UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-00066

American Balanced Fund

(Exact Name of Registrant as Specified in Charter)

6455 Irvine Center Drive

Irvine, California 92618

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (949) 975-5000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2014

Michael W. Stockton

American Balanced Fund

6455 Irvine Center Drive

Irvine, California 92618

(Name and Address of Agent for Service)

Copies to:

Michael Glazer

Morgan, Lewis & Bockius LLP

355 South Grand Avenue, Suite 4400

Los Angeles, California 90071

(Counsel for the Registrant)

ITEM 1 – Reports to Stockholders

Find balance that is

actively achieved and

maintained over time.

Special feature page 6

| American Balanced Fund® Annual report

for the year ended

December 31, 2014 |

American Balanced Fund seeks conservation of capital, current income, and long-term growth of both capital and income.

This fund is one of more than 40 offered by one of the nation’s largest mutual fund families, American Funds, from Capital Group. For more than 80 years, Capital has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

See page 4 for Class A share results with relevant sales charges deducted. For other share class results, visit americanfunds.com and americanfundsretirement.com.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

The fund’s 30-day yield for Class A shares as of January 31, 2015, calculated in accordance with the U.S. Securities and Exchange Commission (SEC) formula, was 1.40%. The fund’s 12-month distribution rate for Class A shares as of that date was 1.41%. Both reflect the 5.75% maximum sales charge. The SEC yield reflects the rate at which the fund is earning income on its current portfolio of securities while the distribution rate reflects the fund’s past dividends paid to shareholders. Accordingly, the fund’s SEC yield and distribution rate may differ.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Fellow investors:

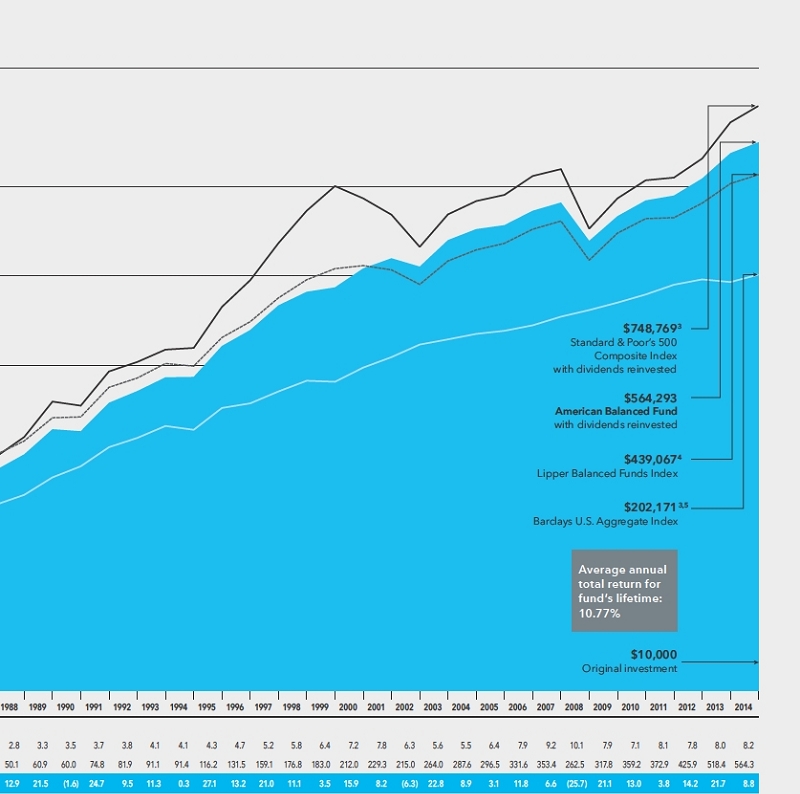

In a market environment that favored equities over fixed-income securities, American Balanced Fund gained 8.85% for the 12-month period ended December 31, 2014, exceeding the 7.21% return of the Lipper Balanced Funds Index. American Balanced Fund’s returns for the past three-, five- and 10-year periods were 14.80%, 12.17% and 6.97% — all outpacing the Lipper index returns of 11.78%, 9.50% and 6.01%, respectively. Looking at the bigger, long-term picture, over the near-40 years that Capital Research and Management Company has managed the fund, American Balanced Fund realized an average annual total return of 10.94%, compared with 10.07% for the Lipper index.

In short, fund investors seeking to increase their wealth — prudently, over time, through a balanced approach —historically have been rewarded as the fund has invested primarily in blue-chip equities and investment-grade (rated BBB/Baa and above) fixed-income securities with a U.S. emphasis.

For many investors, their introduction to American Balanced Fund has been through their employer’s retirement plan. In 2014, the fund continued to help Americans prepare for retirement as one of the most widely used balanced funds in defined benefit 401(k)s, with over $16.3 billion in participant contributions, according to Pensions & Investments (September 2014).

2014 market review

The U.S. economy started the year on shaky ground, due to an unusually harsh winter. As temperatures rose, the equity markets picked up steam — soon at record-breaking levels — extending one of the longest-running bull markets in history. The unmanaged Standard & Poor’s 500 Composite Index climbed above 2,000 for the first time ever, as it gained 13.66% for the year, with dividends reinvested. The Dow Jones Industrial Average surpassed the 18,000 mark during the year and ended 2014 with a 10.02% annual gain, with dividends reinvested.

Investors, it seems, were encouraged by the U.S. economy’s gradual improvement, high corporate profits and attractive stock valuations compared to fixed-income securities.

Uncertainty about interest rates and how they would affect investments had investors taking a cautious approach to fixed-income markets through much of 2014. Month after month, many investors expected rates to go up but, in fact, they continued to do the exact opposite. This can be attributed to economic weakness in the rest of the world, rising geopolitical risks and a lower-than-anticipated level of inflation. Finally, in mid-December, the Fed shifted its position on the timing of future interest rate hikes. That day, there was a 288-point gain (+1.69%) in the Dow Jones Industrial Average. The next day, the Dow was up 421 points (+2.43%), its best day of the year.

Despite concerns investors may have about interest rates, a sound fixed-income investment strategy can provide current income and potentially mitigate volatility associated with equity investing. Furthermore, the very strong U.S. equity

We’ve made a conscious effort to adjust the equity portion of American Balanced Fund from 74%, where it started the year, to 67% to help protect gains our investors were able to make in 2014.

results of the past few years and the associated rise in valuations argues for a more cautious equity investment position. To that end, we’ve made a conscious effort to adjust the equity portion of American Balanced Fund from 74%, where it started the year, to 67%, and increase the fixed-income allocation from 23% to 28%. Our goal is to help our investors protect gains they were able to make during the year in 2014. (To learn more about balanced investing, read the special feature beginning on page 6.)

AMBAL portfolio highlights

Most sectors of the S&P 500 advanced in 2014, led by a 28.98% rise in utilities. Health care and information technology rose at notable rates, gaining 25.34% and 20.12%, respectively. But energy stocks, hurt by plunging crude oil prices in the second half of the year, lost 7.78%.

AMBAL’s lower-than-index position in energy companies proved positive for relative results, and careful investment selection further helped to lift returns. Similarly, having fewer investments in telecommunication services companies was additive to the fund’s relative returns.

While health care companies outpaced the broader market, AMBAL’s smaller position dampened returns and became one of the fund’s largest detractors. A notable bright spot in our health care investment strategy was UnitedHealth Group (+34.25%), which served as one of the fund’s top 10 contributors for 2014. (See page 11 for more information about UnitedHealth.)

Two stocks that have helped the fund in the past but detracted from results in 2014 were Amazon (–22.18%) and Boeing (–4.77%). On the plus side, Lockheed Martin (+29.54%) and Microsoft (+24.10%) buoyed results (see pages 10 and 11, respectively). We continue to be enthusiastic about all four of these securities on a long-term basis.

