UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-7120

HARTE-HANKS, INC.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 74-1677284 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

200 Concord Plaza Drive, Suite 800, San Antonio, Texas 78216

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code — 210-829-9000

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the closing price ($25.68) as of the last business day of the registrant’s most recently completed second fiscal quarter (June 30, 2007), was approximately $1,280,015,000.

The number of shares outstanding of each of the registrant’s classes of common stock as of January 31, 2008 was 66,756,439 shares of common stock, all of one class.

Documents incorporated by reference:

Portions of the Proxy Statement to be filed for the Company’s 2008 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

THIS ANNUAL REPORT ON FORM 10-K IS BEING DISTRIBUTED TO STOCKHOLDERS IN LIEU OF A SEPARATE ANNUAL REPORT PURSUANT TO RULE 14a-3(b) OF THE ACT AND SECTION 203.01 OF THE NEW YORK STOCK EXCHANGE LISTED COMPANY MANUAL.

Harte-Hanks, Inc. and Subsidiaries

Table of Contents

Form 10-K Report

December 31, 2007

2

PART I

INTRODUCTION

Harte-Hanks, Inc. (Harte-Hanks) is a worldwide direct and targeted marketing company that provides direct marketing services and shopper advertising opportunities to a wide range of local, regional, national and international consumer and business-to-business marketers. We manage our operations through two operating segments: Direct Marketing, which operates both nationally and internationally, and Shoppers, which operates in local and regional markets in California and Florida.

Marketing today is under intense focus in many organizations. Many corporations have a chief-level executive charged with marketing who is under pressure to utilize a combination of data, technology, channels and resources to demonstrate a return on marketing investment. This has led many to use direct and targeted marketing, as accountability and measurability are hallmarks of the discipline, allowing customer insight to be leveraged to create and accelerate value. Direct Marketing, which represented 63% of our total revenues in 2007, is a leader in the movement toward highly targeted marketing. Our Shoppers business applies geographic targeting principles. Our strategy is based on six key elements:

| | • | | Being a market leader in each of our businesses; |

| | • | | Increasing revenues through growing our base businesses; |

| | • | | Introducing new services, products and innovations; |

| | • | | Entering new markets and making acquisitions; |

| | • | | Using technology to create competitive advantages; and |

| | • | | Employing people who understand our clients’ businesses and markets; |

Harte-Hanks is the successor to a newspaper business begun in Texas in the early 1920s by Houston Harte and Bernard Hanks. In 1972, Harte-Hanks went public and was listed on the New York Stock Exchange (NYSE). We became private in a leveraged buyout initiated by management in 1984. In 1993, we again went public and listed our common stock on the NYSE. In 1997, we sold all of our remaining traditional media operations (consisting of newspapers, television and radio companies) in order to focus all of our efforts on two business segments—Direct Marketing and Shoppers. See segment financial information in Note O “Business Segments” in the Notes to Consolidated Financial Statements.

Harte-Hanks provides public access to all reports filed with the Securities and Exchange Commission (SEC) under the Securities Exchange Act of 1934, as amended (the 1934 Act). These documents may be accessed free of charge on our website at the following address:http://www.harte-hanks.com. Since November 15, 2002, these documents have been provided as soon as practical after they are filed with the SEC. The documents may also be found at the SEC’s website athttp://www.sec.gov. Additionally, we have adopted and posted on our website a code of ethics that applies to our principal executive officer, principal financial officer and principal accounting officer. Our website also includes our corporate governance guidelines and the charters for each of our audit, compensation, and nominating and corporate governance committees. We will provide a printed copy of any of the aforementioned documents to any requesting stockholder.

DIRECT MARKETING

General

Direct marketing services are targeted to specific industries or markets with services and software products tailored to each industry or market. Our Direct Marketing clients include many of the largest retailers; financial companies including banks, financing companies, mutual funds and insurance companies; high-tech and telecommunications companies; and pharmaceutical companies and healthcare organizations. Direct Marketing

3

clients are also from such selected markets as automotive, consumer packaged goods, government/not-for-profit, business services, energy, publishing, travel/hospitality and utilities. We believe that we generally have the ability to provide services to new industries and markets by modifying our services and applications as opportunities are presented. In 2007, 2006 and 2005, Harte-Hanks Direct Marketing had revenues of $732.5 million, $709.7 million, and $694.6 million, respectively, which accounted for approximately 63%, 60%, and 61% of our total revenues, respectively.

Depending on the needs of our clients, our Direct Marketing capabilities are provided in an integrated approach through more than 30 facilities worldwide, more than 10 of which are located outside of the United States. Each of these centers possesses some specialization and is linked with others to support the needs of our clients.

We use various capabilities and technologies to enable our clients to identify, reach, influence and nurture their customers. Harte-Hanks Direct Marketing improves the return on its clients’ marketing investment by increasing their prospect and customer value through solutions and services organized around five groupings of integrated activities:

| | • | | Information (data collection/management); |

| | • | | Opportunity (data access/utilization); |

| | • | | Insight (data analysis/interpretation); |

| | • | | Engagement (program and campaign creation and development); and |

| | • | | Interaction (program execution). |

Harte-Hanks Direct Marketing uses various capabilities and technologies as enablers to capture, analyze and disseminate customer and prospect data across all points of customer contact. Using both proprietary software and open software solutions, we build contact databases for our clients using the information gained from the client’s marketing and communication activities across different media such as mail, websites, e-mail, inbound and outbound teleservices, trade shows, point-of-sale and other sources. We believe that these databases enable clients to measure the return on their marketing communications investments and make more informed decisions about future marketing efforts. We help clients manage the inquiries they receive from a myriad of sources related to their marketing efforts. These inquiries, or leads, are qualified, tracked and distributed both to appropriate sales channels and to client management for analysis, decision-making and/or additional interaction in order for clients to manage their customer and prospect relationships more effectively. These leads are also developed for business-to-business clients through our CI Technology Database and through research efforts of our Aberdeen business.

Our Direct Marketing activities often start with the development of a roadmap, followed by building customized marketing databases for specific clients and providing them with easy-to-use tools to perform analysis and to target their best customers and prospects. Using our proprietary name and address matching software, the Trillium Software System®, we investigate and standardize large numbers of customer records from multiple sources, integrate them into a single database for each client and, if needed, append demographic and lifestyle information.

Our Allink® databases are built for clients and tailored to specific market segments. These databases are moved to the client’s site or maintained at Harte-Hanks with online access from client locations. In addition to building a client’s database and providing solutions for analytics and campaign management, we perform regular database updates.

These solutions are linked to our service bureau. Our service bureau services include preparing list selections, maximizing deliverability and reducing clients’ mailing costs through our Advanced Data Quality services, including Trillium Software and Global Address capabilities in addition to sophisticated postal coding, hygiene and address updates through a non-exclusive National Change of Address license with the U.S. Postal Service.

4

As a further extension of the client’s marketing arm, we provide customer insight by using marketing research and analytics services. Specific capabilities include tracking and reporting, media analysis, modeling, database profiling, primary data collection, marketing applications, consulting and program development.

We engage with our client’s customers by offering direct marketing agency services that combine information-based strategy and brand-building creative efforts that are channel independent, using both traditional direct and interactive media.

