UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________________________________

FORM 10-K

_________________________________

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 27, 2021

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 0-6365

_________________________________

APOGEE ENTERPRISES, INC.

(Exact name of registrant as specified in its charter)

_________________________________

| | | | | | | | | | | | | | | | | |

| Minnesota | | | | | 41-0919654 |

(State or other jurisdiction of

incorporation or organization) | | | | | (I.R.S. Employer

Identification No.) |

| | | | | |

| 4400 West 78th Street | Suite 520 | Minneapolis | Minnesota | | 55435 |

| (Address of principal executive offices) | | | | (Zip Code) |

Registrant’s telephone number, including area code: (952) 835-1874

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, $0.33 1/3 Par Value | | APOG | | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | | ☐ | | Accelerated Filer | | ☒ |

| | | | | | |

| Non-accelerated Filer | | ☐ | | Smaller Reporting Company | | ☐ |

| Emerging Growth Company | | ☐ | | | | |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | | ☐ |

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

As of August 28, 2020, the last business day of the registrant's most recently completed second fiscal quarter, the approximate aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant was $560,000,000 (based on the closing price of $21.69 per share as reported on the NASDAQ Stock Market LLC as of that date).

As of April 20, 2021, 25,781,624 shares of the registrant’s common stock, par value $0.33 1/3 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

In accordance with General Instruction G(3) of Form 10-K, certain information required by Part III hereof will either be incorporated into this Annual Report on Form 10-K by reference to our Definitive Proxy Statement for our Annual Meeting of Shareholders filed within 120 days of our fiscal year ended February 27, 2021 or will be included in an amendment to this Annual Report on Form 10-K filed within 120 days of February 27, 2021.

APOGEE ENTERPRISES, INC.

Annual Report on Form 10-K

For the fiscal year ended February 27, 2021

TABLE OF CONTENTS

PART I

ITEM 1. BUSINESS

The Company

Apogee Enterprises, Inc. (Apogee, the Company or we) was incorporated under the laws of the State of Minnesota in 1949. We are a leader in the design and development of architectural building products and services.

Our Company has four reporting segments, with three of the segments serving the commercial construction market:

•The Architectural Framing Systems segment designs, engineers, fabricates and finishes aluminum window, curtainwall, storefront and entrance systems comprising the exterior of buildings. In fiscal 2021, this segment accounted for approximately 46 percent of our net sales.

•The Architectural Glass segment coats and fabricates, high-performance glass used in custom window and wall systems on commercial buildings. In fiscal 2021, this segment accounted for approximately 24 percent of our net sales.

•The Architectural Services segment integrates technical services, project management, and field installation services to design, engineer, fabricate, and install building glass and curtainwall systems. In fiscal 2021, this segment accounted for approximately 24 percent of our net sales.

•The Large-Scale Optical Technologies (LSO) segment manufactures value-added coated glass and acrylic products for custom framing, museum, and technical glass markets. In fiscal 2021, this segment accounted for approximately 6 percent of our net sales.

Strategy

Our strategy is to diversify revenue streams within the commercial construction industry, providing revenue growth and profit generation over an economic cycle, and utilize our capabilities to enter adjacent segments. We work to diversify end markets served through growth from new geographies, new products and new market segments, while working to improve margins through productivity, integration, project selection and rigorous cost management.

In an effort to drive growth and reduce our exposure to the cyclical nature of the large-building segment of the commercial construction industry, we are working to expand our capabilities to serve small- and mid-sized projects across our architectural segments and working to expand our North American geographic reach.

Specifically over the past fiscal year, in the Architectural Framing Systems segment, our focus was to drive margin improvement through increased productivity, cost management, integration, supply chain optimization, and new product development. In the Architectural Glass segment, we began operation of our new fabrication facility designed to serve small-sized and quick-turn projects in Dallas, Texas. In the Architectural Services segment, our emphasis is to generate consistent margins through focused project selection and execution, while continuing to deliver long-term organic growth through targeted geographic expansion.

Within the LSO segment, we are working to grow in new channels, markets and geographies that desire the value-added properties that our glass and acrylics products provide.

Across all our segments, we regularly evaluate business development opportunities in adjacent sectors that will complement our existing portfolio. Finally, we are constantly working to improve the efficiency and productivity of our operations by implementing continuous improvement, lean manufacturing principles and automation where we can achieve solid return on investment.

Products and Services

Architectural Framing Systems, Architectural Glass and Architectural Services segments

These three segments serve the commercial construction industry and participate in various phases of the value stream to design, engineer, fabricate and install custom glass and aluminum window, curtainwall, storefront and entrance systems comprising the exterior of buildings, primarily in the commercial, institutional and multi-family residential construction sectors.

Within our Architectural Framing Systems segment, we design, engineer and fabricate aluminum window, curtainwall, storefront and entrance systems. We also extrude aluminum and provide finishing services for metal components used in a variety of building materials applications, as well as plastic components for other markets.

In our Architectural Glass segment, we fabricate coated glass and apply high-performance coatings to uncoated glass to create a variety of aesthetic characteristics, unique designs and energy-efficient qualities. We also laminate and temper layers of glass and vinyl for protection and strength against hazards such as severe weather and blasts. Much of our high-performance glass is

made-to-order and is typically fabricated into insulating and/or laminated glass units for window, curtainwall, storefront or entrance systems.

Our Architectural Services segment delivers value by integrating technical capabilities, project management skills and field installation services, to provide design, engineering, fabrication and installation services for the exteriors of commercial buildings. Our ability to efficiently design high-quality window and curtainwall systems and effectively manage the installation of building façades enables our customers to meet schedule and cost requirements of their projects.

Our product and service offerings across these architectural segments allow architects to create distinctive looks for buildings such as office towers, hotels, education and athletic facilities, health care facilities, government buildings, retail centers, mixed use and multi-family residential buildings, while also meeting functional requirements such as energy efficiency, hurricane, blast and other impact resistance and/or sound control.

Many of our architectural products and services help architects, developers, and building owners achieve their energy-efficiency and sustainability goals, by improving energy performance, thereby reducing greenhouse gas emissions, providing daylight and natural ventilation, and increasing comfort and safety for occupants. These products include high-performance thermal framing systems, energy efficient glass coatings, and sun control products such as sunshades and light shelves. Many of our framing systems products can be specified with recycled aluminum content and utilize environmentally friendly anodize and paint finishes. In addition, we offer a wide range of renovation solutions to help modernize aging buildings, providing significantly improved energy performance, while preserving historically accurate aesthetics.

LSO segment

The LSO segment provides coated glass and acrylic primarily for use in custom picture framing, museum framing, wall decor and technical glass for other display applications. Products vary based on size and coatings to provide conservation-grade UV protection, anti-reflective and anti-static properties and/or security features.

Product Demand and Distribution Channels

Architectural Framing Systems, Architectural Glass and Architectural Services segments

Demand for the products and services offered by our architectural segments is affected by changes in the North American commercial construction industry, as well as by changes in general economic conditions. Additionally, the Architectural Glass segment has Brazilian operations which are impacted by Brazil's commercial construction industry and general economic conditions.

We look at several external indicators to analyze potential demand for our products and services, such as U.S. and Canadian job growth, office vacancy rates, credit and interest rates available for commercial construction projects, architectural billing statistics and material costs. We also rely on internal indicators to analyze demand, including our sales pipeline, which is made up of contracts in review, projects awarded or committed, and bidding activity. Our sales pipeline, together with ongoing feedback, analysis and data from our customers, architects and building owners, provide visibility into near- and medium-term future demand. Additionally, we evaluate data on U.S. and Canadian non-residential construction market activity, industry analysis and longer-term trends provided by external data sources.

