| |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM 10-K |

| (Mark One) |

| [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2007 |

| OR |

| [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from | | to |

| Commission File Number: 001-07791 |

|

| McMoRan Exploration Co. |

| (Exact name of registrant as specified in its charter) |

| Delaware | 72-1424200 | |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

| | | |

| 1615 Poydras Street | | |

| New Orleans, Louisiana | 70112 | |

| (Address of principal executive offices) | (Zip Code) | |

| | |

| (504) 582-4000 | |

| (Registrant's telephone number, including area code) | |

| | |

| Securities registered pursuant to Section 12(b) of the Act: | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | New York Stock Exchange |

| 6.75% Mandatory Convertible Preferred Stock | | New York Stock Exchange |

| Preferred Stock Purchase Rights | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act

0 Yes SNo

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

0 Yes SNo

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. S Yes 0 No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. 0

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

0 Large accelerated filer S Accelerated filer 0 Non-accelerated filer (Do not check if a smaller reporting company) 0 Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). 0 Yes S No

The aggregate market value of classes of common stock held by non-affiliates of the registrant was approximately $706 million on February 29, 2008, and approximately $322 million on June 30, 2007.

On February 29, 2008, there were issued and outstanding 54,381,818 shares of the registrant’s Common Stock and on June 30, 2007, there were issued and outstanding 34,692,490 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of our Proxy Statement for our 2008 Annual Meeting to be held on June 5, 2008 are incorporated by reference into Part III (Items 10, 11, 12, 13 and 14) of this report. |

McMoRan Exploration Co.

Annual Report on Form 10-K for

the Fiscal Year ended December 31, 2007

|

| | |

| | Page |

| |

| 1 |

| 13 |

| 24 |

| 24 |

| 24 |

| 24 |

| | |

| |

| 26 |

| 28 |

| |

| 30 |

| 50 |

| 99 |

| 99 |

| 99 |

| | 99 |

| |

| 99 |

| 99 |

| |

| 100 |

| 100 |

| 100 |

| | |

| |

| | |

| 100 |

| | |

| 100 |

| | |

| S-1 |

| | |

| E-1 |

Except as otherwise described herein or the context otherwise requires, all references to “McMoRan,” “MMR,” “we,” “us,” and “our” in this Form 10-K refer to McMoRan Exploration Co. and all entities owned or controlled by McMoRan Exploration Co.

All of our periodic report filings with the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, through our website located at www.mcmoran.com, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and any amendments to those reports. These reports and amendments are available through our website as soon as reasonably practicable after we electronically file or furnish such materials with the SEC. All references to Notes in this report refer to the Notes to the Consolidated Financial Statements located in Item 8. of this Form 10-K. We have also provided a glossary of definitions for some of the oil and gas industry terms we use in this Form 10-K beginning on page 100.

BUSINESS

General. We engage in the exploration, development and production of oil and natural gas offshore in the Gulf of Mexico and onshore in the Gulf Coast area. We have one of the largest acreage positions in the shallow waters of the Gulf of Mexico and Gulf Coast areas, our regions of focus. Our focused strategy enables us to efficiently use our strong base of geologic, engineering, and production experience in these regions in which we have operated for more than 35 years. We also believe that our scale of operations in the Gulf of Mexico provides synergies and a strong platform from which to pursue our business strategy. Our oil and gas operations are conducted through McMoRan Oil & Gas LLC (MOXY), our principal operating subsidiary. In addition to our oil and gas operations, we are pursuing the development of the Main Pass Energy Hubtm (MPEHtm) project for the development of a liquefied natural gas (LNG) regasification and storage facility through our wholly owned subsidiary, Freeport-McMoRan Energy LLC (Freeport Energy) (see “— Main Pass Energy Hubtm Project” below).

We conduct substantially all of our operations in the shallow waters of the Gulf of Mexico, commonly referred to as the “shelf,” and onshore in the Gulf Coast region. We believe that we have significant exploration opportunities in large, deep geologic structures located beneath the shallow waters of the Gulf of Mexico shelf and often lying beneath shallow reservoirs where significant reserves have already been produced, commonly referred to as “deep gas” or the “deep shelf” (prospects with drilling depths between 15,000 feet to 25,000 feet). In 2007, we acquired substantially all of the proved property interests and related assets of Newfield Exploration Company (Newfield) located on the outer continental shelf of the Gulf of Mexico, which significantly enhanced our portfolio of shelf opportunities by increasing our gross acreage position from approximately 0.3 million acres to approximately 1.5 million acres as of December 31, 2007. The acquisition also increased our deep gas exploration potential, provided access to new “ultra deep” exploration opportunities (prospects with total drilling depths in excess of 25,000 feet) and established us as one of the largest producers on the “traditional shelf” (prospects located at drilling depths not exceeding 15,000 feet) of the Gulf of Mexico (see “—Newfield Property Acquisition” below). Additionally, the proximity of our shelf prospects to an already existing oil and gas infrastructure generally lowers development costs and the time needed to bring production on-line.

We have significant expertise in various exploration and production technologies, including incorporating 3-D seismic interpretation capabilities with traditional structural geological techniques, offshore drilling to significant total depths and horizontal drilling. We employ 65 oil and gas technical professionals, including geophysicists, geologists, petroleum engineers, production and reservoir engineers and technical professionals who have extensive experience in their fields. We also own or have rights to an extensive seismic database, including 3-D seismic data on substantially all of our acreage. We leverage our extensive in-house expertise and advanced technologies to benefit our operations and identify high potential, high risk drilling prospects in the Gulf of Mexico, which is our primary area of expertise. We continue to focus on enhancing reserve and production growth in the Gulf of Mexico by emphasizing and applying these technologies.

Our experience and recognition in the industry as a leader in drilling deep gas wells in the Gulf of Mexico also provides us with opportunities to partner with other established oil and gas companies. These partnerships typically involve the exploration of our identified prospects or prospects that are brought to us by third parties and allow us to diversify our risks and better manage costs.

Business Strategy. We expect to continue to pursue growth in reserves and production through the exploration, exploitation and development of our existing prospects and new potential prospects. Exploration will continue to be the focus in efforts to maximize value. Our acquisition of the Newfield properties and other recent discoveries has also afforded us with the opportunity to generate value through additional exploration, development and exploitation activities. For 2008, we have allocated approximately 40 percent of our planned capital expenditures for development activities, and we expect to continue to allocate a significant portion of our total capital expenditures to future development activities.

Our exploration strategy, which we refer to as the “deeper pool concept,” involves exploring prospects that lie beneath shallower intervals on the Deep Miocene geologic trend where there has been significant past production. Exploration drilling on these deep prospects involve significant costs and risk. A significant advantage to our “deeper pool” exploration strategy is that the infrastructure is in most cases already available, meaning discoveries generally can be brought on line quickly and at generally lower development costs. We believe our ability to identify structures below 15,000 feet by using structural geology augmented by 3-D seismic data will enable us to identify and exploit additional “deeper pool” prospects.

We use our expertise and a rigorous analytical process in conducting our exploration and development activities. While implementing our drilling plans, we focus on:

| | • | allocating investment capital based on the potential risk and reward for each exploratory and developmental opportunity; |

| | • | increasing the efficiency of our production practices; |

| | • | attracting professionals with geophysical and geological expertise; |

| | • | employing advanced seismic applications; and |

| | • | using new technology applications in drilling and completion practices. |

We intend to continue to strengthen our financial profile and maximize the cash flow from our assets through increased production and aggressive cost management.

The acquired Newfield properties provide us with assets capable of generating significant cash flow, which we plan to use to reduce our current indebtedness and invest in our future growth. Since future oil and gas prices are a significant factor in determining the extent of our potential cash flow, in connection with the acquisition, we entered into derivative contracts for a portion of the anticipated production for 2008, 2009 and 2010. As of December 31, 2007, our hedged position represents approximately 12 percent of our estimated proved reserves, with approximately 9 percent hedged under swap contracts and 3 percent under put contracts (Note 7). We may review future opportunities to hedge an additional portion of our production.