In addition, Harte-Hanks provides a variety of services to help clients develop and execute targeted marketing communication programs. These include services such as telephone, email using our proprietary Postfuture® offering, website development and search marketing, personalization of communication pieces using laser and inkjet printing, targeted mail and fulfillment, transportation logistics, and print-on-demand as well as traditional printing.

Our mail tracking capability and long-standing relationship with the U.S. Postal Service assist our customer’s mailings to reach their destinations on time. By controlling the final stage of the print distribution process through its logistics operations, we facilitate the delivery of our clients’ materials while also managing costs.

Customers

Direct marketing services are marketed to specific industries or markets with services and software products tailored to each industry or market. We believe that we are generally able to provide services to new industries and markets by modifying our existing services and applications. We currently provide direct marketing services to the retail, high-tech/telecom, financial services and pharmaceutical/healthcare vertical markets, in addition to a range of selected markets. Our Direct Marketing business is not overly dependent on any one client or any group of clients. The largest client, measured in revenue, comprised 8% of total Direct Marketing revenues in 2007 and 5% of our total revenues in 2007. The largest 25 clients, measured in revenue, comprised 41% of total Direct Marketing revenues in 2007 and 26% of our total revenues in 2007.

Sales and Marketing

Our national direct marketing sales force is headquartered in Cincinnati, Ohio, with additional offices maintained throughout the United States. There are also product specific sales forces and sales groups in Europe, Australia, South America and Asia. The sales forces, with industry-specific knowledge and experience, emphasize the cross-selling of a full range of direct marketing services and are supported by employees in each sector. The overall sales focus is to position Harte-Hanks as a marketing partner offering various services and solutions (including end-to-end) as required to meet our client’s targeted marketing needs.

5

Direct Marketing Facilities

Direct marketing services are provided at the following facilities:

| | |

National Offices | | Shawnee, Kansas |

Austin, Texas | | Texarkana, Texas |

Baltimore, Maryland | | Troy, Michigan |

Billerica, Massachusetts | | Wilkes-Barre, Pennsylvania |

Bloomfield, Connecticut | | Yardley, Pennsylvania |

Boston, Massachusetts | | |

Cincinnati, Ohio | | National Markets Headquarters |

Clearwater, Florida | | Cincinnati, Ohio |

Deerfield Beach, Florida | | |

East Bridgewater, Massachusetts | | International Offices |

Fort Worth, Texas | | Aldermaston, United Kingdom |

Fullerton, California | | Böblingen, Germany |

Glen Burnie, Maryland | | Bristol, United Kingdom |

Grand Prairie, Texas | | Frenchs Forest (Sydney), Australia |

Jacksonville, Florida | | Hasselt, Belgium |

Lake Mary, Florida | | Iasi, Romania |

Langhorne, Pennsylvania | | Les Ulis, France |

Monroe Township, New Jersey | | Madrid, Spain |

New York, New York | | Manila, Philippines |

Ontario, California | | Melbourne, Australia |

Pennsauken, New Jersey | | São Paulo, Brazil |

Richardson, Texas | | Uxbridge, United Kingdom |

San Diego, California | | |

For more information please refer to Item 2 - Properties.

6

Competition

Our Direct Marketing business faces competition in all of its offerings and within each of its vertical markets. Direct marketing is a dynamic business, subject to technological advancements, high turnover of client personnel who make buying decisions, client consolidations, changing client needs and preferences, continual development of competing products and services and an evolving competitive landscape. This competition comes from numerous local, national and international direct marketing and advertising companies against whom we compete for individual projects, entire client relationships and marketing expenditures by clients and prospective clients. There are various competitive factors in our industry, including the quality and scope of services, technical and strategic expertise, the value of the services provided as compared to the price of the services, reputation and brand recognition. We also compete against print and electronic media and other forms of advertising for marketing and advertising dollars in general. Failure to continually improve our current processes, advance and upgrade our technology applications and to develop new products and services in a timely and cost-effective manner could result in the loss of our clients or prospective clients to current or future competitors. In addition, failure to gain market acceptance of new products and services could adversely affect our growth. Although we believe that our capabilities and breadth of services, combined with our national and worldwide production capability, industry focus and ability to offer a broad range of integrated services enable us to compete effectively, our business results may be adversely impacted by competition. Please refer to Item 1A, “Risk Factors” for additional information regarding risks related to competition.

Seasonality

Our Direct Marketing business is somewhat seasonal as revenues in the fourth quarter tend to be higher than revenues in other quarters during a given year. This increased revenue is a result of overall increased marketing activity prior to and during the holiday season, primarily related to our retail vertical.

SHOPPERS

General

Harte-Hanks Shoppers is North America’s largest owner, operator and distributor of shopper publications, based on weekly circulation and revenues. Shoppers are weekly advertising publications delivered free by Standard Mail to households and businesses in a particular geographic area. Shoppers offer advertisers a targeted, cost-effective local advertising system, with virtually 100% penetration in their area of distribution. Shoppers are particularly effective in large markets with high media fragmentation in which major metropolitan newspapers generally have low penetration.

As of December 31, 2007, Shoppers delivered approximately 13 million shopper packages in five major markets each week covering the greater Los Angeles market (Los Angeles County, Orange County, Riverside County, San Bernardino County, Ventura County and Kern County), the greater San Diego market, Northern California (San Jose, Sacramento, Stockton and Modesto), South Florida (Dade County and Broward County) and the greater Tampa market. Two editions of the shopper publication are delivered to approximately 239,000 households and businesses in South Orange County where both an “early” and “late” editionPennySaverUSA.com are published each week. Our California publications account for approximately 80% of Shoppers’ weekly circulation.

Harte-Hanks publishes 1,077 individual shopper editions each week distributed to zones with circulation of approximately 12,000 each. This allows single-location, local advertisers to saturate a single geographic zone, while enabling multiple-location advertisers to saturate multiple zones. This unique delivery system gives large and small advertisers alike a cost-effective way to reach their target markets. We believe that our zoning capabilities and production technologies have enabled us to saturate and target areas in a number of ways including geographic, demographic, lifestyle, behavioral and language allowing our advertisers to effectively target their customers. Our strategy is to increase our share of local advertising in our existing circulation areas, and, over time, to increase circulation through internal expansion into contiguous areas. In 2007, 2006, and 2005, Harte-Hanks Shoppers had revenues of $430.4 million, $475.0 million, and $440.4 million, respectively, accounting for approximately 37%, 40%, and 39% of our total revenues, respectively.

7

As a result of the difficult economic environment in California, we shut down approximately 600,000 of unprofitable circulation at the end of June 2007. This consisted of approximately 380,000 of circulation in the greater Los Angeles market and approximately 220,000 of circulation in the Northern California market. We will continue to evaluate all of our circulation performance, but do not currently anticipate further circulation reductions of this magnitude in the near future. Despite this recent circulation reduction, we continue to believe that future expansions may provide increased revenue opportunities in the long term.

