UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03416

THE CALVERT FUND

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

Ivy Wafford Duke, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: September 30

Date of reporting period: Six months ended March 31, 2015

Item 1. Report to Stockholders.

[Calvert Income Fund Semi-Annual Report to Shareholders]

[Calvert Short-Duration Income Fund Semi-Annual Report to Shareholders]

[Calvert Long-Term Income Fund Semi-Annual Report to Shareholders]

[Calvert Ultra-Short Income Fund Semi-Annual Report to Shareholders]

[Calvert Government Fund Semi-Annual Report to Shareholders]

[Calvert High-Yield Bond Fund Semi-Annual Report to Shareholders]

|

| |

Semi-Annual Report March 31, 2015

E-Delivery Sign-Up — Details Inside | |

Choose Planet-friendly E-delivery!

Sign up now for on-line statements, prospectuses, and fund reports. In less than five minutes you can help reduce paper mail and lower fund costs.

Just go to www.calvert.com. If you already have an online account at Calvert, click on Login, to access your Account, and select the documents you would like to receive via e-mail.

If you’re new to online account access, click on Login, then Register to create your user name and password. Once you’re in, click on the E-delivery sign-up on the Account Portfolio page and follow the quick, easy steps.

Note: if your shares are not held directly at Calvert but through a brokerage firm, you must contact your broker for electronic delivery options available through their firm.

|

| | | |

| TABLE OF CONTENTS |

| | | | |

| | | | President's Letter |

| | | | Portfolio Management Discussion |

| | | | Shareholder Advocacy Update |

| | | | Shareholder Expense Example |

| | | | Statement of Net Assets |

| | | | Statement of Operations |

| | | | Statements of Changes in Net Assets |

| | | | Notes to Financial Statements |

| | | | Financial Highlights |

| | | | Explanation of Financial Tables |

| | | | Proxy Voting |

| | | | Availability of Quarterly Portfolio Holdings |

| | | | Basis for Board’s Approval of Investment Advisory Contract |

|

| |

| John Streur President and Chief Executive Officer, Calvert Investments, Inc. |

Dear Calvert Shareowner,

The United States economy improved throughout 2014 and into the first quarter of 2015, while major economies in other regions of the world struggled to regain momentum or saw slowing growth. It is still too early to declare victory, but one may say that while the United States led the world into financial crisis nearly eight years ago, the innovative and aggressive responses to the crisis by our policymakers are allowing the United States to recover more quickly. Granted, the United States has the benefit of possessing the world’s reserve currency and our monetary maneuvers in our self-interest are not without cost to economies in other regions.

As 2014 drew to a close, the United States was winding down the quantitative easing portion of its post-crisis monetary policy while the European and Japanese central banks were finding it necessary to increase their own forms of quantitative easing in efforts to support asset prices and spur economic growth.

The impact of modestly improving economic activity in the U.S. and ongoing low global interest rates on financial assets in 2014 created positive returns for most stocks and bonds for the previous 12 months, a condition that gave benefit to most Calvert Funds. The exceptions are assets tied to the price of oil, which collapsed during the second half of the year. Energy industries and natural resource based companies, including renewable energy companies and water related companies, saw their stock valuations drop in reaction.

Across our fixed income and equity strategies, Calvert finds more utility in conducting fundamental research in order to find relative values in securities of individual companies than we do in attempting to anticipate or time changes in global economic indicators. Broadly, we are mindful of the fact that stocks and bonds have benefitted substantially from the easy monetary policies and ultra-low interest rates of the post-crisis era. We believe markets are more or less fairly valued and we have taken steps seeking to moderate the risk across our portfolios.

As I take the helm at Calvert and look back at the 39 years since the firm’s founding in 1976, I note the substantial growth in the world’s population, the massive increase in the industrialization of our global society, and the associated change in the role of corporations in societal and environmental outcomes for our future.

4 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

Public companies have created tremendous net benefits to society through advances in health care, food systems, energy efficiency, communications and technology, and access to finance and other products and services too vast to detail. Hundreds of millions of people throughout the world have seen their standard of living increased through benefits created by corporate activity.

Along with the obvious net benefits to society, we are aware of the substantial stresses placed upon society and the environment from corporate behaviors. At the same time, society has awarded corporations an increasingly prominent role in the day-to-day outcomes of our lives and in the societal and environmental outcomes that will determine the future direction of the world.

Calvert, as a global investment management firm and a steward of client assets, has a growing and evolving role as a leader in responsible investing. Calvert has a rich history as a socially responsible investor and has made many contributions to public policy and corporate governance. Today we are bringing Calvert’s deep expertise in socially responsible investing, public and private policy work, and investment management to a new level with a focus on developing principles and setting standards for use in our investment management processes, our active ownership and engagement discipline and within our investment risk management processes.

As a long-term investor with unique insights into environmental, social, and governance activities of companies throughout the world, Calvert is able to develop a holistic view of companies’ operations. Our ability to use our insights for the benefit of the stewardship of client assets, both to produce desirable investment outcomes for our clients and to assist companies in evolving their role in society along a responsible path has never been more important.

As fellow shareowners of Calvert Funds, you and I know that it is essential to pursue the type of enduring value that Calvert seeks to create, through excellence in financial results balanced with the evolving needs of society and the environment.

Thank you for your share ownership in Calvert Funds; all of us at Calvert Investments, Inc. appreciate the confidence and trust you have placed in us.

John Streur

April 2015

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 5

|

| |

| PORTFOLIO MANAGEMENT DISCUSSION |

|

| |

| Catherine Roy, CFA Senior Vice President and Chief Investment Officer, Fixed Income |

Investment Climate

A very divergent economic picture between the United States and much of the rest of the world prompted central bank actions that affected global currencies and drove financial-market returns over the six-month reporting period. The markets also reacted to new information on key geopolitical situations, notably in the Ukraine.

The economic divergence theme was apparent in Europe, which featured consumer price deflation in many countries. China and Japan also experienced slower growth. In the United States, economic growth pulled back from the strong pace set in mid-2014 to a rate more in line with the Fed’s projected long-run average of 2.2%. While modest, this growth rate was superior to that of many other countries. The U.S. headline Consumer Price Index, which measures inflation excluding volatile food and energy prices, became slightly negative towards the end of the reporting period.

In January, the European Central Bank (ECB) announced a long-awaited quantitative easing program, which had significant market impact. In anticipation of the January ECB decision, some other European central banks, as well as Japan and China, increased monetary accommodation through interest-rate cuts and/or expanded bond purchase programs. In stark contrast, the U.S. Federal Reserve prepared markets for a small and slow series of interest-rate increases, slated to start sometime in 2015. The Fed anticipates that extremely low domestic inflation will be transitory, driven by the drop in energy prices, and is not a problem brought on by lack of consumer demand. In addition, the U.S. labor market is relatively strong, which has long been one condition the Fed required to start a slow removal of monetary accommodation.

Big moves in the world’s major currencies were a byproduct of these central bank actions. In the middle of 2014, the U.S. dollar began a sharp climb against other currencies that drove it to multi-year highs. The Bloomberg DXY, an index that measures the dollar against major currencies, appreciated 14.5% over the six-month reporting period. Tightly correlated to the dollar’s rally was a sharp drop in the price of oil—a market set up for a price collapse due to a massive demand-supply imbalance.

Bonds Provided Positive Returns

The global fixed-income markets generally reacted positively to the ECB-led central bank easing. U.S. bond yields gyrated over the reporting period, but at the end tended to be lower and so bond returns were positive.

6 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | |

| | | | |

| | CALVERT

INCOME FUND | |

| | MARCH 31, 2015 | |

| | | | |

| | ECONOMIC SECTORS | % OF TOTAL INVESTMENTS | |

| | Corporate | 68.8 | % | |

| | Financial Institutions | 19.8 | % | |

| | Industrial | 48.3 | % | |

| | Utility | 0.7 | % | |

| | Government Related | 0.2 | % | |

| | Supranational | 0.2 | % | |

| | Municipal | 0.3 | % | |

| | Utility | 0.3 | % | |

| | Securitized | 21.6 | % | |

| | Asset-Backed Securities | 13.3 | % | |

| | Commercial Mortgage- Backed Securities | 6.9 | % | |

| | Mortgage-Backed Pass- Through | 1.4 | % | |

| | Short-Term Investments | 0.9 | % | |

| | Treasury | 8.2 | % | |

| | Total | 100 | % | |

| | | | |

The ten-year T-note yield fell 58 basis points1 (bps) to 1.94%, while the 30-year fixed-rate mortgage average fell 50 bps to 3.69%. The Barclays U.S. Credit Index average yield declined 18 bps to 2.83%.

In terms of total return, the Barclays Long Credit Index rose 7.24%, the broad intermediate Barclays U.S. Credit Index returned 3.96%, and the shorter-term Barclays 1-5 Year U.S. Credit Index was up 1.48%. The Barclays US Aggregate Index returned 3.43% and the Bank of America Merrill Lynch High Yield Master II Index was little changed, up 1.45%.