Moving forward, the overall mix of the fund’s portfolio has been adjusted to be more defensive. We’ve increased our investment in more defensive sectors such as consumer staples. Fixed income has also been increased, so U.S. Treasury, U.S. agency and agency pass-through securities, as well as other high-quality mortgage and investment-grade corporate bonds, will play an important role for our investors, helping to provide income and mitigating volatility. And the fund’s level of cash is higher as well.

Thank you for your support

We welcome our many new shareholders to the fund and assure all of our investors that we will continue to follow our prudent, research-driven approach to investing that has characterized American Balanced Fund for almost 40 years. We look forward to reporting to you again in six months’ time.

Sincerely,

Gregory D. Johnson

Vice Chairman of the Board and President

February 10, 2015

For current information about the fund, visit americanfunds.com.

History of American Balanced Fund

A historical view of the comparative total returns of stocks, bonds, the 60%/40% S&P/BC Index, the Lipper Balanced Funds Index and AMBAL.

Stocks, bonds and balance (July 26, 1975, to December 31, 2014)

Total

returns (through December 31) | | U.S.

stocks | | U.S.

bonds | | 60%/40%

S&P/BC Index | | Lipper

Balanced

Funds Index | | American

Balanced

Fund |

| 1975 (from July 26) | | | 3.14 | % | | | 5.58 | % | | | 4.16 | % | | | 3.40 | % | | | 5.58 | % |

| 1976 | | | 23.93 | | | | 15.60 | | | | 20.74 | | | | 26.03 | | | | 25.98 | |

| 1977 | | | –7.16 | | | | 3.04 | | | | –3.13 | | | | –0.72 | | | | 0.70 | |

| 1978 | | | 6.57 | | | | 1.39 | | | | 4.74 | | | | 4.80 | | | | 6.21 | |

| 1979 | | | 18.61 | | | | 1.93 | | | | 11.77 | | | | 14.67 | | | | 7.63 | |

| 1980 | | | 32.50 | | | | 2.71 | | | | 20.43 | | | | 19.70 | | | | 14.36 | |

| 1981 | | | –4.92 | | | | 6.25 | | | | –0.47 | | | | 1.86 | | | | 4.40 | |

| 1982 | | | 21.55 | | | | 32.62 | | | | 26.19 | | | | 30.63 | | | | 29.36 | |

| 1983 | | | 22.56 | | | | 8.36 | | | | 16.76 | | | | 17.44 | | | | 16.11 | |

| 1984 | | | 6.27 | | | | 15.15 | | | | 9.96 | | | | 7.46 | | | | 9.36 | |

| 1985 | | | 31.73 | | | | 22.10 | | | | 27.94 | | | | 29.83 | | | | 29.11 | |

| 1986 | | | 18.67 | | | | 15.26 | | | | 17.61 | | | | 18.43 | | | | 16.87 | |

| 1987 | | | 5.25 | | | | 2.76 | | | | 5.65 | | | | 4.13 | | | | 4.02 | |

| 1988 | | | 16.56 | | | | 7.89 | | | | 13.07 | | | | 11.18 | | | | 12.87 | |

| 1989 | | | 31.63 | | | | 14.53 | | | | 24.72 | | | | 19.70 | | | | 21.53 | |

| 1990 | | | –3.11 | | | | 8.96 | | | | 1.81 | | | | 0.66 | | | | –1.57 | |

| 1991 | | | 30.40 | | | | 16.00 | | | | 24.73 | | | | 25.83 | | | | 24.69 | |

| 1992 | | | 7.61 | | | | 7.40 | | | | 7.58 | | | | 7.46 | | | | 9.48 | |

| 1993 | | | 10.06 | | | | 9.75 | | | | 9.98 | | | | 11.95 | | | | 11.27 | |

| 1994 | | | 1.32 | | | | –2.92 | | | | –0.33 | | | | –2.05 | | | | 0.34 | |

| 1995 | | | 37.53 | | | | 18.47 | | | | 29.64 | | | | 24.89 | | | | 27.13 | |

| 1996 | | | 22.95 | | | | 3.63 | | | | 14.96 | | | | 13.05 | | | | 13.16 | |

| 1997 | | | 33.35 | | | | 9.65 | | | | 23.61 | | | | 20.30 | | | | 21.04 | |

| 1998 | | | 28.58 | | | | 8.69 | | | | 20.98 | | | | 15.09 | | | | 11.13 | |

| 1999 | | | 21.04 | | | | –0.82 | | | | 12.00 | | | | 8.98 | | | | 3.47 | |

| 2000 | | | –9.10 | | | | 11.63 | | | | –0.99 | | | | 2.39 | | | | 15.85 | |

| 2001 | | | –11.88 | | | | 8.44 | | | | –3.71 | | | | –3.24 | | | | 8.19 | |

| 2002 | | | –22.09 | | | | 10.26 | | | | –9.82 | | | | –10.69 | | | | –6.27 | |

| 2003 | | | 28.67 | | | | 4.10 | | | | 18.47 | | | | 19.94 | | | | 22.82 | |

| 2004 | | | 10.87 | | | | 4.34 | | | | 8.29 | | | | 8.99 | | | | 8.92 | |

| 2005 | | | 4.91 | | | | 2.43 | | | | 4.00 | | | | 5.20 | | | | 3.12 | |

| 2006 | | | 15.78 | | | | 4.33 | | | | 11.11 | | | | 11.60 | | | | 11.80 | |

| 2007 | | | 5.49 | | | | 6.97 | | | | 6.22 | | | | 6.53 | | | | 6.60 | |

| 2008 | | | –36.99 | | | | 5.24 | | | | –22.06 | | | | –26.18 | | | | –25.73 | |

| 2009 | | | 26.47 | | | | 5.93 | | | | 18.40 | | | | 23.35 | | | | 21.08 | |

| 2010 | | | 15.08 | | | | 6.54 | | | | 12.14 | | | | 11.90 | | | | 13.02 | |

| 2011 | | | 2.09 | | | | 7.84 | | | | 4.67 | | | | 0.74 | | | | 3.82 | |

| 2012 | | | 15.99 | | | | 4.21 | | | | 11.30 | | | | 11.94 | | | | 14.19 | |

| 2013 | | | 32.37 | | | | –2.02 | | | | 17.55 | | | | 16.39 | | | | 21.73 | |

| 2014 | | | 13.66 | | | | 5.97 | | | | 10.60 | | | | 7.21 | | | | 8.85 | |

| Average annual total returns | | | 11.57 | % | | | 7.92 | % | | | 10.39 | % | | | 10.07 | % | | | 10.94 | % |

| Volatility | | | 14.95 | % | | | 5.47 | % | | | 9.70 | % | | | 10.12 | % | | | 9.68 | % |

Figures assume reinvestment of all distributions.

Sources: Stocks — S&P 500; Bonds — Barclays U.S. Aggregate Index. Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market. For the period July 31, 1975, to December 31, 1975, Barclays Government/Credit Bond Index was used.

The 60%/40% S&P/BC Index blends the S&P 500 with the Barclays U.S. Aggregate Index by weighting their total returns at 60% and 40%, respectively. The portfolio is rebalanced monthly.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

The Lipper Balanced Funds Index is an equally weighted index of the 30 largest U.S. balanced funds.

Capital Research and Management Company became the fund’s investment adviser on July 26, 1975.

Volatility is calculated using annualized standard deviation (based on monthly returns), a measure of how returns over time have varied from the mean; a lower number signifies lower volatility.

Fund results shown are for Class A shares and reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.1 Thus, the net amount invested was $9,425.2 Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

The results shown are before taxes on fund distributions and sale of fund shares.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | The maximum initial sales charge was 8.50% prior to July 1, 1988. |

| 3 | The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index. |

| 4 | Results of the Lipper Balanced Funds Index do not reflect any sales charges. |

| 5 | Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market. For the period July 31, 1975, to December 1, 1975, Barclays Government/Credit Bond Index was used. |

| 6 | For the period July 26, 1975 (when Capital Research and Management Company became the fund’s investment adviser) through December 31, 1975. |

The value of a long-term perspective

How a $10,000 investment has grown

This chart shows how a hypothetical $10,000 investment in American Balanced Fund grew from July 26, 1975 — when Capital Research and Management Company became the fund’s investment adviser — to December 31, 2014. As you can see, the investment grew to $564,293 with all distributions reinvested. The fund’s year-by-year results appear under the chart. You can use this table to estimate how the value of your own holdings has grown.

