Exhibit 99(d)

<PAGE> 1

FINANCIAL SECTION

| FINANCIAL TABLE OF CONTENTS | ||

3 | Management's Discussion of Financial Responsibility | |

4 | Independent Auditors' Report | |

5 | Management's Discussion and Analysis | |

| 5 | Operations | |

| 5 | Consolidated Operations | |

| 12 | Segment Operations | |

| 25 | International Operations | |

| 28 | Financial Resources and Liquidity | |

| 39 | Selected Financial Data | |

| 39 | Critical Accounting Policies | |

| 43 | Audited Financial Statements | |

| 43 | Earnings | |

| 43 | Changes in Share Owners' Equity | |

| 45 | Financial Position | |

| 47 | Cash Flows | |

| 49 | Notes to Consolidated Financial Statements | |

| 110 | Our Businesses | |

| 112 | Glossary | |

112 | Corporate Management | |

112 | Operating Management | |

| 114 | Corporate Information | |

<PAGE> 2

ABOUT THESE FINANCIAL STATEMENTS

At GE, all of our businesses share common values and objectives, each striving to deliver excellent performance and generate increasing share owner value. However, our businesses are also diverse. With this diversity comes enormous opportunity, as well as significant challenges. One example of this combination of opportunity and challenge is our need to share our financial statements in the most meaningful way possible. To fulfill this objective we continue to present our consolidated financial information as well as information divided into two major categories – industrial (GE) and financial services (GECS). By reviewing the two major categories, you can gain a meaningful assessment of our performance in measures like leverage, asset turnover and cash flow. While our financial report is longer than it has been historically, that additional length arose from your requests for information. Our discussion of segment results includes asset details for the major financial services businesses, for example, since portfolio size is significant to earnings of those businesses.

When we committed to increasing our transparency, we expected that this report would be a primary vehicle that provides a reference source for your questions about us. We started that process last year, and the 2002 report continues the trend. You will see that our financial section, 69 pages long, contains significantly more information than our 2000 report contained in its 44 pages. We sincerely believe that we have progressed towards our transparency objective, and believe that you will find the important financial information you need in the pages that follow.

We are available to answer your questions, and, when those questions would be of interest to a broader audience, we will include that information in our financial reports. Following are among the other important changes this year, changes that we trust will assist you in using these financial statements:

- We present our financial information electronically atwww.ge.com/investor. This site is much more than an electronic reproduction of the following pages. It is interactive and informative, and we believe it gives a glimpse into the future of financial reporting. We invite you to help us accelerate this process by giving us feedback on the website.

- We changed the way that we manage certain financial services businesses, increasing the total number of reporting segments from eight to 12. We have recast all comparative financial data to provide an accurate basis for comparison.

- We describe our businesses on pages 110 and 111.

- We have included a glossary of key financial and business terms on pages 112 -115.

<PAGE> 3

MANAGEMENT’S DISCUSSION OF FINANCIAL RESPONSIBILITY

One of our most crucial management objectives is to ensure that our investors are well informed. We take full responsibility for meeting this objective, adopting appropriate accounting policies and devoting our full, unyielding commitment to ensuring that those policies are applied properly and consistently. We make every effort to report in a manner that is relevant, complete and clear, and we welcome and evaluate each suggestion from those who use our reports.

Rigorous Management Oversight

Members of our corporate leadership team review each of our businesses constantly, on matters that range from overall strategy and financial performance, to staffing and compliance. Our business leaders constantly monitor real-time financial and operating systems, enabling us to identify potential opportunities and concerns at an early stage, and positioning us to develop and execute rapid responses. Our Board of Directors oversees management’s business conduct, and our Audit Committee, which consists entirely of independent directors, oversees our system of internal financial controls and disclosure controls. We have taken a number of recent governance actions intended to enhance investor trust and improve the board’s overall effectiveness. These actions include increasing to a majority the number of independent directors, naming a Presiding Director who will conduct at least three meetings per year with non-employee directors, requiring each non-employee director to visit two of GE’s businesses annually to meet directly with operating leadership and voluntarily expensing our stock options.

Dedication to Controllership

We maintain a dynamic system of disclosure controls and procedures—including internal controls over financial reporting—designed to ensure reliable financial record-keeping, transparent financial reporting and disclosure, protection of physical and intellectual property, and efficient use of resources. We recruit and retain a world-class financial team, including 450 internal auditors who conduct thousands of audits each year, in every geographic area, at every GE business. Senior management and the Audit Committee oversee the scope and results of these reviews. We also maintain a set of integrity policies—our “Spirit & Letter”—which require compliance with law and policy, and which pertain to such vital issues as upholding financial integrity and avoiding conflicts of interest. We have published these integrity policies in 27 languages, and we have provided them to every one of GE’s more than 300,000 global employees, holding each of these individuals—from our top management on down—personally accountable for compliance with them. Our integrity policies serve to reinforce key employee responsibilities around the world, and we inquire extensively about compliance. Our strong compliance culture reinforces these efforts by requiring employees to raise any compliance concerns and by prohibiting retribution for doing so.

Visibility to Investors

We are keenly aware of the importance of full and open presentation of our financial position and operating results. To facilitate this, we maintain a Disclosure Committee, which includes senior executives who possess exceptional knowledge of our businesses and our investors. We have asked this committee to evaluate the fairness of our financial disclosures, and to report their findings to us and to the Audit Committee. We further ensure strong disclosure by holding more than 250 analyst and investor meetings every year, and by communicating all material information covered in those meetings to the public. In testament to the effectiveness of our stringent disclosure policies, investors surveyed annually by Investor Relations magazine have awarded GE Best Overall Investor Relations Program by a mega-cap company for six consecutive years, and 15 awards in other categories in the past seven years. We are in regular contact with representatives of the major rating agencies, and our debt continues to receive their highest ratings. We welcome the strong oversight of our financial reporting activities by our independent audit firm, KPMG LLP, who are engaged by and report directly to the Audit Committee. Their report for 2002 appears on page 4.

Great companies are built on the foundation of reliable financial information and compliance with the law. For GE, the financial disclosures made in this report are a vital part of that foundation. We present this information proudly, with the expectation that those who use it will understand our company, recognize our commitment to performance with integrity, and share our confidence in GE’s future.

/s/ Jeffrey R. Immelt

Jeffrey R. Immelt

Chairman of the Board

and Chief Executive Officer

/s/ Keith S. Sherin

Keith S. Sherin

Senior Vice President, Finance, and

Chief Financial Officer

February 7, 2003

<PAGE> 4

INDEPENDENT AUDITORS’ REPORT

To Share Owners and Board of Directors of

General Electric Company:

We have audited the accompanying statement of financial position of General Electric Company and consolidated affiliates ("GE") as of December 31, 2002 and 2001, and the related statements of earnings, changes in share owners' equity and cash flows for each of the years in the three-year period ended December 31, 2002. These consolidated financial statements are the responsibility of GE management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the aforementioned financial statements appearing on pages 43, 45, 47, 23, and 49 to 111 present fairly, in all material respects, the financial position of General Electric Company and consolidated affiliates at December 31, 2002 and 2001, and the results of their operations and their cash flows for each of the years in the three-year period ended December 31, 2002, in conformity with accounting principles generally accepted in the United States of America.

As discussed in note 1 to the consolidated financial statements, GE in 2002 changed its methods of accounting for goodwill and other intangible assets and for stock-based compensation, and in 2001 changed its methods of accounting for derivative instruments and hedging activities and impairment of certain beneficial interests in securitized assets.

Our audits were made for the purpose of forming an opinion on the consolidated financial statements taken as whole. The accompanying consolidating information appearing on pages 44, 46, and 48 is presented for purposes of additional analysis of the consolidated financial statements rather than to present the financial position, results of operations and cash flows of the individual entities. The consolidating information has been subjected to the auditing procedures applied in the audits of the consolidated financial statements and, in our opinion, is fairly stated in all material respects in relation to the consolidated financial statements taken as a whole.

/s/ KPMG LLP

KPMG LLP

Stamford, Connecticut

February 7, 2003, except as to notes 10, 16, and 27, which are as of April 10, 2003.

<PAGE> 5

MANAGEMENT’S DISCUSSION AND ANALYSIS

MANAGEMENT’S DISCUSSION OF OPERATIONS

Overview

General Electric Company’s consolidated financial statements represent the combination of the industrial manufacturing and product services businesses of General Electric Company (GE) and the financial services businesses of General Electric Capital Services, Inc. (GECS or financial services).

