UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3430

Oppenheimer Limited-Term Bond Fund

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Arthur S. Gabinet

OFI Global Asset Management, Inc.

Two World Financial Center, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: August 31

Date of reporting period: 8/30/2013

Item 1. Reports to Stockholders.

Table of Contents

Class A Shares

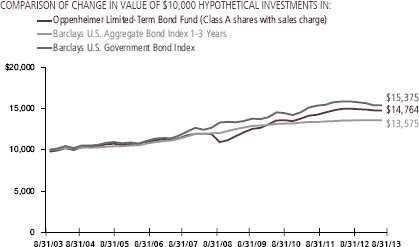

AVERAGE ANNUAL TOTAL RETURNS AT 8/30/13*

| | | | | | | | |

| | | Class A Shares of the Fund | | | | |

| | | Without Sales Charge | | With Sales Charge | | Barclays U.S.

Aggregate Bond Index

1-3 Years | | Barclays U.S.

Government Bond

Index |

1-Year | | -1.21% | | -3.43% | | 0.33% | | -2.91% |

5-Year | | 4.45 | | 3.97 | | 2.49 | | 3.94 |

10-Year | | 4.21 | | 3.97 | | 3.10 | | 4.40 |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund returns include changes in share price, reinvested distributions, and a 2.25% maximum applicable sales charge except where “without sales charge” is indicated. Prior to August 1, 2013, the maximum initial sales charge for Class A shares of the Fund was 4.75%. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. Returns for periods of less than one year are cumulative and not annualized. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677).

*August 30, 2013, was the last business day of the Fund’s fiscal year. See Note 1 of the accompanying Notes to Financial Statements. Index returns are calculated through August 31, 2013.

Prior to August 1, 2013, Oppenheimer Limited-Term Bond Fund was named Oppenheimer U.S. Government Trust.

2 OPPENHEIMER LIMITED-TERM BOND FUND

Fund Performance Discussion

The Fund’s Class A shares (without sales charge) produced a return of -1.21% during the reporting period. On a relative basis, the Fund outperformed the Barclays U.S. Government Bond Index’s return of -2.91%. The Fund experienced declines in what was a difficult environment for fixed-income, particularly over the second half of the period after the Federal Reserve (the “Fed”) discussed the potential for tapering of its quantitative easing program.

On August 1, 2013, the Fund changed its name from Oppenheimer U.S. Government Trust to Oppenheimer Limited-Term Bond Fund, and its primary benchmark became the Barclays U.S. Aggregate Bond Index 1-3 Years. For the one-year period, the Barclays U.S. Aggregate Bond Index 1-3 Years returned 0.33%. The Fund will primarily invest in the debt securities of investment-grade issuers. This includes the debt of the U.S. Government (and its agencies), corporations, mortgage-related securities, and asset-backed securities. In an attempt to decrease volatility, the Fund will seek to maintain an average effective duration between 1 and 3.5 years. The change allows the Fund to invest in a more diversified opportunity set of securities and is intended to reduce its overall interest rate risk.

MARKET OVERVIEW

For the one-year reporting period, market movements were largely driven by central

bank policies. Over the first half of the period, central banks throughout the world

3 OPPENHEIMER LIMITED-TERM BOND FUND

established accommodative policies that resulted in a rally among risk markets. In the U.S., the Federal Reserve (the “Fed”) launched an open-ended quantitative easing program involving monthly purchases of $85 billion of U.S. government securities. The quantitative easing program was designed to help boost the U.S. economy by keeping mortgage rates and other long-term interest rates low. While Europe continued to struggle with its sovereign debt crisis, analysts were encouraged when the head of the European Central Bank publicly stated his intent to support the euro as the European Union’s common currency. Even in Japan, which had been mired in economic weakness for years, new government leadership adopted economic policies and its central bank announced a massive quantitative easing program.

At the end of May, market volatility picked up measurably as comments from Fed Chairman Ben Bernanke at a Congressional hearing surprised the market when he indicated a possible slowdown of the central bank’s asset purchase program if the economy continued to show improvement. Additionally, fears began to creep into the market about a possible slowdown in the world’s emerging economies. As a result, risk assets sold off across the board, with Japanese stocks and emerging market debt absorbing the brunt of the selling, although investment grade credit was certainly not immune. Simultaneously, the intermediate and long-end of the U.S. Treasury curve steepened quite dramatically as investors began to price in the likelihood

of higher interest rates in the future. The volatility continued through June as the Federal Open Market Committee (FOMC) issued a statement indicating again that if the U.S. economy continued to improve the Fed would begin to slow down its quantitative easing program.

Equity markets in the U.S. stabilized over the final months of the reporting period when investors came to the realization that an end to the quantitative easing program did not necessarily imply an imminent increase in short-term interest rates. However, fixed-income markets remained volatile.

FUND REVIEW

Throughout the reporting period, the Fund maintained minimal exposure to U.S. Treasuries. This contributed positively to the Fund’s performance as U.S. Treasuries suffered throughout this reporting period and particularly after the Fed’s announcement of potential tapering. Instead, the Fund remained most heavily invested in mortgage-backed securities (“MBS”) and agency securities for the majority of the period. These investments benefited the Fund over the first half of the reporting period when they rallied and outperformed U.S. Treasuries on the back of positive economic surprises, despite the Cyprus banking crisis, deteriorating conditions in the Eurozone and moderating growth in emerging markets. However, beginning in May, volatility impacted most fixed-income markets after the Fed began to discuss tapering. Before the Fed’s comments, we had already started reducing our position

4 OPPENHEIMER LIMITED-TERM BOND FUND

in MBS since we felt they were vulnerable to policy changes. At the same time, we increased our allocation to agency debt and initiated positions in investment grade and high yield debt. While the decreased exposure to MBS limited the negative impact on Fund performance, MBS still detracted from performance for the overall reporting period. Agency debt also detracted from performance this period, while investment grade and high yield produced modest positive results.

STRATEGY & OUTLOOK

Although it appears that all eyes remain firmly fixated on the Fed and its eventual asset purchase unwind and the perceived growth slowdown within the emerging markets, we believe there is reason for optimism. By historical standards central banks around the globe are executing exceedingly loose monetary policy, which provides plenty of liquidity to the markets. U.S. growth appears to be a surprising bright

spot and we are even beginning to see early signs that growth within Europe may be turning the corner. And while it may be clear that China’s growth trajectory is slowing, we believe policy makers have the situation in hand and the probability of a hard landing is still quite low.

In a “yield-starved” domestic fixed income market dominated by U.S. Treasuries hovering near historic lows, we continue to favor higher-yielding investments to seek a carry, or yield advantage. Given current conditions, we believe the additional carry of the Fund is positioned to help returns even in the context of spreads remaining at their current levels.

| | |

| |  |

| | Peter A. Strzalkowski, CFA |

| | Portfolio Manager |

5 OPPENHEIMER LIMITED-TERM BOND FUND

Top Holdings and Allocations*

| | | | |

PORTFOLIO ALLOCATION | | | | |

Mortgage-Backed Obligations: | | | | |

Government Agency | | | 40 .1 | % |

Non-Agency | | | 7 .9 | |

U.S. Government Obligations | | | 29 .6 | |

Corporate Bonds and Notes | | | 18 .1 | |

Asset-Backed Securities | | | 4 .3 | |

Over-the-Counter Interest Rate | | | | |

Swaptions Purchased | | | – | ** |

Portfolio holdings and allocations are subject to change. Percentages are as of August 30, 2013, and are based on the total market value of investments.

*August 30, 2013, was the last business day of the Fund’s fiscal year. See Note 1 of the accompanying Notes to Financial Statements.

**Represents a value of less than 0.05%.

| | | | |

CREDIT RATING BREAKDOWN | | NRSRO

ONLY

TOTAL | |

AAA | | | 70 .0 | % |

AA | | | 1 .3 | |

A | | | 5 .2 | |

BBB | | | 15 .5 | |

BB | | | 5 .3 | |

B | | | 1 .1 | |

CCC | | | 0 .6 | |

CC | | | 0 .7 | |

D | | | 0 .3 | |

Total | | | 100 .0 | % |

The percentages above are based on the market value of the Fund’s securities as of August 30, 2013, and are subject to change. Except for certain securities issued or guaranteed by a foreign sovereign, all securities have been rated by at least one Nationally Recognized Statistical Rating Organization (“NRSRO”), such as Standard & Poor’s (“S&P”). For securities rated only by an NRSRO other than S&P, OppenheimerFunds, Inc. converts that rating to the equivalent S&P rating. If two or more NRSROs have assigned a rating to a security, the highest S&P equivalent rating is used. Unrated securities issued or guaranteed by a foreign sovereign are assigned a credit rating equal to the highest NRSRO rating assigned to that foreign sovereign. Fund assets invested in Oppenheimer Institutional Money Market Fund are assigned that fund’s S&P rating, which is currently AAA. For the purposes of this table, “investment-grade” securities are securities rated within the NRSROs’ four highest rating categories (AAA, AA, A and BBB). Unrated securities do not necessarily indicate low credit quality, and may or may not be the equivalent of investment-grade. Please consult the Fund’s prospectus and Statement of Additional Information for further information.

6 OPPENHEIMER LIMITED-TERM BOND FUND

Share Class Performance

AVERAGE ANNUAL TOTAL RETURNS WITHOUT SALES CHARGE AS OF 8/30/13

| | | | | | | | | | | | | | | | |

| | | Inception Date | | | 1-Year | | | 5-Year | | | 10-Year | |

Class A (OUSGX) | | | 8/16/85 | | | | -1.21% | | | | 4.45% | | | | 4.21% | |

Class B (UGTBX) | | | 7/21/95 | | | | -1.94% | | | | 3.67% | | | | 3.74% | |

Class C (OUSCX) | | | 12/1/93 | | | | -1.84% | | | | 3.69% | | | | 3.44% | |

Class I (OUSIX) | | | 8/1/13 | | | | -0.20% | * | | | N/A | | | | N/A | |

Class N (OUSNX) | | | 3/1/01 | | | | -1.45% | | | | 4.19% | | | | 3.94% | |

Class Y (OUSYX) | | | 5/18/98 | | | | -1.05% | | | | 4.72% | | | | 4.53% | |

|

AVERAGE ANNUAL TOTAL RETURNS WITH SALES CHARGE AS OF 8/30/13 | |

| | | Inception Date | | | 1-Year | | | 5-Year | | | 10-Year | |

Class A (OUSGX) | | | 8/16/85 | | | | -3.43% | | | | 3.97% | | | | 3.97% | |

Class B (UGTBX) | | | 7/21/95 | | | | -5.72% | | | | 3.50% | | | | 3.74% | |

Class C (OUSCX) | | | 12/1/93 | | | | -2.79% | | | | 3.69% | | | | 3.44% | |

Class I (OUSIX) | | | 8/1/13 | | | | -0.20% | * | | | N/A | | | | N/A | |

Class N (OUSNX) | | | 3/1/01 | | | | -2.40% | | | | 4.19% | | | | 3.94% | |

Class Y (OUSYX) | | | 5/18/98 | | | | -1.05% | | | | 4.72% | | | | 4.53% | |

*Shows performance since inception.