We take an active hand in maintaining a balance of growth and stability.

Balance. We can see it in nature. Many of us seek it in our everyday lives. And investment professionals stress its importance as we pursue our long-term financial goals.

But when it comes to the right mix of investments, balance isn’t so much found as created. And once achieved, it must be maintained. The portfolio managers and analysts of American Balanced Fund (AMBAL) are dedicated to this task.

| |  | |  |

| | | | | |

| Greg Johnson | | Hilda Applbaum | | Jim Mulally |

| Portfolio Manager | | Portfolio Manager | | Portfolio Manager |

The role of balanced investing

“Our job is to help investors grow their wealth and generate income without keeping them up all night worrying about volatility,” says Greg Johnson, president and portfolio manager of AMBAL.

Balanced funds, like AMBAL, combine equity and fixed-income securities to enable investors to mitigate downside risk while still being able to take advantage of some upside market potential. By nature, balanced funds typically lag pure equity funds in a sharply rising market but tend to hold up better during a decline.

The concept of balanced investing isn’t new. The potential benefits of this strategy probably first became clear when the stock market crash of 1929 wiped out 89% of stock market value, as measured by the Dow Jones Industrial Average excluding dividends. Over the years, the popularity of balanced funds has grown as more and more investors have sought relative safety in addition to growth.

AMBAL can serve as a complete investment program for an investor. It may be particularly attractive to those who don’t keep up with the markets and aren’t sure how to create a balanced investment strategy on their own. Older investors nearing retirement may find some peace of mind from a conservative approach designed to help them preserve their hard-earned nest eggs while seeking growth to last through their golden years.

Why investors choose AMBAL

“AMBAL has proven over time to be an investment vehicle for all seasons,” says Greg.

The fund’s objectives — conservation of capital, current income and long-term growth of capital and income — may not be so different from other balanced funds. It’s in the execution of these goals that AMBAL can be distinguished.

Investors should start by asking “What exactly does ‘balanced’ mean?” suggests Greg. “At American Funds, balance is not only the allocation between equity and fixed income, though that’s obviously one piece of it. To us, balance is also strategic diversification of investments in both areas.”

Portfolio Manager Hilda Applbaum adds, “Diversification isn’t necessarily about the number of securities you invest in. You can hold hundreds of stocks and not be diversified if they’re all basically doing the same thing. True diversification requires different ideas working together within the fund.” In AMBAL, these ideas are introduced through a diversified team of investment professionals with different backgrounds, each owning their best ideas. The fund operates in a research-driven environment that enables these portfolio managers and analysts to identify investment opportunities and manage risk.

AMBAL’s asset allocation in action

AMBAL’s balance of equity and fixed-income investments can be re-aligned to more effectively pursue the fund’s objectives. “If you look at the fund’s allocation over time,” suggests Portfolio Manager Jim Mulally, “you’ll see that it adjusts to economic and market conditions — not in a daily, tactical way but as a strategic mix.” Consider these two different points in history:

| 1999: Potentially overvalued market | | | 2013: Strong market growth |

| | | | |

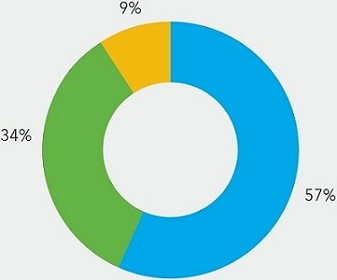

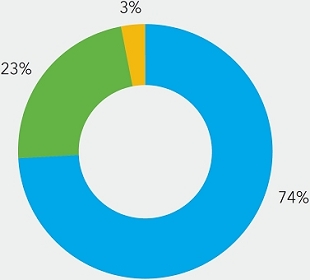

| Wall Street closed its books on a century of unprecedented growth with the Dow Jones Industrial Average, the Nasdaq Composite Index and Standard & Poor’s 500 Composite Index reaching record highs. Already concerned about the sustainability of high stock valuations, AMBAL’s portfolio managers kept the fund’s portfolio close to the levels they had set in 1996 – ending the year just 57% in equities (with 34% in fixed income and 9% in cash). | | | Five years after a devastating crash, the equity market had not only recovered, it rewarded those who remained invested with substantial growth. The Dow and the S&P 500 posted their largest gains since the late 1990s. The Nasdaq rose almost 40% to levels it hadn’t reached since 2000. In order to help investors take advantage of the strong 2013 market, AMBAL maintained an equity allocation over 70%, ending the year almost 74% invested in equities (23% in fixed income and 3% in cash). |

| | | | |

| | |  |

| | | | |

| ■ Total equities ■ Total fixed income ■ Cash & equivalents |

Source: Capital Group (as of December 31, 2013).

Two keys to AMBAL’s success are its asset allocation strategy and time-tested investment process called The Capital System.SM

AMBAL’s dynamic asset allocation strategy

Many balanced funds available today remain at a target asset allocation of approximately 60% equities and 40% fixed-income securities, regardless of market environment.

In contrast, AMBAL seeks a better balance at any given point in time through built-in flexibility. “By design,” explains Greg, “equities can account for as much as 75% and no less than 50% of the AMBAL portfolio. Sometimes, we’ve found that 65% in equities and 35% in fixed-income and cash is where we need to be to effectively pursue the fund’s objectives. There are, however, times when it may be more prudent to move that allocation to one extreme or the other.”

According to Greg, “There are a number of factors we consider as we assess where AMBAL should be in terms of asset allocation, including equity valuations, the term structure of interest rates and our fixed-income professionals’ forecasts on the direction of rates.”

A time-tested system

Balance can be a very personal concept. American Funds understands the value of individual perspectives, even within the structure of a common objective. In AMBAL, as with all of the American Funds, a combination of

| |  | |  |

| | | | | |

| John Smet | | Wesley Phoa | | Andy Barth |

| Portfolio Manager | | Portfolio Manager | | Portfolio Manager |

independence and teamwork defines The Capital System — a process that has, over time, benefited investors as it has enabled each of the portfolio managers and analysts to invest in their strongest convictions. Blended together, these holdings create a broadly diversified portfolio of equity and fixed-income securities that the team believes are most likely to succeed.

“This philosophy,” says Portfolio Manager Wesley Phoa, “has been tried and tested for decades through many, many different market environments. So when you invest in AMBAL, you’re not putting your money into something that has worked well for three or five years. This investment philosophy was working long ago, when the world was totally different from the way it is today. We’re confident that it can continue to work over the next 20 years and beyond, as the world continues to change.”

Research is the backbone of The Capital System. “The amount of deep, fundamental research that goes into every one of the investments in AMBAL is extraordinarily rigorous,” says Justin Toner, investment analyst and coordinator of AMBAL’s research portfolio. Each of the 23 investment analysts in the research portfolio study individual industries and companies in depth — actually visiting these companies in person and meeting with company executives, employees, suppliers, customers and even competitors. Portfolio managers tap this knowledge when making investment decisions on their portion of the overall fund portfolio.

Additionally, AMBAL’s investment analysts, led by Justin, use the research portfolio to invest a portion of the fund based on the sectors they cover. The goal is to own a stock, for example, alongside one of the portfolio managers in the fund, although that’s not a requirement.

“As coordinator of the research portfolio, I keep track of what the analysts are recommending and their level of conviction for each investment,” explains Justin. “If I have an analyst who wants to buy a stock but for some reason didn’t get a portfolio manager to buy it with them, I might typically encourage them to make a larger investment so that it can have a meaningful impact on the overall fund.”