Our architectural products and services are used in subsets of the construction industry differentiated by the following types of factors:

•Building type - Our products and services are primarily used in commercial buildings (office buildings, hotels and retail centers), institutional buildings (education facilities, health care facilities and government buildings), and multi-family residential buildings (a subset of residential construction).

•Level of customization - Many of our projects involve a high degree of customization, as the product or service is designed to meet customer-specified requirements for aesthetics, performance and size, and local building codes.

•Customers and distribution channels - Our customers are mainly glazing subcontractors and general contractors, with project design being influenced by architects and building owners. Our high-performance architectural glass is primarily sold using both a direct sales force and independent sales representatives. Our installation services are sold by a direct sales force in certain metropolitan areas in the U.S. Our window, curtainwall, storefront and entrance systems are sold using a combination of direct sales forces, independent sales representatives and distributors.

•Geographic location - We primarily supply architectural glass products and aluminum framing systems, including window, curtainwall, storefront and entrance systems, to customers in North America. We are one of only a few

architectural glass installation service companies in the U.S. to have a national presence and we have the ability to provide remote installation project management throughout the U.S. Our Architectural Glass segment also supplies architectural glass products to customers in Brazil and certain other international locations.

LSO segment

In our LSO segment, we have a leading brand of value-added coated glass and acrylic used in the custom picture-framing market and museum market. Under the Tru Vue brand, products are sold primarily in North America through national and regional retail chains using a direct sales force, as well as through local retailers using an independent distribution network. We also supply our glass, acrylic and other products to museums, galleries and other organizations in Europe and other international locations through independent distributors.

Competitive Conditions

Architectural Framing Systems, Architectural Glass and Architectural Services segments

The North American commercial construction market is highly fragmented. Competitive factors include price, product quality, product attributes and performance, reliable service, on-time delivery, lead-time, warranty and the ability to provide project management, technical engineering and design services. To protect and enhance our competitive position, we maintain strong relationships with building owners and architects, who influence the selection of products and services on a project, and with general contractors, who initiate projects and develop specifications.

There is a great deal of competition in the North American commercial window and storefront manufacturing industry, and our Architectural Framing Systems segment competes against several national, regional and local aluminum window and storefront manufacturers, as well as regional paint and anodizing finishing companies. Our businesses compete by providing high-quality products, innovation, reliable on-time delivery and short lead times.

In our Architectural Glass segment, we experience competition from regional glass fabricators who can provide certain products with attributes similar to our products. Within the market sector for large, complex projects, we encounter competition from international companies and large regional fabricators, some of which have benefited from the relative strength of the U.S. dollar and lower fabrication costs in recent years. We differentiate ourselves by providing high-quality, innovative and customizable products, short lead times, and strong customer service.

Our Architectural Services segment competes against national and regional glass installation companies. We distinguish ourselves from these competitors through our strong project management and our track record of regularly meeting each project's unique execution requirements.

LSO segment

Product attributes, price, quality, marketing and service are the primary competitive factors in the LSO segment. Our competitive strengths include our excellent relationships with customers, innovative marketing programs and the performance of our value-added products. We compete with certain European and U.S. valued-added glass and acrylic companies.

Warranties

We offer product and service warranties that we believe are competitive for the markets in which our products and services are sold. The nature and extent of these warranties depend upon the product or service, the market and, in some cases, the customer being served. Our standard warranties are generally from two to 10 years for our architectural glass, curtainwall and window system products, while we generally offer warranties of two years or less on our other products and services.

Sources and Availability of Raw Materials

Materials used in the Architectural Framing Systems segment include aluminum billet and extrusions, fabricated glass, plastic extrusions, hardware, paint and chemicals. Raw materials used within the Architectural Glass segment include flat glass, vinyl, silicone sealants and lumber. Within the Architectural Services segment, materials used include fabricated glass, finished aluminum extrusions, fabricated metal panels and hardware. Materials used in the LSO segment are primarily glass and acrylic. Most of our raw materials are readily available from a variety of domestic and international sources.

Trademarks and Patents

We have several trademarks and trade names that we believe have significant value in the marketing of our products, including APOGEE®. Trademark registrations in the U.S. are generally for a term of 10 years, renewable every 10 years as long as the trademark is used in the regular course of trade.

Within the Architectural Framing Systems segment, LINETEC®, WAUSAU WINDOW AND WALL SYSTEMS®, TUBELITE®, ADVANTAGE BY WAUSAU®, 300ES®, FINISHER OF CHOICE®, THERML=BLOCK®, MAXBLOCK®,

DFG®, ECOLUMINUM®, ALUMINATE®, GET THE POINT!®, FORCEFRONT®, SOTAWALL®, SOTA®, HYBRID-WALL®, EFCO®, TERRASTILE®, THERMASTILE®, TRIPLE SET®, ULTRADIZE®, ULTRAFLUR®, ULTRALINE®, ULTRAPON® and XTHERM® are registered trademarks. CUSTOM WINDOW™, INVENT™, INVENT.PLUS™, INVENT RETRO™, INVISION™, CLEARSTORY™, EPIC™, HERITAGE™, VISULINE™, SEAL™, SUPERWALL™, CROSSTRAK™, HP-Wall™, VersaTherm™, E-Strut™, E-Shade™, E-Lite™, Series 960 Wall™, Durastile™ and X Force™ are unregistered trademarks. ALUMICOR™, BUILDING EXCELLENCE™, TerraPorte 7600 Out-Swing accessABLE™, ThermaSlide™ 7000, Integra 6000™, ThermaSlide™ and SecureSash™ are unregistered trademarks in Canada.

Within the Architectural Glass segment, VIRACON®, DIGITALDISTINCTIONS®, ROOMSIDE®, GLASS IS EVERYTHING®, CLEARPOINT®, CYBERSHIELD®, STORMGUARD®, ACCELERATING YOUR ARCHITECTURAL GLASS®, VELOCITY, AN APOGEE COMPANY® and VTS® are registered trademarks. VIRASPAN™ is an unregistered trademark. In addition, GLASSECVIRACON®, GLASSEC®, INSULATTO® and GV PRIME® are registered trademarks in Brazil.

Within the Architectural Services segment, HARMON®, H DESIGN®, HARMON GLASS®, HI-7000®, and BUILDING TRUST IN EVERYTHING WE DO® are registered trademarks. UCW-8000™, HI-8500™, HI-9000™, SMU-6000™ and HPW-250™ are unregistered trademarks.

Within the LSO segment, TRU VUE®, CONSERVATION CLEAR®, CONSERVATION REFLECTION CONTROL®, ULTRAVUE®, MUSEUM GLASS®, OPTIUM®, PREMIUM CLEAN®, REFLECTION CONTROL®, AR REFLECTION-FREE®, OPTIUM ACRYLIC®, OPTIUM MUSEUM ACRYLIC®, CONSERVATION MASTERPIECE®, CONSERVATION MASTERPIECE ACRYLIC®, TRU VUE AR®, STATICSHIELD®, TRULIFE®, and VISTA AR® are registered trademarks. TRULIFE INFINITY FRAME™, PREMIUM CLEAR™, THE DIFFERENCE IS CLEAR™ and TRU FRAMEABLE MOMENTS™ are unregistered trademarks and TRUBARRIER™ is pending federal registration.

We have several patents pertaining to our glass coating methods and products, for hybrid window wall/curtainwall systems and methods of installation, and for our UV coating and etch processes for anti-reflective glass for the picture framing industry and fine art market. Despite being a point of differentiation from our competitors, no single patent is considered to be material.

