OMB APPROVAL

OMB Number: 3235-0570

Expires: October 31, 2006

Estimated average burden hours per response...19.3

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3486

Mosaic Tax-Free Trust

(Exact name of registrant as specified in charter)

550 Science Drive, Madison, WI 53711

(Address of principal executive offices)(Zip code)

W. Richard Mason

Madison/Mosaic Legal and Compliance Department

8777 N. Gainey Center Drive, Suite 220

Scottsdale, AZ 85258

(Name and address of agent for service)

Registrant's telephone number, including area code: 608-274-0300

Date of fiscal year end: September 30

Date of reporting period: September 30, 2003

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspoection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. s 3507.

Item 1. Report to Shareholders.

ANNUAL REPORT

September 30, 2003

Mosaic Tax-Free Trust

- Mosaic Arizona Tax-Free Fund

- Mosaic Missouri Tax-Free Fund

- Mosaic Virginia Tax-Free Fund

- Mosaic Tax-Free National Fund

- Mosaic Tax-Free Money Market

Mosaic Funds

Mosaic Funds

www.mosaicfunds.com

Contents

Management’s Discussion of Fund Performance

The annual period ended September 30, 2003 was another positive stretch for holders of Mosaic Tax-Free Trust Funds. One-year total returns for the bond funds in Tax-Free Trust were: 2.72% for Tax-Free National; 3.17% for Tax-Free Arizona; 2.24% for Tax-Free Missouri; and 3.35% for Tax-Free Virginia. As of September 30, 2003, with Federal Reserve Rates at historic lows, Mosaic Tax-Free Money Market was yielding 0.57% (after expense waivers) on a seven-day basis. Over the same period, the Lipper General Municipal Debt Index was up 3.38%. The Lehman Municipal Index, which provides a fee-free benchmark for the industry, was up 3.89% for the year. While positive, these returns were considerably lower than the previous few annual periods, which were characterized by a deep bear market in stocks and steadily dropping interest rates. Beginning in the fall of 2002, there was a broadening anticipation of economic recovery, which put pressure on the valuation of municipal bonds, particularly in the early part of the annual period and this past July.

Not all municipal bonds weathered the period equally well. For instance, the fiscal crisis in California generally hurt valuations of bonds issued from within that state’s borders. Mosaic’s Tax-Free portfolios always have an emphasis on high-quality, investment-grade bonds, and we held no California securities during the course of this annual period.

Another source of strength in our holdings was the high percentage of non-callable bonds. Whenever possible, we opt for these bonds, which continue to yield high rates, even when the overall interest rate environment dips. Callable bonds, on the other hand, allow the issuer to reclaim the bonds when their yield appears to be high compared to current rates. To an important extent, the variance of return in our state tax-free funds represents the availability of non-callable bonds within that state.

Economic Overview

The one-year period was a strong one for stock returns, and overall cash flows showed investor movement from bonds to stocks. Expectations of economic expansion were in the air at the beginning of the fiscal year, but only more recently did indicators begin confirming these predictions. By the end of September 2003, consumer sentiment was improving, manufacturing and non-manufacturing activities were demonstrating expansion, and capital spending was growing. Corporate profit growth continued to improve through the period. A continued recovery in corporate profits is a precursor to sustained business capital spending and new job creation.

Record fiscal and monetary stimulus—including two Federal Reserve Board rate cuts during the past year—appeared to be driving the recovery. However, increased Federal spending and tax cuts have led to a large Federal budget deficit. And while these stimulative measures promote economic growth, left too long they could rekindle inflation, leading to higher interest rates. Recent weakness in the U.S. dollar is also problematic. Foreign investors, particularly in Japan and China, have been willing lenders to the U.S. to finance our large deficits. Should dollar weakness persist, attracting foreign capital may require higher interest rates.

Outlook

The condition of the labor market is vital to the economic recovery. Most labor market readings remain weak, but should begin to firm in coming months. The labor market lags the economic cycle, with employers slow to trim payrolls heading into a recession, and slow to hire in the early stages of an expansion. So far, companies have been able to meet rising demand through longer hours and better use of productive capacity. However, cost-cutting has about run its course, and employers will increasingly need to add workers to meet rising demand.

Looking forward, despite the third quarter’s jump in rates, long-term yields remain lower than they were last year when economic prospects were more tenuous. Our outlook is for continued economic improvement, fueled by record monetary and fiscal stimulus and a gradually improving labor market. Although the interest rate environment is always subject to unexpected change, we think the most likely scenario over the upcoming months is for longer maturity rates to continue their ascent from current levels, while very short interest rates remain stable.

ARIZONA FUND

Arizona continues to enjoy a strong, well-diversified service and tourism based economy. The State does not have a credit rating because it does not issue general obligation bonds. The Fund had a total return of 3.17% for the annual period and the 30-day SEC yield was 2.89% as of September 30, 2003. The Mosaic Tax-Free Arizona Fund underperformed the Lipper General Municipal Bond Index, which advanced 3.38%, and the Lehman Municipal Index, which advanced 3.89%, largely due to its maintenance of a shorter average maturity throughout the 12-month period. This defensive positioning was done in anticipation of increasing interest rates during the year. However, rates initially fell to record lows before rising towards the end of the third quarter of 2003. We continue to believe that the risks of higher interest rates over the near term outweigh the benefits of extending maturities and therefore maintain a shorter duration posture. As of September 30, 2003, the Lehman Index’s duration was 8.19 years. The duration of the portfolio was 6.19 years while the average credit quality remained at AA. Purchases made during the period included the Greater Arizona Development Authority Infrastructure Revenue Authority and the University of Arizona Certificates of Participation. Arizona ranked 16th in the country in terms of issuance on a year-to-date basis.

Comparison of Changes in the Value of a $10,000 Investment with the Lehman Municipal Bond Index and Lipper General Municipal Bond Index for Mosaic Arizona Fund

Past performance is not predictive of future performance. Graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

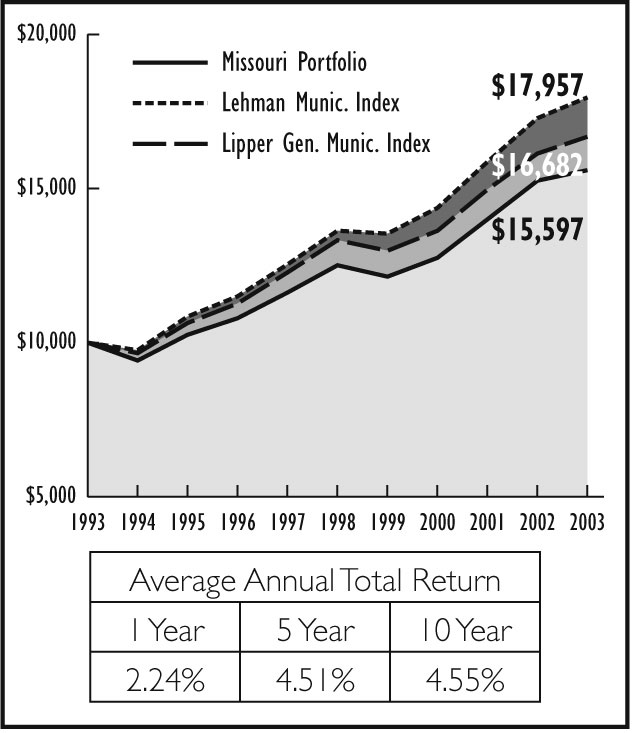

MISSOURI FUND

Missouri has a broad-based and diversified economy that is service-sector oriented. The State’s general obligation bonds are rated AAA. The Fund had a total return of 2.24% for the annual period and the 30-day SEC yield was 2.88% as of September 30, 2003. The Mosaic Tax-Free Missouri Fund underperformed the Lipper General Municipal Bond Index, which advanced 3.38%, and the Lehman Municipal Index, which advanced 3.89% due largely to its maintenance of a shorter average maturity throughout the 12-month period. This defensive positioning was done in anticipation of increasing interest rates during the year. However, rates initially fell to record lows before rising towards the end of the third quarter of 2003. We continue to believe that the risks of higher interest rates over the near term outweigh the benefits of extending maturities and therefore maintain a shorter duration posture. As of September 30, 2003, the Lehman Index’s duration was 8.19 years. The duration of the portfolio was 7.33 years while the average credit quality was maintained at AA. Purchases during the period included the North Kansas City School District and Lees Summit General Obligation bonds. Missouri ranked 18th in the country in terms of issuance on a year-to-date basis.

Comparison of Changes in the Value of a $10,000 Investment with the Lehman Municipal Bond Index and Lipper General Municipal Bond Index for Mosaic Missouri Fund

Past performance is not predictive of future performance. Graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

VIRGINIA FUND

The Commonwealth of Virginia maintains a AAA general obligation bond rating based on a well-diversified economy that emphasizes services and government. The Fund had a total return of 3.35% for the annual period and the 30-day SEC yield was 3.24% as of September 30, 2003. The Mosaic Tax-Free Virginia Fund performed in line with the Lipper General Municipal Bond Index, which advanced 3.38%, but underperformed the Lehman Municipal Index, which advanced 3.89%, largely due to its maintenance of a shorter average maturity throughout the 12-month period. This defensive positioning was done in anticipation of increasing interest rates during the year. However, rates initially fell to record lows before rising towards the end of the third quarter of 2003. We continue to believe that the risks of higher interest rates over the near term outweigh the benefits of extending maturities and therefore maintain a shorter duration posture. As of September 30, 2003, the Lehman Index’s duration was 8.19 years. The duration of the portfolio was 7.21 years while the average credit quality was maintained at AA. Purchases during the period included Loudoun County Refunding General Obligations and the Frederick-Winchester Regional Sewer System Authority. Virginia ranked 14th in the country in terms of issuance on a year-to-date basis.