Publications

The following table sets forth certain information with respect to Shoppers publications:

| | | | | | |

| | | | | December 31, 2007 |

Market | | Publication Name | | Circulation | | Number of

Zones |

Greater Los Angeles | | PennySaverUSA.com | | 5,650,000 | | 504 |

| | | |

Northern California | | PennySaverUSA.com | | 2,600,500 | | 207 |

| | | |

Greater San Diego | | PennySaverUSA.com | | 1,887,500 | | 157 |

| | | |

South Florida | | TheFlyer.com | | 1,459,500 | | 116 |

| | | |

Greater Tampa | | TheFlyer.com | | 1,314,500 | | 93 |

| | | | | | |

Total | | | | 12,912,000 | | 1,077 |

| | | | | | |

Our Shopper publications contain classified and display advertising and are delivered by Standard Mail saturation. The typical shopper publication contains approximately 41 pages and is 7 by 9-1/2 inches in size. Each edition, or zone, is targeted around a natural neighborhood marketing pattern. Shoppers also serve as a distribution vehicle for multiple ads from national and regional advertisers; "print and deliver" single-sheet inserts designed and printed by us, coupon books, preprinted inserts, and four-color glossy flyers printed by third party printers. In addition, our Shoppers also provide advertising and other services online through our websites –PennySaverUSA.com andTheFlyer.com.PennySaverUSA.com displays the ads published in the print versions of thePennySaverUSA.com (California) andTheFlyer.com (Florida) publications, and is a leader in the aggregation of online classified ads from free community papers and shoppers across the country. It is our current policy that customers who purchase a classified ad in one of our weekly publications, also receive a posting on our website.

We have acquired, developed and applied innovative technology and customized equipment in the publication of our Shoppers, contributing to efficiency and growth. A proprietary pagination system has made it possible for over a thousand weekly zoned editions to be designed, built and output to plate-ready negatives in a paperless, digital environment. Automating the production process saves on labor, newsprint, and overweight postage. This software also allows for better ad tracking, immediate checks on individual zone and ad status, and more on-time press starts with less manpower.

Customers

Shoppers serves both business and individual advertisers in a wide range of industries, including real estate, employment, automotive, retail, high-tech/telecom, financial services, and a number of other industries. Shoppers is not overly dependent on any one client or any group of clients. The largest client, measured in revenue, comprised 2% of total Shoppers revenue in 2007 and 1% of our total revenue in 2007. The top 25 clients in terms of revenue comprised 15% of Shoppers revenues in 2007 and 6% of our total revenues in 2007.

8

Sales and Marketing

We maintain local Shoppers sales offices throughout our geographic markets and employ more than 700 commissioned sales representatives who develop both targeted and saturation advertising programs for clients. The sales organization provides service to national, regional and local advertisers through its telemarketing departments and field sales representatives. Shoppers clients vary from individuals with a single item for sale to local neighborhood advertisers to large multi-location advertisers. The core clients continue to be local service businesses and small retailers. We also focus our marketing efforts on larger national accounts by emphasizing our ability to deliver saturation advertising in defined zones, or even partial zones for inserts, in combination with advertising in the Shopper publication.

Additional focus is placed on particular industries/categories through the use of sales specialists. These sales specialists are primarily used to target automotive, real estate and employment advertisers.

We utilize proprietary sales and marketing systems to enter client orders directly from the field, instantly checking space availability, ad costs and other pertinent information. These systems efficiently facilitate the placement of advertising into multiple-zoned editions and include built-in error-reducing safeguards that aid in minimizing costly sales adjustments. In addition to allowing advertising information to be entered for immediate publication, these systems feed a relational client database enabling sales personnel to access client history by designated variables to facilitate the identification of similar potential clients and to assist with timely follow-up on existing clients.

Shoppers Facilities

Our Shoppers are produced at owned or leased facilities in the markets they serve. We have six production facilities – three in Southern California, one in Northern California, one in Southern Florida and one in Tampa, Florida – and more than 30 sales offices.

For more information please refer to Item 2—Properties.

Competition

Our Shoppers business competes for advertising, as well as for readers, with other print and electronic media. Competition comes from local and regional newspapers, magazines, radio, broadcast, satellite and cable television, other shoppers, the internet, other communications media and other advertising printers that operate in our markets. The extent and nature of such competition are, in large part, determined by the location and demographics of the markets targeted by a particular advertiser, and the number of media alternatives in those markets. Failure to continually improve our current processes, advance and upgrade our technology applications and to develop new products and services in a timely and cost-effective manner could result in the loss of our clients to current or future competitors. In addition, failure to gain market acceptance of new products and services and geographic areas could adversely affect our growth. We believe that our production systems and technology, which enable us to publish separate editions in narrowly targeted zones, and our local ad content, allow us to compete effectively, particularly in large markets with high media fragmentation. However, our business results may be adversely impacted by competition. Please refer to Item 1A, “Risk Factors” for additional information regarding risks related to competition.

Seasonality

Our Shoppers business is somewhat seasonal in that revenues from the last two publication dates in December and first two to three publication dates in January each year are affected by a slowdown in advertising by businesses and individuals after the holidays. In general the second and third quarters are the highest revenue quarters for our Shopper business.

9

U.S. AND FOREIGN GOVERNMENT REGULATIONS

As a company with business activities around the world, we are subject to a variety of domestic and international legal and regulatory requirements that impact our business, including, for example, regulations governing consumer protection and unfair business practices, contracts, e-commerce, intellectual property, labor and employment, securities, tax, and other laws that are generally applicable to commercial activities.

We are also subject to, or affected by, numerous domestic and foreign laws, regulations and industry standards that regulate direct marketing activities, including those that address privacy, data security and unsolicited marketing communications. Examples of some of these laws and regulations that may be applied to, or affect, our business or the businesses of our clients include the following:

| | • | | The Financial Services Modernization Act of 1999, or Gramm-Leach-Bliley Act (GLB), which, among other things, regulates the use for marketing purposes of non-public personal financial information of consumers that is held by financial institutions. Although Harte-Hanks is not considered a financial institution, many of our clients are subject to the GLB. The GLB also includes rules relating to the physical, administrative and technological protection of non-public personal financial information. |

| | • | | The Health Insurance Portability and Accountability Act of 1996 (HIPAA), which regulates the use of personal health information for marketing purposes and requires reasonable safeguards designed to prevent intentional or unintentional use or disclosure of protected health information. |

| | • | | Federal and state laws governing the use of the Internet and regulating telemarketing, including the federal Controlling the Assault of Non-Solicited Pornography and Marketing Act of 2003 (CAN-SPAM), which regulates commercial email and requires that commercial emails give recipients an opt-out method. Telemarketing activities are regulated by, among other requirements, the Federal Trade Commission’s Telemarketing Sales Rule (TSR), the Federal Communications Commission’s Telephone Consumer Protection Act (TCPA) and various state do-not-call laws. |

| | • | | A number of states in the U.S. have passed versions of security breach notification laws, which generally require timely notifications to affected persons in the event of data security breaches or other unauthorized access to certain types of protected personal data. |

| | • | | The Fair Credit Reporting Act (FCRA), which governs among other things, the sharing of consumer report information, access to credit scores, and requirements for users of consumer report information. |

| | • | | The Fair and Accurate Credit Transactions Act of 2003 (FACT Act), which amended the FCRA and requires, among other things, consumer credit report notice requirements for creditors that use consumer credit report information in connection with risk-based credit pricing actions and also prohibits a business that receives consumer information from an affiliate from using that information for marketing purposes unless the consumer is first provided a notice and an opportunity to direct the business not to use the information for such marketing purposes, subject to certain exceptions. |

| | • | | The European Union (EU) data protection laws, including the comprehensive EU Directive on Data Protection (1995), which imposes a number of obligations with respect to use of personal data, and includes a prohibition on the transfer of personal information from the EU to other countries that do not provide consumers with an “adequate” level of privacy or security. The EU standard for adequacy is generally stricter and more comprehensive than that of the U.S. and most other countries. |

There are additional consumer protection, privacy and data security regulations domestically and in other countries in which we or our clients do business. These laws regulate the collection, use, disclosure and

10

retention of personal data and may require consent from consumers and grant consumers other rights, such as the ability to access their personal data and to correct information in the possession of data controllers. We and many of our clients also belong to trade associations that impose guidelines that regulate direct marketing activities, such as the Direct Marketing Association’s Commitment to Consumer Choice.

