UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-03451

SEI Daily Income Trust

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices)

Timothy D. Barto, Esq.

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-610-676-1000

Date of fiscal year end: January 31, 2023

Date of reporting period: January 31, 2023

Item 1. Reports to Stockholders.

January 31, 2023

ANNUAL REPORT

SEI Daily Income Trust

❯ | Government Fund |

❯ | Government II Fund |

❯ | Treasury II Fund |

❯ | Ultra Short Duration Bond Fund |

❯ | Short-Duration Government Fund |

❯ | GNMA Fund |

Paper copies of the Funds’ shareholder reports are no longer sent by mail, unless you specifically request them from the Funds or from your financial intermediary, such as a broker-dealer or bank. Shareholder reports are available online and you will be notified by mail each time a report is posted on the Funds’ website and provided with a link to access the report online.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with the Funds, you can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by calling 1-800-DIAL-SEI. Your election to receive reports in paper will apply to all funds held with the SEI Funds or your financial intermediary.

seic.com

TABLE OF CONTENTS

| Letter to Shareholders | 1 |

| Management’s Discussion and Analysis of Fund Performance | 4 |

| Schedules of Investments | 11 |

| Statements of Assets and Liabilities | 48 |

| Statements of Operations | 50 |

| Statements of Changes in Net Assets | 52 |

| Financial Highlights | 56 |

| Notes to Financial Statements | 58 |

| Report of Independent Registered Public Accounting Firm | 71 |

| Trustees and Officers of the Trust | 72 |

| Disclosure of Fund Expenses | 75 |

| Liquidity Risk Management Program | 77 |

| Board of Trustees’ Considerations in Approving the Advisory Agreement | 78 |

| Notice to Shareholders | 84 |

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarter of each fiscal year on Form N-PORT for Ultra Short Duration Bond Fund, Short-Duration Government Fund & GNMA Fund. Additionally, for Government Fund, Government II Fund & Treasury II Fund, the Trust files monthly its complete schedule of portfolio holdings with the Securities and Exchange Commission on Form N-MFP. The Trust’s Forms N-PORT and N-MFP are available on the Commission’s website at http://www.sec.gov.

Since the Funds in SEI Daily Income Trust typically hold only fixed income securities, they generally are not expected to hold securities for which they may be required to vote proxies. Regardless, in light of the possibility that a Fund could hold a security for which a proxy is voted, the Trust has adopted proxy voting policies. A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

LETTER TO SHAREHOLDERS

January 31, 2023

To Our Shareholders

All eyes (and ears) were on U.S. Federal Reserve (Fed) during the 12-month period ended January 31, 2023. The U.S. equity market gyrated as the central bank began and then maintained its interest rate-hiking cycle in an effort to tame inflation. Headline inflation in the U.S., as measured by the consumer-price-index, reached a peak of 9.1% in June 2022, before decelerating as energy prices declined. However, yet core inflation (excluding food and energy costs) remained stubbornly high for much of the period.

As inflationary pressures persisted, the Fed raised its benchmark interest rate eight times by an aggregate of 450 basis points (4.50%) over the reporting period to a range of 4.25% to 4.50%. However, the central bank slowed the pace of its 75-basis-point increases following its meetings in September and November to 50 basis points and 25 basis points in December and late January.

Geopolitical Events

Russia’s ongoing invasion of Ukraine dominated the geopolitical news during the reporting period. In November, Ukraine’s military regained control of the southern city of Kherson as Russian Defense Minister Sergei Shoigu ordered his troops to retreat from what had been the sole regional Ukrainian capital Moscow had held since invading the country in late February 2022. This was a major setback for Russia’s Vladimir Putin. Ukraine’s president, Volodymyr Zelenskyy, addressed a joint session of the U.S. Congress in late December in an effort to secure additional financial aid from the U.S. and its allies. President Joe Biden reiterated the U.S. government’s support for Ukraine in its conflict with Russia. In late December, the U.S. Congress approved $US 45 billion in additional financial assistance to Ukraine. The U.S., Germany, and several other European allies agreed to send tanks to Ukraine in support of its defense against Russia’s ongoing invasion.

The Republican Party secured a slim majority in the U.S. House of Representatives in the general election in November. One of the first moves by party leaders was the refusal to approve an increased debt limit (commonly referred to as the “debt ceiling”) unless the administration of President Joe Biden, a Democrat, agreed to specific spending cuts. U.S. Treasury Secretary Janet Yellen announced that the Treasury Department began taking “extraordinary measures” after the government reached its $31.4 trillion borrowing limit on January 19, 2023. Yellen estimated that the U.S. government might run out of money and be unable to meet its financial obligations in early June if the House of Representatives does not vote to raise the debt ceiling. She urged Congress to “act promptly to protect the full faith and credit of the United States.”

Liz Truss was elected U.K. prime minister in September but served just seven weeks before resigning after the disastrous reception of her fiscal program sent gilt and sterling markets reeling, collapsing her support within the Conservative Party. Her departure cleared the way for Rishi Sunak to ascend as Conservative leader and prime minister.

Economic Performance

Inflation showed signs of cooling over the reporting period. According to the Department of Labor, the U.S. Consumer Price Index (CPI) advanced 0.5% in January 2023, up from the 0.1% rise in December of last year. The year-over-year increase of 6.4%, down marginally from the 6.5% rise in December, was the smallest annual gain in the CPI since the 12-month period ending October 2021. The personal-consumption-expenditures index (PCE) posted increases of 0.6% in January and 5.4% over the previous 12-month period. The core PCE index, which excludes volatile food and energy prices, was also up 0.6% for the month and 4.7% year-over-year. The PCE price index tracks the change in prices paid by or on behalf of consumers for a more comprehensive set of goods and services than that of the CPI. Consequently, the PCE index is the Fed’s preferred gauge of inflation.

The Department of Commerce reported that the U.S. economy expanded at annualized rates of 3.2% and 2.7% in the third and fourth quarters of 2022, respectively. These gains reversed the corresponding 1.6% and 0.6% declines in GDP in the first and second quarters of the year. The U.S. economy expanded by 2.1% for the 2022 calendar year—from the 37-year high of 5.7% in 2021. The government attributed the rise in GDP in 2022 mainly to upturns in consumer spending and exports, which were partly offset by decreases in residential fixed investment (purchases of private residential structures and residential equipment that is owned by landlords and rented to tenants) and federal government spending, as well as an increase in imports (which are subtracted from the calculation of GDP).

The U.S. unemployment rate dipped 0.4% to 3.4% during the reporting period. The labor-force participation rate ended the period at 62.4%, up marginally from 62.2% in January 2022. Average hourly earnings rose 4.4% over the reporting period.

SEI Daily Income Trust / Annual Report / January 31, 2023

1

LETTER TO SHAREHOLDERS (Concluded)

January 31, 2023

The Federal Open Market Committee (FOMC) met most recently at the end of the reporting period. In its post-meeting statement on February 1, the central bank noted that it will continue to monitor information regarding the economic outlook, including labor market conditions, inflation pressures, and financial and international developments. The Fed reiterated its commitment to restricting inflation to its 2% target rate.

Market Developments

A theme for U.S. fixed-income markets over the reporting period was the inversion of the U.S. Treasury yield curve; yields on shorter-term bonds rose by more than those on longer-term securities (bond prices move inversely to interest rates). The significant upturn in shorter-term bond yields reflected expectations for continued rate hikes by the Fed, while longer-term bonds showed signs of concern for how monetary tightening might have a negative effect on economic growth. Yields on two-year Treasury notes ended the 12-month period up 303 basis points to 4.21%, while 10-year yields gained 173 basis points during the fiscal year.

Despite posting losses during the reporting period, U.S. high-yield bonds outperformed U.S. government and corporate bonds as they have less interest-rate sensitivity. The U.S. government bond market, as measured by the Bloomberg U.S. Government Index, was down 8.43% during the reporting period, while U.S. high-yield bonds, as measured by the ICE BofA US High Yield Constrained Index, fell 5.14%. The ICE BofA U.S. Corporate Index declined 9.32%. U.S. asset- and mortgage-backed securities also moved lower during the period.

Commodity prices rose during the reporting period, with the Bloomberg Commodity Total Return Index (which represents the broad commodity market) returning 6.20%. Precious metals prices rallied sharply in the second half of the reporting period as the U.S. dollar weakened and the Fed’s interest-rate hikes started to moderate. However, prices for West Texas Intermediate crude oil and Brent crude oil fell amid concerns that additional interest-rate hikes from central banks will weigh on global economic growth and reduce demand. Wheat prices moved higher for the first several months of the reporting period before decreasing after Russia renewed a deal with the UN, Ukraine, and Turkey that allows the shipment of Ukrainian grain through the Black Sea.

Our View

We are projecting a less robust global economy in 2023 than the one witnessed in the past year. Volatility is expected across asset classes as investors face familiar headwinds: inflation rates exceeding the targets of major central banks, interest-rate increases continuing throughout the first half of the year, and quantitative easing shifting to quantitative tightening. The expected result for many countries is stagnant or recessionary economies through 2023 and perhaps into 2024. While these obstacles are bad news for stock prices and depress the value of current bond holdings, there is a silver lining for long-suffering income-seeking investors, as fixed-income markets now offer better yields than they have in decades.

In the U.S., wages are down in inflation-adjusted terms, the housing market is suffering a severe contraction, and some industries (notably within technology) are losing a significant number of jobs. However, the overall economy still isn’t declining in the pronounced, pervasive, and persistent manner that characterizes a typical recession.

With regard to inflation, there is good reason to believe that inflation rates have peaked for most countries. We don’t expect to see inflation fall back to the 2% target that central banks of advanced economies set for themselves. This is especially true in the U.S. and other countries challenged by exceptionally tight labor markets and already-high wage inflation.

Moving on to monetary policy, further Fed interest-rate hikes are expected for the remainder of 2023. As widely expected, following its meeting on January 31-February 1, the Federal Open Market Committee (FOMC) raised the federal-funds rate by 0.25% to a range of 4.50% to 4.75%—the smallest increase since its rate-hiking policy began in March 2022. The central bank’s policymakers reiterated their commitment to reducing inflation to the 2% target rate, and said they would continue to monitor the labor market, inflation pressures and expectations, and financial and international developments to inform its economic outlook. Whether this proves sufficient to tame inflation remains to be seen.

