UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-524 |

| |

| The Dreyfus/Laurel Funds Trust | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Michael A. Rosenberg, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 12/31 | |

Date of reporting period: | 6/30/2010 | |

| | | | | | |

The following N-CSR relates only to the series of the Registrant listed below, and does not affect the other series of the Registrant, which have different fiscal year ends and, therefore, different N-CSR reporting requirements. Separate N-CSR Forms will be filed for those series, as appropriate.

Dreyfus Core Value Fund

Dreyfus High Yield Fund

FORM N-CSR

Item 1. Reports to Stockholders.

SEMIANNUAL REPORT June 30, 2010

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

| | Contents |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Understanding Your Fund’s Expenses |

| 6 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 7 | Statement of Investments |

| 17 | Statement of Assets and Liabilities |

| 18 | Statement of Operations |

| 19 | Statement of Changes in Net Assets |

| 21 | Financial Highlights |

| 25 | Notes to Financial Statements |

| 38 | Information About the Review and Approval of the Fund’s Investment Management Agreement |

| | FOR MORE INFORMATION |

| | Back Cover |

Dreyfus

High Yield Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this semiannual report for Dreyfus High Yield Fund, covering the six-month period from January 1, 2010, through June 30, 2010.

After posting solid gains over the first quarter of 2010, the financial markets encountered renewed volatility in the second quarter, which caused some of the bond market’s higher yielding sectors to erase their previous gains and end the reporting period lower than where they began. Conversely, traditional safe havens such as U.S.Treasury securities gained value as investors became more risk-averse.

The second-quarter swoon occurred despite continued U.S. economic growth, as manufacturing activity improved and unemployment began to moderate in a recovery that has so far proved sustainable but milder than historical averages. Indeed, many of the headlines that spooked investors emanated from overseas markets, including a sovereign debt crisis in Europe.

Despite recent headlines about the current state of the U.S. economy, we still believe that it is unlikely that we’ll encounter a “double-dip” recession. Instead, we expect current financial strains to ease and the domestic economy to expand at a moderate pace over the second half of the year. However, we currently see a number of downside risks that could result in volatility over the short term, which is why we still believe that a long-term investment focus with an emphasis on higher quality bonds may be advisable for many investors. As always, your financial advisor can help you assess both the risks and opportunities provided by the financial markets in this investment climate.

For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

July 15, 2010

2

DISCUSSION OF FUND PERFORMANCE

For the period of January 1, 2010, through June 30, 2010, as provided by Karen Bater, Portfolio Manager

Fund and Market Performance Overview

For the six-month period ended June 30, 2010, Dreyfus High Yield Fund’s Class A shares produced a total return of 1.66%, Class B shares returned 1.41%, Class C shares returned 1.28% and Class I shares returned 1.63%.1 In comparison, the BofA Merrill Lynch U.S. High Yield Master II Constrained Index (the “Index”), the fund’s benchmark, achieved a total return of 4.74% over the same period.2

After rallying early in the reporting period, high yield bonds fell sharply in May and June when new developments caused investors to question the strength and sustainability of the global economic recovery. The fund produced lower returns than its benchmark, primarily due to overweighted exposure to “triple-C” rated bonds and underweighted positions in the better-quality tiers of the high yield spectrum.

The Fund’s Investment Approach

The fund seeks to maximize total return, consisting of capital appreciation and current income.

At least 80% of the fund’s assets are invested in fixed-income securities that are rated below investment grade (“high yield” or “junk” bonds) or are the unrated equivalent as determined by Dreyfus. Individual issues are selected based on careful credit analysis.We thoroughly analyze the business, management and financial strength of each of the companies whose bonds we buy, then project each issuer’s ability to repay its debt.

Renewed Uncertainty Derailed a Bond Market Rally

U.S. and global economic recoveries persisted during the first quarter of 2010 as manufacturing activity increased, housing prices appeared to bottom and the domestic labor market showed early evidence of modest improvement. The U.S. economic rebound was sparked, in part, by historically low short-term interest rates from the Federal Reserve Board and a massive stimulus program adopted by the federal government. Improving economic conditions helped lift the prices of

DISCUSSION OF FUND PERFORMANCE (continued)

higher yielding fixed-income securities, including high yield corporate bonds. In contrast, U.S. government securities lagged market averages as investors favored riskier investments.

However, investor sentiment changed sharply in the second quarter of 2010, when a number of new developments brought the economic recovery into question. A sovereign debt crisis roiled Europe when Greece found itself unable to finance a heavy debt load, requiring intervention from the International Monetary Fund and the European Union. Meanwhile, surging property values in China kindled local inflation fears, and investors grew concerned that higher short-term interest rates and other remedial measures might constrain growth in Asia.The United States also encountered greater economic uncertainty when retail sales, employment and housing data sent mixed signals regarding the strength and sustainability of the economic recovery.

As a result of these economic setbacks, higher yielding sectors of the U.S. bond market lost value, giving back many of the reporting period’s previous gains, and traditionally defensive U.S. government securities generally rallied. High yield bonds had led the bond market rally early in the year and ranked among the more severe decliners during the market correction in May and June.

Constructive Investment Posture Dampened Results

In the midst of the economic recovery, we had positioned the fund to participate fully in the bond market rally through an emphasis on securities that historically have tended to be more sensitive than average to changing economic conditions. Consequently, we generally favored high yield bonds with relatively generous coupons and lower credit ratings, including those in the triple-C rating tier. Conversely, the fund held underweighted exposure to high yield bonds with single-B and double-B ratings. This relatively constructive investment posture enhanced the fund’s relative performance early in the reporting period, but it proved detrimental during the May/June reversal. The fund also invested a relatively larger portion of its assets in investment-grade corporate bonds than the benchmark, but these higher-quality securities were not sufficient to offset weakness among lower-rated high yield credits.

The fund’s constructive investment posture reflected an emphasis on relatively economically sensitive industry groups, including media,

4

technology and telecommunications services companies. Conversely, the fund held underweighted exposure to the energy, building products, leisure and chemicals industry groups, which we regarded as richly valued. In addition, one of the fund’s holdings, telecommunications service provider Sorenson Communications, suffered when the Federal Communications Commission reduced rates for a service that enables hearing-impaired callers to place and receive telephone calls through sign language interpreters.

Positioned for a Mild Recovery

Although we are concerned regarding recent economic and market setbacks, we believe a return to recession is unlikely. In addition, high yield bonds have reached more attractive valuations, default rates have been declining and an active new-issue market has provided ample financing to high yield companies. Therefore, we have maintained the fund’s relatively constructive positioning, focusing on growth opportunities in industry groups that have demonstrated an ability to grow their revenues, generate free cash flow and provide reasonable asset protection.

July 15, 2010

Bond funds are subject generally to interest rate, credit, liquidity and market risks, to varying degrees, all of which are more fully described in the fund’s prospectus. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines. High yield bonds are subject to increased credit risk and are considered speculative in terms of the issuer’s perceived ability to continue making interest payments on a timely basis and to repay principal upon maturity.

| |

| 1 | Total return includes reinvestment of dividends and any capital gains paid, and does not take into |

| | consideration the maximum initial sales charge in the case of Class A shares, or the applicable |

| | contingent deferred sales charges imposed on redemptions in the case of Class B and Class C |

| | shares. Had these charges been reflected, returns would have been lower. Past performance is no |

| | guarantee of future results. Share price, yield and investment return fluctuate such that upon |

| | redemption, fund shares may be worth more or less than their original cost. Return figure provided |

| | for Class I shares reflects the absorption of certain fund expenses by The Dreyfus Corporation |

| | pursuant to an agreement in effect through September 30, 2010, at which time it may be |

| | extended, modified or terminated. Had these expenses not been absorbed, the fund’s Class I return |

| | would have been lower. |

| 2 | SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where applicable, capital |

| | gain distributions.The BofA Merrill Lynch U.S. HighYield Master II Constrained Index is an |

| | unmanaged performance benchmark composed of U.S. dollar-denominated domestic andYankee |

| | bonds rated below investment grade with at least $100 million par amount outstanding and at |

| | least one year remaining to maturity. Bonds are capitalization-weighted.Total allocations to an |

| | issuer are capped at 2%.The index does not reflect fees and expenses to which the fund is subject. |

