UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-1512

Oppenheimer Capital Income Fund

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Cynthia Lo Bessette

OFI Global Asset Management, Inc.

225 Liberty Street, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: August 31

Date of reporting period: 8/31/2018

Item 1. Reports to Stockholders.

Class A Shares

AVERAGE ANNUAL TOTAL RETURNS AT 8/31/18

| | | | | | | | | | | | | | | | | | | | |

| | | Class A Shares of the Fund | | | | | | | | | | |

| | | | | | | | | | | | Bloomberg | | | | |

| | | Without Sales | | | With Sales | | | Russell 3000 | | | Barclays U.S. | | | Reference Index | |

| | | Charge | | | Charge | | | Index | | | Aggregate Bond | | | | |

| | | | | | | | | | | | Index | | | | |

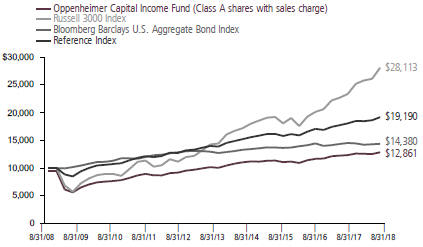

| 1-Year | | | 4.10% | | | | -1.88% | | | | 20.25% | | | | -1.05% | | | | 6.15% | |

| 5-Year | | | 5.05 | | | | 3.81 | | | | 14.25 | | | | 2.49 | | | | 6.69 | |

| 10-Year | | | 3.16 | | | | 2.55 | | | | 10.89 | | | | 3.70 | | | | 6.73 | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund returns include changes in share price, reinvested distributions, and a 5.75% maximum applicable sales charge except where “without sales charge” is indicated. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. Returns for periods of less than one year are cumulative and not annualized. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677). See Fund prospectuses and summary prospectuses for more information on share classes and sales charges.

2 OPPENHEIMER CAPITAL INCOME FUND

Fund Performance Discussion

The Fund’s Class A shares (without sales charge) generated a total return of 4.10% during the one-year period ended 8/31/18. On a relative basis, the Fund underperformed its Reference Index, a customized weighted index comprised of 65% Bloomberg Barclays U.S. Aggregate Bond Index (Bloomberg Barclays Index) and 35% Russell 3000 Index, which returned 6.15%. Measured separately, the Bloomberg Barclays Index returned -1.05% and the Russell 3000 Index returned 20.25%. The Fund marginally underperformed the Morningstar 30-50% Equity Category average, which returned 4.35%.

All three of the Fund’s strategies generated positive returns during the reporting period. The High Grade Fixed Income and Opportunistic strategies both outperformed the return of the Bloomberg Barclays Index. The Equity & Equity Like strategy generated a double-digit return, but underperformed the Russell 3000 Index. The underperformance of the Fund versus its Reference Index

was the result of underperformance in the equity strategy. During the reporting period, in equities broadly speaking, growth substantially outperformed value and the strong performance was driven by a narrow handful of stocks. Given these dynamics, it is not surprising that a core domestic-focused equity portfolio with a conservative tilt underperformed. The Opportunistic strategy

COMPARISON OF CHANGE IN VALUE OF $10,000 HYPOTHETICAL INVESTMENTS IN:

3 OPPENHEIMER CAPITAL INCOME FUND

outperformed the Bloomberg Barclays Index by more than 650 basis points (bps) during the period on the back of strong security selection. The Fund has continued to deliver on its value proposition of attractive total returns combined with low volatility (3.63% standard deviation versus 9.08% for the S&P 500 and 8.64% for the Russell 3000 Index during the reporting period), good downside risk mitigation, an attractive yield, and high risk-adjusted returns. For the period from April 2009 to August 2018 (the time that Michelle Borré has been lead portfolio manager), the Fund has generated a Sharpe Ratio of 1.69 versus 1.25 for the Morningstar 30-50% Equity Allocation Category peer group average and a Sortino Ratio of 3.88 versus 2.39 for the peer group average. (A higher number indicates a superior risk-adjusted return.)

The Fund’s Class A shares paid four dividends during the period: $0.0609 per share in June 2018, $0.0608 per share in March 2018, $0.0856 per share in December 2017 and $0.0613 per share in September 2017 for a total of $0.2686 per share in the last 12 months. (The Fund’s Class A shares had a net asset value (NAV) of $10.28 per share on 8/31/18.) In addition, we believe that upside/ downside capture ratios provide a good measure of the Fund’s downside protection. The upside capture ratio is the cumulative performance of the Fund in all up months of positive return divided by the cumulative performance of the index in those months. The downside capture ratio is the cumulative performance of the Fund in all down months

of negative return divided by the cumulative performance of the index in those months. For the period from April 2009 to August 2018 (the time that Michelle Borré has been lead portfolio manager), the Fund’s upside capture has been 94% of the Morningstar 30-50% Equity Allocation Category peer group average and its downside capture has been 60%. For the same period, the Fund’s upside capture has been 98% of the Reference Index and its downside capture has been 90%. This level of asymmetry means that the Fund has delivered significantly more upside than downside during that period. In our view, these distributions, combined with our upside/ downside capture ratios, are a testament to the Fund’s intelligent blending of multiple asset classes.

More broadly, the Fund seeks to deliver total return by providing a stream of income along with capital appreciation while attempting to mitigate downside risk. The Fund invests opportunistically in a broad range of securities across asset classes and capital structures. The portfolio is designed as a conservative investment vehicle with income, upside potential, strong risk-adjusted returns, controlled drawdowns and low volatility. Our investment process combines top down and bottom up analyses both within and across asset classes. We are fundamentally driven and longer-term, value-oriented investors.

MARKET OVERVIEW

Regarding the macro environment, risk assets around the world rallied from the date of

4 OPPENHEIMER CAPITAL INCOME FUND

President Donald Trump’s election victory in November 2016 through 12/31/17, pushing valuations close to all-time highs for a variety of asset classes. During the first eight months of 2018, however, many of these asset classes have reversed course and posted losses. For example, although the S&P 500 generated a positive total return of 9.94% in the first eight months of 2018, the DAX Index (a measure of blue chip German stocks) has fallen 4.29%, the MSCI Emerging Markets Index has fallen 6.99%, and the Shanghai Composite Index has fallen 15.72% over the same period. In addition, the performance difference between growth and value equities has continued to be enormous, with the Russell 1000 Growth Index generating a 27.23% return during the reporting period compared to the 12.47% return for the Russell 1000 Value Index. Against this backdrop, interest rates have continued to climb higher, with the yield on the 10-year Treasury note rising from 1.85% on election day to 2.86% by the end of the reporting period for an increase of 101 bps. Fixed income has come under pressure as rates have continued to back up, with the Bloomberg Barclays Index falling 1.05% during the reporting period. In our view, Treasuries could become less helpful to investors during market selloffs, in part because they offer low yields, making the risk/ reward tradeoff unattractive. We believe this is especially true as the Federal Reserve (Fed) continues on its well-telegraphed path of raising rates while simultaneously shrinking its balance sheet.

The Trump administration has injected a level of policy uncertainty into the markets that investors have not seen in quite a while. At the same time, we believe structural flaws in both Europe and Japan remain unresolved. China and other emerging markets will likely eventually face slower long-term growth because the current growth is overly reliant, in our view, on excessive credit expansion. Meanwhile, we believe that in a number of countries there has been a meaningful change in the relationship between elected representatives and voters, or stated differently, between those who make policies and those who actually pay for those policies. We have discussed in previous commentaries the impact of Brexit along with the rise of populist parties in Europe. In March 2018, Italian voters shunned center left parties and instead voted for populist and center right candidates, resulting in a hung parliament. Although the Euro-skeptic/ populist Five Star party and the anti-immigrant League party have subsequently formed a ruling coalition, it remains to be seen how effectively they can govern and for how long. The new government is also likely to test the existing budget constraints in the EU. More recently, in September 2018, Sweden held elections but no single party won enough votes to form a government. The nationalist Sweden Democrats (SD) won 18% of the vote although the center-left ruling coalition and the center-right alliance (both with approximately 40% of the vote) have refused to govern with SD. Shortly after that election, Prime Minister Stefan Löfven lost a no-confidence vote and will be forced

5 OPPENHEIMER CAPITAL INCOME FUND

to step down. A major issue in the election was Sweden’s immigration policy. Joining the EU opened the door to new problems like immigration and the need to bail out peripheral nations. However, the EU does not seem capable of solving these issues, in our opinion, which has caused significant internal tension. We believe the EU in its current form is unsustainable, although we do not know what specific catalysts might cause changes in its structure or when those changes might occur.

Moreover, we believe investors now face rising geopolitical risks both in the U.S. and around the world. Trade disputes between the U.S. and China, Europe, Japan, Canada and Mexico have the potential to escalate meaningfully. At the same time, the Trump administration faces challenges at home including an investigation by special counsel Robert Mueller, a growing list of announced retirements by Republicans in Congress, and looming mid-term elections. Under these circumstances, we believe investors could benefit from a broader toolkit than was needed during the risk-on, quantitative easing (QE)-supported market of the past several years and a different toolkit than has been effective in the past because of the unfavorable risk/reward in conservative fixed income. Part of this broader toolkit could include the Fund’s ability to take short positions, which can profit from market declines. This kind of short exposure is available through the Opportunistic strategy of the Fund. (Because the Fund does not have a prime broker, we do not short

individual securities. However, we can take negative positions, or the functional equivalent of short exposures, through a variety of different financial instruments.)

FUND REVIEW

Equity & Equity Like Strategy. The Fund’s Equity & Equity-Like strategy may include common stocks, equity derivatives and hybrid securities with equity sensitivity. This strategy generated a double-digit return during the reporting period, but underperformed the Russell 3000 Index. The strongest contributors to performance were our call options on the S&P 500 and our positions in Cisco and Apple. The largest detractors were our positions in Philip Morris International, General Electric, and Dish Network.

Our call options on the S&P 500 contributed to performance as the index climbed 19.66% in the period on the back of strong earnings acceleration, solid quarterly results, and continued economic growth in the U.S. We like the asymmetry of the call options, which we believe have limited downside and considerably more potential upside.