The global banking system itself appears to be in decent shape following the regulatory and capital-enhancement reforms put in place after the global financial crisis. On the geopolitical front, energy prices posted surprisingly sharp declines. Natural gas prices in Europe are the exception. With the war in Ukraine appearing likely to drag on for the foreseeable future, the possibility exists for more surprises that will keep energy prices quite volatile, with current prices likely at the low end of a wide trading range.

2

SEI Daily Income Trust / Annual Report / January 31, 2023

LETTER TO SHAREHOLDERS (Concluded)

January 31, 2023

On the geopolitical front, Russia’s war in Ukraine rages on. Energy prices are expected to remain volatile. Despite military aid to Ukraine from the U.S. and some of its allies, the country’s war with Russia appears likely to persist well into this year at the very least. As Russia is a major exporter of oil and natural gas to Europe, the possibility exists for more surprises that will keep energy prices quite volatile.

The Chinese government’s easing of the most onerous COVID-19 should help offset, at least partially, the impact of a global slowdown in advanced countries. It also eventually could exert upward pressure on commodity prices, especially for energy and metals. This would benefit commodity-oriented exporters in Latin America and the Middle East, along with South Africa, Indonesia, and Malaysia.

Looking ahead, there are numerous challenges for the global economy. Nonetheless, we believe any recession will likely be fairly shallow. Inflation may continue to run above its long-term trend for some time, but it appears that central banks have at least begun to rein it in. Value-oriented stocks had strong relative performance in 2022, and we believe they remain attractive. As inflation pressures ease and the pace of central bank rate hikes slows, we believe that the fixed-income environment should be more compelling.

Sincerely,

James Smigiel

Chief Investment Officer

SEI Daily Income Trust / Annual Report / January 31, 2023

3

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

January 31, 2023

Ultra Short Duration Bond Fund

I. Objective

The Ultra Short Duration Bond Fund (the “Fund”) seeks to provide higher current income than that typically offered by a money-market fund while maintaining a high degree of liquidity and a correspondingly higher risk of principal volatility.

II. Investment Approach

The Fund uses a multi-manager approach, relying on a number of subadvisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (SIMC). For the 12-month period ending January 31, 2023, the sub-advisors were MetLife Investment Management, LLC (MetLife) and Wellington Management Company LLP (Wellington). There were no manager changes during the period.

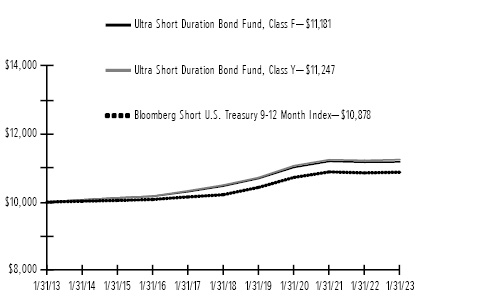

III. Returns

For the 12-month period ending January 31, 2023, the Ultra Short Duration Bond Fund, Class F, returned 0.09%. The Fund’s benchmark—the Bloomberg Short U.S. Treasury 9-12 Month Index (which tracks the performance of U.S. Treasury securities that have a remaining maturity between 9 and 12 months)—returned 0.18%.

IV. Performance Discussion

As noted in the shareholder letter, the U.S. Federal Reserve (Fed) increased the target range on the federal funds rate from a range of 0.00%-0.25% at the start of the reporting period to 4.25%-4.50% by the end of the period on January 31, 2023, in an effort to combat persistent inflation, including an unprecedented four consecutive interest-rate hikes of 0.75 basis points. The lagged effects of the Fed’s tighter monetary policy started to work its way through the economy as inflation began to moderate during the fourth quarter of 2022, with the Consumer Price Index (CPI) declining to 6.5% in December after peaking at 9.1% in June. In addition to raising rates, the Fed commenced its balance sheet run-off during the reporting period, and while the central bank hasn’t directly sold any securities, it has set caps of $60 billion of U.S. Treasurys and $35 billion of agency mortgage-backed securities (MBS) each month. Performance was mixed across spread sectors, over the 12-month period. Corporate bonds produced positive excess returns following a rebound during the fourth quarter of 2022, as inflation began to moderate and investors became more optimistic that the Fed was getting closer to the end of its rate-hiking cycle. The reporting period was challenging for agency MBS, which continue to face technical headwinds as the Fed

reduced the size of its balance sheet and rate volatility was elevated. The performance of asset-backed securities (ABS) was mixed over the period, with the sector overall slightly underperforming U.S. Treasury. While recessionary risks have increased and economic growth appears to be slowing, the U.S. consumer remains in relative strong shape as the nation’s unemployment rate trickled down to 3.4% in January of 2023—the lowest level in more than 50 years.

Fund performance over the reporting period benefited from an allocation to corporate credit. While spreads widened for much of the period as firms came under margin pressure given rising labor and input costs, corporate credit generated positive excess returns following a strong fourth quarter of 2022, as inflation moderated and investors became more optimistic that the Fed was near the top of its rate-hiking cycle. The Fund’s performance within the ABS sector was mixed during the period, with security selection in credit cards and auto loans bolstered performance and an allocation to student loans was a detractor. The Fund’s allocation to non-agency MBS had a negative impact on performance, as housing affordability declined significantly given rising mortgage rates and home price appreciation. The Fund’s duration positioning had a minimal impact on performance as managers oscillated between slightly short and slightly long, but never deviated far from neutral. An allocation to commercial mortgage-backed securities (CMBS) weighed on Fund performance as the sector generated negative excess returns over the period.

Both of the Fund’s subadvisors, MetLife and Wellington, contributed to Fund performance for the reporting period, and benefited from similar exposures, including corporate bonds and ABS. Wellington’s allocation to non-agency MBS detracted from Fund performance, while MetLife’s security selection within ABS had a positive impact.

The Fund used Treasury futures in an effort to efficiently manage duration and yield-curve exposures. Additionally, the Fund used to-be-announced (TBA) forward contracts (TBA forward contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS: Fannie Mae, Freddie Mac and GNMA) to manage market exposures. None of these had a meaningful impact on Fund performance during the reporting period.

Investing is subject to risk, including the possible loss of principal. Past performance is not an indication of future results.

4

SEI Daily Income Trust / Annual Report / January 31, 2023

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

January 31, 2023

Ultra Short Duration Bond Fund (Concluded)

Ultra Short Duration Bond Fund:

AVERAGE ANNUAL TOTAL RETURN1 | |||||

One Year | Annualized | Annualized | Annualized | Annualized | |

Class F | 0.09% | 0.49% | 1.33% | 1.12% | 2.77% |

Class Y | 0.18% | 0.53% | 1.38% | N/A | 1.39% |

Bloomberg Short U.S. Treasury 9-12 Month Index | 0.18% | 0.47% | 1.26% | 0.85% | 1.06% |

Comparison of Change in the Value of a $10,000 Investment in the Ultra Short Duration Bond Fund, Class F and Class Y, versus the Bloomberg Short U.S. Treasury 9-12 Month Index.

1 | For the periods ended January 31, 2023. Past performance is no indication of future performance. Class F Shares were offered beginning 9/28/93. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Class Y Shares were offered beginning 8/31/15. |

N/A — Not Available.

SEI Daily Income Trust / Annual Report / January 31, 2023

5

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

January 31, 2023

Short-Duration Government Fund

I. Objective

The Short-Duration Government Fund (the “Fund”) seeks to preserve principal value and maintain a high degree of liquidity while providing current income.

II. Investment Approach

The Fund uses a subadvisor to manage the Fund under the supervision of SEI Investments Management Corporation (SIMC). For the 12-month period ending January 31, 2023, the subadvisor was Wellington Management Company LLP (Wellington). No manager changes were made during the period.

III. Returns

For the 12-month period ending January 31, 2023, the Short-Duration Government Fund, Class F, returned -2.74%. The Fund’s benchmark—the ICE BofA 1-3 Year U.S. Treasury Index (which tracks the performance of direct sovereign debt of the U.S. government having a maturity of at least one year and less than three years)—returned -2.35%.

IV. Performance Discussion

As noted in the shareholder letter, the U.S. Federal Reserve (Fed) increased the target range on the federal funds rate from a range of 0.00%-0.25% at the start of the reporting period to 4.25%-4.50% by the end of the period on January 31, 2023, in an effort to combat persistent inflation, including an unprecedented four consecutive interest-rate hikes of 0.75 basis points. The lagged effects of the Fed’s tighter monetary policy started to work its way through the economy as inflation began to moderate during the fourth quarter of 2022, with the Consumer Price Index (CPI) declining to 6.5% in December after peaking at 9.1% in June. In addition to raising rates, the Fed commenced its balance sheet run-off during the reporting period, and while the central bank hasn’t directly sold any securities, it has set caps of $60 billion of U.S. Treasurys and $35 billion of agency mortgage-backed securities (MBS) each month. Performance was mixed across spread sectors, over the 12-month period. Corporate bonds produced positive excess returns following a rebound during the fourth quarter of 2022, as inflation began to moderate and investors became more optimistic that the Fed was getting closer to the end of its rate-hiking cycle. The reporting period was challenging for agency MBS, which continue to face technical headwinds as the Fed reduced the size of its balance sheet and rate volatility was elevated. The performance of asset-backed securities (ABS) was mixed over the period, with the sector overall slightly underperforming U.S. Treasury. While recessionary risks have increased and economic growth appears to be

slowing, the U.S. consumer remains in relative strong shape as the nation’s unemployment rate trickled down to 3.4% in January of 2023—the lowest level in more than 50 years.

The Fund’s allocation to agency MBS detracted from performance for the reporting period as the sector generated negative excess returns. Agency MBS lagged as the Fed began reducing the size of its balance sheet during the second quarter in 2022, and then accelerated the pace of run-off during the fourth quarter of the year. Security selection within the sector had a positive impact on performance as specified pools outperformed to-be-announced (TBA) securities and higher-coupon credits fared better than lower-coupon issues given the technical environment. An overweight to agency collateralized mortgage obligations (CMOs) also contributed positively to Fund performance. Wellington, the Fund’ subadvisor, likes the sector due to its predictable cash flows. An overweight to agency commercial mortgage-backed securities (CMBS) detracted from Fund performance as the sector underperformed duration-neutral Treasurys for the period.

The Fund used derivatives on a limited basis during the reporting period. The Fund employed U.S. Treasury futures to manage yield-curve exposure and overall portfolio duration. The Fund used Treasury futures and TBA forward contracts to manage duration, yield-curve and market exposures (TBA forward contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS: Fannie Mae, Freddie Mac and GNMA). Treasury futures did not have a material impact on Fund performance for the period.

