UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811- 01494

General Electric RSP U.S. Equity Fund

(Exact name of registrant as specified in charter)

1600 Summer Street

Stamford, Connecticut 06905

(Address of principal executive offices)(Zip code)

GE Asset Management, Inc.

1600 Summer Street

Stamford, Connecticut 06905

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: 800-242-0134

Date of fiscal year end: 12/31

Date of reporting period: 12/31/15

| Item 1. | Reports to Stockholders |

GE RSP Funds

U.S. Equity Fund

Income Fund

Annual Report

December 31, 2015

The information provided on the performance pages relates to the GE RSP U.S. Equity Fund and GE RSP Income Fund (each a “Fund” and collectively the “Funds”).

Total returns take into account changes in share price and assume reinvestment of dividends and capital gains distributions, if any. Total returns shown are net of Fund expenses.

The performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Periods less than one year are not annualized. Please call toll-free (800) 242-0134 or visit the Funds’ website at http://www.geam.com for the most recent month-end performance data.

An investment in a Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. An investment in a Fund is subject to risk, including possible loss of principal invested.

The Standard & Poor’s (“S&P”) 500® Composite Price Index of stocks (“S&P 500 Index”) is an unmanaged, market capitalization-weighted index of stocks of 500 large U.S. companies, which is widely used as a measure of large-cap stock market performance.

The Barclays U.S. Aggregate Bond Index is an unmanaged market value-weighted index of taxable investment grade debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of one year or more. This index is designed to represent the performance of the U.S. investment-grade first rate bond market.

The results shown for the foregoing indices assume the reinvestment of net dividends or interest and do not reflect fees, expenses, or taxes. As such, index returns do not reflect the actual cost of investing in the instruments that comprise an index.

The peer universe of underlying funds used for the peer group average annual total return calculation is based on a blend of Morningstar peer categories, as shown.

Morningstar is an independent mutual fund rating service. A Fund’s performance may be compared to or ranked within a universe of mutual funds with investment objectives and policies similar but not necessarily identical to that of the Fund.

©2016 Morningstar, Inc. All Rights Reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damage or losses relating from any use of this information. Past performance is no guarantee of future results.

The views expressed in this document reflect our judgment as of the publication date and are subject to change at any time without notice.

1

(Unaudited)

David B. Carlson

Chief Investment Officer — U.S. Equities

Stephen V. Gelhaus

Senior Vice President

Paul C. Reinhardt

Senior Vice President

The GE RSP U.S. Equity Fund is managed by a team of portfolio managers that includes David B. Carlson, Stephen V. Gelhaus, and Paul C. Reinhardt. Each of the foregoing portfolio managers manages one of three sub-portfolios, which comprise the Fund. A sub-portfolio refers to the portion of the Fund’s assets that are allocated to, and managed by, a particular portfolio manager on the Fund’s portfolio management team. The three sub-portfolios are managed independently of each other and the portfolio managers have full discretion over their sub-portfolio. However, as lead portfolio manager for the Fund, Mr. Carlson is vested with the authority to adjust the allocation of assets to each sub-portfolio.

David B. Carlson is Chief Investment Officer — U.S. Equities at GE Asset Management (GEAM). He manages the overall U.S. equity investments for GEAM. Mr. Carlson has served as a portfolio manager for the GE RSP U.S. Equity Fund since May 2011. Mr. Carlson joined GEAM in 1982 as a securities analyst for investment operations. He became a Vice President for Mutual Fund Portfolios in 1987, a Senior Vice President in 1989 and an Executive Vice President in 2003.

Stephen V. Gelhaus is a Senior Vice President of GEAM. He has served as a portfolio manager for the GE RSP U.S. Equity Fund since January 2002. Mr. Gelhaus joined GEAM in June 1991 and was a research analyst in the U.S. Equities group from 1995 through 2001.

Paul C. Reinhardt is a Senior Vice President of GEAM. He has served as a portfolio manager for the GE RSP U.S. Equity Fund since January 2001. Mr. Reinhardt joined GEAM in 1982 as an equity analyst and has been a portfolio manager since 1987.

| Q. | How did the GE RSP U.S. Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended December 31, 2015? |

| A. | For the twelve-month period ended December 31, 2015, the Fund returned -2.05%. The S&P 500® Index (S&P 500 Index), the Fund’s benchmark, returned 1.38% and the Fund’s Morningstar peer group of 1,650 U.S. Large Blend Funds returned an average of -1.46% over the same period. |

| Q. | What market factors affected the Fund’s performance? |

| A. | From a price perspective, the flat performance of the S&P 500 Index belied tremendous volatility in sectors of the economy and markets around the globe. Several macro themes have driven the market, including the strengthening U.S. dollar, low interest rates and falling energy prices. Energy dropped 21% — the worst performing S&P 500 Index sector. Growth concerns stemming from China and the emerging markets exacerbated commodity weakness, creating headwinds for materials and industrial companies, while a strong dollar pressured many multi-nationals. In the past year the growth style of investing has significantly outperformed value, in part because of relative strength in some of the higher-priced momentum driven Internet and technology stocks. The Fund underperformed the S&P 500 Index due in part due to its valuation-conscious discipline in each of the underlying portfolios in this multi-manager Fund. It also seems that a portfolio’s positioning in what have been dubbed the “FANG” stocks mattered (i.e., Facebook, Amazon, Netflix and Google). |

| Q. | What were the primary drivers behind Fund performance? |

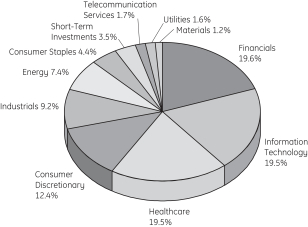

| A. | The Fund’s sector allocation effect was positive, bolstered by overweights in consumer discretionary and health care; two of the period’s strongest performing S&P 500 sectors. In these sectors, Amazon (+118%), Boston Scientific (+42%), Actavis (+23%), and Lowe’s (+14%) contributed most positively to portfolio returns. Underweighting the struggling energy and materials sectors was another positive factor. Underperformance for the Fund, therefore, was driven mostly by positioning for higher interest rates and individual stock selections within sectors. |

| | Stock selection among technology companies was a key driver of Fund |

2

(Unaudited)

| | performance relative to the S&P 500 Index. Western Digital (-35%) paid dearly for its SanDisk acquisition and we reduced the position. Qualcomm (-29%) suffered unexpected market share losses and we trimmed the holding to reflect changing market dynamics. Baidu (-17%) weighed on returns as it invested in new businesses to bolster its leading on-line presence in China. We believed Baidu’s margin compression would be short-lived and added to the position on weakness (in fact, it was performing better in the last quarter of 2015). Other lagging older-line tech names included Hewlett Packard (-32% and reduced) and EMC (-12% and eliminated). Fed tightening expectations got pushed out over the course of the year, and our tilt towards higher rates was not rewarded in this scenario. The Fund was underweight in the high yielding REITs, and over weighted interest-rate and market sensitive financials holdings (e.g., Ameriprise -15% Invesco -13%, and State Street -10%). American Express (-16%) underperformed as profit outlook dimmed, losing key customers (we eliminated the name). As oil prices pulled back, commodity-sensitive companies like Cenovus (-36%), Hess (-31%), Archer Daniels Midland (-26%), Monsanto (-14%) and Schlumberger (-14%) underperformed. |

| Q. | Were there any significant changes in the Fund during the period? |

| A. | The Fund ended the year with 94 equity holdings, exactly flat with the beginning of 2015. There were no changes in terms of the process; however we took advantage of market swings to upgrade certain holdings. For example, media was a challenging place to invest this year, as investors grew concerned about cord-cutting and the demise of traditional media. We eliminated Discovery — a content provider caught in the cross hairs of this debate — and added SiriusXM, a satellite radio broadcaster immune to cord-cutting fears. We eliminated EMC in technology, for example, as fears of slowing growth in traditional enterprise storage impaired its growth rate. We added to Google and initiated a new position in VMWare, with more exposure to Cloud data storage. In industrials we added to more domestically-oriented industries including defense/aerospace, professional services, and the airlines which |

| | benefitted from falling oil prices. We switched from Dover to United Rentals to reduce energy end-market exposure in the industrial sector. |

| | At year-end, the Fund’s largest sector overweights were in health care and financials. Consumer discretionary went from a key overweight to an underweight, due to eliminations of some auto-related companies (BorgWarner and AutoZone), selected retailers (Target and Dick’s Sporting Goods) and Discovery in media. Despite any changes in positioning, the Fund maintained its bottom-up stock selection approach with a focus on the long-term investment horizon. We believe the Fund is well-positioned to add value through active stock selection going into the next year. |

3

(Unaudited)

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in shares of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended December 31, 2015.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given under the heading “Expenses paid during

the period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs, such as sales charges or redemption fees, if any. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

July 1, 2015 – December 31, 2015

| | | | | | | | | | | | |

| | | Account value at

the beginning of

the period ($) | | | Account value

at the end of

the period ($) | | | Expenses

paid during

the period ($)* | |

Actual Fund Return | | | 1,000.00 | | | | 967.00 | | | | 0.84 | |

Hypothetical 5% Return

(2.5% for the period) | | | 1,000.00 | | | | 1,024.35 | | | | 0.87 | |

| * | | Expenses are equal to the Fund’s annualized net expense ratio of 0.17%** (for the period July 1, 2015 – December 31, 2015), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| ** | | May differ from expense ratio disclosed in the financial highlights, which is calculated based on the entire fiscal year’s data. |

4

(Unaudited)

A mutual fund designed for investors who seek long-term growth of capital and income. The Fund seeks to achieve its investment objectives by investing at least 80% of its net assets under normal circumstances in equity securities of U.S. companies, such as common and preferred stocks.