Our position in Cisco Systems (CSCO), a manufacturer of networking hardware and telecommunications equipment, also contributed to performance. The company’s shares have benefited from a variety of factors. First, Cisco is showing tangible evidence of its ability to transition to a higher mix of recurring revenue through a

6 OPPENHEIMER CAPITAL INCOME FUND

subscription model. Second, the company has been a major beneficiary of capital repatriation enabled by the recently enacted tax reforms. Management has made clear that it will use these funds to improve its shareholder capital allocation program. Finally, Cisco has benefited from overall improvement in the enterprise spending environment on the back of improved economic conditions, higher corporate cash flows (resulting from lower taxes), and accelerated depreciation available under the new tax laws.

Our position in Apple Inc. (AAPL), a technology company that designs and sells consumer electronics and online services, contributed to performance as the company benefited from investor anticipation surrounding its upcoming product cycle. In addition, investors have gained a better appreciation of the benefit of Apple’s recurring revenue stream from services as well as its aggressive plans to return capital to shareholders. In this regard, in May 2018, management announced a new $100 billion share repurchase program and increased the dividend by 16%. The buyback program commenced in June 2018 and management expects to complete it at a fast pace. The increase in the dividend is the largest since the company re-introduced the dividend in 2012.

In contrast, our position in Philip Morris International (PM), a cigarette and tobacco company, detracted from performance. The shares suffered as investors have become

concerned about possible market saturation for iQOS in Japan. Although we expect growth to slow in that market, the global rollout of iQOS is still in the early stages. We expect the heat-not-burn technology to enjoy a multi-year penetration trend and expect iQOS to be accretive to market share and potentially to margins for the company.

Our holdings in General Electric (GE), an industrial conglomerate focused on aviation, power, energy, and healthcare, underperformed during the period in part due to investors’ concerns about the magnitude of revisions to the earnings outlook for 2017-2018. The concerns stem from a weaker global gas power generation outlook, a longer recovery period for the Oil & Gas business and a slowing wide-body aerospace cycle. The market has also been penalizing GE’s lower free cash flow conversion rate of 65% versus its historical rate of 80%. The announced 50% dividend cut in November 2017 was also a negative that hurt the stock, but gives the company needed flexibility to fund future capital expenditures. The January 2018 announcement of a reinsurance charge and required cash contribution for GE Capital compounded the problem. However, subsequent to the end of the reporting period, the company announced the appointment of a new CEO, Larry Culp, to help turn the company around. Mr. Culp’s success in leading Danaher for 14 years and his reputation for operating excellence, combined with investors’ confidence in his strategic vision, has resulted in GE’s stock moving noticeably higher since the announcement.

7 OPPENHEIMER CAPITAL INCOME FUND

We believe these actions should translate into improved free cash flow generation over time.

Our position in Dish Network (DISH), a television services provider, was also a detractor. The shares have suffered as there had been investor expectations that management could monetize the company’s existing spectrum holdings now that all service providers are free to discuss mergers, joint ventures and partnerships. For the last few years, these conversations weren’t possible because of anti-collusion rules that were in place as the government executed several spectrum auctions. While it’s uncertain when, or if, DISH will partner with another company, we are confident that in a capacity-constrained world, its spectrum is valuable and management will be opportunistic in monetizing these assets.

Opportunistic strategy. In this strategy we seek asymmetric risk/reward opportunities and investments where the return profile has a low correlation to traditional investment strategies. We also seek investments that can help to achieve the broader objectives of the Fund. At the end of the reporting period, this strategy included investments in senior loans through Oppenheimer Master Loan Fund, LLC, asset-backed securities (ABS), corporate bonds, and certain derivatives. This strategy outperformed the Bloomberg Barclays Index by over 650 bps during the reporting period, largely on the back of strong security selection. Among the top performers in this strategy were our positions in senior bank loans, the preferred stock of Citigroup, and

our spread position in European sovereign debt. The biggest detractors were our position in gold, our pair trade that was long the U.S. dollar and short the Thai baht, and our holdings in bonds issued by Wells Fargo.

Our holdings in the Oppenheimer Master Loan Fund, LLC contributed to performance in the period. The economy continued to grow while still easy financial conditions prevailed. Floating rate loans have benefited from the rise in U.S. interest rates as well as the rise in Libor since Trump’s election victory. The floating rate nature of these securities tends to make them more attractive than fixed rate securities in a rising rate environment. Credit spreads tightened in the period as solid economic growth continues to support asset prices. Default rates remain under 2%, which is below the historical average.

Our position in the preferred stock of Citigroup also contributed to performance. Citigroup Capital XIII is a trust preferred security that pays a floating interest rate of 3-month Libor plus 637 bps; currently, 3-month Libor is 234 bps. Since this is a floating rate security, it contributed to performance during a period of rising yields on longer-dated Treasuries. In addition, Citigroup Capital XIII outperformed the S&P Preferred Stock Index during the twelve months ended 8/31/18.

Our long/short position in European credit spreads contributed to performance as well. This position benefits from wider spreads between Germany and less creditworthy

8 OPPENHEIMER CAPITAL INCOME FUND

European sovereigns (i.e., Italy, Spain and France). In March 2018, Italian voters shunned center left parties and instead voted for populist and center right candidates, resulting in a hung parliament. Since then, the Euro-skeptic/populist Five Star party and the anti-immigrant League party have formed a ruling coalition. The government’s plans call for a larger fiscal deficit, which detracts from Italy’s credit profile. Furthermore, we believe it increases the strain on the EU. Both of these factors caused Italian credit spreads to widen, benefiting our position.

In contrast, our position in gold (GLD) detracted from performance as the yellow metal declined by 9.1% to $1,201 per troy ounce in the period. Gold bullion, which began the period at $1,321, oscillated in a $206 range before ending the period with a loss of $120 per ounce. The precious metals complex fell on the back of a stronger dollar (the U.S. Dollar Index climbed 2.7% in the period), continued solid economic growth, rising U.S. interest rates, and moderate inflation expectations. We believe some investors are increasingly viewing gold and other precious metals as warrants (i.e., long-dated options) on monetary policy going off the rails or a potential hedge against competitive currency debasement or adverse geopolitical events.

Our pair trade that was long U.S. dollar / short Thai baht detracted from performance as well. We exited this position in June. These bonds were fixed to floating rate securities that were paying a fixed rate of

5.9%. If these securities were not called (redeemed) in June of 2024, they would pay a floating rate of 3-month Libor plus 311 bps. The bonds were negatively impacted in the period by rising yields on longer-dated Treasuries as well as by widening credit spreads. Wider spreads reduced the probability that these bonds would be called, which in turn negatively impacted performance. During the twelve months ended 8/31/18, the total return from these securities outperformed the return from longer-dated Treasuries, but underperformed the return from the S&P Preferred Stock Index.

High Grade Fixed Income strategy.

The High Grade Fixed Income strategy generated positive returns and outperformed the Bloomberg Barclays Index during the reporting period. This strategy continues to favor corporate bonds, mortgages, and other securitized products over government debt. The dollar was generally stronger during the period against a basket of currencies for the largest trading partners of the U.S. In addition, the yield on the 10-year Treasury note climbed from 1.85% to 2.86% by the end of the period. Contributing to this strategy’s outperformance was an allocation to non-agency mortgage-backed securities (MBS), which benefited from solid fundamentals and a strong technical environment. Also benefiting relative performance was an allocation to BB-rated corporate bonds, an underweight to U.S. Treasuries, and solid security selection.

9 OPPENHEIMER CAPITAL INCOME FUND

The economic expansion continues as the U.S. economy is nearing the Fed’s dual mandate of full employment and price stability. Underlying inflation is converging toward the Fed’s 2% target. The High Grade Fixed Income Team believes the Fed is on track to deliver two additional rate hikes in 2018 after hiking by 25 bps three separate times during the reporting period. The Fed has signaled that it will tighten policy gradually, and so far, the hiking cycle has been orderly.

The High Grade Fixed Income Team believes macroeconomic fundamentals should remain solid with a continued increase in U.S. growth resulting from fiscal stimulus and tax reform. Although the Team generally remains neutral duration, in light of rising Treasury yields, particularly at the front of the curve, the Team maintained its slightly shorter effective duration than the Bloomberg Barclays Index at the end of the reporting period. At the sector level, the Team continues to maintain its strategic underweight to U.S. Treasuries. In lieu of Treasuries, the Team continues to maintain its overweight in agency MBS relative to the Bloomberg Barclays Index. The Team believes the sector’s high quality and spread above Treasuries make it an attractive area to add incremental yield potential to the portfolio. Within structured credit, the Team continues to favor auto ABS given their attractive fundamentals, carry and solid structures. The Team has also maintained a small overweight in commercial mortgage-backed securities (CMBS) and remains up-in-structure. Overall, the High Grade Fixed Income Team is more cautious on

credit as it believes we currently reside in the fourth quarter of the credit cycle. The Team remains cautiously engaged in investment grade corporate credit with modest exposure to typically high Sharpe Ratio BB-rated corporates. As a result, the Team is less likely to increase credit risk meaningfully, absent specific relative value opportunities. The Team typically avoids corporate bonds that are rated B or below and also avoids emerging market debt.

STRATEGY & OUTLOOK

After a nearly two-year hiatus, volatility and drawdowns have returned. In our view, the sudden spike in volatility and 10% drop in the S&P 500 in January were overdue. We believe the actual outlier was 2017 with its 50-year lows in equity volatility, 30-year lows in Treasury volatility, and a maximum drawdown of 2.8% on the S&P 500—well below the annual average of more than 10%. In particular, by the end of 2017, it had been more than 380 days since the last 5% drawdown on the S&P 500, far longer than the 90-day average of the last nine decades. The market was due for a spike in volatility and a meaningful drawdown, both of which occurred in late January as the CBOE Volatility Index (VIX Index) jumped more than 250% and the S&P 500 fell 10.1%. The bumpiness continued as the VIX Index spiked 65% in late March and the S&P 500 sold off 7.5%. Prolonged periods of low volatility breed complacency and a lack of mindfulness about downside risk, in our view. We believe many investors are starting to pay attention again.

