| UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 |

FORM N-CSR

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES |

Investment Company Act file number 811- 2402

| John Hancock Sovereign Bond Fund (Exact name of registrant as specified in charter) |

601 Congress Street, Boston, Massachusetts 02210

(Address of principal executive offices) (Zip code)

| Alfred P. Ouellette Senior Attorney and Assistant Secretary |

601 Congress Street

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-663-4324

| Date of fiscal year end: | May | 31 | ||

| Date of reporting period: | May | 31, 2006 |

ITEM 1. REPORT TO SHAREHOLDERS.

| Table of contents |

| Your fund at a glance |

| page 1 |

| Managers’ report |

| page 2 |

| A look at performance |

| page 6 |

| Growth of $10,000 |

| page 7 |

| Your expenses |

| page 8 |

| Fund’s investments |

| page 10 |

| Financial statements |

| page 25 |

| Trustees & officers |

| page 45 |

| For more information |

| page 49 |

To Our Shareholders,

After producing modest returns in 2005, the stock market advanced smartly in the first four months of 2006. Investors were encouraged by solid corporate earnings, a healthy economy and stable inflation, which suggested the Federal Reserve could be coming close to the end of its 18-month campaign of raising interest rates. Those hopes were dashed in May, however, when economic data suggested a resurgence of inflation and more Fed rate hikes. The result was a significant market pullback that continued into June, erasing much of the earlier gains. Inflation and rate hike concerns also worked on the bond market, which, with the exception of low-quality bonds, made little headway over the last 12 months.

With the financial markets’ about-face and increased volatility, it is anyone’s guess where the market will end 2006, especially given the wild cards of interest rate moves and record-high energy prices and their impact on corporate profits and the economy.

One thing we do know, however, is that the stock market’s pattern is one of extremes. Consider the last 10 years. From 1995 through 1999, we saw double-digit returns in excess of 20% per year, only to have 2000 through 2002 produce ever-increasing negative results, followed by another 20%-plus up year in 2004 and a less than 5% advance in 2005. Since 1926, the market, as measured by the Standard & Poor’s 500 Index, has produced average annual results of 10.4% . However, that “normal” return is rarely produced in any given year. In fact, calendar-year returns of 8% to 12% have occurred only five times in the 80 years since 1926.

Although the past in no way predicts the future, we have learned at least one lesson from history: Expect highs and lows in the short term, but always invest for the long term. Equally important: Work with your financial professional to maintain a diversified portfolio, spread out among not only different asset classes — stocks, bonds and cash — but also among various investment styles. It’s the best way we know of to benefit from, and weather, the market’s extremes.

Sincerely,

| Keith F. Hartstein, President and Chief Executive Officer |

This commentary reflects the CEO’s views as of May 31, 2006. They are subject to change at any time.

| YOUR FUND AT A GLANCE |

| The Fund seeks a high level of current income consistent with prudent invest- ment risk by investing at least 80% of its assets in a diversified portfolio of bonds and other debt securities, including corporate bonds and U.S. government and agency securities. |

Over the last twelve months

* Rising interest rates, resulting from a healthy economy and higher inflation, led to modestly negative returns in the bond market.

* Treasury and corporate bonds posted the largest declines, while high-yield corporate bonds continued to produce positive results.

* The Fund’s defensive positioning and increased emphasis on mortgage-backed securities contributed to its outperformance of its benchmark index.

Total returns for the Fund are at net asset value with all distributions reinvested. These returns do not reflect the deduction of the maximum sales charge, which would reduce the performance shown above.

| Top 10 issuers | ||

| 22.0% | Federal National Mortgage Association | |

| 13.4% | United States Treasury | |

| 7.2% | Federal Home Loan Mortgage Corp. | |

| 2.5% | JP Morgan Chase | |

| 1.9% | Goldman Sachs Group | |

| 1.6% | Bear Stearns Co., Inc. | |

| 1.6% | Countrywide Home Loans | |

| 1.6% | Citigroup, Inc. | |

| 1.5% | Morgan Stanley Capital | |

| 1.1% | Bank of America | |

As a percentage of net assets on May 31, 2006.

1

| BY HOWARD C. GREENE, CFA, BARRY H. EVANS, CFA AND JEFFREY N. GIVEN, CFA, FOR THE SOVEREIGN ASSET MANAGEMENT LLC PORTFOLIO MANAGEMENT TEAM |

| MANAGERS’ REPORT |

| JOHN HANCOCK Bond Fund |

Recently, Jeffrey N. Given joined the Fund’s portfolio management team, replacing Benjamin Matthews, who has retired. Mr. Given, a second vice president, joined John Hancock in 1993 and is currently on the portfolio management teams for several other John Hancock fixed-income funds. He has more than 13 years of experience in the investment industry.

Rising interest rates — resulting from a strong economy and higher inflation — led to modestly negative returns for bonds during the year ended May 31, 2006. The U.S. economy grew by a healthy 3.5% in 2005, and growth was even stronger in the first quarter of 2006, as the economy rebounded from a hurricane-related slowdown in late 2005. Inflation also picked up significantly during the period — the consumer price index rose by 4.2% for the year ended May 31, 2006, up from 2.8% for the previous 12 months. The inflation increase was driven primarily by soaring energy and commodity prices.

| “Rising interest rates — resulting from a strong economy and higher inflation — led to modestly negative returns for bonds during the year ended May 31, 2006.” |

In this environment, the Federal Reserve extended its program of short-term interest rate increases, raising its federal funds rate target from 3% to 5% over the past year via eight quarter-point rate hikes. This is the highest level for the federal funds rate since April 2001.

Although bond yields generally rose across the board, short-term yields increased more than long-term yields — the two-year Treasury note yield rose from 3.6% to 5.0% during the one-year period, while the 30-year Treasury yield climbed from 4.3% to 5.2% . This yield convergence produced a “flat” yield curve, where bond yields were virtually equal across the maturity spectrum.

Sector performance was mixed but generally negative. Treasury bonds, which are most sensitive to interest rate fluctuations, and investment-grade corporate bonds posted the biggest declines. High yield corporate bonds bucked the trend, producing strong

2

gains during the period. Mortgage-backed securities also held up well as the combination of relatively high yields and high credit quality attracted investor demand.

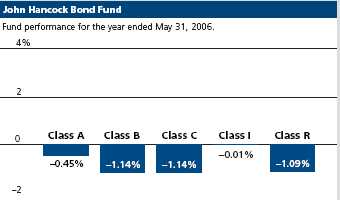

Fund performance

For the year ended May 31, 2006, John Hancock Bond Fund’s Class A, Class B, Class C, Class I and Class R shares posted total returns of –0.45%, –1.14%, –1.14%, –0.01% and –1.09%, respectively, at net asset value. The Fund’s performance was ahead of the –1.10% return of the Lehman Brothers Government/Credit Bond Index and in line with the –0.43% average return of the Morningstar intermediate-term bond category.1 Keep in mind that your net asset value return will differ from the Fund’s performance if you were not invested in the Fund for the entire period and did not reinvest all distributions. See pages six and seven for historical performance information.

Shifting into neutral

One factor that contributed to the Fund’s outperformance of its benchmark index was our defensive positioning, especially in the first half of the period. To lower the portfolio’s risk profile, we reduced its interest rate sensitivity and boosted overall credit quality. We also adjusted the maturity structure to benefit from the convergence of short- and long-term bond yields.

Since the beginning of 2006, however, we have been scaling back our defensive approach and moving toward a more neutral position with regard to interest rate sensitivity and maturity structure. With the yield convergence largely played out, we are starting to position for the inevitable widening of short- and long-term yields.

| “One factor that contributed to the Fund’s outperformance of its benchmark index was our defen- sive positioning, especially in the first half of the period.” |

Cutting back on corporates

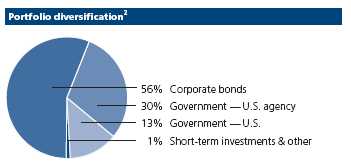

The one plank of our defensive strategy that remained in place throughout the one-year period was upgrading the portfolio’s credit quality. Toward that end, we reduced our holdings of corporate bonds, which comprised the portfolio’s largest sector weighting at the beginning of the period. In particular, we cut back on high yield corporate bonds, becoming more selective in our lower-rated holdings.

3

| Sector | |

| distribution2 | |

| Government — | |

| U.S. agency | 30% |

| Financials | 25% |

| Government — | |

| U.S. | 13% |

| Mortgage | |

| bonds | 8% |

| Utilities | 7% |

| Consumer | |

| discretionary | 4% |

| Industrials | 2% |

| Health care | 2% |

| Telecommunication | |

| services | 2% |

| Materials | 2% |

| Information | |

| technology | 2% |

| Consumer | |

| staples | 1% |

| Energy | 1% |

With the housing market starting to cool off and consumer spending expected to slow, we limited our exposure to bonds issued by consumer-oriented companies, automakers and homebuilders. We also remained wary of companies under pressure from equity investors to reduce cash and/or take on more debt to boost stockholder returns, because these moves generally weaken a company’s financial position. Consequently, we focused on securities issued by utilities, banks and finance-related companies, which are typically unwilling or unable to compromise their balance sheets and credit ratings.

Adding to mortgages

We added significantly to our holdings of mortgage-backed securities over the past year, making them the biggest sector weighting in the portfolio by the end of the period. In part, this reflected our efforts to improve portfolio credit quality, but it was also where we found the most attractive values in the bond market.

We focused our purchases on commercial mortgages and adjustable-rate mortgages, both of which offered yields comparable to ordinary fixed-rate mortgages but held up better in a rising interest rate environment.

Leaders and laggards

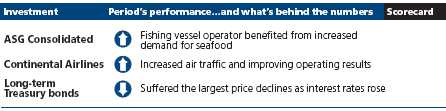

Among individual securities, the portfolio benefited from its modest exposure to emerging markets, which performed very well over the past year. A good example is our floating-rate holding of Bosphorous Financial Services, a securitized transaction of Finansbank, one of the larger banks in Turkey. This security got a boost after Finansbank agreed to sell approximately 45% of its stock to the National Bank of Greece.

4

Bonds issued by gaming companies also produced strong results; they are considered stable, defensive issues that typically hold up well during periods of market weakness. One of our top performers was MTR Gaming Group, Inc., which reported favorable financial results.

| “We believe that several factors — including a softening housing mar- ket, high energy prices and rising interest rates — suggest that an economic slowdown is forthcoming.” |

The weakest performers in the portfolio were all longer-term bonds, which declined the most as interest rates rose. Ocean Spray Cranberries, Inc., which we own as a preferred stock, fell because of the increase in long-term interest rates.

