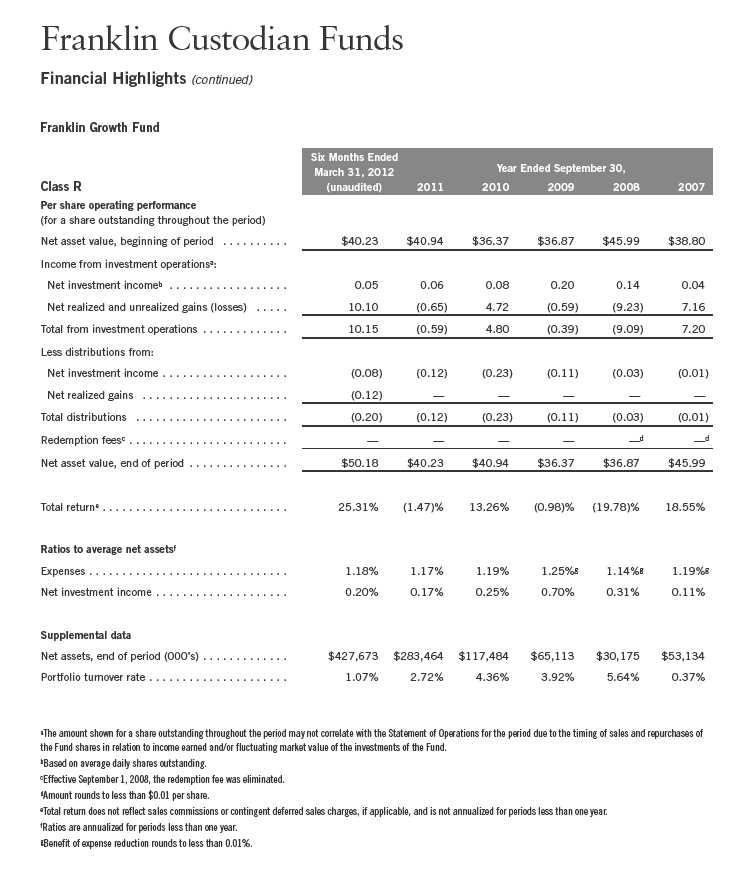

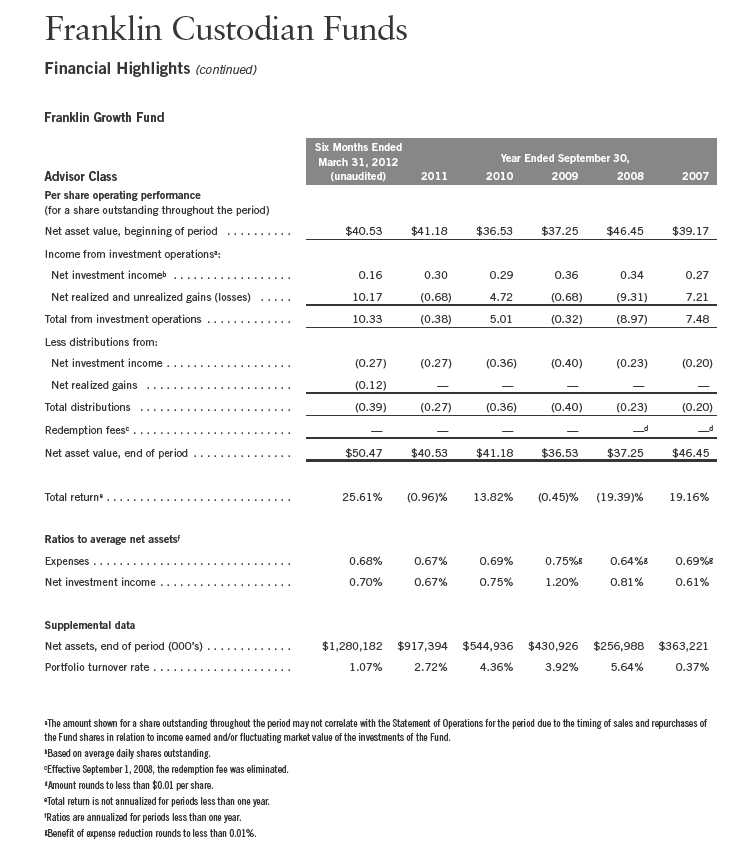

Franklin Growth Fund

Your Fund’s Goal and Main Investments: Franklin Growth Fund seeks capital appreciation by investing substantially in equity securities of companies that are leaders in their industries.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

We are pleased to bring you Franklin Growth Fund’s semiannual report for the period ended March 31, 2012.

Performance Overview

Franklin Growth Fund – Class A delivered a +25.49% cumulative total return for the six months under review. The Fund performed comparably to the +25.89% total return of its benchmark, the Standard & Poor’s 500 Index (S&P 500), which is a broad measure of U.S. stock performance.1 You can find the Fund’s long-term performance data in the Performance Summary beginning on page 16.

Investment Strategy

We use fundamental, bottom-up research to seek companies meeting our criteria of growth potential, quality and valuation. In seeking sustainable growth characteristics, we look for companies we believe can produce sustainable earnings and cash flow growth, evaluating the long-term market opportunity and competitive structure of an industry to target leaders and emerging leaders. We define quality companies as those with strong and improving competitive positions in attractive markets. We also believe important attributes of quality are experienced and talented management teams as well as financial strength reflected in the capital structure, gross and operating margins, free cash flow generation and returns on capital employed. Our valuation analysis includes a range of potential outcomes based on an assessment of multiple scenarios. In assessing value, we consider whether security prices fully reflect the balance of the sustainable growth opportunities relative to business and financial risks.

1. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. The index is unmanaged and includes reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