Outlook

The United States economy is expanding moderately and has weathered global weakness better than other most other major economies. The 5.5% headline unemployment rate is just above the Federal Open Market Commission’s (FOMC)

|

| | | | | | |

| | | | | |

| | CALVERT

INCOME FUND | |

| | MARCH 31, 2015 | |

| | | | | |

| | INVESTMENT PERFORMANCE | |

| | (TOTAL RETURN AT NAV*) | |

| | | 6 MONTHS ENDED 3/31/15 | 12 MONTHS ENDED 3/31/15

| |

| | Class A | 2.83 | % | 4.60 | % | |

| | Class B | 2.47 | % | 3.60 | % | |

| | Class C | 2.55 | % | 3.87 | % | |

| | Class I | 3.21 | % | 5.21 | % | |

| | Class R | 2.78 | % | 4.30 | % | |

| | Class Y | 3.07 | % | 4.96 | % | |

| | | | | |

| | Barclays U.S. Credit Index | 3.96 | % | 6.74 | % | |

| | | | | |

| | Lipper BBB-Rated Corporate Debt Funds Average | 3.78 | % | 6.75 | % | |

| | | | | |

| | | 30 DAYS ENDED | |

| | SEC YIELD | 3/31/15 | 9/30/14 | |

| | Class A | 2.10 | % | 2.35 | % | |

| | Class B | 1.34 | % | 1.10 | % | |

| | Class C | 1.33 | % | 1.96 | % | |

| | Class I | 2.81 | % | 3.28 | % | |

| | Class R | 2.00 | % | 2.33 | % | |

| | Class Y | 2.51 | % | 2.95 | % | |

| | | |

| | * Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 3.75% front-end sales charge or any deferred sales charge. | |

| | | | | |

long-term target range. Wage growth is modest but steady. The labor-force participation rate, however, remains low—influenced by demographics and the long-term loss of traditional middle-wage jobs to overseas competition and automation. Workers in general, however, are in improved bargaining positions. The Fed’s benchmark consumer inflation rate hovers around zero, sharply below the 2% target.

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 7

Despite another cold winter, U.S. economic growth in 2015 could approach 3% in the absence of a material systemic shock. We expect inflation to continue well below the Fed’s 2% target. Improvement in the labor market should continue, with unemployment below 5.5%. Discord on Capitol Hill promises to add some uncertainty to late-summer debt-ceiling negotiations. Household consumption remains the major engine of growth and should be supported by lower energy prices. Lower energy prices, however, are likely to depress earnings and investment from energy-industry companies and the much-stronger dollar may dampen overall U.S. corporate earnings. Housing-sector activity remains a disappointment, despite very low mortgage rates, and residential mortgage lending remains relatively restrained in the post-crisis market. The U.S. trade situation may deteriorate given continued strength of the dollar, which could drive up import costs.

If U.S. data trends hold, within the context of the global backdrop of disinflation and central bank easing, we expect the Fed to raise short-term interest rates by late 2015. If lift-off is in 2015, however, we expect no more than two quarter-point increases over the balance of the year. If the weaker global picture and price disinflation persist, there is a reasonable chance the Fed will delay any rate increases into 2016.

Over the longer term, we expect the benchmark 10-year T-note yield to fluctuate between 2% and 3%, influenced by the trend in economic data surprises, major central bank forward guidance, expected low global inflation rates, and flows in global fixed-income markets. We expect short-term money markets rates to remain close to zero percent for much of 2015.

Calvert Investment Management, Inc.

April 2015

1. A basis point is 0.01 percentage points.

|

| | | | |

| | | | |

| | CALVERT

INCOME FUND | |

| | MARCH 31, 2015 | |

| | | | |

| | AVERAGE ANNUAL TOTAL RETURNS | |

| | | | |

| | CLASS A SHARES | (WITH MAX. LOAD) | |

| | One year | 0.65 | % | |

| | Five year | 3.46 | % | |

| | Ten year | 3.52 | % | |

| | | | |

| | CLASS B SHARES | (WITH MAX. LOAD) | |

| | One year | -0.40 | % | |

| | Five year | 3.38 | % | |

| | Ten year | 3.05 | % | |

| | | | |

| | CLASS C SHARES | (WITH MAX. LOAD) | |

| | One year | 2.87 | % | |

| | Five year | 3.53 | % | |

| | Ten year | 3.19 | % | |

| | | | |

| | CLASS I SHARES | | |

| | One year | 5.21 | % | |

| | Five year | 4.93 | % | |

| | Ten year | 4.59 | % | |

| | | | |

| | CLASS R SHARES* | | |

| | One year | 4.30 | % | |

| | Five year | 4.05 | % | |

| | Ten year | 3.72 | % | |

| | | | |

| | CLASS Y SHARES** | | |

| | One year | 4.96 | % | |

| | Five year | 4.63 | % | |

| | Ten year | 4.19 | % | |

| | | | |

| | * Performance results for Class R shares prior to October 31, 2006 reflect the performance of Class A shares at net asset value (NAV). Actual Class R share performance would have been lower than Class A share performance because of higher Rule 12b-1 fees and other class-specific expenses that apply to the Class R shares. ** Performance for Class Y Shares prior to February 29, 2008 reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different. | |

| | | | |

8 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

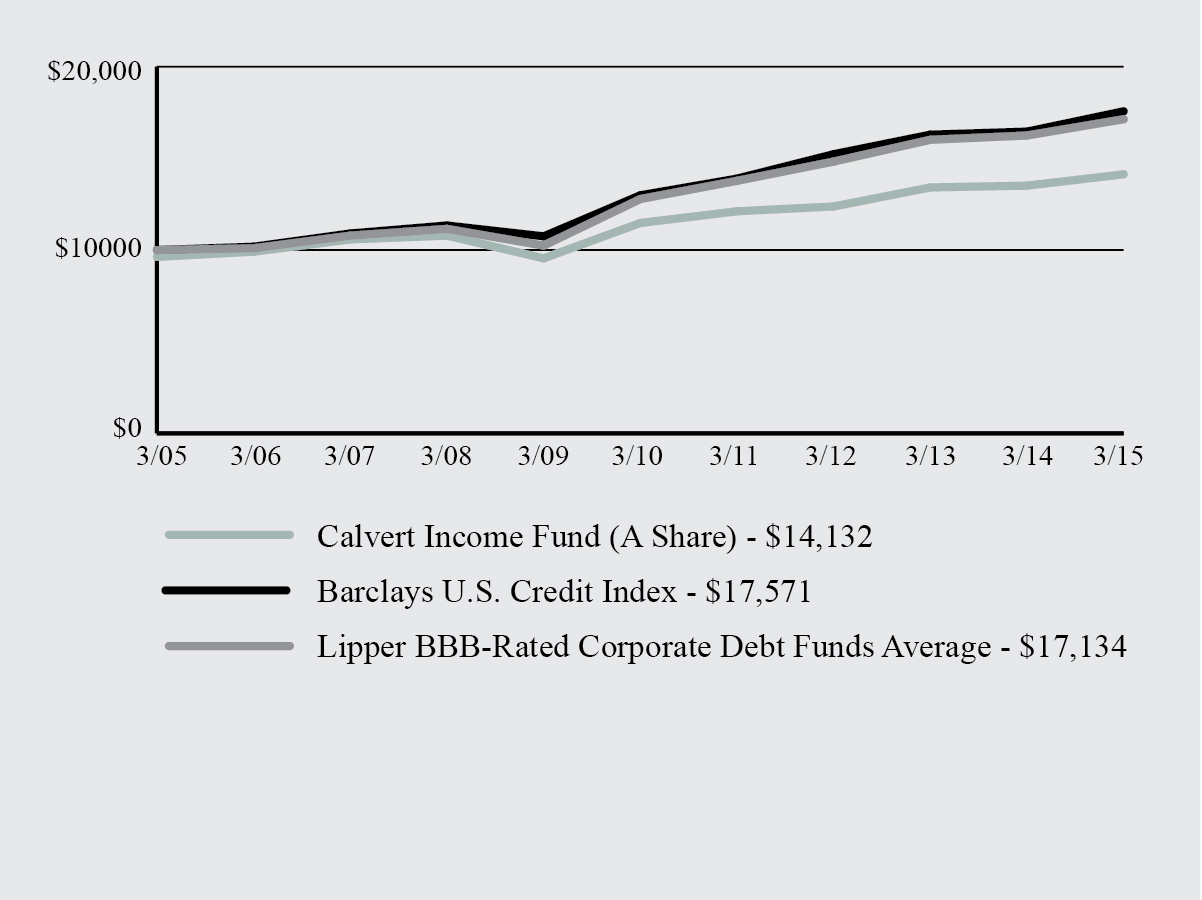

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal year periods. The results shown are for Class A shares and reflect the deduction of the maximum front-end Class A sales charge of 3.75%, and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund shares. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.25%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s operating expenses.

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 9

SHAREHOLDER ADVOCACY UPDATE

2014 Corporate Diversity Report Findings Released

In March, Calvert published its 2014 survey findings on the corporate diversity practices of the largely multinational companies that make up the Standard & Poor’s 100 Index (S&P 100), in follow-up to reports published in 2012 and 2010. Calvert believes companies that fully commit to providing a fair and equitable working environment will recognize gains in both the workplace and marketplace.

Key findings from the 2014 survey include:

| |

| • | Milestone for women in the board room. In 2014, every company in the S&P 100 had at least one woman on its board of directors. In addition, there was a 17% increase in companies with three or more women and/or minorities on their boards. |

| |

| • | Diversity commitment on the rise. In the past two years, top scores related to overall corporate commitment have increased by 45%.This stems primarily from greater board oversight of diversity initiatives and increased CEO and/or chair involvement. |

| |

| • | LGBT policies have advanced overall. However, initiatives for persons with disabilities continue to fall behind other groups. |

Overall, in 2014, we saw growing commitment to women and minority employees, momentum around family-friendly work environments, and accelerated progress in support of LGBT employees. Looking ahead, we hope to see enhanced corporate diversity commitments, greater representation of women and minorities on boards, improved EEO1-disclosure, and expanded diversity initiatives for persons with disabilities.