Seasonality

Activity in the construction industry is impacted by the seasonal impact of weather and weather events in our operating locations, with activity in some markets reduced in winter due to inclement weather.

Working Capital Requirements

Trade and contract-related receivables and other contract assets are the largest components of our working capital. Inventory requirements, mainly related to raw materials, are most significant in our Architectural Framing Systems and Architectural Glass segments.

Backlog

Backlog represents the dollar amount of signed contracts or firm orders, generally as a result of a competitive bidding process, which may be expected to be recognized as revenue in the future. Backlog is not a term defined under U.S. GAAP and is not a measure of contract profitability. In addition to backlog, we have a substantial amount of projects with short lead times that book-and-bill within the same reporting period and are not included in backlog. We have good visibility beyond backlog, as projects awarded, verbal commitments and bidding activities are not included in backlog.

Architectural Framing Systems segment backlog as of year-end was $411.3 million, compared to $429.6 million at the end of the prior year, reflecting a decline in order volume. We expect approximately 60 percent of the backlog in this segment to be fulfilled in fiscal 2022, with the remainder expected to be filled in fiscal 2023 and beyond; however, the timing of backlog may be impacted by project delays.

Architectural Glass segment backlog as of year-end was $43.5 million, net of intersegment eliminations, compared to $31.0 million at the end of the prior year, due to extended lead times and order activity. We expect this backlog to be fulfilled in fiscal 2022.

Backlog in the Architectural Services segment as of year-end was $570.9 million, compared to $659.7 million at the end of the prior year, due to timing of firm orders, signed contracts and the broader industry slow-down that occurred in fiscal 2021. We expect approximately 50 percent of the backlog in this segment to be filled during fiscal 2022, with the remainder expected to be filled in fiscal 2023 and beyond; however, the timing of backlog may be impacted by project delays.

Backlog is not a significant metric for the LSO segment, as orders are typically booked and billed within a short time-frame.

Compliance with Government Regulations

We are subject to extensive regulation under environmental and occupational safety and health laws and regulations in the United States and in other countries in which we operate. These laws and regulations relate to, among other things, our use and storage of hazardous materials in our manufacturing operations and associated air emissions and discharges to surface and underground waters. We have several continuing programs designed to ensure compliance with foreign, federal, state and local environmental and occupational safety and health laws and regulations. We contract with outside vendors to collect and dispose of waste at our production facilities in compliance with applicable environmental laws. In addition, we have procedures in place that enable us to properly manage the regulated materials used in and wastes created by our manufacturing processes. We believe we are currently in material compliance with all such laws and regulations. While we will continue to incur costs for compliance with government regulations for our ongoing operations, we do not expect these to have a material effect upon our capital expenditures, earnings or competitive position. At one manufacturing facility in our Architectural Framing Systems segment, we are continuing to work to remediate historical environmental impacts. These remediation activities are being conducted without significant disruption to our operations.

Impact of COVID-19 on Our Business

The ongoing COVID-19 pandemic continues to cause uncertainty in global markets. During fiscal 2021, we experienced delays in commercial construction projects and orders because of COVID-19 and other disruptions to our business, including various physical distancing and health-related precautions, and we were required to close operations at two facilities in our LSO segment for a portion of the year due to governmental orders. Earlier in the pandemic, we were impacted by quarantine-related absenteeism among our production workforce, resulting in labor constraints at some of our facilities. While our efforts to mitigate the impacts of the pandemic have evolved positively, the extent to which COVID-19 will continue to impact our business will depend in part on the effectiveness of ongoing public health initiatives, which have been buoyed by vaccine production and distribution.

In response to this pandemic, we took several cost actions, including a merit and hiring freeze, temporary pay reductions, temporary suspension of the Company's 401(k) matching program, and made short term reductions in capital expenses, while emphasizing spending controls across the company. These temporary cost actions were mostly lifted during the fourth quarter of fiscal 2021.

Human Capital Resources

The Company had approximately 6,100 employees on February 27, 2021, down from 7,200 employees on February 29, 2020. As of February 27, 2021, approximately 560 of these employees were represented by U.S. labor unions.

Competition for qualified employees in the markets and industries in which we operate is strong, and the success of our Company depends on our ability to attract, select, develop and retain a productive and engaged workforce. Investing in our employees and their well-being, offering competitive compensation and benefits, promoting diversity and inclusion, and adopting positive human capital management practices are critical components of our corporate strategy.

Health, Wellness and Safety

The safety of our employees is integral to our Company. Providing a safe and secure work environment is one of our highest priorities and we devote significant time and resources to workplace safety. Our safety program is directed by our Risk Roundtable, comprised of safety leaders from across our Company. This group meets quarterly to review safety performance, share best practices, set goals and objectives for the organization, and plan safety culture assessments. In support of our safety efforts, we identify, assess and investigate incidents and injury data, and each year set goals to improve key safety performance indicators. We train, promote, consult and communicate with our workforce during this process.

We offer a comprehensive health and wellness program for our employees. In addition to standard health programs including medical insurance and preventive care, we have a variety of resources available to employees relating to physical and mental wellness.

The COVID-19 pandemic has magnified the importance of keeping our employees safe and healthy. In response to the pandemic, we have taken actions consistent with recommendations of the U.S. Centers for Disease Control and Prevention to protect our workforce. We will continue to emphasize the health and safety of our employees going forward.

Diversity, Equity and Inclusion

Our diversity, equity and inclusion program promotes a workplace where each employee’s abilities are recognized, respected, and utilized to further the Company’s goals. Our aim is to create an environment where people feel included as a part of a team

because of their diversity of outlooks, perspectives, and characteristics, which ultimately adds value for our company. We strive to create a culture of inclusion, reduce bias in our talent practices, and invest in and engage with our communities. We conduct diversity and code of conduct trainings with employees and managers to promote an inclusive and diverse workplace, where all individuals feel respected and part of a team regardless of their race, national origin, ethnicity, gender, age, religion, disability, sexual orientation or gender identity.

Talent Management and Development

Our talent management program is focused on developing employees and leaders to meet the Company’s evolving needs. Managers actively engage with their employees to provide coaching and feedback and identify training and development opportunities to improve performance in the employee’s current role and to position the employee for future growth. Training and development opportunities include new-hire training, job specific training, stretch assignments, and safety training. The company also offers leadership development opportunities, such as our Apogee Leadership Program, along with technical training for engineers, designers and sales staff. In addition, the company offers an education assistance program in which certain eligible employees receive tuition reimbursement to help defray the costs associated with their continuing education. Our executive leadership and Human Resources teams regularly conduct talent reviews and succession planning to assist with meeting critical talent and leadership needs.

International Sales

Information regarding export and international sales is included in Item 8, Financial Statements and Supplementary Data, within Note 15 of our Consolidated Financial Statements.

Available Information

The Company maintains a website at www.apog.com. Through a link to a third-party content provider, our website provides free access to the Company's Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and, if applicable, amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the Exchange Act), as soon as reasonably practicable after electronic filing such material with, or furnishing it to, the Securities and Exchange Commission (SEC). These reports are also available on the SEC's website at www.sec.gov. Also available on our website are various corporate governance documents, including our Code of Business Ethics and Conduct, Corporate Governance Guidelines, and charters for the Audit, Compensation, and Nominating and Corporate Governance Committees of the Board of Directors.