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus High Yield Fund from January 1, 2010 to June 30, 2010. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment

assuming actual returns for the six months ended June 30, 2010

| | | | |

| | Class A | Class B | Class C | Class I |

| Expenses paid per $1,000† | $ 4.75 | $ 7.24 | $ 8.48 | $ 3.50 |

| Ending value (after expenses) | $1,016.60 | $1,014.10 | $1,012.80 | $1,016.30 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment

assuming a hypothetical 5% annualized return for the six months ended June 30, 2010

| | | | |

| | Class A | Class B | Class C | Class I |

| Expenses paid per $1,000† | $ 4.76 | $ 7.25 | $ 8.50 | $ 3.51 |

| Ending value (after expenses) | $1,020.08 | $1,017.60 | $1,016.36 | $1,021.32 |

|

| † Expenses are equal to the fund’s annualized expense ratio of .95% for Class A, 1.45% for Class B, 1.70% for |

| Class C and .70% for Class I, multiplied by the average account value over the period, multiplied by 181/365 (to |

| reflect the one-half year period). |

6

| | | | | |

| STATEMENT OF INVESTMENTS | | | | |

| June 30, 2010 (Unaudited) | | | | | |

| |

| |

| |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes—96.0% | Rate (%) | Date | Amount ($) | | Value ($) |

| Automotive—4.5% | | | | | |

| Ford Motor Credit, | | | | | |

| Sr. Unscd. Notes | 8.00 | 12/15/16 | 2,805,000 | | 2,871,947 |

| Ford Motor Credit, | | | | | |

| Sr. Unscd. Notes | 8.70 | 10/1/14 | 8,580,000 | | 8,949,849 |

| Ford Motor, | | | | | |

| Sr. Unscd. Debs | 6.50 | 8/1/18 | 730,000 | a | 675,250 |

| Ford Motor, | | | | | |

| Sr. Unscd. Notes | 7.45 | 7/16/31 | 7,485,000 | a | 6,792,637 |

| Goodyear Tire & Rubber, | | | | | |

| Sr. Unscd. Notes | 10.50 | 5/15/16 | 3,460,000 | | 3,780,050 |

| Lear, | | | | | |

| Gtd. Bonds | 7.88 | 3/15/18 | 1,760,000 | | 1,773,200 |

| Lear, | | | | | |

| Gtd. Notes | 8.13 | 3/15/20 | 1,575,000 | | 1,586,812 |

| Motors Liquidation, | | | | | |

| Sr. Unscd. Notes | 8.38 | 7/15/33 | 7,605,000 | a,b | 2,471,625 |

| Navistar International, | | | | | |

| Gtd. Notes | 8.25 | 11/1/21 | 4,595,000 | | 4,686,900 |

| TRW Automotive, | | | | | |

| Gtd. Notes | 7.25 | 3/15/17 | 4,240,000 | c | 4,134,000 |

| United Components, | | | | | |

| Gtd. Notes | 9.38 | 6/15/13 | 1,268,000 | | 1,280,680 |

| | | | | | 39,002,950 |

| Cable/Satellite TV—3.5% | | | | | |

| CCH II Capital, | | | | | |

| Gtd. Notes | 13.50 | 11/30/16 | 18,924,136 | | 22,141,239 |

| Cequel Communications Holdings I, | | | | | |

| Sr. Unscd. Notes | 8.63 | 11/15/17 | 2,375,000 | c | 2,377,969 |

| Dish DBS, | | | | | |

| Gtd. Notes | 7.88 | 9/1/19 | 1,675,000 | | 1,750,375 |

| Insight Communications, | | | | | |

| Sr. Notes | 9.38 | 7/15/18 | 4,100,000 | c | 4,100,000 |

| | | | | | 30,369,583 |

| Capital Goods—1.4% | | | | | |

| Leucadia National, | | | | | |

| Sr. Unscd. Notes | 7.13 | 3/15/17 | 2,545,000 | | 2,468,650 |

| RBS Global and Rexnord, | | | | | |

| Gtd. Notes | 8.50 | 5/1/18 | 5,395,000 | c | 5,260,125 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Capital Goods (continued) | | | | | |

| Wireco WorldGroup, | | | | | |

| Sr. Unscd. Notes | 9.50 | 5/15/17 | 4,415,000 | c | 4,326,700 |

| | | | | | 12,055,475 |

| Chemicals—1.0% | | | | | |

| Huntsman International, | | | | | |

| Gtd. Notes | 7.88 | 11/15/14 | 915,000 | | 887,550 |

| Huntsman International, | | | | | |

| Gtd. Notes | 8.63 | 3/15/20 | 2,990,000 | c | 2,773,225 |

| Ineos Finance, | | | | | |

| Sr. Scd. Notes | 9.00 | 5/15/15 | 1,600,000 | c | 1,604,000 |

| Invista, | | | | | |

| Sr. Unscd. Notes | 9.25 | 5/1/12 | 1,945,000 | c | 1,979,038 |

| LBI Escrow, | | | | | |

| Sr. Scd. Notes | 8.00 | 11/1/17 | 1,420,000 | c | 1,466,150 |

| | | | | | 8,709,963 |

| Consumer Products—1.0% | | | | | |

| Reddy Ice, | | | | | |

| Sr. Scd. Notes | 11.25 | 3/15/15 | 8,215,000 | a,c | 8,502,525 |

| Containers—3.1% | | | | | |

| AEP Industries, | | | | | |

| Sr. Unscd. Notes | 7.88 | 3/15/13 | 8,321,000 | | 8,237,790 |

| BWAY Holding, | | | | | |

| Gtd. Notes | 10.00 | 6/15/18 | 2,380,000 | c | 2,493,050 |

| Plastipak Holdings, | | | | | |

| Sr. Notes | 10.63 | 8/15/19 | 2,435,000 | c | 2,715,025 |

| Reynolds Group Issuer, | | | | | |

| Sr. Notes | 8.50 | 5/15/18 | 9,445,000 | c | 9,315,131 |

| Solo Cup, | | | | | |

| Sr. Scd. Notes | 10.50 | 11/1/13 | 3,545,000 | | 3,682,369 |

| | | | | | 26,443,365 |

| Energy—4.0% | | | | | |

| American Petroleum Tankers, | | | | | |

| Sr. Scd. Notes | 10.25 | 5/1/15 | 2,395,000 | c | 2,412,962 |

| Aquilex Holdings, | | | | | |

| Sr. Notes | 11.13 | 12/15/16 | 4,245,000 | c | 4,266,225 |

| Chesapeake Energy, | | | | | |

| Gtd. Notes | 9.50 | 2/15/15 | 6,135,000 | | 6,809,850 |

| Cie Generale de | | | | | |

| Geophysique-Veritas, Gtd. Notes | 9.50 | 5/15/16 | 2,635,000 | | 2,687,700 |

8

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Energy (continued) | | | | | |

| Ferrellgas Partners, | | | | | |

| Sr. Unscd. Notes | 8.63 | 6/15/20 | 3,550,000 | | 3,567,750 |

| Ferrellgas Partners, | | | | | |

| Sr. Unscd. Notes | 9.13 | 10/1/17 | 3,025,000 | c | 3,168,687 |

| McJunkin Red Man, | | | | | |

| Sr. Scd. Notes | 9.50 | 12/15/16 | 7,905,000 | a,c | 7,707,375 |

| Petrohawk Energy, | | | | | |

| Gtd. Notes | 10.50 | 8/1/14 | 2,180,000 | | 2,354,400 |

| Sabine Pass LNG, | | | | | |

| Sr. Scd. Notes | 7.50 | 11/30/16 | 2,385,000 | | 1,997,437 |

| | | | | | 34,972,386 |

| Finance—9.0% | | | | | |

| Ally Financial, | | | | | |

| Gtd. Notes | 8.00 | 11/1/31 | 16,010,000 | | 14,849,275 |

| Ally Financial, | | | | | |

| Gtd. Notes | 8.30 | 2/12/15 | 1,955,000 | c | 1,984,325 |

| BAC Capital Trust XIV, | | | | | |

| Gtd. Notes | 5.63 | 9/29/49 | 11,750,000 | d | 8,019,375 |

| Citigroup Capital XXI, | | | | | |

| Gtd. Bonds | 8.30 | 12/21/77 | 11,891,000 | d | 11,640,552 |

| Developers Diversified Realty, | | | | | |

| Sr. Unscd. Notes | 9.63 | 3/15/16 | 3,425,000 | | 3,720,115 |

| HUB International Holdings, | | | | | |

| Sr. Sub. Notes | 10.25 | 6/15/15 | 10,376,000 | c | 9,571,860 |

| Icahn Enterprises Finance, | | | | | |

| Gtd. Notes | 8.00 | 1/15/18 | 9,350,000 | a,c | 9,116,250 |

| International Lease Finance, | | | | | |

| Sr. Unscd. Notes | 8.63 | 9/15/15 | 9,421,000 | c | 8,949,950 |

| iPayment, | | | | | |

| Gtd. Notes | 9.75 | 5/15/14 | 6,010,000 | | 5,499,150 |

| USI Holdings, | | | | | |

| Sr. Sub. Notes | 9.75 | 5/15/15 | 4,475,000 | c | 4,128,187 |

| | | | | | 77,479,039 |

| Food, Beverage & | | | | | |

| Tobacco—1.6% | | | | | |

| Bolthouse Farms, | | | | | |

| Bank Notes | 9.50 | 7/25/16 | 6,300,000 | e | 6,307,875 |

| Dean Foods, | | | | | |

| Gtd. Notes | 7.00 | 6/1/16 | 4,844,000 | | 4,553,360 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Food, Beverage & | | | | | |