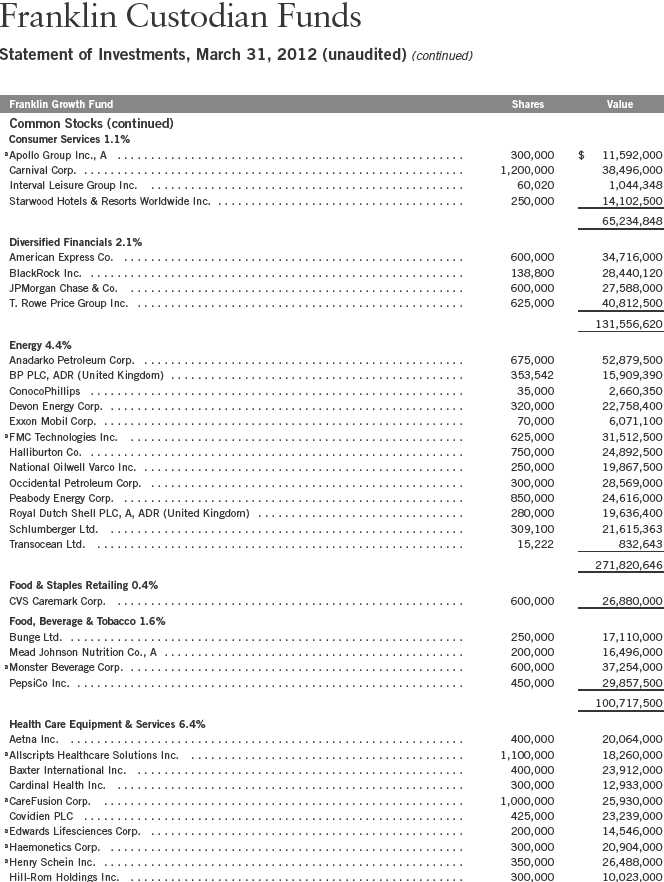

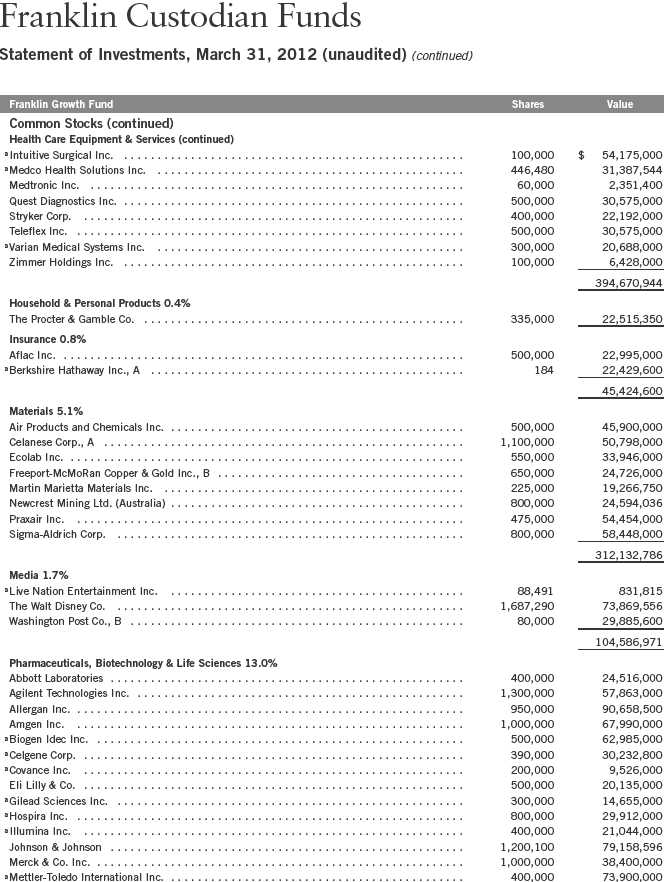

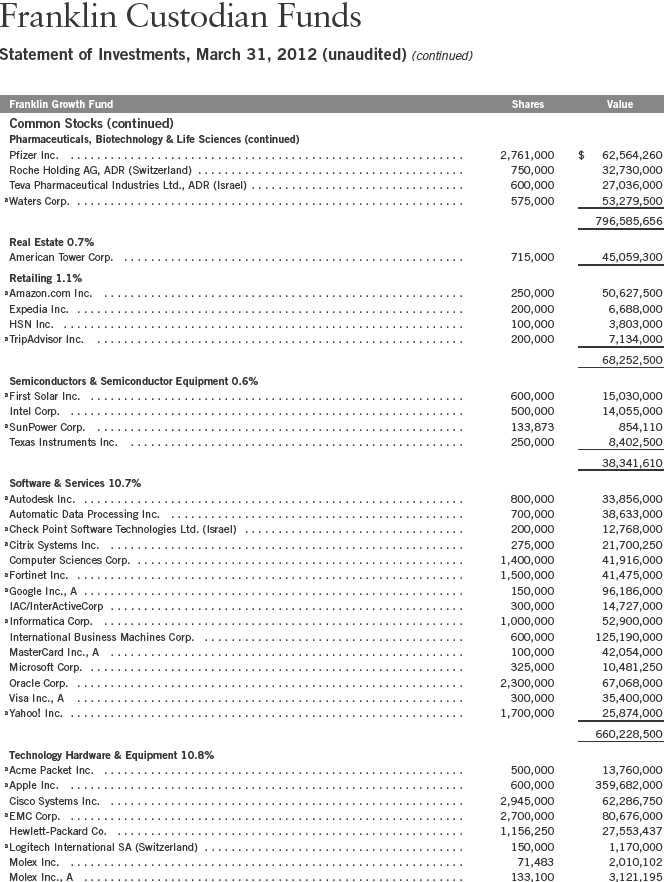

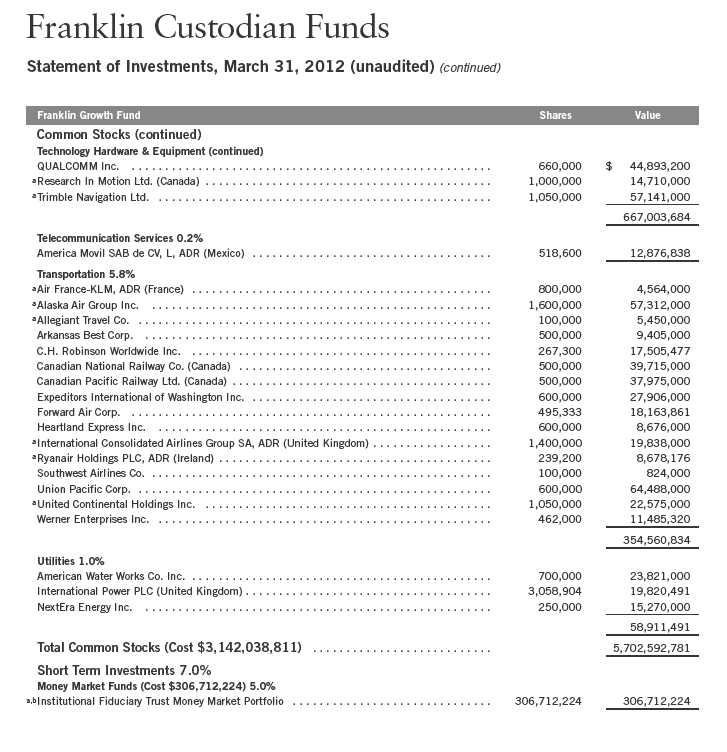

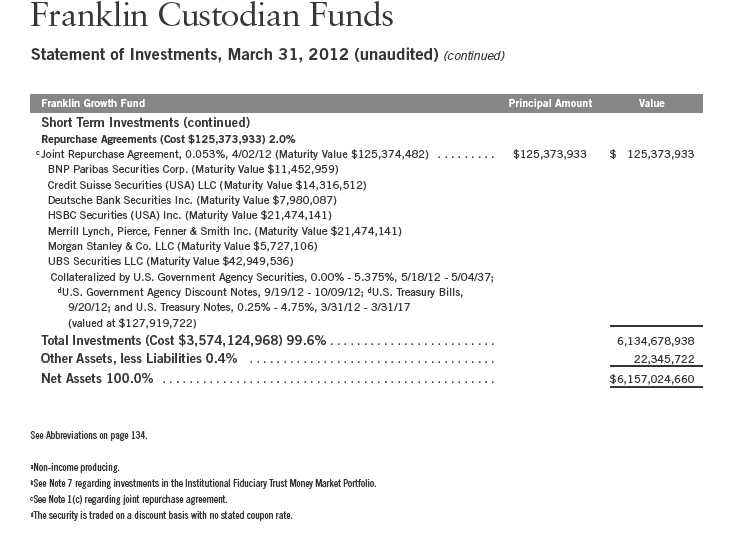

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 61.

Semiannual Report | 13

Manager’s Discussion

Franklin Growth Fund owned shares of 167 companies at period-end. We continue to invest in a broad array of companies of all sizes and in varied industries.

During the six months under review, the Fund’s holdings in the industrials, information technology and consumer discretionary sectors made key contributions to performance.2 Industrial supply company W.W. Grainger and electrical equipment designer and manufacturer Thomas & Betts were leading performers in the industrials sector. W.W. Grainger sales increased early in 2012 amid strong volume and following acquisitions. In addition, the firm’s quarterly earnings rose as profit margins improved. Thomas & Betts agreed to a purchase offer from Switzerland-based ABB Limited, although the offer was awaiting approval from a forthcoming Thomas & Betts shareholder vote. In the information technology sector, several holdings were major contributors. Personal computer designer and manufacturer Apple benefited from robust demand for its iPhones and iPads. Share prices for EMC, the leading global disk storage systems firm, advanced as the storage support market expanded in the fourth quarter of 2011. GPS and control systems manufacturer Trimble Navigation reported favorable results for the quarter ended December 2011, as the domestic construction market for navigation products showed strength. Measurement products firm Agilent Technologies also boosted returns, as the health care sector firm’s first-quarter profit increased amid rising sales from its chemicals and life sciences division. Outside of these sectors, global entertainment and media firm Walt Disney also made a notable positive contribution to performance as the firm’s first-quarter net income jumped 12%.

Performance was more muted, but still positive, for the Fund’s telecommunication services and utilities holdings. Mexico-based wireless services provider America Movil’s performance trailed that of other Fund holdings as higher debt levels and weakness for the peso contributed to profit levels declining in the fourth quarter. Renewable energy services firm NextEra Energy’s power and gas trading businesses endured low prices and volatility in trading markets, and the firm’s Florida utility froze base rates for customers as the state navigated adverse economic conditions. Certain positions lost value, including BlackBerry smartphone maker Research in Motion. Tepid sales for the company’s handsets

2. The industrials sector comprises capital goods, commercial and professional services, and transportation in the SOI. The information technology sector comprises semiconductors and semiconductor equipment, software and services, and technology hardware and equipment in the SOI. The consumer discretionary sector comprises automobiles and components, consumer durables and apparel, consumer services, media and retailing in the SOI.

14 | Semiannual Report

and PlayBook tablet computers weighed on its share price. Elsewhere, an unprofitable quarter for solar module manufacturer First Solar resulted in negative returns, and network communications equipment firm Acme Packet trimmed its estimates for earnings and sales in 2012. However, few holdings posted negative performance during the six-month period.

Thank you for your continued participation in Franklin Growth Fund. We look forward to serving your future investment needs.

CFA® is a trademark owned by CFA Institute.

The foregoing information reflects our analysis, opinions and portfolio holdings as of March 31, 2012, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Semiannual Report | 15

Performance Summary as of 3/31/12

Franklin Growth Fund

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

16 | Semiannual Report

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Average annual total return and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class B: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only;

Class R/Advisor Class: no sales charges.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Semiannual Report | 17

Performance Summary (continued)

Endnotes

All investments involve risks, including possible loss of principal. Historically, the Fund has focused on larger companies. The Fund may also invest in small, relatively new and/or unseasoned companies, which involves additional risks, as the price of these securities can be volatile, particularly over the short term. In addition, the Fund may invest up to 40% of its net assets in stocks of foreign companies, which involve special risks, including currency fluctuations and economic as well as political uncertainty. The portfolio includes investments in the technology sector, which has been one of the most volatile sectors of the market. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class B: Class C: | These shares have higher annual fees and expenses than Class A shares. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Class R: | Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not been annualized.

3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

18 | Semiannual Report

Your Fund’s Expenses

Franklin Growth Fund

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. | |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 19

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 0.93%; B: 1.67%; C: 1.68%; R: 1.18%; and Advisor: 0.68%), multiplied by the average account value over the period, multiplied by 183/366 to reflect the one-half year period.