Comparison of Changes in the Value of a $10,000 Investment with the Lehman Municipal Bond Index and Lipper General Municipal Bond Index for Mosaic Virginia Fund

Past performance is not predictive of future performance. Graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

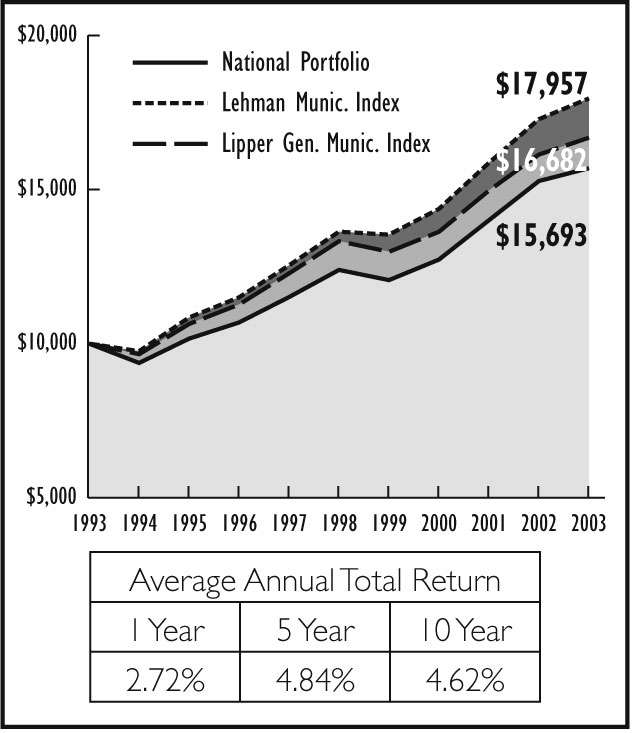

NATIONAL FUND

The National Fund had a total return of 2.72% for the annual period and the 30-day SEC yield was 2.72% as of September 30, 2003. The Mosaic Tax-Free National Fund underperformed the Lipper General Municipal Bond Index which advanced 3.38%, and the Lehman Municipal Index, which was up 3.89%, largely due to its maintenance of a shorter average maturity throughout the 12-month period. This defensive positioning was done in anticipation of increasing interest rates during the year. However, rates initially fell to record lows before rising towards the end of the third quarter of 2003. We continue to believe that the risks of higher interest rates over the near term outweigh the benefits of extending maturities and therefore maintain a shorter duration posture than the Index. As of September 30, 2003, the Lehman Index’s duration was 8.19 years. The duration of the portfolio was 6.61 years while the average credit quality was maintained at AA. Purchases made during the period included the First Florida Government Finance Authority and Redford, Michigan Unified School District General Obligation bonds. The United States and its territories has issued $287 billion in muni bonds year-to-date through the end of September which represents a 13% increase in volume over the same period last year.

Comparison of Changes in the Value of a $10,000 Investment with the Lehman Municipal Bond Index and Lipper General Municipal Bond Index for Mosaic National Fund

Past performance is not predictive of future performance. Graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

MONEY MARKET

The fund continues to provide a high degree of liquidity and safety of principal. As of September 30, 2003, the fund’s seven-day yield was 0.57% after expense waivers. The average maturity of the fund stood at 38 days at the end of the annual period.

We appreciate your confidence in Mosaic Funds and reaffirm our commitment to provide you with competitive returns to meet your investment objectives.

Sincerely,

(signature)

Michael J. Peters, CFA

Vice President

TO THE BOARD OF TRUSTEES AND SHAREHOLDERS OF

MOSAIC TAX-FREE TRUST

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of Mosaic Tax-Free Trust (the "Trust"), including Arizona Fund, Missouri Fund, Virginia Fund, National Fund, and Tax-Free Money Market (collectively, the "Funds"), as of September 30, 2003, the related statements of operations for the year then ended, statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Trust’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights. Our procedures included confirmation of securities owned as of September 30, 2003, by correspondence with the Funds’ custodian and brokers. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of each of the Funds constituting the Mosaic Tax-Free Trust as of September 30, 2003, the results of their operations, the changes in their net assets, and their financial highlights for the respective stated periods, in conformity with accounting principles generally accepted in the United States of America.

Deloitte & Touche LLP

(signature)

Chicago, Illinois

November 11, 2003

Arizona Fund • Portfolio of Investments

Credit Rating* | Principal | Market | ||

| Moody’s | S&P | |||

| LONG TERM MUNICIPAL BONDS: 102.1% of net assets | ||||

| EDUCATION: 29.6% | ||||

| Aa3 | AA | Maricopa County Unified School District #210 (Phoenix), 5.375%, 7/1/13 | $400,000 | $447,888 |

| Aaa | AAA | Maricopa County Unified School District #41 (Gilbert), 5.8%, 7/1/14 | 250,000 | 297,405 |

| Baa2 | nr | Maricopa County, Unified School District #090 Saddle Mountain, 5%, 7/1/14 | 75,000 | 76,593 |

| Aaa | AAA | Mohave County Elementary School District #16 (Mohave Valley) (MBIA Insured), 5.375%, 7/1/13 | 100,000 | 113,197 |

| Aaa# | AAA | Mohave County Elementary School District #1 (Lake Havasu) (FGIC Insured), 5.9%, 7/1/15 | 200,000 | 226,766 |

| Aaa | AAA | Pima County Unified School District #10 (Amphitheater), (FGIC Insured), 5.1%, 7/1/11 | 190,000 | 217,039 |

| Aaa | AAA | Pima County, Arizona School District, (MBIA Insured), 5%, 7/1/09 | 125,000 | 138,705 |

| Aaa | AAA | University of Arizona, (AMBAC Insured) 5%, 6/1/17 | 125,000 | 135,018 |

| Aaa | AAA | University of Arizona Board of Regents, (FGIC Insured) 5.8%, 6/1/24 | 275,000 | 304,307 |

| GENERAL OBLIGATION: 13.7% | ||||

| Baa1 | A- | Puerto Rico Commonwealth, 6.5%, 7/1/14 | 320,000 | 390,544 |

| Aaa# | AAA | Scottsdale Preserve Authority Excise Tax Revenue (FGIC Insured), 5.625%, 7/1/22 | 225,000 | 245,158 |

| Aa2 | AA | Tucson Recreational Facility Improvements, 5.25%, 7/1/19 | 250,000 | 268,935 |

| HOSPITAL: 6.6% | ||||

| Aaa# | AAA | Arizona Health Facilities Authority, Hospital Revenue (Phoenix Baptist Hospital) (MBIA Insured), 6.25%, 9/1/11 | 155,000 | 157,899 |

| Aaa | AAA | Pima County Industrial Development Authority Revenue (Refunding Bonds), 5.625%, 4/1/14 | 250,000 | 276,917 |

| HOUSING: 4.2% | ||||

| nr | AA | Maricopa County Industrial Development Authority, Multifamily Housing Revenue, (Pines at Camelback Apartments), 5.45%, 5/1/28 | 150,000 | 150,009 |

| Aaa | nr | Maricopa County Industrial Development Authority, Single Family Mortgage Revenue, 4.3%, 12/1/06 | 120,000 | 126,074 |

| INDUSTRIAL DEVELOPMENT: 1.7% | ||||

| Aaa | AAA | Phoenix Civic Improvement Corp. Excise Tax, 4.5%, 7/1/08 | $100,000 | $110,258 |

| LEASING AND OTHER FACILITIES: 22.9% | ||||

| Aaa | AAA | Arizona Board of Regents Certificate Participation, (AMBAC Insured), 5.5%, 6/1/13 | 320,000 | 365,437 |

| Baa1 | nr | Arizona Tourism & Sports Authority Tax Revenue Bond, 5%, 7/1/16 | 100,000 | 102,789 |

| A1 | A | Greater Arizona Development Authority Infrastructure Revenue Bond, 4.85%, 8/1/20 | 300,000 | 302,784 |

| Aaa | nr | Maricopa County Public Corp. Lease Revenue Bond, (AMBAC Insured), 5.5% 7/1/10 | 280,000 | 323,364 |

| Aaa | nr | Maricopa County Stadium Revenue Bond, (AMBAC Insured), 5.25% 6/1/12 | 250,000 | 283,832 |

| Aaa | AAA | Rio Nuevo Multipurpose Facilities, Certificate Participation, (FGIC Insured), 4.5%, 7/1/08 | 125,000 | 137,822 |

| POLLUTION CONTROL: 3.9% | ||||

| Aaa | AAA | Navajo County Arizona Pollution Control Corporate (MBIA-IBC Insured), 5.875%, 8/15/28 | 250,000 | 256,070 |

| TRANSPORTATION: 10.9% | ||||

| Aaa | AAA | Flagstaff Street and Highway User Revenue, Junior Lien (FGIC Insured), 5.9%, 7/1/10 | 500,000 | 589,585 |

| Aaa | AAA | Mesa Street and Highway Revenue Bond, (FSA Insured), 4%, 7/1/14 | 130,000 | 133,375 |

| WATER AND SEWER: 8.6% | ||||

| nr | AA | Buckeye Water and Sewer Improvements, 5.45%, 1/1/10 | 235,000 | 265,411 |