| Tobacco (continued) | | | | | |

| Michael Foods, | | | | | |

| Sr. Notes | 9.75 | 7/15/18 | 2,665,000 | c | 2,751,612 |

| | | | | | 13,612,847 |

| Gaming—6.4% | | | | | |

| Ameristar Casinos, | | | | | |

| Gtd. Notes | 9.25 | 6/1/14 | 3,395,000 | | 3,573,237 |

| Boyd Gaming, | | | | | |

| Sr. Sub. Notes | 6.75 | 4/15/14 | 1,425,000 | a | 1,254,000 |

| Boyd Gaming, | | | | | |

| Sr. Sub. Notes | 7.13 | 2/1/16 | 4,385,000 | a | 3,628,588 |

| Harrahs Operating Co., | | | | | |

| Sr. Scd. Notes | 10.00 | 12/15/18 | 2,080,000 | a | 1,716,000 |

| Isle of Capri Casinos, | | | | | |

| Gtd. Notes | 7.00 | 3/1/14 | 5,517,000 | a | 4,992,885 |

| MGM Mirage, | | | | | |

| Gtd. Notes | 4.25 | 4/15/15 | 2,300,000 | c | 1,831,375 |

| MGM Mirage, | | | | | |

| Gtd. Notes | 6.75 | 4/1/13 | 3,115,000 | | 2,795,712 |

| MGM Mirage, | | | | | |

| Gtd. Notes | 7.50 | 6/1/16 | 10,590,000 | a | 8,392,575 |

| MGM Mirage, | | | | | |

| Sr. Unscd. Notes | 11.38 | 3/1/18 | 17,585,000 | a,c | 16,617,825 |

| Penn National Gaming, | | | | | |

| Sr. Sub. Notes | 8.75 | 8/15/19 | 4,115,000 | | 4,248,738 |

| Pokagon Gaming Authority, | | | | | |

| Sr. Notes | 10.38 | 6/15/14 | 4,288,000 | c | 4,459,520 |

| Shingle Springs Tribal Gaming | | | | | |

| Authority, Sr. Notes | 9.38 | 6/15/15 | 2,795,000 | c | 2,229,012 |

| | | | | | 55,739,467 |

| Health Care—6.5% | | | | | |

| American Renal Holdings, | | | | | |

| Sr. Scd. Notes | 8.38 | 5/15/18 | 530,000 | c | 527,350 |

| Bausch & Lomb, | | | | | |

| Sr. Unscd. Notes | 9.88 | 11/1/15 | 8,445,000 | | 8,719,463 |

| Biomet, | | | | | |

| Gtd. Notes | 11.63 | 10/15/17 | 30,930,000 | | 33,636,375 |

| Capella Healthcare, | | | | | |

| Gtd. Notes | 9.25 | 7/1/17 | 2,020,000 | c | 2,045,250 |

10

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Health Care (continued) | | | | | |

| Inverness Medical Innovations, | | | | | |

| Sr. Unscd. Notes | 7.88 | 2/1/16 | 3,240,000 | | 3,183,300 |

| Inverness Medical Innovations, | | | | | |

| Gtd. Notes | 9.00 | 5/15/16 | 5,940,000 | | 5,969,700 |

| Radiation Therapy Services, | | | | | |

| Sr. Sub. Notes | 9.88 | 4/15/17 | 2,210,000 | c | 2,132,650 |

| | | | | | 56,214,088 |

| Media—12.0% | | | | | |

| Allbritton Communications, | | | | | |

| Sr. Unscd. Notes | 8.00 | 5/15/18 | 5,830,000 | c | 5,800,850 |

| Clear Channel Communications, | | | | | |

| Sr. Unscd. Notes | 4.90 | 5/15/15 | 8,375,000 | | 4,396,875 |

| Clear Channel Communications, | | | | | |

| Sr. Unscd. Notes | 5.00 | 3/15/12 | 4,726,000 | a | 4,052,545 |

| Clear Channel Communications, | | | | | |

| Sr. Unscd. Notes | 5.50 | 9/15/14 | 20,639,000 | a | 11,454,645 |

| Clear Channel Communications, | | | | | |

| Sr. Unscd. Notes | 5.50 | 12/15/16 | 9,188,000 | | 4,456,180 |

| Clear Channel Communications, | | | | | |

| Sr. Unscd. Notes | 5.75 | 1/15/13 | 11,368,000 | a | 8,753,360 |

| Clear Channel Communications, | | | | | |

| Sr. Unscd. Debs | 6.88 | 6/15/18 | 3,880,000 | | 1,901,200 |

| Clear Channel Communications, | | | | | |

| Gtd. Notes | 10.75 | 8/1/16 | 3,330,000 | a | 2,355,975 |

| Gray Television, | | | | | |

| Sr. Scd. Notes | 10.50 | 6/29/15 | 12,900,000 | a,c | 12,577,500 |

| LBI Media, | | | | | |

| Sr. Sub. Notes | 8.50 | 8/1/17 | 9,807,000 | c | 8,458,538 |

| LIN Television, | | | | | |

| Gtd. Notes, Ser. B | 6.50 | 5/15/13 | 4,635,000 | | 4,472,775 |

| Nexstar Broadcasting, | | | | | |

| Gtd. Notes | 0.50 | 1/15/14 | 722,089 | c | 646,270 |

| Nexstar Broadcasting, | | | | | |

| Gtd. Notes | 7.00 | 1/15/14 | 201,000 | | 179,895 |

| Nexstar Finance Holdings, | | | | | |

| Sr. Discount Notes | 11.38 | 4/1/13 | 1,348,032 | d | 1,317,702 |

| Nexstar/Mission Broadcasting, | | | | | |

| Sr. Scd. Notes | 8.88 | 4/15/17 | 780,000 | c | 787,800 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Media (continued) | | | | | |