20 | Semiannual Report

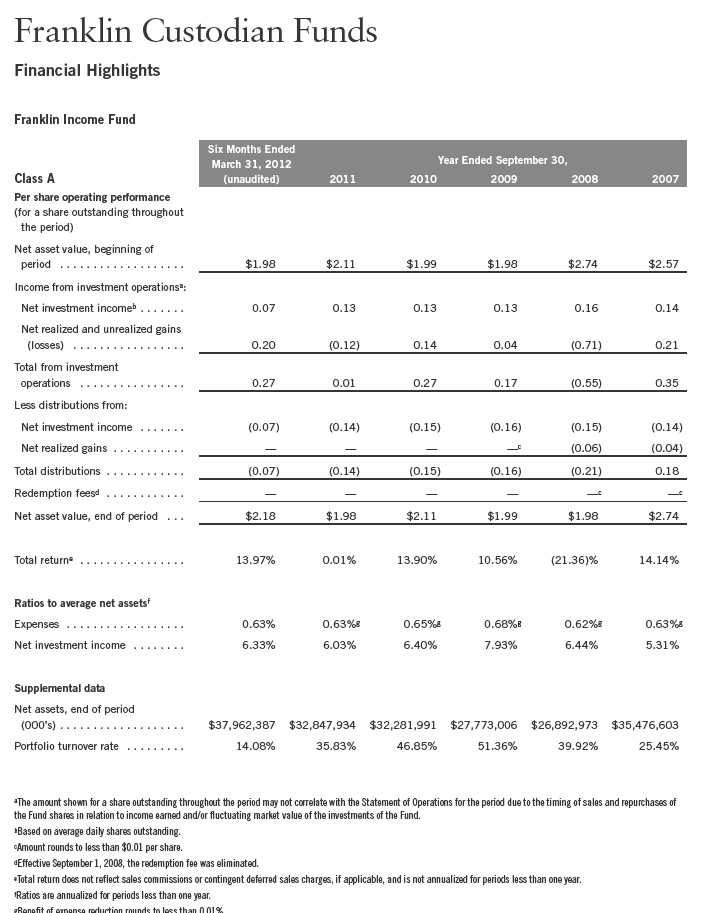

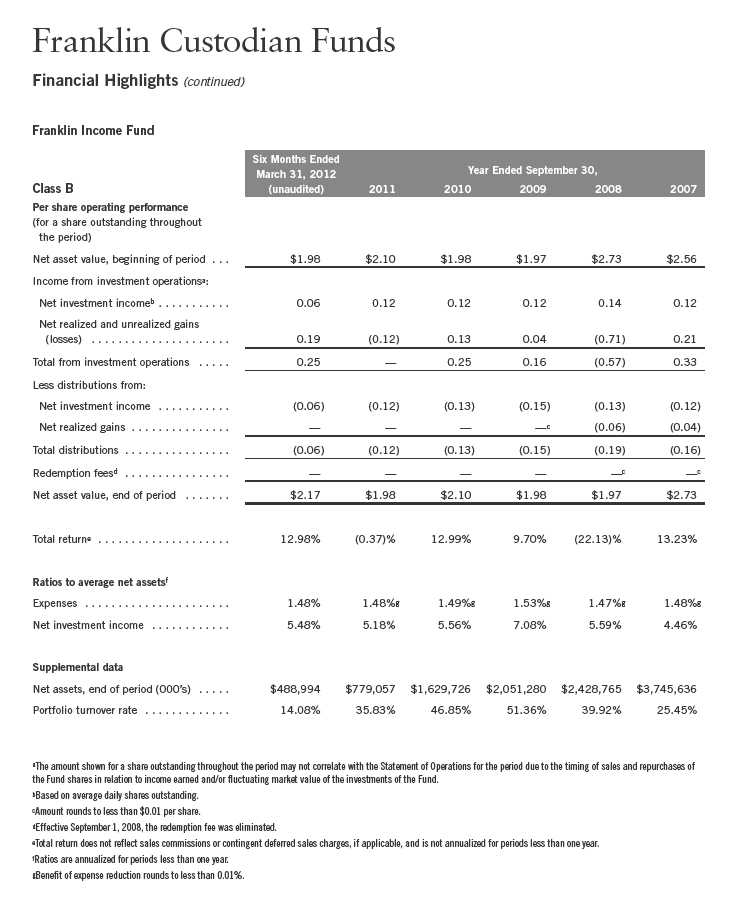

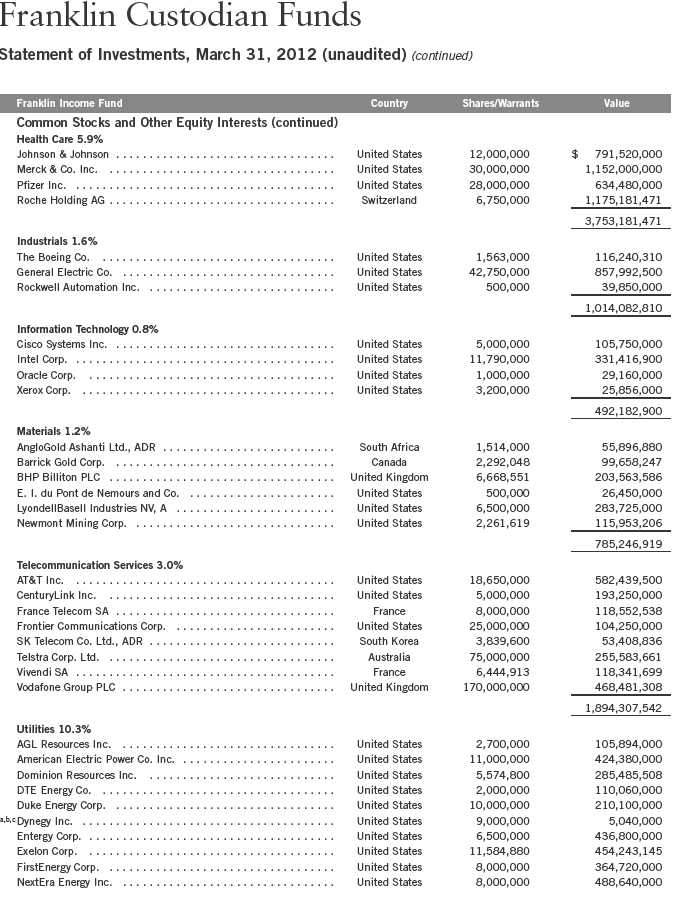

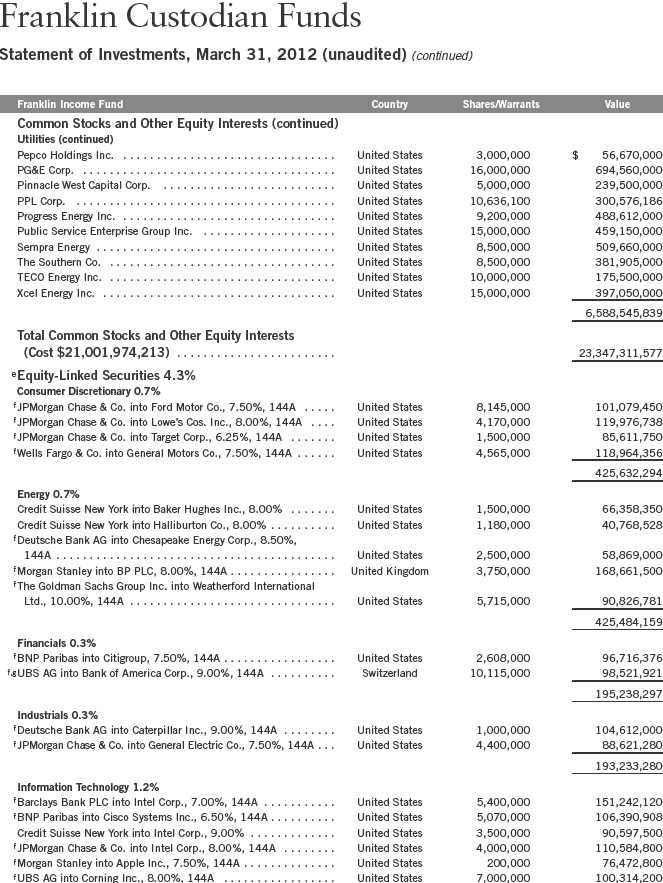

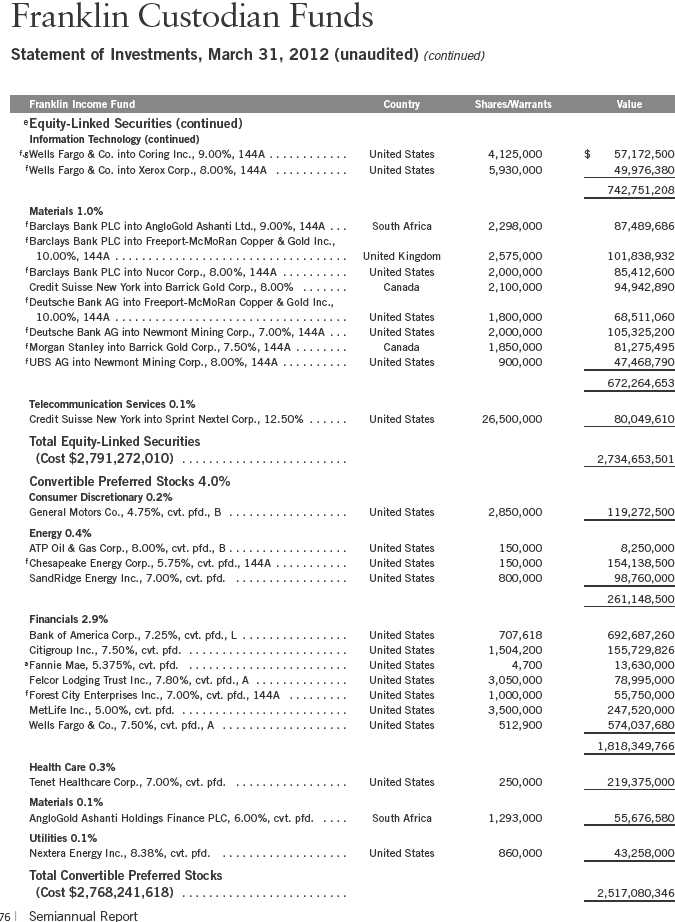

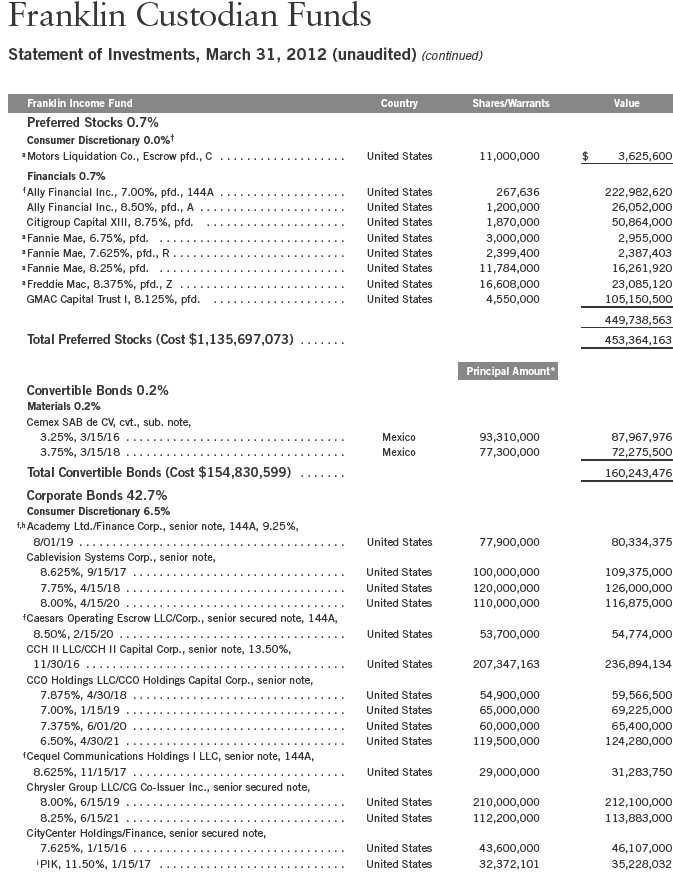

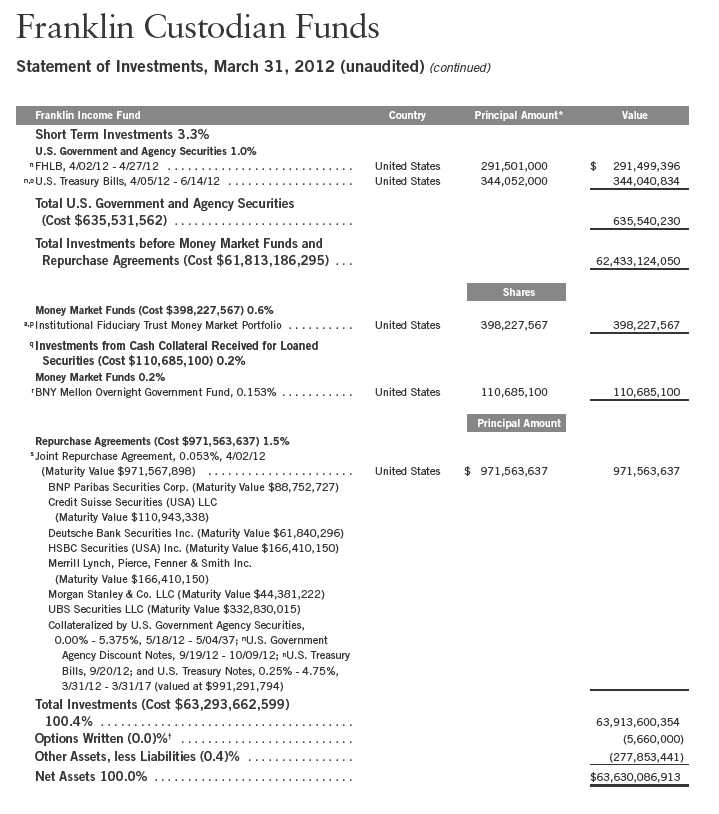

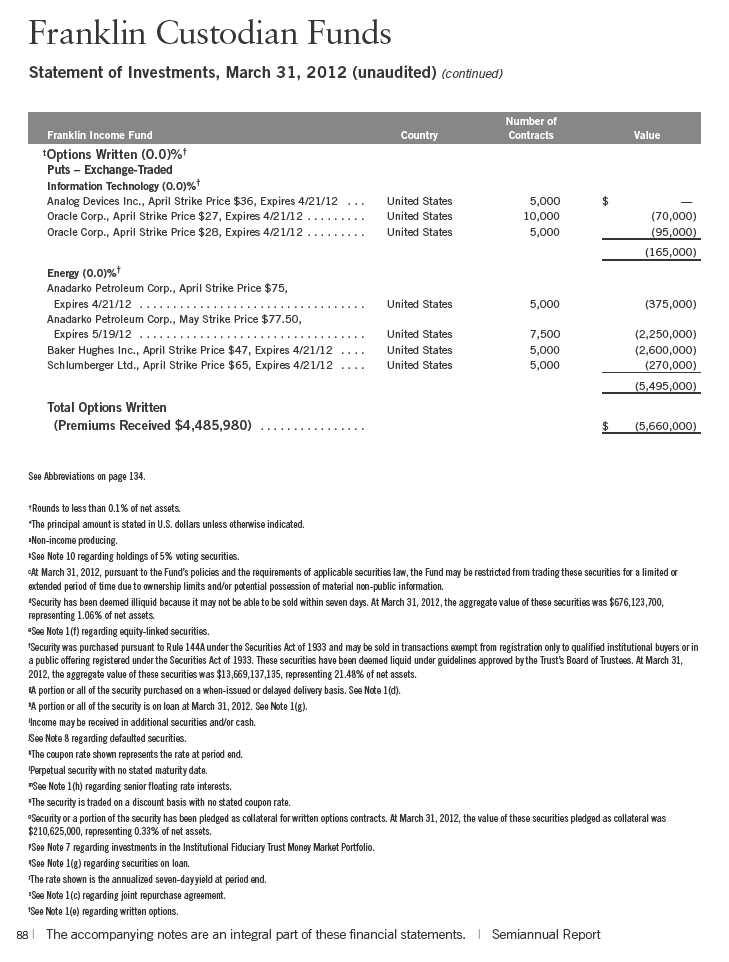

Franklin Income Fund

Your Fund’s Goal and Main Investments: Franklin Income Fund seeks to maximize income while maintaining prospects for capital appreciation by investing, under normal market conditions, in a diversified portfolio of debt and equity securities.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

This semiannual report for Franklin Income Fund covers the period ended March 31, 2012.

Performance Overview

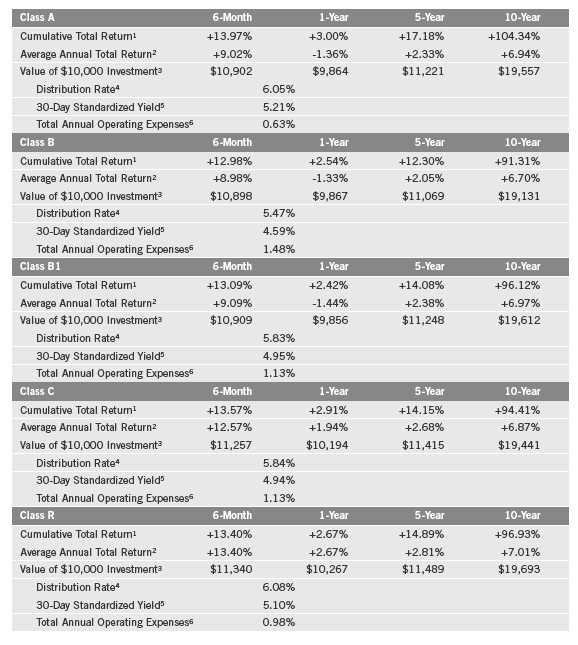

Franklin Income Fund – Class A delivered a +13.97% cumulative total return for the six months under review. The Fund underperformed the +25.89% total return of its equity benchmark, the Standard & Poor’s 500 Index (S&P 500), which is a broad measure of U.S. stock performance.1 The Fund outperformed the +1.43% total return of its fixed income benchmark, the Barclays Capital (BC) U.S. Aggregate Index, which tracks the U.S. investment-grade, taxable bond market.1 The Fund performed comparably to the +13.96% total return of its peers as measured by the Lipper Mixed-Asset Target Allocation Moderate Funds Classification Average, which consists of funds chosen by Lipper that, by practice, maintain a mix of 40% to 60% equity securities, with the remainder in bonds and cash.2 You can find the Fund’s long-term performance data in the Performance Summary beginning on page 26.