We present Management’s Discussion of Operations in three parts: Consolidated Operations, Segment Operations and International Operations.

Consolidated Operations

We achieved record earnings in 2002, demonstrating the benefits of our diverse business portfolio and continuing emphasis on globalization, technology, growth in services, digitization and the Six Sigma Quality initiative.

Our consolidated revenues were $131.7 billion in 2002, an increase of 5% over revenues of $125.9 billion in 2001, reflecting a 7% increase in our industrial businesses and a slight decrease in financial services. Our consolidated revenues of $125.9 billion in 2001 decreased 3% from $129.9 billion in 2000, reflecting a 6% increase in industrial business revenues partially offsetting a 12% decrease in financial services—the result of significant strategic repositioning activities.

Our earnings before accounting changes increased to a record $15.1 billion in 2002, a 7% increase from $14.1 billion in 2001. Per-share earnings before accounting changes increased to $1.51 during 2002, up 7% from the prior year’s $1.41. (Except as otherwise noted, when we refer to “per-share earnings” or “earnings per share,” we mean earnings per share on a diluted basis.)

Contributions from acquisitions affect earnings comparisons. Our consolidated net earnings in 2002, 2001 and 2000 include approximately $636 million, $225 million and $345 million, respectively, from acquired businesses. We integrate acquisitions as quickly as possible and only earnings during the first 12 months following the quarter in which we complete the acquisition are considered to be related to acquired businesses.

RETURN ON AVERAGE SHARE OWNERS’ EQUITY (excluding the effect of accounting changes) was 25.8% in 2002, compared with 27.1% in 2001, which was about the same as in 2000.

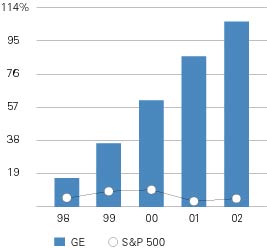

WE DECLARED $7.3 BILLION IN DIVIDENDS IN 2002. Per-share dividends of $0.73 were up 11% from 2001, following a 16% increase from the preceding year. We have rewarded our share owners with 27 consecutive years of dividend growth. Our dividend growth for the past five years has significantly outpaced dividend growth of companies in the Standard & Poor’s 500 stock index.

Except as otherwise noted, the analysis in the remainder of this section presents the results of GE (with GECS included on a one-line basis) and GECS. See the Segment Operations section on page 12 for a more detailed discussion of the businesses within GE and GECS.

<PAGE> 6

GE TOTAL REVENUES were $79.0 billion in 2002, compared with $74.0 billion in 2001 and $69.5 billion in 2000.

GE sales of goods and services were $73.3 billion in 2002, an increase of 8% from 2001, which in turn was 7% higher than in 2000. Volume was about 9% higher in 2002, reflecting double-digit increases at Power Systems, NBC, Medical Systems, Specialty Materials and Industrial Systems, partially offset by decreases at Aircraft Engines and Transportation Systems. Selling prices were lower across most segments other than NBC and Power Systems. The net effect in 2002 of exchange rates on sales denominated in currencies other than the U.S. dollar was slightly positive. Volume in 2001 was about 7% higher than in 2000, with selling price and currency effects both slightly negative.

| GE/S&P CUMULATIVE DIVIDEND GROWTH SINCE 1997

|

For purposes of the financial statement display of sales and costs of sales on pages 43 and 44, “goods” is required by U.S. Securities and Exchange Commission regulations to include all sales of tangible products, and “services” must include all other sales, including broadcasting and information services activities. We refer to sales of both spare parts (goods) and repair services as sales of “product services,” which is an important part of our operations. Sales of product services were $20.8 billion in 2002, an 11% increase over 2001. Increases in product services in 2002 and 2001 were widespread, led by continued strong growth at Power Systems, Medical Systems and Transportation Systems. Operating margin from product services was approximately $5.2 billion, up 11% from 2001. The increase reflected improvements in most product services businesses and was led by Power Systems and Medical Systems.

<PAGE> 7

GE OTHER INCOME, earned from a wide variety of sources, was $1.1 billion, $0.4 billion and $0.5 billion in 2002, 2001 and 2000, respectively. Other income in 2002 included a $0.6 billion pre-tax gain resulting from NBC’s exchange of certain assets for the cable network Bravo and a $0.5 billion pre-tax gain on the sale of 90% of Global eXchange Services.

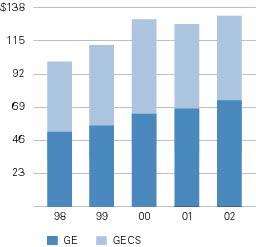

GECS TOTAL REVENUES decreased slightly to $58.2 billion in 2002, following a 12% decrease to $58.4 billion in 2001. The largest single factor affecting 2002 revenues was growth from increases in acquisitions and originations—primarily at Commercial Finance. This growth was more than offset by the absence of revenues from Americom after its sale in late 2001 ($1.7 billion), increased estimates of prior-year loss events and lower investment gains at Insurance ($0.9 billion), lower securitization activity in all segments ($0.6 billion), and lower market interest rates.

| CONSOLIDATED REVENUES (In billions)

|

The three principal reasons for the decrease in revenues in 2001 compared with 2000 were: the deconsolidation of Montgomery Ward LLC (Wards) and resulting absence of sales in 2001 ($3.2 billion); the effects of rationalization of operations and market conditions at Commercial Finance and IT Solutions ($1.5 billion and $1.4 billion, respectively); and reduced surrender fees ($1.2 billion) associated with the planned run-off of restructured insurance policies of Toho Mutual Life Insurance Company (Toho) at GE Financial Assurance. Additional information about other revenue items is provided in the Segment Operations section on page 12.

Despite good growth in underlying operations, GECS earnings before accounting changes of $4.6 billion in 2002 were down 17% from 2001. The Insurance segment more than accounted for the decline, with $2.3 billion after tax of adverse development and adjustments to estimates of prior-year loss events. Realized investment gains and gains on asset securitization declined by $0.8 billion after tax. Partial offsets were goodwill amortization that ceased at the beginning of 2002 ($0.6 billion in 2001) and lower taxes ($0.6 billion).

GECS earnings before accounting changes in 2001 increased 8% from 2000. Principal factors in the 2001 increase were strong productivity ($0.7 billion) and lower taxes ($0.5 billion) partially offset by reduced earnings at GE Global Insurance Holding Corporation (GE Global Insurance Holding), the parent of Employers Reinsurance Corporation ($0.5 billion) reflecting the events of September 11, 2001, losses and lower realized gains on financial instruments. Excluding effects of Paine Webber Group, Inc. (PaineWebber) in 2000 and Americom in 2001, such pre-tax gains were lower in 2001 by $0.5 billion ($0.3 billion after tax). Pre-tax gains on sales of investment securities declined in 2001 by $0.5 billion, of which $0.4 billion related to GE Equity; other GE Equity gains were $0.8 billion lower; while gains on securitizations were up $0.8 billion from 2000.

<PAGE> 8

PRINCIPAL COSTS AND EXPENSES FOR GE are those classified as costs of goods and services sold, and selling, general and administrative expenses. Several of our ongoing initiatives had significant effects on costs:

- The Six Sigma Quality initiative continues to reduce rework, simplify processes and reduce direct material costs.

- Globalization continues to reduce costs through sourcing of products and services in lower-cost countries.

- Digitization has also enabled us to simplify and streamline processes while investing in internal infrastructure hardware and software. We conduct a growing portion of our business over the Internet. Benefits from this initiative include improved customer service, expanded product and service offerings and increased operating efficiency for us and our customers.

Our principal U.S. postretirement benefit plans (plans) contributed $806 million to pre-tax earnings in 2002, or 3.5% of earnings before accounting changes, compared with $1,480 million (6.8%) and $1,266 million (6.5%) in 2001 and 2000, respectively. Considering current and expected asset allocations, as well as historical and expected returns on various categories of assets in which our plans are invested, we assumed that long-term returns on our pension plan assets would be 8.5% in 2002 and 9.5% in 2001 and 2000. Reducing the assumed return by 100 basis points in 2002 increased annual pension costs by about $480 million pretax. Of course, actual annual investment returns can be extremely volatile. Because this short-term market volatility occurs in context of the long-term nature of pension plans, U.S. accounting principles provide that differences between assumed and actual returns are recognized over the average future service of employees.