| Quebecor Media, | | | | | |

| Sr. Unscd. Notes | 7.75 | 3/15/16 | 3,275,000 | | 3,225,875 |

| Quebecor Media, | | | | | |

| Sr. Unscd. Notes | 7.75 | 3/15/16 | 8,325,000 | | 8,200,125 |

| Salem Communications, | | | | | |

| Sr. Scd. Notes | 9.63 | 12/15/16 | 4,713,000 | a | 4,877,955 |

| Sinclair Broadcast Group, | | | | | |

| Gtd. Notes | 8.00 | 3/15/12 | 11,929,000 | a | 11,675,509 |

| Sinclair Television Group, | | | | | |

| Sr. Scd. Notes | 9.25 | 11/1/17 | 3,885,000 | c | 3,943,275 |

| | | | | | 103,534,849 |

| Metals Mining—2.6% | | | | | |

| Drummond, | | | | | |

| Sr. Unscd. Notes | 7.38 | 2/15/16 | 4,705,000 | | 4,446,225 |

| Murray Energy, | | | | | |

| Gtd. Notes | 10.25 | 10/15/15 | 3,750,000 | c | 3,750,000 |

| Severstal Columbus, | | | | | |

| Sr. Scd. Notes | 10.25 | 2/15/18 | 13,700,000 | c | 14,213,750 |

| | | | | | 22,409,975 |

| Paper—3.0% | | | | | |

| Abitibi-Consolidated of Canada, | | | | | |

| Sr. Scd. Notes | 13.75 | 4/1/11 | 2,182,582 | b,c | 2,318,994 |

| Newpage, | | | | | |

| Sr. Scd. Notes | 11.38 | 12/31/14 | 17,034,000 | a | 15,543,525 |

| Smurfit Kappa Funding, | | | | | |

| Sr. Sub. Notes | 7.75 | 4/1/15 | 2,115,000 | | 2,099,138 |

| Verso Paper Holdings, | | | | | |

| Gtd. Notes, Ser. B | 11.38 | 8/1/16 | 4,500,000 | a | 3,858,750 |

| Verso Paper Holdings, | | | | | |

| Sr. Scd. Notes | 11.50 | 7/1/14 | 1,875,000 | a | 2,029,688 |

| | | | | | 25,850,095 |

| Printing & Publishing—1.0% | | | | | |

| Cenveo, | | | | | |

| Sr. Scd. Notes | 8.88 | 2/1/18 | 8,120,000 | a | 7,835,800 |

| Cenveo, | | | | | |

| Gtd. Notes | 10.50 | 8/15/16 | 650,000 | a,c | 664,625 |

| | | | | | 8,500,425 |

12

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Retail—2.7% | | | | | |

| Hillman Group, | | | | | |

| Gtd. Notes | 10.88 | 6/1/18 | 3,960,000 | c | 4,098,600 |

| Neiman Marcus Group, | | | | | |

| Gtd. Notes | 10.38 | 10/15/15 | 12,881,000 | a | 13,170,822 |

| QVC, | | | | | |

| Sr. Scd. Notes | 7.13 | 4/15/17 | 1,900,000 | c | 1,871,500 |

| QVC, | | | | | |

| Sr. Scd. Notes | 7.50 | 10/1/19 | 3,160,000 | c | 3,120,500 |

| Susser Holdings and Finance, | | | | | |

| Gtd. Notes | 8.50 | 5/15/16 | 1,050,000 | c | 1,055,250 |

| | | | | | 23,316,672 |

| Retail-Food & Drug—2.4% | | | | | |

| Rite Aid, | | | | | |

| Gtd. Notes | 9.50 | 6/15/17 | 8,625,000 | a | 6,878,438 |

| Rite Aid, | | | | | |

| Sr. Scd. Notes | 10.38 | 7/15/16 | 8,680,000 | a | 8,799,350 |

| Stater Brothers Holdings, | | | | | |

| Gtd. Notes | 7.75 | 4/15/15 | 4,695,000 | | 4,706,737 |

| | | | | | 20,384,525 |

| Services—3.5% | | | | | |

| Aramark, | | | | | |

| Gtd. Notes | 8.50 | 2/1/15 | 3,250,000 | | 3,298,750 |

| Dyncorp International, | | | | | |

| Sr. Unscd. Notes | 10.38 | 7/1/17 | 3,110,000 | c | 3,102,225 |

| Garda World Security, | | | | | |

| Sr. Unscd. Notes | 9.75 | 3/15/17 | 4,485,000 | c | 4,574,700 |

| General Maritime, | | | | | |

| Gtd. Notes | 12.00 | 11/15/17 | 8,200,000 | c | 8,405,000 |

| Marquette Transportation Finance, | | | | | |

| Sr. Scd. Notes | 10.88 | 1/15/17 | 6,565,000 | c | 6,466,525 |

| Navios Maritime Holdings, | | | | | |

| Sr. Scd. Notes | 8.88 | 11/1/17 | 2,005,000 | a,c | 2,030,063 |

| Ultrapetrol Bahamas, | | | | | |

| First Mortgage Notes | 9.00 | 11/24/14 | 1,817,000 | | 1,762,490 |

| WCA Waste, | | | | | |

| Gtd. Notes | 9.25 | 6/15/14 | 1,075,000 | | 1,079,031 |

| | | | | | 30,718,784 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Technology—9.2% | | | | | |

| Alion Science and Technology, | | | | | |

| Sr. Scd. Notes | 12.00 | 11/1/14 | 1,393,015 | c | 1,399,980 |

| Ceridian, | | | | | |

| Gtd. Notes | 11.25 | 11/15/15 | 19,028,000 | d | 17,267,910 |

| Ceridian, | | | | | |

| Gtd. Notes | 12.25 | 11/15/15 | 16,461,490 | a | 14,897,648 |

| First Data, | | | | | |

| Gtd. Notes | 9.88 | 9/24/15 | 2,565,000 | | 1,936,575 |

| First Data, | | | | | |

| Gtd. Notes | 9.88 | 9/24/15 | 4,550,000 | a | 3,480,750 |

| Sorenson Communications, | | | | | |

| Sr. Scd. Notes | 10.50 | 2/1/15 | 21,725,000 | a,c | 13,795,375 |

| Sungard Data Systems, | | | | | |

| Gtd. Notes | 10.25 | 8/15/15 | 22,167,000 | a | 22,998,263 |

| Sungard Data Systems, | | | | | |

| Gtd. Notes | 10.63 | 5/15/15 | 3,460,000 | | 3,715,175 |

| | | | | | 79,491,676 |

| Telecommunications—13.8% | | | | | |

| Digicel Group, | | | | | |

| Sr. Unscd. Notes | 8.88 | 1/15/15 | 22,285,000 | c | 21,895,013 |

| Digicel Group, | | | | | |

| Sr. Unscd. Notes | 9.13 | 1/15/15 | 3,542,457 | c | 3,493,748 |

| Digicel Group, | | | | | |

| Sr. Notes | 10.50 | 4/15/18 | 1,408,000 | a,c | 1,459,040 |

| Digicel, | | | | | |

| Sr. Unscd. Notes | 12.00 | 4/1/14 | 1,700,000 | c | 1,908,250 |

| Intelsat Bermuda, | | | | | |

| Gtd. Notes | 11.25 | 2/4/17 | 26,575,000 | d | 27,040,062 |

| Intelsat Jackson Holdings, | | | | | |

| Gtd. Notes | 11.25 | 6/15/16 | 12,735,000 | | 13,626,450 |

| Telesat Canada, | | | | | |

| Sr. Unscd. Notes | 11.00 | 11/1/15 | 6,790,000 | | 7,367,150 |

| Telesat Canada, | | | | | |

| Sr. Sub. Notes | 12.50 | 11/1/17 | 2,415,000 | | 2,716,875 |

| Wind Acquisition Finance, | | | | | |

| Scd. Notes | 11.75 | 7/15/17 | 8,830,000 | c | 9,094,900 |

| Wind Acquisition Finance, | | | | | |

| Scd. Bonds | 12.00 | 12/1/15 | 1,100,000 | c,d | 1,144,000 |

14

| | | | | |

| | Coupon | Maturity | Principal | | |

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Telecommunications (continued) | | | | | |

| Wind Acquisition Holdings, | | | | | |

| Sr. Scd. Notes | 12.25 | 7/15/17 | 32,115,000 | a,c | 29,385,225 |

| | | | | | 119,130,713 |

| Utilities—3.8% | | | | | |

| AES, | | | | | |

| Sr. Unscd. Notes | 8.00 | 10/15/17 | 5,325,000 | | 5,404,875 |

| AES, | | | | | |

| Sr. Unscd. Notes | 9.75 | 4/15/16 | 3,765,000 | c | 4,066,200 |

| Dynegy Holdings, | | | | | |

| Sr. Unscd. Notes | 8.38 | 5/1/16 | 5,235,000 | a | 4,168,369 |

| Energy Future Holdings, | | | | | |

| Gtd. Notes | 10.88 | 11/1/17 | 4,725,000 | a,d | 3,520,125 |

| North American | | | | | |

| Energy Alliance, | | | | | |

| Sr. Scd. Notes | 10.88 | 6/1/16 | 2,935,000 | c | 3,037,725 |

| NRG Energy, | | | | | |

| Gtd. Notes | 7.38 | 1/15/17 | 8,465,000 | | 8,401,513 |

| RRI Energy, | | | | | |

| Sr. Unscd. Notes | 7.63 | 6/15/14 | 4,165,000 | a | 4,123,350 |

| | | | | | 32,722,157 |

| Total Bonds and Notes | | | | | |

| (cost $819,174,854) | | | | | 829,161,559 |

| |

| Preferred Stocks—.1% | | | Shares | | Value ($) |

| Media | | | | | |

| Spanish Broadcasting System, | | | | | |

| Ser. B, Cum. $26.875 | | | | | |

| (cost $1,598,517) | | | 1,523 f | 1,065,752 |

| |

| Common Stocks—.3% | | | | | |

| Cable/Satellite TV—.2% | | | | | |

| Charter Communications, Cl. A | | | 55,002 g | 1,941,571 |

| Media—.1% | | | | | |

| LIN TV, Cl. A | | | 180,000 g | 973,800 |

| Total Common Stocks | | | | | |

| (cost $1,860,749) | | | | | 2,915,371 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | |

| Other Investment—2.1% | Shares | Value ($) |

| Registered Investment Company; | | |

| Dreyfus Institutional Preferred | | |

| Plus Money Market Fund | | |

| (cost $18,203,000) | 18,203,000 h | 18,203,000 |

| |

| Investment of Cash Collateral | | |

| for Securities Loaned—16.1% | | |

| Registered Investment Company; | | |

| Dreyfus Institutional Cash Advantage Fund | | |

| (cost $138,868,515) | 138,868,515 h | 138,868,515 |

| |

| Total Investments (cost $979,705,635) | 114.6% | 990,214,197 |

| Liabilities, Less Cash and Receivables | (14.6%) | (126,440,102) |

| Net Assets | 100.0% | 863,774,095 |

|

| a Security, or portion thereof, on loan. At June 30, 2010, the total market value of the fund’s securities on loan is |

| $131,403,757 and the total market value of the collateral held by the fund is $139,066,113, consisting of cash |

| collateral of $138,868,515 and U.S. Government and agencies securities valued at $197,598. |

| b Non-income producing—security in default. |

| c Securities exempt from registration under Rule 144A of the Securities Act of 1933.These securities may be resold in |

| transactions exempt from registration, normally to qualified institutional buyers. At June 30, 2010, these securities |

| had a total market value of $313,512,774 or 36.3% of net assets. |

| d Variable rate security—interest rate subject to periodic change. |

| e The valuation of this security has been determined in good faith by management under the direction of the Board of |

| Directors. At June 30, 2010, the value of this security amounted to $ 6,307,875 or 0.7% of net assets. |

| f Illiquid security.The valuation of this security has been determined in good faith by management under the direction of |

| the Board of Directors.At June 30, 2010, the value of this security amounted to $ 1,065,752 or 0.1% of net assets |

| g Non-income producing security. |

| h Investment in affiliated money market mutual fund. |

| | | |

| Portfolio Summary (Unaudited)† | | |

| |

| | Value (%) | | Value (%) |

| Corporate Bonds | 96.0 | Preferred Stocks | .1 |

| Money Market Investments | 18.2 | | |

| Common Stocks | .3 | | 114.6 |

| |

| † Based on net assets. | | | |

| See notes to financial statements. | | | |

16

|

| STATEMENT OF ASSETS AND LIABILITIES |

| June 30, 2010 (Unaudited) |

| | | | |

| | | | Cost | Value |

| Assets ($): | | | | |

| Investments in securities—See Statement of Investments (including | | |

| securities on loan, valued at $131,403,757)—Note 1(c): | | |

| Unaffiliated issuers | | | 822,634,120 | 833,142,682 |

| Affiliated issuers | | | 157,071,515 | 157,071,515 |

| Cash | | | | 164,108 |

| Cash denominated in foreign currencies | | 49 | 43 |

| Dividends and interest receivable | | | | 20,986,721 |

| Receivable for shares of Beneficial Interest subscribed | | 886,716 |

| Receivable for investment securities sold | | | 461,680 |

| | | | | 1,012,713,465 |

| Liabilities ($): | | | | |

| Due to The Dreyfus Corporation and affiliates—Note 3(b) | | 670,698 |

| Liability for securities on loan—Note 1(c) | | | 138,868,515 |

| Payable for investment securities purchased | | | 7,211,068 |

| Payable for shares of Beneficial Interest redeemed | | | 2,189,089 |

| | | | | 148,939,370 |

| Net Assets ($) | | | | 863,774,095 |

| Composition of Net Assets ($): | | | |

| Paid-in capital | | | | 1,148,572,335 |

| Accumulated distributions in excess of investment income—net | | (2,391,732) |

| Accumulated net realized gain (loss) on investments | | | (292,915,064) |

| Accumulated net unrealized appreciation (depreciation) | | |

| on investments and foreign currency transactions | | | 10,508,556 |

| Net Assets ($) | | | | 863,774,095 |

| |

| |

| Net Asset Value Per Share | | | |

| | Class A | Class B | Class C | Class I |

| Net Assets ($) | 323,195,607 | 13,574,191 | 118,924,478 | 408,079,819 |

| Shares Outstanding | 51,644,492 | 2,168,248 | 18,997,253 | 65,159,594 |

| Net Asset Value Per Share ($) | 6.26 | 6.26 | 6.26 | 6.26 |

| |

| See notes to financial statements. | | | | |

|

| STATEMENT OF OPERATIONS |

| Six Months Ended June 30, 2010 (Unaudited) |

| |

| Investment Income ($): | |

| Income: | |

| Interest | 46,171,105 |

| Income from securities lending—Note 1(c) | 339,634 |

| Dividends: | |

| Unaffiliated issuers | 40,917 |

| Affiliated issuers | 9,358 |

| Total Income | 46,561,014 |

| Expenses: | |

| Management fee—Note 3(a) | 3,137,119 |

| Distribution and service fees—Note 3(b) | 1,110,875 |

| Trustees’ fees—Note 3(a) | 34,994 |

| Loan commitment fees—Note 2 | 12,186 |

| Interest expense—Note 2 | 153 |

| Total Expenses | 4,295,327 |

| Less—Trustees’ fees reimbursed by the Manager—Note 3(a) | (34,994) |

| Net Expenses | 4,260,333 |

| Investment Income—Net | 42,300,681 |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | |

| Net realized gain (loss) on investments and foreign currency transactions | 20,519,959 |

| Net realized gain (loss) on forward foreign currency exchange contracts | 31,046 |

| Net Realized Gain (Loss) | 20,551,005 |

| Net unrealized appreciation (depreciation) on | |

| investments and foreign currency transactions | (48,561,893) |

| Net unrealized appreciation (depreciation) on | |

| forward foreign currency exchange contracts | (2,968) |

| Net Unrealized Appreciation (Depreciation) | (48,564,861) |

| Net Realized and Unrealized Gain (Loss) on Investments | (28,013,856) |

| Net Increase in Net Assets Resulting from Operations | 14,286,825 |

| |

| See notes to financial statements. | |

18

STATEMENT OF CHANGES IN NET ASSETS

| | |

| | Six Months Ended | |

| | June 30, 2010 | Year Ended |

| | (Unaudited) | December 31, 2009 |

| Operations ($): | | |

| Investment income—net | 42,300,681 | 66,290,493 |

| Net realized gain (loss) on investments | 20,551,005 | (6,401,619) |

| Net unrealized appreciation | | |

| (depreciation) on investments | (48,564,861) | 181,196,172 |

| Net Increase (Decrease) in Net Assets | | |

| Resulting from Operations | 14,286,825 | 241,085,046 |

| Dividends to Shareholders from ($): | | |

| Investment income—net: | | |

| Class A Shares | (17,824,154) | (29,894,758) |

| Class B Shares | (852,786) | (2,849,188) |

| Class C Shares | (5,856,163) | (8,775,809) |

| Class I Shares | (21,580,635) | (27,846,038) |

| Total Dividends | (46,113,738) | (69,365,793) |

| Beneficial Interest Transactions ($): | | |

| Net proceeds from shares sold: | | |

| Class A Shares | 53,580,312 | 286,678,813 |

| Class B Shares | 239,602 | 1,476,907 |

| Class C Shares | 8,944,905 | 44,838,158 |

| Class I Shares | 89,129,488 | 232,223,371 |

| Net assets received in connection | | |

| with reorganization—Note 1 | — | 129,672,713 |

| Dividends reinvested: | | |

| Class A Shares | 14,451,212 | 22,562,646 |

| Class B Shares | 628,070 | 1,872,480 |

| Class C Shares | 3,596,200 | 5,010,735 |

| Class I Shares | 6,677,725 | 6,001,284 |

| Cost of shares redeemed: | | |

| Class A Shares | (93,793,847) | (198,188,481) |

| Class B Shares | (9,217,249) | (31,665,643) |

| Class C Shares | (14,973,961) | (19,316,179) |

| Class I Shares | (72,910,209) | (98,684,961) |

| Increase (Decrease) in Net Assets from | | |

| Beneficial Interest Transactions | (13,647,752) | 382,481,843 |

| Total Increase (Decrease) in Net Assets | (45,474,665) | 554,201,096 |

| Net Assets ($): | | |

| Beginning of Period | 909,248,760 | 355,047,664 |

| End of Period | 863,774,095 | 909,248,760 |

| Undistributed (distributions in excess of) | | |

| investment income—net | (2,391,732) | 1,421,325 |

STATEMENT OF CHANGES IN NET ASSETS (continued)