It’s all about balance

Deep fundamental research. A dynamic asset allocation strategy that has historically added to the fund. And a process for investing that has stood the test of time. “It’s all about balance,” says Portfolio Manager Andy Barth. “The structure of AMBAL gives us the flexibility to do what we believe is right for our investors.” ■

How the fund is managed

Portfolio managers

AMBAL’s 10 portfolio managers have an average of 30 years of investment experience.* The knowledge and wisdom they have accumulated over the years have helped them manage your fund through many different stock market cycles.

| Hilda L. Applbaum | 28 years | James R. Mulally | 39 years |

| Andrew F. Barth | 30 years | Dina N. Perry | 37 years |

| Alan N. Berro | 29 years | Wesley K.-S. Phoa | 21 years |

| Gregory D. Johnson | 21 years | John H. Smet | 33 years |

| Jeffrey T. Lager | 20 years | Eugene P. Stein | 44 years |

Investment analysts

The analysts invest in their strongest convictions through the research portfolio, which is coordinated by Justin Toner.

| * | List of investment professionals and their years of experience are as of the prospectus dated March 1, 2015 (unaudited). |

A closer look at the fixed-income portfolio

In 2008, there were few safe harbors for investors. In the fixed-income market, many were surprised at the volatility of high-grade corporate bonds. Only Treasuries did well.

“Since then, the fixed-income market has become even more complex,” says Portfolio Manager John Smet. “More instruments are available and the number of players, including non-U.S. investors, has grown dramatically.”

To effectively cover this market, AMBAL has five fixed-income portfolio managers. John Smet, Jim Mulally and Hilda Applbaum are generalists who buy U.S. Treasury bonds, investment-grade bonds issued by governments and corporations, and securities backed by home mortgages from Fannie Mae, Freddie Mac and Ginnie Mae. Wesley Phoa and Andy Barth together act as a fourth generalist manager; Wesley focuses on Treasuries, government agencies and mortgages, while Andy specializes in credit securities, which are primarily investment-grade corporate bonds (rated BBB/Baa and above).

“One of the main things we all try to remember is that fixed income is meant to be a part of AMBAL that is stable and generates income. It’s an important part of the balance for our investors,” describes Wesley.

Research is a critical component of their efforts. Andy explains, “I think our investors are fully aware of the strong research capability that Capital brings on the equity side. We’re doing that very same thing in fixed income as well in order to make informed decisions.”

As part of that initiative, two groups were introduced, post-2008, to better leverage the power of The Capital System of investing:

Portfolio Strategy Group (PSG): “The PSG is a part of The Capital System that’s unique to fixed income,” explains Jim. “It provides discipline to the portfolio through top-down guidance, which helps us make more consistent investment decisions.” Specifically, the PSG establishes broad, strategic parameters that act as a guide in the construction of AMBAL’s fixed-income portfolio. It is then up to the portfolio managers to use their own creativity within those guidelines. The overall goal of the PSG is to promote good investment results over full market cycles.

Risk and Quantitative Solutions Group (RQS): This team of risk analysts are integrated into Capital Group’s fixed-income organization to contribute to superior long-term investment results through rigorous discipline and quantitative analysis based on computer modeling. A “virtual” portfolio of the fund’s holdings is subjected to a variety of simulations designed to mirror the effects of potential economic scenarios and market movements over time. “Future risk is a big challenge for anyone in the fixed-income market,” says John. “The simulation work done by RQS is an effective way to understand the risk in our portfolios.”

Inside the research portfolio:

Justin Toner

Sectors

U.S. Aerospace and defense

U.S. and Japanese automobiles

Waste services (environmental services)

Beyond coordinating the overall research portfolio, Justin invests in three equities in AMBAL, including Lockheed Martin, one of the fund’s top industrial holdings. “This has been a large investment for us for many years, and we invested a lot more in it fairly recently,” says Justin. “Lockheed Martin is an extremely well-managed, cash-generative company. And management returns that cash to shareholders through dividends and share re-purchases.

“It was an extremely cheap equity in early 2013, when it looked like defense spending was going to be hit hard in Washington. But it’s often when sentiment is most negative that you have the opportunity to invest in a good company at a great price. Even now, as it appears defense spending may rise again, albeit modestly, the company remains a reasonably valued investment.”

Four of our investment analysts describe the conviction behind a key AMBAL investment each holds.

Diana Wagner

Sectors

Health care services

Semi-conductor equipment

Paper and forest products

UnitedHealth Group is not only Diana’s largest holding, it represents one of AMBAL’s top holdings in the health care sector.

Diana explains, “Many worried that the Affordable Care Act (ACA) was a government takeover of health care, but I think it further promoted the role of the private sector. UnitedHealth is already, in many ways, enabling the country’s health care agenda as the government’s contractor for the federal health insurance exchange through its Optum subsidiary. Optum is now one-third of profits and also sells services to help hospitals, doctors, employers and even other insurers adapt to the changing health care environment.

“However, the biggest growth opportunity I see for UnitedHealth is the continued privatization of Medicare and Medicaid, which is still in the early stages.”

Paul Benjamin

Sectors

Information technology hardware

Information technology software

One of Paul’s investments, Microsoft, is AMBAL’s largest holding. “We’ve been building our position in Microsoft in a material way, especially in 2013,” says Paul. “The stock was downgraded, partly due to weak investments in the consumer franchise area — such as the Surface tablet, retail stores and Bing. But that’s only 20% of the picture.

“The other 80% of the profits comes from a very healthy enterprise business that’s growing 8% to 10% a year. Today, Microsoft is the second-largest infrastructure cloud vendor, after Amazon. As more people turn to these services, I feel confident that Microsoft is the one legacy IT company best positioned to succeed in the cloud — even more so under the direction of new CEO Satya Nadella and new Chairman John Thompson, whose background from IBM and Symantec should prove valuable to Microsoft moving forward.”

Andrei Muresianu

Sectors

Telecommunications

Cable and satellite

Traditional U.S. media

Andrei invests in Comcast, a top AMBAL holding in the consumer discretionary area. “In addition to a steady cash flow from their core cable TV business, I was attracted to Comcast’s position as a leader in broadband communications. A lot of Americans are interested in getting broadband at home and upgrading the speed of their service.

“Another reason for my conviction is Comcast’s acquisition of NBC/Universal from General Electric. This could enable Comcast to become a very profitable integrated media company with the means to shape the evolution of the media ecosystem, ranging from video-on-demand to dynamic addressable advertising to out-of-home TV-everywhere rights that can make their product mobile and customizable.”