STANDARDIZED YIELDS

| | | | |

| For the 30 Days Ended 8/31/13 | | | | |

Class A | | | 2.49 | % |

Class B | | | 1.80 | |

Class C | | | 1.80 | |

Class I | | | 2.90 | |

Class N | | | 2.30 | |

Class Y | | | 2.77 | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677). Fund returns include changes in share price, reinvested distributions, and the applicable sales charge: for Class A shares, the current maximum initial sales charge of 2.25%; for Class B shares, the contingent deferred sales charge of 4% (1-year) and 1% (5-year); and for Class C and N shares, the contingent deferred sales charge of 1% for the 1-year period. There is no sales charge for Class I and Y shares. Prior to August 1, 2013, the maximum initial sales charge for Class A shares of the Fund was 4.75%; for Class B shares, the contingent deferred sales charge was 5% (1-year) and 2% (5-year). Because Class B shares convert to Class A shares 72 months after purchase, the 10-year return for Class B shares uses Class A performance for the period after conversion. Returns for periods of less than one year are cumulative and not annualized.

7 OPPENHEIMER LIMITED-TERM BOND FUND

Standardized yield is based on net investment income for the 30-day period ended 8/31/13 and the maximum offering price at the end of the period for Class A shares and the net asset value for Class B, Class C, Class I, Class N and Class Y shares. Each result is compounded semiannually and then annualized. Falling share prices will tend to artificially raise yields.

The Fund’s performance is compared to that of the Barclays U.S. Aggregate Bond Index 1-3 Years and the Barclays U.S. Government Bond Index. The Barclays U.S. Aggregate Bond Index 1-3 Years is an unmanaged index of publicly issued investment grade corporate, U.S. Treasury and government agency securities with remaining maturities of one to three years. The Barclays U.S. Government Bond Index is composed of publicly issued, nonconvertible, domestic debt of the U.S. Government or any agency thereof, quasi-federal corporations, or corporate debt guaranteed by the U.S. Government. Flower bonds and pass-through issues are excluded. The Fund has changed its benchmark from the Barclays U.S. Government Bond Index to the Barclays U.S. Aggregate Bond Index 1-3 Years, which it believes is a more appropriate measure of the Fund’s performance. The indices are unmanaged and cannot be purchased directly by investors. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

The Fund’s investment strategy and focus can change over time. The mention of specific fund holdings does not constitute a recommendation by OppenheimerFunds, Inc. or its affiliates.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking your financial advisor, visiting oppenheimerfunds.com, or calling 1.800.CALL OPP (225.5677). Read prospectuses and summary prospectuses carefully before investing.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

6 OPPENHEIMER LIMITED-TERM BOND FUND

Fund Expenses

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions; and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire 6-month period ended August 30, 2013.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or contingent deferred sales charges (loads), or a $12.00 fee imposed annually on accounts valued at less than $500.00 (subject to exceptions described in the Statement of Additional Information). Therefore, the “hypothetical” section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

9 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | | | | | | | | | |

| Actual | | Beginning

Account

Value

March 1, 2013 | | | Ending

Account

Value

August 30, 2013 | | | Expenses

Paid During

6 Months Ended

August 30, 2013 | |

Class A | | $ | 1,000 .00 | | | $ | 989 .90 | | | $ | 4 .55 | |

Class B | | | 1,000 .00 | | | | 987 .10 | | | | 8 .35 | |

Class C | | | 1,000 .00 | | | | 987 .10 | | | | 8 .35 | |

Class I | | | 1,000 .00 | | | | 998 .00 | | | | 2 .20 | |

Class N | | | 1,000 .00 | | | | 988 .60 | | | | 5 .80 | |

Class Y | | | 1,000 .00 | | | | 991 .20 | | | | 3 .35 | |

| | | |

Hypothetical

(5% return before expenses) | | | | | | | | | |

Class A | | | 1,000 .00 | | | | 1,020 .51 | | | | 4 .62 | |

Class B | | | 1,000 .00 | | | | 1,016 .70 | | | | 8 .48 | |

Class C | | | 1,000 .00 | | | | 1,016 .70 | | | | 8 .48 | |

Class I | | | 1,000 .00 | | | | 1,022 .86 | | | | 2 .23 | |

Class N | | | 1,000 .00 | | | | 1,019 .25 | | | | 5 .89 | |

Class Y | | | 1,000 .00 | | | | 1,021 .71 | | | | 3 .40 | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended August 30, 2013 are as follows:

| | | | |

| Class | | Expense Ratios | |

Class A | | | 0 .91 | % |

Class B | | | 1 .67 | |

Class C | | | 1 .67 | |

Class I | | | 0 .44 | |

Class N | | | 1 .16 | |

Class Y | | | 0 .67 | |

The expense ratios reflect voluntary waivers and/or reimbursements of expenses by the Fund’s Manager. Some of these undertakings may be modified or terminated at any time, as indicated in the Fund’s prospectus. The “Financial Highlights” tables in the Fund’s financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

10 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS August 30, 2013* | | |

| | | | | | | | |

| |

| Principal

Amount |

| | | Value | |

Asset-Backed Securities—5.2% | | | | | | | | |

American Credit Acceptance Receivables Trust, Series 2012-3, Cl. C, 2.78%, 9/17/181 | | $ | 505,000 | | | $ | 502,192 | |

AmeriCredit Automobile Receivables Trust: | | | | | | | | |

Series 2012-3, Cl. E, 4.46%, 11/8/191 | | | 1,305,000 | | | | 1,342,877 | |

Series 2012-4, Cl. D, 2.68%, 10/9/18 | | | 950,000 | | | | 944,449 | |

Series 2013-1, Cl. D, 2.09%, 2/8/19 | | | 1,675,000 | | | | 1,618,069 | |

Series 2013-2, Cl. D, 2.42%, 5/8/19 | | | 2,505,000 | | | | 2,434,628 | |

Series 2013-3, Cl. D, 3.00%, 7/8/19 | | | 1,600,000 | | | | 1,577,624 | |

Avis Budget Rental Car Funding AESOP LLC, Series 2011-3A, Cl. B, 4.74%, 11/20/171 | | | 995,000 | | | | 1,054,645 | |

Capital Auto Receivables Asset Trust, Series 2013-1, Cl. D, 2.19%, 9/20/21 | | | 1,085,000 | | | | 1,049,431 | |

CarMax Auto Owner Trust, Series 2013-1, Cl. D, 1.99%, 8/15/19 | | | 730,000 | | | | 710,624 | |

CPS Auto Receivables Trust, Series 2012-C, Cl. A, 1.82%, 12/16/191 | | | 722,474 | | | | 725,948 | |

Credit Acceptance Auto Loan Trust, Series 2012-2A, Cl. B, 2.21%, 9/15/201 | | | 430,000 | | | | 431,264 | |

DT Auto Owner Trust: | | | | | | | | |

Series 2012-2A, Cl. D, 4.35%, 3/15/191 | | | 2,305,000 | | | | 2,364,394 | |

Series 2013-1A, Cl. D, 3.74%, 5/15/201 | | | 965,000 | | | | 962,623 | |

Exeter Automobile Receivables Trust, Series 2012-2A, Cl. C, 3.06%, 7/16/181 | | | 170,000 | | | | 170,179 | |

First Investors Auto Owner Trust, Series 2012-1A, Cl. D, 5.65%, 4/15/181 | | | 810,000 | | | | 852,834 | |

Ford Credit Floorplan Master Owner Trust A, Series 2013-3, Cl. D, 1.74%, 6/15/17 | | | 860,000 | | | | 860,599 | |

Santander Drive Auto Receivables Trust: | | | | | | | | |

Series 2011-S1A, Cl. D, 3.10%, 5/15/172 | | | 51,970 | | | | 52,018 | |

Series 2012-3, Cl. D, 3.64%, 5/15/18 | | | 3,305,000 | | | | 3,362,301 | |

Series 2012-5, Cl. D, 3.30%, 9/17/18 | | | 1,480,000 | | | | 1,485,144 | |

Series 2012-AA, Cl. D, 2.46%, 12/17/181 | | | 3,500,000 | | | | 3,414,215 | |

Series 2013-1, Cl. D, 2.27%, 1/15/19 | | | 3,450,000 | | | | 3,348,389 | |

Series 2013-2, Cl. D, 2.57%, 3/15/19 | | | 4,110,000 | | | | 3,984,086 | |

Series 2013-3, Cl. D, 2.42%, 4/15/19 | | | 3,465,000 | | | | 3,297,848 | |

SNAAC Auto Receivables Trust: | | | | | | | | |

Series 2012-1A, Cl. C, 4.38%, 6/15/171 | | | 60,000 | | | | 61,435 | |

Series 2013-1A, Cl. B, 2.09%, 7/16/181 | | | 745,000 | | | | 739,226 | |

Series 2013-1A, Cl. C, 3.07%, 8/15/181 | | | 830,000 | | | | 819,599 | |

Structured Asset Securities Corp., Interest-Only Stripped Pass-Through | | | | | | | | |

Certificates, Series 2002-AL1, Cl. AIO, 8.14%, 2/25/325 | | | 6,492,983 | | | | 584,668 | |

United Auto Credit Securitization Trust: | | | | | | | | |

Series 2012-1, Cl. B, 1.87%, 9/15/151 | | | 1,435,000 | | | | 1,434,481 | |

Series 2012-1, Cl. C, 2.52%, 3/15/161 | | | 1,040,000 | | | | 1,038,975 | |

Series 2013-1, Cl. B, 1.74%, 4/15/161 | | | 1,285,000 | | | | 1,281,910 | |

Series 2013-1, Cl. C, 2.22%, 12/15/171 | | | 820,000 | | | | 817,141 | |

Series 2013-1, Cl. D, 2.90%, 12/15/171 | | | 145,000 | | | | 144,263 | |

| | | | | | | | |

Total Asset-Backed Securities (Cost $44,138,895) | | | | | | | 43,468,079 | |

Mortgage-Backed Obligations—57.4% | | | | | | | | |

Government Agency—47.7% | | | | | | | | |

FHLMC/FNMA/FHLB/Sponsored—46.9% | | | | | | | | |

Federal Home Loan Mortgage Corp. Gold Pool: | | | | | | | | |

4.50%, 5/1/19 | | | 58,004 | | | | 61,150 | |

5.00%, 7/1/33-6/1/34 | | | 1,336,316 | | | | 1,445,794 | |

5.50%, 9/1/39 | | | 4,457,388 | | | | 4,859,639 | |

11 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS Continued | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

FHLMC/FNMA/FHLB/Sponsored Continued | | | | | | | | |

Federal Home Loan Mortgage Corp. Gold Pool: Continued | | | | | | | | |

6.00%, 1/1/22-7/1/24 | | $ | 1,547,216 | | | $ | 1,694,339 | |

6.50%, 4/1/18-4/1/34 | | | 1,023,215 | | | | 1,109,554 | |

7.00%, 8/1/16-3/1/35 | | | 3,187,236 | | | | 3,672,213 | |

7.50%, 1/1/32-2/1/32 | | | 1,938,788 | | | | 2,290,468 | |

8.00%, 4/1/16 | | | 163,035 | | | | 170,955 | |

9.00%, 8/1/22-5/1/25 | | | 69,972 | | | | 78,175 | |

11.50%, 6/1/20-11/17/20 | | | 14,607 | | | | 14,743 | |

12.50%, 7/1/19 | | | 1,691 | | | | 1,732 | |

13.00%, 8/1/15 | | | 1,764 | | | | 1,790 | |

Federal Home Loan Mortgage Corp., Interest-Only Stripped Mtg.-Backed Security: | | | | | | | | |