Outlook

We believe that several factors — including a softening housing market, high energy prices and rising interest rates — suggest that an economic slowdown is forthcoming. This should bring about the end of the Fed’s rate-hike cycle, after one more likely increase in June. The Fed’s focus, however, has shifted from economic growth to inflation, which has risen sharply in recent months. Another uncertain factor is new Fed chairman Ben Bernanke, who took over from Alan Greenspan in January and is facing his first challenge. We expect to maintain the portfolio’s neutral stance while continuing our emphasis on credit quality upgrades and individual security selection.

| Quality | ||

| distribution2 | ||

| AAA | 63% | |

| AA | 2% | |

| A | 7% | |

| BBB | 14% | |

| BB | 8% | |

| B | 4% | |

This commentary reflects the views of the portfolio managers through the end of the Fund’s period discussed in this report. The managers’ statements reflect their own opinions. As such, they are in no way guarantees of future events and are not intended to be used as investment advice or a recommendation regarding any specific security. They are also subject to change at any time as market and other conditions warrant.

1 Figures from Morningstar, Inc. include reinvested dividends and do not take into account sales charges. Actual load-adjusted performance is lower.

2 As a percentage of net assets on May 31, 2006.

5

| A LOOK AT PERFORMANCE |

| For the period ended May 31, 2006 |

| Class A | Class B | Class C | Class I1 | Class R1 | ||||||

| Inception date | 11-9-73 | 11-23-93 | 10-1-98 | 9-4-01 | 8-5-03 | |||||

| Average annual returns with maximum sales charge (POP) | ||||||||||

| One year | –4.92% | –5.88% | –2.09% | –0.01% | –1.09% | |||||

| Five years | 4.00 | 3.90 | 4.23 | — | — | |||||

| Ten years | 5.54 | 5.45 | — | — | — | |||||

| Since inception | — | — | 3.99 | 4.96 | 3.57 | |||||

| Cumulative total returns with maximum sales charge (POP) | ||||||||||

| One year | –4.92 | –5.88 | –2.09 | –0.01 | –1.09 | |||||

| Five years | 21.68 | 21.06 | 23.03 | — | — | |||||

| Ten years | 71.52 | 69.97 | — | — | — | |||||

| Since inception | — | — | 35.00 | 25.78 | 10.39 | |||||

| SEC 30-day yield as of May 31, 2006 | ||||||||||

| 4.71 | 4.24 | 4.23 | 5.33 | 3.33 | ||||||

Performance figures assume all distributions are reinvested. Returns with maximum sales charge reflect a sales charge on Class A shares of 4.5% and the applicable contingent deferred sales charge (CDSC) on Class B and Class C shares. The returns for Class C shares have been adjusted to reflect the elimination of the front-end sales charge effective July 15, 2004. The Class B shares’ CDSC declines annually between years 1–6 according to the following schedule: 5, 4, 3, 3, 2, 1%. No sales charge will be assessed after the sixth year. Class C shares held for less than one year are subject to a 1% CDSC. Sales charge is not applicable for Class I and Class R shares.

The returns reflect past results and should not be considered indicative of future performance. The return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Due to market volatility, the Fund’s current performance may be higher or lower than the performance shown. For performance data current to the most recent month-end, please call 1-800-225-5291 or visit the Fund’s Web site at www.jhfunds.com.

The performance table above and the chart on the next page do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Fund’s performance results reflect any applicable expense reductions, without which the expenses would increase and results would have been less favorable.

1For certain types of investors as described in the Fund’s Class I and Class R share prospectuses.

6

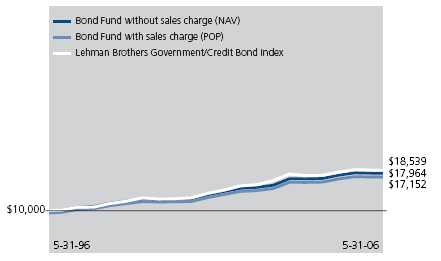

| GROWTH OF $10,000 |

This chart shows what happened to a hypothetical $10,000 investment in Class A shares for the period indicated. For comparison, we’ve shown the same investment in the Lehman Brothers Government/Credit Bond Index.

| Class B1 | Class C1 | Class I2 | Class R2 | |||||

| Period beginning | 5-31-96 | 10-1-98 | 9-4-01 | 8-5-03 | ||||

| Bond Fund | $16,997 | $13,500 | $12,578 | $11,039 | ||||

| Index | 18,539 | 14,447 | 12,453 | 10,925 | ||||

Assuming all distributions were reinvested for the period indicated, the table above shows the value of a $10,000 investment in the Fund’s Class B, Class C, Class I and Class R shares, respectively, as of May 31, 2006. The Class C shares investment with maximum sales charge has been adjusted to reflect the elimination of the front-end sales charge effective July 15, 2004. Performance of the classes will vary based on the difference in sales charges paid by shareholders investing in the different classes and the fee structure of those classes.

Lehman Brothers Government/Credit Bond Index is an unmanaged index that measures the performance of U.S. government bonds, U.S. corporate bonds and Yankee bonds.

It is not possible to invest directly in an index. Index figures do not reflect sales charges and would be lower if they did.

1 No contingent deferred sales charge applicable.

2 For certain types of investors as described in the Fund’s Class I and Class R share prospectuses.

7

| YOUR EXPENSES |

These examples are intended to help you understand your ongoing operating expenses.

Understanding fund expenses

As a shareholder of the Fund, you incur two types of costs:

* Transaction costs which include sales charges (loads) on purchases or redemptions (varies by share class), minimum account fee charge, etc.

* Ongoing operating expenses including management fees, distribution and service fees (if applicable) and other fund expenses.

We are going to present only your ongoing operating expenses here.

Actual expenses/actual returns

This example is intended to provide information about your fund’s actual ongoing operating expenses, and is based on your fund’s actual return. It assumes an account value of $1,000.00 on November 30, 2005, with the same investment held until May 31, 2006.

| Account value | Expenses paid | |||

| $1,000.00 | Ending value | during year | ||

| on 11-30-05 | on 5-31-06 | ended 5-31-061 | ||

| Class A | $999.70 | $5.29 | ||

| Class B | 996.20 | 8.77 | ||

| Class C | 996.20 | 8.77 | ||

| Class I | 1,001.90 | 3.13 | ||

| Class R | 994.30 | 10.04 | ||

Together with the value of your account, you may use this information to estimate the operating expenses that you paid over the period. Simply divide your account value at May 31, 2006 by $1,000.00, then multiply it by the “expenses paid” for your share class from the table above. For example, for an account value of $8,600.00, the operating expenses should be calculated as follows:

8

Hypothetical example for comparison purposes

This table allows you to compare your fund’s ongoing operating expenses with those of any other fund. It provides an example of the Fund’s hypothetical account values and hypothetical expenses based on each class’s actual expense ratio and an assumed 5% annual return before expenses (which is not your fund’s actual return). It assumes an account value of $1,000.00 on November 30, 2005, with the same investment held until May 31, 2006. Look in any other fund shareholder report to find its hypothetical example and you will be able to compare these expenses.

| Account value | Expenses paid | |||

| $1,000.00 | Ending value | during year | ||

| on 11-30-05 | on 5-31-06 | ended 5-31-061 | ||

| Class A | $1,019.64 | $5.35 | ||

| Class B | 1,016.15 | 8.86 | ||

| Class C | 1,016.15 | 8.86 | ||

| Class I | 1,021.80 | 3.16 | ||

| Class R | 1,014.86 | 10.15 | ||

Remember, these examples do not include any transaction costs, such as sales charges; therefore, these examples will not help you to determine the relative total costs of owning different funds. If transaction costs were included, your expenses would have been higher. See the prospectus for details regarding transaction costs.

1 Expenses are equal to the Fund’s annualized expense ratio of 1.06%, 1.76%, 1.76%, 0.63% and 2.02% for Class A, Class B, Class C, Class I and Class R respectively, multiplied by the average account value over the period, multiplied by number of days in most recent fiscal half-year/365 or 366 (to reflect the one-half year period).

9

F I N A N C I A L S TAT E M E N T S

| FUND’S INVESTMENTS |

| Securities owned by the Fund on May 31, 2006 |

This schedule is divided into four main categories: bonds, preferred stocks, U.S. government and agencies securities and short-term investments. Bonds, preferred stocks and U.S. government and agencies securities are further broken down by industry group. Short-term investments, which represent the Fund’s cash position, are listed last.

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

| Bonds 55.69% | $565,992,493 | |||||||||

| (Cost $580,829,764) | ||||||||||

Airlines 0.36% | 3,701,542 | |||||||||

| Continental Airlines, Inc., | ||||||||||

| Pass Thru Ctf Ser 1999-1A | 6.545% | 02-02-19 | A– | $980 | 972,314 | |||||

| Pass Thru Ctf Ser 2000-2 Class B | 8.307 | 04-02-18 | BB– | 1,302 | 1,250,918 | |||||

| Pass Thru Ctf Ser 2001-1 Class C | 7.033 | 06-15-11 | BB– | 1,516 | 1,477,730 | |||||

| Jet Equipment Trust, | ||||||||||

| Equip Trust Ctf Ser 1995-B2 (B)(H)(S) | 10.910 | 08-15-14 | D | 5,800 | 580 | |||||

Asset Management & Custody Banks 0.40% | 4,021,021 | |||||||||

| Rabobank Capital Fund II, | ||||||||||

| Perpetual Bond (5.260% to 12-31-13 | ||||||||||

| then variable) (L)(S) | 5.260 | 12-29-49 | AA | 4,230 | 4,021,021 | |||||

Broadcasting & Cable TV 1.24% | 12,588,162 | |||||||||

| Clear Channel Communications, Inc., | ||||||||||

| Note | 5.500 | 09-15-14 | BBB– | 1,900 | 1,738,065 | |||||

| Comcast Corp., | ||||||||||

| Gtd Note | 5.900 | 03-15-16 | BBB+ | 1,860 | 1,797,541 | |||||

| Cox Communications, Inc., | ||||||||||

| Note | 7.125 | 10-01-12 | BBB | 2,295 | 2,383,718 | |||||

| Shaw Communications, Inc., | ||||||||||

| Sr Note (Canada) | 8.250 | 04-11-10 | BB+ | 2,040 | 2,131,800 | |||||

| TCI Communications, Inc., | ||||||||||

| Deb | 9.800 | 02-01-12 | BBB | 1,990 | 2,314,338 | |||||

| XM Satellite Radio, Inc., | ||||||||||

| Sr Note (S) | 9.750 | 05-01-14 | CCC | 2,390 | 2,222,700 | |||||

Building Products 0.26% | 2,697,262 | |||||||||

| Home Depot, Inc. (The), | ||||||||||

| Sr Note | 5.400 | 03-01-16 | AA | 2,800 | 2,697,262 | |||||

| See notes to financial statements. |

10

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Casinos & Gaming 1.51% | $15,376,632 | |||||||||