10 OPPENHEIMER CAPITAL INCOME FUND

The combination of tax cuts, fiscal stimulus and a tight labor market could lead to higher inflation and higher rates than many investors expect. The Trump administration is pursuing a triple play of tax cuts, higher federal spending, and a major proposed infrastructure plan. Significantly, these efforts are taking place as the economy is accelerating and during a tight labor market. The fact that the administration is pursuing these policies in the absence of a recession makes them unusual. The fact that it is pursuing them all at the same time and so late in the economic cycle makes them highly unusual. We believe this stimulus increases the dual risks of higher inflation and tighter monetary policy.

U.S. Equities are Outperforming International Equities for a Reason this Year. The S&P 500 is meaningfully outperforming most developed and emerging market equity indices thus far in 2018—and there is a reason why. In the fourth quarter of 2017, the Fed was raising interest rates and starting to shrink its balance sheet. Simply put, quantitative easing was morphing into quantitative tightening. By the end of the reporting period, Congress had enacted tax reforms, it had agreed to two years of fiscal stimulus, and the Trump administration had drafted an infrastructure program. As a result, the federal government was borrowing more at a time when the U.S. Treasury was selling assets. This combination of factors effectively pulled U.S. dollars out of the rest of the world, making it more expensive to borrow in

dollars. The good news for U.S. companies is that they have enjoyed the benefits of several offsets in the form of lower tax rates, increased fiscal stimulus, consistent deregulation by the Trump administration, and accelerating economic growth. In contrast, companies in other developed markets as well as those in the emerging markets have enjoyed few (if any) such offsets. This is part of the reason why economic growth in the U.S. and earnings growth for the S&P 500 have been so robust relative to other markets thus far in 2018, in our view.

The trade winds are shifting but by how much remains to be seen. In the wake of Trump’s election victory, we wrote in our fourth quarter commentary for 2016 that international trade was one area of public policy where Trump did not need the approval of Congress to effect meaningful change. That view has proved to be correct so far as the U.S. has engaged in simultaneous trade disputes with China, Europe, Japan, Mexico, and Canada. The dispute with Mexico may be heading toward resolution, but the other disputes remain outstanding and how or when they are resolved remains uncertain. We do know, however, that trade barriers tend to make goods and services more expensive, and on a longer-term basis, they tend to slow economic growth, although the impact may not be apparent for some time.

There is a changing of the guard at the Fed. Jerome Powell became the new Chairman of the Federal Reserve when Janet

11 OPPENHEIMER CAPITAL INCOME FUND

Yellen’s term expired in February. Richard Clarida recently joined the Fed as Vice Chairman and Randy Quarles joined the Fed in early 2018. Trump has also nominated Professor Marvin Goodfriend and Michelle Bowman to positions as Fed Governors. Their confirmation hearings took place earlier this year but the Senate has yet to vote on these nominees. If a newly reconstituted Fed is more hawkish than investors currently expect, then the Trump administration could ultimately shift the tide away from the current easy money policies of central banks around the world. The Fed has raised the Fed Funds rate by 25 bps seven times since December 2015, including twice in 2018, and indicated that it plans two additional hikes in 2018, three in 2019, and one in 2020. It also started to normalize its $4.5 trillion balance sheet in October, which is effectively additional monetary policy tightening. At the Fed’s stated pace, that balance sheet should shrink below $4.0 trillion by the end of 2018.

The Fed is not alone—other central banks are moving in the same direction. Almost a dozen central banks around the world have started hiking rates this year in response to rising inflation and a falling local currency. Among the G-4 central banks, the Bank of England recently hiked rates for the second time in a decade, the European Central Bank is currently tapering its QE program (which is expected to end in December 2018), and the Bank of Japan has signaled that it could let the yield on 10-year Japanese government bonds start to rise

next year. All of this is a notable regime shift after years of coordinated monetary policy easing on a global basis. We could possibly see the first reduction of QE on a global basis in a while in 2019 as other central banks follow the U.S. in reducing stimulus. In fact, the rate at which G-4 central bank balance sheets are expanding has already slowed dramatically since the Fed started shrinking its balance sheet in October 2017. In our opinion, the next step is for the collective size of those balance sheets to start contracting. Today, only the Fed’s balance sheet is contracting. This change could be significant because central bank buying of assets globally has impacted interest rates around the world. We have constructed the portfolio with an eye toward delivering low volatility, effective diversification, strong downside risk mitigation, and high risk-adjusted returns in a variety of market conditions.

U.S. stocks and bonds remain expensive. Valuations for stocks and bonds in the U.S. are at or near their highest deciles going back 100 years. The fact that both asset classes are so expensive at the same time is unusual. Regarding equities, there is an earnings boost coming from tax reform but in the long term, buying stocks at high valuations typically means lower expected future returns for investors. At the same time, U.S. fixed income is expensive relative to historical valuations and the Fed has repeatedly warned of additional rate hikes through 2020. Moreover, the Trump administration’s fiscal and economic policies have caused a meaningful change in the

12 OPPENHEIMER CAPITAL INCOME FUND

outlook for fixed income. Treasury rates had been range bound for some time, with yields oscillating between 1.25% to 3.0%. In the longer run, however, we did not believe rates this low were sustainable. Trump’s election victory sent rates higher as the 10-year yield jumped from 1.85% on election day to 2.86% by 8/31/18. We have become more bearish on fixed income after the election. In our view, a strong focus on valuations is critical at this point in the economic, equity and credit cycles.

Seeking attractive investment opportunities later in the cycle. We believe the U.S. economy still has attractive growth potential in certain areas, and are waiting to see what additional pro-growth policies the Trump administration can actually implement. We recognize that there are pockets of innovation and disruption in different industries including consumer packaged goods, pharmaceuticals, consumer discretionary, real estate, and technology. Nonetheless, we are mindful that the U.S. equity bull market became the longest on record as of 8/22/18, eclipsing the prior record which ran from October 1990 to March 2000. We also recognize that extended periods of low equity volatility historically have not been sustainable, and they typically resolve with a period of meaningfully higher volatility. In part because of the Fed’s multiple rounds of quantitative easing in the wake of the global financial crisis, the U.S. equity market entered an extended period of

low volatility that began in early 2012 and continues through today. Over the last 30 years, the average maximum drawdown for the S&P 500 during periods of low volatility has been just under 10%. In sharp contrast, the average maximum drawdown for the S&P 500 during periods of high volatility has been just over 40%. The dual risks for investors are that volatility moves meaningfully higher and drawdowns become much more severe.

Moreover, we recognize that U.S. equity valuations are pushing up against the edge of bubble territory after several years when S&P 500 Index performance ran well ahead of earnings growth, leading to significant multiple expansion. (Since the S&P 500 bottomed in March 2009, it has climbed by more than 330% through 8/31/18, while S&P earnings have grown by less than one third of that figure.) In fact, the only time in the last four decades when the S&P 500 Index has traded at a higher price-earnings multiple on next 12 months’ consensus earnings was during the Tech Bubble in 1997-2000.

Accordingly, we continue to pick our spots, selecting securities that we believe offer attractive risk-adjusted returns. We remain focused, as always, on controlling volatility and mitigating downside risk. We expect to be in a cross-current heavy world for a while. We believe that the ability to generate attractive returns efficiently and without taking on undue risk, controlling volatility and limiting drawdowns will be of greater value to

13 OPPENHEIMER CAPITAL INCOME FUND

investors in this kind of environment, and that is where our investment team’s efforts are focused.

| | |

| |

Michelle Borré, CFA Portfolio Manager |

|

| | |

| |

Krishna Memani Portfolio Manager |

|

14 OPPENHEIMER CAPITAL INCOME FUND

Portfolio Positioning

| | | | | | | | | | | | |

| PORTFOLIO POSITIONING | | | | | | | | | | | | |

| | | Long | | | Short | | | Net | |

High-Grade Fixed Income Strategy | | | 42.4% | | | | -20.5% | | | | 21.9% | |

Equity Strategy | | | 39.3 | | | | -0.6 | | | | 38.7 | |

Opportunistic Strategy | | | 30.9 | | | | -14.6 | | | | 16.3 | |

| | | |

| HIGH-GRADE FIXED INCOME STRATEGY | | | | | | | | | | | | |

| | | Long | | | Short | | | Net | |

Corporate Bonds | | | 18.2% | | | | 0.0% | | | | 18.2% | |

Mortgage Related Securities | | | 16.4 | | | | 0.0 | | | | 16.4 | |

Asset Backed Securities | | | 5.2 | | | | 0.0 | | | | 5.2 | |

Duration Hedges | | | 2.7 | | | | -20.5 | | | | -17.8 | |

Credit Default Swaps | | | 0.0 | | | | 0.0 | | | | 0.0 | |

| | | |

| TOP TEN EQUITY HOLDINGS | | | | | | | | | | | | |

| | | Long | | | Short | | | Net | |

Apple, Inc. | | | 1.3% | | | | 0.0% | | | | 1.3% | |

M&T Bank Corp. | | | 1.2 | | | | 0.0 | | | | 1.2 | |

Chubb Ltd. | | | 1.2 | | | | 0.0 | | | | 1.2 | |

Alphabet, Inc., Cl. A | | | 1.1 | | | | 0.0 | | | | 1.1 | |

UnitedHealth Group, Inc. | | | 1.1 | | | | 0.0 | | | | 1.1 | |

Philip Morris International, Inc. | | | 1.1 | | | | 0.0 | | | | 1.1 | |

Blackstone Mortgage Trust, Inc., Cl. A | | | 1.0 | | | | 0.0 | | | | 1.0 | |

Lockheed Martin Corp. | | | 1.0 | | | | 0.0 | | | | 1.0 | |

Cisco Systems, Inc. | | | 0.9 | | | | 0.0 | | | | 0.9 | |

Xilinx, Inc. | | | 0.9 | | | | 0.0 | | | | 0.9 | |

Portfolio holdings and allocations are dollar-weighted based on total net assets and are subject to change. Percentages are as of August 31, 2018. Holdings exclude cash and cash equivalents. As of August 31, 2018, the Fund held approximately 6.6% in cash and cash equivalents. Negative weightings may result from the use of leverage. Leverage involves the use of various financial instruments or borrowed capital in an attempt to increase investment return. Leverage risks include potential for higher volatility, greater decline of the Fund’s net asset value and fluctuations of dividends and distributions paid by the Fund. Asset tables may not display cash weightings. Net total exposure may not equal the sum of long and short exposure due to rounding. For more current Fund holdings, please visit oppenheimerfunds.com.