To learn the highest- and lowest-rated companies in the report, A Survey of Corporate Diversity Practices of the S&P 100, and to find out more about the report’s methodology and findings, visit www.calvert.com.

2015 Shareholder Resolutions

Building on our initiatives from 2014, Calvert was the lead filer on 38 shareholder resolutions for the 2015 proxy season, and co-filer on another 18 proposals. Key topics include “big data” and civil rights issues, sustainability reporting, board of director oversight of environmental and social matters, water risk, climate change and greenhouse gas emissions reductions, supply chain labor issues, and board diversity.

Specifically, Calvert asked 14 companies to set a goal and a timeline for reducing their greenhouse gas emissions and filed seven proposals asking companies to issue a sustainability report describing their environmental, social and governance (ESG) performance and goals. To push for improved boardroom diversity, Calvert filed six proposals with companies requesting they report on their plans to increase minority and women Board representation and assess the effectiveness of these efforts. We also filed seven proposals requesting that companies assess and manage the civil rights’ risks related to their use of big data, which refers to data sets so large or complex that traditional data processing applications are inadequate. We also filed proposals on water risk in the agricultural supply chain and on developing a sustainable agriculture policy.

To keep abreast of the outcomes of these 2015 shareholder resolutions, as well as Calvert’s proxy voting and public policy initiatives, visit the “Resources” section on www.calvert.com.

10 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

SHAREHOLDER EXPENSE EXAMPLE

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2014 to March 31, 2015).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 11

|

| | | |

| | BEGINNING ACCOUNT VALUE 10/1/14 | ENDING ACCOUNT VALUE 3/31/15 | EXPENSES PAID DURING PERIOD* 10/1/14 - 3/31/15 |

CLASS A | | | |

| Actual | $1,000.00 | $1,028.31 | $6.47 |

| Hypothetical | $1,000.00 | $1,018.55 | $6.44 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS B | | | |

| Actual | $1,000.00 | $1,024.73 | $10.75 |

| Hypothetical | $1,000.00 | $1,014.31 | $10.70 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS C | | | |

| Actual | $1,000.00 | $1,025.47 | $9.82 |

| Hypothetical | $1,000.00 | $1,015.23 | $9.77 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS I | | | |

| Actual | $1,000.00 | $1,032.09 | $3.29 |

| Hypothetical | $1,000.00 | $1,021.70 | $3.27 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS R | | | |

| Actual | $1,000.00 | $1,027.77 | $7.43 |

| Hypothetical | $1,000.00 | $1,017.60 | $7.39 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS Y | | | |

| Actual | $1,000.00 | $1,030.75 | $4.46 |

| Hypothetical | $1,000.00 | $1,020.54 | $4.44 |

| (5% return per year before expenses) | | | |

| | | | |

* Expenses are equal to the Fund’s annualized expense ratio of 1.28%, 2.13%, 1.95%, 0.65%, 1.47% and 0.88% for Class A, Class B, Class C, Class I, Class R, and Class Y, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

|

12 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

STATEMENT OF NET ASSETS

MARCH 31, 2015

|

| | | | | | |

ASSET-BACKED SECURITIES - 14.7% | PRINCIPAL AMOUNT | VALUE |

| | | |

| ALM XII Ltd., 3.449%, 4/16/27 (e)(r) |

| $3,400,000 |

|

| $3,363,620 |

|

| American Homes 4 Rent: | | |

| 3.50%, 6/17/31 (e)(r) | 3,000,000 |

| 2,959,749 |

| 4.705%, 10/17/36 (e) | 2,400,000 |

| 2,560,390 |

| 4.596%, 12/17/36 (e) | 2,950,000 |

| 3,121,652 |

| Applebee’s Funding LLC / IHOP Funding LLC, 4.277%, 9/5/44 (e) | 3,050,000 |

| 3,156,890 |

| Avis Budget Rental Car Funding AESOP LLC, 3.04%, 3/20/19 (e) | 4,820,000 |

| 4,803,395 |

| CKE Restaurant Holdings, Inc., 4.474%, 3/20/43 (e) | 4,850,000 |

| 5,007,281 |

| Consumer Credit Origination Loan Trust, 2.82%, 3/15/21 (e) | 4,772,315 |

| 4,789,819 |

| DB Master Finance LLC, 3.98%, 2/20/45 (e) | 2,500,000 |

| 2,553,150 |

| Eagle I Ltd., 2.57%, 12/15/39 (e) | 3,750,000 |

| 3,744,750 |

| Element Rail Leasing I LLC: | | |

| 2.299%, 4/19/44 (e) | 1,208,457 |

| 1,203,464 |

| 3.668%, 4/19/44 (e) | 2,700,000 |

| 2,752,744 |

| 4.406%, 4/19/44 (e) | 2,783,000 |

| 2,850,911 |

| Element Rail Leasing II LLC, 3.585%, 2/19/45 (e) | 3,900,000 |

| 3,942,510 |

| FRS I LLC, 3.08%, 4/15/43 (e) | 5,976,435 |

| 6,020,182 |

| GLC II Trust, 4.00%, 12/18/20 (e) | 3,931,808 |

| 3,953,433 |

| GLC Trust, 3.00%, 7/15/21 (e) | 3,107,249 |

| 3,104,141 |

| Global SC Finance II SRL, 2.98%, 4/17/28 (e) | 2,748,333 |

| 2,757,713 |

| GMAT Trust, 3.721%, 2/25/44 (e)(r) | 2,189,192 |

| 2,185,919 |

| Hilton Grand Vacations Trust, 2.28%, 1/25/26 (e) | 1,246,624 |

| 1,257,416 |

| HOA Funding LLC, 4.846%, 8/20/44 (e) | 4,752,000 |

| 4,763,880 |

| Invitation Homes Trust: | | |

| 1.60%, 12/17/30 (e)(r) | 300,000 |

| 297,875 |

| 2.273%, 6/17/31 (e)(r) | 2,500,000 |

| 2,510,095 |

| 3.878%, 6/17/32 (e)(r) | 1,750,000 |

| 1,750,000 |

| JGWPT XXXI LLC, 4.94%, 3/16/65 (e) | 1,000,000 |

| 1,066,482 |

| JGWPT XXXII LLC, 4.48%, 1/15/75 (e) | 1,450,000 |

| 1,484,249 |

|

| Navient Student Loan Trust, 1.714%, 7/25/52 (r) | 1,200,000 |

| 1,112,720 |

|

| OneMain Financial Issuance Trust, 2.43%, 6/18/24 (e) | 7,400,000 |

| 7,411,174 |

|

| Oxford Finance Funding Trust, 3.475%, 12/15/22 (e) | 2,600,000 |

| 2,602,860 |

|

| Selene Non-Performing Loans LLC, 2.981%, 5/25/54 (e)(r) | 2,806,496 |

| 2,778,552 |

|

| SLM Private Education Loan Trust, 3.00%, 5/16/44 (e) | 2,700,000 |

| 2,661,355 |

|

| SoFi Professional Loan Program LLC, 2.55%, 8/27/29 (e) | 3,828,118 |

| 3,850,750 |

|

| STORE Master Funding LLC, 4.21%, 4/20/44 (e) | 2,887,917 |

| 2,984,662 |

|

| TAL Advantage V LLC: | | |

| 3.33%, 5/20/39 (e) | 3,123,394 |

| 3,171,422 |

|

| 3.97%, 5/20/39 (e) | 916,667 |

| 909,112 |

|

| 3.27%, 11/21/39 (e) | 2,513,333 |

| 2,559,099 |

|

| 4.15%, 11/21/39 (e) | 966,667 |

| 980,143 |

|

| Trinity Rail Leasing LP, 3.525%, 1/15/43 (e) | 3,000,000 |

| 3,029,400 |

|

| US Residential Opportunity Fund Trust, 3.721%, 1/27/35 (e) | 1,979,162 |

| 1,985,764 |

|

| VOLT XIX LLC, 3.875%, 4/25/55 (e)(r) | 5,788,728 |

| 5,810,529 |

|

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 13

|

| | | | | | |

ASSET-BACKED SECURITIES - CONT’D | PRINCIPAL AMOUNT | VALUE |

| | | |

| VOLT XXVII LLC: | | |

| 3.375%, 8/27/57 (e)(r) |

| $2,185,687 |

|

| $2,186,859 |

|

| 4.75%, 8/27/57 (e)(r) | 800,000 |

| 792,978 |

|

| | | |

| Total Asset-Backed Securities (Cost $121,578,878) | | 122,789,089 |

|

| | | |

| | | |

COLLATERALIZED MORTGAGE-BACKED OBLIGATIONS (PRIVATELY ORIGINATED) - 1.9% | | |

| Banc of America Mortgage Trust, 0.301%, 1/25/34 (r) | 18,717,132 |

| 76,459 |

|

| CAM Mortgage Trust: | | |

| 4.45%, 5/15/48 (e)(r) | 3,500,000 |

| 3,512,215 |

|

| 5.50%, 12/15/53 (e)(r) | 404,107 |

| 404,374 |

|

| Fannie Mae Connecticut Avenue Securities: | | |

| CAS 2014-C02 1M2, 2.774%, 5/25/24 (r) | 6,980,000 |

| 6,378,324 |

|

| CAS 2014-C03 1M2, 3.174%, 7/25/24 (r) | 2,000,000 |

| 1,881,648 |

|

| CAS 2014-C03 2M2, 3.074%, 7/25/24 (r) | 1,500,000 |

| 1,402,097 |

|

| CAS 2015-C01 1M2, 4.474%, 2/25/25 (r) | 1,950,000 |

| 1,986,876 |

|

| | | |

Total Collateralized Mortgage-Backed Obligations (Privately Originated) (Cost $16,232,170) | | 15,641,993 |