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

| | | | | | | | | | | | | | |

| Name | | Age | | Positions with Apogee Enterprises and Past Experience |

| Ty R. Silberhorn | | 53 | | Chief Executive Officer of the Company since January 2021. Prior to joining the Company, Mr. Silberhorn worked for 3M, a diversified global manufacturer and technology company, most recently serving as Senior Vice President of 3M's Transformation, Technologies and Services from April 2019 through December 2020. Prior to this position and since 2001, he held several 3M global business unit leadership roles, serving as Vice President and General Manager for divisions within Safety & Industrial, Transportation & Electronics, and the Consumer business groups. |

| Curtis Dobler | | 55 | | Executive Vice President and Chief Human Resources Officer since April 2019. Executive Vice President and Chief Human Resources Officer at Associated Materials, Inc., a manufacturer and distributor of exterior residential building products, from 2015 through 2019. |

| Meghan M. Elliott | | 44 | | Vice President, General Counsel and Secretary of the Company since June 2020. Prior to this role, Ms. Elliot served as Assistant General Counsel for the Company since 2014. |

| Nisheet Gupta | | 46 | | Executive Vice President and Chief Financial Officer of the Company since June 2020. Prior to joining the Company, Mr. Gupta served Vice President of Global Finance Operations at Land O’Lakes, a leading agribusiness and food company, since 2017. Prior to joining Land O’ Lakes, Mr. Gupta worked at Diebold Nixdorf, a banking solutions and retail technology systems company, as Vice President, Finance, Global Transformation from 2016 to 2017, Vice President, Finance and Chief Financial Officer, International from 2014 to 2016 and in various roles of increasing responsibility in Diebold Nixdorf’s financial organization, from 2011 to 2014. |

| Maureen Hayes | | 58 | | Chief Information Officer of the Company since 2012. |

| Gary R. Johnson | | 59 | | Senior Vice President of the Company since 2018, Treasurer and Vice President since 2001 and an employee of the Company since 1995. |

| Greg J. Sachs | | 51 | | Chief Procurement Officer of the Company since January 2020. Prior to joining the Company, Mr. Sachs served as Chief Procurement Officer at Resideo Technologies, Inc., a provider of critical comfort, residential thermal solutions and security solutions, from 2018 through 2020, and previously worked for Honeywell International, Inc. as Chief Procurement Officer from 2016 through 2018 and as Global Vice President of Sourcing from 2014 through 2016. |

ITEM 1A. RISK FACTORS

Our business faces many risks. Any of the risks discussed below, or elsewhere in this Form 10-K or our other filings with the Securities and Exchange Commission, could have a material adverse impact on our business, financial condition or results of operations.

COVID-19 Pandemic Risks

The novel coronavirus (COVID-19) pandemic, efforts to mitigate the pandemic, and the related weakening economic conditions, have impacted our business and could have a significant negative impact on our operations, liquidity, financial condition and financial results

In early 2020, a novel strain of coronavirus, COVID-19, started to impact the global economic environment causing extreme volatility and uncertainty in global markets. In March 2020, the World Health Organization declared COVID-19 to be a global pandemic and we started to see certain impacts to our business. This contagious disease outbreak, which has continued to spread, and the related adverse public health developments, and government orders to "stay in place," have adversely affected work forces, economies and financial markets globally. Quarantines and "stay in place" orders, the timing and length of containment and eradication solutions, travel restrictions, absenteeism by infected workers, labor shortages or other disruptions to our supply chain or to our customers, have adversely impacted our sales and operating results and have resulted in some continued project delays. In addition, the pandemic contributed to an economic downturn that could affect the ability of our customers to obtain financing for projects, which could therefore impact demand for our products and services. Order lead times could be extended or delayed and our pricing or pricing by our suppliers for needed materials could increase. Some critical materials, products or services may become unavailable if the regional or global spread were significant enough to prevent alternative sourcing.

To date, we have experienced delays in commercial construction projects due to COVID-19. While the construction and construction-related industries are considered an "essential service" in most jurisdictions in which we operate, site closures or project delays have occurred and increased social distancing and health-related precautions are required on many work sites, which may cause additional project delays and additional costs to be incurred. Within the LSO segment, we also experienced the temporary closure of many of our customer's retail locations. We also were required temporarily to shut down our factories in this segment to comply with government "stay in place" orders.

We expect this global pandemic to continue to have an impact on our future revenue and results of operations, the size and duration of which we are currently unable to predict. The global outbreak of COVID-19 continues to evolve rapidly. The extent to which COVID-19 will impact our business will depend on future developments, which are highly uncertain and cannot be predicted with confidence, such as the ultimate severity and spread of the disease, the intensity and duration of outbreaks, travel restrictions and social distancing requirements in the United States and other countries, business closures or business disruptions, and the effectiveness of actions taken in the United States and other countries to contain, treat and eradicate the disease.

Given the speed and frequency of continuously evolving developments with respect to this pandemic, we cannot reasonably estimate the magnitude of the impact to our future results of operations, liquidity or financial position. To the extent that our customers and suppliers are adversely impacted by the COVID-19 outbreak, this could reduce the availability, or result in delays, of materials or supplies, or delays in customer payments, which in turn could materially interrupt our business operations and/or impact our results of operations and liquidity.

Market and Industry Risks

North American and global economic and industry-related business conditions materially affect our sales and results of operations

Our Architectural Framing Systems, Architectural Glass and Architectural Services segments are significantly influenced by North American economic conditions and the cyclical nature of the North American commercial construction industry. The commercial construction industry is impacted by macroeconomic trends, such as availability of credit, employment levels, consumer confidence, interest rates and commodity prices. In addition, changes in architectural design trends, demographic trends, and/or remote work trends could negatively impact demand for our products. To the extent changes in these factors negatively impact the overall commercial construction industry, our revenue and profits could be significantly reduced.

Our LSO segment primarily depends on the strength of the retail custom picture framing industry. This industry is dependent on consumer confidence and the conditions of the U.S. economy. A decline in consumer confidence, whether as a result of an economic slowdown (due to COVID-19 concerns discussed above or otherwise), uncertainty regarding the future or other factors, could result in a decrease in net sales and operating income of this segment.

Global instability and uncertainty arising from events outside of our control, such as significant natural disasters, political crises, public health crises and pandemics, and/or other catastrophic events could materially affect our results of operations

Natural disasters, political crises, public health crises, such as the current COVID-19 pandemic, and other catastrophic events or other events outside of our control may damage our facilities or the facilities of third parties on which we depend, have broader adverse impacts on the commercial construction market, consumer confidence and spending, and/or impact both the well-being of our employees and our ability to operate our facilities. These types of disruptions or other events outside of our control could affect our business negatively, cause delays or cancellation of commercial construction projects or cause us to temporarily close our facilities, harming our operating results. In addition, if any of our facilities, including our manufacturing, finishing or distribution facilities, or the facilities of our suppliers, third-party service providers, or customers, is affected by natural disasters, political crises, public health crises, or other catastrophic events or events outside of our control, our business and operating results could suffer.

New competitors or specific actions of our existing competitors could materially harm our business

We operate in competitive industries in which the actions of our existing competitors or new competitors could result in loss of customers and/or market share. Changes in our competitors' products, prices or services could negatively impact our share of demand, net sales or margins.

Our Architectural Framing Systems and Architectural Glass segments have seen an increase in imports of products into the U.S. from international suppliers due to the relative strength of the U.S. dollar. If foreign imports occur at increased levels for extended periods of time, our net sales and margins in those segments could be negatively impacted.

Our LSO segment competes with several international specialty glass manufacturers and international and domestic acrylic suppliers. If these competitors are able to successfully improve their product attributes, service capabilities and production capacity and/or increase their sales and marketing focus in the U.S. custom picture framing market, this segment's net sales and margins could be negatively impacted.