Series 192, Cl. IO, 11.93%, 2/1/285 | | | 116,482 | | | | 22,829 | |

Series 205, Cl. IO, 15.88%, 9/1/295 | | | 861,585 | | | | 175,105 | |

Series 206, Cl. IO, 0.00%, 12/1/295,8 | | | 252,620 | | | | 41,073 | |

Series 243, Cl. 6, 0.00%, 12/15/325,8 | | | 346,661 | | | | 73,042 | |

Federal Home Loan Mortgage Corp., Mtg.-Linked Amortizing Global Debt | | | | | | | | |

Securities, Series 2012-1, Cl. A10, 2.06%, 1/15/22 | | | 4,100,604 | | | | 4,138,104 | |

Federal Home Loan Mortgage Corp., Real Estate Mtg. Investment Conduit | | | | | | | | |

Multiclass Pass-Through Certificates: | | | | | | | | |

Series 151, Cl. F, 9.00%, 5/15/21 | | | 22,111 | | | | 24,633 | |

Series 1644, Cl. S, 2.404%, 12/15/233 | | | 3,802,418 | | | | 3,921,588 | |

Series 2043, Cl. ZP, 6.50%, 4/15/28 | | | 1,941,744 | | | | 2,204,014 | |

Series 2116, Cl. ZA, 6.00%, 1/15/29 | | | 1,131,085 | | | | 1,265,224 | |

Series 2148, Cl. ZA, 6.00%, 4/15/29 | | | 1,798,671 | | | | 2,011,407 | |

Series 2220, Cl. PD, 8.00%, 3/15/30 | | | 128,056 | | | | 149,554 | |

Series 2326, Cl. ZP, 6.50%, 6/15/31 | | | 214,977 | | | | 243,483 | |

Series 2344, Cl. FP, 1.134%, 8/15/313 | | | 310,915 | | | | 318,808 | |

Series 2368, Cl. PR, 6.50%, 10/15/31 | | | 884,094 | | | | 1,001,741 | |

Series 2427, Cl. ZM, 6.50%, 3/15/32 | | | 765,621 | | | | 858,447 | |

Series 2451, Cl. FD, 1.184%, 3/15/323 | | | 205,833 | | | | 211,393 | |

Series 2461, Cl. PZ, 6.50%, 6/15/32 | | | 502,429 | | | | 568,024 | |

Series 2464, Cl. FI, 1.184%, 2/15/323 | | | 193,888 | | | | 198,632 | |

Series 2465, Cl. PG, 6.50%, 6/15/32 | | | 671,968 | | | | 753,228 | |

Series 2470, Cl. LF, 1.184%, 2/15/323 | | | 194,459 | | | | 199,216 | �� |

Series 2471, Cl. FD, 1.184%, 3/15/323 | | | 294,041 | | | | 301,276 | |

Series 2500, Cl. FD, 0.684%, 3/15/323 | | | 383,906 | | | | 388,109 | |

Series 2517, Cl. GF, 1.184%, 2/15/323 | | | 154,109 | | | | 157,879 | |

Series 2526, Cl. FE, 0.584%, 6/15/293 | | | 446,950 | | | | 449,889 | |

Series 2530, Cl. FD, 0.684%, 2/15/323 | | | 400,124 | | | | 404,982 | |

Series 2538, Cl. F, 0.784%, 12/15/323 | | | 405,140 | | | | 409,168 | |

Series 2551, Cl. FD, 0.584%, 1/15/333 | | | 294,502 | | | | 296,612 | |

Series 2551, Cl. LF, 0.684%, 1/15/333 | | | 21,780 | | | | 22,013 | |

Series 2668, Cl. AZ, 4.00%, 9/15/18 | | | 361,086 | | | | 383,179 | |

Series 3015, Cl. GM, 5.00%, 8/15/35 | | | 8,440,000 | | | | 9,193,641 | |

Series 3134, Cl. FA, 0.484%, 3/15/363 | | | 5,076,731 | | | | 5,097,842 | |

Series 3465, Cl. HA, 4.00%, 7/15/17 | | | 179,700 | | | | 184,923 | |

Series 3617, Cl. DC, 4.00%, 7/15/27 | | | 1,324,730 | | | | 1,350,962 | |

Series 3822, Cl. JA, 5.00%, 6/15/40 | | | 1,446,782 | | | | 1,521,650 | |

Series 3848, Cl. WL, 4.00%, 4/15/40 | | | 1,738,773 | | | | 1,845,672 | |

Series 3917, Cl. BA, 4.00%, 6/15/38 | | | 1,726,494 | | | | 1,793,429 | |

12 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | | | | | |

| | | Principal

Amount | | | Value | |

FHLMC/FNMA/FHLB/Sponsored Continued | | | | | | | | |

Federal Home Loan Mortgage Corp., Real Estate Mtg. Investment Conduit | | | | | | | | |

Multiclass Pass-Through Certificates, Interest-Only Stripped Mtg.-Backed | | | | | | | | |

Security: | | | | | | | | |

Series 2074, Cl. S, 55.51%, 7/17/285 | | $ | 181,900 | | | $ | 38,437 | |

Series 2079, Cl. S, 58.44%, 7/17/285 | | | 328,727 | | | | 70,489 | |

Series 2122, Cl. S, 38.90%, 2/15/295 | | | 1,010,065 | | | | 215,636 | |

Series 2304, Cl. SK, 47.80%, 6/15/295 | | | 1,019,170 | | | | 205,507 | |

Series 2493, Cl. S, 50.12%, 9/15/295 | | | 254,925 | | | | 55,033 | |

Series 2526, Cl. SE, 36.56%, 6/15/295 | | | 396,402 | | | | 84,311 | |

Series 2795, Cl. SH, 14.27%, 3/15/245 | | | 3,002,006 | | | | 471,678 | |

Series 2802, Cl. AS, 0.00%, 4/15/335,8 | | | 102,155 | | | | 3,551 | |

Series 2819, Cl. S, 46.32%, 6/15/345 | | | 3,914,041 | | | | 764,495 | |

Series 2920, Cl. S, 56.62%, 1/15/355 | | | 2,377,483 | | | | 474,342 | |

Series 2922, Cl. SE, 8.81%, 2/15/355 | | | 541,514 | | | | 99,875 | |

Series 3004, Cl. SB, 99.99%, 7/15/355 | | | 3,237,627 | | | | 577,485 | |

Series 3201, Cl. SG, 7.78%, 8/15/365 | | | 1,479,752 | | | | 283,317 | |

Series 3397, Cl. GS, 15.34%, 12/15/375 | | | 359,737 | | | | 64,733 | |

Series 3424, Cl. EI, 0.00%, 4/15/385,8 | | | 435,047 | | | | 61,877 | |

Series 3450, Cl. BI, 14.50%, 5/15/385 | | | 4,026,729 | | | | 728,908 | |

Series 3606, Cl. SN, 6.79%, 12/15/395 | | | 859,820 | | | | 102,512 | |

Series 3659, Cl. IE, 0.00%, 3/15/195,8 | | | 3,655,218 | | | | 297,543 | |

Series 3685, Cl. EI, 0.00%, 3/15/195,8 | | | 3,015,514 | | | | 211,395 | |

Series 3736, Cl. SN, 10.77%, 10/15/405 | | | 3,086,407 | | | | 463,756 | |

Federal Home Loan Mortgage Corp., Stripped Mtg.-Backed Security, | | | | | | | | |

Series 237, Cl. F16, 0.684%, 5/15/363 | | | 2,274,582 | | | | 2,306,209 | |

Federal National Mortgage Assn. Pool: | | | | | | | | |

2.50%, 9/1/276 | | | 21,350,000 | | | | 21,193,212 | |

2.667%, 10/1/363 | | | 9,044,895 | | | | 9,594,528 | |

3.00%, 4/25/266 | | | 34,900,000 | | | | 35,723,420 | |

3.50%, 9/1/276 | | | 68,310,000 | | | | 71,437,321 | |

4.00%, 9/1/266 | | | 8,845,000 | | | | 9,339,767 | |

4.50%, 2/1/19-12/1/20 | | | 5,604,949 | | | | 5,952,250 | |

4.50%, 9/1/22-9/1/396 | | | 51,445,000 | | | | 54,367,973 | |

5.00%, 12/1/17-6/1/22 | | | 10,560,386 | | | | 11,247,659 | |

5.00%, 9/1/396 | | | 9,202,000 | | | | 9,896,466 | |

5.50%, 2/1/35-5/1/36 | | | 1,472,840 | | | | 1,614,700 | |

6.00%, 6/1/30-3/1/37 | | | 11,075,061 | | | | 12,208,590 | |

6.50%, 6/1/17-1/1/34 | | | 8,618,852 | | | | 9,479,367 | |

7.00%, 11/1/17-11/1/35 | | | 6,466,504 | | | | 7,299,398 | |

7.50%, 2/1/27-8/1/33 | | | 5,173,568 | | | | 6,096,627 | |

8.00%, 12/1/22 | | | 16,860 | | | | 19,619 | |

8.50%, 7/1/32 | | | 33,603 | | | | 39,059 | |

11.00%, 7/1/16 | | | 7,285 | | | | 7,855 | |

11.50%, 11/1/15 | | | 9,351 | | | | 9,426 | |

Federal National Mortgage Assn., Interest-Only Stripped Mtg.-Backed Security: | | | | | | | | |

Series 221, Cl. 2, 44.31%, 5/1/235 | | | 745,524 | | | | 133,512 | |

Series 252, Cl. 2, 44.22%, 11/1/235 | | | 354,658 | | | | 64,435 | |

Series 303, Cl. IO, 40.74%, 11/1/295 | | | 2,991,628 | | | | 497,879 | |

Series 319, Cl. 2, 22.68%, 2/1/325 | | | 622,985 | | | | 127,229 | |

Series 321, Cl. 2, 9.09%, 4/1/325 | | | 918,239 | | | | 182,482 | |

Series 324, Cl. 2, 4.17%, 7/1/325 | | | 385,581 | | | | 76,559 | |

Series 328, Cl. 2, 0.00%, 12/1/325,8 | | | 2,448,025 | | | | 504,487 | |

13 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS Continued | | |

| | | | | | | | |

| |

| Principal

Amount |

| | | Value | |

FHLMC/FNMA/FHLB/Sponsored Continued | | | | | | | | |

Federal National Mortgage Assn., Interest-Only Stripped Mtg.-Backed Security: Continued | | | | | | | | |