(as a % of Fair Value of Investments of $4,935,053 (in thousands) on December 31, 2015) (a)

| | | | |

Allergan PLC | | | 3.33% | |

JPMorgan Chase & Co. | | | 2.82% | |

Comcast Corp., Class A | | | 2.74% | |

Amgen Inc. | | | 2.72% | |

Apple Inc. | | | 2.40% | |

Johnson & Johnson | | | 2.16% | |

Exxon Mobil Corp. | | | 2.14% | |

Cisco Systems Inc. | | | 2.10% | |

Medtronic PLC | | | 2.03% | |

PepsiCo Inc. | | | 1.99% | |

Portfolio composition as a % of Fair Value of Investments of $4,935,053 (in thousands) on December 31, 2015 (a)

|

| Morningstar Performance Comparison |

Based on average annual returns for periods ended December 31, 2015

| | | | | | | | | | | | |

| | | One

Year | | | Five

Year | | | Ten

Year | |

Number of funds in peer group | | | 1,650 | | | | 1,420 | | | | 1,228 | |

Peer group average annual total return | | | -1.46 | % | | | 10.16 | % | | | 5.95 | % |

Morningstar Category in peer group: U.S. Large Growth | |

|

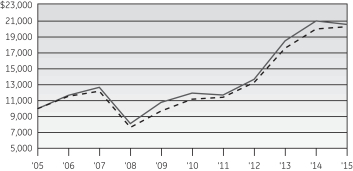

| Change in Value of a $10,000 Investment |

|

| Average Annual Total Return |

For the periods ended December 31, 2015

| | | | | | | | | | | | | | | | | | | | |

| | | One

Year | | Five

Year | | Ten

Year | | Ending value of a

$10,000

investment |

GE RSP U.S. Equity Fund | | | | -2.05% | | | | | 11.37% | | | | | 7.45% | | | | | $20,522 | |

S&P 500 Index | | | | 1.38% | | | | | 12.57% | | | | | 7.31% | | | | | $20,242 | |

| (a) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and does not reflect the fees or charges that would be associated with variable contracts through which shares of the Fund are offered.

5

| | |

GE RSP U.S. Equity Fund | | December 31, 2015 |

| | | | | | | | | | |

| | | Number

of Shares | | | Fair

Value | | | |

Common Stock — 96.4%† |

|

Aerospace & Defense — 4.2% |

| | | |

General Dynamics Corp. | | | 284,343 | | | $ | 39,057,354 | | | |

Hexcel Corp. | | | 784,035 | | | | 36,418,426 | | | |

Honeywell International Inc. | | | 797,991 | | | | 82,647,928 | | | |

The Boeing Co. | | | 165,170 | | | | 23,881,930 | | | |

United Technologies Corp. | | | 250,495 | | | | 24,065,055 | | | |

| | | | | | | 206,070,693 | | | |

|

Agricultural Products — 0.8% |

| | | |

Archer-Daniels-Midland Co. | | | 1,091,523 | | | | 40,037,064 | | | |

|

Air Freight & Logistics — 0.3% |

| | | |

United Parcel Service Inc., Class B | | | 167,261 | | | | 16,095,526 | | | |

|

Airlines — 1.0% |

| | | |

Delta Air Lines Inc. | | | 1,003,565 | | | | 50,870,710 | | | |

|

Application Software — 0.7% |

| | | |

Intuit Inc. | | | 376,337 | | | | 36,316,520 | | | |

|

Asset Management & Custody Banks — 4.0% |

| | | |

Ameriprise Financial Inc. | | | 533,144 | | | | 56,737,185 | | | |

Invesco Ltd. | | | 2,108,356 | | | | 70,587,759 | | | |

State Street Corp. | | | 1,041,198 | | | | 69,093,899 | | | (e) |

| | | | | | | 196,418,843 | | | |

|

Auto Parts & Equipment — 0.7% |

| | | |

Delphi Automotive PLC | | | 382,609 | | | | 32,801,070 | | | |

|

Automobile Manufacturers — 0.6% |

| | | |

Ford Motor Co. | | | 2,090,760 | | | | 29,458,808 | | | |

|

Automotive Retail — 0.2% |

| | | |

Advance Auto Parts Inc. | | | 62,723 | | | | 9,440,439 | | | |

|

Biotechnology — 5.3% |

| | | |

Alexion Pharmaceuticals Inc. | | | 234,165 | | | | 44,666,974 | | | (a) |

Amgen Inc. | | | 825,850 | | | | 134,060,231 | | | |

Gilead Sciences Inc. | | | 829,265 | | | | 83,913,325 | | | |

| | | | | | | 262,640,530 | | | |

|

Broadcasting — 0.3% |

| | | |

CBS Corp., Class B | | | 271,799 | | | | 12,809,887 | | | |

|

Cable & Satellite — 4.3% |

| | | |

Comcast Corp., Class A | | | 2,395,467 | | | | 135,176,203 | | | |

Liberty Global PLC, Class C | | | 1,317,179 | | | | 53,701,388 | | | (a) |

Sirius XM Holdings Inc. | | | 5,435,976 | | | | 22,124,422 | | | (a) |

| | | | | | | 211,002,013 | | | |

| | | | | | | | | | |

| | | Number

of Shares | | | Fair

Value | | | |

|

Casinos & Gaming — 0.3% |

| | | |

Las Vegas Sands Corp. | | | 347,066 | | | $ | 15,215,373 | | | |

|

Communications Equipment — 3.7% |

| | | |

Cisco Systems Inc. | | | 3,815,637 | | | | 103,613,623 | | | |

QUALCOMM Inc. | | | 1,545,665 | | | | 77,260,065 | | | |

| | | | | | | 180,873,688 | | | |

|

Consumer Finance — 1.3% |

| | | |

Discover Financial Services | | | 1,244,002 | | | | 66,703,387 | | | |

|

Data Processing & Outsourced Services — 2.0% |

| | | |

PayPal Holdings Inc. | | | 752,674 | | | | 27,246,799 | | | (a) |

Visa Inc., Class A | | | 919,934 | | | | 71,340,881 | | | |

| | | | | | | 98,587,680 | | | |

|

Diversified Banks — 6.9% |

| | | |

Bank of America Corp. | | | 5,546,264 | | | | 93,343,623 | | | |

Citigroup Inc. | | | 250,891 | | | | 12,983,609 | | | |

JPMorgan Chase & Co. | | | 2,107,207 | | | | 139,138,878 | | | |

Wells Fargo & Co. | | | 1,756,238 | | | | 95,469,098 | | | |

| | | | | | | 340,935,208 | | | |

|

Diversified Chemicals — 0.1% |

| | | |

The Dow Chemical Co. | | | 146,353 | | | | 7,534,252 | | | |

|

Drug Retail — 0.2% |

| | | |

CVS Health Corp. | | | 104,538 | | | | 10,220,680 | | | |

|

Electric Utilities — 0.7% |

| | | |

NextEra Energy Inc. | | | 319,120 | | | | 33,153,377 | | | |

|

Fertilizers & Agricultural Chemicals — 0.9% |

| | | |

Monsanto Co. | | | 439,060 | | | | 43,256,191 | | | |

|

General Merchandise Stores — 0.9% |

| | | |

Dollar General Corp. | | | 614,683 | | | | 44,177,267 | | | |

|

Healthcare Distributors — 0.7% |

| | | |

Cardinal Health Inc. | | | 376,337 | | | | 33,595,604 | | | |

| | | |

Healthcare Equipment — 4.6% | | | | | | | | | | |

| | | |

Abbott Laboratories | | | 1,003,565 | | | | 45,070,104 | | | |

Boston Scientific Corp. | | | 3,491,569 | | | | 64,384,533 | | | (a) |

Medtronic PLC | | | 1,304,634 | | | | 100,352,447 | | | |

Stryker Corp. | | | 183,451 | | | | 17,049,936 | | | |

| | | | | | | 226,857,020 | | | |

|

Healthcare Supplies — 0.6% |

| | | |

The Cooper Companies Inc. | | | 204,894 | | | | 27,496,775 | | | |

|

Home Improvement Retail — 1.7% |

| | | |

Lowe’s Companies Inc. | | | 1,093,467 | | | | 83,147,231 | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

6

| | |

GE RSP U.S. Equity Fund | | December 31, 2015 |

| | | | | | | | | | |

| | | Number

of Shares | | | Fair

Value | | | |

|

Household Products — 0.3% |

| | | |

The Procter & Gamble Co. | | | 165,534 | | | $ | 13,145,055 | | | |

|

Independent Power Producers & Energy Traders — 0.2% |

| | | |

Calpine Corp. | | | 626,599 | | | | 9,066,887 | | | (a) |

|

Industrial Machinery — 1.5% |

| | | |

Dover Corp. | | | 182,519 | | | | 11,190,240 | | | |

Ingersoll-Rand PLC | | | 1,129,010 | | | | 62,422,963 | | | |

| | | | | | | 73,613,203 | | | |

|

Integrated Oil & Gas — 4.9% |

| | | |

Cenovus Energy Inc. | | | 1,998,108 | | | | 25,216,123 | | | |

Chevron Corp. | | | 491,329 | | | | 44,199,957 | | | |

Exxon Mobil Corp. | | | 1,355,108 | | | | 105,630,669 | | | |

Occidental Petroleum Corp. | | | 960,073 | | | | 64,910,535 | | | |

| | | | | | | 239,957,284 | | | |

|

Integrated Telecommunication Services — 0.5% |

| | | |

Verizon Communications Inc. | | | 585,413 | | | | 27,057,789 | | | |

|

Internet Retail — 1.5% |

| | | |

Amazon.com Inc. | | | 108,720 | | | | 73,482,761 | | | (a) |

|

Internet Software & Services — 6.3% |

| | | |

Alphabet Inc., Class A | | | 86,072 | | | | 66,964,877 | | | (a) |

Alphabet Inc., Class C | | | 104,538 | | | | 79,331,797 | | | (a) |

Baidu Inc. ADR | | | 301,069 | | | | 56,914,084 | | | (a) |

eBay Inc. | | | 1,824,560 | | | | 50,138,909 | | | (a) |

Facebook Inc., Class A | | | 355,429 | | | | 37,199,199 | | | (a) |

LinkedIn Corp., Class A | | | 100,356 | | | | 22,588,128 | | | (a) |

| | | | | | | 313,136,994 | | | |

|

Investment Banking & Brokerage — 1.0% |

| | | |

The Charles Schwab Corp. | | | 1,505,347 | | | | 49,571,077 | | | |

|

IT Consulting & Other Services — 0.3% |

| | | |

Cognizant Technology Solutions Corp., Class A | | | 278,013 | | | | 16,686,340 | | | (a) |

|

Life & Health Insurance — 0.5% |

| | | |

Lincoln National Corp. | | | 459,967 | | | | 23,117,941 | | | |

|

Movies & Entertainment — 2.0% |

| | | |

The Walt Disney Co. | | | 401,426 | | | | 42,181,844 | | | |

Time Warner Inc. | | | 909,481 | | | | 58,816,136 | | | |

| | | | | | | 100,997,980 | | | |

|

Multi-Line Insurance — 1.9% |

| | | |

American International Group Inc. | | | 439,235 | | | | 27,219,393 | | | |

The Hartford Financial Services Group Inc. | | | 1,553,448 | | | | 67,512,850 | | | |