<PAGE> 9

Two other significant factors affecting postretirement benefit costs are the discount rate used to measure the present value of plan obligations and changes in postretirement healthcare costs. We reduced our discount rate from 7½% to 7¼% for 2002, a reduction that increased our costs by about $90 million pretax. Postretirement healthcare costs also increased substantially in 2002. See notes 5 and 6 for additional information about funding status, components of earnings effects and actuarial assumptions of the plans. See pages 41-42 for discussion of pension assumptions.

Our postretirement benefit costs will likely increase in 2003 for a number of reasons, including a reduction in the discount rate from 7¼% to 6¾%, amortization of investment losses and sustained increases in healthcare costs. We continue to expect that our plan assets will earn 8½%, on average, over the long term. Our labor agreements with various unions expire in June 2003, and results of union negotiations, which are uncertain, could affect postretirement benefit costs in 2003 and beyond.

We will not make any contributions to the GE Pension Plan in 2003. To the best of our ability to forecast the next five years, we do not anticipate making contributions to that Plan so long as expected investment returns are achieved. The present funding status provides assurance of benefits for our participants, but future effects on operating results and funding depend on economic conditions and investment performance.

OPERATING MARGIN is sales of goods and services less the costs of goods and services sold, as well as selling, general and administrative expenses. GE operating margin was 19.1% of sales in 2002, down from 19.6% in 2001 and about the same as the comparable 18.9% in 2000. The decline in 2002 was attributable to the Plastics segment and the Lighting business in Consumer Products and also reflected restructuring and other charges of $0.6 billion, partially offset by improvements in operating margins at Power Systems and NBC. Restructuring and other charges included $0.4 billion for rationalizing certain operations and facilities of GE’s worldwide industrial businesses. The improvement in operating margin in 2001 was led by Power Systems and Aircraft Engines, reflecting increasing benefits from the digitization, product services and Six Sigma Quality initiatives. Reported operating margin was 18.6% in 2000, including the costs of a one-time retirement benefit provision associated with the labor agreement concluded in that year.

TOTAL COST PRODUCTIVITY (sales in relation to costs, both on a constant dollar basis) for GE in 2002 and 2001 was about 2%. Variable cost productivity improvements (led by Industrial Systems and Plastics) and base cost productivity improvements at Plastics were more than offset by lower base cost productivity primarily at Power Systems, Industrial Systems and Specialty Materials. In 2001, total cost productivity was 2.2% as productivity in Power Systems and Medical Systems was partially offset by negative productivity across several businesses, particularly Plastics, reflecting volume declines.

GE INTEREST AND OTHER FINANCIAL CHARGES in 2002 amounted to $569 million, down 30% from $817 million in 2001, which was about the same as 2000. The decrease in 2002 was primarily the result of lower interest on tax liabilities (see page 11). During 2001, the benefits of lower average interest rates and lower average borrowing levels were partially offset by increased provisions for interest on tax liabilities.

GECS INTEREST EXPENSE ON BORROWINGS in 2002 was $9.9 billion, compared with $10.6 billion in 2001 and $11.1 billion in 2000. Changes in both years reflected the effects of lower interest rates, partially offset by the effects of higher average borrowings used to finance acquisitions and asset growth. The average composite effective interest rate was 4.07% in 2002, compared with 5.11% in 2001 and 5.89% in 2000. In 2002, average assets of $455.2 billion were 18% higher than in 2001, which in turn were 7% higher than in 2000. See page 31 for a discussion of interest rate risk management.

<PAGE> 10

| GECS BORROWINGS (In billions)

|

FINANCING SPREADS. Over the last three years, market interest rates have been more volatile than GECS average composite effective interest rates, principally because of the mix of effectively fixed-rate borrowings in the GECS financing structure. Yields on our portfolio of fixed and floating-rate financial products have behaved similarly; consequently, financing spreads have remained relatively flat over the three-year period.

<PAGE> 11

INCOME TAXES on consolidated earnings before accounting changes were 19.9%, compared with 28.3% in 2001 and 31.0% in 2000. A more detailed analysis of differences between the U.S. federal statutory rate and the consolidated rate, as well as other information about our income tax provisions, is provided in note 7.

The effective tax rate of GE decreased to 20.2% in 2002 from 22.9% in 2001 and 23.0% in 2000. During 2002, GE entered into settlements with the U.S. Internal Revenue Service (IRS) concerning certain export tax benefits. The result of those settlements, included in the line “Tax on international activities including exports” in note 7, was a decrease in the GE effective tax rate of approximately two percentage points. Also during 2002, GE entered into a tax advantaged transaction to exchange certain assets for the cable network Bravo. The effect of this transaction on the GE effective tax rate is included in the line “All other—net” in note 7.

GECS effective tax rate decreased to negative 1.7% in 2002 from 19.8% in 2001 and 26.9% in 2000. The 2002 effective tax rate reflects effects of pre-tax losses at GE Global Insurance Holding (ERC) and GE Equity, the effects of lower taxed earnings from international operations and favorable tax settlements with the IRS discussed below. Pre-tax losses of $2.8 billion at ERC and $0.6 billion at GE Equity reduced the effective tax rate of GECS by approximately 17 percentage points.

During 2002, as a result of revised IRS regulations, GECS reached a settlement with the IRS allowing the deduction of previously realized losses associated with the prior disposition of Kidder Peabody. Also during 2002, a settlement was reached with the IRS regarding the treatment of certain reserves for obligations to policyholders on life insurance contracts in the GE Financial Assurance business. The benefits of these settlements, which reduced the GECS rate approximately four percentage points (excluding the ERC and GE Equity losses), are included in the line “All other—net” in note 7.

The 2001 effective tax rate of GECS reflected the effects of lower taxed earnings from international operations and certain other transactions (see note 7). That rate also included effects of a $0.6 billion pre-tax charge related to the events of September 11, 2001, principally at ERC, which reduced the GECS effective tax rate by one percentage point.

NEW ACCOUNTING STANDARDS. The Financial Accounting Standards Board’s (FASB) Statement of Financial Accounting Standards (SFAS) 142, Goodwill and Other Intangible Assets, generally became effective for us on January 1, 2002. Under SFAS 142, goodwill is no longer amortized but is tested for impairment using a fair value methodology. We stopped amortizing goodwill effective January 1, 2002.

The result of our applying the new rules as of January 1, 2002, was a non-cash charge of $1.2 billion ($1.0 billion after tax, or $0.10 per share), which we reported in the caption “Cumulative effect of accounting changes.” Substantially all of the charge relates to the GECS IT Solutions business and the GECS GE Auto and Home business. Factors contributing to the impairment charge were the difficult economic environment in the information technology sector and heightened price competition in the auto insurance industry. After the required accounting changes, our 2002 earnings and earnings per share were $14.1 billion and $1.41, respectively, compared with $13.7 billion and $1.37, respectively, in 2001.

In 2002, we adopted the stock option expense provisions of SFAS 123, Accounting for Stock-Based Compensation. This accounting change did not result in a cumulative effect charge, but increased 2002 costs by $45 million and reduced net earnings by $27 million. See note 1 on page 49 for additional information.

The cumulative effect of accounting changes in 2001 related to the adoption, as of January 1, 2001, of SFAS 133, Accounting for Derivative Instruments and Hedging Activities, as amended, and the consensus of the FASB’s Emerging Issues Task Force on Issue 99-20, Recognition of Interest Income and Impairment on Purchased and Retained Beneficial Interests in Securitized Financial Assets. Adoption of these standards resulted in a one-time, non-cash charge that reduced our 2001 earnings by $444 million ($0.04 per share). After these required accounting changes, our 2001 earnings and earnings per share were $13.7 billion and $1.37, respectively, compared with $12.7 billion and $1.27, respectively, in 2000.

MAJOR PROVISIONS OF NEW ACCOUNTING STANDARDS that will affect us follow.

SFAS 143, Accounting for Asset Retirement Obligations, requires recognition of the fair value of obligations associated with the retirement of long-lived assets when there is a legal obligation to incur such costs. This amount is accounted for like an additional element of cost, and, like other cost elements, is depreciated over the corresponding asset’s useful life. SFAS 143 primarily affects our accounting for costs associated with the future retirement of facilities used for storage and production of nuclear fuel. On January 1, 2003, we recorded a liability for the expected present value of future retirement costs of $363 million, increased net property, plant and equipment by $24 million and recognized a one-time, cumulative effect charge of $215 million (net of tax). This accounting change will not involve cash and will have only a modest effect on future earnings.