During 2007, we made one of our most significant deep gas discoveries in recent history at the Flatrock discovery at South Marsh Island Block 212. To date, we have drilled three successful wells in this field and plan to pursue further exploration and development in this high-potential area.

Newfield Property Acquisition. As discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operation and Quantitative and Qualitative Disclosures About Market Risk — Operational Activities” included in Items 7. and 7A. in this Form 10-K, on August 6, 2007, we completed the acquisition of substantially all of the proved property interests and related assets of Newfield located on the outer continental shelf of the Gulf of Mexico for total cash consideration of approximately $1.1 billion and the assumption of the related reclamation obligations. The effective date of the acquisition was July 1, 2007.

Our acquisition of the Newfield properties provides us with substantial reserves, production and exploration rights on the shelf of the Gulf of Mexico. At the time of the transaction, the acquired Newfield properties included 124 fields on 148 offshore blocks covering approximately 1.25 million gross acres (approximately 0.5 million acres net to our interests). Estimated proved reserves for the acquired Newfield properties as of July 1, 2007 totaled approximately 321 Bcfe, of which 71 percent represented proved natural gas reserves. The acquired Newfield properties produced an average of approximately 235 MMcfe/d for the quarter ended December 31, 2007.

We also acquired 50 percent of Newfield’s interest in certain unproved exploration leases on the outer continental shelf of the Gulf of Mexico. At December 31, 2007, these interests encompassed 13 primary term blocks covering approximately 64,000 gross acres. In addition, we acquired a majority interest of Newfield’s ownership in leases associated with its Treasure Island and Treasure Bay ultra deep prospects.

The acquired Newfield properties significantly expand our production and cash flow generating capacity and provide us with expanded deep gas opportunities on the shelf of the Gulf of Mexico. The benefits of the acquisition include:

| | • | substantial reserves, production and leasehold interests of approximately 1.25 million gross acres in an area on the outer continental shelf of the Gulf of Mexico, where we have significant experience and expertise; |

| | • | strong cash flows, which will enable us to reduce our debt rapidly and invest in high potential, high risk projects; and |

| | • | increased scale of operations, technical depth and expanded financial resources providing a strong platform from which we will be able to pursue growth opportunities in our core area of operations. |

Main Pass Energy Hubtm Project. We are pursuing the development of a multifaceted energy facility at MPEH™, including the potential development of a facility to receive and process LNG and store and distribute natural gas. We have completed preliminary engineering for the development of the MPEHtm project located at our Main Pass facilities located offshore in the Gulf of Mexico, 38 miles east of Venice, Louisiana. We are continuing discussions with potential energy suppliers to develop commercial arrangements for the facilities.

Following an extensive review, in January 2007 the Maritime Administration (MARAD) approved our license application for the MPEHtm project. MARAD concluded in its Record of Decision that construction and operation of the MPEHtm deepwater port would be in the national interest and consistent with national security and other national policy goals and objectives, including energy sufficiency and environmental quality. MARAD also concluded that MPEHtm would fill a vital role in meeting national energy requirements going forward and the port’s offshore deepwater location would help reduce congestion and enhance safety in receiving LNG cargoes to the U.S.

MARAD’s approval and issuance of the Deepwater Port license for MPEHtm is subject to various terms, criteria and conditions contained in its Record of Decision, including demonstration of financial responsibility, compliance with applicable laws and regulations, environmental monitoring and other customary conditions.

The project’s proximity to large and liquid U.S. gas markets and the significant potential of the onsite cavern storage provide attractive commercial opportunities for energy suppliers and natural gas consumers and marketers. The MPEHtm facility is approved with a capacity of regasifying LNG at a peak rate of 1.6 Bcf per day, storing 28 Bcf of natural gas in salt caverns and delivering 3.1 Bcf per day of natural gas to the U.S. market, including gas from storage.

We believe that a natural gas terminal at Main Pass has numerous potential advantages over other LNG sites including:

| | • | Offshore unloading provides savings compared with land-based facilities. |

| | * | Remote offshore location near major shipping lanes avoids port congestion and offers shipping logistical advantages; and |

| | * | Water depth of 210 feet allows access to the largest LNG carriers. |

| | • | Eastern Gulf of Mexico location offers a premium price to Henry Hub. |

| | * | Our dedicated pipeline system would deliver to eight major interstate pipelines; and |

| | * | Onsite gas conditioning would allow receipt of a wide range of LNG Btu contents. |

| | • | Seasonal arbitrage opportunities through onsite gas cavern storage offer significant added value. |

| | * | Extensive infrastructure allows future expansion; |

| | * | Existing platforms over a large salt dome provide extensive cavern storage capacity; and |

| | * | MPEHtm is the only facility in the United States combining LNG regas, gas conditioning, and onsite cavern storage. |

Prior to commencing construction of the facilities, we expect to enter into commercial arrangements that would enable us to finance the construction costs, projected to be approximately $800 million, with a potential additional investment of up to $600 million for pipelines and cavern storage based on preliminary engineering estimates completed in the second half of 2006. The total project investment will ultimately depend on comprehensive engineering studies, future estimated construction cost levels and project specification requirements for supply.

We currently own 100 percent of the MPEHtm project. However, two entities have separate options to participate as passive equity investors for up to an aggregate of 25 percent of our equity interest in the project. Future financing arrangements may also reduce our equity interest in the project. For additional information regarding the risks associated with the MPEHtm project, our estimated future reclamation costs and risks related to our reclamation obligations associated with the former assets and operations of the Main Pass facilities, see “Risk Factors” included in Item 1A. of this Form 10-K.

Marketing. We currently sell our natural gas in the spot market at prevailing prices. Prices on the spot market fluctuate with demand and as a result of related industry variables. We generally sell our crude oil and condensate one month at a time at prevailing market prices. From time to time, we may enter into transactions that fix the future prices for a portion of oil and natural gas sales volumes, through the issuance of oil and gas derivative contracts. See Note 7 for information regarding our existing oil and natural gas derivative contracts.

REGULATION

General. Our exploration, development and production activities are subject to federal, state and local laws and regulations governing exploration, development, production, environmental matters, occupational health and safety, taxes, labor standards and other matters. All material licenses, permits and other authorizations currently required for our operations have been obtained or timely applied for. Compliance is often burdensome, and failure to comply carries substantial penalties. The regulatory burden on the oil and gas industry increases the cost of doing business and affects profitability. For additional information related to the risks associated with the regulation of our oil and gas activities, see “Risk Factors” included in Item 1A. of this Form 10-K.

Exploration, Production and Development. Our exploration, production and development operations are subject to regulation at both the federal and state levels. Among other things, operators are required to obtain permits to drill wells and to meet bonding and insurance requirements in order to drill, own or operate wells. Regulations also control the location of wells, the method of drilling and casing wells, the restoration of properties upon which wells are drilled and the plugging and abandoning of wells. Our oil and gas operations are also subject to various conservation laws and regulations, which regulate the size

of drilling units, the number of wells that may be drilled in a given area, the levels of production, and the unitization or pooling of oil and gas properties.