| Aaa | AAA | Mesa Recreational, Water and Sewer Improvements (FGIC Insured), 6.5%, 7/1/10 | 250,000 | 303,905 |

| TOTAL INVESTMENTS (Cost $6,200,053) | $6,747,086 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: (2.1%) of net assets | (142,009) | |||

| NET ASSETS: 100% | $6,605,077 | |||

Missouri Fund • Portfolio of Investments

Credit Rating* | Principal | Market | ||

| Moody’s | S&P | |||

| LONG TERM MUNICIPAL BONDS: 96.6% of net assets | ||||

| EDUCATION: 32.9% | ||||

| Aaa | AAA | Jackson County Reorg School District #7, Lees Summit, (FSA Insured), 5.25%, 3/1/14 | $300,000 | $337,026 |

| Aa2 | nr | Jefferson County School District, 6.7%, 3/1/11 | 200,000 | 240,698 |

| Aaa | AAA | Kansas City School District Building (FGIC Insured), 5%, 2/1/14 | 150,000 | 154,645 |

| Aaa | AAA | Mehlville School District R-9, Certificate Participation, (FSA Insured), 5%, 9/1/19 | 300,000 | 318,822 |

| nr | AA+ | Normandy School District General Obligation, 5.4%, 3/1/18 | 325,000 | 348,381 |

| Aa1 | AA+ | North Kansas City School District, 4.25%, 3/1/16 | 300,000 | 305,352 |

| Aa1 | AA+ | Platte County School District Park Hill, 5.5%, 3/1/14 | 300,000 | 325,557 |

| Aaa | AAA | St. Louis Board of Education, 5.5%, 4/1/10 | 275,000 | 318,282 |

| Aaa | AAA | St. Louis County Pattonville R-3 School District (FGIC Insured), 5.75%, 3/1/16 | 200,000 | 229,470 |

| GENERAL OBLIGATION: 14.5% | ||||

| Aa2 | nr | Lees Summit, 4.7%, 4/1/21 | 325,000 | 329,976 |

| Aaa | AAA | Missouri State (Fourth State Building), 5.75%, 8/1/19 | 200,000 | 224,746 |

| Baa1 | A- | Puerto Rico Commonwealth Public Improvement, 6.5%, 7/1/14 | 480,000 | 585,816 |

| HOSPITAL: 1.6% | ||||

| Aa2 | AA+ | Missouri State Certificate Participation, Rehabilitation Center, 6%, 11/1/15 | 115,000 | 124,240 |

| HOUSING: 7.3% | ||||

| nr | AAA# | St. Louis County Mortgage Revenue (AMT), 5.65%, 2/1/20 | 500,000 | 570,960 |

| LEASING AND OTHER FACILITIES: 31.9% | ||||

| A1 | nr | Greene County Certificate Participation, 5.25%, 7/1/11 | $300,000 | $336,060 |

| Aa3 | nr | Jackson County Missouri, Public Building Corp. Leasehold Revenue, 5.1%, 11/1/12 | 200,000 | 219,672 |

| Aaa | AAA | Missouri Development Financial Board Cultural Facilities Revenue Bond, (MBIA Insured), 5.25%, 12/1/17 | 350,000 | 383,506 |

| Baa1 | BBB+ | Missouri Development Financial Board Infrastructure Facilities Revenue Bond, 4.3%, 12/1/12 | 225,000 | 225,497 |

| Aa1 | AA+ | Missouri State Board Public Buildings, 4.0%, 12/1/10 | 75,000 | 79,998 |

| Aaa | AAA | Springfield Public Building Corp. Leasehold Revenue Bond, 5.8%, 6/1/13 | 275,000 | 319,902 |

| Aa3 | nr | Springfield Public Building Corp. Leasehold Revenue Bond, 4.7%, 5/1/12 | 175,000 | 188,625 |

| Aaa | nr | St Louis Municipal Finance Corporation, Leasehold Revenue Bond (AMBAC Insured), 5.75%, 2/15/17 | 300,000 | 343,017 |

| Aaa | AAA | St Louis Parking Facilities Revenue (MBIA Insured), 5.375%, 12/15/21 | 375,000 | 407,456 |

| POLLUTION CONTROL REVENUE: 3.1% | ||||

| A1 | A+ | St Louis Industrial Development Authority Pollution Control Revenue, 6.65%, 5/1/16 | 200,000 | 246,606 |

| TRANSPORTATION: 3.4% | ||||

| Aa2 | AA | Missouri State Highway & Transportation, Street & Road Revenue, 5.25%, 2/1/20 | 250,000 | 267,370 |

| WATER AND SEWER: 1.9% | ||||

| Aaa | nr | Jefferson County Public Water Supply District Number C-1 (AMBAC Insured), 5.25%, 12/1/16 | 130,000 | 144,888 |

| TOTAL INVESTMENTS (Cost $6,917,291) | $7,576,568 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 3.4% of net assets | 264,194 | |||

| NET ASSETS: 100% | $7,840,762 | |||

Virginia Fund • Portfolio of Investments

Credit Rating* | Principal | Market | ||

| Moody’s | S&P | |||

| LONG TERM MUNICIPAL BONDS: 98.4% of net assets | ||||

| EDUCATION: 6.7% | ||||

| A2 | nr | Loudoun County Industrial Development Authority, University Facilities Revenue (George Washington University), 6.25%, 5/15/22 | $500,000 | $506,815 |

| nr | A | Roanoke County Industrial Development Authority, (Hollins College), 5.25%, 3/15/23 | 900,000 | 935,361 |

| Aa2 | AA | Virginia College Building Authority, Educational Facilities Revenue (Washington And Lee University), 5.75%, 1/1/14 | 20,000 | 20,602 |

| A1 | AA- | Virginia State Universities, University Revenue (Virginia Commonwealth University), 5.75%, 5/1/15 | 500,000 | 540,300 |

| GENERAL OBLIGATION: 26.2% | ||||

| Aaa | AAA | Alexandria, 5%, 1/1/16 | 200,000 | 224,984 |

| Aaa | AAA | Arlington County, 5%, 2/1/19 | 250,000 | 264,753 |

| Aaa | AAA | Culpepper County, 6%, 1/15/21 | 500,000 | 595,775 |

| Aaa | AAA | Fairfax County, 4.5%, 6/1/12 | 500,000 | 533,095 |

| A2 | A | Henry County, 6%, 7/15/14 | 500,000 | 529,575 |

| Aaa | AAA | Leesburg, (AMBAC Insured), 5.6%, 6/1/15 | 500,000 | 547,625 |

| Aa1 | AA+ | Loudoun County, 5.25%, 5/1/13 | 750,000 | 848,287 |

| Aa1 | AA+ | Loudoun County, 5%, 10/1/13 | 500,000 | 564,145 |

| Aa3 | AA | Lynchburg, 5.7%, 6/1/25 | 1,170,000 | 1,266,373 |

| A1 | nr | Prince George County, 4.5%, 8/1/12 | 400,000 | 430,764 |

| Baa1 | A- | Puerto Rico Commonwealth, 6.5%, 7/1/14 | 1,115,000 | 1,360,802 |

| Aa1 | AA+ | Virginia Beach, 5%, 3/1/12 | 540,000 | 604,697 |

| HOSPITAL: 18.1% | ||||

| A2 | nr | Arlington County Industrial Development Authority, Hospital Facilities Revenue Bond, 5.5%, 7/1/15 | $1,225,000 | $1,313,776 |

| Aaa# | AAA | Danville Industrial Development Authority, Hospital Revenue (Danville Regional Medical Center) (FGIC Insured) (Prerefunded 10/1/04 @ 101), 6.375%, 10/1/14 | 350,000 | 372,397 |

| Aaa | AAA | Danville Industrial Development Authority, Hospital Revenue (Danville Regional Medical Center) (AMBAC Insured) 5%, 10/1/10 | 250,000 | 281,502 |

| A3 | nr | Fredericksburg Industrial Development Authority Hospital Facilities Revenue, 5%, 8/15/08 | 450,000 | 491,305 |

| Aaa | AAA | Fredericksburg Industrial Development Authority Hospital Facilities Revenue, 5.25%, 6/15/16 | 800,000 | 867,464 |

| Aaa | AAA | Hanover County Industrial Development Authority, Revenue Bon Secours Health System (MBIA Insured), 6%, 8/15/10 | 640,000 | 758,758 |

| Aaa# | nr | Prince William County Industrial Development Authority, Hospital Revenue, (Prerefunded 10/1/05 @ 102), 6.85%, 10/1/25 | 85,000 | 96,279 |

| Aaa | AAA | Roanoke Industrial Development Authority, Hospital Revenue (Carilion Health Systems) (MBIA Insured), 5.5%, 7/1/16 | 500,000 | 567,885 |

| Aaa | AAA | Roanoke Industrial Development Authority, Hospital Revenue (Roanoke Memorial Hospitals) (MBIA Insured), 6.125%, 7/1/17 | 500,000 | 612,660 |

| HOUSING: 8.8% | ||||

| nr | AAA | Fairfax County Redevelopment & Housing Authority, Multi-Family Housing Revenue (Castel Lani Project) (FHA Insured), 5.5%, 4/1/28 | 425,000 | 437,372 |

| nr | A# | Prince William County Industrial Development Authority, Multi-Family Housing Revenue, 5.35%, 7/1/23 | 830,000 | 836,366 |

| nr | AAA | Suffolk Redevelopment & Housing Authority, Multi-Family Housing Revenue, 5.6%, 2/1/33 | 1,250,000 | 1,346,725 |