Our customer dependence in the LSO segment creates a significant risk of reduced demand for our products

The LSO segment is highly dependent on a relatively small number of customers for its sales, while working to grow in new markets and with new customers. Accordingly, loss of a significant customer, a significant reduction in pricing, or a shift to a less favorable mix of value-added picture framing glass or acrylic products for one or more of those customers could materially reduce LSO net sales and operating results. Many customers in this segment temporarily closed retail outlets, during a portion of fiscal 2021, as a result of "stay in place" orders within the United States, resulting in reduced demand for our product. We are unable to estimate the severity or longer-term impact resulting from this COVID-19 pandemic on our business in this segment.

Operational Risks

If we are not able effectively to utilize and manage our manufacturing capacity, our results of operations will be negatively affected

Near-term performance depends, to a significant degree, on our ability to provide sufficient available capacity and appropriately utilize existing production capacity. The failure to successfully maintain existing capacity, or manage unanticipated interruptions in production, successfully implement planned capacity expansions, and/or make timely investments in additional physical capacity and supporting technology systems could adversely affect our operating results.

Loss of key personnel and inability to source sufficient labor could adversely affect our operating results

Our success depends on the skills of the Company's leadership, construction project managers and other key technical personnel, and our ability to secure sufficient manufacturing and installation labor. In recent years, strong residential and commercial construction and low U.S. unemployment has caused increased competition for experienced construction project managers and other labor. If we are unable to retain existing employees, provide a safe and healthy working environment, and/or recruit and train additional employees with the requisite skills and experience, our operating results could be adversely impacted.

If we are unable to manage our supply chain effectively, including availability and price of materials used in our products, our results of operations will be negatively affected

Our Architectural Framing Systems and Architectural Services segments use aluminum as a significant input to their products. While we structure many of our supply agreements in a way to moderate the effects of fluctuations in the market for raw aluminum and we endeavor to adjust our pricing to offset potential impacts, operating results could be negatively impacted by price movements in the market for raw aluminum. In recent years, we have seen increased volatility in the price of aluminum that we purchase from both domestic and international sources. Due to our Architectural Framing Systems segment presence in Canada, we have significant cross-border activity, as our Canadian businesses purchase inputs from U.S.-based suppliers and sell to U.S.-based customers. A significant change in U.S. trade policy with Canada could, therefore, have an adverse impact on our net sales and operating results.

Our Architectural Glass and LSO segments use raw glass as a significant input to their products. We periodically experience a tighter supply of raw glass when there is growth in automotive manufacturing and residential and non-residential construction. Failure to acquire a sufficient amount of raw glass on terms as favorable as current terms, including as a result of a significant unplanned downtime or shift in strategy at one or more of our key suppliers, could negatively impact our operating results.

Our suppliers are subject to the fluctuations in general economic cycles. Global economic conditions may impact their ability to operate their businesses, including recent impacts from the evolving COVID-19 pandemic. They may also be impacted by the increasing costs or availability of raw materials, labor and distribution, resulting in demands for less attractive contract terms or an inability for them to meet our requirements or conduct their own businesses. The performance and financial condition of one or more suppliers may cause us to alter our business terms or to cease doing business with a particular supplier or suppliers, or change our sourcing practices generally, which could in turn adversely affect our business and financial condition.

If we encounter problems with distribution, our ability to deliver our products to market could be adversely affected. Our operations are vulnerable to interruptions in the event of work stoppages, whether due to health concerns, such as COVID-19 or otherwise, labor disputes or shortages, and natural disasters that may affect our distribution and transportation to job sites. Moreover, our distribution system includes computer-controlled and automated equipment, which may be subject to a number of risks related to data and system security or computer viruses, the proper operation of software and hardware, power interruptions or other system failures. If we encounter problems with our distribution systems, our ability to meet customer and consumer expectations, manage inventory, manage transportation-related costs, complete sales and achieve operating efficiencies could be adversely affected.

Product quality issues and product liability claims could adversely affect our operating results

We manufacture and/or install a significant portion of our products based on the specific requirements of each customer. We believe that future orders of our products or services will depend on our ability to maintain the performance, reliability, quality and timely delivery standards required by our customers. We have in the past and are currently subject to product liability and warranty claims, including certain legal claims related to a commercial sealant product formerly incorporated into our products. If our products have performance, reliability or quality problems, or products are installed using incompatible glazing materials or installed improperly (by us or a customer), we may experience additional warranty expense; reduced or canceled orders; higher manufacturing or installation costs; or delays in the collection of accounts receivable. Additionally, product liability and warranty claims, including relating to the performance, reliability or quality of our products and services, could result in costly and time-consuming litigation that could require significant time and attention of management and involve significant monetary damages that could negatively impact our operating results. There is also no assurance that the number and value of product liability and warranty claims will not increase as compared to historical claim rates, or that our warranty reserve at any particular time is sufficient. No assurance can be given that coverage under insurance policies, if applicable, will be adequate to cover future product liability claims against us. If we are unable to recover on an insurance claims, in whole or in part, or if we exhaust our available insurance coverage at some point in the future, then we might be forced to expend legal fees and settlement or judgment costs, which could negatively impact our profitability, results of operations, cash flows and financial condition.

Project management and installation issues could adversely affect our operating results

Some of our segments are awarded fixed-price contracts that include material supply and installation services. Often, bids are required before all aspects of a construction project are known. An underestimate in the amount of labor required and/or cost of materials for a project; a change in the timing of the delivery of product; system design errors; difficulties or errors in execution; or significant project delays, caused by us or other trades, could result in failure to achieve the expected results. Any one or more of such issues could result in losses on individual contracts that could negatively impact our operating results.

Risks related to acquisitions and integration activities could adversely affect our operating results

We have completed and may complete additional acquisitions in the future to accelerate the execution of our growth strategies, including new geographies, adjacent market sectors and new product introductions. There are risks inherent in completing acquisitions, including:

•diversion of management’s attention from existing business activities;

•difficulties or delays in integrating and assimilating information and financial systems, operations and products of an acquired business or other business venture or in realizing projected efficiencies, growth prospects, cost savings and synergies;

•potential loss of key employees, customers and suppliers of the acquired businesses or adverse effects on relationships with existing customers and suppliers;

•adverse impact on overall profitability if the acquired business does not achieve the return on investment projected at the time of acquisition; and

•with respect to the acquired assets and liabilities, inaccurate assessment of additional post-acquisition capital investments; undisclosed, contingent or other liabilities; problems executing backlog of material supply or installation projects; unanticipated costs; and an inability to recover or manage such liabilities and costs.

If one or more of these risks were to arise in a material manner, our operating results could be negatively impacted.

Difficulties in maintaining our information technology systems, and potential security threats, could negatively affect our operating results and/or our reputation

Our operations are dependent upon various information technology systems that are used to process, transmit and store electronic information, and to manage or support our manufacturing operations and a variety of other business processes and activities. We could encounter difficulties in maintaining our existing systems, and developing and implementing new systems. Such difficulties could lead to disruption in business operations and/or significant additional expenses that could adversely affect our results.

Additionally, information technology security threats are increasing in frequency and sophistication. Our information technology and Internet based systems have been in the past, and may be in the future, subject to attempts to gain unauthorized access, breach, malfeasance or other system disruptions, none of which have been material to us to date. These threats pose a risk to the security of our systems and networks, and the confidentiality, availability and integrity of our data. Should such an attack succeed, it could lead to the compromise of confidential information, manipulation and destruction of data and product specifications, production downtimes, disruption in the availability of financial data, or misrepresentation of information via digital media. The occurrence of any of these events could adversely affect our reputation and could result in litigation, regulatory action, project delay claims, and increased costs and operational consequences of implementing further data protection systems.

Violations of legal and regulatory compliance requirements, including environmental laws, and changes in existing legal and regulatory requirements, may have a negative impact on our business and results of operations.