15 OPPENHEIMER CAPITAL INCOME FUND

| | | | | | | | | | | | |

OPPORTUNISTIC STRATEGY | | | | | | | | | | | | |

| | | Long | | | Short | | | Net | |

Senior Loans | | | 13.0% | | | | 0.0% | | | | 13.0% | |

Corporate Bonds & Hybrids | | | 5.7 | | | | 0.0 | | | | 5.7 | |

Asset Backed Securities | | | 5.3 | | | | 0.0 | | | | 5.3 | |

Commodities | | | 1.0 | | | | 0.0 | | | | 1.0 | |

Sovereign | | | 1.9 | | | | -5.3 | | | | -3.4 | |

Interest Rates | | | 0.0 | | | | -3.3 | | | | -3.3 | |

Relative Value | | | 2.8 | | | | -3.6 | | | | -0.8 | |

Currencies | | | 0.0 | | | | -2.4 | | | | -2.4 | |

Catastrophe Bonds | | | 1.1 | | | | 0.0 | | | | 1.1 | |

Portfolio holdings and allocations are dollar-weighted based on total net assets and are subject to change. Percentages are as of August 31, 2018. Holdings exclude cash and cash equivalents. As of August 31, 2018, the Fund held approximately 6.6% in cash and cash equivalents. Negative weightings may result from the use of leverage. Leverage involves the use of various financial instruments or borrowed capital in an attempt to increase investment return. Leverage risks include potential for higher volatility, greater decline of the Fund’s net asset value and fluctuations of dividends and distributions paid by the Fund. Asset tables may not display cash weightings. Net total exposure may not equal the sum of long and short exposure due to rounding. For more current Fund holdings, please visit oppenheimerfunds. com.

16 OPPENHEIMER CAPITAL INCOME FUND

Share Class Performance

AVERAGE ANNUAL TOTAL RETURNS WITHOUT SALES CHARGE AS 8/31/18

| | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1-Year | | | 5-Year | | | 10-Year | | | | |

| Class A (OPPEX) | | | 12/1/70 | | | | 4.10 | % | | | 5.05 | % | | | 3.16 | % | | | | |

| Class C (OPECX) | | | 11/1/95 | | | | 3.24 | | | | 4.25 | | | | 2.32 | | | | | |

| Class I (OCIIX) | | | 12/27/13 | | | | 4.44 | | | | 4.65 | * | | | N/A | | | | | |

| Class R (OCINX) | | | 3/1/01 | | | | 3.73 | | | | 4.75 | | | | 2.82 | | | | | |

| Class Y (OCIYX) | | | 1/28/11 | | | | 4.25 | | | | 5.29 | | | | 5.86 | * | | | | |

| |

AVERAGE ANNUAL TOTAL RETURNS WITH SALES CHARGE AS OF 8/31/18 | | | | | |

| | | Inception

Date | | | 1-Year | | | 5-Year | | | 10-Year | | | | |

| Class A (OPPEX) | | | 12/1/70 | | | | -1.88 | % | | | 3.81 | % | | | 2.55 | % | | | | |

| Class C (OPECX) | | | 11/1/95 | | | | 2.24 | | | | 4.25 | | | | 2.32 | | | | | |

| Class I (OCIIX) | | | 12/27/13 | | | | 4.44 | | | | 4.65 | * | | | N/A | | | | | |

| Class R (OCINX) | | | 3/1/01 | | | | 3.73 | | | | 4.75 | | | | 2.82 | | | | | |

| Class Y (OCIYX) | | | 1/28/11 | | | | 4.25 | | | | 5.29 | | | | 5.86 | * | | | | |

* Shows performance since inception.

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800. CALL OPP (225.5677). Fund returns include changes in share price, reinvested distributions, and the applicable sales charge: for Class A shares, the current maximum initial sales charge of 5.75% and for Class C shares, the contingent deferred sales charge of 1% for the 1-year period. There is no sales charge for Class I, Class R and Class Y shares. Returns for periods of less than one year are cumulative and not annualized. See Fund prospectuses and summary prospectuses for more information on share classes and sales charges.

The Fund’s performance is compared to the performance of the Russell 3000 Index, the Bloomberg Barclays U.S. Aggregate Bond Index and the Fund’s Reference Index. The Russell 3000 Index measures the performance of the largest 3,000 U.S. companies, representing approximately 98% of the investable U.S. equity market. The Bloomberg Barclays U.S. Aggregate Bond Index is an index of U.S. dollar-denominated, investment-grade U.S. corporate government and mortgage-backed securities. The Fund’s Reference Index is a customized weighted index currently comprised of 35% Russell 3000 Index and 65% Bloomberg Barclays U.S. Aggregate Bond Index. The indices are unmanaged and cannot be purchased directly by investors. While index comparisons may be useful to provide a benchmark for the Fund’s performance, it must be noted that the Fund’s investments are not limited to the investments comprising the indices. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict

17 OPPENHEIMER CAPITAL INCOME FUND

performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

The Morningstar 30-50% Equity Allocation Category Average is the average return of the mutual funds within the investment category as defined by Morningstar. Returns include the reinvestment of distributions but do not consider sales charges. The Morningstar 30-50% Equity Category Average performance is shown for illustrative purposes only and does not predict or depict the performance of the Fund.

The views in the Fund Performance Discussion represent the opinions of this Fund’s portfolio manager(s) and are not intended as investment advice or to predict or depict the performance of any investment. These views are as of the close of business on August 31, 2018, and are subject to change based on subsequent developments. The Fund’s portfolio and strategies are subject to change.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking your financial advisor, visiting oppenheimerfunds.com, or calling 1.800.CALL OPP (225.5677). Read prospectuses and summary prospectuses carefully before investing.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

18 OPPENHEIMER CAPITAL INCOME FUND

Fund Expenses

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments and/or contingent deferred sales charges on redemptions; and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire 6-month period ended August 31, 2018.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During 6 Months Ended August 31, 2018” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or contingent deferred sales charges (loads). Therefore, the “hypothetical” section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

19 OPPENHEIMER CAPITAL INCOME FUND

| | | | | | | | | | | | |

| Actual | | Beginning Account Value March 1, 2018 | | Ending Account Value August 31, 2018 | | Expenses Paid During 6 Months Ended August 31, 2018 |

Class A | | $ | 1,000.00 | | | $ | 1,022.20 | | | $ | 4.96 | |

Class C | | | 1,000.00 | | | | 1,018.10 | | | | 8.89 | |

Class I | | | 1,000.00 | | | | 1,024.10 | | | | 2.91 | |

Class R | | | 1,000.00 | | | | 1,020.30 | | | | 6.33 | |

Class Y | | | 1,000.00 | | | | 1,023.30 | | | | 3.78 | |

| | | |

| Hypothetical | | | | | | | | | | | | |

| (5% return before expenses) | | | | | | |

Class A | | | 1,000.00 | | | | 1,020.32 | | | | 4.95 | |

Class C | | | 1,000.00 | | | | 1,016.43 | | | | 8.88 | |

Class I | | | 1,000.00 | | | | 1,022.33 | | | | 2.91 | |

Class R | | | 1,000.00 | | | | 1,018.95 | | | | 6.33 | |

Class Y | | | 1,000.00 | | | | 1,021.48 | | | | 3.78 | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended August 31, 2018 are as follows:

| | | | |

| Class | | Expense Ratios | |

Class A | | | 0.97% | |

Class C | | | 1.74 | |

Class I | | | 0.57 | |

Class R | | | 1.24 | |

Class Y | | | 0.74 | |

The expense ratios reflect voluntary and/or contractual waivers and/or reimbursements of expenses by the Fund’s Manager and Transfer Agent. Some of these undertakings may be modified or terminated at any time, as indicated in the Fund’s prospectus. The “Consolidated Financial Highlights” tables in the Fund’s financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