| | |

| Six Months Ended | |

| | June 30, 2010 | Year Ended |

| | (Unaudited) | December 31, 2009 |

| Capital Share Transactions: | | |

| Class Aa | | |

| Shares sold | 8,309,633 | 51,207,569 |

| Shares issued in connection with | | |

| reorganization—Note 1 | — | 10,690,947 |

| Shares issued for dividends reinvested | 2,251,800 | 3,780,546 |

| Shares redeemed | (14,600,823) | (33,630,114) |

| Net Increase (Decrease) in Shares Outstanding | (4,039,390) | 32,048,948 |

| Class Ba | | |

| Shares sold | 37,160 | 257,820 |

| Shares issued in connection with reorganization—Note 1 | — | 4,883,654 |

| Shares issued for dividends reinvested | 97,770 | 320,812 |

| Shares redeemed | (1,426,420) | (5,472,399) |

| Net Increase (Decrease) in Shares Outstanding | (1,291,490) | (10,113) |

| Class C | | |

| Shares sold | 1,384,553 | 7,842,855 |

| Shares issued in connection with reorganization—Note 1 | — | 7,195,044 |

| Shares issued for dividends reinvested | 560,613 | 837,067 |

| Shares redeemed | (2,339,028) | (3,270,669) |

| Net Increase (Decrease) in Shares Outstanding | (393,862) | 12,604,297 |

| Class I | | |

| Shares sold | 13,813,375 | 39,340,054 |

| Shares issued in connection with reorganization—Note 1 | — | 1,748,575 |

| Shares issued for dividends reinvested | 1,041,599 | 998,987 |

| Shares redeemed | (11,386,824) | (16,641,631) |

| Net Increase (Decrease) in Shares Outstanding | 3,468,150 | 25,445,985 |

|

| a During the period ended June 30, 2010, 483,540 Class B shares representing $3,129,888, were automatically |

| converted to 483,688 Class A shares and during the period ended December 31, 2009, 2,061,607 Class B shares |

| representing $12,009,537 were automatically converted to 2,063,045 Class A shares. |

See notes to financial statements.

20

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated.All information (except portfolio turnover rate) reflects financial results for a single fund share.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | | |

| Six Months Ended | | | | | |

| June 30, 2010 | | Year Ended December 31, | |

| Class A Shares | (Unaudited) | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per Share Data ($): | | | | | | |

| Net asset value, | | | | | | |

| beginning of period | 6.48 | 5.06 | 6.92 | 7.33 | 7.24 | 7.65 |

| Investment Operations: | | | | | | |

| Investment income—neta | .30 | .54 | .50 | .49 | .49 | .51 |

| Net realized and unrealized | | | | | | |

| gain (loss) on investments | (.19) | 1.43 | (1.82) | (.37) | .14 | (.36) |

| Total from Investment Operations | .11 | 1.97 | (1.32) | .12 | .63 | .15 |

| Distributions: | | | | | | |

| Dividends from | | | | | | |

| investment income—net | (.33) | (.55) | (.54) | (.53) | (.54) | (.56) |

| Net asset value, end of period | 6.26 | 6.48 | 5.06 | 6.92 | 7.33 | 7.24 |

| Total Return (%)b | 1.66c | 40.43 | (20.17) | 2.03 | 8.66 | 2.22 |

| Ratios/Supplemental Data (%): | | | | | | |

| Ratio of total expenses | | | | | | |

| to average net assets | .96d | .96 | .96 | .96 | .95 | .95 |

| Ratio of net expenses | | | | | | |

| to average net assets | .95d | .95 | .95 | .95 | .95 | .95 |

| Ratio of net investment income | | | | | | |

| to average net assets | 9.41d | 8.86 | 7.89 | 6.78 | 6.76 | 6.93 |

| Portfolio Turnover Rate | 39.19c | 77.94 | 48.85 | 50.65 | 29.98 | 40.57 |

| Net Assets, end of period | | | | | | |

| ($ x 1,000) | 323,196 | 360,921 | 119,560 | 169,453 | 202,098 | 236,421 |

| |

| a | Based on average shares outstanding at each month end. |

| b | Exclusive of sales charge. |

| c | Not annualized. |

| d | Annualized. |

See notes to financial statements.

FINANCIAL HIGHLIGHTS (continued)

| | | | | | |

| Six Months Ended | | | | | |

| June 30, 2010 | | Year Ended December 31, | |

| Class B Shares | (Unaudited) | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per Share Data ($): | | | | | | |

| Net asset value, | | | | | | |

| beginning of period | 6.48 | 5.06 | 6.93 | 7.34 | 7.24 | 7.65 |

| Investment Operations: | | | | | | |

| Investment income—neta | .27 | .49 | .46 | .45 | .45 | .46 |

| Net realized and unrealized | | | | | | |

| gain (loss) on investments | (.18) | 1.45 | (1.82) | (.37) | .16 | (.35) |

| Total from Investment Operations | .09 | 1.94 | (1.36) | .08 | .61 | .11 |

| Distributions: | | | | | | |

| Dividends from | | | | | | |

| investment income—net | (.31) | (.52) | (.51) | (.49) | (.51) | (.52) |

| Net asset value, end of period | 6.26 | 6.48 | 5.06 | 6.93 | 7.34 | 7.24 |

| Total Return (%)b | 1.41c | 39.78 | (20.69) | 1.53 | 8.12 | 1.73 |

| Ratios/Supplemental Data (%): | | | | | | |

| Ratio of total expenses | | | | | | |

| to average net assets | 1.46d | 1.46 | 1.46 | 1.46 | 1.45 | 1.45 |

| Ratio of net expenses | | | | | | |

| to average net assets | 1.45d | 1.45 | 1.45 | 1.45 | 1.45 | 1.45 |

| Ratio of net investment income | | | | | | |

| to average net assets | 8.61d | 8.35 | 7.31 | 6.24 | 6.25 | 6.36 |

| Portfolio Turnover Rate | 39.19c | 77.94 | 48.85 | 50.65 | 29.98 | 40.57 |

| Net Assets, end of period | | | | | | |

| ($ x 1,000) | 13,574 | 22,434 | 17,568 | 39,892 | 67,834 | 96,334 |

| |

| a | Based on average shares outstanding at each month end. |

| b | Exclusive of sales charge. |

| c | Not annualized. |

| d | Annualized. |

See notes to financial statements.

22

| | | | | | |

| Six Months Ended | | | | | |

| June 30, 2010 | | Year Ended December 31, | |

| Class C Shares | (Unaudited) | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per Share Data ($): | | | | | | |

| Net asset value, | | | | | | |

| beginning of period | 6.48 | 5.06 | 6.93 | 7.34 | 7.24 | 7.65 |

| Investment Operations: | | | | | | |

| Investment income—neta | .28 | .50 | .45 | .43 | .43 | .45 |

| Net realized and unrealized | | | | | | |

| gain (loss) on investments | (.20) | 1.42 | (1.83) | (.36) | .16 | (.36) |

| Total from Investment Operations | .08 | 1.92 | (1.38) | .07 | .59 | .09 |

| Distributions: | | | | | | |

| Dividends from | | | | | | |

| investment income—net | (.30) | (.50) | (.49) | (.48) | (.49) | (.50) |

| Net asset value, end of period | 6.26 | 6.48 | 5.06 | 6.93 | 7.34 | 7.24 |

| Total Return (%)b | 1.28c | 39.41 | (20.89) | 1.28 | 7.85 | 1.48 |

| Ratios/Supplemental Data (%): | | | | | | |

| Ratio of total expenses | | | | | | |

| to average net assets | 1.71d | 1.71 | 1.71 | 1.71 | 1.70 | 1.70 |

| Ratio of net expenses | | | | | | |

| to average net assets | 1.70d | 1.70 | 1.70 | 1.70 | 1.70 | 1.70 |

| Ratio of net investment income | | | | | | |

| to average net assets | 8.70d | 8.15 | 7.12 | 6.02 | 6.01 | 6.14 |

| Portfolio Turnover Rate | 39.19c | 77.94 | 48.85 | 50.65 | 29.98 | 40.57 |

| Net Assets, end of period | | | | | | |

| ($ x 1,000) | 118,924 | 125,724 | 34,374 | 53,294 | 65,728 | 74,770 |

| |

| a | Based on average shares outstanding at each month end. |

| b | Exclusive of sales charge. |

| c | Not annualized. |

| d | Annualized. |

See notes to financial statements.