| | | | | | | 94,732,243 | | | |

| | | | | | | | | | |

| | | Number

of Shares | | | Fair

Value | | | |

|

Multi-Utilities — 0.7% |

| | | |

Dominion Resources Inc. | | | 547,779 | | | $ | 37,051,772 | | | |

|

Oil & Gas Equipment & Services — 1.3% |

| | | |

Schlumberger Ltd. | | | 935,567 | | | | 65,255,798 | | | |

|

Oil & Gas Exploration & Production — 1.2% |

| | | |

Hess Corp. | | | 1,011,762 | | | | 49,050,222 | | | |

Marathon Oil Corp. | | | 838,257 | | | | 10,553,655 | | | |

| | | | | | | 59,603,877 | | | |

|

Packaged Foods & Meats — 1.1% |

| | | |

Mondelez International Inc., Class A | | | 1,170,826 | | | | 52,499,838 | | | |

|

Paper Packaging — 0.2% |

| | | |

Packaging Corporation of America | | | 146,353 | | | | 9,227,557 | | | |

|

Pharmaceuticals — 8.3% |

| | | |

Allergan PLC | | | 526,583 | | | | 164,557,188 | | | (a) |

Johnson & Johnson | | | 1,037,271 | | | | 106,548,477 | | | |

Merck & Company Inc. | | | 1,651,700 | | | | 87,242,794 | | | |

Pfizer Inc. | | | 1,641,247 | | | | 52,979,453 | | | |

| | | | | | | 411,327,912 | | | |

|

Property & Casualty Insurance — 0.9% |

| | | |

ACE Ltd. | | | 375,629 | | | | 43,892,249 | | | |

|

Railroads — 0.2% |

| | | |

CSX Corp. | | | 355,429 | | | | 9,223,382 | | | |

|

Real Estate Services — 0.3% |

| | | |

CBRE Group Inc., Class A | | | 406,524 | | | | 14,057,600 | | | (a) |

|

Regional Banks — 0.2% |

| | | |

First Republic Bank | | | 154,704 | | | | 10,219,746 | | | |

|

Research & Consulting Services — 1.2% |

| | | |

Nielsen Holdings PLC | | | 1,318,563 | | | | 61,445,036 | | | |

|

Semiconductor Equipment — 1.1% |

| | | |

Applied Materials Inc. | | | 2,843,434 | | | | 53,086,913 | | | |

|

Soft Drinks — 2.0% |

| | | |

PepsiCo Inc. | | | 980,566 | | | | 97,978,155 | | | |

|

Specialized Finance — 2.0% |

| | | |

CME Group Inc. | | | 564,505 | | | | 51,144,153 | | | |

McGraw Hill Financial Inc. | | | 501,782 | | | | 49,465,670 | | | |

| | | | | | | 100,609,823 | | | |

|

Specialized REITs — 0.6% |

| | | |

American Tower Corp. | | | 286,511 | | | | 27,777,241 | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

7

| | |

GE RSP U.S. Equity Fund | | December 31, 2015 |

| | | | | | | | | | |

| | | Number

of Shares | | | Fair

Value | | | |

|

Systems Software — 1.5% |

| | | |

Microsoft Corp. | | | 554,051 | | | $ | 30,738,750 | | | |

Oracle Corp. | | | 857,209 | | | | 31,313,845 | | | |

VMware Inc., Class A | | | 257,455 | | | | 14,564,229 | | | (a) |

| | | | | | | 76,616,824 | | | |

|

Technology Hardware, Storage & Peripherals — 3.8% |

| | | |

Apple Inc. | | | 1,124,829 | | | | 118,399,501 | | | |

HP Inc. | | | 2,487,999 | | | | 29,457,908 | | | |

Western Digital Corp. | | | 658,588 | | | | 39,548,209 | | | |

| | | | | | | 187,405,618 | | | |

|

Trading Companies & Distributors — 0.7% |

| | | |

United Rentals Inc. | | | 501,782 | | | | 36,399,266 | | | (a) |

|

Wireless Telecommunication Services — 1.2% |

| | | |

SBA Communications Corp., Class A | | | 561,157 | | | | 58,960,766 | | | (a) |

| | | |

Total Common Stock

(Cost $4,115,867,372) | | | | | | | 4,762,920,763 | | | |

| | | | | | | | | | |

| | | Principal Amount | | | Fair

Value | | | |

Short-Term Investments — 3.5% |

| | |

Time Deposit — 3.5% | | | | | | | |

| | | |

State Street Corp. | | | | | | | | | | |

0.01% 01/04/16 | | $ | 172,132,649 | | | $ | 172,132,649 | | | (e) |

(Cost $172,132,649) | | | | | | | | | | |

| | | |

Total Investments

(Cost $4,288,000,021) | | | | | | | 4,935,053,412 | | | |

| | | |

Other Assets and Liabilities, net — 0.1% | | | | | | | 6,483,867 | | | |

| | | | | | | | | | |

| | | |

NET ASSETS — 100.0% | | | | | | $ | 4,941,537,279 | | | |

| | | | | | | | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

8

(Unaudited)

William M. Healey

Senior Vice

President and

Chief Investment

Officer – Core

Fixed Income

Investments

Mark H. Johnson

Senior Vice

President and

Chief Investment

Officer – Insurance

and Long Duration

The GE RSP Income Fund (the “Fund”) is co-managed by William M. Healey and Mark H. Johnson. Messrs. Healey and Johnson are each responsible for a portion of the Fund, the size of which is determined by consensus and adjusted on a periodic basis, if necessary. Although each portfolio manager manages his portion of the Fund independent of the other, they are highly collaborative and communicative.

William M. Healey is a Senior Vice President and Chief Investment Officer – Core Fixed Income Investments of GEAM. He has served on the portfolio management team for the GE RSP Income Fund since joining GEAM as a portfolio manager in 1996. He became Vice President in June 2001, Senior Vice President in January 2007 and Chief Investment Officer – Core Fixed Income Investments in April 2012. Prior to joining GEAM, Mr. Healey spent over 11 years in the fixed income group at MetLife.

Mark H. Johnson is a Senior Vice President and Chief Investment Officer – Insurance and Long Duration of GEAM. He has been a member of the portfolio management team for the GE RSP Income Fund since 2007. Mr. Johnson joined GE in 1998 and GEAM as a Vice President and portfolio manager in 2002. He became Senior Vice President in 2007 and Chief Investment Officer – Long Duration Fixed Income & Insurance Investments in April 2012. Prior to joining GEAM, Mr. Johnson held positions at various insurance companies and public accounting firms.

| Q. | How did the GE RSP Income Fund perform compared to its benchmark for the twelve-month period ended December 31, 2015? |

| A. | For the twelve-month period ended December 31, 2015, the Fund returned 0.34%. The Barclay’s Capital U.S. Aggregate Bond Index, the Fund’s benchmark, returned 0.55% and the Fund’s Morningstar peer group of 1,086 U.S. Intermediate-Term Funds returned an average of -0.27% over the same period. |

| Q. | What market factors affected the Fund’s performance? |

| A. | The two major factors which affected the Fund’s performance were the movement in |

| | interest rates and credit spreads. The 10-year US Treasury note finished the year at 2.3%, up just 10 bps but traded down to 1.65% in January, then moved to 2.5% by the end of June before drifting down by year end as inflation remained well below the Fed’s target of 2%. The 2-year treasury yield, basically unchanged for the first nine months of the year, jumped from 0.65% to 1.05% in the fourth quarter as expectations for a Fed Funds rate hike became reality in December. Economic growth in the US slowed from 3% in Q1 to 2% (Bloomberg estimate) in Q4 as the price of oil plummeted over 30% and the US dollar rose 9% versus a basket of major world currencies. As economic growth decelerated, credit spreads widened putting pressure on corporate bond prices. The option-adjusted spread (OAS) of the Barclays Investment Grade Bond Index widened 35 bps beginning in May and the OAS of Barclays US High Yield Index hurt primarily by the energy sector widened 180 bps. |

| Q. | What were the primary drivers of Fund performance? |

| A. | The primary driver of the Fund’s underperformance versus its benchmark was the allocation to high yield securities which are not in the index. The significant widening of credit spreads resulted in a negative return for the high yield market of -4.5% and while the Fund was not heavily exposed to energy companies, the allocation was the largest performance detractor. The overweight in high grade corporate bonds also negatively impacted the Fund’s total return. Security selection among the high grade credit sector, primarily underweight commodity-related sectors and overweight financials, and residential mortgage-backed securities contributed positively to the Fund’s performance. Tactically trading the Fund’s duration relative to the index, as treasury yields bounced within a range, also benefited the Fund. |

9

(Unaudited)

| Q. | Were there any significant changes to the Fund during the period? |

| A. | The most significant change to the Fund was a general increase in the allocation to spread sectors during the year. The allocation to high grade credit started the year slightly overweight and ended the year 10% overweight by market value, which added roughly 0.3 years to the Fund’s spread duration. The allocation to commercial mortgage-backed securities was also increased from 3% to 10% overweight by market value and from 0.1 to 0.5 spread duration contribution. The Fund’s duration was tactically traded within neutral to 0.5 years long relative to the benchmark during the period. |

10

(Unaudited)

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in shares of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended December 31, 2015.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given under the heading “Expenses

paid during the period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs, such as sales charges or redemption fees, if any. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

July 1, 2015 – December 31, 2015

| | | | | | | | | | | | |

| | | Account value at

the beginning of

the period ($) | | | Account value

at the end of

the period ($) | | | Expenses

paid during

the period ($)* | |

Actual Fund Return | | | 1,000.00 | | | | 1,003.20 | | | | 1.01 | |

Hypothetical 5% Return

(2.5% for the period) | | | 1,000.00 | | | | 1,024.20 | | | | 1.02 | |

| * | | Expenses are equal to the Fund’s annualized net expense ratio of 0.20%** (for the period July 1, 2015 – December 31, 2015), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| ** | | May differ from expense ratio disclosed in the financial highlights, which is calculated based on the entire fiscal year’s data. |

11

(Unaudited)

A mutual fund designed for investors who seek a high interest rate of return over a long-term period consistent with the preservation of capital. The Fund seeks to achieve its investment objective by investing at least 80% of its net assets under normal circumstances in debt securities and investing primarily in a variety of investment-grade debt securities, such as U.S. Government securities, mortgage-backed securities, corporate bonds, and money market instruments.