Investing is subject to risk, including the possible loss of principal. Past performance is not an indication of future results.

6

SEI Daily Income Trust / Annual Report / January 31, 2023

Short-Duration Government Fund:

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

January 31, 2023

Short-Duration Government Fund (Concluded)

AVERAGE ANNUAL TOTAL RETURN1 | |||||

One Year | Annualized | Annualized | Annualized | Annualized | |

Class F | -2.74% | -0.55% | 0.66% | 0.53% | 3.84% |

Class Y | -2.58% | -0.39% | 0.82% | N/A | 0.72% |

ICE BofA 1-3 Year U.S. Treasury Index | -2.35% | -0.36% | 0.97% | 0.74% | 0.79% |

Comparison of Change in the Value of a $10,000 Investment in the Short-Duration Government Fund, Class F and Class Y, versus the ICE BofA 1-3 Year U.S. Treasury Index.

1 | For the periods ended January 31, 2023. Past performance is no indication of future performance. Class F Shares were offered beginning 2/17/87. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Class Y Shares were offered beginning 12/31/14. |

N/A — Not Available.

SEI Daily Income Trust / Annual Report / January 31, 2023

7

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

January 31, 2023

GNMA Fund

I. Objective

The GNMA Fund (the “Fund”) seeks to preserve principal value and maintain a high degree of liquidity while providing current income.

II. Investment Approach

The Fund uses a subadvisor to manage the Fund under the supervision of SEI Investments Management Corporation (SIMC). For the 12-month period ending January 31, 2023, the subadvisor was Wellington Management Company LLP (Wellington). No manager changes were made during the period.

III. Returns

For the 12-month period ending January 31, 2023, the GNMA Fund, Class F, returned -7.23%. The Fund’s benchmark—the Bloomberg GNMA Index (which tracks the performance of securitized mortgage pools backed by the Government National Mortgage Association (GNMA)—returned -6.69%.

IV. Performance Discussion

As noted in the shareholder letter, the U.S. Federal Reserve (Fed) increased the target range on the federal funds rate from a range of 0.00%-0.25% at the start of the reporting period to 4.25%-4.50% by the end of the period on January 31, 2023, in an effort to combat persistent inflation, including an unprecedented four consecutive interest-rate hikes of 0.75 basis points. The lagged effects of the Fed’s tighter monetary policy started to work its way through the economy as inflation began to moderate during the fourth quarter of 2022, with the Consumer Price Index (CPI) declining to 6.5% in December after peaking at 9.1% in June. In addition to raising rates, the Fed commenced its balance sheet run-off during the reporting period, and while the central bank hasn’t directly sold any securities, it has set caps of $60 billion of U.S. Treasurys and $35 billion of agency mortgage-backed securities (MBS) each month. Performance was mixed across spread sectors, over the 12-month period. Corporate bonds produced positive excess returns following a rebound during the fourth quarter of 2022, as inflation began to moderate and investors became more optimistic that the Fed was getting closer to the end of its rate-hiking cycle. The reporting period was challenging for agency MBS, which continue to face technical headwinds as the Fed reduced the size of its balance sheet and rate volatility was elevated. The performance of asset-backed securities (ABS) was mixed over the period, with the sector overall slightly underperforming U.S. Treasury. While recessionary risks have increased and economic growth appears to be

slowing, the U.S. consumer remains in relative strong shape as the nation’s unemployment rate trickled down to 3.4% in January of 2023—the lowest level in more than 50 years.

An overweight allocation to and security selection in agency collateralized mortgage obligations contributed positively to Fund performance for the reporting period given that the sector has more predictable cash flows than to-be-announced (TBA) securities. Security selection within the agency MBS sector detracted from Fund performance for the period. Performance varied up and down the coupon stack, with higher-coupon MBS outperforming lower-coupon issues. The Fed primarily holds lower-coupon bonds, providing a technical headwind for this segment of the coupon stack. An allocation to agency commercial mortgage-backed securities (CMBS) weighed on Fund performance as the subsector underperformed duration-neutral Treasurys for the period. Wellington, the Fund’s subadvisor, continues to favor specified pools relative to TBA securities.

The Fund used derivatives on a limited basis during the reporting period. The Fund employed U.S. Treasury futures to manage yield-curve exposure and overall portfolio duration. The Fund used Treasury futures and TBA forward contracts to manage duration, yield-curve and market exposures (TBA forward contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS: FNMA, FHLMC and GNMA). Treasury futures had no material impact on Fund performance for the period. The Fund made selective use of mortgage derivatives, such as interest-only STRIPS (Separate Trading of Registered Interest and Principal of Securities), principal-only STRIPS and inverse floaters (a bond with a coupon rate that moves in the opposite direction of short-term interest rates). The yields on these securities are sensitive to the expected or anticipated rate of principal payments on the underlying assets; principal payments may have a material effect on their yields. These instruments are purchased only when rigorous stress-testing and analysis suggest that a higher return can be earned at a similar or lower risk compared to non-derivative securities.

Investing is subject to risk, including the possible loss of principal. Past performance is not an indication of future results.

8

SEI Daily Income Trust / Annual Report / January 31, 2023

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

January 31, 2023

GNMA Fund (Concluded)

GNMA Fund:

AVERAGE ANNUAL TOTAL RETURN1 | |||||

One Year | Annualized | Annualized | Annualized | Annualized | |

Class F | -7.23% | -2.44% | 0.02% | 0.79% | 4.99% |

Class Y | -6.99% | -2.19% | 0.28% | N/A | 0.52% |

Bloomberg GNMA Index | -6.69% | -2.14% | 0.36% | 0.98% | 0.56% |

Comparison of Change in the Value of a $10,000 Investment in the GNMA Fund, Class F and Class Y, versus the Bloomberg GNMA Index.

1 | For the periods ended January 31, 2023. Past performance is no indication of future performance. Class F Shares were offered beginning 3/20/87. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Class Y Shares were offered beginning 10/30/15. |

N/A — Not Available.

SEI Daily Income Trust / Annual Report / January 31, 2023

9

Definition of Indices*

Bloomberg Short U.S. Treasury 9-12 Month Index is a widely-recognized, market weighted index of U.S. Treasury Bonds with remaining maturities between nine and twelve months.

ICE BofA 1-3 Year U.S. Treasury Index is a widely-recognized, unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than 3 years.

Bloomberg GNMA Index is a widely-recognized, capitalization-weighted index of 15-30 year fixed-rate securities backed by mortgage pools of GNMA.

Bloomberg Commodity Total Return Index comprises futures contracts and tracks the performance of a fully collateralized investment in the index. This combines the returns of the index with the returns on cash collateral invested in 13-week (three-month) U.S. Treasury bills.

Bloomberg 1-10 Year U.S. TIPS Index measures the performance of inflation-protected public obligations of the U.S. Treasury that have a remaining maturity of 1 to 10 years.

Bloomberg U.S. Corporate Investment Grade Index includes publicly issued, fixed-rate, nonconvertible investment-grade (rated BBB- or higher by S&P Global Ratings and Fitch Ratings or Baa3 or higher by Moody’s Investors Service) dollar-denominated, U.S. Securities and Exchange (SEC)-registered corporate debt having at least one year to maturity.

Bloomberg U.S. Government Bond Index tracks the performance of U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury.

ICE BofA U.S. High Yield Constrained Index is a market capitalization-weighted index which tracks the performance of U.S. dollar-denominated below-investment-grade (rated BB+ or lower by S&P Global Ratings and Fitch Ratings or Ba1 or lower by Moody’s Investors Service) corporate debt publicly issued in the U.S. domestic market.

* | An Index measures the market price of a specific group of securities in a particular market sector. You cannot invest directly in an index. An index does not have an investment adviser and does not pay any commissions or expenses. If an index had expenses, its performance would be lower. |