<PAGE> 12

In November 2002, the FASB issued Interpretation No. (FIN) 45, Guarantor’s Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees of Indebtedness of Others. Among other things, the Interpretation requires guarantors to recognize, at fair value, their obligations to stand ready to perform under certain guarantees. FIN 45 is effective for guarantees issued or modified on or after January 1, 2003. It will have an inconsequential effect on our financial position and future results of operations.

In January 2003, the FASB issued FIN 46, Consolidation of Variable Interest Entities, which we intend to adopt on July 1, 2003. FIN 46's consolidation criteria are based on analysis of risks and rewards, not control, and represent a significant and complex modification of previous accounting principles. FIN 46 represents an accounting change, not a change in the underlying economics of asset sales. Under its provisions, certain assets previously sold to our special purpose entities (SPEs) could be consolidated on our books, and, if consolidated, any assets and liabilities now on our books related to those SPEs would be removed. In the event we consolidated these assets, we would not reacquire their legal ownership, nor would our legal rights and obligations change. Any consolidated assets would earn returns substantially like the returns we would have earned had we never sold them. Even assuming the legal provisions controlling these SPEs are not changed between now and the July 1 effective date of FIN 46, the very complexity of the new consolidation rules and their evolving clarification make forecasting that July 1 effect impracticable. It is also clear that many alternative structures for sales of financial assets would continue to be reported as sales under FIN 46 with the assets qualifying for sale not consolidated. We are evaluating whether characteristics of those structures can cost-beneficially be applied to our arrangements before the July 1 effective date. Further information about entities that potentially fall within the scope of FIN 46 is provided in note 29.

Segment Operations

REVENUES AND SEGMENT PROFIT FOR OPERATING SEGMENTS are shown on page 23. For additional information, including a description of the products and services included in each segment, see pages 110 and 111.

Segment profit is determined based on internal performance measures used by the Chief Executive Officer to assess performance of each business. Generally, the results of decisions made by the Chief Executive Officer regarding unusual matters are excluded from internal business measurements. Historically, such matters have included charges for restructuring; rationalization or other similar expenses; and litigation settlements or other losses, responsibility for which precedes the current business management team. Segment profit excludes any goodwill amortization, the effects of pensions and other retiree benefit plans and accounting changes. Segment profit excludes or includes interest and other financial charges and segment income taxes according to how segment management is measured -- excluded in determining operating profit for Aircraft Engines, Consumer Products, Industrial Products and Systems, Medical Systems, NBC, Plastics, Power Systems, Specialty Materials and Transportation Systems, but included in determining net earnings for Commercial Finance, Consumer Finance, Equipment Management, Insurance and All Other GECS.

AIRCRAFT ENGINES reported a 2% decrease in revenues in 2002 as commercial engine pricing pressures and reduced commercial product services revenues combined with lower industrial units were substantially offset by increased military sales. Operating profit was 4% lower, primarily as a result of lower pricing for commercial engines, lower product services volume from reduced flight hours and higher labor costs, partially offset by lower material costs and productivity. Revenues and operating profit increased 6% and 7%, respectively, in 2001, reflecting higher volume in product services and higher volume of commercial engines and aero-derivative products. The improvement in operating profit was also attributable to productivity.

<PAGE> 13

OPERATING PROFIT OF GE SEGMENTS

|

In 2002, revenues from sales to the U.S. government were $2.2 billion, compared with $1.9 billion in 2001.

Aircraft Engines received orders of $11.6 billion in 2002, compared with $12.1 billion in 2001. The $11.6 billion total backlog at year-end 2002 comprised unfilled product orders of $9.8 billion (of which 43% was scheduled for delivery in 2003) and product services orders of $1.8 billion scheduled for 2003 delivery. Comparable December 31, 2001, total backlog was $11.2 billion.

<PAGE> 14

Commercial Finance

(In millions) |

| 2002 |

| 2001 |

| 2000 |

|

Revenues |

| ||||||

Commercial Equipment Financing |

| $ 4,539 |

| $ 4,212 |

| $ 3,355 |

|

Real Estate |

| 2,124 |

| 1,886 |

| 1,977 |

|

Commercial Finance (CF) |

| 2,350 |

| 1,758 |

| 1,587 |

|

Structured Finance Group |

| 1,243 |

| 1,093 |

| 999 |

|

Aviation Services |

| 2,694 |

| 2,173 |

| 1,962 |

|

Vendor Financial Services |

| 4,130 |

| 3,954 |

| 5,137 |

|

Other Commercial Finance |

| 701 |

| 683 |

| 316 |

|

Total revenues |

| $ 17,781 |

| $15,759 |

| $ 15,333 |

|

Net earnings |

| ||||||

Commercial Equipment Financing |

| $ 719 |

| $ 640 |

| $ 550 |

|

Real Estate |

| 650 |

| 528 |

| 421 |

|

Commercial Finance (CF) |

| 599 |

| 384 |

| 312 |

|

Structured Finance Group |

| 488 |

| 399 |

| 359 |

|

Aviation Services |

| 454 |

| 497 |

| 501 |

|

Vendor Financial Services |

| 369 |

| 332 |

| 327 |

|

Other Commercial Finance |

| (90 | ) | 8 |

| (54 | ) |

Total net earnings |

| $ 3,189 |

| $ 2,788 |

| $ 2,416 |

|

Charges of $85 million in 2001 were not allocated to this segment because we did not include these costs in measuring the performance of businesses in this segment for internal purposes. Such charges, included in All Other GECS, related to restructuring various global operations and to provisions for disposition of assets. | |||||||

December 31 (In millions) |

| 2002 |

| 2001 |

|

Total assets | |||||

Commercial Equipment Financing |

| $ 51,757 |

| $ 49,360 |

|

Real Estate |

| 29,522 |

| 23,132 |

|

Commercial Finance (CF) |

| 26,897 |

| 25,386 |

|

Structured Finance Group |

| 19,293 |

| 17,130 |

|

Aviation Services |

| 30,512 |

| 24,546 |

|

Vendor Financial Services |

| 25,518 |

| 21,477 |

|

Other Commercial Finance |

| 10,746 |

| 8,838 |

|

Total assets |

| $194,245 |

| $169,869 |

|

Financing receivables -- net |

| $128,277 |

| $117,540 |

|

<PAGE> 15

Commercial Finance revenues increased 13% in 2002 principally reflecting acquisitions and increased originations across substantially all businesses, partially offset by reduced market interest rates and lower securitization activity at CF and Commercial Equipment Financing. The 2001 increase of 3% resulted from acquisition and volume growth at Commercial Equipment Financing, Vendor Financial Services, Aviation Services and CF, including the acquisition of Heller Financial, Inc. in October, volume growth at Structured Finance Group and increased securitization activity partially offset by the effects of rationalization of certain operations at Vendor Financial Services. Net earnings increased 14% in 2002 and 15% in 2001. The 2002 increase in net earnings resulted from acquisitions and origination growth, productivity across all businesses and growth in lower taxed earnings from international operations, partially offset by increased credit losses and lower securitization activity at CF and Commercial Equipment Financing. The 2001 increase reflected securitization gains, asset growth from acquisitions at Commercial Equipment Financing, CF and Vendor Financial Services, origination growth at Structured Finance Group, and higher asset gains and productivity at Real Estate. Other Commercial Finance principally includes 2002 revenues of $665 million and net earnings of $122 million of the Healthcare Financial Services business that we acquired in October 2001, offset by certain costs related to our acquisition of Heller Financial, Inc.