|

| | | |

| | | |

COMMERCIAL MORTGAGE-BACKED SECURITIES - 4.9% | | |

| Citigroup Commercial Mortgage Trust, 3.575%, 9/15/17 (e)(r) | 2,800,000 |

| 2,737,280 |

|

| CSMC Trust, 4.185%, 9/15/37 (e) | 1,800,000 |

| 1,941,214 |

|

| EQTY INNS Mortgage Trust, 3.625%, 5/8/31 (e)(r) | 4,700,000 |

| 4,688,433 |

|

| Extended Stay America Trust: | | |

| 3.604%, 12/5/31 (e) | 2,970,000 |

| 3,093,026 |

|

| 5.053%, 12/5/31 (e)(r) | 1,765,000 |

| 1,833,770 |

|

| Hilton USA Trust: | | |

| 3.714%, 11/5/30 (e) | 1,600,000 |

| 1,633,723 |

|

| 5.222%, 11/5/30 (e)(r) | 3,500,000 |

| 3,595,051 |

|

| JP Morgan Chase Commercial Mortgage Securities Trust: | | |

| 3.771%, 6/10/27 (e) | 2,200,000 |

| 2,282,313 |

|

| 3.805%, 6/10/27 (e)(r) | 1,500,000 |

| 1,517,436 |

|

| 3.775%, 6/15/29 (e)(r) | 3,500,000 |

| 3,495,782 |

|

| Morgan Stanley Capital I Trust, 3.446%, 7/13/29 (e)(r) | 1,700,000 |

| 1,661,670 |

|

| Motel 6 Trust, 5.279%, 2/5/30 (e) | 2,100,000 |

| 2,103,217 |

|

| ORES NPL LLC: | | |

| 6.00%, 3/27/24 (e) | 2,600,000 |

| 2,600,000 |

|

| 3.081%, 9/25/25 (e) | 846,510 |

| 844,393 |

|

| VFC LLC, 5.50%, 7/20/30 (e) | 3,000,000 |

| 2,999,445 |

|

14 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | | |

COMMERCIAL MORTGAGE-BACKED SECURITIES - CONT'D | PRINCIPAL AMOUNT | VALUE |

| | | |

| WFRBS Commercial Mortgage Trust: | | |

| 3.497%, 8/15/47 (e) |

| $1,400,000 |

|

| $1,211,599 |

|

| 4.234%, 8/15/47 (r) | 2,200,000 |

| 2,275,167 |

|

| | | |

| Total Commercial Mortgage-Backed Securities (Cost $40,108,860) | | 40,513,519 |

|

| | | |

| | | |

CORPORATE BONDS - 68.9% | | |

| | | |

| 21st Century Fox America, Inc., 5.40%, 10/1/43 | 1,500,000 |

| 1,826,403 |

|

| Actavis Funding SCS: | | |

| 3.80%, 3/15/25 | 1,150,000 |

| 1,186,834 |

|

| 4.75%, 3/15/45 | 2,300,000 |

| 2,444,569 |

|

Albertsons Holdings LLC/Saturn Acquisition Merger Sub, Inc., 7.75%, 10/15/22 (e) | 1,979,000 |

| 2,117,530 |

|

| Alliance Mortgage Investments, Inc., 12.61%, 6/1/10 (b)(r)(x)* | 3,077,944 |

| — |

|

| Ally Financial, Inc., 3.25%, 2/13/18 | 3,000,000 |

| 2,970,000 |

|

| Amazon.com, Inc., 3.30%, 12/5/21 | 2,000,000 |

| 2,080,064 |

|

| America Movil SAB de CV: | | |

| 2.375%, 9/8/16 | 2,000,000 |

| 2,032,780 |

|

| 4.375%, 7/16/42 | 1,500,000 |

| 1,499,790 |

|

| American Airlines Group, Inc., 4.625%, 3/1/20 (e) | 600,000 |

| 587,625 |

|

| American Airlines Pass Through Trust: | | |

| 5.60%, 1/15/22 (e) | 2,726,425 |

| 2,872,834 |

|

| 3.375%, 11/1/28 | 2,800,000 |

| 2,810,640 |

|

| American International Group, Inc., 4.50%, 7/16/44 | 2,450,000 |

| 2,629,872 |

|

| American Tower Corp.: | | |

| 3.45%, 9/15/21 | 1,000,000 |

| 1,020,766 |

|

| 4.70%, 3/15/22 | 2,000,000 |

| 2,144,920 |

|

| Amgen, Inc.: | | |

| 3.625%, 5/22/24 | 1,000,000 |

| 1,051,647 |

|

| 5.375%, 5/15/43 | 1,500,000 |

| 1,789,594 |

|

| Anadarko Petroleum Corp., 4.50%, 7/15/44 | 1,000,000 |

| 1,023,044 |

|

| Anheuser-Busch InBev Finance, Inc.: | | |

| 2.625%, 1/17/23 | 1,900,000 |

| 1,873,030 |

|

| 4.00%, 1/17/43 | 1,900,000 |

| 1,932,507 |

|

| Anheuser-Busch InBev Worldwide, Inc.: | | |

| 2.50%, 7/15/22 | 1,500,000 |

| 1,479,861 |

|

| 3.75%, 7/15/42 | 1,000,000 |

| 975,180 |

|

| Antero Resources Corp., 6.00%, 12/1/20 | 1,000,000 |

| 1,000,500 |

|

| Anthem, Inc., 4.65%, 1/15/43 | 2,000,000 |

| 2,167,896 |

|

| Apache Corp., 4.75%, 4/15/43 | 1,000,000 |

| 1,045,158 |

|

| Apple, Inc., 3.45%, 2/9/45 | 4,045,000 |

| 3,839,672 |

|

| ArcelorMittal, 6.125%, 6/1/18 | 6,700,000 |

| 7,199,150 |

|

| Asian Development Bank, 2.125%, 3/19/25 | 1,700,000 |

| 1,714,630 |

|

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 15

|

| | | | | | |

CORPORATE BONDS - CONT’D | PRINCIPAL AMOUNT | VALUE |

| | | |

| AT&T, Inc.: | | |

| 2.375%, 11/27/18 |

| $3,500,000 |

|

| $3,545,052 |

|

| 2.30%, 3/11/19 | 1,450,000 |

| 1,461,103 |

|

| 4.35%, 6/15/45 | 2,750,000 |

| 2,630,317 |

|

Avis Budget Car Rental LLC / Avis Budget Finance, Inc., 9.75%, 3/15/20 | 1,400,000 |

| 1,525,160 |

|

| Bank of America Corp.: | | |

| 2.60%, 1/15/19 | 1,650,000 |

| 1,679,357 |

|

| 4.125%, 1/22/24 | 3,190,000 |

| 3,415,967 |

|

| 4.00%, 4/1/24 | 1,850,000 |

| 1,967,875 |

|

| 4.00%, 1/22/25 | 1,500,000 |

| 1,512,140 |

|

| 4.25%, 10/22/26 | 3,450,000 |

| 3,561,580 |

|

| Bank of America NA: | | |

| 5.30%, 3/15/17 | 9,000,000 |

| 9,611,928 |

|

| 6.10%, 6/15/17 | 5,000,000 |

| 5,477,620 |

|

| Berkshire Hathaway Finance Corp., 3.00%, 5/15/22 | 2,500,000 |

| 2,600,075 |

|

BNSF Funding Trust I, 6.613% to 1/15/26, floating rate thereafter to 12/15/55 (r) | 14,501,000 |