Series 334, Cl. 12, 0.00%, 3/1/335,8 | | $ | 1,378,052 | | | $ | 260,629 | |

Series 339, Cl. 7, 0.00%, 8/1/335,8 | | | 1,145,119 | | | | 192,121 | |

Series 351, Cl. 10, 0.00%, 4/1/345,8 | | | 983,173 | | | | 156,520 | |

Series 351, Cl. 8, 0.00%, 4/1/345,8 | | | 896,757 | | | | 142,909 | |

Series 356, Cl. 10, 0.00%, 6/1/355,8 | | | 673,421 | | | | 108,515 | |

Series 356, Cl. 12, 0.00%, 2/1/355,8 | | | 332,726 | | | | 53,646 | |

Series 362, Cl. 13, 0.00%, 8/1/355,8 | | | 598,888 | | | | 104,117 | |

Series 364, Cl. 15, 0.00%, 9/1/355,8 | | | 820,230 | | | | 132,639 | |

Federal National Mortgage Assn., Principal-Only Stripped Mtg.-Backed Security, Series 327, Cl. 1, 11.64%, 9/1/327 | | | 167,715 | | | | 160,399 | |

Federal National Mortgage Assn., Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates: | | | | | | | | |

Series 1992-161, Cl. H, 7.50%, 9/25/22 | | | 2,174,322 | | | | 2,513,900 | |

Series 1993-87, Cl. Z, 6.50%, 6/25/23 | | | 609,463 | | | | 686,772 | |

Series 1999-54, Cl. LH, 6.50%, 11/25/29 | | | 448,577 | | | | 500,030 | |

Series 2001-51, Cl. OD, 6.50%, 10/25/31 | | | 1,943,984 | | | | 2,161,412 | |

Series 2001-69, Cl. PF, 1.184%, 12/25/313 | | | 445,823 | | | | 456,763 | |

Series 2002-29, Cl. F, 1.184%, 4/25/323 | | | 208,132 | | | | 213,290 | |

Series 2002-52, Cl. FD, 0.684%, 9/25/323 | | | 304,943 | | | | 308,674 | |

Series 2002-59, Cl. F, 0.584%, 9/25/323 | | | 883,156 | | | | 888,520 | |

Series 2002-60, Cl. FH, 1.184%, 8/25/323 | | | 373,822 | | | | 383,139 | |

Series 2002-64, Cl. FJ, 1.184%, 4/25/323 | | | 64,068 | | | | 65,656 | |

Series 2002-68, Cl. FH, 0.684%, 10/18/323 | | | 122,113 | | | | 123,445 | |

Series 2003-112, Cl. AN, 4.00%, 11/25/18 | | | 818,263 | | | | 868,740 | |

Series 2003-116, Cl. FA, 0.584%, 11/25/333 | | | 216,510 | | | | 217,847 | |

Series 2003-119, Cl. FK, 0.684%, 5/25/183 | | | 5,418,651 | | | | 5,448,500 | |

Series 2003-130, Cl. CS, 13.732%, 12/25/333 | | | 297,617 | | | | 362,135 | |

Series 2003-26, Cl. XF, 0.634%, 3/25/233 | | | 1,155,978 | | | | 1,163,484 | |

Series 2003-28, Cl. KG, 5.50%, 4/25/23 | | | 2,262,876 | | | | 2,477,993 | |

Series 2004-72, Cl. FB, 0.684%, 9/25/343 | | | 1,547,889 | | | | 1,567,126 | |

Series 2005-104, Cl. MC, 5.50%, 12/25/25 | | | 3,363,599 | | | | 3,686,725 | |

Series 2005-31, Cl. PB, 5.50%, 4/25/35 | | | 2,280,000 | | | | 2,607,644 | |

Series 2005-69, Cl. LE, 5.50%, 11/25/33 | | | 343,502 | | | | 345,820 | |

Series 2006-11, Cl. PS, 23.892%, 3/25/363 | | | 400,530 | | | | 615,078 | |

Series 2006-46, Cl. SW, 23.524%, 6/25/363 | | | 270,724 | | | | 414,214 | |

Series 2006-50, Cl. KS, 23.525%, 6/25/363 | | | 579,246 | | | | 880,270 | |

Series 2006-50, Cl. SK, 23.525%, 6/25/363 | | | 1,117,190 | | | | 1,675,564 | |

Series 2007-109, Cl. NF, 0.734%, 12/25/373 | | | 2,263,807 | | | | 2,292,204 | |

Series 2007-42, Cl. A, 6.00%, 2/25/33 | | | 46,889 | | | | 46,866 | |

Series 2007-9, Cl. LE, 5.50%, 3/25/37 | | | 2,000,000 | | | | 2,293,151 | |

Series 2008-14, Cl. BA, 4.25%, 3/25/23 | | | 365,596 | | | | 389,696 | |

Series 2009-114, Cl. AC, 2.50%, 12/25/23 | | | 1,772,936 | | | | 1,818,987 | |

Series 2009-36, Cl. FA, 1.124%, 6/25/373 | | | 1,634,416 | | | | 1,656,681 | |

Series 2011-122, Cl. EC, 1.50%, 1/25/20 | | | 4,965,772 | | | | 5,028,313 | |

Series 2011-15, Cl. DA, 4.00%, 3/25/41 | | | 1,308,646 | | | | 1,377,223 | |

Series 2011-3, Cl. KA, 5.00%, 4/25/40 | | | 2,019,323 | | | | 2,202,624 | |

Series 2011-6, Cl. BA, 2.75%, 6/25/20 | | | 2,414,833 | | | | 2,510,522 | |

Series 2011-69, Cl. EA, 3.00%, 11/25/29 | | | 1,608,964 | | | | 1,647,836 | |

Series 2011-88, Cl. AB, 2.50%, 9/25/26 | | | 1,467,269 | | | | 1,510,765 | |

Series 2012-20, Cl. FD, 0.584%, 3/25/423 | | | 996,541 | | | | 1,002,930 | |

14 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | | | | | |

| | |

| Principal

Amount |

| | | Value | |

FHLMC/FNMA/FHLB/Sponsored Continued | | | | | | | | |

Federal National Mortgage Assn., Real Estate Mtg. Investment Conduit | | | | | | | | |

Multiclass Pass-Through Certificates, Interest-Only Stripped Mtg.-Backed Security: | | | | | | | | |

Series 2001-61, Cl. SH, 29.98%, 11/18/315 | | $ | 749,057 | | | $ | 160,318 | |

Series 2001-63, Cl. SD, 31.36%, 12/18/315 | | | 301,462 | | | | 60,204 | |

Series 2001-68, Cl. SC, 20.08%, 11/25/315 | | | 193,477 | | | | 40,682 | |

Series 2001-81, Cl. S, 27.10%, 1/25/325 | | | 190,591 | | | | 41,623 | |

Series 2002-28, Cl. SA, 36.93%, 4/25/325 | | | 199,510 | | | | 41,001 | |

Series 2002-38, Cl. SO, 46.04%, 4/25/325 | | | 322,133 | | | | 59,003 | |

Series 2002-39, Cl. SD, 38.75%, 3/18/325 | | | 340,464 | | | | 72,797 | |

Series 2002-41, Cl. S, 59.33%, 7/25/325 | | | 1,146,441 | | | | 240,362 | |

Series 2002-48, Cl. S, 32.88%, 7/25/325 | | | 306,794 | | | | 64,836 | |

Series 2002-52, Cl. SD, 35.60%, 9/25/325 | | | 304,943 | | | | 65,558 | |

Series 2002-52, Cl. SL, 35.17%, 9/25/325 | | | 204,203 | | | | 43,258 | |

Series 2002-53, Cl. SK, 35.96%, 4/25/325 | | | 212,371 | | | | 46,340 | |

Series 2002-56, Cl. SN, 34.64%, 7/25/325 | | | 419,211 | | | | 88,731 | |

Series 2002-77, Cl. IS, 43.37%, 12/18/325 | | | 548,820 | | | | 119,110 | |

Series 2002-77, Cl. SH, 41.04%, 12/18/325 | | | 281,895 | | | | 60,230 | |

Series 2002-9, Cl. MS, 28.75%, 3/25/325 | | | 322,296 | | | | 70,807 | |

Series 2003-23, Cl. ES, 0.00%, 10/25/225,8 | | | 717,182 | | | | 24,617 | |

Series 2003-25, Cl. IK, 23.66%, 4/25/335 | | | 4,871,578 | | | | 881,637 | |

Series 2003-33, Cl. SP, 30.38%, 5/25/335 | | | 725,259 | | | | 138,796 | |

Series 2003-4, Cl. S, 30.32%, 2/25/335 | | | 467,976 | | | | 97,538 | |

Series 2004-65, Cl. SA, 28.03%, 5/25/235 | | | 83,841 | | | | 545 | |

Series 2005-12, Cl. SC, 10.78%, 3/25/355 | | | 269,960 | | | | 57,352 | |

Series 2005-14, Cl. SE, 40.52%, 3/25/355 | | | 2,005,214 | | | | 322,481 | |

Series 2005-40, Cl. SB, 54.01%, 5/25/355 | | | 1,505,664 | | | | 262,243 | |

Series 2005-52, Cl. JH, 8.25%, 5/25/355 | | | 809,600 | | | | 162,393 | |

Series 2005-6, Cl. SE, 17.29%, 2/25/355 | | | 2,894,494 | | | | 539,210 | |

Series 2007-88, Cl. XI, 27.31%, 6/25/375 | | | 1,180,391 | | | | 149,634 | |

Series 2008-55, Cl. SA, 16.58%, 7/25/385 | | | 740,261 | | | | 107,058 | |

Series 2009-8, Cl. BS, 0.00%, 2/25/245,8 | | | 1,726,640 | | | | 150,971 | |

Series 2010-95, Cl. DI, 0.00%, 11/25/205,8 | | | 4,685,654 | | | | 388,471 | |

Series 2012-40, Cl. PI, 3.30%, 4/25/415 | | | 2,191,513 | | | | 397,450 | |

Vendee Mortgage Trust, Interest-Only Stripped Mtg.-Backed Security, | | | | | | | | |

Series 1995-2B, Cl. 2IO, 23.02%, 6/15/255 | | | 4,288,235 | | | | 101,199 | |

| | | | | | | | |

| | | | | | | | 393,054,721 | |

GNMA/Guaranteed—0.8% | | | | | | | | |

Government National Mortgage Assn. I Pool: | | | | | | | | |

6.50%, 11/15/23-12/15/23 | | | 44,066 | | | | 48,653 | |

7.00%, 1/15/28-8/15/28 | | | 261,061 | | | | 302,920 | |

7.50%, 2/15/22-11/15/26 | | | 175,764 | | | | 190,824 | |

8.00%, 9/15/16-8/15/28 | | | 36,999 | | | | 38,584 | |

8.50%, 8/15/17-12/15/17 | | | 109,534 | | | | 116,481 | |

9.50%, 7/15/18-12/15/19 | | | 4,949 | | | | 4,984 | |

10.00%, 8/15/17-8/15/19 | | | 31,768 | | | | 32,420 | |

10.50%, 12/15/15-12/15/20 | | | 84,157 | | | | 86,139 | |

Government National Mortgage Assn. II Pool: | | | | | | | | |

1.625%, 4/20/173 | | | 6,559 | | | | 6,828 | |

7.00%, 1/20/30 | | | 61,533 | | | | 71,545 | |

11.00%, 10/20/19-7/20/20 | | | 68,836 | | | | 71,536 | |

15 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS Continued | | |

| | | | | | | | |

| |

| Principal

Amount |

| | | Value | |

GNMA/Guaranteed Continued | | | | | | | | |

Government National Mortgage Assn., Interest-Only Stripped Mtg.-Backed Security: | | | | | | | | |