20 OPPENHEIMER CAPITAL INCOME FUND

CONSOLIDATED

STATEMENT OF INVESTMENTS August 31, 2018

| | | | | | |

| | | Shares | | | Value |

| Common Stocks—34.8% | | | | | | |

| Consumer Discretionary—1.4% | | | | | | |

| Household Durables—0.2% | | | | | | |

| Mohawk Industries, Inc.1 | | | 30,740 | | | $ 5,889,477 |

| Media—0.8% | | | | | | |

| DISH Network Corp., Cl. A1 | | | 266,644 | | | 9,425,865 |

| Live Nation Entertainment, Inc.1 | | | 196,560 | | | 9,765,101 |

| | | | | | 19,190,966 |

| Specialty Retail—0.4% | | | | | | |

Lowe’s Cos., Inc. | | | 87,440 | | | 9,509,099 |

| Consumer Staples—2.3% | | | | | | |

| Beverages—0.7% | | | | | | |

Coca-Cola Co. (The) | | | 404,900 | | | 18,046,393 |

| Tobacco—1.6% | | | | | | |

| Altria Group, Inc. | | �� | 241,365 | | | 14,124,680 |

| Philip Morris International, Inc. | | | 347,030 | | | 27,030,166 |

| | | | | | 41,154,846 |

| Energy—3.2% | | | | | | |

| Energy Equipment & Services—0.4% | | | | | | |

| Halliburton Co. | | | 93,584 | | | 3,733,066 |

| Schlumberger Ltd. | | | 98,866 | | | 6,244,376 |

| | | | | | 9,977,442 |

| Oil, Gas & Consumable Fuels—2.8% | | | | | | |

| Canadian Natural Resources Ltd. | | | 146,947 | | | 5,017,593 |

| Chevron Corp. | | | 68,018 | | | 8,057,412 |

| ConocoPhillips | | | 126,054 | | | 9,256,145 |

| EOG Resources, Inc. | | | 34,830 | | | 4,117,951 |

| Noble Energy, Inc. | | | 160,008 | | | 4,755,438 |

| Occidental Petroleum Corp. | | | 132,573 | | | 10,588,605 |

| TOTAL SA, Sponsored ADR | | | 289,860 | | | 18,185,816 |

| Valero Energy Corp. | | | 82,120 | | | 9,680,306 |

| | | | | | 69,659,266 |

| Financials—5.8% | | | | | | |

| Capital Markets—1.0% | | | | | | |

| Goldman Sachs Group, Inc. (The) | | | 43,820 | | | 10,420,834 |

| Raymond James Financial, Inc. | | | 56,478 | | | 5,254,713 |

| State Street Corp. | | | 108,930 | | | 9,467,107 |

| | | | | | 25,142,654 |

| Commercial Banks—1.5% | | | | | | |

| M&T Bank Corp. | | | 172,050 | | | 30,478,657 |

21 OPPENHEIMER CAPITAL INCOME FUND

CONSOLIDATED

STATEMENT OF INVESTMENTS Continued

| | | | | | |

| | | Shares | | | Value |

| Commercial Banks (Continued) | | | | | | |

| PNC Financial Services Group, Inc. (The) | | | 47,678 | | | $ 6,843,700 |

| | | | | | 37,322,357 |

| Insurance—1.5% | | | | | | |

| Allstate Corp. (The) | | | 46,334 | | | 4,659,810 |

| Chubb Ltd. | | | 218,727 | | | 29,580,640 |

| Travelers Cos., Inc. (The) | | | 32,690 | | | 4,302,004 |

| | | | | | 38,542,454 |

| Real Estate Investment Trusts (REITs)—1.6% | | | | | | |

| Blackstone Mortgage Trust, Inc., Cl. A | | | 747,750 | | | 25,468,365 |

| Starwood Property Trust, Inc. | | | 742,622 | | | 16,359,963 |

| | | | | | 41,828,328 |

| Thrifts & Mortgage Finance—0.2% | | | | | | |

WSFS Financial Corp. | | | 82,100 | | | 4,006,480 |

| Health Care—6.9% | | | | | | |

| Biotechnology—0.5% | | | | | | |

Shire plc, ADR | | | 70,552 | | | 12,365,649 |

| Health Care Equipment & Supplies—0.7% | | | | | | |

| Abbott Laboratories | | | 107,567 | | | 7,189,778 |

| Medtronic plc | | | 110,011 | | | 10,606,161 |

| | | | | | 17,795,939 |

| Health Care Providers & Services—2.9% | | | | | | |

| AMN Healthcare Services, Inc.1 | | | 68,930 | | | 4,018,619 |

| Cigna Corp. | | | 72,671 | | | 13,686,856 |

| Envision Healthcare Corp.1 | | | 113,090 | | | 5,129,762 |

| HCA Healthcare, Inc. | | | 86,632 | | | 11,618,217 |

| Premier, Inc., Cl. A1 | | | 252,390 | | | 11,163,210 |

| UnitedHealth Group, Inc. | | | 105,460 | | | 28,311,792 |

| | | | | | 73,928,456 |

| Pharmaceuticals—2.8% | | | | | | |

| Allergan plc | | | 37,960 | | | 7,277,312 |

| Johnson & Johnson | | | 89,150 | | | 12,007,614 |

| Merck & Co., Inc. | | | 300,930 | | | 20,640,789 |

| Mylan NV1 | | | 247,740 | | | 9,694,066 |

| Novartis AG, Sponsored ADR | | | 96,520 | | | 8,012,125 |

| Roche Holding AG | | | 48,008 | | | 11,914,632 |

| | | | | | 69,546,538 |

| Industrials—5.0% | | | | | | |

| Aerospace & Defense—2.8% | | | | | | |

| L3 Technologies, Inc. | | | 56,946 | | | 12,170,499 |

| Lockheed Martin Corp. | | | 75,030 | | | 24,040,363 |

| Northrop Grumman Corp. | | | 60,878 | | | 18,171,474 |

22 OPPENHEIMER CAPITAL INCOME FUND

| | | | | | |

| | | Shares | | | Value |

| Aerospace & Defense (Continued) | | | | | | |

| Raytheon Co. | | | 77,570 | | | $ 15,470,561 |

| | | | | | 69,852,897 |

| Air Freight & Couriers—0.2% | | | | | | |

FedEx Corp. | | | 20,444 | | | 4,987,314 |

| Commercial Services & Supplies—0.6% | | | | | | |

Republic Services, Inc., Cl. A | | | 184,790 | | | 13,556,194 |

| Construction & Engineering—0.1% | | | | | | |

Granite Construction, Inc. | | | 75,190 | | | 3,434,679 |

| Industrial Conglomerates—1.0% | | | | | | |

| General Electric Co. | | | 729,100 | | | 9,434,554 |

| Honeywell International, Inc. | | | 96,905 | | | 15,413,709 |

| | | | | | 24,848,263 |

| Machinery—0.3% | | | | | | |

Stanley Black & Decker, Inc. | | | 59,984 | | | 8,429,552 |

| Information Technology—5.0% | | | | | | |

| Communications Equipment—1.3% | | | | | | |

| Cisco Systems, Inc. | | | 499,676 | | | 23,869,523 |

| CommScope Holding Co., Inc.1 | | | 280,590 | | | 8,891,897 |

| | | | | | 32,761,420 |

| Internet Software & Services—1.1% | | | | | | |

Alphabet, Inc., Cl. A1 | | | 23,876 | | | 29,410,457 |

| Semiconductors & Semiconductor Equipment—1.3% | | | | | | |

| QUALCOMM, Inc. | | | 156,413 | | | 10,747,137 |

| Xilinx, Inc. | | | 282,932 | | | 22,020,598 |

| | | | | | 32,767,735 |

| Technology Hardware, Storage & Peripherals—1.3% | | | | | | |

Apple, Inc. | | | 142,315 | | | 32,395,163 |

| Materials—1.8% | | | | | | |

| Chemicals—0.6% | | | | | | |

| Celanese Corp., Cl. A | | | 129,241 | | | 15,099,226 |

| Containers & Packaging—1.0% | | | | | | |

| Packaging Corp. of America | | | 77,325 | | | 8,499,564 |

| Sonoco Products Co. | | | 289,971 | | | 16,249,975 |

| | | | | | 24,749,539 |

| Metals & Mining—0.2% | | | | | | |

| Steel Dynamics, Inc. | | | 92,760 | | | 4,241,915 |

23 OPPENHEIMER CAPITAL INCOME FUND

CONSOLIDATED

STATEMENT OF INVESTMENTS Continued

| | | | | | |

| | | Shares | | | Value |

| Telecommunication Services—1.8% | | | | | | |

| Diversified Telecommunication Services—1.8% | | | | | | |

| AT&T, Inc. | | | 631,170 | | | $ 20,159,570 |

| BCE, Inc. | | | 238,140 | | | 9,708,968 |

| Swisscom AG | | | 18,525 | | | 8,267,491 |

| Verizon Communications, Inc. | | | 154,377 | | | 8,393,477 |

| | | | | | 46,529,506 |

| Utilities—1.6% | | | | | | |

| Electric Utilities—1.0% | | | | | | |

| American Electric Power Co., Inc. | | | 210,180 | | | 15,076,211 |

| Edison International | | | 91,620 | | | 6,022,183 |

| PG&E Corp. | | | 102,530 | | | 4,734,835 |

| | | | | | 25,833,229 |

| Multi-Utilities—0.6% | | | | | | |

| CMS Energy Corp. | | | 319,016 | | | 15,708,348 |

| Total Common Stocks (Cost $927,919,812) | | | | | | 878,511,781 |

| Preferred Stocks—1.5% | | | | | | |

| Citigroup Capital XIII, 7.75% Cum., Non-Vtg. [US0003M+637]2 | | | 1,133,000 | | | 30,806,270 |

| M&T Bank Corp., 6.375% Cum., Series A, Non-Vtg. | | | 1,833 | | | 1,851,330 |

| M&T Bank Corp., 6.375% Cum., Series C, Non-Vtg. | | | 4,500 | | | 4,545,000 |

| Total Preferred Stocks (Cost $36,592,296) | | | | | | 37,202,600 |

| | |

| | | Principal Amount | | | |

| Asset-Backed Securities—9.0% | | | | | | |

| Accredited Mortgage Loan Trust: | | | | | | |

| Series 2005-3, Cl. M3, 2.764% [US0001M+48], 9/25/352 | | $ | 7,222,280 | | | 6,998,143 |

| Series 2005-4, Cl. M1, 2.465% [US0001M+40], 12/25/352 | | | 1,919,000 | | | 1,867,104 |

| American Credit Acceptance Receivables Trust: | | | | | | |

| Series 2015-3, Cl. D, 5.86%, 7/12/223 | | | 955,000 | | | 966,481 |

| Series 2016-4, Cl. B, 2.11%, 2/12/213 | | | 318,519 | | | 318,349 |

| Series 2017-3, Cl. B, 2.25%, 1/11/213 | | | 425,000 | | | 424,374 |

| Series 2017-4, Cl. B, 2.61%, 5/10/213 | | | 477,000 | | | 475,546 |

| Series 2017-4, Cl. C, 2.94%, 1/10/243 | | | 1,351,000 | | | 1,343,725 |

| Series 2017-4, Cl. D, 3.57%, 1/10/243 | | | 1,952,000 | | | 1,937,248 |

| Series 2018-2, Cl. B, 3.46%, 8/10/223 | | | 1,860,000 | | | 1,861,616 |

| Series 2018-2, Cl. C, 3.70%, 7/10/243 | | | 1,835,000 | | | 1,836,305 |

| AmeriCredit Automobile Receivables Trust: | | | | | | |

| Series 2015-2, Cl. D, 3.00%, 6/8/21 | | | 1,555,000 | | | 1,555,450 |

| Series 2017-2, Cl. D, 3.42%, 4/18/23 | | | 2,065,000 | | | 2,055,894 |

| Series 2017-4, Cl. D, 3.08%, 12/18/23 | | | 940,000 | | | 922,562 |

| Bear Stearns Structured Products Trust: | | | | | | |

| Series 2007-EMX1, Cl. A2, 3.365% [US0001M+130], 3/25/372,3 | | | 5,900,000 | | | 6,086,940 |