(as a % of Fair Value of Investments of $2,562,439 (in thousands) on December 31, 2015) (a)

| | | | |

| Moody’s/S&P/Rating * | | Percentage of

Fair Value | |

| |

Aaa / AAA | | | 3.9% | |

| |

Aa / AA | | | 48.7% | |

| |

A / A | | | 9.6% | |

| |

Baa / BBB | | | 20.8% | |

| |

Ba / BB and lower | | | 10.0% | |

| |

NR / Other | | | 7.0% | |

Portfolio composition as a % of Fair Value of Investments of $2,562,439 (in thousands) on December 31, 2015 (a)

|

| Morningstar Performance Comparison |

Based on average annual returns for periods ended December 31, 2015

| | | | | | | | | | | | |

| | | One

Year | | | Five

Year | | | Ten

Year | |

Number of funds in peer group | | | 1,086 | | | | 990 | | | | 860 | |

Peer group average annual total return | | | -0.27 | % | | | 3.17 | % | | | 3.98 | % |

Morningstar Category in peer group: Intermediate-Term Bond | |

|

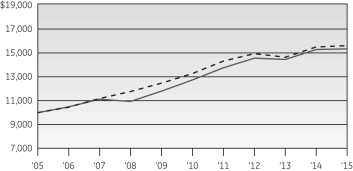

| Change in Value of a $10,000 Investment |

|

| Average Annual Total Return |

For the periods ended December 31, 2015

| | | | | | | | | | | | | | | | | | | | |

| | | One

Year | | Five

Year | | Ten

Year | | Ending value of a

$10,000

investment |

GE RSP Income Fund | | | | 0.34% | | | | | 3.78% | | | | | 4.34% | | | | | $15,300 | |

Barclays U.S. Aggregate Bond Index | | | | 0.55% | | | | | 3.25% | | | | | 4.51% | | | | | $15,552 | |

| (a) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

| * | Moody’s Investors Services, Inc. (“Moody’s”) and Standard & Poor’s Corporation (“S&P”) are nationally recognized statistical rating organizations. The quality ratings represent the lower of Moody’s or S&P credit ratings. When a rating from only one of the rating agencies is available, that rating is used. Securities not rated by Moody’s or S&P are categorized as not rated. Credit quality measures a bond issuer’s ability to repay interest and principal in a timely manner. Credit quality ratings assigned by a rating agency are subject to change periodically and are not absolute standards of quality. In formulating investment decisions for the Fund, GEAM develops its own analysis of the credit quality and risks associated with individual debt instruments, rather than relying exclusively on rating agency ratings. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and does not reflect the fees or charges that would be associated with variable contracts through which shares of the Fund are offered.

12

| | |

GE RSP Income Fund | | December 31, 2015 |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Bonds and Notes – 98.9%† | | | |

| |

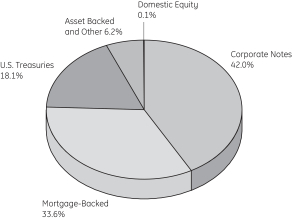

U.S. Treasuries — 18.8% | | | |

| |

U.S. Treasury Bonds | | | |

| 2.50% | | 02/15/45 | | $ | 1,721,000 | | | $ | 1,540,973 | | | (m) |

| 3.13% | | 11/15/41 | | | 61,519,000 | | | | 63,425,658 | | | (m) |

U.S. Treasury Notes | | | |

| 0.63% | | 05/31/17 - 07/31/17 | | | 33,033,500 | | | | 32,874,026 | | | (m) |

| 0.75% | | 12/31/17 | | | 50,000,000 | | | | 49,666,250 | | | (m) |

| 0.88% | | 10/15/18 | | | 44,127,000 | | | | 43,645,177 | | | (m) |

| 1.38% | | 10/31/20 | | | 123,986,200 | | | | 121,826,236 | | | (m) |

| 1.88% | | 10/31/22 | | | 112,680,400 | | | | 111,256,233 | | | (m) |

| 2.00% | | 08/15/25 | | | 40,531,000 | | | | 39,517,077 | | | (m) |

| | | | 463,751,630 | | | |

| |

Agency Mortgage Backed — 23.9% | | | |

| | | |

Federal Home Loan Mortgage Corp. | | | | | | | | | | |

| 4.50% | | 06/01/33 - 02/01/35 | | | 137,387 | | | | 148,537 | | | |

| 5.00% | | 07/01/35 - 06/01/41 | | | 9,461,460 | | | | 10,550,702 | | | |

| 5.50% | | 05/01/20 - 04/01/39 | | | 2,742,363 | | | | 3,084,910 | | | |

| 6.00% | | 04/01/17 - 11/01/37 | | | 5,076,721 | | | | 5,759,293 | | | |

| 6.50% | | 07/01/29 | | | 24,153 | | | | 27,687 | | | |

| 7.00% | | 10/01/16 - 08/01/36 | | | 899,900 | | | | 1,013,268 | | | |

| 7.50% | | 01/01/28 - 09/01/33 | | | 50,779 | | | | 55,090 | | | |

| 8.00% | | 11/01/30 | | | 4,046 | | | | 4,343 | | | |

| 8.50% | | 04/01/30 | | | 11,264 | | | | 13,693 | | | |

| 9.00% | | 05/01/16 - 11/01/16 | | | 5,052 | | | | 5,105 | | | |

Federal National Mortgage Assoc. | | | | | | | | | | |

| 2.22% | | 04/01/37 | | | 18,971 | | | | 19,320 | | | (h) |

| 3.00% | | 02/01/43 - 06/01/43 | | | 103,664,261 | | | | 103,995,438 | | | |

| 3.50% | | 11/01/42 - 08/01/45 | | | 68,812,379 | | | | 71,043,747 | | | |

| 4.00% | | 05/01/19 - 03/01/44 | | | 60,526,313 | | | | 64,297,514 | | | |

| 4.50% | | 05/01/18 - 01/01/41 | | | 52,082,249 | | | | 56,317,687 | | | |

| 5.00% | | 07/01/20 - 06/01/41 | | | 16,226,731 | | | | 18,182,543 | | | |

| 5.50% | | 03/01/16 - 01/01/39 | | | 16,550,667 | | | | 18,488,677 | | | |

| 6.00% | | 05/01/19 - 05/01/41 | | | 24,765,805 | | | | 28,169,721 | | | |

| 6.50% | | 03/01/16 - 08/01/36 | | | 1,086,908 | | | | 1,224,951 | | | |

| 7.00% | | 10/01/16 - 02/01/34 | | | 100,274 | | | | 104,609 | | | |

| 7.50% | | 03/01/17 - 12/01/33 | | | 539,412 | | | | 608,749 | | | |

| 8.00% | | 06/01/24 - 01/01/33 | | | 192,855 | | | | 213,777 | | | |

| 8.50% | | 04/01/30 | | | 30,797 | | | | 38,904 | | | |

| 9.00% | | 01/01/17 - 12/01/22 | | | 120,160 | | | | 129,265 | | | |

| 2.50% | | TBA | | | 31,677,489 | | | | 31,862,956 | | | (c) |

| 3.00% | | TBA | | | 3,215,000 | | | | 3,213,881 | | | (c) |

| 3.50% | | TBA | | | 20,980,779 | | | | 21,639,496 | | | (c) |

| 4.00% | | TBA | | | 10,297,187 | | | | 10,893,503 | | | (c) |

Government National Mortgage Assoc. | | | | | | | | | | |

| 1.63% | | 11/20/21 - 10/20/25 | | | 9,587 | | | | 9,709 | | | (h) |

| 1.75% | | 05/20/21 - 04/20/24 | | | 7,812 | | | | 8,024 | | | (h) |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