| Caesars Entertainment, Inc., | ||||||||||

| Sr Note | 7.000% | 04-15-13 | BBB– | $2,360 | 2,431,289 | |||||

| Chukchansi Economic Development | ||||||||||

| Authority, Sr Note (S) | 8.000 | 11-15-13 | BB– | 570 | 582,113 | |||||

| Jacobs Entertainment, Inc., | ||||||||||

| Sr Sec Note (B) | 11.875 | 02-01-09 | B | 3,235 | 3,427,094 | |||||

| Little Traverse Bay Bands of Odawa Indians, | ||||||||||

| Sr Note (S) | 10.250 | 02-15-14 | B | 1,655 | 1,638,450 | |||||

| Majestic Star Casino, LLC/Cap II, | ||||||||||

| Sr Sec Note (S) | 9.750 | 01-15-11 | B– | 2,060 | 2,121,800 | |||||

| Mashantucket West Pequot, | ||||||||||

| Bond (S) | 5.912 | 09-01-21 | BBB– | 1,250 | 1,157,037 | |||||

| Mohegan Tribal Gaming Authority, | ||||||||||

| Sr Sub Note | 7.125 | 08-15-14 | B+ | 1,050 | 1,023,750 | |||||

| MTR Gaming Group, Inc., | ||||||||||

| Gtd Sr Note Ser B | 9.750 | 04-01-10 | B+ | 1,595 | 1,692,694 | |||||

| Sr Sub Note (S) | 9.000 | 06-01-12 | B– | 420 | 424,725 | |||||

| Waterford Gaming LLC, | ||||||||||

| Sr Note (S) | 8.625 | 09-15-12 | B+ | 828 | 877,680 | |||||

Commercial Printing 0.07% | 754,154 | |||||||||

| Quebecor World Capital Corp., | ||||||||||

| Sr Note (Canada) (S) | 8.750 | 03-15-16 | BB– | 800 | 754,154 | |||||

Commodity Chemicals 0.23% | 2,366,400 | |||||||||

| Lyondell Chemical Co., | ||||||||||

| Gtd Sr Sub Note | 10.875 | 05-01-09 | B | 2,320 | 2,366,400 | |||||

Computer Hardware 0.21% | 2,176,005 | |||||||||

| Activant Solutions, Inc., | ||||||||||

| Sr Sub Note (S) | 9.500 | 05-01-16 | CCC+ | 485 | 476,513 | |||||

| Pioneer Standard Electronics, Inc., | ||||||||||

| Sr Note | 9.500 | 08-01-06 | BB– | 1,695 | 1,699,492 | |||||

Construction Materials 0.34% | 3,419,056 | |||||||||

| Duke Capital LLC, | ||||||||||

| Sr Note | 6.250 | 02-15-13 | BBB | 3,380 | 3,419,056 | |||||

Consumer Finance 1.48% | 15,054,633 | |||||||||

| American General Finance Corp., | ||||||||||

| Med Term Note Ser I | 4.875 | 07-15-12 | A+ | 3,250 | 3,085,742 | |||||

| Ford Motor Credit Co., | ||||||||||

| Floating Rate Note (P) | 6.120 | 11-16-06 | BB+ | 3,325 | 3,320,122 | |||||

| Household Finance Corp., | ||||||||||

| Note | 6.375 | 10-15-11 | A | 1,785 | 1,834,146 | |||||

| See notes to financial statements. |

11

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Consumer Finance (continued) | ||||||||||

| HSBC Finance Capital Trust IX, | ||||||||||

| Note (5.911% to 11-30-15 then variable) | 5.911% | 11-30-35 | BBB+ | $2,600 | $2,504,349 | |||||

| HSBC Finance Corp., | ||||||||||

| Sr Note | 6.750 | 05-15-11 | A | 4,140 | 4,310,274 | |||||

Department Stores 0.35% | 3,536,015 | |||||||||

| J.C. Penney Co., Inc., | ||||||||||

| Deb | 8.125 | 04-01-27 | BBB– | 1,455 | 1,508,138 | |||||

| Deb | 7.650 | 08-15-16 | BBB– | 1,855 | 2,027,877 | |||||

Diversified Banks 1.73% | 17,570,338 | |||||||||

| Bank of New York, | ||||||||||

| Cap Security (S) | 7.780 | 12-01-26 | A– | 4,420 | 4,629,269 | |||||

| BNP Paribas Capital Trust, | ||||||||||

| Sub Bond (9.003% to 10-27-10 | ||||||||||

| then variable) (S) | 9.003 | 12-29-49 | A+ | 2,560 | 2,862,444 | |||||

| Chuo Mitsui Trust & Banking Co., Ltd, | ||||||||||

| Perpetual Sub Note (5.506% to 4-15-15 | ||||||||||

| then variable) (Japan) (S) | 5.506 | 12-15-49 | Baa2 | 2,530 | 2,368,287 | |||||

| HBOS Plc, | ||||||||||

| Perpetual Bond (6.413% to 10-1-35 | ||||||||||

| then variable) (United Kingdom) (S) | 6.413 | 09-29-49 | A | 3,410 | 3,079,823 | |||||

| Royal Bank of Scotland Group Plc, | ||||||||||

| Perpetual Bond (7.648% to 09-30-31 | ||||||||||

| then variable) (United Kingdom) | 7.648 | 08-29-49 | A | 4,140 | 4,630,515 | |||||

Diversified Commercial Services 0.13% | 1,335,000 | |||||||||

| Sotheby’s Holdings, Inc., | ||||||||||

| Note | 6.875 | 02-01-09 | BB– | 1,335 | 1,335,000 | |||||

Diversified Financial Services 1.00% | 10,198,773 | |||||||||

| CIT Group, Inc., | ||||||||||

| Sr Note | 5.600 | 04-27-11 | A | 2,690 | 2,670,810 | |||||

| Nissan Motor Acceptance Corp., | ||||||||||

| Sr Note (S) | 5.625 | 03-14-11 | BBB+ | 2,725 | 2,688,613 | |||||

| St. George Funding Co., | ||||||||||

| Perpetual Bond (8.485% to 06-30-17 | ||||||||||

| then variable) (Australia) (S) | 8.485 | 12-31-49 | Baa1 | 4,555 | 4,839,350 | |||||

Diversified Metals & Mining 0.21% | 2,130,000 | |||||||||

| Freeport-McMoRan Copper & Gold, Inc., | ||||||||||

| Sr Note | 10.125 | 02-01-10 | B+ | 2,000 | 2,130,000 | |||||

Drug Retail 0.17% | 1,703,047 | |||||||||

| Allergan, Inc., | ||||||||||

| Note (S) | 5.750 | 04-01-16 | A | 1,735 | 1,703,047 | |||||

| See notes to financial statements. |

12

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Electric Utilities 6.08% | $61,834,720 | |||||||||

| AES Eastern Energy LP, | ||||||||||

| Pass Thru Ctf Ser 1999-A | 9.000% | 01-02-17 | BB+ | $3,708 | 4,088,855 | |||||

| Beaver Valley Funding Corp., | ||||||||||

| Sec Lease Obligation Bond | 9.000 | 06-01-17 | BBB– | 3,919 | 4,365,100 | |||||

| BVPS II Funding Corp., | ||||||||||

| Collateralized Lease Bond | 8.890 | 06-01-17 | BB+ | 6,387 | 7,212,392 | |||||

| DTE Energy Co., | ||||||||||

| Sr Note Ser B | 6.350 | 06-01-16 | Baa2 | 2,605 | 2,596,417 | |||||

| East Coast Power LLC, | ||||||||||

| Sr Sec Note Ser B | 7.066 | 03-31-12 | BBB– | 3,062 | 3,144,757 | |||||

| Empresa Electrica Guacolda SA, | ||||||||||

| Sr Sec Note (Chile) (S) | 8.625 | 04-30-13 | BBB– | 1,872 | 2,028,431 | |||||

| Entergy Gulf States, Inc., | ||||||||||

| 1st Mtg Note | 5.700 | 06-01-15 | BBB+ | 1,355 | 1,275,926 | |||||

| HQI Transelect Chile SA, | ||||||||||

| Sr Note (Chile) | 7.875 | 04-15-11 | A– | 2,895 | 3,072,869 | |||||

| Indiantown Cogeneration, LP, | ||||||||||

| 1st Mtg Note Ser A-9 | 9.260 | 12-15-10 | BB+ | 1,473 | 1,539,792 | |||||

| IPALCO Enterprises, Inc., | ||||||||||

| Sr Sec Note | 8.625 | 11-14-11 | BB– | 3,000 | 3,217,500 | |||||

| Kansas Gas & Electric Co., | ||||||||||

| Bond | 5.647 | 03-29-21 | BB– | 1,910 | 1,804,835 | |||||

| Midland Funding Corp. II, | ||||||||||

| Lease Obligation Bond Ser B | 13.250 | 07-23-06 | BB– | 4,002 | 4,033,641 | |||||

| Monterrey Power SA de CV, | ||||||||||

| Sr Sec Bond (Mexico) (S) | 9.625 | 11-15-09 | BBB | 2,445 | 2,640,908 | |||||

| Pepco Holdings, Inc., | ||||||||||

| Note | 6.450 | 08-15-12 | BBB | 2,370 | 2,416,267 | |||||

| PNPP II Funding Corp., | ||||||||||

| Deb | 9.120 | 05-30-16 | BB+ | 212 | 238,052 | |||||

| PPL Energy Supply LLC, | ||||||||||

| Sr Note Ser A | 6.400 | 11-01-11 | BBB | 2,645 | 2,701,349 | |||||

| Progress Energy, Inc., | ||||||||||

| Sr Note | 6.850 | 04-15-12 | BBB– | 1,210 | 1,266,451 | |||||

| System Energy Resources, Inc., | ||||||||||

| Sec Bond (S) | 5.129 | 01-15-14 | BBB | 3,219 | 3,103,195 | |||||

| Texas-New Mexico Power Co., | ||||||||||

| Sr Note | 6.125 | 06-01-08 | BBB | 3,350 | 3,352,067 | |||||

| TransAlta Corp., | ||||||||||

| Note (Canada) | 5.750 | 12-15-13 | BBB– | 2,735 | 2,660,991 | |||||

| Waterford 3 Funding Corp., | ||||||||||

| Sec Lease Obligation Bond | 8.090 | 01-02-17 | BBB– | 4,974 | 5,074,925 | |||||

| See notes to financial statements. |

13

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||||

Electrical Components & Equipment 0.24% | $2,479,635 | |||||||||||

| AMETEK, Inc., | ||||||||||||

| Sr Note | 7.200% | 07-15-08 | BBB | $2,425 | 2,479,635 | |||||||

Food Distributors 0.21% | 2,286,276 | |||||||||||

| Tyson Foods, Inc., | ||||||||||||

| Sr Note | 6.600 | 04-01-16 | BBB | 2,320 | 2,286,276 | |||||||

Food Retail 0.75% | 7,636,051 | |||||||||||

| Ahold Finance USA, Inc., | ||||||||||||

| Gtd Pass Thru Ctf Ser 2001A-1 | 7.820 | 01-02-20 | BB | 3,292 | 3,356,491 | |||||||