| Series 2007-EMX1, Cl. M1, 4.065% [US0001M+200], 3/25/372,3 | | | 8,000,000 | | | 7,952,268 |

| Cabela’s Credit Card Master Note Trust: | | | | | | |

| Series 2015-1A, Cl. A2, 2.603% [US0001M+54], 3/15/232 | | | 2,855,000 | | | 2,869,530 |

| Series 2015-2, Cl. A2, 2.733% [US0001M+67], 7/17/232 | | | 3,170,000 | | | 3,194,131 |

| Series 2016-1, Cl. A1, 1.78%, 6/15/22 | | | 3,735,000 | | | 3,707,444 |

24 OPPENHEIMER CAPITAL INCOME FUND

| | | | | | |

| | | Principal Amount | | | Value |

| Asset-Backed Securities (Continued) | | | | | | |

| Cabela’s Credit Card Master Note Trust: (Continued) | | | | | | |

| Series 2016-1, Cl. A2, 2.913% [US0001M+85], 6/15/222 | | $ | 1,745,000 | | | $ 1,754,124 |

| Capital Auto Receivables Asset Trust, Series 2017-1, Cl. D, 3.15%, 2/20/253 | | | 275,000 | | | 273,085 |

| CarFinance Capital Auto Trust, Series 2015-1A, Cl. A, 1.75%, 6/15/213 | | | 41,224 | | | 41,186 |

| CarMax Auto Owner Trust: | | | | | | |

| Series 2015-2, Cl. D, 3.04%, 11/15/21 | | | 655,000 | | | 653,802 |

| Series 2015-3, Cl. D, 3.27%, 3/15/22 | | | 1,975,000 | | | 1,973,884 |

| Series 2016-1, Cl. D, 3.11%, 8/15/22 | | | 1,300,000 | | | 1,295,551 |

| Series 2017-1, Cl. D, 3.43%, 7/17/23 | | | 1,565,000 | | | 1,557,897 |

| Series 2017-4, Cl. D, 3.30%, 5/15/24 | | | 705,000 | | | 694,209 |

| Series 2018-1, Cl. D, 3.37%, 7/15/24 | | | 515,000 | | | 506,977 |

| CCG Receivables Trust: | | | | | | |

| Series 2017-1, Cl. B, 2.75%, 11/14/233 | | | 1,580,000 | | | 1,555,457 |

| Series 2018-1, Cl. B, 3.09%, 6/16/253 | | | 620,000 | | | 613,920 |

| Series 2018-1, Cl. C, 3.42%, 6/16/253 | | | 175,000 | | | 173,179 |

| Series 2018-2, Cl. C, 3.87%, 12/15/253 | | | 415,000 | | | 415,617 |

| CIG Auto Receivables Trust, Series 2017-1A, Cl. A, 2.71%, 5/15/233 | | | 542,289 | | | 538,983 |

| Citibank Credit Card Issuance Trust, Series 2014-A6, Cl. A6, 2.15%, 7/15/21 | | | 3,545,000 | | | 3,528,997 |

| CNH Equipment Trust, Series 2017-C, Cl. B, 2.54%, 5/15/25 | | | 475,000 | | | 464,587 |

| CPS Auto Receivables Trust: | | | | | | |

| Series 2017-C, Cl. A, 1.78%, 9/15/203 | | | 201,547 | | | 201,041 |

| Series 2017-C, Cl. B, 2.30%, 7/15/213 | | | 685,000 | | | 681,143 |

| Series 2017-D, Cl. B, 2.43%, 1/18/223 | | | 1,180,000 | | | 1,169,044 |

| Series 2018-A, Cl. B, 2.77%, 4/18/223 | | | 975,000 | | | 968,089 |

| Series 2018-B, Cl. B, 3.23%, 7/15/223 | | | 1,090,000 | | | 1,087,890 |

| CPS Auto Trust, Series 2017-A, Cl. B, 2.68%, 5/17/213 | | | 210,000 | | | 209,678 |

| Credit Acceptance Auto Loan Trust: | | | | | | |

| Series 2017-3A, Cl. C, 3.48%, 10/15/263 | | | 1,415,000 | | | 1,397,821 |

| Series 2018-1A, Cl. B, 3.60%, 4/15/273 | | | 920,000 | | | 916,427 |

| Series 2018-1A, Cl. C, 3.77%, 6/15/273 | | | 1,305,000 | | | 1,295,079 |

| Series 2018-2A, Cl. C, 4.16%, 9/15/273 | | | 770,000 | | | 775,199 |

| Dell Equipment Finance Trust: | | | | | | |

| Series 2017-2, Cl. B, 2.47%, 10/24/223 | | | 470,000 | | | 464,000 |

| Series 2018-1, Cl. B, 3.34%, 6/22/233 | | | 590,000 | | | 591,912 |

| Drive Auto Receivables Trust: | | | | | | |

| Series 2015-BA, Cl. D, 3.84%, 7/15/213 | | | 113,604 | | | 114,178 |

| Series 2016-CA, Cl. D, 4.18%, 3/15/243 | | | 1,070,000 | | | 1,082,479 |

| Series 2017-3, Cl. C, 2.80%, 7/15/22 | | | 785,000 | | | 782,738 |

| Series 2017-AA, Cl. C, 2.98%, 1/18/223 | | | 1,210,000 | | | 1,209,580 |

| Series 2017-BA, Cl. D, 3.72%, 10/17/223 | | | 1,525,000 | | | 1,532,710 |

| Series 2018-1, Cl. D, 3.81%, 5/15/24 | | | 1,190,000 | | | 1,187,105 |

| Series 2018-2, Cl. D, 4.14%, 8/15/24 | | | 2,160,000 | | | 2,173,706 |

| Series 2018-3, Cl. D, 4.30%, 9/16/24 | | | 1,420,000 | | | 1,437,471 |

| DT Auto Owner Trust: | | | | | | |

| Series 2015-2A, Cl. D, 4.25%, 2/15/223 | | | 685,870 | | | 689,211 |

| Series 2016-4A, Cl. E, 6.49%, 9/15/233 | | | 495,000 | | | 509,749 |

| Series 2017-1A, Cl. C, 2.70%, 11/15/223 | | | 565,000 | | | 563,660 |

| Series 2017-1A, Cl. D, 3.55%, 11/15/223 | | | 1,060,000 | | | 1,061,749 |

25 OPPENHEIMER CAPITAL INCOME FUND

CONSOLIDATED

STATEMENT OF INVESTMENTS Continued

| | | | | | |

| | | Principal Amount | | | Value |

| Asset-Backed Securities (Continued) | | | | | | |

| DT Auto Owner Trust: (Continued) | | | | | | |

| Series 2017-1A, Cl. E, 5.79%, 2/15/243 | | $ | 1,025,000 | | | $ 1,042,308 |

| Series 2017-2A, Cl. D, 3.89%, 1/15/233 | | | 1,165,000 | | | 1,168,244 |

| Series 2017-3A, Cl. B, 2.40%, 5/17/213 | | | 1,235,000 | | | 1,231,510 |

| Series 2017-3A, Cl. E, 5.60%, 8/15/243 | | | 1,015,000 | | | 1,026,975 |

| Series 2017-4A, Cl. C, 2.86%, 7/17/233 | | | 285,000 | | | 283,570 |

| Series 2017-4A, Cl. D, 3.47%, 7/17/233 | | | 1,675,000 | | | 1,664,501 |

| Series 2017-4A, Cl. E, 5.15%, 11/15/243 | | | 990,000 | | | 991,134 |

| Series 2018-1A, Cl. B, 3.04%, 1/18/223 | | | 1,055,000 | | | 1,053,201 |

| Series 2018-2A, Cl. B, 3.43%, 5/16/223 | | | 555,000 | | | 555,323 |

| Element Rail Leasing I LLC, Series 2014-1A, Cl. A1, 2.299%, 4/19/443 | | | 872,515 | | | 860,855 |

| Evergreen Credit Card Trust Series, Series 2018-2, Cl. A, 2.427% [US0001M+35], 7/15/222,3 | | | 2,755,000 | | | 2,758,283 |

| Exeter Automobile Receivables Trust, Series 2018-1A, Cl. B, 2.75%, 4/15/223 | | | 1,065,000 | | | 1,057,157 |

| Fieldstone Mortgage Investment Trust, Series 2004-5, Cl. M3, 4.09% [US0001M+202.5], 2/25/352 | | | 4,434,759 | | | 4,272,103 |

| Flagship Credit Auto Trust: | | | | | | |

| Series 2014-1, Cl. D, 4.83%, 6/15/203 | | | 200,000 | | | 200,848 |

| Series 2016-1, Cl. C, 6.22%, 6/15/223 | | | 2,410,000 | | | 2,501,841 |

| FRS I LLC, Series 2013-1A, Cl. A1, 1.80%, 4/15/433 | | | 53,247 | | | 52,977 |

| GLS Auto Receivables Trust, Series 2018-1A, Cl. A, 2.82%, 7/15/223 | | | 2,038,172 | | | 2,032,307 |

| GM Financial Automobile Leasing Trust: | | | | | | |

| Series 2017-3, Cl. C, 2.73%, 9/20/21 | | | 795,000 | | | 786,991 |

| Series 2018-2, Cl. C, 3.50%, 4/20/22 | | | 965,000 | | | 965,572 |

| GSAMP Trust: | | | | | | |

| Series 2005-HE4, Cl. M3, 2.845% [US0001M+78], 7/25/452 | | | 13,300,000 | | | 13,272,325 |

| Series 2005-HE5, Cl. M3, 2.525% [US0001M+46], 11/25/352 | | | 4,060,889 | | | 3,933,451 |

| Series 2007-HS1, Cl. M4, 4.315% [US0001M+225], 2/25/472 | | | 4,849,000 | | | 4,944,379 |

| JP Morgan Mortgage Acquisition Corp., Series 2005-OPT2, Cl. M2, 2.515% [US0001M+45], 12/25/352 | | | 5,480,000 | | | 5,471,558 |

| JP Morgan Mortgage Acquisition Trust: | | | | | | |

| Series 2007-CH1, Cl. MV10, 3.065% [US0001M+100], 11/25/362,3 | | | 5,010,000 | | | 4,884,491 |