Federal leases. As of December 31, 2007, after giving effect to the acquired Newfield properties, we currently have interests in 291 offshore leases located in federal waters on the Gulf of Mexico’s outer continental shelf. Federal offshore leases are administered by the MMS. These leases were issued through competitive bidding, contain relatively standard terms and require compliance with detailed MMS regulations and the Outer Continental Shelf Lands Act, which are subject to interpretation and change by the MMS. Lessees must obtain MMS approval for exploration, development and production plans prior to the commencement of offshore operations. In addition, approvals and permits are required from other agencies such as the U.S. Coast Guard, the Army Corps of Engineers and the Environmental Protection Agency. The MMS has regulations requiring offshore production facilities and pipelines located on the outer continental shelf to meet stringent engineering and construction specifications, and has proposed and/or promulgated additional safety-related regulations concerning the design and operating procedures of these facilities and pipelines. MMS regulations also restrict the flaring or venting of natural gas and prohibit the flaring of liquid hydrocarbons and oil without prior authorization.

The MMS has regulations governing the plugging and abandonment of wells located offshore and the installation and removal of all fixed drilling and production facilities. The MMS generally requires that lessees have substantial net worth or post supplemental bonds or other acceptable assurances that the obligations will be met. The cost of these bonds or other surety can be substantial, and there is no assurance that supplemental bonds or other surety can be obtained in all cases. We are meeting the supplemental bonding requirements of the MMS by providing financial assurances from MOXY. We and our subsidiaries’ ongoing compliance with applicable MMS requirements will be subject to meeting certain financial and other criteria. Under some circumstances, the MMS could require any of our operations on federal leases to be suspended or terminated. Any suspension or termination of our operations could have a material adverse affect on our financial condition and results of operations.

State and Local Regulation of Drilling and Production. We own interests in properties located in state waters of the Gulf of Mexico, offshore Louisiana and Texas. These states regulate drilling and operating activities by requiring, among other things, drilling permits and bonds and reports concerning operations. The laws of these states also govern a number of environmental and conservation matters, including the handling and disposing of waste materials, unitization and pooling of natural gas and oil properties, and the levels of production from natural gas and oil wells.

Environmental Matters. Our operations are subject to numerous laws relating to environmental protection. These laws impose substantial penalties for any pollution resulting from our operations. We believe that our operations substantially comply with applicable environmental laws. For additional information related to risks associated with these environmental laws and their impact on our operations, see “Risk Factors” included in Item 1A. of this Form 10-K.

Solid Waste. Our operations require the disposal of both hazardous and nonhazardous solid wastes that are subject to the requirements of the Federal Resource Conservation and Recovery Act and comparable state statutes. In addition, the EPA and certain states in which we currently operate are presently in the process of developing stricter disposal standards for nonhazardous waste. Changes in these standards may result in our incurring additional expenditures or operating expenses.

Hazardous Substances. The Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), also known as the “Superfund” law, imposes liability, without regard to fault or the legality of the original conduct, on some classes of persons that are considered to have contributed to the release of a “hazardous substance” into the environment. These persons include but are not limited to the owner or operator of the site or sites where the release occurred, or was threatened and companies that disposed or arranged for the disposal of the hazardous substances found at the site. Persons responsible for releases of hazardous substances under CERCLA may be subject to joint and several liability for the costs of cleaning up the hazardous substances and for damages to natural resources. Despite the “petroleum exclusion” of CERCLA that encompasses wastes directly associated with crude oil and gas production, we may generate or arrange for the disposal of “hazardous substances” within the meaning of CERCLA or comparable state statutes in the course of our ordinary operations. Thus, we may be responsible under CERCLA (or the state equivalents) for costs required to clean up sites where the release of a “hazardous substance” has occurred. Also, it is not uncommon for neighboring landowners

and other third parties to file claims for cleanup costs as well as personal injury and property damage allegedly caused by the hazardous substances released into the environment. Thus, we may be subject to cost recovery and to some other claims as a result of our operations.

Air. Our operations are also subject to regulation of air emissions under the Clean Air Act, comparable state and local requirements and the Outer Continental Shelf Lands Act. The scheduled implementation of these laws could lead to the imposition of new air pollution control requirements on our operations. Therefore, we may incur capital expenditures over the next several years to upgrade our air pollution control equipment. We do not believe that our operations would be materially affected by these requirements, nor do we expect the requirements to be any more burdensome to us than to other companies our size involved in exploration and production activities.

Water. The Clean Water Act prohibits any discharge into waters of the United States except in strict conformance with permits issued by federal and state agencies. Failure to comply with the ongoing requirements of these laws or inadequate cooperation during a spill event may subject a responsible party to civil or criminal enforcement actions. Similarly, the Oil Pollution Act of 1990 imposes liability on “responsible parties” for the discharge or substantial threat of discharge of oil into navigable waters or adjoining shorelines. A “responsible party” includes the owner or operator of a facility or vessel, or the lessee or permittee of the area in which a facility is located. The Oil Pollution Act assigns liability to each responsible party for oil removal costs and a variety of public and private damages. While liability limits apply in some circumstances, a party cannot take advantage of liability limits if the spill was caused by gross negligence or willful misconduct, or resulted from violation of a federal safety, construction or operating regulation. If the party fails to report a spill or to cooperate fully in the cleanup, liability limits likewise do not apply. Even if applicable, the liability limits for offshore facilities require the responsible party to pay all removal costs, plus up to $75 million in other damages. Few defenses exist to the liability imposed by the Oil Pollution Act.

The Oil Pollution Act also requires a responsible party to submit proof of its financial responsibility to cover environmental cleanup and restoration costs that could be incurred in connection with an oil spill. As amended by the Coast Guard Authorization Act of 1996, the Oil Pollution Act requires parties responsible for offshore facilities to provide financial assurance in amounts that vary from $35 million to $150 million depending on a company’s calculation of its “worst case” oil spill. Both Freeport Energy and MOXY currently have insurance to cover its facilities’ “worst case” oil spill under the Oil Pollution Act regulations. Thus, we believe that we are in compliance with this act in this regard.

Endangered Species. Several federal laws impose regulations designed to ensure that endangered or threatened plant and animal species are not jeopardized and their critical habitats are neither destroyed nor modified by federal action. These laws may restrict our exploration, development, and production operations and impose civil or criminal penalties for noncompliance.

Safety and Health Regulations. We are also subject to laws and regulations concerning occupational safety and health. We do not currently anticipate making substantial expenditures because of occupational safety and health laws and regulations. We cannot predict how or when these laws may be changed, or the ultimate cost of compliance with any future changes. However, we do not believe that any action taken will affect us in a way that materially differs from the way it would affect other companies in our industry.

EMPLOYEES

At December 31, 2007, we had a total of 110 employees located at our New Orleans, Louisiana headquarters and the Houston, Texas and Lafayette, Louisiana offices that were established in connection with the Newfield transaction. These employees are primarily devoted to production, regulatory, engineering, land, geological and various administrative functions. Our employees are not represented by any union or covered by a collective bargaining agreement, and we believe our relations with our employees are satisfactory.

Additionally, since January 1, 1996, numerous services necessary for our business and operations, including certain executive, technical, administrative, accounting, financial, tax and other services, have been performed by FM Services Company (FM Services) pursuant to a services

agreement. FM Services is a wholly owned subsidiary of Freeport-McMoRan Copper & Gold Inc. Either party may terminate the services agreement at any time upon 90 days notice (Note 12).

We also use contract personnel to perform various professional and technical services, including but not limited to drilling, construction, well site surveillance, environmental assessment, and field and on-site production operating services. These services are intended to minimize our development and operating costs as well as allow our management staff to focus on directing our oil and gas operations.

We maintain an ethics and business conduct policy applicable to all personnel employed by or affiliated with us. Our corporate governance guidelines and our ethics and business conduct policy are available at www.mcmoran.com and are available in print upon request. We intend to post promptly on our website amendments to or waivers, if any, of our ethics and business conduct policy made with respect to any of our directors and executive officers.

PROPERTIES

Oil and Gas Reserves. Our estimated proved oil and natural gas reserves at December 31, 2007 totaled 363.9 Bcfe, of which 67.5 percent represented natural gas reserves. All of our proved reserve estimates were prepared by Ryder Scott Company, L.P., an independent petroleum engineering firm, in accordance with the rules and regulations required by the SEC.