| INDUSTRIAL DEVELOPMENT: 7.1% | ||||

| Aaa | nr | Fairfax County Economic Development Authority (National Wildlife Assoc.), 5.25%, 9/1/19 | 1,000,000 | 1,089,080 |

| Baa3 | nr | Peninsula Ports Authority Coal Terminal Revenue, 7.375%, 6/1/20 | 1,000,000 | 1,010,000 |

| LEASING AND OTHER FACILITIES: 9.2% | ||||

| Aa1 | AA+ | Fairfax County Economic Development Authority, Lease Revenue, 5.5%, 5/15/18 | $500,000 | $520,920 |

| Aaa | AAA | Portsmouth Industrial Development Authority Revenue, Hotel Conference Center & Parking, 5.125%, 4/1/17 | 1,000,000 | 1,082,070 |

| Aaa | nr | Richmond Industrial Development Authority Government Facilities, 5%, 7/15/13 | 1,000,000 | 1,125,070 |

| MUNICIPAL OTHER: 11.1% | ||||

| Aaa | AAA | Southeastern Public Service Authority Revenue, 5%, 7/1/15 | 1,000,000 | 1,126,940 |

| Aaa | AAA | Southwest Regional Jail Authority Revenue, (MBIA Insured), 4.5% 9/1/10 | 1,000,000 | 1,100,190 |

| Aa1 | AA+ | Virginia State Public Building Authority, Public Facilities Revenue, 5%, 8/01/18 | 1,000,000 | 1,058,300 |

| TRANSPORTATION: 1.3% | ||||

| Aaa | AAA | Richmond Metropolitan Authority Expressway Revenue, (FGIC Insured), 5.25%, 7/15/12 | 350,000 | 398,794 |

| WATER & WASTE: 9.9% | ||||

| Aaa | AAA | Frederick Regional Sewer System Revenue, (AMBAC), 5%, 10/1/15 | 570,000 | 641,256 |

| Aaa | AAA | Henry County Water & Sewer Revenue, (FSA Insured), 5.25%, 11/15/13 | 700,000 | 804,867 |

| Aaa | AAA | Stafford County Water & Sewer Revenue, (FSA Insured), 4.5%, 6/1/11 | 335,000 | 365,083 |

| Aaa | AAA | Upper Occoquan Sewer, Regional Sewer Revenue, (MBIA Insured), 5.15%, 7/1/20 | 1,000,000 | 1,127,530 |

| TOTAL INVESTMENTS (Cost $27,493,755) | $29,206,542 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 1.6% of net assets | 474,327 | |||

| NET ASSETS: 100% | $29,680,869 | |||

National Fund • Portfolio of Investments

Credit Rating* | Principal | Market | ||

| Moody’s | S&P | |||

| LONG TERM MUNICIPAL BONDS: 98.0% of net assets | ||||

| ARIZONA: 5.2% | ||||

| Aaa | AAA | Rio Nuevo Multipurpose Facilities, Certificate Participation, (FGIC Insured), 4.5%, 7/1/08 | $1,100,000 | $1,212,838 |

| FLORIDA: 10.5% | ||||

| Aaa | nr | First Florida Government Community Revenue Bond, (AMBAC Insured), 5.5%, 7/1/16 | 1,000,000 | 1,163,800 |

| Aaa | AAA | Palm Beach County Solid Waste Authority Revenue Bond, (AMBAC Insured), 6%, 10/1/10 | 1,100,000 | 1,306,811 |

| ILLINOIS: 10.5% | ||||

| Aaa | nr | Grundy County School District #054, General Obligation, (AMBAC Insured), 8.35%, 12/1/07 | 720,000 | 900,662 |

| Aaa | AAA | Regional Illinois Transportation Authority, Transit Revenue (AMBAC Insured), 7.2%, 11/1/20 | 300,000 | 404,913 |

| Aaa | AAA | University of Illinois Certificates, Utility Infrastructure Projects (MBIA Insured), 5.75%, 8/15/09 | 1,000,000 | 1,167,970 |

| INDIANA: 2.7% | ||||

| Aaa | AAA | Indiana Bond Bank, 5.75%, 8/1/13 | 550,000 | 635,151 |

| IOWA: 4.6% | ||||

| nr | A | Davenport Community School District, School Improvements, 4.6%, 7/1/09 | 1,000,000 | 1,091,530 |

| KANSAS: 3.7% | ||||

| Aa2 | AA+ | Kansas State Department of Transportation, Hwy Revenue, 6.125%, 9/1/09 | 740,000 | 880,267 |

| MARYLAND: 3.2% | ||||

| Aa1 | AA+ | Anne Arundel County, Solid Waste Projects (AMT), 5.5%, 9/1/16 | $100,000 | $109,419 |

| Aaa | AAA | Baltimore Auto Parking Revenue (FGIC Insured), 5.9%, 7/1/09 | 75,000 | 88,343 |

| Aa3 | AA- | Baltimore, Port Facilities Revenue (Consolidated Coal Sales), 6.5%, 10/1/11 | 100,000 | 102,338 |

| Aa2 | AA | Frederick County, 5.1%, 12/1/17 | 75,000 | 81,386 |

| Aaa | AAA | Maryland State, 5%, 7/15/11 | 50,000 | 56,060 |

| Aaa# | AAA | Maryland State Transportation Authority Transportation Facilities Project Revenue, 6.8%, 7/1/16 | 100,000 | 122,179 |

| nr | AA+ | Montgomery County Revenue Authority, Lease Revenue (Human Services Headquarters), 5.6%, 8/1/14 | 100,000 | 110,587 |

| A2 | nr | Northeast Waste Disposal Authority, Solid Waste Revenue Bond, 5.8%, 7/1/04 | 70,000 | 72,186 |

| MASSACHUSETTS: 5.4% | ||||

| Aa2 | AA | Massachusetts Bay Transportation Authority, Transit Revenue, 7%, 3/1/14 | 1,000,000 | 1,266,350 |

| MICHIGAN: 1.9% | ||||

| Aaa | AAA | Redford United School District, (AMBAC Insured), 5%, 5/1/22 | 410,000 | 442,616 |

| MINNESOTA: 0.9% | ||||

| Aa1 | AA+ | Minnesota State Housing Finance Agency, Housing Revenue (Single-Family Mortgage) (AMT), 6.25%, 7/1/26 | 210,000 | 217,633 |

| MISSISSIPPI: 5.8% | ||||

| Aaa | AAA | Harrison County Wastewater Management District, Sewer Revenue, (Wastewater Treatment Facilities) (FGIC Insured), 7.75%, 2/1/14 | 500,000 | 667,375 |

| Aaa | AAA | Harrison County Wastewater Management District, Sewer Revenue, (Wastewater Treatment Facilities) (FGIC Insured), 8.5%, 2/1/13 | 500,000 | 693,585 |

| MISSOURI: 4.8% | ||||

| Aa1 | AA+ | Missouri State Health & Educational Facilities Authority Revenue Bond, 5%, 11/1/09 | 1,000,000 | 1,135,910 |

| NORTH DAKOTA: 2.3% | ||||

| Baa1 | nr | Grand Forks Health Care Systems Revenue Bond, 7.125%, 8/15/24 | $500,000 | $547,545 |

| PENNSYLVANIA: 5.5% | ||||

| Aaa | AAA | Lehigh County General Obligation (Lehigh Valley Hospital) (MBIA Insured), 7%, 7/1/16 | 1,000,000 | 1,293,670 |

| PUERTO RICO: 0.4% | ||||

| Baa1 | A- | Puerto Rico Commonwealth, 6.5%, 7/1/14 | 85,000 | 103,738 |

| SOUTH CAROLINA: 0.9% | ||||

| Aaa# | AAA | Piedmont Municipal Power Agency Electrical Revenue (FGIC Insured), 6.5%, 1/1/16 | 145,000 | 180,612 |

| TENNESSEE: 3.4% | ||||

| Aa1 | nr | Williamson County, 5.5%, 9/1/14 | 695,000 | 806,450 |

| TEXAS: 17.0% | ||||

| Aaa | AAA | Lower Colorado River Authority, Utility Revenue, (AMBAC Insured), 6%, 1/1/17 | 305,000 | 370,743 |

| Aaa | AAA | North Forest Independent School District, 6%, 8/15/11 | 1,050,000 | 1,246,571 |

| nr | AA | Red River Educational Finance Revenue Bond, 5.75%, 5/15/15 | 1,000,000 | 1,143,250 |

| Aaa# | AAA | Texas Public Building Authority, Building Revenue (MBIA Insured), 7.125%, 8/1/11 | 1,000,000 | 1,224,540 |

| VIRGINIA: 7.8% | ||||

| A3 | nr | Fredericksburg Industrial Development Authority Hospital Facilities Revenue, 5%, 8/15/08 | 175,000 | 191,063 |

| Aaa | AAA | Hanover County Industrial Development Authority Hospital (Bon Secours Health Systems) (MBIA Insured), 6%, 8/15/10 | 500,000 | 592,780 |

| Aa1 | AA+ | Virginia Commonwealth Transportation Board, 4.5%, 4/1/18 | 1,000,000 | 1,027,000 |

| WASHINGTON: 1.5% | ||||

| Aaa | AAA | King County School District #415 Kent, (FSA Insured), 5.5%, 6/1/16 | 300,000 | 348,894 |