| Series 2007-CH1, Cl. MV8, 3.065% [US0001M+100], 11/25/362 | | | 5,400,000 | | | 5,332,171 |

| Long Beach Mortgage Loan Trust, Series 2005-WL3, Cl. M1, 2.71% [US0001M+64.5], 11/25/352 | | | 1,739,910 | | | 1,727,410 |

| Morgan Stanley ABS Capital I, Inc. Trust, Series 2006-NC1, Cl. M1, 2.445% [US0001M+38], 12/25/352 | | | 12,287,000 | | | 12,250,403 |

| Navistar Financial Dealer Note Master Owner Trust II: | | | | | | |

| Series 2016-1, Cl. D, 5.365% [LIBOR01M+330], 9/27/212,3 | | | 495,000 | | | 495,778 |

| Series 2017-1, Cl. C, 3.615% [LIBOR01M+155], 6/27/222,3 | | | 400,000 | | | 401,549 |

| Series 2017-1, Cl. D, 4.365% [LIBOR01M+230], 6/27/222,3 | | | 465,000 | | | 465,548 |

| New Century Home Equity Loan Trust: | | | | | | |

| Series 2005-1, Cl. M2, 2.785% [US0001M+72], 3/25/352 | | | 4,383,661 | | | 4,237,705 |

| Series 2005-2, Cl. M3, 2.80% [US0001M+73.5], 6/25/352 | | | 5,500,000 | | | 5,519,414 |

| RASC Series Trust, Series 2006-KS2, Cl. M2, 2.455% [US0001M+39], 3/25/362 | | | 4,875,000 | | | 4,765,775 |

| Raspro Trust, Series 2005-1A, Cl. G, 2.725% [LIBOR03M+40], 3/23/242,3 | | | 1,405,920 | | | 1,414,398 |

26 OPPENHEIMER CAPITAL INCOME FUND

| | | | | | | | |

| | | Principal Amount | | | Value | |

| Asset-Backed Securities (Continued) | | | | | | | | |

| Santander Drive Auto Receivables Trust: | | | | | | | | |

| Series 2016-2, Cl. D, 3.39%, 4/15/22 | | $ | 825,000 | | | $ | 827,301 | |

| Series 2017-1, Cl. D, 3.17%, 4/17/23 | | | 1,085,000 | | | | 1,078,531 | |

| Series 2017-1, Cl. E, 5.05%, 7/15/243 | | | 2,735,000 | | | | 2,783,054 | |

| Series 2017-2, Cl. D, 3.49%, 7/17/23 | | | 390,000 | | | | 389,700 | |

| Series 2017-3, Cl. D, 3.20%, 11/15/23 | | | 1,900,000 | | | | 1,885,042 | |

| Series 2018-1, Cl. D, 3.32%, 3/15/24 | | | 760,000 | | | | 748,652 | |

| Series 2018-2, Cl. D, 3.88%, 2/15/24 | | | 1,165,000 | | | | 1,162,325 | |

| Series 2018-3, Cl. C, 3.51%, 8/15/23 | | | 2,950,000 | | | | 2,954,164 | |

| Santander Retail Auto Lease Trust, Series 2017-A, Cl. C, 2.96%, 11/21/223 | | | 1,275,000 | | | | 1,258,326 | |

| SG Mortgage Securities Trust, Series 2005-OPT1, Cl. M2, 2.515% [US0001M+45], 10/25/352 | | | 6,129,000 | | | | 6,082,168 | |

| TCF Auto Receivables Owner Trust, Series 2015-1A, Cl. D, 3.53%, 3/15/223 | | | 1,075,000 | | | | 1,070,911 | |

| United Auto Credit Securitization Trust, Series 2018-1, Cl. C, 3.05%, 9/10/213 | | | 1,635,000 | | | | 1,629,639 | |

| Verizon Owner Trust, Series 2017-3A, Cl. A1A, 2.06%, 4/20/223 | | | 1,260,000 | | | | 1,242,845 | |

| Veros Automobile Receivables Trust, Series 2017-1, Cl. A, 2.84%, 4/17/233 | | | 516,264 | | | | 514,515 | |

| Westlake Automobile Receivables Trust: | | | | | | | | |

| Series 2016-1A, Cl. E, 6.52%, 6/15/223 | | | 1,760,000 | | | | 1,793,213 | |

| Series 2017-2A, Cl. E, 4.63%, 7/15/243 | | | 2,090,000 | | | | 2,101,476 | |

| Series 2018-1A, Cl. C, 2.92%, 5/15/233 | | | 1,100,000 | | | | 1,091,800 | |

| Series 2018-1A, Cl. D, 3.41%, 5/15/233 | | | 2,275,000 | | | | 2,262,303 | |

| Series 2018-3A, Cl. B, 3.32%, 10/16/233 | | | 1,019,000 | | | | 1,018,839 | |

| World Financial Network Credit Card Master Trust: | | | | | | | | |

| Series 2012-D, Cl. A, 2.15%, 4/17/23 | | | 1,040,000 | | | | 1,034,626 | |

| Series 2016-C, Cl. A, 1.72%, 8/15/23 | | | 4,470,000 | | | | 4,408,529 | |

| Series 2017-A, Cl. A, 2.12%, 3/15/24 | | | 2,775,000 | | | | 2,732,677 | |

| Series 2017-B, Cl. A, 1.98%, 6/15/23 | | | 2,105,000 | | | | 2,089,886 | |

| Series 2017-C, Cl. A, 2.31%, 8/15/24 | | | 2,845,000 | | | | 2,798,761 | |

| Series 2018-A, Cl. A, 3.07%, 12/16/24 | | | 3,695,000 | | | | 3,680,812 | |

| | | | | | | | |

| Total Asset-Backed Securities (Cost $217,999,419) | | | | | | | 226,778,374 | |

| Mortgage-Backed Obligations—17.7% | | | | | | | | |

| Government Agency—10.5% | | | | | | | | |

| FHLMC/FNMA/FHLB/Sponsored—9.3% | | | | | | | | |

| Federal Home Loan Mortgage Corp. Gold Pool: | | | | | | | | |

| 4.50%, 5/1/19 | | | 51,194 | | | | 51,704 | |

| 5.00%, 12/1/34 | | | 36,024 | | | | 38,362 | |

| 6.50%, 7/1/28-4/1/34 | | | 107,680 | | | | 119,010 | |

| 7.00%, 10/1/31 | | | 79,473 | | | | 86,408 | |

| 9.00%, 8/1/22-5/1/25 | | | 3,514 | | | | 3,737 | |

| Federal Home Loan Mortgage Corp., Interest-Only Stripped Mtg.-Backed Security: | | | | | | | | |

| Series 183,Cl. IO, 80.873%, 4/1/274 | | | 69,924 | | | | 15,771 | |

| Series 192,Cl. IO, 99.999%, 2/1/284 | | | 22,839 | | | | 4,658 | |

| Series 243,Cl. 6, 0.00%, 12/15/324,5 | | | 72,223 | | | | 11,999 | |

| Federal Home Loan Mortgage Corp., Mtg.-Linked Amortizing Global Debt Securities, Series 2012-1, Cl. A10, 2.06%, 1/15/22 | | | 1,748,122 | | | | 1,712,076 | |

| Federal Home Loan Mortgage Corp., Principal-Only Stripped Mtg.- Backed Security, Series 176, Cl. PO, 4.127%, 6/1/266 | | | 22,750 | | | | 20,882 | |

27 OPPENHEIMER CAPITAL INCOME FUND

CONSOLIDATED

STATEMENT OF INVESTMENTS Continued

| | | | | | | | |

| | | Principal Amount | | | Value | |

| FHLMC/FNMA/FHLB/Sponsored (Continued) | | | | | | | | |

| Federal Home Loan Mortgage Corp., Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates: | |

| Series 2034,Cl. Z, 6.50%, 2/15/28 | | $ | 54,740 | | | $ | 59,052 | |

| Series 2043,Cl. ZP, 6.50%, 4/15/28 | | | 240,524 | | | | 263,801 | |

| Series 2053,Cl. Z, 6.50%, 4/15/28 | | | 48,769 | | | | 53,589 | |

| Series 2279,Cl. PK, 6.50%, 1/15/31 | | | 99,208 | | | | 107,969 | |

| Series 2326,Cl. ZP, 6.50%, 6/15/31 | | | 44,100 | | | | 47,417 | |

| Series 2427,Cl. ZM, 6.50%, 3/15/32 | | | 185,175 | | | | 202,484 | |

| Series 2461,Cl. PZ, 6.50%, 6/15/32 | | | 212,172 | | | | 229,782 | |

| Series 2626,Cl. TB, 5.00%, 6/15/33 | | | 167,733 | | | | 173,228 | |

| Series 2635,Cl. AG, 3.50%, 5/15/32 | | | 56,082 | | | | 55,753 | |

| Series 2707,Cl. QE, 4.50%, 11/15/18 | | | 4,763 | | | | 4,759 | |

| Series 2770,Cl. TW, 4.50%, 3/15/19 | | | 4,733 | | | | 4,741 | |

| Series 3010,Cl. WB, 4.50%, 7/15/20 | | | 47,303 | | | | 47,705 | |

| Series 3025,Cl. SJ, 17.187% [-3.667 x LIBOR01M+2,475], 8/15/352 | | | 27,190 | | | | 38,591 | |

| Series 3030,Cl. FL, 2.463% [LIBOR01M+40], 9/15/352 | | | 373,646 | | | | 375,322 | |

| Series 3645,Cl. EH, 3.00%, 12/15/20 | | | 3,715 | | | | 3,714 | |

| Series 3741,Cl. PA, 2.15%, 2/15/35 | | | 14,614 | | | | 14,600 | |

| Series 3815,Cl. BD, 3.00%, 10/15/20 | | | 1,189 | | | | 1,189 | |

| Series 3822,Cl. JA, 5.00%, 6/15/40 | | | 64,583 | | | | 66,081 | |

| Series 3840,Cl. CA, 2.00%, 9/15/18 | | | 162 | | | | 161 | |

| Series 3848,Cl. WL, 4.00%, 4/15/40 | | | 311,628 | | | | 313,930 | |

| Series 3857,Cl. GL, 3.00%, 5/15/40 | | | 29,484 | | | | 29,605 | |

| Series 4221,Cl. HJ, 1.50%, 7/15/23 | | | 738,733 | | | | 721,372 | |

| Federal Home Loan Mortgage Corp., Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates, Interest-Only Stripped Mtg.-Backed Security: | |