<PAGE> 16

Consumer Finance

(In millions) |

| 2002 |

| 2001 |

| 2000 |

|

Revenues |

| ||||||

Global Consumer Finance |

| $ 6,489 |

| $5,561 |

| $5,429 |

|

Card Services |

| 3,777 |

| 3,947 |

| 3,891 |

|

Total revenues |

| $10,266 |

| $9,508 |

| $9,320 |

|

Net earnings |

| ||||||

Global Consumer Finance |

| $ 1,224 |

| $1,034 |

| $ 870 |

|

Card Services |

| 670 |

| 669 |

| 522 |

|

Other Consumer Finance | (95 | ) | (101 | ) | (97 | ) | |

Total net earnings |

| $ 1,799 |

| $1,602 |

| $1,295 |

|

Charges of $57 million in 2001 were not allocated to this segment because we did not include these costs in measuring the performance of businesses in this segment for internal purposes. Such charges, included in All Other GECS, related to unprofitable financing product lines that have been exited. | |||||||

December 31 (In millions) |

| 2002 |

| 2001 |

|

Total assets | |||||

Global Consumer Finance |

| $58,310 |

| $43,893 |

|

Card Services |

| 18,655 |

| 19,085 |

|

Total assets |

| $76,965 |

| $62,978 |

|

Financing receivables -- net |

| $63,254 |

| $47,891 |

|

Consumer Finance revenues increased 8% following a 2% increase in 2001. Revenues increased in 2002 primarily as a result of acquisitions and increased international originations, partially offset by lower securitization activity at Card Services. The revenue performance in 2001 reflected the post-acquisition revenues from acquired businesses and volume growth. Net earnings increased 12% following a 24% increase in 2001, as a result of origination growth, acquisitions, growth in lower taxed earnings from international operations and productivity benefits, partially offset by lower securitization activity at Card Services. The 2001 increase reflected productivity at Global Consumer Finance and volume growth at Card Services.

Consumer Products revenues of $8.5 billion were flat in 2002 as 5% higher Appliances revenues, reflecting success of new products, were offset by a 9% decline in Lighting revenues. Consumer Products pricing was down during the year. Operating profit decreased 24% to $0.5 billion, reflecting adverse results in Lighting, particularly from lower prices, higher base costs and higher charges resulting from customer credit issues. Consumer Products revenues of $8.4 billion in 2001 were 3% lower than in 2000 as price erosion at Appliances and Lighting offset modest market share gains at Appliances. Operating profit decreased by 26% to $0.6 billion in 2001, largely as a result of lower selling prices at Appliances and Lighting and increased program spending on new products at Appliances.

<PAGE> 17

Equipment Management

(In millions) |

| 2002 |

| 2001 |

| 2000 |

|

Revenues |

| $4,254 |

| $4,401 |

| $4,969 |

|

Net earnings |

| $ 313 |

| $ 377 |

| $ 484 |

|

Charges of $17 million in 2001 were not allocated to this segment because we did not include these costs in measuring the performance of businesses in this segment for internal purposes. Such charges, included in All Other GECS, related to the restructuring of various global operations. | |||||||

December 31 (In millions) |

| 2002 |

| 2001 |

|

Total assets |

| $25,222 |

| $24,940 |

|

Equipment leased to others |

| $ 9,416 |

| $ 9,749 |

|

Equipment Management businesses experienced business-wide declining utilization rates throughout the period, resulting in both lower revenues and lower earnings. Equipment Management realized productivity benefits in 2002, partially offsetting the utilization's effect on earnings. In 2001, Equipment Management realized tax benefits from a restructuring of the Penske joint venture, and recognized asset impairments at Transport International Pool/Modular Space and GE European Equipment Management.

Industrial Products and Systems

(In millions) |

| 2002 |

| 2001 |

| 2000 |

|

Revenues | |||||||

Industrial Systems |

| $4,968 |

| $4,440 |

| $4,469 |

|

GE Supply |

| 2,473 |

| 2,302 |

| 2,159 |

|

Total revenues |

| $7,441 |

| $6,742 |

| $6,628 |

|

Operating profit | |||||||

Industrial Systems |

| $ 488 |

| $ 527 |

| $ 596 |

|

GE Supply |

| 109 |

| 99 |

| 80 |

|

Total operating profit |

| $ 597 |

| $ 626 |

| $ 676 |

|

Industrial Products and Systems reported a 10% increase in revenues and 5% lower operating profit as volume increased and selling prices declined across the segments.

Industrial Systems revenues rose 12% compared with 2001, but operating profit declined 7%, reflecting the negative effects of lower selling prices, partially offset by the positive effects of acquisitions and productivity. Industrial Products and Systems revenues in 2001 were 2% higher than in 2000, as higher revenue at GE Supply more than offset selling price decreases across the segment and lower volume at Industrial Systems. Operating profit decreased 7% in 2001 primarily as a result of the decline in selling prices and cost inflation.

<PAGE> 18

Insurance

(In millions) |

| 2002 |

| 2001 |

| 2000 |

|

Revenues | |||||||

GE Financial Assurance |

| $ 12,317 |

| $12,826 |

| $12,888 |

|

Mortgage Insurance |

| 1,090 |

| 1,075 |

| 973 |

|

GE Global Insurance |

| ||||||

Holding (ERC) |

| 9,432 |

| 9,453 |

| 10,223 |

|

Other Insurance |

| 457 |

| 536 |

| 682 |

|

Total revenues |

| $ 23,296 |

| $23,890 |

| $24,766 |

|

Net earnings | |||||||

GE Financial Assurance |

| $ 934 |

| $ 1,088 |

| $ 1,009 |

|

Mortgage Insurance |

| 538 |

| 500 |

| 444 |

|

GE Global Insurance |

| ||||||

Holding (ERC) |

| (1,794 | ) | 78 |

| 566 |

|

Other Insurance |

| 227 |

| 213 |

| 182 |

|

Total net earnings |

| $ (95 | ) | $ 1,879 |

| $ 2,201 |

|

Charges of $306 million in 2001 were not allocated to this segment because we did not include these costs in measuring the performance of businesses in this segment for internal purposes. Such charges, included in All Other GECS, related to unprofitable insurance products and lines that have been exited and to provisions for disposition of nonstrategic investments. | |||||||

Insurance revenues decreased 2% in 2002, because of the ongoing planned run-off of acquired policies at Toho and lower realized investment gains. Segment revenues declined 4% in 2001 on reduced net premiums earned at ERC, reflecting the events of September 11, 2001, decreased investment income, and the planned run-off of restructured insurance policies at Toho. These factors were partially offset by increased premium income associated with origination volume at ERC and by post-acquisition revenues from acquired businesses and volume growth at GE Financial Assurance.

Net pre-tax realized investment gains in the equity and debt securities portfolios amounted to $413 million, $972 million and $818 million in 2002, 2001 and 2000, respectively.

Net earnings decreased $2.0 billion in 2002, following a $0.3 billion decrease in 2001. The 2002 decrease was primarily attributable to the recognition of adverse development related to prior-year loss events at ERC, discussed below. With retrocession coverages previously purchased by ERC, the recording of this adverse development both increased policyholder losses and, to a lesser extent, decreased premium revenues (principally because of higher levels of contingent ceded premiums following these reserve adjustments). Also contributing to the reduction in 2002 net earnings were lower investment gains across all businesses, including a $110 million after-tax impairment on WorldCom, Inc. bonds at GE Financial Assurance. These decreases were partially offset by core premium growth, including higher premium pricing at ERC and the $152 million benefit from recognition of a favorable tax settlement with the IRS related to the treatment of certain reserves for obligations to policyholders on life insurance contracts at GE Financial Assurance.

The level of reported claims activity at ERC related to prior-year loss events, particularly for liability-related exposures underwritten in 1997 through 2001, accelerated at a rate higher than we had anticipated. In 2002, considering the continued acceleration in reported claims activity, we concluded that our best estimate of ultimate losses was higher in the range of reasonably possible loss scenarios than previously estimated. Accordingly, we recognized a fourth quarter pre-tax charge of $2.5 billion to increase recorded reserves to reflect the revised indications of remaining liability. The more significant adverse development was in hospital medical malpractice ($300 million), product liability ($300 million), professional liability ($250 million), umbrella liability ($200 million), workers compensation ($200 million), individual liability ($150 million) and asbestos ($150 million). With amounts recognized in previous quarters of 2002, our overall 2002 pre-tax charge for adverse development amounted to $3.5 billion. Insurance loss provisions are based on the best available estimates at a given time. As described on page 41 under the caption "Insurance Liabilities and Reserves," these estimates will be adjusted in the future as required.

<PAGE> 19

We have continued our rigorous commitment to improved underwriting initiatives at ERC aimed at ensuring that consistent and diligent underwriting standards are applied to all risks. Throughout 2002, we have been disciplined in rejecting risks that either fail to meet the established standards of price or terms and conditions, or that involve areas for which sufficient historical data do not exist to evaluate the risk adequately. For risks that pass our criteria, we have sought to retain or even judiciously expand our business. On the other hand, we have curtailed or exited business in particular property and casualty business channels when expected returns do not appear to justify the risks.