| 16,349,879 |

|

| BP Capital Markets plc: | | |

| 2.75%, 5/10/23 | 1,000,000 |

| 975,503 |

|

| 3.535%, 11/4/24 | 1,000,000 |

| 1,018,385 |

|

| Capital One Bank: | | |

| 2.25%, 2/13/19 | 2,400,000 |

| 2,412,706 |

|

| 3.375%, 2/15/23 | 4,600,000 |

| 4,658,866 |

|

| Celanese US Holdings LLC, 5.875%, 6/15/21 | 1,300,000 |

| 1,404,000 |

|

| Celgene Corp., 3.625%, 5/15/24 | 1,900,000 |

| 1,974,632 |

|

| Cemex SAB de CV: | | |

| 5.273%, 9/30/15 (e)(r) | 6,250,000 |

| 6,280,625 |

|

| 6.50%, 12/10/19 (e) | 1,000,000 |

| 1,062,500 |

|

| CenturyLink, Inc., 7.65%, 3/15/42 | 3,650,000 |

| 3,732,125 |

|

| Cisco Systems, Inc., 3.625%, 3/4/24 | 1,500,000 |

| 1,620,424 |

|

| CIT Group, Inc.: | | |

| 4.25%, 8/15/17 | 1,125,000 |

| 1,139,062 |

|

| 5.25%, 3/15/18 | 4,150,000 |

| 4,295,250 |

|

| Citigroup, Inc.: | | |

| 2.50%, 9/26/18 | 5,000,000 |

| 5,098,000 |

|

| 3.75%, 6/16/24 | 1,000,000 |

| 1,045,162 |

|

| 3.875%, 3/26/25 | 3,750,000 |

| 3,764,085 |

|

| ConAgra Foods, Inc., 4.65%, 1/25/43 | 1,000,000 |

| 1,003,276 |

|

| ConocoPhillips Co.: | | |

| 3.35%, 11/15/24 | 2,000,000 |

| 2,061,004 |

|

| 4.30%, 11/15/44 | 750,000 |

| 796,040 |

|

| Continental Airlines Pass Through Trust, 6.25%, 10/11/21 | 4,282,253 |

| 4,560,600 |

|

| Cott Beverages, Inc., 6.75%, 1/1/20 (e) | 1,000,000 |

| 1,035,000 |

|

| Coveris Holdings SA, 7.875%, 11/1/19 (e) | 1,500,000 |

| 1,533,750 |

|

| Crown Castle Towers LLC: | | |

| 4.174%, 8/15/37 (e) | 825,000 |

| 859,650 |

|

| 4.883%, 8/15/40 (e) | 3,000,000 |

| 3,294,045 |

|

16 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | | |

CORPORATE BONDS - CONT’D | PRINCIPAL AMOUNT | VALUE |

| | | |

| Cummins, Inc., 4.875%, 10/1/43 |

| $1,100,000 |

|

| $1,305,139 |

|

| CVS Pass-Through Trust, 6.036%, 12/10/28 | 3,060,025 |

| 3,617,250 |

|

| DDR Corp., 4.75%, 4/15/18 | 6,700,000 |

| 7,212,858 |

|

| Deutsche Telekom International Finance BV, 4.875%, 3/6/42 (e) | 600,000 |

| 676,588 |

|

| DIRECTV Holdings LLC / DIRECTV Financing Co., Inc.: | | |

| 3.95%, 1/15/25 | 3,000,000 |

| 3,090,831 |

|

| 5.15%, 3/15/42 | 2,000,000 |

| 2,090,144 |

|

| Discover Bank, 7.00%, 4/15/20 | 2,500,000 |

| 2,967,815 |

|

| Dow Chemical Co., 4.625%, 10/1/44 | 1,700,000 |

| 1,777,066 |

|

| Dr Pepper Snapple Group, Inc., 3.20%, 11/15/21 | 2,555,000 |

| 2,657,151 |

|

| Enterprise Products Operating LLC, 7.034% to 1/15/18, floating rate thereafter to 1/15/68 (r) | 12,115,000 |

| 13,097,817 |

|

| ERP Operating LP, 4.625%, 12/15/21 | 1,000,000 |

| 1,117,020 |

|

| Express Scripts Holding Co.: | | |

| 4.75%, 11/15/21 | 1,500,000 |

| 1,687,660 |

|

| 3.90%, 2/15/22 | 1,000,000 |

| 1,061,811 |

|

| Ford Motor Credit Co. LLC: | | |

| 3.984%, 6/15/16 | 1,500,000 |

| 1,546,544 |

|

| 4.25%, 2/3/17 | 5,000,000 |

| 5,250,320 |

|

| 1.684%, 9/8/17 | 2,000,000 |

| 1,997,152 |

|

| 2.145%, 1/9/18 | 1,350,000 |

| 1,365,421 |

|

| 3.219%, 1/9/22 | 1,000,000 |

| 1,021,063 |

|

| General Electric Capital Corp., 4.625%, 1/7/21 | 2,250,000 |

| 2,533,306 |

|

General Electric Capital Corp. / LJ VP Holdings LLC, 3.80%, 6/18/19 (e) | 3,000,000 |

| 3,210,810 |

|

| General Electric Co.: | | |

| 3.375%, 3/11/24 | 4,000,000 |

| 4,231,112 |

|

| 4.50%, 3/11/44 | 4,200,000 |

| 4,714,529 |

|

| General Motors Co., 5.20%, 4/1/45 | 2,750,000 |

| 2,984,674 |

|

| General Motors Financial Co., Inc.: | | |

| 3.50%, 7/10/19 | 1,500,000 |

| 1,539,994 |

|

| 3.15%, 1/15/20 | 600,000 |

| 607,138 |

|

| 4.00%, 1/15/25 | 1,900,000 |

| 1,937,840 |

|

| Genworth Holdings, Inc., 4.80%, 2/15/24 | 3,800,000 |

| 3,196,750 |

|

| Gilead Sciences, Inc., 3.70%, 4/1/24 | 1,000,000 |

| 1,067,804 |

|

| Goldman Sachs Group, Inc.: | | |

| 6.15%, 4/1/18 | 10,975,000 |

| 12,338,545 |

|

| 2.625%, 1/31/19 | 4,000,000 |

| 4,086,664 |

|

| 3.50%, 1/23/25 | 4,150,000 |

| 4,222,849 |

|

| Grain Spectrum Funding II LLC, 3.29%, 10/10/19 (e) | 1,000,000 |

| 1,001,250 |

|

| Health Care REIT, Inc.: | | |

| 5.25%, 1/15/22 | 2,000,000 |

| 2,254,176 |

|

| 3.75%, 3/15/23 | 2,000,000 |

| 2,048,526 |

|

| Home Depot, Inc.: | | |

| 2.70%, 4/1/23 | 2,000,000 |

| 2,030,234 |

|

| 4.20%, 4/1/43 | 1,000,000 |

| 1,092,480 |

|

| 4.40%, 3/15/45 | 600,000 |

| 669,920 |

|

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 17

|

| | | | | | |

CORPORATE BONDS - CONT’D | PRINCIPAL AMOUNT | VALUE |

| | | |

| Host Hotels & Resorts LP, 3.75%, 10/15/23 |

| $2,000,000 |

|

| $2,027,188 |

|

| Hyundai Capital America, 4.00%, 6/8/17 (e) | 2,000,000 |

| 2,099,862 |

|

| Hyundai Capital Services, Inc., 3.50%, 9/13/17 (e) | 3,245,000 |

| 3,366,499 |

|

| Illinois Tool Works, Inc., 3.90%, 9/1/42 | 2,000,000 |

| 2,061,392 |

|

Innovation Ventures LLC / Innovation Ventures Finance Corp., 9.50%, 8/15/19 (e) | 3,000,000 |

| 3,030,000 |

|

| International Lease Finance Corp., 6.75%, 9/1/16 (e) | 2,000,000 |

| 2,125,000 |

|

| Jabil Circuit, Inc., 7.75%, 7/15/16 | 2,000,000 |

| 2,145,000 |

|

| JPMorgan Chase & Co.: | | |

| 2.35%, 1/28/19 | 3,000,000 |

| 3,049,173 |

|

| 3.625%, 5/13/24 | 7,000,000 |

| 7,278,530 |

|

| 3.875%, 9/10/24 | 3,000,000 |

| 3,077,670 |

|

| 3.125%, 1/23/25 | 4,900,000 |

| 4,914,372 |

|

| Kenan Advantage Group, Inc., 8.375%, 12/15/18 (e) | 1,500,000 |

| 1,560,000 |

|

| Kern River Funding Corp., 6.676%, 7/31/16 (e) | 47,598 |

| 50,217 |

|

| Kia Motors Corp., 3.625%, 6/14/16 (e) | 4,000,000 |

| 4,105,784 |

|

| Kinder Morgan Energy Partners LP: | | |

| 4.10%, 11/15/15 | 1,000,000 |

| 1,017,618 |

|

| 4.25%, 9/1/24 | 1,000,000 |

| 1,022,534 |

|

| 5.625%, 9/1/41 | 2,960,000 |

| 3,129,114 |

|

| Kinder Morgan, Inc.: | | |

| 5.55%, 6/1/45 | 1,500,000 |

| 1,581,544 |

|

| 5.05%, 2/15/46 | 4,400,000 |

| 4,394,144 |

|

| Kroger Co., 3.85%, 8/1/23 | 1,900,000 |

| 2,024,912 |

|

| Laboratory Corporation of America Holdings: | | |

| 3.60%, 2/1/25 | 700,000 |

| 702,857 |

|

| 4.70%, 2/1/45 | 700,000 |

| 720,507 |

|

| Land O’Lakes Capital Trust I, 7.45%, 3/15/28 (e) | 8,000,000 |

| 8,640,000 |

|

| Leucadia National Corp.: | | |

| 8.125%, 9/15/15 | 3,320,000 |

| 3,417,309 |

|

| 6.625%, 10/23/43 | 2,925,000 |

| 2,923,622 |

|

| Life Technologies Corp., 6.00%, 3/1/20 | 4,000,000 |

| 4,619,572 |

|

LL & P Wind Energy, Inc. Washington Revenue Bonds, 6.192%, 12/1/27 (e) | 2,675,000 |

| 2,730,613 |

|

| Lowe’s Co.’s, Inc., 4.65%, 4/15/42 | 1,050,000 |

| 1,203,432 |

|

| LYB International Finance BV, 5.25%, 7/15/43 | 1,000,000 |

| 1,114,364 |

|

| Macy’s Retail Holdings, Inc., 4.30%, 2/15/43 | 1,000,000 |

| 1,014,766 |

|

| Masco Corp., 4.45%, 4/1/25 | 850,000 |

| 877,625 |

|

| Massachusetts Institute of Technology, 3.959%, 7/1/38 | 500,000 |

| 537,416 |

|

| Medtronic, Inc., 3.50%, 3/15/25 (e) | 2,000,000 |

| 2,090,782 |

|

| Methanex Corp., 5.65%, 12/1/44 | 3,275,000 |

| 3,439,716 |

|

| MetLife, Inc.: | | |

| 4.875%, 11/13/43 | 2,400,000 |

| 2,770,037 |

|

| 4.05%, 3/1/45 | 900,000 |

| 932,056 |

|

Michaels FinCo Holdings LLC / Michaels FinCo, Inc., 7.50%, 8/1/18 (e) | 752,000 |