Our estimated proved reserves as of December 31, 2007 are summarized in the table below:

| | Gas | | Oil and condensate | | Total |

| | (MMcf) | | (MBbls) | | (MMcfe) |

| Proved developed: | | | | | | | | |

| Producing | | 91,710 | | | 8,049 | | | 140,006 |

| Non-producing | | 98,340 | | | 9,122 | | | 153,069 |

| Shut-in | | 13,545 | | | 281 | | | 15,233 |

| Total proved developed | | 203,595 | | | 17,452 | | | 308,308 |

| Proved undeveloped | | 42,011 | | | 2,265 | | | 55,600 |

| Total proved reserves | | 245,606 | | | 19,717 | | | 363,908 |

The following table presents the present value of estimated future net cash flows before income taxes from the production and sale of our estimated proved reserves as of December 31, 2007 (in thousands).

| | Proved Reserves |

| | Developed | | Undeveloped | | Total |

| Estimated undiscounted future net cash flows before | | | | | | | | |

| income taxes | $ | 2,021,404 | | $ | 306,687 | | $ | 2,328,091 |

| Present value of estimated future net cash flows before | | | | | | | | |

income taxes a | $ | 1,589,089 | | $ | 229,486 | | $ | 1,818,575 |

| a. | Calculated based on the prices and costs prevailing at December 31, 2007 and using a 10 percent per annum discount rate as required by the SEC. The weighted average price for all our properties with proved reserves was $92.69 per barrel of oil and $7.22 per Mcf of natural gas at December 31, 2007. |

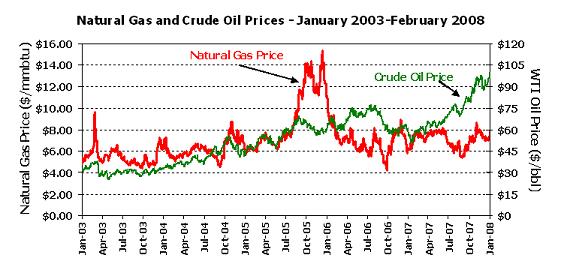

Production, Unit Prices and Costs. Our production during 2007 totaled approximately 39.0 Bcf of natural gas and 2.7 MMBbls of crude oil and condensate or an aggregate of 55.5 Bcfe. Our production during 2006 totaled approximately 14.5 Bcf of natural gas and 1.6 MMBbls of crude oil and condensate or an aggregate of 23.9 Bcfe. Average daily production from our properties, net to our interests, approximated 152 MMcfe/d in 2007, 65 MMcfe/d in 2006 and 36 MMcfe/d in 2005.

The following table shows production volumes, average sales prices and average production (lifting) costs for our oil and natural gas sales for each period indicated. The relationship between our

sales prices and production (lifting) costs depicted in the table is not necessarily indicative of our present or future results of operations.

| | | Years Ended December 31, | |

| | | 2007 | | 2006 | | 2005 | |

| Net natural gas production (Mcf) | | 38,994,000 | | 14,545,600 | | 7,938,000 | |

| Net crude oil and condensate production, excluding Main | | | | | | | |

Pass (Bbls)a | | 1,821,900 | | 779,000 | | 387,100 | |

| Net crude oil production from Main Pass (Bbls) | | 564,000 | | 775,500 | | 463,000 | |

| Sales prices: | | | | | | | |

| Natural gas (per Mcf) | | $ 7.01 | | $ 7.05 | | $ 9.24 | |

Crude oil and condensate, including Main Pass (per Bbl)b | | 76.55 | | 60.55 | | 53.82 | |

Production (lifting) costs: c | | | | | | | |

Per barrel for Main Pass d | | $44.17 | | $35.76 | | $41.46 | |

Per Mcfe for other properties e | | 1.88 | | 1.34 | | 1.06 | |

| a. | The volume produced during 2007 includes approximately 358,900 equivalent barrels of oil and condensate associated with $19.3 million of plant product revenues received for the value of such products recovered from the processing of our natural gas production. Our oil and condensate production includes 178,700 and 106,700 equivalent barrels of oil ($9.6 million and $5.0 million of revenues) associated with plant products during 2006 and 2005, respectively. |

| b. | Realization does not include the effect of the plant product revenues discussed in (a) above. |

| c. | Production costs exclude all depletion, depreciation and amortization expense. The components of production costs may vary substantially among wells depending on the production characteristics of the particular producing formation, method of recovery employed, and other factors. Production costs include charges under transportation agreements as well as all lease operating expenses including well insurance costs. |

| d. | Production costs for Main Pass included approximately $1.8 million, $3.17 per barrel in 2007, $3.6 million, $4.68 per barrel in 2006 and $3.9 million, $8.31 per barrel in 2005, of estimated repair costs for damages sustained during Hurricane Katrina. |

| e. | Production costs were converted to an Mcf equivalent on the basis of one barrel of oil being equivalent to six Mcf of natural gas. Production costs included workover expenses totaling $19.7 million or $0.38 per Mcfe in 2007, $4.5 million or $0.23 per Mcfe in 2006 and $1.2 million or $0.13 per Mcfe in 2005. |

Acreage. As of December 31, 2007, we owned or controlled interests in 603 oil and gas leases in the Gulf of Mexico and onshore Louisiana and Texas covering 1.52 million gross acres (0.64 million acres net to our interests). Our acreage position on the outer continental shelf includes 1.30 million gross acres (0.57 million acres net to our interests). We own leasehold interests to approximately 0.5 million acres, 0.1 million net to our interests, that are scheduled to expire in 2008.

We also hold potential reversionary interests in oil and gas leases that we have farmed-out or sold to other oil and gas exploration companies. Interest in these leases will partially revert to us upon the achievement of specified production thresholds or the realization of specified net production proceeds.

The following table shows the oil and gas acreage in which we held interests as of December 31, 2007. The table does not account for our gross acres associated with our farm-in, or certain other farm-out arrangements (approximately 0.10 million gross acres). For more information regarding our acreage position, see Note 3.

| | | Developed | | Undeveloped |

| | | Gross | | Net | | Gross | | Net |

| | | Acres | | Acres | | Acres | | Acres |

| Offshore (federal waters) | | 709,391 | | 412,034 | | 593,435 | | 162,641 |

| Onshore Louisiana and Texas | | 36,769 | | 18,255 | | 71,898 | | 30,523 |

| Total at December 31, 2007 | | 746,160 | | 430,289 | | 665,333 | | 193,164 |

Oil and Gas Properties. Our properties are primarily located on the outer continental shelf in the shallow waters of the Gulf of Mexico. We classify our activities based upon the drilling depth of our prospects. Our three principal classifications for Gulf of Mexico shelf prospects are traditional shelf, deep shelf and ultra deep shelf. Prospects located at drilling depths not exceeding 15,000 feet are considered to be traditional shelf prospects. Prospects exceeding 15,000 feet but not exceeding 25,000 feet are considered deep shelf prospects. Any prospect located at drilling depths exceeding 25,000 feet is considered to be an ultra deep shelf prospect. Since 2004, we have focused our exploration activities almost exclusively on deep shelf prospects, generally those located beneath shallow reservoirs where significant reserves have already been produced. Our acquisition of the Newfield properties significantly enhances our portfolio of shelf opportunities, increases our deep shelf exploration potential and provides access to new ultra deep shelf opportunities.

In addition to our Gulf of Mexico shelf properties, we also have property interests onshore and in the state waters of Louisiana and Texas and three deepwater properties in the Gulf of Mexico. The deepwater properties involve prospects located in water depths exceeding 1,000 feet.