Federal, state and foreign governmental and industry organizations continue to consider new legislative and regulatory proposals that would impose additional restrictions on direct marketing services and products. We anticipate that such proposals will continue to be introduced in the future, some of which may be adopted. In addition, our business may be affected by the impact of these restrictions on our clients and their marketing activities. These additional regulations could increase compliance requirements and restrict or prevent the collection, management, aggregation, transfer, use or dissemination of information or data that is currently legally available. Additional regulations may also restrict or prevent current practices regarding unsolicited marketing communications. For example, many states are considering implementing do-not-mail legislation that could impact our Direct Marketing and Shoppers businesses and the businesses of our clients and customers. In addition, public interest in individual privacy rights and data security may result in the adoption of further voluntary industry guidelines that could impact our direct marketing activities and business practices.

We cannot predict the scope of any new legislation, regulations or industry guidelines or how courts may interpret existing and new laws. Additionally, enforcement priorities by governmental authorities may change and also impact our business. Compliance with regulations is costly and time-consuming, and we may encounter difficulties, delays or significant expenses in connection with our compliance. There could be a material adverse impact on our business due to the enactment or enforcement of legislation or industry regulations, the issuance of judicial or governmental interpretations, enforcement priorities of governmental agencies or a change in customs arising from public concern over consumer privacy and data security issues.

INTELLECTUAL PROPERTY RIGHTS

Our intellectual property assets include, for example, trademarks and service marks that identify our company and our products and services, software and other technology that we develop, our proprietary collections of data and intellectual property licensed from third parties, such as prospect list providers. We generally seek to protect our intellectual property through a combination of license agreements and trademark, service mark, copyright, patent and trade secret laws. We also enter into confidentiality agreements with many of our employees, vendors and clients and seek to limit access to and distribution of intellectual property and other proprietary information. We pursue the protection of our trademarks and other intellectual property in the United States and internationally. We have also filed certain patent applications in the United States.

Despite our efforts to protect our intellectual property, unauthorized parties may attempt to copy or otherwise obtain and use our proprietary information and technology. Monitoring unauthorized use of our intellectual property is difficult and unauthorized use of our intellectual property may occur. We cannot be certain that patents or trademark registrations will be issued, nor can we be certain that any issued patents or trademark registrations will give us adequate protection from competing products. For example, issued patents may be circumvented or challenged and declared invalid or unenforceable. In addition, others may develop competing technologies or databases on their own. Moreover, there is no assurance that our confidentiality agreements with our employees or third parties will be sufficient to protect our intellectual property and proprietary information.

We may also be subject to infringement claims against us by third parties and may incur substantial costs and devote significant management resources in responding to such claims. We are obligated under some agreements to indemnify our clients as a result of claims that we infringe on the proprietary rights of third parties. These costs and diversions could cause our business to suffer. If any party asserts an infringement claim, we may need to obtain licenses to the disputed intellectual property. We cannot assure you, however, that we will be able to obtain these licenses on commercially reasonable terms or that we will be able to obtain any licenses at all. The failure to obtain necessary licenses or other rights may have an adverse affect on our ability to provide our products and services.

11

EMPLOYEES

As of December 31, 2007, Harte-Hanks employed 6,579 full-time employees and 447 part-time employees, as follows: Direct Marketing – 4,365 full-time and 105 part-time employees; Shoppers – 2,193 full-time and 341 part-time employees; and corporate office – 21 full-time employees and 1 part-time employee. None of the work force is represented by labor unions. We consider our relations with our employees to be good.

Cautionary Note Regarding Forward-Looking Statements

This report, including the Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A), contains “forward-looking statements” within the meaning of the federal securities laws. All such statements are qualified by this cautionary note, which is provided pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933 (1933 Act) and Section 21E of the 1934 Act. Forward-looking statements may also be included in our other public filings, press releases, our website and oral and written presentations by management. Statements other than historical facts are forward-looking and may be identified by words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “seeks,” “could,” “intends,” or words of similar meaning. Examples include statements regarding (1) our strategies and initiatives, (2) our financial outlook, (3) planned adjustments to our cost structure and other actions designed to respond to market conditions and improve our performance, (4) expectations for our businesses and for the industries in which we operate, including with regard to the recent negative performance trends in our Shoppers business, (5) competitive factors, (6) acquisition and development plans, (7) our stock repurchase program, (8) expectations regarding legal proceedings and other contingent liabilities, and (9) other statements regarding future events, conditions or outcomes.

These forward-looking statements are based on current information, expectations and estimates and involve risks, uncertainties, assumptions and other factors that are difficult to predict and that could cause actual results to vary materially from what is expressed in or indicated by the forward-looking statements. In that event, our business, financial condition, results of operations or liquidity could be materially adversely affected and investors in our securities could lose part or all of their investments. Some of these risks, uncertainties, assumptions and other factors can be found in our filings with the SEC, including the factors discussed below in this "Item 1A. Risk Factors" and any updates thereto in our Forms 10-Q. The forward-looking statements included in this report and those included in our other public filings, press releases, our website and oral and written presentations by management are made only as of the respective dates thereof, and we undertake no obligation to update publicly any forward-looking statement in this report or in other documents, our website or oral statements for any reason, even if new information becomes available or other events occur in the future.

In addition to the information set forth elsewhere in this report, including in the MD&A section, the factors described below should be considered carefully in making any investment decisions with respect to our securities. The risks described below are not the only ones we face or may face in the future. Additional risks and uncertainties that are not presently anticipated, or that we may currently believe are immaterial, could also impair our business operations and financial performance.

We face significant competition for individual projects, entire client relationships and advertising dollars in general.

Our Direct Marketing business faces significant competition in all of its offerings and within each of its vertical markets. Direct marketing is a dynamic business, subject to technological advancements, high turnover of client personnel who make buying decisions, client consolidations, changing client needs and preferences, continual development of competing products and services and an evolving competitive landscape. This competition comes from numerous local, national and international direct marketing and advertising companies

12

against whom we compete for individual projects, entire client relationships and marketing expenditures by clients and prospective clients. We also compete against print and electronic media and other forms of advertising for marketing and advertising dollars in general. In addition, our ability to attract new clients and to retain existing clients may, in some cases, be limited by clients’ policies on or perceptions of conflicts of interest. These policies can prevent us from performing similar services for competing products or companies. Our Shoppers business competes for advertising, as well as for readers, with other print and electronic media. Competition comes from local and regional newspapers, magazines, radio, broadcast, satellite and cable television, other shoppers, the internet, other communications media and other advertising printers that operate in our markets. The extent and nature of such competition are, in large part, determined by the location and demographics of the markets targeted by a particular advertiser and the number of media alternatives in those markets. Our failure to improve our current processes or to develop new products and services could result in the loss of our clients to current or future competitors. In addition, failure to gain market acceptance of new products and services could adversely affect our growth.