| 1.88% | | 08/20/23 - 09/20/24 | | $ | 5,416 | | | $ | 5,563 | | | (h) |

| 3.00% | | 04/20/43 - 06/20/43 | | | 30,583,318 | | | | 31,107,220 | | | |

| 3.50% | | 05/20/43 | | | 21,672,361 | | | | 22,647,084 | | | |

| 4.00% | | 01/20/41 - 04/20/43 | | | 26,111,671 | | | | 27,953,585 | | | |

| 4.50% | | 08/15/33 - 03/20/41 | | | 11,521,634 | | | | 12,544,782 | | | |

| 5.00% | | 08/15/33 | | | 537,468 | | | | 597,701 | | | |

| 6.00% | | 04/15/27 - 09/15/36 | | | 1,323,637 | | | | 1,518,959 | | | |

| 6.50% | | 04/15/19 - 09/15/36 | | | 1,181,006 | | | | 1,349,011 | | | |

| 7.00% | | 03/15/26 - 10/15/36 | | | 689,050 | | | | 756,878 | | | |

| 7.50% | | 11/15/22 - 11/15/31 | | | 246,501 | | | | 262,293 | | | |

| 8.00% | | 12/15/29 - 06/15/30 | | | 3,473 | | | | 3,884 | | | |

| 8.50% | | 10/15/17 | | | 33,670 | | | | 34,671 | | | |

| 9.00% | | 11/15/16 - 12/15/21 | | | 162,525 | | | | 168,819 | | | |

| 3.00% | | TBA | | | 16,800,032 | | | | 17,021,713 | | | (c) |

| 4.00% | | TBA | | | 7,679,113 | | | | 8,143,778 | | | (c) |

| 5.00% | | TBA | | | 12,587,000 | | | | 13,787,748 | | | (c) |

| 5.50% | | TBA | | | 1,900,000 | | | | 2,110,717 | | | (c) |

| | | | 591,139,505 | | | |

| |

Agency Collateralized Mortgage Obligations — 0.3% | | | |

| | | |

Collateralized Mortgage Obligation Trust | | | | | | | | | | |

| 0.01% | | 11/01/18 | | | 20,986 | | | | 20,856 | | | (d,f) |

Federal Home Loan Mortgage Corp. | | | | | | | | | | |

| 0.08% | | 09/25/43 | | | 8,778,461 | | | | 24,991 | | | (g,h) |

Federal Home Loan Mortgage Corp. REMIC | | | | | | | | | | |

| 3.50% | | 11/15/24 - 11/15/30 | | | 7,973,940 | | | | 646,449 | | | (g) |

| 5.00% | | 02/15/38 | | | 81,694 | | | | 1,443 | | | (g) |

| 5.50% | | 06/15/33 | | | 465,060 | | | | 97,283 | | | (g) |

| 6.27% | | 08/15/25 | | | 2,901,759 | | | | 285,873 | | | (g,h) |

| 7.50% | | 07/15/27 | | | 17,709 | | | | 2,345 | | | (g) |

| 8.00% | | 04/15/20 | | | 11,103 | | | | 11,489 | | | |

Federal Home Loan Mortgage Corp. STRIPS | | | | | | | | | | |

| 1.47% | | 08/01/27 | | | 12,698 | | | | 11,544 | | | (d,f) |

| 5.62% | | 08/15/43 | | | 6,575,042 | | | | 1,420,816 | | | (g,h) |

| 8.00% | | 02/01/23 - 07/01/24 | | | 45,449 | | | | 9,555 | | | (g) |

Federal National Mortgage Assoc. REMIC | | | | | | | | | | |

| 0.51% | | 12/25/22 | | | 41,756 | | | | 40,391 | | | (d,f) |

| 1.22% | | 12/25/42 | | | 1,332,627 | | | | 44,276 | | | (g,h) |

| 5.00% | | 02/25/40 - 09/25/40 | | | 3,815,616 | | | | 415,844 | | | (g) |

| 5.58% | | 07/25/38 | | | 776,267 | | | | 107,130 | | | (g,h) |

| 7.08% | | 05/25/18 | | | 96,178 | | | | 5,412 | | | (g,h) |

| 8.00% | | 05/25/22 | | | 60 | | | | 971 | | | (g) |

Federal National Mortgage Assoc. STRIPS | | | | | | | | | | |

| 1.87% | | 12/25/34 | | | 472,481 | | | | 436,941 | | | (f,d) |

| 4.50% | | 08/25/35 - 01/25/36 | | | 1,257,569 | | | | 225,804 | | | (g) |

| 5.00% | | 03/25/38 - 05/25/38 | | | 692,776 | | | | 125,446 | | | (g) |

| 5.50% | | 12/25/33 | | | 168,309 | | | | 32,892 | | | (g) |

| 6.00% | | 01/25/35 | | | 649,634 | | | | 134,041 | | | (g) |

| 7.50% | | 11/25/23 | | | 188,824 | | | | 40,480 | | | (g) |

See Notes to Schedules of Investments and Notes to Financial Statements.

13

| | |

GE RSP Income Fund | | December 31, 2015 |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

| 8.00% | | 08/25/23 - 07/25/24 | | $ | 94,006 | | | $ | 19,953 | | | (g) |

| 8.50% | | 03/25/17 - 07/25/22 | | | 66,214 | | | | 7,730 | | | (g) |

| 9.00% | | 05/25/22 | | | 34,535 | | | | 6,052 | | | (g) |

Government National Mortgage Assoc. | | | | | | | | | | |

| 4.50% | | 10/20/37 - 08/16/39 | | | 6,191,630 | | | | 411,300 | | | (g) |

| 5.00% | | 10/20/37 - 09/20/38 | | | 3,131,820 | | | | 185,190 | | | (g) |

| 5.85% | | 02/20/40 | | | 2,695,304 | | | | 461,170 | | | (g,h) |

| 6.46% | | 01/16/40 | | | 4,547,204 | | | | 840,279 | | | (g,h) |

| | | | 6,073,946 | | | |

|

Asset Backed — 0.1% |

| | | |

Capital One Multi-Asset Execution Trust 2006-B1 | | | | | | | | | | |

| 0.61% | | 01/15/19 | | | 1,000,000 | | | | 999,382 | | | (h) |

Chase Funding Trust 2004-1 | | | | | | | | | | |

| 3.99% | | 11/25/33 | | | 1,098,837 | | | | 1,122,146 | | | (i) |

Irwin Home Equity Loan Trust 2006-2 | | | | | | | | | | |

| 0.37% | | 02/25/36 | | | 163,763 | | | | 141,959 | | | (b,h) |

| | | | 2,263,487 | | | |

|

Corporate Notes — 43.5% |

| | | |

21st Century Fox America Inc. | | | | | | | | | | |

| 3.70% | | 10/15/25 | | | 845,000 | | | | 843,476 | | | (b) |

| 4.95% | | 10/15/45 | | | 338,000 | | | | 332,900 | | | (b) |

| 6.65% | | 11/15/37 | | | 1,846,000 | | | | 2,145,165 | | | |

ABB Finance USA Inc. | | | | | | | | | | |

| 1.63% | | 05/08/17 | | | 3,213,000 | | | | 3,215,284 | | | |

AbbVie Inc. | | | | | | | | | | |

| 1.75% | | 11/06/17 | | | 2,949,000 | | | | 2,943,429 | | | |

| 2.00% | | 11/06/18 | | | 2,313,000 | | | | 2,303,285 | | | |

| 2.50% | | 05/14/20 | | | 3,380,000 | | | | 3,346,585 | | | |

| 3.60% | | 05/14/25 | | | 1,360,000 | | | | 1,342,404 | | | |

| 4.70% | | 05/14/45 | | | 675,000 | | | | 660,108 | | | |

Abengoa Greenfield S.A. | | | | | | | | | | |

| 6.50% | | 10/01/19 | | | 2,275,000 | | | | 250,250 | | | (b) |

ACCO Brands Corp. | | | | | | | | | | |

| 6.75% | | 04/30/20 | | | 3,446,000 | | | | 3,549,380 | | | |

ACE INA Holdings Inc. | | | | | | | | | | |

| 2.30% | | 11/03/20 | | | 3,376,000 | | | | 3,353,242 | | | |

| 3.15% | | 03/15/25 | | | 2,365,000 | | | | 2,338,730 | | | |

| 3.35% | | 05/03/26 | | | 2,363,000 | | | | 2,356,185 | | | |

| 4.35% | | 11/03/45 | | | 709,000 | | | | 720,512 | | | |

Actavis Funding SCS | | | | | | | | | | |

| 1.30% | | 06/15/17 | | | 3,992,000 | | | | 3,954,208 | | | |

| 3.00% | | 03/12/20 | | | 1,689,000 | | | | 1,687,654 | | | |

| 3.45% | | 03/15/22 | | | 2,365,000 | | | | 2,368,777 | | | |

| 3.80% | | 03/15/25 | | | 3,378,000 | | | | 3,361,059 | | | |

| 4.75% | | 03/15/45 | | | 338,000 | | | | 329,502 | | | |

Activision Blizzard Inc. | | | | | | | | | | |

| 5.63% | | 09/15/21 | | | 3,378,000 | | | | 3,538,455 | | | (b) |

Aetna Inc. | | | | | | | | | | |

| 3.50% | | 11/15/24 | | | 2,106,000 | | | | 2,103,814 | | | |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Agrium Inc. | | | | | | | | | | |

| 3.38% | | 03/15/25 | | $ | 845,000 | | | $ | 771,385 | | | |

| 4.90% | | 06/01/43 | | | 1,562,000 | | | | 1,397,282 | | | |

Alibaba Group Holding Ltd. | | | | | | | | | | |

| 4.50% | | 11/28/34 | | | 1,350,000 | | | | 1,291,630 | | | |

Altria Group Inc. | | | | | | | | | | |

| 2.95% | | 05/02/23 | | | 1,681,000 | | | | 1,636,062 | | | |

| 4.50% | | 05/02/43 | | | 1,681,000 | | | | 1,594,338 | | | |

America Movil SAB de C.V. | | | | | | | | | | |

| 3.13% | | 07/16/22 | | | 1,670,000 | | | | 1,640,887 | | | |

| 5.00% | | 03/30/20 | | | 2,650,000 | | | | 2,875,838 | | | |

American Axle & Manufacturing Inc. | | | | | | | | | | |

| 6.25% | | 03/15/21 | | | 2,250,000 | | | | 2,328,750 | | | |

| 6.63% | | 10/15/22 | | | 717,000 | | | | 751,058 | | | |

American Campus Communities Operating Partnership LP | | | | | | | | | | |

| 3.35% | | 10/01/20 | | | 1,358,000 | | | | 1,356,413 | | | |

| 4.13% | | 07/01/24 | | | 1,030,000 | | | | 1,022,813 | | | |

American Electric Power Company Inc. | | | | | | | | | | |

| 2.95% | | 12/15/22 | | | 2,694,000 | | | | 2,662,612 | | | |

American Express Co. | | | | | | | | | | |

| 3.63% | | 12/05/24 | | | 3,368,000 | | | | 3,296,164 | | | |

American Express Credit Corp. | | | | | | | | | | |

| 2.60% | | 09/14/20 | | | 3,380,000 | | | | 3,389,515 | | | |

American International Group Inc. | | | | | | | | | | |

| 3.75% | | 07/10/25 | | | 3,381,000 | | | | 3,352,748 | | | |

| 4.13% | | 02/15/24 | | | 1,013,000 | | | | 1,041,078 | | | |

| 4.50% | | 07/16/44 | | | 676,000 | | | | 625,197 | | | |

| 4.80% | | 07/10/45 | | | 1,690,000 | | | | 1,634,139 | | | |

American Tower Corp. (REIT) | | | | | | | | | | |

| 3.40% | | 02/15/19 | | | 4,077,000 | | | | 4,182,957 | | | |

Amgen Inc. | | | | | | | | | | |

| 2.20% | | 05/22/19 | | | 4,996,000 | | | | 4,990,454 | | | |

Amkor Technology Inc. | | | | | | | | | | |

| 6.63% | | 06/01/21 | | | 3,389,000 | | | | 3,363,582 | | | |

Anadarko Petroleum Corp. | | | | | | | | | | |

| 3.45% | | 07/15/24 | | | 672,000 | | | | 597,286 | | | |

| 6.20% | | 03/15/40 | | | 1,766,000 | | | | 1,624,722 | | | |

Anheuser-Busch InBev Worldwide Inc. | | | | | | | | | | |

| 2.50% | | 07/15/22 | | | 4,861,000 | | | | 4,679,014 | | | |

Anthem Inc. | | | | | | | | | | |

| 3.30% | | 01/15/23 | | | 1,732,000 | | | | 1,683,968 | | | |

Apache Corp. | | | | | | | | | | |

| 5.10% | | 09/01/40 | | | 1,689,000 | | | | 1,443,859 | | | |

Apple Inc. | | | | | | | | | | |

| 2.50% | | 02/09/25 | | | 1,831,000 | | | | 1,752,042 | | | |

| 2.85% | | 05/06/21 | | | 5,169,000 | | | | 5,295,961 | | | |

| 3.45% | | 02/09/45 | | | 1,690,000 | | | | 1,454,865 | | | |

Aramark Services Inc. | | | | | | | | | | |

| 5.75% | | 03/15/20 | | | 3,778,000 | | | | 3,907,869 | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