Investment Strategy

By generally performing independent analysis of debt, convertible and equity securities, we search for undervalued or out-of-favor securities we believe offer opportunities for income today and significant growth tomorrow. We consider such factors as a company’s experience and managerial strength; its responsiveness to changes in interest rates and business conditions; debt maturity schedules and borrowing requirements; a company’s changing financial condition and market recognition of the change; and a security’s relative value based on such

1. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

2. Source: Lipper Inc. For the six-month period ended 3/31/12, this category consisted of 496 funds. Lipper calculations do not include sales charges or expense subsidization by a fund’s manager. The Fund’s performance relative to the average may have differed if these and other factors had been considered.

The indexes are unmanaged and include reinvestment of any income or distributions. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

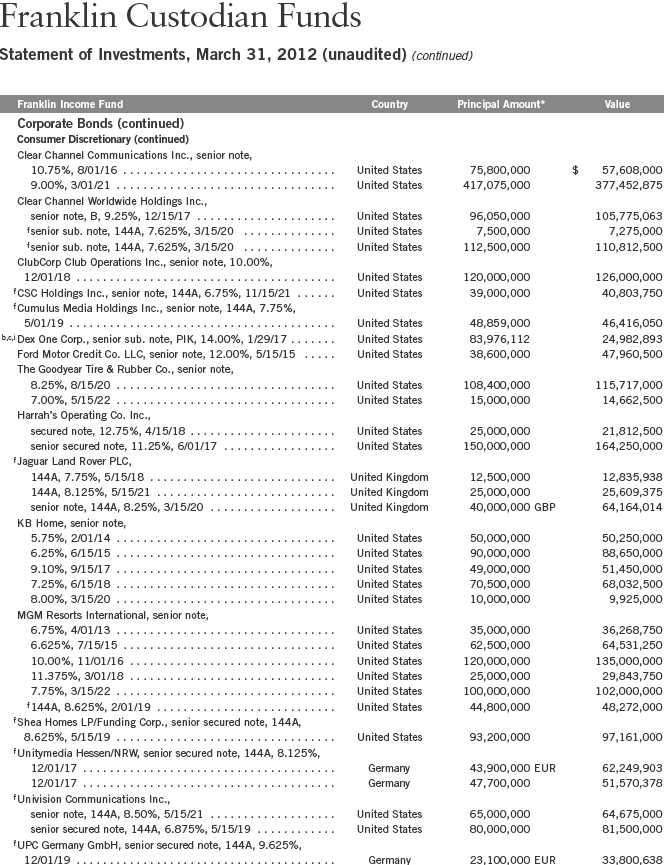

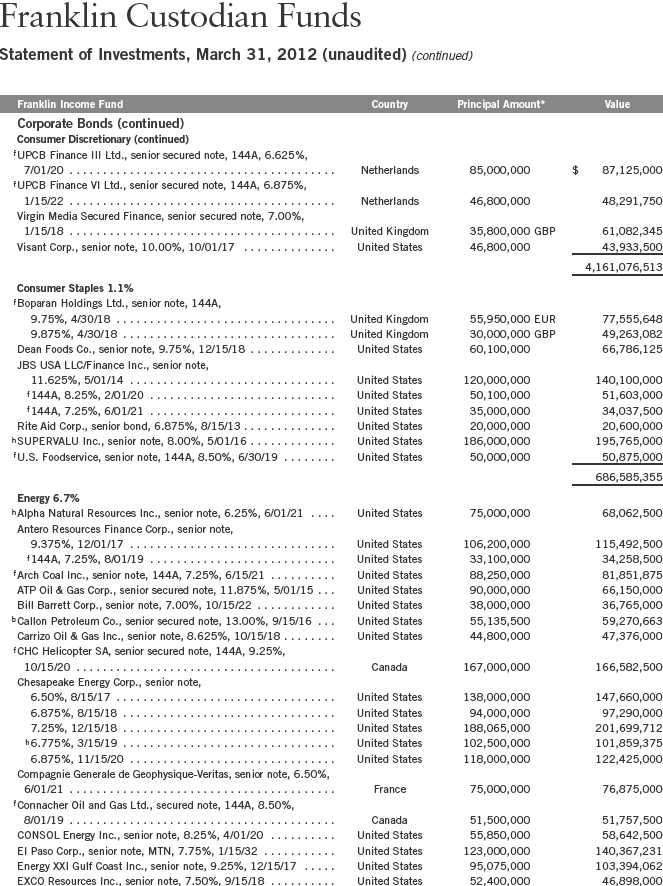

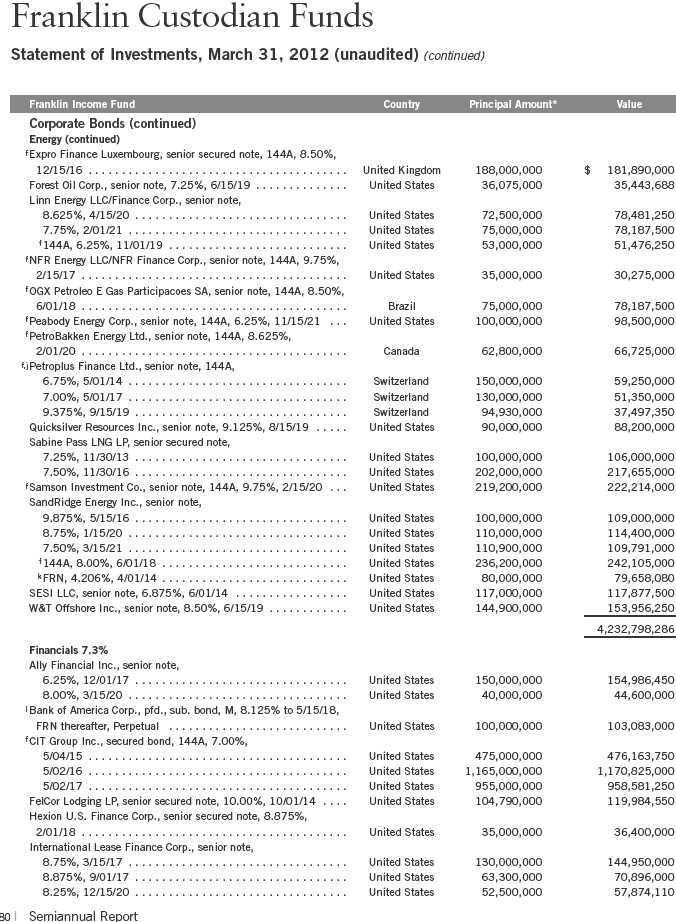

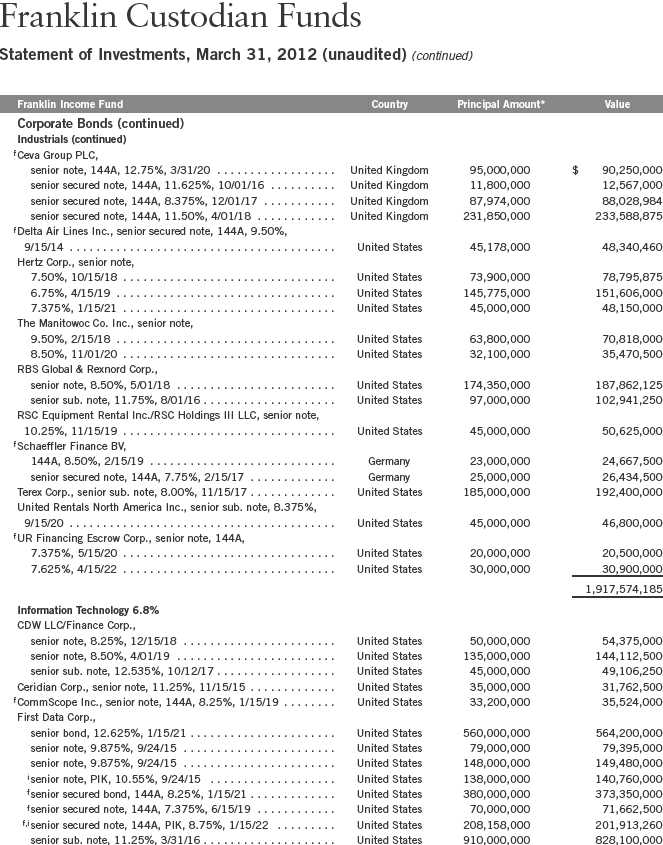

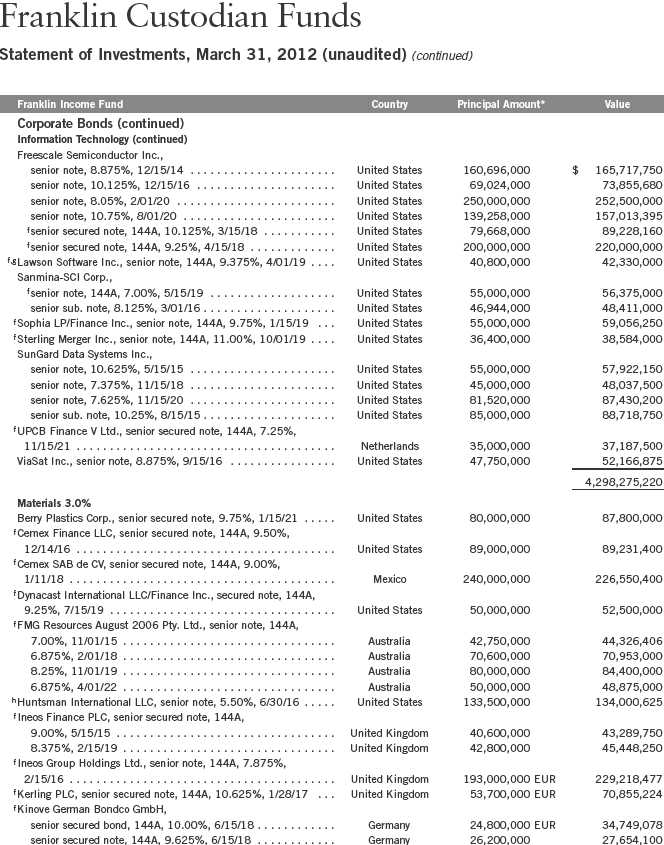

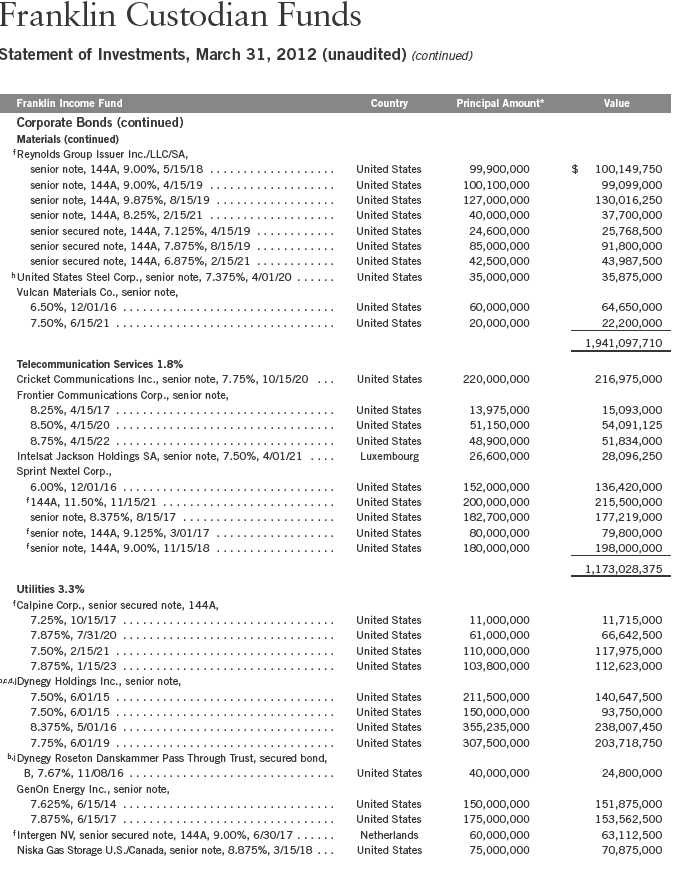

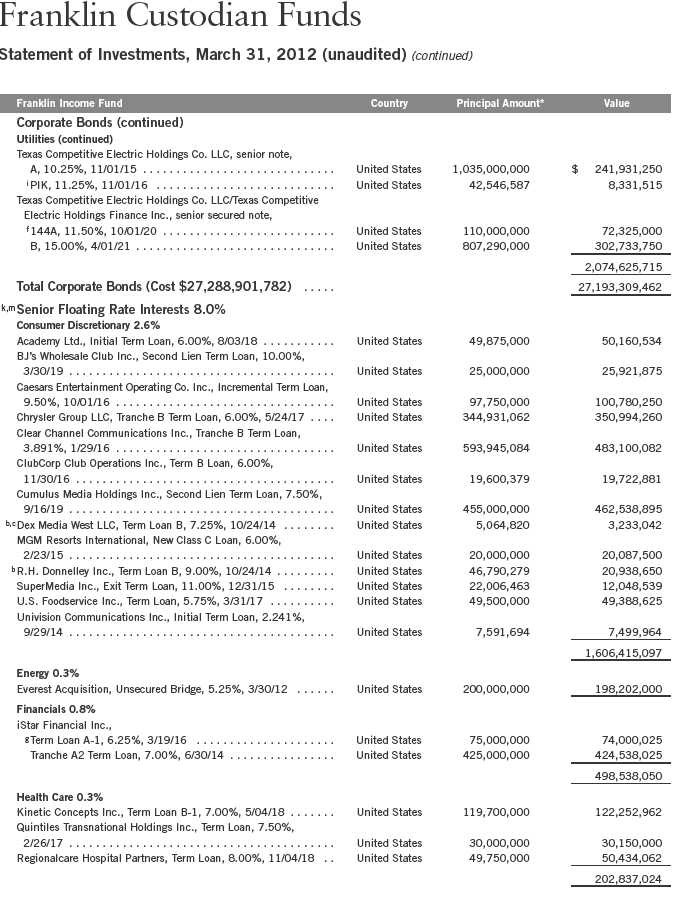

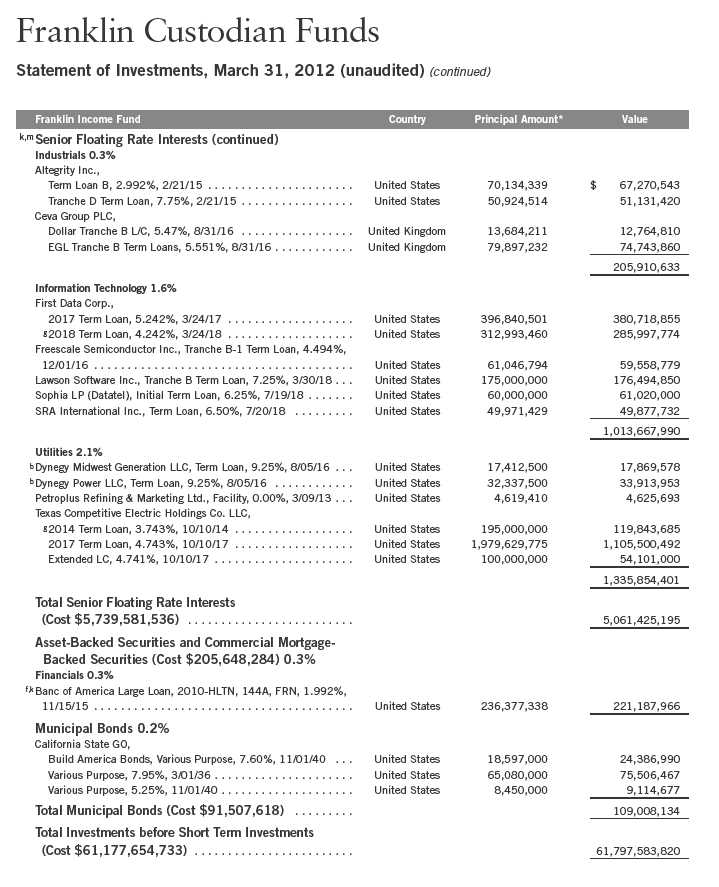

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 73.

Semiannual Report | 21

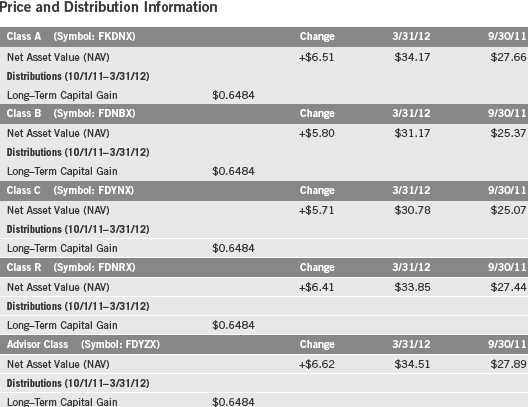

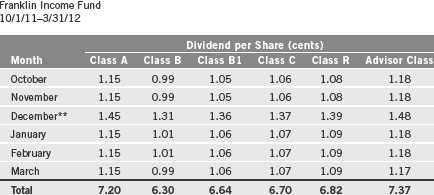

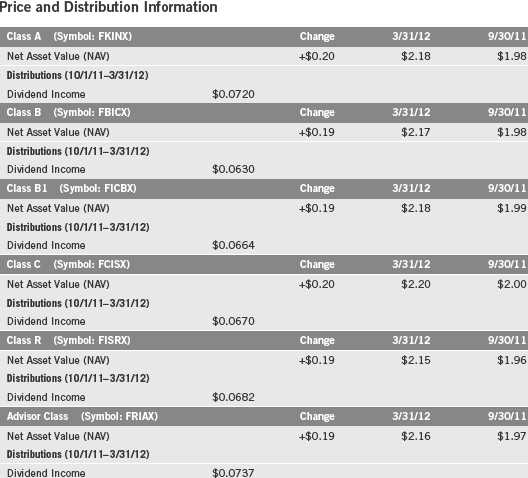

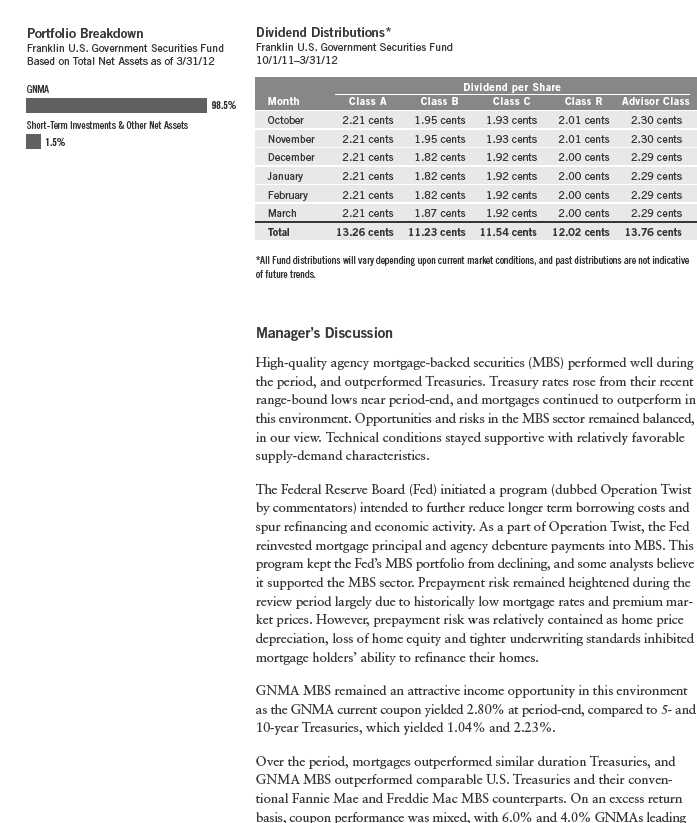

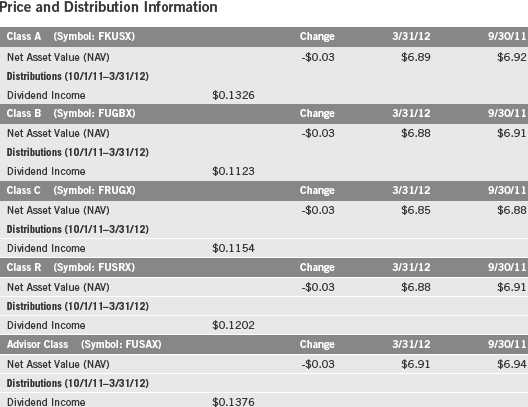

Dividend Distributions*

*All Fund distributions will vary depending upon current market conditions, and past distributions are not indicative of future trends.

**Includes an additional 0.30 cent per share distribution to meet excise tax requirements.

factors as anticipated cash flow, interest or dividend coverage, asset coverage and earnings.