10

SEI Daily Income Trust / Annual Report / January 31, 2023

SCHEDULE OF INVESTMENTS

January 31, 2023

Government Fund

† | Percentages are based on total investments. |

Description | Face Amount | Value | ||||||

U.S. GOVERNMENT AGENCY OBLIGATIONS — 41.9% | ||||||||

FFCB | ||||||||

4.365%, U.S. SOFR + 0.055%, 02/09/2023 (A) | $ | 50,000 | $ | 50,000 | ||||

4.360%, U.S. SOFR + 0.050%, 02/17/2023 (A) | 35,350 | 35,350 | ||||||

4.350%, U.S. SOFR + 0.040%, 03/10/2023 (A) | 24,905 | 24,905 | ||||||

4.325%, U.S. SOFR + 0.015%, 05/16/2023 (A) | 64,290 | 64,290 | ||||||

2.250%, 06/07/2023 | 17,040 | 17,040 | ||||||

4.345%, U.S. SOFR + 0.035%, 07/12/2023 (A) | 6,900 | 6,900 | ||||||

4.360%, U.S. SOFR + 0.050%, 07/20/2023 (A) | 69,555 | 69,555 | ||||||

4.340%, U.S. SOFR + 0.030%, 07/25/2023 (A) | 35,165 | 35,164 | ||||||

4.360%, U.S. SOFR + 0.050%, 08/22/2023 (A) | 45,640 | 45,640 | ||||||

4.355%, U.S. SOFR + 0.045%, 10/16/2023 (A) | 56,020 | 56,020 | ||||||

4.370%, U.S. SOFR + 0.060%, 11/22/2023 (A) | 58,535 | 58,535 | ||||||

4.365%, U.S. SOFR + 0.055%, 01/10/2024 (A) | 9,660 | 9,660 | ||||||

4.360%, U.S. SOFR + 0.050%, 05/09/2024 (A) | 59,285 | 59,285 | ||||||

4.400%, U.S. SOFR + 0.090%, 08/26/2024 (A) | 77,740 | 77,740 | ||||||

4.450%, U.S. SOFR + 0.140%, 11/07/2024 (A) | 51,805 | 51,805 | ||||||

4.480%, U.S. SOFR + 0.170%, 01/23/2025 (A) | 16,755 | 16,755 | ||||||

FFCB DN (B) | ||||||||

1.823%, 02/01/2023 | 54,040 | 54,040 | ||||||

4.383%, 03/16/2023 | 27,765 | 27,622 | ||||||

FHLB | ||||||||

4.350%, U.S. SOFR + 0.040%, 02/10/2023 (A) | 100,000 | 100,000 | ||||||

3.410%, 02/10/2023 | 41,925 | 41,925 | ||||||

2.080%, 02/13/2023 | 94,765 | 94,765 | ||||||

4.340%, U.S. SOFR + 0.030%, 03/02/2023 (A) | 132,480 | 132,480 | ||||||

4.325%, U.S. SOFR + 0.015%, 03/02/2023 (A) | 59,970 | 59,970 | ||||||

4.365%, U.S. SOFR + 0.055%, 03/10/2023 (A) | 115,380 | 115,380 | ||||||

Description | Face Amount | Value | ||||||

U.S. GOVERNMENT AGENCY OBLIGATIONS (continued) | ||||||||

4.330%, U.S. SOFR + 0.020%, 03/13/2023 (A) | $ | 168,800 | $ | 168,800 | ||||

4.350%, U.S. SOFR + 0.040%, 03/23/2023 (A) | 150,000 | 150,000 | ||||||

4.320%, U.S. SOFR + 0.010%, 03/23/2023 (A) | 128,950 | 128,950 | ||||||

4.380%, U.S. SOFR + 0.070%, 03/27/2023 (A) | 41,595 | 41,595 | ||||||

4.380%, U.S. SOFR + 0.070%, 03/28/2023 (A) | 14,910 | 14,910 | ||||||

4.320%, U.S. SOFR + 0.010%, 04/05/2023 (A) | 50,000 | 50,000 | ||||||

4.370%, U.S. SOFR + 0.060%, 04/10/2023 (A) | 85,620 | 85,620 | ||||||

4.370%, U.S. SOFR + 0.060%, 04/18/2023 (A) | 197,440 | 197,440 | ||||||

4.340%, U.S. SOFR + 0.030%, 04/25/2023 (A) | 133,500 | 133,500 | ||||||

4.330%, U.S. SOFR + 0.020%, 05/02/2023 (A) | 15,860 | 15,860 | ||||||

4.350%, U.S. SOFR + 0.040%, 05/03/2023 (A) | 104,800 | 104,800 | ||||||

4.340%, U.S. SOFR + 0.030%, 05/09/2023 (A) | 171,300 | 171,300 | ||||||

4.340%, U.S. SOFR + 0.030%, 05/11/2023 (A) | 75,665 | 75,665 | ||||||

4.340%, U.S. SOFR + 0.030%, 05/17/2023 (A) | 146,875 | 146,875 | ||||||

4.400%, U.S. SOFR + 0.090%, 05/23/2023 (A) | 57,685 | 57,685 | ||||||

4.350%, U.S. SOFR + 0.040%, 05/26/2023 (A) | 155,200 | 155,200 | ||||||

4.360%, U.S. SOFR + 0.050%, 06/02/2023 (A) | 124,610 | 124,610 | ||||||

4.365%, U.S. SOFR + 0.055%, 07/03/2023 (A) | 26,685 | 26,685 | ||||||

3.450%, 09/25/2023 | 52,460 | 52,453 | ||||||

4.390%, U.S. SOFR + 0.080%, 01/24/2024 (A) | 140,000 | 140,000 | ||||||

FHLB DN (B) | ||||||||

1.825%, 02/02/2023 | 169,740 | 169,731 | ||||||

4.260%, 02/15/2023 | 128,510 | 128,299 | ||||||

0.000%, 05/03/2023 | 100,000 | 98,825 | ||||||

Total U.S. Government Agency Obligations | ||||||||

(Cost $3,743,629) ($ Thousands) | 3,743,629 | |||||||

U.S. TREASURY OBLIGATIONS — 6.1% | ||||||||

U.S. Treasury Bills (B) | ||||||||

1.158%, 02/23/2023 | 41,115 | 41,086 | ||||||

3.527%, 03/16/2023 | 119,915 | 119,419 | ||||||

4.377%, 03/21/2023 | 109,900 | 109,268 | ||||||

SEI Daily Income Trust / Annual Report / January 31, 2023

11

SCHEDULE OF INVESTMENTS

January 31, 2023

Government Fund (Concluded)

Description | Face Amount | Value | ||||||

U.S. TREASURY OBLIGATIONS (continued) | ||||||||

0.000%, 05/04/2023 | $ | 29,925 | $ | 29,577 | ||||

2.146%, 05/18/2023 | 52,955 | 52,627 | ||||||

4.561%, 11/30/2023 | 19,875 | 19,147 | ||||||

U.S. Treasury Notes | ||||||||

0.125%, 04/30/2023 | 15,855 | 15,780 | ||||||

4.789%, US Treasury 3 Month Bill Money Market Yield + 0.140%, 10/31/2024 (A) | 68,445 | 68,445 | ||||||

4.849%, US Treasury 3 Month Bill Money Market Yield + 0.200%, 01/31/2025 (A) | 90,000 | 90,000 | ||||||

Total U.S. Treasury Obligations | ||||||||

(Cost $545,349) ($ Thousands) | 545,349 | |||||||

REPURCHASE AGREEMENTS — 49.9% | ||||||||

Barclays Bank | ||||||||

4.300%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $450,053,750 (collateralized by U.S. Treasury Obligations, ranging in par value $217,253,100 - $266,857,000, 0.750% - 3.500%, 09/15/2025 - 05/31/2026, with a total market value of $459,000,456) (C) | 450,000 | 450,000 | ||||||

BNP Paribas | ||||||||

4.270%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $450,053,375 (collateralized by U.S. Treasury Obligations, ranging in par value $5 - $162,387,000, 0.000% - 3.880%, 01/15/2026 - 11/15/2047, with a total market value of $450,053,375) (C) | 450,000 | 450,000 | ||||||

BOFA Securities | ||||||||

4.300%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $505,060,319 (collateralized by various FHLMC Obligations, ranging in par value $7,936,770 - $104,556,825, 1.500% - 7.000%, 05/01/2042 - 02/01/2053, with a total market value of $520,150,000) (C) | 505,000 | 505,000 | ||||||

Citigroup Global Markets | ||||||||

4.270%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $750,088,958 (collateralized by U.S. Obligations, ranging in par value $100 - $360,288,900, 0.750% - 5.500%, 05/31/2028 - 03/02/2157, with a total market value of $765,000,018) (C) | 750,000 | 750,000 | ||||||

Description | Face Amount | Value | ||||||

REPURCHASE AGREEMENTS (continued) | ||||||||

Citigroup Global Markets | ||||||||

4.310%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $5,000,599 (collateralized by GNMA Obligations, ranging in par value $1,000 - $5,866,759, 2.500% - 4.500%, 03/15/2052 - 04/20/2052, with a total market value of $5,100,967) (C) | $ | 5,000 | $ | 5,000 | ||||

Goldman Sachs | ||||||||

4.310%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $460,055,072 (collateralized by U.S. Treasury Obligations, ranging in par value $65,621 - $792,637,440, 2.000% - 6.000%, 04/20/2032 - 06/15/2057, with a total market value of $469,200,000) (C) | 460,000 | 460,000 | ||||||

Goldman Sachs | ||||||||

4.270%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $150,017,792 (collateralized by U.S. Obligations, ranging in par value $200 - $125,547,200, 0.250% - 2.880%, 05/31/2023 - 05/15/2052, with a total market value of $153,000,075) (C) | 150,000 | 150,000 | ||||||

J.P. Morgan Securities | ||||||||

4.290%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $120,014,300 (collateralized by U.S. Treasury Obligation, par value $109,948,700, 4.380%, 02/15/2038, with a total market value of $122,400,029) (C) | 120,000 | 120,000 | ||||||

Mizuho Securities | ||||||||

4.300%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $2,000,239 (collateralized by U.S. Treasury Obligations, ranging in par value $1,052,800 - $1,121,600, 0.250% - 2.250%, 11/15/2024 - 07/31/2025, with a total market value of $2,040,020) (C) | 2,000 | 2,000 | ||||||

MUFG Securities Americas | ||||||||

4.270%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $150,017,792 (collateralized by U.S. Treasury Obligations, ranging in par value $200 - $63,827,300, 0.630% - 5.380%, 11/15/2024 - 02/15/2036, with a total market value of $153,000,003) (C) | 150,000 | 150,000 | ||||||

12

SEI Daily Income Trust / Annual Report / January 31, 2023

SCHEDULE OF INVESTMENTS

January 31, 2023

Government Fund (Concluded)

Description | Face Amount | Value | ||||||

REPURCHASE AGREEMENTS (continued) | ||||||||

Natixis S.A. | ||||||||

4.270%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $750,088,958 (collateralized by U.S. Treasury Obligations, ranging in par value $100 - $190,000,000, 0.000% - 5.380%, 03/09/2023 - 11/15/2052, with a total market value of $765,000,005) (C) | $ | 750,000 | $ | 750,000 | ||||

TD Securities | ||||||||

4.310%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $112,013,409 (collateralized by U.S. Treasury Obligations, ranging in par value $408,400 - $26,047,600, 0.130% - 2.750%, 02/15/2023 - 11/15/2031, with a total market value of $114,240,036) (C) | 112,000 | 112,000 | ||||||

TD Securities | ||||||||

4.290%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $10,001,192 (collateralized by U.S. Treasury Obligations, ranging in par value $2,096,900 - $3,033,200, 1.500% - 3.880%, 02/15/2026 - 11/30/2027, with a total market value of $10,200,015) (C) | 10,000 | 10,000 | ||||||

The Bank of Nova Scotia | ||||||||

4.270%, dated 01/31/23, to be repurchased on 02/01/23, repurchase price $551,065,355 (collateralized by U.S. Treasury Obligations, ranging in par value $152,650,000 - $562,086,725, 0.000% - 4.250%, 02/28/2023 - 05/15/2052, with a total market value of $562,086,725) (C) | 551,000 | 551,000 | ||||||

Total Repurchase Agreements | ||||||||

(Cost $4,465,000) ($ Thousands) | 4,465,000 | |||||||

Total Investments — 97.9% | ||||||||

(Cost $8,753,978) ($ Thousands) | $ | 8,753,978 | ||||||

| Percentages are based on a Net Assets of $8,942,773 ($ Thousands). |

(A) | Variable or floating rate security. The rate shown is the effective interest rate as of period end. The rates on certain securities are not based on published reference rates and spreads and are |

(B) | The rate reported is the effective yield at time of purchase. |

(C) | Tri-Party Repurchase Agreement. |

As of January 31, 2023, all of the Fund's investments were considered Level 2, in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP. |

For more information on valuation inputs, see Note 2—Significant Accounting Policies in Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