We are subject to a legal and regulatory framework imposed under federal and state laws and regulatory agencies, including laws and regulations that apply specifically to U.S. public companies and laws and regulations applicable to our manufacturing and construction site operations. Our efforts to comply with evolving laws, regulations, and reporting standards may increase our general and administrative expenses, divert management time and attention, or limit our operational flexibility, all of which could have a material adverse effect on our business, financial position, and results of operations. Additionally, new laws, rules, and regulations, or changes to existing laws or their interpretations, could create added legal and compliance costs and uncertainty for us.

We use hazardous materials in our manufacturing operations, and have air and water emissions that require controls. Accordingly, we are also subject to federal, state and local environmental laws and regulations, including those governing the storage and use of hazardous materials and disposal of wastes. A violation of such laws and regulations, or a release of such substances, may expose us to various claims, including claims by third parties, as well as remediation costs and fines.

Financial Risks

Due to our self-insurance programs, we may have a material adverse effect on our operating results in the event of a material product liability claim

We obtain third-party insurance to provide coverage for potential risk in areas such as employment practices, workers' compensation, directors and officers, automobile, architect's and engineer's errors and omissions, product rework and general liability, as well as medical insurance and various other coverages. However, we retain a high amount of risk on a self-insured basis, partially through our wholly-owned insurance subsidiary. Therefore, a material architectural product liability event could have a material adverse effect on our operating results.

Foreign currency effects could negatively affect our sales and operating income

When the U.S. dollar strengthens against foreign currencies, imports of products into the U.S. produced by international competitors become more price competitive and exports of our U.S.-fabricated products become less price competitive. If we are not able to counteract these types of price pressures through superior quality and service, our net sales and operating income could be negatively impacted. Additionally, our international subsidiaries report their results of operations and financial position in their relevant functional currencies (local country currency), which are then translated into U.S. dollars. As the relationship between these currencies and the U.S. dollar changes, there could be a negative impact on our reported results and financial position.

Results can differ significantly from our expectations and the expectations of analysts, which could have an adverse affect on the market price of our common stock

Our sales and earnings guidance and resulting external analyst estimates are largely based on our view of our business and the broader commercial construction market. Further, there is additional risk in our ability to accurately forecast and provide guidance in the current environment, given the evolving conditions as a result of the COVID-19 pandemic and related economic downturn. Failure to meet our guidance or analyst expectations for net sales and earnings would have an adverse impact on the market price of our common stock.

We may experience further impairment of our goodwill and indefinite-lived intangible assets, in the future, which could adversely impact our financial condition and results of operations

Our assets include a significant amount of goodwill and indefinite-lived intangible assets. We evaluate goodwill and indefinite-lived intangible assets for impairment annually in our fiscal fourth quarter, or more frequently if events or changes in circumstances indicate that the carrying value of a reporting unit may not be recoverable. The assessment of impairment involves significant judgment and projections about future performance.

Based on our analysis performed in the fourth quarter of fiscal 2021, we determined impairment of goodwill at two of our reporting units within the Architectural Framing Systems segment, EFCO and Sotawall, and we determined impairment of the EFCO tradename. As a result, we recorded a goodwill impairment expense of $63.8 million and an indefinite-lived intangible asset impairment expense of $6.3 million. Refer to additional information included within Notes 1 and 6 to the Financial Statements contained in Item 8 within this Annual Report on Form 10-K.

The discounted cash flow projections and revenue projections used in these analyses are dependent upon achieving forecasted levels of revenue and profitability. If revenue or profitability were to fall below forecasted levels, or if market conditions were to decline in a material or sustained manner, further impairment could be indicated at these or our other reporting units and we could incur an additional non-cash impairment expense that would negatively impact our financial condition and results of operations.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

The following table lists, by segment, the Company's major properties as of February 27, 2021.

| | | | | | | | | | | | | | |

| Property Location | | Owned/ Leased | | Function |

| Architectural Framing Systems segment | | | | |

| Wausau, WI | | Owned | | Manufacturing/Administrative |

| Stratford, WI | | Owned | | Manufacturing |

| Reed City, MI | | Owned | | Manufacturing |

| Walker, MI | | Leased | | Manufacturing/Administrative |

| Dallas, TX | | Leased | | Manufacturing |

| Toronto, ON Canada | | Leased | | Manufacturing/Warehouse/Administrative |

| Brampton, ON Canada | | Leased | | Manufacturing/Warehouse/Administrative |

| | | | |

| | | | |

| Monett, MO | | Owned | | Manufacturing/Warehouse/Administrative |

| | | | |

| Architectural Glass segment | | | | |

| Owatonna, MN | | Owned | | Manufacturing/Administrative |

| | | | |

| Statesboro, GA | | Owned | | Manufacturing/Warehouse |

| Dallas, TX | | Leased | | Manufacturing/Warehouse |

| Nazaré Paulista, Brazil | | Owned(1) | | Manufacturing/Administrative |

| | | | | | | | | | | | | | |

| Property Location | | Owned/ Leased | | Function |

| Architectural Services segment | | | | |

| Minneapolis, MN | | Leased | | Administrative |

| West Chester, OH | | Leased | | Manufacturing |

| Mesquite, TX | | Leased | | Manufacturing |

| Glen Burnie, MD | | Leased | | Manufacturing |

| Orlando, FL | | Leased | | Manufacturing |

| LSO segment | | | | |

| McCook, IL | | Leased | | Manufacturing/Warehouse/Administrative |

| Faribault, MN | | Owned | | Manufacturing/Administrative |

| Other | | | | |

| Minneapolis, MN | | Leased | | Administrative |

(1)This is an owned facility; however, the land is leased from the city.

ITEM 3. LEGAL PROCEEDINGS

From time to time, the Company is a party to various legal proceedings incidental to its normal operating activities. In particular, like others in the construction supply and services industry, the Company is routinely involved in various disputes and claims arising out of construction projects, sometimes involving significant monetary damages or product replacement. We have in the past and are currently subject to product liability and warranty claims, including certain legal claims related to a commercial sealant product formerly incorporated into our products. The Company is also subject to litigation arising out of areas such as employment practices, workers compensation and general liability matters. Although it is very difficult to accurately predict the outcome of any such proceedings, facts currently available indicate that no matters will result in losses that would have a material adverse effect on the results of operations, cash flows or financial condition of the Company.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Apogee common stock is traded on the NASDAQ Stock Market under the ticker symbol "APOG". As of April 7, 2021, there were 1,136 shareholders of record and 9,112 shareholders for whom securities firms acted as nominees.

Dividends

Quarterly, the Board of Directors evaluates declaring dividends based on operating results, available funds and the Company's financial condition. Cash dividends have been paid each quarter since 1974. The chart below shows quarterly and annual cumulative cash dividends per share for the past three fiscal years.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fiscal Year | | First | | Second | | Third | | Fourth | | Total |

| 2021 | | $ | 0.1875 | | | $ | 0.1875 | | | $ | 0.1875 | | | $ | 0.2000 | | | $ | 0.7625 | |

| 2020 | | 0.1750 | | | 0.1750 | | | 0.1750 | | | 0.1875 | | | 0.7125 | |

| 2019 | | 0.1575 | | | 0.1575 | | | 0.1575 | | | 0.1750 | | | 0.6475 | |

| | | | | | | | | | |

| | | | | | | | | | |

Purchases of Equity Securities by the Company

The following table provides information with respect to purchases made by the Company of its own stock during the fourth quarter of fiscal 2021:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Period | | Total Number of Shares Purchased (a) | | Average Price Paid per Share | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (b) | | Maximum Number of Shares that May Yet Be Purchased under the Plans or Programs (b) |

| November 29, 2020 through December 26, 2020 | | — | | | $ | — | | | — | | | 1,443,059 | |

| December 27, 2020 through January 23, 2021 | | 167,567 | | | 37.44 | | | 160,139 | | | 1,282,920 | |

| January 24, 2021 through February 27, 2021 | | 197,680 | | | 37.08 | | | 165,536 | | | 1,117,384 | |

| Total | | 365,247 | | | $ | 37.22 | | | 325,675 | | | 1,117,384 | |

(a) The shares in this column represent the total number of shares that were repurchased by us pursuant to our publicly announced repurchase program, plus the shares surrendered to us by plan participants to satisfy withholding tax obligations related to share-based compensation.