Deep Shelf. The following table identifies select deep shelf discoveries as of December 31, 2007.

| | | Net | | | | | |

| | Working | Revenue | Water | Total | Production a |

| | Interest | Interest | Depth | Depth | Gross | | Net |

| | (%) | (%) | (feet) | (feet) | (MMcfe/d) |

| Louisiana State Lease 18090 | | | | | | | |

“Long Point” b | 37.5 | 26.7 | 8 | 19,000 | 54 | | 14 |

| St. Mary Parish, LA | | | | | | | |

“Laphroaig” c | 50.0 | 38.5 | <10 | 19,060 | 43 | | 16 |

| Louisiana State Lease 18350 | | | | | | | |

| “Point Chevreuil” | 25.0 | 17.5 | <10 | 17,051 | 13 | | 2 |

| Onshore Vermilion Parish, LA | | | | | | | |

“Liberty Canal” c | 37.5 | 27.6 | n/a d | 16,594 | 12 | | 3 |

| South Marsh Island Block 217 | | | | | | | |

“Hurricane” b | 27.5 | 19.4 | 10 | 19,664 | 11 | | 3 |

| Vermilion Blocks 16/17 | | | | | | | |

“King Kong” c | 40.0 | 29.2 | 13 | 18,918 | 3 | | 1 |

| South Marsh Island Block 212 | | | | | | | |

”Flatrock” b, e | 25.0 | 18.8 | 10 | 18,400 | f | | f |

| South Marsh Island Block 217 | | | | | | | |

“Hurricane Deep” b, e | 25.0 | 20.8 | <10 | 21,500 | g | | g |

| a. | Reflects average daily production rates for the fourth quarter of 2007. |

| b. | We were operator for drilling exploratory wells at these prospects. We relinquished being operator following successful completion of the related wells. |

| d. | Prospect is located onshore in Vermilion Parish, Louisiana. |

| e. | Prospect will be eligible for deep gas royalty relief under current MMS guidelines, which could result in an increased net revenue interest for early production. The guidelines exempt from U.S. government royalties production of as much as the first 25 Bcf from a depth of 18,000 feet or greater, and as much as 15 Bcf from depths between 15,000 and 18,000 feet, with gas production from all qualified wells on a lease counting towards the volume eligible for royalty relief. The exact amount of royalty relief depends on eligibility criteria, which include the well depth, nature of the well, and the timing of drilling and production. In addition, the guidelines include price threshold provisions that discontinue royalty relief if natural gas prices exceed a specified level. The price threshold was not exceeded during 2007, 2006 or 2005. |

| f. | The well commenced production on January 28, 2008 and on March 14, 2007 is producing at a gross rate of approximately 48 MMcfe/d and approximately 12 Mmcfe/d net to us. |

| g. | The well commenced production on January 24, 2008 and on March 14, 2007 is currently producing at a rate of approximately 22 MMcfe/d and approximately 5 MMcfe/d net to us. |

Traditional Shelf. The following table identifies select producing traditional shelf properties as of December 31, 2007.

| | | | | Net | | | | | |

| | | Working | | Revenue | | Water | | Production a | |

| Lease | | Interest | | Interest | | Depth | | Gross | | Net | |

| | | (%) | | (%) | | (feet) | | (MMcfe/d) | |

| | | | | | | | | | | | |

Eugene Island Block 182 b ,c | | 66.9 | | 52.8-63.6 | | 88 | | 22 | | 13 | |

Eugene Island Blocks 251/262 b | | 56.9 | | 43.9 | | 160 | | 23 | | 10 | |

Main Pass Block 299 b | | 100.0 | | 83.3 | | 210 | | 11 | | 9 | |

South Marsh Island Block 49 b | | 100.0 | | 83.3 | | 98 | | 10 | | 8 | |

High Island Block 474 c | | 69.2 | | 57.8 | | 180 | | 14 | | 8 | |

Grand Isle Block 3 b | | 50.0 | | 36.5 | | 10 | | 20 | | 7 | |

South Timbalier Block 148 b | | 58.2 | | 40.0 | | 86 | | 17 | | 7 | |

| East Cameron Block 373 | | 40.0 | | 33.3 | | 348 | | 19 | | 6 | |

South Marsh Island Block 141 b | | 87.3 | | 66.0 | | 230 | | 10 | | 6 | |

West Delta Block 133 b | | 75.0 | | 54.3 | | 373 | | 11 | | 6 | |

Vermilion Block 215 b | | 92.0 | | 76.8 | | 115 | | 8 | | 6 | |

| a. | Based on average daily production rates for fourth quarter of 2007. |

| b. | Fields operated by us. |

| c. | This property has multiple wells with varying ownership interests. Interests reflected in this table are approximate average working interest and net revenue interest for the field. |

Ultra Deep Shelf. We currently have no production from our ultra-deep shelf properties. We acquired interests from Newfield in leases associated with its Treasure Island and Treasure Bay ultra-deep gas prospect inventory. This ultra-deep prospect inventory currently consists of 86 lease blocks. We have been designated operator of the Blackbeard prospect, which is located at South Timbalier Block 168 in 70 feet of water (see “Oil and Gas Activities—Discoveries and Development Activities—Blackbeard” below). We currently hold an approximate 87.3 percent working interest in the well but are in discussions with third parties to participate in this prospect, the results of which are expected to decrease our current working interest. We are working to identify “deeper pool” exploration prospects on this ultra deep shelf acreage position.

Deep Water and Other Properties. Our deepwater properties are located in the Gulf of Mexico beyond the outer continental shelf. We currently have interests in three properties in the deepwater of the Gulf of Mexico. Our deepwater properties are the Garden Banks Block 625, 208 and 161 fields.

Oil and Gas Activity.

Discoveries and Development Activities. Since 2004, we have participated in 17 discoveries on 32 prospects that have been drilled and evaluated, including four discoveries announced in 2007. Three additional prospects are not yet fully evaluated.

Flatrock. We are pursuing aggressively the opportunities in the Flatrock area, located on OCS 310 at South Marsh Island Block 212 in approximately 10 feet of water.

The Flatrock No. 1 discovery well was drilled to a total depth of 18,400 feet in August 2007. Wireline and log-while-drilling porosity logs confirmed that the well encountered eight zones totaling 260 net feet of hydrocarbon bearing sands over a combined 637 foot gross interval, including five zones in the Rob-L section and three zones in the Operc section. Initial production was established in the 17,200 foot Operc interval on January 28, 2008. At March 14, 2008, the well was producing at a rate of approximately 48 MMcf/d and 845 barrels of condensate per day, approximately 12 MMcfe/d net to us.

The Flatrock No. 2 delineation well, which commenced drilling on October 7, 2007, is located approximately one mile northwest of the Flatrock discovery well. The well was drilled to a total depth of

17,684 feet and log while-drilling tools have indicated an additional resistive zone totaling 30 net feet of pay below 17,100 feet in the Operc Section. In total, the well encountered eight sands including four zones as indicated by wireline logs which contained 190 net feet of hydrocarbon bearing sands over a combined 318 foot gross interval above 15,500 feet in the Rob-L section and four zones as indicated by log-while-drilling tools totaling 70 net feet of resistivity below 15,500 feet in the Rob-L and Operc sections. Completion operations have commenced with initial production expected to be established in the thickest Rob-L interval by mid-year 2008.

The Flatrock No. 3 delineation well commenced drilling on November 5, 2007 and is located approximately 3,000 feet south of the Flatrock discovery well. The well has encountered a Rob-L interval, which contained 70 net feet of hydrocarbon bearing sands over a combined 280 foot gross interval above 15,500 feet as indicated by wireline logs and log-while-drilling tools have indicated two additional zones, a Rob-L sand and an Operc sand, totaling 40 net feet of resistivity. We are currently drilling in the top of the Operc sand. As anticipated, this Operc sand is consistent with and structurally higher to the sand currently producing in the Flatrock No. 1 discovery well. The well will be deepened to a proposed total depth of 18,800 feet to evaluate additional targets in the Operc sections.