| Delhaize America, Inc., | ||||||||||||

| Gtd Note | 9.000 | 04-15-31 | BB+ | 1,575 | 1,765,625 | |||||||

| Food Lion, Inc., | ||||||||||||

| Note | 8.730 | 08-30-06 | BB+ | 2,500 | 2,513,935 | |||||||

Gas Utilities 0.56% | 5,663,767 | |||||||||||

| Energy Transfer Partners, | ||||||||||||

| Gtd Sr Note (G) | 5.950 | 02-01-15 | BBB– | 2,790 | 2,694,705 | |||||||

| Kinder Morgan Finance Co., | ||||||||||||

| Gtd Sr Note | 6.400 | 01-05-36 | BBB | 2,250 | 1,889,968 | |||||||

| KN Capital Trust I, | ||||||||||||

| Gtd Cap Security Ser B | 8.560 | 04-15-27 | BB+ | 1,030 | 1,079,094 | |||||||

Health Care Facilities 0.18% | 1,854,092 | |||||||||||

| Manor Care, Inc., | ||||||||||||

| Gtd Note | 6.250 | 05-01-13 | BBB | 1,885 | 1,854,092 | |||||||

Health Care Services 0.62% | 6,318,934 | |||||||||||

| Alliance Imaging, Inc., | ||||||||||||

| Sr Sub Note (L) | 7.250 | 12-15-12 | B– | 1,835 | 1,646,913 | |||||||

| Caremark Rx, Inc., | ||||||||||||

| Sr Note | 7.375 | 10-01-06 | BBB– | 1,335 | 1,342,400 | |||||||

| Health Management Associates, Inc., | ||||||||||||

| Sr Sub Note | 6.125 | 04-15-16 | A– | 3,390 | 3,329,621 | |||||||

Hotels, Resorts & Cruise Lines 0.27% | 2,730,032 | |||||||||||

| Hyatt Equities LLC, | ||||||||||||

| Note (S) | 6.875 | 06-15-07 | BBB | 2,705 | 2,730,032 | |||||||

Industrial Conglomerates 0.52% | 5,255,002 | |||||||||||

| General Electric Co., | ||||||||||||

| Note | 5.000 | 02-01-13 | AAA | 5,465 | 5,255,002 | |||||||

Industrial Machinery 0.57% | 5,765,100 | |||||||||||

| Kennametal, Inc., | ||||||||||||

| Sr Note | 7.200 | 06-15-12 | BBB | 2,960 | 3,111,271 | |||||||

| Trinity Industries, Inc., | ||||||||||||

| Pass Thru Ctf (S) | 7.755 | 02-15-09 | Ba1 | 2,615 | 2,653,829 | |||||||

| See notes to financial statements. |

14

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Integrated Oil & Gas 0.22% | $2,193,975 | |||||||||

| Pemex Project Funding Master Trust, | ||||||||||

| Gtd Note | 9.125% | 10-13-10 | BBB | $1,990 | 2,193,975 | |||||

Integrated Telecommunication Services 0.49% | 4,931,006 | |||||||||

| AT&T Corp., | ||||||||||

| Gtd Sr Note | 8.000 | 11-15-31 | A | 3,400 | 3,917,256 | |||||

| Intelsat Subsidiary Holding Co., Ltd., | ||||||||||

| Gtd Floating Rate Sr Note (Bermuda) (P)(S) | 9.614 | 01-15-12 | B+ | 1,000 | 1,013,750 | |||||

Investment Banking & Brokerage 1.11% | 11,241,468 | |||||||||

| Goldman Sachs Group, Inc. (The), | ||||||||||

| Sr Note | 5.350 | 01-15-16 | A+ | 2,770 | 2,619,174 | |||||

| Lehman Brothers Holdings, Inc., | ||||||||||

| Med Term Note Ser H | 5.500 | 04-04-16 | A+ | 2,530 | 2,432,486 | |||||

| Merrill Lynch & Co., Inc., | ||||||||||

| Sub Note | 6.050 | 05-16-16 | A | 2,500 | 2,488,908 | |||||

| Mizuho Finance, | ||||||||||

| Gtd Sub Bond (Cayman Islands) | 8.375 | 12-29-49 | A2 | 3,500 | 3,700,900 | |||||

Leisure Facilities 0.25% | 2,515,585 | |||||||||

| AMC Entertainment, Inc., | ||||||||||

| Sr Sub Note (L) | 9.500 | 02-01-11 | CCC+ | 1,450 | 1,439,241 | |||||

| HRP Myrtle Beach Operations, | ||||||||||

| Floating Rate Sr Sec Note (P)(S) | 9.818 | 04-01-12 | B | 1,075 | 1,076,344 | |||||

Life & Health Insurance 0.82% | 8,292,197 | |||||||||

| AmerUs Group Co., | ||||||||||

| Sr Note | 6.583 | 05-16-11 | Baa3 | 1,870 | 1,878,733 | |||||

| Phoenix Cos., Inc. (The), | ||||||||||

| Bond | 6.675 | 02-16-08 | BBB | 2,205 | 2,212,162 | |||||

| Phoenix Life Insurance Co., | ||||||||||

| Note (S) | 7.150 | 12-15-34 | BBB+ | 1,920 | 1,872,121 | |||||

| Provident Financing Trust I, | ||||||||||

| Gtd Cap Security (L) | 7.405 | 03-15-38 | B+ | 2,585 | 2,329,181 | |||||

Marine 0.26% | 2,667,321 | |||||||||

| CMA CGM SA, | ||||||||||

| Sr Note (France) (S) | 7.250 | 02-01-13 | BB+ | 2,790 | 2,667,321 | |||||

Meat, Poultry & Fish 0.27% | 2,704,000 | |||||||||

| ASG Consolidated LLC, | ||||||||||

| Sr Disc Note (Zero to 11-1-08, | ||||||||||

| then 11.500%) (O)(L) | Zero | 11-01-11 | B– | 3,200 | 2,704,000 | |||||

Metal & Glass Containers 0.17% | 1,740,750 | |||||||||

| BWAY Corp., | ||||||||||

| Gtd Sr Sub Note | 10.000 | 10-15-10 | B– | 1,650 | 1,740,750 | |||||

| See notes to financial statements. |

15

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Metal & Mining 0.13% | $1,284,949 | |||||||||

| Vedanta Resources Plc, | ||||||||||

| Sr Note (United Kingdom) (S) | 6.625% | 02-22-10 | BB+ | $1,320 | 1,284,949 | |||||

Multi-Line Insurance 0.70% | 7,090,375 | |||||||||

| American International Group, | ||||||||||

| Note (S) | 5.050 | 10-01-15 | AA | 3,000 | 2,814,699 | |||||

| Horace Mann Educators Corp., | ||||||||||

| Sr Note | 6.850 | 04-15-16 | BBB | 1,550 | 1,531,333 | |||||

| Zurich Capital Trust I, | ||||||||||

| Gtd Cap Security (S) | 8.376 | 06-01-37 | A– | 2,580 | 2,744,343 | |||||

Multi-Media 0.75% | 7,597,244 | |||||||||

| News America Holdings, Inc., | ||||||||||

| Gtd Sr Deb | 8.250 | 08-10-18 | BBB– | 3,000 | 3,458,706 | |||||

| Time Warner Entertainment Co., | ||||||||||

| Sr Deb | 8.375 | 03-15-23 | BBB+ | 1,990 | 2,223,383 | |||||

| Viacom, Inc., | ||||||||||

| Sr Note (S) | 6.875 | 04-30-36 | BBB | 1,980 | 1,915,155 | |||||

Multi-Utilities & Unregulated Power 0.61% | 6,231,006 | |||||||||

| Dynegy-Roseton Danskamme, | ||||||||||

| Gtd Pass Thru Ctf Ser B | 7.670 | 11-08-16 | B | 2,600 | 2,662,441 | |||||

| Salton Sea Funding Corp., | ||||||||||

| Gtd Sr Sec Note Ser E | 8.300 | 05-30-11 | BB+ | 1,043 | 1,098,204 | |||||

| Sr Sec Bond Ser F | 7.475 | 11-30-18 | BB+ | 2,349 | 2,470,361 | |||||

Oil & Gas Refining, Marketing & Transportation 0.55% | 5,545,387 | |||||||||

| Enterprise Products Operating LP, | ||||||||||

| Gtd Sr Note Ser B | 6.375 | 02-01-13 | BB+ | 4,265 | 4,254,218 | |||||

| Premcor Refining Group, Inc., | ||||||||||

| Sr Note | 9.500 | 02-01-13 | BBB– | 1,175 | 1,291,169 | |||||

Oil & Gas Drilling 0.15% | 1,496,944 | |||||||||

| Delek & Avner-Yam Tethys Ltd., | ||||||||||

| Sr Sec Note (Israel) (S) | 5.326 | 08-01-13 | BBB– | 1,557 | 1,496,944 | |||||

Packaged Foods & Meats 0.11% | 1,146,052 | |||||||||

| General Foods Corp., | ||||||||||

| Deb | 7.000 | 06-15-11 | A– | 1,145 | 1,146,052 | |||||

Paper Packaging 0.17% | 1,761,825 | |||||||||

| MDP Acquisitions Plc, | ||||||||||

| Sr Note (Ireland) | 9.625 | 10-01-12 | B– | 1,690 | 1,761,825 | |||||

| See notes to financial statements. |

16

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Paper Products 0.27% | $2,736,430 | |||||||||

| Abitibi Consolidated, Inc., | ||||||||||

| Note (Canada) | 6.000% | 06-20-13 | B+ | $1,445 | 1,221,025 | |||||

| Plum Creek Timber Co., Inc., | ||||||||||

| Gtd Note | 5.875 | 11-15-15 | BBB– | 1,570 | 1,515,405 | |||||

Pharmaceuticals 0.50% | 5,066,306 | |||||||||

| Medco Health Solutions, Inc., | ||||||||||

| Sr Note | 7.250 | 08-15-13 | BBB | 2,380 | 2,526,042 | |||||

| Wyeth, | ||||||||||

| Note | 5.500 | 02-15-16 | A | 2,650 | 2,540,264 | |||||

Property & Casualty Insurance 0.46% | 4,698,503 | |||||||||

| Markel Corp., | ||||||||||

| Sr Note | 7.350 | 08-15-34 | BBB– | 2,380 | 2,313,298 | |||||

| Ohio Casualty Corp., | ||||||||||

| Sr Note | 7.300 | 06-15-14 | BB+ | 2,330 | 2,385,205 | |||||

Real Estate Management & Development 0.63% | 6,391,627 | |||||||||

| Healthcare Realty Trust, Inc., | ||||||||||

| Sr Note | 8.125 | 05-01-11 | BBB– | 2,515 | 2,717,173 | |||||

| Health Care REIT, Inc., | ||||||||||

| Sr Note | 6.200 | 06-01-16 | BBB– | 1,525 | 1,485,178 | |||||

| Socgen Real Estate Co., LLC, | ||||||||||

| Perpetual Bond Ser A (7.640% to | ||||||||||

| 09-30-07 then variable) (S) | 7.640 | 12-29-49 | A | 2,140 | 2,189,276 | |||||

Regional Banks 1.29% | 13,148,671 | |||||||||

| BankAmerica Institutional Bank, | ||||||||||

| Gtd Cap Security Ser B (S) | 7.700 | 12-31-26 | A | 1,060 | 1,109,752 | |||||

| Colonial Bank, NA, | ||||||||||

| Sub Note | 6.375 | 12-01-15 | BBB– | 2,563 | 2,544,062 | |||||

| Mainstreet Capital Trust I, | ||||||||||

| Gtd Jr Sub Cap Security Ser B (G) | 8.900 | 12-01-27 | A3 | 2,380 | 2,571,590 | |||||

| NB Capital Trust IV, | ||||||||||

| Gtd Cap Security | 8.250 | 04-15-27 | A | 3,030 | 3,201,386 | |||||

| State Street Institutional Capital Trust, | ||||||||||

| Gtd Cap Security Ser A (S) | 7.940 | 12-30-26 | A | 1,325 | 1,390,458 | |||||

| Wachovia Capital Trust II, | ||||||||||

| Gtd Floating Rate Cap Security (P) | 5.568 | 01-15-27 | A– | 2,420 | 2,331,423 | |||||