Series 1998-19, Cl. SB, 54.32%, 7/16/285 | | $ | 735,301 | | | $ | 157,224 | |

Series 1998-6, Cl. SA, 62.05%, 3/16/285 | | | 438,114 | | | | 90,694 | |

Series 2007-17, Cl. AI, 16.85%, 4/16/375 | | | 3,349,823 | | | | 627,127 | |

Series 2010-111, Cl. GI, 28.75%, 9/16/135 | | | 22,212,504 | | | | 1,108 | |

Series 2011-52, Cl. HS, 8.66%, 4/16/415 | | | 5,402,292 | | | | 1,358,449 | |

Government National Mortgage Assn., Real Estate Mtg. Investment Conduit | | | | | | | | |

Multiclass Pass-Through Certificates: | | | | | | | | |

Series 1999-32, Cl. ZB, 8.00%, 9/16/29 | | | 3,111,729 | | | | 3,660,218 | |

Series 2000-12, Cl. ZA, 8.00%, 2/16/30 | | | 778,376 | | | | 911,217 | |

Series 2009-46, Cl. HC, 5.00%, 11/20/34 | | | 160,128 | | | | 163,193 | |

| | | | | | | | |

| | | | | | | 7,940,144 | |

Non-Agency—9.7% | | | | | | | | |

Commercial—7.3% | | | | | | | | |

BCAP LLC Trust, Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2012-RR2, Cl. 6A3, 3.02%, 9/26/351,3 | | | 2,828,205 | | | | 2,882,197 | |

Series 2012-RR6, 2.404%, 11/26/362 | | | 3,354,886 | | | | 3,394,249 | |

Capital Lease Funding Securitization LP, Interest-Only Commercial Mtg. Pass-Through Certificates, Series 1997-CTL1, Cl. IO, 0.00%, 6/22/242,3,5,8 | | | 3,903,186 | | | | 186,856 | |

CHL Mortgage Pass-Through Trust, Mtg. Pass-Through Certificates, Series 2005-17, Cl. 1A8, 5.50%, 9/25/35 | | | 3,285,362 | | | | 3,278,453 | |

Citigroup Commercial Mortgage Trust, Commercial Mtg. Pass-Through | | | | | | | | |

Certificates, Series 20113-GCJ11, 4.459%, 4/10/231 | | | 880,000 | | | | 735,635 | |

Citigroup Mortgage Loan Trust, Inc., Mtg.-Backed Nts.: | | | | | | | | |

Series 2006-AR1, Cl. 1A1, 2.55%, 10/25/353 | | | 4,840,450 | | | | 4,557,138 | |

Series 2012-8, Cl. 1A1, 2.674%, 10/25/351,3 | | | 4,518,219 | | | | 4,545,130 | |

COMM Mortgage Trust, Commercial Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2012-CR4, Cl. D, 4.73%, 10/15/451,3 | | | 270,000 | | | | 235,530 | |

Series 2012-CR5, Cl. E, 4.48%, 12/10/451,3 | | | 420,000 | | | | 351,260 | |

Series 2013-CR7, Cl. D, 4.501%, 3/10/461,3 | | | 955,000 | | | | 779,609 | |

COMM Mortgage Trust, Interest-Only Stripped Mtg.-Backed Security: | | | | | | | | |

Series 2010-C1, Cl. XPA, 0.00%, 7/10/461,3,5,8 | | | 21,552,051 | | | | 974,163 | |

Series 2012-CR5, Cl. XA, 2.33%, 12/10/453,5 | | | 17,534,068 | | | | 1,937,216 | |

Credit Suisse Commercial Mortgage Trust, Commercial Mtg. Pass-Through Certificates, Series 2006-C1, Cl. AJ, 5.567%, 2/15/393 | | | 2,650,000 | | | | 2,847,324 | |

Credit Suisse First Boston Commercial Trust, Commercial Mtg. Pass-Through Certificates, Series 2005-C6, Cl. AJ, 4.94%, 12/15/403 | | | 2,250,000 | | | | 2,352,239 | |

DBUBS Mortgage Trust, Commercial Mtg. Pass-Through Certificates, Series 2011-LC1A, Cl. E, 5.728%, 11/10/461,3 | | | 400,000 | | | | 385,937 | |

EverBank Mortgage Loan Trust, Commercial Mtg. Pass-Through Certificates, | | | | | | | | |

Series 2013-1, Cl. A1, 2.25%, 3/25/431,3 | | | 1,330,664 | | | | 1,205,733 | |

FREMF Mortgage Trust, Commercial Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2013-K25, Cl. C, 3.742%, 11/25/451,3 | | | 515,000 | | | | 420,681 | |

Series 2013-K26, Cl. C, 3.723%, 12/25/451,3 | | | 345,000 | | | | 280,621 | |

Series 2013-K27, Cl. C, 3.616%, 1/25/461,3 | | | 530,000 | | | | 425,169 | |

Series 2013-K28, Cl. C, 3.614%, 6/25/461,3 | | | 530,000 | | | | 425,355 | |

Series 2013-K30, Cl. C, 3.666%, 6/25/451,3 | | | 855,000 | | | | 668,815 | |

Series 2013-K712, Cl. C, 3.483%, 5/25/451,3 | | | 890,000 | | | | 781,691 | |

Series 2013-K713, Cl. C, 3.274%, 4/25/461,3 | | | 2,670,000 | | | | 2,290,506 | |

16 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Commercial Continued | | | | | | | | |

GSR Mortgage Loan Trust, Mtg. Pass-Through Certificates, Series 2005-AR4, Cl. 6A1, 5.25%, 7/25/353 | | $ | 985,613 | | | $ | 971,538 | |

Heller Financial Commercial Mortgage Asset Corp., Interest-Only Commercial Mtg. Pass-Through Certificates, Series 2000-PH1, Cl. X, 0.00%, 1/17/341,3,5,8 | | | 5,425,248 | | | | 67,718 | |

JP Morgan Chase Commercial Mortgage Securities Trust, Commercial Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2006-LDP7, Cl. AJ, 6.056%, 4/15/453 | | | 1,265,000 | | | | 1,265,397 | |

Series 2006-LDP8, Cl. AJ, 5.48%, 5/15/453 | | | 705,000 | | | | 727,248 | |

JP Morgan Mortgage Trust, Mtg. Pass-Through Certificates, Series 2006-A7, Cl. 2A2, 2.837%, 1/25/373 | | | 555,366 | | | | 449,654 | |

JPMBB Commercial Mortgage Securities Trust, Commercial Mtg. Pass- Through Certificates, Series 2013-C14, Cl. D, 4.712%, 8/15/461,3 | | | 855,000 | | | | 733,246 | |

LB-UBS Commercial Mortgage Trust, Commercial Mtg. Pass-Through Certificates, Series 2007-C6, Cl. AM, 6.114%, 7/15/403 | | | 1,010,000 | | | | 1,099,104 | |

Lehman Structured Securities Corp., Commercial Mtg. Pass-Through Certificates, Series 2002-GE1, Cl. A, 2.514%, 7/26/242,3 | | | 150,075 | | | | 131,585 | |

Morgan Stanley Bank of America Merrill Lynch Trust, Commercial Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2012-C6, Cl. E, 4.82%, 11/15/451,3 | | | 810,000 | | | | 695,036 | |

Series 2013-C7, Cl. D, 4.444%, 2/15/461,3 | | | 980,000 | | | | 810,705 | |

Series 2013-C8, Cl. D, 4.312%, 12/15/481,3 | | | 710,000 | | | | 586,570 | |

Morgan Stanley Capital I Trust, Commercial Mtg. Pass-Through Certificates, | | | | | | | | |

Series 2007-IQ13, Cl. AM, 5.406%, 3/15/44 | | | 2,215,000 | | | | 2,357,349 | |

Morgan Stanley Reremic Trust, Re-Securitization Real Estate Mtg. Investment Conduit Multiclass Pass-Through Certificates, Series 2012-R3, Cl. 1A, 2.366%, 11/26/361,3 | | | 4,525,958 | | | | 4,489,675 | |

Sequoia Mortgage Trust, Mtg. Pass-Through Certificates, Series 2012-2, Cl. A2, 3.50%, 4/25/423 | | | 982,589 | | | | 968,829 | |

UBS-Barclays Commercial Mortgage Trust, Commercial Mtg. Pass-Through Certificates, Series 2012-C2, Cl. E, 5.05%, 5/10/631,3 | | | 380,000 | | | | 335,279 | |

Wells Fargo Mortgage-Backed Securities Trust, Mtg. Pass-Through Certificates, Series 2005-AR1, Cl. 1A1, 2.625%, 2/25/353 | | | 4,380,422 | | | | 4,332,073 | |

WF-RBS Commercial Mortgage Trust, Commercial Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2012-C10, Cl. D, 4.609%, 12/15/451,3 | | | 410,000 | | | | 341,020 | |

Series 2012-C7, Cl. E, 5.004%, 6/15/451,3 | | | 710,000 | | | | 621,468 | |

Series 2012-C8, Cl. E, 5.042%, 8/15/451,3 | | | 800,000 | | | | 701,565 | |

Series 2013-C11, Cl. D, 4.324%, 3/15/451,3 | | | 416,000 | | | | 338,432 | |

Series 2013-C15, Cl. D, 4.636%, 8/15/461,3 | | | 725,000 | | | | 589,157 | |

WF-RBS Commercial Mortgage Trust, Interest-Only Commercial Mtg. Pass- Through Certificates, Series 2011-C3, Cl. XA, 1.85%, 3/15/441,3,5 | | | 14,370,078 | | | | 1,023,947 | |

| | | | | | | | |

| | | | | | | | 59,578,102 | |

Multi-Family—0.2% | | | | | | | | |

Wells Fargo Mortgage-Backed Securities Trust, Mtg. Pass Through Certificates, Series 2005-AR15, Cl. 1A2, 2.613%, 9/25/353 | | | 1,273,868 | | | | 1,226,152 | |

Residential—2.2% | | | | | | | | |

Argent Securities, Inc., Asset-Backed Pass-Through Certificates, | | | | | | | | |

Series 2004-W8, Cl. A2, 1.144%, 5/25/343 | | | 3,697,210 | | | | 3,561,275 | |

Banc of America Commercial Mortgage Trust, Commercial Mtg. Pass-Through Certificates, Series 2007-4, Cl. AM, 6.001%, 2/10/513 | | | 2,990,000 | | | | 3,244,709 | |

17 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS Continued | | |

| | | | | | | | |

| | |

| Principal

Amount |

| | | Value | |

Residential Continued | | | | | | | | |

CHL Mortgage Pass-Through Trust, Mtg. Pass-Through Certificates: | | | | | | | | |

Series 2005-J4, Cl. A7, 5.50%, 11/25/35 | | $ | 2,371,463 | | | $ | 2,424,861 | |