| TOTAL LONG TERM MUNICIPAL BONDS | ||||

| (Cost $20,996,112) | $23,006,765 | |||

| SHORT TERM MUNICIPAL BONDS: 0.2% of net assets | ||||

| VMIG1/Aaa | AAA | Palm Beach County Florida Water & Sewer Revenue Bond, 1.2%, 10/1/11^ (Cost $50,000) | $50,000 | $50,000 |

| TOTAL INVESTMENTS (Cost $21,046,112) | $23,056,765 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 1.8% of net assets | 432,357 | |||

| NET ASSETS: 100% | $23,489,122 | |||

Money Market • Portfolio of Investments

Credit Rating* | Principal | Value | ||

| Moody’s | S&P | |||

| SHORT TERM MUNICIPAL SECURITIES: 94.1% of net assets | ||||

| FLORIDA: 11.3% | ||||

| VMIG1/Aa2 | nr | Eustis Florida Health Facilities Authority Revenue, Waterman Medical Center, 1.1%, 12/1/15^ | $265,000 | $265,000 |

| Aaa | AAA | Florida Div. Board Financial Dept. of General Services, 4.5%, 7/1/05 | 165,000 | 170,979 |

| VMIG1/Aaa | AAA | Palm Beach County Florida Water & Sewer Revenue Bond, 1.2%, 10/1/11^ | 100,000 | 100,000 |

| GEORGIA: 8.4% | ||||

| VMIG1/Aaa | A1+/AAA | Atlanta Water and Wastewater Revenue (FSA) (SPA-Dexia Credit Local) 1.2%, 11/1/41^ | 200,000 | 200,000 |

| nr | A1/A | Fulton County Georgia Residential Care Facilities (LOC-Rabobank Nederland), 1.2%, 1/1/18^ | 200,000 | 200,000 |

| KENTUCKY: 6.3% | ||||

| VMIG1/Aa2 | nr | Ashland Pollution Control Revenue (Ashland Oil Inc.) (LOC-Suntrust Bank Nashville), 1%, 4/1/09^ | 300,000 | 300,000 |

| MINNESOTA: 4.0% | ||||

| VMIG1/Aaa | A1+/AAA | Minneapolis & St Paul Housing and Redevelopment Authority Health Care Systems, 1.2%, 8/15/25^ | 190,000 | 190,000 |

| MISSISSIPPI: 4.2% | ||||

| P1/Aa2 | nr | Jackson County Pollution Control Revenue Bond, 1.2%, 6/1/23^ | 200,000 | 200,000 |

| MISSOURI: 4.2% | ||||

| nr | A1+/AA+ | Missouri State Health & Educational Facilities Authority Revenue Bond, 1.2%, 6/1/26^ | 200,000 | 200,000 |

| NEW MEXICO: 4.2% | ||||

| P-1 | A1/AA | Farmington Pollution Control Revenue, 1.2%, 5/1/24^ | 200,000 | 200,000 |

| NEW YORK: 3.6% | ||||

| Aaa | AAA | New York State Government Assistance Corp. (MBIA Insured) (IBC GO of Corp) (Prerefunded 4/1/04 @ 100), 5%, 4/1/23 | $165,000 | $168,128 |

| NORTH CAROLINA: 16.9% | ||||

| VMIG1/Aa1 | A1/AAA | Greensboro, General Obligation (SPA- Wachovia Bank of NC), 1.05%, 4/1/07^ | 300,000 | 300,000 |

| VMIG1/Aaa | A1/AAA | North Carolina Medical Care Commission, Hospital Revenue (Pooled Equipment Project) (MBIA Insured), 1.05%, 12/1/25^ | 300,000 | 300,000 |

| nr | A1/A+ | North Carolina Medical Care Commission, Retirement Facilities Revenue (Aldersgate Project) (LOC-Branch Banking & Trust), 1.15%, 1/1/31^ | 200,000 | 200,000 |

| PENNSYLVANIA: 6.5% | ||||

| Aaa | AAA | Gettysburg Municipal Authority College Project Revenue Bond, (Prerefunded 8/15/04 @ 102), 6.5%, 8/15/09 | 100,000 | 106,600 |

| VMIG1 | nr | Pennsylvania Higher Educational Facilities Authority Revenue Bond, 2.5%, 11/25/03 | 200,000 | 200,340 |

| TENNESSEE: 5.8% | ||||

| VMIG1/Aaa | A1+/AAA | Metropolitan Nashville Airport Authority Revenue (FGIC Insured) (LOC-Societe Generale), 1.05%, 7/1/19 ^ | 275,000 | 275,000 |

| TEXAS: 9.1% | ||||

| Aaa | AAA | Eanes Independent School District, 5.75%, 8/1/09 | 125,000 | 129,771 |

| VMIG1/Aa2 | A1/A+ | Port Development Corporation, Marine Terminal Revenue (Stolt Terminal) (LOC-Canadian Imperial Bank), 1.10%, 1/15/14^ | 300,000 | 300,000 |

| WASHINGTON: 5.4% | ||||

| VMIG1/A3 | nr | Washington State Housing Finance Commission, Housing Revenue (Panorama City Project) (LOC-Key Bank Of Washington), 1.20%, 1/1/27^ | 100,000 | 100,000 |

| VMIG1/Aa2 | nr | Washington State Housing Finance Commission, Non-Profit Housing Revenue, 1.23%, 8/1/19^ | 155,000 | 155,000 |

| WYOMING: 4.2% | ||||

| VMIG1/Aa2 | nr | Uinta County Pollution Control Revenue, 1.20%, 12/1/22^ | $200,000 | $200,000 |

| TOTAL INVESTMENTS (Cost $4,460,818)+ | $4,460,818 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 5.9% of net assets | 279,061 | |||

| NET ASSETS: 100% | $4,739,879 | |||

Notes to Portfolios of Investments:

- ^ Security has a variable coupon rate and/or is subject to a demand feature before final

- maturity. Coupon rate as of September 30, 2003.

- # Refunded or escrowed to maturity

- AMBAC American Municipal Bond Assurance Corporation

- AMT Subject to Alternative Minimum Tax

- FGIC Financial Guaranty Insurance Company

- FHA Federal Housing Administration

- FSA Federal Security Assistance

- GNMA Government National Mortgage Association

- LOC Letter of Credit

- MBIA Municipal Bond Investors Assurance Corporation

- Moody’s Moody’s Investors Service, Inc.

- nr Not rated

- PSF Permanent School Fund

- S&P Standard & Poor’s Corporation

* Credit ratings are unaudited

+ Aggregate cost for federal income tax purposes as of September 30, 2003.

Statements of Assets and Liabilities

Arizona | Missouri | Virginia | National | Money | |

| ASSETS | |||||

| Investments, at value (Note 1) | |||||

| mInvestment securities | $6,747,086 | $7,576,568 | $29,206,542 | $23,006,765 | $-- |

| mShort term securities | -- | -- | -- | 50,000 | 4,460,818 |

| mTotal investments* | 6,747,086 | 7,576,568 | 29,206,542 | 23,056,765 | 4,460,818 |

| Cash | 82,296 | 494,246 | 109,708 | 166,226 | 263,995 |

| Receivables | |||||

| mInterest | 87,791 | 80,355 | 377,224 | 286,545 | 15,056 |

| mCapital shares sold | -- | -- | -- | -- | 17 |

| Total assets | 6,917,173 | 8,151,169 | 29,693,474 | 23,509,536 | 4,739,886 |

| LIABILITIES | |||||

| Payables | |||||

| mInvestment securities purchased | 296,919 | 305,423 | -- | -- | -- |

| mDividends | 5,515 | 4,619 | 8,105 | 6,678 | 7 |

| mCapital shares redeemed | 9,662 | 365 | 4,500 | 13,736 | -- |

| Total Liabilities | 312,096 | 310,407 | 12,605 | 20,414 | 7 |

| NET ASSETS (Note 5) | $6,605,077 | $7,840,762 | $29,680,869 | $23,489,122 | $4,739,879 |

| CAPITAL SHARES OUTSTANDING | 602,645 | 707,422 | 2,460,470 | 2,051,167 | 4,740,696 |

| NET ASSET VALUE PER SHARE | $0(0010.96 | $000,11.08 | $0000,12.06 | $0 00,11.45 | $0000,1.00 |

| *INVESTMENT SECURITIES, AT COST | $6,200,053 | $6,917,291 | $27,493,755 | $21,046,112 | $4,460,818 |

For the year ended September 30, 2003

Arizona | Missouri | Virginia | National | Money | |

| INVESTMENT INCOME (Note 1) | |||||

| Interest income | $295,210 | $367,732 | $1,418,386 | $1,053,260 | $55,922 |

| EXPENSES (Notes 2 and 3) | |||||

| Investment advisory fees | 40,320 | 48,784 | 187,165 | 148,315 | 24,737 |

| Service agreement fees | 30,966 | 35,905 | 116,791 | 104,414 | 17,795 |

| Expenses waived | -- | -- | -- | -- | (14,961) |

| Total expenses | 71,286 | 84,689 | 303,956 | 252,729 | 27,571 |

| NET INVESTMENT INCOME | 223,924 | 283,043 | 1,114,430 | 800,531 | 28,351 |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | |||||

| Net realized gain (loss) on investments | (1,504) | 90,168 | 322,133 | 232,568 | -- |

| Change in net unrealized appreciation (depreciation) of investments | (29,725) | (215,557) | (434,157) | (411,304) | -- |

| NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | (31,229) | (125,389) | (112,024) | (178,736) | -- |

| TOTAL INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $192,695 | $157,654 | $1,002,406 | $621,795 | $28,351 |