Soft Drinks 0.16% | 1,595,213 | |||||||||

| Panamerican Beverages, Inc., | ||||||||||

| Sr Note (Panama) | 7.250 | 07-01-09 | BBB | 1,545 | 1,595,213 | |||||

| See notes to financial statements. |

17

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Specialized Finance 1.60% | $16,245,867 | |||||||||

| Astoria Depositor Corp., | ||||||||||

| Pass Thru Ctf Ser B (G)(S) | 8.144% | 05-01-21 | BB | $3,640 | 3,728,306 | |||||

| Bosphorous Financial Services, | ||||||||||

| Sec Floating Rate Note (P)(S) | 6.970 | 02-15-12 | Baa3 | 2,660 | 2,670,558 | |||||

| ESI Tractebel Acquistion Corp., | ||||||||||

| Gtd Sec Bond Ser B | 7.990 | 12-30-11 | BB | 3,837 | 3,971,038 | |||||

| Humpuss Funding Corp., | ||||||||||

| Gtd Note (S) | 7.720 | 12-15-09 | B2 | 1,516 | 1,492,778 | |||||

| Specialty Underwriting & Residential | ||||||||||

| Finance Trust, Mtg Pass Thru Ctf | ||||||||||

| Ser 2003 BC4 Class A3B | 4.788 | 11-25-34 | AAA | 3,246 | 3,217,012 | |||||

| UCAR Finance, Inc., | ||||||||||

| Gtd Sr Note | 10.250 | 02-15-12 | B– | 1,095 | 1,166,175 | |||||

Specialty Chemicals 0.15% | 1,481,269 | |||||||||

| Nova Chemicals Ltd., | ||||||||||

| Note (Canada) | 7.875 | 09-15-25 | BB+ | 1,545 | 1,481,269 | |||||

Steel 0.23% | 2,386,200 | |||||||||

| Metallurg Holdings, Inc., | ||||||||||

| Sr Sec Note (G)(S) | 10.500 | 10-01-10 | B– | 2,460 | 2,386,200 | |||||

Telecommunications Equipment 0.58% | 5,892,324 | |||||||||

| Corning, Inc., | ||||||||||

| Med Term Note | 8.300 | 04-04-25 | Ba2 | 4,230 | 4,421,742 | |||||

| Note | 6.050 | 06-15-15 | BBB– | 1,515 | 1,470,582 | |||||

Thrifts & Mortgage Finance 21.32% | 216,663,080 | |||||||||

| Banc of America Commercial Mortgage, Inc., | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-4 Class A5A | 4.933 | 07-10-45 | AAA | 1,595 | 1,493,752 | |||||

| Mtg Pass Thru Ctf Ser 2005-6 Class A4 | 5.182 | 09-10-47 | AAA | 3,490 | 3,343,229 | |||||

| Banc of America Funding Corp., | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-B Class 6A1 | 5.901 | 03-20-36 | AAA | 4,211 | 4,190,432 | |||||

| Mtg Pass Thru Ctf Ser 2006-D Class 6B1 | 5.982 | 05-20-36 | AA+ | 1,855 | 1,816,565 | |||||

| Bear Stearns Adjustable Rate Mortgage Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-12 | ||||||||||

| Class 22A1 (P) | 5.762 | 02-25-36 | AAA | 4,024 | 4,011,596 | |||||

| Bear Stearns Alt-A Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-3 Class B2 (P) | 5.341 | 04-25-35 | AA+ | 1,263 | 1,233,037 | |||||

| Mtg Pass Thru Ctf Ser 2006-1 | ||||||||||

| Class 23A1 (P) | 5.681 | 02-25-36 | AAA | 4,623 | 4,576,882 | |||||

| Mtg Pass Thru Ctf Ser 2006-3 Class 34A1 | 6.227 | 05-25-36 | AAA | 5,154 | 5,162,005 | |||||

| Bear Stearns Commercial Mortgage Securities, Inc., | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-T20 | ||||||||||

| Class A4A (P) | 5.156 | 10-12-42 | Aaa | 1,640 | 1,567,652 | |||||

| See notes to financial statements. |

18

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Thrifts & Mortgage Finance (continued) | ||||||||||

| Chaseflex Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-2 Class 4A1 | 5.000% | 05-25-20 | AAA | $4,881 | $4,679,593 | |||||

| Citigroup/Deutsche Bank Commercial | ||||||||||

| Mortgage Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-CD1 | ||||||||||

| Class A4 (P) | 5.226 | 07-15-44 | AAA | 2,470 | 2,375,615 | |||||

| Mtg Pass Thru Ctf Ser 2005-CD1 | ||||||||||

| Class C (P) | 5.226 | 07-15-44 | AA | 1,030 | 981,837 | |||||

| Citigroup Mortgage Loan Trust, Inc., | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-5 | ||||||||||

| Class 2A3 | 5.000 | 08-25-35 | AAA | 3,072 | 3,008,098 | |||||

| Mtg Pass Thru Ctf Ser 2005-10 | ||||||||||

| Class 1A5A (P) | 5.902 | 12-25-35 | AAA | 4,569 | 4,541,806 | |||||

| Citigroup Mortgage Securities, Inc., | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-5 | ||||||||||

| Class 2A3 | 5.000 | 08-25-20 | Aaa | 5,323 | 5,161,120 | |||||

| Commercial Mortgage, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-C7 | ||||||||||

| Class A3 (N) | 5.707 | 06-10-46 | AAA | 3,775 | 3,793,847 | |||||

| ContiMortgage Home Equity Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 1995-2 Class A-5 | 8.100 | 08-15-25 | AAA | 621 | 635,702 | |||||

| Countrywide Alternative Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2004-24CB Class 1A1 | 6.000 | 11-25-34 | AAA | 3,841 | 3,769,366 | |||||

| Mtg Pass Thru Ctf Ser 2005-6 Class 2A1 | 5.500 | 04-25-35 | Aaa | 2,912 | 2,766,760 | |||||

| Mtg Pass Thru Ctf Ser 2005-J1 Class 3A1 | 6.500 | 08-25-32 | AAA | 2,338 | 2,341,247 | |||||

| Mtg Pass thru Ctf 2006-11CB Class 3A1 | 6.500 | 05-25-36 | AAA | 7,287 | 7,275,446 | |||||

| CS First Boston Mortgage Securities Corp., | ||||||||||

| Mtg Pass Thru Ctf Ser 2003-25 Class 2A1 | 4.500 | 10-25-18 | AAA | 1,786 | 1,716,341 | |||||

| Mtg Pass Thru Ctf Ser 2005-5 Class 1A1 | 5.000 | 07-25-20 | AAA | 2,500 | 2,384,906 | |||||

| DB Master Finance LLC, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-1 Class A2 | 5.779 | 06-20-31 | AAA | 1,535 | 1,535,480 | |||||

| Mtg Pass Thru Ctf Ser 2006-1 Class M1 | 8.285 | 06-20-31 | BB | 855 | 859,275 | |||||

| First Horizon Alternative Mortgage Securities, | ||||||||||

| Mtg Pass Thru Ctf Ser 2004-AA5 | ||||||||||

| Class B1 (P) | 5.237 | 12-25-34 | AA | 1,438 | 1,408,227 | |||||

| Mtg Pass Thru Ctf Ser 2006-AA2 | ||||||||||

| Class B1 (G)(P) | 6.269 | 05-25-36 | AA | 1,330 | 1,326,839 | |||||

| Global Signal Trust, | ||||||||||

| Sub Bond Ser 2004-2A Class D (S) | 5.093 | 12-15-14 | Baa2 | 1,820 | 1,771,538 | |||||

| Sub Bond Ser 2006-1 Class E (S) | 6.495 | 02-15-36 | Baa3 | 1,705 | 1,700,762 | |||||

| GMAC Commercial Mortgage Securities, Inc., | ||||||||||

| Mtg Pass Thru Ctf Ser 2002-C1 Class A1 | 5.785 | 11-15-39 | AAA | 3,693 | 3,697,351 | |||||

| See notes to financial statements. |

19

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Thrifts & Mortgage Finance (continued) | ||||||||||

| GMAC Mortgage Corporation Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-AR1 | ||||||||||

| Class 2A1 (P) | 5.665% | 04-19-36 | AAA | $4,627 | $4,578,853 | |||||

| Greenwich Capital Commercial Funding Corp., | ||||||||||

| Mtg Pass Thru Ctf Ser 2003-C2 Class A-2 | 4.022 | 01-05-36 | AAA | 2,410 | 2,314,041 | |||||

| Mtg Pass Thru Ctf Ser 2005-GG5 Class A2 | 5.117 | 04-10-37 | AAA | 5,150 | 5,051,989 | |||||

| GSR Mortgage Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2004-9 | ||||||||||

| Class B1 (G)(P) | 4.520 | 08-25-34 | AA | 3,211 | 3,104,913 | |||||

| Mtg Pass Thru Ctf Ser 2005-5F Class 6A1 | 5.000 | 05-25-20 | AAA | 2,980 | 2,868,788 | |||||

| Mtg Pass Thru Ctf Ser 2005-8F Class 6A1 | 4.500 | 10-25-20 | AAA | 3,210 | 3,069,935 | |||||

| Mtg Pass Thru Ctf Ser 2006-AR1 | ||||||||||

| Class 3A1 (P) | 5.428 | 01-25-36 | AAA | 7,431 | 7,296,021 | |||||

| Indymac Index Mortgage Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2004-AR13 | ||||||||||