Current and future competitors may have significantly greater financial and other resources than we do, and they may sell competing products and services at lower prices or at lower profit margins, resulting in pressures on our prices and margins.

The sizes of our competitors vary across market segments. Therefore, some of our competitors may have significantly greater financial, technical, marketing or other resources than we do in one or more of our market segments, or overall. As a result, our competitors may be in a position to respond more quickly than we can to new or emerging technologies and changes in customer requirements, or may devote greater resources than we can to the development, promotion, sale and support of products and services. Moreover, new competitors or alliances among our competitors may emerge and potentially reduce our market share, revenue or margins. Some of our competitors also may choose to sell products or services competitive to ours at lower prices by accepting lower margins and profitability, or may be able to sell products or services competitive to ours at lower prices given proprietary ownership of data, technical superiority or economies of scale. Price reductions or pricing pressure by our competitors could negatively impact our margins and results of operations, and could also harm our ability to obtain new customers on favorable terms.

We must maintain technological competitiveness, continually improve our processes and develop and introduce new products and services in a timely and cost-effective manner.

We believe that our success depends on, among other things, maintaining technological competitiveness in our Direct Marketing and Shopper products, processing functionality and software systems and services. Technology changes rapidly and there are continuous improvements in computer hardware, network operating systems, programming tools, programming languages, operating systems, database technology and the use of the Internet. Advances in information technology may result in changing client preferences for products and product delivery formats in our industry. We must continually improve our current processes and develop and introduce new products and services in order to match our competitors’ technological developments and other improvements in competing product and service offerings and the increasingly sophisticated requirements of our clients. We may be unable to successfully identify, develop and bring new and enhanced services and products to market in a timely and cost-effective manner, such services and products may not be commercially successful and services, products and technologies developed by others may render our services and products noncompetitive or obsolete.

Our success depends on our ability to consistently and effectively deliver our products and services to our clients.

Our success depends on our ability to effectively and consistently staff and execute client engagements within the agreed upon timeframe and budget. Depending on the needs of our clients, our Direct Marketing engagements may require customization, integration and coordination of a number of complex product and service offerings and execution across many of our facilities worldwide. Moreover, in some of our engagements, we rely on subcontractors and other third parties to provide a portion of our overall services, and we cannot guarantee that these third parties will effectively deliver their services or that we will have adequate

13

recourse against these third parties in the event they fail to effectively deliver their services. Other contingencies and events outside of our control may also impact our ability to provide our products and services. Our failure to effectively and timely staff, coordinate and execute our client engagements may adversely impact existing client relationships, the amount or timing of payments from our clients, our reputation in the marketplace and ability to secure additional business and our resulting financial performance. In addition, our contractual arrangements with our Direct Marketing clients and other customers may not provide us with sufficient protections against claims for lost profits or other claims for damages.

If we lose key management or are unable to attract and retain the talent required for our business, our operating results could suffer.

Our prospects depend in large part upon our ability to attract, train and retain experienced technical, client services, sales, consulting, research and development, marketing, administrative and management personnel. While the demand for personnel is dependent on employment levels, competitive factors and general economic conditions, qualified personnel historically have been in great demand and from time to time and in the foreseeable future may remain a limited resource. The loss or prolonged absence of the services of these individuals could have a material adverse effect on our business, financial position or operating results.

We have previously experienced, and may experience in the future, reduced demand for our products and services because of general economic conditions, the financial conditions and marketing budgets of our clients and other factors that may impact the industry verticals that we serve.

Economic downturns often severely affect the marketing services industry. In the past, our customers have responded, and may respond in the future, to weak economic conditions by reducing their marketing budgets, which are generally discretionary in nature and easier to reduce in the short-term than other expenses. In addition, revenues from our Shoppers business are largely dependent on local advertising expenditures in the markets in which they operate. Such expenditures are substantially affected by the strength of the local economies in those markets. Direct Marketing revenues are dependent on national, regional and international economies and business conditions. A lasting economic recession or downturn in the United States economy and the economies we operate in abroad, could have material adverse effects on our business, financial position or operating results. Similarly, there may be industry or company-specific factors that negatively impact our clients and prospective clients or their industries and result in reduced demand for our products and services. We may also experience reduced demand as a result of consolidation of clients and prospective clients in the industry verticals that we serve.

Our Shoppers business is geographically concentrated and is subject to the California and Florida economies.

Our Shoppers business is concentrated geographically in California and Florida. An economic downturn in these states or a large disaster, such as a flood, hurricane, earthquake or other disaster or condition that disables our facilities, immobilizes the United States Postal Service or causes a significant negative change in the economies of these regions, could have a material adverse effect on our business, financial position or operating results.

Our business plan requires us to effectively manage our costs. If we do not achieve our cost management objectives, our financial results could be adversely affected.

Our business plan and expectations for the future require that we effectively manage our cost structure, including our operating expenses and capital expenditures across our operations. To the extent that we do not effectively manage our costs, our financial results may be adversely affected.

Privacy, security and other direct marketing regulatory requirements may prevent or impair our ability to offer our products and services.

We are subject to, or affected by, numerous laws, regulations and industry standards that regulate direct marketing activities, including those that address privacy, data security and unsolicited marketing communications. Please refer to the section above entitled, “U.S. and Foreign Government Regulations,” for additional information regarding these regulations.

14

Federal, state and foreign governmental and industry organizations continue to consider new legislative and regulatory proposals that would impose additional restrictions on direct marketing services and products. We anticipate that such proposals will continue to be introduced in the future, some of which may be adopted. In addition, our business may be affected by the impact of these restrictions on our clients and their marketing activities. These additional regulations could increase compliance requirements and restrict or prevent the collection, management, aggregation, transfer, use or dissemination of information or data that is currently legally available. Additional regulations may also restrict or prevent current practices regarding unsolicited marketing communications. For example, many states are considering implementing do-not-mail legislation that could impact our Direct Marketing and Shoppers businesses and the businesses of our clients and customers. In addition, public interest in individual privacy rights and data security may result in the adoption of further voluntary industry guidelines that could impact our direct marketing activities and business practices.

We cannot predict the scope of any new legislation, regulations or industry guidelines or how courts may interpret existing and new laws. Additionally, enforcement priorities by governmental authorities may change and also impact our business. Compliance with regulations is costly and time-consuming, and we may encounter difficulties, delays or significant expenses in connection with our compliance. There could be a material adverse impact on our business due to the enactment or enforcement of legislation or industry regulations, the issuance of judicial or governmental interpretations, enforcement priorities of governmental agencies or a change in customs arising from public concern over consumer privacy and data security issues.

Consumer perceptions regarding the privacy and security of their data may prevent or impair our ability to offer our products and services.