SEI Daily Income Trust / Annual Report / January 31, 2023

13

SCHEDULE OF INVESTMENTS

January 31, 2023

Government II Fund

† | Percentages are based on total investments. |

Description | Face Amount | Value | ||||||

U.S. GOVERNMENT AGENCY OBLIGATIONS — 77.0% | ||||||||

FFCB | ||||||||

4.360%, U.S. SOFR + 0.050%, 02/17/2023 (A) | $ | 10,010 | $ | 10,010 | ||||

4.350%, U.S. SOFR + 0.040%, 03/10/2023 (A) | 8,140 | 8,140 | ||||||

4.325%, U.S. SOFR + 0.015%, 05/16/2023 (A) | 16,890 | 16,890 | ||||||

2.250%, 06/07/2023 | 2,930 | 2,930 | ||||||

4.345%, U.S. SOFR + 0.035%, 07/12/2023 (A) | 2,270 | 2,270 | ||||||

4.360%, U.S. SOFR + 0.050%, 07/20/2023 (A) | 22,455 | 22,455 | ||||||

4.340%, U.S. SOFR + 0.030%, 07/25/2023 (A) | 7,495 | 7,495 | ||||||

4.360%, U.S. SOFR + 0.050%, 08/22/2023 (A) | 16,340 | 16,340 | ||||||

4.355%, U.S. SOFR + 0.045%, 10/16/2023 (A) | 18,800 | 18,800 | ||||||

4.330%, U.S. SOFR + 0.020%, 11/15/2023 (A) | 7,790 | 7,788 | ||||||

4.370%, U.S. SOFR + 0.060%, 11/22/2023 (A) | 20,740 | 20,740 | ||||||

4.365%, U.S. SOFR + 0.055%, 01/10/2024 (A) | 3,165 | 3,165 | ||||||

4.360%, U.S. SOFR + 0.050%, 05/09/2024 (A) | 11,010 | 11,010 | ||||||

4.400%, U.S. SOFR + 0.090%, 08/26/2024 (A) | 18,510 | 18,510 | ||||||

4.450%, U.S. SOFR + 0.140%, 11/07/2024 (A) | 11,180 | 11,180 | ||||||

4.480%, U.S. SOFR + 0.170%, 01/23/2025 (A) | 3,245 | 3,245 | ||||||

FFCB DN (B) | ||||||||

1.823%, 02/01/2023 | 9,265 | 9,265 | ||||||

4.481%, 03/03/2023 | 50,000 | 49,815 | ||||||

4.077%, 03/31/2023 | 13,305 | 13,219 | ||||||

4.212%, 04/20/2023 | 14,000 | 13,875 | ||||||

FHLB | ||||||||

4.350%, U.S. SOFR + 0.040%, 02/10/2023 (A) | 26,120 | 26,120 | ||||||

3.410%, 02/10/2023 | 10,530 | 10,530 | ||||||

2.080%, 02/13/2023 | 16,060 | 16,060 | ||||||

4.350%, U.S. SOFR + 0.040%, 02/17/2023 (A) | 2,590 | 2,590 | ||||||

4.340%, U.S. SOFR + 0.030%, 03/02/2023 (A) | 100,000 | 100,000 | ||||||

4.325%, U.S. SOFR + 0.015%, 03/02/2023 (A) | 41,170 | 41,170 | ||||||

Description | Face Amount | Value | ||||||

U.S. GOVERNMENT AGENCY OBLIGATIONS (continued) | ||||||||

4.365%, U.S. SOFR + 0.055%, 03/10/2023 (A) | $ | 23,490 | $ | 23,490 | ||||

4.320%, U.S. SOFR + 0.010%, 03/23/2023 (A) | 22,270 | 22,270 | ||||||

4.380%, U.S. SOFR + 0.070%, 03/27/2023 (A) | 8,605 | 8,605 | ||||||

4.370%, U.S. SOFR + 0.060%, 04/18/2023 (A) | 20,280 | 20,280 | ||||||

4.330%, U.S. SOFR + 0.020%, 05/02/2023 (A) | 4,165 | 4,165 | ||||||

4.350%, U.S. SOFR + 0.040%, 05/03/2023 (A) | 16,545 | 16,545 | ||||||

4.340%, U.S. SOFR + 0.030%, 05/11/2023 (A) | 14,770 | 14,770 | ||||||

4.340%, U.S. SOFR + 0.030%, 05/17/2023 (A) | 28,525 | 28,525 | ||||||

4.360%, U.S. SOFR + 0.050%, 06/02/2023 (A) | 23,730 | 23,730 | ||||||

3.450%, 09/25/2023 | 12,585 | 12,583 | ||||||

4.390%, U.S. SOFR + 0.080%, 01/24/2024 (A) | 13,450 | 13,450 | ||||||

FHLB DN (B) | ||||||||

1.825%, 02/02/2023 | 30,260 | 30,258 | ||||||

4.288%, 02/15/2023 | 175,000 | 174,710 | ||||||

4.331%, 02/17/2023 | 68,000 | 67,870 | ||||||

4.400%, 02/22/2023 | 50,000 | 49,873 | ||||||

4.404%, 02/24/2023 | 50,000 | 49,860 | ||||||

4.440%, 03/01/2023 | 75,000 | 74,743 | ||||||

4.397%, 03/07/2023 | 40,000 | 39,836 | ||||||

4.513%, 03/15/2023 | 35,805 | 35,618 | ||||||

4.484%, 03/22/2023 | 50,000 | 49,698 | ||||||

4.556%, 03/24/2023 | 100,000 | 99,359 | ||||||

4.654%, 04/19/2023 | 25,000 | 24,754 | ||||||

0.000%, 05/03/2023 | 31,000 | 30,636 | ||||||

Total U.S. Government Agency Obligations | ||||||||

(Cost $1,379,240) ($ Thousands) | 1,379,240 | |||||||

U.S. TREASURY OBLIGATIONS — 28.8% | ||||||||

U.S. Treasury Bills (B) | ||||||||

4.104%, 02/02/2023 | 15,000 | 14,998 | ||||||

4.131%, 02/09/2023 | 45,000 | 44,959 | ||||||

4.346%, 02/14/2023 | 22,000 | 21,966 | ||||||

4.056%, 02/21/2023 | 31,805 | 31,734 | ||||||

1.158%, 02/23/2023 | 10,825 | 10,817 | ||||||

4.336%, 03/07/2023 | 50,000 | 49,798 | ||||||

4.496%, 03/14/2023 | 50,000 | 49,746 | ||||||

4.483%, 03/21/2023 | 57,915 | 57,572 | ||||||

4.557%, 03/28/2023 | 40,000 | 39,724 | ||||||

4.496%, 04/04/2023 | 25,000 | 24,809 | ||||||

4.629%, 04/27/2023 | 45,000 | 44,514 | ||||||

0.000%, 05/04/2023 | 50,000 | 49,419 | ||||||

14

SEI Daily Income Trust / Annual Report / January 31, 2023

SCHEDULE OF INVESTMENTS

January 31, 2023

Government II Fund (Concluded)

Description | Face Amount | Value | ||||||

U.S. TREASURY OBLIGATIONS (continued) | ||||||||

2.146%, 05/18/2023 | $ | 8,565 | $ | 8,512 | ||||

4.561%, 11/30/2023 | 3,920 | 3,776 | ||||||

U.S. Treasury Notes | ||||||||

2.000%, 02/15/2023 | 20,000 | 19,983 | ||||||

0.125%, 03/31/2023 | 16,840 | 16,802 | ||||||

0.125%, 04/30/2023 | 2,790 | 2,777 | ||||||

4.634%, US Treasury 3 Month Bill Money Market Yield + -0.015%, 01/31/2024 (A) | 955 | 955 | ||||||

4.686%, US Treasury 3 Month Bill Money Market Yield + 0.037%, 07/31/2024 (A) | 8,000 | 7,994 | ||||||

4.789%, US Treasury 3 Month Bill Money Market Yield + 0.140%, 10/31/2024 (A) | 14,340 | 14,340 | ||||||

Total U.S. Treasury Obligations | ||||||||

(Cost $515,195) ($ Thousands) | 515,195 | |||||||

Total Investments — 105.8% | ||||||||

(Cost $1,894,435) ($ Thousands) | $ | 1,894,435 | ||||||

| Percentages are based on a Net Assets of $1,790,974 ($ Thousands). |

(A) | Variable or floating rate security. The rate shown is the effective interest rate as of period end. The rates on certain securities are not based on published reference rates and spreads and are |

(B) | The rate reported is the effective yield at time of purchase. |

As of January 31, 2023, all of the Fund's investments were considered Level 2, in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP. |

For more information on valuation inputs, see Note 2—Significant Accounting Policies in Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

SEI Daily Income Trust / Annual Report / January 31, 2023

15

SCHEDULE OF INVESTMENTS

January 31, 2023

Treasury II Fund

† | Percentages are based on total investments. |

Description | Face Amount | Value | ||||||

U.S. TREASURY OBLIGATIONS — 102.9% | ||||||||

U.S. Treasury Bills (A) | ||||||||

4.104%, 02/02/2023 | $ | 1,000 | $ | 1,000 | ||||

3.976%, 02/07/2023 | 28,600 | 28,581 | ||||||

4.080%, 02/14/2023 | 48,000 | 47,930 | ||||||

4.049%, 02/21/2023 | 82,195 | 82,012 | ||||||

1.158%, 02/23/2023 | 2,000 | 1,999 | ||||||

4.278%, 02/28/2023 | 25,000 | 24,920 | ||||||

4.339%, 03/07/2023 | 32,530 | 32,399 | ||||||

4.496%, 03/14/2023 | 30,000 | 29,847 | ||||||

3.527%, 03/16/2023 | 6,585 | 6,558 | ||||||

4.460%, 03/21/2023 | 22,000 | 21,871 | ||||||

4.557%, 03/28/2023 | 74,000 | 73,488 | ||||||

4.398%, 03/30/2023 | 10,000 | 9,931 | ||||||

4.496%, 04/04/2023 | 11,210 | 11,124 | ||||||

4.613%, 04/13/2023 | 25,000 | 24,775 | ||||||

4.511%, 04/18/2023 | 3,565 | 3,531 | ||||||

4.629%, 04/27/2023 | 30,000 | 29,676 | ||||||

0.000%, 05/04/2023 | 15,000 | 14,826 | ||||||

2.146%, 05/18/2023 | 1,850 | 1,839 | ||||||

4.561%, 11/30/2023 | 1,180 | 1,137 | ||||||

U.S. Treasury Notes | ||||||||

2.000%, 02/15/2023 | 20,000 | 19,983 | ||||||

0.125%, 03/31/2023 | 3,375 | 3,367 | ||||||

4.683%, US Treasury 3 Month Bill Money Market Yield + 0.034%, 04/30/2023 (B) | 3,100 | 3,100 | ||||||