| 767,040 |

|

| Michaels Stores, Inc., 5.875%, 12/15/20 (e) | 2,650,000 |

| 2,722,875 |

|

18 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | | |

CORPORATE BONDS - CONT’D | PRINCIPAL AMOUNT | VALUE |

| | | |

| Microsoft Corp., 2.70%, 2/12/25 |

| $2,000,000 |

|

| $2,007,712 |

|

| Morgan Stanley: | | |

| 6.25%, 8/28/17 | 2,900,000 |

| 3,203,665 |

|

| 5.50%, 1/26/20 | 2,000,000 |

| 2,272,986 |

|

| 1.396%, 1/27/20 (r) | 2,100,000 |

| 2,131,403 |

|

| 2.65%, 1/27/20 | 3,500,000 |

| 3,548,727 |

|

| 3.70%, 10/23/24 | 2,400,000 |

| 2,502,197 |

|

| 5.00%, 11/24/25 | 4,150,000 |

| 4,584,318 |

|

| NBCUniversal Media LLC: | | |

| 4.375%, 4/1/21 | 9,500,000 |

| 10,584,245 |

|

| 4.45%, 1/15/43 | 2,800,000 |

| 3,040,486 |

|

| NII Capital Corp., 7.625%, 4/1/21 (p)* | 10,600,000 |

| 3,233,000 |

|

| Northrop Grumman Corp., 3.85%, 4/15/45 | 1,000,000 |

| 984,385 |

|

| Numericable-SFR SAS, 6.00%, 5/15/22 (e) | 2,000,000 |

| 2,025,000 |

|

| Oracle Corp., 3.40%, 7/8/24 | 2,000,000 |

| 2,102,378 |

|

| PacifiCorp, 4.10%, 2/1/42 | 4,000,000 |

| 4,314,404 |

|

| Penske Truck Leasing Co. LP / PTL Finance Corp.: | | |

| 3.125%, 5/11/15 (e) | 2,200,000 |

| 2,204,651 |

|

| 3.05%, 1/9/20 (e) | 3,300,000 |

| 3,355,288 |

|

| PepsiCo, Inc., 2.75%, 3/5/22 | 2,000,000 |

| 2,041,222 |

|

| Pernod Ricard SA: | | |

| 4.45%, 1/15/22 (e) | 8,250,000 |

| 8,941,705 |

|

| 4.25%, 7/15/22 (e) | 2,000,000 |

| 2,155,556 |

|

| Pioneer Natural Resources Co., 5.875%, 7/15/16 | 3,340,000 |

| 3,525,554 |

|

| ProLogis LP, 6.875%, 3/15/20 | 1,407,000 |

| 1,659,305 |

|

| Prospect Medical Holdings, Inc., 8.375%, 5/1/19 (e) | 1,000,000 |

| 1,062,500 |

|

| Prudential Financial, Inc., 4.60%, 5/15/44 | 1,000,000 |

| 1,060,261 |

|

| Regions Bank, 7.50%, 5/15/18 | 514,000 |

| 597,439 |

|

| Reliance Steel & Aluminum Co., 4.50%, 4/15/23 | 2,300,000 |

| 2,323,501 |

|

| Rio Tinto Finance USA plc, 3.50%, 3/22/22 | 2,000,000 |

| 2,066,300 |

|

| SABMiller Holdings, Inc.: | | |

| 2.20%, 8/1/18 (e) | 1,300,000 |

| 1,315,040 |

|

| 3.75%, 1/15/22 (e) | 4,215,000 |

| 4,434,007 |

|

| 4.95%, 1/15/42 (e) | 1,500,000 |

| 1,685,379 |

|

| SBA Tower Trust, 3.722%, 4/15/48 (e) | 6,870,000 |

| 7,094,903 |

|

| Shell International Finance BV, 4.55%, 8/12/43 | 2,000,000 |

| 2,267,028 |

|

| Spencer Spirit Holdings, Inc., 9.00%, 5/1/18 (e) | 2,945,000 |

| 2,985,494 |

|

| Sprint Corp., 7.25%, 9/15/21 | 3,150,000 |

| 3,165,750 |

|

| Telefonica Emisiones SAU: | | |

| 3.992%, 2/16/16 | 2,670,000 |

| 2,737,962 |

|

| 3.192%, 4/27/18 | 2,000,000 |

| 2,085,884 |

|

| TerraForm Power Operating LLC, 5.875%, 2/1/23 (e) | 1,500,000 |

| 1,556,250 |

|

| The TJX Co.’s, Inc., 2.50%, 5/15/23 | 2,000,000 |

| 1,971,130 |

|

| Thermo Fisher Scientific, Inc., 4.15%, 2/1/24 | 1,200,000 |

| 1,295,648 |

|

| Time Warner Cable, Inc., 5.50%, 9/1/41 | 4,250,000 |

| 4,882,155 |

|

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 19

|

| | | | | | |

CORPORATE BONDS - CONT’D | PRINCIPAL AMOUNT | VALUE |

| | | |

| Time Warner, Inc.: | | |

| 4.05%, 12/15/23 |

| $1,500,000 |

|

| $1,605,522 |

|

| 5.375%, 10/15/41 | 4,000,000 |

| 4,684,628 |

|

| 4.90%, 6/15/42 | 1,500,000 |

| 1,664,402 |

|

| Total Capital International SA, 2.70%, 1/25/23 | 2,000,000 |

| 1,993,086 |

|

| Turkish Airlines Pass Through Trust, 4.20%, 9/15/28 (e) | 800,000 |

| 808,000 |

|

| United Airlines Pass Through Trust: | | |

| 4.75%, 10/11/23 | 2,904,000 |

| 2,944,075 |

|

| 4.625%, 3/3/24 | 1,600,000 |

| 1,604,480 |

|

| United Technologies Corp., 4.50%, 6/1/42 | 2,900,000 |

| 3,216,503 |

|

| Verizon Communications, Inc.: | | |

| 2.625%, 2/21/20 | 10,765,000 |

| 10,951,880 |

|

| 3.50%, 11/1/24 | 2,400,000 |

| 2,456,076 |

|

| 4.862%, 8/21/46 | 11,945,000 |

| 12,505,639 |

|

| Viacom, Inc.: | | |

| 3.875%, 4/1/24 | 2,000,000 |

| 2,057,724 |

|

| 5.25%, 4/1/44 | 1,950,000 |

| 2,092,325 |

|

| Virgin Australia Trust: | | |

| 6.00%, 4/23/22 (e) | 2,717,984 |

| 2,813,114 |

|

| 5.00%, 4/23/25 (e) | 773,147 |

| 813,737 |

|

| Wachovia Capital Trust III, 5.57%, 3/29/49 (r) | 2,050,000 |

| 2,024,170 |

|

| Walgreens Boots Alliance, Inc.: | | |

| 3.80%, 11/18/24 | 2,200,000 |

| 2,274,694 |

|

| 4.80%, 11/18/44 | 1,600,000 |

| 1,726,950 |

|

| Wal-Mart Stores, Inc., 4.00%, 4/11/43 | 4,150,000 |

| 4,402,067 |

|

| Wells Fargo & Co.: | | |

| 3.45%, 2/13/23 | 2,000,000 |

| 2,046,410 |

|

| 4.10%, 6/3/26 | 2,000,000 |

| 2,110,136 |

|

| Whirlpool Corp., 2.40%, 3/1/19 | 1,000,000 |

| 1,012,996 |

|

| Williams Co.’s, Inc., 5.75%, 6/24/44 | 8,000,000 |

| 7,476,952 |

|

| Williams Partners LP: | | |

| 3.60%, 3/15/22 | 3,400,000 |

| 3,389,382 |

|

| 3.90%, 1/15/25 | 2,000,000 |

| 1,955,462 |

|

| Williams Partners LP / ACMP Finance Corp.: | | |

| 6.125%, 7/15/22 | 2,600,000 |

| 2,754,700 |

|

| 4.875%, 3/15/24 | 4,650,000 |

| 4,673,250 |

|

| Zoetis, Inc., 1.875%, 2/1/18 | 1,500,000 |

| 1,500,855 |

|

| | | |

| Total Corporate Bonds (Cost $549,520,119) | | 575,436,665 |

|

| | | |

| | | |

U.S. GOVERNMENT AGENCIES AND INSTRUMENTALITIES - 0.0% | | |

| Premier Aircraft Leasing EXIM 1 Ltd., 3.547%, 4/10/22 | 95 |

| 101 |

|

| | | |

| Total U.S. Government Agencies and Instrumentalities (Cost $95) | | 101 |

|

| | | |

20 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | | |

U.S. GOVERNMENT AGENCY MORTGAGE-BACKED SECURITIES - 0.0% | PRINCIPAL AMOUNT | VALUE |

| Ginnie Mae, 11.00%, 10/15/15 |

| $8 |

|

| $8 |

|

| | | |

| Total U.S. Government Agency Mortgage-Backed Securities (Cost $8) | | 8 |

|

| | | |

| | | |

U.S. TREASURY OBLIGATIONS - 8.1% | | |

| United States Treasury Bonds, 3.00%, 11/15/44 | 15,125,000 |

| 16,572,508 |

|

| United States Treasury Notes: | | |

| 0.50%, 3/31/17 | 9,980,000 |

| 9,968,303 |

|

| 1.00%, 3/15/18 | 7,950,000 |

| 7,979,192 |

|

| 1.375%, 3/31/20 | 10,235,000 |

| 10,236,597 |

|

| 1.75%, 3/31/22 | 7,910,000 |

| 7,930,392 |

|

| 2.00%, 2/15/25 | 14,945,000 |

| 15,039,572 |

|

| | | |

| Total U.S. Treasury Obligations (Cost $66,781,735) | | 67,726,564 |

|

| | | |

| | | |

TIME DEPOSIT - 0.9% | | |

| State Street Bank Time Deposit, 0.088%, 4/1/15 | 7,870,897 |

| 7,870,897 |

|

| | | |

| Total Time Deposit (Cost $7,870,897) | | 7,870,897 |

|

| | | |

| | | |

| | | |

| TOTAL INVESTMENTS (Cost $802,092,762) - 99.4% | | 829,978,836 |

|

| Other assets and liabilities, net - 0.6% | | 5,297,444 |

|

NET ASSETS - 100% | |

| $835,276,280 |

|

| | | |

| | | |

NET ASSETS CONSIST OF: | | |

| Paid-in capital applicable to the following shares of beneficial interest, unlimited number of no par value shares authorized: | | |