Statements of Changes in Net Assets

For the year ended September 30:

Arizona Fund | Missouri Fund | Virginia Fund | ||||

2003 | 2002 | 2003 | 2002 | 2003 | 2002 | |

| INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | ||||||

| Net investment income | $223,924 | $247,713 | $283,043 | $309,921 | $1,114,430 | $1,182,860 |

| Net realized gain (loss)on investments | (1,504) | 27,750 | 90,168 | 28,681 | 322,133 | 178,807 |

| Net unrealized appreciation (depreciation) on investments | (29,725) | 203,733 | (215,557) | 364,338 | (434,157) | 924,856 |

| Total increase in net assets resulting from operations | 192,695 | 479,196 | 157,654 | 702,940 | 1,002,406 | 2,286,523 |

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||

| From net investment income | (223,924) | (247,713) | (283,043) | (309,921) | (1,114,430) | (1,182,860) |

| From net capital gains | -- | -- | -- | -- | (117,232) | -- |

| Total distributions | (223,924) | (247,713) | (283,043) | (309,921) | (1,231,662) | (1,182,860) |

| CAPITAL SHARE TRANSACTIONS (Note 7) | (164,632) | (313,084) | (602,951) | 233,232 | (170,024) | (770,108) |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | (195,861) | (81,601) | (728,340) | 626,251 | (399,280) | 333,555 |

| NET ASSETS | ||||||

| Beginning of year | $6,800,938 | $6,882,539 | $8,569,102 | $7,942,851 | $30,080,149 | $29,746,594 |

| End of year | $6,605,077 | $6,800,938 | $7,840,762 | $8,569,102 | $29,680,869 | $30,080,149 |

National Fund | Money Market | |||

2003 | 2002 | 2003 | 2002 | |

| INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | ||||

Net investment income | $ 800,531 | $ 880,637 | $ 28,351 | $ 42,909 |

Net realized gain on investments | 232,568 | 344,059 | -- | -- |

Net unrealized appreciation (depreciation) of investments | (411,304) | 864,307 | -- | -- |

Total increase in net assets resulting from operations | 621,795 | 2,089,003 | 28,351 | 42,909 |

| DISTRIBUTIONS TO SHAREHOLDERS | ||||

From net investment income | (800,531) | (880,637) | (28,351) | (43,669) |

From net capital gains | -- | -- | -- | -- |

| Total distributions | (800,531) | (880,637) | (28,351) | (43,669) |

| CAPITAL SHARE TRANSACTIONS (Note 7) | (606,280) | (1,351,644) | (311,210) | (42,967) |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | (785,016) | (143,278) | (311,210) | (43,727) |

| NET ASSETS | ||||

Beginning of year | $24,274,138 | $24,417,416 | $5,051,089 | $5,094,816 |

End of year | $23,489,122 | $24,274,138 | $4,739,879 | $5,051,089 |

Selected data for a share outstanding for the periods indicated.

ARIZONA FUND

Year Ended September 30, | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

| Net asset value, beginning of year | $11.00 | $10.63 | $10.06 | $10.03 | $10.74 |

| Investment operations: | |||||

| Net investment income | 0.38 | 0.39 | 0.42 | 0.45 | 0.44 |

| Net realized and unrealized gain (loss) on investments | (0.04) | 0.37 | 0.57 | 0.03 | (0.71) |

| Total from investment operations | 0.34 | 0.76 | 0.99 | 0.48 | (0.27) |

| Less distributions from net investment income | (0.38) | (0.39) | (0.42) | (0.45) | (0.44) |

| Net asset value, end of year | $10.96 | $11.00 | $10.63 | $10.06 | $10.03 |

| Total return (%) | 3.17 | 7.37 | 10.01 | 4.93 | (2.57) |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $6,605 | $6,801 | $6,883 | $6,451 | $7,175 |

| Ratio of expenses to average net assets (%) | 1.11 | 1.11 | 1.10 | 1.12 | 1.12 |

| Ratio of net investment income to average net assets (%) | 3.47 | 3.69 | 4.01 | 4.53 | 4.23 |

| Portfolio turnover (%) | .5 | .15 | .20 | .29 | .37 |

MISSOURI FUND

Year Ended September 30, | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

| Net asset value, beginning of year | $11.24 | $10.72 | $10.17 | $10.12 | $10.87 |

| Investment operations: | |||||

| Net investment income | 0.40 | 0.41 | 0.43 | 0.44 | 0.44 |

| Net realized and unrealized gain (loss) on investments | (0.16) | 0.52 | 0.55 | 0.05 | (0.75) |

| Total from investment operations | 0.24 | 0.93 | .98 | 0.49 | (0.31) |

| Less distributions from net investment income | (0.40) | (0.41) | (0.43) | (0.44) | (0.44) |

| Net asset value, end of year | $11.08 | $11.24 | $10.72 | $10.17 | $10.12 |

| Total return (%) | 2.24 | 8.96 | 9.79 | 5.03 | (2.95) |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $7,841 | $8,569 | $7,943 | $7,321 | $7,686 |

| Ratio of expenses to average net assets (%) | 1.09 | 1.08 | 1.08 | 1.09 | 1.10 |

| Ratio of net investment income to average net assets (%) | 3.63 | 3.85 | 4.06 | 4.43 | 4.15 |

| Portfolio turnover (%) | .17 | .21 | .16 | .26 | .17 |

VIRGINIA FUND

Year Ended September 30, | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

| Net asset value, beginning of year | $12.16 | $11.70 | $11.14 | $11.13 | $11.93 |

| Investment operations: | |||||

| Net investment income | 0.45 | 0.48 | 0.49 | 0.50 | 0.49 |

| Net realized and unrealized gain (loss) on investments | (0.05) | 0.46 | 0.56 | 0.01 | (0.80) |

| Total from investment operations | 0.40 | 0.94 | 1.05 | 0.51 | (0.31) |

| Less distribution from: | |||||

| net investment income | (0.45) | (0.48) | (0.49) | (0.50) | (0.49) |

| net capital gains | (0.05) | .-- | .-- | .-- | .-- |

| Total distributions | (0.50) | (0.48) | (0.49) | (0.50) | (0.49) |

| Net asset value, end of year | $12.06 | $12.16 | $11.70 | $11.14 | $11.13 |

| Total return (%) | 3.35 | 8.22 | 9.62 | 4.78 | (2.69) |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $29,681 | $30,080 | $29,747 | $28,526 | $30,229 |

| Ratio of expenses to average net assets (%) | 1.01 | 1.01 | 1.01 | 1.02 | 1.02 |

| Ratio of net investment income to average net assets (%) | 3.72 | 4.05 | 4.26 | 4.60 | 4.22 |

| Portfolio turnover (%) | .31 | .27 | .38 | . 24 | .27 |

NATIONAL FUND

Year Ended September 30, | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

| Net asset value, beginning of year | $11.53 | $10.97 | $10.43 | $10.30 | $11.00 |

| Investment operations: | |||||

| Net investment income | 0.38 | 0.41 | 0.49 | 0.42 | 0.42 |

| Net realized and unrealized gain (loss) on investments | (0.08) | 0.56 | 0.54 | 0.13 | (0.70) |

| Total from investment operations | 0.30 | 0.97 | 1.03 | 0.55 | (0.28) |

| Less distribution from net investment income | (0.38) | (0.41) | (0.49) | (0.42) | (0.42) |

| Net asset value, end of year | $11.45 | $11.53 | $10.97 | $10.43 | $10.30 |

| Total return (%) | 2.72 | 9.08 | 10.03 | 5.53 | (2.67) |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $23,489 | $24,274 | $24,417 | $21,951 | $28,838 |

| Ratio of expenses to average net assets (%) | 1.07 | 1.07 | 1.06 | 1.07 | 1.07 |

| Ratio of net investment income to average net assets (%) | 3.37 | 3.70 | 4.48 | 4.15 | 3.87 |

| Portfolio turnover (%) | .21 | .56 | .53 | .78 | .35 |

MONEY MARKET

Year Ended September 30, | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

| Net asset value, beginning of year | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Net investment income | 0.01 | 0.01 | 0.03 | 0.03 | 0.02 |

| Less distribution from net investment income | (0.01) | (0.01) | (0.03) | (0.03) | (0.02) |

| Net asset value, end of year | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total return (%) | 0.58 | 0.86 | 2.72 | 3.06 | 2.49 |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $4,740 | $5,051 | $5,095 | $4,866 | $6,818 |

| Ratio of expenses to average net assets before fee waiver (%) | 0.86 | 0.86 | 0.86 | 0.86 | 0.86 |

| Ratio of expenses to average net assets after fee waiver1 (%) | 0.56 | 0.76 | 0.76 | 0.76 | 0.77 |

| Ratio of net investment income to average net assets before fee waiver (%) | 0.27 | 0.75 | 2.58 | 2.91 | 2.37 |

| Ratio of net investment income to average net assets after fee waiver1 (%) | 0.57 | v0.85 | 2.68 | 3.01 | 2.46 |

1See Notes 2 and 3 to the Financial Statements.

For the year ended September 30, 2003

1. Summary of Significant Accounting Policies.Mosaic Tax-Free Trust (the "Trust") is registered with the Securities and Exchange Commission under the Investment Company Act of 1940 as an open-end, diversified investment management company. The Trust maintains five separate funds (described in the following sentences and defined as the "Funds") which invest principally in securities exempt from federal income taxes, commonly known as "municipal" securities. The Arizona, Missouri and Virginia Funds (the "State Funds") invest solely in securities exempt from both federal and state income taxes in their respective states. The National Fund invests in securities exempt from federal taxes. The National Fund and the State Funds invest in intermediate and long-term securities. The Tax-Free Money Market invests in short-term securities. Because the Trust is 100% no-load, the shares of each fund are offered and redeemed at the net asset value per share.