Our initial production at the Flatrock No. 1 well and drilling results at the Flatrock No. 2 and 3 wells indicate that the Flatrock discovery is potentially significant. These wells are located in shallow water depths in an area with available infrastructure and the expansion of pipeline and facility capacity is currently underway. Depending on production from Flatrock and the development and production activities in the area, additional infrastructure expenditures may be required.

Hurricane Deep. The Hurricane Deep Prospect, located on South Marsh Island Block 217, commenced drilling on October 26, 2006 and was drilled to 20,712 feet true vertical depth. Logs have indicated that an exceptionally thick upper Gyro sand was encountered totaling 900 gross feet. Based on wireline logs, the top of the Gyro sand indicated 40 feet of net hydrocarbons in a 53 foot gross interval. This sand thickness suggests that prospects in the Mound Point/Hurricane/JB Mountain/Blueberry Hill area may have thick sands as potential Gyro reservoirs. The well commenced production from the Gyro sand on January 24, 2008 and at March 14, 2008 was producing at a gross rate of approximately 22 MMcfe/d, 5 MMcfe/d net to us. The Hurricane Deep well has two zones behind pipe in the shallower Rob-L and Operc sections of the well. We have a 25.0 percent working interest and a 17.7 percent net revenue interest in the Hurricane Deep Prospect which is located in twelve feet of water on OCS 310, one mile northeast of the currently producing Hurricane discovery well. We control 7,700 gross acres in this area.

Tiger Shoal/Mound Point. We control approximately 150,000 gross acres in the Tiger Shoal/Mound Point area (OCS Block 310/Louisiana State Lease 340). The addition of the Flatrock discovery follows a series of prior discoveries we have made in this area, including Hurricane, Hurricane Deep, JB Mountain, and Mound Point. Efforts to identify additional prospects in this area are in progress. We have drilled a total of eight successful wells in the OCS Block 310/Louisiana State Lease 340 area. We have multiple additional exploration opportunities with significant potential on this large acreage position.

Cottonwood Point. The Cottonwood Point well located on Vermilion Block 31 commenced drilling on May 1, 2007 and was drilled to 19,987 feet. Wireline logs have indicated approximately 43 net feet of hydrocarbon bearing sands over an approximate 92 foot gross interval in the upper Rob-L section. The targeted deeper Operc objectives were determined not to contain commercial quantities of hydrocarbons. The well was completed in the Rob-L section and production is expected to commence in the second quarter of 2008 following facilities installation.

Blackbeard. We acquired the Blackbeard prospect as part of our acquisition of the Newfield properties. The Blackbeard West well was previously drilled by Newfield and its partners to a total depth of 30,067 feet and encountered a thin gas-bearing sand below 30,000 feet. The well was temporarily abandoned in August 2006 before reaching its primary targets. We have contracted a rig to re-enter and deepen the well to a proposed depth of approximately 31,200 feet. The Blackbeard West well is located at South Timbalier Block 168 in 70 feet of water. The rig is on location and drilling operations are expected to commence in the near term. We currently hold an approximate 87.3 percent working interest in the well but are in discussions with third parties to participate in this prospect, the results of which are expected to decrease our current working interest.

Exploratory and Development Drilling. The following table shows the gross and net number of productive, dry, in-progress and total exploratory and development wells that we drilled in each of the periods presented.

| | | 2007 | | 2006 | | 2005 | |

| | | Gross | | Net | | Gross | | Net | | Gross | | Net | |

| Exploratory | | | | | | | | | | | | | |

| Productive | | 4 | | 1.150 | | 6 | | 2.375 | | 4 | | 1.426 | |

| Dry | | 1 | | 0.150 | | 4 | | 1.185 | a | 6 | | 2.021 | b |

| In-progress | | 5 | | 1.673 | | 4 | | 1.808 | | 5 | | 1.728 | |

| Total | | 10 | | 2.973 | | 14 | | 5.368 | | 15 | | 5.175 | |

| | | | | | | | | | | | | | |

| Development | | | | | | | | | | | | | |

| Productive | | - | | - | | 7 | | 2.613 | | 2 | | 0.667 | |

| Dry | | 1 | | 0.250 | | - | | - | | - | | - | |

In-progress c | | 2 | | 1.091 | | 2 | | 0.854 | | 5 | | 1.904 | |

| Total | | 3 | | 1.341 | | 9 | | 3.467 | | 7 | | 2.571 | |

| a. | Includes the exploratory well at Grand Isle Block 18 (0.26 net) that was determined to be nonproductive in early January 2007. |

| b. | Includes the exploratory wells at South Marsh Island Block 230 (0.25 net) and West Cameron Block 95 (0.50 net) that were determined to be non-productive in early January 2006. |

| c. | Includes the program’s 0.304 net interest in the Mound Point Offset No. 2 well (increased to 0.541 net interest for 2007) and 0.550 net interest in the JB Mountain No. 3, which have been temporarily abandoned. |

Productive Well Interests. The following table shows our interest in productive oil and natural gas wells as of December 31, 2007. For purposes of this table “productive wells” are defined as wells producing hydrocarbons and wells “capable of production” (for example, wells waiting for pipeline connections or wells waiting to be connected to currently installed production facilities). This table does not include (1) exploratory and development wells which have located commercial quantities of oil and natural gas but which are not capable of commercial production without installation of production facilities, or (2) wells that are shut-in and require a recompletion or workover to resume production. “Net wells” for the purposes of this table are defined to mean wells at our net revenue interest.

| | Gas | | Oil | |

| | Gross | | Net | | Gross | | Net | |

| Offshore | 175 | | 81.267 | | 87 | | 47.580 | |

| Onshore | 24 | | 9.078 | | 4 | | 2.251 | |

| Total | 199 | | 90.345 | | 91 | | 49.831 | |

Exploration Agreements.

Newfield. In connection with our acquisition of the Newfield properties, we also acquired 50 percent of Newfield’s interest in certain unproved exploration leases on the outer continental shelf of the Gulf of Mexico. At December 31, 2007, these interests encompassed 13 primary term blocks covering approximately 64,000 gross acres. In addition, we acquired a majority interest of Newfield’s ownership in leases associated with the Treasure Island and Treasure Bay ultra deep prospects. We have not drilled any wells on these acquired interests; however, the Blackbeard West ultra deep well is expected to commence in the first quarter of 2008 (see “Oil and Gas Activity – Discoveries and Development Activities – Blackbeard” above). For additional information about the acquisition of the Newfield properties, see “Business—Newfield Property Acquisition” above.

Plains Exploration & Production Company. Prior to our Newfield acquisition, we entered into an exploration agreement with Plains pursuant to which Plains obtained the right to participate in various exploration prospects in limited areas being explored by us. None of the properties we acquired from Newfield are subject to our agreement with Plains. As of December 31, 2007, Plains has participated in six prospects under the terms of this exploration arrangement.

El Paso Farm-Out Arrangement. We have a farm-out agreement with El Paso Production Company (El Paso) which resulted in the JB Mountain and Mound Point Offset discoveries in the OCS 310 and Louisiana State Lease 340 areas, respectively. Through this arrangement, El Paso currently has rights to an approximate 13,000 gross acres surrounding the JB Mountain prospect (55 percent working interest and a 38.8 percent net revenue interest) and the Mound Point Offset prospect (30.4 percent working interest and a 21.6 percent net revenue interest). El Paso retains 100 percent of the program’s interests until the aggregate production attributable to the program’s net revenue interests reaches 100 Bcfe, after which, ownership of 50 percent of the program’s working and net revenue interests would revert to us. There are three producing wells subject to the 100 Bcfe arrangement, which averaged an aggregate gross rate of approximately 26 MMcfe/d during 2007. We do not expect payout under the 100 Bcfe arrangement will occur in 2008.