FINANCIAL HIGHLIGHTS (continued)

| | | | | | |

| Six Months Ended | | | | | |

| June 30, 2010 | | Year Ended December 31, | |

| Class I Shares | (Unaudited) | 2009 | 2008 | 2007a | 2006 | 2005 |

| Per Share Data ($): | | | | | | |

| Net asset value, | | | | | | |

| beginning of period | 6.49 | 5.06 | 6.92 | 7.33 | 7.24 | 7.65 |

| Investment Operations: | | | | | | |

| Investment income—netb | .31 | .54 | .51 | .52 | .51 | .53 |

| Net realized and unrealized | | | | | | |

| gain (loss) on investments | (.20) | 1.45 | (1.82) | (.38) | .14 | (.36) |

| Total from Investment Operations | .11 | 1.99 | (1.31) | .14 | .65 | .17 |

| Distributions: | | | | | | |

| Dividends from | | | | | | |

| investment income—net | (.34) | (.56) | (.55) | (.55) | (.56) | (.58) |

| Net asset value, end of period | 6.26 | 6.49 | 5.06 | 6.92 | 7.33 | 7.24 |

| Total Return (%) | 1.63c | 40.99 | (20.06) | 2.29 | 8.92 | 2.34 |

| Ratios/Supplemental Data (%): | | | | | | |

| Ratio of total expenses | | | | | | |

| to average net assets | .71d | .71 | .72 | .71 | .70 | .70 |

| Ratio of net expenses | | | | | | |

| to average net assets | .70d | .70 | .69 | .70 | .70 | .70 |

| Ratio of net investment income | | | | | | |

| to average net assets | 9.72d | 9.20 | 9.43 | 7.01 | 7.01 | 7.18 |

| Portfolio Turnover Rate | 39.19c | 77.94 | 48.85 | 50.65 | 29.98 | 40.57 |

| Net Assets, end of period | | | | | | |

| ($ x 1,000) | 408,080 | 400,170 | 183,546 | 17,368 | 18,059 | 18,595 |

| |

| a | Effective June 1, 2007, Class R shares were redesignated as Class I shares. |

| b | Based on average shares outstanding at each month end. |

| c | Not annualized. |

| d | Annualized. |

See notes to financial statements.

24

NOTES TO FINANCIAL STATEMENTS (Unaudited)

NOTE 1—Significant Accounting Policies:

Dreyfus High Yield Fund (the “fund”) is a separate diversified series of The Dreyfus/Laurel FundsTrust (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering seven series, including the fund.The fund’s investment objective seeks to maximize total return, consisting of capital appreciation and current income.The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

As of the close of business on January 8, 2009, pursuant to an Agreement and Plan of Reorganization previously approved by the fund’s Board of Trustees,all of the assets,subject to the liabilities,of Dreyfus High Income Fund (“High Income”) were transferred to the fund in exchange for corresponding class of shares of Beneficial Interest of the fund of equal value. The purpose of the transaction was to combine two funds with comparable investment objectives and strategies. Shareholders of Class A, Class B,Class C and Class I shares of High Income received Class A,Class B, Class C and Class I shares of the fund, respectively, in each case in an amount equal to the aggregate net asset value of their investment in High Income at the time of the exchange.The exchange ratio for Class A,Class B, Class C and Class I shares are 1.96, 1.96, 1.95 and 1.96, respectively. The net asset value of the fund’s shares on the c lose of business January 8, 2009, after the reorganization was $5.29 for Class A, $5.29 for Class B, $5.29 for Class C and $5.29 for Class I shares, and a total of 10,690,947 Class A shares, 4,883,654 Class B shares, 7,195,044 Class C shares and 1,748,575 Class I shares were issued to shareholders of High Income in the exchange. The exchange was a tax-free event to the High Income shareholders. For financial reporting purposes, assets received and shares issued by the fund were recorded at fair value; however, the cost basis of investments received from High Income was carried forward to align ongoing reporting of the fund’s realized and unrealized gains and losses with amounts distributable to shareholders for tax purposes.

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

The net assets and net unrealized (depreciation) immediately before the acquisition were as follows:

| | |

| | Unrealized | |

| | (Depreciation) ($) | Net Assets ($) |

| Dreyfus High Income Fund— | | |

| Target Fund | (23,749,040) | 129,672,713 |

| Dreyfus High Yield Fund— | | |

| Acquiring Fund | (81,332,832) | 382,765,045 |

| Total | (105,081,872) | 512,437,758 |

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares. The fund is authorized to issue an unlimited number of shares of Beneficial Interest in each of the following classes of shares: Class A, Class B, Class C and Class I. Class A, Class B and Class C shares are sold primarily to retail investors through financial intermediaries and bear a distribution fee and/or shareholder services fee. Class A shares are sold with a front-end sales charge, while Class B and Class C shares are subject to a contingent deferred sales charge (“CDSC”). Class B shares automatically convert to Class A shares after six years.The fund does not offer Class B shares, except in connection with dividend reinvestment and permitted exchanges of Class B shares. Class I shares are sold primarily to bank trust departments and other financial service providers (including The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus), acting on behalf of customers having a qualified trust or investment account or relationship at such institution, and bear no distribution or services fees. Class I shares are offered without a front-end sales charge or CDSC. Other differences between the classes include the services offered to and the expenses borne by each class and the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Trust accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

26

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities.Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

(a) Portfolio valuation: Investments in securities excluding short-term investments (other than U.S.Treasury Bills), and forward foreign currency exchange contracts (“forward contracts”) are valued each business day by an independent pricing service (the “Service”) approved by the Board of Trustees. Investments for which quoted bid prices are readily available and are representative of the bid side of the market in the judgment of the Service are valued at the mean between the quoted bid prices (as obtained by the Service from dealers in such securities) and asked prices (as calculated by the Service based upon its evaluation of the market for such securities). Other investments (which constitute a majority of the portfolio securities) are valued as determined by the Service, based on methods which include consideration of: yields o r prices of securities of comparable quality, coupon, maturity and type; indications as to values from dealers; and general market conditions. Restricted securities, as well as securities or other assets for which recent market quotations are not readily available and are not valued by a pricing service approved by the Board of Trustees, or are determined by the fund not to reflect accurately fair value, are valued at fair value as determined in good faith under the direction of the Board of Trustees. The factors that may be considered when fair valuing a security include fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold and public trading in similar securities of the issuer or comparable issuers. Short-term investments, excluding U.S.Treasury Bills, are car-

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

ried at amortized cost, which approximates value. Registered investment companies that are not traded on an exchange are valued at their net asset value. Investments in equity securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Investments denominated in foreign currencies are translated to U.S. dollars at the prevailing rates of exchange. Forward contracts are valued at the forward rate.

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e. the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for

identical investments.

Level 2—other significant observable inputs (including quoted

prices for similar investments, interest rates, prepayment speeds,

credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own

assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

28

The following is a summary of the inputs used as of June 30, 2010 in valuing the fund’s investments:

| | | | |

| | | Level 2—Other | Level 3— | |

| | Level 1— | Significant | Significant | |

| | Unadjusted | Observable | Unobservable | |

| | Quoted Prices | Inputs | Inputs | Total |

| Assets ($) | | | | |

| Investments in Securities: | | | |

| Corporate Bonds† | — | 829,161,559 | — | 829,161,559 |

| Equity Securities— | | | | |

| Domestic† | 2,915,371 | — | 1,065,752 | 3,981,123 |

| Mutual Funds | 157,071,515 | — | — | 157,071,515 |

| † See Statement of Investments for industry classification. | | |

The following is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value:

| |

| | Investments in |

| | Preferred Stock ($) |

| Balance as of 12/31/2009 | 1,523 |

| Realized gain (loss) | — |

| Change in unrealized appreciation (depreciation) | 1,064,229 |

| Net purchases (sales) | — |

| Transfers in and/or out of Level 3 | — |

| Balance as of 6/30/2010 | 1,065,752 |

In January 2010, FASB issued Accounting Standards Update (“ASU”) No. 2010-06 “Improving Disclosures about FairValue Measurements”. The portions of ASU No. 2010-06 which require reporting entities to prepare new disclosures surrounding amounts and reasons for significant transfers in and out of Level 1 and Level 2 fair value measurements as well as inputs and valuation techniques used to measure fair value for both recurring and nonrecurring fair value measurements that fall in either Level 2 or Level 3 have been adopted by the fund.The remaining portion of ASU No. 2010-06 requires reporting entities to make new disclosures about information on purchases, sales, issuances and settlements on a gross basis in the reconciliation of activity in Level 3

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

fair value measurements.These new and revised disclosures are required to be implemented for fiscal years beginning after December 15, 2010. Management is currently evaluating the impact that the adoption of this remaining portion of ASU No. 2010-06 may have on the fund’s financial statement disclosures.