| Class A: 33,992,900 shares outstanding |

| $1,038,140,903 |

|

| Class B: 39,878 shares outstanding | 17,915,201 |

|

| Class C: 6,127,397 shares outstanding | 140,137,913 |

|

| Class I: 5,687,181 shares outstanding | 121,461,709 |

|

| Class R: 324,694 shares outstanding | 4,580,271 |

|

| Class Y: 4,157,540 shares outstanding | 64,943,218 |

|

| Undistributed net investment income | 220,440 |

|

| Accumulated net realized gain (loss) | (580,179,092 | ) |

| Net unrealized appreciation (depreciation) | 28,055,717 |

|

| | | |

NET ASSETS |

| $835,276,280 |

|

| | | |

| See notes to financial statements. |

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 21

|

| | | | | | |

NET ASSET VALUE PER SHARE | | |

| Class A (based on net assets of $563,587,469) | $16.58 |

| Class B (based on net assets of $652,616) | $16.37 |

| Class C (based on net assets of $101,583,095) | $16.58 |

| Class I (based on net assets of $94,345,999) | $16.59 |

| Class R (based on net assets of $5,425,117) | $16.71 |

| Class Y (based on net assets of $69,681,984) | $16.76 |

| | | |

| |

|

| | | | | | | | |

FUTURES | NUMBER OF CONTRACTS | EXPIRATION DATE | UNDERLYING FACE AMOUNT AT VALUE | UNREALIZED APPRECIATION (DEPRECIATION) |

| Purchased: | | | | |

| 2 Year U.S. Treasury Notes | 221 | 6/15 |

| $48,433,531 |

|

| $103,617 |

|

| Ultra U.S. Treasury Bonds | 223 | 6/15 | 37,882,125 |

| 764,118 |

|

| Total Purchased | | | |

| $867,735 |

|

| | | | | |

| Sold: | | | | |

| 5 Year U.S. Treasury Notes | 135 | 6/15 |

| $16,228,477 |

|

| ($196,388 | ) |

| 10 Year U.S. Treasury Notes | 385 | 6/15 | 49,628,906 |

| (501,704 | ) |

| Total Sold | | | |

| ($698,092 | ) |

(b) This security was valued under the direction of the Board of Trustees. See Note A. (e) Security is exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. (p) Security is in default and is no longer accruing interest. (r) The coupon rate shown on floating or adjustable rate securities represents the rate at period end. (x) Alliance Bancorp and its affiliates filed for Chapter 7 bankruptcy on July 13, 2007. This security is no longer accruing interest. * Non-income producing security. Abbreviations: LLC: Limited Liability Corporation LP: Limited Partnership plc: Public Limited Company REIT: Real Estate Investment Trust See notes to financial statements. |

22 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

STATEMENT OF OPERATIONS

SIX MONTHS ENDED MARCH 31, 2015

|

| | | |

NET INVESTMENT INCOME | |

| Investment Income: | |

| Interest income |

| $17,443,856 |

|

| Dividend income | 21,960 |

|

| Total investment income | 17,465,816 |

|

| | |

| Expenses: | |

| Investment advisory fee | 1,720,803 |

|

| Administrative fees | 1,197,811 |

|

| Transfer agency fees and expenses | 916,209 |

|

| Distribution Plan expenses: | |

| Class A | 734,380 |

|

| Class B | 4,879 |

|

| Class C | 519,832 |

|

| Class R | 13,569 |

|

| Trustees' fees and expenses | 63,477 |

|

| Custodian fees | 55,415 |

|

| Registration fees | 42,345 |

|

| Reports to shareholders | 47,535 |

|

| Professional fees | 49,259 |

|

| Accounting fees | 61,102 |

|

| Miscellaneous | 20,696 |

|

| Total expenses | 5,447,312 |

|

| Reimbursement from Advisor: | |

| Class B | (8,766 | ) |

| Class R | (7,741 | ) |

| Net expenses | 5,430,805 |

|

| | |

NET INVESTMENT INCOME | 12,035,011 |

|

| | |

REALIZED AND UNREALIZED GAIN (LOSS) | |

| Net realized gain (loss) on: | |

| Investments | (2,531,538 | ) |

| Futures | 730,060 |

|

| | (1,801,478 | ) |

| Change in unrealized appreciation (depreciation) on: | |

| Investments | 13,973,082 |

|

| Futures | 85,064 |

|

| | 14,058,146 |

|

| | |

NET REALIZED AND UNREALIZED GAIN (LOSS) | 12,256,668 |

|

| | |

INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

| $24,291,679 |

|

| | |

| See notes to financial statements. |

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 23

STATEMENTS OF CHANGES IN NET ASSETS

|

| | | | | | | |

INCREASE (DECREASE) IN NET ASSETS | SIX MONTHS ENDED MARCH 31, 2015 | | YEAR ENDED SEPTEMBER 30, 2014 |

| Operations: | | | |

| Net investment income |

| $12,035,011 |

| |

| $27,594,912 |

|

| Net realized gain (loss) | (1,801,478 | ) | | (16,719,592 | ) |

| Change in unrealized appreciation (depreciation) | 14,058,146 |

| | 36,475,100 |

|

| | | | |

INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | 24,291,679 |

| | 47,350,420 |

|

| | | | |

| Distributions to shareholders from: | | | |

| Net investment income: | | | |

| Class A shares | (8,154,205 | ) | | (19,738,154 | ) |

| Class B shares | (9,440 | ) | | (56,683 | ) |

| Class C shares | (1,097,607 | ) | | (2,557,698 | ) |

| Class I shares | (1,581,109 | ) | | (3,256,812 | ) |

| Class R shares | (70,203 | ) | | (135,730 | ) |

| Class Y shares | (1,107,265 | ) | | (1,844,471 | ) |

| Total distributions | (12,019,829 | ) | | (27,589,548 | ) |

| | | | |

| Capital share transactions: | | | |

| Shares sold: | | | |

| Class A shares | 29,279,386 |

| | 58,135,737 |

|

| Class B shares | 958 |

| | 33,570 |

|

| Class C shares | 2,067,047 |

| | 3,276,853 |

|

| Class I shares | 6,626,071 |

| | 13,628,419 |

|

| Class R shares | 534,623 |

| | 1,176,454 |

|

| Class Y shares | 7,411,511 |

| | 30,347,431 |

|

| Reinvestment of distributions: | | | |

| Class A shares | 7,356,425 |

| | 17,952,323 |

|

| Class B shares | 7,744 |

| | 47,077 |

|

| Class C shares | 735,650 |

| | 1,691,297 |

|

| Class I shares | 1,561,672 |

| | 3,200,584 |

|

| Class R shares | 63,702 |

| | 121,628 |

|

| Class Y shares | 721,224 |

| | 970,884 |

|

| Redemption fees: | | | |

| Class A shares | 720 |

| | 10,939 |

|

| Class C shares | 112 |

| | 41 |

|

| Class I shares | — |

| | 1,209 |

|

| Class R shares | — |

| | 53 |

|

| Class Y shares | 235 |

| | 230 |

|

| See notes to financial statements. |

24 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

STATEMENTS OF CHANGES IN NET ASSETS

|

| | | | | | | |

INCREASE (DECREASE) IN NET ASSETS - CONT'D | SIX MONTHS ENDED MARCH 31, 2015 | | YEAR ENDED SEPTEMBER 30, 2014 |

| Shares redeemed: | | | |

| Class A shares |

| ($97,248,712 | ) | |

| ($247,321,343 | ) |

| Class B shares | (645,436 | ) | | (2,962,693 | ) |

| Class C shares | (10,108,514 | ) | | (31,938,939 | ) |

| Class I shares | (8,163,232 | ) | | (21,901,425 | ) |

| Class R shares | (660,953 | ) | | (1,485,384 | ) |

| Class Y shares | (9,881,222 | ) | | (25,133,677 | ) |

| Total capital share transactions | (70,340,989 | ) | | (200,148,732 | ) |

| | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | (58,069,139 | ) | | (180,387,860 | ) |

| | | | |

NET ASSETS | | | |

| Beginning of period | 893,345,419 |

| | 1,073,733,279 |

|

| End of period (including undistributed net investment income of $220,440 and $205,258, respectively) |