Net earnings decreased $0.3 billion in 2001, reflecting underwriting results at ERC, which were partially offset by productivity benefits at GE Financial Assurance. Net earnings in 2001 at ERC were adversely affected by approximately $575 million ($386 million after tax) related to the insurance losses arising from the events of September 11, 2001. This amount primarily resulted from contingent premium payment provisions contained in certain retrocession agreements. After these particular losses, total losses exceeded retrocession policy limits in place at ERC. Substantially all of the September 11, 2001, losses are recoverable under reinsurance policies that require additional premiums to those retrocessionaires. Therefore, the 2001 Statement of Earnings reflects a $698 million reduction in net premiums earned and $78 million of increased losses, partially offset by $201 million in lower insurance acquisition costs. Historical experience related to large catastrophic events has shown that a broad range of total insurance industry loss estimates often exists following such an event, and it is not unusual for there to be significant subsequent revisions to such estimates. Our best estimate of the existing liability, net of estimated recoveries under retrocession arrangements, has not changed significantly from our initial estimate.

Excluding events of September 11, 2001, net earnings in 2001 and 2000 were also adversely affected by the continued general deterioration of underwriting results at ERC, reflecting higher property and casualty-related losses (principally as a result of adverse development relating to prior-year loss events) and the continued effects of low premiums in the property and casualty insurance/reinsurance industry. ERC underwriting results in 2001 tracked performance in the global property and casualty industry.

The majority of the adverse development at ERC in 2001, and to a lesser extent in 2000, related to higher projected ultimate losses for liability coverages, especially in the hospital liability, nonstandard automobile (automobile insurance extended to higher-risk drivers) and commercial and public entity general liability lines of business. Results in 2000 also reflected an increase in industry-wide loss estimates related to certain large property loss events, with the largest effect resulting from the European windstorms occurring in late 1999.

Our Mortgage Insurance business had favorable loss experience throughout the three years ended December 31, 2002, reflecting continued strength in certain real estate markets and the success of our loss containment initiatives.

MEDICAL SYSTEMS revenues increased 6% to $9.0 billion in 2002, on higher equipment and product services volume, partially offset by weak market conditions in Latin America and Japan. Operating profit rose 3% to $1.5 billion as productivity and increased volume were partially offset by lower pricing. Medical Systems revenues rose 16% to $8.4 billion in 2001, primarily as a result of sharply higher volume. Operating profit grew 13% to $1.5 billion in 2001, largely as a result of productivity and volume growth.

Orders received by Medical Systems in 2002 were $9.6 billion, an 8% increase over 2001. The $4.0 billion total backlog at year-end 2002 comprised unfilled product orders of $2.6 billion (of which 95% was scheduled for delivery in 2003) and product services orders of $1.4 billion scheduled for 2003 delivery. Comparable December 31, 2001, total backlog was $4.1 billion.

<PAGE> 20

NBC reported record revenues of $7.1 billion in 2002, a 24% increase compared with 2001, and operating profit of $1.7 billion, up 18%. Primary factors contributing to this performance included our improved performance in the advertising market, our broadcast of the 2002 Winter Olympics and contributions from the Telemundo acquisition. NBC's 2002 results also included $0.2 billion of the $0.6 billion total gain from the exchange of certain assets for the cable network Bravo and $0.2 billion of other charges for various asset impairments. Revenues declined 15% in 2001, mostly from an industry-wide decline in advertising volume and pricing, as well as lost revenue related to covering the events of September 11, 2001. Operating profit decreased 12% in 2001, reflecting adverse advertising market conditions, the events of September 11, 2001, and charges resulting from dissolving the XFL, which more than offset savings from cost reduction actions.

PLASTICS revenues of $5.2 billion in 2002 were relatively unchanged from 2001 levels, as continued weakness in pricing offset increased volume. Operating profit at Plastics declined 28% to $0.8 billion as productivity and increased volume were not sufficient to offset substantially lower selling prices and increased raw material costs. In 2001, Plastics revenues were 13% lower than the prior year, reflecting increased pricing pressures and lower volume. Plastics experienced continued softness in the automotive, optical media, telecommunications and business equipment markets. Operating profit in 2001 was 23% lower than in 2000, primarily as a result of lower pricing and volume, which more than offset base cost reductions.

POWER SYSTEMS revenues increased 13% to $22.9 billion in 2002, following an increase of 36% in 2001. Operating profit rose 29% to $6.3 billion in 2002, following a 93% increase in 2001. Operating profit improvements at Power Systems reflect the $0.9 billion positive effect of customer contract termination fees, net of associated costs. Results in 2002 also include restructuring and other charges of $0.2 billion as Power Systems adjusted its cost structure.

These results reflected the changing conditions in the power generation business as demand for new power generation equipment declined in 2002 and orders were delayed or cancelled. When orders are cancelled, contractual terms require customers to pay termination fees. In all cases, we expect such fees to cover our investment in the contracts. At least a portion of this investment has generally been received as progress collections. We also expect to recover at least part of lost profits.

Power Systems orders were $14.2 billion in 2002, compared with $24.5 billion in 2001, reflecting the sharp decline in demand for new power generation equipment in the United States. The $16.7 billion total backlog at year-end 2002 comprised unfilled product orders of $13.1 billion (of which 73% was scheduled for delivery in 2003) and product services orders of $3.6 billion scheduled for 2003 delivery. Comparable December 31, 2001, total backlog was $28.9 billion. As a result of current market conditions, we are in discussions with certain customers regarding their equipment requirements. These discussions may result in changes to contractual agreements, including delays or cancellations, and may also result in further termination fees.

SPECIALTY MATERIALSrevenues increased 32% to $2.4 billion in 2002, reflecting the contributions of recent acquisitions, partially offset by lower selling prices. Operating profit at Specialty Materials rose 6% to $0.3 billion, reflecting higher acquisition volume and lower material costs, partially offset by lower pricing and higher base costs. In 2001, Specialty Materials revenues of $1.8 billion were 9% lower than 2000 reflecting lower sales in the semiconductor market.

TRANSPORTATION SYSTEMS revenues of $2.3 billion were 2% lower and operating profit of $0.4 billion was about the same as in 2001, as product services revenues, strong variable cost productivity and lower materials costs offset the effects of lower volume and pricing pressures.

<PAGE> 21

Transportation Systems received orders of $2.8 billion in 2002, compared with $2.6 billion in 2001. The $2.1 billion total backlog at year-end 2002 comprised unfilled product orders of $1.6 billion (of which 53% was scheduled for delivery in 2003) and product services orders of $0.6 billion scheduled for 2003 delivery. Comparable December 31, 2001, total backlog was $1.7 billion.

All Other GECS

(In millions) |

| 2002 |

| 2001 |

| 2000 |

|

Revenues | |||||||

IT Solutions |

| $ 1,992 |

| $ 2,301 |

| $ 3,721 |

|

GE Equity |

| (384 | ) | (126 | ) | 1,079 |

|

Americom gain |

| -- |

| 1,158 |

| -- |

|

Americom |

| -- |

| 540 |

| 594 |

|

Asset impairments |

| -- |

| (383 | ) | (238 | ) |

Product line exits |

| -- |

| (53 | ) | -- |

|

PaineWebber gain |

| -- |

| -- |

| 1,366 |

|

Wards |

| -- |

| -- |

| 3,234 |

|

Other -- All Other GECS |

| 982 |

| 1,358 |

| 2,033 |

|

Total revenues |

| $ 2,590 |

| $ 4,795 |

| $ 11,789 |

|

Net earnings | |||||||

IT Solutions |

| $ (46 | ) | $ 13 |

| $ (243 | ) |

GE Equity |

| (375 | ) | (264 | ) | 532 |

|

Americom gain |

| -- |

| 642 |

| -- |

|

Americom |

| -- |

| 259 |

| 202 |

|

Asset impairments |

| -- |

| (310 | ) | (49 | ) |

Product line exits |

| -- |

| (180 | ) | -- |

|

Restructuring |

| -- |

| (144 | ) | (298 | ) |

PaineWebber gain |

| -- |

| -- |

| 848 |

|

Wards |

| -- |

| (22 | ) | (782 | ) |

Other -- All Other GECS |

| (159 | ) | (502 | ) | (794 | ) |

Total net earnings |

| $ (580 | ) | $ (508 | ) | $ (584 | ) |

All Other GECS includes GECS activities and businesses that we do not measure within one of the other financial services segments.