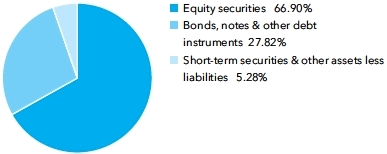

Summary investment portfolio December 31, 2014

| Investment mix by security type | Percent of net assets |

| Common stocks 66.90% | | Shares | | | Value

(000) | |

| Financials 12.36% | | | | | | | | |

| Wells Fargo & Co. | | | 30,902,000 | | | $ | 1,694,048 | |

| Berkshire Hathaway Inc., Class A1 | | | 6,580 | | | | 1,487,080 | |

| JPMorgan Chase & Co. | | | 20,651,000 | | | | 1,292,339 | |

| American Express Co. | | | 11,300,000 | | | | 1,051,352 | |

| ACE Ltd. | | | 5,095,000 | | | | 585,314 | |

| Citigroup Inc. | | | 9,500,000 | | | | 514,045 | |

| Weyerhaeuser Co.1 | | | 13,115,242 | | | | 470,706 | |

| SunTrust Banks, Inc. | | | 11,000,000 | | | | 460,900 | |

| Capital One Financial Corp. | | | 5,569,000 | | | | 459,721 | |

| Other securities | | | | | | | 1,827,034 | |

| | | | | | | | 9,842,539 | |

| | | | | | | | | |

| Consumer discretionary 9.93% | | | | | | | | |

| Comcast Corp., Class A | | | 36,050,000 | | | | 2,091,260 | |

| Home Depot, Inc. | | | 16,929,349 | | | | 1,777,074 | |

| Amazon.com, Inc.1 | | | 4,119,500 | | | | 1,278,487 | |

| Twenty-First Century Fox, Inc., Class A | | | 25,156,900 | | | | 966,151 | |

| Walt Disney Co. | | | 5,220,000 | | | | 491,672 | |

| Other securities | | | | | | | 1,304,966 | |

| | | | | | | | 7,909,610 | |

| | | | | | | | | |

| Information technology 8.84% | | | | | | | | |

| Microsoft Corp. | | | 59,655,000 | | | | 2,770,975 | |

| Texas Instruments Inc. | | | 11,232,000 | | | | 600,519 | |

| ASML Holding NV (New York registered) | | | 4,055,401 | | | | 437,294 | |

| ASML Holding NV2 | | | 1,470,405 | | | | 157,534 | |

| Cisco Systems, Inc. | | | 18,250,000 | | | | 507,624 | |

| TE Connectivity Ltd. | | | 7,805,000 | | | | 493,666 | |

| Other securities | | | | | | | 2,076,570 | |

| | | | | | | | 7,044,182 | |

| | | | | | | | | |

| Industrials 8.49% | | | | | | | | |

| Boeing Co. | | | 12,695,000 | | | | 1,650,096 | |

| Lockheed Martin Corp. | | | 6,574,037 | | | | 1,265,962 | |

| Union Pacific Corp. | | | 7,040,000 | | | | 838,675 | |

| General Electric Co. | | | 23,650,000 | | | | 597,635 | |

| Parker-Hannifin Corp. | | | 4,100,000 | | | | 528,695 | |

| United Technologies Corp. | | | 3,690,000 | | | | 424,350 | |

| Other securities | | | | | | | 1,459,411 | |

| | | | | | | | 6,764,824 | |

| | | | | | | | | |

| Consumer staples 7.61% | | | | | | | | |

| Philip Morris International Inc. | | | 14,750,000 | | | | 1,201,387 | |

| Coca-Cola Co. | | | 27,663,000 | | | | 1,167,932 | |

| Procter & Gamble Co. | | | 9,935,000 | | | | 904,979 | |

| PepsiCo, Inc. | | | 8,766,000 | | | | 828,913 | |

| Costco Wholesale Corp. | | | 5,677,326 | | | | 804,761 | |

| | | Shares | | | Value

(000) | |

| Nestlé SA2 | | | 8,140,000 | | | $ | 596,675 | |

| Nestlé SA (ADR) | | | 1,000,000 | | | | 72,950 | |

| Other securities | | | | | | | 488,725 | |

| | | | | | | | 6,066,322 | |

| | | | | | | | | |

| Health care 6.71% | | | | | | | | |

| Merck & Co., Inc. | | | 22,990,000 | | | | 1,305,602 | |

| UnitedHealth Group Inc. | | | 9,295,000 | | | | 939,632 | |

| Pfizer Inc. | | | 21,905,000 | | | | 682,341 | |

| Roche Holding AG2 | | | 2,358,957 | | | | 639,373 | |

| Bristol-Myers Squibb Co. | | | 9,950,000 | | | | 587,348 | |

| Johnson & Johnson | | | 5,510,000 | | | | 576,181 | |

| Other securities | | | | | | | 618,769 | |

| | | | | | | | 5,349,246 | |

| | | | | | | | | |

| Energy 4.39% | | | | | | | | |

| Chevron Corp. | | | 5,244,755 | | | | 588,357 | |

| Royal Dutch Shell PLC, Class B (ADR) | | | 8,058,000 | | | | 560,514 | |

| Enbridge Inc. | | | 9,795,000 | | | | 503,561 | |

| ConocoPhillips | | | 7,169,508 | | | | 495,126 | |

| Other securities | | | | | | | 1,346,052 | |

| | | | | | | | 3,493,610 | |

| | | | | | | | | |

| Materials 3.07% | | | | | | | | |

| Potash Corp. of Saskatchewan Inc. | | | 19,850,000 | | | | 701,102 | |

| E.I. du Pont de Nemours and Co. | | | 6,750,000 | | | | 499,095 | |

| Other securities | | | | | | | 1,247,313 | |

| | | | | | | | 2,447,510 | |

| | | | | | | | | |

| Other 0.73% | | | | | | | | |

| Other securities | | | | | | | 579,754 | |

| | | | | | | | | |

| Miscellaneous 4.77% | | | | | | | | |

| Other common stocks in initial period of acquisition | | | | | | | 3,797,825 | |

| | | | | | | | | |

| Total common stocks (cost: $32,600,515,000) | | | | | | | 53,295,422 | |

| | | | | | | | | |

| Bonds, notes & other debt instruments 27.82% | | Principal amount

(000) | | | | | |

| Corporate bonds & notes 9.26% | | | | | | | | |

| Financials 2.93% | | | | | | | | |

| American Express Co. 6.15% 2017 | | $ | 22,800 | | | | 25,421 | |

| American Express Credit Co. 1.55% 2017 | | | 15,465 | | | | 15,507 | |

| Berkshire Hathaway Inc. 2.00%–2.90% 2016–2020 | | | 60,840 | | | | 62,108 | |

| JPMorgan Chase & Co. 1.35%–3.88% 2017–2024 | | | 159,365 | | | | 159,511 | |

| JPMorgan Chase & Co., Series S, junior subordinated, perpetual, 6.75% (undated)3 | | | 25,000 | | | | 26,531 | |

| Wells Fargo & Co. 1.25%–4.60% 2016–2024 | | | 111,300 | | | | 115,201 | |

| Other securities | | | | | | | 1,929,647 | |

| | | | | | | | 2,333,926 | |

| | | | | | | | | |

| Consumer discretionary 1.07% | | | | | | | | |

| 21st Century Fox America, Inc. 3.70% 20244 | | | 18,420 | | | | 18,985 | |

| Amazon.com, Inc. 3.80%–4.95% 2024–2044 | | | 109,575 | | | | 113,343 | |

| Comcast Corp. 3.60%–6.45% 2017–2044 | | | 60,350 | | | | 70,803 | |

| Home Depot, Inc. 2.00%–5.95% 2019–2041 | | | 77,700 | | | | 84,241 | |

| News America Inc. 3.00% 2022 | | | 6,000 | | | | 5,970 | |

| Other securities | | | | | | | 556,200 | |

| | | | | | | | 849,542 | |

| | | | | | | | | |

| Consumer staples 0.98% | | | | | | | | |

| Coca-Cola Co. 1.50%–1.80% 2015–2016 | | | 36,470 | | | | 36,961 | |

| PepsiCo, Inc. 7.90% 2018 | | | 15,000 | | | | 18,264 | |

| Philip Morris International Inc. 3.25%–4.88% 2024–2044 | | | 59,800 | | | | 60,616 | |

| Procter & Gamble Co. 1.45% 2016 | | | 13,460 | | | | 13,625 | |

| Other securities | | | | | | | 647,716 | |

| | | | | | | | 777,182 | |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Corporate bonds & notes (continued) | | | | | | | | |

| Health care 0.91% | | | | | | | | |

| UnitedHealth Group Inc. 1.40%–6.00% 2017–2018 | | $ | 67,170 | | | $ | 74,022 | |

| Other securities | | | | | | | 653,041 | |

| | | | | | | | 727,063 | |

| | | | | | | | | |

| Industrials 0.54% | | | | | | | | |

| Boeing Company 0.95% 2018 | | | 12,000 | | | | 11,743 | |

| General Electric Capital Corp. 1.00%–6.00% 2015–2024 | | | 99,605 | | | | 103,139 | |