Series 2007-HY3, Cl. 1A1, 2.758%, 6/25/473 | | | 2,676,444 | | | | 2,331,796 | |

CWABS Asset-Backed Certificates Trust, Asset-Backed Certificates, | | | | | | | | |

Series 2005-16, Cl. 2AF2, 5.098%, 5/25/363 | | | 512,785 | | | | 511,160 | |

Merrill Lynch Mortgage Investors Trust, Mtg. Pass-Through Certificates, | | | | | | | | |

Series 2005-A1, Cl. 2A1, 2.656%, 12/25/343 | | | 238,149 | | | | 239,870 | |

MLCC Mortgage Investors, Inc., Mtg. Pass-Through Certificates, Series 2006- 3, Cl. 2A1, 2.456%, 10/25/363 | | | 2,062,531 | | | | 1,950,277 | |

RALI Trust, Mtg. Asset-Backed Pass-Through Certificates, Series 2006-QS13, Cl. 1A8, 6%, 9/25/36 | | | 17,455 | | | | 13,575 | |

WaMu Mortgage Pass-Through Certificates Trust, Mtg. Pass-Through Certificates, Series 2007-HY1, Cl. 4A1, 2.544%, 2/25/373 | | | 3,712,945 | | | | 3,170,365 | |

Wells Fargo Mortgage-Backed Securities Trust, Mtg. Pass Through Certificates, Series 2005-9, Cl. 2A6, 5.25%, 10/25/35 | | | 771,739 | | | | 794,381 | |

| | | | | | | | |

| | | | | | | 18,242,269 | |

| | | | | | | | |

Total Mortgage-Backed Obligations (Cost $468,085,990) | | | | | | | 480,041,388 | |

| | | | | | | | |

U.S. Government Obligations—35.4% | | | | | | | | |

Federal Home Loan Mortgage Corp. Nts.: | | | | | | | | |

0.875%, 10/14/16-3/7/18 | | | 110,350,000 | | | | 108,392,687 | |

1.375%, 5/1/20 | | | 44,019,000 | | | | 41,102,521 | |

2.375%, 1/13/22 | | | 4,949,000 | | | | 4,745,319 | |

Federal National Mortgage Assn. Nts.: | | | | | | | | |

0.375%, 7/5/16 | | | 32,194,000 | | | | 31,787,744 | |

0.875%, 5/21/18 | | | 8,160,000 | | | | 7,836,799 | |

1.25%, 1/30/17 | | | 47,553,000 | | | | 47,790,908 | |

1.375%, 11/15/16 | | | 16,460,000 | | | | 16,646,854 | |

1.875%, 9/18/18 | | | 32,642,000 | | | | 32,624,830 | |

U.S. Treasury Nts., 0.25%, 2/28/149 | | | 5,000,000 | | | | 5,004,785 | |

| | | | | �� | | | |

Total U.S. Government Obligations (Cost $301,201,824) | | | | | | | 295,932,447 | |

| | | | | | | | |

Corporate Bonds and Notes—21.7% | | | | | | | | |

Consumer Discretionary—2.5% | | | | | | | | |

Automobiles—1.2% | | | | | | | | |

Ford Motor Credit Co. LLC, 3% Sr. Unsec. Nts., 6/12/17 | | | 8,800,000 | | | | 8,864,654 | |

Hyundai Capital America, 1.875% Unsec. Nts., 8/9/161 | | | 1,000,000 | | | | 999,276 | |

| | | | | | | | |

| | | | | | | 9,863,930 | |

| | | | | | | | |

Household Durables—0.4% | | | | | | | | |

Jarden Corp., 7.50% Sr. Sub. Nts., 5/1/17 | | | 1,800,000 | | | | 2,011,500 | |

Lennar Corp., 4.125% Sr. Unsec. Nts., 12/1/181 | | | 2,150,000 | | | | 2,053,250 | |

| | | | | | | | |

| | | | | | | 4,064,750 | |

| | | | | | | | |

Specialty Retail—0.3% | | | | | | | | |

Sally Holdings LLC/Sally Capital, Inc., 6.875% Sr. Unsec. Nts., 11/15/19 | | | 1,900,000 | | | | 2,080,500 | |

| | | | | | | | |

Textiles, Apparel & Luxury Goods—0.6% | | | | | | | | |

Hanesbrands, Inc., 6.375% Sr. Unsec. Unsub. Nts., 12/15/20 | | | 1,900,000 | | | | 2,061,500 | |

Levi Strauss & Co., 7.625% Sr. Unsec. Nts., 5/15/20 | | | 1,900,000 | | | | 2,047,250 | |

PVH Corp., 7.375% Sr. Unsec. Nts., 5/15/20 | | | 1,900,000 | | | | 2,061,500 | |

| | | | | | | | |

| | | | | | | 6,170,250 | |

18 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | | | | | |

| | |

| Principal

Amount |

| | | Value | |

Consumer Staples—0.8% | | | | | | | | |

Food & Staples Retailing—0.3% | | | | | | | | |

Safeway, Inc., 3.40% Sr. Unsec. Nts., 12/1/16 | | $ | 2,000,000 | | | $ | 2,077,746 | |

Personal Products—0.2% | | | | | | | | |

Avon Products, Inc., 4.60% Sr. Unsec. Nts., 3/15/20 | | | 2,000,000 | | | | 2,051,060 | |

Tobacco—0.3% | | | | | | | | |

Lorillard Tobacco Co., 2.30% Sr. Unsec. Nts., 8/21/17 | | | 2,150,000 | | | | 2,115,295 | |

Energy—2.7% | | | | | | | | |

Energy Equipment & Services—0.4% | | | | | | | | |

Pacific Drilling SA, 5.375% Sr. Sec. Nts., 6/1/201 | | | 2,100,000 | | | | 2,031,750 | |

Seadrill Ltd., 5.625% Sr. Unsec. Nts., 9/15/171 | | | 2,000,000 | | | | 2,025,000 | |

| | | | | | | | |

| | | | | | | 4,056,750 | |

| | | | | | | | |

Oil, Gas & Consumable Fuels—2.3% | | | | | | | | |

Access Midstream Partners LP/ACMP Finance Corp., 5.875% Sr. Unsec. Nts., 4/15/21 | | | 2,000,000 | | | | 2,065,000 | |

Continental Resources, Inc., 5% Sr. Unsec. Nts., 9/15/22 | | | 2,100,000 | | | | 2,131,500 | |

DCP Midstream Operating LP, 2.50% Sr. Unsec. Unsub. Nts., 12/1/17 | | | 1,300,000 | | | | 1,278,217 | |

EQT Corp., 5.15% Sr. Unsec. Nts., 3/1/18 | | | 2,000,000 | | | | 2,126,358 | |

Kinder Morgan Energy Partners LP, 2.65% Sr. Unsec. Nts., 2/1/19 | | | 2,000,000 | | | | 1,977,836 | |

MEG Energy Corp., 6.50% Sr. Unsec. Nts., 3/15/211 | | | 1,600,000 | | | | 1,636,000 | |

Oasis Petroleum, Inc., 7.25% Sr. Unsec. Nts., 2/1/19 | | | 2,000,000 | | | | 2,130,000 | |

Pioneer Natural Resources Co., 6.65% Sr. Unsec. Nts., 3/15/17 | | | 2,490,000 | | | | 2,842,938 | |

Rockies Express Pipeline LLC, 3.90% Sr. Unsec. Unsub. Nts., 4/15/151 | | | 1,146,000 | | | | 1,151,730 | |

Spectra Energy Partners LP, 4.60% Sr. Unsec. Nts., 6/15/21 | | | 1,000,000 | | | | 1,023,354 | |

Western Gas Partners LP, 2.60% Sr. Unsec. Nts., 8/15/18 | | | 1,000,000 | | | | 989,220 | |

| | | | | | | | |

| | | | | | | | 19,352,153 | |

Financials—8.0% | | | | | | | | |

Capital Markets—0.8% | | | | | | | | |

Macquarie Bank Ltd., 2% Sr. Unsec. Nts., 8/15/161 | | | 3,400,000 | | | | 3,394,781 | |

UBS Preferred Funding Trust V, 6.243% Jr. Sub. Perpetual Bonds, Series 13,4 | | | 3,500,000 | | | | 3,696,875 | |

| | | | | | | | |

| | | | | | | 7,091,656 | |

| | | | | | | | |

Commercial Banks—3.3% | | | | | | | | |

Abbey National Treasury Services plc, 3.05% Sr. Unsec. Nts., 8/23/18 | | | 3,202,000 | | | | 3,213,345 | |

BNP Paribas SA, 2.70% Sr. Unsec. Nts., 8/20/18 | | | 3,000,000 | | | | 2,987,202 | |

HSBC Finance Capital Trust IX, 5.911% Unsec. Sub. Nts., 11/30/353 | | | 4,500,000 | | | | 4,584,375 | |

Huntington Bancshares, Inc., 2.60% Sr. Unsec. Nts., 8/2/18 | | | 3,400,000 | | | | 3,363,953 | |

LBG Capital No. 1 plc, 7.875% Unsec. Sub. Nts., 11/1/201 | | | 1,900,000 | | | | 2,028,250 | |

Lloyds TSB Bank plc, 6.50% Unsec. Sub. Nts., 9/14/201 | | | 900,000 | | | | 978,943 | |

Rabobank Capital Funding Trust III, 5.254% Jr. Sub. Perpetual Bonds1,3,4 | | | 2,700,000 | | | | 2,754,000 | |

Royal Bank of Scotland Group plc, 7.64% Jr. Sub. Perpetual Bonds, Series U3,4 | | | 2,300,000 | | | | 2,070,000 | |

Santander Holdings USA, Inc., 3.45% Sr. Unsec. Nts., 8/27/18 | | | 760,000 | | | | 769,634 | |

Zions Bancorporation, 4% Sr. Unsec. Nts., 6/20/16 | | | 3,806,000 | | | | 3,937,269 | |

| | | | | | | | |

| | | | | | | 26,686,971 | |

| | | | | | | | |

Consumer Finance—0.8% | | | | | | | | |

Ally Financial, Inc., 3.50% Sr. Unsec. Nts., 7/18/16 | | | 2,100,000 | | | | 2,118,375 | |

Discover Bank, 4.20% Sr. Unsec. Nts., 8/8/23 | | | 2,100,000 | | | | 2,067,549 | |

19 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS Continued | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Consumer Finance Continued | | | | | | | | |

National Rural Utilities Cooperative Finance Corp., 4.75% Sr. Unsec. Sub. Nts., 4/30/433 | | $ | 1,800,000 | | | $ | 1,674,000 | |

| | | | | | | | |

| | | | | | | 5,859,924 | |

| | | | | | | | |

Diversified Financial Services—0.8% | | | | | | | | |

ING US, Inc., 5.65% Jr. Sub. Nts., 5/15/533 | | | 2,250,000 | | | | 2,082,551 | |

JPMorgan Chase & Co., 7.90% Jr. Sub. Perpetual Bonds, Series 13,4 | | | 3,750,000 | | | | 4,138,425 | |

| | | | | | | | |

| | | | | | | 6,220,976 | |

| | | | | | | | |

Insurance—1.7% | | | | | | | | |

Allstate Corp. (The), 5.75% Sub. Nts., 8/15/533 | | | 2,140,000 | | | | 2,111,912 | |