(b) In fiscal 2004, announced on April 10, 2003, the Board of Directors authorized the repurchase of 1,500,000 shares of Company stock. The Board increased the authorization by 750,000 shares, announced on January 24, 2008; by 1,000,000 shares on each of the announcement dates of October 8, 2008, January 13, 2016, January 9, 2018, and January 14, 2020; and by 2,000,000 shares, announced on October 3, 2018. The repurchase program does not have an expiration date.

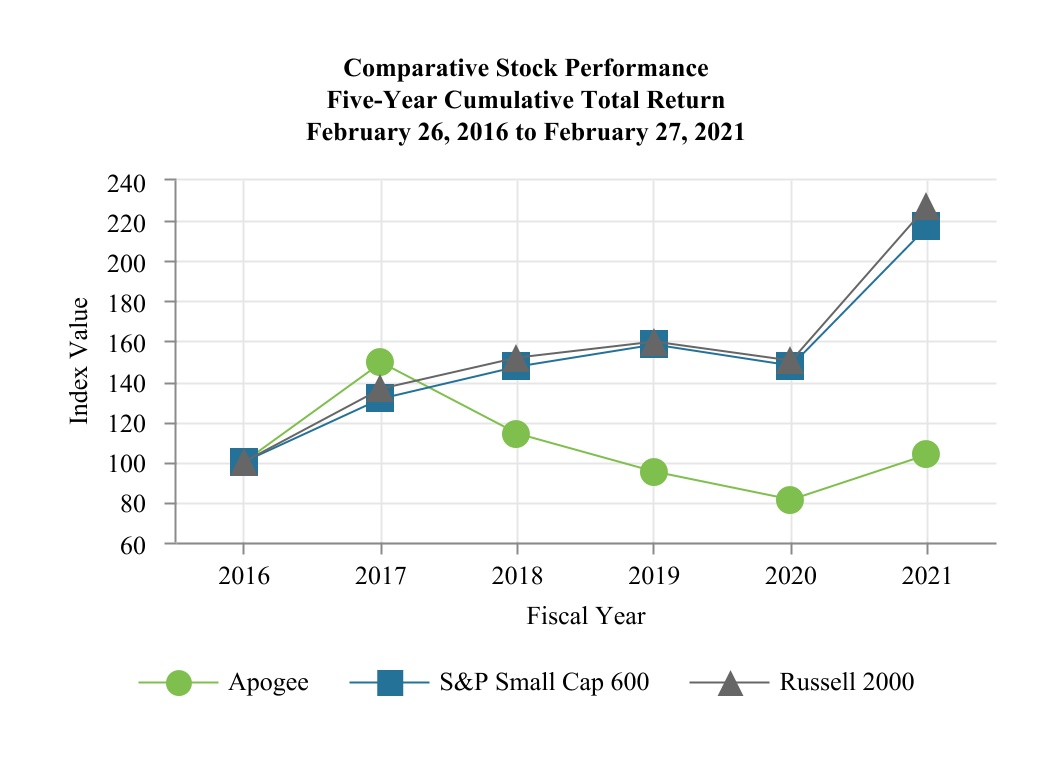

Comparative Stock Performance

The graph below compares the cumulative total shareholder return on a $100 investment in our common stock for the last five fiscal years with the cumulative total return on a $100 investment in the Russell 2000 Index, a broad equity market index, and the Standard & Poor's Small Cap 600 Growth Index, an index that includes companies of similar market capitalization. The graph assumes an investment at the close of trading on February 26, 2016, and also assumes the reinvestment of all dividends.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 2016 | | 2017 | | 2018 | | 2019 | | 2020 | | 2021 |

| Apogee | | $ | 100.00 | | | $ | 149.31 | | | $ | 114.13 | | | $ | 94.99 | | | $ | 81.14 | | | $ | 103.58 | |

| S&P Small Cap 600 Growth Index | | 100.00 | | | 131.15 | | | 147.36 | | | 158.24 | | | 147.84 | | | 217.10 | |

| Russell 2000 Index | | 100.00 | | | 136.51 | | | 151.95 | | | 159.67 | | | 150.44 | | | 227.16 | |

We selected the Standard & Poor's Small Cap 600 Growth Index as an index of companies with similar market capitalization because we are unable to identify a peer group of companies similar to us in size and scope of business activities or a widely recognized published industry index that accurately reflects our diverse business activities. Most of our direct competitors in our various business units are either privately owned or divisions of larger, publicly owned companies.

ITEM 6. SELECTED FINANCIAL DATA

The following information should be read in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations, included in Item 7 of this Annual Report on Form 10-K, and our consolidated financial statements and related notes, included in Item 8 of this Annual Report on Form 10-K.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Fiscal Year | | |

| (In thousands, except per share data and percentages) | | 2021(1) | | 2020 | | 2019 | | 2018(2) | | 2017(3)(4) | | |

| Results of Operations Data | | | | | | | | | | | | |

| Net sales | | $ | 1,230,774 | | | $ | 1,387,439 | | | $ | 1,402,637 | | | $ | 1,326,173 | | | $ | 1,114,533 | | | |

| Gross profit | | 275,689 | | | 318,959 | | | 293,565 | | | 333,518 | | | 292,023 | | | |

| Operating income | | 25,527 | | | 87,848 | | | 67,284 | | | 114,284 | | | 122,225 | | | |

| Net earnings | | 15,436 | | | 61,914 | | | 45,694 | | | 79,488 | | | 85,790 | | | |

| Earnings per share - basic | | 0.59 | | | 2.34 | | | 1.64 | | | 2.79 | | | 2.98 | | | |

| Earnings per share - diluted | | 0.59 | | | 2.32 | | | 1.63 | | | 2.76 | | | 2.97 | | | |

| Cash dividends per share | | 0.7625 | | | 0.7125 | | | 0.6475 | | | 0.5775 | | | 0.5150 | | | |

| Balance Sheet Data | | | | | | | | | | | | |

| | | | | | | | | | | | |

| Total assets | | 1,015,099 | | | 1,128,991 | | | 1,068,168 | | | 1,022,320 | | | 784,658 | | | |

| | | | | | | | | | | | |

| Long-term debt | | 165,000 | | | 217,900 | | | 245,724 | | | 215,860 | | | 65,400 | | | |

| Shareholders' equity | | 492,745 | | | 516,778 | | | 496,317 | | | 511,355 | | | 470,577 | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Other Data | | | | | | | | | | | | |

| Gross profit as a percentage of sales | | 22.4 | % | | 23.0 | % | | 20.9 | % | | 25.1 | % | | 26.2 | % | | |

| Operating income as a percentage of sales | | 2.1 | % | | 6.3 | % | | 4.8 | % | | 8.6 | % | | 11 | % | | |

Return on average invested capital(5) | | 2.6 | % | | 8.4 | % | | 5.6 | % | | 9.3 | % | | 14.3 | % | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

(1)Includes $70.1 million impairment expense on goodwill and indefinite-lived intangible assets.