This report includes "forward looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including statements about our plans, strategies, expectations, assumptions and prospects. "Forward-looking statements" are all statements other than statements of historical fact, or current facts, that address activities, events, outcomes and other matters that we plan, expect, intend, assume, believe, budget, predict, forecast, project, estimate or anticipate (or other similar expressions) will, should or may occur in the future, such as: statements regarding our financial plans; our indebtedness; acquisitions; our exploration and development plans and the potential development of the MPEH™ project; our ability to satisfy the MMS reclamation obligations with respect to Main Pass and our environmental obligations; drilling potential and results; anticipated flow rates of producing wells; anticipated initial flow rates of new wells; reserve estimates and depletion rates; general economic and business conditions; risks and hazards inherent in the production of oil and natural gas; demand and potential demand for oil and natural gas; trends in oil and natural gas prices; amounts and timing of capital expenditures and reclamation costs; and our ability to obtain necessary permits for new operations.

Forward-looking statements are based on assumptions and analyses made in light of our experience and perception of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. These statements are subject to a number of assumptions, risks and uncertainties, including the risk factors discussed below and in our other filings with the SEC, general economic and business conditions, the business opportunities that may be presented to and pursued by us, changes in laws and other factors, many of which are beyond our control. Except for our ongoing obligations under federal securities laws, we do not intend, and we undertake no obligation, to update or revise any forward-looking statements. Readers are cautioned that forward-looking statements are not guarantees of future performance and actual results and developments may differ materially from those projected in the forward-looking statements. Important factors that could cause actual results to differ materially from our expectations include, among others, the following:

Risks Relating to Financial Matters

Our substantial indebtedness, including the indebtedness incurred in connection with the acquisition of the Newfield properties and our recent senior notes offering, could adversely affect our operating results and financial condition.

We incurred significant debt to fund the acquisition of substantially all of the proved property interests and related assets of Newfield Exploration Company (Newfield) located on the outer continental shelf of the Gulf of Mexico, as well as in connection with the offering of our 11.875% Senior Notes to repay a portion of that debt. As of December 31, 2007, the outstanding principal amount of our indebtedness was approximately $800.5 million, including $100.9 million for our 6% convertible senior notes that will mature on July 2, 2008. Our level of indebtedness could have important consequences. For example, it could:

| · | make it difficult for us to service our debt; |

| · | increase our vulnerability to adverse changes in economic and industry conditions; |

| · | require us to dedicate a substantial portion of our cash flow from operations and proceeds of equity issuances or asset sales to pay or provide for our indebtedness, thus reducing the |

availability of cash flows to fund working capital, capital expenditures, acquisitions, investments and other general corporate purposes;

| · | limit our flexibility to plan for, or react to, changes in our businesses and the markets in which we operate; |

| · | place us at a competitive disadvantage to our competitors that have less debt; and |

| · | limit our ability to borrow money or sell stock to fund our working capital, capital expenditures, acquisitions, and debt service requirements and other financing needs. |

In addition, we may need to incur additional indebtedness in the future in the ordinary course of business. The terms of our amended and restated credit facility and other agreements governing our indebtedness allow us to incur limited amounts of additional debt. If new debt is added to current debt levels, the risks described above could intensify. Further, if future debt financing is not available to us when required or is not available on acceptable terms, we may be unable to grow our business, take advantage of business opportunities, respond to competitive pressures or refinance maturing debt, any of which could have a material adverse effect on our operating results and financial condition.

Our future revenues will be reduced as a result of agreements that we have entered into and may enter into in the future with third parties.

We have agreements with third parties to support the funding of the exploration and development of certain of our properties. These agreements will reduce our future revenues. For example, we have entered into a farm-out agreement with El Paso Production Company, a subsidiary of El Paso Corporation (El Paso), to fund the exploration and development of four of our prospects, two of which resulted in discoveries and two of which were nonproductive. We have also participated in a multi-year exploration venture agreement with a private exploration and production company, which generally participated for 50 percent of our interest, paid 50 percent of our costs and assumed 50 percent of our obligations with respect to our prospects in which it elected to participate. Finally, prior to our Newfield acquisition, we entered into an exploration agreement with Plains pursuant to which Plains obtained the right to participate in various exploration prospects in limited areas being explored by us. None of the properties we acquired from Newfield are subject to our agreement with Plains. As of December 31, 2007, Plains has participated in six prospects under the terms of this exploration arrangement.

We may also seek to enter into additional farm-out or other arrangements with other companies. Such arrangements would reduce our share of future revenues associated with our exploration prospects and will defer the realization of the value of our interest in the prospects until specified production quantities have been achieved, or specified net production proceeds have been received by our partners in these ventures. Consequently, even if exploration and development of our prospects is successful, we cannot assure you that such exploration and development will result in an increase in our revenues or our proved oil and gas reserves or when such increases might occur.

We have incurred losses from our operations in the past and may continue to do so in the future. Our failure to achieve profitability in the future could adversely affect the trading price of our common stock and our other securities and our ability to raise additional capital.

Our continuing operations, which include start-up costs for the Main Pass Energy Hubtm (MPEHtm) project, incurred losses of $63.6 million in 2007, $44.7 million in 2006 and $31.5 million in 2005. No assurance can be given that we will achieve profitability or positive cash flows from our operations in the future. Our failure to achieve profitability in the future could adversely affect the trading price of our common stock, our other securities and our ability to raise additional capital.

We are responsible for reclamation, environmental and other obligations relating to both our oil and gas properties, including the acquired Newfield properties and our former sulphur operations, including Main Pass and Port Sulphur.

As of December 31, 2007, we had accrued $294.7 million relating to the reclamation liabilities with respect to our oil and gas properties, including $268.6 million of estimated reclamation liabilities assumed with the acquisition of the Newfield properties. Among these reclamation obligations are the plugging and abandonment of wells, the reclamation and removal of platforms, facilities and pipelines and the repair and replacement of wells, equipment and facilities, including obligations associated with

damages sustained from Hurricanes Ivan, Katrina and Rita. The scope and cost of these obligations may ultimately be materially greater than estimated at the time of the acquisition.

In December 1997, we assumed responsibility for potential liabilities, including environmental liabilities, associated with the prior conduct of the businesses of our predecessors. Among these are potential liabilities arising from sulphur mines that were depleted and closed in accordance with environmental laws in effect at the time, particularly in coastal or marshland areas that have experienced subsidence or erosion that has exposed previously buried pipelines and equipment. New laws or actions by governmental agencies calling for additional reclamation action on those closed operations could result in significant additional reclamation costs for us. We could also be subject to potential liability for personal injury or property damage relating to wellheads or other materials at closed mines in coastal areas that have become exposed through coastal erosion. As of December 31, 2007, we had $10.5 million relating to accrued reclamation liabilities with respect to our discontinued Main Pass sulphur operations of which $2.6 million has been prepaid as of December 31, 2007, and $10.8 million relating to accrued reclamation liabilities with respect to our other discontinued sulphur operations, including $9.6 million for the Port Sulphur facilities. We are in the process of completing closure activities at the Port Sulphur facilities following damages sustained by the facilities from Hurricanes Katrina and Rita in 2005.

We cannot assure you that actual reclamation costs ultimately incurred will not exceed our current and future accruals for reclamation costs, that we will have the necessary resources to satisfy these obligations in the future, or that we will be able to satisfy applicable bonding requirements.

We are subject to indemnification obligations with respect to: (1) the sulphur transportation and terminaling assets that we sold in June 2002, including sulphur and oil and gas obligations arising under environmental laws; and (2) our acquisition of the Newfield properties.