Manager’s Discussion

During the six-month reporting period, renewed investor risk tolerance following a period of heightened economic and systemic risk in mid-2011 drove U.S. equity market gains. Although investor perception of heightened risk related to European and U.S. fiscal challenges dominated the markets from July through September 2011, the reality of sustained moderate economic growth and healthy corporate profit levels buoyed stocks from October 2011 through March 2012. Fixed income market returns remained somewhat challenged due to the combined effects of low overall interest rates and the potential negative impact of rising long-term interest rates.

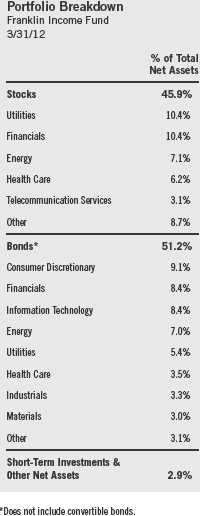

During the period under review, the Fund’s total fixed income exposure decreased to 51.2% from 56.2% of total net assets, and its equity exposure increased to 45.9% from 42.2%. Our cash position increased during the period to 2.9% from 1.6% of total net assets. Within fixed income, the majority of asset declines came from corporate bonds through a combination of profit taking as many long-duration securities traded at significant premiums to par value when corporate spreads tightened, and refinancing because many companies called securities and issued longer maturity debt at lower interest costs. Spread widening pressured high yield markets in August and September 2011, and along with low yields and the broader market’s returns, helped set the bar for a period of stronger performance during the reporting period.

22 | Semiannual Report

Within the Fund’s fixed income investments, corporate bond holdings performed well relative to the broader fixed income market’s lackluster return as favorable credit fundamentals helped drive credit spreads lower and long-term interest rates remained relatively in check. The technology, communications, consumer cyclical and consumer non-cyclical sectors performed well, while the electric utilities sector was a notable laggard.