(2)Includes the acquisition of EFCO in June 2017.

(3)Fiscal 2017 contained 53 weeks. Each of the other periods presented contained 52 weeks.

(4)Includes the acquisition of Sotawall in December 2016.

(5)Return on average invested capital is a non-GAAP financial measure that we define as [operating income x 0.75]/average invested capital. We believe this measure is useful in understanding operational performance over time. This non-GAAP measure should be viewed in addition to, and not as an alternative to, the reported financial results of the company prepared in accordance with GAAP. Other companies may calculate this measure differently from us, thereby limiting the usefulness of the measure for comparison with others.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Forward-Looking Statements

This Annual Report on Form 10-K, including Management's Discussion and Analysis, contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements reflect our current views with respect to future events and financial performance. The words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “forecast,” “project,” “should,” "will," "continue" and similar expressions are intended to identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All forecasts and projections in this document are “forward-looking statements,” and are based on management's current expectations or beliefs of the Company's near-term results, based on current information available pertaining to the Company, including the risk factors noted under Item 1A in this Form 10-K. From time to time, we also may provide oral and written forward-looking statements in other materials we release to the public, such as press releases, presentations to securities analysts or investors, or other communications by the Company. Any or all of our forward-looking statements in this report and in any public statements we make could be materially different from actual results.

Accordingly, we wish to caution investors that any forward-looking statements made by or on behalf of the Company are subject to uncertainties and other factors that could cause actual results to differ materially from such statements. These uncertainties and other risk factors include, but are not limited to, the risks and uncertainties set forth under Item 1A in this Form 10-K, all of which are incorporated by reference into this Item 7.

We wish to caution investors that other factors might in the future prove to be important in affecting the Company's results of operations. New factors emerge from time to time; it is not possible for management to predict all such factors, nor can it assess the impact of each such factor on the business or the extent to which any factor, or a combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Overview

We are a leader in the design and development of value-added glass and metal products and services. Our four reporting segments are: Architectural Framing Systems, Architectural Glass, Architectural Services and Large-Scale Optical Technologies (LSO).

During fiscal 2021, we responded quickly to a challenging environment for our business, driven by the evolving and ongoing impacts of the COVID-19 pandemic and slowness in certain of our end markets. We adapted our business operations so we could continue to serve customers, while keeping the health and safety of our employees a top priority. We focused on driving improvements throughout our business, while using this year to begin positioning the company for sustainable growth and improved profitability in the future. In particular, we paid down a significant percentage of our long-term debt and strengthened our financial position, giving us better financial flexibility going forward. We also made progress on actions to improve our overall cost structure.

Fiscal 2021 summary of results:

•Consolidated net sales were $1.2 billion, a decrease of 11 percent over fiscal 2020.

•Operating income was $25.5 million, a decrease of 71 percent from $87.8 million in the prior year.

•Diluted EPS was $0.59, compared to $2.32 in the prior year, a decrease of 75 percent.

•Adjusted operating income was $87.1 million, a decrease of 3 percent compared to the prior year, and adjusted diluted EPS was $2.40 in fiscal 2021, an increase of 1 percent compared to the prior year. Refer to the table below for a reconciliation to GAAP of these adjusted amounts.

Adjusted operating income and adjusted earnings per diluted share (adjusted diluted EPS) are supplemental non-GAAP financial measures provided by the Company to assess performance on a more comparable basis from period-to-period by excluding amounts that management does not consider part of core operating results. Management uses these non-GAAP measures to evaluate the Company’s historical and prospective financial performance, measure operational profitability on a consistent basis, and provide enhanced transparency to the investment community. These non-GAAP measures should be viewed in addition to, and not as an alternative to, the reported financial results of the company prepared in accordance with GAAP. Other companies may calculate these measures differently, thereby limiting the usefulness of the measures for comparison with other companies.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Reconciliation of Non-GAAP Financial Information |

| Adjusted Operating Income and Adjusted Net Earnings per Diluted Common Share |

| (Unaudited) |

| | | | | | Diluted per share amounts |

| | Year-ended | | Year-ended |

| (In thousands) | | February 27, 2021 | | February 29, 2020 | | February 27, 2021 | | February 29, 2020 |

| Operating income | | $ | 25,527 | | | $ | 87,848 | | | $ | 0.59 | | | $ | 2.32 | |

| Impairment expense on goodwill and intangible assets | | 70,069 | | | — | | | 2.66 | | | — | |

| Restructuring | | 4,884 | | | — | | | 0.19 | | | — | |

| Gain on sale of building | | (19,346) | | | — | | | (0.74) | | | — | |

| COVID-19 | | 4,988 | | | — | | | 0.19 | | | — | |

| Post-acquisition and acquired project matters | | 1,000 | | | (635) | | | 0.04 | | | (0.02) | |

| Cooperation agreement advisory costs | | — | | | 2,776 | | | — | | | 0.10 | |

Income tax impact on above adjustments (1) | | N/A | | N/A | | (0.53) | | | (0.02) | |

| Adjusted operating income | | $ | 87,122 | | | $ | 89,989 | | | $ | 2.40 | | | $ | 2.38 | |

| | | | | | | | |

| (1) Income tax impact calculated using an estimated statutory tax rate of 25%, which reflects the estimated blended statutory tax rate for the jurisdiction in which the charge or income occurred. Income tax impact excludes the amount of each charge that is non-deductible in the applicable jurisdiction. In prior periods, tax impacts were calculated using an effective tax rate. All such periods were recalculated herein using the 25% estimated statutory tax rate for consistency and comparability with the current period presentation. This change did not have a significant impact on the income tax impact or the adjusted net earnings or adjusted earnings per diluted common share amounts that had been reported for the three months or twelve months ended February 29, 2020. |

Results of Operations

Net Sales

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | 2021 | | 2020 | | 2019 | | 2021 vs. 2020 | | 2020 vs. 2019 |

| Net sales | | $ | 1,230,774 | | | $ | 1,387,439 | | | $ | 1,402,637 | | | (11.3) | % | | (1.1) | % |

Fiscal 2021 Compared to Fiscal 2020

Net sales in fiscal 2021 decreased by 11.3 percent compared to fiscal 2020, reflecting end market softness and COVID-19 related volume declines in the Architectural Framing Systems, Architectural Glass and LSO segments, partially offset by increased volume in the Architectural Services segment, driven by execution of projects in backlog.

Fiscal 2020 Compared to Fiscal 2019

Net sales in fiscal 2020 decreased by 1.1 percent compared to fiscal 2019, driven by expected project timing-related decreases within the Architectural Services segment and by lower volumes at certain businesses within the Architectural Framing Systems segment, partially offset by improved volume in the Architectural Glass segment.

Performance

The relationship between various components of operations, as a percentage of net sales, is provided below.

| | | | | | | | | | | | | | | | | | | | |

| (Percentage of net sales) | | 2021 | | 2020 | | 2019 |

| Net sales | | 100.0 | % | | 100.0 | % | | 100.0 | % |

| Cost of sales | | 77.6 | | | 77.0 | | | 79.1 | |

| Gross margin | | 22.4 | | | 23.0 | | | 20.9 | |

| Selling, general and administrative expenses | | 14.6 | | | 16.7 | | | 15.9 | |

| Impairment expense on goodwill and intangible assets | | 5.7 | | | — | | | 0.2 | |

| Operating income | | 2.1 | | | 6.3 | | | 4.8 | |

| | | | | | |

| Interest expense, net | | 0.4 | | | 0.7 | | | 0.6 | |