14

| | |

GE RSP Income Fund | | December 31, 2015 |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Ascension Health | | | | | | | | | | |

| 4.85% | | 11/15/53 | | $ | 2,608,000 | | | $ | 2,809,958 | | | |

AstraZeneca PLC | | | | | | | | | | |

| 2.38% | | 11/16/20 | | | 1,189,000 | | | | 1,180,959 | | | |

| 3.38% | | 11/16/25 | | | 1,689,000 | | | | 1,676,935 | | | |

| 4.38% | | 11/16/45 | | | 673,000 | | | | 674,456 | | | |

AT&T Inc. | | | | | | | | | | |

| 2.38% | | 11/27/18 | | | 3,936,000 | | | | 3,966,331 | | | (m) |

| 2.45% | | 06/30/20 | | | 3,389,000 | | | | 3,338,853 | | | (m) |

| 3.40% | | 05/15/25 | | | 3,389,000 | | | | 3,257,558 | | | (m) |

| 4.50% | | 05/15/35 | | | 1,689,000 | | | | 1,562,251 | | | (m) |

| 4.75% | | 05/15/46 | | | 844,000 | | | | 772,618 | | | (m) |

| 4.80% | | 06/15/44 | | | 1,339,000 | | | | 1,226,706 | | | (m) |

AutoNation Inc. | | | | | | | | | | |

| 4.50% | | 10/01/25 | | | 2,366,000 | | | | 2,401,980 | | | |

AutoZone Inc. | | | | | | | | | | |

| 3.25% | | 04/15/25 | | | 3,378,000 | | | | 3,268,864 | | | |

Bank of America Corp. | | | | | | | | | | |

| 1.70% | | 08/25/17 | | | 8,512,000 | | | | 8,488,337 | | | (m) |

| 2.60% | | 01/15/19 | | | 1,476,000 | | | | 1,481,011 | | | (m) |

| 3.88% | | 08/01/25 | | | 669,000 | | | | 679,186 | | | (m) |

| 3.95% | | 04/21/25 | | | 2,026,000 | | | | 1,973,038 | | | (m) |

| 4.00% | | 01/22/25 | | | 1,691,000 | | | | 1,656,734 | | | (m) |

| 4.10% | | 07/24/23 | | | 1,981,000 | | | | 2,049,150 | | | (m) |

| 4.25% | | 10/22/26 | | | 3,030,000 | | | | 2,999,506 | | | (m) |

Barclays Bank PLC | | | | | | | | | | |

| 2.25% | | 05/10/17 | | | 8,801,000 | | | | 8,894,687 | | | (b) |

Barclays PLC | | | | | | | | | | |

| 5.25% | | 08/17/45 | | | 1,670,000 | | | | 1,682,166 | | | |

Barrick Gold Corp. | | | | | | | | | | |

| 4.10% | | 05/01/23 | | | 530,000 | | | | 454,699 | | | |

Baxalta Inc. | | | | | | | | | | |

| 2.88% | | 06/23/20 | | | 3,381,000 | | | | 3,340,425 | | | (b) |

| 4.00% | | 06/23/25 | | | 2,537,000 | | | | 2,512,003 | | | (b) |

Bed Bath & Beyond Inc. | | | | | | | | | | |

| 4.92% | | 08/01/34 | | | 498,000 | | | | 444,052 | | | |

Berkshire Hathaway Energy Co. | | | | | | | | | | |

| 6.13% | | 04/01/36 | | | 3,165,000 | | | | 3,688,538 | | | |

Berkshire Hathaway Finance Corp. | | | | | | | | | | |

| 3.00% | | 05/15/22 | | | 1,056,000 | | | | 1,074,636 | | | |

Berkshire Hathaway Inc. | | | | | | | | | | |

| 4.50% | | 02/11/43 | | | 521,000 | | | | 524,208 | | | |

Berry Plastics Corp. | | | | | | | | | | |

| 5.13% | | 07/15/23 | | | 2,045,000 | | | | 1,988,763 | | | |

| 6.00% | | 10/15/22 | | | 1,300,000 | | | | 1,322,750 | | | (b) |

BHP Billiton Finance USA Ltd. | | | | | | | | | | |

| 5.00% | | 09/30/43 | | | 924,000 | | | | 837,311 | | | |

Biogen Inc. | | | | | | | | | | |

| 2.90% | | 09/15/20 | | | 1,693,000 | | | | 1,689,284 | | | |

| 4.05% | | 09/15/25 | | | 1,692,000 | | | | 1,700,780 | | | |

| 5.20% | | 09/15/45 | | | 677,000 | | | | 677,194 | | | |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Bombardier Inc. | | | | | | | | | | |

| 4.75% | | 04/15/19 | | $ | 1,371,000 | | | $ | 1,127,648 | | | (b) |

| 6.00% | | 10/15/22 | | | 1,407,000 | | | | 986,307 | | | (b) |

| 7.75% | | 03/15/20 | | | 1,372,000 | | | | 1,107,890 | | | (b) |

Boston Scientific Corp. | | | | | | | | | | |

| 3.85% | | 05/15/25 | | | 1,705,000 | | | | 1,677,904 | | | |

BP Capital Markets PLC | | | | | | | | | | |

| 1.38% | | 05/10/18 | | | 1,688,000 | | | | 1,663,914 | | | |

| 3.81% | | 02/10/24 | | | 1,633,000 | | | | 1,632,685 | | | |

Branch Banking & Trust Co. | | | | | | | | | | |

| 3.63% | | 09/16/25 | | | 3,400,000 | | | | 3,433,667 | | | |

Building Materials Corporation of America | | | | | | | | | | |

| 5.38% | | 11/15/24 | | | 4,068,000 | | | | 4,057,830 | | | (b) |

Burlington Northern Santa Fe LLC | | | | | | | | | | |

| 3.65% | | 09/01/25 | | | 1,165,000 | | | | 1,180,625 | | | |

Calpine Corp. | | | | | | | | | | |

| 5.75% | | 01/15/25 | | | 2,054,000 | | | | 1,812,655 | | | |

| 5.88% | | 01/15/24 | | | 4,556,000 | | | | 4,669,900 | | | (b) |

Calumet Specialty Products Partners LP/Calumet Finance Corp. | | | | | | | | | | |

| 6.50% | | 04/15/21 | | | 3,402,000 | | | | 2,959,740 | | | |

Canadian Pacific Railway Co. | | | | | | | | | | |

| 2.90% | | 02/01/25 | | | 1,690,000 | | | | 1,590,937 | | | |

Capital One Financial Corp. | | | | | | | | | | |

| 4.20% | | 10/29/25 | | | 3,376,000 | | | | 3,335,032 | | | |

Capital One NA | | | | | | | | | | |

| 2.35% | | 08/17/18 | | | 1,340,000 | | | | 1,342,762 | | | |

Caterpillar Inc. | | | | | | | | | | |

| 4.30% | | 05/15/44 | | | 1,089,000 | | | | 1,050,864 | | | |

Catholic Health Initiatives | | | | | | | | | | |

| 2.60% | | 08/01/18 | | | 1,030,000 | | | | 1,034,258 | | | |

| 4.35% | | 11/01/42 | | | 1,029,000 | | | | 962,315 | | | |

CBS Corp. | | | | | | | | | | |

| 3.70% | | 08/15/24 | | | 2,624,000 | | | | 2,553,236 | | | |

CCO Safari II LLC | | | | | | | | | | |

| 3.58% | | 07/23/20 | | | 2,534,000 | | | | 2,519,485 | | | (b) |

| 4.91% | | 07/23/25 | | | 2,534,000 | | | | 2,531,509 | | | (b) |

| 6.38% | | 10/23/35 | | | 338,000 | | | | 341,121 | | | (b) |

| 6.48% | | 10/23/45 | | | 676,000 | | | | 676,240 | | | (b) |

Celgene Corp. | | | | | | | | | | |

| 3.88% | | 08/15/25 | | | 3,380,000 | | | | 3,369,258 | | | |

| 5.00% | | 08/15/45 | | | 1,690,000 | | | | 1,696,466 | | | |

CenturyLink Inc. | | | | | | | | | | |

| 5.80% | | 03/15/22 | | | 6,803,000 | | | | 6,234,949 | | | |

Cequel Capital Corp. | | | | | | | | | | |

| 5.13% | | 12/15/21 | | | 3,893,000 | | | | 3,503,700 | | | (b) |

Chevron Corp. | | | | | | | | | | |

| 3.33% | | 11/17/25 | | | 2,365,000 | | | | 2,382,049 | | | |

Cigna Corp. | | | | | | | | | | |

| 3.25% | | 04/15/25 | | | 3,379,000 | | | | 3,318,472 | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

15

| | |

GE RSP Income Fund | | December 31, 2015 |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Cinemark USA Inc. | | | | | | | | | | |