In addition to comments on All Other GECS elsewhere in this report, the following comments relate to the table above:

IT Solutions (ITS) -- Revenues and net earnings in 2002 decreased primarily as a result of market conditions and 2001 product line and geographic market exits. During 2001 and 2000, in response to intense competition and transition of the computer equipment market to a direct distribution model, ITS exited its underperforming operations in the United Kingdom, France, Brazil and Mexico and significantly reduced its reseller role in the United States. Costs for involuntary termination benefits, asset impairments, facilities exit costs and losses on sales of portions of the business amounted to $45 million ($43 million after tax) and $246 million ($191 million after tax) in 2001 and 2000, respectively, and are included in restructuring in the table above. The number of employees was reduced from a 2000 peak of 10,000 to 6,000 at the end of 2002.

GE Equity -- GE Equity manages equity investments in early-stage, early growth, pre-IPO companies. GE Equity revenues include income, gains and losses on such investments. Revenues and net earnings during 2002 reflected increased losses on investments, including losses in the telecommunications and software industries, and lower gains. Effective in the fourth quarter of 2002, GE Equity will no longer make new investments in private companies. GE Equity will continue to give financial support to companies within its existing portfolio. The existing portfolio will be managed for maximum value over time, eventually winding down. During 2001, losses on GE Equity's investments exceeded gains and other investment income, resulting in negative revenues and a $264 million net loss, which increased over the prior year principally from reduced asset gains.

<PAGE> 22

Americom -- On November 9, 2001, GECS exchanged its satellite operations, comprising the stock of Americom and other related assets and liabilities, for a combination of cash and 31% of the publicly-traded stock of SES Global, a leading satellite company, in order to create the world's largest satellite services provider. The transaction resulted in a gain of $1,158 million ($642 million after tax), representing the difference between the carrying value of the 69% investment in Americom and the amount of cash plus the market value of SES Global shares received at the closing date. No gain was recorded on the 31% interest in Americom that was indirectly retained by GECS. GECS investment in SES Global is accounted for on the equity method in Commercial Finance.

2001 Asset impairments and product line exits -- Operations included $656 million of after-tax charges related to disposing of and providing for disposition of several nonstrategic investments and other assets, to certain unprofitable insurance and financing product lines that were exited, and to restructuring various global operations. These costs, not allocated to the related businesses as we did not include these costs in measuring the performance of those businesses for internal purposes, included $478 million ($310 million after tax) for other-than-temporary impairments of investments, the largest of which were held by GE Financial Assurance, GE Equity and ERC. These losses, $383 million of which were charged to revenues, included $130 million ($84 million after tax) of losses on Enron bonds; such bonds were written down to a cost basis of $32 million at December 31, 2001. Such losses also included investment impairment charges of $199 million ($130 million after tax) on non-U.S. mutual funds and the technology sector.

In response to escalating losses, GECS in 2001 decided to cease further underwriting and exit certain insurance and financing product lines. Charges associated with such loss events and the resulting exits totaled $180 million after tax, of which $149 million related to the loss events in ERC product lines, primarily nonstandard automobile and higher limit industrial property insurance coverages.

Restructuring of several GECS global businesses included consolidation of several European Equipment Management businesses and rationalization of European Equipment Finance businesses. Costs related to the exit of these activities amounted to $144 million after tax and consisted of involuntary termination benefits, facilities exit costs, and asset impairments.

Other -- All Other GECS includes GECS corporate function expenses, liquidating businesses and other non-segment aligned operations, the most significant of which were Auto Financial Services (AFS) and GE Auto and Home. The decrease in revenues in 2002 and 2001 resulted from AFS, which stopped accepting new business in 2000. Net earnings increased in 2002 primarily because of a favorable tax settlement with the IRS allowing the deduction of previously realized losses associated with the prior disposition of Kidder Peabody and tax benefits from growth in lower taxed earnings from international operations.

<PAGE> 23

SUMMARY OF OPERATING SEGMENTS

General Electric Company and consolidated affiliates | ||||||

For the years ended December 31 (In millions) | 2002 | 2001 | 2000 | 1999 | 1998(c) | |

REVENUES | ||||||

| Aircraft Engines | $11,141 | $11,389 | $10,779 | $10,730 | $10,294 |

| Commercial Finance | 17,781 | 15,759 | 15,333 | 12,302 | 8,072 |

| Consumer Finance | 10,266 | 9,508 | 9,320 | 7,562 | 6,750 |

| Consumer Products | 8,456 | 8,435 | 8,717 | 8,525 | 8,520 |

| Equipment Management | 4,254 | 4,401 | 4,969 | 4,789 | 4,234 |

| Industrial Products and Systems | 7,441 | 6,742 | 6,628 | 6,284 | 6,149 |

| Insurance | 23,296 | 23,890 | 24,766 | 19,433 | 16,841 |

| Medical Systems | 8,955 | 8,409 | 7,275 | 6,171 | 4,624 |

| NBC | 7,149 | 5,769 | 6,797 | 5,790 | 5,269 |

Plastics | 5,245 | 5,252 | 6,013 | 5,315 | 5,201 | |

| Power Systems | 22,926 | 20,211 | 14,861 | 10,099 | 8,500 |

| Specialty Materials | 2,406 | 1,817 | 2,007 | 1,803 | 1,595 |

Transportation Systems | 2,314 | 2,355 | 2,263 | 2,358 | 2,156 | |

| All Other GECS | 2,590 | 4,795 | 11,789 | 11,663 | 12,797 |

| Corporate items and eliminations | (2,522) | (2,819) | (1,664) | (1,194) | (533) |

CONSOLIDATED REVENUES | $131,698 | $125,913 | $129,853 | $111,630 | $100,469 | |

SEGMENT PROFIT (See description below) | ||||||

| Aircraft Engines | $2,060 | $2,147 | $2,000 | $1,739 | $1,478 |

| Commercial Finance (a) | 3,189 | 2,788 | 2,416 | 1,834 | 1,492 |

| Consumer Finance (a) | 1,799 | 1,602 | 1,295 | 848 | 631 |

| Consumer Products | 495 | 648 | 879 | 971 | 1,103 |

| Equipment Management (a) | 313 | 377 | 484 | 416 | 476 |

| Industrial Products and Systems | 597 | 626 | 676 | 611 | 497 |

| Insurance (a) | (95) | 1,879 | 2,201 | 2,142 | 1,459 |

| Medical Systems | 1,546 | 1,498 | 1,321 | 1,107 | 844 |

| NBC | 1,658 | 1,408 | 1,609 | 1,427 | 1,225 |

Plastics | 843 | 1,166 | 1,518 | 1,297 | 1,283 | |

| Power Systems | 6,255 | 4,860 | 2,523 | 1,537 | 1,118 |

| Specialty Materials | 282 | 267 | 347 | 293 | 253 |

Transportation Systems | 402 | 400 | 436 | 437 | 377 | |

| All Other GECS (a) | (580) | (508) | (584) | (285) | 146 |

| Total segment profit | 18,764 | 19,158 | 17,121 | 14,374 | 12,382 |

GECS goodwill amortization | -- | (552) | (620) | (512) | (408) | |

GE corporate items and eliminations (b) | 775 | 532 | 844 | 872 | 1,022 | |

GE interest and other financial charges | (569) | (817) | (811) | (810) | (883) | |

GE provision for income taxes | (3,837) | (4,193) | (3,799) | (3,207) | (2,817) | |

Earnings before accounting changes | 15,133 | 14,128 | 12,735 | 10,717 | 9,296 | |