Pursuant to various federal, state, foreign and industry regulations, consumers have control as to how certain data regarding them is collected, used and shared for marketing purposes. If due to privacy or security concerns, consumers exercise their ability to prevent such data collection, use or sharing, this may impair our ability to provide direct marketing to those consumers and limit our clients’ requirements for our services. Additionally, privacy and security concerns may limit consumers’ voluntarily providing data to our customers or marketing companies. Some of our services depend on voluntarily provided data and may be impaired without such data.

Our reputation and business results may be adversely impacted if we, or subcontractors upon whom we rely, do not effectively protect sensitive personal information of our clients and our clients’ customers.

Current privacy and data security laws and industry standards impact the manner in which we capture, handle, analyze and disseminate customer and prospect data as part of our client engagements. In many instances, client contracts also mandate privacy and security practices. If we fail to effectively protect and control sensitive personal information (such as personal health information, social security numbers or credit card numbers) of our clients and their customers or prospects in accordance with these requirements, we may incur significant expenses, suffer reputational harm and loss of business, and, in certain cases, be subjected to regulatory or governmental sanctions or litigation. These risks may be increased due to our reliance on subcontractors and other third parties in providing a portion of our overall services in certain engagements. We cannot guarantee that these third parties will effectively protect and handle sensitive personal information or other confidential information, or that we will have adequate recourse against these third parties in that event.

We may not be able to adequately protect our information systems.

Our ability to protect our information systems against damage from a data loss, security breach, computer virus, fire, power loss, telecommunications failure or other disaster is critical to our future success. Some of these systems may be outsourced to third-party providers from time to time. Any damage to our information systems that causes interruptions in our operations or a loss of data could affect our ability to meet our clients' requirements, which could have a material adverse effect on our business, financial position or operating results. While we take precautions to protect our information systems, such measures may not be effective and existing measures may become inadequate because of changes in future conditions.

15

Breaches of security, or the perception that e-commerce is not secure, could harm our business and reputation.

Business-to-business and business-to-consumer electronic commerce, including that which is Internet-based, requires the secure transmission of confidential information over public networks. Some of our products and services are accessed through the Internet. Security breaches in connection with the delivery of our products and services, or well-publicized security breaches that may affect us or our industry, such as database intrusion, could be detrimental to our business, operating results and financial condition. We cannot be certain that advances in criminal capabilities, new discoveries in the field of cryptography or other developments will not compromise or breach the technology protecting the information systems that access our products, services and proprietary database information.

Data suppliers could withdraw data that we rely on for our products and services.

We purchase or license much of the data we use.There could be a material adverse impact on our Direct Marketing business if owners of the data we use were to withdraw or cease to allow access to the data, or materially restrict the authorized uses of their data. Data providers could withdraw their data if there is a competitive reason to do so, if there is pressure from the consumer community or if additional legislation is passed restricting the use of the data. We also rely upon data from other external sources to maintain our proprietary and non-proprietary databases, including data received from customers and various government and public record sources. If a substantial number of data providers or other key data sources were to withdraw or restrict their data, if we were to lose access to data due to government regulation, or if the collection of data becomes uneconomical, our ability to provide products and services to our clients could be materially adversely affected, which could result in decreased revenues, net income and earnings per share.

We must successfully evaluate acquisition targets and integrate acquisitions.

We frequently evaluate acquisition opportunities to expand our product and service offerings and geographic locations, including potential international acquisitions. Acquisition activities, even if not consummated, require substantial amounts of management time and can distract from normal operations. In addition, we may be unable to achieve the profitability goals, synergies and other objectives initially sought in acquisitions, and any acquired assets, data or businesses may not be successfully integrated into our operations. Acquisitions may result in the impairment of relationships with employees and customers. Moreover, although we review and analyze assets or companies we acquire, such reviews are subject to uncertainties and may not reveal all potential risks and we may incur unanticipated liabilities and expenses as a result of our acquisition activities. The failure to identify appropriate candidates, to negotiate favorable terms, or to successfully integrate future acquisitions into existing operations could result in not achieving planned revenue growth and could negatively impact our net income and earnings per share.

We are vulnerable to increases in paper prices.

In recent years, newsprint prices have fluctuated widely. We maintain, on average, less than 30 days of paper inventory and do not purchase our paper pursuant to long-term paper contracts. Because we have a limited ability to protect ourselves from fluctuations in the price of paper or to pass increased costs along to our clients, these fluctuations could materially affect the results of our operations.

We are vulnerable to increases in postal rates and disruptions in postal services.

Our Shoppers and Direct Marketing services depend on the United States Postal Service to deliver products. Our Shoppers are delivered by Standard Mail, and postage is the second largest expense, behind payroll, in our Shoppers business. Standard postage rates have increased in recent years and are expected to increase again in the first half of 2008. Overall Shoppers postage costs may increase as a result of increases in postage rates, circulation and insert volumes. Postage rates also influence the demand for our Direct Marketing services even though the cost of mailings is typically borne by our clients and is not directly reflected in our revenues or expenses. Accordingly, future postal increases or disruptions in the operations of the U.S. Postal Service may have an adverse impact on us.

16

Our indebtedness may adversely impact our ability to react to changes in our business or changes in general economic conditions.

The amount of our indebtedness and the terms under which we have borrowed money under our credit facilities or other agreements could have important consequences for our business. Our debt covenants require that we maintain certain financial measures and ratios. As a result of these covenants and ratios, we may be limited in the manner in which we can conduct our business, and we may be unable to engage in favorable business activities or finance future operations or capital needs. A failure to comply with these restrictions or to maintain the financial measures and ratios contained in the debt agreements could lead to an event of default that could result in an acceleration of outstanding indebtedness. In addition, the amount and terms of our indebtedness could:

| | • | | limit our flexibility in planning for, or reacting to, changes in our business and the industries in which we operate, including limiting our ability to invest in our strategic initiatives, and, consequently, place us at a competitive disadvantage; |

| | • | | reduce the availability of our cash flows that would otherwise be available to fund working capital, capital expenditures, acquisitions and other general corporate purposes; and |

| | • | | result in higher interest expense in the event of increases in interest rates because some of our borrowings are at variable rates of interest, as discussed below under “Interest rate increases could affect our results of operations, cash flows and financial position.” |

We may incur additional indebtedness in the future and, if new debt is added to our current debt levels, the above risks could be increased.

Interest rate increases could affect our results of operations, cash flows and financial position.

Interest rate movements in Europe and the United States can affect the amount of interest we pay related to our debt and the amount we earn on cash equivalents. Our primary interest rate exposure is to interest rate fluctuations in Europe, specifically Eurodollar rates due to their impact on interest related to our credit facilities. As of December 31, 2007, we had $259.1 million of debt outstanding, all of which was at variable interest rates. We manage a portion of our interest rate exposures by entering into an interest rate swap for a total notional amount of $150.0 million, resulting in a net amount of $109.1 million of variable-rate debt at December 31, 2007. To the extent that we have debt with variable interest rates that is not hedged, our results of operations, cash flows and financial position could be materially adversely affected by significant increases in interest rates. We also have exposure to interest rate fluctuations in the United States, specifically money market, commercial paper and overnight time deposit rates, as these affect our earnings on excess cash. Even with the offsetting increase in earnings on excess cash in the event of an interest rate increase, we cannot be assured that future interest rate increases will not have a material adverse impact on our business, financial position or operating results.