Within equity securities, our common stock holdings increased, while our convertible security holdings decreased modestly. We favored the relative value of stocks over fixed income investments, a sentiment that was supported by a number of trends including stable, albeit modest, economic growth, high corporate profit margins, improved balance sheets (including large cash balances), and renewed evidence of dividend increases and share buybacks. We view dividend increases and share buybacks as shareholder friendly actions, rather than management-driven actions taken to improve credit profiles. Although we still consider convertible securities to be an attractive asset class for the Fund’s strategy over the long term, opportunities were somewhat limited recently due to the low level of new issuance in that market. The Fund’s equity exposure remained broadly diversified, with the largest weightings in utilities, financials, energy and health care. The Fund’s financials exposure increased meaningfully following a period of price volatility during the summer of 2011.

Although the Fund’s cash position increased slightly during the period, our approach is to look for opportunities to meet the Fund’s objective, rather than structurally looking to hold more cash in the portfolio. We are actively looking for what we consider to be attractive investments for the Fund.

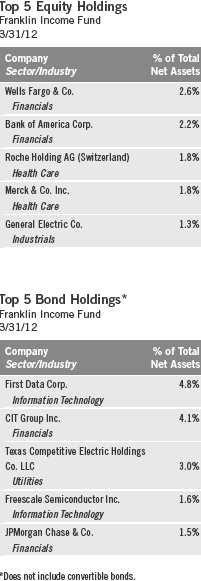

Individual bond issuers that performed well included First Data, a leading electronic transactions processing company, which was a key fixed income contributor. The company benefited from factors including improved spending trends, a better-than-expected outcome related to increased regulation, and specific actions the company took to extend its near-term maturities, providing greater overall balance sheet flexibility. Similarly, our Clear Channel Communications bond holdings benefited from greater demand for advertising services amid the improving economy. Other strong fixed income contributors included CIT Group and JPMorgan Chase & Co. in financials, hospital operators HCA and Tenet Healthcare in health care, and Chrysler Group in consumer discretionary. Chrysler benefited from strengthening auto sales as the economy continued its gradual improvement and from the company’s better offerings, particularly with Jeep models.

Texas Competitive Electric Holdings, a leading electricity generator and retail service provider in Texas, was a major fixed income detractor. Despite robust demand for power over the past year, this coal-based generator’s profitability

Semiannual Report | 23

was hurt by the decline in natural gas prices. Although the company has what we consider to be attractive hedges in place for the next couple of years, we feel long-term improvement will be needed for the company to navigate future debt servicing requirements. Other detractors included Petroplus Finance, an independent refiner in Europe that faced year-end liquidity strains amid weak demand, and Clearwire Communications (sold by period-end), which was pressured by funding concerns as the company sought to build out its network of wireless broadband services.

Among the Fund’s equity holdings, financials led the way with significant gains from Bank of America, Wells Fargo & Co., JPMorgan Chase & Co. and Citigroup. Investors seemed to become more comfortable with capital requirements amid an unpredictable regulatory environment and in the cases of Wells Fargo and JPMorgan Chase & Co., the ability to increase dividends and pursue share buybacks. Other top equity performers included major pharmaceutical companies such as Merck & Co., Pfizer and Roche Holding, which we believe benefited from cheap valuations and attractive dividend yields, as well as the perception that the pharmaceutical industry may finally be moving forward after the negative impact major patent expirations had on its financial results. General Electric and Intel were also key contributors. In our analysis, both holdings are high-quality companies with strong leadership positions and investment-grade quality balance sheets, and could be well positioned to increase dividends.

24 | Semiannual Report

Thank you for your continued participation in Franklin Income Fund.

We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of March 31, 2012, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Semiannual Report | 25

Performance Summary as of 3/31/12

Franklin Income Fund

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

26 | Semiannual Report

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Average annual total return and value of $10,000 investment include maximum sales charges. Class A: 4.25% maximum initial sales charge; Class B/B1: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only;

Class R/Advisor Class: no sales charges.

Semiannual Report | 27

Performance Summary (continued)

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Endnotes

All investments involve risks, including possible loss of principal. The Fund’s share price and yield will be affected by interest rate movements. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in the Fund adjust to a rise in interest rates, the Fund’s share price may decline. The Fund’s portfolio includes a substantial portion of higher yielding, lower-rated corporate bonds because of the relatively higher yields they offer. Floating-rate loans are lower rated, higher yielding instruments, which are subject to increased risk of default and can potentially result in loss of principal. These securities carry a greater degree of credit risk relative to investment grade securities. Stock prices fluctuate, sometimes rapidly and dramatically due to factors affecting individual companies, particular industries or sectors, or general market conditions. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class B: Class B1 (formerly Class B): Class C: | These shares have higher annual fees and expenses than Class A shares. These shares have higher annual fees and expenses than Class A shares. Effective 11/1/01, closed to new investors. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Class R: | Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not been annualized.

3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. Distribution rate is based on an annualization of the respective class’s March dividend and the maximum offering price (NAV for Classes B, B1, C, R and Advisor) per share on 3/31/12.

5. The 30-day standardized yield for the 30 days ended 3/31/12 reflects an estimated yield to maturity (assuming all portfolio securities are held to maturity). It should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate (which reflects the Fund’s past dividends paid to shareholders) or the income reported in the Fund’s financial statements.

6. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

28 | Semiannual Report

Your Fund’s Expenses

Franklin Income Fund

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. | |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 29

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 0.63%; B: 1.48%; B1: 1.13%; C: 1.13%; R: 0.98%; and Advisor: 0.48%), multiplied by the average account value over the period, multiplied by 183/366 to reflect the one-half year period.

30 | Semiannual Report

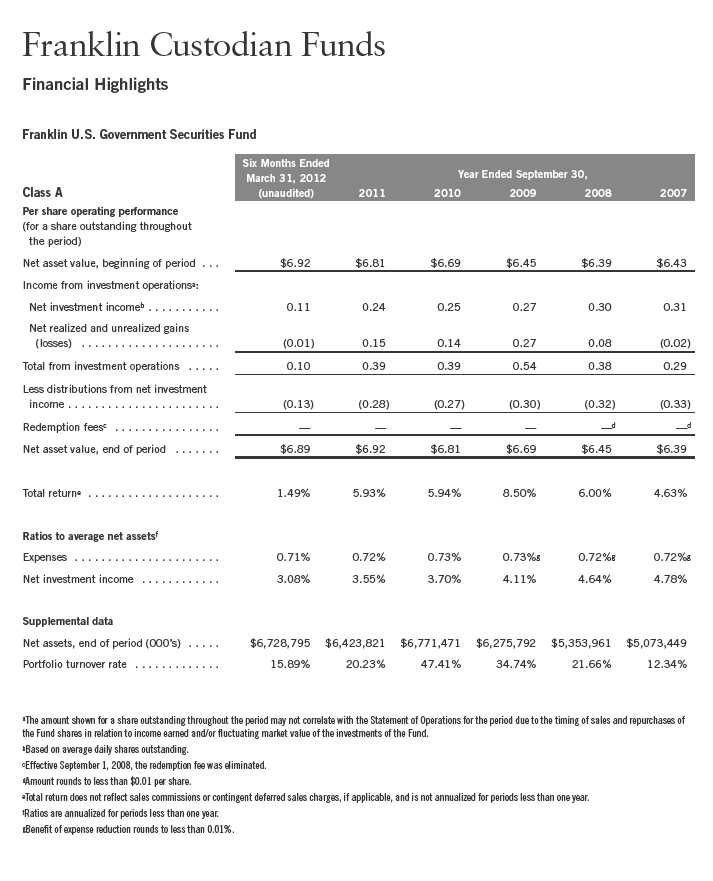

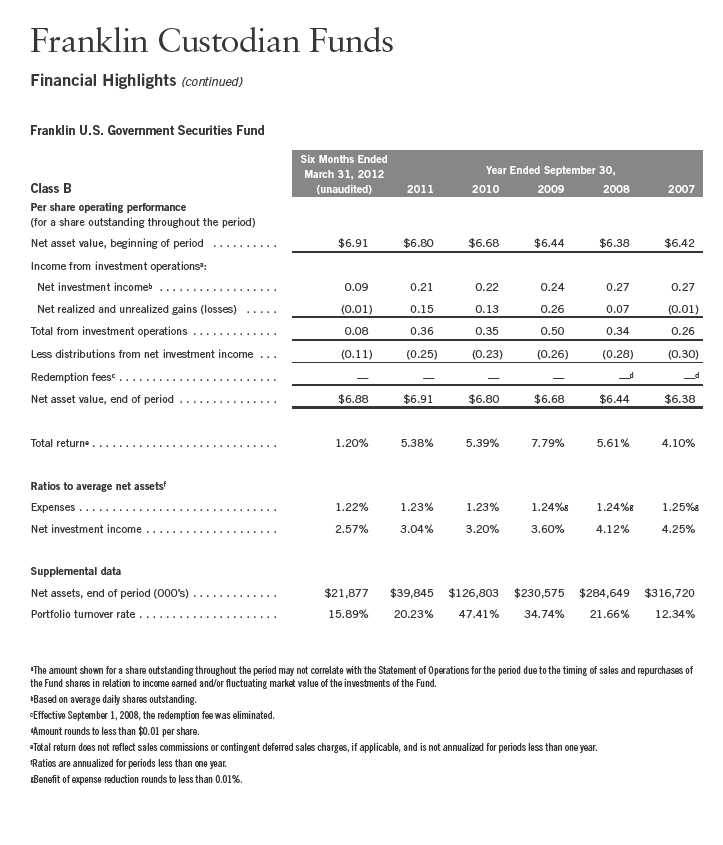

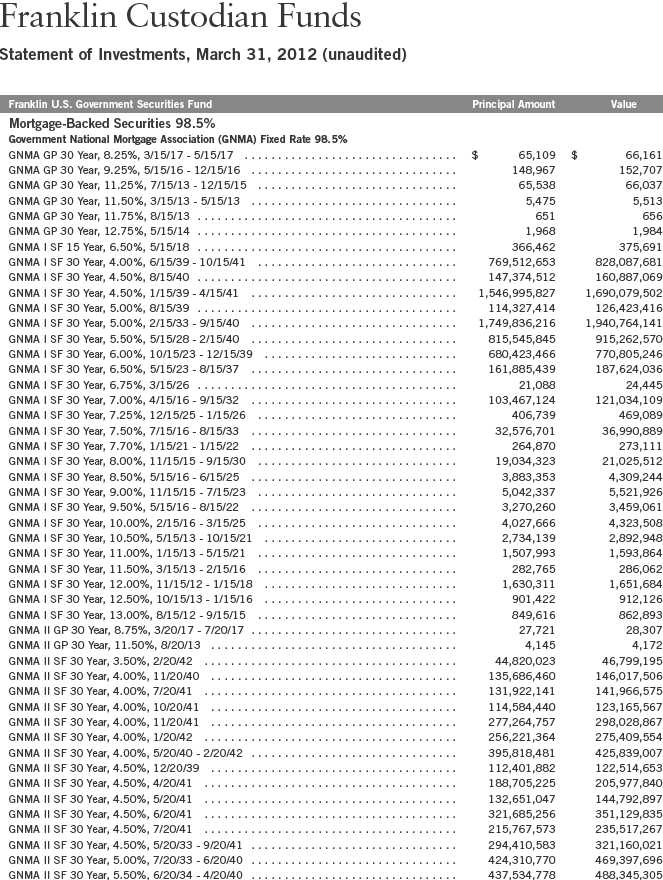

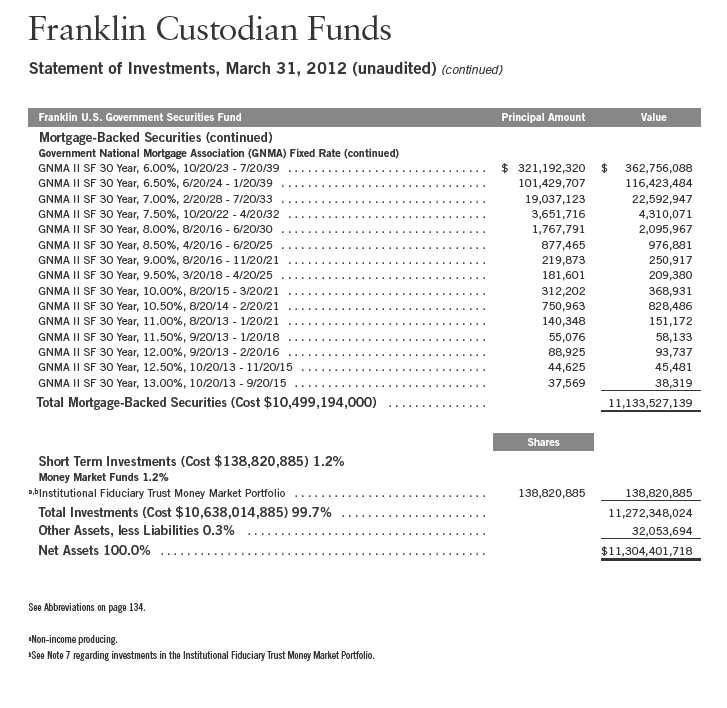

Franklin U.S. Government Securities Fund

Your Fund’s Goal and Main Investments: Franklin U.S. Government Securities Fund seeks income by investing at least 80% of its net assets in U.S. government securities. The Fund presently invests substantially all of its assets in Government National Mortgage Association obligations (Ginnie Maes).