| 4.88% | | 06/01/23 | | $ | 3,403,000 | | | $ | 3,317,925 | | | |

Citigroup Inc. | | | | | | | | | | |

| 1.55% | | 08/14/17 | | | 7,436,000 | | | | 7,405,944 | | | (m) |

| 1.75% | | 05/01/18 | | | 3,366,000 | | | | 3,337,746 | | | (m) |

| 1.85% | | 11/24/17 | | | 1,625,000 | | | | 1,622,686 | | | (m) |

| 2.05% | | 12/07/18 | | | 3,069,000 | | | | 3,052,722 | | | (m) |

| 2.65% | | 10/26/20 | | | 1,680,000 | | | | 1,667,798 | | | (m) |

| 4.40% | | 06/10/25 | | | 1,693,000 | | | | 1,710,743 | | | (m) |

| 4.45% | | 09/29/27 | | | 1,000,000 | | | | 994,048 | | | (m) |

| 4.65% | | 07/30/45 | | | 2,704,000 | | | | 2,734,899 | | | (m) |

CMS Energy Corp. | | | | | | | | | | |

| 4.88% | | 03/01/44 | | | 1,699,000 | | | | 1,722,852 | | | |

CNA Financial Corp. | | | | | | | | | | |

| 5.88% | | 08/15/20 | | | 2,898,000 | | | | 3,212,572 | | | |

CNOOC Nexen Finance 2014 ULC | | | | | | | | | | |

| 4.25% | | 04/30/24 | | | 3,448,000 | | | | 3,475,322 | | | |

Cogeco Cable Inc. | | | | | | | | | | |

| 4.88% | | 05/01/20 | | | 3,215,000 | | | | 3,206,963 | | | (b) |

Colgate-Palmolive Co. | | | | | | | | | | |

| 4.00% | | 08/15/45 | | | 1,690,000 | | | | 1,693,747 | | | |

Columbia Pipeline Group Inc. | | | | | | | | | | |

| 3.30% | | 06/01/20 | | | 2,366,000 | | | | 2,304,723 | | | (b) |

| 4.50% | | 06/01/25 | | | 1,689,000 | | | | 1,530,879 | | | (b) |

Comcast Corp. | | | | | | | | | | |

| 3.38% | | 08/15/25 | | | 5,747,000 | | | | 5,821,556 | | | |

| 4.20% | | 08/15/34 | | | 1,693,000 | | | | 1,676,808 | | | |

| 4.60% | | 08/15/45 | | | 1,690,000 | | | | 1,710,997 | | | |

ConocoPhillips Co. | | | | | | | | | | |

| 3.35% | | 11/15/24 | | | 1,000,000 | | | | 914,965 | | | |

Continental Resources Inc. | | | | | | | | | | |

| 3.80% | | 06/01/24 | | | 735,000 | | | | 517,950 | | | |

| 4.50% | | 04/15/23 | | | 677,000 | | | | 486,680 | | | |

| 4.90% | | 06/01/44 | | | 399,000 | | | | 240,668 | | | |

Corp Andina de Fomento | | | | | | | | | | |

| 4.38% | | 06/15/22 | | | 4,826,000 | | | | 5,137,760 | | | |

Credit Suisse AG | | | | | | | | | | |

| 1.70% | | 04/27/18 | | | 3,437,000 | | | | 3,412,542 | | | |

| 2.60% | | 05/27/16 | | | 3,681,000 | | | | 3,700,697 | | | (b) |

Credit Suisse Group Funding Guernsey Ltd. | | | | | | | | | | |

| 3.75% | | 03/26/25 | | | 3,390,000 | | | | 3,275,069 | | | (b) |

Crown Americas LLC/Crown Americas Capital Corp. IV | | | | | | | | | | |

| 4.50% | | 01/15/23 | | | 4,092,000 | | | | 3,999,930 | | | |

CSX Corp. | | | | | | | | | | |

| 4.50% | | 08/01/54 | | | 1,018,000 | | | | 923,377 | | | |

CubeSmart LP | | | | | | | | | | |

| 4.00% | | 11/15/25 | | | 946,000 | | | | 939,289 | | | |

CVS Health Corp. | | | | | | | | | | |

| 2.25% | | 08/12/19 | | | 5,080,000 | | | | 5,075,204 | | | |

| 3.88% | | 07/20/25 | | | 3,381,000 | | | | 3,451,142 | | | |

| 5.13% | | 07/20/45 | | | 2,536,000 | | | | 2,671,504 | | | |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Daimler Finance North America LLC | | | | | | | | | | |

| 2.38% | | 08/01/18 | | $ | 8,030,000 | | | $ | 8,042,230 | | | (b) |

Danaher Corp. | | | | | | | | | | |

| 2.40% | | 09/15/20 | | | 1,689,000 | | | | 1,689,130 | | | |

| 3.35% | | 09/15/25 | | | 1,693,000 | | | | 1,719,688 | | | |

| 4.38% | | 09/15/45 | | | 902,000 | | | | 931,701 | | | |

Denbury Resources Inc. | | | | | | | | | | |

| 5.50% | | 05/01/22 | | | 3,402,000 | | | | 1,129,396 | | | |

| 6.38% | | 08/15/21 | | | 2,076,000 | | | | 747,360 | | | |

Deutsche Bank AG | | | | | | | | | | |

| 4.50% | | 04/01/25 | | | 3,426,000 | | | | 3,151,992 | | | |

Devon Energy Corp. | | | | | | | | | | |

| 5.85% | | 12/15/25 | | | 1,388,000 | | | | 1,350,012 | | | |

Dexia Credit Local S.A. | | | | | | | | | | |

| 2.25% | | 01/30/19 | | | 6,894,000 | | | | 6,938,873 | | | (b) |

Diageo Investment Corp. | | | | | | | | | | |

| 2.88% | | 05/11/22 | | | 4,105,000 | | | | 4,069,512 | | | |

DigitalGlobe Inc. | | | | | | | | | | |

| 5.25% | | 02/01/21 | | | 3,520,000 | | | | 2,956,800 | | | (b) |

DIRECTV Holdings LLC/DIRECTV Financing Company Inc. | | | | | | | | | | |

| 4.45% | | 04/01/24 | | | 2,595,000 | | | | 2,665,519 | | | |

Discover Bank | | | | | | | | | | |

| 3.10% | | 06/04/20 | | | 2,360,000 | | | | 2,366,464 | | | |

Dollar General Corp. | | | | | | | | | | |

| 1.88% | | 04/15/18 | | | 3,370,000 | | | | 3,337,584 | | | |

| 4.13% | | 07/15/17 | | | 3,373,000 | | | | 3,463,835 | | | |

| 4.15% | | 11/01/25 | | | 1,688,000 | | | | 1,677,992 | | | |

Dollar Tree Inc. | | | | | | | | | | |

| 5.75% | | 03/01/23 | | | 4,084,000 | | | | 4,257,570 | | | (b) |

Dominion Resources Inc. | | | | | | | | | | |

| 1.95% | | 08/15/16 | | | 3,151,000 | | | | 3,158,915 | | | |

Dr Pepper Snapple Group Inc. | | | | | | | | | | |

| 3.40% | | 11/15/25 | | | 3,376,000 | | | | 3,316,616 | | | |

Duke Energy Progress LLC | | | | | | | | | | |

| 4.15% | | 12/01/44 | | | 1,010,000 | | | | 986,400 | | | |

Eastman Chemical Co. | | | | | | | | | | |

| 3.60% | | 08/15/22 | | | 3,368,000 | | | | 3,353,386 | | | |

Ecopetrol S.A. | | | | | | | | | | |

| 5.88% | | 05/28/45 | | | 851,000 | | | | 604,210 | | | |

Electricite de France S.A. | | | | | | | | | | |

| 2.15% | | 01/22/19 | | | 6,811,000 | | | | 6,779,349 | | | (b) |

Eli Lilly & Co. | | | | | | | | | | |

| 3.70% | | 03/01/45 | | | 338,000 | | | | 316,138 | | | |

EMD Finance LLC | | | | | | | | | | |

| 3.25% | | 03/19/25 | | | 1,689,000 | | | | 1,601,572 | | | (b) |

Energizer Holdings Inc. | | | | | | | | | | |

| 5.50% | | 06/15/25 | | | 3,394,000 | | | | 3,190,360 | | | (b) |

Energy Transfer Equity LP | | | | | | | | | | |

| 5.88% | | 01/15/24 | | | 6,800,000 | | | | 5,542,000 | | | |

Energy Transfer Partners LP | | | | | | | | | | |

| 4.05% | | 03/15/25 | | | 675,000 | | | | 554,653 | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

16

| | |

GE RSP Income Fund | | December 31, 2015 |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

| 5.15% | | 03/15/45 | | $ | 1,182,000 | | | $ | 835,545 | | | |

| 6.50% | | 02/01/42 | | | 2,729,000 | | | | 2,219,635 | | | |

Ensco PLC | | | | | | | | | | |

| 4.50% | | 10/01/24 | | | 1,678,000 | | | | 1,155,588 | | | |

| 5.20% | | 03/15/25 | | | 1,014,000 | | | | 721,972 | | | |

| 5.75% | | 10/01/44 | | | 676,000 | | | | 445,365 | | | |

Enterprise Products Operating LLC | | | | | | | | | | |

| 3.70% | | 02/15/26 | | | 3,380,000 | | | | 3,034,385 | | | |

Equinix Inc. | | | | | | | | | | |

| 5.88% | | 01/15/26 | | | 675,000 | | | | 695,250 | | | |

ERP Operating LP | | | | | | | | | | |

| 4.50% | | 07/01/44 | | | 688,000 | | | | 690,408 | | | |

European Investment Bank | | | | | | | | | | |

| 4.88% | | 01/17/17 | | | 6,925,000 | | | | 7,200,033 | | | |

FedEx Corp. | | | | | | | | | | |

| 3.20% | | 02/01/25 | | | 1,073,000 | | | | 1,044,498 | | | |

Fiat Chrysler Automobiles N.V. | | | | | | | | | | |

| 4.50% | | 04/15/20 | | | 2,050,000 | | | | 2,075,625 | | | |

| 5.25% | | 04/15/23 | | | 1,400,000 | | | | 1,375,500 | | | |

Five Corners Funding Trust | | | | | | | | | | |

| 4.42% | | 11/15/23 | | | 3,703,000 | | | | 3,866,291 | | | (b) |

Florida Power & Light Co. | | | | | | | | | | |

| 4.13% | | 02/01/42 | | | 1,675,000 | | | | 1,667,020 | | | |

Ford Motor Credit Company LLC | | | | | | | | | | |

| 3.20% | | 01/15/21 | | | 3,401,000 | | | | 3,378,251 | | | |

| 3.22% | | 01/09/22 | | | 3,400,000 | | | | 3,328,889 | | | |

| 5.88% | | 08/02/21 | | | 2,569,000 | | | | 2,864,892 | | | |

Fresenius Medical Care US Finance Inc. | | | | | | | | | | |

| 5.75% | | 02/15/21 | | | 3,833,000 | | | | 4,101,310 | | | (b) |

Frontier Communications Corp. | | | | | | | | | | |

| 7.13% | | 03/15/19 | | | 3,979,000 | | | | 3,978,602 | | | |

| 11.00% | | 09/15/25 | | | 3,069,000 | | | | 3,038,310 | | | (b) |

General Motors Co. | | | | | | | | | | |

| 5.20% | | 04/01/45 | | | 338,000 | | | | 318,204 | | | (m) |

General Motors Financial Company Inc. | | | | | | | | | | |

| 3.15% | | 01/15/20 | | | 2,366,000 | | | | 2,344,969 | | | |

| 3.20% | | 07/13/20 | | | 6,761,000 | | | | 6,656,887 | | | (m) |

| 4.30% | | 07/13/25 | | | 3,380,000 | | | | 3,279,766 | | | (m) |

Georgia-Pacific LLC | | | | | | | | | | |

| 3.60% | | 03/01/25 | | | 2,545,000 | | | | 2,516,779 | | | (b) |

Gilead Sciences Inc. | | | | | | | | | | |

| 2.55% | | 09/01/20 | | | 1,690,000 | | | | 1,690,155 | | | |

| 3.65% | | 03/01/26 | | | 1,895,000 | | | | 1,911,841 | | | |

| 4.80% | | 04/01/44 | | | 767,000 | | | | 769,419 | | | |

Grupo Televisa SAB | | | | | | | | | | |

| 5.00% | | 05/13/45 | | | 967,000 | | | | 830,822 | | | |

Halliburton Co. | | | | | | | | | | |

| 2.70% | | 11/15/20 | | | 1,689,000 | | | | 1,670,179 | | | |

| 3.80% | | 11/15/25 | | | 1,696,000 | | | | 1,652,489 | | | |

| 5.00% | | 11/15/45 | | | 1,013,000 | | | | 1,000,672 | | | |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