Securities Valuation: The State and National Funds value securities having maturities of 60 days or less at amortized cost, which approximates market value. Securities having longer maturities, for which market quotations are readily available are valued at the mean between their bid and ask prices. Securities for which market quotations are not readily available are valued at their fair value as determined in good faith under procedures approved by the Board of Trustees. The Money Market uses the amortized cost method of valuation whereby portfolio securities are valued at acquisi-tion cost as adjusted for amortization of premium or accretion of discount.

Investment Transactions: Investment transactions are recorded on a trade date basis. The cost of investments sold is determined on the identified cost basis for financial statement and federal income tax purposes.

Investment Income: Interest income is recorded on an accrual basis. Bond premium is amortized and original issue discount and market discount are accreted over the expected life of each applicable security using the effective interest method.

Distribution of Income and Gains: Net invest-ment income, determined as gross invest--ment income less total expenses, is declared as a regular dividend monthly for the State and National Funds and daily for the Money Market. Dividends are distributed to share-holders or reinvested in additional shares as of the close of business at the end of each month. Capital gain distributions, if any, are declared and paid annually at year-end. Additional distributions may be made if necessary. Distributions paid during the years ended September 30, 2003 and 2002 were identical for book purposes and tax purposes.

Income Tax: No provision is made for Federal income taxes since it is the intention of the Funds to comply with the provisions of the Internal Revenue Code available to investment companies and to make the requisite distribu-tion to shareholders of taxable income which will be sufficient to relieve it from all or substantially all Federal Income Taxes. As of September 30, 2003, capital loss carryovers available to offset future capital gains for federal income tax purposes and the years they expire are as follows:

| Expiration Date | Arizona Fund |

| September 30, 2008 | $22,638 |

| September 30, 2011 | 1,504 |

| Expiration Date | Missouri Fund |

| September 30, 2008 | $71,053 |

| Expiration Date | National Fund |

| September 30, 2008 | $160,551 |

| Expiration Date | Money Market |

| September 30, 2007 | $ 9 |

| September 30, 2008 | 751 |

Due to inherent differences in the recognition of income, expenses, and realized gains/losses under generally accepted accounting principles and federal income tax purposes, permanent differences between financial and tax basis reporting for the 2003 fiscal year have been identified and appropriately reclassified. In the Tax-Free Arizona Fund and Tax-Free National Fund, permanent differences relating to expired capital loss carryovers totaling $202,304 and $618,019, respectively were reclassified from accumulated undistributed net realized losses to paid in capital.

Use of Estimates: The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions. Such estimates affect the reported amounts of assets and liabilities and reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

2. Investment Advisory Fees and Other Transactions with Affiliates. The investment advisor to the Trust, Madison Mosaic, LLC, a wholly owned subsidiary of Madison Investment Advisors, Inc. ("the Advisor"), earns an advisory fee equal to 0.625% per annum of the average net assets of the State and National Funds and 0.5% per annum of the average net assets of the Money Market. The fees are accrued daily and are paid monthly. Effective December 9, 2002, the Advisor irrevocably waived 0.25% of this fee for the Money Market fund totaling $10,019 for the year ended September 30, 2003. This waiver may end at any time.

3. Service Agreement Fees. Under a separate Services Agreement, the Advisor will provide or arrange for each Fund to have all other necessary operational and support services for a fee based on a percentage of average net assets. This percentage is 0.48% for the Arizona Fund, 0.46% for the Missouri Fund, 0.39% for the Virginia Fund, 0.44% for the National Fund and 0.36% for the Money Market. During the years ended September 30, 2003, 2002, 2001, 2000 and 1999, the Advisor irrevocably waived $4,942, $5,036, $5,006, $6,075, and $6,062, respectively of this fee for the Money Market. This waiver may end at any time.

The Advisor is also responsible for the fees and expenses of Trustees who are affiliated with the Advisor and for certain promotional expenses.

4. Aggregate Cost and Unrealized Appreciation. The aggregate cost for federal income tax purposes and the net unrealized appreciation (depreciation) are stated as follows as of September 30, 2003:

Arizona Fund | Missouri Fund | |

| Aggregate Cost | $6,200,053 | $6,917,291 |

| Gross unrealized appreciation | 547,033 | 659,277 |

| Gross unrealized depreciation | --) | -- |

| Net unrealized appreciation | $ 547,033) | $ 659,277 |

Virginia Fund | National Fund | |

| Aggregate Cost | $27,493,755) | $21,046,112 |

| Gross unrealized appreciation | 1,717,939) | 2,050,552 |

| Gross unrealized depreciation | (5,152) | (39,899) |

| Net unrealized appreciation | $1,712,787 | $2,010,653 |

5. Net Assets. At September 30, 2003, net assets included the following:

Arizona Fund | Missouri Fund | |

| Paid in capital | $6,082,186 | $7,252,538 |

| Accumulated net realized losses | (24,142) | (71,053) |

| Net unrealized appreciation on investments | 547,033 | 659,277 |

| Total Net Assets | $6,605,077 | $7,840,762 |

Virginia Fund | National Fund | |

| Paid in capital | $27,645,949) | $21,639,020 |

| Accumulated net realized gains (losses) | 322,133 | (160,551) |

| Net unrealized appreciation on investments | 1,712,787 | 2,010,653 |

| Total Net Assets | $29,680,869 | $23,489,122 |

Money Market | |

| Paid in capital | $4,740,639 |

| Accumulated net realized losses | (760) |

| Total Net Assets | $4,739,879 |

6. Investment Transactions. Purchases and sales of securities (excluding short-term securities) for the year ended September 30, 2003, were as follows:

Purchases | Sales | |

| Arizona Fund | $ 604,029 | $ 298,000 |

| Missouri Fund | 1,178,085 | 1,865,314 |

| Virginia Fund | 8,622,788 | 8,788,835 |

| National Fund | 4,546,936 | 5,036,954 |

| Money Market | -- | -- |

7. Capital Share Transactions. An unlimited number of capital shares, without par value, are authorized. Transactions in capital shares were as follows:

Year Ended September 30, | ||

| Arizona Fund | 2003 | 2002 |

| In Dollars | ||

| Shares sold | $ 441,441 | $ 526,148 |

| Shares issued in reinvestment of dividends | 162,775 | 184,798 |

| Total shares issued | 604,216 | 710,946 |

| Shares redeemed | (768,848) | (1,024,030) |

| Net decrease | $(164,632) | $(313,084) |

| In Shares | ||

| Shares sold | 40,876 | 49,142 |

| Shares issued in reinvestment of dividends | 14,975 | 17,398 |

| Total shares issued | 55,851 | 66,540 |

| Shares redeemed | (71,281) | (96,133) |

| Net decrease | (15,430) | (29,593) |

Year Ended September 30, | ||

| Missouri Fund | 2003 | 2002 |

| In Dollars | ||

| Shares sold | $ 183,604 | $ 529,230 |

| Shares issued in reinvestment of dividends | 223,156 | 249,809 |

| Total shares issued | 406,760 | 779,039 |

| Shares redeemed | (1,009,711) | (545,807) |

| Net increase (decrease) | $(602,951) | $ 233,232 |

| In Shares | ||

| Shares sold | 16,654 | 49,223 |

| Shares issued in reinvestment of dividends | 20,316 | 23,240 |

| Total shares issued | 36,970 | 72,463 |

| Shares redeemed | (92,033) | (50,957) |

| Net increase (decrease) | (55,063) | 21,506 |

Year Ended September 30, | ||

| Virginia Fund | 2003 | 2002 |

| In Dollars | ||

| Shares sold | $3,139,443 | $2,726,222 |

| Shares issued in reinvestment of dividends | 1,121,658 | 1,075,387 |

| Total shares issued | 4,261,101 | 3,801,609 |

| Shares redeemed | (4,431,125) | (4,571,717) |

| Net decrease | $(170,024) | $(770,108) |

| In Shares | ||

| Shares sold | 261,864 | 232,752 |

| Shares issued in reinvestment of dividends | 93,984 | 91,649 |

| Total shares issued | 355,848 | 324,401 |

| Shares redeemed | (369,794) | (391,517) |

| Net decrease | (13,946) | (67,116) |

Year Ended September 30, | ||

| National Fund | 2003 | 2002 |

| In Dollars | ||

| Shares sold | $4,033,258 | $3,654,029 |

| Shares issued in reinvestment of dividends | 717,333 | 791,858 |

| Total shares issued | 4,750,591 | 4,445,887 |

| Shares redeemed | (5,356,871) | (5,797,531) |

| Net decrease | $(606,280) | $(1,351,644) |

| In Shares | ||

| Shares sold | 355,713 | 332,628 |

| Shares issued in reinvestment of dividends | 63,288 | 72,095 |

| Total shares issued | 419,001 | 404,723 |

| Shares redeemed | (472,860) | (526,348) |

| Net decrease | (53,859) | (121,625) |

Year Ended September 30, | ||

| Money Market | 2003 | 2002 |

| In Dollars & Shares | ||

| Shares sold | $1,320,767 | $1,351,168 |

| Shares issued in reinvestment of dividends | 27,815 | 42,728 |

| Total shares issued | 1,348,582 | 1,393,896 |

| Shares redeemed | (1,659,792) | (1,436,863) |

| Net decrease | (311,210) | $ (42,967) |

8. Subsequent Event. On October 20, 2003, the Board of Trustees approved a resolution to recommend to the shareholders of Tax-Free Money Market to approve its liquidation. As a result, Tax-Free Money Market will be closed to new investors and additional investments effective November 15, 2003.