| Class B1 | 5.296 | 01-25-35 | AA | 2,179 | 2,140,936 | |||||

| Mtg Pass Thru Ctf Ser 2005-AR5 | ||||||||||

| Class B1 (P) | 5.415 | 05-25-35 | AA | 2,355 | 2,306,766 | |||||

| Mtg Pass Thru Ctf Ser 2006-AR3 | ||||||||||

| Class 3A1A (P) | 6.197 | 04-25-36 | AAA | 4,559 | 4,562,768 | |||||

| JP Morgan Alternative Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-A1 | ||||||||||

| Class 4A1 | 6.092 | 03-25-36 | AAA | 5,747 | 5,742,018 | |||||

| JP Morgan Chase Commercial Mortgage | ||||||||||

| Security Corp., | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-LDP3 | ||||||||||

| Class A4B | 4.996 | 08-15-42 | AAA | 3,995 | 3,746,740 | |||||

| Mtg Pass Thru Ctf Ser 2005-LDP4 Class B | 5.129 | 10-15-42 | Aa2 | 2,126 | 2,002,395 | |||||

| JP Morgan Mortgage Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-S2 Class 2A16 | 6.500 | 09-25-35 | AAA | 4,336 | 4,345,435 | |||||

| Mtg Pass Thru Ctf Ser 2005-S3 Class 2A2 | 5.500 | 01-25-21 | AAA | 4,580 | 4,498,478 | |||||

| Lehman Mortgage Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-1 Class 6A1 | 5.000 | 11-25-20 | AAA | 4,262 | 4,133,890 | |||||

| Master Adjustable Rate Mortgages Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-2 Class 4A1 | 4.995 | 02-25-36 | AAA | 5,424 | 5,286,510 | |||||

| Merrill Lynch Mortgage Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-CKI1 | ||||||||||

| Class A6 (P) | 5.240 | 11-12-37 | AAA | 3,685 | 3,546,549 | |||||

| Morgan Stanley Capital I, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-HQ7 | ||||||||||

| Class A4 | 5.205 | 11-14-42 | AAA | 3,765 | 3,616,181 | |||||

| Mtg Pass Thru Ctf Ser 2005-IQ10 | ||||||||||

| Class A4A | 5.230 | 09-15-42 | AAA | 5,270 | 5,041,858 | |||||

| See notes to financial statements. |

20

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Thrifts & Mortgage Finance (continued) | ||||||||||

| Morgan Stanley Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-3AR | ||||||||||

| Class 3A1 | 6.120% | 03-25-36 | AAA | $6,198 | $6,180,919 | |||||

| Nomura Asset Acceptance Corp., | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-AF1 | ||||||||||

| Class CB1 | 6.540 | 06-25-36 | AA | 1,615 | 1,628,374 | |||||

| Prime Mortgage Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-2 Class 1A2 | 5.000 | 07-25-20 | Aaa | 6,175 | 6,044,052 | |||||

| Provident Funding Mortgage Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-1 Class B1 (P) | 4.367 | 05-25-35 | AAA | 1,620 | 1,545,102 | |||||

| Renaissance Home Equity Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-2 Class AF3 | 4.499 | 08-25-35 | AAA | 2,080 | 2,028,119 | |||||

| Mtg Pass Thru Ctf Ser 2005-2 Class AF4 | 4.934 | 08-25-35 | AAA | 2,365 | 2,260,297 | |||||

| Residential Accredit Loans, Inc., | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-QA12 | ||||||||||

| Class NB5 (P) | 5.997 | 12-25-35 | AAA | 4,334 | 4,346,296 | |||||

| Mtg Pass Thru Ctf Ser 2006-QA1 | ||||||||||

| Class A31 | 6.305 | 01-25-36 | AAA | 6,133 | 6,152,256 | |||||

| Residential Asset Securitization Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2006-A7CB | ||||||||||

| Class 2A1 | 6.500 | 07-25-36 | AAA | 5,225 | 5,251,125 | |||||

| SBA CMBS Trust, | ||||||||||

| Sub Bond Ser 2005-1A Class A (S) | 5.369 | 11-15-35 | Aaa | 1,310 | 1,289,293 | |||||

| Sub Bond Ser 2005-1A Class B (S) | 5.565 | 11-15-35 | Aa2 | 1,300 | 1,283,574 | |||||

| Sub Bond Ser 2005-1A Class D (S) | 6.219 | 11-15-35 | Baa2 | 750 | 746,959 | |||||

| Sub Bond Ser 2005-1A Class E (S) | 6.706 | 11-15-35 | Baa3 | 795 | 797,851 | |||||

| Sovereign Capital Trust I, | ||||||||||

| Gtd Cap Security | 9.000 | 04-01-27 | BB | 3,840 | 4,076,210 | |||||

| Washington Mutual Alternative Loan Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2005-6 Class 1CB | 6.500 | 08-25-35 | AAA | 2,713 | 2,715,873 | |||||

| Wells Fargo Mortgage Backed Securities Trust, | ||||||||||

| Mtg Pass Thru Ctf Ser 2004-7 Class 2A2 | 5.000 | 07-25-19 | AAA | 3,039 | 2,923,526 | |||||

| Mtg Pass Thru Ctf Ser 2005-AR2 | ||||||||||

| Class 3A1 (P) | 4.945 | 03-25-35 | Aaa | 3,093 | 3,011,884 | |||||

Tobacco 0.16% | 1,634,370 | |||||||||

| Reynolds American, Inc., | ||||||||||

| Sr Sec Note (S) | 7.250 | 06-01-13 | BB | 1,655 | 1,634,370 | |||||

Utilities Other 0.26% | 2,619,688 | |||||||||

| Magellan Midstream Partners, LP, | ||||||||||

| Note | 6.450 | 06-01-14 | BBB | 2,570 | 2,619,688 | |||||

| See notes to financial statements. |

21

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Wireless Telecommunication Service 1.63% | $16,541,212 | |||||||||

| America Movil SA de CV, | ||||||||||

| Sr Note (Mexico) | 5.750% | 01-15-15 | BBB | $1,905 | 1,792,022 | |||||

| AT&T Wireless Services , Inc., | ||||||||||

| Sr Note | 8.125 | 05-01-12 | A | 1,700 | 1,884,836 | |||||

| Crown Castle Towers LLC, | ||||||||||

| Sub Bond Ser 2005-1A Class A | 4.643 | 06-15-35 | Aaa | 2,050 | 1,970,753 | |||||

| Sub Bond Ser 2005-1A Class D | 5.612 | 06-15-35 | Baa2 | 2,460 | 2,409,660 | |||||

| Embarq Corp., | ||||||||||

| Note | 6.738 | 06-01-13 | BBB– | 1,130 | 1,131,417 | |||||

| Nextel Communications, Inc., | ||||||||||

| Sr Note Ser F | 5.950 | 03-15-14 | BB | 3,000 | 2,915,268 | |||||

| Nextel Partners, Inc., | ||||||||||

| Sr Note | 8.125 | 07-01-11 | BB– | 2,820 | 2,961,000 | |||||

| Rogers Wireless, Inc., | ||||||||||

| Sr Sub Note (Canada) | 8.000 | 12-15-12 | B+ | 1,435 | 1,476,256 | |||||

| Credit | ||||||||||

| Issuer, description | rating (A) | Shares | Value | |||||||

Preferred stocks 0.17% | $1,740,095 | |||||||||

| (Cost $1,886,000) | ||||||||||

Agricultural Products 0.17% | 1,740,095 | |||||||||

| Ocean Spray Cranberries, Inc., 6.25%, Ser A (S) | BB+ | 23,000 | 1,740,095 | |||||||

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

U.S. government and agencies securities 43.27% | $439,846,215 | |||||||||

| (Cost $451,950,773) | ||||||||||

Government U.S. 13.40% | 136,256,353 | |||||||||

| United States Treasury, | ||||||||||

| Bond (L) | 6.875% | 08-15-25 | AAA | $38,635 | 45,607,420 | |||||

| Bond (L) | 5.375 | 02-15-31 | AAA | 7,415 | 7,499,576 | |||||

| Inflation Indexed Note (L) | 3.500 | 01-15-11 | AAA | 22,732 | 23,953,408 | |||||

| Note (L) | 5.125 | 05-15-16 | AAA | 11,890 | 11,899,286 | |||||

| Note | 4.875 | 04-30-11 | AAA | 10,625 | 10,546,556 | |||||

| Note (L) | 4.250 | 10-15-10 | AAA | 31,305 | 30,359,746 | |||||

| Note (L) | 4.250 | 11-15-13 | AAA | 6,745 | 6,390,361 | |||||

Government U.S. Agency 29.87% | 303,589,862 | |||||||||

| Federal Home Loan Mortgage Corp., | ||||||||||

| 20 Yr Pass Thru Ctf | 11.250 | 01-01-16 | AAA | 59 | 61,691 | |||||

| 30 Yr Adj Rate Pass Thru Ctf | 5.285 | 12-01-35 | AAA | 9,321 | 9,041,110 | |||||

| 30 Yr Pass Thru Ctf | 6.000 | 01-01-36 | AAA | 22,748 | 22,493,852 | |||||

| 30 Yr Pass Thru Ctf | 5.164 | 11-01-35 | AAA | 9,553 | 9,268,845 | |||||

| See notes to financial statements. |

22

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Government U.S. Agency (continued) | ||||||||||

| Federal Home Loan Mortgage Corp., (continued) | ||||||||||

| 30 Yr Pass Thru Ctf | 5.000% | 07-01-35 | AAA | $10,677 | $10,016,406 | |||||

| 30 Yr Pass Thru Ctf | 5.000 | 09-01-35 | AAA | 1,228 | 1,151,566 | |||||

| CMO REMIC 2489-PE | 6.000 | 08-15-32 | AAA | 2,785 | 2,752,826 | |||||

| CMO REMIC 2640-WA (G) | 3.500 | 03-15-33 | AAA | 1,382 | 1,317,449 | |||||

| CMO REMIC 3033-JH (G) | 5.000 | 06-15-32 | AAA | 5,109 | 4,967,221 | |||||

| CMO REMIC 3046-BA (G) | 5.000 | 10-15-24 | AAA | 6,913 | 6,732,410 | |||||

| Note | 5.300 | 11-17-10 | AAA | 5,835 | 5,754,074 | |||||

| Federal National Mortgage Assn., | ||||||||||

| 15 Yr Pass Thru Ctf | 9.000 | 06-01-10 | AAA | 568 | 608,171 | |||||

| 15 Yr Pass Thru Ctf | 7.500 | 02-01-08 | AAA | 54 | 54,044 | |||||

| 15 Yr Pass Thru Ctf | 7.000 | 09-01-10 | AAA | 135 | 137,289 | |||||

| 15 Yr Pass Thru Ctf | 7.000 | 04-01-17 | AAA | 671 | 689,057 | |||||

| 15 Yr Pass Thru Ctf | 7.000 | 06-01-17 | AAA | 166 | 170,256 | |||||

| 15 Yr Pass Thru Ctf | 5.500 | 11-01-20 | AAA | 1,876 | 1,848,223 | |||||

| 15 Yr Pass Thru Ctf | 5.500 | 12-01-20 | AAA | 11,248 | 11,083,100 | |||||

| 15 Yr Pass Thru Ctf | 5.000 | 05-01-18 | AAA | 7,510 | 7,274,282 | |||||

| 15 Yr Pass Thru Ctf | 5.000 | 08-01-19 | AAA | 9,768 | 9,435,740 | |||||

| 15 Yr Pass Thru Ctf | 5.000 | 10-01-19 | AAA | 7,530 | 7,286,325 | |||||

| 15 Yr Pass Thru Ctf | 4.500 | 05-01-18 | AAA | 7,903 | 7,502,868 | |||||

| 15 Yr Pass Thru Ctf | 4.500 | 10-01-18 | AAA | 17,968 | 17,058,228 | |||||

| 30 Yr Adj Rate Pass Thru Ctf | 5.000 | 08-01-35 | AAA | 6,417 | 6,023,116 | |||||