We could fail to adequately protect our intellectual property rights and may face claims for intellectual property infringement.

Our ability to compete effectively depends in part on the protection of our technology, products, services and brands through intellectual property right protections, including patents, copyrights, database rights, trade secrets and trademarks. The extent to which such rights can be protected and enforced varies in different jurisdictions. There is also a risk of litigation relating to our use or future use of intellectual property rights of third parties. Third-party infringement claims and any related litigation against us could subject us to liability for damages, restrict us from using and providing our technologies, products or services or operating our business generally, or require changes to be made to our technologies, products and services. Please refer to the section above entitled, “Intellectual Property Rights,” for additional information regarding our intellectual property and associated risks.

17

Our international operations subject us to risks associated with operations outside the U.S.

Harte Hanks Direct Marketing conducts business outside of the United States. During 2007, approximately 8.5% of Harte Hanks Direct Marketing’s revenues were derived from businesses outside the United States, primarily Europe, Asia and South America. We may expand our international operations in the future as part of our growth strategy. Accordingly, our future operating results could be negatively affected by a variety of factors, some of which are beyond our control, including:

| | • | | social, economic and political instability; |

| | • | | changes in U.S. and foreign governmental legal requirements or policies resulting in burdensome government controls, tariffs, restrictions, embargoes or export license requirements; |

| | • | | the potential for nationalization of enterprises; |

| | • | | potentially adverse tax treatment; |

| | • | | less favorable foreign intellectual property laws that would make it more difficult to protect our intellectual properties from appropriation by competitors; |

| | • | | more onerous or differing data privacy and security requirements or other marketing regulations; |

| | • | | longer payment cycles for sales in foreign countries; and |

| | • | | the costs and difficulties of managing international operations. |

In addition, exchange rate movements may have an impact on our future costs or on future cash flows from foreign investments. We have not entered into any foreign currency forward exchange contracts or other derivative instruments to hedge the effects of adverse fluctuations in foreign currency exchange rates. The various risks that are inherent in doing business in the United States are also generally applicable to doing business outside of the United States, and may be exaggerated by the difficulty of doing business in numerous sovereign jurisdictions due to differences in culture, laws and regulations.

We must maintain effective internal controls.

In designing and evaluating our internal controls over financial reporting, we recognize that any internal control or procedure, no matter how well designed and operated, can provide only reasonable assurance of achieving desired control objectives and that no system of internal controls can be designed to provide absolute assurance of effectiveness. If we fail to maintain a system of effective internal controls, it could have a material adverse effect on our business, financial position or operating results. Additionally, adverse publicity related to a failure in our internal controls over financial reporting could have a negative impact on our reputation and business.

Fluctuation in our revenue and operating results may impact our stock price.

From time to time, we may provide forward-looking statements regarding our anticipated or targeted financial and operating performance, including with respect to our earnings per share and revenue growth. Fluctuations in our quarterly revenues and operating results in any future period that fall below the performance indicated by our forward-looking statements or the expectations of securities analysts and investors could cause a decline in our stock price. These fluctuations could be caused by a variety of factors, including unanticipated variations in the size, budget, or progress toward the completion of our engagements, variability in the market demand for our services, client consolidations, the unanticipated termination of several major client engagements or other factors discussed in this Item 1A. “Risk Factors.”

The granting of stock-based awards to our employees affects our expenses and our stock price.

Effective January 1, 2006, we became subject to new stock-based compensation accounting rules that require that compensation costs related to stock-based payment transactions, including stock options, restricted stock and performance stock units, be recognized in our financial statements. Previously, we accounted for stock-based

18

compensation of employees using the intrinsic value method, which resulted in no compensation expense charged against income for stock option grants to employees where the exercise price was equal to the market price of the underlying stock at the date of grant. Beginning January 1, 2006, grants of options, stock or other forms of equity have been recognized as compensation expense in our statement of operations, increasing our reported expenses for the same activities and negatively impacting our earnings per share. These increased expenses could affect the price of our common shares.

War or terrorism could affect our business.

War and/or terrorism or the threat of war and/or terrorism involving the United States could have a significant impact on our business, financial position or operating results. War or the threat of war could substantially affect the levels of advertising expenditures by clients in each of our businesses. In addition, each of our businesses could be affected by operation disruptions and a shortage of supplies and labor related to such a war or threat of war.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

Our headquarters are located in San Antonio, Texas and we occupy approximately 17,000 square feet of leased premises at that location. Our business is conducted in facilities worldwide containing aggregate space of approximately 3.6 million square feet. Approximately 3.4 million square feet are held under leases, which expire at dates through 2023. The balance of the properties, used in our Southern California Shopper operations and Hasselt, Belgium Direct Marketing operations, are owned.

We are subject to various legal proceedings in the course of conducting our businesses and, from time to time, we may become involved in additional claims and lawsuits incidental to our businesses. In the opinion of management, after consultation with counsel, any ultimate liability arising out of currently pending claims and lawsuits is not currently expected to have a material effect on our consolidated financial position or results of operations. Nevertheless, we cannot predict the impact of future developments affecting our pending or future claims and lawsuits.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted to a vote of security holders during the fourth quarter of 2007.

19

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Common Stock

Our common stock is listed on the NYSE (symbol: HHS). The reported high and low quarterly sales price ranges for 2007 and 2006 were as follows:

| | | | | | | | |

| | | 2007 | | 2006 |

| | | High | | Low | | High | | Low |

First Quarter | | 28.78 | | 25.81 | | 31.00 | | 25.60 |

Second Quarter | | 27.85 | | 25.07 | | 28.21 | | 24.33 |

Third Quarter | | 26.67 | | 19.62 | | 27.17 | | 22.35 |

Fourth Quarter | | 20.52 | | 15.50 | | 27.84 | | 25.03 |

In 2007, quarterly dividends were paid at the rate of 7.0 cents per share. In 2006, quarterly dividends were paid at the rate of 6.0 cents per share.

In January 2008, we announced an increase in the regular quarterly dividend from 7.0 cents per share to 7.5 cents per share, payable March 14, 2008 to holders of record on February 29, 2008.

As of February 1, 2008, there are approximately 2,750 holders of record.