Cumulative effect of accounting changes | (1,015) | (444) | -- | -- | -- | |

CONSOLIDATED NET EARNINGS | $14,118 | $13,684 | $12,735 | $10,717 | $9,296 | |

(a) Segment profit measured as net earnings. (b) Corporate items include the effect of pension and other benefit plans that are not allocated to segment results as well as income, principally from licensing activities, of $97 million, $88 million, $79 million, $62 million and $271 million in 2002, 2001, 2000, 1999 and 1998, respectively. In 2002, corporate items include $341 million of the total gain of $571 million resulting from NBC's exchange of certain assets for the cable network Bravo and a $488 million gain from the sale of 90% of Global eXchange Services. Also included in 2002 are $175 million of the total restructuring and other charges of $556 million, which related to segment activities as follows: Aircraft Engines -- $55 million, Industrial Products and Systems -- $30 million, Medical Systems -- $30 million, Plastics -- $51 million, and other -- $9 million. In 1999, corporate items include $176 million of the total restructuring and other charges of $265 million, which related to segment activities as follows: Aircraft Engines -- $42 million, Consumer Products -- $80 million, Medical Systems -- $34 million and other -- $20 million. (c) 1998 revenues and segment profit for Commercial Finance, Consumer Finance, Equipment Management, Insurance and All Other GECS have not been recast to reflect the debt leverage ratios and financial services' organizational changes that became effective January 1, 2003. | ||||||

<PAGE> 24

SEGMENT PROFIT is defined in this paragraph. The notes to consolidated financial statements on pages 49-111 are an integral part of this statement. Segment profit excludes goodwill amortization, the effects of pensions and other retiree benefit plans and accounting changes. The segment profit measure for GE industrial businesses -- Aircraft Engines, Consumer Products, Industrial Products and Systems, Medical Systems, NBC, Plastics, Power Systems, Specialty Materials and Transportation Systems -- is operating profit (earnings before interest and other financial charges, income taxes and accounting changes). The segment profit measure for Commercial Finance, Consumer Finance, Equipment Management, Insurance and All Other GECS is after-tax earnings before accounting changes, reflecting the importance of financing and tax considerations to their operating activities.

JANUARY 1, 2003, RECLASSIFICATION OF FINANCIAL SERVICES SEGMENT PROFIT. GE Capital historically has issued about $8 of debt for each $1 of equity -- a "leverage ratio" of 8:1. For purposes of measuring segment profit, each of our financial services businesses was also assigned debt and interest costs on the basis of that consolidated 8:1 leverage ratio. In evaluating expected returns on potential investments, however, we also used business-specific, market-based leverage ratios. As of January 1, 2003, we extended the business-specific, market-based leverage to the performance measurement of each of our financial services businesses, and consequently to the definition of segment profit. As a result, at January 1, 2003, debt of $12.5 billion previously allocated to the segments was allocated to the All Other GECS segment. At the same time, we revised our historical techniques for allocating shared costs and unusual items to financial services businesses. The results of our financial services segments had previously been presented on the historic 8:1 leverage ratio basis. Beginning in 2003, the new leverage ratios and recast comparative historical results will be as follows:

(Dollars in millions) |

| 2002 |

| 2001 |

| 2000 |

| 1999 |

|

COMMERCIAL FINANCE | |||||||||

Leverage ratio |

| 7.4:1 |

| 7.5:1 |

| 7.4:1 |

| 7.5:1 |

|

Adjusted net earnings |

| $ 3,189 |

| $ 2,788 |

| $ 2,416 |

| $ 1,834 |

|

| |||||||||

CONSUMER FINANCE | |||||||||

Leverage ratio |

| 12.4:1 |

| 12.3:1 |

| 12.3:1 |

| 12.4:1 |

|

Adjusted net earnings |

| $ 1,799 |

| $ 1,602 |

| $ 1,295 |

| $ 848 |

|

| |||||||||

EQUIPMENT MANAGEMENT | |||||||||

Leverage ratio |

| 5.0:1 |

| 5.1:1 |

| 5.1:1 |

| 4.9:1 |

|

Adjusted net earnings |

| $ 313 |

| $ 377 |

| $ 484 |

| $ 416 |

|

| |||||||||

INSURANCE | |||||||||

Leverage ratio |

| 0.4:1 |

| 0.4:1 |

| 0.4:1 |

| 0.4:1 |

|

Adjusted net earnings |

| $ (95 | ) | $ 1,879 |

| $ 2,201 |

| $ 2,142 |

|

| |||||||||

ALL OTHER GECS | |||||||||

Adjusted net earnings |

| $ (580 | ) | $ (508 | ) | $ (584 | ) | $ (285 | ) |

<PAGE> 25

International Operations

Estimated results of international activities include the results of our operations located outside the United States plus all U.S. exports. We classify certain GECS operations that cannot meaningfully be associated with specific geographic areas as “Other international” for this purpose.

International revenues of $52.9 billion, $51.4 billion and $53.0 billion in 2002, 2001 and 2000, respectively, represented about 40% of consolidated revenues in each year.

Consolidated international revenues

| (In millions) | 2002 | 2001 | 2000 | ||||

| Europe | $24,301 | $23,878 | $24,144 | ||||

| Pacific Basin | 12,026 | 11,447 | 12,921 | ||||

| Americas | 5,165 | 5,507 | 5,912 | ||||

| Other international | 3,911 | 3,456 | 2,842 | ||||

| 45,403 | 44,288 | 45,819 | |||||

| Exports from the U.S. to external customers | 7,481 | 7,149 | 7,138 | ||||

| $52,884 | $51,437 | $52,957 | |||||

GE international revenues were $29.0 billion, $28.3 billion and $26.7 billion in 2002, 2001 and 2000, respectively. GE international revenues of $29.0 billion in 2002 were $0.7 billion higher than in 2001. Revenues in 2001 of $28.3 billion increased $1.6 billion over 2000. The increase in 2002 related to both an increase in operations outside the U.S. and higher U.S. exports. Revenue increases in Europe were led by Medical Systems and Industrial Systems. Growth in Specialty Materials revenues across all geographic areas was partially offset by lower sales in all areas by Aircraft Engines. Increases in U.S. export sales in 2002 were primarily in Plastics and Power Systems, partially offset by lower exports by Medical Systems and Transportation Systems.

| 2002 CONSOLIDATED INTERNATIONAL REVENUES BY REGION (INCLUDING EXPORTS FROM THE U.S.)

|

GECS international revenues were $23.9 billion in 2002, an increase of 3% from $23.1 billion in 2001. GECS revenues in the Pacific Basin increased 9% in 2002, as a result of acquisitions and origination growth, primarily at Consumer Finance and Commercial Finance. Revenues in “Other international” increased 11% in 2002, primarily as a result of origination growth at Aviation Services. Revenues in Europe decreased 2% as a result of lower investment gains and adjustments to estimates of prior year loss events at Insurance, the 2001 divestiture of Americom, and market conditions and geographic market exits at IT Solutions, partially offset by acquisitions at Consumer Finance and Commercial Finance.

<PAGE> 26

Consolidated international operating profit was $6.5 billion in 2002, an increase of 7% over 2001, which was 11% lower than in 2000. Operating profit rose 24% to $1.2 billion in the Americas and 28% to $0.9 billion in “Other international” and was relatively unchanged in Europe ($2.1 billion) and the Pacific Basin ($2.3 billion).

Total assets of international operations were $229.0 billion in 2002 (40% of consolidated assets), an increase of $49.0 billion, or 27%, over 2001. GECS international assets grew 28% from $161.6 billion at year-end 2001 to $207.5 billion at the end of 2002. GECS assets increased 41% and 26% in the Pacific Basin and Europe, respectively, resulting from acquisitions and origination growth.

Our international activities span all global regions and primarily encompass manufacturing for local and export markets, import and sale of products produced in other regions, leasing of aircraft, sourcing for our plants domiciled in other global regions and provision of financial services within these regional economies. Thus, when countries or regions experience currency and/or economic stress, we may have increased exposure to certain risks, but also may have new profit opportunities. Potential increased risks include, among other things, higher receivables delinquencies and bad debts, delays or cancellation of sales and orders principally related to power and aircraft equipment, higher local currency financing costs and a slowdown in established financial services activities. New profit opportunities include, among other things, lower costs of goods sourced from countries with weakened currencies, more opportunities for lower cost outsourcing, expansion of industrial and financial services activities through purchases of companies or assets at reduced prices and lower U.S. debt financing costs.

| 2002 TOTAL ASSETS OF INTERNATIONAL OPERATIONS

|

Financial results of our international activities reported in U.S. dollars are affected by currency exchange. We use a number of techniques to manage the effects of currency exchange, including selective borrowings in local currencies and selective hedging of significant cross-currency transactions. Principal currencies are the euro, the Japanese yen and the Canadian dollar.

<PAGE> 27

Environmental Matters

Our operations, like operations of other companies engaged in similar businesses, involve the use, disposal and cleanup of substances regulated under environmental protection laws.