| 30 Yr Pass Thru Ctf | 6.000 | 11-01-34 | AAA | 750 | 742,195 | |||||

| 30 Yr Pass Thru Ctf | 6.000 | 09-01-35 | AAA | 10,604 | 10,489,738 | |||||

| 30 Yr Pass Thru Ctf | 6.000 | 10-01-35 | AAA | 506 | 500,571 | |||||

| 30 Yr Pass Thru Ctf | 6.000 | 05-01-36 | AAA | 20,145 | 19,900,627 | |||||

| 30 Yr Pass Thru Ctf (N) | 6.000 | 06-01-36 | AAA | 3,445 | 3,401,938 | |||||

| 30 Yr Pass Thru Ctf | 5.500 | 05-01-35 | AAA | 53,171 | 51,405,074 | |||||

| 30 Yr Pass Thru Ctf | 5.500 | 01-01-36 | AAA | 14,626 | 14,093,278 | |||||

| 30 Yr Pass Thru Ctf | 5.500 | 02-01-36 | AAA | 16,927 | 16,312,921 | |||||

| 30 Yr Pass Thru Ctf | 5.000 | 08-01-35 | AAA | 10,517 | 9,871,452 | |||||

| 30 Yr Pass Thru Ctf | 5.000 | 10-01-35 | AAA | 5,784 | 5,428,896 | |||||

| 30 Yr Pass Thru Ctf | 5.000 | 03-01-36 | AAA | 5,494 | 5,153,816 | |||||

| 30 Yr Pass Thru Ctf | 4.500 | 09-01-35 | AAA | 9,657 | 8,783,861 | |||||

| CMO REMIC 2003-33-AC (G) | 4.250 | 03-25-33 | AAA | 1,127 | 1,059,986 | |||||

| CMO REMIC 2003-49-JE (G) | 3.000 | 04-25-33 | AAA | 3,137 | 2,720,898 | |||||

| CMO REMIC 2003-58-AD (G) | 3.250 | 07-25-33 | AAA | 3,084 | 2,746,924 | |||||

| CMO REMIC 2003-63-PE (G) | 3.500 | 07-25-33 | AAA | 2,542 | 2,267,119 | |||||

| Financing Corp., | ||||||||||

| Bond | 10.350 | 08-03-18 | Aaa | 3,545 | 5,025,147 | |||||

| Government National Mortgage Assn., | ||||||||||

| 30 Yr Pass Thru Ctf | 10.500 | 01-15-16 | AAA | 25 | 26,883 | |||||

| 30 Yr Pass Thru Ctf | 10.000 | 06-15-20 | AAA | 35 | 37,909 | |||||

| 30 Yr Pass Thru Ctf | 10.000 | 11-15-20 | AAA | 12 | 12,602 | |||||

| 30 Yr Pass Thru Ctf | 9.500 | 03-15-20 | AAA | 37 | 41,004 | |||||

| 30 Yr Pass Thru Ctf | 9.500 | 06-15-20 | AAA | 10 | 11,139 | |||||

| See notes to financial statements. |

23

F I N A N C I A L S TAT E M E N T S

| Interest | Maturity | Credit | Par value | |||||||

| Issuer, description | rate | date | rating (A) | (000) | Value | |||||

Government U.S. Agency (continued) | ||||||||||

| Government National Mortgage Assn., (continued) | ||||||||||

| 30 Yr Pass Thru Ctf | 9.500% | 01-15-21 | AAA | $47 | $51,749 | |||||

| 30 Yr Pass Thru Ctf | 9.500 | 05-15-21 | AAA | 22 | 24,017 | |||||

| CMO Remic 2003-42-XA | 3.750 | 05-16-33 | AAA | 821 | 751,969 | |||||

| Interest | Par value | |||||||||

| Issuer, description, maturity date | rate | (000) | Value | |||||||

Short-term investments 0.20% | $2,017,000 | |||||||||

| (Cost $2,017,000) | ||||||||||

Joint Repurchase Agreement 0.20% | 2,017,000 | |||||||||

| Investment in a joint repurchase agreement transaction | ||||||||||

| with Bank of America. — Dated 5-31-06, due | ||||||||||

| 6-01-06 (Secured by U.S. Treasury Inflation Indexed | ||||||||||

| Bonds 3.625%, due 4-15-28 and 2.375%, due | ||||||||||

| 1-15-25, and U.S. Treasury Inflation Indexed Note | ||||||||||

| 4.250%, due 1-15-10) | 4.900% | $2,017 | 2,017,000 | |||||||

| Total investments 99.33% | $1,009,595,803 | |||||||||

| Other assets and liabilities, net 0.67% | $6,804,438 | |||||||||

| Total net assets 100.00% | $1,016,400,241 | |||||||||

(A) Credit ratings are unaudited and are rated by Moody’s Investors Service where Standard & Poor’s ratings are not available unless indicated otherwise.

(B) This security is fair valued in good faith under procedures established by the Board of Trustees.

(G) Security rated internally by John Hancock Advisers, LLC.

(H) Non-income-producing issuer filed for protection under the Federal Bankruptcy Code or is in default of interest payment.

(L) All or a portion of this security is on loan as of May 31, 2006.

(N) These securities having an aggregate value of $7,195,785 or 0.71% of the Fund’s net assets, have been purchased on a when-issued basis. The purchase price and the interest rate of such securities are fixed at trade date, although the Fund does not earn any interest on such securities until settlement date. The Fund has instructed its custodian bank to segregate assets with a current value at least equal to the amount of its when-issued commitments. Accordingly, the market value of $7,444,284 of Federal National Mortgage Assn., 5.500%, 5-1-35 has been segregated to cover the when-issued commitments.

(O) Cash interest will be paid on this obligation at the stated rate beginning on the stated date. (P) Represents rate in effect on May 31, 2006.

(S) These securities are exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be resold, normally to qualified institutional buyers, in transactions exempt from registration. Rule 144A securities amounted to $92,421,397 or 9.09% of the Fund’s net assets as of May 31, 2006.

Parenthetical disclosure of a foreign country in the security description represents country of a foreign issuer; however, security is U.S. dollar-denominated.

The percentage shown for each investment category is the total value of that category as a percentage of the net assets of the Fund.

| See notes to financial statements. |

24

F I N A N C I A L S TAT E M E N T S

| ASSETS AND LIABILITIES |

May 31, 2006

| This Statement of Assets and Liabilities is the Fund’s balance sheet. It shows the value of what the Fund owns, is due and owes. You’ll also find the net asset value and the maximum offering price per share. |

| Assets | ||

| Investments at value (cost $1,036,683,537) | ||

| including $124,148,336 of securities loaned | $1,009,595,803 | |

| Cash | 53,730 | |

| Receivable for investments sold | 12,874,540 | |

| Receivable for shares sold | 497,612 | |

| Interest receivable | 10,760,121 | |

| Variation margin receivable | 476 | |

| Other assets | 126,041 | |

| Total assets | 1,033,908,323 | |

| Liabilities | ||

| Payable for investments purchased | 15,218,381 | |

| Payable for shares repurchased | 1,150,838 | |

| Dividends payable | 147,413 | |

| Payable to affiliates | ||

| Management fees | 462,491 | |

| Distribution and service fees | 62,666 | |

| Other | 186,059 | |

| Variation margin payable | 12,892 | |

| Other payables and accrued expenses | 267,342 | |

| Total liabilities | 17,508,082 | |

| Net assets | ||

| Capital paid-in | 1,067,189,468 | |

| Accumulated net realized loss on investments, | ||

| financial futures contracts and swap contracts | (23,442,230) | |

| Net unrealized depreciation of investments | ||

| and financial futures contracts | (27,100,150) | |

| Distributions in excess of net investment income | (246,847) | |

| Net assets | $1,016,400,241 | |

| Net asset value per share | ||

| Based on net asset values and shares outstanding — | ||

| the Fund has an unlimited number of shares | ||

| authorized with no par value | ||

| Class A ($899,310,850 ÷ 61,971,220 shares) | $14.51 | |

| Class B ($86,918,769 ÷ 5,989,732 shares) | $14.51 | |

| Class C ($23,946,969 ÷ 1,650,203 shares) | $14.51 | |

| Class I ($5,465,060 ÷ 376,623 shares) | $14.51 | |

| Class R ($758,593 ÷ 52,274 shares) | $14.51 | |

| Maximum offering price per share | ||

| Class A1 ($14.51 ÷ 95.5%) | $15.19 | |

1 On single retail sales of less than $100,000. On sales of $100,000 or more and on group sales the offering price is reduced.