| General Electric Co. 0.85%–4.50% 2015–2044 | | | 44,100 | | | | 44,881 | |

| General Electric Corp. 5.25% 2017 | | | 16,000 | | | | 17,758 | |

| Union Pacific Corp. 5.70% 2018 | | | 11,150 | | | | 12,711 | |

| Other securities | | | | | | | 240,145 | |

| | | | | | | | 430,377 | |

| | | | | | | | | |

| Other 2.83% | | | | | | | | |

| Other securities | | | | | | | 2,258,557 | |

| | | | | | | | | |

| Total corporate bonds & notes | | | | | | | 7,376,647 | |

| | | | | | | | | |

| U.S. Treasury bonds & notes 7.90% | | | | | | | | |

| U.S. Treasury 6.34% | | | | | | | | |

| U.S. Treasury 0.25% 2015 | | | 489,000 | | | | 489,323 | |

| U.S. Treasury 0.38%–5.50% 2015–2044 | | | 3,128,524 | | | | 3,297,525 | |

| U.S. Treasury 0.625% 2018 | | | 775,000 | | | | 759,438 | |

| U.S. Treasury 1.50% 2019 | | | 511,500 | | | | 508,201 | |

| | | | | | | | 5,054,487 | |

| | | | | | | | | |

| U.S. Treasury inflation-protected securities 1.56% | | | | | | | | |

| U.S. Treasury Inflation-Protected Security 0.13%–2.38% 2015–20435 | | | 729,170 | | | | 740,096 | |

| U.S. Treasury Inflation-Protected Security 1.375% 20445 | | | 438,688 | | | | 501,401 | |

| | | | | | | | 1,241,497 | |

| | | | | | | | | |

| Total U.S. Treasury bonds & notes | | | | | | | 6,295,984 | |

| | | | | | | | | |

| Mortgage-backed obligations 6.67% | | | | | | | | |

| Federal agency mortgage-backed obligations 4.45% | | | | | | | | |

| Fannie Mae 0.00%–11.01% 2018–20473,6,7 | | | 2,504,771 | | | | 2,647,668 | |

| Freddie Mac 0.00%–6.50% 2023–20443,6 | | | 200,498 | | | | 213,297 | |

| Other securities | | | | | | | 683,771 | |

| | | | | | | | 3,544,736 | |

| | | | | | | | | |

| Other 2.22% | | | | | | | | |

| Other securities | | | | | | | 1,771,509 | |

| | | | | | | | | |

| Total mortgage-backed obligations | | | | | | | 5,316,245 | |

| | | | | | | | | |

| Federal agency bonds & notes 2.30% | | | | | | | | |

| Fannie Mae 0.38%–6.25% 2015–20293,6 | | | 759,454 | | | | 770,848 | |

| Federal Home Loan Bank 0.38%–5.50% 2016–2036 | | | 171,405 | | | | 174,107 | |

| Freddie Mac 0.50%–3.53% 2015–20243,6 | | | 723,416 | | | | 729,247 | |

| Other securities | | | | | | | 158,950 | |

| | | | | | | | 1,833,152 | |

| | | | | | | | | |

| Other 1.64% | | | | | | | | |

| Other securities | | | | | | | 1,302,738 | |

| | | | | | | | | |

| Miscellaneous 0.05% | | | | | | | | |

| Other bonds, notes and other debt instruments in initial period of acquisition | | | | | | | 39,507 | |

| | | | | | | | | |

| Total bonds, notes & other debt instruments (cost: $21,574,677,000) | | | | | | | 22,164,273 | |

| | | | | | | | | |

| Short-term securities 5.97% | | | | | | | | |

| Chariot Funding, LLC 0.25%–0.27% due 5/21/2015–8/26/20154 | | | 120,600 | | | | 120,428 | |

| Coca-Cola Co. 0.13%–0.19% due 1/8/2015–4/23/20154 | | | 162,100 | | | | 162,069 | |

| Fannie Mae 0.06%–0.16% due 1/7/2015–10/1/2015 | | | 1,172,994 | | | | 1,172,609 | |

| Federal Home Loan Bank 0.07%–0.17% due 1/14/2015–11/4/2015 | | | 1,491,397 | | | | 1,491,012 | |

| Freddie Mac 0.07%–0.17% due 1/12/2015–8/18/2015 | | | 698,400 | | | | 698,185 | |

| | | Principal amount

(000) | | | Value

(000) | |

| General Electric Capital Corp. 0.19%–0.20% due 5/5/2015–5/13/2015 | | $ | 120,000 | | | $ | 119,923 | |

| JPMorgan Chase & Co. 0.25% due 3/11/20154 | | | 25,000 | | | | 24,991 | |

| Jupiter Securitization Co., LLC 0.21% due 5/5/20154 | | | 25,000 | | | | 24,980 | |

| Procter & Gamble Co. 0.08%–0.15% due 1/5/2015–2/9/20154 | | | 140,000 | | | | 139,995 | |

| Other securities | | | | | | | 802,842 | |

| | | | | | | | | |

| Total short-term securities (cost: $4,756,675,000) | | | | | | | 4,757,034 | |

| Total investment securities 100.69% (cost: $58,931,867,000) | | | | | | | 80,216,729 | |

| Other assets less liabilities (0.69)% | | | | | | | (553,050 | ) |

| | | | | | | | | |

| Net assets 100.00% | | | | | | $ | 79,663,679 | |

This summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio, including loan participations and assignments which may be subject to legal or contractual restrictions on resale. The total value of all such loans was $5,506,000, which represented .01% of the net assets of the fund.

The following footnotes apply to either the individual securities noted or one or more of the securities aggregated and listed as a single line item.

| 1 | Security did not produce income during the last 12 months. |

| 2 | Valued under fair value procedures adopted by authority of the board of trustees. The total value of all such securities, including those in “Miscellaneous” and “Other securities,” was $1,785,370,000, which represented 2.24% of the net assets of the fund. This amount includes $1,773,228,000 related to certain securities trading outside the U.S. whose values were adjusted as a result of significant market movements following the close of local trading. |

| 3 | Coupon rate may change periodically. |

| 4 | Acquired in a transaction exempt from registration under Rule 144A or Section 4(2) of the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities, including those in “Other securities,” was $3,055,295,000, which represented 3.84% of the net assets of the fund. |

| 5 | Index-linked bond whose principal amount moves with a government price index. |

| 6 | Principal payments may be made periodically. Therefore, the effective maturity date may be earlier than the stated maturity date. |

| 7 | A portion or all of the security purchased on a TBA basis. |

Key to abbreviations

ADR = American Depository Receipts

TBA = To be announced

See Notes to Financial Statements

Financial statements

| Statement of assets and liabilities | | | | | | |

| at December 31, 2014 | (dollars in thousands) | |

| | |

| Assets: | | | | | | | | |

| Investment securities, at value (cost: $58,931,867) | | | | | | $ | 80,216,729 | |

| Cash | | | | | | | 1,163 | |

| Receivables for: | | | | | | | | |

| Sales of investments | | $ | 755,690 | | | | | |

| Sales of fund’s shares | | | 337,088 | | | | | |

| Dividends and interest | | | 196,414 | | | | 1,289,192 | |

| | | | | | | | 81,507,084 | |

| Liabilities: | | | | | | | | |

| Payables for: | | | | | | | | |

| Purchases of investments | | | 1,559,586 | | | | | |

| Repurchases of fund’s shares | | | 233,196 | | | | | |

| Investment advisory services | | | 15,589 | | | | | |

| Services provided by related parties | | | 29,073 | | | | | |

| Trustees’ deferred compensation | | | 4,227 | | | | | |

| Other | | | 1,734 | | | | 1,843,405 | |

| Net assets at December 31, 2014 | | | | | | $ | 79,663,679 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Capital paid in on shares of beneficial interest | | | | | | $ | 58,078,777 | |

| Undistributed net investment income | | | | | | | 122,668 | |

| Undistributed net realized gain | | | | | | | 178,586 | |

| Net unrealized appreciation | | | | | | | 21,283,648 | |

| Net assets at December 31, 2014 | | | | | | $ | 79,663,679 | |

(dollars and shares in thousands, except per-share amounts)