American International Group, Inc., 3.375% Sr. Unsec. Nts., 8/15/20 | | | 1,700,000 | | | | 1,678,772 | |

Lincoln National Corp., 6.05% Jr. Unsec. Sub. Nts., 4/20/673 | | | 2,700,000 | | | | 2,686,500 | |

Prudential Financial, Inc., 5.20% Jr. Sub. Nts., 3/15/443 | | | 2,285,000 | | | | 2,067,925 | |

Swiss Re Capital I LP, 6.854% Jr. Sub. Perpetual Bonds1,3,4 | | | 4,400,000 | | | | 4,620,000 | |

| | | | | | | | |

| | | | | | | 13,165,109 | |

| | | | | | | | |

Real Estate Investment Trusts (REITs)—0.6% | | | | | | | | |

American Tower Corp., 5.05% Sr. Unsec. Unsub. Nts., 9/1/20 | | | 2,000,000 | | | | 2,072,192 | |

Host Hotels & Resorts LP, 5.875%, 6/15/19 | | | 2,350,000 | | | | 2,553,000 | |

| | | | | | | | |

| | | | | | | | 4,625,192 | |

Health Care—0.4% | | | | | | | | |

Health Care Providers & Services—0.2% | | | | | | | | |

Omnicare, Inc., 7.75% Sr. Sub. Nts., 6/1/20 | | | 1,850,000 | | | | 2,044,250 | |

| | | | | | | | |

Pharmaceuticals—0.2% | | | | | | | | |

Hospira, Inc., 6.05% Sr. Unsec. Nts., 3/30/17 | | | 1,900,000 | | | | 2,045,814 | |

Industrials—2.4% | | | | | | | | |

Aerospace & Defense—0.2% | | | | | | | | |

Huntington Ingalls Industries, Inc., 6.875% Sr. Unsec. Nts., 3/15/18 | | | 1,900,000 | | | | 2,056,750 | |

Building Products—0.2% | | | | | | | | |

Masco Corp., 5.85% Sr. Unsec. Nts., 3/15/17 | | | 1,900,000 | | | | 2,042,500 | |

Commercial Services & Supplies—0.6% | | | | | | | | |

Clean Harbors, Inc., 5.25% Sr. Unsec. Unsub. Nts., 8/1/20 | | | 2,130,000 | | | | 2,114,025 | |

RR Donnelley & Sons Co., 8.25% Sr. Unsec. Nts., 3/15/19 | | | 1,900,000 | | | | 2,104,250 | |

| | | | | | | | |

| | | | | | | | 4,218,275 | |

Industrial Conglomerates—0.5% | | | | | | | | |

General Electric Capital Corp., 6.375% Unsec. Sub. Nts., 11/15/673 | | | 3,900,000 | | | | 4,129,125 | |

Machinery—0.3% | | | | | | | | |

Oshkosh Corp., 8.50% Sr. Unsec. Nts., 3/1/20 | | | 1,100,000 | | | | 1,218,250 | |

Xylem, Inc., 3.55% Sr. Unsec. Nts., 9/20/16 | | | 1,600,000 | | | | 1,672,803 | |

| | | | | | | | |

| | | | | | | | 2,891,053 | |

Professional Services—0.2% | | | | | | | | |

Nielsen Finance LLC/Nielsen Finance Co., 4.50% Sr. Unsec. Nts., 10/1/20 | | | 2,120,000 | | | | 2,024,600 | |

Road & Rail—0.2% | | | | | | | | |

Penske Truck Leasing Co. LP/PTL Finance Corp., 2.50% Sr. Unsec. Nts., 3/15/161 | | | 1,500,000 | | | | 1,518,379 | |

20 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Trading Companies & Distributors—0.2% | | | | | | | | |

International Lease Finance Corp., 5.875% Sr. Unsec. Unsub. Nts., 4/1/19 | | $ | 2,000,000 | | | $ | 2,036,240 | |

Information Technology—0.2% | | | | | | | | |

IT Services—0.2% | | | | | | | | |

Fidelity National Information Services, Inc., 7.875% Sr. Unsec. Nts., 7/15/20 | | | 1,500,000 | | | | 1,662,600 | |

Materials—1.6% | | | | | | | | |

Containers & Packaging—0.4% | | | | | | | | |

Cascades, Inc., 7.875% Sr. Unsec. Nts., 1/15/20 | | | 1,200,000 | | | | 1,269,000 | |

Sealed Air Corp., 8.125% Sr. Unsec. Nts., 9/15/191 | | | 1,850,000 | | | | 2,062,750 | |

| | | | | | | 3,331,750 | |

| | | | | | | | |

Metals & Mining—1.2% | | | | | | | | |

Barrick Gold Corp., 2.90% Sr. Unsec. Nts., 5/30/16 | | | 1,700,000 | | | | 1,710,589 | |

Freeport-McMoRan Copper & Gold, Inc., 2.375% Sr. Unsec. Nts., 3/15/181 | | | 2,250,000 | | | | 2,102,161 | |

Plains Exploration & Production Co., 8.625% Sr. Unsec. Nts., 10/15/19 | | | 1,500,000 | | | | 1,665,025 | |

Steel Dynamics, Inc., 7.625% Sr. Unsec. Nts., 3/15/20 | | | 1,850,000 | | | | 2,007,250 | |

Xstrata Finance Canada Ltd., 2.05% Sr. Unsec. Nts., 10/23/151 | | | 2,100,000 | | | | 2,091,762 | |

| | | | | | | | 9,576,787 | |

Telecommunication Services—2.0% | | | | | | | | |

Diversified Telecommunication Services—1.8% | | | | | | | | |

Frontier Communications Corp., 8.50% Sr. Unsec. Nts., 4/15/20 | | | 1,830,000 | | | | 2,008,425 | |

Koninklijke KPN NV, 7% Sr. Sub. Nts., 3/28/731,3 | | | 2,100,000 | | | | 2,106,180 | |

Telecom Italia Capital SA, 7.175% Sr. Unsec. Nts., 6/18/19 | | | 1,900,000 | | | | 2,074,230 | |

Telefonica Emisiones SAU, 5.877% Sr. Unsec. Nts., 7/15/19 | | | 4,100,000 | | | | 4,374,659 | |

T-Mobile USA, Inc., 5.25% Sr. Unsec. Nts., 9/1/181 | | | 2,100,000 | | | | 2,130,188 | |

Windstream Corp., 7.875% Sr. Unsec. Nts., 11/1/17 | | | 1,850,000 | | | | 2,062,750 | |

| | | | | | | 14,756,432 | |

| | | | | | | | |

Wireless Telecommunication Services—0.2% | | | | | | | | |

Crown Castle International Corp., 7.125% Sr. Unsec. Nts., 11/1/19 | | | 1,900,000 | | | | 2,052,000 | |

Utilities—1.1% | | | | | | | | |

Electric Utilities—0.8% | | | | | | | | |

EDP Finance BV, 6% Sr. Unsec. Nts., 2/2/181 | | | 1,850,000 | | | | 1,926,312 | |

Electricite de France SA, 5.25% Jr. Sub. Perpetual Bonds1,3,4 | | | 1,200,000 | | | | 1,127,040 | |

Great Plains Energy, Inc., 6.875% Sr. Unsec. Nts., 9/15/17 | | | 1,368,000 | | | | 1,571,468 | |

Iberdrola Finance Ireland Ltd., 5% Sr. Unsec. Nts., 9/11/191 | | | 2,000,000 | | | | 2,106,808 | |

| | | | | | | 6,731,628 | |

| | | | | | | | |

Multi-Utilities—0.3% | | | | | | | | |

CMS Energy Corp., 6.55% Sr. Unsec. Nts., 7/17/17 | | | 2,200,000 | | | | 2,528,768 | |

Total Corporate Bonds and Notes (Cost $181,434,076) | | | | | | | 181,129,213 | |

21 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF INVESTMENTS Continued | | |

| | | | | | | | | | | | |

| | | Swaption

Expiration

Date | | | Notional

Amount | | | Value | |

Over-the-Counter Interest Rate Swaptions Purchased—0.0% | | | | | | | | | | | | |

JPMorgan Chase Bank NA; Interest Rate Swaption (European); Swap Terms: Paid: Three-Month USD BBA LIBOR; Received: 1.74%; Termination Date: 12/10/2310 (Cost $200,000) | | | 12/6/13 | | | $ | 100,000,000 | | | $ | 128 | |

Total Investments, at Value (Cost $995,060,785) | | | 119.7 | % | | | | | | | 1,000,571,255 | |

Liabilities in Excess of Other Assets | | | (19.7 | ) | | | | | | | (164,671,688 | ) |

| | | | |

Net Assets | | | 100.0 | % | | | | | | $ | 835,899,567 | |

| | | | |

Footnotes to Statement of Investments

*August 30, 2013 represents the last business day of the Fund’s 2013 fiscal year. See Note 1 of the accompanying Notes.

1. Represents securities sold under Rule 144A, which are exempt from registration under the Securities Act of 1933, as amended. These securities have been determined to be liquid under guidelines established by the Board of Trustees. These securities amount to $87,724,611 or 10.49% of the Fund’s net assets as of August 30, 2013.

2. Restricted security. The aggregate value of restricted securities as of August 30, 2013 was $3,764,708, which represents 0.45% of the Fund’s net assets. See Note 7 of the accompanying Notes. Information concerning restricted securities is as follows:

| | | | | | | | | | | | | | | | |

| Security | | Acquisition

Dates | | | Cost | | | Value | | | Unrealized

Appreciation/

(Depreciation) | |

BCAP LLC Trust, Mtg. Pass- Through Certificates, Series 2012-RR6, 2.404%, 11/26/36 | | | 6/14/12 | | | $ | 3,308,416 | | | $ | 3,394,249 | | | $ | 85,833 | |

Capital Lease Funding Securitization LP, Interest-Only Commercial Mtg. Pass-Through Certificates, Series 1997-CTL1, Cl. IO, 0.00%, 6/22/24 | | | 4/21/97-6/27/97 | | | | 789,752 | | | | 186,856 | | | | (602,896 | ) |

Lehman Structured Securities Corp., Commercial Mtg. Pass- Through Certificates, Series 2002-GE1, Cl. A, 2.514%, 7/26/24 | | | 1/28/02 | | | | 147,044 | | | | 131,585 | | | | (15,459 | ) |

Santander Drive Auto Receivables Trust, Series 2011- S1A, Cl. D, 3.10%, 5/15/17 | | | 2/4/11-4/14/11 | | | | 52,020 | | | | 52,018 | | | | (2 | ) |

| | | | | | | | |

| | | | | | $ | 4,297,232 | | | $ | 3,764,708 | | | $ | (532,524 | ) |

| | | | | | | | |

3. Represents the current interest rate for a variable or increasing rate security.

4. This bond has no contractual maturity date, is not redeemable and contractually pays an indefinite stream of interest. Rate reported represents the current interest rate for this variable rate security.