| See notes to financial statements. |

25

F I N A N C I A L S TAT E M E N T S

OPERATIONS

| For the year ended May 31, 2006 |

| This Statement of Operations summarizes the Fund’s investment income earned and expenses incurred in operating the Fund. It also shows net gains (losses) for the period stated. |

| Investment income | ||

| Interest | $61,359,421 | |

| Securities lending | 402,278 | |

| Dividends | 297,704 | |

| Total investment income | 62,059,403 | |

| Expenses | ||

| Investment management fees | 5,516,990 | |

| Class A distribution and service fees | 2,884,839 | |

| Class B distribution and service fees | 1,093,533 | |

| Class C distribution and service fees | 261,334 | |

| Class R distribution and service fees | 2,257 | |

| Class A, B and C transfer agent fees | 2,048,332 | |

| Class I transfer agent fees | 2,923 | |

| Class R transfer agent fees | 3,024 | |

| Accounting and legal services fees | 254,709 | |

| Custodian fees | 220,232 | |

| Printing | 134,851 | |

| Miscellaneous | 79,609 | |

| Trustees’ fees | 77,230 | |

| Registration and filing fees | 72,352 | |

| Professional fees | 51,511 | |

| Compliance fees | 46,442 | |

| Securities lending fees | 17,276 | |

| Interest | 14,916 | |

| Total expenses | 12,782,360 | |

| Less expense reductions | (68,893) | |

| Net expenses | 12,713,467 | |

| Net investment income | 49,345,936 | |

| Realized and unrealized gain (loss) | ||

| Net realized gain (loss) on | ||

| Investments | (5,090,076) | |

| Financial futures contracts | 353,112 | |

| Swap contracts | (16,389) | |

| Change in net unrealized appreciation (depreciation) of | ||

| Investments | (50,042,126) | |

| Financial futures contracts | 325,821 | |

| Net realized and unrealized loss | (54,469,658) | |

| Decrease in net assets from operations | ($5,123,722) | |

| See notes to financial statements. |

26

F I N A N C I A L S TAT E M E N T S

| CHANGES IN NET ASSETS |

| These Statements of Changes in Net Assets show how the value of the Fund’s net assets has changed during the last two periods. The difference reflects earnings less expenses, any investment gains and losses, distributions, if any, paid to shareholders and the net of Fund share transactions. |

| Year | Year | |||

| ended | ended | |||

| 5-31-05 | 5-31-06 | |||

| Increase (decrease) in net assets | ||||

| From operations | ||||

| Net investment income | $52,262,850 | $49,345,936 | ||

| Net realized gain (loss) | 5,559,997 | (4,753,353) | ||

| Change in net unrealized | ||||

| appreciation (depreciation) | 24,622,118 | (49,716,305) | ||

| Increase (decrease) in net assets | ||||

| resulting from operations | 82,444,965 | (5,123,722) | ||

| Distributions to shareholders | ||||

| From net investment income | ||||

| Class A | (49,122,496) | (46,118,272) | ||

| Class B | (5,941,309) | (4,473,822) | ||

| Class C | (1,227,067) | (1,070,734) | ||

| Class I | (254,528) | (306,121) | ||

| Class R | (8,053) | (18,727) | ||

| From capital paid-in | ||||

| Class A | — | (482,923) | ||

| Class B | — | (46,686) | ||

| Class C | — | (12,857) | ||

| Class I | — | (2,928) | ||

| Class R | — | (409) | ||

| (56,553,453) | (52,533,479) | |||

| From Fund share transactions | (98,851,379) | (100,388,082) | ||

| Net assets | ||||

| Beginning of period | 1,247,405,391 | 1,174,445,524 | ||

| End of period1 | $1,174,445,524 | $1,016,400,241 | ||

1 Includes distributions in excess of net investment of $228,662 and $246,847, respectively.

| See notes to financial statements. |

27

F I N A N C I A L H I G H L I G H T S

| FINANCIAL HIGHLIGHTS |

CLASS A SHARES

The Financial Highlights show how the Fund’s net asset value for a share has changed since the end of the previous period.

| Year ended | 5-31-021,2 | 5-31-03 | 5-31-04 | 5-31-05 | 5-31-06 | |||||

| Per share operating performance | ||||||||||

| Net asset value, | ||||||||||

| beginning of period | $14.69 | $14.71 | $15.69 | $14.98 | $15.30 | |||||

| Net investment income3 | 0.82 | 0.72 | 0.70 | 0.67 | 0.68 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | 0.06 | 1.02 | (0.65) | 0.38 | (0.74) | |||||

| Total from investment operations | 0.88 | 1.74 | 0.05 | 1.05 | (0.06) | |||||

| Less distributions | ||||||||||

| From net investment income | (0.86) | (0.76) | (0.76) | (0.73) | (0.72) | |||||

| From capital paid-in | — | — | — | — | (0.01) | |||||

| (0.86) | (0.76) | (0.76) | (0.73) | (0.73) | ||||||

| Net asset value, end of period | $14.71 | $15.69 | $14.98 | $15.30 | $14.51 | |||||

| Total return4 (%) | 6.1 | 12.26 | 0.31 | 7.115 | (0.45) | |||||

| Ratios and supplemental data | ||||||||||

| Net assets, end of period | ||||||||||

| (in millions) | $1,144 | $1,192 | $1,047 | $1,012 | $899 | |||||

| Ratio of expenses | ||||||||||

| to average net assets (%) | 1.11 | 1.12 | 1.09 | 1.05 | 1.07 | |||||

| Ratio of gross expenses | ||||||||||

| to average net assets6 (%) | — | — | — | 1.06 | 1.08 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets (%) | 5.51 | 4.84 | 4.55 | 4.41 | 4.56 | |||||

| Portfolio turnover (%) | 189 | 273 | 241 | 139 | 135 | |||||

| See notes to financial statements. |

28

F I N A N C I A L H I G H L I G H T S

CLASS B SHARES

| Year ended | 5-31-021,2 | 5-31-03 | 5-31-04 | 5-31-05 | 5-31-06 | |||||

| Per share operating performance | ||||||||||

| Net asset value, | ||||||||||

| beginning of period | $14.69 | $14.71 | $15.69 | $14.98 | $15.30 | |||||

| Net investment income3 | 0.72 | 0.62 | 0.59 | 0.57 | 0.58 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | 0.06 | 1.02 | (0.65) | 0.37 | (0.74) | |||||

| Total from investment operations | 0.78 | 1.64 | (0.06) | 0.94 | (0.16) | |||||

| Less distributions | ||||||||||

| From net investment income | (0.76) | (0.66) | (0.65) | (0.62) | (0.62) | |||||

| From capital paid-in | — | — | — | — | (0.01) | |||||

| (0.76) | (0.66) | (0.65) | (0.62) | (0.63) | ||||||

| Net asset value, end of period | $14.71 | $15.69 | $14.98 | $15.30 | $14.51 | |||||

| Total return4 (%) | 5.37 | 11.48 | (0.39) | 6.375 | (1.14) | |||||

| Ratios and supplemental data | ||||||||||

| Net assets, end of period | ||||||||||

| (in millions) | $236 | $233 | $164 | $128 | $87 | |||||

| Ratio of expenses | ||||||||||

| to average net assets (%) | 1.81 | 1.82 | 1.79 | 1.75 | 1.77 | |||||

| Ratio of gross expenses | ||||||||||

| to average net assets6 (%) | — | — | — | 1.76 | 1.78 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets (%) | 4.81 | 4.15 | 3.84 | 3.70 | 3.84 | |||||

| Portfolio turnover (%) | 189 | 273 | 241 | 139 | 135 | |||||

| See notes to financial statements. |

29

F I N A N C I A L H I G H L I G H T S

CLASS C SHARES

| Year ended | 5-31-021,2 | 5-31-03 | 5-31-04 | 5-31-05 | 5-31-06 | |||||

| Per share operating performance | ||||||||||

| Net asset value, | ||||||||||

| beginning of period | $14.69 | $14.71 | $15.69 | $14.98 | $15.30 | |||||

| Net investment income3 | 0.72 | 0.62 | 0.59 | 0.57 | 0.58 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | 0.06 | 1.02 | (0.64) | 0.37 | (0.74) | |||||

| Total from | ||||||||||

| investment operations | 0.78 | 1.64 | (0.05) | 0.94 | (0.16) | |||||

| Less distributions | ||||||||||

| From net investment income | (0.76) | (0.66) | (0.66) | (0.62) | (0.62) | |||||

| From capital paid-in | — | — | — | — | (0.01) | |||||

| (0.76) | (0.66) | (0.66) | (0.62) | (0.63) | ||||||

| Net asset value, end of period | $14.71 | $15.69 | $14.98 | $15.30 | $14.51 | |||||

| Total return4 (%) | 5.36 | 11.48 | (0.39) | 6.375 | (1.14) | |||||

| Ratios and supplemental data | ||||||||||

| Net assets, end of period | ||||||||||

| (in millions) | $44 | $45 | $32 | $28 | $24 | |||||

| Ratio of expenses to | ||||||||||

| average net assets (%) | 1.81 | 1.82 | 1.79 | 1.75 | 1.77 | |||||

| Ratio of gross expenses | ||||||||||

| to average net assets6 (%) | — | — | — | 1.76 | 1.78 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets (%) | 4.81 | 4.15 | 3.84 | 3.71 | 3.86 | |||||

| Portfolio turnover (%) | 189 | 273 | 241 | 139 | 135 | |||||

| See notes to financial statements. |

30

F I N A N C I A L H I G H L I G H T S

CLASS I SHARES

| Year ended | 5-31-021,2,7 | 5-31-03 | 5-31-04 | 5-31-05 | 5-31-06 | |||||

| Per share operating performance | ||||||||||

| Net asset value, beginning of period | $14.96 | $14.71 | $15.69 | $14.98 | $15.30 | |||||

| Net investment income3 | 0.66 | 0.78 | 0.76 | 0.73 | 0.75 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | (0.21) | 1.02 | (0.64) | 0.38 | (0.74) | |||||

| Total from investment operations | 0.45 | 1.80 | 0.12 | 1.11 | 0.01 | |||||

| Less distributions | ||||||||||

| From net investment income | (0.70) | (0.82) | (0.83) | (0.79) | (0.79) | |||||

| From capital paid-in | — | — | — | — | (0.01) | |||||

| (0.70) | (0.82) | (0.83) | (0.79) | (0.80) | ||||||

| Net asset value, end of period | $14.71 | $15.69 | $14.98 | $15.30 | $14.51 | |||||

| Total return4 (%) | 3.048 | 12.71 | 0.78 | 7.55 | (0.01) | |||||

| Ratios and supplemental data | ||||||||||

| Net assets, end of period | ||||||||||

| (in millions) | —9 | $9 | $5 | $5 | $5 | |||||

| Ratio of expenses | ||||||||||

| to average net assets (%) | 0.6810 | 0.72 | 0.63 | 0.65 | 0.64 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets (%) | 5.9410 | 5.23 | 4.98 | 4.82 | 4.99 | |||||

| Portfolio turnover (%) | 189 | 273 | 241 | 139 | 135 | |||||

| See notes to financial statements. |

31

F I N A N C I A L H I G H L I G H T S

CLASS R SHARES

| Year ended | 5-31-047 | 5-31-05 | 5-31-06 | |||

| Per share operating performance | ||||||

| Net asset value, | ||||||

| beginning of period | $14.93 | $14.98 | $15.30 | |||

| Net investment income3 | 0.54 | 0.67 | 0.59 | |||

| Net realized and unrealized | ||||||

| gain (loss) on investments | 0.10 | 0.36 | (0.75) | |||

| Total from investment operations | 0.64 | 1.03 | (0.16) | |||

| Less distributions | ||||||

| From net investment income | (0.59) | (0.71) | (0.62) | |||

| From capital paid-in | — | — | (0.01) | |||

| (0.59) | (0.71) | (0.63) | ||||

| Net asset value, end of period | $14.98 | $15.30 | $14.51 | |||

| Total return4 (%) | 4.308 | 7.02 | (1.09) | |||

| Ratios and supplemental data | ||||||

| Net assets, end of period | ||||||

| (in millions) | —9 | —9 | 1 | |||

| Ratio of expenses | ||||||

| to average net assets (%) | 1.3810 | 1.12 | 1.76 | |||

| Ratio of net investment income | ||||||

| to average net assets (%) | 4.4010 | 4.44 | 3.95 | |||

| Portfolio turnover (%) | 241 | 139 | 135 | |||

1 Audited by previous auditor.