Shares of beneficial interest issued and outstanding (no stated par value) —

unlimited shares authorized (3,220,722 total shares outstanding)

| | | Net assets | | | Shares

outstanding | | | Net asset

value per share | |

| Class A | | $ | 46,916,623 | | | | 1,895,258 | | | $ | 24.75 | |

| Class B | | | 541,503 | | | | 21,915 | | | | 24.71 | |

| Class C | | | 5,573,575 | | | | 226,297 | | | | 24.63 | |

| Class F-1 | | | 2,841,081 | | | | 114,837 | | | | 24.74 | |

| Class F-2 | | | 1,869,537 | | | | 75,555 | | | | 24.74 | |

| Class 529-A | | | 2,831,067 | | | | 114,526 | | | | 24.72 | |

| Class 529-B | | | 72,769 | | | | 2,939 | | | | 24.76 | |

| Class 529-C | | | 904,726 | | | | 36,622 | | | | 24.70 | |

| Class 529-E | | | 144,261 | | | | 5,839 | | | | 24.71 | |

| Class 529-F-1 | | | 110,888 | | | | 4,489 | | | | 24.71 | |

| Class R-1 | | | 157,898 | | | | 6,417 | | | | 24.61 | |

| Class R-2 | | | 1,307,723 | | | | 53,115 | | | | 24.62 | |

| Class R-2E | | | 10 | | | | — | * | | | 24.75 | |

| Class R-3 | | | 3,315,311 | | | | 134,519 | | | | 24.65 | |

| Class R-4 | | | 4,384,832 | | | | 177,399 | | | | 24.72 | |

| Class R-5 | | | 2,616,255 | | | | 105,610 | | | | 24.77 | |

| Class R-6 | | | 6,075,620 | | | | 245,385 | | | | 24.76 | |

*Amount less than one thousand.

See Notes to Financial Statements

| Statement of operations | | |

| for the year ended December 31, 2014 | | (dollars in thousands) | |

| | | |

| Investment income: | | | | | | | | |

| Income: | | | | | | | | |

| Dividends (net of non-U.S. taxes of $13,991) | | $ | 1,173,278 | | | | | |

| Interest | | | 486,595 | | | $ | 1,659,873 | |

| Fees and expenses*: | | | | | | | | |

| Investment advisory services | | | 173,885 | | | | | |

| Distribution services | | | 227,751 | | | | | |

| Transfer agent services | | | 74,564 | | | | | |

| Administrative services | | | 19,275 | | | | | |

| Reports to shareholders | | | 2,326 | | | | | |

| Registration statement and prospectus | | | 1,058 | | | | | |

| Trustees’ compensation | | | 703 | | | | | |

| Auditing and legal | | | 142 | | | | | |

| Custodian | | | 609 | | | | | |

| Other | | | 3,814 | | | | 504,127 | |

| Net investment income | | | | | | | 1,155,746 | |

| | | | | | | | | |

| | | | | | | | | |

| Net realized gain and unrealized appreciation on investments and currency: | | | | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments | | | 4,942,260 | | | | | |

| Currency transactions | | | (906 | ) | | | 4,941,354 | |

| Net unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments (net of non-U.S. taxes of $511) | | | 272,453 | | | | | |

| Currency translations | | | (926 | ) | | | 271,527 | |

| Net realized gain and unrealized appreciation on investments and currency | | | | | | | 5,212,881 | |

| | | | | | | | | |

| Net increase in net assets resulting from operations | | | | | | $ | 6,368,627 | |

*Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements.

| Statements of changes in net assets | | | | | | |

| | | (dollars in thousands) |

| | | | |

| | | Year ended December 31 | |

| | | 2014 | | | 2013 | |

| | | | | | | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 1,155,746 | | | $ | 970,228 | |

| Net realized gain on investments and currency transactions | | | 4,941,354 | | | | 1,873,080 | |

| Net unrealized appreciation on investments and currency translations | | | 271,527 | | | | 9,504,575 | |

| Net increase in net assets resulting from operations | | | 6,368,627 | | | | 12,347,883 | |

| | | | | | | | | |

| Dividends and distributions paid to shareholders: | | | | | | | | |

| Dividends from net investment income | | | (1,089,310 | ) | | | (1,016,591 | ) |

| Distributions from net realized gain on investments | | | (4,365,643 | ) | | | — | |

| Total dividends and distributions paid to shareholders | | | (5,454,953 | ) | | | (1,016,591 | ) |

| | | | | | | | | |

| Net capital share transactions | | | 7,862,108 | | | | 3,682,825 | |

| | | | | | | | | |

| Total increase in net assets | | | 8,775,782 | | | | 15,014,117 | |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of year | | | 70,887,897 | | | | 55,873,780 | |

| End of year (including undistributed net investment income: $122,668 and $45,929, respectively) | | $ | 79,663,679 | | | $ | 70,887,897 | |

See Notes to Financial Statements

Notes to financial statements

1. Organization

American Balanced Fund (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified investment company. The fund seeks conservation of capital, current income, and long-term growth of both capital and income.

The fund has 17 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and seven retirement plan share classes (Classes R-1, R-2, R2-E, R-3, R-4, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are described further in the following table:

| Share class | | Initial sales

charge | | Contingent deferred sales

charge upon redemption | | Conversion feature | |

| Classes A and 529-A | | Up to 5.75% | | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | | None | |

| Classes B and 529-B* | | None | | Declines from 5% to 0% for redemptions within six years of purchase | | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years | |

| Class C | | None | | 1% for redemptions within one year of purchase | | Class C converts to Class F-1 after 10 years | |

| Class 529-C | | None | | 1% for redemptions within one year of purchase | | None | |

| Class 529-E | | None | | None | | None | |

| Classes F-1, F-2 and 529-F-1 | | None | | None | | None | |

| Classes R-1, R-2, R-2E, R-3, R-4, R-5 and R-6 | | None | | None | | None | |

*Class B and 529-B shares of the fund are not available for purchase.

On August 29, 2014, the fund made an additional retirement plan share class (Class R-2E) available for sale pursuant to an amendment to its registration statement filed with the U.S. Securities and Exchange Commission. Refer to the fund’s prospectus for more details.

Holders of all share classes have equal pro rata rights to the assets, dividends and liquidation proceeds of the fund. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, transfer agent and administrative services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board. The fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require the fund’s investment adviser to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. The fund follows the significant accounting policies described in this section, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, transfer agent and administrative services, are charged directly to the respective share class.

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. The effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments in the fund’s statement of operations. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by U.S. GAAP. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities |

| Mortgage-backed; asset-backed obligations | Standard inputs and cash flows, prepayment information, default rates, delinquency and loss assumptions, collateral characteristics, credit enhancements and specific deal information |

| Municipal securities | Standard inputs and, for certain distressed securities, cash flows or liquidation values using a net present value calculation based on inputs that include, but are not limited to, financial statements and debt contracts |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or deemed to be not representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described above for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of trustees as further described. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to

a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure — The fund’s board of trustees has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the board of trustees with supplemental information to support the changes. The fund’s board and audit committee also regularly review reports that describe fair value determinations and methods.

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications — The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following table presents the fund’s valuation levels as of December 31, 2014 (dollars in thousands):

| | | Investment securities | |

| | | Level 1 | | | Level 2* | | | Level 3 | | | Total | |

| Assets: | | | | | | | | | | | | | | | | |

| Common stocks: | | | | | | | | | | | | | | | | |

| Financials | | $ | 9,842,539 | | | $ | — | | | $ | — | | | $ | 9,842,539 | |

| Consumer discretionary | | | 7,909,610 | | | | — | | | | — | | | | 7,909,610 | |

| Information technology | | | 6,886,648 | | | | 157,534 | | | | — | | | | 7,044,182 | |

| Industrials | | | 6,764,824 | | | | — | | | | — | | | | 6,764,824 | |

| Consumer staples | | | 5,469,647 | | | | 596,675 | | | | — | | | | 6,066,322 | |

| Health care | | | 4,709,873 | | | | 639,373 | | | | — | | | | 5,349,246 | |

| Energy | | | 3,493,610 | | | | — | | | | — | | | | 3,493,610 | |

| Materials | | | 2,447,510 | | | | — | | | | — | | | | 2,447,510 | |

| Other | | | 579,754 | | | | — | | | | — | | | | 579,754 | |

| Miscellaneous | | | 3,418,178 | | | | 379,647 | | | | — | | | | 3,797,825 | |

| Bonds, notes & other debt instruments: | | | | | | | | | | | | | | | | |

| Corporate bonds & notes | | | — | | | | 7,376,647 | | | | — | | | | 7,376,647 | |