| Independent Trustees | |||||

| Name, Address and Age | Position(s) Held with Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen | Other Directorships Held |

| Philip E. Blake 550 Science Drive Madison, WI 53711 Born 11/07/1944 | Trustee | Indefinite Term since May 2001 | Retired investor; formerly publisher of Madison’s Wisconsin State Journal newspaper. | All 13 Mosaic Funds | Madison Newspapers, Inc. of Madison, WI |

| James R. Imhoff, Jr. 550 Science Drive Madison, WI 53711 Born 5/20/1944 | Trustee | Indefinite Term since July 1996 | Chairman and CEO of First Weber Group, Inc. (real estate brokers) of Madison, WI. | All 13 Mosaic Funds | None |

| Lorence D. Wheeler 550 Science Drive Madison, WI 53711 Born 1/31/1938 | Trustee | Indefinite Term since July 1996 | Retired investor; formerly Pension Specialist for CUNA Mutual Group (insurance) and President of Credit Union Benefits Services, Inc. (a provider of retirement plans and related services for credit union employees nationwide). | All 13 Mosaic Funds | None |

| Interested Trustees* | |||||

| Frank E. Burgess 550 Science Drive Madison, WI 53711 Born 8/04/1942 | Trustee and Vice President | Indefinite Terms since July 1996 | Founder, President and Director of Madison Investment Advisors, Inc. | All 13 Mosaic Funds | None |

| Katherine L. Frank 550 Science Drive Madison, WI 53711 Born 11/27/1960 | Trustee and President | Indefinite Terms President since July 1996, Trustee since May 2001 | Principal and Vice President of Madison Investment Advisors, Inc. and President of Madison Mosaic, LLC | All 13 Mosaic Funds, but does not serve as Trustee of Mosaic Equity Trust | None |

| Officers* | |||||

| Jay R. Sekelsky 550 Science Drive Madison, WI 53711 Born 9/14/1959 | Vice President | Indefinite Term since July 1996 | Principal and Vice President of Madison Investment Advisors, Inc. and Vice President of Madison Mosaic, LLC | All 13 Mosaic Funds | None |

| Christopher Berberet 550 Science Drive Madison, WI 53711 Born 7/31/1959 | Vice President | Indefinite Term since July 1996 | Principal and Vice President of Madison Investment Advisors, Inc. and Vice President of Madison Mosaic, LLC | All 13 Mosaic Funds | None |

| W. Richard Mason 8777 N. Gainey Center Drive, #220 Scottsdale, AZ 85258 Born 5/13/1960 | Secretary and General Counsel | Indefinite Terms since November 1992 | Principal of Mosaic Funds Distributor, LLC; General Counsel for Madison Investment Advisors, Madison Scottsdale, LC and Madison Mosaic, LLC | All 13 Mosaic Funds | None |

| Greg Hoppe 550 Science Drive Madison, WI 53711 Born 4/28/1969 | Chief Financial Officer | Indefinite Term since August 1999 | Vice President of Madison Mosaic, LLC; formerly CFO of Amcore Bank-South Central and auditor for McGladrey & Pullen accounting firm. | All 13 Mosaic Funds | None |

*All interested Trustees and Officers of the Trust are employees and/or owners of Madison Investment Advisors, Inc. Since Madison Investment Advisors, Inc. serves as the investment advisor to the Trust, each of these individuals is considered an "interested person" of the Trust as the term is defined in the Investment Company Act of 1940.

The Statement of Additional Information contains more information about the Trustees and is available upon request. To request a free copy, call Mosaic Funds at 1-800-368-3195.

For federal income tax purposes, the following information is furnished with respect to the distributions paid by the Funds during their taxable year ended September 30, 2003. The Funds designated 100% of each of their income distributions as tax-exempt income distributions.

Proxy Voting Information. The Trust adopted policies that provide guidance and set forth parameters for the voting of proxies relating to securities held in the Fund’s portfolios. These policies are available to you upon request and free of charge by writing to Mosaic Funds, 550 Science Drive, Madison, WI 53711 or by calling toll-free at 1-800-368-3195. Beginning next year, the Trust’s proxy voting policies may also be obtained by visiting the Securities and Exchange Commission web site at www.sec.gov. The Trust will respond to shareholder requests for copies of our policies within two business days of request by first-class mail or other means designed to ensure prompt delivery.

Change of Independent Auditors. In October 2003, the Board of Trustees decided that, effective for the fiscal year beginning October 1, 2003, for matters relating to such fiscal years, the firm of Grant Thornton, LLP shall serve as the certifying accountant for the Trust, replacing Deloitte & Touche LLP at the conclusion of its engagement certifying the financial statements for the Trust’s fiscal year ended September 30, 2003 and attendant matters related to fiscal years ended prior to September 30, 2004. For the Trust’s last two fiscal years, Deloitte & Touche LLP has not issued to the Trust an adverse opinion or a disclaimer of opinion, or qualified or modified an opinion as to uncertainty, audit scope, or accounting principles. There has been no disagreement with Deloitte & Touche LLP on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which disagreement, if not resolved to the satisfaction of Deloitte & Touche LLP, would have caused it to make reference to the subject matter of the disagreement in connection with its report. There have been no events listed in paragraphs (a)(1)(v)(A) through (D) of 17 CFR 229.304(a)(1).

The Mosaic Family of Mutual Funds

Mosaic Equity Trust

Mosaic Investors Fund

Mosaic Balanced Fund

Mosaic Mid-Cap Fund

Mosaic Foresight Fund

Mosaic Income Trust

Mosaic Government Fund

Mosaic Intermediate Income Fund

Mosaic Institutional Bond Fund

Mosaic Tax-Free Trust

Mosaic Arizona Tax-Free Fund

Mosaic Missouri Tax-Free Fund

Mosaic Virginia Tax-Free Fund

Mosaic Tax-Free National Fund

Mosaic Tax-Free Money Market

Mosaic Government Money Market

For more complete information on any Mosaic fund, including charges and expenses, request a prospectus by calling 1-800-368-3195. Read it carefully before you invest or send money. This document does not constitute an offering by the distributor in any jurisdiction in which such offering may not be lawfully made. Mosaic Funds Distributor, LLC.

TRANSER AGENT

Mosaic Funds

c/o US Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

TELEPHONE NUMBERS

Shareholder Service

Toll-free nationwide: 888-670-3600

Mosaic Tiles (24 hour automated information)

Toll-free nationwide: 800-336-3600

550 Science Drive

Madison, Wisconsin 53711

Mosaic Funds

www.mosaicfunds.com

SEC File Number 811-3486

Item 2. Code of Ethics.

The Trust has adopted a code of ethics that applies to the Trust’s principal executive officer, principal financial officer, principal accounting officer or controller or persons performing similar functions, regardless of whether these individuals are employed by the Trust or a third party. The code was first adopted during the period covered by this report and was not subsequently amended. The Trust granted no waivers from the code during the period covered by this report. Any person may obtain a complete copy of the code without charge by calling Mosaic Funds at 800-368-3195 and requesting a copy of the Mosaic Funds Sarbanes Oxley Code of Ethics.

Item 3. Audit Committee Financial Expert.

At a meeting held during the period covered by this report, The Trust’s Board of Trustees elected Philip Blake, an “independent” Trustee and a member of the Trust’s audit committee, to serve as the Trust’s audit committee financial expert among the three Mosaic independent Trustees who so qualify to serve in that capacity.

Item 4. Principal Accountant Fees and Services.

(a) Note that audit fees are paid pursuant to the Services Agreement between the Trust and Madison Mosaic, LLC and are not paid directly to the accountants. Total audit fees paid to the registrant's principal accountant for the fiscal years ended September 30, 2002 and 2003, respectively, out of the Services Agreement fees collected from all Mosaic Funds were $98,900 and $92,500. Of these amounts, approximately $37,300 and $35,577, respectively, was attributable to the registrant and the remainder attributable to audit services provided to other Mosaic Funds registrants.

(b) Not applicable.

(c) Not applicable.

(d) Not applicable.

(e) (1) Before any accountant is engaged by the registrant to render audit or non-audit services, the engagement must be approved by the audit committee as contemplated by paragraph (c)(7)(i)(A) of Rule 2-01of Regulation S-X.

(2) Not applicable.

(f) Not applicable.

(g) Not applicable.

(h) Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. [Reserved]

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. [Reserved]

Item 9. Controls and Procedures.

Trust’s principal executive officer and principal financial officer determined that the Trust’s disclosure controls and procedures are effective, based on their evaluation of these controls and procedures within 90 days of the date of this report. There were no significant changes in the Trust’s internal controls or in other factors that could significantly affect these controls subsequent to the date of their evaluation. The officers identified no significant deficiencies or material weaknesses.

Item 10. Exhibits.

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940.

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this Report to be signed on its behalf by the undersigned, thereunto duly authorized.

Mosaic Tax-Free Trust

By: (signature)

W. Richard Mason, Secretary

Date: November 12, 2003

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this Report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated.

By: (signature)

Katherine L. Frank, Chief Executive Officer

Date: November 12, 2003

By: (signature)

Greg Hoppe, Chief Financial Officer

Date: November 12, 2003