0.125%, 04/30/2023 | 640 | 637 | ||||||

4.678%, US Treasury 3 Month Bill Money Market Yield + 0.029%, 07/31/2023 (B) | 10,035 | 10,037 | ||||||

4.574%, US Treasury 3 Month Bill Money Market Yield + -0.075%, 04/30/2024 (B) | 5,890 | 5,885 | ||||||

4.686%, US Treasury 3 Month Bill Money Market Yield + 0.037%, 07/31/2024 (B) | 3,000 | 2,998 | ||||||

4.789%, US Treasury 3 Month Bill Money Market Yield + 0.140%, 10/31/2024 (B) | 14,725 | 14,710 | ||||||

Total U.S. Treasury Obligations | ||||||||

(Cost $508,161) ($ Thousands) | 508,161 | |||||||

Total Investments — 102.9% | ||||||||

(Cost $508,161) ($ Thousands) | $ | 508,161 | ||||||

| Percentages are based on a Net Assets of $494,060 ($ Thousands). |

(A) | The rate reported is the effective yield at time of purchase. |

(B) | Variable or floating rate security. The rate shown is the effective interest rate as of period end. The rates on certain securities are not based on published reference rates and spreads and are |

As of January 31, 2023, all of the Fund's investments were considered Level 2, in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP. |

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

16

SEI Daily Income Trust / Annual Report / January 31, 2023

SCHEDULE OF INVESTMENTS

January 31, 2023

Ultra Short Duration Bond Fund

† | Percentages are based on total investments. Total investments exclude options, futures contracts, forward contracts, and swap contracts, if applicable. |

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS — 37.6% | ||||||||

Communication Services — 2.0% | ||||||||

AT&T | ||||||||

9.150%, 02/01/2023 | $ | 600 | $ | 600 | ||||

4.970%, SOFRINDX + 0.640%, 03/25/2024 (A) | 650 | 650 | ||||||

NTT Finance | ||||||||

0.373%, 03/03/2023 (B) | 1,950 | 1,943 | ||||||

Take-Two Interactive Software | ||||||||

3.300%, 03/28/2024 | 525 | 515 | ||||||

Verizon Communications | ||||||||

5.119%, SOFRINDX + 0.790%, 03/20/2026 (A) | 500 | 498 | ||||||

4.829%, SOFRINDX + 0.500%, 03/22/2024 (A) | 500 | 499 | ||||||

Warnermedia Holdings | ||||||||

3.428%, 03/15/2024 (B) | 750 | 734 | ||||||

| 5,439 | ||||||||

Consumer Discretionary — 3.0% | ||||||||

7-Eleven | ||||||||

0.625%, 02/10/2023 (B) | 360 | 360 | ||||||

American Honda Finance MTN | ||||||||

0.875%, 07/07/2023 | 300 | 295 | ||||||

Daimler Truck Finance North America LLC | ||||||||

5.331%, U.S. SOFR + 1.000%, 04/05/2024 (A)(B) | 450 | 450 | ||||||

5.068%, U.S. SOFR + 0.750%, 12/13/2024 (A)(B) | 600 | 597 | ||||||

General Motors Financial | ||||||||

5.038%, U.S. SOFR + 0.760%, 03/08/2024 (A) | 500 | 496 | ||||||

4.951%, U.S. SOFR + 0.620%, 10/15/2024 (A) | 2,895 | 2,847 | ||||||

4.250%, 05/15/2023 | 525 | 524 | ||||||

Home Depot | ||||||||

4.000%, 09/15/2025 | 45 | 45 | ||||||

Howard University | ||||||||

2.801%, 10/01/2023 | 380 | 374 | ||||||

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Hyatt Hotels | ||||||||

1.300%, 10/01/2023 | $ | 175 | $ | 170 | ||||

Hyundai Capital America MTN | ||||||||

0.800%, 04/03/2023 (B) | 450 | 447 | ||||||

Nordstrom | ||||||||

2.300%, 04/08/2024 | 210 | 199 | ||||||

Starbucks | ||||||||

4.551%, SOFRINDX + 0.420%, 02/14/2024 (A) | 345 | 344 | ||||||

Volkswagen Group of America Finance LLC | ||||||||

3.125%, 05/12/2023 (B) | 1,275 | 1,269 | ||||||

| 8,417 | ||||||||

Consumer Staples — 1.7% | ||||||||

Coca-Cola Europacific Partners PLC | ||||||||

0.500%, 05/05/2023 (B) | 975 | 964 | ||||||

Conagra Brands | ||||||||

0.500%, 08/11/2023 | 325 | 317 | ||||||

Constellation Brands | ||||||||

3.600%, 05/09/2024 | 350 | 345 | ||||||

General Mills | ||||||||

5.241%, 11/18/2025 | 320 | 322 | ||||||

JDE Peet's | ||||||||

0.800%, 09/24/2024 (B) | 500 | 462 | ||||||

Keurig Dr Pepper | ||||||||

0.750%, 03/15/2024 | 2,010 | 1,920 | ||||||

Mondelez International | ||||||||

2.125%, 03/17/2024 | 290 | 282 | ||||||

| 4,612 | ||||||||

Energy — 1.9% | ||||||||

ConocoPhillips | ||||||||

2.125%, 03/08/2024 | 450 | 438 | ||||||

Enbridge | ||||||||

4.787%, SOFRINDX + 0.630%, 02/16/2024 (A) | 775 | 772 | ||||||

Energy Transfer | ||||||||

5.875%, 01/15/2024 | 1,370 | 1,376 | ||||||

EQT | ||||||||

5.678%, 10/01/2025 | 305 | 305 | ||||||

Pioneer Natural Resources | ||||||||

0.550%, 05/15/2023 | 830 | 820 | ||||||

Saudi Arabian Oil | ||||||||

1.250%, 11/24/2023 (B) | 200 | 193 | ||||||

Saudi Arabian Oil MTN | ||||||||

2.875%, 04/16/2024 (B) | 1,230 | 1,198 | ||||||

| 5,102 | ||||||||

Financials — 16.1% | ||||||||

American Express | ||||||||

3.950%, 08/01/2025 | 325 | 320 | ||||||

3.375%, 05/03/2024 | 350 | 344 | ||||||

SEI Daily Income Trust / Annual Report / January 31, 2023

17

SCHEDULE OF INVESTMENTS

January 31, 2023

Ultra Short Duration Bond Fund (Continued)

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

0.750%, 11/03/2023 | $ | 2,005 | $ | 1,948 | ||||

Athene Global Funding | ||||||||

4.902%, SOFRINDX + 0.700%, 05/24/2024 (A)(B) | 825 | 818 | ||||||

Banco Santander | ||||||||

3.892%, 05/24/2024 | 400 | 394 | ||||||

Bank of America | ||||||||

5.080%, U.S. SOFR + 1.290%, 01/20/2027 (A) | 275 | 276 | ||||||

5.022%, U.S. SOFR + 0.690%, 04/22/2025 (A) | 650 | 646 | ||||||

Bank of America MTN | ||||||||

4.992%, U.S. SOFR + 0.660%, 02/04/2025 (A) | 510 | 507 | ||||||

4.963%, BSBY3M + 0.430%, 05/28/2024 (A) | 575 | 572 | ||||||

1.486%, U.S. SOFR + 1.460%, 05/19/2024 (A) | 300 | 297 | ||||||

Bank of Montreal | ||||||||

4.628%, SOFRINDX + 0.350%, 12/08/2023 (A) | 600 | 599 | ||||||

Bank of Montreal MTN | ||||||||

4.938%, SOFRINDX + 0.620%, 09/15/2026 (A) | 675 | 661 | ||||||

4.651%, SOFRINDX + 0.320%, 07/09/2024 (A) | 325 | 324 | ||||||

Bank of Nova Scotia | ||||||||

4.564%, U.S. SOFR + 0.380%, 07/31/2024 (A) | 650 | 648 | ||||||

Banque Federative du Credit Mutuel | ||||||||

4.935%, 01/26/2026 (B) | 350 | 350 | ||||||

4.524%, 07/13/2025 (B) | 250 | 247 | ||||||

BPCE | ||||||||

5.029%, 01/15/2025 (B) | 345 | 345 | ||||||

Brighthouse Financial Global Funding MTN | ||||||||

5.091%, U.S. SOFR + 0.760%, 04/12/2024 (A)(B) | 445 | 443 | ||||||

Canadian Imperial Bank of Commerce | ||||||||

5.129%, U.S. SOFR + 0.800%, 03/17/2023 (A) | 500 | 500 | ||||||

4.711%, SOFRINDX + 0.400%, 12/14/2023 (A) | 575 | 575 | ||||||

Capital One Financial | ||||||||

4.985%, U.S. SOFR + 2.160%, 07/24/2026 (A) | 250 | 248 | ||||||

4.968%, U.S. SOFR + 0.690%, 12/06/2024 (A) | 425 | 421 | ||||||

Citigroup | ||||||||

5.026%, U.S. SOFR + 0.694%, 01/25/2026 (A) | 350 | 346 | ||||||

5.001%, U.S. SOFR + 0.669%, 05/01/2025 (A) | 250 | 248 | ||||||

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Citizens Bank | ||||||||

4.119%, U.S. SOFR + 1.395%, 05/23/2025 (A) | $ | 250 | $ | 246 | ||||

CNA Financial | ||||||||

7.250%, 11/15/2023 | 200 | 203 | ||||||

Commonwealth Bank of Australia | ||||||||

4.838%, U.S. SOFR + 0.520%, 06/15/2026 (A)(B) | 425 | 420 | ||||||

Corebridge Financial | ||||||||

3.500%, 04/04/2025 (B) | 230 | 222 | ||||||

Corebridge Global Funding | ||||||||

0.800%, 07/07/2023 (B) | 315 | 309 | ||||||

Credit Suisse NY | ||||||||

4.750%, 08/09/2024 | 250 | 245 | ||||||

4.722%, SOFRINDX + 0.390%, 02/02/2024 (A) | 2,280 | 2,229 | ||||||

0.520%, 08/09/2023 | 650 | 629 | ||||||

Danske Bank | ||||||||

6.466%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 2.100%, 01/09/2026 (A)(B) | 350 | 355 | ||||||