| U.S. Treasury bonds & notes | | | — | | | | 6,295,984 | | | | — | | | | 6,295,984 | |

| Mortgage-backed obligations | | | — | | | | 5,316,245 | | | | — | | | | 5,316,245 | |

| Federal agency bonds & notes | | | — | | | | 1,833,152 | | | | — | | | | 1,833,152 | |

| Other | | | — | | | | 1,302,738 | | | | — | | | | 1,302,738 | |

| Miscellaneous | | | — | | | | 39,507 | | | | — | | | | 39,507 | |

| Short-term securities | | | — | | | | 4,757,034 | | | | — | | | | 4,757,034 | |

| Total | | $ | 51,522,193 | | | $ | 28,694,536 | | | $ | — | | | $ | 80,216,729 | |

| * | Securities with a value of $1,393,582,000, which represented 1.75% of the net assets of the fund, transferred from Level 1 to Level 2 since the prior fiscal year-end, primarily due to significant market movements following the close of local trading. |

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions — The prices of, and the income generated by, the common stocks, bonds and other securities held by the fund may decline – sometimes rapidly or unpredictably – due to various factors, including events or conditions affecting the general economy or particular industries; overall market changes; local, regional or global political, social or economic instability; governmental or governmental agency responses to economic conditions; and currency exchange, interest rate and commodity price fluctuations.

Issuer risks — The prices of, and the income generated by, securities held by the fund may decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance and strategic initiatives such as mergers, acquisitions or dispositions and the market response to any such initiatives.

Investing in growth-oriented stocks — Growth-oriented common stocks and other equity-type securities (such as preferred stocks, convertible preferred stocks and convertible bonds) may involve larger price swings and greater potential for loss than other types of investments.

Investing in income-oriented stocks — Income provided by the fund may be reduced by changes in the dividend policies of, and the capital resources available for dividend payments at, the companies in which the fund invests.

Investing in debt instruments — The prices of, and the income generated by, bonds and other debt securities held by the fund may be affected by changing interest rates and by changes in the effective maturities and credit ratings of these securities.

Rising interest rates will generally cause the prices of bonds and other debt securities to fall. Falling interest rates may cause an issuer to redeem, call or refinance a debt security before its stated maturity, which may result in the fund having to reinvest the proceeds in lower yielding securities. Longer maturity debt securities generally have greater sensitivity to changes in interest rates and may be subject to greater price fluctuations than shorter maturity debt securities.

Bonds and other debt securities are also subject to credit risk, which is the possibility that the credit strength of an issuer will weaken and/or an issuer of a debt security will fail to make timely payments of principal or interest and the security will go into default. Lower quality debt securities generally have higher rates of interest and may be subject to greater price fluctuations than higher quality debt securities. Credit risk is gauged, in part, by the credit ratings of the debt securities in which the fund invests. However, ratings are only the opinions of the rating agencies issuing them and are not guarantees as to credit quality or an evaluation of market risk. The fund’s investment adviser relies on its own credit analysts to research issuers and issues in seeking to mitigate various credit and default risks.

Investing in securities backed by the U.S. government — Securities backed by the U.S. Treasury or the full faith and credit of the U.S. government are guaranteed only as to the timely payment of interest and principal when held to maturity. Accordingly, the current market values for these securities will fluctuate with changes in interest rates. Securities issued by government-sponsored entities and federal agencies and instrumentalities that are not backed by the full faith and credit of the U.S. government are neither issued nor guaranteed by the U.S. government.

Investing in mortgage-related and other asset-backed securities — Mortgage-related securities, such as mortgage-backed securities, and other asset-backed securities, include debt obligations that represent interests in pools of mortgages or other income-bearing assets, such as consumer loans or receivables. Such securities often involve risks that are different from or more acute than the risks associated with investing in other types of debt securities. Mortgage-backed and other asset-backed securities are subject to changes in the payment patterns of borrowers of the underlying debt. When interest rates fall, borrowers are more likely to refinance or prepay their debt before its stated maturity. This may result in the fund having to reinvest the proceeds in lower yielding securities, effectively reducing the fund’s income. Conversely, if interest rates rise and borrowers repay their debt more slowly than expected, the time in which the mortgage-backed and other asset-backed securities are paid off could be extended, reducing the fund’s cash available for reinvestment in higher yielding securities.

Thinly traded securities — There may be little trading in the secondary market for particular bonds or other debt securities, which may make them more difficult to value, acquire or sell.

Investing outside the U.S. — Securities of issuers domiciled outside the U.S., or with significant operations or revenues outside the U.S., may lose value because of adverse political, social, economic or market developments (including social instability, regional conflicts, terrorism and war) in the countries or regions in which the issuers operate or generate revenue. These securities may also lose value due

to changes in foreign currency exchange rates against the U.S. dollar and/or currencies of other countries. Issuers of these securities may be more susceptible to actions of foreign governments, such as the imposition of price controls or punitive taxes, that could adversely impact revenues. Securities markets in certain countries may be more volatile and/or less liquid than those in the U.S. Investments outside the U.S. may also be subject to different accounting practices and different regulatory, legal and reporting standards and practices, and may be more difficult to value, than those in the U.S. In addition, the value of investments outside the U.S. may be reduced by foreign taxes, including foreign withholding taxes on interest and dividends. Further, there may be increased risks of delayed settlement of securities purchased or sold by the fund. The risks of investing outside the U.S. may be heightened in connection with investments in emerging markets.

Management — The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses employed by the investment adviser in this process may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

5. Certain investment techniques

Index-linked bonds — The fund has invested in index-linked bonds, which are fixed-income securities whose principal value is periodically adjusted to a government price index. Over the life of an index-linked bond, interest is paid on the adjusted principal value. Increases or decreases in the principal value of index-linked bonds are recorded as interest income in the fund’s statement of operations.

Mortgage dollar rolls — The fund has entered into mortgage dollar roll transactions in which the fund sells a mortgage-backed security to a counterparty and simultaneously enters into an agreement with the same counterparty to buy back a similar security on a specific future date at a predetermined price. Mortgage dollar rolls are accounted for as purchase and sale transactions, which may increase the fund’s portfolio turnover rate.

Loan transactions — The fund has entered into loan transactions in which the fund acquires a loan either through an agent, by assignment from another holder, or as a participation interest in another holder’s portion of a loan. The loan is often administered by a financial institution that acts as agent for the holders of the loan, and the fund may be required to receive approval from the agent and/or borrower prior to the sale of the investment. The loan’s interest rate and maturity date may change based on the terms of the loan, including potential early payments of principal.

6. Taxation and distributions

Federal income taxation — The fund complies with the requirements under Subchapter M of the Internal Revenue Code applicable to mutual funds and intends to distribute substantially all of its net taxable income and net capital gains each year. The fund is not subject to income taxes to the extent such distributions are made. Therefore, no federal income tax provision is required.

As of and during the period ended December 31, 2014, the fund did not have a liability for any unrecognized tax benefits. The fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the fund did not incur any interest or penalties.

The fund is not subject to examination by U.S. federal tax authorities for tax years before 2011 and by state tax authorities for tax years before 2010.

Non-U.S. taxation — Dividend and interest income are recorded net of non-U.S. taxes paid.

Distributions — Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax basis, which may differ from net investment income and net realized gains for financial reporting purposes. These differences are due primarily to different treatment for items such as currency gains and losses; short-term capital gains and losses; capital losses related to sales of certain securities within 30 days of purchase; deferred expenses; cost of investments sold; and paydowns on fixed-income securities. The fiscal year in which amounts are distributed may differ from the year in which the net investment income and net realized gains are recorded by the fund for financial reporting purposes. The fund may also designate a portion of the amount paid to redeeming shareholders as a distribution for tax purposes.