| $835,276,280 |

| |

| $893,345,419 |

|

| | | | |

CAPITAL SHARE ACTIVITY | | | |

| Shares sold: | | | |

| Class A shares | 1,777,939 |

| | 3,560,530 |

|

| Class B shares | 59 |

| | 2,075 |

|

| Class C shares | 125,623 |

| | 200,327 |

|

| Class I shares | 402,283 |

| | 831,692 |

|

| Class R shares | 32,203 |

| | 71,261 |

|

| Class Y shares | 445,524 |

| | 1,822,323 |

|

| Reinvestment of distributions: | | | |

| Class A shares | 447,197 |

| | 1,097,697 |

|

| Class B shares | 477 |

| | 2,905 |

|

| Class C shares | 44,729 |

| | 103,441 |

|

| Class I shares | 94,882 |

| | 195,595 |

|

| Class R shares | 3,843 |

| | 7,377 |

|

| Class Y shares | 43,367 |

| | 58,714 |

|

| Shares redeemed: | | | |

| Class A shares | (5,908,161 | ) | | (15,168,560 | ) |

| Class B shares | (39,800 | ) | | (182,955 | ) |

| Class C shares | (614,292 | ) | | (1,961,250 | ) |

| Class I shares | (495,573 | ) | | (1,344,465 | ) |

| Class R shares | (39,840 | ) | | (90,945 | ) |

| Class Y shares | (593,713 | ) | | (1,527,005 | ) |

| Total capital share activity | (4,273,253 | ) | | (12,321,243 | ) |

| | | | |

| See notes to financial statements. |

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 25

NOTES TO FINANCIAL STATEMENTS

NOTE A — SIGNIFICANT ACCOUNTING POLICIES

General: Calvert Income Fund (the “Fund”), a series of The Calvert Fund, is registered under the Investment Company Act of 1940 as a non-diversified, open-end management investment company. The Calvert Fund is comprised of six separate series. The operations of each series are accounted for separately. The Fund offers six classes of shares of beneficial interest - Classes A, B, C, I, R, and Y. Class A shares are sold with a maximum front-end sales charge of 3.75%. Class B shares are sold without a front-end sales charge and, with certain exceptions, will be charged a deferred sales charge at the time of redemption, depending on how long investors have owned the shares. Class B shares are no longer offered for purchase, except through reinvestment of dividends and/or distributions and through certain exchanges. Class B shares were closed effective April 20, 2015. Class C shares are sold without a front-end sales charge and, with certain exceptions, will be charged a deferred sales charge on shares sold within one year of purchase. Class B and Class C shares have higher levels of expenses than Class A shares. Class I shares require a minimum account balance of $1,000,000. The $1 million minimum initial investment is waived for retirement plans that trade through omnibus accounts and may be waived for certain other institutional accounts where it is believed to be in the best interest of the Fund and its shareholders. Class I shares have no front-end or deferred sales charge and have lower levels of expenses than Class A shares. Class R shares are generally only available to certain retirement plans where plan level or omnibus accounts are held on the books of the Fund. Class R shares have no front-end or deferred sales charge and have a higher level of expenses than Class A Shares. Class Y shares are generally only available to wrap or similar fee-based programs offered by financial intermediaries, foundations, and endowments that have entered into an agreement with the Fund’s Distributor to offer Class Y shares. Class Y shares have no front-end or deferred sales charge and have lower levels of expenses than Class A shares. Each class has different: (a) dividend rates due to differences in Distribution Plan expenses and other class specific expenses, (b) exchange privileges and (c) class specific voting rights.

Security Valuation: Net asset value per share is determined every business day as of the close of the regular session of the New York Stock Exchange (generally 4:00 p.m. Eastern time). The Fund uses independent pricing services approved by the Board of Trustees (“the Board”) to value its investments wherever possible. Investments for which market quotations are not available or deemed not reliable are fair valued in good faith under the direction of the Board.

The Board has adopted Valuation Procedures (the “Procedures”) to determine the fair value of securities and other financial instruments for which market prices are not readily available or which may not be reliably priced. The Board has delegated the day-to-day responsibility for determining the fair value of assets of the Fund to Calvert Investment Management, Inc. (the “Advisor” or “Calvert”) and has provided these Procedures to govern Calvert in its valuation duties.

Calvert has chartered an internal Valuation Committee to oversee the implementation of these Procedures and to assist it in carrying out the valuation responsibilities that the Board has delegated.

The Valuation Committee meets on a regular basis to review illiquid securities and other investments which may not have readily available market prices. The Valuation Committee’s fair valuation determinations are subject to review, approval and ratification by the Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation was determined.

26 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

The Valuation Committee utilizes various methods to measure the fair value of the Fund’s investments. Generally Accepted Accounting Principles (GAAP) establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

Level 1 - quoted prices in active markets for identical securities

Level 2 - other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 - significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an investment’s assigned level within the hierarchy during the period. There were no such transfers during the period. Valuation techniques used to value the Fund’s investments by major category are as follows:

Debt securities, including restricted securities, are valued based on evaluated prices received from independent pricing services or from dealers who make markets in such securities. For corporate bonds, municipal securities, and U.S. government and government agency obligations, pricing services utilize matrix pricing which considers yield or price of bonds of comparable quality, coupon, maturity and type as well as dealer supplied prices and such securities are generally categorized as Level 2 in the hierarchy. For asset-backed securities, collateralized mortgage-backed obligations, commercial mortgage-backed securities and U.S. government agency mortgage-backed securities, pricing services utilize matrix pricing which considers prepayment speed assumptions, attributes of the collateral, yield or price of bonds of comparable quality, coupon, maturity and type as well as dealer supplied prices and, accordingly, such securities are generally categorized as Level 2 in the hierarchy. Short-term securities of sufficient credit quality with remaining maturities of sixty days or less for which quotations are not readily available are valued at amortized cost, which approximates fair value, and are categorized as Level 2 in the hierarchy.

When independent prices are unavailable or unreliable, debt securities may be valued utilizing pricing matrices which consider similar factors that would be used by independent pricing services. These are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

Futures contracts are valued at the settlement price established each day by the board of trade or exchange on which they are traded and are categorized as Level 1 in the hierarchy.

If a market value cannot be determined for a security using the methodologies described above, or if, in the good faith opinion of the Advisor, the market value does not constitute a readily available market quotation, or if a significant event has occurred that would materially affect the value of the security, the security will be fair valued as determined in good faith by the Valuation Committee.

The Valuation Committee considers a number of factors, including significant unobservable valuation inputs when arriving at fair value. It considers all significant facts that are reasonably available and relevant to the determination of fair value.

The Valuation Committee primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and

www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED) 27

other relevant information for the investment to determine the fair value of the investment. When more appropriate, the fund may employ an income-based or cost approach. An income-based valuation approach discounts anticipated future cash flows of the investment to calculate a present amount (discounted). The measurement is based on the value indicated by current market expectations about those future amounts. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. A cost based approach is based on the amount that currently would be required to replace the service capacity of an asset (current replacement cost). From the seller’s perspective, the price that would be received for the asset is determined based on the cost to a buyer to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence.

The values assigned to fair value investments are based on available information and do not necessarily represent amounts that might ultimately be realized. Further, due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed, and the differences could be material. The Valuation Committee employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis and reviews of any related market activity.

At March 31, 2015, securities valued at $0, or 0.0% of net assets, were fair valued in good faith under the direction of the Board.

The following table summarizes the market value of the Fund’s holdings as of March 31, 2015, based on the inputs used to value them:

|

| | | | | | | | | | | | | | |

| | VALUATION INPUTS |

INVESTMENTS IN SECURITIES* | LEVEL 1 | | LEVEL 2 | | LEVEL 3 | | TOTAL |

| Asset backed securities | __ |

| |

| $122,789,089 |

| | __ |

| |

| $122,789,089 |

|

| Collateralized mortgage-backed obligations | — |

| | 15,641,993 |

| | — |

| | 15,641,993 |

|

| Commercial mortgage-backed securities | — |

| | 40,513,519 |

| | — |

| | 40,513,519 |

|

| Corporate debt | — |

| | 575,436,665 |

| | ** |

| | 575,436,665 |

|

| U.S. government obligations | — |

| | 67,726,673 |

| | — |

| | 61,726,673 |

|

| Other debt obligations | — |

| | 7,870,897 |

| | — |

| | 7,870,897 |

|

| TOTAL | — |

| |

| $829,978,836 |

| | ** |

| |

| $829,978,836 |

|

| Other financial instruments*** |

| $169,643 |

| | — |

| | — |

| |

| $169,643 |

|

| | | | | | | | |

* For a complete listing of investments, please refer to the Statement of Net Assets. ** Level 3 Securities are valued at $0 and represent 0.0% of net assets. *** Other financial instruments are derivative instruments not reflected in the Total Investments in the Statement of Net Assets, such as futures, which are valued at the unrealized appreciation/depreciation of the instrument. |

Loan Participations and Assignments: The Fund may invest in direct debt instruments which are interests in amounts owed to lenders or lending syndicates by corporate, governmental, or other borrowers. A Fund’s investments in loans may be in the form of participations in loans or assignments of all or a portion of loans from third parties. A loan is often administered by a bank or other financial institution (the “lender”) that acts as agent for all holders. The agent administers the terms of the loan, as specified in the loan agreement. A Fund may invest in multiple series or tranches of a loan, which may have varying terms and

28 www.calvert.com CALVERT INCOME FUND SEMI-ANNUAL REPORT (UNAUDITED)

carry different associated risks. A Fund generally has no right to enforce compliance with the terms of the loan agreement with the borrower. As a result, a Fund may be subject to the credit risk of both the borrower and the lender that is selling the loan agreement. When a Fund purchases assignments from lenders it acquires direct rights against the borrower of the loan. When investing in a loan participation, a Fund has the right to receive payments of principal, interest and any fees to which it is entitled only from the lender selling the loan agreement and only upon receipt of payments by the lender from the borrower.