Since 1983, the Fund has invested substantially in Ginnie Mae securities, which carry a guarantee backed by the full faith and credit of the U.S. government as to the timely payment of interest and principal.1 Issued by the Government National Mortgage Association (GNMA), Ginnie Maes have been among the highest yielding U.S. government obligations available.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

We are pleased to bring you Franklin U.S. Government Securities Fund’s semiannual report for the period ended March 31, 2012.

Performance Overview

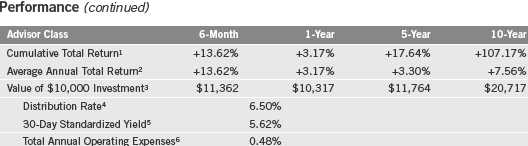

Franklin U.S. Government Securities Fund – Class A posted a +1.49% cumulative total return for the six months under review. The Fund performed comparably to the +1.46% total return of its peers as measured by the Lipper GNMA Funds Classification Average, which consists of funds chosen by Lipper that invest primarily in GNMAs.2 In comparison, the Fund outperformed the Barclays Capital (BC) U.S. Government Index: Intermediate Component, the intermediate component of the BC U.S. Government Index, which returned +0.30% for the same period.3 The Fund’s return reflects the effect of management fees and expenses, while the BC U.S. Government Index: Intermediate Component does not have such costs. You can find the Fund’s long-term performance data in the Performance Summary beginning on page 34.

Investment Strategy

We currently invest all the Fund’s assets predominantly in GNMA (Ginnie Mae) obligations. We analyze securities using proprietary models to help us identify attractive investment opportunities. The Fund’s short-term investments may include short-term government securities and cash or cash equivalents.

1. Securities owned by the Fund, but not shares of the Fund, are guaranteed by the U.S. government, its agencies or instrumentalities as to timely payment of principal and interest. The Fund’s yield and share price are not guaranteed and will vary with market conditions.

2. Source: Lipper Inc. For the six-month period ended 3/31/12, this category consisted of 69 funds. Lipper calculations do not include sales charges or expense subsidization by a fund’s manager. The Fund’s performance relative to the average may have differed if these or other factors had been considered.

3. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

The indexes are unmanaged and include reinvestment of any income or distributions. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 94.

Semiannual Report | 31

32 | Semiannual Report

and 4.5% and 5.0% GNMAs lagging. We remained weighted to GNMA I securities (comprising single-issuer pools), although our exposure to GNMA II securities (comprising multiple-issuer pools) increased over the period. We increased the Fund’s allocation to some 4.0% and 4.5% GNMA I’s. Our heaviest allocation remained in 4.0% through 5.0% coupons.

Franklin U.S. Government Securities Fund takes a consistent and disciplined approach and invests in GNMA mortgage pass-throughs, which remained the only MBS backed by the full faith and credit of the U.S. government.1 The Fund takes a collateral-intensive research approach to uncover opportunities across the GNMA universe. We believe our experience and continual investment in new technologies can help us identify specified pools and individual securities that offer strong cash flow fundamentals and valuations.

Thank you for your continued participation in Franklin U.S. Government Securities Fund. We welcome your comments and questions and look forward to serving your investment needs in the years ahead.

The foregoing information reflects our analysis, opinions and portfolio holdings as of March 31, 2012, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Semiannual Report | 33

Performance Summary as of 3/31/12

Franklin U.S. Government Securities Fund

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

34 | Semiannual Report

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Average annual total return includes maximum sales charges. Class A: 4.25% maximum initial sales charge; Class B: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only; Class R/Advisor Class: no sales charges.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Semiannual Report | 35

Performance Summary (continued)

Endnotes

All investments involve risks, including possible loss of principal. The Fund’s share price and yield will be affected by interest rate movements and mortgage prepayments. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in the Fund adjust to a rise in interest rates, the Fund’s share price may decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class B: Class C: | These shares have higher annual fees and expenses than Class A shares. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Class R: | Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not been annualized.

3. Distribution rate is based on an annualization of the respective class’s March dividend and the maximum offering price (NAV for Classes B, C, R and Advisor) per share on 3/31/12.

4. The 30-day standardized yield for the 30 days ended 3/31/12 reflects an estimated yield to maturity (assuming all portfolio securities are held to maturity). It should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate (which reflects the Fund’s past dividends paid to shareholders) or the income reported in the Fund’s financial statements.

5. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

36 | Semiannual Report

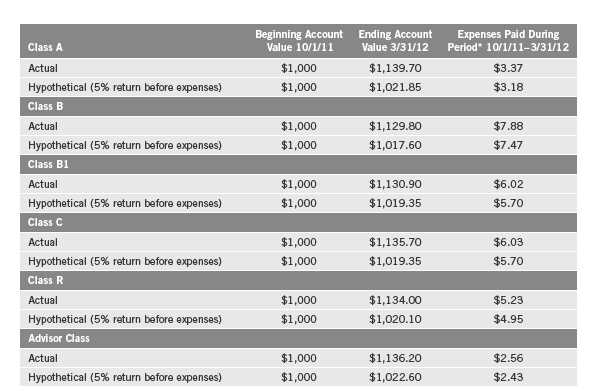

Your Fund’s Expenses

Franklin U.S. Government Securities Fund

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. | |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 37

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 0.71%; B: 1.22%; C: 1.22%; R: 1.07%; and Advisor: 0.57%), multiplied by the average account value over the period, multiplied by 183/366 to reflect the one-half year period.