Deutsche Bank NY | ||||||||

5.376%, U.S. SOFR + 1.219%, 11/16/2027 (A) | 550 | 519 | ||||||

4.605%, U.S. SOFR + 0.500%, 11/08/2023 (A) | 600 | 598 | ||||||

DNB Bank | ||||||||

2.968%, SOFRINDX + 0.810%, 03/28/2025 (A)(B) | 275 | 267 | ||||||

Equitable Financial Life Global Funding | ||||||||

5.500%, 12/02/2025 (B) | 300 | 303 | ||||||

4.721%, U.S. SOFR + 0.390%, 04/06/2023 (A)(B) | 575 | 575 | ||||||

Fifth Third Bank | ||||||||

5.852%, U.S. SOFR + 1.230%, 10/27/2025 (A) | 470 | 477 | ||||||

GA Global Funding Trust | ||||||||

4.795%, U.S. SOFR + 0.500%, 09/13/2024 (A)(B) | 1,745 | 1,701 | ||||||

Goldman Sachs Group | ||||||||

5.032%, U.S. SOFR + 0.700%, 01/24/2025 (A) | 425 | 423 | ||||||

4.789%, U.S. SOFR + 0.500%, 09/10/2024 (A) | 250 | 249 | ||||||

3.200%, 02/23/2023 | 1,315 | 1,314 | ||||||

HSBC Bank Canada | ||||||||

0.950%, 05/14/2023 (B) | 2,775 | 2,744 | ||||||

HSBC Holdings PLC | ||||||||

7.336%, U.S. SOFR + 3.030%, 11/03/2026 (A) | 300 | 317 | ||||||

4.752%, U.S. SOFR + 0.580%, 11/22/2024 (A) | 425 | 418 | ||||||

18

SEI Daily Income Trust / Annual Report / January 31, 2023

SCHEDULE OF INVESTMENTS

January 31, 2023

Ultra Short Duration Bond Fund (Continued)

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Huntington National Bank | ||||||||

4.008%, U.S. SOFR + 1.205%, 05/16/2025 (A) | $ | 250 | $ | 246 | ||||

Jackson Financial | ||||||||

1.125%, 11/22/2023 | 425 | 411 | ||||||

JPMorgan Chase | ||||||||

5.217%, U.S. SOFR + 0.885%, 04/22/2027 (A) | 650 | 640 | ||||||

4.909%, U.S. SOFR + 0.580%, 06/23/2025 (A) | 325 | 322 | ||||||

4.904%, U.S. SOFR + 0.580%, 03/16/2024 (A) | 500 | 500 | ||||||

4.774%, U.S. SOFR + 0.535%, 06/01/2025 (A) | 400 | 396 | ||||||

KeyBank | ||||||||

4.671%, SOFRINDX + 0.340%, 01/03/2024 (A) | 575 | 574 | ||||||

4.631%, SOFRINDX + 0.320%, 06/14/2024 (A) | 400 | 399 | ||||||

Macquarie Group MTN | ||||||||

5.041%, U.S. SOFR + 0.710%, 10/14/2025 (A)(B) | 425 | 419 | ||||||

Manufacturers & Traders Trust | ||||||||

5.400%, 11/21/2025 | 300 | 305 | ||||||

4.650%, 01/27/2026 | 460 | 459 | ||||||

MassMutual Global Funding II | ||||||||

4.691%, U.S. SOFR + 0.360%, 04/12/2024 (A)(B) | 400 | 400 | ||||||

MassMutual Global Funding II MTN | ||||||||

0.850%, 06/09/2023 (B) | 448 | 442 | ||||||

Mitsubishi UFJ Financial Group | ||||||||

4.788%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 1.700%, 07/18/2025 (A) | 325 | 323 | ||||||

Mizuho Financial Group | ||||||||

5.387%, ICE LIBOR USD 3 Month + 0.630%, 05/25/2024 (A) | 775 | 774 | ||||||

Morgan Stanley | ||||||||

5.050%, U.S. SOFR + 1.295%, 01/28/2027 (A) | 275 | 276 | ||||||

3.620%, U.S. SOFR + 1.160%, 04/17/2025 (A) | 350 | 344 | ||||||

0.731%, U.S. SOFR + 0.616%, 04/05/2024 (A) | 250 | 248 | ||||||

Morgan Stanley MTN | ||||||||

3.750%, 02/25/2023 | 2,170 | 2,168 | ||||||

National Bank of Canada | ||||||||

0.750%, 08/06/2024 | 325 | 306 | ||||||

Nationwide Building Society | ||||||||

0.550%, 01/22/2024 (B) | 400 | 382 | ||||||

NatWest Markets PLC | ||||||||

4.658%, U.S. SOFR + 0.530%, 08/12/2024 (A)(B) | 490 | 486 | ||||||

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Nordea Bank Abp | ||||||||

1.000%, 06/09/2023 (B) | $ | 300 | $ | 296 | ||||

Pacific Life Global Funding II | ||||||||

0.500%, 09/23/2023 (B) | 400 | 389 | ||||||

PNC Financial Services Group | ||||||||

5.671%, SOFRINDX + 1.090%, 10/28/2025 (A) | 425 | 431 | ||||||

Principal Life Global Funding II | ||||||||

4.781%, U.S. SOFR + 0.450%, 04/12/2024 (A)(B) | 170 | 169 | ||||||

4.584%, U.S. SOFR + 0.380%, 08/23/2024 (A)(B) | 665 | 658 | ||||||

Protective Life Global Funding | ||||||||

1.082%, 06/09/2023 (B) | 255 | 251 | ||||||

Royal Bank of Canada MTN | ||||||||

4.782%, SOFRINDX + 0.450%, 10/26/2023 (A) | 400 | 400 | ||||||

Skandinaviska Enskilda Banken | ||||||||

0.550%, 09/01/2023 (B) | 250 | 243 | ||||||

Societe Generale | ||||||||

5.382%, U.S. SOFR + 1.050%, 01/21/2026 (A)(B) | 425 | 417 | ||||||

4.351%, 06/13/2025 (B) | 500 | 492 | ||||||

Standard Chartered PLC | ||||||||

7.776%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 3.100%, 11/16/2025 (A)(B) | 300 | 313 | ||||||

6.170%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 2.050%, 01/09/2027 (A)(B) | 350 | 359 | ||||||

Sumitomo Mitsui Trust Bank MTN | ||||||||

4.751%, U.S. SOFR + 0.440%, 09/16/2024 (A)(B) | 500 | 498 | ||||||

Toronto-Dominion Bank MTN | ||||||||

4.879%, U.S. SOFR + 0.590%, 09/10/2026 (A) | 425 | 416 | ||||||

4.639%, U.S. SOFR + 0.350%, 09/10/2024 (A) | 500 | 498 | ||||||

4.606%, U.S. SOFR + 0.355%, 03/04/2024 (A) | 575 | 574 | ||||||

Truist Financial MTN | ||||||||

4.684%, U.S. SOFR + 0.400%, 06/09/2025 (A) | 400 | 395 | ||||||

UBS | ||||||||

0.700%, 08/09/2024 (B) | 400 | 375 | ||||||

UBS MTN | ||||||||

4.476%, U.S. SOFR + 0.360%, 02/09/2024 (A)(B) | 400 | 400 | ||||||

| 45,234 | ||||||||

Health Care — 4.1% | ||||||||

AmerisourceBergen | ||||||||

0.737%, 03/15/2023 | 200 | 199 | ||||||

SEI Daily Income Trust / Annual Report / January 31, 2023

19

SCHEDULE OF INVESTMENTS

January 31, 2023

Ultra Short Duration Bond Fund (Continued)

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Baxter International | ||||||||

4.658%, SOFRINDX + 0.440%, 11/29/2024 (A) | $ | 425 | $ | 418 | ||||

Bristol-Myers Squibb | ||||||||

0.537%, 11/13/2023 | 425 | 411 | ||||||

Cigna | ||||||||

3.750%, 07/15/2023 | 1,775 | 1,765 | ||||||

0.613%, 03/15/2024 | 190 | 181 | ||||||

CommonSpirit Health | ||||||||

4.200%, 08/01/2023 | 1,115 | 1,109 | ||||||

GE HealthCare Technologies | ||||||||

5.550%, 11/15/2024 (B) | 375 | 378 | ||||||

GSK Consumer Healthcare Capital US LLC | ||||||||

3.024%, 03/24/2024 | 420 | 410 | ||||||

Humana | ||||||||

0.650%, 08/03/2023 | 1,700 | 1,662 | ||||||

Illumina | ||||||||

5.800%, 12/12/2025 | 300 | 306 | ||||||

0.550%, 03/23/2023 | 400 | 398 | ||||||

PerkinElmer | ||||||||

0.550%, 09/15/2023 | 600 | 582 | ||||||

Royalty Pharma PLC | ||||||||

0.750%, 09/02/2023 | 700 | 682 | ||||||

SSM Health Care | ||||||||

3.688%, 06/01/2023 | 970 | 967 | ||||||

Stryker | ||||||||

0.600%, 12/01/2023 | 230 | 222 | ||||||

Thermo Fisher Scientific | ||||||||

4.861%, SOFRINDX + 0.530%, 10/18/2024 (A) | 1,810 | 1,805 | ||||||

| 11,495 | ||||||||

Industrials — 1.3% | ||||||||

AerCap Ireland Capital DAC / AerCap Global Aviation Trust | ||||||||

5.010%, U.S. SOFR + 0.680%, 09/29/2023 (A) | 700 | 696 | ||||||

Boeing | ||||||||

4.508%, 05/01/2023 | 1,245 | 1,243 | ||||||

1.950%, 02/01/2024 | 425 | 412 | ||||||

1.167%, 02/04/2023 | 475 | 475 | ||||||

Cargill | ||||||||

1.375%, 07/23/2023 (B) | 300 | 295 | ||||||

Carlisle | ||||||||

0.550%, 09/01/2023 | 175 | 171 | ||||||

DAE Funding LLC MTN | ||||||||

1.550%, 08/01/2024 (B) | 450 | 425 | ||||||

| 3,717 | ||||||||

Information Technology — 1.9% | ||||||||

Fidelity National Information Services | ||||||||

0.375%, 03/01/2023 | 425 | 424 | ||||||

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Hewlett Packard Enterprise | ||||||||