22 OPPENHEIMER LIMITED-TERM BOND FUND

5. Interest-Only Strips represent the right to receive the monthly interest payments on an underlying pool of mortgage loans. These securities typically decline in price as interest rates decline. Most other fixed income securities increase in price when interest rates decline. The principal amount of the underlying pool represents the notional amount on which current interest is calculated. The price of these securities is typically more sensitive to changes in prepayment rates than traditional mortgage-backed securities (for example, GNMA pass-throughs). Interest rates disclosed represent current yields based upon the current cost basis and estimated timing and amount of future cash flows. These securities amount to $20,390,233 or 2.44% of the Fund’s net assets as of August 30, 2013.

6. All or a portion of the security position is when-issued or delayed delivery to be delivered and settled after August 30, 2013. See Note 1 of the accompanying Notes.

7. Principal-Only Strips represent the right to receive the monthly principal payments on an underlying pool of mortgage loans. The value of these securities generally increases as interest rates decline and prepayment rates rise. The price of these securities is typically more volatile than that of coupon-bearing bonds of the same maturity. Interest rates disclosed represent current yields based upon the current cost basis and estimated timing of future cash flows. These securities amount to $160,399 or 0.02% of the Fund’s net assets as of August 30, 2013.

8. Interest rate is less than 0.0005%.

9. All or a portion of the security position is held in accounts at a futures clearing merchant and pledged to cover margin requirements on open futures contracts and written options on futures, if applicable. The aggregate market value of such securities is $5,004,785. See Note 6 of the accompanying Notes.

10. Non-income producing security.

| | | | | | | | | | | | | | | | | | | | |

| Futures Contracts as of August 30, 2013 are as follows: | | | | | | | | | | | | | | | |

| | | | | |

| Contract Description | | Buy/Sell | | | Number of

Contracts | | | Expiration

Date | | | Value | | | Unrealized

Appreciation (Depreciation) | |

U.S. Treasury Long Bonds | | | Sell | | | | 1,066 | | | | 12/19/13 | | | $ | 140,612,063 | | | $ | (1,716,956 | ) |

U.S. Treasury Nts., 2 yr. | | | Sell | | | | 32 | | | | 12/31/13 | | | | 7,032,000 | | | | (2,396 | ) |

U.S. Treasury Nts., 5 yr. | | | Sell | | | | 997 | | | | 12/31/13 | | | | 119,320,651 | | | | (274,364 | ) |

U.S. Treasury Nts., 10 yr. | | | Sell | | | | 1,063 | | | | 12/19/13 | | | | 132,110,969 | | | | (544,317 | ) |

U.S. Treasury Ultra Bonds | | | Buy | | | | 395 | | | | 12/19/13 | | | | 56,040,625 | | | | 1,618,013 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | (920,020 | ) |

| | | | | | | | | | | | | | | | | | | | |

See accompanying Notes to Financial Statements.

23 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF ASSETS AND LIABILITIES August 30, 20131 | | |

| | | | |

Assets | | | | |

Investments, at value (cost $995,060,785)—see accompanying statement of investments | | $ | 1,000,571,255 | |

Cash | | | 40,863,520 | |

Receivables and other assets: | | | | |

Investments sold on a when-issued or delayed delivery basis | | | 132,831,415 | |

Interest and principal paydowns | | | 5,030,775 | |

Shares of beneficial interest sold | | | 3,687,060 | |

Variation margin receivable | | | 416,998 | |

Expense waivers/reimbursements due from manager | | | 18,266 | |

Other | | | 137,891 | |

| | | | |

Total assets | | | 1,183,557,180 | |

Liabilities | | | | |

Payables and other liabilities: | | | | |

Investments purchased (including $335,480,199 purchased on a when-issued or delayed delivery basis) | | | 345,499,051 | |

Shares of beneficial interest redeemed | | | 1,053,204 | |

Variation margin payable | | | 233,031 | |

Trustees’ compensation | | | 228,454 | |

Distribution and service plan fees | | | 185,779 | |

Transfer and shareholder servicing agent fees | | | 167,669 | |

Dividends | | | 119,599 | |

Shareholder communications | | | 39,736 | |

Other | | | 131,090 | |

| | | | |

Total liabilities | | | 347,657,613 | |

Net Assets | | $ | 835,899,567 | |

| | | | |

| | | | |

Composition of Net Assets | | | | |

Par value of shares of beneficial interest | | $ | 89,688 | |

Additional paid-in capital | | | 826,007,456 | |

Accumulated net investment income | | | 6,854,883 | |

Accumulated net realized loss on investments | | | (1,642,910 | ) |

Net unrealized appreciation on investments | | | 4,590,450 | |

| | | | |

Net Assets | | $ | 835,899,567 | |

| | | | |

1. August 30, 2013 represents the last business day of the Fund’s 2013 fiscal year. See Note 1 of the accompanying Notes.

24 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

Net Asset Value Per Share | | | | |

Class A Shares: | | | | |

| Net asset value and redemption price per share (based on net assets of $632,387,117 and 67,837,522 shares of beneficial interest outstanding) | | $ | 9.32 | |

| Maximum offering price per share (net asset value plus sales charge of 2.25% of offering price) | | $ | 9.53 | |

| Class B Shares: | | | | |

| Net asset value, redemption price (excludes applicable contingent deferred sales charge) and offering price per share (based on net assets of $34,045,225 and 3,656,923 shares of beneficial interest outstanding) | | $ | 9.31 | |

| Class C Shares: | | | | |

| Net asset value, redemption price (excludes applicable contingent deferred sales charge) and offering price per share (based on net assets of $119,677,069 and 12,858,365 shares of beneficial interest outstanding) | | $ | 9.31 | |

| Class I Shares: | | | | |

| Net asset value, redemption price and offering price per share (based on net assets of $9,958 and 1,065 shares of beneficial interest outstanding) | | $ | 9.35 | |

| Class N Shares: | | | | |

| Net asset value, redemption price (excludes applicable contingent deferred sales charge) and offering price per share (based on net assets of $33,368,206 and 3,579,706 shares of beneficial interest outstanding) | | $ | 9.32 | |

| Class Y Shares: | | | | |

| Net asset value, redemption price and offering price per share (based on net assets of $16,411,992 and 1,754,543 shares of beneficial interest outstanding) | | $ | 9.35 | |

See accompanying Notes to Financial Statements

25 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENT OF OPERATIONS For the Year Ended August 30, 20131 | | |

| | | | |

Investment Income | | | | |

Interest | | $ | 20,449,526 | |

Fee income on when-issued securities | | | 6,336,109 | |

Other income | | | 16,976 | |

| | | | |

Total investment income | | | 26,802,611 | |

Expenses | | | | |

Management fees | | | 5,350,077 | |

Distribution and service plan fees: | | | | |

Class A | | | 1,750,669 | |

Class B | | | 452,807 | |

Class C | | | 1,461,289 | |

Class N | | | 193,767 | |

Transfer and shareholder servicing agent fees: | | | | |

Class A | | | 1,193,306 | |

Class B | | | 144,339 | |

Class C | | | 269,081 | |

Class N | | | 103,267 | |

Class Y | | | 25,306 | |

Shareholder communications: | | | | |

Class A | | | 193,722 | |

Class B | | | 22,194 | |

Class C | | | 39,875 | |

Class N | | | 8,251 | |

Class Y | | | 810 | |

Trustees’ compensation | | | 33,427 | |

Custodian fees and expenses | | | 12,361 | |

Other | | | 70,831 | |

| | | | |

Total expenses | | | 11,325,379 | |

Less waivers and reimbursements of expenses | | | (1,053,426 | ) |

| | | | |

Net expenses | | | 10,271,953 | |

Net Investment Income | | | 16,530,658 | |

1. August 30, 2013 represents the last business day of the Fund’s 2013 fiscal year. See Note 1 of the accompanying Notes.

26 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

Realized and Unrealized Gain (Loss) | | | | |

Net realized gain (loss) on: | | | | |

Investments from unaffiliated companies | | $ | (7,830,795) | |

Closing and expiration of option contracts written | | | 266,954 | |

Closing and expiration of futures contracts | | | 8,766,788 | |

Swap contracts | | | 1,095,902 | |

Closing and expiration of swaption contracts written | | | (28,188 | ) |

| | | | |

Net realized gain | | | 2,270,661 | |

Net change in unrealized appreciation/depreciation on: | | | | |

Investments | | | (28,649,012 | ) |

Futures contracts | | | (2,813,629 | ) |

Option contracts written | | | (10,948 | ) |

Swaption contracts written | | | (23,454 | ) |

| | | | |

Net change in unrealized appreciation/depreciation | | | (31,497,043 | ) |

Net Decrease in Net Assets Resulting from Operations | | $ | (12,695,724) | |

| | | | |

See accompanying Notes to Financial Statements.

27 OPPENHEIMER LIMITED-TERM BOND FUND

| | | | |

| | |

| | STATEMENTS OF CHANGES IN NET ASSETS | | |

| | | | | | | | |

| | | Year Ended

August 30, 20131 | | | Year Ended

August 31, 2012 | |

Operations | | | | | | | | |

Net investment income | | $ | 16,530,658 | | | $ | 21,003,600 | |

Net realized gain | | | 2,270,661 | | | | 30,533,605 | |

Net change in unrealized appreciation/depreciation | | | (31,497,043 | ) | | | 2,015,161 | |

| | | | |

Net increase (decrease) in net assets resulting from operations | | | (12,695,724 | ) | | | 53,552,366 | |

Dividends and/or Distributions to Shareholders | | | | | | | | |

Dividends from net investment income: | | | | | | | | |

Class A | | | (13,419,150 | ) | | | (16,439,582 | ) |

Class B | | | (495,091 | ) | | | (852,759 | ) |

Class C | | | (1,604,046 | ) | | | (2,367,467 | ) |

Class I | | | (23 | ) | | | — | |

Class N | | | (639,805 | ) | | | (904,244 | ) |

Class Y | | | (392,846 | ) | | | (439,548 | ) |

| | | | |

| | | | (16,550,961 | ) | | | (21,003,600 | ) |

Distributions from net realized gain: | | | | | | | | |

Class A | | | (19,333,828 | ) | | | (7,801,334 | ) |

Class B | | | (1,285,124 | ) | | | (610,058 | ) |

Class C | | | (3,996,405 | ) | | | (1,683,231 | ) |

Class I | | | — | | | | — | |

Class N | | | (1,089,754 | ) | | | (470,053 | ) |

Class Y | | | (553,853 | ) | | | (193,052 | ) |

| | | | |

| | | (26,258,964 | ) | | | (10,757,728 | ) |

Beneficial Interest Transactions | | | | | | | | |

Net increase (decrease) in net assets resulting from beneficial interest transactions: | | | | | | | | |

Class A | | | (80,858,211 | ) | | | 72,277,182 | |

Class B | | | (17,415,152 | ) | | | (2,200,733 | ) |

Class C | | | (33,492,002 | ) | | | 16,611,652 | |

Class I | | | 10,000 | | | | — | |

Class N | | | (8,831,574 | ) | | | 617,176 | |

Class Y | | | 812,977 | | | | 4,592,329 | |

| | | | |

| | | (139,773,962 | ) | | | 91,897,606 | |

Net Assets | | | | | | | | |