We are subject to indemnification obligations with respect to the sulphur operations previously engaged in by us and our predecessor companies. In addition, we assumed, and agreed to indemnify IMC Global Inc. (now a subsidiary of Mosaic Company) from certain potential obligations, including environmental obligations relating to historical oil and gas operations conducted by the Freeport-McMoRan companies prior to the 1997 merger of Freeport-McMoRan Inc. and IMC Global. We have also assumed and agreed to indemnify Newfield from certain potential obligations, including environmental obligations relating to our acquisition of the Newfield properties. The scope and cost of these obligations may ultimately be materially greater than estimated at the time of the acquisition. Our liabilities with respect to those obligations could adversely affect our operations and liquidity.

Our ability to collect our accounts receivable depends on the continuing creditworthiness of our customers.

The majority of our accounts receivable result from oil and natural gas sales or joint interest billings to third parties in the energy industry. Our credit risk associated with these third parties may increase as we produce and sell oil and natural gas on a larger scale. These third parties may be affected by adverse changes in market conditions resulting in downgrades to credit ratings or other consequences. While we sell oil and natural gas to companies that we believe are reasonable credit risks, there is no guaranty that the risk associated with the creditworthiness of these parties will not increase.

Risks Relating to our Operations

Acquisitions involve risks, including unanticipated liabilities and expenses associated with acquired properties, difficulties in integrating acquired properties into our business, diversion of management attention, and increases in the scope and complexity of our operations.

We completed the Newfield acquisition on August 6, 2007 with an effective date of July 1, 2007. We were only able to complete a limited review of the acquired properties by the time of the August 6 closing and we may have not identified all existing or potential contingent exposures to which we could be subject in the future from the acquisition. It is possible that we will discover issues with an acquired property asset or potential liability that we did not anticipate at the time the acquisition was completed. These issues may be material and could include, among other things, unexpected environmental issues,

title defects or other liabilities. Often, we acquire properties on an “as is” basis and have limited or no remedies against the seller, including Newfield, with respect to these potential exposures.

The failure to successfully integrate acquired operations into our existing operations may affect our ability to operate at optimal performance levels and may require significant management attention and financial resources that would otherwise be available for the ongoing development or expansion of our existing operations. Challenges involved in the integration process may include retaining key employees, maintaining key employee morale, addressing differences in business cultures, processes and systems and developing internal expertise regarding the acquired properties and assets.

The high-rate production characteristics of our Gulf of Mexico properties and our ownership interests in prospects subject to farm-out arrangements subject us to high reserve replacement needs.

Our future financial performance depends in large part on our ability to find, develop and produce oil and natural gas reserves, and we cannot make any assurances that we will be able to do so profitably. Unless we conduct successful exploration and development activities, acquire properties with proved reserves, or meet certain production and related thresholds in our prospects subject to farm-out arrangements, our proved reserves will decline as they are produced.

Producing natural gas and oil reservoirs are generally characterized by declining production rates that vary depending on reservoir characteristics and other factors. Production from the Gulf of Mexico shelf generally declines at a faster rate than in other producing regions of the world. Reservoirs in the Gulf of Mexico shelf are generally sandstone reservoirs characterized by high porosity and high permeability that results in an accelerated recovery of production in a relatively short period of time, with a generally more rapid decline near the end of the life of the reservoir. This results in recovery of a relatively higher percentage of reserves during the initial years of production, and a corresponding need to replace these reserves with discoveries at new prospects at a relatively rapid rate.

Additionally, our ownership interests in prospects subject to farm-out or other exploration arrangements will revert to us only upon the achievement of a specified production threshold or the receipt of specified net production proceeds. As a result, significant discoveries on these prospects will be needed before we can increase our revenues or our proved oil and gas reserves. We cannot predict with certainty that our exploration or farm-out arrangements will result in an increase in our revenues or proved oil and gas reserves, or if they do result in an increase, when that increase might occur.

We will require additional capital to fund our future drilling activities and the development of other projects. If we fail to obtain additional capital, we may not be able to continue our operations or the development of these projects.

Historically, we have funded our operations and capital expenditures through:

| | • | our cash flow from operations; |

| | • | entering into exploration arrangements with other third parties; |

| | • | selling oil and gas properties; |

| | • | borrowing money from banks; |

• issuance of senior notes; and

| | • | selling preferred stock, common stock and securities convertible into common stock. |

In the near-term, we plan to continue to pursue the drilling of our exploration prospects and the development of other projects, such as the MPEH TM project. We incurred $153.2 million in capital expenditures in 2007. We expect that our capital expenditures during 2008 will total approximately $225 million, including $40 million of carryover costs from 2007, $90 million for costs associated with Flatrock, Blackbeard West and other exploration opportunities and approximately $95 million for anticipated development costs. These expenditures could increase if our drilling efforts are successful. Although we intend to fund our near-term expenditures with available cash, operating cash flows and

borrowings under our senior secured revolving credit facility, we may need to raise additional capital through future equity or debt transactions to continue our drilling activities and other project developments.

Our exploration and development activities may not be commercially successful.

Oil and natural gas exploration and development activities involve a high degree of risk that hydrocarbons will not be found, that they will not be found in commercial quantities, or that the value produced will be less than the related drilling, completion and operating costs. The 3-D seismic data and other technologies that we use provide no assurance prior to drilling a well that oil or natural gas is present or economically producible. The cost of drilling, completing and operating a well is often uncertain, especially when drilling offshore and when drilling deep wells. Our drilling operations may be changed, delayed or canceled as a result of numerous factors, including:

| | • | the market price of oil and natural gas; |

| | • | unexpected drilling conditions; |

| | • | unexpected pressure or irregularities in geologic formations; |

| | • | equipment failures or accidents; |

| | • | tropical storms, hurricanes and other adverse weather conditions, which are common in the Gulf of Mexico during certain times of the year; |

| | • | regulatory requirements; and |

| | • | equipment and labor shortages resulting in cost overruns. |

Additionally, completion of a well does not guarantee that it will be profitable or even that it will result in recovery of the related drilling, completion and operating costs.

We plan to conduct most of our near-term exploration and development activities on deep shelf prospects in the shallow waters of the Gulf of Mexico, an area that has had limited historical drilling activity due, in part, to its geologic complexity. Deeper targets are more difficult to detect with traditional seismic processing and the expense of drilling deep shelf wells and the risk of mechanical failure is significantly higher because of the higher temperatures and pressure found at greater depths. Our exploratory wells require significant capital expenditures (typically ranging between $15-$20 million, net to our interests) before we can ascertain whether they contain commercially recoverable oil and natural gas reserves. Prior experience also suggests that the gross drilling costs for deep shelf exploratory wells can potentially exceed as much as $50 million per well. Accordingly, we cannot assure you that our oil and natural gas exploration activities, either on the deep shelf or elsewhere, will be commercially successful.

The future results of our oil and natural gas business are difficult to forecast, primarily because the results of our exploration strategy are unpredictable.

A significant portion of our oil and natural gas business is devoted to exploration, the results of which are unpredictable. In addition, we use the successful efforts accounting method for our oil and natural gas exploration and development activities. This method requires us to expense geologic and geophysical costs and the costs of unsuccessful exploration wells as they are incurred, rather than capitalizing these costs up to a specified limit as permitted pursuant to the full cost accounting method. Because the timing difference between incurring exploration costs and realizing revenues from successful properties can be significant, losses may be reported even though exploration activities may be successful during a reporting period. Accordingly, depending on our exploration results, we may incur significant additional losses as we continue to pursue our exploration activities. We cannot assure you that our oil and gas operations will enable us to achieve or sustain positive earnings or cash flows from operations in the future.

To sell our natural gas and oil we depend upon the availability, proximity and capacity of natural gas gathering systems, pipelines and processing facilities, which are owned by others.