Issuer Purchases of Equity Securities

The following table contains information about our purchases of our equity securities during the fourth quarter of 2007:

| | | | | | | | | |

Period | | Total

Number of

Shares

Purchased | | Average

Price

Paid per

Share | | Total Number

of Shares

Purchased

as Part of

a Publicly

Announced Plan (1) | | Maximum

Number of

Shares that

May Yet Be

Purchased Under

the Plan(2) |

October 1 – 31, 2007 | | 860,000 | | $ | 18.69 | | 860,000 | | 5,651,991 |

November 1 – 30, 2007 | | 1,564,136 | | $ | 16.61 | | 1,451,300 | | 4,200,691 |

December 1 – 31, 2007(3) | | 1,300,000 | | $ | 16.97 | | 1,300,000 | | 2,900,691 |

| | | | | | | | | |

Total | | 3,724,136 | | $ | 17.21 | | 3,611,300 | | |

| | | | | | | | | |

| (1) | During the fourth quarter of 2007, 3,611,300 shares were purchased through our stock repurchase program that was publicly announced in January 1997. Under this program shares can be purchased in the open market or through privately negotiated transactions. As of December 31, 2007, our Board had authorized the repurchase of up to 61.9 million shares of our outstanding common stock. As of December 31, 2007, we had repurchased a total of 59.0 million shares at an average price of $19.11 per share under this program. |

| (2) | Subsequent to year end, on January 29, 2008, our Board authorized an additional 12.5 million shares under our stock repurchase program, bringing the total repurchase authorization to 74.4 million shares. |

| (3) | On December 10, 2007, we purchased 0.1 million shares of our common stock from The Shelton Family Foundation (Foundation) and 0.1 million shares of our common stock from The Scottie Ann Shelton Trust (Trust). These purchases were made at a price of $16.93 per share (the closing price per share of our common stock on December 10, 2007). Mr. Larry D. Franklin, the Chairman of our Board of Directors, and David L. Copeland, a member of our Board of Directors, both served as directors on the Foundation and trustees of the Trust at the time of these purchases and both disclaim beneficial ownership of any shares held by the Foundation or the Trust. In January 2008, Mr. Franklin resigned from the Board of the Foundation. |

20

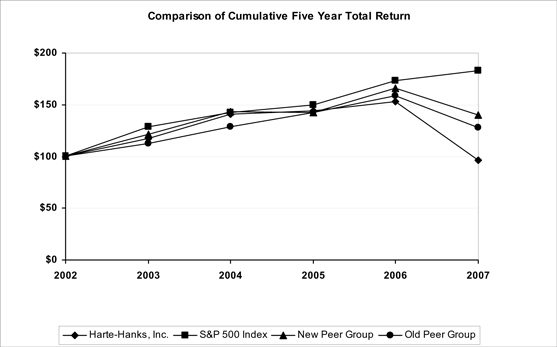

Comparison of Stockholder Returns

The material under this heading is not “soliciting material,” is not deemed “filed” with the SEC, and is not to be incorporated by reference into any filing under the 1933 Act or the 1934 Act, whether made before or after the date hereof and irrespective of any general incorporation language in such filing.

The following graph compares the cumulative total return of our common stock during the period December 31, 2002 to December 31, 2007 with the Standard & Poor’s 500 Stock Index (S&P 500 Index) and with two peer groups. We made modifications to our peer group in this 2007 Annual Report on Form 10-K compared to our previous peer group in order to be consistent with the modified 2008 peer group used by our Compensation Committee in evaluating management compensation.

Our former peer group included Acxiom Corporation, Catalina Marketing Corporation, Choicepoint, Inc., Convergys Corporation, Equifax, Inc., Fair Isaac and Company, Incorporated, infoUSA, Inc., Sykes Enterprises, Incorporated, and Teletech Holdings, Inc.

Our current peer group includes Acxiom Corporation, Alliance Data Systems Corporation, Catalina Marketing Corporation, Choicepoint, Inc., Consolidated Graphics, Inc., Dun & Bradstreet Corporation, Equifax, Inc., Fair Isaac and Company, Incorporated, ICT Group, Inc., infoUSA, Inc., Interpublic Group of Companies, Inc., PC Mall, Inc., R.H. Donnelley Corporation, Source Interlink Companies, Inc., Sykes Enterprises, Incorporated, Teletech Holdings, Inc., Valassis Communications, Inc., ValueClick, Inc., and Viad Corp.

The S&P Index includes 500 United States companies in the industrial, transportation, utilities and financial sectors and is weighted by market capitalization. The peer groups are also weighted by market capitalization.

21

The graph depicts the results of investing $100 in our common stock, the S&P 500 Index and the peer groups at closing prices on December 31, 2002.

| | | | | | | | | | | | |

| | | Base

Period

Dec-02 | | Years Ending |

| | | | Dec-03 | | Dec-04 | | Dec-05 | | Dec-06 | | Dec-07 |

Harte-Hanks, Inc. | | 100 | | 117.23 | | 140.97 | | 144.25 | | 152.80 | | 96.64 |

S&P 500 Index | | 100 | | 128.68 | | 142.69 | | 149.70 | | 173.34 | | 182.86 |

New Peer Group | | 100 | | 121.11 | | 143.30 | | 142.51 | | 166.03 | | 140.12 |

Old Peer Group | | 100 | | 112.11 | | 129.12 | | 142.27 | | 158.91 | | 128.32 |

22

| ITEM 6. | SELECTED FINANCIAL DATA |

Five-Year Financial Summary

| | | | | | | | | | | | | | | | | | | | |

In thousands, except per share amounts | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

Statement of Operations Data | | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 1,162,886 | | | $ | 1,184,688 | | | $ | 1,134,993 | | | $ | 1,030,461 | | | $ | 944,576 | |

Operating expenses | | | | | | | | | | | | | | | | | | | | |

Payroll, production and distribution | | | 871,468 | | | | 874,088 | | | | 825,568 | | | | 755,715 | | | | 692,170 | |

Advertising, selling, general and administrative | | | 89,787 | | | | 90,516 | | | | 88,067 | | | | 80,682 | | | | 75,886 | |

Depreciation | | | 33,195 | | | | 31,566 | | | | 29,918 | | | | 28,169 | | | | 29,433 | |

Intangible amortization | | | 3,509 | | | | 2,466 | | | | 1,427 | | | | 600 | | | | 600 | |

| | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 997,959 | | | | 998,636 | | | | 944,980 | | | | 865,166 | | | | 798,089 | |

| | | | | | | | | | | | | | | | | | | | |

Operating income | | | 164,927 | | | | 186,052 | | | | 190,013 | | | | 165,295 | | | | 146,487 | |

Interest expense, net | | | 12,453 | | | | 6,102 | | | | 1,760 | | | | 679 | | | | 687 | |

Net Income | | $ | 92,640 | | | $ | 111,792 | | | $ | 114,458 | | | $ | 97,568 | | | $ | 87,362 | |

Earnings per common share—diluted | | $ | 1.26 | | | $ | 1.39 | | | $ | 1.34 | | | $ | 1.11 | | | $ | 0.97 | |

Cash dividends per common share | | $ | 0.28 | | | $ | 0.24 | | | $ | 0.20 | | | $ | 0.16 | | | $ | 0.12 | |

Weighted-average common and common equivalent shares outstanding—diluted | | | 73,703 | | | | 80,646 | | | | 85,406 | | | | 87,806 | | | | 89,982 | |

| | | | | |

Segment Data | | | | | | | | | | | | | | | | | | | | |

Revenues | | | | | | | | | | | | | | | | | | | | |

Direct Marketing | | $ | 732,461 | | | $ | 709,728 | | | $ | 694,558 | | | $ | 641,214 | | | $ | 584,804 | |

Shoppers | | | 430,425 | | | | 474,960 | | | | 440,435 | | | | 389,247 | | | | 359,772 | |

| | | | | | | | | | | | | | | | | | | | |

Total revenues | | $ | 1,162,886 | | | $ | 1,184,688 | | | $ | 1,134,993 | | | $ | 1,030,461 | | | $ | 944,576 | |