HCA Inc. | | | | | | | | | | |

| 4.75% | | 05/01/23 | | $ | 5,690,000 | | | $ | 5,633,100 | | | |

| 6.50% | | 02/15/20 | | | 2,903,000 | | | | 3,162,819 | | | |

HSBC Holdings PLC | | | | | | | | | | |

| 4.25% | | 08/18/25 | | | 1,357,000 | | | | 1,346,917 | | | |

HSBC USA Inc. | | | | | | | | | | |

| 2.75% | | 08/07/20 | | | 5,059,000 | | | | 5,061,671 | | | |

Hyundai Capital America | | | | | | | | | | |

| 2.13% | | 10/02/17 | | | 1,488,000 | | | | 1,479,149 | | | (b) |

Illinois Tool Works Inc. | | | | | | | | | | |

| 3.50% | | 03/01/24 | | | 3,402,000 | | | | 3,497,603 | | | |

ING Bank N.V. | | | | | | | | | | |

| 2.70% | | 08/17/20 | | | 1,400,000 | | | | 1,406,833 | | | (b) |

Ingersoll-Rand Luxembourg Finance S.A. | | | | | | | | | | |

| 3.55% | | 11/01/24 | | | 2,358,000 | | | | 2,308,664 | | | |

Ingles Markets Inc. | | | | | | | | | | |

| 5.75% | | 06/15/23 | | | 5,729,000 | | | | 5,714,677 | | | |

Intel Corp. | | | | | | | | | | |

| 2.45% | | 07/29/20 | | | 1,690,000 | | | | 1,710,064 | | | |

Intelsat Jackson Holdings S.A. | | | | | | | | | | |

| 5.50% | | 08/01/23 | | | 3,422,000 | | | | 2,686,270 | | | |

International Business Machines Corp. | | | | | | | | | | |

| 3.63% | | 02/12/24 | | | 3,479,000 | | | | 3,583,106 | | | |

Interstate Power & Light Co. | | | | | | | | | | |

| 3.40% | | 08/15/25 | | | 3,380,000 | | | | 3,400,364 | | | |

Intesa Sanpaolo S.p.A. | | | | | | | | | | |

| 5.02% | | 06/26/24 | | | 1,167,000 | | | | 1,148,733 | | | (b) |

Invesco Finance PLC | | | | | | | | | | |

| 3.13% | | 11/30/22 | | | 4,673,000 | | | | 4,610,017 | | | |

JB Poindexter & Company Inc. | | | | | | | | | | |

| 9.00% | | 04/01/22 | | | 962,000 | | | | 1,005,290 | | | (b) |

JBS USA LLC/JBS USA Finance Inc. | | | | | | | | | | |

| 5.75% | | 06/15/25 | | | 2,722,000 | | | | 2,368,140 | | | (b) |

| 5.88% | | 07/15/24 | | | 1,896,000 | | | | 1,715,880 | | | (b) |

Jefferies Group LLC | | | | | | | | | | |

| 5.13% | | 01/20/23 | | | 1,378,000 | | | | 1,367,279 | | | |

| 6.50% | | 01/20/43 | | | 1,123,000 | | | | 1,038,248 | | | |

Johnson Controls Inc. | | | | | | | | | | |

| 4.63% | | 07/02/44 | | | 1,663,000 | | | | 1,409,378 | | | |

JPMorgan Chase & Co. | | | | | | | | | | |

| 2.55% | | 10/29/20 | | | 1,679,000 | | | | 1,664,052 | | | (m) |

| 3.88% | | 09/10/24 | | | 5,053,000 | | | | 5,029,008 | | | (m) |

| 3.90% | | 07/15/25 | | | 3,000 | | | | 3,090 | | | (m) |

| 4.25% | | 10/01/27 | | | 1,000,000 | | | | 998,575 | | | (m) |

| 5.00% | | 12/29/49 | | | 2,443,000 | | | | 2,320,850 | | | (h,m) |

| 6.10% | | 10/29/49 | | | 4,040,000 | | | | 4,060,604 | | | (h,m) |

KB Home | | | | | | | | | | |

| 7.00% | | 12/15/21 | | | 4,119,000 | | | | 4,062,364 | | | |

Keysight Technologies Inc. | | | | | | | | | | |

| 4.55% | | 10/30/24 | | | 3,365,000 | | | | 3,235,209 | | | |

See Notes to Schedules of Investments and Notes to Financial Statements.

17

| | |

GE RSP Income Fund | | December 31, 2015 |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

KFW | | | | | | | | | | | | |

| 2.00% | | 10/04/22 | | $ | 10,325,000 | | | $ | 10,158,478 | | | |

| 4.50% | | 07/16/18 | | | 2,938,000 | | | | 3,158,418 | | | |

Kinder Morgan Energy Partners LP | | | | | | | | | | |

| 3.50% | | 09/01/23 | | | 1,096,000 | | | | 909,226 | | | |

| 4.30% | | 05/01/24 | | | 1,756,000 | | | | 1,509,953 | | | |

Kinder Morgan Inc. | | | | | | | | | | |

| 3.05% | | 12/01/19 | | | 673,000 | | | | 623,094 | | | |

| 4.30% | | 06/01/25 | | | 1,346,000 | | | | 1,163,559 | | | |

| 5.55% | | 06/01/45 | | | 1,014,000 | | | | 791,845 | | | |

Kinross Gold Corp. | | | | | | | | | | |

| 6.88% | | 09/01/41 | | | 225,000 | | | | 123,282 | | | |

Kraft Heinz Foods Co. | | | | | | | | | | |

| 2.80% | | 07/02/20 | | | 5,071,000 | | | | 5,059,114 | | | (b,m) |

| 3.95% | | 07/15/25 | | | 4,395,000 | | | | 4,437,548 | | | (b,m) |

L Brands Inc. | | | | | | | | | | |

| 5.63% | | 02/15/22 | | | 3,628,000 | | | | 3,854,750 | | | |

L-3 Communications Corp. | | | | | | | | | | |

| 1.50% | | 05/28/17 | | | 2,332,000 | | | | 2,303,069 | | | |

Lee Enterprises Inc. | | | | | | | | | | |

| 9.50% | | 03/15/22 | | | 2,712,000 | | | | 2,495,040 | | | (b) |

Lennar Corp. | | | | | | | | | | |

| 4.50% | | 11/15/19 | | | 4,067,000 | | | | 4,135,631 | | | |

| 4.75% | | 05/30/25 | | | 1,355,000 | | | | 1,324,513 | | | |

Levi Strauss & Co. | | | | | | | | | | |

| 5.00% | | 05/01/25 | | | 2,041,000 | | | | 2,030,795 | | | |

Lockheed Martin Corp. | | | | | | | | | | |

| 2.50% | | 11/23/20 | | | 2,365,000 | | | | 2,356,678 | | | (m) |

| 3.55% | | 01/15/26 | | | 3,379,000 | | | | 3,396,351 | | | (m) |

| 3.80% | | 03/01/45 | | | 705,000 | | | | 624,464 | | | (m) |

| 4.70% | | 05/15/46 | | | 761,000 | | | | 783,082 | | | (m) |

Lowe’s Companies Inc. | | | | | | | | | | |

| 4.38% | | 09/15/45 | | | 1,350,000 | | | | 1,387,600 | | | |

LyondellBasell Industries N.V. | | | | | | | | | | |

| 4.63% | | 02/26/55 | | | 676,000 | | | | 548,205 | | | |

Macquarie Bank Ltd. | | | | | | | | | | |

| 4.88% | | 06/10/25 | | | 3,428,000 | | | | 3,385,164 | | | (b) |

Marathon Petroleum Corp. | | | | | | | | | | |

| 3.63% | | 09/15/24 | | | 3,370,000 | | | | 3,141,993 | | | |

Marsh & McLennan Companies Inc. | | | | | | | | | | |

| 3.50% | | 03/10/25 | | | 2,383,000 | | | | 2,347,362 | | | |

| 3.75% | | 03/14/26 | | | 2,365,000 | | | | 2,365,147 | | | |

Mattel Inc. | | | | | | | | | | |

| 2.35% | | 05/06/19 | | | 5,171,000 | | | | 5,127,951 | | | |

McDonald’s Corp. | | | | | | | | | | |

| 2.75% | | 12/09/20 | | | 921,000 | | | | 920,546 | | | |

| 3.70% | | 01/30/26 | | | 2,148,000 | | | | 2,146,769 | | | |

| 4.88% | | 12/09/45 | | | 706,000 | | | | 709,802 | | | |

Mead Johnson Nutrition Co. | | | | | | | | | | |

| 3.00% | | 11/15/20 | | | 2,363,000 | | | | 2,363,347 | | | |

| 4.13% | | 11/15/25 | | | 2,363,000 | | | | 2,381,996 | | | |

| | | | | | | | | | | | |

| | | Principal

Amount | | | Fair

Value | | | |

Medtronic Inc. | | | | | | | | | | |

| 2.50% | | 03/15/20 | | $ | 1,009,000 | | | $ | 1,016,426 | | | |

| 3.50% | | 03/15/25 | | | 4,042,000 | | | | 4,089,853 | | | |

| 4.63% | | 03/15/45 | | | 1,685,000 | | | | 1,737,281 | | | |

Memorial Sloan-Kettering Cancer Center | | | | | | | | | | |

| 4.13% | | 07/01/52 | | | 1,325,000 | | | | 1,235,993 | | | |

Merck & Company Inc. | | | | | | | | | | |

| 2.75% | | 02/10/25 | | | 3,380,000 | | | | 3,290,775 | | | |

MetLife Inc. | | | | | | | | | | |

| 3.60% | | 11/13/25 | | | 1,690,000 | | | | 1,703,016 | | | |

| 4.05% | | 03/01/45 | | | 843,000 | | | | 781,029 | | | |

| 4.72% | | 12/15/44 | | | 1,036,000 | | | | 1,058,017 | | | |

MGM Resorts International | | | | | | | | | | |

| 5.25% | | 03/31/20 | | | 2,037,000 | | | | 2,016,630 | | | |

| 6.63% | | 12/15/21 | | | 3,402,000 | | | | 3,482,797 | | | |

Microsoft Corp. | | | | | | | | | | |

| 4.00% | | 02/12/55 | | | 1,600,000 | | | | 1,436,139 | | | |

Mid-America Apartments LP | | | | | | | | | | |

| 4.00% | | 11/15/25 | | | 1,696,000 | | | | 1,684,952 | | | |

Mizuho Bank Ltd. | | | | | | | | | | |