(b) Foreign currency transactions: The fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in the market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized on securities transactions between trade and settlement date, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the value of assets and liabilities other than investments resulting from changes in exchange rates. Foreign currency gains and losses on investments are included with net realized and unrealized gain or loss on investments.

(c) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

Pursuant to a securities lending agreement withThe Bank of NewYork Mellon, the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral

30

is either in the form of cash, which can be invested in certain money market mutual funds managed by the Manager, U.S. Government and Agency securities or letters of credit.The fund is entitled to receive all income on securities loaned, in addition to income earned as a result of the lending transaction.Although each security loaned is fully collateralized, the fund bears the risk of delay in recovery of, or loss of rights in, the securities loaned should a borrower fail to return the securities in a timely manner. During the period ended June 30, 2010,The Bank of New York Mellon earned $182,880 from lending portfolio securities, pursuant to the securities lending agreement.

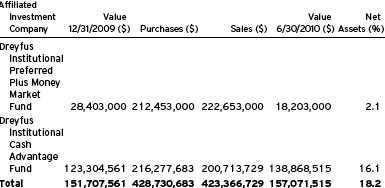

(d) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” in the Act.

The fund may invest in shares of certain affiliated investment companies also advised or managed by Dreyfus. Investments in affiliated investment companies for the period ended June 30, 2010 were as follows:

(e) Concentration of Risk: The fund invests primarily in debt securities. Failure of an issuer of the debt securities to make timely interest or principal payments, or a decline or the perception of a decline in the credit quality of a debt security, can cause the debt security’s price to fall, potentially lowering the fund’s share price. High yield (“junk”)

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

bonds involve greater credit risk, including the risk of default, than investment grade bonds, and are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. In addition, the value of debt securities may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment. They may also decline because of factors that affect a particular industry.

(f) Dividends to shareholders: It is the policy of the fund to declare dividends daily from investment income-net. Such dividends are paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(g) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended June 30, 2010, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the three-year period ended December 31, 2009 remains subject to examination by the Internal Revenue Service and state taxing authorities.

32

The fund has an unused capital loss carryover of $309,880,382 available for federal income tax purposes to be applied against future net securities profits, if any, realized subsequent to December 31, 2009. If not applied, $138,776,715 of the carryover expires in fiscal 2010, $72,493,638 expires in fiscal 2011, $1,917,623 expires in fiscal 2012, $11,766,163 expires in fiscal 2013, $2,406,483 expires in fiscal 2014, $16,497,195 expires in fiscal 2015, $42,229,566 expires in fiscal 2016 and $23,792,999 expires in fiscal 2017. Based on certain provisions in the Code, various limitations regarding the future utilization of these carryforwards, brought forward as a result of the fund’s merger with the following funds may apply: HighYield Total Fund, BNY Hamilton High Yield Fund and Dreyfus High Income Fund. It is possible that the fund will not be able to utilize most of its capital loss carryover prior to its expiration date.

The tax character of distributions paid to shareholders during the fiscal year ended December 31, 2009 was as follows: ordinary income $69,365,793. The tax character of current year distributions will be determined at the end of the current fiscal year.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $225 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon (each, a “Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended June 30, 2010, was approximately $22,200 with a related weighted average annualized interest rate of 1.40%.

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

NOTE 3—Investment Management Fee and Other Transactions with Affiliates:

(a) Pursuant to an investment management agreement with the Manager, the Manager provides or arranges for one or more third parties and/or affiliates to provide investment advisory, administrative, custody, fund accounting and transfer agency services to the fund. The Manager also directs the investments of the fund in accordance with its investment objective, policies and limitations. For these services, the fund is contractually obligated to pay the Manager a fee, calculated daily and paid monthly, at the annual rate of .70% of the value of the fund’s average daily net assets. Out of its fee, the Manager pays all of the expenses of the fund except brokerage fees, taxes, interest, commitment fees, Rule 12b-1 distribution fees and expenses, shareholder service fees, fees and expenses of non-interested Trustees (including counsel fees) and extraord inary expenses. In addition, the Manager is required to reduce its fee in an amount equal to the fund’s allocable portion of fees and expenses of the non-interested Trustees (including counsel fees). Effective January 1, 2010, each Trustee who is not an “interested person” of the Trust (as defined in the Act) received $60,000 per annum, plus $7,000 per joint Board meeting of the Trust, The Dreyfus/Laurel Funds, Inc., The Dreyfus/Laurel Tax-Free Municipal Funds, Dreyfus Investment Funds and Dreyfus Funds, Inc. (collectively, the “Board Group Open-end Funds”) attended, $2,500 for separate in-person committee meetings attended which are not held in conjunction with a regularly scheduled Board meeting and $2,000 for Board meetings and separate committee meetings attended that are conducted by telephone.The Board Group Open-end Funds also reimburse each Trustee who is not an “interested person” of the Trust (as defined in the Act) for travel and out-of-pocket expenses.With respe ct to Board meetings, the Chairman of the Board receives an additional 25% of such compensation (with the exception of reimbursable amounts). Effective January 1, 2010, the Chair of each of the Board’s committees, unless the Chair also serves as Chair of the Board, receives $1,350 per applicable committee meeting. In the event that there is an in-person joint committee meeting or a joint telephone

34

meeting of the Board Group Open-end Funds and Dreyfus HighYield Strategies Fund, the $2,500 or $2,000 fee, as applicable, is allocated between the Board Group Open-end Funds and Dreyfus High Yield Strategies Fund. The Trust’s portion of these fees and expenses are charged and allocated to each series based on net assets. Amounts required to be paid by the Trust directly to the non-interested Trustees, that would be applied to offset a portion of the management fee payable to the Manager, are in fact paid directly by the Manager to the non-interested Trustees.

The Manager has contractually agreed, until September 30, 2010, to waive receipt of its fees and/or assume the expenses of Class I shares of the fund so that the annual operating expenses (excluding taxes, interest, brokerage commissions, commitment fees on borrowings and extraordinary expenses) do not exceed .81% of the value of the fund’s average daily net assets. No expense reimbursement was required pursuant to the agreement for the period ended June 30, 2010.

During the period ended June 30, 2010, the Distributor retained $15,460 from commissions earned on sales of the fund’s Class A shares and $12,387 and $15,344 from CDSCs on redemptions of the fund’s Class B and Class C shares, respectively.

(b) Under separate Distribution Plans (the “Plans”) adopted pursuant to Rule 12b-1 under the Act, Class A shares pay annually up to .25% of the value of the average daily net assets to compensate the Distributor for shareholder servicing activities and expenses primarily intended to result in the sale of Class A shares. Class B and Class C shares pay the Distributor for distributing their shares at an aggregate annual rate of .50% and .75% of the value of the average daily net assets of Class B and Class C shares, respectively. Class B and Class C shares are also subject to a Service Plan adopted pursuant to Rule 12b-1 (the “Service Plan”), under which Class B and Class C shares pay the Distributor for providing certain services to the holders of their shares a fee at the annual rate of .25% of the value of the average daily net ass ets of Class B and Class

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

C shares. During the period ended June 30, 2010, Class A, Class B and Class C shares were charged $432,590, $43,280 and $460,024, respectively, pursuant to their respective Plans. During the period ended June 30, 2010, Class B and Class C shares were charged $21,640 and $153,341, respectively, pursuant to the Service Plan.

Under its terms, the Plans and Service Plan shall remain in effect from year to year, provided such continuance is approved annually by a vote of a majority of those Trustees who are not “interested persons” of the Trust and who have no direct or indirect financial interest in the operation of or in any agreement related to the Plans or Service Plan.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $497,592, Rule 12b-1 distribution plan fees $145,806 and service plan fees $27,300.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales (including paydowns) of investment securities, excluding short-term securities and forward contracts, during the period ended June 30, 2010, amounted to $342,005,063 and $352,281,597, respectively.

The provisions of ASC Topic 815 “Derivatives and Hedging” require qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of gains and losses on derivative instruments and disclosures about credit-risk-related contingent features in derivative agreements. The disclosure requirements distinguish between derivatives, which are accounted for as “hedges” and those that do not qualify for hedge accounting. Because investment companies value their derivatives at fair value and recognize changes in fair value through the Statement of Operations, they do not qualify for such accounting. Accordingly, even though a fund’s investments in derivatives may represent economic hedges, they are considered to be non-hedge transactions for purposes of this disclosure.

36