| Series 2130,Cl. SC, 83.043%, 3/15/294 | | | 52,142 | | | | 6,605 | |

| Series 2796,Cl. SD, 99.999%, 7/15/264 | | | 90,872 | | | | 10,479 | |

| Series 2920,Cl. S, 56.073%, 1/15/354 | | | 572,702 | | | | 75,911 | |

| Series 2922,Cl. SE, 20.242%, 2/15/354 | | | 134,620 | | | | 16,842 | |

| Series 2937,Cl. SY, 11.389%, 2/15/354 | | | 1,521,027 | | | | 183,850 | |

| Series 2981,Cl. AS, 2.531%, 5/15/354 | | | 1,066,655 | | | | 110,510 | |

| Series 3397,Cl. GS, 0.00%, 12/15/374,5 | | | 277,754 | | | | 43,303 | |

| Series 3424,Cl. EI, 0.00%, 4/15/384,5 | | | 81,213 | | | | 6,651 | |

| Series 3450,Cl. BI, 12.817%, 5/15/384 | | | 653,295 | | | | 87,754 | |

| Series 3606,Cl. SN, 13.929%, 12/15/394 | | | 269,546 | | | | 32,639 | |

| Series 4057,Cl. QI, 5.741%, 6/15/274 | | | 4,514,720 | | | | 377,571 | |

| Series 4818,Cl. BI, 2.648%, 3/15/454 | | | 1,524,299 | | | | 284,594 | |

| Federal National Mortgage Assn.: | | | | | | | | |

| 2.50%, 9/1/337 | | | 13,260,000 | | | | 12,894,104 | |

| 3.00%, 9/1/33-9/1/487 | | | 29,295,000 | | | | 28,623,681 | |

| 3.50%, 9/1/33-9/1/487 | | | 93,390,000 | | | | 93,103,899 | |

| 4.00%, 9/1/33-9/1/487 | | | 28,015,000 | | | | 28,569,883 | |

| 4.50%, 9/1/487 | | | 43,650,000 | | | | 45,323,748 | |

| 5.00%, 9/1/487 | | | 8,525,000 | | | | 9,012,886 | |

| Federal National Mortgage Assn. Pool: | | | | | | | | |

| 5.00%, 3/1/21 | | | 5,644 | | | | 5,786 | |

| 5.50%, 2/1/35-4/1/39 | | | 716,525 | | | | 775,884 | |

| 6.50%, 10/1/19-11/1/31 | | | 268,470 | | | | 294,401 | |

| 7.00%, 12/1/32-4/1/35 | | | 22,544 | | | | 23,900 | |

28 OPPENHEIMER CAPITAL INCOME FUND

| | | | | | |

| | | Principal Amount | | | Value |

| FHLMC/FNMA/FHLB/Sponsored (Continued) | | | | | | |

| Federal National Mortgage Assn. Pool: (Continued) | | | | | | |

| 7.50%, 1/1/33-3/1/33 | | $ | 1,318,570 | | | $ 1,510,730 |

| 8.50%, 7/1/32 | | | 2,423 | | | 2,460 |

| Federal National Mortgage Assn., Interest-Only Stripped Mtg.-Backed Security: | | | | | | |

| Series 222,Cl. 2, 99.999%, 6/25/234 | | | 130,822 | | | 15,466 |

| Series 252,Cl. 2, 99.999%, 11/25/234 | | | 109,737 | | | 14,871 |

| Series 303,Cl. IO, 97.675%, 11/25/294 | | | 64,235 | | | 14,939 |

| Series 308,Cl. 2, 79.058%, 9/25/304 | | | 162,017 | | | 38,478 |

| Series 320,Cl. 2, 52.582%, 4/25/324 | | | 584,210 | | | 141,937 |

| Series 321,Cl. 2, 23.601%, 4/25/324 | | | 403,509 | | | 95,319 |

| Series 331,Cl. 9, 20.612%, 2/25/334 | | | 156,202 | | | 31,121 |

| Series 334,Cl. 17, 27.725%, 2/25/334 | | | 83,413 | | | 20,087 |

| Series 339,Cl. 12, 0.00%, 6/25/334,5 | | | 279,172 | | | 70,963 |

| Series 339,Cl. 7, 0.00%, 11/25/334,5 | | | 330,876 | | | 72,704 |

| Series 343,Cl. 13, 0.00%, 9/25/334,5 | | | 289,309 | | | 55,398 |

| Series 343,Cl. 18, 0.00%, 5/25/344,5 | | | 78,623 | | | 18,591 |

| Series 345,Cl. 9, 0.00%, 1/25/344,5 | | | 134,397 | | | 30,689 |

| Series 351,Cl. 10, 0.00%, 4/25/344,5 | | | 88,303 | | | 21,423 |

| Series 351,Cl. 8, 0.00%, 4/25/344,5 | | | 156,555 | | | 30,710 |

| Series 356,Cl. 10, 0.00%, 6/25/354,5 | | | 111,532 | | | 23,491 |

| Series 356,Cl. 12, 0.00%, 2/25/354,5 | | | 54,849 | | | 11,953 |

| Series 362,Cl. 13, 0.00%, 8/25/354,5 | | | 197,936 | | | 40,381 |

| Series 364,Cl. 16, 0.00%, 9/25/354,5 | | | 239,062 | | | 48,224 |

| Series 365,Cl. 16, 0.00%, 3/25/364,5 | | | 520,400 | | | 106,253 |

| Federal National Mortgage Assn., Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates: | | | | | | |

| Series 1993-87,Cl. Z, 6.50%, 6/25/23 | | | 113,480 | | | 119,283 |

| Series 1998-61,Cl. PL, 6.00%, 11/25/28 | | | 64,947 | | | 70,061 |

| Series 1999-54,Cl. LH, 6.50%, 11/25/29 | | | 105,634 | | | 114,315 |

| Series 2001-51,Cl. OD, 6.50%, 10/25/31 | | | 154,762 | | | 163,462 |

| Series 2003-130,Cl. CS, 9.971% [-2 x LIBOR01M+1,410], 12/25/332 | | | 42,983 | | | 44,096 |

| Series 2003-28,Cl. KG, 5.50%, 4/25/23 | | | 242,993 | | | 251,969 |

| Series 2003-84,Cl. GE, 4.50%, 9/25/18 | | | 5 | | | 5 |

| Series 2004-25,Cl. PC, 5.50%, 1/25/34 | | | 27,066 | | | 27,169 |

| Series 2005-104,Cl. MC, 5.50%, 12/25/25 | | | 1,327,772 | | | 1,394,550 |

| Series 2005-31,Cl. PB, 5.50%, 4/25/35 | | | 1,430,000 | | | 1,556,460 |

| Series 2005-73,Cl. DF, 2.315% [LIBOR01M+25], 8/25/352 | | | 329,762 | | | 330,922 |

| Series 2006-11,Cl. PS, 16.996% [-3.667 x LIBOR01M+2,456.67], 3/25/362 | | | 94,073 | | | 134,306 |

| Series 2006-46,Cl. SW, 16.629% [-3.667 x LIBOR01M+2,419.92], 6/25/362 | | | 67,420 | | | 92,673 |

| Series 2006-50,Cl. KS, 16.629% [-3.667 x LIBOR01M+2,420], 6/25/362 | | | 126,001 | | | 176,730 |

| Series 2006-50,Cl. SK, 16.629% [-3.667 x LIBOR01M+2,420], 6/25/362 | | | 26,010 | | | 35,791 |

| Series 2008-75,Cl. DB, 4.50%, 9/25/23 | | | 8,281 | | | 8,280 |

| Series 2009-113,Cl. DB, 3.00%, 12/25/20 | | | 49,907 | | | 49,844 |

| Series 2009-36,Cl. FA, 3.005% [LIBOR01M+94], 6/25/372 | | | 122,048 | | | 124,855 |

| Series 2009-70,Cl. TL, 4.00%, 8/25/19 | | | 7,992 | | | 7,986 |

29 OPPENHEIMER CAPITAL INCOME FUND

CONSOLIDATED

STATEMENT OF INVESTMENTS Continued

| | | | | | |

| | | Principal Amount | | | Value |

| FHLMC/FNMA/FHLB/Sponsored (Continued) | | | | | | |

| Federal National Mortgage Assn., Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates: (Continued) |

| Series 2010-43,Cl. KG, 3.00%, 1/25/21 | | $ | 39,811 | | | $ 39,787 |

| Series 2011-15,Cl. DA, 4.00%, 3/25/41 | | | 68,811 | | | 68,486 |

| Series 2011-3,Cl. EL, 3.00%, 5/25/20 | | | 56,107 | | | 56,022 |

| Series 2011-3,Cl. KA, 5.00%, 4/25/40 | | | 464,680 | | | 482,464 |

| Series 2011-38,Cl. AH, 2.75%, 5/25/20 | | | 178 | | | 177 |

| Series 2011-82,Cl. AD, 4.00%, 8/25/26 | | | 136,318 | | | 136,411 |

| Federal National Mortgage Assn., Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates, Interest-Only Stripped Mtg.-Backed Security: |

| Series 2001-15,Cl. SA, 99.999%, 3/17/314 | | | 9,373 | | | 712 |

| Series 2001-65,Cl. S, 47.49%, 11/25/314 | | | 137,248 | | | 25,804 |

| Series 2001-81,Cl. S, 48.553%, 1/25/324 | | | 36,299 | | | 5,880 |

| Series 2002-47,Cl. NS, 32.314%, 4/25/324 | | | 87,766 | | | 15,221 |

| Series 2002-51,Cl. S, 32.965%, 8/25/324 | | | 80,581 | | | 13,975 |

| Series 2002-52,Cl. SD, 63.988%, 9/25/324 | | | 123,551 | | | 20,711 |

| Series 2002-60,Cl. SM, 22.84%, 8/25/324 | | | 108,087 | | | 14,394 |