38 | Semiannual Report

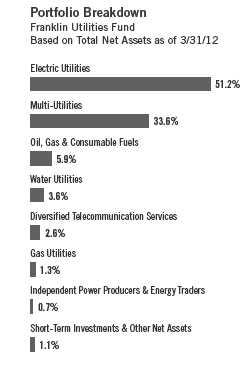

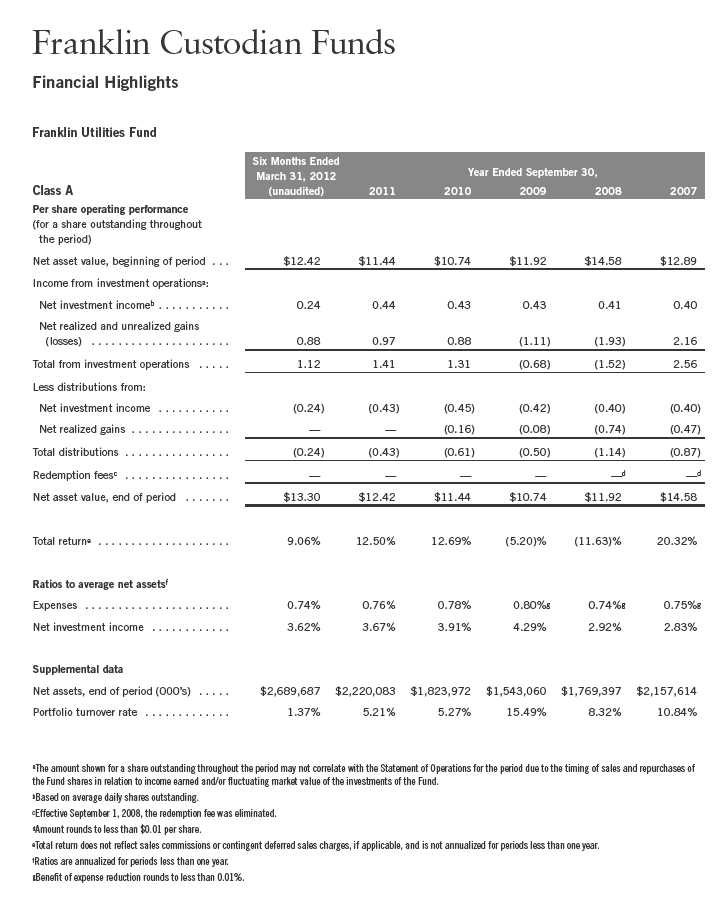

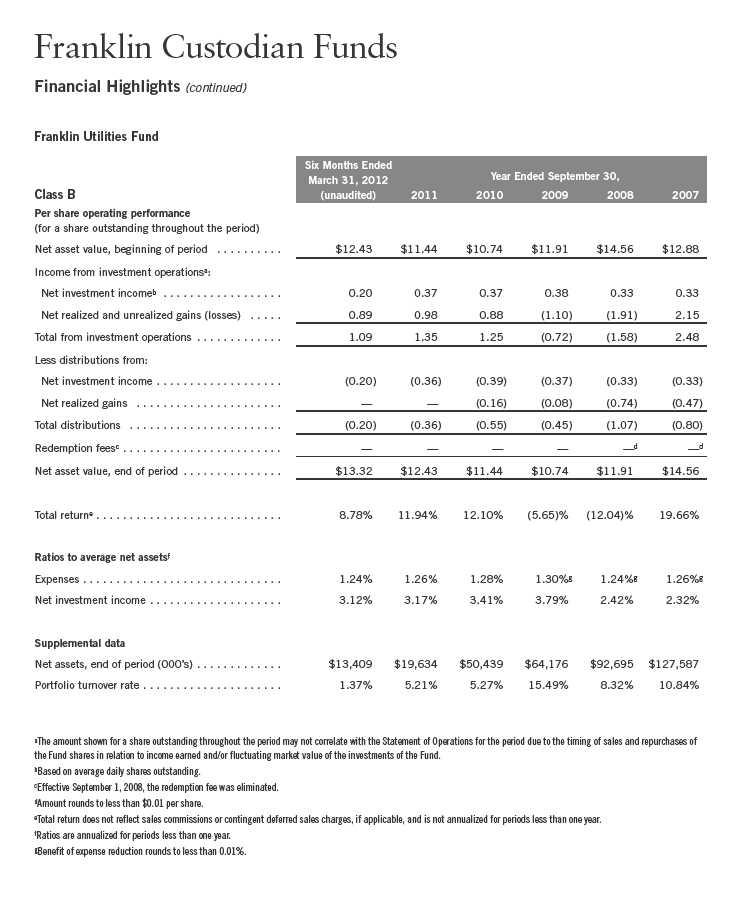

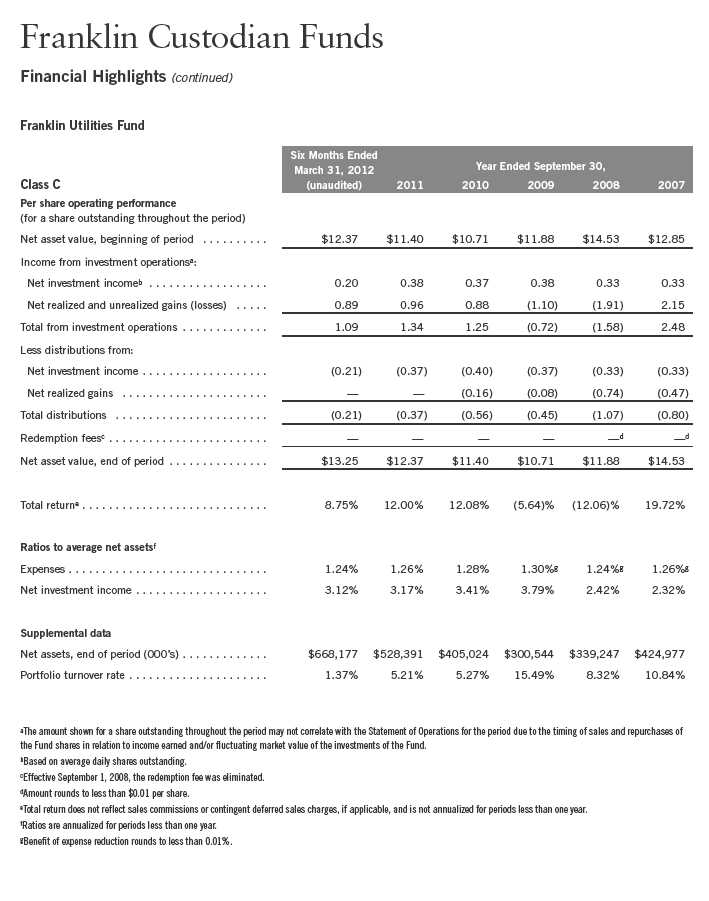

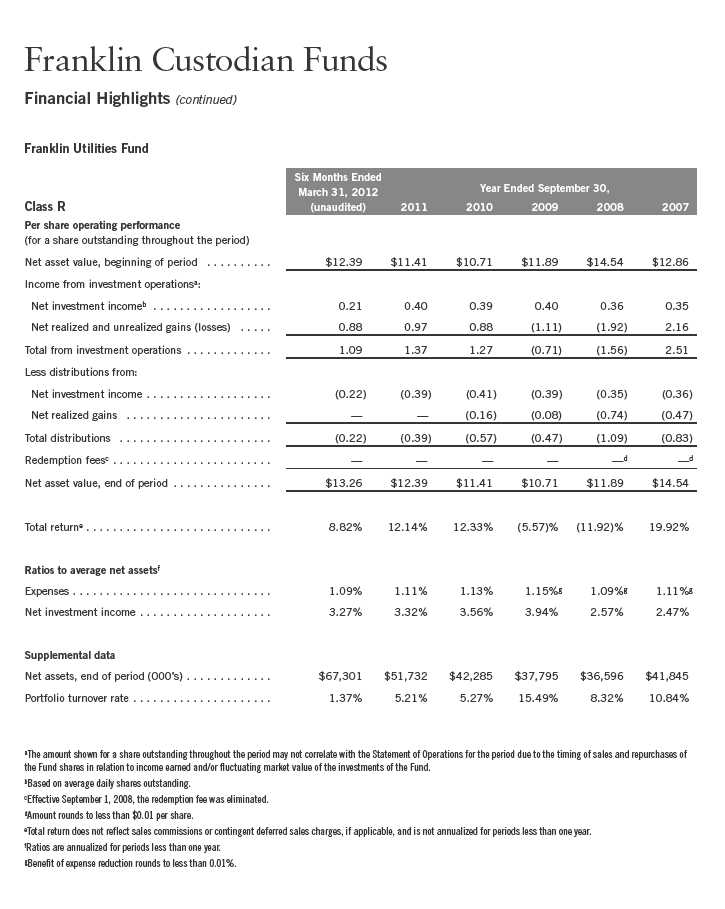

Franklin Utilities Fund

Your Fund’s Goal and Main Investments: Franklin Utilities Fund seeks both capital appreciation and current income by investing at least 80% of its net assets in public utility company securities.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

This semiannual report for Franklin Utilities Fund covers the period ended March 31, 2012.

Performance Overview

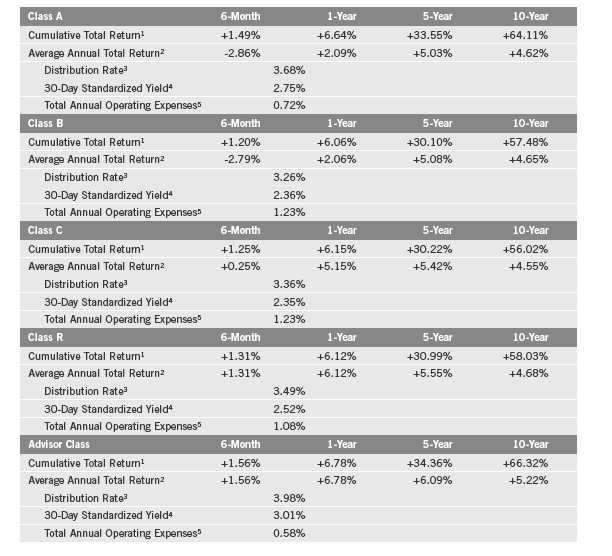

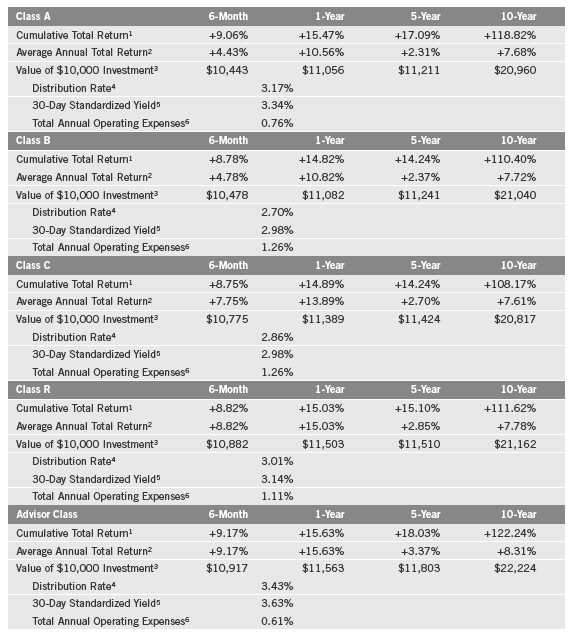

Franklin Utilities Fund – Class A delivered a +9.06% cumulative total return for the six months under review. The Fund’s Class A shares underperformed the +25.89% total return of its broad benchmark, the Standard & Poor’s 500 (S&P 500) Index, which is a broad measure of U.S. stock performance.1 The Fund outperformed the +6.53% total return of its narrow benchmark, the S&P 500 Utilities Index, which measures the performance of all utilities stocks in the S&P 500 Index.1 You can find the Fund’s long-term performance data in the Performance Summary beginning on page 42.

Investment Strategy

We search for the best return opportunities available in the global utilities arena with a specific focus on the U.S. electricity and gas sector. Generally, we look for companies producing a high percentage of earnings from regulated utility franchise operations.

Manager’s Discussion

For the six months under review, utilities produced the weakest performance of the S&P 500 Index’s 10 major sector groups, a reversal of its leading performer status for the 12-month period ended September 30, 2011, the date of the previous annual report. However, stock selection aided the Fund’s performance relative to the S&P 500 Utilities Index.

1. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. The indexes are unmanaged and include reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 101.

Semiannual Report | 39

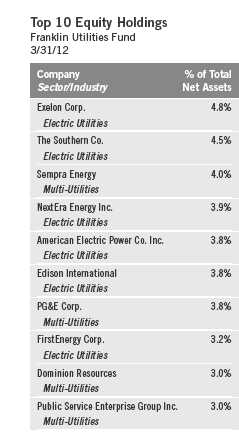

Although the majority of Fund holdings lie within the utilities sector, positions in the energy sector performed particularly well during the six-month reporting period.2 The Williams Cos., which owns and operates natural gas pipelines in North America, was a leading contributor from the energy sector. The firm acquired a company involved in gathering, treating and transporting natural gas. The Williams Cos. also announced higher planned increases in dividend payment. Pipeline transportation and energy storage provider Kinder Morgan’s share price climbed as its announced acquisition of El Paso Corp. was expected to close in the first half of 2012. Infrastructure and utilities firm Sempra Energy posted gains as profits and revenues increased and it announced a dividend increase. In the utilities sector, NextEra Energy, North America’s largest producer of solar and wind energy, posted gains as fourth quarter 2011 earnings doubled compared to the previous year.

Positions that declined in value for the six-month period included Public Service Enterprise Group and Exelon. Public Service Enterprise Group operates gas, nuclear, coal and oil-fired power facilities serving the Northeast and mid-Atlantic regions of the U.S. The firm’s shares fell amid multi-year lows for natural gas prices. Utility services provider Exelon’s investment-grade ratings were downgraded by Moody’s Investor Service, an independent credit rating agency, after Exelon acquired Constellation Energy Group. Moody’s expected negative cash flow for the combined entity, and with Exelon’s sizable capital requirements and dividend, the transaction weighed on investor sentiment.

2. The utilities sector comprises electric utilities, gas utilities and water utilities in the SOI. The energy sector comprises multi-utilities and oil, gas and consumable fuels in the SOI.

40 | Semiannual Report

Thank you for your continued participation in Franklin Utilities Fund.

We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of March 31, 2012, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Semiannual Report | 41

Performance Summary as of 3/31/12

Franklin Utilities Fund

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

42 | Semiannual Report

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Average annual total return and value of $10,000 investment include maximum sales charges. Class A: 4.25% maximum initial sales charge; Class B: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only; Class R/Advisor Class: no sales charges.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Semiannual Report | 43

Performance Summary (continued)

Endnotes

All investments involve risks, including possible loss of principal. In addition to being sensitive to other factors, securities issued by utility companies have been historically sensitive to interest rate changes. When interest rates fall, utility securities prices, and thus a utilities fund’s share price, tend to rise; when interest rates rise, their prices generally fall. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class B: Class C: | These shares have higher annual fees and expenses than Class A shares. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Class R: | Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not been annualized.

3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. Distribution rate is based on an annualization of the respective class’s current quarterly dividend and the maximum offering price (NAV for Classes B, C, R and Advisor) per share on 3/31/12.

5. The 30-day standardized yield for the 30 days ended 3/31/12 reflects an estimated yield to maturity (assuming all portfolio securities are held to maturity). It should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate (which reflects the Fund’s past dividends paid to shareholders) or the income reported in the Fund’s financial statements.

6. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

44 | Semiannual Report

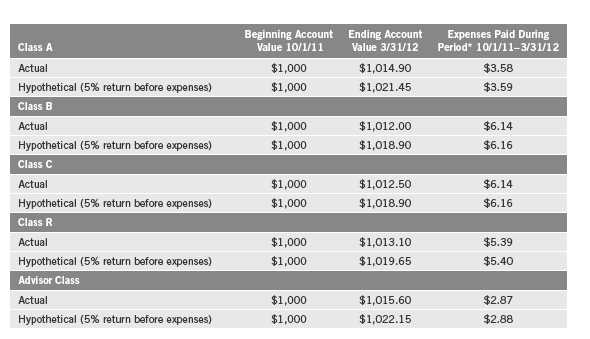

Your Fund’s Expenses

Franklin Utilities Fund

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. | |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 45

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 0.74%; B: 1.24%; C: 1.24%; R: 1.09%; and Advisor: 0.59%), multiplied by the average account value over the period, multiplied by 183/366 to reflect the one-half year period.

46 | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 47

48 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 49

50 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 51

52 | Semiannual Report

Semiannual Report | 53

54 | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 55

56 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 57

58 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 59

60 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | 61

62 | Semiannual Report

Semiannual Report | 63

64 | Semiannual Report

Semiannual Report | 65

66 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 67

68 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 69

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 71

72 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | 73

74 | Semiannual Report

Semiannual Report | 75

Semiannual Report | 77

78 | Semiannual Report

Semiannual Report | 79

Semiannual Report | 81

82 | Semiannual Report

Semiannual Report | 83

84 | Semiannual Report

Semiannual Report | 85

86 | Semiannual Report

Semiannual Report | 87

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 89

90 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 91

92 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 93

94 | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 95

96 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 97

98 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 99

100 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 103

Franklin Custodian Funds

Financial Statements (continued)

Statements of Assets and Liabilities (continued)

March 31, 2012 (unaudited)

104 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 105

106 | The accompanying notes are an integral part of these financial statements. | Semiannual Report