4.450%, 10/02/2023 | $ | 250 | $ | 249 | ||||

Microchip Technology | ||||||||

0.972%, 02/15/2024 | 375 | 359 | ||||||

Salesforce | ||||||||

0.625%, 07/15/2024 | 1,560 | 1,473 | ||||||

Skyworks Solutions | ||||||||

0.900%, 06/01/2023 | 855 | 842 | ||||||

TD SYNNEX | ||||||||

1.250%, 08/09/2024 | 650 | 611 | ||||||

VMware | ||||||||

1.000%, 08/15/2024 | 1,445 | 1,358 | ||||||

| 5,316 | ||||||||

Materials — 0.5% | ||||||||

Celanese US Holdings LLC | ||||||||

5.900%, 07/05/2024 | 325 | 327 | ||||||

Martin Marietta Materials | ||||||||

0.650%, 07/15/2023 | 480 | 470 | ||||||

Nutrien | ||||||||

5.900%, 11/07/2024 | 175 | 178 | ||||||

Sherwin-Williams | ||||||||

4.050%, 08/08/2024 | 250 | 247 | ||||||

| 1,222 | ||||||||

Real Estate — 0.1% | ||||||||

Realty Income | ||||||||

5.050%, 01/13/2026 | 350 | 351 | ||||||

Utilities — 5.0% | ||||||||

American Electric Power | ||||||||

5.294%, ICE LIBOR USD 3 Month + 0.480%, 11/01/2023 (A) | 1,060 | 1,056 | ||||||

Atmos Energy | ||||||||

0.625%, 03/09/2023 | 425 | 423 | ||||||

CenterPoint Energy | ||||||||

4.778%, SOFRINDX + 0.650%, 05/13/2024 (A) | 325 | 321 | ||||||

CenterPoint Energy Resources | ||||||||

5.279%, ICE LIBOR USD 3 Month + 0.500%, 03/02/2023 (A) | 368 | 368 | ||||||

Dominion Energy | ||||||||

5.299%, ICE LIBOR USD 3 Month + 0.530%, 09/15/2023 (A) | 1,445 | 1,447 | ||||||

Duke Energy | ||||||||

4.539%, U.S. SOFR + 0.250%, 06/10/2023 (A) | 500 | 499 | ||||||

Edison International | ||||||||

3.550%, 11/15/2024 | 275 | 268 | ||||||

Eversource Energy | ||||||||

2.800%, 05/01/2023 | 810 | 806 | ||||||

20

SEI Daily Income Trust / Annual Report / January 31, 2023

SCHEDULE OF INVESTMENTS

January 31, 2023

Ultra Short Duration Bond Fund (Continued)

Description | Face Amount | Market Value | ||||||

CORPORATE OBLIGATIONS (continued) | ||||||||

Mississippi Power | ||||||||

4.630%, U.S. SOFR + 0.300%, 06/28/2024 (A) | $ | 350 | $ | 345 | ||||

NextEra Energy Capital Holdings | ||||||||

4.779%, SOFRINDX + 0.540%, 03/01/2023 (A) | 375 | 375 | ||||||

4.733%, SOFRINDX + 0.400%, 11/03/2023 (A) | 705 | 704 | ||||||

2.940%, 03/21/2024 | 450 | 441 | ||||||

OGE Energy | ||||||||

0.703%, 05/26/2023 | 245 | 242 | ||||||

Pacific Gas and Electric | ||||||||

3.250%, 02/16/2024 | 350 | 343 | ||||||

1.700%, 11/15/2023 | 275 | 268 | ||||||

PPL Electric Utilities | ||||||||

4.974%, ICE LIBOR USD 3 Month + 0.250%, 09/28/2023 (A) | 875 | 872 | ||||||

4.659%, U.S. SOFR + 0.330%, 06/24/2024 (A) | 465 | 459 | ||||||

Public Service Enterprise Group | ||||||||

0.841%, 11/08/2023 | 2,370 | 2,293 | ||||||

Southern California Edison | ||||||||

5.161%, SOFRINDX + 0.830%, 04/01/2024 (A) | 960 | 959 | ||||||

Southern California Gas | ||||||||

5.103%, ICE LIBOR USD 3 Month + 0.350%, 09/14/2023 (A) | 970 | 968 | ||||||

Tampa Electric | ||||||||

3.875%, 07/12/2024 | 325 | 319 | ||||||

WEC Energy Group | ||||||||

4.750%, 01/09/2026 | 275 | 276 | ||||||

| 14,052 | ||||||||

Total Corporate Obligations | ||||||||

(Cost $106,358) ($ Thousands) | 104,957 | |||||||

ASSET-BACKED SECURITIES — 22.5% | ||||||||

Automotive — 10.9% | ||||||||

American Credit Acceptance Receivables Trust, Ser 2021-3, Cl B | ||||||||

0.660%, 02/13/2026 (B) | 76 | 76 | ||||||

American Credit Acceptance Receivables Trust, Ser 2021-4, Cl A | ||||||||

0.450%, 09/15/2025 (B) | 7 | 7 | ||||||

American Credit Acceptance Receivables Trust, Ser 2022-1, Cl A | ||||||||

0.990%, 12/15/2025 (B) | 135 | 134 | ||||||

American Credit Acceptance Receivables Trust, Ser 2022-2, Cl A | ||||||||

2.660%, 02/13/2026 (B) | 237 | 235 | ||||||

Description | Face Amount | Market Value | ||||||

ASSET-BACKED SECURITIES (continued) | ||||||||

American Credit Acceptance Receivables Trust, Ser 2023-1, Cl A | ||||||||

5.450%, 09/14/2026 (B) | $ | 435 | $ | 435 | ||||

AmeriCredit Automobile Receivables Trust, Ser 2019-3, Cl C | ||||||||

2.320%, 07/18/2025 | 422 | 416 | ||||||

ARI Fleet Lease Trust, Ser 2021-A, Cl A2 | ||||||||

0.370%, 03/15/2030 (B) | 73 | 72 | ||||||

Avid Automobile Receivables Trust, Ser 2021-1, Cl A | ||||||||

0.610%, 01/15/2025 (B) | 9 | 9 | ||||||

Capital One Prime Auto Receivables Trust, Ser 2022-2, Cl A2A | ||||||||

3.740%, 09/15/2025 | 565 | 560 | ||||||

Carmax Auto Owner Trust, Ser 2019-3, Cl C | ||||||||

2.600%, 06/16/2025 | 375 | 368 | ||||||

Carmax Auto Owner Trust, Ser 2021-1, Cl A3 | ||||||||

0.340%, 12/15/2025 | 630 | 607 | ||||||

Carmax Auto Owner Trust, Ser 2021-2, Cl A3 | ||||||||

0.520%, 02/17/2026 | 568 | 548 | ||||||

Carmax Auto Owner Trust, Ser 2022-3, Cl A2A | ||||||||

3.810%, 09/15/2025 | 547 | 542 | ||||||

CarMax Auto Owner Trust, Ser 2023-1, Cl A2A | ||||||||

5.230%, 01/15/2026 | 555 | 555 | ||||||

Carvana Auto Receivables Trust, Ser 2021-N1, Cl A | ||||||||

0.700%, 01/10/2028 | 573 | 536 | ||||||

Carvana Auto Receivables Trust, Ser 2021-N2, Cl A1 | ||||||||

0.320%, 03/10/2028 | 11 | 11 | ||||||

Carvana Auto Receivables Trust, Ser 2021-N2, Cl B | ||||||||

0.750%, 03/10/2028 | 80 | 73 | ||||||

Carvana Auto Receivables Trust, Ser 2021-N3, Cl B | ||||||||

0.660%, 06/12/2028 | 195 | 179 | ||||||

Carvana Auto Receivables Trust, Ser 2021-P3, Cl A2 | ||||||||

0.380%, 01/10/2025 | 56 | 56 | ||||||

CFMT LLC, Ser 2021-AL1, Cl B | ||||||||

1.390%, 09/22/2031 (B) | 383 | 365 | ||||||

Chesapeake Funding II LLC, Ser 2019-2A, Cl A1 | ||||||||

1.950%, 09/15/2031 (B) | 20 | 19 | ||||||

Chesapeake Funding II LLC, Ser 2021-1A, Cl A2 | ||||||||

4.684%, ICE LIBOR USD 1 Month + 0.230%, 04/15/2033 (A)(B) | 147 | 147 | ||||||

CPS Auto Receivables Trust, Ser 2021-B, Cl B | ||||||||

0.810%, 12/15/2025 (B) | 191 | 189 | ||||||

SEI Daily Income Trust / Annual Report / January 31, 2023

21

SCHEDULE OF INVESTMENTS

January 31, 2023

Ultra Short Duration Bond Fund (Continued)

Description | Face Amount | Market Value | ||||||

ASSET-BACKED SECURITIES (continued) | ||||||||

CPS Auto Receivables Trust, Ser 2021-C, Cl B | ||||||||

0.840%, 07/15/2025 (B) | $ | 495 | $ | 490 | ||||

CPS Auto Receivables Trust, Ser 2022-A, Cl A | ||||||||

0.980%, 04/16/2029 (B) | 488 | 481 | ||||||

CPS Auto Receivables Trust, Ser 2023-A, Cl A | ||||||||

5.540%, 03/16/2026 (B) | 680 | 680 | ||||||

Credit Acceptance Auto Loan Trust, Ser 2021-3A, Cl A | ||||||||

1.000%, 05/15/2030 (B) | 250 | 240 | ||||||

Donlen Fleet Lease Funding 2 LLC, Ser 2021-2, Cl A2 | ||||||||

0.560%, 12/11/2034 (B) | 214 | 208 | ||||||

DT Auto Owner Trust, Ser 2020-1A, Cl C | ||||||||

2.290%, 11/17/2025 (B) | 230 | 229 | ||||||

DT Auto Owner Trust, Ser 2020-3A, Cl B | ||||||||

0.910%, 12/16/2024 (B) | 81 | 81 | ||||||

DT Auto Owner Trust, Ser 2021-1A, Cl B | ||||||||

0.620%, 09/15/2025 (B) | 249 | 248 | ||||||

DT Auto Owner Trust, Ser 2021-2A, Cl A | ||||||||

0.410%, 03/17/2025 (B) | 7 | 7 | ||||||

DT Auto Owner Trust, Ser 2021-2A, Cl B | ||||||||

0.810%, 01/15/2027 (B) | 220 | 217 | ||||||

DT Auto Owner Trust, Ser 2021-3A, Cl A | ||||||||

0.330%, 04/15/2025 (B) | 96 | 96 | ||||||

DT Auto Owner Trust, Ser 2021-4A, Cl A | ||||||||

0.560%, 09/15/2025 (B) | 385 | 380 | ||||||

DT Auto Owner Trust, Ser 2023-1A, Cl A | ||||||||

5.480%, 04/15/2027 (B) | 610 | 610 | ||||||